CASE NO.: SCU- H0) - Florida's Supreme Court

13

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of CASE NO.: SCU- H0) - Florida's Supreme Court

¥-.

SUPREME COURT OF FLORIDA

CASE NO.: SCU- H0)On Discretionary Review From

The Fourth District Court ofAppeal

(4D10-674)

JACQUELINE HARVEY,

Petitioner,

VS.

DEUTSCHE BANK NATIONAL TRUST COMPANY

AS INDENTURE TRUSTEE FOR AMERICAN HOME

MORTGAGE INVESTMENT TRUST 2005-1, MORTGAGE-BACKED

NOTES SERIES 2005-1

Respondent.

PETITIONER'S BRIEF ON JURISDICTION

Respectfully submitted by,

Jacqueline Harvey

Pro se Petitioner

2359 SW Brookwood Lane

Palm City, Florida 34990

(561) 677-8485

TABLE OF CONTENTS

Page

TABLE OF AUTHORITIES ii

I. INTRODUCTION 1

II. STATEMENT OF THE CASE AND FACTS 2

III. ARGUMENT 5

A. STANDARD OF REVIEW 5

B. THIS COURT SHOULD REVIEW THE OPINION, WHICH

CONFLICTS WITH MANY DECISIONS FROM THIS

COURT AND FROM OTHER DISTRICTS 5

1. THE FOURTH DISTRICT'S ASSUMPTION THE

ORIGINAL PROMISSORY NOTE WAS IN THE

POSSISSION OF DEUTSCHE BANK IS

MISPLACED 6

2. THE FOURTH DISTRICT'S RELIANCE ON RIGGS

V. AURORA IS MISPLACED 6

3. THE FOURTH DISTRICT'S HOLDING THAT

FRAUDULENT ASSIGNMENTS OF MORTGAGES

ARE IRRELEVANT IS INCONSISTENT AND

CONFLICTS WITH THIS COURT'S PREVIOUS

DECISIONS 7

CONCLUSION 8

CERTIFICATE OF SERVICE 9

CERTIFICATE OF FONT COMPLIANCE 10

APPENDIX Tab

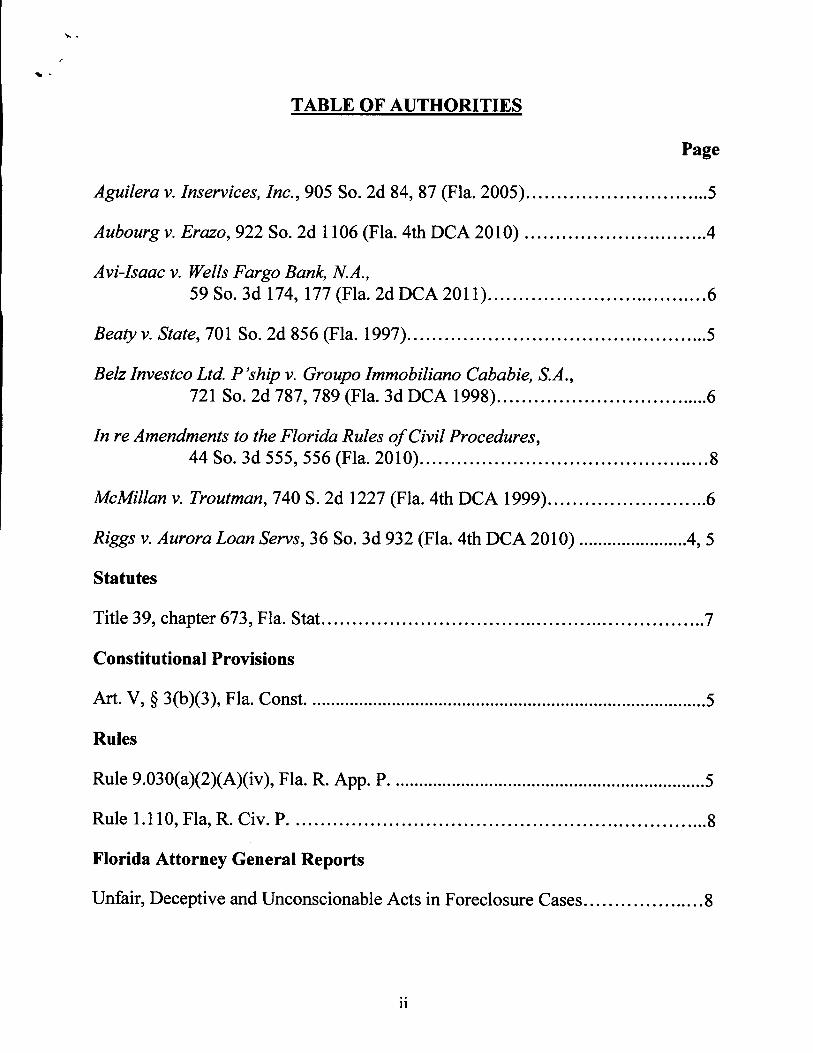

TABLE OF AUTHORITIES

Page

Aguilera v. Inservices, Inc., 905 So. 2d 84, 87 (Fla. 2005) 5

Aubourg v.Erazo,922 So. 2d 1106 (Fla. 4th DCA 2010) 4

Avi-Isaac v. Wells Forgo Bank, N.A.,

59 So. 3d 174, 177 (Fla. 2d DCA 2011) 6

Beatyv. State, 701 So. 2d 856 (Fla. 1997) 5

Belz Investco Ltd. P'shipv. Groupo Immobiliano Cababie, S.A.,

721 So. 2d 787, 789 (Fla. 3d DCA 1998) 6

In re Amendments to the Florida Rules ofCivil Procedures,

44 So. 3d 555, 556 (Fla. 2010) 8

McMillan v. Troutman, 740 S. 2d 1227 (Fla. 4th DCA 1999) 6

Riggs v. Aurora Loan Servs, 36 So. 3d 932 (Fla. 4th DCA 2010) 4, 5

Statutes

Title 39, chapter 673, Fla. Stat 7

Constitutional Provisions

Art. V, § 3(b)(3), Fla. Const 5

Rules

Rule 9.030(a)(2)(A)(iv), Fla. R. App. P 5

Rule 1.110, Fla, R. Civ. P 8

Florida Attorney General Reports

Unfair, Deceptive and Unconscionable Acts in Foreclosure Cases 8

ii

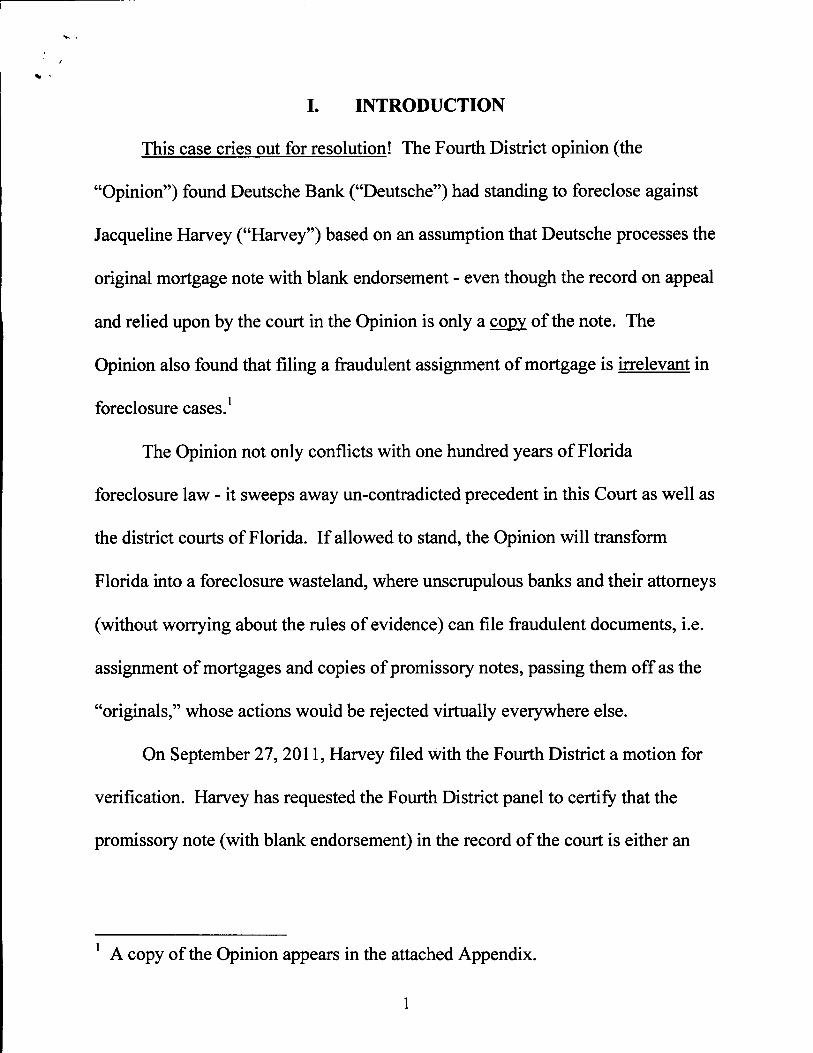

I. INTRODUCTION

This case cries out for resolution! The Fourth District opinion (the

"Opinion") found Deutsche Bank ("Deutsche") had standing to foreclose against

Jacqueline Harvey ("Harvey") based on an assumption that Deutsche processes the

original mortgage note with blank endorsement - even though the record on appeal

and relied upon by the court in the Opinion is only a copy of the note. The

Opinion also found that filing a fraudulent assignment of mortgage is irrelevant in

foreclosure cases.1

The Opinion not only conflicts with one hundred years of Florida

foreclosure law - it sweeps away un-contradicted precedent in this Court as well as

the district courts of Florida. If allowed to stand, the Opinion will transform

Florida into a foreclosure wasteland, where unscrupulous banks and their attorneys

(without worrying about the rules of evidence) can file fraudulent documents, i.e.

assignment ofmortgages and copies of promissory notes, passing them off as the

"originals," whose actions would be rejected virtually everywhere else.

On September 27, 2011, Harvey filed with the Fourth District a motion for

verification. Harvey has requested the Fourth District panel to certify that the

promissory note (with blank endorsement) in the record of the court is either an

A copy ofthe Opinion appears in the attached Appendix.

original promissory or a copy ofthe promissory note. This motion is still pending

in the Fourth District.

II. STATEMENT OF THE CASE AND FACTS

On April 6,2009, Deutsche Bank ("Deutsche") filed a two-count foreclosure

count against Jacqueline Harvey ("Harvey"). Count I ofthe complaint sought to

reestablish the lost note. Attached to the complaint were copies of the promissory

note and a copy of the mortgage, showing American Home Mortgage Acceptance,

Inc. ("AHMAI") as the lender and Mortgage Electronic Registration Systems, Inc.

("MERS") as the nominee mortgagee.

On September 17, 2009, Deutsche filed a motion for summary judgment,

along with an affidavit of indebtedness. On September 30, 2009, Deutsche filed an

affidavit of lost note. A hearing on Deutsche's motion for summary judgment was

held on October 12, 2009. At the hearing, the judge determined that the lost note

affidavit was not in the case file and declined to rule on the motion without first

reviewing the lost note affidavit.

On October 29, 2009, Deutsche filed a re-notice of hearing on the motion for

summary judgment, a Notice of Withdrawal of Count I ofplaintiff s complaint, a

copy of an assignment ofmortgage from MERS to Deutsche Bank and a Notice of

Filing Attached Original Note with Blank Endorsement (along with attached note).

The hearing was held on January 11, 2010. During this hearing the judge stated

the original note was in the file. Harvey asked the judge to see the alleged

"original" note. The trial judge refused and the following discussion took place.

Ms. Harvey: I would like to be able to see that, (the alleged "original"

note).

The Court: You have been given every opportunity to see it; they

gave you notice that they filed it, you could have looked.

Ms. Harvey: I went to the court - I went to the record myself and

looked and it was not the original.

Harvey argued that the assignment ofmortgage was fraudulent and Deutsche

did not have standing when they filed the foreclosure proceeding because the

assignment was not filed until twenty days after it filed the foreclosure. The judge

dismissed Harvey's argument and final foreclosure judgment was entered on

January 14,2010.

Harvey filed a noticed motion for reconsideration arguing that Deutsche

lacked standing to bring the foreclosure action and the assignment ofmortgage

contains questionable signatures. At the reconsideration hearing the trial denied

Harvey's motion. The judge stated: "I've already denied your motion, I did that in

chambers. So there's nothing for us to do today. Okay?"

Harvey appealed to the Fourth District, arguing that the trial court erred in

granting summary judgment because (1) a genuine issue of material fact existed as

to Deutsche's standing to foreclose; (2) the assignment of mortgage contained

questionable signatures in order to commit fraud upon the court; and (3) the trial

court abused its discretion by denying Harvey's motion for reconsideration and

violated her due process right by denying her an opportunity to be heard.

Deutsche argued that, as holder of the "original" note, endorsed in blank it

had standing to enforce the note, and that the trial court properly entered final

summary judgment.

On April 20, 2011, the Fourth District affirmed the summary judgment per

curiam citing Riggs v. Aurora Loan Servs., LLC, 36 So. 3d 932 (Fla. 4th DCA

2010) and Aubourg v. Erazo, 922 So. 2d 1106 (Fla. 4th DCA 2010). On May 4,

2011 filed a motion for rehearing. In this motion for rehearing Harvey again

argued that (1) Deutsche Bank did not have physical possession of the original

promissory note as evidenced in the Record and (2) the assignment of mortgage

contained questionable authorized signatures.

On June 29, 2011, the Fourth District denied Harvey's motion for

rehearing, but addressed some points argued by Harvey in her brief.

The Opinion citing Riggs concluded that since Deutsche possessed the

original note and filed it with the circuit court, its standing may be established from

its standing as note holder, regardless of any recorded assignment. Addressing

Harvey's argument regarding "questionable signatures" contained in the

assignment of mortgage, the Opinion concludes: "Even if Harvey could prove this,

the dispute would be between AHMAI and Deutsche."

On July 13, 2011, Harvey filed a Motion for rehearing en bane and motion

for certification. The motion for rehearing en bane and motion for certification

was denied on September 1,2011.

Harvey timely filed a notice to invoke the discretionary jurisdiction ofthis

Court to review the Fourth District opinions.

III. ARGUMENT

A. STANDARD OF REVIEW.

This Court may exercise jurisdiction to review the district court Opinion

because: (1) it misapplies this Court's precedent; and (2) it expressly and directly

conflicts with decisions ofthis Court and other district courts on the same question

of law. See Fla. Const, art. V, § 3(b)(3); Fla. R. App. P. 9.030(a)(2)(A)(iv); see

also Aguilera v. Inservices, Inc._, 905 So. 2d 84, 87 (Fla. 2005) ("misapplication of

decisional law creates conflict jurisdiction"); Beaty v. State, 701 So. 2d 856 (Fla.

1997) (noting that conflict must be express and direct).

B. THIS COURT SHOULD REVIEW THE OPINION, WHICH

CONFLICTS WITH MANY DECISIONS FROM THIS COURT

AND FROM OTHER DISTRICTS.

The Opinion's holding derives from a misapplication ofRiggs v. Aurora, a

case that did not even address the issue of a copy of a promissory note filed in a

foreclosure case or a fraudulent assignment of mortgage. This Court should take

jurisdiction to resolve the conflict created by the Opinion.

V

1. The Fourth District's Assumption the Original Promissory Note

was in the Possession of Deutsche Bank is Misplaced.

It is still in dispute whether the promissory note contained in the record

which the Fourth District relied upon as a basis for the Opinion is in fact the

original note. At the summary judgment hearing, Harvey's request to see the note

was denied by the trial judge. When the authenticity of the note was raised by

Harvey during summary judgment this conflict should have been reconciled at an

evidentiary hearing not at summary judgment. Belz Investco Ltd. P 'ship v. Groupo

Immobiliano Cababie, S.A., 721 So. 2d 787, 789 (Fla. 3d DCA 1998). McMillan

v. Troutman, 740 So.2d 1227 (Fla. 4th DCA 1999). Further, "it is reversible error

for a trial judge to deny a party an evidentiary hearing to which [the party] is

entitled." Avi-Isaac v, Wells Fargo Bank, N.A., 59 So. 3d 174, 177 (Fla. 2d DCA

2011) (quoting Sperdute v. Household Realty Corp., 585 So. 2d 1168, 1169 (Fla.

4th DCA 1991)

2. The Fourth District's Reliance on Riggs v. Aurora is Misplaced.

The Opinion also affirmed summary judgment on the basis that Deutsche's

actual possession of the original promissory note supported its claim that it was the

proper holder of the note thereby satisfied the requirements under the Uniform

Commercial Code.

In Harvey's May 4, 2011 motion for rehearing, Harvey stated, "In Riggs

where it is undisputed that Aurora had physical possession of the original note and

mortgage, in the instant case, Deutsche Bank did not have physical possession of

the original promissory note as evidenced in the Record." The existence of the

"original" promissory note still remains in question.

By applying Riggs to this instant case, without resolving the issue ofwhether

the note presented at summary judgment was in fact authentic and not a mere copy,

the Opinion altered decades of case law and seemingly rewrote Chapter 673, which

is the Florida equivalent of Article 3 ofthe Uniform Commercial Code governing

"negotiable instruments" by converting a copy ofpromissory note into a valid

negotiable instrument. If left to stand, the Opinion will have a tremendous

impact on all foreclosures in this state and will significantly impact future real

estate transactions.

3. The Fourth District Holding that Fraudulent Assignments of

Mortgages are Irrelevant is Inconsistent and Conflicts With This

Court's Previous Decisions

The assignment ofmortgage in this case contained a conflict on its face as to

Deutsche Bank's right to foreclose. By declaring that: "Even ifHarvey could

prove [the assignment was fraudulent], the dispute would be between AHMAI

[original lender] and Deutsche [the Plaintiff]", the Opinion announces a new rule

in foreclosure cases that actual ownership of the loan is irrelevant once the Plaintiff

makes aprimafacie showing of the right to enforce the note as its holder. It

cannot be disputed the assignment of mortgage contained the signatures ofthree

known Robo-Signers. See: Unfair, Deceptive and Unconscionable Acts in

Foreclosure Cases " (Florida Attorney General, Economic Crimes Division Report

2011). By holding that fraudulent assignments ofmortgages are irrelevant in

foreclosure cases, the Opinion altered decades of case law and seemingly

undermines and ignores the mandate set down by this Court when it addressed the

problem ofthe plethora of fraudulently executed documents in statewide

foreclosure cases. Acknowledging the importance of this problem and finding that

the veracity ofbanks and their chosen counsel is so often in questions, this Court

changed Florida Rules of Civil Procedure 1.110 to require that foreclosure

complaints be verified. In re Amendments to the Florida Rules ofCivil

Procedures, 44 So. 3d 555, 556 (Fla. 2010). The objective of this Court is largely

undermined by the Fourth District Opinion as it now stands.

If left to stand, the Opinion will have a tremendous impact on all pending

and future foreclosure cases in the State of Florida and will significantly limit

valid foreclosure defenses in such cases.

This Court should take jurisdiction to address the conflict and to correct the

Fourth District's serious error.

CONCLUSION

For the foregoing reasons, the Court should accept jurisdiction to review the

district court's decision and allow full briefing on the merits.

t

Respectfully submitted,

Jac^ueli^Harvey2359 SW Brookwood Lane

Palm City, Florida 34990

(561) 667-8485

CERTIFICATE OF SERVICE

I HEREBY CERTIFY that a true copy hereof has been furnished by United

States Mail to Katherine E. Giddings, Esq., and Nancy M. Wallace, Esq.,

AKERMAN SENTERFITT, 106 East College Avenue, Suite 1200, Tallahassee,

Florida 32301, this 1st day of October, 2011.

Jac^Geli^Harvey

CERTIFICATE OF FONT COMPLIANCE

I HEREBY CERTIFY that the font used in this brief is Times New Roman

14-point font and that the brief complies with the font requirements of Rule

9.210(a)(2).

Jac^neTme^arvey

10