BEFORE THE FEDERAL ENERGY REGULATORY ... - Tampa Electric

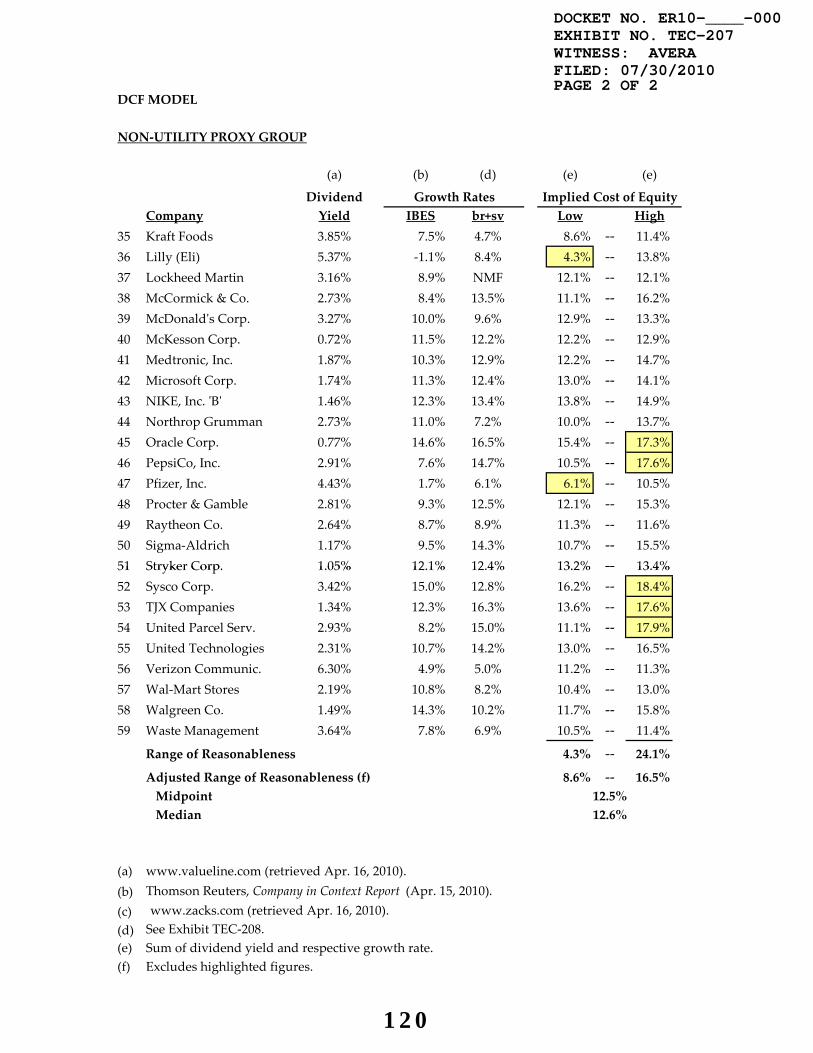

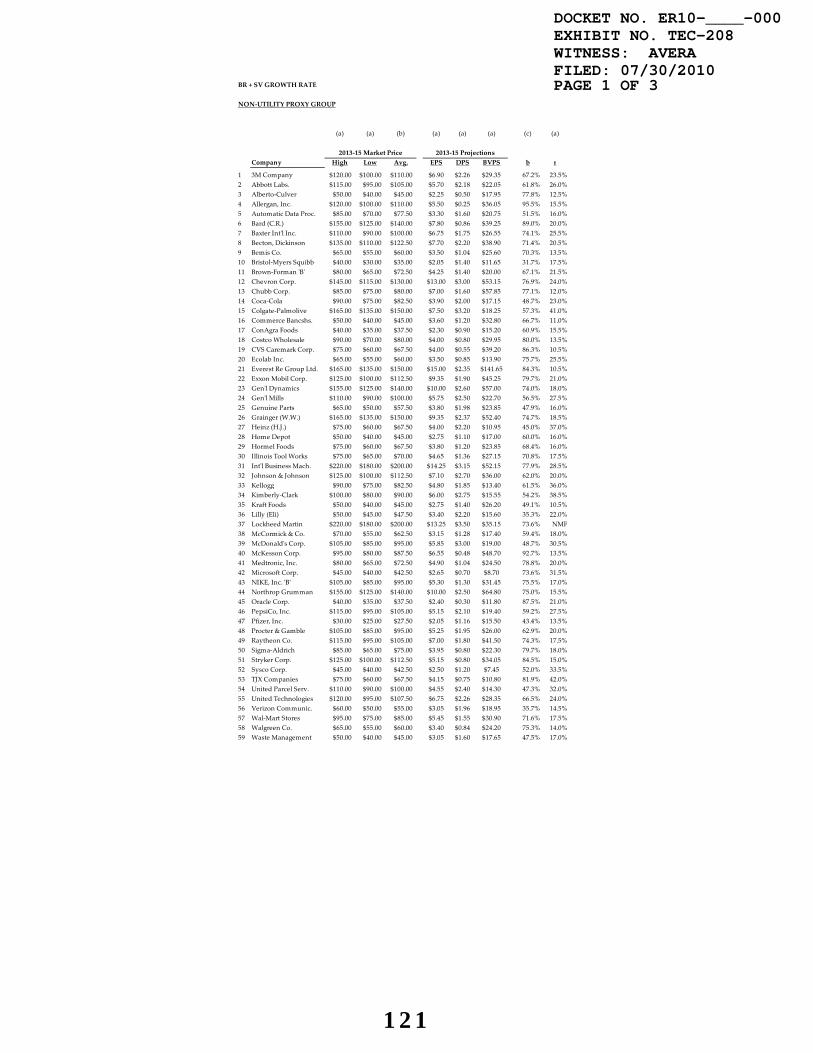

132

BEFORE THE FEDERAL ENERGY REGULATORY COMMISSION DOCKET NO. ER10-____-000 DIRECT TESTIMONY AND EXHIBIT OF WILLIAM E. AVERA ON BEHALF OF TAMPA ELECTRIC COMPANY

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of BEFORE THE FEDERAL ENERGY REGULATORY ... - Tampa Electric

BEFORE THE

FEDERAL ENERGY REGULATORY COMMISSION

DOCKET NO. ER10-____-000

DIRECT TESTIMONY AND EXHIBIT

OF

WILLIAM E. AVERA

ON BEHALF OF TAMPA ELECTRIC COMPANY

DOCKET NO. ER10-____-000 EXHIBIT NO. TEC-200 FILED: 07/30/2010

WILLIAM E. AVERA 1

DIRECT TESTIMONY AND EXHIBIT INDEX 2

3

INTRODUCTION AND EXPERIENCE................................1 4

Qualifications........................................1 5

Overview..............................................4 6

Summary and Conclusions...............................7 7

FUNDAMENTAL ANALYSES.......................................9 8

Tampa Electric Company................................9 9

Electric Power Industry..............................12 10

Impact of Capital Market Conditions..................21 11

CAPITAL MARKET ESTIMATES..................................26 12

Cost of Equity Concept...............................26 13

Development and Selection of a Proxy Group...........31 14

DCF Model ...........................................44 15

Evaluation of DCF Results............................49 16

Evaluating an ROE Point Estimate.....................59 17

Flotation Costs......................................67 18

ROE BENCHMARKS............................................70 19

Non-Utility DCF Model................................73 20

Expected Earnings Approach...........................79 21

ROE FOR TAMPA ELECTRIC....................................83 22

Implications for Financial Integrity.................84 23

Capital Structure....................................92 24

ROE Recommendation...................................99 25

DOCKET NO. ER10-____-000 EXHIBIT NO. TEC-200 FILED: 07/30/2010

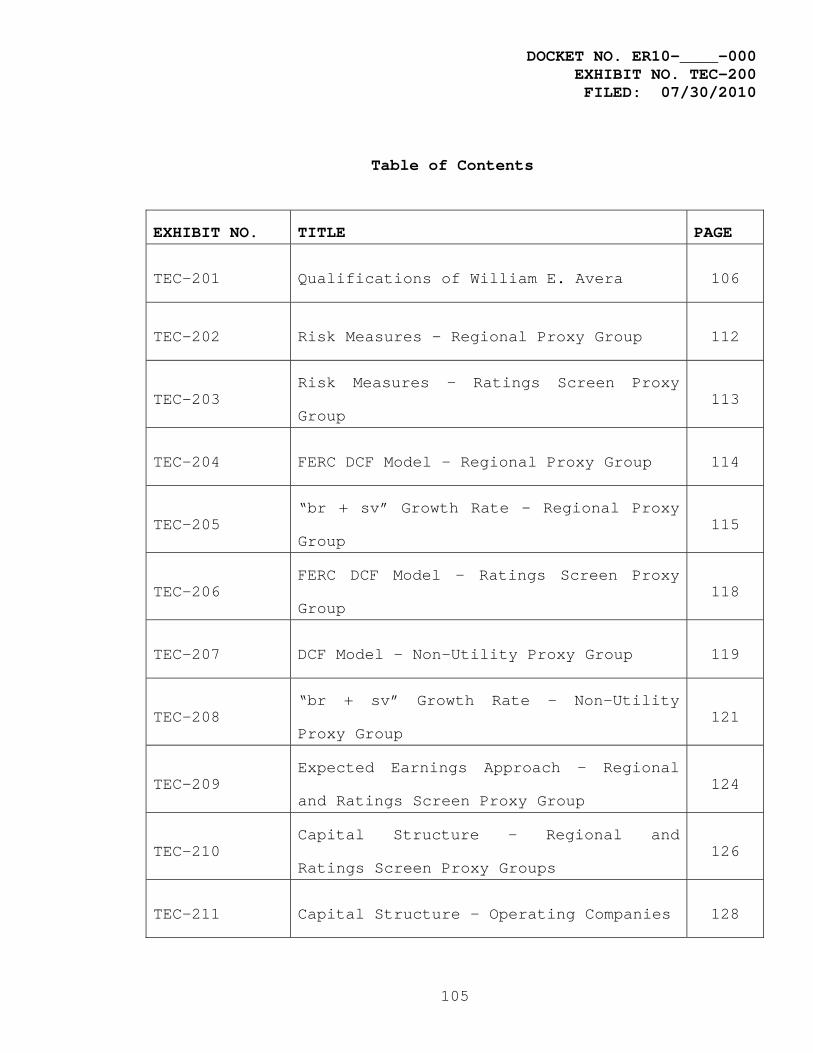

EXHIBITS.................................................104 1

2

Exhibit No. Description 3

TEC-201 Qualifications of William E. Avera 4

TEC-202 Risk Measures – Regional Proxy Group 5

TEC-203 Risk Measures – Ratings Screen Proxy Group 6

TEC-204 FERC DCF Model – Regional Proxy Group 7

TEC-205 “br + sv” Growth Rate – Regional Proxy Group 8

TEC-206 FERC DCF Model – Ratings Screen Proxy Group 9

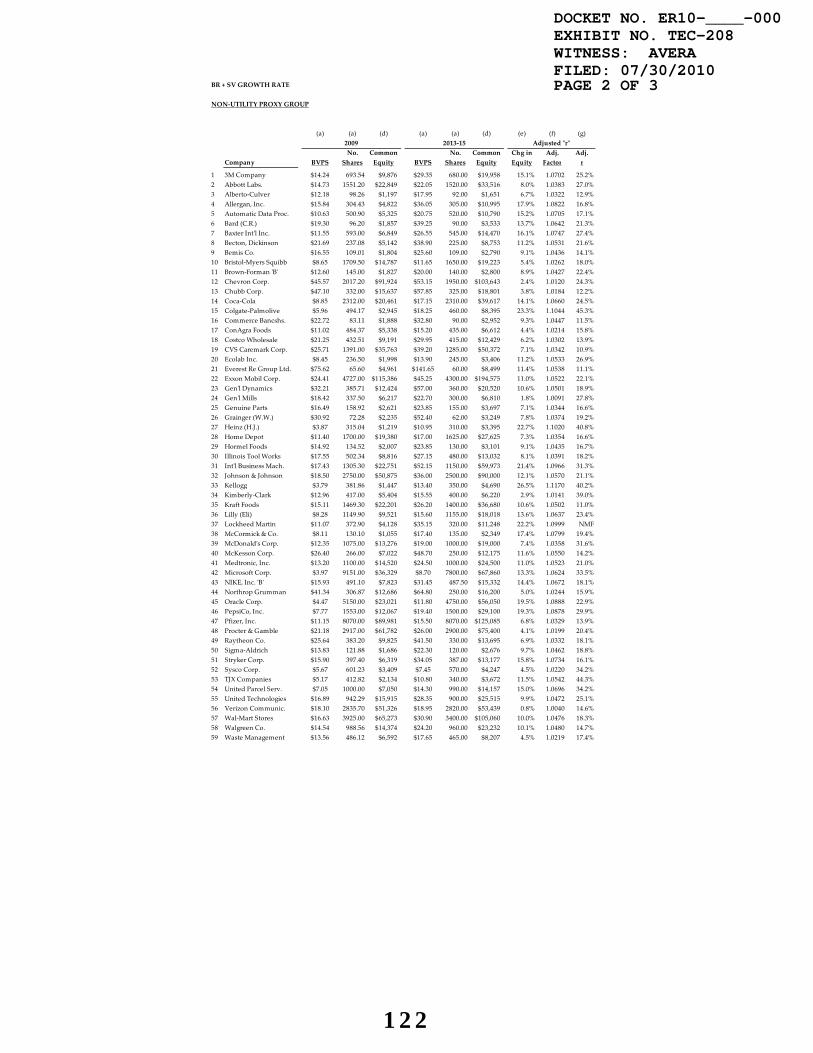

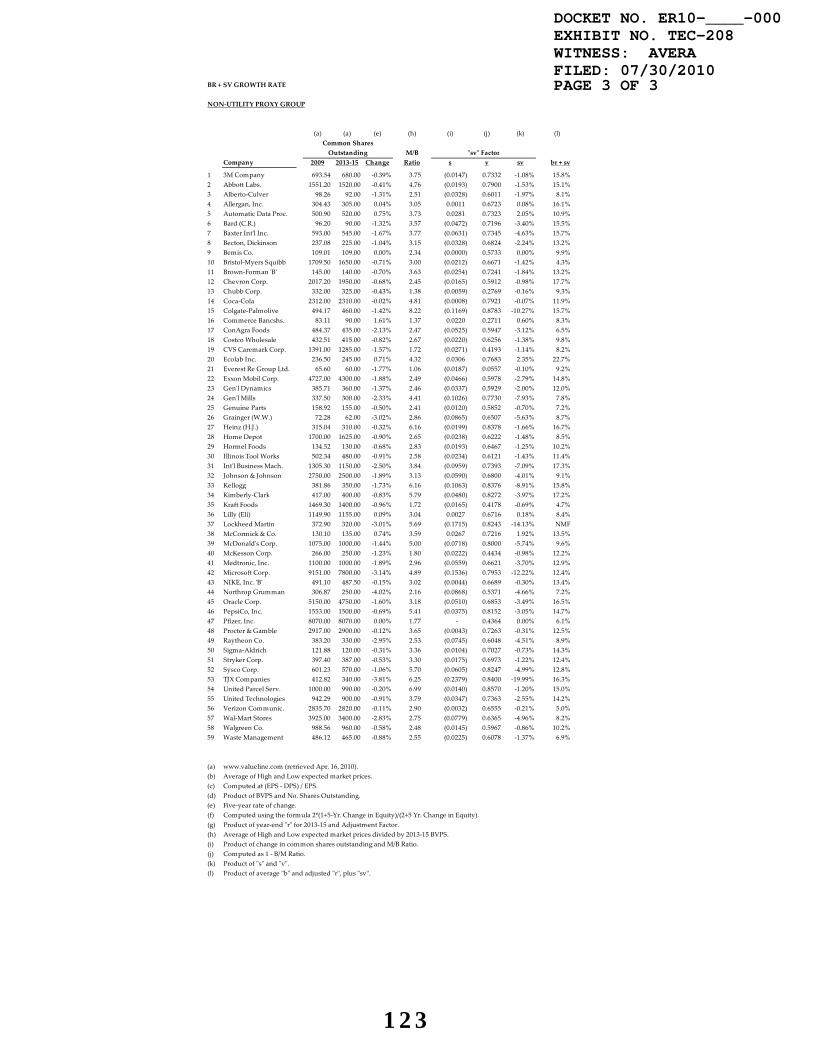

TEC-207 DCF Model – Non-Utility Proxy Group 10

TEC-208 “br + sv” Growth Rate – Non-Utility Proxy Group 11

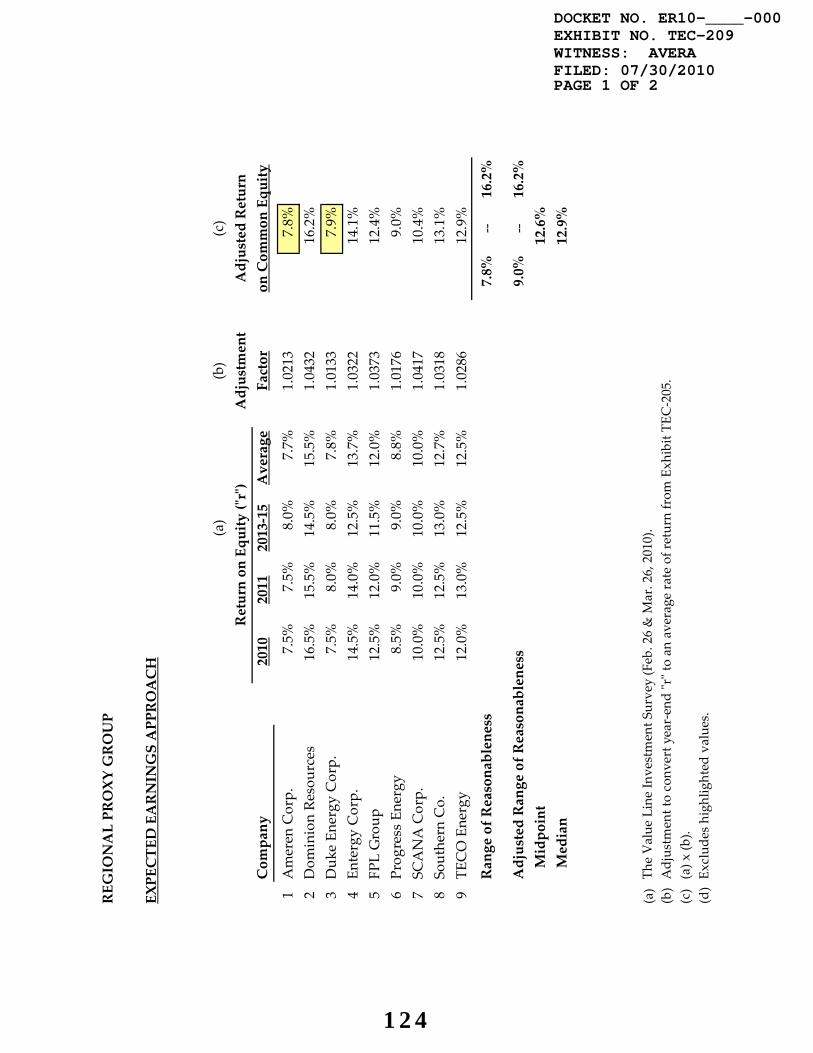

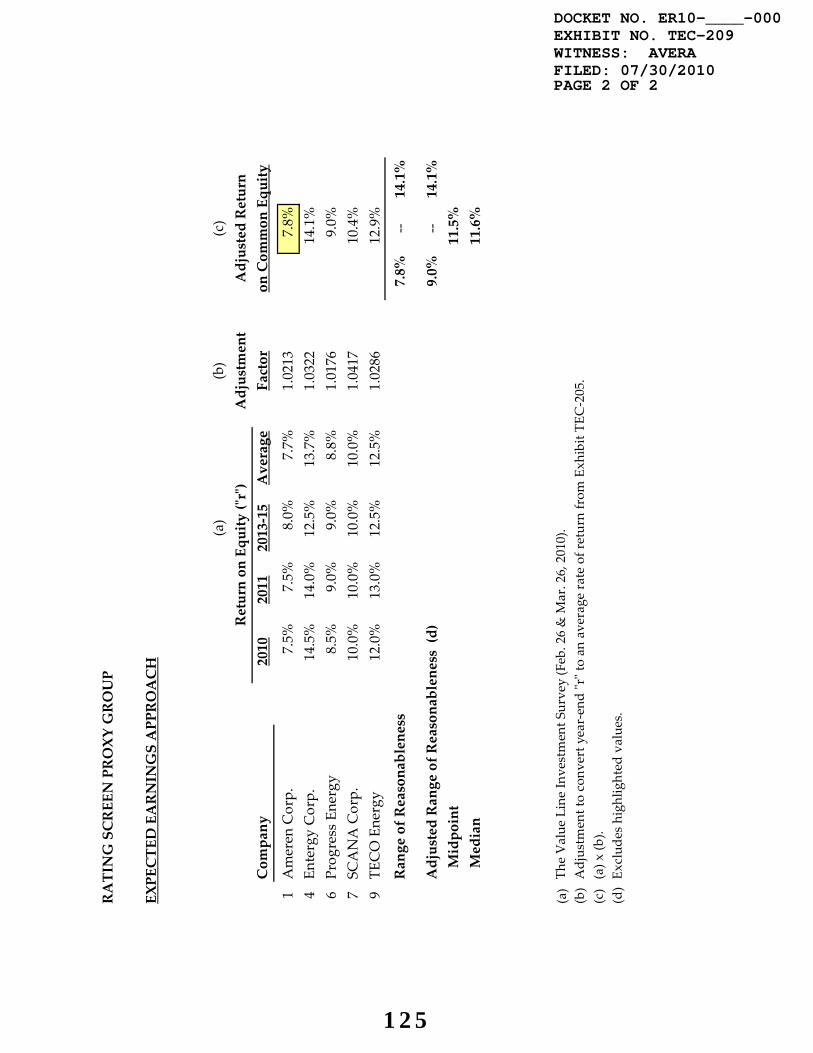

TEC-209 Expected Earnings Approach – Regional and 12

Ratings Screen Proxy Groups 13

TEC-210 Capital Structure – Regional and Ratings Screen 14

Proxy Groups 15

TEC-211 Capital Structure – Operating Companies 16

17

18

19

20

21

22

23

24

25

DOCKET NO. ER10-____-000 EXHIBIT NO. TEC-200 FILED: 07/30/2010

BEFORE THE FEDERAL ENERGY REGULATORY COMMISSION 1

PREPARED DIRECT TESTIMONY 2

OF 3

WILLIAM E. AVERA 4

ON BEHALF OF TAMPA ELECTRIC COMPANY 5

6

INTRODUCTION AND EXPERIENCE 7

Q. Please state your name and business address. 8

9

A. William E. Avera, 3907 Red River, Austin, Texas, 78751. 10

11

Q. In what capacity are you employed? 12

13

A. I am the President of FINCAP, Inc., a firm providing 14

financial, economic, and policy consulting services to 15

business and government. 16

17

Qualifications 18

Q. What are your qualifications? 19

20

A. I received a B.A. degree with a major in economics from 21

Emory University. After serving in the U.S. Navy, I 22

entered the doctoral program in economics at the 23

University of North Carolina at Chapel Hill. Upon 24

receiving my Ph.D., I joined the faculty at the 25

DOCKET NO. ER10-____-000 EXHIBIT NO. TEC-200 FILED: 07/30/2010

2

University of North Carolina and taught finance in the 1

Graduate School of Business. I subsequently accepted a 2

position at the University of Texas at Austin where I 3

taught courses in financial management and investment 4

analysis. I then went to work for International Paper 5

Company in New York City as Manager of Financial 6

Education, a position in which I had responsibility for 7

all corporate education programs in finance, accounting, 8

and economics. 9

10

In 1977, I joined the staff of the Public Utility 11

Commission of Texas (“PUCT”) as Director of the Economic 12

Research Division. During my tenure at the PUCT, I 13

managed a division responsible for financial analysis, 14

cost allocation and rate design, economic and financial 15

research, and data processing systems, and I testified in 16

cases on a variety of financial and economic issues. 17

Since leaving the PUCT in 1979, I have been engaged as a 18

consultant. I have participated in a wide range of 19

assignments involving utility-related matters on behalf 20

of utilities, industrial customers, municipalities, and 21

regulatory commissions. I have previously testified 22

before the Federal Energy Regulatory Commission (“FERC” 23

or the “Commission”), as well as the Federal 24

Communications Commission (“FCC”), the Surface 25

DOCKET NO. ER10-____-000 EXHIBIT NO. TEC-200 FILED: 07/30/2010

3

Transportation Board (and its predecessor, the Interstate 1

Commerce Commission), the Canadian Radio-Television and 2

Telecommunications Commission, and regulatory agencies, 3

courts, and legislative committees in over 40 states. 4

5

In 1995, I was appointed by the PUCT, with the approval 6

of the Governor, to the Synchronous Interconnection 7

Committee to advise the Texas legislature on the costs 8

and benefits of connecting Texas to the national electric 9

transmission grid. In addition, I served as an outside 10

director of Georgia System Operations Corporation, the 11

system operator for electric cooperatives in Georgia. 12

13

I have served as Lecturer in the Finance Department at 14

the University of Texas at Austin and taught in the 15

evening graduate program at St. Edward’s University for 16

twenty years. In addition, I have lectured on economic 17

and regulatory topics in programs sponsored by 18

universities and industry groups. I have taught in 19

hundreds of educational programs for financial analysts 20

in programs sponsored by the Association for Investment 21

Management and Research, the Financial Analysts Review, 22

and local financial analysts societies. These programs 23

have been presented in Asia, Europe, and North America, 24

including the Financial Analysts Seminar at Northwestern 25

DOCKET NO. ER10-____-000 EXHIBIT NO. TEC-200 FILED: 07/30/2010

4

University. I hold the Chartered Financial Analyst (CFA®) 1

designation and have served as Vice President for 2

Membership of the Financial Management Association. I 3

have also served on the Board of Directors of the North 4

Carolina Society of Financial Analysts. I was elected 5

Vice Chairman of the National Association of Regulatory 6

Utility Commissioners (“NARUC”) Subcommittee on Economics 7

and appointed to NARUC’s Technical Subcommittee on the 8

National Energy Act. I have also served as an officer of 9

various other professional organizations and societies. 10

11

Overview 12

Q. What is the purpose of your testimony? 13

14

A. The purpose of my testimony is to present to the FERC my 15

independent analysis of a fair rate of Return on Equity 16

(“ROE”) for the jurisdictional wholesale electric utility 17

operations of Tampa Electric Company (“Tampa Electric” or 18

“the Company”). My evaluation considered FERC’s 19

established precedent and policy objectives, industry 20

conditions and fundamentals, independent estimates of the 21

ROE for alternative benchmark groups of electric 22

utilities, as well as the particular exposures 23

confronting the Company and its electric production and 24

transmission systems. 25

DOCKET NO. ER10-____-000 EXHIBIT NO. TEC-200 FILED: 07/30/2010

5

Q. Please summarize the basis of your knowledge and 1

conclusions concerning the issues to which you are 2

testifying in this case. 3

4

A. To prepare my testimony, I used information from a 5

variety of sources that would normally be relied upon by 6

a person in my capacity. In connection with the present 7

filing, I considered and relied upon corporate 8

disclosures, publicly available financial reports and 9

filings, and other published information relating to 10

Tampa Electric. In addition, I am familiar with FERC 11

policy generally and have submitted testimony in numerous 12

proceedings at the Commission dealing with required rates 13

of return for electric utilities.1 I also reviewed 14

information relating generally to capital markets and 15

specifically to investor perceptions, requirements, and 16

expectations for regulated utilities in a restructured 17

wholesale electric power market. These sources, coupled 18

with my experience in the fields of finance and utility 19

regulation, have given me a working knowledge of ROE 20

issues affecting Tampa Electric and are the basis of my 21

conclusions. 22

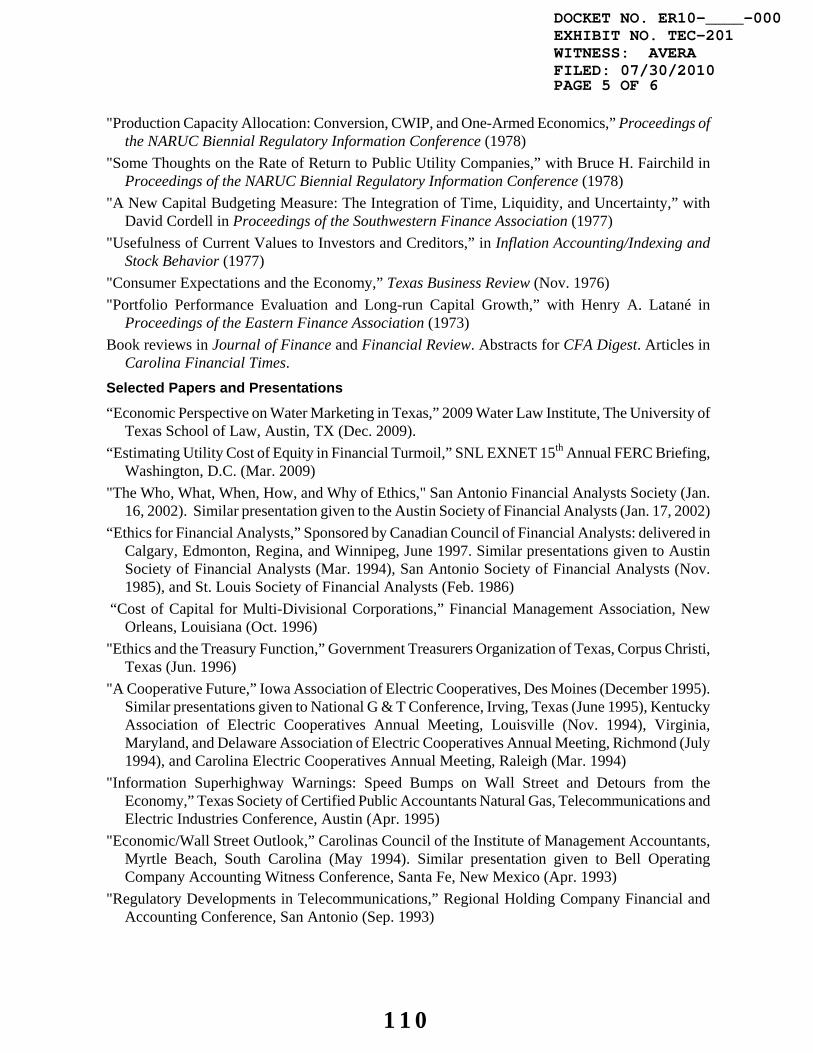

1 See, e.g., Docket No. ER00-3316-000 on behalf of American Transmission Company, LLC, Docket No. ER02-485-000 involving the Midwest Independent Transmission System Operator, Inc., Docket No. ER04-157-000 on behalf of the transmission-owning members of the ISO New England, Inc., Docket No. ER07-562-000 on behalf of Trans-Allegheny Interstate Line Company, Docket No. ER08-386-000 on behalf of Potomac-Appalachian Transmission Highline, LLC, Docket No. EL08-31-000 on behalf of Westar Energy, Inc., and Docket No. ER08-686-000 on behalf of Pepco Holdings, Inc.

DOCKET NO. ER10-____-000 EXHIBIT NO. TEC-200 FILED: 07/30/2010

6

Q. What is the role of the ROE in setting a utility’s rates? 1

2

A. The rate of return on common equity compensates 3

shareholders for the use of their capital to finance the 4

plant and equipment necessary to provide utility service. 5

Investors commit capital only if they expect to earn a 6

return on their investment commensurate with returns 7

available from alternative investments with comparable 8

risks. To be consistent with sound regulatory economics 9

and the standards set forth by the Supreme Court in the 10

Bluefield2 and Hope3 cases, a utility’s allowed return on 11

common equity should be sufficient to: (1) fairly 12

compensate investors for capital they have invested in 13

the utility, (2) enable the utility to offer a return 14

adequate to attract new capital on reasonable terms, and 15

(3) maintain the utility’s financial integrity. 16

17

Q. How did you go about evaluating the ROE for Tampa 18

Electric? 19

20

A. I first reviewed the operations and finances of Tampa 21

Electric, as well as the general conditions in the 22

electric utility industry. With this background, I 23

2 Bluefield Water Works & Improvement Co. v. Pub. Serv. Comm’n, 262 U.S. 679 (1923).

3 FPC v. Hope Natural Gas Co., 320 U.S. 591 (1944).

DOCKET NO. ER10-____-000 EXHIBIT NO. TEC-200 FILED: 07/30/2010

7

examined current capital market conditions and conducted 1

quantitative analyses to estimate the current cost of 2

equity. Consistent with Commission precedent,4 I relied 3

on the Discounted Cash Flow (“DCF”) methodology, 4

currently prescribed by FERC, and applied it to a proxy 5

group of other electric utilities with a direct 6

correlation to Tampa Electric and the broader markets in 7

which the Company operates. In addition, I examined 8

alternative ROE benchmarks that included DCF cost of 9

equity estimates for a proxy group of low-risk industrial 10

firms and expected earned rates of return for utilities. 11

12

Summary and Conclusions 13

Q. Based on your evaluation, what did you conclude regarding 14

a fair ROE for Tampa Electric? 15

16

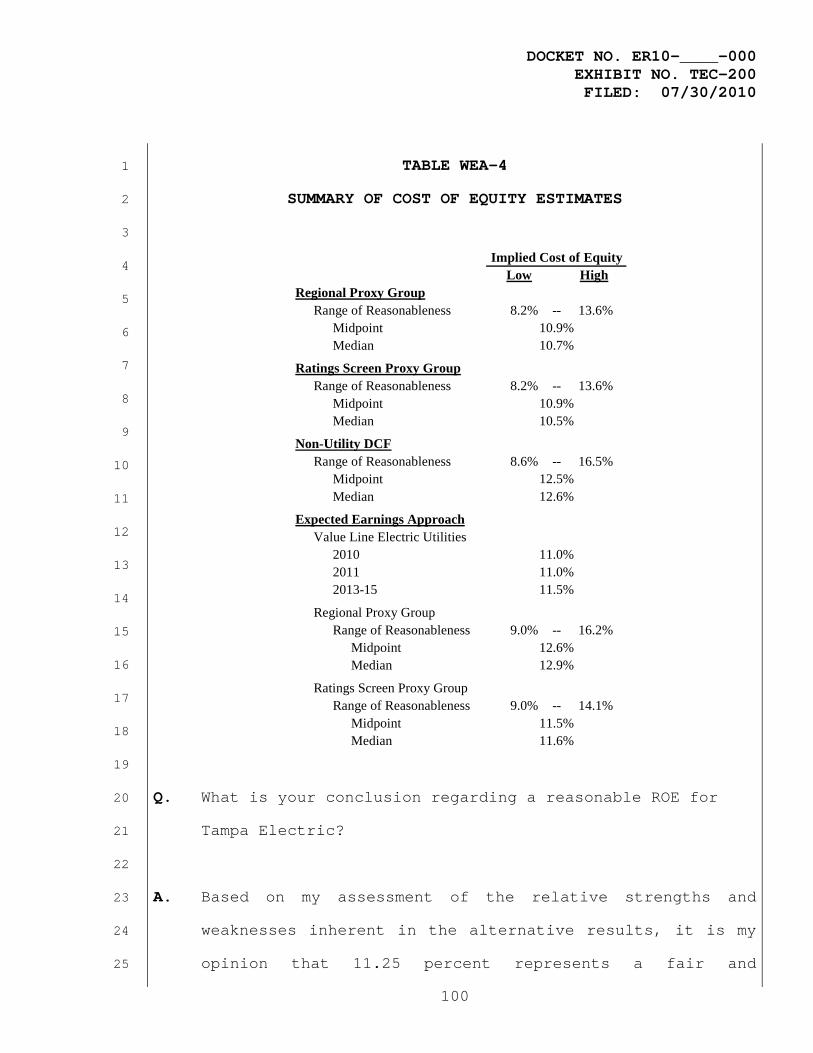

A. I recommend an ROE for Tampa Electric of 11.25 percent. 17

My recommendation falls well within the 8.2 percent to 18

13.6 percent zone of reasonableness produced by applying 19

the Commission-approved DCF approach to the proxy group 20

of nine regional electric utilities. While my 11.25 21

percent ROE recommendation exceeds the midpoint and 22

4 See, e.g., Bangor Hydro-Elec. Co., 117 FERC ¶ 61,129 (2006) (“Bangor Hydro”); Midwest

Indep. Transmission Sys. Operator, Inc., 100 FERC ¶ 61,292 (2002) (“Midwest ISO”), reh’g denied, 102 FERC ¶ 61,143 (2003), modified on other grounds sub nom. Pub. Serv. Comm’n v. FERC, 397 F.3d 1004 (D.C. Cir. 2005); S. Cal. Edison Co., 92 FERC ¶ 61,070 (2000) (“Southern California Edison”), reh’g denied, 108 FERC ¶ 61,085 (2004).

DOCKET NO. ER10-____-000 EXHIBIT NO. TEC-200 FILED: 07/30/2010

8

median produced using the Commission’s DCF approach, an 1

ROE above these values is supported by reference to 2

alternative ROE benchmarks, which consistently support a 3

higher allowed return. In evaluating the ROE for 4

jurisdictional utility operations, it is also important 5

to consider the uncertainties associated with Tampa 6

Electric and the challenges the Company faces in raising 7

the capital required to finance significant planned 8

infrastructure investment – including a renewed focus on 9

regulatory uncertainties. 10

11

My conclusions are reinforced by the need to consider 12

flotation costs, and the fact that current cost of 13

capital estimates are likely to understate investors’ 14

requirements at the time the outcome of this proceeding 15

becomes effective and beyond. Moreover, ongoing turmoil 16

in the domestic and global financial markets and 17

continued economic uncertainties have exacerbated the 18

risks faced by utilities and their investors. In 19

addition, my recommendation also considers the 20

Commission’s policy goal of attracting the capital 21

investment to expand utility infrastructure necessary to 22

support efficient, reliable wholesale power markets. 23

Taken together, these considerations confirm the 24

reasonableness of my recommended range and support an 25

DOCKET NO. ER10-____-000 EXHIBIT NO. TEC-200 FILED: 07/30/2010

9

11.25 percent ROE for Tampa Electric. 1

2

FUNDAMENTAL ANALYSES 3

Q. What is the purpose of this section? 4

5

A. As a predicate to the quantitative analyses that I 6

address later in this testimony, this section briefly 7

reviews the operations and finances of Tampa Electric. In 8

addition, it examines the risks and prospects for the 9

electric utility industry and conditions in the capital 10

markets and the general economy. An understanding of the 11

fundamental factors driving the risks and prospects of 12

electric utilities is essential in developing an informed 13

opinion of investors’ expectations and requirements that 14

are the basis of a fair rate of return. 15

16

Tampa Electric Company 17

Q. Please briefly describe Tampa Electric. 18

19

A. Tampa Electric is the principal subsidiary of TECO 20

Energy, Inc. (“TECO Energy”). Headquartered in Tampa, 21

Florida, Tampa Electric provides electric generation, 22

transmission, and distribution utility services 23

throughout an area of approximately 2,000 square miles in 24

West Central Florida, including Hillsborough County and 25

DOCKET NO. ER10-____-000 EXHIBIT NO. TEC-200 FILED: 07/30/2010

10

parts of Polk, Pasco and Pinellas Counties, with an 1

estimated population of over one million. The principal 2

communities served are Tampa, Winter Haven, Plant City 3

and Dade City. In addition, Tampa Electric engages in 4

wholesale sales to utilities and other resellers of 5

electricity. Through its Peoples Gas System division, 6

Tampa Electric also purchases, distributes and markets 7

natural gas to more than 334,000 residential, commercial, 8

industrial and electric power generation customers in the 9

state of Florida. 10

11

During 2009, approximately 49 percent of Tampa Electric’s 12

total operating revenue was derived from residential 13

sales, 31 percent from commercial sales, 9 percent from 14

industrial sales, and 11 percent from other sales, 15

including bulk power sales for resale. Tampa Electric’s 16

generating resources have a combined capacity of 17

approximately 4,700 megawatts. Approximately 55 percent 18

of Tampa Electric’s generation of electricity for 2009 19

was coal-fired, with natural gas representing 20

approximately 45 percent and oil representing less than 1 21

percent. Tampa Electric used its generating units to meet 22

approximately 91 percent of the total system load 23

requirements, with the remaining 9 percent coming from 24

purchased power. 25

DOCKET NO. ER10-____-000 EXHIBIT NO. TEC-200 FILED: 07/30/2010

11

Tampa Electric's transmission and distribution facilities 1

include over 7,700 miles of overhead lines and 2

approximately 4,470 miles of underground cables. At 3

December 31, 2009, Tampa Electric’s investment in assets 4

amounted to approximately $6.3 billion, with revenues 5

totaling approximately $2.9 billion. Tampa Electric's 6

retail electric operations are subject to the 7

jurisdiction of the Florida Public Service Commission 8

(“FPSC”), with wholesale power and interstate 9

transmission service regulated by FERC. 10

11

Q. Is Tampa Electric interconnected with other utilities 12

through a regional reliability organization? 13

14

A. Yes. Tampa Electric is interconnected with electric 15

power systems in the southeast through the Florida 16

Reliability Coordinating Council, Inc. (“FRCC”), which 17

serves as a regional entity for the purpose of proposing 18

and enforcing reliability standards and coordinating and 19

planning the bulk electric system in Florida. The area 20

of Florida that is within the FRCC region is peninsular 21

Florida east of the Apalachicola River, while the 22

panhandle area west of the Apalachicola River is within 23

the scope of the SERC Reliability Corporation (“SERC”). 24

25

DOCKET NO. ER10-____-000 EXHIBIT NO. TEC-200 FILED: 07/30/2010

12

Q. What credit ratings have been assigned to Tampa Electric? 1

2

A. Currently, Tampa Electric is assigned a corporate credit 3

rating of “BBB” by Standard & Poor’s Corporation (“S&P”), 4

with Moody’s Investors Service (“Moody’s”) assigning an 5

issuer rating of “Baa1”. Meanwhile, Fitch Ratings Ltd. 6

(“Fitch”) has assigned the Company a “BBB” issuer default 7

rating. 8

9

Electric Power Industry 10

Q. What general conditions have characterized the electric 11

power industry? 12

13

A. Since the 1990s, the industry has experienced significant 14

structural change resulting from market forces and 15

regulatory initiatives. At least initially, this process 16

was largely driven by regulatory reforms at the federal 17

level. The Energy Policy Act of 1992 greatly facilitated 18

competition for the production and sale of power at the 19

wholesale level, with FERC being a proponent of actions 20

designed to foster greater competition in markets for 21

wholesale power supply. 22

23

In April 1996, the Commission adopted Order No. 888,5 24

5 Promoting Wholesale Competition Through Open Access Non-Discriminatory Transmission Services by Public Utilities; Recovery of Stranded Costs by Public Utilities and Transmitting Utilities, Order No. 888, 1991-1996 FERC Stats. & Regs., Regs. Preambles ¶ 31,036 (1996), order on reh’g, Order No. 888-A, 1996-2000 FERC Stats. & Regs., Regs. Preambles ¶ 31,048, order on reh’g, Order No. 888-B, 81 FERC ¶ 61,248 (1997), reh’g denied, Order No. 888-C, 82 FERC ¶ 61,046 (1998), aff’d in part and remanded in part sub nom. Transmission Access Policy Study Group v. FERC, 225 F.3d 667 (D.C. Cir. 2000), aff’d sub nom. N.Y. v. FERC, 535 U.S. 1 (2002).

DOCKET NO. ER10-____-000 EXHIBIT NO. TEC-200 FILED: 07/30/2010

13

which mandated open access to the wholesale transmission 1

facilities of jurisdictional electric utilities. The 2

Commission later promoted improvements to the 3

transmission system and has continued to pursue the goal 4

of creating “seamless” wholesale power markets that 5

facilitate transactions across transmission grid 6

boundaries, among other objectives. In response to the 7

passage of the Energy Policy Act of 2005 (“EPAct 2005”), 8

FERC also issued its Order Nos. 679 and 679-A, 9

establishing incentive-based rate treatments to promote 10

greater capital investment in electric utility 11

infrastructure. 12

13

Q. How have investors’ risk perceptions for the utility 14

industry evolved? 15

16

A. Implementation of these structural changes and related 17

events have caused investors to rethink their assessment 18

of the relative risks associated with the utility 19

industry. The past decade witnessed steady erosion in 20

credit quality throughout the electric power industry, 21

both as a result of revised perceptions of the risks in 22

the industry and the weakened finances of industry 23

participants themselves. Late last year, S&P observed 24

with respect to the industry’s future that: 25

26

DOCKET NO. ER10-____-000 EXHIBIT NO. TEC-200 FILED: 07/30/2010

14

Looming costs associated with environmental 1 compliance, slack demand caused by economic 2 weakness, the potential for permanent demand 3 destruction caused by changes in consumer 4 behavior and closing of manufacturing 5 facilities, and numerous regulatory filings 6 seeking recovery of costs are some of the 7 significant challenges the industry has to deal 8 with.6 9

10

Q. Does Tampa Electric anticipate the need to access 11

the capital markets going forward? 12

13

A. Yes. Tampa Electric will require capital investment to 14

provide for necessary maintenance and replacements and 15

fund new investments in the facilities needed to 16

generate, transmit and distribute electricity, which are 17

expected to total over $1.2 billion over the years 2011 18

to 2014.7 19

20

Continued support for Tampa Electric’s financial 21

integrity and flexibility will be instrumental in 22

attracting the long-term capital necessary to fund these 23

projects in an effective manner. In addition, Tampa 24

Electric will be required to refinance maturing debt 25

issues and must meet short-term liquidity needs arising 26

from seasonal cash flows and ongoing construction 27

6 Standard & Poor’s Corporation, “U.S. Regulated Electric Utilities Head Into 2010 With Familiar Concerns,” RatingsDirect (Dec. 28, 2009).

7 TECO Energy, Inc., 2009 Form 10-K Report at 57.

DOCKET NO. ER10-____-000 EXHIBIT NO. TEC-200 FILED: 07/30/2010

15

programs. Tampa Electric’s exposure to storm restoration 1

activities magnifies the importance of maintaining 2

financial flexibility, which is essential to guarantee 3

access to the cash resources and interim financing 4

required to cover operating cash flows and fund required 5

investments in the utility system. 6

7

Q. Is the potential for energy market volatility an ongoing 8

concern for investors? 9

10

A. Yes. In recent years, utilities and their customers have 11

had to contend with dramatic fluctuations in energy costs 12

due to ongoing price volatility in the spot markets and 13

investors recognize the prospect of further turmoil in 14

energy markets. In times of extreme volatility, 15

utilities can quickly find themselves in a significant 16

under-recovery position with respect to power costs, 17

which can severely stress liquidity. Moody’s has warned 18

investors of ongoing exposure to “extremely volatile” 19

energy commodity costs, including purchased power prices, 20

which are heavily influenced by fuel costs,8 and Fitch 21

noted that rapidly rising energy costs created 22

vulnerability in the utility industry.9 23

8 Moody’s Investors Service, “Storm Clouds Gathering on the Horizon for the North American Electric Utility Sector,” Special Comment (Aug. 2007).

9 Fitch Ratings Ltd., “Staying Afloat: Downstream Liquidity in the Energy and Power Sectors,” Oil & Gas / Global Power Special Report (June 16, 2008).

DOCKET NO. ER10-____-000 EXHIBIT NO. TEC-200 FILED: 07/30/2010

16

For example, while coal has historically provided 1

relative stability with respect to fuel costs, the Energy 2

Information Administration (“EIA”), a statistical agency 3

of the U.S. Department of Energy (“DOE”), reported that 4

prices for Central and Northern Appalachia coal spiked 5

from approximately $45 per ton in June 2007 to over $140 6

per ton in September 2008, before falling back into the 7

$40 to $50 range in September 2009.10 8

9

The power industry and its customers have also had to 10

contend with dramatic fluctuations in gas costs due to 11

ongoing price volatility in the spot markets. Fitch has 12

highlighted the challenges that fluctuations in energy 13

prices can have for utilities and noted that: 14

15

The sharp run-up and subsequent collapse of 16 natural gas prices in 2008 is emblematic of the 17 extreme price volatility that characterizes the 18 commodity and is likely to persist in the 19 future.11 20

21

Moody’s concluded that natural gas “remains highly 22

volatile,” and warned that such price fluctuations “could 23

have a significant impact on a utility’s liquidity 24

10 Energy Information Administration, Coal News and Markets (Jun. 20 & Sep. 26, 2008, Oct. 13, 2009).

11 Fitch Ratings, Ltd., “U.S. Utilities, Power and Gas 2009 Outlook,” Global Power North American Special Report (Dec. 22, 2008).

DOCKET NO. ER10-____-000 EXHIBIT NO. TEC-200 FILED: 07/30/2010

17

profile.”12 1

2

While expectations for significantly lower power prices 3

reflect weaker fundamentals affecting current load and 4

fuel prices, investors recognize the potential that such 5

trends could quickly reverse. S&P observed that “short-6

term price volatility from numerous possibilities … is 7

always possible”,13 while Fitch noted, “uncertainty 8

regarding fuel prices, in particular natural gas costs, 9

has made planning for the future even more problematic.”14 10

Moody’s concluded that utilities remain exposed to 11

“volatile commodity prices … which can wreak havoc on 12

even the strongest utility liquidity profiles.”15 13

14

Q. What other financial pressures impact investors’ risk 15

assessment of electric utilities? 16

17

A. Investors are aware of the financial and regulatory 18

pressures faced by utilities associated with both rising 19

costs and the need to undertake significant capital 20

investments. As Moody’s observed: 21

12 Moody’s Investors Service, “Carbon Risks Becoming More Imminent for U.S. Electric Utility Sector,” Special Comment (March 2009).

13 Standard & Poor’s Corporation, “Top 10 Investor Questions: U.S. Regulated Electric Utilities,” RatingsDirect (Jan. 22, 2010).

14 Fitch Ratings, Ltd., “Electric Utility Capital Spending: The Show Will Go On,” Global Power U.S. and Canada Special Report (Oct. 14, 2009).

15 Moody’s Investors Service, “U.S. Electric Utilities Face Challenges Beyond Near-Term,” Industry Outlook (Jan. 2010).

DOCKET NO. ER10-____-000 EXHIBIT NO. TEC-200 FILED: 07/30/2010

18

Utilities remain exposed to large, long-term 1 capital investment challenges, volatile 2 commodity prices and legal judgments that can 3 wreak havoc on even the strongest liquidity 4 profiles.16 5

6

Similarly, S&P recently noted that cost increases and 7

capital projects, along with uncertain load growth, were 8

a significant challenge to the utility industry.17 Fitch 9

reached similar conclusions: 10

11

The combination of high capital expenditures 12 and relatively weak electricity demand will 13 continue to pressure credit quality and require 14 base rate increases in 2010 and beyond.18 15

16

As noted earlier, investors are aware that Tampa Electric 17

will undertake significant electric utility capital 18

expenditures. Providing the infrastructure necessary to 19

meet the energy needs of customers imposes additional 20

financial responsibilities and risks on Tampa Electric. 21

22

Q. Are environmental considerations also affecting 23

investors’ evaluation of electric utilities? 24

25

A. Yes. Although Tampa Electric’s exposure has been 26

16 Moody’s Investors Service, “U.S. Electric Utilities Face Challenges Beyond Near-Term,” Industry Outlook (Jan. 2010).

17 Standard & Poor’s Corporation, “Industry Economic And Ratings Outlook,” RatingsDirect (Feb. 2, 2010).

18 Fitch Ratings Ltd., “U.S. Utilities, Power, and Gas 2010 Outlook,” Global Power North America Special Report (Dec. 4, 2009).

DOCKET NO. ER10-____-000 EXHIBIT NO. TEC-200 FILED: 07/30/2010

19

moderated through its ability to recoup certain 1

environmental and conservation costs through a surcharge 2

recovery mechanism at the retail level in Florida, 3

utilities are confronting increased environmental 4

pressures that could impose significant uncertainties and 5

costs. In early 2007 S&P cited environmental mandates, 6

including emissions, conservation, and renewable 7

resources, as one of the top ten credit issues facing 8

U.S. utilities.19 Similarly, Moody’s noted that “the 9

prospect for new environmental emission legislation – 10

particularly concerning carbon dioxide – represents the 11

biggest emerging issue for electric utilities.”20 12

13

Compliance with these evolving standards will undoubtedly 14

require significant capital expenditures, especially for 15

utilities like Tampa Electric that depend significantly 16

on coal-fired generation. S&P concluded, “Although we 17

expect the cap-and-trade program to be economy wide and 18

affect a variety of sectors, it will disproportionately 19

affect the power sector.”21 S&P recently emphasized that 20

because of uncertainty over the details and timing of 21

future limits on CO2 emissions, existing ratings do not 22

19 Standard & Poor’s Corporation, “Top Ten Credit Issues Facing U.S. Utilities,” RatingsDirect (Jan. 29, 2007).

20 Moody’s Investors Service, “U.S. Investor-Owned Electric Utilities,” Industry Outlook (Jan. 2009).

21 Standard & Poor’s Corporation, “The Potential Credit Impact Of Carbon Cap-And-Trade Legislation On U.S. Companies,” RatingsDirect (Sep. 14, 2009).

DOCKET NO. ER10-____-000 EXHIBIT NO. TEC-200 FILED: 07/30/2010

20

fully reflect the impact of carbon risks.22 1

2

Q. Have investors recognized that electric utilities face 3

additional risks because of the impact of industry 4

restructuring on transmission operations? 5

6

A. Yes. Transmission operations have become increasingly 7

complex, and investors have recognized that difficulties 8

in obtaining permits and uncertainty over the adequacy of 9

allowed rates of return have contributed to heightened 10

risk and fueled concerns regarding the adequacy of 11

investment in the transmission sector of the electric 12

power industry. 13

14

At the same time, the development of competitive 15

wholesale power markets has resulted in increased demand 16

for transmission resources. Concerns regarding the need 17

to encourage further investment in the transmission 18

sector were exemplified by the Commission’s observations 19

in Order No. 679:23 20

21

[I]nvestment in transmission facilities in real 22 dollar terms declined significantly between 23 1975 and 1998. Although the amount of 24

22 Id.

23 Promoting Transmission Investment through Pricing Reform, Order No. 679, FERC Stats. & Regs. ¶ 31,222 (“Order No. 679”), order on reh’g, Order No. 679-A, FERC Stats. & Regs.¶ 31,236 (2006), order on reh’g, 119 FERC ¶ 61,062 (2007).

DOCKET NO. ER10-____-000 EXHIBIT NO. TEC-200 FILED: 07/30/2010

21

investment has increased somewhat in the past 1 few years, data for the most recent year 2 available, 2003, shows investment levels still 3 below the 1975 level in real dollars. This 4 decline in transmission investment in real 5 dollars has occurred while the electric load 6 using the nation’s grid more than doubled. 7 Further, the record shows that the growth rate 8 in transmission mileage since 1999 is not 9 sufficient to meet the expected 50 percent 10 growth in consumer demand for electricity over 11 the next two decades.24 12

13

The challenges posed by an increasingly complex 14

marketplace heighten the uncertainties associated with 15

transmission operations while requiring the commitment of 16

significant new capital investment to maintain and 17

enhance service capabilities. 18

19

Impact of Capital Market Conditions 20

Q. What are the implications of recent capital market 21

conditions? 22

23

A. The deep financial and real estate crisis that the 24

country experienced in late 2008, and continuing into 25

2009 led to unprecedented price fluctuations in the 26

capital markets as investors dramatically revised their 27

risk perceptions and required returns. As a result of 28

investors’ trepidation to commit capital, stock prices 29

24 Order No. 679 at P 10.

DOCKET NO. ER10-____-000 EXHIBIT NO. TEC-200 FILED: 07/30/2010

22

declined sharply while the yields on corporate bonds 1

experienced a dramatic increase. 2

3

With respect to utilities specifically, as of April 2010, 4

the Dow Jones Utility Average stock index remained almost 5

30 percent below the previous high reached in May 2008. 6

This sell-off in common stocks and sharp fluctuations in 7

utility bond yields reflect the fact that the utility 8

industry was not immune to the impact of financial market 9

turmoil and the ongoing economic downturn. As the Edison 10

Electric Institute (“EEI”) noted in a letter to 11

congressional representatives as the financial crisis 12

intensified, capital market uncertainties have serious 13

implications for utilities and their customers: 14

15

In the wake of the continuing upheaval on Wall 16 Street, capital markets are all but 17 immobilized, and short-term borrowing costs to 18 utilities have already increased substantially. 19 If the financial crisis is not resolved 20 quickly, financial pressures on utilities will 21 intensify sharply, resulting in higher costs to 22 our customers and, ultimately, could compromise 23 service reliability.25 24

25

Similarly, an October 1, 2008 Wall Street Journal report 26

confirmed that utilities had been forced to delay 27

25 Letter to House of Representatives, Thomas R. Kuhn, President, Edison Electric Institute (Sep. 24, 2008).

DOCKET NO. ER10-____-000 EXHIBIT NO. TEC-200 FILED: 07/30/2010

23

borrowing or pursue more costly alternatives to raise 1

funds.26 In December 2008, Fitch confirmed “sharp 2

repricing of and aversion to risk in the investment 3

community,” and noted that the disruptions in financial 4

markets and the fundamental shift in investors’ risk 5

perceptions had increased the cost of capital for 6

utilities.27 7

8

More recently, in assessing the impact of the downturn on 9

the utility sector, Fitch concluded, “While utilities 10

maintained relatively good market access during the 11

credit crisis, the cost of capital is higher than prior 12

to the credit crisis, and bank credit remains relatively 13

tight.”28 Similarly, S&P noted that while utilities are 14

expected to maintain access to credit in 2010, such 15

access will be “on more demanding terms than in previous 16

years,”29 with Moody’s noting that “costs associated with 17

credit facilities have increased significantly.”30 18

19

Q. How do interest rates on long-term bonds compare with 20

26 Smith, Rebecca, “Corporate News: Utilities’ Plans Hit by Credit Markets,” Wall Street Journal at B4 (Oct. 1, 2008).

27 Fitch Ratings Ltd., “U.S. Utilities, Power and Gas 2009 Outlook,” Global Power North America Special Report (Dec. 22. 2008).

28 Fitch Ratings Ltd., “Electric Utility Capital Spending: The Show Will Go On,” Global Power U.S. and Canada Special Report (Oct. 14, 2009).

29 Standard & Poor’s Corporation, “Ratings Roundup: Ratings Trend In Electric Utility Sector Turns More Negative In First Quarter Of 2010,” RatingsDirect (Apr. 16, 2010).

30 Moody’s Investors Service, “U.S. Electric Utilities Face Challenges Beyond Near-Term,” Industry Outlook (Jan. 2010).

DOCKET NO. ER10-____-000 EXHIBIT NO. TEC-200 FILED: 07/30/2010

24

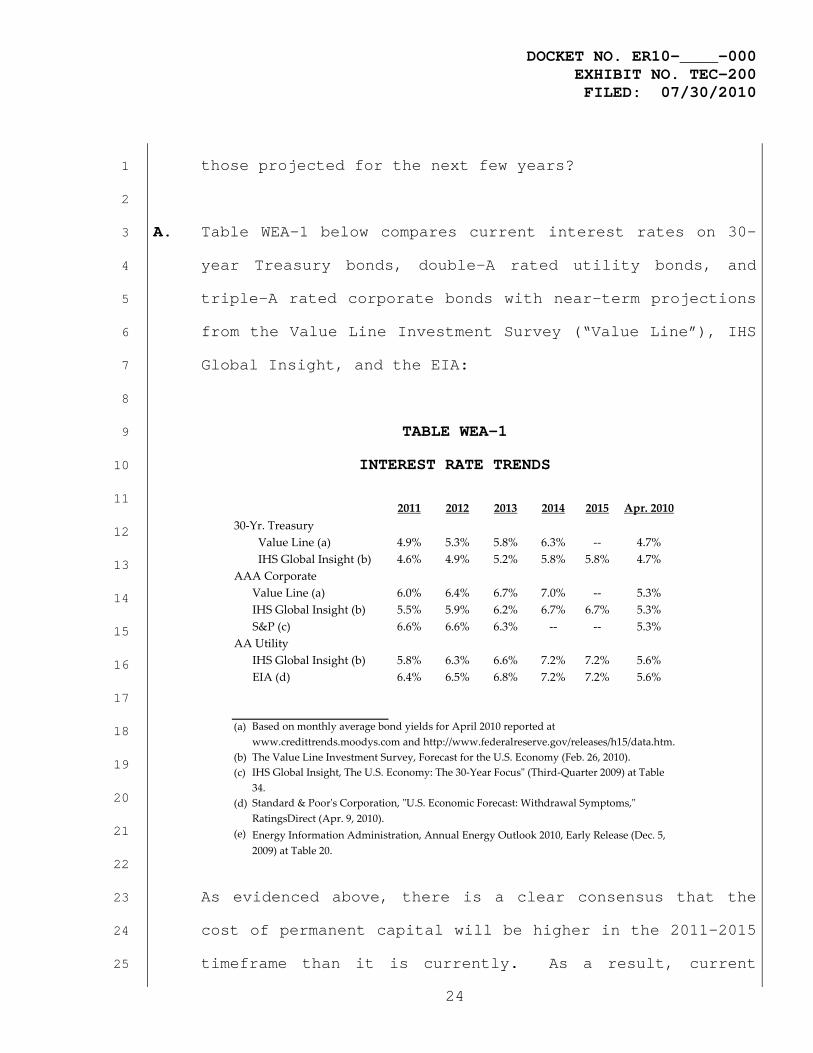

those projected for the next few years? 1

2

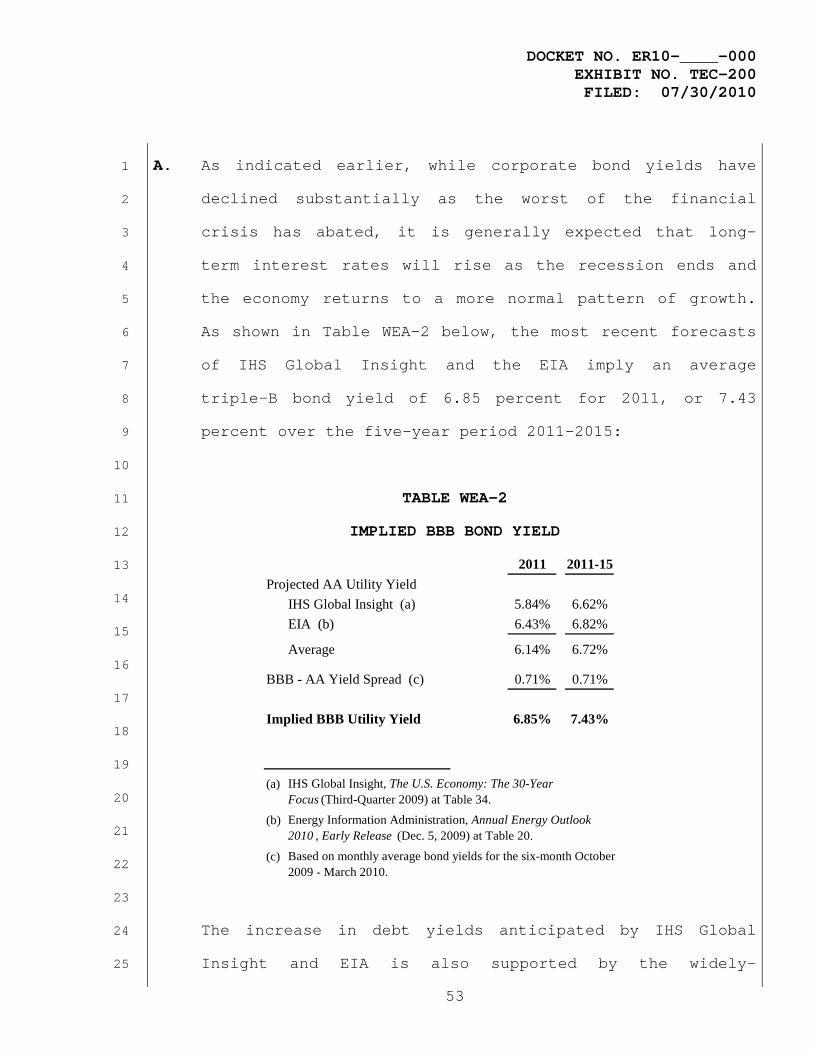

A. Table WEA-1 below compares current interest rates on 30-3

year Treasury bonds, double-A rated utility bonds, and 4

triple-A rated corporate bonds with near-term projections 5

from the Value Line Investment Survey (“Value Line”), IHS 6

Global Insight, and the EIA: 7

8

TABLE WEA-1 9

INTEREST RATE TRENDS 10

11

12

13

14

15

16

17

18

19

20

21

22

As evidenced above, there is a clear consensus that the 23

cost of permanent capital will be higher in the 2011-2015 24

timeframe than it is currently. As a result, current 25

2011 2012 2013 2014 2015 Apr. 201030‐Yr. Treasury

Value Line (a) 4.9% 5.3% 5.8% 6.3% ‐‐ 4.7% IHS Global Insight (b) 4.6% 4.9% 5.2% 5.8% 5.8% 4.7%

AAA CorporateValue Line (a) 6.0% 6.4% 6.7% 7.0% ‐‐ 5.3%IHS Global Insight (b) 5.5% 5.9% 6.2% 6.7% 6.7% 5.3%S&P (c) 6.6% 6.6% 6.3% ‐‐ ‐‐ 5.3%

AA UtilityIHS Global Insight (b) 5.8% 6.3% 6.6% 7.2% 7.2% 5.6%EIA (d) 6.4% 6.5% 6.8% 7.2% 7.2% 5.6%

(a)

(b) The Value Line Investment Survey, Forecast for the U.S. Economy (Feb. 26, 2010).(c)

(d)

(e)

Based on monthly average bond yields for April 2010 reported at www.credittrends.moodys.com and http://www.federalreserve.gov/releases/h15/data.htm.

Standard & Poorʹs Corporation, ʺU.S. Economic Forecast: Withdrawal Symptoms,ʺ RatingsDirect (Apr. 9, 2010).Energy Information Administration, Annual Energy Outlook 2010, Early Release (Dec. 5, 2009) at Table 20.

IHS Global Insight, The U.S. Economy: The 30‐Year Focusʺ (Third‐Quarter 2009) at Table 34.

DOCKET NO. ER10-____-000 EXHIBIT NO. TEC-200 FILED: 07/30/2010

25

cost of capital estimates are likely to understate 1

investors’ requirements at the time the outcome of this 2

proceeding becomes effective and beyond. 3

4

Q. What do these events imply with respect to the ROE for 5

Tampa Electric? 6

7

A. No one knows the future of our complex global economy. 8

We know that the financial crisis had been building for a 9

long time, and few predicted that the economy would fall 10

as rapidly as it has, or that corporate bond yields would 11

fluctuate as dramatically as they did. While conditions 12

in the economy and capital markets appear to have 13

stabilized, investors are apt to react swiftly and 14

negatively to any future signs of trouble in the 15

financial system or economy. As the Wall Street Journal 16

noted in February: 17

18

Stocks pulled out of a 167-point hole with a 19 late rally Friday, capping a wild week 20 reminiscent of the most volatile days of the 21 credit crisis. … It was a return to the unusual 22 relationships, or correlations, seen at major 23 flash points over the past two years when 24 investors fled risky assets and jumped into 25 safe havens. This market behavior, which has 26 reasserted itself repeatedly since the 27 financial crisis began, suggests that 28 investment decisions are still being driven 29 more by government support and liquidity 30

DOCKET NO. ER10-____-000 EXHIBIT NO. TEC-200 FILED: 07/30/2010

26

concerns than market fundamentals.31 1

2

More recently, the European debt crisis has sparked 3

renewed share price volatility and stress in the credit 4

markets. Given the importance of reliable utility 5

service for customers and the economy, it would be unwise 6

to ignore investors’ increased sensitivity to risk in 7

evaluating a fair ROE for Tampa Electric in this case. 8

9

CAPITAL MARKET ESTIMATES 10

Q. What is the purpose of this section of your testimony? 11

12

A. In this section, I develop DCF estimates of the cost of 13

equity for proxy groups of electric utilities. First, I 14

address the concept of the cost of equity, along with the 15

risk-return tradeoff principle fundamental to capital 16

markets. Next, I describe the specific DCF analyses I 17

conducted to estimate the current cost of equity for the 18

alternative proxy groups. 19

20

Cost of Equity Concept 21

Q. What role does the return on common equity play in a 22

utility’s rates? 23

24

31 Gongloff, Mark, “Stock Rebound Is a Crisis Flashback – Late Surge Recalls Market’s Volatility at Peak of Credit Difficulties; Unusual Correlations,” Wall Street Journal at B1 (Feb. 6, 2010).

DOCKET NO. ER10-____-000 EXHIBIT NO. TEC-200 FILED: 07/30/2010

27

A. The return on common equity is the cost of inducing and 1

retaining investment in the utility’s physical plant and 2

assets. This investment is necessary to finance the 3

asset base needed to provide utility service. Competition 4

for investor funds is intense and investors are free to 5

invest their funds wherever they choose. They will commit 6

money to a particular investment only if they expect it 7

to produce a return commensurate with those from other 8

investments with comparable risks. 9

10

Q. What fundamental economic principle underlies this cost 11

of equity concept? 12

13

A. The fundamental economic principle underlying the cost of 14

equity concept is the notion that investors are risk 15

averse. In capital markets where relatively risk-free 16

assets are available (e.g., U.S. Treasury securities), 17

investors can be induced to hold riskier assets only if 18

they are offered a premium, or additional return, above 19

the rate of return on a risk-free asset. Since all 20

assets compete with each other for investor funds, 21

riskier assets must yield a higher expected rate of 22

return than safer assets to induce investors to hold 23

them. 24

25

DOCKET NO. ER10-____-000 EXHIBIT NO. TEC-200 FILED: 07/30/2010

28

Given this risk-return tradeoff, the required rate of 1

return (k) from an asset (i) can generally be expressed 2

as 3

ki = Rf +RPi 4

5

where: Rf = Risk-free rate of return, and 6

RPi = Risk premium required to hold 7

riskier asset i. 8

9

Thus, the required rate of return for a particular asset 10

is a function of: (1) the yield on risk-free assets and 11

(2) the asset’s relative risk, with investors demanding 12

correspondingly larger risk premiums for bearing greater 13

risk. 14

15

Q. Is there evidence that the risk-return tradeoff principle 16

actually operates in the capital markets? 17

18

A. Yes. The risk-return tradeoff can be readily documented 19

in segments of the capital markets where required rates 20

of return can be directly inferred from market data and 21

where generally accepted measures of risk exist. Bond 22

yields, for example, reflect investors’ expected rates of 23

return, and bond ratings measure the risk of individual 24

bond issues. The observed yields on government 25

DOCKET NO. ER10-____-000 EXHIBIT NO. TEC-200 FILED: 07/30/2010

29

securities, which are considered free of default risk, 1

and bonds of various rating categories demonstrate that 2

the risk-return tradeoff does, in fact, exist in the 3

capital markets. 4

5

Q. Does the risk-return tradeoff observed with fixed income 6

securities extend to common stocks and other assets? 7

8

A. It is generally accepted that the risk-return tradeoff 9

evidenced with long-term debt extends to all assets. 10

Documenting the risk-return tradeoff for assets other 11

than fixed income securities, however, is complicated by 12

two factors. First, there is no standard measure of risk 13

applicable to all assets. Second, for most assets – 14

including common stock – required rates of return cannot 15

be directly observed. Yet there is every reason to 16

believe that investors exhibit risk aversion in deciding 17

whether or not to hold common stocks and other assets, 18

just as when choosing among fixed-income securities. 19

20

Q. Is this risk-return tradeoff limited to differences 21

between firms? 22

23

A. No. The risk-return tradeoff principle applies not only 24

to investments in different firms, but also to different 25

DOCKET NO. ER10-____-000 EXHIBIT NO. TEC-200 FILED: 07/30/2010

30

securities issued by the same firm. The securities issued 1

by a utility vary considerably in risk because they have 2

different characteristics and priorities. Long-term debt 3

secured by a mortgage on property is senior among all 4

capital in its claim on a utility’s net revenues and is, 5

therefore, the least risky. Following first mortgage 6

bonds are other debt instruments also holding contractual 7

claims on the utility’s net revenues, such as 8

subordinated debentures. The last investors in line with 9

respect to a claim on the utility’s assets are common 10

shareholders. They receive only the net revenues, if any, 11

which remain after all other claimants have been paid. 12

As a result, the rate of return that investors require 13

from a utility’s common stock, the most junior and 14

riskiest of its securities, must be considerably higher 15

than the yield offered by the utility’s senior, long-term 16

debt. 17

18

Q. What does the above discussion imply with respect to 19

estimating the cost of equity? 20

21

A. Although the cost of equity cannot be observed directly, 22

it is a function of the returns available from other 23

investment alternatives and the risks to which the equity 24

capital is exposed. Because it is unobservable, the cost 25

DOCKET NO. ER10-____-000 EXHIBIT NO. TEC-200 FILED: 07/30/2010

31

of equity for a particular utility must be estimated by 1

analyzing information about capital market conditions 2

generally, assessing the relative risks of the company 3

specifically, and employing various quantitative methods 4

that focus on investors’ required rates of return. These 5

various quantitative methods typically attempt to infer 6

investors’ required rates of return from stock prices, 7

interest rates, or other capital market data. 8

9

Q. What method did you use to evaluate the cost of equity 10

for Tampa Electric? 11

12

A. Consistent with FERC precedent, my analysis applied the 13

Commission’s one-step DCF methodology for electric 14

utilities. In recognition of the fact that no single 15

approach to estimating a utility’s cost of equity can be 16

regarded as definitive, I also developed an alternative 17

DCF benchmark using a proxy group of non-utility 18

companies. In addition, I also evaluated a fair ROE 19

using an earnings approach based on investors’ current 20

expectations in the capital markets. 21

22

Development and Selection of a Proxy Group 23

Q. How did you implement the DCF method to estimate the cost 24

of common equity for Tampa Electric? 25

DOCKET NO. ER10-____-000 EXHIBIT NO. TEC-200 FILED: 07/30/2010

32

A. Application of the DCF model to estimate the cost of 1

equity requires observable capital market data, such as 2

stock prices. Tampa Electric does not have publicly 3

traded common stock, but even for a publicly traded firm, 4

the cost of equity can only be estimated. As a result, 5

applying quantitative models using observable market data 6

produces only a result that inherently includes some 7

degree of observation error. Thus, the accepted approach 8

to increase confidence in the results is to apply the DCF 9

model to a proxy group of publicly traded companies that 10

investors regard as risk comparable. The results of the 11

analysis on the sample of companies are relied upon to 12

establish a range of reasonableness for the cost of 13

equity for the specific company at issue. 14

15

Q. What specific proxy group did you rely on for your 16

analyses? 17

18

A. Following the same general approach approved by the 19

Commission in Bangor Hydro and Westar,32 my analyses 20

focused on regional utilities located in adjacent 21

reliability organizations. My initial proxy group 22

consisted of the investor-owned members of FRCC and SERC 23

with publicly traded stock. Excluded from my analyses 24

32 Westar Energy, Inc., 122 FERC ¶ 61,268 at P 94 (2008) (“Westar”).

DOCKET NO. ER10-____-000 EXHIBIT NO. TEC-200 FILED: 07/30/2010

33

was one firm (E.ON AG) for which no data from IBES or 1

Value Line was currently available.33 Finally, I also 2

verified that Value Line, S&P, and IBES classify all of 3

the proxy companies predominantly as electric utilities.34 4

I refer to the resulting group of nine utilities as the 5

“Regional Proxy Group.” 6

7

Q. Has the Commission previously considered membership in a 8

regional reliability or transmission organization when 9

establishing proxy groups? 10

11

A. Yes. The ultimate goal of assembling a proxy group for 12

purposes of performing the DCF analysis is to calculate a 13

return for the utility in question that is analogous to 14

returns on comparable investments with a similar risk 15

profile.35 The Commission has recognized that being 16

located in the same geographical market is a relevant 17

factor in determining whether companies face comparable 18

risks. Consideration of geography as a proxy group 19

criterion first arose where the Commission established a 20

single ROE that was to be implemented across an entire 21

regional organization, as was the case in Midwest ISO.36 22

33 Formerly I/B/E/S International, Inc., IBES growth rates are now compiled and published by Thomson Reuters.

34 See, e.g., Tallgrass Transmission, LLC, 125 FERC ¶ 61,248 at P 77 (2008) (“Tallgrass”).

35 See, e.g., Southern California Edison Co., at 61,266 (2000).

36 Midwest ISO Inc., 100 FERC ¶ 61,292 (2002).

DOCKET NO. ER10-____-000 EXHIBIT NO. TEC-200 FILED: 07/30/2010

34

Subsequently, in cases involving services provided within 1

the context of well-integrated and coordinated market 2

operations, the Commission has accepted proxy groups 3

composed of members of adjacent regional transmission 4

organizations.37 In other words, in the specific case 5

where participating utilities face comparable risks due 6

to a high degree of similarity in market and regulatory 7

circumstances, geography has been accepted as a valid 8

proxy for risks. 9

10

Similarly, the Commission’s decision in Atlantic Path 15 11

premised its ROE findings on DCF results for the 12

applicant’s proposed proxy group of companies within the 13

footprint of the Western Electricity Coordinating Council 14

(“WECC”).38 The Atlantic Path 15 decision observed that 15

WECC utilities are electrically integrated and that being 16

located in the same geographic market is a relevant 17

factor to consider in determining whether companies face 18

similar risks.39 In Atlantic Path 15, the Commission 19

reasoned that adopting a region-wide proxy group, 20

modified through application of additional risk-based 21

screens, “will provide a significant measure of 22

37 See, e.g., Bangor Hydro; Potomac-Appalachian Transmission Highline, LLC, 122 FERC ¶ 61,188 (2008) (“PATH”); Westar; Virginia Electric Power Co., 123 FERC ¶ 61,098 (2008) (“VEPCO”).

38 Atlantic Path 15, 122 FERC ¶ 61,135 at P 19 (2008) (“Atlantic Path 15”).

39 Id. at PP 25-26.

DOCKET NO. ER10-____-000 EXHIBIT NO. TEC-200 FILED: 07/30/2010

35

regulatory certainty” and “improve the Commission’s 1

ability to decide cases quickly for entities seeking 2

financing of necessary infrastructure.”40 The decision 3

also suggested that the use of such proxy group might 4

“simplify rate proceedings and reduce litigation costs.”41 5

Thus, while there is no general policy requiring that 6

proxy companies be chosen based on geography, in those 7

instances where there is a clear link between location 8

and key operational characteristics that help to define 9

risks in the minds of investors, membership in a regional 10

reliability or transmission organization can serve as 11

valid criteria in defining proxy companies. 12

13

Q. Does the use of the Regional Proxy Group to establish a 14

reasonable ROE for Tampa Electric follow the Commission’s 15

precedent? 16

17

A. Yes. Consistent with FERC’s guidance, this proxy group 18

is composed of utilities “with a direct correlation” to 19

Tampa Electric and “the broader markets” with which Tampa 20

Electric interacts.42 In fact, geographic location is a 21

primary characteristic that shapes the risks and 22

challenges faced by Tampa Electric and its investors. 23

40 Id. at P 23.

41 Id.

42 Duquesne Light Co., 118 FERC ¶ 61,087 at P 73 (2007).

DOCKET NO. ER10-____-000 EXHIBIT NO. TEC-200 FILED: 07/30/2010

36

Because of its location on the Florida peninsula, Tampa 1

Electric is exposed to potential fuel supply 2

interruptions and transmission disturbances, and the 3

Company faces the ever-present danger of catastrophic 4

damage from recurring tropical storms. 5

6

Moreover, use of the Regional Proxy Group to determine 7

the ROE range of reasonableness is also consistent with 8

the high degree of integration between the FRCC and SERC 9

members, with three of the four publicly traded FRCC 10

member utilities also being members of SERC. Given the 11

history of regional planning, coordination and system 12

operations among these utilities and within the region, 13

there is a very direct link in the minds of investors 14

between Tampa Electric’s operating environment and that 15

of the other members of the FRCC and SERC. Reference to 16

the Regional Proxy Group also recognizes that these firms 17

compete for investment funds from the same pool of 18

potential capital. Considering these common traits, the 19

companies in the Regional Proxy Group provide a sound 20

basis on which to estimate investors’ required returns 21

and establish the ROE range of reasonableness for Tampa 22

Electric. 23

24

Q. Did your analysis also consider reported risk measures? 25

DOCKET NO. ER10-____-000 EXHIBIT NO. TEC-200 FILED: 07/30/2010

37

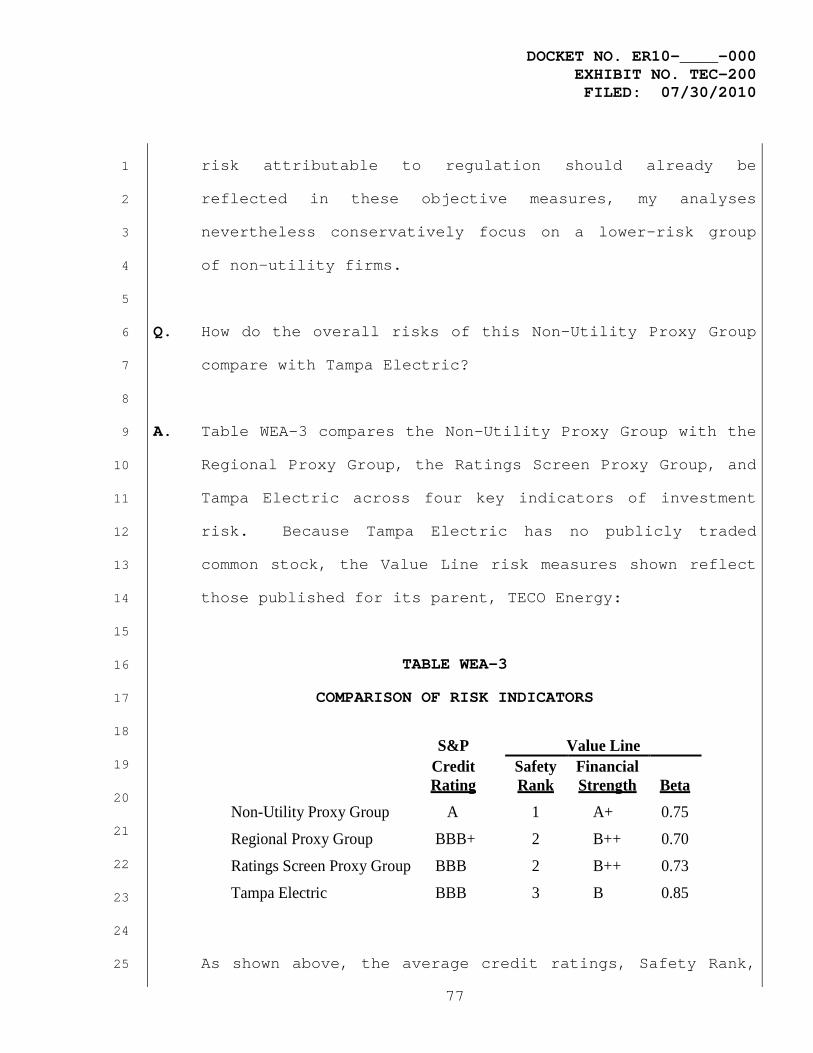

A. Yes. My evaluation also included a comparison of four 1

objective measures of the investment risks associated 2

with bonds and common stocks – S&P’s corporate credit 3

rating and Value Line’s Safety Rank, Financial Strength 4

Rating, and beta. 5

6

Credit ratings are assigned by independent rating 7

agencies to provide investors with a broad assessment of 8

the creditworthiness of a firm. Because the rating 9

agencies’ evaluation includes virtually all of the 10

factors normally considered important in assessing a 11

firm’s relative credit standing, corporate credit ratings 12

provide a broad measure of overall investment risk that 13

is readily available to investors. Widely cited in the 14

investment community and referenced by investors as an 15

objective measure of risk, credit ratings are also 16

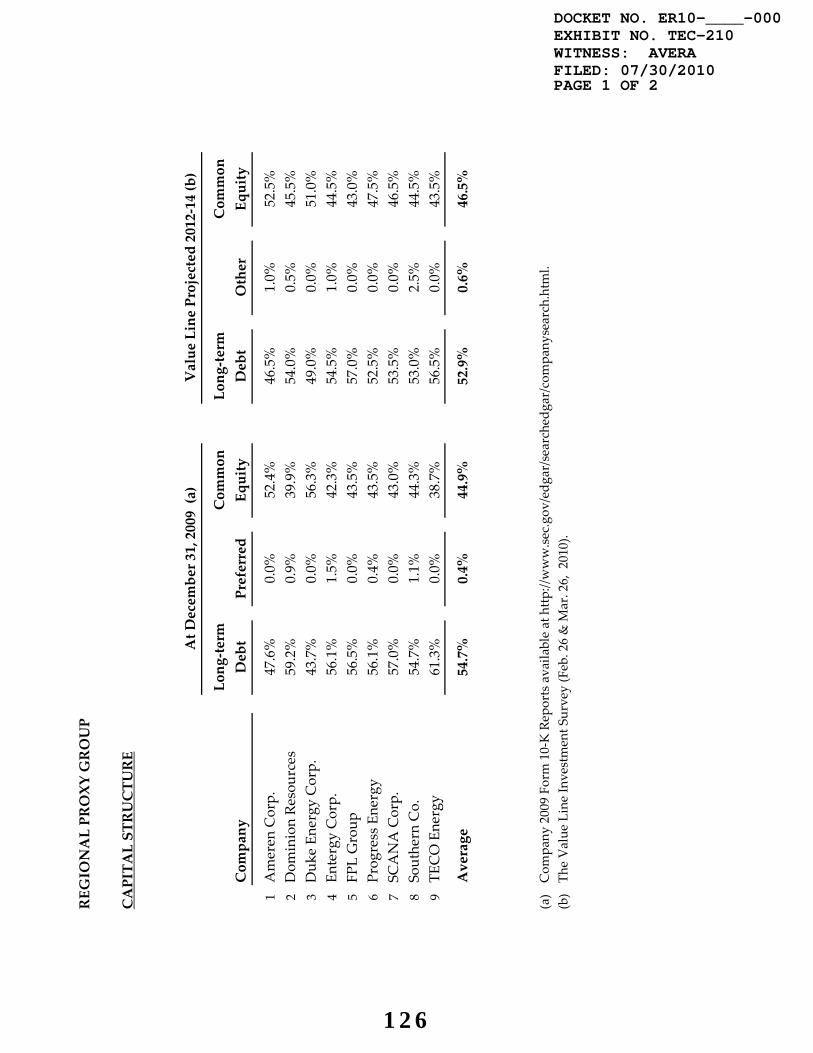

frequently used as a primary risk indicator in 17

establishing proxy groups to estimate the cost of equity. 18

19

Apart from the broad assessment of investment risk 20

provided by credit ratings, other quality rankings 21

published by investment advisory services also provide 22

relative assessments of risk that are considered by 23

investors in forming their expectations. Given that Value 24

Line is perhaps the most widely available source of 25

DOCKET NO. ER10-____-000 EXHIBIT NO. TEC-200 FILED: 07/30/2010

38

investment advisory information, its rankings provide 1

useful guidance regarding the risk perceptions of 2

investors. The Safety Rank is Value Line’s primary risk 3

indicator and ranges from “1” (Safest) to “5” (Most 4

Risky). This overall risk measure is intended to capture 5

the total risk of a stock, and incorporates elements of 6

stock price stability and financial strength. The 7

Financial Strength Rating is designed as a guide to 8

overall financial strength and creditworthiness, with the 9

key inputs including financial leverage, business 10

volatility measures, and company size. Value Line’s 11

Financial Strength Ratings range from “A++” (strongest) 12

down to “C” (weakest) in nine steps. Finally, Value 13

Line’s beta, which measures the volatility of a 14

security's price relative to the market as a whole. A 15

stock that tends to respond less to market movements has 16

a beta less than 1.00, while stocks that tend to move 17

more than the market have betas greater than 1.00. 18

19

Q. What do these criteria indicate with respect to the 20

investment risks of the Regional Proxy Group and Tampa 21

Electric? 22

23

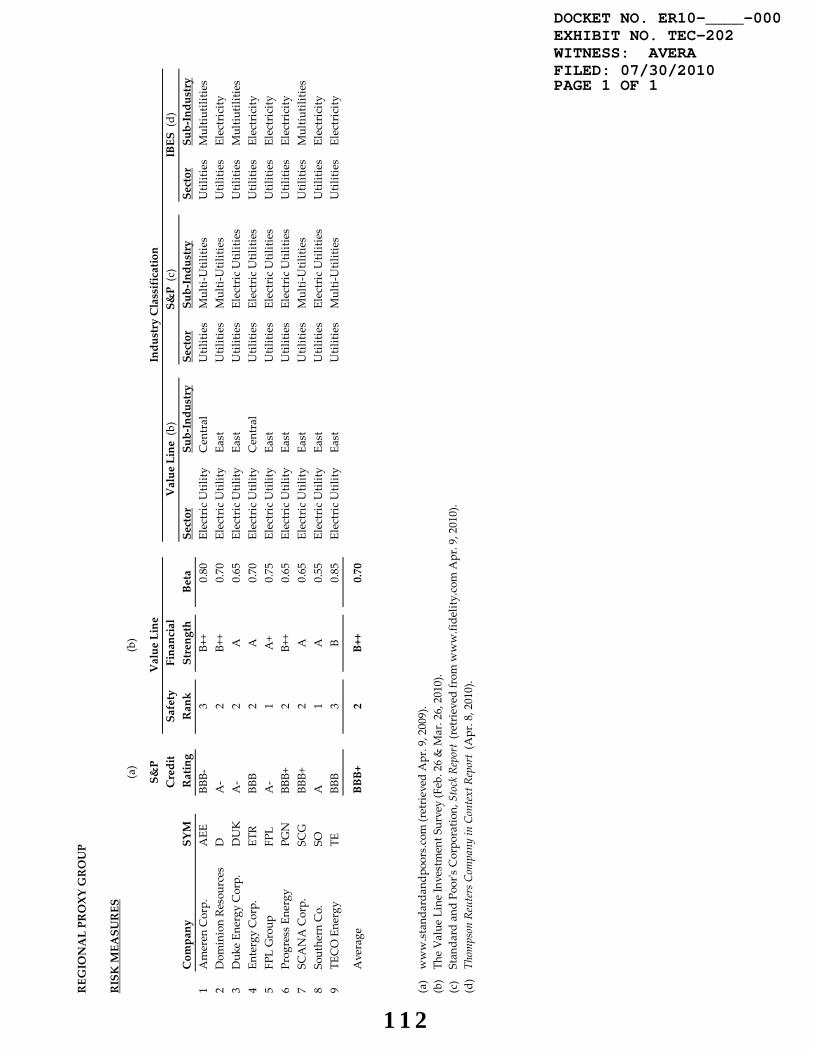

A. The risk measures for the Regional Proxy Group are shown 24

on Exhibit No. TEC-202. The average S&P corporate credit 25

DOCKET NO. ER10-____-000 EXHIBIT NO. TEC-200 FILED: 07/30/2010

39

rating for the utilities in the Regional Proxy Group is 1

“BBB+”, with four companies having ratings in the single-2

A category. Meanwhile, the average Value Line Safety 3

Rank for the utilities in the Regional Proxy Group is 4

“2”, while the Financial Strength Ratings for the proxy 5

firms averaged “B++”. Finally, the average beta value 6

for the Regional Proxy Group is 0.70. As discussed 7

earlier, Tampa Electric is rated “BBB” by S&P. Value 8

Line has assigned TECO Energy a Safety Rank of “3” and a 9

Financial Strength Rating of “B”, and reports a beta 10

value of 0.85.43 Based on these criteria, which reflect 11

objective, published indicators that incorporate 12

consideration of a broad spectrum of risks, including 13

financial and business position and exposure to company 14

specific factors, investors are likely to regard the 15

risks and prospects of the Utility Proxy Group as being 16

lower than those of Tampa Electric. 17

18

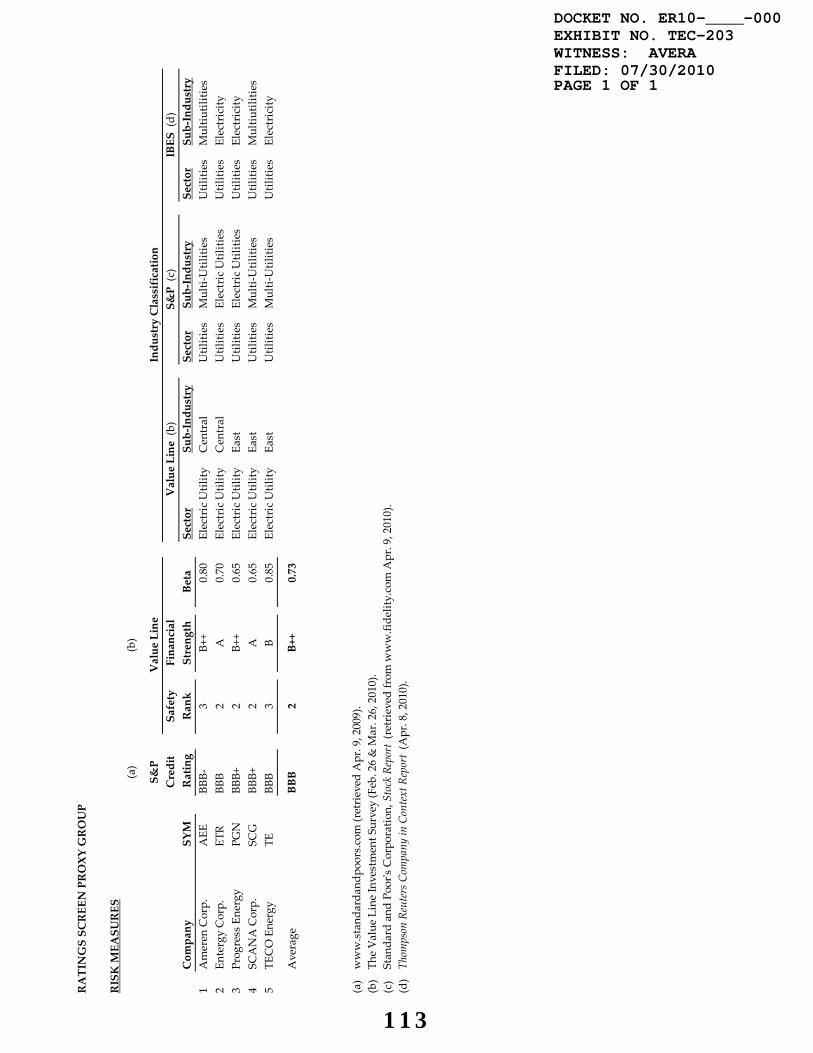

Q. Did you also evaluate DCF results after narrowing the 19

Regional Proxy Group based on credit ratings? 20

21

A. Yes. In developing a regional proxy group, the Commission 22

has also recognized that it may be appropriate to 23

43 Because Tampa Electric has no publicly traded common stock, I referenced the Value Line risk measures for its parent, TECO Energy.

DOCKET NO. ER10-____-000 EXHIBIT NO. TEC-200 FILED: 07/30/2010

40

eliminate firms based on reference to corporate credit 1

ratings. Consistent with this practice, I also examined 2

the results of the Commission’s DCF model after screening 3

the Regional Proxy Group to eliminate utilities with 4

corporate credit ratings outside a “comparable risk 5

band”, which the Commission has interpreted as one 6

“notch” higher or lower than the corporate ratings of the 7

utility at issue. With TECO Energy being rated “BBB” by 8

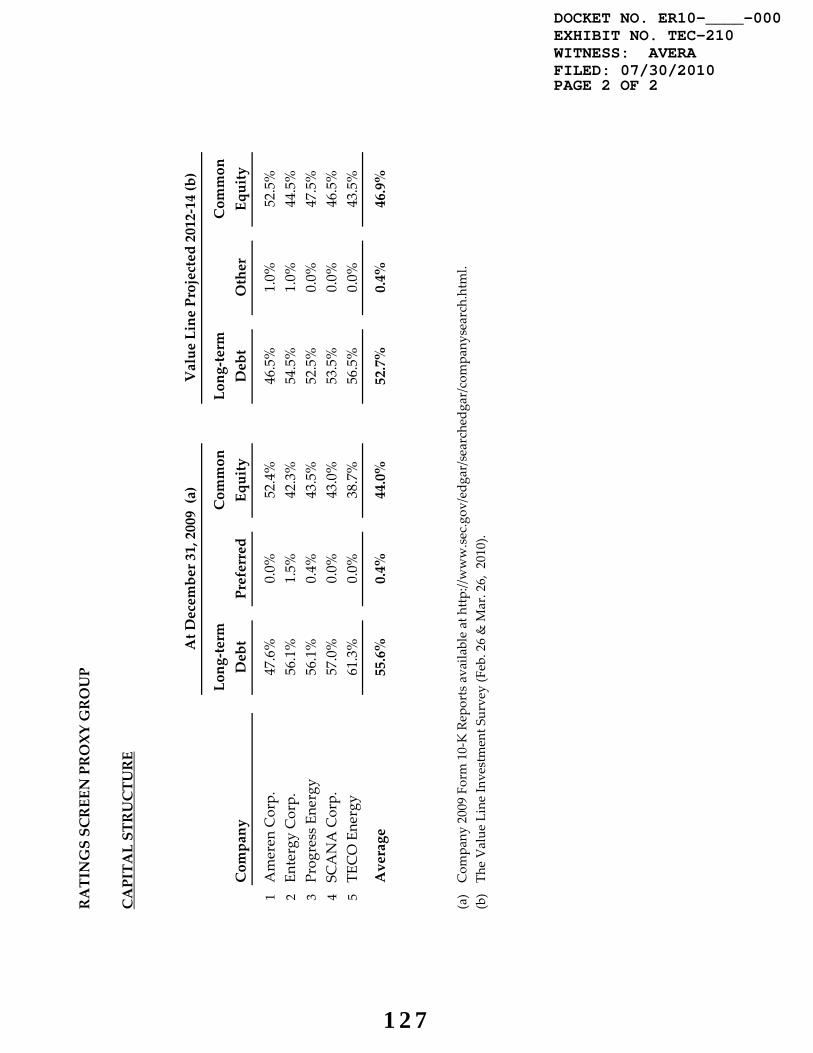

S&P, application of this criterion resulted in a proxy 9

group of five electric utilities with corporate credit 10

ratings in the “BBB-” to “BBB+” range, which I refer to 11

as the “Ratings Screen Proxy Group”. These utilities are 12

shown on Exhibit No. TEC-203. 13

14

Q. Do you believe that it is necessary to impose this credit 15

ratings screen in defining a proxy group for Tampa 16

Electric? 17

18

A. No. The ultimate goal of assembling a proxy group for 19

purposes of performing the DCF analysis is to calculate a 20

return for the utility in question that is analogous to 21

returns on comparable investments with a similar risk 22

profile. In cases involving services provided within the 23

context of well-integrated and coordinated market 24

operations, the Commission has recognized that geography 25

DOCKET NO. ER10-____-000 EXHIBIT NO. TEC-200 FILED: 07/30/2010

41

can serve as a proxy for comparable risk. In other 1

words, in geographic markets where participating 2

utilities face comparable risks due to similar market 3

circumstances, membership in adjacent regional 4

organizations has been accepted as a valid proxy for 5

risks in the context of establishing rates for wholesale 6

utility services. 7

8

I agree that credit ratings are a meaningful measure of 9

investment risks and that the overall risk profile of the 10

Regional Proxy Group should be considered, as I have 11

done; but narrowing a geographically-based proxy group 12

based on additional criteria runs counter to the 13

fundamental notion underlying this approach. Namely, 14

that participation in integrated, adjacent wholesale 15

markets with similar regulatory and operating 16

environments is a valid proxy for risk. The Regional 17

Proxy Group is consistent with the Commission’s 18

determination that members of well-integrated regional 19

markets face similar risks because of common 20

characteristics that are related to geographical 21

location. Moreover, as I demonstrated earlier, the 22

average investment risks attributable to the Regional 23

Proxy Group is generally comparable to those that 24

investors associate with Tampa Electric. Under these 25

DOCKET NO. ER10-____-000 EXHIBIT NO. TEC-200 FILED: 07/30/2010

42

circumstances, there is no need for additional screening 1

criteria. 2

3

Q. What potential problems are associated with employing 4

credit ratings to further narrow the Regional Proxy 5

Group? 6

7

A. If membership in regional organizations and geographic 8

proximity are accepted as the primary risk factors in 9

determining whether a utility should be included in a 10

proxy group, imposing additional screens can weaken the 11

ability of the proxy group to serve its intended purpose 12

of most closely approximating the risks entailed in 13

providing jurisdictional wholesale utility service. 14

Narrowing the regional proxy groups using additional risk 15

screens, such as corporate credit ratings, increases the 16

potential that the resulting subset will be insufficient 17

to reflect industry conditions and investor expectations 18

and ROE requirements. As noted earlier, the cost of 19

equity is inherently unobservable and because the DCF 20

model depends on estimates it is subject to measurement 21

error, with FERC having acknowledged the pitfalls of a 22

constrained proxy group.44 23

44 Application of the credit rating screen reduces the size of the proxy group, and while the

Commission has on occasion accepted proxy groups as small as four companies, FERC has generally recognized that a constrained proxy group “may not be representative of industry conditions.” See, e.g., Enbridge Pipelines (KPC), 100 FERC ¶ 61,260 at P 237 (2002) (citing Transcontinental Gas Pipe Line Corp., 60 FERC ¶ 63,001, at 65,041, aff'd in part, rev'd in part, 60 FERC ¶ 61,246, at 61,826 (1992), rev'd and remanded, N. C. Util. v. FERC, 42 F.3d 659 (1994), order on reh’g, Transco, 71 FERC ¶ 61,305, at 62,195 (1995)).

DOCKET NO. ER10-____-000 EXHIBIT NO. TEC-200 FILED: 07/30/2010

43

Even though corporate credit ratings provide a widely 1

accepted, objective benchmark for investment risks, the 2

inherent limitations of the DCF approach mean that the 3

potential to misjudge investors’ required return 4

increases as the size of the proxy group shrinks. In a 5

perfect world, bond ratings and DCF results would always 6

be inversely correlated, with DCF estimates for higher 7

rated companies being lower than for utilities with 8

inferior ratings. But because the true cost of equity is 9

unobservable and our estimating tools (e.g., applications 10

of the DCF model based on observable data) provide 11

imperfect readings, this is not always the case. 12

Consider the Commission’s decision in VEPCO, for example. 13

There, the Commission excluded FPL Group, Inc. (“FPL 14

Group,” now NextEra Energy, Inc.) from the proxy group 15

because its credit rating indicated lower risk than the 16

top threshold of its “BBB” to “A-” range, while the 17

average DCF estimate implied for FPL Group exceeded the 18

10.9 percent ROE determined based on the remaining proxy 19

companies.45 Conversely, while Central Vermont Public 20

Service Corporation was eliminated because its lower bond 21

rating was indicative of greater risk, its implied 22

average DCF estimate of 9.6 percent fell 130 basis points 23

below the 10.9 percent estimate for the proxy group. 24

Because the application of quantitative methods to 25

45 VEPCO at P 63; Supplemental Protest of Central Virginia Electric Cooperative, Craig-Botetourt Electric Cooperative, North Carolina Electric Membership Corporation, and Old Dominion Electric Cooperative, Exhibit INC-1.

DOCKET NO. ER10-____-000 EXHIBIT NO. TEC-200 FILED: 07/30/2010

44

estimate the cost of equity is inherently imprecise, the 1

potential for anomalous conclusions rises as the proxy 2

group is narrowed. As a result, while imposing an 3

additional risk screen may impart a patina of refinement, 4

it is more likely to increase, rather than ameliorate, 5

the potential for error. 6

7

DCF Model 8

Q. How is the DCF model used to estimate the cost of equity? 9

10

A. DCF models attempt to replicate the market valuation 11

process that sets the price investors are willing to pay 12

for a share of a company’s stock. The model rests on the 13

assumption that investors evaluate the risks and expected 14

rates of return from all securities in the capital 15

markets. Given these expectations, the price of each 16

stock is adjusted by the market until investors are 17

adequately compensated for the risks they bear. 18

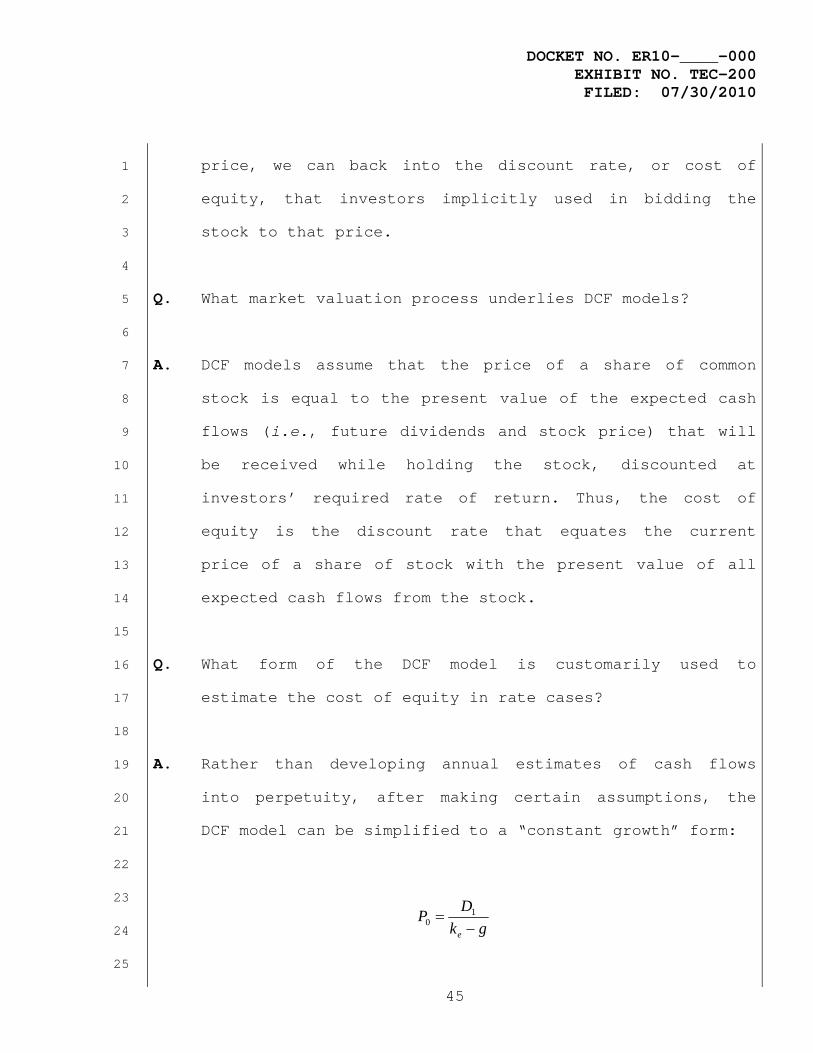

Therefore, we can look to the market to determine what 19

investors believe a share of common stock is worth. By 20

estimating the cash flows investors expect to receive 21

from the stock in the way of future dividends and capital 22

gains, we can calculate their required rate of return. 23

Thus, the cash flows that investors expect from a stock 24

are estimated, and given the stock’s current market 25

DOCKET NO. ER10-____-000 EXHIBIT NO. TEC-200 FILED: 07/30/2010

45

price, we can back into the discount rate, or cost of 1

equity, that investors implicitly used in bidding the 2

stock to that price. 3

4

Q. What market valuation process underlies DCF models? 5

6

A. DCF models assume that the price of a share of common 7

stock is equal to the present value of the expected cash 8

flows (i.e., future dividends and stock price) that will 9

be received while holding the stock, discounted at 10

investors’ required rate of return. Thus, the cost of 11

equity is the discount rate that equates the current 12

price of a share of stock with the present value of all 13

expected cash flows from the stock. 14

15

Q. What form of the DCF model is customarily used to 16

estimate the cost of equity in rate cases? 17

18

A. Rather than developing annual estimates of cash flows 19

into perpetuity, after making certain assumptions, the 20

DCF model can be simplified to a “constant growth” form: 21

22

23

24

25

gkDP

e −= 1

0

DOCKET NO. ER10-____-000 EXHIBIT NO. TEC-200 FILED: 07/30/2010

46

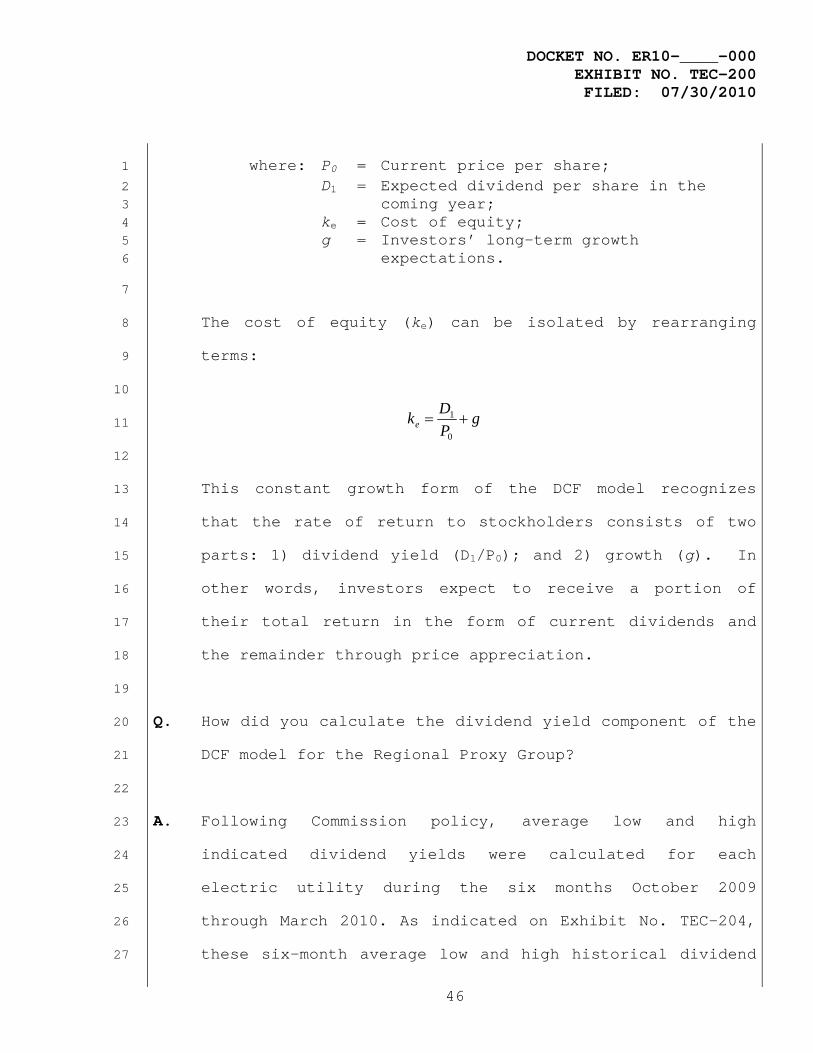

where: P0 = Current price per share; 1

D1 = Expected dividend per share in the 2 coming year; 3

ke = Cost of equity; 4 g = Investors’ long-term growth 5 expectations. 6

7

The cost of equity (ke) can be isolated by rearranging 8

terms: 9

10

11

12

This constant growth form of the DCF model recognizes 13

that the rate of return to stockholders consists of two 14

parts: 1) dividend yield (D1/P0); and 2) growth (g). In 15

other words, investors expect to receive a portion of 16

their total return in the form of current dividends and 17

the remainder through price appreciation. 18

19

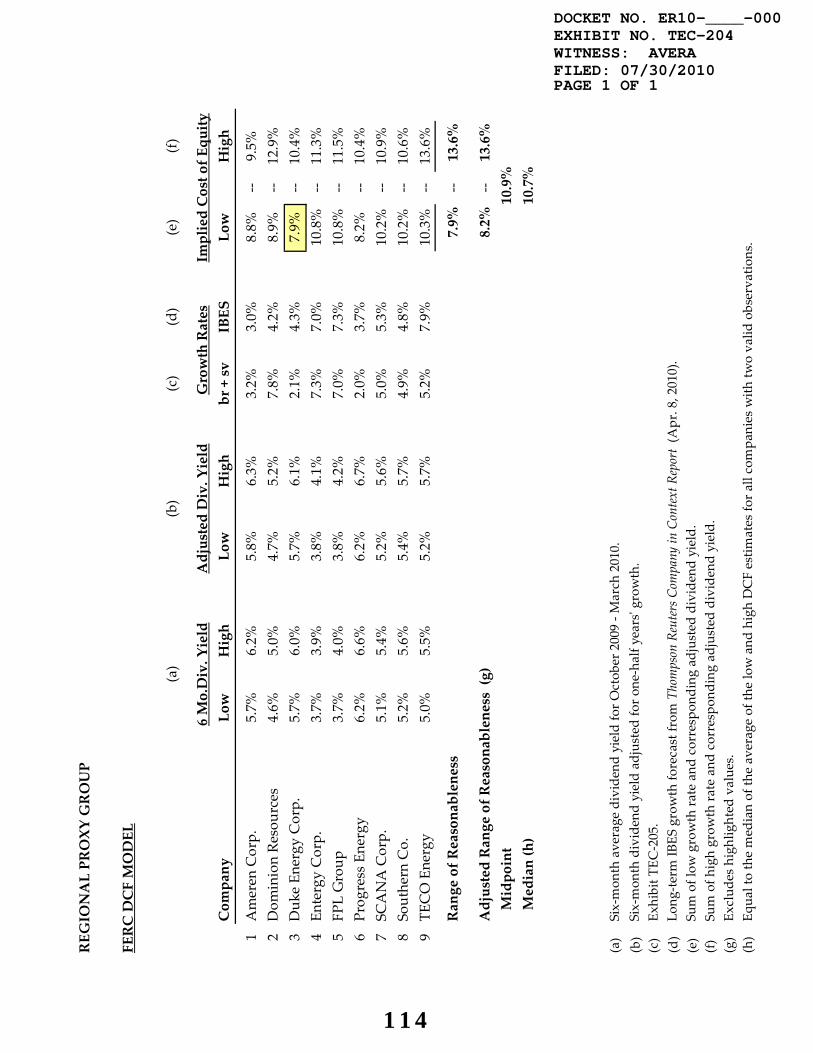

Q. How did you calculate the dividend yield component of the 20

DCF model for the Regional Proxy Group? 21

22

A. Following Commission policy, average low and high 23

indicated dividend yields were calculated for each 24

electric utility during the six months October 2009 25

through March 2010. As indicated on Exhibit No. TEC-204, 26

these six-month average low and high historical dividend 27

gPDke +=

0

1

DOCKET NO. ER10-____-000 EXHIBIT NO. TEC-200 FILED: 07/30/2010

47

yields were also increased by one-half of the low and 1

high growth rates discussed subsequently (1 + 0.5g) to 2

convert them to adjusted dividend yields. 3

4

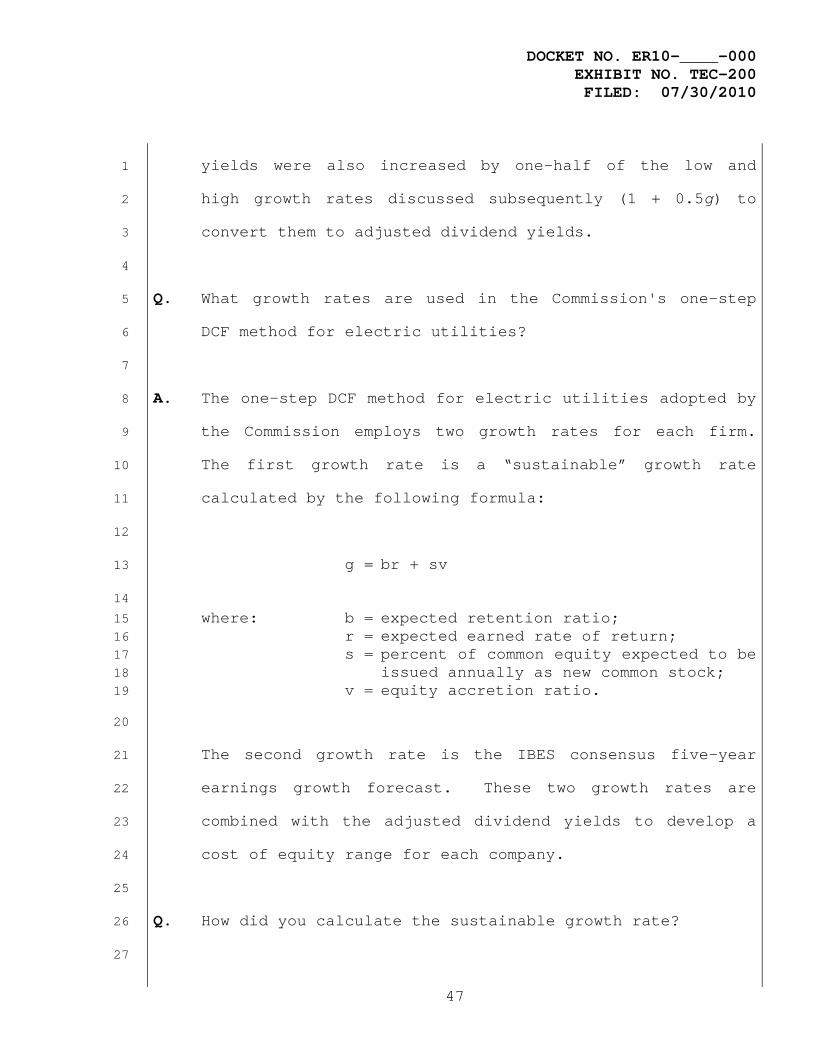

Q. What growth rates are used in the Commission's one-step 5

DCF method for electric utilities? 6

7

A. The one-step DCF method for electric utilities adopted by 8

the Commission employs two growth rates for each firm. 9

The first growth rate is a “sustainable” growth rate 10

calculated by the following formula: 11

12

g = br + sv 13

14

where: b = expected retention ratio; 15 r = expected earned rate of return; 16 s = percent of common equity expected to be 17

issued annually as new common stock; 18 v = equity accretion ratio. 19

20

The second growth rate is the IBES consensus five-year 21

earnings growth forecast. These two growth rates are 22

combined with the adjusted dividend yields to develop a 23

cost of equity range for each company. 24

25

Q. How did you calculate the sustainable growth rate? 26

27

DOCKET NO. ER10-____-000 EXHIBIT NO. TEC-200 FILED: 07/30/2010

48

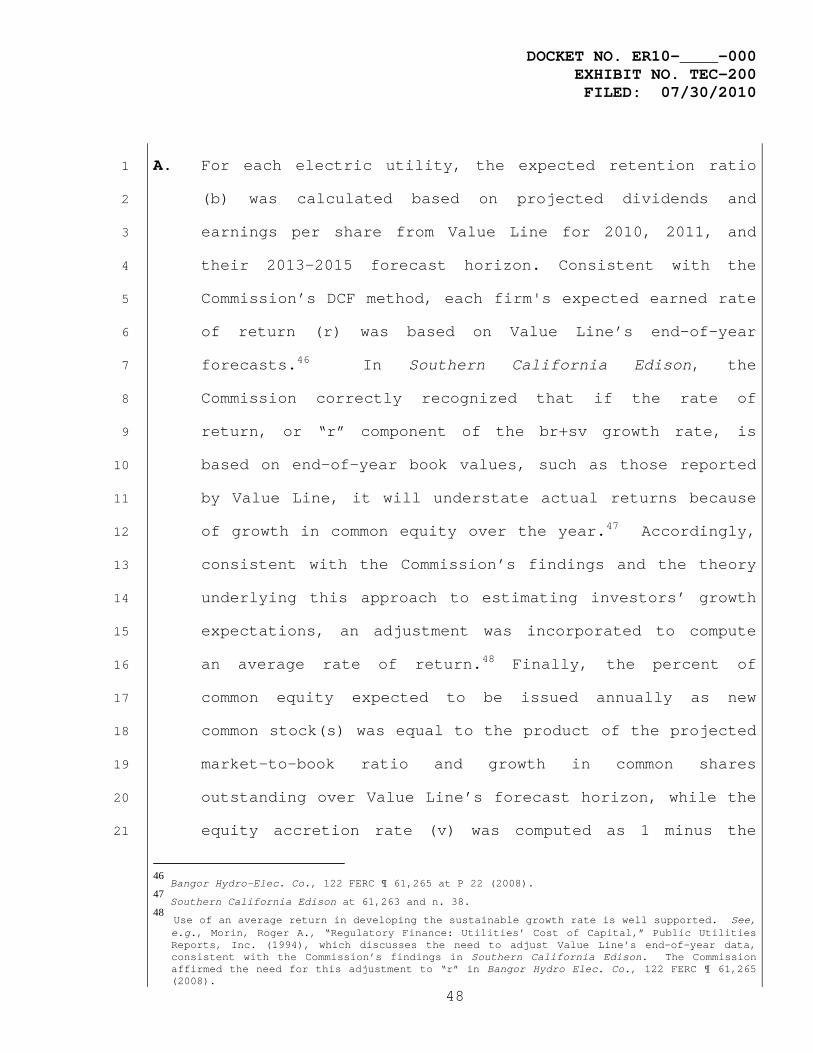

A. For each electric utility, the expected retention ratio 1

(b) was calculated based on projected dividends and 2

earnings per share from Value Line for 2010, 2011, and 3

their 2013-2015 forecast horizon. Consistent with the 4

Commission’s DCF method, each firm's expected earned rate 5

of return (r) was based on Value Line’s end-of-year 6

forecasts.46 In Southern California Edison, the 7

Commission correctly recognized that if the rate of 8

return, or “r” component of the br+sv growth rate, is 9

based on end-of-year book values, such as those reported 10

by Value Line, it will understate actual returns because 11

of growth in common equity over the year.47 Accordingly, 12

consistent with the Commission’s findings and the theory 13

underlying this approach to estimating investors’ growth 14

expectations, an adjustment was incorporated to compute 15

an average rate of return.48 Finally, the percent of 16

common equity expected to be issued annually as new 17

common stock(s) was equal to the product of the projected 18

market-to-book ratio and growth in common shares 19

outstanding over Value Line’s forecast horizon, while the 20

equity accretion rate (v) was computed as 1 minus the 21

46 Bangor Hydro-Elec. Co., 122 FERC ¶ 61,265 at P 22 (2008).

47 Southern California Edison at 61,263 and n. 38.

48 Use of an average return in developing the sustainable growth rate is well supported. See, e.g., Morin, Roger A., “Regulatory Finance: Utilities’ Cost of Capital,” Public Utilities Reports, Inc. (1994), which discusses the need to adjust Value Line’s end-of-year data, consistent with the Commission’s findings in Southern California Edison. The Commission affirmed the need for this adjustment to “r” in Bangor Hydro Elec. Co., 122 FERC ¶ 61,265 (2008).

DOCKET NO. ER10-____-000 EXHIBIT NO. TEC-200 FILED: 07/30/2010

49

inverse of the projected market-to-book ratio. The 1

calculation of the sustainable growth rate for each 2

electric utility in the Regional Proxy Group is shown on 3

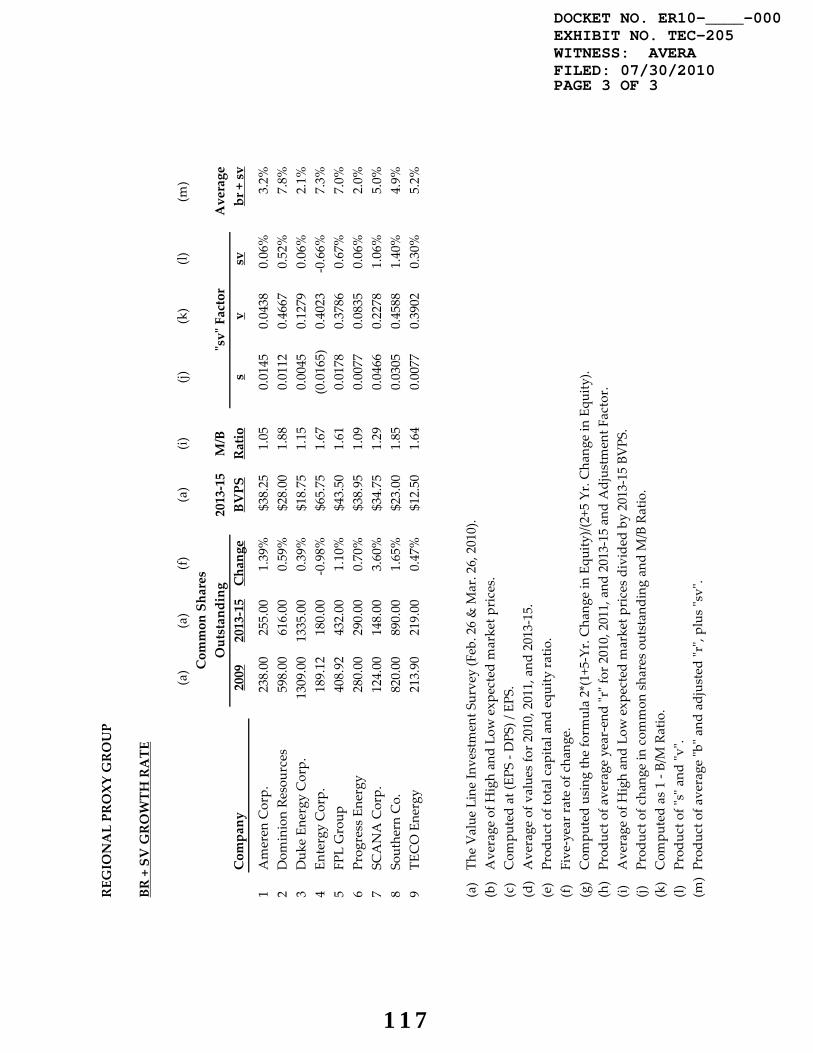

Exhibit No. TEC-205. 4

5

Q. What are investment analysts' projected growth rates for 6

the companies in the Regional Proxy Group? 7

8

A. The five-year IBES earnings growth forecasts for each 9

electric utility in the proxy group are shown in column 10

(d) on Exhibit No. TEC-204. 11

12

Q. What were the results of applying the Commission’s one-13

step DCF approach to the Regional Proxy Group? 14

15

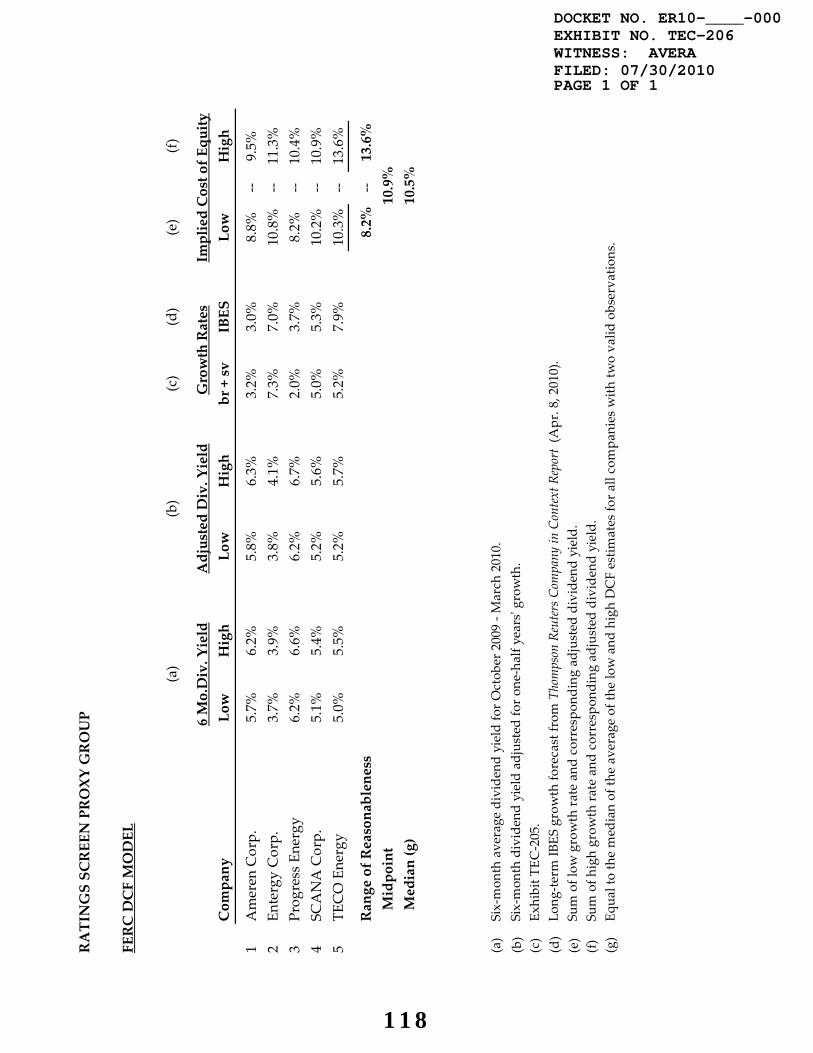

A. As shown on Exhibit No. TEC-204, application of the 16

Commission’s DCF model to the Regional Proxy Group 17

resulted in current cost of equity estimates ranging from 18

7.9 percent to 13.6 percent. 19

20

Evaluation of DCF Results 21

Q. In evaluating the results of the constant growth DCF 22

model, is it appropriate to eliminate cost of equity 23

estimates that are extreme outliers? 24

25

DOCKET NO. ER10-____-000 EXHIBIT NO. TEC-200 FILED: 07/30/2010

50

A. Yes. In applying quantitative methods to estimate the 1

cost of equity, it is essential that the resulting values 2

pass fundamental tests of reasonableness and economic 3

logic. Accordingly, DCF estimates that are implausibly 4

low or high should be eliminated when evaluating the 5

results of this method. 6

7

Q. How did you evaluate DCF estimates at the low end of the 8

range? 9

10

A. It is a basic economic principle that investors can be 11

induced to hold more risky assets only if they expect to 12

earn a return to compensate them for their risk bearing. 13

As a result, the rate of return that investors require 14

from a utility’s common stock, the most junior and 15

riskiest of its securities, must be considerably higher 16

than the yield offered by senior, long-term debt. 17

Consistent with this principle, the DCF range must be 18

adjusted to eliminate cost of equity estimates that are 19

determined to be extreme low outliers when compared 20