Copyright by Colin Koutney 2018 - The University of Texas at ...

75

Copyright by Colin Koutney 2018

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Copyright by Colin Koutney 2018 - The University of Texas at ...

Copyright

by

Colin Koutney

2018

The Dissertation Committee for Colin Koutney Certifies that this is the approved

version of the following Dissertation:

Do Analysts Improve on Managers’ Voluntary ETR Forecasts?

Committee: Lillian Mills, Supervisor Michael Clement Jonathan Cohn Dain Donelson Braden Williams

Do Analysts Improve on Managers’ Voluntary ETR Forecasts?

by

Colin Koutney

Dissertation

Presented to the Faculty of the Graduate School of

The University of Texas at Austin

in Partial Fulfillment

of the Requirements

for the Degree of

Doctor of Philosophy

The University of Texas at Austin

December 2018

Dedication

To Mama, Daddy, and Lenore

v

Acknowledgements

This dissertation benefited from the suggestions of my dissertation committee:

Michael Clement, Jonathan Cohn, Dain Donelson, Lillian Mills (Chair), and Braden

Williams. I thank you for your feedback and encouragement throughout the process. I also

thank Alejandra Flores and Vincent Truong for their research assistance and the McCombs

Research Excellence Fund for funding.

I am very grateful to my advisor, Lillian Mills, for her mentorship on all things

research, teaching, and life. With her passion for academia and engagement with the

profession, Lil exemplifies the accounting scholar that I aspire to be.

During the program, I was lucky to meet many great colleagues who helped me in

countless small and large ways. I am very appreciative and grateful to you. I am especially

thankful to Ken Brown, Jakob Infuehr, Prasart Jongjaroenkamol, Antonis Kartapanis,

Daehyun Kim, and Zheng Leitter. Your friendship means a lot to me. Finally, I thank Xinyu

Zhang for helping me to be better each day.

vi

Abstract

Do Analysts Improve on Managers’ Voluntary ETR Forecasts?

Colin Koutney, Ph.D.

The University of Texas at Austin, 2018

Supervisor: Lillian Mills

This study examines whether analysts improve on managers’ voluntary annual

effective tax rate (ETR) forecasts. Although managers frequently issue voluntary ETR

forecasts, we know little about how analysts use this information. I find approximately 33

percent of analyst ETR forecasts materially deviate from management’s ETR forecast (i.e.,

more than half a percentage point). I also find (1) analysts’ after-tax, pretax, and ETR

forecasts are less accurate when deviating from managers’ ETR forecasts, even when

controlling for analyst characteristics; (2) less experienced analysts deviate more often than

more experienced analysts; and (3) investors do not differentiate between analyst forecasts

that deviate versus forecasts that follow managers’ ETR forecasts, suggesting investors do

not find incremental information in these forecasts. Overall, my results indicate that

analysts can be overconfident about their private information and underweight

management information.

vii

Table of Contents

List of Tables ..................................................................................................................... ix

Chapter 1: Introduction ........................................................................................................1

Chapter 2: Background and Hypotheses Development .......................................................6

2.1 Management earnings forecasts ............................................................................6

2.2 Analyst herding literature ...................................................................................10

2.3 Are analyst earnings forecasts that disagree with managers’ ETR forecasts more accurate? ....................................................................................................12

2.4 Do investors react more to analyst forecasts with disagreeing ETR forecasts? ............................................................................................................14

Chapter 3: Sample and Descriptive Statistics ....................................................................15

Chapter 4: Research Design and Empirical Analyses ........................................................18

4.1 Determinants of disagreement (H1) ....................................................................18

4.2 Analyst forecast accuracy (H2)...........................................................................23

4.3 Investor reaction to analyst forecast revisions (H3) ...........................................26

Chapter 5: Supplemental Analyses ....................................................................................28

5.1 What information do disagreeing analysts use to forecast ETR? .......................28

5.2 What firm characteristics influence the percentage of analysts who disagree with management ETR forecasts? ......................................................................30

5.3 Why do managers issue ETR forecasts? .............................................................32

5.4 Does ETR forecasting complexity moderate the association between analyst ETR forecast disagreement and forecast accuracy? ...........................................34

Chapter 6: Robustness Tests ..............................................................................................35

6.1 Minority interest and other income item adjustments ........................................35

6.2 Placebo test .........................................................................................................36

viii

Chapter 7: Discussion and Conclusion ..............................................................................37

Tables .................................................................................................................................38

Appendices .........................................................................................................................51

Appendix A: Example of a Management ETR Forecast—Abbot Laboratories’ 2005 Guidance from 2004 Q4 Earnings Conference Call (Tax-related forecasts underlined) ...........................................................................................52

Appendix B: Examples of Voluntary Management ETR Forecasts—Abbot Laboratories’ time-series of ETR forecasts, 2004-2015 .....................................53

Appendix C: Variable Definitions ............................................................................54

References ..........................................................................................................................58

ix

List of Tables

Table 1: Sample Construction Procedure ..........................................................................39

Table 2: Frequency of Management Voluntary ETR Forecasts ........................................40

Table 3: Descriptive Statistics ...........................................................................................41

Table 4: Analyst Characteristics and Disagreement with Management ETR Forecasts ...42

Table 5: Analyst Absolute After-tax Forecast Error ..........................................................44

Table 6: Analyst Absolute Pretax Forecast Error ..............................................................45

Table 7: Analyst Absolute ETR Forecast Error .................................................................46

Table 8: Stock Return to Analysts Forecasts and Disagreement with Management

ETR Forecasts ...............................................................................................47

Table 9: What Do Disagreeing Analysts Forecast as ETR? ..............................................48

Table 10: What Firm Characteristics Influence the Percent of Analysts Who Disagree

with Management ETR Forecasts? ...............................................................49

Table 11: Which Firms Issue ETR Forecasts? ...................................................................50

1

Chapter 1: Introduction

Do analysts improve on managers’ voluntary effective tax rate (ETR) forecasts?

The question is important because ETR forecasts are the second most common forecast

issued by managers (Lansford, Lev, and Tucker [2013]; NIRI [2016]; Chapman and Green

[2018]). In addition, investors could benefit from comparing analyst and voluntary

manager tax rate forecasts to understand the recent and continuing volatility in tax expense

resulting from 2017 U.S. corporate tax reform and potential future adjustments for its

unintended consequences (Tankersley and Rappeport [2018]; Rubin [2018]; Deloitte

[2018]). Moreover, analysts regularly disagree with managers on ETR forecasts: about 33

percent of analyst forecasts deviate from managers’ voluntary ETR forecasts by more than

half a percentage point.1

Current research suggests several reasons why analysts can improve on managers’

ETR forecasts. First, analysts sometimes have information to improve on management

forecasts. Concerning net earnings forecasts, analysts issue more accurate forecasts than

management when earnings are highly correlated with macroeconomic indicators (Hutton,

Lee, and Shu [2012]). Second, when analysts deviate from public information like analyst

consensus forecasts, they issue more accurate and informative forecasts (Gleason and Lee

[2003]; Clement and Tse [2005]). Third, analysts can improve on managers’ mandatory

quarterly ETR forecasts (Bratten, Gleason, Larocque, and Mills [2017]). In contrast to

these reasons, prior studies find analysts generally do not improve on management net

earnings forecasts by showing analysts’ and managers’ forecasts are equally accurate

1 Hereafter, I use the terms ‘deviate’ and ‘disagree’ to refer to cases when the absolute difference between analysts’ and managers’ voluntary ETR forecasts is greater than 0.5%.

2

(Hutton et al. [2012]; Ruland [1978]; Waymire [1986]). Thus, I examine whether analyst

forecasts that deviate from managers’ ETR forecasts improve on managers’ ETR forecasts.

To investigate this question, I examine the characteristics of analysts that disagree

with managers’ ETR forecasts, whether analyst forecasts with disagreement are more

accurate than forecasts following managers’ ETR forecasts, and whether investors

differentiate between analyst earnings forecasts that disagree versus forecasts that follow

managers’ ETR forecasts. Using firm-year fixed effects and other controls, I can compare

analyst characteristics and forecast accuracy of analysts who disagree to those who agree

with managers’ ETR forecasts. To analyze investor reaction, I examine narrow return

windows centered at the release of the analyst forecast to ensure the forecast is the primary

news event.

I hand-collect managers’ annual voluntary ETR forecasts from S&P 500

corporations between 2004 and 2015 from fourth-quarter earnings conference calls.2 I find

managers frequently issue voluntary ETR forecasts: 2,347 out of 5,411 firm-years (43

percent) have ETR forecasts. I match managers’ annual ETR forecasts to I/B/E/S analyst

forecasts for a total of 44,114 firm-year-analyst forecasts. The large sample allows for

panel and cross-sectional analysis of firms that issue ETR forecasts and an examination of

whether individual analysts improve on managers’ forecasts.

Overall, the results suggest that analysts who disagree with managers’ ETR

forecasts do not improve on managers’ forecasts. First, the analyst characteristics

associated with ETR disagreement portray analysts who are overconfident in their abilities.

2 Throughout the paper, I refer to management voluntary ETR forecasts as simply management ETR forecasts, except to distinguish them from quarterly GAAP ETRs, which are essentially mandatory ETR forecasts. Quarterly GAAP ETRs, calculated as the year-to-date tax expense divided by pretax income, are mandatory because interim period tax expense is reported using estimated annual ETRs based the view that interim periods are integral parts of the annual period (ASC 740-270), but their use as forecasts is distorted because quarterly GAAP tax expense includes discrete items (Bratten et al. [2017]).

3

I find analysts who disagree work at larger brokerages but also have less work experience.

Also, ETR forecast disagreement is not significantly associated with analysts’ workloads

because analysts who follow more companies or industries do not disagree more often than

analysts who follow fewer companies or industries. These findings are contrary to

implications from the analyst herding literature because they suggest analysts who disagree

with public information about taxes do not necessarily have greater access to private

information.

Second, I find analyst forecasts are less accurate when analysts disagree with

managers’ voluntary ETR forecasts, which contrasts with recent evidence (Bratten et al.

[2017]) that analysts are more accurate when disagreeing with mandatory ETR forecasts.

On average, analysts issue less accurate ETR, after-tax earnings, and pretax earnings

forecasts when disagreeing with management’s voluntary ETR forecast. These results are

robust to controlling for analyst characteristics. These results are also robust to specifying

the regression using ranked analyst forecast accuracy to mitigate concerns that inaccurate

and outlier forecasts explain the results.

Third, investors do not appear to differentiate between analyst forecasts that

disagree with managers’ ETR forecasts and analyst forecasts following managers’

forecasts. I examine investor reaction in addition to forecast accuracy because investors

could value analyst forecast deviations from managers’ forecasts for reasons other than

greater accuracy.3 To compare investor reactions, I examine stock price changes in the 40-

minute window centered at the release of the analyst forecast. I do not find a significant

3 Whether analysts contribute tax information to investors is an important question. Lev and Nissim [2004] and Thomas and Zhang [2011] show that current tax information predicts future stock returns. Weber [2009] argues the association between tax information and stock returns is due to the inability of analysts to incorporate tax information into their forecasts.

4

association between analyst forecasts that disagree and stock return, suggesting that

investors do not differentiate between the forecasts.

In two supplemental analyses, I examine why analysts do not appear to improve on

managers’ forecasts. First, I investigate whether mistakes explain why analysts disagree

with managers’ ETR forecasts. I find disagreeing analysts incorporate management’s ETR

forecast, analysts’ own ETR forecast issued before management’s forecast, and the prior

year Street ETR. In addition, analysts do not appear to use GAAP ETRs or a statutory tax

rate. Thus, rather than a mistake, analysts appear to disagree because they attempt to

contribute incremental information. However, it appears they overweight historical

information.

I also examine why managers forecast ETRs. I find managers are more likely to

forecast ETRs when transitory items (special items and nonrecurring income taxes) are

present. Thus, managers’ voluntary ETR forecasts could help investors calculate a

persistent tax rate. Moreover, Bratten et al. [2017] find that analysts do not mimic

managers’ mandatory ETR forecasts when discrete items are present, which implies that

managers’ voluntary ETR forecasts meet a demand for tax rate information from analysts.

These findings imply disagreeing analysts potentially ignore important information in

managers’ ETR forecasts.

This study contributes to the literature in several ways. While my paper is the first

to my knowledge to examine whether analysts improve on managers’ voluntary ETR

forecasts, prior studies compare analysts’ and managers’ EPS forecasts (Hutton et al.

[2012]; Louis, Sun, and Urcan [2013]) and analyst ETR forecasts and managers’

mandatory GAAP ETR forecasts (Bratten et al. [2017]). I highlight some differences

between my study and these to clarify the interpretation of my study. First, I find analysts

do not appear to improve on managers’ voluntary ETR forecasts in normal operating

5

circumstances. In contrast, Hutton et al. [2012] show analysts do not improve on

management EPS forecasts when firms face unusual operating circumstances. Together,

both studies broadly suggest that analysts do not improve on managers’ forecasts that

require firm-specific knowledge. Second, Louis et al. [2013] argue that analysts deviate

from management forecasts to add information for their clients (such as to adjust for

earnings management). My results suggest that although analysts who disagree with

management ETR forecasts attempted to improve on management ETR forecasts, analysts

generally do not succeed. Third, Bratten et al. [2017] find analysts improve on implied

ETR forecasts from GAAP interim reporting by comparing analysts’ non-GAAP ETR

forecasts to managers’ GAAP ETRs. Thus, while analysts improve on managers’

mandatory ETR forecasts, they do not appear to improve on managers’ voluntary ETR

forecasts and my study cautions against broad conclusions that analysts generally out-

perform managers on ETR forecasts.

More broadly, my paper contributes to the analyst herding literature by suggesting

that analysts underweight some public information from managers. It is also important to

note that the empirical analyst herding research finds analysts who deviate from public

information (represented by other analysts’ forecasts) issue more accurate forecasts. Based

on this literature, my findings that analysts issue less accurate ETR forecasts are surprising

because they always have the option to simply copy managers’ public ETR forecasts.

Finally, the findings could be useful for investors who seek additional tax

information due to the uncertainty from 2017 U.S. tax code reform. As investors estimate

the implications of the new tax code to earnings, they could view analyst forecasts as an

alternative to management forecasts, but the findings suggest that managers issue the most

accurate ETR forecasts.

6

Chapter 2: Background and Hypotheses Development

2.1 MANAGEMENT EARNINGS FORECASTS

Management earnings forecasts are important because they provide timely

information about firm earnings. They explain about 55 percent of stock returns—more

than any other accounting-related disclosure, like actual earnings announcements,

mandatory SEC filings, or analyst forecasts (Beyer, Cohen, Lys, and Walther [2010]).

Moreover, an increasing number of firms issue earnings forecasts, rising from about 15

percent in the 1990s to 65 percent in 2013 (Anilowski, Feng, and Skinner [2007]; Chapman

and Green [2018]). Due to the importance and increasing regularity of management

forecasts, numerous studies examine them.

Surveying the literature, Hirst, Koonce, and Venkataraman [2008] organize

management earnings forecast studies into three components: antecedents, characteristics,

and consequences.4 My study relates a forecast characteristic (forecast disaggregation) to

a forecast consequence (whether analysts follow management’s ETR forecast).5

Specifically, I examine whether analysts improve on managers’ ETR forecasts for analyst

forecasts issued after managers’ forecasts. This section discusses prior literature with

respect to the informativeness of management forecasts and whether analysts and investors

use management forecasts.

Prior to the 1970s, the U.S. Securities and Exchange Commission (SEC) prohibited

the issuance of forecasts because managers were considered to be too biased to issue useful

information in voluntary and unverified disclosures. However, after the SEC changed

4 Earlier reviews include Cameron [1986], King, Pownall, and Waymire [1990], and Healy and Palepu [2001]. 5 When issuing a forecast, managers choose forecast characteristics, which encompass decisions managers make about the content in their forecasts. Forecast consequences are the reactions to managers’ forecasts.

7

regulations to allow management forecasts, early studies find that they are informative.6,7

These studies generally find that management earnings forecasts are more accurate than

naïve earnings models and are at least as accurate as analyst consensus earnings forecasts

(Copeland and Marioni [1972]; McDonald [1973]; Basi, Carey, and Twark [1976]; Imhoff

[1978]; Ruland [1978]; Waymire [1986]; Jaggi [1980]; Imhoff and Pare [1982]).8 Given

the substantial research, King, Pownall, and Waymire [1990, p. 117] conclude that “the

evidence indicates that management forecasts are more accurate than analyst forecasts

available to investors prior to release of the management forecast.”

Early studies also show that investors react to management earnings forecasts

(Foster [1973]; Gonedes, Dopuch, and Penman [1976]; Patell [1976]; Jaggi [1978];

Nichols and Tsay [1979]; Penman [1980]; Penman [1983]; Anjinkya and Gift [1984];

Waymire [1984]; McNichols [1989]). Investor reaction suggests managers convey new

information with their forecasts. King et al. [1990, p. 117] conclude that “the literature

unambiguously suggests that management forecasts are price informative.” Thus, despite

the managers’ incentives to issue biased forecasts, management earnings forecasts are

generally accurate and useful to investors.

Moreover, the SEC effectively increased the relative informativeness of

management forecasts with the implementation of Regulation Fair Disclosure (Reg FD) in

6 In addition to removing the prohibition on issuing management forecasts, the SEC reduced the litigation risk associated with the issuance of a management forecast. In 1979, the SEC provided ‘safe harbor’ for good faith forecasts and, in 1996, the Private Securities Litigation Reform Act increased the standard to file lawsuits. These changes likely increased the frequency of management forecasts. 7 Cameron (1986) writes that the SEC allowed forecasts because managers were privately conveying earnings forecasts to analysts, thereby creating an uneven playing field for investors without access to analysts. 8 The timing of analysts’ forecasts relative to the manager’s forecast generally does not matter for relative forecast accuracy. Basi et al. [1976] and Imhoff [1978] examine analyst forecasts issued before managers’ forecasts while Imhoff and Pare [1982] study analyst forecasts issued after management forecasts. Ruland [1978], Jaggi [1980], and Waymire [1986] examine analyst forecasts issued both before and after managers’ forecasts. Regardless of the timing, the results often find analysts and managers have similar forecast accuracy.

8

2000. Reg FD restricts managers from selectively disclosing material information. Before

Reg FD, analysts could improve on managers’ public forecasts simply because analysts

had additional private information from management. Consistent with analysts relying on

private information from managers, Bailey et al. [2003] find analyst forecast dispersion

increases and conclude that analysts have greater difficulty to form forecasts after the

adoption of Reg FD.

Furthermore, analyst incentives or ability could prevent them from improving on

managers’ forecasts. For example, studies show analysts have incentives to disseminate

opportunistic management forecasts and analysts lack expertise to de-bias managers’

opportunistic forecasts (Kasznik [1999]; Matsumoto [2002]; Rogers and Stocken [2005];

Cotter, Tuna, and Wysocki [2006]; Feng and McVay [2010]; Kross, Ro, and Suk [2011];

Larocque [2010]). Thus, in the current environment, it appears difficult for analysts to

improve on management forecasts.

Nevertheless, prior studies find analyst forecasts are just as accurate as management

earnings forecasts both before Reg FD (Ruland [1978]; Imhoff and Pare [1982]; Imhoff

[1978]; Waymire [1986]) and after Reg FD (Hutton et al. [2012]). So why aren’t analyst

forecasts less accurate than management forecasts?

Hutton et al. [2012] argues that analysts have certain information advantages over

management: (1) greater access to macroeconomic forecasts; (2) more objectivity when

evaluating information; and (3) higher ability to process industry-wide information. Hutton

et al. [2012] find that the consensus analyst forecast is more accurate than managers’

forecasts when firm earnings are correlated with macroeconomic trends like gross domestic

product and energy costs. But they also find that the consensus analyst forecast is less

accurate when firms have abnormally high inventories, excess operational capacities, or an

9

operating loss. Thus, whether analysts improve on management earnings forecasts is a

question about the quality of private information that analysts have relative to managers.

For ETR forecasts, analysts’ sources of private tax information are difficult to

identify and it is also unclear why analysts deviate from managers’ public and voluntary

ETR forecasts without relying on useful private information. However, prior research on

analyst herding examines why analysts deviate from public information and the

consequences of deviation. Thus, the analyst herding literature provides relevant

theoretical and empirical findings to examine determinants and consequences of analyst

forecasts deviating from managers’ ETR forecasts.

10

2.2 ANALYST HERDING LITERATURE

Broadly, the subset of analyst literature on “herding” investigates how analysts

weight public and private information in their earnings forecasts. Herding refers to the

phenomenon of many different agents taking similar actions at roughly the same time

(Jegadeesh and Kim [2010]).

Although the financial press criticizes analysts for displaying herding behavior in

their stock recommendations and earnings forecasts, theoretical studies show that analysts

rationally bias their forecasts toward the consensus view in response to career and

reputational concerns (Scharfstein and Stein [1990]; Trueman [1994]). For example,

‘weak’ analysts who lack ability, expertise, or private information strategically herd to

avoid being identified as a weak analyst. In contrast, ‘strong’ analysts (those with higher

ability, greater expertise, or access to private information) issue bold forecasts to showcase

their ability.9 Consistent with these predictions, empirical studies find weak analysts are

more likely to issue herding forecasts (Hong, Kubik, and Solomon [2000]; Clement and

Tse [2005]).

Although the analyst herding literature focuses on analyst reactions to the public

information from other analysts’ forecasts, this paper focuses on analyst reactions to public

information from managers in the form of voluntary ETR forecasts. I classify analyst ETR

forecasts as either agreeing or disagreeing with public management ETR forecasts. When

analysts disagree with a manager’s forecast, analysts reveal that they place heavier weight

on their private information than the manager’s forecast. Alternatively, disagreeing

9 Other analyst herding studies reconsider whether analysts herd and whether analysts who herd are stronger analysts. For example, Bernhardt et al. [2006] find that analysts who issue contrarian (anti-herding) forecasts overweight their private information. In a theoretical study, Aharoni et al. [2017] show that strong analysts rationally herd. In circumstances when information is difficult to obtain, they find that analysts with private information can underweight their private information and strategically bias their forecast toward the consensus. These findings suggest that the type of analyst who herds is not resolved by prior literature.

11

analysts could simply have failed to copy the firm’s ETR forecast. Prior studies note cases

where analysts do not incorporate publicly available tax information into their forecasts

(Plumlee [2003]; Hoopes [2017]). Thus, analysts who disagree with management ETR

forecasts could be weaker analysts. On the other hand, prior research shows that analysts

react to management forecasts (Waymire [1986]; Jennings [1987]; Hassell, Jennings, and

Lasser [1988]; Clement, Frankel, and Miller [2003]). Thus, analysts who disagree with

manager’s ETR forecast should only do so when they have good reasons to disagree.

In summary, the herding literature implies that weaker analysts are more likely to

herd on management’s ETR forecast. However, the tax literature and management earnings

forecast literature suggest that weaker analysts are more likely deviate from management’s

ETR forecast because it is not clear what private information analysts have about taxes.

Given the evidence for opposing predictions, I state my hypothesis in the null form:

H1: The likelihood that analysts disagree with managers’ voluntary ETR forecasts

is not systematically associated with an analyst’s experience and resources.

12

2.3 ARE ANALYST EARNINGS FORECASTS THAT DISAGREE WITH MANAGERS’ ETR

FORECASTS MORE ACCURATE?

In addition to examining characteristics of analysts who herd, analyst herding

studies investigate the effect of analyst herding on forecast accuracy. Analysts have

incentives to issue profitable stock recommendations and accurate forecasts (Keane and

Runkle [1998]; Brown, Call, Clement, and Sharp [2015]). Clement and Tse [2005] find

that bold forecasts are more accurate than herding forecasts. Their finding is consistent

with theoretical arguments that herding represents analysts biasing toward the consensus

(although not necessarily mimicking) and underweighting their useful private information.

Clement and Tse [2005] also find that when analysts issue forecast revisions, the

improvement in forecast accuracy is greater for bold forecasts than herding forecasts. This

finding further suggests that bold forecasts are more reflective of private information than

herding forecasts.

For ETR forecasts, Bratten et al. [2017] show that analysts improve on managers’

mandatory ETR forecasts implied from GAAP interim reporting of tax expense and pretax

earnings. In the presence of complexity (such as discrete tax items), they find analysts tend

not to mimic managers’ mandatory GAAP ETR forecasts. By not mimicking, analysts

could be considered bold forecasters who assign higher weights to their private information

relative to their peers who mimic managers. In addition, Bratten et al. [2017] find analysts

who do not mimic managers’ GAAP ETR forecasts issue more accurate earnings forecasts

than analysts who did mimic. In summary, Bratten et al.’s [2017] results are consistent with

Clement and Tse’s [2005] results as we can view non-mimicking analysts as bold

forecasters and mimicking analysts as herd forecasters. These results would suggest that

analyst forecasts with disagreement over managers’ non-GAAP ETR forecasts are more

accurate than analyst forecasts that agree with managers’ non-GAAP ETR forecasts.

13

However, analysts who disagree with management ETR forecasts potentially issue

less accurate forecasts than analysts who agree for multiple reasons. First, numerous tax

studies argue that analysts are often either unable or unwilling to process tax information.

For example, Donelson et al. [2018] find that analyst forecast accuracy suffers when

managers strategically retain nonrecurring income taxes in non-GAAP earnings. Second,

tax information is difficult for firm outsiders to obtain (Graham et al. [2012]), so it is

unclear what private information analysts use to incrementally improve upon managers’

forecasts. Third, managers have the most useful information for calculating a forecast, so

biased management forecasts can still be informative. In addition, even when analysts can

anticipate managerial forecast bias, they do not entirely correct for the bias (Gong, Li, and

Wang [2010]). Fourth, although Bratten et al. [2017] show that analysts’ non-GAAP ETR

forecasts improve on managers’ GAAP ETR forecasts, it is unclear whether their findings

generalize to non-GAAP ETR forecasts from analysts and managers.

Moreover, analysts’ primary objective when issuing forecasts is to inform clients.

If forecast informativeness and accuracy are conflicting objectives, then analysts could

decide to issue less accurate forecasts. Louis et al. [2013] argue that analyst forecasts

deviate from managers’ pre-announcement earnings guidance to correct for earnings

management, even though deviations result in less accurate analyst forecasts. Overall, these

reasons suggest that analysts who disagree with managers’ voluntary ETR forecasts are

less accurate than analysts who agree.

Given the opposing predictions from the tax literature and the analyst herding

literature, I state my hypothesis in the null form as follows:

H2: Analyst disagreement with managers’ voluntary ETR forecasts is not

systematically associated with their earnings forecast accuracy.

14

2.4 DO INVESTORS REACT MORE TO ANALYST FORECASTS WITH DISAGREEING ETR

FORECASTS?

Prior research on investor reactions to analyst forecasts suggests that investors react

to the incremental information in analyst forecasts. For example, analyst EPS forecasts

with sales forecast information have a greater market reaction than EPS forecasts without

sales forecast information (Keung [2010]). In addition, investors react less to analyst

herding forecasts (Cooper, Day, and Lewis [2001]; Gleason and Lee [2003]). Analysts

could also sacrifice their forecast accuracy to increase the usefulness of their forecast to

clients (Louis et al. [2013]). Thus, even if disagreeing analyst forecasts are less accurate,

investors would still react more strongly to disagreeing analyst forecasts if investors find

useful information in the forecasts relative to agreeing analyst forecasts.

On the other hand, investors could react less to disagreeing analyst forecasts for the

same reasons that suggest disagreeing analyst forecasts are less accurate than agreeing

analyst forecasts. Because investor reaction could be greater or weaker to analysts’

forecasts with ETR disagreement relative to agreeing ETR forecasts, I state my hypothesis

in the null form:

H3: Investor reaction to an analyst’s forecast is not systematically associated with

whether the analyst’s ETR forecast disagrees with voluntary management ETR forecasts.

15

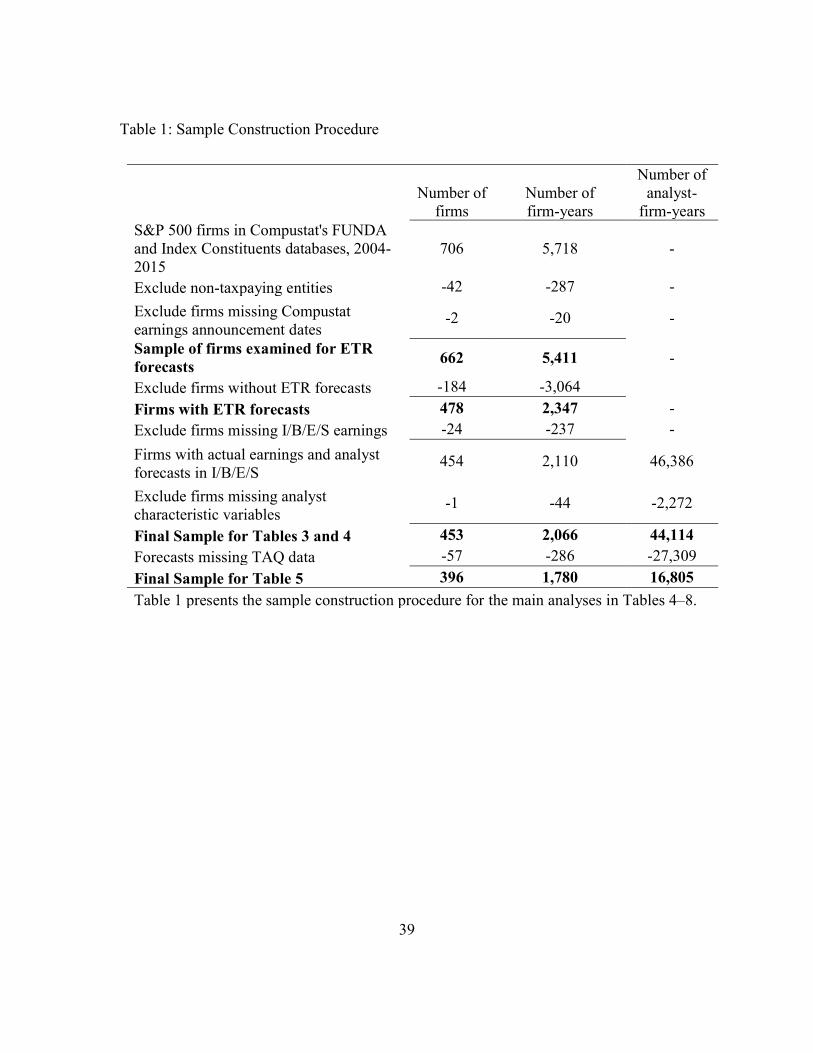

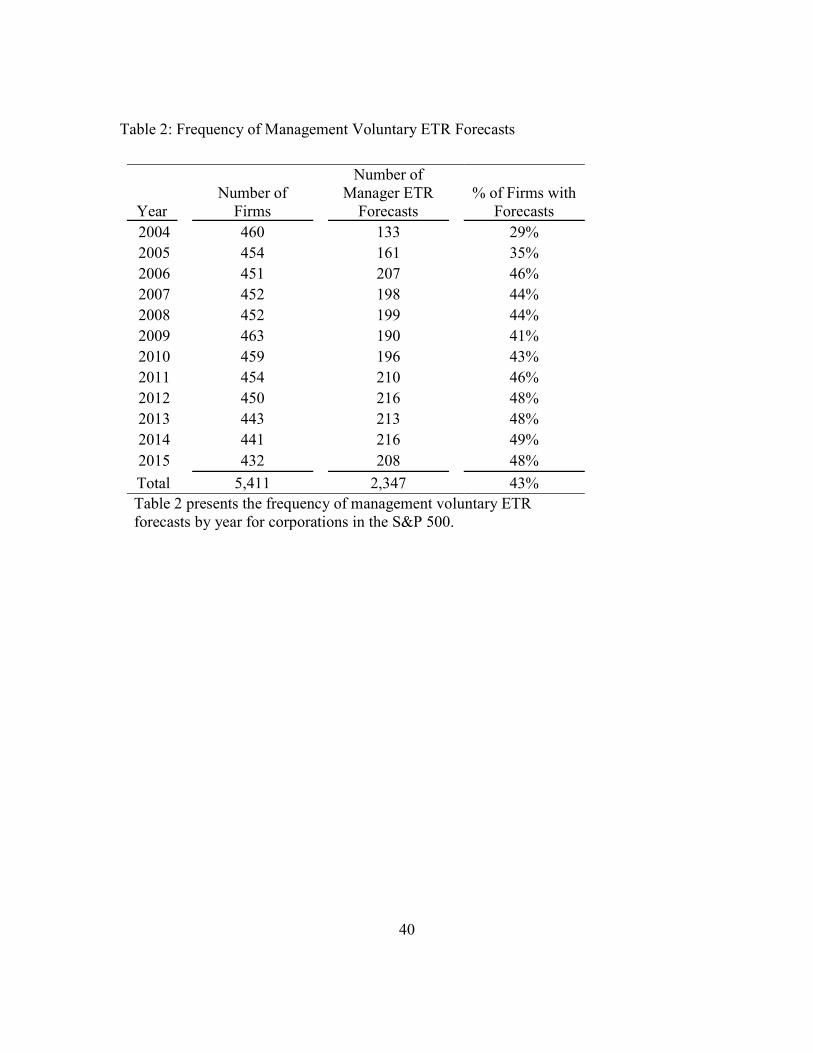

Chapter 3: Sample and Descriptive Statistics

I collect managers’ voluntary ETR forecasts from earnings conference calls on

Thomson Reuters ONE for S&P 500 corporations in Compustat between 2004 and 2015

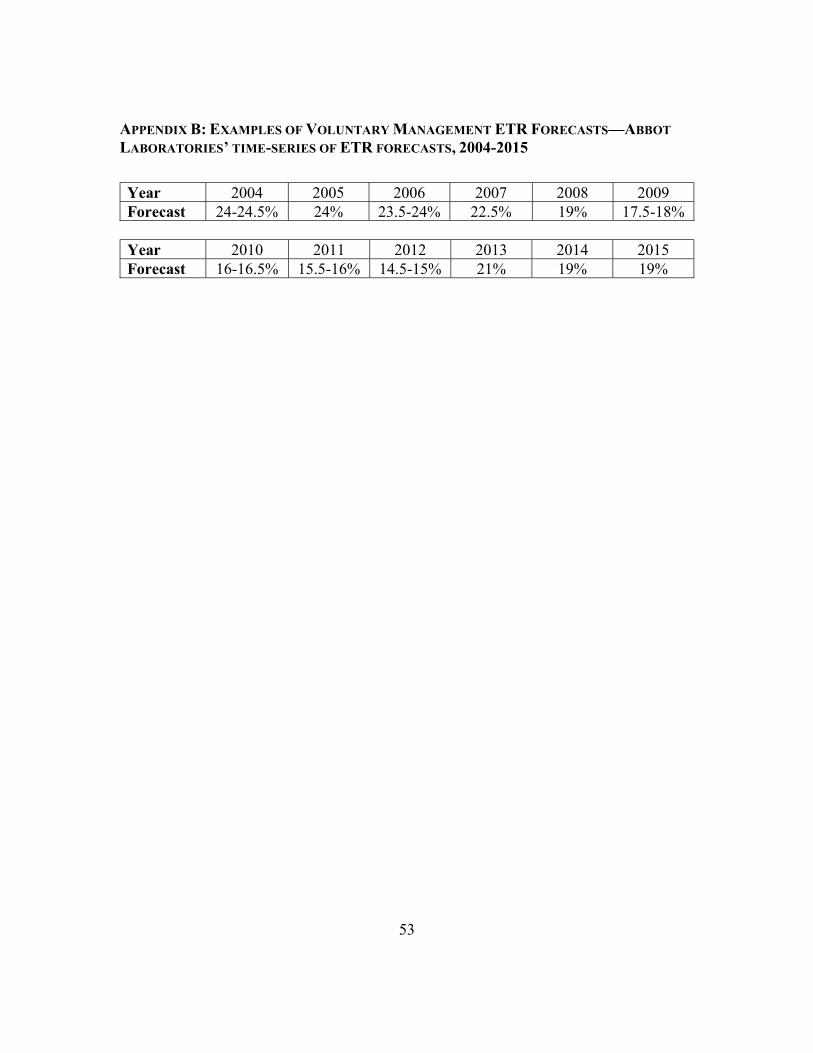

incorporated in the U.S. as shown in Table 1.10,11 I hand-collect ETR forecasts because

machine-readable databases like First Call Company Issued Guidance (CIG) have sparse

coverage of non-EPS forecasts (Chuk, Matsumoto, and Miller [2013]). A total of 5,411

firm-years (about 451 firms per year) meet the initial sample requirements and potentially

issue ETR forecasts. Like Hutton et al. [2012], my sample consists of annual ETR forecasts

made early in the fiscal year.12 I read fourth-quarter earnings conference calls to find

management ETR forecasts (Appendix A presents an example of ETR guidance from

Abbot Laboratories and Appendix B presents their ETR forecasts from 2004-2015). I find

managers voluntarily issued ETR forecasts in about 43 percent of firm-years (2,347 out of

5,411 firm-years). Table 2 shows that the percentage of firm managers issuing ETR

forecasts ranges from a minimum of 29 percent in 2004 to a maximum of 49 percent in

2014. After excluding observations missing information from I/B/E/S, I have 2,110 firm-

years with ETR forecasts.

I match managers’ voluntary ETR forecasts to analyst forecasts from I/B/E/S for a

total sample of 44,114 analyst-firm-year forecasts issued in the period between the prior

year’s fourth quarter earnings release and before the current fiscal year’s first quarter

10 All analysts should have to access to managers’ voluntary ETR forecasts because my sample begins several years after the implementation of Reg FD in 2000. I do not expect Reg FD to influence my findings, which significantly changed firms’ information environments (Heflin, Subramanyam, and Zhang [2003]; Wang [2007]). Thus, I expect analysts to disagree with managers’ ETR forecasts because they had different expectations of ETR rather than because they did not know managers’ forecasts. 11 I exclude 287 firm-years of non-taxable entities including real estate investment trusts (SIC code 6798), limited partnerships (names ending in “-LP”), trusts (names containing “TRUST”), and mutual funds, because these entities often have insignificant income tax burdens. 12 Manager and analyst forecasts issued later in the year suffer from larger confounding incentives to beat forecasts.

16

earnings release.13 I study analyst forecasts between these dates to keep information

available to analysts consistent across firms. Outside of these dates, other information will

be increasingly important to forecast ETR relative to managers’ ETR forecasts.14 The

sample contains forecasts from 3,178 analysts from 272 brokerages.

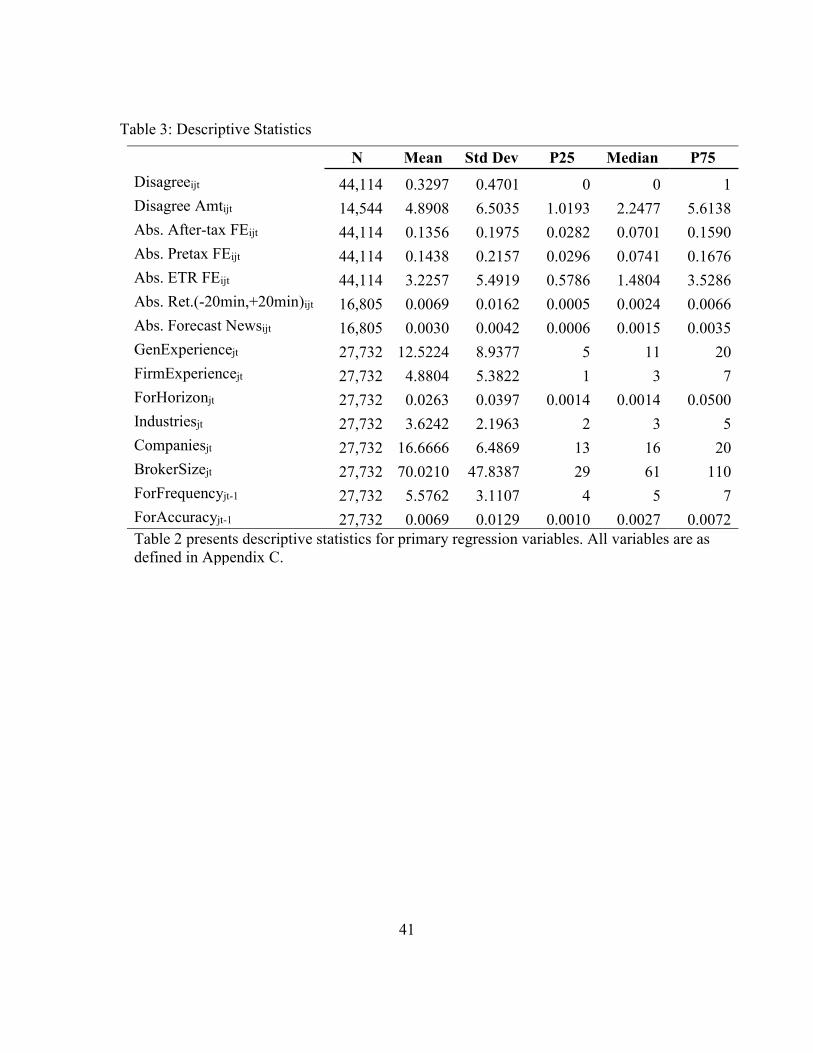

Table 3 presents descriptive statistics for regression variables of my main tests. I

document that 33 percent of analyst forecasts disagree with management ETR forecasts.15

Among the analysts with ETR forecast disagreement, the mean (median) absolute ETR

forecast disagreement difference between analysts and managers is 4.8 percent (2.2

percent). Thus, analyst ETR disagreement appears material to the overall earnings forecast.

Descriptive statistics for analyst characteristics exclude duplicate analyst forecasts

in a firm-year. Analysts have a mean (median) of 12.5 (11) years of general forecasting

experience. In a fiscal year, analysts issued a mean (median) of 5.5 (5) forecasts per firm.

They cover a mean (median) of 3.6 (3) industries and 16.6 (16) companies. Thus, analysts

in the sample have significant forecasting experience, update their forecasts throughout the

year, and follow multiple industries and companies.

13 My sample includes all analyst forecasts issued in a firm-year between the prior year’s fourth-quarter earnings release and the current year’s first-quarter earnings release. Thus, the sample can include multiple forecasts by an individual analyst for a single firm-year and it reflects a null hypothesis that analysts update their forecasts to fully reflect their expectations. However, my results are robust to restricting the sample of forecasts to either an analyst’s first-issued forecast or last-issued forecast in a firm-year and including analyst fixed effects. 14 Specifically, I only consider analyst forecasts issued after the fourth-quarter earnings release so analysts can update for managers’ ETR forecasts and the prior fiscal year’s financial performance. I also do not examine analyst forecasts issued after the first-quarter earnings release because first-quarter earnings provide new information about firm prospects. Finally, analyst forecasts issued during this period are less likely to rely on stale information because analysts often update their forecasts following fiscal year-end earnings releases (Asquith et al. [2005]). 15 Bratten et al. [2017] document 73.6 percent of analysts’ ETR forecasts differ from managers’ implied GAAP ETR forecasts by greater than half a percent. As expected, their disagreement frequency is greater than the one reported in this study because they show mandatory inclusion of discrete tax items pollute GAAP ETR forecasts. This paper compares analysts’ and managers’ non-GAAP ETR forecasts, which are generally free of discrete tax items.

17

The main dependent variables for examining the consequences of ETR

disagreement are absolute after-tax forecast error and stock price changes in the 40-minute

windows centered at the releases of analyst forecasts. The mean (median) of absolute after-

tax forecast error is 0.13 (0.07), with slightly larger values for absolute pretax forecast

error. The absolute stock price change in the 40-minute window has a mean (median) of

0.0069 (0.0024), and the forecasts news (the difference between the analyst after-tax

forecast and the consensus analyst forecast) has a mean (median) of 0.0030 (0.0015).

18

Chapter 4: Research Design and Empirical Analyses

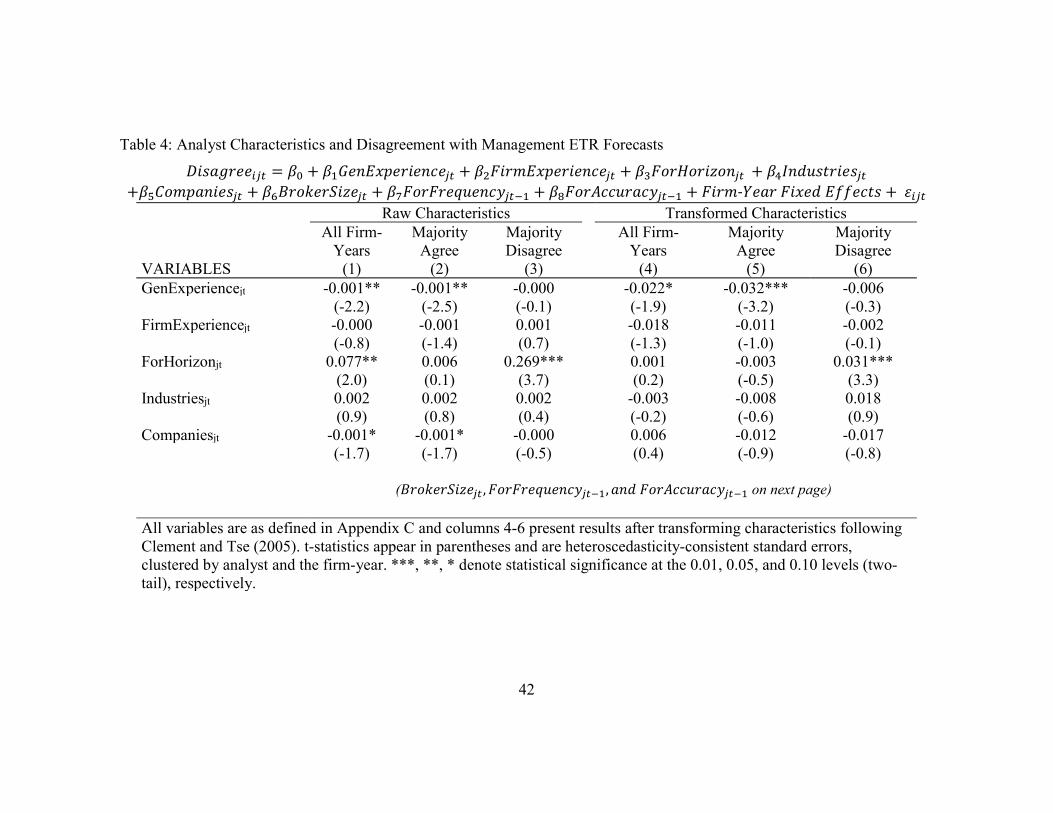

4.1 DETERMINANTS OF DISAGREEMENT (H1)

My first research question studies the association between analyst characteristics

and analyst disagreement with managers over ETR forecasts. I use a linear probability

model because nonlinear models with large numbers of fixed effects produce biased

coefficient estimates.16 My dependent variable (Disagreeijt) is an indicator variable for

analyst disagreement. Consistent with Bratten et al. [2017], Disagreeijt equals 1 when

analyst ETR forecasts deviate from manager’s ETR forecast by more the 0.5 percent and

equals 0 otherwise. When managers issue ETR forecast ranges, analyst disagreement

equals 1 if analyst ETR forecasts are outside of a manager’s forecast range by greater than

or equal to 0.5 percent, and equals 0 otherwise.17

I examine analyst characteristics studied by Clement [1999] and Clement and Tse

[2005]. Specifically, I test the association between analyst disagreement with management

ETR forecasts and general forecasting experience, firm forecasting experience, forecast

horizon, number of industries followed, number of companies followed, the size of the

brokerage that employs the analyst, how many forecasts the analysts issued for the firm in

the previous year, and the accuracy of the analyst’s last forecast for the firm in the prior

year. My empirical regression model is as follows:

16 I have 2,066 unique firm-years with manager ETR forecasts. Greene [2004] shows nonlinear fixed effects models such as logit and probit produce biased coefficient estimates because of the incidental parameter problem. 17 Results are not sensitive to measuring analyst disagreement as occurring when an analysts’ ETR forecast differs from the manager’s range midpoint by greater than or equal to 0.5 percent.

19

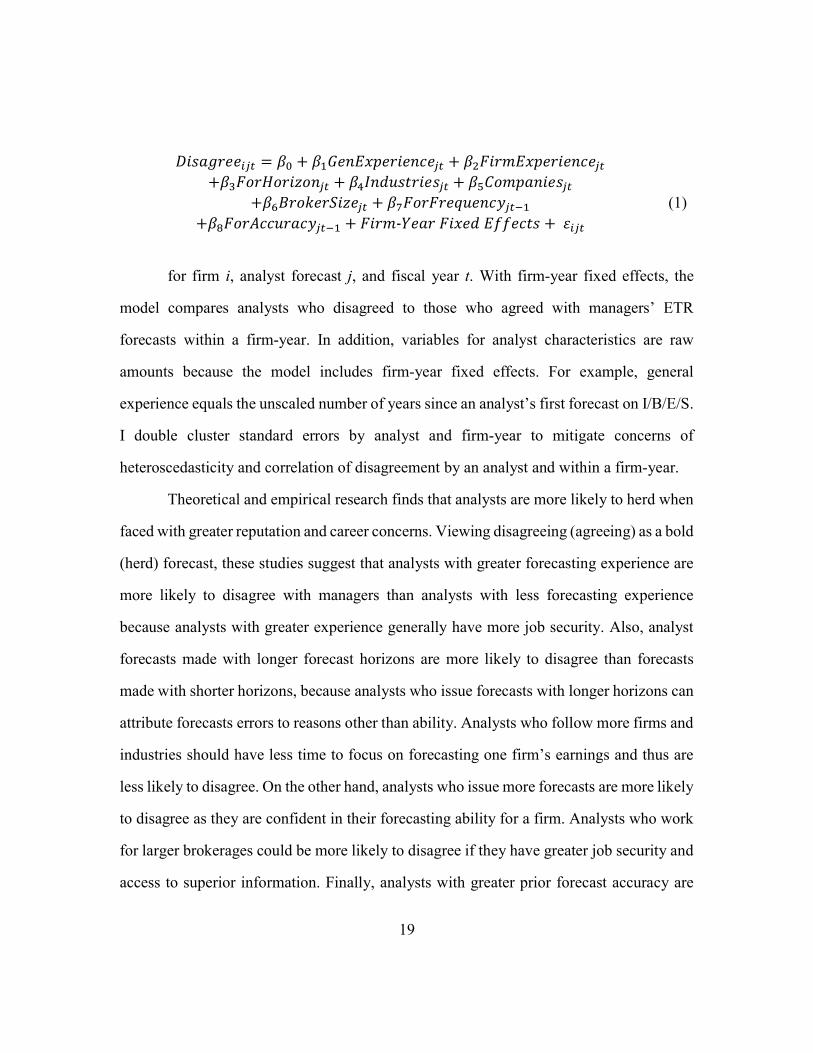

𝐷𝑖𝑠𝑎𝑔𝑟𝑒𝑒 = 𝛽 + 𝛽 𝐺𝑒𝑛𝐸𝑥𝑝𝑒𝑟𝑖𝑒𝑛𝑐𝑒 + 𝛽 𝐹𝑖𝑟𝑚𝐸𝑥𝑝𝑒𝑟𝑖𝑒𝑛𝑐𝑒

+𝛽 𝐹𝑜𝑟𝐻𝑜𝑟𝑖𝑧𝑜𝑛 + 𝛽 𝐼𝑛𝑑𝑢𝑠𝑡𝑟𝑖𝑒𝑠 + 𝛽 𝐶𝑜𝑚𝑝𝑎𝑛𝑖𝑒𝑠 +𝛽 𝐵𝑟𝑜𝑘𝑒𝑟𝑆𝑖𝑧𝑒 + 𝛽 𝐹𝑜𝑟𝐹𝑟𝑒𝑞𝑢𝑒𝑛𝑐𝑦

+𝛽 𝐹𝑜𝑟𝐴𝑐𝑐𝑢𝑟𝑎𝑐𝑦 + 𝐹𝑖𝑟𝑚-𝑌𝑒𝑎𝑟 𝐹𝑖𝑥𝑒𝑑 𝐸𝑓𝑓𝑒𝑐𝑡𝑠 + 𝜀 (1)

for firm i, analyst forecast j, and fiscal year t. With firm-year fixed effects, the

model compares analysts who disagreed to those who agreed with managers’ ETR

forecasts within a firm-year. In addition, variables for analyst characteristics are raw

amounts because the model includes firm-year fixed effects. For example, general

experience equals the unscaled number of years since an analyst’s first forecast on I/B/E/S.

I double cluster standard errors by analyst and firm-year to mitigate concerns of

heteroscedasticity and correlation of disagreement by an analyst and within a firm-year.

Theoretical and empirical research finds that analysts are more likely to herd when

faced with greater reputation and career concerns. Viewing disagreeing (agreeing) as a bold

(herd) forecast, these studies suggest that analysts with greater forecasting experience are

more likely to disagree with managers than analysts with less forecasting experience

because analysts with greater experience generally have more job security. Also, analyst

forecasts made with longer forecast horizons are more likely to disagree than forecasts

made with shorter horizons, because analysts who issue forecasts with longer horizons can

attribute forecasts errors to reasons other than ability. Analysts who follow more firms and

industries should have less time to focus on forecasting one firm’s earnings and thus are

less likely to disagree. On the other hand, analysts who issue more forecasts are more likely

to disagree as they are confident in their forecasting ability for a firm. Analysts who work

for larger brokerages could be more likely to disagree if they have greater job security and

access to superior information. Finally, analysts with greater prior forecast accuracy are

20

more likely to disagree because prior forecast accuracy could increase general confidence

in forecasting ability. On the other hand, Aharoni et al. [2017] show that strong analysts

underweight their private information. If so, then the associations between analyst

disagreement and career/reputational concerns described above switch from positive to

negative and vice versa.

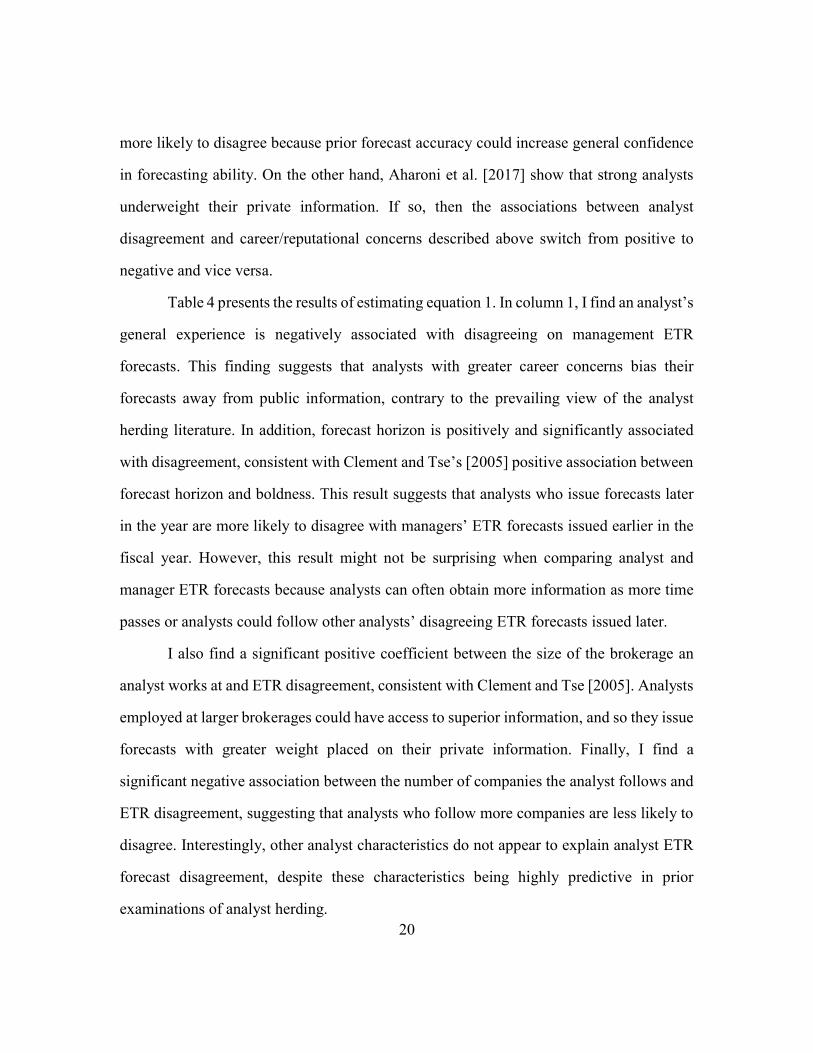

Table 4 presents the results of estimating equation 1. In column 1, I find an analyst’s

general experience is negatively associated with disagreeing on management ETR

forecasts. This finding suggests that analysts with greater career concerns bias their

forecasts away from public information, contrary to the prevailing view of the analyst

herding literature. In addition, forecast horizon is positively and significantly associated

with disagreement, consistent with Clement and Tse’s [2005] positive association between

forecast horizon and boldness. This result suggests that analysts who issue forecasts later

in the year are more likely to disagree with managers’ ETR forecasts issued earlier in the

fiscal year. However, this result might not be surprising when comparing analyst and

manager ETR forecasts because analysts can often obtain more information as more time

passes or analysts could follow other analysts’ disagreeing ETR forecasts issued later.

I also find a significant positive coefficient between the size of the brokerage an

analyst works at and ETR disagreement, consistent with Clement and Tse [2005]. Analysts

employed at larger brokerages could have access to superior information, and so they issue

forecasts with greater weight placed on their private information. Finally, I find a

significant negative association between the number of companies the analyst follows and

ETR disagreement, suggesting that analysts who follow more companies are less likely to

disagree. Interestingly, other analyst characteristics do not appear to explain analyst ETR

forecast disagreement, despite these characteristics being highly predictive in prior

examinations of analyst herding.

21

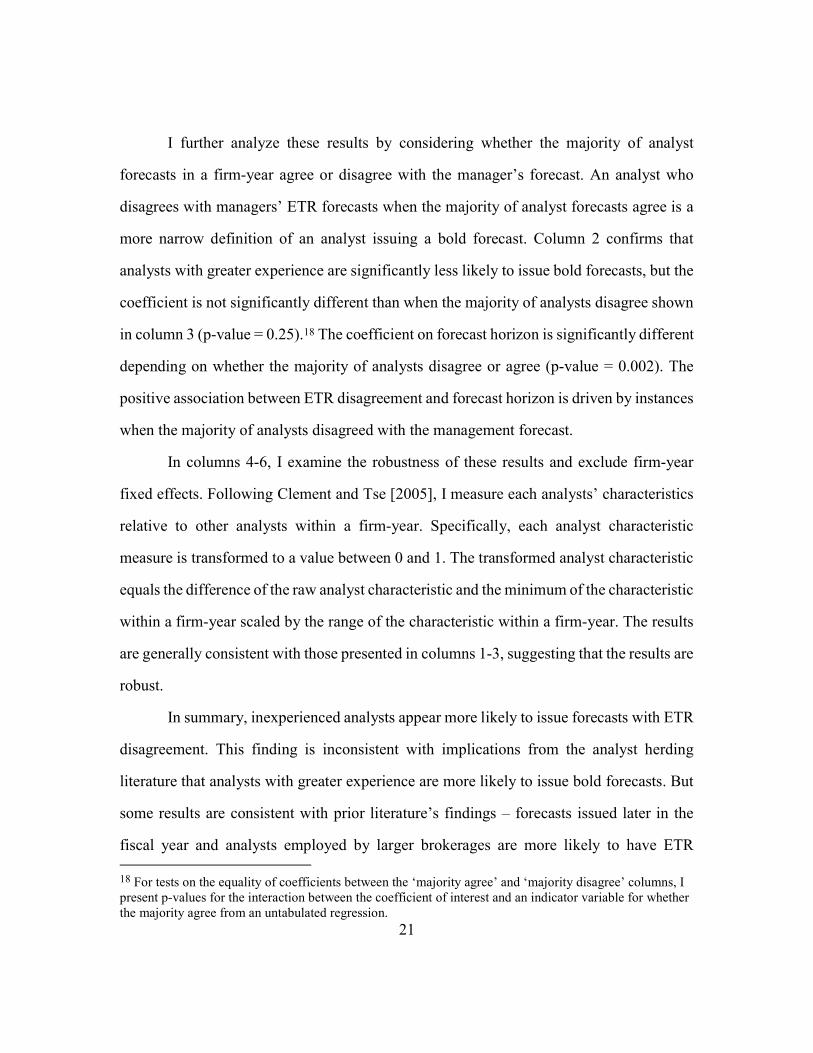

I further analyze these results by considering whether the majority of analyst

forecasts in a firm-year agree or disagree with the manager’s forecast. An analyst who

disagrees with managers’ ETR forecasts when the majority of analyst forecasts agree is a

more narrow definition of an analyst issuing a bold forecast. Column 2 confirms that

analysts with greater experience are significantly less likely to issue bold forecasts, but the

coefficient is not significantly different than when the majority of analysts disagree shown

in column 3 (p-value = 0.25).18 The coefficient on forecast horizon is significantly different

depending on whether the majority of analysts disagree or agree (p-value = 0.002). The

positive association between ETR disagreement and forecast horizon is driven by instances

when the majority of analysts disagreed with the management forecast.

In columns 4-6, I examine the robustness of these results and exclude firm-year

fixed effects. Following Clement and Tse [2005], I measure each analysts’ characteristics

relative to other analysts within a firm-year. Specifically, each analyst characteristic

measure is transformed to a value between 0 and 1. The transformed analyst characteristic

equals the difference of the raw analyst characteristic and the minimum of the characteristic

within a firm-year scaled by the range of the characteristic within a firm-year. The results

are generally consistent with those presented in columns 1-3, suggesting that the results are

robust.

In summary, inexperienced analysts appear more likely to issue forecasts with ETR

disagreement. This finding is inconsistent with implications from the analyst herding

literature that analysts with greater experience are more likely to issue bold forecasts. But

some results are consistent with prior literature’s findings – forecasts issued later in the

fiscal year and analysts employed by larger brokerages are more likely to have ETR 18 For tests on the equality of coefficients between the ‘majority agree’ and ‘majority disagree’ columns, I present p-values for the interaction between the coefficient of interest and an indicator variable for whether the majority agree from an untabulated regression.

22

disagreement. Overall, the results appear to portray analyst ETR disagreement as resulting

from analyst overconfidence in their private information. However, based on evidence of

analyst characteristics alone, it is unclear whether analysts’ ETR disagreement forecasts

have consequences for forecast accuracy and investor reaction consistent with prior

literature on analyst herding.

23

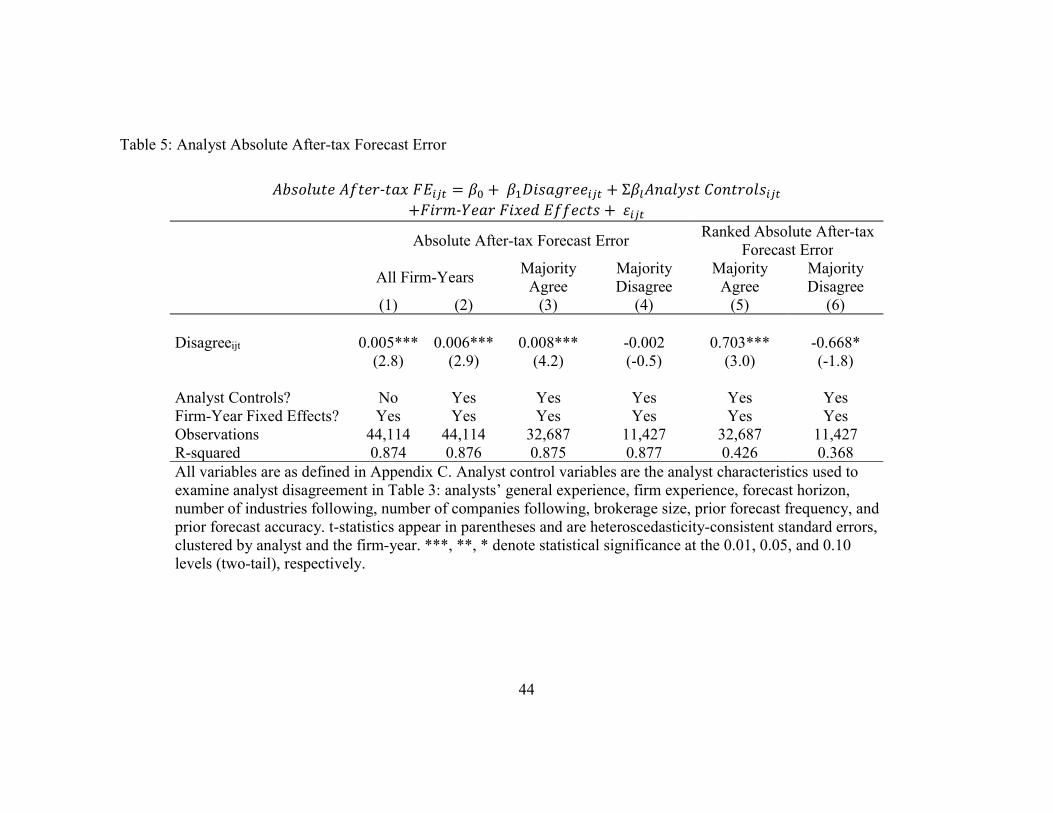

4.2 ANALYST FORECAST ACCURACY (H2)

My second research question investigates the consequence of ETR forecast

disagreement for forecast accuracy. Specifically, I examine the association between analyst

disagreement and forecast accuracy using the following regression:

𝐴𝑏𝑠𝑜𝑙𝑢𝑡𝑒 𝐴𝑓𝑡𝑒𝑟-𝑡𝑎𝑥 𝐹𝐸 = 𝛽 + 𝛽 𝐷𝑖𝑠𝑎𝑔𝑟𝑒𝑒 + Σ𝛽 𝐴𝑛𝑎𝑙𝑦𝑠𝑡 𝐶𝑜𝑛𝑡𝑟𝑜𝑙𝑠

+𝐹𝑖𝑟𝑚-𝑌𝑒𝑎𝑟 𝐹𝑖𝑥𝑒𝑑 𝐸𝑓𝑓𝑒𝑐𝑡𝑠 + 𝜀 (2)

Absolute After-tax FEijt is defined as the absolute value of the after-tax forecast

error (the difference of after-tax earnings forecast and I/B/E/S actual earnings) scaled by

absolute I/B/E/S actual earnings.19 I control for analyst characteristics described in

equation 1 and I include firm-year fixed effects, which allows a comparison of the average

absolute forecast error of agreeing analysts versus disagreeing analysts within a firm-year.

I also double cluster standard errors on analyst and firm-year.

Because absolute forecast error measures the distance between the forecast and

actual amount, a positive coefficient on Disagreeijt (β1) suggests that disagreement leads to

less accurate forecasts and a negative coefficient suggests a more accurate forecast. I also

examine the accuracy of analyst pretax forecasts with Absolute Pretax FEijt, defined as the

absolute value of pretax forecast error scaled by absolute I/B/E/S pretax actual earnings.

Finally, I test the accuracy of analyst ETR forecasts with Absolute ETR FEijt, defined as

the absolute value of the analyst ETR forecast minus the Street ETR forecast.

Table 5 shows the results to estimating equation 2. Column 1 reports the empirical

estimates of the model including only an indicator for analyst disagreement and firm-year

fixed effects. Column 2 adds controls for analyst characteristics to the model. Both columns

19 Absolute forecast error results are robust to scaling the absolute difference of analyst earnings forecast and the I/B/E/S actual earnings forecast by fiscal year-end market value of equity.

24

have significantly positive coefficients on Disagreeijt, which suggests that analyst after-tax

forecasts with ETR disagreement are less accurate than analyst after-tax forecasts without

ETR disagreement.

In columns 3 and 4, I examine whether the association between analyst forecast

accuracy and ETR disagreement depends on whether the majority of analyst forecasts agree

or disagree with the manager’s ETR forecast. I find the association between ETR

disagreement and absolute forecast error is driven by analysts who disagreed when the

majority of analysts agreed (column 3). In contrast, when the majority of analyst forecasts

disagree with a manager’s ETR forecast, I do not find evidence of a significant association

between analysts’ forecasts that disagree and absolute forecast error (column 4). The

coefficients in column 3 and 4 are significantly different (p-value = 0.04), suggesting that

it is important to consider public information available to analysts from managers and the

consensus analyst behavior.

Columns 5 and 6 repeat the analysis of columns 3 and 4 using ranked absolute after-

tax forecast errors as the dependent variable. By ranking on absolute forecast error, the

results speak to an analyst’s goal to achieve relative forecast accuracy rather than absolute

forecast accuracy (Aharoni et al. 2017). Moreover, ranking absolute forecast errors

mitigates concerns that results can be attributed to inaccurate outlier forecasts. Column 5

shows a positive and statistically significant coefficient on Disagreeijt, which suggests that

forecasts are less accurate when the majority of analysts agreed. Column 6 shows a

negative and statistically significant coefficient on Disagreeijt, which suggests that

forecasts with ETR agreement are less accurate when the majority of forecasts have ETR

disagreement. In addition, the coefficients in columns 5 and 6 are significantly different

(p-value = 0.002). The results on ranked absolute forecast error confirm those presented

for absolute forecast error.

25

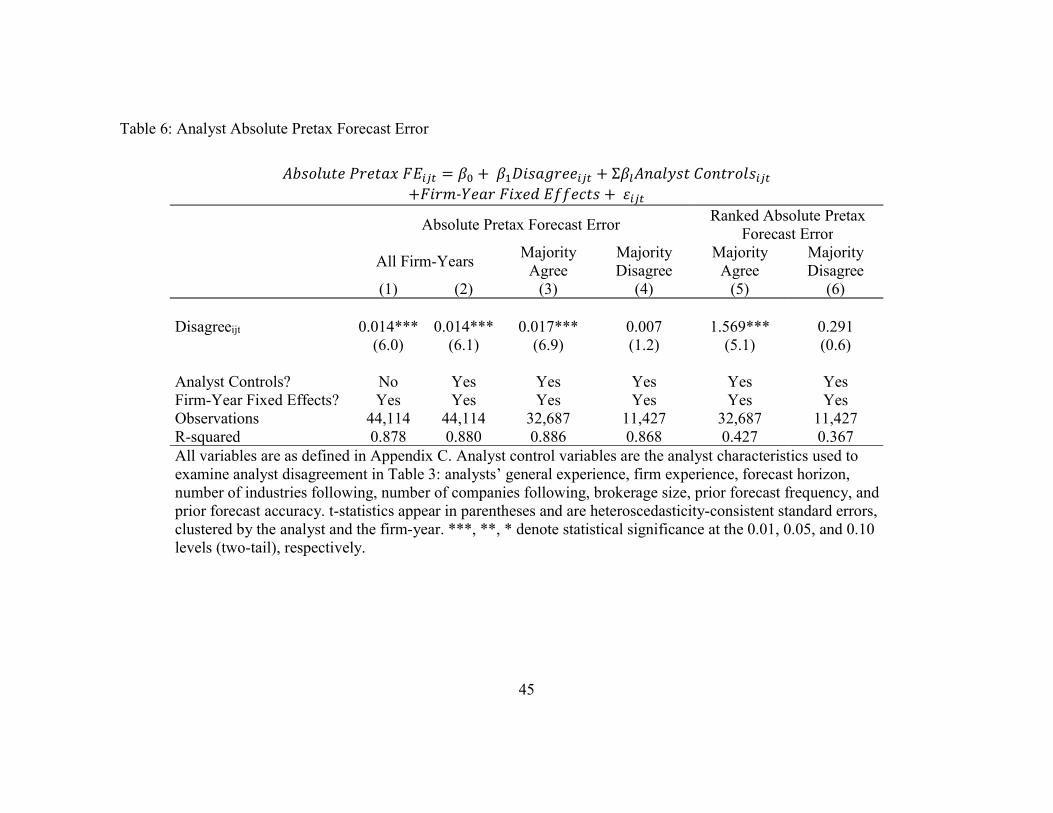

Table 6 shows the analysis for absolute pretax forecast error. Analyst disagreement

over ETR forecasts is associated with less accurate pretax forecasts. Thus, analysts appear

to disagree with managers about firm prospects, which leads to less accurate forecasts

rather than inaccurate forecasts being solely driven by disagreement over ETR. In

untabulated analysis, I also examine whether the differences in pretax forecast accuracy

are material to analyst after-tax earnings forecast accuracy. Specifically, I re-calculate

analysts’ after-tax earnings forecasts so that all forecasts use managers’ ETR forecasts. I

find analysts’ after-tax earnings forecasts adjusted to use managers’ ETR forecasts are

significantly less accurate than after-tax earnings forecasts following managers’ ETR

forecasts. Thus, analysts’ ETR forecast disagreements are associated with disagreements

in pretax earnings forecasts that are material to after-tax earnings overall.

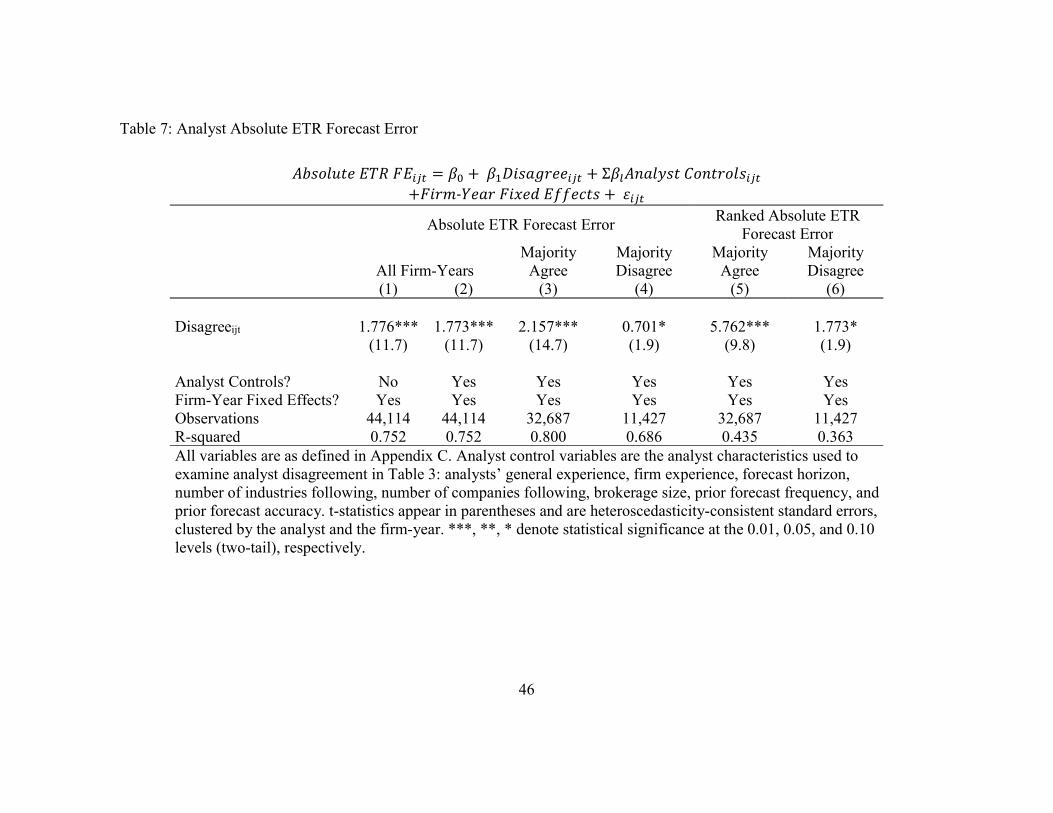

In Table 7, I examine analyst absolute ETR forecast error. Column 1 shows that the

average absolute difference between the actual ETR and the analyst disagreeing ETR

forecast is 1.7%, which likely materially impacts analyst after-tax earnings forecast

accuracy.

In summary, results in Tables 5-7 show a strong association between analyst

absolute forecast errors and whether analyst ETR forecasts disagree with voluntary

management ETR forecasts. These findings speak to the herding literature because the

results suggest that disagreeing analysts are most inaccurate when they issue disagreeing

forecasts and the majority of analysts issued agreeing forecasts.

26

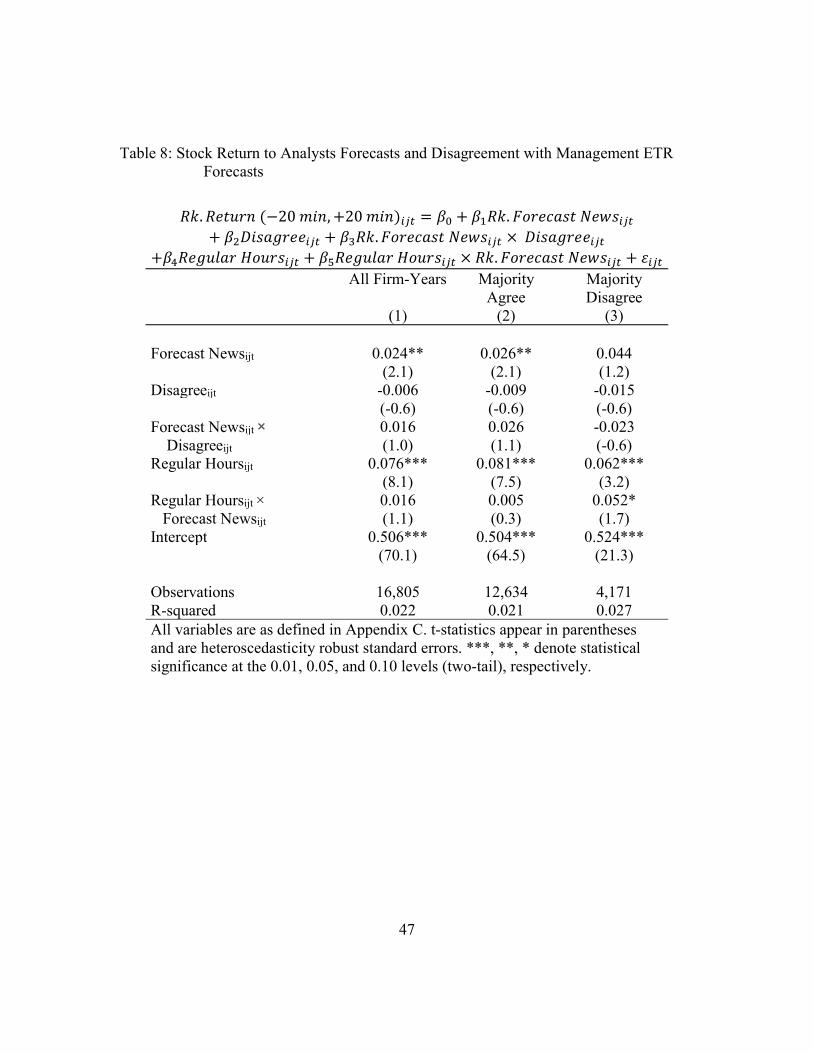

4.3 INVESTOR REACTION TO ANALYST FORECAST REVISIONS (H3)

My final research question examines investor reactions to analyst forecast revisions

when the analyst forecasts disagree with management ETR forecasts. Prior literature shows

that analyst revisions are positively associated with stock price changes, so I control for

analyst revisions and interact the revision with the indicator variable Disagreeijt. My model

is as follows:

𝑅𝑘. 𝑅𝑒𝑡𝑢𝑟𝑛 (−20𝑚𝑖𝑛, +20 𝑚𝑖𝑛) = 𝛽 + 𝛽 𝑅𝑘. 𝐹𝑜𝑟𝑒𝑐𝑎𝑠𝑡 𝑁𝑒𝑤𝑠

+ 𝛽 𝐷𝑖𝑠𝑎𝑔𝑟𝑒𝑒 + 𝛽 𝐹𝑜𝑟𝑒𝑐𝑎𝑠𝑡 𝑁𝑒𝑤𝑠 × 𝐷𝑖𝑠𝑎𝑔𝑟𝑒𝑒 + 𝜀 (3)

Rk. Return (-20min, +20min)ijt is the absolute stock price change in the 40-minute

window beginning 20 minutes before an analyst issue his forecast and ending 20 minutes

after, ranked within the firm-year and scaled by the number of forecasts in a firm-year.20,21

Prior studies use narrow return windows to examine whether analyst stock

recommendations are informative to investors (Altınkılıc and Hansen [2009]; Li et al.

[2015]). I calculate stock return as the change in stock price (proxied as the midpoint of

the national best bid and offer from NYSE Trade and Quote (TAQ) data between 2005-

2014).22 I also control for whether the forecast is issued during regular trading hours

20 I do not use daily stock returns because analysts often issue forecasts on the day of the earnings release or soon after. As a result, daily stock returns comingle investor reactions to an analyst’s forecast with the earnings release and other analyst forecasts. In untabulated robustness test of daily returns, I do not find investors react more analyst forecasts with ETR disagreement than analyst forecasts that follow managers’ ETR forecasts. 21 Similar to Altınkılıc and Hansen [2009], my main results use the 40-minute window centered at the announcement time. I find results similar to those presented in three additional time periods of narrow return windows: (0 min, +10 min), (-10 min, +10 min), and (0 min, +20 min). In addition, while other studies using TAQ data calculate stock returns by averaging the price of actual trades over ten-minute periods, I use the midpoint of bid-ask spreads because bid-ask spread data are available even without actual trades. When using actual trade data and following the return calculation methodology in Altınkılıc and Hansen [2009], the results are similar to those presented, but with a smaller sample. 22 I use ‘monthly product’ TAQ data, which provides intraday transaction data for years between 1993 and 2014.

27

(between 9:30 am and 4:00 pm) or in extended trading hours (including pre-trading hours

between 4:00 am and 9:30 am and after-hours trading between 4:00 pm and 8:00 pm). I

exclude analyst forecasts issued outside of regular and extended trading hours.

Rk. Forecast Newsijt equals the absolute difference between an analyst’s current

forecast and the consensus analyst forecast (calculated as the average of all analyst

forecasts issued before the analyst’s forecast), and ranked within the firm-year and scaled

by the number of forecasts in the firm-year. Standard errors are clustered by forecast

issuance date.

I expect a positive value of Rk. Forecast Newsijt (β1>0) because investors should

react to forecasts with greater news (Ivković and Jegadeesh [2004]). The coefficients of

interest are on Disagreeijt (β2) and the interaction term (β3) between Rk. Forecast Newsijt

and Disagreeijt. The coefficient on Disagreeijt suggests how investors react to analyst

forecasts, irrespective of news in the analyst forecast. The coefficient on the interaction

term between Rk. Forecast Newsijt and Disagreeijt suggests whether analysts disagreement

influences how investors perceive the usefulness of the forecast news.

Table 8 presents results of market reaction to analyst forecasts. As expected,

investors react to analyst forecast news: in the 40-minute window, stock returns are

positively associated with analyst forecasts displaying more forecast news. However,

investors do not distinguish between analyst forecasts that disagree with managers’ ETR

forecast versus analyst forecasts that follow. In addition, disagreeing forecasts do not

moderate the association between investor reaction and forecast news. These results do not

depend on whether the majority of analyst forecasts agree or disagree. In summary,

investors do not appear to find analysts’ disagreeing ETR forecasts as improvements on

managers’ ETR forecasts.

28

Chapter 5: Supplemental Analyses

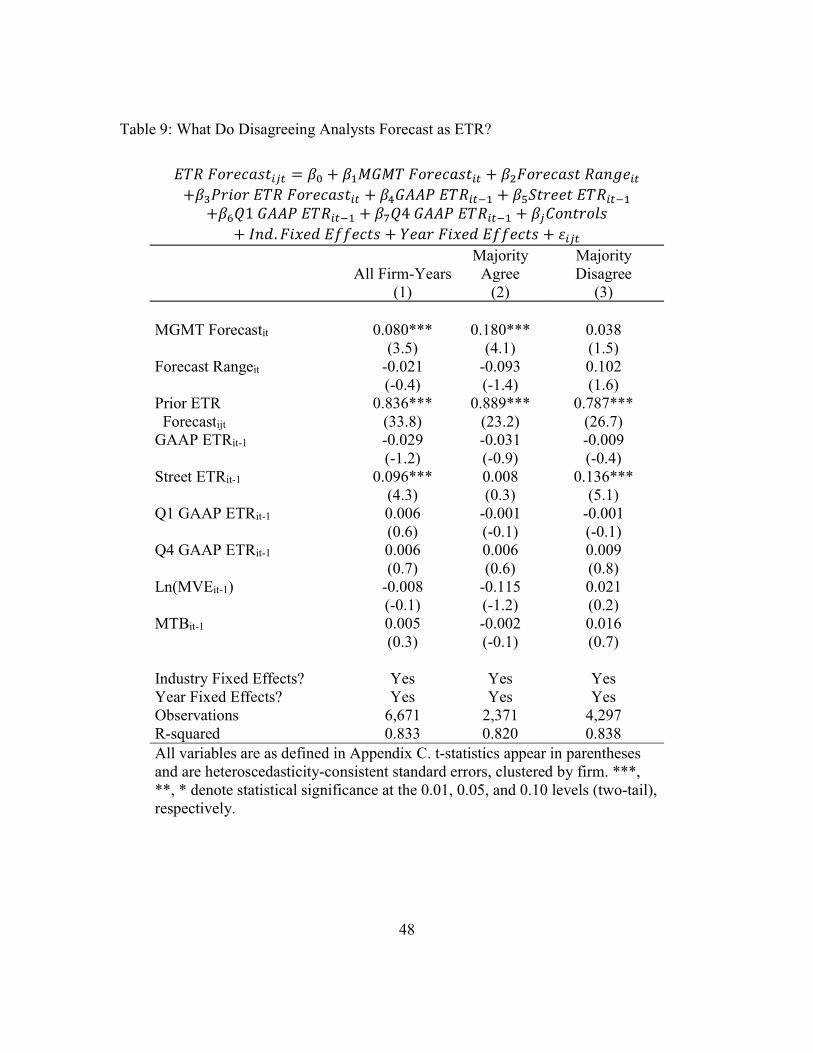

5.1 WHAT INFORMATION DO DISAGREEING ANALYSTS USE TO FORECAST ETR?

The findings suggest that analysts do not improve on managers’ ETR forecasts.

Given that analysts can use managers’ forecasts rather than forecasting their own ETR,

analysts could have made a mistake when forecasting disagreeing ETRs. I consider this

explanation for disagreeing with managers’ ETR forecasts by examining what information

analysts use when they disagree. Specifically, I consider whether analysts use information

from manager’s ETR forecast range, the analyst’s own prior ETR forecast, the prior year

GAAP ETR, the prior year Street ETR, the prior year Q1 GAAP ETR, and the prior year

Q4 GAAP ETR.23 I also control for firm size and firm growth potential to proxy for the

general complexity of the firm’s business operation. The sample of analyst forecasts

contains only analysts’ ETR disagreement forecasts and it contains only the first forecast

issued by an analyst in a fiscal year to ensure analysts’ revisions are for information in the

fourth-quarter earnings release.

Column 1 of Table 9 shows that an analyst’s prior ETR forecast is significantly

associated with their subsequent ETR forecast. This evidence suggests that analysts have

information influencing their prior forecast that continues to influence their current

forecast, as if they are anchored on using their own prior forecast. Although the sample

contains only analyst forecasts that disagree with management ETR forecasts, I also find a

significant association between management ETR forecasts and analyst ETR forecasts.

Thus, analysts appear to use some of the managers’ ETR forecast information.24

23 Analysts can use the U.S. statutory tax rate as their ETR forecast, but a histogram of disagreeing ETR forecasts does not show “bunching” at the maximum U.S. statutory tax rate in the sample period (35 percent). 24 Because the evidence suggests analysts heavily rely on their prior ETR forecast, I examine whether analysts update their forecasts when managers issue new forecasts. In untabulated tests, I examine the association between analysts’ ETR revisions (the absolute difference between analysts’ current and last

29

Furthermore, the coefficients on management ETR forecast in columns 2 and 3 are

significantly different from one another (p-value = 0.002). This difference suggests that the

association between managers’ and analysts’ ETR forecasts is driven by situations when

the analyst disagreed, but the majority of analysts agreed. Finally, the prior year Street ETR

is significantly associated with analyst current ETR forecasts, suggesting the use of

historical tax information. However, columns 2 and 3 show that the coefficient on prior

year Street ETR is only significant when the majority of analysts disagreed (and

significantly different; p-value = 0.008).25 In summary, these results suggests that analysts

rely on their prior efforts to forecast ETR, but their use of manager’s ETR forecast and

historical ETR information depends on whether the majority of analysts agreed or

disagreed with manager’s forecast. Thus, analysts appear to exert effort to disagree with

managers’ ETR forecasts rather than disagreeing resulting from a casual error.

ETR forecasts) and managers’ forecast updates (the absolute difference between a manager’s ETR forecast and the analyst’s last forecast). For example, if an analyst forecasts a 24.5 percent ETR prior to an earnings announcement and then the manager issues a 26 percent ETR forecast, a disagreeing analyst forecast can revise their ETR upward 0.5 percent to a 25 percent ETR, rather than the full 1.5 percent. Adding to the findings in Table 6, the results suggest that analysts do not substantially revise their forecasts to match managers’ ETR forecasts and appear to be anchored on their prior ETR forecast. 25 These results are consistent with conversations with financial analysts, which confirm that analysts forecast ETRs. In general, they employ various methods to forecast ETRs and they believe ETRs should be stable across years so prior year Street ETRs are useful.

30

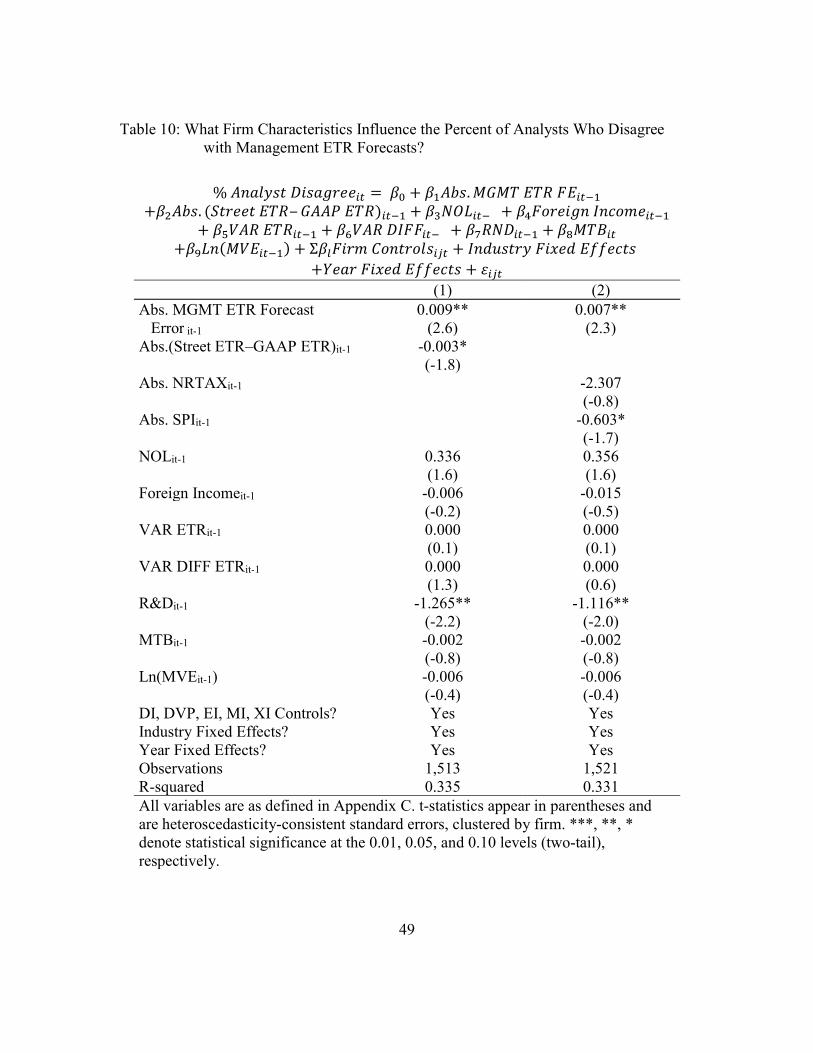

5.2 WHAT FIRM CHARACTERISTICS INFLUENCE THE PERCENTAGE OF ANALYSTS WHO

DISAGREE WITH MANAGEMENT ETR FORECASTS?

To understand why analysts disagree with managers, I examine the determinants of

the percentage of analysts’ forecasts that disagree with managers’ ETR forecasts. For

example, analysts potentially disagree with managers in complex situations because

analysts interpret complex information differently. On the other hand, analysts could be

more likely to follow the manager’s ETR forecast when forecasting is complicated because

they realize managers are more informed. I use the absolute difference between Street and

GAAP ETR in the prior year as a proxy for ETR forecast complexity because the absolute

difference between Street and GAAP ETR represents discrete items (Bratten et al. [2017]).

In Column 1 of Table 10, I find that a negative association between the prior-year

absolute difference between Street and GAAP ETR and the percentage of analysts

disagreeing. The result suggests fewer analysts disagree with managers when forecasting

ETR is more complex. I also find a positive association between the prior-year absolute

management ETR forecast error and the percentage of analysts disagreeing, suggesting that

more analysts follow managers’ ETR forecasts when managers are accurate forecasters and

that management credibility is important to analysts (Williams [1996]).

In Column 2, I exclude the absolute difference between Street and GAAP ETR and

include the absolute value of nonrecurring income taxes and special items, because these

items often generate differences between Street and GAAP ETR. The negative signs on

absolute nonrecurring income taxes is consistent with the negative sign on Abs. (Street‒

GAAP ETR)it-1 in column 1, but not statistically significant, which could reflect insufficient

power to observe the effect of nonrecurring income taxes on analyst disagreement.

The negative and statistically significant coefficient on special items suggests that

more analysts follow managers’ ETR forecast when managers disclosed special items in

31

the previous year. In addition, fewer analysts disagree when firms have greater R&D

spending. R&D spending makes forecasting ETR more difficult because R&D expense

generates tax credits in the jurisdiction where the spending occurs. The result further

suggests that greater ETR forecasting complexity is associated with less analyst

disagreement.

In general, these results imply that ETR forecasting complexity is associated with

more analysts following of managers’ ETR forecasts. Analysts also consider past

forecasting accuracy by managers when deciding their forecast. Because analysts appear

to disagree in less complex situations, these findings contribute additional evidence to the

perspective that when analysts disagree with managers’ ETR forecast, the analyst

characteristics describe overconfidence.

32

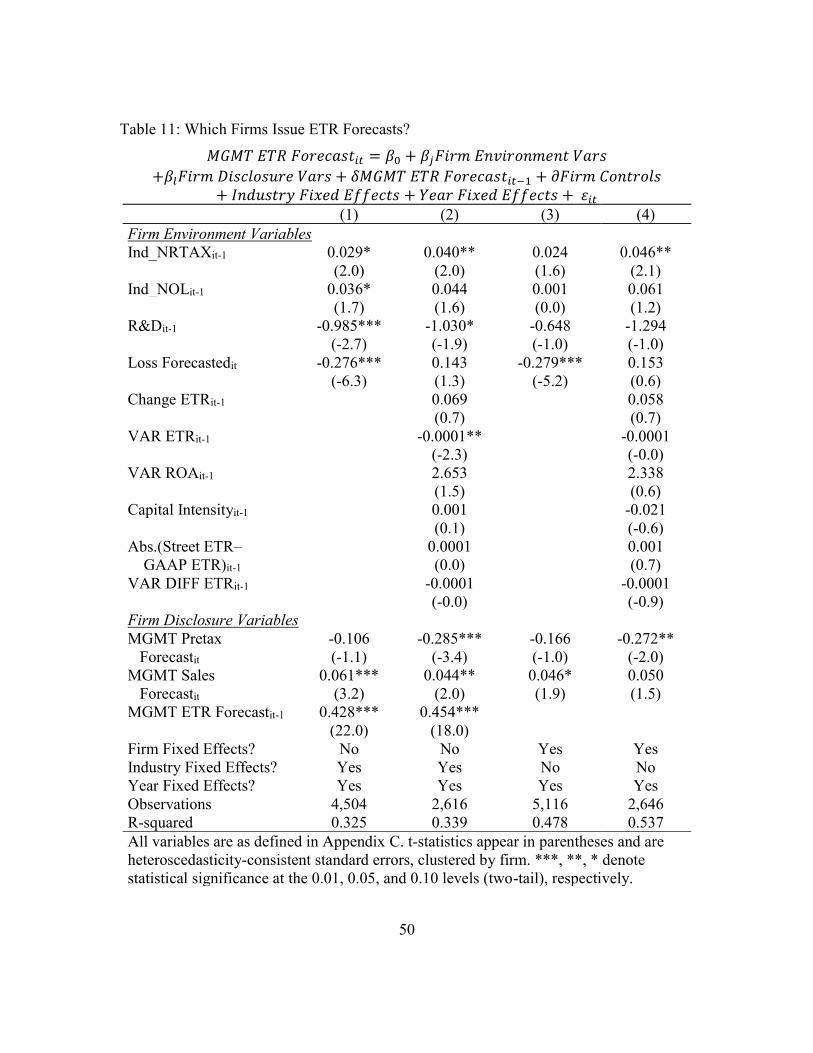

5.3 WHY DO MANAGERS ISSUE ETR FORECASTS?

Next, I explore why managers issue ETR forecasts. If managers primarily want to

inform market participants of firm-specific events when issuing ETR forecasts, then

analysts are unlikely to have information that improves on managers’ forecasts. Prior

research suggests that managers voluntarily disclose to meet outside demand for

information, such as when environments are complex (Graham et al. [2005]). Wasley and

Wu [2006] find that managers issue cash flow forecasts to signal good news, especially

about cash flows, and conclude that different incentives will drive different disclosures.

Thus, the incentives for managers to forecast ETR could be different than those for

forecasts of net earnings and cash flows.

Higgins [2013] argues that ETR forecasting difficulty motivates managers to issue

ETR forecasts. However, greater ETR forecasting difficulty could lead to increased

differences of opinion between analysts and managers about future ETRs. My study adds

to Higgins [2013] because I collect managers’ ETR forecasts from earnings conference

calls while she collects forecasts from 10-Ks. In general, managers issue forecasts at

earnings releases rather than in 10-Ks so my sample is larger and more representative of

firms that issue ETR forecasts. In Table 11, I examine whether managers issue ETR

forecasts in response to forecasting complexity, while controlling for the firms’ overall

disclosure strategy. MGMT ETR Forecastit is an indicator variable equal to 1 when a

manager issued an ETR forecast and 0 otherwise. My variables of interest proxy for the

firm environment, especially for ETR forecast complexity. To control for managers’

general disclosure strategies, I include indicator variables for whether a manager issued a

pretax earnings forecast or a sales forecast. Thus, the analysis speaks to why managers

issue tax information forecasts rather than why they generally forecast.

33

I find evidence that temporary complexity in ETR is associated with a greater

likelihood that managers issue an ETR forecast, but persistent complexity is associated

with less likelihood that managers issue an ETR forecast. Specifically, in Column 1, I find

a positive association between the issuance of an ETR forecast and whether the firm

reported a nonrecurring income tax in the prior year, but when firms have greater R&D

spending or potential negative earnings, managers are less likely to forecast an ETR. Thus,

managers appear to issue ETR forecasts when prior year’s ETR is temporarily complex

and managers appear less likely to issue ETR forecasts when they also face complexity to

forecast an ETR. In column 2, I add control variables for the historical complexity of ETR,

but I do not find these variables influence managers’ decisions to issue ETR forecasts.

Columns 3 and 4 show similar results when controlling for firm fixed effects rather than

an indicator variable of whether managers issued an ETR in the prior fiscal year. Thus,

managers appear to issue ETR forecasts to communicate firm-specific information.

34

5.4 DOES ETR FORECASTING COMPLEXITY MODERATE THE ASSOCIATION BETWEEN

ANALYST ETR FORECAST DISAGREEMENT AND FORECAST ACCURACY?

Analysts could have information to add to managers’ forecasts under certain types

of complexity, especially when analysts can reply on their macroeconomic information,

unbiased perspectives, or industry knowledge (Hutton et al. [2012]). Thus, I examine

whether complexity moderates the association between analyst ETR forecast disagreement

and forecast accuracy. I identify three situations when forecasting an ETR is potentially

more complex and analysts could rely on their information advantages: (1) firms that

operate in many countries, (2) firms with many legal entities in tax havens, and (3) firms

with weak corporate governance (measured as the percentage of independent directors in

the board).26 In untabulated analyses, I do not find the proxies of ETR forecast complexity

moderate the association between ETR forecast disagreement and forecast accuracy.

Specifically, I compare firms with greater than or equal to the median level of the

complexity proxy to firms with less than the median level. In both subsamples, analysts

issue less accurate forecasts when they disagree with managers’ ETR forecasts and the

average forecast error is about equal. Thus, analysts do not appear improve on managers’

ETR forecasts even in complex forecasting circumstances.

26 Dyreng and Lindsey [2009] find that U.S. firms with subsidiaries in at least one tax haven country have lower ETRs than firms without subsidiaries in tax havens. I thank Scott Dyreng for providing the Exhibit 21 data at https://sites.google.com/site/scottdyreng/Home/data-and-code.

35

Chapter 6: Robustness Tests

6.1 MINORITY INTEREST AND OTHER INCOME ITEM ADJUSTMENTS

Although I calculate analysts’ ETR forecasts following methodology in current

literature (Bratten et al. [2017]; Hutchens [2017]): the difference between pretax and after-

tax earnings forecasts, scaled by the pretax forecast with forecast values from I/B/E/S, this

calculation of analysts’ ETR forecast can lead to inaccurate values because analysts

sometimes submit their after-tax earnings forecasts with other income item adjustments,

but analysts’ pretax forecasts do not include these items.27 Mitigating concerns about

estimation error in analyst ETR forecasts, my results are robust (untabulated) to three large-

sample tests designed to eliminate noise from other income item adjustments. I construct

samples of firm-years with no other income item adjustments (1) in the fiscal year before

the forecast year; (2) in the forecast year; and (3) in both the prior and current forecast year.

Analyst ETR disagreement remains significantly associated with less accurate earnings

forecasts in all three subsamples, so other income item adjustments do not appear to explain

the results.28

27 Consistent with Bratten et al. [2017], other income item adjustments are from minority interest, discontinued operations, extraordinary income, equity in earnings affiliates, and preferred dividends. 28 I also randomly sample 60 firm-years and match analyst forecasts from I/B/E/S to their research reports on Thomson Reuters ONE. Analyst research reports provide the true analyst ETR forecast. However, I lose about 60 percent of analyst forecasts when matching I/B/E/S to Thomson Reuters ONE. Consistent with a loss of statistical power, untabulated results show coefficient signs consistent with the main analysis, but not statistically significant.

36

6.2 PLACEBO TEST

Do analysts who disagree have lower forecasting ability? I examine this possibility

with placebo dates to match analyst and manager forecasts. Specifically, I lag analyst ETR

forecast disagreement (e.g., if an analyst disagrees with the manager in the year 2010, I

examine whether the analyst’s forecast in the year 2009 is less accurate than peer analyst

forecasts who agreed with managers in the year 2010). If analysts of weaker ability issue

forecasts with ETR disagreement, then I should find roughly similar results using placebo

dates. In an untabulated regression, I find no evidence of a relationship between analyst

disagreement and absolute forecast error using a lagged one-year placebo date. Thus, my

results do not appear to result from analysts of weaker ability issuing forecasts with ETR

disagreement.

37

Chapter 7: Discussion and Conclusion

This study examines determinants and consequences of analyst ETR forecast

disagreement with managers. To my knowledge, my study is the first to examine whether

analysts improve on managers’ voluntary ETR forecasts. When viewing analyst forecasts

that disagree with managers’ ETR forecasts as bold forecasts, the results contrast with

implications from the analyst herding literature. I find that analysts with less work

experience and analysts working at larger brokerages are more likely to disagree with

managers. I also find analyst forecasts with disagreement over ETR are less accurate, and

investors do not appear to differentiate between the types of forecasts. These results suggest

that analysts do not improve on management ETR forecasts. While Hutton et al. [2012]

find that analysts do not improve on managers’ forecasts when firms face unusual

circumstances, my findings suggest that, even under regular operating circumstances,

analysts do not improve on managers’ forecasts of firm-specific information like taxes.

Finally, my study informs investors looking to analysts to understand the impact of

taxes on corporate earnings, especially given the 2017 reform of the U.S. corporate income

tax code. Tax reform had a material and complex impact on corporate earnings due to the

reduction of the statutory tax rate and deemed repatriation of permanently reinvested

foreign earnings. In situations of temporary complexity, this study finds evidence that

managers are more likely to issue forecasts and analysts appear more likely to follow

managers’ ETR forecast. However, some of the tax law’s implications remain unclear and