CSR in Microfinance: A Tripple Bottom Line Approach

29

NORUWA, OSARETIN VICTOR COURSE NAME: Corporate Social Responsibility (CSR) Essay Title: CSR IN MICROFINANCE: A TRIPLE BOTTOM-LINE APPROACH ATLANTIC INTERNATIONAL UNIVERSITY December, 2014

Transcript of CSR in Microfinance: A Tripple Bottom Line Approach

NORUWA, OSARETIN VICTOR

COURSE NAME: Corporate Social

Responsibility (CSR)

Essay Title:

CSR IN MICROFINANCE: A TRIPLE BOTTOM-LINE APPROACH

ATLANTIC INTERNATIONAL UNIVERSITY

December, 2014

CSR in Microfinance: A Triple Bottom-Line Approach Page 2

TABLE OF CONTENTS

1.0. Introduction ………………………..……………………………………….3

2.0. Corporate Social Responsibility (CSR) and Microfinance……..………4

2.1. What is Corporate Social Responsibility (CSR)? ………………4

2.2. Arguments for and Against CSR ……..…………………………6

2.3. CSR in Nigerian MFBs Today …..……………………………….9

3.0. Microfinance as a Development and Poverty Reduction Tool ……….9

3.1. The Concept of Development ………………………………….10

3.2. Poverty Cycle ………………….………………………………..11

3.3. The Objective of the Nigerian Microfinance Framework ……13

4.0. CSR: The Triple Bottom Approach to Microfinance …………………15

4.1. Financial Sustainability: The Bases for Business Ventures ..15

4.2. Social Mission: A Necessary consideration for MFBs ………16

4.3. CSR: Thorough Blend ………………………………………….17

5.0. Conclusion ………………………………………………………………20

Appendix 1 ………………………………………………………………21

Bibliography …………………………………………………………….26

CSR in Microfinance: A Triple Bottom-Line Approach Page 3

1.0. INTRODUCTION:

Microfinance generally refers to the provision of small financial services to the informal

sector in a cost effective manner that is convenient for the intended users of the services.

These intended users include low income households, micro entrepreneurs/enterprises, the

under-banked and unbanked public. This definition is supported by Megan (2009) when he

wrote that “Microfinance essentially consist of a combination of financial products (micro-

credit, micro-leasing, micro-insurance, micro-savings, and money transfer) targeting

specific client groups. Recipients of these services generally represent micro-business and

economically active, but poor citizens”. This implies that microfinance tends to focus

primarily on the provision of sustainable economic support for the income generating

activities (IGAs) of those at the lower end of the national economy. Microfinance Institutions

(MFIs) seeks to facilitate better living for its staff and clients while making good returns for

its shareholder. This is commonly referred to as the “Double Bottom-Line” approach to

microfinance. Lyudvig (2013)

From the above, microfinance actually facilitates the development, growth and sustenance

of micro/small enterprises whose activities directly or indirectly impact negatively on the

environment. Bellow is an extract from a post by Anna Lyudvig, in the African AM Online

Magazine:

“In 1953 Howard R. Bowen, a distinguished American economist,

educator and administrator was perhaps the first person to talk of

CSR in Microfinance: A Triple Bottom-Line Approach Page 4

CSR in his book, Social Responsibilities of the Businessmen, defining

CSR as the “the obligations of businessmen to pursue those policies, to

make those decisions, or to follow those lines of action which are

desirable in terms of the objectives and values of our society.”

Small as their individual activities may be, microenterprises cumulatively contribute

significantly to environment pollutions and degradation. The focus of this paper is to

highlight the need to consider and minimize environmental cost in our effort to fight poverty

and enhance the living standards of our target clients; that is making the MFIs and their

clients “Socially Responsible”, thus making it a “Triple Bottom” approach: social mission,

profit motive and environmental consideration, better put – “People, Profit and Planet”-

Mallireddy Charan, 2011. This would be considered in four sub-topics.

The first part will consider the fundamental principles of Microfinance as focusing more on

the Double Bottom-line. The next would focus on the relevance of CSR in Microfinance.

The essence of this part would be the laying of emphasis on the need to take microfinance

beyond service delivery to demonstrating corporate social responsibility towards the host

community of the institution. The third part showcases the “Triple Bottom-line” approach to

CSR; while in the conclusion, I shall make effort to summarize the main idea of this paper

and attempt some recommendations for Microfinance practitioners.

2.0. Corporate Social Responsibility (CSR) and Microfinance: An assessment

2.1. What is Corporate Social Responsibility (CSR)?

A review of different literatures on this subject shows that “there is no agreed definition of

CSR”, Crowther & Aras (2008). Ramon Mullerat equally expatiated on some of the reasons

CSR in Microfinance: A Triple Bottom-Line Approach Page 5

why CSR is difficult to define in a universally acceptable manner, as follows: (1) it is a

relatively new concept, (2) it is rapidly evolving, (3) adopted CSR campaigns depend on the

size of the business organization- its services and products, (4) company owners have

different objectives, and ultimately, (5) more and more elements are implemented in the

concept of CSR (Mullerat 2010). There however seems to be a general consensus that

CSR expresses the relationship that or should exist between a corporation/organization

and the community in which it operates its business activities.

For the purpose of this paper, I shall align with some of the definitions available in different

literatures as presented below:

“…CSR is a concept whereby companies integrate social and environmental concerns in

their business operations and their interaction with their stakeholders on a voluntary

basis.”- EU Commission, quoted in Crowther & Aras (2008).

(CSR) can be defined as the "economic, legal, ethical, and discretionary expectations that

society has of organizations at a given point in time" - Carroll and Buchholtz quoted in

Tim Barnett (2012), retrieved from: http://www.referenceforbusiness.com/management/Comp-

De/Corporate-Social-Responsibility.html

The second definition above presents CSR as a kind of “social contract” between a

business entity and its immediate communities by emphasizing “society’s expectations” on

the basis of economic, legal and ethical principles. The first definition lays its emphasis on

the fact that the social contract has to be adopted or implemented on a “voluntary basis”.

CSR in Microfinance: A Triple Bottom-Line Approach Page 6

The very fact that it is “voluntary” makes it somewhat ambiguous to define as each

organization can customize the content of its “social contract” with its own community

relative to its business philosophy. Hence, Tim Barnett (2012) argued that “The concept of

corporate social responsibility means that organizations have moral, ethical, and

philanthropic responsibilities in addition to their responsibilities to earn a fair return for

investors and comply with the law”. Since most businesses are set up to make good returns

on investment, the level of priority given to it pursuit of profitability in relation to its “social

responsibility” will vary from one organization to another.

It is also necessary to note that CSR though related to business ethics, is much different

and broader than it. Barnett (2012) elucidated this when he wrote, “While CSR

encompasses the economic, legal, ethical, and discretionary responsibilities of

organizations, business ethics usually focuses on the moral judgments and behavior of

individuals and groups within organizations. Thus, the study of business ethics may be

regarded as a component of the larger study of corporate social responsibility.”

2.2. Arguments for and Against CSR

While the awareness of and the debate on the concept of CSR seems to be growing

rapidly, there are also growing arguments for and against it. One of such arguments

against it is attributed to Milton Friedman 1970, as quoted in Crowther and Aras (2008)

which states thus, “there is only one social responsibility of business – to use its resources

CSR in Microfinance: A Triple Bottom-Line Approach Page 7

and engage in activities designed to increase its profits so long as it stays within the rules

of the game, which is to say, engages in open and free competition without deception or

fraud”. These arguments have been summarized by Barnett (2012) as shown below:

Exhibit 1 Arguments For and Against CSR

FOR AGAINST

The rise of the modern corporation created and continues to create many social problems. Therefore, the corporate world should assume responsibility for addressing these problems.

Taking on social and moral issues is not economically feasible. Corporations should focus on earning a profit for their shareholders and leave social issues to others.

In the long run, it is in corporations' best interest to assume social responsibilities. It will increase the chances that they will have a future and reduce the chances of increased governmental regulation.

Assuming social responsibilities places those corporations doing so at a competitive disadvantage relative to those who do not.

Large corporations have huge reserves of human and financial capital. They should devote at least some of their resources to addressing social issues.

Those who are most capable should address social issues. Those in the corporate world are not equipped to deal with social problems.

Arguing from a “competitive” perspective will certainly lay emphasis on the fact that

addressing social issues has its attendant cost to a business entity. This implies that

absolving the cost of socially responsible actions could impact negatively on an institutions

CSR in Microfinance: A Triple Bottom-Line Approach Page 8

competitive advantage in relation to the competition. However, in line with the first

argument for CSR as stated above, “The rise of the modern corporation created and

continues to create many social problems. Therefore, the corporate world should assume

responsibility for addressing these problems”, corporate institutions should see themselves

as “corporate citizen” who should share in the responsibility for building a better society.

This could be possible if they engage in producing quality and safe products/services and

ensure that they conduct their businesses in an open and honest manner.

The second argument in favor as highlighted above relates to the future self-interest of the

business entity. This argument tends to focus on the future benefits the entity may stand to

enjoy later as opposed to considerations for present benefits. This argument thus suggests

that business entities should conduct themselves in such a way in the present so as to

assure themselves of a favorable operating environment in the future.

The last argument in favor of CSR above sees the business entity as a socially responsible

“corporate citizen”. Just like every other citizen in the community, the “corporate citizen”

has a duty to contribute to the development of the society beyond tax payment. For

example, Forbes.com in November 2012 published a list of “30 Most Generous

Celebrities”, who contributed to various developmental and social courses in their

respective societies around the world. These celebrities would obviously be “Tax

responsible” citizens in their respective communities and yet still see the need to contribute

meaningfully to their societies. It is in this perspective that “corporate citizen” are expected

CSR in Microfinance: A Triple Bottom-Line Approach Page 9

to see their roles in the community.

2.3. CSR in Nigerian MFBs Today

As part of this write up, a sample survey was conducted via questionnaires to ascertain

how well MFBs appreciate and incorporate CSR into their business operation. A total

twenty (20) questionnaires (see appendix 1) were sent via email to different MFBs across

the country, however only two (2) responses were received. This could be seen as a

reflection of how CSR is appreciated among MFBs in Nigeria.

From the two responses received, both said the CSR occupied a prominent place in their

institutions program. While it is considered as part of the regular day-to-day business in one

institution, it is considered as a periodic event in the other. Both respondents stated that the

focus of their CSR was education and that a dedicated department was saddled with CSR

responsibilities in their respective institutions. They also stated that CSR was explicitly

stated in their annual financial budgets, but as to the impact of their respective institutions

CSR initiatives on their financial performance, while one believed there was no significant

impact, the other was not sure. Regarding the level of impact of CSR on their rates of

customer acquisition and retention, one respondent believe it was very helpful while the

other stated that it was somewhat helpful. However both respondents sounded very

positive on how enthusiastic they would be to recommend CSR to their banks.

3.0. Microfinance as a Developmental and Poverty reduction tool.

Poverty has been defined as “a state or condition in which a person or community lacks the

CSR in Microfinance: A Triple Bottom-Line Approach Page 10

financial resources and essentials to enjoy a minimum standard of life and well-being that's

considered acceptable in society” – Investopedia.com. As have been mentioned earlier in

the introduction, “Microfinance essentially consist of a combination of financial products

(micro-credit, micro-leasing, micro-insurance, micro-savings, and money transfer) targeting

specific client groups. Recipients of these services generally represent micro-business and

economically active, but poor citizens” - Megan, (2009). The emphasis here is on the target

client group, - “the poor”. This implies that the primary goal of microfinance is to address

the challenge of poverty in an economy.

In many countries like Nigeria, poverty is a key developmental challenge. The level of

poverty is often viewed from the perspective of financial inclusion or access to financial

services. CBN 2011. In the light of this perspective, a survey carried out by EFInA in 2012,

showed that 34.9million of the Nigerian adult population (above 18years), representing

39.7% were completely excluded from financial services. Another 15.2m which represents

17.3% had access to informal financial services which are largely unregulated. These

together account for a total of 57% of the adult population, living only 43% (37m) that have

access to formal financial services. A nation that has 57% of its productive population

below the “poverty line” is certainly having serious developmental issue.

3.1. The Concept of Development

“Economic development is the sustained, concerted actions of policy makers and

communities that promote the standard of living and economic health of a specific

area. Economic development can also be referred to as the quantitative and qualitative

CSR in Microfinance: A Triple Bottom-Line Approach Page 11

changes in the economy” – Wikipedia. For the purpose of this paper, I shall conceptualize

development in relation to the local communities in terms of “available and accessible

economic capacities and resources needed to improve the living standard of a people”.

2005 was tagged the international year of microfinance – UNCDF, 2005. The UNCDF

stated as part of its millennium development goals that “Microfinance is one of the

practical development strategies and approaches that should be implemented and

supported to attain the bold ambition of reducing world poverty by half. Indeed,

microfinance is interwoven into many of the recommended strategies to achieve the

Millennium Development Goals. It is an important means of halving poverty by 2015”. This

goes to shows the level of importance that is attached to Microfinance in terms of tackling

the challenges posed by under-development around the globe. Developmental efforts from

Microfinance Banks (MFBs)/Microfinance Institutions (MFIs) go beyond the provision of

access to financial service. This is because the concept of poverty as defined and

illustrated in section 3.2 below, goes beyond lack of financial resource to other indexes

such as poor or lack of formal education, poor hygiene or access to good health care

services, as well as the lack of adequate resources needed to create wealth. Thus

developmental efforts from MFBs/MFIs should be viewed holistically to include other

factors that tend to perpetuate poverty among low income earners.

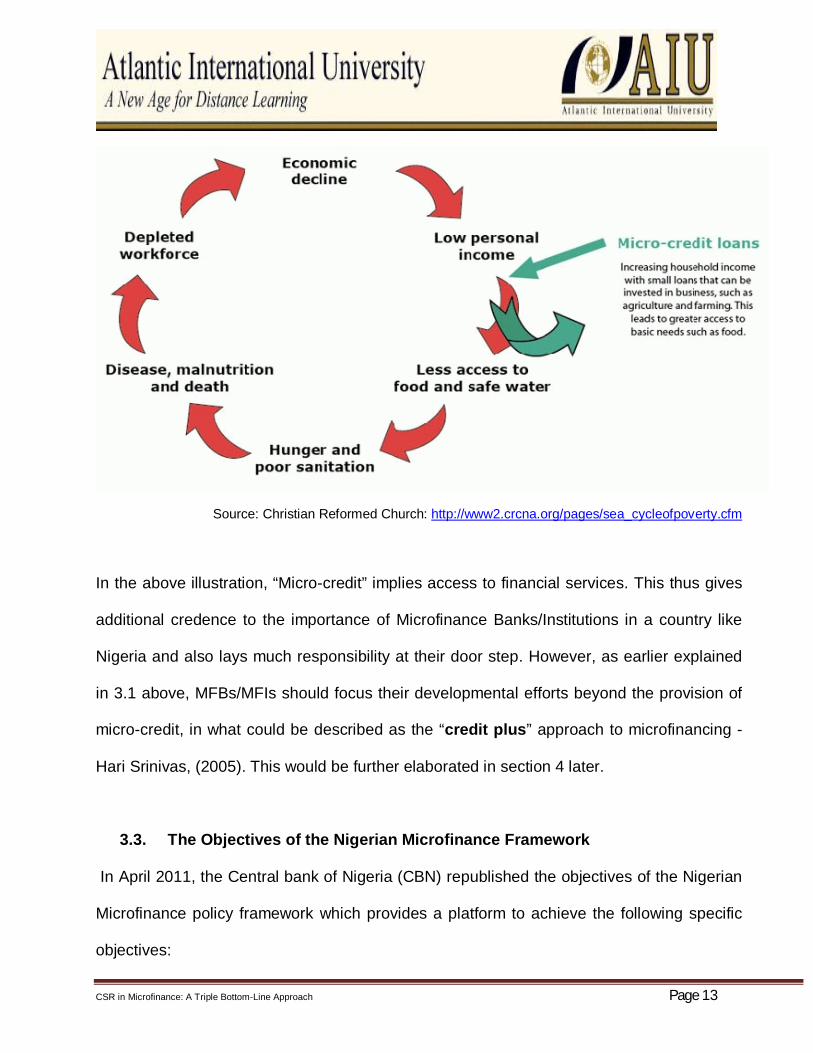

3.2. The Poverty Cycle

“The cycle of poverty has been described as a phenomenon where poor families become

CSR in Microfinance: A Triple Bottom-Line Approach Page 12

trapped in poverty for generations. Because they have no or limited access to critical

resources, such as education and financial services, subsequent generations are also

impoverished” - Christian Reformed Church. A similar definition given by Business

Dictionary.Com postulates that the low level of resourcefulness or income leads to

a chain of events that tends to perpetuate the situation. Some of these events are

highlighted as follows: “progressively lower levels of education and training leading to lack

of employment opportunities, leading to criminal activity (such as sale of illegal drugs) for

survival, leading to addiction, shattered health, early death, and breakup of family, leading

to even bleaker future for the next generation” - Business Dictionary.com.

The Reformed church illustrated the challenge posed by poverty in a community and the

role of microcredit in helping clients break out of the cycle, pictorially as shown below:

Figure 1: The Cycle of Poverty

CSR in Microfinance: A Triple Bottom-Line Approach Page 13

Source: Christian Reformed Church: http://www2.crcna.org/pages/sea_cycleofpoverty.cfm

In the above illustration, “Micro-credit” implies access to financial services. This thus gives

additional credence to the importance of Microfinance Banks/Institutions in a country like

Nigeria and also lays much responsibility at their door step. However, as earlier explained

in 3.1 above, MFBs/MFIs should focus their developmental efforts beyond the provision of

micro-credit, in what could be described as the “credit plus” approach to microfinancing -

Hari Srinivas, (2005). This would be further elaborated in section 4 later.

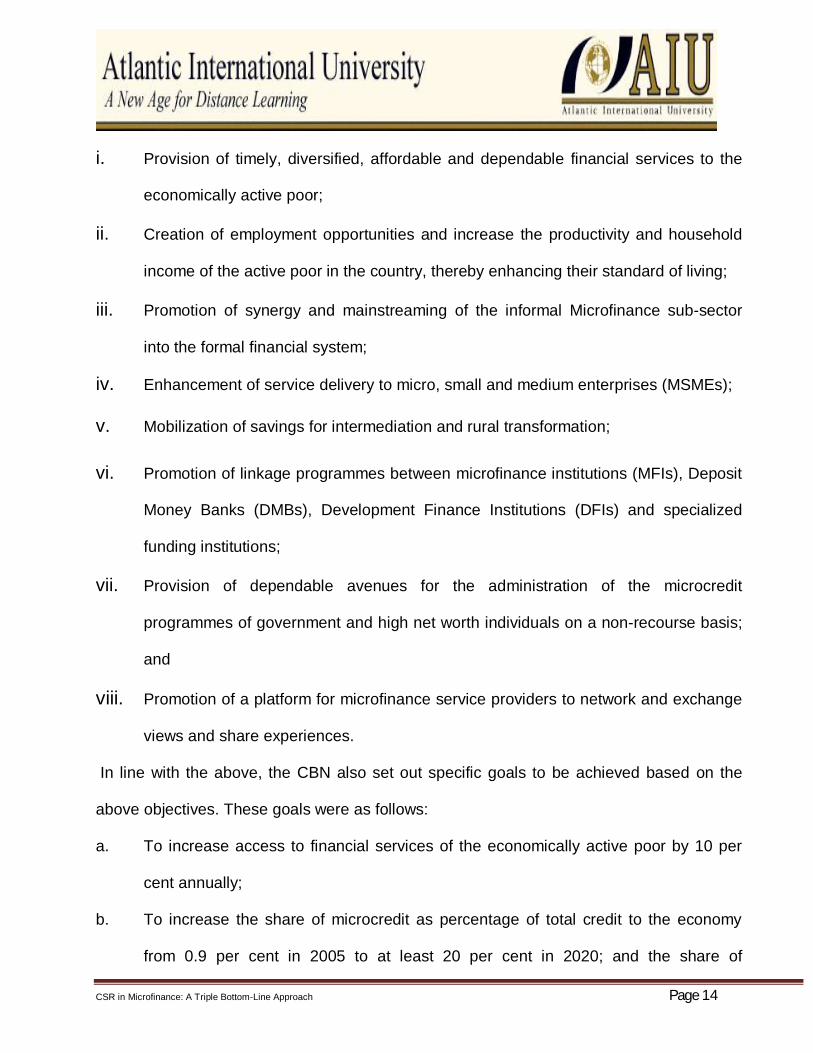

3.3. The Objectives of the Nigerian Microfinance Framework

In April 2011, the Central bank of Nigeria (CBN) republished the objectives of the Nigerian

Microfinance policy framework which provides a platform to achieve the following specific

objectives:

CSR in Microfinance: A Triple Bottom-Line Approach Page 14

i. Provision of timely, diversified, affordable and dependable financial services to the

economically active poor;

ii. Creation of employment opportunities and increase the productivity and household

income of the active poor in the country, thereby enhancing their standard of living;

iii. Promotion of synergy and mainstreaming of the informal Microfinance sub-sector

into the formal financial system;

iv. Enhancement of service delivery to micro, small and medium enterprises (MSMEs); v. Mobilization of savings for intermediation and rural transformation; vi. Promotion of linkage programmes between microfinance institutions (MFIs), Deposit

Money Banks (DMBs), Development Finance Institutions (DFIs) and specialized

funding institutions;

vii. Provision of dependable avenues for the administration of the microcredit

programmes of government and high net worth individuals on a non-recourse basis;

and

viii. Promotion of a platform for microfinance service providers to network and exchange

views and share experiences.

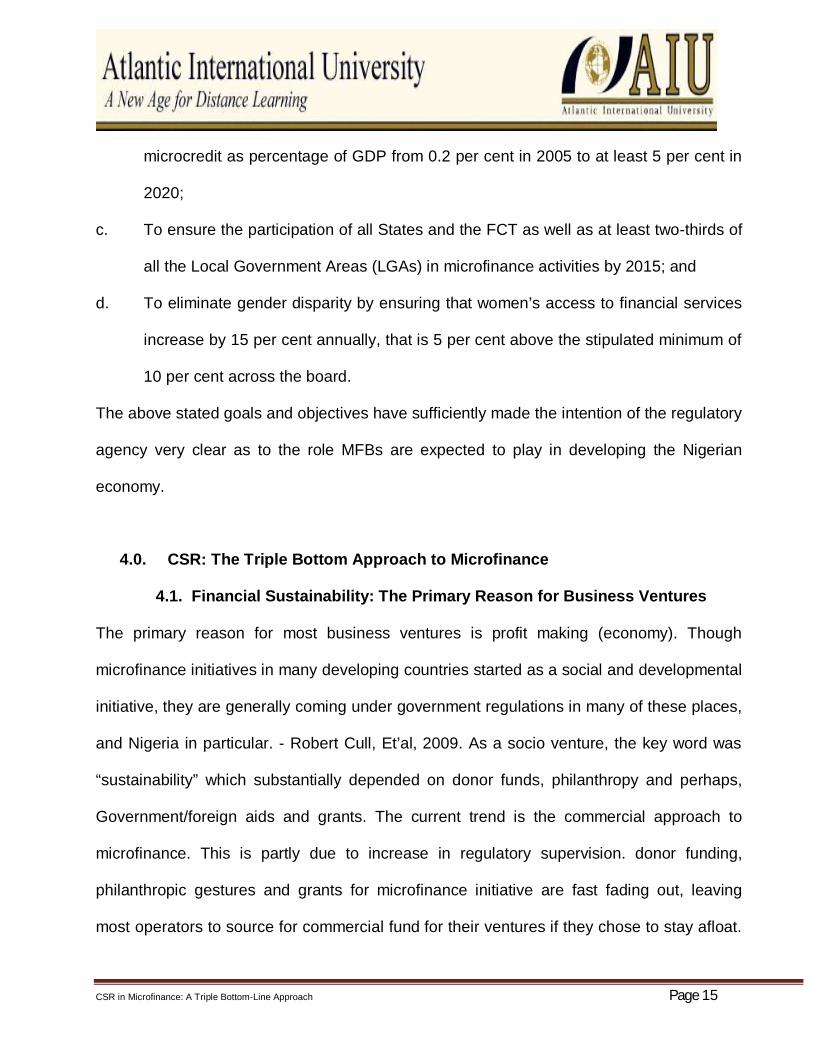

In line with the above, the CBN also set out specific goals to be achieved based on the

above objectives. These goals were as follows:

a. To increase access to financial services of the economically active poor by 10 per

cent annually;

b. To increase the share of microcredit as percentage of total credit to the economy

from 0.9 per cent in 2005 to at least 20 per cent in 2020; and the share of

CSR in Microfinance: A Triple Bottom-Line Approach Page 15

microcredit as percentage of GDP from 0.2 per cent in 2005 to at least 5 per cent in

2020;

c. To ensure the participation of all States and the FCT as well as at least two-thirds of

all the Local Government Areas (LGAs) in microfinance activities by 2015; and

d. To eliminate gender disparity by ensuring that women’s access to financial services

increase by 15 per cent annually, that is 5 per cent above the stipulated minimum of

10 per cent across the board.

The above stated goals and objectives have sufficiently made the intention of the regulatory

agency very clear as to the role MFBs are expected to play in developing the Nigerian

economy.

4.0. CSR: The Triple Bottom Approach to Microfinance

4.1. Financial Sustainability: The Primary Reason for Business Ventures

The primary reason for most business ventures is profit making (economy). Though

microfinance initiatives in many developing countries started as a social and developmental

initiative, they are generally coming under government regulations in many of these places,

and Nigeria in particular. - Robert Cull, Et’al, 2009. As a socio venture, the key word was

“sustainability” which substantially depended on donor funds, philanthropy and perhaps,

Government/foreign aids and grants. The current trend is the commercial approach to

microfinance. This is partly due to increase in regulatory supervision. donor funding,

philanthropic gestures and grants for microfinance initiative are fast fading out, leaving

most operators to source for commercial fund for their ventures if they chose to stay afloat.

CSR in Microfinance: A Triple Bottom-Line Approach Page 16

All of these have implications for profitability to be at the fore of many microfinance

initiatives, just like in any other business ventures.

Regulated microfinance initiatives, in particular, are costlier to run. This is largely due to the

huge cost of complying with regulatory requirements. - Robert Cull, Et’al, 2009. In Nigeria,

the nature of regulation requires Microfinance banks to be a commercial venture and to be

profitable. – CBN 2013. Therefore, profit orientation is a norm in the Nigerian Microfinance

parlance, it is however not intended to be the sole objective of the venture, from the

perspective of the regulators and certainly, the public.

4.2. Social Mission: A Necessary Consideration for MFBs

Social orientation seems to be a natural component of any microfinance initiative. The

target client group (active poor/ low income earners), the unit transaction sizes, the breadth

(the number of client groups) and depth (the type and level of vulnerable client group) of

outreaches, etc all combine to make the “colour” of socio orientation very prominent in any

“picture” of microfinance initiative. The following statement posted on the website of

Deutsche Bank, Germany, corroborates this assertion succinctly:

“Microfinance is a proven and effective tool to empower marginalized

populations through the provision of small loans and other financial services.

More than 60 percent of people in the developing world do not have access

to formal job opportunities; microfinance enables the poor to generate income

through self-employment.” Retrieved on December 5, 2014, from:

https://www.db.com/cr/en/concrete-funds.htm

Many major microfinance initiatives are highly gender biased. This is because very high

CSR in Microfinance: A Triple Bottom-Line Approach Page 17

percentages of their clients are women, which further buttresses the assertion of social

orientation. According to a statement posted on the website of ACCION International, about

500 MFIs around the world report to the MIX market (www.mixmarket.org) as at 2008. “The

MIX 500 MFIs serve an estimated 65 million borrowers among the self-employed poor

worldwide, 70 percent of them women.” - http://www.accion.org.

The belief that the concept of microfinance incorporates socio mission accounts for why

many stakeholders today are concerned about the socio impact of microfinance initiatives.

Maintaining the institution’s focus on the core client group (the active poor, low income

earners and the most vulnerable) and making consistent effort to provide mutually

beneficial services to them should suffice for socio mission.

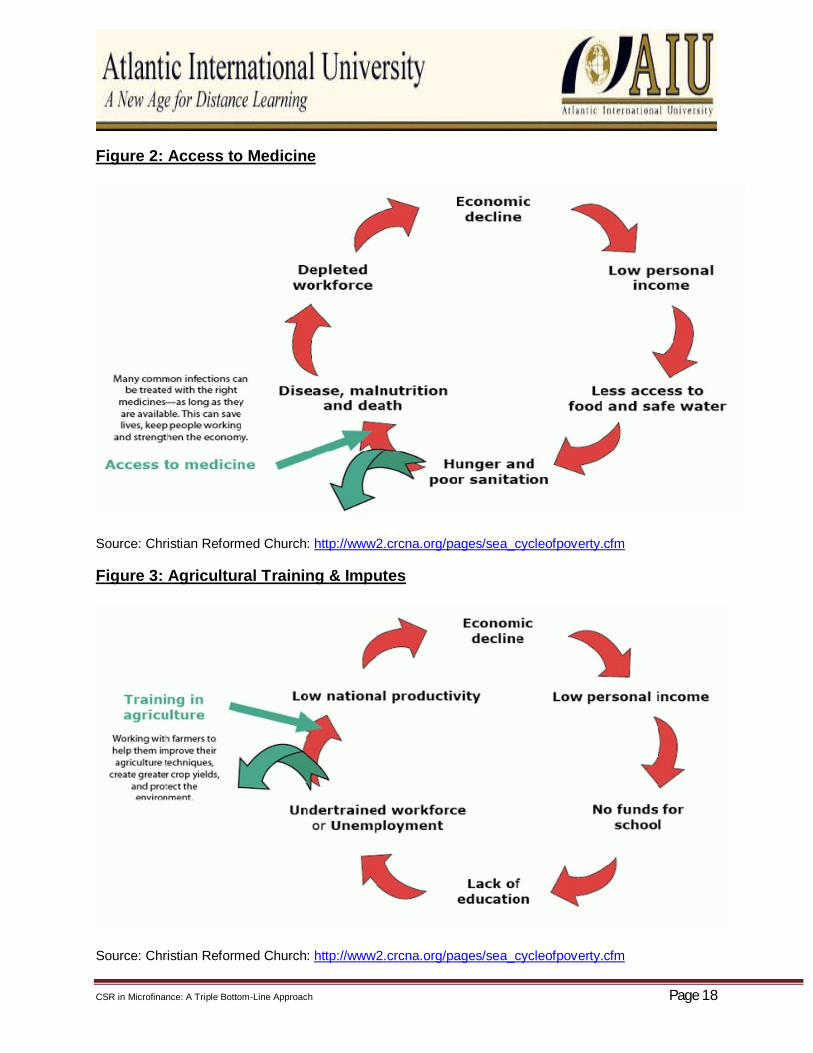

4.3. CSR: A Thorough blend

As earlier explained in 3.2 above, some of the factors that tend to perpetuate the cycle of

poverty include, lack of access to good education and training, conventional health care

system, as well as other resources that can be used to create wealth. MFBs and MFIs can

incorporate these needs into their programs as part of their CSR initiatives. Beside the

provision of microcredits as illustrated in 3.2, figure 1 above, figures 2 and 3 below

illustrates other ways that CSR initiative could help a community to break out of the cycle of

poverty.

CSR in Microfinance: A Triple Bottom-Line Approach Page 18

Figure 2: Access to Medicine

Source: Christian Reformed Church: http://www2.crcna.org/pages/sea_cycleofpoverty.cfm

Figure 3: Agricultural Training & Imputes

Source: Christian Reformed Church: http://www2.crcna.org/pages/sea_cycleofpoverty.cfm

CSR in Microfinance: A Triple Bottom-Line Approach Page 19

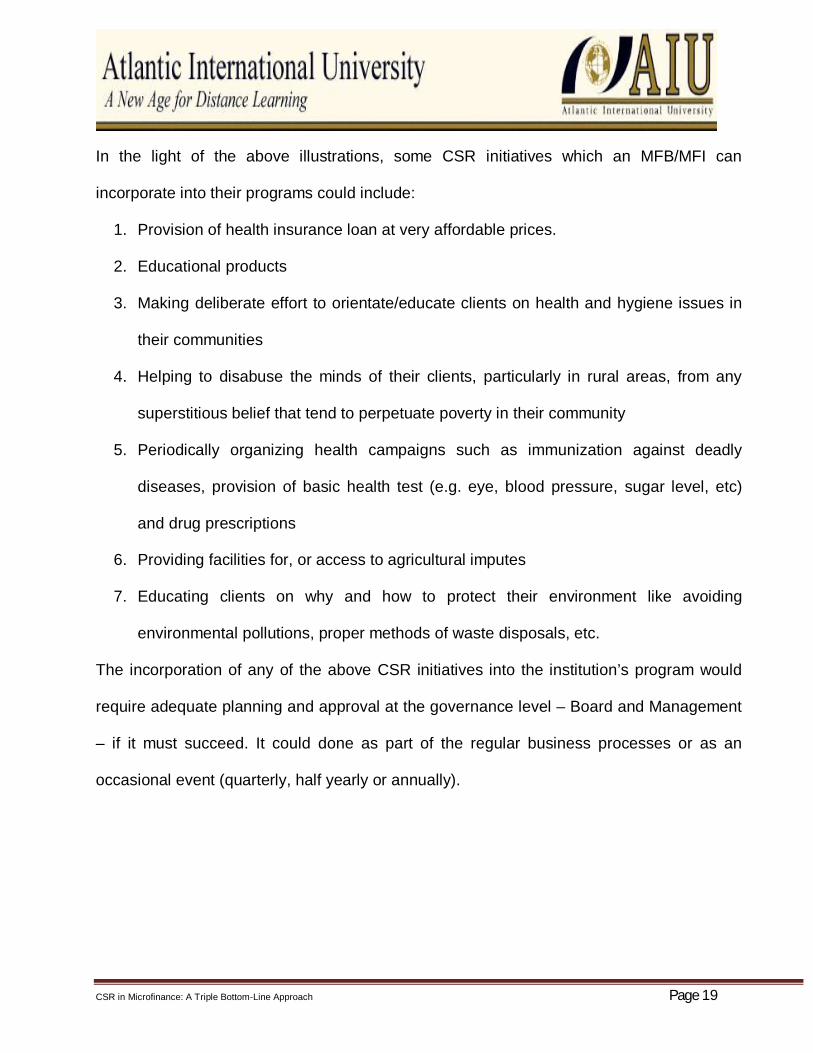

In the light of the above illustrations, some CSR initiatives which an MFB/MFI can

incorporate into their programs could include:

1. Provision of health insurance loan at very affordable prices.

2. Educational products

3. Making deliberate effort to orientate/educate clients on health and hygiene issues in

their communities

4. Helping to disabuse the minds of their clients, particularly in rural areas, from any

superstitious belief that tend to perpetuate poverty in their community

5. Periodically organizing health campaigns such as immunization against deadly

diseases, provision of basic health test (e.g. eye, blood pressure, sugar level, etc)

and drug prescriptions

6. Providing facilities for, or access to agricultural imputes

7. Educating clients on why and how to protect their environment like avoiding

environmental pollutions, proper methods of waste disposals, etc.

The incorporation of any of the above CSR initiatives into the institution’s program would

require adequate planning and approval at the governance level – Board and Management

– if it must succeed. It could done as part of the regular business processes or as an

occasional event (quarterly, half yearly or annually).

CSR in Microfinance: A Triple Bottom-Line Approach Page 20

5.0. Conclusion

Microfinance has been considered as a veritable tool for reducing poverty and developing

the community, particularly in developing economies. It is the provision of financial services

with a socio mission. The target client groups for its initiative include the active poor, low

income earners, “unbanked” and “under-banked” population of an economy. Lack of access

to financial services is not the only cause or perpetuator of poverty. Other factors that have

been considered as perpetuators of poverty include: lack of access to good education and

training, good health care services, and inadequate resources needed to break out of the

poverty cycle.

CSR requires that microfinance service providers should demonstrate a balanced

responsibility to all stakeholders rather that to the shareholders alone. Stakeholders in this

sense would include: shareholders, staff, clients/customers, the Government and the

community/environment in which they operate. Balanced responsibility on the other hand

entails good financial returns to shareholder, carrying out its business to the target client

groups with an intention to alleviate socio ill in the society and helping to both protect and

improve the environment/community by deliberately investing in it.

CSR in Microfinance: A Triple Bottom-Line Approach Page 21

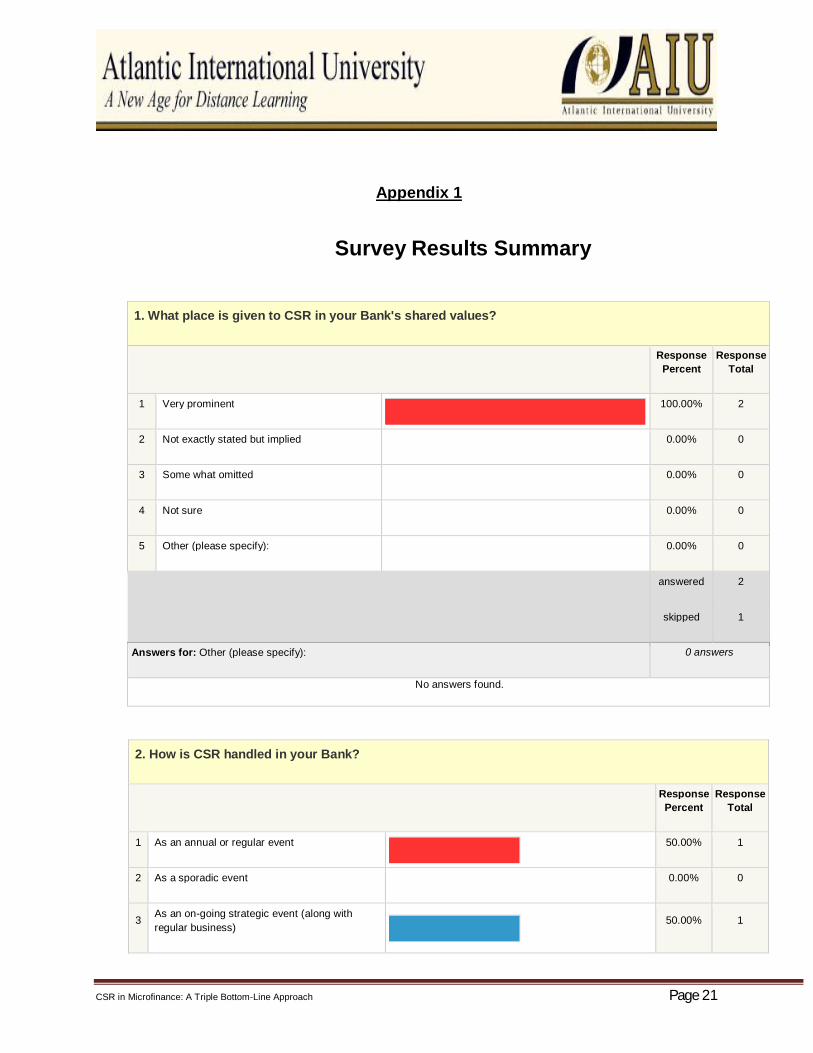

Appendix 1

Survey Results Summary

1. What place is given to CSR in your Bank's shared values?

Response Percent

Response Total

1 Very prominent

100.00% 2

2 Not exactly stated but implied 0.00% 0

3 Some what omitted 0.00% 0

4 Not sure 0.00% 0

5 Other (please specify): 0.00% 0

answered 2

skipped 1

Answers for: Other (please specify): 0 answers

No answers found.

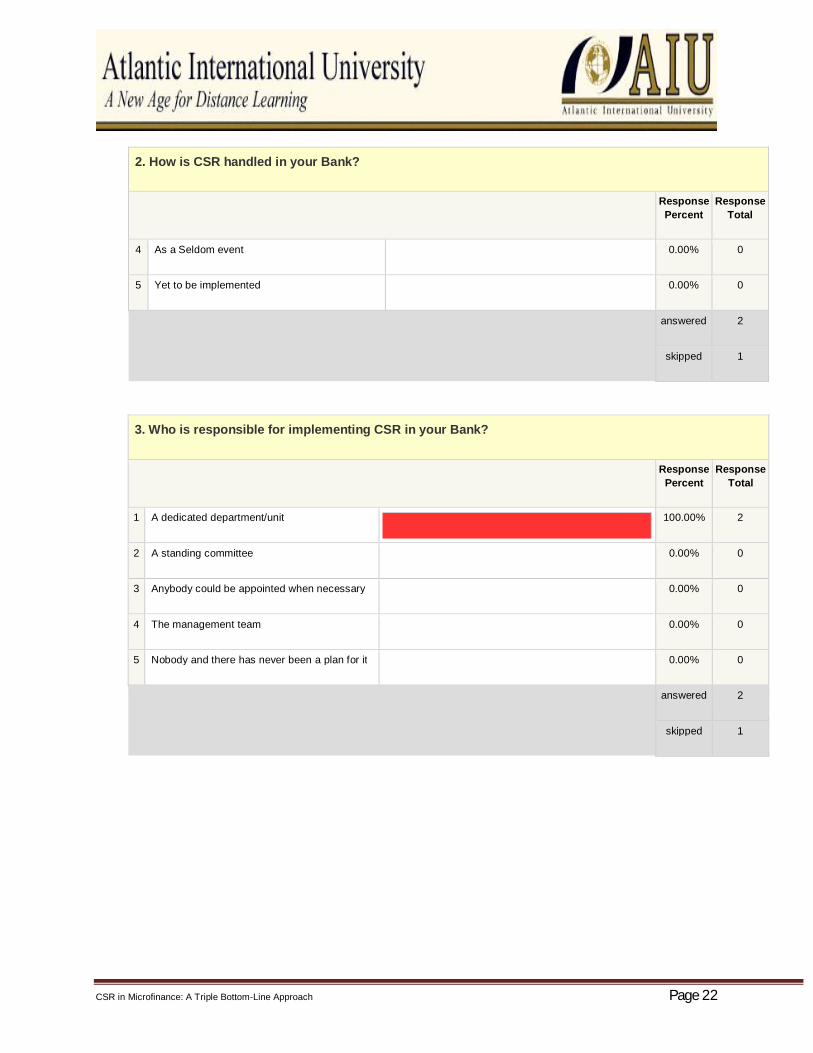

2. How is CSR handled in your Bank?

Response Percent

Response Total

1 As an annual or regular event

50.00% 1

2 As a sporadic event 0.00% 0

3 As an on-going strategic event (along with regular business)

50.00% 1

CSR in Microfinance: A Triple Bottom-Line Approach Page 22

2. How is CSR handled in your Bank?

Response Percent

Response Total

4 As a Seldom event 0.00% 0

5 Yet to be implemented 0.00% 0

answered 2

skipped 1

3. Who is responsible for implementing CSR in your Bank?

Response Percent

Response Total

1 A dedicated department/unit

100.00% 2

2 A standing committee 0.00% 0

3 Anybody could be appointed when necessary 0.00% 0

4 The management team 0.00% 0

5 Nobody and there has never been a plan for it 0.00% 0

answered 2

skipped 1

CSR in Microfinance: A Triple Bottom-Line Approach Page 23

4. What is the focus of your Bank's CSR?

Response Percent

Response Total

1 Education

100.00% 2

2 Health 0.00% 0

3 Social, political and religious orientation 0.00% 0

4 Provision of social amenities/community development

0.00% 0

5 Other (please specify): 0.00% 0

answered 2

skipped 1

Answers for: Other (please specify): 0 answers

No answers found.

5. Is CSR usually incorporated in your bank's annual budgets?

Response Percent

Response Total

1 Explicitly stated

100.00% 2

2 Incorporated under other budget items but implied

0.00% 0

3 incorporated as part of miscellaneous expenses 0.00% 0

4 Not in anyway budgeted for and thus not implemented

0.00% 0

5 Taken as extra budgetary expenses 0.00% 0

answered 2

CSR in Microfinance: A Triple Bottom-Line Approach Page 24

5. Is CSR usually incorporated in your bank's annual budgets?

Response Percent

Response Total

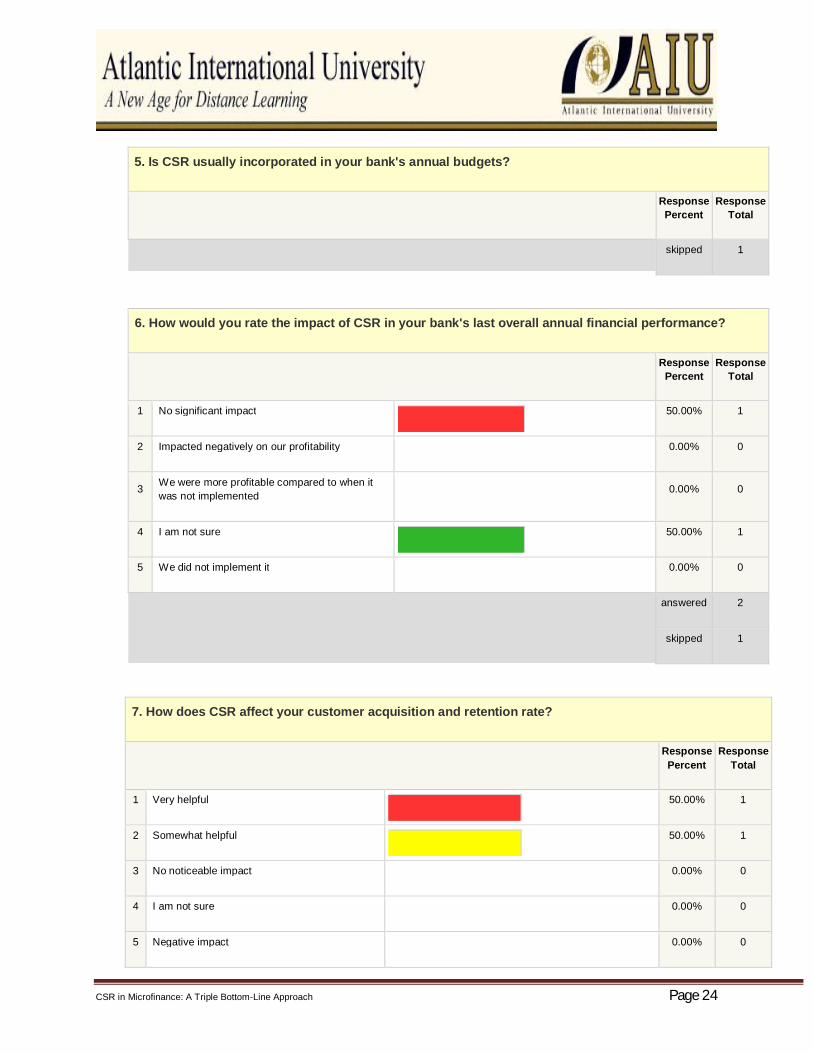

skipped 1

6. How would you rate the impact of CSR in your bank's last overall annual financial performance?

Response Percent

Response Total

1 No significant impact

50.00% 1

2 Impacted negatively on our profitability 0.00% 0

3 We were more profitable compared to when it was not implemented

0.00% 0

4 I am not sure

50.00% 1

5 We did not implement it 0.00% 0

answered 2

skipped 1

7. How does CSR affect your customer acquisition and retention rate?

Response Percent

Response Total

1 Very helpful

50.00% 1

2 Somewhat helpful

50.00% 1

3 No noticeable impact 0.00% 0

4 I am not sure 0.00% 0

5 Negative impact 0.00% 0

CSR in Microfinance: A Triple Bottom-Line Approach Page 25

7. How does CSR affect your customer acquisition and retention rate?

Response Percent

Response Total

answered 2

skipped 1

8. Would you be willing to recommend CSR for your bank?

Response Percent

Response Total

1 Absolutely

100.00% 2

2 May be 0.00% 0

3 I am indifferent 0.00% 0

4 I do not see the need 0.00% 0

5 No 0.00% 0

answered 2

skipped 1

CSR in Microfinance: A Triple Bottom-Line Approach Page 26

BIBLIOGRAPHY

1. ACCION International, 2008. Retrieved on December 5, 2014 from:

www.accion.org/content/microfinance-leaders-launch-campaign-client-protection-clinton-global-

initiative

2. Anna Lyudvig (2013), Making Impact, Retrieved from:

http://www.africaammagazine.com/tag/triple-bottom-line/

3. Business Dictionary.Com. retrieved on November 26, 2014, from:

http://www.businessdictionary.com/definition/poverty-cycle.html.

4. CBN, 2011. Microfinance Policy Framework for Nigeria. Central Bank of Nigeria, Abuja.

5. CBN4 (2012), Revised Regulatory and Supervisory Guidelines for Microfinance Banks

(MFBs) in Nigeria, CBN Abuja, Nigeria.

6. CBN5 (2012), Launching of Nigeria’s National Financial Inclusion Strategy (Programme),

CBN Abuja, Nigeria

7. CBN 2013. Revised Regulatory and supervisory Guidelines for Microfinance Banks

(MFBs) in Nigeria. CBN Abuja, Nigeria.

8. CGAP (2012), A Guide to Regulation and Supervision of Microfinance, Consensus

Guideline; The World Bank, Washington DC.

9. Christian Reformed Church. Retrieved on November 26, 2014, from:

http://www2.crcna.org/pages/sea_cycleofpoverty.cfm

10. David Crowther & Guler Aras (2008), Corporate Social Responsibility, Venture

Publishing Aps, Retrieved from: Bookboon.com.

11. Deutsche bank. Retrieved on December 5, 2014, from:

https://www.db.com/cr/en/concrete-funds.htm

CSR in Microfinance: A Triple Bottom-Line Approach Page 27

12. EFInA, 2012. EFInA Access to Financial Services in Nigeria 2012 Survey- Key Findings,

EFInA Lagos, Nigeria.

13. Forbes.com, 2012. Retrieved from:

http://www.forbes.com/sites/andersonantunes/2012/01/11/the-30-most-generous-

celebrities/

14. Hari Srinivas (2005), Microfinance and Community Development- Environmental Colors

of Microfinance, Retrieved from: www.gdrc.org.

15. Investopedia.com. retrieved on November 26, 2014, from:

http://www.investopedia.com/terms/p/poverty.asp

16. Jose M. Salazar-Xirinachs (2012), Breaking New Grounds: Partnership for More &

Better Jobs for Young People, ILO, New York.

17. Mallireddy Charan, 2011. Triple Bottom Line. Retrieved from:

http://www.slideshare.net/cherryharanreddy11/triple-bottom-line-7664625

18. Marjon Van Opijnen (2008), MESO-FINANCING, Round Table Africa, Retrieved from:

www.roundtableafrica.net.

19. Megan Yuenger (2009), Microfinance as an Economic Development Tool in Uzbekistan,

Indiana University, Bloomington,

20. Microfinance Certification Programme (2012), A Study Manual (Revised), CBN/NDIC

Abuja, Nigeria.

21. Milford Bateman (2011), Background Note- Microfinance as a Development and Poverty

Reduction Policy: is it Everything it’s Cracked Up to Be? Oversea Development

Institute, Retrieved from; http://www.odi.org.uk.

CSR in Microfinance: A Triple Bottom-Line Approach Page 28

22. Milford Bateman and Ha-Joon Chang (2009), The Microfinance Illusion, Retrieved from:

www.hajoonchang.net.

23. My Global Classroom (2008), From Microfinance to Meso-Finance, Retrieved from:

www.muglobalclassroom.blogspot.com.

24. Nwankwo Odi, et’al (2013), Impact of Microfinance on Rural Transformation in Nigeria,

International Journal of Business and Management, Vol.8, No.19 (2013).

25. Ramon Mullerat (2010), Corporate Social Responsibility: The Corporate Governance of

the 21st Century - 2nd edition. Kluwer Law International. The Netherlands.

26. Robert Cull, Et’al, 2009. Does Regulatory Supervision Curtail Microfinance Profitability and Outreach? (WPS4948) The World Bank.

27. Scott Gaul (2011), Mapping Nigerian Microfinance Banks, Microfinance Information

Exchange (MIX), Retrieved from: http://www.themix.org.

28. Stephen O. Obajaja (2008), Legal Matters in Development of Small, Medium Scale

Enterprises, The Nation Newspaper, Nigeria.

29. The World Bank, www.worldbank.org/country/nigeria.

30. Thierry Sanders and Carolien Wegener (2006), Meso-Finance: Filling the Financial

Service Gap for Small Businesses in Developing Countries, NCDO, Retrieved from:

www.bidnetwork.org.

31. Tim Barnett (2012), Corporate Social Responsibility, retrieved from:

http://www.referenceforbusiness.com/management/Comp-De/Corporate-Social-Responsibility.html.

32. UNCDF, 2005. Microfinance and the Millennium Development Goals. UNCDF. New

York.

33. UN Millennium Project (2005), Investing in Development- A Practical Plan to Achieve

CSR in Microfinance: A Triple Bottom-Line Approach Page 29

the Millennium Development Goals, UNDP/Earthiscan, UK.

34. Wikipedia. Economic Development. Retrieved on November 26, 2014, from:

http://en.wikipedia.org/wiki/Economic_development