BPO Europe & Africa

18

-

Upload

independent -

Category

Documents

-

view

4 -

download

0

Transcript of BPO Europe & Africa

!"#$%#&'(!#)!*)+#&$

,-+./&++!0$)1&++!2**3

"4)$./'

5&&/

7-$)8&%/!%/9! *$.1%/!":7+

2

3

1. Executive Summary .........................................................................................................4

2. Business Process Outsourcing and Off-Shoring ..............................................................5

2.1 From BPO to KPO ...................................................................................................5

2.2 Current Developments..............................................................................................6

2.3 Structural changes: the end of captive centres .........................................................7

2.4 The Global View ......................................................................................................8

2.5 Success factors .........................................................................................................9

3. The European Market.......................................................................................................9

3.1 Overview ..................................................................................................................9

3.2 A brief view on the main European IT service markets.........................................10

3.2.1 Germany......................................................................................................10

3.2.2 France..........................................................................................................10

3.2.3 UK...............................................................................................................10

4. The potential of the Sub-Saharan Countries ..................................................................11

4.1 The current players.................................................................................................11

4.1.1 South Africa................................................................................................11

4.1.2 Mauritius.....................................................................................................11

4.1.3 Ghana ..........................................................................................................12

4.1.4 Senegal........................................................................................................13

4.2 Potential newcomers ..............................................................................................13

4.2.1 Kenya ..........................................................................................................13

4.2.2 Botswana.....................................................................................................14

4.2.3 Nigeria ........................................................................................................14

5. Developing a Strategy....................................................................................................15

5.1 Recommendations ..................................................................................................15

6. References ......................................................................................................................17

4

1. Executive Summary

The global off-shoring market has matured over the past decade and reached an esti-mated volume of $30 billion in revenues over the past two years, where India and thePhilippines account for 50% of the world-wide BPO market.

The share of this market by Sub-Saharan countries is small, but a number of them haveestablished a good position on the international ranking index.

This report provides an overview of the current developments and future trends in thefield of Business Processing Outsourcing and analyses some of the most important Sub-Saharan countries. From this analysis it concludes with some recommendations of howto support the development in the selected countries to increase their competitiveness inthe current BPO markets and at the same time highlighting the importance to move toKnowledge Process Off-Shoring services in the future.

November, 2009

5

2. Business Process Outsourcing and Off-Shoring

Business Process Outsourcing and Off-shoring has been quite popular in the US for along time and is receiving rapidly increasing attention in Europe. On the IT side, Out-sourcing started with data entry services many years ago and then moved to more com-plex services (e.g. pay roll administration) and has currently arrived at ‘smart sourcing’,where not only business processes are outsourced, but parts of the business as well (inform of partnerships) allowing the outsourcing company to concentrate on their corebusiness. Outsourcing, in whatever form, does not automatically imply outsourcing toother (and cheaper) countries. Business processes are often outsourced to companies inthe same country, in particular the more complex processes. Increasing complexity of-ten goes hand in hand with increased sensitivity of the related data and companies pre-fer to outsource them to service providers close by they not only can trust but also eas-ily check.

Off-shoring refers to the acquisition of intermediate inputs by companies from locationsoutside the consuming country. It is the crossing of international borders that distin-guishes it from outsourcing in general. It is important to realize that this phenomenon isnot new and has been going on since at least the industrial revolution. It is effectivelysynonymous with the distribution of labour and with companies remaining competitiveand cost-conscious while specializing in what they do best. What is new, however, isthat information and communication technology (ICT) in recent years has made out-sourcing of whole new types of services possible. IT and cheap communication todayfacilitate companies to outsource most things that can be reproduced/conducted in digi-tal form, such as IT support, back office (payroll administration and accounting), call-centres, software programming, and some R&D functions. Similarly, ICT has enabledadditional outsourcing in goods manufacturing, as intermediate inputs can now beseamlessly sourced from multiple suppliers.1

One highly popular type of outsourcing is the Call Centre market and although only asmall percentage of Call Centre activities is outsourced and off-shored, it is a large andhighly competitive market. It is interesting to note that the demand for call centre agentsin India has grown so fast that the labour supply has been unable to keep up with it: by2009, the demand for agents in India is projected to be over 1 million, and more than20% of those positions will be unfilled because of a shortage of available skilled la-bour.2

2.1 From BPO to KPO

There is no clear definition of the processes that are usually out-sourced and off-shoredunder the term 'BPO'. But it isgenerally accepted that theseencompass processes that re-quire a low to medium-skilledworkforce at the off-shoringdestination. It is important tonote that these off-shoringservices provide little to noneadded value for the countriesproviding them, apart fromproving jobs. At the same

Data entry /preparation

Document management

Data processing

Forms and report generation

Card processing

Inbound only

Inbound/outbound

Outbound only

General back-

office

Consumer

Contact

Business

Process

Outsourcing

6

time, working at off-shore service providers does not provide any career view for theemployees and hence the attrition rate is usually very high. Furthermore, the attractive-ness of an off-shore location for these types of services hinges almost entirely on the la-bour rate.

Countries like India have reacted to this situation by moving increasing into the domainof Knowledge Process Outsourcing where the main indicator of competitiveness is theskill level of the local workforce. Off-shoring is no longer simply about obtaining low-cost resources elsewhere; it is now about accessing specific types of talent and gainingentry points to serve new and broader markets. Global companies are now incorporatingoff-shoring as part of their forward-looking strategies rather employing it as a knee-jerkreaction to cost pressures. Encouraged by the early success of off-shoring in the ITOand BPO sectors, companies are increasingly exploring the value of sending high-endprocesses offshore, including ones that directly affect their revenue generation capabili-ties. Typical Knowledge Process Outsourcing services are3:

Type of Activity Examples

Investment research: equities, derivatives, credit research,valuation and accounting

Financial modelling

Company, industry and sector reports

Credit risk management

Normalizing accounting standards

Valuation of companies

Equity and Finan-cial Research andAnalytics

Tracking of stock markets and analysis thereof

Market Analysis: market segmentation, marketing stimulus andspend optimization, need gap analysis, market mapping

Data mining: mining the Internet, databases and company web-sites and preparation of reports with analysis, data processingand analysis

Report preparation: company and sector reports; editing andformatting of reports

Business and Mar-keting Researchand Analytics

Customer Analytics: customer satisfactions surveys, customerand segmentation, price sensitivity/pricing analysis, benchmark-ing

Very Large Scale Integration (VLSI) design

Simulations

Chip design

Vehicle design support

Engineering andDesign Services

Prototype development

Offshore drug discoveryPharmaceutical re-search outsourcing Clinical research

2.2 Current Developments

North American companies still account for about 70% of offshore outsourcing spend-ing, but Europe is catching up with their spending on off-shoring is rising faster thanthat of their counterparts in North America. However, the interest from Europe is morein near-shore locations where English is not the dominant language, including locations

7

in Central and Eastern Europe, and the Middle-East and North Africa. Sub-Saharan Af-rica is not in the main focus of European companies.

The economic crisis has affected the off-shoring business as well, but the full effects arestill not clear. For example, the Indian software association NASSCOM states:

After several years of unbridled growth, the Indian IT-BPO industry is fac-ing a challenging global economic environment as a result of the crisis inthe US that has impacted the international financial services sector andcredit markets. While timely Government intervention and a series of bail-out packages are expected to stabilise Western economies, the current un-certainties are expected to persist until market conditions improve.

The recessionary wave sweeping the world, however, is having a directbearing on the outsourcing industry in India, with demand dipping as globalcompanies adopt a “wait and watch approach.” While the economic down-turn has compelled companies to relook at their outsourcing strategies in abid to cut costs, the interesting fact remains that outsourcing can in fact helporganisations tide over tough times and maintain competitiveness.4

The value of new off-shoring deals signed worldwide during the three-month period be-tween October 2008 and January 2009, as reported by research service Datamonitor,declined by 38% compared to the same period the previous year. Compensation hasbeen frozen among several outsourcing providers in India and attrition rates havedropped in half compared to the previous year - sure signs that the industry is slowingdown.5

The Plunkett Research reports6:

As of mid-2009, outsourcing of BPO and other services was continuing tosuffer a difficult adjustment due to the global recession. For example, the fi-nancial services industry was one of the largest industry sectors that hadturned to outsourced call centres. The downsizing of the global banking andinvestment sector meant a significant reduction in the need for services. Inother types of services, such as BPO and knowledge management, majorproviders of outsourced services reported that clients were delaying or can-celling projects in large numbers.

2.3 Structural changes: the end of captive centres

Numerous large organisations had created their captive centres in off-shore location.Captive Centres can be best characterised by:

• Dedicated set of resources offshore• Created specifically for the “parent”• 100% dependant on parent for business• Commercial relationship is time and material• True extension of onshore teams

Apart from the expected cost effectiveness they were mainly motivated by control as-pects (concerning people, processes, technology …), and IP considerations. Howevermany captive centres failed to contain costs efficiently and more companies are optingto buy the services they need from outsourcing providers. For example Citibank soldtheir captive operations to Tata Consultancy Services and Philips to Infosys. Such moveincreases flexibility on both sides and in particular the service providers are rapidly in-

8

creasing their global footprint to seek for talents in new markets as their home locationscannot supply the needed labour force. As Nimish Soni, CEO - BPO Division, Cam-bridge Solution, said when asked what the best happenings in 2008 were: "The exit ofthe ‘captives’ – the inefficiencies of the captives finally pull them down. The captivemodel is now ‘dead’."

2.4 The Global View

The most comprehensive view on the off-shoring business, or Global Services, is pro-vided by A.T. Kearney. Since 2004 the Global Services Location Index is prepared onan annual basis ranking the top 50 off-shoring countries world-wide. The index metricsare based on three categories: Financial Attractiveness (covering compensation cost, in-frastructure cost, and tax and regulatory costs), People Skills and Availability (includ-ing for example labour force availability, education and language and attrition risks),and Business environment (including amongst others the infrastructure, security risks,and security of intellectual property). Data are collected from a variety of sources in-cluding client engagements, and should not be viewed as absolute figures. Countriesthat are not on this list should by no means be ignored; they can be highly attractive forspecific clients or services. Furthermore, the off-shoring market is highly dynamic withchanging patterns of demand leading to considerable fluctuation of the position ofsmaller countries in this index. While the big players have maintained their positionsince 2004, a number of countries have dropped off the list while others entered.

The above figure highlights the Sub-Saharan countries (red) and the North-African andMiddle-East ones (yellow) that can be considered as the strongest competitors forEuropean clients.

Compared with the 2007 Index Mauritius has maintained its rank (25), while Ghanamoved up from rank 27 to 15 and Senegal from rank 39 to 26. South Africa hasdropped from rank 31 to 39, after it lost points in all three categories with the deteriora-tion of the infrastructure being the most striking drop among the individual metrics.

While the top three countries - India, China, and Malaysia - maintain there safe positionin the 2009 index, the Middle East and North Africa region is emerging as a hot off-

9

shoring destination for the world. They have a large and well-educated population, lowcosts and are close to Europe. Egypt is now on rank 6 - up from rank 13 in 2007 - andbefore the Philippines, Jordan moved up from rank 14 to 9, and Tunisia from rank 26 to17.

2.5 Success factors

Low compensation rates, high education standards or favourable business environmentsare without doubt a prerequisite for attracting off-shore business, but are no longer suf-ficient to ensure success. Regional Off-shoring has become an important factor in orderto gain more independence from large international clients. Just as it makes sense foradvanced economies to trade business services with lower-cost countries, it also makessense for low-cost countries to off-shore to each other. For example, Egypt has suppliedskilled migrant labour to the Gulf region for many years but now is gradually changingto remote delivering from the home country, and Saudi software companies have estab-lished the IT development centres in Cairo.

Mauritius is a service exporter to Europe and now several local Mauritius BPO compa-nies that provide services for France have opened their offshore centres in Madagascar,hiring French speaking workers at significantly lower cost. Consequently, for smallercountries and newcomers in the field it could be much more profitable to enter the BPObusiness by providing off-shore services to other off-shore countries than directly to theEuropean or North American clients.

3. The European Market

3.1 Overview

Publicly available information on recent markets trends for BPO from Europe is nolonger available. Market reports are offered by numerous market research organisationsbut for a very high price7,8.

However, there are some data available that give at least a view on future developmentand prospects in this field.

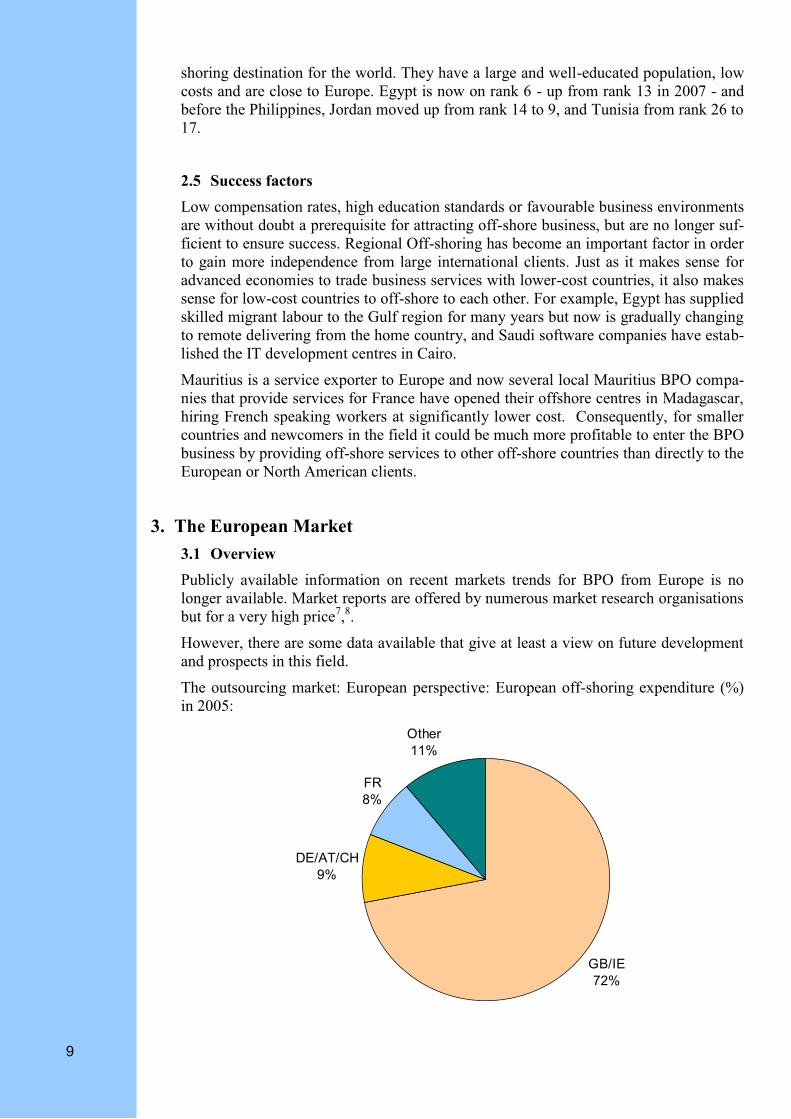

The outsourcing market: European perspective: European off-shoring expenditure (%)in 2005:

GB/IE

72%

DE/AT/CH

9%

FR

8%

Other

11%

10

Outsourcing remains the fastest growing market trend in Europe and there is a cleartendency towards smaller and shorter projects.

The typical growth drivers in outsourcing are

- Application management outsourcing

- Network and desktop outsourcing

- Information system outsourcing & hosting infrastructure services

In general Off-shoring is becoming an important element of IT services delivery withconsiderable growth of this IT off-shoring market in Europe with an expected16.5%/year until 2009. There is also an important and still largely untapped market po-tential with SMEs, who are increasingly interested in outsourcing and off-shoring.

3.2 A brief view on the main European IT service markets

3.2.1 Germany

Continuous and stable growth track:• 4.7% (2006)• 5.0 (2007)

Growth driver: outsourcing (ca. 10% growth in 2006) Market volume outsourcing: € 14 billion (2006) Motivation for outsourcing:

• IT staff shortage• Reduction of market risks• Cost pressure & international competition

Important target market: SMEs Off-shoring preference: near-shoring/Eastern Europe

3.2.2 France

Stable growth track:• 5.5% (2006)• 5.8% (2007)

Outsourcing market is growing but companies still reluctant to outsource becauseof cultural barriers and labour laws

Outsourcing market bound to grow dynamically due to:• Cost pressure• IT staff shortage

Focus on BPO Vertical drivers: banking and insurance industry

3.2.3 UK

Solid growth but on a smaller scale:• 5.9% (2006)• 5.6% (2007)

Mature market but still the most dynamic and advanced outsourcing market in theEU

70% of European off-shoring spending in the UK & Ireland (2005) Off-shoring preference: India

11

4. The potential of the Sub-Saharan Countries

A number of Sub-Saharan countries are active as BPO providers and some have made itinto the league of the top 50 outsourcing hubs world-wide.

However, detailed information about the type of services, the volume of contracts, orthe expected market development is very sparse. This chapter gives a brief overview ofsome countries that are known as successful players, based on publicly available infor-mation.

4.1 The current players

4.1.1 South Africa

South Africa is by far the strongest play in the BPO field in Africa. The prediction in2007 was the South Africa is expected to nearly double the number of contact centresthey had in 2003. It had brought the country on a respectable rank 31 in the Kearny In-dex in 2007. However, South Africa dropped to rank 39 only two years later, loosingpoints on all the three Kearny categories. The deterioration of the infrastructure was themost striking one.

Currently, the government is backing huge infrastructure investments in advance of the2010 FIFA World Cup which South Africa will host, and those can only aid the off-shore outsourcing case. So there is a chance that South Africa moves some ranks higheragain in the coming years.

In 2006 DTI launched a Business Process Outsourcing Sector Support Programme inSouth Africa, since despite its success in BPO it faced a number of critical challenges:

- a shortage of entry and middle managers;- higher cost of operations than key competitors;- negative perceptions of operational risks;- relative difficulty in setting up new operations in South Africa;- some restrictive regulations;- a limited number of BPO service vendors with major anchor clients;- an uncompetitive and comparatively expensive technology infrastructure; and- an ineffective marketing effort.

The results of this support programme as at March 2008 are as follows:

ObjectiveActual at March

2008Target to Dec

2009

Firms attracted or expanded 9 43

Jobs created 39 936 109 852

People trained 17 279 35 000

4.1.2 Mauritius

Mauritius, despite having the smallest labour force in the index, ranks well at 25 be-cause of strong people skills and favourable business environment. According to theWorld Bank, it is the 24th most attractive business environment globally. Large compa-nies like Accenture and Infosys also use Mauritius for their global delivery functions.

12

Mauritius has developed a National ICT Strategic Plan (2006 – 2010) to achieve the vi-sion of the Government to make the ICT sector the fifth pillar of the economy and Mau-ritius a regional ICT hub.

Major BPO Services in Mauritius:

The development of the BPO Industry in Mauritius has been quite rapid until 2007; fig-ures relating to 2009 are not yet available.

4.1.3 Ghana

Ghana, the Sub-Saharan pioneer in IT and off-shore services, is doing exceptionallywell, now positioned on rank 15 - up from 27 in 2007.

In 2003, the MoC issued a policy for the overall ICT sector. The objective of this ICTfor Accelerated Development (ICT4AD) policy is “to engineer an ICT led socio-development process with the potential to transform Ghana into a middle income in-formation-rich, knowledge-based and technology-driven economy and society.” TheICT4AD policy outlined some of the initial steps being adopted by the government ofGhana to increase the ICT competitiveness of the country.

With one of the most competitive demographics in the ITES-BPO world, Ghana has thepotential of developing itself as the preferred ITES-BPO destination in the region. Thecountry benefits from a stable and supportive political scenario as well as a latent talent

13

pool which, if trained, can provide the necessary scale for growth of the industry.

However, to achieve the desired success, Ghana will need to develop cost-effective andsuitable infrastructure, Moreover, the country will need to develop the talent pool, aswell as introduce the necessary policy and regulatory frameworks.

The Ghana Association of Software and IT Services Companies (GASSCOM) isGhana’s premier trade association for the IT software and services industry. GASS-COM is registered as a non-profit company limited by guarantee under company’s codeof the Republic of Ghana. GASSCOM's member companies are in the business of soft-ware development, software services, IT-enabled/BPO services and e-commerce.

4.1.4 Senegal

Senegal's strengths as an off-shore location are mainly due to its financial attractivenessand a favourable business environment, but it suffers under a low availability of peopleand skills.

At present (2008), there is a dozen call centres active in the country, most of which spe-cialized in telemarketing. Altogether, they have 1200 seats and employ some 2200 staff.The largest one, the Premium Contact Center International (PCCI), accounts alone for60% of seats, and it employs about 1,000 people. The others are mainly medium-sized,ranging from 100 employees, Center Value, Africatel AVS, to 200, like Call Me. Thereare also smaller ones such as Senetel, 20 employees, and Quality Center, 40 employees,the latter being the only one not based in Dakar, but in St. Louis. The BPO sub-sector isinstead not very developed. There are just few players active in database management,financial and accountant services and other back-office operation. The largest companyin this segment is Global Outsourcing who employs more than 300 staff, while otherplayers, like SESI, Jouve Sénégal, Senescan, and Sinti Senegal have from 40 to 80 em-ployees. PCCI as well, has recently diversified its activities to include some BPO ser-vices. The interest in this field is indeed increasing, and large international players aremore and more interested to open offshore facilities in the country. For instance,TRG—a group with 1,000 centres worldwide—has recently inaugurated a 300-seats fa-cility in Dakar, which will provide a vast range of BPO services.

4.2 Potential newcomers

4.2.1 Kenya

The National ICT Strategy issued by the government of Kenya in January 2006, under-line the key role of call centres and business process outsourcing services (BPO) toachieve the strategy’s goal of “making Kenya the ICT capital of Africa”.

According to the plan, outsourcing can contribute to create some 30,000 jobs in the nearfuture. The National ICT Strategy has been adopted by ICTPark, a consortium of local,regional, and global organizations working together for the development of ICT sectorin Kenya. The consortium focuses on facilitating the development of BPO and call cen-tres in Kenya by working in close relation with facility owners, business operators andoutsourcing clients.

Kenya BPO and Contact Society (KBPOCCS) is the private sector association repre-senting the needs of the Contact Centre and Business Process Outsourcing industry inKenya.

The Kenyan government has created the right environment for the BPO sector to takeoff, particularly through investing in an undersea-fibre cables. In July 2009, SEACOM

14

went live in several African Countries including Kenya. When the TEAMS cable goeslive later this year, and the EASSY cable goes live next year, Kenya will have an abun-dance of high speed internet connectivity to the rest of the world. Internet are expectedto drop by as much as 70% in due course.

4.2.2 Botswana

In 2007 Botswana published an edited draft of their proposed National Information andCommunications Technology Policy to provide Botswana with a clear and compellingroadmap that will drive social, economic, cultural and political transformation throughthe effective use of Information and Communications Technology (ICT) in the yearsahead. The Policy complements and builds upon Vision 2016 and provides many of thekey strategies essential for achieving Botswana’s national development targets.

One of the Policy Recommendations under 'ICT and Economic Diversification' is to"support the introduction and growth of Business Process Outsourcing (BPO) withinBotswana. Although the economic upside to this endeavour is extremely positive, thereare considerable challenges in areas such as lack of skilled workers, lack of call centremanagement expertise and inadequate physical infrastructure. These challenges arevery similar to those mentioned in other ICT key programmes and highlight the criticalneed for continuous investment in infrastructure, education and skills development."

The potential for Botswana to benefit from the development of BPO/call centre opera-tions had been under discussion since 2004 when the IFSC (Botswana International Fi-nancial Services Centre) conducted a diagnostic study on the sector. Subsequently, Out-source Botswana was founded as a private sector representative association in 2006,aiming at promoting the BPO and Call Centre industry in Botswana through publicawareness. The 'Botswana International BPO & Call Centre Conference 2007' was heldin July 2007 but apparently no tangible activities have followed since. One of the mainproblem seems to be the low and expensive bandwidth under which the country stillsuffers.

4.2.3 Nigeria

In 2007 the Nigerian government had appointed the National Information TechnologyDevelopment Agency (NITDA) as responsible for the execution of a National Out-sourcing Strategy. It also announced that it will hold the first Nigerian InternationalOutsourcing Conference in Abuja over 21-23 March, 2007, as a platform to launch thethis National Outsourcing Strategy.

However, nothing much seems to have happened since. Sean Moroney, Chairman ofAITEC Africa, said in an interview9 in November 2009: "In Nigeria, which should bethe powerhouse of Africa, the lack of electrical power drives up costs as all enterpriseshave to spend huge amounts on diesel for their own generators. Further than that, Nige-ria has an appalling service culture, partly inherited from its history of military regimes,partly from an arrogance derived from its oil wealth, where its enterprises feel they donot have to deliver service to earn and retain customer support. For example, Nigeriahas made very little effort to develop a tourism industry. In contrast, Kenya has a thriv-ing tourism industry, which is highly service-oriented – and this feeds well into anotherservice industry like outsourcing. "

15

5. Developing a Strategy

A clear picture of the BPO potential in the Sub-Saharan countries has not yet emerged.However, two main problem areas are clearly visible:

- All countries still suffer under inadequate IT infrastructure and expensive tele-communication costs. To address these problems, African governments havecome up with bandwidth subsidies to help guarantee survival and aid competi-tion with cheaper destinations such as India and the Philippines. But this doesnot work everywhere, for example in Ghana there is no bandwidth subsidy.

- Sub-Saharan countries have been quite successful with simple BPO operationslike call-centres but are loosing out against the Indian and Asian competitionwith respect to higher value processes, since there is a shortage of skilled humanresources. Training or support programmes like the one carried out by DTI,South Africa, should be carried out in other countries as well.

A strategy to foster BPO between European and Sub-Saharan Africa, to be imple-mented by a support agency like CDE, is not obvious. Training programmes that trainthousands of people would certainly be helpful, but are clearly too costly. Infrastructureproblems and provision of sufficient and affordable bandwidth need to be addressed bythe target countries and could possibly be supported by large development aid pro-grammes.

This leaves the 'marketing' aspects. Apart from South Africa, most countries have arelatively small potential for BPO, which could of course be developed in the future,provided they can attract sufficient customers. However, most Sub-Saharan countriesare not very well known in Europe, which makes it very difficult to market their ser-vices, in particular to smaller clients.

The competition with India, China, and other big players is obvious, but these are play-ing in a different league, not necessarily addressing smaller companies in EU who havea need for BPO. So in that sense, this competition is not as critical as it may seem.However, there are new competitors coming up, first of all Egypt, but also in otherMENA countries. In particular with a view on European customers, the MENA regioncan be considered as Near-shore and hence more attractive. As described earlier, thereis a new move of "Sub-outsourcing", or as it is also called "expanding the global foot-print". Again, India is leading in this respect by off-shoring their work to smaller coun-tries, including African ones. But also African outsourcing locations, like Mauritius,outsource some of their work to other neighbouring countries, in this case Madagascar.Such move is indeed a chance for many Sub-Saharan countries as it does not require di-rect marketing of their services to the end clients - say in Europe - but to BPO serviceproviders in their own geographic and cultural vicinity.

5.1 Recommendations

A more intensive approach of promoting BPO between Europe and the sub-Saharancountries in general - as originally foreseen - would be very difficult due to the largedifferences across the two regions - both in terms of market demands and services of-fered - and probably not of any significant value.

There are a number of successful BPO activities in several sub-Saharan countries, butthere seems to be little or no real support by agencies or ministries. Hence the businessthat is being done in this field is based on individual contacts and the success cases thatexist are not due to any form of policy support or state-driven initiatives.

16

Furthermore, a sufficiently homogenous situation across the sub-Saharan countries (forexample in terms of human resources, skills, or infrastructure) does not exist, whichmakes a general approach of promotion of BPO difficult if not impossible. A similarsituation can be observed in Europe, where the attitude towards BPO varies quite sig-nificantly from one country to the other.

Therefore, it might be more beneficial to focus on one or two African countries, whereBPO activities already exist and which could provide a more promising entry point fordeeper analysis and subsequent promotion.

As mentioned earlier, the classical BPO market, and in particular the flourishing callcentres, produces only little added value to the economic development of the countries.The long-term aim should be to help the Sub-Saharan in moving to higher level proc-esses, from fro example software development services to the full scale of KnowledgeProcess Services.

Hence, fostering BPO in the Sub-Saharan countries should focus on the following is-sues:

1. As a first step, addressing some of the countries that already have a proven off-shoring potential, like Ghana, Senegal, Mauritius, and possibly Kenya.

2. Initiate a policy dialogue with those ministries or governmental agencies that are re-sponsible for the telecommunications network to develop a preferential tariff systemto strengthen the position of the current BPO service providers. Bandwidth costs areone of the main factors that determine competiveness in the global BPO market.10

3. Assist the main players in the selected countries to develop a market strategy thatfocuses on "sub-off-shoring" with the larger global companies for example in India.This would allow them to strengthen their positions and give more weight towardspotential EU clients.

4. Launch a targeted awareness campaign on the different types of BPO to raise thelevel of services in the future and develop a perspective to capture the KPO market.As this would not only require different marketing approaches but also higher skilllevels, such campaign should address both service providers and through a targetedpolicy dialogue the education ministries.

17

6. References

1 Jacob Funk Kirkegaard: Outsourcing and O shoring: Pushing the European Model Over

the Hill, Rather Than O the Cli . Working Paper WP 05-1 March 2005, Institute for In-

ternational Economics, Washington

2 Aksin, Armony, and Mehrotra: The Modern Call Center. Production and OperationsManagement 16(6), pp. 665–688, 2007, Production and Operations Management Society

3 TPI Research Report, Technology Partners International, Inc., July 2007

4 NASSCOM : Annual Report 2008-09. See www.nasscom.org

5 The Shifting Geography of Offshoring. The 2009 A.T. Kearney Global Services LocationIndex. A.T. Kearney, Chicago 2009

6 Plunkett Research Ltd, 2009, http://www.plunkettresearch.com

7 Western European BPO Market Estimates 2008 and Forecasts 2009-2013

Published by: IDCPublished: Apr. 16, 2009 - 21 PagesUS$ 6,400.00AbstractThis IDC study forecasts market demand in Western Europe for "key horizontal" BPO services(customer care, finance and accounting, human resources procurement BPO) and for the period2008-2013. This IDC study gives decision makers information on:The size of demand for providing key horizontal BPO services in Western Europe in 2009-2103IDC's predictions and assumptions concerning the drivers shaping the Western European BPOservices market, and what impact they have on demand development Key recommendations forvendors from IDC for maintaining and growing BPO services revenues in the coming yearsOverall, demand in Western Europe for "key horizontal" BPO services continues to grow, albeitat a slightly lowered rate than in our previous forecast published in December 2008. IDC is fore-casting a CAGR of 6.9% for the period between 2008 and 2013, including the relatively slow-growing HR processing market. Excluding HR processing services), IDC is forecasting a CAGRof 9.4% during this period."While economic recession makes many enterprises more interested in adopting BPO, it simulta-neously restricts the cash they have for investing in new outsourcing projects and it makes manyexecutives more risk-averse," said Douglas Hayward, research manager at IDC. "The bottom lineis that BPO demand remains relatively strong, but economic recession has taken demand growthdown by about a percentage point of growth."

8 Call Center Outsourcing in Western Europe

Published by: DatamonitorFeatures of this market research:

- Direct strategic recommendations for vendors either already present, or looking to enter,the Western European outsourcing market.

- Complete market sizing and forecasts across geographies, verticals and presented invalue, number of call centers and agent positions.

- Coverage across the ten key vertical markets in the outsourcing space with year-on-yearcomparisons of growth.

- Key trends in technology, product, pricing and business drivers are identified and dis-cussed.

102 pages3.395,00$Reports among others on:OFFSHORING `

Key findingsOffshore outsourcing’s impact on Western Europe

18

The market by countryUKFranceBeneluxSpainGermanyItaly

MARKET FORECAST AND GROWTHIntroductionKey findingsWestern Europe as a wholeOutsourced call centers in Western EuropeThe value of the marketOutsourcing traffic in Western EuropeTraffic by business functionThe Market by verticalVertical sizingVertical focus

9 See: http://www.aitecafrica.com/news/view/94

10 The success of Egypt as a major call-centre service provider is due to the decision of theCommunication and IT Minister to substantially reduce the bandwidth cost for the firstcall centre Xceed, at a time were the standard rates were prohibitive for this type of in-dustry.