ENHANCING THE IMAGE OF PROFESSIONAL ACCOUNTANTS THROUGH ETHICS FOR NATIONAL DEVELOPMEN1 Copy

26

ENHANCING THE IMAGE OF PROFESSIONAL ACCOUNTANTS THROUGH ETHICS MBONU CHIKWELU .M.ESQ EMAIL: [email protected] DEPARTMENT OF ACCOUNTANCY FEDERAL POLYTECHNIC, OKO PRESENTED AT THE FIRST NATIONAL CONFERENCE OF DEPARTMENT OF BANKING AND FINANCE FEDERAL POLYTECHNIC, OKO

-

Upload

federalpolyoko -

Category

Documents

-

view

1 -

download

0

Transcript of ENHANCING THE IMAGE OF PROFESSIONAL ACCOUNTANTS THROUGH ETHICS FOR NATIONAL DEVELOPMEN1 Copy

ENHANCING THE IMAGE OF PROFESSIONAL ACCOUNTANTSTHROUGH

ETHICS

MBONU CHIKWELU .M.ESQ

EMAIL: [email protected]

DEPARTMENT OF ACCOUNTANCY

FEDERAL POLYTECHNIC, OKO

PRESENTED AT THE

FIRST NATIONAL CONFERENCE OF

DEPARTMENT OF BANKING AND FINANCE

FEDERAL POLYTECHNIC, OKO

2

THEME: RE-BRANDING THE PROFESSIONAL IMAGE IN THEFINANCIAL AND BUSINESS WORLD FOR SUSTAINABLE NATIONAL

DEVELOPMENT

DATE: 15TH – 17TH JUNE, 2011

ABSTRACT

Recent collapse of big firms like Enron, World Com etc. aroundthe globe have battered the image of the professional accountant and made the credibility of professional accountants to be in doubt. Little wonder that the National Board for Technical Education (NBTE) introduced professional ethics as a course of study in all the tertiary institutions under it’s jurisprudence. In the paper, the use of ethics in restoring the image of professional accountants was discussed.The social and ethical environment in the context of ethical challenges, social responsibility and business were considered. Ethics in organisations and approaches in managingethics were further discussed. Professional ethics of some foreign and local professional accounting bodies were focussed. The paper argues that the employees, the customers, the suppliers and the society as a whole will attain their respective goals if ethics is given its rightful place.

INTRODUCTION

Background of Study

3

During the industrial revolution, of the 20th century, as the

manufacturing concerns grew in size, their owners began to use

service of hired managers. With this separation of the

ownership from the management groups, the absentee owners

turned increasingly to professional accountant (auditors) to

protect themselves against the danger of intentional errors as

well as fraud committed by managers and employees. If it turns

out that the report of the professional accountant who is

supposed to be an independent person of integrity cannot be

relied upon, a problem arises. This was witnessed in USA in

the year 2000, where at the request of the Security and

Exchange Commission; the accounting profession established a

Panel on Audit Effectiveness. The Panel was charged with the

responsibility to review and evaluate how independent audits

of financial statement are performed and to assess whether

recent trends in audit practices serve the public interest.

Recommendation from the panel resulted in changes in auditing

standards. However, even before these changes in audit

requirement could be implemented, a series of events in the

capital markets produced a chain reaction that caused

4

unprecedented reforms in the accounting profession

(Whittington R.O and K. Pany: 2004:9)

In December 2001 Enron Corporation filed for bankruptcy

shortly after acknowledging that accounting irregularities had

been used to significantly inflate earnings in the current and

preceding years. Shortly thereafter, it was discovered that

WorldCom had used ACCOUNTING FRAUD to significantly overstate

its reported income. In addition to these two very visible

cases, a record number of public companies reported prior-

period financial statements, and almost weekly the Security

and Exchange commission announce a new investigation into

another company’s accounting practices. Investor uncertainty

about reliability of financial statements rocked an already

weak financial market during the later part of 2001 and first

half of 2002. It brought into question the effectiveness of

the financial statement audits and created a crisis of

credibility for the accounting profession. More significantly,

highly publicised conviction of Andersen LLP, one of the then

‘Big 5’ accounting firms, on changes of destruction of

documents of related to the Enron case brought into question

5

the ethical principles of the public accounting profession

(Whittington R.O and K. Pany, 2004:10).

These events drew quick responses from a number of

congressional committees, the SEC and the U.S Justice

Department, as they began investigating corporate management

and the accounting profession. By the summer of 2002, congress

had passed the Sarbanes – Oxley Act of 2002, that included a

set of reforms toughening penalties for corporate fraud,

restricting the type of consulting Professional Accountants

(CPAs) many perform for audit clients, and creating the Public

Company Accounting Oversight Board (PCAOB) to oversee the

accounting profession. The establishment of the PCAOB

eliminated a significant portion of the accounting

profession’s system of self regulation.

In Nigeria, the financial industry have witnessed two

periods of distress in 1990s and 2000s. The distressed banks

had published financial statements which did not give any

cause for worry before their distress. It is therefore argued

that the professional accountants in Nigeria cannot completely

exonerate themselves from complicity in the events. Concerning

the five failed banks, Salu(2009:3) queried:

6

“Don’t they ever get audited? Who looks at the books and

passes them fit to declare billions in profits thereby

deceiving the unsuspecting ordinary Nigerians who some go as

far as borrow money from banks to buy share in the same banks.

The target of these queries appear to be on the mega auditor

firms: Price Water House Coopers(PWC) and Akintola

Deloite(AD).These two auditing firms with international

reputations to keep were the auditors to the five distressed

banks. While PWC was the auditor to Intercontinental bank and

Oceanic bank, AD was the auditor to Union bank, Afribank and

Finbank. The argument that companies are not answerable to

shareholders did not sound convincing in the circumstance.

However, as the audited report is handed over to the committee

of the bank made up Executive Directors(ED) and Non-Executive

Directors of equal numbers, it is expected that the non-Eds

would be transparent enough to fight on behalf of ordinary

shareholders. Also the reputation of the auditing firm would

be largely based on the management report that ought to have

been sent in to the audit committee to alert them of the

7

anomalies. We wait with vested interest to see how these firms

would redeem their image.”

Illustrative case 1

In 2002 WorldCom reported over $7 billion in accounting

irregularities, completely eliminating the company’s previously

reported profit for all of 2000 and 2001, and causing the company to

declare bankruptcy. At one time WorldCom had reported total assets

in excess of $100billion and in market value in excess of $150

billion making it the largest bankruptcy in American history.

STATEMENT OF THE PROBLEM

The financial statements audited by the professional

accountant will obviously lack

Credibility as the auditor fails to discharge their duty with

the due ethical principles. This will lower the morale of

investing public and will reduce the level of investments in

the country. The economy will suffer for it as foreign direct

investment (FDI) and economic growth will be abysmal. The

professional accountant is bound to lose their rights in the

8

society as was the case in USA as the auditor cannot be

trusted.

Ethical problems arising from firm and individuals abound in

the society such as environmental pollution from firms,

employee’s lack of job satisfaction, and poor quality goods

among others. However, the broad objective of this study is to

determine how good ethical conduct can restore the image of

professional accountant and encourage investment in stock

market.

METHODOLOGY

This is a descriptive study be of the role of ethics in

enhancing the image of the professional accountant. It

employed the secondary source of data collection by making use

of available literature on ethics and how it can enhance the

image of the professional accountant.

LITERATURE REVIEW

THE NATURE OF ETHICS

9

According to Wittington R.O and K.Pany (2004:57) “Ethics

has been defined as the study of moral principles and values

that govern the actions and decision of an individual or

group”. ACCA (2007:24) defined ethics as “a set of moral

principles to guide behaviour”. While personal ethics vary

from individual to individual, at any point in time, most

people within the society are able to agree as to what is

considered ethical and unethical behaviour.

A good starting point for considering ethics is to

examine the context in which most ethical question arises -

relationships among people. Any relationships between two or

more individuals carries with it sets of expectations by each

of the individuals involved. Certainly, the relationship

between a professional accountant and a client offers a number

of interesting challenges. For example, is it ethical for a

senior auditor to underreport the number hours worked in audit

engagement?

ETHICAL DILEMMAS AND PROBLEMS FACING PROFESSIONAL

MANAGERS

10

An ethical dilemma is a situation that an individual faces involving a

decision about appropriate behaviour (Whittington: 58).An ethical dilemma

generally involves a situation in which the welfare of one or more other

individual is affected by the result of the decision. Ethical dilemmas faced

by auditors often have an effect on the welfare of a large

number of individuals or groups. As an example, if an auditor

makes an unethical decision about the content of an auditor

report, the wealth of thousands of investors and creditors may

be affected.

Managers have a duty (in most entities) to aim for

profit. At the same time, modern ethical standards impose a

duty to guard, preserve and enhance the value of the entity

for the good of all touched by it, including the general

public. Large organisation tend to be more often held to

account over this than small ones.BPP learning media (2008:25)

identified two areas that managers face ethical problem.

1. In the area of products and production, managers have

responsibility to ensure that the public and their own

employees are protected from danger. Attempts to increase

profitability by cutting cost may lead to dangerous

working conditions or to inadequate safety standards. In

11

the United States, product liability litigation is so

common that this legal threat may be a more effective

deterrent than general ethical standards. In Nigeria,

consumer protection council has been established by the

government.

2. Another ethical problems concern payment by companies to

government or municipal officials who have power to help

or hinder the payers operation.

Four ways in which this take place are

1. extortion

2. Bribery

3. Grease money

4. gifts

In Nigeria the Halliburton oil company tax scandal in

which $198Million taxes were evaded by the company through

bribery (Agbambu.C: 2010)

FRAME WORK FOR ETHICAL DECISION

How do we make decision about an appropriate course of

action when faced with an ethical dilemma? (Wittington R.O and

12

K. Pany :58) identified formal decision process to use. The

steps involved in making any decision generally include:

1. Identify the problem.

2. Identify possible courses of action.

3. Identify any constraints relating to the decision

4. Analyse the likely effects of the possible courses of

action.

5. Select the best course of action

THE SOCIAL AND ETHICAL ENVIRONMENT

Firms have to ensure they obey the law; about they also face ethical

concerns, because their reputations depend on a good image. Whereas the

political environment in which an organisation operates consists of laws,

regulations and government agencies, the social environment consists of the

customs beliefs and education of the society as a whole, or of different groups

in society and the ethical environment consists of a set (or sets) of well

established rules of personal and organisational behaviour.

EXAMPLES OF SOCIAL AND ETHICAL OBJECTIVES

Companies are not passive in the social and ethical

environment

13

1. Employees:

(a) A minimum wage, perhaps with adequate differentials for

skilled labour.

(b) Job security (over and above the protection afforded to

employees by government legislation.

(c) Good conditions of work (labour the legal minimum)

(d) Job satisfaction

2. Customers: may be regarded as entitled to receive a

product of good quality at a reasonable price.

3. Suppliers: may be offered regular orders and timely

payment in return for the reliable delivery and good

service.

4. Society as a whole:

(a) Control of pollution

(b) Provision of financial assistant to charities, sports and

community activities

(c) Co-operation with government authorities in identifying

and preventing health hazards in the products sold.

14

SOCIAL RESPONSIBILITY AND BUSINESS

There are two schools of thought in respect of social

responsibility: Share holder and stakeholder paradigm.

According to Bello A. (2011:76). In its simplest form, the

shareholder wealth maximization paradigm takes a clear-cut

position in giving share holders the superior accounting

status and subordinating other constituencies’ interest to

them. Managers’ accountability is owned only to shareholders

while other constituencies do not enjoy it. In contrast, the

stakeholder paradigm requires corporations and their

management constantly to juggle between conflicting interests

in an effort to avoid extreme harm to any one of them,

inevitably at the expense of some constituencies.

Today, the shareholders paradigm appears to be the

dominant paradigm as a matter of law as well as of practice

hansman and Kraakman (2001).

APPROACHES TO MANAGING ETHICS

15

Paine L. (1994) suggests that there are two approaches to

the management of ethics in organisations: - Compliance based

and (b) Integrity based.

COMPLIANCE BASED APPROACH: A compliance base approach is

primarily designed to ensure that the company acts within the

letter of the law, and that violations are prevented, detected

and punished. Some organisations faced with the legal

consequences of unethical behaviour take legal precautions

such as those below:-

1. Compliance procedures

2. Audits of contracts

3. System for employees to inform superiors about criminal

misconduct without fear of retribution.

4. Disciplinary procedures

Corporate compliance is limited in that it refers only to

the law, but legal compliance is not an adequate means for

addressing the full range of ethical issues that arises every

day. Furthermore, mere compliance with the law is no guide to

exemplary behaviour. INTEGRITY BASED PROGRAMMES: An

16

integrity based approach combines a concern for the law with

an emphasis on managerial responsibility for ethical

behaviour. Integrity strategies strive to define companies

guiding values, aspirations and patterns of thought and

conduct. When integrated into the day to day operation of an

organisation, such strategies can help prevent damaging

ethical lapses, while tapping into powerful human impulses for

moral thought and action.

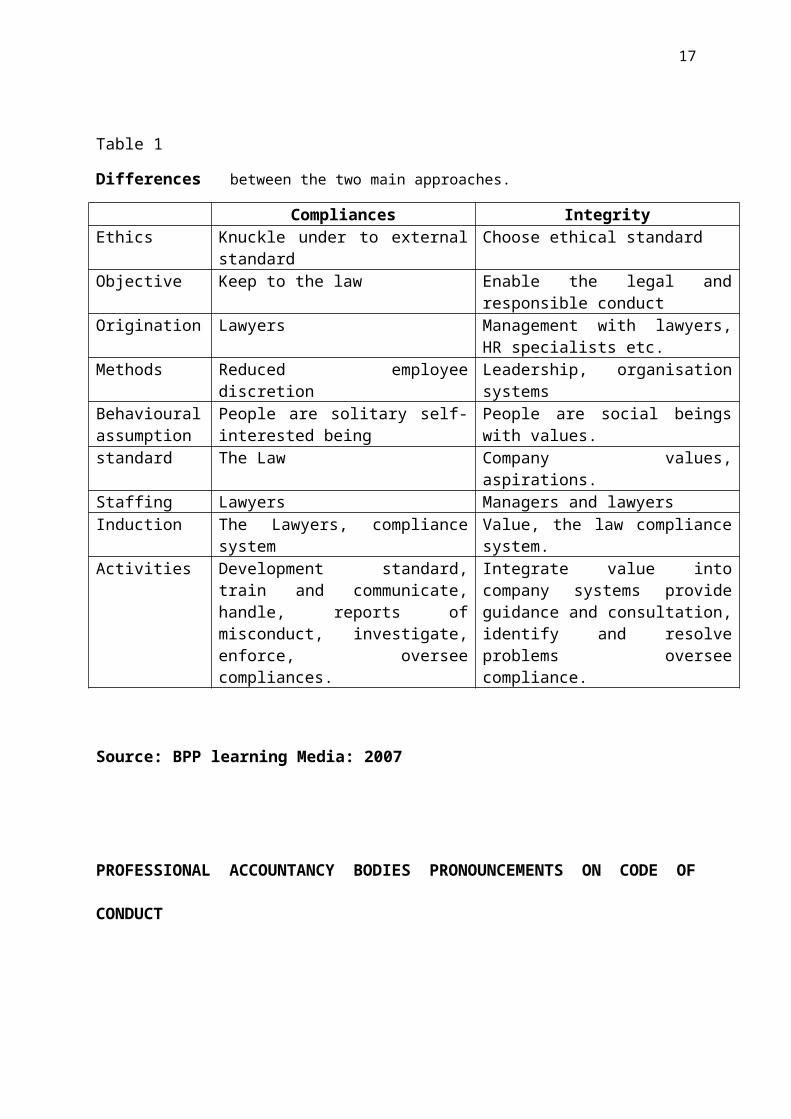

17

Table 1

Differences between the two main approaches.

Compliances IntegrityEthics Knuckle under to external

standard Choose ethical standard

Objective Keep to the law Enable the legal andresponsible conduct

Origination Lawyers Management with lawyers,HR specialists etc.

Methods Reduced employeediscretion

Leadership, organisationsystems

Behaviouralassumption

People are solitary self-interested being

People are social beingswith values.

standard The Law Company values,aspirations.

Staffing Lawyers Managers and lawyersInduction The Lawyers, compliance

systemValue, the law compliancesystem.

Activities Development standard,train and communicate,handle, reports ofmisconduct, investigate,enforce, overseecompliances.

Integrate value intocompany systems provideguidance and consultation,identify and resolveproblems overseecompliance.

Source: BPP learning Media: 2007

PROFESSIONAL ACCOUNTANCY BODIES PRONOUNCEMENTS ON CODE OF

CONDUCT

18

A distinguishing mark of accountancy profession is it’s

acceptance of responsibility to act in public interest.

Therefore, a professional accountant’s responsibility is not

exclusively to satisfy the needs of individual client or

employer. The public interest is considered to be collective

well-being of the community of people, institutions, the

professional accountant serves, including clients, lenders,

governments, employers, employees, investors, the business and

financial community and others who rely on the work of the

professional accountants.

Accountancy profession is founded on code of conduct. In this

respect different professional bodies have made pronouncements

on code of conduct.

CHARTERED ASSOCIATION OF CERTIFIED ACCOUNTANTS (ACCA)

The ACCA rule fundamental principles and the general

rules.

The five fundamental principles are:

Integrity Objectivity Professional competence and the care. Confidentiality Professional behaviour

19

The general rules include:

Confidentiality Money laundering Whistle blowing Independence conflicts interest advertising publicity obtaining professional work remuneration insider dealing

AMERICAN INSTITUTE OF CERTIFIED PUBLIC ACCOUNTANTS (AICPA)

The AICPA code of professional conduct consists of two

sections. The first section, the principles is a goal-

oriented, positively stated discussion of the public, clients,

and fellow practitioners. The principles provide the framework

for the rules, the second section of the code. The rules are

enforceable application of the principles. They define

acceptable behaviour and identify sources of authority for

performance standards.

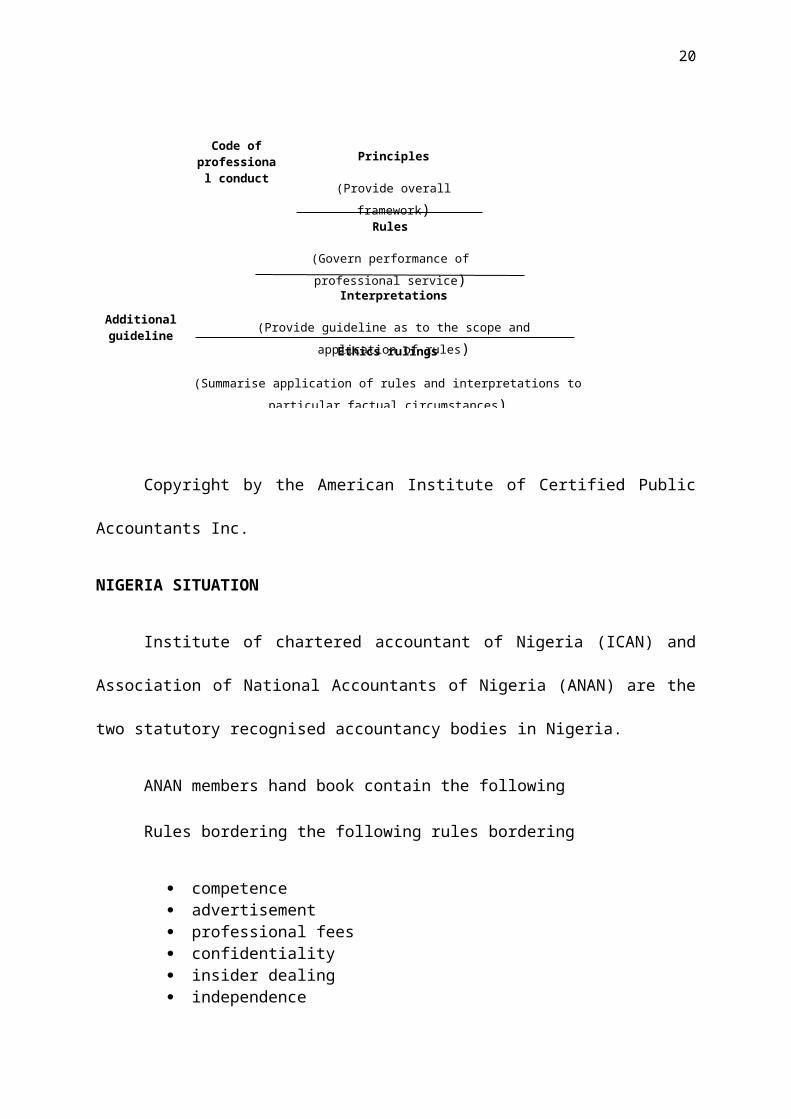

Fig 1 AICA Professional ethics

20

Copyright by the American Institute of Certified Public

Accountants Inc.

NIGERIA SITUATION

Institute of chartered accountant of Nigeria (ICAN) and

Association of National Accountants of Nigeria (ANAN) are the

two statutory recognised accountancy bodies in Nigeria.

ANAN members hand book contain the following

Rules bordering the following rules bordering

competence advertisement professional fees confidentiality insider dealing independence

Principles

(Provide overallframework)

Rules

(Govern performance ofprofessional service)

Interpretations

(Provide guideline as to the scope andapplication of rules)Ethics rulings

(Summarise application of rules and interpretations toparticular factual circumstances)

Code ofprofessional conduct

Additionalguideline

21

handling of client’s money

ICAN has ethical guidelines for their members in relation to

the following:

Professional independence

confidentiality of information

rules on advertising and publicity including house

journals produced

description of designatory letters

determination of fees

custody of money held by clients

exchange of correspondence with former incumbent

before accepting engagements

lien in client’s documents for unpaid fees

and some others

22

CONCLUSION

The professional accountant has public trust and

therefore his negative action are bound to affect the society

as a whole. Ethics comes in place to guide the professional

towards positive discharge of his duties. The national woes

can be traceable to a lot of unethical practices of the

government official, the manufactures, the employers, the

employees and the entire citizenry.

Accountants are not only the watchdog, but the custodians of

the conscience and guidance of the interest of the investing

public and the general public. They help to restore investor’s

confidence. Inculcation of ethical values will go a lot in

rebranding the image of the professional accountant. Thus the

credibility and reliability of financial statements will be

far stronger and with a higher positive impact on the capital

market and industry.

23

RECOMMENDATIONS

1. Ethical training is recommended for the employed of both

private and public sectors of the economy. Training

should also be intensified by professional accountancy

bodies and tertiary institutions in Nigeria. A course in

ethics should be offered separately in their

examinations.

2. Organisation should set up departments that will fashion

out strategies in handling their ethical challenges.

24

3. Government should enable legislations to check unethical

practices in the country.

4. Government should copy the United States example in

investigating the professional accountants in Nigeria so

that culprits will be convicted like in the case of

Andersen LLP and Enron Plc.

25

REFERENCES

Agbambu .C.(2010)”$198M Halliburton Scandal: Presidency orders prosecution of

suspects”

www.tribune.com.ng/index.php/news/6563-198m

Aguolu. O.(1998) Fundamentals of Auditing, Nimo: Rex Charles &

Patrick

Bello. A(2011) Corporate Governance and Accountability, Lagos: ANAN

MCPD

BPP Learning Media (2008) ACCA Paper 2-Corporate Reporting, London:

BPP Learning Media

Coopers and Lybrand (1985) Student’s Manual of Auditing, Berkshire: Van

Nostrand

Reinhold (UK) Ltd

Hansmann. H. And R. Kraakman (2001The End of History for Corporate Law,

89 GEO. LJ.439

Izedonmi .P.F. (2008) Review of Accounting Ethics Curriculum, Lagos:

ICAN/World Bank

26

Workshop

Jide. S.(2009) Nigeria’s Distress Available at

www.http://babajidesalu.wordpress.com

Lander. G.P. (2004What is Sarbanes-Oxley? New York: McGraw-Hill

Millichamp A.H.(2002)Auditing, London: Book Power/ ELST edition

Oyeyemi.F.O.(2007)Manual of Advanced Auditing, Professional Practice,

Investigation

& Other Assurance Services for Professional Accountant, Jos: Seeye

Prints

Whittington.R.O and K. Pany(2004) Principles of Auditing and other

Assurance Services,

New York: McGraw-Hill/Irwin

BPP Learning Media (2008) ACCA

Paper 2 – corporate reporting Whittington R.O and K Pany

(2004)