Enhancing ASEAN Minerals Trade and Investment

134

Enhancing ASEAN Minerals Trade and Investment REPSF Project No. 04/009b Authors: ABARE Jane Mélanie, Marina Kim, Sam Hester, Peter Berry, Allison Ball and Karen Schneider Mekong Economics Paul Burke, Le Hoa Au Duong and Adam McCarty Final Report December 2005 The views expressed in this report are those of the authors, and not necessarily those of the ASEAN Secretariat and/or the Australian Government.

Transcript of Enhancing ASEAN Minerals Trade and Investment

Enhancing ASEAN Minerals Trade and Investment REPSF Project No. 04/009b Authors: ABARE Jane Mélanie, Marina Kim, Sam Hester, Peter Berry, Allison Ball and Karen Schneider

Mekong Economics Paul Burke, Le Hoa Au Duong and Adam McCarty

Final Report December 2005

The views expressed in this report are those of the authors, and not necessarily those of the ASEAN Secretariat and/or the Australian Government.

Enhancing ASEAN Minerals Trade and Investment

REPSF Project 04/009b: Final Report i

ABSTRACT

The development of mineral resources has contributed to economic growth and development in many of the world’s economies. The mining sector has the potential to boost economic growth through the provision of employment, export revenues and investment in infrastructure and human capital. Most ASEAN member countries are highly prospective in terms of minerals. However, to date, much of this potential has remained largely untapped.

In this study, the factors underlying the relatively weak performance of the minerals sector in ASEAN member countries are investigated. The assessment reveals that the sector remains constrained by economy wide impediments, such as weak governance and underdeveloped infrastructure, and minerals sector issues, such as poor geological information and regulatory uncertainty. These factors affect the ability of ASEAN member countries to secure the necessary investment to sustain the development of capital intensive and long term minerals projects.

The prospects for the minerals sector in ASEAN will be influenced not only by the emerging opportunities in global minerals markets, but critically on the readiness and capacity of individual ASEAN member countries to address the major obstacles to the development of the sector within their respective economic, social and political settings.

Enhancing ASEAN Minerals Trade and Investment

REPSF Project 04/009b: Final Report iii

CONTENTS

ABSTRACT.............................................................................................................................. I CONTENTS............................................................................................................................ III LIST OF TABLES ...................................................................................................................V LIST OF FIGURES.................................................................................................................VI LIST OF BOXES ...................................................................................................................VII ABBREVIATIONS................................................................................................................VIII ACKNOWLEDGMENTS ........................................................................................................IX EXECUTIVE SUMMARY ........................................................................................................X

A. Study objectives ........................................................................................................ x B. Minerals sectors of the ASEAN region.................................................................... x C. Global outlook for minerals .................................................................................... xii D. Investment in the minerals sector......................................................................... xiii E. Policy recommendations ........................................................................................ xv F. The role of regional cooperation......................................................................... xviii

I. INTRODUCTION ............................................................................................................... 1 II. OVERVIEW OF THE ASEAN MINERALS SECTOR........................................................ 3

A. Economic contribution of the minerals sector ....................................................... 3 B. Mineral reserves ........................................................................................................ 4 C. Minerals production .................................................................................................. 6 D. Minerals consumption............................................................................................... 9 E. Minerals trade .......................................................................................................... 10

III. GLOBAL OUTLOOK FOR MINERALS .......................................................................... 13 A. Outlook overview..................................................................................................... 15

1. Aluminium .......................................................................................................... 15 2. Bauxite................................................................................................................ 17 3. Copper ................................................................................................................ 17 4. Gold..................................................................................................................... 20 5. Lead .................................................................................................................... 22 6. Nickel .................................................................................................................. 23 7. Tin ....................................................................................................................... 25 8. Zinc ..................................................................................................................... 26 9. Gemstones ......................................................................................................... 28

B. The role of China ..................................................................................................... 30 C. Implications of global minerals outlook for ASEAN............................................. 30 D. Sensitivity of outlook to key variables .................................................................. 31 E. Market access issues.............................................................................................. 35

1. Global trade environment for minerals............................................................ 35 2. The proposed EU REACH legislation .............................................................. 39

IV. INVESTMENT IN THE MINERALS SECTOR IN ASEAN............................................... 41 A. Investment flows in the minerals sector ............................................................... 42

1. Total investment ................................................................................................ 42 2. Foreign direct investment................................................................................. 43 3. Future investment prospects ........................................................................... 46

B. Institutional and regulatory arrangements affecting investment in the minerals sector........................................................................................................................ 47

Enhancing ASEAN Minerals Trade and Investment

iv REPSF Project 04/009b: Final Report

1. National institutions and regulations .............................................................. 47 2. Regional investment frameworks .................................................................... 54

C. Key determinants of minerals sector investment................................................. 55 1. Minerals sector investment decision criteria.................................................. 55

Economy wide factors.......................................................................................... 56 Minerals sector factors......................................................................................... 58 Environmental and social factors......................................................................... 58

2. Minerals sector investment decision model ................................................... 59 D. Key impediments to minerals sector investment in ASEAN ............................... 60

1. Economy wide impediments ............................................................................ 61 2. Minerals sector impediments ........................................................................... 63 3. Environmental and social issues ..................................................................... 66

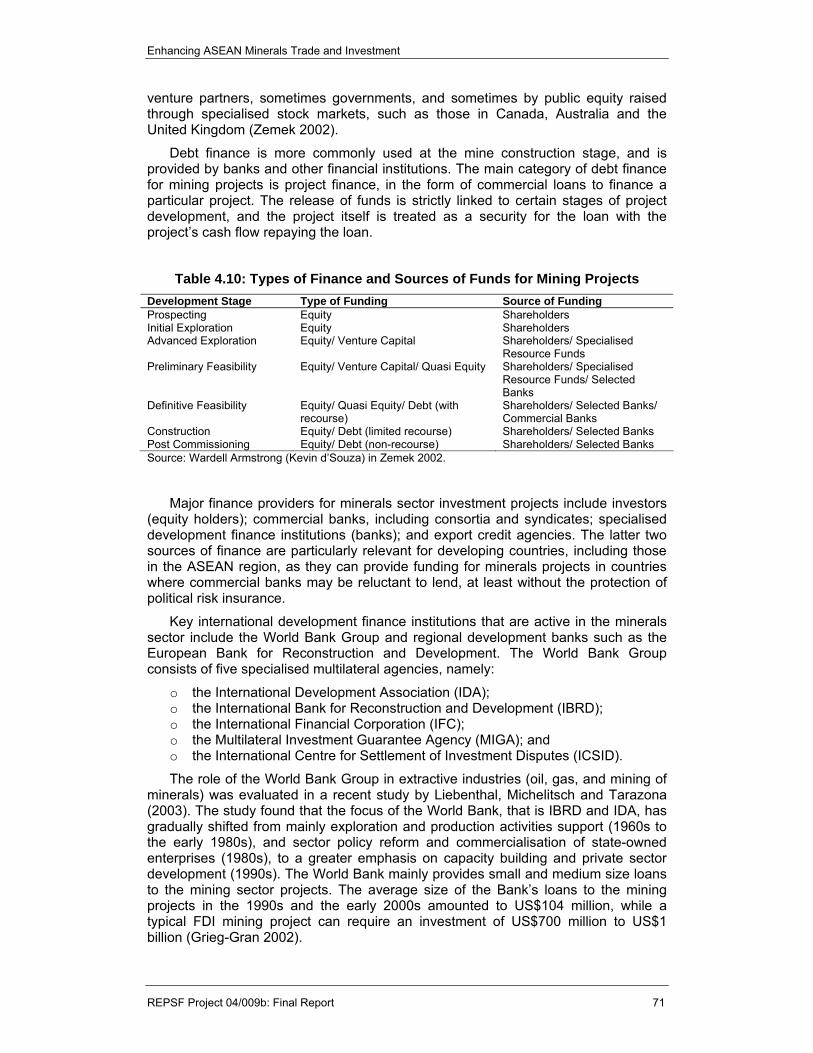

E. Risk, investment and economic activity................................................................ 67 F. Funding investment................................................................................................. 70

V. POLICY RECOMMENDATIONS..................................................................................... 75 A. Economy wide recommendations.......................................................................... 76

1. AMCAP Strategy 1: Facilitating trade and investment................................... 76 Competitive neutrality .......................................................................................... 76 Trading rights....................................................................................................... 76 Foreign direct investment .................................................................................... 76 Infrastructure development .................................................................................. 76 Access to finance................................................................................................. 77

2. AMCAP Strategy 3: Strengthening institutional and human capacities....... 77 Governance ......................................................................................................... 77

B. Minerals sector recommendations ........................................................................ 77 1. AMCAP Strategy 1: Facilitating trade and investment................................... 77

Reliability and availability of basic geological information ................................... 77 Land access......................................................................................................... 78 Regulatory certainty............................................................................................. 78 Security of tenure................................................................................................. 79 Competitive taxation regime ................................................................................ 79

2. AMCAP Strategy 2: Promoting environmentally and socially sustainable mineral development............................................................................................... 80 3. AMCAP Strategy 3: Strengthening institutional and human capacities....... 81

VI. ASEAN COOPERATION IN MINERALS: MAXIMISING OPPORTUNITIES.................. 83 A. Potential benefits of ASEAN cooperation in minerals ......................................... 83 B. ASEAN minerals cooperation to date .................................................................... 84 C. AMCAP 2005-2010 and the prospects for regional cooperation ......................... 90 D. Conclusion ............................................................................................................... 92

REFERENCES...................................................................................................................... 95 APPENDIXES .....................................................................................................................101

A. Appendix 1: A brief technical description of the GTEM model ......................... 101 B. Appendix 2: Interview program............................................................................ 104 C. Appendix 3: About the authors ............................................................................ 110

Enhancing ASEAN Minerals Trade and Investment

REPSF Project 04/009b: Final Report v

LIST OF TABLES

Table 1: FDI in Mining and Quarrying, ASEAN member countries, 1999-2003, US$ Million ...................................................................................................................... xiii

Table 2.1: Distribution of Metallic Mineral Reserves in ASEAN.................................. 4 Table 2.2: Estimated Reserves of ASEAN Key Metallic Minerals ............................... 5 Table 2.3: Distribution of Non-Metallic Mineral Reserves in ASEAN.......................... 5 Table 2.4: ASEAN Production of Key Minerals, 2003................................................... 7 Table 2.5: ASEAN Gemstones Production, 2003.......................................................... 9 Table 3.1: World Aluminium Outlook........................................................................... 16 Table 3.2: World Copper Outlook................................................................................. 18 Table 3.3: World Gold Outlook ..................................................................................... 20 Table 3.4: World Lead Outlook..................................................................................... 22 Table 3.5: World Nickel Outlook................................................................................... 24 Table 3.6: World Tin Outlook........................................................................................ 26 Table 3.7: World Zinc Outlook...................................................................................... 27 Table 3.8: Most-Favoured-Nation Applied Duties on Selected Mineral Ores and

Concentrates and Metal Products.......................................................................... 37 Table 3.9: Common Effective Preferential Tariffs under the AFTA Scheme, 2005..37 Table 4.1: Minerals Sector Investment in ASEAN member countries, 1997-2004, $US

Million ....................................................................................................................... 43 Table 4.2: FDI in Mining and Quarrying, ASEAN member countries, 1999-2003, US$

Million ....................................................................................................................... 45 Table 4.3: FDI in the ASEAN Mining and Quarrying Sector by Major Source

Country, 1999-2003, US$ Million ............................................................................ 45 Table 4.4: Major Recently Approved Investment Projects in the Metallic Minerals

Sector in ASEAN...................................................................................................... 46 Table 4.5: Summary of Minerals Regulations in ASEAN member countries ........... 51 Table 4.6: Timeframes for the Phasing Out of Temporary Exclusion List ............... 55 Table 4.7: Ranking of Investment Decision Factors at the Exploration and Mining

Stages....................................................................................................................... 56 Table 4.8: Credit Risk Assessments of ASEAN member countries and Associated

GTEM Risk Classifications ..................................................................................... 69 Table 4.9: Assumed Increase in Investment for Each Country Risk Group, Relative

to the Reference Case at 2010................................................................................ 69 Table 4.10: Types of Finance and Sources of Funds for Mining Projects ............... 71

Enhancing ASEAN Minerals Trade and Investment

vi REPSF Project 04/009b: Final Report

LIST OF FIGURES

Figure 1: Production of Key Metallic Minerals in ASEAN, 2003................................. xi Figure 2: Forecast Average Annual Growth in World Metals Consumption, 2004-

2010...........................................................................................................................xii Figure 3: Key Impediments to Minerals Sector Investment in ASEAN.................... xiv Figure 2.1: ASEAN Minerals Production as a Share of GDP (%), 2003 ...................... 4 Figure 2.2: Production of Key Minerals in ASEAN, 2003 ............................................. 6 Figure 2.3: ASEAN Share of World Minerals Production (%), 2003 ............................ 7 Figure 2.4: ASEAN Production of Key Minerals by Country, 1990-2004 .................... 8 Figure 2.5: ASEAN Production of Key Minerals, 1990-2004 ........................................ 8 Figure 2.6: ASEAN Consumption of Key Metals, 1990-2004 ..................................... 10 Figure 2.7: ASEAN Trade in Key Minerals, 2003......................................................... 11 Figure 3.1: Forecast Average Annual Growth in World Metals Consumption, 2004-

2010...........................................................................................................................15 Figure 3.2: Outlook for World Metals Consumption to 2010 ..................................... 15 Figure 3.3: Forecast Average Annual Growth in China’s Metals Consumption, 2004-

2010...........................................................................................................................30 Figure 3.4: Per cent Change in Global Consumption of Selected Mineral

Commodities under Higher Economic Growth in China, Relative to the Reference Case at 2010........................................................................................... 33

Figure 3.5: Per cent Change in ASEAN Production of Selected Mineral Commodities under High Productivity Growth Assumptions in ASEAN Mining, Relative to the Reference Case at 2010................................................................. 34

Figure 3.6: Per cent Change in ASEAN Exports of Selected Mineral Commodities under High Productivity Growth Assumptions in ASEAN Mining, Relative to the Reference Case at 2010........................................................................................... 35

Figure 4.1: Minerals Sector Investment Decision Model ........................................... 60 Figure 4.2 Key Impediments to Minerals Sector Investment in ASEAN................... 61 Figure 4.3: Change in GDP in ASEAN under Alternative Scenarios of Investment

Growth, Relative to the Reference Case at 2010 .................................................. 70 Figure 4.4: IFC’s Extractive Industries Approvals, 1990-2002 .................................. 72 Figure 6.1: ASEAN Minerals Cooperation ................................................................... 85 Figure 6.2: ASEAN Minerals Cooperation Areas ........................................................ 87 Figure 6.3: Regional Cooperation Spectrum .............................................................. 89

Enhancing ASEAN Minerals Trade and Investment

REPSF Project 04/009b: Final Report vii

LIST OF BOXES

Box 3.1: Key Characteristics of Selected Metallic Minerals ...................................... 14 Box 3.2: ABARE’s Global Trade and Environment Model (GTEM) ........................... 32 Box 4.1: Taxes Affecting the Minerals Sector............................................................. 48 Box 4.2: Types of Mineral Royalties ............................................................................ 49 Box 4.3: Minerals Sector Risks .................................................................................... 57

Enhancing ASEAN Minerals Trade and Investment

viii REPSF Project 04/009b: Final Report

ABBREVIATIONS

AADCP ASEAN – Australia Development Cooperation Program

ABARE Australian Bureau of Agricultural and Resource Economics

AFTA ASEAN Free Trade Area

AIA ASEAN Investment Area

AMCAP ASEAN Minerals Cooperation Action Plan

AMMin ASEAN Ministerial Meeting on Minerals

APEC Asia Pacific Economic Cooperation

ASEAN Association of Southeast Asian Nations

ASOMM ASEAN Senior Officials Meeting on Minerals

CEPT Common Effective Preferential Tariff

ECA Export Credit Agency

FDI Foreign Direct Investment

GDP Gross Domestic Product

GEMEED Expert Group on Minerals and Energy Exploration and Development

GTAP Global Trade Analysis Project

GTEM Global Trade and Environment Model

IBRD International Bank for Reconstruction and Development

ICSID International Centre for Settlement of Investment Disputes

IDA International Development Association

IFC International Financial Corporation

MIGA Multilateral Investment Guarantee Agency

MKE Mekong Economics Ltd

NGO Non-Government Organisation

OECD Organisation for Economic Cooperation and Development

REACH Registration, Evaluation and Authorisation of Chemicals

REPSF Regional Economic Policy Support Facility

WTO World Trade Organisation

Enhancing ASEAN Minerals Trade and Investment

REPSF Project 04/009b: Final Report ix

ACKNOWLEDGMENTS

This study was made possible by funding support from the Regional Economic Policy Support Facility under the ASEAN–Australia Development Cooperation Program.

The authors gratefully acknowledge the assistance provided by government and industry organisations that were consulted throughout the preparation of this report. While the extensive list of participants in the interview program (see Appendix 2) makes it impractical to thank each interviewee individually, we are highly appreciative of the valuable insights, information and comments provided by all. The authors also thank national study coordinators and Australian Embassy officers for facilitating consultations with industry and government organisations.

We would also like to acknowledge the constructive feedback of participants at the following meetings: the 2nd Special ASEAN Senior Officials Meeting of Minerals Experts (9 June 2005 – Langkawi), the 2nd Private Sector Forum on Minerals Cooperation (1 August 2005 – Kuching) and the 7th ASEAN Senior Officials Meeting on Minerals (2 August 2005 – Kuching).

We are also grateful for valuable contributions to the project made by ABARE colleagues. In particular, thanks are due to Andrew Maurer (formerly of ABARE), Frank Drum, Wil Mollard, Simon Richmond and Ryan Wilson for the commodity outlook notes, and to Lindsay Hogan, Jammie Penm and Don Gunasekera for helpful advice and comments.

Enhancing ASEAN Minerals Trade and Investment

x REPSF Project 04/009b: Final Report

EXECUTIVE SUMMARY

The Association of Southeast Asian Nations (ASEAN) region is well endowed with mineral resources. However, to date, the minerals sector has performed below its potential in the majority of member countries, reflecting a diverse set of regulatory and institutional constraints. In an environment of growing global demand for mineral based commodities, the sustainable development of these resources has the potential to deliver substantial economic benefits to ASEAN member countries. In some of these countries, the mining sector represents a large potential source of government revenue, that could contribute to the resources required to finance social and physical infrastructure to support economic growth and alleviate poverty. In other countries, the development of the sector also provides an opportunity to create a diversified and more resilient economic portfolio.

A. STUDY OBJECTIVES The key objectives in this study, undertaken jointly by the Australian Bureau of

Agricultural and Resource Economics (ABARE) and Mekong Economics Ltd (MKE) for the ASEAN Secretariat, through the ASEAN-Australia Development Cooperation Program (AADCP) Regional Economic Policy Support Facility (REPSF), are as follows:

o identify key mineral commodities in ASEAN in terms of resources, production and trade;

o assess the international market outlook for minerals, including mineral processing activities, and examine ASEAN’s actual and potential economic and trade performance in the light of the policy and market environment;

o evaluate current regulatory and institutional arrangements in ASEAN member countries that govern investment, including foreign direct investment, in the minerals sector, and identify the factors determining the attractiveness of investment in that sector; and

o provide recommendations for enhancing the attractiveness of investment in the minerals sector in ASEAN, taking into account the potential role of regional cooperation.

The focus in this study is primarily on high value globally traded non-energy minerals significant in the ASEAN region. These include metallic minerals such as gold, copper and tin, and gemstones. It should be noted, however, that locally and regionally traded mineral products, in particular non-metallic minerals, often dominate in volume terms in several ASEAN member countries.

B. MINERALS SECTORS OF THE ASEAN REGION From a regional perspective, ASEAN’s role in global minerals production, consumption

and trade is currently relatively limited, with the exception of tin, nickel and copper for which the region contributes a significant share of world production and trade. Minerals production accounted for 0.9% of ASEAN gross domestic product (GDP) in 2003. However, within the region, there is significant variation in the composition and volume of minerals produced, reflecting different resource endowments, economic structures and socio-political settings. The contribution of minerals production to GDP is highest in Indonesia (2.3%), followed by the Lao PDR (1.7%), and the Philippines (1.6%).

Minerals production in ASEAN is backed by diverse reserves of both metallic and non-metallic minerals. A lack of consistent reserves data across all ASEAN member countries makes it difficult to provide definitive estimates for the region as a whole. Indonesia accounts for a significant share of ASEAN and world mineral reserves, including 7.5% of the world’s

Enhancing ASEAN Minerals Trade and Investment

REPSF Project 04/009b: Final Report xi

known reserves of copper, more than 13% of known reserves of tin, more than 5% of known reserves of nickel, and more than 4% of the world’s known gold reserves (USGS 2005). Myanmar, the Philippines, Thailand and Viet Nam are also well endowed with substantial mineral wealth.

Different resource endowments, risk profiles, levels of economic development and regulatory and institutional factors account for the considerable diversity in the size and scope of minerals production across countries in the region (Figure 1). Indonesia is by far the largest producer of a number of metallic mineral commodities, mainly as a result of its rich mineral endowment and government promotion of investment in the mining sector. In value terms, the key minerals produced in ASEAN member countries are nickel, copper, tin and gold, with Indonesia being the main producer of these metals. For tin, nickel and copper, ASEAN production represents a significant share of world production, accounting for 29%, 11% and 8% of global production respectively. Other metallic minerals produced on a smaller scale in the region include bauxite, lead, zinc and iron ore. In 2003, ASEAN total minerals production was valued at around US$5.9 billion.

ASEAN member countries are also significant producers of a wide array of non-metallic minerals, including gemstones, gypsum, limestone, kaolin, phosphate rock, sand, gravel and a wide range of other industrial minerals. Non-metallic minerals production is important for the economies of the Lao PDR, Malaysia and Myanmar, and constitutes a significant share of total minerals production in Thailand and Viet Nam.

There are limited processing facilities in ASEAN and most of the production of metallic minerals is exported as ores and concentrates for processing/refining outside the region. However, some mineral processing occurs in the region, particularly of copper, bauxite, lead, zinc and tin. As the largest producer of mineral ores and concentrates, Indonesia is also the main producer of refined mineral products. Some of the refined metals produced locally in ASEAN member countries are consumed by domestic manufacturing and construction industries, although the region generally relies on imports of refined metals to meet consumption requirements.

Figure 1: Production of Key Metallic Minerals in ASEAN, 2003

Note: Production in thousand tonnes; gold production is in tonnes. Source: World Bureau of Metal Statistics 2005.

Enhancing ASEAN Minerals Trade and Investment

xii REPSF Project 04/009b: Final Report

ASEAN accounts for a substantial share of world trade in tin, copper and nickel, although its role in world markets for other mineral commodities is relatively minor. In 2003, ASEAN export volumes of refined tin accounted for 58% of world trade, while exports of unrefined and refined copper accounted for 16% and 6% of world trade respectively. In value terms, the key ASEAN minerals exports over the 10 years to 2003 were copper, aluminium, tin and nickel. The value of ASEAN exports of metallic minerals grew rapidly until 1995, largely led by strong growth in copper and aluminium. From this peak, the value of minerals exports declined, to be more than 8% below the 1995 level in 2002, reflecting lower world prices for copper, nickel, zinc and tin over the period. However, world demand for metals rose significantly in 2003 and 2004, resulting in strong price rises for mineral commodities. As a consequence, the value of ASEAN exports of copper, nickel, aluminium, lead, zinc, tin and other base metals rose by more than 62% to US$7.1 billion in 2003 (AFTA 2005). With increased ASEAN minerals production and stronger metals prices, the value of ASEAN minerals exports has risen significantly in 2004 and 2005.

In contrast with metallic minerals, a significant proportion of ASEAN non-metallic minerals production is consumed locally. Some higher value non-metallic minerals, such as gemstones, are largely exported, both to foreign countries and other ASEAN member countries.

C. GLOBAL OUTLOOK FOR MINERALS Economic growth, supported by growth in the construction, infrastructure and

manufacturing sectors, will remain the key driver of world minerals and metals consumption over the medium to longer term. Also important will be continued population growth and rising per person incomes.

Global consumption of most refined minerals considered in this study is projected to grow by more than 3% a year between 2004 and 2010 (Figure 2). The strongest growth in consumption is expected to occur in aluminium, followed by nickel, tin and zinc. World gold consumption is projected to grow at a slower rate, at around 1.5% a year out to 2010.

Figure 2: Forecast Average Annual Growth in World Metals Consumption, 2004-2010

Source: ABARE.

Continued growth in demand in China is expected to be one of the key drivers of world metals consumption in the coming years. In the medium term, China’s consumption of all mineral commodities is expected to grow well above the average world growth rates. More specifically, annual growth of more than 10% is expected in China’s consumption of nickel,

Enhancing ASEAN Minerals Trade and Investment

REPSF Project 04/009b: Final Report xiii

tin and zinc. Aluminium and copper consumption in China are forecast to grow by 9% a year over the period to 2010. The strong demand for minerals in China can be expected to provide significant opportunities for minerals producers worldwide. In 2003, China accounted for close to 7% of total exports of mineral products from ASEAN (AFTA 2005). The expected growth in China’s minerals demand represents an important opportunity for ASEAN member countries to become more prominent players on the international minerals scene by taking advantage of their mineral prospectivity, geographical proximity to key markets and relatively low labor costs.

D. INVESTMENT IN THE MINERALS SECTOR A key determinant of ASEAN member countries’ ability to capitalise on future growth

opportunities in world minerals markets is their capacity to secure the necessary investment to support long term capital intensive mining projects. Domestic sources of finance are often constrained and unable to satisfy total demand for investment, making minerals sector developments in ASEAN strongly dependent on inflows of foreign direct investment (FDI).

Investment in the ASEAN minerals sector over the past decade has remained relatively limited and concentrated in a handful of member countries. Mining sector investment typically contributes a small percentage of total investment in ASEAN, representing less than 5% of total investment in most ASEAN member countries in recent years. As can be expected, countries with a more established minerals sector, such as Indonesia, have received larger investment inflows than countries where the minerals sector is less mature, such as Cambodia.

Over time, foreign investment has increasingly become a dominant factor in total capital flows in a number of countries in the region. However, while several ASEAN member countries have established minerals sectors built on FDI, the relatively new ASEAN members have opened their doors to foreign investment only recently. Over the period 1999-2003 (the period for which data are available), FDI in the ASEAN mining and quarrying sector was highly variable, with a low of US$635 million in 2000 and a peak of US$1.6 billion in 2001. Similarly, the share of FDI in the ASEAN mining and quarrying sector as a proportion of total FDI in ASEAN fluctuated widely, ranging from 3% in 2000 to 10% in 2002 (Table 1).

Table 1: FDI in Mining and Quarrying, ASEAN member countries, 1999-2003, US$ Million

1999 2000 2001 2002 2003 1999-2003 Share of FDI in mining and quarrying,

1999-2003a (%) Indonesia (211.0) (275.3) (233.7) (242.3) 232.3 (729.9) - Lao PDR 12.2 9.2 2.0 4.8 9.5 37.7 1 Malaysia 722.4 677.4 911.1 1,089.0 253.0 3,652.8 61 Myanmar 220.2 107.2 111.2 162.9 112.7 714.1 12 The Philippines 379.0 79.9 (1.0) 22.3 (7.5) 472.7 8 Thailand (41.8) (274.7) 518.0 (97.0) (5.0) 99.4 2 Viet Nam 264.6 311.2 298.6 406.7 431.8 1,712.8 29 ASEAN 1,345.6 634.9 1,606.2 1,346.4 1,026.8 5,959.6 100 Share of total FDI in ASEAN (%)

5 3 8 10 5 3

a: Indonesia had a negative net FDI flow over the period 1999-2003. The share is not reported to avoid confusion related to the sign of the percentage. FDI = foreign direct investment. Note: negative numbers are enclosed in parentheses. Source: ASEAN Secretariat 2004a.

Enhancing ASEAN Minerals Trade and Investment

xiv REPSF Project 04/009b: Final Report

This broad regional profile is underpinned by significant diversity across individual countries. In particular, in the period between 1999 and 2003, FDI in mining and quarrying declined in the Philippines, while rising sharply in the Lao PDR, and more moderately in Myanmar since 2001. Indonesia and Thailand mostly saw FDI outflows from the sector over the 5-year period to 2003. More than 60% of total FDI in ASEAN mining and quarrying was directed to Malaysia and was largely associated with oil and natural gas.

There is a wide assortment of factors that determine a country’s ability to attract foreign investment in the minerals sector. Some factors are common to investment decisions across all sectors. Typically, these relate to the maturity and stability of the political, economic and legal systems in a potential host country, and the availability of infrastructure. Other factors are more specific to the minerals sector and include geological potential, security of tenure, taxation regimes, and access to technologies and skilled labor.

Importantly, environmental and social considerations are also having a strong bearing on investment decisions pertaining to the minerals sector. Poor environmental management during the early development of the industry has tarnished the image of the sector in several ASEAN member countries, giving rise to strong anti-mining sentiments. Further, it is increasingly recognised that much of the environmental damage caused by mining activities has a direct impact on local communities in terms of their livelihoods and health. Against this background, it is becoming increasingly clear that the institutions and systems that countries establish to regulate, manage and monitor the environmental impact of mining operations directly influence the extent of investors’ interest in starting up a particular mining operation.

In view of the general objective to increase FDI in the region, ASEAN member countries have achieved significant progress in liberalising their trade and investment regimes. However, to date, the minerals sector has not been successful in attracting a significant share of total FDI inflows in the majority of ASEAN member countries. This reflects a wide spectrum of economy wide and sector specific impediments that have constrained the development of the sector. An assessment of the key impediments, as identified through the extensive consultation program in individual ASEAN member countries, is summarised in Figure 3.

Figure 3: Key Impediments to Minerals Sector Investment in ASEAN

A key impediment at the economy wide level is weak governance at many levels including weak rule of law, lack of transparency and accountability, and lack of partnership between government and non-government organisations.

Enhancing ASEAN Minerals Trade and Investment

REPSF Project 04/009b: Final Report xv

In terms of sector specific issues, uncertainty, whether related to the scope and implementation of regulations, the process for obtaining exploration and mining licences, or the resolution of land access issues, represents a significant impediment to investment in many of the countries in the ASEAN region. These factors, combined with shortcomings at the broader economy wide level, contribute to raise the risks associated with mining activities in the region. The higher the risks involved, the higher the rate of return required to attract investment in the minerals sector.

E. POLICY RECOMMENDATIONS The development of the minerals sector within a country calls for a strong and effective

policy framework. Governments are ultimately responsible for the regulatory and institutional settings within which mining takes place in a given jurisdiction, and their actions are critical to achieving sustainable benefits from the minerals industry for the national economy. More specifically, the sustainable development of the minerals sector is contingent on the provision of strategic direction; the requisite legal, regulatory and institutional frameworks to pursue economic, social and environmental objectives; accountability, transparency, and stakeholder consultation; and systems to deliver tangible benefits to the country’s citizens.

These conditions are also necessary for attracting the substantial levels of private sector investment, particularly FDI, required to underpin the development of the minerals sector in ASEAN member countries. At a time when globalisation is creating new opportunities for investment and increasing competition for mining capital, maintaining a stable and facilitative policy climate is becoming more important, and more challenging than it has ever been.

Key policy recommendations to address the wide spectrum of shortcomings identified in the report are summarised below. These recommendations are structured within the framework of the ASEAN Minerals Action Plan (AMCAP) 2005-2010. Country specific recommendations to improve the trade and investment environment in individual ASEAN member countries are provided in the Country Reports (see Volume II).

Economy wide recommendations In order to enhance trade and investment in the minerals sector, governments in

ASEAN member countries should address issues at the economy wide level. In particular, governments should:

AMCAP Strategy 1: Facilitating trade and investment o have a clear sense of direction, vision and purposeful commitment to ensure that

there is a level playing field across all economic sectors in terms of fiscal and other economic conditions;

o convey their commitment to the community through targeted and sustained education programs designed to enhance the profile of the minerals sector in terms of its potential economic benefits and environmental performance;

o minimise the involvement of state-owned enterprises in the operation of resources sectors and remove any conflict of interest between the government as a regulator and developer of natural resources;

o remove all non-tariff barriers to trade affecting the minerals sector both directly and indirectly;

o remove restrictions on FDI in order to facilitate further development of the region’s minerals sector. In some countries, this would involve removing quotas for domestic

Enhancing ASEAN Minerals Trade and Investment

xvi REPSF Project 04/009b: Final Report

investment in minerals sector enterprises. In several other countries, the relaxation of joint venture requirements would also assist to stimulate foreign investors’ participation in the development of extractive industries;

o create and maintain an environment characterised by a liberal trade and investment regime and stable macroeconomic conditions;

o reduce the commercial and political risks faced by potential investors;

o strengthen domestic capital markets through the provision of stable and unambiguous regulatory environments;

o consider the consolidation of equity markets across ASEAN member countries. Such a consolidated market would benefit from higher volumes, reduced trading costs and harmonised regulations;

AMCAP Strategy 3: Strengthening institutional and human capacities o continue to invest in capacity building programs to strengthen the technical,

regulatory, legal, commercial and administrative skills of public sector agencies involved in regulation of the minerals and other sectors;

o pay particular attention to capacity building at the local government level in terms of personnel, financial resource management, and intra- and intergovernmental relationships;

o focus on delivering accountable, participative and results-oriented governance outcomes in countries where significant policy reform initiatives are already in place; and

o pursue an integrated and sustainable reform strategy, backed by strong political will and appropriate resourcing.

Minerals sector recommendations In addition to addressing economy wide issues, governments in ASEAN member

countries should address issues that affect the minerals sector specifically. In this context, governments should:

AMCAP Strategy 1: Facilitating trade and investment o strive to provide high level geoscientific information;

o in the presence of limited government resources, explore the opportunities for partnerships with industry, academia and community organisations to provide that information;

o generate support for collaborative research programs designed to add to the region’s mineral reserves by developing ways of finding new ores and extracting currently uneconomic resources in a sustainable manner;

o investigate the potential for donor funding to improve the capacity of ASEAN member countries to collect, compile and disseminate geological information;

o adopt a market based system for determining the optimal allocation of land resources, in cases where property rights can be assigned to particular land uses;

o devote additional resources to the development of regulatory frameworks for allocating and securing property rights over land resources where property rights are not clearly defined;

Enhancing ASEAN Minerals Trade and Investment

REPSF Project 04/009b: Final Report xvii

o where property rights cannot be defined, adopt transparent and consistent administrative processes and procedures to remove the uncertainty surrounding access to land resources;

o ensure that these processes and procedures are flexible enough to allow new information related to mining technologies, for example, as well as changes in economic factors such as minerals prices, to be taken into account;

o ensure that the licensing process is clear, efficient and transparent, while acknowledging that improving regulatory certainty in the minerals sector requires an enhancement of both regulations themselves and institutions that carry out their implementation;

o where laws are vague or incomplete, pay attention to improving their clarity and broadening their scope;

o strengthen institutions to ensure that government agencies are consistent in their application of regulations, acknowledging that improving regulatory certainty in the minerals sector is closely linked to the broader issues of improving governance generally and reducing sovereign risk;

o provide clear information about existing regulations and procedures, including licensing processes, to potential investors in a readily accessible form;

o consider the establishment of a ‘one-stop shop’ for minerals sector investment;

o consider the potential contribution of the private sector in identifying the weaknesses in existing regulations and procedures and in designing and delivering appropriate capacity building programs;

o ensure that the requirements for investors to proceed from an exploration licence to a mining licence are clear and transparent so as to reduce the actual and perceived risks involved in allocating substantial capital resources at the high risk exploration stage;

o specify the conditions under which a title can be revoked;

o ensure that minerals rights are exclusive, and transferable to other enterprises, provided that all technical, financial, environmental and other requirements are met;

o move toward mining taxation regimes that are:

- internationally competitive and allow a fair share of benefits between governments and investors;

- easy to understand;

- easy to administer;

- stable and predictable over time;

- non-discriminatory;

- transparent; and

- provide a level playing field for all participants.

o consider their minerals sector taxation regimes in comparison with those of countries with more established minerals sectors and countries that have had recent success in attracting substantial capital inflows to their minerals sector (Chile and Mongolia, for example), taking into consideration that the mix of minerals produced, the degree of decentralisation and the level of economic development will affect the composition of minerals taxation regimes across countries;

Enhancing ASEAN Minerals Trade and Investment

xviii REPSF Project 04/009b: Final Report

o develop taxation regimes for the minerals sector with a full understanding of the international context in which mining companies operate;

o move toward the adoption of royalty arrangements that are linked to profitability, given the cyclical nature of minerals markets;

AMCAP Strategy 2: Promoting environmentally and socially sustainable mineral development o demonstrate their commitment and ability to set appropriate and reliable

environmental rules, at acceptable international standards, and to monitor these standards in a credible manner;

o where the legal and institutional settings are not in place, initiate a process of gradually establishing:

- a legal basis for environmental regulation;

- basic institutional responsibilities;

- essential regulatory frameworks;

- monitoring and enforcement procedures, including public disclosure; and

- human and financial resources to address priority issues, taking into account that the methods employed for achieving environmental objectives will vary considerably on the basis of different local, natural, socio-economic and cultural conditions;

o where the legal and related institutional mechanisms are already in place, focus on the implementation of these frameworks and in finding pragmatic solutions that take into account resource and capacity constraints;

o work with the private sector to address the environmental liabilities that the mining sector has inherited from past operations;

o provide strong underlying regulatory regimes to encourage the development of, participation in, and continued evolution of effective voluntary initiatives;

o consider more explicitly the social impact of mining, particularly on local communities that rely on the natural environment for their livelihoods; and

AMCAP Strategy 3: Strengthening institutional and human capacities o seek to improve technical skills in geology, mine engineering, environmental sciences

and other disciplines related to the mining sector through regional cooperation initiatives and public-private sector partnerships.

F. THE ROLE OF REGIONAL COOPERATION The majority of constraints to the development of the minerals sectors in ASEAN member

countries are driven by domestic policies. Consequently, most of the reforms required to improve the investment environment in the minerals sector are also domestic in nature.

However, significant potential also exists for regional cooperation to complement domestic efforts to improve the trade and investment environment in the minerals sector. Governments have a role to play in the provision of public goods such as high level geological information, and the facilitation of an enabling regime for private sector investment. ASEAN cooperation in minerals can enhance the ability of ASEAN governments to carry out these functions at both the domestic and regional levels through activities

Enhancing ASEAN Minerals Trade and Investment

REPSF Project 04/009b: Final Report xix

ranging from the development of policy frameworks to the undertaking of joint scientific and economic research. Further, regional cooperation provides an opportunity to benefit from the potential economies of scale and scope in activities such as those involved in undertaking geological surveys.

To date, the role of ASEAN cooperation in the development of the minerals sector has been limited. However, recent advances under the ASEAN minerals cooperation umbrella have generated significant momentum in fostering stronger ties across ASEAN member countries. In particular, the ASEAN Minerals Cooperation Action Plan (AMCAP) 2005-2010, adopted at the first ASEAN Ministerial Meeting on Minerals (AMMin) in Malaysia in August 2005, is poised to become one of the most comprehensive regional minerals cooperation programs in the world. The AMCAP 2005-2010 identifies a comprehensive list of activities and projects to be carried out toward:

o facilitating and enhancing trade and investment in minerals; o promoting environmentally and socially sustainable mineral development; and o strengthening institutional and human capacities.

Importantly, the outcomes of the plan will be highly contingent on its effective implementation over the next 5 years. Implementation of the AMCAP will require resources, careful project planning, institutions that are capable of implementing the plan, and ongoing political will in ASEAN member countries.

Enhancing ASEAN Minerals Trade and Investment

xx REPSF Project 04/009b: Final Report

This page has intentionally been left blank

Enhancing ASEAN Minerals Trade and Investment

REPSF Project 04/009b: Final Report 1

I. INTRODUCTION

The development of mineral resources has contributed to economic growth and development in many of the world’s economies. The mining sector can boost economic growth and raise living standards through the provision of employment, both directly and indirectly, export revenues and investment in infrastructure and human capital. Minerals sector development can make a significant contribution not only in developing countries that may have few alternative drivers of economic growth, but also in countries that are seeking to diversify their economic structures in response to global market forces.

The Association of Southeast Asian Nations (ASEAN) region has abundant natural resources and is prospective in terms of both metallic and non-metallic minerals. Individual ASEAN member countries have a diverse mix of mineral endowments, different economic structures and political settings. In terms of the development of their mineral resources, they can be broadly categorised into three groups:

(i) those countries with more mature minerals sectors - Indonesia, Malaysia, the Philippines and Thailand;

(ii) those countries that have prospective yet immature minerals sectors - Cambodia, the Lao PDR, Myanmar and Viet Nam; and

(iii) those countries that do not have a strong mineral resource base - Brunei Darussalam and Singapore.

In comparison with its mineral wealth, ASEAN’s contribution to world non-energy minerals production, consumption and trade is generally relatively small, notwithstanding the region’s significant production of tin, nickel and copper. This reflects a range of factors, including limited access to capital, unsupportive regulatory regimes and weak institutions. Further, the bulk of ASEAN minerals production and trade currently occurs in ores and concentrates, rather than refined metals, with much of the value adding (and economic benefit) occurring outside the region.

In recent years, strong world economic growth has fuelled global demand for mineral commodities. This has resulted in significantly higher commodity prices that have created incentives and opportunities for ASEAN member countries to further develop their mineral resources. With strong global demand for mineral commodities expected to continue, ASEAN member countries will be well placed to boost economic growth and contribute to poverty alleviation through increased investment in the minerals sector. However, this will be depend on a number of factors. These revolve largely around the ability to provide and maintain a stable and constructive investment climate in the region, within a global context characterised by growing competition for limited capital resources.

This study, undertaken for the ASEAN Secretariat, through the ASEAN-Australia Development Cooperation Program (AADCP) Regional Economic Policy Support Facility (REPSF), has the following key objectives:

o identify key mineral commodities in ASEAN in terms of resources, production and trade;

o assess the international market outlook for minerals, including mineral processing activities, and examine ASEAN’s actual and potential economic and trade performance in the light of the policy and market environment;

o evaluate current regulatory and institutional arrangements in ASEAN member countries that govern investment, including foreign direct investment, in the minerals sector, and identify the factors determining the attractiveness of investment in that sector; and

o provide recommendations for enhancing the attractiveness of investment in the minerals sector in ASEAN, taking into account the potential role of regional cooperation.

Enhancing ASEAN Minerals Trade and Investment

2 REPSF Project 04/009b: Final Report

The focus in the study is primarily on high value, globally traded non-energy minerals significant in the ASEAN region. These include metallic minerals such as gold, copper and tin, and gemstones. It should be noted, however, that locally and regionally traded mineral products, in particular non-metallic minerals, often dominate in volume terms in several ASEAN member countries.

The report is structured as follows. An overview of the minerals sector in ASEAN member countries is presented in Chapter II. This is followed by an analysis of the global medium term outlook for key mineral commodities from the region’s perspective (bauxite, aluminium, copper, gold, lead, nickel, tin, zinc and gemstones). The implications of the outlook for ASEAN in terms of future trade prospects are also highlighted in Chapter III, taking into consideration market access issues relevant to minerals trade.

The focus of Chapter IV is on investment in the minerals sector in ASEAN. Recent patterns of investment, including foreign direct investment (FDI), in the minerals sector are examined. Existing regulatory and institutional arrangements affecting investment flows to the sector are also reviewed. Drawing on the extensive consultation program undertaken in ASEAN member countries (Appendix 2), this chapter also presents an assessment of the major impediments to attracting investment flows to the region’s mining sector.

In the light of the assessment presented in Chapter IV, key domestic policy recommendations to enhance trade and investment in the ASEAN minerals sector are provided in Chapter V. This is supplemented in Chapter VI by a discussion of the potential role of regional cooperation in pursuing the development of minerals sectors in ASEAN. Country specific recommendations are provided in Country Reports – Volume II (Mélanie, Kim, Hester, Berry, Ball, Schneider, Burke, Au Duong and McCarty 2005) that accompany this report (henceforth, referred to as Country Reports).

Enhancing ASEAN Minerals Trade and Investment

REPSF Project 04/009b: Final Report 3

II. OVERVIEW OF THE ASEAN MINERALS SECTOR o Most countries in the ASEAN region are prospective in terms of both metallic and

non-metallic mineral resources. However, despite this rich mineral potential, the contribution of the minerals sector to regional economic development is relatively limited. Minerals production accounted for around 0.9% of ASEAN gross domestic product (GDP) in 2003.

o There is considerable diversity in the size and scope of minerals production across countries in the region. This reflects varying resource endowments, risk profiles and levels of economic development, and the effectiveness of regulatory regimes and institutions. Indonesia is by far the largest producer of a number of metallic mineral commodities in ASEAN.

o For the region generally, metallic minerals production is more significant in value terms, while non-metallic minerals represent a larger share of production in volume terms. However, in Thailand and Viet Nam, non-metallic minerals are also more significant in value terms. Key metallic minerals produced in ASEAN include nickel, copper, tin and gold. Major non-metallic minerals produced in the region comprise gemstones, gypsum, limestone, kaolin and a wide range of other industrial minerals.

o Minerals consumption in ASEAN has been increasing, in parallel with the growth in manufacturing, infrastructure development and rising incomes in the region. Major processed metallic minerals consumed in ASEAN include aluminium, copper, zinc, lead, tin and nickel. However, much of the indigenous production of metallic minerals tends to be exported as ores and concentrates for processing outside the region, rather than being consumed in domestic mineral processing sectors.

o ASEAN has a substantial share of world trade in tin, copper and nickel, with major trading partners comprising Japan, the Republic of Korea and China, as well as other ASEAN member countries.

A. ECONOMIC CONTRIBUTION OF THE MINERALS SECTOR Reflecting the large variations in the maturity and intensity of development within the

minerals sector, the contribution of mining to overall economic development varies considerably across the ASEAN region. For the region as a whole, the minerals sector accounts for a relatively small share of GDP, with minerals production accounting for 0.9% of ASEAN GDP in 2003. The contribution of minerals production to GDP is highest in Indonesia (2.3%), followed by the Lao PDR (1.7%) and the Philippines (1.6%) (Figure 2.1). For comparison, production of metallic and non-metallic minerals accounts for 2.9% of GDP in Australia (ABARE 2004). Further, the mining sector makes an important contribution to GDP in Latin American economies, such as Chile, where it accounts for 8% of GDP. Notably, the contribution of the minerals sector to economic activity varies significantly on a provincial basis within some ASEAN member countries. In Indonesia, for example, the PT Freeport Indonesia copper mine contributed almost 50% of gross regional product in Papua province in 2000.

The minerals sector is also not a significant contributor to total employment in ASEAN, reflecting the small contribution of mining to economic activity and the capital intensive nature of the industry. However, the minerals sector has the potential to boost local employment in some of the least developed parts of the region, both directly and indirectly. It is estimated that at least 300,000 workers were directly employed in the ASEAN minerals sector in 2004. This figure is unlikely to include workers at unregulated and sometimes illegal small scale mining enterprises, which in some ASEAN member countries may be significant. For example, the Philippines has a large number of self-employed informal sector miners operating small scale gold mines. In addition, considerable numbers of workers in ASEAN

Enhancing ASEAN Minerals Trade and Investment

4 REPSF Project 04/009b: Final Report

member countries are employed indirectly by the sector, largely through the provision of goods and services to mining operations and their employees.

Figure 2.1: ASEAN Minerals Production as a Share of GDP (%), 2003

Sources: Country reports.

Incomes and revenues raised from the minerals sector can make an important contribution to economic development, both nationally and on a regional basis. The contribution of the minerals sector to government revenues varies significantly across ASEAN member countries. For example, in Indonesia, ASEAN’s largest minerals producer, an estimated US$1.1 billion, accounting for 2.7% of total government revenues, was raised from the mining industry in 2003 (Indonesia Country Report). In the Philippines, mining activities generated less than 1% of total government revenues in 2004.

B. MINERAL RESERVES Across ASEAN, known reserves are diverse and extensive for both metallic and non-

metallic minerals. However, the lack of consistent reserves data across all ASEAN member countries makes it difficult to provide definitive estimates for the region as a whole. Indonesia accounts for a significant share of ASEAN and world mineral reserves. Indonesia’s mineral reserves include 7.5% of the world’s known reserves of copper, more than 13% of known reserves of tin, more than 5% of known reserves of nickel, and more than 4% of the world’s known gold reserves (USGS 2005). Myanmar, the Philippines, Thailand and Viet Nam are also well endowed with substantial mineral wealth (Table 2.1). Where available, estimated reserves of key metallic minerals are summarised in Table 2.2.

Table 2.1: Distribution of Metallic Mineral Reserves in ASEAN Bauxite Copper Gold Iron

Ore Lead Nickel Silver Tin Zinc Other

Cambodia Indonesia Lao PDR Malaysia Myanmar The Philippines Thailand Viet Nam Sources: Country reports.

Enhancing ASEAN Minerals Trade and Investment

REPSF Project 04/009b: Final Report 5

Table 2.2: Estimated Reserves of ASEAN Key Metallic Minerals Bauxite Copper Gold Nickel Tin

Mt Mt kt Mt Mt Indonesiaa 2.8 4,772.2 3,379,486.0 598.9 0.5 Lao PDRb - 3.8 0.1 - 21.7 Malaysiac 18.0 0.8 0.1 75.0 0.9 The Philippines - 6,473.0 2,163,000.0 3,385.0 - Thailand - 96.5 2,746.0 - 0.3 Viet Namd 4,175.0 0.8 0.4 0.1 0.1 a: Includes proven plus probable reserves; b: Includes indicated, inferred and hypothetic resources; c: Indicative mineral reserves; d: Excludes possible resources. kt = thousand tonnes; Mt = million tonnes. Note: Reserves data refer to mineral ores. Reserves in terms of metal content is significantly lower. For example, gold reserves in Indonesia amount to 3000 tonnes in metal content. Sources: Country Reports.

Many ASEAN member countries are also endowed with significant reserves of non-metallic minerals, including gemstones, potash, silica, limestone, marble, gypsum and kaolin (Table 2.3). In a number of ASEAN member countries, including Indonesia, the Philippines and Thailand, non-metallic mineral reserves are larger than those of metallic minerals. However, in value terms, reserves of metallic minerals tend to be higher, reflecting the relatively higher prices for globally traded minerals.

Table 2.3: Distribution of Non-Metallic Mineral Reserves in ASEAN Gemstones Sands Clays Stones Gypsum Lime

stone Marble Granite Potash Other

Cambodia Indonesia Lao PDR Malaysia Myanmar The Philippines Thailand Viet Nam

Sources: Country reports.

There are large differences in the intensity of exploration that has been conducted and the known reserves of various minerals across ASEAN member countries. In Indonesia, for example, there is a significant amount of ongoing mineral exploration. However, in some other countries, there has been minimal exploration and limited data are available on mineral reserves. Brunei Darussalam and Singapore have little or no mineral potential.

In Indonesia, mining and exploration permits cover 2% of the country’s landmass, with actual mining projects covering less than 0.1% of the landmass. Permits cover 1.4% and 0.3% of the landmass in the Philippines and Malaysia, respectively. Other ASEAN member countries such as Cambodia, the Lao PDR, Myanmar and Viet Nam also have significant mineral prospectivity, but remain relatively unexplored. For example, based on available data, mineral resources of the Lao PDR are comparable to those of several countries in the region with larger mining industries such as Indonesia and the Philippines (World Bank 2003). Myanmar has the highest quality rubies and jade in the world and world-class deposits of lead-zinc-silver, tin-tungsten, fine rubies, sapphires and jade, while Viet Nam’s bauxite deposits are estimated to be among the largest in the world.

Enhancing ASEAN Minerals Trade and Investment

6 REPSF Project 04/009b: Final Report

C. MINERALS PRODUCTION Historically, mining activity has been unevenly distributed across ASEAN, reflecting a mix

of factors. These include varying resource endowments, risk profiles, levels of economic development, and regulatory and institutional settings. As a result, there is considerable diversity in the size and scope of minerals production across countries in the region (Figure 2.2). Indonesia is by far the largest producer of a number of metallic mineral commodities, mainly as a result of its rich mineral endowment and government promotion of investment in the mining sector. In Malaysia, which has a long and important history of tin mining, metallic minerals production has generally been declining over the past two decades, reflecting to a large extent the Government’s prioritisation of manufacturing as a pillar of economic development. Similarly, the Philippines mining sector has languished since the mid-1980s as a result of domestic factors such as political instability and restrictive minerals policies, and external factors, including sluggish commodity prices and natural disasters. The minerals sector in many less developed ASEAN member countries has typically lacked the investment and exploration needed to develop a sustainable minerals industry.

Figure 2.2: Production of Key Minerals in ASEAN, 2003

Note: Production in thousand tonnes; gold production in tonnes. Production data refer to metal content only. Source: World Bureau of Metal Statistics 2005.

In value terms, the key minerals produced in ASEAN member countries are nickel, copper, tin and gold, with Indonesia being ASEAN’s largest producer of these minerals. Other major metallic minerals produced in ASEAN include bauxite, lead, zinc and iron ore. Production of these minerals is widely dispersed across countries (Table 2.4). In 2003, ASEAN total minerals production was valued at around US$5.9 billion.

ASEAN production of tin, nickel and copper accounts for a significant share of world production of these commodities. ASEAN mine and refined tin production accounted for 29% and 33% of world production respectively in 2003. For nickel, ASEAN mine and refined production accounted for 11% and 1% of world production. For copper, ores and refined production in ASEAN member countries accounted for 8% and 3% of world production respectively (Figure 2.3).

Enhancing ASEAN Minerals Trade and Investment

REPSF Project 04/009b: Final Report 7

Table 2.4: ASEAN Production of Key Minerals, 2003 Bauxite Copper Gold Nickel Tin Zinc kt kt t kt kt kt

Indonesia 1,262.7 1,003.4 164.4 103.5 64.0 - Lao PDR - - 5.1 - 1.1 0.6 Malaysia 5.7 - 4.7 - 3.4 - Myanmar - 27.9 - - 1.3 1.0 The Philippines - 20.4 39.0 19.5 - - Thailand - - - - 0.9 25.9 Viet Nam 20.0 1.2 - - 2.1 26.1 ASEAN 1,288.4 1,052.9 213.2 123.0 72.8 53.6 kt = thousand tonnes; t = tonnes; - = nil. Note: Data for Cambodia are not available. To allow for comparison, data for the above table were sourced from the World Bureau of Metal Statistics (2005). Therefore, some inconsistency may occur with the data reported in individual country reports, based on in-country data sources. Mine production data refer to metal content only. Source: World Bureau of Metal Statistics 2005.

Figure 2.3: ASEAN Share of World Minerals Production (%), 2003

Note: To allow for comparison, the above graph is based on data from the World Bureau of Metal Statistics (2005). Therefore, some inconsistency may occur with the data reported in individual country reports, based on in-country data sources. Source: World Bureau of Metal Statistics 2005.

Notwithstanding the decline in mine output in some ASEAN member countries, total production of ASEAN four key minerals — copper, gold, nickel and tin — doubled between 1990 and 2004, driven primarily by Indonesia, and reached its peak in 2002 (Figure 2.4). In particular, copper production increased by 130%, gold by 369%, nickel by 35%, and tin by 17% over that period. ASEAN production of copper and gold — which are extracted jointly — has increased more rapidly than for other minerals, mainly as a result of the new production from the very large Grasberg and Batu Hijau copper/gold mines in Indonesia (Figure 2.5). Also contributing to the rise in copper production over the period was increased output from the Monywa mine in Myanmar. However, total ASEAN copper production has fallen over the past few years as a result of unstable mine conditions at Grasberg that have sharply reduced output. In addition, copper production in the Philippines has declined steadily over the past decade primarily as a result of mine closures. Mine closures also led to the cessation of copper mining in Malaysia in 1999.

ASEAN tin production has grown moderately since 2002 (after a period of flat production since 1990) as a result of rising production in Indonesia, the Lao PDR and Myanmar. However, growth in overall production was partially offset by declining production in Malaysia and Thailand as a result of lower grades of ore and mine depletion, together with decreased replacement capacity coming on stream in those countries. ASEAN nickel production has

Enhancing ASEAN Minerals Trade and Investment

8 REPSF Project 04/009b: Final Report

risen slowly since the late 1990s, largely as a result of increased production in Indonesia and the Philippines.

Figure 2.4: ASEAN Production of Key Minerals by Country, 1990-2004

a: For Viet Nam, base year is 1996. Note: Mine production has increased in recent years in the Lao PDR and Myanmar, albeit from a low base. Source: World Bureau of Metal Statistics 2005.

Figure 2.5: ASEAN Production of Key Minerals, 1990-2004

kt = thousand tonnes. Sources: Country Reports; World Bureau of Metal Statistics 2005, International Nickel Study Group 2005.

ASEAN member countries also produce significant volumes of a wide range of non-metallic minerals, including gemstones, gypsum, limestone, kaolin, phosphate rock, sand, gravel and other industrial minerals. Much of this non-metallic minerals production comes from a large number of small scale mining and quarrying operations that are typically operated by small private concerns. Apart from gemstones (Table 2.5), a small proportion of this production is traded within the Asian region, with the vast bulk of non-metallic minerals production consumed by domestic industries such as construction. Local production of cement, for example, consumes large quantities of sand and limestone.

Enhancing ASEAN Minerals Trade and Investment

REPSF Project 04/009b: Final Report 9

Table 2.5: ASEAN Gemstones Production, 2003 Thousand Carats

Cambodia 50 Indonesia 30 Lao PDR 2,303 Myanmar 45,442 Thailand 716 Sources: Country reports.

In some ASEAN member countries, the production of non-metallic minerals is higher than the production of metallic minerals in volume terms. Non-metallic minerals production is important for the economies of the Lao PDR, Malaysia and Myanmar, and constitutes a significant share of total minerals production in Thailand and Viet Nam. In particular, non-metallic minerals accounted for 80% and 55% of the total value of minerals production in 2004 in Thailand and Viet Nam respectively.

D. MINERALS CONSUMPTION Much of ASEAN production of metallic minerals tends to be exported as ores and

concentrates for processing/refining outside the region, rather than being consumed in domestic mineral processing sectors. However, some mineral processing occurs in the region. The main minerals processed in ASEAN include copper, bauxite, lead, zinc and tin, with Indonesia being the main producer of refined mineral products. Copper refineries are located in Indonesia, Myanmar and the Philippines, while the region’s only aluminium smelter is located in Indonesia. Lead refining, primarily from used batteries, occurs in Indonesia, Malaysia, Myanmar, the Philippines and Thailand, while Thailand has the region’s only zinc smelter. Indonesia is the second largest refined tin producer in the world, with smaller scale facilities also located in Malaysia, Myanmar, Thailand and Viet Nam.

Some of the processed minerals produced locally in ASEAN member countries are consumed by domestic manufacturing and construction industries, although the region generally relies on imports of metals to meet demand. Rapid industrialisation — particularly in Malaysia and Singapore — combined with rising incomes in several ASEAN member countries has resulted in strong increases in demand for metals as inputs to industrial production and final consumption. Aluminium and copper are the major processed minerals consumed in ASEAN, together with smaller volumes of zinc, lead, tin and nickel. ASEAN consumption of lead, tin, copper and zinc accounted for between 3% and 5% of total world consumption of these commodities in 2003 (World Bureau of Metal Statistics 2005).

Growth in ASEAN metals consumption is strongly correlated with growth in manufacturing, infrastructure development and rising incomes in the region. ASEAN manufacturing activity grew rapidly between 1990 and 2004, with average industrial production growth rates of between 3.4% and 6.3% a year for the ASEAN member countries of Indonesia, Malaysia, the Philippines, Singapore, and Thailand. This growth has been driven largely by rising demand for consumer durables such as cars, whitegoods and home electronics, together with the expansion of infrastructure for electricity generation and supply, transport and communications. Much of this increased manufacturing activity and infrastructure development is highly metals intensive and has resulted in strong and expanding markets for metals within the ASEAN region.

However, with the Asian financial downturn in 1997, there was a sharp contraction in economic activity in the ASEAN region. As a consequence, there were significant falls in the region’s production of metals intensive products such as consumer durables. However, by 1999 ASEAN industrial production had begun to improve, with metals consumption having largely recovered to previous levels by 2001 (Figure 2.6).

Enhancing ASEAN Minerals Trade and Investment

10 REPSF Project 04/009b: Final Report

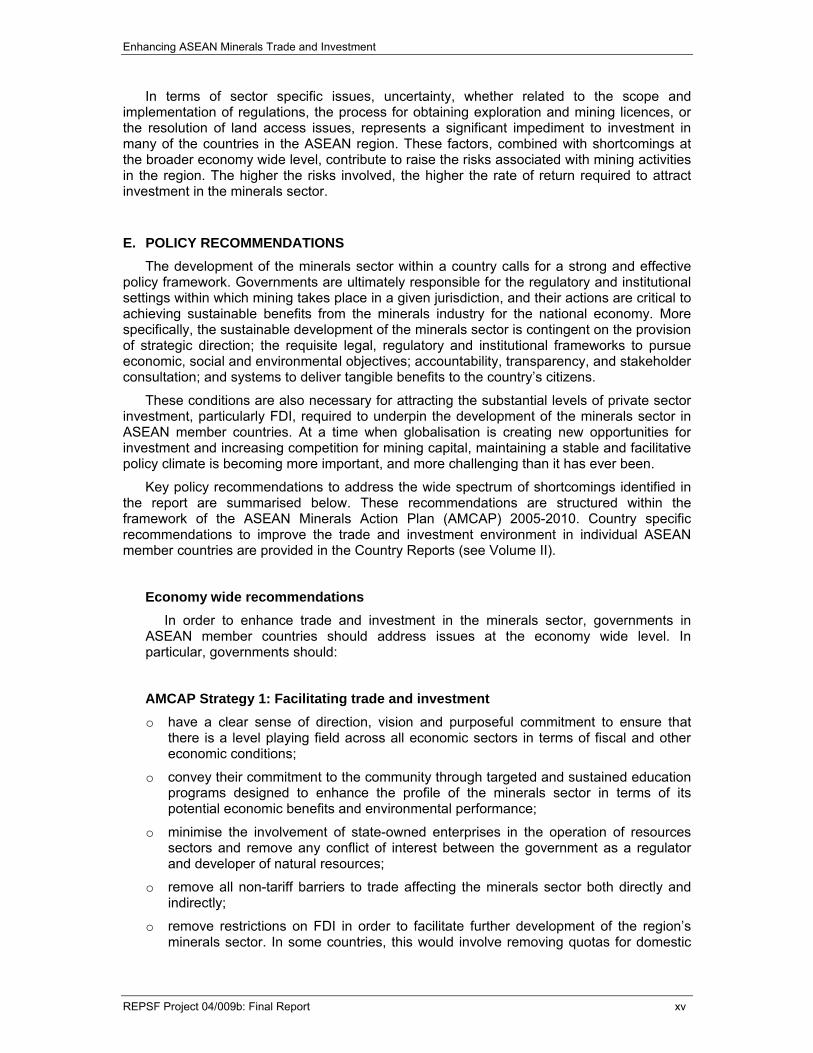

Non-metallic minerals are also in strong demand in ASEAN member countries. Non-metallic minerals consumed in ASEAN include limestone, aggregates and sand for construction of buildings and transport infrastructure, as well as clays and other minerals for a variety of industrial and consumer applications.

Figure 2.6: ASEAN Consumption of Key Metals, 1990-2004

kt = thousand tonnes. Sources: World Bureau of Metal Statistics 2005; International Lead-Zinc Study Group 2005.

E. MINERALS TRADE The bulk of ASEAN metallic minerals production is exported, with only a relatively small

proportion of local minerals production consumed by industries within the region. For example, over the 10 years to 2004, Indonesia exported 87% of its copper production, 84% of gold, 98% of nickel and 97% of bauxite production, respectively. Other ASEAN member countries that produce metallic minerals also export a significant share of their production, with the bulk of ASEAN minerals exports going to markets in the Asia Pacific region. Major trading partners include Japan, the Republic of Korea and China as well as other ASEAN member countries.

ASEAN has a substantial share of world trade in tin, copper and nickel, although its role in world markets for other mineral commodities is relatively limited. In 2003, ASEAN export volumes of refined tin accounted for 58% of world trade, while exports of unrefined and refined copper accounted for 16% and 6% of global trade respectively. The region is also becoming an increasingly significant exporter of nickel and aluminium as a result of increased productive capacity.