Equinox - HotCopper

88

Into Production Equinox Annual Report 2008

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of Equinox - HotCopper

Equinox Minerals Limited

Equinox Canada155 University Avenue, Toronto Ontario, Canada M5H 3B7Telephone: +1 (416) 865 3393 Facsimile: +1 (416) 865 3394

Equinox Australia50 Kings Park Road, West Perth, Western Australia, Australia 6005Telephone: +61 (8) 9322 3318 Facsimile: +61 (8) 9324 1195

[email protected] www.equinoxminerals.com

Eq

uin

ox Min

erals Lim

ited A

nn

ual R

eport 2008

Into Production

Equinox Annual Report 2008

Equinox Minerals Limited Tenement Schedule

PROJECTS TENEMENTS EQUINOX INTEREST JOINT VENTURE PARTNER

ZAMBIA

Lumwana LML49 100% Mwombezhi Dome PLLS148Kabompo PLLS027 Kitwe PLLS026 100%# * Mwekere PLLS176 Kasanka PLLS081 Mutapanda To be advised 100% AUSTRALIA Curnamona Craton Ethiudna EL3714 100% Uranium One Australia Pty Ltd

EL = Exploration Licence; PLLS = Prospecting Licence; LML = Large scale Mining Lease.

# Anglo American have a 70% clawback option should a mineral resource > 3 million tonnes copper metal (or equivalent) be discovered.

* Prospecting Licences are in the process of being converted to Retention Licences, final approval is pending.

Equinox Minerals Limited Offices

Canada155 University Avenue, Toronto Ontario, Canada M5H 3B7Telephone: +1 (416) 865 3393 Facsimile: +1 (416) 865 3394

Australia50 Kings Park Road, West Perth, Western Australia, Australia 6005Telephone: +61 (8) 9322 3318 Facsimile: +61 (8) 9324 1195 Email: [email protected] Website: www.equinoxminerals.com

Stock SymbolEQN – Toronto Stock Exchange, Australian Stock Exchange

AuditorsPricewaterhouseCoopers LLPSuite 3000, Box 82, Royal Trust Tower, TD Centre Toronto Ontario, Canada M5K 1G8

Transfer AgentsCIBC Mellon Trust Company199 Bay Street, Commercial Court West, Securities Level Toronto Ontario, Canada M5L 1G9Telephone: +1 416 643 5500

Advanced Share Registry Services150 Stirling Highway, Nedlands, Perth, Western Australia, 6009, AustraliaTelephone: +61 (8) 9389 8033

Corporate Directory

Directors and Officers

Peter Tomsett Chairman

Craig Williams President & CEO

David McAusland Director

Harry Michael Director, Vice President Operations & COO

Dave Mosher Director

Jim Pantelidis Director

Brian Penny Director

Michael Klessens Vice President Finance CFO & Company Secretary

Kevin van Niekerk Vice President Investor Relations & Corporate

Development

Robert Rigo Vice President Project Development

Ralph Gibson Vice President Project Finance

Contents

Corporate Profile 1Equinox at a Glance 2Chairman’s Letter to Shareholders 5President/CEO’s Letter to Shareholders 8 Lumwana Project Summary 10Equinox Exploration 17Corporate Responsibility 19The Equinox Team 20MD&A 22Financial Statements & Notes 39Statement of Corporate Governance 74

Cautionary Language and Forward Looking Statements

This document contains ‘forward-looking statements’ and ‘forward-looking information’, which may include, but is not limited to, statements with respect to the future financial or operating performances of Equinox, its subsidiaries and their respective projects, the future price of copper and uranium, the estimation of mineral reserves and resources, the realization of mineral reserve estimates, the timing and amount of estimated future production, estimated costs of future production, the sale of future production, capital, operating and exploration expenditures, the costs of Equinox’s hedging policy, costs and timing of future exploration, requirements for additional capital, government regulation of exploration, development and mining operations, environmental risks, reclamation and rehabilitation expenses, title disputes or claims, and limitations of insurance coverage. Often, but not always, forward-looking information can be identified by the use of words such as ‘plans’, ‘expects’, ‘is expected’, ‘is expecting’, ‘budget’, ‘scheduled’, ‘estimates’, ‘forecasts’, ‘intends’, ‘anticipates’, or ‘believes’, or variations (including negative variations) of such words and phrases, or state that certain actions, events or results ‘may’, ‘could’, ‘would’, ‘might’, or ‘will’ be taken, occur or be achieved. The purpose of forward-looking information is to provide the reader with information about management’s expectations and plans for the Company. Readers are cautioned that forward-looking information involves known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of Equinox and/or its subsidiaries to be materially different from any future results, performance or achievements expressed or implied by the forward-looking information. Such factors include, among others, those factors discussed in the section entitled ‘Risk Factors’ in the Company’s annual information form, which is available at www.SEDAR.com. Although Equinox has attempted to identify statements containing important factors that could cause actual actions, events or results to differ materially from those described in forward-looking information, there may be other factors that cause actions, events or results to differ from those anticipated, estimated or intended. Forward-looking information contained herein is made as of the date of this document based on the opinions and estimates of management on the date statements containing such forward looking information are made, and Equinox disclaims any obligation to update any forward-looking information, whether as a result of new information, estimates or opinions, future events or results or otherwise. There can be no assurance that forward-looking information will prove to be accurate, as actual results and future events could differ materially from those anticipated in such information. Accordingly, readers should not place undue reliance on forward looking information.

The Company has included a non-GAAP performance measure in this news release: ‘cash (C1) operating cost’. The Company believes that, in addition to conventional measures prepared in accordance with GAAP, certain investors use this information to evaluate the Company. It is intended to provide additional information and should not be considered in isolation or as a substitute for measures of performance prepared with GAAP. Cash (C1) operating cost is a common performance measure in the copper industry and is prepared and presented herein on a basis consistent with the industry standard Brook Hunt definitions. Cash (C1) operating cost includes direct cash costs, minesite and realization costs through to refined metal.

Scientific and technical information contained in this press release has been prepared under the supervision of Robert Rigo, Vice President, Project Development of Equinox who is a ‘Qualified Person’ in accordance with National Instrument 43-101 - Standards of Disclosure for Mineral Projects.Readers are cautioned not to rely solely on the summary of information contained in this release, but should read the Amended Technical Report which is posted on Equinox’s website (www.equinoxminerals.com) and filed on SEDAR (www.sedar.com) and any future amendments to such report. Readers are also directed to the cautionary notices and disclaimers contained therein. All currency in this release is U.S. dollars unless otherwise stated.

Readers are cautioned not to rely solely on the summary of such information contained in this release, but should read the Amended Technical Report which is posted on Equinox’s website www.equinoxminerals.com and filed on SEDAR www.sedar.com and any future amendments to such report. Readers are also directed to the cautionary notices and disclaimers contained herein. All currency in this release is U.S. dollars unless otherwise stated.

In this report ‘Equinox’, ‘the Company’ and/or ‘the Corporation’ refer to Equinox Minerals Limited.

Lumwana, owned 100% by Equinox, is situated 220 km northwest of the world-renowned Zambian Copperbelt. With proven and probable reserves totaling 321 million tonnes of ore grading at 0.73% copper, Lumwana represents the single largest new copper mine coming into production anywhere in the world in 2008/2009*.

At full capacity, mine production rates will process in excess of 20 million tonnes of ore per year mined at a strip ratio of 4.2:1. Lumwana ore, which is predominantly sulphide, is treated through a large, yet conventional plant which produces a sulphide concentrate which is being sold to offtakers.

Concentrate production commenced in December 2008 and ramp-up is expected to be completed in mid-2009. At this time, Equinox will operate one of the largest copper mines in Africa with expected production in 2009 of 170,000 tonnes of copper in concentrate at an average cash cost of $1.15 per pound of copper for the 2009 year.

The project has significant potential for organic expansion and the Company believes that Lumwana represents the cornerstone for its objective to build a new mining house.

In 2009 Equinox will be one of the world’s top 20 copper producing companies.

Corporate ProfileEquinox Minerals Limited (EQN on TSX and ASX) is an international mine development and exploration company operating the flagship Lumwana copper mine in Zambia.

1

2008 Highlights

2

n Commissioning of the Lumwana Copper Project commenced in April 2008 with the electrification of the main Lumwana 33kV substation and subsequent reticulation of power around the site;

n Equinox secured the long-term land title to approximately 35 thousand hectares (350 square kilometres) of township and mine operating areas at the Company’s Lumwana mining license;

n In June the Lumwana SAG mill was fully energized and rotated by the engineering contractor and commissioning of the primary crusher also commenced;

n A fire on July 7, 2008, caused damage to the main transformer and adjacent substation causing a four and a half month delay to project completion and handover;

n In September, crushing of material at the primary crusher commenced with the 4.5 kilometre conveying circuit commissioned, transporting crushed material to the fine ore stockpile at the copper concentrator;

n In October 2008, Equinox secured an additional US$80.0 million project debt facility to enable the Company to meet additional working capital requirements resulting from the transformer fire and subsequent delayed startup;

n The large scale Hitachi EX5500 electric face shovels were successfully commissioned and put into production commencing in October 2008;

n Equinox accepted handover of the Lumwana processing facilities and associate infrastructure from the engineering contractor in November 2008;

n Equinox produced its first copper concentrate at Lumwana during December 2008. Wet commissioning of the final stage of the process plant filter-press commenced;

n First commercial quantities of copper concentrate were made to off-take customers during December 2008;

n The Lumwana Property Development Company, a special purpose vehicle established for the new Lumwana town, secured an additional US$25 million debt facility with FMO to cover infrastructure costs; and

n Lumwana achieved an excellent health and safety record, with over 5 million man hours without a lost time injury and producing a lost-time-injury frequency rate of 0.3 (per 200 thousand hours), an achievement management believes to be an outstanding result.

The Company estimates copper production for 2009 will total 170,000 tonnes (375 million pounds) of copper metal in concentrates at an average cash operating (C1) cost of US$1.15 per pound. As can be expected, unit production costs are anticipated to be higher in the early part of 2009 until steady state production activities are reached, which is expected by mid-2009 at which time Equinox will be operating one of the largest copper mines in Africa.

Lumwana Uranium ProjectIn April 2008, Equinox published the Lumwana uranium feasibility study (‘UFS’) on the design of a treatment facility for the uranium ore stockpile that will result from the selective mining of the discrete, high grade uranium zones within the Lumwana copper orebodies presently being mined. This facility would cost about $200 million and could recover approximately 2 million pounds of uranium oxide (U3O8) and 12,800 tonnes of copper concentrate per year.

ExplorationExploration drilling at Kanga proved successful and extended the Malundwe deposit to the south with an additional inferred resource of 78 million tones of 0.76% copper. Whilst this additional resource is yet to be optimized within the Lumwana pit designs, such an extension may materially impact the economics of Lumwana with higher grade Kanga ore possibly being able to displace lower grade Chimiwungo ore in the mine development schedule.

Further exploration opportunities are recognized both near Lumwana and elsewhere on the Company’s extensive regional property holdings in Zambia.

Equinox CorporateEquinox shareholders elected two additional independent directors, Mr. David McAusland and Mr. Jim Pantelidis, to serve on the Board of Directors of the Company.

ObjectivesLumwana holds significant potential for organic expansion and the Company expects the mine will provide a solid foundation from which to build a new Mining House:

n The Company estimates copper production for 2009 will total 170,000 tonnes (375 million pounds) of copper metal in concentrates at an average cash operating (C1) cost of US$1.15 per pound for the 2009 year;

n Steady state production activities are expected to be reached by mid-2009 at which time Equinox will be operating one of the largest copper mines in Africa;

n To increase process plant design capacity throughput by 20% from 20 million tonnes per year to 24 million tonnes per year increasing Lumwana mine copper output;

n Complete a feasibility study for the medium-term objective of expanding Lumwana process plant throughput further (stage two expansion) to between 30 to 35 million tonnes per year:

n Develop a uranium facility to process the uranium ore stockpiles, subject to favorable financing and uranium market conditions;

n Continue exploration activities close to Lumwana and on regional exploration properties; and

n Actively monitor and evaluate new projects and corporate opportunities.

3

Chairman’s Letter to Shareholders

4

The year has been dominated by the global financial crisis and has been a real roller coaster ride, but for Equinox at least has ended on an upward path.

With hindsight, the first half of the year was relatively uneventful, as we progressed site construction works at Lumwana towards our planned mid year commissioning. However, in early July, just as the site crews were about to commence feeding ore into the mills, we suffered a severe fire, which destroyed a major transformer and important electrical control systems. Our site personnel and the construction contractor performed an outstanding recovery effort, and allowed us to start up in late November, having sourced replacement components in very fast time. While the 5 month delay was unfortunate, it has not significantly diminished the long term value of the project, given it’s 37 year mine life.

The project is now complete, at a cost of $814 million, slightly over budget due to the extra costs associated with the fire. Some of these costs were mitigated by insurance claims and drawing on the construction contractor’s Liquidated Damages.

Since then, the plant has performed well, and we fully expect to be consistently producing at a rate above the nameplate capacity of 20 million tonnes per annum as 2009 progresses.

The completion of such a large and complex plant in a logistically difficult environment has been an outstanding achievement by all those associated with the project. We were particularly pleased that the project was completed with an excellent safety record, recording over 5 million hours worked without a lost time injury.

Of course, even being in a remote part of Zambia, we have not been immune to the dramatic changes in the financial world during 2008. The fire and subsequent rectification work led to increased costs, and we were very pleased to be able to secure an $80 million extension to our debt facility in October, at a time when the credit markets had virtually dried up. This is a tribute to the quality of our project, and the level of support from our banking syndicate.

Another major change has been the dramatic fall in all commodity prices, and copper has not been immune to the global recession. The copper price fell very quickly in the second half of 2008, from over $3.00/lb, to it’s level in February 2009 of around $1.50/lb. Obviously we would have preferred to start production into a better market, but we will still be able to generate strong cashflow, and service our debt at these levels.

Our prudent copper hedging program has also served us well, and at year end our hedge book had a positive mark to market value of $243 million. However, we must remember that copper is a cyclic commodity, and one of the great advantages of having such a long mine life is that it will allow us to take advantage of higher prices through future peaks in

the cycle. Copper continues to have the best supply-demand fundamentals of all the base metals.

Falling uranium prices and the difficult financing environment also caused us to put our uranium project on hold. The uranium ore falls within the copper pit, so we are currently stockpiling uranium ore in the expectation that conditions will improve, and the project will go ahead at some future time.

There were also many changes within Zambia, following the tragic death of the country’s President Mwanawasa. We were very pleased to see the peaceful transition of power to his deputy. President Banda, like his predecessor, is a great supporter of the Lumwana project, and we look forward to working with him and his administration. Changes have already been made. The government recognized that the tax changes made last year were a serious disincentive to investment, and many of the more onerous provisions have been removed. Furthermore, we have always maintained that we have a binding Development Agreement with the government, and we have been pleased to see that the tax provisions contained in that agreement have been largely honoured, though the mechanism of Statutory Instruments.

The Zambian Government has clearly stated that it expects mining companies to be good corporate citizens, and we believe that Equinox continues to be at the forefront of that process.

We continue to contribute to job creation, town and infrastructure development including schools and medical clinics, and helping develop small businesses, such as craft, textiles, agriculture and fisheries. We look forward to continuing government support, and will play our part in making Zambia a better place for it’s citizens to live.

As foreshadowed last year, we have added significant strength to your Board of Directors, with the addition of David McAusland and Jim Pantelidis. They both bring many years of varied, international business experience to the table, and I believe we now have the right board to take us thought the challenges of the years ahead.

I would like to thanks all those people in Zambia who have been working tirelessly to bring this great project to fruition. With the help of Craig and his outstanding management team, I am sure they will make 2009, our first year of copper production, a safe and memorable one.

Peter TomsettChairman of the Board

5

Dear ShareholderWhen I wrote to you this time last year, little did any of us know what a tumultuous time was in store for us.

6

Lumwana

Lumwana –Africa’s largest copper producing mine. The Project is expected to process 20 million tonnes per year of ore over an expected lifespan of 37 years.

7

8

President/CEO’s Letter to Shareholders

8

9

Our driving focus for the last nine and a half years has been bringing Lumwana into production – this goal was finally achieved in December 2008 and is a tribute to the determination, skill and perseverance of the Equinox team.

This goal was achieved through overcoming the numerous challenges thrown in our path – the raising of over US$800 million to finance the project through the international debt and equity markets; the technical challenges of designing and ultimately building a project of the massive scale of Lumwana, in a remote region of Zambia; the fight for recognition of Lumwana as a world class project and Equinox as a significant player in the international copper industry.

Of course the global financial crisis has had a severe impact on the Equinox share price and the copper price that underpins Lumwana revenue generation. Whilst we are fortunate that we financed and built the Lumwana Project during better times in the resources industry, today’s copper prices do not provide the ideal environment for commissioning such a large copper mine. Without the 5 month delay resulting from the transformer fire in July, we would have been commissioning at copper prices of US$3.00 per pound of copper, rather than US$1.40/lb in January 2009. Nevertheless, Lumwana has been built for the long term – with a 37 year mine life, the current downturn in the metals market is the first, but not the last, low point in the commodities cycle that Lumwana will experience. This project has been designed for the long term, to survive the lows of the cycle and profit from the highs.

Lumwana Project ramp up is progressing well, with the processing plant showing the capacity to operate at nameplate design of 20 million tonnes per year (20 Mtpa) and the potential to exceed this throughput. We expect that ramp up will be completed by mid-2009. The challenge at present is for mine productivity to match processing throughput. Ramping up mine production in the middle of the Zambian wet season has presented a considerable challenge, but as the rains subside into Q2-09 we expect that mine productivity will increase towards matching mill throughput.

So what of the year ahead? Our focus is well and truly on the ramping up of Lumwana to full production by mid-2009. The cash flow generation will facilitate debt payback, strengthen our financial position and enhance future opportunities. We have mid-term objectives to further increase plant throughput by optimisation and de-bottlenecking, and an increase in mine production – our target is reaching a 24 Mtpa throughput rate in 2010.With the very large resource and long mine life at Lumwana, we believe that there is the potential for further expansion over a time line of 4 to 5 years, up to a stage two production target of about 30 Mtpa, although this will require a feasibility study to determine what will be required.

A further opportunity for organic expansion is the building of a plant to treat the uranium-rich ore that is already being mined and stockpiled from discrete areas of the copper pit. While we have put the construction of this plant on hold until financing and uranium market conditions improve, it is likely that this opportunity could ultimately provide an important by-product for Lumwana.

Equinox holds a large and highly prospective area surrounding Lumwana and has already made discoveries at Kanga and Chimiwungo North. There is clearly substantial exploration potential both close to Lumwana and further afield in our exploration properties elsewhere in Zambia. The Company intends to maintain an active exploration presence in the country.

Lastly, the flip-side to the difficult period in the metals market is one of opportunity for those companies with the ability to survive the downturn. As we come out of this trough, numerous acquisition opportunities are presenting that could offer Equinox with its next level of growth. Lumwana is our cornerstone project that should provide the cash generation to facilitate both organic expansion and company diversification through acquisition, building Equinox into an important next generation mid-tier producer.

Craig R. WilliamsPresident and Chief Executive Officer

9

Dear Shareholder2008 has been a year of challenges and achievements for Equinox.

Lumwana is now a major copper mine which will establish Equinox in 2009 as one of the World’s Top 20 copper producing companies.

Lumwana

10

Lumwana Summary

Situated 220 km northwest of the Zambian Copperbelt, Lumwana hosts a proven and probable mineral reserve of 321 million tonnes of ore grading 0.73% copper. Lumwana is now a major copper mine which will establish Equinox in 2009 as one of the World’s Top 20 copper producing companies. At full capacity, mine production rates will process in excess of 20 million tonnes of ore per year, mined at a strip ratio of 4.2:1. Lumwana ore, which is predominantly sulphide, is treated through a large, yet conventional plant completed in November 2008, producing a sulphide concentrate for sale to offtakers.

Mine commissioning and ramp-up is expected to be achieved by mid-2009 at which time Equinox will operate one of the largest copper mines in Africa, producing an average of 172,000 tonnes per year (or 380 million lbs per year) of copper in concentrate for the first six years of an expected 37 year mine life.

Project LocationLocated in the North Western Province of Zambia, 220 kilometres west of the Copperbelt and 65 kilometres west of the town of Solwezi, Lumwana is easily accessed by the T-5 Northwest Highway.

The Copperbelt, one of the world’s greatest concentrations of copper-cobalt deposits, has been a centre of commercial copper production for over 80 years.

Mining LicenseThe Lumwana Large Scale Mining License, LML-49, covers 1,355 square kilometres, and includes two major copper deposits, Malundwe and Chimiwungo. Equinox owns 100% of LML-49.

InfrastructureThe recently refurbished T-5 Northwest Highway, which links the Lumwana region, Solwezi and the Copperbelt, passes within 3 kilometres of the project.

ZESCO, the Zambian national power generation and distribution company, commissioned the 330kV power line from Solwezi to the Lumwana sub-station. Equinox has a long-term (15 year) power supply off-take agreement with ZESCO.

Mine PlanThe Company’s optimized mine plan (published in the June 2008 Technical Report) is based on the ‘Development Case’ which contemplates a mining schedule that contains 45% Measured and Indicated Resources and 55% Inferred Resources to be mined over a 37 year mine life on the basis of processing 20 million tones per year of ore at an average strip ratio of 4.2:1.

The mine development of the Malundwe and Chimiwungo deposits, which are 7 kilometres apart, is by open-pit mining methods. The ore bodies are 95% sulphide (with only 5% oxide) and very consistent, so large scale bulk-mining methods are being employed utilizing equipment that includes a total of 27 x 240 tonne capacity diesel-electric drive hybrid

11

haulage trucks and 7 x 518 tonne diesel and electric loaders (excavators and face shovels). The mining fleet utilizes ‘trolley assist’ whereby the trucks switch from diesel operation to grid electricity as they make the run up the ramp from the pit to the ore and waste dumps. This trolley assist technology provides substantial fuel and operating cost savings for the Lumwana mining fleet.

Lumwana Construction and OperationsSulphide ore is being processed on-site by conventional crushing, grinding and flotation to produce copper concentrates that are being delivered to offtakers, predominantly to local Zambian smelters. Metallurgical test work has indicated recoveries of greater than 95% copper, producing average concentrate grades of 43.3% Cu for Malundwe and 29.5% Cu for Chimiwungo and initial commissioning production figures indicate that these specifications will be achievable. The flotation plant has a design capacity to treat at least 20 million tonnes per year of ore and in the first 6 year period, should produce in concentrate, 172,000 tonnes of copper metal per year (380 million lbs per year).

Equinox accepted handover of the Lumwana Copper Plant and other associated infrastructure from the engineering contractor in November 2008. Mine commissioning and ramp-up is underway and commercial concentrate deliveries have commenced. During the year the following activities, in chronological order, contributed to this significant milestone:

n Commissioning of the Lumwana Copper Project commenced in April 2008 with the electrification of the main Lumwana 33 kV substation and subsequent reticulation of power around the site;

n Equinox secured long-term land title to approximately 35 thousand hectares (350 square kilometres) of township and mine operating areas at the Company’s Lumwana mining license. In May 2008, this grant permitted the Company to manage and administer the Lumwana surface rights, in particular the planned Lumwana town sub-division, thus enabling the Company to deliver employee home ownership and other commercial developments within the township;

n In June the Lumwana SAG mill was fully energized and rotated by the engineering contractor using Siemens gearless mill drives and commissioning of the primary crusher also commenced;

n A fire on July 7, 2008 caused damage to a main

transformer and adjacent substation, causing a four and a half month delay to project completion and handover;

n In September, crushing of material at the primary crusher commenced with the 4.5 kilometre conveying circuit commissioned transporting crushed material to the fine ore stockpile at the copper concentrator;

n In October 2008, Equinox secured an additional $80.0 million project debt facility to enable the Company to meet additional working capital requirements resulting from the transformer fire and subsequently delayed startup;

n The large scale Hitachi EX5500 electric face shovels were successfully commissioned and put into production commencing in October 2008;

n Equinox accepted handover of the Lumwana processing facilities and other associated infrastructure from the engineering contractor in November 2008;

n Equinox produced its first copper concentrate at Lumwana during December 2008. Wet commissioning of the final stage of the process plant filter-press commenced;

n First commercial quantities of copper concentrate deliveries were made to off-take customers during December 2008;

n Mine activities continued to ramp-up towards steady state commercial production;

n The Lumwana Property Development Company, a special purpose vehicle established to own and manage the new Lumwana town secured a $25 million debt facility with Nederlandse Financierings-Maatshappij voor Ontwikkelingslanden N.V., the Dutch development funding institution, to cover town infrastructure costs. Debt drawdown can commence once Equinox meets a number of conditions precedent; and

n The Lumwana Project achieved an excellent health and safety record, with over 5 million man hours without a lost time injury, producing a lost-time-injury frequency rate of 0.3 (per 200,000 hours).

The Company expects that it will produce 170,000 tonnes (375 million pounds) of copper metal in concentrates in 2009 at a cash (C1) operating cost of $1.15 per pound.

As can be expected, unit production costs are anticipated to be higher in the early part of 2009 until steady state production activities are reached, which is expected by mid-2009 at which time Equinox will be operating one of the largest copper mines in Africa.

12

Lumwana

13

Lumwana

Copper Concentrate OfftakeDuring 2007 Equinox signed offtake contracts for 100% of its copper concentrate production for the first 5 years of the mine life.

The Company’s primary offtake contract is with Chambishi Copper Smelter Limited, a joint venture between China Nonferrous Metal Mining (Group) Co. Ltd. and Yunnan Copper Industry (Group) Co. Ltd. which has commissioned a new copper smelter at the Chambishi mine on the Zambian Copperbelt. Equinox is supplying this new smelter with concentrate under a 5-year ‘take and pay’ contract, with annual commitments to Chambishi of 100,000 tonnes of copper contained in concentrates or approximately 230,000 tonnes of Lumwana concentrates per year.

The balance of Equinox’s concentrate production is currently being delivered under short term contracts to traders in Zambia and the Company is in discussions with other smelters for longer term contracts.

Uranium Feasibility StudyIn April 2008, Equinox published the Lumwana UFS on the design of a treatment facility for the uranium ore stockpile that will result from the selective mining of the discrete, high grade uranium zones within the Lumwana copper orebodies presently being mined. This facility would cost about $200 million and could recover approximately 2 million pounds of uranium oxide (U3O8) and 12,800 tonnes of copper concentrate per year.

Subsequent to the release of the UFS, the Government of the Republic of Zambia (‘GRZ’) implemented its guidelines for uranium mining, processing and export that are consistent with International Atomic Energy Agency guidelines and the Nuclear Non-proliferation Treaty. The GRZ has recently approved the Lumwana Uranium Environmental Impact Assessment which was finalized and submitted to the Environmental Council of Zambia by Equinox in June 2008 as part of the required permitting process.

The decision to proceed with development of the Lumwana Uranium Project will depend, subject to board approval, on a number of factors including, improvements in the international project financing climate, as well as current market prices for uranium oxide. In the interim, high grade uranium ore will be stockpiled at Lumwana.

Potential Project ExpansionThe Lumwana process plant is conservatively rated at 20 million tonnes per year throughput. By optimizing and ‘de-bottlenecking’ the plant, Equinox engineers believe that throughput could potentially, at limited additional capital cost, be increased by 20% to about 24 million tonnes per year, increasing copper output to above 200,000 tonnes per year.

Given the very large resource and long mine life at Lumwana there is an opportunity to further expand throughput to about 30 million tonnes per year. Such further expansion would require significant additional capital cost and be subject to the completion of a feasibility study.

Project Debt and Equity FinancingIn December 2006, Equinox signed a US$582.7 million senior and subordinated Project finance facility for the completion of development and construction of the Lumwana Project. The facility is comprised of three tranches, $54.0 million subordinated debt facility, $364.0 million senior debt facility and $164.7 million asset backed facility. In response to the delay in commencement of commercial production caused by the fire incident at the Lumwana Project, the Company signed an $80.0 million extension to the above senior debt facility in September 2008.

As a requirement of the Lumwana Project financing facility, the Company also established a $45.0 million cost overrun facility for the Lumwana Project should any cost overrun occur, but in certain circumstances can also be utilized for debt repayment.

The cost overrun facility is structured as letters of credit which convert to Equinox common shares at a 6.75% discount to the prevailing TSX share price at the time of draw down, should that be required. As at 31 December, 2008, this $45m facility has not been utilized and remains available.

On March 26, 2009 the Company reached agreement with its debt financiers to restructure its debt repayment schedule. The main terms of the agreement are to smooth the principal debt repayments more evenly over the life of the loans without changing the tenor of the various facilities.

The effect on the 2009 calendar year repayments is a reduction of $87 million to $138 million the majority of which is payable in September 2009.

14

Notes to Resources & Reserves Tables

The Mineral Reserve and Resource within engineered pits were determined by Golder on the basis of 12.5mx12.5mx4m block models, including mining dilution and recovery, and optimized by Whittle 4X software with associated pit designs generated using Vulcan software. The cut-offs applied were based on $1.20/lb Cu, resulting in sulphide cut-off grades of 0.16% for Malundwe and 0.21% for Chimiwungo. These pit designs constitute the Development Case. The Lumwana Uranium resource estimate was carried out based on a 0.01% U3O8 cutoff, ordinary kriging on 2m composite samples using 25mx25mx4m and 5mx5mx2m blocks, within a $1.00/lb Cu pit design.

Competent PersonsThe estimates of mineral resources and ore reserveswere prepared in accordance with the standards setout in the Australasian Code for Reporting of Identified Mineral Resources and Ore Reserves (The JORC Code) and in accordance with CIM standards as prescribed by National Instrument 43-101. Mineral resource and reserve data is based on information compiled by persons who are members of the Australasian Institute of Mining and Metallurgy or the Australian Institute of Geoscientists and who have the relevant experience as ‘competent persons’ as defined in the JORC Code and as a ‘Qualified Person’ in accordance with National Instrument 43-101 in relation to the mineralization being reported on.

Technical information in this publication is summarized or extracted from the ‘Amended Technical Report on the Lumwana Copper Project, North West Province, Republic of Zambia’ dated October 2006, prepared by Michael Davis, Process Manager, Ausenco Ltd., Ross Bertinshaw, Principal of Golder Associates Pty Ltd., Tim Miller, Director, of Investor Resources Finance Pty Ltd, and Robert Hanbury, Associate Director, of Knight Piésold PtyLtd., each of whom is a ‘Qualifed Person’ who is either a corporate member of the Australasian Institute of Mining and Metallurgy, Australian Institute of Geoscientists or the CIM.

Forward Looking StatementsStatements within this publication are forward-looking, which are subject to various risks and uncertainties that could cause actual results and future events to differ materially from those expressed or implied by such statements. Investors are cautioned that such statements are not guarantees of future performance and results. Risks and uncertainties about the Company’s businessare more fully discussed in the Company’s disclosure documents filed from time to time with the Canadian and Australian securities authorities. See the October 2006 Technical Report and the last Annual Information Form on SEDAR at www.sedar.com for further details.

The Lumwana Project includes the Malundwe and Chimiwungo deposits.The Lumwana resource, defined by Golder Associates Pty. Ltd. (‘Golder’) inaccordance with the JORC Code and CIM Standards NI43-101 and using a0.2% copper cut-off, has been defined as follows:

Lumwana Resources: Measured + Indicated + Inferred

Class Tonnes Cu Co Au (Mt) (%) (ppm) (g/t)

Measured 129.5 0.89 238 0.03Indicated 228.7 0.68 153 0.02Total (Measured and Indicated) 358.2 0.76 184 0.02Inferred 564.4 0.63 46 0.01

Uranium within the Malundwe and Chimiwungo copper deposits occurs as discrete uranium-enriched zones that will be separately mined and stockpiled during the copper mining operation and as such, processing of the copper ore does not produce any uranium ‘contamination’ of resultant copper concentrate. The Lumwana uranium resource has been estimated using a 0.01% uranium cut-off grade as shown below:

Lumwana Uranium Mineral Resources (2003 BFS)

Class Tonnes Grade Contained Metal (Mt) U3O8 % U3O8 lbs

Indicated 9.5 0.093 19 408 000Inferred 2.6 0.042 2 035 000

Lumwana Uranium Resources within the Copper Pits

Class Tonnes Grade Contained Metal (Mt) U3O8 % U3O8 lbs

Indicated 7.2 0.083 13 094 000Inferred 0.5 0.051 545 000

Lumwana Sulphide Reserves & Resources within Designed Pits –Development Case

Class Tonnes Cu (Mt) (%)

Malundwe Proved 42.9 1.09Probable 78.2 0.79Total Mineral Reserves 121.1 0.89Inferred Resource 4.2 0.77 Chimiwungo Proved 81.5 0.70Probable 118.7 0.57Total Mineral Reserves 200.2 0.62Inferred Resource 413.0 0.60 Combined Malundwe + Chimiwungo Proved 124.4 0.83Probable 196.9 0.66Total Mineral Reserves 321.3 0.73Total Inferred Resource 417.2 0.60

Reserves and ResourcesLumwana

15

Development AgreementThe Lumwana Development Agreement between Equinox and the GRZ was signed on 16th December 2005 and provides a 10 year stability period for the key fiscal and taxation provisions related to the Lumwana Project.

Key issues defined in the Lumwana Development Agreement include a corporate tax rate of 25% and a mineral royalty of 0.6% of gross product. Capital expenditures are allowed to be deducted in the year incurred and losses can be carried forward for up to 10 years. There has also been permitted a deferral of payment of various customs and excise duties and imposts and a confirmation that there will be no withholding tax payable on the remission of profits or the repatriation of capital. Other provisions contained in the Lumwana Development Agreement deal with:

n Arbitration;n Employment;n Energy and supply;n Exchange control;n Export regulations and procedures;n Regulations and management of companies;n Mining operation, curtailment of production,

resumption of production and closure;n Waiver of Government’s sovereign immunity; andn Investment agreements and enforcement of

foreign awards.

Incorporated in the Lumwana Development Agreement is a Copper Price Participation Agreement (the ‘PPA’). The PPA is triggered upon the extinguishment of the Lumwana Project debt facilities and only if the margin between the copper price and Lumwana operating costs is above an agreed threshold. The total amount due in the event of the above occurring is capped at $50 million with a further $50 million potentially payable for a ‘windfall’ margin between copper price and Lumwana operating costs.

The GRZ enacted in April 2008, a number of changes to the tax regime in the country that included an increase in the corporate tax rate to 30%, the mining royalty to 3%, a variable profits tax and a windfall tax. Further, in January 2009, the GRZ announced a plan to withdraw some of these tax changes, including the controversial windfall tax, in order to protect foreign investment and Zambian mining industry jobs. In Equinox’s view the Development Agreement overrides these tax changes

Lumwana

16

17

n The Kanga prospect, located south of the Malundwe pit at Lumwana where mining has commenced. Continued drilling throughout 2008 in the Kanga area completed 55 reverse circulation holes and 10 diamond holes for an aggregate project metreage of 18,100 metres and has shown that it is a southerly extension of the Malundwe deposit, extending for at least 1 kilometre south of the Malundwe pit.

n Drilling along the western flank of the Malundwe deposit has intersected significant copper mineralization of up to 10m thick at ~1% copper outside the current pit design;

n The Kababisa prospect northeast of the Malundwe deposit has been reconnaissance drilled by 34 reverse circulation holes and two diamond drill holes on lines 200 metres apart along a strike length of 1000 metres. Copper mineralization was successfully intersected along the entire strike length, over thicknesses of 6 metres to 14 metres. Holes of note at this prospect are LUM501, 6 metres at 1.15% copper from 18 metres (oxide) and LUM504, 6 metres at 0.89% copper from 62 metres (sulphide).

Equinox considers Kanga, Chimiwungo North and the other ‘near mine’ targets as showing significant potential to develop into resources which could be exploited during the Lumwana mine life.

Equinox holds extensive exploration permits in Zambia, around the Copperbelt (one of the world’s most significant copper producing regions), to the east around Kasanka, to the northwest surrounding the Lumwana Mining License and in the Kabompo region further to the northwest.

Expansion of the exploration teams throughout 2008 has enabled a marked increase in on-ground reconnaissance work at targets previously identified from remotely sensed data in 2007, and this will form the basis of work into 2009.

Exploration

Equinox has identified numerous targets at Lumwana including:

Throughout 2008, Equinox maintained an accelerated exploration effort in parallel with Lumwana development to generate a suite of exploration projects.

18

19

Equinox has already had a direct positive impact on the local community at Lumwana, and will continue to do so as it builds sustainable community programs that will grow and develop long after the mine is exhausted. Equinox has developed and fosters a strong relationship with each of the three traditional chiefs and their chiefdoms in which contain the Lumwana large scale mining licence.

Employment preference and sourcing initially is done via these Chiefs to ensure maximum local participation in employment opportunities as well as ensuring the Company fully harnesses local available skills. This alone has had a dramatic impact in this largely undeveloped part of the country. This relationship has gone much further and is now extended beyond direct employment alone to infrastructural projects as well as capacity building training in many and diverse areas.

The Company implements education and training programs, including sponsoring 54 scholarships to the University of Zambia as well as 90 high school scholarships and traineeships. Equinox also provides local capacity building programs for small to medium scale businesses, in conjunction with carefully selected NGO partners, in such areas as textiles, floral products and supporting local market days.

In addition, the development of agriculture and aquaculture into commercial operations capable of providing primary produce to the surrounding areas has been a priority. Equinox has established the Lumwana Development Trust Fund that has so far built 30 classrooms for local schools, 4 teacher’s houses, 3 medical clinics, a community library and 2 women’s development centres.

Equinox and Lumwana will continue to play a pivotal role in the development of local community capacity and empowerment as well as the broader impact it has on Zambia as a nation. The Company’s next milestone is in conjunction with the GRZ to develop a multi-facility economic zone to attract other investors for economic diversification in the surrounding Lumwana area.

Corporate Responsibility

Lumwana and Sustainability of the Local Community

20

The TeamThe Board and focused management team comprise the blend of corporate experience, financial management, project management, technical expertise, mine development, operational experience and financing expertise required for the success and dynamic growth of the Company in Africa and beyond.

BoardPeter Tomsett (Non-Executive Chairman) is a mining engineer with over 26 years of experience in the mining industry, including 20 years with Placer Dome Inc. He served as President and Chief Executive Officer of Place Dome Inc, until its acquisition by Barrick Gold in January 2006. After starting his career with CRA Ltd at Broken Hill, Mr Tomsett joined Placer in 1986 in the Project Development group and subsequently held senior executive roles including responsibility for Placer’s Asia Pacific region as Executive Vice-President and later also took on responsibility for Placer Dome Africa, which operated mines in South Africa and Tanzania. He was appointed as President and Chief Executive Officer of Placer Dome in September 2004. Peter joined the Equinox board as Non-executive Chairman in July 2007.

Craig Williams (President and Chief Executive Officer) is a geologist involved in mineral exploration and development for over 33 years, co-founding Equinox in 1993 along with the late Dr Bruce Nisbet. He has been directly involved in several significant discoveries, including the Ernest Henry Deposit in Queensland and a series of gold deposits in Western Australia. Mr Williams and the late Dr Nisbet were jointly awarded ‘Prospector of the Year’ in 1994 by the Australian Association of Mining and Exploration Companies in recognition of their track record of discovery. Mr Williams has extensive corporate management and financing experience.

Harry Michael (Executive Director, Vice-President Operations and Chief Operating Officer) is a mining engineer with extensive mine development and operational experience, both within Australia and internationally. Of particular relevance is his experience as CEO of Geita Gold Mining Ltd, one of the largest open cut mines in Africa and as General Manager of the large open cut Iduapriem Gold Mine in Ghana. Mr Michael joined Equinox in 2004 as Chief Operating Officer and Lumwana Project Manager. He is based on-site at Lumwana, running the operation and managing all of the Company’s interests in Zambia.

David McAusland (Non-Executive Director and Chair of the Corporate Governance and Nominating Committee) is a highly experienced senior executive, lawyer and corporate executive. From 1999 to February 2008, he held the position of Executive Vice-President, Corporate Development and Chief Legal Officer of Alcan Inc. Prior to joining Alcan, Mr McAusland was the managing partner of a major Canadian law firm. Mr. McAusland holds a Bachelor of Law and a Bachelor of Civil Law and has had global responsibilities including strategy, major transactions, legal and regulatory affairs, and government relations.

David Mosher (Non-Executive Director and Chair of the Health, Safety, Environment and Sustainability Committee) is a former gold mining company CEO experienced in operations in Canada, Russia and Burkina Faso. He has over 36 years as a geologist and mining executive with experience in Australia, North America, Russia, Asia and Africa with extensive experience in mine development, corporate management and financing.

Jim Pantelidis (Non-Executive Director and Chair of the Compensation and Human Resources Committee) is a highly experienced senior executive and is currently Chairman of the Board of Parkland Income Fund and has served as a director of Parkland since 1999. Mr Pantelidis is Chairman and Director of The Consumers Waterheater Income Fund since 2002. From 1999 to 2002 he served as Chairman and Chief Executive Officer for the Bata Shoe Organization. He also spent 30 years in the petroleum industry and was at one time President of both the upstream and downstream divisions of Petro-Canada.

Brian Penny (Non-Executive Director and Chair of the Audit Committee) is Vice President Finance of Western Goldfields Inc and Vice President Finance and CFO of Silver Bear Resources and formerly, Vice President, Finance and Chief Financial Officer of Toronto based Kinross Gold Corporation. He is a Certified Management Accountant (Ontario) and has in excess of 21 years experience of accounting, financial and corporate management, and corporate governance within the mining industry.

ManagementMichael Klessens (Vice President Finance, Chief Financial Officer and Company Secretary) has over 21 years of experience in the mining industry, particularly corporate and financial management, project financing and the development of mining operations.

Robert Rigo (Vice President Project Development) is an engineer with over 31 years experience in the mining and mineral processing industry and particularly the management of major open pit mining operations and feasibility studies. At Lumwana he managed the feasibility study that was completed in 2003 and has had ongoing responsibility for project implementation, EPC contract management and offtake management.

Kevin van Niekerk (Vice President Investor Relations & Corporate Development) is an engineer with substantial African experience who manages the Toronto office and the Company’s investor relations in North America and Europe.

Ralph Gibson (Vice President Project Finance) has extensive experience in mining project finance, having worked for financial institutions in Australia and the UK providing debt and hedging facilities to mining companies in Australia, Africa, the former Soviet Union and the Americas. Mr Gibson manages the Company’s banking syndicate, debt facilities and hedging transactions.

Equinox Minerals Limited

Consolidated

For the year ended December 31, 2008 Expressed in US Dollars unless otherwise stated

Financial Statements

21

This document provides management’s discussion and analysis (‘MD&A’) of the financial condition of Equinox Minerals Limited (‘Equinox’ or the ‘Company’) as at and for the year ended December 31, 2008, compared to the corresponding period in 2007. This MD&A should be read in conjunction with the December 31, 2008 and December 31, 2007 audited consolidated financial statements of Equinox and related notes thereto. This information is presented as of March 27, 2009 and is current to that date unless otherwise stated. The financial information contained in this document is derived from the Company’s consolidated financial statements prepared in accordance with Canadian Generally Accepted Accounting Principles (‘Canadian GAAP’). All amounts in this discussion are expressed in U.S. dollars, unless identified otherwise.

The following discussion contains forward-looking statements that involve numerous risks and uncertainties. Actual results of the Company could differ materially from those discussed in such forward-looking statements as a result of these risks and uncertainties, including those set forth in this MD&A under ‘Forward-Looking Statements’ and under ‘Risk Factors.’

Additional information about the Company and its business activities, including the Company’s annual information form dated March 27, 2009 (the ‘AIF’) and its other continuous disclosure documents, is available on SEDAR at www.sedar.com.

Equinox is an international mining and exploration company, dual listed on the Toronto Stock Exchange (the ‘TSX’) and the Australian Securities Exchange (the ‘ASX’) under the symbol ‘EQN’. The Company is focused on operating its 100% owned Lumwana copper mine in Zambia. The Lumwana copper mine is expected to produce an average of 172,000 tonnes per year of copper metal contained in concentrates for the first 6 years of its 37 year mine life. The 20 million tonnes per annum plant is now operational and production commenced in early December 2008. Full production is expected to be reached mid-2009 at which time Lumwana will be one of Africa’s largest copper mines.

The Company believes that there are significant opportunities at the Lumwana copper mine to expand and optimize the concentrator and mine throughput rate, and to assess and evaluate the additional near mine deposits discovered to date.

Equinox maintains an active ‘pipeline’ of exploration projects on its Zambian tenements which presently total some 6,284 square kilometres. In particular, exploration of targets on properties near the Lumwana copper mine is focused on resource definition which if successful, could deliver additional ore to the Lumwana mill.

Equinox will continue to review and assess opportunities for organic growth and expansion, and corporate opportunities to grow the Company.

Management Discussion and AnalysisFor the year ended December 31, 2008

22

HIGHLIGHTS FOR THE YEAR

LUMWANA PROJECT

Equinox accepted handover of the Lumwana Copper Plant and other associated infrastructure from the engineering contractor in November 2008. Mine commissioning and ramp-up is underway and commercial concentrate deliveries have commenced. During the year the following activities, in chronological order, contributed to this significant milestone:

n Commissioning of the Lumwana Copper Project commenced in April 2008 with the electrification of the main Lumwana 33 kV substation and subsequent reticulation of power around the site;

n Equinox secured long-term land title to approximately 35 thousand hectares (350 square kilometres) of township and mine operating areas at the Company’s Lumwana mining license. In May 2008 this grant permited the Company to manage and administer the Lumwana surface rights, in particular the planned Lumwana town sub-division, thus enabling the Company to deliver employee home ownership and other commercial developments within the township;

n In June the Lumwana mine SAG mill (18 megawatts) was fully energized and rotated in June 2008 by the engineering contractor using Siemens gearless mill drives and commissioning of the primary crusher also commenced in June 2008;

n A fire on July 7, 2008, caused damage to a main transformer and adjacent substation, causing a four and a half month delay to project completion and handover;

n In September, crushing of material at the primary crusher commenced, with the 4.5 kilometre conveying circuit commissioned transporting crushed material to the fine ore stockpile at the copper concentrator;

n In October 2008, Equinox secured an additional $80.0 million project debt facility to enable the Company to meet additional working capital requirements resulting from the transformer fire and subsequently delayed startup;

n The large scale Hitachi EX5500 electric face shovels were successfully commissioned and put into production commencing in October 2008;

n Equinox accepted handover of the Lumwana processing facilities and other associated infrastructure from the engineering contractor in November 2008;

n Equinox produced its first copper concentrate at Lumwana during December 2008. Wet commissioning of the final stage of the process plant filter-press commenced;

n First commercial quantities of copper concentrate deliveries were made to off-taker customers during December 2008;

n Mine activities continued to ramp-up towards steady state commercial production; and

n The Lumwana Project achieved an excellent health and safety record, with over 5 million man hours without a lost time injury, producing a lost-time-injury frequency rate of 0.3 (per 200,000 hours).

The Company expects that it will produce 170,000 tonnes (375 million pounds) of copper metal in concentrates in 2009 at a cash (C1) operating cost of $1.15 per pound. As can be expected, unit production costs are anticipated to be higher in the early part of 2009 until steady state production activities are reached, which is expected by mid-2009 at which time Equinox will be operating one of the largest copper mines in Africa.

23

URANIUM FEASIBILITY STUDY

In April 2008, Equinox published the Lumwana uranium feasibility study (‘UFS’) on the design of a treatment facility for the uranium ore stockpile that will result from the selective mining of the discrete, high grade uranium zones within the Lumwana copper orebodies presently being mined. This facility would cost about $200 million and could recover approximately 2 million pounds of uranium oxide (U3O8) and 12,800 tonnes of copper concentrate per year.

Subsequent to the release of the UFS, the Government of the Republic of Zambia (‘GRZ’) implemented its guidelines for uranium mining, processing and export that are consistent with International Atomic Energy Agency guidelines and the Nuclear Non-proliferation Treaty. The GRZ has recently approved the Lumwana Uranium Environmental Impact Assessment which was finalized and submitted to the Environmental Council of Zambia by Equinox in June 2008 as part of the required permitting process.

The decision to proceed with development of the Lumwana Uranium Project will depend, subject to board approval, on a number of factors including, improvements in the international project financing climate, as well as current market prices for uranium oxide. In the interim, high grade uranium ore will be stockpiled at Lumwana.

EXPLORATION

Throughout 2008, Equinox maintained an accelerated exploration effort in parallel with Lumwana development to generate a suite of exploration projects.

Equinox has identified numerous targets at Lumwana including:

n The Kanga prospect, located south of the Malundwe pit at Lumwana where mining has commenced. Continued drilling throughout 2008 in the Kanga area completed 55 reverse circulation holes and 10 diamond holes for an aggregate project metreage of 18,100 metre and has shown that it is a southerly extension of the Malundwe deposit, extending for at least 1 kilometre south of the Malundwe pit;

n Drilling along the western flank of the Malundwe deposit has intersected significant copper mineralization of up to 10 metres thick at ~1% copper outside the current pit design; and

n The Kababisa prospect northeast of the Malundwe deposit has been reconnaissance drilled by 34 reverse circulation holes and two diamond drill holes on lines 200 metres apart along a strike length of 1000 metres. Copper mineralization was successfully intersected along the entire strike length, over thicknesses of 6 metres to 14 metres. Holes of note at this prospect are LUM501, 6 metres at 1.15% copper from 18 metres (oxide) and LUM504, 6 metres at 0.89% copper from 62 metres (sulphide).

Equinox considers Kanga, Chimiwungo North and the other ‘near mine’ targets as showing significant potential to develop into resources which could be exploited during the Lumwana mine life.

Equinox holds extensive exploration permits in Zambia, around the Copperbelt (one of the world’s most significant copper producing regions), to the east around Kasanka, to the northwest surrounding the Lumwana Mining License and in the Kabompo region further to the northwest. Expansion of the exploration teams throughout 2008 has enabled a marked increase in on-ground reconnaissance work at targets previously identified from remotely sensed data in 2007, and this will form the basis of work into 2009.

24

Management Discussion and AnalysisFor the year ended December 31, 2008

CORPORATE

The Lumwana Property Development Company, a special purpose vehicle established to own and manage the new Lumwana town secured a $25 million debt facility with Nederlandse Financierings-Maatshappij voor Ontwikkelingslanden N.V., (‘FMO’)the Dutch development funding institution, to cover town infrastructure costs. Debt drawdown can commence once Equinox meets a number of conditions precedent.

Equinox identified two additional independent director candidates, Mr. David McAusland of Beaconsfield, Québec and Mr. Jim Pantelidis of Toronto, Ontario, who were duly elected to serve on the Board of Directors of the Company in May 2008.

SELECTED FINANCIAL INFORMATION

The table below sets forth selected financial data relating to the Company’s years ended December 31, 2008, December 31, 2007 and December 31, 2006. This financial data is derived from the Company’s audited consolidated financial statements, which are prepared in accordance with Canadian GAAP. Year ended December 31 Fourth QuarterEARNINGS AND DEFICIT 2008 2007 2006 2008 2007 2006 $’000 $’000 $’000 $’000 $’000 $’000

Other Income / (Expenses) 268,195 4,805 9,302 255,206 1,936 2,988 Exploration Expense 10,262 7,114 2,456 2,977 2,746 667 General and Administration 8,388 11,194 5,601 2,600 2,739 1,424 Financing Costs 3,660 2,595 0 685 2,595 0 Incentive Stock Option Expense 4,953 11,993 16,064 908 2,083 1,041 Share of loss of equity accounted investee 0 867 458 0 0 307 Amortization of property, plant and equipment 314 145 100 107 49 29 Income tax expense/(recovery) 67,937 312 983 64,632 (823) 983 Net Income/(Loss) 172,681 (29,415) (16,177) 183,296 (9,099) (3,467)Basic earnings/(Loss) per share (dollars) 0.30 (0.06) (0.04) 0.31 (0.02) 0.00Diluted earnings per share (dollars) 0.29 (0.05) (0.04) 0.30 (0.02) 0.00Basic weighted avg # of shares (000’s) 583,800 538,313 372,903 593,651 564,708 435,302 Diluted weighted avg # of shares (000’s) 601,312 577,155 399,569 611,163 603,550 461,967

BALANCE SHEET Total Assets 1,471,131 828,002 357,174 Total Liabilities 760,923 409,664 68,944 Shareholders’ Equity 710,208 418,338 288,230

25

RESULTS OF OPERATIONS

Year ended December 31, 2008 compared to the year ended December 31, 2007

n Other income/(expense) was $268.2 million for 2008 (2007: $4.8 million) mainly due to derivative instrument fair value gains of $361.0 million (2007: $nil) as a result of the copper price dropping to $1.38 per pound at December 31, 2008, offset by derivative instrument losses transferred from equity of $89.5 million (2007: $nil). Foreign exchange losses of $4.2 million (2007: gain of $0.6 million) were incurred as a result of the strengthening U.S. dollar. Impairment losses of $1.7 million (2007: $nil) were recorded on available-for-sale financial assets and a promissory note receivable. Interest income contributed $2.2 million (2007: $4.4 million). See ‘Discussion of Financial Position and Liquidity – Derivative Instruments’ for an explanation of the cash flow hedge related items included in other income/(expense).

n Exploration expenditures were $10.3 million for 2008 (2007: $7.1 million) due to continued work carried out on the Lumwana UFS and exploration activities elsewhere in Zambia.

n General and administrative (‘G&A’) costs were $8.4 million for 2008 (2007: $11.2 million). The reduction was due to the 2007 figures including a $1.5 million success fee paid in association with a Lumwana mine copper concentrate off-take agreement, a payment of $0.75 million made to a former Chairman on his resignation and contract dispute settlement costs of $2.3 million (€1.7 million) relating to Komatsu mining equipment for the Lumwana Project. Otherwise the 2008 G&A costs have generally increased due to higher staffing levels and costs, an increase in the number of directors, increased insurance and premises rental costs.

n Financing costs associated with the Lumwana Project debt facilities, other than capitalized interest and commitment fees, were $3.7 million for 2008 (2007: $2.6 million).

n The incentive stock option expense was $5.0 million for 2008 (2007: $12.0 million) resulting from the vesting of options granted and/or approved to employees and directors during the year.

The recognized a future income tax expense of $67.9 million for 2008 (2007: $0.3 million) in response to recent changes enacted (and substantially enacted) to the Zambian tax regime by the Government of the Republic of Zambia (the ‘GRZ’) (see ‘Critical Accounting Estimates – Future Income Taxes’ for an explanation of the future income taxes). Realized and unrealized derivative instrument gains have generated a future income tax expense of $82.8 million which has been partially sheltered by previously unrecognized losses equaling $16.0 million. The remainder of the tax expense was recognized on interest income earned and unrealized changes in available-for-sale financial assets.

Three months ended December 31, 2008 compared to the three months ended December 31, 2007

n Other income/(expense) was $255.2 million for the quarter ended December 31, 2008 (2007: $1.9 million) mainly due to derivative instrument fair value gains of $333.5 million (2007: $nil) as a result of the copper price dropping to $1.38 per pound at December 31, 2008, offset by derivative instrument losses transferred from equity of $71.0 million (2007: $nil). Foreign exchange losses of $6.8 million (2007: gain of $0.4 million) were incurred as a result of the strengthening U.S. dollar. Impairment losses of $1.5 million (2007: $nil) were recorded available-for-sale financial assets and a promissory note receivable. Interest income contributed $0.5 million (2007: $1.0 million). See ‘Discussion of Financial Position and Liquidity - Derivative Instruments’ for an explanation of the cash flow hedge related items included in other income/(expense).

n Exploration expenditures were $3.0 million for the quarter ended December 31, 2008 (2007: $2.7 million) due to continued work carried out on the Lumwana UFS and exploration activities elsewhere in Zambia.

n G&A costs were $2.6 million for the quarter ended December 31, 2008 (2007: $2.7 million).

n Financing costs associated with the Lumwana Project debt facilities, other than capitalized interest and commitment fees, were $0.7 million for the quarter ended December 31, 2008 (2007: $2.6 million).

26

Management Discussion and AnalysisFor the year ended December 31, 2008

n The incentive stock option expense was $0.9 million for the quarter ended December 31, 2008 (2007: $2.1 million) resulting from the vesting of options granted and/or approved to employees and directors during the quarter.

n Future income tax expense was $64.6 million for the quarter ended December 31, 2008 (2007: benefit of $0.8 million). Of this amount, $80.6 million was recognized in relation to the $262.5 million net hedging gain booked which has been partially sheltered by previously unrecognized losses equaling $16.0 million. See ‘Critical Accounting Estimates – Future Income Taxes’ for an explanation of the future income taxes.

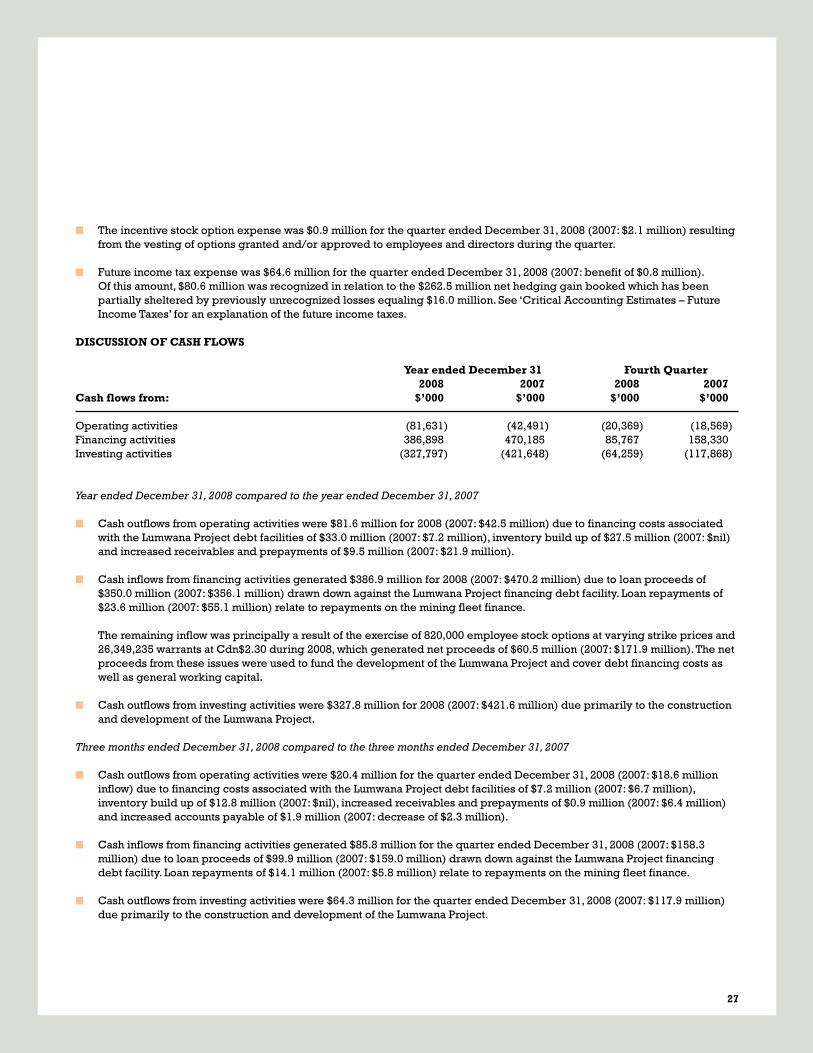

DISCUSSION OF CASH FLOWS Year ended December 31 Fourth Quarter 2008 2007 2008 2007Cash flows from: $’000 $’000 $’000 $’000

Operating activities (81,631) (42,491) (20,369) (18,569)Financing activities 386,898 470,185 85,767 158,330 Investing activities (327,797) (421,648) (64,259) (117,868)

Year ended December 31, 2008 compared to the year ended December 31, 2007

n Cash outflows from operating activities were $81.6 million for 2008 (2007: $42.5 million) due to financing costs associated with the Lumwana Project debt facilities of $33.0 million (2007: $7.2 million), inventory build up of $27.5 million (2007: $nil) and increased receivables and prepayments of $9.5 million (2007: $21.9 million).

n Cash inflows from financing activities generated $386.9 million for 2008 (2007: $470.2 million) due to loan proceeds of $350.0 million (2007: $356.1 million) drawn down against the Lumwana Project financing debt facility. Loan repayments of $23.6 million (2007: $55.1 million) relate to repayments on the mining fleet finance.

The remaining inflow was principally a result of the exercise of 820,000 employee stock options at varying strike prices and 26,349,235 warrants at Cdn$2.30 during 2008, which generated net proceeds of $60.5 million (2007: $171.9 million). The net proceeds from these issues were used to fund the development of the Lumwana Project and cover debt financing costs as well as general working capital.

n Cash outflows from investing activities were $327.8 million for 2008 (2007: $421.6 million) due primarily to the construction and development of the Lumwana Project.

Three months ended December 31, 2008 compared to the three months ended December 31, 2007

n Cash outflows from operating activities were $20.4 million for the quarter ended December 31, 2008 (2007: $18.6 million inflow) due to financing costs associated with the Lumwana Project debt facilities of $7.2 million (2007: $6.7 million), inventory build up of $12.8 million (2007: $nil), increased receivables and prepayments of $0.9 million (2007: $6.4 million) and increased accounts payable of $1.9 million (2007: decrease of $2.3 million).

n Cash inflows from financing activities generated $85.8 million for the quarter ended December 31, 2008 (2007: $158.3 million) due to loan proceeds of $99.9 million (2007: $159.0 million) drawn down against the Lumwana Project financing debt facility. Loan repayments of $14.1 million (2007: $5.8 million) relate to repayments on the mining fleet finance.

n Cash outflows from investing activities were $64.3 million for the quarter ended December 31, 2008 (2007: $117.9 million) due primarily to the construction and development of the Lumwana Project.

27

DISCUSSION OF FINANCIAL POSITION AND LIQUIDITY

December 31 December 31 2008 2007 $’000 $’000

Assets Cash and cash equivalents 51,327 73,367 Current portion of derivative instruments 127,570 0 Other current assets 69,353 24,886 Restricted cash 26,076 25,601 Derivative instruments 129,109 0 Capital assets 1,067,290 684,249 Future tax assets 0 15,555 Other non-current assets 406 4,344 Total Assets 1,471,131 828,002

Liabilities Current liabilities 225,708 83,374 Long-term debt 475,040 263,107 Finance leases 3,418 0Future tax liability 48,963 0 Asset retirement obligation 5,358 3,025 Long term compensation 269 421 Derivative instruments 0 59,694 Other provisions 2,167 43 Total Liabilities 760,923 409,664

Shareholders’ Equity 710,208 418,338

Outstanding number of shares 596,933,212 564,966,871

Cash and Cash EquivalentsCash and cash equivalents were $51.3 million at December 31, 2008 (December 31, 2007: $73.4 million) due to proceeds from borrowings and issues of equity offset by expenditures on capital assets for the Lumwana Project.

Derivative InstrumentsAs at December 31, 2008 and pursuant to the lending requirements for the Lumwana Project debt facility, the Company has entered into a number of copper put option and forward contracts relating to a portion of its expected copper production at the Lumwana mine. These contracts are designed to provide protection against fluctuations in the copper price.

Upon entering into the copper put option contracts the Company incurred a premium of $86.5 million which is due and payable on expiry of the underlying contracts between October 2008 and March 2011. There is no premium or cost associated with the copper forward contracts.

For accounting purposes, these contracts were designated at inception as hedges of the anticipated sale of copper cathode. Due to contractual uncertainties relating to a tolling off-take agreement the Lumwana mine will not produce copper cathode for sale as it’s off-take contracts relate to the sale of copper concentrate, not copper cathode. As a result, it is probable that the forecasted transactions that were being hedged will no longer occur, therefore hedge accounting has been discontinued.

28

Management Discussion and AnalysisFor the year ended December 31, 2008

Where hedge accounting is discontinued in these circumstances, gains or losses on the hedge instruments in that period must be recognized in the income statement. Furthermore, any cumulative gain or loss on those hedge instruments, previously reported in other comprehensive income, are immediately transferred to the income statement.

A mark to market gain of $361.0 million on the bought put options and forward contracts has been recorded in the income statement in the current period. The mark to market loss on those hedge contracts previously deferred in other comprehensive income of $89.5 million has been recorded in the income statement in the current period.

The mark to market fair value of all contracts is based on independently provided market rates and determined using standard valuation techniques. These techniques include the impact of counterparty credit risk which was determined to be $10.1 million. The spot price of copper at December 31, 2008 used for the mark to market valuations was $1.38 per pound.

Other Current AssetsOther current assets were $69.4 million at December 31, 2008 (December 31, 2007: $24.9 million) primarily due to the increase in inventories of $27.5 million (December 31, 2007: $Nil) and an accounts receivable balance of $35.4 million (December 31, 2007: $18.9 million).

Restricted CashRestricted cash of $26.1 million at December 31, 2008 (December 31, 2007: $25.6 million) resulted from $25.3 million plus accrued interest being deposited in a demobilization cost reserve account as required under the terms of the Lumwana Project finance facility for the mining fleet.

Capital AssetsCapital assets were $1,067.3 million at December 31, 2008 (December 31, 2007: $684.2 million) largely due to construction and development of the Lumwana Project. Construction in progress has increased to $548.3 million (December 31, 2007: $397.6 million). Mine development costs are $342.7 million (December 31, 2007 $204.9 million), and other property, plant and equipment has increased to $170.1 million (December 31, 2007 $81.7 million).

Future Tax AssetsThe GRZ enacted on April 1, 2008, a number of changes to the tax regime in the country, particularly in relation to mining companies. In light of this, at 31 March 2008, the Company conservatively recognized a valuation allowance up to the value of the future tax asset arising on unrealized losses on its derivative instruments. These adjustments are recorded in other comprehensive income. See ‘Critical Accounting Estimates - Future Income Taxes’ below for an explanation of the future income taxes.

Other Non-Current AssetsEquinox holds a promissory note issued by Alturas for $0.375 million, which is non interest bearing and payable on March 31, 2010. An impairment loss of $0.34 million was recognized in the income statement during the year ended December 31, 2008. This represents the remaining balance receivable on the promissory note. In making this determination, the Company considered the financial health and business outlook for Alturas.

At December 31, 2008, Equinox owned approximately 17.6% of the outstanding shares of Alturas Minerals Corp. (‘Alturas’) (listed on the TSX Venture Exchange under the trading Symbol ‘ALT’). The market value of the Company’s investment in Alturas, based on the closing TSX-V share price of C$0.045 at December 31, 2008, is $0.3 million (December 31, 2007: $2.2 million). For the year ended December 31, 2008, the Company has determined that this investment is impaired. In making this determination, the Company considered the decline in the investment’s fair value against its cost, along with the financial health of and business outlook for Alturas. An impairment loss of $0.2 million was recognized in the income statement for the year ended December 31, 2008.