Explanatory notes: SECTION A – Multiple-choice ... - Audentia

Upload

khangminh22Category

view

0download

0

Partnership – Basic Considerations and Formation 1

CHAPTER 1

MULTIPLE CHOICE ANSWERS AND SOLUTIONS 1-1: a

Jose's capital should be credited for the market value of the computer contributed by him.

1-2: b (40,000 + 80,000) ÷ 2/3 = 180,000 x 1/3 = 60,000. 1-3: a Cash P100,000 Land 300,000 Mortgage payable ( 50,000)

Net assets (Julio, capital) P350,000 1-4: b Total Capital (P300,000/60%) P500,000 Perla's interest ______40%

Perla's capital P200,000 Less: Non-cash asset contributed at market value Land P 70,000 Building 90,000 Mortgage Payable ( 40,000) _120,000

Cash contribution P 80,000 1-5: d - Zero, because under the bonus method, a transfer of capital is only required. 1-6: b Reyes Santos

Cash P200,000 P300,000 Inventory – 150,000 Building – 400,000 Equipment 150,000 Mortgage payable ________ ( 100,000)

Net asset (capital) P350,000 P750,000 1-7: c AA BB CC

Cash P 50,000 Property at Market Value P 80,000 Mortgage payable ( 35,000) Equipment at Market Value _______ _______ P55,000

Capital P 50,000 P 45,000 P55,000

2 Chapter 1 1-8: a PP RR SS

Cash P 50,000 P 80,000 P 25,000 Computer at Market Value __25,000 _______ __60,000

Capital P 75,000 P 80,000 P 85,000 1-9: c Maria Nora

Cash P 30,000 Merchandise inventory P 90,000 Computer equipment 160,000 Liability ( 60,000) Furniture and Fixtures 200,000 ________

Total contribution P230,000 P190,000 Total agreed capital (P230,000/40%) P575,000 Nora's interest ______60%

Nora's agreed capital P345,000 Less: investment 190,000

Cash to be invested P155,000 1-10: d Roy Sam Tim

Cash P140,000 – – Office Equipment – P220,000 – Note payable ________ _( 60,000) ______

Net asset invested P140,000 P160,000 P – Agreed capitals, equally (P300,000/3) = P100,000 1-11: a Lara Mitra

Cash P130,000 P200,000 Computer equipment – 50,000 Note payable ________ _( 10,000)

Net asset invested P130,000 P240,000 Goodwill (P240,000 - P130,000) = P110,000 1-12: a Perez Reyes

Cash P 50,000 P 70,000 Office Equipment 30,000 – Merchandise – 110,000 Furniture 100,000 Notes payable _______ ( 50,000)

Net asset invested P 80,000 P230,000

Partnership – Basic Considerations and Formation 3

1-12: Continued Bonus Method: Total capital (net asset invested) P310,000 Goodwill Method: Net assets invested P310,000 Add: Goodwill (P230,000-P80,000) _150,000

Net capital P460,000 1-13: b Required capital of each partner (P300,000/2) P150,000 Contributed capital of Ruiz: Total assets P105,000 Less Liabilities __15,000 __90,000

Cash to be contributed by Ruiz P 60,000 1-14: d Total assets: Cash P 70,000 Machinery 75,000 Building _225,000 P370,000 Less: Liabilities (Mortgage payable) __90,000

Net assets (equal to Ferrer's capital account) P280,000 Divide by Ferrer's P & L share percentage ____70%

Total partnership capital P400,000 Required capital of Cruz (P400,000 X 30%) P120,000 Less Assets already contributed: Cash P 30,000 Machinery and equipment 25,000 Furniture and fixtures __10,000 __65,000

Cash to be invested by Cruz P 55,000 1-15: d Adjusted assets of C Borja Cash P 2,500 Accounts Receivable (P10,000-P500) 9,500 Merchandise inventory (P15,000-P3,000) 12,000 Fixtures __20,000 P 44,000 Asset contributed by D. Arce: Cash P 20,000 Merchandise __10,000 __30,000

Total assets of the partnership P 74,000

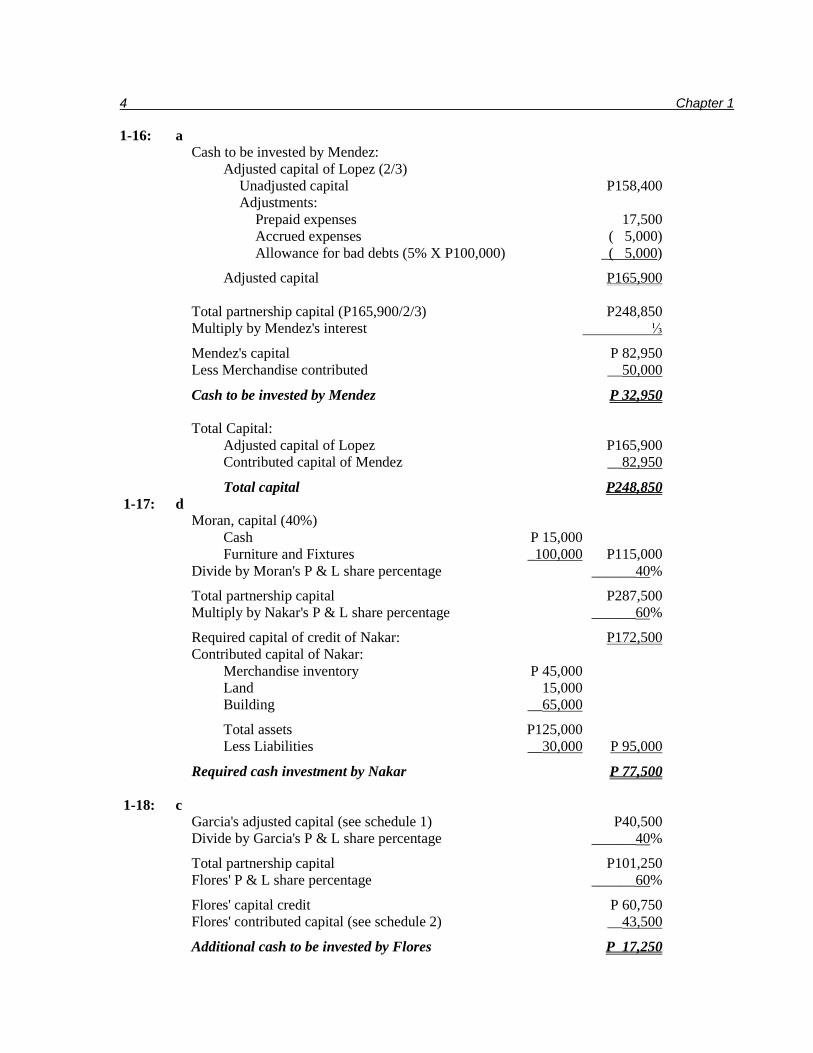

4 Chapter 1 1-16: a Cash to be invested by Mendez: Adjusted capital of Lopez (2/3) Unadjusted capital P158,400 Adjustments: Prepaid expenses 17,500 Accrued expenses ( 5,000) Allowance for bad debts (5% X P100,000) _( 5,000)

Adjusted capital P165,900 Total partnership capital (P165,900/2/3) P248,850 Multiply by Mendez's interest ⅓

Mendez's capital P 82,950 Less Merchandise contributed __50,000

Cash to be invested by Mendez P 32,950 Total Capital: Adjusted capital of Lopez P165,900 Contributed capital of Mendez __82,950

Total capital P248,850 1-17: d Moran, capital (40%) Cash P 15,000 Furniture and Fixtures _100,000 P115,000 Divide by Moran's P & L share percentage ______40%

Total partnership capital P287,500 Multiply by Nakar's P & L share percentage ______60%

Required capital of credit of Nakar: P172,500 Contributed capital of Nakar: Merchandise inventory P 45,000 Land 15,000 Building __65,000

Total assets P125,000 Less Liabilities __30,000 P 95,000

Required cash investment by Nakar P 77,500 1-18: c Garcia's adjusted capital (see schedule 1) P40,500 Divide by Garcia's P & L share percentage ______40%

Total partnership capital P101,250 Flores' P & L share percentage ______60%

Flores' capital credit P 60,750 Flores' contributed capital (see schedule 2) __43,500

Additional cash to be invested by Flores P 17,250

Partnership – Basic Considerations and Formation 5 1-18: Continued Schedule 1: Garcia, capital: Unadjusted balance P 49,500 Adjustments: Accumulated depreciation ( 4,500) Allowance for doubtful account ( 4,500)

Adjusted balance P 40,500 Schedule 2: Flores capital: Unadjusted balance P 57,000 Adjustments: Accumulated depreciation ( 1,500) Allowance for doubtful accounts ( 12,000)

Adjusted balance P 43,500 1-19: d Ortiz Ponce Total

( 60%) ( 40%) Unadjusted capital balances P133,000 P108,000 P241,000 Adjustments: Allowance for bad debts ( 2,700) ( 1,800) ( 4,500) Inventories 3,000 2,000 5,000 Accrued expenses _( 2,400) ( 1,600) ( 4,000)

Adjusted capital balances P130,900 P106,000 P237,500 Total capital before the formation of the new partnership (see above) P237,500 Divide by the total percentage share of Ortiz and Ponce (50% + 30%) ______80%

Total capital of the partnership before the admission of Roxas P296,875 Multiply by Roxas' interest ______20%

Cash to be invested by Roxas P 59,375 1-20: d Merchandise to be invested by Gomez: Total partnership capital (P180,000/60%) P300,000 Gomez's capital (P300,000 X 40%) P120,000 Less Cash investment __30,000

Merchandise to be invested by Gomez P 90,000 Cash to be invested by Jocson: Adjusted capital of Jocson: Total assets (at agreed valuations) P180,000 Less Accounts payable __48,000 P132,000 Required capital of Jocson _180,000

Cash to be invested by Jocson P 48,000

6 Chapter 1 1-21: b Unadjusted Ell, capital (P75,000 – P5,000) P 70,000 Allowance for doubtful accounts ( 1,000) Accounts payable ( 4,000)

Adjusted Ell, capital P 65,000 1-22: c Total partnership capital (P113,640/1/3) P340,920 Less Divino's capital _113,640

Cortez's capital after adjustments P227,280 Adjustments made: Allowance for doubtful account (2% X P96,000) 1,920 Merchandise inventory ( 16,000) Prepaid expenses ( 5,200) Accrued expenses ___3,200

Cortez's capital before admission of Divino P211,200 1-23: a Total assets at fair value P4,625,000 Liabilities (1,125,000) Capital balance of Flora P3,500,000 1-24: c Total capital of the partnership (P3,500,000 ÷ 70%) P5,000,000 Eden agreed profit & loss ratio 30% Eden agreed capital 1,500,000 Eden contributed capital at fair value 812,000 Allocated cash to be invested by Eden P 688,000 1-25: c __Rey __Sam_ __Tim __Total_ Contributed capital (assets-liabilities)P471,000 P291,000 P195,000 P957,000 Agreed capital (profit and loss ratio) 382,800 382,800 191,400 957,000 Capital transfer (Bonus) P 88,200 P(91,800) P 3,600 - 1-26: d Total agreed capital (P90,000 ÷ 40%) P225,000 Contributed capital of Candy (P126,000+P36,000-P12,000) 150,000 Total agreed capital (P90,000 ÷ 40%) 225,000 Candy, agreed capital interest 60% Agreed capital of Candy 135,000 Contributed capital of Candy 150,000 Withdrawal of Candy P 15,000

Partnership – Basic Considerations and Formation 7 1-27: a Total agreed capital (210,000 ÷ 70%) P300,000 Nora’s interest 30% Agreed capital of Nora P 90,000 Cash invested 42,000 Merchandise to be invested by Nora P 48,000 1-28: a Contributed capital of May (P194,000 - P56,000) P138,000 Agreed capital of May (P300,000 x 70%) 210,000 Cash to be invested by May P 72,000 1-29: d Zero, because the bonus method involves only a transfer of capital. 1-30: b Noy Bi Cash P 10,000 P 14,000 Accounts receivable- Net 92,000 92,000 Merchandise inventory 216,000 150,000 Computer equipment 24,000 14,000 Furniture and fixtures 18,000 ---- Total assets at fair value 360,000 270,000 Accounts payable (108,000) (72,000) Net assets invested 252,000 198,000 Agreed capital 250,000 200,000 Goodwill (withdrawal) P (2,000) P 2,000 1-31: c Villar Roxas Cash P 2,205,000 P - Office equipment 630,000 - Merchandise inventory - 1,575,000 Notes payable ( 210,000) - Contributed capital 2,625,000 1,575,000 Agreed capital 2,520,000 1,680,000 Bonus to Roxas P( 105,000) P 105,000 1-32: b Total capital before adjustments (P210,750 + P103,000) P313,750 Allowance for doubtful accounts ( 10,000) Accumulated depreciation (P1,000 – P500) 500 Obsolete inventory ( 3,500) Total assets of the partnership P300,750

8 Chapter 1 1-33: b Gibo Edu Cash P 19,200 P136,800 Accounts receivable 163,200 129,600 Merchandise inventory 240,000 216,000 Equipment 60,000 - Accounts payable (60,000) (96,000) Notes payable (12,000) - Contributed capital 410,400 386,400 Loss on sale of equipment (1,800) 1,800 Net assets 408,600 388,200 Additional investment by Edu - 20,400 Agreed capital P408,600 P408,600 1-34: a Garnett Bryant Unadjusted capital P2,443,364 P3,097,528 Accumulated depreciation ( 80,000) 200,000 Accounts receivable written off ( 108,000) ( 140,000) Adjusted capital contributed 2,255,364 3,157,528 Agreed capital 2,255,364 1,503,576* Capital withdrawal P - P 1,653,952 * Total agreed capital (P2,255,364 / 60%) P3,758,940 Bryant’s interest 40% Agreed capital of Bryant P1,503,576 1-35: a Total capital P3,758,940 Total liabilities 4,299,396 Total assets P8,058,336 1-36: a Gordon Fernando Unadjusted capital P220,000 P309,375 Undervaluation of inventory 11,000 - Allowance for doubtful accounts (2,750) ( 4,125) Accrued expenses - (20,250) Contributed capital 228,250 285,000 Agreed capital of Gordon (P285,000/75%) x 25% 133,250 285,000 Capital withdrawal by Gordon P 95,000 P -

Partnership – Basic Considerations and Formation 9

SOLUTIONS TO PROBLEMS

Problem 1 – 1

1. a. Books of Pedro Castro will be retained by the partnership To adjust the assets and liabilities of Pedro Castro. 1. Pedro Castro, Capital ............................................................. 600 Merchandise Inventory ...................................................... 600 2. Pedro Castro, Capital ............................................................. 200 Allowance for Bad Debts .................................................. 200 3. Accrued Interest Receivable .................................................. 35 Pedro Castro, Capital ......................................................... 35 Computation: P1,000 x 6% x 3/12 = P15 P2,000 x 6% x 2/12 = _20

Total ......................... ...... P35 4. Pedro Castro, Capital ............................................................. 100 Accrued Interest Payable ................................................... 100 (P4,000 x 5% x 6/12 = P100) 5. Pedro Castro, Capital ............................................................. 800 Accumulated Depreciation – Furniture and Fixtures ........ 800 6. Office Supplies ...................................................................... 400 Pedro Castro, Capital ......................................................... 400 To record the investment of Jose Bunag. Cash .. ........................................................................................... 15,067.50 Jose Bunag, Capital ............................................................... 15,067.50 Computation:

Pedro Castro, Capital (1) P600 P31,400 (2) 200 35 (3) (4) 100 400 (6) (5) ___800 P1,700 P31,835 P30,135

Jose Bunag, Capital : 1/2 x P30,135 = P15,067.50

10 Chapter 1 b. A new set of books will be used

Books of Pedro Castro To adjust the assets and liabilities. See Requirement (a). To close the books. Notes Payable ............................................................................... 4,000 Accounts Payable ......................................................................... 10,000 Accrued Interest Payable .............................................................. 100 Allowance for Bad Debts ............................................................. 1,200 Accumulated Depreciation – Furniture and Fixtures ................... 1,400 Pedro Castro, Capital ................................................................... 30,135 Cash ....................................................................................... 6,000 Notes Receivable ................................................................... 3,000 Accounts Receivable ............................................................. 24,000 Accrued Interest Receivable .................................................. 35 Merchandise Inventory .......................................................... 7,400 Office Supplies ...................................................................... 400 Furniture and Fixtures............................................................ 6,000

New Partnership Books To record the investment of Pedro Castro. Cash ........................................................................................... 6,000 Notes Receivable .......................................................................... 3,000 Accounts Receivable .................................................................... 24,000 Accrued Interest Receivable......................................................... 35 Merchandise Inventory ................................................................. 7,400 Office Supplies ............................................................................. 400 Furniture and Fixtures .................................................................. 6,000 Notes Payable ........................................................................ 4,000 Accounts Payable................................................................... 10,000 Accrued Interest Payable ....................................................... 100 Allowance for Bad Debts ....................................................... 1,200 Accumulated Depreciation – Furniture and Fixtures ............. 1,400 Pedro Castro, Capital ............................................................. 30,135 To record the investment of Jose Bunag. Cash .. ........................................................................................... 15,067.50 Jose Bunag, Capital ............................................................... 15,067.50

Partnership – Basic Considerations and Formation 11 2. Castro and Bunag Partnership

Statement of Financial Position October 1, 2011

A s s e t s Cash ..... ...... ... ........................................................................................... P21,067.50 Notes receivable .......................................................................................... 3,000.00 Accounts receivable .................................................................................... P 24,000 Less Allowance for bad debts...................................................................... ___1,200 22,800.00 Accrued interest receivable ......................................................................... 35.00 Merchandise inventory ................................................................................ 7,400.00 Office supplies ........................................................................................... 400.00 Furniture and fixtures .................................................................................. 6,000 Less Accumulated depreciation ................................................................... ___1,400 __4,600.00 Total Assets ........................................................................................ P59,302.50

Liabilities and Capital Notes payable ........................................................................................... P 4,000.00 Accounts payable ........................................................................................ 10,000.00 Accrued interest payable ............................................................................. 100.00 Pedro Castro, Capital ................................................................................... 30,135.00 Jose Bunag, Capital ..................................................................................... _15,067.50 Total Liabilities and Capital ............................................................... P59,302.50

Problem 1 – 2

Contributed Capitals: Jose: Capital before adjustment ...................................................... P 85,000 Notes Payable ........................................................................ 62,000 Undervaluation of inventory .................................................. 13,000 Underdepreciation.................................................................. ( 25,000) P 135,000 Pedro: Cash ....................................................................................... 28,000 Pablo: Cash ....................................................................................... 11,000 Marketable securities ............................................................. _57,500 ___68,500 Total contributed capital .............................................................................. P 231,500 Agreed Capitals: Bonus Method: Jose (P231,500 x 50%) ................................................................. P115,750 Pedro (P231,500 x 25%) .............................................................. 57,875 Pablo (P231,500 x 25%)............................................................... __57,875 Total . ........................................................................................... P231,500

12 Chapter 1 Goodwill Method. To have a goodwill, the only possible base is the capital of Pablo. The computation is: Contributed Agreed Capital Capital Goodwill

Jose P135,000 P137,000 (50%) 2,000 Pedro 28,000 68,500 (25%) 40,500 Pablo __68,500 __68,500 (25%) _____– Total P231,500 274,000 42,500 Total agreed capital (P68,500 ÷ 25%) = 274,000

Jose, Pedro and Pablo Partnership Statement of Financial Position

June 30, 2011 Bonus Method Goodwill Method Assets: Cash P 49,000 P 49,000 Accounts receivable (net) 48,000 48,000 Marketable securities 57,500 57,500 Inventory 85,000 85,000 Equipment (net) 45,000 45,000 Goodwill ______– __42,500 Total P284,500 P327,000 Liabilities and Capital: Accounts payable P 53,000 P 53,000 Jose, capital (50%) 115,750 137,000 Pedro, capital (25%) 57,875 68,500 Pablo, capital (25%) __57,875 __68,500 Total P284,500 P327,000

Problem 1 – 3

1. Books of Pepe Basco To adjust the assets. a. Pepe Basco, Capital ...................................................................... 3,200 Estimated Uncollectible Account .......................................... 3,200 b. Pepe Basco, Capital ...................................................................... 500 Accumulated Depreciation – Furniture and Fixtures ............. 500

Partnership Basic Considerations and Formation 13 To close the books. Estimated Uncollectible Account ....................................................... 4,800 Accumulated Depreciation – Furniture and Fixtures .......................... 1,500 Accounts Payable ................................................................................ 3,600 Pepe Basco, Capital ............................................................................ 31,500 Cash .. ........................................................................................... 400 Accounts Receivable .................................................................... 16,000 Merchandise Inventory ................................................................. 20,000 Furniture and Fixtures .................................................................. 5,000 2. Books of the Partnership To record the investment of Pepe Basco. Cash .... ... ........................................................................................... 400 Accounts Receivable .......................................................................... 16,000 Merchandise Inventory ....................................................................... 20,000 Furniture and Fixtures ......................................................................... 5,000 Estimated Uncollectible account .................................................. 4,800 Accumulated Depreciation – Furniture and Fixtures ................... 1,500 Accounts Payable ......................................................................... 3,600 Pepe Basco, Capital ...................................................................... 31,500 To record the investment of Carlo Torre. Cash .... ... ........................................................................................... 47,250 Carlo Torre, Capital ..................................................................... 47,250 Computation: Pepe Basco, capital (Base) ........................................................... P31,500 Divide by Pepe Basco's P & L ratio ............................................. ___40% Total agreed capital ...................................................................... P78,750 Multiply by Carlo Torre's P & L ratio .......................................... ___60% Cash to be invested by Carlo Torre .............................................. P47,250

Problem 1 – 4 a. Roces' books will be used by the partnership

Books of Sales 1. Adjusting Entries (a) Sales, Capital ......................................................................... 3,200 Accumulated Depreciation – Fixtures ............................... 3,200 (b) Goodwill ................................................................................ 32,000 Sales, Capital ..................................................................... 32,000

14 Chapter 1 2. Closing Entry Allowance for Bad Debts ............................................................. 12,800 Accumulated Depreciation – Delivery Equipment ...................... 8,000 Accumulated Depreciation – Fixtures .......................................... 91,200 Accounts Payable ......................................................................... 64,000 Notes Payable ............................................................................... 40,000 Accrued Taxes .............................................................................. 8,000 Sales, Capital ................................................................................ 224,000 Cash ....................................................................................... 4,800 Accounts Inventory ................................................................ 72,000 Merchandise Inventory .......................................................... 192,000 Prepaid Insurance................................................................... 3,200 Delivery Equipment ............................................................... 48,000 Fixtures .................................................................................. 96,000 Goodwill ................................................................................ 32,000

Books of Roces (Books of the Partnership) 1. Adjusting Entries (a) Roces, Capital .............................................................................. 1,600 Allowance for Bad Debts ....................................................... 1,600 (b) Accumulated Depreciation – Fixtures .......................................... 16,000 Roces, Capital ........................................................................ 16,000 (c) Merchandise Inventory ................................................................. 8,000 Roces, Capital ........................................................................ 8,000 (d) Goodwill ....................................................................................... 40,000 Roces, Capital ........................................................................ 40,000 2. To record the investment of Sales. Cash .... ... ........................................................................................... 4,800 Accounts Receivable .......................................................................... 72,000 Merchandise Inventory ....................................................................... 192,000 Prepaid Insurance ................................................................................ 3,200 Delivery Equipment ............................................................................ 48,000 Fixtures ... ........................................................................................... 96,000 Goodwill . ........................................................................................... 32,000 Allowance for Bad Debts ............................................................. 12,800 Accumulated Depreciation – Delivery Equipment ...................... 8,000 Accumulated Depreciation – Fixtures .......................................... 91,200 Accounts Payable ......................................................................... 64,000 Notes Payable ............................................................................... 40,000 Accrued Taxes .............................................................................. 8,000 Sales, Capital ................................................................................ 224,000

Partnership – Basic Considerations and Formatio 15 b. Sales' books will be used by the partnership

Books of Roces 1. Adjusting Entries See Requirement (a). 2. Closing Entry Allowance for Bad Debts ............................................................. 1,600 Accumulated Depreciation – Delivery Equipment ...................... 12,800 Accumulated Depreciation – Fixtures .......................................... 64,000 Accounts Payable ......................................................................... 104,000 Accrued Taxes .............................................................................. 6,400 Roces, Capital .............................................................................. 224,000 Cash ....................................................................................... 14,400 Accounts Receivable ............................................................. 57,600 Merchandise Inventory .......................................................... 132,800 Prepaid Insurance................................................................... 4,800 Delivery Equipment ............................................................... 19,200 Fixtures .................................................................................. 144,000 Goodwill ................................................................................ 40,000

Books of Sales (Books of the Partnership) 1. Adjusting Entries See Requirement (a). 2. To record the investment of Roces. Cash .... ... ........................................................................................... 14,400 Accounts Receivable .......................................................................... 57,600 Merchandise Inventory ....................................................................... 132,800 Prepaid Insurance ................................................................................ 4,800 Delivery Equipment ............................................................................ 19,200 Fixtures ... ........................................................................................... 144,000 Goodwill . ........................................................................................... 40,000 Allowance for Bad Debts ............................................................. 1,600 Accumulated Depreciation – Delivery Equipment ...................... 12,800 Accumulated Depreciation – Fixtures .......................................... 64,000 Accounts Payable ......................................................................... 104,000 Accrued Taxes .............................................................................. 6,400 Roces, Capital .............................................................................. 224,000

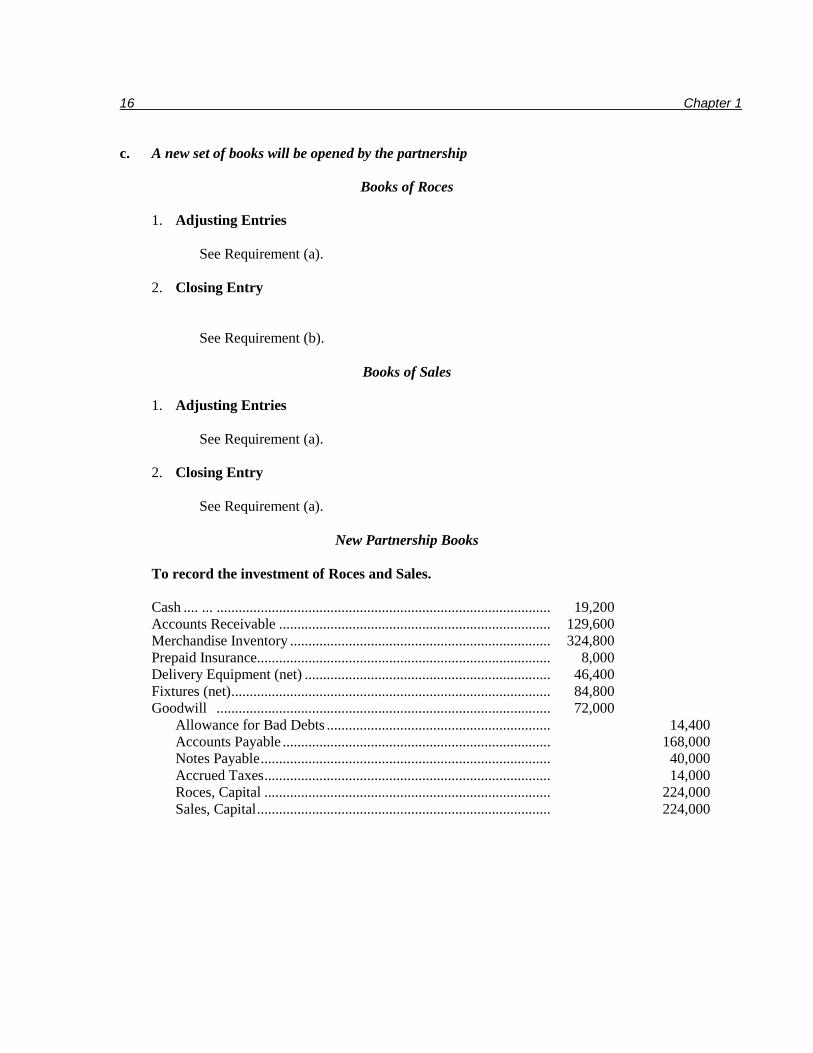

16 Chapter 1 c. A new set of books will be opened by the partnership

Books of Roces 1. Adjusting Entries See Requirement (a). 2. Closing Entry See Requirement (b).

Books of Sales 1. Adjusting Entries See Requirement (a). 2. Closing Entry See Requirement (a).

New Partnership Books To record the investment of Roces and Sales. Cash .... ... ........................................................................................... 19,200 Accounts Receivable .......................................................................... 129,600 Merchandise Inventory ....................................................................... 324,800 Prepaid Insurance ................................................................................ 8,000 Delivery Equipment (net) ................................................................... 46,400 Fixtures (net) ....................................................................................... 84,800 Goodwill ........................................................................................... 72,000 Allowance for Bad Debts ............................................................. 14,400 Accounts Payable ......................................................................... 168,000 Notes Payable ............................................................................... 40,000 Accrued Taxes .............................................................................. 14,000 Roces, Capital .............................................................................. 224,000 Sales, Capital ................................................................................ 224,000

Partnership – Basic Considerations and Formation 17

Problem 1 – 5 1. To close Magno's books. Allowance for Bad Debts .................................................................... 1,000 Accounts Payable ................................................................................ 6,000 Notes Payable ..................................................................................... 10,000 Accrued Interest Payable .................................................................... 300 R. Magno, Capital ............................................................................... 24,700 Cash .. ........................................................................................... 5,000 Accounts Receivable .................................................................... 13,000 Merchandise Inventory ................................................................. 12,000 Equipment .................................................................................... 3,000 Other Assets ................................................................................. 9,000 2. To adjust the books of Lagman. Goodwill . ........................................................................................... 8,000 Allowance for Bad Debts ............................................................. 210 J. Lagman, Capital ........................................................................ 7,790 3. To record the investment of Magno. Cash .... ... ........................................................................................... 5,000 Accounts Receivable .......................................................................... 13,000 Merchandise Inventory ....................................................................... 12,000 Equipment ........................................................................................... 3,000 Other Assets ........................................................................................ 9,000 Allowance for Bad Debts ............................................................. 1,000 Accounts Payable ......................................................................... 6,000 Notes Payable ............................................................................... 10,000 Accrued Interest Payable .............................................................. 300 R. Magno, Capital ........................................................................ 24,700 To adjust the investments of the partners. Cash .... ... ........................................................................................... 10,300 R. Magno, Capital ........................................................................ 10,300 (P35,000 – P24,700 = P10,300) J. Lagman, Capital .............................................................................. 35,790 Cash .. ........................................................................................... 23,300 Accounts Payable to J. Lagman ................................................... 12,490 (P63,000 + P7,790 = P70,790 – P35,000 = P35,790)

18 Chapter 1

4. Lagman and Magno Statement of Financial Position

December 31, 2011

A s s e t s Cash .... ... ........................................................................................... P – Accounts receivable ............................................................................ P34,000 Less Allowance for bad debts ............................................................. 1,210 32,790 Merchandise inventory ....................................................................... 21,000 Equipment ........................................................................................... 8,000 Other assets ......................................................................................... 46,000 Goodwill ........................................................................................... ___8,000 Total Assets .................................................................................. P115,790

Liabilities and Capital Accounts payable ................................................................................ P 18,000 Notes payable...................................................................................... 15,000 Accrued interest payable ..................................................................... 300 Accounts payable to J. Lagman .......................................................... 12,490 J. Lagman, capital ............................................................................... 35,000 R. Magno, capital ................................................................................ __35,000 Total Liabilities and Capital ......................................................... P115,790

Problem 1 – 6

1. Books of Toledo Toledo, Capital ............................................................................. 4,800 Allowance for Bad Debts (15% x P32,000) .......................... 4,800 Books of Ureta Ureta, Capital ............................................................................... 2,400 Allowance for Bad Debts (10% x P24,000) .......................... 2,400 Cash (90% x P12,000) .................................................................. 10,800 Loss from Sale of Office Equipment ............................................ 1,200 Office Equipment................................................................... 12,000 Toledo, Capital (1/4 x P1,200) ..................................................... 300 Ureta, Capital ............................................................................... 900 Loss from Sale of Office Equipment ..................................... 1,200

Partnership – Basic Considerations and Formation 19 2. New Partnership Books Cash .. ........................................................................................... 3,200 Accounts Receivable .................................................................... 32,000 Merchandise ................................................................................. 40,000 Office Equipment ......................................................................... 10,000 Allowance for Bad Debts ....................................................... 4,800 Accounts Payable................................................................... 10,000 Notes Payable ........................................................................ 2,000 Toledo, Capital ...................................................................... 68,400 To record the investment of Toledo. Cash .. ........................................................................................... 22,800 Accounts Receivable .................................................................... 24,000 Merchandise ................................................................................. 36,000 Toledo, Capital ............................................................................. 300 Allowable for Bad Debts ....................................................... 2,400 Accounts Payable................................................................... 16,000 Ureta, Capital ......................................................................... 64,700 To record the investment of Ureta. 3. Cash .... ... ........................................................................................... 3,400 Ureta, Capital ............................................................................... 3,400 To record Ureta's cash contribution. Computation: Toledo, capital (P68,400 – P300) ................................................. P 68,100 Divide by Toledo's profit share percentage .................................. ____50% Total agreed capital of the partnership ......................................... P136,200 Multiply by Ureta's profit share percentage ................................. ____50% Agreed capital of Ureta ................................................................ P 68,100 Ureta, capital ................................................................................ __64,700 Cash contribution of Ureta ........................................................... P 3,400

or Toledo, capital (P68,400 – P300) ................................................. P 68,100 Less Ureta, capital ........................................................................ __64,700 Cash contribution of Ureta ........................................................... P 3,400

20 Chapter 1 4. Toledo and Ureta Partnership

Statement of Financial Position July 1, 2011

A s s e t s

Cash .... ... ........................................................................................... P 29,400 Accounts receivable ............................................................................ P56,000 Less Allowance for bad debts ............................................................. __7,200 48,800 Merchandise ........................................................................................ 76,000 Office equipment ................................................................................ __10,000 Total Assets .................................................................................. P164,200

Liabilities and Capital Accounts payable ................................................................................ P 26,000 Notes payable...................................................................................... 2,000 Toledo, capital .................................................................................... 68,100 Ureta, capital ....................................................................................... __68,100 Total Liabilities and Capital ......................................................... P164,200

Partnership Operations 21

CHAPTER 2

MULTIPLE CHOICE ANSWERS AND SOLUTIONS 2-1: d Jordan Pippen Total Annual salary P120,000 P80,000 P200,000 Balance, equally ( 10,000) ( 10,000) ( 20,000) Total P110,000 P 70,000 P180,000 2-2: a JJ KK LL Total Bonus (.20 X P90,000) P18,000 – – P 18,000 Interest JJ (.15 X P100,000) P15,000 – –) KK (.15 X P200,000) P 30,000 –) LL (.15 X P300,000) P45,000) 90,000 Balance, equally ( 6,000) ( 6,000) ( 6,000) ( 18,000) Total profit share P27,000 P 24,000 P39,000 P 90,000 2-3: a 2-4: a Allan Michael Total Interest Allan - .10 X (P40,000 + 60,000 /2) P 5,000 ) Michael - .10 X (P60,000 + 70,000/2) P 6,500) P 11,500 Balance, equally _14,000 _14,000 __28,000 Total P 19,000 P20,500 P 28,000 2-5: a Fred Greg Henry Total Interest (.10 of average capital) P12,000 P 6,000 P 4,000 P 22,000 Salaries 30,000 20,000 50,000 Balance, equally ( 35,000) ( 35,000) ( 35,000) (105,000) Total P 7,000 ( P29,000) (P11,000) (P 33,000) 2-6: b Average Capital Capital Months Peso Date Balance Unchanged Months January 1 140,000 6 P 840,000 July 1 180,000 1 180,000 August 1 165,000 5 __825,000 12 P1,845,000 Average capital - P1,845,000/12 = P153,750 Interest (P153,750 X 10%) = P 15,375

22 Chapter 2 2-7: c Capital Months Peso Date Balance Unchanged Months January 1 P16,000 3 P 48,000 April 1 17,600 2 35,200 June 1 19,200 3 57,600 September 1 15,200 4 __60,800 12 P201,600 Average Capital(P201,600/12) = P16,800 2-8: a Net profit before bonus P 24,000 Net profit after bonus (P24,000/120%) __20,000 Bonus to RJ 4,000 Balance (P24,000-P4,000)X3/5 __12,000 Total profit share P 16,000 2-9: a LT AM Total Interest P3,200 P 3,600 P 6,800 Salaries 15,000 7,500 22,500 Balance, 3:2 (11,580) ( 7,720) ( 19,300) Total P 6,620 P 3,380 P 10,000 2-10: b Net income after salary, interest and bonus P467,500 Add back: Salary (P10,000 X 12) P120,000 Interest (P250,000 X .05) __12,500 _132,500 Net income after bonus (80%) P600,000 Net income before bonus (P600,000/80%) _750,000 Paul's bonus P150,000 2-11: b CC DD EE Total Salary P 14,000 P 14,000 Balance P14,000 P 8,400 5,600 28,000 Additional profit to DD ( 1,500) __2,100 ( 600) ______– Total P12,500 P10,500 P 19,000 P 42,000 Net income Fees Earned P90,000 Expenses _48,000 Net Income P42,000

Partnership Operations 23 2-12: c LL MM NN Total Interest P 2,000 P 1,250 P 750 P 4,000 Annual Salary 8,500 – – 8,500 Additional profit to give LL, P20,000 9,500 5,700 3,800 19,000* Additional profit to give MM, P14,000 _____– __7,050 _____– __7,050 Total P20,000 P14,000 P 4,550 P 38,550 *(P9,500/50%) = P19,000 2-13: a RR SS TT Total Excess (Deficiency) RR (P80,000 - P95,000) P15,000 – –) SS (P50,000 - P40,000) – (P10,000) –) P 5,000 Balance 4:3:1 _47,500 _35,625 _11,875 __95,000 Total P62,500 P25,625 P11,875 P100,000 Net Income (200,000 - 100,000) = P100,000 2-14: b AA BB CC Total AA - 100,000 X 10% P 10,000 ) 150,000 X 20% 30,000 ) P 40,000 Remainder, 210,000 BB (60,000 X .05) P 3,000 ) CC (60,000 X .05) P 3,000 6,000 Balance, equally __68,000 _68,000 _68,000 _204,000 Total P108,000 P71,000 P71,000 P250,000 2-15: a AJ BJ CJ Total Bonus to CJ Net profit before bonus P44,000 Net profit after bonus (P44,000/110%)P40,000 – – P4,000 P4,000 Interest to BJ – P1,000 – 1,000 Salaries P 10,000 – 12,000 22,000 Balance, 4:4:2 __6,800 _6,800 __3,400 _17,000 Total P 16,800 P7,800 P19,400 P44,000 2-16: c Total profit share of Pedro P200,000 Less: Salary to Pedro P 50,000 Interest __20,000 __70,000 Share in the balance (40%) P130,000 Net profit after salary and interest (130,000/40%) P325,000 Add: Total Salaries P150,000 Total Interest __70,000 _220,000 Total Partnership Income P545,000

24 Chapter 2 2-17: c Net income before extraordinary gain and bonus (69,600-12,000) P 57,600 Net income after bonus (57,600/120%) _48,000 Bonus to RR P 9,600 Distribution of Net Income: JJ RR Total Bonus – P 9,600 P 9,600 Balance, equally P 24,000 24,000 48,000 Net profit before extraordinary gain P 24,000 P 33,600 P 57,600 Extraordinary gain __4,800 __7,200 _12,000 Total P 28,800 P 40,800 P 69,600 2-18: a Mel Jay Total Interest P 20,000 P 12,000 P 32,000 Annual Salary 36,000 – 36,000 Remainder 60:40 __60,000 _40,000 _100,000 Total P116,000 P 52,000 P168,000 2-19: a DV JE FR Total Interest on excess (Deficiency) P 15,000 P 3,750 (P 7,500) P 11,250 Remainder 5:3:2 ( 36,875) ( 22,125) ( 14,750) ( 73,750) Total (P 21,875) (P 18,375) (P 22,250) (P 62,500) 2-20: c Correction of 1998 profit: Net income per books P 19,500 Understatement of depreciation ( 2,100) Overstatement of inventory, December 31 ( 11,400) Adjusted net income P 6,000 Pete Rico Total Distribution of net income per book: Equally P 9,750 P 9,750 P 19,500 Distribution of adjusted net income Equally ( 3,000) ( 3,000) ( 6,000) Required Decrease P 6,750 P 6,750 P 13,500 2-21: a Tiger Woods Total Salaries P 64,000 P100,000 P164,000 Interest 24,000 30,000 54,000 Bonus (P360,000-P54,000)X.25 76,500 – 76,500 Remainder, 30:70 __19,650 __45,850 __65,500 Total P184,150 P175,850 P360,000

Partnership Operations 25 2-22: a Clotty Cotto Total Salaries P 20,000 – P 20,000 Commission – P 25,000 25,000 Interest 32,000 33,600 65,600 Bonus, schedule 1 30,000 – 30,000 Remainder, 60:40 __35,640 _23,760 __59,400 Total P117,640 P 82,360 P200,000 Schedule 1 Net income before salary, commission, interest and bonus P200,000 Less: salaries __20,000 Net income before bonus P180,000 Net income after bonus (P180,000/120%) _150,000 Bonus P 30,000 2-23: a Mike Tyson Total Capital balance, beginning P600,000 P400,000 P1,000,000 Additional investment 100,000 200,000 300,000 Capital withdrawal -200,000 ( 100,000) _-300,000 Capital balance before profit and loss distribution P500,000 P500,000 P1,000,000 Net income: Salary P200,000 P300,000 P 500,000 Balance, 3:2 __60,000 __40,000 __100,000 Total P260,000 P340,000 P 600,000 Total P760,000 P840,000 P1,600,000 Drawings ( 200,000) ( 300,000) ( 500,000) Capital balance, end P560,000 P540,000 P1,100,000 2-24: d Average Capital - King: Capital Months Peso Date Balance Unchanged Months January 1 P40,000 3 P120,000 April 1 55,000 9 _495,000 12 P615,000 Average capital – P615,000/12 = P51,250 Average Capital - Queen: Capital Months Peso Date Balance Unchanged Months January 1 P100,000 7 P700,000 April 1 130,000 5 __650,000 12 P1,350,000 Average capital - P1,350,000 / 12 =P112,500

26 Chapter 2 2-24: Continued Distribution of Net Income - Schedule 1 King Queen Total Interest P 5,125 P11,250 P16,375 Bonus, Schedule 2 12,725 – 12,725 Salaries 25,000 30,000 55,000 Residual, 50:50 ( 2,050) _(2,050) _(4,100) Total P40,800 P39,200 P80,000 Schedule 2 Net income before allocation P80,000 Less: Interest _16,375 Net income before bonus P63,625 Net income after bonus (P63,625/125%) _50,900 Bonus P12,725 Capital Balance December 31: King Queen Total Capital balance, January 1 P40,000 P100,000 P140,000 Additional investment _15,000 __30,000 __45,000 Capital balance before profit and loss distribution P55,000 P130,000 P185,000 Net income (Schedule 2) 40,800 39,000 80,000 Drawings (P400 X 52) ( 20,800) ( 20,800) ( 41,600) Capital balance, December 31 P75,000 P148,400 P223,400 2-25: d Total receipts (P1,500,000 + P1,625,000) P3,125,000 Expenses ( 1,080,000) Net income P2,045,000 Distribution to Partners Red – P1,500,000/P3,125,000 X P2,045,000 = P 981,600 (1) Blue – P1,625,000/P3,125,000 X P2,045,000 = _1,063,400 P2,045,000 Capital balance of Blue Dec. 31 Capital Balance, Jan. 1 P 374,000 Additional investment ___22,000 Capital balance before profit and loss distribution P 396,000 Profit share 1,063,400 Drawings ( 750,000) Capital balance, Dec. 31 P 709,400 (2)

Partnership Operations 27 2-26: a Ray Sam Total Capital balances, March 1 P150,000 P180,000 P330,000 Additional investment, Nov. 1 _______ __60,000 __60,000

Capital balances before salaries, profit and Drawings 150,000 240,000 390,000 Profit share: Interest 15,000 20,000 35,000 Balance, 60:40 51,000 34,000 85,000

Total 66,000 54,000 120,000

Total 216,000 294,000 510,000 Salaries _18,000 _24,000 _42,000

Total 234,000 318,000 552,000 Drawings (18,000) (24,000) (42,000)

Capital balances, Feb. 28 P216,000 P294,000 P510,000 2-27: a Susan Tanny Total Capital balances, 1/1 P150,000 P30,000 P180,000 Additional investment, 4/1 8,000 8,000 Capital withdrawals, 7/1 _______ (6,000) _(6,000)

Balances before profit distribution 158,000 24,000 182,000 Profit distribution: Interest 23,400 4,050 27,450 Bonus (20% x P30,000) 6,000 6,000 Balance, equally (1,725) (1,725) (3,450)

Total 21,675 _8,325 30,000

Total 179,675 32,325 212,000 Drawings (12,000) (12,000) (24,000)

Capital balances, 12/31 P167,675 P20,325 P188,000

28 Chapter 2 2-28: a Sin Tan Uy Total Capital balances, beg. 1st year P110,000 P80,000 P110,000 P300,000 Loss distribution, 1st year: Salaries 20,000 10,000 30,000 Interest 11,000 8,000 11,000 30,000 Balance, 5:3:2 (40,000) (16,000) (24,000) (80,000) Total ( 9,000) ( 8,000) ( 3,000) (20,000) Total 101,000 72,000 107,000 280,000 Drawings (10,000) (10,000) (10,000) (30,000) Capital balances, beg. 2nd year 91,000 62,000 97,000 250,000 Profit distribution, 2nd year: Salaries 20,000 10,000 30,000 Interest 9,100 6,200 9,700 25,000 Balance, 5:3:2 ( 7,500) ( 4,500) ( 3,000) (15,000) Total 21,600 _1,700 16,700 40,000 Total 112,600 63,700 113,700 290,000 Drawings _(10,000) (10,000) _(10,000) _(30,000) Capital balances, end of 2nd year P102,600 P53,700 P103,700 P260,000 2-29: c Jay Kay Loi Total Capital balances, 1/1/06 P30,000 P30,000 P30,000 P90,000 Additional investment, 2006 5,000 5,000 Capital withdrawal, 2006 _(5,000) _(4,000) ______ _(9,000) Capital balances 25,000 26,000 35,000 86,000 Profit distribution, 2006: Interest 3,000 3,000 3,000 9,000 Salary 7,000 7,000 Balance, equally _1,000 _1,000 _1,000 __3,000 Capital balances, 1/1/07 36,000 30,000 39,000 105,000 Additional investment, 2007 5,000 5,000 Capital withdrawal, 2002 ______ _(3,000) _(8,000) (11,000) Capital balances 41,000 27,000 31,000 99,000 Profit distribution, 2007: Interest 3,600 3,000 3,900 10,500 Salary 7,000 7,000 Balance, equally _1,500 _1,500 _1,500 __4,500 Capital balances, 1/1/08 53,100 31,500 36,400 121,000 Additional investment, 2008 6,000 6,000 Capital withdrawal, 2008 ______ _(4,000) _(2,000) _(6,000) Capital balances 53,100 27,500 40,400 121,000 Profit distribution, 2008: Interest 5,310 3,150 3,640 12,100 Salary 7,000 7,000 Balance, equally __3,300 __3,300 __3,300 ___9,900 Capital balances, 12/31/08 per books P68,710 P33,950 P47,340 P150,000 Understatement of depreciation (2,000) (2,000) (2,000) (6,000) Adjusted capital balances, 12/31/08 P66,710 P31,950 P45,340 P144,000

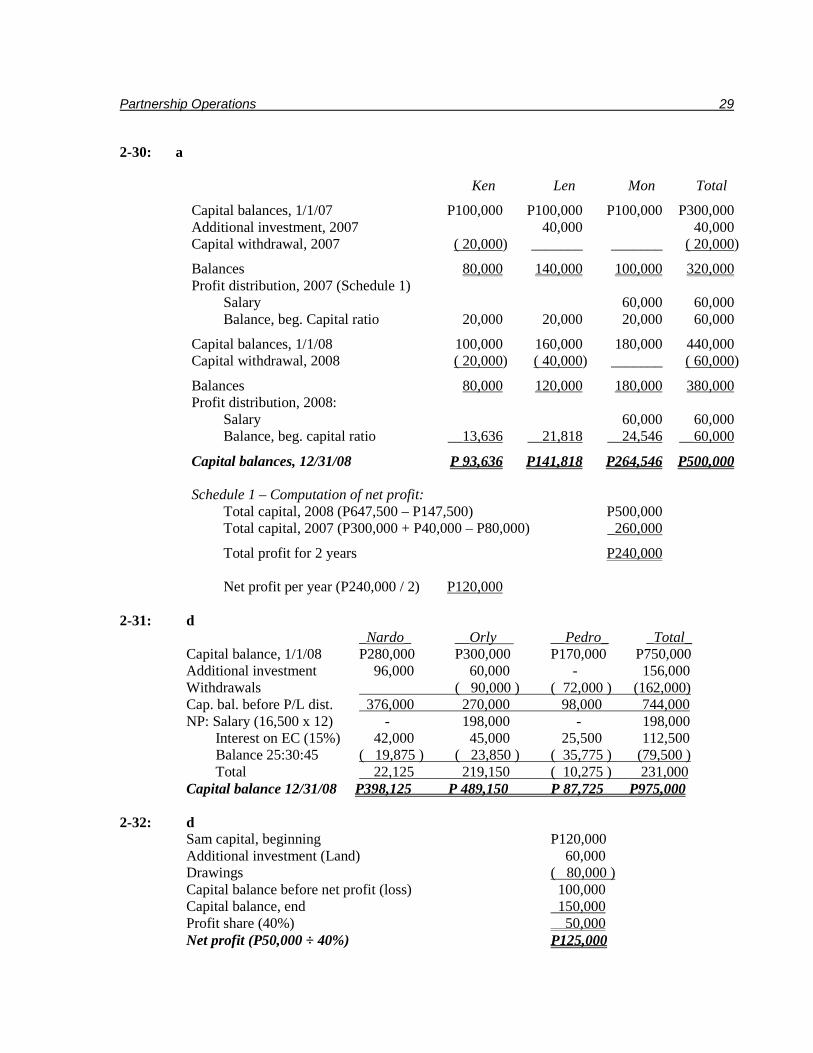

Partnership Operations 29 2-30: a Ken Len Mon Total

Capital balances, 1/1/07 P100,000 P100,000 P100,000 P300,000 Additional investment, 2007 40,000 40,000 Capital withdrawal, 2007 ( 20,000) _______ _______ ( 20,000)

Balances 80,000 140,000 100,000 320,000 Profit distribution, 2007 (Schedule 1) Salary 60,000 60,000 Balance, beg. Capital ratio 20,000 20,000 20,000 60,000

Capital balances, 1/1/08 100,000 160,000 180,000 440,000 Capital withdrawal, 2008 ( 20,000) ( 40,000) _______ ( 60,000)

Balances 80,000 120,000 180,000 380,000 Profit distribution, 2008: Salary 60,000 60,000 Balance, beg. capital ratio __13,636 __21,818 __24,546 __60,000

Capital balances, 12/31/08 P 93,636 P141,818 P264,546 P500,000 Schedule 1 – Computation of net profit: Total capital, 2008 (P647,500 – P147,500) P500,000 Total capital, 2007 (P300,000 + P40,000 – P80,000) _260,000

Total profit for 2 years P240,000 Net profit per year (P240,000 / 2) P120,000 2-31: d _Nardo_ __Orly __Pedro_ _Total_ Capital balance, 1/1/08 P280,000 P300,000 P170,000 P750,000 Additional investment 96,000 60,000 - 156,000 Withdrawals ( 90,000 ) ( 72,000 ) (162,000) Cap. bal. before P/L dist. 376,000 270,000 98,000 744,000 NP: Salary (16,500 x 12) - 198,000 - 198,000 Interest on EC (15%) 42,000 45,000 25,500 112,500 Balance 25:30:45 ( 19,875 ) ( 23,850 ) ( 35,775 ) (79,500 ) Total 22,125 219,150 ( 10,275 ) 231,000 Capital balance 12/31/08 P398,125 P 489,150 P 87,725 P975,000 2-32: d Sam capital, beginning P120,000 Additional investment (Land) 60,000 Drawings ( 80,000 ) Capital balance before net profit (loss) 100,000 Capital balance, end 150,000 Profit share (40%) 50,000 Net profit (P50,000 ÷ 40%) P125,000

30 Chapter 2 2-33: a __Joe__ __Tom__ __Total__ Capital balance, 1/2/07 P 80,000 P 40,000 P120,000 Net loss- 2007: Annual salary 96,000 48,000 144,000 10% interest on beg. capital 8,000 4,000 12,000 Bal. beg. cap. ratio: 8:4 ( 108,000) ( 54,000) ( 162,000) Total ( 4,000) ( 2,000) ( 6,000) Capital balance 76,000 38,000 114,000 Drawings ( 4,000) ( 4,000) ( 8,000) Capital balance, 12/31/07 72,000 34,000 106,000 Net profit- 2008: Annual salary 96,000 48,000 144,000 10% interest on BC 7,200 3,400 10,600 Bonus to Joe–NPBB – P 22000 NPAB (22000/110%)20000 2,000 2,000 Balance equally ( 67,300) ( 67,300) ( 134,600) Total 37,900 ( 15,900) 22,000 Total 109,900 18,100 128,000 Drawings ( 4,000) ( 4,000) ( 8,000) Capital balance, 12/31/08 105,900 14,100 120,000 2-34: a Decrease in capital P 60,000 Drawings ( 130,000) Contribution 25,000 Profit share 45,000 Net income (45,000 ÷ 30) P150,000 2-35: b

2009: Original profit allocation Cris Paul Bryan Total Salaries P 80,000 P 60,000 P 60,000 P200,000 Balance of profit 100,000 100,000 100,000 300,000 Total P180,000 P160,000 P160,000 P500,000 Revised profit allocation Salaries P 80,000 P 60,000 P 60,000 P200,000 Interest on capital (Sch. A) 7,500 13,200 5,700 26,400 Balance of profit 91,200 91,200 91,200 273,600 Total P178,799 P164,400 P156,900 P500,000 Difference in total P 1,300 P (4,400) P 3,100 P 0

Partnership Operations 31 2-35: Continued 2010

Original profit allocation: Cris Paul Bryan Total Salaries P 80,000 P 60,000 P 60,000 P200,000 Balance of profit 70,000 70,000 70,000 210,000 Total P150,000 P130,000 P130,000 P410,000 Revised allocation: Salaries P 80,000 P 60,000 P 60,000 P200,000 Interest on capital (Sch. B) 3,944 2,428 3,528 9,900 Balance of profit 66,700 P 66,700 P 66,700 P200,000 Total P150,644 P129,128 P130,228 P410,000 Difference in totals P (644) P 872 P (228) P 0 Total of differences P 656 P (3,528) P 2,872 P 0

Therefore Paul capital should be increased by P3,528 Schedule A: Revised Computation of Interest on Average Capital

Capital Fraction of Average Partner Date Balance Year Unchanged Capital Cris January 1 P180,000 3/12 P45,000 March 31 30,000 6/12 15,000 September 30 10,000 3/12 2,500 P62,500 Paul January 1 P250,000 3/12 P62,500 March 31 80,000 6/12 40,000 September 30 30,000 3/12 7,500 P110,000 Bryan January 1 P60,000 9/12 P45,000 September 30 10,000 3/12 2,500 P47,500

Interest at 12%: Cris: P62,500 x 12% = P7,500 Paul: P110,000 x 12%= P13,200 Bryan: P47,500 x 12% = P5,700

32 Chapter 2 2-35: Continued Schedule B: Revised Computation of Interest on Average Capital

Capital Fraction of Average Partner Date Balance Year Unchanged Capital Cris January 1 P188,700 1/12 P15,725 March 31 18,700 11/12 17,142 P32,867 Paul January 1 P194,400 1/12 P16,200 March 31 4,400 11/12 4,033 P20,233 Bryan January 1 P166,900 1/12 P13,908 September 30 16,900 11/12 15,492 P29,400

Interest at 12%: Cris: P32,867 x 12% = P3,944 Paul: P20,233 x 12%= P2,428 Bryan: P29,400 x 12% = P3,528 2-36: a

Gabriel Harry Cumulative Total Salaries P35,000 P40,000 P 75,000 Bonus (Sch. A) 12,000 87,000 Interest on capital (Sch. B) 11,467 5,333 103,800 Remainder of profit 11,280 16,920 132,000 Total P69,747 P62,253

Schedule A: Computation of Bonus to Gabriel Bonus = 10% (net income – Bonus) 110% Bonus = 10% (net income) 110% Bonus = P13,200 Bonus = P12,000 Schedule B: Calculation of average capital balances:

Partner Date Capital Balance Fraction Average Capital Gabriel January 1 P120,000 3/12 P 30,000 April 1 140,000 512 58,333 November 1 170,000 2/12 28,333 November 1 160,000 2/12 26,667 P143,333

Partnership Operations 33 2-36: Continued:

Partner Date Capital Balance Fraction Average Capital Harry January 1 60,000 10/12 P50,000 November 1 100,000 2/12 16,667 P66,667

Interest therefore: Gabriel: P143,333 x 8% = P11,467 Harry: P66,667 x 8% = P5,333 2-37: a Adjustments to Income:

2009 2010 Amortization of business name P(5,000) P (5,000) Prepaid expenses, 2009 3,000 (3,000) Accrued expenses, 2009 (2,000) 2,000 Fees billed in 2010 8,400 (8,400) Inventory overstatement 4,000 Accrued expenses, 2010 (8,600) Accrued income, 2010 (3,000) Adjustments to income P 4,400 P(22,000)

Computations of Adjusted Capital Balances:

Cory Dory Eva Unadjusted balances, December 31, 2010 P25,000 P30,000 P28,000 Bonus to Cory on change in 2009 income (Sch. 1) 400 Allocation of remaining adjustments to 2009 income 1,200 1,200 1,600 Bonus to Cory on change in 2010 income (Sch. 2) (2,000) Allocation of remaining adjustments to 2010 income (7,000) (7,000) (6,000) Correction of capital withdrawal (5,000) Adjusted capital balances, December 31, 2010 P12,600 P24,200) P23,600

Schedule 1: Bonus = 10% (1 - Bonus) Bonus = 10% (P4,400 – Bonus) 110% Bonus = P440 Bonus = P400 Schedule 2: Bonus = 10% )1 – Bonus) Bonus = 10% (P22,000 – Bonus) 110% Bonus = (P2,200) Bonus = (P2,000)

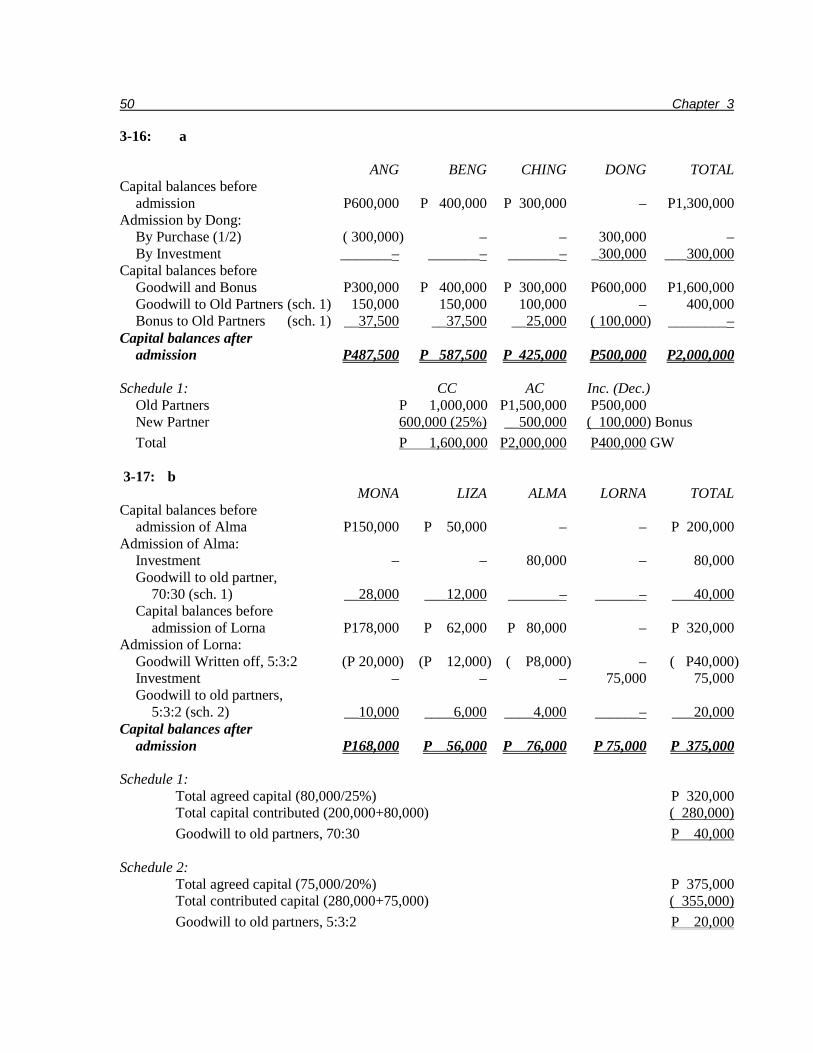

34 Chapter 2 2-38: b Old Partners Capital Balances before Admission of New Partner:

Alma Betty Total Capital balances, March 1, 2009 P480,000 P240,000 P720,000 2009 net loss: Salaries (10 months) 480,000 240,000 720,000 Interest on beginning capital balances 48,000 24,000 72,000 Balance, beginning capital ratio (552,000) (276,000) (828,000) Total (24,000) (12,000) (36,000) Total 456,000 228,000 684,000 Drawings (24,000) (24,000) (48,000) Capital balances, 1/1/2010 432,000 204,000 636,000 2010 net profit: Salaries

576,000

288,000

864,000

Interest on beginning capital balances 43,200 20,400 63,600 Balance, equally (397,800) (397,800) (795,600) Total 221,400 (89,400) 132,000 Total 653,400 114,600 768,000 Drawings (24,000) (24,000) (48,000) Capital balances, 12/31/010 P629,400 P90,600 P720,000

Contributed capital of new partner Cora P400,000 Agreed capital of Cora (P720,000 + P400,000) x 40% 448,000 Bonus from Alma and Betty, original capital ratio(reduction from capital) P 48,000 Therefore entry a is correct.

Partnership Operations 35

SOLUTIONS TO PROBLEMS

Problem 2 – 1

1. Castro : (P26,000/P42,500) x P23,800 = P14,560 Diaz : (P16,500/P42,500) x P23,800 = __9,240 P23,800 2. Castro : (P31,250/P50,000) x P23,800 = P14,875 Diaz : (P18,750/P50,000) x P23,800 = __8,925 P23,800 Computation of Average Capitals: Castro: Capital Months Peso Date Balances Unchanged Months 1/1 ..................................... P26,000 3 P 78,000 4/10 ................................... 29,000 1 29,000 5/1 ..................................... 36,000 3 108,000 8/1 ..................................... 32,000 5 _160,000 12 P375,000 Average capital = P375,000 ÷ 12 months = P31,250 Diaz: Capital Months Peso Date Balances Unchanged Months 1/1 ..................................... P16,500 5 P 82,500 6/1 ..................................... 21,500 3 64,500 9/1 ..................................... 19,500 4 __78,000 12 P225,000 Average capital = P225,000 – 12 months = P18,750 3. Castro Diaz Total Interest ........................................................ P 7,500 P4,500 P12,000 Salaries ........................................................ 36,000 24,000 60,000 Balance, equally .......................................... ( 24,100) (24,100) ( 48,200) Total ............................................................ P19,400 P 4,400 P23,800 4. Castro Diaz Total Bonus (a) .................................................... P 4,760 P – P 4,760 Interest (b) ................................................... 1,100 – 1,100 Balance, 3:2 ................................................ _10,764 _7,176 _17,940 Total ............................................................ P16,624 P7,176 P23,800

36 Chapter 2 Computations: a. Net profit before bonus................................................. P23,800 Net profit after bonus (P23,800 ÷ 125%) ..................... _19,040 Bonus ............................................................................ P 4,760 b. Average capital of Castro [(P26,000 + P32,000) ÷ 2] ........................... P29,000 Average of Diaz [(P16,500 + P18,500) ÷ 2]....... .................................. _18,000 Castro's excess ..................................................... .................................. P11,000 Multiply by .......................................................... .................................. ___10% Interest ................................................................. .................................. P 1,100 5. Castro : (P3,000/P5,000) x P23,800 = P14,280 Diaz : (P2,000/P5,000) x P23,800 = __9,520 P23,800

Problem 2 – 2

a. Average Capital: Robin: Date Balances Months Peso Unchanged Months Jan. 1 P135,000 2 P270,000 Feb. 28 95,000 2 190,000 Apr. 30 175,000 5 875,000 Sept. 30 195,000 3 __585,000 12 P1,920,000 Ave. Capital (P1,920,000 ÷ 12) = P160,000 Hood: Date Balances Months Peso Unchanged Months Jan. 1 P140,000 3 P420,000 Mar. 31 200,000 3 600,000 June 30 150,000 2 300,000 Aug. 31 220,000 2 440,000 Oct. 31 200,000 2 __400,000 12 P2,160,000 Ave. Capital (P2,160,000 ÷ 12) = P180,000 Profit Distribution: Robin : P160,000 ÷ P340,000 x P510,000 = P240,000 Hood : P180,000 ÷ P340,000 x P510,000 = _270,000 P510,000

Partnership Operations 37 b. Robin Hood Total Interest on ave. capital ......................................... P 14,400 P 16,200 P 30,600 Salaries ................................................................. 60,000 100,000 160,000 Bonus (P510,000 – 30,600 – 160,000) x 25%) .... 78,850 – 79,850 Balance, equally ................................................... _119,775 _119,775 _239,550 Totals ................................................................... P274,025 P235,975 P510,000 c. Robin Hood Totals Interest: Robin (P195,000 – P135,000) 10%............. P 6,000 Hood (P200,000 – P140,000) 10% ............. P 6,000 P 12,000 Balance, equally ................................................... 249,000 249,000 498,000 Totals ................................................................... 255,000 255,000 510,000 d. Robin Hood Total Salaries ................................................................. P 80,000 P120,000 P200,000 Bonus (see computations below) ......................... 62,000 62,000 Balance, equally ................................................... _124,000 _124,000 _248,000 Totals ................................................................... P266,000 P244,000 P510,000 Bonus Computations: Net income before salaries and bonus ......... ..................... ....................... P510,000 Less Salaries ................................................ ..................... ....................... 200,000 Net income before bonus ............................ ..................... ....................... 310,000 Net income after bonus (P310,000 ÷ 125%) ..................... ....................... _248,000 Bonus .......................................................... ..................... ....................... P 62,000

Problem 2 – 3 a. De Villa De Vera Total Salaries ................................................................. P 30,000 – P 30,000 Commission (2% x P1,000,000) .......................... P 20,000 20,000 Interest of 8% on average capital ......................... 32,800 31,200 64,000 Bonus (see computations below) ......................... 9,818 9,818 19,636 Balance, equally ................................................... __44,182 __44,182 __88,364 Total ..................................................................... P116,800 P105,200 P222,000 Bonus Computations: Income before salary, commissions, interest & bonus ...... ....................... P222,000 Salary and commission (P30,000 + P20,000) ................... ....................... ( 50,000) Interest ......................................................... ..................... ....................... ( 64,000) Income before bonus ................................... ..................... ....................... 108,000 Income after bonus (P108,000 ÷ 110%) ..... ..................... ....................... _98,182 Bonus .......................................................... ..................... ....................... P 9,818 b. Income Summary ................................................. P 222,000 De Villa, capital .......................................... 116,800 De Vera, capital........................................... 105,200

38 Chapter 2

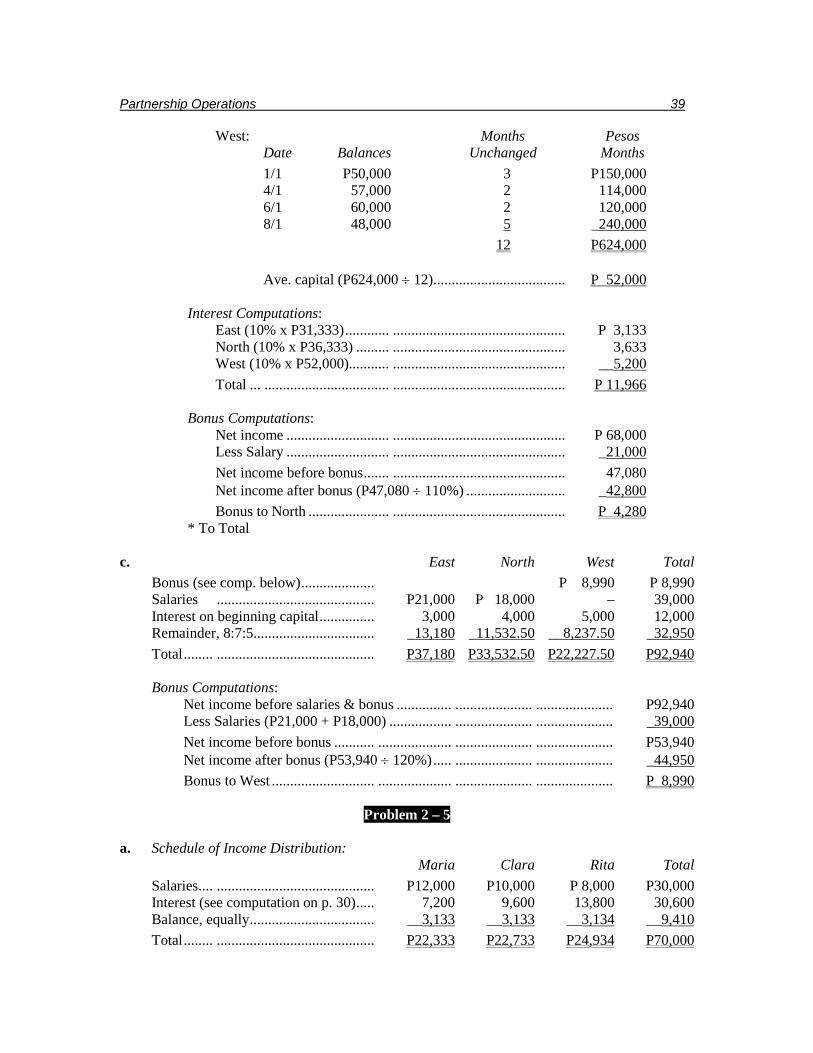

Problem 2 – 4 a. East North West Total Salaries ................................................ P15,000 P20,000 P18,000 P53,000 Bonus (see computation below) .......... 3,760 3,760 Interest (see computation below) ........ 2,800 4,000 4,800 11,600 Balance, 3:3:4 ..................................... __3,180 __3,180 __4,240 _10,600 Total .................................................... P24,740 P27,180 P27,040 P78,960 Bonus computations: Net income before bonus ........... .................... ..................... ..................... P78,960 Net income after bonus (P78,960 ÷ 105%) ..... ..................... ..................... _75,200 Bonus ......................................... .................... ..................... ..................... P 3,760 Interest computations: East (10% x P28,000)................. .................... ..................... ..................... P 2,800 North (10% x P40,000) .............. .................... ..................... ..................... 4,000 West (10% x P48,000) ............... .................... ..................... ..................... __4,800 Total ........................................... .................... ..................... ..................... P11,600 b. East North West Total Interest (see computations below) ...... P 3,133 P 3,633 P 5,200 P11,966 Salaries ................................................ 24,000 21,000 25,000 70,000 Bonus (see computations below) ........ 4,280 4,280 Balance, equally .................................. ( 6,056) ( 6,055) ( 6,055) ( 18,166) Total .................................................... P 21,077 P 22,858 P 24,145 P 68,080 Interest computations: Average capitals: East: Months Pesos Date Balances Unchanged Months 1/1 P30,000 4 P120,000 5/1 36,000 4 144,000 9/1 28,000 4 _112,000 12 P376,000 Average capital (P376,000 ÷ 12) .......................................... P 31,333 North: Months Pesos Date Balances Unchanged Months 1/1 P40,000 2 P80,000 3/1 31,000 4 124,000 7/1 36,000 2 72,000 9/1 40,000 4 _160,000 12 P436,000 Average capital (P436,000 ÷ 12) ........................................... P 36,333

Partnership Operations 39 West: Months Pesos Date Balances Unchanged Months 1/1 P50,000 3 P150,000 4/1 57,000 2 114,000 6/1 60,000 2 120,000 8/1 48,000 5 _240,000 12 P624,000 Ave. capital (P624,000 ÷ 12) .................................... P 52,000 Interest Computations: East (10% x P31,333) ............ ............................................... P 3,133 North (10% x P36,333) ......... ............................................... 3,633 West (10% x P52,000)........... ............................................... __5,200 Total ... .................................. ............................................... P 11,966 Bonus Computations: Net income ............................ ............................................... P 68,000 Less Salary ............................ ............................................... _21,000 Net income before bonus ....... ............................................... 47,080 Net income after bonus (P47,080 ÷ 110%) ........................... _42,800 Bonus to North ...................... ............................................... P 4,280 * To Total c. East North West Total Bonus (see comp. below) .................... P 8,990 P 8,990 Salaries ........................................... P21,000 P 18,000 – 39,000 Interest on beginning capital ............... 3,000 4,000 5,000 12,000 Remainder, 8:7:5 ................................. _13,180 _11,532.50 __8,237.50 _32,950 Total ........ ........................................... P37,180 P33,532.50 P22,227.50 P92,940 Bonus Computations: Net income before salaries & bonus ............... ..................... ..................... P92,940 Less Salaries (P21,000 + P18,000) ................. ..................... ..................... _39,000 Net income before bonus ........... .................... ..................... ..................... P53,940 Net income after bonus (P53,940 ÷ 120%) ..... ..................... ..................... _44,950 Bonus to West ............................ .................... ..................... ..................... P 8,990

Problem 2 – 5 a. Schedule of Income Distribution: Maria Clara Rita Total Salaries .... ........................................... P12,000 P10,000 P 8,000 P30,000 Interest (see computation on p. 30) ..... 7,200 9,600 13,800 30,600 Balance, equally .................................. __3,133 __3,133 __3,134 __9,410 Total ........ ........................................... P22,333 P22,733 P24,934 P70,000

40 Chapter 2 Problem 2-5: Continued Interest on Average Capital: Maria: P80,000 x 8% x 6 months .. .................... P 3,200 P100,000 x 5% x 6 months .................... __4,000 P 7,200 Clara: P120,000 x 8% .................. .................... 9,600 Rita: P180,000 x 8% x 9 Mos. ... .................... P10,800 P150,000 x 8% x 3 Mos. ... .................... __3,000 _13,800 Total ........................................... .................... P30,600 b. Statement of Partners Capital: Maria Clara Rita Total Balances, Jan. 1................................... P 80,000 P120,000 P180,000 P380,000 Additional Investment ........................ 20,000 – – 20,000 Capital Withdrawal ............................. – – ( 30,000) ( 30,000) Net Income.......................................... 22,333 22,733 24,934 70,000 Drawings ........................................... ( 10,000) ( 10,000) ( 10,000) ( 30,000) Balance, Dec. 31 ................................. P112,333 P132,733 P164,934 P410,000

Problem 2 – 6

1. Allocation of net loss for 2011: Alvin Benny Celia Total Salary to Alvin .................................... P 20,000 P20,000 Interests on average capital: Alvin (P120,000 x 10%) ............ 12,000 Benny (P200,000 x 10%) ........... 20,000 Celia (P220,000 x 10%) ............. 22,000 54,000 Balance, 30:30:40 ............................... (29,400) _(29,400) _(39,200) _(98,000) Total ........ ........................................... P 2,600 P( 9,400) P(17,200) P(24,000) 2. Statement of Partnership Capital Year Ended December 31, 2011 Alvin Benny Celia Total Capitals, January 1, 2011 .................... P120,000 P180,000 P220,000 P520,000 Additional investments ....................... 60,000 40,000 100,000 Capital withdrawals ............................ _______ ________ _(20,000) _(20,000) Balances .. ........................................... 120,000 240,000 240,000 600,000 Net loss (see above) ............................ __2,600 __(9,400) _(17,200) _(24,000) Balances .. ........................................... 122,600 230,600 222,800 576,000 Drawings . ........................................... _(16,000) _______ _______ _(16,000) Capitals, December 31, 2011 .............. P106,600 P230,600 P222,800 P560,000

Partnership Operations ..................................... 41 Problem 2-6: Continued 3. Correcting entry: Celia capital ........................................ 2,400 Alvin capital ............................... 2,200 Benny capital ............................. 200 To correct capital accounts for error in loss allocation computed as follows: Alvin Benny Celia Correct loss allocation ........................ P2,600 P(9,400) P(17,200) Actual loss allocation .......................... __(400) __9,600 __14,800 Adjustment .......................................... P2,200 P 200 P ( 2,400)

Problem 2 – 7 Dino Nelson Oscar Total Capital balances, 1/2/09............................... P45,000 P45,000 P45,000 P135,000 Additional investment, 2009 ....................... _15,000 _15,000 __6,000 __36,000 Balances....................................................... 60,000 60,000 51,000 171,000 Net income (Loss) - 2009, equally .............. (1,800) ( 1,800) ( 1,800) ( 5,400) Withdrawals, 2009 ....................................... (17,000) ( 7,000) ( 3,200) ( 27,200) Capital balances, 12/31/09........................... 41,200 51,200 46,000 138,400 Additional investment, 2010 ....................... _____– _____– __6,000 ___6,000 Balances....................................................... 41,200 51,200 52,000 144,400 Net income - 2010, 40: 30: 30 ..................... 10,800 8,100 8,100 27,000 Withdrawals, 2010 ....................................... (17,000) ( 7,000) ( 3,200) ( 27,200) Capital Balances, 12/31/010 ........................ 35,000 52,300 56,900 144,200 Additional investment, 2011 ....................... ______– ______– ___6,000 ___6,000 Balances....................................................... 35,000 52,300 62,900 150,200 Net income, 2011 (schedule 1) .................... 56,365 42,272 20,363 120,000 Withdrawals, 2011 ....................................... (19,000) ( 9,000) ( 3,200) ( 31,200) Capital balances, 12/31/011......................... P72,365 P86,572 P80,063 P239,000 Schedule 1: Dino Nelson Oscar Total Annual salaries.................................... P48,000 P24,000 P12,000 P84,000 Bonus (see computations below) ........ – 10,909 – 10,909 Interest ................................................ 3,600 3,600 3,600 10,800 Balance, equally .................................. _* 4,765 __4,763 __4,763 __14,291 Totals .................................................. P56,365 P43,272 P20,363 P120,000 Bonus computations: Net income before bonus ........... ................ ..................... ..................... P120,000 Net income after bonus (P120,000 ÷ 110%) ..................... ..................... _109,091 Bonus to Nelson ......................... ................ ..................... ..................... P 10,909 * To Total

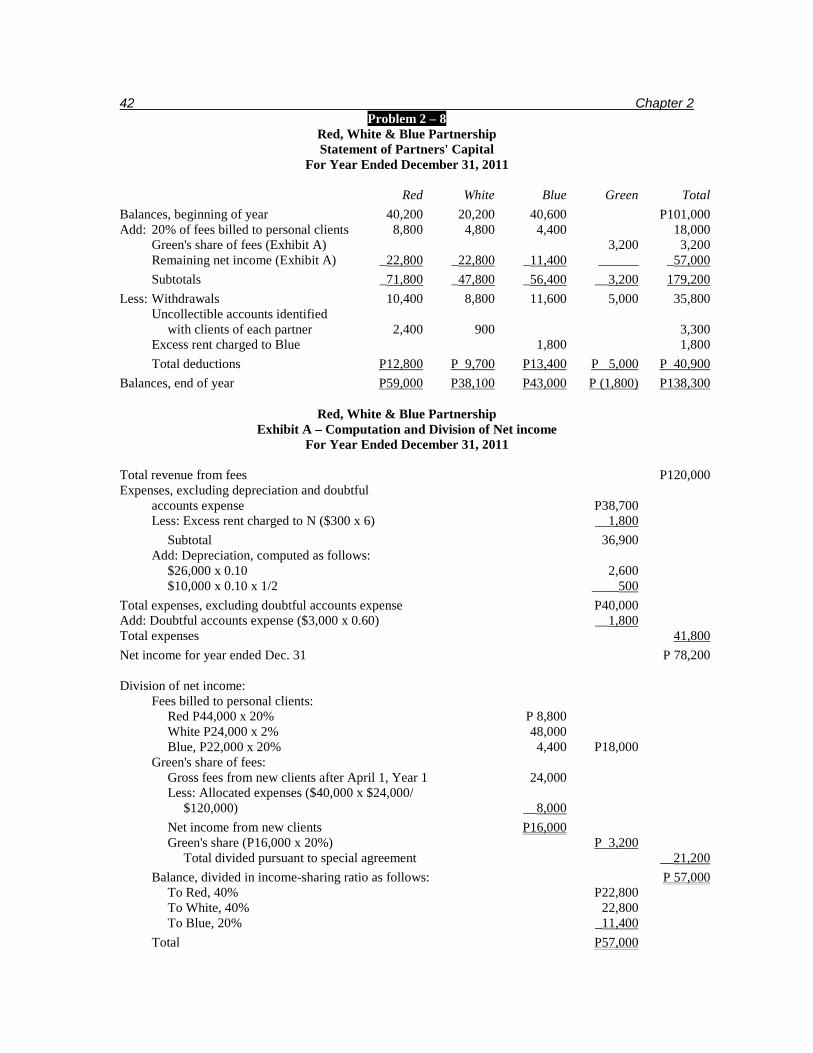

42 Chapter 2 Problem 2 – 8

Red, White & Blue Partnership Statement of Partners' Capital

For Year Ended December 31, 2011 Red White Blue Green Total Balances, beginning of year 40,200 20,200 40,600 P101,000 Add: 20% of fees billed to personal clients 8,800 4,800 4,400 18,000 Green's share of fees (Exhibit A) 3,200 3,200 Remaining net income (Exhibit A) _22,800 _22,800 _11,400 ______ _57,000 Subtotals _71,800 _47,800 _56,400 __3,200 179,200 Less: Withdrawals 10,400 8,800 11,600 5,000 35,800 Uncollectible accounts identified with clients of each partner 2,400 900 3,300 Excess rent charged to Blue 1,800 1,800 Total deductions P12,800 P 9,700 P13,400 P 5,000 P 40,900 Balances, end of year P59,000 P38,100 P43,000 P (1,800) P138,300

Red, White & Blue Partnership Exhibit A – Computation and Division of Net income

For Year Ended December 31, 2011 Total revenue from fees P120,000 Expenses, excluding depreciation and doubtful accounts expense P38,700 Less: Excess rent charged to N ($300 x 6) __1,800 Subtotal 36,900 Add: Depreciation, computed as follows: $26,000 x 0.10 2,600 $10,000 x 0.10 x 1/2 ____500 Total expenses, excluding doubtful accounts expense P40,000 Add: Doubtful accounts expense ($3,000 x 0.60) __1,800 Total expenses 41,800 Net income for year ended Dec. 31 P 78,200 Division of net income: Fees billed to personal clients: Red P44,000 x 20% P 8,800 White P24,000 x 2% 48,000 Blue, P22,000 x 20% 4,400 P18,000 Green's share of fees: Gross fees from new clients after April 1, Year 1 24,000 Less: Allocated expenses ($40,000 x $24,000/ $120,000) __8,000 Net income from new clients P16,000 Green's share (P16,000 x 20%) P 3,200 Total divided pursuant to special agreement __21,200 Balance, divided in income-sharing ratio as follows: P 57,000 To Red, 40% P22,800 To White, 40% 22,800 To Blue, 20% _11,400 Total P57,000

Partnership Operations 43

Problem 2 – 9 Allan, Eman and Gino Partnership Statement of Profit Distribution Year Ended December 31, 2011 Allan Eman Gino Total

Interest P 4,000 P 750 P 250 P 5,000 Commission (P16,120 – P5,000) x 10% – 1,112 1,112 2,224 Balance, equally __5,926 _5,925 _5,925 _17,776

Total P 9,926 P7,787 P7,287 P25,000 Adjustments (50% of P25,000 to Allan) __2,574 (1,287) (1,287) _____–

Total P12,500 P6,500 P6,000 P25,000

Problem 2 – 10 Gary, Sonny, and Letty Partnership Statement of Partners' Capital Accounts Year Ended December 31, 2011 Gary Sonny Letty Total

Capital balances, 1/1/08 P210,000 P180,000 P 90,000 P480,000 Additional investments ___9,100 _______ _______ __9,100

Total _219,100 _180,000 _90,000 489,100 Profit distribution: Salaries 13,680 11,520 10,640 35,840 Interest 25,920 21,600 10,800 58,320 Bonus to Gary and Sonny (Schedule 1) – – – Balance, equally __(9,720) _(9,720) _(9,720) (29,160)

Total __29,880 _23,400 _11,720 _65,000

Total 248,980 203,400 101,720 554,100 Drawings _(21,000) (18,000) __(9,000) _(48,000)

Capital balances, 12/31/08 P227,980 P185,400 P 92,720 P506,100 Schedule 1: Computation of the bonus. Net profit before interest, salaries and bonus P 65,000 Less: Salaries P35,840 Interest _58,320 __94,160

Net profit (loss) before bonus P(29,160) Therefore no bonus is to be given to Gary and Sonny.

44 Chapter 2

Problem 2 – 11 a. Entries to record the formation of the partnership and the events that occurred during 2008: Cash 1,100,000 Inventory 800,000 Land 1,300,000 Equipment 1,000,000 Mortgage payable 500,000 Installment note payable 200,000 Kobe, capital (P600,000 + P800,000 + P1,000,000 – P200,000) 2,200,000 Lebron, capital (P500,000 + P1,300,000 - P500,000) 1,300,000 (1) Inventory 300,000 Cash 240,000 Accounts payable 60,000 (2) Mortgage payable 50,000 Interest expense 20,000 Cash 70,000 (3) Installment note payable 35,000 Interest expense 20,000 Cash 55,000 (4) Accounts receivable 210,000 Cash 1,340,000 Sales 1,550,000 (5) Selling and general expenses 340,000 Cash 278,000 Accrued expenses payable 62,000 (6) Depreciation expense 60,000 Accumulated depreciation 60,000 (7) Kobe, drawing 104,000 Lebron, drawing 104,000 Cash 208,000 (8) Sales 1,550,000 Income summary 1,550,000 (9) Cost of goods sold 900,000 Inventory 900,000 P900,000 = P800,000 + P300,000 – P200,000