Mechanisms for stakeholder integration: Bringing virtual stakeholder dialogue into organizations

Archives Des Sciences Vol 65, No. 5;May 2012

204 ISSN 1661-464X

Applying Stakeholder Approach in Developing Charity Disclosure

Index

Saunah Zainon (Corresponding author)

Accounting Research Institute, Faculty of Accountancy, Universiti Teknologi MARA

40450 Shah Alam, Selangor, Malaysia

Tel: +6019-776-2627 E-mail: [email protected]

Ruhaya Atan

Accounting Research Institute, Faculty of Accountancy, Universiti Teknologi MARA

40450 Shah Alam, Selangor, Malaysia

Tel: +6019-759-8710 E-mail: [email protected]

Yap Bee Wah

Department of Statistics, Faculty of Computer & Mathematical Sciences, Universiti Teknologi MARA

40450 Shah Alam, Selangor, Malaysia

Tel: +6012-634-4464 E-mail: [email protected]

The research is financed by the Prototype Research Grant Scheme (PRGS) under the Ministry of Higher

Education (MOHE), Malaysia

Abstract

The objective of this paper is to develop the Charity Disclosure Index (ChDI) by applying a stakeholder

approach. The large scale web survey was used to obtain the weight by its importance from the

institutional donors as respondents, representing the key stakeholders of the charity organizations. This

paper offers an acceptable charity disclosure instrument with the assignment of weight, based on the

stakeholder approach. The results indicate that the stakeholders had assigned the financial information

and governance information as the highest weight out of five categories of information in the charity

organizations. This study focuses on a single country study. Therefore, findings of this study might not

be comparative to other country that use different disclosure index. Nevertheless, it presents the original

work of self-developed ChDI instrument to measure the extent of charity disclosure in which it can be used

as a basis to improve the quality of charity reporting.

Keywords: Charity Disclosure Index, Instrument, Stakeholder, Reporting

1. Introduction

Disclosure of information is essential for the functioning of efficient charity organizations. Information is

disclosed through regulated financial reports, including financial statements and notes to the accounts,

service efforts and accomplishment (SEA) reports and other regulatory filings. In recent years, the nature of

charity organizations has changed from merely the traditional financial reporting model to the performance

Archives Des Sciences Vol 65, No. 5;May 2012

205 ISSN 1661-464X

reporting of information (Beattie, McInnes, & Fearnley, 2004). Performance reporting information

emphasizes backward-looking, quantified, financial, forward-looking and non-financial in nature. This is to

satisfy the stakeholders’ needs for information that provide disclosure of information for accountability and

transparency. In recent times, demand for disclosure by charity organizations has also increased due to

the increased in charity organizations wrongdoings and fraud (Cordery & Baskerville, 2011). Thus,

disclosure continues to become a major mechanism to sustain charity fraud and improving charity reporting

quality.

In addition, recent action of South East Asia countries such as Singapore and Thailand through their

Charity Councils have been actively reviewing and improving their non-profits regulatory framework and

enhancing their disclosure policies. In contrast, Malaysia, as one of the South East Asia countries where

the levels of transparency and governance controls are not prescribed by law, is lacked by the disclosure

policy. Hence, proactive action should be taken to improve the situation because accountability,

transparency and good governance are the keys to enhance the relationships between NPOs and

stakeholders. This proactive action may be taken by means of information disclosure. However, some

relevant questions are still open, such as the measurement of information for disclosure quality for charity

organizations. Another limitation encountered in charity disclosure studies is the difficulty in measuring

the extent of disclosure. This is because measurement of information disclosed by charity organizations is

a complex task since there is no uniform disclosure index can be applied in charity organizations.

This paper stimulates the interest and motivation of charity organization disclosure studies to coincide with

the moves of accounting and regulatory bodies to enhance accountability. In order to reduce information

asymmetry, an organization must consistently provide stakeholders with reliable and relevant information.

This is particularly to fulfill donors accountability by developing a disclosure index through the improved

in reporting (IASB, 2009; Narain, 2009) based on Malaysia regulatory environment. The objective of this

paper is to describe the process of developing the Charity Disclosure Index (ChDI) instrument, which

attempts to consider the needs for information of the stakeholders. This paper contributes to the existing

literature in three unique ways. First, as far as our knowledge reaches, there is no disclosure index

designed for charity organizations. This help assist the difficulties associated to information disclosure

measurement in charity organizations. Second, ChDI developed in this study has a multidimensional in

character that covers comprehensive elements of information such as the background, financial,

non-financial, governance and future information. Third, this index is developed using both the

qualitative and quantitative research methods and finally, a further contribution of ChDI is it should be a

value in an attempt to fill a gap in charity disclosure measurement instrument.

The rest of the paper is organized as follows: for the next section in Section 2 we review the literature

related to our research. Section 3 describes the process of developing ChDI and the final section

concludes the paper.

Archives Des Sciences Vol 65, No. 5;May 2012

206 ISSN 1661-464X

2.0 Review of Literature

Some researchers have argued that for the charity organizations, the discharged of accountability by means

of disclosure may attract the existing and potential donors (Banks, Fisher, & Nelson, 1997; D Coy, 1995;

Waters, 2010). Disclosure of information becomes important in tandem with the financial meltdowns

seen and related to non-profit organizations (Chandranayagam, 2010). He stated that “there just does not

seem to be enough transparency and publicly available information on projects done by non-profit

organizations, or projects in which such charitable organizations have invested.” Such disclosures aim to

demonstrate accountability and transparency, reporting the proper utilization of resources. Evidence from

previous studies showed that non-profits’ lack of disclosure and asymmetric information dissemination

among stakeholders may not only cause to inefficient resource allocations (Behn, DeVries, & Lin, 2007)

but leads to undermine the credibility of non-profits. Therefore, there is a concern to measure the extent

of disclosure in charity annual reports. In particular, this can be done through the use of disclosure index

to measure the extent of disclosure.

In the context of charity, disclosure plays an important role in the aspect of charity governance and

accountability (Saxton & Guo, 2011; Sinclair, Hooper, & Ayoub, 2010). Disclosure also fills financial

reporting function. Disclosure through financial reporting can be employed to reduce the undesirable

influences of information asymmetry. However, the most difficulty encountered in charity disclosure

studies is on disclosure measurement for a better disclosure quality. Disclosure quality is a complex

concept, multifaceted and subjective (Beattie et al., 2004). Often, there is lack of theory in support that

enables the construction of disclosure index for this concept. The extant of literature adopts a variety of

approaches to disclosure measurement, under the implicit assumption for disclosure quality. According to

Beattie et al. (2004), the approaches to measure disclosure can be classified in two categories: subjective

ratings and semi-objective approach.

The first approach has been to use subjective ratings that refer to analysts’ score on disclosure quality

rankings. This approach is not without conceptual problems involve the subjective judgement and

self-selection bias. In order to overcome limitations of subjective ratings, the second approach has been to

use researcher-constructed disclosure indices or semi-objective approach. Under this approach,

self-constructed disclosure index is developed by the researcher to measure the level of both mandatory and

voluntary information. Semi-objective approach also includes the use of tools such as thematic content

analysis, readability studies, linguistic analysis and disclosure indices (Urquiza, Navarro, & Trombetta,

2009).

2.1 Disclosure Index

One way of measuring information disclosed is through the use of disclosure index. An index comprises

numbers that encapsulate, in single figures, objects in the set that one wants to measure and that are capable

of measurement (D. Coy & Dixon, 2004, p. 82). The extensive used of disclosure index not only in

corporate annual reports (Alanezi & Albuloushi, 2011; Ho & Wong, 2001; Marston & Shrives, 1991), but

also applied in the context of various categories of non-profits such as colleges, universities, schools and

Archives Des Sciences Vol 65, No. 5;May 2012

207 ISSN 1661-464X

museums. For example, the colleges and universities (D. Coy & Dixon, 2004; Gordon, Fisher, Malone, &

Tower, 2002; Posey, 1980), the schools (Tooley & Guthrie, 2001), the museums (Christensen & Mohr,

2003; Wei, Davey, & Coy, 2008) and the charities (Connolly & Hyndman, 2000, 2001, 2004; Jetty &

Beattie, 2009).

It is common to design an index that takes into account several items of information, which are

dichotomous measured in terms of two possibilities of disclosure (value of 1 for disclosure) and

non-disclosure (value of 0 for non-disclosure). Various scholars have adopted a dichotomous approach in

order to assess the extent of disclosure in annual reports (Gandia, 2011; Gordon et al., 2002; Wei et al.,

2008). Alternatively, items of information are weighted in correspondence with their relative importance.

This alternative approach of a weighted disclosure index were used by Chow and Wong-Boren (1987),

Coy, Tower and Dixon (1993), and Fischer, Gordon and Kraut (2010) although there is no consensus about

the convenience of weighting them. In fact, in some cases, the researcher argued that predetermined the

weights are subjective (Ahmed, Dey, Akhter, & Raza, 2011). Furthermore, it is also argued weighted

indices have no difference or empirical advantage over an unweighted index (M. Fischer et al., 2010).

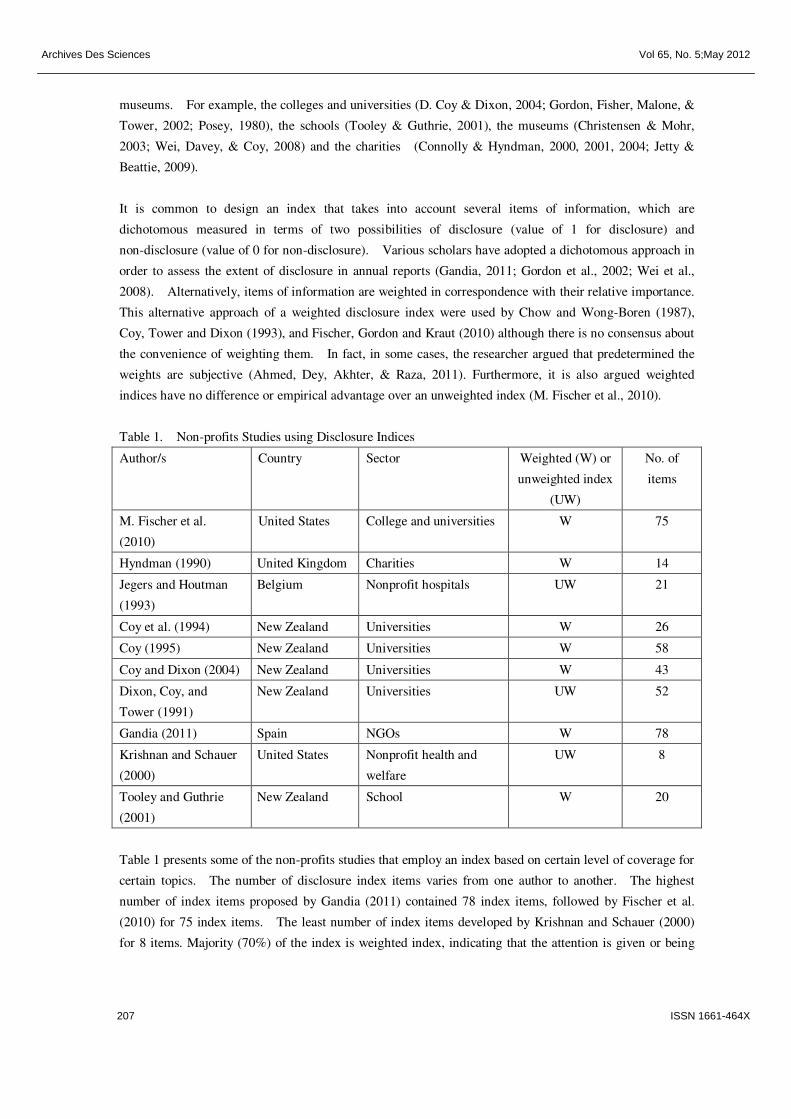

Table 1. Non-profits Studies using Disclosure Indices

Author/s Country Sector Weighted (W) or

unweighted index

(UW)

No. of

items

M. Fischer et al.

(2010)

United States College and universities W 75

Hyndman (1990) United Kingdom Charities W 14

Jegers and Houtman

(1993)

Belgium Nonprofit hospitals UW 21

Coy et al. (1994) New Zealand Universities W 26

Coy (1995) New Zealand Universities W 58

Coy and Dixon (2004) New Zealand Universities W 43

Dixon, Coy, and

Tower (1991)

New Zealand Universities UW 52

Gandia (2011) Spain NGOs W 78

Krishnan and Schauer

(2000)

United States Nonprofit health and

welfare

UW 8

Tooley and Guthrie

(2001)

New Zealand School W 20

Table 1 presents some of the non-profits studies that employ an index based on certain level of coverage for

certain topics. The number of disclosure index items varies from one author to another. The highest

number of index items proposed by Gandia (2011) contained 78 index items, followed by Fischer et al.

(2010) for 75 index items. The least number of index items developed by Krishnan and Schauer (2000)

for 8 items. Majority (70%) of the index is weighted index, indicating that the attention is given or being

Archives Des Sciences Vol 65, No. 5;May 2012

208 ISSN 1661-464X

emphasized for weighted index, in particular the weight of importance for information given by the

stakeholders. This shows stakeholders have long been considered as important target group for items of

information in disclosure (Elkington, 1993).

2.2 Items of Information for Disclosures

The direction for non-profit disclosure movement began with a call for better reporting within charity sector

in the United Kingdom (UK) with the first study by Bird and Morgan-Jones (1981). Their study found

great diversity in financial accounting practices of charities which, in turn, affect the use and understanding

of the disclosures by stakeholders. The findings of Bird and Morgan-Jones’s resulted in the introduction

of the 1988 Statement of Recommended Practice (SORP) by the Accounting Standards Committee (ASC,

1988), which was subsequently revised in 1995 (Charity Accounting Review Committee 1995), in 2000

(Charity Commission 2000) and in 2005 (Charity Commission 2005).

Other studies conducted by Hines and Jones (1992) and, William and Palmer (1998), also found varying

practices among the United Kingdom (UK) charities. Hines and Jones (1992) found that the original

SORP (1988) had little impact in reducing the variations in practices and this was supported by William

and Palmer (1998). Both studies suggested a change in direction towards improving the quality of

reporting through the user needs model. Soon after, research on charity onwards appears to follow user

needs model as suggested by them. Studies by Connolly and Hyndman (2003, 2004), and Christensen and

Mohr (2003), for example, have specifically examined the extent of narrative disclosure presented in

charities’ annual reports. Specifically, Connolly and Hyndman (2003, 2004) investigated the level of

disclosures, with specific information about background and performance indicators within the annual

reports narrative section. They found that the charities were only reporting background information but

seems to lack in disclosure of performance, with regards to efficiency and effectiveness. They concluded

that even the charity management are aware of the needs of users, but no provisions are made to meet the

performance disclosure of information.

Similarly, the study conducted by Christensen and Mohr (2003) in the United States (US), showed that the

contents of 172 not-for-profit museums annual reports were highly variable. They vary in overall content

of annual reports, from short descriptions of museum’s aims and activities to a comprehensive overview of

the charity’s mission, objectives and accomplishments. Financial data disclosure of information also

differs from no information to a complete set of audited financial statements. A content analysis study by

Connolly and Dhanani (2004) in assessing the disclosure patterns of accounting narratives within 71 UK

fund-raising charities revealed that: practices vary considerably, disclosure patterns are diverse depending

on the type of information disclosed; and charities report are mainly descriptive in nature, does not compare

activities and operations over time and does not provide explanations for significant changes reported.

Hyndman (1989) initially examined ten types of information in meeting stakeholders’ needs. In a later

study Hyndman (1990) identified four more information commonly disclosed by charities. He concluded

that charity reports are led by financial information, which stakeholders perceive as relatively less

important than the non-financial information. His studies proposed a priori model of reporting based on

Archives Des Sciences Vol 65, No. 5;May 2012

209 ISSN 1661-464X

information types suggested and needed by stakeholders. In addition, Hyndman recommended the need

towards moving the central focus from financial to non-financial disclosure for quality reporting.

Similarly, Khumawala and Gordon (1997) found that donors are more interested in non-financial

information such as the purpose of the organization, service efforts and accomplishments, the statement of

activities, programs provided, organizational goals and achievement, and the classification of expenses.

Kilcullen et al. (2007) identified four types of information – the first type of information identified is on

donation and grants or non-reciprocal transfers (NRT) including additional disclosure on the contribution

of volunteers in hours and dollars, the uses of NRT and the sources of funds. The remaining type of

information in their study also covers the financial and the non-financial information on the service

performance, fund accounting and budget information. The four types of information were from the

guidance provided to not-for-profit entities by standard setters from New Zealand, the U.S.A., Canada and

the U.K. and prior research on charities by Hyndman (1990) and, Khumawala and Gordon (1997).

The studies on information disclosure were further extended recently by Hancock et al. (2010) who

investigated the extent to which information is useful for assessing accountability and for decision making.

He found that the users and preparers have different perspectives, and they are able to differentiate the

usefulness of information for the purpose of decision making and accountability. Respondents are also

able to distinguish between different types of information for each category.

As evidence from the above literature, there appears a great motivation towards identifying items of

information to be considered by the charity in their disclosure reporting and the next section describes the

process of developing the charity disclosure index instrument for charity organizations.

3.0 The Process of Developing the ChDI

The main objective of this study is to describe the process of developing the ChDI. ChDI is the

instrument in the form of disclosure index that can be used to measure the extent of charity organizations

disclosure of information in their annual returns. A disclosure index indicate the extent to which the list of

selected items are disclosed in annual reports (Marston & Shrives, 1991). Coy (1995, p. 121) states that a

disclosure index is: ‘... a quantitative-based instrument designed to measure a series of items which, when

the scores for the items are aggregated, gives surrogate score indicative of the level of disclosure in a

specific context for which the index was devised.....’

The development of the ChDI in this study was initiated through a four-step process taking into

consideration the views from the needs of the stakeholders on their needs for information. The four-step

processes are as follows:

1. Identification of information items from review of literature, the statutory and regulations, and

semi-structured interviews with the key stakeholders.

2. Identification of measurement, structure and scoring procedures.

3. Assignment of weights.

Archives Des Sciences Vol 65, No. 5;May 2012

210 ISSN 1661-464X

4. Assessment of validity.

Many of early works view disclosure from the perspective of the information provider. As a result, the

disclosure studies may not say much about how the disclosures match the stakeholders’ needs for

information. Therefore, the development of ChDI contains both the qualitative and quantitative research

methods to take into account the stakeholders’ needs for information. Figure 1 below presents the process

of ChDI development.

Figure 1. The Process of ChDI Development

Process Description of

Process

Instrument Information Item Status

New Retained Modified Deleted

Process 1

A. Identification of

information

items from

review of

literature , the

statutory and

regulations

34

B. Semi-structured

Interviews with

key stakeholders

4

38

0

0

Process 2 Identification of

Measurement,

Structure and

Scoring Procedures

Process 3 Assignment of

Weights

Process 4 Assessment of

Validity

A. Expert Review

B. Survey

21

3

85

88

28

0

2

0

Initial ChDI

Validated CHDI

R E

V I S

I O N

Validated and tested

ChDI

Archives Des Sciences Vol 65, No. 5;May 2012

211 ISSN 1661-464X

3.1 Process 1A - The Identification of Information Items

Although there was no commonly specific theory used to determine the number of items for disclosure

index (Hooks, Coy, & Davey, 2002), the list of information items is primarily determined through a

review of literature. The number of information items developed by Coy (1995) contained 58 items in

Public Accountability Index (PAI), which were grouped into three broad categories: the Overview,

Financial and Service disclosures. The use of PAI in a study of annual reports in universities is built on

the predecessor of Modified Accountability Disclosure (MAD-score) index which consists of 26 items (Coy

et al. 1994). Hyndman (1990), on the other hand, used only 14 items of information in a charity

disclosure study. Figure 2 below presents the sources of the information items for the ChDI, mainly derived

from the Societies Act 1966 (Act 335) & Regulations, Malaysia Income Tax Act (ITA) 1967 and

Hyndman’s priori model.

Figure 2. Sources of the Items of Information

���� Name of the organization.

���� Registered address of the organization.

���� List of office bearers’ name.

���� Statement of financial position or balance sheet.

���� Statement of receipts and payments.

���� Name of associated or affiliated society, association,

trade union, or any other body of persons,

incorporated or unincorporated, outside Malaysia.

Societies

Act 1966 (Act 335) &

Regulations

���� Address of associated or affiliated society,

association, trade union, or any other body of

persons, incorporated or unincorporated, outside

Malaysia.

���� Minutes of annual general meeting (AGM).

���� Date of registration.

���� Description of financial support or aid by any

person outside Malaysia.

���� Description of financial support or aid by any

organization outside Malaysia.

Section 44(6) Malaysia

ITA 1967

���� Audited financial statements.

���� List of committee members stating the names, full

addresses, identity card numbers, occupation and the

positions held in the committee.

���� List of activities.

Archives Des Sciences Vol 65, No. 5;May 2012

212 ISSN 1661-464X

Priori Model of

Hyndman (1990)

� Statement of goals.

� Statement of objectives.

� Problem/need area information.

� Measure (s) of output.

� Measure (s) of efficiency.

� Administration cot percentage information.

� Simplified operating statement.

� Simplified balance sheet.

� Statement of future objectives.

� Budget information.

Basically, there are eleven items of information that need to be furnished by the registered charity

organizations under the Registry of Society (ROS). The information need to be furnished by submitting

Form 9 that consists of the Statement of Receipts and Payments of the last financial year, together with a

balance sheet showing the financial position at the close of the last financial year to the ROS within sixty

days after holding its AGM. This requirement is in accordance with Section 14(d) of the Societies Act 1966

(Act 335) & Regulations. However, the accounts submitted may not necessarily be audited. The other

statements that supplements financial statements such a Cash Flow Statement, Statement of Changes in

General Fund and Notes, comprising a summary of significant accounting policies and other explanatory

notes are not required by the ROS.

For tax-exempt purposes, the Inland Revenue Department (IRD) of Malaysia is the body that responsible

for granting the status. On the other hand, charitable organizations that may formally apply for tax

exemptions under Section 44(6) of the ITA 1967 from the IRD. However, the IRD guidelines for

application of Section 44(6) approval only requires general requirement of audited financial statements for

the preceding two years without the breakdown of the detail components of the financial statements to be

submitted. The other requirement for tax-exempt status application is the list of committee members (with

full details) and the list of activities of the organizations. In addition, Hyndman’s priori model was also

used as a benchmark in the identification of the items of information. As a result, the initial list of the

ChDI contained 34 items of information.

3.2 Process 1B – Semi-structured Interviews with Key Stakeholders

With the original list of 34 information items identified based on the review of the literature, the ChDI is

further developed through the interview process with the key stakeholders, represented by the institutional

donors. Semi-structured interviews were used to obtain items of information needs by the institutional

donors. The donors are major institutional donors with charitable donations of RM10,000 and above.

There were five companies that agreed to participate in this study. Three companies comprises of private

companies (family-owned business), in which the shares are not publicly traded. One of the companies is

an international foreign bank and the other is a main board public listed company.

Archives Des Sciences Vol 65, No. 5;May 2012

213 ISSN 1661-464X

All interviews were conducted in the interviewee’s office to allow the researcher and participant to interact

more freely. The questions were open-ended. Each interview was recorded and transcribed. The

interview session took place between 45-90 minutes. The interviews were chosen as the most appropriate

research approach because the people being interviewed are informants towards donations decision making.

Moir (2004) who undertook exploratory interviews with three different types of organizations (a large bank,

an international accounting firm and a large law firm) to sensitize the issues and to develop ease of

interviewing and analyzing data. Semi-structured interviews in this study foster the structuring and finding

of common patterns in relatively unknown fields of research (Eisenhardt, 1989). Interviews can provide

important information which is difficult to obtain via survey.

Based on the interviews, four more items of information were added to the ChDI list. The extra

information needed by the institutional donors from the charity organizations are: award winning for

participation in projects, participation in regional events, involvement in international events and the

statistics of their clients. These four items of information were all non-financial information (performance

information) category items and were added into the existing ChDI resulting in 38 items of information

listed in the list.

3.3 Process 2 – Identification of Measurement, Structure and Scoring Procedures

The 38 items of information were then structured accordingly into its categories. Coy and Dixon (2004)

found it is useful to structure an index into separate categories. Thus, the ChDI is structured into five

categories as follows: Basic Background Information (BBI), Financial Information (FI), Non-Financial or

Performance Information (NFI), Future Information (FUI) and Governance Information (GI). BBI has a list

of 13 items. There are 30 items which fall under FI, 19 items for NFI, eight items under FUI and GI has 18

items. These categories are then structured accordingly based on its categories. Table 2 below

summarizes the major elements of the ChDI. Altogether there are 88 items of information listed in ChDI.

Table 2. Items of Information in ChDI

Category Items of Information

Basic Background

Information

(BBI)

1. Name of the charity organization

2. Registered address of the organization

3. Nature of the organization services

4. List of office bearers’ name

5.

Name of associated or affiliated society, association, trade union, or any other body

of persons, incorporated or unincorporated, outside Malaysia

6. Address of associated or affiliated society, association, trade union, or any other

body of persons, incorporated or unincorporated, outside Malaysia

7. Minutes of AGM*

8. Legal and regulatory formation

9. Date of registration

10. Registration Number

11. Tax-exempt status

Archives Des Sciences Vol 65, No. 5;May 2012

214 ISSN 1661-464X

12. Governing Act [eg. Societies Act 1966, Trustees (Incorporation Act (Act 258]

13. Type of organization (eg. public-funded organization or private-funded

organization)

Financial Information

(FI)

1. Statement of Receipts and Payments

2. Description of financial support or aid by any person outside Malaysia

3. Description of financial support or aid by any organization outside Malaysia

4. Non-current assets

5. Current assets

6. Long-term liabilities

7. Current liabilities

8. Charitable funds

9. Statement of changes in charitable funds

10. Surplus or deficit

11. Cash flow from operating activities

12. Cash flow from investing activities

13. Cash flow from financing activities

14. Method of cash flow preparation

15. Financial resources

16. Disclosure of accounting policies

17. List of expenses (without classification)

18. Functional classification of expenses into charitable expenses

19. Functional classification of expenses into administration expenses

20. Percentage of charitable expenses out of total expenses

21. Percentage of administration expenses out of total expenses

22. Benefit-in-kind (in monetary terms)

23. Financial risk management

24. Total sources of income (without classification of income)

25. Classification of income such as donation income

26. Classification of income such as membership fees

27. Classification of income such as fundraising income

28. Classification of income such as other income

29. Government grants

30. Private grants

1. Clients’ satisfaction

2. Well-managed clients’ complaints

3. Investment in technology and computer system

4. New programs and services generated for new clients’ needs

5. New programs and services launch

Archives Des Sciences Vol 65, No. 5;May 2012

215 ISSN 1661-464X

Non-Financial

Information

(NFI)

6. Increase in clients each year

7. High level programs and service’s quality

8. The use of performance criteria to evaluate programs and services

9. Increase in number of staffs in training course

10. Improvement of skills and performance of staffs every year

11. High success rates maintained each year

12. High level program and services completion

13. Staff training

14. Non-financial resources (benefit-in-kind)

15. Participation in special projects

16. Participation in regional events

17. Participation in international events

18. Statistics of clients

19. List of activities

Future Information

(FUI)

1. Budget information for future expansion

2.

3.

Strategic planning for organizational development

Statement of future activities that benefit clients

4. Vision statement

5.

6.

Mission statement

Statement of objectives in a specific programs

7.

8.

Core values of the organization

Next year’s coming target future donations

Governance

Information (GI)

1. Patron’s message

2. Statement of principal officers (eg. Chairman, President, Director, etc.)

3. Statement of key committee members

4. List of names of major donors

5. Sponsorship

6. Calendar of events

7. Community services

8. Internal audit committee

9. Audit certification by independent auditor

10. Corporate partnership involvement

11. Founder of the organization

12. Patron of the organization

13. Committee members’ background

14. Committee members’ experience

15. Committee members’ qualification

16. Race of the committee members

Archives Des Sciences Vol 65, No. 5;May 2012

216 ISSN 1661-464X

17. Gender of the committee members

18. Number of the committee members

Basic Background Information (BBI)

Basic background information such as the name, nature of the services, registered address and the list of

office bearers’ name are not only compulsory requirement by the Societies Act 1966 (Act 335) and

Regulations but served as useful information to stakeholders, such as the institutional donors because it

provides a basic context of the organization prior detailed information about the organization. With BBI,

the stakeholders may have the overall picture of the organizations’ service operations and status for them to

make donation decision making for that charity organization.

Financial Information (FI)

Financial information is essential for the stakeholders to know the economic situation of the organizations

and they are able to evaluate on the use of funds that controlled and monitored by the board of trustees.

The Societies Act 1966 (Act 335) & Regulations requires the financial information about the organization

from the Statement of Receipts and Payments and related items in the Balance Sheet such as the current

assets, non-current assets and related disclosures of accounting policies to provide the stakeholders with

important financial information.

Non-Financial Information (NFI)

The non-financial information category includes clients’ satisfaction, clients’ complaints, and an increase in

clients, staff training and non-financial resources. The non-financial information is often regarded as

important information in charity organization. Hyndman’s (1990) and, Khumawala and Gordon’s (1997)

reported that in charity surveys, non-financial information is regarded most important by the users

compared to financial information.

Future Information (FUI)

Hyndman’s (1990) priori model provide a basis for the future information that is not covered in the

financial information or non-financial information category. This is considered the most important

information for charity. Such information includes budget information, strategic planning, mission and

vision statement and the core values of the organization.

Governance Information (GI)

This information is mostly obtained from the panel expert review during the content validity process. In

well-organized charity organizations, it is essential to have good charity governance for accountability

purposes. Governance matters such as the name list of major donors, statement of principal officers,

community services, establishment of internal audit committee or the founder of the organization are all

information items that might be required by the charity stakeholders.

Archives Des Sciences Vol 65, No. 5;May 2012

217 ISSN 1661-464X

3.4 Process 3 – Assignment of Weights

In computing the index score, either weighted or unweighted approach can be used to measure the extent of

disclosure. Previous studies have shown the use of weights (Fischer, Gordon, & Khumawala, 2008:

Fischer et al. 2010; Gandia, 2011; Gordon et al. 2002; Tooley & Guthrie, 2001) in measuring the extent of

disclosures in annual reports. The annual report is a vehicle for communicating information to enable the

performance and position of the organizations to be measured, classified, quantified and evaluated.

To be an index, ChDI has to provide a single number that aggregate the scores of all information. The

weights for the reporting index will be derived from the importance of information (e.g. information by

category such as the BBI, FI, NFI, FUI and GI). Some items of information might be recognized or

considered to be more important than others by the stakeholders. Therefore, it is detrimental to treat all

items of equal value. Weightings allows greater recognition of items that are essentially extensive such as

the non-current assets compared to items that are inherently limited in extent such as movement in equity.

To calculate the disclosure index, the weightings indicate the importance of the information items and are

measured using a seven-point scale (1= not at all important to 7= extremely important). Study

participants were asked to rate the relative importance of each of the identified disclosure items based on

this seven-point scale. The overall median weighted score were computed to provide a single figure

which summarizes the responses and serves as a basis for comparing the level of importance the study

participants attribute to each item of information. A median was used to denote the weight of

importance for the information items because it is more representative and meaningful for the ordinal scale

data (Agresti, 2010).

3.5 Process 4A – Assessment of Validity (Expert Review)

The final step involved in developing the ChDI is to test the validity of the items. Validity refers to the

degree to which it measures what it is suppose to measure and the reliability of a scale indicates how free it is

from random error (Pallant, 2007). The main types of validity used in this study were both the face and the

content validity. Face validity is the degree to which a survey questionnaire or other measurement appears

to reflect the variable it has been designed to measure. On the other hand, content validity or logical validity

seeks to establish that the items or questions are a well-balanced sample of the content domain to be measured

(Oppenheim, 1992, p. 162). This is an important process since the quality of the research instrument

becomes a central focus point of the study. Therefore, before it was pretested, the questionnaire has been

reviewed by the experts in their own field for face and content validity. Both local and international experts

participated in the validity process of ChDI. Local panel experts included the institutional donor who was

also the member of the National Council of Welfare and Social Development (NCSWD) of Malaysia, the

charity representatives and academic researchers from accounting, management and law backgrounds. The

expert from the non-profit regulatory body, i.e. the ROS was also invited in reviewing this validity process.

The recognized local experts were asked to review whether all items of information had been covered, and

consequently, from the 38 items of information, two information items deleted, additional 21 new

information items and 28-modified items were added, giving 85 items of information in the list.

Example of deleted item was ‘Balance Sheet’ and this item was replaced by the details of the balance sheet

Archives Des Sciences Vol 65, No. 5;May 2012

218 ISSN 1661-464X

items such as ‘the non-current assets, current assets, current liabilities and long-term liabilities.’ On the

modified items, the unfamiliar term by certain respondents such as ‘the ratio of charitable expenses’ was

changed to ‘percentage of charitable expenses to total expenses.” The ChDI was then sent for international

experts review.

Two international experts in survey research and non-financial performance measures were selected. The

ChDI was further improved by recommendation by the international expert to consider expanding the scale

measurement. The scale was then was then expanded to 7 points (1-Not at all important to 7-Extremely

important), this allowing the respondent to select some more point, with 4 being neutral. It was suggested

that a 7-point scale of evaluation would provide better accuracy to differentiate the total score of category

items and the aggregate total score of the index items (Ritchie & Eastwood, 2006). Other items in the

ChDI were considered adequate for the ChDI to be used as the instrument to measure the extent of

disclosure practices by the charity organizations. The index scores are considered reliable if the results

can be replicated by other researcher and valid if the index mean what the researchers intended (Marston &

Shrives, 1991). A reliable index is reached uniformly by determining scores for each of, possibly, many

component items, which have been identified as relevant to the set and the purposes of the index. This is

to ensure the practicality so that there will be enough variance in the responses.

3.6 Process 4B – Assessment of Validity (Survey)

The ChDI is intended to capture the institutional donors’ needs for information that should be disclosed and

the relative importance of the information items from the charity organizations. The validated ChDI were

then further validated through the survey before it is ready to be applied and used as validated ChDI. Since

the questionnaire design has impact on response rate and validity of the data (Rea & Parker, 2005), there

is a need to revise and improve the questionnaire design through pilot testing. The questionnaire was

revised and improved accordingly before it was distributed to respondents. Additional three items of

financial information considered important by the respondents such as the information on ‘cash flow from

financing activities,’ ‘private grants’ and ‘financial risk management’ were added as a result of pilot testing.

The revised and validated ChDI consists of 88 items of information. Figure 3 below summarizes the

category of information accordingly in the form of numbers and percentage.

Figure 3. Category of Information by Numbers and Percentage

Archives Des Sciences Vol 65, No. 5;May 2012

219 ISSN 1661-464X

The above graph shows that the most of 34.1% items of information under the FI category, followed by the

NFI items (21.6%) and the least of 9.1% items of information in the FUI category. The extent of validity

and reliability of ChDI were further validated by means of large-scale data for the final survey in order to

confirm the importance of information needed by the stakeholders. For this purpose, data was collected via

a structured questionnaire using web application survey (perseus.surveysolutions®/EFM). This choice of

methods is chosen due to many claims made about the advantages of conducting surveys on the web.

The web or online survey is a cost effective way of administering a survey that allows large amount of

information collected. The web survey may also save time by allowing the researchers to collect data

while they working on other tasks or projects (Andrews, Nonnecke, & Peece, 2003). After an invitation

to participate in a survey is posted to the website, the responses to web survey can be transmitted to the

researcher through e-mail or immediately posted to an HTML document or database file. This would

allow the researcher to perform preliminary analyses while waiting for the desired number of targeted

responses.

As discussed above, web survey offers many benefits over traditional surveys. However, there are some

drawbacks that should also be considered by researchers using web survey methodology. Although many

problems in survey methods are also inherent in traditional survey methods, but some are unique to only the

computer medium. Sampling is one of the issues encountered in web survey method. Concerning sampling

representatives (Dillman, 2000; Swoboda, Muehlberger, Weitkunat, & Schneeweiss, 1997; Tse, 1998) that

many populations are geographically diverse, do not receive the attention they deserved since e-mail

sampling is necessarily limited to e-email users.

Kittleson (1995) argued that the US Postal Service is the best way of getting a satisfactory response rate

that could not be achieved among active e-mail users. Few studies that noted low e-mail survey response

rate, among others, Couper, Blair and Triplett (1997) achieved a 43% web survey response rate versus 71%

from mail, Schuldt and Totten (1994) reported only 19% compared to a 57% mail response and Swoboda et

al. (1997) received a 21% response rate from e-mail survey. In contrast to the results noted, there are

some web survey studies perform well beyond expectations. Indeed, some could reach as high as 70%.

An e-mail survey to Lotus Development Corporation employees conducted by Bachmann and Elfrink (1996)

achieved 56% response rate. Also, Kiesler and Sproull’s (1986) e-mail survey to college students

achieved a 67% response rate. Mehta and Sivadas (1995) concluded that e-mail surveys with pre-notice

and follow up prompts can generally achieve higher response rates.

This study uses the web survey design methodology for the purpose of assigning the weights for the

instrument through the conduct of larger scale web-based survey before it can be used. For this, the target

respondents are those institutional donors from the main public listed companies in the Bursa Malaysia and

the respondents were guaranteed of ethics and confidentiality; as they are assured that identifying

information will not be made available to anyone who is not directly involved in the study. This is the

principle of anonymity which essentially means that the respondents will remain anonymous throughout the

study.

Archives Des Sciences Vol 65, No. 5;May 2012

220 ISSN 1661-464X

As at 10 May 2011, there are 839 main public listed companies in the Bursa Malaysia. Not all companies

having had established the corporate social responsibility department. However, the chosen companies

were based on the basis that the companies have made sum amount of donations as one of the corporate

social responsibility (CSR) pillars. Data collection for the web survey took about two months from 16th of

May 2011 to 15th of June 2011. Respondents were assured of confidentiality and anonymity of their

returned questionnaires. The response rate was very low in the first two weeks. During the two-month

period, three e-mail reminders were sent out to them in order to increase the response rate.

By 15th of June 2011, a total of 140 institutional donors participated. Out of 140 returned questionnaires,

16.4% were incomplete responses and therefore only 117 fully completed questionnaires can be used for

further analysis. This contributed to 13.9% of response rate. The respondents were majority from the

industrial products sector (35%) and consumer products sector (25.6%). This is followed by the trading

and services (12%), construction (9.4%), plantation (4.3%), properties (3.4%) and others (10.3%). Table 3

presents the result of median and standard deviation for the final survey.

Table 3. Median and standard deviations for information items listed in ChDI for Main Survey

Rank Information items Category Median Standard

deviation

Min. Max.

Extremely

Important

1 Cash flow from operating

activities

FI 7.00 0.906 2 7

2 Internal audit committee GI 7.00 0.772 4 7

3 Audit certification by

independent auditor

GI 7.00 0.960 1 7

Very

Important

4 Improvement of skills and

performance of staffs every

year

NFI 6.00 0.911 1 7

5 Staff training NFI 6.00 0.868 3 7

6 Statistics of clients NFI 6.00 0.902 3 7

7 List of activities NFI 6.00 0.923 1 7

8 Budget information for

future expansion

FUI 6.00 0.845 3 7

9 Strategic planning for

organizational development

FUI 6.00 0.830 3 7

10 Statement of future

activities that benefit clients

FUI 6.00 0.868 3 7

Archives Des Sciences Vol 65, No. 5;May 2012

221 ISSN 1661-464X

11 Vision statement FUI 6.00 0.835 3 7

12 Mission statement FUI 6.00 0.866 3 7

13 Statement of objectives in

a specific programme

FUI 6.00 1.019 1 7

14 Core values of the

organization

FUI 6.00 0.881 1 7

15 Next year’s coming target

future donations

FUI 6.00 1.126 1 7

16 Patron’s message GI 6.00 1.445 1 7

17 Statement of principal

officers

GI 6.00 1.082 1 7

18 List of names of major

donors

GI 6.00 1.190 1 7

19 Sponsorship GI 6.00 1.064 1 7

20 Calendar of events GI 6.00 0.710 3 7

21 Community services GI 6.00 0.689 4 7

22 Corporate partnership

involvement

GI 6.00 0.803 1 7

23 Founder of the organization GI 6.00 1.054 1 7

24 Patron of the organization GI 6.00 1.144 1 7

25 Committee members’

background

GI 6.00 0.655 4 7

26 Committee members’

experience

GI 6.00 0.662 4 7

27 Committee members’

qualification

GI 6.00 0.709 3 7

28 Number of committee

members

GI 6.00 0.869 1 7

29 Name of the organization BBI 6.00 0.802 3 7

30 Registered address of the

organization

BBI 6.00 0.889 2 7

31 Nature of the organization

services

BBI 6.00 0.966 3 7

32 List of office bearer’s name BBI 6.00 1.105 1 7

33 Legal and regulatory

formation

BBI 6.00 0.847 1 7

34 Date of registration BBI 6.00 0.970 3 7

35 Registration number BBI 6.00 0.854 3 7

36 Tax exempt status BBI 6.00 0.826 3 7

37 Governing Act BBI 6.00 0.826 3 7

Archives Des Sciences Vol 65, No. 5;May 2012

222 ISSN 1661-464X

38 Type of organization BBI 6.00 0.805 3 7

39 Statement of Receipts and

Payments

FI 6.00 0.713 4 7

40 Surplus or deficit FI 6.00 0.978 1 7

41 Cash flow from investing

activities

FI 6.00 0.912 2 7

42 Cash flow from financing

activities

FI 6.00 1.045 1 7

43 Method of cash flow

preparation

FI 6.00 0.875 3 7

44 Financial resources FI 6.00 0.772 3 7

45 Disclosure of accounting

policies

FI 6.00 0.860 1 7

46 List of expenses (without

classification)

FI 6.00 0.797 4 7

47 Functional classification of

expenses into charitable

expenses

FI 6.00 0.701 4 7

48 Functional classification of

expenses into

administration expenses

FI 6.00 0.681 4 7

49 Percentage of charitable

expenses out of total

expenses

FI 6.00 0.775 3 7

50 Percentage of

administration expenses out

of total expenses

FI 6.00 0.822 3 7

51 Benefit in kind (in

monetary terms)

FI 6.00 0.725 3 7

52 Financial risk management FI 6.00 0.698 4 7

53 Total sources of income

(without classification of

income)

FI 6.00 0.701 4 7

54 Classification of income

such as donation income

FI 6.00 0.833 1 7

55 Classification of income

such as membership fees

FI 6.00 0.682 4 7

56 Classification of income

such as fundraising income

FI 6.00 0.682 4 7

57 Classification of income FI 6.00 0.695 4 7

Archives Des Sciences Vol 65, No. 5;May 2012

223 ISSN 1661-464X

such as other income

58 Government grants FI 6.00 0.754 4 7

59 Private grants FI 6.00 0.748 4 7

60 Clients’ satisfaction NFI 6.00 0.701 3 7

61 Well-managed clients’

complaints

NFI 6.00 0.750 3 7

Moderately

Important

62 Increase in number of staffs

in training courses

NFI 5.00 0.844 1 7

63 High success rates

maintained each year

NFI 5.00 0.903 1 7

64 High –level programme and

services completion

NFI 5.00 0.815 3 7

65 Non-financial resources

(Benefit in kind)

NFI 5.00 0.751 3 7

66 Winner or participation in

special projects

NFI 5.00 0.764 3 7

67 Participation in regional

events

NFI 5.00 0.738 3 7

68 Participation in

international events

NFI 5.00 0.752 3 7

69 Statement of key committee

members

NFI 5.00 1.357 1 7

70 Race of committee

members

GI 5.00 1.462 1 7

71 Gender of committee

members

GI 5.00 1.399 1 7

72 Non-current assets FI 5.00 0.776 3 7

73 Current assets FI 5.00 0.779 3 7

74 Long-term liabilities FI 5.00 0.808 3 7

75 Current liabilities FI 5.00 0.919 1 7

76 Charitable funds FI 5.00 0.705 3 7

77 Statement of changes in

charitable funds

FI 5.00 0.756 3 7

78 Investment in technology

and computer system

NFI 5.00 0.743 3 7

79 New programmes and

services generated for new

clients’ needs

NFI 5.00 0.788 3 7

Archives Des Sciences Vol 65, No. 5;May 2012

224 ISSN 1661-464X

80 New programmes and

services launch

NFI 5.00 0.782 3 7

81 Increase in clients NFI 5.00 0.715 3 7

82 High level programme and

service’s quality

NFI 5.00 0.845 1 7

83 The use of performance

criteria to evaluate

programme and services

NFI 5.00 0.894 1 7

Neutral

84 Name of associated or

affiliated society outside

Malaysia

BBI 4.00 1.807 1 7

85 Address of associated or

affiliated society outside

Malaysia

BBI 4.00 1.703 1 7

86 Financial support from

person outside Malaysia

BBI 4.00 1.799 1 7

87 Financial support from

organization outside

Malaysia

BBI 4.00 1.758 1 7

Slightly

Important

88 Minutes of AGM BBI 3.00 1.715 1 7

It was noted that the first three items that carried the highest weight (median of 7.00) were both from the

financial information category (cash flow from operating activities) and the governance category of

information (i.e. the internal audit and audit certification by independent auditor). Minutes of AGM, the

item of information that is required by the ROS carried the least weight (median of 3.00). The remaining

items of information follows their respective importance-weight assigned, making this instrument ready and

complete for practical usage.

4.0 Conclusion

One of the major purposes of disclosure in annual reports is to inform stakeholders about the organizations’

affairs. Therefore, it is likely that the stakeholders use the disclosed information to meet their interests

and needs. Because non-profits sector may possess characteristics that differ from profit sector, it is

important to have a specifically designed disclosure measurement instrument.

The process of ChDI development in this study has provided new insight regarding the assessment of the

stakeholders’ needs for information from the charity organizations. This is true for two reasons. First,

the items of information included in the index were based from both the review of literature, interviews and

subject to confirmation and scrutiny by the key stakeholders through a survey. Second, this process

Archives Des Sciences Vol 65, No. 5;May 2012

225 ISSN 1661-464X

demonstrated a comprehensive reference made from both the primary and secondary information. Hence,

ChDI can be a meaningful instrument that can be used as to provide a framework to guide the preparation

of charity reporting. ChDI has its unique novelty by incorporating a polychotomous approach of 7-point

likert scale to assess items of information, meaning that ChDI is considered weighted-importance index that

generate ratio scale for the use in parametric statistical analyses.

The development of ChDI considering the key stakeholders in the process of developing the disclosure

indices to measure the extent of disclosure is very practical and applicable in the context of charity annual

reports, particularly in Malaysia. However, because of the nature of this study, it might not be possible to

make general statements about the information needs of all the diverse charity stakeholders. As to this

study without limitations, the researchers’ discretion on certain information items has been used but

notwithstanding the stakeholders’ opinions dominates the judgement and discretion.

One important issue that relates to the application of ChDI is whether the ChDI can be applicable in other

charity organizations from other countries, or on other parts of the NPOs, such as the human resource,

women, youth or culture categorization of NPOs. As far as NPOs are generally concerned, the generic

features on the basic and financial category of information can be applied elsewhere, but it would be

meaningful if some medication could be made to suit several special features based on other countries

environment.

The disclosure index developed in this study is also a valuable instrument to measure the accountability of

the information disclosed in the annual reports of charity organizations. It also provides an acceptable

charity disclosure instrument with weight assigned, which can be used by the regulators to assess the

adequacy of charity disclosure reporting.

References

Agresti, A. (2010). Analysis of ordinal categorical data (2nd ed.). New Jersey: John Wiley & Sons.

Ahmed, A. A. A., Dey, M. M., Akhter, W., & Raza, A. (2011). Timeliness attributes and the extent of

accounting disclosure: A study of banking companies in Bangladesh. Interdisciplinary Journal of

Contemporary Research in Business, 3(1), 915-925.

Alanezi, F. S., & Albuloushi, S. S. (2011). Does the existence of voluntary audit committees really affect

IFRS-required disclosure? The Kuwaiti evidence. International Journal of Disclosure and

Governance, 8(2), 148-173.

Andrews, D., Nonnecke, B., & Peece, J. (2003). Electronic survey methodology: A case study in reaching

hard-to-involve internet users. International Journal of Human-Computer Interaction 16(2),

185-210.

Bachmann, D., & Elfrink, J. (1996). Tracking the progress of e-mail versus snail-mail. Marketing Research,

8(2), 31-35.

Banks, W., Fisher, J., & Nelson, M. (1997). University accountability in England, Wales, and Northern

Ireland: 1992-1994. Journal of International Accounting, Auditing & Taxation, 6(2), 211-226.

Beattie, V., McInnes, B., & Fearnley, S. (2004). A methodology for analysing and evaluating narratives in

Archives Des Sciences Vol 65, No. 5;May 2012

226 ISSN 1661-464X

annual reports: A comprehensive descriptive profile and metrics for disclosure quality attributes.

Accounting Forum, 28(3), 205-236. doi: 10.1016/j.accfor.2004.07.001

Behn, B., DeVries, D., & Lin, J. (2007). Voluntary disclosure in nonprofit organizations: An exploratory

study. Retrieved 11 November 2009 http://ssrn.com/abstract=727363

Bird, P., & Morgan-Jones, P. (1981). Financial reporting by charities. London: The Institute of Chartered

Accountants of England and Wales.

Chandranayagam, D. (2010, 20 January ). Charities must tell us more, The Sun, p. 13.

Chow, C. W., & Wong-Boren, A. (1987). Voluntary financial disclosure by Mexican corporations. The

Accounting Review, July, 533-541.

Christensen, A., & Mohr, R. (2003). Not-for-profit annual reports: What do museum managers

communicate? Financial Accountability & Management, 19(2), 139-158.

Connolly, C., & Dhanani, A. (2004). Narrative reporting practices in United Kingdom charities Working

Paper: Cardiff Business School.

Connolly, C., & Hyndman, N. (2000). Charity accounting: An empirical analysis of the impact of recent

changes. The British Accounting Review, 32(1), 77-100.

Connolly, C., & Hyndman, N. (2001). A comparative study on the impact of revised SORP 2 on British and

Irish charities. Financial Accountability & Management, 17(1), 73-97.

Connolly, C., & Hyndman, N. (2003). Performance reporting by UK charities: Approaches, difficulties and

current practice: The Institute of Chartered Accountants of Scotland.

Connolly, C., & Hyndman, N. (2004). Performance reporting: A comparative study of British and Irish

chatities. The British Accounting Review, 36, 127-154.

Cordery, C. J., & Baskerville, R. F. (2011). Charity transgressions, trust and accountability. Voluntas:

International Journal of Voluntary and Nonprofit Organizations(22), 197-213.

Couper, M. P., Blair, J., & Triplett, T. (1997). A comparison of mail and e-mail for a survey of employees in

federal statistical agencies. Paper presented at the American Association for Public Opinion

Research.

Coy, D. (1995). A public accountability index for annual reporting by NZ Universities. University of

Waikato. Hamilton.

Coy, D., & Dixon, K. (2004). The public accountability index: Crafting a parametric disclosure index for

annual reports. British Accounting Review, 36(1), 79-106.

Coy, D., Tower, G., & Dixon, K. (1993). Quantifying the quality of tertiary education annual reports.

Accounting and Finance, 33(2), 121-129.

Coy, D., Tower, G., & Dixon, K. (1994). Public sector reform in New Zealand: the progress of tertiary

education annual reports, 1990-92. Financial Accountability & Management, 10(3), 253-261.

Dillman, D. A. (2000). Mail and internet surveys: The tailored design method (2nd ed.). New York: Wiley.

Dixon, K., Coy, D., & Tower, G. D. (1991). External reporting by New Zealand universities 1985-1989:

Improving accountability. Financial Accountability & Management, 7, 159-178.

Eisenhardt, K. M. (1989). Building theories from case study research. Academy of Management Review,

14(4), 532-550.

Elkington, J. (1993). Coming clean: The rise and rise of the corporate environmental report. Business

Strategy and the Environmental, 2, 42-44.

Archives Des Sciences Vol 65, No. 5;May 2012

227 ISSN 1661-464X

Fischer, M., Gordon, T. P., & Khumawala, S. B. (2008). Tax-exempt organizations and nonarticulation:

Estimates are no substitute for disclosure of cash provided by operations. Accounting Horizons,

22(2), 133-158.

Fischer, M., Gordon, T. P., & Kraut, M. A. (2010). Meeting user information needs: The impact of major

changes in FASB and GASB standards on financial reporting by colleges and universities Journal

of Accounting and Public Policy (Vol. 29, pp. 374-399).

Gandia, J. L. (2011). Internet disclosure by nonprofit organizations: Empirical evidence of

nongovernmental organizations for development in Spain. Nonprofit and Voluntary Sector

Quarterly, 40(1), 57-78. doi: 10.1177/0899764009343782

Gordon, T., Fisher, M., Malone, D., & Tower, G. (2002). A comparative empirical examination of extent of

disclosure by private and public colleges and universities in the United States. Journal of

Accounting and Public Policy, 21(3), 235-275.

Hancock, P., Izan, I., & Kilcullen, L. (2010, 4-6 July). Useful information in the external financial reports

of private sector NFP entities - a user perspective. Paper presented at the Accounting and

Finance Association of Australia and New Zealand (AFAANZ) Conference, Christchurch, New

Zealand.

Hines, A., & Jones, M. J. (1992). The impact of SORP2 on the UK charitable sector: An empirical study.

Financial Accountability & Management, 8(1), 49-67.

Ho, S. S. M., & Wong, K. S. (2001). A study of the relationship between corporate govenance structures

and the extent of voluntary disclosure Journal of International Accounting, Auditing & Taxation,

10(2), 139-156.

Hooks, J., Coy, D., & Davey, H. (2002). The information gap in annual reports. Accounting, Auditing and

Accountability Journal, 15(4), 501-522.

Hyndman, N. (1990). Charity accounting: An empirical study of the information needs of contributors to

UK fundraising charities. Financial Accountability & Management, 6(4), 295-307.

Hyndman, N. S. (1989). Charity accounting: A comparison of contributors' information needs and the ASC

approach. Paper presented at the Irish Accounting Association Annual Conference, Cork.

IASB. (2009). Exposure Draft Management Commentary.

Jegers, M., & Houtman, C. (1993). Accounting theory and compliance with accounting regulations: The

case of hospitals. Financial Accountability & Management, 9(4), 267-278.

Jetty, J., & Beattie, V. (2009). RR108 - Disclosure practices and policies of UK Charities ACCA Research

Report No. 108: ACCA.

Khumawala, S. B., & Gordon, T. P. (1997). Bridging the credibility of GAAP: Individual donors and the

new accounting standards for nonprofit organizations. Accounting Horizons, 11(3), 45-68.

Kiesler, S., & Sproull, L. S. (1986). Response effects in the electronic survey. Public Opinion Quarterly, 50,

402-413.

Kilcullen, L., Hancock, P., & Izan, H. Y. (2007). User requirements for not-for-profit entity financial

reporting: An international comparison. Australian Accounting Review, 17(1), 26.

Kittleson, M. J. (1995). An assessment of the response rate via the postal service and e-mail. Health Values,

19(2), 27-39.

Krishnan, J., & Schauer, P. C. (2000). The differentiation of quality among auditors: Evidence from the

Archives Des Sciences Vol 65, No. 5;May 2012

228 ISSN 1661-464X

not-for-profit sector. Auditing: A Journal of Theory and Practice, 19(1), 9-25.

Marston, C. L., & Shrives, P. J. (1991). The use of disclosure indices in accounting research: A review of

article. British Accounting Review, 23(3), 195-210.

Mehta, R., & Sivadas, E. (1995). Comparing response rates and response content in mail versus electronic

mail surveys. Journal of the Market Research Society, 37(4), 429-439.

Moir, L. (2004). Why does business support the arts? Philanthropy, marketing or legitimation. Cranfield

University, London.

Narain, L. S. (2009). Implications of the Sarbanes-Oxley Act for nonprofit organizations. The Business

Review, Cambridge, 13(2), 16-23.

Oppenheim, A. N. (1992). Questionnaire design, interviewing and attitude measurement. New York: Basic

Books Inc.

Pallant, J. (2007). SPSS: Survival manual (3rd ed.). Crows Nest NSW 2065: Allen & Unwin.

Posey, R. B. (1980). An investigation of the differences in bond disclosures made by public and private

colleges. Oklahoma State University

Rea, L. M., & Parker, R. A. (2005). Designing and conducting survey research: A comprehensive guide.

San Francisco: Jossey-Bass.

Ritchie, W. J., & Eastwood, K. (2006). Executive functional experience and its relationship to the financial

performance of nonprofit organizations. Nonprofit Management and Leadership, 17(1), 67-82.

Saxton, G. D., & Guo, C. (2011). Accountability online: Understanding the web-based accountability

practices of nonprofit organizations. Nonprofit and Voluntary Sector Quarterly, 40(2), 270-295.

Schuldt, B. A., & Totten, J. W. (1994). Electronic mail vs. mail survey response rates. Marketing Research,

6(1), 36-39.

Sinclair, R., Hooper, K., & Ayoub, S. (2010). Perspectives of accountability in charities. Paper presented at

the Sixth Asia Pacific Interdisciplinary Research in Accounting Conference, University of Sydney,

Australia.

Swoboda, S. J., Muehlberger, N., Weitkunat, R., & Schneeweiss, S. (1997). Internet surveys by direct

mailing: An innovative way of collecting data. Social Science Computer Review, 15(3), 242-255.

Tooley, S., & Guthrie, J. (2001). Performance accountability disclosures in annual reports: An application

in the New Zealand compulsory school sector. Paper presented at the Third Asian Pacific

Interdisciplinary Research in Accounting Conference, Adelaide.

Tse, A. (1998). Comparing the response rate, response speed and response quality of two methods of

sending questionnaires: E-mail vs. mail. Journal of the Market Research Society, 40(4), 353-361.

Urquiza, F. B., Navarro, M. C. A., & Trombetta, M. (2009). Disclosure Indices Design: Does it make a

difference? Revista de Contabilidad-Spanish Accounting Review, 12(2), 253-277.

Waters, R. D. (2010). Increasing fundraising efficiency through evaluation: Applying communication

theory to the nonprofit organizations-donor relationship. Nonprofit and Voluntary Sector Quarterly

Retrieved 17 March, 2010, from http://nvs.sagepub.com/content/early/2010/03/17/0899764009354322

Wei, T. L., Davey, H., & Coy, D. (2008). A disclosure index to measure the quality of annual reporting by

museums in New Zealand and the UK. Journal of Applied Accounting Research, 9(1), 29-51. doi:

10.1108/09675420810886114

Williams, S., & Palmer, P. (1998). The state of charity accounting - developments, improvement and

Archives Des Sciences Vol 65, No. 5;May 2012

229 ISSN 1661-464X

continuing problems. Financial Accountability & Management, 14(4), 265-279.

Copyright © 2022 FDOKUMEN