Covering "FInancial Terrorism"

18

This article was downloaded by: [Florida Atlantic University] On: 06 May 2012, At: 19:29 Publisher: Routledge Informa Ltd Registered in England and Wales Registered Number: 1072954 Registered office: Mortimer House, 37-41 Mortimer Street, London W1T 3JH, UK Journalism Practice Publication details, including instructions for authors and subscription information: http://www.tandfonline.com/loi/rjop20 COVERING “FINANCIAL TERRORISM” James F. Tracy Available online: 29 Nov 2011 To cite this article: James F. Tracy (2011): COVERING “FINANCIAL TERRORISM”, Journalism Practice, DOI:10.1080/17512786.2011.633789 To link to this article: http://dx.doi.org/10.1080/17512786.2011.633789 PLEASE SCROLL DOWN FOR ARTICLE Full terms and conditions of use: http://www.tandfonline.com/page/terms-and- conditions This article may be used for research, teaching, and private study purposes. Any substantial or systematic reproduction, redistribution, reselling, loan, sub-licensing, systematic supply, or distribution in any form to anyone is expressly forbidden. The publisher does not give any warranty express or implied or make any representation that the contents will be complete or accurate or up to date. The accuracy of any instructions, formulae, and drug doses should be independently verified with primary sources. The publisher shall not be liable for any loss, actions, claims, proceedings, demand, or costs or damages whatsoever or howsoever caused arising directly or indirectly in connection with or arising out of the use of this material.

Transcript of Covering "FInancial Terrorism"

This article was downloaded by: [Florida Atlantic University]On: 06 May 2012, At: 19:29Publisher: RoutledgeInforma Ltd Registered in England and Wales Registered Number: 1072954 Registeredoffice: Mortimer House, 37-41 Mortimer Street, London W1T 3JH, UK

Journalism PracticePublication details, including instructions for authors andsubscription information:http://www.tandfonline.com/loi/rjop20

COVERING “FINANCIAL TERRORISM”James F. Tracy

Available online: 29 Nov 2011

To cite this article: James F. Tracy (2011): COVERING “FINANCIAL TERRORISM”, JournalismPractice, DOI:10.1080/17512786.2011.633789

To link to this article: http://dx.doi.org/10.1080/17512786.2011.633789

PLEASE SCROLL DOWN FOR ARTICLE

Full terms and conditions of use: http://www.tandfonline.com/page/terms-and-conditions

This article may be used for research, teaching, and private study purposes. Anysubstantial or systematic reproduction, redistribution, reselling, loan, sub-licensing,systematic supply, or distribution in any form to anyone is expressly forbidden.

The publisher does not give any warranty express or implied or make any representationthat the contents will be complete or accurate or up to date. The accuracy of anyinstructions, formulae, and drug doses should be independently verified with primarysources. The publisher shall not be liable for any loss, actions, claims, proceedings,demand, or costs or damages whatsoever or howsoever caused arising directly orindirectly in connection with or arising out of the use of this material.

COVERING ‘‘FINANCIAL TERRORISM’’

The Greek debt crisis in US news media

James F. Tracy

The 2010 Greek financial crisis marks an important chapter in an era where the underlying

maneuvers of private financial entities figure centrally in the wherewithal of Western nation

states. Utilizing framing research, this study examines representation of the Greek crisis by US

news media from December 2009 to July 2010. In contrast to the incident’s coverage in the

European and business press initially attributing the crisis to speculation and the manipulation of

Greek debt, major US news media presented the event through specific event-driven frames that

obscured knowledge of deeper causes. By drawing attention to dramatic events in Athens and the

American stock markets, US outlets presented the financial crisis in narrow terms that blamed

the event on alleged character flaws and ineptitudes of a nation and its people. This reportage

legitimized proposals of economic austerity as reparation. In the midst of excessive business and

financial-related information, the ability of US journalism to explain how and for whom

transnational economic processes proceed remains provisional. Journalism prompting public

discourse on such dynamics is crucial at present as the formulas hastening the Greek crisis now

threaten industrialized countries throughout the West.

KEYWORDS business journalism; European debt crisis; European Union; financial news;

framing research; neoliberalism

Introduction

As third-generation Greek premier George Papandreou was running for office in

2009 he promised to forge a new social welfare state based on outlays for public health,

education, and attending to poverty. Upon his election, however, the new prime minister

reversed himself completely, claiming that Greece’s coffers were depleted and asserting

that the only remedy was for the country to commit to severe cutbacks in public spending

and reduce overall living standards so that Greece could make good on its loans to

international banks (Petras, 2010). Following Papandreou’s disclosure, the country’s

bondholders lost confidence in Greece’s ability to meet its obligations. The expressed

opinion of government officials and the financial community was that if Greece defaulted

the economic tumult would spread to other European Union (EU) countries, possibly

undermining the euro currency and spelling the fate of the EU as a whole.

Subsequent reports, however, revealed that within days of assuming power

Papandreou began talks with the International Monetary Fund (IMF) for a bailout

(ekathinerini, 2011; European Tribune, 2011). Several Greek political leaders also accused

Papandreou and his political alliance of purchasing $1.3 billion in credit default swaps

(CDS)*basically high-stakes bets against an entity’s debt*on Greek bonds in early 2009

and selling them to a private investment firm shortly after assuming power. At the time of

the sale the CDS were worth $40 million, yet their value swelled to $27 billion as

Papandreou steered Greece toward austerity measures and bailouts.

Journalism Practice, 2011, iFirst Article, 1!17ISSN 1751-2786 print/1751-2794 online# 2011 Taylor & Francis http://dx.doi.org/10.1080/17512786.2011.633789

Dow

nloa

ded

by [F

lorid

a A

tlant

ic U

nive

rsity

] at 1

9:29

06

May

201

2

The initial stages of the Greek debt crisis mark an important episode in the

recent history of Western economies, and charting how the event emerged in public

discourse provides an opportunity to assess more closely how such a crisis is presented

in news media. Guided by framing research, this study examines how news outlets

interpreted and related the Greek debt crisis in dissimilar ways over an eight-month

period*first to the financial community by way of the business and European press,

and subsequently through mainstream channels in the United States. In the most

simplistic of terms, the study seeks to examine how despite the excess of business and

financial-related information today, an understanding of the economic processes

impacting on everyday lives remains fleeting. Indeed, the extent of public discourse

prompting knowledge on the dynamics of transnational financial actors is crucial in the

United States and elsewhere because similar conditions contributing to the Greek

financial crisis are now in play against multiple Western economies (Elk, 2011; Lopez,

2011).

Neo-liberalism and the Nation State

Financial crises are inherent to a neo-liberal economic program where, through

indebtedness, the economies and infrastructures of sovereign nation states are taken

over by powerful transnational actors. Loans to governments, while ostensibly justified

for projects advancing gross domestic product, typically only benefit a tiny financial

elite while securing their unbounded loyalty (Perkins, 2004, pp. 16!17). Through much

of the twentieth century such policies were methodically directed at developing

countries (Lichensztejn and Quijano, 1982; Palast, 2003), yet they are now being

implemented in industrialized nations in a broader global transition to private

ownership of social space and institutions. Under neo-liberalism the state’s formal

role is narrowly circumscribed in terms of enforcing private property rights and

ensuring the performance of a market mechanism for acquisition and exchange. The

logic of the market must be extended to all areas of social life*including basic

requirements such as electricity and water, education, and the environment. Where

markets do not exist they must be created (Harvey, 2005). A fundamental contradiction

in the neo-liberal program is that without regulation capital and its attendant ability to

wield market and extra-market power accumulates in fewer and fewer hands. Thus the

fabled ‘‘free market’’ becomes increasingly subject to manipulation by a select few

participants.Neo-liberalism has been substantially augmented through the ‘‘financialization’’ of

capitalism over the past 40 years. In the United States and other Western nations,

opportunities for investment dried up due to an overabundance of productive capacity

and decreasing consumption. The answer to the lack of economic stimulus has been non-

productive speculation with a new assortment of complex financial instruments*futures,

options, derivatives, and so on. In turn, speculation has been the primary economic engine

since the 1970s (Foster and Magdoff, 2009, p. 79). With investment banks and hedge funds

the principal accumulators of capital, and in the absence of state intervention, the power

of such outlets to undermine other institutions through speculative financial maneuvers

now extends to the conquest of entire nation states.

2 JAMES F. TRACY

Dow

nloa

ded

by [F

lorid

a A

tlant

ic U

nive

rsity

] at 1

9:29

06

May

201

2

Neo-liberal Newspeak and ‘‘Financial Terrorism’’

The ascendance of neo-liberal thought and intensified programs of privatization

have been accompanied by an overwhelming tide of news and information specifically

targeting the business and investor classes (Chakavartty and Schiller, 2009; Corcoran and

Fahy, 2009; Doyle, 2006; Martin, 2002; Miller, 2009). As Chakavartty and Schiller explain, ‘‘In

a short period of time, across most of the news-producing world, the print news media

began in the mid-1980s to shift in their attention from a broad economy and society

coverage to business and finance’’ (2010, p. 677). Accelerated by increased concentration

of media ownership (Bagdikian, 2004) business journalism, with its valorization of risk,

entrepreneurialism and finance, predominantly serves the interests of an affluent

minority*the 6!7 percent who trade securities on a regular basis (Pew Research Center,

2008a). Despite this development, public opinion suggests abundant interest in economic

news, even if such news is difficult to find, does not speak to more immediate social

concerns, or involves economic conditions elsewhere in the world (Pew Research Center,

2008b).

The neo-liberal turn in news has produced a news discourse that ‘‘operates largely

within the parameters and presuppositions of the world of business, markets and finances

and addresses its readers likewise, as interested observers and potentially affected

consumers’’ (Cottle, 2009, p. 14). Exempted from this equation are most citizens who have

much at stake yet limited means for understanding economic vicissitudes. Yet ‘‘day to day

instability and swings in stock market values are the source of large windfall profits

accruing to ‘institutional speculators’ and hedge funds’’ (Chossudovsky, 2010, p. 7). In this

way, the Greek crisis afforded financial syndicates with tremendous opportunity via CDS

and the euro’s marked drop in value against the dollar (Pullman et al., 2010).

In April 2010 a criminal complaint of fraud was filed with Greece’s Attorney General,

likening the Greek debt crisis to a coordinated act of ‘‘financial terrorism’’ (Tobras and

Noulas, 2010). The grievance pointed to how Greece’s government and consumer debt as

a percent of GDP was less than the same figures for the Netherlands, Ireland, Belgium,

Spain, Portugal, and Italy, and that what actually took place in late 2009 and early 2010

was major credit rating agencies Moody’s, Standard & Poor’s, Fitch, and European and

international financial firms including Morgan Stanley, Goldman Sachs, JP Morgan, Royal

Bank of Scotland, and Credit Suisse, colluded to undermine Greek government finances.

This was accomplished by lowering Greece’s bond rating while purchasing large quantities

of CDS on Greek bonds, thus driving up Greece’s borrowing costs and making it

impossible to finance its debt (Tobras and Noulas, 2010).When Greece sought entry into the EU in the early 2000s, US-based investment bank

Goldman Sachs aided the Greek government in hiding public debt through foreign

currency swaps to meet EU national liability protocols (Story et al., 2010). These

transactions are routine to government refinancing. ‘‘But in the Greek case the US

bankers devised a special kind of swap with fictional exchange rates. That enabled Greece

to receive a far higher sum than the actual euro market value of 10 billion dollars or yen’’

(Baizil, 2010). Having extensive knowledge of the country’s financial profile, Goldman was

a principle purveyor of Greek bonds and encouraged investors to purchase CDS on Greek

debt (Tobras, 2010; Tobras and Noulas, 2010).As news of Greece’s situation emerged in December 2009, hedge funds increasingly

targeted what they termed the ‘‘PIIGS’’ (Portugal, Ireland, Italy, Greece, Spain) through

massive purchases of CDS (Slater et al., 2009, p. C1). By February 2010 targeting vulnerable

COVERING ‘‘FINANCIAL TERRORISM’’ 3

Dow

nloa

ded

by [F

lorid

a A

tlant

ic U

nive

rsity

] at 1

9:29

06

May

201

2

EU countries developed into a more coordinated speculative assault by traders and a

select number of hedge funds against the euro currency by way of Greece, then

recognized as the EU’s weakest flank. A total of 60,000 CDS contracts totaling $84.8 billion

had been sold through 2009 (Pullman et al., 2010), while 40,000 contracts against the euro

valued at $7.6 billion represented the largest ever bet against a single currency (Garnham

et al., 2010). Yet as we shall see, the roles played by investment banks, hedge funds, and

rating agencies were close to non-existent in most US media coverage of the unfolding

events.

Framing Economic Crises

Erving Goffman (1986) explains framing as the taken-for-granted cognitive ritual

whereby individuals understand the world and act within it. In this view frames are, as

Lippmann (1922) famously remarked, ‘‘the pictures in our heads.’’ In a similar vein, when

journalists ‘‘frame’’ issues or events through certain formulae*selection of sources,

rhetorical style, positioning of pieces in the newspaper or newscast*they direct onlookers

to certain features of the object deemed worthy of emphasis, while downplaying others.

Obtaining its authority through the audience’s perception of journalistic objectivity, ‘‘the

news necessarily selects facts that support a particular view of the world; that is, it

provides us with a (perhaps unconscious) bounded view of the world, a ‘frame’’’ (Rojecki,

1999, p. 16).

Frames take shape through the assembling of journalistic narrative*of answering

‘‘the who, what, where, why, how, and when’’ (Bennett and Edelman, 1985, p. 159). In this

process certain words, phrases, or audio and video clips are juxtaposed to render an event

comprehensible and imbue it with meaning. Briefly, this involves telling a story, and stories

may be told in many ways. As Hackett and Zhao observe, ‘‘the storytellers need to have a

narrative to thread the story together, to determine what counts as a relevant and

noticeable fact or event, and to hold the audience’s attention (1998, p. 119). Thus news

frames, in concert with the emotions, values, and judgments they evoke, present and

define social problems and their causes while suggesting potential remedies (Entman,

2004).

Coverage of the Greek crisis shares common ground with coverage of labor

unionism and the economy (Goldman and Rajagopal, 1991; Goss, 2001; Kumar, 2007;

Martin, 2004; Puette, 1992). Indeed, labor and economics involve the selection and

interpretation of certain phenomena to explain complex processes within specific

institutional and communicative constraints. Like workers picketing an employer, a

demonstration against public cutbacks may be held up as an explanation for*and even

cause of*calamities defying quick and tidy explanations.

Along these lines, Iyengar (1991) explains how news media overall present

phenomena in terms of thematic or episodic frames, and this notion is helpful for further

distinguishing coverage of the Greek events between coverage in financial and foreign

versus US news media. A thematic frame provides an occurrence with some historical,

social, and even economic context for an audience to understand why something is

happening. On the other hand, in an episodic frame the journalist mainly attends to

circumstances as they proceed without historical context. As Bennett notes, ‘‘such news is

personalized, dramatized, and fragmented; it often tells stories about social order and

4 JAMES F. TRACY

Dow

nloa

ded

by [F

lorid

a A

tlant

ic U

nive

rsity

] at 1

9:29

06

May

201

2

disorder’’ (2012, p. 44). In turn, audiences subject to viewing national and world eventsthrough the episodic frame often look to the people depicted or vague institutions for the

causes of social problems rather than recognizing larger, less observable political and

socioeconomic processes at play. The Greek crisis progresses in intermittent thematicframes in the financial and foreign press in the several months before May 2010, with

attention to the role speculation played in the predicament, while it was subsequently

presented in episodic frames in the US news media. Detailed consideration of both ofthese journalistic locations is not permissible in this avenue given space constraints.

Methodology

The following provides a quantitative overview through which to qualitatively assesshow the Greek debt crisis was presented by two US newspapers, two national

newsweeklies, and three broadcast television networks between December 1, 2009 and

July 31, 2010. Content collection via digital archives is not always the most reliablemethod. Such ‘‘push-button’’ investigation (Deacon, 2007) has its drawbacks in the form of

potentially flawed data samples. With this in mind, several varied searches were conducted

and examined with a variety of terms to identify and assemble the data set using thefollowing parameters. A total of 115 pieces were retrieved in a search on LexisNexis

Academic using ‘‘Greece’’ in the headline or lead and ‘‘European Union or financial crisis or

economic crisis and debt or default or credit rating’’ for ABC (13 transcripts), CBS (sixtranscripts), NBC (14 transcripts), Newsweek (27 combined articles from US and Interna-

tional editions), New York Times (25 articles) USA Today (16 articles), and a separate search

on the EBSCO Business Source Premier database of Time (US and International, 14 articles).The New York Times published 175 articles on the crisis. To reduce this sample in scale

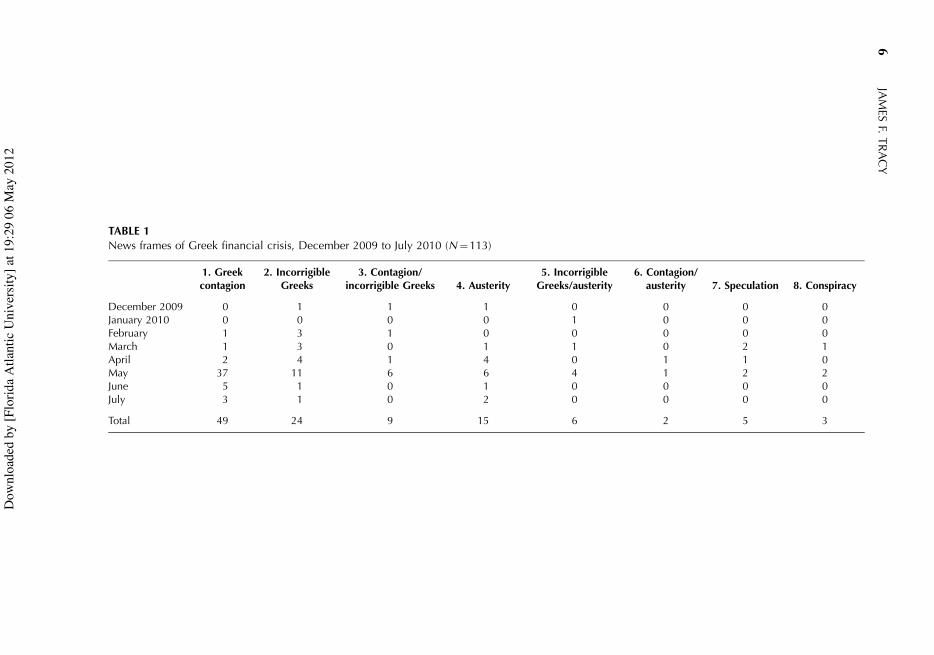

every seventh article was selected chronologically for a sample of 25. The first story from

the overall sample appeared on December 21, 2009 and the last on July 24, 2010. Twoarticles defied categorization in the News Frames (Table 1).

Dominant Frames of the Greek Crisis in US Coverage

Unlike the prolific and glowing coverage afforded protests throughout MiddleEastern countries during ‘‘Arab Spring’’ by US news media, the Greek crisis was presented

through specific episodic frames that sequentially present a problem*‘‘Greek Contagion,’’

a cause*‘‘Incorrigible Greeks,’’ and a solution*‘‘Austerity.’’ ‘‘Greek Contagion’’ (Table 1,column 1) is characterized by an explicit anxiety that the Greek crisis threatens the euro

through its potential to spread to other EU countries and perhaps throughout the world.

‘‘Incorrigible Greeks’’ (Table 1, column 2) situates Greek government officials and people asspendthrift, unruly, irredeemable, and thus perpetrators of the event. ‘‘Austerity’’ (Table 1,

column 4) cites Greece’s fiscal recklessness and proposes slashing public spending as the

sole remedy.As columns 3, 5, and 7 in Table 1 indicate, the above frames frequently overlap

within the same stories and are deemed so where characteristics of two frames are present

in a story lead. This may be found in reports on the ‘‘Incorrigible’’ Greek peopledemonstrating in the streets vis-a-vis assertions relating the protests to a drop in the stock

market (Contagion). For example,

COVERING ‘‘FINANCIAL TERRORISM’’ 5

Dow

nloa

ded

by [F

lorid

a A

tlant

ic U

nive

rsity

] at 1

9:29

06

May

201

2

TABLE 1News frames of Greek financial crisis, December 2009 to July 2010 (N"113)

1. Greekcontagion

2. IncorrigibleGreeks

3. Contagion/incorrigible Greeks 4. Austerity

5. IncorrigibleGreeks/austerity

6. Contagion/austerity 7. Speculation 8. Conspiracy

December 2009 0 1 1 1 0 0 0 0January 2010 0 0 0 0 1 0 0 0February 1 3 1 0 0 0 0 0March 1 3 0 1 1 0 2 1April 2 4 1 4 0 1 1 0May 37 11 6 6 4 1 2 2June 5 1 0 1 0 0 0 0July 3 1 0 2 0 0 0 0

Total 49 24 9 15 6 2 5 3

6JA

MES

F.TR

AC

Y

Dow

nloa

ded

by [F

lorid

a A

tlant

ic U

nive

rsity

] at 1

9:29

06

May

201

2

Protesters are furious about massive spending cutbacks required by the bailout plan

that’s supposed to help Greece out of its debt crisis. Concerns that those problems won’t

be solved and will, in fact, spread to other nations in Europe sent stocks down hard in

this country today. The Dow lost 225 points. (NBC News, 2010b)

The monthly metric in the leftmost column of Table 1 illustrates how over half of the

stories appeared in May. This is due to the episodic, event-driven nature of the coveragecentering around three incidents: the deaths of three bank employees in Athens on May 5

when protesters allegedly set the bank ablaze; the May 6 Dow Jones Industrial Average

‘‘flash crash’’ where the index dropped 1000 points; the multibillion-euro bailout of Greeceby the EU and IMF in mid-May.

Tables 2 and 3 show how the majority of sources for the stories are financial

industry, government, or academic or think-tank economists, at least some of whom sharefairly similar beliefs about economic dynamics as they relate to Greece. On the other hand,

sources that may provide countervailing views, such as union leaders or workers, are

poorly represented. The absence of these voices invariably plays into how the prevalentframes take shape. As Touri explains, ‘‘news stories become a platform for framing

contests, where political actors compete by sponsoring their preferred meanings’’ (2008,

p. 172). Since much of the coverage leaves unexamined the more opaque dimension offinancial speculation and manipulation discussed at length on blogs and similar alternative

outlets, the causes and consequences of the crisis remained obscure. For a moment these

unusual analyses also appear in mainstream outlets. With this in mind, closer considerationof the story’s less-examined features can help to place the dominant frames in a broader

perspective. I return to the three dominant frames below, but to provide some additional

historical context for the reader I briefly turn to examine the thematic frames less salient inmost US crisis coverage.

Speculation, Regulation, and Conspiracies

Two thematic frames centering on ‘‘Speculation’’ and ‘‘Regulation’’ (Table 1, columns

7 and 8), each of which figure in New York Times coverage, are subtly interrelated and bear

upon how the episodic frames emerge. In early 2010 European and US financial newsmedia, including the New York Times, published numerous pieces on the probable role

TABLE 2Sources cited by US broadcast networks ABC, CBS, and NBC (N"35)

SourceABC (13

transcripts)CBS (6

transcripts)NBC (14

transcripts) Total

Present/former government official 0 0 0 0Government economist 0 0 0 0Financial industry economist 8 8 0 16Non-financial business

representative0 0 0 0

Academic or think-tank economist 2 1 1 4Network correspondent or pundit 2 4 3 9Guest journalist or pundit 0 0 1 1Union representative 0 0 0 0Citizen/worker 1 0 4 5

COVERING ‘‘FINANCIAL TERRORISM’’ 7

Dow

nloa

ded

by [F

lorid

a A

tlant

ic U

nive

rsity

] at 1

9:29

06

May

201

2

speculation played in bringing about the Greek crisis (e.g. Baizil, 2010; Garnham et al.,

2010; Pullman et al., 2010; Slater et al., 2009, p. C1). The issue of speculation was

underlined in March when European Central Bank president Jean-Claude Trichet, German

Chancellor Angela Merkel, French President Nicolas Sarkozy, and Britain’s Prime Minister

Gordon Brown strongly criticized the role of offshore banks and hedge funds in

exacerbating financial crises and called for their regulation (Ewing and Werdigier, 2010).

Likewise Greece’s Papandreou cited CDS for playing a major role in the Greek crisis. On a

similar note, credit ratings agencies were referenced for their ‘‘megaphone effect’’ which

influenced financial predicaments (Dixon and Swann, 2010, p. B2).

Meaningful regulatory action did not come to pass and discussions ceased as the

case for financial speculation or manipulation was decried as conspiratorial in several

prominent venues (Bratich, 2008). ‘‘Talk in continental Europe of an ‘Anglo-Saxon’

conspiracy of greedy speculators is . . . dishonest,’’ The Economist (2010) argued. ‘‘The

speculators did not invent the deficits.’’ Citing European leaders’ claims that speculators

undermined Greece’s finances, Newsweek warned that if the EU suppressed the use of

credit default swaps ‘‘and other derivatives, it will hurt, not help, the continent’s sickly

economies. To start, there is simply no evidence that swaps were really to blame for the

Greek crisis’’ (Sheridan, 2010). Newsweek misleadingly points to how ‘‘the volume of

activity in the Greek swaps market stayed constant at about $9 billion since mid-January’’

(Sheridan, 2010) without noting this figure was without precedent (Garnham et al., 2010).When Germany banned CDS in May (an action of little consequence since most

CDS trading is done in London and New York), USA Today suggested how the move

disturbed markets, ‘‘spooked investors’’ and left European bankers holding Greek debt

on a precipice (Lynch, 2010b, p. 6A). Echoing the notion of conspiracy, a Greek public-

sector union official is quoted, claiming that for now ‘‘Greece is the target. But Wall

Street needs more easy targets. They need Spain. They need Portugal.’’ The unionist’s

hypothesis is dismissed by USA Today as one of ‘‘many conspiracy theories’’ without

credibility because the $8 billion in credit default swaps is ‘‘dwarfed by the more than

$400 billion total Greek debt’’ (Lynch, 2010a, p. 1A). The observation mistakes the figure

of CDS against the euro for the $85 billion taken out against Greek debt throughout

2009 to early 2010 (Pullman et al., 2010).

TABLE 3Sources cited by US newspaper and news periodicals sources (N"196)

SourceNew York Times

(25 articles)USA Today (16

articles)Time (13articles)

Newsweek (27articles) Total

Present/formergovernment official

24 6 2 4 36

Government economist 8 5 0 2 15Financial industry

economist30 33 2 10 75

Non-financial businessrepresentative

4 5 5 1 15

Academic or think-tankeconomist

21 2 5 6 34

Network correspondent orpundit

1 1 0 0 2

Union representative 3 11 5 0 19

8 JAMES F. TRACY

Dow

nloa

ded

by [F

lorid

a A

tlant

ic U

nive

rsity

] at 1

9:29

06

May

201

2

Greek Contagion

The Greek debt crisis is related in sampled coverage solely or partly to convey the

impression of Contagion*that Greece’s default would impact on the euro currency and

affect other nations, perhaps on a scale akin to the 2008 global liquidity crisis. The bulk of

such reports emerged in the wake of tentative loan negotiations between Greece, the EU

and the IMF, with their frequency intensifying after the Athens bank workers’ deaths and

the US stock market’s ‘‘flash crash.’’ While news of the Greek financial situation was well

known in the international and business press, the contagion theme in mainstream

coverage was established in late April, when Standard & Poor’s lowered its rating on Greek

bonds to ‘‘junk.’’In the Contagion frame anxiety reigns and little can be done to stave off the

creeping contamination. USA Today reported that the ensuing market turmoil brought

‘‘fresh fears that a $143 billion Greek bailout plan may not be enough to stem the spread

of the debt crisis to other struggling eurozone countries’’ (Shell, 2010, p. 3B). Shortly

thereafter a $1 trillion reserve was established by the EU and IMF to shore up other ailing

peripheral countries. This effort, Time suggests, finally ‘‘may be enough to keep the Greek

disease from infecting Spain, Portugal, Ireland and other overleveraged European

countries.’’ Still, the broader problem of risk ‘‘is no longer over there; it’s here. It isn’t in

exotic parts of the world; it’s in the cradle of Western civilization’’ (Karabell, 2010, p. 20).

The Contagion premise was largely fueled through reliance on explanations of

financial industry representatives and economists. For example, an analyst tells USA Today,

‘‘‘What happens in Athens doesn’t stay in Athens. Eventually, it comes to an Athens near

you, like Athens, Ohio’’’ (Shell, 2010, p. 3B). ABC reporter Juju Chang noted, ‘‘A leading

credit rating agency said this morning that the Greek debt crisis could spread and affect

the banking systems of other nations, like Portugal, Italy, Spain, Ireland, even the UK’’ (ABC

News, 2010a). Similarly, prominent mutual fund chief Mohamed El-Erian remarked, ‘‘To the

extent that European banks are under pressure, then it will make the whole banking

system much more difficult to navigate’’ (ABC News, 2010b). Hours before the May 6 crash

NBC commented, ‘‘There is growing concern that the bailout for Greece may not be big

enough and that other heavily indebted European countries . . . may need a bailout too’’

(NBC News, 2010c). A representative of UBS, Art Cashin, noted, ‘‘We hope it*that the

people in the European Union can come together and resolve this: that it does not turn

out to be the first domino to fall’’ (CBS News, 2010b).

Underscored by the May 6 flash crash, the Contagion frame proceeds with news

reports intimating that Greece was the cause of the crash. In an example of the Contagion

and Austerity themes overlapping, CBS correspondent Anthony Mason points to the

market’s abrupt and terrifying drop. ‘‘What pushed it to the edge? Well, it all started in

Athens.’’ A segue to a scene of Greek citizens protesting is followed by an inquiring

financial industry analyst: ‘‘‘Does Europe, in fact, have the ability to take the tough

medicine it needs to take and get back on its feet economically to start to grow again?’’

Mason continues, ‘‘The fear is that the Greek debt crisis could become contagious’’ (CBS

News, 2010a). Newsweek’s report on the package of loans extended to Greece by the EU

and IMF, ‘‘Greece May Not Be the End of It’’ (Theil, 2010b, p. 7), explained how ‘‘Europe

stood on the edge of another financial crisis,’’ while ‘‘Greece, for all intents and purposes,

went bankrupt.’’ Time (2010, p. 24) likewise summarized how Greece’s bond downgrade

‘‘deepened fears that Europe’s debt crisis could soon spiral out of control.’’

COVERING ‘‘FINANCIAL TERRORISM’’ 9

Dow

nloa

ded

by [F

lorid

a A

tlant

ic U

nive

rsity

] at 1

9:29

06

May

201

2

Contagion is also a basis framing how the crisis threatens the euro currency, and

even the global economic recovery. For example, financial historian Niall Ferguson (2010,

p. 46) muses, ‘‘Just when it seemed safe to start using the word ‘recovery,’ a Greek crisis

threatened to choke off the global rebound, and to terminate the very existence of the

world’s second biggest currency.’’ Echoing Ferguson, Time proclaimed how ‘‘the sickly

currency now threatens the global economic recovery’’ even though EU ‘‘leaders remain

committed to their great experiment with monetary union’’ (Schuman, 2010b, p. 18). As

highlighted above, however, undermining the euro was a central reason for speculators’

attacks on peripheral EU countries.

In a peculiar turn the Contagion frame also presents speculators as victims rather

than culprits or accessories of market tumult. ‘‘We know volatility scares the pants off

investors,’’ USA Today points out. Traders must therefore contend with gee-whiz confusion

and uncertainty. ‘‘Do I get out? Do I get in? If I got out, do I get back in? What gives? Is it

2008 again?’’ (Shell, 2010, p. 3B). Referencing the 1997 Asian financial crisis, Time similarly

attributes attacks on currencies and credit to a vague tyranny of anxiousness, versus

calculation. ‘‘Just because country A falls into a debt crisis doesn’t mean countries B, C or G

should as well. But that’s not how investors think in times of uncertainty. Instead, they look

for other potential trouble spots, then try to get out’’ (Schuman, 2010c, p. 18).The Contagion frame is closely accompanied by that of the Incorrigible Greeks.

Through the merger, responsibility for the crisis is situated not in financial and regulatory

systems facilitating speculation and manipulation of markets, nor with powerful financial

entities profiting from the confusion, but rather in myriad cultural and social characteristics

of the Greek people themselves*from their supposedly inept or corrupt government

officials to the reckless belligerents protesting in the streets because they refuse to accept

that they could no longer live beyond their means.

Incorrigible Greeks

The notion of morality is linked to myth in framing the Greek debt crisis, specifically

the powerful western notion of the competitive ‘‘free market,’’ where all individuals and

countries are equally equipped to thrive. As Hertog and MacLeod explain, myths ‘‘are

widely shared and understood within the culture, and are especially prone to drawing in a

wide array of additional beliefs, feelings, expectations, and values. That is, they are

especially efficient in making meaning’’ (2001, p. 148). And research suggests how

audiences are persistently in search of cues to render things meaningful. Neuman et al.

found in their development of the ‘‘human impact frame’’ how audience members have a

tendency to ‘‘overlay the frame with a moral or evaluative dimension’’ (1992, p. 63). In

rendering moral judgment there is a responsibility frame that explains an issue or event in

terms of who or what is accountable (Semetko and Valkenburg, 2000). Within the

Incorrigible Greeks frame moral judgment is prompted by presenting Greeks as

blameworthy for the financial crisis.As discontent over austerity measures and outrage toward government corruption

grew, Greeks poured into the streets. US news media, however, were almost uniform in

censuring the Greek people for their plight. Time explained how Greece joined the EU ‘‘by

the skin of its teeth,’’ yet the ‘‘decision makers in Athens with responsibility for fiscal policy

continued to blunder’’ by running big deficits (Fox, 2010, p. 24). Newsweek deemed Greece

10 JAMES F. TRACY

Dow

nloa

ded

by [F

lorid

a A

tlant

ic U

nive

rsity

] at 1

9:29

06

May

201

2

as having ‘‘the record for the developed world’s most crooked economy’’ because of an

inability to tax under-the-table economic activities (Theil, 2010a, p. 6). A March NBC Nightly

News piece begins with Brian Williams reminding viewers how the US’s economic setbacks

‘‘are truly global’’ with ‘‘a debt crisis that is shaking [Greece] to the core.’’ Amid scenes of

an Athens protest, the reporter explains how police

fired tear gas at angry demonstrators and dodged Molotov cocktails for the second time

in only two weeks. Tens of thousands of protestors, including nurses, firemen and

teachers, walked off their jobs for 24 hours, angry at painful government budget cuts,

slashed salaries, frozen pensions and higher taxes. (NBC News, 2010a)

Yet the Greeks’ outrage is offset with representatives of the higher market morality.

A Greek official explains, ‘‘The country was spending more than it was earning.’’ An

economics professor likens a default to ‘‘Armageddon.’’ The reporter adds, ‘‘The reckless

spending was further fueled 10 years ago with the launch of a single currency in Europe’’

that led to ‘‘a flood of cheap loans’’ (NBC News, 2010a).

With the events in the first week of May the notion of Incorrigible Greeks became

increasingly valid, with attempts to tie the country’s plight to those familiar to Americans.

‘‘Greece is the General Motors of countries,’’ New York Times columnist Tom Friedman

remarked, because of its ‘‘generous contracts to its unions’’ and early retirement age (ABC

News, 2010c). Remarking on footage of over 100,000 Greeks who ‘‘took to the streets to

protest the country’s financial catastrophe,’’ ABC News (2010d) anchors explained at the

outset how the ‘‘debt crisis half a world away . . . could be affecting your retirement.’’ CBS

News (2010c) reported on the EU/IMF loan package to Greece designed to rescue the

country ‘‘from its self-inflicted wounds, crippling national debt and angry protests that

broke out over an austerity plan to reduce it [sic].’’ CNBC’s Trish Regan compared Greece, a

country ‘‘that didn’t necessarily play by the same economic rules,’’ to a shirking US

mortgagor. ‘‘[T]he banks over in Europe are getting nervous that that sub prime borrower,

Greece, is essentially going to walk away from the mortgage that they owe the bank’’ (NBC

News, 2010d). The lead to a Time profile of an Athens nightclub exemplifies the

Incorrigible Greeks frame: ‘‘Following years of free spending, Greeks find themselves in

deep debt. That hasn’t stopped the party. Keeping the good times alive in Greece’s

bouzouki clubs’’ (Itano, 2010, p. 10).

The Incorrigible Greeks frame also acts as a precursor to and rationale for the

Austerity frame. Time (Joffe, 2010, p. 48) highlighted Germany’s ‘‘tough line with Europe’s

spendthrifts’’ with regard to loan conditions. Likening the eurozone to ‘‘a train stringing

together 16 engines,’’ the PIIGS, by spending lavishly on ‘‘entitlements’’ and public-sector

salaries, are using

too much coal . . . What do you do when you shovel coal and run out of fuel? You

borrow*as the PIIGS have done. The markets have cast their verdict on that. Now,

Greece has to borrow at twice the interest rate that German bonds fetch.

An example of the Incorrigible Greeks and Austerity frames’ subtle mergence may

be found in Newsweek’s comparison of Greece and Ireland’s ability to endure austerity

measures. After the Irish people’s ‘‘wild lending and spending binge ended with a burst

housing bubble and the near collapse of its banks,’’ they acknowledged their mistake with

‘‘a rare understanding that the country’s plight demands sacrifice.’’ The Irish approach

contrasts with some of the other ‘‘PIIGS’’*the ‘‘big-time losers whose feckless behavior

COVERING ‘‘FINANCIAL TERRORISM’’ 11

Dow

nloa

ded

by [F

lorid

a A

tlant

ic U

nive

rsity

] at 1

9:29

06

May

201

2

threatened the future of the entire euro zone . . . There’s no Greek-style fudging or fingerpointing at the demons of Anglo Saxon capitalism’’ (Underhill, 2010).

Austerity

While the Contagion and Incorrigible Greeks frames episodically draw attention to

alleged perils and causes of the crisis, the austerity frame is thematic in nature, using theevent as the basis for a larger discussion of reining in the public sector, with the inevitable

corollary of expanding privatization. ‘‘The meaning of Greece transcends high finance,’’

Newsweek signals in a lead. ‘‘Every advanced society, including the United States, has awelfare state.’’ Yet social programs are irreconcilable with too much debt. ‘‘It’s an open

question whether the collision will cause social and economic turmoil’’ as has been thecase in Greece. Most wealthy countries will eventually face ‘‘unpleasant choices’’ between

taking care of their own citizenry or servicing the loans to ‘‘banks and other investors’’

(Samuelson, 2010, p. 19). Emphasizing the austerity theme, Newsweek asks Papandreou,‘‘Are you prepared to make additional budget cuts, sack public employees, and lower

labor costs?’’ ‘‘We will do whatever we need to do,’’ the Prime Minister responds. ‘‘And this

isn’t puff talk. We’ve already done it. We’re not renewing tens of thousands of contracts inthe public sector. We are moving to close down or merge hundreds of public sector

organizations. We’re shrinking local government, scrapping some 6,000 semi-official

operations. That shows our political will and determination’’ (Samuelson, 2010, p. 19).In the wake of the early May protests and market crash, USA Today suggests

increased taxes and cutbacks in Medicare and Social Security as remedies, reminding

Americans in light of the Greek events that even though their country prints the world’sreserve currency ‘‘they should note the obvious: Debt is debt. If too much Greek

borrowing can send world financial markets into turmoil like that of the past couple of

days, imagine the damage a U.S. debt crisis would inflict’’ (2010, p. 12A). Driving this pointhome, George Will compares Greece to some US state economies that portend a

‘‘collapse’’ of ‘‘a welfare state model, that says you can constantly enlarge government on

a narrower and narrower tax base, producing more and more people dependent on thegovernment’’ (ABC News, 2010e).

Taking an explicit view toward neo-liberal restructuring, Time proposes an array of

measures to ‘‘fix’’ what it deems to be overregulated EU member states. ‘‘Many [investors]remain doubtful that Greece and other euro-zone members . . . can undertake the drastic

fiscal adjustments necessary to avoid defaults or debt restructurings.’’ A solution is ‘‘even

greater integration,’’ letting corporations ‘‘take advantage of a true single market.’’ In oneinstance, Time notes, ‘‘the E.U. has tried for years to pry open national gas and power

markets to more union wide [sic] competition, which could reduce energy prices for

companies, but has faced resistance from member states with large, dominant utilities’’(Schuman, 2010a, pp. 38!41).

Conclusion

By situating consideration of news on the economy in the context of broadereconomic processes this study has sought to examine how such news perpetuates these

very activities. Mainstream US news media reduced the Greek financial crisis to the alleged

12 JAMES F. TRACY

Dow

nloa

ded

by [F

lorid

a A

tlant

ic U

nive

rsity

] at 1

9:29

06

May

201

2

shortcomings of a nation and its people. This was accomplished by presenting the event in

narrative frameworks that draw attention to and define certain phenomena, thereby

setting the stage for the proposal of seemingly commonsensical solutions including

austerity, privatization, and further deregulation. Were these media outlets so inclined in

terms of journalistic practice, another set of frames highlighting the less examined

techniques of investment banks and hedge funds, and their probable collusion with

government actors, might bring about a different set of breakdowns and recommenda-

tions. Restating the neo-liberal formula discussed at the outset, the designs and actions of

financial saboteurs are safely concealed behind a carefully crafted set of cultural

caricatures and seemingly expert rationales that serve to legitimize, normalize, and

perpetuate such processes. By keeping public attention focused on the surface

phenomena of financial crises without probing their deeper causes and the implications

for other advanced economies, major news media all but ensure the increased frequency

and severity of similar crises.The problems commercial news outlets pose for journalism practice and much

needed public awareness of pressing economic concerns are not new. Yet given the scale

of present crises the consequences of this communication breakdown will likely be far

greater. For example, as McChesney (2004) has noted, the Enron and WorldCom debacles

were abetted by mainstream business journalism’s failure to identify and report on the

raging corruption of these entities. Yet all the while alternative news media were pointing

to Enron and WorldCom’s malfeasances that resulted in significant financial losses for

stockholders, pensioners, and taxpayers (McChesney, 2004, p. 90).

Coverage of the Greek debt crisis shares a similar dynamic. Yet given the colossal

stakes*the fate of one or more nation states*the failure of journalism here has far

greater consequences. Advocates of privatization*investment banks, hedge funds, and

sovereign wealth funds*are employing similar if not identical practices in the United

States to privatize highways and other public infrastructure paid for by American

taxpayers over past decades. Without reporting and analysis explaining how such

processes similarly affect individuals of all modern states, the public will lack the

knowledge of and thereby means to understand and defend itself against continued

acts of financial terrorism.

REFERENCES

ABC NEWS (2010a) ‘‘Headline News’’, Good Morning America, 6 May, http://www.lexisnexis.com/

hottopics/lnacademic/, accessed 6 May 2011.

ABC NEWS (2010b) ‘‘Big Plunge; free fall’’, World News with Diane Sawyer, 6 May, http://www.

lexisnexis.com/hottopics/lnacademic/, accessed 6 May 2011.

ABC NEWS (2010c) ‘‘Markets in Turmoil: why Greece matters to us’’, Good Morning America, 6 May,

http://www.lexisnexis.com/hottopics/lnacademic/, accessed 6 May 2011.

ABC NEWS (2010d) ‘‘Markets in Turmoil: US suffers if Greece fails’’, Good Morning America, 6 May,

http://www.lexisnexis.com/hottopics/lnacademic/, accessed 6 May 2011.

ABC NEWS (2010e) ‘‘The Roundtable: the week’s politics’’, This Week, 9 May, http://www.lexisnexis.

com/hottopics/lnacademic/, accessed 6 May 2011.

BAGDIKIAN, BEN (2004) The New Media Monopoly, Boston: Beacon Press.

COVERING ‘‘FINANCIAL TERRORISM’’ 13

Dow

nloa

ded

by [F

lorid

a A

tlant

ic U

nive

rsity

] at 1

9:29

06

May

201

2

BALZLI, BEAT (2010) ‘‘How Goldman Sachs Helped Greece to Mask its True Debt’’, 8 February,

http://www.spiegel.de/international/europe/0,1518,676634,00.html, accessed 16 Novem-

ber 2011.

BENNETT, W. LANCE (2012) News: the politics of illusion, 9th edn, New York: Longman.

BENNETT, W. LANCE and MURRAY, EDELMAN (1985) ‘‘Toward a New Political Narrative’’, Journal of

Communication 35(4), pp. 156!71.

BRATICH, JACK Z. (2008) Conspiracy Panics: political rationality and popular culture, Albany: State

University of New York Press.

CBS NEWS (2010a) CBS Evening News, 6 May, http://www.lexisnexis.com/hottopics/lnacademic/,

accessed 6 May 2011.

CBS NEWS (2010b) ‘‘The Dow Plunges Nearly a Thousand Points, But Rebounds’’, CBS The Early

Show, 7 May, http://www.lexisnexis.com/hottopics/lnacademic/, accessed 6 May 2011.

CBS NEWS (2010c) CBS Evening News, Sunday Edition, 9 May, http://www.lexisnexis.com/

hottopics/lnacademic/, accessed 6 May 2011.

CHAKRAVARTTY, PAULA and SCHILLER, DAN (2010) ‘‘Neoliberal Newspeak and Digital Capitalism in

Crisis’’, International Journal of Communication 4, pp. 670!92.

CHOSSUDOVSKY, MICHEL (2010) ‘‘The Global Economic Crisis: an overview’’, in: Michel

Chossudovsky and Andrew Gavin Marshall (Eds), The Global Economic Crisis: the Great

Depression of the XXI century, Ottawa: Centre for Research on Globalization, pp. 3!60.

CORCORAN, FARREL and FAHY, DECLAN (2009) ‘‘Exploring the European Elite Sphere: the role of the

Financial Times’’, Journalism Studies 10(1), pp. 100!13.

COTTLE, SIMON (2009) Global Crisis Reporting: journalism in the global age, New York: Open

University Press/McGraw Hill.

DEACON, DAVID (2007) ‘‘Yesterday’s Papers and Today’s Technology: digital newspaper archives

and ‘push button’ content analysis’’, European Journal of Communication 22(1), pp. 5!25.

DIXON, HUGO and CHRISTOPHER SWANN (2010) ‘‘Agencies Are Overrated’’, New York Times, 29 April,

p. B2.

DOYLE, GILLIAM (2006) ‘‘Financial News Journalism: a post-Enron analysis of approaches toward

economic and financial news production in the UK’’, Journalism 4, pp. 433!52.

EKATHIMERINI (2011) ‘‘IMF Chief Quotes Put PM on Spot’’, 4 May, http://www.ekathimerini.com/

4dcgi/_w_articles_wsite1_1_04/05/2011_389638, accessed 21 May 2011.

ELK, MIKE (2011) ‘‘How Big Banks Greek-style Schemes Are Bankrupting States Across the US’’, 25

May, Huffingtonpost.com, http://www.huffingtonpost.com/mike-elk/how-big-banks-

greek-style_b_476809.html, accessed 13 June 2011.

ENTMAN, ROBERT M. (2004) Projections of Power: framing news, public opinion, and US foreign policy,

Chicago: University of Chicago Press.

EUROPEAN TRIBUNE (2011) ‘‘The Revelations of Strauss Kahn’’, 6 May, http://www.eurotrib.com/

story/2011/5/4/194747/6846, accessed 11 May 2011.

EWING, JACK and JULIE WERDIGIER (2010) ‘‘Trichet Sides With Advocates of Crackdown on Banks’’,

New York Times, 13 March, http://www.nytimes.com/2010/03/13/business/global/

13trichet.html, accessed 29 September 2011.

FERGUSON, NIALL (2010) ‘‘Euro Trashed: the Greek debt crisis could be the beginning of the end of

Europe’s answer to the dollar’’, Newsweek, 31 May, p. 46.

FOSTER, JOHN BELLAMY and MAGDOFF, FRED (2009) The Great Financial Crisis: causes and

consequences, New York: Monthly Review Press.

FOX, JUSTIN (2010) ‘‘Minor Tragedy’’, Time, 22 February, p. 24.

14 JAMES F. TRACY

Dow

nloa

ded

by [F

lorid

a A

tlant

ic U

nive

rsity

] at 1

9:29

06

May

201

2

GARNHAM, PETER, MALLET, VICTOR and OAKLEY, DAVID (2010) ‘‘Traders Make $8bn Bet Against Euro’’,

Financial Times, 8 Feburary, http://www.lexisnexis.com/hottopics/lnacademic/, 6 May

2011.

GOFFMAN, ERVING (1986) Frame Analysis: an essay on the organization of experience, Cambridge,

MA: Harvard University Press.

GOLDMAN, ROBERT and RAJAGOPAL, ARVIND (1991) Mapping Hegemony: television news coverage of

industrial conflict, Norwood, NJ: Ablex Publishing.

GOSS, BRIAN MICHAEL (2001) ‘‘All Our Kids Get Better Jobs Tomorrow: the North American Free

Trade Agreement in the New York Times’’, Journalism and Communication Monographs

3(1), pp. 3!47.

HACKETT, ROBERT and ZHAO, YHEZH (1998) Sustaining Democracy? Journalism and the Politics of

Objectivity, Toronto: Garamond Press.

HARVEY, DAVID (2005) A Brief History of Neoliberalism, New York: Oxford University Press.

HERTOG, JAMES K. and MCLEOD, DOUGLAS M. (2001) ‘‘A Multiperspectival Approach to Framing

Analysis: a field guide’’, in: Stephen D. Reese, Oscar H. (Eds), Gandy Jr. and August E. Grant

(Eds), Framing Public Life: perspectives on Media and Our Understanding of the Social World,

Mahwah, NJ and London: Lawrence Erlbaum Associates.

ITANO, NICOLE (2010) ‘‘Postcard: Athens’’, Time, 21 June, p. 10.

IYENGAR, SHANTO (1991) Is Anyone Responsible? How television frames political issues, Chicago:

University of Chicago Press.

JOFFE, JOSEF (2010) ‘‘German Rules: Chancellor Angela Merkel is right to take a tough line with

Europe’s spendthrifts’’, Time, International Edition, 12 April, p. 48.

KARABELL, ZACHARY (2010) ‘‘Risk Inverse’’, Time, 24 May, p. 20.

KUMAR, DEEPA (2007) Outside the Box: corporate media, globalization, and the UPS strike, Urbana:

University of Illinois Press.

LICHENSZTEJN, SAMUEL and QUIJANO, JOSE MANUEL (1982) ‘‘The External Indebtedness of the

Developing Countries to International Private Banks’’, in: J.C. Sanchez Arnau (Ed.), Debt

and Development, New York: Praeger Publishers.

LIPPMANN, WALTER (1922) Public Opinion, Harcourt, Brace and Company, Inc.

LOPEZ, LUCIANA (2011) ‘‘IMF Cuts U.S. Growth Forecast: warns of crisis’’, Reuters, 17 June, http://

www.reuters.com/article/2011/06/17/us-imf-idUSTRE75G2VD20110617, 29 September

2011.

LYNCH, DAVID A. (2010a) ‘‘Greece’s Financial Pain Could Ripple Across USA; how Athens handles

its crisis affects our economy’’, USA Today, 10 May, p. 1A.

LYNCH, DAVID A. (2010b) ‘‘Europe’s Debt Woes Still an Albatross on U.S. Markets; ‘It looks like the

policy makers in Europe are just sort of flailing’’’, USA Today, 19 May, p. 6A.

MARTIN, CHRISTOPHER R. (2004) Framed! Labor and the corporate media, New York: Cornell

University Press.

MARTIN, RANDY (2002) Financialization of Daily Life, Philadelphia: Temple University Press.

MCCHESNEY, ROBERT W. (2004) The Problem of the Media: communication politics in the 21st century,

New York: Monthly Review Press.

MILLER, TOBY (2009) ‘‘Journalism and the Question of Citizenship’’, in: S. Allan (Ed.), Routledge

Companion to News and Journalism, London: Routledge, pp. 397!406.

NBC NEWS (2010a) ‘‘Greek Financial Crisis’’, NBC Nightly News, 11 March, http://www.lexisnexis.

com/hottopics/lnacademic/, accessed 6 May 2011.

NBC NEWS (2010b) ‘‘Protests in Greece; stock market report’’, NBC Nightly News, 5 May, http://

www.lexisnexis.com/hottopics/lnacademic/, accessed 6 May 2011.

COVERING ‘‘FINANCIAL TERRORISM’’ 15

Dow

nloa

ded

by [F

lorid

a A

tlant

ic U

nive

rsity

] at 1

9:29

06

May

201

2

NBC NEWS (2010c) ‘‘Overseas Markets Mostly Down This Morning’’, Today, 6 May, http://www.

lexisnexis.com/hottopics/lnacademic/, accessed 6 May 2011.

NBC NEWS (2010d) ‘‘Problems with Euro and European Union Affecting US Stock Market’’, NBC

Nightly News, 22 May, http://www.lexisnexis.com/hottopics/lnacademic/, accessed 6 May

2011.

NEUMAN, W. RUSSELL, JUST, MARION R. and CRIGLER, ANN N. (1992) ‘‘Common Knowledge: news and the

construction of political meaning’’, Chicago: University of Chicago Press.

PALAST, GREG (2002) The Best Democracy Money Can Buy: the truth about corporate cons,

globalization, and high finance fraudsters, New York: Penguin Group.

PERKINS, JOHN (2004) Confessions of an Economic Hit Man, San Francisco: Berrett-Koehler

Publishers.

PETRAS, JAMES (2010) ‘‘Greece: the curse of three generations of Papandreou’s’’, The James Petras

Website, 23 March, http://petras.lahaine.org/articulo.php?p"1800&more"1&c",

accessed 21 June 2011.

PEW RESEARCH CENTER (2008a) ‘‘Growing Rich!Poor Divide in Affording Necessities: economic

discontent deepens as inflation concerns rise’’, Washington, DC: Pew Research Center for

the People & the Press, http://www.people-press.org/files/legacy-pdf/395, accessed 29

September 2011.

PEW RESEARCH CENTER (2008b) ‘‘News Interest Index Omnibus Survey, Q.3: ‘Did you follow [reports

about the condition of the U.S. economy] very closely, fairly closely, not too closely, or

not at all closely?’’’, Washington, DC: Pew Research Center for the People & the Press,

http://www.people-press.org/files/legacy-questionnaires/526.pdf, accessed 29

September 2011.

PUETTE, WILLIAM J. (1992) Through Jaundiced Eyes: how the media view organized labor, New York:

Institute for Labor Research.

PULLMAN, SUSAN, KELLY, KATE and MOLLENKAMP, CARRICK (2010) ‘‘Hedge Funds Try ‘Career Trade’

Against Euro’’, Wall Street Journal, 26 February, http://www.lexisnexis.com/hottopics/

lnacademic/, accessed 6 May 2011.

ROJECKI, ANDREW (1999) Silencing the Opposition: antinuclear movements & the media in the Cold

War, Urbana: University of Illinois Press.

SAMUELSON, ROBERT J. (2010) ‘‘The Real Greek Tragedy; why this is just the opening act’’,

Newsweek, 1 March, p. 19.

SCHUMAN, MICHAEL (2010a) ‘‘How to Fix Europe’’, Time, 12 May, pp. 38!41, http://www.lexisnexis.

com/hottopics/Inacademic/, accessed 6 May 2011.

SCHUMAN, MICHAEL (2010b) ‘‘Ragin’ Contagion’’, Time, 17 May, p. 18.

SCHUMAN, MICHAEL (2010c) ‘‘We’re Eurosceptic’’, Time, 31 May, p. 19.

SEMETKO, HOLLI A. and PATTI, M. VALENBURG (2000) ‘‘Framing European Politics: a content analysis of

press and television news’’, Journal of Communication 50(2), pp. 93!109.

SHELL, ADAM (2010) ‘‘It Takes Guts to Stomach Today’s Volatility: swings scare investors into

regrettable actions’’, USA Today, 13 May, p. 3B.

SHERIDAN, BARRETT (2010) ‘‘Greece’s Crisis Smoke Screen’’, Newsweek, 22 March.

SLATER, JOANNA, ZUCKERMAN, GREGORY and BRYAN-LOW, CASSELL (2009) ‘‘Hedge Funds Make Some

‘Piigs’ Pay*now they expand their bets of financial trouble in euro-zone’s weaker

members; S&P hits Spain’’, Wall Street Journal, 10 December, http://www.lexisnexis.com/

hottopics/lnacademic/, accessed 6 May 2011.

16 JAMES F. TRACY

Dow

nloa

ded

by [F

lorid

a A

tlant

ic U

nive

rsity

] at 1

9:29

06

May

201

2

STORY, LOUISE, LANDON, THOMAS and SCHWARTZ, NELSON D. (2010) ‘‘Wall St. Helped to Mask Debt

Fueling Europe’s Crisis’’, New York Times, 14 February, http://www.lexisnexis.com/

hottopics/lnacademic/, accessed 6 May 2011.

THE ECONOMIST (2010) ‘‘Who Pays the Bill? dealing with budget deficits’’, 6 March, http://www.

lexisnexis.com.ezproxy.fau.edu/inacui2api/delivery/, accessed 10 May 2011.

THEIL, STEFAN (2010a) ‘‘The Long Shadow of Greece’’, Newsweek, 8 March, p. 6.

THEIL, STEFAN (2010b) ‘‘Greece May Not Be the End of It’’, Newsweek, 10 May, p. 7.

TIME (2010) ‘‘The World: 10 essential stories’’, 10 May, pp. 24!5.

TOBRAS, KIRKAKOS (2010) ‘‘Interview with Max Keiser’’, Keiser Report 102, 9 December, http://www.

youtube.com/watch?v"7zXxwYt737o.

TOBRAS, KIRKAKOS and NOULAS, GEORGE (2010) ‘‘Criminal Fraud Charge Report Against Speculators

and Their Greek Accomplices and Partners’’, http://www.stopspeculators.gr/, accessed 21

June 2011.

TOURI, MARIA (2008) ‘‘News Blogs: strengthening democracy through conflict prevention’’, Aslib

Proceedings 61(2), pp. 170!84.

UNDERHILL, WILLIAM (2010) ‘‘The Anti-Greece: why Dublin isn’t burning like Athens’’, Newsweek,

International Edition, 19 May, http://www.lexisnexis.com/hottopics/lnacademic/,

accessed 6 May 2011.

USA TODAY (2010) ‘‘Greek Debt Crisis Offers Preview of What Awaits U.S’’, 6 May, p. 12A.

James F. Tracy, School of Communication and Multimedia Studies, Florida Atlantic

University, Culture & Society Building 220, 777 Glades Road, Boca Raton, FL 33431,

USA. E-mail: [email protected]

COVERING ‘‘FINANCIAL TERRORISM’’ 17

Dow

nloa

ded

by [F

lorid

a A

tlant

ic U

nive

rsity

] at 1

9:29

06

May

201

2