FILE COP ' IReport No.AF-79a - World Bank Documents

100

FILE COP ' IReport No.AF-79a This report was prepared for use within the Bank and its affiliated organizations. They do not accept responsibility for its accuracy or completeness. The report may not be published nor may it be quoted as representing their views. INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT INTERNATIONAL DEVELOPMENT ASSOCIATION CURRENT ECONOMIC POSITION AND PROSPECTS OF THE REPUBLIC OF CAMEROON August 8, 1968 Africa Department Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of FILE COP ' IReport No.AF-79a - World Bank Documents

FILE COP ' IReport No.AF-79a

This report was prepared for use within the Bank and its affiliated organizations.They do not accept responsibility for its accuracy or completeness. The report maynot be published nor may it be quoted as representing their views.

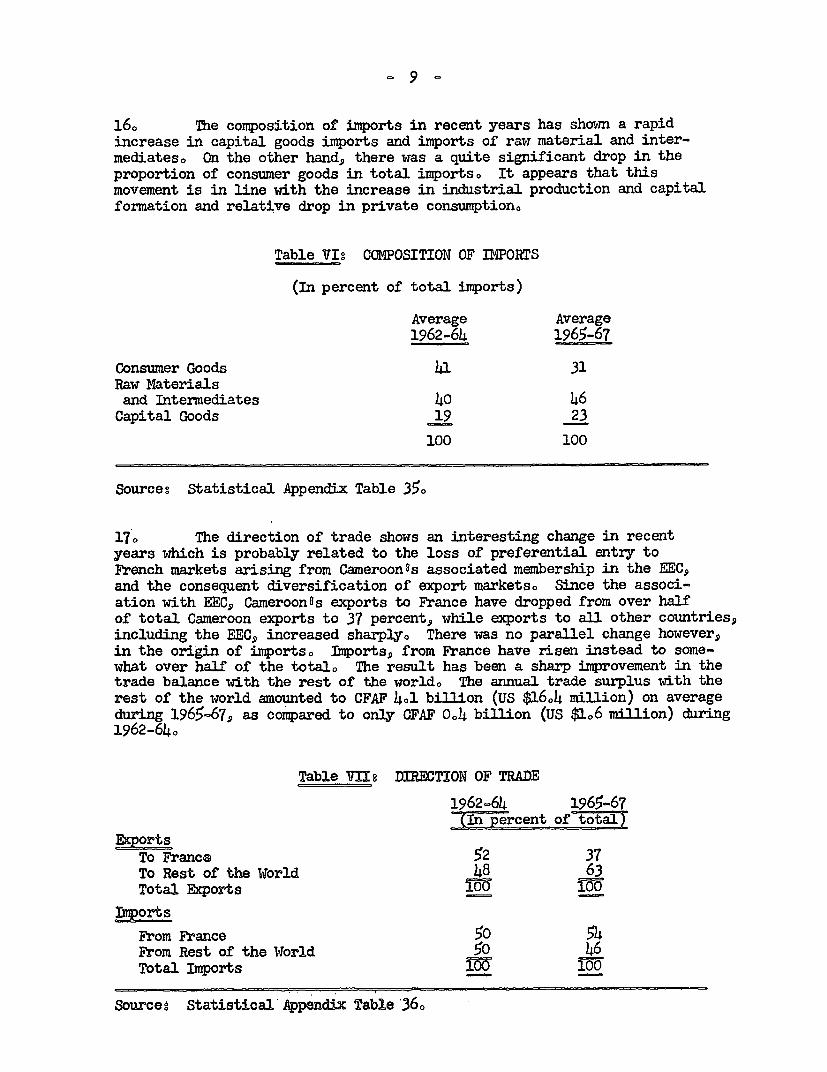

INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT

INTERNATIONAL DEVELOPMENT ASSOCIATION

CURRENT ECONOMIC POSITION

AND PROSPECTS

OF THE

REPUBLIC OF CAMEROON

August 8, 1968

Africa Department

Pub

lic D

iscl

osur

e A

utho

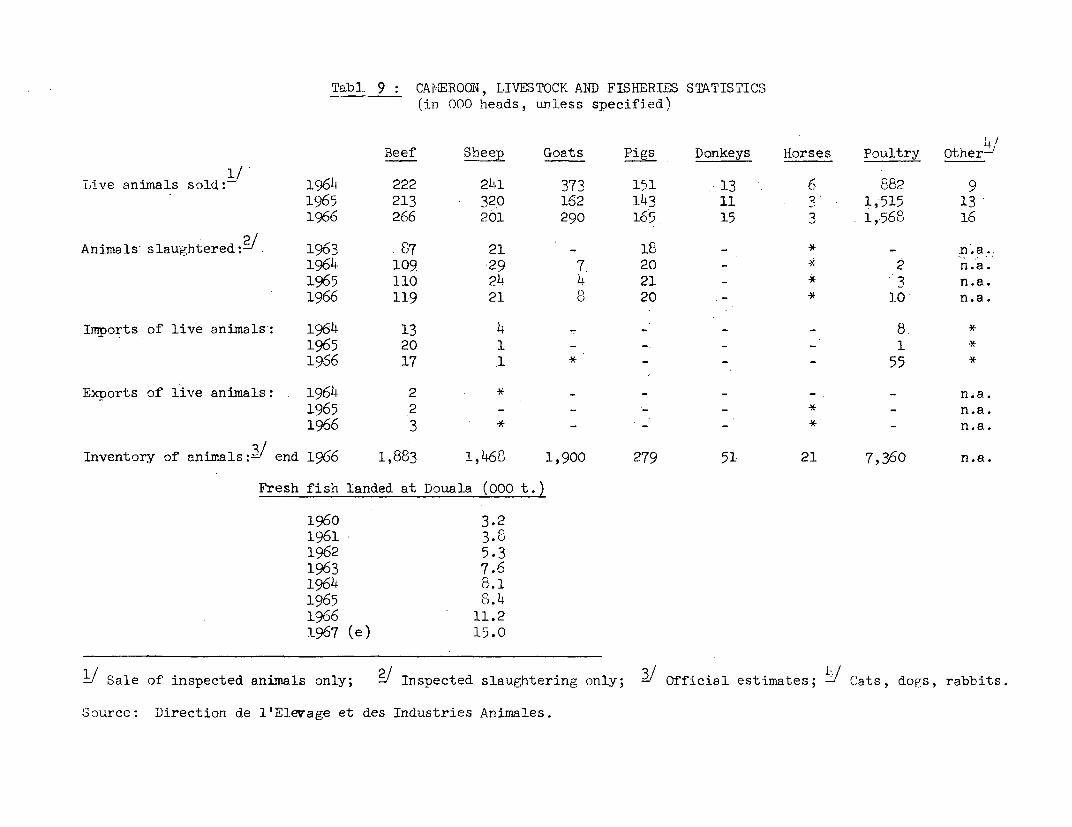

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

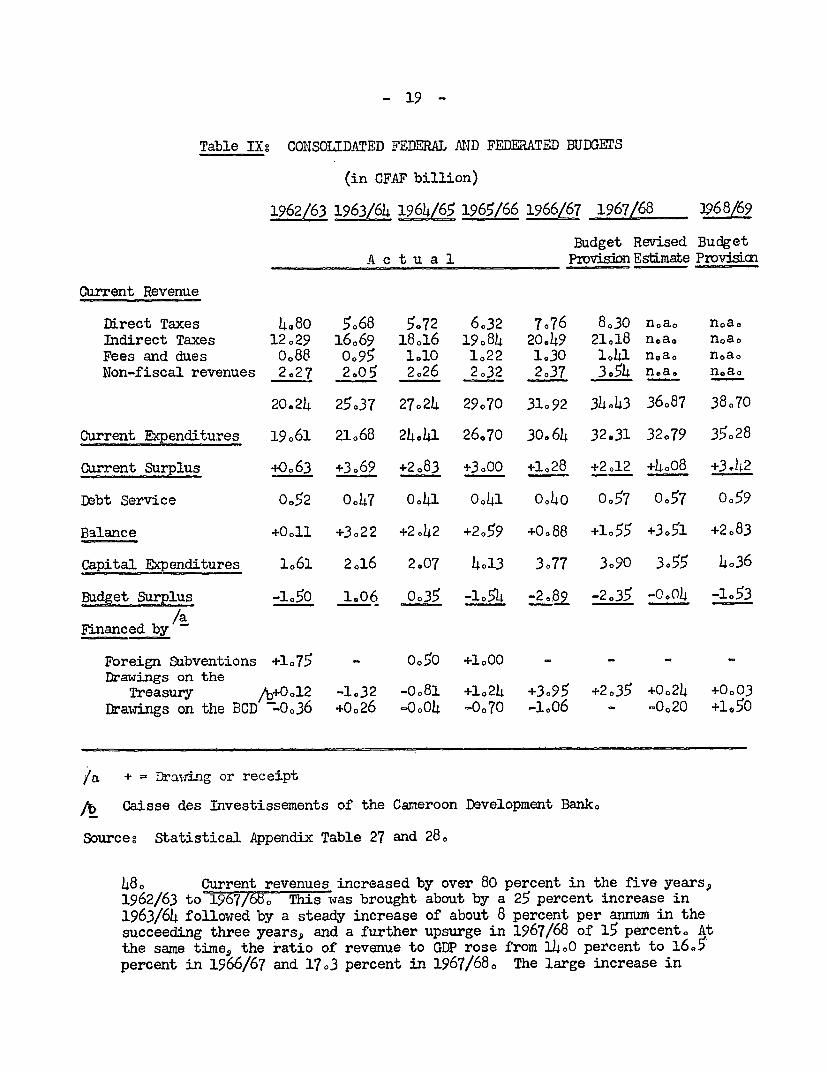

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

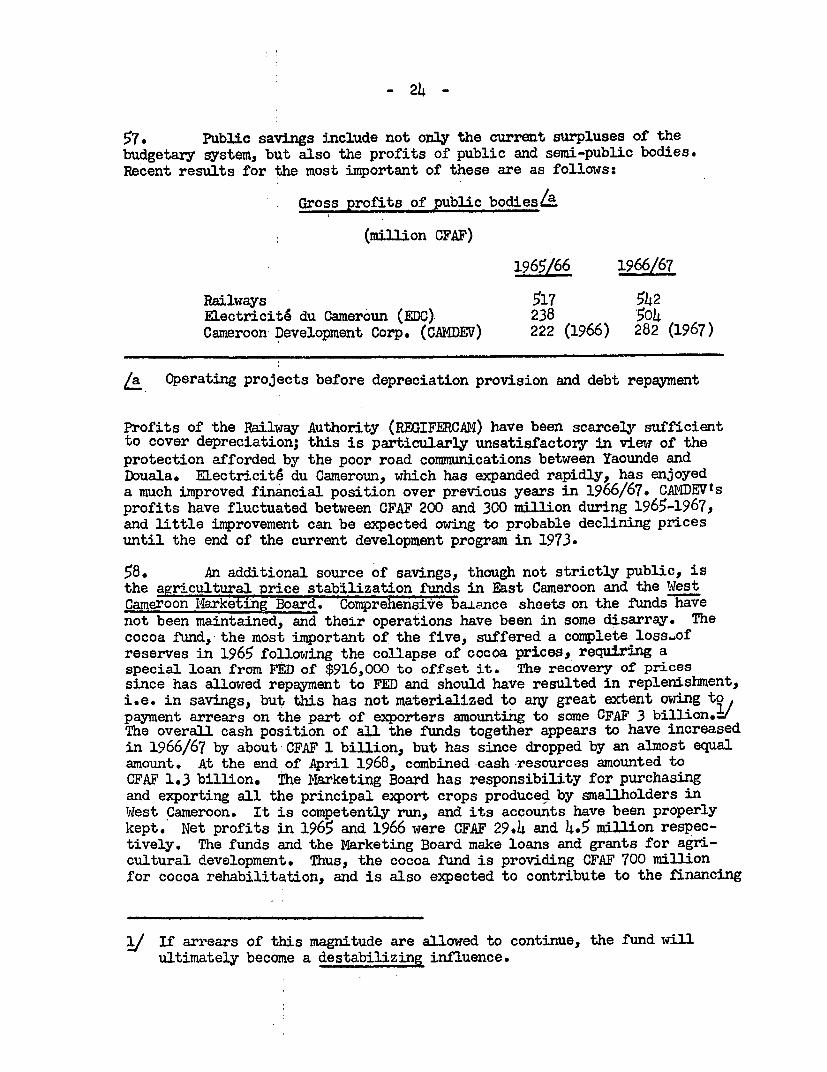

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTS

Currency Unit: CFA francs (CFAF)

U.S. $1 = CFAF Z46.85CFAF 100 = U. S. $0. 4051CFAF 1, 000, 000 = U. S. $4, 051. 04

This report was prepared by Miessrz-.. Cornrlis JO A. Jansen

(Ghief of Mission), Timothy Lankester and Hanms Peter Muth

following a mission to Cameroon in May 19680

TABLE OF CONTENTSPageNo.

BASIC DATA (i)

SUNOARY AND CONCLUSIONS (iii)

I0 BACKGROUND 1

II. RECENT ECONOMIC DEVELOPMENTS

A. Origin and Expenditures on GDP 5

B. Fbreign Trade 7

C0 Sectoral Growth

(i) Agriculture 10(ii) Manufacturing Industry 13

(iii) Transportation 14(iv) Power 16

III. THE-FINAnCIAI, SITUATION.

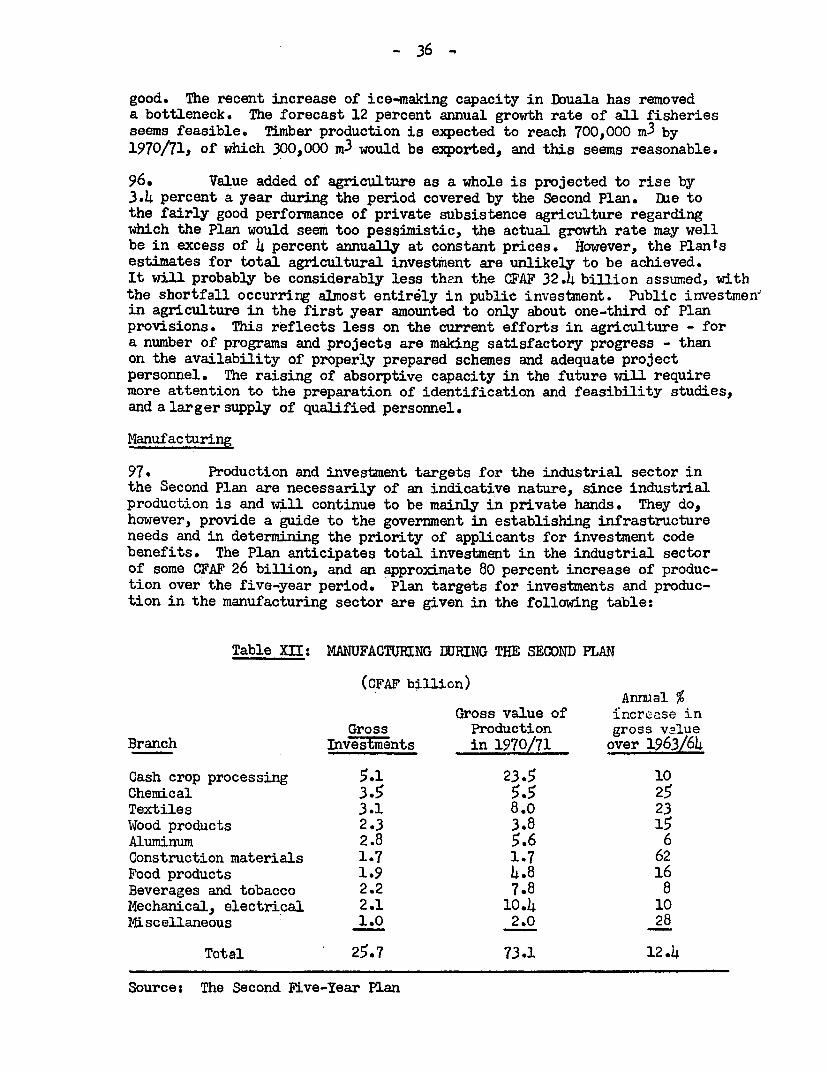

A. Public Finance 18

B. Money, Credit, Prices, Wages 25

C0 Balance of Payments and Foreign Aid 27

IV. PROSPECTS FOR PRODUCTION AND CAPITAL FORIIATION

A. Introduction 29

B. Development Plans 30

C0 Sectoral Policies

(i) Agriculture 33(ii) Manufacturing 36(iii) Transportation 38(iv) Power 39(v) Education 40

D. Conclusion 40

V0 FINANCIAL PROSPECTS

A. Introduction 42

B0 Public Finance 43

C0 Private Sector Savings e5

D. Foreign Resources 46

VI. STATISTICAL APPENDIX

Map

BASIC DATA

Area: 183, 24 square miles; 475,450 square kilometers

Population (1968): 5v,49,000 (of which about 15,000 non-Africans)

Rate of growth: 2.1%Density: 29.7 per sq. mile

Political Status:

East Cameroon independent January 1, 1960;West Cameroon October 1. 1961;Federation October 20, 1961.Member Equatorial African Monetary Union andFranc Zone, Eauatorial African Economic andCustoms Union; Associated Member EEC.

Gross Domnestic Product (Est. 1967/68): $860 million(subsistence 20%)

Per capita: $157

Primary sector 37%Secondary sector 16%Transport, Trade, Services 47%

Rate of growth,1962/63 - 1966/67 7o3% (at current prices)

4i7% (at constant prices)

Percent of GDP at Market Prices

1962/63 - 196364 1964/65 - 196

Gross investment 10.8 14.9Gross savings 9e8 12.8Net import of goods

and services 10 2.1Balance of payments current -

account surplus o.6 -o.5Investmnent income payments net 1.4 1.2Government taxation revenue

(hbede:l.ratin 15.1 16 .4

Average ArmualIncrease

Money, Credit and Prices (CFAF billion) December 1967 196h - 1967

Total money supply 27.1 903%Quasi-money 2.9 1303%Commercial bank credit to private sector 3402 8 3%Rate of change in prices 3 -

Public Sector Operations (CFAF billion) 1966/67 1 / (revisedestimate

Governient current receipts 3109 3609Government current expenditures 3006 3208Surplus/Deficit +103 +401Government capital expenditures 308 306Public investment expenditures 105 10.5

External Public Debt (US$ million) 1967

Total debt (including undisbursed)at December 31, 1967 133

Total debt service 306Debt service ratio U02% of exports

Balance of Payrments (US$ million) Average annualincrease

1967 196)4 - 1967

Total exports 154 203%Total imports 186 1203%Current account deficit -45 téForeign aid disbursements 31 901%

Commodity concentration of exports 1967 196h

Coffee, Cocoa, Aluminurm 28%; 27%; 1i% 27%; 20%; 15%

Gross foreign exchange reserves 1967 196h

US$ million (end of year) 27 45

1I4F Position 31 Dec. 1967

Quota $1606 million

Drawings no ne

Bank/IDA Operations (in $million, at March 31, 1968)Amount committed Amount disbursed

Bank 1100IDA 7>55 o-85

2/ Current account in 1964 was in surplus.

SUIIMARY AND CONCLUSIONS

1. The Federal Republic of Cameroon, established in October 1961,consists of territories formerly administered by France and the UnitedISingdom. The govermnent of President Abidjo has handled post-independenceproblems firmly but with a sense of compromise, and bas successfully wea-thered tribal insurrection and the strains imposed by two administrativesystems and official languages. The governnent maintains close relationswith France and the European Common Market. It is a member of the franczone, ard the convertibility of its currency, the CFA franc, is guaranteedby the French treasury. Moreover, French aid and technical assistance playa vital role in the financing of economic development. As an associatedmember, the country also receives considerable aid from the European Com-mon Market. Cameroon has been trying to intensify economic cooperationwith its neighbors. In 1966 it entered into a customs and economic unionwith four of them. In May 1968, Chad and Central African RepXublicleft the unmon. A liberal policy bas been followed towards private ini-tiative; foreign private investment and management play a leading rolein manufacturing, banking and part of commerce and agricultural estates.Aware of the significant contribution of foreign capital and personnel,the government bas hitherto pursued its long-term goal of cameroonizationwitb moderation.

2. Per capita GDP stands at about 1 In recent years, GDP basgrown at about 5 per cent per year in real terms. This is well in excessof population growth, estimated at 2.1 per cent per year. Investment basincreased significantly as a proportion of GDP. Domestic savings havealso increased, and until recently almost matched total investment. Atthe same time, bowever, Cameroon bas been receiving substantial amountsof foreign aid and foreign private capital, but these have been nearlybalanced by transfers abroad of profits and incomes by foreign companiesoperating in the country and by the large number of expatriate personnel.

3. Foreign trade is the equivalent of about 40 per cent of GDP.Exports comprise a variety of agricultural crops, the môst important beingcocoa and coffee; and also aluminum. After impressive growth in theearly 60's, exports have scarcely risen in the past two years, largely owingto unfavorable prices and adverse weather conditions. The composition ofimports bas changed quite markedly in favor of raw materials and interme-diate and capital goods, reflecting the growth of consumer goods manufac-turing in the country. Total imports have grown fairly steadily, and havebeen on average covered by export earnings. However, in 1967 they increasedsharply leaving a substantial trade deficit for the first time.

4. About three-quarters of the working population is engaged in agri-culture, predominantly on a smallholder basis. Most farmers produce acombination of subsistence and export crops, and specialization is quitelimited. The contribution of agriculture to GDP bas dropped from about47 per cent to around 37 per cent since 1959. Nevertheless, though laggingbehind other sectors of the economy, production bas increased. Output of

- ii -

food crops appears to have been rising faster than population. Importsof foodstuffs are considerable, but mainly consist of items wbich cannotbe produced economically in Cameroon. Nutritional levels on the wholeare not unsatisfactory. The performance of export crops bas been mixed.Coffee, tbe most important foreign excbange earner, bas increased rapidly,witb the more valuable Arabica variety almost doubling in the past sixyears. Cocoa production grew considerably in the early 60's. But since1965, it bas stagnated under the effects of widespread disease. On theother hand, quality bas recently sbown a great improvement, and an importantdisease fighting and rebabilitation scheme launched in 1967 promises toraise output again. Banana production, once a major export, bas declineddrastically owing to Panama disease, and conversion to the more resistantand bigher yielding Poyo type has been slow. Output of rubber bas risenslowly, while tbat of paln products has stagnated. Cotton production, onthe other hand, has continued to grow rapidly since its introduction inthe 1950's, more than doubling over the past ten years.

5. Agricultural development bas been hampered by poor transportationand absence of regular marketing circuits. Land tenure problems and lackof credit have also been a constraint. The government bas recently passedlegislation clarif'ying the procedures for the expropriation of land forprojects in the public interest. It is also considering the possibilityof setting up an agricultural credit bank. However, it seems preferablethat credit be provided in connsction with specific schemes as is the casewith the current successful cocoa program. Progress in the future willdepend on overcoming these bottlenecks and also on the greater effective-ness of the extension services. The quality of extension personnel is good,but their work needs to be concentrated in productive schemos, and coordinatedto avoid contradictory instruction at the village level.

6. Manufacturing, though still a comparatively small sector, has pro-gressed extremely rapidly. In the past few years, industrial turnover basincreased by about 17 per cent annually. The main elements in this growthhave been import substitution of simple consumer goods and processing forexport, including aluminum. Industry has prospered with the help of astable political climate and generous fiscal benefits under Cameroon'sinvestment code. Opportunities for furtber import substitutions remain inmany lines, but increasingly industrial growth will depend on the expansionof tbe national and neighboring countries' markets.

7. Transportation is of decisive importance to the country's develop-ment. At present the network does not match up to its needs. Roads andrailways are few, and these are mostly in a poor state of repair. Theinadequacy of the road system is especially unfavorable for rural develop-ment. There has been some progress in improving the system recently, indlu-ding the establishment of a large maintenance equipment pool and the startof construction on a trunk road linking the major economic centers of Eastand West Cameroon. However, for the future more attention will need to begiven to the development of feeder roads. The Trans-Cameroon railway, wbich

- iii -

will eventually link the population centers of north and soutb, is advancingwell, and an urgently needed program to improve the central line bas justbegun. Cameroonts port capacity is nearing saturation; a study is beingundertaken to determine the most economic means for its expansion.

8. The educational system has grown rapidly and relatively satisfactoryschool attendance rates have been achieved. But shortage of trained teachersandothernecessaryinputs has lowered its effectivEmess. Izthe past twoyears,the government bas rightly re-oriented its policy to improving the qualityof the system and to expanding vocational instruction.

9. Cameroon bas enjoyed a generally stable financial situation, wbichhowever weakened to some extent in 1966 and 1967. In the early 1960's,budgetary operations, if anything, bad a deflationary effect. In 1965/66and 1966/67, however, tbey were expansionary. Substantial overall deficitsoccurred, coinciding with the phasing out of French budgetary support, andthus necessitated drawings on reserves. At the same tine, credit to theprivate sector expanded rapidly, leading to the increase in imports in1967, and consequently to a sharp fall in foreign exchange reserves. In1967/68 the fiscal situation has improved greatly, and measures have recentlybeen taken to curb the growth of credit. These, together with more favorableexport results, have led to a recovery of reserves in the first months of 1968.

10. Fiscal performance has improved quite impressively since indepen-dence. Budgetary savings have increased from a negative amount in 1961/62to about CFAF 4 billion ($16 million) in 1967/68. Current expenditureshave increased rapidly mainly on account of the growth of governnent sala-ries and allowances, but these have been more than matched by revenue growth.The latter has been due principally to the expansion of taxed activities,rather than to increases in tax rates. Capital expenditures on budgetaryaccount have also risen quite fast, altbough a higb proportion have goneinto adninistrative facilities. The one exception to this generally favor-able picture was 1966/67, when government savings fell off sharply owingto an extraordinary increase in current expenditures urnatched by revenues.But in 1967/68, renewed restraint on the expenditure side and a largeincrease in revenues bave brought about a strong recovery, with the largestcurrent surplus ever achieved. The government is determined to maintainthis improvement in the coming years, and is talidng action to hold downsalaries and allowances.

11. The goverrrnent's development strategy is outlined in its SecondFive-Year Development Plan (1966/67 - 1970/71). The Plan is framed withinthe perspective of doubling per capita income between 1960 and 1980, whichwould require an annual GDP growth of slightly below six per cent. Toachieve this, capital formation is projected to increase to 16 per cent ofGDP, as compared with 10 - 11 per cent during the First Plan period (1960/61 -1961/65), and it is expected to be split about equally between public andprivate sectors. Private investment is to be encouraged by maintaining aliberal attitude to foreign capital and through the benefits of the invest-ment code. Almost 50 per cent of public investment is intended for infra-

- iv -

structure, compared with 18 per cent for agriculture. Agriculture, however,will also indirectly benefit from investments in infrastructure, educationand health. Foreign aid is-expected to finance over one-third of totalinvestment and almost three-quarters of public, but a considerable increasein domestic public savings is also required.

12. The relative emphasis of the Plan is sound, as is the government'sconcentration on infrastructure, agriculture and social services whilerelying on the private sector to develop manufacturing. The excellent per-formance of the manufacturing sector in the last two years and immediateprospects indicate that the Plan's projections for private investment arelikely to be realized. Plan implementation in the public sector, however,has been somewhat disappointing. Public investment, while higher than inthe pre-Plan period, has fallen well below expectations, largely owing tothe shortage of qualified project personnel and adequately prepared projects.This is especiaUy the case in agriculture. Moreover, the composition ofpublic investment has diverged from that planned, mainly on account of thegovernment's excessive spending on administrative facilities. In this res-pect, as inthe Firet Plan period, the government bas failed to take the leadin pursuing the priorities it set. However, the capital budgets for thecoming year show a marked improvement, with closer adherence to Plan provi-sions.

13. The capacity for implementing projects bas been improving, and thestatus of projects and programs under execution indicate that public invest-ment could be increased significantly in the coming three years, resultingin total public investments for the five-year period of $288 million, 85 percent of the Plan target. Whether this can be achieved depends on financialavailabilities.

14. In the past, financial capacity was not on the whole a constraint,but it is likely to become increasingly so in the future. Public savingshave increased greatly since the early sixties, but on present revenue andexpenditure trends they are unlikely to contribute more than 27 per centover the next three years to the public investment total warranted by thecountry's increasing absorptive capacity. With the present institutionalarrangements, it is difficult for the government to tap domestic privatesavings. The mission's estimate of public investment in the coming threeyears therefore leaves a gap of about $150 million, and of $168 million ifdebt repayment and a small amount of foreign aid for schemes in the privatesector are included. Disbursements on already committed or near-committedaid are likely to be just over $100 million, so that $65 million would beneeded out of new commitments. In view of the relatively small contribu-tion of public savings to total public investment, and since part of publicsavings will be needed for sehemes unsuitable for external financing, it isnecessary that aid should cover a high portion of the costs of foreign-financed projects; this will require, particularly for agricultural pro-jects, a degree of local cost financing.

15. Aid prospects are sormewbat 'ess certain than hitherto. The gov-ernment should therefore seek to strengthen the revenue system in order to

increase public savings, and thereby reduce its reliance on foreign

assistance. This will require examining the possibilities of improving

tax administration and of increasing company and income tax. A cost/benefit

study of the investment code would also be desirable to determine whether

or not the fiscal benefits granted to companies under it bave been fully

justified. In addition, steps might also be considered to retain a

larger part oaZ private savings in the country.

16. Prospects for continued overall growth in the next few years appear

favorable. They will depend partly on the availability of finance forpublic investment. But assuming the level of public investment estimated

by the mission can be achieved, and given the expectation of continued

buoyancy in private sector investment, then the GDP growth rate of 5.8 per

cent projected in the Plan is likely to be somewhat exceeded. For the longer

termn, the probable increase in the population growth rate to about 3 per

cent per year as a result of falling death rates could impair the prospectsfor both total and per capita growtb. It would therefore be useful for the

government to start a study of the many problens connected with a possiblepopulation control program.

17. Servica on Cameroon's currently incurred public debt will reach a

peak of about $7 million, 4 - 5 per cent of projected exports in the early1970's, and a modest increase in debt on conventional terms would be jus-tified. However, in view of the country's poverty, and the size andduration of its need for development aid, most foreign assistance should

be on concessional terms.

THE ECONOMY OF CAMEROON

I. BACKGROUND

1. The purpose of this report is to upqate the analysis and conclusionsin the previous economic report on Cameroon.Y The encouraging progress ofthe economy noted in that report was the result of large infrastructureinvestments since the early l95Ots and various programs and projects inexport agriculture and manufacturing. According to the report, GDP in realterms had been increasing during the years 1959-1964 at an average yearly rateof about five percent. In the public sector, government had been successfulin raising current savings and development expenditures, while private sectordevelopment had been stimulated by the establishment of a favorable investmentclimate. Economic growth had been much helped by the monetary ties with Franceand the financial assistance from France and the European Economic Community(EEC).

2. As far as the future was concerned, the report felt that the govern-mentts Second Five-Year Plan (1966/67-1970/71) was unlikely to be fully imple-mented during the plan period. In view of political and economic uncertaintiesand administrative weaknesses,total investment would probably not exceed 80percent of the amount proposed in the Plan. At the same time, the report wasless optimistic than the planners about the scope for increasing domesticsavings, especially those in the public sector. The GDP growth rate for thePlan period was estimated in the report at 4-5 percent a year, well ahead ofthe estimated population growth of 2.1 percent.

3. In view of the light debt burden and at least moderately good exportprospects, the report felt that Cameroon was creditworthy for borrowing limitedamounts of capital on conventional terms. But in view of the countryts povertyand the likelihood that economic progress in the foreseeable future would berelatively slow, it was recommended that the major proportion of foreign finan-cial assistance be extended on concessional terms.

4. The Federal Republic of Cameroon, almost las large as France but withonly 5.4 million inhabitants, is a poor country. Per capita GDP is estimatedat CFAF 39,000 or $157 at the official exchange rate. About three-quarters ofthe population depends on agriculture for its livelihood, of which the vastmajority are smallholders. Nearly all farmers produce a mixture of cash andsubsistence crops, and thus, while subsistence cultivation accounts for about20% of GIP, a subsistence sector (i.e. producing wholly for self-consumption)as such is virtually non-existent. Except in West Cameroon, plantation agri-culture is relatively unimportant. Establishment of estate-type operations inEast Cameroon has been hampered by difficulties in establishing legal title toland under the prevailing land tenure system. Recently, however, steps havebeen taken to solve this problem. The country has considerable ecologicaldiversity which permits the cultivation of a large variety of crops; this isone of the strong points of the economy. The coastal, southern and south-eastern parts of the country are covered with tropical rain forests withsuitable conditions for tropical tree crops such as coffee, cocoa, palm oil,

] "The Economy of the Federal Republic of Caameroon", No. AF-48b datedNovember 3, 1966

- 2-

rubber, bananas. In the north, near Lake Chad, where rainfall is seasonal,cotton, groundnuts, rice and other cereals are grown. Between these regionsthere is a considerable area of higher lands with generally lower tempera-tures and sufficient rainfall for good grazing potential. With the exceptionof smaller areas of volcanic and alluvial terrains, soil fertility is nothigh. But thanks to good growing conditions (rainfall, sunshine) the nutri-tional position of the population is not unfavorable and there is no largeprevalence of hungeri/ S here are few known minerai resources that are com-mercially exploitable, However, ongoing exploration of oil deposits on andoff the liest Cameroon shore has shown favorable initial results. The rivershave good hydropotential, but little significance for navigation.

5. The Federation consists of the states qf East and West Cameroon,formerly U.N. Trust Territories, administered by France and the United Kingdom,respectively. It was established in October 1961. The former French territory,now the State of East Cameroon, is by far the larger of the two occupying 91percent of the total land area and comprising 79 percent of the population.The constitution gives wide powers to the President, who is chosen by directpopular vote. The President has the initiative for legislative proposalsincluding the formulation of the Federal budget which he subnits for approvalto the unicameral National Assembly. The President also appoints the minis-terial cabinet of the Federal and the Prime Ministers of the two State govern-ments. There is only one political party.

6. There is considerable ethnic, social and religious diversity withinthe country. In the north, the population is predominantly Sudanic, thesociety is semi-feudal, and Islam is the common religion. In the southernand coastal regions, the people are mainly Bantu, but comprise a multiplicityof tribes, languages, and customs. Christianity and animism are the mainforms of religion. In spite of these differences, Cameroon has enjoyedpolitical stability for the last six years. President Ahidjo, a northerner,has maintained a government of truly national complexion, and the task ofunifying the country, both politically and economically, is being pursuedwith energy and success. Post-independence problems have generally beenhandled with a sense of compromise, but not without firmness. The insur-rection in the early 1960's of the Bamileke, a major tribe living on high,fertile and very densely populated lands, on the border of East and WestCareroon, was brought under control with the use of military force. Anothermajor problem, the unification of East and West Cameroone is not yet fullysolved. Steps have been taken to harmonize the administration and taxes inthe two parts of the country. In 1966, the Federation introduced uniformcustoms duties, chiefly by raising West Cameroonts duties to the much higherlevel prevailing in the East. Direct taxes however are still much higher inthe West than in East Cameroon. The Federation has tlfo official languages,French and English. In order to improve day-to-day communications betweenthe two territories, the Federal Governrent is promoting bilingual instructionon a limited scale.

1 In several regions there are qualitative deficiencies, particularly ofproteins, fat, calcium, vitamins A, B2 and C. Cf. G. Winters, Méthodologedes enquêtes "Niveau de vie" en milieu rural Africain (Yaoundé, August 1967)

- 3 -

7. Cameroon maintains close financial and economic connections withFrance and the EEC, of which it is an associated member. It is a member ofthe franc zone and its currency, the CFA franc, which is in circulationthroughout former French Equatorial Africa, is fully convertible with theFrench franc. Cameroon shares with Gabon, Congo (Brazzaville), Chad andthe Central African Republic, a common central bank, the BCEAEC,1J whichwas established with French financial assistance, and whose headquartersis in Paris. Financial aid from France, mostly on a grant basis, has playeda vital role in the financing of Cameroonis development effort. Specialmarketing arrangements, however, for Cameroon 's export products in France arebeing phased out in line with the Yaoundé convention. According to theconvention, which established the ground rules for associated membershipin the Common Market, the EEC common outer tariff is to be applied to theproducts of associated members. However, in order to facilitate the tran-sition to competition on the basis of world market prices, the EuropeanDevelopment Fund (FED) of the EEC is providing, for a transitional period,price support for a number of products and aid for production diversification.Both these are coming up for re-negotiation in 1969. The government hasestablished friendly relations with its neighbors. The country is a memberof the Organization of African States and Madagascar (OCAM) and on January 1,1966, it formed, with four neighbor countries,d/ an economic and customsunion. The total number of inhabitants of the member countries is 11.6 million.their average per capita income about $110 and their combined imports in 1965amounted to $338 million. This union, the Union Douanière et Economique deltAfrique Centrale (UDEAC) introduced a conmon outer tariff and aimed atharmonization of investment decisions and investment encouragement laws withinthe union. A solidarity fund was established to provide compensation to Chadand Central African Republic for the loss of customs revenues arising fromthe union. In 1967/68 Cameroon contributed CFAF 500 million ($2 million)to it.In early May 1968 Chad and the Central African Republic left UDEAC to form anew association with Congo (Kinshasa). The other three members have statedthat they will continue the union. The departure of Chad and Central AfricanRepublic, the most;backward of the five, is likely to have little effect onCameroon. UDEACts existence has been too brief to have made already asubstantial contribution to regional development and at the present stageof development of member countries spectacular results are not to be expected.However, it is certainly desirable that this constructive attempt to widenthe scope for industrial development be continued.

8. While progress has been made in the field of education (in the moredensely populated areas primary school attendance and literacy among theyoung are high), the country still does not supply sufficient numbers ofhighly skilled administrative, professional and managerial personnel. African-ization of top civil service posts proceeded rapidly in the first few yearsof independence, but since 1964 the pace has slackened. A large number of

lJ Banque Centrale des Etats de l'Afrique Equatoriale et du Cameroun (CentralBank of the states of Equatorial Africa and Cameroon).

2| Central African Republic, Chad, Congo (Brazzaville), and Gabon.

expatriate advisers, many of them with previous administrative experiencein Cameroon 9 is assisting the goverrnnent. As far as the private sector isconcernedp government has maintained a liberal visa policy and most of theresponsible positions in industrys commerce and banking are held by foreigners.Meanwhile a large number of Cameroonians are pursuing advanced studies abroad.When these students will have obtained professional qualifications and sub-sequently the necessary career experience, they should eventually be able toreplace the expatriate element. Of necessity this is a slow process andpolitical pressure to accelerate it unduly should be resisted.

9. Population density is low in most of the country, about 11.5 persquare km for the country as a whole. This fact has contributed to a feelingamong policy makers that population growth (now estimated at 201 percent ayear) does not pose a serious economic problem and consequently governmenthas not yet formulated a policy of population control. Howeverg if preventivemedicines on which public health programs are now concentratingS proves suc-cessful, the death rate might drop quite drastically in a relatively shortperiod from its present estimated level of 26 per l,OOOc As has happened inmany other less-developed countriess the result would be a sharp rise in thepopulation growth probably to over three percent a year. Since this wouldlead to a lower savings rate (because of the increased dependency ratio) andincreased expenditures on high capital-output ratio activities such as edu-cation and pîob'lc administration9 the result would be perceptibly smallerannual GDP increases to be shared by much larger numbers. Under such condi-tions per capita income growth would slow down and the outlook for the countrywould be less favorable. These considerations suggest that it would be usefulfor the government to start, perhaps in cooperation with appropriate advisoryagencies, a study of the many difficult social9 cultural and medical problemsconnected with a possible population control program.

II. RECENT ECONOMIC DEVELOPMTS

A. Origin and Expenditures on GDP

10. The most recent official national accounts estimates relate tothe financial year 1964/65. For the three years that have passed sincethen there are no official estimates. In order to obtain a view of overalldevelopments in these recent years, the mission has attempted to piecetogether, from various sources of statistical informations tables showilngGDP by industrial origin and expenditure categories. In view of the scar-city and unreliability of statistical data the results are necessariytentative, but it is felt that they do provide an approximation of whathas happened in the economy and at the same time help judging the prospectsof the econony.

il. The first conclusion from these calculations is that the grow4thof GDP has remained well ahead of population growth. Annual GDP growthover the five-year period 1962/63 to 1966/67 is estimated at 7.3 percentin eurrent and .?7 percent in constant prices. The origin of GDP by prin-cipal economic sectors is shown in Table I.

Table I: GROSS DOMESTIC PROLWUCT BY INDUSTRIAL ORIGIN

(at current market prices, CFAF billion)

1959 1962/63 1963/64 1964/65 1965/66 1966/67 1967/68

Agriculture %4.o 61.2 64.6 68.2 70.7 72.1 77.8Manutacturing 16.7 19.2 22.1 25.4Construction 11.3 17.4 19.6 5.9 6.5 7,2 7.9Electricity,Gas, Water 1.0 1.3 1.5 1.7 1.9 2.0 2.2

Transport, Storage 3.4 5.8 6.8 10.6 12.7 14.7 16.7Commerce 29.4 37.1 39.9 38.4 40.5 42.6 46.6Public AdminisirationLa 10.4 13.9 15.0 19.7 21.7 25.9 27.9Other Servicest.2 4.1 8.0 9.1 6.7 6.9 6.9 8.4

GDP 113.6 144,7 156.5 168.1 180.1 193.5 212.9

9 No provision made for imputed rent of governnent buildings..Apparently no provision included for owner-occupied dwellings.

Sources: 1959-1963/64: Previous economic report (AF-48)1964/65: Direction de la Statistique, slightly adjusted by mission.1965/66-1967/68:Mission estimates.

The growth pattern in recent years bas been different for the various sectors.Agriculture felt the impact of very low cooea prices in 1965 and of drought

affecting the production of coffee, cotton and a number of other productsin 1966. This temporary slow-down in the growth of agricultural value addeddid not check the fairly fast growth rates of manufacturing production,transportation and construction activity. The proportion of these sectorsin GDP has been increasing significantly, On the other hand, the contribu-tion of agriculture has dropped to 37 percent, a level that is low in com-parison with other African countries./

12. The statistical basis of the table on expenditures on GDP (Table II;see also Statistical Appendix Table 25) is not strong, so that conclusionsmust be drawn with caution. It would appear that a considerable shift hastaken place from consumption to investment. Investment rose from 11 percentof GDP in 1962-64 to 15 percent in 1964-67. Public and private sectors bothparticipated in the upsurge of investment. The increase in private sectorinvestment is probably closely related to the earlier mentioned sharp increasein manufacturing production and the expansion in recent years of moderntransportation and distribution activities. The rapid increase in investmentand savings shown in the table would be a favorable development althoughthe level of investment is still low by international comparison (20-25percent of GDP in highly developed economies and 15-20 percent in a numberof fast growing developing economies).

Table II: EXPENDITURES ON GDP

(In percent of GDP)

Average Average

1 l96h/65 - 1966/67

Consumption 90.2 87.2

Private 75.3 69.3Public 14.9 17.9

Investment 10.8 1h.9

Private 7.0 9.5Public 3.8 5.5

Dmport Surplus 1.0 2.1

GOP 100 100

Savings 9.8 12.8

Source: Statistical Appendix, Table 25.

1| The average contribution of agriculture to GDP in French speakingcountries south of the Sahara is 45 percent, but this does not includea number of the more backward countries which rely probably even moreon agriculture. Source: IBRD World Tables.

-7-

13. Most of the increase in investment appears to be covered bdomestic savings. In fact, the net participation of foreign savingsiYin the financing of Cameroonts total investment, although on the rise, isquite small, only two percent of GDP and only 13 percent of total invest-ment. This is in apparent contradiction with the countryts heavy relianceon foreign aid and the evidently substantial private foreign investments,especially in the industrial sector. The explanation is that transfersout of private current income, and perhaps also capital by foreign enter-prises and residents are large, in fact almost as large as the capitalinflow. From 1962 to 1966 the net outflow of private funds on current andcapital account averaged about CFAF 4.1 billion. In this situation, thenet contribution to Cameroon of foreign aid and foreign private investmentconsists in the additions resulting from it to productive capacity ratherthan in a net strengthening of the savings-investment balance.

B. Foreign Trade

14. The basic importance of foreign trade to the Cameroon economyderives from the countryls meagre resource endowment and early stage ofindustrial development. These make it necessary to import most of therequirements for raw materials and intermediate products as well asvirtually all capital goods. The country also needs certain food imports.Recent overail developments in foreign trade are given in the followingtable:

Table III: EXPORTS AND IOPORTS

(In CFAF billion)

1962 1963 1964 1965 1966 1967

Exports 30.0 34.8 36.1 35.4 36.9 38.6Imports 28.3 31.6 32.8 37.4 36.1 46.4Trade Balance + 1.7 + 3.2 + 3.3 - 2.0 + 0.8 - 7.8

Source: Statistical Appendix Table 38.

Cameroonis tropical tree crops and, since the early 19 6 01s, aluminumexports, have provided foreign exchange earnings roughly equivalent tomerchandise importsa with the notable exception of 1967, which showeda substantial trade deficit. This i;as caused by a sharp increase inimports in the latter half of the year. The total value of foreign tradeas a percentage of GDPF, has fluctuated as follows:

1] Net import of goods and services

- 8 -

Table IV: FOREIGN TRADE AS PERCENT OF GDP

1959 1962/63 1963/64 1964/65 1965/66 1966/67

Exports 23.6; 21.5 23.9 22.9 20,9 19.8Imports 17.7 20.3 20.7 22.3 20.9 19.4

TOTAL 41.3 41.8 44.6 45.2 41.8 39.2

Source: Table I and Quarterly Economic Bulletin for trade on a fiscal year basis.

Betwfeen 1959 and 1964/65, the export ratio remained fairly steady, whilethe import ratio increased; since 1964/65, both ratios have declined,although in 1967/68 the import ratio has almost certainly risen again.

15. As pointed out before, the variety of export products has ensureda greater stability than experienced by some primary commodity exporters.For this reason, the 28 percent drop in cocoa prices in 1965/66, at the timeCameroonts largest export p,oduct led to only a 7 percent drop in the weightedaverage of export prices f Although the development of export prices since1962 has, on the whole, not been unfavorable, growth of total export valueshas not been very high, about 3.5 a year (comparing 1965-67 exports with1962-64 exports). Growth in export volume is shown in the following table(Table V). Of the principal products only coffee has had a high growthrate. In a few cases the fairly poor export showing is also due to increaseddomestie consumption. This is true for cotton, cocoa (recent establishmentof cocoa butter and chocolate factories) and groundnuts.

Table V: GROWTH OF VOLUME AND VALUE COMPOSITION OF EXPORTS

Average Average Average Value CompositionExport Volume Export Volume Annual Growth in 1967

1962-64 1965-67 Rate (in % of total(in thousand tons) (in %) export value)

Coffee 46.2 59.5 8.8 28.8Cocoa 69.7 744.9 2.5 25.2Aluminum 50o.7 46.9 -2,4 13.6Timber 236.7 254,1 2.4 6.9Cotton 14.8 17.2 5.1 4.7Rubber 8.2 10.7 9.3 2.9Bananas 117.>4 77.1 -13.1 1.9Palm kernels 17.9 18.3 0.8 1.4Palm oil 5.7 9.5 18.6 1.2

Source: Statistical Appendix Table 34.

1J According to mission calculation of export price index (1964/65 100):1962/63 1963/64 1964/65 1965/66 1966/67 1967/68

95 96 100 93 98 100

16. The composition of imports in recent years has shown a rapidincrease in capital goods imports and imports of raw material and inter-mediatesa On the other hand, there was a quite significant drop in theproportion of consumer goods in total imports, It appears that thismovement is in line with the increase in industrial production and capitalformation and relative drop in private consunptiono

Table VID CCWPOSITION OF IMPORTS

(In percent of total imports)

Average Average1962-64 1965-67

Consumer Goods 41 31Raw Materialsand Intermediates 40 46

Capital Goods 19 23

100 100

Source: Statistical Appendix Table 35o

170 The direction of trade shows an interesting change in recentyears which is probably related to the loss of preferential entry toFrench markets arising from Cameroon8s associated membership in the EEC9and the consequent diversification of export markets. Since the associ-ation with EECg Cameroon2s exports to France have dropped from over halfof total Cameroon exports to 37 percent, while exports to ail other countries,including the EEC, increased sharply. There was no parallel change however,in the origin of importsa Imports, from France have risen instead to some-what over half of the total. The result has been a sharp improvement in thetrade balance with the rest of the world, The annual trade surplus with therest of the world amounted to CFAF 4L1 billion (US $16,4 million) on averageduring 1965-67, as compared to only CFAF 04 billion (US $1o6 million) duringi962-64o

Table VIIg DIRECTION OF TRADE

1962-64 1965-67=Inpercent of

ExportsTo France 52 37To Rest of the World 48 63Total Exports îo100y

Iineorts

From France 50 54From Rest of the World 5° 46Total Imports 100 100

Sources Statistical'Appendi:x Table 36o

- 10 -

C. Sectoral Growth

Agriculture

18. The economy of Cameroon remains, to a large extent, based onagriculture. Roughly 80 percent of the population still live in ruralareas, compared to 87 percent in 1959. Agriculturets contribution to GDPis estimated at 37 percent in 1967/68 as against 47 percent in 1959. Thesector earns almost ail of Cameroonls foreign exchange, largely by exportingcocoa, coffee, cotton, bananas, lumber and a variety of other products.The country is, hcwever, not self-suufficient in food production. Food andbeverage imports have averaged CFAF 5.3 billion ($21 million) since 1963 ofwhich about a quarter consisted of "luxury-foods" - alcoholic beverages,Eiropean meats, fruits and vegetables, canned food. The three most im-portant single food items have been on the increase, as the followingtable shows:

Table VIII: IMPORTS

(In thousand tons)

1964 1965 1966 1967

Rice 6.8 9.9 7.9 10.1Flour 16.9 22.3 24.7 30.9Sugar 8.o 10.1 9.5 13.7

19. In East Camaeroon agricultural production is largely in the handsof smallgrowers. The normal pattern is for farmers to produce partly forcash and partly for subsistence0 Plot sizes average between one and threehectares. Two postwar attempts at creating a strong cooperative structurehave failed, chiefly because of lack of proper guidance and of understandingof cooperative principles and practices among leaders and peasant members.The major exception is the successful union of Arabica cooperatives (UCCAO)IJwhich provides technical and marketing guidance to the growers through theircooperatives. UCCAO markets the entire East Cameroon Arabica production. Afresh attempt at reorganizing the cooperative system was launched in 1965.The government is trying to avoid the flaws of earlier attempts, and indi-cations are that the movement may succeed among producers of export cropsfor whom cooperation in disease control, plant rejuvenation, harvesting andconditioning, and marketing usually means substantially higher cash incomes.Plantations exist on a limited scale, principally for oil palm and rubber.

20. In West Cameroon plantation agriculture is relatively more important.The Cameroon Development Corporation (oDC), a statutory authority of thegovernment, is much the largest agricultural enterprise, and controls some22,900 hectares. Rubber accounted for 54 percent and oil palms for 36 percent

1j Union des Coopératives de Café Arabica de l'ouest.

of the area. The planting estimate for 1968 is 3,700 hectares, of which73 percent for oil palms. Each year the corporation produces about 30percent of West Cameroonts exports.

21. There is little reliable information about the production ofsubsistence cropsl4' but it appears that output of the most important cropshas been increasing somewhat faster than population growth since the early1960's, although years with poor rainfaJ. have periodically damaged par-ticular crops. Maize, manioc, millet and sorghum, arrow-root, plantainsand yams are the basic staples. IWest Cameroon staples include potatoesand vegetables. Cultivation methods in subsistence agriculture are stillprimitive and the use of fertilizers and pesticides has remained very limitede

22. The possibilities of import substitution are limited by consumerpreferences and by climatic factors. Expatriates will probably continue toconsume imported goods, such as beverages, milk products and meat, in pre-ference for domestic produce and some staple products, notably wheat, cannotbe economically produced in Cameroon. However, the production of rice hasincreased quite rapidly since 1960, and industrial-type sugar cane productionstarted in 1967.

23. Production trends in several export crops appear encouraging.Several of these crops benefit from more intensive government financialand technical assistance. In the field of coffee, the government isencouraging conversion from the Robusta to the Arabica variety wherealtitude and climate permit. Arabica production, for which higher worldmarket prices prevail, has increased froxm about 11,000 tons in 1961/62to an estimated 21,000 tons in 1967/68_ In the same period the outputof Robusta increased from about 38,000 to some 52,000 tons. The 1968International Coffee Agreement raises Cameroonts official basic quotafrom 45,0oo to 60,000 tons. Cameroon has been selling well in non-quotamarkets, particularly Japan and Eastern Birope, but this trade is strictlybilateral and may fluctuate from one year to the next.

24. Cocoa production increased considerably between 1961/62 and1964/65, froma77,000 to 98,000 t, and has remained at or somewhat belowthis level since then. In part this is due to the sharp price drop in1965 which temporarily reduced the interest of growers. Meanwhile,quality improved. Only 21 percent of the 1963/64 crop was of superior

1/ In this report crops are categorized as subsistence and export orcash according to official Cameroonian terminology. Subsistencecrops include non-exported cash crops such as rice and sugar cane.

2 Agricultural production figures for East and lWest Cameroon aredifficult to reconcile since the former are kept for "campaignyears" and the latter for calendar years. All additions aretherefore somewhat arbitrary, particularly where productionfluctuates greatly from one year to the next. Neverthelessefor lack of more precise data, the data for East and West Cameroonhave been added without making any adjustments.

- 12 -

quality, but this share rose to 89 percent in the current (1967/68) campaign.After a USAID financed pilot program and a larger FAC supported prograrn,the Cocoa Price Stabilization Fund has launched in 1967 a cocoa rehabilitationscheme which is to cover 250,000 hectares in five years' time.

25. Banana production, once a major export product, has crumbled owingto the Panama disease. Conversion to the sturdier, disease resistant "Poyoa"variety is possible as far as growing conditions are concerned. However,the "Poyo" banana needs more attention from the farmer - irrigation, ferti-lization, support of the stems carrying the heavy bunches - which makesconversion based on sma11grower care a difficult venture. The added effortproduces Poyo yields up to four times higher than those common with GrosMichel plants. While Ivory Coast converted to Payo and rapidly increasedits banana production, Cameroon has hesitated and saw its output dwindlefrom an estimated 160,000 t in 1961/62 to less than 90,000 t in 1967/68(estimate). Poyo production in 1967/68 will exceed 30,000 t for the firsttime and has doubled every year since 1964/65. The goverrnment has requestedFMD financing for a large-scale conversion scheme, but there is still un-certainty whether to proceed on the basis of plantations or a smallholderscheme with intensive supervision.

26. Cotton production and harvest is managed by a French non-profitorganization (the Compagnie Française pour le Dléveloppement des FibresTextiles)o Cotton is grown in the North of the country. Production wasstarted in 1951/52, It had reached 20,000 t by 1957/58, and had increasedto 56,o0o t in 1966/67. Yield per hectare has increased somewhat erratically,due to great variation in annual rainfaU and to the policy of expandingcotton acreage every few years, since the extensive cultivation of new fieldsmakes for lower average yields. In 1966/67 average yield per hectare was570 kg. Tests at Guetale indicate that yields could be considerably increasedwith the use of fertilizer. An obstacle to more regular fertilization isthe high cost of transport.

27. In East Cameroon the output of palm oil and pal kernels hasfollowed a dowward trend in recent years. Production is la-rgely in thehands of smallgrowers who have shown growing aversion to the laborioustask of climbing the palm trees. (Wild palms are generally much higherthan plantation trees), East Cameroon used to export palm oil regularlyup to about 1961.- Since then domestic production has been supplemented byimports from West Cameroon. The Bank has been asked to help finance a 9,OOOhadevelopzr.ent prograrn in East Camneroon uzhich will assure the supply of thedomestic market and also produce exportable surpluses of palm oil. In WestCameroon the production of palm oil and palm kernels is largely in the handsof CDC and Paniol (Unilever). In 1967 Bank and IDA lent $18 million to CDCwhich intends to increase its oil palm plantations from 8,800 ha at the endof 1967 to 21,000 ha by 1973.

28. R&ibber production in East Cameroon has been stagnating at around4,o500 t aniually throughout the 19601s. Low world market prices are adducedas reasons for bad plantation maintenance. On the other hand, CDC in WestCameroon has almost doubled its output from 3,800 tons in 1961 to 7,300 tonsin 1967. Practically the entire output of East and West Cameroon is exported.

- 13 -

29. Production data for timber are available only for East Cameroon.Although the southeastern part of the country is heavily forested, productionhas not developed spectacularly. The yield per hectare in valuable timberis very low - much lower, for example, than in neighboring Gabon - and vastareas are virtually inaccessible. Lack of roads and high transportationcosts in general limit the scope for expansion.

30, The main livestock producing areas are the region around Adamoua,northern Cameroon and West Cameroon. Cattle and goat herds numbered about1.9 million each at the end of 1966, and there were about 1.5 million sheep,280,000 pigs and almost 7.4 million head of poultry. Inadequate transportis a serious problem for cattle and beef trade. Cattle are mainly transportedon hoof over large distances with severe loss in weight and quality. In theshort run, development of production is hampered by high mortality due todiseases, lack of care aild mneconomic slaughtering. For the long term, poorbreeds wiil be a constraint on output, but there are on-going experiments toimprove domestic types by cross-breeding with imported animals. Scantyavailable data suggest slow growth of beef production, considerable increasesin poultry sales, and little development for sheep, goats and pigs. Datafor production and sales outside the control of official inspectors -probably quite high - are not available.

31. - ProC.ction of fresh-water fish yields annually between 40,000 and45,000 tons. Three-fourths are caught in Lake Chad, the rest in the numerousrivers and in artificial fish ponds, a large number of which have been createdsince 1960. Fishing gear ard processing are still primitive which leads towaste and spoilage, Since the early sixties there has been marine fishingwith motorized. vessels on a commercial basis. These vessels landed about15,000 tons of fresh fish at Douala during 1967. In 1960 landings hadtotalled only 3,200 tons, No precise data exist on the production of tra-ditional sea fishing, but rough estimates indicate that annual productionis 10,000 tons.

Manufacturing Industry

32. Manufacturing consists primarily of agricultural processing plantsand import substitution ventures suitable for a small market: beverages,footwear, textiles and garments, bicycle assembly, paint, matches, soap.The large hydro-potential has led to the establishment of a large aluminumfactory based on imported alumina. Most of the industry is located in theport city Douala, where the infrastructure is adequate for many industrialpurposes. Growth of industry has been favored by political stability,liberal government attitude towards foreign investment and industrial creditfrom financial institutions at moderate cost. Credits of the government--owned Banque Camerounaise de Développement (BCD) bear interest rates of 6-7percent a year. Commercial bank interest rates respond to Central Bankdiscount rates which, depending on the kind of paper discounted, rangedfrom 2.5 to 6 percent in mid-1967. New BCD credits to industry (includinghandicraft) amounted to about $2.5 million a year during the last two yearsand long- and medium-term commercial bank credit to larger industrialenterprises amounted in 1967 to somewhat over $1 million. In addition, thegovernment-owned Société Nationale dlInvestissement (MNI) has since 1964 made

- 4 -

minority participations in the capital of industrial enterprises at anaverage annual rate of $1 million. Many industrial enterprises are sub-sidiaries of foreign concerns and as such have access to the funds andcredit of the mother organization. In order to increase domestic andforeign industrial investment, government adopted in 1960 an investmentct1e under which eligible enterprises are exempted for a period up to 10years from paying import duties and up to three years from paying otherindirect taxes. Some enterprises are also exempted from profits taxesand a number of large enterprises have been given under the code guaranteesof fiscal stability for up to 25 years. The enterprises that have receivedthis guarantee are the aluminum factory, the two largest power companies,the recently established sugar and fLour mills and the two companies searchingfor oil. In all, 11O firms have been granted benefits under the code, underthe UDEAC investment code which affords similar benefits to enterpriseswishing to export to other UDEAC members or under other Cameroon investmentlegislation. Total planned investment of the 110 firms amounted to $160million. It seems likely that a major part of this investment has beenrealized. Benefits under the investment code are generous. Even the minimumbenefit of exemption from import duties and indirect taxes amounts to 40-50percent of the value of the products concerned0 It is hard to judge whetherthe revenue loss represented by the benefits is matched by increases ininvestment, national income and, later, increased tax revenue.

33. The manufacturing sector as a whole has grown rapidlyo In recentyears, aggregate industrial turnover (including processing of export crops)increased by over 17 percent per annum at constant prices to over $180 millionequivalent in 1966/67. The number of employees increased by 14.5 percentannually to 15,O00. In the past, most of the progress has been derived fromnew plants manufacturing hitherto imported products. Opportunities forfurther import substitution remain in many lines, but increasingly industrialgrowth will depend on the expansion of the national and neighboring countriesmarkets. The UDEAC carries the promise of a larger market, although mostplants established in Cameroon under the UDEAC investmpent code so far havesold almost all of their output in Cameroon itself.L' Four firms in the shoeand textile branch sold more than 20 percent of their output to Chad and theCentral African Republic, which now have left UDEAC; these firms may facesome difficulties in the future.

Transportation

34. Given the wide geographic distribution of productive resources aswell as the limited degree of economic self-sufficiency of most parts of thecountry, the development of the transportation network is of decisive impor-tance for economic progress. The present transportation infrastructure doesnot measure up to this task in spite of some recent progress, There are fewroads and railwaysj and these are mostly in poor state. The country's major

1] Out of 43 such plants only one sold more than 40 percent of its outputin other UDEAC countries, while 26 sold over 90 percent in Cameroon itself(January-June 1967 data).

g/ There is 1 km of railroad and 2.4 km of asphalted road for every 1,000 kma2of surface. This compares with 5.2 and 8 lm., respectively in Senegal,1.9 and 2.6 lm in Ivory Coast, and 1.5 and 3.1 lm in M4adagascar.

sea port is becoming congested, and rapid increase of air traffic demandsadditional investments. The transportation problem is complicated by thefact that the central part of the country is one of the least populatedregions (4 inhabitants per km2 ), a vast economic no-man's land whichaccounts for 30 percent of the total land area of East Cameroon. Theeconomic return of north-south transportation projects is adversely af-fected by the long distances separating the two regions in the absenceof a sizable flow of goods originating in the central region.

35. In 1966 Cameroon had 14,700 km of roads of which 1,200 km wereasphalted and another 3,600 km were all-weather earth roads. About 9,800 kmwere secondary earth roads which permit only slow, high-cost and at timesdangerous vehicle traffic. An additional 17,000 km of tracks are practi-cally inaccessible for trucks and cars. The road network is primarilyconcentrated in the south-west (Douala-Yaounde region), the Bamileke regionand in the north. Large parts of the country have no road or rail connection.

36. The First Plan projected investments for roads and brid es totallingCFAF ll.8 billion ($47 million) for the five-year period. Foreign aid com-mitments during the same period and for the same purpose totalled CFAF 6.6billion. Although precise data on the First Plan are not available, it isvirtually certain that investments fell short of the Plan target, mainlyo%wing to deficiencies in project preparation and execution. In mid-1966projects involving CFAF 2.8 billion in foreign funds had not been completed.The Second Plan envisaged much larger investments in roads and bridgestotalling CFAF 16.5 billion, with CFAF 9.9 billion foreign financing andCFAF 1.0 billion to be contributed in labor. However, first year realizationsamounted to only about 56 percent of the Plants first year target, for thesame reason as during the First Plan. -

37. There are no reliable statistics on road traffic, but the numberof truck registrations suggests a growth rate of about 6 percent in recentyears of transportation of goods. Registration of passenger cars and buseswould indicate a growth rate of passenger traffic of between 13 and 17 percenta year. About 16,000 trucks are engaged in commercial transportation. Twoexpatriate companies dominate the business, but individual foreigners andCameroonians play a growing role in road transportation. Freight rates varyaccording to distance, state of the road, load factor (including possibilityof a return load). For distances in excess of 800 kms, they average aroundCFAF 10 per t/hm (US 40).

38. The railway net consists of a connection between Douala and Yaounde(345 km, the "central line") and a line from Dbuala to Nkongsamba (172 km).Passenger traffic-increased at a rate of about 6 percent in the last twoyears. Freight transportation has been more or less stationary, apparentlybecause the system in its present state cannot carry more traffic.

39. The central line which accounted for about 64 percent of passengertraffic in 1966/67 and for 82 percent of freight traffic is in a bad stateof repair. Some of the rail was laid before the First World lWar. Accidentsare frequent and there are long delays in the shipment of goods. In May ofthis year the railways started at $4.7 million rehabilitation program for thecentral line which would replace 146 km of rail laid between 1910 and 1926.

- 16 -

The financial position of the railway worsened in recent years, larogelybecause of increased financial charges and personnel and materials costs.The ratio of expenditures (excluding depreciation and taxes) to revenuesrose from 096:1 in 1964/65 to 0.8:1 in 1967/68.

40. The construction of the TransCameroon railway which is to linkYaounde with Ngaoundere (630 km) in the north is progressing well. Thefirst 100 km section was opened in July and early next year another 193 kmwill be completed. The financing of these first 293 km was secured fromFED ($17.3 nillion), USAID ($9.2 million) and FAC ($8.2 million).

41. At the end of 1967 Cameroon had two major commercial airports,Yaounde which can accommodate Caravelle jets and Douala which can accomodateail international jet planes. There is a large number of secondary airports.Table 20 in the appendix shows rapid increase in plane movements, passengerand freight traffic between 1963 and 1967. A new terminal building in Yaoundewas opened in 1968, and plans exist to construct a modern terminal at Douala,the old one being no longer adequate to handle traffic. Airport fees wereincreased in 1967 for the purpose of repaying borrowed funds for the Yaoundeterminal and establishing a special fund for the Douala terminus.

42. Cameroon has four sea ports handling about 1.5 million tons of freighteach year. Doueala, which accounts for 90 percent of merchandise traffic, haseleven bertlhs and is linlced to the railway system. Estimates of Doualals capacity,range up to 2.0 million tons a year. However, attainment of this would requireimportant changes, particularly as regards urarehouse and storage fees. Thereis little question that ,the eleven berths can accommodate vessels loadingand unloading 2 million tons, but the port has little space for lateralexpansion of storage facilities. The rates for storage should take this intoaccount and, after allowing for the necessary time for the removal of importedmerchandise and margins for the temporary storage of goods to be exported, asteep gradation of fees is needed to provide incentive for importers andexporters to occupy scarce space for a minimum of time. Currently, however,annual flat rates per square meter are charged which, in addition, are so lowthat the alternative of constructing storage space elsewhere in DDuala isunattractive to traders. For open storage, rates vary between US $0.40 and$2.23 per mn /year(9.6 square feet), and for magazine and hangar space betweenUS $3.04 and $7.29 per r2/year.

43. Dredging operations at Douala are not carried out regu.larly orefficiently. Draft alongside quay is 8 to 10 meters, but in the accesschannel it is between 4.7 and 5 meters; high tide adds up to 0.6 meters, sothat vessels up to about 5.2 meters draft can be accommodated safely.

Power

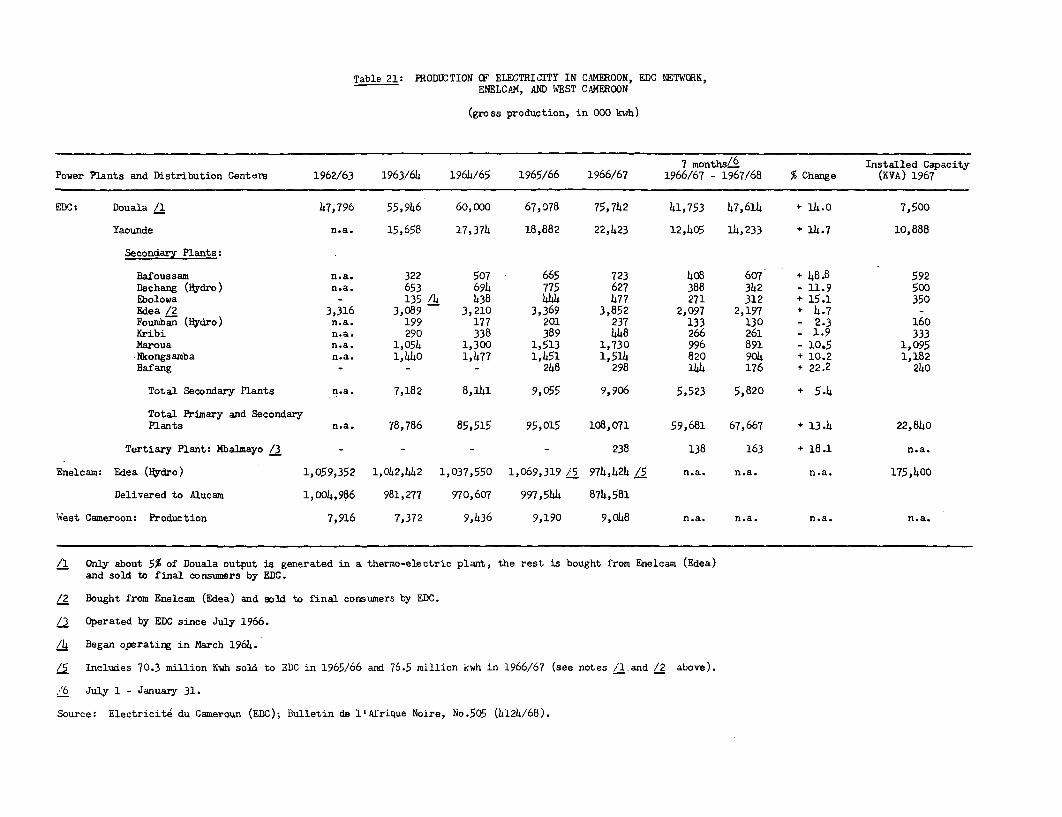

44. The major producer of electrical energy is Ehelcam (Energie Electriquedu Cameroun) which operates the Edea dam and power plant with an installedcapacity of 175,400 KVA. Enelcamn has only two clients, the aluminum plant(Alucam), also at Edea, which takes about 85-90 percent of MielcamIs production,and EDC (Electricité du Cameroun), the largest distributor of energy, whichabsorbs the rest. Enelcam is obliged to supply on demand a minimum (20,000 kwh)of electricity to EDC at all times. Thi.s limits Alucamts share, and thus

- 17

its output of aluminum during the dry season; but the completion of newinstallations by 1970 will aller full-scale operation the year round.Production by Enelcam has fluctuated bet.ween 0.98 and 1,07 billion ktvrhin the past five years. Fluctuations are due to variations in rainfail.Sales of pawer to EDC have risen from 50 to 76.5 million kwh between1962/63 and 1966/67. EDC operates a 609000 volt transmission line fromEdea to Douala, and a 909000 volt line from Edea to Yaounde will beinaugurated in July 1968. This line will cover Yaoundels needs for thenext 25 yearso Production in Wpest Cameroon made a big leap between 1962/63and 1964/65, but has declined slightly thereafter due to lack of rainfall,and stood at about 9.1 million kwh in 1965/66 and 1966/67. Consumption ofelectricity, Alucam apart9 has increased regularly by 13 percent in recentyears. The largest increases occurred in high tension power, which in Doualaincreased fronm 16.8 to 28.9 million kwh in three years, and in Yaounde from3.5 to 5'3 million kwh during the same period.

III. TE FINZCIAL SITUATION

45. The financial situation of Cameroon is characterized by closerelations with France and the Common Market. Ful currency convertibilityhas been guaranteed by an agreement with the French Treasury and monetarydevelopnents are supervised by a monetary conmittee with French represen-tation. Official aid from France is large and the flow of private capitalbetween the two countries is free from controls. In recent years aid andtrade with the Common 1<arket gained in importance. Cameroon has, on thewhole, enjoyed a stable financial position, although it has weakened tosome extent recently.

A. Public Pinance '

46. Government financial operations consist principally of the budgetsof the federal and two federated governments. The federal budget has thedominant position, accounting for over 60 percent of the budget expendituresand over 70 percent of revenues, The federated governments, whose main areaof responsibility are local administration, agriculture, road maintenanceand primary education, receive annual subventions from the federal budget.The Federal Government receives the proceeds of ah1 customs duties, whilethe states collect the bulk of direct taxes. Except for specific Frenchbudgetary support, which was terminated in 1965, the budgets do not includeforeign aid. This is normally channelled direct to the recipient concernedor through the Cameroon Developaent Bank.

47. As indicated in the last Bank report, the early 1960ts saw amarked improvement in budgetary performance* In 1962/63, the current accountdeficit was eliminated and in 1963/64 and 1964/65 a current surplus emergedwhich was more than sufficient to cover capital expenditures. In 1965/66the current surplus remained substantial, although a sharp rise in capitaloutlays necessitated additional financingo In 1966/67, however, there wasa sharp retrogression with the current surplus falling off and, in spite ofa reduction in capital expenditures, causing a large overall deficit. Thisdeterioration appears to have been only temporary and was caused basicallyby an extraordinary increase in current expenditures. In 1967/68, based onresults for the first nine months, there has been an impressive recovery,and it appears thatthe current surplus wiI1 be the largest ever achieved.This has resulted from a large increase in revenue, especially from customsrevenue, and renewed restraint an the expenditure side. Furthermore, theoverall deficit has been practically eliminated. A consolidated statementof the budgetary operations of the three governments is given in the followingtable:

1] Cameroonts fiscal year runs from July 1 to June 30. For the Federaland East-Cameroon governments there is an additional 3 months"complementary" period during which expenditures if authorizedbefore the end of June may take place, and their accounts are closedat the end of September.

- 19 -

Table IX: CONSOLIDATED FEDERAL ANID FEDERTED BUDGETS

(in OFAF billion)

1962/63 1963/65 1964/65 196/66 196667 1967/68 1968/69

Budget Revised BudgetA c t u a 1 PovisiDn Estimate Pzvvi3ian

Current Revenue

Direct Taxes 4080 5.68 5,72 6.32 7.76 8.30 n.a. noa.Indirect Taxes 12.29 16.69 18.16 19.84 20.49 2118 n.a. n.aoFees and dues 0088 0o95 lelO 122 130 1041 n.a0 n.aoNon-fiscal revenues 2.27 2e05 2.26 2.32 2.37 3e54 n.a, n.ao

20.24 25-37 27024 29-70 31-92 34.43 36-87 38-70

Current EXpenditures 19.61 21.68 24.41 26.70 30.64 32.31 32-79 35.28

Current Surplus +0o63 +3.69 +2.83 +3.00 +1,28 +2012 +4 008 +3.42

Debt Service o052 0047 0041 0041 o0 4o 0o57 0°57 °o59

Balance +0011 +3.22 +2.42 +2059 +0.88 +1.55 +3.51 +2.83

Capital Expenditures 1061 2.16 2.07 4013 3077 3.90 3.55 4036

Budget Surplus -1l50 1.06 035 -1054 -2.8 -2.35 -0004 -153

Financed by

Foreign Subventions +175 - 0o05 +loOO - - -Drawings on the

Treasury /bh+ol 2 -1e32 -0o81 +1 024 +3.95 +2.35 +024 +003Drawings on the BCD -O.o36 +0.26 -0 004 -0-70 -1î06 - -0,20 +1,50

ja + - Drawi-ng or receipt

/b Caisse des Investissements of the Cameroon Development Bank,

Sourcee Statistical Appendix Table 27 and 28.

480 Current revenues increased by over 80 percent in the five yearsy1962/63 to 1967/6th This was brought about by a 25 percent increase in1963/64 followed by a steady increase of about 8 percent per annum in thesucceeding three years, and a further upsurge in 1967/68 of 15 percent. Atthe same timeS the ratio of revenue to GDP rose from 14i0 percent to 16.5percent in 1966/67 and 17.3 percent in 1967/68o The large increase in

_ 20 -

receipts in 1963/64 is explained by the introduction of a tax on businesstransactions in that year; thereafter, there have been no significantincreases in tax rates, except for the increase in duties on goods enteringWest Cameroon as a result of the harconization of customs duties in 1966,which may have brought in an additional CFAF 0.7 billion. The upward trendin revenues has been due primarily to the expansion of taxable activities.With indirect taxes accounting for about 65 percent of total revenues, andimport and export duties contributing about 75 and 15 percent respectivelyto these, the key element in 1964/65 and 1965/66 was the increase in foreigntrade. Foreign trade more or less stagnated in the following two years, butrevenues continued to rise, owing partly to deferred iimport duty payments,and partly to the continuing growth of the modern sector. The sharp increaseof revenues in 1967/68 appears to be due to the upsurge of imports in thesecond half of 1967. Direct taxes have increased, but their ratio to totalrevenue has remained roughly constant, The coming into force of the UDEACin 1966 may, if anything, have increased tax revenues. Certain tax lawshad to be adjusted, but the Governnent estimated in the 1966/67 budget thatCameroon would obtain CFAF 0.3 billion additional tax revenue from the UDEACarrangements. This was offset, however, by contributions to the UDEACsolidarity fund.

49. Cirrent exprenditures are fairly high because of the costly adminis-trative structure of two full-fledged state governments and a federal govern-ment. They would be higher still were it not for the annual payment of aboutCFAF 1 billion by France towards the salaries of expatriate school-teachersand civil servants. Without these payments, which would otherwise come withinthe purview of current budgetary expenditures, the overall budgetary situationwould be less favorable. On the whole, current expenditures have barely laggedbehind revenues, !with an average annual increase of 11 percent over the lastfive years. The largest increase took place in 1966/67, when expendituresrose by 15 percent as compared with the preceding year. Determined effortsby the governnent have reduced the increase to only 7.5 percent in 1967/68.An important element in this expansion has been the extension of governmentservices, particularly education and health. Another has been the rapidgrowth of government contributions and subsidies, particularly for educationand healthe augmented during the last two years by payments to the UDEACsolidarity fund (CFAF 0.3 billion and CFAF 0.5 billion respectively), andby measures to improve the distribution of food in West Cameroon followingthe rise in the cost of living resulting from tariff harmonization. Theoverriding factor, however, has been the rapid growth of personal emoluments.Governnent salary scales have in fact remained practically unchanged sinceindependence, but upgrading has caused a fast increase in wages and salaries.Between 1962/63 and 1967/68, while the number of Federal government employeesincreased by only about 4 percent, average salaries rose by almost 60 percent.In addition, civil servants receive extremely generous housing and familyallowances both of which have been on the increase. The governments are awareof the deleterious effect of these increases on public savings, and moregenerally on the rural-urban wage differential. Curtailment of civilservants emoluments is politically difficult, as in other African countries.Nevertheless, as a start the Federal Governinent is intending to pass legis-lation which would restrict the level of family allowances. Governnent alsointends to reduce sharply the number of civil servants annually promoted to

_ 21 -

a higher rank and to freeze the amount paid on rent allowances. The WestCameroon governnent has also recently reduced the number of its ministriesby three in an effort to economize.

50. Compared with many countries, governnent debt service payMentsi/have been small. This is because of the favorable terms on which aid hasbeen obtained in the past: in 1967/68, service payments were only about3 percent of total governinent debt outstanding (excluding guarantees).Consequently, current savings could be used largely for financing capitalexpenditures.

51. Capital expenditures / have risen impressively since the earlysixties; they have been almost twice as high in the years 1965/66 to1967/68 as in the preceding three years. The largest outlay, CFAF 4.13billion, occurred in 1965/66, after which expenditures declined somewhat.Over a third of the total in the most recent years has been spent onadministrative buildings and equipment, about a third on infrastructure,and the remainder about equally on agriculture and social services. Althoughin some cases necessary for governmentts efficient functioning, the outlayson administrative facilities have been excessive, and as pointed out in ChapterIV they threaten to jeopardize the success of the Second Plan. Capitalexpenditures on budgetary account constitute well under half of total publicinvestr,xents. Nevertheless, the over-concentration on slow yielding ormarginally productive schemes on budgetary account reflects the government1 sfailure to take the lead in following the priorities set out in the Plan.

1] It has not been possible to separate interest and amortization. Sincethe latter are the larger, total debt service payments have beenconsidered as falling outside current expenditure.

2] One idiosyncrasy of the budgetary system requires explanation at thispoint. Current expenditures, as shown in the final governnent accounts,refer to actual outlays. Capital expenditures, on the other hand, forthe Federation and East Cameroon, refer to authorizations only. At theend of each fiscal year, the unspent portion of authorizations istransferred to a special fund (Caisse des Investissements) held withthe Banque Camerounaise de Développement (BCD). Thereafter, disbursementsare made out of this fund as and when expenditure takes place. Sincetransfers to the fund have exceeded disbursements from it in most years,the governnent accounts give an inflated picture of capital expenditures.This confusing practice has been put to an end in the 1968/69 budget,and in future capital expenditures will be on the same footing ascurrent. However, disbursements will continue for at least two yearson the sizable funds built up in the BCD as a result of earlier transfers.The capital expenditure figures shown in Table IX and referred to areadjusted on the basis of information obtained from the BCD.

- 22 -

52. As indicated in the above table, capital expenditures anddebt service have been financed partly by current savings, partly by Frenchbudgetary support, and partly by drawings on the Treasury. In 1963/64 and1964/65 they were covered entirely by current savings; in 1965/66 they werefinanced in part by all three items. French budgetary support was terminatedin the same year, and in 1966/67 the sharp deterioration in savings resultedin drawings on the Treasury to the extent of almost CFAF 4 billion. melatter were accentuated by substantial transfers to the BCD for unspentcapital commitments (see previous footnote). In 1967/68, the recovery ofcurrent savings accompanied by lower investment outlays has practicallyeliminated the need for deficit financing, although again continued drawingson the Treasury have been necessary owing to additional net transfers to theBCD.