Determinants of Entry Mode Choice of MNCs into Emerging Markets:Some Evidence from South Africa and...

21

Determinants of Entry Mode Choice of MNCs in Emerging Markets: Evidence from South Africa and Egypt Author(s): Sumon Kumar Bhaumik and Stephen Gelb Source: Emerging Markets Finance & Trade, Vol. 41, No. 2 (Mar. - Apr., 2005), pp. 5-24 Published by: M.E. Sharpe, Inc. Stable URL: http://www.jstor.org/stable/27750436 . Accessed: 04/04/2014 03:27 Your use of the JSTOR archive indicates your acceptance of the Terms & Conditions of Use, available at . http://www.jstor.org/page/info/about/policies/terms.jsp . JSTOR is a not-for-profit service that helps scholars, researchers, and students discover, use, and build upon a wide range of content in a trusted digital archive. We use information technology and tools to increase productivity and facilitate new forms of scholarship. For more information about JSTOR, please contact [email protected]. . M.E. Sharpe, Inc. is collaborating with JSTOR to digitize, preserve and extend access to Emerging Markets Finance &Trade. http://www.jstor.org This content downloaded from 130.92.9.58 on Fri, 4 Apr 2014 03:27:24 AM All use subject to JSTOR Terms and Conditions

-

Upload

johannesburg -

Category

Documents

-

view

1 -

download

0

Transcript of Determinants of Entry Mode Choice of MNCs into Emerging Markets:Some Evidence from South Africa and...

Determinants of Entry Mode Choice of MNCs in Emerging Markets: Evidence from SouthAfrica and EgyptAuthor(s): Sumon Kumar Bhaumik and Stephen GelbSource: Emerging Markets Finance & Trade, Vol. 41, No. 2 (Mar. - Apr., 2005), pp. 5-24Published by: M.E. Sharpe, Inc.Stable URL: http://www.jstor.org/stable/27750436 .

Accessed: 04/04/2014 03:27

Your use of the JSTOR archive indicates your acceptance of the Terms & Conditions of Use, available at .http://www.jstor.org/page/info/about/policies/terms.jsp

.JSTOR is a not-for-profit service that helps scholars, researchers, and students discover, use, and build upon a wide range ofcontent in a trusted digital archive. We use information technology and tools to increase productivity and facilitate new formsof scholarship. For more information about JSTOR, please contact [email protected].

.

M.E. Sharpe, Inc. is collaborating with JSTOR to digitize, preserve and extend access to Emerging MarketsFinance &Trade.

http://www.jstor.org

This content downloaded from 130.92.9.58 on Fri, 4 Apr 2014 03:27:24 AMAll use subject to JSTOR Terms and Conditions

Emerging Markets Finance and Trade, vol. 41, no. 2,

March-April 2005, pp. 5-24. ? 2005 M.E. Sharpe, Inc. All rights reserved. ISSN 1540-496X/2005 $9.50 + 0.00.

Sumon Kumar Bhaumik and Stephen Gelb

Determinants of Entry Mode Choice of MNCs in Emerging Markets

Evidence from South Africa and Egypt

Abstract: It is now stylized that the importance of foreign direct investment for developing countries and emerging markets arises from the impact of the presence of multinational

corporations (MNCs) in the host country on the productivity of local firms, by way of tech

nology diffusion and competition. There is also general agreement that the extent of tech

nology transfer by an MNC to a developing country affiliate depends on the extent of its control on the local affiliate and that, in turn, the extent of this control depends on the mode

of entry of the MNC into the host country. However, the existing literature is based on the

experience of developed countries and as such does not contribute to the literature on

development economics. This article addresses this lacuna using unique firm-level data

from South Africa and Egypt. Our results indicate that the determinants of entry mode

choice not only differ between developed and developing countries, but also among devel

oping countries. They also bring into question the role of MNCs in fostering productivity

growth in developing countries.

Key words: entry mode choice, local institutions, local knowledge, multinational corpora tions (MNC), technology transfer.

Sumon Kumar Bhaumik ([email protected]) is lecturer at the School of Manage ment and Economics, Queen's University Economics, Belfast, UK; research associate at

the Centre for New and Emerging Markets, London Business School, UK; and research

fellow at William Davidson Institute, Ann Arbor, Michigan. Stephen Gelb (sgelb@the

edge.org.za) is director of the EDGE Institute, Johannesburg, South Africa. The authors are

grateful to the Economic Research Forum, Cairo, for firm-level data from Egypt and back

ground information about the Egyptian economy; Paul Cousins, Saul Estrin, Klaus Meyer, Simon Commander, Jeffrey Nugent, and seminar participants at the 2003 annual meeting of

the Allied Social Science Association for valuable comments; and to Caitlin Frost, Maria

Bytchkova, and Gherardo Girardi for research assistance. The authors remain responsible for all remaining errors. The research was made possible by a grant from the Department for International Development of the British government.

5

This content downloaded from 130.92.9.58 on Fri, 4 Apr 2014 03:27:24 AMAll use subject to JSTOR Terms and Conditions

6 EMERGING MARKETS FINANCE AND TRADE

By the end of the twentieth century, foreign direct investment (FDI) had effec

tively replaced trade as a driver of economic growth in less developed and emerg ing economies. In 2002, there were an estimated 65,000 multinational corporations (MNCs) with about 850,000 worldwide affiliates employing about 54 million

employees, a rise of 141 percent over the 1990 employment figure for MNCs

(UNCTAD 2002). Over the same period, the stock of outward FDI increased from

$1 trillion to $6.6 trillion, and MNCs accounted for about 10 percent of the world's GDP and about 33 percent of the world's exports.

The developing world continues to receive a minuscule proportion of global FDI flows. In 2001, for example, developing countries received a paltry $205 bil lion in FDI, or less than 5 percent of the global FDI, with China alone accounting for more than a quarter of the developing world's FDI flows. In other words, it is difficult to conceive of FDI as a major future source of financial resource for de

veloping countries and emerging markets, with the possible exception of large countries like Russia and India. The importance of FDI, however, stems from the

proposition that MNCs are instrumental in transferring technology from devel

oped to developing countries. It has been pointed out that the presence of MNCs in a country does not by any

means guarantee the transfer of technology. MNCs may be reluctant to transfer

technology to developing country affiliates if they do not have complete control over the operations of these affiliates (Blomstrom and Zejan 1989; Ramachandran

1993). Further, even if the MNCs do transfer advanced technology to their devel

oping-country affiliates, and even if this technology subsequently becomes avail able to other firms operating in the industry, the domestic firms may not be able to

adapt to this technology on account of technology gaps between the MNCs and the domestic firms (Lapan and Bardhan 1973; Glass and Saggi 1998).

However, there is some evidence to suggest that the presence of MNCs in de

veloping-country industries has spillover effects that add to the productivity of the domestic firms operating in these industries (Patibandla and Petersen 2002). There is also counterevidence to suggest that the presence of MNCs can sometimes af fect the productivity of domestic firms adversely (Aitken and Harrison 1999). But there is a fair degree of unanimity that MNC affiliates in developing countries

usually have more technology-intensive production means (Vishwasrao and Bosshardt 2001) and higher labor productivity (Blomstrom and Sjoholm 1999). Hence, it is not unreasonable to believe that, in the presence of appropriate policies that both liberalize the economy and build institutions that can sustain free-market

competition, MNC affiliates in developing countries would provide domestic firms with a benchmark that would eventually lead to enhanced productivity over time.

The plausible causal chain of events is as follows: MNC affiliates will adopt relatively technology-intensive production practices in developing countries, aided

by technology transfer from the parent MNC. This technology can be passed on to domestic firms in the developing country directly by way of, for example, inter firm migration of labor. Alternatively (or in addition to this), in the presence of

This content downloaded from 130.92.9.58 on Fri, 4 Apr 2014 03:27:24 AMAll use subject to JSTOR Terms and Conditions

MARCH-APRIL 2005 7

appropriate policies and institutions, domestic firms can experience productivity growth by way of competition with MNC affiliates. Clearly, the productivity of the

developing-country MNC affiliate, and, through direct or indirect linkage, that of the domestic firms, depends on the extent of technology transferred by the parent

MNCs to their affiliates. As mentioned, the extent of technology transfer depends significantly on the

extent of control that a parent MNC has on the activities of its affiliate. It has been

argued, for example, that, contrary to popular wisdom in the policy circles of many developing countries, joint ventures (JVs) do not encourage transfer of technology from MNCs to their developing-country partners. MNCs typically use the JVs as vehicles toward gaining knowledge about the business environment in the devel

oping economy, and once they have absorbed this knowledge, they usually initiate their own business operations by opting out of the JVs (Sinha 2001). In other

words, the "form" in which an MNC affiliate exists in a developing country or an

emerging market may significantly determine the extent of technology transfer and productivity spillover.

Arguably, this form is captured by the mode of entry of MNCs into developing countries and other new countries of operation. Greenfield entry provides an MNC with complete control over its affiliate's operations, and hence the possibility of

technology transfer is the highest with this mode of entry. Correspondingly, if an MNC has only partial control of its affiliate, as in the case of a JV, the probability of such a transfer is low. Finally, if an MNC enters a country by way of an acqui sition, the extent of technology transfer would depend on the extent of control the

MNC has on the incumbent management and on the expected rate of technology diffusion by way of the interfirm mobility of incumbent managers and techno crats. An important empirical question, therefore, is what determines the entry mode choice of an MNC when it enters a developing country.

The entry mode choice of an MNC while entering a new country has received

significant attention in the literature (see, e.g., Agarwal and Ramaswami 1992; Caves and Mehra 1986; Cho and Padmanabhan 1995; Erramilli and Rao 1993; Gorg 2000; Hennart and Park 1993; Kogut and Singh 1988; Luo 2001; Zejan 1990). A major shortcoming of the literature on entry mode choice is that it has

largely explored the strategic decisions of developed-country MNCs entering other

developed countries. Indeed, research that has taken into account developing coun tries too has limited itself mostly to China (Gleason et al. 2002; Tse et al. 1997) and the transition economies of Central and Eastern Europe (Meyer 2001). Fur ther, the literature has focused itself almost entirely on testing hypotheses gener ated from transactions-cost and resource-based theories of international business,

thereby limiting the analyses to the implications of empirical results for the busi ness strategies of MNCs. The implications of the results for the development eco nomics literature have been almost completely ignored.

Our paper addresses this lacuna in the literature using unique firm-level data collected from MNC affiliates in South Africa and Egypt, two major African countries

This content downloaded from 130.92.9.58 on Fri, 4 Apr 2014 03:27:24 AMAll use subject to JSTOR Terms and Conditions

8 EMERGING MARKETS FINANCE AND TRADE

for neither of whom oil is a major resource or export product. As we shall see, these two countries are sufficiently different in terms of their political and economic legacy, as well as in terms of their stages of development. They therefore provide us with a

quasi-controlled experiment that highlights the differences in the determinants of choice of entry mode in different developing-country or emerging market contexts. Our results suggest that perceptions of MNCs about local institutions have an im

pact on their entry mode choice in both South Africa and Egypt. However, there are also some noticeable differences. In South Africa, factors like the resource needs of the MNC and the extent of competition that they are likely to face play an important role in determining the choice of the mode of entry. In Egypt, on the other hand, a

major determinant of the entry mode decision is the familiarity of the MNC with local conditions and the business environment in developing countries and emerg

ing markets in general. Importantly, our results indicate that factors such as the technology intensive

ness of an MNCs product, the extent of income risk it is exposed to by way of

competition, and the size of the developing-country affiliate relative to the MNCs

global operations are not significant determinants of entry mode choice. They are consistent with the conventional wisdom. Empirical evidence suggests that devel

oping-country operations usually represent a very small fraction of MNCs' global operations and that they usually do not produce technology-intensive products in

developing countries, usually opting for products that are either in the low-tech

nology downstream segments of their supply chain or are nearing the end of their

product cycles (Estrin and Meyer 2004). The estimated impact of local competi tion on entry mode choice is also weak, and this is consistent with evidence that

suggests that MNCs' affiliates in developing countries can operate in niche mar kets (Kokko 1994) and thereby avoid competition. These results bring into ques tion the role of MNCs in generating productivity growth in a developing country or emerging market.

Determinants of Entry Mode Choice in a

Developing Country

By definition, an MNC is a firm that has ownership of a technology (which in cludes business practice) that gives it a competitive edge in a product market (Ethier 1986). An MNC spreads it operations around the world either to access resources in other countries, whether petroleum in Nigeria or software professionals in In

dia, say, so as to add to its competitive edge, or to use its competitive/technological advantage to sell its product in the local/host country market. Given its technologi cal advantage over competing firms in the local market, the biggest challenge fac

ing an MNC is informational asymmetry with respect to potential business partners and the business environment in the host country.

Entering a new country in partnership with a local firm alleviates this problem, as partnership allows the MNC ready access to a local firm's private information

This content downloaded from 130.92.9.58 on Fri, 4 Apr 2014 03:27:24 AMAll use subject to JSTOR Terms and Conditions

MARCH-APRIL 2005 9

about the local business environment, and to the partner's contacts with other local firms and the host country's government and regulatory authorities. In other words,

entry into a country in the form of a JV or an acquisition reduces the MNCs transaction cost of doing business. The benefit accruing to the MNC from the reduction of transactions cost is greater if the MNC has significant need for local

resources, whether tangible or intangible (Gomes-Casseres 1989). The benefits will also be large if the official procedures and institutions supporting local busi ness doings are underdeveloped, and if the government is potentially a hindrance to profitable economic activity. Hence, if an MNC has significant need for local

resources, or if the local institutions, business regulations, and governance are not conducive to carrying on business efficiently (Agarwal and Ramaswami 1992;

Gatignon and Anderson 1988), an MNC is more likely to opt for a local partner, either by way of a JV or by acquiring a local firm that can give the MNC quick access to the required resources (Asiedu and Esfahani 2001; Teece 1986). An ac

quisition, and perhaps also a JV, is even more likely if the MNC feels that the

quality of the local managerial labor is high, such that dependence on a local part ner would not compromise the quality of the MNCs organizational integrity and

quality of products and services. This alleviation of transactions cost, however, comes at a price. If the MNC

enters the new country with a local JV partner, it faces a stylized agency problem; while the MNCs main objective is to learn more about the local firms and busi ness conditions, its JV partner's objective is usually to access the proprietary tech

nology that gives the MNC its competitive edge. As we mentioned above, this

agency conflict usually results in dissolution of JVs after a few years of operation. If, on the other hand, the MNC enters the host country by way of an acquisition, it has to deal with the problem of restructuring the acquired organization (such that its business culture is similar to that of the parent MNC) and the cost associated

with such restructuring. Given the cost associated with JVs and acquisitions, an MNC would prefer to

enter a new country on its own, by way of a greenfield project, if the technology intensiveness of its products, and hence the potential cost of losing a technological edge over its rivals, is high (Cho and Padmanabhan 1995; Hennart 1991), and if the extent of its informational problem is not significant. Hence, a greenfield entry would be more likely if the MNC has prior operating experience in the host coun

try, or in similar developing countries or emerging markets (Barbosa et al. 2004). It is also less likely to opt for a JV or the acquisition mode of entry if the rules

governing FDI and industry-specific regulations have been significantly liberal ized, such that business operations in the host country do not involve licenses and

repeated interaction with the domestic government and domestic regulatory agen cies.1 Greenfield entry is also more likely if the "cultural" distance between the

MNCs home country and the host country of operations is minor, such that it is

relatively easy for the MNC to understand and accurately interpret local norms, governance structure, and business practices (Yip 1982).

This content downloaded from 130.92.9.58 on Fri, 4 Apr 2014 03:27:24 AMAll use subject to JSTOR Terms and Conditions

10 EMERGING MARKETS FINANCE AND TRADE

Even though economic logic suggests that the size of an MNCs developing country operations, relative to its global operations, would affect its choice of entry mode, it is difficult to predict exactly how the relative size of the local operations would affect the choice of entry mode. On the one hand, a greenfield entry is also more likely if the host country-based operations constitute a significant proportion of an MNCs assets and turnover because the MNC would want tight control over an affiliate whose performance would have a significant impact on its global perfor

mance. On the other hand, if the host country-based project is large on account of factors like economies of scale, the MNC might want to minimize its risk by sharing it with a local firm, a move that might also reduce transactional uncertainties for the local affiliate (Caves and Mehra 1986). Risk-averse behavior might also lead to an abandonment of the greenfield mode of entry if the local market is very competitive, such that, despite the technological/competitive edge, the magnitude of returns on the investment made in the host country is uncertain (Hennart and Park 1993).

Finally, the choice of the entry mode would depend on the rate of growth of the local industry, and on whether, broadly speaking, the MNC operates in a manufac

turing or a services-sector industry. As with the relative size of the local affiliate, the impact of the rate of growth of the industry on the entry mode choice is uncer tain (Agarwal and Ramaswami 1992; Barbosa and Louri 2002; Horstman and

Markusen 1996). On one hand, if an industry is fast growing, and therefore fast

changing, it may be essential for an MNC to quickly have a stake in it, so as not to lose its first-mover advantage to other MNCs or local firms. In such an event, an

entry by way of acquisition, for example, may be more suitable. On the other hand, if a rapidly growing industry also promises high rates of return on invest ment well into the future, it may be reasonable for the MNC to minimize its agency and restructuring costs by opting for a greenfield project, even though such a move would increase the transactions cost in the short run. The importance of the sector of operation of the MNC lies in the possibility that the manufacturing sector is more intensive in investment in tangible resources than the services sector, such that a manufacturing MNC is likely to be more responsive to factors that affect the transactions cost of operations in a host country than a service-sector MNC (Brouthers and Brouthers 2003)

In other words, the specification underlying any econometric analysis of the choice of entry mode would be as follows:

Entry mode = /(Growth of local industry, Technology-intensiveness of

product, Competition in the local market, Resource needs of the MNC, Local institutions, governance, and business

regulations, Prior operating experience in developing-country environments, Cultural distance between MNCs home

country and host country, Extent of liberalization of FDI

regulations and industry-specific regulations, Perceptions about quality of host country's managerial labor, Sector of

operation of the MNC) (1)

This content downloaded from 130.92.9.58 on Fri, 4 Apr 2014 03:27:24 AMAll use subject to JSTOR Terms and Conditions

MARCH-APRIL 2005 11

In addition, given that developing economies and emerging markets experience

significant and different systemic shocks during different time periods, the speci fication has to include controls for the year of entry of an MNC into a host country. The entry mode choices facing the MNC are greenfield, acquisition of a host country firm, or a JV with a local firm. The measurement of the variables is discussed in the next section.

Choice of Countries, Data, and Variable Measurement

Choice of Countries

We estimate specification (1) using firm-level data collected from South Africa and Egypt. Although both these countries are of the same continent, they have few similarities. Egypt has enjoyed significant political stability since the 1970s, in the form of the same administration. However, the country has experienced a struc tural break in its economic policy paradigm because of the government's move

away from central planning toward market-based allocation of resources, since the

early 1990s. Unlike Egypt, South Africa has had a fairly long history of private enterprise and export orientation. However, during the late 1980s and early 1990s, the South African economy had to endure a period of economic flux when major world economies imposed sanctions in protest against apartheid. Almost simulta

neously, the country underwent profound political change. Since the early 1990s, South Africa has retraced its steps toward private enterprise and export orientation amid profound social and economic change. The policy environments of these two

countries, as witnessed during the 1990s, are discussed in detail in Gelb (2003) and Louis and Handoussa (2003).

In other words, during the 1990s, an MNC contemplating investment in Egypt was unlikely to have experienced major surprises with respect to its political economy and corresponding institutions. Indeed, the relevant issue was more likely to be whether the policy and institutional changes that accompanied the move from central planning to a market-oriented economy were actually significant. In the context of South Africa, on the other hand, the changes to the political economy and the corresponding institutions were expected to be significant, and the main issue was the extent to which the new political regime would preserve the country's legacy of private enterprise, given the past concentration of productive resources in the hands of a small minority, and maintain its links with the European and

North American economies.

The differences in legacy are also reflected in economic facts and figures. South Africa is a quasi-industrialized country with reasonably good infrastructure in

comparison with other emerging markets, and which has played host to firms from advanced industrialized nations for decades. Despite the sharp depreciation of its

currency toward the end of the 1990s, its per capita GDP in terms of nominal dollars stood at $2,685 at the turn of the century. At the same time, the income and

This content downloaded from 130.92.9.58 on Fri, 4 Apr 2014 03:27:24 AMAll use subject to JSTOR Terms and Conditions

12 EMERGING MARKETS FINANCE AND TRADE

wealth distribution in the country remains skewed, resulting in a Gini coefficient of 0.59. Egypt, by contrast, has a moribund industrial sector and lower average levels of infrastructure. The per capita GDP of the country has increased continu

ally over time, but in 2000, at $1,425, it was still about half that of South Africa. On the other hand, the socialist legacy of Egypt's economic policy has led to a much lower level of inequality, as indicated by the Gini coefficient of 0.29.

There are, of course, points of similarity between the countries. For example, in both the countries, about a fifth of the people have had tertiary education, indicat

ing a similar proportion of high-skilled laborers in both populations. Further, as of

2000, both countries had similar levels of net FDI inflow, whether measured as a

percentage of GDP or in terms of FDI per capita. However, the political and eco nomic legacies of the two countries are sufficiently different to provide a sharp contrast in terms of the knowledge and the expectations that MNCs may have had about the two countries. Because choice of entry mode depends significantly on such knowledge and on the perceptions of the MNCs of the resource availability, business environment, and so on, in host countries, we believe that it is instructive to undertake a comparative study of the entry mode choice of MNCs entering South Africa and Egypt.

Data and Variable Measurement

The data were gathered with the help of a common questionnaire that was admin istered to foreign investment companies in the two countries between November 2000 and April 2001. Prior to administration of the survey instrument, it was pi loted and refined during the summer of 2000. The base population for the survey study was defined as all registered FDI projects that have been started in the coun tries between 1990 and 2000, have a minimum employment of 10 persons, and a have minimum foreign equity stake of 10 percent. The time limit ensures that information concerning relevant establishments was still within their organiza tional memory and, therefore, available at the time of the survey.

The MNC affiliates responding to the survey instrument categorized themselves as belonging to one of four categories: greenfield project, JV, acquisition with

complete control, and acquisition with less than complete control. The incidence of acquisition with less than complete control accounted for less than 5 percent of the total number of responses, net of the observations dropped on account of miss

ing values. Arguably, there is little difference between an acquisition with less than complete control and a JV; the agency conflict in the former involves an

MNC and its local partner, while the conflict in the latter involves an MNC as a new strategic shareholder and local incumbent shareholders. Hence, for our pur poses, we consider acquisitions with less than complete control as JVs. Our de

pendent variable, therefore, takes the value 1 if the entry mode is greenfield, the value 2 if the entry mode is acquisition, and the value 3 if the entry mode is JV.

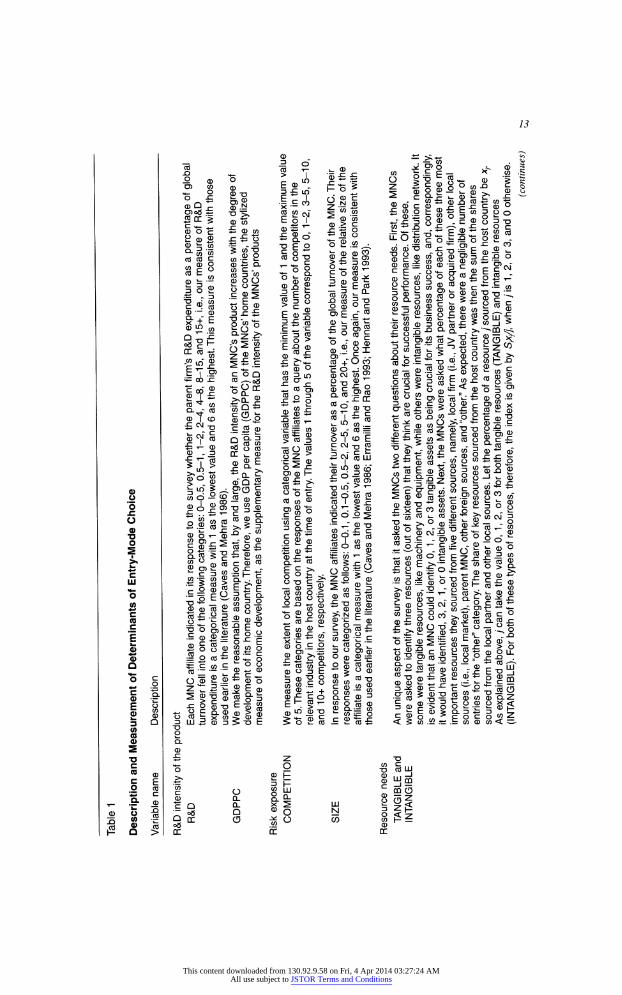

The measurement of the explanatory variables is reported in Table 1.

This content downloaded from 130.92.9.58 on Fri, 4 Apr 2014 03:27:24 AMAll use subject to JSTOR Terms and Conditions

Table

1

Description and Measurement

of Determinants

of Entry-Mode Choice

Variable name Description R&D

intensity

of the product

R&D Each MNC affiliate indicated in its response to the survey

whether

the parent firm's R&D expenditure as a percentage of global

turnover fell into one of the following categories: 0-0.5, 0.5-1, 1-2, 2-4, 4-8, 8-15, and 15+, i.e., our measure of R&D

expenditure is a categorical measure with 1 as the lowest value and 6 as the highest. This measure is consistent with those

used earlier in the

literature

(Caves and Mehra 1986).

GDPPC We make the reasonable assumption that, by and

large, the R&D intensity of an MNCs product increases with the degree of

development of its home country. Therefore, we use

GDP per capita (GDPPC) of the MNCs' home countries, the stylized

measure of economic development, as the

supplementary

measure for the R&D intensity of the MNCs' products

Risk exposure

COMPETITION We measure the extent of local competition using a

categorical

variable that has the minimum value of 1 and the maximum value

of 5. These categories are based on the responses of the

MNC

affiliates to a query about the number of competitors in the relevant industry in the host country at the time of entry

The

values 1 through 5 of the variable correspond to 0, 1-2, 3-5, 5-10,

and 10+ competitors,

respectively.

SIZE In response to our survey, the MNC affiliates indicated

their

turnover as a percentage of the global turnover of the MNC. Their

responses were categorized as follows: 0-0.1, 0.1-0.5,

0.5-2,

2-5, 5-10, and 20+, i.e., our measure of the relative size of the affiliate is a categorical measure with 1 as the lowest value and 6 as the highest. Once again, our measure is consistent with

those used earlier in the literature (Caves and

Mehra

1986; Erramilli and Rao 1993; Hennart and Park 1993).

Resource needs

TANGIBLE and An unique aspect of the survey is that it asked the

MNCs

two different questions about their resource needs. First, the MNCs

INTANGIBLE were asked to identify three resources (out of sixteen) that they think are crucial for successful performance. Of these,

some were tangible resources, like machinery and equipment, while others were intangible resources, like distribution network. It is evident that an MNC could identify 0, 1, 2, or 3 tangible

assets

as being crucial for its business success, and, correspondingly,

it would have identified, 3, 2, 1, or 0 intangible assets.

Next,

the MNCs were asked what percentage of each of these three most

important resources they sourced from five different

sources, namely, local firm (i.e., JV partner or acquired firm), other local

sources (i.e., local market), parent MNC, other foreign

sources,

and "other." As expected, there were a negligible number of entries for the "other" category. The share of key

resources

sourced from the host country was then the sum of the shares

sourced from the local partner and other local sources.

Let

the percentage of a resource j sourced from the host country be xr As explained above, yean take the value 0, 1, 2, or 3 for

both

tangible resources (TANGIBLE) and intangible resources (INTANGIBLE). For both of these types of resources,

therefore,

the index is given by Sp/l when /is 1, 2, or 3, and 0 otherwise.

(continues) ^

This content downloaded from 130.92.9.58 on Fri, 4 Apr 2014 03:27:24 AMAll use subject to JSTOR Terms and Conditions

Table

1 (continued)

Variable name Description

Institutions,

governance,

and business environment

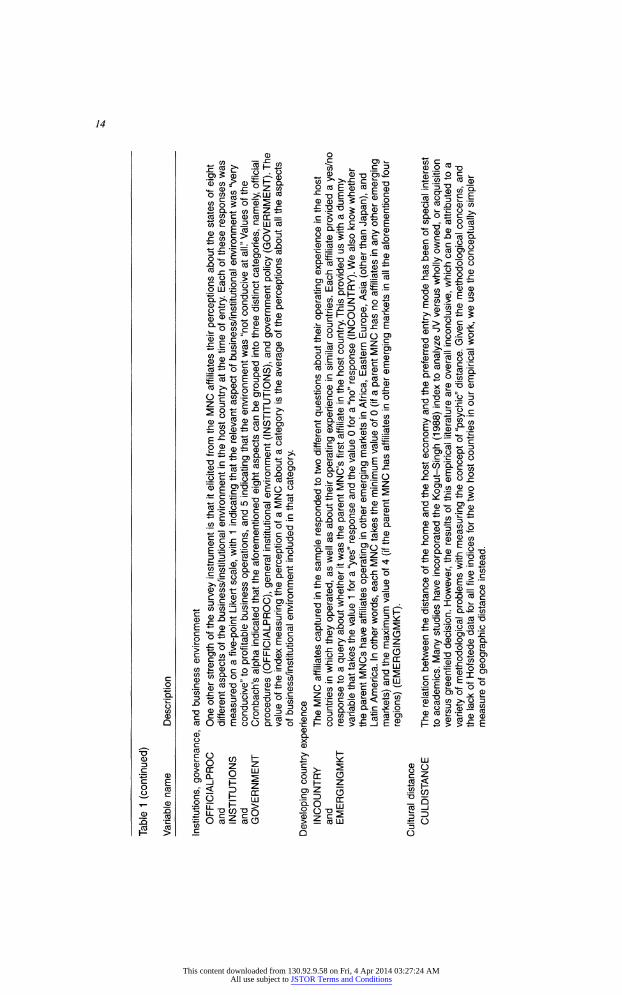

OFFICIALPROC One other strength of the survey instrument is that

it elicited

from the MNC affiliates their perceptions about the states of eight and different aspects of the business/institutional environment in the host country at the time of entry. Each of these responses was INSTITUTIONS measured on a five-point Likert scale, with 1

indicating

that the relevant aspect of business/institutional environment was "very and conducive" to profitable business operations, and 5 indicating that the environment was "not conducive at all." Values of the GOVERNMENT Cronbach's alpha indicated that the aforementioned eight aspects can be grouped into three distinct categories, namely, official procedures (OFFICIALPROC), general institutional environment (INSTITUTIONS), and government policy (GOVERNMENT). The

value of the index measuring the perception of a MNC about a category is the average of the perceptions about all the aspects

of business/institutional environment included in that category.

Developing country experience

INCOUNTRY The MNC affiliates captured in the sample responded to two different questions about their operating experience in the host

and countries in which they operated, as well as about their

operating

experience in similar countries. Each affiliate provided a yes/no

EMERGINGMKT response to a query about whether it was the parent

MNC's

first affiliate in the host country. This provided us with a dummy variable that takes the value 1 for a "yes" response and the value 0 for a "no" response (INCOUNTRY). We also know whether

the parent MNCs have affiliates operating in other

emerging markets

in Africa, Eastern Europe, Asia (other than Japan), and Latin America. In other words, each MNC takes the minimum value of 0 (if a parent MNC has no affiliates in any other emerging

markets) and the maximum value of 4 (if the parent MNC has affiliates in other emerging markets in all the aforementioned four

regions) (EMERGINGMKT).

Cultural distance CULDISTANCE

The relation between the distance of the home and the host economy and the preferred entry mode has been of special interest to academics. Many studies have incorporated the Kogut-Singh (1988) index to analyze JV versus wholly owned, or acquisition versus greenfield decision. However, the results of this empirical literature are overall inconclusive, which can be attributed to a variety of methodological problems with measuring the concept of "psychic" distance. Given the methodological concerns, and

the lack of Hofstede data for all five indices for the two

host countries in our empirical work, we use the conceptually simpler

measure of geographic distance instead.

This content downloaded from 130.92.9.58 on Fri, 4 Apr 2014 03:27:24 AMAll use subject to JSTOR Terms and Conditions

Perceptions about quality of local managerial labor

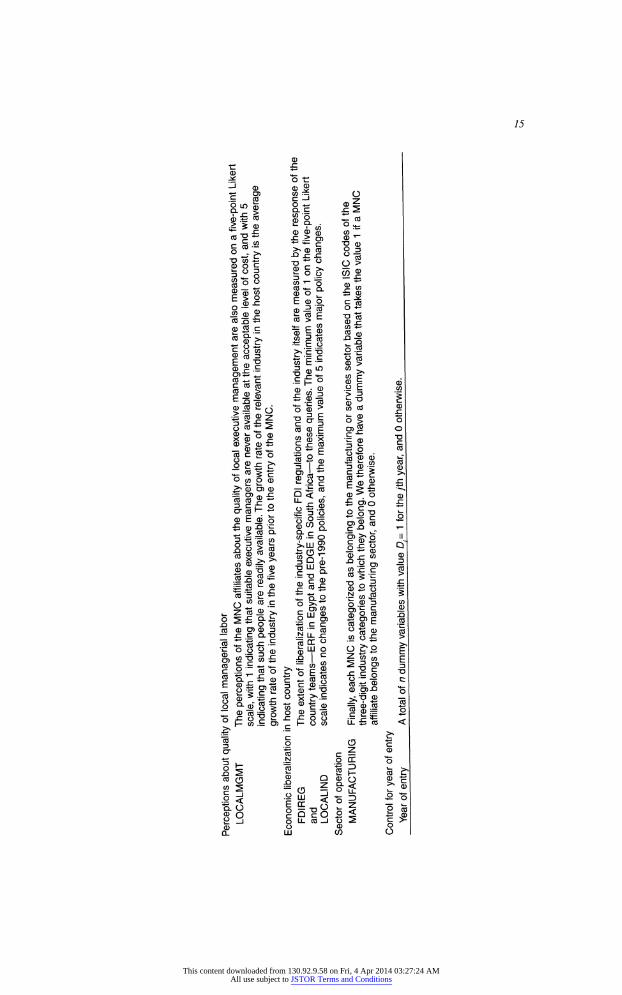

LOCALMGMT The perceptions of the MNC affiliates about the

quality

of local executive management are also measured on a five-point Likert scale, with 1 indicating that suitable executive managers are never available at the acceptable level of cost, and with 5 indicating that such people are readily available. The growth rate of the relevant industry in the host country is the average

growth rate of the industry in

the

five years prior to the entry of the MNC.

Economic liberalization in host country

FDIREG The extent of liberalization of the industry-specific FDI regulations and of the industry itself are measured by the response of the

and country teams?ERF in Egypt and EDGE in South

Africa?to these queries. The minimum value of 1 on the five-point Likert

LOCALIND scale indicates no changes to the pre-1990

policies,

and the maximum value of 5 indicates major policy changes.

Sector of operation

MANUFACTURING Finally, each MNC is categorized as

belonging to the manufacturing or services sector based on the ISIC codes of the

three-digit industry categories to which they belong.

We

therefore have a dummy variable that takes the value 1 if a MNC

affiliate belongs to the manufacturing sector, and 0 otherwise.

Control for year of entry

Year of entry_A total of n dummy variables

with value Df = 1 for the yth year, and 0 otherwise._

This content downloaded from 130.92.9.58 on Fri, 4 Apr 2014 03:27:24 AMAll use subject to JSTOR Terms and Conditions

16 EMERGING MARKETS FINANCE AND TRADE

Table 2

Descriptive Statistics

South Africa Egypt

Mean Std. Dev. Mean Std. Dev.

R&D 3.85 GDPPC (USD) 22,841 INDGROWTH 13.64

COMPETITION 3.50 SIZE 3.00 TANGIBLE 19.83 INTANGIBLE 50.61

OFFICIALPROC 2.45 INSTITUTIONS 2.42

GOVERNMENT 2.68 INCOUNTRY 0.72 EMERGINGMKT 0.87 LOCALMGMT 3.42 CULDISTANCE (KMS) 10,182 FDIREG 1.96 LOCALIND 1.96 MANUFACTURING 0.53

2.02 2.37 1.82

9,817 18,795 11,358 11.64 15.42 28.02

1.30 3.22 1.45

1.61 3.29 1.96

35.99 23.25 37.82

35.74 44.74 34.81

0.71 2.77 0.82

0.78 3.15 0.99

0.89 3.08 1.08

0.44 0.63 0.48

0.32 0.88 0.32

1.17 3.60 1.42

1,962 3,856 3,324 0.95 3.19 1.29

1.03 3.24 1.23

0.50 0.43 0.49

Descriptive Statistics

The South African sample includes forty cases of greenfield entry, forty-seven cases of acquisition and twenty-seven cases of JV. The corresponding figures for

Egypt are fifty-one, nineteen, and forty, respectively. The relatively high propor tion of acquisition in the South African context is consistent with the pattern ob served in the context of FDI among developed countries. The relatively high proportion of JV in the Egyptian context, on the other hand, is consistent with the usual experiences of developing countries.

The descriptive statistics for the explanatory variables for the choice of entry mode for the two countries are presented in Table 2. The descriptive statistics

suggest the following:

1. South Africa attracts more sophisticated MNCs, that spend a greater share of their sales revenues on research and development (R&D), as compared with the MNCs that enter Egypt. The former are also from more developed coun

tries, as indicated by the per capita GDP of these countries. This is consis tent with the fact that, as suggested by the variable capturing cultural distance

This content downloaded from 130.92.9.58 on Fri, 4 Apr 2014 03:27:24 AMAll use subject to JSTOR Terms and Conditions

MARCH-APRIL 2005 17

between the home and host countries, MNCs operating in South Africa came largely from North America and north/west Europe, while a signifi cant proportion of the investors in Egypt are from the Middle East/North Africa region.

2. Neither the affiliates in South Africa nor those in Egypt constitute a significant part of the worldwide operations of the parent MNCs; an average local affili ate contributing to 2 percent or less of the parent MNCs global turnover.

3. The MNCs entering both countries source a small fraction of their required tangible resources from the hosts, but they do source a significant part of their intangible assets therein. This is consistent with the prior theory that an

MNCs success in an emerging market depends more on its ability to de

velop business networks involving firms in the supply chain as well as the

government machinery than on acquisitions of resources like labor and raw materials.

The business and institutional environments of South Africa are not dissimilar.

However, local FDI-specific and industry-specific regulations are rated more in vestor friendly by MNCs operating in Egypt than by those operating in South Africa.

Regression Results

As mentioned earlier, the MNCs in our sample made one of three different choices, namely, greenfield entry, acquisition of a local firm, or JV with a local firm. We therefore estimate specification (1) using a multinomial logit regression model. The appropriate Hausman test did not reject the null hypothesis of IIA (indepen dence of irrelevant alternatives) at the 10 percent level of significance, thereby supporting our prior theory that the aforementioned three modes of entry are inde

pendent of each other. The marginal effects generated from the multinomial logit estimates are presented in Tables 3 and 4 for South Africa and Egypt, respectively. The pseudo ^-square values for the regressions?0.34 for South Africa and 0.32 for Egypt?indicate a fairly good fit for the specification, given the cross-sectional nature of the data and the sample size.

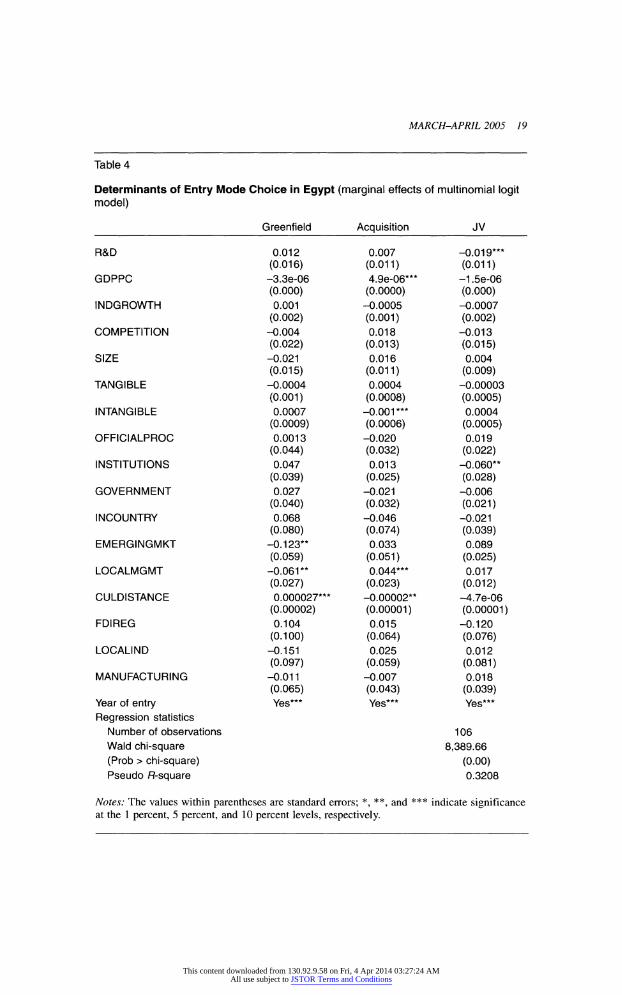

The regression results highlight some important aspects of the entry mode deci sion of MNCs into developing countries or emerging markets. First, the R&D

intensity of an MNCs product, which lies at the heart of the literature that has

developed around experiences and strategies of MNCs in developed markets, does not play an important role in determining the mode of entry. It does not matter at all in South Africa, and it matters only marginally in Egypt. However, in the Egyp tian context, the coefficient estimate for the R&D variable is consistent with the

prior idea presented that high R&D intensity of an MNCs product would reduce the probability of a JV.

Contrary to expectations, a higher value of the GDP per capita of the MNCs' home countries (GDPPC) is associated with a higher probability for acquisition of

This content downloaded from 130.92.9.58 on Fri, 4 Apr 2014 03:27:24 AMAll use subject to JSTOR Terms and Conditions

18 EMERGING MARKETS FINANCE AND TRADE

Table 3

Determinants of Entry Mode Choice in South Africa (marginal effects of multinomial logit model)

Greenfield Acquisition JV

R&D

GDPPC

INDGROWTH

COMPETITION

SIZE

TANGIBLE

INTANGIBLE

OFFICIALPROC

INSTITUTIONS

GOVERNMENT

INCOUNTRY

EMERGINGMKT

LOCALMGMT

CULDISTANCE

FDIREG

LOCALIND

MANUFACTURING

Year of entry

Regression statistics

Number of observations

Wald chi-square

(Prob > chi-square) Pseudo fi-square

Notes: The values within parentheses are standard errors; *, at the 1 percent, 5 percent, and 10 percent levels.

-0.013

(0.036) -0.000019*

(0.00001) 0.012

(0.008) 0.079

(0.057) 0.006

(0.047) -0.006**

(0.002) -0.002

(0.002) 0.065

(0.009) 0.009

(0.104) -0.107

(0.094) -0.149

(0.145) -0.231

(0.229) -0.118***

(0.063) -0.00002

(0.00003) 0.011

(0.101) 0.055

(0.091) -0.336**

(0.150) Yes**

0.004

(0.025) 0.000016*

(0.00001) -0.004

(0.005) 0.029

(0.043) 0.025

(0.031) 0.001

(0.001) 0.004*

(0.001) -0.041

(0.082) -0.145***

(0.088) 0.140**

(0.070) -0.029

(0.121) -0.037

(0.198) -0.009

(0.047) -0.00001

(0.00003) 0.005

(0.073) 0.016

(0.067) 0.122

(0.122) Yes**

0.009

(0.028) 2.5e-06

(0.00001) -0.007

(0.006) -0.108**

(0.057) -0.032

(0.042) 0.004**

(0.001) -0.001

(0.001) -0.024

(0.090) 0.136***

(0.082) -0.032

(0.079) 0.179

(0.123) 0.269**

(0.124) 0.128**

(0.064) 0.00004

(0.00003) -0.017

(0.074) -0.071

(0.078) 0.213***

(0.124) Yes**

114 10,614.41

(0.00) 0.3486

and *** indicate significance

This content downloaded from 130.92.9.58 on Fri, 4 Apr 2014 03:27:24 AMAll use subject to JSTOR Terms and Conditions

MARCH-APRIL 2005 19

Table 4

Determinants of Entry Mode Choice in Egypt (marginal effects of multinomial logit model)

Greenfield Acquisition JV

R&D

GDPPC

INDGROWTH

COMPETITION

SIZE

TANGIBLE

INTANGIBLE

OFFICIALPROC

INSTITUTIONS

GOVERNMENT

INCOUNTRY

EMERGINGMKT

LOCALMGMT

CULDISTANCE

FDIREG

LOCALIND

MANUFACTURING

Year of entry

Regression statistics

Number of observations

Wald chi-square

(Prob > chi-square) Pseudo ft-square

Notes: The values within parentheses are standard errors; *, **

at the 1 percent, 5 percent, and 10 percent levels, respectively.

0.012

(0.016) -3.3e-06

(0.000) 0.001

(0.002) -0.004

(0.022) -0.021

(0.015) -0.0004

(0.001) 0.0007

(0.0009) 0.0013

(0.044) 0.047

(0.039) 0.027

(0.040) 0.068

(0.080) -0.123**

(0.059) -0.061**

(0.027) 0.000027*

(0.00002) 0.104

(0.100) -0.151

(0.097) -0.011

(0.065) Yes***

0.007

(0.011) 4.9e-06***

(0.0000) -0.0005

(0.001) 0.018

(0.013) 0.016

(0.011) 0.0004

(0.0008) -0.001***

(0.0006) -0.020

(0.032) 0.013

(0.025) -0.021

(0.032) -0.046

(0.074) 0.033

(0.051) 0.044***

(0.023) -0.00002**

(0.00001) 0.015

(0.064) 0.025

(0.059) -0.007

(0.043) Yes***

-0.019***

(0.011) -1.5e-06

(0.000) -0.0007

(0.002) -0.013

(0.015) 0.004

(0.009) -0.00003

(0.0005) 0.0004

(0.0005) 0.019

(0.022) -0.060**

(0.028) -0.006

(0.021) -0.021

(0.039) 0.089

(0.025) 0.017

(0.012) -4.7e-06

(0.00001) -0.120

(0.076) 0.012

(0.081) 0.018

(0.039) Yes***

106 8,389.66

(0.00) 0.3208

and *** indicate significance

This content downloaded from 130.92.9.58 on Fri, 4 Apr 2014 03:27:24 AMAll use subject to JSTOR Terms and Conditions

20 EMERGING MARKETS FINANCE AND TRADE

a local firm, both in South Africa and Egypt, and with a lower probability for

greenfield projects in South Africa. This indicates that GDPPC captures the home

country effect, rather than the R&D intensity of an MNC's product. MNCs from richer countries have deep pockets, and also a higher propensity to invest in for

eign countries by way of cross-border acquisitions (UNCTAD 2002). Second, the South African data find support in favor of the prior hypothesis that

MNCs that have relatively high need for tangible and intangible resources from the host country are less likely to opt for greenfield projects and are more likely to

opt for JV and acquisitions of local firms. However, in Egypt, an MNC's need for

tangible resources does not have any impact on its choice of entry mode, and its need for intangible resources makes an acquisition less likely, albeit only at the 10

percent level of significance. This counterintuitive result, which implies that the

restructuring cost associated with an acquisition is perceived to be higher than the reduction in the resource-seeking MNC's transactions cost on account of the ac

quisition, is difficult to explain. But it does raise questions about the perceptions of the MNCs regarding the organizational structures and business cultures of Egyp tian firms.

Third, in both South Africa and Egypt, perceptions of the MNCs about the

quality of the local institutions and governance, as well as about the business pro cedures, play a significant role in determining the choice of entry mode. However, the nature of the impact in the two countries is noticeably different, In South Af

rica, a low perceived quality of the institutions, as manifested by a high value of institutions (see Table 1), is associated with a lower probability for acquisitions and with a higher probability for JV relationships. In Egypt, on the other hand, a

high value of institutions is associated with a lower probability for JV and a higher (though not statistically significant) probability for acquisitions. The results sug gest that, ceteris paribus, a low quality of institutions increases restructuring cost in South Africa and agency costs in Egypt. This is consistent with the perception about the complex political economy of restructuring a firm in South Africa, given the high rates of unemployment, and so on, and raises questions about the percep tion of the MNCs regarding the reliability of Egyptian firms as partners in an environment where contract enforcement may be both difficult and costly.

The question about the perception of MNCs regarding Egyptian firms is once

again brought to the fore by the result that an increase in the cultural (or geo graphical) distance between an MNC's home country and Egypt increases the

probability of a greenfield project and reduces the probability of acquisitions. Once

again, this result is counterintuitive in light of the evidence accumulated from

developed-country experiences. It suggests that if an MNC's parent management feels that it would find it difficult to understand the local norms (or be able to

effectively monitor the local partner), it would prefer to opt for a greenfield project, even though this would increase the MNC's transactions cost of doing business.

Finally, the regression results confirm, in the Egyptian context, the prior theory about the relationship between the choice of entry mode and the perception of the

This content downloaded from 130.92.9.58 on Fri, 4 Apr 2014 03:27:24 AMAll use subject to JSTOR Terms and Conditions

MARCH-APRIL 2005 21

MNCs about the quality of the local management. The probability of an acquisi tion in Egypt increases with improvement in the perception about the quality of the local managerial labor, and, correspondingly, the probability of a greenfield entry decreases.

Concluding Remarks

In this study, we extend the existing literature involving the strategic decision of an

MNC concerning the mode of entering an emerging market to two relatively large, yet different, African countries. The importance of the choice of the entry mode, from a policy-making perspective, is a consequence of the stylized result that the extent of technology transfer by an MNC to a developing or emerging country affiliate depends significantly on the extent to which the parent can exert control over the affiliate, which, in turn, is determined by the mode of entry of the MNC into that country. Our results indicate that the nature of impact of the perceived determinants of entry mode choice may be very different between developed and

developing countries, leading to counterintuitive results in the latter when viewed in light of the literature that is based on the experiences of the former. The results also indicate that the determinants of entry mode choice vary significantly across

developing countries, with local knowledge playing a more significant role in rela

tively less-developed countries (e.g., Egypt) than in relatively more developed ones

(e.g., South Africa). From a policy-making perspective, however, an important result is that factors

such as the technology intensiveness of an MNCs product, the extent of income risk it is exposed to by way of competition, and the size of the developing-country affiliate relative to the MNCs global operations are not significant determinants of entry mode choice. They are consistent with the conventional wisdom, as also is the empirical evidence, which suggests that developing-country operations usu

ally represent a very small fraction of the MNCs' global operations, and that they usually do not produce technology-intensive products in developing countries, but rather products that are either in the low-technology downstream segments of their

supply chain or are nearing the end of their product cycle (Estrin and Meyer 2004). The weak impact of local competition on entry mode choice is consistent with evidence that suggests that MNCs' affiliates in developing countries can operate in niche markets (Kokko 1994) and thereby avoid competition. These results bring into question the ability of FDI to raise productivity in developing countries, both

directly by way of technology transfer and indirectly by way of competition from MNC affiliates.

Ironically, the data, which are one of the strengths of this paper, are also the source of its shortcomings. While it is unique in its coverage and scope, and pro vides an insight into the strategic decision-making process of MNCs entering emerg ing markets, it has a significant missing value problem that has led to a loss of

nearly 25 percent of the observations. Also, we were forced to adopt the qualita

This content downloaded from 130.92.9.58 on Fri, 4 Apr 2014 03:27:24 AMAll use subject to JSTOR Terms and Conditions

22 EMERGING MARKETS FINANCE AND TRADE

tive/categorical measures of some of the variables (e.g., competition) when, ide

ally, we should have used measures like industry-level Herfindahl indices. How

ever, the cost of obtaining data of this quality is prohibitively high at present. This endeavor should, therefore, be left for the future.

Note

1. As argued by Gomes-Casseres (1990), FDI-related regulations may also play a role

in determining entry mode choice by restricting the options of an MNC.

References

Agarwal, S., and S.N. Ramaswami. 1992. "Choice of Foreign Market Entry Mode: Impact of Ownership, Location, and Internalization Factors." Journal of International Business

Studies 23, no. 1: 1-27.

Aitken, B.J., and A.E. Harrison. 1999. "Do Domestic Firms Benefit from Direct Foreign Investment? Evidence from Venezuela." American Economic Review 89, no. 3:605-618.

Asiedu, E., and H.S. Esfahani. 2001. "Ownership Structure in Foreign Direct Investment

Projects." Review of Economics and Statistics 83, no. 4: 647-662.

Barbosa, N., and H. Louri. 2002. "On the Determinants of Multinationals' Ownership Pref

erences: Evidence from Greece and Portugal." International Journal of Industrial Or

ganization 20, no. 4: 493-515.

Barbosa, N.; P. Guimaraes; and D. Woodward. 2004. "Foreign Firm Entry in Portugal: An

Application of Event Count Models " Applied Economics 36, no. 5: 465-472.

Blomstrom, M., and F. Sjoholm. 1999. "Technology Transfer and Spillovers: Does Local

Participation with the Multinationals Matter?" European Economic Review 43, no. 4-6:

915-923.

Blomstrom, M., and M. Zejan. 1989. "Why do Multinational Firms Seek Out Joint Ven

tures?" Working Paper no. 2987, National Bureau of Economic Research, Cambridge, MA.

Brouthers, K.D., and L.E. Brouthers. 2003. "Why Service and Manufacturing Entry Mode

Choices Differ: The Influence of Transaction Cost Factors, Risk and Trust." Journal of

Management Studies 40, no. 5: 1179-1204.

Caves, R. E., and S. Mehra. 1986. "Entry of Foreign Multinationals into US Manufacturing Industries." In Competition in Global Industries, ed. M. Porter, pp. 449^4-82. Boston:

Harvard Business School Press.

Cho, K.R., and P. Padmanabhan. 1995. "Acquisition Versus New Venture: The Choice of

Foreign Establishment Mode by Japanese Firms." Journal of International Manage ment 1, no. 3: 255-285.

Erramilli, K.M., and CP. Rao. 1993. "Service Firms' International Entry-Mode Choice: A

Modified Transactions-Cost Analysis Approach." Journal of Marketing 57: 19-38.

Estrin, S., and K.E. Meyer. 2004. Investment Strategies in Emerging Markets. Cheltenham, UK: Edward Elgar.

Ethier, WJ. 1986. "The Multinational Firm." Quarterly Journal of Economics 101, no. 4:

805-834.

Gatignon, H., and E. Anderson. 1988. "The Multinational Corporation's Degree of Control

over Foreign Subsidiaries: An Empirical Test of Transactions Cost Explanation" Jour

nal of Law Economics and Organization 4, no. 2: 305-336.

This content downloaded from 130.92.9.58 on Fri, 4 Apr 2014 03:27:24 AMAll use subject to JSTOR Terms and Conditions

MARCH-APRIL 2005 23

Gelb, S. 2003. "Background Paper: Institutional Development and FDI in South Africa."

DRC Working Paper no. 7, Centre for New and Emerging Markets, London Business

School.

Glass, A.J., and K. Saggi. 1998. "International Technology Transfer and the Technology

Gap." Journal of Development Economics 55, no. 2: 369-398.

Gleason, K.G.; C.I. Lee; and I. Mathur. 2002. "Dimensions of International Expansions by U.S. Firms to China: Wealth Effects, Mode Selection and Firm Specific Factors." Inter

national Review of Economics and Finance 11, no. 2: 139-154.

Gomes-Casseres, B. 1989. "Ownership Structures of Foreign Business Subsidiaries." Jour

nal of Economic Behavior and Organization 11, no. 1: 1-25. -. 1990. "Firm Ownership Preferences and Host Government Restrictions: An Inte

grated Approach." Journal of International Business Studies 21, no. 1: 1-22.

Gorg, H. 2000. "Analysing Foreign Market Entry: The Choice Between Greenfield Invest

ments and Acquisitions." Journal of Economic Studies 27, no. 3: 165-181.

Hennart, J.F. 1991. "The Transactions Cost Theory of Joint Ventures: An Empirical Study of Japanese Subsidiaries in the United States." Management Science 37, no. 4:483-497.

Hennart, J.F., and Y.R. Park. 1993. "Greenfield vs. Acquisition: The Strategy of Japanese Investors in the United States." Management Science 39, no. 9: 1054-1070.

Horstman, I.J., and J.R. Markusen. 1996. "Exploring New Markets; Direct Investment, Contractual Relations and the Multinational Exercise." International Economic Review

37, no. 1: 1-19.

Kogut, B., and H. Singh. 1988. "Entering United States by Joint Venture: Competitive

Rivalry and Industry Structure." In Cooperative Strategies in Business, ed. F. Contractor

and P. Lorange. Lexington, MA: Lexington Books.

Kokko, A. 1994. "Technology, Market Characteristics, and Spillovers." Journal of Devel

opment Economics 43, no. 2: 279-293.

Lapan, H., and P. Bardhan. 1973. "Localized Technical Progress and Transfer of Technol

ogy and Economic Development." Journal of Economic Theory 6, no 6: 585-595.

Louis, M., and H. Handoussa. 2003. "Institutional Development and FDI in Egypt." DRC Working Paper No. 1, Centre for New and Emerging Markets, London Busi ness School.

Luo, Y. 2001. "Determinants of Entry in an Emerging Economy: A Multilevel Approach," Journal of Management Studies 38, no. 3: 443^+72.

Meyer, K.E. 2001. "International Business Research on Transition Economies." In Oxford Handbook of International Business, ed. A. Rugman and T. Brewer. Oxford: Oxford

University Press (available at www.oxfordscholarship.com/oso/public/content/

economicsfmance/0199241821/toe.html).

Patibandla, M., and B. Petersen. 2002. "Role of Transnational Corporations in the Evolu

tion of a High-Tech Industry: The Case of India's Software Industry." World Develop ments, no. 9: 1561-1577.

Ramachandran, V. 1993. "Technology Transfer, Firm Ownership, and Investment in Hu

man Capital." Review of Economics and Statistics 75, no. 4: 664-670.

Sinha, U.B. 2001. "International Joint Venture, Licensing and Buy-out Under Asymmetric Information." Journal of Development Economics 66, no. 1: 127-151.

Teece, D. 1986. "Transactions Cost Economics and the Multinational Enterprise: An As

sessment." Journal of Economic Behavior and Organization 7, no. 1: 21-45.

Tse, D.K.; Y. Pan; and KY. Au. 1997. "How MNCs Choose Entry Modes and Form Alli ances: The China Experience." Journal of International Business Studies 28, no. 4:

779-805.

This content downloaded from 130.92.9.58 on Fri, 4 Apr 2014 03:27:24 AMAll use subject to JSTOR Terms and Conditions

24 EMERGING MARKETS FINANCE AND TRADE

UNCTAD. 2002. World Investment Report: Transnational Corporations and Export Com

petitiveness. United Nations, Geneva.

Vishwasrao, S., and W. Bosshardt. 2001. "Foreign Ownership and Technology Adoption: Evidence from Indian Firms." Journal of Development Economics 65, no. 2: 367-387.

Yip, G. 1982. "Diversification Entry: Internal Development Versus Acquisition." Strategic

Management Journal 3, no. 3: 331-345.

Zejan, M.C. 1990. "New Ventures or Acquisitions. The Choice of Swedish Multinational

Enterprises." Journal of Industrial Economics 38, no. 3: 349-355.

To order reprints, call 1-800-352-2210; outside the United States, call 717-632-3535.

This content downloaded from 130.92.9.58 on Fri, 4 Apr 2014 03:27:24 AMAll use subject to JSTOR Terms and Conditions