Analysis Fraud

127

A A i i i g g g l l l i i i R R R i i z z o o o u u u SUPERVISORS PROF. J. SOLDATOS PROF. I. CHRISTOU MASTER OF ASTER OF ASTER OF ASTER OF SCIENCE IN CIENCE IN CIENCE IN CIENCE IN INFORMATION NFORMATION NFORMATION NFORMATION & TELECOMMUNICATIONS ELECOMMUNICATIONS ELECOMMUNICATIONS ELECOMMUNICATIONS TECHNOLOGIES ECHNOLOGIES ECHNOLOGIES ECHNOLOGIES ATHENS ATHENS ATHENS ATHENS , OCTOBER OCTOBER OCTOBER OCTOBER 2010 2010 2010 2010

-

Upload

independent -

Category

Documents

-

view

4 -

download

0

Transcript of Analysis Fraud

AAAAAAAAAAAA iiiiiiiiiiii gggggggggggg llllllllllll iiiiiiiiiiii RRRRRRRRRRRR iiiiiiiiiiii zzzzzzzzzzzz oooooooooooo uuuuuuuuuuuu

SSSSSSSSUUUUUUUUPPPPPPPPEEEEEEEERRRRRRRRVVVVVVVVIIIIIIIISSSSSSSSOOOOOOOORRRRRRRRSSSSSSSS

PPPPPPPPRRRRRRRROOOOOOOOFFFFFFFF........ JJJJJJJJ ........ SSSSSSSSOOOOOOOOLLLLLLLLDDDDDDDDAAAAAAAATTTTTTTTOOOOOOOOSSSSSSSS

PPPPPPPPRRRRRRRROOOOOOOOFFFFFFFF........ IIIIIIII ........ CCCCCCCCHHHHHHHHRRRRRRRRIIIIIIIISSSSSSSSTTTTTTTTOOOOOOOOUUUUUUUU

MMMMAS TE R O F A S T E R O F A S T E R O F A S T E R O F SSSS C I ENC E I N C I ENC E I N C I ENC E I N C I ENC E I N IIII N FORMAT I ON N FORMAT I ON N FORMAT I ON N FORMAT I ON

&&&& TTTT E L E COMMUN ICA T I ON S E L E COMMUN ICA T I ON S E L E COMMUN ICA T I ON S E L E COMMUN ICA T I ON S TTTT E CHNO LOG I E SE CHNO LOG I E SE CHNO LOG I E SE CHNO LOG I E S

ATHENSATHENSATHENSATHENS ,,,, OCTOBER OCTOBER OCTOBER OCTOBER 2010201020102010

Analysis of Fraud Detection

Aigli Rizou – MSITT 2010 2

ABSTRACTABSTRACTABSTRACTABSTRACT

Fraud plays a leading role in most aspects of social and economical life

worldwide. The expansion of modern technology resulted in the facilitation of

our daily activities, but rendered our lives more vulnerable to fraud attacks.

Intense financial pressure during the economic crisis has, also, led to a bulge

in fraud and increasing number of victims. Banking, telecommunications

insurance, internet and enterprises are the sectors which suffer significant

losses and they are the basic parts the current thesis disserts. The

economical impact of fraud made fraud prevention and detection a dire

necessity. Fraud detection theoretical background stems from scientific fields,

such as data mining, machine learning, artificial intelligence and statistics.

Supervised and unsupervised learning algorithms have contributed to the

evolvement of fraud detection. Moreover, several academic studies have

indulged in the research of various promising fraud techniques, with a view to

encounter the evolving nature of fraud. The presentation of a real-life fraud

detection system of a Greek Bank aims at giving a more practical view of the

problem. A short description of the system reveals the way the Bank deals

with fraud cases. Based on a real data set labeled by the system, another

machine learning tool is used in order to check the reliability of the running

supervised algorithms. Finally, the proposed fraud detection solution aims at

offering a robust fraud detection system with improved performance,

constituting a subject for future work.

Keywords: fraud detection, fraud losses, classification, clustering, confusion

matrix, false alarm rate, classifier ensembles, class label

Analysis of Fraud Detection

Aigli Rizou – MSITT 2010 3

ACKNOWLEDGMENTSACKNOWLEDGMENTSACKNOWLEDGMENTSACKNOWLEDGMENTS

I w o u l d l i ke t o e x p r e s s m y g r a t i t u d e a n d a p p r e c i a t i o n t o

m y s u p e r v i s o r s , P r o f . J . S o l d a t o s a n d P r o f . I . C h r i s t o u ,

w h o s e v a l u a b l e g u i d a n c e a n d h a r mo n i o u s c o l l a b o r a t i o n

e n c o u r a g e d m e t o d i s c o v e r u n kn o w n a s p e c t s o f t h e

s u b j e c t .

Analysis of Fraud Detection

Aigli Rizou – MSITT 2010 4

DECLARATIONDECLARATIONDECLARATIONDECLARATIONSSSS

I , A i g l i R i z o u , d e c l a r e t h a t t h e w o r k p r e s e n t e d i n t h i s

t h e s i s w a s c a r r i e d o u t i n a c c o r d a n c e w i t h t h e r e g u l a t i o n s

o f t h e A t h e n s I n f o r m a t i o n T e c h n o l o g y I n s t i t u t e . A n y

v i e w s e x p r e s s e d i n t h i s d i s s e r t a t i o n a r e t h o s e o f t h e

a u t h o r a n d i n n o w a y r e p r e s e n t t h o s e o f t h e A t h e n s

In f o r m a t i o n Te c h n o l o g y ( A I T ) I n s t i t u t e .

Aigli Rizou

22/10/2010

Th e w o r k c o n t a i n e d i n t h i s t h e s i s “ A n a l ys i s o f F r a u d

D e t e c t i o n ” b y A i g l i R i z o u h a s b e e n c a r r i e d o u t u n d e r m y

s u p e r v i s i o n .

J. Soldatos I. Christou

22/10/2010 22 /10/2010

Athens Information Technology Athens Information Technology

Analysis of Fraud Detection

Aigli Rizou – MSITT 2010 5

TABLE OF CONTENTSTABLE OF CONTENTSTABLE OF CONTENTSTABLE OF CONTENTS

1 . I N T R O D UC T I O N .............................................................................11

1 . 1 . H i s t o r y ............................................................................................11

1 . 2 . O b j e c t i v e .......................................................................................12

1 . 3 . S t r u c tu r e .......................................................................................13

2 FRAUD DETECTION (FD) OVERVIEW .................................................15

22 .. 11 .. FF rr aa uu dd DD ee ff ii nn ii tt ii oo nn .......................................................................15

2 . 2 . F r a u d D e t e c t i o n & P r e v e n t i o n .........................................15

2 . 3 . F r a u d T y p e s ................................................................................16

2 . 3 . 1 . B a n k i n g ...............................................................................16

2 . 3 . 2 . In s u r a n c e ...........................................................................18

2 . 3 . 3 . In t e r n e t ................................................................................18

2 . 3 . 4 . T e l e c o m m u n i c a t i o n s ...................................................19

2 . 3 . 5 . E n t e r p r i s e s .......................................................................19

2 . 3 . 6 . G e n e r a l ................................................................................19

2 . 4 . F r a u d T e c h n i q u e s ....................................................................20

2 . 4 . 1 . B a n k i n g ...............................................................................20

2 . 4 . 2 . In s u r a n c e ...........................................................................22

2 . 4 . 3 . In t e r n e t ................................................................................23

2 . 4 . 4 . T e l e c o m m u n i c a t i o n s ...................................................24

2 . 4 . 5 . E n t e r p r i s e s .......................................................................25

2 . 5 . F r a u d s t e r s T y p e ........................................................................26

2 . 6 . E c o n o m i c a l I m p a c t o f F r a u d .............................................27

2 . 6 . 1 . G e n e r a l ................................................................................28

2 . 6 . 2 . B a n k i n g ...............................................................................30

2 . 6 . 2 . 1 . C r e d i t / D e b i t c a r d s ...................................................30

2 . 6 . 2 . 2 . I d e n t i t y T h e f t ..............................................................34

2 . 6 . 3 . E n t e r p r i s e s .......................................................................34

2 . 6 . 4 . In s u r a n c e ...........................................................................36

2 . 6 . 5 . In t e r n e t ................................................................................36

2 . 6 . 5 . 1 . A d v a n c e F e e F r a u d – 4 1 9 S c a m ......................37

Analysis of Fraud Detection

Aigli Rizou – MSITT 2010 6

2 . 6 . 6 . T e l e c o m m u n i c a t i o n s ...................................................38

2 . 7 . D i f f i c u l t i e s i n F D .....................................................................39

2 . 8 . F D S y s t e m R e q u i r e m e n t s ....................................................41

2 . 8 . 1 . B u s i n e s s R e q u i r e m e n t s ............................................41

2 . 8 . 2 . T e c h n i c a l R e q u i r e m e n t s ...........................................41

2 . 8 . 3 . F u n c t i o n a l R e q u i r e m e n t s .........................................42

2.9. P e r f o r m a n c e M e t r i c s ..............................................................42

2 . 9 . 1 . R e c e i v e r O p e r a t i n g C h a r a c t e r i s t i c ( R O C ) .....44

3 THEORETICAL PERSPECTIVE ............................................................46

3.1. F D M e t h o d s ..................................................................................46

3 . 2 . S u p e r v i s e d & U n s u p e r v i s e d L e a r n i n g M e t h o d s ....46

3 . 2 . 1 . C l a s s i f i c a t i o n ..................................................................47

3 . 2 . 1 . 1 . D e c i s i o n T r e e ( D T ) ..................................................48

3 . 2 . 1 . 1 . 1 . C 4 . 5 ( J 4 8 ) ..............................................................49

3 . 2 . 1 . 2 . A r t i f i c i a l N e u r a l N e t w o r k s ( A N N ) ...................50

3 . 2 . 1 . 3 . F u z z y L o g i c ( F L ) .......................................................53

3 . 2 . 1 . 4 . F u z z y N e u r a l Ne t w o r k ( F N N) .............................54

3 . 2 . 1 . 5 . N a ï v e B a y e s ( N B ) .....................................................55

3 . 2 . 1 . 6 . S u p p o r t V e c t o r M a c h i n e s ( S V M ) .....................55

3 . 2 . 2 . L i n e a r a n d L o g i s t i c R e g r e s s i o n ..........................57

3 . 2 . 3 . C l u s t e r i n g ..........................................................................57

3 . 2 . 3 . 1 . O u t l i e r D e t e c t i o n ......................................................57

3 . 2 . 4 . Me t a - l e a r n i n g ..................................................................58

3 . 2 . 4 . 1 . B a g g i n g ( B o o t s t r a p A g g r e g a t i n g ) ..................59

3 . 2 . 4 . 2 . S t a c k i n g ( S t a c k e d G e n e r a l i z a t i o n ) ...............60

3 . 2 . 4 . 3 . B o o s t i n g .......................................................................60

4 ACADEMIC PERSPECTIVE ..................................................................61

4 . 1 . S c i e n t i f i c R e s e a r c h ................................................................61

4 . 1 . 1 . C a r d F D ...............................................................................61

4 . 1 . 1 . 1 . E x p e r i m e n t 1 - D e s c r i p t i o n ................................61

4 . 1 . 1 . 2 . E x p e r i m e n t 1 – R e s u l t s ........................................63

4 . 1 . 2 . In s u r a n c e F D ....................................................................66

4 . 1 . 2 . 1 . E x p e r i m e n t 1 - D e s c r i p t i o n ................................66

Analysis of Fraud Detection

Aigli Rizou – MSITT 2010 7

4 . 1 . 2 . 2 . E x p e r i m e n t 1 - R e s u l t s .........................................68

4 . 1 . 3 . T e l e c o m m u n i c a t i o n s F D ............................................69

4 . 1 . 3 . 1 . E x p e r i m e n t 1 - D e s c r i p t i o n ................................69

4 . 1 . 3 . 2 . E x p e r i m e n t 1 - R e s u l t s .........................................72

5 PRACTICAL PERSPECTIVE .................................................................76

5 . 1 . B a n k An t i - F r a u d S y s t e m ......................................................76

5 . 1 . 1 . T h e S o f t w a r e ....................................................................78

5 . 1 . 1 . 1 . S e r v i c e C o n s u m e r T i e r .........................................78

5 . 1 . 1 . 2 . S e r v i c e P r o v i d e r T i e r ............................................79

5 . 1 . 1 . 3 . C l i e n t T i e r .....................................................................79

5 . 1 . 1 . 4 . C o m m u n i c a t i o n ..........................................................79

5 . 1 . 2 . F L S o f t w a r e ......................................................................80

5 . 1 . 2 . 1 . R i s k S h i e l d P r o j e c t ..................................................82

5 . 1 . 2 . 1 . 1 . I n p u t V a r i a b l e s ...................................................82

5 . 1 . 2 . 1 . 2 . F i n g e r p r i n t s .........................................................83

5 . 1 . 2 . 1 . 3 . C a l c u l a t i o n U n i t s ..............................................85

5 . 1 . 2 . 1 . 4 . O u t p u t V a r i a b l e s ...............................................85

5 . 1 . 2 . 1 . 5 . D e c i s i o n V a r i a b l e .............................................85

5 . 1 . 2 . 1 . 6 . C a s e Ma n a g e m e n t .............................................86

5 . 2 . W a i k a t o E n vi r o n m e n t f o r K n o w l e d g e An a l y s i s ( W E K A) ......................................................................................................86

5 . 2 . 1 . P r e p r o c e s s ........................................................................87

5 . 2 . 1 . 1 . D a t a s e t ..........................................................................88

5 . 2 . 2 . C l a s s i f i c a t i o n ..................................................................89

5 . 2 . 2 . 1 . P e r f o r m a n c e M e t r i c s ..............................................90

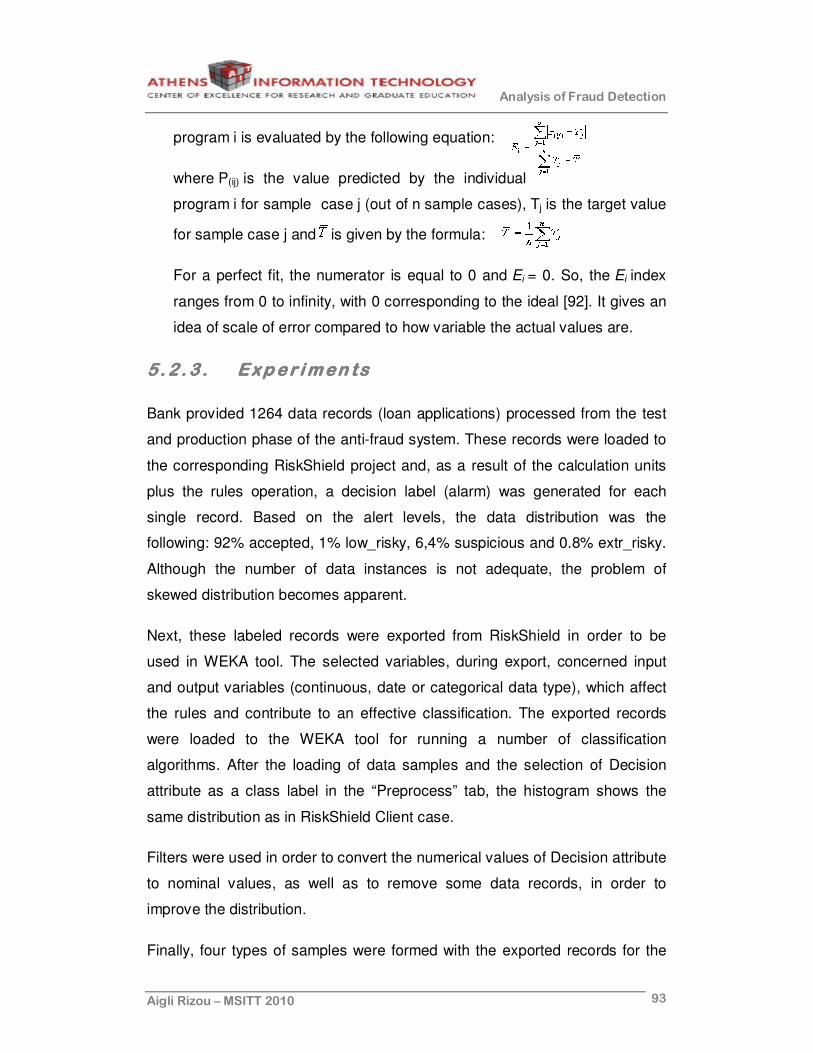

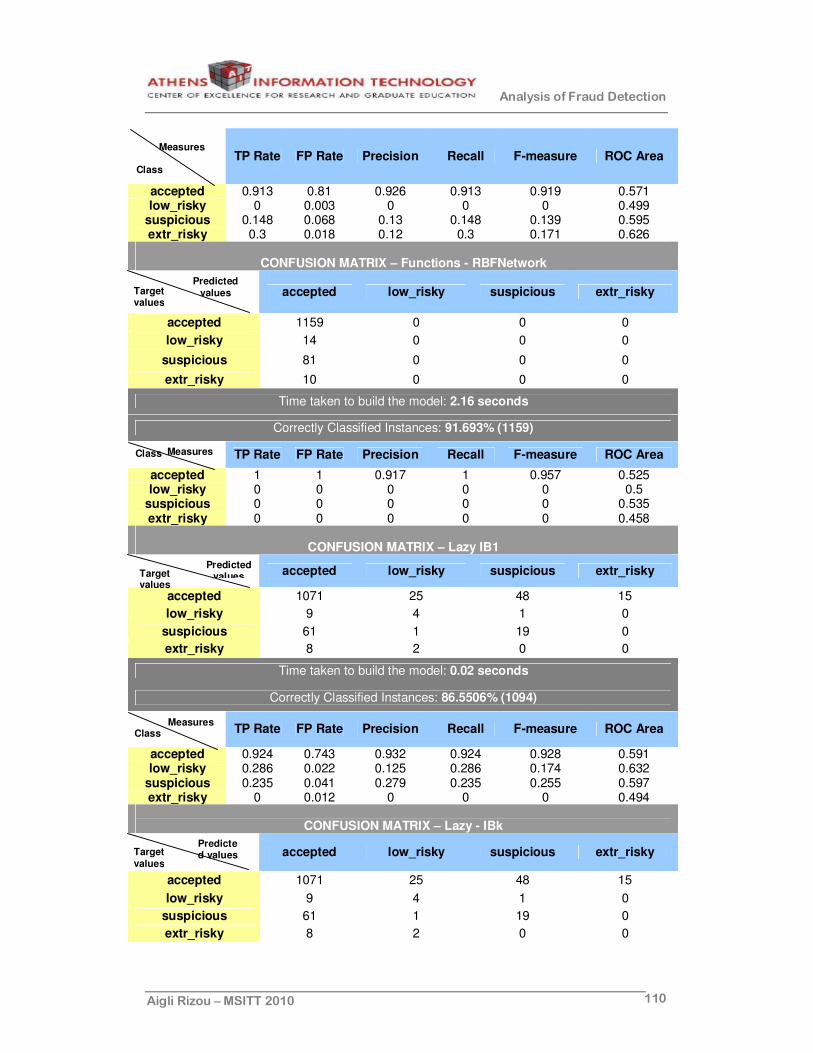

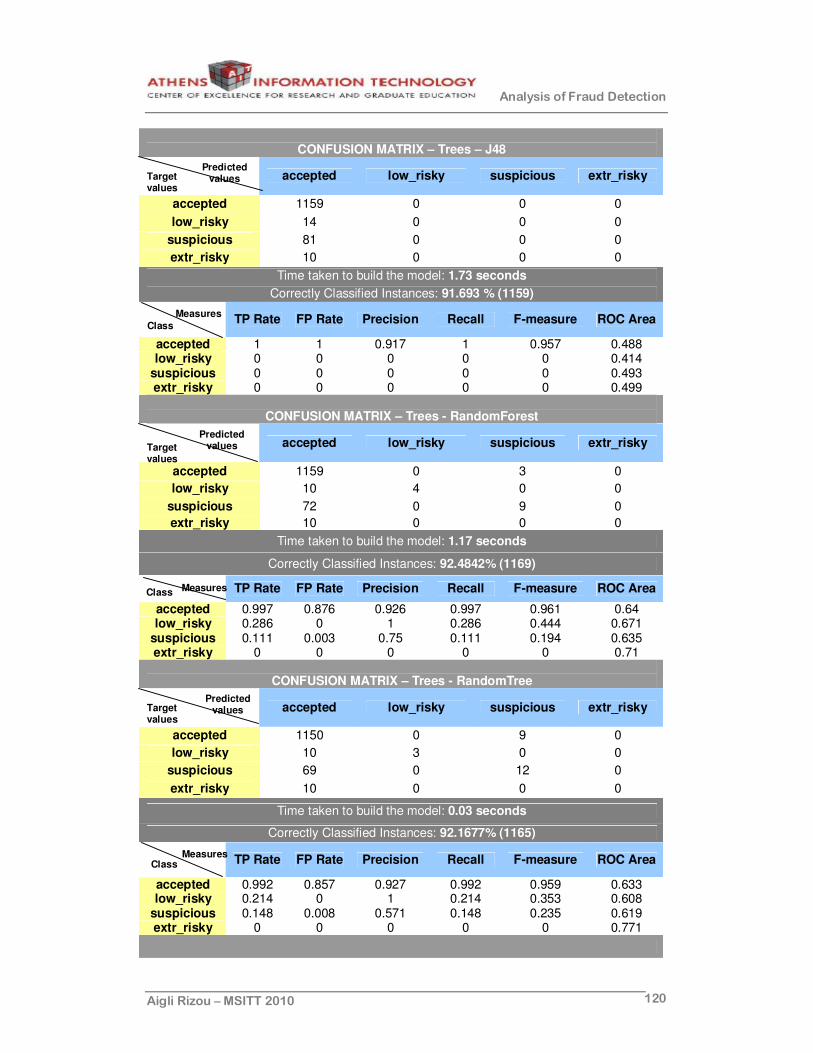

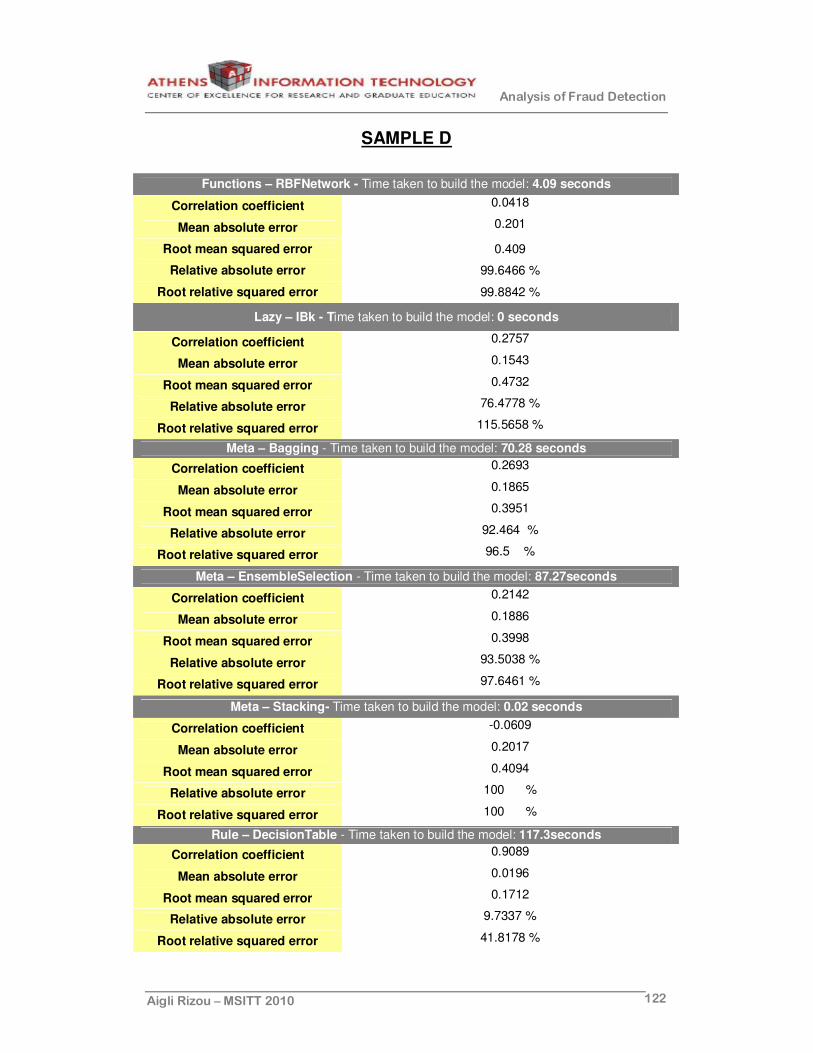

5 . 2 . 3 . E x p e r i m e n t s .....................................................................93

5 . 3 . R e s u l t s ...........................................................................................94

5 . 4 . C o n c l u s i o n s & F u t u r e W o r k ..............................................99

R E F E R E N C E S ......................................................................................103

A P P E N D I X A .........................................................................................109

A P P E N D I X B .........................................................................................124

Analysis of Fraud Detection

Aigli Rizou – MSITT 2010 8

LIST OF FIGURESLIST OF FIGURESLIST OF FIGURESLIST OF FIGURES

Figure 1: Bar chart of fraud types from 51 unique and published FD papers [76].................................................................................................................20

Figure 2: Hierarchy chart of white-collar crime perpetrators from both firm-level and community-level perspectives [76]..................................................26

Figure 3: Breakdown of fraud losses in UK for 2008 according to NFA [48] ..30

Figure 4: Breakdown of card losses in UK during 2008 according to FFA [48].......................................................................................................................31

Figure 5: UK Fraud loss ratios by card type according to Visa estimates for 2008 [16]. .......................................................................................................31

Figure 6: Comparative overview of European countries based on Visa estimates in 2008 [16]....................................................................................32

Figure 7: Fraud loss ratios of 2008 according to Visa [16]. ............................33

Figure 8: Card fraud losses in the US for 2006..............................................33

Figure 9: Distribution of occupational fraud losses worldwide according to ACFE [25]. .....................................................................................................34

Figure 10: Proportion analysis per fraud category according to ACFE [25]....35

Figure 11: Median occupational fraud losses by category for 106 nations according to ACFE [25]..................................................................................35

Figure 12: Annual dollar loss of referred complaints according to IC3 (in millions) [46]...................................................................................................36

Figure 13:Advance fee fraud losses for Greece (419 Unit of Ultrascan AGI) [54].................................................................................................................37

Figure 14: Advance fee fraud losses worldwide in 2009 in million $ (Ultrascan AGI) [54].........................................................................................................38

Figure 15: Receiver Operating Characteristic curve & the Area Under the Curve [84]. .....................................................................................................45

Figure 16: A Simple Linear Classification Boundary for the Loan Data Set, where the shaped region denotes class no loan [85]. ....................................48

Figure 17: An indicative DT example [61]. .....................................................49

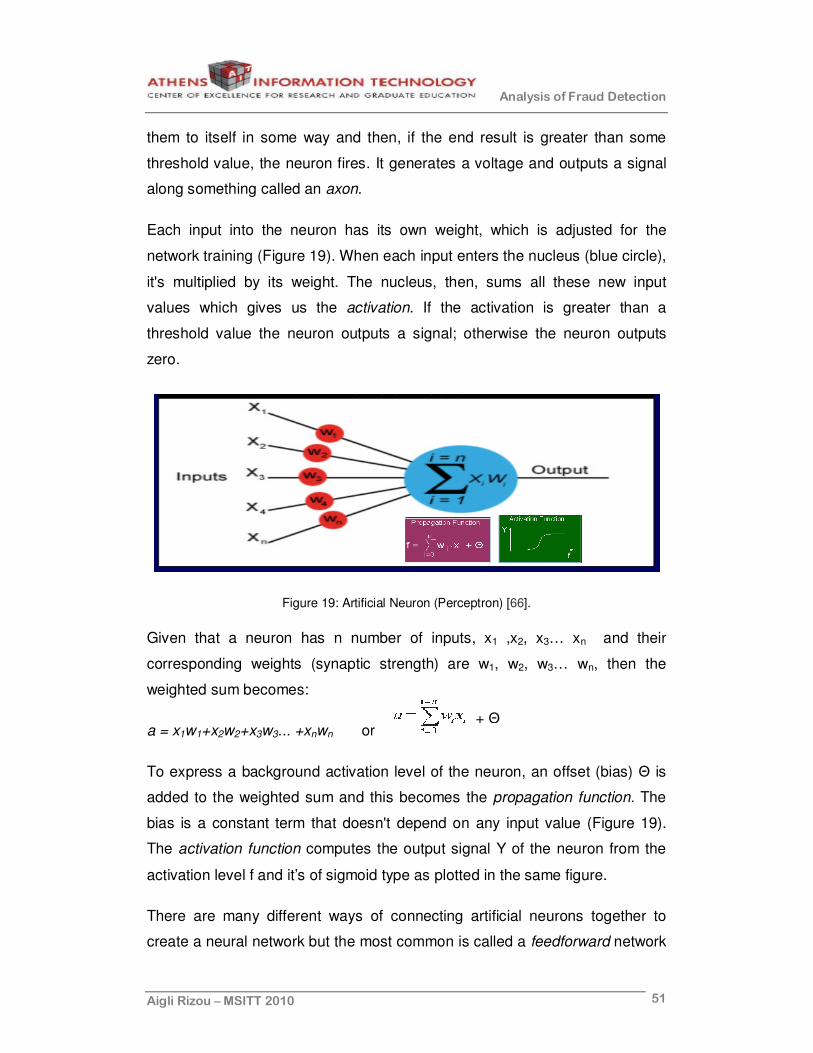

Figure 18: A human neuron forming a chemical synapse [66]. .....................50

Figure 19: Artificial Neuron (Perceptron) [66].................................................51

Figure 20: Three-Layer feedforward ANN......................................................52

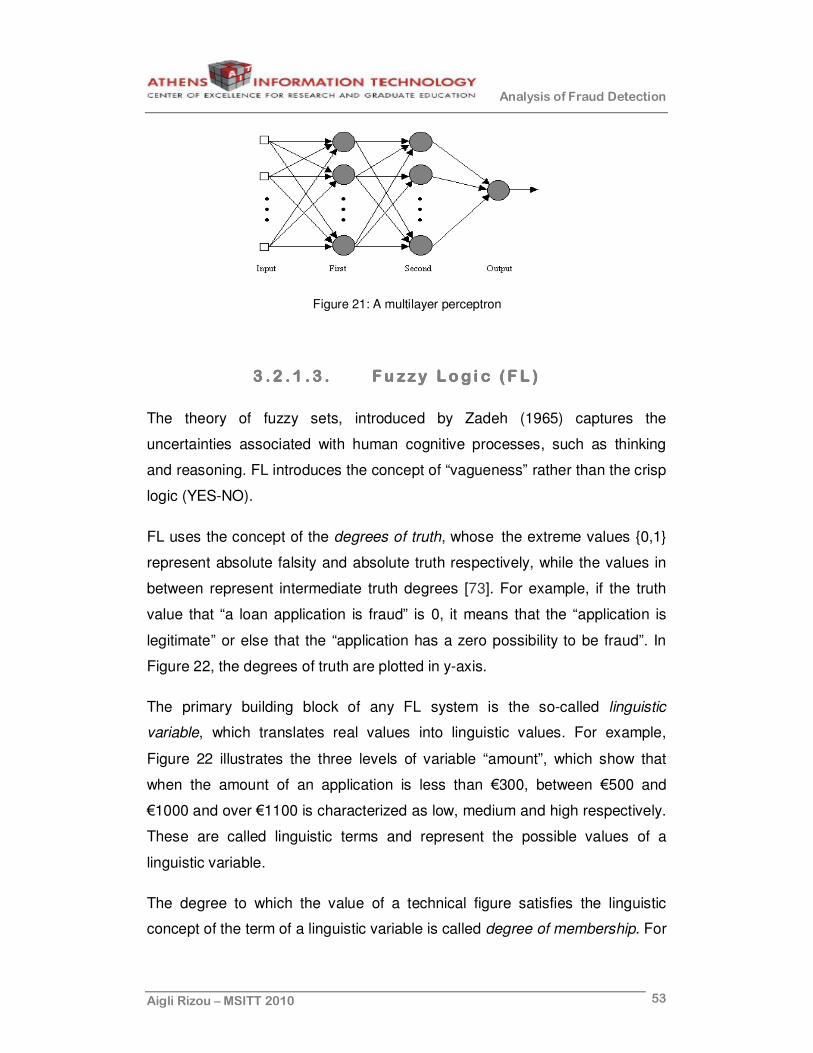

Figure 21: A multilayer perceptron .................................................................53

Analysis of Fraud Detection

Aigli Rizou – MSITT 2010 9

Figure 22: Membership function of the linguistic variable “amount” in FL ......54

Figure 23: Margins and Support Vectors in a two-dimensional example [65].56

Figure 24: Example of clustering [85].............................................................58

Figure 25: Graphical representation of bagging. ............................................59

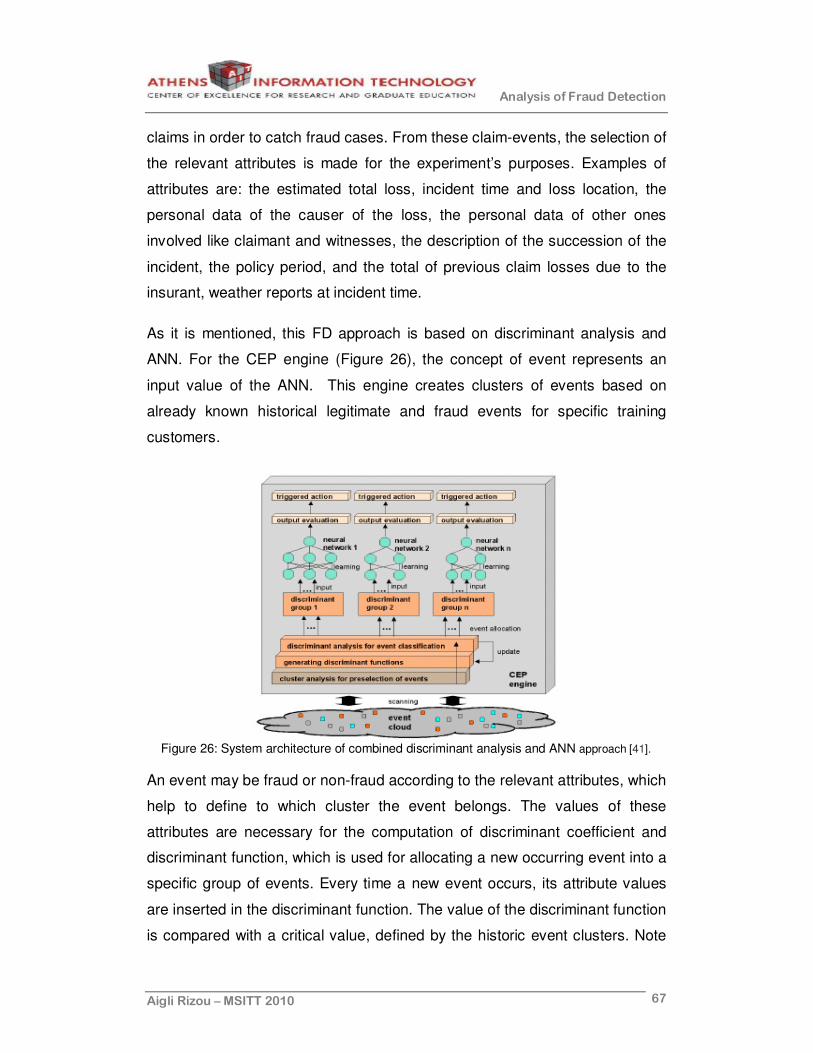

Figure 26: System architecture of combined discriminant analysis and ANN approach [41]. ................................................................................................67

Figure 27: The vector of comparison [30].......................................................70

Figure 28: An example of similarity vectors of 3 user profile – test sets (Group 1) [30].............................................................................................................72

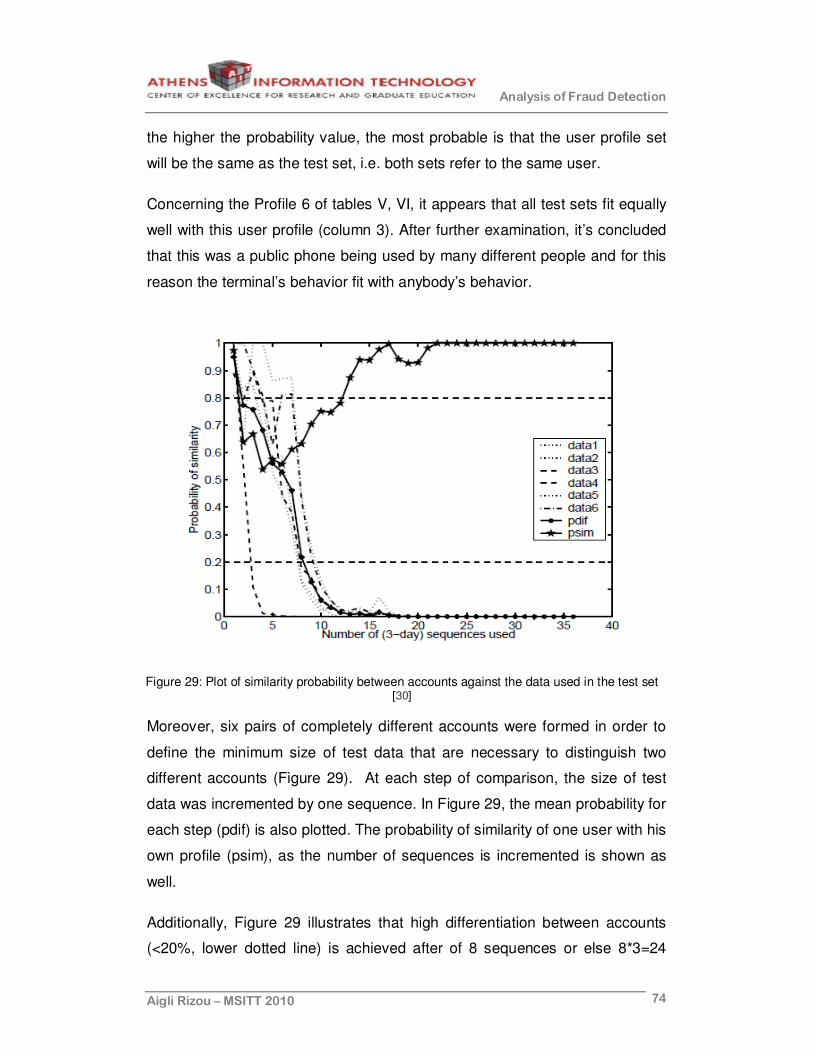

Figure 29: Plot of similarity probability between accounts against the data used in the test set [30]..................................................................................74

Figure 30: RiskShield architecture [79]. .........................................................78

Figure 31: A simplified FL environment – fuzzyTECH software .....................81

Figure 32: RiskShield-Client project...............................................................83

Figure 33: Fingerprint.....................................................................................84

Figure 34: Preprocess tab of WEKA ..............................................................87

Figure 35: arff file ...........................................................................................88

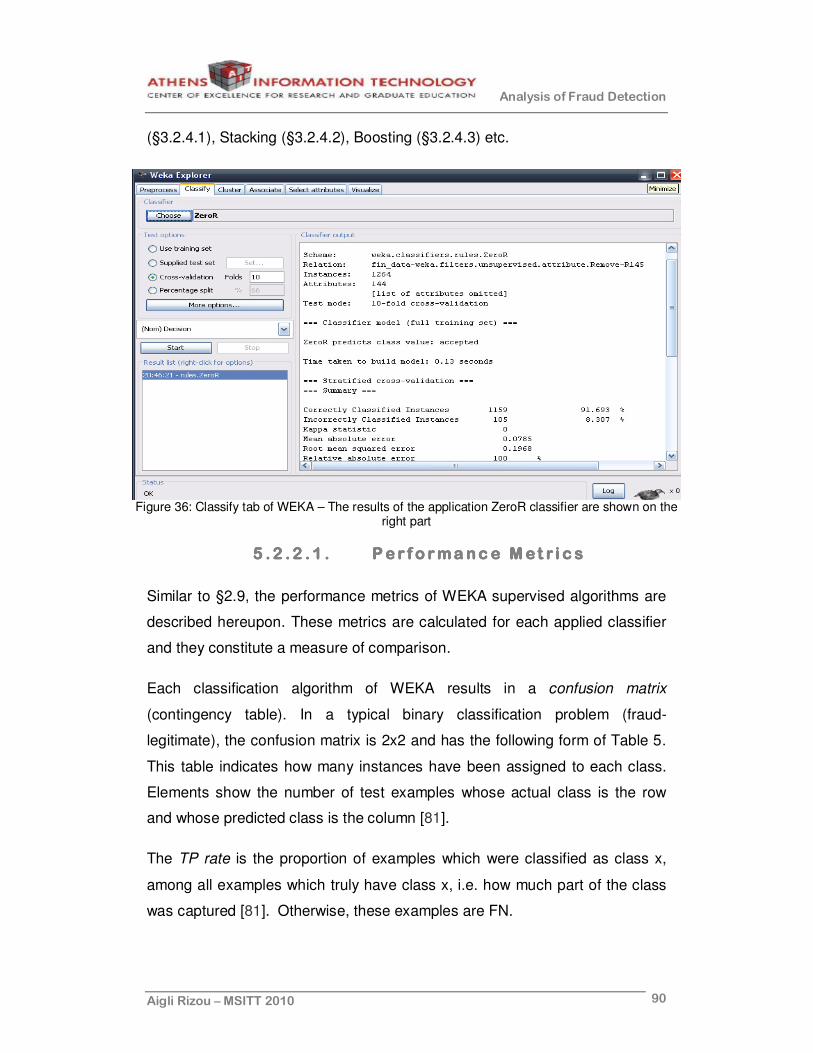

Figure 36: Classify tab of WEKA – The results of the application ZeroR classifier are shown on the right part .............................................................90

Figure 37: LOF proposed solution [84].........................................................100

Figure 38: The general framework for combining outlier detection techniques [84]...............................................................................................................101

LIS T O F TABLES

Table 1: Annual Fraud losses per fraud sector and country...........................29

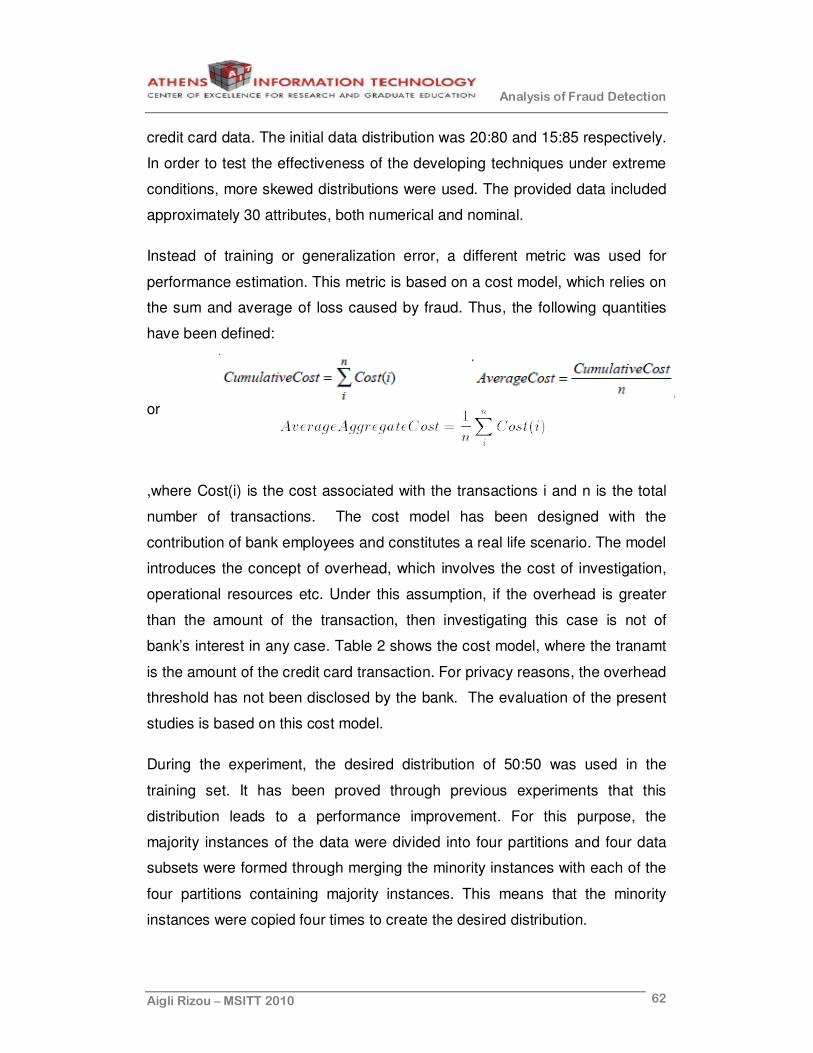

Table 2: Cost model assuming a fixed overhead [17]. ...................................63

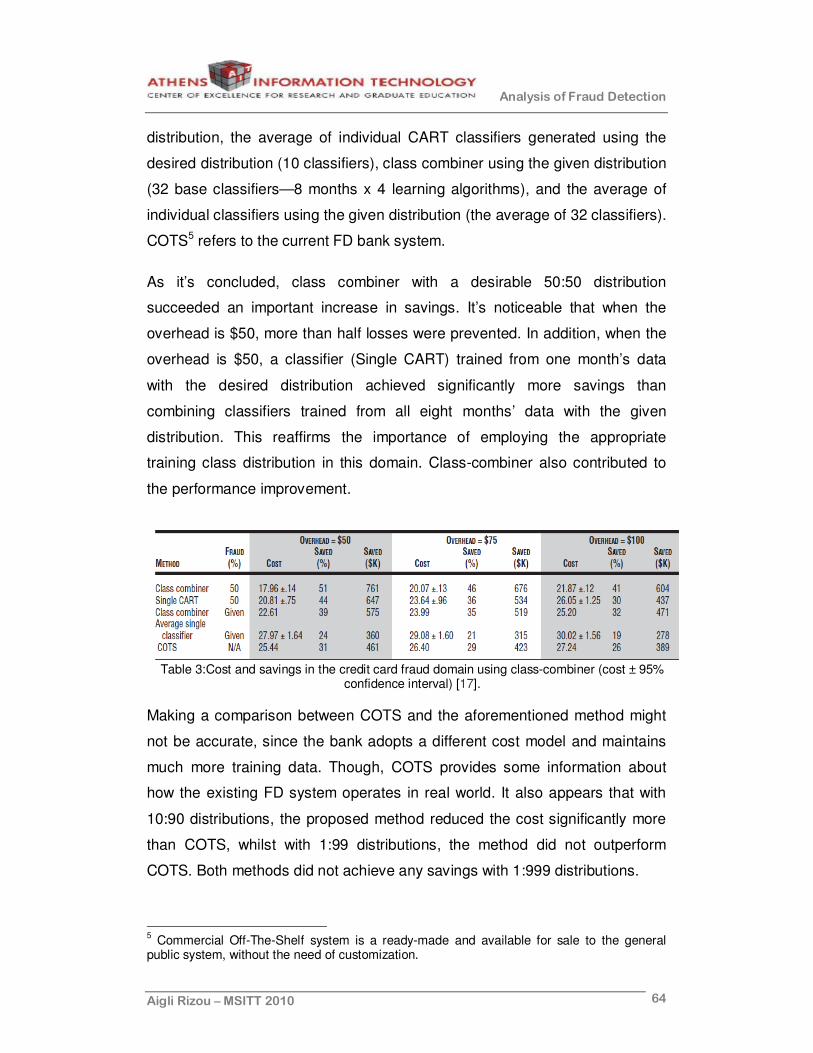

Table 3:Cost and savings in the credit card fraud domain using class-combiner (cost ± 95% confidence interval) [17]. ............................................64

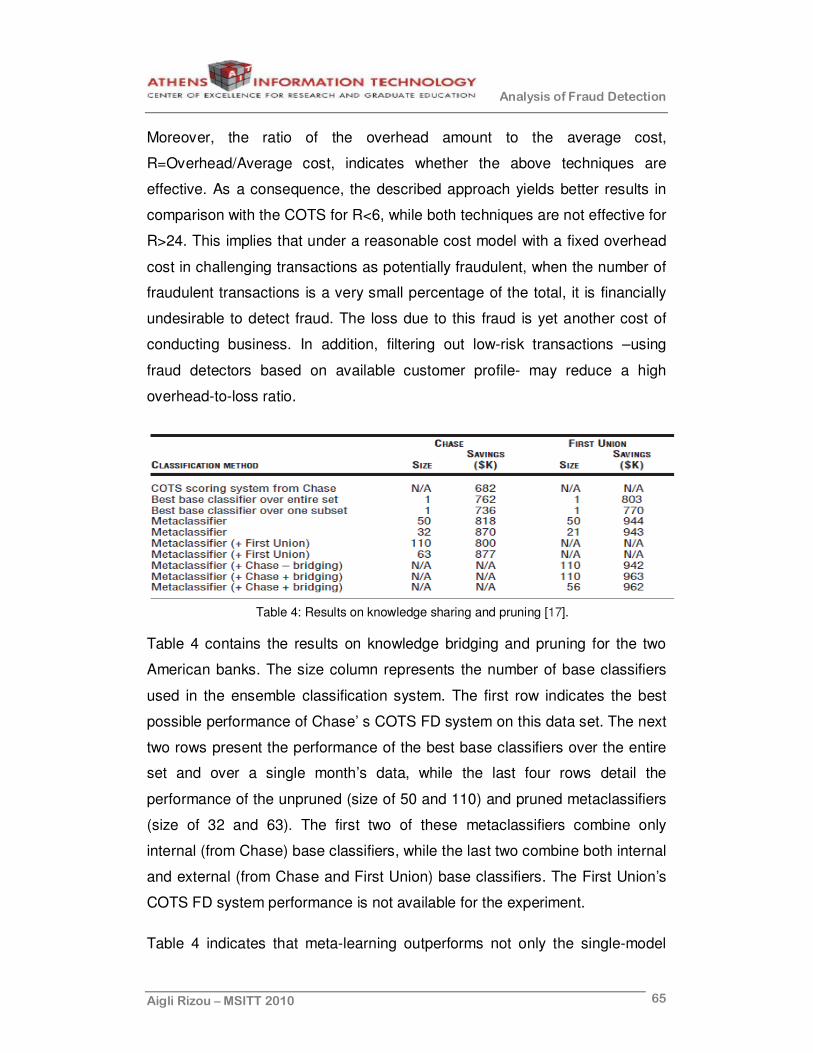

Table 4: Results on knowledge sharing and pruning [17]...............................65

Table 5: Confusion matrix for binary problems...............................................91

Analysis of Fraud Detection

Aigli Rizou – MSITT 2010 10

Analysis of Fraud Detection

Aigli Rizou – MSITT 2010 11

1.1.1.1. INTRODUCTIONINTRODUCTIONINTRODUCTIONINTRODUCTION

1 .1.1.1.1.1.1.1. H is toryHis toryHis toryHis tory

The phenomenon of fraud dates back centuries ago and it’s believed that its

presence coincides with the dawn of commerce. A true history of fraud has

been recorded in 300 B.C. in Greece, when a merchant named Hegestratus

took out a large insurance policy known as bottomry. In essence, the

merchant borrowed money and agreed to pay back with interest as soon as

the cargo (i.e. corn) was delivered. If the loan was not paid back, then the

lender had the right to acquire the boat and the cargo as well. Hegestratus

decided to sink his empty boat, keep the loan and sell the corn. However, he

didn’t manage to deceive the lender, as he drowned when trying to escape his

crew passengers when they caught him in the act. This is regarded as the first

recorded incident of insurance fraud worldwide [9].

Fraud, undoubtedly, keeps up with the social, economical and technological

evolution and thus it appears with different intensity and form, depending on

the epoch. The expansion of modern technology and the global

superhighways of communications in combination with the fraudsters’

“professionalism” have led to a dramatic increase on fraud incidents and fraud

losses.

The modern trend is the appearance of new fraud forms on the scene, as an

attempt to establish the financial crime as a part of the organized crime.

Financial crime is a global phenomenon and poses a threat not only to

organizations and businesses, but also to individuals, through international

organized bands of criminals, who take advantage of the sophisticated means

of technology and of course worldwide web. As a result, fraudsters are no

INTRODUCTION

Analysis of Fraud Detection

Aigli Rizou – MSITT 2010 12

more naïve and entrepreneurs but more cautious and intelligent, developing

new adaptive ways to deceive the potential victims.

The fraud loss of billion of dollars worldwide each year has sparked a search

for effective countermeasures to those who exploit security vulnerabilities to

commit any kind of fraud. Under this scope, fraud prevention and detection

technologies have become an imperative need. However, the effectiveness of

these techniques is based on their flexibility towards fraudsters’ evolving

behavior.

1.2.1.2.1.2.1.2. Object iveObject iveObject iveObject ive

The present study addresses the fraud detection issue, focusing in particular

fraud sectors, such as banking, insurance, internet and telecommunications.

The citation of some statistical figures worldwide indicates the recent aspect

of the problem. Irrespective of the fraud type and the obstacles during fraud

detection, the requirements of each fraud detection system are common.

Various scientific areas offer the means for developing a number of fraud

detection methods, which are applicable in real life scenarios. In addition,

some indicative scientific experiments are presented in order to provide the

results of the utilization of the previous methods and to give motivations for

further research.

The final part of the thesis includes the analysis of a real life fraud detection

scenario of application fraud and the description of the implemented software

in order to explain the operation and the requirements of a real fraud detection

system. In the context of this thesis, a number of algorithms have been

applied as part of another kind of open source machine learning tool.

Providing that the real fraud detection system exhibits a high degree of

accuracy, a comparative evaluation of the algorithms’ performance is

accomplished. The ultimate goal is to propose an optimized solution, which

will yield improved results in real life fraud detection systems.

Analysis of Fraud Detection

Aigli Rizou – MSITT 2010 13

1.3 .1.3 .1.3 .1.3 . S t ruc tureSt ruc tureSt ruc tureSt ruc ture

The present thesis has been organized in the following way.

Chapter 2 introduces the fraud concept through various definitions. Banking,

telecommunications, insurance, internet and enterprises are the sectors under

consideration. Depending on fraud type, different techniques have been

developed so far by the perpetrators. This chapter, also, describes the typical

characteristics of fraudsters’ profile. In order to highlight the magnitude of the

problem, figures concerning fraud losses of Europe and the U.S. for the last

years are quoted. In addition, chapter 2 refers to the obstacles during FD so

that it brings out the complexity of the problem. The last part includes the

requirements of a reliable FD system as well as the metrics used for the

evaluation of its performance.

Chapter 3 provides a theoretical background of FD, introducing fundamental

concepts, necessary for the next chapters. The existing FD methods, used in

modern FD tools, proceed from various scientific fields and they are divided

into two categories, supervised and unsupervised methods. A special

reference to metalearning algorithms is given, since they have proven to be

very effective means of FD.

Chapter 4 contains a number of experiments carried out in the scientific field,

divided per fraud sector as in chapter 2. The experiments exploit the

algorithms of chapter 3, providing useful results for future considerations.

Chapter 5 constitutes the practical part of the thesis and describes a real FD

system, implemented by a Greek bank, which detects fraud behaviors among

loan applications. In the first place, the real application fraud data, provided by

the bank, are loaded in the system and the results are recorded. Next, the

same data set is loaded in an open source machine learning tool in order to

record the results of the running algorithms. The comparison of both result

sets helps to draw conclusions for the effectiveness of the algorithms as a

Analysis of Fraud Detection

Aigli Rizou – MSITT 2010 14

standalone tool. Finally, a potential ideal FD solution is proposed as an object

for future work.

Analysis of Fraud Detection

Aigli Rizou – MSITT 2010 15

2222 FRAUD DFRAUD DFRAUD DFRAUD DETECTION OVERVIEWETECTION OVERVIEWETECTION OVERVIEWETECTION OVERVIEW

22222222 ........ 11111111 ........ FFFFFFFF rrrrrrrr aaaaaaaa uuuuuuuu dddddddd DDDDDDDD eeeeeeee ffffffff iiiiiiii nnnnnnnn iiiiiiii tttttttt iiiiiiii oooooooo nnnnnnnn

Fraud is the crime of obtaining money by deceiving people (Cambridge

Advanced Learner’s Dictionary).

Fraud is a criminal deception; the use of false representations to gain an

unjust advantage (Concise Oxford Dictionary).

Fraud is an intentional deception made for personal gain or to damage

another individual and undoubtedly it’s considered to be a crime and a civil

law violation [2].

Fraud is an intentional act meant to induce another person to part with

something of value, or to surrender a legal right. It is a deliberate

misrepresentation or concealment of information in order to deceive or

mislead [31].

Fraud occurs in most of the areas of human endeavour, causing significant

financial losses not only to the individuals but also to various enterprises. No

matter in which domain fraudsters commit fraud, their primary motivation is

money and secondarily power, peer regard, appreciation and greed.

2.2.2.2.2.2.2.2. Fraud Detect ionFraud Detect ionFraud Detect ionFraud Detect ion & Prevent ion& Prevent ion& Prevent ion& Prevent ion

As fraud increases dramatically with the expansion of modern technologies,

there is an urgent need that sophisticated technologies and fraud experts’

knowledge should be combined in order to ensure against fraud attacks.

FRAUD

DETECTION (FD)

OVERVIEW

Analysis of Fraud Detection

Aigli Rizou – MSITT 2010 16

Nowadays, individuals, organizations or companies apply various fraud

prevention and detection methods, aiming at minimizing their losses as soon

as possible.

In particular, fraud prevention involves measures to inhibit fraud at an early

stage, such as personal identification number for bank cards, chip-based EMV

payment cards, Internet security systems for credit card transactions,

Subscriber Identity Module (SIM) cards for mobile phones, laminated metal

strips and holographs on banknotes etc. However, none of these measures

acts as panacea in practice. What is more, there should be a trade-off

between expense and inconvenience (e.g. to a customer) on the one hand

and effectiveness on the other.

Unlike prevention, fraud detection implies identifying fraud as soon as

possible once it has been perpetrated. FD comes into effect, after fraud

prevention has failed. Hence, FD must be applied constantly, since failure of

fraud prevention is not always verified. For example, although individuals

guard their cards against fraudsters very meticulously, card’s data can be

stolen and then it’s crucial to be able to detect as fast as possible that fraud is

being committed.

2.3.2.3.2.3.2.3. Fraud TypesFraud TypesFraud TypesFraud Types

There are at least as many types of fraud as there are types of people who

commit it, but in every case the deception is their common denominator. The

common fraud types per sector are the following.

2 .3 .1 .2 .3 .1 .2 .3 .1 .2 .3 .1 . Bank ing Bank ing Bank ing Bank ing

Bank fraud is an attempt to deceptively earn money, assets or property owned

or held by a financial institution [2]. In this case, not only banks but also

millions of people fall victim to monetary damages caused by bank fraud.

There are countless ways that bank fraud can occur, but only two main

Analysis of Fraud Detection

Aigli Rizou – MSITT 2010 17

categories can be distinguished, insider and outsider bank fraud.

Insider Bank Fraud is perpetrated by people who work inside or have access

to restricted areas of information inside of the financial institution [4]. This type

of fraud is difficult for banks to combat, since the number of people who hold

positions with responsibilities for handling large amount of money is

significantly high. Hence, there is an urgent need for banks to constantly

update security measures. Here are some of the common forms of insider

fraud.

Illegal Insider Trading: When someone has the authority to make

investments on behalf of the bank without the bank being aware of it. This

type of fraud may lead to an irreparable damage for the bank.

Identity theft: It is often the case that a bank employee uses customers’

personal information with a view to selling this information or making

fraudulent purchases.

Fraudulent loans: When a loan officer within a bank forges documents,

creates false entities or lies about the ability of the applicant to repay in order

to “borrow” a sum of money from the bank that they never intend to repay.

Wire Fraud: There are cases where insiders attempt to use fraudulent or

forged documents which claim to request a bank depositor’s money be wired

to another bank often an offshore account in some distant foreign country. It

may take a bank months or even longer to notice the missing funds.

Outsider bank fraud or fraud perpetrated by outside parties is not limited to

persons working inside the financial institutions. Some of the common ways to

accomplish this form of fraud are the following [4].

Debit/Credit card fraud: It’s described as the unauthorized use of a

debit/credit card to obtain goods of value. It includes counterfeiting cards,

using lost or stolen cards and fraudulently acquiring credit cards through the

mail. In all of these cases, the fraudster uses a physical card, but physical

Analysis of Fraud Detection

Aigli Rizou – MSITT 2010 18

possession is not essential to perpetrate credit card fraud. Typical case is the

“cardholder-not- present” fraud, where only the card’s details are given (e.g.

over the phone) [44]. Apart from internet, card fraud occurs in ATM and POS

transactions.

Identity theft: It’s considered to be one of the most popular schemes today

and occurs when someone steals the identity of another person to perform an

illegal action. Fraudsters obtain useful information from a variety of sources,

such as the victim’s wallet, trash, fake websites of internet, fake documents

etc [6]. Identity theft is strongly connected with other types of fraud, such as

application fraud, which is described subsequently.

Application fraud: It refers to the theft of an individual’s personal data such

as name, address, telephone and mobile numbers, id number, passports,

social security number and their use in financial credit products applications in

someone’s name. Credit cards, bank accounts, loans are examples of such

applications which are recorded fraudulently in victim’s name, leaving her/him

liable for any resulting charges and fees [5].

Money Laundering: It involves the investment or transfer of money from

racketeering, drug transactions or other embezzlement schemes so that the

original source either is concealed or it appears to be legitimate [6].

Purchasing and selling securities, using the funds as collateral on the loans,

and even writing off the money as business expenses are all common forms

of money laundering.

2 .3 .2 .2 .3 .2 .2 .3 .2 .2 .3 .2 . I ns ur anceIns ur anceIns ur anceIns ur ance

It’s any act perpetrated with the fraudulent intent to obtain payment from an

insurer agent. Although insurance fraud is not a highly visible crime, it costs

insurance companies great deal of money annually [2, 3].

2 .3 .3 .2 .3 .3 .2 .3 .3 .2 .3 .3 . I n t er ne tIn t er ne tIn t er ne tIn t er ne t

This type of fraud varies and it’s intended to intercept, view or redirect

Analysis of Fraud Detection

Aigli Rizou – MSITT 2010 19

confidential information about the client and the client’s financial information in

order to compromise accounts and commit fraud. A common practice is to

create fake websites which deceive clients, extorting them great amounts of

money [6].

2 .3 .4 .2 .3 .4 .2 .3 .4 .2 .3 .4 . Te l ecommun ica t i onsTe l ecommun ica t i onsTe l ecommun ica t i onsTe l ecommun ica t i ons

Fraudsters steal or use telecommunication service (telephones, cell, phones,

computers etc.) to commit other types of fraud, deceiving consumers,

businesses and communication service providers. This type of fraud can only

be detected once it has occurred [7, 30].

2 .3 .5 .2 .3 .5 .2 .3 .5 .2 .3 .5 . Ente rpr i sesEn te r pr i sesEn te r pr i sesEn te r pr i ses

The occupational fraud is described as the abuse of one’s occupation for

personal enrichment through the deliberate misuse of the employing

enterprises’s resources or assets [24].

2 .3 .6 .2 .3 .6 .2 .3 .6 .2 .3 .6 . GeneralGener alGener alGener al

Referring to the above fraud types, Figure 1 [76] displays the most popular

subgroups of occupational, insurance, credit card and telecommunications

fraud, studied in published FD papers. Occupational FD is concerned with

determining fraudulent financial reporting by management and abnormal retail

transactions by employees. Referring to insurance fraud, four groups exist: a)

home insurance, b) crop insurance, c) automobile insurance and d) medical

insurance. Credit FD involves screening credit applications and/or logged

credit card transactions. In telecommunications fraud, subscription data and/or

wire-line and wireless phone calls are monitored [76].

Analysis of Fraud Detection

Aigli Rizou – MSITT 2010 20

Figure 1: Bar chart of fraud types from 51 unique and published FD papers [76].

2.4.2.4.2.4.2.4. Fraud TechnFraud TechnFraud TechnFraud Techn iquesiquesiquesiques

Depending on the sector and the type, fraud is committed in various ways

which are described in the following paragraphs. Note that there are also

combinations of these types.

2 .4 .1 .2 .4 .1 .2 .4 .1 .2 .4 .1 . Bank ingBank ingBank ingBank ing

There are numerous ways to impose credit or debit card fraud is committed

and the following are the most typical.

- Phishing: Phishing attacks are considered to be one of the fastest growing

fraud trends and potential victims are customers of both large and small

financial institutions. It is a criminal scam whereby Internet perpetrators try to

steal cardholder’s pertinent and sensitive data through e-mail. This will result

in committing identity theft fraud and possible account hijacking. The e-mails

appear to come from a well-known organization –with which victim does not

even have an account- and ask for victims’ personal information, such as card

number, social security number, account number or password. The fraudster

leads cardholders to a website so that he/she will be able to “phish” their

personal information. Phishing e-mails almost always urge victims to click a

link, which results in a site for entering their personal information. However,

legitimate organizations would never request personal information of

Analysis of Fraud Detection

Aigli Rizou – MSITT 2010 21

cardholders via email.

- Skimming: Card skimming is the most traditional method for defrauding

cardholders, which takes place in public areas with internet access, such as

airports, gas stations, supermarkets, gas stations and Internet cafes. It, also,

takes place in ATMs and POS and involves illegal copying of information from

the magnetic strip of a credit or debit card. It is a more direct version of a

phishing scam. Scammers use a “wedge”, that is a device that captures and

stores the full magnetic stripe tract data, to steal the account number

information. Some wedges can store large volumes of track information

versus some that are wireless and send data to the scammer in the parking lot

or outside the merchant establishment. Once criminals have skimmed the

card, they are able to create a fake or ‘cloned’ card with victim’s details on it.

Then, they run up charges on victim’s account.

Card skimming is an alternative way for fraudsters to steal cardholder’s

identity and use it to commit identity fraud, i.e. to borrow money or take out

loans in victim’s name [19, 21].

Money Laundering: Main precondition is the physical disposal of cash. The

next step is known as layering and involves carrying out complex layers of

financial transactions to separate the illicit proceeds from their source and

disguise the audit trail. Finally, the perpetrator makes the wealth derived from

the illicit proceeds appear legitimate.

Identity theft is strongly connected with other types of fraud, such as credit

card or application fraud, and the common techniques used are the following

[2, 37].

- Shoulder surfing: Perpetrators observe directly victims from a nearby

location, such as looking over someone’s shoulder to extract valuable

information. It is especially effective in crowded places and it’s relatively easy

for fraudsters to observe victims as they fill out a form, enter their PIN at an

ATM or a POS terminal, enter passwords at an internet café, public and

Analysis of Fraud Detection

Aigli Rizou – MSITT 2010 22

university libraries or airport kiosks or use a calling card a public pay phone.

Shoulder surfing is accomplished at a distance using binoculars or other

vision-enhancing devices. Inexpensive, miniature closed-circuit television

cameras can be concealed in ceilings, walls or fixtures to observe data entry.

- Dumpster diving: When criminals go through victims’ garbage cans or a

communal dumpster or trash bin to obtain copies of their checks, credit card

or bank statements or other records that typically bear their name, address,

and even their telephone number. These types of records make it easier for

criminals to get control over accounts in victim's name and assume his/her

identity.

The way to commit application fraud is divided into 2 categories: a) when the

fraudster assumes another person’s identity, solely for the purpose of

receiving another individual’ s credit cards or loans and b) when the fraudster

applies for a loan or a credit card, but gives false personal details on purpose.

2 .4 .2 .2 .4 .2 .2 .4 .2 .2 .4 .2 . I ns ur anceIns ur anceIns ur anceIns ur ance

Fraudsters use four kinds of techniques in order to perpetrate insurance fraud

[22]:

- Exploited accidents: They refer to actual accidents which did occur and

they’re exploited in order to get reimbursed for pre-existing damage or the

damage increased on purpose at fraudster’s interest.

- Fabricated accidents: In this case, an accident either did not take place or

at least not as stated and fraudster merely pretends it did occur in order to

proceed to a legitimate claim.

- Provoked accidents: One driver intentionally involves another innocent

driver in an accident, which is crafted cleverly to make the latter appear as the

one at fault. A typical case is when the fraudster accelerates before a yellow

traffic light and brakes hard or perhaps reverse in front of a red light. Potential

locations for these accidents are blind corners, where accomplices are always

Analysis of Fraud Detection

Aigli Rizou – MSITT 2010 23

on hand to coordinate the accident and act as witnesses.

- Staged accidents: An accident did occur but, if one strictly applies the laws

of coincidence, an accident did not really take place. It’s common practice that

rental vehicles are involved and sometimes more than once. The damage

incurred is either not repaired or only to the extent absolutely necessary.

2 .4 .3 .2 .4 .3 .2 .4 .3 .2 .4 .3 . I n ter ne t I n ter ne t I n ter ne t I n ter ne t

Apart from the Phishing, Skimming, techniques already mentioned, internet

fraud can be committed through the following ways as well [26]:

- Trojan horse: It appears to be a useful, legitimate software program or file,

but once installed, it causes havoc with a computer by damaging or deleting

files. Such scam may claim to have pornographic element or to have a

program which removes computer viruses. When the unsuspecting user

opens the file or downloads the software, then the damage has happened.

Unlike viruses or worms, Trojan horse is not designed to replicate itself. Some

Trojan horse programs open a backdoor into the computer, allowing

unscrupulous users to steal sensitive financial and identity information [19,

20].

- Advance Fee: An incident involving communications that would have people

believe that to receive something, they must first pay money to cover some

sort of incidental cost or expense. Among the variations on this type of scam

is the Nigerian letter or 419 scam [46].

- Nigerian Letter or 419 scam: The fraudster sends spam e-mails to

numerous recipients and narrates a fake story about a money transfer which

is not able to make. Usually, these e-mails contain the famous subject line

“Your assistance is needed”. The potential victim answers this e-mail and the

perpetrator either steals money from his/her bank account or steals sensitive

card data [28]. The majority of Nigerian Advance fee fraud is still organized by

Nigerians, but no longer initially from Nigeria [46].

Analysis of Fraud Detection

Aigli Rizou – MSITT 2010 24

- Lottery scam: Scammers send e-mails/letters/faxes which claim that the

potential victim has already won a great deal of money in an international

lottery, even though he/she has never taken part in. They also claim that

victim’s address has been randomly chosen out of a large pool of addresses

as a ‘winning entry’. In some cases, the emails claim to be endorsed by well-

known companies such as Microsoft or include links to legitimate lottery

organization websites. Any relationships implied by these endorsements and

links will be completely bogus.

2 .4 .4 .2 .4 .4 .2 .4 .4 .2 .4 .4 . Te l ecommun ica t i onsTe l ecommun ica t i onsTe l ecommun ica t i onsTe l ecommun ica t i ons

Methods of telecommunications fraud are grouped into four categories [44]:

- Contractual fraud: In this case, perpetrators generate revenue through the

normal use of a service, whilst having no intention of paying for use.

Subscription and Premium Rate fraud are some of the examples of

contractual fraud. In Subscription fraud, the fraudster subscribes to the mobile

network using a false identity and then sells the use of his phone to

unscrupulous customers (typically for international calls to distant foreign

countries) at a rate lower than the regular tariff. A large number of expensive

calls is accumulated, but the fraudster disappears before the bill can be

collected [40].

- Technical fraud: It is connected with attacks against weaknesses in the

technology of the mobile system. The perpetrator should have technical skills

and abilities, but once a weakness is discovered then this information is often

quickly distributed in a form that non-technical people can use.

- Hacking fraud: The fraudster generates revenue by breaking into insecure

systems and exploiting or selling on any available functionality.

- Procedural fraud: It involves attacks against the procedures followed to

minimize the exposure to fraud. The perpetrator often attacks the weaknesses

in the business procedures used to grant access to the system.

Analysis of Fraud Detection

Aigli Rizou – MSITT 2010 25

Apart from the above, there are combinations of these techniques. For

example, there are cases where fraudsters obtain the ability to place

international and mobile calls, by gaining a legitimate PIN to use with the

private PABX1 of an organization as employees of the organization, but have

no intention of paying for these services (contractual fraud). Additionally,

fraudsters give the PIN to others (hacking fraud) who also used the service,

without paying. There is often the case where an employee of the

organization with special technical knowledge manages to deceive the system

and obtain a PIN that belongs to another person. The fraudster then starts

using this PIN, pretending to be the legitimate user and burdens the legitimate

user’s account [30].

2 .4 .5 .2 .4 .5 .2 .4 .5 .2 .4 .5 . Ente rpr i sesEn te r pr i sesEn te r pr i sesEn te r pr i ses

According to the Association of Certified Fraud Examiners (ACFE),

occupational fraud is committed mainly through the following ways [23]:

- Asset misappropriation: In this case, the perpetrator steals or misuses an

organization’s resources, like false invoicing, payroll fraud and skimming.

- Corruption: Fraudsters use the influence in business transactions so that

their duty to their employer is violated aiming at obtaining for themselves.

Employees might receive or offer bribes, extort funds from third parties or

engage in conflicts of interest.

- Financial statement fraud: It involves the intentional misstatement or

omission of material information from the organization’s financial reports.

These are the cases of “cooking the books” that often make front page

headlines. Financial statement fraud cases often involve the reporting of

fictitious revenues or the concealment of expenses or liabilities in order to

make an organization appear more profitable than it really is.

1 Private Automated Branch Exchange (PABX), this telephone network is commonly used

by call centres and other organizations. PABX allows a single access number to offer multiple lines to outside callers while providing a range of external lines to internal callers or staff [75]

Analysis of Fraud Detection

Aigli Rizou – MSITT 2010 26

2.5.2.5.2.5.2.5. FFFFrauds tersrauds tersrauds tersrauds ters T T T Typeypeypeype

Figure 2 illustrates the types of profit-motivated fraudsters and affected

industries [76]. It stands to reason that, each business is susceptible to

internal fraud or corruption not only from the high level employees

(managers), but also the low level employees.

Fraudsters can be an external party (or parties) or can perpetrate fraud in the

form of prospective/existing customer or supplier. The external fraudster has

three basic profiles: the average offender, the criminal offender and the

organized crime offender.

Figure 2: Hierarchy chart of white-collar crime perpetrators from both firm-level and

community-level perspectives [76]

Average offenders display random and/or occasional dishonest behaviour

when there is opportunity, sudden temptation, or when suffering from financial

problems. In contrast, the more risky external fraudsters are individual criminal

offenders and organised/group crime offenders (professional/career

fraudsters) because they repeatedly disguise their true identities and/or evolve

their modus operandi over time to approximate legal forms and to counter FD

systems. Hence, it’s very important that business should take effective

countermeasure concerning their FD systems and algorithms according to

professional fraudsters’ modus operandi. Occupational and insurance fraud is

mainly committed by average offenders, while credit and telecommunications

Analysis of Fraud Detection

Aigli Rizou – MSITT 2010 27

fraud is more vulnerable to professional fraudsters.

2.6.2.6.2.6.2.6. Economical Impac t o f F raudEconomical Impac t o f F raudEconomical Impac t o f F raudEconomical Impac t o f F raud

Fraud is a considerable and increasing financial risk which threatens the

profitability and status of enterprises and causes great inconvenience to

individuals and merchants worldwide. The financial and economic result of

fraud is obviously the worst aspect of the problem.

In contrast with fraud costs, business costs, such as utility, accommodation,

salaries or procurement costs are usually known and predictable. The attitude

of denying the existence of fraud or reacting after the losses have been

occurred, surely, doesn’t help to mitigate the problem. It’s often the case that

the necessary protection measures against fraud are taken after the fraud

losses have occurred or after the resources have been diverted from where

they were intended and of course after the economic damage has happened.

Furthermore, fraud losses affect individuals not only in a direct but also in an

indirect way. For instance, when banks lose money because of credit card

fraud, cardholders pay for all of that loss through higher interest rates, higher

fees, and reduced benefits. In case of insurance companies, policyholders

pay fraud losses through high premiums.

The key to successful loss reduction is measurement methodologies, which

have been developed and implemented over the last decade by various

associations and organizations. Measuring fraud costs contributes to draw

useful conclusions about the investment to be made in moderating them and

the financial benefits from their reduction [89].

Of course, fraud scientific observation or measurement is not an easy task

because of its complicated nature. However, in the cost of fraud the following

parameters should be taken into account [11]:

− immediate direct loss due to fraud

Analysis of Fraud Detection

Aigli Rizou – MSITT 2010 28

− cost of fraud prevention and detection

− cost of lost business (when replacing card)

− opportunity cost of fraud prevention/detection

− deterrent effect on spread of e-commerce

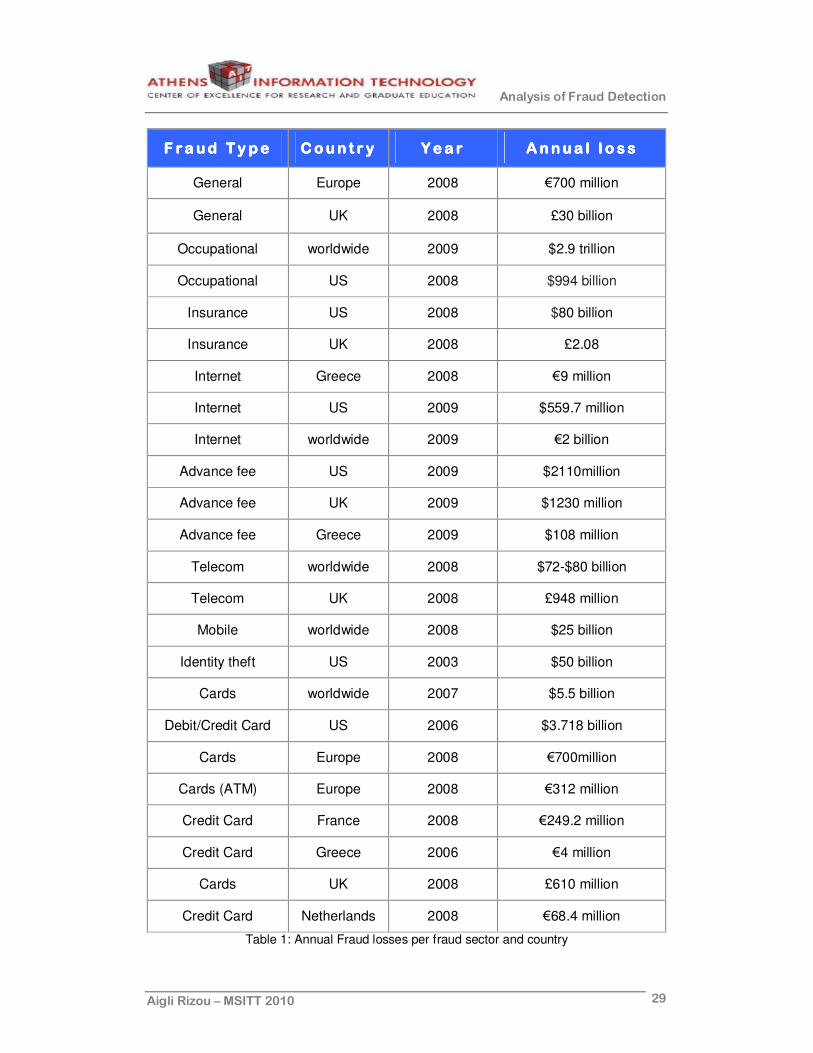

Table 1 contains the size of annual fraud losses of various countries and time

periods based on fraud sector, interpreted in actual figures. Some comments

on the losses are given in the following paragraphs.

It’s important to mention that if detected fraud losses increase, this doesn’t

necessarily mean that there is more fraud or the FD systems improved;

similarly, if detected fraud losses drop, this doesn’t mean that there is less

fraud or worse detection [89].

2 .6 .1 .2 .6 .1 .2 .6 .1 .2 .6 .1 . Genera lGenera lGenera lGenera l

Using fraud figures that are currently available, the National Fraud Authority

(NFA) estimates that fraud cost the UK economy £30.5 billion during 2008

[48]. However, these estimations suggest that public sector losses accounted

for 58% of all fraud loss, with estimated fraud losses of £17.6 billion for the

public sector alone (Figure 3). Next, the private sector losses, which

accounted for 30% of, total loss or £9.3 billion. The individual and charity

sector represents the rest 12% of the total loss, which is translated to £3.5

billion and £32 million respectively.

Analysis of Fraud Detection

Aigli Rizou – MSITT 2010 29

F raud T y peF raud T y peF raud T y peF raud T y pe C oun t r yCoun t r yCoun t r yCoun t r y Y e a rYea rYea rYea r A nnua l l o s sAnnua l l o s sAnnua l l o s sAnnua l l o s s

General Europe 2008 €700 million

General UK 2008 £30 billion

Occupational worldwide 2009 $2.9 trillion

Occupational US 2008 $994 billion

Insurance US 2008 $80 billion

Insurance UK 2008 £2.08

Internet Greece 2008 €9 million

Internet US 2009 $559.7 million

Internet worldwide 2009 €2 billion

Advance fee US 2009 $2110million

Advance fee UK 2009 $1230 million

Advance fee Greece 2009 $108 million

Telecom worldwide 2008 $72-$80 billion

Telecom UK 2008 £948 million

Mobile worldwide 2008 $25 billion

Identity theft US 2003 $50 billion

Cards worldwide 2007 $5.5 billion

Debit/Credit Card US 2006 $3.718 billion

Cards Europe 2008 €700million

Cards (ATM) Europe 2008 €312 million

Credit Card France 2008 €249.2 million

Credit Card Greece 2006 €4 million

Cards UK 2008 £610 million

Credit Card Netherlands 2008 €68.4 million

Table 1: Annual Fraud losses per fraud sector and country

Analysis of Fraud Detection

Aigli Rizou – MSITT 2010 30

Figure 3: Breakdown of fraud losses in UK for 2008 according to NFA [48]

2 .6 .2 .2 .6 .2 .2 .6 .2 .2 .6 .2 . Bank ingBank ingBank ingBank ing

2 .6 .2 .1 .2 .6 .2 .1 .2 .6 .2 .1 .2 .6 .2 .1 . Cred i t /Deb i t ca rdsC red i t /Deb i t ca rdsC red i t /Deb i t ca rdsC red i t /Deb i t ca rds

In 2007, card fraud globally took in an estimated $5.5 billion, based on a

worldwide survey conducted by Kroll Consulting Services in collaboration with

the Economist Intelligence Unit [51].

Concerning Europe figures, the European ATM Security Team (EAST)

estimates that losses of card fraud referring to ATM transactions fell from

€485 million to €312 million during 2008, despite a rise in attacks [15]. Based

on EAST’s estimates international losses due to skimming attacks fell by 43%

from €393 million to €226 million, continuing a downward trend from 2007

[15]. Furthermore, according to Visa, 0.055% of the cards transactions is

considered to be fraudulent and the card fraud turnover is estimated at

€700million [53].

Analysis of Fraud Detection

Aigli Rizou – MSITT 2010 31

Figure 4: Breakdown of card losses in UK during 2008 according to FFA [48]

Figure 5: UK Fraud loss ratios by card type according to Visa estimates for 2008 [16].

Financial Fraud Action (FFA) has reported that over 10.5 billion UK card

transactions have taken place in 2008, with spending amount £397 billion and

card fraud loss up to £610 million, up 14% from 2007 [48]. The majority of

card losses resulted from card-not-present scheme and accounted for over a

Analysis of Fraud Detection

Aigli Rizou – MSITT 2010 32

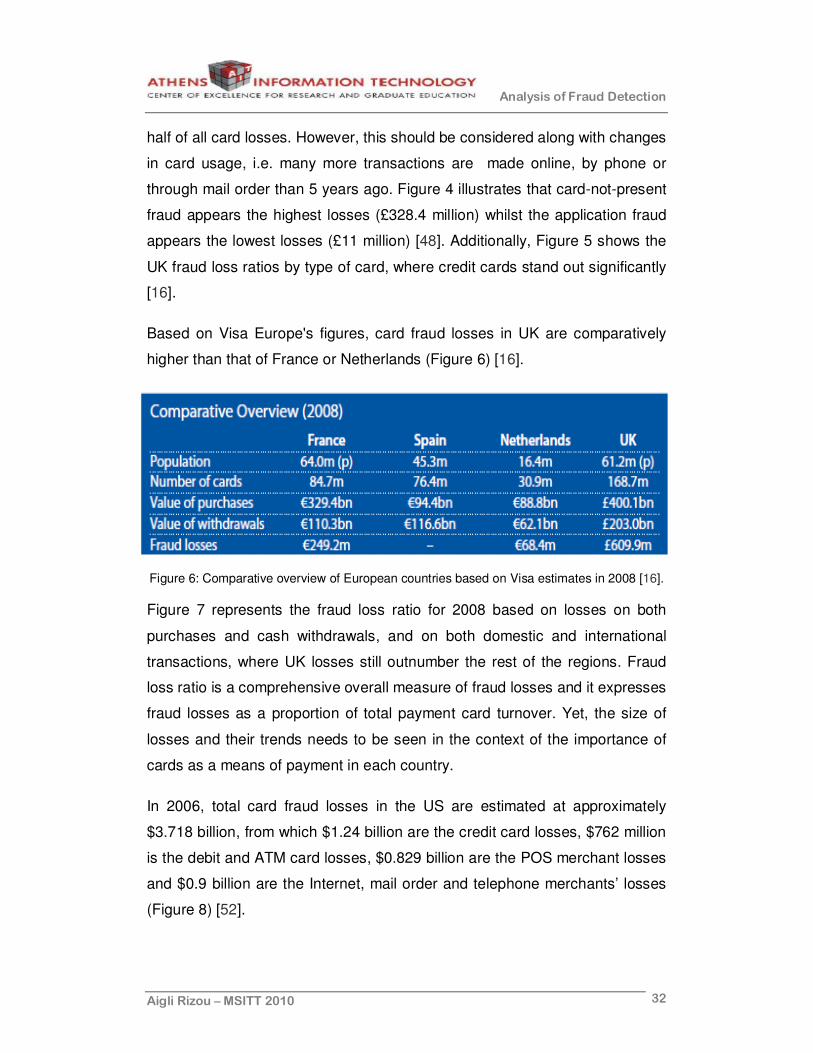

half of all card losses. However, this should be considered along with changes

in card usage, i.e. many more transactions are made online, by phone or

through mail order than 5 years ago. Figure 4 illustrates that card-not-present

fraud appears the highest losses (£328.4 million) whilst the application fraud

appears the lowest losses (£11 million) [48]. Additionally, Figure 5 shows the

UK fraud loss ratios by type of card, where credit cards stand out significantly

[16].

Based on Visa Europe's figures, card fraud losses in UK are comparatively

higher than that of France or Netherlands (Figure 6) [16].

Figure 6: Comparative overview of European countries based on Visa estimates in 2008 [16].

Figure 7 represents the fraud loss ratio for 2008 based on losses on both

purchases and cash withdrawals, and on both domestic and international

transactions, where UK losses still outnumber the rest of the regions. Fraud

loss ratio is a comprehensive overall measure of fraud losses and it expresses

fraud losses as a proportion of total payment card turnover. Yet, the size of

losses and their trends needs to be seen in the context of the importance of

cards as a means of payment in each country.

In 2006, total card fraud losses in the US are estimated at approximately

$3.718 billion, from which $1.24 billion are the credit card losses, $762 million

is the debit and ATM card losses, $0.829 billion are the POS merchant losses

and $0.9 billion are the Internet, mail order and telephone merchants’ losses

(Figure 8) [52].

Analysis of Fraud Detection

Aigli Rizou – MSITT 2010 33

Figure 7: Fraud loss ratios of 2008 according to Visa [16].

Greek banks and financial institutions as well as Visa and MasterCard

estimate that card fraud loss in Greece is half than the corresponding

European losses. For every, €1000 transaction, €0.35 is the result of fraud,

while in Europe the corresponding amount is €0.75 and the total turnover is

estimated to €1,2-€1,5 billion. This implies that debit and credit card fraud

turnover is calculated around €4 million and concerns 2.500 cardholders, with

average loss €110 each. The most frequent fraud types in Greece are: 23%

counterfeiting, 24% stolen cards, 26% lost cards and 27% other types. The

corresponding percentages in Europe are 35%, 19%, 17% and 29% [28].

Card fraud losses in billions $ (US, 2006)

0,7620,829

0,9

1,24

0

0,2

0,4

0,6

0,8

1

1,2

1,4

credit card debit and ATM POS merchant losses Internet, mail order and telephone merchants’

Figure 8: Card fraud losses in the US for 2006

Analysis of Fraud Detection

Aigli Rizou – MSITT 2010 34

2 .6 .2 .2 .2 .6 .2 .2 .2 .6 .2 .2 .2 .6 .2 .2 . I d en t i t y TI den t i t y TI den t i t y TI den t i t y T he f the f th e f th e f t

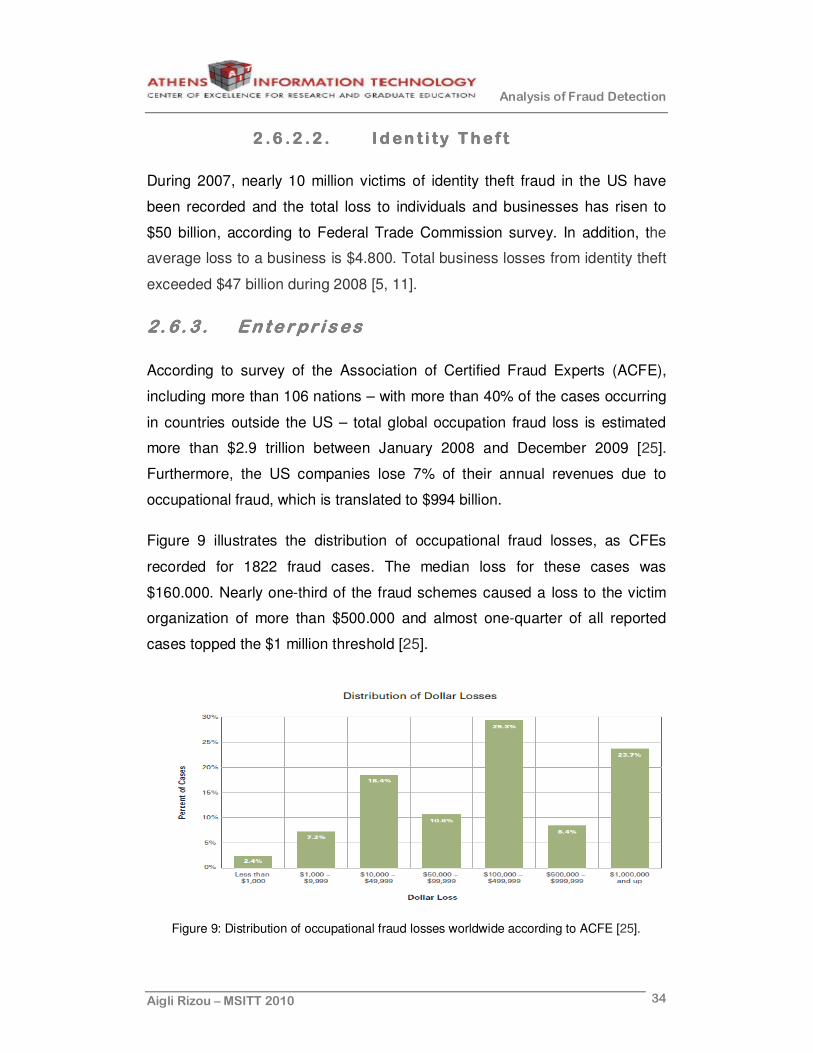

During 2007, nearly 10 million victims of identity theft fraud in the US have

been recorded and the total loss to individuals and businesses has risen to

$50 billion, according to Federal Trade Commission survey. In addition, the

average loss to a business is $4.800. Total business losses from identity theft

exceeded $47 billion during 2008 [5, 11].

2 .6 .3 .2 .6 .3 .2 .6 .3 .2 .6 .3 . Ente rpr i sesEn te r pr i sesEn te r pr i sesEn te r pr i ses

According to survey of the Association of Certified Fraud Experts (ACFE),

including more than 106 nations – with more than 40% of the cases occurring

in countries outside the US – total global occupation fraud loss is estimated

more than $2.9 trillion between January 2008 and December 2009 [25].

Furthermore, the US companies lose 7% of their annual revenues due to

occupational fraud, which is translated to $994 billion.

Figure 9 illustrates the distribution of occupational fraud losses, as CFEs

recorded for 1822 fraud cases. The median loss for these cases was

$160.000. Nearly one-third of the fraud schemes caused a loss to the victim

organization of more than $500.000 and almost one-quarter of all reported

cases topped the $1 million threshold [25].

Figure 9: Distribution of occupational fraud losses worldwide according to ACFE [25].

Analysis of Fraud Detection

Aigli Rizou – MSITT 2010 35

In addition, Figure 10 shows the proportion of the total losses based on fraud

category. Referring to cases which cost more than $18 billion, 21% were

caused by asset misappropriation, 11% by corruption and 68% by fraudulent

financial statements.

Figure 10: Proportion analysis per fraud category according to ACFE

[25].

Analyzing the median losses of occupational fraud per scheme worldwide

(Figure 11), the asset misappropriation appears to be the least costly, despite

its high frequency. In contrast, financial statement fraud caused a loss of more

than $4 million and corruption schemes fell in the middle category, creating a

median loss of $250.000.

Figure 11: Median occupational fraud losses by category for 106 nations according to ACFE [25].

Analysis of Fraud Detection

Aigli Rizou – MSITT 2010 36

2 .6 .4 .2 .6 .4 .2 .6 .4 .2 .6 .4 . I ns ur anceIns ur anceIns ur anceIns ur ance

The annual losses of fraudulent insurance claims are calculated nearly $80

billion in the US, according to the estimates of the Coalition Against Insurance

Fraud. This figure includes all lines of insurance. It’s also a conservative figure

because much insurance fraud goes undetected and unreported. As it’s

mentioned in §2.6, fraud contributes to higher insurance premiums because

insurance companies generally must pass the costs of bogus claims — and of

fighting fraud — onto policyholders [48].

According to Association of British Insurers (ABI), losses occurred by both

detected and undetected insurance fraud in the UK during 2008 reach £2.08

billion. It’s worth mentioning that the UK insurance industry is the largest in

Europe and the third largest in the world accounting for 11% of total worldwide

premium income [47].

2 .6 .5 .2 .6 .5 .2 .6 .5 .2 .6 .5 . I n t er ne tIn t er ne tIn t er ne tIn t er ne t

Internet fraud losses in the USA referred to law enforcement amounts to

$559.7 million in 2009 according to the Internet Crime Complaint Center (IC3)

[46]. Figure 12 shows the increasing internet fraud losses of referred

complaints from 2001 until 2009 for the US.

Figure 12: Annual dollar loss of referred complaints according to IC3 (in millions) [46].

On the other hand, the total turnover per year in Greece reached from €3,2

million in 2007 to €9 million in 2008. At the same time, the global turnover is

Analysis of Fraud Detection

Aigli Rizou – MSITT 2010 37

estimated more than €2 billion.

2 .6 .5 .1 .2 .6 .5 .1 .2 .6 .5 .1 .2 .6 .5 .1 . Advance Advance Advance Advance Fe e F raud Fe e F raud Fe e F raud Fe e F raud –––– 41 9 S 41 9 S 41 9 S 41 9 S camcamcamcam

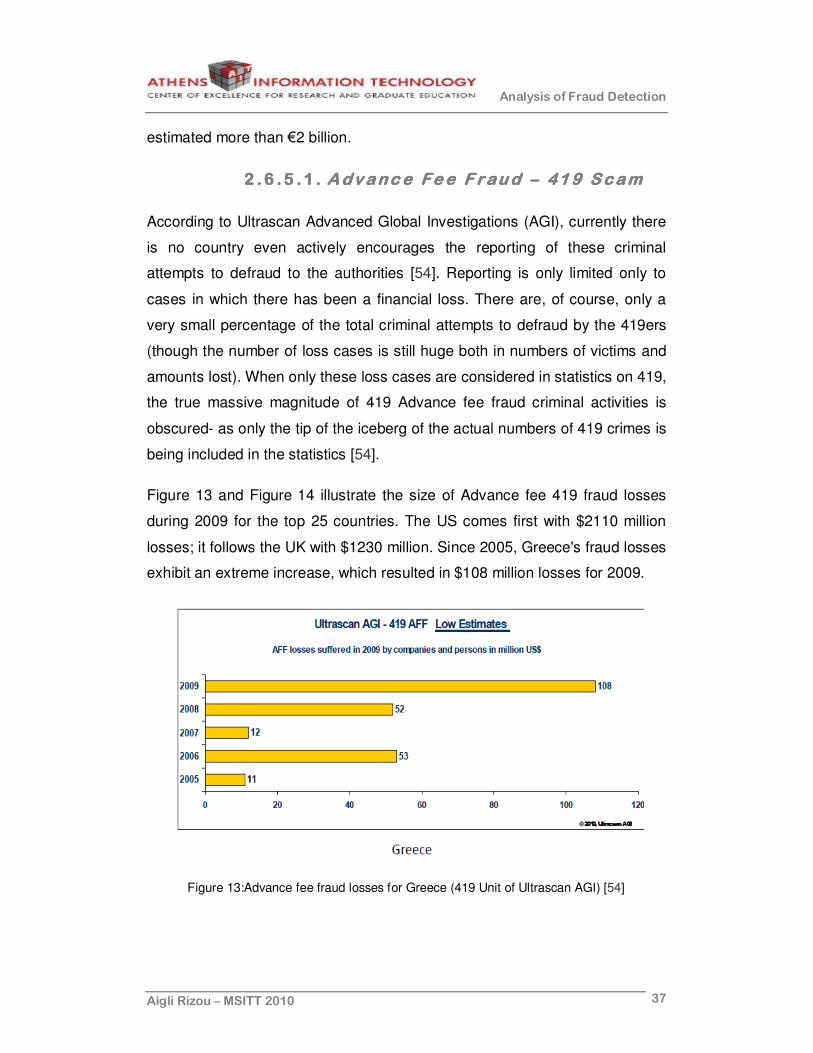

According to Ultrascan Advanced Global Investigations (AGI), currently there

is no country even actively encourages the reporting of these criminal

attempts to defraud to the authorities [54]. Reporting is only limited only to

cases in which there has been a financial loss. There are, of course, only a

very small percentage of the total criminal attempts to defraud by the 419ers

(though the number of loss cases is still huge both in numbers of victims and

amounts lost). When only these loss cases are considered in statistics on 419,

the true massive magnitude of 419 Advance fee fraud criminal activities is

obscured- as only the tip of the iceberg of the actual numbers of 419 crimes is

being included in the statistics [54].

Figure 13 and Figure 14 illustrate the size of Advance fee 419 fraud losses

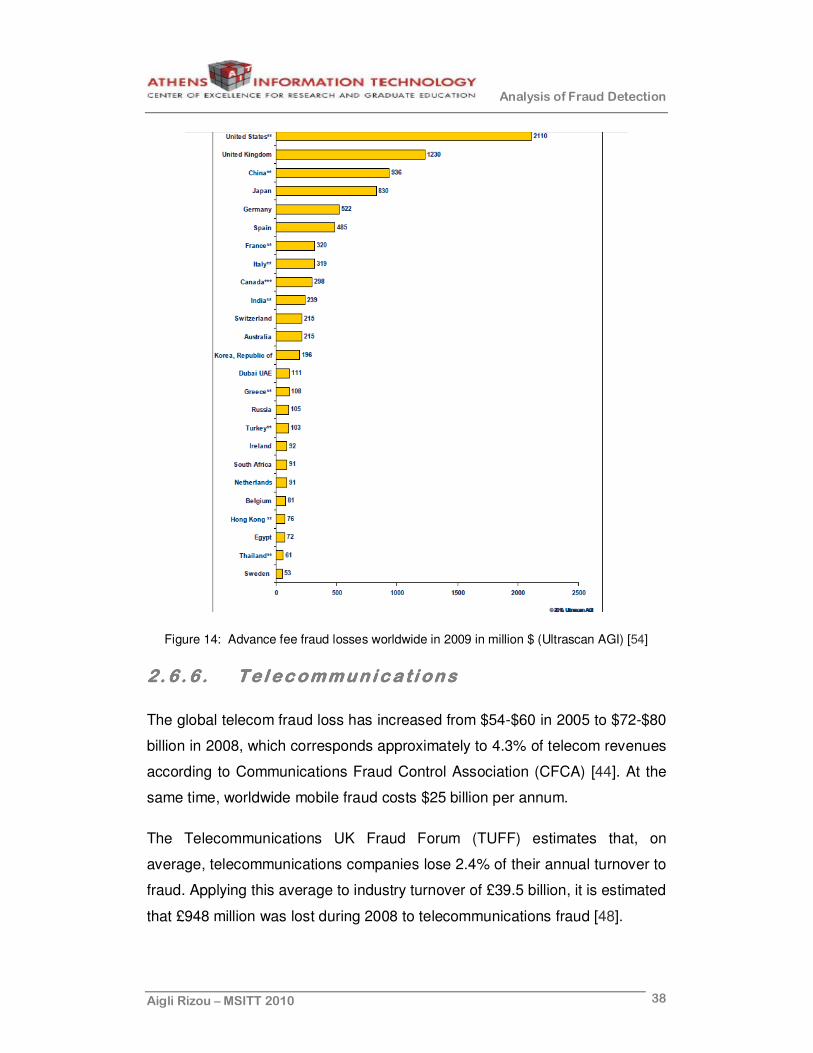

during 2009 for the top 25 countries. The US comes first with $2110 million

losses; it follows the UK with $1230 million. Since 2005, Greece's fraud losses

exhibit an extreme increase, which resulted in $108 million losses for 2009.

Figure 13:Advance fee fraud losses for Greece (419 Unit of Ultrascan AGI) [54]

Analysis of Fraud Detection

Aigli Rizou – MSITT 2010 38

Figure 14: Advance fee fraud losses worldwide in 2009 in million $ (Ultrascan AGI) [54]

2 .6 .6 .2 .6 .6 .2 .6 .6 .2 .6 .6 . Te l ecommun ica t i onTe l ecommun ica t i onTe l ecommun ica t i onTe l ecommun ica t i on ssss

The global telecom fraud loss has increased from $54-$60 in 2005 to $72-$80

billion in 2008, which corresponds approximately to 4.3% of telecom revenues

according to Communications Fraud Control Association (CFCA) [44]. At the

same time, worldwide mobile fraud costs $25 billion per annum.

The Telecommunications UK Fraud Forum (TUFF) estimates that, on

average, telecommunications companies lose 2.4% of their annual turnover to

fraud. Applying this average to industry turnover of £39.5 billion, it is estimated

that £948 million was lost during 2008 to telecommunications fraud [48].

Analysis of Fraud Detection

Aigli Rizou – MSITT 2010 39

2.7.2.7.2.7.2.7. D i f f i cu l t ies in FDD i f f i cu l t ies in FDD i f f i cu l t ies in FDD i f f i cu l t ies in FD

Fraud is a constantly evolving discipline and a hard task to deal with, so it’s

not surprising that many FD systems exhibit serious limitations. Depending on

the fraud type, different systems with different parameters, database

interfaces, procedures and case management tools should be developed.

Hence, nowadays FD is considered to be a great challenge for numerous

reasons.

Whenever it becomes known that FD method is in place, criminals adapt their

strategies rapidly. To avoid information leaks to fraudsters, FD methods must

be kept secret. New criminals that will enter the field may not be aware of

these FD methods and adopt strategies which lead to identifiable frauds [32].

It’s often the case that there is a subtle distinction between a fraudulent and a

legitimate behaviour, since legitimate account users may gradually change

their behaviour over a long period of time and it’s important to avoid spurious

alarms [32].

Another fundamental problem of FD is the unwillingness of financial

institutions, organizations or companies to admit being defrauded in order to

preserve a good reputation in the market. Due to the severely limited

exchange of ideas in FD, data sets do not become available and the results

are often censored, encumbering the measurement of fraud losses [32].

Beyond these limitations, FD requires the analysis of massive amounts of

transactions data. For example, the credit card company Barclaycard carries

approximately 350 million transactions a year in the United Kingdom alone

(Hand, Blunt, Kelly and Adams, 2000), the Royal Bank of Scotland - which

has the largest credit card merchant acquiring business in Europe - carries

over a billion transactions a year and AT&T carries around 275 million calls

each weekday (Cortes and Pregibon, 1998) [32]. As a consequence,

assuming that the fraudulent transaction represent the 0,1% out of 100 million

transactions and for each fraud case the company loses €10, this implies that

Analysis of Fraud Detection

Aigli Rizou – MSITT 2010 40

the fraud cost or alternatively the potential value of FD amounts to €1 million.

Processing huge data sets in a search for fraudulent transactions in a timely

manner is an important problem [32]. Experienced and well-trained employees

are capable of effective manual classification of transactions, comparing with

historical data. Yet, time and cost requirements render this aspect prohibitive

[18].

High dimensionality of the input, i.e. the number of attributes, is another point

to be considered. This implies that the search space also increases in an

exponential manner and thus the processing time is affected [57].

There is no doubt that the correct choice of data attributes is often a tricky

task. The existence of both irrelative variables and mixed attribute data-sets

(i.e. data-sets containing both nominal and continuous attributes) or even

complex data types such as text, signals, images is a crucial factor during FD

[11].

Moreover, the FD task exhibits technical problems because the available

training data are highly skewed, i.e. legitimate transactions outnumber

fraudulent ones [11, 17]. It's estimated that 1 out of 1000 transactions is

fraudulent. This percentage is lower in case of debit card fraud and even

lower in case of web-based banking transactions and money laundering [18].

An additional difficulty in FD procedure lies in the typical validity of

transactions for classification. In particular, almost all transactions concerning

electronic payments are typical valid, since fraudsters do not commit fraud

with an expired card [18].

Because of this the typical validity, it is possible that some transaction records

contain original and fake subsets at the same time (class overlapping).

Consequently, the finding of suitable business rules for the discrimination

between original and fraud cases becomes a hard task [18].

Finally, it's noteworthy that the variable misclassification cost per error type

Analysis of Fraud Detection

Aigli Rizou – MSITT 2010 41

burdens significantly the FD process. For example, credit card transactions

may be labelled incorrectly: a fraudulent transaction may remain unobserved

and thus be labelled legitimate (and the extent of this may remain unknown)

or a legitimate transaction may be misreported as fraudulent [32].

2.8.2.8.2.8.2.8. FD SFD SFD SFD Sys temys temys temys tem Requi rements Requi rements Requi rements Requi rements

All the aforementioned difficulties generate the need of a number of business,

technical and functional requirements for the development of a robust FD

system.

2 .8 .1 .2 .8 .1 .2 .8 .1 .2 .8 .1 . Bus iness Bus iness Bus iness Bus iness RRRRequ i r emen tsequ i r emen tsequ i r emen tsequ i r emen ts

As it’s already mentioned, fraud losses may imperil the good name and the

profitability of the businesses. In this case, there is a dual impact, which

involves not only the lost amounts but also the internal cost, generated due to

the settlement of the fraud case. So, the reference point for money saving is

the following: spare as less money as possible for fraud cases and their

settlement [18].

Obviously, every time a fraud case appears, the relationship between

customer and the particular organization is put on a risk. So, the point is that a

reliable FD system should produce a minimum number of false alarms for

preserving the customer’s satisfaction [18].

Another key issue in FD is the interception of authorization request in real

time, since fraudsters constitute a serious threat as long as they act

inconspicuously [18], especially in cases such as card fraud.

2 .8 .2 .2 .8 .2 .2 .8 .2 .2 .8 .2 . Techn ica l Techn ica l Techn ica l Techn ica l RRRRequi r emen tsequi r emen tsequi r emen tsequi r emen ts

The connection and the integration of new FD solutions in an existent

business environment cause many problems due to the high cost. Hence, the

FD solution should be flexible and available for the majority of technological

Analysis of Fraud Detection

Aigli Rizou – MSITT 2010 42

platforms and should allow the easy integration and interconnection. Thus, the

implementation and maintenance cost remains low [18].

2 .8 .3 .2 .8 .3 .2 .8 .3 .2 .8 .3 . Funct ional Requi rements

The percentage of false alarms is slightly connected with the percentage of

response. This means that when there is high percentage of responses, then

several false alarms are produced, which leads to customers’ inconvenience.

Consequently, the number of the accepted false alarms helps to define how

many cases will be investigated. This suggests that there should be a

balance between the number of false alarms and responses [18].

Usually, each service provider knows better the fraud issues that encounters.

For this reason, the internal design of an FD system is a secure approach. In

addition, fraud experts should be very precise and studious during the system

design and the goal is to create an FD system totally transparent to them [18].

Some fraud types are global and other appear in specific areas or in specific

service providers. These are the rarest ones, but they can cause great losses.

Given the rampant change of fraud types, it’s very important to use FD safety

measures as fast as possible. Hence, the system processor should be

capable of preserving the decision logic in an independent way [18].

Last but not least, fraud systems should not be awkward to use. The goal is to

facilitate fraud experts during FD, so as to avoid wasting time on simple tasks,

such as retrieving the necessary analytical data of the transaction from

several disparate databases.

2.9.2.9.2.9.2.9. PerformanPerformanPerformanPerformance Mce Mce Mce Metr icsetr icsetr icsetr ics

The performance of a FD system is a subtle matter with many pitfalls and

ambiguous opinions. The performance is usually defined by each service

provider’s needs and requirements and it’s strongly connected with the losses

a service provider is able to prevent. Because measuring averted losses is not

Analysis of Fraud Detection

Aigli Rizou – MSITT 2010 43

a feasible task, service providers use metrics as detection rate and false

alarm rate [39]. Additional information for classifiers’ performance metrics is

given in §5.2.2.1.

An ideal FD system would have 0% false alarms and 100% hits with

instantaneous detection. Though, the successful detection of all fraud cases

as soon as fraud starts implies that many legitimate cases will be mislabelled

as fraudulent at least once. In fact, in a real FD system there is a trade-off of

the above performance criteria.

False alarm rate refers to the percentage of legitimate instances mislabelled

as fraud. In case of 1000000 legitimate instances in the total population out of

which 100 cases are mislabelled as fraud, this gives a false alarm rate of

0.01%. This measure is considered to be important especially in the flagging

phase, where fraud experts aim at reducing the number of cases that have to

be investigated for fraud to just those that involve actual fraud [39].

As it is mentioned in §5.1, when there is no clear evidence of fraud, there

should be a further analysis by the fraud analysts, before the interception of a

transaction, the restriction of an account or the denial of an insurance claim. In

this case, the flagged instances with the highest priority in the queue are

investigated first, whenever a fraud analyst is available. A queue may

prioritize instances by the number of fraudulent minutes accumulated to date

or by the time of the most recent high scoring call, for example. Performance

can then be evaluated after flagging or after prioritization. For example, the

flagging detection rate is the fraction of compromised accounts in the