CORPORATE GOVERNANCE AND PROFITABILITY OF LISTED COMPANIES A CASE STUDY OF BANK OF BARODA (BOBU)...

106

CORPORATE GOVERNANCE AND PROFITABILITY OF LISTED COMPANIES A CASE STUDY OF BANK OF BARODA (BOBU) UGANDA MBARARA BRANCH, MBARARA DISTRICT BY MARIAM BIRUNGI 2011/BBA/098/PS A RESEARCH REPORT SUBMITTED TO THE INSTITUTE OF MANAGEMENT SCIENCE IN PARTIAL FULFILLMENT OF THE REQUIREMENTS FOR THE AWARD OF BACHELOR’S DEGREE OF BUSINESS ADMINISTRATION OF MBARARA UNIVERSITY OF SCIENCE AND TECHNOLOGY MAY, 2014

Transcript of CORPORATE GOVERNANCE AND PROFITABILITY OF LISTED COMPANIES A CASE STUDY OF BANK OF BARODA (BOBU)...

CORPORATE GOVERNANCE AND PROFITABILITY OF LISTED COMPANIES

A CASE STUDY OF BANK OF BARODA (BOBU) UGANDA

MBARARA BRANCH, MBARARA DISTRICT

BY

MARIAM BIRUNGI

2011/BBA/098/PS

A RESEARCH REPORT SUBMITTED TO THE INSTITUTE OF MANAGEMENT SCIENCE IN

PARTIAL FULFILLMENT OF THE REQUIREMENTS FOR

THE AWARD OF BACHELOR’S DEGREE OF BUSINESS

ADMINISTRATION OF MBARARA UNIVERSITY

OF SCIENCE AND TECHNOLOGY

MAY, 2014

DECLARATION

I hereby declare that, this is my original piece of work which is as a

result of my tireless effort into the research so as to ensure

reliability of information. It has never been submitted for the award

of a degree or diploma in any university or higher institution of

learning except where references to other research reports have been

made.

Signature……………………. Date……………………………

BIRUNGI MARIAM

2011/BBA/098/PS

APPROVAL

This research report has been submitted for examination with my

approval as the university supervisor.

Signature…………………………… ……………………………..

ASSOC. PROF. CHARLES TUSHABOMWE -KAZOOBA DATE

ii

DEDICATION

I declare this research report to my beloved father Mr.kasaija Martin.

Thank you for the love you have always shown to sacrifice the small

meager resources for my academic success and the advice and

inspiration during my struggle. I am really grateful to you and may the

lord reward you abundantly.

iii

ACKNOWLEGDEMENT

Firstly, to God for inspiration, strength and vision to complete my

course, wisdom and understanding. I am therefore grateful to Him. “If

you want something very badly, you can achieve it, it may take patience, very

hard work, a real struggle, and along time but it can be done, that much faith is a

prerequisite of any undertaking, artistic or otherwise ” margo jones (1913-1955).

I would sincerely like to thank my supervisor Assoc. Prof. Charles

Tushabomwe -Kazooba whose commitment, relentless support and

guidance helped me to sew together the threads of my research. Your

constant encouragement showed me that “ by believing passionately in something

that does not yet exist, we create it. ” (Nikos Kazantzakis). So, to you I am

forever grateful. I cannot fail to appreciate all my Lecturers who have

imparted knowledge and skills since year one, and provided constant

iv

guidance towards my academic career during this course. May God bless

you all. More appreciation goes to you my father kasaija martin and

brother kerathum Juma for your love and financial support and the words

of wisdom and encouragement at the university.

I would like to also show my gratitude to all the staff of Bank of Baroda

Mbarara Branch who rendered me access and assisted me with the data

necessary in the compilation of this report you have really made this a

success. I am indeed so grateful to all my dear friends, Golden,

SebAlright, Esau Muhwezi, James Bwambale and Natasha kamwine for the

love and academic support. May the lord richly bless you.

v

TABLE OF CONTENTS

DECLARATION....................................................i

APPROVAL.......................................................i

DEDICATION....................................................ii

ACKNOWLEGDEMENT..............................................iii

LIST OF TABLES..................................................ix

LIST OF ABBREVIATIONS (ACRONYMS)................................xi

ABSTRACT.....................................................xii

CHAPTER ONE:INTRODUCTION........................................1

1.0 Introduction................................................1

1.1 Background of the study.......................................1

1.2 Motivation of the study.......................................5

1.3. Statement of the problem.....................................6

1.4. Objectives of the study......................................6

1.5. Research questions..........................................6

1.6. Scope of the study...........................................7

1.7 Significance of the study.....................................8

LITERATURE REVIEW..............................................10

2.1 History of Corporate Governance..............................10

2.1.1Conceptual meaning of corporate governance..................10

vi

2.2 Elements of corporate governance systems.....................12

2.2.1 Board size................................................12

2.2.2 Board roles...............................................13

2.2.2.1 Policy and decision making...............................13

2.2.2.2 Strategizing role.......................................13

2.2.2.3 Monitoring and control..................................14

2.2.2.4 Advice and counsel......................................14

2.2.3 Board effectiveness.......................................14

2.2.3.1 Committees.............................................15

2.2.3.2 Skills and knowledge (Management experience).............15

2.2.3.3 Risk Management.........................................16

2.2.3.4. Delegation............................................16

2.2.3.5 Information and communication...........................17

2.3. Definition of profitability................................17

2.3.1 Measuring profitability...................................18

2.3.2 Elements of profitability.................................18

2.3.2.1 Cost control............................................18

2.3.2.2. Revenue/ Turnover adequacy.............................18

2.3.2.3. Required rate of return.................................19

vii

2.3.2.4. Market share...........................................19

2.3.2.5 Pricing................................................19

2.3.2.6. Entry barriers.........................................19

2.3.2.7. Asset adequacy.........................................20

2.4. Relationship between Corporate Governance & Profitability level

..............................................................20

2.4.1. Relationship between Board roles and Profitability level.. . 21

2.4.2. Relationship between monitoring and control and Profitability

levels........................................................21

2.4.3. Relationship between Board size and Profitability level....21

2.4.4. Relationship between Policy and Decision making and

Profitability.................................................21

2.4.5. Relationship between strategizing role and profitability

level.........................................................21

2.4.6. Relationship between Board effectiveness and Profitability. 22

2.5. Conclusion................................................22

RESEARCH METHODOLOGY...........................................23

3.0Introduction...............................................23

3.1. Research design............................................23

3.2. Study population...........................................23

3.3. Sampling..................................................23

viii

3.3.1. Sampling size and Sampling Procedure......................23

3.4. Sources of data............................................24

3.4.1. Primary source...........................................24

3.4.2. Secondary source.........................................24

3.5. Data collection instruments................................24

3.5.1. Questionnaire...........................................24

3.5.2. Interview...............................................25

3.5.3 Documentation/ secondary data.............................25

3.6 Reliability and validity....................................25

3.7. Data collection procedure..................................26

3.8. Measuring study variables..................................26

3.9 Data Presentation and Analysis...............................26

3.10 Ethical Consideration......................................27

3.11 Limitations of the study....................................27

CHAPTER TWO: PRESENTATION, DISCUSSION AND ANALYSIS OF FINDINGS.....29

2.0 Introduction...............................................29

2.2 Corporate Governance systems................................29

2.2.4 Whether board sets strategic objectives for management to

implement.....................................................32

ix

4.2.2 Whether well defined strategy keeps the company in the right

direction.....................................................33

2.2.2 Whether board monitors and reviews the implementation of

strategic plan and objectives...................................34

4.2.1 Whether board members provide advice and counsel to the

Management....................................................35

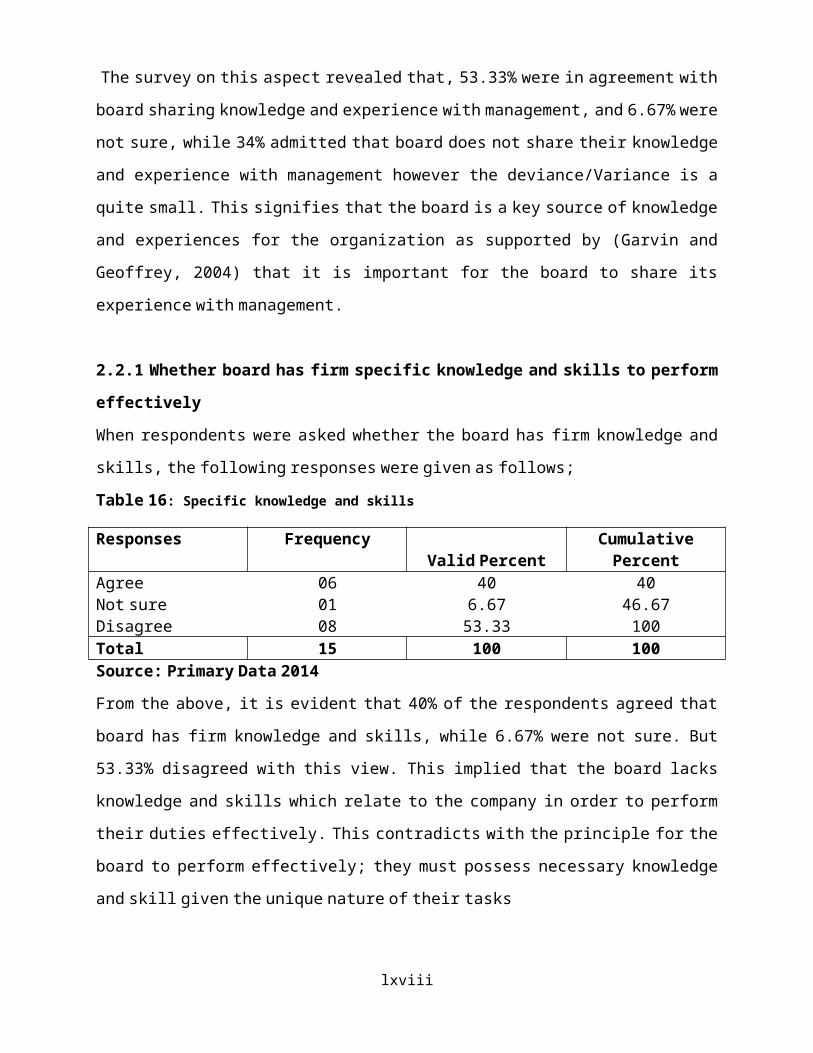

2.2.1 Whether board has firm specific knowledge and skills to perform

effectively...................................................37

2.2.3 Board members integrate knowledge of the firm with their

expertise to accomplish tasks...................................38

2.4 Establishment of the relationship between Corporate Governance

and Profitability level.........................................45

CHAPTER THREE: SUMMARY, CONCLUSIONS AND RECOMMENDATIONS...........47

3.0 Introduction...............................................47

3.1 Summary of major findings of the study........................47

3.1.1 Findings on demographic characteristics of respondents......47

3.1.3 Findings on profitability level............................48

3.1.4 Findings on the relationship between corporate governance and

profitability level............................................49

3.2 Conclusions................................................49

3.3 Recommendations............................................49

3.3.1 Recommendations on corporate governance....................50

x

3.3.2 Recommendations on profitability level.....................51

3.4 Areas for further Research...................................52

REFERENCES....................................................53

APPENDIX I: QUESTIONNAIRE.......................................58

APPENDIX II: WORK PLAN..........................................62

APPENDIX III: ESTIMATED BUDGET..................................63

APPENDIX IV: INTRODUCTORY LETTER................................64

xi

LIST OF TABLES Table 1: Maximum level for board positions.......................29

Table 2 : Effectiveness of small sized boards.....................30

Table 3: Directors increasing pool of expertise and resource pool...30

Table 4: Information for decision making.........................31

Table 5: Board developing methods for decision making.............31

Table 6 : Management allowed taking part in decision making process. 32

Table 7: Setting strategic objectives for implementation..........32

Table 8: Keeping in the right direction...........................33

Table 9: Management involvement in strategic planning process.....33

Table 10: Monitoring internal system.............................34

Table 11 : Monitoring and reviewing strategic plan and objectives...34

Table 12: Monitoring performance of the firm......................35

Table 13: Providing advice and counsel...........................35

Table 14 :Advising the CEO.......................................36

Table 15 : Sharing knowledge and experience.......................36

Table 16: Specific knowledge and skills..........................37

Table 17: Training and supervision...............................37

xii

Table 18 :Integrating knowledge of the firm with expertise.........38

Table 19 :Ensuring quality decision making.......................38

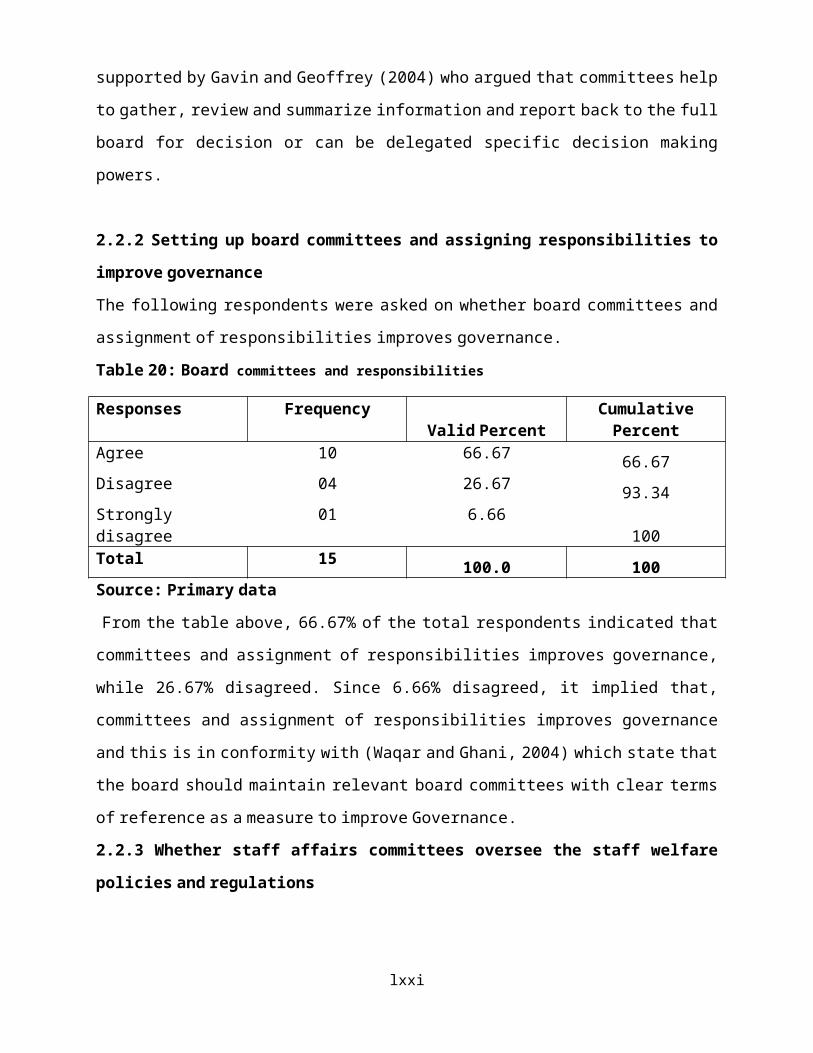

Table 20: Board committees and responsibilities..................39

Table 21: Staff affairs and welfare policies and regulations.......39

Table 22 : Appropriate policies to moderate risk..................40

Table 23 :Risk management identification.........................40

Table 24 :Regular review of risk management.......................41

Table 25 :Boosting morale of employee and management..............41

Table 26 : Authority and responsibilities........................42

Table 27: Articulating and documenting delegated tasks............42

Table 28 : Revenue targets......................................43

Table 29 :Cost control measures to minimize cost..................43

Table 30: Optimal use of assets..................................44

Table 31 : Role of Required Rate of Return (RRR)....................44

Table 32 : Competition with other institutions in the business......45

Table 33: Responses on the relationship between Corporate Governance

and Profitability level.........................................45

xiii

LIST OF ABBREVIATIONS (ACRONYMS)

ACCA : ASSOCIATION OF CHARTED CERTIFIED ACCOUNTANT.

BIS : BANK FOR INTERNATIONAL SETTLEMENTS.

BOBU : BANK OF BARODA UGANDA.

BOD : BOARD OF DIRECTORS.

BOU : BANK OF UGANDA

CAMEL : CAPITAL ADEQUACY MODEL

CAR : CAPITAL ADEQUACY RATIO

CEO : CHIEF EXECUTIVE OFFICER

CK : CORE CAPITAL

CLERP : CORPORATE LAW ECONOMIC REFORM PROGRAM PAPER

CPA : CERTIFIED PUBLIC ACCOUNTANTS

GBL : GREENLAND BANK

ICB : INTERNATIONAL CREDIT BANK

xiv

ICGU : INSTITUTE OF CORPORATE GOVERNANCE

ICSA : INSTITUTE OF CHARTED SECURITIES AND ADMINISTRATION

MD : MANAGING DIRECTOR

NPA : NON PERFORMING ASSETS

ROA : RETURN ON ASSETS

ROE : RETURN ON EQUITY

SPSS : STATISTICAL PACKAGES FOR SOCIAL SCIENCES

USAID : UNITED STATES AGENCY FOR INTERNATIONAL DEVELOPMENT

ABSTRACT

The research was carried out to determine the relationship between

Corporate Governance Systems and the level of profitability level of

BOBU limited using a case study of Mbarara Branch- Mbarara

Municipality on Mbarara High Street in Mbarara District as a case

study. The research arose due to the deteriorating profitability level

of BOBU. The objectives of the study were to examine the corporate

governance systems in Bank of Baroda Uganda, to establish

profitability levels in Bank of Baroda Uganda, and to establish the

relationship between corporate governance and profitability level in

Bank of Baroda Uganda.

The research was carried in Bank of Baroda, Mbarara Branch in Mbarara

Municipality. Sources of data were both primary and secondary. Primary

data was gathered using questionnaires while secondary data was got

from documents and journals obtained from libraries, professional

xv

journals from the internet, financial reports and published

literature like text books. A descriptive and analytical research

design was used employing both qualitative and quantitative approach,

to establish the relationship between the two variables and this

assisted the researcher in arriving at an appropriate conclusion.

This study required the use of computer applications such as Ms Excel,

Ms Word that helped in analyzing and editing data. Spearman’s rank

correlation coefficient was used to determine the magnitude of the

relationship and prediction of profitability level of Bank of Baroda

Uganda mbarara.The findings of the study revealed that corporate

governance has got a significant influence on the profitability of

Bank of Baroda Uganda as an organization in question which was

represented by a strong positive relationship of r=0.900 between the

study variables.

It is thus within Bank of Baroda’s role to set and establish policies

and procedures that can stand a test of time. There is need for constant

reviews and improvements amongst board members and their employees to

help in the achievement of the set target profits. Efforts should

further be devoted to training and supervision of the Bank’s staff to

help improve their competencies and the company’s profitability too.

From the findings, the researcher concluded that corporate governance

greatly affects profitability of companies rendering the fact that

these two variables are correlated. Thus for companies to perform

effectively, corporate governance systems should be set.

xvi

CHAPTER ONE

INTRODUCTION

1.0 Introduction

This chapter covers the background of the study, statement of the

study, objectives of the study, research questions, description of the

study area and scope of study, significance of the study and

conclusion.

1.1 Background of the study

The International financial landscape is changing rapidly; economies

and financial systems are undergoing traumatic years. Globalization

and technology have continuing speed, financial arenas are becoming

more open, new products and services are being invented and marketed

and regulators everywhere are scrambling to assess the changes and

master the turbulence. An international wave of mergers and

acquisitions has swept the banking industry as boundaries between

financial sectors and products have blurred dramatically. In this

brave new world, one fact remains unchanged. The need for countries to

have sound resilient banking systems and strong banks with good

Corporate Governance then will use competition to strengthen and

upgrade their institutions that will survive in an increasingly open

environment (Kaheeru, 2001).

According to James Wolfensohn former World Bank Group President,

Corporate governance is about promoting corporate fairness,

transparency and accountability (Financial Times, 1999). Governance

is a requisite for survival and a gauge of how predictable the system

xvii

for doing business in any country is. In developing countries, the

importance of governance is to strengthen the foundation of society

and chip into the global economy. Governance is concerned with

structures and processes for decision making, accountability,

control and behavior at the top of organisations. Corporate governance

is a concept that involves practices that entail the organization of

management and control of companies. Corporate governance is the means

by which an organization is directed and controlled. In broad terms,

corporate governance refers to the processes by which organizations

are directed, controlled and held accountable. Corporate governance

encompasses authority, accountability, stewardship, leadership,

direction and control exercised in corporations. It reflects the

interaction among those persons and groups, which provide resources to

the company and contribute to its performance such as shareholders,

employees, creditors, long-term suppliers and subcontractors

(Brownbridge, 2007).

Corporate governance helps in defining the relation between the

company and its general environment, the social and political systems

in which it operates. Corporate governance is linked to economic

performance. The way management and control are organized affects the

company's performance and it's long run competitiveness. It

determines the conditions for access to capital markets and the degree

of investors‟ confidence (Brownbridge, 2007). Corporate governance

is the set of processes, customs, policies, Laws and institutions

affecting the- way a corporation is directed, administered or

controlled (Knell 2006). Corporate governance also includes the

xviii

relationships among the many players involved (the stakeholders) and

the goals for which the corporation is governed. The principal players

are the shareholders, management and the board of directors. Other

stakeholders include employees, suppliers, customers, bankers and

other lenders, regulators, the environment and the community at large

(Knell 2006).

On a Global scale, corporate governance largely concentrates in

management of Financial Institutions. Efficient corporate governance

greatly helps a nation’s economy to grow. However, inefficiencies in

corporate governance grossly lead to economic crises and economic

slowdown. (Brandil Micheal; 2011): The aims of corporate governance

are to promote achievement of the highest sustainable economic growth

and raise standard of living, while maintaining financial stability,

and thus contribute to the development of the world economy, OECD

(2004). The principles of corporate Governance include: a) Ensuring

existence of a Basis for an Effective Corporate Governance Framework

to promote transparent and efficient markets. This should be

consistent with the rule of law and clearly articulate the division of

responsibilities among different supervisory, regulatory and

enforcement authorities; b) Observance of the Rights of Shareholders

and Key Ownership Functions; 1) Secure methods of ownership

registration; 2) convey or transfer shares; 3) obtain relevant and

material information on the corporation on a timely and regular basis;

4) participate and vote in general shareholder meetings; 5) elect and

remove members of the board; and 6) share in the profits of the

corporation; c) Observance of Equitable Treatment of Shareholders to

xix

ensure the equitable treatment of all the shareholders, including

minority and foreign shareholders. This also includes the opportunity

for all stakeholders to obtain effective redress for violation of

their rights; d) The Role of Stakeholders in Corporate Governance

should recognize the rights of stakeholders established by law or

through mutual agreements. This should also encourage active co-

operation between corporations and stakeholders in creating wealth,

jobs, and the sustainability of financially sound enterprises; e) a

framework that ensures timely, transparent, and accurate disclosure

on all material matters regarding the corporation, including the

financial situation, performance, ownership, and governance of the

company; f) The Responsibilities of the Board. The corporate

governance framework should ensure the strategic guidance of the

company, the effective monitoring of management by the board, and the

board’s accountability to the company and the shareholders.

In Uganda, the factors responsible for poor corporate performance

especially in banks emanate from lack of transparency, accountability

and poor ethical conduct (Kibirango,1999). Commercial banks failures

have been linked to self-inflicted causes resulting from bank owners;

ICB(International Credit Bank), GBL(Greenland Bank), and Coop Bank

were afflicted with the one-man management syndrome of corporate

governance exemplified by Thomas Kato (ICB), Sulaiman Kiggundu (GBL)

and USAID (Co-op Bank). There was no separation between senior

management and the board of directors in ICB or GBL and that management

took little account of depositor’s interests. The board of ICB

consisted of 4 members of the Kato family including a six -year- old

xx

child. GBL had two boards of directors but neither had a say in the

running of the bank for instance ICBs audit report cited connected or

insider lending to a tune of UShs. 4 billion. In the case of GBL the July

1998 Bank of Uganda (BOU) Audit Report stated that as per

30th June 1998, Insider lending stood at Ushs.22, 722 million

representing 47 percent of customer deposits and accounting for 55

percent of the total loan portfolio yet the maximum amount the bank

could lend according to FIS 1993 was Ushs.975 million only. The report

also cited that in most cases credit was extended on sole instructions

of then Managing Director without any or minimal documentation (BOU,

1999).

According to shliefer et al.., (1997), corporate governance is about

promoting fairness and transparency to ensure satisfactory return on

the investment. It is also defined as a system by which businesses and

corporations are directed and controlled (Oola, 2002; Institute of

Corporate Governance Manual on Corporate Governance, 2005) and is

concerned with distribution of rights and responsibilities among

different participants in the management of the corporation. Well

defined and enforced corporate governance provides a structure that,

at least in theory, works for the benefit of everyone concerned by

ensuring that the enterprise adheres to accepted ethical standards and

best practices as well as to formal laws.

To that end, organizations have been formed at the regional, national

and global levels. In recent years, corporate governance has received

increased attention because of high-profile scandals involving abuse

xxi

of corporate power and in some cases, alleged criminal activity by

corporate officers. Corporate Governance comprises of company board

size, board roles, policy and decision making, board effectiveness and

compliance with laws and best practices (larker et al, 2005).

Corporate governance systems are founded on pillars of board sizes,

board role and board effectiveness.

Profitability refers to the ability of a company to generate returns

for the shareholders in light of the investment committed (Frank,

2002). It is further defined as the efficiency of a company to yield a

targeted level of income. It is measured as gross revenue less expenses

and tax (ACCA, 2002). It is the most used and preferred financial

performance indicator for companies. Profitability is a primary goal

of the business ventures, without which the business will not exist in

the long run (Don, 2006). It is a revealing indicator of a company’s

competitive position in markets and its quality of management (Ariho,

2006). Profitability is the most important variable for determining

business performance, as other factors and variables tend to be

subjective (Balunywa, 1992). It provides a follow up of how resources

are being managed and utilized.

Profitability is shown by the cost control, required rate of return,

pricing, asset adequacy, and revenues/turnover (Hampton, 2001)

market share and entry barriers. These show that the firm is making

profits. Corporate profits may be viewed as the return to share holders

for their invested resources. The employees of the institution should

be held to occupy a strategic role in corporate success. Policy agendas

xxii

should be formulated to form a relationship between the employees and

the Board of Directors to support and achieve the business objectives.

Thus, due to proper Corporate Governance that has been seen in Bank of

Baroda, there has been a notable rise in the Bank’s net profits which

increased by 23.95% in 2010 to shs 16.7b, up from shs 13.4b earned in

2008, (New vision: Tuesday, 2nd March 12, 2010). Deposits also

increased to shs 271.7b, up from shs 214.1b collected in 2008, while

total income rose to shs 445b, translating into a 20.49% growth. It is

also noted that customer loyalty was a key factor for Bank of Baroda

(Uganda) progress.

In a bid to improve corporate governance practices, directors face

various huddles throughout their tenure to balance numerous

conflicting demands by shareholders, staff and regulators and manage

conflict of interest. (The exchange, 2007). The major challenges

involve, operating costs, high taxes levied (Ariho, 2006) changes in

share prices, interest rate risk (Bank of Baroda (UG) Annual report

2009.) capital inadequacy, changes in technology, loss of

shareholders and low sales volumes. These major come about due to poor

corporate governance practices such as lack of responsibility by Board

members, poor communication means, poor advertising programs, poor

technology and the weak legal regulatory system.

1.2 Motivation of the study The last ten years have seen the emergence of a new field within the

corporate governance literature dedicated to the corporate

governance of banks, which has especially focused on Uganda banks.

This research report contributes to this stream of research by

xxiii

studying diverse features of the corporate governance of banks in the

Uganda Commercial Bank case. There are two main reasons why we should

study the corporate governance of banks: its relevance and its

possible specificity. First, banks are important. While efficient

banks can stimulate the prosperity and growth of the whole economy,

banking crises are able to destabilize the economic and political

situation of nations. This central role that banks play in any economy

makes the study of their corporate governance a fundamental issue, not

only from a private, but also from a public viewpoint. Second,

corporate governance in banking might be different than in other

industries. It has been argued that one reason behind the difficulty of

identifying the effect of corporate governance on performance may be

the existence of different optimal structures across industries which

would be even more patent in the presence of regulation. Corporate

governance has a central role in sustainable wealth creation,

particularly in the area of the private sector development, as it

establishes transparency in enterprises while ensuring corporate

accountability. This in turn helps to build the confidence required

for development and operation of efficient financial markets. At the

level of individual firms, strengthened governance facilitates

access to diverse forms of business finance. Thus the motivation of the

study was intended to establish the relationship between corporate

governance and profitability of Bank of Baroda (Uganda) Mbarara

branch.

1.3. Statement of the problem.

In recent years, the profitability level of Bank of Baroda (Uganda)

Mbarara branch has been low and declining. Although Bank of Baroda

xxiv

(Uganda) Mbarara branch has tried to set up various rules, and

regulations to attract and retain shareholders, reduce share prices,

follow listing rules, carry out massive advertising programs,

improved technology, good communication channels, conforming to

international standards and encouraging responsibility , the company

still continues to evidence a decline in the profitability levels.

This could be due to poor corporate governance problems arising out of

mis-management of the company, poor communication means, weak legal

and regulatory systems, poor advertising mediums caused by poor

technology and generally lack of responsibility. In persistence of

the above situation, the company may face operational problems such as

excessive borrowing, loss of business partners and customers,

excessive borrowing and under capitalization which might threaten its

long run survival amidst the ever increasing competition and may face

closure.

1.4. Objectives of the study

This study was based on the following objectives

i. To examine the corporate governance systems in Bank of Baroda (Uganda) Mbarara branch.

ii. To establish profitability levels in Bank of Baroda (Uganda) Mbarara branch.

iii. To establish the relationship between corporate governance and profitability levels in Bank of Baroda (Uganda) Mbarara branch.

1.5. Research questions

This research was set to answer the following research questions:

xxv

i. What are the corporate governance systems in Bank of Baroda

(Uganda) Mbarara branch?

ii. What is the profitability level of Bank of Baroda (Uganda)

Mbarara branch?

iii. What is the relationship between corporate governance and

profitability in Bank of Baroda (Uganda) Mbarara branch?

1.6. Scope of the study

The study was limited to Bank of Baroda (Uganda) Mbarara Branch, in

Mbarara District. This was because of the convenience and familiarity

of the location to the researcher. Mbarara Branch in Mbarara

municipality in Mbarara district Mbarara town has a number of streets

which include Mbarara High Street, Mbaguta Street, Bishop Willis

Street Garage Street, Markhansingh Street, Bulemba Road and Bucunku

Street. Mbarara town is located about 266 kilometres (165 mi)

southwest of Kampala. Population Estimates of Ugandan Cities and Towns

(2002 and 2008).

The current study focuses on the corporate governance as an

independent variable in terms of board size, policy and decision

making, board roles in terms of monitoring and control, advice and

counsel, board effectiveness in terms of skills and knowledge,

committees, delegation and risk management. The study will also

acknowledged profitability as a dependent variable was measured using

the cost control, turnover, assets, pricing, required rate of return

as well as market share.

xxvi

This study was to cover the period between 2010 up to 2013 for

provision of updated information. The area scope was limited to only

Bank of Baroda (Uganda) Mbarara Branch, in Mbarara municipality to

avoid too much complexity in research findings and also Mbarara

municipality having many commercial banks that can enable access to

the information needed by the researcher.

Table 1 Summery of the financial statement (2008 to 2013)

PATICULARS 2010

(Shs.’000)

2011

(Shs.’000)

2012

Shs.’000)

2013

Shs.’000)

After tax profit 22,588,800 28,191,520

29,471,732 30,883,725

Total assets 252,801,140 256,595,450

948,676,593 709,176,711

Net loan andadvances

226,324,000 293,241,000

61,722,194 61,085,712

Deposits 1,559,331 26,735,652

647,540,368 524,301,572

Retained earnings 70,215,003 82,306,2 123,576,288 111,418

xxvii

69 ,571

Source: financial statement from Bank of Baroda Uganda Limited

(www.bankof baroda.ug/reports/barodaFS-2010-2013)

1.7 Significance of the study

The study will help to make contribution in terms of knowledge for

policy makers and regulators in areas of corporate governance and

profitability levels of Bank of Baroda (Uganda) Mbarara branch.

The study also will provide alternatives that form a foundation of

other corporate governance research for scholars in various

institutions.

The resolutions and recommendations of this research may help the

corporate directors and managers in implementing efficient and

effective corporate governance practices to archive target profits.

The study will help the researcher to gain skills of handling research

issues. This helps the researcher in pursuance of further studies and

in office.

The study will identify other areas of corporate governance and

profitability where not much research has been made.

The study will generate data that will contribute to the formulation of

appropriate corporate governance policies by the ministry of

finance, planning and economic development.

xxviii

The study will provide a strategy that will help improve the financial

performance of tropical bank of Africa in Uganda.

The study will provide a basis on how to improve the financial

performance of other commercial banks in Uganda.

The study will provide a basis for further research in corporate

governance and performance of commercial banks in Uganda.

LITERATURE REVIEW 2.0 Introduction

xxix

This critically reviews the existing literature on the subject of

corporate governance and profitability the theoretical framework was

based on various perspectives of corporate governance systems which

included board roles, board size and board effectiveness and the

theories involved in functional profitability performance such as

cost control among others and the entire relationship between

corporate governance and profitability

2.1 History of Corporate Governance

The origins of corporate governance go back to thousands of years; when

ownership and management of enterprises were first separated thus the

owners had a need for mechanism to monitor the performance of managers.

The concept of stewardship and the role of the auditor as someone would

check that proper stewardship had taken place, emerged from this

separation of ownership and management. Corporate governance has

emerged as a key issue in the economic well being of countries and

companies. Africa in 2004 posted a brilliant growth rate and projected

brighter times ahead because some countries effected brighter times

ahead because some countries effected some regulatory reforms and

maintained good governance ( national informant ; issue 11 ,wed 25-31

may 2005). Globalization, information and communication technology,

and financial reporting requirements have driven corporate

governance to the centre stage.

2.1.1 Conceptual meaning of corporate governance

Institute of corporate governance Uganda (ICGU) defines corporate

governance as the system by which companies and corporations are

directed and controlled .this definition recognizes that any

xxx

enterprise whether public or private is entrusted with the power and

must to adhere to established principles and practices governing the

apportionment and exercise this power .ICGU has noted that the current

global economic environment is grounded in free trade ,significant

private sector influences mind market driven economic development .

Corporate governance has a central role in sustainable wealth

creation, particularly in the area of the private sector development,

as it establishes transparency in enterprises while ensuring

corporate accountability .This in turn helps to build the confidence

required for development and operation of efficient financial

markets. At the level of individual firms, strengthened governance

facilitates access to diverse forms of business finance. Gabrielle

O’Donovan ( A broad culture of corporate governance ) a business

author, defines corporate governance as an internal system

encompassing policies, processes and people, which serves the needs of

shareholders and other stakeholders by directing and controlling

management activities with good business savvy, objectivity,

accountability and integrity . Sound corporate governance is reliant

on external market place commitment and legislation, plus a healthy

board culture which safeguards policies and processes.

O’Donovan goes to say that “the perceived quality of a company’s

corporate governance can influence its share price as well as the cost

of raising capital. Quality is determined by the financial markets

legislation and other external market forces plus how policies and

processes are implemented and how people are led, external forces are

to a large extent; outside the circle of control of any board. The

internal environment id quite a different matter and offers companies

xxxi

the opportunity to differentiate form competitors through their board

culture. To date too much of corporate governance debate has centered

on legislative policy, to deter fraudulent activities and

transparency policy which misleads executives to treat the symptoms

and not the cause.”

Corporate governance is about building credibility, ensuring

transparency and accountability as well as maintaining an effective

channel of information disclosure that would foster good corporate

performance. It is also about how to build trust and sustain confidence

among the various interest groups that make up an organization (mark,

2000). Transparency is integral to corporate governance. A higher

transparency reduces the information asymmetry between firm’s

management and financial stakeholders (equity holders and bond

holders), mitigating the firm’s problems in corporate governance

(Sandeep et al, 2002). In Uganda lack of transparency is attributed to

the closures of commercial banks (Yunusu, 2001). Corporate Governance

as an organizational concept refers to the manner in which the power of

an organization is exercised in the steward of the corporation’s total

portfolio of assets and resources with the intention of increasing and

maintaining shareholder value and satisfaction of other stakeholders

in the context of its corporate mission (Private Sector Corporate

Governance Trust, 1999.)

The ultimate goal and objective of promoting corporate governance is

to improve and strengthen leadership, credibility, stability, Board

efficiency and competitiveness of existing corporate business

entities. This will enhance the creation of new ones and enable their

xxxii

sustained ability to produce wealth, create employment and compete in

the Global market (ICGG,2005).It focuses on the relationship among

directors, officers, shareholders and regulators and how these

parties interact to monitor the operations of the company.

Corporate Governance goes beyond the simple concept of who is in charge

and who has the power. It includes the notion of accountability and

responsibility and involves an alignment of interests among

directors, employees and investors. Therefore the chief among its

goals are improving shareholder value and supporting a continuing

commitment to growth. Subsequently, the concept is gradually warming

itself to the top of policy agenda in the African continent. Indeed it

is believed that the Asian crisis and the seemingly poor performance of

the corporate sector in Africa have made the concept of Corporate

Governance a catch phrase in the development debate.(Berglof and Von

Thadden,1999).It is believed that good governance generates investor

Good will and confidence.

Again, poorly governed firms are expected to be less

profitable .Claessens et al. (2003) provides that a better corporate

framework benefits firms through greater access to financing ,better

performance and more favorable treatment of all stakeholders. They

further argue that weak corporate governance does not only lead to poor

performances and risky financing patterns, but also renders

conducive/possibility for macroeconomic crisis like the 1997 East-

Asian crisis.

xxxiii

2.2 Elements of corporate governance systems

2.2.1 Board size

Board size is defined as the total number of Directors on a board.

(Panasian et al, 2003).It is regarded as an important determinant of

effective corporate governance. According to Goshi et al., (2002) the

optimal board size includes the executive directors and non executive

directors. Consideration has to be given to the size of the board

itself. Questions like, is the board too small or too large to

adequately fulfill its requirements, given the size and complexity of

the organization, Does board size have an effect on board functioning?

It is stated that large boards perform better compared to smaller

boards, because a great number of directors increases available

expertise and resource pool.

Expanding the size of the Board provides an increased pool of

expertise, information and advice quality and board’s monitoring

capacity, not obtained from other corporate staff. Thus in contrast,

small boards cannot enjoy the advantages of the pool of expertise,

information and advice quality of the larger boards.

2.2.2 Board roles

Board effectiveness occurs via the execution of roles set as proposed

by different researchers in various ways Hung(1998).Defining a clear

role set is difficult since different disciplines concentrate on

different areas of interest.

xxxiv

Though there are various roles as per chairperson, chief executive and

Director’s offices, there are several board roles that must receive

board support as indicated below;

2.2.2.1 Policy and decision making

The final function that a board needs to consider is its duty with

respect to delegating authority. Due to the complexity of the business

environment, it is impossible for the board to be the sole decision

making body in the company.

Each board needs to work on developing an appropriate method that

involves everybody in decision making. Obviously, this will again vary

with the context facing the board but in all circumstances, the board

needs to clearly articulate and document the delegations it makes

(Gavin & Geoffrey, 2004).

Managers at the top level usually do not involve their subordinates in

decision making and tend to drive the organization in their own

interests. Once corporate governance policies are under looked, it may

create problems in the management as it was the case in Greenland Bank.

2.2.2.2 Strategizing role

The board’s objective in strategy formulation is aimed at ensuring

that the strategy of the company will lead to the long term creation of

shareholder wealth or goals and values upheld by the organization. The

strategizing role is included for three reasons, increasing

performance pressure being applied by institutional shareholders,

Board perception of the importance of the strategizing role,(Triker

1998) and recent legal precedent that places corporate goal setting

xxxv

and strategic direction squarely within the board’s

charter(Baxt,2002).A well laid and defined strategy drives the

company in the right direction.

2.2.2.3 Monitoring and control

The prime role of the board is control and monitoring management

performance of financial institutions, (Rosnik, 1987, 1990) a role

made necessary by the separation of ownership from control. Meigs and

Meigs (1984) contend that internal control system need to be monitored

if an entity is to realize its profitability objective and this is

accomplished through ongoing monitoring activities and separate

evaluations.

It includes regular management and supervisory activities and other

actions personnel take in performing their duties such as Risk

assessment, effectiveness and reporting deficiencies to top

management and board to design appropriate actions.

The board should frequently monitor and endeavor to review the

management’s implementation of strategic plan and objectives to

ensure management efficiency and accuracy. It is therefore predicted

that if the Board performs its duties effectively, the value of the

firm is predicted to increase and wealth of the shareholders would also

be enhanced accordingly. The Board monitors and controls the

performance of the firm. In case Managers fail to put the company’s

interests at the forefront, it may offer room for inefficient

practices to occur.

xxxvi

2.2.2.4 Advice and counsel

The Directors help in providing advice to the CEO who is obliged to act

prudently in the management of the company and its day to day

implementation of the direction to success. The Board is a key source

of knowledge and experience for the organization it governs. It is thus

important for the Board to share its experience with Management

particularly the CEO, to serve the interests of the company (Garvin &

Geoffrey, 2004).

2.2.3 Board effectiveness

According to Forbes and Daniel (1999), Board effectiveness refers to

the Board’s ability to perform its control and service tasks

effectively. It is therefore a mix of executive and non executive

directors. Most people believe that the more the outside Directors a

board has, the more effective the board (Weisbach, 1998).

The perception of Board effectiveness widely differs from one

individual to another, thus to Jackson & Holland (1998) board

effectiveness is measured and based on individual experience. Whereas

Huat & David (2001) argued that board effectiveness is measured as the

ability of the board to perform its functions. Therefore, there is need

to identify the control variables and gaps in understanding how the

Board can impact on the firm performance. A board dominated by Insiders

is not expected to play their role as effective monitors and

supervisors of management especially when the Board chairman is also

the firm’s CEO (katto, 2001).

Basing on the above literature, it’s fairly held that Board

performance is largely defined in terms of the role played by the Board

xxxvii

of Directors. Some of these roles are inter-related and using these

perspectives, the following have been identified;

2.2.3.1 Committees

A committee is a specific group of people to whom a specific task has

been assigned and delegated by the full board. These may be

remuneration committees, Audit committees Klein (2002) and

nominating committees vafeas (1999).It is stipulated under the audit

profession, that to ensure a balance of power, an audit committee

should comprise of at least three non-executive directors (ACCA,

2002).The set up of committees ensures that no key decisions of the

board are individually made, since vesting too much power in

individuals breeds inefficiencies and leads to poor governance. Board

committees will therefore improve on decision making in the BOD. It

further enables board effectiveness and profitability level also

increases.

These committees help to gather, review and summarize information and

report back to the full Board for decisions or can also be delegated

specific decision making powers, Gavin and Geoffrey (2004).Some

committees may be appointed and may be composed of family members and

relatives who will always act in the Board’s favour.

2.2.3.2 Skills and knowledge (Management experience)

Board members must have the right mix of skills and knowledge, that is,

functional knowledge in various business areas such as accounting,

finance, legal and marketing as well as Industry specific knowledge to

clearly understand specific company issues and challenges. In

addition, board members must have enough general knowledge to provide

xxxviii

input to all topics of discussion, ask questions of all special

interest until they are comfortable enough to cast votes, Espstein et

al., (2002).

Thus for the board to work effectively, the members must possess

necessary knowledge and skills given the unique nature of their tasks.

However, availability of expertise in a group does not guarantee the

use of that expertise. Companies need to be aware that the use of

knowledge and skills is as important as its expertise. Therefore the

board should integrate the knowledge of the firm with their expertise

in the areas of law and strategy if they are to exercise the control

task effectively. However, recruitment of inexperienced staff will be

reflected in the weakness of the management and this compromises good

corporate governance practices.

2.2.3.3 Risk Management

Risk is about uncertainty of events happening. It involves a

probability of a good or bad outcome. Risk management therefore

revolves around the techniques devised in order to promote and ensure

the effective control of risks. It involves set procedures devised to

minimize adverse effects of possible financial and business losses.

Such procedures include identifying potential sources of measuring

the financial consequences of a loss occurring and using control to

minimize actual losses. The risk process takes into account the

diversification of risk, sharing the risk and establishing controls.

Risk management further focuses on the unpredictability of financial

markets and seeks to minimize the possible effects on financial

performance. This is carried out by the treasury department under

xxxix

policies of the Board. Because of the dynamic economic and operating

conditions, mechanisms must be in place to identify and deal with the

various risks associated with change to safeguard the company’s

survival. Due to uncertainities it may not be simple to predict the

outcomes of good corporate governance thus corrective measures have to

be set in advance.

2.2.3.4. Delegation

As evidenced in company operations, due to the wide spread technical

issues involved, the board cannot be the sole decision making body in

the company. It is therefore in principle to develop an appropriate

method and level of delegation of authority. It requires the board to

document well and monitor the delegations it makes.

Delegation helps to boost the morale of the persons given the

opportunity to carry on a particular task and provides a sense of

leadership and responsibility to the entire company members. The

reluctance and negligence of managers to delegate authority to other

parties probably caused by the fear of competition violates the

corporate governance policies and principles.

2.2.3.5 Information and communication

In principle it is relevant and vital for the Board to keep its

subordinates informed of the goals, objectives, policies and

constraints to which the organization is expected to conform (Arora,

1995). Budgets are an important channel for the dissemination of this

information to the managers to fully coordinate their activities

efficiently (Nixon, 2001).

xl

Information preferably should be in writing and the managers should be

able to listen to their subjects’ ideas.

This helps to build team work in the company which ensures good

performances. Effective communication must occur in a broader sense,

flowing down, across and up the organization.

Poor communication renders Board inefficiency and ineffectiveness as

there will be no direction of orders and commands hence poor

performance accompanied by low profitability. All personnel must be

fully informed of their responsibilities and roles in the internal

control. The company should enhance a proper communication flow with

entire community that embodies the suppliers, customers,

stakeholders, external auditors to ensure the set Goals are attained.

2.3. Definition of profitability

Profitability refers to the ability of the company to generate returns

for the shareholders in light of their investment committed; Frank

(2002).Profit is measured as the difference between revenues and

expenses incurred in the trading period. Profit is the ultimate goal of

a company and in case of failure to achieve the target profit; the

company ceases to exist (Ariho, 2006). Profitability indicates the

firms’ professional management of its operations. Profits are seen as

a return to the shareholders for their resources invested in the

company, and also help to reveal the enterprise’s competitive position

in the market it operates.

The earning of profits is a major goal of almost every business

enterprise be it large or small. Economists define profits as the

xli

amount by which an entity becomes “better off” during a period of time

(kamara, 1998). This enables the businesses’ existence over a period

of time unlike the non profitable businesses which are unlikely to

continue operating for long. Measuring profitability helps to assess

business success, as per current, past profitability and projecting

future profitability.

2.3.1 Measuring profitability

Business profits perform a vital economic function in any

organization. They are relevant in improving standard of living,

achieving high employment and expanding the national economy. There

are various methods of measuring profits, such as subtracting expenses

from sales. The most common measure of profits however is profit after

tax which is a result of the impact of all factors on the firm’s

earnings.

However, profitability of the business enterprise is hard to determine

and calculate since there are some other factors that have a great

impact on it and therefore hard to predict. The factors that need

consideration here are; cost control, sales turn over, required rate

of return, asset adequacy, and market share and entry barriers.

2.3.2 Elements of profitability

2.3.2.1 Cost control

A cost is a foregoing or sacrifice, measured in monetary terms,

incurred to achieve a purpose, (Pandey, 1992). Cost control is taken up

after an event has happened, it points out the deviations that require

xlii

the Manager’s investigation, survey and addressing these issues to

bridge the gap after influencing factors have been identified.

Cost control requires the reduction of various costs for instance

financial, cost of sales and operating expenses to improve

profitability (Hampton, 2001). These costs must be reduced or

minimized to ensure a desired level of profitability.

2.3.2.2. Revenue/ Turnover adequacy

This accrues from the sale of goods and services in the course of the

business. Thus the more the sales in the specified period, the more the

returns reaped. In case the sales margin of profit is less, it results

into the inability of the firm to cover fixed costs and fixed charges

like debts and profits for its shareholders. A firm’s sales revenue is

affected by the expenses a firm incurs in raising sales such as

promotions, remuneration expenses which reduce the intended profits

of the company. But at least there should be a given range to be

maintained over time to avoid inadequacies in financing the business.

2.3.2.3. Required rate of return

This is defined as the risk free rate plus risk premium. It is also the

rate of return expected by investors (Pandey, 1994) from a proposal

before it can be accepted. When a firm invests in capital, it must make

a risk return decision. Therefore the determination of required rate

of return is a profitability function.

2.3.2.4. Market share

This relates to the entire customer population that a company commands

as defined by the number of customers (kawere, 2007). A large market

xliii

share is characterized by high sales revenue which offers high

profitability level compared to a small market share company. However

the entry of more companies into the industry renders the share up of

profits and in the long run some exit the market

2.3.2.5 Pricing

This is determined by the cost of production involved in the process of

providing or availing a service. The price charged should fairly

reflect the time taken and it should be competitive in relation to that

of the competitor since they may use it to take over your customers.

Proper pricing involves analyzing profit requirements in pricing

decisions which leads to the formulation of pricing policies.

Therefore, a good price should be able to earn a business profits

because no business will survive without profits in the long run (Don,

2006). But also its stated that if the market price of the company’s

share is high, it may not appeal to small investors. If it is brought

down to a desired range, trading activities would increase.

2.3.2.6. Entry barriers

Entry barriers are most commonly evident in industries with high

profitability. These influence the conduct and ability of the firm in

generation of adequate profits.

Economies characterized by absence of competition and barriers are

centers for competitors and therefore profits have to be distributed

among the competing firms and hence reducing the profits reaped.

xliv

2.3.2.7. Asset adequacy

Assets can be real assets such as property, plant and machinery or

financial assets such as shares and bonds. The assets held by the

company are important determinants of its profitability (Pandey,

2004). How resourceful are the assets available? Assets that are of no

purpose lie idle and therefore provide little if no impact to the

company thus yield no profits. Companies with a low asset base reap low

profits compared to others with a high asset base.

2.4. Relationship between Corporate Governance & Profitability level

Corporate Governance from the perspective of the investor is defined

as “both the promise to repay a fair return on capital invested and the

commitment to operate a firm efficiently given investment.” Metrick

and Ishii, (2002).

Corporate Governance is seen as concerned with ways of bringing the

interests of (investors & managers) into line and ensuring that firms

are run for the benefit of Investors. It is also concerned with the

relationship between the internal governance mechanisms of

corporations and society’s conception of the scope of corporate

accountability.

It should be noted that companies with an adequate mix of executive and

non executive directors have registered good performance (Yoshikawa &

Phan, 2004). Firms with stronger shareholder rights have higher firm

value, higher sales growth, high profits and lower capital

expenditure. (Gompers & Metrick, 2003). Further companies that

emphasize corporate governance will overtime generate superior

returns and economic performance and lower their cost of capital as

xlv

compared to those with weak corporate governance that face high risks

resulting in higher cost of capital and poor performance.

The company management should be able to turn business plans into

reality and also improve the firm’s profitability. These can be

achieved through good board size where every member plays a role to

improve a company’s efficiency. The assumption among researchers is

that effective corporate governance policies like board sizes and

board roles lead to effective organization. There should be positive

relationship in firm performance and a number of mechanisms should be

put in place, such as sucking of ineffective and non performing

managers to ensure that profitability is achieved.

2.4.1. Relationship between Board roles and Profitability level

Profitability levels can be raised through proper execution of Board

roles set by the personnel concerned. If some tend to be inactive,

reshuffles can be made and roles redefined to ensure management

efficiency and compliance with the laws therein corporate governance.

2.4.2. Relationship between monitoring and control and Profitability

levels

The Board’s role is to monitor the various elements that would

influence and have an impact as per the profitability levels. It

includes evaluation and scrutinizing the spending efficiency and

impact of various expenditure, Bakunda (2001). Monitoring of the

market and all companies activities offers proper accountability and

flow of activities to attain a preferred and set profitability levels.

xlvi

2.4.3. Relationship between Board size and Profitability level

The size of the Board is a crucial element in an organization. But a

prudent decision has to be made in respect of the Board size and the

company’s profitability levels since profits are got after expenses

are offset. In management, an optimal Board size is preferable because

of the low cost attached to it, and the ease with which decisions

regarding the direction of the company are made. A large Board size

presents high staff costs hence cutting the profits that the company

has to gain.

2.4.4. Relationship between Policy and Decision making and

Profitability

The policies set matter most as to how the company is to be run and the

decision making should involve every one since ideas help to build

proper systems that maintain better services that cut the would be

costs hence increasing the profitability levels.

2.4.5. Relationship between strategizing role and profitability

level

Strategies formed are driven at ensuring that the company is in

position of achieving the set Goals such as accumulating the desired

wealth to earn a pay back to the shareholders as a long-term goal.

2.4.6. Relationship between Board effectiveness and Profitability

Board effectiveness depends on the execution of the three board roles

that include; monitoring and control, policy and decision making,

providing counsel and advice).

xlvii

Board effectiveness is measured in terms of individual experience,

Board dynamics and continuous evaluation and review to keep a track of

the profitability level. Therefore, higher levels of Board

effectiveness ensure high profitability level since the costs of

business will be lowered down. Board effectiveness through proper

communication skills, risk management and team work provide room for

proper conduct and good performances that ensure profitability in the

company.

2.5. Conclusion

Research dedicated to Corporate Governance and Profitability

indicates that these two variables are inter-related in various

aspects and as such, the existence of proper corporate principles and

practices ensures set up of reliable internal controls that improve

the company’s profitability.

It should also be understood that corporate governance can be used as a

tool to promote young businesses’ profitability but also, the fact

that corporate governance not being the absolute measure of

profitability should be taken into account.

xlviii

RESEARCH METHODOLOGY

3.0Introduction This gives a description of the various methods that the researcher

used in collecting data and achieving the objectives of the study on

corporate governance and profitability. The subsections beneath it

include, research design, study population, sampling designs, sample

size, sampling procedures, sources of data, data collection methods,

data collection procedure, measurements of variables and instruments

and data processing and data analysis and ethical issues and

limitations during the study. It provides a thorough description on

how the relevant information was obtained to enable research to be

carried on. Findings of the study were assessed and conclusions drawn.

3.1. Research design

The research was to be designed in manners that enable the researcher

to collect data that was to meet the objectives of the study.

descriptive and analytical research designs were used in addition to

the qualitative and quantitative approach to solicit inform on

corporate governance and profitability level in Bank of Baroda Uganda.

Qualitative approach involves the use of interview. Quantitative

approach also involved the use of structured questionnaires which were

to be used to capture data about respondent’s attitudes and behaviors

from the field and to establish the relationship between two

variables. This enabled the attainment of adequate information and

making of an appropriate conclusion.

xlix

3.2. Study population

The study population involved administrators such as Directors,

Managers and all various employees such as Accountants, Managers,

Auditors, and Banking tellers and cashiers.

3.3. Sampling

3.3.1. Sampling size and Sampling Procedure

Data was collected from 15 respondents from the Bank, comprising of 3

managers and 12 Employees at the different levels (positions and

posts). These were chosen basing on the level of education and position

held. This sample size selected is a representative of the entire

population study. The sampling procedure involved purposive sampling

in which Directors and Managers who have relevant knowledge to the

purpose of the investigation are chosen. With expert sampling, the

sample was considered one with the desired expertise and expertise in

the area under investigation.

Simple random sampling was used on other employees such as Accountants

and Bank Tellers. The procedure here involved the researcher

identifying few members and assigned numbers using papers that are

mixed up and employees are required to pick recommended numbers from

one to twenty three (23) to form the sample for the study.

3.4. Sources of data

The data researcher was gathered data from both primary and secondary

sources of data.

l

3.4.1. Primary source

Primary data was gathered from respondents at Bank of Baroda Uganda

Mbarara branch management who were assumed to give first hand

information on the subject under study.

3.4.2. Secondary source

Secondary data was extracted from text books, and other related

written literature such as research reports, journal, magazines and

financial reports availed in the library. Also internet source was

vital during the compilation of data.

3.5. Data collection instruments

These instruments included questionnaires and interviews to enable

the capturing and analysis of data. The methods that were used

included;

3.5.1. Questionnaire

These were well documented structured and semi structured questions

printed in simple precise and concise language for the respondent to

understand, based in a five point Likert scale. These questionnaires

involved some that were to be mailed to the directors, managers and

other chosen employees while others were self administered

questionnaires which were land delivered to the respondents, to have

them filled. The questionnaire were piloted as recommended by Saunder

et al and other (2003) who writes that, piloting helps ensure validity

and reliability and also said that piloting helps to refine the

questionnaire so that respondents have no problem in answering the

questions and there would be no problems in recording the data.

li

3.5.2. Interview

An interview is a conversation between two people (the interviewer and

the interviewee) where questions are asked by the interviewer to

obtain information from the interviewee. The qualitative research

interview seeks to describe and the meanings of central themes in the

life world of the subjects. The main task in interviewing is to

understand the meaning of what the interviewees say. (Kvale, 1996).

The researcher used formal interviewing as a method of data collection

and the interviews offered a chance to explore topics in depth and

allowed interaction between the researcher and the respondents such

that any misunderstanding of the questions and answers provided could

easily be corrected. The researcher interviewed the respondent of the

Bank of Baroda Mbarara branch using the interview guide. This was used

to tap the vital information that may not be collected using the

questionnaires from Bank of Baroda Mbarara branch employees, manager &

administrators.

3.5.3 Documentation/ secondary data : Secondary data was also used in

this study as; the researcher collected secondary information from

different sources like; text books, internet, news paper, magazines,

journals among other sources. This information reviewed by visiting

places like libraries and internet cafes.

3.6 Reliability and validity

Validity of an instrument was used in this study where consistent with

the definition provided by Miles and Huberman (1994), as the” extent to

which the items in the instrument measure what they are set out to

lii

measure.” The validity of the instruments was established by the

supervisor.

Reliability, according to Miles and Huberman (1994), has to do with the

extent to which the items in an instrument generate consistent

responses over several trials with different audiences in the same

setting or circumstances”. The reliability of the instruments and data

was established following a pre-test procedure of the instruments

before their use with actual research respondents.

3.7. Data collection procedure

The researcher got an introductory letter from Mbarara University of

Science And Technology, Department Of Management Science which was

presented to the respondents, who kindly provided the researcher with

the required information about the company. Questionnaires were to be

self-administered and respondents were guaranteed of

confidentiality.

3.8. Measuring study variables

The two variables independent and dependent were measured.

Corporate governance as the independent variable was used as an

indicator of how companies are controlled, managed and directed, this

was measured in terms of board roles, board size and board

effectiveness. Profitability as dependent variable was measured in

terms of cost control, sales turnover, required rate of return and the

market share powered by the company. A five-point response scale

ranging from strongly agrees, agree, unfair, disagree to strongly

disagree was chosen to help in the assessment of these indicators

through the various responses forwarded.

liii

3.9 Data Presentation and Analysis

Data analysis ; A both quantitative and qualitative method were used

during data analysis. Quantitative data involved use of frequencies,

tables against their percentages, that is pie chart and this was

showing values that aided in data interpretation. Qualitative data

presented in writing useful information from the respondents as

presented in relation to the study variables. After collecting all the

necessary data, this data was recorded and edited, analyzed and

rephrased to eliminate errors and ensure consistency. Both

qualitative and quantitative data analysis was used. Qualitative data

was analyzed in the field as it was collected (verbatim reporting)

using coding sheets while quantitative was analyzed by using computer

programs like Microsoft word and Microsoft excel. Also under

qualitative analysis, thematic analysis was used and in quantitative

data analysis; graphs, tables and pie charts were used for data

analysis and presentations of findings.

Data Editing: The collected data was edited for accuracy,

completeness. Editing was done to find out how well the answered

questionnaires were done in line with consideration paid to questions

and responses from interview guide answered by the study respondents.

Data Coding: The edited data was coded. Coding involve assigning

numbers to similar questions from which answers were given unique

looks to make the work easier. In this case computer Packages was used

to analyze the code data.

Data presentation ; After the data , was edited, it was presented

inform of frequency and tables after which the data was analyzed in

liv

form of pie-charts which may be developed using Micro Soft Word and

Micro Soft Excel, this was done to only quantitative edited data.

Quantitative data were grouped and statistical description such as

tables showing frequencies and percentages and pie- charts as well as

graphs for better interpretation. However, qualitative data was

analyzed in a way of identifying the responses from respondents that