Compiled & Solved by: Sameer Hussain - a4accounting

14

ACCOUNTING – XI 2016 –Regular & Private – Solved Paper Compiled & Solved by: Sameer Hussain www.a4accounting.weebly.com www.facebook.com/a4accounting.net www.twitter.com/a4accounting2 [email protected]

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Compiled & Solved by: Sameer Hussain - a4accounting

ACCOUNTING – XI

2016 –Regular & Private – Solved Paper

Compiled & Solved by: Sameer Hussain

www.a4accounting.weebly.com

www.facebook.com/a4accounting.net

www.twitter.com/a4accounting2

Compiled & Solved by: Sameer Hussain www.a4accounting.weebly.com

www.facebook.com/a4accounting.net www.twitter.com/a4accounting2

Accounting – XI – 2016 Regular & Private Solution 1

Time: 20 Minutes Max. Marks: 20 SECTION “A” (MULTIPLE CHOICE QUESTIONS)

Note: (i) This section contains of 20 part questions and all are to be answered. Each question carries equal marks. (ii) Do not copy down the part question in your answer book. Write only the answer in full against the proper number of the question and its part. (iv) The code of your question paper must be mentioned in bold letters in the beginning. Q.No.1 Choose the correct answer for each from the given options:

(1) If total assets are Rs.50,000 and liabilities are 20% of assets, then capital is: (a) Rs.10,000. (b) Rs.40,000. (c) Rs.50,000. (d) Rs.60,000.

(2) Un-earned income is a/an:

(a) Assets. (b) Liabilities. (c) Owner’s equity. (d) Expense.

(3) The term cost of goods sold means:

(a) Sales + Gross profit. (b) Sales – Net profit. (c) Sales + Net profit. (d) Sales – Gross profit.

(4) Closing entries are made to close:

(a) Assets account. (b) Liabilities account. (c) Capital account. (d) Revenues and expenses account.

(5) The owner’s claim to the assets of the business is:

(a) Assets. (b) Expense. (c) Liability. (d) Owner’s equity.

(6) A business that purchases and sells goods is called:

(a) Manufacturing. (b) Servicing. (c) Trading. (d) None of these.

Compiled & Solved by: Sameer Hussain www.a4accounting.weebly.com

www.facebook.com/a4accounting.net www.twitter.com/a4accounting2

Accounting – XI – 2016 Regular & Private Solution 2

(7) These accounts normally have credit balances except: (a) Bank loan. (b) Sales. (c) Sales return. (d) Accounts payable.

(8) This is non – current asset:

(a) Inventories. (b) Equipments. (c) Office supplies. (d) Accounts receivable.

(9) Amount paid for servicing of owner’s car will be recorded as:

(a) Assets. (b) Liability. (c) Expense. (d) Drawings.

(10) The excess of asset over capital is:

(a) Income. (b) Expense. (c) Profit. (d) Liability.

(11) Revenue of business is Rs.60,000, while net loss is Rs.15,000 then expenses are:

(a) Rs.15,000. (b) Rs.45,000. (c) Rs.60,000. (d) Rs.75,000.

(12) All cash receipts and payments are recorded in:

(a) Purchase journal. (b) Sales journal. (c) Petty book. (d) Cash book.

(13) Contra entry appears on this side of cash book:

(a) Payment side. (b) Receipt side. (c) Both sides. (d) None of these.

(14) Journals are also called:

(a) Ledgers. (b) Books of final entry. (c) Books of primary entry. (d) Financial statements.

Compiled & Solved by: Sameer Hussain www.a4accounting.weebly.com

www.facebook.com/a4accounting.net www.twitter.com/a4accounting2

Accounting – XI – 2016 Regular & Private Solution 3

(15) Overdraft in the bank statement is shown as: (a) Credit balance. (b) Debit balance. (c) Zero balance. (d) Both debit and credit balance.

(16) Ending stock is:

(a) Liability. (b) Income. (c) Asset. (d) Capital.

(17) This shows the financial position of the business:

(a) Income statement. (b) Cash book. (c) Balance sheet. (d) Bank statement.

(18) Cost of goods sold is a part of:

(a) Equities. (b) Balance sheet. (c) Income statement. (d) Cash book.

(19) This account will be credited, if Mr. A started business with cash:

(a) Capital. (b) Cash. (c) Drawings. (d) Expense.

(20) An entry with more than one debit or credit is called:

(a) Double entry. (b) Compound entry. (c) Contra entry. (d) Triple entry.

Compiled & Solved by: Sameer Hussain www.a4accounting.weebly.com

www.facebook.com/a4accounting.net www.twitter.com/a4accounting2

Accounting – XI – 2016 Regular & Private Solution 4

Time: 2 Hours 40 Minutes Max. Marks: 80 SECTION “B” (SHORT – ANSWER QUESTIONS) (50)

Note: Attempt any Four questions. All questions carry equal marks. The use of calculator is allowed. Q.No.2 ACCOUNTING EQUATION (a) Define the term accounting. (b) State fundamental accounting equation. (c) Give rules of debit and credit in terms of increase and decrease. (d) Write the steps of accounting cycle. SOLUTION 2 (a) Accounting: Accounting is the process of identifying, measuring, recording and communicating economic transactions. Measurement is normally made in monetary terms and accountant will prepare records in the form of financial statements, such as income statement and balance sheet. SOLUTION 2 (b) Accounting equation: Assets = Liabilities + Owner’s Equity SOLUTION 2 (c) Rules of Debit & Credit:

Head of Accounts Increases Decreases

Assets Recorded as Debit Recorded as Credit

Liabilities Recorded as Credit Recorded as Debit

Owner’s Equity Recorded as Credit Recorded as Debit

Revenue & Income Recorded as Credit Recorded as Debit

Expenses Recorded as Debit Recorded as Credit

SOLUTION 2 (d) Steps of Accounting Cycle:

Journal entries.

Post to ledger.

Trial balance.

Adjusting entries.

Adjusted trial balance.

Financial statement.

Closing entries.

After-closing trial balance.

Reversing entries.

Compiled & Solved by: Sameer Hussain www.a4accounting.weebly.com

www.facebook.com/a4accounting.net www.twitter.com/a4accounting2

Accounting – XI – 2016 Regular & Private Solution 5

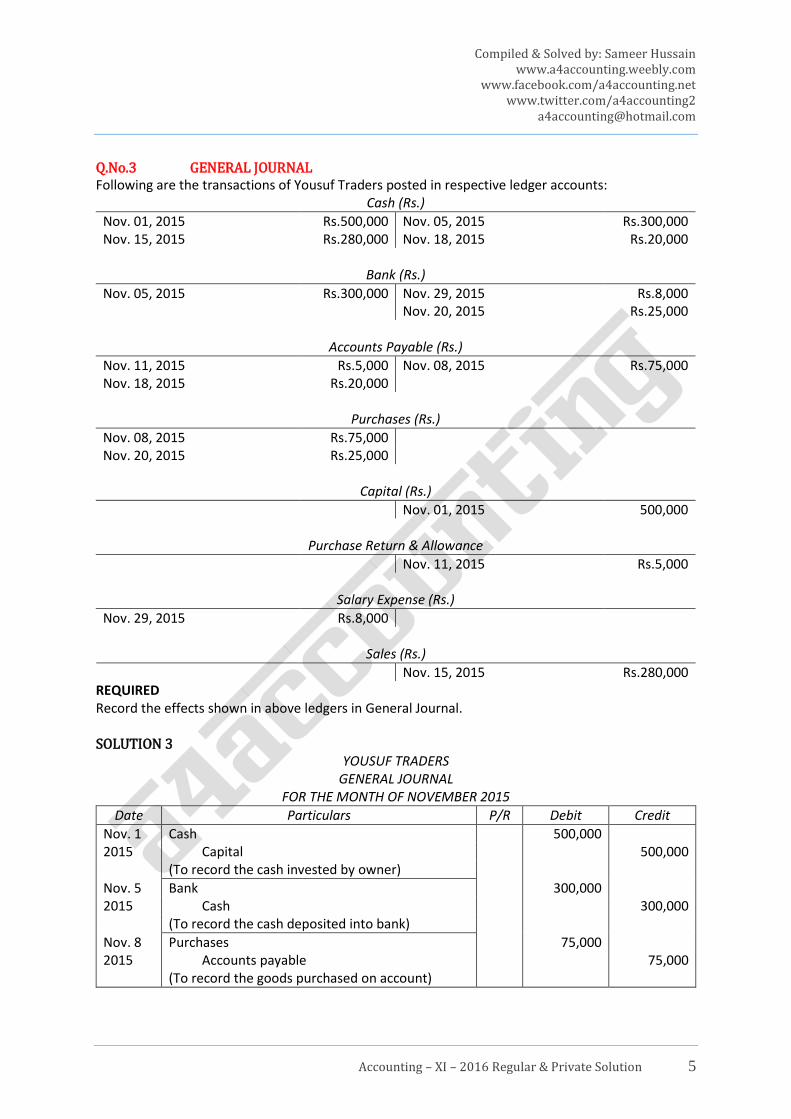

Q.No.3 GENERAL JOURNAL Following are the transactions of Yousuf Traders posted in respective ledger accounts:

Cash (Rs.)

Nov. 01, 2015 Rs.500,000 Nov. 05, 2015 Rs.300,000 Nov. 15, 2015 Rs.280,000 Nov. 18, 2015 Rs.20,000

Bank (Rs.)

Nov. 05, 2015 Rs.300,000 Nov. 29, 2015 Rs.8,000 Nov. 20, 2015 Rs.25,000

Accounts Payable (Rs.)

Nov. 11, 2015 Rs.5,000 Nov. 08, 2015 Rs.75,000 Nov. 18, 2015 Rs.20,000

Purchases (Rs.)

Nov. 08, 2015 Rs.75,000 Nov. 20, 2015 Rs.25,000

Capital (Rs.)

Nov. 01, 2015 500,000

Purchase Return & Allowance

Nov. 11, 2015 Rs.5,000

Salary Expense (Rs.)

Nov. 29, 2015 Rs.8,000

Sales (Rs.)

Nov. 15, 2015 Rs.280,000 REQUIRED Record the effects shown in above ledgers in General Journal. SOLUTION 3

YOUSUF TRADERS GENERAL JOURNAL

FOR THE MONTH OF NOVEMBER 2015

Date Particulars P/R Debit Credit

Nov. 1 Cash 500,000 2015 Capital 500,000 (To record the cash invested by owner)

Nov. 5 Bank 300,000 2015 Cash 300,000 (To record the cash deposited into bank)

Nov. 8 Purchases 75,000 2015 Accounts payable 75,000 (To record the goods purchased on account)

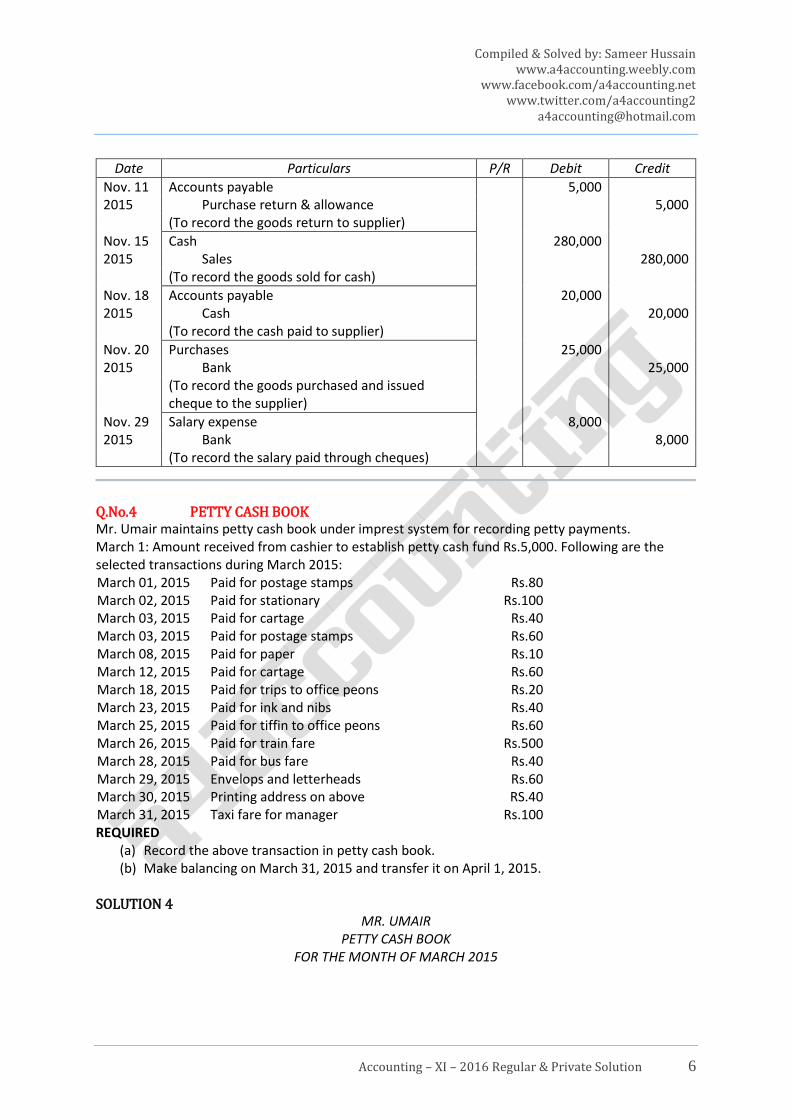

Compiled & Solved by: Sameer Hussain www.a4accounting.weebly.com

www.facebook.com/a4accounting.net www.twitter.com/a4accounting2

Accounting – XI – 2016 Regular & Private Solution 6

Date Particulars P/R Debit Credit

Nov. 11 Accounts payable 5,000 2015 Purchase return & allowance 5,000 (To record the goods return to supplier)

Nov. 15 Cash 280,000 2015 Sales 280,000 (To record the goods sold for cash)

Nov. 18 Accounts payable 20,000 2015 Cash 20,000 (To record the cash paid to supplier)

Nov. 20 Purchases 25,000 2015 Bank 25,000 (To record the goods purchased and issued

cheque to the supplier)

Nov. 29 Salary expense 8,000 2015 Bank 8,000 (To record the salary paid through cheques)

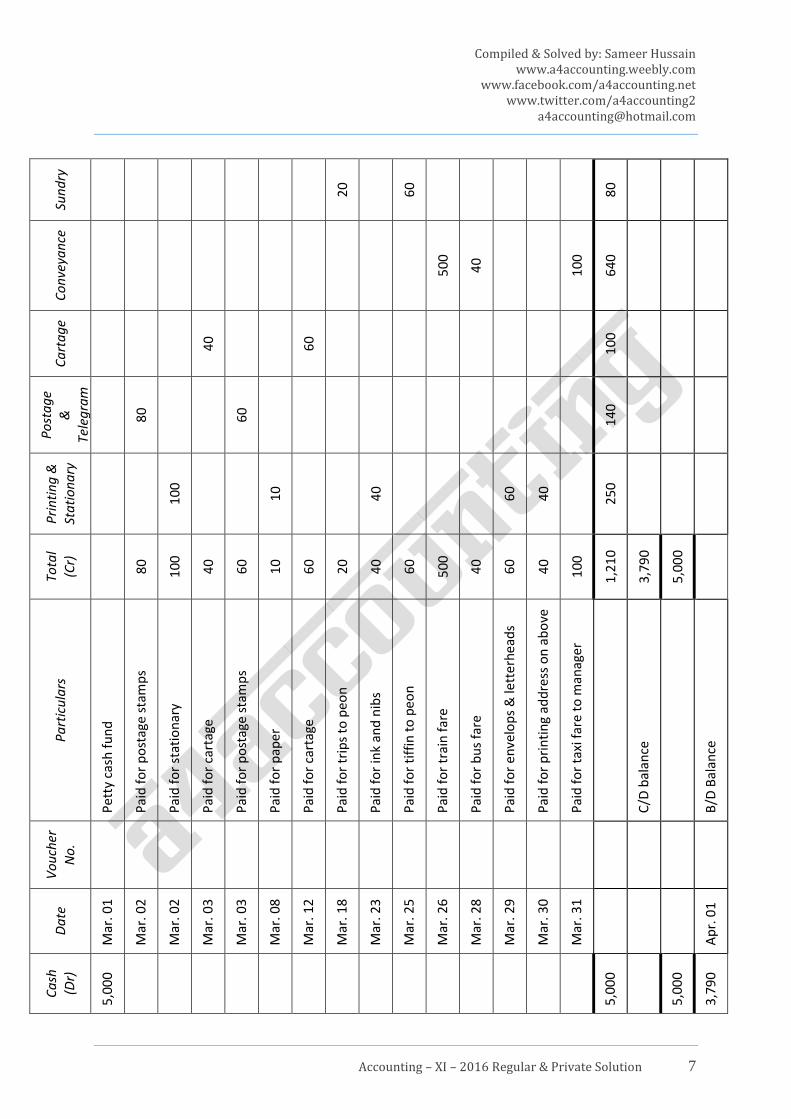

Q.No.4 PETTY CASH BOOK Mr. Umair maintains petty cash book under imprest system for recording petty payments. March 1: Amount received from cashier to establish petty cash fund Rs.5,000. Following are the selected transactions during March 2015: March 01, 2015 Paid for postage stamps Rs.80 March 02, 2015 Paid for stationary Rs.100 March 03, 2015 Paid for cartage Rs.40 March 03, 2015 Paid for postage stamps Rs.60 March 08, 2015 Paid for paper Rs.10 March 12, 2015 Paid for cartage Rs.60 March 18, 2015 Paid for trips to office peons Rs.20 March 23, 2015 Paid for ink and nibs Rs.40 March 25, 2015 Paid for tiffin to office peons Rs.60 March 26, 2015 Paid for train fare Rs.500 March 28, 2015 Paid for bus fare Rs.40 March 29, 2015 Envelops and letterheads Rs.60 March 30, 2015 Printing address on above RS.40 March 31, 2015 Taxi fare for manager Rs.100 REQUIRED

(a) Record the above transaction in petty cash book. (b) Make balancing on March 31, 2015 and transfer it on April 1, 2015.

SOLUTION 4

MR. UMAIR PETTY CASH BOOK

FOR THE MONTH OF MARCH 2015

Compiled & Solved by: Sameer Hussain www.a4accounting.weebly.com

www.facebook.com/a4accounting.net www.twitter.com/a4accounting2

Accounting – XI – 2016 Regular & Private Solution 7

Sun

dry

20

60

80

Co

nve

yan

ce

50

0

40

10

0

64

0

Ca

rta

ge

40

60

10

0

Po

sta

ge

&

Tele

gra

m

80

60

14

0

Pri

nti

ng

&

Sta

tio

na

ry

10

0

10

40

60

40

25

0

Tota

l (C

r)

80

10

0

40

60

10

60

20

40

60

50

0

40

60

40

10

0

1,2

10

3,7

90

5,0

00

Pa

rtic

ula

rs

Pet

ty c

ash

fu

nd

Pai

d f

or

po

stag

e st

amp

s

Pai

d f

or

stat

ion

ary

Pai

d f

or

cart

age

Pai

d f

or

po

stag

e st

amp

s

Pai

d f

or

pap

er

Pai

d f

or

cart

age

Pai

d f

or

trip

s to

peo

n

Pai

d f

or

ink

and

nib

s

Pai

d f

or

tiff

in t

o p

eon

Pai

d f

or

trai

n f

are

Pai

d f

or

bu

s fa

re

Pai

d f

or

enve

lop

s &

lett

erh

ead

s

Pai

d f

or

pri

nti

ng

add

ress

on

ab

ove

Pai

d f

or

taxi

far

e to

man

ager

C/D

bal

ance

B/D

Bal

ance

Vo

uch

er

No

.

Da

te

Mar

. 01

Mar

. 02

Mar

. 02

Mar

. 03

Mar

. 03

Mar

. 08

Mar

. 12

Mar

. 18

Mar

. 23

Mar

. 25

Mar

. 26

Mar

. 28

Mar

. 29

Mar

. 30

Mar

. 31

Ap

r. 0

1

Ca

sh

(Dr)

5,0

00

5,0

00

5,0

00

3,7

90

Compiled & Solved by: Sameer Hussain www.a4accounting.weebly.com

www.facebook.com/a4accounting.net www.twitter.com/a4accounting2

Accounting – XI – 2016 Regular & Private Solution 8

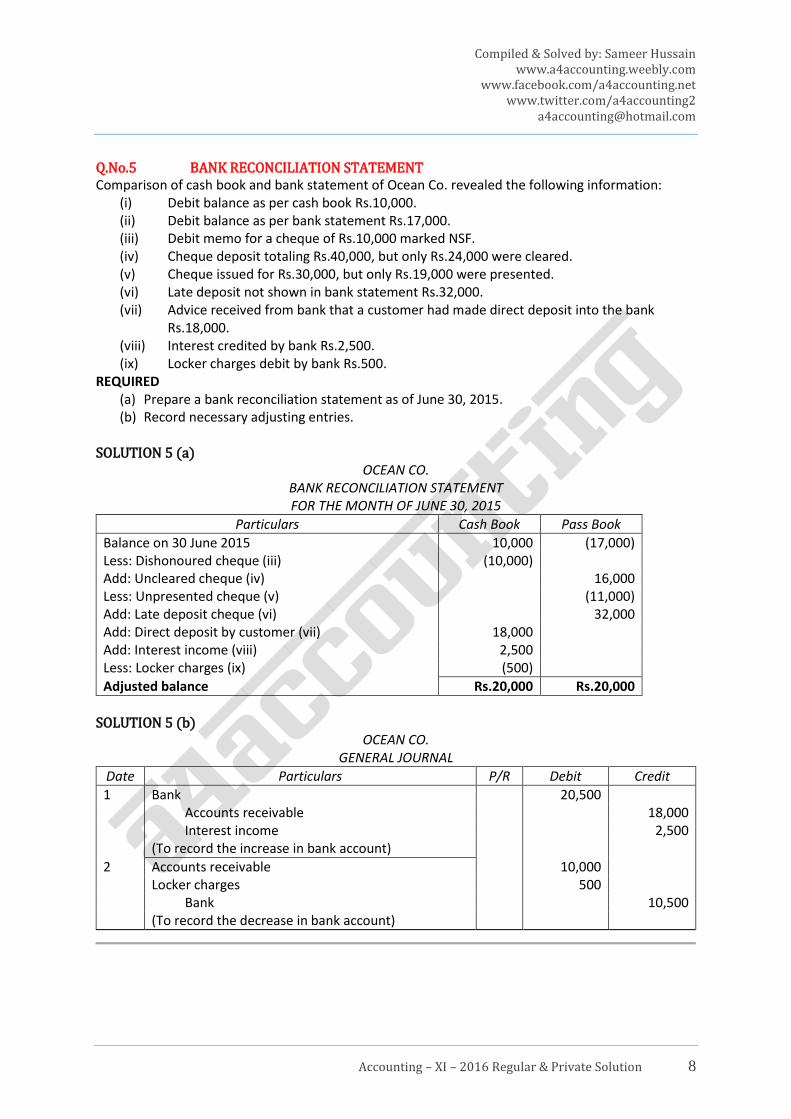

Q.No.5 BANK RECONCILIATION STATEMENT Comparison of cash book and bank statement of Ocean Co. revealed the following information:

(i) Debit balance as per cash book Rs.10,000. (ii) Debit balance as per bank statement Rs.17,000. (iii) Debit memo for a cheque of Rs.10,000 marked NSF. (iv) Cheque deposit totaling Rs.40,000, but only Rs.24,000 were cleared. (v) Cheque issued for Rs.30,000, but only Rs.19,000 were presented. (vi) Late deposit not shown in bank statement Rs.32,000. (vii) Advice received from bank that a customer had made direct deposit into the bank

Rs.18,000. (viii) Interest credited by bank Rs.2,500. (ix) Locker charges debit by bank Rs.500.

REQUIRED (a) Prepare a bank reconciliation statement as of June 30, 2015. (b) Record necessary adjusting entries.

SOLUTION 5 (a)

OCEAN CO. BANK RECONCILIATION STATEMENT FOR THE MONTH OF JUNE 30, 2015

Particulars Cash Book Pass Book

Balance on 30 June 2015 10,000 (17,000) Less: Dishonoured cheque (iii) (10,000) Add: Uncleared cheque (iv) 16,000 Less: Unpresented cheque (v) (11,000) Add: Late deposit cheque (vi) 32,000 Add: Direct deposit by customer (vii) 18,000 Add: Interest income (viii) 2,500 Less: Locker charges (ix) (500)

Adjusted balance Rs.20,000 Rs.20,000

SOLUTION 5 (b)

OCEAN CO. GENERAL JOURNAL

Date Particulars P/R Debit Credit

1 Bank 20,500 Accounts receivable 18,000 Interest income 2,500 (To record the increase in bank account)

2 Accounts receivable 10,000 Locker charges 500 Bank 10,500 (To record the decrease in bank account)

Compiled & Solved by: Sameer Hussain www.a4accounting.weebly.com

www.facebook.com/a4accounting.net www.twitter.com/a4accounting2

Accounting – XI – 2016 Regular & Private Solution 9

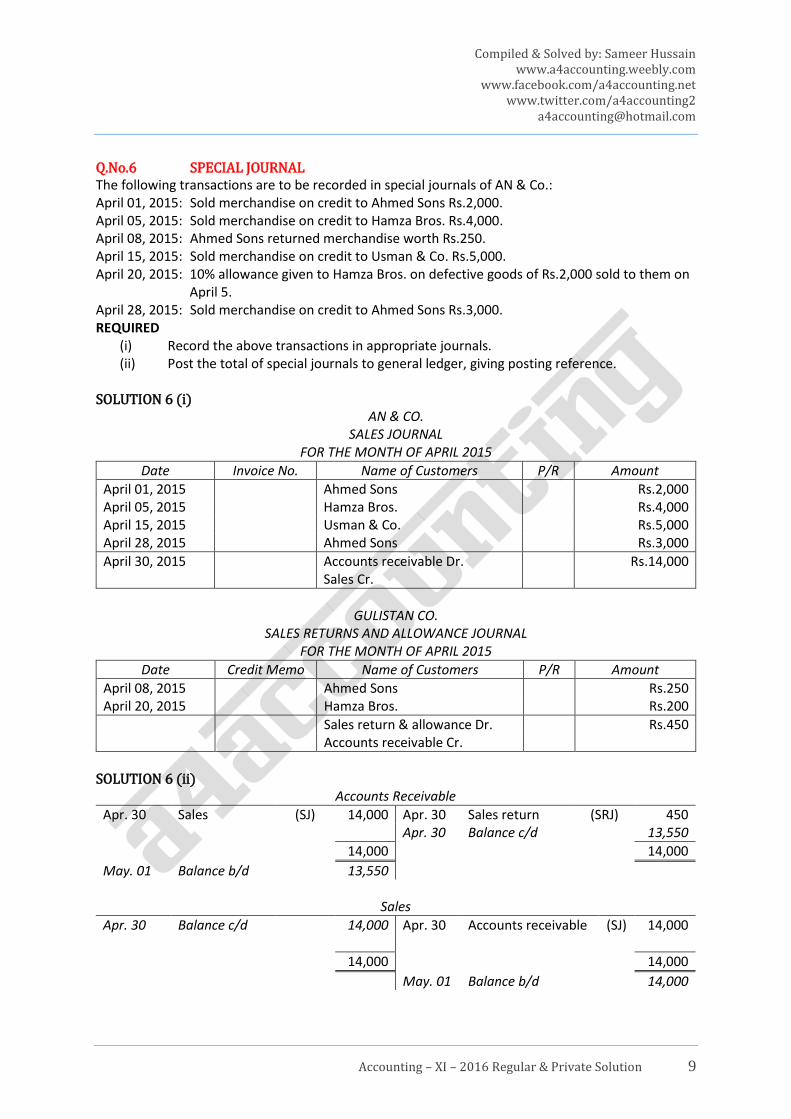

Q.No.6 SPECIAL JOURNAL The following transactions are to be recorded in special journals of AN & Co.: April 01, 2015: Sold merchandise on credit to Ahmed Sons Rs.2,000. April 05, 2015: Sold merchandise on credit to Hamza Bros. Rs.4,000. April 08, 2015: Ahmed Sons returned merchandise worth Rs.250. April 15, 2015: Sold merchandise on credit to Usman & Co. Rs.5,000. April 20, 2015: 10% allowance given to Hamza Bros. on defective goods of Rs.2,000 sold to them on

April 5. April 28, 2015: Sold merchandise on credit to Ahmed Sons Rs.3,000. REQUIRED

(i) Record the above transactions in appropriate journals. (ii) Post the total of special journals to general ledger, giving posting reference.

SOLUTION 6 (i)

AN & CO. SALES JOURNAL

FOR THE MONTH OF APRIL 2015

Date Invoice No. Name of Customers P/R Amount

April 01, 2015 Ahmed Sons Rs.2,000 April 05, 2015 Hamza Bros. Rs.4,000 April 15, 2015 Usman & Co. Rs.5,000 April 28, 2015 Ahmed Sons Rs.3,000

April 30, 2015 Accounts receivable Dr. Rs.14,000 Sales Cr.

GULISTAN CO.

SALES RETURNS AND ALLOWANCE JOURNAL FOR THE MONTH OF APRIL 2015

Date Credit Memo Name of Customers P/R Amount

April 08, 2015 Ahmed Sons Rs.250 April 20, 2015 Hamza Bros. Rs.200

Sales return & allowance Dr. Rs.450 Accounts receivable Cr.

SOLUTION 6 (ii)

Accounts Receivable

Apr. 30 Sales (SJ) 14,000 Apr. 30 Sales return (SRJ) 450 Apr. 30 Balance c/d 13,550

14,000 14,000

May. 01 Balance b/d 13,550

Sales

Apr. 30 Balance c/d 14,000 Apr. 30 Accounts receivable (SJ) 14,000

14,000 14,000

May. 01 Balance b/d 14,000

Compiled & Solved by: Sameer Hussain www.a4accounting.weebly.com

www.facebook.com/a4accounting.net www.twitter.com/a4accounting2

Accounting – XI – 2016 Regular & Private Solution 10

Sales Return & Allowances

Apr. 30 Sales return (SRJ) 450 Apr. 30 Balance c/d 450

450 450

May. 01 Balance b/d 450

Q.No.7 CORRECTION OF ERRORS Following errors were discovered before the closing of books of Hydride Co. Give entries in general journal to correct each of the following:

(a) Purchase of furniture Rs.12,000 was wrongly debit to purchase account. (b) Salaries expense Rs.15,000 were recorded as service expense. (c) Depreciation was overcharged by Rs.3,000 through allowance for depreciation account. (d) Return of defective furniture worth Rs.2,000 was recorded as purchase return account. (e) Sale of old equipment worth Rs.10,000 recorded as sale account. (f) Payment of owner’s club fee Rs.6,000 was recorded as fee expense.

SOLUTION 7

HYDRIDE CO. CORRECTING ENTRIES

Date Particulars P/R Debit Credit

(a) Furniture 12,000 Purchase 12,000 (To correct the purchase of furniture)

(b) Salaries expense 15,000 Service expense 15,000 (To correct the payment of salaries)

(c) Allowance for depreciation 3,000 Depreciation expense 3,000 (To correct the depreciation expense)

(d) Purchase return 2,000 Furniture 2,000 (To correct the return of furniture)

(e) Sales 10,000 Equipment 10,000 (To correct the sale of old equipment)

(f) Drawings 6,000 Fee expense 6,000 (To correct the payment of owner’s club fee)

Compiled & Solved by: Sameer Hussain www.a4accounting.weebly.com

www.facebook.com/a4accounting.net www.twitter.com/a4accounting2

Accounting – XI – 2016 Regular & Private Solution 11

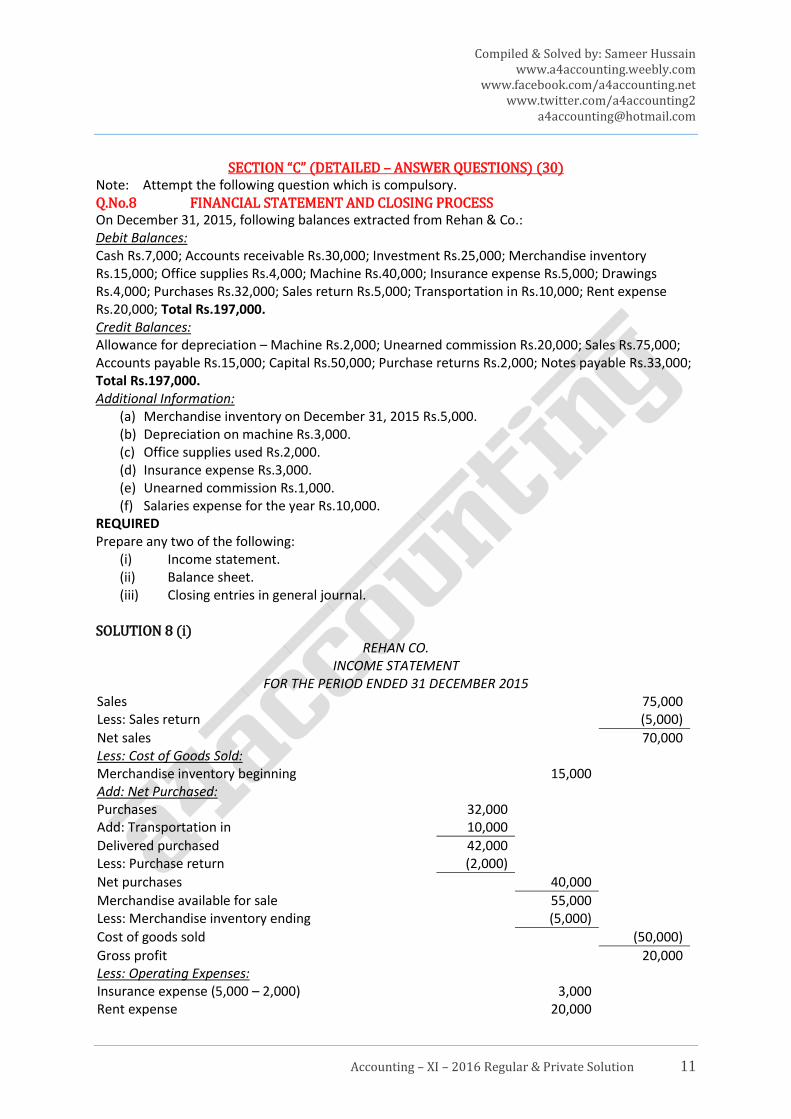

SECTION “C” (DETAILED – ANSWER QUESTIONS) (30) Note: Attempt the following question which is compulsory. Q.No.8 FINANCIAL STATEMENT AND CLOSING PROCESS On December 31, 2015, following balances extracted from Rehan & Co.: Debit Balances: Cash Rs.7,000; Accounts receivable Rs.30,000; Investment Rs.25,000; Merchandise inventory Rs.15,000; Office supplies Rs.4,000; Machine Rs.40,000; Insurance expense Rs.5,000; Drawings Rs.4,000; Purchases Rs.32,000; Sales return Rs.5,000; Transportation in Rs.10,000; Rent expense Rs.20,000; Total Rs.197,000. Credit Balances: Allowance for depreciation – Machine Rs.2,000; Unearned commission Rs.20,000; Sales Rs.75,000; Accounts payable Rs.15,000; Capital Rs.50,000; Purchase returns Rs.2,000; Notes payable Rs.33,000; Total Rs.197,000. Additional Information:

(a) Merchandise inventory on December 31, 2015 Rs.5,000. (b) Depreciation on machine Rs.3,000. (c) Office supplies used Rs.2,000. (d) Insurance expense Rs.3,000. (e) Unearned commission Rs.1,000. (f) Salaries expense for the year Rs.10,000.

REQUIRED Prepare any two of the following:

(i) Income statement. (ii) Balance sheet. (iii) Closing entries in general journal.

SOLUTION 8 (i)

REHAN CO. INCOME STATEMENT

FOR THE PERIOD ENDED 31 DECEMBER 2015 Sales 75,000 Less: Sales return (5,000)

Net sales 70,000 Less: Cost of Goods Sold: Merchandise inventory beginning 15,000 Add: Net Purchased: Purchases 32,000 Add: Transportation in 10,000

Delivered purchased 42,000 Less: Purchase return (2,000)

Net purchases 40,000

Merchandise available for sale 55,000 Less: Merchandise inventory ending (5,000)

Cost of goods sold (50,000)

Gross profit 20,000 Less: Operating Expenses: Insurance expense (5,000 – 2,000) 3,000 Rent expense 20,000

Compiled & Solved by: Sameer Hussain www.a4accounting.weebly.com

www.facebook.com/a4accounting.net www.twitter.com/a4accounting2

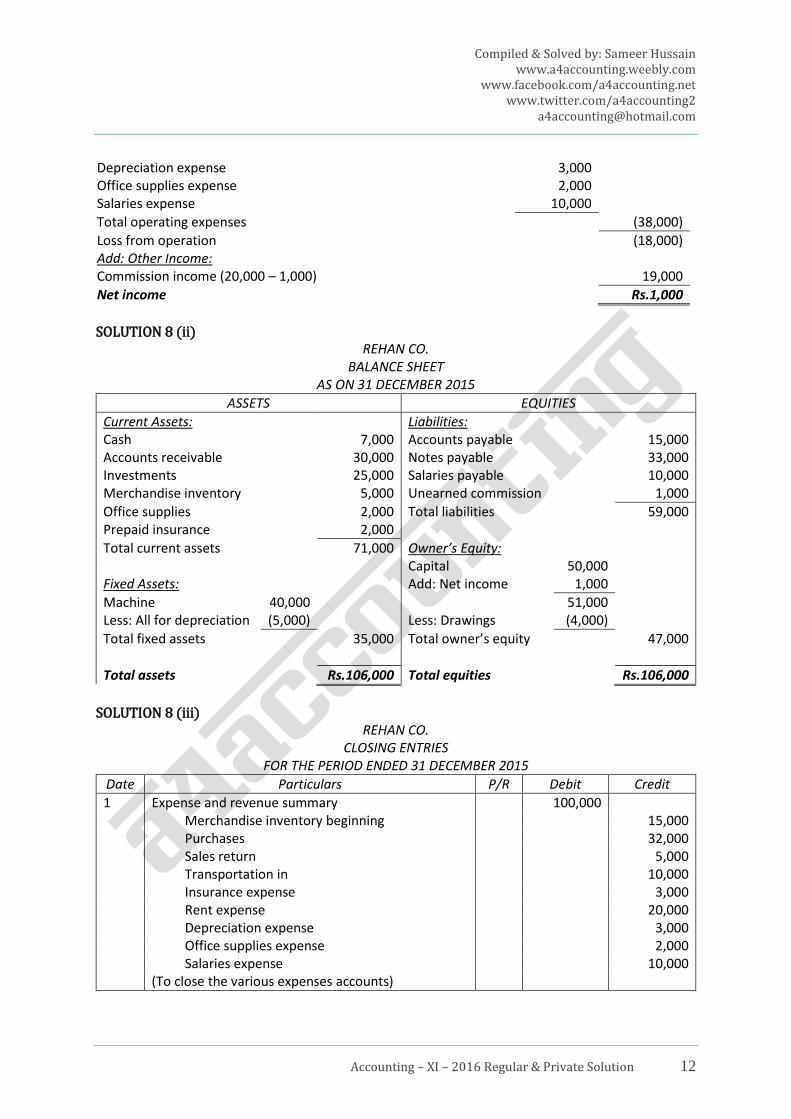

Accounting – XI – 2016 Regular & Private Solution 12

Depreciation expense 3,000 Office supplies expense 2,000 Salaries expense 10,000

Total operating expenses (38,000)

Loss from operation (18,000) Add: Other Income: Commission income (20,000 – 1,000) 19,000

Net income Rs.1,000

SOLUTION 8 (ii)

REHAN CO. BALANCE SHEET

AS ON 31 DECEMBER 2015

ASSETS EQUITIES

Current Assets: Liabilities: Cash 7,000 Accounts payable 15,000 Accounts receivable 30,000 Notes payable 33,000 Investments 25,000 Salaries payable 10,000 Merchandise inventory 5,000 Unearned commission 1,000

Office supplies 2,000 Total liabilities 59,000 Prepaid insurance 2,000

Total current assets 71,000 Owner’s Equity: Capital 50,000 Fixed Assets: Add: Net income 1,000

Machine 40,000 51,000 Less: All for depreciation (5,000) Less: Drawings (4,000)

Total fixed assets 35,000 Total owner’s equity 47,000

Total assets Rs.106,000 Total equities Rs.106,000

SOLUTION 8 (iii)

REHAN CO. CLOSING ENTRIES

FOR THE PERIOD ENDED 31 DECEMBER 2015

Date Particulars P/R Debit Credit

1 Expense and revenue summary 100,000 Merchandise inventory beginning 15,000 Purchases 32,000 Sales return 5,000 Transportation in 10,000 Insurance expense 3,000 Rent expense 20,000 Depreciation expense 3,000 Office supplies expense 2,000 Salaries expense 10,000 (To close the various expenses accounts)

Compiled & Solved by: Sameer Hussain www.a4accounting.weebly.com

www.facebook.com/a4accounting.net www.twitter.com/a4accounting2

Accounting – XI – 2016 Regular & Private Solution 13

Date Particulars P/R Debit Credit

2 Sales 75,000 Purchase return 2,000 Merchandise inventory ending 5,000 Commission income 19,000 Expense and revenue summary 101,000 (To close the various income accounts)

3 Expense and revenue summary 1,000 Capital 1,000 (To transfer the net income to the capital account)

4 Capital 4,000 Drawings 4,000 (To close the drawings account)

Additional Working:

REHAN CO. ADJUSTING ENTRIES

FOR THE PERIOD ENDED 31 DECEMBER 2015

Date Particulars P/R Debit Credit

1 Merchandise inventory 5,000 Expense and revenue summary 5,000 (To adjust the merchandise inventory)

2 Depreciation expense 3,000 Allowance for depreciation – Machine 3,000 (To adjust the depreciation expense)

3 Office supplies expense 2,000 Office supplies 2,000 (To adjust the office supplies)

4 Prepaid insurance 2,000 Insurance expense 2,000 (To adjust the insurance expense)

5 Unearned commission 19,000 Commission income 19,000 (To adjust the unearned commission)

6 Salaries expense 10,000 Salaries payable 10,000 (To adjust the unpaid salaries)