Evaluations of Outcome Sequences

22

Organizational Behavior and Human Decision Processes Vol. 83, No. 2, November, pp. 331–352, 2000 doi:10.1006/obhd.2000.2913, available online at http://www.idealibrary.com on Evaluations of Outcome Sequences Dawn Matsumoto Harvard University Mark E. Peecher University of Illinois at Urbana–Champaign and Jay S. Rich University of Connecticut We extend the literature on intertemporal choice by investigat- ing how possession of knowledge related to the present value of future outcomes (PV knowledge) affects the extent to which individuals weight certain attributes when evaluating outcome sequences. While PV-knowledgeable individuals can ascribe value to attributes according to their PV relevance (or irrele- vance), unknowledgeable individuals cannot do so. Such knowl- edge, therefore, likely interacts with outcome-sequence attributes to affect the extent to which individuals exhibit impa- tience when evaluating outcome sequences. The main experimen- tal findings indicate that higher PV knowledge increases the extent to which individuals value impatience (as opposed to improvement). However, these findings also reinforce a need to distinguish among impatience, improvement, and PV because some higher PV knowledge participants willingly sacrifice PV while exhibiting impatience (while others do so in order to gain improvement). Overall, PV considerations appear central, but not determinative, in higher PV-knowledgeable individuals’ evalua- tions of outcome sequences. q 2000 Academic Press We thank S. Biggs, M. Shelley, R. Tubbs, as well as workshop participants at theUniversity of Iowa’s Judgment and Decision-Making Colloquium, the University of Utah, the University of Connecticut, and Rutgers University for their helpful comments. Address correspondence and reprint requests to Mark E. Peecher, Department of Accountancy, College of Commerce and Business Administration, University of Illinois at Urbana–Champaign, 284 Commerce West Building, 1206 South Sixth Street, Champaign, IL 61820. E-mail: [email protected]. 331 0749-5978/00 $35.00 Copyright q 2000 by Academic Press All rights of reproduction in any form reserved.

-

Upload

independent -

Category

Documents

-

view

1 -

download

0

Transcript of Evaluations of Outcome Sequences

Organizational Behavior and Human Decision ProcessesVol. 83, No. 2, November, pp. 331–352, 2000doi:10.1006/obhd.2000.2913, available online at http://www.idealibrary.com on

Evaluations of Outcome SequencesDawn Matsumoto

Harvard University

Mark E. Peecher

University of Illinois at Urbana–Champaign

and

Jay S. Rich

University of Connecticut

We extend the literature on intertemporal choice by investigat-ing how possession of knowledge related to the present valueof future outcomes (PV knowledge) affects the extent to whichindividuals weight certain attributes when evaluating outcomesequences. While PV-knowledgeable individuals can ascribevalue to attributes according to their PV relevance (or irrele-vance), unknowledgeable individuals cannot do so. Such knowl-edge, therefore, likely interacts with outcome-sequenceattributes to affect the extent to which individuals exhibit impa-tience when evaluating outcome sequences. The main experimen-tal findings indicate that higher PV knowledge increases theextent to which individuals value impatience (as opposed toimprovement). However, these findings also reinforce a need todistinguish among impatience, improvement, and PV becausesome higher PV knowledge participants willingly sacrifice PVwhile exhibiting impatience (while others do so in order to gainimprovement). Overall, PV considerations appear central, but notdeterminative, in higher PV-knowledgeable individuals’ evalua-tions of outcome sequences. q 2000 Academic Press

We thank S. Biggs, M. Shelley, R. Tubbs, as well as workshop participants at the University ofIowa’s Judgment and Decision-Making Colloquium, the University of Utah, the University ofConnecticut, and Rutgers University for their helpful comments.

Address correspondence and reprint requests to Mark E. Peecher, Department of Accountancy,College of Commerce and Business Administration, University of Illinois at Urbana–Champaign,284 Commerce West Building, 1206 South Sixth Street, Champaign, IL 61820. E-mail:[email protected].

3310749-5978/00 $35.00

Copyright q 2000 by Academic PressAll rights of reproduction in any form reserved.

332 MATSUMOTO, PEECHER, AND RICH

Key Words: intertemporal choice; impatience; improvement; time valueof money; present value; outcome sequences.

Many decisions have intertemporal effects. By consuming all today, oneleaves nothing for tomorrow. By saving all for tomorrow, one goes withouttoday. Between these extremes an infinite number of possible sequences exist.If individuals had complete control over the timing of receipt, what sequencewould they choose? One can decompose this descriptive research question intoat least two related questions. The first question concerns the attributes thatindividuals generally consider when evaluating sequences. The second questionconcerns more primitive factors that affect the extent to which certain individu-als weight these various attributes. The experiments reported in this articleaddress both questions.

Three goals motivated the research. First, as business researchers, we areespecially interested in how people evaluate certain types of sequences (e.g.,earnings, stock returns, and so on). A popular assumption in business researchis that managers and other stakeholders are impatient at least in the sensethat they homogeneously maximize present value (PV). While impatience asa construct need not require PV maximization (i.e., impatience can manifestwhen persons choose among alternatives of equal PV), many common behaviorsand experimental findings contradict even broad conceptualizations of impa-tience, including PV maximization. Why do academics frequently opt to be paidover 12 instead of 9 months (Loewenstein & Thaler, 1981)? Why do participantsin experiments frequently choose improving outcome sequences(Loewenstein & Sicherman, 1991)? Why do over 70% of individual taxpayersmake interest-free loans to the IRS (Omer & Shelley, 1998)? Why does themarket reward firms who report patterns of increasing earnings after control-ling for growth and risk (Barth, Elliott, & Finn, 1999)? These behaviors raisequestions about the relative importance of PV maximization in the outcome-sequence evaluation process (Shefrin & Thaler, 1992).

Second, with the exception Benzion, Rapoport, and Yagil (1989), much of theexperimental support for the aforementioned “anomalous behaviors” stemsfrom participants who are relatively unknowledgeable about PV concepts. Arbi-trage theory suggests that relatively unknowledgeable but capable individualsseek to acquire knowledge to avoid being driven from markets (Loewenstein &Thaler, 1981), and expert performance research suggests that knowledge likelymoderates how individuals mentally represent and evaluate outcome sequences(Chi, Feltovich, & Glaser, 1981). While Loewenstein and Sicherman (1991)provide hints of the moderating role of knowledge in that PV maximizationincreases for college graduates and high-wage-earners, no research of whichwe are aware directly investigates the influence of PV knowledge on individuals’outcome-sequence evaluations.

Third, we conjecture that an interaction between sequence-evaluator’s PVknowledge and attributes of sequences shape the extent to which evaluationsreflect impatience as opposed to improvement. Knowledgeable individuals canchoose to weight or ignore attributes of sequences because of their PV relevance

EVALUATIONS OF OUTCOME SEQUENCES 333

(or irrelevance). Unknowledgeable individuals are constrained to the use ofalternative grounds in determining which attributes to weight or ignore. Toillustrate, consider how evaluators react to the attribute of outcome sequenceliquidity. Liquid sequences feature goods that are themselves cash or readilyconvertible to cash (e.g., commodities) or are thought of by evaluators as such(e.g., tickets to major sporting events routinely are scalped, whereas tickets tohigh school musicals typically are not). Holding all else constant, relativelyliquid sequences likely instigate greater impatience in higher, as opposed tolower, PV-knowledge individuals.

HYPOTHESIS DEVELOPMENT

Background Literature

Most theoretical discussions of the evaluation of outcome sequences assumeindividuals should use a positive discount rate (i.e., delayed outcomes haveless value today). The quantitative expression of this process for a given eventsequence, X 5 (x1, x2, . . . , xn), is:

V(X ) 5 on

t51wtu(xt), (1)

where u(x) is the undiscounted utility for event x and wt is a discount factorapplied to period t, such that 0 , wt # 1, wt21 . wt , and wt11/wt 5 k, wherek is a constant marginal utility of substitution between discount factors foradjacent periods.

Normative considerations aside, psychology research on intertemporal choiceprovides evidence that individuals often want to delay desired outcomes (e.g.,Loewenstein, 1987), especially when they evaluate outcome sequences (e.g.,Chapman, 1996; Hsee & Abelson, 1991, Loewenstein & Sicherman, 1991;Loewenstein & Prelec, 1993). Loewenstein and Prelec (1993), for example, ask95 Harvard University students, “Which would you prefer if both were free?‘‘dinner at a fancy French restaurant’’ or ‘‘dinner at a local Greek restaurant.” ”Eighty-two students (86%) choose the French restaurant. Those preferring theFrench restaurant answer a second and a third question. The second questionasks students to choose between “dinner at the French restaurant on Fridayin 1 month” or “dinner at the French restaurant on Friday in 2 months.”Consistent with PV, 78% prefer the French dinner earlier. The third questionasks students to choose between “dinner at the French restaurant on Fridayin 1 month and dinner at the Greek restaurant on Friday in 2 months” or“dinner at the Greek restaurant on Friday in 1 month and dinner at the Frenchrestaurant on Friday in 2 months.” Surprisingly, 57% defer consumption of theFrench dinner when it is part of an outcome sequence, whereas only 22% ofstudents do so when it is framed as an isolated event. In terms of Eq. (1), thesedata violate the assumption that wt21 . wt for all t and imply nonstationarydiscount factors. To see the latter, note that most question two responses sug-gest w1 . w2, whereas a majority of question three responses suggest w1 , w2

334 MATSUMOTO, PEECHER, AND RICH

(as long as French dinners are preferred to Greek dinners, which is establishedby question one).

One could argue that the above data reveal little about how individualsevaluate business-related sequences comprised of items such as dividends,operating cash flows, and accounting earnings. For such sequences, one canargue that “time is money.” There is, however, similar anomalous evidence forliquid, monetary sequences. Loewenstein and Sicherman (1991) report thatvisitors to Chicago’s Museum of Science and Industry overwhelmingly chooseincreasing over decreasing cash flows, even when the total cash over 6 yearsis fixed. This finding holds across two sequence domains, wages and rent, anddespite an explanation of some PV concepts. In particular, the percentage ofsubjects choosing PV-maximizing sequences ranges from 7 to 28%, with lowerpercentages associated with the wage context (roughly 15%) than with the rentcontext (roughly 26%).

Drawing on these data and a number of other studies’ findings, Loewensteinand Prelec (1993) develop a descriptive model that expresses the value ofintertemporal event sequences as a weighted average of three attributes. Twoof these attributes run counter to positive time discounting/PV assumptions.The LP model can be expressed as:

V(X ) 5 on

t51ut 1 b o

n

t51dt 1 s o

n

t51.dt., (2)

where ut is the undiscounted utility received from an event at time t; b and sare parameters indicating that an individual prefers improving (b . 0) ordeclining (b , 0) sequences and uniform (s , 0) or nonuniform (s . 0) se-

quences; and where dt 5tn o

n

i51ui 2 o

t

i51ui, or the difference between the cumula-

tive utility that would have been received if the outcomes were uniformlyallocated across the n periods and the cumulative utility actually received upto period t.1

Our concern primarily is with factors that influence the sign of the model’sb parameter, which reflects an impatience-to-improvement continuum.

1 Another way of expressing dt is in terms of anticipation utility (AU) and recollection utility(RU). In the LP model, anticipation utility is a linear function of the undiscounted utility of agiven future event and the number of periods that precede realization of the future event (t 2 1):

AU 5 ot

(t 2 1)ut.

Recollection utility (RU) similarly is the sum of given utility levels multiplied by the number ofsubsequent event periods (n 2 t):

RU 5 ot

(n 2 t)ut.

As an example, suppose that one frames two vacations—one on March 1st and one on July 1st—asa calendar year’s worth of vacations. The first vacation would have 3 months of anticipation and9 months of recollection and the second vacation would have 6 months of anticipation and 6 monthsof recollection.

EVALUATIONS OF OUTCOME SEQUENCES 335

Loewenstein and Prelec find that, consistent with much prior research, b ispositive for the majority of their experiments’ participants. Specifically, theyask 52 visitors at Chicago’s Museum of Science and Industry to evaluate se-quences of five consecutive weekends. Of the five weekends, one is very enjoy-able, two are moderately enjoyable, and one is boring. Bar graphs reflect therelative enjoyability of the five different weekends. Subjects’ rank orderingsimply a positive b estimate for 77% of the subjects. Further, a second reportedexperiment also provides evidence that b . 0, as participants prefer increasingsequences roughly 80% of the time (cf. Ross & Simonson, 1991). In fact, thefinding of b . 0 is empirically supported in a number of other studies. Thepreference for improvement holds for aversive sequences (e.g., Fredrickson &Kahneman 1993), and it intensifies for sequences that improve faster thanothers, especially near the end of the sequence (Hsee, Salovey, & Abelson,1994). Finally, Schmitt and Kemper (1996) show that although differencesbetween anticipated and experienced utilities exist for outcome sequences,improvement itself is valued in both measures of utility.

Relatively few studies investigate evaluator-specific determinants of the signof b. Chapman (1996), however, does so by examining how evaluator-specificexpectations influence outcome-sequence evaluations. She initially observes adomain effect (i.e., health versus wages) in that, on average, undergraduatesmore frequently prefer decreasing sequences in a health, as opposed to a wage,domain. Regardless of domain, undergraduates who expect their wages orhealth to increase (or decrease) also tend to prefer increasing (decreasing)sequences. Overall, expectations partially mediate the effects of domain on theundergraduates’ preferences.

Hypotheses

We predict the sign of b to be a function of individuals’ PV knowledge andoutcome-sequence attributes. We also predict that knowledge and outcome-sequence attributes interactively affect the sign of b. We examine both nonmon-etary and monetary outcome sequences. Because PV concepts are rooted in thetime value of money (e.g., interest), we predict that the extent to which PVknowledge induces impatience will be greater in liquid, monetary sequencesthan in less liquid, nonmonetary sequences.

Within the monetary sequences, we examine evaluators’ sensitivity to domain(wage vs rent) and to interchangeability (cash flows held constant vs PV heldconstant). With respect to interchangeability, we expect PV knowledge to in-crease the extent to which impatience is exhibited so long as total cash flow,not total PV, is held constant across alternative sequences. When cash flows areheld constant, higher PV knowledge participants will recognize that impatiencemaximizes PV. When PV is held constant, the time value of money becomesless relevant, so that higher and lower PV knowledge participants likely willexhibit similar degrees of impatience. With respect to domain, we expect PVknowledge to mitigate the prior research finding in which greater impatiencewas exhibited in cash flow sequences involving rent as opposed to wages

336 MATSUMOTO, PEECHER, AND RICH

(Loewenstein & Sicherman, 1991). From a PV perspective, the key point isthat both wages and rents are cash flows.

Finally, while we anticipate that domain, interchangeability, and liquiditymay themselves interactively affect evaluators’ assessments of outcomes, ourinvestigation is somewhat exploratory with respect to higher order interactions.Exploration is necessary in this regard because no descriptive theory currentlyexists which is sufficiently precise to pinpoint predictions concerning how allthese factors simultaneously interact. To summarize, we investigate the follow-ing hypotheses:

H1: Ceteris paribus, greater knowledge of PV concepts produces more impatience in outcome-sequence evaluations.H2: Ceteris paribus, greater PV knowledge increases (decreases) the weight ascribed to out-come-sequence attributes that are PV relevant (PV irrelevant).

EXPERIMENT 1

The purpose of the first experiment is to provide an initial test of the general-izability of b . 0. Consequently, we recruited relatively high-knowledge partici-pants and employed liquid, monetary outcome sequences. Our thinking wasthat if b . 0 given these participants and sequences, there would be no compel-ling reason to conduct additional experimentation to test whether b/K isnegative.

Method

Participants. Fifty-four undergraduate seniors majoring in accounting atthe University of Washington participated in exchange for a free cafe latte. Weconstrued these participants to be knowledgeable relative to subjects typicallytested in psychology. Unlike most psychology-study participants, by the timeaccounting undergraduates are seniors, they have taken several courses thatexplicitly focus on and test PV concepts. For example, several accountingcourses test students’ knowledge of specific financial accounting standards thatrequire application of such PV concepts.

Materials and procedure. The instrument was a pencil-and-paper task witha format quite similar to that used by Loewenstein and Sicherman (1991). Itwas composed of three parts (i.e., Parts 1, 2, and 3), followed by four shortpostexperimental questions. The administrator read aloud cover-page direc-tions that emphasized that participation was voluntary, that preferences werebeing solicited, and that no single “right” or “wrong” answers existed. Partici-pants started the materials in unison. They were allowed to look through thethree-page instrument before completing individual parts.

Part 1 asked participants to rank order six outcome sequences, and Part 2asked them to estimate and briefly justify the amount they would pay for theirpreferred sequence. Part 3 asked participants to choose between two outcomesequences after providing some reasons in support of each sequence. Stated

EVALUATIONS OF OUTCOME SEQUENCES 337

reasons in support of the “present-value maximizing” alternative were thatfront-ended cash can be put into a bank and earn interest so that one can havemore money every year. For the “non-present-value maximizing” sequence,stated reasons were that it can be satisfying to get bigger payments each year,that it is often difficult to save money, and that selecting it would give morespending later without worrying about putting money away in the earlier years.Appendix A contains excerpts of the Experiment 1 instrument.

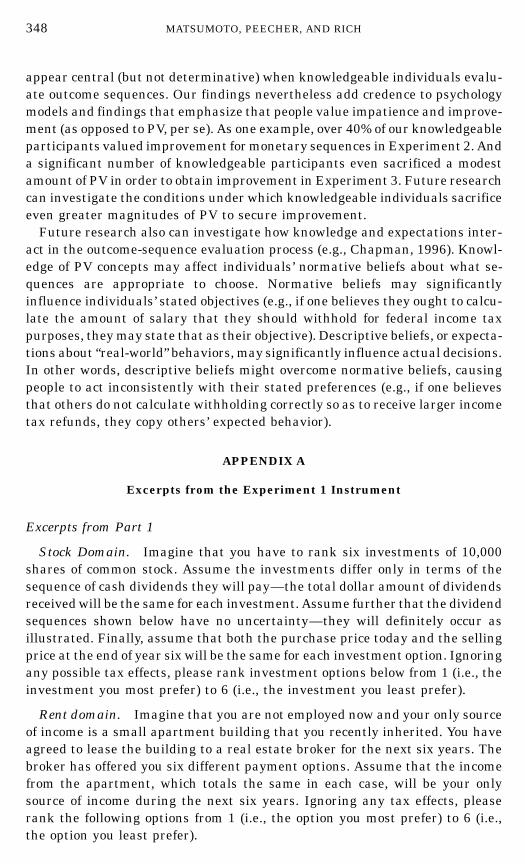

Although we concentrated on highly liquid, monetary sequences, we manipu-lated sequence domain, between subjects, to enhance generalizability. Therewere two such manipulations, each at two levels; one was for Part 1 sequences,and the other was for Part 3 sequences. In Part 1, one domain was dividendsfrom a common stock investment. Six 6-year investment alternatives werepresented, with total dividends received held constant. Instructions empha-sized that the alternatives differed only in sequencing and that both the pur-chase and future selling prices were identical. The other Part 1 domain wasrental income, with the rent hypothetically being the participants’ only sourceof income for 6 years. Both the rental and stock dividend scenarios askedparticipants to ignore tax effects.

The Part 3 manipulation also varied domains, but they also altered theduration and outcome amounts of the sequences. One domain pitted two 6-year, context-free sequences of $150,000 in total cash flows against each other.These alternative cash-flow sequences mirrored each other, with periodic cashflows increasing in one and decreasing in the other. The other Part 3 domainwas lifetime wages. Participants were asked to imagine that they knew theirwages until retirement (i.e., 30 to 40 years) and to choose between an immedi-ate, lump-sum payout and any other self-specified allocation. Last, participantsbriefly justified their choices in Part 3.

Results

We categorized participant responses according to whether they strictly wereconsistent with impatience (i.e., b , 0) or improvement (i.e., b . 0). Becausethe sequences in Part 1 decreased in present value going from option 1 tooption 6, strict impatience requires a rank ordering of 1st, 2nd, 3rd, 4th, 5th,and 6th. At the other extreme, strict improvement requires a rank ordering of6th, 5th, 4th, 3rd, 2nd, and 1st. For Part 3, the categorization process wassimpler: the participants’ dichotomous choice reflected either impatience orimprovement.

Panel A of Table 1 presents pooled data for all 324 Part 1 rankings (54subjects 3 6 rankings), while Panel B presents data partitioned by participantsfor both Parts 1 and 3. The pooled data show that roughly 3 of every 4 Part 1rankings strictly fit impatience (72.5% in Panel A). Similarly, the participant-specific data show that roughly two of every three participants strictly fitimpatience (63% in Panel B). Further, evidence for improvement is minimalin both the pooled and participant-specific data (12.3% in Panel A and 6% inPanel B). In Part 3, impatience also dominates improvement (70 versus 30%

338 MATSUMOTO, PEECHER, AND RICH

TABLE 1

Implied Signs of b for the High-Knowledge Participants in Experiment 1

Panel A: Part 1 data pooled across all participantsRanking according to strict-PV heuristic

Participants’ rankings 1 2 3 4 5 6

1 44 0 0 0 0 102 2 42 1 2 7 03 1 1 37 10 3 24 1 5 5 38 3 25 2 4 5 3 37 36 4 2 6 1 4 37

Panel B: Participant-level data from Parts 1 and 3Implications for b

Strict impatience Strict improvementPart of instrument (b , 0) (b . 0) Other

Part 1 34 3 1763% 6% 31%

Part 2 38 1670% 30% n/a

Note. In Panel A, data in each of the six columns and rows total n 5 54, for a population ofobservations totaling n 5 324. Numbers in bold denote impatience (235/324 5 72.5%); impatienceimplies b , 0. Numbers underlined denote improvement (40/324 5 12.3%); improvement impliesb . 0. In Panel B, data are aggregated at the participant level so that each row totals N 5 54.

of responses; see Panel B). The extent to which the Panel B participant-specificdata suggest that impatience dominates improvement is significantly greaterthan one would expect by chance for both Part 1 [X2(2) 5 26.78, p , .001] andPart 3 [X2(1) 5 8.96, p 5 .006]. And, interestingly, impatience prevails morefrequently here than in Loewenstein and Sicherman (1991), where impatienceaccounted for less than 30% of responses. Thus, at a minimum, our data allow usto reject the proposition that b . 0 for relatively high-PV-knowledge individualswhen they evaluate liquid outcome sequences.

EXPERIMENT 2

While Experiment 1 demonstrates that b , 0 for individuals who are rela-tively knowledgeable of PV concepts, it does not directly test whether the signof b differs with PV knowledge. Experiment 1 also does not explicitly testwhether differential PV knowledge is associated with differential weighting ofcertain attributes of outcome sequences. We designed Experiment 2 to addressthese issues.

EVALUATIONS OF OUTCOME SEQUENCES 339

Method

Participants. We recruited 85 higher PV-knowledge participants and 291lower PV-knowledge participants, or 376 participants in total, from two under-graduate accounting courses at the University of Illinois at Urbana–Champaign. Participants received nominal course credit for participating. Our“higher knowledge” participants were students in an advanced managerialaccounting course. These students were juniors and seniors, and they hadtaken between four and five other accounting classes, on average. In contrast,our “lower knowledge” participants were students in a second-semester intro-ductory accounting course. These students were almost exclusively sophomores,and they had taken one other accounting class. Due to course sequencing,about half of our “lower knowledge” participants were concurrent enrollees inan introductory finance course that focuses heavily on PV concepts. In ancillaryanalysis, we single out these participants, whom we would expect to behavemore like our higher PV-knowledge participants than the rest of our lowerknowledge participants.

Materials. The instrument featured two main parts followed by a question-naire devoted to demographic information (Appendix B contains excerpts fromthe Experiment 2 instrument). We used these two main parts to manipulatesequence liquidity within subjects at two levels (i.e., monetary versus nonmone-tary). We counterbalanced the presentation order. The liquid, monetary domainconsisted of cash-flow sequences that were similar to those used in Experiment1 [i.e., consistent with Loewenstein & Sicherman (1991)]. The illiquid, nonmon-etary domain consisted of restaurant sequences like those adopted byLoewenstein & Prelec (1993).2

Design. We manipulated two additional factors, between subjects, that varyin PV relevance. These factors were manipulated only within the monetarysequences. First, we manipulated domain at two levels (i.e., wages versus rent).We expect lower PV-knowledge individuals to assign greater importance to thisattribute. Specifically, wage levels often reflect mastery with a profession (cf.Loewenstein & Sicherman, 1991), and individuals seldom have the option tofront-end lifetime wages. In contrast, rental domains offer no synonym formastery and front-ending rent over a multiyear contract is common (e.g., auto-mobile leases). Consequently, in the absence of PV knowledge, individualsare expected to value improvement more in the wage domain than in therent domain.

Second, we manipulated interchangeability at two levels. We operationalized

2 Holding all else constant, more impatience is invoked by monetary than by nonmonetarysequences. Relative to our monetary sequences, however, our nonmonetary sequences featureshorter durations and smaller amounts. Since shorter durations and smaller amounts both invokeimpatience, we cannot here predict a main effect for liquidity (i.e., the monetary versus nonmonetarymanipulation). We made this design choice because it simultaneously facilitates direct comparisonswith our Experiment 1 and allows testing of our hypotheses, which concern a PV knowledge 3

liquidity interaction but not a liquidity main effect.

340 MATSUMOTO, PEECHER, AND RICH

higher and lower interchangeability by holding constant either total cash flowor total PV, respectively, across the six alternative sequences. According to PVtheory, cash flows in different periods should be weighted by different discountfactors and, thus, are not interchangeable. We effected the interchangeabilitymanipulation by including, at the bottom of graphs depicting each sequence,either “Total Cashflows 5 $150,000” or “Total Present Value 5 $106,800.”We expected this manipulation to seem more important to higher knowledgeparticipants and that they would be more impatient when total cash flowwas held constant. Viewed slightly differently, by holding total present-valueconstant, we provided an opportunity for higher PV-knowledge participants todemonstrate that they ascribe at least some value to improvement.3

To summarize, the design of Experiment 2 consists of four two-level indepen-dent variables, one of which we measured and three of which we manipulated.The measured variable is PV knowledge. The three manipulated variablesare liquidity, domain, and interchangeability. Liquidity is manipulated withinsubjects with sequences being either monetary or nonmonetary. Between sub-jects, domain is manipulated by using either wages or rent, and interchange-ability is manipulated by holding constant either total cash flow or presentvalue.

Results

Primary results As before, we coded the participants’ responses accordingto whether they suggested impatience (i.e., b , 0) or improvement (i.e., b .

0). A coding scheme categorized each participant’s monetary ranking as beingpredominantly consistent with either impatience or improvement. Specifically,we multiplied each participant’s row matrix of rankings of options 1 through6, R 5 (r1, r2, . . . , r6) by a column matrix ranking the options strictly accordingto PV 5 (pv1, pv2, . . . , pv6) 5 (1,2,3,4,5,6). The cross product (i.e., R ∗ PVT)for strict adherence to PV (improvement) is 91 (56). The midpoint of theserankings [i.e., (1,4,6,5,3,2) and (2,3,5,6,4,1)] produces products of 74 and 73,respectively. We chose 73.5 as a partition and code higher products as “impa-tience” and lower products as “improvement.” Use of other reasonable cutoffssuch as .78 [i.e., (5,3,1,2,4,6)] for impatient and ,69 [i.e., 6,4,2,1,3,5)] forimprovement do not affect our inferences because our data are bimodal, mani-festing heavily on the end points of the 56-to-91 distribution (only 26 of the376 participants’ responses fall between 67.5 and 79.5).

Each participant provided a response for the monetary sequence and for thenonmonetary sequence, with the order of presentation counterbalanced. Eachof these responses could comply with either impatience or improvement. So,each participant could respond in one of four ways: (1) value impatience forboth the monetary and nonmonetary sequences (i.e., always impatient); (2)

3 We note that if one holds PV constant across increasing and decreasing sequences, the firstterm of the Loewenstein and Prelec model (i.e., undiscounted utility of the individual outcomes)likely would differ across the alternative sequences as the total cash flow varies.

EVALUATIONS OF OUTCOME SEQUENCES 341

value impatience for the monetary sequence but improvement for the nonmone-tary sequence (i.e., impatient only for monetary); (3) value improvement forthe monetary sequence but impatience for the nonmonetary sequence (i.e.,impatient only for nonmonetary); and (4) value improvement for the monetaryand nonmonetary sequences (i.e., never impatient). Panels A and B of Table 2provide frequency and percentage data that summarize the responses of lowerand higher knowledge participants across these four profiles.

To test our hypotheses, we ran a repeated-measures Categorical Model (CAT-MOD) ANOVA (see Table 3A). Because the order of monetary and nonmonetarysequences does not interact with any of our independent variables and affectsnone of our inferences, we simplify presentation of our analyses by excluding

TABLE 2

Response Profile Frequencies and Percentages in Experiment 2

Experimental condition

Rent domain Wage domain

Cash flow PV Cash flow PV Columnconstant constant constant constant averages

Panel A: Response profile frequenciesLower knowledge participants

(1) Always impatient 23 21 18 13 75(2) Impatient only for monetary 14 9 17 7 47(3) Impatient only for nonmonetary 24 25 22 25 96(4) Never impatient 18 17 16 22 73

Row totals 79 72 73 67 291

Higher knowledge participants(1) Always impatient 8 11 10 3 32(2) Impatient only for monetary 6 5 4 2 17(3) Impatient only for nonmonetary 4 3 5 13 25(4) Never impatient 2 3 3 3 11

Row totals 20 22 22 21 85

Panel B: Response profile percentagesLower knowledge participants

(1) Always impatient 29 29 25 19 26(2) Impatient only for monetary 18 13 23 10 16(3) Impatient only for nonmonetary 30 35 30 37 33(4) Never impatient 23 24 22 33 25

Higher knowledge participants(1) Always impatient 40 50 45 14 38(2) Impatient only for monetary 30 23 18 10 20(3) Impatient only for nonmonetary 20 14 23 62 29(4) Never impatient 10 14 14 14 13

Note. In Panel B, percentage columns sum to 100% for lower and higher knowledge participants.

342 MATSUMOTO, PEECHER, AND RICH

TABLE 3A

Repeated-Measures Analysis of Variance for Experiment 2

Source Chi-squarea

Intercept 458.84**Knowledge (Lower vs Higher) 8.79**Domain (Rent vs Wages) 3.05Interchangeability (Total cash vs Present value) 1.68Liquidity (Monetary vs Nonmonetary) 10.77**Knowledge 3 Domain 0.13Knowledge 3 Interchangeability 0.07Domain 3 Interchangeability 2.68Knowledge 3 Liquidity 0.90Domain 3 Liquidity 5.33*Interchangeability 3 Liquidity 5.83*Knowledge 3 Domain 3 Liquidity 5.66*Knowledge 3 Interchangeability 3 Liquidity 0.35Knowledge 3 Domain 3 Interchangeability 0.49Domain 3 Interchangeability 3 Liquidity 3.13Knowledge 3 Domain 3 Interchangeability 3 Liquidity 1.26

a For each chi-square test df 5 1.* p , .05.** p , .005.

the order-related explanatory variables.4 Five effects are significant at conven-tional levels. Four of these five effects stem from a three-way (Knowledge 3

Domain 3 Liquidity) interaction, which subsumes the Domain 3 Liquidityinteraction as well as the Knowledge and Liquidity main effects. The remainingeffect is a two-way (Interchangeability 3 Liquidity) interaction. We first discussthe Knowledge 3 Domain 3 Liquidity interaction and then comment on theless complex Interchangeability 3 Liquidity interaction.

To investigate the Knowledge 3 Domain 3 Liquidity three-way interaction,we collapse the data across Interchangeability and again present responseprofiles (1) through (4) (see Table 3B). Table 3B also presents the percentageof participants who exhibited impatience for monetary sequences (5) by sum-ming the percentages in response profiles (1) and (2). Similarly, it sums thepercentages in response profiles (1) and (3) to yield the percentage of partici-pants who were impatient for nonmonetary sequences (6). Lines (5) and (6)provide the summary data for the Knowledge 3 Domain 3 Liquidity interac-tion. We next discuss the Knowledge 3 Domain 3 Liquidity interaction interms of the Domain and Liquidity main effects and the interaction thereof,as applicable, separately for lower and higher knowledge participants.

For lower knowledge participants, a significant Liquidity main effect obtains

4 While intuition might suggest that responding to monetary sequences would increase thedegree of impatience exhibited on nonmonetary sequences, whether monetary sequences werecompleted before or after nonmonetary sequences did not significantly affect the degree of impa-tience exhibited on nonmonetary sequences [X2(1) 5 3.24, p 5 .174].

EVALUATIONS OF OUTCOME SEQUENCES 343

TABLE 3B

Response Profiles Collapsed across Interchangeability for Experiment 2

Domain (percentages)

Rent Wage Both

Lower knowledge participants(1) Always impatient 29 22 26(2) Impatient only for monetary 15 17 16(3) Impatient only for nonmonetary 33 34 33(4) Never impatient 23 27 25

Totals 100 100 100

(5) Impatient on monetary 5 (1) 1 (2) 44 39 42(6) Impatient on nonmonetary 5 (1) 1 (3) 62 56 58

Higher knowledge participants(1) Always impatient 45 30 38(2) Impatient only for monetary 26 14 20(3) Impatient only for nonmonetary 17 42 29(4) Never impatient 12 14 13

Totals 100 100 100

(5) Impatient on monetary 5 (1) 1 (2) 71 44 57(6) Impatient on nonmonetary 5 (1) 1 (3) 62 72 66

[X2(1) 5 18.77, p , .001]. These participants were more impatient for nonmone-tary (58%) than for monetary sequences (42%). Neither the Domain main effectnor the Domain 3 Liquidity interaction affected their responses (lowestp 5 .175). Thus, as reported in Table 3B, their most popular response was“impatient only for nonmonetary” (about 33% of their responses), followed by“always impatient” (26%), “never impatient” (25%), and “impatient only formonetary” (16%).

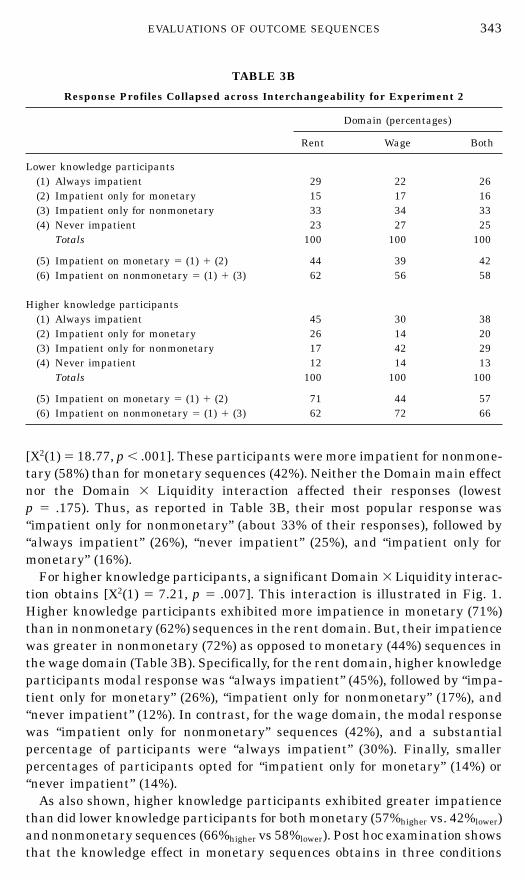

For higher knowledge participants, a significant Domain 3 Liquidity interac-tion obtains [X2(1) 5 7.21, p 5 .007]. This interaction is illustrated in Fig. 1.Higher knowledge participants exhibited more impatience in monetary (71%)than in nonmonetary (62%) sequences in the rent domain. But, their impatiencewas greater in nonmonetary (72%) as opposed to monetary (44%) sequences inthe wage domain (Table 3B). Specifically, for the rent domain, higher knowledgeparticipants modal response was “always impatient” (45%), followed by “impa-tient only for monetary” (26%), “impatient only for nonmonetary” (17%), and“never impatient” (12%). In contrast, for the wage domain, the modal responsewas “impatient only for nonmonetary” sequences (42%), and a substantialpercentage of participants were “always impatient” (30%). Finally, smallerpercentages of participants opted for “impatient only for monetary” (14%) or“never impatient” (14%).

As also shown, higher knowledge participants exhibited greater impatiencethan did lower knowledge participants for both monetary (57%higher vs. 42%lower)and nonmonetary sequences (66%higher vs 58%lower). Post hoc examination showsthat the knowledge effect in monetary sequences obtains in three conditions

344 MATSUMOTO, PEECHER, AND RICH

FIG. 1. Higher knowledge participants’ (Domain 3 Liquidity) interaction in Experiment 2.( ) never impatient; (m) impatient only for nonmonetary; (□) impatient only for monetary; ( )always impatient.

(69%higher versus 46%lower; p , .001 in the conditions of Rent/Cash flow, Rent/PV,and Wages/Cash flow). In these same conditions, knowledge does not influenceparticipants’ impatience in nonmonetary sequences ( p 5 .451). In the re-maining Wages/PV condition, however, the knowledge effect is essentially theopposite. Knowledge does not influence participants’ impatience for monetarysequences ( p 5 .545), but higher knowledge produces marginally greater impa-tience for nonmonetary sequences (75% vs 56%; p 5 .072).

We now discuss the remaining two-way (Interchangeability 3 Liquidity)interaction ( p 5 .016) without reference to any table. Whether Interchangeabil-ity was high (i.e., cash flow constant) or low (i.e., PV constant) did not influencethe extent to which participants exhibited impatience for nonmonetary se-quences (61%cash flow vs 65%PV ). The Interchangeability distinction mattered,though, for monetary sequences. Specifically, when PV was held constant, fewerparticipants exhibited impatience in the monetary sequences (57%cash flow vs42%PV ) without regard to their PV knowledge.

We expected some of these results, but not others. One, we expected higherknowledge to increase impatience for monetary sequences because the timevalue of money underlies PV concepts. We found higher PV knowledge to resultin greater impatience across the board, for both monetary and nonmonetarysequences. Similarly, we expected PV knowledge to moderate the difference inimpatience observed in monetary sequences when cash flow, as opposed to PV,was held constant. While our findings show higher knowledge participantswere more impatient in monetary sequences when total cash flow (67%) instead

EVALUATIONS OF OUTCOME SEQUENCES 345

of PV (49%) was held constant; the same was true for lower knowledge partici-pants (cash flow 60%; PV 36%). Finally, we had expected a significant domaineffect to obtain for lower knowledge participants, but we found domain tomatter more for our higher knowledge participants.

From a different perspective, it is notable that we observe significant knowl-edge effects even though our lower knowledge participants exhibit more impa-tience than has been exhibited by participants in previous research (see Table4). Specifically, for monetary sequences, our lower knowledge participants ex-hibit greater impatience than did participants in Loewenstein and Sicherman(1991). And, for nonmonetary sequences, they exhibit greater impatience thandid participants in Loewenstein and Prelec (1993). It is possible that theseinterstudy differences in impatience stem from both impatient persons self-selecting into business courses and to instruction about PV altering preferences.

Ancillary findings. Because it would be presumptuous to label any of theExperiment 2 participants as being naive with respect to PV concepts, oneshould limit how broadly they interpret the knowledge main effect and relatedinteractions. Persons may react differently to PV concepts depending on theirpredisposition to seek PV knowledge in the first place. That is, knowledge ofPV might reinforce preexisting tendencies to be impatient that exist in ourparticipants but not in the general population. While we leave direct investiga-tion of this possibility to future research, we examine here whether instructioninfluences the preferences of our lower PV-knowledge participants. We parti-tioned these participants into two groups based on whether they currentlywere enrolled in or had finished an introductory finance course that presents PVconcepts. We ran a categorical model, using the finance class as a partitioningvariable to proxy for PV knowledge. Suggestive that initial instruction in PVconcepts alters preferences, instruction in PV increases impatience in our lowerknowledge participants [55% versus 45%, X2(1) 5 6.13, p 5 .013].

TABLE 4

Comparison of Experiment 2 Results to Previous Psychology Research

Wages Rent

Panel A: Monetary sequencesExperiment 2

Higher knowledge 43% 72%Lower knowledge 38% 44%

Loewenstein and Sicherman (1991) 15% 26%

Panel B: Nonmonetary sequencesExperiment 2

Higher knowledge 67%Lower knowledge 59%

Loewenstein and Prelec (1993) 43%

346 MATSUMOTO, PEECHER, AND RICH

EXPERIMENT 3

Experiment 2 suggests that individuals who possess relatively high PVknowledge value impatience more than do those with relatively low PV knowl-edge. In Experiment 2, individuals who value improvement when cash flowswere held constant act as if they willingly sacrifice PV in order to gain improve-ment. In Experiment 3, we make PV trade-offs more salient by informingparticipants whether the PV of outcome sequences increase or decrease acrossoptions 1 through 6. Consequently, in Experiment 3, we explicitly (1) distinguishimpatience from PV and (2) investigate whether PV-knowledgeable people con-sciously sacrifice PV because of impatience or desires for improvement.

Method

Participants. Fifty undergraduate accounting majors at the University ofConnecticut participated in exchange for nominal course credit. Over 90% ofthe students were within 1 month of graduating. They had earned an average(range) of 25 (15 to 34) h of accounting credit at a time when 24 h of account-ing credit was required in order to take the Uniform CPA Examination inConnecticut.

Materials. The instrument employed three primary parts followed by collec-tion of demographic information. Each of the three parts asked participantsto rank order six outcome sequences in the wage domain. All three partsincluded bar graphs of the different wage sequences, just as in Experiments1 and 2. We manipulated one independent variable, PV, within subjects atthree levels by varying the discount rate. In a control condition, the outcomeshave identical PV. In a second condition, we disentangle PV from impatienceby having PV increase when going from option 1 ($112,400) to option 6($113,940). For example, participants who prefer option 1 the most are impa-tient, but they sacrifice PV. Finally, in a third condition, we disentangle PVfrom improvement by having PV decrease from option 1 ($103,660) to option6 ($102,660). In this case, participants who prefer, for example, option 6 valueimprovement but sacrifice PV. Panel A of Table 5 summarizes the PV amountsused in all three conditions of Experiment 3.

Results. As in Experiment 2, we multiplied each participant’s row matrixof rankings of options 1 through 6, R 5 (r1, r2, . . . , r6) by a column matrixranking the options strictly according to impatience, I 5 (1,2,3,4,5,6). All indi-viduals whose product was above 73.5 in the control condition were coded as“impatient,” while individuals whose product was below 73.5 were coded as“improvement.” As before, the results are not sensitive to changes in the cutoff.

Panel B of Table 5 shows that in the PV-constant (control) condition, 14participants valued impatience (m 5 88.50; maximum possible of 91) and 36valued improvement (m 5 59.67; minimum possible of 56). Of the 36 partici-pants who valued improvement in the control condition, only six switched toimpatience in order to avoid sacrificing PV in condition 3. Conversely, 30 of

EVALUATIONS OF OUTCOME SEQUENCES 347

TABLE 5

Present Values in and Results of Experiment 3

Panel A: Present values presented to participants

Condition Option 1 Option 2 Option 3 Option 4 Option 5 Option 6

PV Constant (Control) $108,400 $108,400 $108,400 $108,400 $108,400 $108,400PV Improving $112,940 $113,370 $113,550 $113,620 $113,880 $113,940PV Declining $103,660 $103,240 $103,060 $102,990 $102,740 $102,660

Panel B: ResultsPreference

Impatience Improvement Total

PV Constant (Control) 14 36 50Sacrifice PV and maintain preferenceRevealed in control condition 11 30 41Avoid sacrificing PV and switch fromPreference revealed in control condition 3 6 9

the 36 participants who valued improvement in the control condition willinglysacrificed PV to secure improvement. The number of participants who willinglysacrificed PV is greater than one would expect by chance ( p , .001). Becauseknowledgeable participants forgo at least some PV to obtain improvement, PVunlikely is determinative in their evaluations of outcome sequences. Last, ofthe 14 individuals who valued impatience in the control condition, 11 continuedto be impatient in condition 2. In this condition impatience resulted in a salientPV loss ( p , .001). Revealed preferences that imply impatience is sought atthe cost of forgone PV suggests a need to distinguish between impatience andPV—even for people knowledgeable of the time value of money.

CONCLUSIONS

Our experimental evidence suggests that evaluators who are relativelyknowledgeable about present value (PV) tend to favor being impatient overseeking improvement when evaluating monetary and nonmonetary sequences.Evidence also suggests that the acquisition of PV knowledge significantly in-creases participants’ tendency to exhibit impatience on such sequences. Theincreased tendency to exhibit impatience due to PV knowledge does appearto have some bounds, however. For some types of monetary sequences, PVknowledge does not increase impatience (e.g., sequences of wages where PV isheld constant). Finally, the experimental evidence indicates that impatiencedoes not necessarily coincide with a desire to maximize PV in that some knowl-edgeable participants exhibited impatience while willingly sacrificing PV.

Our findings relate back to our three motives for conducting the study. Busi-ness researchers will be comforted by our findings because PV considerations

348 MATSUMOTO, PEECHER, AND RICH

appear central (but not determinative) when knowledgeable individuals evalu-ate outcome sequences. Our findings nevertheless add credence to psychologymodels and findings that emphasize that people value impatience and improve-ment (as opposed to PV, per se). As one example, over 40% of our knowledgeableparticipants valued improvement for monetary sequences in Experiment 2. Anda significant number of knowledgeable participants even sacrificed a modestamount of PV in order to obtain improvement in Experiment 3. Future researchcan investigate the conditions under which knowledgeable individuals sacrificeeven greater magnitudes of PV to secure improvement.

Future research also can investigate how knowledge and expectations inter-act in the outcome-sequence evaluation process (e.g., Chapman, 1996). Knowl-edge of PV concepts may affect individuals’ normative beliefs about what se-quences are appropriate to choose. Normative beliefs may significantlyinfluence individuals’ stated objectives (e.g., if one believes they ought to calcu-late the amount of salary that they should withhold for federal income taxpurposes, they may state that as their objective). Descriptive beliefs, or expecta-tions about “real-world” behaviors, may significantly influence actual decisions.In other words, descriptive beliefs might overcome normative beliefs, causingpeople to act inconsistently with their stated preferences (e.g., if one believesthat others do not calculate withholding correctly so as to receive larger incometax refunds, they copy others’ expected behavior).

APPENDIX A

Excerpts from the Experiment 1 Instrument

Excerpts from Part 1

Stock Domain. Imagine that you have to rank six investments of 10,000shares of common stock. Assume the investments differ only in terms of thesequence of cash dividends they will pay—the total dollar amount of dividendsreceived will be the same for each investment. Assume further that the dividendsequences shown below have no uncertainty—they will definitely occur asillustrated. Finally, assume that both the purchase price today and the sellingprice at the end of year six will be the same for each investment option. Ignoringany possible tax effects, please rank investment options below from 1 (i.e., theinvestment you most prefer) to 6 (i.e., the investment you least prefer).

Rent domain. Imagine that you are not employed now and your only sourceof income is a small apartment building that you recently inherited. You haveagreed to lease the building to a real estate broker for the next six years. Thebroker has offered you six different payment options. Assume that the incomefrom the apartment, which totals the same in each case, will be your onlysource of income during the next six years. Ignoring any tax effects, pleaserank the following options from 1 (i.e., the option you most prefer) to 6 (i.e.,the option you least prefer).

EVALUATIONS OF OUTCOME SEQUENCES 349

Excerpts from Part 3

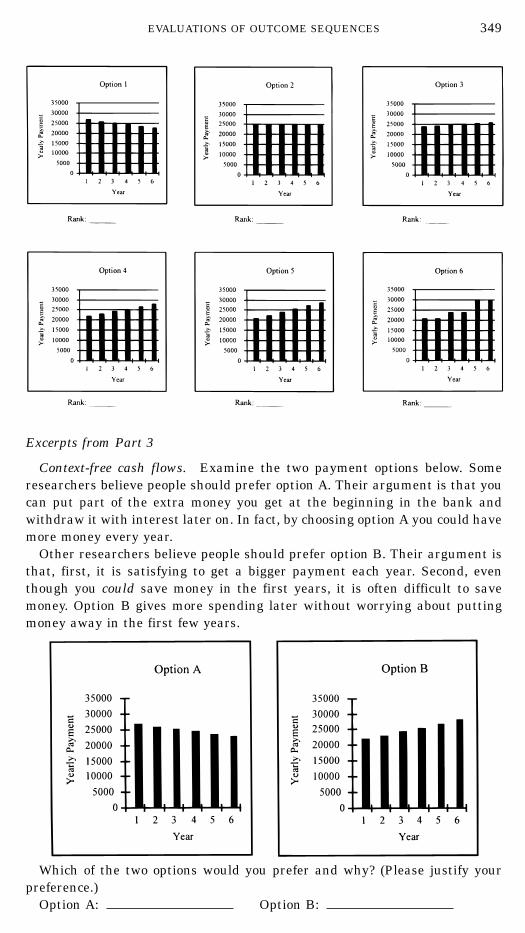

Context-free cash flows. Examine the two payment options below. Someresearchers believe people should prefer option A. Their argument is that youcan put part of the extra money you get at the beginning in the bank andwithdraw it with interest later on. In fact, by choosing option A you could havemore money every year.

Other researchers believe people should prefer option B. Their argument isthat, first, it is satisfying to get a bigger payment each year. Second, eventhough you could save money in the first years, it is often difficult to savemoney. Option B gives more spending later without worrying about puttingmoney away in the first few years.

Which of the two options would you prefer and why? (Please justify yourpreference.)

Option A: Option B:

350 MATSUMOTO, PEECHER, AND RICH

Wages until retirement. Assume it were possible to perfectly forecast yourtotal “wages until retirement” and that you had the following choice. You couldreceive all your “wages until retirement” in a lump sum today, or you couldallocate whatever portions of your “wages until retirement” to your variousworking years.

Some researchers think that given such a hypothetical circumstance youshould prefer the lump sum. Their argument is that you can put the lump suminto a bank and/or other investments and withdraw it with interest later on.In fact, by choosing the lump sum option, you could have more money every year.

Other researchers think that given such a hypothetical circumstance youshould allocate your wages over the working years of your life, so that yourwages are greater in later years than in early years. Their argument is that,first, it is satisfying to get bigger wages each year. Second, even though youcould save and/or the money from a lump sum, it is often difficult to save and/or invest money. Allocating some of your wages to your later years gives morespending later without worrying about saving and/or investing an initiallump sum.

Which of these two options would you prefer and why? (Please justify yourpreference below).

Lump Sum: Some Other Allocation:

APPENDIX B

Excerpts From the Experiment 2 Instrument

Monetary Context—Wage Domain

Imagine that you are not working now, but have been offered a six year job,and are presented with a choice between different payment options. You arecertain that you will work at this job for the next six years. The wages, whichtotal $150,000 in each option, will be your only source of income over the nextsix years. Finally, the payment option you select will not affect your futurejobs or income from those jobs in any way. Ignoring any possible tax effects,please rank the payment options below from 1 (i.e., the option you most prefer)to 6 (i.e., the option you least prefer).

Nonmonetary Context

Ignore personal scheduling considerations (e.g., your preexisting plans) whenresponding to the following questions.

Which would you prefer if both were free? (mark only one).A. Dinner for two at a fancy French restaurant.B. Dinner for two at a local Greek restaurant.

If you prefer the French restaurant, which of the following would you prefer?(mark only one).

C. Dinner for two at a fancy French restaurant on a Friday in 1 month.D. Dinner for two at a fancy French restaurant on a Friday in 2

months.

EVALUATIONS OF OUTCOME SEQUENCES 351

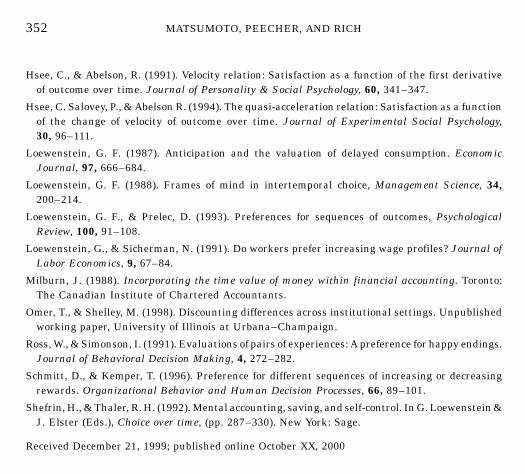

Which would you prefer? (mark only one).E. Dinner for two the fancy French restaurant on Friday in 1 month

and dinner for two at the local Greek restaurant on Friday in 2 months.F. Dinner for two at the local Greek restaurant on Friday in 1 month

and dinner for two at the fancy French restaurant on Friday in 2 months.

REFERENCES

Barth, M., Elliott, J., & Finn, M. (1999). Market rewards associated with patterns of increasingearnings. Journal of Accounting Research, 37, 387–413.

Benzion, U., Rapoport, A., & Yagil, J. (1989). Discount rates inferred from decisions: An experimen-tal study. Management Science, 35, 270–284.

Chapman, G. (1996). Expectations and preferences for sequences of health and money. Organiza-tional Behavior and Human Decision Processes, 67, 59–75.

Chi, M., Feltovich, P., & Glaser, R. (1981). Categorization and representation of physics problemsby experts and novices. Cognitive Science, 5, 121–152.

Fredrickson, B., & Kahneman, D. (1993). Duration neglect in retrospective evaluations of affectiveepisodes. Journal of Personality and Social Psychology, 65, 45–55.

352 MATSUMOTO, PEECHER, AND RICH

Hsee, C., & Abelson, R. (1991). Velocity relation: Satisfaction as a function of the first derivativeof outcome over time. Journal of Personality & Social Psychology, 60, 341–347.

Hsee, C. Salovey, P., & Abelson R. (1994). The quasi-acceleration relation: Satisfaction as a functionof the change of velocity of outcome over time. Journal of Experimental Social Psychology,30, 96–111.

Loewenstein, G. F. (1987). Anticipation and the valuation of delayed consumption. EconomicJournal, 97, 666–684.

Loewenstein, G. F. (1988). Frames of mind in intertemporal choice, Management Science, 34,200–214.

Loewenstein, G. F., & Prelec, D. (1993). Preferences for sequences of outcomes, PsychologicalReview, 100, 91–108.

Loewenstein, G., & Sicherman, N. (1991). Do workers prefer increasing wage profiles? Journal ofLabor Economics, 9, 67–84.

Milburn, J. (1988). Incorporating the time value of money within financial accounting. Toronto:The Canadian Institute of Chartered Accountants.

Omer, T., & Shelley, M. (1998). Discounting differences across institutional settings. Unpublishedworking paper, University of Illinois at Urbana–Champaign.

Ross, W., & Simonson, I. (1991). Evaluations of pairs of experiences: A preference for happy endings.Journal of Behavioral Decision Making, 4, 272–282.

Schmitt, D., & Kemper, T. (1996). Preference for different sequences of increasing or decreasingrewards. Organizational Behavior and Human Decision Processes, 66, 89–101.

Shefrin, H., & Thaler, R. H. (1992). Mental accounting, saving, and self-control. In G. Loewenstein &J. Elster (Eds.), Choice over time, (pp. 287–330). New York: Sage.

Received December 21, 1999; published online October XX, 2000