3. MARKETING Y MERCHANDISING............................. 27

Voluntas (2006) 17:99–113DOI 10.1007/s11266-006-9012-6

ORIGINAL PAPER

Caveat Venditor? Museum Merchandising, NonprofitCommercialization, and the Case of the MetropolitanMuseum in New York

Stefan Toepler

Published online: 25 August 2006C© International Society for Third-Sector Research and The Johns Hopkins University 2006

Abstract This paper reviews some of the underpinnings of the current commercializationdebate in the nonprofit sector, based on an analysis of Metropolitan Museum of Art data from1960 to 2002. The case suggests at least two avenues for additional research: First, whileanalysts tend to see the origins of the commercialization phenomenon in the fiscal setbacksof the 1980s, the economic crisis of the 1970s and the resulting erosion of endowment fundsmay also have been an as of yet unexplored driving force behind the commercializationtrend. Second, current conceptual frameworks of the phenomenon adequately explain themotivations behind the observable rise of the museum’s commercial activities. However,the changing rationales as well as economic fortunes of commercial activities in this casehighlight the need for a better understanding of the long-term effects and consequences ofcommercial activity by nonprofit organizations, particularly in light of the current push forincreased entrepreneurialism.

Keywords Museums . Merchandising . Earned income . Commercialization . Socialentrepreneurship . Metropolitan Museum in New York

Introduction

Although historians have noted that commercial means have always contributed to thefinancing of charitable enterprises (Wilson, 1998), analysts have recently paid heightenedattention to the commercial activities of nonprofit institutions (Lyman & Hodgkinson, 1989;Salamon, 1993; Weisbrod, 1998a). Commercialization in this context can be understood as agreater propensity of nonprofit managers to rely less on donative sources of income and focusmore heavily on fees for related services, sales of goods and services that are either relatedor unrelated to the organization’s mission, and other forms of earned rather than contributed

S. Toepler (�)Nonprofit Studies Program, Department of Public and International Affairs, George Mason University,3401 N. Fairfax Drive, MSN 4D5, Arlington, Virginia 22201, USAe-mail: [email protected]

Springer

100 Voluntas (2006) 17:99–113

income. Somewhat generalizing, two contrary strands of argument on this issue are moreor less clearly discernible in the current debate. Under headings such as self-sustainabilityand social entrepreneurship, the first strand is hands-on and largely celebratory in natureand posits that the adoption of commercial means and mechanisms to conduct the nonprofitbusiness is a positive development (e.g., Bornstein, 2004; Brinckerhoff, 2000; Larson, 2002).As frequently pushed by consultants and private funders, a more business-like approach tononprofit management is seen as resulting in greater efficiency as well as new and innovativeways of addressing protracted social problems.

A second view of commercialization, by contrast, holds that the opposite is true. The coreargument here is that a decline of private and public contributed revenues in relative terms hasforced (reluctant) nonprofit managers to seek recourse to commercial-like income sourcesin order to sustain growth and meet societal needs. Charging fees and selling goods at bestincidental to the mission only takes place to cross-subsidize the collective good provision(James, 1983). For instance, social service organizations may explore commercial venturesto help finance services to low-income clients who would otherwise be unable to afford them(Alexander, 2000). In doing so, however, nonprofit institutions face significant threats. Indeveloping commercial activities and revenues, the self-generation of income—or “makingmoney”—may become an end in itself, nonprofit managers may get distracted from theirpursuit of the mission, and the organization’s original goals may get displaced (DiMaggio,1986b; Weisbrod, 1998b).

In this paper, focus falls on one prominent cultural institution—the Metropolitan Museumof Art in New York—to suggest that there are a number of key generalized assumptionsunderlying both points of view that require a closer evaluation. If so, the current theoreticaland analytical frameworks for explaining the commercialization phenomenon may not besufficient to fully understand the causes and impacts of this trend. The intention behindusing a case study is to search for counterfactual evidence. The Metropolitan is amongthose museums that have pursued merchandising with some degree of intensity over the pastcouple of years. If current commercialization theories are valid, they should have considerableexplanatory power in this case. If the case presents evidence that cannot be easily reconciledwith theory, it would point to areas where our understanding of the commercialization issuerequires further theoretical elaboration.

Assumptions underlying the commercialization debate

There are two general assumptions that shape the commercialization debate. The first as-sumption concerns the historical roots of the commercialization issue. It is generally takenfor granted that increased commercialism is largely a result of developments in the 1980sand that entrepreneurial approaches to financing the private provision of collective goods andservices have only been adopted since (Young & Salamon, 2002; Zietlow, 2001). In the past,prevailing notions hold that nonprofits were largely funded through private philanthropy.Beginning in the post-war era and amplified in the 1960s, government funding became in-creasingly prevalent in most policy areas in which nonprofits are active ranging from healthand education to social services and community development to the arts (Salamon, 1995;Smith & Lipsky, 1993). The tremendous expansion of the nonprofit sector in the second halfof the twentieth century was thus largely fueled by donative sources of income—whetherprivate donations or public subsidies and contracts. In the 1980s, however, this began tochange. Reductions in federal programs sharply decreased overall support, while socialneeds and demand for nonprofit services increased (Salamon, 1995). Though growing in

Springer

Voluntas (2006) 17:99–113 101

absolute terms, private philanthropy did not compensate for losses in public support or helpclose funding gaps due to need-based growth of nonprofit programs (Abramson et al., 1999).The resulting relative decline of public and private donative support thus forced nonprofitsto rely increasingly on program and other market-based revenues (Salamon, 2002). Com-mercialization emerged as a serious issue. Since theories about the motivations of nonprofitmanagers suggest that commercial activities are non-preferred as long as preferred donativefinancing sources are sufficiently available (Weisbrod, 1998b), there is little reason to assumethat nonprofits did engage in commercial ventures in substantial ways before the 1980s.

A second assumption suggests that commercial activities are pursued to generate newresources in order to offset declining donative income in an effort to cross-subsidize mission-related activities. Since there is little point in undertaking these activities if they do not servethis purpose, this implies in turn that commercial ventures do indeed generate significantincome for nonprofit institutions. With few exceptions (Zimmerman & Dart, 1998), however,the issue of the efficiency of commercial activities is typically not much thematized and thebelief that entrepreneurial ventures are a viable solution for cash-strapped institutions haslargely gone unquestioned. While there is considerable concern about possible negativeimpacts on the missions and the very nature of nonprofits, there appears still to be littleconcern about the economic viability of business ventures. The fact that nonprofit managersare increasingly reverting to commercial means by itself however should not be taken toimply that the desired outcomes are indeed achieved. By contrast, there are two reasons thatshould lead us to expect that the opposite may be true: First, the majority of start-ups inthe business sector fail within a few years and there are no good reasons to assume that thecommercial start-ups of nonprofit firms should fare better (Dees, 1998). Second, businessplanning is still not widely employed in the nonprofit sector (and much less so in the arts) andcommercial undertakings of nonprofits may more likely be based on hunches and perceivedopportunities than on sound planning (Zietlow, 2001).

Since this paper presents a case study of an art museum, attention is given to the appli-cability of the commercialization issues to the arts and the museum field in particular. Aftera brief description of the data and methodology, findings of an analysis of the Museum’sAnnual Reports from 1960 to 2002 are presented. The paper ends with a discussion ofthe findings and suggests additional areas of inquiry that could usefully inform the furtherevolution of commercialization theory.

Commercialization and the arts

The arts provide a useful case to explore the type of larger dynamics within the nonprofitsector that sparked the commercialization phenomenon. Over the four decades that the fol-lowing analysis examines, what should we expect to find? First, until the 1960s, high culturalinstitutions, such as art museums and symphony orchestras, remained tightly controlled andfinancially dependent on the local urban elites that had founded many of these institutions to-wards the end of the nineteenth century (DiMaggio 1986a; Stevens, 1996). Wealthy patronsaccordingly controlled key resources, that is individual gifts as well as occasionally sub-stantial municipal appropriations. In the 1960s, however, private foundations became moresystematically involved in funding the arts and in 1965 the federal government establishedthe National Endowment for the Arts, in turn spurring the development of new state andlocal level public funding agencies. With the entrance of corporations as sponsors, the 1970sthus saw the rise of new public and private funding mechanisms that began to diminish thedominant role of local elite patrons and municipalities. While state and local government

Springer

102 Voluntas (2006) 17:99–113

continued to grow, federal funding, however, began to stagnate in the 1980s, while privategrants and giving did not keep up with the growth of the field (Cobb, 1996; Stevens, 1996).

Within the arts field, art museums in particular constitute an ideal exemplar of the tensionsinherent in the commercialization issue. Perceived as secluded temples of culture in the past,museums have long resisted mixing commerce and the muse. Criticism of commercializationand undue corporate influence flared up as soon as corporations began to show greater interestin sponsoring art exhibitions in the 1970s (Alexander, 1996) and has in one form or the othercontinued until today. Nevertheless, the work of museum directors has become “a constanttug-of-war between artistic mission and commercial consideration.” (The Economist, April21, 2001, p. 65). In many ways, the wariness in the museum field about the potentialinfluence of corporate and commercial interests (Malaro, 1994) corresponds closely withthe goal or mission displacement concern in the commercialization debate. To a large part,the perceived commercialization of museums beginning in the 1980s was driven by theexpansion of merchandising, and the increase in retail activities was, like the advent ofcorporate sponsorship, not greeted with unanimous approval. Somewhat tongue-in-cheek,the director the Cleveland Museum of Art, for example, wrote in the institution’s 1990 annualreport:

The Museum’s steady pursuit of new monies to offset operating costs continues its upward energeticway . . . The institution of parking fees . . . aroused a fair amount of warmly expressed indignation(which for a time reduced Museum attendance). The decision to expand the Museum Store has nurtureda comparable expression of delight.

Regardless of how traditional museum constituencies felt about this issue, the tide wasincreasingly difficult to stem by the 1990s. While museums did pursue other forms ofcommercialization, including the raising of admission fees where feasible, merchandisingappeared to have become a strategy of choice. Museums expanded on-site store space, devel-oped permanent or temporary off-site shops in shopping malls, and—with the developmentof e-tailing technologies—took merchandising into cyberspace. As indicated in the abovequote, the key rationale behind this trend was to develop new financing sources to help closefunding gaps.

Data and methodology

In the absence of useful historical data, the extent of commercialization in the past isnotoriously hard to trace. Analysts typically have to rely on highly aggregated Censusdata (e.g., Salamon, 1993) or IRS form 990 information or survey data (Weisbrod, 1998a).However, all of these data sources have significant limitations, particularly when it comes toinferring organizational strategies and managerial behavior. Moreover, the key data sourcesthat have made it possible to chart the size, scope, and financing of the nonprofit sectorin empirical terms (e.g., the Census of Service Industries and IRS data) are only availablefrom the late 1970s and early 1980s. As this coincides with the presumed on-set of thecommercialization phenomenon, they only allow a very limited comparison to presumablyless commercial prior decades.

For this reason, this paper takes a different route in trying to trace these develop-ments. More specifically, financial information is collected from the Annual Reports ofthe Metropolitan Museum of Art for a more than 40-year period from 1960 to 2002. Be-ginning the analysis in 1960 provides a glimpse into the way the Metropolitan Museumand similar institutions were funded before the large-scale advent of external foundation,government, and corporate funders. Although the analysis presented here is based on a

Springer

Voluntas (2006) 17:99–113 103

single case, it will demonstrate both the usefulness as well as feasibility of approachingthe commercialization issue from this vantage point. The Annual Reports were collectedfrom various local academic and museum libraries. Data reported here represent operat-ing revenues, excluding capital support. Changing reporting and accounting standards overthe period required a number of adjustments to the data, although key revenue sourceswere reported continuously and with a high degree of consistency. Between the late 1970sand the early 1980s, the museum introduced an important reporting change that could noteasily be adjusted for. Specifically, before the end of the 1970s, only direct expenses of pub-lications and merchandising were reported. Since, reported expenses also include supportservices charges. Thus, pre-and post-1980 merchandising net income is not fully comparable.To eliminate the effects of inflation, the data were converted into constant 1960 dollars.

In this context, it is important to point out that the Metropolitan Museum is chosen toillustrate larger trends and dynamics. The paper should not be construed as a judgment ofmanagerial decisions of the past or an indictment of the Museum on commercializationcharges. While the Metropolitan, by its own admission, has been on the very forefront ofthese developments, the underlying issue is endemic to the art museum field, perhaps themuseum field at large. Moreover, as suggested below, it may be worthwhile exploring howwell the findings of this case translate to other types of institutions, such as colleges anduniversities or hospitals, which have undergone similar, if not even greater, commercialtransformations.

Charting the Metropolitan Museum’s revenue structure

The following first presents an overview of the major changes in the Museum’s revenuestructure that have occurred over the four decades, and then traces the development of, andshifting rationales and reasons for, the commercial activities of the Museum. Commercialactivities essentially comprise admissions (i.e., the museum equivalent to fees for service),on the one hand, and what museums usually refer to as auxiliary activities—auxiliary, thatis, to the main mission of the institutions—on the other. For the most part, the latter includemuseum shop and other merchandising activities, restaurant and food services, as well asparking. For practical purposes, merchandising includes the sale of highly mission-relevantproducts (e.g., exhibition catalogues and scholarly publications of museum staff), marginallymission-relevant products that are still considered educational and tax-exempt under the taxcode (e.g., coffee mugs or ties depicting items from the collection), and unrelated products(e.g., coffee mugs with the museum’s logo).

A commercial transformation?

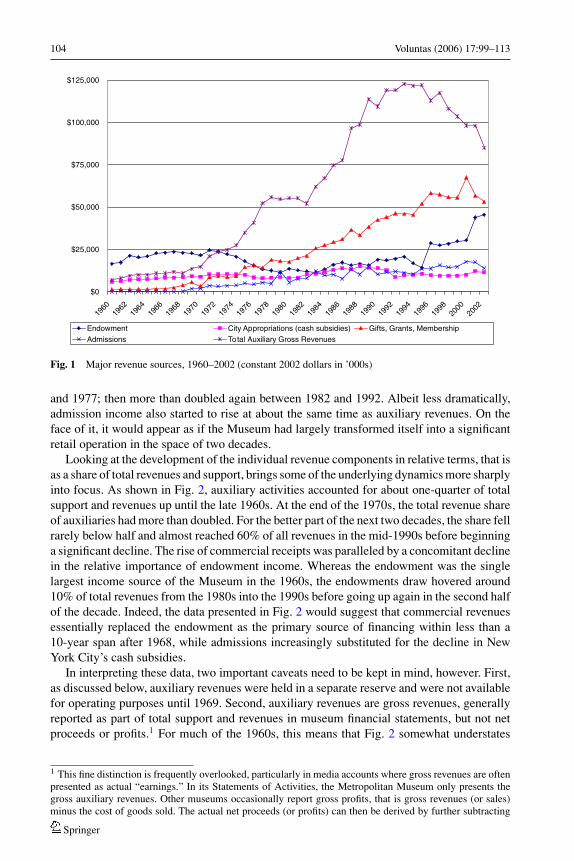

A review of the overall revenue structure suggests that a significant commercial transforma-tion of the Museum did indeed happen in the period under consideration. Figure 1 traces theMuseum’s main revenue sources from 1960 to 2002 in constant 2002 dollars. Endowmentincome and city subsidies had their ups and downs over the years, but the figure shows astriking upsurge of auxiliary gross revenues as well as gifts, grants, and membership. The lat-ter started to go up in the mid-1970s when the museum began to benefit from the emergenceof foundation funders, corporate sponsors, as well as state and federal government support,as discussed earlier. The climb of donative income was, however, eclipsed by an earlierand much more pronounced rise in the gross revenues of the Museum’s merchandising andother auxiliary activities. These revenues more than tripled in constant dollars between 1967

Springer

104 Voluntas (2006) 17:99–113

$0

$25,000

$50,000

$75,000

$100,000

$125,000

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

Endowment City Appropriations (cash subsidies) Gifts, Grants, MembershipAdmissions Total Auxiliary Gross Revenues

Fig. 1 Major revenue sources, 1960–2002 (constant 2002 dollars in ’000s)

and 1977; then more than doubled again between 1982 and 1992. Albeit less dramatically,admission income also started to rise at about the same time as auxiliary revenues. On theface of it, it would appear as if the Museum had largely transformed itself into a significantretail operation in the space of two decades.

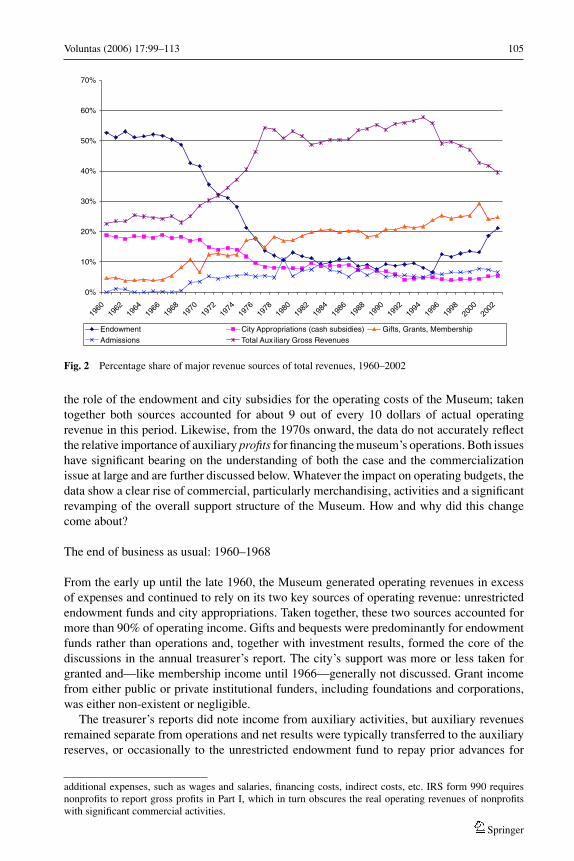

Looking at the development of the individual revenue components in relative terms, that isas a share of total revenues and support, brings some of the underlying dynamics more sharplyinto focus. As shown in Fig. 2, auxiliary activities accounted for about one-quarter of totalsupport and revenues up until the late 1960s. At the end of the 1970s, the total revenue shareof auxiliaries had more than doubled. For the better part of the next two decades, the share fellrarely below half and almost reached 60% of all revenues in the mid-1990s before beginninga significant decline. The rise of commercial receipts was paralleled by a concomitant declinein the relative importance of endowment income. Whereas the endowment was the singlelargest income source of the Museum in the 1960s, the endowments draw hovered around10% of total revenues from the 1980s into the 1990s before going up again in the second halfof the decade. Indeed, the data presented in Fig. 2 would suggest that commercial revenuesessentially replaced the endowment as the primary source of financing within less than a10-year span after 1968, while admissions increasingly substituted for the decline in NewYork City’s cash subsidies.

In interpreting these data, two important caveats need to be kept in mind, however. First,as discussed below, auxiliary revenues were held in a separate reserve and were not availablefor operating purposes until 1969. Second, auxiliary revenues are gross revenues, generallyreported as part of total support and revenues in museum financial statements, but not netproceeds or profits.1 For much of the 1960s, this means that Fig. 2 somewhat understates

1 This fine distinction is frequently overlooked, particularly in media accounts where gross revenues are oftenpresented as actual “earnings.” In its Statements of Activities, the Metropolitan Museum only presents thegross auxiliary revenues. Other museums occasionally report gross profits, that is gross revenues (or sales)minus the cost of goods sold. The actual net proceeds (or profits) can then be derived by further subtracting

Springer

Voluntas (2006) 17:99–113 105

0%

10%

20%

30%

40%

50%

60%

70%

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

Endowment City Appropriations (cash subsidies) Gifts, Grants, MembershipAdmissions Total Aux iliary Gross Revenues

Fig. 2 Percentage share of major revenue sources of total revenues, 1960–2002

the role of the endowment and city subsidies for the operating costs of the Museum; takentogether both sources accounted for about 9 out of every 10 dollars of actual operatingrevenue in this period. Likewise, from the 1970s onward, the data do not accurately reflectthe relative importance of auxiliary profits for financing the museum’s operations. Both issueshave significant bearing on the understanding of both the case and the commercializationissue at large and are further discussed below. Whatever the impact on operating budgets, thedata show a clear rise of commercial, particularly merchandising, activities and a significantrevamping of the overall support structure of the Museum. How and why did this changecome about?

The end of business as usual: 1960–1968

From the early up until the late 1960, the Museum generated operating revenues in excessof expenses and continued to rely on its two key sources of operating revenue: unrestrictedendowment funds and city appropriations. Taken together, these two sources accounted formore than 90% of operating income. Gifts and bequests were predominantly for endowmentfunds rather than operations and, together with investment results, formed the core of thediscussions in the annual treasurer’s report. The city’s support was more or less taken forgranted and—like membership income until 1966—generally not discussed. Grant incomefrom either public or private institutional funders, including foundations and corporations,was either non-existent or negligible.

The treasurer’s reports did note income from auxiliary activities, but auxiliary revenuesremained separate from operations and net results were typically transferred to the auxiliaryreserves, or occasionally to the unrestricted endowment fund to repay prior advances for

additional expenses, such as wages and salaries, financing costs, indirect costs, etc. IRS form 990 requiresnonprofits to report gross profits in Part I, which in turn obscures the real operating revenues of nonprofitswith significant commercial activities.

Springer

106 Voluntas (2006) 17:99–113

building programs. The publications department produced art books, print reproductions,and some casts of items in the collection, as well as Christmas cards and an engagementcalendar. These activities were seen as an outreach or educational device. The distribution ofa new publication series through the Book-of-the-Month Club won the Museum “new friendsin widely scattered quarters” and the Christmas card catalogue “was a widely appreciatedservice of the Museum” (Annual Report, 1960), that also provided “a unique means ofexploring the reserves of the departmental storerooms, and illustrate rarely exhibited worksof art as well as familiar ones” (Annual Report, 1967).

Although the Museum continuously generated surpluses, the reports unfailing pointedto the problem of rising costs of operations, acquisitions, and building needs that would“continue to require more current income through annual giving and increases in the Unre-stricted Endowment Funds” (Annual Report, 1960). The strategy of choice in the early tolate 1960s was thus to further develop the traditional donative revenue sources. The pursuitof commercial revenues was a non-issue: Admission to the Museum and special exhibitionswas free of charge and auxiliary income was essentially used to finance future publicationsand high quality reproductions.

The origins of commercialization: 1969–1971

At the end of the 1960s and the beginning of the 1970s, however, several factors cametogether that culminated in major changes in the way the Museum would be financed inthe future. First, the staff build-up and other preparations for the Centennial Celebrationin 1970 (the Museum was founded in 1870) accelerated existing cost pressures. Second,Thomas Hoving, an energetic new leader, was appointed director in 1967. Early in histerm, Hoving aggressively pursued the acquisition of major private collections as well as anew building master plan that would expand the Museum to the limits of its Central Parklocation. Hoving also begun to change the basic orientation of the museum (and the USmuseum field at large) towards education and public access (Hoving, 1993). The 1959–60Annual Report had already noted that the “traditional idea of the Museum as a repositoryof objects tends to obscure its growing likeness to other educational institutions” (p. 31),but the 1970–71 Annual Report took this trend to its logical conclusion: “The period ofquantitative amassment has closed; the epoch of education and communication has openedin earnest” (p. 3). Pursuing these functions, in turn, required additional operating revenues.Third, the budgetary problems of New York City during FY 1968–69 led to an announcementof reductions in support of cultural institutions (including the Metropolitan) that was laterwithdrawn. Nevertheless, it sent a clear signal to the Museum’s leadership that municipalsupport could not be taken for granted anymore, and after 1969, city support was dutifullyacknowledged in the financial reports. Finally, the Museum was beginning to feel the on-setof the inflation of the 1970s, as the Annual Report for 1969–70 emphasized in somewhatdramatic terms:

Inflation has hit all nonprofit institutions hard. The Metropolitan Museum is no exception . . . this is asituation that neither trustees nor administration can permit to continue, or the days of the Museum’sexistence will be numbered. (pp. 35–36)

Thus, while the museum was expanding both physically and in its functions, it becameclear that its two key traditional revenue sources would not suffice anymore. The City’s bud-getary problems threatened municipal support and inflation threatened endowment support.In response, the Museum begun to pursue more aggressively alternative sources of grantsupport, calling on corporations, foundations, individuals, and government to pick up the

Springer

Voluntas (2006) 17:99–113 107

“challenge that members, trustees, and a few wealthy individuals have hitherto carried alone”(Annual Report, 1969–70, p. 45).

Perhaps even more importantly, the need for “vigorous action” also led to a re-examinationof Museum attitudes towards more commercial means of income. In fact, within less than3 years, the Museum set changes in place that marked the beginning of what we would nowterm a growing commercialization. First, income from auxiliary activities was no longerset aside for auxiliary purposes or to help defray costs of extraordinary expenses, such asbuilding needs. “Recognizing that auxiliary activities are an integral part of the Museum,”notes the Treasurer’s Report in the 1968–69 Annual Report, “the Board of Trustees transferred[funds] from the Reserve for Auxiliary Activities to be used for 1969 operating purposes”(p. 122). Henceforth, auxiliary activities ceased to be an end in themselves, but becamea means to cross-subsidize basic Museum operations. Second, in the same fiscal year theMuseum instituted a new policy of charging admissions for special exhibitions (ibid.); andintroduced voluntary admissions at the main building (Annual Report, 1970–71, p. 42).

Non-profit cultural institutions today are subject to the same economic hazards of life as is a profit-making business but without adequate cushions. Non-profit status and tax privileges were originallyaccorded museums to offset the fiscal disadvantages of serving the public good, but they no longerwork adequately to keep museum budgets balanced. (Annual Report, 1971–72, p. 7)

Using auxiliary activity profits for operations and charging fees thus now seemed anappropriate means of cushioning the new economic realities.

The rise of commercialization: 1972–1990

By 1972, the new policies were beginning to bear fruit. While the Museum was forced tolay-off staff and leave vacant positions unfilled, the “dynamic and imaginative leadership”in the bookshop and reproduction division provided some hope in otherwise dire economiccircumstances:

Over the past six years revenue from sales of books, catalogues, calendars and reproductions of worksof art from our collection have risen . . . It is hoped that this significant and much needed source ofincome will continue to increase in the future. (Annual Report, 1972–73, p. 8)

Three developments came together during the decade that forced an ever-growing re-liance on commercial income as an essential source of financing. First and foremost, eco-nomic recession and inflation began to undermine the endowment as the traditional pillarof the museum’s finances, necessitating “vigorous attention to revenue-producing activities”(Annual Report, 1974–75, p. 11). Indeed, by the middle of the decade, endowment incomewas rapidly declining, while earned income gained sharply. Commercial and membershipincome, with close to 26% of total income by 1975, was:

. . . exceeded only by our income from endowment which is now 33.2 percent of total income ascompared with 40.1 percent last year and 65 percent in 1966. Clearly, in the absence of these, in effect,self-generated revenues—virtually all of which have become significant only within the last eightyears—the Museum would have been even more painfully plagued by the financial woes afflicting somany of our sister institutions.

Grim as the prospects for the coming years may seem, we can be proud to have been at the forefrontin seeking alternatives to the traditional sources of support which are clearly no longer adequate tosustain the services we provide. (Annual Report, 1974–75, p. 12)

With endowment income as a share of total income cut in half between 1966 and 1975,the Museum’s exploration of commercial income was essentially validated and there wasno thought to return the Museum to its traditional revenue structure. Perhaps the clearest

Springer

108 Voluntas (2006) 17:99–113

indication of the new attitude was the decision to use endowment funds to finance merchan-dising expansions. In 1978, a $3 million shop expansion was financed through an advanceof endowment funds and a commercial loan (secured with endowment securities) in equalmeasure to be repaid from merchandising sales (Annual Report, 1977–78). Two years later,another 10% of the endowment was advanced to finance merchandising inventories, theparking garage construction, and another bookshop expansion (Annual Report, 1979–80).The belief in the potential of commercialism was not unfettered, as the 1976 President’sReport indicates:

Nevertheless, there is a limit, no matter how inventive our merchandising or how generous the publicresponse to our pay-what-you-wish admissions, beyond which the Museum cannot expect to go inthe realm of self-sufficiency. We exist, after all, to offer maximum services and we cannot adopt themeasures of an ordinary business by curtailing services when finances so dictate without underminingour very reason for being. (Annual Report, 1975–76, p. 4)

This warning spoke to the other two developments in this decade that ultimately helpedto cement the importance of commercial revenues. First, whereas an “ordinary business”might have considered postponing expansion plans during a period of sustained recessionand inflation, the Metropolitan’s building and expansion plans continued throughout thedecade without any obvious signs of scaling back. By 1980, the Museum had opened “noless than eight major facilities” despite the unanticipated “double-digit rate of inflation andconsecutive annual increases in inflation” that had occurred since the new facilities and theresulting new expenses were planned a decade earlier (Annual Report, 1981–82, p. 68).Second, the caution regarding the limits of self-sustainability was repeated in 1977 with anunequivocal statement of its intention: “the gap which always remains between incomeand operating expenses can only be filled by government” (Annual Report, 1976–77,p. 5). However, while federal arts appropriations increased in the 1970s, there was nogeneral bailout of cultural institutions. Moreover, the Museum increasingly faced cuts instate aid and reductions in city cash subsidies and, faced with its own economic problems,New York City proved unwilling and unable to keep covering fully the growing maintenanceand protection needs of the Museum. With the endowment and city aid in continuous decline,commercial income was the Museum’s best chance to have its expansion and finance it too.Accordingly, suggested admission fees were raised in 1976 and 1977 and then again in 1980,1981, and 1982. (At the same time, investments in merchandising operations and new shopscontinued.)

Yet, the limits to self-sustainability were beginning to show at the end of the 1970s. TheMuseum faced a string of record deficits and hired a consulting firm to develop a 5-year plantowards a financial equilibrium. The plan foresaw a three-pronged strategy of: (1) increasingadmissions, membership, and auxiliary income; (2) reducing costs; and, (3) rebuilding “thetraditional strength of the endowment and its role as the financial heart of the Museum”(Annual Report, 1980–81, p. 77). While the first two strategies were essentially what theMuseum had pursued over the past decade, the third strategy constituted an effort to changecourse. A new capital campaign, the Fund for the Met, was now seen as the “principal meansby which we can begin to overcome the problem of recurring operating deficits and movetowards a state of financial equilibrium” (Annual Report, 1981–82, p. 5).

Although the goals of the Fund for the Met campaign were reached in 1986, it neitherachieved the hoped-for financial equilibrium nor did it reduce the Museum’s quest of com-mercial income. By contrast, the King Tut exhibition that the Met had orchestrated at theend of the 1970s had ushered in the age of the blockbuster exhibition. That “large atten-dance figures, not surprisingly, also mean substantial revenues from auxiliary activities”(Annual Report, 1973–74, p. 11) was an old insight, but beginning in the early 1980s the

Springer

Voluntas (2006) 17:99–113 109

Metropolitan mounted a string of hugely successful special exhibitions that boosted bothadmissions and auxiliary income to new heights: The Vatican Collections (1983), Manet(1984), van Gogh in Arles (1985), van Gogh in Saint-Remy and Auvers (1987), Degas,Goya, and O’Keeffe (1989). While endowment gains battled further reductions in New YorkCity subsidies throughout much of the 1980s, “blockbuster economics” (Temin, 1991) heldthe perpetual operating deficits at bay.

With blockbuster induced merchandising profits so strong that endowment advances forretail expansions were repaid faster than expected in 1985, the Museum was weary of:

what all of us agree to be an overdependence on special exhibition revenues. Overall, the Metropolitanhas a long way to go before it can be said to have truly achieved financial stability—stability thatwould reduce our dependence on highly popular exhibitions. (Annual Report, 1983–84, p. 4)

With “the lengthening chain of income . . . only as strong as the weakest link” (ibid., p. 78),the Museum remained nevertheless determined to preserve the strength of merchandisingoperations by way of lengthening the retail chain. As concerns mounted towards the end ofthe 1980s that the overall economic situation might negatively impact merchandising results,the Museum responded by increasing retail operations—opening seven new off-site storesacross the country over the next 3 years.2

Reaching the plateau: 1991–2002

Despite the off-site store expansion, the Museum was beginning to wonder about the futureof commercial activities. Summing up the pursuit of the past 20 years, the 1990–91 AnnualReport acknowledged for the first time that there might be a limit to growth:

Fortunately, the Metropolitan spent much of the 1970s and early 1980s on diversifying its revenuebase to avoid excessive dependence on a single source of funds. As a result, there are now eight majorrevenue streams supporting the operations of the Museum, including the city. However, while weforecast continued growth in many of these areas, we are concerned that some sources of income, suchas merchandising and admissions, may be approaching plateaus beyond which sustainable growth isuncertain. (p. 75)

In part, this gloomy assessment may have been due to declines in the mail-order business,attributed to “industry trends,” that led to losses in the merchandising operations during therecession of the early 1990s. Nevertheless, with auxiliary activities as one of the eight majorrevenue sources and “chronic uncertainty of city funding levels” (Annual Report, 1991–92,p. 88) coupled with continued operating deficits, a retreat in the merchandising arena wasnot seen as an option. By contrast, the Museum pursued further expansion. Faced with asluggish economy at home, the Museum began to seek out foreign ventures. Nevertheless,merchandising operations began to incur net losses from the mid-1990s to the end of thedecade. The Annual Reports effectively ceased to discuss auxiliary activities until 1999rather concentrating on endowment funds and a new capital campaign launched in 1994.Merchandising operations bounced briefly back to profitability in 2001, but, after peaking inthe mid-1990s, gross revenues as well as expenses went on a precipitous slide. In constantdollars, the Museum had brought down its annual merchandising expenditures in 2002 tothe 1987 level. In relative terms, 2002 merchandising gross revenues dropped down to 40%of total revenues and support—the lowest share since 1975.

2 There are a total of 20 “Met Stores” across the United States (California, Colorado, Florida, Georgia,Nevada, New Jersey, New York, Texas) and another 13 abroad (Australia, Austria, Japan, Mexico, Philippines,Singapore, Thailand). See website: www.metmuseum.org

Springer

110 Voluntas (2006) 17:99–113

Discussion and conclusion

The case study presented here has been exploratory and illustrative in nature and, as such,defies easy generalizability. As far as the Metropolitan’s experience over the past decadeis concerned, however, other evidence suggests that other museums have followed similartrajectories. Many large museums—the Smithsonian and the Museum of Fine Arts, Bostonto name but a few—also experienced problems with their retail divisions in the late 1990s.In their sample of 15 larger museums, Toepler and Kirchberg (2002) detected a decline ofmerchandising gross revenues and net profits in the same period, speculating that there maynot have been any net proceeds across the sample. Comparing Economic Census and IRSStatistics of Income (SOI) data for the museum field at large, Toepler and Dewees (2005)noted that the growth of sales revenue of the largest museums, as represented in the SOIsample, had come to a virtual standstill by the mid-1990s and suggested the on-set of apotential “decommercialization” trend. In some respects, at least, the present case may thusnot be too overly idiosyncratic. Although the economic history of one institution cannot bemore than suggestive in the end, there are nevertheless potentially important implications forfuture commercialization research. What conclusions can be drawn from this case study?

Insofar as this case is any indication, the roots of the rise of commercialization may liein the late 1960s and 1970s. Explaining the commercialization development as a result oftrends in the 1980s and early 1990s (e.g., decreasing government support, increased for-profit competition) may therefore not be sufficient. As in this case, it seems equally, if notmore likely, that the economic crisis of the 1970s took substantial tolls on institutions thatrelied heavily on endowment income before and forced them to develop alternative financingmethods. If that is so, the loss of endowment support in real terms in the 1970s may in facthave been an important contributing factor to the commercial transformation in fields beyondthe arts, such as the hospital industry and higher education. Additional work in this respectin other nonprofit sub-sectors may provide useful new insights.

Conceptually, Weisbrod (1998b) has offered the most concise framework of the com-mercialization issue yet. To recapitulate briefly, Weisbrod posits that nonprofit organizationsproduce both public and private goods and that managers have pronounced preferences thatshape the product mix. The public good output, such as collection, conservation, and schol-arly research in the museum case, is the most preferred, but requires potentially limiteddonations and subsidies. To supplement donative support and cross-subsidize the publicgood provision, nonprofits also produce private goods. Private goods are preferred if closelyrelated to mission, such as admission charges for both the permanent as well as specialexhibitions. Other private goods that are at best indirectly related to the mission, such asauxiliary activities, are non-preferred and will only be produced at a minimum unless do-native income and preferred private good provision are insufficient to finance the desiredlevel of public good output. Once nonprofit managers engage in private good production,there is the possibility that economic and financial considerations begin to override missionconsiderations and mission displacement may take place.

The Metropolitan case fits this framework neatly. In the pre-1969 era, the Museumcommanded sufficient donative resources through its endowment (i.e., accumulated priordonations) and municipal subsidies to pursue its public good production. Preferred privategoods were not needed and admission was free. As the continued adequateness of donativerevenues came into question at the turn of the decade, admission fees were introduced, butthese “preferred private good” charges were kept voluntary on a pay-as-you-wish (or can)basis and labeled “suggested contributions” rather than fees. At their inception, the Museum

Springer

Voluntas (2006) 17:99–113 111

Table 1 Suggested and average admission contributions

Year of increase Suggested contribution Average contribution Ratio suggested/average (%)

1971 $1.50 $0.65 431976 $1.75 $0.98 561977 $2.00 $1.05 531980 $2.50 $1.44 581981 $3.50 $1.96 561982 $4.00 $2.19 551986 $4.50 $2.80 621991 $6.00 $3.72 621995 $7.00 n/a —1999 $10.00 n/a —

was clearly concerned about a potential negative impact on access. Noting that more thanhalf of all visitors entered for free, the Annual Report for 1972–73 held:

We are gratified that the pay-as-you-wish concept continues to produce a critically important amountof revenue without impeding or discouraging visits from large numbers of the interested public. (p. 8)

Later increases were done in response to pressing needs, and the fact that average con-tributions never reached as much as two-thirds of the suggestion (see Table 1), never ledthe Museum to change the voluntary nature of admission fees over three decades of nearcontinuous operating deficits.

Similarly, the crucial change in the late 1960s to start using auxiliary activity surplusesfor operating purposes was as much motivated by cross-subsidy considerations as was theintroduction of admission fees. This was made clear in the 1974–74 Annual Report:

Admissions and auxiliary activity revenues generated from the popular response to many of themajor exhibitions made possible, in turn, the mounting of the many unfunded, but highly important,exhibitions . . . (p. 90)

But this also shows the beginnings of programmatic impact as the statement alreadyencapsulates the very idea of blockbuster economics, that is the mounting of “fundable”and “profitable” popular exhibitions to help support unfundable, but “highly important”(i.e., scholarly) exhibitions without much popular appeal. While the popularity of specialexhibitions was more or less a lucky happenstance into the 1970s, the pursuit of popularblockbusters became effectively an outright strategy in the 1980s and 1990s, no matter howuncomfortable the Museum was with it at times.

While Weisbrod’s framework thus adequately explains the emergence of the commercial-ization phenomenon (both in terms of admissions and auxiliary activities) in the MetropolitanMuseum, the case suggests two issues that may require further conceptual elaboration. Themodel so far is essentially static and both issues have to do with changes over time. First,retail and merchandising activities in the museum case are generally not too easily catego-rized into preferred and non-preferred, public and private. A full reproduction of a collectionitem in its own shape or form may be preferable over its reproduction on a silk scarf. Thelatter may be preferable over using a motif of the item for the design of an earring and this,in turn, more preferable than a piece of jewelry with no connection to the collection at all.However, the boundaries are very fluid. Perhaps more importantly though, the case suggeststhat the relative “preferentiality” of commercial activities may not be stable over time.

As discussed earlier, the volume of “retail” activities was all but insignificant in the early1960s, although the proceeds were not used for operations. Arguably, however, the sales

Springer

112 Voluntas (2006) 17:99–113

of reproductions and publications were in effect a “preferred” contribution to the publicgood output at the time. While there was a certain visitor and/or patron service elementto it, the Museum’s concern about the quality of reproductions and the desire to share inthis way items from the collection that were otherwise rarely shown indicate that theseactivities were originally much closer to preferred public goods than non-preferred privateones. Indeed, many museums started to make postcards and reproductions available in the latenineteenth century in an effort to aid art and design students, researchers as well as craftsmenin their work. While some of the products remained the same, the nature of the businesschanged fundamentally from the 1970s on, however. Financial (i.e., non-preferred, private)aspects became dominant and there has been little, if any, indication that the Museum valuedits merchandising expansion for any other than purely economic reasons. More broadlyspeaking, this example underlines the possibility that even commercial ventures, whichoriginally developed out of mission-related activity, might eventually turn into somethingless desirable or preferable. That ventures may take on a life of their own and gradually pushnonprofits in unforeseen directions over time is possibly where the mission threat lies ratherthan in an abrupt and wholesale change of the managerial mindset. In the current context, thissuggests that a more cautious approach to pushing mission-based social entrepreneurshipmight be in order until we begin to understand better what the long-term effects may be.

On the other hand, there is nothing inherently wrong with the shift from the preferrednessto the non-preferredness of the commercial venture in question, as long as it continues tocontribute to the cross-subsidization of the mission good. Even if the auxiliary activities ofthe Metropolitan have largely taken on a non-preferred private good character, they havelong served the museum well in this respect. Auxiliary profits lessened the deficits in theearly 1970s and early 1980s, kept the Museum around the break-even level in the mid-1970sand mid-1980s, and were the reason for a brief period of substantial excesses of revenue overexpenses in the late 1980s. While auxiliary operations were therefore arguably crucial forthe survival of the Museum in the 1970s and 1980s, the situation changed in the 1990s, whenauxiliary deficits began to occur. This, in turn, points to another, quite fundamental issuewith entrepreneurial ventures of nonprofits: the possibility of downturns in the business cycleand the occurrence of losses. This generally suggests the need to emphasize contingencyplanning in any entrepreneurship scheme, both in form of building operating reserves toguard against short-term losses and exit strategies if the business conditions decline overthe long-term. Otherwise, revenue diversification by commercial means can as likely be abane as a boon. All in all, the present case suggests that both the potentially shifting natureand the long-term unpredictability of commercial ventures can play against the economicsof nonprofit organizations. Further exploring such changes over time may usefully informthe current commercialization and social entrepreneurship debates, in conceptual as well aspractical terms.

Acknowledgment Part of this work was completed while the author was a Fellow in Museum Practice atthe Smithsonian Center for Education and Museum Studies.

References

Abramson, A., Salamon, L. M., & Steuerle, C. E. (1999). The nonprofit sector and the Federal budget: Recenthistory and future directions. In E. Boris & C. E. Steuerle (Eds.), Nonprofits & government: collaborationand conflict. Washington, DC: Urban Institute Press, pp. 99–139.

Alexander, V. (1996). Museums & money: The impact of funding on exhibitions, scholarship, and management.Bloomington: Indiana University Press.

Springer

Voluntas (2006) 17:99–113 113

Alexander, J. (2000). Adaptive strategies of nonprofit human service organizations in an era of devolution andnew public management. Nonprofit Management and Leadership, 10(3), 287–303.

Anheier, H. K., & Toepler, S. (1998). Commerce and the muse: Are art museums becoming commercial?In B. Weisbrod (Ed.), To profit or not to profit? The commercial transformation of the nonprofit sector.New York: Cambridge University Press, pp. 233–248.

Bornstein, D. (2004). How to change the world: Social entrepreneurs and the power of new ideas. New York:Oxford University Press.

Brinckerhoff, P. (2000). Social entrepreneurship: The art of mission-based venture development. New York:John Wiley.

Cobb, N. (1996). Looking ahead: Private sector giving to the arts and humanities. Washington, DC: President’sCommittee on the Arts and the Humanities.

Dees, J. (1998). Enterprising nonprofits. Harvard Business Review, 76(1), 54–69.Dees, J., Emerson, J., & Economy, P. (2001). Enterprising nonprofits: A toolkit for social entrepreneurs. New

York: John Wiley.Dees, J., Emerson, J., & Economy, P. (2002). Strategic tools for social entrepreneurs: Enhancing the perfor-

mance of your enterprising nonprofit. New York: John Wiley.DiMaggio, P. (1986a). Cultural entrepreneurship in nineteenth-century Boston. In P. DiMaggio (Ed.), Nonprofit

enterprise in the arts: Studies in mission & constraint. New York: Oxford University Press, pp. 41–61.DiMaggio, P. (1986b). Can culture survive the marketplace? In P. DiMaggio (Ed.), Nonprofit enterprise in the

arts: Studies in mission & constraint. New York: Oxford University Press, pp. 65–92.James, E. (1983). How nonprofits grow: A model. Journal of Policy Analysis and Management, 2(3), 350–365.Larson, R. (2002). Venture forth!the essential guide to starting a moneymaking business in your nonprofit

organization. St. Paul, MN: Amherst H. Wilder Foundation.Lyman, R., & Hodgkinson, V. (Eds.) (1989). The future of the nonprofit sector: Challenges, changes, and

policy considerations. San Francisco: Jossey-Bass.Malaro, M. (1994). Museum governance: mission, ethics, policy. Washington, DC: Smithsonian Institution

Press.Salamon, L. (1993). The marketization of welfare: Changing nonprofit and for-profit roles in the American

welfare state. Social Service Review, 67(1), 17–39.Salamon, L. M. (1995). Partners in public service: Government-nonprofit relations in the modern welfare

state. Baltimore: Johns Hopkins University Press.Smith, S. R., & Lipsky, M. (1993). Nonprofits for hire: The welfare state in the age of contracting. Cambridge,

MA: Harvard University Press.Stevens, L. (1996). The earnings shift: The new bottom line paradigm for the arts industry in a market-driven

era. Journal of Arts Management, Law and Society, 26(2), 101–114.Temin, P. (1991). An economic history of American art museums. In M. Feldstein (Ed.), The economics of

art museums. Chicago: University of Chicago Press, pp. 179–193.Toepler, S., & Dewees, S. (2005). Are there limits to financing culture through the market? Evidence from the

U.S. museum field. International Journal of Public Administration, 28(1/2), 131–146.Toepler, S., & Kirchberg, V. (2002). Museums, merchandising and nonprofit commercialization. National

Center for Nonprofit Enterprise Working Paper, available at www.nationalnce.orgWeisbrod, B. (1997). The future of the nonprofit sector: Its entwining with private enterprise and government.

Journal of Policy Analysis and Management, 16(4), 541–555.Weisbrod, B. (Ed.) (1998a). To profit or not to profit? The commercial transformation of the nonprofit sector.

New York: Cambridge University Press.Weisbrod, B. (1998b). Modeling the nonprofit organization as a multiproduct firm: A framework for choice.

In B. Weisbrod (Ed.), To profit or not to profit? The commercial transformation of the nonprofit sector.New York: Cambridge University Press, pp. 47–64.

Wilson, R. (1998). Philanthropy in 18th-century Central Europe: Evangelical reform and commerce. Voluntas,9(1), 81–102.

Young, D., & Salamon, L. (2002). Commercialization, social ventures, and for-profit competition. In L. M.Salamon (Ed.), The state of nonprofit america. Washington, DC: Brookings Institution Press, pp. 423–446.

Zietlow, J. (2001). Social entrepreneurship: Managerial, finance and marketing aspects. Journal of Nonprofit& Public Sector Marketing, 9(1/2), 19–43.

Zimmerman, B., & Dart, R. (1998). Charities doing commercial ventures: Societal and organizational impli-cations. Ottawa, Canada: CPRN and the Trillium Foundation.

Springer

Copyright © 2022 FDOKUMEN