Cambodia's taxation compared to Vietnam's

33

1 Bowdoin College Taxation in Cambodia Keavatey Srun Econ 2210: Economics in the Public Sector John Fitzgerald December 17, 2014

-

Upload

independent -

Category

Documents

-

view

0 -

download

0

Transcript of Cambodia's taxation compared to Vietnam's

1

Bowdoin College

Taxation in Cambodia

Keavatey Srun Econ 2210: Economics in the Public Sector John Fitzgerald

December 17, 2014

2

Table of Contents

I. Introduction …...................................................................................................………3

II. Types of taxes. ….......................................................................................................... 6

1. Profit Tax …............................................................................................................. 7

2. Value Added Tax …................................................................................................. 8

3. Excise Tax …............................................................................................................ 9

4. Salary Tax …............................................................................................................ 9

5. Registration Tax …................................................................................................. 10

6. Tax on Means of Transportation …........................................................................ 10

7. Property Tax …...................................................................................................... 10

8. Public Lighting Tax …........................................................................................... 10

9. Other Taxes …........................................................................................................ 11

III. Major Reforms and Tax Performance after Reforms …………………………...… 13

1. Major Reforms …................................................................................................... 13

2. Tax Performance after Reforms.............................................................................. 14

IV. Challenges ………………………………………………………………….…….. 18

1. Tax Administration Issues …................................................................................. 18

2. Tax Incentives…..................................................................................................... 19

3. Tax Evasion…........................................................................................................ 21

V. Comparative Study of Cambodian and Vietnamese Tax Systems …......................... 23

1. Tax Structure…....................................................................................................... 24

2. Tax Composition…................................................................................................ 27

3. Tax Administration…............................................................................................. 28

VI. Conclusion and Recommendations…......................................................................... 30

Bibliography …........................................................................................................... 32

3

I. Introduction

Given Cambodia’s high level of dollarization, the state loses most of the authority to

manage monetary policy in the country. This causes fiscal policy play very significant role in

Cambodian economic system. Macroeconomic stability depends soundly on prudent fiscal

policy and debt management in this developing country. Since Cambodia do not earn money

from bond issuing nor from Seigniorage, government revenue comes mainly from tax

collection revenue and foreign aid.

Cambodia has shown a sound macroeconomic performance over the past decades

with around 10 percent of GDP growth rate annually until 2008 (WB 2014). Because of the

disruption by the global economic downturn during 2008 and 2009, growth dropped to 0

percent in 2009. Then it returned to 6 percent in 2010 before reaching about 7 percent in the

last several years (WB 2014).

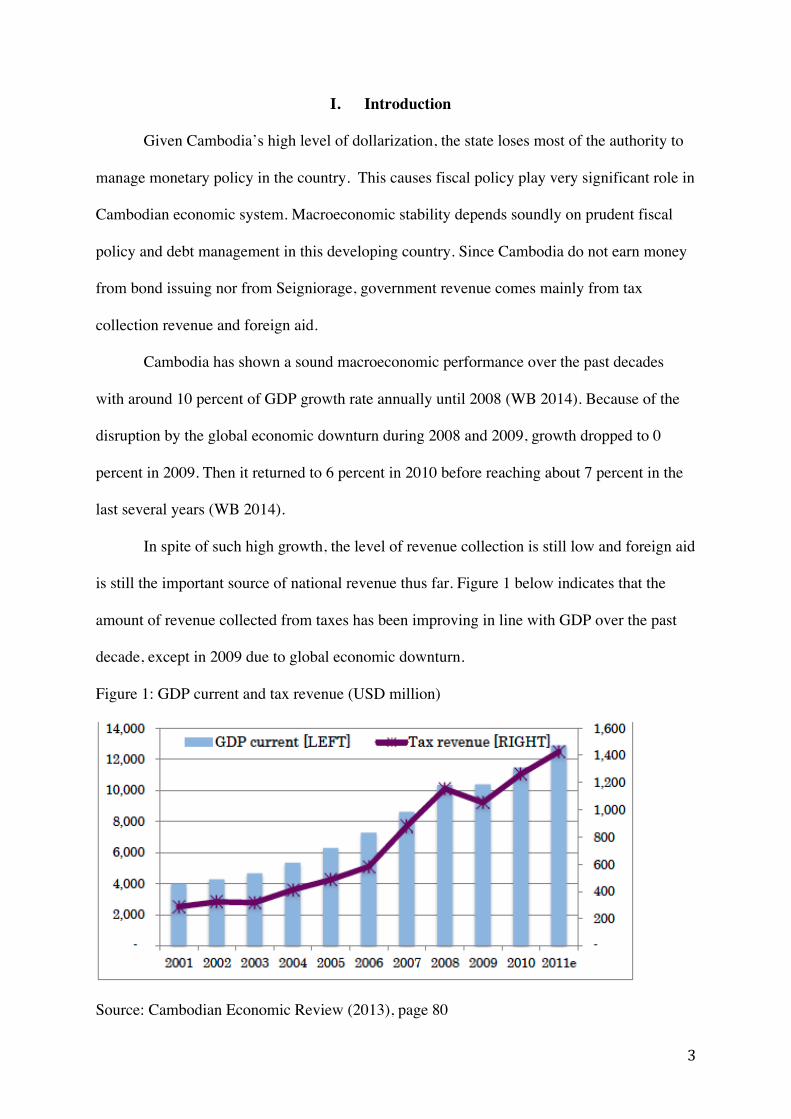

In spite of such high growth, the level of revenue collection is still low and foreign aid

is still the important source of national revenue thus far. Figure 1 below indicates that the

amount of revenue collected from taxes has been improving in line with GDP over the past

decade, except in 2009 due to global economic downturn.

Figure 1: GDP current and tax revenue (USD million)

Source: Cambodian Economic Review (2013), page 80

4

It is also noted that the ratio of tax revenue to GDP in Cambodia remains low

compared to other low-income countries (May 2012). It remains the lowest compared to other

countries as seen figure 2, and this results from challenges described in detail in the following

section of this paper.

Figure 2: Cambodian tax revenue compared to other countries

Source: World Bank (2013)

The tax system in Cambodia has had significant reform since 1997 when the Law on

Taxation was introduced, and it has continued being reformed each year until present. The

Cambodian government has continued reforming the tax collection system, especially the

profit taxes, salary tax, VAT and excise tax, by reforming tax policy and tax administration. A

new property tax was introduced in 2011 (Norregaard 2013). The reforms include introducing

new taxes (property tax, personal income tax) and some new tax regulations, widening the tax

base, increasing the tax rate on some items of excise tax, limiting tax exemption,

strengthening tax compliance and tightening tax administration (MEF 2010). However, the

new property tax is only being piloted in a limited number of urban areas.

Cambodian taxation has been improving over the past decade in terms of tax

collection policy and tax administration. The ratio of annual tax revenue to GDP has

increased, and large proportion of the revenue still comes from indirect tax including VAT,

import duties and excise tax. However, the revenue is still relatively low compared to other

5

countries in the same stage of development. Cambodia loses a significant amount of revenue

every year resulting from ineffective tax administration, very long tax holidays (Profit Tax

holiday up to 6 years and exemption from import duties and export tax) and all forms of tax

evasion in the country. Thus, this paper will explore more detail on tax system in Cambodia,

which will address answers to the following sub questions:

1. What are the major types of tax in Cambodia?

2. What are the main reforms that Cambodia has reform in tax system from 1997 till

present? And what are the outcomes of the reforms?

3. What are the challenges that make Cambodian tax revenue remains lower than others

low income countries?

4. What are the differences between tax system in Vietnam and Cambodia?

This paper organized as followed. Following this introductory section, section II

presents the types of taxes in Cambodia. Section III specifies major reforms and tax

performance resulting from outcomes of reforms. In section IV, we will compare the tax

system in Cambodia to tax system in Vietnam. Finally, section V is a conclusion and

recommendations.

6

II. Types of Tax in Cambodia

There are two major tax regimes, which are currently applied in Cambodia: real and

estimated regimes.

The real regime is applied to registered companies, state-owned companies, semi state-own companies, import-export companies, qualified investment projects, and other business enterprises that meet the following criteria: i) annual turnover exceeding 500 million riels (about USD 125,000) in case of supplying goods or both goods and services; ii) annual turnover exceeding 250 million riels (about USD 62,500) in case of providing services; and iii) annual turnover exceeding 125 million riels (about USD 31,250) in case of doing business with the government (bidding). Enterprises other than those mentioned above are subject to the estimated regime in which the taxable amount is estimated based on the discussion between taxpayers and tax officials. (Ngo 2013) It simply means real regime is applied to large and medium taxpayers while estimate regime

is applied to small taxpayers. Moreover, all types of taxes are applied equally to all level of

government throughout the country though people in the provinces can pay their taxes

directly to provincial tax department.

According to Law of taxation in Cambodia, there are different types of taxes, which

will be described more detail below. Among these, the Tax on Profit, VAT and Excise tax

share first, second and third biggest proportion of tax collected revenue respectively in 2012

as seen in figure 3.

Figure 3: Shares Percentage of Different Taxes in Tax Revenue

Source: The Fourth IMF-Japan High-Level Tax Conference for Asian Countries (2013)

7

Following section will describe each type of tax in detail including Profit Tax, the

VAT, Excise Tax, Tax on Salary Registration Tax, Tax on Means of Transportation,

Property Tax, Public Lighting Tax and other taxes. It will explain how each tax is applied

in Cambodia.

1. Profit Tax

Tax on Profit is owed by a resident taxpayer on income from Cambodian and foreign

sources. For a non-resident taxpayer, the tax is calculated on income from Cambodian

sources only.

The rates of the tax on profit are the tax rates on the annual profit as following:

§ 20% for the profit realized by a legal person. “The term ‘legal person’ means any

enterprise or organizations carrying on a business officially recognized by the

competent institutions of the Royal Government. It includes any government

institution, religious organizations, charitable organization, or non-profit organization.”

(Law of Taxation of the Kingdom of Cambodia, art. 3)

§ 30% for profit realized under an oil or natural gas production sharing contract and

the exploitation of natural resources including timber, ore, gold, and precious stones.

§ 9% for the profit of Qualified Investment Projects, an investment that has

received a Final Registration Certificate approved by Cambodia Development Council,

to be entitled to the 5-year transitional period determined by Cambodia Development

Council.

§ 0% for the profit of qualified investment projects during the tax exemption period.

Source: Ministry of Economy and Finance

8

§ 5% of the gross premiums received in the tax year for the insurance or

reinsurance

§ Progressive tax rates for profit earned by physical persons and dividend of

shareholders

Percentages of annual profit that is taxed Rate

From 0 to 6,000,000 Riels (USD 1,500) 0%

From 6,000,001 to 15,000,000 Riels (greater than USD 1,500 to USD 3,750) 5%

From 15,000,001 to 102,000,000 Riels (greater than USD 3,750 to USD 25,500) 10%

From 102,000,001 to 150,000,000 Riels (greater than USD 25, 500 to USD 37,500) 15%

Greater than 150,000,000 Riels (greater than USD 37,500) 20%

2. Value Added Tax (VAT)

The Value added tax has been implemented in Cambodia since early 1999. The VAT

is collected from the supply of goods or services. VAT rate is 0 percent for exported goods

from Cambodia and services consumed outside Cambodia and 10 percent for all supplies

other than exports and non-taxable supplies. Exports include international transportation of

passengers and goods.

VAT due = Output Tax – Input Tax

§ Output Tax is the VAT charged on supplying of goods and services to customers.

§ Input Tax is the VAT paid on import of goods or the VAT on local purchase of goods

or services for the business.

When goods are imported, they are assessed on Input Tax at the border. When they

are sold, customers pay the Output Tax. Thus, by 20th of each month tax payers must file the

VAT return if the units of goods they sell is less than the units of goods they pay input tax, or

9

they pay more VAT tax collected from their customers if they sell more units of goods than

the units they are tax. This is called the “invoice method”.

3. Specific Tax on Certain Merchandise and Services (Excise Tax)

The specific tax is imposed on a number of local and imported products and services

including tickets for local and international air transportation (10%); beverage (20%);

Tobacco, entertainment, large automobile, motorcycles from 125 cc upwards (10% each);

entertainment services, air transport of passenger (10% each); local and international

telecommunication (3%); petroleum products, and automobile more than 2,000cc (30%

each).

4. Tax on Salary

The Tax on Salary is a monthly tax imposed on salary that has been received within

the framework of fulfilling employment activities. A resident in Cambodia is liable to the Tax

on Salary from Cambodian sources and foreign sources while a non-resident person is liable

to the tax on salary from Cambodian source only.

Tax on salary of resident employees is determined on monthly basis and is withheld to

the progressive tax rate below:

Monthly Salary (Riels) Rate

0 – 500,000 (Approx. USD 125 or less) 0%

500,001 – 1,250,000 (over USD 125 – USD 312.5) 5%

1,250,001 – 8,500,000 (over USD 312.5 – USD 2,215) 10%

8,500,001 – 12,500,000 (over USD 2,215 – USD 3,125) 15%

12,500,001 – upwards (over 3,125) 20%

Fringe benefits 20% on market value

Non-residents Flat rate of 20%

*Note: USD 1 ≈ 4, 000 Riels

10

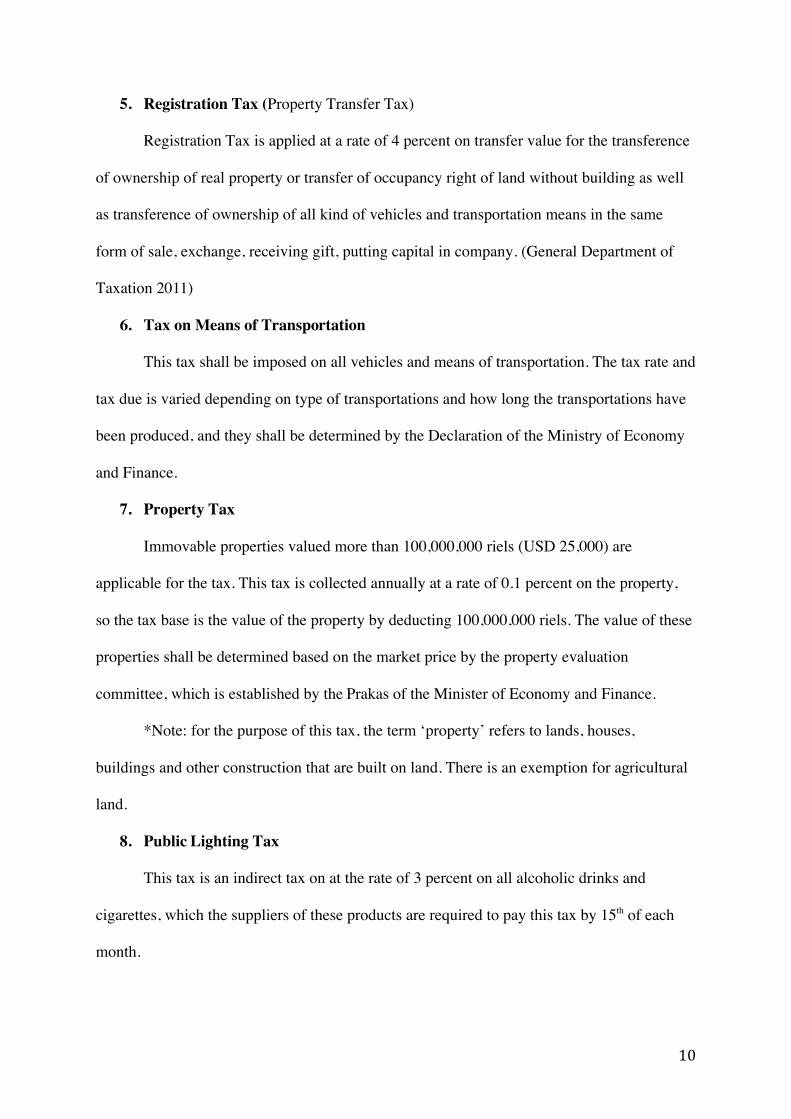

5. Registration Tax (Property Transfer Tax)

Registration Tax is applied at a rate of 4 percent on transfer value for the transference

of ownership of real property or transfer of occupancy right of land without building as well

as transference of ownership of all kind of vehicles and transportation means in the same

form of sale, exchange, receiving gift, putting capital in company. (General Department of

Taxation 2011)

6. Tax on Means of Transportation

This tax shall be imposed on all vehicles and means of transportation. The tax rate and

tax due is varied depending on type of transportations and how long the transportations have

been produced, and they shall be determined by the Declaration of the Ministry of Economy

and Finance.

7. Property Tax

Immovable properties valued more than 100,000,000 riels (USD 25,000) are

applicable for the tax. This tax is collected annually at a rate of 0.1 percent on the property,

so the tax base is the value of the property by deducting 100,000,000 riels. The value of these

properties shall be determined based on the market price by the property evaluation

committee, which is established by the Prakas of the Minister of Economy and Finance.

*Note: for the purpose of this tax, the term ‘property’ refers to lands, houses,

buildings and other construction that are built on land. There is an exemption for agricultural

land.

8. Public Lighting Tax

This tax is an indirect tax on at the rate of 3 percent on all alcoholic drinks and

cigarettes, which the suppliers of these products are required to pay this tax by 15th of each

month.

11

9. Other taxes

Ø Tax on Unused Land

The tax rate is 2 percent on the assessed value of unused land.

Ø Patent Tax

It is charged approximately USD 300 for annual business registration on Patent Tax

Payment, and it is required to pay in accordance with type of business and location.

Ø Minimum Tax

The Minimum Tax is a distinct tax from the profit tax. The Minimum tax is imposed

on taxpayers subject to the real regime system of taxation, except the qualified investment

projects determined by the Council for the Development of Cambodia. The Minimum Tax is

imposed at the rate of 1 percent of the annual turnover inclusive of all taxes, except for VAT,

and is payable at the time of the annual liquidation of the tax on profit. If the profit tax

amount exceeds 1 percent of annual turnover, the taxpayer pays only the tax on profit.

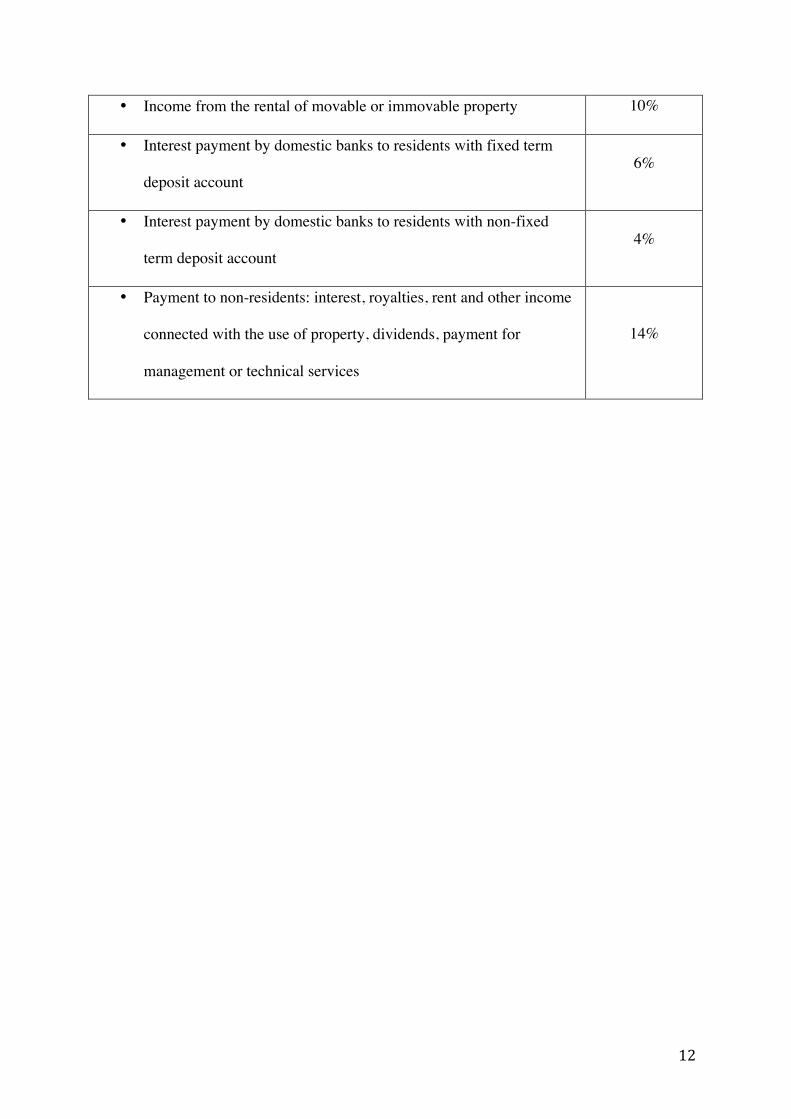

Ø Withholding Tax

The Withholding Tax is applied to certain payments for services and other payments

made to suppliers (VDB Loi 2012).

The withholding tax is assessed at the following rates:

Payments that withholding tax is applied on Rate

• Income received by individuals for services such as management,

consulting, etc.

• Payment of royalties for intangibles and interests in mineral

resources

• Payment of interest by a resident taxpayer carrying on business,

other than domestic banks or financial institutions

15%

12

• Income from the rental of movable or immovable property 10%

• Interest payment by domestic banks to residents with fixed term

deposit account 6%

• Interest payment by domestic banks to residents with non-fixed

term deposit account 4%

• Payment to non-residents: interest, royalties, rent and other income

connected with the use of property, dividends, payment for

management or technical services

14%

13

III. Major Reforms & Tax Performance after reform

1. Major Reforms

There are three important periods of tax reform in Cambodia including pre-reform

period from 1982 to 1993, reform period from 1994 to 1996, and tax reform period from

1997 until present. This part will focus on the tax reform from 1997 to present.

According to Sim Eang and Um Seiha (2005), the reforms include as following. Law

on Taxation was promulgated in 1997, which introduced profit tax, salary tax, VAT, excise

tax, withholding tax, and administrative rules and procedures. Moreover, self-assessment

system was applied in only Phnom Penh before 2000, but it was extended to five provinces in

2001 and 16 provinces in 2003. Plus, Large taxpayer unit was established in 2001 in Phnom

Penh, which covers 600 taxpayers and gets USD 250, 000 annual turnover. Equally

important, there is tax reform measure on different aspects including reform measure for

taxpayer services, reform measure of bookkeeping, tax reform measure of SMEs, reform

measure of tax audit, reform measure of staff training and reform measure of Information

Technology.

Important revenue-enhancing provisions were included in 1997 Law on Taxation as

following:

§ Levying a turnover tax on the first sale after importation (previously exempt); § Broadening the coverage of the excise duties on automobiles, international air travel, and

international telecommunication services; § Introducing taxes on interest and dividends; § Strengthening the application of a minimum tax on enterprises, including those granted tax

holidays under the Investment Law; applying a 30 percent of profit tax rate for oil and gas production-sharing contracts, and for exploiting natural resources, including timber, ores, gas and precious stones;

§ Extending coverage of taxes on salaries to government employees, elected officials and employees of NGOs;

§ Introducing the withholding of taxes; and § Replacing taxes on turnover and consumption with a value-added tax (VAT for the 600 largest

taxpayers (from 1 January 1998), and extending it gradually. (Chan et al. 1998, 39)

14

2. Tax Performance after Reforms

This section will discuss the tax performance after the major reforms from 1997 to

present.

Two major types of indirect tax are the VAT and excise tax. While the VAT is at 10

percent for all goods and services, the excise tax rate varies for different products. These two

taxes are generally regarded as regressive because the lower income people will bear a

relatively greater burden than the rich despite the flat rate. Simply, the rich pay smaller

percentage of their income as tax compared to the poor because they consume a lower

proportion of income. Unlike indirect tax, direct taxes such as profit tax and salary tax are

progressive because the rich pay a higher proportion of their income as tax. Generally, the

corporation or owners of the capital may still carry most of the burden even if the corporation

or owners of the capital might be able to pass some of the burden of direct tax to customers.

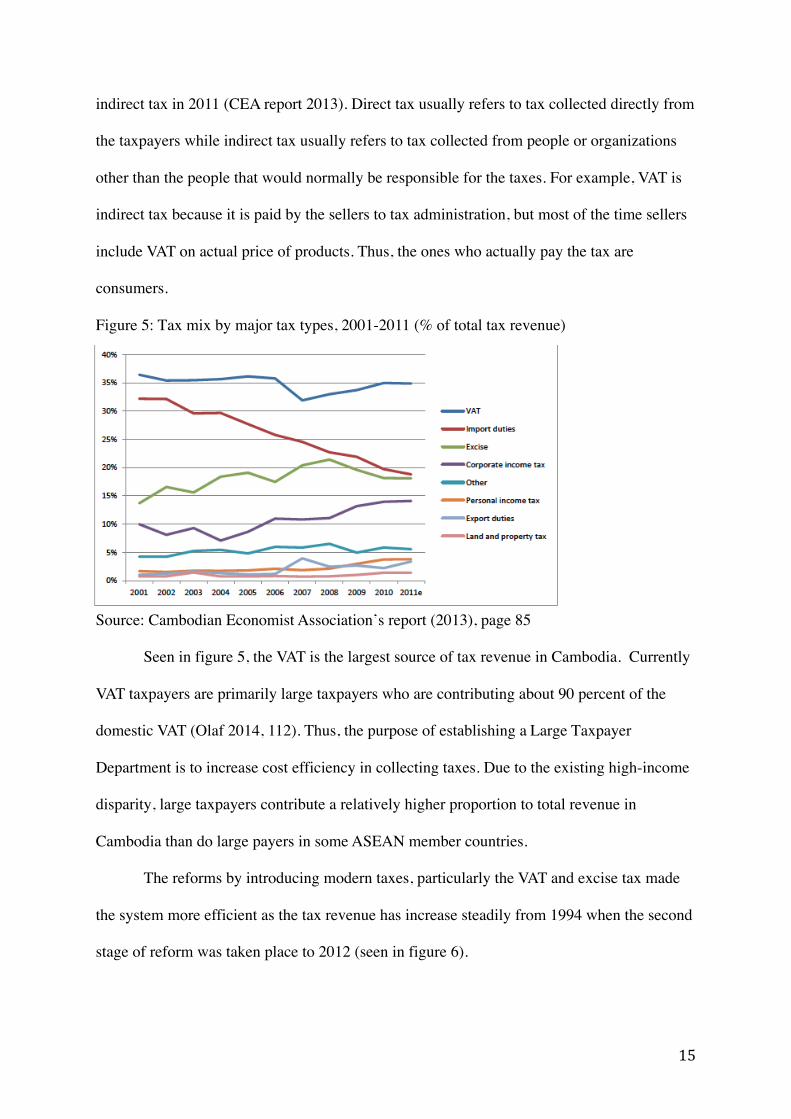

Since indirect taxes contribute very over 50 percent of total tax revenue as seen in

figure 4, we can speculate the whole tax system in Cambodia is regressive.

Figure 4: Composition of tax revenue, 2001-2011

Source: Cambodian Economist Association’s report (2013), page 83

Based on figure 5 above, the three major tax types that share a very large proportion

of total tax revenue are VAT, import duties and excise tax. VAT and excise tax together are

the main indirect tax types in Cambodia. Together they contributed around 98 percent of all

15

indirect tax in 2011 (CEA report 2013). Direct tax usually refers to tax collected directly from

the taxpayers while indirect tax usually refers to tax collected from people or organizations

other than the people that would normally be responsible for the taxes. For example, VAT is

indirect tax because it is paid by the sellers to tax administration, but most of the time sellers

include VAT on actual price of products. Thus, the ones who actually pay the tax are

consumers.

Figure 5: Tax mix by major tax types, 2001-2011 (% of total tax revenue)

Source: Cambodian Economist Association’s report (2013), page 85

Seen in figure 5, the VAT is the largest source of tax revenue in Cambodia. Currently

VAT taxpayers are primarily large taxpayers who are contributing about 90 percent of the

domestic VAT (Olaf 2014, 112). Thus, the purpose of establishing a Large Taxpayer

Department is to increase cost efficiency in collecting taxes. Due to the existing high-income

disparity, large taxpayers contribute a relatively higher proportion to total revenue in

Cambodia than do large payers in some ASEAN member countries.

The reforms by introducing modern taxes, particularly the VAT and excise tax made

the system more efficient as the tax revenue has increase steadily from 1994 when the second

stage of reform was taken place to 2012 (seen in figure 6).

16

Figure 6: Tax Revenue collected from 1994 - 2012

Source: The Fourth IMF-Japan High-Level Tax Conference for Asian Countries (2013)

Figure 7: Overall trend of tax revenues (% of GDP)

Source: Cambodian Economic Review (2013), page 81

This figure 7 shows that Cambodia increased the domestic revenue from 10 percent in

2001 to 13 percent in 2011. However, World Bank (2011) shows that the level of domestic

17

revenue collection in Cambodia is still lower than the average for low-income countries of

about 15 percent, the average for ASEAN members of around 23 percent.

The performance of tax collection has been improving but very slowly. Next section,

we will discuss challenges that make the improvement slow and compare Cambodian tax

system to another developing country tax system, which is successfully reformed.

18

IV. Challenges

Tax revenue in Cambodia has increased but still relative low compared to other low

income countries in the region. The inefficiency in tax collection is resulted from some

challenges described below.

1. Tax Administration Issues

Eng (2013) have examined problems in tax administration and describes the issue as

following. Though Cambodian tax administration was created in 1982, it is still quite young

and still lack of experiences because Cambodia was still in critical period (civil war) from

1982 to 1993. Just since 1997 when Lax of Taxation was promulgated, tax performance has

improved, and Tax Department was upgraded to General Department of Taxation in 2008.

Moreover, after having gone through civil war for quite long, tax paying has become new

culture to Cambodian people. Thus, many of them, especially poor people are not really

happy and have not yet accustomed to tax culture. Plus, there is lack of information sharing to

people and amongst related government entities. Similarly, a lot of Cambodian human

resources were killed during Khmer Rouge regime, so Cambodia still needs time to rebuild

capacity of human resources to work in this sector. Moreover, low salary of tax officials and

poorly organized procedure of staff performance review also discourage people to work in

this field. Therefore, limited number and capacity of tax officials, limited resources allocation

could slow down the process of tax reform and contribute to ineffective policies. In addition,

most of procedures in tax collection are manual and paper-based since Information

Technology in Cambodia is still limited. Thus, it slows down the procedure. At the same

time, system and procedures to monitor and control the work of General Department of

Taxation’s officials are still underdeveloped. Furthermore, audition issue including

19

underdeveloped audit guidelines, lack of tax auditors’ skill, insufficient intelligence/risk

assessment still remain as problems for General Department of Taxation.

2. Tax Incentives

Most developing countries have used tax incentives or holidays to influence

corporations to invest their money in development projects in their countries. Tax incentives

have become an instrument to attract inflow of foreign direct investment (FDI). Cambodia

started implementing this tool by providing tax incentives as stipulated in its Law on

Investment in 1994. Later, Cambodia also benefits from export exemption by U.S through

Generalized System of Preferences (GSP), a U.S trade program designed to promote

economic growth in the developing countries by providing preferential duty-free entry for up

to 4, 800 products into the U.S and Everything But Arms (EBA), a policy initiated by the EU

providing duty free access to the EU for exports of all products except arms and ammunition.

The Law on Investment was promulgated in 1994 in the purpose of encouraging

participation from the private sector, and especially to attract FDI. When the law was

amended in 2003, all domestic or foreign Qualified Investment Projects became entitled to

the following incentives (Law on the Amendment to the Law on Investment of the Kingdom

of Cambodia 2013, art. 14):

§ Free from 20 percent profit tax imposed by the Law on Taxation for up to nine

years of three periods (trigger, 3 years period, and priority periods mentioned

above).

§ 100 percent exemption from import duties on production equipment,

construction materials, raw materials, intermediate goods, and production input

accessories.

§ 100 percent exemption from export tax.

20

§ Employment of foreign nationals who are management personnel and experts,

technical personnel, and skilled workers.

§ Repatriation of profit and no restriction on currency conversion.

In addition to the above incentives, there are some income sources that are exempt

from profit tax including income from government revenue, NGOs and labor organizations,

and sales of own-produced agricultural products of a person who is not subject to the real

regime. The estimation in 2011 showed that Cambodia’s revenue loss was equivalent to about

6 to 7 percent of GDP per annum resulted from tax incentives. 4 percent of it was derived

from exemptions on customs duties while another 2 to 3 percent resulted from other

incentives such as exemptions on corporate income taxes for qualified investment projects

approved by the Council for the Development of Cambodia (WB 2011).

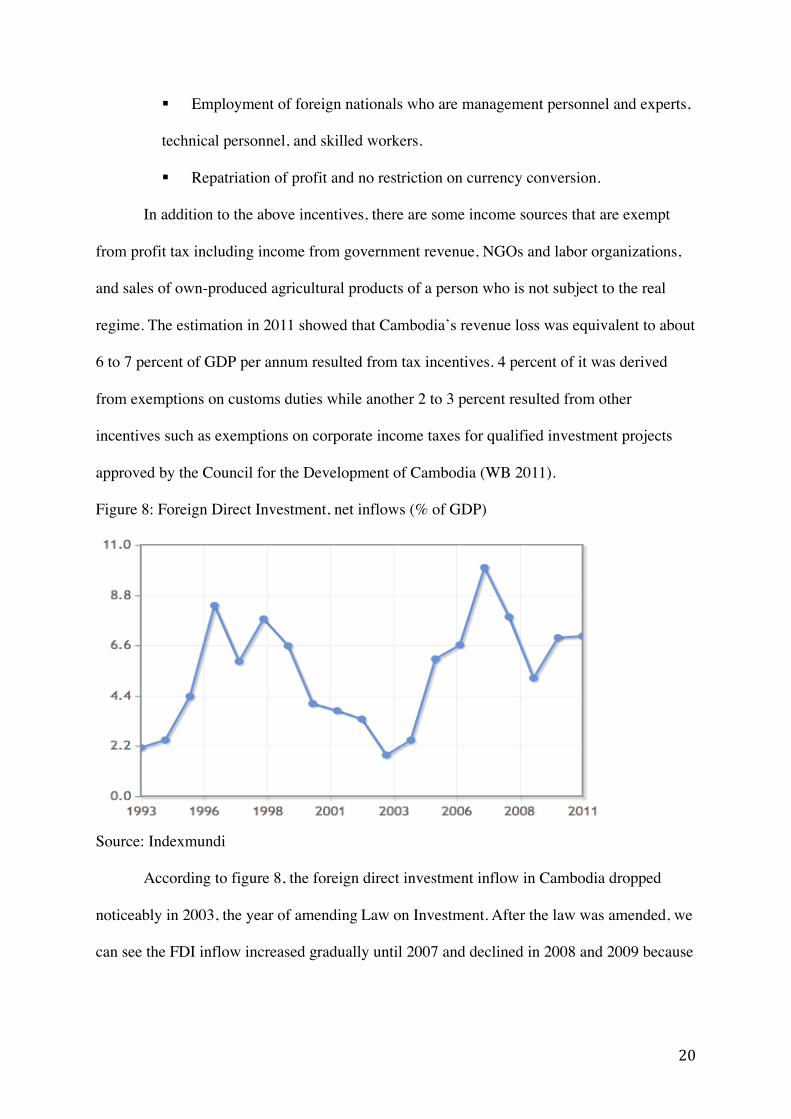

Figure 8: Foreign Direct Investment, net inflows (% of GDP)

Source: Indexmundi

According to figure 8, the foreign direct investment inflow in Cambodia dropped

noticeably in 2003, the year of amending Law on Investment. After the law was amended, we

can see the FDI inflow increased gradually until 2007 and declined in 2008 and 2009 because

21

of global financial crisis. This shows that tax incentives helps to attract more FDI into the

country.

3. Tax Evasion

In addition from benefiting from tax incentives, companies usually find their ways to

evade tax payment. For instance, one of the possible ways that a company can avoid paying

tax is to get the business closed down at the end of the tax incentive period and re-registered

under a new name to benefit from the tax incentive once again. Though this practice is

happening in Cambodia, there is neither proof nor effective means to detect and discourage it.

Moreover, since two tax regimes are applicable in the system as mentioned above,

there are loopholes that allow noncompliant taxpayers to shift their income through the

regimes for avoidance and evasion of taxes. As stated in Cambodia Economic Review (2013),

the 1997 Law of Taxation contained a loophole for tax evasion, particularly by enterprises

that are applicable under the estimated regime. Taxpayers could easily manipulate the amount

of business turnover because the law does not require enterprises in this regime to submit

regular financial reports. Thus, it is tough for tax officers to uncover the actual size of

turnover and profit for tax calculation. Furthermore, based on the law, the amount of

estimated profit shall be determined by the tax administration after verification and

discussion with taxpayers. This procedure seems to leave a chance for tax officers to abuse

the rule and for taxpayers to evade the tax by underreporting the actual taxable amount. It

also makes bribery from taxpayers to tax officers possible.

Besides the above-mentioned loophole, underreporting existing enterprises,

underreporting sales and cross-border smuggling are other forms of tax evasion in Cambodia.

All forms of tax evasion cause the significant loss of national revenue. Ngo (2013) claims

there is no recent data to prove the loss of national revenue caused by tax evasion, but the lost

amount through tax evasion by business enterprises was about USD 400 million in 2005,

22

which was equal about 6 percent of Cambodia’s GDP at that time. Plus, data in 2007 showed

the smuggled beer across border accounted for 29 percent of the total beer market in

Cambodia or 6 percent more than the legal imports, which would have cost Cambodia about

3 percent (USD 22 million) of Cambodia’s total revenue (Ngo 2013, 96).

23

IV. A Comparison of Cambodian and Vietnamese Tax Systems

Among the low-income countries in Asian, particularly known as CLMV, Vietnam

has the highest tax revenue in ASEAN and in the world as seen in the figure 9 below.

Vietnamese tax revenue is 23 percent of GDP while Cambodian tax revenue is only around

10 percent of GDP, which is even below Laos PDR’s. This section will look at the similarities

and differences between tax system in Cambodia and Vietnam by looking at 3 aspects

including tax structure, tax composition, and tax administration.

Figure 9: Tax Collection in Asian Low Income Countries

Source: IMF’s staff report (Feb 2014)

According to Nguyen (n.d), Vietnam tax system has undergone three phase of reform

and has successful. The first phase was from 1990 to 1995, with a result of introduction of a

unified tax system. Turnover tax, profit tax and export-import tax played an important role in

this stage of reform. The second phase (1997-2005) introduced VAT and corporate income

tax, amended the regulations on import and export duties and on special consumption tax

(excise tax) to ensure consistency in the tax system. The third phase (2006-2010) is a five-

year Tax Reform Plan to simplify tax policies and strengthen tax administration.

24

1. Tax Structure

First, the VAT in Cambodia is at flat rate of 10 percent for all supplies other

than exports and non-taxable supplies while the VAT in Vietnam has three applicable rates: 0

percent, 5 percent, and 10 percent. Goods and services traded across borders are taxed at 0

percent, 26 goods and services are exempt from VAT, while 15 categories of goods and

services are taxed at 5 percent. The standard rate is still at 10 percent. This shows the

similarity between the tax systems in both countries. However, during the last phase of

reform in Vietnam (2006-2010), VAT rate structure was reformed by restricting zero-rating to

exports, expanding scope of 10 percent rate and narrowing scope of 5 percent rate,

eliminating the discrimination between domestic and imported products, and reducing

exemptions (Olaf 2014, 106). Also, the calculation method was improved by setting

requirement to input VAT deduction as to make payments through the banking system

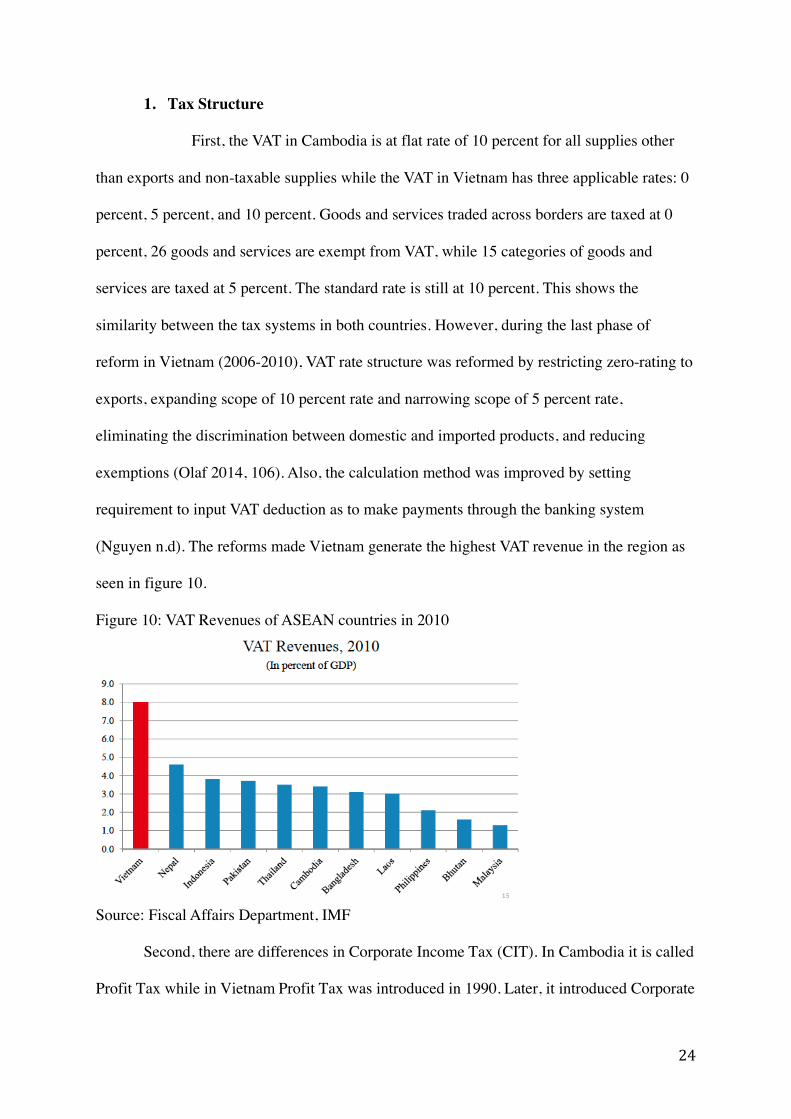

(Nguyen n.d). The reforms made Vietnam generate the highest VAT revenue in the region as

seen in figure 10.

Figure 10: VAT Revenues of ASEAN countries in 2010

Source: Fiscal Affairs Department, IMF

Second, there are differences in Corporate Income Tax (CIT). In Cambodia it is called

Profit Tax while in Vietnam Profit Tax was introduced in 1990. Later, it introduced Corporate

25

Income Tax in 1999, and it has amended several times to build a business-friendly

environment. The current CIT enacted in 2009 does not make any discrimination between

enterprises of different sectors. CIT in Vietnam applies higher rates varying between 32 and

50 percent on oil, gas and other precious material while in Cambodia they are taxed at 30

percent. The CIT in Vietnam has been strengthened by unifying the rate structure, removing

some incentives, permitting deductions, and transferring unincorporated businesses to the

Personal Income Tax (Nguyen n.d & Olaf 2014).

Table 1: Corporate tax rates in ASEAN since 2007 (%)

According to table 1, in total corporate tax rate in Vietnam is still higher than one in

Cambodia though it decreases from 28 percent in 2006 to 22 percent in 2014.

Third, the Personal Income Tax (PIT) has reformed by introducing a tax on capital

income, broadening the tax brackets, and lowering the top marginal rate (Nguyen n.d). There

are seven tax brackets in 2009 PIT in Vietnam: 5, 10, 15, 20, 25, 30, and 35 percent.

However, there are only 5 tax brackets in Tax on Salary in Cambodia: 0, 5, 10, 15, and 20

percent. These two taxes are applied similarly but at different rate.

Fourth, for Excise or Special Consumption Tax, the tax rate on goods vary from 10

percent (gasoline, air conditioners of 90, 000 BTU or less, and electrically operated passenger

cars of between 16 seats and under 24 seats) to 70 percent (votive gilt papers and votive

objects) and on services between 15 percent (lottery business) to 40 percent (dance halls)

26

(Gangadha et all. 2011, 34). However, in Cambodia it varies from only 3 percent to 30

percent as mentioned in the previous section. The excise tax rate in Vietnam is much higher

than one in Cambodia. Table 1 and 2 shows the examples of the differences in tax rate of

alcohol and package tobacco in both countries and other ASEAN countries.

Table 2: A comparative analysis of alcohol excise duties in ASEAN

Source: Preece 2012

Table 3: A comparative analysis of packaged tobacco excise duties in ASEAN

Source: Preece 2012

27

Fifth, Vietnam has adopted Natural Resources Tax law, which has a wide range of

royalty rates from 1 percent to the high of 40 percent. Minerals, both metallic and

nonmetallic, are subjected to the range of 5 to 30 percent. The range for most natural forest

products is between 10 to 30 percent. Among many types of natural resources, royalty rates

on crude oil could reach the highest rate of 40 percent. This tax was adopted in 2009 to

increase revenue and help protect natural resources (Nguyen n.d).

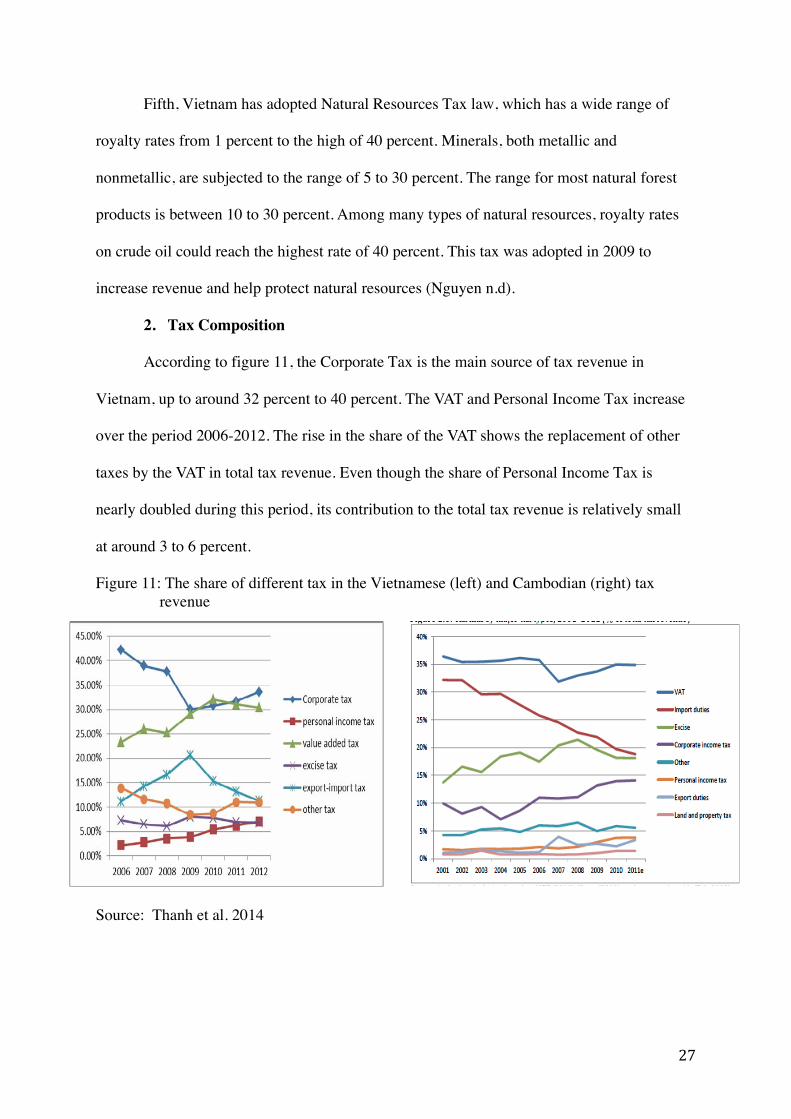

2. Tax Composition According to figure 11, the Corporate Tax is the main source of tax revenue in

Vietnam, up to around 32 percent to 40 percent. The VAT and Personal Income Tax increase

over the period 2006-2012. The rise in the share of the VAT shows the replacement of other

taxes by the VAT in total tax revenue. Even though the share of Personal Income Tax is

nearly doubled during this period, its contribution to the total tax revenue is relatively small

at around 3 to 6 percent.

Figure 11: The share of different tax in the Vietnamese (left) and Cambodian (right) tax revenue

Source: Thanh et al. 2014

28

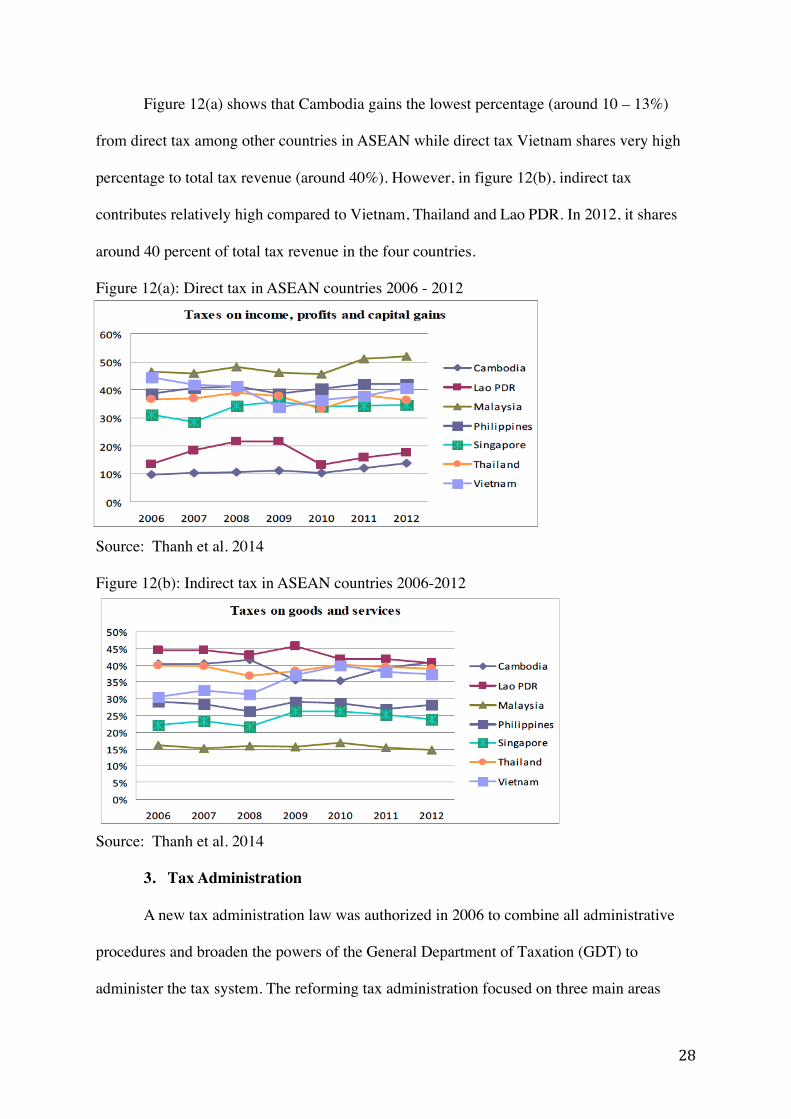

Figure 12(a) shows that Cambodia gains the lowest percentage (around 10 – 13%)

from direct tax among other countries in ASEAN while direct tax Vietnam shares very high

percentage to total tax revenue (around 40%). However, in figure 12(b), indirect tax

contributes relatively high compared to Vietnam, Thailand and Lao PDR. In 2012, it shares

around 40 percent of total tax revenue in the four countries.

Figure 12(a): Direct tax in ASEAN countries 2006 - 2012

Source: Thanh et al. 2014

Figure 12(b): Indirect tax in ASEAN countries 2006-2012

Source: Thanh et al. 2014

3. Tax Administration

A new tax administration law was authorized in 2006 to combine all administrative

procedures and broaden the powers of the General Department of Taxation (GDT) to

administer the tax system. The reforming tax administration focused on three main areas

29

(Pham & Engelschalk 2011). First, modernization tax administration system by reorganizing

the GDT’s headquarters and its network of tax officers into based unites. Second, all tax

headquarters and offices are equipped with technology. Computer network was connected

and a broad range of electronic applications was implemented. Last, reform focused on

personnel development by taking into account the upgrading staff skills.

However, Vietnam still ranks very low in tax paying because individuals and

businesses need to spend 872 hours to make payments for their tax liabilities while in

Cambodia they need to spend only 173 hours to do so as shown in table 4.

Table 4: Comparison in paying tax between countries in ASEAN

Table 5 shows that Vietnam’s CIT is the second highest in the region while

Cambodia’s CIT is the second lowest. However, indirect tax rate in both countries are equal.

These make Vietnam generates higher tax collection revenue because Vietnam has higher

CIP and indirect tax rate compared to Cambodia, and Cambodia’s tax revenue depends

mainly on indirect tax collection in the time being.

Table 5: Corporate and Indirect Tax Rates of ASEAN countries in 2012

30

V. Conclusion and Recommendation

To conclude, Cambodian taxation has been improving over the past decade in terms

of tax collection policy and tax administration such as Law of Taxation was adopted in 1997,

tax administration including procedures, IT, capacity of tax official have been improved

gradually, and more effective and wider covered taxes have been imposed. As a result, the

annual tax revenue to GDP has increased steadily over the past decade. However, the revenue

is still relatively low compared to other countries in the region and other low-income

countries since there are many challenges especially tax administration issues, long tax

holidays and all forms of tax evasion in the country that Cambodia needs more time to tackle

of.

In comparison of tax system in Cambodia and Vietnam, tax rates in each type in

Vietnam are higher than tax rates in Cambodia. Also, Vietnam has applied the tax on Natural

Resource, which has not appeared yet in Cambodia. Moreover, while Corporate Income Tax

and VAT is the first and second biggest source of tax revenue in Vietnam, Cambodia still

depends mainly on indirect tax, particularly VAT and excise tax in revenue collection. Also,

Corporate Income Tax in Cambodia is still relatively low, which could not generate

significant amount of income to the country. Furthermore, Vietnam has enacted the tax

administrative law to strengthen the tax administrative system, improve technology, and

develop tax officials. But Cambodia is still facing challenges in this area, which need further

improvements.

In order to further strengthen tax system, Cambodian government should consider

some suggestions as following:

• Reform the VAT and excise taxes since it will generate an immediate revenue impact

• Continue tax policy reforms by reducing exemptions and incentives, rationalizing

corporate and persona income taxes, and implementing property taxes

31

• Improve tax administration by collecting debts and improving performance of the

Large Taxpayer Department because it will raise additional revenue in the near term.

• Establish taxpayer services to reduce compliance costs

• Develop human resources by arranging important training to old and new recruited

staffs, evaluating staffs’ performance regularly and giving incentives to well-

performed staffs

• Strengthen oversight and accountability of tax institutions and promoting

transparency to avoid fraud and tax evasion

• Improve Information Technology

• The system of negotiation in determining tax in the estimated regime should be

removed to improve transparency and help taxpayers meet their tax obligations.

32

Bibliography

Chan et al. 1998. Cambodia: Challenges and Options of Regional Economic Integration. Conference Papers, 38-40. Phnom Penh: Cambodia Development Resource Institute. Council for the Development of Cambodia. 2014. “Taxation and Accounting.” Investor’s Information. Accessed October 19, 2014. http://www.cambodiainvestment.gov.kh/investors-information/taxation-and- accounting.html Eng, Ratana. 2013. “The Fourth IMF-Japan High-Level Tax Conference for Asian Countries.” Enforcement Trends and Compliance Challenges in Cambodia. General Department of Taxation. “Taxes in Brief.” Accessed October 19, 2014. http://www.tax.gov.kh/en/btop.php Indexmundi. “Cambodia – Foreign direct investment.” Accessed December 17, 2014 http://www.indexmundi.com/facts/cambodia/foreign-direct-investment International Moneytary Fund. 2014. “Cambodia: 2013 Article IV Consultation.” Staff Country Reports. IMF Country Report No. 14/33. Washington, D.C. International Moneytary Fund. 2007. “Cambodia: A Note on the Tax System.” Staff Country Reports. IMF Country Report No. 07/291. Washington, D.C. InvestorGuide. 2012. “The Difference Between Direct Tax and Indirect Tax.” Accessed November 12, 2014. http://www.investorguide.com/article/11164/the-difference- between-direct-tax-and-indirect-tax-igu/ KMPG. 2014. Corporate tax rates table. KPMG. 2012. Corporate and Indirect Tax Survey 2012. KPMG. Law on the Amentment to the Law on Investment of the Kingdome of Cambodia. 2003. “Chapter 5: Investment Incentives. Article 14: New.” Law on Taxation. 2004. Kingdom of Cambodia. May, Kunmakara. 2012. “Criticism for Cambodia's Tax Revenue.” The Phnom Penh Post, July 12. Accessed October 19, 2014. http://www.phnompenhpost.com/business/criticism-cambodia’s-tax-revenue Ministry of Economy and Finance. 2010. “Opening Address.” Paper presented at the seventh meeeting of the Asia Tax Forum by deputy prime minister Keat Chhon, Siem Reap- Angkor, Cambodia. Ngo, Sothath. 2013. “A Review of Taxation in Cambodia”. Cambodia Economic Review. Issue 6, 78-98. Phnom Penh: Cambodian Economic Association.

33

Nguyen, Van P. n.d. Tax Reform in Vietnam: Main accomplishments and lessons. Vietnam: Tax Policy Department, Ministry of Finance. Norregaard, John. 2013. Taxing Immovable Property Revenue Potential and Implementation Challenges. Working paper, Fiscal Affairs Department, International Monetary Fund, Washington D.C: IMF. Norregaard, Matheson, Mullins, Schatan. N.d. Tax Reform in Vietnam Issues for 2011-2015. Fiscal Affairs Department, International Monetary Fund. Olaf, Unteroberdoerster, ed. 2014. Cambodia Entering a New Phase of Growth. Washington D.C.: International Monetary Fund. Pham, Duc M., & Engelschalk, Michael. 2011. “Tax Administration.” Tax Reform in Vietnam. The World Bank, 66317. Preece, Rob. 2012. “Excise taxation of key commodities across South East Asia: a comparative analysis ahead of the ASEAN Economic Community in 2015.” World Customs Journal 6. Sim, Eang, and Um Seiha. 2005. Cambodia Tax Reform and Self-Assessment System. Cambodia: Tax Department. Thanh, Su D., Trung, Bui T., Kien, Tran T. 2014. Reforms of Tax System in Vietnam Toward International Integration Commitments Until 2020. Vietnam: University of Economics Ho Chi Minh City. VDB Loi. 2012. “Withholding Tax in Cambodia.” Updates & Analysis. Accessed November 10, 2014. http://www.vdb-loi.com/analysis/withholding-tax-wht-in-cambodia/ World Bank. 2014. “GDP Growth (annual %).” Accessed October 19, 2014. http://data.worldbank.org/indicator/NY.GDP.MKTP.KD.ZG World Bank. 2013. Doing Business 2014: Understanding Regulations for Small and Medium- Size Enterprises. World Bank Group: Washington D.C. World Bank. 2013. “More Efficient Public Expenditur for Strong and Inclusive Growth.” Public Financial Management Reforms, Policy Note 83079. Cambodia: The World Bank Office. World Bank. 2011. “Cambodia: More Efficient Government Spending for Strong and Inclusive Growth.” Integrated Fiduciary Assessment and Public Expenditure Review. Report No. 61691-KH. Washington D.C.