Comparative ratio analysis of SHINEPUKUR & RAK Ceramics Ltd.

34

North South University School Of Business Summer 2013 Course Name – Financial Accounting Course code - ACT 201 Section – 23 Submitted to - Sayeba Kamal Athoi (SBK) Submission Date: 1 st September, 2013 Submitted by: Group 2 Name ID Riad Ahmed 1310266030 Refat Bin Wadud 1310693630 Tanzirul Islam 1310784630 Md. Naim 1310427630 1

Transcript of Comparative ratio analysis of SHINEPUKUR & RAK Ceramics Ltd.

North South UniversitySchool Of Business

Summer 2013

Course Name – Financial Accounting

Course code - ACT 201

Section – 23

Submitted to - Sayeba Kamal Athoi (SBK)

Submission Date: 1st September, 2013

Submitted by: Group 2

Name ID

Riad Ahmed 1310266030

Refat Bin Wadud 1310693630

Tanzirul Islam 1310784630

Md. Naim 1310427630

1

Akhi Shikder 1311200630

April 12, 2013

Sayeba Kamal AthoiLecturerSchool of BusinessNorth South University

Subject: Submission of Financial Accounting Project

Dear Madam,

We are submitting herewith our project entitled “Financial statement analysis of RAK Ceramics Ltd. and SHINEPUKUR Ceramics Ltd.” as per your instruction to fulfill the Financial Accountingcourse requirement.

The main purpose of this report is to study and compare the analysis of financial statements and ratios of the two companies.We decided to conduct the report on RAK Ceramics and SHINEPUKUR Ceramics keeping in mind their contribution in the economy and importance.

We can assure you the authenticity of this report. We sincerely hope that this report will merit your approval. We are grateful to you for giving us the opportunity to study the analysis of annual reports of both companies and to compile this report.

Respectfully yours,GROUP 2

2

IntroductionWe have decided to select ceramics industry of Bangladesh for ourproject. We will be comparing and analyzing the performance of the two major ceramic companies. RAK Ceramics Ltd and SHINEPUKUR Ceramics Ltd. We decided to select this industry because of its huge contribution to improve the economic condition of our country.

Ceramics has a high demand in the world. Bangladesh apparently has the perfect geographical position, supply of raw materials and labor available to meet this demand. Ceramics industry of Bangladesh produces wall and floor tiles, sanitary ware, ceramicsplate and cup, tableware etc. Ceramic industry of Bangladesh is abooming sector and the great potential of both domestic and foreign market.

Background of the companies

3

RAK Ceramics: RAK Ceramics (Bangladesh) Ltd incorporated in Bangladesh on 26 November, 1998 as a private company limited by ashare under the company act 1994. It is engaged in manufacturing and marketing of ceramic tiles, bathroom sets and all types of sanitary ware. It has started its commercial production 0n 12 November, 20000. RAK Ceramics Ltd, 90% held by RAK Ceramics PSC and its nominees, a company incorporated under the laws of UAE and remaining 10% owned by local investor Mr. S.A.K. Ekramuzzaman. With an annual turnover of over BDT 3248 million, within the short span of 11 years RAK has firmly established itself as one of the leading manufacturer of high quality ceramicwall floor tiles, and sanitary wares products in Bangladesh. The core business of RAK Ceramics Ltd is to manufacture and sell of tiles and sanitary wares. The company has over 1000 models activein the ceramic and porcelain tile business and regularly adds several new designs to the product portfolio. The company manufactures tiles in a very wide range of tiles in the size from20 cm x 30 cm up to 60 cm x 60 cm in Bangladesh location. The company has over 40 models an exclusive range of sanitary ware tooffer with a very wide choice. Most of production is consumed in local market and balance gets exported to UAE. RAK ceramics Bangladesh Ltd is an ISO certified organization.

SHINEPUKUR Ceramics: SCL is a member of BEXIMCO group which is the largest private business conglomerate in Bangladesh. SHINEPUKUR ceramics has been registered in Bangladesh in 1997 andplants were commissioned in 1998. Total investment in the companyis US$ 35 million. The company has already made additional investment of US$ 10 million to expand its Bone china unit. SHINEPUKUR has well control laboratory facilities, and has its disposal, own captive gas-based power generation capability, own water supply, and medical and sanitary facilities. The company was certified ISO in Aug 2001. SCL produces variety and a wide range of Bone china and porcelain tableware for retail as well ashotel, and Ivory china for retail house ware. Complementing its superb range of bone china, SHINEPUKUR also offers porcelain, ivory china, high alumina table ware for all different market

4

segments and they produce dinner to tea plates, soup tureens to soup spoons, retail tabletop to industrial. They export their products in Australia, Argentina, Canada, Denmark, France, India and many other countries.

CompetitorsSome of the major competitors of these two companies are Peoples Ceramics Industry Ltd, FARR Ceramics, Mirpur Ceramics Works Ltd, Fu-Wang Ceramic Industry Ltd.

5

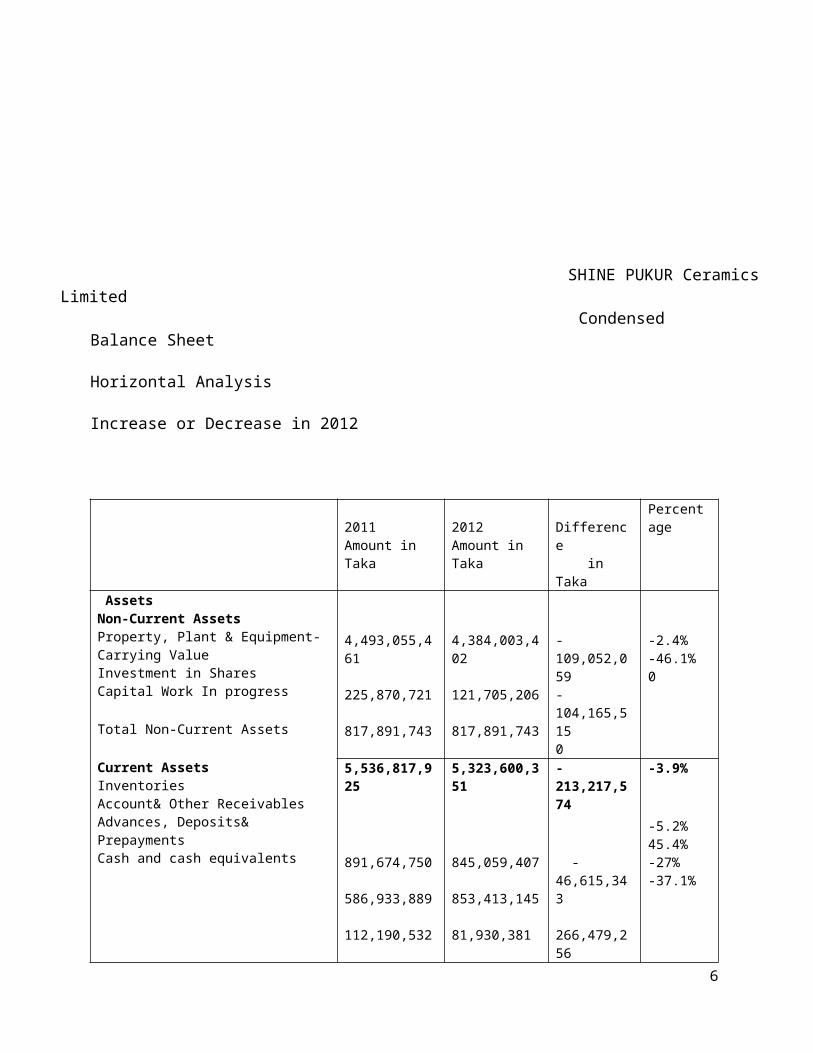

SHINE PUKUR Ceramics Limited

Condensed Balance Sheet Horizontal Analysis Increase or Decrease in 2012

2011Amount in Taka

2012Amount in Taka

Difference in Taka

Percentage

AssetsNon-Current AssetsProperty, Plant & Equipment-Carrying ValueInvestment in SharesCapital Work In progress

Total Non-Current Assets

Current Assets InventoriesAccount& Other ReceivablesAdvances, Deposits& Prepayments Cash and cash equivalents

4,493,055,461 225,870,721 817,891,743

4,384,003,402 121,705,206 817,891,743

-109,052,059-104,165,5150

-2.4%-46.1%0

5,536,817,925

891,674,750 586,933,889 112,190,532

5,323,600,351

845,059,407 853,413,145 81,930,381

-213,217,574

-46,615,343 266,479,256

-3.9%

-5.2%45.4%-27%-37.1%

6

25,432,780 16,009,871 -30,260,151 -9,422,909

Total Current assets

Total Assets

Equity and LiabilitiesShareholder’s Equity Issued Shared Capital Revaluation surplus Retained Earnings

1,617,231,951

7,154,049,876

1,796,412,804

7,120,013,155

179,180,853

-34,036,721

11.1%

-0.5%

1,111,274,5302,953,318,420 435,167,473

1,277,965,7002,907,734,989 358,761,360

166,691,170 -45,583,431 -76,406,113

15%-1.5%-17.6%

Total Shareholder’s Equity

Non-Current LiabilitiesLong term loan-Net Off Current Maturity(secured)Long Term Loan (Unsecured)Deferred Tax Liability

4,499,760,423

396,579,272

598,837,779 9,965,449

4,544,462,049

296,189,631

498,837,779 8,456,579

44,701,626

-100,389,641

-100,000,000 1,508,870

1%

-25.3%

-16.7%15.1%

Total Non-Current Liabilities

Current LiabilitiesShort Term Loan from Banks (secured)Long Term Loan-Current Maturity(Secured)Creditor, Accruals & Other Payables

1,005,382,500

1,147,673,708 91,818,692 409,414,553

803,483,989

1,183,795,749 143,242,382 445,028,986

201,898,511

36,122,041 51,423,69

20.1%

3.1%56%8.7%

7

0 35,614,433

Total Current Liabilities

Total Equity and Liabilities

1,648,906,953

7,154,049,876

1,772,067,117

7,120,013,155

123,160,164

-34,036,721

7.5%

-o.5%

SHINEPUKUR Ceramics Limited Comprehensive Income Statement Horizontal Analysis Increase or Decrease in 2012

2011Amount in Taka

2012Amount in Taka

Difference in Taka

Percentage

Sales RevenueCost of goods sold

Gross Profit

Operating expenses:Administrative expenses Selling and distribution expensesExchange loss

1,901,129,192(1,248,024,942)

1,942,350,752(1,268,312,998)

41,221,560 (20,288,056)

3.8%1.6%

653,104,250

(61,433,037)

674,037,754

(54,107,127)

20,933,504

(-7,325,910) (2,217,558)

3.2%

-11.9%4.5%-1%

8

(49,547,627) (10,120,204)

(51,765,185) ----

-10,120,204

In totalProfit from operationsGain/Loss on sale shareFinance costProfit before contribution toWPFFContribution to worker’s Profit participation/welfare fundsNet Profit before TaxIncome Tax expenseNet Profit after Tax for the year

Other comprehensive Income:Revaluation surplus on Property, Plant & EquipmentsFair value loss on investmentin Shares

(121,100,868) 532,003,382 315,370 (306,604,938)

(105,872,312) 568,165,442 (19,649,764) (364,625,228)

(-15,228,556) 36,162,060 (19,334,394) (58,020,290)

-12.6%6.8%

18.9%

225,713,814

(10,748,277)

183,890,450

(8,756,688)

-41,823,364

(-1,991,589)

-18.5%

-18.5%

214,965,537 (46,197,435)

175,133,762 (84,848,705)

-39,831,775 (38,651,270)

-18.5%18%

168,768,102

1,612,405,062

(13,371,595)

90,285,057

----

(45,583,431)

-78,483,045

-1,612,405,062

(32,211,836)

-46.5%

-1%

241%

Total Comprehensive Income for the year

1,767,801,569

44,701,626

-1,723,099,943

-97.5%

9

Horizontal analysis also known as Trend analysis is a financial statement analysis technique that shows changes in the amounts ofcorresponding financial statement items over a period of time. Itis a useful tool to evaluate the trend situations. Its purpose isto determine the increase or decrease that has taken place.

SHINEPUKUR Ceramics: The comparative balance sheet of SHINEPUKURstates that a number of significant changes have occurred from 2011 to 1012.

Total non-current assets decreased by 3.9% and non-current liabilities increased by 20.1% which suggests that the company isn’t expanding its business rather its been sellingoff its assets to pay for the non-current liabilities.

SHNINEPUKUR’s current assets increased by 11.1% and current liabilities increased by 7.5%. So this company is more than able to pay for its day to day operations expenses

Increase in “issued share capital” by 15% indicates that thecompany issuing 15% more share than before probably to pay-off its fixed debts or to finance its operations.

Its retain earnings decreased by 17.6% which suggests that the company’s been earning less.

In short, SHINEPUKUR isn’t doing very well. Its been reducing itsbusiness and not getting enough profit.

10

The comparative income statement of SHINEPUKUR shows some changeslike:

Sales revenue increased by 3.8% and COGS increased by only 1.6%. It suggests that the company’s selling enough productsand it also means that their operational activities are good

Operating expense decreased by 12.6%. Although gross profit increased by 3.2% net income decreased

by 97.5% in 2012. It indicates that 2012 was not a good timefor SHINEPUKUR.

In short, SHINEPUKUR Ceramics doesn’t appear to be favorable.

RAK Ceramics Limited Condensed Balance sheet Horizontal Analysis Increase or decrease in 2012

2011Amount in Taka

2012Amount in Taka

Difference in Taka

Percentage

11

AssetsNon-Current AssetsProperty, Plant & EquipmentEquity Accounted Investees Intangible AssetsCapital Work in ProgressInvestment in Shares of Listed companiesLoan to AssociatesPreliminary & Pre-operating Expenses

Total Non-Current Assets

Current Assets InventoriesTrade & Other ReceivablesLoan AssociatesAdvances, Deposits and Pre-paymentsAdvance Income TaxCash & Cash equivalents

2,725,576,102 82,955,354 113,928,723 36,578,205 3,176,995 --- 10,926,364

3,000,994,834 99,935,330 112,670,334 30,955,703 2,189,065 95,204,185 ---

275,418,732 16,979,976 -1,258,389 -5,622,502 -987,930 95,204,185 10,926,364

10.1%20.5%-1.1%-15.4%-31.2% --100%

2,973,141,743

1,658,062,569 526,123,351 ----- 194,219,227 948,002,438 1,442,035,679

3,341,949,451

1,777,888,718 621,590,397 4,795,815 217,599,7381,303,890,755 988,298,905

368,807,708

119,826,149 95,467,046 4,795,815 23,380,511 355,888,317 -453,736,774

12.4%

7.2%18.1%----12.3%37.5%-31.5%

Total Current assets

Total Assets

4,768,443,264

7,741,585,0

4,913,984,328

8,255,933,779

145,541,064

514,348,7

3.1%

6.6%

12

Equity and Liabilities Equity Share Capital Share Premium Retained EarningsNon-Controlling Interests

07 72

2,530,808,5001,473,647,9791,318,178,608 173,866,834

2,783,889,3501,473,647,9791,293,599,640 108,824,662

253,080,850

0 -24,578,968 -65,421,172

10%0-1.9%-37.6%

Total Equity

Non-Current LiabilitiesBorrowingsDeferred Tax Liability

5,496,501,921

32,931,914 134,641,798

6,659,961,631

18,567,275 121,162,388

1,163,459,710

-14,364,639 -13,479,410

21.2%

-43.6%-10%

Total Non-Current LiabilitiesCurrent LiabilitiesProvision for Employee BenefitsBorrowingsTrade & Other PayablesProvision for ExpensesProvision for Royalty and Technical Know-How FeesProvision for Income Taxes

167,573,712

11,356,382 392,682,041 316,506,302 165,098,899

106,399,3301,085,466,420

139,729,663

21,856,218 389,152,953 197,523,746 172,927,231

219,094,8681,455,687,469

-27,844,049

10,499,836 -3,529,088 -118,982,556 7,828,332

112,695,538 370,221,049

-16.6%

92.4%-0.9%-37.6%4.8%

105.9%34.1%

Total Current Liabilities

Total Equity and Liabilities

2,077,509,374

2,456,242,485

378,733,111

18.2%

6.6%

13

7,741,585,007

8,255,933,779

514,348,772

RAK Ceramics Limited Comprehensive Income Statement Horizontal Analysis Increase or Decrease in 2012

2011Amount in

Taka

2012Amount in Taka

Difference in Taka

Percentage

SalesCost of goods soldGross ProfitOther IncomeAdministrative expensesMarketing and Selling expenses

4,580,008,209(2,693,596,290)

4,908,171,279(2,979,160,088)

328,163,070(285,563,798)

7.2%10.6%

1,886,411,919 6,076,938(255,823,055)(641,800,857)

1,929,011,1919,570,670(297,250,162)(730,822,714)

42,599,272 3,494,732 (41,427,107) (89,021,857)

2.3%57.5%16.2%13.9%

Profit from Operating activitiesFinance incomeFinance costsNet finance incomeShare of Profit/loss of equity accounted investeesProfit before contribution to worker’s

(891,546,974)994,864,945147,136,340(61,462,408)85,673,732

(1,018,502,206)910,508,985102,831,687(25,867,434)76,964,253

(73,020,024)

(126,955,232) -84,356,960 -44,304,653 (-35,594,974) -

14.2%-8.5%-30.1%-57.9%10.2%

28.9%

14

Profit Participation fund

Contribution to worker’s Profit Participation fund

(56,644,648)

8,709,479

(16,375,376)

1,023,894,029

(63,193,326)

914,453,214

(57,500,590)

-109,440,815

(-5,692,736)

-10.7%

-9%

Profit before Income Tax

Income Tax expense: Current tax Deferred taxProfit for the year

Profit attributable to:Equity holders of the companyNon-controlling interestsProfit after Tax for the year

960,700,703

(323,570,136)4,606,626(318,963,510)

856,952,624

(370,221,049)13,479,410(356,741,639)

-103,748,079

(46,650,913) 8,872,784 (37,778,129)

-10.8%

1.4%192.6%11.8%

641,737,193

500,210,985 -141,526,208

-22.1%

756,952,645(115,215,452)

608,123,157(107,912,172)

-148,829,488 (-7,303,280)

-19.7%-6.3%

641,737,193

500,210,985 -141,526,208

-22.1%

15

RAK Ceramics: The important changes in the comparative balance sheet from 2011 to 2012 are as follows:

Total non-current assets have increased by 12.4% which meansthat the company is buying more fixed assets probably for expanding its business.

Non-current liabilities decreased by 16.6% which suggests improvement.

Its current asset increased by 3.2% whereas current liabilities increased 18.2%. It indicates that RAK isn’t able to pay off its current debts even if it’s doing well.

Its retained earnings decreased by only 1.9%.In short, RAK ceramics is doing better. Its been expanding its business which means its getting enough profit from business.

The changes in income statement in 2011 to 2012 indicates that :

Sales grew by 7.2% and COGS grew by 10.6% which means that RAK isn’t selling as much as it should probably because of its poor operating activities.

Operating expenses grew by 14%. Gross profit increased by 2.3% and net income decreased by

22.1%

The changes above suggests that although gross profit increased, the net income decreased by 22.1%..

16

SHINE PUKUR Ceramics Limited Condensed Balance Sheet Vertical analysis

2011Amount in Taka

2012Amount in Taka

Percentage2011

Percentage 2012

AssetsNon-Current AssetsProperty, Plant & Equipment-Carrying ValueInvestment in SharesCapital Work In progressTotal Non-Current Assets

4,493,055,461 225,870,721 817,891,743

4,384,003,402 121,705,206 817,891,743

62.8%3.2%11.4%

61.6%1.7%11.5%

Current Assets InventoriesAccount& Other ReceivablesAdvances, Deposits& Prepayments Cash and cash equivalents

5,536,817,925 891,674,750 586,933,889

5,323,600,351

845,059,407

77.4%

12.5%8.2%1.6%0.4%

74.8%

11.9%12%1.2%0.2%

17

112,190,532 25,432,780

853,413,145 81,930,381 16,009,871

Total Current assets

Total Assets

1,617,231,951

7,154,049,876

1,796,412,804

7,120,013,155

22.6%

100%

25.2%

100%

Equity and LiabilitiesShareholder’s Equity Issued Share Capital Revaluation surplus Retained Earnings

1,111,274,5302,953,318,420 435,167,473

1,277,965,7002,907,734,989 358,761,360

15.5%41.9%6.1%

17.9%40.8%5%

Total Shareholder’s Equity

Non-Current LiabilitiesLong term loan-Net Off Current Maturity(secured)Long Term Loan (Unsecured)Deferred Tax Liability

4,499,760,423

396,579,272

598,837,779 9,965,449

4,544,462,049

296,189,631

498,837,779 8,456,579

62.9%

5.5%

8.4%0.14%

63.8%

4.2%

7%0.12%

Total Non-Current Liabilities

Current LiabilitiesShort Term Loan from Banks (secured)Long Term Loan-Current Maturity(Secured)Creditor, Accruals & Other Payables

1,005,382,500

1,147,673,708 91,818,692 409,414,553

803,483,989

1,183,795,749 143,242,382 445,028,98

14.1%

16%1.3%

5.7%

11.3%

16.6%2.1%

6.3%

18

6Total Current Liabilities

Total Equity and Liabilities

1,648,906,953

7,154,049,876

1,772,067,117

7,120,013,155

23%

100%

24.9%

100%

SHINEPUKUR Ceramics Limited Comprehensive Income Statement Vertical Analysis

2011Amount in Taka

2012Amount in Taka

Percentage 2011

Percentage 2012

Sales RevenueCost of goods soldGross Profit

Operating expenses:Administrative expenses Selling and distribution expensesExchange loss

1,901,129,192(1,248,024,942)

1,942,350,752(1,268,312,998)

100%65.6%

100%65.3%

653,104,250

(61,433,037) (49,547,627)

674,037,754

(54,107,127) (51,765,185)

34.4%

3.2%2.6%0.5%

34.7%

2.8%2.7%0%

19

(10,120,204)

----

In totalProfit from operationsGain/Loss on sale shareFinance costProfit before contribution toWPFFContribution to worker’s Profit participation/welfare fundsNet Profit before TaxIncome Tax expenseNet Profit after Tax for the year

Other comprehensive Income:Revaluation surplus on Property, Plant & EquipmentsFair value loss on investmentin Shares

Total Comprehensive Income for the year

(121,100,868) 532,003,382 315,370 (306,604,938)

(105,872,312) 568,165,442 (19,649,764) (364,625,228)

6.4%28%0.02%16.1%

5.5%29.3%1%18.8%

225,713,814

(10,748,277)

183,890,450

8,756,688

11.9%

0.6%

9.5%

0.5%

214,965,537 (46,197,435)

175,133,762 (84,848,705)

11.3%2.4%

9%4.4%

168,768,102

1,612,405,062

(13,371,595)

90,285,057

----

(45,583,431)

8.9%

84.8%

0.7%

4.6%

0%

2.3%

1,767,801,569

44,701,626

93% 2.3%

20

Vertical Analysis: Vertical analysis is the proportional analysis of a financial statement, where each line item on a financial statement is listed as a percentage of another item. Typically, this means that every line item on an income statement is stated as a percentage of gross sales, while every line item on a balance sheet is stated as a percentage of total assets.

SHINEPUKUR Ceramics: In the comparative balance sheet , we can see that:

Current asset increased from 22.6% to 25.2% of total assets. Fixed assets decreased from77.4% to 74.8% of total assets. Issued share capital increased from 15.5% to 17.9%. Retained earnings decreased from 6.1% to 5%

Like mentioned before, SHINEPUKUR isn’t expanding its business. Its paying for its liabilities and financing its operation by issuing more bonds and selling off its fixed assets. Retained earnings decreased means they aren’t doing well enough.

In the comparative income statement, we can see that,

SHINEPUKUR’s cost of goods sold decreased by 0.3%(65.6-65.3).

Its operating expenses is down by 0.9%(6.4-5.5). Revaluation surplus on plant and assets of 1,612,405,062

which is 84.8% of sales

21

This emphasizes on the assumption that, SHINEPUKUR’s net income went down from 93% to 2.3% because it didn’t have a huge revaluation surplus on plant and assets like it had in 2011.

RAK Ceramics Limited Condensed Balance sheet Vertical Analysis

2011Amount in Taka

2012Amount in Taka

Percentage 2011

Percentage 2012

AssetsNon-Current AssetsProperty, Plant & EquipmentEquity Accounted Investees Intangible AssetsCapital Work in ProgressInvestment in Shares of Listed companiesLoan to AssociatesPreliminary & Pre-operating Expenses

2,725,576,102 82,955,354 113,928,723 36,578,205 3,176,995

3,000,994,834 99,935,330 112,670,334 30,955,703 2,189,065

35.2%1.1%1.5%0.5%0.04%0%0.1%

36.3%1.2%1.4%0.4%0.03%1.2%0%

22

--- 10,926,364

95,204,185 ---

Total Non-Current Assets

Current Assets InventoriesTrade & Other ReceivablesLoan AssociatesAdvances, Deposits and Pre-paymentsAdvance Income TaxCash & Cash equivalents

2,973,141,743

1,658,062,569 526,123,351 ----- 194,219,227 948,002,438 1,442,035,679

3,341,949,451

1,777,888,718 621,590,397 4,795,815 217,599,7381,303,890,755 988,298,905

38.5%

21.4%6.8%0%2.5%12.2%18.6%

40.5%

21.5%7.5%0.06%2.6%15.8%12%

Total Current assets

Total Assets

Equity and Liabilities Equity Share Capital Share Premium Retained EarningsNon-Controlling Interests

4,768,443,264

7,741,585,007

4,913,984,328

8,255,933,779

61.6%

100%

59.5%

100%

2,530,808,5001,473,647,9791,318,178,608 173,866,834

2,783,889,3501,473,647,9791,293,599,640 108,824,662

32.7%19%17% 2.2%

33.7%17.8%15.7%1.3%

Total Equity

Non-Current LiabilitiesBorrowingsDeferred Tax Liability

5,496,501,921

32,931,914 134,641,798

6,659,961,631

18,567,275 121,162,388

71%

0.4%1.7%

80.7%

0.2%1.5%

Total Non-Current Liabilities 2.2% 1.7%

23

Current LiabilitiesProvision for Employee BenefitsBorrowingsTrade & Other PayablesProvision for ExpensesProvision for Royalty and Technical Know-How FeesProvision for Income Taxes

167,573,712

11,356,382 392,682,041 316,506,302 165,098,899

106,399,3301,085,466,420

139,729,663

21,856,218 389,152,953 197,523,746 172,927,231

219,094,8681,455,687,469

0.1%5%4.1%2.1%

1.4%14%

0.3%4.7%2.4%2.1%

2.7%17.6%

Total Current Liabilities

Total Equity and Liabilities

2,077,509,374

7,741,585,007

2,456,242,485

8,255,933,779

26.8%

100%

29.8%

100%

RAK Ceramics Limited Comprehensive Income Statement Vertical Analysis

2011Amount in

Taka

2012Amount in Taka

Percentage 2011

Percentage 2012

SalesCost of goods soldGross ProfitOther IncomeAdministrative expensesMarketing and Selling expenses

4,580,008,209(2,693,596,290)

4,908,171,279(2,979,160,088)

100%58.8%

100%60.7%

1,886,411,919 6,076,938

1,929,011,1919,570,670(297,250,16

41.2%0.1%5.6%14%

39.3%0.2%6.1%14.9%

24

Profit from Operating activitiesFinance incomeFinance costsNet finance incomeShare of Profit/loss of equity accounted investeesProfit before contribution to worker’sProfit Participation fund

Contribution to worker’s Profit Participation fund

(255,823,055)(641,800,857)

2)(730,822,714)

(891,546,974)994,864,945147,136,340(61,462,408)85,673,732

(56,644,648)

(1,018,502,206)910,508,985102,831,687(25,867,434)76,964,253

(73,020,024)

19.5%21.7%3.2%1.3%1.9%

1.2%

20.8%18.6%2.1%0.5%1.6%

1.5%

1,023,894,029

(63,193,326)

914,453,214

(57,500,590)

22.4%

1.4%

18.6%

1.2%

Profit before Income TaxIncome Tax expense: Current tax Deferred tax

Profit for the year

Profit attributable to:Equity holders of the companyNon-controlling interests

960,700,703

(323,570,136)4,606,626(318,963,510)

856,952,624

(370,221,049)13,479,410(356,741,639)

21%

7.1%0.1%7%

17.5%

7.5%0.3%7.3%

641,737,193

500,210,985 14% 10.2%

756,952,645(115,215,452)

608,123,157(107,912,172)

16.5%2.5%

12.4%2.2%

Profit after Tax for the year

641,737,193

500,210,985 14% 10.2%

25

RAK Ceramics: The comparative balance sheet of RAK ceramics shows:

Fixed assets increased by 2%(40.5-38.5). Current decreased from 61.6% to 59.5%. Non-current liabilities decreased by 5%(2.2-1.7). Share capital increased from 32.7% to 33.7% only.

Above changes suggest that the company is doing well enough to expand its business and that’s why it’s buying more fixed assets.Decrease in non-current liabilities suggests that it’s been paying off its long term debts. Rise in share capital by 1% only indicates that RAK Ceramics is earning enough profit to run its business that’s why they didn’t need to issue that much share.

The changes in the income statements shows that:

COGS has increased from 57.8% to 58.7% . Operating expenses increased by 1.3%(20.8-19.5) Net income decreased by 1.8%(14-10.2)

The changes above indicates that RAK’s COGS and operating expenses both have risen and that’s why it’s net income decreased.

26

Ratios

SHINEPUKURCeramics Analysis

2011 2012Current Ratio 0.98:1 1.01:1 For 1 taka worth of current liabilities

SHINEPUKUR has 1.01 taka worth of currentassets. This ratio has increased.

Acid-test(Quick)Ratio

0.37:1 0.49:1 Quick ratio has decreased.

Receivable turn-over Ratio

3.57Times

2.70Times

The Business collected its receivables 2.70 times in 365 days which means once in every 135 days. This amount reduced in 2012.

Profit MarginRatio

8.82% 4.64% SHINE PUKUR earns profit of 4.6 taka in every100 taka. Its twice as low as 2011.

Asset Turn overRatio

0.31Times

0.27Times

For investing 1 taka SHINEPUKUR is generating0.27 taka worth of revenue. The company isn’t using it assets efficiently.

Inventory Turn-over Ratio

1.4Times

1.5Times

SHINEPUKUR Ceramics sells its Inventory oncein ever 243 days

27

Return onAsset(ROA)

2.75% 1.27% 1.27 taka is earned on every 100 taka assets.

Return onEquity(ROE)

4.67% 2.00%

A net income of 2.0 taka is earned for every100 taka invested by the owners.

Debt to TotalRatio

30% 40%

40% of the company’s assets are provided bycreditor.

Earnings perShare(EPS)

1.32 0.71

SHINEPUKUR earned 0.71 taka per share.

Ratios

RAK Ceramics Analysis

2011 2012Current Ratio 2.30:1

2:1

For 1 taka worth of current liabilitiesSHINEPUKUR has 2 taka worth of currentassets. Although it has decreased, it isstill an ideal ratio for the company.

28

Acid-test(Quick)Ratio

0.95:1 0.66:1

Quick ratio has decreased.

Receivable turn-over Ratio

10.73Times

7.98Times

The Business collected its receivables 7.98times in 365 days which means once in every

45 days. So the company efficiency incollecting receivable decreased but its still

in a good position.Profit Margin

Ratio14.01%

10.19%RAK earns profit of 10.19 taka in every 100

taka. It decreased by 3.8%.

Asset Turn-overRatio

0.62Times

0.61Times

For investing 1 taka RAK is generating 0.61 taka worth of revenue. The company is using its assets in the same way as before.

Inventory Turn-Over ratio

1.71Times

1.73Times

SHINEPUKUR Ceramics sells its inventory oncein every 210 days.

Return on Asset(ROA)

8.68% 6.25%

6.25 taka is earned on every 100 taka assets

Return onEquity(ROE)

12.33% 8.23%

A net income of 8.23 taka is earned for every100 taka invested by the owners.

Debt to TotalRatio

29% 31 %

31% of the company’s assets are provided bycreditor

Earnings perShare(EPS)

2.72 2.18

RAK earned 2.18 taka per share.

29

Comments:

Current Ratio: For RAK ceramic, in 2012 Ratio of 2:1 means thatfor every TK of current liability RAK has TK 2 current assets.RAK current Ratio has decreased in the current year than previousyear. For SHINEPUKUR ceramic, In 2012 Ratio of 1.01:1 means thatfor every TK of current liability SHINEPUKUR ceramic has TK 1.01current assets. SHINEPUKUR current Ratio has increased in thecurrent year than previous year.

Profitability Ratio: As per profit margin ratio shows thatSHINEPUKUR ceramic’s profit margin is more than 2 times greaterthan RAK ceramic’s profit margin.

Asset Turnover Ratio: Asset Turnover Ratio shows that RAKceramics assets turnover Ratio is more than 2 times greater thanSHINEPUKUR ceramics.

Return on Asset (ROA) Ratio: In RAK ceramics, return on asset isabout 4 times greater than SHINEPUKUR ceramics, so RAK ceramicsgenerates more profits from its asset which is good for thecompany.

Return on Equity (ROE) Ratio: ROE position is very good for RAKceramics than SHINEPUKUR ceramics so it generates higher returnfor the shareholders.

Earnings per Share (EPS) Ratio: In 2012 RAK ceramics EPS is 3times more than in 2011 and SHINEPUKUR ceramics EPS in 2012 is

30

less than EPS in 2011 here RAK ceramics EPS is greater thanSHINEPUKUR ceramics.

Now, judging by the ratio analysis of these two companies, it isclear that both companies have suffered loss in 2012. But RAKCeramics is still profitable and much more better than SHINEPUKURCeramics because in 2012:

RAK Ceramic’s current ratio is 2:1whereas SHINEPUKUR’s is1.01:1.

RAK’s profit margin is almost 3times bigger than that ofSHINEPUR’S

Return on asset of RAK Ceramics is 6.25% but SHINEPUKUR’sreturn on asset is only 1.27%.

Creditors provide money 31% of RAK’s assets whereas creditorsprovide money for 40% of SHINEPUKUR’s assets.

Lastly, RAK earns 2.18 taka in each share, but SHINEPUKUR earnsonly 0.71 taka per every share.

The points above make it obvious that RAK Ceramics is doing muchmore better than SHINEPUKUR. So, it’s clear that investing in RAKCeramics is a comparatively safe, profitable, and smart choice.

Appendix 01:

RAK Ceramics Ltd.

Ratio 2012 2011

Current Ratio 49139843282456242485

= 2:1

47684432642077509374= 2.30:1

31

Acid-Test(Quick)Ratio

988298905+6215903972456242485

= 0.66

1442035679+5261233512077509374

= 0.95

Receivable TurnoverRatio

4580008209(621590397+526123351)/2

= 7.98 Times

4908171279(526123351+388310742)/

2=10.73 Times

Profit Margin Ratio 500210985*1004908171279= 10.19%

641737193*1004580008209= 14.01%

Asset TurnoverRatio

4908171279(8255933779+7741585007)

/2= 0.61 Times

4580008209(7741585007+7041094354

)/2= 0.62 Times

Inventory Turn-Overratio

2979160088(1658062569+1777888718)

/2= 1.73 Times

2,693,596,290(1487724337+1658062569

)/2= 1.71 Times

Debt to Total Ratio 139,729,663+ 2,456,242,495 8255933779

= 0.31 Times

167,573,712+2,077,509,374

7,741,585,007= 0.29 Times

Return onAsset(ROA)

500210985*100(8255933779+7741585007)

/2= 6.25%

641737193*100(7741585007+7041094354

)/2=8.68%

Return onEquity(ROE)

500210985*100(5496501921+6659961631)

/2= 8.23%

641737193*100(5496501921+4910792692

)/2=12.33%

Earnings PerShare(EPS)

2.18 2.72

32

Appendix 02:

SHINEPUKUR Ceramics Ltd.

Ratio 2012 2011

Current Ratio 17964128041772067117= 1.01:1

16172319511648906953= 0.98:1

Acid-Test(Quick)Ratio

16009871+8534131451772067117= 0.49:1

25431780+5869338891648906953= 0.37:1

Receivable TurnoverRatio

1942350752(853413145+856933889)

/2= 2.70 Times

1901129192(586933889+477473540

)/2=3.75 Times

Profit Margin Ratio 90285057*1001942350750= 4.64%

168768102*1001901129192= 8.82%

Asset TurnoverRatio

1942350752(7120013155+7154049876)

/2= 0.27 Times

1901129192(7154049876+5125726997

)/2= 0.31 Times

Inventory Turn-overRatio

1,268,312,998(845059407+891,674,750)/

2= 1.5 Times

1,248,024,942(891,674,750+845,195,056

)/2=1.4 Times

Debt to Total Ratio (803483989+1772067117)7120013155= 0.4Times

( 1,005,382,500+ 1,648,906,953 ) 7,154,049,876

= .3 Times

33

Return onAsset(ROA)

90285057*100(7120013155+7154049876)

/2= 1.27%

168768102*100(7154049876+5125726997

)/2=2.75%

Return onEquity(ROE)

90285057*100 (4544462049+4499760423

)/2= 2.00%

168768102*100 (4499760423+273195885

4)/2=4.67%

Earnings PerShare(EPS)

0.71 1.32

All information regarding the two competitor companies has been obtained from their respective sites.The annual reports have been attached for your convenience.The sites and persons from which information has been used are listed below.

http://www.fuwanggroup.com/financial.html

http://www.amclpran.com/investor.php

34