ANNuAL - REPORT - For personal use only

88

ANNUAL REPORT ACN: 057 140 922 …a period marked by our transition from iron ore developer to iron ore producer… in parallel with significant gains in our maiden thermal coal initiatives… For personal use only

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of ANNuAL - REPORT - For personal use only

ANNuAL REPORT

ACN: 057 140 922

…a period marked by our transition from iron

ore developer to iron ore producer…

in parallel with signifi cant gains in our

maiden thermal coal initiatives…

For

per

sona

l use

onl

y

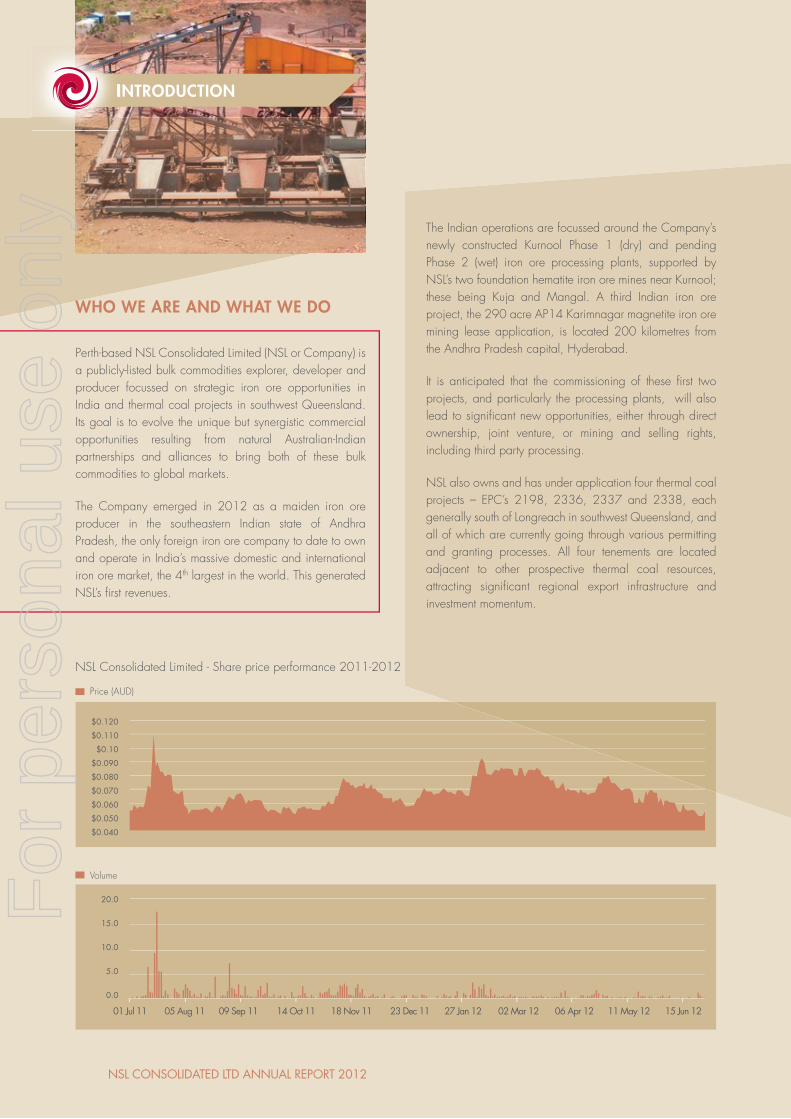

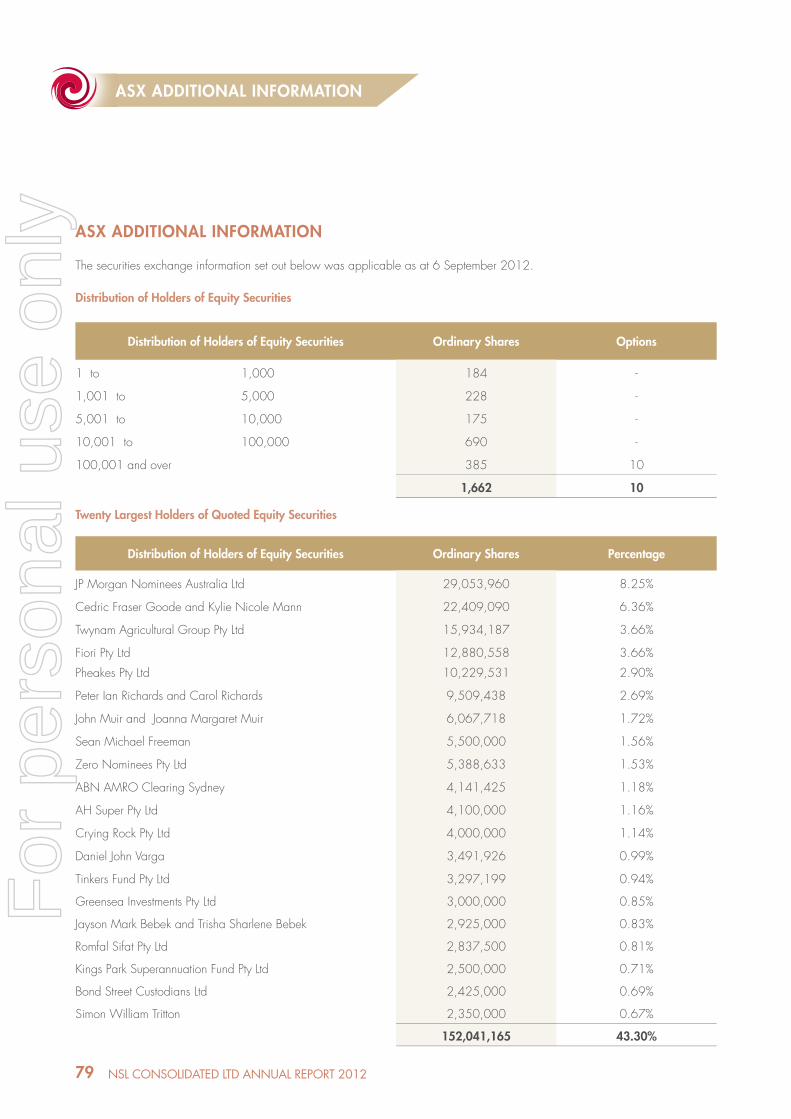

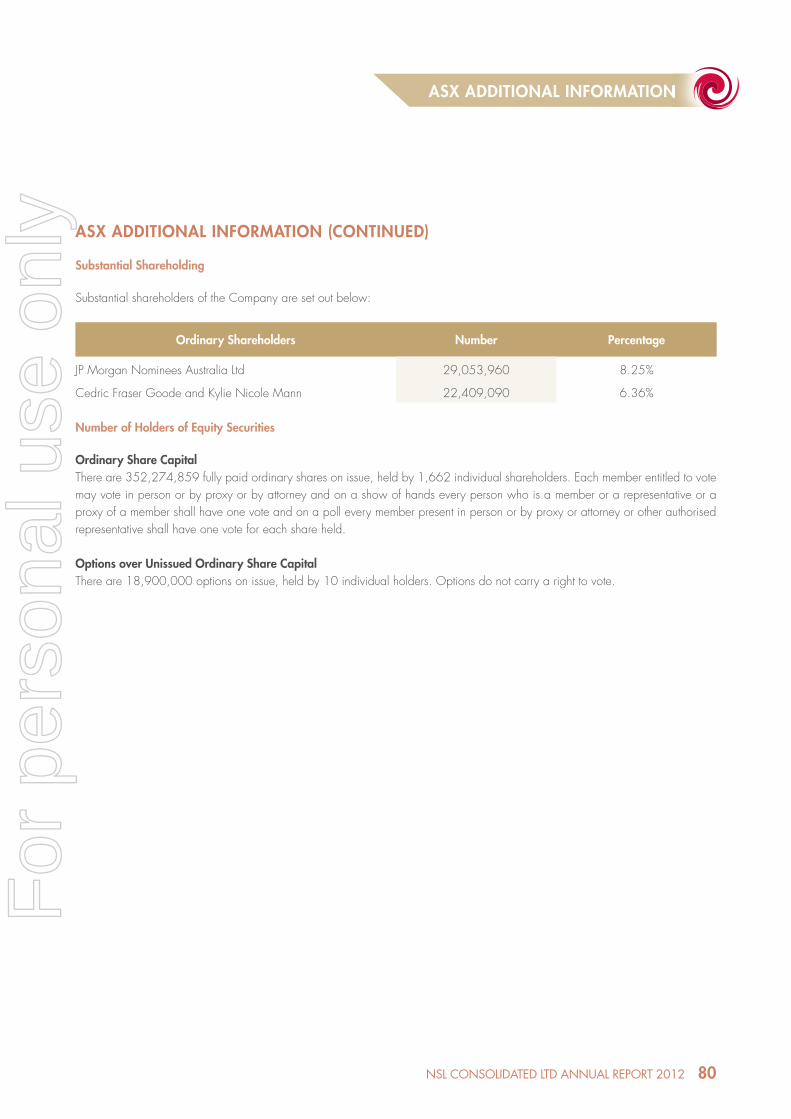

The Indian operations are focussed around the Company’s newly constructed Kurnool Phase 1 (dry) and pending Phase 2 (wet) iron ore processing plants, supported by NSL’s two foundation hematite iron ore mines near Kurnool; these being Kuja and Mangal. A third Indian iron ore project, the 290 acre AP14 Karimnagar magnetite iron ore mining lease application, is located 200 kilometres from the Andhra Pradesh capital, Hyderabad.

It is anticipated that the commissioning of these fi rst two projects, and particularly the processing plants, will also lead to signifi cant new opportunities, either through direct ownership, joint venture, or mining and selling rights, including third party processing.

NSL also owns and has under application four thermal coal projects – EPC’s 2198, 2336, 2337 and 2338, each generally south of Longreach in southwest Queensland, and all of which are currently going through various permitting and granting processes. All four tenements are located adjacent to other prospective thermal coal resources, attracting signifi cant regional export infrastructure and investment momentum.

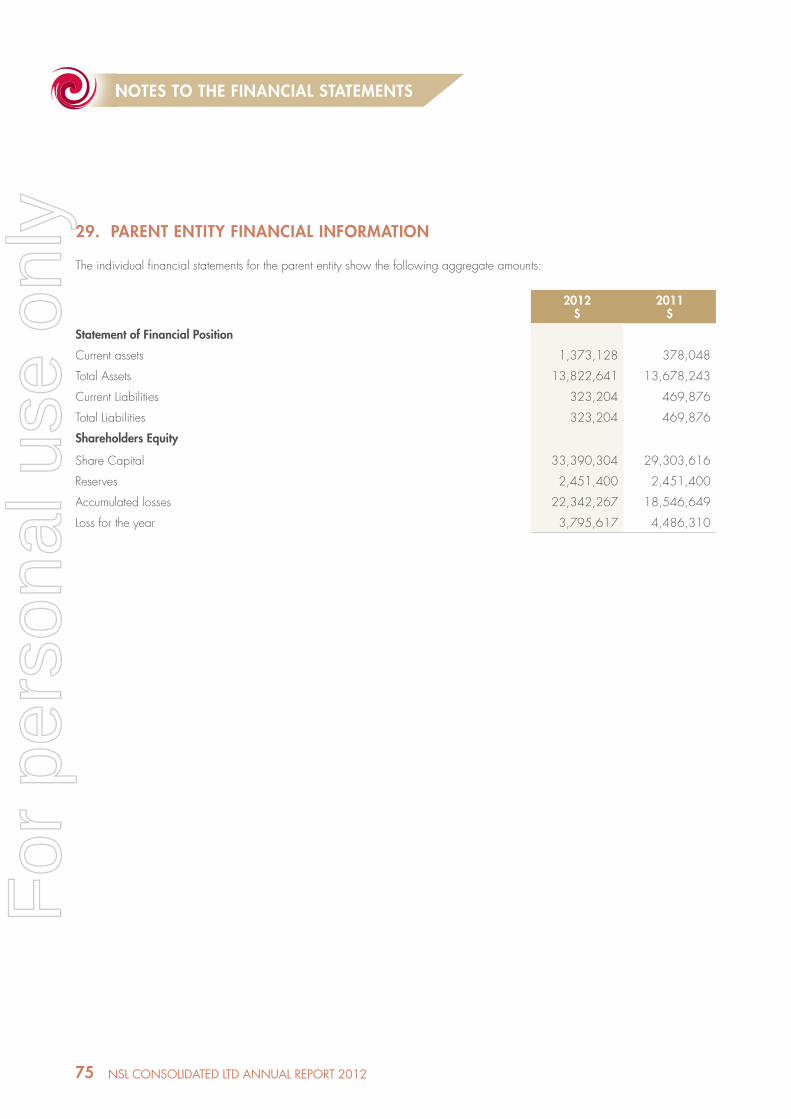

WHO WE ARE AND WHAT WE DO

Perth-based NSL Consolidated Limited (NSL or Company) is a publicly-listed bulk commodities explorer, developer and producer focussed on strategic iron ore opportunities in India and thermal coal projects in southwest Queensland. Its goal is to evolve the unique but synergistic commercial opportunities resulting from natural Australian-Indian partnerships and alliances to bring both of these bulk commodities to global markets.

The Company emerged in 2012 as a maiden iron ore producer in the southeastern Indian state of Andhra Pradesh, the only foreign iron ore company to date to own and operate in India’s massive domestic and international iron ore market, the 4th largest in the world. This generated NSL’s fi rst revenues.

NSL CONSOLIDATED LTD ANNuAL REPORT 2012

$0.120

$0.110

$0.10

$0.090

$0.080

$0.070

$0.060

$0.050

$0.040

Price (AUD)

Volume

20.0

15.0

10.0

5.0

0.0

01 Jul 11 05 Aug 11 09 Sep 11 14 Oct 11 18 Nov 11 23 Dec 11 27 Jan 12 02 Mar 12 06 Apr 12 11 May 12 15 Jun 12

INTRODUCTIONINTRODUCTION

NSL Consolidated Limited - Share price performance 2011-2012

For

per

sona

l use

onl

y

INTRODUCTIONINTRODUCTION

Magnetite can be combined with bentonite (a clay) and heat to produce high quality pellets preferred by steelmakers for use in their blast furnaces as they are more effi cient and reduce costs and pollution. Magnetite pellets attract a higher price over hematite ores. Magnetite is the main product of the world’s largest producer of iron ore and steel, China. With hematite grades dropping, more and more magnetite is being used in blends. Magnetite processing is decades old, well understood and low risk.

What is thermal coal?

Thermal coal, also known as steaming coal, is generally used to generate power used in either public electricity grids or directly by industry consuming electrical power (such as chemical industries, paper manufacturers, cement works and brickworks). For use in power generation, the coal is ground to a powder and fi red into a boiler to produce steam to drive turbines that produce electricity.

It is different to coking coal which is metallurgical coal used as a reducing agent in a blast furnace to temper iron ore into steel products. Since 2000, global coal consumption has grown faster than any other fuel. The fi ve largest coal users - China, USA, India, Russia and Japan - account for around 77% of total global coal use. The biggest market for coal is Asia, which currently accounts for over 65% of global coal consumption. Many countries do not have natural energy resources suffi cient to cover their energy needs, and therefore need to import energy to help meet their requirements. India, Japan, Chinese Taipei and Korea import signifi cant quantities of steam coal for electricity generation and coking coal for steel production. (Source: World Coal Association)

OUR COMMODITIES

What is hematite iron ore?

Hematite (Fe2O3) is a non magnetic style of iron ore oxide mineral and in pure form contains 69.9% iron ore. It has been the dominant iron ore mined in Australia since the early 1960s. High grade hematite ores are referred to as Direct Shipping Ore (DSO) because they are mined and benefi ciated using a relatively simple crushing and screening process before being exported for use in steel making. Australia’s hematite DSO averages 56% to 62% iron ore content, without treatment. Hematite ores tend however to have higher levels of impurities such as phosphorous, sulphur and aluminium. Hematite DSO ores are exploited on all continents except Antarctica, with the largest intensity in South America, Australia and Asia. Most large hematite iron ore deposits are sourced from altered banded iron ore formations. DSO deposits are typically rarer than the magnetite-bearing strata but are considerably cheaper to mine and process as they require less benefi ciation due to the higher iron ore content.

What is magnetite iron ore?

Magnetite (Fe3O4) is a magnetic mineral ore that can be crushed and passed over a magnet and the magnetite extracted leaving a clean high grade product. It occurs as four general types: 1) Banded iron ore formation (BIFs) or BIF/gneiss 2) Taconite 3) Skarn and 4) Siltstone. Magnetite ore in the ground is of lower grade than commercially exploited hematite ores but after processing, a product with much higher iron ore grades and much lower costly impurities is produced.

Magnetite can be combined with bentonite (a clay) and heat to produce high quality pellets preferred by steelmakers for use in their blast furnaces as they are more effi cient and reduce costs and pollution. Magnetite pellets attract a higher price over hematite ores. Magnetite is the main product of the world’s largest producer of iron ore and steel, China. With hematite grades dropping, more and more magnetite is being used in blends. Magnetite processing is decades old, well understood and low risk.

What is thermal coal?

Thermal coal, also known as steaming coal, is generally used to generate power used in either public electricity grids or directly by industry consuming electrical power (such as chemical industries, paper manufacturers, cement works and brickworks). For use in power generation, the coal is ground to a powder and fi red into a boiler to produce steam to drive turbines that produce electricity.

It is different to coking coal which is metallurgical coal used as a reducing agent in a blast furnace to temper iron ore into steel products. Since 2000, global coal consumption has grown faster than any other fuel. The fi ve largest coal users - China, USA, India, Russia and Japan - account for around 77% of total global coal use. The biggest market for coal is Asia, which currently accounts for over 65% of global coal consumption. Many countries do not have natural energy resources suffi cient to cover their energy needs, and therefore need to import energy to help meet their requirements. India, Japan, Chinese Taipei and Korea import signifi cant quantities of steam coal for electricity generation and coking coal for steel production. (Source: World Coal Association)

OUR COMMODITIES

What is hematite iron ore?

Hematite (Fe2O3) is a non magnetic style of iron ore oxide mineral and in pure form contains 69.9% iron ore. It has been the dominant iron ore mined in Australia since the early 1960s. High grade hematite ores are referred to as Direct Shipping Ore (DSO) because they are mined and benefi ciated using a relatively simple crushing and screening process before being exported for use in steel making. Australia’s hematite DSO averages 56% to 62% iron ore content, without treatment. Hematite ores tend however to have higher levels of impurities such as phosphorous, sulphur and aluminium. Hematite DSO ores are exploited on all continents except Antarctica, with the largest intensity in South America, Australia and Asia. Most large hematite iron ore deposits are sourced from altered banded iron ore formations. DSO deposits are typically rarer than the magnetite-bearing strata but are considerably cheaper to mine and process as they require less benefi ciation due to the higher iron ore content.

What is magnetite iron ore?

Magnetite (Fe3O4) is a magnetic mineral ore that can be crushed and passed over a magnet and the magnetite extracted leaving a clean high grade product. It occurs as four general types: 1) Banded iron ore formation (BIFs) or BIF/gneiss 2) Taconite 3) Skarn and 4) Siltstone. Magnetite ore in the ground is of lower grade than commercially exploited hematite ores but after processing, a product with much higher iron ore grades and much lower costly impurities is produced.

NSL CONSOLIDATED LTD ANNuAL REPORT 2012

For

per

sona

l use

onl

y

HIGHLIGHTSHIGHLIGHTS

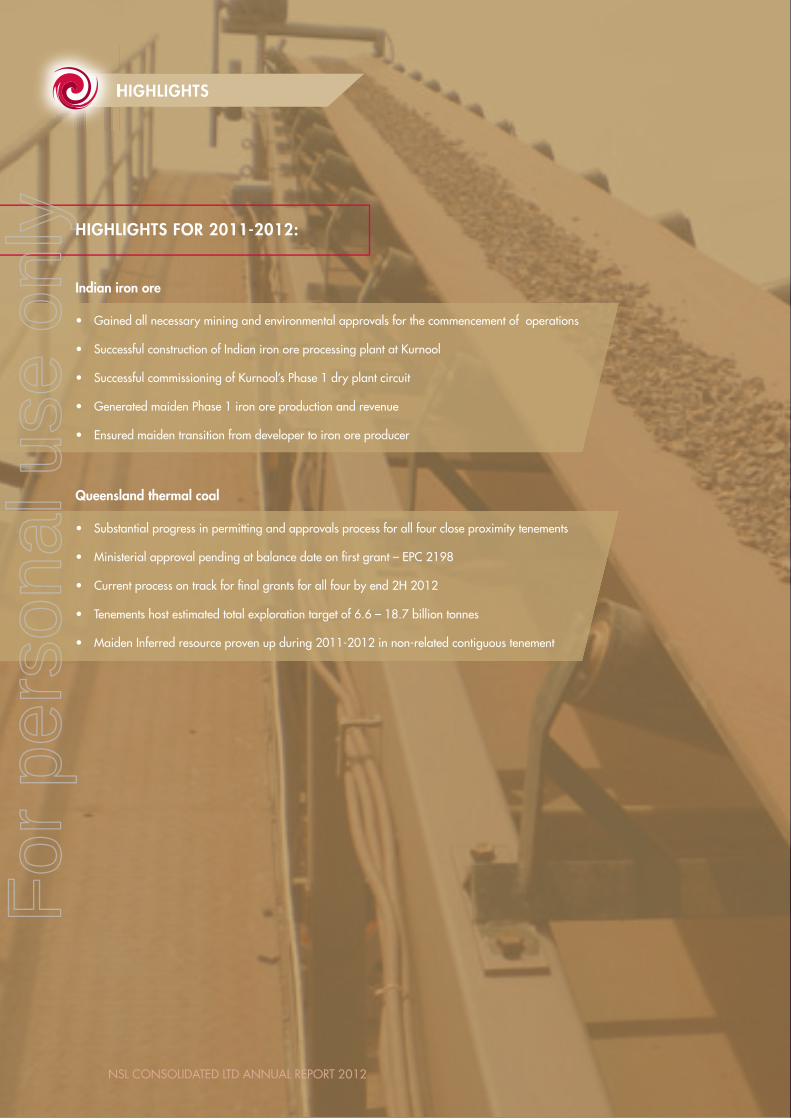

HIGHLIGHTS FOR 2011-2012:

Indian iron ore

• Gained all necessary mining and environmental approvals for the commencement of operations

• Successful construction of Indian iron ore processing plant at Kurnool

• Successful commissioning of Kurnool’s Phase 1 dry plant circuit

• Generated maiden Phase 1 iron ore production and revenue

• Ensured maiden transition from developer to iron ore producer

Queensland thermal coal

• Substantial progress in permitting and approvals process for all four close proximity tenements

• Ministerial approval pending at balance date on fi rst grant – EPC 2198

• Current process on track for fi nal grants for all four by end 2H 2012

• Tenements host estimated total exploration target of 6.6 – 18.7 billion tonnes

• Maiden Inferred resource proven up during 2011-2012 in non-related contiguous tenement

NSL CONSOLIDATED LTD ANNuAL REPORT 2012

For

per

sona

l use

onl

y

NSL CONSOLIDATED LTD ANNuAL REPORT 2012

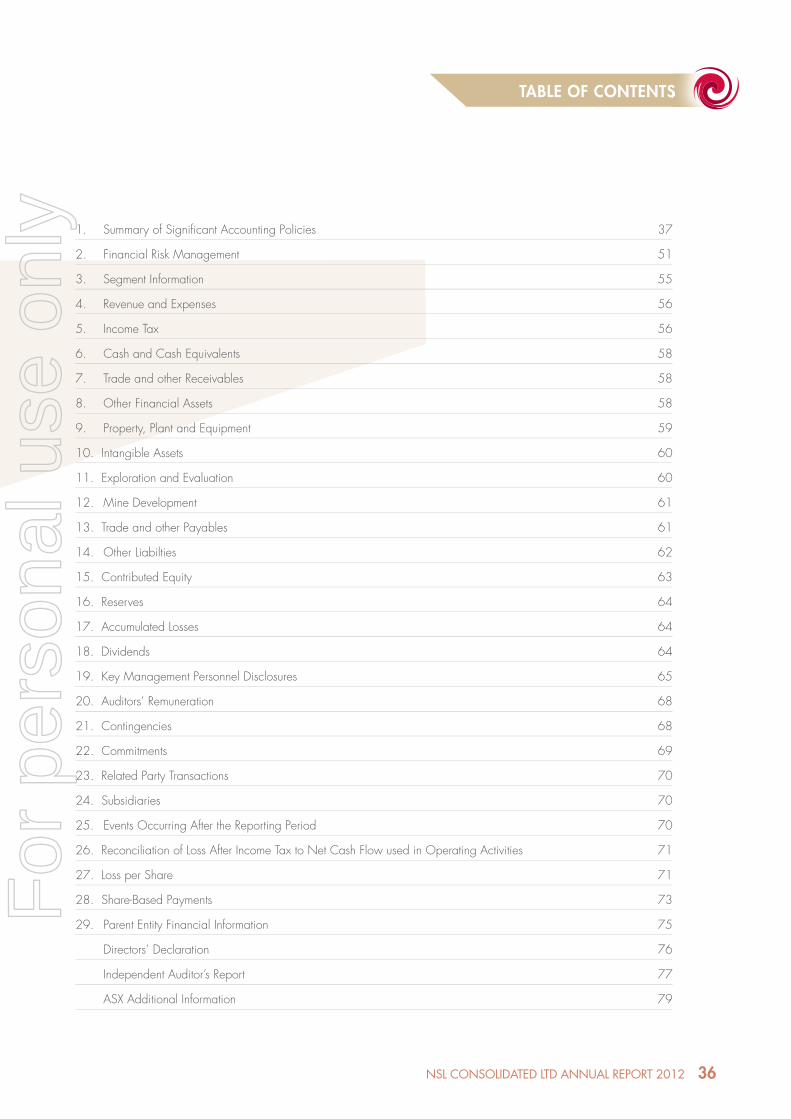

CONTENTS

Corporate Directory 1

Chairman’s Letter 2

Managing Director’s Report 3

Directors’ Report 9

Auditor’s Independence Declaration 23

Corporate Governance Statement 24

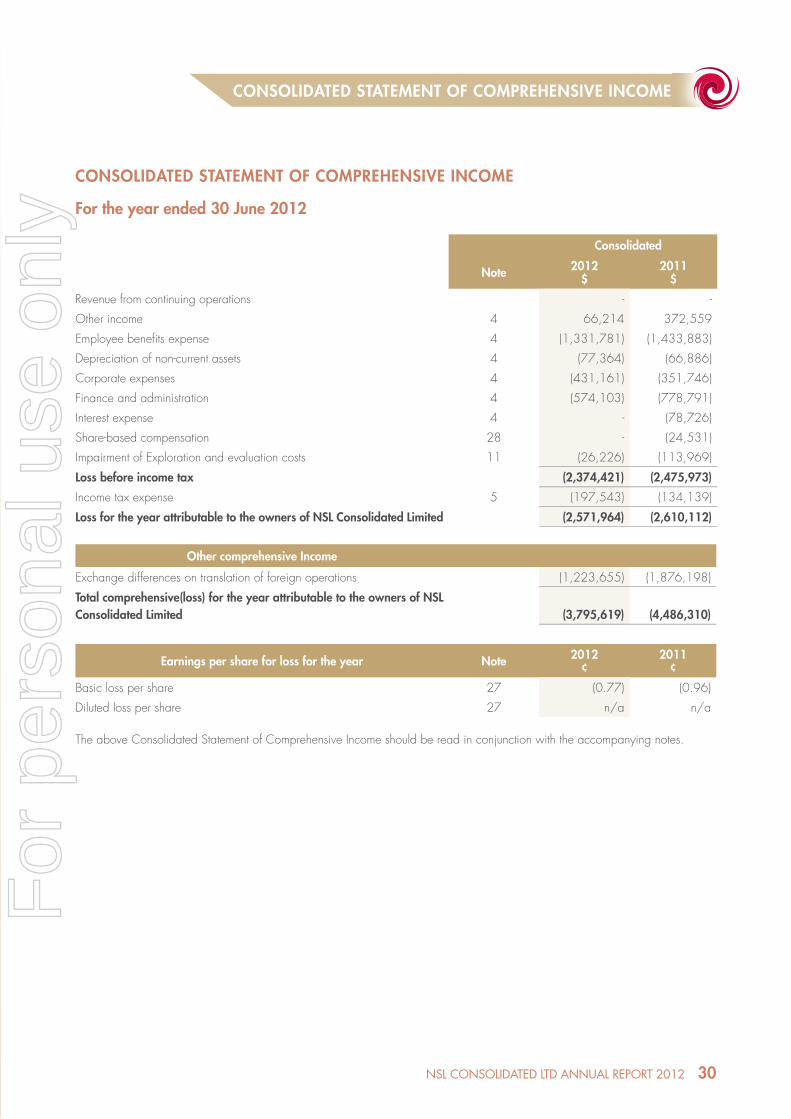

Consolidated Statement of Comprehensive Income 30

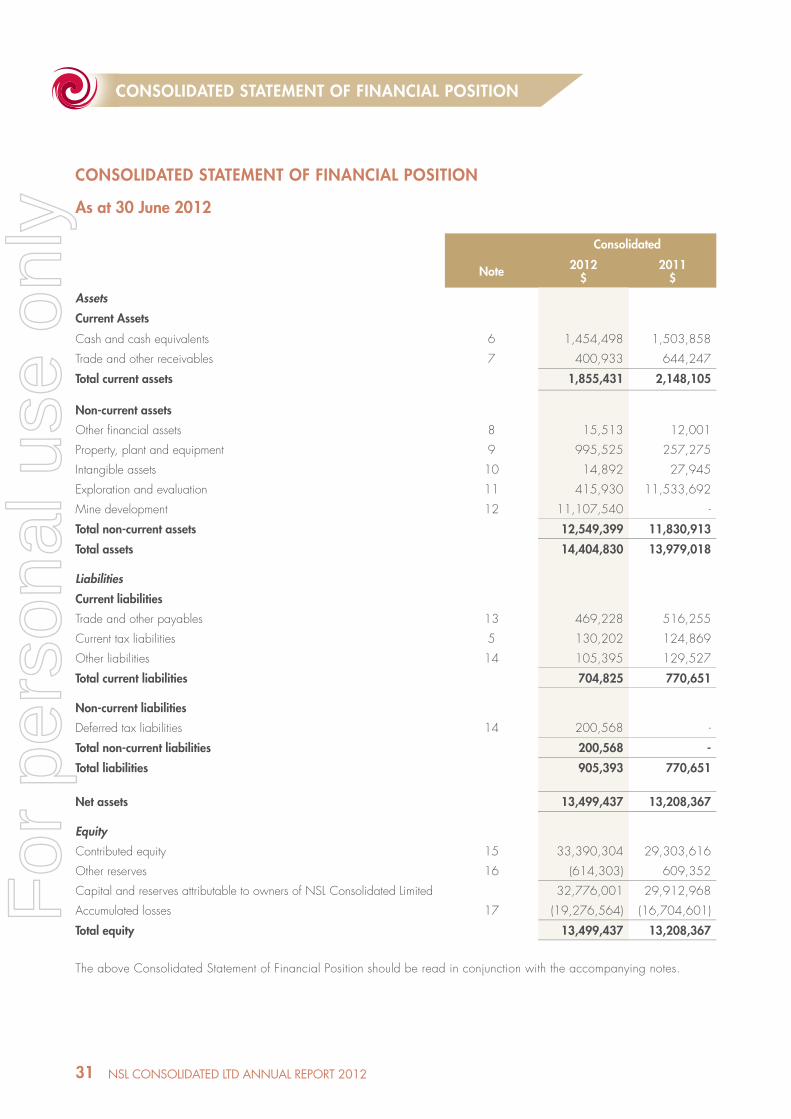

Consolidated Statement of Financial Position 31

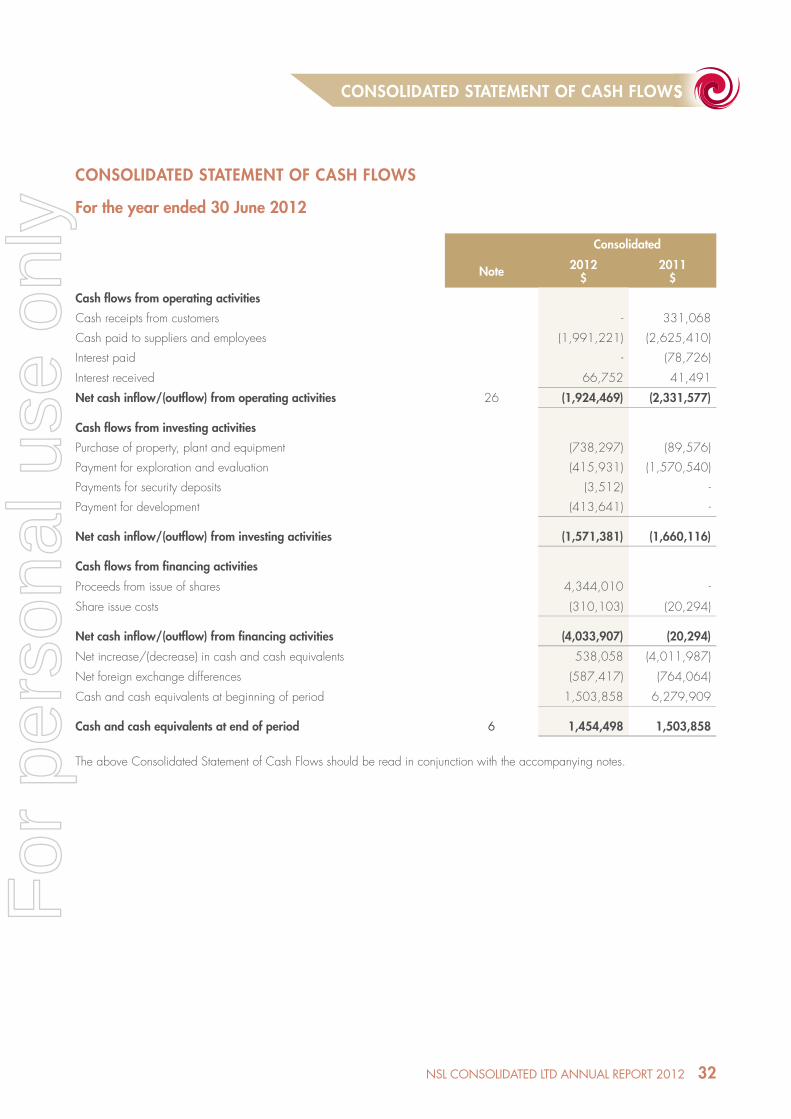

Consolidated Statement of Cash Flows 32

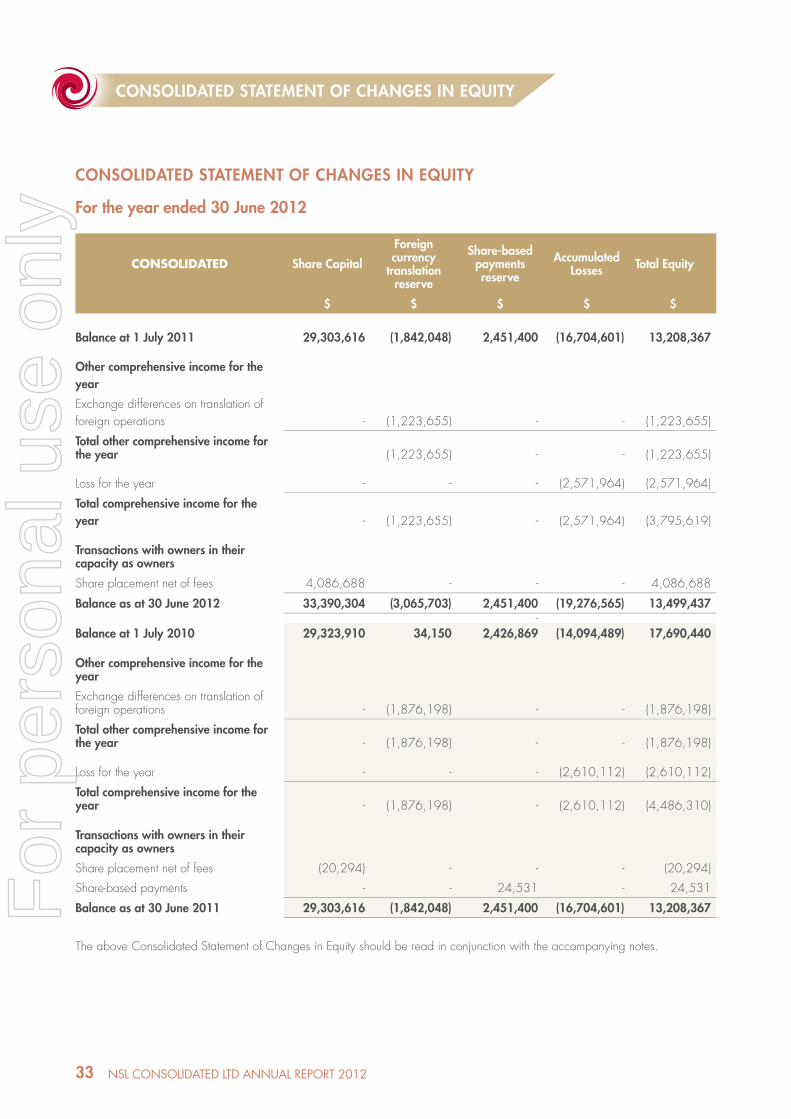

Consolidated Statement of Changes in Equity 33

Notes to the Financial Statements 36

CONTENTSCONTENTS

For

per

sona

l use

onl

y

CORPORATE DIRECTORY CORPORATE DIRECTORY

1

DIRECTORSJ Muir ACA

Chairman / Non-Executive Director

C F Goode MBA

Managing Director / CEO

P C Wall LLB, B.Comm, M.App.Fin

Non-Executive Director

P I Richards B.Comm

Non-Executive Director

COMPANY SECRETARY S P Henbury

REGISTERED OFFICEc/- FJH Solutions

21 Teddington Road

Burswood WA 6100

Telephone: (08) 9486 2333

Facsimile: (08) 9355 4580

CORPORATE OFFICE Level 1, 30 Ord Street

West Perth WA 6005

Telephone: (08) 9322 5562

Facsimile: (08) 9322 5563

WEB SITE ADDRESSwww.nslconsolidated.com

SHARE REGISTRY Security Transfer Registrars

770 Canning Highway

Applecross WA 6153

Telephone: (08) 9315 2333

Facsimile: (08) 9315 2233

AUDITORS BDO Audit (WA) P/L

38 Station Street

Subiaco WA 6008

SOLICITORS TO THE COMPANY Steinepreis Paganin Lawyers and Consultants

Level 4, The Read Buildings

16 Milligan Street

Perth WA 6000

STOCK EXCHANGE LISTING NSL Consolidated Limited’s shares are listed on the Australian Securities Exchange and Frankfurt Stock Exchange

Australian Stock Exchange Code: NSL

Frankfurt Stock Exchange Code: 2NC

NSL CONSOLIDATED LTD ANNuAL REPORT 2012

For

per

sona

l use

onl

y

CHAIRMAN’S LETTERCHAIRMAN’S LETTER

Dear Fellow Shareholders,

The continuing global economic uncertainty and its effect on commodity prices and capital markets make it very diffi cult to forecast the future in any detail. This is refl ected in a tough year for the junior end of the resources market, with many participants entering 2012-2013 focussed on survival measures and protection of cash reserves.

Your company is subject to these pressures as much as any other company at this stage of its development. Where we differ from our peers is our geographical positioning which puts us right in the middle of a growing market and a low cost environment, and importantly, at the threshold of generating positive cash fl ows.

India’s appetite for iron ore is driven by its need to upgrade infrastructure over the next 10-20 years and that requires steel (and also energy). The iron ore mining industry, with the exception of mines associated with steel mills is fragmented and security of supply will be a major factor in our success. While our operations are close to many Indian steel mills which will enable us to supply directly into the domestic market, importantly we are also within easy reach of East Coast ports for the short shipping distance to China.

While global seaborne iron ore prices have been drifting down, Indian domestic iron ore prices continue to strongly rise, highlighting the existing domestic supply and demand imbalance associated with iron ore. The result of this imbalance highlights the unique opportunity your company has as the only foreign company to own and operate iron ore mines in India.

The Indian mining environment is very different to that in Australia but the hard won experience we have gained over the last three years shows in where we are today.

Our major achievements this year are the commissioning of our dry benefi ciation plant and our fi rst sales. The building and commissioning of the plant was completed on schedule with zero harm to our employees and contractors. We are also working with the local communities to ensure that we have a social license to operate. The longer we operate in India the more we understand how to work within a different business environment and the better we become in getting things done.

Your Directors were also pleased to note continued investment and thermal coal resource estimations during the year in Queensland’s prolifi c thermal coal province in the State’s southwest, where our four thermal coal tenements are undergoing approvals processes. Subject to approvals, it is our objective to commence our maiden thermal coal exploration campaign with substantive on-ground survey, exploration and drilling to be programmed and scheduled.

This again should deliver to the equities markets an assurance that NSL’s plan to deliver production and development milestones are on track.

We thank you sincerely for your loyalty as shareholders during the past challenging 12 months. Finally the board sincerely thanks the hard work of our Australian and Indian staff in building up the business for the future.

Jock MuirChairman

2NSL CONSOLIDATED LTD ANNuAL REPORT 2012

For

per

sona

l use

onl

y

MANAGING DIRECTOR’S REPORTMANAGING DIRECTOR’S REPORT

3 NSL CONSOLIDATED LTD ANNuAL REPORT 2012

Why Indian iron ore?

With signifi cant investment to be made in upgrading India’s infrastructure in the next 10 years (estimated to be US$1.7 trillion) India’s Government is taking various steps to further encourage private and foreign investments. NSL is positioned to be part of that growth plan – a plan which has to service strong domestic consumption, higher workforce numbers, and emerging middle classes. India’s wealthiest consumers (those earning US$1m or more in PPP terms) will increase by 40 million in the next 10 years! Every sector within India’s consumer market is booming, making India far less vulnerable to external shocks and pressures than other emerging markets.

It may be the world’s 4th largest steel producer and is the 3rd

largest iron ore exporter, but India’s iron ore market, though large, is fragmented, with many small-scale operations. Its iron ore sector boasts about 80 companies operating over 250 mines to produce approximately160Mtpa.

As a participant in the local market, India’s economic growth and stability therefore favours NSL’s long-term presence in India and provides high leverage to attractive iron ore prices, both domestic and export, while it can also leverage its cash fl ow and asset base in line with India’s economic growth.

No junior resources developer should, however, focus all of their resources into a single market or commodity. Encouraged by our Indian alliances, NSL moved into Queensland’s bulk commodities market, focussing on thermal coal opportunities, a commodity that is well understood by domestic and international consumers, joint venture partners, fi nanciers and the equities market.

Our entry has been at low cost but with strong upside. While the early period has serviced the requirements of applications and approvals necessary before exploration can commence, nonetheless all four tenements are expected to be licensed by year’s end. This will facilitate the commencement of substantive on-ground survey, exploration and drilling campaigns to be planned and scheduled in the near future. We see the projects as having company maker potential.

THE REASONS BEHIND OUR BUSINESS STRATEGY…

Why India?

India’s GDP is currently US$1.3 trillion, making it the 8th largest economy in the world. However, in Purchasing Power Parity (PPP) terms, which recognises India’s low cost base, the GDP notionally rises to three times this amount (US$3.8 trillion) which places it on a similar size to Japan. By 2013, it is expected to become the third largest economy in the world (after the USA and China) in PPP terms.

India’s economy grew by 8.4% per annum (in 2010-11). High GDP growth rate is expected to be maintained over the next 10 years. India’s GDP will grow fi ve times in the next 20 years, and GDP per capita will almost quadruple. The country is also one of the youngest countries in the world, with an average age of 25 and likely to get younger. India’s working-age population will increase by 240 million over the next 20 years. With a population of 1.2 billion, a strong work ethic, high levels of education, democracy, English language skills and an entrepreneurial culture, demand for energy commodities will continue to grow. This is supported by its national savings rate of 37% of GDP, a rate which fuels most of its investment requirements. Not surprisingly, only 20% of India’s total public debt is sourced from foreign borrowings.

No junior resources developer should, however, focus all of their resources into a single market or commodity. Encouraged by our Indian alliances, NSL moved into Queensland’s bulk commodities market, focussing on thermal coal opportunities, a commodity that is well understood by domestic and international consumers, joint venture partners, fi nanciers and the equities market.

Our entry has been at low cost but with strong upside. While the early period has serviced the requirements of applications and approvals necessary before exploration can commence, nonetheless all four tenements are expected to be licensed by year’s end. This will facilitate the commencement of substantive on-ground survey, exploration and drilling campaigns to be planned and scheduled in the near future. We see the projects as having company maker potential.

For

per

sona

l use

onl

y

MANAGING DIRECTOR’S REPORTMANAGING DIRECTOR’S REPORT

4NSL CONSOLIDATED LTD ANNuAL REPORT 2012

Our Qld coal for India?

In addition NSL’s strategy includes the option to examine and where possible develop opportunities to supply our Australian thermal coal, if proven up as mineable resource, into the expanding Indian market. This opportunity is no better demonstrated than in October last year when most of India’s 86 coal-based power projects were operating with less than a week’s coal supply – in a country that has the 5th largest generation capacity in the world – 83GW (Aug 2010) rising to an expected ~ 240 GW over the next four years. Its acute power defi cit of ~15% was no better demonstrated than in the massive blackout that struck most of the country’s north in July this year.

Its thermal power sector is facing a 15% shortage (50-60 Mt) of domestically supplied coal, yet owing to its rapid economic growth creating increasing energy needs, thermal coal requirement growth in India is likely to outstrip domestic thermal coal supply growth. Domestic coal defi cit for thermal power plants is expected to touch 30% and 32% in FY 2012 and FY 2017 respectively. As coal assumes an even greater role in India’s energy supply, the projected coal shortage is likely to lead to increased coal imports in the future – the gateway targeted by NSL for our Queensland projects

Indian Iron Ore

This year has delivered a number of milestones, culminating in the commissioning in June of Phase 1 of the Company’s wholly-owned Kurnool iron ore dry separation plant in Andhra Pradesh, southeast India.

That has set the stage for a build-up during the new fi nancial year to Kurnool’s anticipated 200,000 tonnes per annum rate while NSL installs the Phase 2 wet benefi ciation plant to add an anticipated additional 200,000 tpa capacity (for 400,000 tpa total).

Increased buyer interest generated by plant completion and start-up bodes well for fi rst sales from the Phase 2 output in the opening half of calendar 2013.

The achievements were driven by the Company’s Australian and Indian based operational and management teams.

NSL’s Mangal hematite mine, just fi ve kilometres from the stockyard servicing the Kurnool dry plant, is now fully operational with a permanent fl eet of excavators and trucks on site. These fl eet levels will be increased as Kurnool moves towards nameplate production capacity.

The nearby Kuja hematite mine, immediately adjacent to NSL’s stockyard facilities is on track to commence mine start up during the September 2012 quarter, with an initial fl eet of excavators and trucks servicing deliveries into Kurnool.

Major construction and commissioning gains were made during the year at the Kurnool operations, including start-up on the weighbridge, developing the site’s laboratory and commissioning the Phase 1 dry separation plant. This plant is capable of delivering iron ore grades of 54-58% Fe in 5-20mm sized material.

For

per

sona

l use

onl

y

5 NSL CONSOLIDATED LTD ANNuAL REPORT 2012

MANAGING DIRECTOR’S REPORT

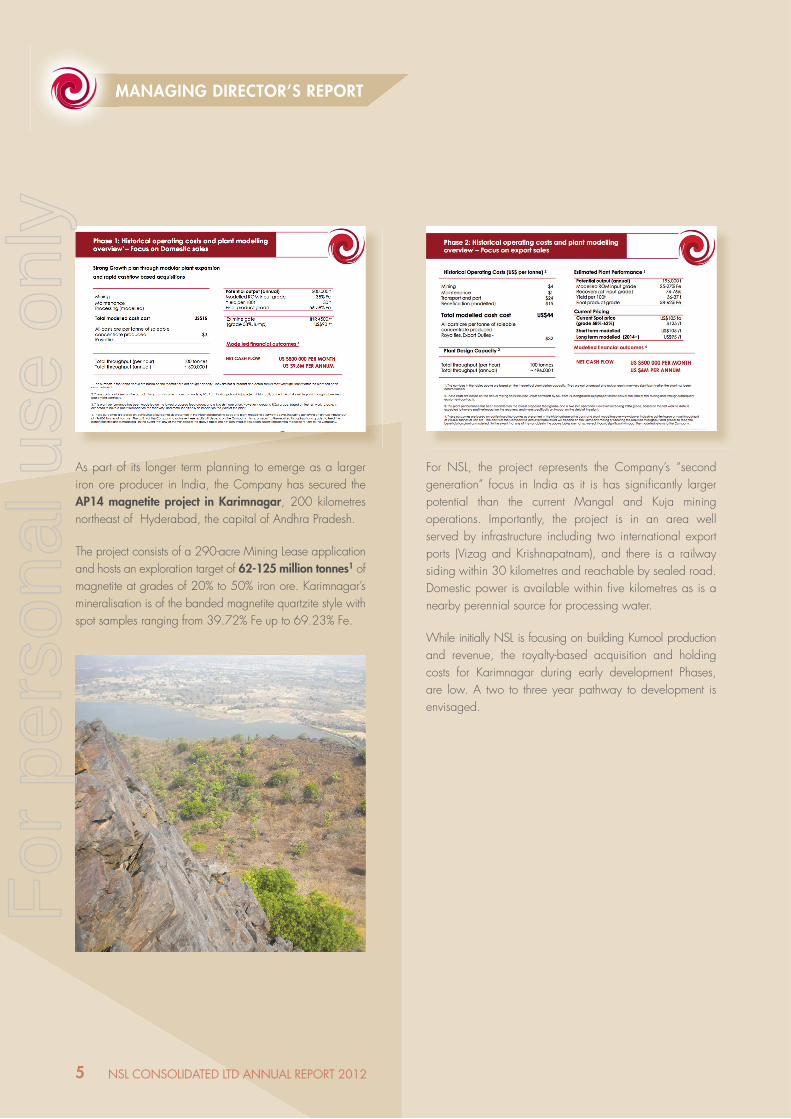

As part of its longer term planning to emerge as a larger iron ore producer in India, the Company has secured the AP14 magnetite project in Karimnagar, 200 kilometres northeast of Hyderabad, the capital of Andhra Pradesh.

The project consists of a 290-acre Mining Lease application and hosts an exploration target of 62-125 million tonnes1 of magnetite at grades of 20% to 50% iron ore. Karimnagar’s mineralisation is of the banded magnetite quartzite style with spot samples ranging from 39.72% Fe up to 69.23% Fe.

For NSL, the project represents the Company’s “second generation” focus in India as it is has signifi cantly larger potential than the current Mangal and Kuja mining operations. Importantly, the project is in an area well served by infrastructure including two international export ports (Vizag and Krishnapatnam), and there is a railway siding within 30 kilometres and reachable by sealed road. Domestic power is available within fi ve kilometres as is a nearby perennial source for processing water.

While initially NSL is focusing on building Kurnool production and revenue, the royalty-based acquisition and holding costs for Karimnagar during early development Phases, are low. A two to three year pathway to development is envisaged.

MANAGING DIRECTOR’S REPORT

For

per

sona

l use

onl

y

6NSL CONSOLIDATED LTD ANNuAL REPORT 2012

The Company’s development timeline then for our Indian iron ore operations is as follows:

NSL IRON ORE - STRONG GROWTH PIPELINE

Ramp up production from Kuja, Mangal and Phase 1 plant Cash fl ows commenced

Phase 2 construction,commissioning

Close proximity opportunities withtimely access to material Strong expanded cashfl ows

DSO and low grade benefi ciation projects

Target run rate of 1.5million tonnes per annumStrict criteria

One to two year timehorizon to production

Finalise Mining Leaseapproval

Two to three year timehorizon to production

Initial review - scopeproject Establish JORC resource

Kurnool Expansion - leveraged existing asset base - 2nd half 2012 to 2013

Target acquisitions - 2012 to 2014

Continue AP14 development

Unlock further value throughbenefi ciation

Pelletisation offers attractivemargins

Government incentives to valueadd - no export duty

Move up the value chain

Queenslandthermal

coal evaluation continues

MANAGING DIRECTOR’S REPORTMANAGING DIRECTOR’S REPORT

Queenslandthermal

coal evaluation continues

Existing production from Kurnool (via Mangal / Kuja)

For

per

sona

l use

onl

y

7 NSL CONSOLIDATED LTD ANNuAL REPORT 2012

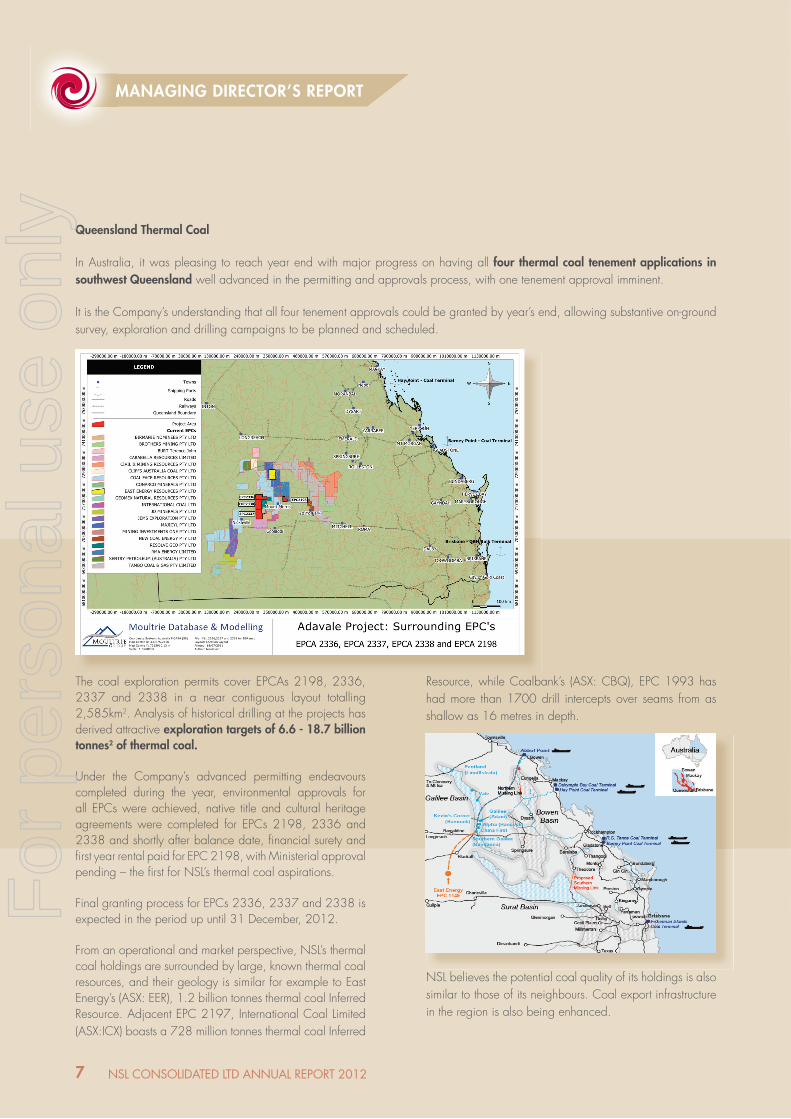

The coal exploration permits cover EPCAs 2198, 2336, 2337 and 2338 in a near contiguous layout totalling 2,585km2. Analysis of historical drilling at the projects has derived attractive exploration targets of 6.6 - 18.7 billion tonnes2 of thermal coal.

Under the Company’s advanced permitting endeavours completed during the year, environmental approvals for all EPCs were achieved, native title and cultural heritage agreements were completed for EPCs 2198, 2336 and 2338 and shortly after balance date, fi nancial surety and fi rst year rental paid for EPC 2198, with Ministerial approval pending – the fi rst for NSL’s thermal coal aspirations.

Final granting process for EPCs 2336, 2337 and 2338 is expected in the period up until 31 December, 2012.

From an operational and market perspective, NSL’s thermal coal holdings are surrounded by large, known thermal coal resources, and their geology is similar for example to East Energy’s (ASX: EER), 1.2 billion tonnes thermal coal Inferred Resource. Adjacent EPC 2197, International Coal Limited (ASX:ICX) boasts a 728 million tonnes thermal coal Inferred

Resource, while Coalbank’s (ASX: CBQ), EPC 1993 has had more than 1700 drill intercepts over seams from as shallow as 16 metres in depth.

NSL believes the potential coal quality of its holdings is also similar to those of its neighbours. Coal export infrastructure in the region is also being enhanced.

MANAGING DIRECTOR’S REPORTMANAGING DIRECTOR’S REPORT

Queensland Thermal Coal

In Australia, it was pleasing to reach year end with major progress on having all four thermal coal tenement applications in southwest Queensland well advanced in the permitting and approvals process, with one tenement approval imminent.

It is the Company’s understanding that all four tenement approvals could be granted by year’s end, allowing substantive on-ground survey, exploration and drilling campaigns to be planned and scheduled.

For

per

sona

l use

onl

y

8NSL CONSOLIDATED LTD ANNuAL REPORT 2012

MANAGING DIRECTOR’S REPORTMANAGING DIRECTOR’S REPORT

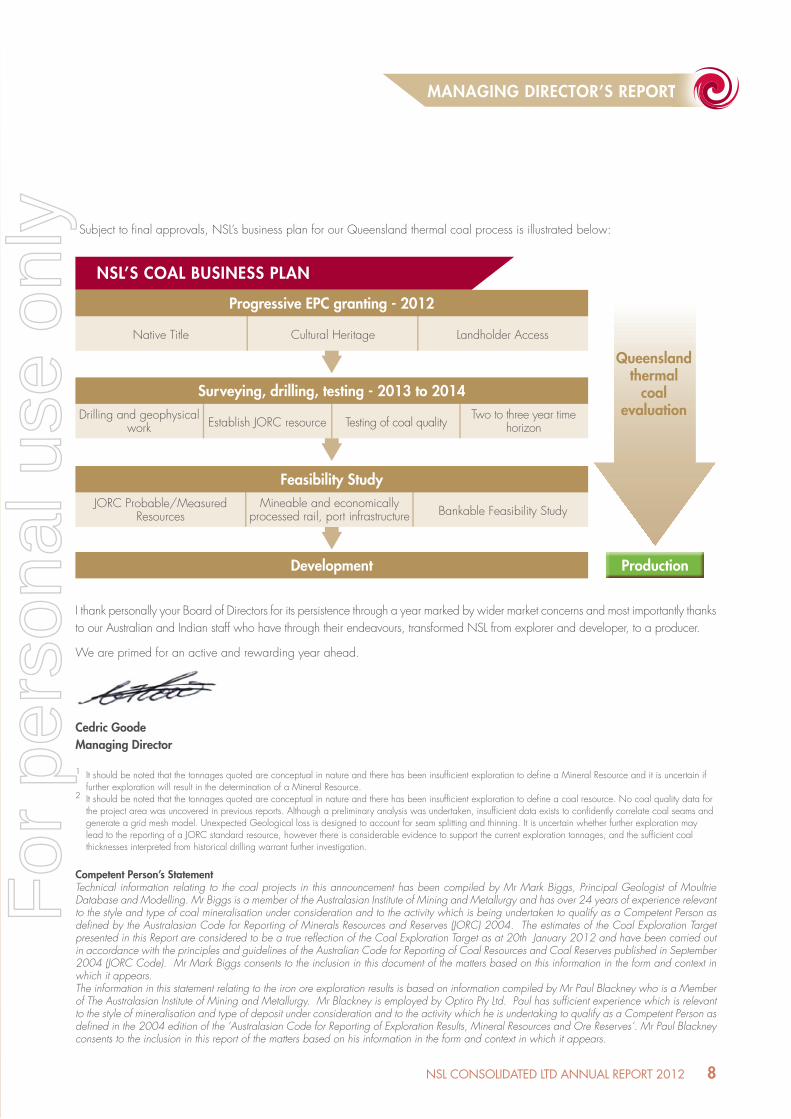

Subject to fi nal approvals, NSL’s business plan for our Queensland thermal coal process is illustrated below:

NSL’S COAL BUSINESS PLAN

Landholder Access

Progressive EPC granting - 2012

JORC Probable/MeasuredResources

Mineable and economicallyprocessed rail, port infrastructure Bankable Feasibility Study

Feasibility Study

Queenslandthermal

coal evaluation

Native Title Cultural Heritage

Drilling and geophysical work Testing of coal qualityEstablish JORC resource

Two to three year timehorizon

Surveying, drilling, testing - 2013 to 2014

Development Production

I thank personally your Board of Directors for its persistence through a year marked by wider market concerns and most importantly thanks to our Australian and Indian staff who have through their endeavours, transformed NSL from explorer and developer, to a producer.

We are primed for an active and rewarding year ahead.

Cedric GoodeManaging Director

1 It should be noted that the tonnages quoted are conceptual in nature and there has been insuffi cient exploration to defi ne a Mineral Resource and it is uncertain if further exploration will result in the determination of a Mineral Resource.2 It should be noted that the tonnages quoted are conceptual in nature and there has been insuffi cient exploration to defi ne a coal resource. No coal quality data for the project area was uncovered in previous reports. Although a preliminary analysis was undertaken, insuffi cient data exists to confi dently correlate coal seams and generate a grid mesh model. Unexpected Geological loss is designed to account for seam splitting and thinning. It is uncertain whether further exploration may lead to the reporting of a JORC standard resource, however there is considerable evidence to support the current exploration tonnages, and the suffi cient coal thicknesses interpreted from historical drilling warrant further investigation.

Competent Person’s StatementTechnical information relating to the coal projects in this announcement has been compiled by Mr Mark Biggs, Principal Geologist of Moultrie Database and Modelling. Mr Biggs is a member of the Australasian Institute of Mining and Metallurgy and has over 24 years of experience relevant to the style and type of coal mineralisation under consideration and to the activity which is being undertaken to qualify as a Competent Person as defi ned by the Australasian Code for Reporting of Minerals Resources and Reserves (JORC) 2004. The estimates of the Coal Exploration Target presented in this Report are considered to be a true refl ection of the Coal Exploration Target as at 20th January 2012 and have been carried out in accordance with the principles and guidelines of the Australian Code for Reporting of Coal Resources and Coal Reserves published in September 2004 (JORC Code). Mr Mark Biggs consents to the inclusion in this document of the matters based on this information in the form and context in which it appears. The information in this statement relating to the iron ore exploration results is based on information compiled by Mr Paul Blackney who is a Member of The Australasian Institute of Mining and Metallurgy. Mr Blackney is employed by Optiro Pty Ltd. Paul has suffi cient experience which is relevant to the style of mineralisation and type of deposit under consideration and to the activity which he is undertaking to qualify as a Competent Person as defi ned in the 2004 edition of the ‘Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves’. Mr Paul Blackney consents to the inclusion in this report of the matters based on his information in the form and context in which it appears.

For

per

sona

l use

onl

y

9 NSL CONSOLIDATED LTD ANNuAL REPORT 2012

The Directors of NSL Consolidated Limited (the Company or NSL) present their report on the consolidated entity (referred to hereafter as the Group), consisting of NSL Consolidated Limited and the entities it controlled at the end of, and during, the fi nancial year ended 30 June 2012.

DIRECTORS

The following persons were Directors of NSL Consolidated Limited during the whole of the fi nancial year and up to the date of this report, unless otherwise stated:

Jock Muir Chairman/Non-Executive

Cedric Goode Managing Director/CEO

Peter Wall Non-Executive Director

Peter Richards Non-Executive Director

PRINCIPAL ACTIVITIESThe principal activity of the Group during the fi nancial year was review, assessment, exploration, development and strategic investment in Indian iron ore and Queensland Coal projects.

DIVIDENDSThe Directors do not recommend the payment of a dividend and no amounts have been paid or declared by way of dividend since the start of the fi nancial year.

REVIEW OF OPERATIONSNSL is an Australian-based mining Company focussed on developing iron ore projects in India and coal projects in Queensland.

The Indian iron ore mining industry is highly fragmented, with a large number of relatively small, potentially high value operations and available near-term production targets.

The relatively small scale and fragmented nature of Indian iron ore production, as well as low capital and infrastructure costs, provide an opportunity for NSL to use Australian mining expertise to aggregate strategically placed smaller operations to realise economies of scale.

India has several important advantages that favour the development of its iron ore industry, including having a highly educated workforce, reliable existing transport infrastructure in place with third party access regimes, an established domestic steel industry and proximity to and established ties with major iron ore markets, such as China.

Indian Iron Ore Projects - Kuja and Mangal

NSL has two foundation projects, Kuja and Mangal, located in the south eastern province of Andhra Pradesh, India. During the year NSL conducted various testing and technical studies on a Benefi ciation process capable of producing iron ore of 58-62% Fe from low grade 25-27% iron ore.

As the Company improves its knowledge base, it intends to expand its mining portfolio through further acquisitions. Based on exploration results and regional geological consistency on sites the Company has under due diligence, NSL has assessed that these could contain DSO and signifi cant tonnage of low grade hematite and magnetite amenable to benefi ciation.

This work has enabled NSL to refi ne its strategy to include both Direct Shipping Ore and low grade, hematite and magnetite deposits amenable to benefi ciation.

To support this key initiative, NSL has fi nalised the full project plans for design, fabrication, shipping, construction, commissioning and continued onsite technical expertise of plant requirements for the Phase 1 dry separation plant and the Phase 2 wet benefi ciation plant to support bulk mining and processing of the iron ore from Kuja and Mangal.

India Iron Ore Project – AP14 Karimnagar

NSL bolstered its Indian iron ore business, with the acquisition of AP14 consisting of a Mining Lease application over 290 acre property in Karimnagar (200 km North East of Hyderabad), which contains signifi cant Banded Magnetite Quartzite mineralisation. AP14 is estimated to have a JORC Exploration Target at the project of 62 million to 125 million tonnes1 at grades of 20% to 50% Fe.

DIRECTORS’ REPORTDIRECTORS’ REPORT

For

per

sona

l use

onl

y

In addition to the unsecured Convertible Note, the Company has also entered into a Marketing Agreement with Resources First Pte Ltd to market the Company’s iron ore and procure sales contracts in a manner and at a price consistent with industry standards. This can include Resources First Pte Ltd directly purchasing the iron ore. NSL retain the ultimate and fi nal say to whom, and for what price the iron ore is sold.

The non-exclusive Marketing Agreement is for a three year period (shortened to two years from the date of early conversion of all Notes).

NSL will pay a 2.5% commission for any sales secured to or by Resources First Pte Ltd from Kurnool. The agreement does not apply to any other iron production projects which may be developed by NSL in India.

The agreement caps Resources First Pte Ltd commissioned sales to 300,000 tpa – or about three quarters of Kurnool’s current anticipated total output of 400,000 tpa.

Queensland thermal coal project EPC 2198 granted

As announced on 13 August 2012, the fi rst of the Companys four thermal coal tenements, EPC 2198 has now been formally granted.

10NSL CONSOLIDATED LTD ANNuAL REPORT 2012

DIRECTORS’ REPORTDIRECTORS’ REPORT

Queensland Coal Assets

In conjunction with our Indian iron ore strategy and following enquiries from our Indian and Chinese contacts,

the Company has expanded its commodity portfolio and added value in Queensland with the acquisition of thermal coal exploration permits (EPC Applications) 2198, 2336, 2337 and 2338.

NSL has an Exploration Target of 6.6-18.7 billion tonnes2 of thermal coal across of 4 EPC Applications.

A detailed discussion and analysis of NSL’s operations will be set out in the annual report.

SIGNIFICANT CHANGES IN STATE OF AFFAIRSDuring the fi nancial year the nature of the business changed from an exploration phase to a development phase.

MATTERS SUBSEQUENT TO THE END OF THE FINANCIAL YEARConvertible Note and Marketing Agreement

As announced on 8 August 2012, the Company has entered into a low cost three-year unsecured US$2.5 million Convertible Note with Resources First Pte Ltd at an interest rate of 6%pa.

Interest payments will be yearly on an arrears basis, with the Notes convertible in two tranches at a 10% discount to the 20 VWAP (Volume Weighted Average Price) of Ordinary Shares on issue. The tranche conversion dates are any time after 12 months and 24 months respectively from date of issue, with the conversion price set at a discount to the 20 day VWAP prior to the time of conversion.

NSL can elect to buy some or all of the Notes at its election at any time during the three year term without penalties.

Any shares issued from converted Notes will be voluntarily escrowed for a period of three months post conversion.

The Notes in no way prohibit the Company from undertaking any equity capital raising activities.

NSL CONSOLIDATED LTD ANNuAL REPORT 2012 10

For

per

sona

l use

onl

y

11 NSL CONSOLIDATED LTD ANNuAL REPORT 2012

INFORMATION ON DIRECTORS

The Directors of the Company at any time during or since the end of the fi nancial year are set out below, together with details of qualifi cations, experience and responsibilities.

DIRECTORS’ REPORTDIRECTORS’ REPORT

LIKELY DEVELOPMENT AND EXPECTED RESULTS OF OPERATIONS

Further information as to likely developments in the operations of the Group and the expected results of those operations in subsequent fi nancial years have not been included in this report because the Directors believe it would be likely to result in unreasonable prejudice to the Group.

ENVIRONMENTAL REGULATION

The Group’s current Australian operations are subject to environmental regulation under the laws of the Commonwealth and or State of Queensland.

The Indian entity, NSL Mining Resources India Pvt Ltd, is subject to environmental regulations / legislation in respect of its mines in Andhra Pradesh.

The Directors have considered compliance with the National Greenhouse and Energy Reporting Act 2007 which requires entities to report annual greenhouse gas emissions and energy use. For the period 1 July 2011 to 30 June 2012 the directors have assessed that there are no current reporting requirements, but may be required to do so in the future.

J Muir ACA. Non-Executive/Chairman

Appointed as a Non-Executive Chairman on 13 August 2009

Experience and expertiseMr. Muir brings more than 30 years’ experience in global mining and mining services. Most recently, Jock held the position of Non-Executive Director of Dyno Nobel Ltd, an ASX 200 company, prior to a merger with Incitec Pivot in 2008. In his 15 year career with Dyno Nobel, Mr Muir also held the positions of Managing Director of the Asia Pacifi c Region, Senior Vice President for Global Initiation Systems (based in the USA) and Senior Vice President for Global Marketing and Business Development. His experience in these roles included the development of new businesses in China and Russia. Prior to Dyno Nobel Mr Muir held the position of Managing Director of Mitchell Cotts Australia, a subsidiary of a British public company, specialising in mining services and process engineering.

Other current directorshipsBarminco Ltd – Non-Executive Chairman

Special responsibilitiesNon-Executive Chairman

Interest in shares and options6,067,718 shares and 2,000,000 options in NSL Consolidated Ltd

For

per

sona

l use

onl

y

C F Goode MBA. Managing Director/Chief Executive Offi cer

Appointed as a Managing Director / CEO on 1 December 2008

Experience and expertiseMr Goode brings more than 20 years of mining industry experience. With industry experience focussed in the Iron Ore, Coal and Gold sectors Mr Goode has held a variety of technical, commercial, operational and strategic roles both domestically and internationally with mining and mining services companies. Mr Goode has a proven track record in global strategic planning, global new business acquisitions, merger integration, joint venture establishment and profi t and loss responsibility.

Other current directorshipsNone

Former directorship in last 3 yearsNone

Special responsibilitiesManaging Director

Interest in shares and options22,409,090 shares and 8,000,000 options in NSL Consolidated Ltd

Interest in shares and options22,409,090 shares and 8,000,000 options in NSL

12NSL CONSOLIDATED LTD ANNuAL REPORT 2012

DIRECTORS’ REPORTDIRECTORS’ REPORT

P C Wall LLB, B.Comm, M.App.Fin. Non-Executive Director

Appointed as a Non-Executive Director on 11 April 2007

Experience and expertiseFollowing graduation from UWA, Mr Wall commenced employment at a large Perth based law fi rm and later joined Steinepreis Paganin in January 2000. (Appointed as a Partner in July 2005). He has a wide range of experience in all forms of corporate and commercial law with specifi c expertise in equity capital markets, mergers and acquisitions and resources law.

Other current directorshipsPTO Consolidated Ltd – March 2012 to presentDiscovery Resources Ltd – June 2012 to presentPartner of Steinepreis Paganin

Special responsibilitiesNon-Executive Director

Interest in shares and options12,229,531 shares and 2,000,000 options in NSL Consolidated Ltd

For

per

sona

l use

onl

y

13 NSL CONSOLIDATED LTD ANNuAL REPORT 2012

DIRECTORS’ REPORTDIRECTORS’ REPORT

INFORMATION ON DIRECTORS (CONTINUED)

MEETINGS OF DIRECTORS

The number of meetings of the Company’s board of directors and of each board committee held during the year ended 30 June 2012, and the numbers of meetings attended by each director were:

Name Board Audit Committee RemunerationCommittee

Other(include details)

Held Attended Held Attended Held Attended Held Attended

J Muir 5 5 2 2 1 1 - -

C F Goode 5 5 2 2 1 1 - -

P C Wall 5 5 2 2 1 1 - -

P I Richards 5 5 2 2 1 1 - -

P I Richards B.Comm. Non-Executive Director

Appointed as a Non-Executive Director on 13 August 2009

Experience and expertiseMr Richards has more than 30 years of business and international experience with Gloabl companies including BP plc, Wesfarmers Limited and Dyno Nobel Limited. He recently retired as CEO of Dyno Nobel following its takeover. During his time with Dyno Nobel, Perter successfully led the Asia Pacifi c operation based in Sydney and then the North American business unit based in Utah, USA. After becoming CEO, Peter expanded the business into China, Southern Africa and Europe while continuing to build upon its core Australian and North American operations.

Peter’s experience has afforded signifi cant exposure to the investment, broking and analyst community and his global experience provides him with direct exposure to diverse cultures and societies and has equipped him to develop businesses in a range of locations, including South Africa, Indonesia and Turkey.

Other current directorshipsBradken LimitedEmeco Holdings Limited Norfolk Group LimitedKangaroo Resources LimitedMinbos Resources LimitedSedgman Limited

Special responsibilitiesNon-Executive Director.

Interest in shares and options9,509,438 shares and 2,000,000 options in NSL Consolidated Ltd

COMPANY SECRETARY

The Company secretary is Mr Sean P Henbury. Mr Henbury was appointed to the position of the Company secretary in 2007. Mr Henbury (CA, FITA) is a Chartered Accountant with over 13 years experience in public practice with three of Perth’s major Accounting fi rms. He was a founding director of the accounting fi rm FJH Solutions Pty Ltd, where he continues to provide client support across a wide range of industries including mining, exploration, research and development, construction and manufacturing. Mr Henbury’s primary areas of expertise include taxation consulting, taxation compliance, corporate restructuring, fi nancial reporting, and Company secretarial requirements.

Mr Henbury has been company secretary of a number of companies and is regularly called upon to advise Directors of their duties.

For

per

sona

l use

onl

y

MEETINGS OF DIRECTORS (CONTINUED)

The audit committee and remuneration committee functions are performed by the full board. Please refer the Corporate Governance Statement section under the heading Principle 2: Structure the Board to add value.

REMUNERATION REPORT – AUDITED

This remuneration report sets out remuneration information for the Company’s non-executive directors, executive director and other key management personnel.

Directors and executives disclosed in this report

14NSL CONSOLIDATED LTD ANNuAL REPORT 2012

DIRECTORS’ REPORTDIRECTORS’ REPORT

Role of the remuneration committeeThe remuneration committee is a committee of the board. It is primary responsible for making recommendation to the board on: – non-executive director fees– executive remuneration (directors and other executives), and– the over-arching executive remuneration framework and incentive plan policies.

Their objective is to ensure that remuneration policies and structures are fair and competitive and aligned with long-term interests of the Company.

The Corporate Governance Statement provides further information on the role of this committee.

Name Position

Non-executive and executive directors – see page 11 to 13 above

Other key management personnel of the Group.

J S M Tambyrajah Chief Financial Offi cer (resigned 30 March 2012)

S M Freeman Chief Operating Offi cer

T K S Lee Financial Controller (commenced 16 March 2012)

For

per

sona

l use

onl

y

15 NSL CONSOLIDATED LTD ANNuAL REPORT 2012

REMUNERATION REPORT – AUDITED (CONTINUED)

Principles used to determine the nature and amount of remuneration

Non-Executive DirectorFees and payments to the non-executive directors refl ect the demands which are made on, and the responsibilities of, the directors. Non-executive directors’ fees and payments are reviewed annually by the Board. The Non-executive Chairman fees are determined independently to the fees of non-executive directors based on comparative roles in the external market. The Chairman is not present at any discussions relating to the determination of his own remuneration.

Non-executive directors have received short term incentive options but do not receive performance bonuses.

Directors’ feesThe current base remuneration was last reviewed with effect from 1 July 2011. The Chairman currently receives a fi xed fee for his services.

Non-executive directors’ fees are determined within an aggregate directors’ fee pool limit, which is periodically recommended for approval by shareholders. The maximum currently stands at $250,000 per annum and was approved by shareholders at the annual general meeting on 30 November 2011.

The following non-executive director fees have applied to the respective fi nancial years:

Name 2012$

2011$

Chairman 60,000 60,000

Other non-executive directors (in aggregate) 96,000 96,000

Retirement allowances for non-executive directorsNo retirement benefi ts are provided.

Executive DirectorsThe Company had one Executive Director during the year. The executive pay and reward framework has two components being base pay and benefi ts, including superannuation, and incentive share options granted. The Group does not offer any retirement benefi ts to Executive Directors. The only performance related links to the existing remuneration policies are the vesting conditions placed upon the performance share options granted and the cash bonus.

Use of remuneration consultantsDuring the year 30 June 2012 the Company did not engage any remuneration consultants.

Voting and comments made at the company’s 2011 Annual General MeetingThe Company received more than 91% of “yes” votes on its remuneration report for the 2011 fi nancial year. The Company did not receive any specifi c feedback at the AGM or throughout the year on its remuneration practices.

Relationship of Rewards and PerformanceThe value of incentive options, performance options and performance bonuses can represent a signifi cant portion of an executive’s salary package. The ultimate value to the executives of and link to remuneration policies are the vesting conditions placed upon performance share options and bonuses and or the share price as the realised value arising from options issued is dependent upon an increase in the share price to above the exercise price of the options.

The details of the vesting conditions associated with performance shares and bonuses are disclosed in the service agreement and share-based compensation section of the remuneration report.

DIRECTORS’ REPORT

For

per

sona

l use

onl

y

2012

Short-term employee benefi tsPost-

employment benefi ts

Long-termbenefi ts

Share-based

payments

Proportion of remuneration

that is performance

based

% of Value of remune-ration that consists of optionsCash salary

and feesCash bonus

Non-monetary benefi ts

Super-annuation

Long service leave

Termination benefi ts

Options Total

$ $ $ $ $ $ $ $ % %

Non-Executive Directors

J Muir 60,000 - - - - - - 60,000 - -

P C Wall 48,000 - - - - - - 48,000 - -

P I Richards 48,000 - - - - - - 48,000 - -

Executive Director

C F Goode 350,000 - 9,077 42,000 - - - 401,077 - -

Other key management personnel

J S M Tambyrajah* 169,902 - - 20,388 - - - 190,290 - -

S M Freeman 250,000 - 6,796 30,000 - - - 286,796 - -

T K S Lee** 52,159 - - 4,694 - - - 56,853 - -

Specifi ed executive

S P Henbury - - - - - - - - - -

Total key management personnel compensation

978,061 - 15,873 97,082 - - - 1,091,016 - -

Details of Remuneration Details of the remuneration of the directors and the key management personnel of the Group (as defi ned in AASB 124 Related Party Disclosures) are set out in the following tables.

Key management personnel of the Group and other executives of the Company and the Group

16NSL CONSOLIDATED LTD ANNuAL REPORT 2012

DIRECTORS’ REPORTDIRECTORS’ REPORT

REMUNERATION REPORT – AUDITED (CONTINUED)

Company performance, shareholder wealth and Director and Executive remunerationAs the Company is not yet generating earnings nor paying dividends, the share price is the key measure of shareholder value. The table below shows the performance in share price over the year and previous 3 years.

Year 30 June 2009$

30 June 2010$

30 June 2011$

30 June 2012$

Closing Share price 0.01 0.062 0.055 0.054

% Change - 520% -11% -1.8%

The issuing of share options under Director and Employee share option plans helps align the Boards personal interests to that of the shareholders.

* Resigned 30 March 2012 as Chief Financial Offi cer ** Commenced 16 March 2012 as Financial Controll

For

per

sona

l use

onl

y

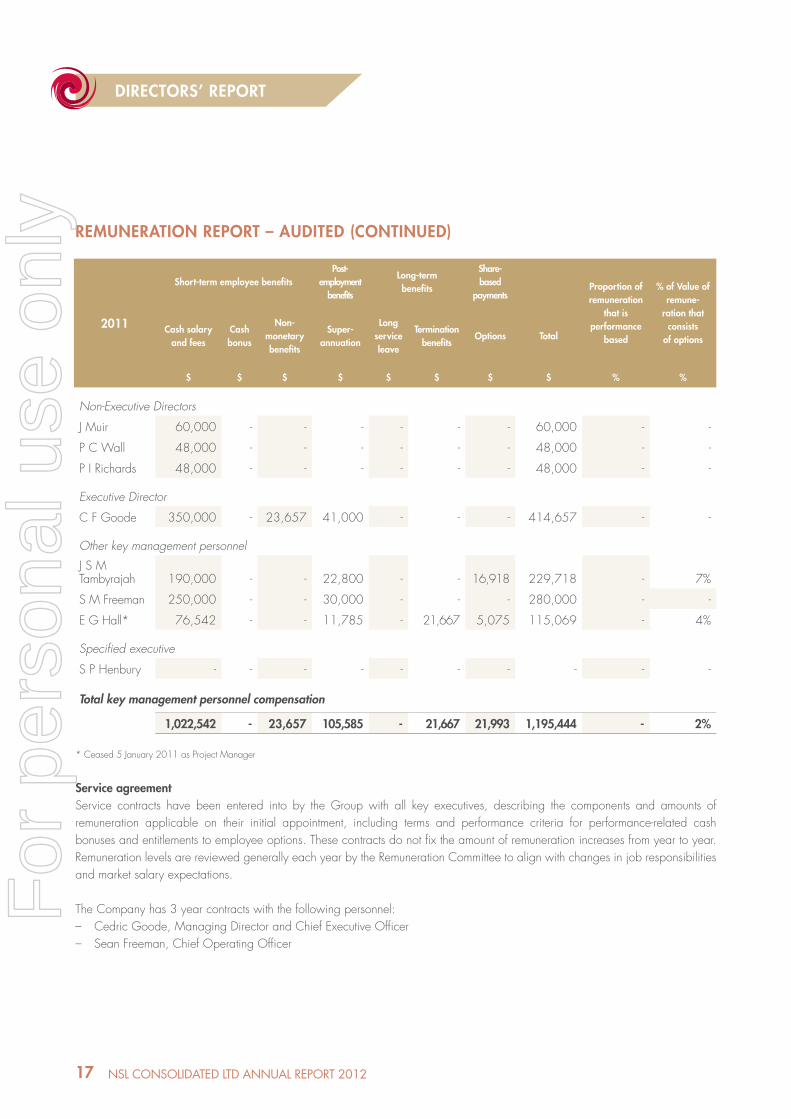

2011

Short-term employee benefi tsPost-

employment benefits

Long-termbenefi ts

Share-based

paymentsProportion of remuneration

that is performance

based

% of Value of remune-

ration that consists

of optionsCash salary

and feesCash bonus

Non-monetary benefi ts

Super-annuation

Long service leave

Termination benefi ts

Options Total

$ $ $ $ $ $ $ $ % %

Non-Executive Directors

J Muir 60,000 - - - - - - 60,000 - -

P C Wall 48,000 - - - - - - 48,000 - -

P I Richards 48,000 - - - - - - 48,000 - -

Executive Director

C F Goode 350,000 - 23,657 41,000 - - - 414,657 - -

Other key management personnel

J S M Tambyrajah 190,000 - - 22,800 - - 16,918 229,718 - 7%

S M Freeman 250,000 - - 30,000 - - - 280,000 - -

E G Hall* 76,542 - - 11,785 - 21,667 5,075 115,069 - 4%

Specifi ed executive

S P Henbury - - - - - - - - - -

Total key management personnel compensation

1,022,542 - 23,657 105,585 - 21,667 21,993 1,195,444 - 2%

60

REMUNERATION REPORT – AUDITED (CONTINUED)

Service agreementService contracts have been entered into by the Group with all key executives, describing the components and amounts of remuneration applicable on their initial appointment, including terms and performance criteria for performance-related cash bonuses and entitlements to employee options. These contracts do not fi x the amount of remuneration increases from year to year. Remuneration levels are reviewed generally each year by the Remuneration Committee to align with changes in job responsibilities and market salary expectations.

The Company has 3 year contracts with the following personnel:– Cedric Goode, Managing Director and Chief Executive Offi cer– Sean Freeman, Chief Operating Offi cer

* Ceased 5 January 2011 as Project Manager

17 NSL CONSOLIDATED LTD ANNuAL REPORT 2012

DIRECTORS’ REPORT

For

per

sona

l use

onl

y

REMUNERATION REPORT – AUDITED (CONTINUED)

Service agreement (continued)These contracts are renewable on expiry. A summary of the terms and conditions of the service agreements is as follows:

– Cedric Goode – 3 years commencing on 1st September 2009.

Annual salary is $350,000. Other benefi ts include a Company provided car, 12% superannuation contribution by the employer, short term incentive options, long term performance options and performance based bonus.

The performance bonus will be awarded on milestones, subject to production and profi tability conditions which are; (a) 0.25 years Salary on achievement of 20kt ore shipped from acquired mine(s); (b) 0.5 years Salary on achievement of 250kt ore shipped from acquired mine(s; (c) 0.75 years Salary on achievement of 500kt ore shipped from acquired mine(s); (d) 1.5 years Salary on achievement of 1Mt ore shipped from acquired mine(s); and (e) 2 years Salary on achievement of 2Mt ore shipped from acquired mine(s).

Performance based bonuses (c), (d) and (e) above: (f) will be paid in the year following achievement after the audited fi nancial report for the prior year is available; and (g) are subject to the net profi t before tax and fi nancing costs (NPBTFC) per tonne of ore mined and sold: - US$12 per tonne NPBTFC = pay performance bonuses in full; and - US$6 per tonne NPBTFC = 50% of performance bonus to be paid.

The performance bonus will be paid pro-rata between US$6 per tonne and US$12 per tonne, with no additional bonus being payable if NPBTFC is greater than US$12.

Termination benefi ts The Company may at its sole discretion terminate the employment with reasons according to clause 14.1 of the service agreement, or without reason by giving 6 months written notice and making a payment of 12 months salary after the expiry of the 6 months written notice period. If the Company elects to pay the equivalent of the 6 months salary and dispense with the notice period, the total payment inclusive of the 12 months notice period will be equivalent of 18 months salary.

– Sean Freeman – 3 years commencing on 1st July 2009.

Annual salary is $250,000. Other benefi ts include 12% superannuation contribution by the employer, short term incentive options, long term performance options and performance based bonus.

The performance bonus will be awarded on milestones, subject to production and profi tability conditions which are; (a) 0.25 years Salary on achievement of 20kt ore shipped from acquired mine(s); (b) 0.25 years Salary on achievement of 250kt ore shipped from acquired mine(s; (c) 0.5 years Salary on achievement of 500kt ore shipped from acquired mine(s); (d) 0.5 years Salary on achievement of 1Mt ore shipped from acquired mine(s); and (e) 1 years Salary on achievement of 2Mt ore shipped from acquired mine(s).

18NSL CONSOLIDATED LTD ANNuAL REPORT 2012

DIRECTORS’ REPORTDIRECTORS’ REPORT

For

per

sona

l use

onl

y

REMUNERATION REPORT – AUDITED (CONTINUED)

Service agreement (continued) Performance based bonuses (c), (d) and (e) above: (f) will be paid in the year following achievement after the audited financial report for the prior year is available; and (g) are subject to the net profit before tax and financing costs (NPBTFC) per tonne of ore mined and sold: - US$12 per tonne NPBTFC = pay performance bonuses in full; and - US$6 per tonne NPBTFC = 50% of performance bonus to be paid.

The performance bonus will be paid pro-rata between US$6 per tonne and US$12 per tonne, with no additional bonus being payable if NPBTFC is greater than US$12.

Termination benefits The Company may at its sole discretion terminate the employment with reasons according to clause 14.1 of the service agreement or without reason by giving three months written notice and making a payment of six month’s salary after the expiry of the written three months notice. If the Company elects to pay the equivalent of three month’s salary and dispense with the notice period, the total payment inclusive of six months notice period will be the equivalent of nine month’s salary.

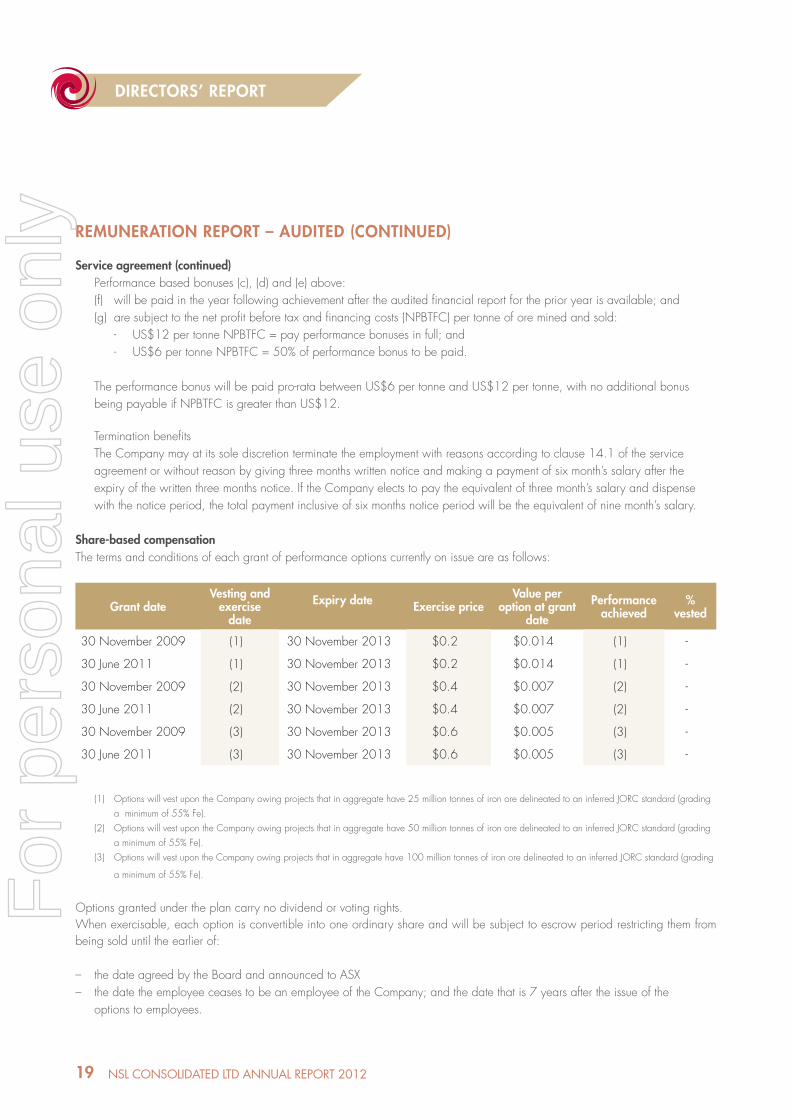

Share-based compensationThe terms and conditions of each grant of performance options currently on issue are as follows:

(1) Options will vest upon the Company owing projects that in aggregate have 25 million tonnes of iron ore delineated to an inferred JORC standard (grading a minimum of 55% Fe). (2) Options will vest upon the Company owing projects that in aggregate have 50 million tonnes of iron ore delineated to an inferred JORC standard (grading a minimum of 55% Fe). (3) Options will vest upon the Company owing projects that in aggregate have 100 million tonnes of iron ore delineated to an inferred JORC standard (grading

a minimum of 55% Fe).

Options granted under the plan carry no dividend or voting rights.When exercisable, each option is convertible into one ordinary share and will be subject to escrow period restricting them from being sold until the earlier of:

– the date agreed by the Board and announced to ASX– the date the employee ceases to be an employee of the Company; and the date that is 7 years after the issue of the options to employees.

Grant dateVesting and

exercise date

Expiry date Exercise priceValue per

option at grant date

Performance achieved

% vested

30 November 2009 (1) 30 November 2013 $0.2 $0.014 (1) -

30 June 2011 (1) 30 November 2013 $0.2 $0.014 (1) -

30 November 2009 (2) 30 November 2013 $0.4 $0.007 (2) -

30 June 2011 (2) 30 November 2013 $0.4 $0.007 (2) -

30 November 2009 (3) 30 November 2013 $0.6 $0.005 (3) -

30 June 2011 (3) 30 November 2013 $0.6 $0.005 (3) -

19 NSL CONSOLIDATED LTD ANNuAL REPORT 2012

DIRECTORS’ REPORT

For

per

sona

l use

onl

y

REMUNERATION REPORT – AUDITED (CONTINUED)

Share-based compensation (continued)The assessed fair value at grant date of options granted to the individuals is allocated equally over the period from grant date to vesting date, and the amount is included in the remuneration tables above. Fair values at grant date are independently determined using a Black-Scholes option pricing model that takes into account the exercise price, the term of the option, the impact of dilution, the share price at grant date and expected price volatility of the underlying share, the expected dividend yield and the risk-free interest rate for the term of the option.

Shares provided on exercise of remuneration optionsThere was no option exercised during the year.

Employee share schemeNone of the directors of the Company, other key management personnel of the Group or the Group Company Secretary is eligible to participate in the Company’s employee share scheme.

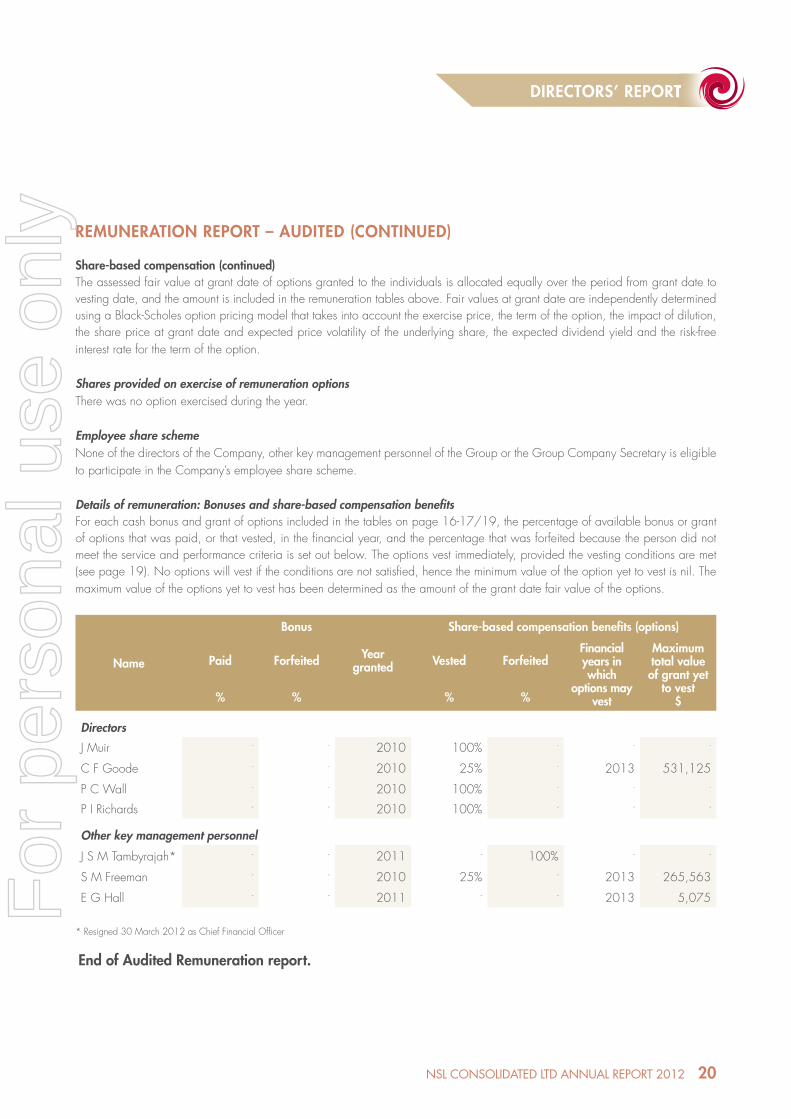

Details of remuneration: Bonuses and share-based compensation benefi tsFor each cash bonus and grant of options included in the tables on page 16-17/19, the percentage of available bonus or grant of options that was paid, or that vested, in the fi nancial year, and the percentage that was forfeited because the person did not meet the service and performance criteria is set out below. The options vest immediately, provided the vesting conditions are met (see page 19). No options will vest if the conditions are not satisfi ed, hence the minimum value of the option yet to vest is nil. The maximum value of the options yet to vest has been determined as the amount of the grant date fair value of the options.

Name

Bonus Share-based compensation benefi ts (options)

Paid Forfeited Year granted Vested Forfeited

Financial years in which

options may vest

Maximum total value of grant yet

to vest$% % % %

Directors

J Muir - - 2010 100% - - -

C F Goode - - 2010 25% - 2013 531,125

P C Wall - - 2010 100% - - -

P I Richards - - 2010 100% - - -

Other key management personnel

J S M Tambyrajah* - - 2011 - 100% - -

S M Freeman - - 2010 25% - 2013 265,563

E G Hall - - 2011 - - 2013 5,07560

End of Audited Remuneration report.

20NSL CONSOLIDATED LTD ANNuAL REPORT 2012

DIRECTORS’ REPORTDIRECTORS’ REPORT

* Resigned 30 March 2012 as Chief Financial Offi cer

For

per

sona

l use

onl

y

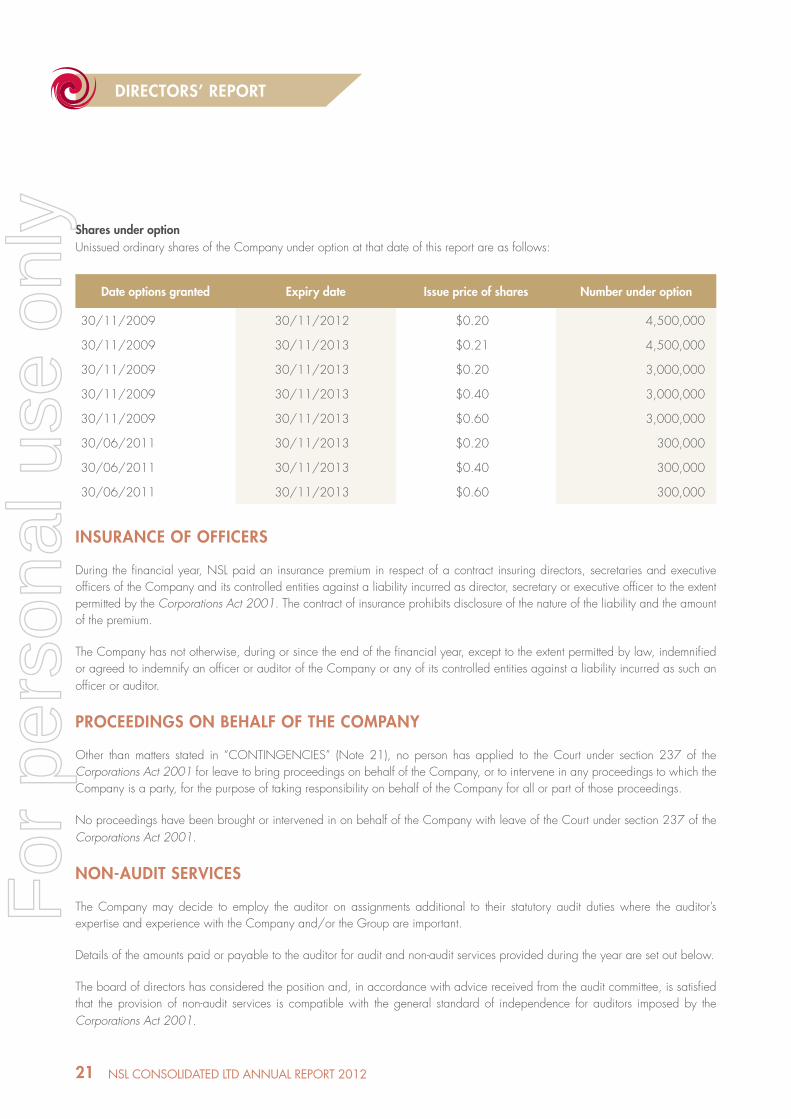

Shares under optionUnissued ordinary shares of the Company under option at that date of this report are as follows:

Date options granted Expiry date Issue price of shares Number under option

30/11/2009 30/11/2012 $0.20 4,500,000

30/11/2009 30/11/2013 $0.21 4,500,000

30/11/2009 30/11/2013 $0.20 3,000,000

30/11/2009 30/11/2013 $0.40 3,000,000

30/11/2009 30/11/2013 $0.60 3,000,000

30/06/2011 30/11/2013 $0.20 300,000

30/06/2011 30/11/2013 $0.40 300,000

30/06/2011 30/11/2013 $0.60 300,000

INSURANCE OF OFFICERS

During the financial year, NSL paid an insurance premium in respect of a contract insuring directors, secretaries and executive officers of the Company and its controlled entities against a liability incurred as director, secretary or executive officer to the extent permitted by the Corporations Act 2001. The contract of insurance prohibits disclosure of the nature of the liability and the amount of the premium.

The Company has not otherwise, during or since the end of the financial year, except to the extent permitted by law, indemnified or agreed to indemnify an officer or auditor of the Company or any of its controlled entities against a liability incurred as such an officer or auditor.

PROCEEDINGS ON BEHALF OF THE COMPANY

Other than matters stated in “CONTINGENCIES” (Note 21), no person has applied to the Court under section 237 of the Corporations Act 2001 for leave to bring proceedings on behalf of the Company, or to intervene in any proceedings to which the Company is a party, for the purpose of taking responsibility on behalf of the Company for all or part of those proceedings.

No proceedings have been brought or intervened in on behalf of the Company with leave of the Court under section 237 of the Corporations Act 2001.

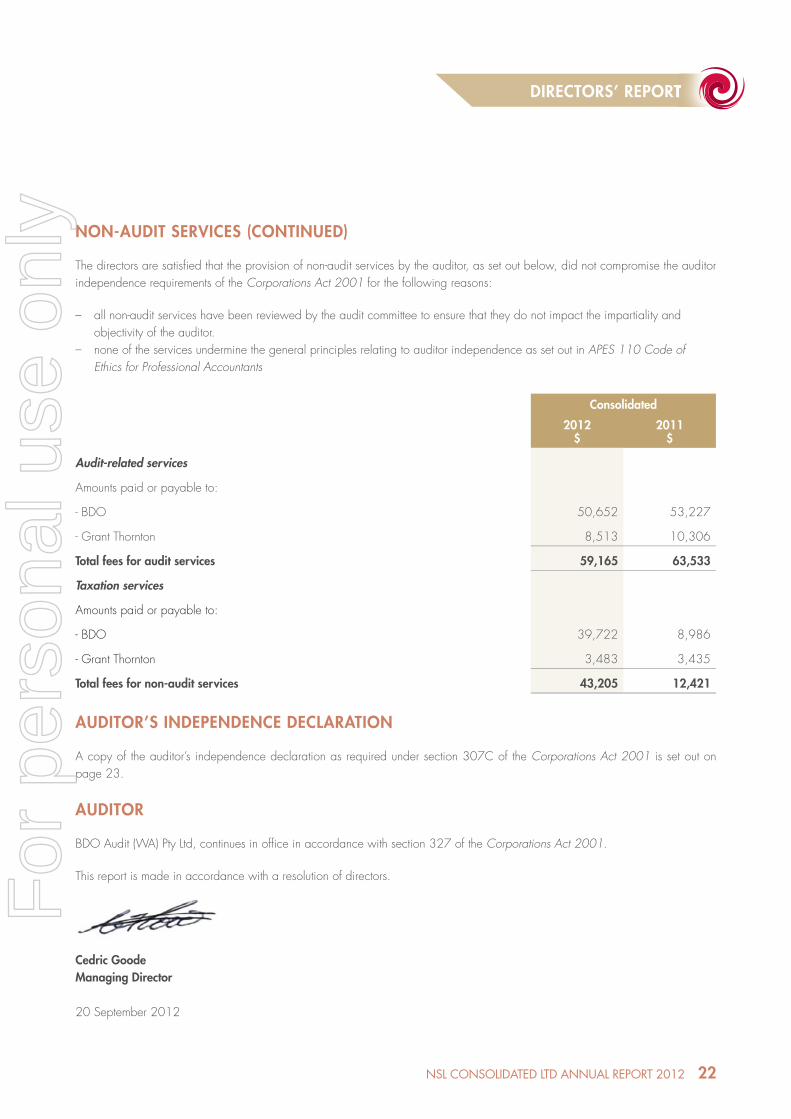

NON-AUDIT SERVICES

The Company may decide to employ the auditor on assignments additional to their statutory audit duties where the auditor’s expertise and experience with the Company and/or the Group are important.

Details of the amounts paid or payable to the auditor for audit and non-audit services provided during the year are set out below.

The board of directors has considered the position and, in accordance with advice received from the audit committee, is satisfied that the provision of non-audit services is compatible with the general standard of independence for auditors imposed by the Corporations Act 2001.

DIRECTORS’ REPORT

21 NSL CONSOLIDATED LTD ANNuAL REPORT 2012

For

per

sona

l use

onl

y

DIRECTORS’ REPORTDIRECTORS’ REPORT

NON-AUDIT SERVICES (CONTINUED)

The directors are satisfi ed that the provision of non-audit services by the auditor, as set out below, did not compromise the auditor independence requirements of the Corporations Act 2001 for the following reasons:

– all non-audit services have been reviewed by the audit committee to ensure that they do not impact the impartiality and objectivity of the auditor.– none of the services undermine the general principles relating to auditor independence as set out in APES 110 Code of Ethics for Professional Accountants

Consolidated

2012$

2011$

Audit-related services

Amounts paid or payable to:

- BDO 50,652 53,227

- Grant Thornton 8,513 10,306

Total fees for audit services 59,165 63,533

Taxation services

Amounts paid or payable to:

- BDO 39,722 8,986

- Grant Thornton 3,483 3,435

Total fees for non-audit services 43,205 12,421

AUDITOR’S INDEPENDENCE DECLARATION

A copy of the auditor’s independence declaration as required under section 307C of the Corporations Act 2001 is set out on page 23.

AUDITOR

BDO Audit (WA) Pty Ltd, continues in offi ce in accordance with section 327 of the Corporations Act 2001.

This report is made in accordance with a resolution of directors.

Cedric GoodeManaging Director

20 September 2012

22NSL CONSOLIDATED LTD ANNuAL REPORT 2012

For

per

sona

l use

onl

y

AUDITOR’S INDEPENDANCE DECLARATION

23 NSL CONSOLIDATED LTD ANNuAL REPORT 2012

23

Tel: +8 6382 4600 Fax: +8 6382 4601 www.bdo.com.au

38 Station Street Subiaco, WA 6008 PO Box 700 West Perth WA 6872 Australia

BDO Audit (WA) Pty Ltd ABN 79 112 284 787 is a member of a national association of independent entities which are all members of BDO (Australia) Ltd ABN 77 050 110 275, an Australian company limited by guarantee. BDO Audit (WA) Pty Ltd and BDO (Australia) Ltd are members of BDO International Ltd, a UK company limited by guarantee, and form part of the international BDO network of independent member firms. Liability limited by a scheme approved under Professional Standards Legislation (other than for the acts or omissions of financial services licensees) in each State or Territory other than Tasmania.

20 September 2012 The Directors NSL Consolidated Limited Level 1, 30 Ord Street WEST PERTH WA 6005 Dear Sirs, DECLARATION OF INDEPENDENCE BY PHILLIP MURDOCH TO THE DIRECTORS OF NSL CONSOLIDATED LIMITED As lead auditor of NSL Consolidated Limited for the year ended 30 June 2012, I declare that, to the best of my knowledge and belief, there have been no contraventions of: • the auditor independence requirements of the Corporations Act 2001 in relation to the audit

• any applicable code of professional conduct in relation to the audit. This declaration is in respect of NSL Consolidated Limited and the entities it controlled during the year.

Phillip Murdoch Director BDO Audit (WA) Pty Ltd Perth, Western Australia

For

per

sona

l use

onl

y

CORPORATE GOVERNANCE STATEMENT

Corporate governance is the system by which companies are directed and managed. It infl uences how the objectives of the Company are set and achieved, how risk is monitored and assessed, and how performance is optimised. Good corporate governance structures encourage companies to create value through entrepreneurism, innovation, development and exploration and provide accountability and control systems commensurate with risks involved.

Good corporate governance will evolve with the changing circumstances of a Company and must be tailored to meet these circumstances. NSL is a junior mining and exploration Company.

The Company’s Board and management are committed to a high standard of corporate governance practices, ensuring that the Company complies with the Corporations Act 2001, Australian Securities Exchange (ASX) Listing Rules, Company Constitution and other applicable laws and regulations.

However, at this stage of the Company’s corporate development, implementation of the ASX Corporate Governance Principles and Recommendations, whilst wholeheartedly supported, is not practical in every instance given the modest size and simplicity of the business. The principles and recommendations and details of the current and evolving governance practices are identifi ed in the following pages.

Principle 1: Lay solid foundations for management and oversight

The Board has the responsibility of protecting the rights and interests of shareholders and enhancement of long-term shareholder value. To fulfi ll this role, the Board is responsible for:

– Appointment of the Chief Executive Offi cer and other senior executives and the determination of their terms and conditions including remuneration and termination;– Driving the strategic direction of the Company, ensuring appropriate resources are available to meet objectives and monitoring management’s performance;– Reviewing and ratifying systems of risk management and internal compliance and control, codes of conduct and legal compliance;– Approving and monitoring the progress of major capital expenditure, capital management and signifi cant acquisitions and divestitures;– Approving and monitoring the budget and the adequacy and integrity of fi nancial and other reporting;– Approving the annual, half yearly and quarterly accounts;– Approving signifi cant changes to the organisational structure;– Approving the issue of any shares, options, equity instruments or other securities in the Company;– Ensuring a high standard of corporate governance practice and regulatory compliance and promoting ethical and responsible decision making;– Recommending to shareholders the appointment of the external auditor as and when their appointment or re-appointment is required to be approved by them; and– Meeting with the external auditor, at their request, without management being present.

24NSL CONSOLIDATED LTD ANNuAL REPORT 2012

CORPORATE GOVERNANCE STATEMENTCORPORATE GOVERNANCE STATEMENT

For

per

sona

l use

onl

y

CORPORATE GOVERNANCE STATEMENT (CONTINUED)

Principle 2: Structure the Board to add value

The Board is currently made up of four directors, two (Jock Muir and Peter Richards) of whom are considered independent. The Board considers a director to be independent where he or she is not a member of management and is free of any business or other relationship that could materially interfere with, or could reasonably be perceived to materially interfere with, the director’s ability to act in the best interests of the Company. This is not compliant with the ASX Corporate Governance Councils recommendations that the majority of Directors should be independent non-executives and the Chairman should be independent. The Board considers the current composition to be both satisfactory and realistic under the present circumstances.

Under the Company’s Constitution and the Australian Stock Exchange Listing Rules, all directors are subject to shareholder re-election every three years.

The full Board currently hold a number of scheduled meetings each year, plus strategy meetings and any extraordinary meetings at such other times as may be necessary to address signifi cant matters as they arise.

Standing Board meeting agenda items include the Managing Director’s report, fi nancial reports, strategic matters, governance and compliance.

Board members possess complementary business disciplines and experience aligned with the Company objectives. The experience and qualifi cations of directors are noted in the Directors’ Report.

Where any director has a personal interest in a matter, the director is not permitted to be present during discussions or to vote on the matter. The enforcement of this requirement ensures that the interest of shareholders, as a whole, are pursued and not jeopardised by a lack of a majority of independent directors.

The Company has developed Board committee charters for both the Audit Committee and Remuneration Committee, however due to the size of the Company the Board has not established committees to review compensation arrangements of senior executives or to manage Board succession. The full board approves all management remuneration including the allocation of options and involves itself in the nomination, selection and retirement of directors.

The Company will give consideration at an appropriate juncture in the Company’s development, for the creation of a Nomination and Remuneration Committee. The current size of the full Board permits it to act as this committee and to regularly review membership. The Board will give consideration to appointment of specialist and independent directors when the activities and scale of operation of the Company warrant such appointments.

The Board reviews the performance of Board members regularly on an on-going basis. The reviews are conducted by the Chairman and involve an exchange of views with all the members of the Board. In particular, the Board assesses the appropriate mix of skills, experience and expertise required by the Board and assesses the extent to which the required skills and experience are represented on the Board.

The Board intends to formally introduce a formal process of self assessment of its collective performance, the performance of individual directors and of Board committees.

CORPORATE GOVERNANCE STATEMENTCORPORATE GOVERNANCE STATEMENT

25 NSL CONSOLIDATED LTD ANNuAL REPORT 2012

For

per

sona

l use

onl

y

CORPORATE GOVERNANCE STATEMENT (CONTINUED)

Principle 3: Promote ethical and responsible decision making

The Company actively promotes ethical and responsible decision-making. The Company has established a formal code of conduct that addresses practices necessary to maintain confi dence in the Company’s integrity. The code takes into account the Board’s legal obligations and the reasonable expectations of its stakeholders. In addition, it is a condition of each employee’s employment contract that they uphold minimum standards of generally accepted ethical conduct.

Dealing in Company sharesThe Board has formally instituted a Company requirement that limits the purchase or disposal of shares by directors, offi cers and employees to the period of four weeks from the:a) date of the Company’s Annual General Meeting;b) release of the quarterly results announcement to the Australia Stock Exchange (ASX);c) release of the half yearly results announcement to the ASX;d) release of the preliminary fi nal results announcement to the ASX; ore) release of a disclosure document offering securities in the Company.

NSL has a policy agreed to by the Board members, other Company offi cers and employees that any proposed trade in the Company’s securities is to be fi rstly advised to the Chairman. Once the Chairman has given approval, the relevant person may execute the trade. Such policy clearly mitigates the risk of breaching the insider trading provisions and gives the Chairman control to restrict trading if the Chairman may be privy to sensitive information before the other Company offi cers and personnel are, or the Chairman has knowledge that certain sensitive information (eg. exploration results) are due for receipt within a short term timeframe.

Directors, offi cers and employees with any non-public sensitive information are prohibited from purchasing or disposing of Company shares, in accordance with the Corporations Act 2001.

Directors must advise the Company of any transactions conducted by them in the shares of the Company, in accordance with the Corporations Act 2001 and ASX Listing Rules.

The Board has approved and published in the public domain the Guidelines for Buying and Selling Securities which details the points listed above.

Diversity PolicyThe Company recognises the benefi ts arising from employee and board diversity, including a broader pool of high quality employees, improving employee retention, accessing different perspectives and ideas and benefi ting from all available talent.