CSR IN THE BANGLADESH TEXTILE INDUSTRY: Responsible Supply Chain Managemet

Upload

khangminh22Category

view

0download

0

CHAPTER II

A. TEXTILE INDUSTRY IN INDIA

2.1 Introduction

2.2 New Economic Policy

2.3 GATT & Textile Industry

2.4 World Trade Organization

2.5 WTO - Textile & Clothing

2.6 Origin & Growth of Spinning Mills in India

2.7 Current Scenario

2.8 Recent Amendments in Textile Industry

2.9 Buoyancy in Cotton Yarn Industry

B. TEXTILE INDUSTRY IN MAHARASHTRA

2.10 Introduction

2.11 Details of Co-operative Spinning Mills in

Maharashtra (2004-05)

2.12 Review of the Performance of the Co

operative Spinning Mills in Production

C. TEXTILE INDUSTRY IN ICHALKARANTI

2.13 Historical Background

2.14 Growth of Textile Industry during

Independence

2.15 Growth of Powerlooms in Ichalkaranji.

8

CHAPTER II

A. TEXTILE INDUSTRY IN INDIA

2.1 INTRODUCTION

The Textile Industry occupies a unique place in our

Country and it is oldest Industry in India. It accounts for

14% of the total industrial production and contributes

nearly 30% of the total exports and is the second largest

employment generator after agriculture.

Textile Industry is providing one of the most basic

needs of people and it holds importance, maintaining

sustained growth for improving quality of life. It has a

unique position as a self-reliant industry. From the

production of raw materials to the delivery of finished

products with substantial value-addition to each stage of

processing.

It has the vast potential for creation of employment

opportunities in the agricultural, industrial, organized and

decentralized sectors both in rural and urban areas,

particularly for women.

The Government accepted a new economic policy in

the year 1991. It gave stress on the liberalization and

globalization. The policy has made some fundamental

9

changes in the trade and commerce in order to promote the

free trade policy. It aimed at competitive environment,

product quality and participation in the globalization

programme and using all resources for the good of the

common people. This policy has proved good results on the

economic front of our nation and is going to promote

industrial development in India. There are also some

negative impacts on our economy also.

Co-operative sector is the golden mean between

capitalism and socialism, (i.e. Private & Public Sector). It

gives equal importance to capital and labour. But now a

days, the Co-operative Sector is becoming a sick sector due

to outdated technology and machinery, inefficiency,

unhealthy competition, decreasing productivity, corruption,

nepotism and political interference in the administration

etc.

2.2 NEW ECONOMIC POLICY

It is evident that the new economic policy and WTO

have passed a challenge to the Co-operative sector. Hence,

it has to prove its efficiency in work, performance and

capacity to raise capital & ability to complete with other

industry. If it does not accept this challenge, its very

existence is likely to be in danger. In such circumstances,

10wumneb mmm lihuit

IVAJI UBIVEBS1TY. ItOLMAraa.

the co-operative sector has to be vigilant. It should adopt

scientific and effective method of management and work

consciously & honestly to become self-sufficient. It should

prove that the co-operative sector is an inevitable factor in

the balanced and healthy progress of Nation.

2.3 GATT AND TEXTILE INDUSTRY

The General Agreement on Tariff & Trade ( GATT )

was established in 1948 in Geneva.

OBJECTIVES :

The objective of free trade is order to encourage

growth and development of all member countries.

THE PRINCIPLE PURPOSE :

GATT was to ensure competition in commodity trade

through the removal or reduction of trade barriers.

GATT held seven rounds of talks at different places to

remove obstacles in world trade. The first seven rounds of

negotiations conducted under GATT were aimed at

stimulating international trade through reduction in tariff

restrictions on imports imposed by member countries.

The eight rounds of talks known as Uruguay started

in 1986 and continued till recently in Uruguay. The issues

covered in earlier rounds have been —

1. Tariffs.

n

2. Protection

3. Production in Arid lands.

4. Production in Natural resources.

5. Textile.

6. Agriculture Production and Price etc.

7. GATT Laws.

8. Restrictions

9. Multi Negotiations

10. Subsidies etc.

11. Dispute Settlement System

12. Working System of GATT.

GATT & Textile & Clothing

GATT agreement has made certain proposal; to

liberalize the trade of textile and clothing. These proposals

are very important for developing countries since textile

export. Ironically, developed countries that claim to be the

greatest champions of free trade have imposed most

comprehensive quota restrictions under the Multi-Fibre

Agreement [MFA] quotas over a ten year period (1993 to

2003) and to fully liberalize the textile sector at the end of

the ten years period.

The act was divided the 10 years period into the

phases of three years. In the first phase, 16 percent of the

12

textile exports to the developed countries will be liberalized

to be followed by 17 percent in the second phase and

another 18 percent in the third phase. Thus, the end of the

10 years period. Thus, only 51 percent of Textile market

will be liberalized. Thus a substantial portion (49 percent)

shall have to wait for the second wave of liberalization after

2003 A.D. What is intriguing is that textiles are defined in

such a way that textile sector included items that are not

currently under quota restrictions in developing countries.

Thus creating real liberalization and withdrawing non-tariff

restrictions in developed countries.. Thus, instead of

creating real liberalization and withdrawing non-tariff

restrictions, the myth of liberalization has been created.

The Ministry of Commerce has made this Point Clear. " It

is a fact that the Textile agreement is not evenly balanced

in the sense in the initial years. There is minimal

liberalization and significant steps for liberalization are left

only to last three years. This is one of the points of

dissatisfaction for India and we are strongly urging the

importing countries to bring forward the liberalization

processes".

13

2.4 WORLD TRADE ORGANIZATION: -

The World Trade Organization (WTO) contained in the

final act was established on the 1st Jan. 1995 and India

became a founder member of WTO by ratifying the WTO

agreement on 30th Dec. 1994. This World Trade

Organization is administering the new global trade rules

establishing the rule of law in International Trade.

WTO works towards mutually supportive and trade

and environment policies and promotion of sustainable

development.

2.5 WTO : TEXTILE AND CLOTHING :-

The WTO has adopted discriminatory quantitative

restrictions in the textile and clothing sector by over 30

years under short-term agreement, long term agreements

in 1974 and multi-fibre agreement (MFA) upto 31st

December 1994. The MFA is a series of bilaterally

negotiated quotas to limit the access of developing country.

Textile exports to the developed countries during the fifties.

It was assigned to protect the US Textile Producers for the

booming Japanese Textile export. Later on it was extended

to many other developing countries including India. These

quantitative restrictions had covered a growing number of

14

products over the years and had become increasingly

restrictive.

1. The agreement on Textiles and Clothing has the

provision for prohibitions on any such restriction on

free exports and elimination of MFA arrangement.

The quantitative restrictions only affect exports of

developing Countries to the industrial countries and

not the trade among the industrial countries

themselves. The implementation of the agreement by

the WTO on Textile and clothing would mean the

elimination of all non-tariff measures in textile and

clothing industries over a period of 10 years (1994-

2004). Thus, it is integration of textile and clothing

sector on January 1, 2005 into free trade system

under WTO.

15

2. Division of 10 Years Period was in three Stages: -

Stages Time period Percentage of Phasing

Out

Phase I January 1, 1998 16% of total 1990

imports

Phase II January 1, 1998 17% of total 1990

imports

Phase III January 1, 2002 18% of total 1990 ^

imports

Phase IV January 1, 2005 Remainder of Textile

Imports

3. The countries can introduce discriminatory

restrictions on the products under WTO Provision,

which were not already made subject to GATT or WTO

rules or which they do not have under existing

bilateral agreement.

4. The interest of developing countries has been kept

safe under certain safeguards mechanism which is

applicable maximum for three years period. The

developing countries allowed to follow non-tariff

16

measures in certain circumstances if imports are

threat to their domestic industries.

The Textile and Clothing is very sensitive sector and

significant for developing and least developing countries.

As simple industrial countries embarking on

industrialization usually begin with textile & clothing

industries. They account 24% of export for sub-saharan

Africa, 14% Asia & 8% for Latin America. For Bangla Desh

and Sri Lanka, they account for half of all export earnings.

Through the quota system 18% developing countries export

was affected. The agreement on Textile and Clothing aims

to remove both (over 10 years period) the non-tariff and

tariff barriers. Through the reduction of tariff barriers is

less satisfactory than the non-tariff barriers. The

advalorem tariff for Textiles and Clothing is 12% just more

than times higher tariffs level than the 3.8% advalorem

average tariffs for all industrial products. Similarly, 22%

tariffs cut in industrial countries for textile and clothing fall

short of the average tariffs out of 38%. For more than half

of the textile and clothing goods tariff remains above 10%,

for more than one quarter of goods tariff will be charged

13.25% and only 4% of the textile clothing trade will be

17

duty free, after the implementation of the reduction

commitments.

The major benefit occurring from it is that the

exceptional treatment of textiles and clothing products will

come to a half and industrial products will be treated

equally. Tariffs, either than quotas, will remain the

principle trade policy instruments. Under MFA (Multi Fibre

Agreement) quotas were more restrictive factor than the

tariffs. A key effect of MFA had/has to restrain countries to

developed countries. Many studies have established the

link between export of textile and clothing and interest of

developing countries. In 1986, UNCTAD ( United Nations

Conference on Trade & Development ) made an estimate

that complete non-discriminatoiy liberalization (involving

tariff & quota) could increase developing country export of

clothing by 135% and textiles by 78%. According to a

study by Kirmani, Molajani & Mayer, developing country

exports to Major OCED countries could increase by 82% for

textile & 93% for clothing if both restrictions were removed.

While developing countries have experienced a cap on

their export through the MFA, it should be said that many

of them have benefited from the system through the

18

predictable environment, which it has created, as well as

through the quota results. So the magnitude of the gains

for developing countries will be influenced by the actual

method used to allocated internal KFA quota. At the same

time, however, there is no unanimous view as to what the

real implications of MFA on developing countries have

been, ipso facto, the real effects of liberalization.

The scope of the application of safeguard measure has

been tested by WTO Dispute Settlement Body in the case of

US Measures affecting imports of Woven Wool Shirts &

Blouses from India. The Panel in this Case concluded that

the US restraint on Imports of Woven Wool Shirts &

Blouses, Category 440 from India and its extensions had

violated the Provisions of Articles 2 of the Conclusions of

the Panel had been upheld by the Appellate Body. Thus,

India's Fundamental Stand taken through out the long run

and arduous Process of bilateral consultations and two

reviews by the Textile Monitoring Body (TMB) that the US

safeguard action was unjustified had been upheld by the

Panel and Appellate Body.

In this case, the panel pursued jurisprudence on

onus probandi in two layers. The first is that the

19

complainant should submit a prima facie case of violation

and then after the complained party has to prove that at

the time of its determination, it had respected the

requirements of Article 6 of the ATC. It is well known that

the Article 6 of the ATC is the only Provision in the WTO

legal framework that permitted Members to impose

discriminatory trade measures to protect domestic

procedures against legitimate trade, during the transition

period. Due to its special nature, India had argued that the

Art 6 is to consider as an exception measure under

ATC. But the Appellate Body declined to consider Article 6

as an exception and applying the GATT 1947's

jurisprudence in this regard.

The appellate Body citing from the previous report on

US Restrictions on Imports of Cotton & Man-made Fibre,

used the argument of the balance of rights and obligation

for opposite ends. In these two cases, the Appellate Body

applied two different approaches, in one case to justify a

narrow interpretation and in the other to arrive at an

expansive interpretation of the same provision of the ATC.

Though, on the question of burden of Proof, the Appellate

Body laid down the real-presumption, which states that "

20

We agree with the Panel that it was upto India to present

evidence and arguments sufficient to establish a

Presumption that the transitional safeguard determination

by the US was inconsistent with its obligations under

Article 6 of the ATC. With this presumption thus

established, it was then up to the US to bring evidence and

arguments to rebut the presumption

Capability of developing countries in one side and

brought textile 86 clothing from the grip of Protection to the

rule based multilateral system in another side, which

undoubtedly, facilitates benefit to developing and least

developing countries.

Although the development of textile sector was earlier

taking place in terms of general policies, in recognition of

the importance of this sector, for the first time a separate

policy statement was made in 1985 with regard to

development of textile sector.

The textile policy of 2000 aims at achieving the target

of textile and apparel exports of Us $ 50 billion by 2010 of

which the share of garments will be Us $ 25 billion. The

main market for Indian textiles and apparels are USA, UK,

21

UAE, Germany, France, Italy, Russia, Canada, Bangladesh

and Japan.

The main objective of the textile policy 2000 is to

provide cloth of acceptable quality at reasonable prices for

the vast majority of the population of the Country, to

increasingly contribute to the provision of sustainable

employment and the economic growth of the nation and to

compete with confidence for an increasing share of the

global market.

2.6 : ORIGIN & GROWTH OF SPINNING MILLS IN

INDIA.

The Co-operative movement was started in India as

early as 1891 in Punjab. But the Co-operative movement in

India began actually in 1904, with the enactment of Co

operative Credit Societies Act. However, systematic and

integrated programmes for development of co-operatives in

the field of agricultural credit, marketing, processing of

agricultural produce and supply of agricultural inputs were

developments in the second, third, fourth and fifth Five

Years Plans. During the Fourth Plan, the objective was to

encourage the growth of Co-operatives and integrated

development of various types of Co-operative Organizations.

22

The Fifth Five Years Plan aims at strengthening

agricultural co-operatives, marking consumer co-operative

more viable, correcting the regional imbalances and

focussing the activities of the Co-operative more and more

on small / marginal farmers and workers sections of the

population.

The co-operative movement has branched out in

diverse such as credit, marketing, processing and storage

for agricultural credit, processing manufacturing and

distribution of supplies for small and medium industries,

rural electrification and public distribution of goods and

food grains. Although the beginning of the processing

industry in the Co-operative Sector can be traced back to

1917 when cotton ginning and pressing unit was

established in the erstwhile Mysore state, the real start

was, however, taken after 1908 with the establishment of

the Co-operative Sector at Prawaranagar in the

Maharashtra State.

Today, the Co-operative industry has diversified itself

in different directions and sectors of the economic activity.

The establishment of Spinning Mills in Co-operative

Sector in India is relatively of recent Origin (In 1951 at

23

Guntkal sponsored by the Madras State Handloom

Weavers' Federal Co-operative Society) in 1958 another Co

operative Spinning Mill was registered in the State of

Madras with the special objective of providing employment

mainly to Indian repatriates from Sri Lanka and Burma. By

the end of the Second Five Year Plan, as many as 21 Co

operative Spinning Mills have been organized in the

Country. During the third Year Plan period, the

programme for establishment of Co-operative Spinning

Mills classed as processing Co-operatives, was launched

with the help of the National Development Corporation of

India. As a result, by 1973, 24 co-operative spinning mills

of cotton growers were registered in the Country. Besides

the Co-operative Spinning Mills of Weavers and Cotton

growers, a third category came into existence during 1961-

62 in which both the growers and weavers were enrolled as

members. Such mills were classed as mixed sector Mills.

There are in all 82 Co-operative Spinning Mills in

production in the Country having a total spindleage of

20.58 lakhs. This accounts for just over 8 percent of the

total spindleage. Out of the 82 installed Mills, 38 mills are

of growers and 44 of weavers.

24

2.7 EXPORT ORIENTED UNITS IN INDIA

Foreign capital helps in the development of a country

by filling two gaps, viz. Resource gap & foreign exchange

gap. In the initial level of development, the country is not

able to generate enough resources over & above the

consumption requirement of the country. In the absence of

enough savings coming forward for capital formation the

country remains under the vicious circle of under

development.

Foreign capital provides the essential resources &

helps in breaking this vicious circle. It also helps in the

development process, by providing the essential foreign

exchange that enables the purchases of imported raw

materials, improved machinery & advanced technology.

Most of the under developed countries try to

channelise these flows in the areas & sectors that are

highly export oriented with the aim that along with the

overall production with higher level of exports are achieved

which then could be used to meet the foreign exchange

requirement of the Country.

It has also pursued a similar kind of strategy over a

period of time and started Export Oriented Unit by

providing a traditional sector like Textile and tea have

25

faired much better than modem sector like Engineering

and Chemical because of high export intensity of export. In

textile export oriented Unit, many of Units uses indigenous

raw material and this textile sector is having much higher

export intensity of the sales, which helps in higher foreign

currency for the Country. As far as import intensity of

export is concerned, in many of the Mills imported

improved machinery and advanced technology to produce

high quality of textile for exports market. This is one time

investment that is at time of starting of the mill and

because of this for longer period of time the overall import

intensity of export for textile export oriented unit became

very low. For ideal case, the export intensity of export for a

EOU is zero.

The Government has given concessions to these

EOUs in the excise duties on purchase of raw material

machinery imports and exports of good to enhance the

export of the country. The Government has also put higher

excise duty on selling of goods in local market from these

export oriented Unit.

2.8 CURRENT SCENARIO

Developing countries with both textile and clothing

capacity may be able to prosper in the new competitive

26

environment after the textile quota regime of quantitative

import restriction under the multi-fibre agreement (MFA)

came to an end on 1st January 2005 under the World

Trade Organization (WTO) Agreement on Textile 8b Clothing.

As a result, the textile industry in developed countries

will face intensified competition in both, their export and

domestic markets. However, the migration of textile

capacity will be influenced by the objective competitive

factors and will be hampered by the presence of distorting

domestic developed countries. The elimination of quota

restriction will open the way for the most competitive

developing countries to develop stronger clusters of textile

expertise, enabling them to handle all stages of the

production chain from growing natural fibers to producing

finished clothing.

The OECD Paper says that while low wages can still

give developing countries a competitive edge in world

markets, time factors now play a far more crucial role in

determining international competitiveness. Countries that

aspire to maintain an export-led in textile and clothing

need to complement their cluster of expertise in

manufacturing by developing their expertise in the high

27

value-added service segments of the supply chain such as

design, sourcing or retail distribution. To pursue these

avenues, national suppliers need to place greater emphasis

on education and training of service-related skills and to

encourage the establishment of joint structures where

domestic suppliers can share market knowledge and offer

more integrated solutions to prospective buyers.

The textile industry is undergoing a major

reorientation towards non-clothing applications of textiles,

known as technical textiles, which are growing roughly at

twice rate of textile production. The Processes involved in

producing technical textiles require expansive equipments

and skilled workers and are, for the moment, concentrated

in developed countries. Technical textiles have many

applications, including bed sheets, filtration and abrasive

materials, Furniture and healthcare upholstery, thermal

protection and blood absorbing and applications. India

must take adequate measures for capturing its market by

promoting research and development in this Sector.

The mood in the Indian textile industry given the

phase-out of the quota regime of the multi-fibre

arrangement (MFA) is upbeat with new investment flowing

28

in and increased orders for the industry as a result of

which capacities are fully booked up to April, 2005. As a

result of various initiatives taken by the Government, there

has been new investment of Rs.50,000/- Crore in the

textile industry in last five years. Nine textile majors

invested Rs.2,600/- Crore and Plan to invest another

Rs.6,400/- Crore. Further, India's Cotton Production

increased by 57% over the last five years and 3 million

additional spindles and 30,000 Shuttle-less looms were

installed.

The Industry expected investment of Rs. 1,40,000/-

Crore in this sector in the Post-MFA Phase. A vision 2010

for textile formulated by the Government after intensive

interaction with the industry and Export Promotion

Councils to capitalize on the upbeat mood aims to increase

India's Share in World's textile trade from the current 4%

to 8% by 2010 and to achieve export value of US $ 50

billion by 2010 vision 2010 for textiles envisages growth in

Indian textile economy from the current US $ 37 billion to

85 billion by 2010 creation of 12 billion new jobs in the

textile sector and modernization and consolidation for

creating a globally competitive textile industry.

29

There will be opportunities as well as challenges for

the Indian Textile Industry in the Post-MFA era. But India

has natural advantages which can be capitalized on strongV,

raw material base - cotton, man-made fibers, jute, silk large

production capacity ( Spinning - 21% of World capacity &

Weaving - 33% of World capacity but of low technology )

vast pool of skilled manpower entrepreneurship, Flexibility

in Production Process and long experience with US / EU (

European Union ). At the same time, there are constraints

relating to fragmented industry, constraints of Processing

quality of Cotton, Concerns over Power Cost, labour

reforms and other infrastructural constraints and

bottlenecks, e.g. cost of power was Rs.8/~ per garment in

India whereas in China it was only Rs.2/- per garment.

Further, for the benefit of exporters, there should be

'State-Owned Cargo Shipping Mechanism, Several

initiatives have already been taken by the Government to

overcome some of these concerns including through the

Technology Upgradation Fund Scheme (TUFS) setting up of

Apparel Parks & liberalization of respective regulatory

practices. Shri Kamal Nath, Union Minister of Commerce &

Industry, has said that India will take up the issue of non-

30

tariff barriers (NTBs) in the World Trade Organization

(WTO), Doha round of multilateral trade negotiations,

which are expected to gather steam from March 2005

onwards.

On the eve of Republic Day, Hon. President Shri

Kalam said that" India is presently exporting six billion US

Dollars worth of garments, whereas with the WTO regime in

place, we can increase the production and export of

garments upto 18 to 20 billion US Dollars within next Five

years. This will enable generation of employment in general

and in rural areas in particular. By tripping the export of

apparels, we can add more than 5 million direct jobs and 7

million indirect jobs in the allied sector, primarily in the

cultivation of Cotton. Concerted efforts are needed in

cotton research, technology generation, transfer of

technology, modernization and upgrading of ginning and

1. Ministiy of Finance has added 165 new textile

products under duty drawback schedule. The new

products included wool tops, cotton yam, acrylic

31

yam, viscose yam, various blended yam/fabrics,

fishing nets etc. Further, the existing entries in the

drawback schedule relating to garments have been

expanded to create separate entries of garments made

up of (1) cotton, (2) man made fibers blend and (3)

MMF, Separate rates have been prescribed for these

categories of garments on the basis of composition of

textiles.

2. After the phasing out of quota regime under the

multi-fibre pact, India can envisage its textile sector

becoming $100b industry by 2010. This will include

exports of 50b. The proposed targets would be

achieved provided reforms are initiated in textile

sector and local manufacturers adopt measures to

improve their competitiveness. A 5-pronged strategy

aiming to attract FDI by making reforms in local

market, replacement of existing indirect taxes with a

single nationwide VAT, liberalization of contract

norms for textile and garment units, elimination of

restrictions that cause poor operational and

organizational performance of manufacturers, was

suggested.

32

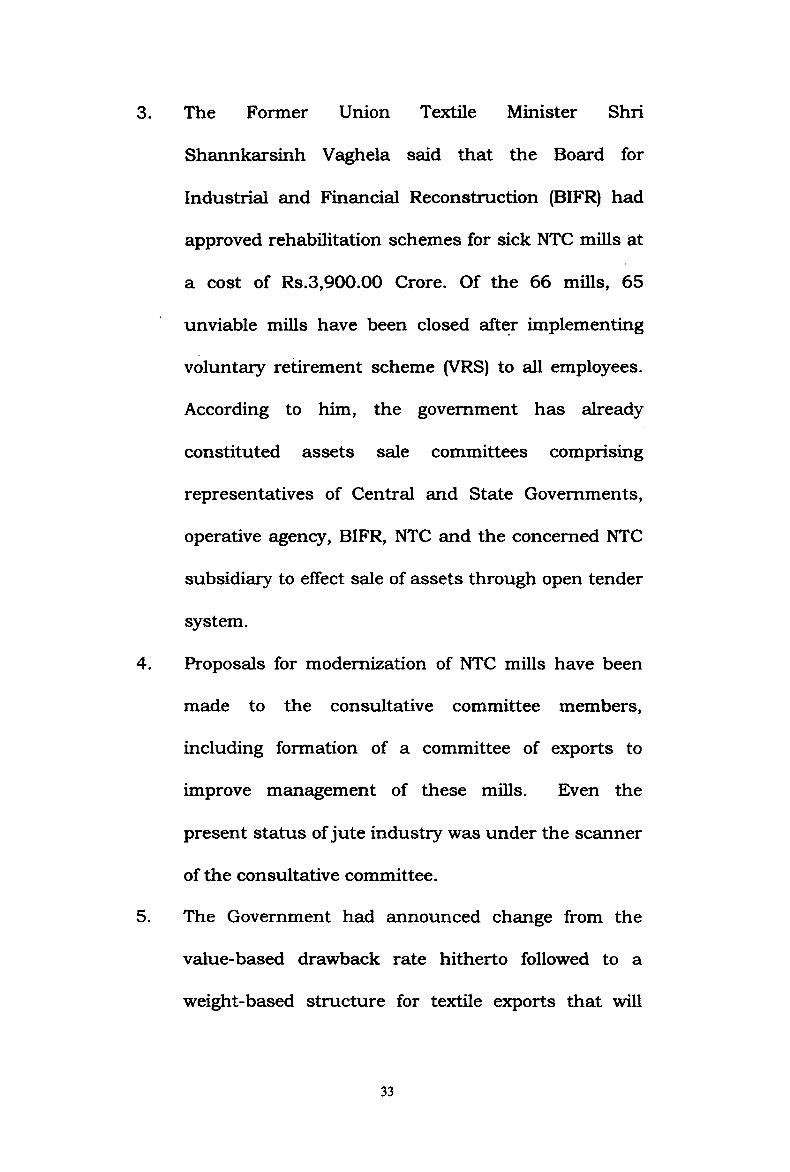

3. The Former Union Textile Minister Shri

Shannkarsinh Vaghela said that the Board for

Industrial and Financial Reconstruction (BIFR) had

approved rehabilitation schemes for sick NTC mills at

a cost of Rs.3,900.00 Crore. Of the 66 mills, 65

unviable mills have been closed after implementing

voluntary retirement scheme (VRS) to all employees.

According to him, the government has already

constituted assets sale committees comprising

representatives of Central and State Governments,

operative agency, BIFR, NTC and the concerned NTC

subsidiary to effect sale of assets through open tender

system.

4. Proposals for modernization of NTC mills have been

made to the consultative committee members,

including formation of a committee of exports to

improve management of these mills. Even the

present status of jute industry was under the scanner

of the consultative committee.

5. The Government had announced change from the

value-based drawback rate hitherto followed to a

weight-based structure for textile exports that will

33

discourage raw material exports and also curtail the

scope for misusing the drawback claims by boosting

invoice value of exports.

6. NCDEX launched its silk contract (raw silk and

cocoon) on Thursday, January 20, 2005. With this

launch, the total number of products offered by

NCDEX goes up to 27. The launch of the silk contract

will offer the entire suite of fibres to the entire value

chain ranging from farmers to textile mills. With the

objective of protecting the interests of the those

affected but WTO agreements and globalization

process, Government of India jointly with NCDEX has

adopted a policy of encouraging future contracts of

silk. The Ministry of Textiles and the Central Silk

Board (CSB) had decided to introduce futures trading

in mulberry cocoons and raw silk on NCDEX. The

basic purpose is to mitigate the risk associated with

the changing prices through an efficient price

discovery mechanism. Features of Trading on the

NCDEX will provide an alternative trading avenue for

farmers, weavers and traders and help them make a

better price discovery for their produce. It will also

34

help them to reduce risks associated with price

volatility through hedging.

2.10 BUOYANCY IN COTTON YARN INDUSTRY

The removal of quotas on January 1, 2005 has

ushered in a new era in world textiles. This move has

created to a large extent a level playing field for all players

in the Industry/Countries. In other words, the need for a

sustainable global competitiveness can never be

overemphasized as today our economy is being integrated

with the world economy. Local problems can not be an

excuse for being uncompetitive - and no one can save a

company, there will be no Government, no restrictive

policies to protect a unit/company. However, differential

tariffs and regional trade agreements would keep

influencing the movement of goods and trade flow for times

to come.

In anticipation of removal of quantitative restrictions,

countries like China and to a lesser extent India had

started building capacities and preparing itself to increase

it's share in the global textile market. There is an expected

restricting of the sourcing strategies of the developed

countries and economics are seen to be the main driver of

deciding where to buy. The textile manufacturing base is

35

fast falling in Europe and North America and Asian and

African countries are filling up the gap at an increasing

pace - the removal of quotas has hastened the process, as

there are no limitations on quantities purchased from any

country.

CHINA THE LARGEST BENEFICIARY :

China was expected and is the largest beneficiary of

the new order in the textiles world. They have been

installing capacities at a rapid pace in anticipation since

1999 and today have the capacity to make huge supplies at

very competitive rates to the developed world. In short,

they are the first choice of every buyer. India did not plan

its expansion in a systematic way and the industry /

Government only woke up in 2004 to the impending

opportunity. The result ? The gap between China and

India has become so large, that it is unfair to call India

No.2 player in the global textile industry. However, as the

saying goes: 'Do not put all your eggs in one basket", every

large buyer wants to diversify its sourcing base and

countries like India / Pakistan / Bangladesh are a ready

choice depending on the type of item.

It is clear that the textile world of manufacturing is

undergoing restructuring and new buying strategies are

36

evolving. Textile clusters are getting stronger around a

limited number of countries. India is gaining because of its

strong textile background on both technical and raw

material base - it is the second best alternative to China

especially for Cotton Textiles - yam /fabric /garments.

However, things are not as rosy as it seems and sounds.

Pre-2005, many Indian suppliers who held quotas were

able to get premium equivalent to the quota prices for the

products. They overnight lost that, leading to a reduction

in their realizations. There has been a drop in prices due to

removal of quota in order to match prices of China and

other low cost countries - this however has been coupled

with volumetric growth in garment orders. Orders are

increasing from the West, but prices are very tight (as that

is the incentive to come to India).

This pressure on garment suppliers to deliver more

and more - means more demand for downstream raw

materials like fabric and yam. India's base of manmade

fibres is not very strong and hence India does not have a

cost advantage on this side, hence import of blended fabric

would grow from China / Pakistan / Indonesia / Thailand.

However, on the cotton side, India is very strong. India has

37

a large and growing raw cotton fibre base, which, is more

than sufficient to meet, expected future demand of the

Industry. Hence, this is where opportunities lie. There

would be tremendous demand pull for cotton yam and

fabric from the garment industry. India is one of the lowest

cost manufactures of cotton based raw materials in the

world and the Indian garment industry would be largely

dependent on the domestic industry for its needs.

INDIA AND TEXTILE INDUSTRY :

In India a major expansion of domestic demand for

cotton yam/fabric in increasing. Today, India has 40%

market share of the global combed yarn trade - however

with the growing need of quality yam by the domestic

industry, exports would be replaced by domestic sales.

Realisation in export sales are 3-5% lower than domestic

sales. However, due to lack of volume demand companies

had to export. This scenario is fast changing, which means

that margins for quality yam manufacturing companies

would go up. Further, it is important to note that gestation

/ lead time for garment / fabric unit is 6 months, while for

a yam unit it is 18-24 months. Hence, there would be a

mismatch in growth of capacity in these two sectors leading

to a tight yam supply situation leading to upward pressure

38

on prices. An example of this is China, which is still

importing a lot of cotton yam to meet its demand of fabric /

garments.

Today, India has about 37 million spindles out of

which may be about 25 million spindles are worthy to give

quality yam. The two main suppliers of spindles in India

have a maximum capacity of 2 million spindles, hence we

cannot add more than 8% yam capacity annually unless

whose go for Chinese machinery - which is yet to be tested

or used in India and whose quality delivery is under

question (Indian yam is expected to be better than Chinese

yam in terms of consistency and quality). The Government

is envisaging multiple fold growth for textiles exports in the

next 5 to 10 years, and not to forget the growing domestic

market - this means major pressure on downstream inputs

which are more commodities in nature - fibre and yam. As

it is well known the price - demand elasticity for commodity

type products is very high and this means the yam

industry can see very high upward movement of prices in

the coming few years.

39

B. TEXTILE INDUSTRY IN MAHARASHTRA

2.11 INTRODUCTION

. Maharashtra possesses a large number of Powerlooms

and Handlooms. There are about 627 lakh Powerlooms in

Maharashtra, which requires Cotton Yam. Powerlooms are

concentrated in sizable numbers around Mumbai,

Bhiwandi, Thane, Malegaon, Ichalkaranji, Solapur, Dhule

and Sangli in the state of Maharashtra. Merely half of

Powerlooms are located in Maharashtra. Handlooms and

Powerlooms get their supplies of raw material, i.e. cotton

yam from Cotton Mills. With a view to protect the interests

of Handlooms & Powerlooms, the Govt, of Maharashtra

have adopted a number of measures relating to financial

assistance, differential rates of excise duties, reservation of

certain cloth varieties etc. for Handloom & Powerloom

Weavers in decentralized sector. A notable feature in the

history of Co-operative Spinning Mills in the year of 1960 in

which first Co-operative Spinning Mills was established in

Maharashtra, i.e. The Deccan Co-operative Spinning Mills

Ltd., at Ichalkaranji, District Kolhapur.

40

In 1950, a typical attempt to run a mill on co

operative basis was made at Bhor. In 1943, Shri Laxmi

Textile Mills was established at Bhor as Private Company

by State Government of Raja of Bhor. In 1953, Laxmi

closed down. In 1959, the workers of closed Unit formed a

Co-operative Society, i.e. Shri Shivaji Textile Workers Co

op. Spinning Mills Ltd. with the assistance of State.

The concept of Co-operative Spinning Mills Ltd. was

thus rooted in Maharashtra in 1959-60 in the form of two

significant attempt denoted the desire to step into a new

field of individual activity with a view to secure economic

benefits for these numbers. Then the Proposals for the

establishment of Co-operative Spinning Mills were received

from Weavers of Nagpur and Solpaur on the lines of Deccan

and the units were installed and went into production in

1968 and 1967 (Solapur). In third Five-Year Plan Period

(Nagpur) Government Of India decided to give preference to

Co-operative Department. In pursuance of the policy, 14

proposals were prepared with the help of National Co

operative Development Corporation. In 1964, Yeotmal

District Cotton Growers Co-op. Spinning Mills Ltd. was

established out of these 14 Co-operative Spinning Mills

14788A41

licensed in growers sector Kolhapur, Amaravati,

Shrirampur, Latur, Bhusawal, Nanded. Units were

installed in 1969 while other Units installed later.

Industrial Finance Corporation, Maharashtra Co-op. Bank

Ltd. provided financial aid for the installation of Co

operative Spinning Mills.

The present condition of the Textile Industry in

Maharashtra can be seen from number of Spinning Mills as

44 installed, 78 composite mills, total spindles of the State

49,77,000 of rotors 5012.

In 1988-99, textile industry in Maharashtra belongs

to Co-operative Sector as 40 Co-op. Spinning Mills, 613

Powerloom Co-operatives, 685 Handloom Co-operatives,

and three Co-op. Processing Houses.

Maharashtra State plays very important role in

respect of Co-op. Spinning Mills in India of which 40 Co

operative Spinning Mills are installed in Maharashtra.

2.12 DETAILS OF CO-OPERATIVE SPINNING MILLS IN

MAHARASHTRA (2004-051

Table No. 2.1

42

DET

AIL

S O

F C

O-O

PER

ATI

VE S

PIN

NIN

G M

ILLS

IN M

AH

AR

ASH

TRA

1515

205

8864

+ 4

32 T

extu

risin

g Sp

indl

es97

0717

5520

1015

lakh

Kgs.

7.5

lakh

Bal

es

Inst

alle

d S

pind

les

Inst

alle

d R

otor

s W

orki

ng S

pind

les

Wor

king

Rot

ors

Annu

al Y

arn

Prod

uctio

n (la

kh K

gs.)

Annu

al C

otto

n R

equi

red

I Total Cap

acity

1171

177

+151

2R

2306

4 +

5336

R43

2 Te

xt.

I Spdls.

I32

0964

+ 20

16 R

CO

122

I 151520

5 II

8854

|

a

I Prim

ary I

Stag

eII « CM - CO

I Under I

Con

stru

ctio

n

I Spindle

s |T“ t ' 36 CM 39

I Liqu

idat

ed I

and

sold ©

*oC& 10

1308

I» l

I 101308

I

Liqu

idat

ion

Spin

dles

I Roto

rs I

T—

3461

88

1175

CM

968

CO

[ 34

6188

I I m

2

j

I Conv

erte

d IM

ills 1 CM t li CM

I C

lose

d M

ills

j

Spin

dles

I Roto

rs

iO

9699

2 3 12

00 432

(Tex

t. (O■o a c0 |

00

I 96

992

8CMt— 43

2 |

I W

orki

ng M

ills

Spin

dles

I Roto

rs

CDT—

6266

89

336

o>

2306

4 31

68

2232

0964

20

16

50i 97071

7I

5520

I Tota - Mills

I

43 to s ,, CO 122

I Fi

ve Y

ear P

lan

j

Upt

o 6th Fiv

e Year

Plan 7t

h Fi

ve Y

ear P

lan

8th

Five

Yea

r Pla

n

10th

Yea

r Pla

n

Tota

l Mill

s <0©*oC‘5

O) Rot

ors

Tota

l Tex

. Spi

ndle

s

v.> No. - CM CO Sour

ces :

MAH

ARAS

HTR

A S

TATE

CO

-OPE

RAT

IVE

TEXT

ILE

FED

ERAT

ION

LIM

ITED

2.13 : REVIEW OF THE PERFORMANCE OF THE

CO-OPERATIVE SPINNING MILLS IN PRODUCTION

IN MAHARASHTRA FOR THE YEAR - 2004-05.

At the end of March 2005 there dare 77 Spinning

Mills and one texturising Unit in Co-operative Sector of the

State of Maharashtra. The board break-up of these Mills is

as under.

1. 60 Mills of Ring Spinning are having 14,81,749

Spindles and 840 Rotors.

2. 11 Mills of Open End Spinning are having 6008

Rotors.

3. 6 Mills of Mixed Pattern are having 33,456 spindles &

2016 Rotors.

4. 1 Texturising Unit is of 432 Spindles.

Total installed capacity of Co-operative Spinning Mills

in 2004-05 in the State was 15,15,205 Spindles, 8,864

rotors and 432 Spindles of texturising.

Classification of the Performance For the Year 2004-05

The efficient management in both technical and

financial aspects of a Spinning Mill, by effective use of main

resources, (i.e. main, machine, material and methods ) is

43

very essential for obtaining good results. Considering the

above factors, exercise is made to find out the top five Mills

which can be classified as technically and financially " Best

Managed Mills ", Machine Productivity Index, Productivity

Index & Cash Gain/Loss earned per workable Spindle in

rupees are the factors considered for ranking purpose.

The following Mills have been considered as the First

Five Best managed Mills for over all performance during the

year 2004-05.

Sr.No. Name of the Mills

1. Sagareshwar Sahakari Soot Girani Ltd. Kadegaon

2. Shri Swami Samarth Shetkari Wa Vinkari Sahakari

Soot Girani Ltd. Valsang.

3. Shetkari Sashakari Soot Girani Ltd. Sangole.

4. Babasaheb Kedar Shetakari Sahakari Soot Gimi Ltd.,

Hingna, Nagpur.

5. Loknayak Jayprakash Narayan Shetkari Sahakari

Soot Gimi Ltd. Shahada.

As regards Technical Performance, since MPI is the

combination of capacity utilization and 40s converted

production, this index plays a more important role in

operational performance. Considering " Machine

44

Productivity Index and Productivity Index " the ranking for

" Best Technical Performance " is done.

Following First Five Mills have been considered for "

Best Technical Performance " during the Year 2004-05.

Sr.No. Name of the Mill

1. Mahalaxmi Magasvargiya Sahakari Soot Gimi Ltd.

Kadepur

2. Indira Gandhi Mahila Sahakari Soot Gimi Ltd.

Ichalkaranji.

3. Mahatma Phule Magasvargiya Shetkari Sahakari Soot

Gimi Ltd., Peth Vadgaon.

4. Loknayak Jayprakash Narayan Shetkari Sahakari

Soot Gimi Ltd., Shahada.

5. Shetkari Sahakari Soot Gimi Ltd. Sangola.

45

C. TEXTILE INDUSTRY IN ICHALKARANJI

2.14 HISTORICAL BACKGROUND

By the turn of the last century, Ichalkaranji

was a small unimposing town devoid of any industrial

activity. It was connected with main places of

business, with no source of assured raw material

supply in the vicinity, nor that of skilled workers. The

growth of the powerloom industry in Ichalkaranji has

come up by passing all text-book laws of economics.

It goes to the credit of erstwhile Jahagirdar of

Ichalkaranji Shrimant Narayanrao Ghorapade that no

conceived an establishment and a development of the

industry and set in motion factors conducive for it.

The first powerloom unit started in the town in 1904,

was also the first one to start in the decentralised

textile sector, in India. The Jahagirdar, induced

many skilled handloom weavers to shift their families

from the surrounding handloom centres like Rabkavi,

Rendal, Budhgaon and Banhatti and made

arrangements for them f land, water and housing at

only a token cost. Finance made available on easy

terms and concessions granted in taxes proved to be

46

the decisive factors in fostering the development of

the industry in the town. Thanks to these benevolent

steps. The weaving industry settled down in the town

and by 1950, about 15,000 Handlooms and about

2,000 Powerlooms were working in the Town.

During the first half of the century, the town

developed mainly as a handloom centre, and

Powerlooms existed but in a scattered manner.

The production was concentrated as fancy

coloured sarees "Patalas" a typical local sort, which

became extremely popular all over the State and had

a large demand even, as far as, in the upper Indian

States. With the increased demand pushing up the

need to step up the pace and quantum of production,

the handloom weaver could no longer cling to the

slow working Handloom. Thus, obliging him to shift

production from Handlooom to Powerloom.

A close study of this phenomenon will ally the

fears of some of the Advocates of the Handloom

industry, that the transformation brings in its wake a

displacement of labour. AS a matter of fact, even with

47

100% increase in the labour force during this period,

Ichalkaranji has been still running short of labour.

As a measure of providing protection to the

Handloom weavers, the Government of India put a

ban on the production of coloured sarees on

Powerlooms. This posed serious problem to the

Industry since the entire loomage in Ichalkaranji then

was displaced on the production of coloured sarees.

The weavers in Ichalkaranji, however, took up the

challenge and with the characteristic ingenuity

devised a system of providing sized beams and weft

pirns to the weavers for the manufacture of dhoties

and mulls. This system fitted in so well, that within a

very short period, entire production in the town was

shifted from the coloured sarees to dhoties and mulls.

The basic short-coming of the weaver is the

dirth of finance, which gave rise to a system of

'Master-Weavers' or 'Middle-Men' who supplied them

raw material and took back cloth woven on their

looms. Although this system solved the weaver's

problems of the supply of raw material and of

marketing of the cloth, it made him totally dependent

48

on the Master Weavers. As a matter of fact, the

Government's short-sighted policy of levying excise

duty on slab basis has worked as a deterrent to the

process of integration in the industry. So long as this

policy continues, there is no change of industry

grouping itself into an economically viable units and

running their businesses in open competition of the

market. The need to give protection to the small units

in the sector cannot be over-emphasized. But the

care must be taken to see that such a policy itself

does not induce owners to remain small perpetually.*

ORGANIZATIONS :

In 1961, some enterprising weavers came

together to form a Co-operative Society with a view to

providing weavers sized beams and pirns and thereby

eliminating the need for a master weaver. Named and

styled as Yantramag Audyogik Sahakari Society Ltd.

it aimed at ensuring fair returns to the weavers for

their fair day's work. But the Society could not do

much progress for want of adequate current capital

and the command over marketing. The Society was

only in the initial stqge of development and could not

withstand the sti^ips of fierce competition of the

49

speculative cloth market. These good efforts would

not have gone in vain had the Government lent the

Society a helping hand.

On the top of these difficulties was the

prejudicial view taken by the Government in judging

the role of this benevolent Society. The Society was

bracketed with the master weavers only because it

supplied yam to the Members and their cloth was

taken back by the Society. It took great efforts to

convince the authorities the impropriety of measuring

the role of the society and of the master weavers with

the common rod.

The Ichalkaranji Powerloom Weavers Co

operative Association Ltd. registered in 1948, is the

Central body in the town having a majority of looms

under their membership. Apart from redressing the

grievances of the industry to the Governments, State

and the Central, the Association conducts many

useful activities in matters of excise, labour and

textile problems.

In 1973, during the period of yam control, the

Association acted as the nominee of the Maharashtra

50

State Powerloom Corporation Ltd. for the distribution

of yam to the Weavers in Ichalkaranji.

In 1974, the Association started a production

programme on a modest scale. The working of the

Scheme is similar to that of the programme run by

the Maharashtra State Powerloom Corporation Ltd.

described elaborately in this note.

SPINNING MILLS :

Having studied over year, the problem of the

occasional shortages in the supply of yam and the

fluctuations in its prices arising out of the same, it

became evident that the ultimate solution lies in

establishing the Spinning Mills owned by the Weavers

themselves.

In pursuance of this aim, The Deccan Co

operative Spinning Mills Ltd. was started in 1960 with

the pioneering efforts of Shri Abasaheb Kulkami,

M.P., Shri Dattajirao Kadam, M.P. and Shri Anantrao

Bhide. It needs a special mention that many persons

who took Shares of this Mills had no enough financial

resources at their command. The experiment of

establishing the Mill was completely new to the

weavers. On the background of this fact the weavers

51

ran a risk in raising the loan from the Ichalkaranji

Urban Co-operative Bank Ltd. for buying of Shares.

The faith reposed by them in the leadership proved

worth the risk, since the economic position of all

these weavers today has improved beyond

recognition. Another Co-operative Spinning Mills was

brought into being in 1965 under the leadership of

Veteran Co-operator, Shri Ratnappa Kumbhar, viz.

Kolhapur Zilha Shetkari Vinkari Sahakri Soot Gimi

Ltd.

Yet another Spinning Mill is being set up with

25,000 Spindles capacity, viz. The Ichalkaranji Co

operative Spinning Mills Ltd. and is expected to go in

production in the near future. It is pertinent to note

here that even after the completion of the third Mill,

the total loomage that can be served by these Mills

will be about 3,000 or merely 14% of the total

loomage working in the town. The rest of the looms

will inevitably remain dependent on the supply of

yam from the outstations.

PROCESSING HOUSE

Lack of processing facilities has been working as

an another serious impediment in the progress of the

52

Industry. Embolden by the success met within the

establishment of the Spinning Mill, v the weavers

launched two co-operative processing houses under

the name and style of The Laxmi Co-operative

Processors Ltd. (1959) and The Yashwant Co

operative Processors Ltd. (1963). This has provided a

new dimension to the Powerloom Industry in

Ichalkaranji.

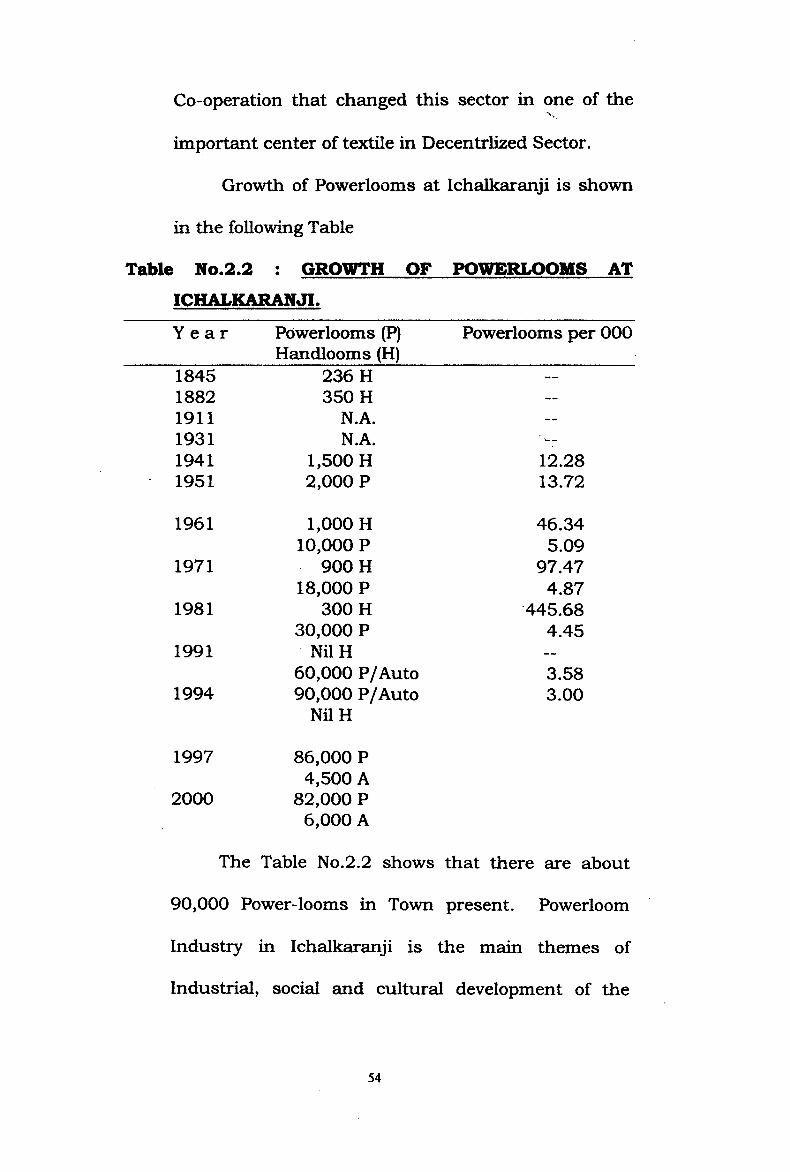

2.15 GROWTH OF POWERLOOMS IN ICHALKARANJI

Ichalkaranji is one of the biggest and most important

Centre of Textile Industry in Western Maharashtra. It

is a humming Centre of Powerloom Industry. The

Centre is producing mainly Cotton and Polyester

Cloth on the powerlooms. Dhoti, Sarees, Papline,

Cambric, Mulls, Khadi, etc. are different varieties

manufactured at Ichalkaranji.

Around 1945, there were hardly 1600 to 1800

Powerlooms. The number gradually increased to

around about 5000 in late fifties. With the spread of

Spinning Mills and other ancillary Industries in and

around the Town, Powerloom Industry took a great

leap in the last three decades. It is the magic touch of

53

Co-operation that changed this sector in one of the

important center of textile in Decentrlized Sector.

Growth of Powerlooms at lchalkaranji is shown

in the following Table

Table No.2.2 : GROWTH OF POWERLOOMS ATICHALKARANJI.

Year POwerlooms (P) Handlooms (H)

Powerlooms per 000

1845 236 H —1882 350 H —

1911 N.A. —

1931 N.A. ■ —1941 1,500 H 12.281951 2,000 P 13.72

1961 1,000 H 46.3410,000 P 5.09

1971 900 H 97.4718,000 P 4.87

1981 300 H 445.6830,000 P 4.45

1991 Nil H —

60,000 P/Auto 3.581994 90,000 P/Auto

Nil H3.00

1997 86,000 P4,500 A

2000 82,000 P6,000 A

The Table No.2.2 shows that there are about

90,000 Power-looms in Town present. Powerloom

Industry in lchalkaranji is the main themes of

Industrial, social and cultural development of the

54

town. The significant role being played by Powerloom

Industry with regard to Country's Economy is well-

accepted. Today it has became centre of attrition for

national, as well as foreign traders. The population of

Ichalkaranji has been growing rapidly. This is due to

rapid expansion of the industries at the Ichalkaranji.

The number of job opportunities have given impetus

to migration and growth of the town. The powerloom

town of Ichalkaranji drew up the jobless, landless

common workers and it offered a fair scope for the

ambition, enterprising people who rushed to the town

to make their fortune. The main cause for the growth

of population in the town is the powerloom industry,

which attracted people from the neighboring areas

and villages in the vicinity of the town. The

immigration can be attributed to the rising Industrial

and commercial activities that boosted up within a

short period of time. One notable feature is that

almost 2/8 of the population of the city is connected

with the powerloom industry.

It would be rather increasing to get acquainted

with other factors apart from powerloom industry,

55

which have humble claim of having a small

contribribution in the spread of the name of

Ichalkaranji as Manchester of Maharashtra.

2.16 ICHALKARANJI CLUSTER AT A GLANCE

-2005

Workers in the Textile

Number of Sizing Units

Number of Hand Processing Units-

Number of Power Processing- 23

Number of Yam Merchants

Number of Fabrics Merchants

Number of Powerlooms

@ 1.2 lakh

@120

@50

@110

@300

@ 1,13,500

Number of Technical Institutions

Number of Training Facilities

Number of Financial Institutions

Number of Industrial Estates

Number of Spinning Units

Item of Manufactured Yam Blended

1

1 (BTRA PSC)

28

4

@15

Cotton,

Yam

T^pe of Fabrics manu- - Dhoti,Poplin,Cambric,facturedShirting, Suitings,Canvas,Wider width Fabrics, Dobby,design Fabrics etc.

56

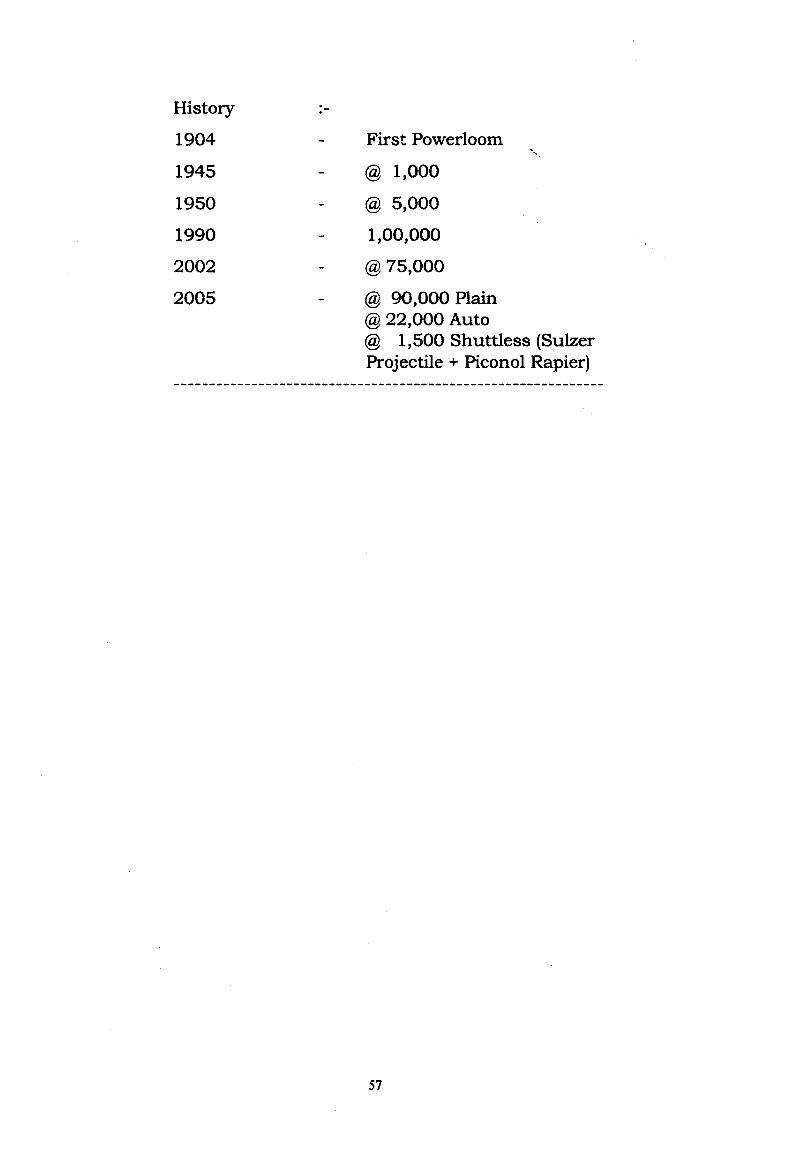

History

1904 First Powerloom

1945 @ 1,000

1950 @ 5,000

1990 1,00,000

2002 @ 75,000

2005 @ 90,000 Plain @ 22,000 Auto @ 1,500 Shuttless (Sulzer Projectile + Piconol Rapier)

57

Copyright © 2022 FDOKUMEN