Auctions of contracts and energy call options to ensure supply adequacy in the second stage of the...

8

1 Auctions of Contracts and Energy Call Options to Ensure Supply Adequacy in the Second Stage of the Brazilian Power Sector Reform Luiz Augusto Barroso, Member, IEEE, José Rosenblatt, André Guimarães, Bernardo Bezerra, and Mario Veiga Pereira, Member, IEEE 1 Abstract— the reform process in the electricity sector of any country has as main objective the design of a power market capable to induce a reliable and efficient energy supply, translated into adequate tariffs. Brazil started its reform process in 1996, inspired by similar schemes in the electricity sector of more developed countries. However, the existence of particularities in the country’s hydroelectric energy market, such as weak spot price signals for system expansion and difficulties to determine benchmark prices, avoided a smooth transition to a fully deregulated market. In 2004, a revisited power sector model was launched, aiming at alleviating the difficulties of the first model. The core of the new proposals lies on the use of contract obligation and energy supply auctions as the backbone for the efficient contracting and supply adequacy. Supply auctions were held in 2004-2005, with a volume of about 20,000 average MW contracted involving about 60 billion USD in financial transactions. This work discusses the implementation of auctions of energy contracts and call options in Brazil as part of the mechanisms to ensure supply adequacy adopted in the second stage of its power sector reform. Index Terms-- Power system economics, power system planning, supply adequacy. I. INTRODUCTION he most fundamental characteristic of the restructuring process that took place in numerous countries around the world in the 1990s was the replacement of regulated procedures used in the decision-making processes under the traditional regulation by market mechanisms. In particular, within a liberalized market there are no mandatory expansion plans that determine which generation units have to be installed in the system and when to meet a demand projection. Instead, market participants decide on their own, according to their business expectations, whether they want to build a certain facility or not, while distribution companies and free consumers are the main responsible to assure their own supply. Following these guidelines, the several electricity markets have been designed worldwide, with the main objective of inducing a reliable and efficient energy supply, translated into adequate tariffs for end-users. Although differing in the degrees and details of implementation, the power sector reform in many countries All authors are with Power Systems Research/Mercados de Energia, Rio de Janeiro, Brazil (e-mail: [email protected]) (including the majority of the South American countries, plus some regions in the US, UK, Spain, etc) shared a common two stage process, where a “second stage” of reforms took place to keep the positive aspects of the “first stage”, but correcting the issues that have not worked as expected (such as flawed capacity payments schemes, weaken signals for system expansion that resulted in power crises and rationing, inefficiencies in the energy purchase, etc). The case of Brazil is not different. The country started its power sector reform in mid 90s, following the general guidelines of more developed countries. After a successful start, with strong interest by private investors on privatization and new projects’ concession auctions, the reform process was disrupted by a severe energy crisis that affected the country for 9 months during 2001-2002. The main consequences were a severe economic loss, on the order of tens of billions of US dollars, and a jump from energy scarcity to energy surplus in the system, motivated by efficient gains on the consumption habits by consumers during the crisis. During and after the crisis, independent panels of experts were set up to discuss what went wrong in the market design and the key common diagnoses were the recognition that the use of spot price as a signal for system expansion was not enough and distribution companies (Discos) needed more effective mechanisms to promote efficient contracting and pass-through limits to end-users. In 2004 a revisited power sector model was launched, inaugurating a second stage of the Brazilian power sector reform. The revisited market design maintains the positive aspects of the first reform, introducing a balance of planning with competition and private investment. It relies on a strong contract obligation with physical coverage gathered with supply auctions of standardized blocks of forward contracts and energy call options to induce system expansion, efficient contracting and signals for end-users. The first auctions were carried out in the past year (2004-2005) and some 20,000 average MW (including contract renewal and new capacity) corresponding to US$ 60 billion in contracts, were contracted. The objective of this work is to analyze the Brazilian experience in its avenue towards the second stage of its power sector reform and provide the results obtained with the supply auctions carried out so far. This work serves as the basis for discussion in the panel session “Market Mechanisms and Supply Adequacy in the T

-

Upload

independent -

Category

Documents

-

view

3 -

download

0

Transcript of Auctions of contracts and energy call options to ensure supply adequacy in the second stage of the...

1

Auctions of Contracts and Energy Call Options to Ensure Supply Adequacy in the Second Stage

of the Brazilian Power Sector Reform Luiz Augusto Barroso, Member, IEEE, José Rosenblatt, André Guimarães, Bernardo Bezerra, and

Mario Veiga Pereira, Member, IEEE

1

Abstract— the reform process in the electricity sector of any country has as main objective the design of a power market capable to induce a reliable and efficient energy supply, translated into adequate tariffs. Brazil started its reform process in 1996, inspired by similar schemes in the electricity sector of more developed countries. However, the existence of particularities in the country’s hydroelectric energy market, such as weak spot price signals for system expansion and difficulties to determine benchmark prices, avoided a smooth transition to a fully deregulated market. In 2004, a revisited power sector model was launched, aiming at alleviating the difficulties of the first model. The core of the new proposals lies on the use of contract obligation and energy supply auctions as the backbone for the efficient contracting and supply adequacy. Supply auctions were held in 2004-2005, with a volume of about 20,000 average MW contracted involving about 60 billion USD in financial transactions. This work discusses the implementation of auctions of energy contracts and call options in Brazil as part of the mechanisms to ensure supply adequacy adopted in the second stage of its power sector reform.

Index Terms-- Power system economics, power system planning, supply adequacy.

I. INTRODUCTION he most fundamental characteristic of the restructuring process that took place in numerous countries around the world in the 1990s was the replacement of regulated

procedures used in the decision-making processes under the traditional regulation by market mechanisms. In particular, within a liberalized market there are no mandatory expansion plans that determine which generation units have to be installed in the system and when to meet a demand projection. Instead, market participants decide on their own, according to their business expectations, whether they want to build a certain facility or not, while distribution companies and free consumers are the main responsible to assure their own supply. Following these guidelines, the several electricity markets have been designed worldwide, with the main objective of inducing a reliable and efficient energy supply, translated into adequate tariffs for end-users.

Although differing in the degrees and details of implementation, the power sector reform in many countries

All authors are with Power Systems Research/Mercados de Energia, Rio

de Janeiro, Brazil (e-mail: [email protected])

(including the majority of the South American countries, plus some regions in the US, UK, Spain, etc) shared a common two stage process, where a “second stage” of reforms took place to keep the positive aspects of the “first stage”, but correcting the issues that have not worked as expected (such as flawed capacity payments schemes, weaken signals for system expansion that resulted in power crises and rationing, inefficiencies in the energy purchase, etc).

The case of Brazil is not different. The country started its power sector reform in mid 90s, following the general guidelines of more developed countries. After a successful start, with strong interest by private investors on privatization and new projects’ concession auctions, the reform process was disrupted by a severe energy crisis that affected the country for 9 months during 2001-2002. The main consequences were a severe economic loss, on the order of tens of billions of US dollars, and a jump from energy scarcity to energy surplus in the system, motivated by efficient gains on the consumption habits by consumers during the crisis.

During and after the crisis, independent panels of experts were set up to discuss what went wrong in the market design and the key common diagnoses were the recognition that the use of spot price as a signal for system expansion was not enough and distribution companies (Discos) needed more effective mechanisms to promote efficient contracting and pass-through limits to end-users.

In 2004 a revisited power sector model was launched, inaugurating a second stage of the Brazilian power sector reform. The revisited market design maintains the positive aspects of the first reform, introducing a balance of planning with competition and private investment. It relies on a strong contract obligation with physical coverage gathered with supply auctions of standardized blocks of forward contracts and energy call options to induce system expansion, efficient contracting and signals for end-users. The first auctions were carried out in the past year (2004-2005) and some 20,000 average MW (including contract renewal and new capacity) corresponding to US$ 60 billion in contracts, were contracted.

The objective of this work is to analyze the Brazilian experience in its avenue towards the second stage of its power sector reform and provide the results obtained with the supply auctions carried out so far.

This work serves as the basis for discussion in the panel session “Market Mechanisms and Supply Adequacy in the

T

2

Second Wave of Power Sector Reforms in Latin America”, to be held in the IEEE General Meeting in Montréal, 2006 and is organized as follows: sections II presents the main system characteristics of the Brazilian interconnected power system. Section III describes the first stage of the sector reform, analyzing drivers, constraints, results achieved and problems observed. Section IV discusses what went wrong with the sector reform and the corrective regulatory measures proposed immediately afterwards, which motivated the design of the second stage of its reform, which in turn is discussed in Section V. Section VI addresses the energy supply auctions carried out so far to deal with the issue of supply adequacy and Section VII presents the conclusions of this work.

II. OVERVIEW OF THE BRAZILIAN POWER SECTOR

A. Physical system Brazil has an installed capacity of 91 GW (2005), where

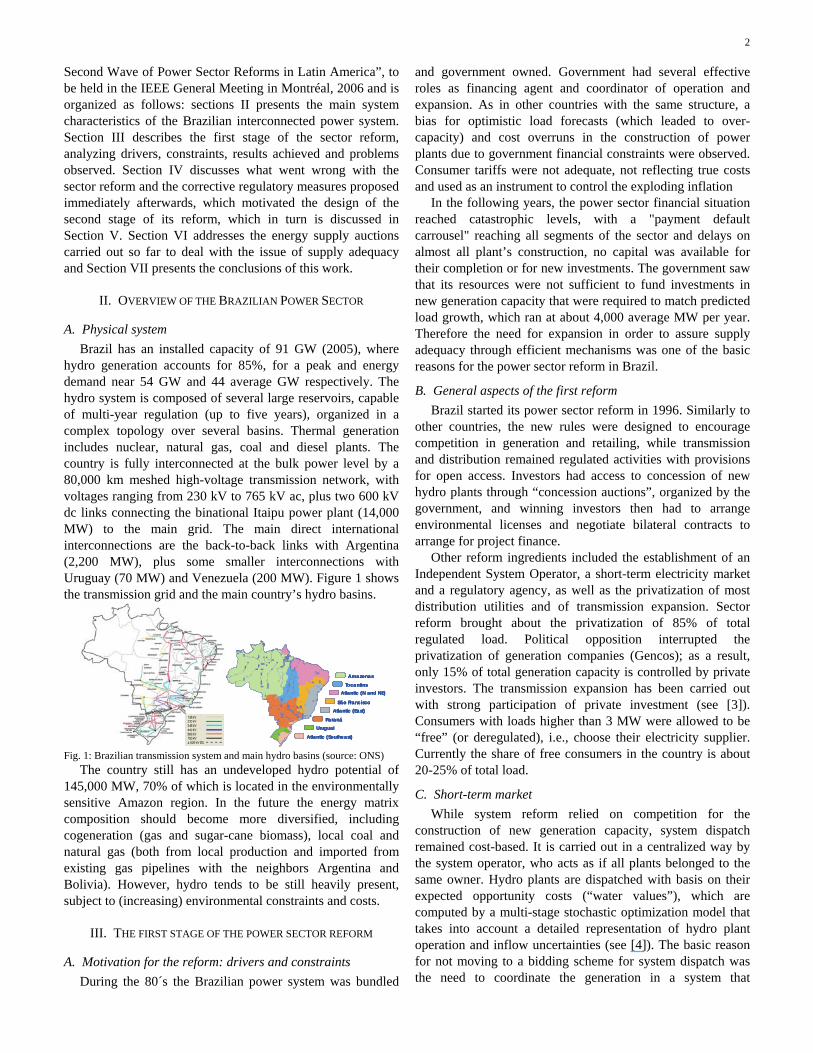

hydro generation accounts for 85%, for a peak and energy demand near 54 GW and 44 average GW respectively. The hydro system is composed of several large reservoirs, capable of multi-year regulation (up to five years), organized in a complex topology over several basins. Thermal generation includes nuclear, natural gas, coal and diesel plants. The country is fully interconnected at the bulk power level by a 80,000 km meshed high-voltage transmission network, with voltages ranging from 230 kV to 765 kV ac, plus two 600 kV dc links connecting the binational Itaipu power plant (14,000 MW) to the main grid. The main direct international interconnections are the back-to-back links with Argentina (2,200 MW), plus some smaller interconnections with Uruguay (70 MW) and Venezuela (200 MW). Figure 1 shows the transmission grid and the main country’s hydro basins.

AmazonasAmazonasTocantinsTocantins

Atlantic (N and NE)Atlantic (N and NE)

São São FranciscoFranciscoAtlantic (East)Atlantic (East)

ParanáParanáUruguaiUruguai

Atlantic (Southeast)Atlantic (Southeast)

AmazonasAmazonasTocantinsTocantins

Atlantic (N and NE)Atlantic (N and NE)

São São FranciscoFranciscoAtlantic (East)Atlantic (East)

ParanáParanáUruguaiUruguai

Atlantic (Southeast)Atlantic (Southeast)

AmazonasAmazonasTocantinsTocantins

Atlantic (N and NE)Atlantic (N and NE)

São São FranciscoFranciscoAtlantic (East)Atlantic (East)

ParanáParanáUruguaiUruguai

Atlantic (Southeast)Atlantic (Southeast)

Fig. 1: Brazilian transmission system and main hydro basins (source: ONS)

The country still has an undeveloped hydro potential of 145,000 MW, 70% of which is located in the environmentally sensitive Amazon region. In the future the energy matrix composition should become more diversified, including cogeneration (gas and sugar-cane biomass), local coal and natural gas (both from local production and imported from existing gas pipelines with the neighbors Argentina and Bolivia). However, hydro tends to be still heavily present, subject to (increasing) environmental constraints and costs.

III. THE FIRST STAGE OF THE POWER SECTOR REFORM

A. Motivation for the reform: drivers and constraints During the 80´s the Brazilian power system was bundled

and government owned. Government had several effective roles as financing agent and coordinator of operation and expansion. As in other countries with the same structure, a bias for optimistic load forecasts (which leaded to over-capacity) and cost overruns in the construction of power plants due to government financial constraints were observed. Consumer tariffs were not adequate, not reflecting true costs and used as an instrument to control the exploding inflation

In the following years, the power sector financial situation reached catastrophic levels, with a "payment default carrousel" reaching all segments of the sector and delays on almost all plant’s construction, no capital was available for their completion or for new investments. The government saw that its resources were not sufficient to fund investments in new generation capacity that were required to match predicted load growth, which ran at about 4,000 average MW per year. Therefore the need for expansion in order to assure supply adequacy through efficient mechanisms was one of the basic reasons for the power sector reform in Brazil.

B. General aspects of the first reform Brazil started its power sector reform in 1996. Similarly to

other countries, the new rules were designed to encourage competition in generation and retailing, while transmission and distribution remained regulated activities with provisions for open access. Investors had access to concession of new hydro plants through “concession auctions”, organized by the government, and winning investors then had to arrange environmental licenses and negotiate bilateral contracts to arrange for project finance.

Other reform ingredients included the establishment of an Independent System Operator, a short-term electricity market and a regulatory agency, as well as the privatization of most distribution utilities and of transmission expansion. Sector reform brought about the privatization of 85% of total regulated load. Political opposition interrupted the privatization of generation companies (Gencos); as a result, only 15% of total generation capacity is controlled by private investors. The transmission expansion has been carried out with strong participation of private investment (see [3]). Consumers with loads higher than 3 MW were allowed to be “free” (or deregulated), i.e., choose their electricity supplier. Currently the share of free consumers in the country is about 20-25% of total load.

C. Short-term market While system reform relied on competition for the

construction of new generation capacity, system dispatch remained cost-based. It is carried out in a centralized way by the system operator, who acts as if all plants belonged to the same owner. Hydro plants are dispatched with basis on their expected opportunity costs (“water values”), which are computed by a multi-stage stochastic optimization model that takes into account a detailed representation of hydro plant operation and inflow uncertainties (see [4]). The basic reason for not moving to a bidding scheme for system dispatch was the need to coordinate the generation in a system that

3

contained several cascaded hydro plants with different owners, taking into account multiple uses of water and constraints such as irrigation and flood control. In particular, it was shown that a bidding scheme based only on the hydro plant’s energy production would not lead to an efficient use of reservoir storage; the reason is that the benefits of the decisions such as sending water downstream or storing it are not properly allocated among generators (see [10]).

Because system dispatch is cost-based, there are no “real” short-term prices, based on the equilibrium between supply and demand. Short-run marginal costs, calculated from the Lagrange multipliers the stochastic dispatch model mentioned above, are used as the clearing price in the short-term wholesale energy market. In addition, because the dispatch model’s objective is to minimize expected operation costs along the study period, these “spot prices” correspond to a “risk neutral” valuation, in the sense that they do not take into account that individual plant owners might be, for instance, risk-averse, and would be willing to trade part of their average profit for a more secure mode of operation.

D. Capacity expansion Capacity expansion was supposed to be induced by a

combination of signals from the spot market and energy forward contract obligations: discos and free consumers were forced to be at least 85% contracted. Although forward contracts were financial instruments, with no influence in the system dispatch, they required physical coverage (firm supply capability) by the part of the seller. The rationale was straightforward: discos and free consumers would have to search for contracts to cover their load growth and these contracts would, at the same time, induce generation expansion (due to the regulatory requirement of physical coverage) and provide investors in new generation with a stable and reliable income source that is necessary for financing. Due to the strong spot price volatility, the contracting level was expected to be high (close to 100%).

Both Discos, which buys energy on the behalf of regulated consumers, and free consumers could negotiate bilaterally their contracts and self-dealing was allowed up to a certain limit. In the case of Discos, contract costs could be passed though consumers up to a benchmark price, established by the regulator. This price should induce efficient contracting.

E. First results The first results of the sector reform (1998-2000) were

encouraging. Privatization of utilities led to approximately US$10 billion in revenues for the Government and a greater efficiency of the “new” private utilities was observed. From 1998 to 2001, about 10,000 MW of new hydro concessions were auctioned off, with a strong participation of private agents. Construction costs and times were reduced by 40%. The creation of free consumers had the positive effect as market benchmark and the transparency brought by the regulatory agencies provided confidence for investors. Along with these results, the international electricity and gas interconnections with Argentina and Bolivia respectively were

conceived and constructed.

F. The supply crisis of 2001 and its aftershocks Notwithstanding in 2001 the sector reform was disrupted in

2001 by a severe energy crisis. As a result of a continued decrease in the storage levels of the system’s reservoirs, during 9 consecutive months during 2001 and 2002 rationing was imposed to all classes of consumers in regions corresponding to 80% of consumption, in order to reduce total load by 20%. The rationing episode is analyzed in [2].

Rationing resulted in a severe economic loss, on the order of billions of US dollars and played a prominent role in the 2002 presidential elections, which were won by the opposition. However, its main consequence for the power sector was a jump to energy surplus: consumption did not rise back to previous levels, leading to the “loss” of approximately 3 years of demand growth and an excess of firm energy of 20% of the market - about 8 average GW (energy, not peak). Discos were in financial problems as a result of the reduced demand, but by that same time, end-user tariffs from privatized Discos started to increase, a consequence of expensive power projects contracted under allowed self-dealing and pass-through rules. Furthermore, the reduced demand and excess supply scenario lead also to low spot prices and financial trouble for the generators with expiring vesting contracts.

IV. WHAT WENT WRONG? During and after the rationing episode, independent panels

of experts were set up to discuss what went wrong in the market design. The common diagnoses pointed out to imperfections mainly in the mechanism for system expansion and in the scheme adopted to induce efficient contracting.

A. Signals for system expansion are inadequate A first reason for the supply difficulty was that the

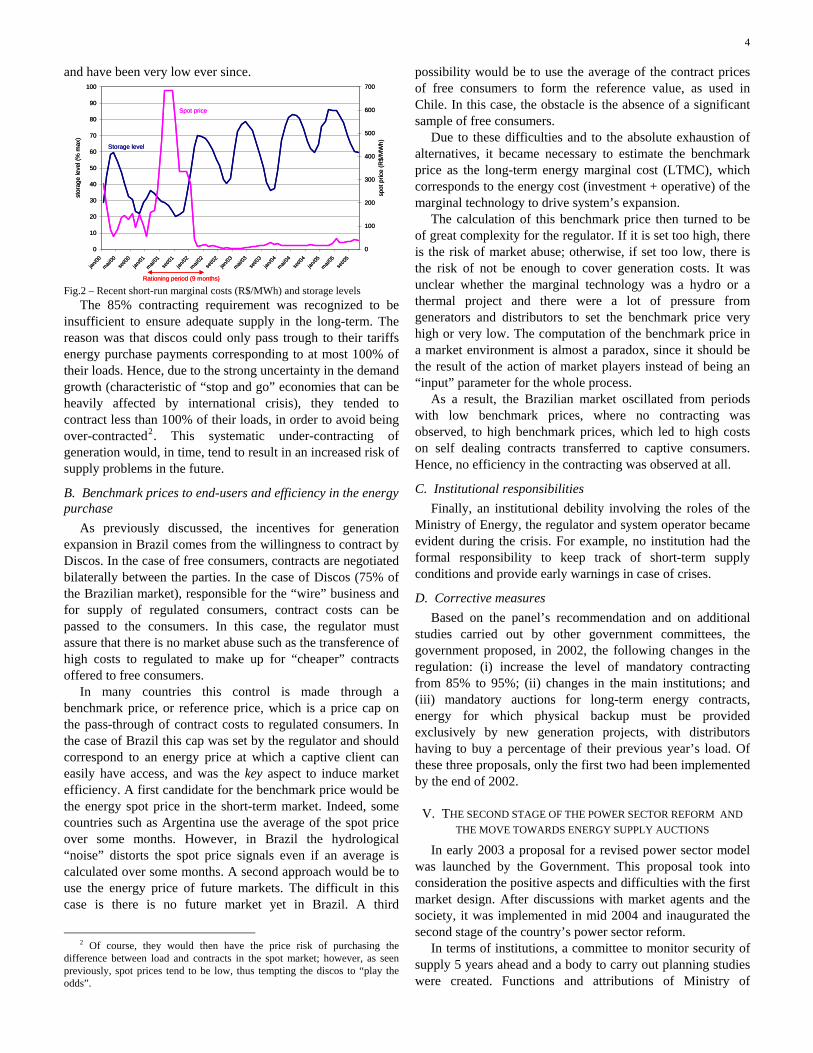

economical signal provided by the spot market is too volatile to correctly indicate and stimulate the entrance of new capacity. This is especially true for the countries with a strong hydro-share, where the occurrence of conjuncture favorable hydro conditions can drive downwards the spot prices even if there are structural problems with supply. For example, in the case of Brazil, due to the size of reservoirs and the multi-year storage capacity, spot prices may be very low for several years (reflecting wet hydro conditions) and then increase sharply for a few months (reflecting dry hydro conditions) before going back to the “normal” levels. In other words, the hydrological “noise” disturbs the correct price signals and the spot price increases substantially only when the system is “too close” from a power crisis, when there is not time anymore to make investments (see [2] for details).

This pattern is shown in Fig 2, which presents the evolution of spot prices and stored energy for the largest price zone in Brazil before, during and after the 2001-2002 crisis. Notice that shortly before rationing started prices still did not reflect the scarcity of energy and after the rationing was over, prices immediately dropped to values close to 6 US$/MWh

4

and have been very low ever since.

0

10

20

30

40

50

60

70

80

90

100

jan/00

mai/00

set/0

0jan

/01

mai/01

set/0

1jan

/02

mai/02

set/0

2jan

/03

mai/03

set/0

3jan

/04

mai/04

set/0

4jan

/05

mai/05

set/0

5

stor

age

leve

l (%

max

)

0

100

200

300

400

500

600

700

spot

pric

e (R

$/M

Wh)

Spot price

Storage level

Rationing period (9 months)

0

10

20

30

40

50

60

70

80

90

100

jan/00

mai/00

set/0

0jan

/01

mai/01

set/0

1jan

/02

mai/02

set/0

2jan

/03

mai/03

set/0

3jan

/04

mai/04

set/0

4jan

/05

mai/05

set/0

5

stor

age

leve

l (%

max

)

0

100

200

300

400

500

600

700

spot

pric

e (R

$/M

Wh)

Spot price

Storage level

Rationing period (9 months) Fig.2 – Recent short-run marginal costs (R$/MWh) and storage levels

The 85% contracting requirement was recognized to be insufficient to ensure adequate supply in the long-term. The reason was that discos could only pass trough to their tariffs energy purchase payments corresponding to at most 100% of their loads. Hence, due to the strong uncertainty in the demand growth (characteristic of “stop and go” economies that can be heavily affected by international crisis), they tended to contract less than 100% of their loads, in order to avoid being over-contracted2. This systematic under-contracting of generation would, in time, tend to result in an increased risk of supply problems in the future.

B. Benchmark prices to end-users and efficiency in the energy purchase

As previously discussed, the incentives for generation expansion in Brazil comes from the willingness to contract by Discos. In the case of free consumers, contracts are negotiated bilaterally between the parties. In the case of Discos (75% of the Brazilian market), responsible for the “wire” business and for supply of regulated consumers, contract costs can be passed to the consumers. In this case, the regulator must assure that there is no market abuse such as the transference of high costs to regulated to make up for “cheaper” contracts offered to free consumers.

In many countries this control is made through a benchmark price, or reference price, which is a price cap on the pass-through of contract costs to regulated consumers. In the case of Brazil this cap was set by the regulator and should correspond to an energy price at which a captive client can easily have access, and was the key aspect to induce market efficiency. A first candidate for the benchmark price would be the energy spot price in the short-term market. Indeed, some countries such as Argentina use the average of the spot price over some months. However, in Brazil the hydrological “noise” distorts the spot price signals even if an average is calculated over some months. A second approach would be to use the energy price of future markets. The difficult in this case is there is no future market yet in Brazil. A third

2 Of course, they would then have the price risk of purchasing the

difference between load and contracts in the spot market; however, as seen previously, spot prices tend to be low, thus tempting the discos to “play the odds”.

possibility would be to use the average of the contract prices of free consumers to form the reference value, as used in Chile. In this case, the obstacle is the absence of a significant sample of free consumers.

Due to these difficulties and to the absolute exhaustion of alternatives, it became necessary to estimate the benchmark price as the long-term energy marginal cost (LTMC), which corresponds to the energy cost (investment + operative) of the marginal technology to drive system’s expansion.

The calculation of this benchmark price then turned to be of great complexity for the regulator. If it is set too high, there is the risk of market abuse; otherwise, if set too low, there is the risk of not be enough to cover generation costs. It was unclear whether the marginal technology was a hydro or a thermal project and there were a lot of pressure from generators and distributors to set the benchmark price very high or very low. The computation of the benchmark price in a market environment is almost a paradox, since it should be the result of the action of market players instead of being an “input” parameter for the whole process.

As a result, the Brazilian market oscillated from periods with low benchmark prices, where no contracting was observed, to high benchmark prices, which led to high costs on self dealing contracts transferred to captive consumers. Hence, no efficiency in the contracting was observed at all.

C. Institutional responsibilities Finally, an institutional debility involving the roles of the

Ministry of Energy, the regulator and system operator became evident during the crisis. For example, no institution had the formal responsibility to keep track of short-term supply conditions and provide early warnings in case of crises.

D. Corrective measures Based on the panel’s recommendation and on additional

studies carried out by other government committees, the government proposed, in 2002, the following changes in the regulation: (i) increase the level of mandatory contracting from 85% to 95%; (ii) changes in the main institutions; and (iii) mandatory auctions for long-term energy contracts, energy for which physical backup must be provided exclusively by new generation projects, with distributors having to buy a percentage of their previous year’s load. Of these three proposals, only the first two had been implemented by the end of 2002.

V. THE SECOND STAGE OF THE POWER SECTOR REFORM AND THE MOVE TOWARDS ENERGY SUPPLY AUCTIONS

In early 2003 a proposal for a revised power sector model was launched by the Government. This proposal took into consideration the positive aspects and difficulties with the first market design. After discussions with market agents and the society, it was implemented in mid 2004 and inaugurated the second stage of the country’s power sector reform.

In terms of institutions, a committee to monitor security of supply 5 years ahead and a body to carry out planning studies were created. Functions and attributions of Ministry of

5

Energy, system operator and regulator were reviewed. In terms of market design, this “second stage” recognizes

that competition is not in the spot market but in contracts with the demands that result in the entrance of new capacity (the so-called competition “for markets”, instead of “within markets”) and is based on: (i) to uphold and increase the level of compulsory contracting to 100% of the load; and (ii) to couple the mandatory contracting requirements with contract auctions as the mechanism to promote efficiency in the energy purchase by discos, and thus providing “real” benchmark prices as auction results. This is discussed next.

A. Mandatory contract obligation One of the consequences of the spot price characteristic in

Brazil is a difficulty for investors to know the “right time” to build new plants, to arrange for project financing and start construction. In order to alleviate this difficulty, the security of supply in Brazil is guaranteed by two Basic Rules: (i) every load in the system must be 100% supplied by a

financial energy supply contract, which means that there should be contracts for the supply of each kWh consumed in the system. This obligation to contract applies for Discos and free consumers, which face penalties on the uncontracted part in case of non compliance;

(ii) every energy contract must be backed up by a physical plant capable of producing the contracted energy in a sustainable (firm) way. The rationale of this scheme is to rely on contracts as

inducers of system expansion. If the system is 100% contracted and contracts have physical coverage, then supply reliability is assured within the “supply risk” defined in the calculation of the physical coverage capacity of each plant, which is calculated by the Government for hydro and thermal projects. Discos are allowed to pass-through to tariffs energy purchase expenses for contracts corresponding up to 103% of their loads. The objective is to replace the “under-contracting” bias discussed previously with a small “over-contracting” bias, to manage the demand uncertainty.

B. Contracting Obligations through Public Auctions In order to promote the most efficient purchase mechanism,

the contract obligation scheme for Discos was coupled with the use of regulated procurement auctions as the main scheme for contracting. Regulated auctions for energy contracts are therefore the backbone for the induction of efficient purchases for regulated consumers. The criterion for contracting in auctions is the smallest tariff and the contracts are standardized, with terms from 5 to 30 years as discussed next. Free consumers can negotiate their energy needs as they please as long as they are 100% contracted.

C. Types of auctions In order to give Discos a portfolio of contracts with

different terms, needed to manage demand uncertainty, and at the same time to allow long-term contracts, that reduce risks for investors, promote competition and attract greenfield (new) generation, there are two main types of auction held

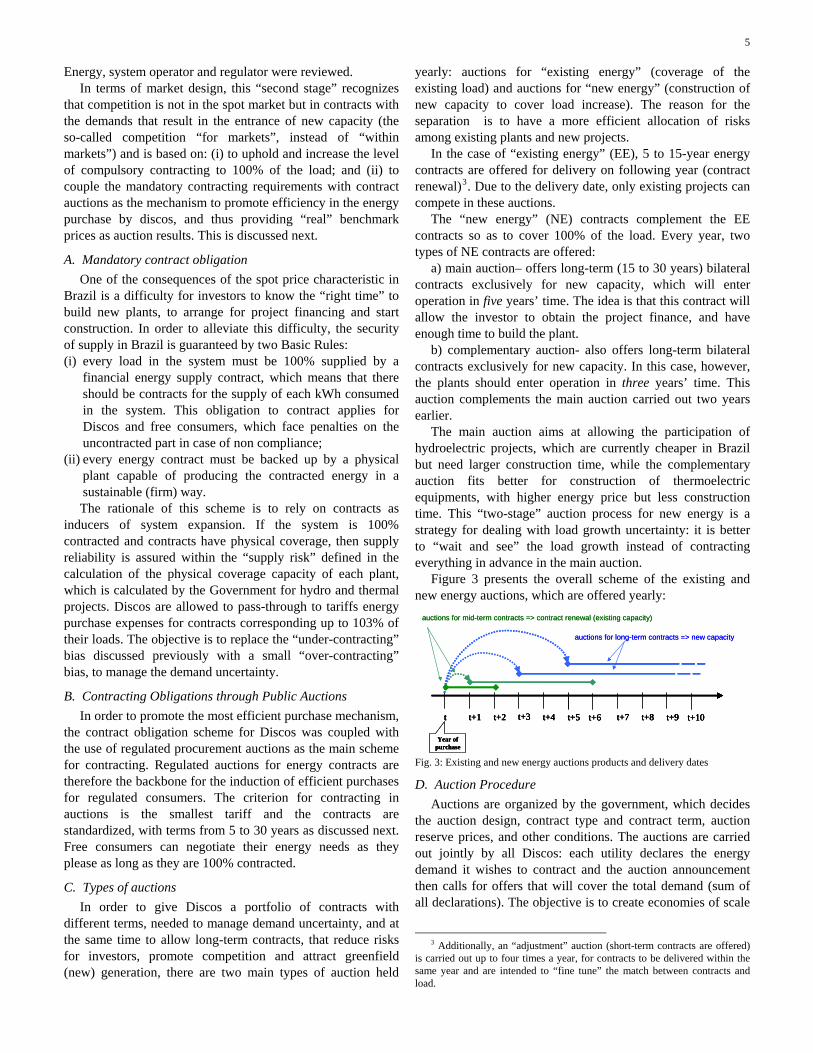

yearly: auctions for “existing energy” (coverage of the existing load) and auctions for “new energy” (construction of new capacity to cover load increase). The reason for the separation is to have a more efficient allocation of risks among existing plants and new projects.

In the case of “existing energy” (EE), 5 to 15-year energy contracts are offered for delivery on following year (contract renewal)3. Due to the delivery date, only existing projects can compete in these auctions.

The “new energy” (NE) contracts complement the EE contracts so as to cover 100% of the load. Every year, two types of NE contracts are offered:

a) main auction– offers long-term (15 to 30 years) bilateral contracts exclusively for new capacity, which will enter operation in five years’ time. The idea is that this contract will allow the investor to obtain the project finance, and have enough time to build the plant.

b) complementary auction- also offers long-term bilateral contracts exclusively for new capacity. In this case, however, the plants should enter operation in three years’ time. This auction complements the main auction carried out two years earlier.

The main auction aims at allowing the participation of hydroelectric projects, which are currently cheaper in Brazil but need larger construction time, while the complementary auction fits better for construction of thermoelectric equipments, with higher energy price but less construction time. This “two-stage” auction process for new energy is a strategy for dealing with load growth uncertainty: it is better to “wait and see” the load growth instead of contracting everything in advance in the main auction.

Figure 3 presents the overall scheme of the existing and new energy auctions, which are offered yearly:

t t+1 t+2 t+3 t+4 t+5 t+6 t+7 t+8 t+9 t+10

Year of purchase

auctions for long-term contracts => new capacity

auctions for mid-term contracts => contract renewal (existing capacity)

t t+1 t+2 t+3 t+4 t+5 t+6 t+7 t+8 t+9 t+10t t+1 t+2 t+3 t+4 t+5 t+6 t+7 t+8 t+9 t+10t t+1 t+2 t+3 t+4 t+5 t+6 t+7 t+8 t+9 t+10

Year of purchaseYear of

purchase

auctions for long-term contracts => new capacity

auctions for mid-term contracts => contract renewal (existing capacity)

Fig. 3: Existing and new energy auctions products and delivery dates

D. Auction Procedure Auctions are organized by the government, which decides

the auction design, contract type and contract term, auction reserve prices, and other conditions. The auctions are carried out jointly by all Discos: each utility declares the energy demand it wishes to contract and the auction announcement then calls for offers that will cover the total demand (sum of all declarations). The objective is to create economies of scale

3 Additionally, an “adjustment” auction (short-term contracts are offered)

is carried out up to four times a year, for contracts to be delivered within the same year and are intended to “fine tune” the match between contracts and load.

6

to contract cheaper projects. Although a “central procurement” is made, Discos are responsible for deciding how much energy they wish to contract and contract costs can be passed through to customers up to a benchmark price (discussed next). Also, separate each winner of an auction will sign individual bilateral contracts with each Disco participating in the auction, being the energy amount of each contract proportional to the Disco’s declared demand, and the total contracted quantity for each Genco matches its offered quantity. In other words, this is not a single buyer model, the Government does not interfere in the contracts nor provides payments guarantees.

For the NE auctions, the Government is responsible to provide an initial “menu” of new generation capacity options (new hydro projects with pre-granted environmental licenses), which are provided from studies of the planning agency. Investors are encouraged to add other projects, i.e., thermal plants, international interconnections, etc. All quantity bids in the auction should be “anchored” by physical coverage.

E. Contract type: forward, call or put options Energy supply contracts to be auctioned can be standard

financial forward contracts or energy call options, the latter is the great novelty. The decision on the contract type is of Government’s responsibility.

Also, the EE contracted amount can be reduced, at any time, to match the Disco’ load reduction in case a qualified captive consumer becomes a free consumer. Finally, the EE contracted amount can be reduced, at the utilities’ discretion, up to 4% in each year to make up for demand uncertainty. This makes these contracts similar to financial “put” options in the Disco’s portfolio.

F. Benchmark price for regulated consumers As discussed in Section IV.B, one of the main difficulties

in the first stage of the Brazilian power sector reform was the definition of the benchmark price to regulate pass-through to end-users. Its “external” definition following a “technocratic” approach (long-term marginal cost) resulted in overall lack of efficiency and undesired results.

With the introduction of auctions, yearly benchmark prices will be determined by the weighted average of total amounts and prices of the new energy auctions and used to regulate the energy cost pass-through to end-consumers. Therefore, the benchmark price is now the result of the market, not an input.

G. Role of the short-term spot market The existence of trading environment strongly based on

financial contracts does not eliminate the need for a place where the differences between actual production or consumption by individual market players and the energy amounts supplied by contracts can be settled, which is the main role of the short-term “spot market”. Prices of this short-term market are derived from dispatch computations as described in section II.B. It is also the place where all wholesale energy contracts are registered, it performs the auctions prescribed in the regulations; and it checks whether

the Basic Rules are being obeyed (i.e. it checks if each consumer is 100% contracted, and if each contract has physical coverage), and applies penalties when they are not.

H. Risk management challenges for Discos and Gencos Under the new market design, Discos run the risk of

penalties in case of under-contracting and the absence of pass-through in case of over-contracting (more than 103% of verified consumption) or in case of purchases at high prices (the pass-though is limited by the benchmark price). However, the market design also provides several risk management instruments to manage its contracting obligation and mitigate the aforementioned risks. The set of regulated auctions previously described can be used as instruments to acquire energy to avoid under-contracting. Moreover, in the case of over-contracting in more than 3% of its load, Discos can count on the reduction flexibilities of the existing energy contracts. Therefore, their main challenges for a distribution company is to establish a contracting portfolio strategy under load uncertainty to meet its contracting obligation taking into account the set of contracts available in the different auctions and the penalties in case of under and over contracting.

The revisited market design also brought new risk management challenges for Gencos. In their case, the objective is to develop a bidding strategy for the contract auction pricing the relevant risks such as (i) hydrological price-quantity market risk; (ii) credit risk in the joint contracting and (iii) put option risk, besides opportunities in spot market selling and trading with free consumers.

I. Implementation The second stage of the power sector reform was

implemented in mid-2004. Up to now two main auctions for mid-term contracts and one auction for long-term contracts (greenfield capacity) – all carried out during the past year (2004-2005) - were the main landmarks in terms of supply auctions to jumpstart the revisited market design. Additional auctions were carried out in October. They are discussed next.

VI. ENERGY SUPPLY AUCTIONS SO FAR

A. Forward Contracts and Existing Energy Auctions The first regulated energy auctions organized under the

new rules were carried out during 2004 and 2005. The first auction, carried out in December 2004, auctioned standard 8-year financial forward contracts for delivery in 2005, 2006 and 2007. A second contract auction was carried out in April 2005 for energy delivery in 2008 and 2009.

Since Brazil still had a high overcapacity when the revisited market design was implemented, these first auctions had as main objective the renewal of energy contracts between existing capacity and Disco as Vesting Contracts expired and jumpstart the model. A subsequent objective was to pre-contract all existing capacity before the entrance of new capacity, which were going to be auctioned in a different auction for long-term contracts (discussed in Section VI.B).

7

Discos declared the load they wanted to contract for each year about 60 days before the auction and the auction’s objective was to call for offers to cover the total demand (sum of all declarations) in each year. For example, contracting needs for 2005, 2006 and 2007 were declared 60 days before the first auction. 1) Auction design

A multi-product simultaneous auction was carried out in each occasion. For instance, the 8-year contracts starting in 2005, 2006 and 2007 were simultaneously sold in the first auction and contracts for delivery in 2008 and 2009 were auctioned in the second auction. Auction design had very special characteristics. In essence, the auction scheme was a hybrid auction divided into two phases, where the first phase was an iterative and simultaneous “descending price clock auction”, and the second phase was a final “pay as bid” round through sealed-bids (see [5]). 2) Auction Results4

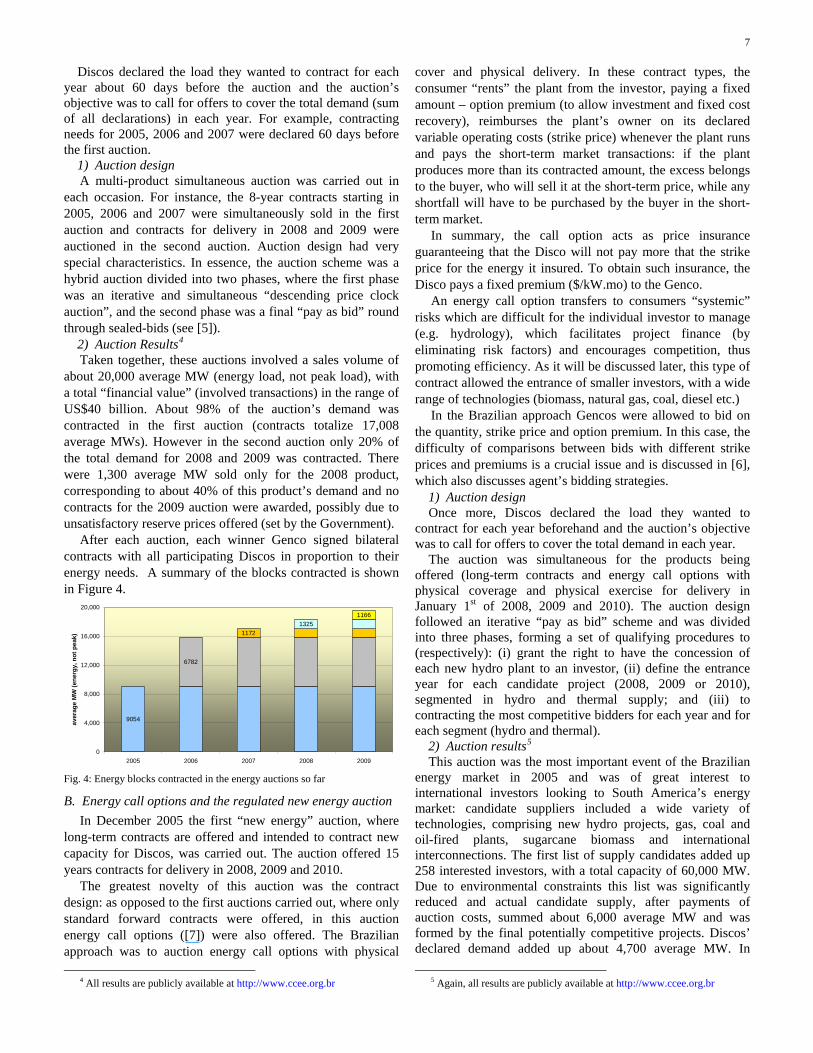

Taken together, these auctions involved a sales volume of about 20,000 average MW (energy load, not peak load), with a total “financial value” (involved transactions) in the range of US$40 billion. About 98% of the auction’s demand was contracted in the first auction (contracts totalize 17,008 average MWs). However in the second auction only 20% of the total demand for 2008 and 2009 was contracted. There were 1,300 average MW sold only for the 2008 product, corresponding to about 40% of this product’s demand and no contracts for the 2009 auction were awarded, possibly due to unsatisfactory reserve prices offered (set by the Government).

After each auction, each winner Genco signed bilateral contracts with all participating Discos in proportion to their energy needs. A summary of the blocks contracted is shown in Figure 4.

9054

6782

11721325

1166

0

4,000

8,000

12,000

16,000

20,000

2005 2006 2007 2008 2009

aver

age

MW

(ene

rgy,

not

pea

k)

Fig. 4: Energy blocks contracted in the energy auctions so far

B. Energy call options and the regulated new energy auction In December 2005 the first “new energy” auction, where

long-term contracts are offered and intended to contract new capacity for Discos, was carried out. The auction offered 15 years contracts for delivery in 2008, 2009 and 2010.

The greatest novelty of this auction was the contract design: as opposed to the first auctions carried out, where only standard forward contracts were offered, in this auction energy call options ([7]) were also offered. The Brazilian approach was to auction energy call options with physical

4 All results are publicly available at http://www.ccee.org.br

cover and physical delivery. In these contract types, the consumer “rents” the plant from the investor, paying a fixed amount – option premium (to allow investment and fixed cost recovery), reimburses the plant’s owner on its declared variable operating costs (strike price) whenever the plant runs and pays the short-term market transactions: if the plant produces more than its contracted amount, the excess belongs to the buyer, who will sell it at the short-term price, while any shortfall will have to be purchased by the buyer in the short-term market.

In summary, the call option acts as price insurance guaranteeing that the Disco will not pay more that the strike price for the energy it insured. To obtain such insurance, the Disco pays a fixed premium ($/kW.mo) to the Genco.

An energy call option transfers to consumers “systemic” risks which are difficult for the individual investor to manage (e.g. hydrology), which facilitates project finance (by eliminating risk factors) and encourages competition, thus promoting efficiency. As it will be discussed later, this type of contract allowed the entrance of smaller investors, with a wide range of technologies (biomass, natural gas, coal, diesel etc.)

In the Brazilian approach Gencos were allowed to bid on the quantity, strike price and option premium. In this case, the difficulty of comparisons between bids with different strike prices and premiums is a crucial issue and is discussed in [6], which also discusses agent’s bidding strategies. 1) Auction design

Once more, Discos declared the load they wanted to contract for each year beforehand and the auction’s objective was to call for offers to cover the total demand in each year.

The auction was simultaneous for the products being offered (long-term contracts and energy call options with physical coverage and physical exercise for delivery in January 1st of 2008, 2009 and 2010). The auction design followed an iterative “pay as bid” scheme and was divided into three phases, forming a set of qualifying procedures to (respectively): (i) grant the right to have the concession of each new hydro plant to an investor, (ii) define the entrance year for each candidate project (2008, 2009 or 2010), segmented in hydro and thermal supply; and (iii) to contracting the most competitive bidders for each year and for each segment (hydro and thermal). 2) Auction results5

This auction was the most important event of the Brazilian energy market in 2005 and was of great interest to international investors looking to South America’s energy market: candidate suppliers included a wide variety of technologies, comprising new hydro projects, gas, coal and oil-fired plants, sugarcane biomass and international interconnections. The first list of supply candidates added up 258 interested investors, with a total capacity of 60,000 MW. Due to environmental constraints this list was significantly reduced and actual candidate supply, after payments of auction costs, summed about 6,000 average MW and was formed by the final potentially competitive projects. Discos’ declared demand added up about 4,700 average MW. In

5 Again, all results are publicly available at http://www.ccee.org.br

8

overall, the auction contracted some 3,300 MW (71% of auction demand) and contracted generation included a mix of technology from all candidate suppliers.

The reason for not having contracted 100% of auction demand was because candidate suppliers felt that reserve prices were not satisfactory or because they had other opportunities in the deregulated market (remember this auction was for the regulated market).

VII. CONCLUSIONS The primary goal of the reform process is Brazil was to

ensure sufficient capacity and investment to serve reliably the country’s growing economy. This work discussed the difficulties that were identified in its design and the proposals of a revisited sector reform to correct them and to implement a design that reconciles competition in generation with a guarantee of adequate supply to ensure the construction of new capacity in an efficient way, based on private investment. The new design is very much auction-based, where contract auctions play an essential role to drive system expansion and provide efficiency gains to consumers. In the past year (2004-2005) Brazil carried out three energy contract auctions (it is not a single buyer model, the discos contract directly) where overall, some 20 thousand average MW were contracting, corresponding to US$ 60 billion in contracts. In particular, the candidate supply for the new capacity auction was large and quite diversified, which is a positive sign (the use of energy call options as contract type helped to increase competition).

In overall, the use of auctions to contract energy is a positive move, as it promotes transparency and increases competition. Other South America’s countries (such as Chile, Peru and perhaps Ecuador and Bolivia) are moving towards similar contracting schemes.

VIII. WHAT’S NEXT: THE CHALLENGES OF ENVIRONMENTAL CONSTRAINTS AND ELECTRICITY-GAS INTEGRATION

Among the issues that still need to be reviewed we can mention the environmental licensing process, which depends on entities completely outside the power sector and it has shown to be very complex (the issuance of a prior license is just its first step). Environmental licensing has become a key factor in system expansion. Hydro power plants have become increasingly more expensive due to environmental compensation programs demanded by Federal and state environmental offices. Future regulatory developments include upholding electricity-gas integration, designing a common framework for electricity and gas markets [9] and incentives to international interconnections.

IX. REFERENCES [1] H. Rudnick; L.A. Barroso; C. Skerk; A. Blanco, “South American

reform lessons - twenty years of restructuring and reform in Argentina, Brazil, and Chile”, IEEE Power and Energy Magazine, Vol 3, July-Aug. 2005.

[2] M. Pereira, L. A. Barroso and J. Rosenblatt “Supply adequacy in the Brazilian power market” Proceedings of the IEEE General Meeting, Denver, 2004.

[3] L.A.Barroso, J.M.Bressane, L.M.Thomé, M.Junqueira, I. Camargo, G. Oliveira, S. Binato, M.V. Pereira, “Transmission Structure in Brazil: Organization, Evaluation and Trends” Proceedings of the IEEE General Meeting, Denver, 2004.

[4] M. Pereira, N. Campodónico, and R. Kelman, “Long-term hydro scheduling based on stochastic models”, Proceedings of EPSOM Conference, Zurich, 1998

[5] Krishna, V. (2002) Auction Theory, Academic Press, San Diego, CA. [6] B.Bezerra, L.A.Barroso, M.V.Pereira, S.Granville, A.Guimarães,

A.Street, “Energy Call Options Auctions for Generation Adequacy in Brazil and Assessment of Gencos Bidding Strategies”, Proceedings of IEEE General Meeting 2006, Montreal.

[7] S. Oren., “Generation Adequacy via Call Options Obligations: Safe Passage to the Promised Land”, 16, UCEI Publications, September 2005.

[8] C. Vazquez., M. River and I.P. Arriaga., 2002. “A market approach to long-term security of supply”, IEEE Trans. on Power Systems, 17 (2)

[9] L.A.Barroso; B. Flach, R. Kelman, B. Bezerra, S. Binato, J.M. Bressane, M.V.Pereira; “Integrated gas-electricity adequacy planning in Brazil: technical and economical aspects” Proceedings of the IEEE PES General Meeting, San Francisco, 2005.

[10] P. Lino, L.A. Barroso, M. Fampa., M.V. Pereira, R. Kelman, “Bid-Based Dispatch of Hydrothermal Systems in Competitive Markets”, Annals of Operations Research, Vol. 120, pp. 81-97, 2003

X. BIOGRAPHIES

Luiz Augusto Barroso has a BSc in Mathematics and a PhD in OR. He joined PSR/Mercados in 1999, where he has been working and researching on power systems economics, planning and operation, focusing on hydro systems. He has been a speaker on these subjects in Latin America, Europe and US/Canada.

José Rosenblatt has a BSc in EE from PUC/Rio, a MSc in OR from Stanford University and an Executive MBA degree at UFRJ's Economics Institute. He joined PSR in 2000, where he is responsible for regulatory and market studies.

André Guimarães has a BSc in EE and a MSc degree in OR. He joined PSR in 2003 and is currently involved with auction modeling and expansion planning models.

Bernardo Bezerra has a BSc in EE and a MSc degree in OR. He joined PSR/Mercados in 2004 and has been working in projects related to gas and electricity integration and pricing of energy call options.

Mario Veiga Pereira has a BSc in EE from PUC/Rio and PhD in OR. He is the president of PSR/Mercados. He is currently engaged in regulatory studies and development of new methodologies and tools for risk management in energy markets. Previously he was a project manager at EPRI's PSPO program and research coordinator at Cepel, where he developed methodologies and software for expansion planning, and hydrothermal scheduling. He was one of the recipients of the Franz Edelman Award for Management Science Achievement, granted by ORSA/TIMS for his work on stochastic optimization applied to hydro scheduling.