Collaborative Stakeholders’ Engagement for Reliable Technology Driven Financial Service Delivery...

38

1 Collaborative Stakeholders’ Engagement for Reliable Technology Driven Financial Service Delivery in Nigeria Kabir Tahir Hamid, PhD., FCIFC Department of Accounting Bayero University, Kano-Nigeria GSM: 08028376563, 08168743809 Email: [email protected] [email protected] Being a Paper Presented at Seminar/Induction Programme of Associate Grade of the Chartered Institute of Finance and Control (CIFCN) with the theme Sustaining Financial Services Delivery in a Technological Driven Environment: Nigeria in Perspective held at Eden Comfort Plaza, 17, Alade Avenue, Off Obafemi Awolowo Way, Ikeja, Lagos (Opposite Lagos Airport Hotel),13 th December, 2014

Transcript of Collaborative Stakeholders’ Engagement for Reliable Technology Driven Financial Service Delivery...

1

Collaborative Stakeholders’ Engagement for Reliable Technology Driven Financial Service Delivery in Nigeria

Kabir Tahir Hamid, PhD., FCIFCDepartment of Accounting

Bayero University, Kano-NigeriaGSM: 08028376563, 08168743809Email: [email protected] [email protected]

Being a Paper Presented at Seminar/Induction Programme of Associate Grade of the Chartered

Institute of Finance and Control (CIFCN) with the theme Sustaining Financial Services Delivery in a Technological

Driven Environment: Nigeria in Perspective held at Eden Comfort Plaza, 17, Alade Avenue, Off Obafemi

Awolowo Way, Ikeja, Lagos (Opposite Lagos Airport Hotel),13th December, 2014

2

Outline of the Presentation1. Introduction2. Historical development of finance

technology infrastructure3. Techno-driven financial services3.1 the concept of financial services3.2 Technology Driven Financial Services

Delivery Methods3.3 Stakeholders in Providing Techno-Driven

Financial Services in Nigeria4. Stakeholders’ collaboration in providing

e-Finance in Nigeria5. Summary, Conclusion and Recommendations References

Introduction Advancement in technology has had a profound effect on the delivery of financial services over the last few decades, and the pace of change and level of impact is continually increasing. Technology was first used as a means of enhancing speed, effectiveness and reducing errors of many routine processes, through centralization and automation. Now it provides a cost-effective and competitive solution to the delivery of financial services.

3

Introduction… Cont’d Electronic channels for payments and financial services delivery are increasingly taking advantage of networks and existing delivery channels such as Automated Teller Machines (ATMs), Point of Sales/Service (PoS), telephone banking (Tele-banking), Electronic Funds Transfer (EFT), brokerage and central securities clearing system, among others. The Internet and private or restricted networks (intranets and extranets) have transformed both operations within financial institutions and communications between customers.

4

Introduction… Cont’d Before the 2005 banking sector consolidation, there were

few opportunities and isolated cases of few banks offering e-banking. Cheque clearing takes 21 days for upcountry instruments and about 6 days for local cheques to receive value. However, the advent of the third generation banks in the late 1980s and early 1990s, led to a significant leap in e-banking by introducing few ATMs into circulation and telephone banking which enable customers to obtain bank balances through their telephone lines. Internet banking followed with few valued customers granted access to track movement in their bank accounts on their computers. Shared services companies that would enable e-payment solutions and cash management were established. Thus, where established ATMC for ATMs, ValuCard for Point of Sales, Interswitch for switching solutions and the Nigerian Interbank Settlement System Limited (NIBSS) for settlements and funds transfers .

5

HISTORICAL DEVELOPMENT OF FINANCE TECHNOLOGY INFRASTRUCTURE (FTI)

The word technology is said to have been derived from the Greek word techne which means “craft” and logy which means “scientific study of”. So technology means the “scientific study of craft.” Craft in this case, means any method or invention that allows humans to control or adapt to their environment. Inventions and tool making have been around since when mankind walked on the surface of the earth. But modern technology began since when scientific thought (philosophy), astronomy and mathematics began to blend together sometimes after the 15th century. Technology is comprised of the products and processes created by engineers to meet our needs and wants. While technology studies human-made world and deals with “what can be”, science studies the natural world and deals with “what is”.

6

HISTORY OF FTI … Cont’d Before formal scientific disciplines, such as chemistry, physics, astronomy and biology were defined, many early inventors simply experimented with items around them trying to come up with ways to improve their lives, and inventions/discoveries often happen by accident. The first inventor who combined engineering with science was Archimedes of Syracuse (287 BC to 212 BC). He is credited with inventing the Archimedian screw for raising water, which is still used in Egypt. He is also credited with inventing the cross-staff for use in astronomy, and the odometer which measures how far someone has traveled.

7

HISTORY OF FTI … Cont’d The abacus, which emerged about 5,000 years ago in

Asia and is still in use today in places like China, Japan and Russia, may be considered the first computer. The word Abacus is said to have been derived from the Greek word ‘abax’, meaning ‘calculating board’ or ‘calculating table’. Early merchants used the abacus to keep trading transactions. But as the use of paper and pencil spread, particularly in Europe, the abacus lost its importance. It took nearly 12 centuries, however, for the next significant advance in computing devices to emerge.

8

HISTORY OF FTI … Cont’d Notable among the significant inventions for finance technology infrastructure were:

First, the invention of first general-purpose programmable computer by Charles Babbage (1791-1871) -"Grand Father" of the computer- with the support of his assistant Augusta Ada King (1815-1842) in 1837 who created the instruction routines (programs) to be fed into the computer, making her the first female computer programmer. Babbage noticed a natural harmony between machines and mathematics: machines were best at performing tasks repeatedly without mistake; while mathematics, particularly the production of mathematics tables, often required the simple repetition of steps. The problem centered on applying the ability of machines to the needs of mathematics.

9

HISTORY OF FTI … Cont’d Second, the invention of the Telephone in 1876 by Alexander Graham Bell (1847-1922) with the support of Thomas Watson (1854- 1934). Third, the invention of the ATM by Luther Simjian (1905-1997) in 1939 and its re-invention and installation at a Barclays Bank in London in 1967 by John Adrian Shepherd-Barron (1925-2010). Forth, the invention of the PoS machine in 1970s by IBM to keep track of monetary transactions in an effort to prevent employees from pocketing payment for goods. IBM was founded by Herman Hollerith (1860-1929) who counted the subsequent US census in 6 weeks after the 1880 census which was counted in about seven years using his Hollerith machine.

10

HISTORY OF FTI … Cont’d Fifth, the invention of the GSM (Global System for Mobile Communications) originally called (Groupe Spécial Mobile), by the European Telecommunications Standards Institute (ETSI) in 1987 with the world's first GSM call by the former Finnish Prime Minister Harri Holkeri to Kaarina Suonio (Mayor in city of Tampere) on July 1, 1991 and the first Short Messaging Service (SMS) in 1992. Sixth, the invention of the web browser, the WWW (World Wide Web) by Tim Berners-Lee (1955-Date) in 1989 along with the standards and protocols that would be used in the exchange of information [HTTP (Hypertext Transfer Protocol), HTML (HyperText Markup Language), and URL (Uniform Resource Locator)].

11

HISTORY OF FTI … Cont’d Despite the advancement in finance technology

infrastructure in the world, there exist vast differential in the extent, quality and versatility of information and communication infrastructure and networking capability between the industrial world and the developing world. This differential (which is generally referred to as digital divide) exists not only between nations, but also within regions and countries, and even within cities and local communities. People with connections to suprateritorial spaces have access to important resources and influence that are denied to those who are left outside, thus resulting in inequalities and different levels of access to techno-driven financial service delivery across the Globe.

12

The Concept of Financial Services

Financial services are the economic services provided by the finance industry, which encompasses a broad range of organizations that manage money, including credit unions, banks, investment banks, credit card companies, insurance companies, accountancy companies, consumer finance companies, stock brokerages, investment funds, real estate funds, pension funds, stock brokerages, payments, savings, credit and some government sponsored enterprises. Financial Services are generally not limited to the field of deposit-taking, loan and investment services, but is also present in the fields of insurance, estate, trust and agency services, securities, and all forms of financial or market intermediation including the distribution of financial products.

13

The Concept of FS… Cont’d The challenges faced by the financial services market are

forcing market participants to keep pace with technological advances for better service delivery. However, in order to effectively serve the needs customers reliability is essential in financial service delivery. Reliability is, literally, the extent to which customers can obtain a dependable uninterrupted service that is within reach, with high data integrity and security, trustworthy, unfailing, fraud-free, competitive, cost effective, efficient, speedy, value-adding and reputable for the achievement of their personal and organizational objectives. The number of reported cases of fraud and forgery in the banking industry increased in 2012. There were 4,527 cases of fraud and forgery involving the sum of N14.8 billion perpetrated mostly by outsiders and some bank staff, through a number of means including illegal funds transfer and fraudulent ATM withdrawals (CBN, 2012), thus re-emphasizing the need for reliability and integrity in e-finance.

14

Technology Driven Financial Services Delivery Methods

1. Automated Teller Machine (ATM): ATM machines were largely cash-dispensing terminals which were originally put in place to reduce queues in branches at peak times, cut down the amount of paperwork and cash handling and free up staff time in branches. There are two kinds of ATM, namely single function cash dispensing and multi-functions offering customers the choice of balance enquiries, mini-statements, cheque book ordering services as well as accessing information on a range of other financial services.

2. Electronic Funds Transfer at Point of Sale (EFTPOS): EFTPOS supports the use of smart cards and enable consumers to achieve easier methods of payment, retailers to reduce the amount of cash in the payment system, financial institutions to reduce the amount of cheque-based payments and provided technology suppliers with outlet for their product.

15

Technology Driven Financial Services Delivery Methods… Cont’d

3.Telebanking: Telebanking involves conducting one’s financial transactions over the telephone. The cost advantages of telephone banking are very attractive when compared with the costs associated with a branch network. The cost of serving retail bank customers by telephone can be as little as 10 percent of the cost of similar transaction via a branch teller. For telephone services operated from call centers closer to customers, there is an additional cost advantage.

Most Deposit Money Banks in Nigeria offer mobile and/or SMS banking services which enables customers to carry out basic banking transactions including but not limited to: balance enquiry, statement request, transfers between own accounts, third party transfer and airtime purchase. SMS banking services, on the other hand, are messages that the bank chooses to send out to a customer's mobile phone, without the customer initiating a request for the information. Typically messages could be :messages alerting debit or credit transactions in the customer's bank account and marketing messages on product and services.

4. 16

Technology Driven Financial Services Delivery Methods… Cont’d

4. Online/Internet Banking: Online banking consists of home banking and internet banking. Home Banking services include: the ability to check account balances, view transactions records and account history, pay bills, apply for other services, communicate with the financial institution, and transfer money instantly between accounts.

5. Smart cards: Smart cards can be used between individuals to exchange electronic cash or can interface with ATMs, telephones and retailers Card based payments which include debit cards, credit cards and prepaid/cash cards are gaining popularity for ATM, Pos and online/web-based transactions. Card based payments are more prevalent in urban areas due to insufficient infrastructure and distribution channels in rural areas. The market is dominated by the domestic card network Interswitch. However, since 2008, Visa and MasterCard have been more active in the Nigerian card market. With some banks migrating from the Interswitch card network to the Visa or MasterCard network.

17

Technology Driven Financial Services Delivery Methods… Cont’d

CBN (2012) report indicates that the volume and value of electronic card (e-card) transactions increased from 355,252,401 and N1,671.4 billion in 2011 to 382,616,953 and N2,095.7 billion in 2012, reflecting an increase of 7.7 and 25.4 per cent, respectively. The increase was attributed to enhanced public confidence in electronic card payments. Similarly, data on various e-payment channels for the period under review indicated that Automated Teller Machines (ATMs) remained the most patronised, accounting for 98.1 per cent, followed by point-of-sale (PoS) terminals at 0.7 per cent. Web and mobile payments accounted for 0.6 per cent each. Similarly, in value terms, ATM accounted for 94.7 per cent, PoS 2.3 per cent, Web and mobile payments, 1.5 per cent each. This can be seen on Table 1.

18

Table 1: Market Share in the e-Payment Mkt, 2009 – 2012

19

Source: CBN Annual Report, 2012 Pp 88

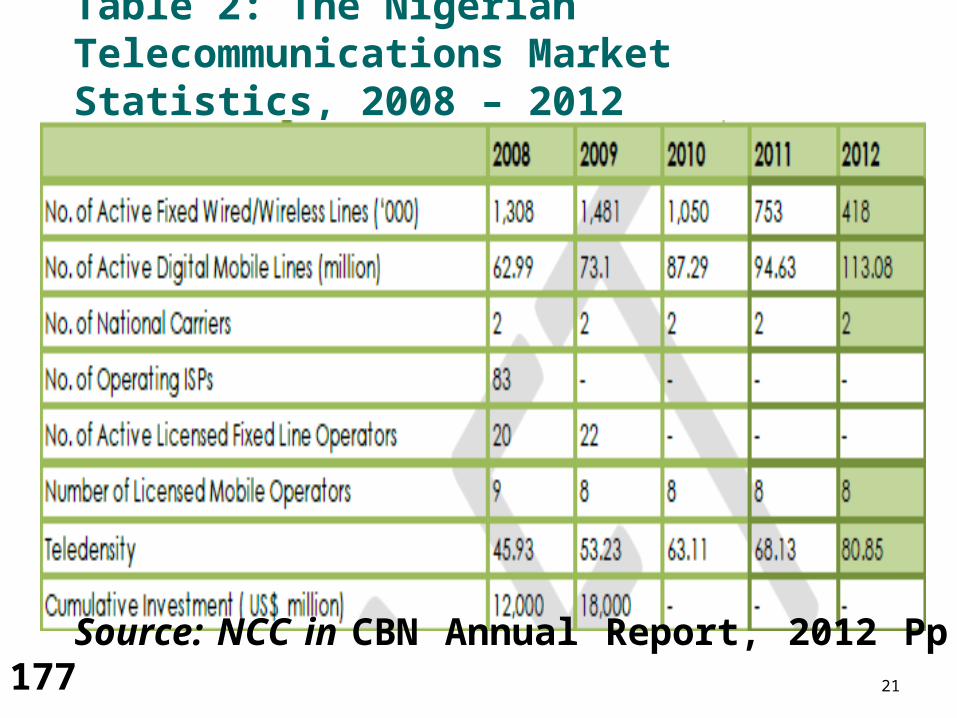

The Nigerian Telecommunications CBN (2012) reports that growth in the communications

sector, which is essential for techno-driven financial service delivery was moderate in 2012 following security challenges and flood that disrupted telecommunication services. This led to a loss of about N75 billion by the telecoms operators during the year including 150 Base Transceiver Stations (BTS). However, The CBN indicates that the combined active subscriber base of the telecommunications sub-sector rose to 113,195,951 active lines (418,166 fixed wired/wireless and 112,777,2785 mobile lines) as at end-December 2012; an increase of 18.1 per cent over its level in December 2011. This led to an increase in Teledensity from 68.1 to 80.9 lines per 100 inhabitants thereby exceeding the International Telecommunication Union (ITU) minimum standard of 1:100. Furthermore, the sub-sector grew by 32.1 per cent in 2012, accounting for 7.0 per cent of the GDP (CBN, 2012). This can be seen on Table 2.

20

Table 2: The Nigerian Telecommunications Market Statistics, 2008 – 2012

Source: CBN Annual Report, 2012 Pp 88

21

Source: NCC in CBN Annual Report, 2012 Pp 177

Figure I: Stakeholders in Providing Techno-Driven Financial Services in Nigeria

22

Source: Adopted by the Author from Financial Inclusion National Policy Framework (2012) Pp 8

Stakeholders in Providing Techno-Driven Financial Services in Nigeria … Cont’d The seven stakeholders identified above, can for the sake of

convenience be broadly grouped into three (3) namely providers, enablers and supporters. Providers are institutions that provide financial products and services, and their partner infrastructure and technology providers. Providers include banks, other financial intuitions, insurance firms and technology/telecommunications firms. Enablers are institutions responsible for setting regulations and policies with regards to e-finance, including regulators and public institutions. While supporters are institutions that can provide technical and funding assistance that enhance techno-driven financial service delivery and support the CBN in achieving its IT policy for the Nigerian banking sector. Supporters include development partners and experts and other bodies like Nigeria Computer Society (NCS), Nigeria Internet Group (NIG), Information Technology Association of Nigeria (ITAN), Institute of Software Practitioners of Nigeria (ISPON), Association of Telecom Companies of Nigeria (ATCON) amongst others.

23

Stakeholders in Providing Techno-Driven Financial Services in Nigeria … Cont’d Association of Telecom Companies of Nigeria (ATCON) Bank of Agriculture (BoA) Bank of Industry (BoI) Bureau De Changes (BDCs) Central Bank of Nigeria (CBN) Computer Professionals Registration Council of Nigeria (CPN) Deposit Money Banks (DMBs) Development Finance Institutions (DFIs) Discount Houses (DHs) Federal Mortgage Bank of Nigeria (FMBN) Finance Companies (FCs) Finance Companies (FCs) Information Technology Association of Nigeria (ITAN) Institute of Software Practitioners of Nigeria (ISPON) Microfinance Banks (MFBs) Mobile Network Operators (MNOs)

24

Stakeholders in Providing Techno-Driven Financial Services in Nigeria … Cont’d

National Identity Management Commission (NIMC) National Identity Management Commission (NIMC) National Insurance Commission (NIC)National IT Development Agency (NITDA) National Pension Commission (PenCom) National Planning Commission (NPC) Nigeria Communications Commission (NCC) Nigeria Computer Society (NCS)Nigeria Computer Society (NCS) Nigeria Export and Import Bank (Nexim) Nigeria Internet Group (NIG) Nigerian Deposit Insurance Corporation (NDIC) Nigerian Social Insurance Trust Fund (NSITF)Pension Fund Administrators (PFAs) Pension Fund Custodians (PFCs) Power Holding Company of Nigeria (PHCN)Primary Mortgage Banks (PMBs) Primary Mortgage Institutions (PMIs) The Nigerian Postal Service (NIPOST)

25

STAKEHOLDERS’ COLLABORATION IN PROVIDING E-FINANCE IN NIGERIA

A Techno-driven financial service has the potentials to enhance financial inclusion for economic growth and development of Nigeria. Poor people do not find formal financial services worthwhile due to the inconvenience and high cost involved in accessing these services (travel time and expense, queuing times, high minimum balance requirements) relative to the more local and informal alternatives they have traditionally used (cash under the mattress, informal deposit collectors, friends and family, storage of value in physical goods). However, e-finance has drastically reduced the inconvenience and the cost associated with formal financial services.

26

STAKEHOLDERS’ COLLABORATION IN PROVIDING E-FINANCE IN NIGERIA … Cont’d

Despite the enormous benefits of e-finance an estimated 2.5 billion world adult’s lack access to basic techno-driven financial services. This situation arises because banks do not find it economically attractive to deploy banking infrastructure (branches, ATMs) and market financial services (savings, insurance, credit) where the majority of poor people live and work.

Delivery of reliable techno-driven financial services cannot be achieved without the active involvement of all stakeholders, namely financial regulators, banks, governments, NGOs, civil societies, policymakers, IT solution providers, payment service providers, mobile network operators, development institutions, Central Bank of Nigeria, NSE, SEC, NIPOST and the public at large.

27

STAKEHOLDERS’ COLLABORATION IN PROVIDING E-FINANCE IN NIGERIA … Cont’d

All the stakeholders, therefore, need to join hands to enhance and sustain the reliability of technology driven financial services for sustainable economic growth and development of Nigeria. The collaboration should be in terms of reducing IT cost in the Nigerian Financial Services industry, enhancing investments in finance technology infrastructure, enhancing power supply and provision of infrastructural facilities in the rural areas, eliminating non-standard systems and infrastructure, enhancing efficiency of electronic information exchange and enhancing data security and integrity issues.

28

STAKEHOLDERS’ COLLABORATION IN PROVIDING E-FINANCE IN NIGERIA … Cont’d

Neither the public nor private sector can stand alone. There is a need for coordination and collective implementation of the National ICT Strategic Plan as most sub plans are dependent on other sub plans. Similarly, as goals are set there is a need for rigorous implementation, monitoring, evaluation and review by all concerned. Since ICT development is multidimensional, the public sector must partner with the private sector in a creative and mutually beneficial manner. Ideas and policies are not enough. Sustainable development is achieved when stakeholders share a common vision and agree on the same national interest. This requires close coordination, coherence and commitment for Nigeria to use ICT to drive social and economic development.

29

30

SUMMARY AND CONCLUSION Enhancing the coverage and reliability

of techno-driven financial services would help in making financial services accessible to the poor, especially those residing in the rural areas which can reduce income inequality and foster economic growth of Nigeria. This will in the long run enhance financial inclusion which is the delivery of financial services, including banking services and credit, at an affordable cost to the vast sections of disadvantaged and low-income groups who tend to be excluded.

31

SUMMARY AND CONCLUSION … Cont’d Bank customers now receive value for cheques in

clearing in three days (instead of the previous 21 days). Settlements of transactions above Ten Million Naira are now done through the National Electronic Funds Transfer (NEFT) with value delivered the same day in most cases. There are ATM machines in major cities and towns in Nigeria. The Point of Sales (PoS) terminals are being aggressively deployed with over 30,000 of them connected to Nigerian Interbank Settlement System Limited (NIBSS) infrastructure and accept all major cards. With some cards, Visa or Master cards, Cardholders now withdraw money in foreign currencies out of the country, while some companies have been licensed to provide Telephone mobile banking services.

Recommendations Nigeria need to improve in the dilapidated state of

infrastructures in both the urban and rural areas and enhancing communication links in the Country through public-private partnership is very crucial to effectively harness the benefit of technology advancement in financial services delivery in Nigeria.

Government and Private sector should partner to provide the basic techno-driven financial service infrastructure to enhance efficient service delivery from banks, telecommunication companies, financial services payment solutions and credit infrastructure. The provision of uninterrupted power supply. There should be public private partnership to make internet facility available and affordable in all parts of the country. This would reduce network failure and enable better and reliable delivery of techno-driven financial services in the Country than what is now available at affordable cost.

32

Recommendations… Cont’d It is imperative to enact appropriate legislations and promote efficient judicial system with a view to promoting a robust consumer protection and safeguard financial institutions against unscrupulous customers. Both customers and providers of financial services should also be able to get justice, swiftly, when they have been defrauded.

ATMs have been deployed predominantly in urban areas due to infrastructure challenges (electricity supply and communication links) which make the deployment of ATMs largely inappropriate for rural areas. In order to increase ATM transaction flows, Independent ATM Deployers (IADs) and banks should consider partnering with retail outlets/ local shops to serve semi-urban and rural customers.

33

Recommendations… Cont’d The adoption of the e-payment channels as a preferred channel of payment increases due to the CBN cashless policy increases the incidence of electronic fraud. This heightened incidence of fraud therefore brought to the fore the need to actively and proactively reacting to this challenge by all concerned to safeguard integrity of the e-payment channels.

34

35

Thank you for the attention

References Allen, F., Demirguc-Kunt, A., Klapper, L. and Martinez, P.

M.S. (2012). Policies to Expand Financial Inclusion, Development Research Group, World Bank, Washington, DC. Available online at siteresources.worldbank.org/EXTGLOBALFINREPORT/Resources/ Accessed 8th December, 2014

CBN (2012). Central Bank of Nigeria Annual Report. Available online at www.cenbank.org/out/2012/ccd/2012%20half%20year%20report.pdf. Accessed 8th December, 2014

CBN (2013). Nigeria Financial Services IT Standards Blueprint. Available online at www.cenbank.org/ITStandards/IT_Standards_Blueprint_Final_revised%. Accessed 8th December, 2014

Claessens, S., Glaessner, T. and Klingebiel, D. (2002). Electronic Finance: A New Approach to Financial Sector Development. World Bank iscussion Paper No. 431. World Bank, Washington D.C. Available online at documents.worldbank.org/.../electronic-finance-new-approach-financial. Accessed 8th November, 2014

36

References… Cont’d Dev, S.M. (2006). Financial Inclusion: Issues and Challenges,

Economic & Political Weekly , 41, p. 416. Available online at businessperspectives.org/journals.../BBS_en_2014_02_Oluwatayo.pdf. Accessed 18th November, 2014

EFInA -Enhancing Financial Innovation and Access- (2010). Scoping Study on Payment Systems in Nigeria: Supply Side Key Findings. Available online at www.efina.org.ng/.../EFInAScoping-Study-on-Payment-Systems-in-Nigeria. Accessed 18/11/2014

Hamid, K.T. (2014a). Globalization and Infrastructure for Virtual Learning: Where Does Africa Stands? Being a Paper Intended for Presentation at CSAE Conference 2014: Economic Development in Africa, to be held from 23rd - 25th March 2014, St Catherine's College, Oxford, United Kingdom.

Hamid, K.T. (2014b). Application of Computer in Accounting. Available online at www.academia.edu/.../ACC_2306_Application_of_Computer_in_Accouting. Accessed 7/12/2014

37

References… Cont’d Ogunsola, L. A. and Okusaga, T. O. (2006). Digital Divide Between

Developed and Less-Developed Countries: The Way Forward. Journal of Social Sciences. 13(2):137-146. web.library.uiuc.edu/asp/agx/acdc/view.asp?ID=C27438 - Cached (Accessed 3rd July, 2012).

Oluwatayo, I.B. (2014). Techno-driven Financial Inclusion in Rural Nigeria: Challenges and Opportunities for Pro-Poor Service Delivery, Banks and Bank System, Vol. 9, Issue 2,Pp 95-99

Popoola, A. T. (2014). The Challenge of Financial Infrastructure in Nigeria. Available online at www.nigeriadevelopmentandfinanceforum.org/.../Dialogue.aspx?Edition. Accessed 7/12/2014.

Roland, B. (2012). National Financial Inclusion Strategy, Summary Report Abuja, 20 January 2012

State Street (2011). The Evolving Role Technology in Financial Services, Vision, Volume VI Issue. Available online at www.statestreet.com/vision/technology/pdf/TheEvolvingRoleTech.pdf. Accessed 7/11/2014.

WOCCU (2012). Using Mobile Technology to Expand Financial Inclusion: The Credit Union Experience, World Council of Credit Unions (WOCCU) Technical Guide, p.16. Available at: www.woccu.org/financialinclusion. Accessed 7/10/2014.

38