A Secure and Efficient Protocol for Electronic Treasury Auctions

Upload

uni-frankfurtCategory

view

0download

0

Institut für Höhere Studien (IHS), Wien Institute for Advanced Studies, Vienna Reihe Ökonomie / Economics Series No. 39

Auctions −− A Survey

René Böheim, Christine Zulehner

Auctions −− A Survey

René Böheim, Christine Zulehner

Reihe Ökonomie / Economics Series No. 39

December 1996

René Böheim ESRC University of Essex Colchester C04 3SQ United Kingdom Phone: ++44 (0) 1206-873901 Fax: ++44 (0) 1206-873151 e-mail: [email protected] Christine Zulehner Department of Finance Institute for Advanced Studies Stumpergasse 56 A-1060 Vienna, Austria Phone: ++43/1/599 91-150 Fax: ++43/1/599 91-163 e-mail: [email protected]

Institut für Höhere Studien (IHS), Wien Institute for Advanced Studies, Vienna

The Institute for Advanced Studies in Vienna is an independent center of postgraduate training and research in the social sciences. The Economics Series presents research done at the Economics Department of the Institute for Advanced Studies. Department members, guests, visitors, and other researchers are invited to contribute and to submit manuscripts to the editors. All papers are subjected to an internal refereeing process.

Editorial Main Editor: Robert M. Kunst (Econometrics) Associate Editors: Christian Helmenstein (Macroeconomics) Arno Riedl (Microeconomics)

Abstract

The importance of auction theory has gained increased recognition in the scientific community,

the latest recognition being the award of the Nobel price to Vickrey and Mirrlees. Auction

theory has been used in quite different fields, both theoretically and empirically. This paper

connects recent developments in theoretical and empirical works, providing a survey about

theoretical, empirical, and experimental results.

Keywords Auction theory, information and uncertainty, asymmetric and private information.

JEL-Classifications D44

Comments

We would like to thank Arno Riedl for his comments. All remaining faults are ours.

I H S | B�oheim, Zulehner / Auctions { A Survey 1

1 Introduction

Auctions are one of the oldest forms to determine transaction prices. One of the earliest

reports of an auction is attributed to the Greek historian Herodotus. He described the

sale of women to men willing to get married in Babylonia around the �fth century B.C..

Historical sources tell us about various auctions taking place in Greece, the Roman

Empire, China, and Japan. Not only history is witness of this economic institution,

but also nowadays auctions are used in a remarkable range of situations. There are

auctions for livestock, owers, antiques, artwork, stamps, wine, real estate, publishing

rights, timber rights, used cars, contracts and land, and for equipment and supplies of

bankrupt �rms and farms. Auctions are of special interest to economists because they

are explicit mechanisms, which describe how prices are formed.

The continuing popularity of auctions makes one wonder about the reasons why. One

explanation is that auctions often yield outcomes that are e�cient and stable. Or to say

it more formally, in a static deterministic model, the set of perfect equilibrium trading

outcomes obtained in an auction game (as the minimum bid is varied) coincides with

the set of core allocations(Milgrom [43]).

A second explanation might be that a seller in a relatively weak bargaining position,

consider the case where the seller is the owner of a nearly bankrupt �rm, can do as well

as a strong bargainer by conducting an auction (Milgrom [43]). However, she then can

not use strategic policies like imposing a reserve price or charging entry fees. Even a

seller in a strong bargaining position will decide to sell via auction, if it is optimal in

relation to other exchange institutions. These three partly complementary explanations

provide a cogent set of reasons for a seller to use an auction when selling an indivisible

object.

The four most common auction forms are the �rst and second price sealed-bid, the

English, and the Dutch auction. The description of all these kinds is given in Section 1.1.

Depending on what kind of good is to be sold we talk about private or common values

auctions. The private value assumption is most nearly satis�ed for nondurable goods.

Because we can say that the consumption of such a good is a personal matter. In

contrast, if we consider durable goods the private value assumption is not ful�lled

anymore. There is the possibility of resale and therefore there is a market price. The

di�erence between these two auction forms is described in more detail in Section 2.

Usually the seller and the bidders are assumed to be risk-neutral. Nevertheless there

are papers dealing with risk-averse bidders. The same is true for symmetry. Symmetry

or asymmetry among bidders means that we have to take into consideration whether

the buyers draw their signals from a symmetric or an asymmetric probability distribu-

tion. The former implies that all bidders are homogeneous, whereas the latter allows

heterogeneity among them.

2 B�oheim, Zulehner / Auctions { A Survey | I H S

The paper is organized as follows: In Section 3 we give a short overview about optimal

auction design. In Section 4 a general auction model is introduced. Section 4.1 gives the

equilibria for the four most common auction types. We also have a look at auctions with

reserve prices and entry fees and what happens if we allow the bidders to be risk averse.

Section 5 considers auctions with asymmetry, royalties, and collusion. In Section 6 the

most prominent results of case studies concerning auctions used in "the real world" are

compared, whereas Section 7 gives a summary of experimental outcomes. The preceding

Section 8 deals with the econometrics of auctions. Results and an overview of used

methods are given. The concluding Section 9 gives a summary and refers to those

auction types, which have been omitted.

1.1 Description of Various Auction Forms

First and Second-Price Sealed Bid Auction The �rst-price auction is a sealed

bid auction in which the buyer with the highest bid obtains the object and pays the

amount she has bid. Whereas in the second-price auction the item still goes to the

bidder with the highest bid, but she pays only the amount of the second highest bid.

This arrangement does not necessarily mean a loss of revenue for the seller, as in this

auction form the buyers will generally bid higher than in the �rst-price auction. The

second-price auction is also known as "Vickrey" auction.

Dutch Auction The Dutch auction, also called descending auction, is conducted by

an auctioneer who initially calls for a very high price and then continuously lowers the

price until some bidder stops the auction and claims the good for that price. This kind

of auction is frequently used in the agricultural sector.

English Auction There is more than one variant of the English auction. In some

the bidders themselves are calling the bids and when nobody is willing to raise the

bid anymore the auction ends. Another possibility is that the auctioneer calls the bids

and the bidders indicate their assents by a slight gesture. Yet there is another form

of the English auction. There the price is posted using an electronic display and is

raised continuously. A bidder who is active at the current price presses a button. In the

moment she releases the button she has withdrawn from the auction. This variant is in

particular used in Japan. These are three quite di�erent forms of the English auction

with three quite di�erent corresponding games.

I H S | B�oheim, Zulehner / Auctions { A Survey 3

2 Private vs. Common Value Auctions

Di�erences among the bidders' valuations of the auctioned object can have two pos-

sible reasons: di�erences in the bidders' tastes or the bidders have access to di�erent

information.

To be more explicit, suppose that each bidder knows exactly how highly she values

the item to be sold. Further she knows nothing about the other bidders valuations, she

perceives any other bidder's valuation as a draw from some probability distribution

and she is aware that the other bidders regard her valuation to be drawn from some

probability distribution as well. These probability distributions are common knowledge

and the valuations of the bidders are statistically independent. In general this is called

the independent private value model.

Now consider the case where the auctioned object has a value known to everyone.

Namely the amount of this item on the market. However nobody knows the true value,

but has some information about the item. And the bidders' perceived values are condi-

tional on the unobserved value independent draws from some probability distribution.

This is called the common value model or the mineral rights model.

The �rst situation applies, for example, to an auction of an antique, where the bidders

buy for their own and will not resale it. Whereas in the latter situation an auction for

an antique that is being bid for by dealers who intend to resell it is described.

The independent private value model and the common value model describe two ex-

tremes. In reality one might �nd auction situations lying between these two cases. A

general model that allows for correlation among the bidders' valuations and that takes

into consideration the two above described special cases, was developed by Milgrom

and Weber [44]. This general model is explained in more detail in Section 4.

To go back to the example given above, an auction of an antique cannot be fully

described in either of the two extreme cases. As the dealers may be guessing about the

ultimative market value of the object, but they may di�er in their selling abilities, so

that the market value depends on which dealer wins the bidding. This arguing asks for

a more general model.

2.1 The Independent Private Value Model

Much of the existing literature on auction theory deals with the independent private

value paradigm in a risk neutral setting. In this section we now want to list the re-

sults and conclusions emerging from the independent private value model. As described

above, in that model a single indivisible good is to be sold to one of n bidders. Any of

the bidders knows the value of the item to herself, and nothing about the values of the

4 B�oheim, Zulehner / Auctions { A Survey | I H S

other bidders. The values are then modeled to be independent draws from some con-

tinuous probability distribution. As the bidders are assumed to behave competitively,

i.e. there are no collusions, the auction can be treated as a non-cooperative game.

There are several important results for this game (see among others Milgrom and

Weber [44]):

Res.1 The Dutch and the �rst-price auctions are strategically equivalent.

Res.2 In the context of the private value model the English and second price auctions

are equivalent as well, although in a somewhat weaker sense than the "strategi-

cally equivalence" of the Dutch and second-price auctions. That means, that in

the latter case no assumptions about the values to the bidders of various outcomes

is required. In particular, the bidder does not need to know the value of the item

to herself.

Res.3 The outcome of the English and second-price auctions is Pareto optimal. In

symmetric models the Dutch and �rst-price auctions also yield Pareto optimal

allocations.

Res.4 The expected revenue generated for the seller by a given mechanism is precisely

the expected value of the object to the second-highest evaluator.

Res.5 All four auctions, i.e. �rst-price, second-price, Dutch, and English 1, lead to

identical expected revenues for the seller (Vickrey [56], Riley and Samuelson [53]).

This is the so-called revenue-equivalence result.

Res.6 For many common sample distributions - including the normal, exponential

and uniform distributions - the four standard auction forms with suitably cho-

sen reserve prices or entry fees are optimal auctions (Myerson [45], Riley and

Samuelson [53]).

Res.7 In case of either a risk-averse buyer or risk-averse seller the seller will strictly

prefer the Dutch or �rst-price to the English or second-price auction.

2.2 The Common Value Model

In the common value auction we assume that the bidders make (conditionally) inde-

pendent estimates of the common value of the item to be sold. The bidder making

the largest estimate will make the highest bid. A consequence of this bidding strategy

is that the winner will �nd that she had overestimated on average the value of the

item she has won, even if all other bidders are making unbiased estimates as well. This

1In the remainder of the paper we denote these four kinds of auctions to be the four standard auction

forms.

I H S | B�oheim, Zulehner / Auctions { A Survey 5

phenomenon is known as the winner's curse. It was �rst described by Capen, Clapp

and Campbell [7], who claimed that this phenomenon is the reason for the low pro�ts

earned by oil companies on o�shore tracts in the 1960's in the US.

In the case of �rst-price auctions the equilibrium of this model has been studied exten-

sively. Those results dealing with the relations between information, prices, and bidder

pro�ts are one of the more interesting ones. For example, Milgrom [41] and Wilson [57]

showed that { under certain regularity assumptions { the equilibrium price in a �rst-

price auction is a consistent estimator of the true value, i.e., that although no bidder

knows the true value of the item, the seller will receive that value as the sale price. In a

common value auction the price can therefore be e�ective in aggregating private infor-

mation. Furthermore, the bidder's expected pro�ts depend more on the privacy than

on the accuracy of the information about the common value of the good (Milgrom [42],

Milgrom and Weber [44]).

3 Optimal Auctions

The theory of optimal auction design addresses the question which auction maximizes

the expected revenue of the seller, given a single object to sell. The decision which kind

of auction is the best is a problem of decision in the face of uncertainty. The seller does

not know the value of the item to be sold to the bidders. Otherwise she would announce

a non negotiable price at or just below the highest bidder's valuation. However, as the

seller does not know the bidder's true valuations she is forced to choose among auction

mechanism which are almost surely going to give her less than this perfect information

optimum (Myerson [46]).

The tool to answer this question is the Revelation Principle. It shows that the seller

can restrict herself to the class of direct and incentive compatible mechanisms. In a

direct mechanism each bidder is simply asked to report her true valuation. Whereas in

an incentive compatible mechanism the bidder �nds it in her own interest to report her

valuation honestly. The direct revelation game has one equilibrium that leads to the

same allocation as the original equilibrium. But this equilibrium need not be unique

(see also Fudenberg and Tirol [15]).

The optimal direct mechanism is found as the solution to a mathematical programming

problem with two constraints: First, incentive-compatibility or self-selection constraints,

which state that the bidders cannot gain by not truthfully reporting their valuations

and second, individual-rationality or free-exit constraints, which guarantee that the

bidders are not better o� if they refuse to take part.

In most of the literature on optimal auction design the independent private value as-

sumption is made. In this setup following results have been shown:

6 B�oheim, Zulehner / Auctions { A Survey | I H S

Res.1 The auction that maximizes the expected price has the following characteristics:

(i) The seller optimally sets a reserve price and does not sell the item if all bidders'

valuations are too low. (ii) Otherwise she sells to the bidder with the highest

valuation (Myerson [45], Riley and Samuelson [53], Milgrom [43]).

Res.2 Any of the English, Dutch, �rst-price, and second-price auctions is the optimal

selling mechanism provided it is supplemented by the optimally set reserve price

(Myerson [45], Riley and Samuelson [53]).

Bulow and Roberts [6] have shown that the seller's problem in devising an optimal

auction is virtually identical to the monopolist's problem in third-degree price discrim-

ination.reinterpretation of the auction

The question whether a public auction or an optimally structured negotiation is more

pro�table to sell a company was answered by Bulow and Klemperer [5]. They found that

under standard assumptions, like risk-neutrality, independence of signals, or increasing

bid functions, the public auction is always preferable. The result holds both for the

independent private value and the common value model.

Relaxing the Independence Assumption Myerson [45] has provided an optimal

auction mechanism for an example with dependent bidders' values. The optimal auction

includes side-bets, which are not possible in the independent case. In the general non-

independent case we can expect side-bets more commonly. With carefully designed

side-bets the seller can counterbalance the bidders' incentive to lie to buy the object

at a lower price.

4 A General Symmetric Model

In Milgrom and Weber's paper [44] a general model for risk neutral bidders was de-

veloped. In the their model there is space for cases like the independent private value

model and the common value model, as well as a range of intermediate models. In this

section we will heavily draw on this paper.

Consider now an auction in which a single object is to be sold and in which n risk

neutral bidders compete for the possession of that object. Each of these bidders has

some information about the object.

Let X = (X1; : : : ;Xn) be a vector. The components of this vector are real-valued

signals observed by the individual bidders. And let Y1; : : : ; Yn�1 denote the largest,

: : :, smallest estimates from among X2; : : : ;Xn. Let S = (S1; : : : ; Sm) be a vector of

additional real-valued variables which in uence the value of the object to the bidders.

The seller might observe some of the components of S. Let Vi = ui(S;X) denote the

I H S | B�oheim, Zulehner / Auctions { A Survey 7

actual value of the object to bidder i, and f(s; x) denotes the joint probability density

of the random elements of the model. Following assumptions are made:

Ass.1: 9 function u on Rm+n such that 8i, ui(S;X) = u(S;Xi; fXjgj 6=i). That means,

that all of the bidders' valuations depend on S in the same manner and that each

bidder's valuation is a symmetric function of the other bidders' signals.

Ass.2: u is nonnegative, continuous, and nondecreasing in its variables.

Ass.3: For each i, E[Vi] <1.

Ass.4: The bidders' valuations are in monetary units and the bidders are risk neutral.

Therefore, bidder i's payo� is Vi� b, if she receives the auctioned object and pays

the amount b.

Ass.5: f is symmetric in its last n arguments.

Ass.6: The variables S1; : : : ; Sm; X1; : : : ;Xn are a�liated. More precisely, let x and x0

represent a pair of (m+ n) vectors, let f(x) denote the joint probability density

of the random variables x, and let x _ x0 and x ^ x

0 denote the component-wise

maximum and minimum of x and x0, respectively. Then the variables are de�ned

to be a�liated if, 8x; x0,

f(x _ x0)f(x ^ x

0) � f(x)f(x0): (1)

Roughly speaking, this condition means that large values for some of the variables make

the other variables more likely to be large rather than small (Milgrom and Weber [44],

p.1098). We refer to (1) as the "a�liation-inequality".

In this general setting both the independent private value paradigm and the common

value paradigm can be treated. In the �rst case m = 0 and each Vi = Xi. Therefore the

only random variables are X1; : : : ;Xn. They are statistically independent and ful�ll (1)

with equality, i.e. independent variables are always a�liated.

In the second casem = 1 and each Vi = S1. Let g(xijs), h(s) and f(s; x) = h(s)g(x1js) : : :

g(xnjs) denote the conditional density of any Xi given the common value S, the

marginal density of S and the joint density of any Xi and S, respectively. Assum-

ing that the density g ful�lls the monotone likelihood ratio property 2 one gets that

g also ful�lls Equation (1). It can be shown that f also ful�lls Equation (1) 3. As a

consequence the common value model de�ned in Section 2.2 meets the the formulation

of the general model, if the density g has the monotone likelihood ratio property.

2Fore a de�nition see Section A.1.3This can be shown by applying Theorem 1, which is listed in the Appendix (see Milgrom and

Weber [44]).

8 B�oheim, Zulehner / Auctions { A Survey | I H S

As the auction is supposed to be symmetric we can focus on bidder 1 4. We can now

rewrite bidder 1's value as follows:

V1 = u(S1; : : : ; Sm;X1; Y1; : : : ; Yn�1): (2)

The joint density of S1; : : : ; Sm;X1; Y1; : : : ; Yn�1 is

(n� 1)!f(s1; : : : ; sm; x1; y1; : : : ; yn�1)1fy1�:::�yn�1g;

where the last term is an indicator function. If the condition in parenthesis is met

it is equal to one, otherwise it is equal to zero. It can be shown that the function

E[V1jX1 = x; Y1 = y1; : : : ; Yn�1 = yn�1] is nondecreasing in x5.

4.1 Results

We now list Milgrom and Weber's results concerning the optimal strategies in the stan-

dard auction forms. In this symmetric bidding environment they identify competitive

behaviour with symmetric Nash equilibrium behaviour. Further we give a summary of

results concerning revealing information, entry fees, reserve price, and risk aversion.

4.1.1 Second-Price Auction

A strategy for bidder i is a function mapping her value estimate xi into a bid b =

bi(xi) � 0. Supposing bidders j 6= 1 adopt strategy bj then the highest bid among them

will be W := maxj 6=1bj(xj). Bidder 1 will win the auction if her bid exceeds W , which

will also be the price bidder 1 has to pay. The decision problem bidder 1 is facing now is

to choose a bid b that maximizes the expected actual value minus the price conditional

on her signal, ignoring the cases where her bid is not the highest. It can be shown that

the equilibrium strategy in a second-price auction is to bid b�(x) = v(x; x) for every

player. The function v is de�ned by v(x; y) := E[V1jX1 = x; Y1 = y]. It can be shown

that v is nondecreasing.

The expected selling price is the expected price paid when bidder 1 wins conditional

on her winning the auction: R = E[v(Y1; Y1)jfX1 > Y1g]. Publicly revealing some

credible information X0 by the seller raises the expected selling price and therefore

revenues. That means announcing information X0 is better, on average, than revealing

no information. Furthermore it can be shown that in a second-price auction, no other

reporting policy, i.e. to censor information sometimes, yield a higher expected price

than the policy of always reporting information X0.

4From now we will retain this simpli�cation. It allows us to identify the winning bidder with bidder

1, which will in particular be used in section 4.1.5For this purpose Theorems 2-5 are engaged, which are all listed in the Appendix

I H S | B�oheim, Zulehner / Auctions { A Survey 9

4.1.2 English Auction

As in section 1.1 described there are several variants of the English auction. Milgrom

and Weber developed a game model which corresponds most closely to the Japanese,

so called press-button, auction: In the very beginning all bidders are active at a price of

zero. The auctioneer raises the price and the bidders drop out one by one and can not

become active anymore. Furthermore all other bidders know the price at which someone

has quit the auction. A strategy for bidder i speci�es whether, at any price level p, she

will stay in the auction or not, as a function of her signal, the number of bidders having

already quit, and the price levels at which they quit. Let k and p1 � : : : � pk denote the

number of bidders who have quit and the levels at which they leave, respectively. Then

bidder i's strategy can be described by a function bik(xi j p1; : : : ; pk) which specify the

price at which bidder i will quit if, at that point, k other bidders have left at the prices

p1; : : : ; pk. Naturally bik(xi j p1; : : : ; pk) is required to be at least pk.

Milgrom and Weber showed that there exists a symmetric equilibrium point in this

setup. The optimal bidding strategy b� = (b�0; : : : ; b�

k) for any bidder is de�ned iteratively

b�

0(x) = E[V1 j X1 = x; Y1 = x; : : : ; Yn�1 = x]

b�

k(x j p1; : : : ; pk) = E[V1 j X1 = x; Y1 = x; : : : ; Yn�1 = x;

b�

k�1(Yn�k j p1; : : : ; pk�1) = pk; : : : ;

b�

0(Yn�1) = p1]:

where b�

0(x) de�nes the optimal bid as long as nobody has left the auctions and

b�

k(x j p1; : : : ; pk) is the equilibrium bid after k bidders have quit.

Further can be shown the English auction is not less than in the second-price auction. In

e�ect, the English auction can be divided into two parts: First, the n�2 bidders with the

lowest estimates reveal their signal publicly through their bidding behaviour. The last

two players are then engaged in a second-price auction. Again, revealing information

X0 publicly raises revenues and no other reporting policy yields a higher expected price

than the policy of always reporting X0.

4.1.3 First-Price and Dutch Auction

Because of the strategic equivalence of the �rst-price and Dutch auction both auction

forms can be treated equally. First, Milgrom and Weber derived necessary conditions

for an n-tuple (b�; : : : ; b�) to be an equilibrium point, when b� is increasing and di�er-

entiable. Then the optimal strategy for any bidder in this setup is de�ned as follows

b�(x) = v(x; x)�

Zx

x

L(� j x)dt(�) with

t(x) = v(x; x) and L(� j x) = exp(�

Zx

�

fY1(s j s)

FY1(s j s)ds):

10 B�oheim, Zulehner / Auctions { A Survey | I H S

where FY1 denotes the cumulative distribution of Y1 corresponding to the density fY1 .

Additionally Milgrom and Weber proved that the expected selling price in the second-

price auction is at least as large as in the �rst-price auction. And again, a policy of

publicly revealing the seller's information can not lower, and may raise, the expected

price in a �rst-price auction. As in the two other auction forms no reporting policy

leads to a higher expected price than the policy of always reporting X0.

4.1.4 Reserve Prices and Entry Fees

In Section 4.1.1- 4.1.3 any mention of the seller setting a reserve price or charging an

entry fee has been omitted. Although in auctions these tools are commonly used and are

thought of to raise the seller's revenue. Milgrom and Weber have shown how to adapt

the optimal strategies in the case of a �rst-price auction. With a �xed reserve price the

ordering of average prices does not alter. The English auction generates higher expected

prices than the second-price auction, which in turn produces higher expected prices than

the �rst-price auction does. However, given any reserve price for one of the standard

auction forms a policy of announcing information X0 and setting the corresponding

reserve price raises expected revenues. A further result shows under some additional

conditions, that it pays to set high entry fees and low reserve prices, rather than the

reverse.

4.1.5 Risk Aversion

Risk aversion raises the expected selling price. In models combining risk aversion and

a�liation it is generally not possible to rank the �rst- and second-price auction by their

average prices. This is in contrast to the case of independent private values with risk

aversion where the �rst-price auction yield higher prices than the second-price auction.

Generally it is not true that partially resolving uncertainty reduces the risk-premium.

The class of utility functions for which any partially resolving uncertainty tends to

reduce the risk premium is a very narrow one. It is the class of increasing utility

functions with constant absolute risk aversion.

If one assumes that bidders are risk averse with constant absolute risk aversion, then

in the second-price and the English auction revealing public information raises the

expected price and among all possible reporting policies for the seller full reporting

leads to the highest expected price. Additionally, the expected price in the English

auction is at least as large as in the second-price auction.

I H S | B�oheim, Zulehner / Auctions { A Survey 11

4.1.6 Summary

When bidders' valuations are a�liated, the English auction yields a higher expected

revenue than the �rst-price, the second-price, or the Dutch auction. Additionally it is

true that the second-price auction leads to higher expected revenue than the �rst-price

auction, which yields the same revenue as the Dutch auction.

In the standard auction forms the seller can raise her expected revenue by having a

reporting policy of revealing any information she has about the item's true value. If one

bidder's information is available to another bidder, her expected surplus is zero (see

Milgrom[42], Milgrom and Weber [44]). This result means that privacy of information

is of more importance than precision of the information.

5 Further Topics

We now consider the assumptions of the independent private value model. These are

independent private values, bidders' risk neutrality, and symmetry, and that payment

is a function of bids alone. Relaxing the �rst assumption leads to the common value

or general model (see Section 2.2 and 4). Results concerning risk aversion are given in

Section 4.1.5. The next two Sections 5.1 and 5.2 are dealing with relaxing one of the

last two assumptions, whereby the �rst two are recovered again. The last Section 5.3

deals with collusion among bidders.

5.1 Asymmetric Bidders

Following McAfee and McMillan [35] we now assume that the bidders fall into separate

groups. Therefore we do not have one distribution of private values anymore, but two

di�erent ones. Bidders of every type draw their valuations still independently from their

speci�c probability distribution.

In this setting the English auction operates much as in the private value model. The

bidder with the highest valuation wins and therefore the outcome is e�cient. As the

�rst-price auction yields a di�erent price as the English auction does, revenue equiva-

lence breaks down. Vickrey [56] among others has constructed examples in which the

price in the English auction can be on average higher or lower than the price in the

�rst-price auction.

In the special case that the two distributions are only distinguishable by their mean,

i.e. the shape of the distribution is the same, only the means di�er, the class of bidders

with the lower average valuation are favoured in the optimal auction (McAfee and

McMillan [35]). The bene�t from such a policy is that the bidders with the higher

average valuation are forced to bid higher than they otherwise would. Thus the price

will drive up on average.

12 B�oheim, Zulehner / Auctions { A Survey | I H S

5.2 Royalties

So far payment was dependent only on bids. Consider now the auction of publishing

rights for books with payment to the author depending on the bid and, via royalty,

on the book's ultimative sales. It is in the seller's interest to condition the bidders'

payments on any information about the winner's valuation (McAfee and McMillan [35]).

Ex post the seller observes an estimate of the winning bidder's true valuation. In this

setup the payment to the seller by the winning bidder is modeled as a linear function of

the bid and the royalty rate times the estimate of the winning bidder's true valuation.

There are three possibilities for bidding mechanism for this linear relationship. First,

the seller can set the royalty rate and call for bids. Second, she can set the �xed payment

and call for bids on the royalty rate, and third she can call on both.

Considering the �rst type of bidding mechanism the following results can be shown:

If the distribution of the observed estimate of the winning bidder's true valuation

is exogenous, the seller's expected revenue is an increasing function of the royalty

rate (McAfee and McMillan [33]). This suggests a royalty rate of hundred percent. An

increasing royalty rate also serves to increase the bidding competition and raises the

bids. However, an increase in the royalty rate reduces the return to the winning bidder

on her own actions after the auction. This in turn tends to lower the seller's expected

revenue. With moral hazard the optimal royalty is less than hundred percent and the

optimal contract is linear in the observed estimate of the winning bidder's valuation

but nonlinear in the winning bidder's bid (McAfee and McMillan [35]). Considering

risk-averse bidders one gets that the higher bidders' risk aversion compared to the

seller's, the higher the optimal royalty rate should be (McAfee and McMillan [33],

Samuelson [54]).

The second type of bidding mechanism has been investigated by Riley [52]. He showed

that under certain assumptions the expected payment by the winning bidder is strictly

greater under royalty bidding than under pure fee bidding and that the expected revenue

from a high bid auction is a strictly increasing function of the royalty rate.

Samuelson [54] has taken the more general case, where the bidder submits a bid repre-

sented by an ordered pair, one bid for the royalty rate and one bid for a �xed payment.

The seller "orders" the bids according to a preannounced selection function. Under

these assumptions the seller seeks a selection function which maximizes her expected

revenue.

5.3 Collusion

So far it was always assumed that the bidders act non cooperatively, i.e. they do not

coordinate their bids. However, in reality this assumption is not always met. Collusion

between bidders in form of cartels or bidding rings are built to prevent too high prices.

I H S | B�oheim, Zulehner / Auctions { A Survey 13

In English auctions a common method in practice is for one member arbitrarily to be

assigned to bid for the item without competition from his fellow cartel members. After-

wards, the item is re-auctioned among the cartel members (McAfee and McMillan [33]).

Milgrom [43] examined that auction forms di�er in their degrees of susceptibility to

collusion. According to Mead's hypothesis [40] he pointed out that in an ascending

auction collusion is easier to support than in sealed-bid auctions. This would explain

why a seller might choose a sealed-bid auction. This holds despite the fact that the

ascending auction is theoretically superior when bidders behave competitively. Instead

of changing the auction form the seller can also use a reserve price. Under the private

value assumptions it can be shown that the optimal anti-cartel reserve price can be

calculated from a relation, where the seller's valuation is a function of the reserve price,

and the number of bidders (McAfee and McMillan[33]). This formula also implies that

the anti-cartel reserve price increases with the number of cartel members and that the

anti-cartel reserve price is higher than the optimal reserve price without collusion.

6 The Real World

Empirical work on auctions have mostly been asking questions like "Does the bidder

with the highest valuation get the object?" or, "Does the seller get all pro�t?", etc.

That is to say, questions concerned with e�ciency and optimality of the auction. Key

parameters to these questions are the reserve prices and the mechanism designs.

In this section we will compare di�erent markets where auctions have been used to sell

the object. We will consider here only the most prominent results, since the current

volume of EconLit (WinSPIRS) produces 162 hits for the search string "auction* AND

empiri*".

6.1 Oil and Gas Lease Auctions in the U.S.A.

The most prominent authors concerning oil lease auctions are Hendricks and Porter.

In their AER 1988 paper [18] they analyse drainage lease auctions on the Outer Con-

tinental Shelf (Louisiana and Texas) from 1959 to 1969. The reason for using this type

of auctions is that the data set is very rich, i.e. it is possible to identify the buyers, the

bidders, and, ex post, the pro�ts of the oil �elds. For each tract that receives at least one

bid following information is obtainable from the U. S. Department of the Interior: date

of sale, location and acreage, the identity of all bidders and the amount they bid, the

identity of participants in joint bids, acceptance of the bid, number and date of drilled

wells, monthly production through 1991 of oil, condensate, gas, and other substances.

The objects were classi�ed in two categories, drainage and wildcat leases. A drainage

sale consists of simultaneous auctioning of tracts which neighbour tracts on which

14 B�oheim, Zulehner / Auctions { A Survey | I H S

deposits have been discovered. Wildcat tracts are in areas where no previous drilling

has occurred. Bidding, drilling behaviour, and pro�ts di�er signi�cantly on these two

types of tracts.

The main di�erence between wildcat and drainage auctions is the distribution of in-

formation. For wildcat leases information is essentially symmetric, since no company

is allowed to engage in explorative drilling. For drainage tracts the neighbouring �rm

has the possibility to obtain seismic information. Non-neighbouring �rms have the pos-

sibility to obtain information from private seismic surveys and from observation of

production by their competitors. Neighbouring �rms tend to be better informed than

the non-neighbouring rivals. This would give them an advantage and could result in

the winner's curse for the actual winner of a lease.

The �nding is that the data strongly support this hypothesis. The decisions of the

neighbouring �rms are signi�cantly better predictors. The predictions of the Bayesian

Nash equilibrium model of bidding in �rst-price, sealed bid auctions with asymmetric

information are consistent with the data. Non-neighbouring �rms earned approximately

zero pro�ts whereas neighbouring �rms were able to gain substantially higher returns.

Hendricks and Porter [20] focus on the role of joint bidders in OCS auctions. They

again take data for the period 1954 till 1979 for U.S. land o� Louisiana and Texas.

The hypothesis that joint ventures enhance competition by allowing smaller �rms (the

"fringe") entry to the market is investigated. The participation of the fringe happened

predominantly via joint bidding, but usually with a big �rm, not together with others

from the fringe. However, in this sample the most pro�table bids came from large

companies bidding either solo or with each other. The participation of the fringe in

joint ventures seems to be motivated mostly by capital constraints. This interpretation

is consistent with several aspects, namely the size of the venture, di�erences of pro�ts,

etc. The discussion of this issue is taken up again in Porter [51], see also below.

In their European Economic Review article Hendricks and Porter [21] analyse oil lease

auctions o� the coasts of Texas and Louisiana, U.S.A., by the U.S. federal government.

The period investigated is 1954 to 1979, using �rst-price sealed bid auctions as the

theoretical model.

The objects were classi�ed in three categories, wildcat, development, and drainage

leases. Drainage and development leases are adjacent to existing areas where oil has

been found (after 1979 this distinction was no longer used), whereas wildcat leases are

in regions where no previous drilling has been undertaken. In the case of drainage and

development leases, owners of neighbouring tracts have data from their own drilling.

For the wildcat leases potential buyers are allowed to gather seismic information but

no on-site drilling is permitted. Development leases were mostly re-o�ers of previously

sold tracts with relinquished leases, or of leases where the bids were rejected as too low.

The bid is a dollar amount which the �rm agrees to pay to the government if it is

I H S | B�oheim, Zulehner / Auctions { A Survey 15

awarded the lease. There is also a �xed fraction, known as royalty, of any production

revenues that the �rm has to pay to the government (in this case mostly 1/6).

To account for the role of information asymmetry the authors distinguished between

neighbouring and non-neighbouring �rms. A regression of ex post pro�ts on partici-

pation and bids of the �rms veri�ed the informational advantage of the neighbouring

company.

The �ndings of this paper are that information plays a crucial role, neighbouring �rms

earning signi�cantly more than non-neighbouring. Furthermore, the returns for non-

neighbouring �rms were lower if neighbouring �rms did not bid. These results are

consistent with the theoretical predictions.

As in the above paper, Porter [51] analyses the sale of oil and gas tracts o� Texas and

Louisiana. The oil and gas production in this area accounts for about 12 percent of

U.S. oil production (25 percent of gas production). The data set runs from 1954 to

1990 (till 1979 for wildcat sales). The article addresses both symmetric (wildcat leases)

and asymmetric (drainage leases) situation, the role of the government, whether and

how bidding consortia acted, and the incidence and timing of exploratory drilling after

a tract was acquired.

In the wildcat lease auctions the presence of the winner's curse might be shown by

the data. A substantial dispersion in the number of submitted bids is reported. Out

of 2.255 purchased tracts on a fraction of 78 percent exploratory drilling was under-

taken. Conditional on being explored, tracts receiving more bids are more likely to be

productive and to have larger deposits if productive.

An interesting question is the behaviour once a site has been bought. Buying a tract does

not force the buyer to engage in exploratory drilling, however, if no drilling is undertaken

the lease is relinquished and reverts to the government. There is a clear deadline e�ect

as the �ve year deadline approaches. This is consistent with a war of attrition if the

�rm prefers its neighbour to drill �rst. Relative to the optimal coordinated plan (where

sequential search would be carried out) the non cooperative equilibrium is ine�cient

(delay of drilling).

The rejection policy of the government is studied. The government rejected bids more

often if there were few bidders. It seemed that the government's rejection policy was to

discourage low bids. Porter noted that the long period between rejection and reo�ering

may be inconsistent with revenue maximization.

Porter [20] looked at the behaviour of joint bidders for the period 1954{79, computing

a ex post value for the tracts. The most pro�table bids have been made from large

�rms bidding either solo or jointly with each other. The average ex post value was

lower than that of tracts bought by consortia of large and small �rms, but the lower

purchase prices more than o�set the di�erence. The participation of small �rms was

16 B�oheim, Zulehner / Auctions { A Survey | I H S

predominantly together with large �rms for high-price tracts. This behaviour can be

explained by capital constraints, however it cannot be the explanation of why large

�rms bid together. Here the motivation could be to reduce competition and lower the

prices.

6.2 Auctions of Contracts

Paarsch [48] uses auctions of tree planting contracts in British Columbia, Canada, from

1985 to 1988, to �nd whether this auctions fall within the private or common value

paradigm framework. The contracts are awarded to the lowest bid, which is typically

the cost per tree planted, in a sealed bid �rst-price auction. Di�erences in bidding

behaviour can be a result of two di�erent (and opposing) paradigms. In the �rst case,

the cost of planting a tree is unknown to all, but the same to all bidders. If this is true,

then a sealed-bid framework o�ers no additional help in �nding out the most e�cient

since all are equally e�cient.

If, on the other hand, there are di�erences in the planting costs then the use of the

sealed-bid framework will induce the bidder with the lowest cost to submit the lowest

bid.

Which paradigm applies will be re ected in the bidders' bidding functions and in the

winning bids. For common value auctions, the bid functions will increase in the number

of bidders, n, where in auctions within the private value setting the bids will decrease

monotonically. The expected value of the winning bid will have no relationship with the

number of bidders in a common value setting, in private value auctions it will decrease

in n.

Sadly, the distribution of the winning bids do not provide enough information to dis-

criminate between the models. Neither the shape nor the mean of the data allows dis-

crimination. Employing several empirical speci�cations (proportional bids, cost additive

bid functions, nonlinear functions of cost) all versions of the private value paradigm are

rejected and there is consistency between the data and the common value paradigm.

Pesendorfer [50] investigates collusion behaviour in milk contract auctions in Florida

and Texas, U.S.A., from 1980 to 1991. Here a �rst-price sealed bid mechanism is em-

ployed, too. The lowest bid is accepted, all bidders have to sign a non-collusion state-

ment, using this framework some 200 million $in school milk contracts were auctioned

between 1980 and 1989, around 200 contracts per year. Between 1988 and 1993 45 com-

panies and 26 persons have been convicted for bid-rigging. There are several aspects

in this specialised market that may encourage collusion. Firms have to agree only on

a price since quality and quantity of milk contracts are prespeci�ed. On top of that

there are many contracts, so that pro�ts can be divided amongst partners. There is

no coordination between di�erent districts, the contracts are awarded only on the bids

I H S | B�oheim, Zulehner / Auctions { A Survey 17

submitted to the speci�c Board of Education. Colluders can detect de�ants easily (an-

nouncement of bids) and react within the same year. The demand elasticity is very low

and the market highly concentrated (8 �rms won 90 percent of all contracts).

The author �nds that both markets are consistent with game theoretic models. In the

case of Florida, a cartel with sidepayments, in Texas, a cartel without side-payments

are consistent with the data.

In a very in uential6 paper Thiel [55] investigated the highway construction auctions. In

this setup contracts are awarded to quali�ed �rms entering the lowest bid. Usually the

highway agency does not reveal its estimate of the value of the contract7. The author

uses a GLS regression under the hypothesis that the sampling distribution is normal

to identify the bidding behaviour. There is consistency in the sense that bidders seem

to be aware of the winner's curse and modify their bids accordingly. The drawback of

the model, highly critised, is the speci�c econometric specifaction right down to the

functional forms.

6.3 Radio

McMillan [39] investigated the mechanisms used in the selling of radio frequences in

the USA.

The author reports the di�culties New Zealand faced when TV licenses were auctioned:

Second-price auctions were used, but no reserve price was imposed. This led to a massive

loss for the government (after massive critisism now �rst-price sealed bid auctions are

used).

The Federal Communications Commission (FCC) chose to use a very complicated mech-

anism, a simultaneuous open multiple-round auction. An open auction was chosen since

it reduces the winner's curse. The FCC chose to run multiple rounds of sealed bids and

announced the bids after each round. This simulates an open outcry auction giving

extra control to the government. With this setup the government has control over col-

lusion, since bidders do not know with whom they are competing. Reserve prices were

used only for licenses that attracted three or fewer bids. Bidders who withdraw a win-

ning bid, or, in case of minorities, who had privileged access to frequencies, resold their

right, had to pay a penalty for doing so. The FCC did not use royalties, although theory

shows that royalties bene�t the seller.

6This paper led to a debate, some of which was reprinted in the AER 1991, cf. Levin and Smith [32],

Kagel and Levin [27], and Hansen and Lott [17].7There are agencies that do tell the estimated value. But this causes drastic change in the bidding

behaviour and is not dealt with in the article.

18 B�oheim, Zulehner / Auctions { A Survey | I H S

6.4 Other Markets

La�ont, Ossard and Vuong [30] used data from French eggplant auctions to test their

model proposed in the article (the method used will be presented in Section 8). The

obtained results are consistent with the theory, i.e. higher quality receives higher prices.

The relative importance of local produce is somewhat surprising but not inconsistent.

McAfee and Vincent [36] and Ashenfelter [1] investigated wine auctions and noted

something that became known as the "price-decline anomaly".

Ashenfelter and Genesove [2] investigated auctions of condominiums. The mechanism

that is used to sell condominiums is a "pooled auction", in which all units are combined

and the highest bidder has the right to choose among the units. This procedure is

repeated untill all the products are sold, resp. no one bids any longer. Prices usually

decline since the early bidder pay a premium for the selection right. Three important

�ndings were reported: First, the prices did decline in the progress of the auction.

Second, the prices of the items showed little or no relationship to the order of selling.

Third, a large price discount was seen in items sold at the beginning of the auction,

which is evidence that the prices did not re ect higher quality. The buyers fell pray to

the winner's curse.

McAfee and Vincent [37] tested for the optimal participation in these auctions. They

have found that the reserve price should be raised, thereby lowering the participation

rate and increasing government's expected revenue. The reserve price, according to

their model (see Section 8), should be 40 times higher than it was.

7 Experimental Auctions

Hendricks and Paarsch [19] see the role for auctions in experiments to test the be-

havioural predictions of game theoretic analysis. If the valuations and the underlying

probability distribution is know to the experimenter, than a comparison of the equi-

librium strategy and agents' behaviour can tell something about the relevance of the

theory.

Another important issue is that each year many goods are actually auctioned, from art

to wine. Auctions constitute one of the simplest way of price determination and are

easily carried out.

One predominant question in auction theory is the winner's curse. This question was

�rst posed in the seminal work of Capen, Clapp, and Campbell [7], who noted that in

case of oil �elds the winning bid usually received unexpectedly low returns.

In experimental settings auctions have been used to analyse a wide �eld of issues, from

bargaining models to political stock markets (double-sided auctions).

I H S | B�oheim, Zulehner / Auctions { A Survey 19

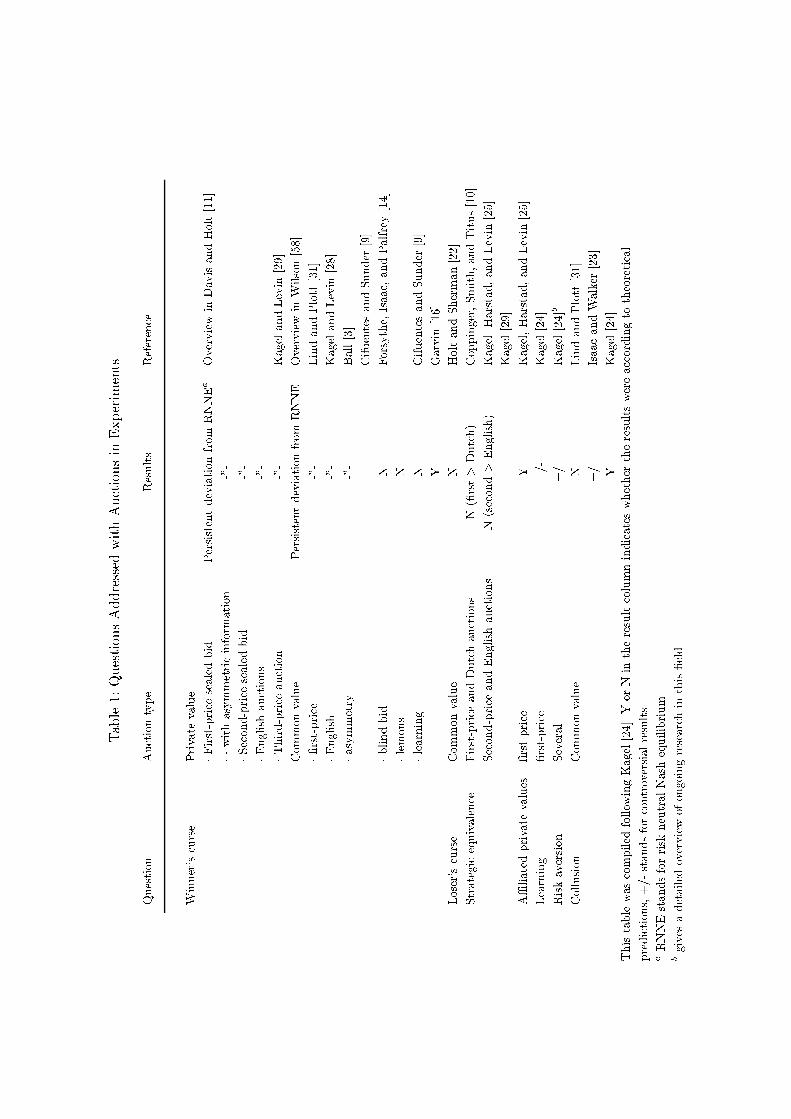

Kagel [24] gives a very detailed survey of results in experimental auctions. He himself

draws on the work of Wilson [58] and McAfee and McMillan [34]. For the sake of com-

pleteness and comparability with Section 6 we will reproduce here the most important

�ndings, listed also in Table 1.

Table1:QuestionsAddressedwithAuctionsinExperiments.

Question

Auctiontype

Results

Reference

Winner'scurse

Privatevalue

�

First-pricesealedbid

Persistentdeviationfrom

RNNEa

OverviewinDavisandHolt[11]

�

�

withasymmetricinformation

-"-

�

Second-pricesealedbid

-"-

�

Englishauctions

-"-

�

Third-priceauction

-"-

KagelandLevin[29]

Commonvalue

Persistentdeviationfrom

RNNE

OverviewinWilson[58]

�

�rst-price

-"-

LindandPlott[31]

�

English

-"-

KagelandLevin[28]

�

asymmetry

-"-

Ball[3]

CifuentesandSunder[9]

�

blindbid

N

Forsythe,Isaac,andPalfrey[14]

�

lemons

N

�

learning

N

CifuentesandSunder[9]

Y

Garvin[16]

Loser'scurse

Commonvalue

N

HoltandSherman[22]

Strategicequivalence

First-priceandDutchauctions

N(�rst>

Dutch)

Coppinger,Smith,andTitus[10]

Second-priceandEnglishauctions

N(second>

English)

Kagel.Harstad,andLevin[25]

Kagel[29]

A�liatedprivatevalues

�rst-price

Y

Kagel,Harstad,andLevin[25]

Learning

�rst-price

+/-

Kagel[24]

Riskaversion

Several

+/-

Kagel[24]b

Collusion

Commonvalue

N

LindandPlott[31]

+/-

IsaacandWalker[23]

Y

Kagel[24]

ThistablewascompiledfollowingKagel[24].YorNintheresultcolumnindicateswhethertheresultswereaccordingtotheoretical

predictions,+/-standsforcontroversialresults.

a

RNNEstandsforrisk-neutralNashequilibrium.

b

givesadetailedoverviewofongoingresearchinthis�eld.

I H S | B�oheim, Zulehner / Auctions { A Survey 21

The questions addressed deal with the most important questions theory is faced within

the �eld analysis. These questions are { amongst others { the winner's curse, the strate-

gic equivalence of certain types of auctions, whether learning does alter the bidding

behaviour, and, if collusive behaviour can be studied.

7.1 Results

In �eld data the question of whether the winner's curse is present is not easily answered,

the setting is usually very complex, in some cases (oil �elds) the value is not known for

years after the bidder bought the drilling rights.

In a seminal paper Bazerman and Samuelson [4] conducted an experiment mainly to

�nd out if the winner's curse is present in a laboratory situation. They observe a clear

winner's curse where the average winning bid was some 25 per cent over the value of

the object (10 $ as opposed to 8 $).

In this experiment the main results could have come from other factors as well. The

bidders were untrained and there were no repeated experiments. Kagel and Levin [26]

designed an experiment to deal with these issues. The main result was that the win-

ning bids were higher than the Nash equilibrium bids, but declined with participants'

experience.

In the laboratory the real value of the object is known to the experimenter, this is not

possible in the real world, where sometimes the real value of the object is known only

to the victims of the winner's curse.

But clearly, all experiments reported the presence of the winner's curse, even the very

unrealistic setup of Kagel, Harstad, and Levin [25] of the third price auction generates

overbidding. So, this seems still to be a very important feature one has to bear in

mind when using auctions. Several countries have already introduced guidelines against

overbidding in selling of public contracts, see e.g. Finsinger [13].

Other results from experiments are not as easily interpreted than the former ones.

The winner's curse being the most important researched topic in this context, other

questions have only recently been investigated. And, furthermore, some of the results

obtained do not allow a straightforward conclusion.

What can be said, however, is that there is a rich �eld of scienti�c research and that

it is still very important to consider other in uences to the outcome of auctions { like

repeated participation or risk aversion.

22 B�oheim, Zulehner / Auctions { A Survey | I H S

8 The Econometrics of Auctions

Many recent papers in auction literature are concerned with the possibility of for-

mulating and testing hypotheses. Hendricks and Paarsch [19] give an introduction to

structural and non-structural models. Both draw on previous work (e.g. Hendricks and

Porter [20] or Paarsch [48]) to distinguish between this two approaches.

One aim of recent work in auction theory was to identify the probability law behind the

valuations of potential bidders. This is essential if one wants to implement an optimal

auction mechanism. Bayesian Nash Equilibrium behaviour imposes restrictions upon

the relationships amongst bidders (e.g. between informed and uninformed bidders)

which do not depend on the functional form of the probability law for the valuations.

If one assumes that there is no unobserved heterogeneity the actual knowledge of this

probability law is unnecessary to test these restrictions (therefore "non-structural ap-

proach").

In contrast to the former approach, among others Paarsch [47], [48] has proposed to

use the entire structure of the auction to derive the data generating process. There is

admittance of heterogeneity, observed and unobserved, in this approach (the "structural

approach"). The complexity of the equilibrium bid functions are the main di�culty this

approach faces.

8.1 The Non-Structural Approach

The sale of drainage leases as described in Section 6 was described as following a

common value auction with a �rst-price sealed-bid mechanism.

Hendricks and Porter [20] imposed a�liation on the joint distribution of values, signals,

and reserve price.

Following this approach Hendricks and Porter [21] derived three restrictions governing

the behaviour of informed and uninformed bidders in the OCS auctions. First, a lower

participation rate of non-neighbouring �rms; second, few non-neighbouring bids below

some de facto reserve price; third, distributional equivalence above some level (where

bids are almost never rejected, a de facto acceptance price). They report tests on

these restrictions and the empirical distributions of bids produced "remarkable strong

support" for the theory. However, there are two caveats: Firstly, the distribution of

data was truncated, but that can be accommodated by imposing a condition on the

�rst order stochastic dominance. Secondly, the assumption of independent distribution

might not be ful�lled and for this reason the asymptotic distribution of the test statistic

is almost surely not standard (and up to some calculational di�culties).

La�ont, Ossard, and Vuong [30] propose a structural estimation method for the empir-

ical study of �rst-price, sealed bid and descending auctions. This method is based on

I H S | B�oheim, Zulehner / Auctions { A Survey 23

simulations relying on nonlinear least squares objective functions. The authors adopt

the private value paradigm where each bidder is supposed to have a di�erent private

value drawn independently from a probability distribution and use the structure of the

winning bid prediction as an estimate for the underlying structure.

McAfee and Vincent [37] use data from Hendricks and Porter [20] for OCS auctions.

They extended the generalized mineral-rights model 8 to allow for stochastic endogenous

participation.

In this model we have nature as a player that determines the number of possible bid-

ders, n, with some probability qn. Out of these a subset of the potential bidders is

drawn at random. The true value is v and the bidders receive some signal, xi, which is

independently distributed. A theorem is derived that provides a distribution-free test to

test whether participation is optimal. The auction is attracting ine�ciently few bidders

whenever net revenues exceed the values of tracts that attracted two or more bids.

8.2 The Structural Approach

8.2.1 English Auctions

Under the private value paradigm the setup of the English auction is the simplest to

estimate the joint distribution function on the n valuations. This is because of two

important assumptions: First, the independence of valuations, and, second, the failure

to distinguish between buyers. This means, that the marginal distributions of the joint

distributions are identical (n-times). If the task is to estimate F , the cumulative dis-

tribution function, this can be accomplished by recovering the entire joint distribution

for the buyers' valuations. A parametric formulation can now be derived (see Hendricks

and Porter [21] for a formal derivation):

Ft(v) = F (v; �; Zt);

where Zt is vector of characteristics which are observable, t indicates one auction out

of T auctions, and � is the unknown value. From this a likelihood-function can be

calculated and tested, given the results of an experiment.

Hendricks and Porter [21] reports results from Paarsch [47] who used this methods in

the British-Columbia timber auctions.

8.2.2 First-Price Sealed Bid Auctions

The winning bid in a �rst-price sealed bid auction, under independent private values, is

a function of the set fvign

i=1. As in the previous section, Ft(v) = F (v; �; Zt) represents

8The generalized mineral rights model is the same as the common value model without the (condi-

tional) independence assumption (Milgrom and Weber [44]).

24 B�oheim, Zulehner / Auctions { A Survey | I H S

a parametric speci�cation for each auction t, where t = 1; : : : ; T . The di�culty in

this framework is the fact that the upper bound of the support of the winning bid

depends on the parameters of interest | this violates the asymptotic consistency of

the maximum-likelihood estimator.

Paarsch [47] has used this framework for the aforementioned timber-sales. The results

showed variation in F depending on the use of English auctions or �rst-price sealed bid

auctions. The bidding behaviour di�ered in that the winning bid was more often the

reserve price with English auctions than with �rst-price sealed bid auctions. Moreover,

the amount of rent government accrued was negative.

8.2.3 Simulated Non-Linear Least Squares

The drawback of the last estimation method is the computational complexity. In gen-

eral the involved functions will not have an analytic solution and have to be solved

numerically.

The proposed alternative of La�ont, Ossard, and Vuong [30] is related to the method

of simulated moments (McFadden [38], and Pakes and Pollard [49]). The simulated

non-linear least squares estimator can be derived by minimizing the following objective

function:

Q(�) =TXt=1

[(wt � �m(�; Zt; Nt))2 �

1

J(J � 1)

JXj=1

(mj(�; Zt; Nt)� �m(�; Zt; Nt))2];

where � is the parameter to be estimated from �nite (�xed) J simulations. �m(�) is an

estimator for �(�), which is an estimate for E[wt]. Asymptotically the estimation error

generated by �m is eliminated by the estimate for the sample variance, the second term

in brackets. They have shown that the asymptotic distribution is normal.

8.2.4 Non-Parametric Estimation

The main criticism of the maximum likelihood method or the simulated non-linear least

squares is that an explicit assumption concerning the density functions, f(v), is needed.

The non-parametric approach, however, has to use all of the bids, not just the win-

ning bid, which the above methods used. The assumptions that are made is that each

potential buyer is bidding optimally against the opponent's bidding strategy, potential

buyers are using the same strategy, and this strategy is increasing in v.

The procedure consists of two steps. The �rst step involves the estimation of the condi-

tional density, gS(sjZ), in a non-parametric way. The estimation of the "hazard rate",

I H S | B�oheim, Zulehner / Auctions { A Survey 25

gS(sjZ)

GS(sjZ), is then used to estimate the bidding-strategy and the conditional density of

valuations. This provides a test of the behavioural hypothesis, which is carried out for

timber sales (Elyakime, La�ont, Loisel, and Vuong [12]). The auction is interesting in

that the seller's reserve price is not announced until the bids have been submitted. The-

oretically, from the point of the buyers, the seller is another buyer, but with a di�erent

payo� function. This implies a di�erent bidding strategy and a lot of trouble for the

researcher.

9 Conclusion

In this paper we have given an overview on auctions with an indivisible single object to

be sold to one of several buyers by one seller. Addressing the theoretical conditions for

which this setup can be analysed as a non cooperative game we have listed the main

results.

With these �ndings markets for quite di�erent objects have been investigated. The

problem is that the fundamental parameters of the game are neither known to the

researcher, nor to the buyers themselves.

To pin down strategic behaviour two possible approaches are considered: First, ex-

perimental economics, second, econometric analysis. From experiments scientists can

conclude from results to theoretical shortcomings, although { since the laboratory does

not re ect the complexity of \real markets" { in a limited way. The econometric ap-

proach is still in its beginning, using quite distinct ways of modeling estimators.

One striking feature with auction theory is that theory determines the market setup,

for instance designing the rules for radio frequencies auctions, whereas on the other

hand e�ort is being made to analyse the outcome of market behaviour.

The models we have considered in this survey are the standard models. Some cases,

which have been treated in the literature we have omitted, e.g. multiple and double-

sided auctions. For other more complicated cases no results have been obtained yet.

We tried to show that auction theory can deal with complex strategies and might be a

tool much needed in future research.

26 B�oheim, Zulehner / Auctions { A Survey | I H S

References

[1] Ashenfelter, O. (1989): "How Auctions Work for Wine and Art," Journal of Eco-nomic Perspectives, 3, 23-26.

[2] Ashenfelter, O. and D. Genesove (1992): Testing for Price Anomalies in RealestateAuctions," American Economic Review (Papers and Proceedings), 82(2), 501-5.

[3] Ball, S.B. (1991): "Experimental Evidence on the Winner's Curse in Negotiations,"Diss. Northwestern University, (quoted in Kagel [24]).

[4] Bazerman, M.H. and W.F. Samuelson (1983): "I Won the Auction but Don't Wantthe Prize," Journal of Con icts Resolutions, 27, 618-34.

[5] Bulow, J. and P. Klemperer (1994): "Auctions vs. Negotiations," NBER WorkingPaper 4608.

[6] Bulow, J. and J. Roberts (1989): "The Simple Economics of Optimal Auctions,"Journal of Political Economy, 97, 1060-1090.

[7] Capen, E.C., R.V. Clapp, and W.M. Campbell (1971): "Competetive Bidding inHigh-Risk Situations," Journal of Petroleum Technology, 23, 641-653.

[8] Cassady, R. (1967): Auctions and Auctioneering, Berkeley: University of CaliforniaPress (quoted in McAfee and McMillan [33]).

[9] Cifuentes, L.A. and S. Sunder (1991): "Some Further Evidence on the Winner'sCurse," Mimeo. Caranegie Mellon University.

[10] Coppinger, V.M., V.L. Smith, and J.A. Titus (1980): "Incentives and Behaviourin English, Dutch, and Sealed-Bid Auctions," Economic Inquiry, 43, 517-20.

[11] Davis, D.D. and C.A. Holt (1993): Experimental Economics, Princeton UniversityPress.

[12] Elyakime, B., J.J. La�ont, H. Ossard and Q. Vuong (1994): "First-Price Sealed-BidAuctions with Secret Reservation Prices," Annales d'Econmie et de Statistique, 34,115-141.

[13] Finsinger, J. (1987): "The Consequences of Non-Competitive and ProtectionistGovernment Purchasing Behaviour," Schweizerische Zeitschrift f�ur Volkswirtschaftund Statistik, 123(2), 147-73.

[14] Forsythe, R., R.M. Isaac, and T.R. Palfrey (1989): "Theories and Tests of "BlindBidding" in Sealed Bid Auctions. Rand Journal of Economics, 20, 214-38.

[15] Fudenberg, D. and J. Tirole (1991): Game Theory, MIT Press, Cambridge Mas-sachusetts.

[16] Garvin, S.(1994): Learning in Common Value Auctions: Some Initial Observa-tions," Journal of Economic Behaviour and Organisation, 25(3), 351-72.

[17] Hansen, R.G. and J.R. Lott (1991): "The Winner's Curse and Public Informationin Common-Value Auctions: Comment. American Economic Review, 81(1), 347-61.Theory," American Economic Review, AEA Papers and Proceedings, 75, 862-865.

[18] Hendricks, K. and R.H. Porter (1988): "An Empirical Study of an Auction withAsymmetric Information," American Economic Review, 78, 865-883.

[19] Hendricks, K. and H.J. Paarsch (1993): "A Survey of Recent Empirical WorkConcerning Auctions," Working Paper, Department of Economics, University ofWestern Ontario.

I H S | B�oheim, Zulehner / Auctions { A Survey 27

[20] Hendricks, K. and R.H. Porter (1992): "Joint Bidding in Federal OSC Auctions,"American Economic Review (Papers and Proceedings), 82(2), 506-11.

[21] Hendricks, K. and R.H. Porter (1993): "Bidding Behaviour in OSC Drainage Auc-tions," European Economic Review, 37, 320-8.

[22] Holt, C.A. and R. Sherman (1994): "The Loser's Curse and Bidder's Bias," Amer-ican Economic Review, 84, 642-52.

[23] Isaac, R.M. and J.M. Walker (1985): "Information and Conspiracy in Sealed-BidAuctions," Journal of Economic Behaviour and Organisation, 6, 139-59.

[24] Kagel, J.H. (1995): "Auctions: A Survey of Experimental Research," in The Hand-book of Experimental Economics, edited by J.H. Kagel and A.E. Roth, PrinctonUniversity Press.

[25] Kagel, J.H., R.M. Harstad, and D. Levin (1987): "Information Impact and Al-location Rules in Auctions with A�liated Private Values: A Laboratory Study.Econometrica, 55, 1275-1304.

[26] Kagel, J. and D. Levin (1986): "The Winner's Curse and Public Information inCommon Value Auctions," American Economic Review, 76, 894-920.

[27] Kagel, J. and D. Levin (1991): "The Winner's Curse and Public Information inCommon Value Auctions: A Reply," American Economic Review, 81, 362-9.

[28] Kagel, J. and D. Levin (1992): "Revenue Raising and Information Processing inEnglish Common-Value Auctions," Mimeo. University of Pittsburgh, (quoted in:Kagel [24].

[29] Kagel, J. and D. Levin (1993): "Independent Private Value Auctions: Bidder Be-haviour in First-, Second-, and Third-Price Auctions with Varying Number ofBidders. Economic Journal, 103, 868-79.

[30] La�ont, J.J., H. Ossard and Q. Vuong (1995): "Econometrics of First-Price Auc-tions," Econometrica, 63, 953-980.

[31] Lind, B. and C.R. Plott (1991): "The Winner's Curse: Experiments with Buyersand with Sellers, American Economic Review, 81, 335-46.

[32] Levin, D. and J.L. Smith (1991): "Some Evidence on the Winner's Curse: A Com-ment, American Economic Review, 81(1), 370-5.

[33] McAfee, R.P. and J. McMillan (1986): "Bidding for Contracts: A Principle-AgentAnalysis," Rand Journal of Economics, 17, 326-38.

[34] McAfee, R.P. and J. McMillan (1987): "Auctions and Biddings," Journal of Eco-nomic Literature, 25, 708-747.

[35] McAfee, R.P. and J. McMillan (1987): "Competion for Agency Contracts," RandJournal of Economics, 18, 296-307.

[36] McAfee, R.P. and D. Vincent (1991): "The Afternoon E�ect," CMSEMS Discus-sion Paper 961.

[37] McAfee, R.P. and D. Vincent (1992): "Updateing the Reserve Price in Common-Value Auctions," American Economic Review (Papers and Proceedings), 82(2),512-8.

[38] McFadden, D. (1989): "A Method of SimulatedMoments for Estimation of DiscreteResponse Models," Econometrica, 57, 995-1026.

[39] McMillan, J. (1989): "Selling Spectrum Rights," Journal of Economic Perspectives,8(3), 145-62.

28 B�oheim, Zulehner / Auctions { A Survey | I H S

[40] Mead, W. (1967): "Natural Resource Disposel Policy - Oral Versus Sealed Bids,"Natural Resource Planning Journal, M, 195-224 (quoted in [43]).

[41] Milgrom, P.R. (1979): "A Convergence Theorem for Competitive Bidding withDi�erential Information," Econometrica, 49, 679-688.

[42] Milgrom, P. (1981): "Rational Expectations, Information Acquisition, and Com-petitive Bidding," Econometrica, 49, 921-943.

[43] Milgrom, P. (1987): "Auction Theory," in Advances in Economic Theory, editedby T.Bewley. Cambridge: Cambridge University Press.

[44] Milgrom, P.R. and R.J. Weber (1982): "A Theory of Auctions and CompetitiveBidding," Econometrica, 50, 1089-1122.

[45] Myerson, R. (1981): "Optimal Auction Design," Mathematics of Operation Re-search, 6, 58-73.

[46] Myerson, R. : "The Basic Theory of Optimal Auctions," Mimeo. Lecture Notes ofJ. Swinkels at IAS, Vienna, 1995.

[47] Paarsch, H.J. (1991): "Empirical Models of Auctions and an Application toBritish Columbian Timber Sales," Discussion Paper 91-19, University of BritishColumbia, (quoted in: Hendricks and Porter [21]).

[48] Paarsch, H.J. (1992): "Deciding Between the Common and Private ValueParadigms in Empirical Models of Auctions," Journal of Econometrics, 51, 192-215.

[49] Pakes, A. and D. Pollard, (1989): "Simulation and the Asymptotics of OptimizationEstimators," Econometrica, 57, 1027-1057.

[50] Pesendorfer, M. (1996): "A Study of Collusion in First- Price Auctions," Mimeo.Yale University.

[51] Porter, R.H. (1995): The Role of Information in US O�shore and Gas Lease Auc-tions," Econometrica, 63(1), 1-27.

[52] Riley, J. (1988): "Ex Post Information in Auctions," Review of Economic Studies,55, 409-429.

[53] Riley, J. and W. Samuelson (1981): "Optimal Auctions," American Economic Re-view, 71, 381-392.

[54] Samuelson, W. (1986): "Bidding for Contracts," Management Science, 32, 1533-1550.

[55] Thiel S.E. (1988): "Some Evidence On The Winner's Curse," American EconomicReview, 78, 381-95.

[56] Vickrey, W. (1961): "Counterspeculation, Auctions and Competitive Sealed Ten-ders," Journal of Finance, 16, 8-37.

[57] Wilson, R. (1977): "A Bidding Model of Perfect Competion," Review of EconomicsStudies, 4, 511-518.

[58] Wilson, R. (1992): "Strategic Analysis of Auctions", in Handbook of Game Theorywith Economic Applications, edited by R. Aumann and S. Hart. New York: NorthHolland.

I H S | B�oheim, Zulehner / Auctions { A Survey 29

A Appendix

A.1 De�nitions

Def.1: The density g has the monotone likelihood ratio property if for all s0 > s and

x0> x, g(x j s)=g(x j s0) � g(x0 j s)=g(x0 j s0). This is equivalent to the a�liation

inequality.

A.2 Used Theorems

We now list all theorems used in the paper. Theorem (1)-(5) are concerned with a�l-

iation. They are taken from Milgrom and Weber [44], where the proofs are given, as

well. For more detailed de�nitions the reader is refered to the appendix of that paper.

Theorem 1: Let f : Rk ! R. (i) If f is strictly positive and twice continuously

di�erentiable, then f is a�liated if and only if for i 6= j, @2lnf=@xi@xj � 0. (ii) If

f(x) = g(x)h(x) where g and h are nonnegative and a�liated, then f is a�liated.

Theorem 2: If f is a�liated and symmetric inX2; : : : ; Xn, then S1; : : : ; Sm; X1; Y1; : : : ;

Yn�1 are a�liated.