CUSTOM PROCEDURES

16

CUSTOM PROCEDURES Goods are imported or exported in India through air,sea,land. goods can come to India through baggage with customers. procedures generally vary with the mode of import and export.

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of CUSTOM PROCEDURES

CUSTOM PROCEDURES

Goods are imported or exported in India

through air,sea,land.

goods can come to India through baggage with

customers.

procedures generally vary with the mode of

import and export.

IMPORT PROCEDURE

bill of entry.

import general manifest

passenger and crew arrival manifest

grant of entry inwards by custom officer

unloading

payment of duty

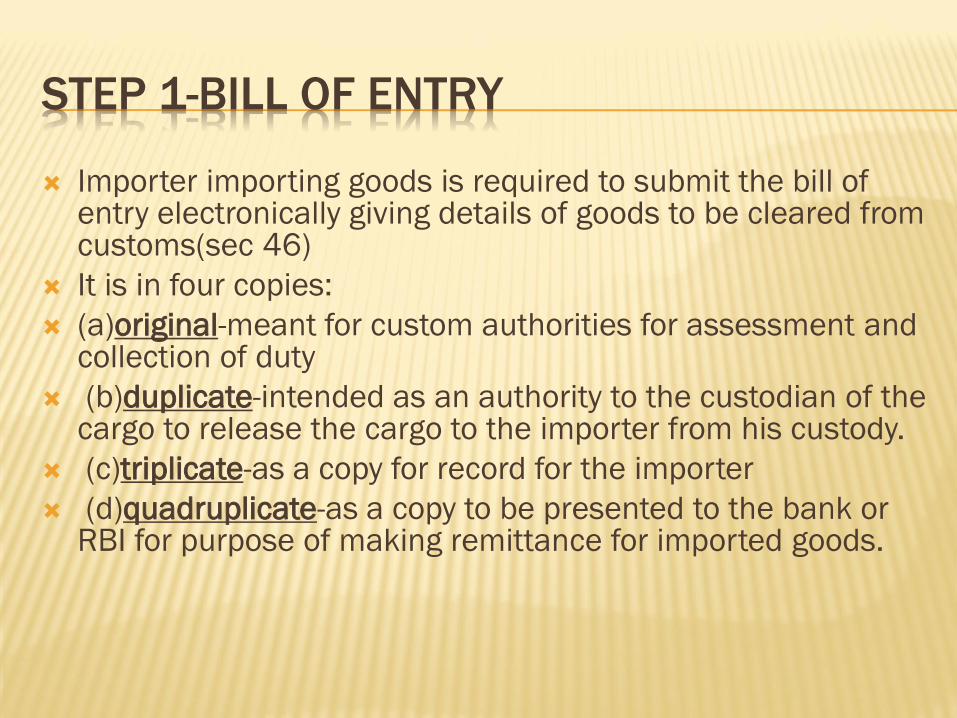

STEP 1-BILL OF ENTRY

Importer importing goods is required to submit the bill of entry electronically giving details of goods to be cleared from customs(sec 46)

It is in four copies:

(a)original-meant for custom authorities for assessment and collection of duty

(b)duplicate-intended as an authority to the custodian of the cargo to release the cargo to the importer from his custody.

(c)triplicate-as a copy for record for the importer

(d)quadruplicate-as a copy to be presented to the bank or RBI for purpose of making remittance for imported goods.

STEP 2-IMPORT GENERAL MANIFEST

Import General Manifest is filed by the carrier of goods once its arrival at a destination port customs location. Once after arrival of goods at destination port, filing of Import General Manifest is mandatory.

Import General Manifest (IGM) notifies customs department of importing country by carrier of goods about the details of goods arrived to such customs location. Once after arrival of goods the carrier files details of cargo about shipper, consignee, number of packages, kind of packages, description of goods, airway bill or bill of lading number and date, flight or vessel details etc. with customs department. In some countries, the IGM can also be filed before arrival of goods.

STEP 3-PASSENGER AND CREW ARRIVAL

MANIFEST

manifest, customs manifest or cargo document is a document listing the cargo, passengers, and crew of a ship, aircraft, or vehicle, for the use of customs and other officials. Where such a list is limited to identifying passengers, it is a passenger manifest or passenger list; conversely, a list limited to identifying cargo is a cargo manifest or cargo list. The manifest may be used by people having an interest in the transport to ensure that passengers and cargo listed as having been placed on board the transport at the beginning of its passage continue to be on board when it arrives at its destination.

STEP 4-GRANT OF ENTRY INWARD

“Entry Inward” refers to the permission granted by proper officer to the master of vessel to unload goods. Entry inwards is granted to the vessel under Section 31 of the Customs Act. Section 31 prohibits unloading of goods before grant of entry inwards. It provides that no imported goods shall be unloaded from the vessel unless an entry inward has been granted to the vessel.

Entry inward is granted only when IGM (Import General Manifest) has been filed by the master of vessel[Master of Vessel = Person-In- Charge of Vessel]. However, if proper officer is satisfied that there is sufficient cause for non-filing of vessel, then he can grant entry inward prior to filing of IGM.

Baggage, mail bags, animals and any perishable or hazardous goods can be unloaded without obtaining “entry inward”.

STEP 5-UNLOADING

Unloading of cargo can start after the custom

officer grant entry inwards.

Section 32 of customs act provides that only

the goods mentioned in the import manifest

can be unloaded. such unloading can be only

at approved places and under the supervision

of custom officer.

STEP 6- PAYMENT OF DUTY

Now custom duty is paid electronically. It should

be paid within one working day(excluding

holidays) after the bill of entry is returned to the

importer for payment of duty.

If duty is not paid within one working day, interest

is payable at 15%.

EXPORT PROCEDURE

entry of goods for exportation

export declaration

export manifest/export report

entry outward

no conveyance to leave without written order

clearance of goods for exportation

difference b/w transit and transshipment

STEP 1-ENTRY OF GOODS FOR EXPORTATION

Entry of goods for exportation.—

(1) The exporter of any goods shall make entry thereof by presenting to the proper officer in the case of goods to be exported in a vessel or aircraft, a shipping bill, and in the case of goods to be exported by land, a bill of export in the prescribed form.

(2) The exporter of any goods, while presenting a shipping bill or bill of export, shall at the foot thereof make and subscribe to a declaration as to the truth of its contents.

STEP 2- EXPORT DECLARATION

As per rule 7 of custom valuation rules

2007,the exporter has to file declaration about

full value of the goods.

STEP 3-EXPORT MANIFEST/REPORT

Export General Manifest is a legal document mandatory to be filed by carrier of goods wit customs department. This document is used by government authorities as proof of export. The customs officials certify proof of export on shipping documents to exporters on the basis of EGM. With such copies or certificates, exporters claim export benefits based on such document, along with other documents like bill of lading as proof of exports.

STEP 4- ENTRY OUTWARD

Entry outward is the permission granted by the Customs Officer to master-of-vessel to receive and load the export goods from the exporter and proceed for its foreign journey. This is granted under section 39 of the Customs Act, 1962. Unless and until ‘entry outward’ order is obtained, no export goods can be loaded in the vessel. However, baggage and mail bags can be loaded in the vessel even prior to grant of entry outward.

STEP 5- NO CONVEYANCE TO LEAVE WITHOUT

WRITTEN ORDER(SEC 42)

The person in charge of the of the conveyance

which has loaded any export goods at a

customs station shall not cause or permit the

conveyance to depart from that customs

station until a written order to that effect has

been given by proper officer's

STEP 6- CLEARANCE OF GOODS FOR

EXPORTATION(SECTION 51)

Clearance of goods for exportation.—Where the

proper officer is satisfied that any goods

entered for export are not prohibited goods and

the exporter has paid the duty, if any, assessed

thereon and any charges payable under this Act

in respect of the same, the proper officer may

make an order permitting clearance and

loading of the goods for exportation.

DIFFERENCE BETWEEN TRANSIT AND

TRANSSHIPMENT

TRANSIT TRANSHIPMENT

1.Section 53 provides 1.section 54 provides for

For transit of goods transshipment of goods.

2.In case of transit, 2.in case of transshipment

Goods Are allowed to of goods the conveyance

remain On the same changes.

conveyance.

3.No separate document 3. separate document is

Is required. To be filled.