CHAPTER 1 ---INCOME TAXATION OF CORPORATIONS I. BASIC BUSINESS FORMS

12

CHAPTER 1 --- INCOME TAXATION OF CORPORATIONS I. BASIC BUSINESS FORMS Businesses in the United States may be operated as sole proprietorships , partnerships , or corporations . The choice is dependent upon nontax as well as tax factors. Examples of nontax factors that can determine the form of business are the number of owners or the desire for limited liability. Although there are many more nontax factors, the emphasis in this chapter is on the tax factors. A. Sole Proprietorships 1. More businesses are operated as proprietorships than any other business form. It is the simplest form, personally, legally, and for tax purposes. Since the proprietorship is not separate from its owner, the owner cannot enter into taxable transactions with the proprietorship. The owner is also personally liable for the proprietorship’s debts (unlimited liability). 2. Proprietorship ordinary income and deductions are reported on Schedule C (or Schedule F if a farming operation) as a support document to the owner’s Form 1040. The owner is subject to self-employment tax based on the proprietorship’s net ordinary income. Items such as proprietorship interest income, dividend income, capital gains and losses, charitable contributions, and state income taxes attributable to the business are reported as though incurred by the owner, not the proprietorship, on the appropriate tax schedules. B. Partnerships (see Chapters 9 and 10 for greater detail) 1. There are two types of partnerships: general and limited. a. General partnerships are owned solely by general partners. General partners are required to participate in management and have personal liability for partnership debts. b. Limited partnerships must have at least one general partner and one limited partner. Limited partners cannot participate in management nor do they have personal liability for partnership debts. 2. Partnership ordinary income and deductions are reported on Form 1065. Each owner’s share of net ordinary income or loss is reported on his or her personal return (Schedule E and Form 1040). All other items flow through to the partners and are reported on the appropriate schedules. 3. A partnership meeting the definition of a publicly traded partnership (PTP) will not be subject to the treatment 1

-

Upload

independent -

Category

Documents

-

view

3 -

download

0

Transcript of CHAPTER 1 ---INCOME TAXATION OF CORPORATIONS I. BASIC BUSINESS FORMS

CHAPTER 1 --- INCOME TAXATION OF CORPORATIONS

I. BASIC BUSINESS FORMS

Businesses in the United States may be operated as sole proprietorships, partnerships, or corporations. The choice is dependent upon nontax as well as tax factors. Examples of nontax factors that can determine the form of business are the number of owners or the desire for limited liability. Although there are many more nontax factors, the emphasis in this chapter is on the tax factors.

A. Sole Proprietorships

1. More businesses are operated as proprietorships than any otherbusiness form. It is the simplest form, personally, legally, and for tax purposes. Since the proprietorship is not separatefrom its owner, the owner cannot enter into taxable transactions with the proprietorship. The owner is also personally liable for the proprietorship’s debts (unlimited liability).

2. Proprietorship ordinary income and deductions are reported on Schedule C (or Schedule F if a farming operation) as a supportdocument to the owner’s Form 1040. The owner is subject to self-employment tax based on the proprietorship’s net ordinaryincome. Items such as proprietorship interest income, dividendincome, capital gains and losses, charitable contributions, and state income taxes attributable to the business are reported as though incurred by the owner, not the proprietorship, on the appropriate tax schedules.

B. Partnerships (see Chapters 9 and 10 for greater detail)

1. There are two types of partnerships: general and limited.a. General partnerships are owned solely by general partners.

General partners are required to participate in management and have personal liability for partnership debts.

b. Limited partnerships must have at least one general partner and one limited partner. Limited partners cannot participatein management nor do they have personal liability for partnership debts.

2. Partnership ordinary income and deductions are reported on Form 1065. Each owner’s share of net ordinary income or loss is reported on his or her personal return (Schedule E and Form1040). All other items flow through to the partners and are reported on the appropriate schedules.

3. A partnership meeting the definition of a publicly traded partnership (PTP) will not be subject to the treatment

1

identified above. Instead, a PTP will be treated and taxed as a regular corporation for Federal income tax purposes.a. Until defined as publicly traded partnerships in the Revenue

Act of 1987, these entities were more commonly called masterlimited partnerships, or simply MLPs.

b. A partnership is a PTP if:1. It is a limited partnership;2. It is organized after December 17, 1987; and3. Its interests are traded on an established securities

market or are readily tradable on a secondary market.c. Partnerships meeting the definition of PTPs, but which were

in existence on December 17, 1987, have ten years to liquidate or be subject to taxation as a regular corporation.

d. Exception: PTPs/MLPs can be treated as partnerships if 90%or more of their income consists of interest, dividends, real property rental income, gains from sale of capital and Sec. 1231 assets, and/or income/gains from development, mining, production, refining, transportation, or marketing of any mineral or natural resource. There are many real estate and oil and gas MLPs that are publicly traded but enjoy pass-through partnership taxation due to this exception.

C. S Corporations (see Chapter 11 and 12 for greater detail)

1. S corporations are regular corporations whose shareholders have elected to be taxed under Subchapter S of the Internal Revenue Code. The election requirements are that the corporation (a) have only one class of stock outstanding, (b) have no more than 100 eligible shareholders, and (c) be an eligible corporation.

2. S shareholders are taxed similarly to partners. The conduit concept generally applies to both partnerships and S corporations.a. Similar to the partnership, S corporation ordinary income

and deductions are reported on Form 1120S.b. Each stockholder’s share of net ordinary income or loss is

reported on his or her personal return in a similar manner as a partner’s share.

c. Since shareholders may be employees of their S corporations,their salaries are subject to withholding and, therefore, their share of net ordinary income is not subject to self-employment tax.

D. C Corporations (see Chapters 1-6 for greater detail)

2

1. Of the four business forms, only the C corporation is a taxable entity.a. All revenues and deductions are taxable to the corporation

and none flows through to the owners. (Special rules regarding corporate income and deductions are discussed below.)

2. A corporation’s income, expenses, gains, and losses are reported on Form 1120.a. Owner/employee salaries are treated the same as they are for

S corporations. That is, they are deductible corporate expenses, subject to withholding but not subject to self-employment taxes.

b. All special rules regarding corporate income and deductions are discussed below.

E. Limited Liability Companies (LLCs) (See chapters 9 and 10 for

greater detail)

1. Limited liability companies blend the corporate feature of limited liability with partnership tax attributes. For some taxpayers, this may be an ideal way of doing business. While professionals (e.g., doctors, dentists, attorneys) may use this entity, professionals may not limit their personal tort liability to their patients and clients, (although they are protected from tort liability arising from their associates).

2. Under ‘‘Check-the-box’’ regulations that became effective in 1997, an LLC will be taxed as a partnership unless it affirmatively elects to be taxed as C corporation.

II. WHAT IS A CORPORATION?

Legally, a corporation is an artificial ‘‘person’’ created by state law. For tax purposes, § 7701 defines a corporation as including associations, joint-stock companies, and insurance companies.A. Historically, an association that was not treated as a

corporation under state or Federal law (e.g., a partnership) could be classified as a corporation for Federal income tax purposes and thus be inadvertently exposed to the disadvantages of the regular (C) corporate form of doing business. The aspects that were addressed in determining whether an association should be classified and taxed as a corporation included:1. Continuity of life,2. Centralized management,3. Limited liability, and4. Free transferability of ownership interests

3

If three of these four characteristics were satisfied, an entity would be taxed as a corporation, even if the entity was treated differently under state law. For example, a limited liability partnership (LLP) or a limited liability company (LLC) could be treated as a corporation for tax purposes if it had, along with limited liability, two of the other three characteristics (e.g., centralized management and no restrictions on the transfer of interests).

B. Naturally, the above classification rules led to a great number of conflicts between the IRS and taxpayers. To simplify this process, the IRS issued regulations effective January 1, 1997 that replace the old rules for classifying entities with a ‘‘check-the-box’’ system. Under the new rules, an entity organized as a corporation under state law, or an entity classified under the Code as a corporation, will be treated as a corporation and will not be allowed to make an election. However,any other business entity (e.g., an LLC) that has at least two members may elect to be treated as a corporation or a partnershipfor tax purposes (an entity with only one member will be treated as a corporation or a sole proprietorship). In general, existing entities will continue to operate as they are as long as there isa reasonable basis for the current classification.

C. The IRS can and will ignore sham corporations, regardless of their legal status. However, the Supreme Court in Bollinger stated that, under certain conditions, a corporation can be considered anontaxable agent of the taxpayer.

III. CORPORATE TAXABLE INCOMEComputations are much closer to generally accepted accounting principles than are those for individuals.A. See corporate tax formula. Individual deductions denied

corporations include the following:

1. Personal exemptions;2. A standard deduction; and3. Itemized deductions.

B. Certain items receive unique treatment by corporations.

1. Dividends received deduction (DRD).a. The DRD equals 70% or 80% of the lesser of dividend income

or taxable income before four items are considered ---the dividends-received deduction, net operating loss carryforwards or carrybacks, capital loss carrybacks, and the domestic production activities deduction.

b. The corporation can deduct 70% or 80% of dividend income even though larger than taxable income if the corporation has an NOL for the year, or the dividends-received deduction creates an NOL for that year.

4

c. Dividends qualifying for the deduction must be receivedfrom taxable domestic U.S. corporations, the stock must be held for more than 45 days prior to the ex-dividend date, and must not have been purchased with borrowed funds unpaid at the date of the dividend (debt-financed stock).d. The recipient corporation is allowed an 80 percent, rather

than the usual 70 percent, dividends-received deduction ifit owns at least 20 (but less than 80) percent of the dividend-paying corporation’s stock.

e. If the recipient corporation owns 80 percent or more of the dividend-paying corporation’s stock, the dividends-received deduction becomes 100 percent regardless of the corporation’s taxable income.

2. Organization expenses (Sec. 248) and start-up costs (Sec. 195).a. Organization expenses and start-up costs normally must be

capitalized but at the election of the corporation are eligible for special treatment.1. Both C and S corporations may elect to deduct

organization expenses up to $5,000 of qualifying expenses and the excess must be amortized over the 180 month period (15 years) beginning with the month in which the business begins. The same rule applies separately to start-up cost.

2. If the organization expenses exceed $50,000, the immediate $5,000 expense is reduced dollar-for-dollar by the amount of the excess, with the remainder being amortized over 180 months. The same rule applies separately to start-up costs.

b. Organization expenses and start-up costs include expenses incident to the creation and start-up of the corporation. 1. Organization expenses include expenses incident to

creation of the corporation. Eligible expenses include fees for attorneys, accountants, state filing charges, temporary directors’ fees and meetings, and similar expenses incident to organization. Expenses do not include stock issue costs which are the costs to print and sell stocks. These issue costs reduced the capital stock accounts

2. Start-up costs are expenses incurred prior to opening the business. Eligible expenses include employee training, pre-opening advertising, cost of lining up suppliers and potential customers, and pre-opening market research.

c. Only those expenses incurred prior to the close of year inwhich business begins qualify

5

1. In determining eligibility, it is irrelevant whether the taxpayer is a cash or accrual basis taxpayer. The expenses merely need to be incurred during the first year.

2. Expenses that are not incurred in the first year must be capitalized and cannot be amortized. Such costs are recovered only upon a sale of all of the corporation’s assets or upon liquidation.

3. Net operating loss.a. There are only two modifications to taxable income when

computing NOL. They are: 1. NOL from previous years must be added back (each year’s NOL is accounted for separately),

2. The dividends-received deduction is calculated basedon 70 (or 80) percent of dividend income (without regard to the taxable income limitation).

b. The carryover periods for NOLs are the same as they are for individuals. There is a carryback of 2 years and a carryforward of 20 years or a carryforward only of 20 years.

4. Charitable contributions.a. Unlike individuals, an accrual basis corporation can

deduct accrued but unpaid contributions in the current year provided the contribution is actually made by the 15th day of the third month following the close of the year.

b. Corporations can deduct basis plus one-half of the appreciation of ordinary income property (limited to twicethe basis) given for the care of the ill, needy, or infants, or for scientific equipment donated to universities.

c. Corporations are limited to an annual deduction (includingcarryforwards) of 10 percent of taxable income. In computing taxable income, omit the charitable contributions, the dividends-received deduction, any NOL and capital loss carrybacks, and the domestic production activities deduction.

d. Excess charitable contributions are carried forward and deducted in any of the five succeeding years (on a FIFO basis), after current year contributions are deducted.

e. It is not uncommon for business to contribute patents and other intangibles. To prohibit deductions for inflated values, §170(e)(1)(B)(iii) limits the amount of the contribution of any patent, certain copyrights, trademark,trade name, trade secret, know-how, software or similar property.

6

1. The FMV of the property must be reduced by the amount of long term capital that would have been recognized had the property been sold. The effect is to limit the contribution deduction to the lesser of the property’s FMV or adjusted basis.

2. However, §170(m) permits an additional charitable deduction is available in future years based on a certain percentage of the ‘‘qualified donee income’’ received or accrued by the charity from the donated property. The effect is to permit a deduction for the value of the property as determined by the income, if any, generated from the property after the donation.

5. Capital gains and losses.a. Capital assets have the same definition for corporations

as they do for individuals. The computation of the amount of gain or loss is also the same.1. Unlike individuals, corporations are not allowed to

deduct capital losses against ordinary income (i.e., there is no capital loss deduction). Instead, a corporation’s capital losses can only be used to offsetcapital gains.

2. Unused capital losses may be carried back 3 years and then forward 5 years to offset capital gains. They are treated as short-term capital losses, regardless of their original character.

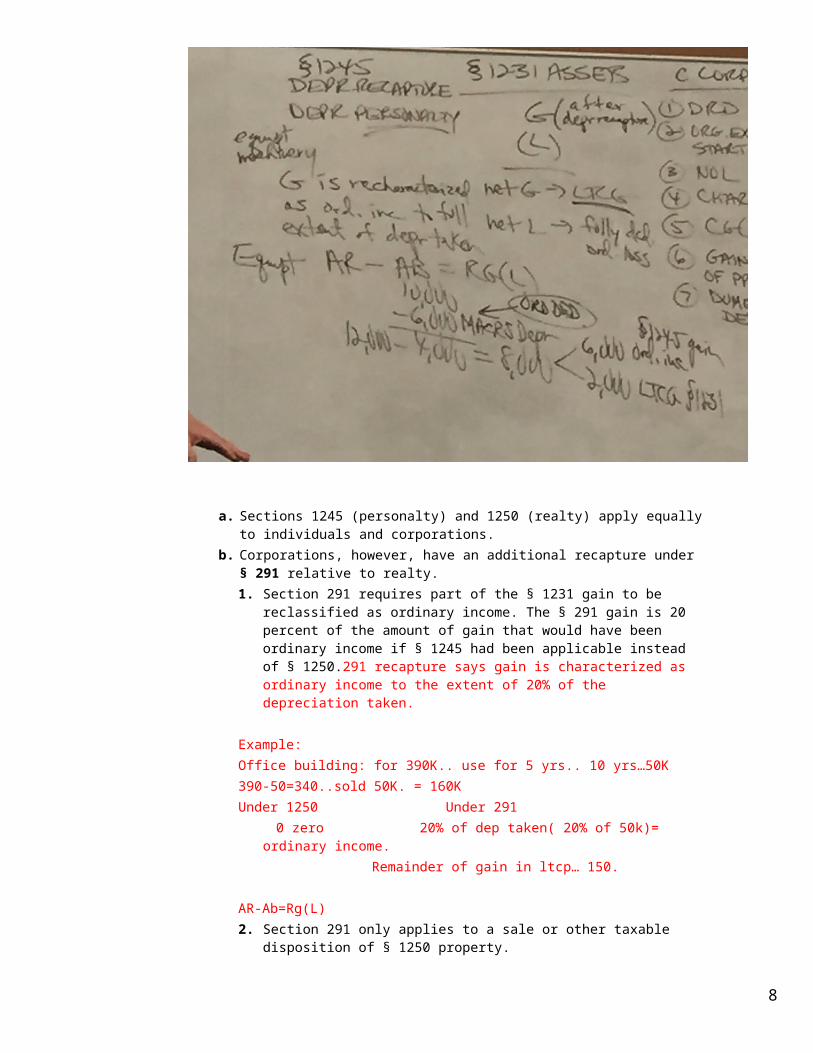

6. Sale of depreciable property. we are talking about 1231 assets(PPE held more than year).

________Net G> LTCGNet L? fully ded ord assetsSection 1245Deprecable recapture ( gain is recharaterized as orginary income

to full extend of dep)

7

a. Sections 1245 (personalty) and 1250 (realty) apply equallyto individuals and corporations.

b. Corporations, however, have an additional recapture under § 291 relative to realty.1. Section 291 requires part of the § 1231 gain to be

reclassified as ordinary income. The § 291 gain is 20 percent of the amount of gain that would have been ordinary income if § 1245 had been applicable instead of § 1250.291 recapture says gain is characterized as ordinary income to the extent of 20% of the depreciation taken.

Example:Office building: for 390K.. use for 5 yrs.. 10 yrs…50K390-50=340..sold 50K. = 160K Under 1250 Under 291

0 zero 20% of dep taken( 20% of 50k)= ordinary income.

Remainder of gain in ltcp… 150.

AR-Ab=Rg(L)2. Section 291 only applies to a sale or other taxable

disposition of § 1250 property.

8

3. Beginning in 2005, the §1250 recapture amount–generallythe excess of accelerated depreciation over straight-line–for most §1250 properties will become zero. Residential buildings acquired during 1981-1986 were normally depreciated using at most a 19 year life. These buildings will be fully depreciated in 2005 and there will be no §1250 recapture.

Also applies to 1250> it says gain characterized in ord inc to the extent of the dep taken in excess of SL dep.There is no dep recapture under 1250.

7. Domestic production activities deduction.: not in book, domestic production encourage. Go usa ( 9% deduction )

a. The domestic manufacturing deduction, or Section 199 deduction, was enacted to encourage US production activities. All taxpayers with qualifying production are entitled to this deduction,including corporations, sole proprietorships, partnerships, S corporations, and estates and trusts.

b. The deduction equals 9 percent of the lesser of qualified production activities income (QPAI) ortaxable income. The deduction is limited to 50 percent of theentity’s domestic W-2 wages.c. Qualified production activities income (QPAI) equals domestic production gross receipts less cost ofgoods sold and directly allocable expenses and certain indirect expenses.d. Domestic production gross receipts are gross receipts from the sale, lease, or exchange of qualifying production property (tangible personal property, computer software, and sound recordings) manufactured, produced, grown or extracted by the taxpayer in whole or in significant part within the U.S. It includes construction performed in the U.S. and engineering

9

or architectural services performed in the U.S. or for U.S. construction projects.

e. It does not include receipts from the sale of food and beverages prepared at a retail establishment (i.e. restaurants), but does include wholesale sales of such prepared items. For example, it would not include the sale of coffee at a Starbucks Coffee Shop but it would include the sale of coffee beans roasted at a Starbucksplant.

IV. COMPUTATION OF INCOME TAXA. Corporations use a four-step progressive rate schedule.

Currently, the tax rates are 15, 25, 34, and 35 percent. See corporate tax rate schedule – inside back cover of textbook.

B. Corporations are denied the benefits of the progressive rates by the imposition of a 5 percent and 3 percent surtax. See corporate tax rate schedule. A controlled group of corporations,either parent/sub or brother/sister, may only use one tax rate schedule, one AMT exemption amount, one Sec. 179 amount, and so forth. To be a controlled group, the parent must own at least 80% of the subsidiary and for a brother/sister controlled group five or fewer individuals must own over 50% of the total voting power of all classes of stock, taking into account the lowest identical ownership of each shareholder.

C. Qualified personal service corporations (PSCs) are taxed at a flat rate of 35 percent. Qualified PSCs are corporations principally performing certain personal services, the employee-owners (who own at least 95% of the stock) perform the services. At least 95% of the services performed must be one of these eighttypes: health, law, engineering, architecture, accounting, actuarial science, performing arts, or consulting.

D. Alternative minimum tax (AMT). See AMT formula – Exhibit 1-8.

1. Like individuals, corporations are subject to the AMT. The taxis imposed at the rate of 20 percent on alternative minimum taxable income (AMTI) in excess of $40,000.

2. Exception: C corporations that have average annual gross receipts for all prior years of no greater than $5,000,000 aregenerally not subject to the AMT; in addition, once average receipts hit $5,000,000, there is no AMT if receipts do not exceed $7,500,000.

3. A corporation’s $40,000 exemption is reduced by 25 percent of the amount its AMTI exceeds $150,000. Thus, the exemption is eliminated for a corporation with AMTI of $310,000 or more.

4. The most significant difference in the AMT rules for corporatetaxpayers, when compared with individuals, is that 75 percent of the excess of adjusted current earnings (ACE) over AMTI

10

(computed without regard to the ACE adjustment) is treated as an adjustment item.

V. FORMS AND FILING REQUIREMENTSA. Corporations are required to file Form 1120. A corporation must

file a return whether or not it has taxable income. See chapter 1, pages 43-48, for an example of Form 1120.1. The form requests data, in addition to the computation of

taxable income and tax, such as comparative balance sheets (Schedule L) and a retained earnings statement (Schedule M-2).

2. The form also requests a reconciliation of taxable income withaccounting income.a. M-1 Reconciliation of book income to taxable income (before

NOLs and dividends received deduction)b. M-3, similar to the M-1 but more exhaustive and detailed,

must be filed in lieu of the M-1 if the corporation has $10million or more in total assets.

c. M-2 Analysis of Retained EarningsB. The corporate income tax return is due the 15th day of the third

month following the close of the corporation’s tax year (i.e., March 15th for calendar year corporations).1. A corporation is entitled to an automatic six-month extension

of time to file the income tax return by filing Form 7004.2. An extension of the due date for filing a corporate tax return

does not extend the date for paying any additional tax due. There is a failure to file penalty (5% per month, up to 5 months) and a failure to pay penalty (0.5% per month, up to 25%) on the amount owed after the due date of the return.

C. Corporations are required to pay estimated taxes.1. The due date for corporate estimated tax payments is the 15th

day of the fourth, sixth, ninth, and twelfth months.2. To avoid the underpayment penalty, corporations must pay

estimated taxes if their total tax liability is $500 or more. The amount that must be paid depends on whether the corporation is a larger corporation. If the corporation is not‘‘large’’ it must pay the lesser ofa. 100% (90% for individuals) of current year’s tax

1. 25% evenly per installment or unevenly if using the annualized income method

2. Installments for calendar year taxpayers are due on 4-15, 6-15, 9-15, 12-15 and the remainder is paid with thereturn

b. 100% of last year’s tax (must be return for 12 months and must be a tax liability)1. 25% evenly per installment (safe harbor)

11

2. For a calendar year taxpayer 25% on 4-15, 6-15, 9-15, 12-15; and balance with return

3. To use the safe harbor, the tax return must be for 12months and show a tax liability in the preceding year. Unlike individuals, the safe harbor cannot be used if the prior year tax was zero.

3. Limitation for large corporation (i.e., at least $1,000,000 oftaxable income in any of the last 3 taxable years not including current year; e.g. if current year is 20X7 then lookat 20X6, 20X5 and 20X4). A large corporation must pay the lesser ofa. 100% of the current taxb. 100% of last year’s tax for first installment only; any

shortfall between installment based on last year’s tax and current year’s must be made up in second installment.

D. Accounting Periods and Methods

1. C corporations can choose to be calendar year or fiscal year. However, S corporations and personal service corporations (PSCs) are generally required to be calendar year since they must have the same tax year as that of their shareholders, who are normally calendar-year individuals.

2. C corporations must use the accrual method if their average annual gross receipts total over $5 million. S corporations and PSCs can always use the cash method. All entities must use the accrual method to account for the salesand costs of inventories sold.

12