determinants of corporate social responsibility for sustainable ...

339

i DETERMINANTS OF CORPORATE SOCIAL RESPONSIBILITY FOR SUSTAINABLE DEVELOPMENT PHD DISSERTATION Submitted By Nasir Hussain NDU-LMS/PhD-13/F-011 Supervisor Dr. Saman Attiq Co-Supervisor Dr. Hassan Jalil Shah SI (M) Department of Leadership and Management Studies Faculty of Contemporary Studies National Defence University Islamabad Pakistan 2019

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of determinants of corporate social responsibility for sustainable ...

i

DETERMINANTS OF CORPORATE SOCIAL

RESPONSIBILITY FOR SUSTAINABLE

DEVELOPMENT

PHD DISSERTATION

Submitted By

Nasir Hussain

NDU-LMS/PhD-13/F-011

Supervisor

Dr. Saman Attiq

Co-Supervisor

Dr. Hassan Jalil Shah SI (M)

Department of Leadership and Management Studies

Faculty of Contemporary Studies

National Defence University

Islamabad Pakistan

2019

i

DETERMINANTS OF CORPORATE SOCIAL

RESPONSIBILITY FOR SUSTAINABLE

DEVELOPMENT

PHD DISSERTATION

Submitted By

Nasir Hussain

NDU-LMS/PhD-13/F-011

Supervisor

Dr. Saman Attiq

Co-Supervisor

Dr. Hassan Jalil Shah SI (M)

This Dissertation is submitted to National Defence University,

Islamabad in partial fulfillment for the degree of Doctor of

Philosophy in Leadership and Management Studies

Department of Leadership and Management Studies

Faculty of Contemporary Studies

National Defence University

Islamabad Pakistan

2019

ii

Dedication

I would like to dedicate this study to my beloved parents. Their unprecedented love & affection,

tenderness & generosity have made me able to do this. Their prayers have relentlessly been the

guiding ways for me in my entire life.

iii

Abstract

Corporate social responsibility (CSR) is a phenomenon that has received considerable

attention not only from academicians & from researchers but also from corporate sector since it

has multidimensional effects on their performance. It is imperative to note that companies may

use CSR as a tool to manage many types of stakeholders, including stakeholders outside of the

organization and outcomes that go beyond financial result. This notion will lead the companies

towards new era mostly stated as sustainability, where companies act responsibly towards social,

environmental and societal issues at large. The current study seeks to model and empirically test

the relationship amongst determinants and outcomes (i.e. psychological and performance) of

corporate social responsibility, specifically this study probe into relationship between ethical

leadership, corporate social responsibility, trust and performance variables (organizational

citizenship behavior, task performance behavior & counterproductive work behavior).

Furthermore, this study also examines the role of ethical climate between the relationships of

ethical leadership and CSR (ethical climate acts as a moderator).

The current study has used mix methods approach i.e. quantitative and qualitative

research design. The population of the study is scheduled and listed commercial banks in

Pakistan. The study has used both simple random probability sampling technique and purposive

sampling technique. Data was collected using mix methods from the sampled individuals for

quantitative analysis. 500 responses were received back from the employees of banks from major

cities (i.e. Karachi, Lahore, Islamabad, Rawalpindi and Peshawar) however, only 420 were

useable. Fifteen top executives were interviewed out of the thirty-five listed commercial banks

for qualitative analysis in respect to sustainable development.

Data was analyzed using Partial Least Square Structural Equation Modeling (PLS-SEM).

Furthermore, necessary tests were conducted using Statistical Package for Social Sciences

iv

(SPSS) version 23. Findings indicate that ethical leadership has positive impact on CSR and

significantly contributes towards defining the underlying processes of CSR. Results confirmed

that ethical climate acts as a moderator between the relationship of ethical leadership & CSR.

The CSR activities are project based and identified through an internal mechanism sometimes

based on need and philanthropic prospective.

The integrated conceptual framework of the current study will be helpful in decision

making as to determine the impact of CSR on performance variables. Similarly, the current study

will help corporate sector in devising strategies and policies of sustainability for competitive

advantages.

The researcher contends that this is one of the few studies in Pakistani context to

understand the underlying processes linking ethical leadership with CSR along with the

performance outcomes and ethical climate as moderator. This will certainly provide a

comprehensive overview of CSR and sustainability prospective in Pakistan.

Keywords: Ethical leadership; Ethical climate; corporate social responsibility; trust;

organizational citizenship behavior; task performance behavior; counter work

productive behavior

1

ACKNOWLEDGEMENTS

I would like to pay my sincere heartfelt gratitude‘s to my parents for their prayers and affection. I

would also pay my esteem to my wife Shaista Nasir whose contribution has been the potency and

impudence for me.

I would also like to thank my supervisor Dr. Saman Attiq for her brilliant and unforgettable

supervision and guidance. I could not complete this study without her support. She has been very

affectionate, unrivaled & kind to me. I also want to thank Dr. Hassan Jalil Shah SI (M) for his

consistent support and valuable guidance as co-supervisor.

Finally, I would like to thanks all my friends of NDU for their bounteousness and support. I

thank my office collogues as well because they cooperated with me all the way to success.

NASIR HUSSAIN

2

LIST OF ABBREVIATIONS& ACRONYMS

Corporate social responsibility CSR

Counter work productive behavior CWPB

Economic survey report ESR

Environment social and governance ESG

European union EU

Habib Bank Limited HBL

International Union for Conservation of Nature IUCN

Millennium Development Goals MDG‘s

National Bank of Pakistan NBP

National Forum for Environment and Health NFEH

Non-governmental organizations NGO‘s

Organization for Economic Co-operation and Development OECD

Organizational citizenship behavior OCB

Pakistan Stock Exchange PSE

Securities and exchange commission of Pakistan SECP

State Bank of Pakistan SBP

Statistical Package for the Social Sciences SPSS

Structural Equation Model SEM

Sustainable development SD

Sustainable Development Goals SDG‘s

Task performance behavior TPB

United Bank Limited UBL

United Nations UN

United Nations Conference on Environment and Development UNCED

United Nations Development Program UNDP

World Bank WB

World Business Council for Sustainable Development WBCSD

World Commission on Environmental Development WCED

World Wide Fund for Nature WWF

3

TABLE OF CONTENTS

Abstract ......................................................................................................................................... iii LIST OF TABLES ........................................................................................................................ 9 LIST OF FIGURES .................................................................................................................... 10 CHAPTER 1 ................................................................................................................................ 14 INTRODUCTION....................................................................................................................... 14

1. Introduction ......................................................................................................................................... 14

1.1 CSR in Developing Economies ....................................................................................................... 18

1.2 CSR Practice Reference to South Asian Context ........................................................................... 20

1.3 CSR in Pakistan’s Context .............................................................................................................. 21

1.4 CSR and Multi-National Companies in Pakistan ............................................................................ 24

1.5 Large Local Companies in Pakistan ............................................................................................... 24

1.6 Pakistan’s Economic & Social Developments................................................................................ 26

1.7 Background ....................................................................................................................................... 27

1.8 Problem Statement ............................................................................................................................ 32

1.9 Research Questions ........................................................................................................................... 33

1.10 Knowledge Gap Identification ........................................................................................................ 34

1.10.1 Knowledge Gap for Sustainability ....................................................................................... 34

1.10.2 Knowledge Gap for CSR ........................................................................................................... 34

1.10.2 Knowledge Gap for Ethical Leadership .................................................................................... 35

1.10.3 Knowledge Gap for Ethical Climate.......................................................................................... 36

1.10.4 Knowledge Gap for Trust ......................................................................................................... 38

1.10.5 Knowledge Gap for Performance Variables ............................................................................. 39

1.11 Research Objectives .................................................................................................................... 40

1.12 Significance of the Study ................................................................................................................ 41

1.12.1 Theoretical Significance ........................................................................................................... 41

1.12.2 Practical Significance ................................................................................................................ 41

1.14 Structure of the Complete Thesis .................................................................................................... 44

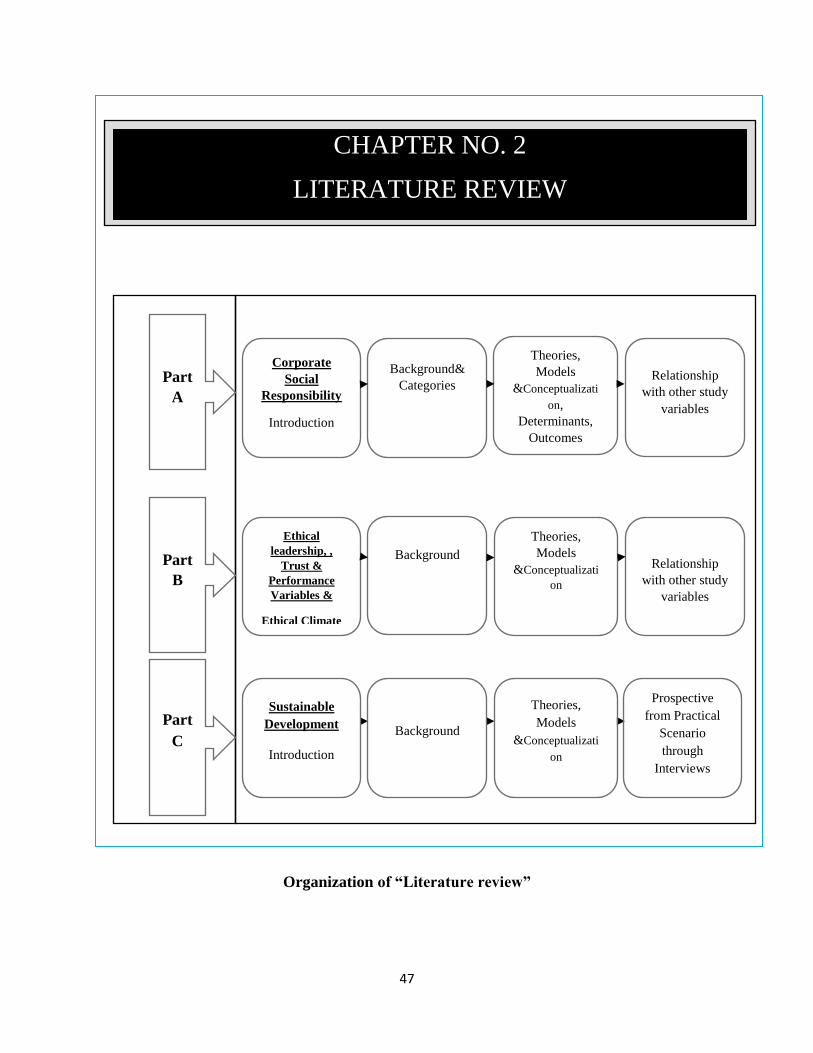

CHAPTER 2 ................................................................................................................................ 48

LITERATURE REVIEW .......................................................................................................... 48 2.1 Introduction ....................................................................................................................................... 48

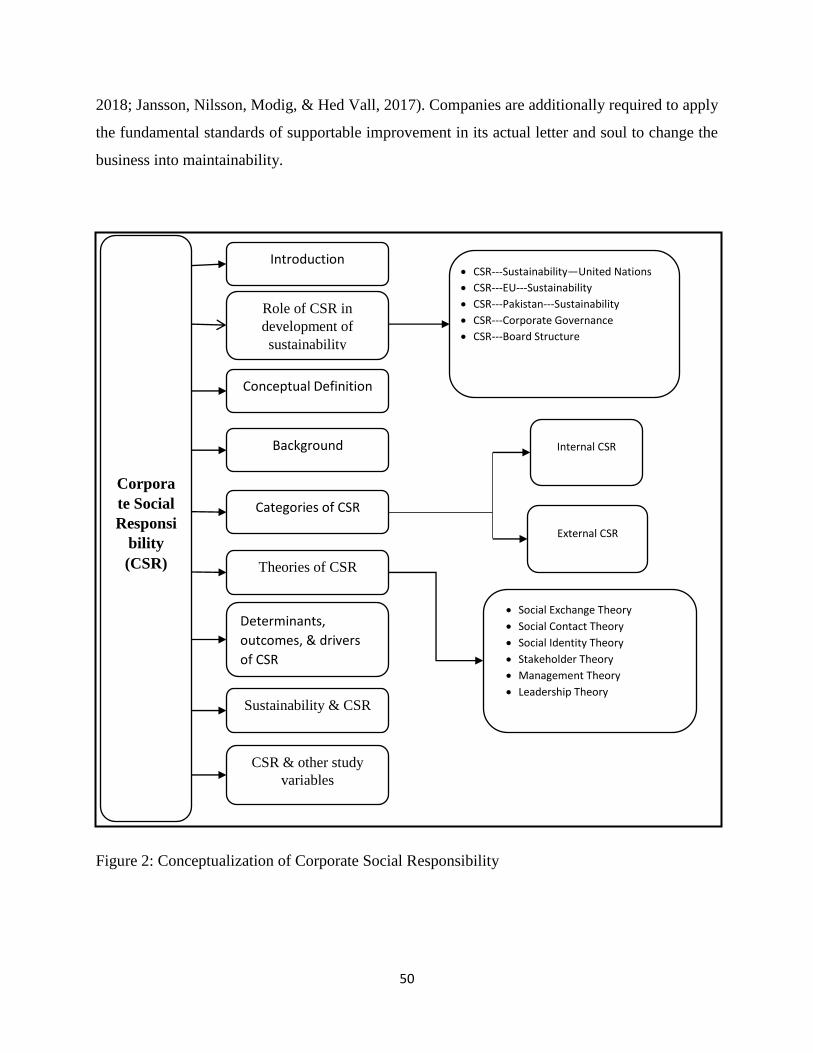

2.2 Corporate Social Responsibility........................................................................................................ 48

2.2.1 Conceptual Definitions of CSR ................................................................................................... 51

2.2.2 Background ................................................................................................................................ 52

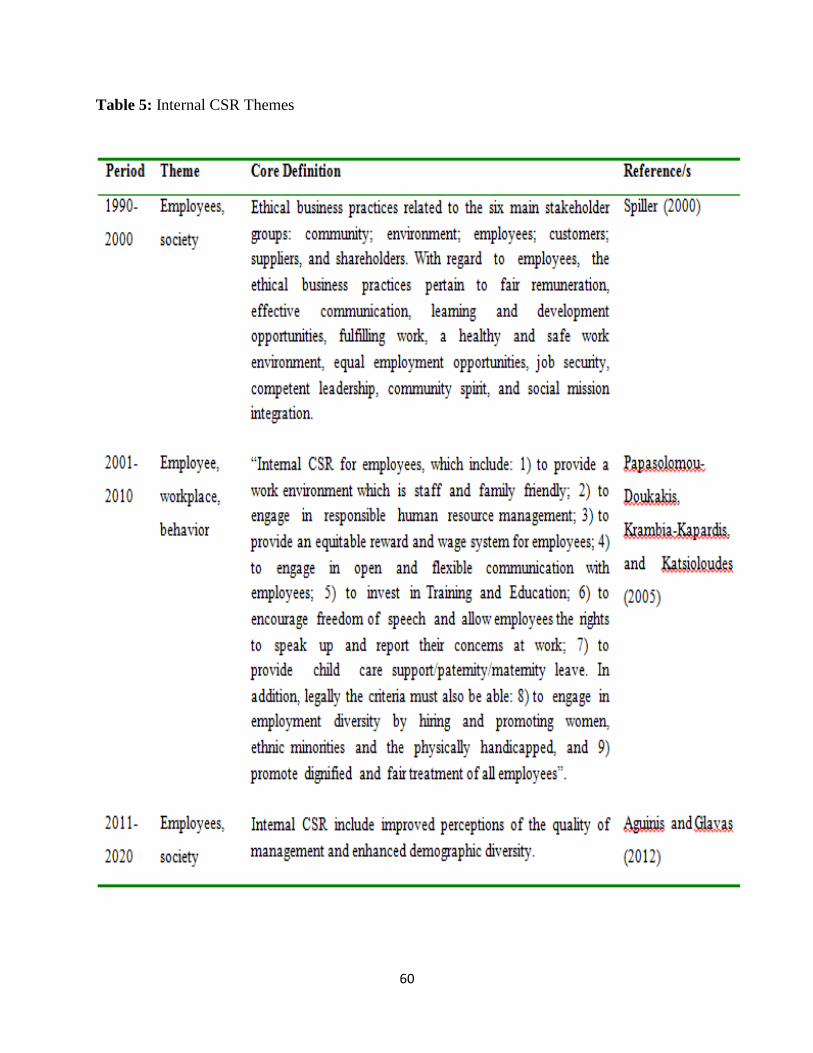

2.2.3 Categories of Corporate Social Responsibility .............................................................................. 58

4

2.2.3.1 Internal CSR ............................................................................................................................. 58

2.2.3.2 External CSR ............................................................................................................................ 61

2.2.4 Theoretical Perspectives of Corporate Social Responsibility ........................................................ 63

2.2.4.1 Stakeholder Theory ................................................................................................................. 63

2.2.4.2 Social Exchange Theory ........................................................................................................... 63

2.2.4.3 Social Identity Theory ............................................................................................................. 64

2.2.4.4 Social Contract Theory ............................................................................................................ 64

2.2.4.5 Legitimacy Theory ................................................................................................................... 65

2.2.4.6 Institutional Theory ................................................................................................................. 65

2.2.4.7 Cultural Theory ....................................................................................................................... 66

2.2.4.8 Management Theory............................................................................................................... 66

2.2.5 Leadership Theories ....................................................................................................................... 66

2.2.5.1 CSR and Transformational Leadership Theory ........................................................................ 66

2.2.5.2 CSR and Transactional Leadership Theory .............................................................................. 68

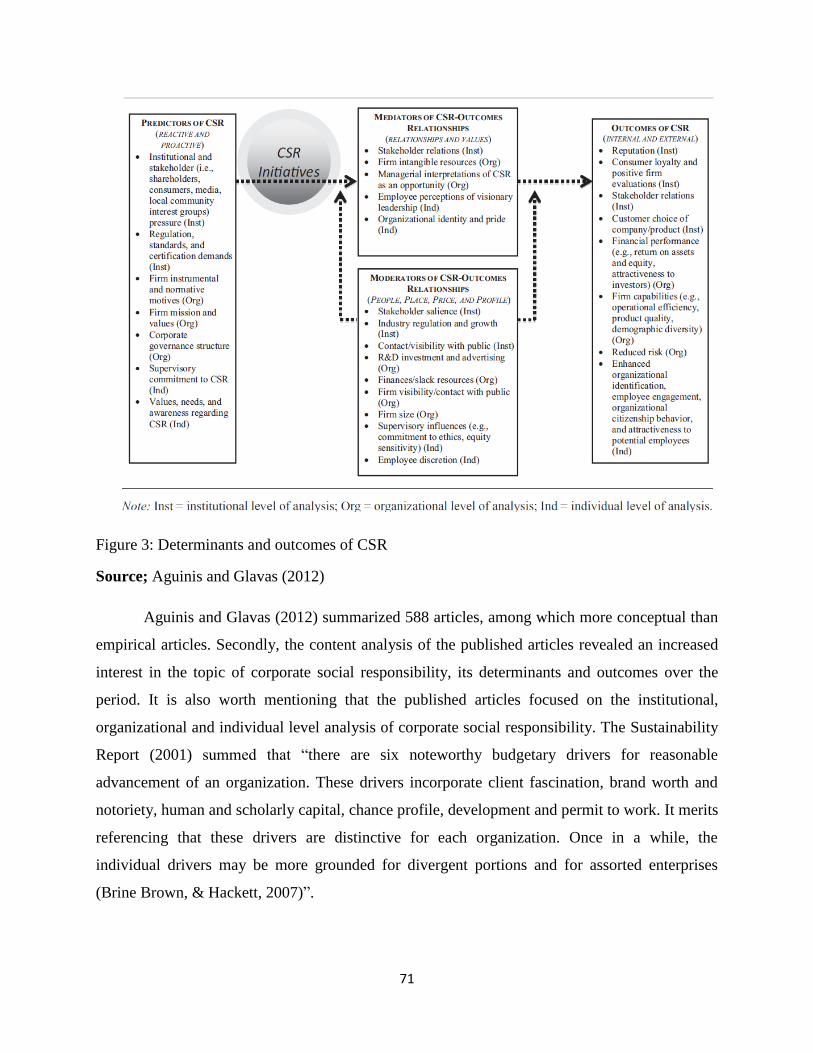

2.2.6 Determinants and outcomes of CSR .............................................................................................. 68

2.2.7 Relationship between CSR & Sustainability ................................................................................. 72

2.2.7.1 CSR & United Nations ............................................................................................................. 73

2.2.7.2 CSR & Corporate Governance ................................................................................................. 74

2.2.7.3 CSR & Role of Corporate Management / Board Structure ..................................................... 75

2.2.8 Outcomes of Corporate Social Responsibility ............................................................................... 76

2.3 Ethical Leadership ............................................................................................................................ 80

2.3.1 Conceptual Definitions of ethical leadership ................................................................................. 80

2.3.2 Background .................................................................................................................................... 81

2.3.3 Theories of Ethical Leadership ...................................................................................................... 83

2.3.3.1 Social Learning Theory ............................................................................................................ 83

2.3.3.2 Transformational Theory ........................................................................................................ 84

2.3.3.4 Spiritual and Authentic Leadership Theory............................................................................. 84

2.3.4 Models of Ethical Leadership ........................................................................................................ 85

2.3.5 Relationship of Ethical Leadership with Other Study Variables ................................................... 86

2.3.5.1 Ethical leadership and Corporate Social Responsibility .......................................................... 86

2.3.5.2 Ethical Leadership and Ethical Climate ................................................................................... 87

2.3.5.3 Ethical Leadership and Transformational Leadership ............................................................. 87

5

2.3.5.4 Ethical Leadership with reference to situation ....................................................................... 88

2.3.5.5 Ethical Leadership with reference to context ......................................................................... 88

2.4 Trust .................................................................................................................................................. 89

2.4.1 Conceptual Definition of Trust ...................................................................................................... 89

2.4.2 Theoretical base for Trust .............................................................................................................. 90

2.4.3 Dimensions of Trust ....................................................................................................................... 91

2.4.3.1 Affect & Cognition-Based Trust............................................................................................... 91

2.4.4 The Model of Trust ........................................................................................................................ 92

2.4.5 Determinants of Trust .................................................................................................................... 93

2.4.6 Relationship of Trust with study variables..................................................................................... 94

2.4.7 Relationship of trust with other variables ...................................................................................... 95

2.5 Performance Behavior ...................................................................................................................... 96

2.5.1 TPB ................................................................................................................................................ 97

2.5.2 Conceptual Definition of Task Performance Behavior ............................................................... 97

2.5.3 Task Performance Vs Contextual performance ......................................................................... 98

2.5.4 Task Performance and Theory of individual differences ........................................................... 98

2.6.1 Conceptual Definition of OCB .................................................................................................... 99

2.6.2 Background ................................................................................................................................ 99

2.6.3 Determinants of OCB ............................................................................................................... 100

2.7 Counterproductive Work Behavior ................................................................................................. 101

2.7.1 Conceptual Definition of CWP ................................................................................................. 101

2.7.2 Determinants of Counterproductive Behaviors ....................................................................... 102

2.8 Ethical Climate ................................................................................................................................ 104

2.8.1 Conceptual Definition of ethical climate ..................................................................................... 104

2.8.2 Types of Ethical Climate.............................................................................................................. 105

2.8.4 Theories of Ethical Climate ......................................................................................................... 105

2.8.4.1 Moral Development Theory .................................................................................................. 105

2.8.4.2 Ethical Climate Theory .......................................................................................................... 105

2.8.5 Determinants of Ethical Climate .................................................................................................. 106

2.8.6 Outcomes of Ethical Climate ....................................................................................................... 107

2.8.7 Relationship with other study variables ....................................................................................... 108

2.8.8 Ethical Climate as Moderator ...................................................................................................... 109

2.9 Sustainable Development ................................................................................................................ 110

6

2.9.1 Definition of Sustainable Development ................................................................................... 112

2.9.2 Background .............................................................................................................................. 112

2.9.3 Theories of Sustainable Development ......................................................................................... 118

2.9.3.1 Signaling theory .................................................................................................................... 118

2.9.3.2 Legitimacy theory .................................................................................................................. 118

2.9.3.3 Stakeholder theory ............................................................................................................... 118

2.9.4 The Evolution from Conventional to Sustainable Development ................................................. 119

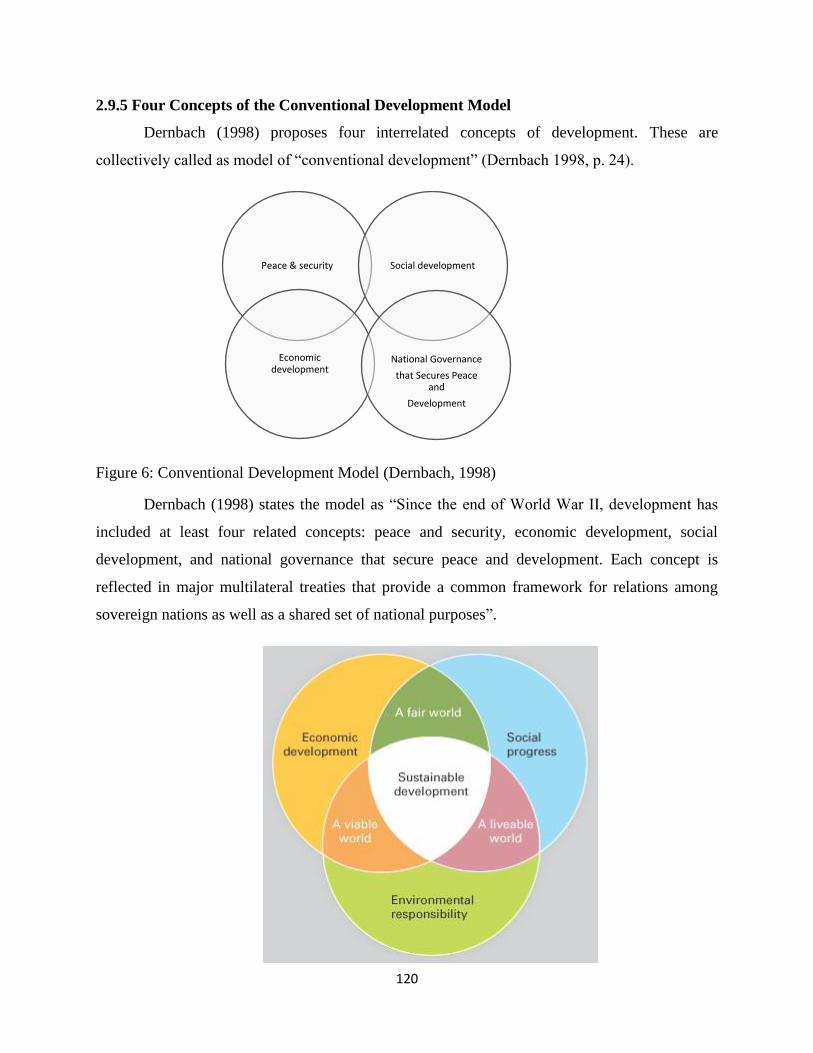

2.9.5 Four Concepts of the Conventional Development Model ............................................................ 120

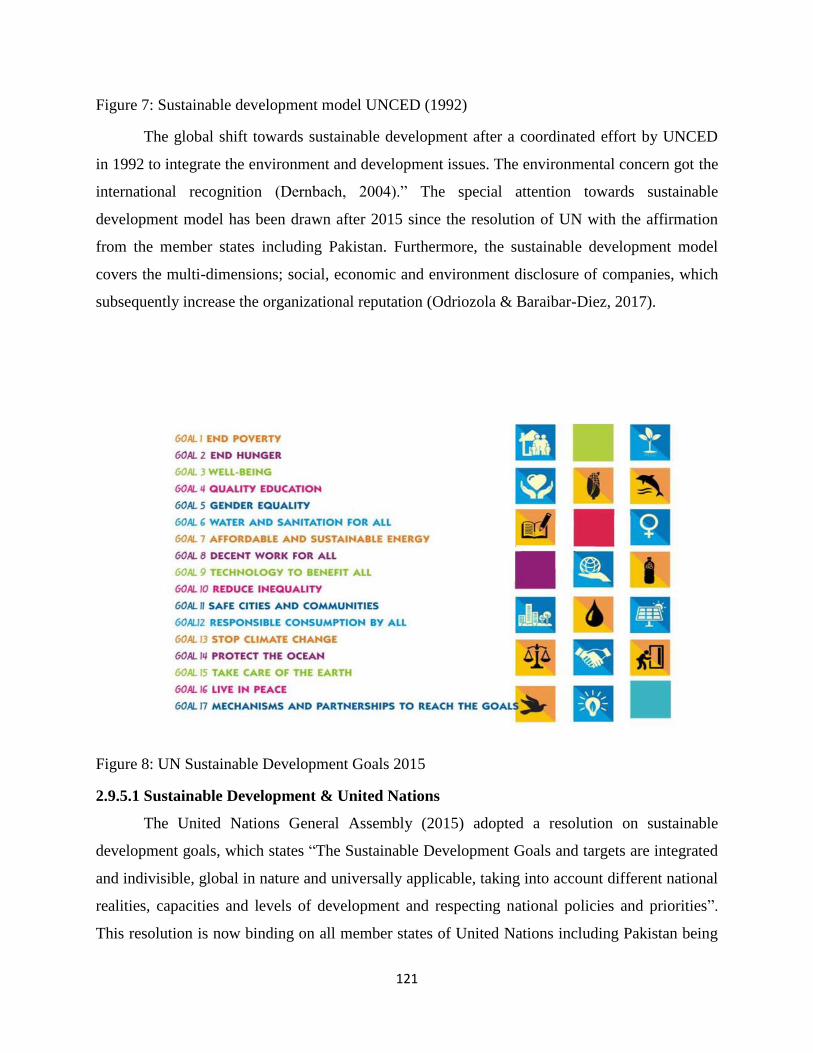

2.9.5.1 Sustainable Development & United Nations ........................................................................ 121

2.9.5.2 Pakistan and Sustainable Development................................................................................ 122

2.9.6 Sustainable Development & CSR Link ....................................................................................... 123

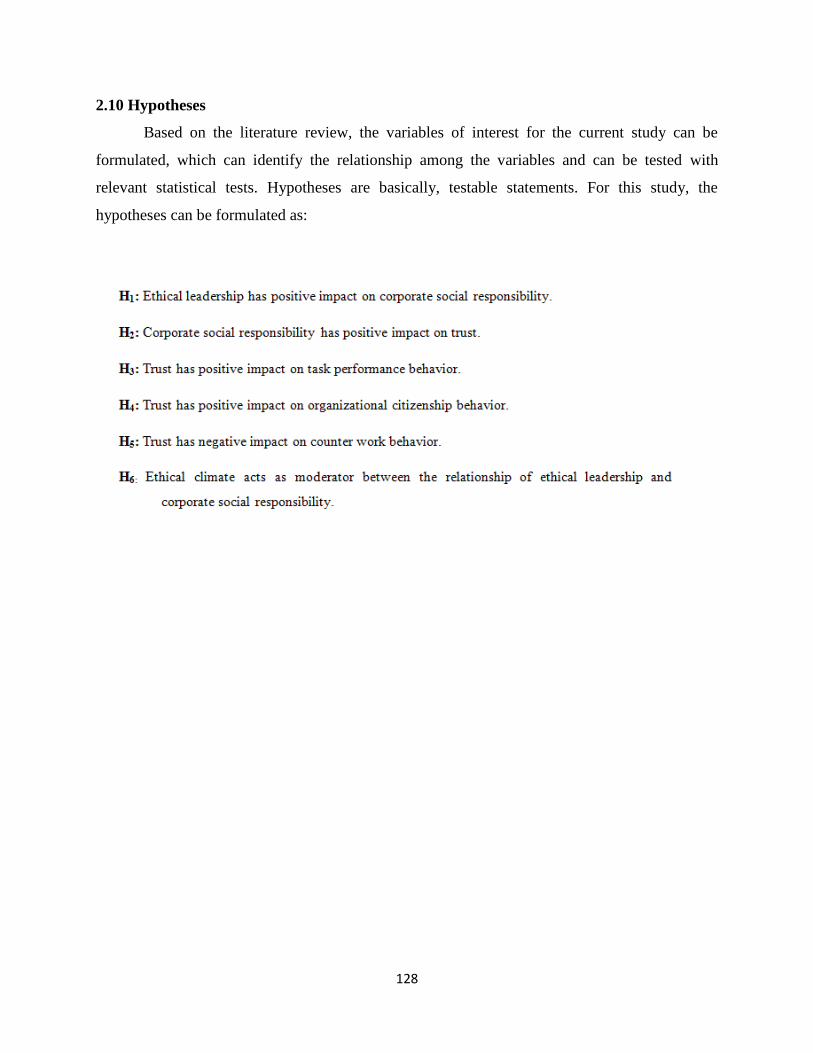

2.10 Hypotheses .................................................................................................................................... 128

Chapter 3 ................................................................................................................................... 131 Research Methodology ............................................................................................................. 131

3.1 Research Design Mix Method Approach ........................................................................................ 131

3.1.1 Research Design for Quantitative Part ......................................................................................... 132

3.1.2 Research Design for Qualitative Part ........................................................................................... 133

3.2 Population Framework .................................................................................................................... 133

3.3 Sample and Data Collection ............................................................................................................ 134

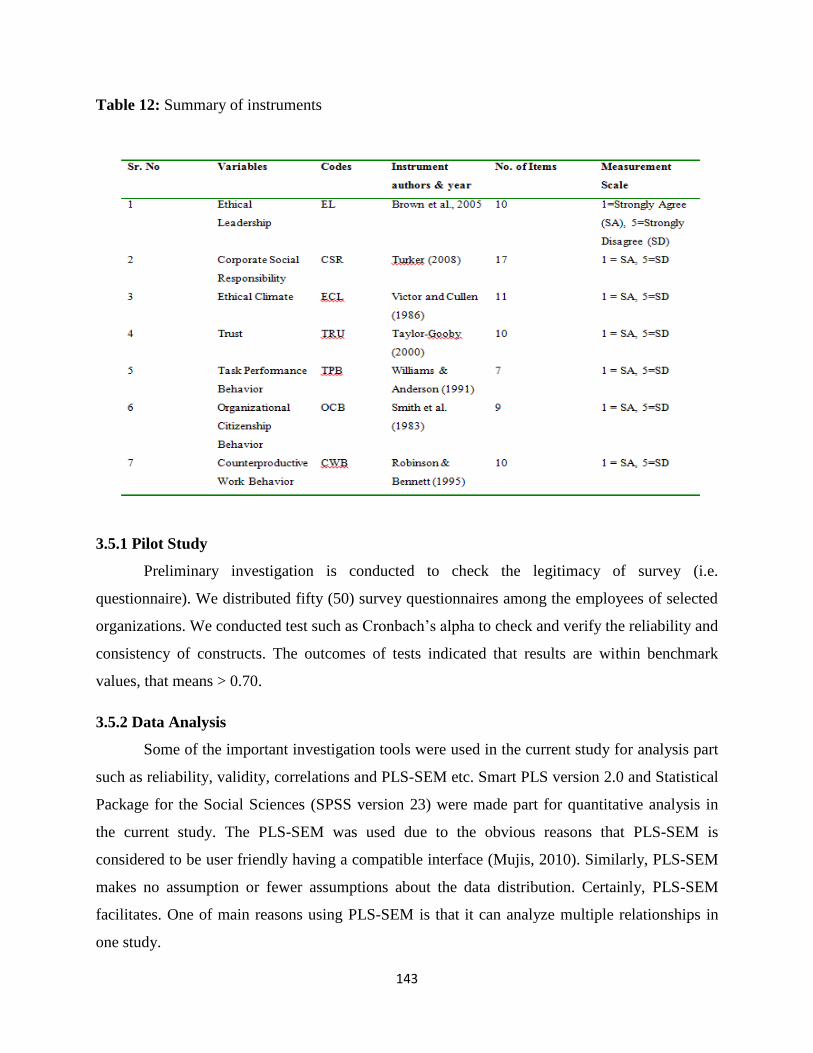

3.4 Measures ......................................................................................................................................... 139

3.4.1 Ethical Leadership .................................................................................................................... 140

3.4.2 Corporate Social Responsibility ............................................................................................... 140

3.4.3 Ethical Climate ......................................................................................................................... 140

3.4.4 Trust ......................................................................................................................................... 140

3.4.5 Counterwork Productive Behavior ........................................................................................... 141

3.4.6 Task Performance Behavior ..................................................................................................... 141

3.4.7 Organizational Citizenship Behavior ........................................................................................ 141

3.4.8 Sustainable Development ............................................................................................................. 141

3.5 Procedure ........................................................................................................................................ 142

3.5.1 Pilot Study ................................................................................................................................ 143

3.5.2 Data Analysis ............................................................................................................................ 143

3.5.3 Data Screening ......................................................................................................................... 144

3.5.4 Normality Analysis ................................................................................................................... 144

7

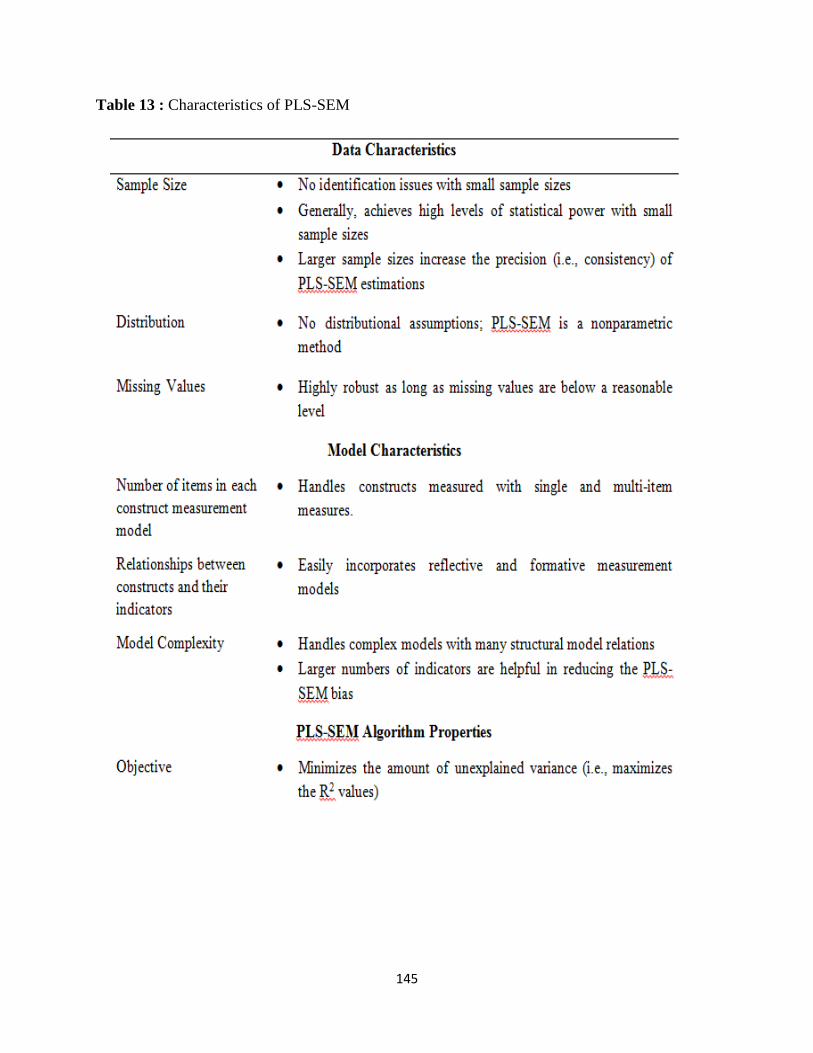

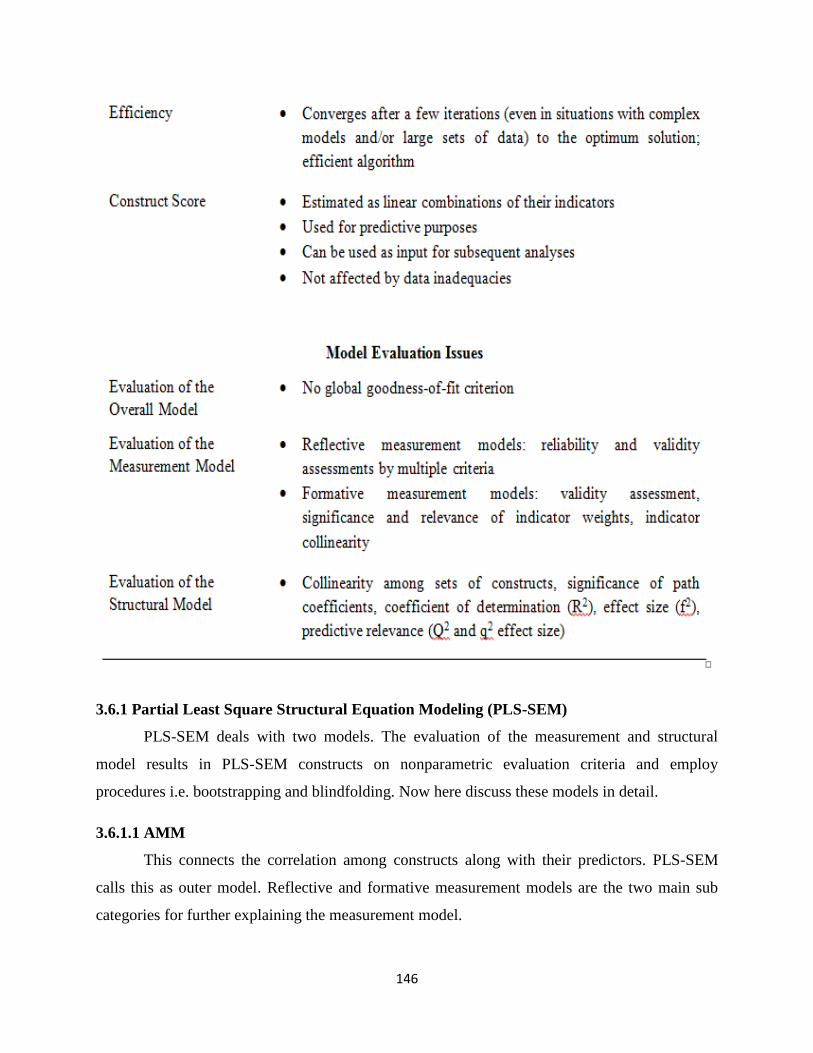

3.6 SEM ................................................................................................................................................ 144

3.6.1 Partial Least Square Structural Equation Modeling (PLS-SEM) ................................................ 146

Chapter 4 ................................................................................................................................... 152 Results & Analysis .................................................................................................................... 152

4. Introduction ....................................................................................................................................... 152

4.1 Scheme of Analyses ........................................................................................................................ 152

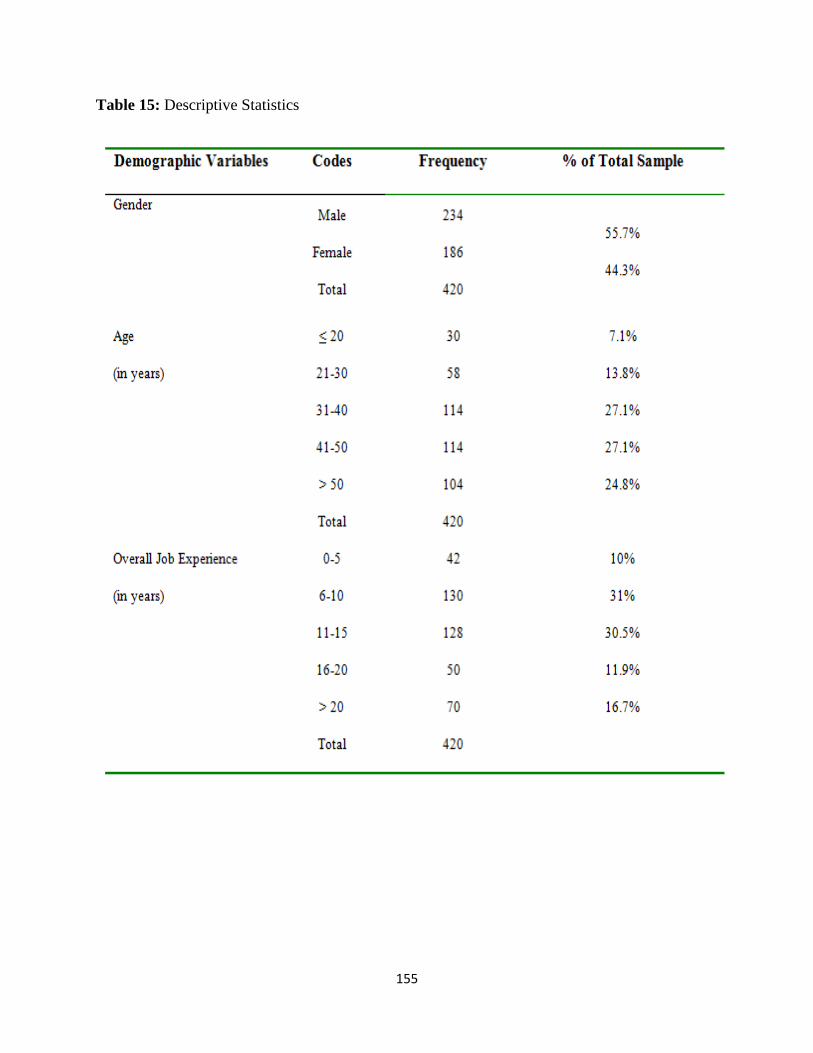

4.2 Response Pattern of Quantitative Part ............................................................................................ 153

4.2.1 Demographic Characteristics of Sample ...................................................................................... 154

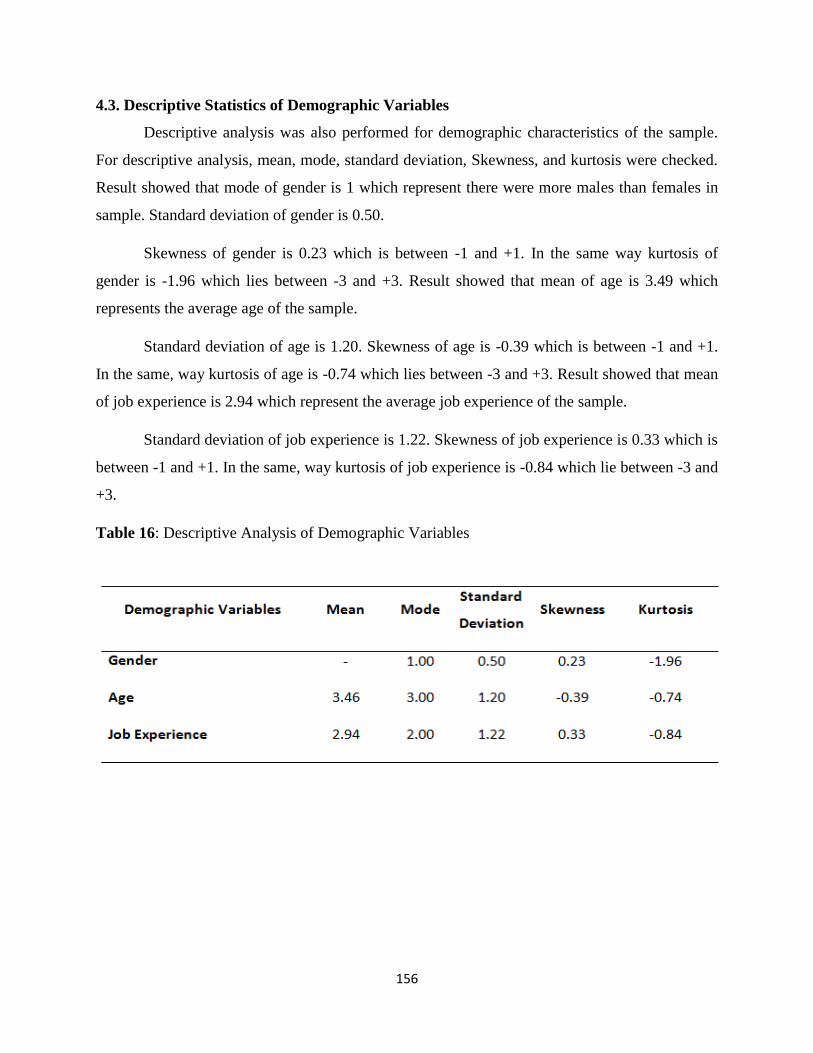

4.3. Descriptive Statistics of Demographic Variables .......................................................................... 156

4.4. Descriptive Analysis of Study Variables ....................................................................................... 157

4.5. Partial least square-structural equation Modeling (PLS-SEM) ...................................................... 163

4.5.1. Reflective Measurement Model .................................................................................................. 163

4.5.1.1 OLs ......................................................................................................................................... 163

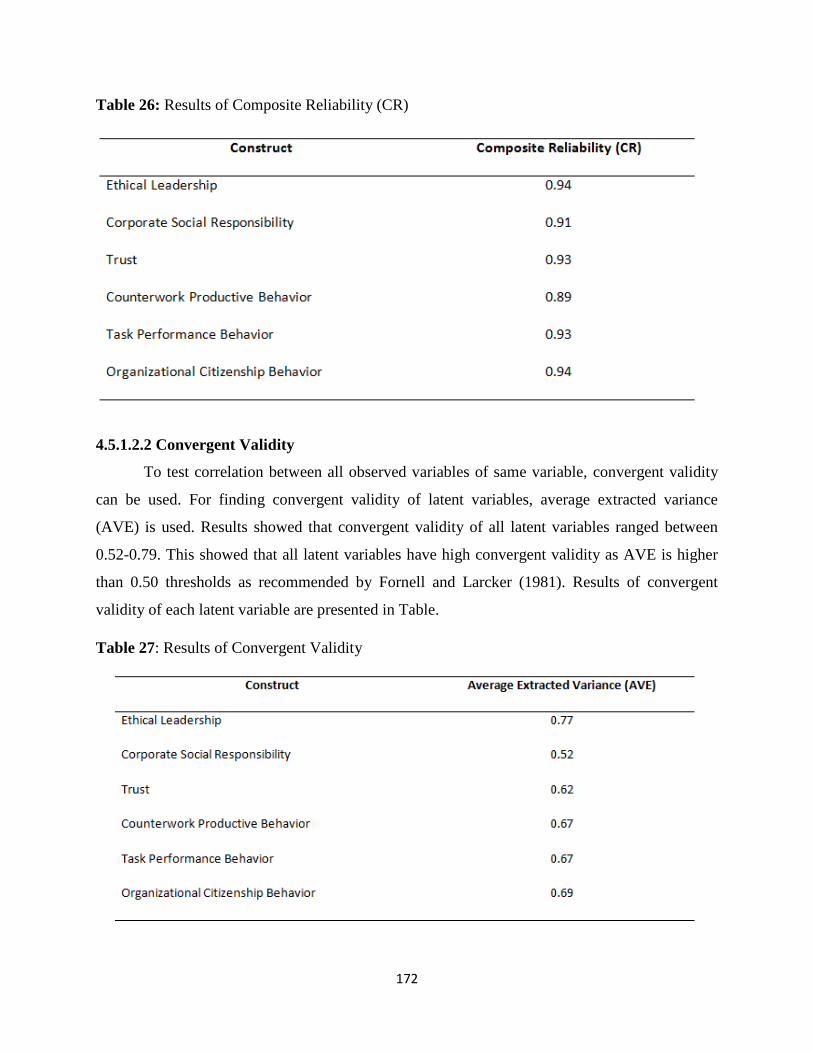

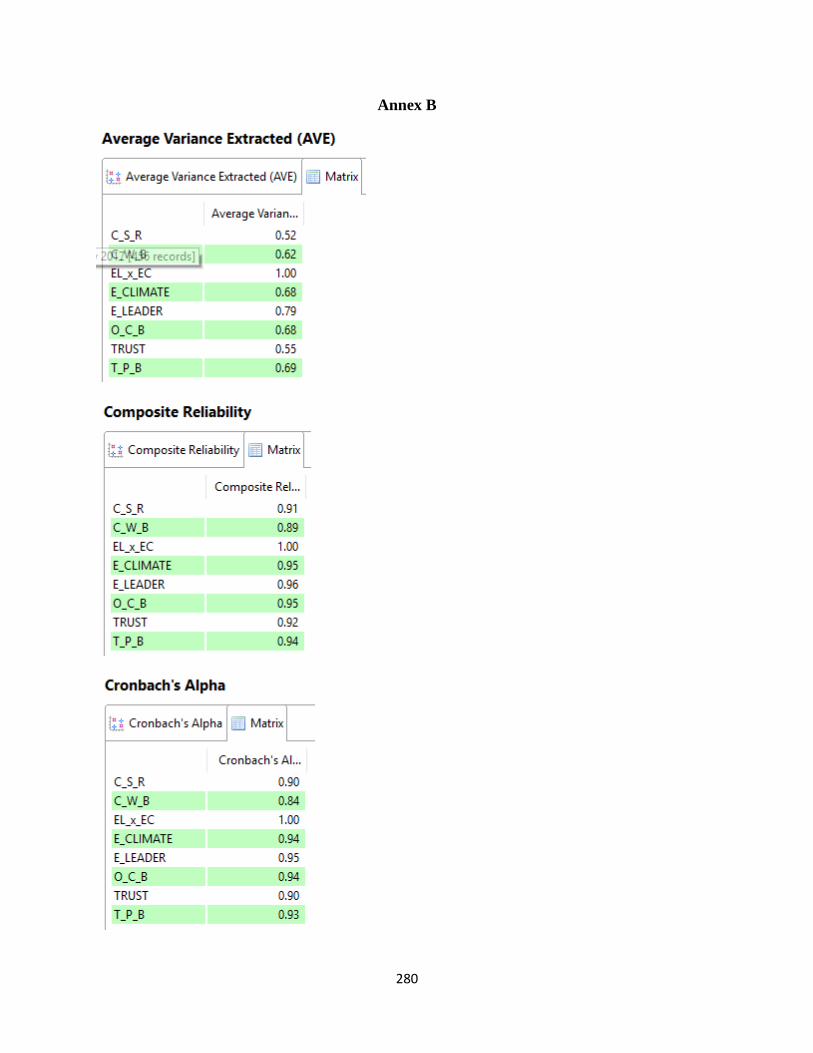

4.5.1.2 Reliability and Validity Analysis .............................................................................................. 170

4.5.1.2.1 Internal Consistency (Reliability) ....................................................................................... 170

4.5.1.2.1.1 Cronbach Alpha ............................................................................................................... 170

4.5.1.2.1.2 Composite Reliability (CR) ............................................................................................... 171

4.5.1.2.2 Convergent Validity ............................................................................................................ 172

4.5.1.2.3 Discriminant Validity .......................................................................................................... 173

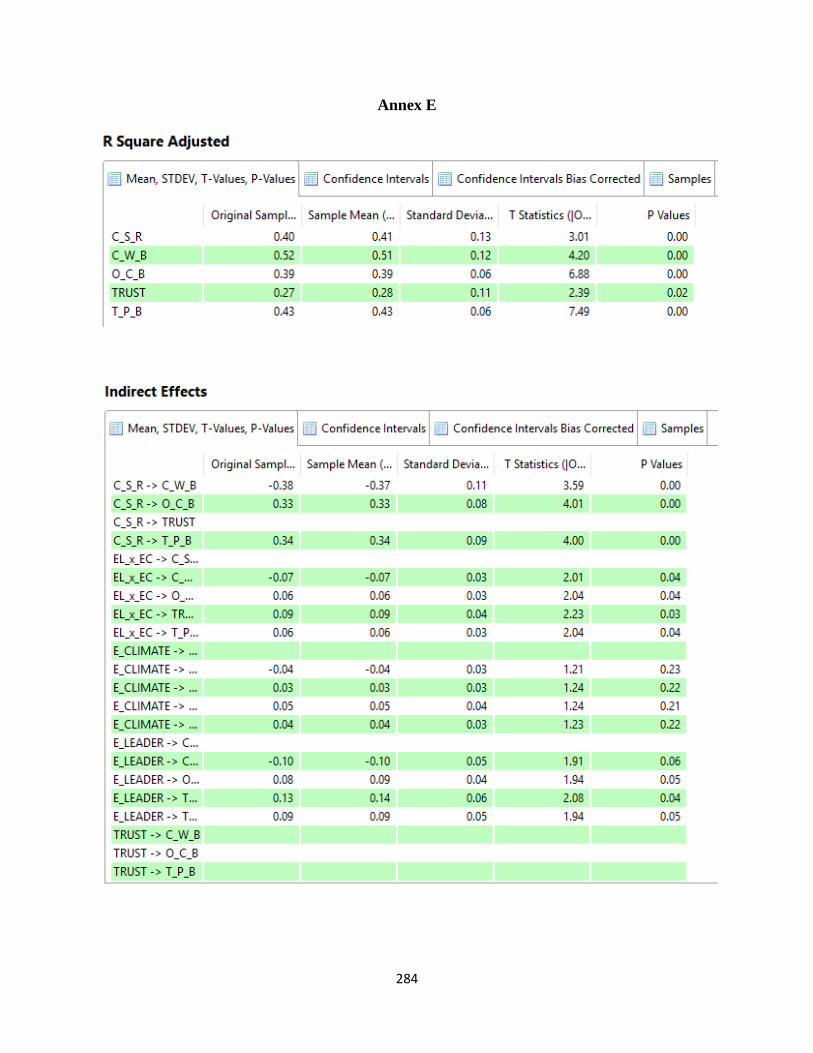

4.5.2 Structural Model .......................................................................................................................... 175

4.5.2.1 Specification of Structural Model ......................................................................................... 175

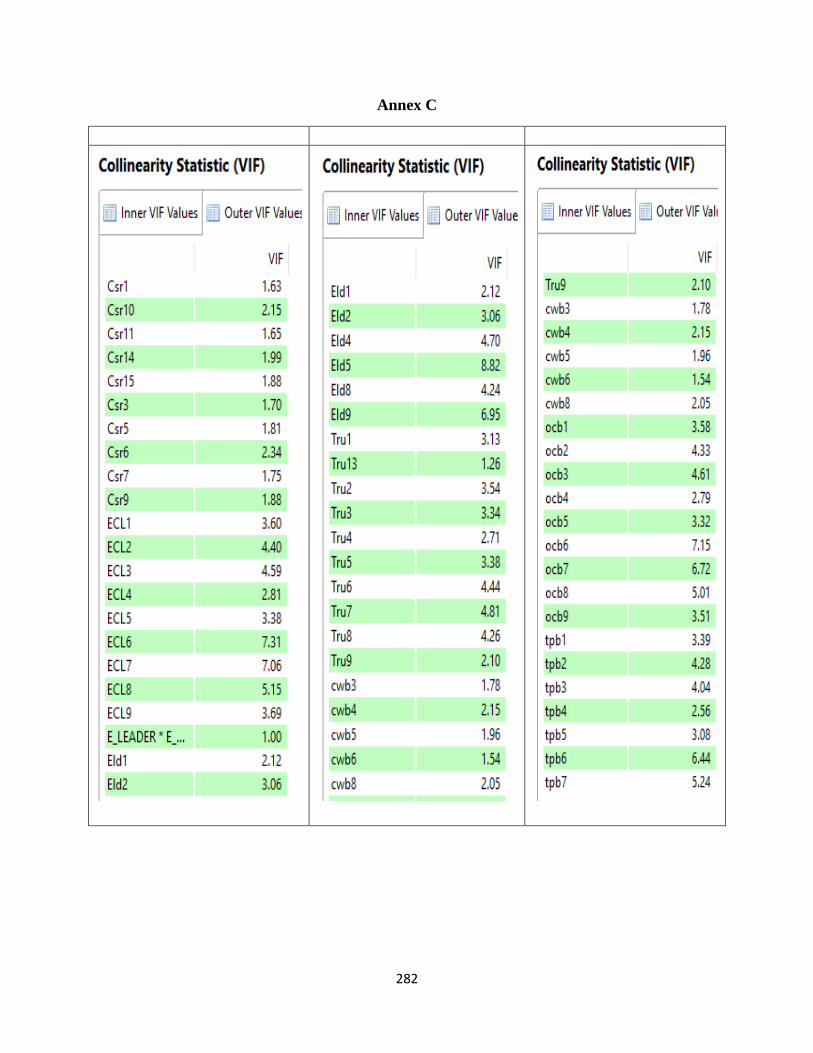

4.5.2.3 Step – 1 Assessment of Collinearity ...................................................................................... 176

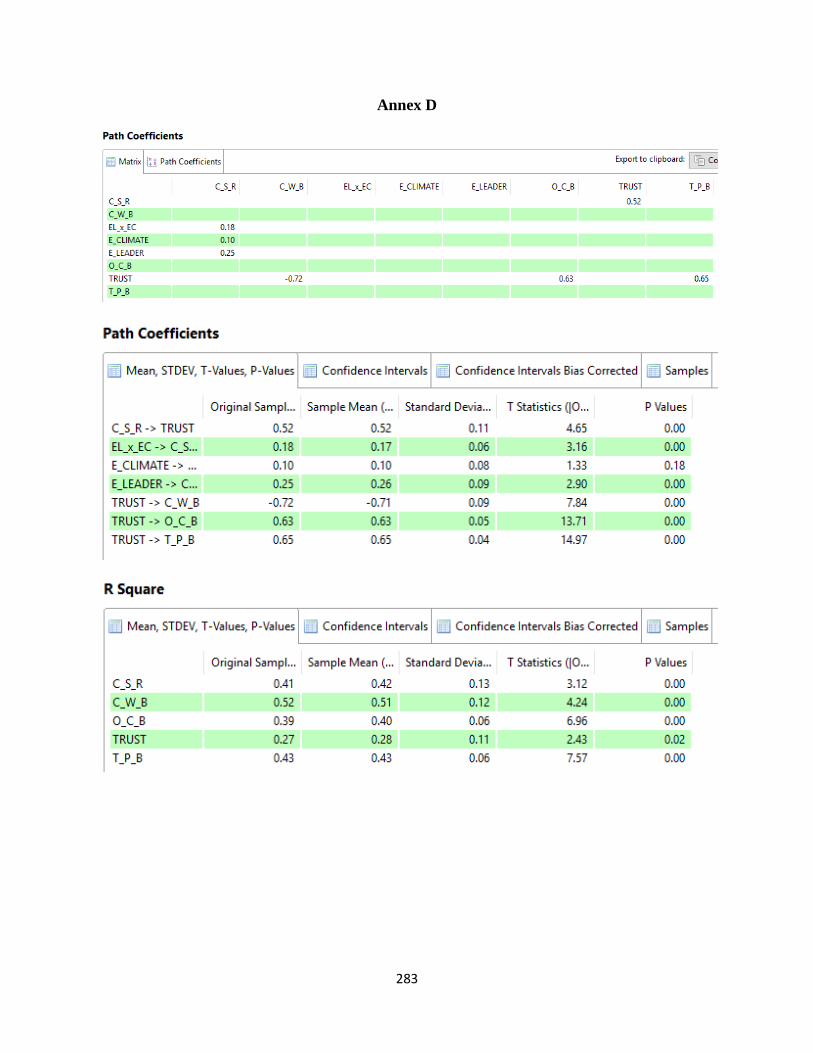

4.5.2.4 Step – 2 Path Coefficient of Structural Model ...................................................................... 177

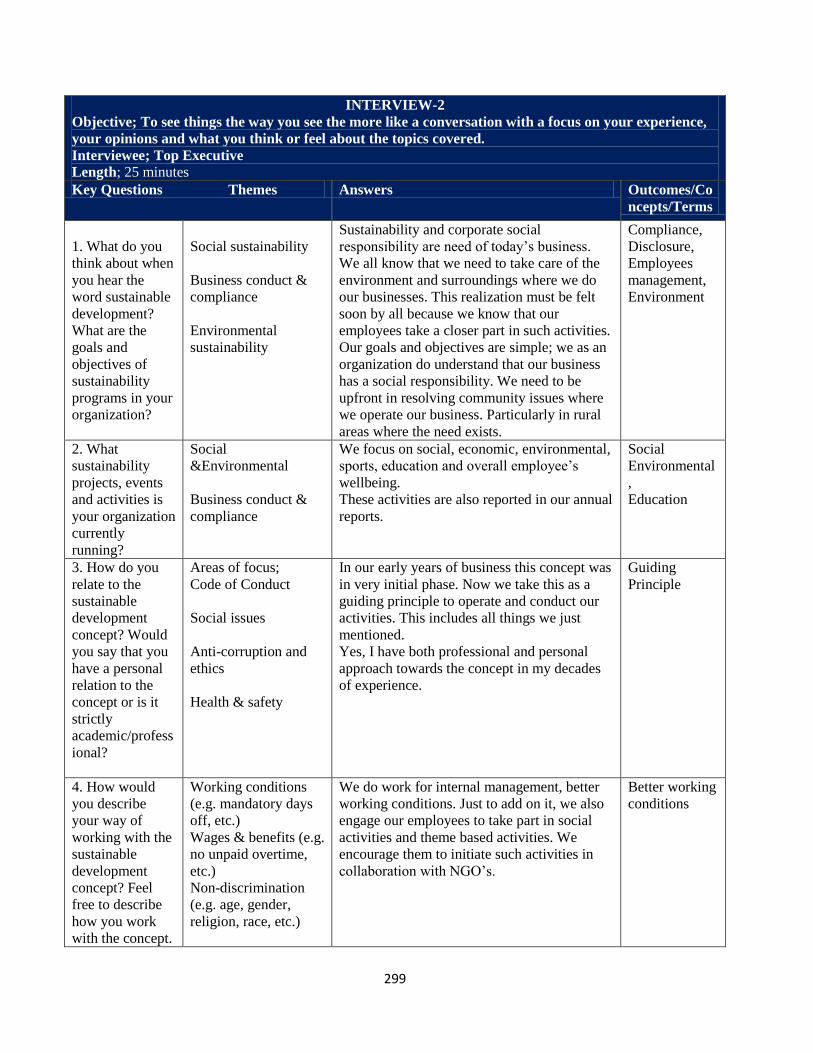

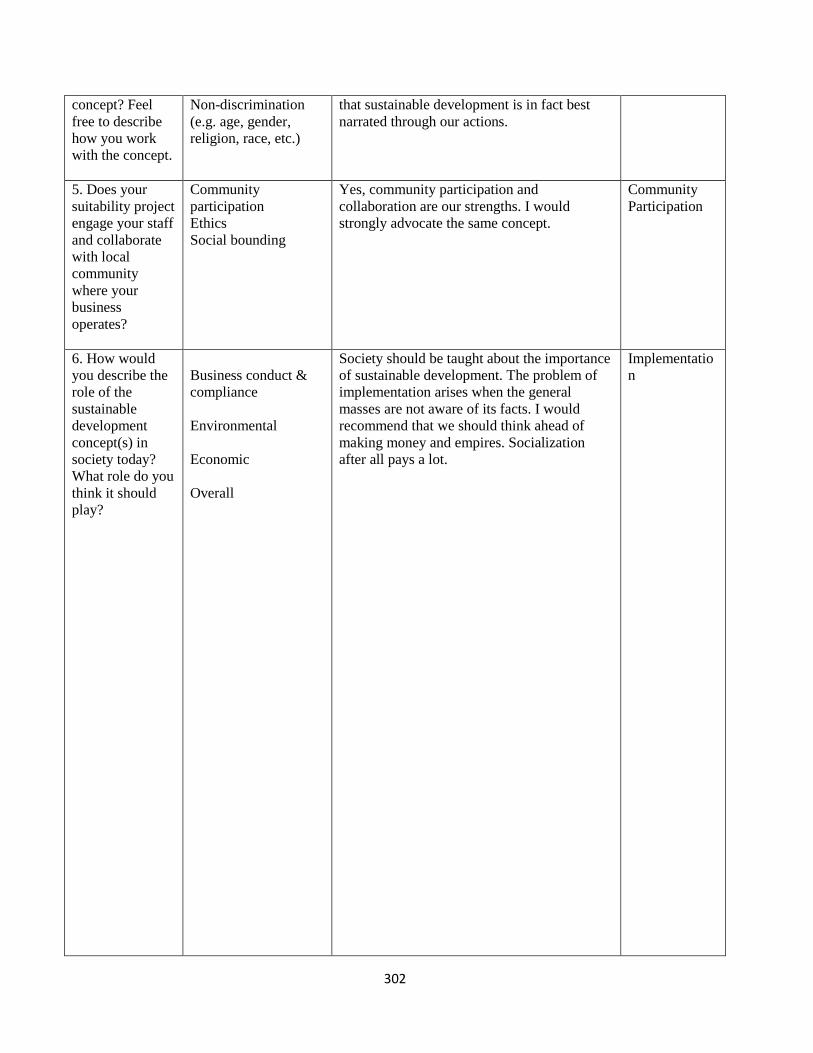

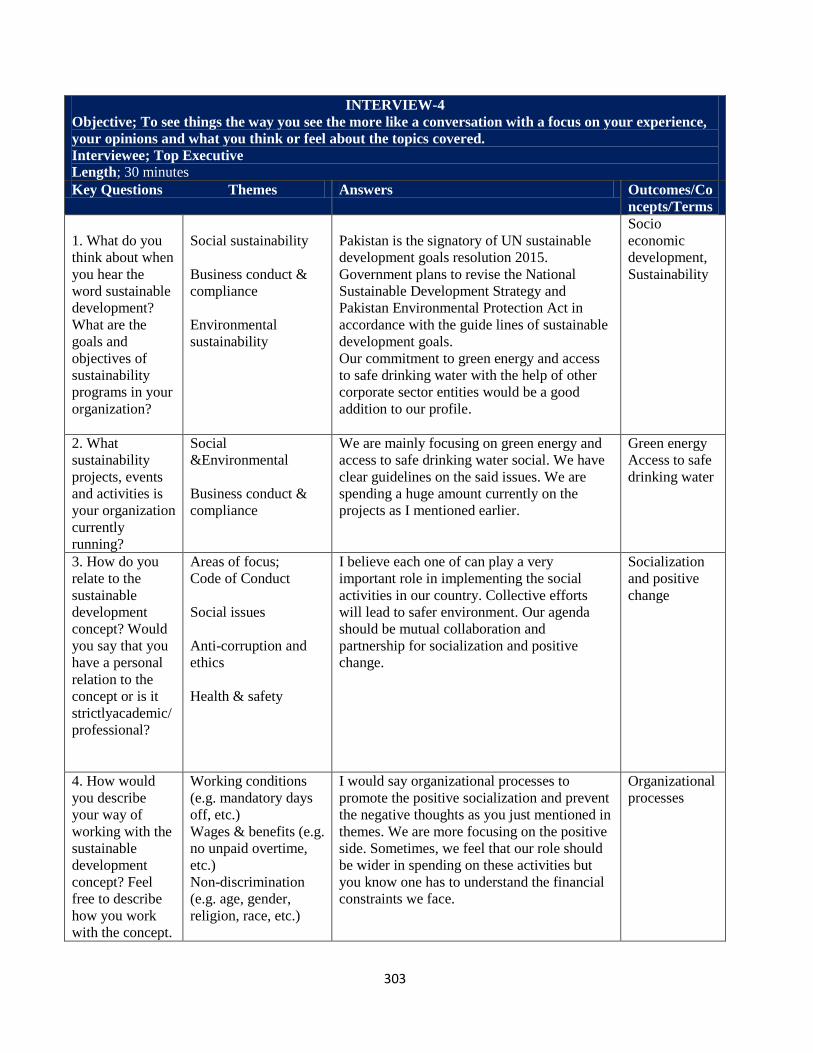

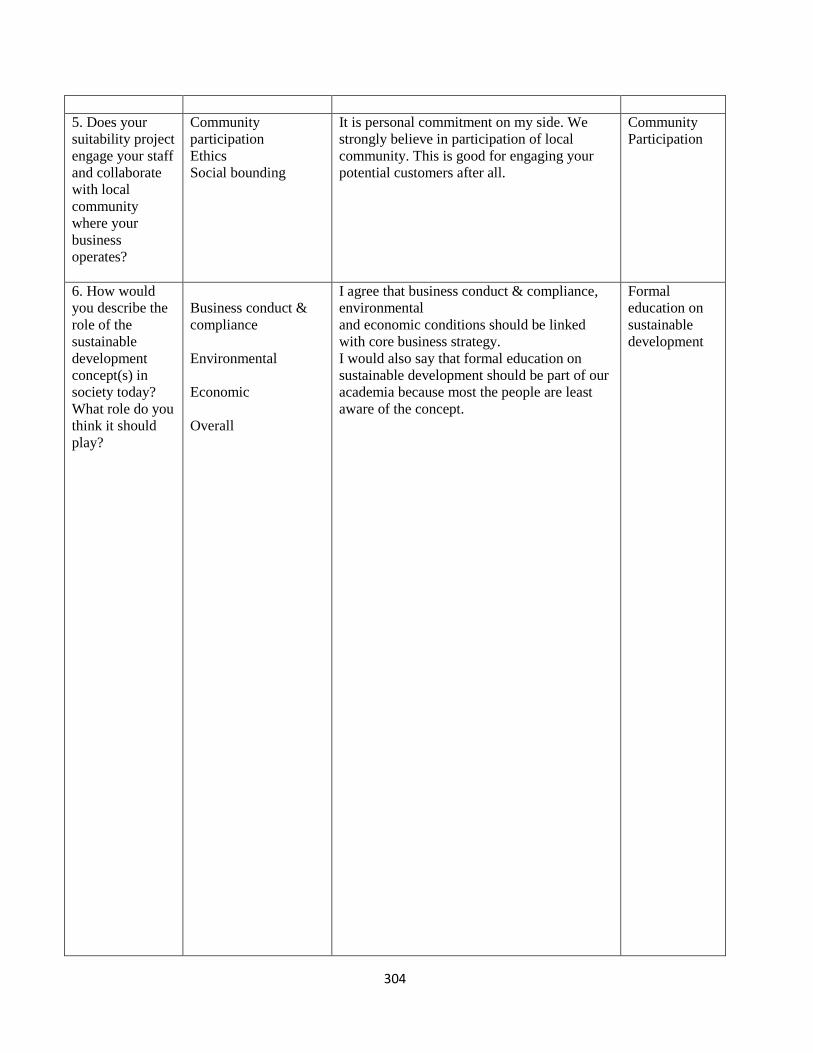

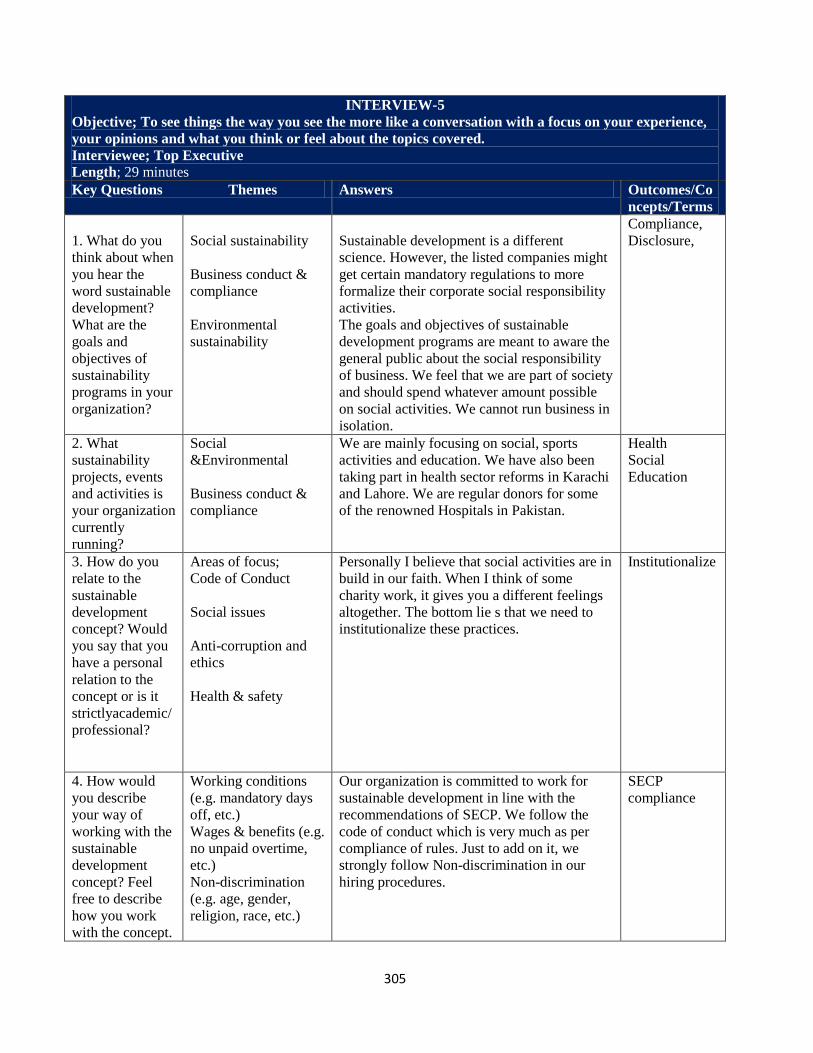

4.6. Response Pattern for Qualitative Part ............................................................................................ 184

4.6.1 Sustainable Development ............................................................................................................. 184

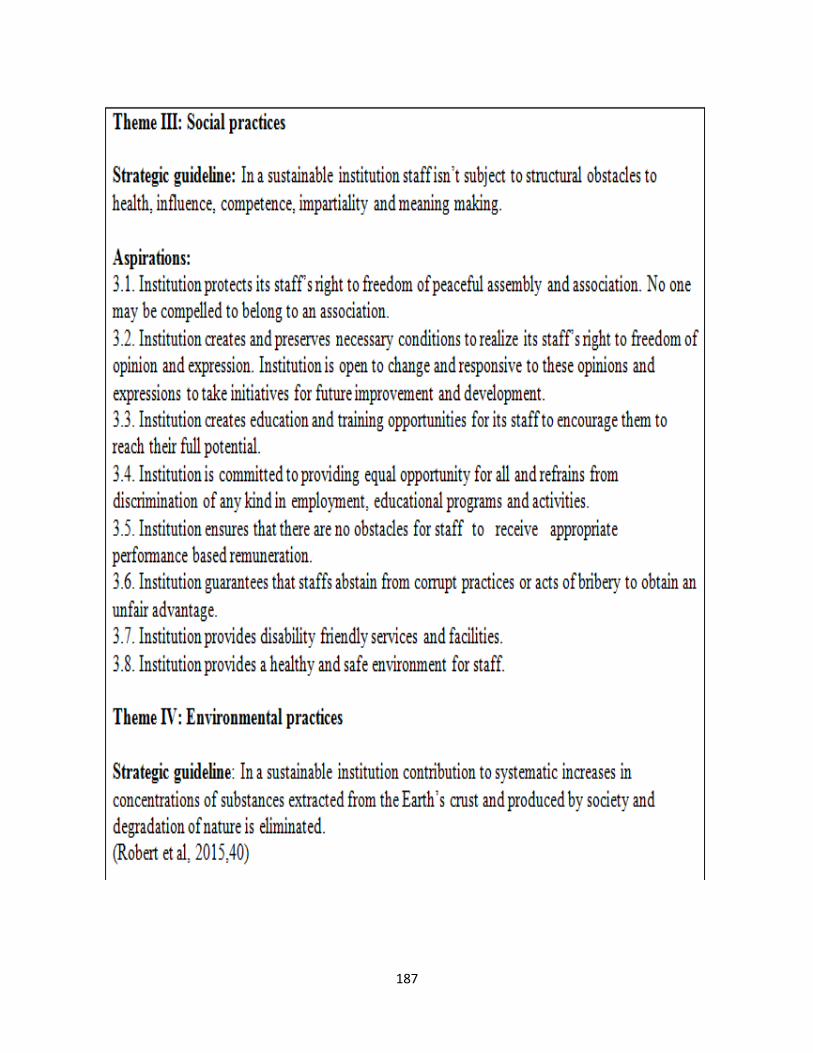

4.6.2 Themes and framework for sustainable development ............................................................ 185

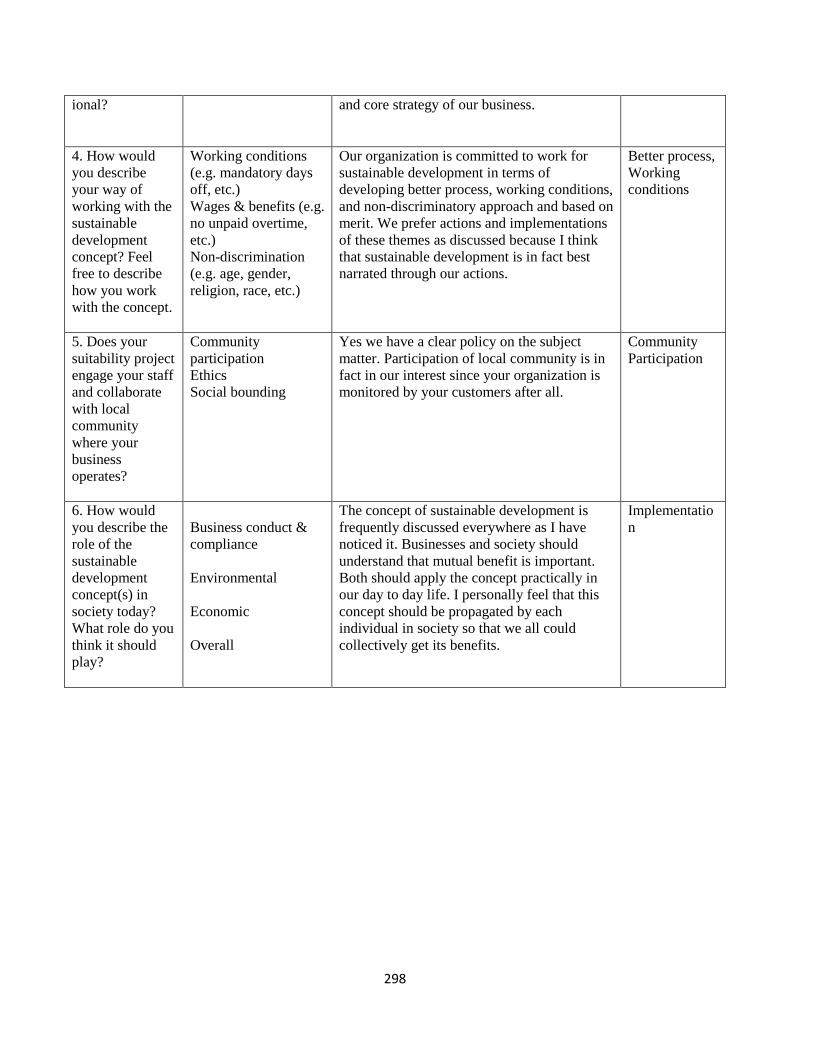

4.6.3 Key Results of Interviews ............................................................................................................ 188

Chapter 5 ................................................................................................................................... 196

Discussion, Implication & Conclusion .................................................................................... 196 5.1 Discussion ....................................................................................................................................... 196

5.1.2 Discussion on Quantitative Part ................................................................................................... 198

5.1.3 Discussion on Qualitative Part (Sustainable Development) ........................................................ 204

5.1.3.1 Theme wise discussion on sustainability .............................................................................. 205

5.2 Implications for Research and Practice ........................................................................................... 209

8

5.2.1 Theoretical Implications ........................................................................................................... 210

5.2.1.1 Better understanding of CSR/SD ........................................................................................... 210

5.2.2 Practical Implications ............................................................................................................... 211

5.2.3 Implications to Banking & other Sector ................................................................................... 212

5.2.4 Implications to the Policy Makers ............................................................................................ 214

5.2.5 Implications to the Society ....................................................................................................... 215

5.3 Limitations and Future Research .................................................................................................... 217

5.4 Conclusion ...................................................................................................................................... 219

References .................................................................................................................................. 223 Appendixes................................................................................................................................. 278

9

LIST OF TABLES

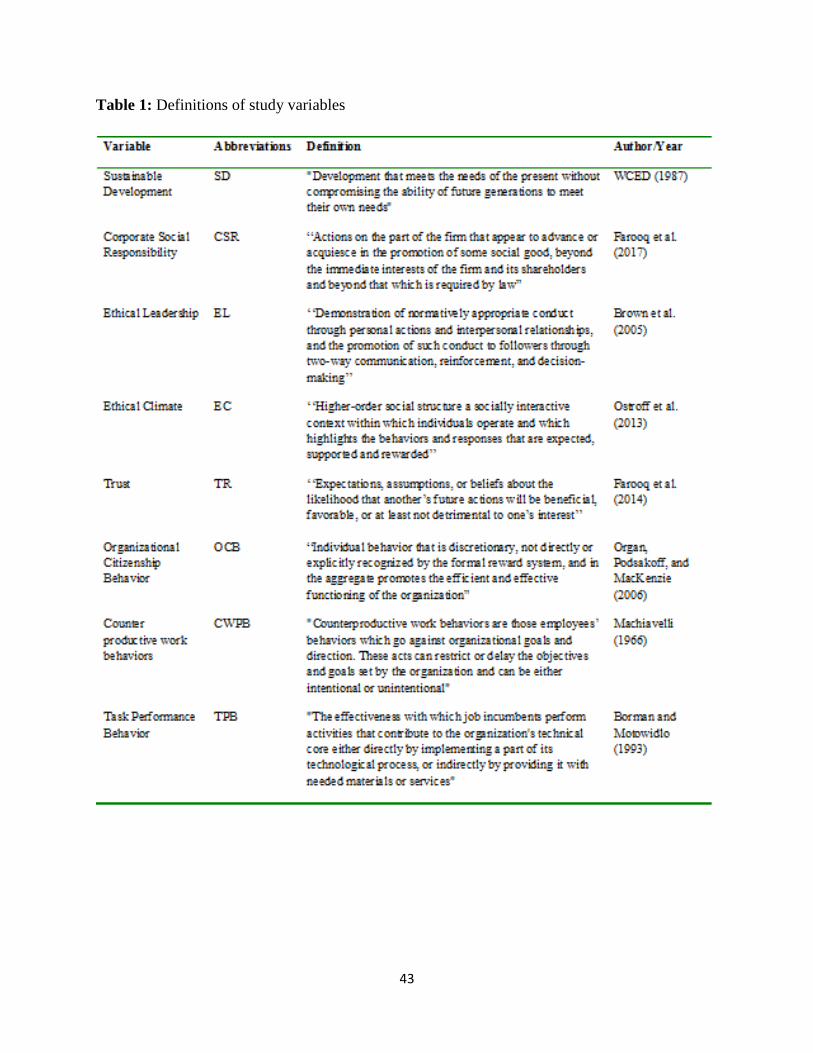

Table 1: Definitions of study variables ....................................................................................................... 43

Table 2: Organization of the Thesis ............................................................................................................ 45

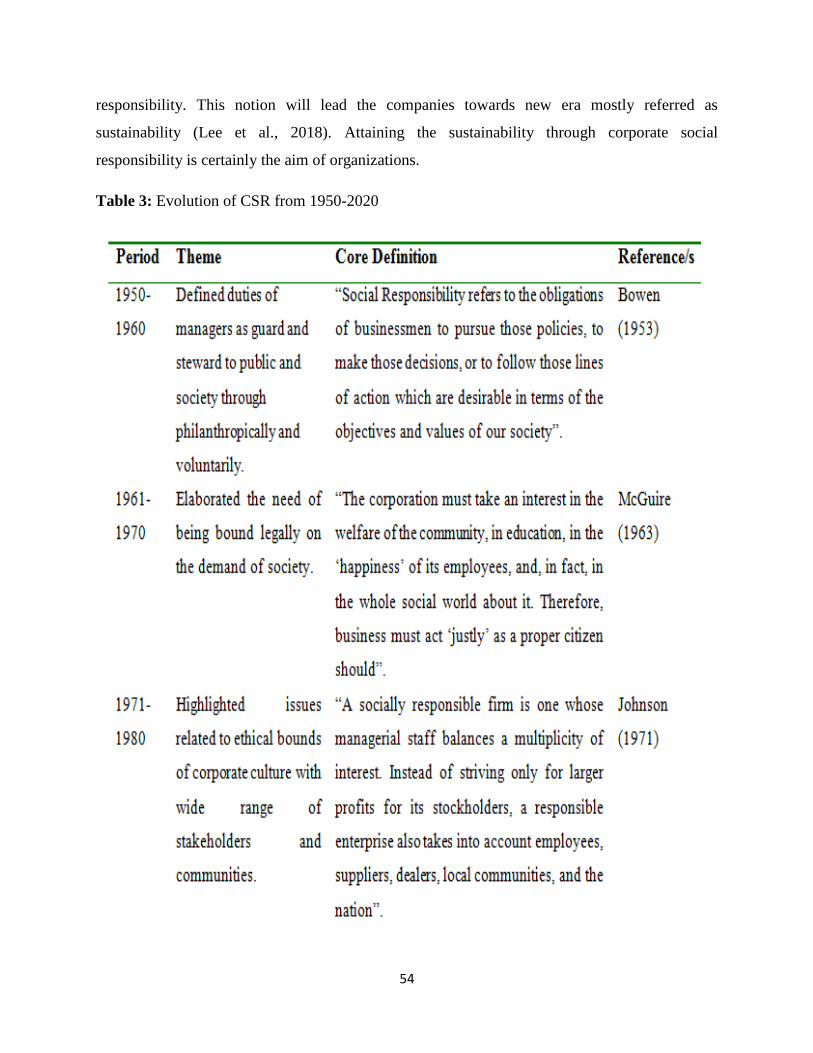

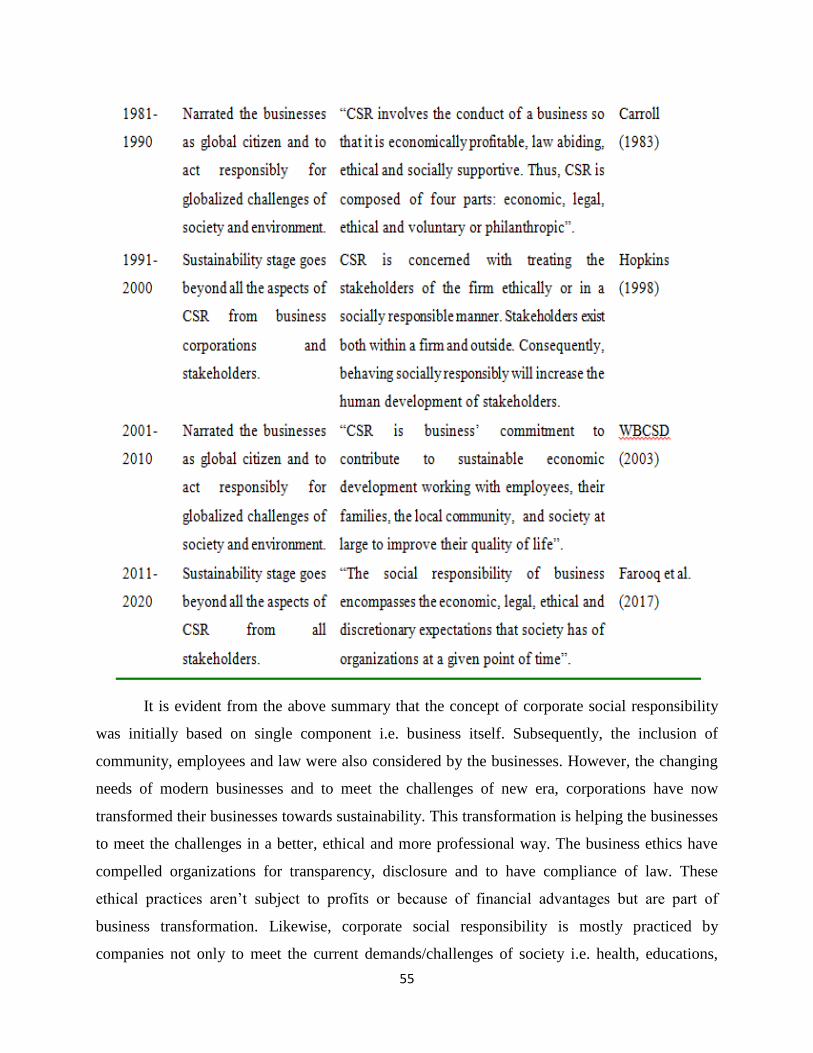

Table 3: Evolution of CSR from 1950-2020 ................................................................................................. 54

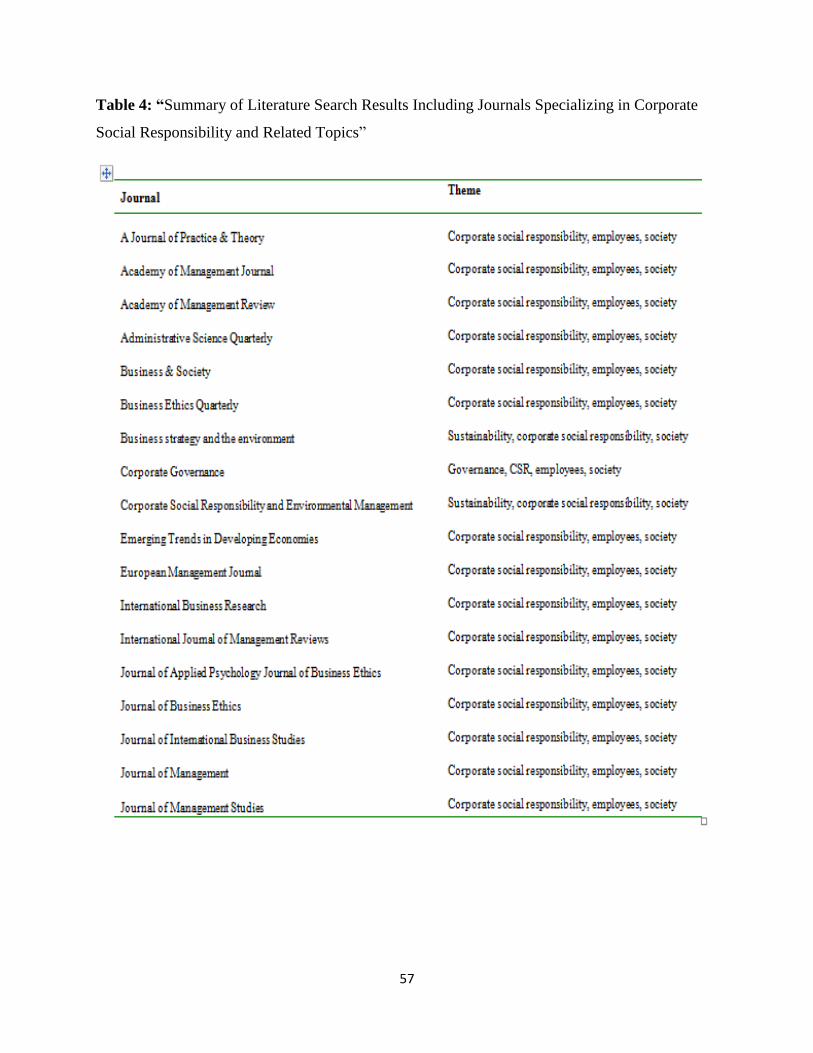

Table 4: “Summary of Literature Search Results Including Journals Specializing in Corporate Social

Responsibility and Related Topics‖ ............................................................................................................ 57

Table 5: Internal CSR Themes ..................................................................................................................... 60

Table 6: External CSR Themes..................................................................................................................... 62

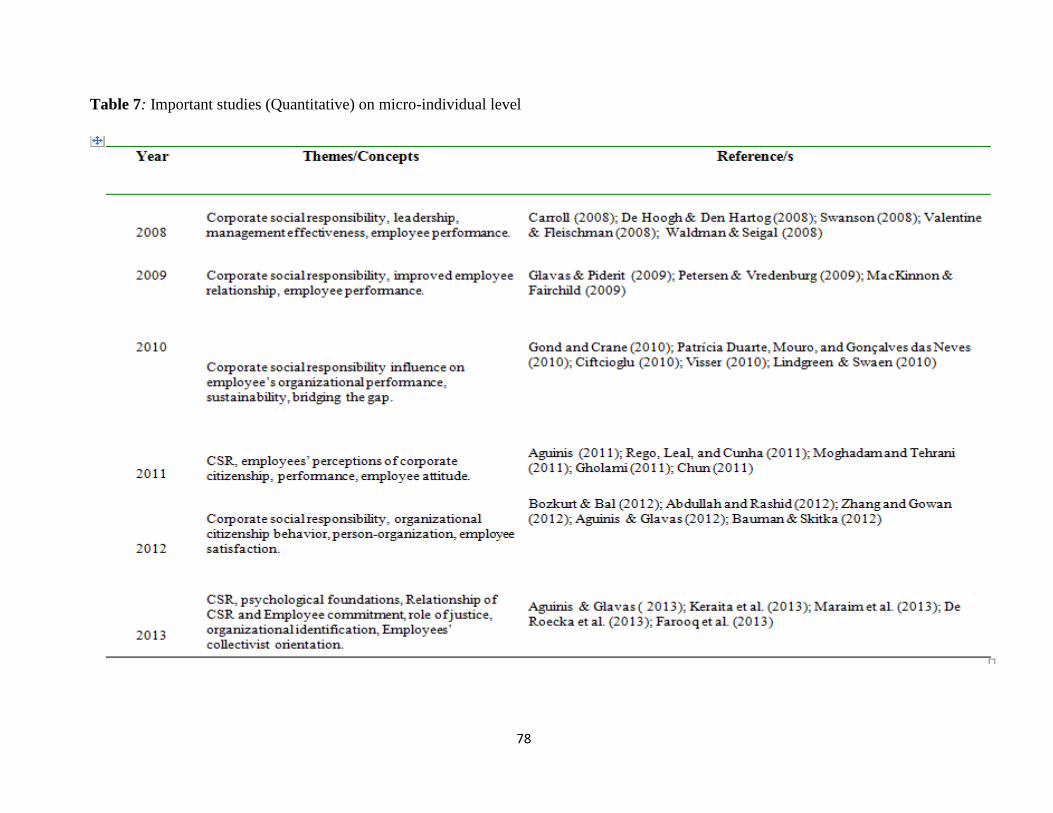

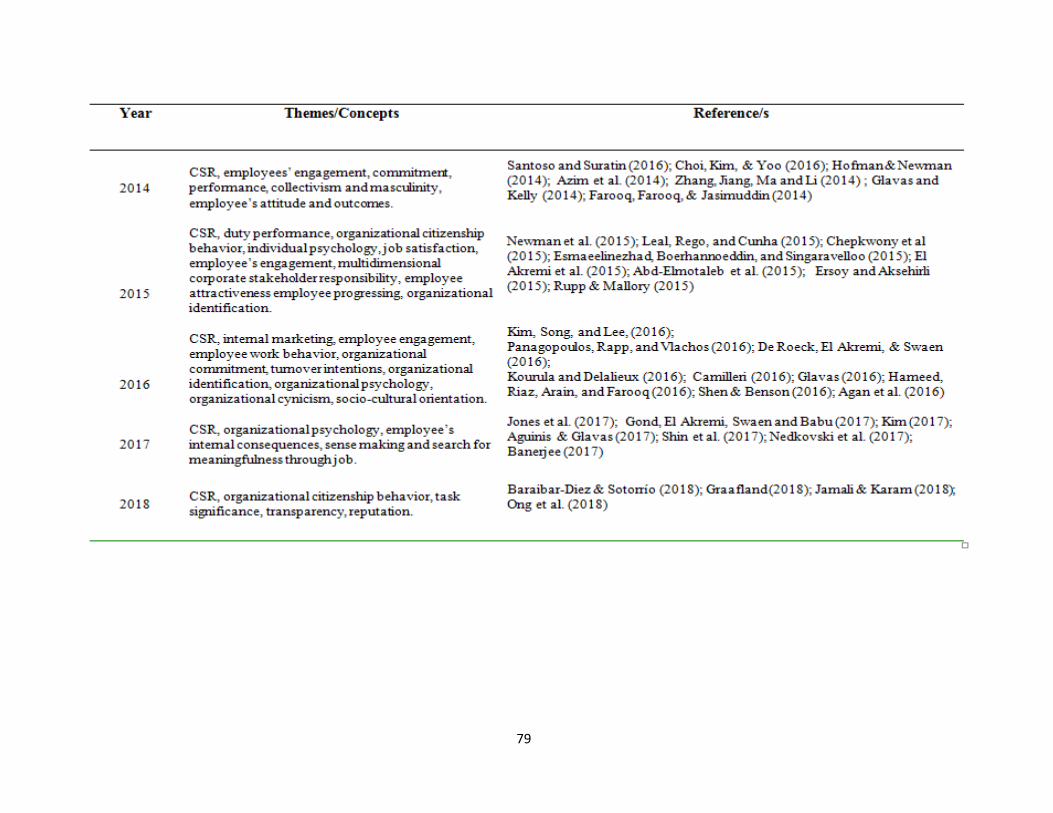

Table 7: Important studies (Quantitative) on micro-individual level ......................................................... 78

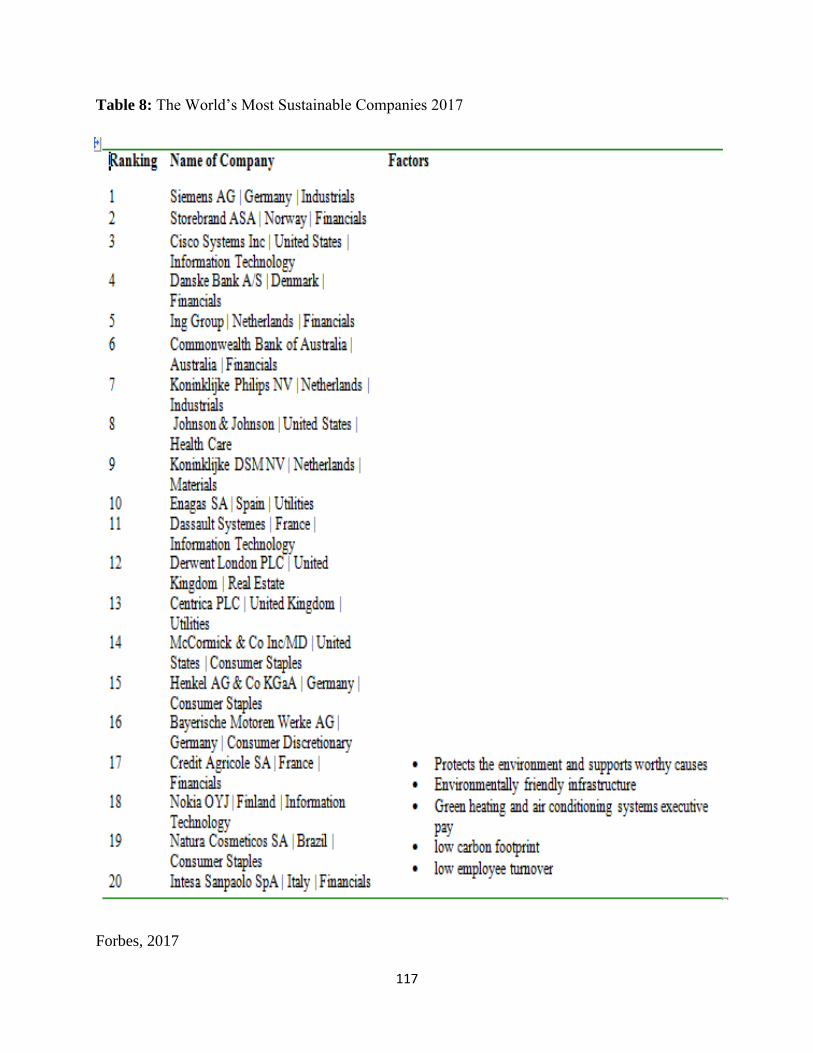

Table 8: The World’s Most Sustainable Companies 2017 ........................................................................ 117

Table 9: Summary of theories defined the constructs ............................................................................. 119

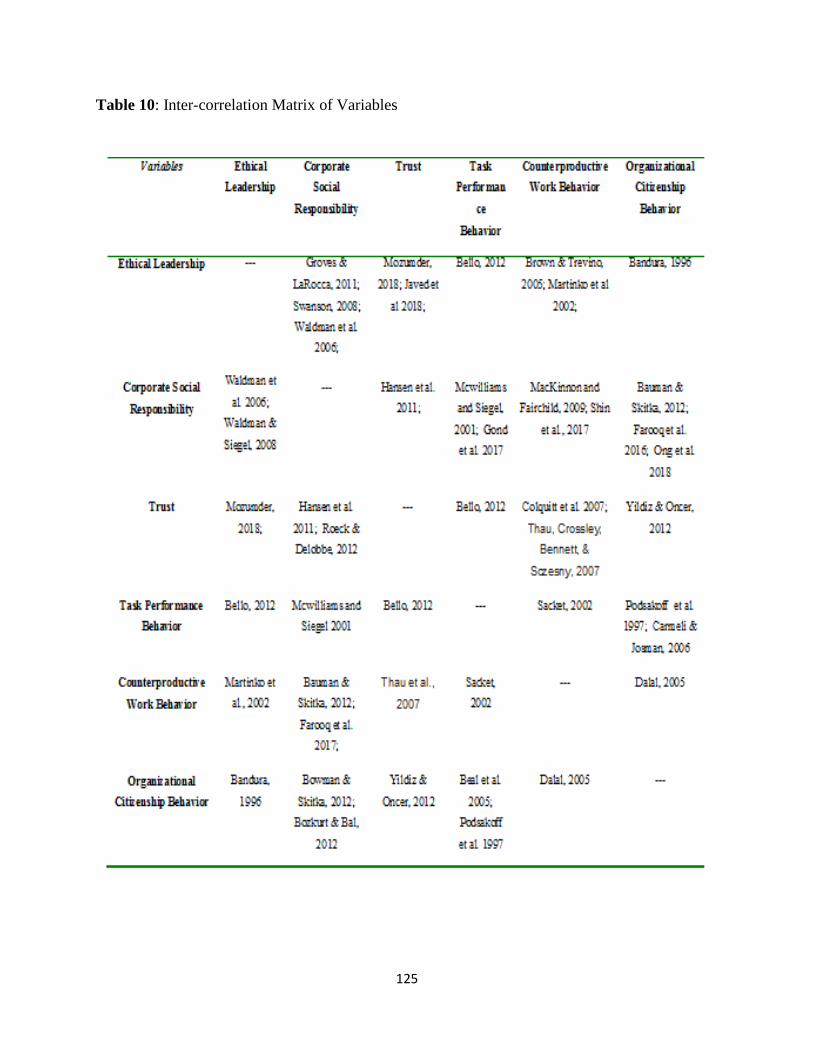

Table 10: Inter-correlation Matrix of Variables ........................................................................................ 125

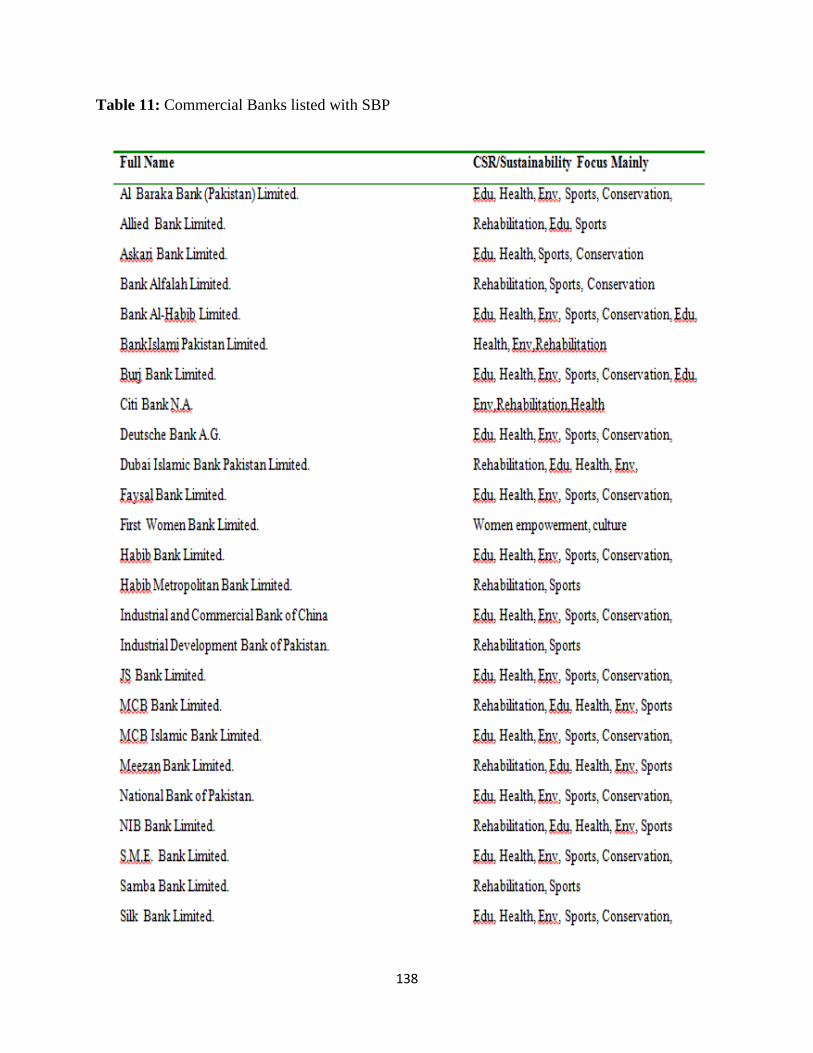

Table 11: Commercial Banks listed with SBP ............................................................................................ 138

Table 12: Summary of instruments .......................................................................................................... 143

Table 13 : Characteristics of PLS-SEM ....................................................................................................... 145

Table 14: Scheme of Analyses ................................................................................................................. 153

Table 15: Descriptive Statistics ................................................................................................................. 155

Table 16: Descriptive Analysis of Demographic Variables ........................................................................ 156

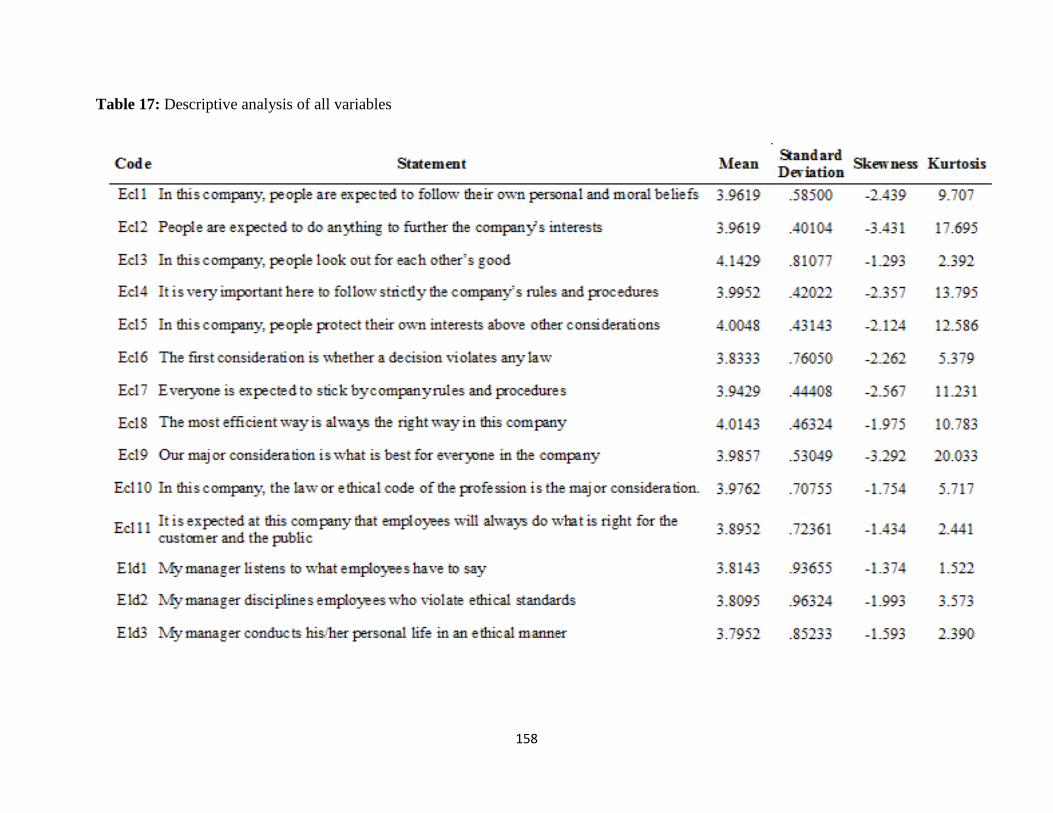

Table 17: Descriptive analysis of all variables........................................................................................... 158

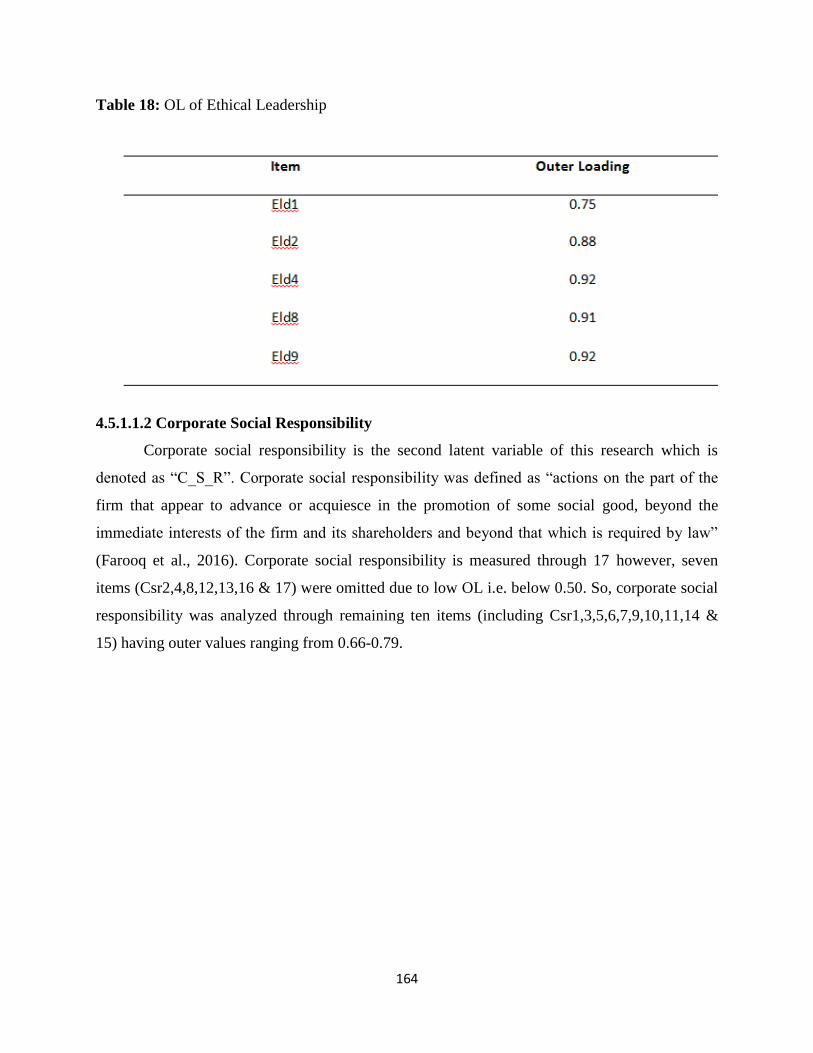

Table 18: OL of Ethical Leadership ............................................................................................................ 164

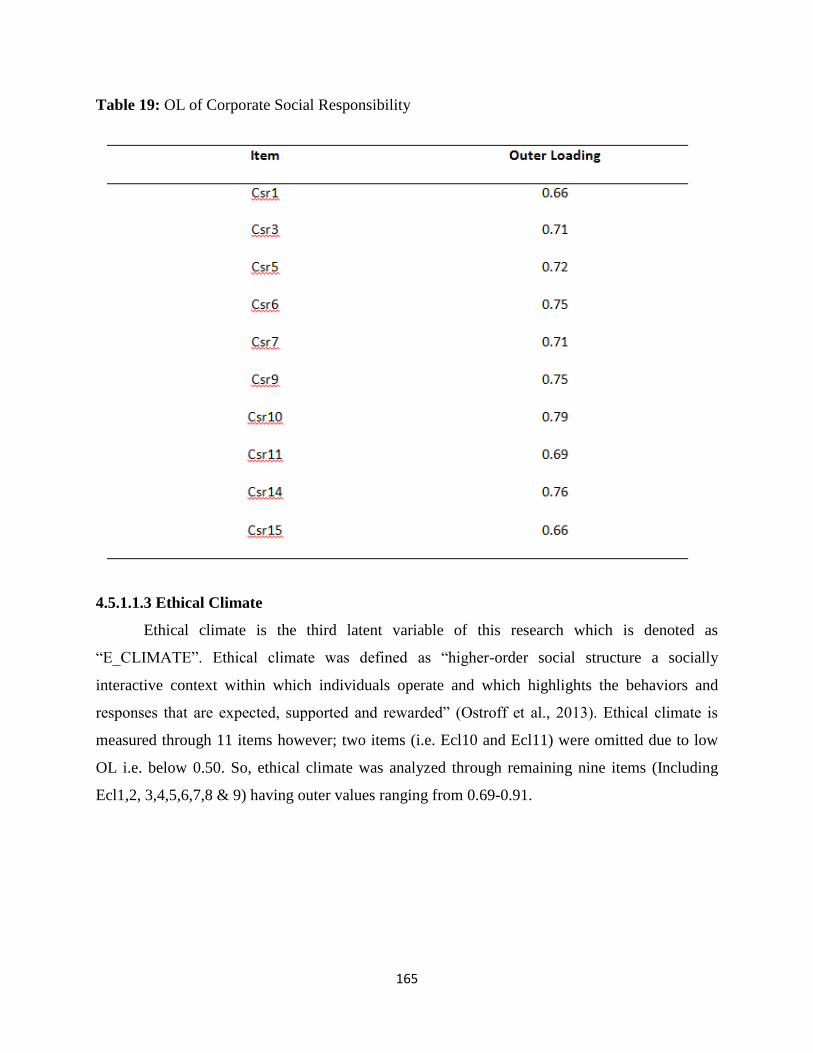

Table 19: OL of Corporate Social Responsibility ....................................................................................... 165

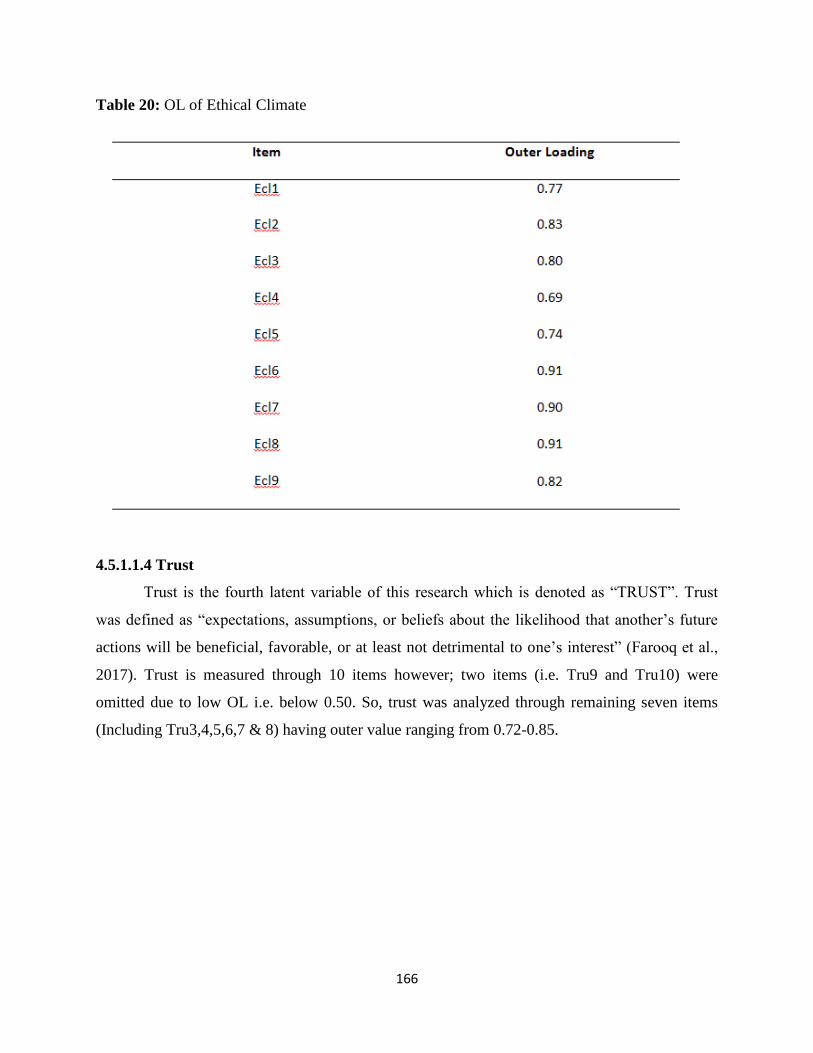

Table 20: OL of Ethical Climate ................................................................................................................. 166

Table 21: OL of Trust ................................................................................................................................. 167

Table 22: OL of Counterwork Productive Behavior .................................................................................. 168

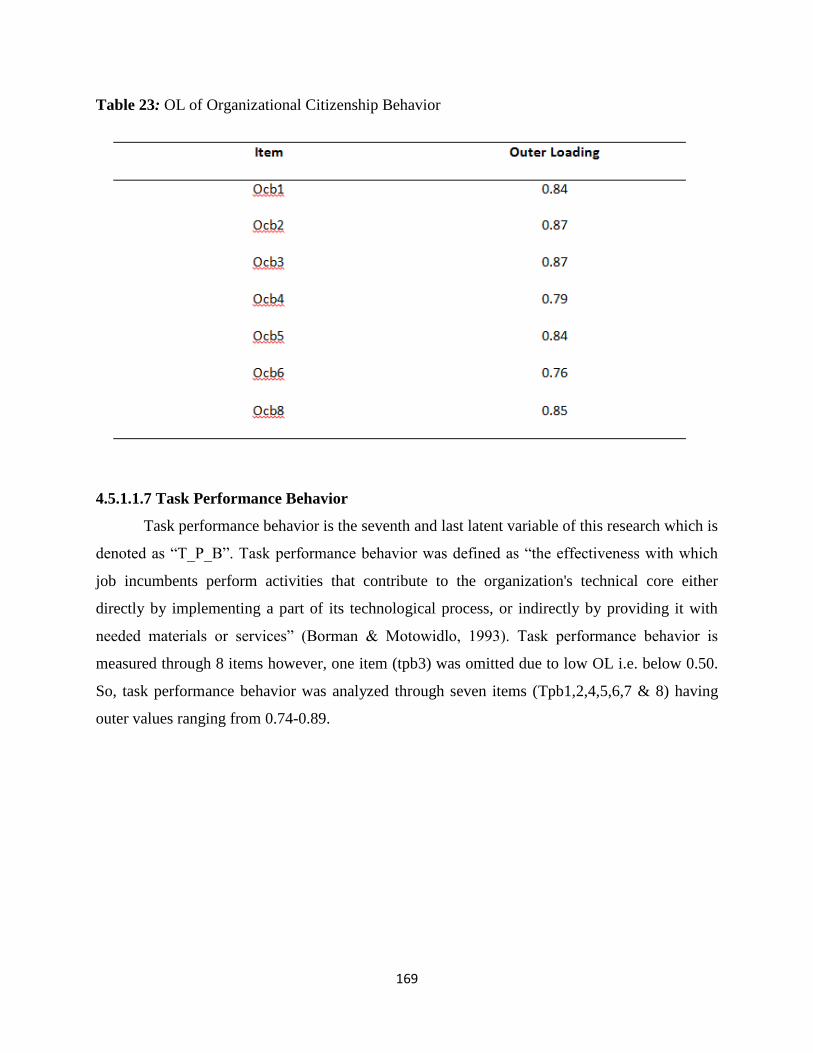

Table 23: OL of Organizational Citizenship Behavior ................................................................................ 169

Table 24: OL of Task Performance Behavior ............................................................................................. 170

Table 25: Results of Cronbach Alpha ........................................................................................................ 171

Table 26: Results of Composite Reliability (CR) ........................................................................................ 172

Table 27: Results of Convergent Validity .................................................................................................. 172

Table 28: Discriminant Validity Fornell-Larcker Criterion ......................................................................... 173

Table 29: Summary of Reflective Measurement Model ........................................................................... 174

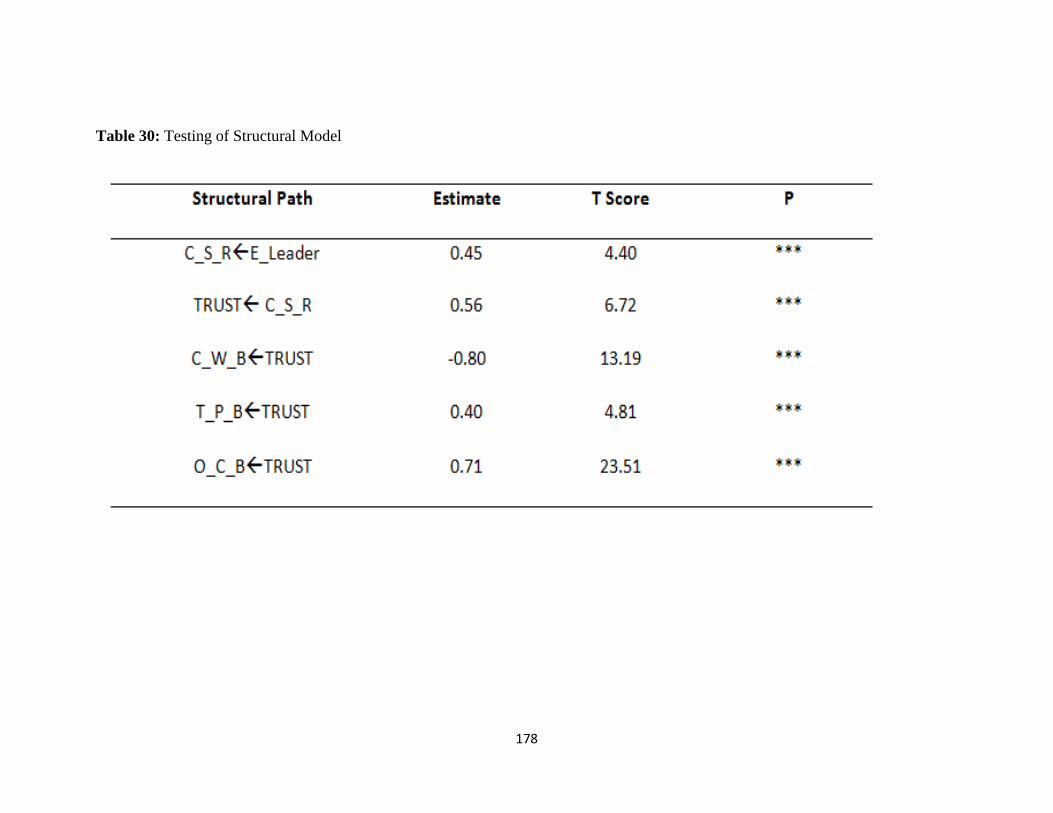

Table 30: Testing of Structural Model ...................................................................................................... 178

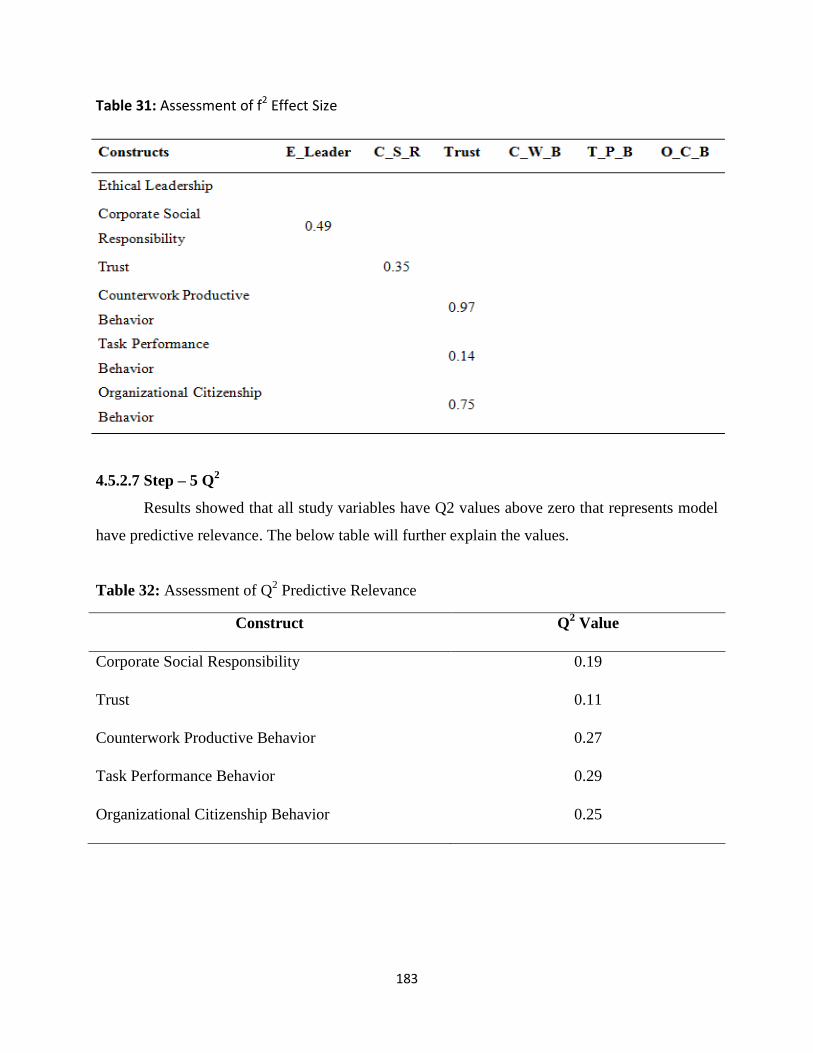

Table 31: Assessment of f2 Effect Size ...................................................................................................... 183

Table 32: Assessment of Q2 Predictive Relevance .................................................................................... 183

Table 33: Details of Interviews with Top Executives ................................................................................ 193

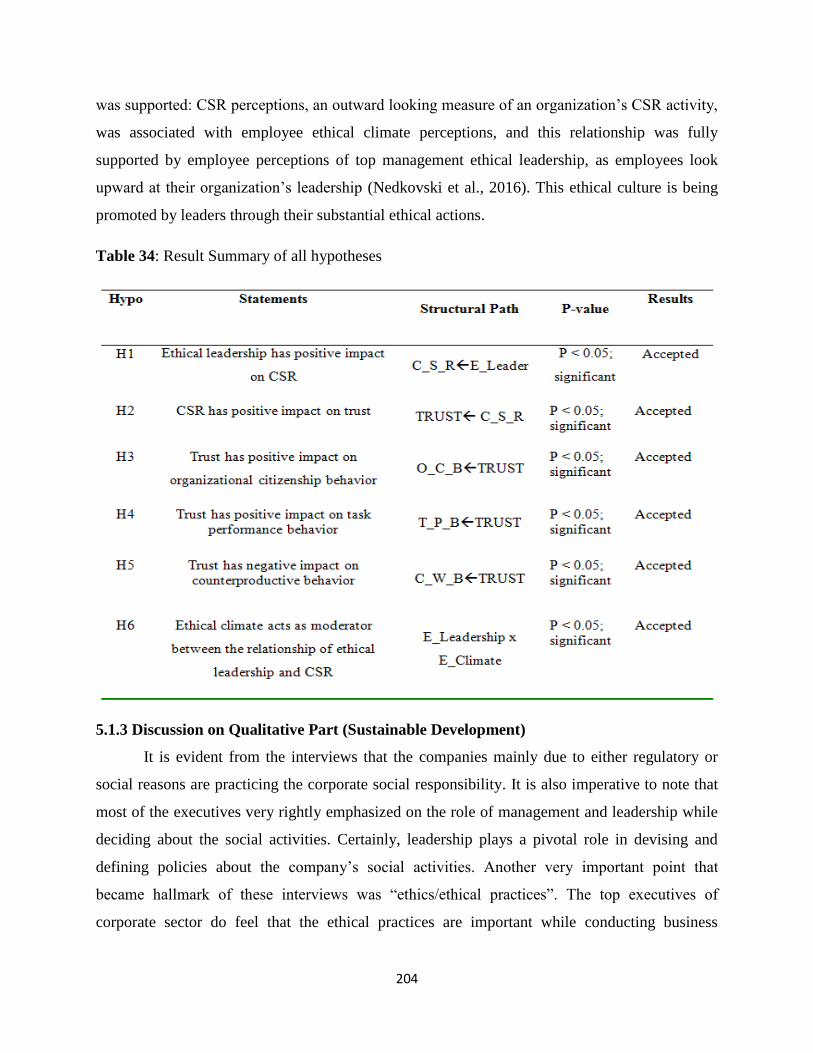

Table 34: Result Summary of all hypotheses ............................................................................................ 204

10

LIST OF FIGURES

Figure 1: CSR pyramid for developing countries ......................................................................................... 20

Figure 2: Conceptualization of Corporate Social Responsibility ................................................................. 50

Figure 3: Determinants and outcomes of CSR ............................................................................................ 71

Figure 4: Drivers of CSR in developing countries ........................................................................................ 72

Figure 5: Model of Trust by Mayer et al. (1995) ......................................................................................... 93

Figure 6: Conventional Development Model (Dernbach, 1998) ............................................................... 120

Figure 7: Sustainable development model UNCED (1992) ....................................................................... 121

Figure 8: UN Sustainable Development Goals 2015 ................................................................................. 121

Figure 9: Conceptual Framework .............................................................................................................. 127

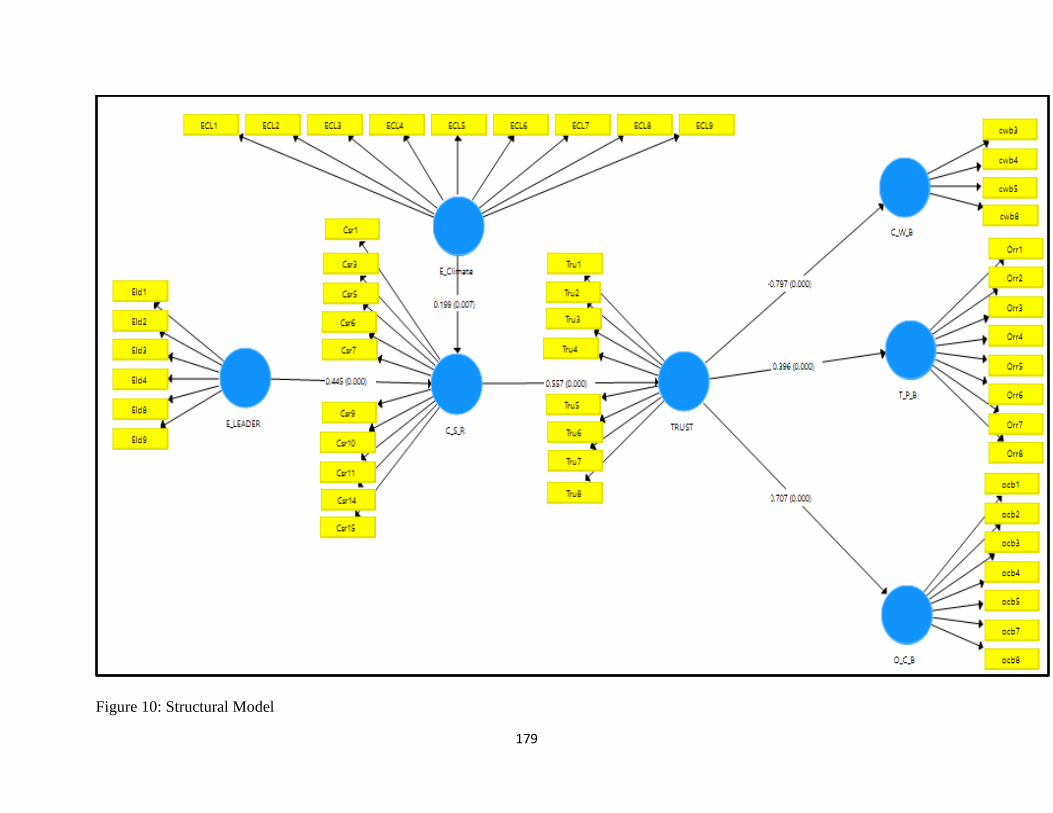

Figure 10: Structural Model ...................................................................................................................... 179

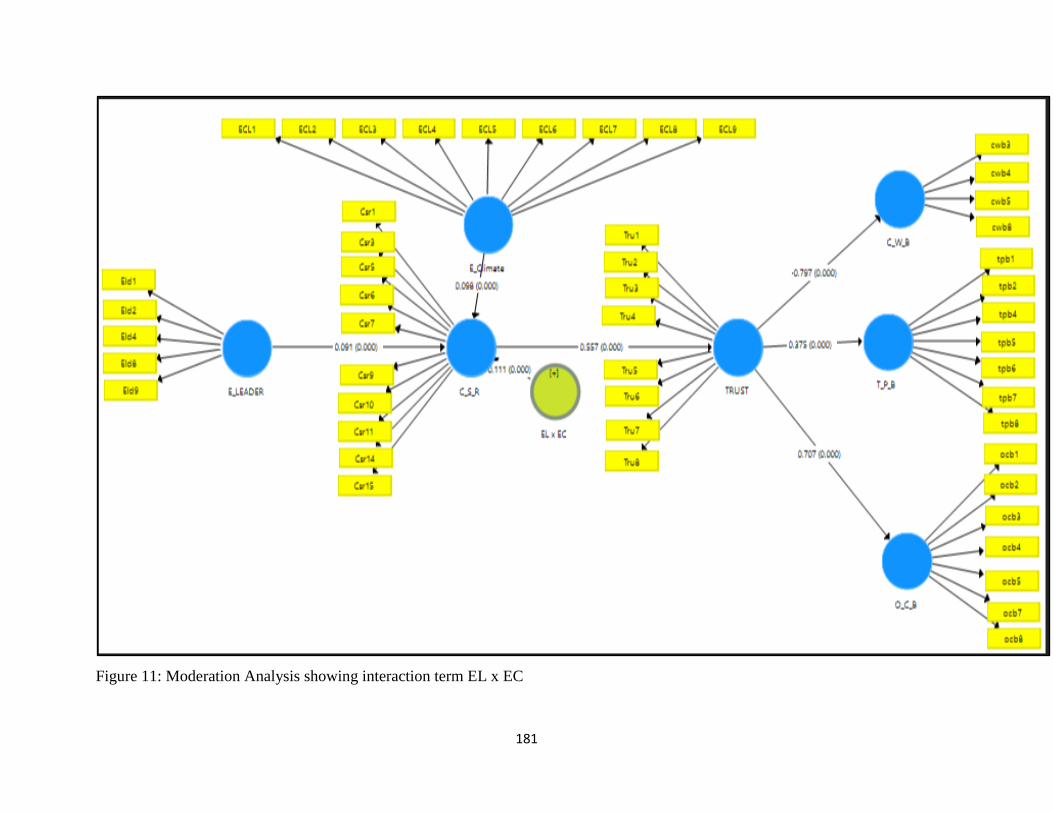

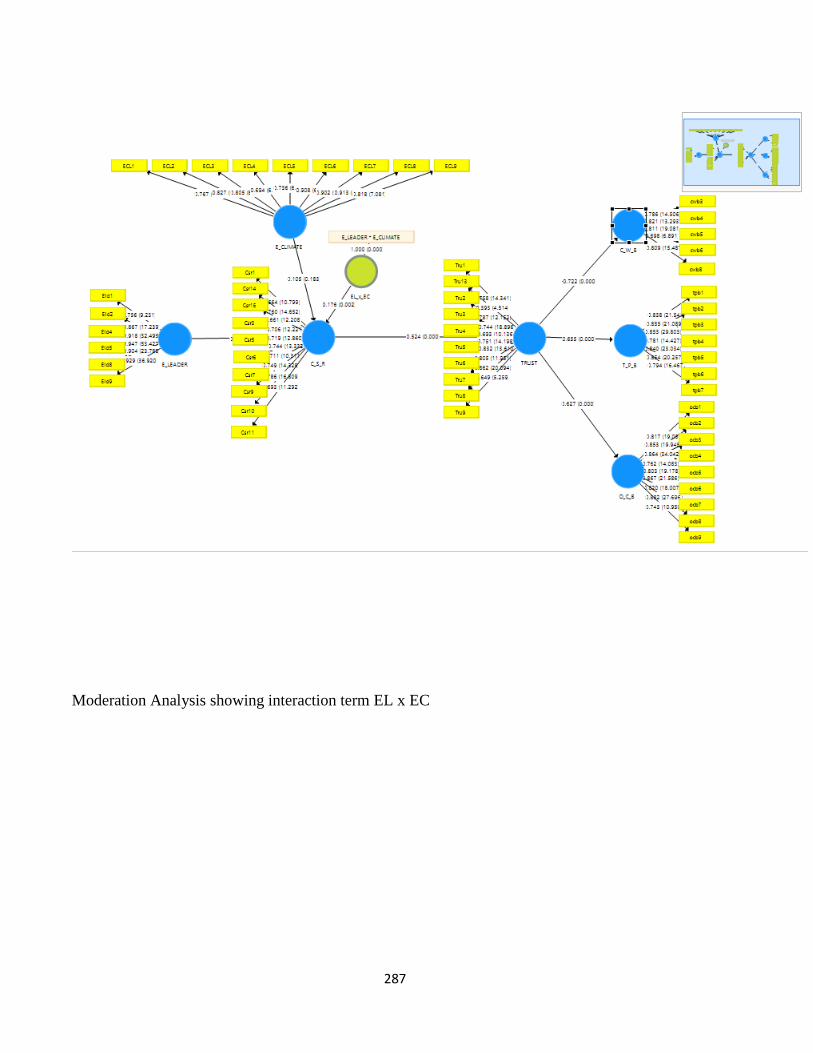

Figure 11: Moderation Analysis showing interaction term EL x EC .......................................................... 181

11

LIST OF SUMMARIES

S. # Title Page no.

1 Summary # 1; Chap-1 ‗Introduction‘ 46

2 Summary # 1; Chap-2 ‗Literature review‘ 129

3 Summary # 1; Chap-3 ‗Research methodology‘ 150

4 Summary # 1; Chap-4 ‗Results and analysis‘ 195

5 Summary # 1; Chap-5 ‗Discussion, implications and future

recommendations‘

222

12

LIST OF APPENDICES

Appendix. No Title Page No.

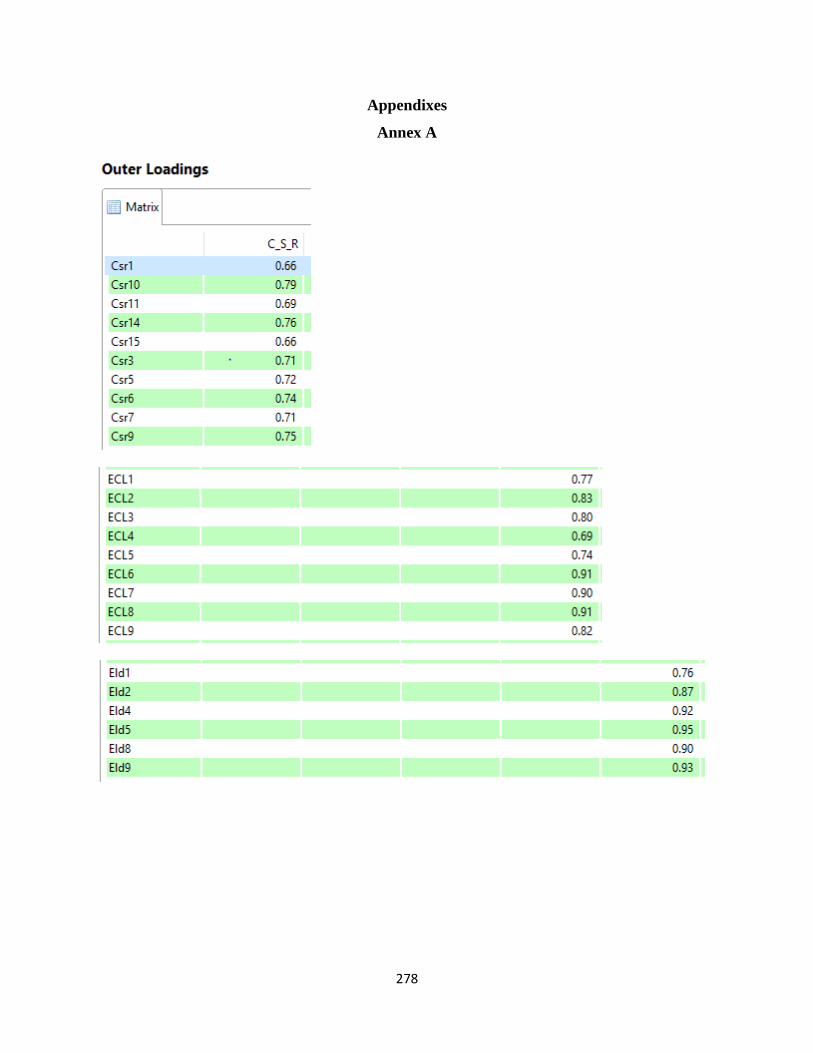

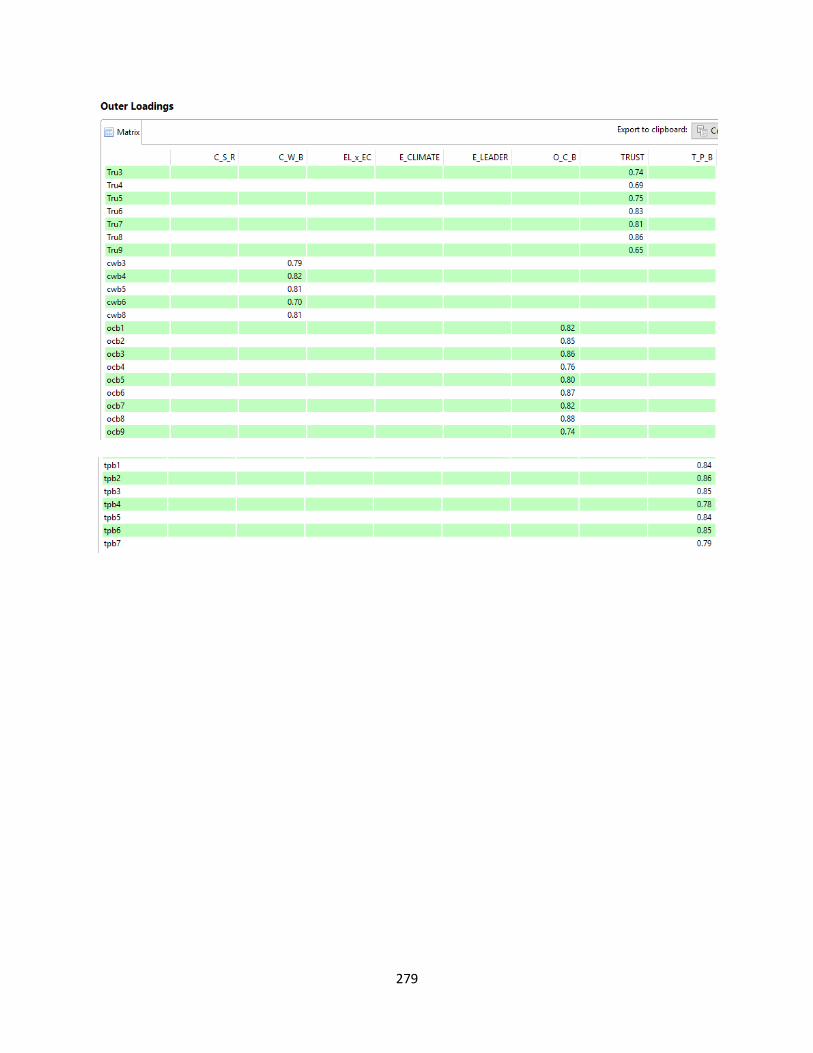

Appendix A Outer Loadings 278

Appendix B Average Variance 280

Appendix C Collinearity statistics 282

Appendix D Path coefficient 283

Appendix E Adjusted R Square 284

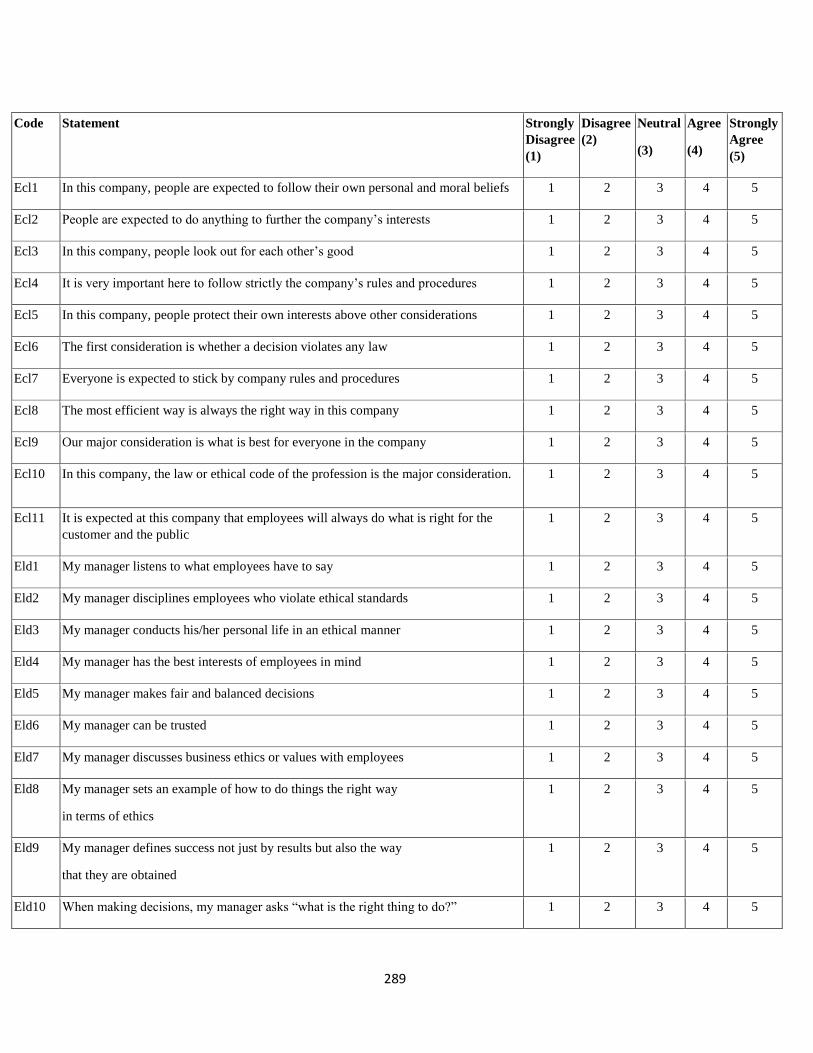

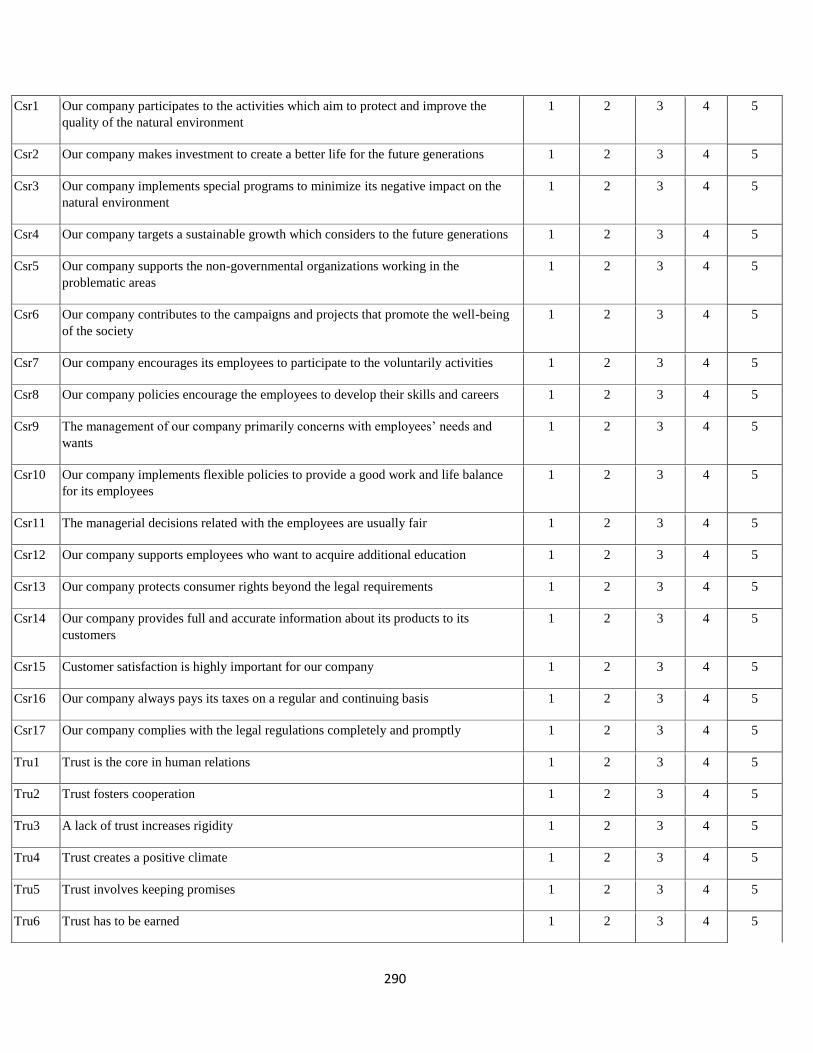

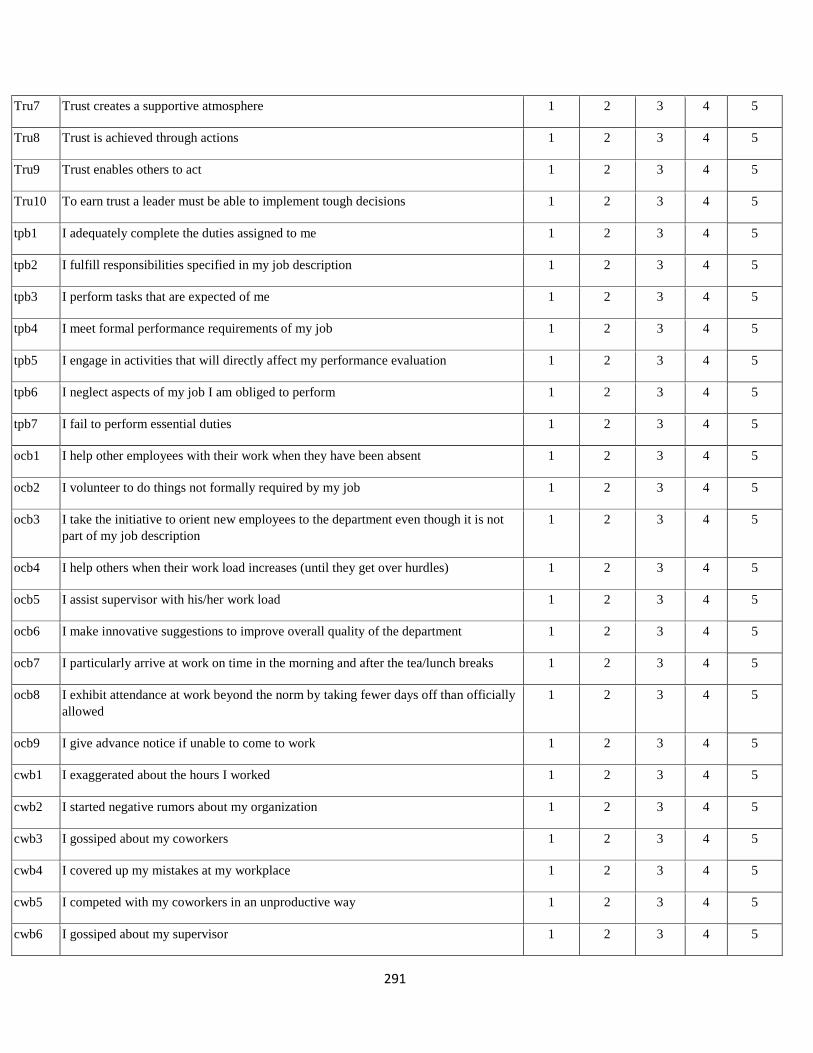

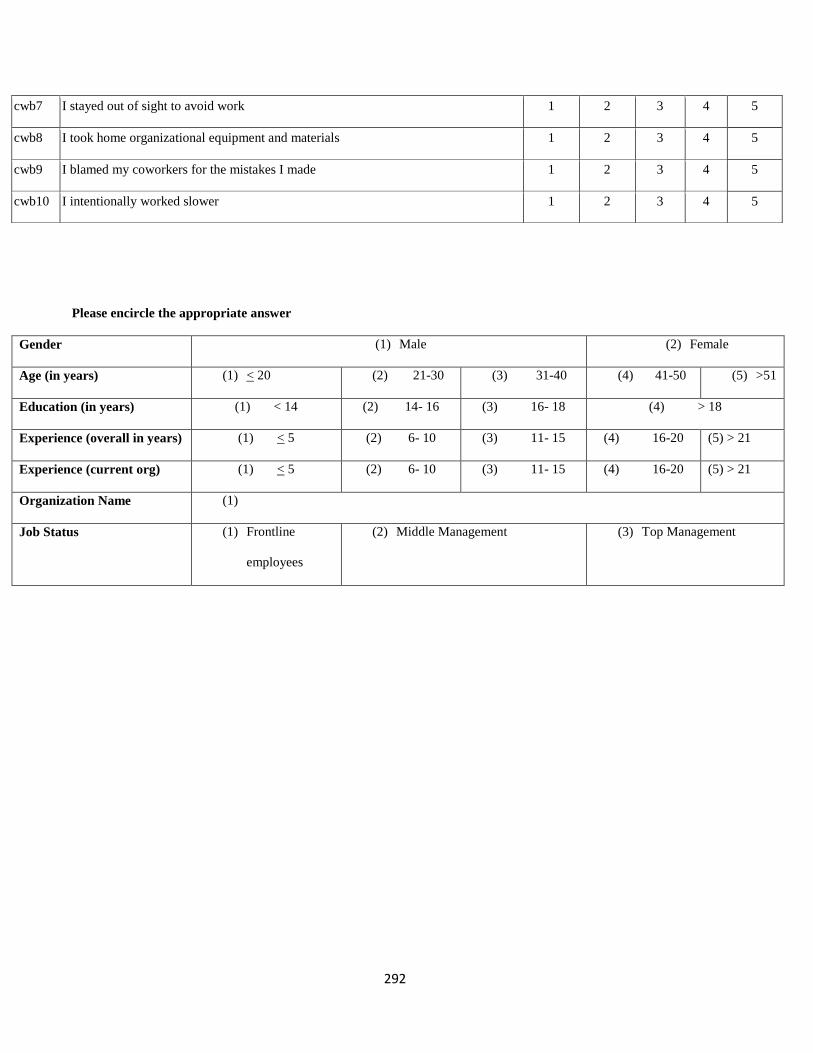

Appendix F Questionnaire for Quantitative Study 288

Appendix G Information Sheet and Consent Form Qualitative

Study

293

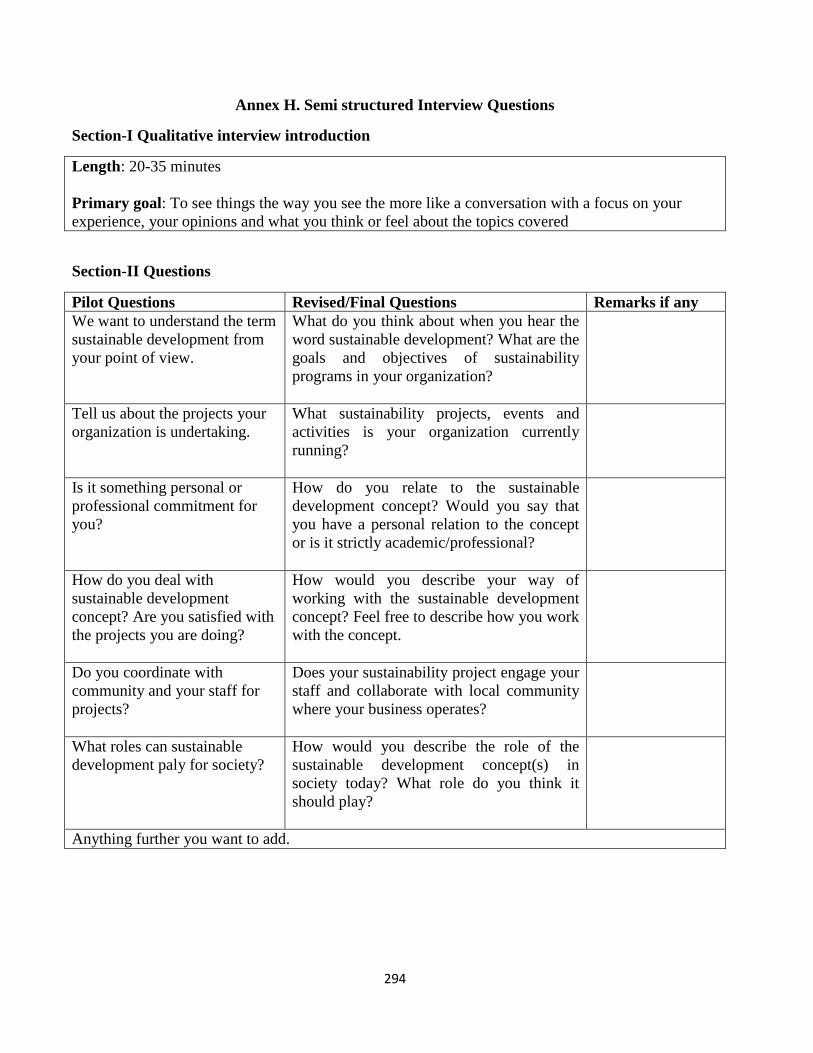

Appendix H Semi structured Interview Questions 294

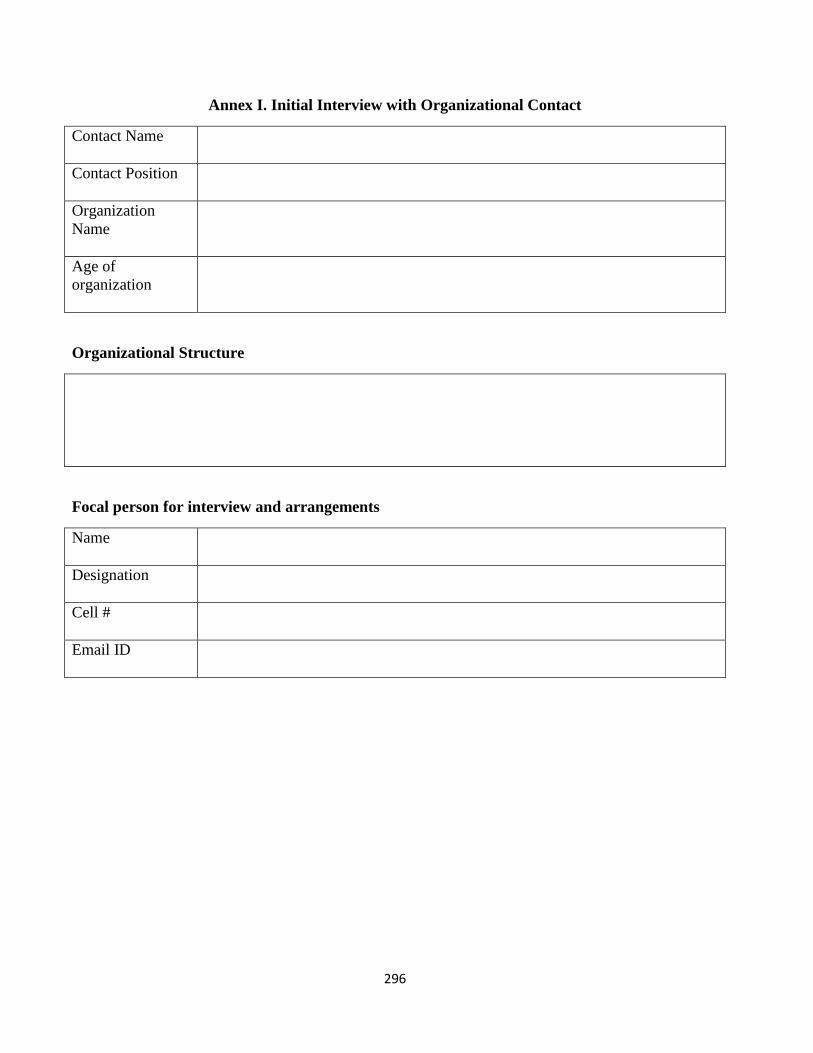

Appendix I Initial Interview with Organizational Contact 296

Appendix J Detailed Interviews Proceedings 297

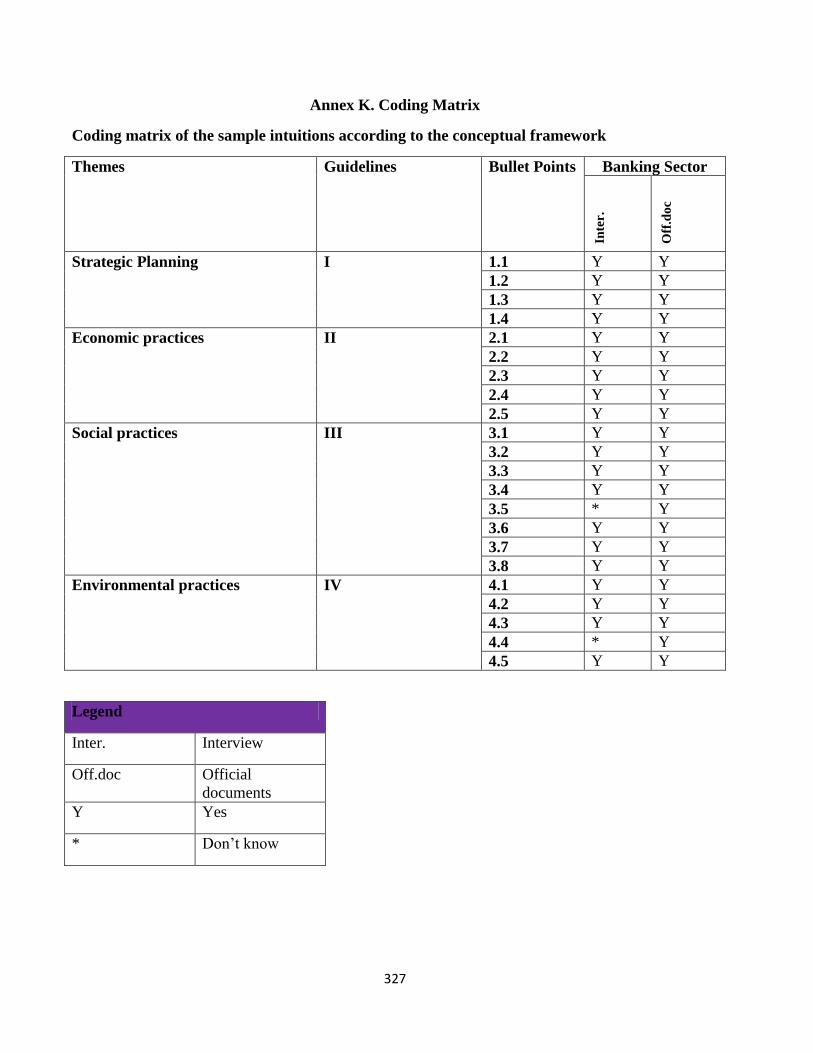

Appendix K Coding Matrix 327

Appendix L Qualitative Research Sample Profile 328

Appendix M Measurement indicators for sustainability 329

Appendix N The Conceptual Framework for Sustainable

Development

333

13

14

____________________________________________________________________________

CHAPTER 1

INTRODUCTION

_____________________________________________________________________________

1. Introduction

Corporate social responsibility is a widely studied construct because it has

multidimensional impact on the economic, environmental, legal & social changes in the

globalized world (Bowen, 1953; Lee, Kim, & Kim, 2018). The rapid business growth in today‘s

world faces both internal and external challenges. Internal challenges include employee‘s

retention, profitability and growth, whereas external challenges cover areas such as tough

competition, maintaining organizational reputation, prestige, environmental impacts and

customerization. These challenges have certainly compelled the organizations to think beyond

financial gains. However, to surmount these challenges, companies now focus on corporate

social responsibility, which may manage many types of stakeholders and outcomes, including;

stakeholders outside of the organization and outcomes that go beyond financial results (Aguinis

& Glavas, 2017). This notion will lead the companies towards a new era of doing business where

the corporate sector aligns its goals, keeping the society‘s interest in priority for growth,

sustainability and economic prosperity.

In today‘s fast growing economic, environmental and social changes, corporate world is

struggling with a new and dynamic role, which is to meet the needs of the present generation

without compromising the ability of the next generations to meet their own needs. This notion is

precisely known as sustainable development model, which is being used to address the massive

issues faced in environmental, social and economic fronts (Charles Jr, Schmidheiny, & Watts,

2017). Corporations often have a substantial impact in eradicating the inequalities in global

development by adopting sustainable development as a model with action-oriented approaches

(Carley & Christie, 2017). In achieving the goals and objectives of the sustainable development

model, it is very much dependent that organizations are taking responsibility for the ways their

actions or operations may impact human needs, culture, societies and the natural environment in

which they operate (Ayuso & Navarrete-Baez, 2018; Jansson, Nilsson, Modig, & Hed Vall,

15

2017). Corporations are also required to apply the basic principles of sustainable development in

its true letter and spirit to transform the business into sustainability. Sustainability often denotes

to activities of organizations, where the inclusion of environmental, economic and social

apprehensions in enterprise‘s operations may be considered in stakeholder‘s management

(Bernal-Conesa, Nieves-Nieto, & Briones‐Penalver, 2017).Sustainability has a set of defined

attributes or characteristics, known as corporate social responsibility (CSR), which may be

termed as the fundamental principles which must be respected by the corporations while doing

the business (Epstein & Buhovac, 2017).

Sustainability and corporate social responsibility are viewed as appropriate highlights of

the cutting edge business and society while tending to corporate social execution, corporate

morals, worldwide corporate citizenship and partner the board (Hall, 2008; Visser & Tolhurst,

2017). The idea of corporate social obligation incorporates the general conviction by the majority

that organizations have a duty to society, which is past the financial specialists and investors of

the firm (Kim & Thapa, 2018). Of course, that responsibility is not only to make money or

profits for the owners but extends to work for the betterment of community at large, government

and the natural environment. In a nutshell, the concept of corporate social responsibility certainly

guarantees a prominent role in addressing the modern challenges of sustainability by contributing

in stirring and heading society towards a sustainable future and economic prosperity of

corporations (Hall, 2008; Ioannou & Serafeim, 2017).

However, the economic prosperity of corporations is no longer acceptable in isolation

from the society and allied forces, which are being impacted by their actions (Kim & Thapa,

2018). Corporate world is required now to focus its attention on both increasing profitability and

work for sustainability through adopting corporate social responsibility. Today‘s organizations

are being forced by a host of factors like social, economic and environmental to reshape their

frameworks, rules, and business models (Gillis & Spring, 2001). The most socially responsible

organizations always try to encompass their efforts to revise their short and long-term goals and

strategies, to meet the global challenges. In the above context, the fundamental concepts of CSR,

whether internal or external, are yet to be explored to further delineate the construct as per

modern era which means beyond financial recompenses. Nevertheless, over the period, the

underlying notions of CSR have gained significant attention of not only corporate giants but also

16

academicians and practitioners (Loosemore & Lim, 2016; Rupp & Mallory, 2015). The corporate

sector has realized that CSR is in fact part of their core business activity and working for society

and planet is the duty of these organizations (Engro Corporation Limited, 2016). In fact, this

concept is being transformed into practice since the modern businesses can feel the pace that

CSR may not only positively enhance organizational credibility (Rasche, 2011) but also impact

open discernment, increment piece of the overall industry, improve partner relations and ensure

corporate notoriety (Ali, Frynas, & Mahmood, 2017; Moratis, 2015) which is certainly the goal

of every organization across the board. Nevertheless, we categorize the CSR activities into three

main facets i.e. micro, macro and strategic based on their outcomes.

Micro CSR is largely concerned with internal organizational activities of management

(Scherer & Bauman, 2007). These activities include the welfare of employees, which is beyond

the financial, strategic and legal bounds of organization (Cooper, 2017; Mehta, Arekar, & Jain,

2014). Micro CSR has its own importance since it deals primarily with employees and the

internal sanctity of the organizations. The study of Rasool (2017) termed micro corporate social

responsibility ―as a psychological endowment for working environment‖. On the other hand,

macro or external CSR is recognized as an excellent tool of credibility-enhancing strategy

(Moratis, 2015) since the external stakeholders may form opinion based on the available

information, which may consequently effect the market share and business growth.

The strategic CSR serves as a tool of strategy formulation for strategic concern, while the

results may help in business integration as a strategy (Loosemore & Lim, 2016). However, the

strategic dimensions of CSR (such as environmental, economic & legal etc.) need to carefully

comprehend because the socio economic context along with the cultural impediments may affect

the results otherwise. The study of Wang, Tong, Takeuchi, and George (2016) concluded that for

a company, strategic CSR is fretful about the long haul accomplishment of the business and its

key situating as to a scope of factors (i.e. environmental, economic & legal etc.). Similarly,

strategic CSR is concerned with customers, suppliers, employees, networks, culture, etc. These

builds may influence the long haul accomplishment of the business and the nature of the

business' vital 'fit' into its condition (Planer-Friedrich & Sahm, 2017). However, the strategic

concept of CSR is in fact influenced by many other contextual factors such as environmental and

legal challenges while the political and regional issues are accumulation to the subject matter.

17

Tilt (2016) contends that while understanding the strategic concept of CSR, researchers should

also study the contextual factors, which means that these factors will certainly differentiate the

outcomes (Ali et al., 2017). It is also important that along with the contextual factors, the

determinants of CSR need to be identified because of socio-political, cultural and environmental

influences. Similarly, the broader concept of CSR along with its determinants, antecedents or

facets might need to be revisited as per the needs of modern businesses and as per the conditions

of various regions, countries and contexts (Campbell, 2007; Carroll, 2015; Tilt, 2016).

The determinants of CSR whether institutional, organizational or individual level, have

gained attention since it‘s important to understand whether, CSR as a construct is being effected

by internal or external factors (Aguinis & Glavas, 2017). The institutional level of determinants

are certainly important factors effecting CSR policies of the companies such as government

regulations (Rizk, Dixon, & Woodhead, 2008), financial performance (Campbell, 2007),

mimetic/simulated forces (Nikolaeva & Bicho, 2011), stakeholder influence/pressure (Brammer

& Millington, 2008) and trade/industry related pressures (Muller & Kolk, 2010). While the

organizational level of antecedents such as board management and governance (Aguilera &

Jackson, 2003), individualistic, relational, collectivist, characteristics of organization and identity

(Brickson, 2007), competitiveness (Bansal & Roth, 2000) and international diversification are

considered important when it comes to institutionalize the concept.

Similarly, individual level factors such as leaders‘ character and moral development

(Snell, 2000), CSR discernments of employees (Rupp, Ganapathi, Aguilera, & Williams, 2006),

psychological needs of employees (Aguilera, Rupp, Williams, &Ganapathi, 2007; Rupp, 2011),

moral values of employee and character attributes and mentalities (Mudrack, 2007), workers

apprehension (Bansal, 2003; Bansal & Roth, 2000; Mudrack, 2007), employee psychological

needs (Trevino, Weaver,& Reynolds, 2006), dispositions and points of view (Mudrack, 2007),

superior‘s promises to CSR (Muller & Kolk, 2010) and CEO intellectual stimulation (Waldman,

Siegel,& Javidan, 2006) attract widespread propositions underlying the specific conditions

(Campbell, 2007; Peng et al., 2016) under which companies could behave socially more

responsible (Ortas, Gallegao,&Alvarez, 2015; Sierra, Zorio,& Garcia, 2015). Nevertheless,

leaders facilitate, encourage and promote the culture where social activities of organization

18

become norms. Similarly, the supervisory commitment to corporate social responsibility is yet

another part where social activities are promoted.

CSR activities are probably an indication of responsible culture promulgated in

companies by their top management (Petrenko, Aime, Ridge, & Hill, 2016). However,

CEO‘s/leaders in firms are motivated for corporate social responsibility activities & policies by

normative/psychological or moral/ethical motives (Bansal & Roth, 2000; Peng et al., 2016; Shin,

2012). This notion becomes itself important at times when leaders practice highly ethical

practices such as CSR, disclosure, compliance and promotion of dutifulness in their operational

affairs by transforming their leadership skills (Abd Rahim, 2016; Sanchez, Bolivar, &

Hernandez, 2017). This transformational process is mostly encouraged by substantial support of

top leaders in companies. Research has demonstrated that transformational pioneers adjust the

qualities, crucial vision of association with CSR arrangements to standardize (Marcus &

Anderson, 2006) and value creation (Gholami, 2011; Neubaum & Zahra, 2006; Obeidat, Tarhini,

& Aqqad, 2016).

Interestingly, research has also emphasized on the leadership qualities including authentic

leadership (Avolio et al., 2004) and types of leadership in relation to CSR policies (Aguilera et

al., 2007) since charismatic leaders at their own may play a vital role in developing these

activities for strategic gains (Carroll, 2015; Waldman et al., 2006). Nevertheless, studies have

just centered around transformational or appealing authority style while evaluating CSR

exercises (Verissimo & Lacerda, 2015). To fill this gap, other leadership styles may be studied

(Frynas & Yamahaki, 2016) such as principled headship (Kalshoven, Den Hartog, & De Hoogh,

2011; Shantz, Alfes, & Latham, 2016).

1.1 CSR in Developing Economies

According to Visser (2006) and the United Nations Development Program (UNDP)

(2006), ―developing economies can be defined as the less industrialized nations with a relatively

low per capita income‖. A study by Belal and Momin (2009) has noticed that the researchers

have focused on the CSR studies in such regions, which are considered as developing economies.

Probably, it is because the developing countries have not been on focus of researchers for many

years (Kratou & Goaied, 2016).

19

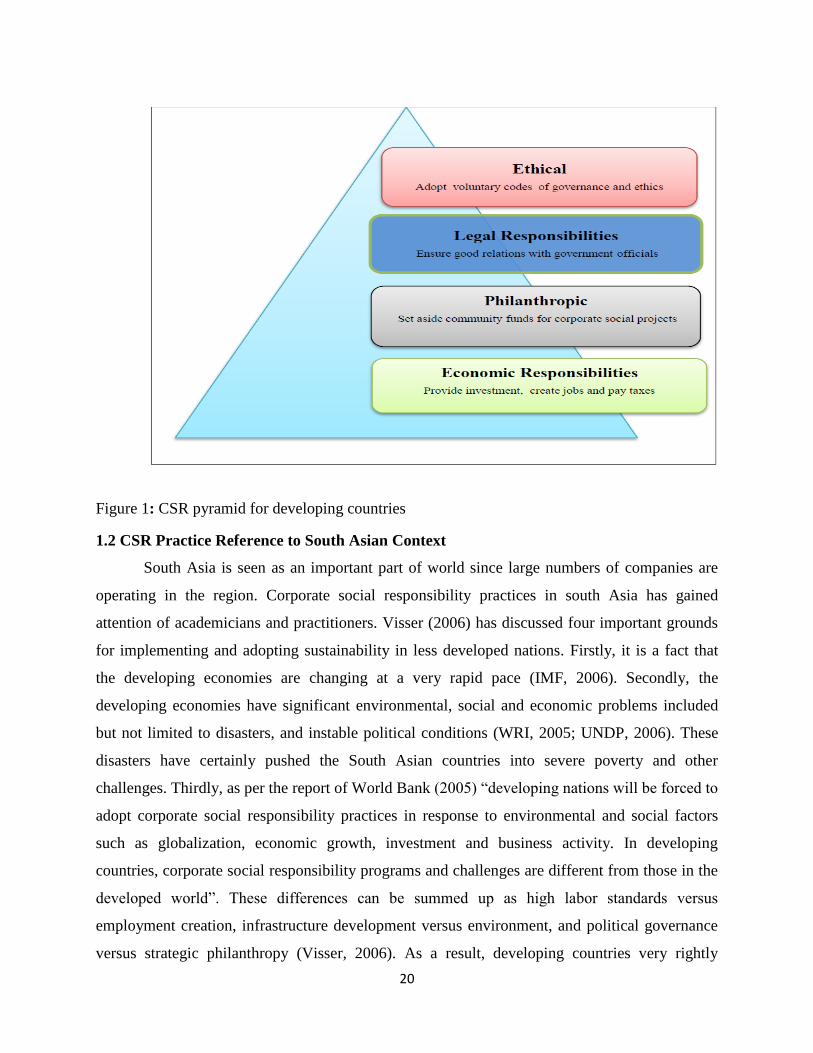

The developing economies are struggling to meet the challenges of globalization,

millennium development goals (MDG‘s) and sustainable development agenda. Notwithstanding

less awareness and having no strict regulations for corporate social responsibility, a substantial

work has been done in the developing countries over the last twenty years (Giuliani, 2016;

Jamali & Sidani, 2012). Corporations today work jointly with civil society and other

stakeholders in developing countries to achieve the goals of sustainability, though the parameters

are different for each individual to define the concept in large (Crane & Matten, 2016; Jamali,

Lund-Thomsen, & Khara, 2017). A continuous debate in this regard is going on over the last few

years (Adams, 2006; Ott, 2003) as sustainability addresses the societal, social and ethical

dimensions along with the economic and environmental concerns (Crane & Matten, 2016). In the

context of addressing the ethical and societal concepts of sustainability, CSR encompasses

strategic framework for achieving the goals of sustainability by framing the concerns in society

regarding the environmental and social valor (Baumgartner & Rauter, 2017; Dahlsrud, 2005;

Vitolla, Rubino, & Garzoni, 2017).

A study conducted by Kemp (2001) summed up as ―there are numerous obstacles to

achieving corporate responsibility, particularly in many developing countries where the

institutions, standards and appeals system, which give life to CSR in North America and Europe,

are relatively weak‖. Similarly, a study by Jamali and Mirshak (2007) has suggested and

highlighted that the developing world can modify and fit the CSR plans which have already been

developed in the Western countries. This way, the developing economies can be benefited in

devising and implementing the CSR plans which are integral part of the business enterprises.

However, the developing world should concentrate on the consequences, outcomes, potential

limits and effects of CSR in developing countries (Jamali et al., 2017; Jamali & Sidani, 2012).

20

Figure 1: CSR pyramid for developing countries

1.2 CSR Practice Reference to South Asian Context

South Asia is seen as an important part of world since large numbers of companies are

operating in the region. Corporate social responsibility practices in south Asia has gained

attention of academicians and practitioners. Visser (2006) has discussed four important grounds

for implementing and adopting sustainability in less developed nations. Firstly, it is a fact that

the developing economies are changing at a very rapid pace (IMF, 2006). Secondly, the

developing economies have significant environmental, social and economic problems included

but not limited to disasters, and instable political conditions (WRI, 2005; UNDP, 2006). These

disasters have certainly pushed the South Asian countries into severe poverty and other

challenges. Thirdly, as per the report of World Bank (2005) ―developing nations will be forced to

adopt corporate social responsibility practices in response to environmental and social factors

such as globalization, economic growth, investment and business activity. In developing

countries, corporate social responsibility programs and challenges are different from those in the

developed world‖. These differences can be summed up as high labor standards versus

employment creation, infrastructure development versus environment, and political governance

versus strategic philanthropy (Visser, 2006). As a result, developing countries very rightly

21

prioritize these issues under the label of corporate social responsibility since these are the critical

problems faced by many people living therein. Some of the major problems faced by many Asian

countries and Africa are severe poverty, tackling HIV/AIDS, infrastructure development and the

basic human needs (World Bank, 2017).

Corporate social responsibility is purely based on humanitarian and philanthropic

perspectives in developing economies (Visser, 2006). It is imperative to note that due to the fact

that this region is under severe pressures of natural and economic nature, companies spend

money in building the infrastructure development. However, other studies suggest that these

countries maintain corporate social responsibility activities beyond philanthropic perspectives

(Belal, 2001; Kemp, 2001; Welford 2005). The present study has focused on the literature related

to corporate social responsibility across the world, to further develop a corporate social

responsibility framework for Pakistan.

1.3 CSR in Pakistan’s Context

It is a fact that the interest in understanding the concept of corporate social responsibility

has increased over the period of time; however, it is still relatively a new phenomenon in

Pakistan (Khan, 2015; Qazi, Ahmed, Kashif, & Qureshi, 2015). In the developed economies, the

long-term sustainability and survival of business is largely correlated with CSR since it creates a

link between business and society. Contrarary to the developed world, in Pakistani corporate

sector, CSR is still a growing concept sometimes misunderstood by these companies (Sajjad &

Eweje, 2014; Waheed, 2005). As rightly identified by many researchers (i.e. Khan, 2015; Safi &

Ramay, 2013), that the concept of corporate social responsibility is often mixed with

philanthropic or charitable activities undertaken by corporate sector. It‘s a common dilemma in

developing economies that the concept of CSR is confused with humanitarian activities.

Probably the practitioners of corporate sector are not fully aware of their social responsibilities

and its subsequent impact on their business empires (Khan, 2015; Waheed, 2005). In Pakistan,

on one side the common public has no awareness about the role of corporate sector in society, on

the other end the corporate sector has yet to understand the true philosophy of CSR as being

practiced in the western world (Ehsan & Kaleem, 2012).

22

Pakistani corporate sector need to understand that corporate social responsibility is a

multidimensional concept such as realization of sense of responsibility for society and

environment. Similarly, the corporate social responsibility is altogether a different phenomenon

since it is way beyond the charitable work or community development initiatives (Mahapatra &

Visalaksh, 2011). Additionally, the corporate world in Pakistan now realizes that corporate social

responsibility is one of their main responsibilities since it is difficult to operate in isolation in

twenty first century. This realization is transformed into social, economic and environmental

activities undertaken by many companies in Pakistan. Similarly, it is also a fact that CSR is now

beyond financial gains and customer sensitivity is becoming priority for business organizations

(Waheed, 2005, p. 12).

The study of Khan (2015) concluded that corporate social responsibility is purely on

voluntary basis since there are no mandatory laws for corporate social responsibility. The

mandatory laws might have enforced companies to undertake the specific social activities as part

of their business responsibility. However, Securities and Exchange Commission of Pakistan

(SECP) introduced voluntary guidelines on CSR in 2013 (SECP, 2013). These guidelines are

promulgated with the intention to promote corporate social activities to further ensure

compliance, transparency and due diligence. Similarly, many of non-governmental

organizations, policy makers and advocacy groups in Pakistan are also working to promote CSR

practices. The study of Sajjad and Eweje (2014) concluded that some of the well-organized

organizations including Triple Bottom Line Pakistan, Sustainable Development Policy Institute,

CSR Association of Pakistan, Corporate Social Responsibility Center Pakistan, National Forum

for Environment and Health (NFEH), Responsible Business Initiative Pakistan and Corporate

Social Responsibility Pakistan are promoting corporate social responsibility culture and

awareness in the Pakistani private sector.

Naeem and Welford (2009) stated in their study that the concept of corporate social

responsibility is in growing stage in Pakistan. Many companies in the country are still working

for inter social responsibility such as employee empowerment, equality, compensations, child

labor and other issues. Similarly, Baughn, Bodie, and McIntosh (2007) examined the concept of

corporate social responsibility of fifteen Asian countries and found that the performance of

Pakistan is probably below average compare to other countries of the region. Similarly,

23

sustainability practices in Pakistan aren‘t reported properly since there is no defined standard or

mechanism as compared to the western world (Mahmood, Kouser, & Iqbal, 2017; Naeem &

Welford, 2009; Kemp & Vinke, 2012). These issues are probably because of multiple reasons

such as social, political and economic instability.

Baughn et al. (2007) pointed that country‘s profile (economic & social) is significantly

linked with CSR activities undertaken because these activities are largely dependent on

economic prosperity of the country. Pakistan has suffered a lot in the past few years because of

war on terror and other natural calamities such as floods and earthquakes in year 2005 and 2011

respectively. Resultantly, the investment and business growth hasn‘t been exemplary in the

country compare to modern world. Jeswani, Wehrmeyer and Mulugetta (2008) categorized and

termed performance of CSR as indifferent, beginner, emerging, and active in case of

environmental perspectives. Most of the Pakistani companies were considered in category of

―indifferent, beginner‖ which means that Pakistani companies have to work hard towards the

environmental CSR in upcoming days. Similarly, Pakistani companies are less aware of

environmental regulations and workers safety and security (Jeswani et al., 2008). In year 2012

over 300 workers died because of fire breakout in a factory in Karachi. The human lives could

have been saved if proper safety measures and environmental regulations would have been

followed (ur-Rehman, Walsh, & Masood, 2012). Nevertheless, these kinds of issues have fully

exposed the safety and security arrangements of these companies and also show failure of

government in implementation of existing rules (Awan, 2001; Human Rights Commission of

Pakistan, 2010; Pasha & Liesivuori, 2003).

Interestingly, health and safety regulations in Pakistan have attracted numerous attentions

from around the world due to series of incidents as discussed above. Some of most recent issues

highlighted are extra working hours, less safety measures, less awareness of regulations and non-

compliance of regulations (Kamal, Malik, Fatima, & Rashid, 2012; Pasha & Liesivuori, 2003).

One of the major issues faced by industry is of no doubt that the workers are less literate and

despite trainings their understating of health and safety regulations is not satisfactory (Kamal et

al., 2012). However, it is pertinent to note that the corporate sector is certainly realizing the

importance of making ethical rules since these might turned up as mandatory rules for these

sectors in upcoming years.

24

1.4 CSR and Multi-National Companies in Pakistan

Multinational companies (MNC‘s) have a significant role in uplifting the economic

activities followed by social activism. In recent times, these MNC‘s have enhanced their

presence across the world including Pakistan in promoting the social, ethical and other various

activities. The MNC‘s in Pakistan are mostly conscious about their social responsibility since

their global presence, reputation, transparency and disclosure policies are in line with the global

reporting standards. Nevertheless, these companies are mostly dominated by their country of

origin (Ali, 2004), ethical practices as per policy and their intrinsic sustainability values. Some of

the notable MNC‘s such as Shell, Siemens, Procter and Gamble, Imperial Chemical Industries,

Nestle, Telenor, Standard Chartered Bank, Microsoft etc. are working to provide better health

infrastructure particularly in rural areas, quality education, and poverty reduction and

rehabilitation programs. These MNC‘s have served millions of people in rural areas in

collaboration with local partners, government and other policy makers.

Siemens spent over Euros 2.5 million during flood in 2010 and 2011, which helped

hundreds of displaced people (Siemens, 2012). Similarly, Unilever Pakistan, worked for quality

of education including developing early childhood centers in collaboration with local partners

(Sajjad & Eweje, 2014). Subsequently, Unilever disbursed over Rs. 29.2 million for health and

education in year 2012 followed by Rs. 128.7 million expended on welfare of community across

the board (UPL, 2012a). Unilever Pakistan, CSR activities are ranging from sustainable sourcing,

packaging, work diversity and health and safety of workers (UPL, 2010) and using the resources

with responsibility (UPL, 2012b).

1.5 Large Local Companies in Pakistan

According to state bank of Pakistan (SBP) Pakistani banking sector is among vibrant and

growing sectors since the banking sector continues its steady expansion as both investments and

advances are showing growth (SBP, 2018). As a component of CSR, Pakistani banks are

spending huge amount on education, health, environment, cultural activities and sports and other

community services (Iqbal, Ahmed, & Kanwal, 2013; Yunis, Durrani, & Khan, 2017). United

bank limited (UBL) ―symbolizes sustainability as the highest standards in terms of well-being

and social responsibility (UBL, 2016)‖. UBL has been one of the donors for The Forman

Christian College (FCC) Lahore where the School of Business and Social Sciences, was

25

inaugurated in 2014 worth Rs. 150 million (UBL, 2016). UBL has contributed millions of funds

for the establishment of four state of the art computer labs at Namal College in Mianwali. UBL

also regularly contribute towards the scholarship programs at Lahore University of Management

Sciences and Bahauddin Zakariya University Multan. Similarly, in health sector, UBL spent a

huge amount in year 2016 including donations to the Marie Adelaide Leprosy Center Karachi,

Shaukat Khanum Memorial Cancer Hospital Lahore and Shalamar Hospital Lahore (UBL,

2016).

Habib bank limited (HBL) is committed to responsible social, environment and

governance practices. HBL spent a huge amount for safe drinking water at Thar, Sindh in

collaboration with Amir Khan Trust in year 2016. During the year 2016, HBL donated 380

million to both HBL foundation and directly to different causes. HBL foundation spent 144

million in 14 different endowment funds of govt and NGO based hospitals across Pakistan. HBL

foundation spent over 104 million in 21 different schools across Pakistan. The foundation also

collaborated with the Marie Adelaide Leprosy Center Karachi to further help in Baluchistan and

also contributed towards purchase of 21 large ambulances for Edhi Foundation. HBL partnered

with Azad foundation in promoting sports activities in Pakistan (HBL, 2016).

The cement sector i.e. Bestway cement is spending 3.5 million US dollars on education

and scholarship programs. The group has spent 2.5 million US dollars for relief and other

activities (Bestway, 2015). The Bestway Foundation contributed £1 million towards disaster

relief in 2005 after the earthquake in Pakistan. Similarly, the group also contributed a substantial

amount for the rehabilitation of 2010 floods in Pakistan (Bestway, 2015). For example, there is

an increasingly trend concerning with social, environmental, and economic impacts of decisions

made by small and medium enterprises. However, it is yet to be explored further in Pakistan

(Sajjad and Eweje, 2014). Similarly, small and medium enterprises is facing numerous

challenges (such as obsolete production facilities, inadequate industrial infrastructure) which are

probably another obstacle in performing social responsibility (Khalique, Bontis, Abdul Nassir

bin Shaari, & Hassan Md. Isa, 2015). Contrary to small and medium enterprises, large companies

such as Fauji Fertilizer Limited, United Bank Limited, English Biscuit Manufacturing Limited,

Engro Corporation Limited, Pakistan State Oil and other companies are having more sense of

responsibility towards sustainability. Similarly banks like UBL, HBL, National Bank of Pakistan

26

(NBP) and other major banks are actively participating in CSR activities across country.

Research has established that banks use CSR as a tool to attract more customers (Abdillah &

Husin, 2016; Mocan, Rus, Draghici, & Ivascu, 2015). Similarly, Engro Corporation limited has

contributed towards social activities ranging from environmental, social, educational and

sustainable green environment in last few years. The company has a clear policy of CSR and

sustainability, which is itself a great success (Engro Corporation Limited, 2011).

1.6 Pakistan’s Economic & Social Developments

Pakistan is an emerging economy, having enormous natural resources, located in South

Asia, having a strategic importance with over 207 million populations (Economic Survey of

Pakistan, 2017; 6th

Population & Census Report, 2017). The country is blessed with numerous

resources such fertile agricultural land, feasible climatic conditions, water and other uncounted

resources. Though initially faced with the severe economic challenges, Pakistan has shown a

significant progress in maintaining macroeconomic stability in last couple of years by shrinking

the fiscal deficit from 8 percent to below 5 percent with gross domestic product growth (GDP) of

over 4.7 percent (World Bank, 2017). Pakistan realizes that controlling the fiscal deficit will lead

the country towards macroeconomic stability, yielding long-term growth and creating a better

environment for businesses. Pakistan has also embarked on an ambitious structural reforms

program. The reforms programs include the restructuring the government owned entities,

privatizing the loss making organizations and introduce information technology across

organizations for better service management. However, due to certain other factors such as

energy crisis, devaluation of rupee against dollars and trade deficit, macroeconomic stability is

still under question (Asian Development Bank, 2013; World Bank, 2017). Certainly, macro-

economic instability has its own repercussions on business and trade. Like in case of Pakistan

stock exchange, it has come down from 50,000 to 40,000 base points within few months of time.

Similarly, the devaluation of rupee is all time higher compare to any other currencies of the

world. Of course, businesses suffer a lot due to all these constraints and at the end of the day;

they strive for their survival instead of doing the social work. In the past country has suffered a

lot due to war on terror, floods in year 2010 and 2011 and power crises from 2007-2017 (ESP,

2012 & 2017; ul Hasan & Zaidi, 2012). Over 5.3 million jobs (direct or indirect including

agricultural) got affected due to the heavy floods in 2010 as per the International Labor

Organization (ILO) (2011). The combine loss for all these constraints (war on terror & floods)

27

caused the economy US $ 68 billion followed by loss of thousands of human live (ESP, 2011 &

2017).

Despite the hardships, poverty ratio in Pakistan has dropped off compare to previous

years; however, sustaining the current reduction rate would be a challenge in upcoming years

(Economic Survey of Pakistan, 2017; World Bank, 2013, 2017). Similarly, spending on human

development, education and health has been substantially increased in recent years in contour

with the ratifications of SDG‘s (Economic Survey of Pakistan, 2018). The United Nations

(2013a) alerted Pakistan to improve it‘s ranking on ―Human Development Index‖ (HDI). World

Economic Forum (2017) revealed that Pakistan is improving in its ranking on the ―Global

Competitive Index‖ (GCI) as compared to previous years.

1.7 Background

Bowen (1953) did the first complete dialog of business morals and corporate social duty.

This notion created a foundation by which business executives and academics could consider

CSR as part of strategic planning and managerial decision-making process (Bowen, 1953). CSR

whether individual, organizational or contextual in nature, has been discussed extensively over

the period. Historically, CSR can be divided into two broader categories; internal and external.

Internal CSR deals with internal organizational activities. Whereas, externally CSR is recognized

as a tool for increased market share and business growth. People, idea generation and social

change were interrelated in 1960s whereas; there were lack of innovative ideas in dealing the

upcoming issues of CSR in 1970s as reported by Friedman (1982). Friedman (1982) summarized

that corporate social responsibility is all about making more profits but in a responsible way

staying within the rules of business.

Freeman's (1984) stakeholder theory summed, ―Managers should tailor their policies to

satisfy stakeholders such as workers, customers, suppliers, and community organizations, in

addition to satisfying their shareholders‖. Stakeholder theory suggests that CSR can be used as a

device for new opportunities and value creation (Obeidat et al., 2016) or value maximization for

strategic gains and competitive advantage, corporate citizenship and sustainability (Parsons,

1997). Based on the discussed theory, some of the researchers have categorized stakeholders as

primary and secondary since business environment, capacity and size are important factor while

adopting and sustaining CSR activities. Employees are considered as the primary stakeholders

28

because CSR activities & policies increase their motivation (Bansal & Roth, 2000) and develop

―higher order or morals‖. After 2000s, the importance of CSR converted into the strategic level

having multiple effects on the organization and was rightly owned by businesses (Zakirova,

2001).

Corporate social responsibility from year 2011 and onwards has witnessed that instead of

a one of assistance, companies have worked towards institutionalization of corporate

philanthropy (Corbett, 2003). The firms have realized that transforming and synergizing the

corporate socialization, with its core strategy is certainly in the interest of firms (Cheng, Ioannou,

& Serafeim, 2004). The study of Donker, Poff, and Zahir, 2008, contended the performance and

corporate social responsibility index are interrelated. Furthermore, both financial (i.e.

profitability etc.) and non-financial outcomes (i.e. reputation, image, trust, motivation etc.) of

CSR are now seen as business strategies (Aguinis & Glavas, 2012).

Lee, Park, and Lee (2013) contended that social activities are basically a fit between

employees‘ perception and organizational culture followed by organizational capabilities to

undertake such activities. The secondary stakeholders don‘t directly affect the CSR policies.

However, these policies may affect the perception towards organization which subsequently may

largely affect the organizational reputation and image (Lee at al., 2013). Research has established