DeCAD70-18 - Budget Policies and Procedures - Commissaries

152

DEPARTMENT OF DEFENSE DeCA DIRECTIVE 70-18 HEADQUARTERS DEFENSE COMMISSARY AGENCY Fort Lee VA 28301-6300 April 10, 1995 Resources Management BUDGET POLICIES AND PROCEDURES BY ORDER OF THE DIRECTOR RONALD P. McCOY Colonel, USAF Chief of Staff RALPH R. TATE Acting Chief, Safety, Security and Administration AUTHORITY: Defense Commissary Agency Directives Management Program is established in compliance with DoD Directive 5105.55, Defense Commissary Agency (DeCA), November 1990. MANAGEMENT CONTROLS: This directive contains Management Control provisions that are subject to evaluation and testing as required by DeCAD 70-2 and as scheduled in DeCAD 70-3. The Management Control Checklist to be used by assessable unit managers to conduct the evaluation and test management controls is at Appendix A. APPLICABILITY: This directive applies to the Defense Commissary Agency (DeCA) activities. HOW TO SUPPLEMENT: Regions may not supplement this directive. HOW TO ORDER COPIES: Stores needing additional copies will submit requirements on DeCA Form 30-21 to Region/IM. Regions will consolidate requirements and order per published schedule. SUMMARY: This directive describes budget policies and procedures to include the process of determining requirements, obtaining resources and effectively applying those resources to accomplish planned goals and objectives of the Defense Commissary Agency. OFFICE OF PRIMARY RESPONSIBILITY (OPR): HQ DeCA/RM COORDINATORS: HQ DeCA Directorates and Regions DISTRIBUTION: E

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of DeCAD70-18 - Budget Policies and Procedures - Commissaries

DEPARTMENT OF DEFENSE DeCA DIRECTIVE 70-18HEADQUARTERS DEFENSE COMMISSARY AGENCYFort Lee VA 28301-6300 April 10, 1995

Resources Management

BUDGET POLICIES AND PROCEDURES

BY ORDER OF THE DIRECTOR

RONALD P. McCOYColonel, USAFChief of Staff

RALPH R. TATEActing Chief, Safety, Security and Administration

AUTHORITY: Defense Commissary Agency Directives Management Program is established in compliancewith DoD Directive 5105.55, Defense Commissary Agency (DeCA), November 1990.

MANAGEMENT CONTROLS: This directive contains Management Control provisions that are subjectto evaluation and testing as required by DeCAD 70-2 and as scheduled in DeCAD 70-3. The ManagementControl Checklist to be used by assessable unit managers to conduct the evaluation and test managementcontrols is at Appendix A.

APPLICABILITY: This directive applies to the Defense Commissary Agency (DeCA) activities.

HOW TO SUPPLEMENT: Regions may not supplement this directive.

HOW TO ORDER COPIES: Stores needing additional copies will submit requirements on DeCA Form30-21 to Region/IM. Regions will consolidate requirements and order per published schedule.

SUMMARY: This directive describes budget policies and procedures to include the process of determiningrequirements, obtaining resources and effectively applying those resources to accomplish planned goals andobjectives of the Defense Commissary Agency.

OFFICE OF PRIMARY RESPONSIBILITY (OPR): HQ DeCA/RMCOORDINATORS: HQ DeCA Directorates and RegionsDISTRIBUTION: E

DeCAD 70-18 April 10, 1995

i

TABLE OF CONTENTS

Para PageChapter 1 - Financial Management in DeCA

General Information ...................................................................................................... 1-1 1-1Basis for Financial Management................................................................................... 1-2 1-1Role of Directors and Managers ................................................................................... 1-3 1-1The Primary Role of Budget ......................................................................................... 1-4 1-2Responsibilities of the Budget Officer at HQ DeCA ................................................... 1-5 1-2Responsibilities of the Budget Officer at Regions ....................................................... 1-6 1-3Headquarters Supervision of Subordinate Budget Offices........................................... 1-7 1-4Participatory Financial Management ............................................................................ 1-8 1-4

Chapter 2 - Biennial Planning, Programming and Budgeting System

Overview ....................................................................................................................... 2-1 2-1Defense Review Board.................................................................................................. 2-2 2-1Continuous Process ....................................................................................................... 2-3 2-1Defense Guidance.......................................................................................................... 2-4 2-1Future Years Defense Program (FYDP)....................................................................... 2-5 2-1FYDP Elements............................................................................................................. 2-6 2-2FYDP Updates .............................................................................................................. 2-7 2-2Program Objective Memorandum (POM) .................................................................... 2-8 2-2Budget Process .............................................................................................................. 2-9 2-3Budget Submission........................................................................................................ 2-10 2-3SECDEF and Office of Management and Budget (OMB) Review.............................. 2-11 2-3Congressional Review................................................................................................... 2-12 2-3Hearings......................................................................................................................... 2-13 2-4Authorization/Appropriation ........................................................................................ 2-14 2-4Congressional Budget and Impoundment Act of 1974................................................. 2-15 2-4Budget Execution .......................................................................................................... 2-16 2-5Flexibility in Budget Operations................................................................................... 2-17 2-5

Chapter 3 - Fund Control

General Information ...................................................................................................... 3-1 3-1Apportionment Process ................................................................................................. 3-2 3-1Appropriation Warrants ................................................................................................ 3-3 3-2Apportionment of Funds ............................................................................................... 3-4 3-2Transfer Actions............................................................................................................ 3-5 3-3Reprogramming............................................................................................................. 3-6 3-3Supplemental Appropriations ....................................................................................... 3-7 3-4Deferrals and Rescissions ............................................................................................. 3-8 3-4Fund Distribution .......................................................................................................... 3-9 3-6Funding Authorization Document (FAD), DeCA Form 70-7 ...................................... 3-10 3-6Funding Targets ............................................................................................................ 3-11 3-6Military Interdepartmental Purchase Request (MIPR), DD Form 448 ........................ 3-12 3-7MIPR Categories........................................................................................................... 3-13 3-7Preparation of MIPR, DD Form 448 and Acceptance of MIPR, DD Form 448-2 ...... 3-14 3-7MIPR Commitment and Obligation.............................................................................. 3-15 3-8

DeCAD 70-18 April 10, 1995

ii

Para PageChapter 4 - Sources and Uses of Funds

Section A - General Information

Purpose .......................................................................................................................... 4-1 4-1Funds ............................................................................................................................. 4-2 4-1

Section B - Sources of Funds

DBOF - Resale Stocks .................................................................................................. 4-3 4-1DBOF - Commissary Operations.................................................................................. 4-4 4-1Surcharge Collections.................................................................................................... 4-5 4-1

Section C - Uses of Funds

DBOF - Resale Stocks .................................................................................................. 4-6 4-2DBOF - Commissary Operations.................................................................................. 4-7 4-2Surcharge Collections.................................................................................................... 4-8 4-2General Policy ............................................................................................................... 4-9 4-2

Chapter 5 - Defense Business Operations Fund (DBOF)

Section A - General

Purpose .......................................................................................................................... 5-1 5-1Background ................................................................................................................... 5-2 5-1

Section B - DBOF Terminology

Definition of DBOF Terms........................................................................................... 5-3 5-2

Section C - DBOF Financial Management Policies and Procedures

Operating Budget .......................................................................................................... 5-4 5-3Capital Budget............................................................................................................... 5-5 5-3Mobilization/Surge Costs and ar Reserve Materiel...................................................... 5-6 5-4Military Personnel ......................................................................................................... 5-7 5-4Full Recovery of Costs and the Setting of Prices.......................................................... 5-8 5-4Revenue Recognition Policy for the Defense Business Operations Fund .................... 5-9 5-5

Section D - Rate Setting in the Business Areas

Use of Rates in DBOF .................................................................................................. 5-10 5-5

Section E - Submission Requirements and Preparation of Materials

General Guidance.......................................................................................................... 5-11 5-6

Section F - Budget Formulation

Purpose .......................................................................................................................... 5-12 5-6

DeCAD 70-18 April 10, 1995

iii

Para Page

General .......................................................................................................................... 5-13 5-6

Submission Requirements............................................................................................. 5-14 5-6

Section G - Congressional Justification/Presentation

Purpose .......................................................................................................................... 5-15 5-7Organization of Justification Books ............................................................................. 5-16 5-7

Chapter 6 - DBOF - Commissary Operations Fund

Section A - General Information

General .......................................................................................................................... 6-1 6-1Responsibilities ............................................................................................................. 6-2 6-1

Section B - Budget Formulation and Justification

Annual Operating Budget (AOB)................................................................................. 6-3 6-1Director's Statement ...................................................................................................... 6-4 6-1Supporting Schedules.................................................................................................... 6-5 6-1OCONUS Requirements............................................................................................... 6-6 6-2

Section C - Budget Execution and Analysis

Expense Plan ................................................................................................................. 6-7 6-2Monthly Variance Analysis........................................................................................... 6-8 6-2Cost Authority............................................................................................................... 6-9 6-3OCONUS Reporting Requirements.............................................................................. 6-10 6-3

Section D - Midyear Review

Midyear Review ............................................................................................................ 6-11 6-3Unit Cost ....................................................................................................................... 6-12 6-4

Section E - Year-End Closeout Procedures

Year-end ........................................................................................................................ 6-13 6-4Review of Unobligated Balances .................................................................................. 6-14 6-4Review of Unliquidated Obligation Balances............................................................... 6-15 6-4Accountability for Fixed Assets.................................................................................... 6-16 6-5Year-end Cutoff............................................................................................................. 6-17 6-5Certification................................................................................................................... 6-18 6-5

Chapter 7 - General and Administrative (G&A) Costs

Background ................................................................................................................... 7-1 7-1References ..................................................................................................................... 7-2 7-1Interservice Support Agreements.................................................................................. 7-3 7-1Terminate Services ........................................................................................................ 7-4 7-1

DeCAD 70-18 April 10, 1995

iv

Para Page

Fund Distribution and Control ...................................................................................... 7-5 7-2G&A Funding for Navy Location Stores (NEXMARTS)............................................ 7-6 7-2Major Real Property Maintenance and Repair (MRPM&R)........................................ 7-7 7-2

Defense Logistics Agency............................................................................................. 7-8 7-3Worker's Compensation ................................................................................................ 7-9 7-3Defense Finance and Accounting Service (DFAS)....................................................... 7-10 7-3Appellate Review .......................................................................................................... 7-11 7-4Personnel Security Program.......................................................................................... 7-12 7-4

Chapter 8 - Civilian Personnel Services

General Information ..................................................................................................... 8-1 8-1Basis for Rates of Pay ................................................................................................... 8-2 8-1Implementing Directives ............................................................................................... 8-3 8-1Direct Hire Pay Systems Categories ............................................................................. 8-4 8-1Indirect Hire Foreign National Personnel, Labor Contracts With Foreign Governments 8-5 8-2Types of Payments to Employees ................................................................................. 8-6 8-2Compensable Hours ...................................................................................................... 8-7 8-4Workyears ..................................................................................................................... 8-8 8-4Average Costs Computation ......................................................................................... 8-9 8-4Manpower Utilization ................................................................................................... 8-10 8-4Manpower Conversion .................................................................................................. 8-11 8-4

Chapter 9 - Programs Requiring Reimbursement

Purpose .......................................................................................................................... 9-1 9-1Military Personnel (MILPERS) .................................................................................... 9-2 9-1NEXMART Operations ................................................................................................ 9-3 9-1AAFES Exchange/Commissary Marts ......................................................................... 9-4 9-2

Chapter 10 - Transportation Policies and Procedures

Background ................................................................................................................... 10-1 10-1Definitions ..................................................................................................................... 10-2 10-1Scope ............................................................................................................................. 10-3 10-2Transportation of Items Other than Personnel.............................................................. 10-4 10-2Transportation Account Codes (TAC) ......................................................................... 10-5 10-2Transportation of Subsistence....................................................................................... 10-6 10-3Transportation of Equipment........................................................................................ 10-7 10-3Other Transportation..................................................................................................... 10-8 10-4Transportation Budget ................................................................................................. 10-9 10-5Transportation Budget Formulation and Justification.................................................. 10-10 10-5Transportation Budget Execution ................................................................................. 10-11 10-5Transportation Bill Paying............................................................................................ 10-12 10-6Enhanced Transportation Automated Documentation System (ETADS).................... 10-13 10-6References ..................................................................................................................... 10-14 10-7

Chapter 11 - Reimburseable Programs

DeCAD 70-18 April 10, 1995

v

Para Page

Purpose .......................................................................................................................... 11-1 11-1General Information ...................................................................................................... 11-2 11-1Vendor Coupons............................................................................................................ 11-3 11-1Commercial Activities (CA) Contracts......................................................................... 11-4 11-1Foreign Government Burdensharing............................................................................. 11-5 11-2

Coast Guard Commissary Operations .......................................................................... 11-6 11-2

Chapter 12 - Unit Cost Resourcing

Section A - General

Purpose .......................................................................................................................... 12-1 12-1Background ................................................................................................................... 12-2 12-1Unit Cost Definition...................................................................................................... 12-3 12-1Concept.......................................................................................................................... 12-4 12-2Unit Cost Goals............................................................................................................. 12-5 12-3

Section B - Setting Unit Cost Goals

Identification of Outputs ............................................................................................... 12-6 12-3Allocation of Unit Cost Goals....................................................................................... 12-7 12-3

Section C - Budget Submission Review and Execution

Operating and Capital Budgets..................................................................................... 12-8 12-4Budget Execution .......................................................................................................... 12-9 12-4Administrative Control of Funding Limitations ........................................................... 12-10 12-5"Cost Only" Transactions ............................................................................................. 12-11 12-5Reimbursements ............................................................................................................ 12-12 12-5

Section D - Accounting and Classification of Costs

Accounting for Costs..................................................................................................... 12-13 12-6Depreciation Policies..................................................................................................... 12-14 12-6Amortization/Depletion/Prepaid Expenses/Capital...................................................... 12-15 12-6Military Personnel Expense Policies............................................................................. 12-16 12-7General and Administrative (G&A) Cost Policies ....................................................... 12-17 12-7

Chapter 13 - General Policies

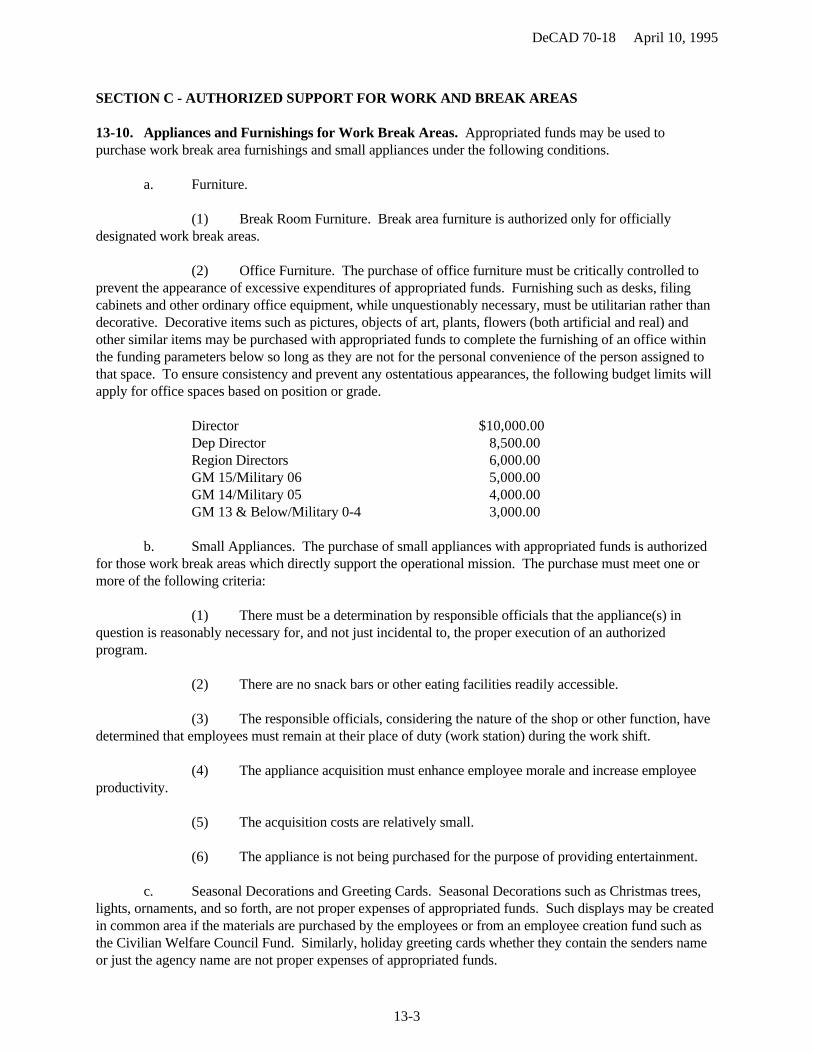

Section A - General Information

Purpose .......................................................................................................................... 13-1 13-1

Section B - Travel and Transportation

Temporary Duty Travel (TDY)..................................................................................... 13-2 13-1

Travel Related to Disability Retirement Processing..................................................... 13-3 13-1

DeCAD 70-18 April 10, 1995

vi

Para Page

Travel Related to Equal Employment Opportunity (EEO) Complaints....................... 13-4 13-1Travel Related to Emergency Leave ............................................................................. 13-5 13-2Dependent Student Travel............................................................................................. 13-6 13-2Passport Fees................................................................................................................. 13-7 13-2Contact Quarters for DoD Employees in a Travel Status............................................. 13-8 13-2Transportation for Defense Property Disposal Offices ................................................ 13-9 13-2

Section C - Authorized Support for Work and Break Areas

Appliances and Furnishings for Work Break Areas ..................................................... 13-10 13-3Personalized Stationery................................................................................................. 13-11 13-4Business Cards .............................................................................................................. 13-12 13-4Entertainment ................................................................................................................ 13-13 13-4Special Drinking Water................................................................................................. 13-14 13-5

Section D - Ethnic and Holiday Observances

Funding Policies ............................................................................................................ 13-15 13-5

Section E - Registration Fees, Professional Memberships and Honorarium and Speaking Fees

Registration Fees for Meetings and Conferences ......................................................... 13-16 13-6Membership in Professional Organizations.................................................................. 13-17 13-7Honorarium and Speaking Fee Policies ........................................................................ 13-18 13-7

Section F - Ceremonies and Refreshments

Traditional Ceremonies ................................................................................................. 13-19 13-7Refreshments at Awards Ceremonies ........................................................................... 13-20 13-7

Section G - Contracted Advisory and Assistance Services (CAAS)

General Information ...................................................................................................... 13-21 13-8

Section H - Awards

General Information ...................................................................................................... 13-22 13-8Civilian Performance Awards ....................................................................................... 13-23 13-9

Section I - Individual Clothing

General Information ...................................................................................................... 13-24 13-9Issue of Military Grade Insignia ................................................................................... 13-25 13-9Distinctive Uniforms and Functional Clothing............................................................. 13-26 13-9

Section J - Refunds and Cash Collections

Witness and Jury Fees................................................................................................... 13-27 13-9

Lump-Sum Leave Payment ........................................................................................... 13-28 13-10

DeCAD 70-18 April 10, 1995

vii

Para Page

Travel Over-Advances .................................................................................................. 13-29 13-10

Section K - Contracts

Early Contract Termination........................................................................................... 13-30 13-10

Section L - Base Realignment and Closures (BRAC)

General Information ...................................................................................................... 13-31 13-10

Accessing BRAC Funds................................................................................................ 13-32 13-10

Chapter 14 - Defense Business Operations Funds (DBOF) - Commissary resale Stocks

General .......................................................................................................................... 14-1 14-1Scope ............................................................................................................................. 14-2 14-1Annual Budget Operating Instruction........................................................................... 14-3 14-1Budget Execution .......................................................................................................... 14-4 14-3Reports .......................................................................................................................... 14-5 14-5Performance Measures .................................................................................................. 14-6 14-6Year-end Closeout Procedures ...................................................................................... 14-7 14-7Central Distribution Centers (CDCs), Reference DeCAD 40-23 ................................ 14-8 14-8

Chapter 15 - Surcharge Collections

Section A - Background and Policy

General .......................................................................................................................... 15-1 15-1Surcharge Collections Apportionment.......................................................................... 15-2 15-1Cash Flow Management................................................................................................ 15-3 15-2Responsibilities ............................................................................................................. 15-4 15-3Surcharge Collections Budgeting.................................................................................. 15-5 15-3Financial Management Procedures ............................................................................... 15-6 15-4Funding for Directorate of Facilities Programs ............................................................ 15-7 15-5

Section B - Region Procedures

Budget Call.................................................................................................................... 15-8 15-6Heating, Ventilation and Air Conditioning (HVAC) and Refrigeration Maintenance Contracts (CONUS Only)......................................................................................... 15-9 15-7Planning Program.......................................................................................................... 15-10 15-7Action taken Upon Receipt of Initial FAD ................................................................... 15-11 15-8On Going Procedures .................................................................................................... 15-12 15-9Monthly Exception Report............................................................................................ 15-13 15-10Changes tot the Surcharge Collections Obligation Execution Plan.............................. 15-14 15-10

Section C - Commissary and Central Distribution Center Procedures

Submission of Annual Budget Requirements to DeCA Region................................... 15-15 15-10

DeCAD 70-18 April 10, 1995

viii

Para Page

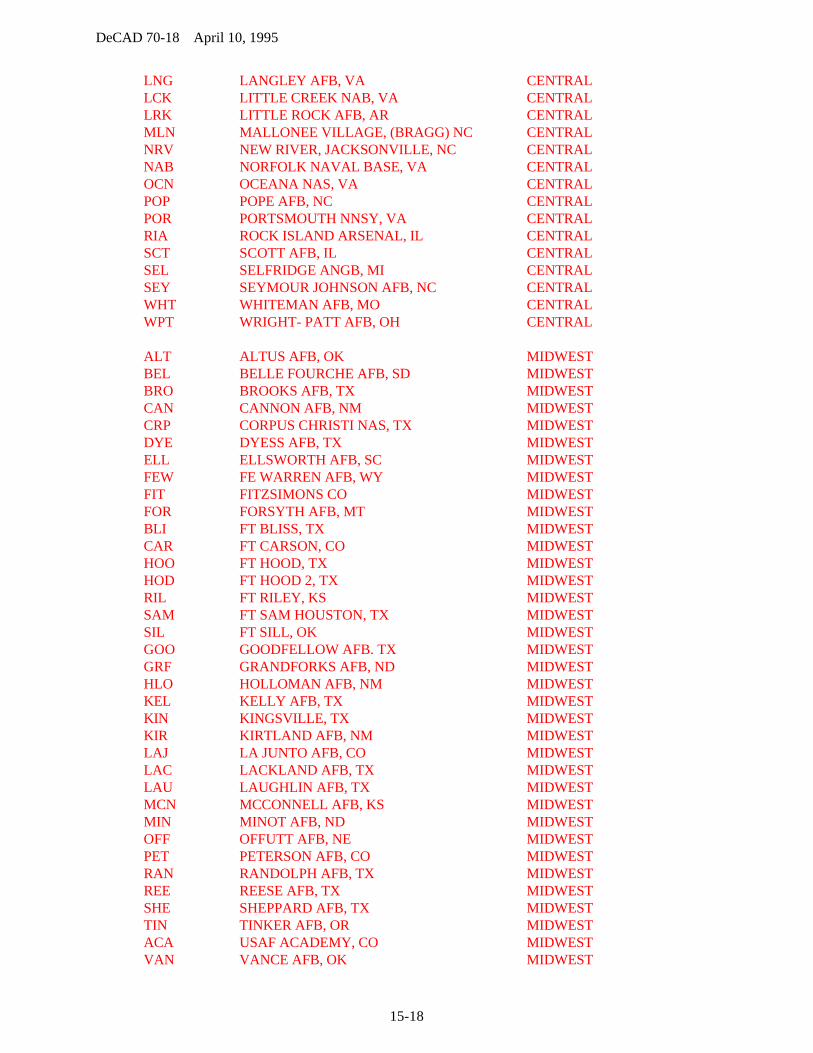

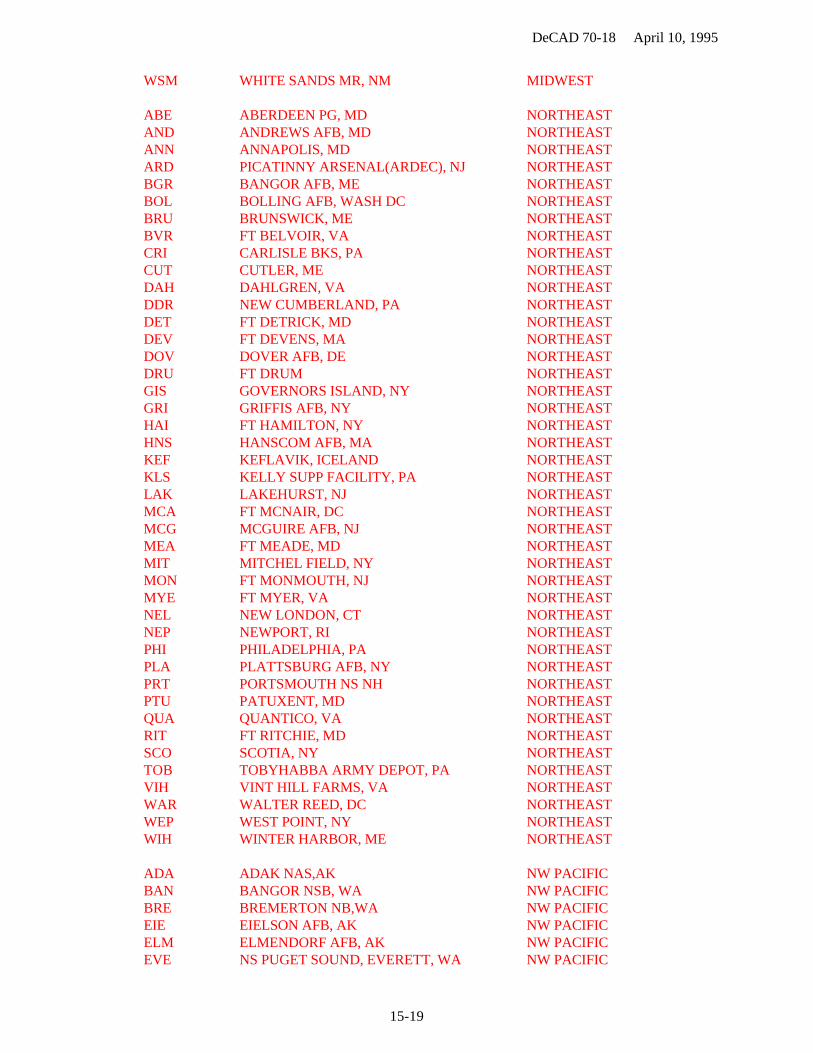

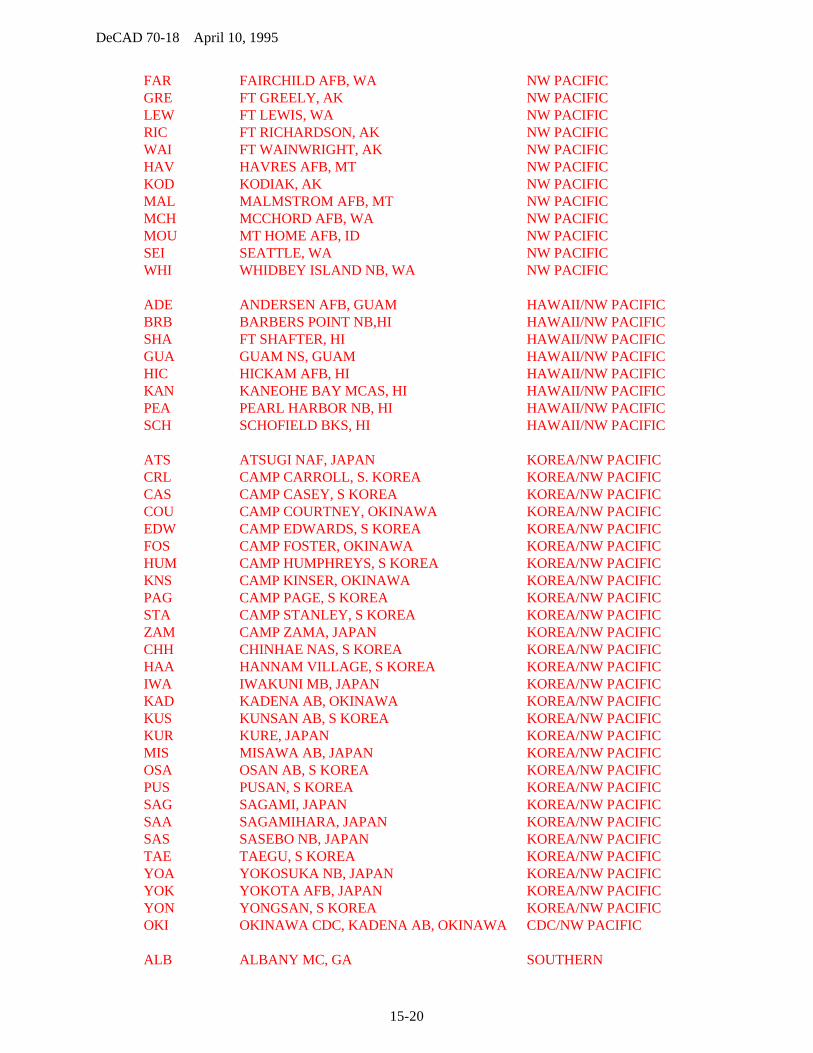

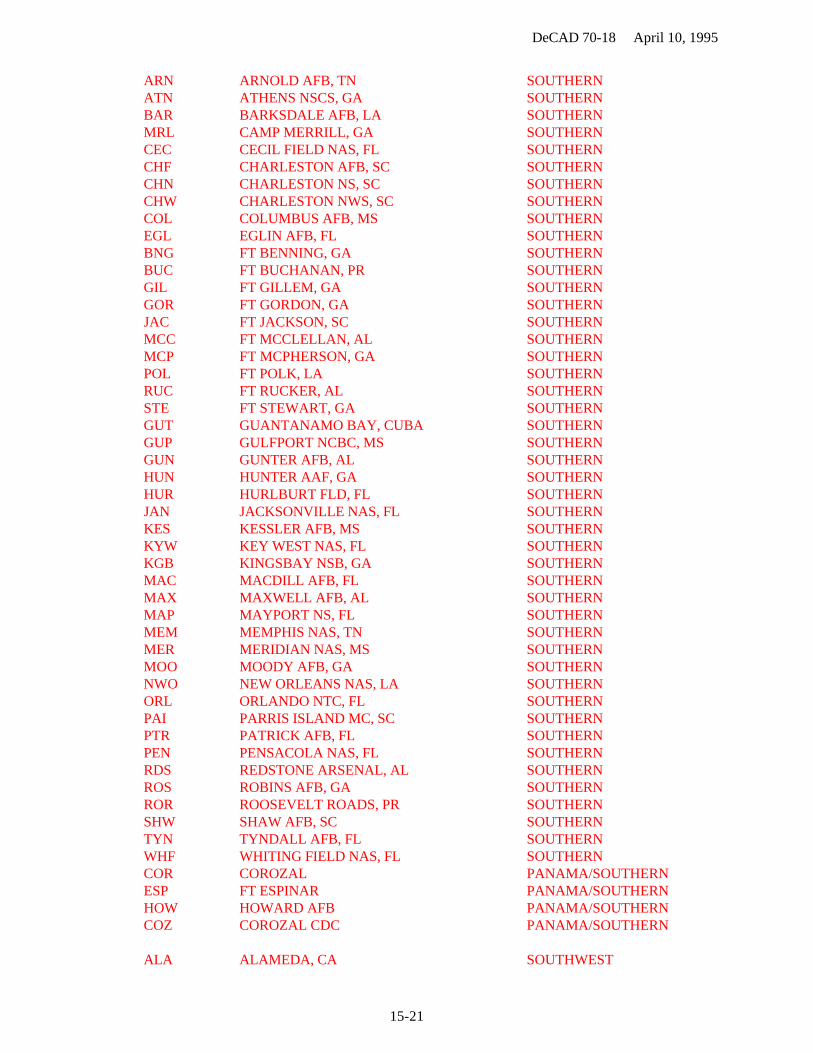

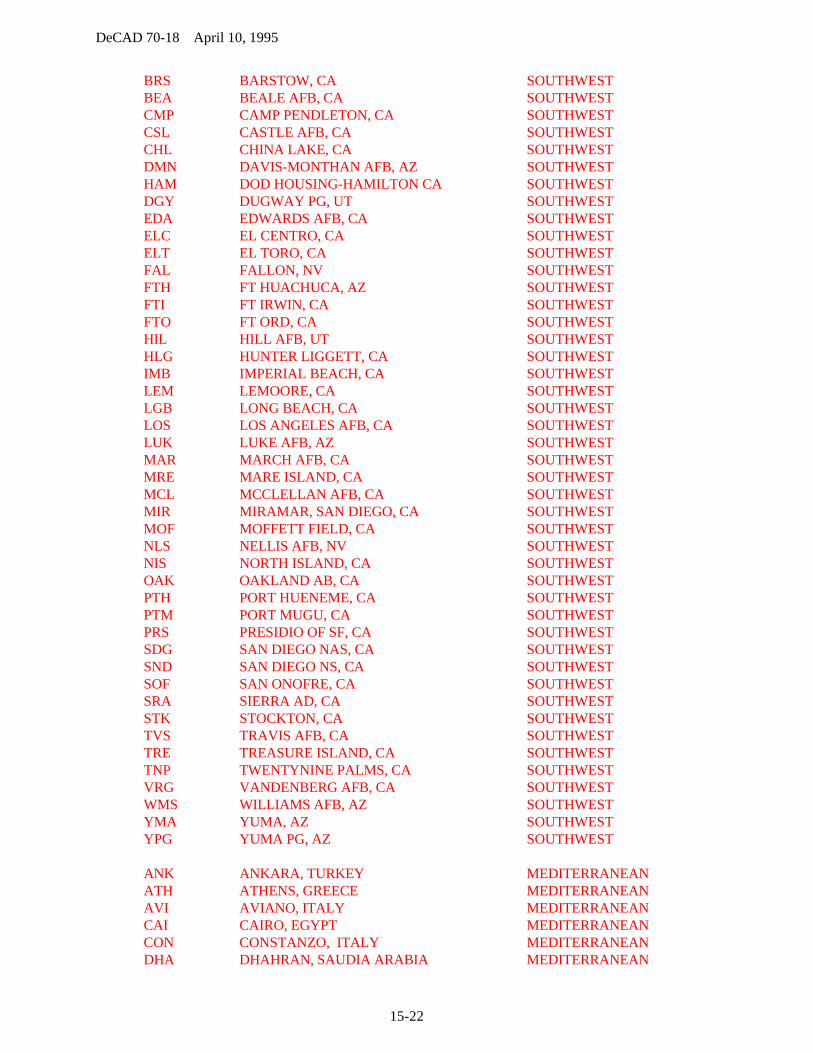

Funding for Installation Support................................................................................... 15-16 15-10CONUS Region Stores Only......................................................................................... 15-17 15-11European Region ........................................................................................................... 15-18 15-12Supplies Drawn from a CDC ........................................................................................ 15-19 15-12Sale or Salvage of Equipment ....................................................................................... 15-20 15-12Transfer of Equipment .................................................................................................. 15-21 15-13Budget Formulation....................................................................................................... 15-22 15-13Budget Execution .......................................................................................................... 15-23 15-14Prior Year Funds ........................................................................................................... 15-24 15-17Commissary Codes........................................................................................................ 15-25 15-17

Chapter 16 - Performance Measures

General .......................................................................................................................... 16-1 16-1Performance Measures .................................................................................................. 16-2 16-1Types of Performance Measures................................................................................... 16-3 16-1Outcome Measures........................................................................................................ 16-4 16-3Work Process Measures ................................................................................................ 16-5 16-3Requirements for Performance Measurement............................................................... 16-6 16-4DeCA Workload Indicators for the Commissary Operations Business Area .............. 16-7 16-5DeCA Workload Indicators for the Commissary Resale Stocks Business Area.......... 16-8 16-5

Chapter 17 - Financial System Reports

Background ................................................................................................................... 17-1 17-1General Provisions ........................................................................................................ 17-2 17-1Defense Business Management System Reports .......................................................... 17-3 17-1DBMS Reports.............................................................................................................. 17-4 17-2DBMS Regulations ....................................................................................................... 17-5 17-5Communications............................................................................................................ 17-6 17-5STANFINS Reports ...................................................................................................... 17-7 17-5Automated System for Army Commissaries (ASAC).................................................. 17-8 17-7STANFINS and ASAC Regulations............................................................................. 17-9 17-7

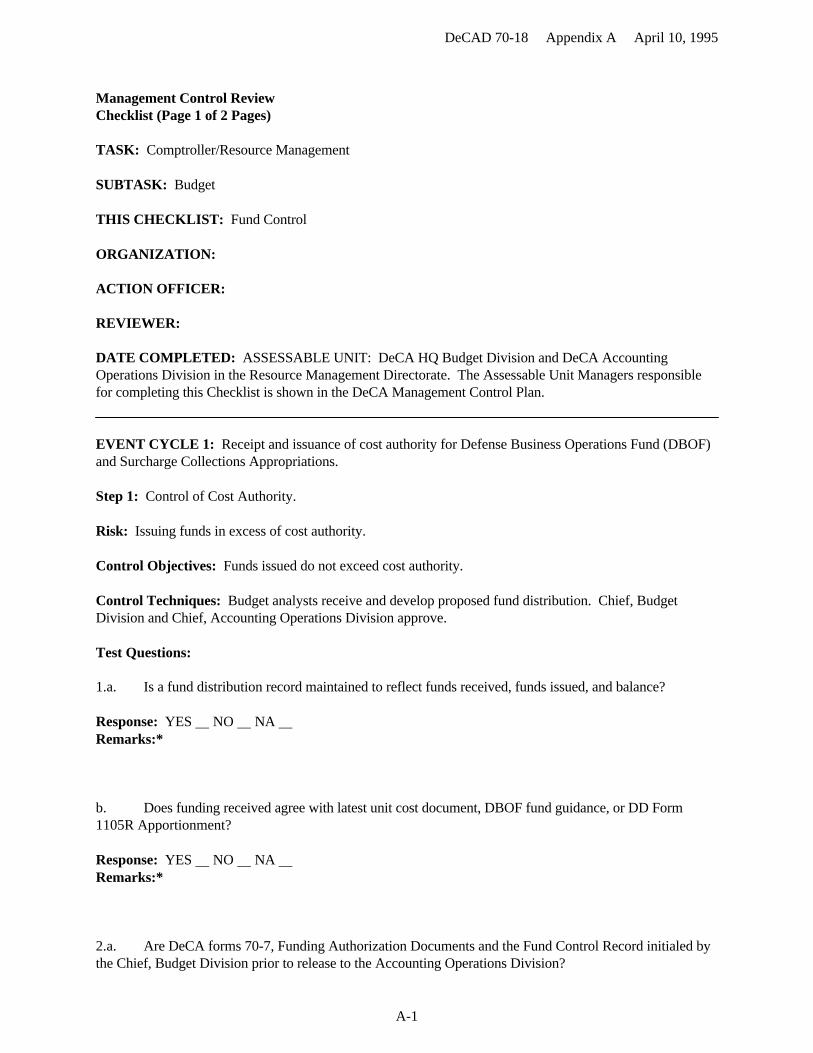

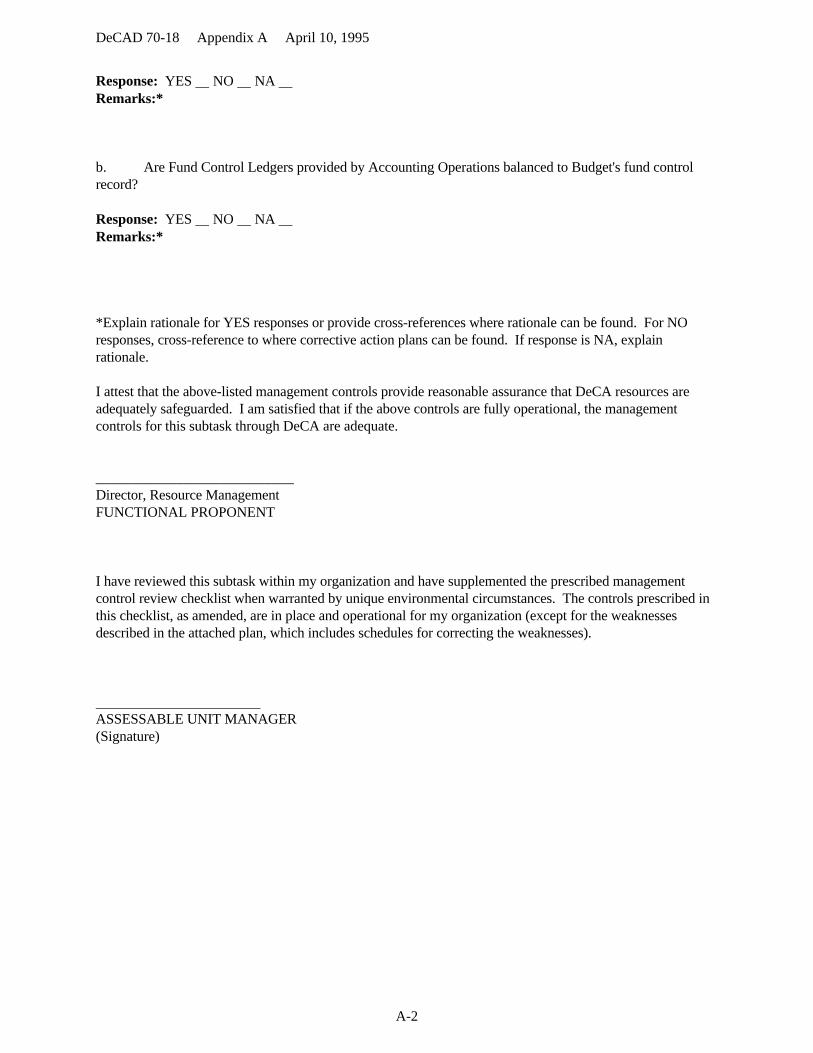

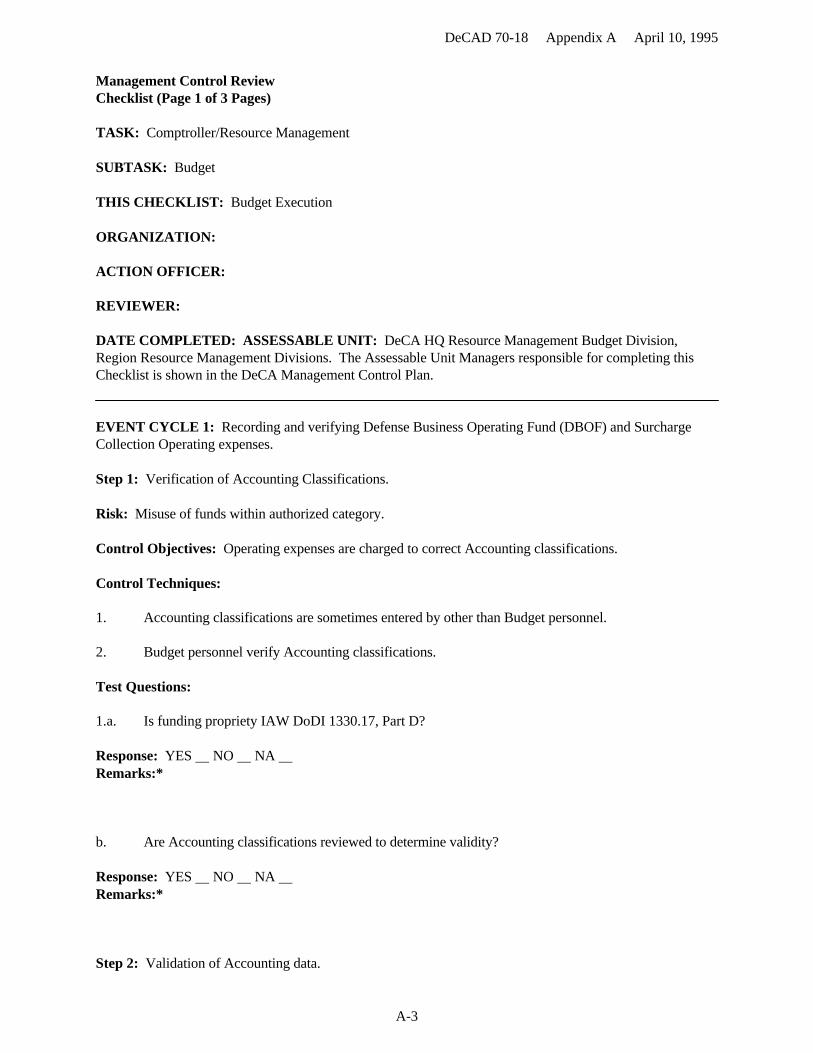

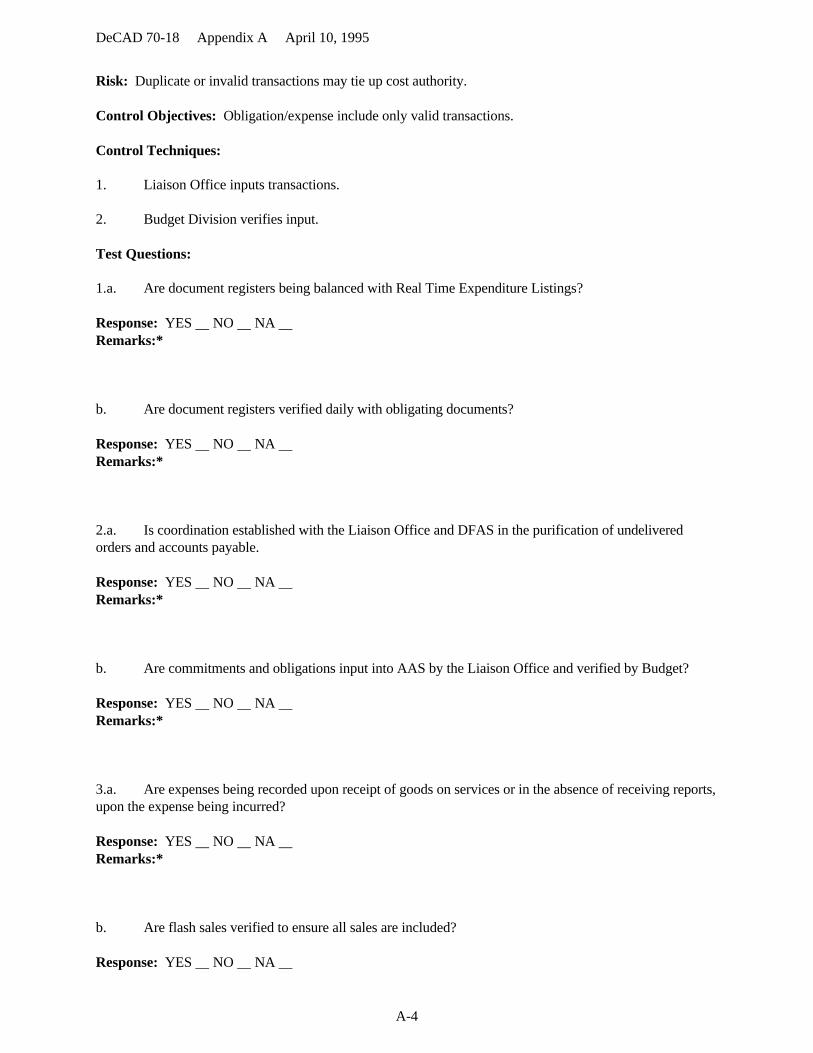

Appendixes

A -Management Control Review Checklist ................................................................. A-1B - Glossary................................................................................................................... B-1

Tables

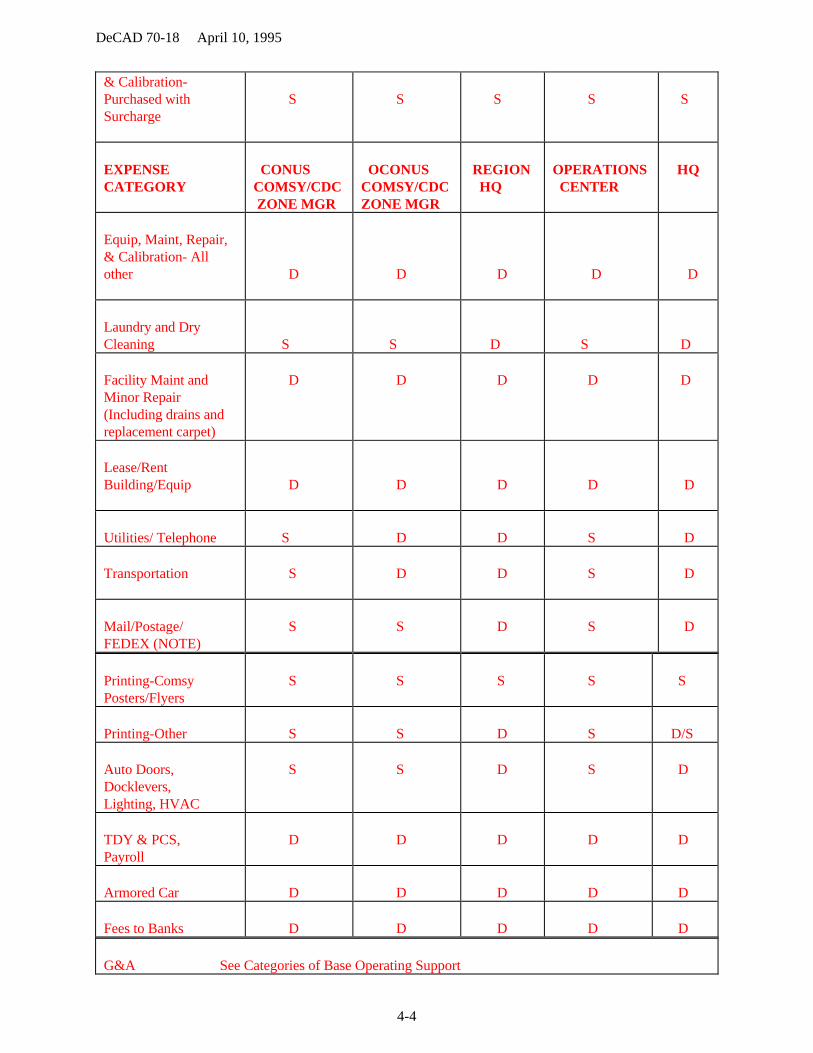

DeCA Funding Matrix by Expense............................................................................... 4-3DeCA Transportation Account Codes .......................................................................... 10-3Commissary Operating Program (COP)....................................................................... 14-1Commissary Operating Program Interpretive Key (CDCs).......................................... 14-2

DeCAD 70-18 April 10, 1995

1-1

Chapter 1

FINANCIAL MANAGEMENT IN DeCA

1-1. General Information. Financial management is the process of determining requirements, obtainingresources and judiciously applying those resources to accomplish planned goals and objectives. Within theDefense Commissary Agency (DeCA), financial management is the effective and efficient use of resources tomeet both the direct mission and support responsibilities of the commissary system. Responsibility for thisprocess is charged to commanders, directors, and managers at the Headquarters, Regions, and ServiceCenters.

1-2. Basis for Financial Management. Financial management is an integral part of resourcemanagement systems in the Department of Defense (DoD) (DoDD 7000.1), and includes the different fundsrequired to defend this nation. DeCA's mission is to:

a. Provide a non-pay benefit through a worldwide commissary system for the resale ofgroceries and household supplies to authorized patrons.

b. Operate designated worldwide troop subsistence supply functions and field exchanges inboth peacetime and war.

1-3. Role of Directors and Managers. Each director and manager, at every level of the organization, isresponsible for the effective, efficient, and economical use of all resources made available to his or herorganization. The extent to which each director and manager directly influences the budgeting, allocation,composition, and distribution of these resources depends on the degree of centralization of authority. Thedegree of centralization is the prerogative of each echelon of command and is determined by mission needs,resources involved, and managerial environment. Regardless of the level of centralization, operating levelmanagers are directly involved and responsible for managing resources used. It is DeCA's intent todecentralize financial management as much as possible.

a. There are positive means for a manager to directly influence the effectiveness, efficiency,and economy with which all resources are used to perform assigned missions and operations. The individualmanager assists in budget formulation and resource allocation by recommending the best mix of availableresources to ensure their most efficient use. Each manager should take an active part in the formulation andexecution of operating budgets. Participatory management includes the use of both a financial managementexecuting and working committee to advise and assist the commander in the decision-making process.

b. The Resource Manager assists by assuring fiduciary accounting and control of obligationsand providing expense data through the accounting system. Both obligation and expense data are importantbecause each involves distinct but related aspects of financial management. Managers must have obligationdata to monitor availability of funds. Expense data is important because it is the basis for measuringperformance of the organization. Relating expenses to production for a given period tells a manager how wellthe manager has done compared to a standard or to past activity. For the Defense Business Operations Fund(DBOF) Commissary Operating Fund obligations and expenses should generally be close to the same, at theend of the fiscal year. The Resource Manager also provides training in resource management and in the useof expense data in financial management.

c. Managers either control or significantly influence expenditures for civilian labor (includingovertime), utilities, transportation, communications, contractual services, supplies, and equipment. Significant management flexibility exists in these areas. Managers also have direct control over TDY funds

DeCAD 70-18 April 10, 1995

1-2

by deciding the necessity and frequency of mission and administrative TDY, mode of travel, and number oftravelers. The same controls can be applied to command directed TDY.

d. An integral part of the resource management process is performance evaluation andproductivity measurement. Individual managers and commanders must have tools, techniques, and analyticalsupport to interpret available data and evaluate performance. The Resource Manager assists in this phase ofresource management.

1-4. The Primary Role of Budget.

a. The primary role of Budget in DeCA is to develop budget estimate guides and directpreparation of budget justification, present and defend DeCA's budget and financial policies to OSD/OMB,and aid in the orderly administration of all appropriated funds available to DeCA. In this role, the budgetofficer functions as the primary technical advisor to the director in the administration of all funds provided byDepartment of Defense (Comptroller) (DoD(C)).

b. The budget process relies heavily on self-control, self-direction, and self-discipline byencouraging the acceptance of budget responsibility at the organizational level where funds are spent. Budgetofficers are responsible along with staff operating personnel, for preparation and execution of the operatingbudget and financial plan. They have stewardship responsibilities for the funding authorities available toregions, and help organizational managers achieve and justify their goals from a financial managementstandpoint. Particular attention and effort must be directed toward managing within the Future Year DefenseProgram (FYDP) structure with detailed identification by program element (PE).

c. Formulation of budget requirements is the responsibility of Budget in conjunction withorganizational managers at each successive level of command, culminating with the submission of the budgetto the Secretary of Defense (SECDEF).

d. All budget submissions and financial plans must be given critical review and approval byoperating activities at each successive level of command in the process of submission to HQ DeCA. Theestimates are then reviewed by DeCA/Resource Management Budget (RMB) and designated DeCA FinancialAdvisory Committee Members to ensure adherence to programs and instructions and achievement of theproper operational balance.

e. In each DeCA organization, the Budget staff will use their experience, functional area data,and financial information to help commanders and organizational managers effectively accomplish theirmissions at the most economical cost.

1-5. Responsibilities of the Budget Officer at HQ DeCA. The budget officer participates actively inthe preparation of operating budgets and financial plans and revisions; guides and counsels operatingpersonnel about plans, assumptions, and technical data; and during the execution phase, explores ways andmeans of accomplishing objectives within the limits of the budgetary authority.

a. The budget officer should view the budget process as an integral part of overall financialmanagement, where programs and requirements compete for limited financial resources.

b. Accounting systems neither manage nor solve the problem of how to match available fundsagainst programmed requirements. Accounting systems and reports provide little management benefit unlessthey are reviewed, analyzed, and put to appropriate use. Proper matching of limited funds with essentialrequirements can only be accomplished by an informed and prudent management. The following pitfallsmust be avoided:

(1) One flawed approach is to determine the initial statement of requirements and then

DeCAD 70-18 April 10, 1995

1-3

encourage the consumption of resources to validate this premise. While this may achieve a temporary andsuperficial form of perceived accuracy and credibility, it is accomplished at the expense of effectivemanagement. Neither the operating budget nor financial plan is cast in concrete and is constantly subject tochange and reprogramming to accommodate revised missions and requirements.

(2) Another faulty approach is to avoid any possibility of withdrawal of financialauthority without regard to the consequences. This self-interest is an attitude of proprietorship at the expenseof good overall management and negates the concept and intent of the DeCA financial management system.

(3) No amount of statistics can perform management. Management can only beperformed by people with a good management attitude. The budget officer can do much toward instilling theproper attitude in subordinates and among operating managers. Do not allow a negative attitude to prevail. When skillful control is exercised with a positive attitude of selflessness and dedication, we are approachingmanagement with the proper perspective.

1-6. Responsibilities of the Budget Officer at Region:

a. Develop, with appropriate staff, budgets and financial plans for the various appropriationsaccording to instructions from higher authority.

b. Receive budget authorities.

c. Determine, with the participation of the staff, distribution of budget authorizations.

d. Monitor funding which has been transferred to subordinate echelons for reporting.

e. Provide guidance and assistance to subordinate organizations, including program andfunding guidance.

f. Plan and perform continuous analysis and evaluation of programs of subordinateorganizations and bases to determine:

(1) Actual accomplishments as compared to planned programs.

(2) Availability of resources to achieve the remainder of approved objectives.

(3) Areas in which financial plan reprogramming may be necessary to accomplishplanned programs.

(4) Funding impact of proposed mission program changes and reprogramming actions.

g. Advise the staff on results of analyses and make appropriate recommendations.

h. Adjust the financial plan or operating budget according to revised objectives, and whennecessary prepare and submit narrative justification for increased or decreased requirements.

i. Adjust distribution of the amounts within the approved financial plan to meet currentrequirements.

j. Conduct special studies pertaining to forecasts, projections, or estimates of requirements.

k. Advise the staff on the propriety of proposed use of financial resources.

DeCAD 70-18 April 10, 1995

1-4

l. Advise, assist, and provide training to base-level organizations.

m. Develop specific policies and procedures for use at region and store level in administrationof operating budgets and financial plans.

n. Develop emergency operating plans and special program reporting instructions andrequirements.

o. Supplement DeCA directives to accommodate region uniques.

p. Monitor preparation of store-level financial management directives.

q. Review and coordinate concurrent use and support agreements.

r. Review and ensure that corrective action is taken on reports of audit and Inspector General(IG) inspection reports.

1-7. Headquarters Supervision of Subordinate Budget Offices. An important function ofDeCA/RMB is to exercise technical supervision and provide all required assistance to the budget offices ofits subordinate echelons. This supervision includes review of estimates and status reports. DeCA/RMBshould also exercise constructive supervision over subordinate budget offices to ensure compliance withbudget policies, procedures, objectives, instructions, and all applicable directives. Representatives ofDeCA/RMB should schedule periodic visits to subordinate budget offices to advise, assist, and review theirprocedures. Headquarters representatives should also be available to visit subordinate offices on request orwhenever review of reports or other information indicates the need for in-person assistance. The primarypurpose of these visits is to provide technical supervision and assistance rather than audit or inspect. However, attention should be given to the propriety of obligations and expenses as recorded in the variousreports. Reports of inspections and visits made by other staff offices may indicate the need for closesupervision.

1-8. Participatory Financial Management. In financial management, the corporate organizationalapproach has proven to be the most effective in achieving a balanced application of resources. Traditionally,funds furnished to an organization or activity do not satisfy total requirements. As a result, a reduction in thescope of certain programs and the deferment or elimination of other programs become necessary toaccomplish the overall mission. Decisions to reduce, defer, or eliminate programs or establish priorities aremost effective when accomplished through the combined efforts of the commander and supporting staff. Unilateral management of programs, in which other programs competing for the same limited resources areignored, often results in poor decisions when measured against the total mission. To provide the basis forcollective resource management action, DeCA must establish and maintain a corporate financial managementstructure. The formal structure consists of two financial management committees: a Financial ExecutiveBoard and a Financial Advisory Committee.

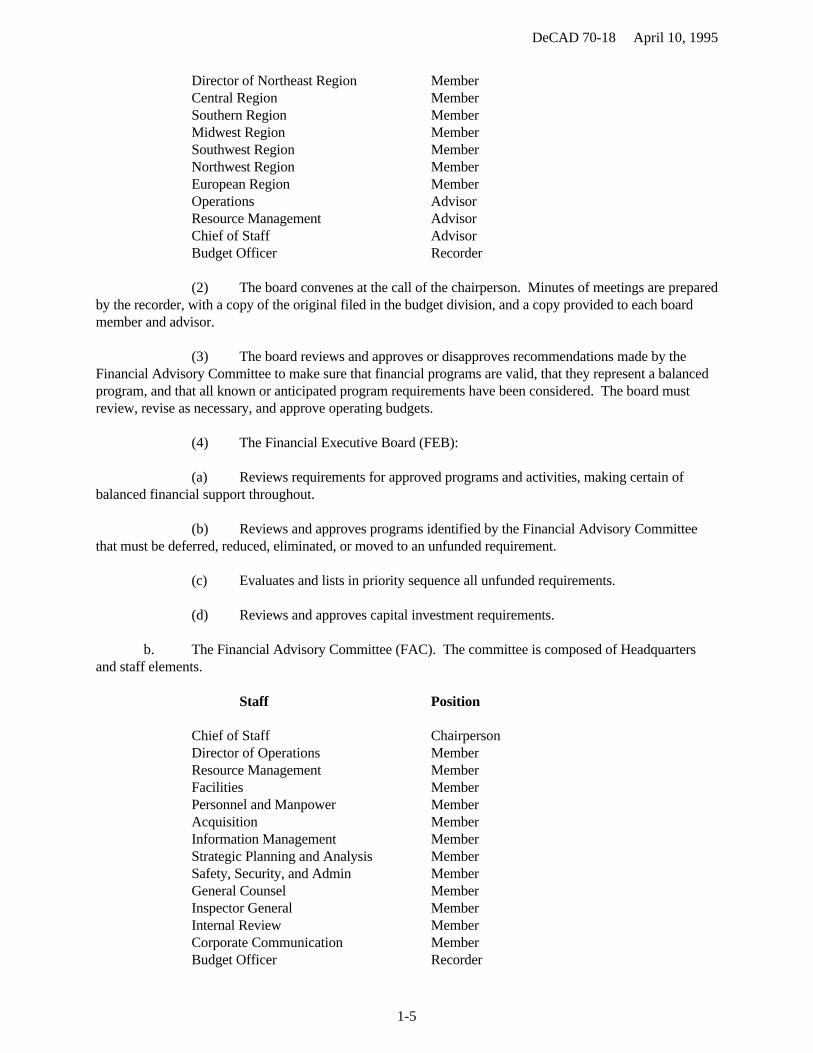

a. The Financial Executive Board (FEB). The board determines program priorities for theAgency and makes sure that resources are effectively allocated.

(1) The board is composed of top-level managers.

Staff Position

Chief Executive Officer Chairperson

DeCAD 70-18 April 10, 1995

1-5

Director of Northeast Region MemberCentral Region MemberSouthern Region MemberMidwest Region MemberSouthwest Region MemberNorthwest Region MemberEuropean Region MemberOperations AdvisorResource Management AdvisorChief of Staff AdvisorBudget Officer Recorder

(2) The board convenes at the call of the chairperson. Minutes of meetings are preparedby the recorder, with a copy of the original filed in the budget division, and a copy provided to each boardmember and advisor.

(3) The board reviews and approves or disapproves recommendations made by theFinancial Advisory Committee to make sure that financial programs are valid, that they represent a balancedprogram, and that all known or anticipated program requirements have been considered. The board mustreview, revise as necessary, and approve operating budgets.

(4) The Financial Executive Board (FEB):

(a) Reviews requirements for approved programs and activities, making certain ofbalanced financial support throughout.

(b) Reviews and approves programs identified by the Financial Advisory Committeethat must be deferred, reduced, eliminated, or moved to an unfunded requirement.

(c) Evaluates and lists in priority sequence all unfunded requirements.

(d) Reviews and approves capital investment requirements.

b. The Financial Advisory Committee (FAC). The committee is composed of Headquartersand staff elements.

Staff Position

Chief of Staff ChairpersonDirector of Operations MemberResource Management MemberFacilities MemberPersonnel and Manpower MemberAcquisition MemberInformation Management MemberStrategic Planning and Analysis MemberSafety, Security, and Admin MemberGeneral Counsel MemberInspector General MemberInternal Review MemberCorporate Communication MemberBudget Officer Recorder

DeCAD 70-18 April 10, 1995

1-6

(1) Committee meetings are convened as necessary to support the deliberation anddecision process of the Financial Executive Board. Minutes of the meetings are prepared by the Recorder,filed in the budget office, and a copy provided to each committee member and each Financial ExecutiveBoard member.

(2) The Committee develops requirements for inclusion in the operating budget, andrevisions thereto. The preparation of operating budgets is a vital part of the overall financial plans, and thecommittee makes recommendations to the Financial Executive Board for final approval. The committeeensures:

(a) Operating budget estimates represent the total amounts required to accomplishassigned missions and approved programs for the regions and headquarters.

(b) Organizations list in order of priority financial requirements to accomplish missionobjectives and, at the same time, provide for a balanced program of mission and support requirements.

(c) Operating budgets achieve a high degree of credibility through an in-depth andimpartial analysis.

(d) Committee members are agents of the Director, as well as representatives of theirparent activity, during the review.

(3) The committee identifies unfunded requirements, establishes a recommendedpriority, and presents them to the Financial Executive Board for review and approval or disapproval.

(4) The committee recommends adjustment or redistribution of financial targetsbetween activities when imbalances in resource distribution are noted. This action requires FinancialExecutive Board approval.

DeCAD 70-18 April 10, 1995

2-1

Chapter 2

BIENNIAL PLANNING, PROGRAMMING AND BUDGETING SYSTEM

2-1. Overview. The Biennial Planning, Programming and Budgeting System (BPPBS) provides MilitaryDepartments and Defense Agencies a method to achieve objectives established by the President and Secretaryof Defense (SECDEF). The process begins with translating guidance into operational plans designed tosafeguard our national security interests. Streamlined planning documents and mission area analyses helpprioritize objectives and assess strategies while providing the all important link between planning andprogramming. Programming includes developing a proposed program by Military Departments and DefenseAgencies and a formal program review and approval by the SECDEF. Initial program costing is establishedduring the programming phase. In the budgeting process, costs are updated and a proposed budget issubmitted to the SECDEF for review and approval. The result becomes part of the President's Budget (PB).

2-2. Defense Review Board. This board is the SECDEF's corporate review body and is responsible formanaging the BPPBS. It is chaired by the Deputy SECDEF and is primarily comprised of the Under andAssistant Secretaries of Defense, Military Secretaries, Chairman of Joint Chiefs of Staffs, and Military Chiefsof Staff. Another key member is the Associate Director, Office of Management and Budget (OMB), NationalSecurity and International Affairs. OMB participation is very useful because this precludes the need for anadditional OMB review following the completion of the DoD budget. This unique procedure allows theSECDEF to submit the DoD budget later than any other department in the execution branch.

2-3. Continuous Process. The BPPBS is an ever-evolving process without a definitive start or end. Furthermore, the segments of a single BPPBS cycle overlap and do not evolve in isolation. This is significantbecause unexpected events occurring in one cycle can impact other cycles. For example, during presidentialelection years, overlap is complicated by supplemental budget requests or major programmatic decisions. Each cycle provides three "snapshots" of the DoD program: (1) Program Objective Memorandum (POM),(2) Budget Estimate Submission (BES), and (3) President's Budget (PB).

2-4. Defense Guidance. The Defense Guidance provides Department of Defense (Comptroller)(DoD(C)) direction to the Military Departments and Defense Agencies for developing the POM. Nationalsecurity policy provides the basis for the Defense Guidance. The Defense Guidance provides SECDEFpolicy, strategy, force planning, resource planning, and fiscal guidance to all DoD organizations. Based onDefense Guidance, DoD(C) sends out fiscal guidance which determines the Total Obligation Authority(TOA) needed to execute the DoD program for the next six years. This amount reflects Presidential andOMB decisions concerning real growth and inflation rates used to develop Military Department and DefenseAgency programs. In other words, Fiscal Guidance provides the overall constraint, or dollar ceiling forconstructing programs.

2-5. Future Years Defense Program (FYDP). The FYDP is the official document that summarizesSECDEF approved programs and captures the three updates to the DoD program. It is a detailed compilationof the total resources (forces, manpower, and dollars for each appropriation) programmed for DoD, arrangedby major force program (MFP) and appropriation. Within each MFP, requirements are arranged by programelement (PE). This structure is used as a basis for internal DoD program review. The appropriation structureis used by Congress in its review of the DoD budget request and differs from the MFP approach. Bysatisfying both requirements, the FYDP serves as an interface between the two methods of portrayingprogram and budget data. The FYDP projects all data except forces for six years; forces extend an additionalthree years. For the FYDP to be used effectively as a management tool at higher echelons of command, itmust be carefully costed. Such costing is accomplished by linking plans and programs to budget estimatesreflecting desired program levels, and to budget authorities representing approved program levels. The

DeCAD 70-18 April 10, 1995

2-2

budgeting system defines resources to be consumed and the accounting system keeps track of what resourceshave been consumed. Therefore, an important link in the DoD financial management system is theaccounting system for research and development, investments, and operations.

2-6. FYDP Elements. The elements of the operating budget structure recorded in the accounting systemfor operations are:

(1) Major Force Program (MFP). The MFP is the major budget program in theoperating budget structure. The DoD MFP structure is:

MFP Description

1 Strategic Forces2 General Purpose Forces3 Intelligence and Communications4 Airlift/Sealift5 Guard and Reserve Forces6 Research and Development7 Central Supply and Maintenance8a Training and Other General Personnel Activities8b Medical9 Administration and Associated Activities10 Support of Other Nations11 Special Operational Forces

(2) Program Element (PE). PEs describe all forces, activities, and support required toaccomplish the DoD mission with associated costs. There are more than 1600 PEs in the DoD. DeCA hastwo PEs, 0702840DBC -- Commissary Resale Stocks and 0702841DBC -- Commissary Operations.

2-7. FYDP Updates. The FYDP is updated three times during each BPPBS cycle; in May (even years)to reflect program proposals as a first step toward the next President's Budget; in September (even years) toreflect Military Departments and Defense Agencies budget estimates resulting from SECDEF decisions onprogram proposals from May; and in January (odd years) to reflect the President's Budget. The final updatebecomes the departure point for developing the program proposal for the next budget year.

2-8. Program Objective Memorandum (POM). Each Military Department and Defense Agencybiennially prepares and submits its POM to the SECDEF. The POM expresses the DeCA FYDPrecommendations to DoD(C) to meet the objectives of the Defense Guidance.

a. The POM is submitted to DoD(C) in April of the even years. DoD(C) reviews each POMtransmittal to determine compliance with Defense Guidance and to develop more cost-effective alternatives toproposed programs.

b. DoD(C) can propose program alternatives to the POM. These alternatives are called issues,which include a discussion section followed by several alternatives. Alternative 1 is always the POMposition. DoD(C) scrubs all issues and develops issue books to submit to the Defense Review Board for theirreview and evaluation.

c. Final decisions on issues are recorded on a Program Decision Memorandum (PDM). ThePDM modifies and approves the POM which becomes the basis for the Budget Estimate Submission.

2-9. Budget Process. The budget process is the final phase in the BPPBS cycle. The budget expresses

DeCAD 70-18 April 10, 1995

2-3

financial requirements necessary to support approved DoD programs developed during preceding phases ofplanning and programming. The approved programs are those which evolve from incorporating all decisiondocuments received through a predetermined date announced by the BPPBS review schedule memorandum. It is through the budget that planning and programming are translated into annual funding requirements. Each budget estimate, therefore, sets forth precisely what DoD expects to accomplish with the resourcesrequested for the year. The budget process is divided into three phases.

a. Formulation. Formulation is planning and developing the budget for a fiscal year or yearsbeginning 1 October. This phase begins when DeCA/RM issues a call for budget estimates. This call isbased on guidance received from DoD(C). Formulation continues with review, modification, and approval ofthe estimates at all echelons of the Military Departments and Defense Agencies, with review, amendment, andfinal approval by the SECDEF, OMB, and the President.

b. Justification. Justification is presenting and justifying the budget to the Congress.

c. Execution. Execution is obligating and expending Congressionally appropriated andrevolving funds for the current and prior fiscal year. Budgets are formulated, justified, and executed on thebasis of appropriations. Appropriations are subdivided into budget activities, sub-heads, programs, project,and so forth. The format and structure of the various appropriations are controlled by Congress and representthe manner in which Congress desired Military Departments and Defense Agencies to express requirementsfor funds.

2-10. Budget Submission. Normally, the Budget Estimate Submission (BES) to the SECDEF is made on15 September, 15 months prior to the first applicable fiscal year. DeCA/RM issues the call for thesubmission of budget estimates from DeCA Regions in early May of each year prior to the budget submissionto SECDEF on 15 September. DeCA/RM instructions prescribes the content and format for budget estimatesand promulgates the required budget relationship to the POM, the decision documents, and to the SECDEFFiscal Guidance or modification thereof. After review and final decision, the DeCA Director submitsproposed budget to SECDEF.

2-11. SECDEF and Office of Management and Budget (OMB) Review. Budget analysts from DoD(C)and OMB normally make a joint review of the budgets submitted to verify pricing adjustments and to identifylesser cost alternatives which can either be pricing or program adjustments. OMB analysts have the authorityto submit separate decisions on the reviews. After this review, witnesses from the Military Departments andDefense Agencies appear to answer any questions and to provide further justification for their estimates. DoD(C) and OMB document their budget decisions in Program Budget Decisions (PBD). PBDs maypropose one or more alternatives to budget estimates and are sent out to the Military Departments andDefense Agencies for an opportunity to develop position papers on each PBD with which there is adisagreement. Decisions contained in the PBDs automatically become final if not appealed. These positionpapers are evaluated by senior officials who determine which disagreements should be major budget issues. Normally, if someone is trying to restore a budget cut, they must provide an offset in the form of existingbudget authority. Final decisions are made by OSD and Military Secretaries and are communicated to theMilitary Departments and Defense Agencies which prepare the budget schedules for inclusion in thePresident's budget. Military Departments and Defense Agencies reflect the results of the PBD process in theJanuary update of the FYDP.

2-12. Congressional Review. The President presents the Defense Budget to Congress as a part of thenational budget in January of each year. Congressional staffs review the overall budget and backup papersbriefly with congressional review commencing early in February.

2-13. Hearings. Hearings begin with "posture" statements from SECDEF, Chairman JCS, ServiceSecretaries, and Service Chiefs made to the congressional committees. Following delivery of posture

DeCAD 70-18 April 10, 1995

2-4

statements, detailed hearings involving Service witnesses are initiated.

a. Congressional review of the Defense portion of the President's Budget is undertaken fromthe separate standpoints of authorization of programs and appropriation of funds. Annual authorizinglegislation for appropriation funds is required for major procurement items (aircraft, missiles, naval vessels,tracked combat vehicles, torpedoes, and other weapons); research, development, test, and evaluation;authorized active duty military personnel end strengths; setting authorized personnel strength of the SelectedReserve components; and for the authorization of the construction program. Authorizing legislation isprepared by the Armed Services Committees of the House and Senate. All appropriation legislation,including that requiring prior authorization, is prepared by the Defense Subcommittees of the House andSenate Appropriations Committees. The military construction appropriation is reviewed and acted upon by aseparate Military Construction Subcommittee and is enacted as a separate appropriation.

b. The committees conduct formal hearings at which the SECDEF and Secretaries of the Army,Navy, and Air Force testify on the overall DoD budget. In subsequent hearings, staff representatives of theMilitary Departments and Defense Agencies are then questioned by congressional subcommittees and staffmembers on details of the programs and estimates of requirements as supported in the budget document.

2-14. Authorization/Appropriation. When the House Armed Services Committee completes itshearings, it publishes a report containing committee recommendations and brings before the House ofRepresentatives an authorization bill based on those recommendations. The House-passed bill is consideredby the Senate Armed Services Committee, hearings are held, the Senate Committee reports to the Senate, andthe full Senate passes a bill.

a. If there are differences between the House and Senate versions of the bill, they are resolvedby a Joint conference of a small number of members from each of the two committees. The conference reportis brought before each of the two legislative bodies, and the final bill is forwarded to the President forsignature to complete the enactment process.

b. The same process is followed in enacting the "appropriations" legislation except that it goesthrough the respective Appropriations Committees rather than the Armed Services Committees. Whensigned by the President, the legislation becomes an effective Public Law called "Department of DefenseAppropriations Act." Ideally, this occurs before October.

c. In instances where appropriation laws are delayed in enactment past 1 October, the Congresspasses a joint resolution to provide authority to continue operations pending a passage of the appropriation. This so-called "continuing resolution" authorizes rates of expenditure not to exceed the lesser rate of: (1) that achieved in the preceding fiscal year, or (2) that reflected in any prior action of either body of Congress. Obligations must also be in consonance with approved programs and the rate of obligation established by theSECDEF as well as any deferrals made in programs.

2-15. Congressional Budget and Impoundment Act of 1974. The Congressional Budget andImpoundment Act of 1974 set forth a new foundation for budget decisions in Congress by reorganizing thebudget cycle and created three new institutions: The Budget Committees of the House and Senate and theCongressional Budget Office. The Congressional Budget Office is a non-partisan agency designed to provideCongress with information and analyses needed to make informed decisions about budget policy and nationalpriorities. Specific areas of responsibility for the Congressional Budget Office fall into three categories: (1)monitoring the economy and estimating the impact of government actions upon it, (2) improving the flow andquality of budget information, and (3) analyzing the costs and effects of alternative budget choices.

2-16. Budget Execution. Once appropriation bills are passed into law they bind the Military Departmentsand Defense Agencies to given labels of obligation and within broad categories to services or items that may

DeCAD 70-18 April 10, 1995

2-5

be purchased. There are other constraints subsequently exercised at various levels of government.

a. The apportionment process, exercised through OMB, reflects presidential control andrestricts the rate or purpose of obligations as provided for by law. It is designed to prevent overobligationsby encouraging the most economical and efficient use of obligational authority. Funds are made available ona quarterly, annual, or other periodic basis. Apportionments are made on the basis of hearings conducted byDoD(C) and OMB wherein apportionment requests are considered.

b. The apportionment process also serves the important function of updating the budget whichwas submitted to DoD(C) more than a year previously. In the absence of an enacted appropriation, theSECDEF establishes authorized obligation rates for each appropriation. After the appropriation is enactedand the apportionment is released by OMB, the apportionment becomes SECDEF's authorized obligationrate.

c. Another financial control technique used by DoD(C) is to defer approved programs untillater in the budget execution period. This can be used to restrict the flow of funds into the economy, as wellas to control programs by withholding funding authorization until complete justification provided.

d. A further OSD technique is the imposition of recoupment objectives on the MilitaryDepartments. A recoupment objective represents the amount of money that DoD(C) estimates can be savedin construction, procurement, and RDT&E accounts in current or prior year programs. Thus, the recoupmentobjective is the amount by which the funding of a budget year program is reduced in anticipation of suchrecovery.

2-17. Flexibility in Budget Operations. To meet changing needs, the SECDEF has the authority, with theapproval of OMB, to transfer funds from one appropriation to another if such transfers do not exceedstatutory limits. There are four other methods besides the transfer authority available to DoD(C) whichprovide flexibility within appropriations: (1) Supplement Budget, (2) Contract Authorization (Section 3772Revised Statutes), (3) Deficiency Budgets, and (4) Reprogramming (DoD INST 7250.10).

a. Supplemental and deficiency budgets are in essence additions to the annual budget proposedby SECDEF requesting funds for major, unforeseen emergencies arising during a current year. The SECDEFhas a separate emergency fund for R&D programs. The amount authorized by Congress for this purposevaries from year to year.

b. The Military Departments are authorized by Section 3732 Revised Statutes to incur certainobligations for clothing, transportation, supplies, and so forth, pending passage of supplemental or deficiencybudget. This authority may be invoked under certain emergency circumstances requiring immediate actionthat cannot be delayed due to nonavailability of sufficient funds.

c. Military Departments and Defense Agencies may recommend reprogramming to savefinancial shortfalls or to adjust programs. This involves the reapplication of funds between programs withina particular appropriation. Dollar limits, referred to as thresholds, dictate who may approve the reapplicationof funds. Changes exceeding certain thresholds or meeting other substantive criteria require notification orprior approval of Congressional committees.

DeCAD 70-18 April 10, 1995

3-1

Chapter 3

FUND CONTROL

3-1. General Information.

a. Fund control is the authority exercised over the receipt, distribution, use, and management ofBudget or Cost Authority to ensure:

(1) Funds are used only for authorized purposes.

(2) Funds are used economically and efficiently.

(3) Distributions, commitments, obligations and expenditures do not exceed amountsauthorized and available.

(4) Distribution, obligation, or disbursement of funds is not reserved or otherwisewithheld without Congressional knowledge and approval. This does not preclude deferral or withholdingaction to provide reserves for contingencies or reprogramming within delegated authority.

b. Fund control includes all systems and operational procedures used in this process.

c. All fund control systems and administrative procedures will:

(1) Provide for segregation of duties in the fund distribution, obligation, anddisbursement process.

(2) Require clear delegation of all funding authority in writing to lower echelonofficials.

(3) Perpetuate administrative and statutory limitations established by higher authority.

(4) Distribute, monitor, and control funds at the highest level possible.

(5) Establish appropriate reserves or other withholding of funds for contingencies.

(6) Ensure that fund withdrawals are coordinated with recipient before being made.

(7) Control reimbursement authority on funding documents.

(8) Provide a mechanism to update amounts available. This includes preventing anddetecting the overdistribution, over-commitment, overobligation, and over-disbursement of funds atappropriate levels.

d. All personnel directly involved in budget and accounting will be familiar with the provisionsof the Anti-Deficiency Act (31 U.S.C. 1517) and how it relates to informal and formal subdivisions of funds.

3-2. Apportionment Process.a. Certain actions are necessary before funds appropriated to the Military Departments and

Defense Agencies can be legally obligated and expended. An appropriation bill becomes law (enacted) on

DeCAD 70-18 April 10, 1995

3-2

the date of the President's approval, or on the date Congress passes it over the President's veto, unless itexpressly provides a different effective date. After an appropriation is enacted, an appropriation warrantmust be issued by the Treasury Department and the appropriation must be apportioned by the Office ofManagement and Budget (OMB). The criteria for apportionment is contained in Title 31 U.S.C., Section1512a.

b. A request for apportionment is submitted in accordance with DoD 7110-1-M, BudgetGuidance Manual, chapter 412, Apportionment and Reapportionment Schedule. An apportionment requestmay include anticipated reimbursements in addition to the direct obligational authority provided in anappropriation act. In addition to new appropriation amounts, obligational authority in an appropriation actmay include unobligated balances carried forward from prior years and unfunded contract authority.

c. If the Department of Defense (DoD) appropriation act has not been enacted by the beginningof the new fiscal year, Congress usually passes a "continuing resolution" authority (CRA) that authorizesobligations and expenditures for ongoing programs at the minimum rate necessary to orderly continueactivities. As a general rule, new program starts are not authorized under continuing resolutions. TheMilitary Departments and Defense Agencies must request temporary appropriation warrants from theTreasury Department for amounts required during the period covered by the CRA. When issued by theTreasury Department, the temporary appropriation warrants constitute authority to incur obligations againstthe direct program, thus providing the basis for distributing such authority to field activities. The MilitaryDepartments and Defense Agencies must submit an initial apportionment request to OSD within 5 calendardays after completion of congressional action. Funding documents are issued after Treasury issues temporaryappropriation warrants and OMB approves request.

d. If the DoD appropriation act is not enacted and a CRA is not passed, there is an absence offunding authorization referred to as appropriation hiatus.

3-3. Appropriation Warrants.

a. An appropriation warrant, Treasury Form TFS 6200, is the document used by the TreasuryDepartment to formally document the funds appropriated by Congress against which obligations may beincurred and payments made. The form is signed by a representative of the Treasury.

b. Temporary appropriation warrants are issued during periods when CRAs are in effect, andare based on requests from the agencies as prescribed by OMB, Treasury and DoD directives. Each DoDcomponent must submit a request to the Treasury Department for temporary appropriation warrants as soonas possible after the passage of the CRA. These requests must be according to OMB Bulletin 73-1 and mustinclude a certification by the head of the agency, or a designated representative, that the amounts requestedare consistent with the provisions of the continuing resolution. Temporary appropriation warrants are signedby a representative of the Treasury and countersigned by a representative of the General Accounting Officeon behalf of the Comptroller General. The temporary warrants are supplemented by the regular appropriationwarrants when the actual appropriate bill is enacted.

3-4. Apportionment of Funds.

a. The apportionment process operates as an Executive Branch control over using, planning,and managing obligation authority made available by Congress. In addition, Title 31 U.S.C., Section 1512provides that: "...an appropriation of funds available for obligation for a definite period shall be apportionedto prevent obligation or expenditure at a rate that would indicate a necessity for a deficiency or supplementalappropriation for the period. An appropriation for an indefinite period and authority to make obligations bycontract before appropriations shall be apportioned to achieve the most effective and economical use."

DeCAD 70-18 April 10, 1995

3-3

b. Apportionments are usually made at the appropriation level. However, on determination ofOMB, apportionment may be made below the appropriation level such as by activity, function, or project. For example, apportionment is usually by individual construction project under the Military ConstructionAppropriation. The time period covered by apportionments may be calendar quarter, or may cover a fullyear. The amount apportioned is available for obligation under the terms of the appropriation on acumulative basis unless reapportioned, 31 U.S.C., Section 1512. A reapportionment supersedes all previousapportionments and covers transactions from the beginning of the fiscal year. The unobligated balances ofapportionments made in previous years for multiple-year appropriations remain available until revisedapportionments are made. Unexpired multiple-year appropriations remain available until expiration of theapplicable appropriation act.

3-5. Transfer Actions.

a. Transfers are legal transactions that move appropriated funds from one appropriationaccount with the Treasury to another account. Requirements for funding certain essential increases to higherpriority programs are met by transfer according to the DoD appropriation act and supplements thereto,Congressionally directed transfers in appropriation language, and other statutory authority. Transfers can bemade only with specific reference to legal authority.