COMMITTEE PUBLIC ACCOUNTS (2008-2011)

23

TWELFTH KERALA LEGISLATIVE ASSEMBLY COMMITTEE ON PUBLIC ACCOUNTS (2008-2011) ONE HUNDRED AND SEVENTY FIRST REPORT (Presented on 23rd February, 2011) SECRETARIAT OF THE KERALA LEGISLATURE THIRUVANANTHAPURAM 2011

-

Upload

khangminh22 -

Category

Documents

-

view

4 -

download

0

Transcript of COMMITTEE PUBLIC ACCOUNTS (2008-2011)

TWELFTH KERALA LEGISLATIVE ASSEMBLY

COMMITTEEON

PUBLIC ACCOUNTS(2008-2011)

ONE HUNDRED AND SEVENTY FIRST REPORT

(Presented on 23rd February, 2011)

SECRETARIAT OF THE KERALA LEGISLATURETHIRUVANANTHAPURAM

2011

TWELFTH KERALA LEGISLATIVE ASSEMBLY

COMMITTEEON

PUBLIC ACCOUNTS(2008-2011)

ONE HUNDRED AND SEVENTY FIRST REPORT

On

Action Taken by Government on the Recommendationscontained in the Hundred and Sixteenth Report of the

Committee on Public Accounts (1995-96)

386/2011.

CONTENTS

Page

Composition of the Committee .. v

Introduction .. vii

Report .. 1

Appendix I : Lr. No. E-1363/1995/SP/VIG/HQT .. 5 dated 29-4-1997 (Enquiry Report)

COMMITTEE ON PUBLIC ACCOUNTS (2008-2011)

Chairman :

Shri Aryadan Muhammed

Members :Shri C. T. Ahammed Ali

,, Anathalavattom Anandan,, Babu Paul*,, K. C. Joseph,, K. M. Mani,, A. C. Moideen

,, M. Prakashan Master

Smt. K. K. Shylaja Teacher

Shri M. V. Sreyams Kumar ,, V. J. Thankappan †

Legislature Secretariat :

Shri P. D. Rajan, Secretary ,, K. Mohana Kumar, Additional Secretary ,, Wilson V. John, Deputy Secretary ,, K. Gopakumaran Pillai, Under Secretary.

* Elected to serve as memeber with effect from 19-3-2009 due to the resignation of Shri N. Anirudhan, MLA and from the Committee.† Elected to serve as member with effect from 14-9-2009 due to the appointment of Shri Ramachandran Kadannappally, MLA and member as Minister.

INTRODUCTION

I, the Chairman, Committee on Public Accounts, having been authorisedby the Committee to present this Report on their behalf present the OneHundred and Seventy First Report on Action Taken by Government on theRecommendations contained in the Hundred and Sixteenth Report of theCommittee on Public Accounts (1995-96).

The Committee considered and finalised this Report at the meeting held on21st February, 2011.

ARYADAN MUHAMMED,

Thiruvananthapuram, Chairman,23rd February, 2011. Committee on Public Accounts.

REPORT

This report deals with the action taken by Government on therecommendations contained in the 116th Report of the Committee onPublic Accounts (1995-96).

The 116th Report of Committee on Public Accounts (1995-96) waspresented to the House on 14th March 1996. The Report contained4 recommendations relating to Local Self Government Department.Government were addressed on 3-4-1996 to furnish Statements of ActionTaken on the recommendations contained in the Report and the finalreplies were received on 13th April 2010.

The Committee examined the action taken statement at its meetingheld on 7-11-2001 and 5-5-2010 and decided not to pursue further actionin the light of the replies furnished by the Government but made remarkson the Government reply on paras 16, 17 and 18. The recommendationsof the Committee, Action Taken Statements furnished by the Governmentand the remarks of the Committee are incorporated in this report.

RECOMMENDATIONS OF THE COMMITTEE AND THE REPLIES

FURNISHED BY GOVERNMENT

LOCAL SELF GOVERNMENT DEPARTMENT

Recommendation

(Sl. No.1 Para No. 15)

The Committee observe that even though the Kerala Slum Areas(Improvement and Clearance) Act was promulgated in 1981 to facilitateClearance and Improvement of Slum Areas, the necessary rules for theeffective implementation of the scheme have not yet been framed by theLocal Administration Department. The Committee are at a loss tounderstand the opinion of the Government Secretary that the Departmenthad acquired powers from other existing rules not inconsistent with theprovision of this Act and also from guidelines issued earlier for theimplementation of the scheme. The Committee like to point out the factthat once an Act is passed by the Legislature for a specific purpose allregulations and guidelines issued by Government for that purpose earlierwould become redundant. While taking strong objection to this kind ofattitude of the Government in closing eyes towards an Act passed byLegislature, the Committee recommend to issue necessary rules

386/2011.

2

immediately invoking the provisions contained in the Act.The Committee also find it reprehensible the method employed by theGovernment in issuing rules i.e. passing on the responsibilities of theGovernment to the Director of Municipalities and other subordinates forframing the rules. In fact many slum clearance development works remainincomplete and some schemes were put in to jittery for want of powers tobe denied out of Rules to be specified and presented by Government asenunciated in the Act.

Action Taken

In regard to the Kerala Slum Areas (Improvement and Clearance)Act, 1981, the Committee on Decentralisation of Powers has remarked thatmany of its provisions are outdated and the implementation of theschemes envisaged therein impracticable or expensive. As regards certainprovisions, it taken up for implementation, there will be resistance fromthe slum dwellers. Therefore, the CDP has recommended to make a freshlegislation instead of implementing the present Act. Government havedecided to make fresh legislation and proposals are being drafted inconsultation with Director of Municipal Administration and Chief TownPlanner. As and when a new Act is adopted, Rules will be framed.

Recommendation

(Sl. No. 2, Para No. 16)

The Committee observe that there is lack of proper planning in thepreparation and execution of slum improvement schemes. The Director ofMunicipalities, who is the nodal officer expected to co-ordinate andstreamline the scheme had totally failed in ensuring prompt execution ofthe works. The Committee recommend that Government should conduct adetailed survey regarding the nature of execution of all the works takenup under the scheme to identity the lapses and short comings and evolvemeasures to avoid them in future.

Recommendation

(Sl. No. 3, Para No. 17)

Many instances of delays and grave irregularities in the constructionof dwelling units as part of the slum eradication work in theChengalchoola slum area in Thiruvananthapuram City were exposed duringthe examination of the audit paragraph. A huge quantity of timberreceived free of cost from the Forest Department for construction of the

3

houses, remain unaccounted and no one is aware of the whereabouts ofthe unaccounted wood to the tune of 67 cubic meters, out of a total717 Cu.M. supplied by Forest Department and entrusted to the KeralaState Construction Corporation. Even though more than 15 years haveelapsed after the completion of the works, no earnest efforts have beeninitiated by Government to reconcile the accounts to ascertain whetherthe timber supplied to KSCC was properly utilised, especially since thetimber was supplied free of cost by Government.

Recommendation

(Sl. No.4, Para No. 18)

The Committee understand that a vigilance enquiry had beenordered into the affair. The Committee recommend that the vigilanceenquiry should be completed immediately and the result intimated to them.The Committee also recommend to take strong action against the culpritsin line with the enquiry report.

Action Taken

(Para Nos. 16, 17 and 18)

The proposed vigilance enquiry has been completed and thefollowing action has been taken.

The Vigilance Enquiry Report had been furnished to Vigilance (E)Department in Government by the Director, Vigilance and Anti-CorruptionBureau with the recommendation to register a criminal case by LocalPolice against Sri C. N. Sadanandan, Contractor. No action wasrecommended against any other officer. The above recommendation wascommunicated to Home Department in Government by Vigilance (E)Department vide letter No. 2466/E2/98/Vigi., dated 29-9-1998. Accordinglya case was registered and is being investigated by the local police.

As far as this Department is concerned, the direction of PublicAccounts Committee to complete the Vigilance Enquiry has been compliedwith. A copy of the vigilance enquiry report is also enclosed as(Appendix I).

Remarks

The Committee remarks that not only the department has notfurnished reply to the recommendations contained in Para Nos. 16 and 17,but the reply furnished on Para No. 18 is vague also. It is mentioned in

4

the Government reply that Vigilance Enquiry has been completed and noofficer if found guilty except the contractor of the work and that acriminal case has been registered against him by the local police. But theGovernment reply is silent about the present position of the case. TheCommittee views this type of irresponsible attitude very seriously andcriticise the department for furnishing such an evasive reply. Yet, theCommittee do not pursue further action in the matter considering thedistance of time.

ARYADAN MUHAMMED,Thiruvananthapuram, Chairman,23rd February, 2011. Committee on Public Accounts.

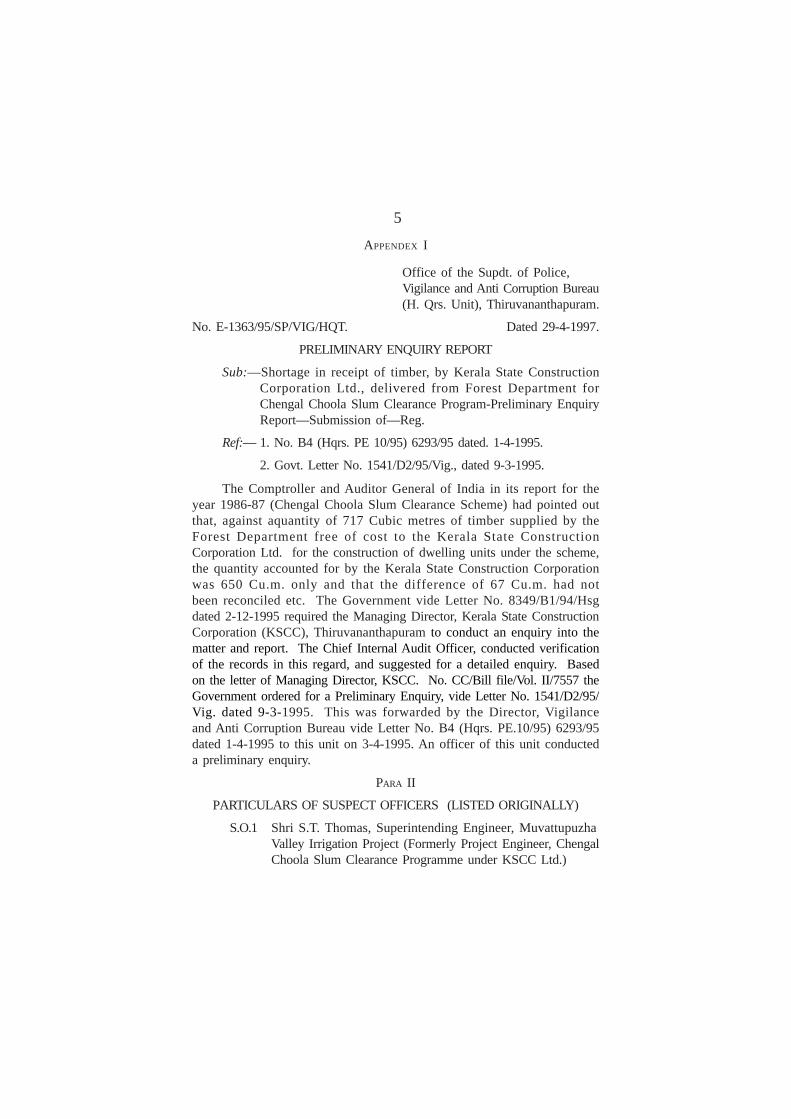

5

APPENDEX I

Office of the Supdt. of Police,Vigilance and Anti Corruption Bureau(H. Qrs. Unit), Thiruvananthapuram.

No. E-1363/95/SP/VIG/HQT. Dated 29-4-1997.

PRELIMINARY ENQUIRY REPORT

Sub:—Shortage in receipt of timber, by Kerala State ConstructionCorporation Ltd., delivered from Forest Department forChengal Choola Slum Clearance Program-Preliminary EnquiryReport—Submission of—Reg.

Ref:— 1. No. B4 (Hqrs. PE 10/95) 6293/95 dated. 1-4-1995.

2. Govt. Letter No. 1541/D2/95/Vig., dated 9-3-1995.

The Comptroller and Auditor General of India in its report for theyear 1986-87 (Chengal Choola Slum Clearance Scheme) had pointed outthat, against aquantity of 717 Cubic metres of timber supplied by theForest Department free of cost to the Kerala State ConstructionCorporation Ltd. for the construction of dwelling units under the scheme,the quantity accounted for by the Kerala State Construction Corporationwas 650 Cu.m. only and that the difference of 67 Cu.m. had notbeen reconciled etc. The Government vide Letter No. 8349/B1/94/Hsgdated 2-12-1995 required the Managing Director, Kerala State ConstructionCorporation (KSCC), Thiruvananthapuram to conduct an enquiry into thematter and report. The Chief Internal Audit Officer, conducted verificationof the records in this regard, and suggested for a detailed enquiry. Basedon the letter of Managing Director, KSCC. No. CC/Bill file/Vol. II/7557 theGovernment ordered for a Preliminary Enquiry, vide Letter No. 1541/D2/95/Vig. dated 9-3-1995. This was forwarded by the Director, Vigilanceand Anti Corruption Bureau vide Letter No. B4 (Hqrs. PE.10/95) 6293/95dated 1-4-1995 to this unit on 3-4-1995. An officer of this unit conducteda preliminary enquiry.

PARA II

PARTICULARS OF SUSPECT OFFICERS (LISTED ORIGINALLY)

S.O.1 Shri S.T. Thomas, Superintending Engineer, MuvattupuzhaValley Irrigation Project (Formerly Project Engineer, ChengalChoola Slum Clearance Programme under KSCC Ltd.)

6

Gazetted Officer, Date of retirement on 31-3-2001

S.O.2 Shri C.A. Narayanan (Contractor), Anil Cottage, Thycaud,Thiruvananthapuram (Expired on 11-12-1995)Private Individual

S.O.3 Shri C.N. Sadanandan (Contractor), Anil Cottage, Thycaud,Thiruvananthapuram.Private Individual.

PARA III

PARTICULARS OF SUSPECT OFFICERS (ADDITIONALLY FOUND)

Nil.

PARA IV

PARTICULARS OF SUSPECT OFFICERS (LISTED ORIGINALLY)

That Suspect Officer (S.O.) 1. Shri S.T. Thomas (NowSuperintending Engineer, Muvattupuzha Valley Irrigation Project) whileholding the post of Project Engineer, Chengal Choola, Slum ClearanceProgramme, under the Kerala State Construction Corporation (KSCC) Ltd.during the period form 13-10-1978 to 10-3-1986 and S.O.2,Sri C. A. Narayanan, Anil Cottage, Thycaud, Thiruvananthapuram (expiredon 11-12-1995) and his son, S.O.3 Sri C. N. Sadanandan, Anil Cottage,Thycaud, Thiruvananthapuram both transporting contractors had causedthe short accounting of 67.481 Cu.m. of timber from a total quantity of717.35 Cu.m. of timber transported by them from various timber depots ofForest Department and that, the records regarding the receipt of timber,were not maintained properly.

PARA V

PARTICULARS OF ALLEGATIONS (ADDITIONALLY FOUND)

Nil.

PARA VI

PARTICULARS OF WITNESS EXAMINED

W1. Shri O. K. Abraham, S/o O. A. Kurian, Age 58/97, Abeylands,Pappanamcode, Thiruvananthapuram. Retired Asst. Engineer.Questioned on 19-3-1997. His Statement is available on

7

pages 1 and 2 of the statement file.

W2. Shri N. Ramakrishnan Pillai, Asst. Conservator, ForestVigilance, Thiruvananthapuram.

Questioned on 10-4-1997. Statement available on page 3 ofthe statement file.

W3. Shri K.M. Hassan Rawther, Regional Manager II Kerala StateConstruction Corporation Ltd., Thiruvananthapuram.

He was questioned on 10-4-1997. Statement available on page 4 ofthe statement file.

PARA VII

DETAILS OF DOCUMENTS ENCLOSED (ORIGINAL/CERTIFIED COPY)

Ext. A:— File No. CC/ROW/80/80 of Kerala State ConstructionCorporation Ltd., Thiruvananthapuram, (Pages 1 to 254).

This document contains the Statements of timber sent by the ForestDepartment and received by KSCC Ltd. This document also contains theverification report of witness No.1, and the comparative statement oftimber sent by the Forest Dept. and received by KSCC Ltd., and theshortage etc.

Ext. B:— File No. CC/RM-II/TVM/5/80/Vo1.IV of KSCC Ltd.,Thiruvananthapuram.

This document contains photocopy of timber pass Nos. 322/79 and355/79 and the details of timber sent from the Forest Dept.

Ext. C:— Measurement Book No. 1486 of Kerala State ConstructionCorporation Ltd., Thiruvananthapuram.

This document contains the details of timber received by KSCC Ltd.,as per timber pass Nos. 8/83, 10/83 and 49/83 issued from ForestDepartment.

Ext. D:—Measurement Book No. 814 of Kerala State ConstructionCorporation Ltd., Thiruvananthapuram.

This document contains the details of timber received by KSCC Ltd.,as per pass No. 143/83 issued from Forest Dept.

Ext. E:— Measurement Book No. 812 of Kerala State ConstructionCorporation Ltd., Thiruvananthapuram.

This document contains the details of timber received by KSCC Ltd.,

8

as per pass Nos. 143/83, 224/79, 289/79, 322/79 and 355/79.

Ext. F:— Measurement Book No. 827 of Kerala State ConstructionCorporation Ltd., Thiruvananthapuram.

This document contains the details of timber received by KSCC asper pass No. 3/85.

Ext. G:— Stock Register of materials of Kerala State ConstructionCorporation Ltd., Thiruvananthapuram, Vol. I(Pages 1 to 152)

This document contains the details of timber received by KSCC Ltd.,as per pass Nos. 8/83, 49/83, 145/83 and 3/85 (Page No. 130).

Ext. H:— Stock Register of materials of Kerala State ConstructionCorporation Ltd., Thiruvananthapuram, Vol. II.

Page Nos. 71 and 72 of this document shows, entries regarding thereceipt of a portion of timber. The entries are vague.

PARA VIII

STATEMENT OF SUSPECT OFFICERS

1. Shri S.T. Thomas, Superintending Engineer, MuvattupuzhaValley Irrigation Project (Formerly Project Engineer,Chengal Choola Slum Clearance Programme).

The Suspect Officer in his statement stated that, he had worked asProject Engineer of the Chengalchoola, Slum Clearance Programme, underKSCC Ltd., Thiruvananthapuram, for the period from 13-10-1978 to10-3-1986. One C. N. Sadanandan was authorised to transport the timberfrom 4 different Forest depots. But there was no written agreement withShri Sadanandan. During his tenure, no comparison of quantity of timber,received by KSCC was made with the quantity of timber, sent from Forestdepots. Therefore, no shortage of timber was noticed. During his period,he had sent, statements of timber received by the KSCC to the ForestDepartment. The Suspect Officer has also stated that, the conveyancecontractor, Shri Sadanandan, had obtained the passes issued by ForestDepartment from the depots, and that all the passes, after conveyancewere collected and kept by himself and he had left these passes withother records at KSCC Office, Tvpm. etc.

2. Shri C. A. Narayanan, Anil Cottage, Thycaud,Thiruvananthapuram. This suspect person expired

9

on 11-12-1995.

3. Shri C. N. Sadanandan, S/o Narayanan, Anil Cottage, Age 46/97,Thycaud, Thiruvananthapuram.

This suspect person who is a private individual stated that he hadconveyed, timber, from four Forest depots to Thiruvananthapuram, duringthe period from 1979 to 1985 for the Changalchoola Slum ClearanceProgramme. Shri S. T. Thomas was the Project Engineer. There was nowritten agreement for the timber conveyance. He had collected the timberpasses from the various Forest depots and conveyed the timber toThiruvananthapuram as per the direction of the Project Engineer and hecollected his charges then and there. He also stated that he hadconveyed all the timber. He received from the depots and handed overthe passes to the Project Engineer and that, he could not remember howmuch quantity of timber he had conveyed.

PARA IX

The allegation is that the suspect officer and suspect personscaused the short accounting of 67.8 cubic meter of timber from a totalquantity of 717.35 cubic metre transported by them from various forestdepots to Trivandrum for Chengal Choola slum clearance programmeundertaken by Kerala State Construction Corporation Ltd.

Three witnesses and two suspect persons were examined and adocuments were perused during the enquiry.

According to the report of Divisional Forest Officer,Thiruvananthapuram, dated 15-11-1990 (As supported by Ext. ‘A’ Pages74 to 76) the Forest department had released 717.350 cubic metre oftimber from their 4 depots, viz. Achancoil, Thirumala, Kulathupuzha andChenkotta during the period from 1978 to 1985. But according to thestatement of Kerala State Construction Corporation (As supported by Ext.A pages 126 to 132) only 649.869 Cu.m., of timber were received by them.So there is a difference of 67.481 Cu.M. of timber between supply andreceipt. This difference in quantity of timber was never reconciled.

Witness 1, Shri O.K. Abraham, conducted a detailed enquiry in orderto find out the reason for difference in supply and receipt of timber andsubmitted his verification report on 23-5-1991 (Ext. A, pages 109 to 118).

10

He has prepared the report after verifying the records available with theForest Department and therefore, this report can be rolled upon as a basicdocument.

As per the comparative statement of timber received by Kerala StateConstruction Corporation and delivered by the Forest Department (Ext. A,Page 132) the difference are as follows:

Name of Depot Pass No. Date of Shortage/MissionIssue (in Cu.m.)

1. Achancoil 16/83 17-1-1983 8.522

2. Achancoil 72/83 3-3-1983 8.893

3. Achancoil 131/83 9-5-1983 8.974

4. Thirumala 48/78 .. 1.275

5. Kulathupuzha 163/78 4-4-1978 1.000, 3.582

6. Kulathupuzha 289/79 7-7-1979 1.000

7. Kulathupuzha 322/79 28-7-1979 1.124

8. Kulathupuzha 355/79 26-8-1979 33.111

Total 67.481 Cu.M.

Enquiry revealed that, regarding Pass Nos. 16/83, 72/83 and 131/83neither the Pass, nor the timber had reached Trivandrum though deliveredfrom the Forest depot. There is no record to show that the timber, as perthese three passes, were received by Kerala Construction Corporation.At the same time, there is proof for the timber having delivered from theForest depot. The conveyance contractor (S.O.3) Shri C. N. Sadanandanhad signed on the overleaf of the copy of pass kept at the depot intoken of having received the pass and timber (As supported by Ext.A, pages 109 to 118). So it is evident that the timber as per the abovethree passes were received from the depots by S.O.3. and he disposedthe whole timber for his own benefits. This attracts the mischief ofCriminal Breach of Trust in respect of the timber received by him fortransportation only.

Regarding Pass No. 48/78, S.137 Cu.ms. of timber were deliveredfrom Thirumala Depot, but only 6.862 Cu.ms. were received by KeralaState Construction Corporation. So there is a shortage of 1.275 Cu.m. oftimber. Enquiry revealed that Suspect Officer, Shri Narayanan had

11

acknowledged receipt of full quantity of timber and pass from the forestdepot. But the Kerala State Construction Corporation had received only6.862 m3 of timber. In order to find out the reason for shortage the passissued by the forest depot along with the details of loge delivered shouldbe made available. The details of the logs delivered will be given alongwith the pass, (As corroborated by W2). But the pass is not forthcomingwith the Kerala State Construction Corporation (As Corroborated by W3).W3 had intimated that the passes could not be located at this distanceof time.

Regarding Pass No. 163/78, issued from Kulathupuzha depot, dated19-4-1978, 59.619 Cu.m. timber were delivered from the depot. But only55.037 Cu.m. of timber were received by Kerala State ConstructionCorporation. Enquiry revealed that, out of 105 logs, only 97 logs weredelivered. This is as per the records maintained at the Forest Depots(As supported by Ext. A, Page No. 114 and corroborated by W1). Butaccording to the statement given by the Forest depot, the whole quantityas per the pass had been delivered. Viewed with Ext. A, this statementcannot be true. So obviously the balance quantity i.e., 4.582 Cu.m. oftimber was removed from the depot, unauthorizedly which would amountto theft.

Regarding Pass No. 285/79 issued from Kulathupuzha Forest depot,dated 7-7-1979, enquiry revealed that the whole quantity delivered fromthe depot was received by Kerala State Construction Corporation i.e.,41.702 Cu.m. of timber was delivered and the same quantity had beenreceived (As supported by Ext. E, Page No. 38). The mistake occurredwas in the statement given by Kerala State Construction Corporation.Therefore, there is no shortage.

Regarding Pass No. 322/79, issued from Kulathupuzha depot, dated28-7-1979, 58.431 Cu.m. of timber were delivered but only 57.312 Cu.m.were received by Kerala State Construction Corporation. Enquiryrevealed that out of 81 logs, only 79 logs were delivered from the depot.Logs having Nos. 3763 (0.665 Cu.m.) and 5941 (0.459 Cu.m.) were notactually delivered. Total quantity of two logs will amount to 1.124 Cu.m.which is the shortage (As supported by Ext. B Page Nos. 91, 92 and 93and Ext. A, Page No. 110 and corroborated by W1). Since not deliveredfrom the depot these 2 logs having measurement equal to the shortageshould be at the depot itself. But according to the forest department, thewhole timber as per the pass had been delivered. Therefore, it is

12

revealed that, these two logs had been removed from the depot whichwould amount to theft.

Regarding Pass No. 355/79 as per the statement of forestdepartment, the full quantity had been delivered (Total 129 logs). Butaccording to the statement of Kerala State Construction Corporation only55.361 Cu.m. were received by them. The shortage is 33.111 Cu.m.Enquiry revealed that out of 129 logs only 78 logs were delivered fromthe depot according to the Pass (As corroborated by W1 and supportedby Ext. A, Page No. 110 and Ext. B, Page Nos. 94 to 97). Therefore theshortage quantity of 33.111 Cu.m., should have been at the depot itself.Since these logs are not at the depot, according to the statement offorest depot it is revealed that the same was removed unauthorized fromthe depot which would amount to theft.

From the foregoing discussions, it is revealed that, out of 717.350Cu.m. of timber the Kerala State Construction Corporation had receivedonly 650.869 Cu.m. of timber. The shortage quantity is 66.481 Cu.m. outof this quantity of timber, 26.389 Cu.m. of timber was taken delivery fromAchancoil Depot as per Pass Nos. 16/83, 72/83 and 131/83 by Suspectperson 3, Shri C.N. Sadanandan but the same had not reacheddestination. 4.582 Cu.m. of timber as per Pass No. 163/78, 1.124 Cu.m. oftimber as per Pass No. 322/79 and 33.111 Cu.m. of timber as perPass No. 355/79 were not actually delivered form Kulathupuzha ForestDepot as per passes, but were removed subsequently unauthorized(Total quantity 38.817 Cu.m.) 8.137 Cu.m. of timber as per Pass No. 48/78was taken delivery from Thirumala depot by suspect person No. 2,Shri C. A. Narayanan but only 6.862 Cu.m. reached the destination. Theshortage is 1.275, since no record, regarding this pass could be traced atthis distance of time, the point, where the timber were missed could notbe located. But it is obvious that this quantity of timber was alsomisappropriated. Thus it is revealed that the missing quantity of timberis 66.481 Cu.m. were stolen or misappropriated either from the ForestDepot or on transit from the depot to Trivandrum.

It is also revealed that the records relating to the receipt of timberwere not maintained properly. The stock registers (Ext. G, Pages 123 and130, Ext. H, Pages 71 & 72) were maintained in a careless manner withincomplete entries. S.O. 1, Shri S. T. Thomas is responsible for thisirregularity.

PARA X : CONCLUSION

13

The allegation is that 66.481 Cu.m. timber was short accorded.Enquiry revised that out of 66.481 Cu.m. of timber, Suspect personNo. 3, Shri C. N. Sadanandan, Contractor had committed criminal breachof Trust in respect of 26.389 Cu.m. of timber, entrusted with him forconveyance from Achan Coil Forest Depot vide Pass No. 16/83 dated17-1-1989, 72/83 dated 3-3-83 and 131/83 dated 9-5-1983 (Ext. A, Page 116,117). The remaining 40.692 Cu.m. of timber were unauthorisedly removedor stolen from Kulathupuzha and Tirumala Forest Depot.

It is also proved that S.O.1 had not maintained proper recordsregarding the receipt of timber.

There is no evidence to suggest that S.O.1 had any involvement inthe Criminal Breach of Trust/Theft mentioned above.

PARA XI

S.O.1— Shri S. T. Thomas, Superintending Engineer, MuvattupuzhaValley Irrigation Project and Formerly Project Engineer, Chengal Choolaslum Clearance Programme under Kerala State Construction CorporationLimited.

Satisfactory.

The others are private individuals

PARA XII

S.O.1—Shri S. T. Thomas, Superintending Engineer,

Government.

The others are private individuals.

PARA XIII

S. R. Gopalakrishnan Nair, Superintendent of Police, Vigilance andAnti-Corruption Bureau, (H.Qrs.Unit), Thiruvananthapuram.

PARA XIV

1. Original Petition

2. Exhibits A, C, D, E & F (Original) and Exhibits B, G and H (Photocopy)

14

{io. H. sI. F{_mlmw, S/o O. A. Ipcy≥ age 58/97, A{U v

]m∏-\w-tImSv, Xncp-h-\-¥-]pcw F∂bm-tfmSp tNmZn-®-Xn¬ ]d-™-Xv.

Rm≥ PWD bn¬ \n∂pw AE Bbn 1994 -˛¬ dn´ -b¿ sNbvXp.

Ct∏mƒ ho´n¬ shdp-sX-bn-cn-°p-I-bm-Wv. 1962-˛¬ Hmh¿ko-b¿ BbmWv

k¿∆o-kn¬ {]th-in-®-Xv. IqSp-X¬ Imehpw Xncp-h-\-¥-]p-cØv PWD bn¬

Bbn-cp-∂p. c≠p-{]m-hiyw tIcfm tÉv I¨kv{S-£≥ tIm¿∏-td-j-\n¬

sU]yq-t´-j-\n¬ tPmen sNbvXn-´p-≠v. 1991-˛92 Ime-L-´-Øn¬ C{]-Imcw

KSCC-bn¬ AEbmbn tPmen t\m°n-bn-cp-∂p. MDbpsS Hm^o-kn-em-bn-cp∂p

tPmen. sN¶¬Nqf …w ¢o-b-d≥kv ]≤-Xn-°p-th≠n t^mdÃv Un∏m¿´p-

sa‚ n¬ \n∂pw 1978 apX¬ 1985 hsc, XSn sIm≠p -h -∂-Xn¬,

67 Iyp. ao‰-tdmfw XSn Ipd-hp-Im-W-s∏-´Xp kw_-‘n®v KSCC P\-d¬

amt\-P-cpsS 8˛5-̨ 1991 Xob-Xn-bnse IØns‚ ASn-ÿm-\-Øn¬ Rm≥ hnhn[

Unt∏m-I-fn¬ t]mbn t\cn´v At\z-jWw \S-Øn-bn-cp-∂p. A∂sØ

doPnb-W¬ amt\-P¿ I Bbn-cp∂ tPmtjzm-bpsS ta¬t\m-́ -Øn-emWv Cu

tPmen Rm≥ sNbvX-Xv. Unt∏m-I-fn¬ shcn-^n-t°-j≥ \S-Øn-bXpw

dnt∏m¿´v Xøm-dm°n ka¿∏n-®Xpw Rm\m-Wv. Ct∏mƒ Fs∂ ImWn-®,

^b¬ \º¿ CC/ROW/80/80-se 109 apX¬ 118 hsc-bp≈ t]Pp-I-fn-te-

°p≈ dnt∏m¿´v Rm≥ Xøm-dm-°n-b-Xm-Wv. B dnt∏m¿´ns‚ ASn-ÿm-

\Øn¬ 23-̨ 5-̨ 1991-̨ ¬ ................ dnt∏m¿´ns‚ BZy-̀ m-KØv .................. sa‚n¬

\n∂pw Ab-®-Xmbn ImWn-®n-´p≈....................tÉv-sa‚pw, KSCCbn¬ e`n-®-

Xm-bn-́ p≈ ac-Øns‚ tÃ-‰p-sa‚pw tN¿Øv comparative statement Xøm-dm-°n-

bn-́ p-≠v. B ac-Øn¬, KSCC bn¬ Ipd-hm-bn-In´nb ]m p-Isf kw_-‘n®v

Unt∏m-I-fn¬ At\z-jWw \S-Øn-bpw, In´nb hnh-c-ß-fpsS ASn-ÿm-\-Øn¬

dnt∏m¿´v Xøm-dm-°p-I-bp-amWv sNbvXn-´p-≈-Xv. t^mdÃv -Un-∏m¿´p-sa‚n¬

\n∂pw 717.350 m3 acw Ab-®-Xm-bn-́ mWv t^md-Ãv Un-∏m¿´p-sa‚n¬ \n∂pw

Ab®p-X∂ tÉv-sa‚n¬ ImWp-∂-Xv. F∂m¬ KSCC bn¬ doPnb-W¬

amt\-P-cpsS tÉv-sa‚p{]Imcw 649.869 m3 acw am{X-ta, e`n-®n-́ p-≈q. 67.481 m3

acw Ipd-hm-bn-´mWv KSCCbn¬ In´n-b-Xmbn ImWp-∂-Xv. A®≥tIm-hn¬

Unt∏m-bn¬ \n∂pw Pass No 16/83 Bbn 17˛1˛83˛\v Ab® 8.522 m3

achpw, Pass No. 72/83 Bbn 3˛3˛83˛\v Ab® 8.893 m3 achpw, Pass No.131/83 Bbn 9-5-83-\v Ab® 8.974m3 achpw KSCC °v e`n-®n-t´-bn-√.

Cu ac-Øns‚ ]m p-I-fpw, KSCC bn¬ e`n-®-Xm-bn-Im-Wp-∂n-√. Rm≥

Unt∏m-bn¬ ]cn-tim-[n-®-Xn¬ Cu ]m p-I-fp-tS-bpw, Unt∏m-bn¬ kq£n-®n-

´p≈ ]I¿∏p-I-fn¬ tIm¨{Sm-Œ¿ kZm-\-µ≥ H∏p-h-®n-́ p-≈-Xmbn ImW-s∏-́ p.

]m pw XSnbpw G‰p-hm-ßp-∂-Xn-\p≈ cko-Xm-bn-́ mWv ]m ns‚ tIm∏n-bn¬

H∏n-´n -´p -≈Xv F∂v At\z-j-W-Øn¬ Adn-bm≥ Ign-™p. Xncp-ae

Unt∏m-bn¬ \n∂pw Pass No. 48/78 Bbn 8.137 m3 XSn Ab-®-Xn¬ 275 m3

Ipd-hmbn 6.862 m3 am{Xta KSCCbpsS A°u≠p{]mIcw e`n-®n-´p-≈q.

F∂m¬ Unt∏m-bnse ]m ns‚ tIm∏n-bn¬ ‘received logs and pass’ F∂v

15

FgpXn Narayanan F∂-bmƒ H∏n-´n -´p≈Xmbn ImW-s∏-´p. XobXn

31-˛1-˛1978 BWv ]m n¬ C´n-cp-∂-Xv. Ipf-Øq-∏pg Unt∏m-bn¬ \n∂pw

pass No. 163/78 Bbn 19-˛4-˛1978-˛\v Ab® 56.037m3 ac-Øn¬ 1m3 Ipd®v

55.037 m3 Dw, 3.582 m3 acw apgp-h-\mbn In´n-bn-´n-√m-sXbpw BWv KSCCbpsS tÉv-sa‚n¬ ImWp-∂-Xv. Cu ]m n¬ samØw 105 XSn-Iƒ BWp-

≈-Xv. Unt∏m-bn¬ kq£n-®n-´p≈ ]Xn-hp-_p°v ]cn-tim-[n-®-Xn¬ BsI

97 XSn-Iƒ am{Xta Ab-®-Xmbn tcJ-s∏-Sp-Øn-bn-́ p-≈q. _m°n Ab-°mØ

8 XSn-I-fpsS Af-hv, samØw Ipd-hp≈ 4.582m3 Bbn-cn-°m-\mWv km[y-X.

Aß-s\-bm-sW-¶n¬ 8 XSn-Iƒ Unt∏m-bn¬ Xs∂ D≠m-bn-cn-°-Ww. Ipf-Øp-∏pg

Unt∏m-bn¬ \n∂pw 289/79 ]mkp-{]-Imcw 7.79-˛\v Ab-®-Xmb 40 XSn-Iƒ

41.702-̨ \v XSnbn¬ 1m3 Ipd®v _m°n 40.702m3 XSn KSCC bn¬ In´n-b-Xm-bn-

´mWv tÉp-sa‚ v Unt∏m-bn¬ \n∂pw, tÉp-sa‚ v ]m n¬ H∏phm-ßn-b-

Xmbn ImWp-∂-Xv. Rm≥ Fs‚ dnt∏m¿´n¬ AX-\p-k-cn®v FgpXn-bn-́ p-≠v.

F∂m¬ Ct∏mƒ measurement Book No. 812- ¬ Page 35 {]Imcw ]mkv

\w. 289/79˛se 40 XSn-Ifpw 111.70m3 XSn apgp-h-\pw, KSCC bn¬ In´n-b-Xmbn

ImWp-∂p-≠v. {io. F≥. cma-Ir-jvW-]n-≈, I¨k¿th-‰¿, t^mdÃv

hnPn-e≥kv, Xncp-h-\-¥-]pcw F∂-bm-tfm-Sp-tNm-Zn-®-Xn¬˛

Rm≥ Xncp-h-\-¥-]p-cØv t^mdÃv hnPn-e≥kn¬ Akn. I¨k¿th-

‰-dm-Wv. t^mdÃv Unt∏m-I-fn¬\n∂v acw ]pd-tØ°v sImSp-°p-∂Xv ]m p-

Iƒ aptJ-\-bm-Wv. ]m p-I-fn¬, acw ISØn sIm≠p-t]m-Ip-∂-Xn\v ]cn-[n-

h®v XobXn h®n-cn-°pw. ]m n¬X-s∂, A\p-h-Zn® tem´n-ep≈ XSn-I-fpsS

\º¿ sImSp-Øn-cn-°pw. IqSp-X¬ XSn-I-fp-s≠-¶n¬, ]m n-t\m-Sp-IqSn

{]tXyIw ISemkvv tN¿Ø-Xn¬ \º-cp-Iƒ sImSp-Øn-cn-°pw. XSn temUv-

sNbvXv ]pd-tØ°v Abbv -°p∂ ka-bw, t^mdÃv Unt∏m-bn -ep≈

hm®¿am¿, ]m n¬ Xob-Xn-h®v Abbv°p-∂ -X-Sn-I-fpsS \º¿ FgpXn

sImSp-°-Ww. CtX hnh-cw, Unt∏m-bn¬ h®n-´p≈ ]Xn-hp-_p-°nepw

tN¿°-Ww. ]Xn-hp-_p-°n-epw ]m nepw XSn-I-fpsS IW°v Ft∏m-gpw

HØp t]mI-Ww. ]m n¬ am¿°p-sN-ømsX GsX-¶nepw XSn- In-S-∏p-s≠-

¶n¬ ............... Xs∂ D≠m-hWw. ]m v km[m-cW AXXv ...............]mkv

\º¿ 322/79 {]Imcw Ab® ................... XSn Ipd-hp-≈-Xmbn ImWp-∂p-≠v.

]cn-tim-[n-®-Xn¬ c≠p-X-Sn-Iƒ Unt∏m-bn¬ D≈-Xmbn I≠p. B c≠p XSn-

I-fpsS BWv 1.124 m3 F¶n¬ Unt∏m-bn¬ \n∂pw Ab® XSn apgp-h≥

KSCC bn¬ In´n-bn-́ p-≠v. ]mkv \º¿ 355/79 {]Imcw 26-̨ 8-̨ 1979-̨ \v Ab®

88.472m3 XSn-bn¬ 33.111.m3 Ipd®v 55.361 m3 XSn am{Xta KSCCbn¬ In´n-

bn-́ p-≈q. Unt∏m-bn¬ day pass ]cn-tim-[n-®-Xn¬ BsI 129 XSn-I-fn¬ 79

FÆw am{X-ta, sUen-hdn FSp-Øn-´p≈q F∂v ImWp-∂p. _m°n 50 XSn-

Iƒ sUen-hdn FSp-Øn-´n-√. B XSn-Ifpw Unt∏m-bn¬ Xs∂-bmWv

D≠mth-≠Xpw

samgn- hm-bn®p tI´p. icn-bm-Wv.

Recorded by me

16

K. S. Skaria,Inspector, Vigilance HQ Unit,

Trivandrum, 19-3-1997.

{io. sI. Fw. l ≥ dmhp-ج, doPnb-W¬ amt\-P¿ II, tIcfm

tÉv I¨kv{S-£≥ tIm¿∏-td-j≥, Xncp-h-\-¥-]pcw F∂-bm-tfmSp tNmZn-®-

Xn¬ ]d-™-Xv.

Rm≥ kpam¿ 3 h¿j-ambn PWDbn¬ \n∂pw sU]yq-t´-j-\n¬

KSCC bn¬ tPmen sNøp-I-bm-Wv. Akn-Â v t{]mPŒv F©n-\o-b-dm-bn-́ mWv

KSCC bn¬ h∂Xv. 22-̨ 10-̨ 1996 apX¬ doPnbW¬ amt\-P¿ II˛s‚ Nm¿÷v

IqSn hln-°p-∂p-≠v. Cu Hm^o-knse dnt°m¿Up-I-fmb M Book No. 812,File No. CC/RM2/TVM/5/80 Vol. IV, Stock Register Vol. I and II F∂n-h

hnPn-e≥kv C≥kvs]-Œ¿°v ]cn-tim-[-\-bv°mbn Rm≥ C∂v G¿∏n-®p-sIm-Sp-

Øn-´p-≠v. Ct∏mƒ Fs∂- Im-Wn-® M Book No. 814, 827, 1486 Ch Cu

Hm^o-kn-te-Xm-Wv. AXv apºv hnPn-e≥kn¬ lmP-cm-°n- sIm-Sp-Ø-Xm-Wv.

File No. CC/ROW/80/80 ^b¬ ChnsS Fw.-Un.bpsS Hm^o-kn-te-Xm-Wv.

sN¶¬Nqf ]≤-Xn-°p-th≠n XSn-sIm-≠p-h∂ ]mkp-Iƒ Cu Hm^o-kn¬

]cn-tim-[n-®n v́ In´n-bn-́ n-√.

samgn- hm-bn®v tI´p. icn-bm-Wv.

Recorded by meK. S. Skaria,

Inspector, Vigilance HQ Unit,Trivandrum, 10-4-1997.

Bƒ°m¿ Xs∂ h∂p hmß-Wwsa∂p≈q. Bƒ°m¿°v HmX-ssd-tk-j≥

Ds≠-¶nte sImSp-°m≥ ]mSp-≈q. ]mkns‚ Unt∏m-bn-ep≈ tIm∏n-bn¬ H∏n-

´p-sIm-Sp-Øm¬ AXn-\¿∞w ]m pw XSnbpw In´n F∂m-Wv.

samgn hmbn-®p-tI´p. icn-bm-Wv.

Recorded by meK. S. Skaria,

Inspector, Vigilance HQ Unit,Trivandrum, 10-4-1997.

{io. Fkv. ‰n. tXma-kv, kq{]-≠nwKv F©n-\o-b¿, aqhm-‰p-]p-g- hmen

Cdn-tK-j≥ t{]mP-Œv, F∂-bm-tfmSv tNmZn-®-Xn¬ ]d-™-Xv:

Rm≥ Ct∏mƒ aqhm-‰p-]pg hmen Cdn-tK-j≥ ]≤-Xn-bn¬ kq{]-≠nwKv

F©n-\o-b-dmbn tPmen t\m°p-I-bm-Wv. Rm≥ 1978 apX¬ 1986 hsc,

Xncp -h -\ -¥-]p -cØv tIcfm tÉv I¨kv{S -£≥ tIm¿∏-td -j-\n¬

17

sU]yq-t -́j-\n¬ Bbn-cp-∂p. C°mew apgp-h\pw F\n-°v, sN¶¬Nq-f …w

¢o-b-d-≥kv ]≤-Xn-bp-sS, t{]mPŒv Hm^o-k-dpsS Nm¿Pv Bbn-cp -∂p.

sN¶¬Nqf ]≤-Xn°v sN¶¬Nqf-bn¬ Xs∂ Hcp Xm¬°m-enI Hm^okv

D≠m-bn-cp-∂p. 1978 apX¬ 1985 hsc, Kh. Hm¿U¿ {]Im-cw, ]W-sam∂pw

sImSp -°m-sX, t^mdÃv Un∏m¿´p -sa‚ n¬\n∂pw, sN¶¬Nq-f -bnse

sI´nSw ]Wn-bp-∂-Xn-\p-th-≠n, [mcmfw XSn-sIm-≠p-h-∂n-´p-≠m-bn-cp-∂p.

kn. F≥. kZm-\-µ≥ F∂ Bfm-bn-cp∂p tIm¨{Sm-Œ¿. kZm-\-µ\v sXm´p-

apºv Ipd-®p-\mƒ Abm-fpsS A—≥ \mcm-b-W-\pw XSnsIm≠p-h-cp-∂-Xn\v

tIm¨{SmŒv ]Wn-sb-Sp-Øn-cp-∂p. C{]-Imcw XSn-sIm-≠p-h-cp-∂-Xn\v

I¨kv-{S-£≥ tIm¿∏-td-j\pw tIm¨{Sm-IvS¿amcp-ambn F{Kn-sa‚ v H∂pw

D≠m-°n-bn-cp-∂n-√. t^mdÃv Un∏m¿´p-sa‚n¬\n∂pw Ab® XSn-bpsS

IW°v t^mdÃv Un∏m¿´p-sa‚pambn HØp-t\m-°n-bn-´n-√. AXp-sIm≠v

Ab® XSn-bn¬ Ipdhp h∂n-´pt≠m F∂v Adn-bm≥ Ign -™n-´n -√.

F∂m¬ Fs‚ ]oco-Un¬ In´nb XSn-bpsS tÉv-sa‚ v Rm≥ CS-bv°n-Sbv°v

t^md-Ãv -Un-∏m¿´p-sa‚n\v Ab-®p-sIm-Sp-Øn-´p-≠m-bn-cp-∂p. t^md-Ãv

-Un-t∏m-I-fn¬ \n∂pw ]m p-Iƒ hmßp-∂Xpw XSn G‰p-hm-ßp-∂-Xpw

tIm¨{Sm-Œ-dm-bn-cp-∂p. tIm¨{Sm-Œ¿, GsX-¶nepw Hcp ]m nse XSn

apgp-h≥ am‰n-b-ti-jw, ]m v Xcm-sX-bn-cp-∂m¬, t^mdÃv Un∏m¿´p-sa‚ns‚

IW-°p-ambn HØp-t\m-°p-tºmƒ am{Xta hyXymkw a\- n-em-°m≥

km[n-°q. Fs‚ ]°¬h∂ ]m p-I-sf-√mw, Rm≥ {Sm≥kv^-dmbn

t]mb-t∏mƒ, I¨kv{S-£≥ tIm¿∏-td-js‚ Hm^o-kn¬ G¬∏n-®n-cp-∂p.

IqSp-X-embn F\n-s°m∂pw Adn-bn-√.

samgn hmbn-®p-tI´p. icn-bm-Wv.

Recorded by meK. S. Skaria,

Inspector, Vigilance HQ Unit,Trivandrum, 25-3-1997.

{io. kZm-\-µ≥, S/o \mcm-b-W≥, age 46/97 T.C. 24/153, ssX°m-Sv,

Xncp-h-\-¥-]pcw F∂-bm-tfmSp tNmZn-®-Xn¬ ]d-™-Xv:

Fs‚ A—≥ 11-̨ 12-̨ 1995-̨ ¬ acn-®p. A—≥ t^md-Ãv tdbv©¿ Bbn

1975-˛¬ dn´-b¿ sNbvX-Xm-Wv. Xncp-h-\-¥-]p-cw t^mdÃv skbn¬kv

Unhn-j-\n¬ \n∂mWv dn´-b¿ sN-bvX-Xv. dn´b¿ sNbvX-tijw A—\v

tIm¨{SmŒv ]Wn-Ifpw a‰p-am-bn-cp-∂p. an°-hmdpw t^md-Ãp-ambn _‘-s∏´

tPmen-I-fm-bn-cp-∂p. 1978-̨ ¬ sN¶¬Nq-f ]≤-Xn-bn¬ sI´nSw ]Wn°v ]okv

h¿°v te_¿ tIm¨{SmŒv FSp-Øn-cp-∂p. A°m-e-Øp-Xs∂ Rm\pw, Nne

tIm¨{SmŒv ]Wn-I-fn¬ G¿s∏-´n -cp -∂p. t^md-Ãp-ambn _‘-s∏´

h¿°p-I-fmWv Rm\pw sNbvXn-cp -∂-Xv. I√m¿ hmen `mKØpw a‰pw

t^md-Ãn¬ Civil work \S-Øn-bn-cp-∂p. sN¶¬Nqf ]≤-Xn°v XSn-I-S-Øn-s°m-

≠p-h-cm-\p≈ tIm¨{SmŒv A—-\m-bn-cp-∂p. F∂m¬ A—\v a‰v k_v

18

tIm¨{SmŒv ]Wn-I-fp-≠m-bn-cp-∂-Xp-sIm≠v XSn Fs‚ ta¬t\m -́Øn-emWv

IqSp-Xepw \S-Øn-b-Xv. t^mdÃv Unt∏m-bn¬ XSn tem´m-bn-°-gn-™m¬

I¨kv{S-£≥ tIm¿∏-td-js\ Adn-bn-°p∂X-\p-k-cn®v Ahn-SsØ t{]mPŒv

F©n-\o-b¿ h∂v XSn I≠v- \º-dp-Iƒ Xn´-s∏-Sp-Øn-t]m-Ipw. ]n∂o-Sv,

t^mdÃv Unt∏m ]mkv A\p-h-Zn-°pw. Cu ]mkv hmßm-dp-≠v. ]mkv

hmßp-tºmƒ AXns‚ tIm∏nbn¬ H∏n-́ p-sIm-Sp-°pw. ]n∂oSv Rm≥ temdn

G¿∏m-Sm°n Unt∏m-bn¬\n∂v XSn Ib-‰pw. Unt∏m-bnse hm®v-am≥,

]m n¬, Hmtcm {]mh-iyhpw Ib-‰n-hn-Sp-∂ -X-Sn-I-fpsS \º¿ t\m´p-sN-bvXmWv

Ab-bv°p-∂-Xv. XSn-bpsS IqsS ]mkpw, Xncp-h-\-¥-]p-cØv sIm≠p-h∂v

an√n¬ XSn- C-d-°n, F©n-\o-b¿ h∂v, XSn ]mkp-ambn HØp-t\m°n

F\n°v Fs‚ I¨sh-b≥kv Nm¿÷v Xcn-I-bmWv sNbvXn-´p-≈-Xv. Rm≥

1979 -˛\pw 1985 -˛ -\p -an -S -bn¬ C{]-Imcw [mcmfw temUv XSn hnhn[

Unt∏m-I-fn¬ \n∂v I¨kv{S-£≥ tIm¿∏-td-j-\p-th≠n sIm≠p-h-∂n-́ p-≠v.

sIm≠p-h∂ XSn-bn¬ Ipd-hp-≈-Xmbn A∂v bmsXm-cp-]-cm-Xnbpw D≠mbn´n√.

]m p-{]-Imcw Hmtcm {]mh-iyhpw Ib-‰nhnSp∂ -XSn IrXy-ambpw Rm≥

]d-bp∂ an√n¬ Cd-°n-sIm-Sp-Øn-́ p-≠v. I¨sh-b≥kv tIm¨{Sm-Œn\v Rm≥

tIm¿∏-td-j-\p-ambn F{Kn-sa‚ v H∂pw Fgp-Xn-h-®n-́ n-√. A—≥ F{Kn-sa‚ v

FgpXn h®n-cp -∂pthm F∂v F\n-°-dn -bn -√. Rm≥ XSn Cd-°p∂

ka-bØpw Fkv. - ‰n. tXmakv F∂ t]cp≈ F©n-\o-b-dm-bn -cp∂p

sN¶¬Nqf ]≤-Xn-bpsS t{]mPŒv F©n-\o-b¿. XSn Cd-°n-°-gn-™m¬

]m p-Iƒ Rm≥ At±-l-sØ-bmWv G¬∏n-°m-dv. Fs‚ I¨sh-b≥kv

Nm¿÷p-Iƒ X∂n-cp-∂Xpw At±lw Xs∂-bm-Wv. samgn hmbn®p-tI´p.

icn-bm-Wv.

Recorded by meK. S. Skaria,

Inspector, Vigilance HQ Unit,Trivandrum.