An Empirical Survey on Potential Customers' Perception towards Islamic Bank.

37

An Empirical Survey of Potential Customers’ Perception towards Islamic Bank By Areeb Saleem 1524 Danial Maroof Shaikh 1475 Danish Mansoor 1355 Maheen Siddiqui 1487 Research paper submitted in partial fulfillment of the requirements for the degree of Bachelors in Business Administration at Research Centre in Iqra University North Nazimabad, Karachi. Iqra University 8 th January, 2015

-

Upload

iqrauniversity -

Category

Documents

-

view

8 -

download

0

Transcript of An Empirical Survey on Potential Customers' Perception towards Islamic Bank.

An Empirical Survey of Potential Customers’ Perception towards Islamic Bank

By

Areeb Saleem 1524

Danial Maroof Shaikh 1475

Danish Mansoor 1355

Maheen Siddiqui 1487

Research paper submitted in partial

fulfillment of the requirements for the

degree of Bachelors in Business

Administration at Research Centre in Iqra

University North Nazimabad, Karachi.

Iqra University

8th January, 2015

ACKNOWLEDGEMENTS

Foremost, we are grateful to thank the Almighty Allah that due to His kindness and

benevolence, we accomplished our academic’s final project before deadline.

Then, we owe our sincere gratitude to our subject teacher Dr. Najmunnisa Siddiqui.

Without her continual support, guidance and best wishes throughout the semester we

wouldn’t be able to accomplish our final project. As it was a group project, so we are

thankful to the team members who stood firm and worked enthusiastically and least,

those respondents who participated willingly.

ii

ABSTRACT:

The research emphasizing major factors of bank selection criteria has been the hot topic for

many bank marketing managers, but this type of research is hardly available for an Islamic

banking system. The main aim of the study is to investigate the major factors which

influence perception of potential customers towards Islamic bank. To achieve this goal, The

Iqra University NC was selected for the investigation. A structured questionnaire was

designed to know the perception of customers which are currently not engaged with an

Islamic bank. A questionnaire was distributed among 120 students including teachers. The

Spearman Correlation technique was used to identify the relationship among major

influencing factors. The results revealed that bank image is the top influencing factor while

choosing an Islamic bank rated by respondents. The other factors include awareness,

religious-orientation and, perceived services & product quality also have an impact on an

individual's decision to select an Islamic bank. Based on the results, mostly respondents are

not willing to deal with an Islamic bank due to the lack of awareness. The study offers

researchers with insight of major factors who directly affect customers' selection criteria.

iii

CONTENTS

ACKNOWLEDGEMENT.............................................................................................. ii

ABSTRACT................................................................................................................. iii

LIST OF TABLES ..............................................................................................v

CHAPTER 1: INTRODUCTION ............................................................................... 6

1.1 Background of the Study............................................................................ 6

1.2 Statement of the Problem ........................................................................... 7

1.3 Research Objectives and/or Questions ....................................................... 8

1.4 Structure of the Study.................................................................................. 9

1.5 Definition of Terms (If required) ................................................................9

1.5.1 Perception of Potential Customers (DV)…………………………...…9

1.5.2 Awareness (IV)…………………………………………………..…...10

1.5.3 Religious Orientation (IV)……………………………………...…….10

1.5.4 Perceived Services & Product Quality (IV)…………………......…..10

1.5.5 Bank Image (IV)……………………………………………..……….11

CHAPTER 2: LITERATURE REVIEW ................................................................. 12

2.1 INTRODUCTION OF ISLAMIC BANKING………………………………...12

2.2 AWARENESS OF PRODUCTS/SERVICES………………………………....14

2.3 RELIGIOUS ORIENTATION………………………………………………...15

2.4 PERCEIVED SERVICE/PRODUCT QUALITY……………………………..17

2.5 BANK IMAGE………………………………………………………………...19

CHAPTER 3: RESEARCH METHOD.................................................................... ..20

3.1 Theoretical Framework ............................................................................20

3.1.1 Type and Nature of Research……………………………………….20

3.1.2 Instrument………………………………………..............................20

3.1.3 Validity and Reliability……………………………………………....20

3.1.3.1 Validity……………………………………………….........20

3.1.3.2 Reliability.........................................................................20

3.1.4 Procedure of Data Collection………………………………………..20

3.1.5 Statistical Technique……………………………………………...….21

3.1.6 Ethical Consideration………………………………………………...21

3.2 Theoretical Framework..................................................................................22

3.3 Research Hypothesis.................................................................................23

3.4 Sampling Design.......................................................................................24

3.4.1 Sampling Technique....... ...................................................................24

3.4.2 Sampling size...... ...............................................................................24

CHAPTER 4: RESULTS ............................................................................................. 25

4.1 Frequency of Demographic Factors................................................................ 25

4.2 Hypotheses Testing ....................................................................................27

4.3 Hypotheses Assessment Summary.............................................................31

CHAPTER 5: CONCLUSION ....................................................................................32

5.1 Conclusion.................................................................................................32

5.2 Discussions................................................................................................33

5.3 Limitations ................................................................................................35

5.4 Future Research Recommendations ...........................................................35

REFERENCES ............................................................................................................ 36

iv

LIST OF TABLES

S. No. Table Page Number

1. Table 4.1.1: Age 25

2. Table 4.1.2: Gender 25

3. Table 4.1.3: Qualification 26

4. Table 4.2.1: Awareness 27

5. Table 4.2.2: Religious Orientation 28

6. Table 4.2.3: Perceived Services & Product Quality 29

7. Table 4.2.4: Bank Image 30

8. Table 4.3: Hypothesis Assessment Summary 31

v

An Empirical Survey of Potential Customers’ Perception

towards Islamic Bank

Page 6 of 37

CHAPTER 1: INTRODUCTION

1.1 Background of the Study:

Banking is an important part of any economic system. They provide

various products and services to different segments. Islamic banking is getting common now

days. It is based on Islamic laws known as Shari’ah and guided by Islamic principles. It is

based on TWO principles including Profit and Loss Sharing principle and Prohibition of

collection on payment of Interest (Kadubo, 2010). Meezan Bank was the first Islamic bank

in Pakistan incorporated in 2002. Now this banking sector has become the reality which

cannot be ignored because society is now embracing Islam as the way to lead its life

(Ahmed, Rehman, & Saif, 2010)

It has been explored that the most important factor which directs customers towards Islamic

Banking in Shari’ah compliance (Khan & Asghar, 2012) The Relegious oriented people are

mostly attracted towards Islamic Banking system nevertheless; it is also providing services

for non-Muslims as well (Kishada & Wahab, 2013, p. 264). This system provides Muslims

with lot of investment opportunities complined with religious faith and non-Muslims are

free to choose between Islamic and conventional banks for investment.

As Islamic banking is newly introduced in Pakistan so the advertising campaign has a

positive impact on the perception of potential customers. According to the literature review,

religious orientation also has a significant impact on the perception of potential customers as

they are aware of risk sharing principle in Islamic economic system. Appropriate awareness

regarding Islamic products and services i.e. Musharaka, Mudarabah, Murabaha, Ijara

financing etc. also directs potential customers toward Islamic Banking (Khattak & Rehman,

2010) In a short period, Islamic banks in Pakistan have shown remarkable performance

capturing the market and getting to the bars set by conventional banks.

An Empirical Survey of Potential Customers’ Perception

towards Islamic Bank

Page 7 of 37

The main objective of this research is to explore the factors that pursue and influence

potential customers towards Islamic banking. The factors mainly include awareness,

religious orientation, perceived product and service quality and banki image/reputation.

Further in this chapter, the problem statement, research objectives and questions and

structure of the study will be discussed.

1.2 Statement of the Problem:

Islamic banking is newly introduced in Pakistan but has shown

commendable performance giving tough competition to conventional banks operating

already. As the name shows, this banking system follows Islamic laws strictly which is

mainly based on TWO principles i.e. Profit and Loss Sharing Priciple being one and the

other being Prohibition of collection on payment of Interest (Gait & Worthington, 2007)

In accordance to the literature reviewed, the ideal situation of perception of customers

towards Islamic banking is noted positive due to Islamic banking being interest free banking

where there is no fixed rate of return (Ashraf, 2013) People also trust that Islamic banking

does not invest in illegal/sin sectors i.e. alcohol, pornography and gambling (Iqbal,

1997)The main cause of Islamic banks restriction on interest is to eliminate the source of

unjust income and to earn with assuming risk factor (Siddiqui, 2001, p. 71) As Pakistan is a

Muslim majority country, so people here abide by Shari’ah and prefer Islamic banking so it

has grown in Pakistan in recent years (Economic Survey of Pakistan 2007-2008)

However, there is no research carried out regarding the perception of potential customers

towards Islamic Banking. This system has shown an increasing trend in recent years but

still, it lacks behind conventional banks due to unawareness among people about the Islamic

banks (Gerrard & Cunningham, 1997)

An Empirical Survey of Potential Customers’ Perception

towards Islamic Bank

Page 8 of 37

Looking at the scenario, the aim to this study is to explore the impact of core factors i.e.

awareness, relegious orientation, perceived product and service quality and bank

image/reputation on the perception of potential customers towars Islamic banking in

Pakistan.

1.3 Research Objectives and/or Questions:

Research Objectives:

RO1: To analyse the relationship between awareness and potential customers’ perception

towards Islamic bank.

RO2:To analyse the relationship between religious orientation and potential customers’

perception towards Islamic bank.

RO3:To analyse the relationship between perceived services & product quality and potential

customers’ perception towards Islamic bank.

RO4:To analyse the relationship between bank image and potential customers’ perception

towards Islamic bank.

Research Questions:

Q1.What is the impact of awareness on the potential customers’ perception towards Islamic

bank?

Q2.What is the impact of religious orientation on the potential customers’ perception

towards Islamic bank?

Q3. What is the impact of perceived product and service quality on the potential customers’

perception towards Islamic bank?

Q4. What is the impact of bank image and reputation on potential customers’ perception

towards Islamic bank?

An Empirical Survey of Potential Customers’ Perception

towards Islamic Bank

Page 9 of 37

1.4 Structure of the Study

This dissertation is arranged in different sections and each section covers some areas

ofresearch. Before proceeding any further it is necessary to understand these sections

andstructure of the report.

Chapter 1 is an introductory chapter which inculdes the Background of the Study,

Statement of the Problem, Research Objectives / Questions and Operational Definations.

Chapter 2 contains Literature Review over the perception of potential customers towards

Islamic Banks which is collected from many sources(mentioned in Literature Review).

In Chapter 3 we list down the Research Methodology which is further divided into

Theoratical Framework, Hypothesis and Research Design.

Then in Chapter 4 we give all the results of the study such as Descriptive Profile of the

data, Hypothesis Testing and Hypothesis Assesment Summary.

In the last Chapter 5 we conclude our Research by showing Conclusion of study,

Discussion on study, Limitations we found and Future Research Recommendations.

At the end, we show the references from where we collect our data

Then the research is finished with Appendix.

1.5 Operational Definitions:

Following are the terms defined operationally regarding the entire research.

1.5.1 Perception of Potential Customers (DV):

By the term ‘potential customers’ researchers meant those customers who are not engaged

with Islamic banks or who are willing to open their accounts in future or not willing to deal

with Islamic banks due to some reasons discussed below. The perception of potential

customers can be measured by comprising of different demographics i.e. gender, age,

An Empirical Survey of Potential Customers’ Perception

towards Islamic Bank

Page 10 of 37

qualification, the level of awareness, religious orientation, the perceived services and

product quality offered by an Islamic bank and, the bank image/reputation.

1.5.2 Awareness (IV):

By the term ‘awareness’ researchers meant those customers who have complete knowledge

regarding the concept of Islamic banking system and the products/services provided by the

Islamic banks. The awareness can be measured by the extent of knowledge of Islamic

banks’ Shari’ah compliance, the level of knowledge of Islamic banks’ products & services,

advertising through television or print media and, the information gained through relatives

and colleagues.

1.5.3 Religious Orientation:

By the tern ‘religious orientation’ researchers meant an individual’s attitude towards religion

and religious beliefs and practices. The level of religious orientation in this study is

measured by the religious knowledge, the deep concerned with religion and, the impact of

surroundings.

1.5.4 Perceived Services & Product Quality (IV):

In the research context, the term ‘perceived services and product quality’ is defined as the

level of insight\knowledge of potential customers regarding the quality of products and

services. Perceived service quality can easily be measured by the friendliness of employees,

efficiency of transactions, consultancy and coaching and, online banking opportunity.

Perceived product quality can easily be measured by risk of return and variety of investment

opportunities.

1.5.5 Bank Image (IV):

In the research context, the term ‘bank image’ is defined as the reputation of Islamic banks

in the eyes of potential customers. Generally, if the goodwill of an Islamic bank in the eyes

of future customers is good or respectable, then there are more chances of customers opt for

An Empirical Survey of Potential Customers’ Perception

towards Islamic Bank

Page 11 of 37

Islamic banks and vice versa. The term ‘bank image’ is measured by the pure Shari’ah

compliance, the time period of a particular bank, and the recommendation to other relatives

or peers.

An Empirical Survey of Potential Customers’ Perception

towards Islamic Bank

Page 12 of 37

CHAPTER 2: LITERATURE REVIEW

2.1 INTRODUCTION OF ISLAMIC BANKING:

The purpose of making Islamic laws is to encourage welfare of mankind, promote

justice, and to safeguard religion and wealth. To protect above mentioned objective, an

Islamic legal system plays a vital role which smoothest the progress of Islamic finance and

to assist the other financial markets, (Ahmed H. , 2006). Considering the previous

researches, no matter all the Muslims incorporate religion in all their life dealings but they

are willing to lead their lives as according to the Islamic Shari’ah and laws., which states

that all sort of interest are totally forbidden in Islam because not only it pushes the economy

into crises but also affect the entire society, (Ahmad, 2008).

As Islamic Banks are newly introduced system, they are struggling to acquire abundant

number of customers just to give tough competition to conventional banks who already have

perfect brand imaging in customers’ mind. As conventional banks provide interest based

products which means they give surety to their customers regarding the return on

investment, On the contrary, Islamic banks have found a way to attract more of the potential

customers by providing interest free products/services therefore; they started progressing by

leaps and bounds. Strictly speaking, since the payment on fixed dividends is prohibited in

Islamic law (Shari’ah) therefore, no preferred shares will be issued by Islamic banks,

(Kadubo, 2010).

An Islamic bank is considered as a mediator and trustee of the customers’ money but it

shares profit and loss with the depositors. Mainly, both conventional and Islamic banks have

the same working structure and functions, (Dar & Presley, 2000). “Islamic banking is

incredibly profitable because, although its underlying funding mechanism is the same

as conventional banking, its default experience is better, and its charges higher and less

crystal clear” (Cook, 2006, p. 16).

An Empirical Survey of Potential Customers’ Perception

towards Islamic Bank

Page 13 of 37

It is proved from the above statement that Islamic banking is not purely different from that

of conventional banking. They are doing almost same practices i.e. saving deposits and

consumer finances, but there exist some major differences in the objectives that Islamic

banking is not based on interest and mainly emphasis on equal distribution of wealth which

directly decreases the poverty and enhances more investment opportunities.

Clearly, the main aim of Islamic banks is not purely profit maximization but instead they

strive hard to promote Islamic values, (Farook, Hassan, & Lanis, 2011). In several countries,

it has been discovered through researches that the customer satisfaction level is more

towards the Islamic banks as compared to the conventional banks, (Nadia Asghar cited

“Ahmed et al. (2010)).

To be more specific, Islamic banking that is operated on Shari’ah laws while conventional

banking focuses on profit maximization, lending and borrowing, many researchers have

revealed that when considering cost efficiency Islamic banks perform more better than the

other conventional banks, and on the other hand when considering technical efficiency

conventional banks give tough competition to Islamic banks, (Nadia Asghar cited Shahid et

al. (2010)). In Pakistan, the comparison between Islamic banking and conventional banking

system indicated the declining stage of conventional banks because of the financial crises at

global level, while Islamic banking moving ahead and making a strong financial position on

the basis of assets, financing, efficiency and profitability etc., (Awan, 2009).

Muslims who seek assistance in all of their financial matters as according to the religion

should opt for Islamic banks. According to the surveys, it has been revealed that there are

numerous Islamic and some high street commercial banks offer products and services which

are based on Shari’ah laws. (www.standardcharterd.com).

An Empirical Survey of Potential Customers’ Perception

towards Islamic Bank

Page 14 of 37

DETERMINANT FACTORS OF A CUSTOMERS’ SELECTION OF AN

ISLAMICBANK:

Following are the main factors which act positively while selecting an Islamic bank:

Awareness of Islamic banking products and services.

Compliance with religion.

Positive perception of products and services offered by Islamic banks.

Good image and reputation of a bank.

2.2 AWARENESS OF PRODUCTS/SERVICES:

As Islamic banks and conventional banks offer different products/services, so awareness

related to provision of services is a key element to attract potential customers. Many

researches up till now have been conducted to find out a relationship between customer’s

awareness and the bank selection. To begin with, a famous research (Gerrard &

Cunningham, 1997) and (Ellahi, Khattak, Rehman, & Jamil, 2010) conducted in Singapore

and Pakistan which revealed that religious factor is not the most essential key element to

drive customer’s towards Islamic banks but knowledge of products is very important. They

discovered that there is a general lack of awareness among people which hinders them to

choose Islamic banks. To support the argument i.e. awareness has an impact on the selection

of an Islamic bank; a study has been conducted by (Ahmad & Haron, 2000) which states

that degree of knowledge of Islamic bank products/services, marketing strategies and service

quality have contributed to increase the market share. A research conducted in UK by

(Ahmad W. , 2008) gave more importance on awareness as he stated that it is most essential

for growth and progress of Islamic banking system to increase the number of its users. But

in due course proper awareness is a source to increase account holders. To clearly

understand the variable awareness, a research was conducted by (Ahmad, 2010) who stated

the importance of service quality in terms of awareness. His study revealed that the

An Empirical Survey of Potential Customers’ Perception

towards Islamic Bank

Page 15 of 37

provision of improved service quality would only satisfy those customers who are well-

aware of the products and services.

On the contrary, findings haven’t been the same always. (Naseer, Jamal, & Al-Khatib, 1999)

conducted an empirical research in Jordan to find out a relationship between customer

awareness and satisfaction, the results showed the other side of an attraction that people do

have awareness of specific products of Islamic banks but due to dissatisfaction towards

some services they refused to choose Islamic banks. By the above statement, it can be stated

that awareness is less important than the service quality.

Similarly, another study was conducted by (Naser, Jamal, & Khatib, 1999) in which they

came out with the idea that most of the customers do have a little bit knowledge about

particular products i.e. Mudarabah and Murabaha but, most of them are not willing to use

these products. Thus, we can say there is a balance between awareness of products/service

and service quality as some people weigh awareness as a priority to select an Islamic bank

while other researches proved that service quality is a key element to select any bank.

2.3 RELIGIOUS ORIENTATION:

In simple words religious orientation can be defined as a person's strong association with his

religion and religious beliefs. Through various researches it has been proved that religious

orientation has been one of the most essential elements of selecting an Islamic banking

system. A famous study conducted by (Omer, 1992) in which he revealed that majority of

Muslims selected Islamic banking system due to religious factor and found that mostly

Muslims were enrolled to Islamic banks and the conventional banks who have Islamic

windows. He further elaborated that majority of customers were ignorant of the

products/services offered by the Islamic banks but the only reason of choosing an Islamic

bank is the religious factor and the strong belief that it is an interest-free banking system.

This research cannot be generalized as the research was conducted in Malaysia, if it was

conducted in an Un-Islamic state the results would be absolutely different, as they would

have considered service quality and the wide range of services as the major factors to deal

An Empirical Survey of Potential Customers’ Perception

towards Islamic Bank

Page 16 of 37

with an Islamic bank. One more research conducted by famous researchers (Metawa &

Almossawi, 1998) who also supported the idea that the religious orientation is primarily the

essential element of selecting an Islamic bank. For further validity one more remarkable

study conducted by (Bashir, 1999) in Kuwait and (Naseer, Jamal, & Al-Khatib, 1999) in

Jordan who mainly focused the Islamic banking selection criteria and found out that

religious belief served as a major motivational element of selecting an Islamic bank which

was rated by the 70% of the respondents. Additional researches conducted by (Ahmad &

Haron, 2000), (Bley & Kuehn, 2004) and (Worthington, 2005) supported the idea that

people's strong religious association has been considered the most essential factor of

choosing an Islamic banking system as Muslims consider Islamic banking as an ethical

banking system that is operated as Riba-free banking which is strongly prohibited in Islamic

Shari'ah. (Dusuki & Abdullah, 2007)Also found out by their research that most of the

customers regarded religious orientation as the most essential element while dealing with

Islamic banking system.

A remarkable study conducted by (Gerrard & Cunningham, 1997) in which he revealed that

62.1% Muslims are willing to keep their deposits in Islamic banks no matter if they get

sufficient returns because of the strong religious association that Riba-free banking will

direct to wellbeing of the society.

Previous were the favorable researches but contradiction always exists. A research

conducted by (El-Bdour, 1989) and (Al-Ajmi, 2009) revealed that religious factor is not

considered as the major factor but still through various evidences it has been proved that

Shari'ah compliance is must for customers. Further they described in their research that

religious motives are not only the key element but people also consider various investment

opportunities provided by an Islamic banking system is simple words, they stated that

majority of bank customers are profit motivated. One more research conducted by (Al-Ajmi,

Al-Saleh, & Hussain, 2009) in which they described various other motivational factors other

than religion like friendly and well-informed bank staff, and considered service quality as a

An Empirical Survey of Potential Customers’ Perception

towards Islamic Bank

Page 17 of 37

key element to attract and retain customers. From which we can easily come to the

conclusion that mostly Muslims give importance to religious beliefs if the study is

conducted in an Un-Islamic state the results would vary as not only few Muslims but

majority of non-Muslims consider other factors i.e. bank image, service quality and

investment opportunities.

2.4 PERCEIVED SERVICE/PRODUCT QUALITY:

To conduct a research related to banks, different aspects are to be studied e.g. employee and

customer satisfaction, product and service quality, banking efficiency, financial performance

etc. as the main elements of research. All the banks are operating in an extremely

competitive environment thus they have realized that to survive successfully in today’s

global environment; they must offer the best quality oriented products/services, (Wang,

2003). A word Service is defined as a set of benefits which are delivered from the service

provider to the service consumer. These include intangible products such as teaching,

coaching, consultancy and other ways to assist the customers. To begin with the concept,

(Lehtimen, 1982) and (Gronroos, 1984) gave first thought to the importance of service

quality. Perceived service quality signifies the customer’s feelings or thoughts over service

provider’s efficiency and it’s notably linked with customer satisfaction. (Shin & Kim, 2008).

Banks provides number of services e.g. acts as a financial intermediation, gives consultancy

and provides agency services that are widespread with the passage of time. It has four main

key features: intangibility, inseparability, perishability and heterogeneity, (Hoffman &

Bateson, 2002). It has been discovered that customer selection criteria comprises of a variety

of features of item. Research showed that there are mainly two characteristics; product

quality and its features, and eminence or differentiation of service, (Awan & Bukhari,

2011).Moreover, service quality is divided into several sub parts. To clearly understand the

impact of service quality on customers a research conducted by (Ringim, 2013) explored

that customers who value time and expects that transactions should be completed before

An Empirical Survey of Potential Customers’ Perception

towards Islamic Bank

Page 18 of 37

time always regard effectiveness and efficiency of services as a high-quality services

provided by banks. Furthermore, improved quality services also represent personnel’s

friendliness, communication methods, dress code and customer relations. (Haron, 1994).

Service quality standards are very essential to maintain in the banking industry. Previous

researchers highlighted its importance (Berry & Thompson, 1982) recommended that strong

relationship between customers and financial organizations gives customers a reason to stay

loyal and therefore provides competitive advantage to financial institutions. Likewise, (Teas,

1993) revealed that the most essential feature of a customer’s dealing with a bank indicates

the long-term relationship that buildup with the bank.

(Al-Ajmi, Al-Saleh, & Hussain, 2009) emphasized mainly on service quality provided by

banks. They argued that not only religious orientation attracts customers but the quality of

customer services plays vital role while selecting an Islamic bank. They furthermore divided

this factor into friendly bank staff, well-educated, experienced and competent staff.

If we talk about perceived service quality it has been explored from previous research

conducted by (Othman, 2001) that the scope of service quality can be evaluated by

measuring a difference between customer’s expectations and perception of a service. The

lesser the difference between customer’s expectations and perception, the more high quality

of service is noted. Modern researchers gave attention to achieve service quality standards

importantly, which directly encourages sales and profits as well, (Kassim & Abdullah,

2010).

(Jones, 2002)Highlighted that there is a pure positive relationship between service quality

and consumers repurchase intention, recommendation to others, and refusing to opt for

better alternatives. All of the above elements ensure customer loyalty and alter behavioral

intentions rapidly in a positive way. One more research conducted by (Levesque &

McDougall, 1996) argued that the service quality and customer satisfaction have a strong

impact on each other as poor service quality will dissatisfy existing customers thus, they

An Empirical Survey of Potential Customers’ Perception

towards Islamic Bank

Page 19 of 37

would prefer switching the bank and might possible the poor quality service would restrict

them to join Islamic banks as well.

It is a misconception that Islamic banks are only for Muslims; instead they facilitate non-

Muslims as well. To check the perception of non-Muslims towards Islamic banks; a research

has been conducted by (Hidayat & Al-Bawardi, 2012) assessed the perception related to

products and services of non-Muslims expatriates in Saudi. The study revealed that cheaper

transaction cost and better quality services are the main reasons to attract them.

2.5 BANK IMAGE:

Bank image can be defined as the perceived reputation about a particular bank or banking

system. The attraction of customers depends on this factor as it plays vital role. The stronger

the bank image in mind of customers, the more new customers it will attract and vice versa.

The customers choose Islamic banks in both aspects, that is, Islamic and economic aspects.

To support this idea, study regarding this was conducted by (Kazeh, 1993) and (El-Bdour,

1989) surveyed 209 university students in Maryland, USA, their main focus was to obtain

information related to major determinants which attract customers towards Islamic banking

system. Study outlined the major factors but the dominant attributes were bank image,

service charges, friendly staff and service quality. They explored that people get attracted by

the bank's image or reputation very likely. Some other important factors that customers

keep in mind while choosing Islamic bank for financial services are name and image

(Ahmad & Haroon, 2002), and other equally important factor is confidentiality as discussed

by the author.(Abbas, 2003) Another is the influence of friends and family. (Metawa &

Almossawi, 1998)Also the perceived quality of service(Owen, 2002).

Concluding, not only spiritual factors attract and retain customers, but non-spiritual factors

also play vital role while choosing an Islamic bank.

An Empirical Survey of Potential Customers’ Perception

towards Islamic Bank

Page 20 of 37

CHAPTER 3: RESEARCH METHOD

3.1 Research Design

3.1.1 Type and Nature of Research

The research approach selected by researchers is quantitative approach. The purpose of this

research is descriptive.

3.1.2 Instrument

The instrument is the self made structured questionnaire by the researchers.

3.1.3 Validity and Reliability

3.1.3.1 Validity

Content Validity

Content validity of the tool was ensured by reviewing literature. Item was developed

with the understanding of literature review.

Face Validity

Face validity is ensured by expert's opinion and tool was reviewed by teacher and

experts from the field.

3.1.3.2 Reliability

The reliability of the data collection tool was ensured by conducting a pilot study of

small sample size (10 respondents).

3.1.4 Procedure of Data Collection

The researchers conducted face to face survey with the help of structured questionnaire. The

questionnaire was distributed among the professionals and students of Iqra University to

collect data. The researchers collected data with the consent of respondents without any

influence and administered the research personally.

An Empirical Survey of Potential Customers’ Perception

towards Islamic Bank

Page 21 of 37

3.1.5 Statistical Technique

The statistical technique used is spearman correlation because the data of dependent variable

is categorical.

3.1.6 Ethical Consideration

The personal information of the respondents is kept confidential and identity has remained

anonymous. Moreover, the physical, emotional and social harm has not been encouraged.

The gender biasness also was not encouraged.

An Empirical Survey of Potential Customers’ Perception

towards Islamic Bank

Page 22 of 37

3.2 Theoretical Framework

Awareness

Religious Oriented

Perceived Services

& Product Quality

Bank Image

Perception of Potential

Customers towards Islamic

Banks

An Empirical Survey of Potential Customers’ Perception

towards Islamic Bank

Page 23 of 37

3.3 Research Hypothesis

Ho1: There is no significant relationship between awareness and the potential customers’

perception towards Islamic banking.

Ho2: There is no significant relationship between religious orientation and the potential

customers’ perception towards Islamic banking.

Ho3: There is no significant relationship between perceived service & product quality and

the potential customers’ perception towards Islamic banking.

Ho4: There is no significant relationship between bank image and the potential customers’

perception towards Islamic banking.

Ha1: There is a significant relationship between awareness and the potential customers’

perception towards Islamic banking.

Ha2: There is a significant relationship between religious orientation and the potential

customers’ perception towards Islamic banking.

Ha3: There is a significant relationship between perceived service & product quality and the

potential customers’ perception towards Islamic banking.

Ha4: There is a significant relationship between bank image and the potential customers’

perception towards Islamic banking.

An Empirical Survey of Potential Customers’ Perception

towards Islamic Bank

Page 24 of 37

3.4 Sampling Design

The population of the study consists of the potential customers of Islamic Banks operating in

Pakistan and the sample of the study is the professionals and students of Iqra University,

Karachi.

3.4.1 Sampling Technique:

The researchers have chosen simple, random and convenient sampling technique.

3.4.2 Sample Size:

The sample size chosen for the study is 100 - 120 samples and is heterogeneous.

An Empirical Survey of Potential Customers’ Perception

towards Islamic Bank

Page 25 of 37

CHAPTER 4: RESULTS

4.1 Frequency of Demographic Factors

Table 4.1.1: Gender

Frequency Percent Valid Percent Cumulative Percent

Valid

Male

47 47.0 47.0 47.0

Female 53 53.0 53.0 100.0

Total 100 100.0 100.0

Interpretation: The researchers conducted this study in a regional university of Karachi

where the sample of students and teachers were asked to give their perception about Islamic

banking system. To accomplish our investigation, 120 questionnaires were distributed out of

which 100 were returned. Females were more willing to participate therefore 53% were

females and 47% of males responded.

Table 4.1.2: Age

Frequency Percent Valid Percent Cumulative Percent

Valid

20 or Less 39 39.0 39.0 39.0

21-30 53 53.0 53.0 92.0

31-40 7 7.0 7.0 99.0

40 Above 1 1.0 1.0 100.0

Total 100 100.0 100.0

An Empirical Survey of Potential Customers’ Perception

towards Islamic Bank

Page 26 of 37

Interpretation: In this study, the highest frequency of participants participated are of

between the age of 21-30. The second highest frequency is of the participants who were less

than 20 years or equal to. Only 7 respondents were of the age 32 - 40 and only one

respondent was above 40.

Interpretation: To accomplish the investigation, it was important to know the educational

level of the participants. In this study, 74% of the respondents were at the bachelor’s level

therefore labeled as the highest frequency participated in the study. Questionnaire was also

distributed among the respondents who had done or currently doing masters. 20% of the

respondents were doing masters and remaining respondents were professionals or holding

any other degree.

Table 4.1.3: Academic Qualification

Frequency Percent Valid Percent Cumulative

Percent

Valid

Bachelor

74 74.0 74.0 74.0

Masters 20 20.0 20.0 94.0

Professional 4 4.0 4.0 98.0

Any Other 2 2.0 2.0 100.0

Total 100 100.0 100.0

An Empirical Survey of Potential Customers’ Perception

towards Islamic Bank

Page 27 of 37

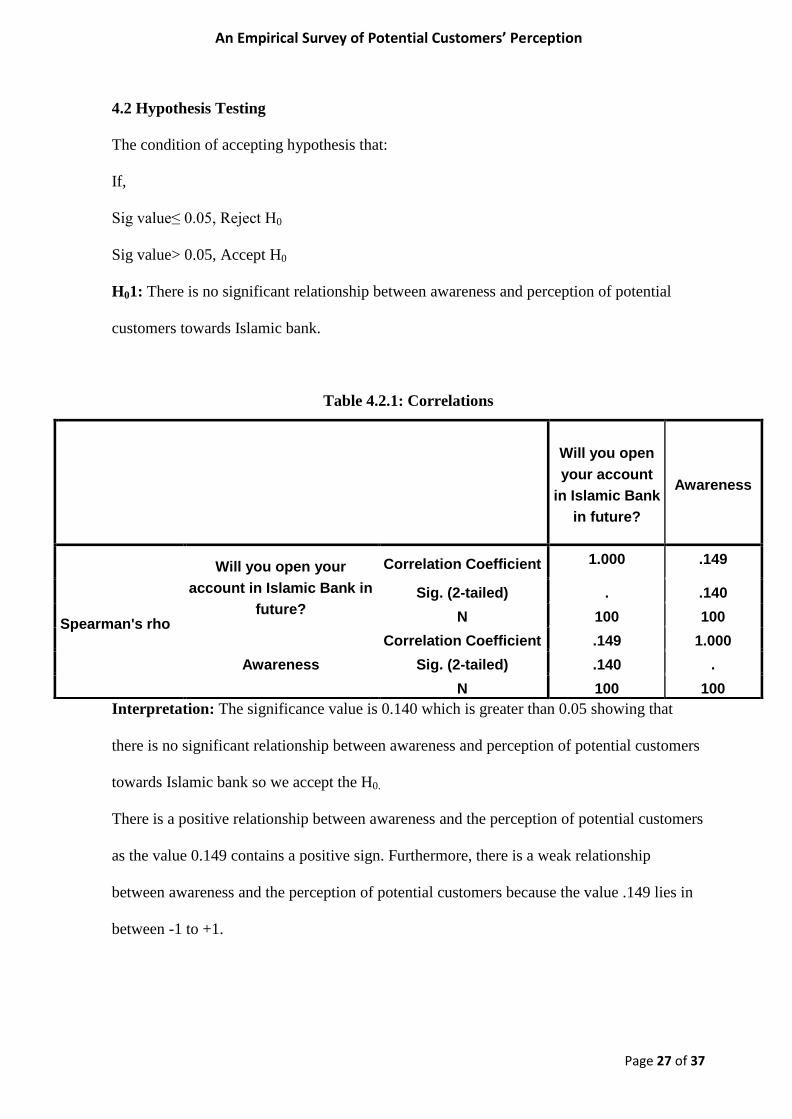

4.2 Hypothesis Testing

The condition of accepting hypothesis that:

If,

Sig value≤ 0.05, Reject H0

Sig value> 0.05, Accept H0

H01: There is no significant relationship between awareness and perception of potential

customers towards Islamic bank.

Interpretation: The significance value is 0.140 which is greater than 0.05 showing that

there is no significant relationship between awareness and perception of potential customers

towards Islamic bank so we accept the H0.

There is a positive relationship between awareness and the perception of potential customers

as the value 0.149 contains a positive sign. Furthermore, there is a weak relationship

between awareness and the perception of potential customers because the value .149 lies in

between -1 to +1.

Table 4.2.1: Correlations

Will you open

your account

in Islamic Bank

in future?

Awareness

Spearman's rho

Will you open your

account in Islamic Bank in

future?

Correlation Coefficient 1.000 .149

Sig. (2-tailed) . .140

N 100 100

Awareness

Correlation Coefficient .149 1.000

Sig. (2-tailed) .140 .

N 100 100

An Empirical Survey of Potential Customers’ Perception

towards Islamic Bank

Page 28 of 37

H02: There is no significant relationship between orientation and perception of potential

customers towards Islamic bank.

Interpretation: The sig value in the above table is equal to 0.05 which means that there is a

significant relationship between religious orientation and perception of potential customers

towards Islamic bank. In the above analysis, H0 is rejected.

The correlation coefficient that is 0.278 shows a weak positive relationship between the two

variables analyzed in the table. The direction is positive because the coefficient has a

positive sign and the strength is weak because of the value being closed to 0.

Table 4.2.2: Correlations

Religious

Orientation

Will you open

your account

in Islamic

Bank in

future?

Spearman's rho

Religious Orientation Correlation

Coefficient

1.000 .278**

Sig. (2-tailed) . .005

N 100 100

Will you open your

account in Islamic Bank

in future?

Correlation

Coefficient

.278** 1.000

Sig. (2-tailed) .005 .

N 100 100

**. Correlation is significant at the 0.01 level (2-tailed).

An Empirical Survey of Potential Customers’ Perception

towards Islamic Bank

Page 29 of 37

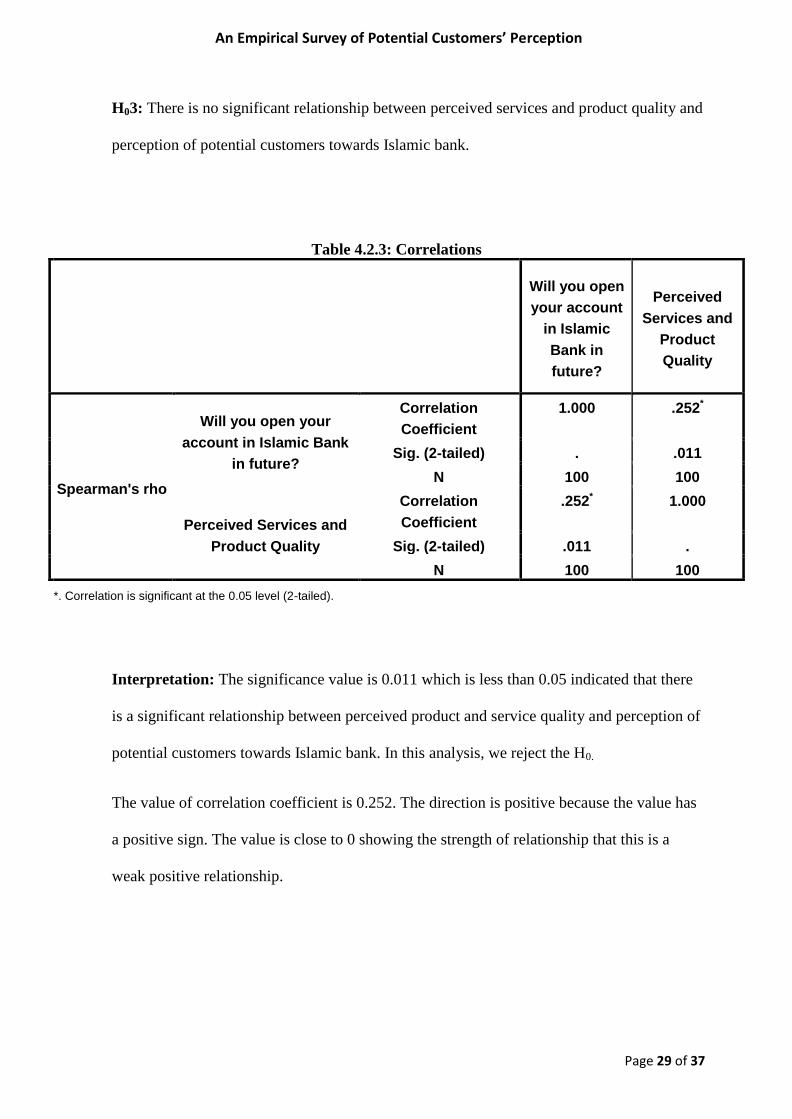

H03: There is no significant relationship between perceived services and product quality and

perception of potential customers towards Islamic bank.

Interpretation: The significance value is 0.011 which is less than 0.05 indicated that there

is a significant relationship between perceived product and service quality and perception of

potential customers towards Islamic bank. In this analysis, we reject the H0.

The value of correlation coefficient is 0.252. The direction is positive because the value has

a positive sign. The value is close to 0 showing the strength of relationship that this is a

weak positive relationship.

Table 4.2.3: Correlations

Will you open

your account

in Islamic

Bank in

future?

Perceived

Services and

Product

Quality

Spearman's rho

Will you open your

account in Islamic Bank

in future?

Correlation

Coefficient

1.000 .252*

Sig. (2-tailed) . .011

N 100 100

Perceived Services and

Product Quality

Correlation

Coefficient

.252* 1.000

Sig. (2-tailed) .011 .

N 100 100

*. Correlation is significant at the 0.05 level (2-tailed).

An Empirical Survey of Potential Customers’ Perception

towards Islamic Bank

Page 30 of 37

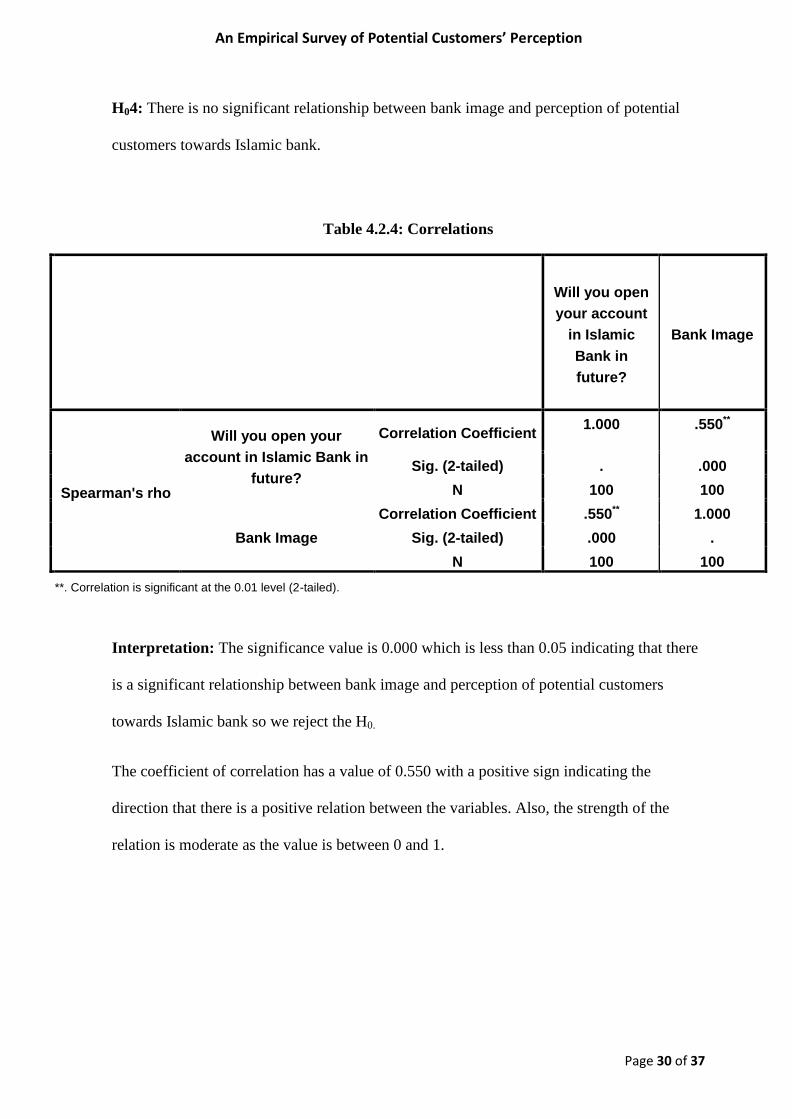

H04: There is no significant relationship between bank image and perception of potential

customers towards Islamic bank.

Interpretation: The significance value is 0.000 which is less than 0.05 indicating that there

is a significant relationship between bank image and perception of potential customers

towards Islamic bank so we reject the H0.

The coefficient of correlation has a value of 0.550 with a positive sign indicating the

direction that there is a positive relation between the variables. Also, the strength of the

relation is moderate as the value is between 0 and 1.

Table 4.2.4: Correlations

Will you open

your account

in Islamic

Bank in

future?

Bank Image

Spearman's rho

Will you open your

account in Islamic Bank in

future?

Correlation Coefficient 1.000 .550**

Sig. (2-tailed) . .000

N 100 100

Bank Image

Correlation Coefficient .550** 1.000

Sig. (2-tailed) .000 .

N 100 100

**. Correlation is significant at the 0.01 level (2-tailed).

An Empirical Survey of Potential Customers’ Perception

towards Islamic Bank

Page 31 of 37

Table 4.3: Hypothesis Assessment Summary:

Hypothesis Direction Correlation

coefficient (r)

Spearman

correlation (p-

value)

Decision

H01: Relationship between

awareness and perception of

potential customers’ towards

Islamic Banks.

- 0.149 0.140 H01 Accepted.

H02: Relationship between

religious orientation and

perception of potential

customers’ towards Islamic

Banks.

+ 0.278 0.005 H02 Rejected.

H03: Relationship between

perceived service & product

quality and perception of

potential customers’ towards

Islamic Banks.

+ 0.252 0.011 H03 Rejected.

H0.4: Relationship between bank

image and perception of

potential customers’ towards

Islamic Banks.

+ 0.550 0.000 H04 Rejected.

An Empirical Survey of Potential Customers’ Perception

towards Islamic Bank

Page 32 of 37

CHAPTER 5: CONCLUSION

5.1 Conclusion

The core objective of this research was to find out that whether there is any significant

impact of the Awareness, Religious Orientation, Perceived Product and Service Quality and

Bank Image on the perception of potential customers towards Islamic banks.

Through the in-depth research on “An Empirical Survey of Potential Customers’ Perception

Towards Islamic Bank” the researchers had concluded that the impact of awareness on

potential customers was against the thoughts, not indeed very affective.

However, Religious Orientation does made a good impact on the perception of potential

customers towards Islamic Banks. The reason behind this healthy impact could be that

Pakistan is an Islamic state and the majority of its nation is Muslim, so people are leaner

towards Islamic Shari’ah than conventional rules.

Feedback researchers received for perception of potential customers towards Islamic Banks

by their Perceived Product and Service Quality was meeting the expectations as it showed

significant relationship. In general, potential customers have a positive sight for Islamic

Banks’ service and product quality; here, the concept of Riba free banking could have made

a good impact on their thoughts.

Bank Image is something which is not often known to general public but the researchers

were intended to know how much people are influenced by the image of bank and how? So

the conclusion came as a significant relationship of Bank Image with the perception of

potential customers towards Islamic Banks. And that is because greater number of people

were agreed to follow the Shari’ah compliance and was likely to recommend such services

to others. All the research conclusions were tested by spearman’s correlation and results

were developed by the appropriate testing.

An Empirical Survey of Potential Customers’ Perception

towards Islamic Bank

Page 33 of 37

5.2 Discussions

Earlier, several researches have been conducted to know the perception of the customers of

Islamic banks, but no researches carried out to know the perception of potential customers

of Islamic banks in Pakistan. The proposed research discussed the perception of future

customers and researches have tried their very best to measure the accurate data with the

help of independent variables. In this study, it has been revealed that the first proposed

hypothesis has been accepted, it contains a value 0.149 which means even if people have

awareness regarding the Islamic banking concept and, the products/services offered by an

Islamic bank, it would not affect peoples’ decision to opt for Islamic banking system.

Though it is not common but this hypothesis has been proved by previous research

conducted by (Naseer, Jamal, & Al-Khatib, 1999) and (Saduman & Okumus, 2005) state

that people do possess knowledge regarding the specific products/services provided by the

Islamic banks but still they are not eager to use Islamic banking system and willingly stick

to the conventional banks. Most of the researches reviewed by the researchers of this study

found out that the improved level of awareness of products/services directs potential

customers towards Islamic banks, but only the research conducted by the above mentioned

authors support the idea that awareness does not have a greater impact on the potential

customers’ perception towards Islamic banks.

In this study, the second proposed hypothesis has been rejected as it contains the significant

value 0.005 and coefficient 0.278 which states there is a weak positive relationship. As this

research has been conducted in an Islamic state so according to the expectations the

religious orientation i.e. deep concerened with relation has greater impact on the perception

of potential customers towards Islamic banks.More specifically, the deeper and stronger the

religious beliefs, the more adoption of Islamic banking system in a society. Many

researchers have agreed with this point that religious orientation has an impact on the

selection of a particular Islamic bank. A research conducted by (Metawa & Almossawi,

1998) reveals that religious factor is the most influential factor which directs customers

An Empirical Survey of Potential Customers’ Perception

towards Islamic Bank

Page 34 of 37

towards Islamic banks moreover, they argued that people do not have sufficient knowledge

regarding the Islamic banking products/services but they have a firm belief that Islamic

banks do not invest in sinful projects and are strictly against giving interest.

The third proposed hypothesis has been rejected which states that there is no significant

relationship between perceived services & product quality on the perception of potential

customers towards Islamic banks. The correlation coefficient 0.252 states that there is a

weak but positive relationship between both variables. Specifically, the more good

perception of products/services offered by Islamic banks the more chances of future

customers directing towards Islamic banking system. According to several researches,

service quality has the greatest impact among all supporting factors. The research conducted

by (Ringim, 2013) and (Haron, 1994) agrees with the proposed hypothesis that quality of

service, efficiency of transactions and friendliness of employees have an utmost impact on

the perception of future customers towards Islamic banks. Thus, the rejection of null

hypothesis fully supported the previous researches conducted in an Islamic states.

The last null hypothesis has also been rejected which states that bank image does not have

an impact on the potential customers’ perception towards Islamic banks. The 0.550

coefficient correlation indicates the moderate but postive relationship between two

variables. In particular it reveals that; the higher the goodwill in the eyes of future

customers, the more they will attract towards Islamic banks i.e. increase in variable X, in

result variable Y also tends to increase. To support the hypothesis, a remarkable research

conducted by (Ahmad & Haroon, 2002) reveals that customers mainly focus on name and

reputation of a particular bank specially when choosing an Islamic bank. Overall, the result

obtained in this study is completely supporting the previous researches but the results are not

accurate due to some restrictions highlighted below.

An Empirical Survey of Potential Customers’ Perception

towards Islamic Bank

Page 35 of 37

5.3 Limitations

The researchers confronted with several limitations while conducting this study. Firstly, the

main purpose is to identify the perception of potential customers towards Islamic banks in

Pakistan. Therefore, the result obtained by the respondents couldn't be generalized as the

sample chosen was too small to predict the same results existing in the remaining

population. The second limitation throughout the study was the time constraint. Each

respondent has different class schedule so it was hard to get accurate data moreover,

researchers had limited time to complete the research within 3 months as this type of

research requires lots of articles, journals and other better quality information and were

unable to compile relevant information. Mainly there was limitation that the research was at

Academic level so it shrinks the scope of researchers. The last limitation which sustained

throughout the research was the lack of interest towards the selected topic. Respondents

were found with very limited or no knowledge towards Islamic banking so it was hard to

analyze the accurate results as expected. Future researches can eliminate these limitations by

switching to multiple relevant resources.

5.4 Future Research Recommendations:

The research conducted is very limited to regional university students only, so it is

recommended that further research should be conducted at a broader level to find out more

accurate perceptions of potential customers towards Islamic banks. Moreover, the

respondents were mostly females; it is recommended that more accurate data can be

gathered by taking responses from males as males are more directed towards any banking

system instead of females. In addition, the study revealed that there is a lack of awareness

among the general public regarding Islamic banking products and services, so in order to

increase the level of understanding it is recommended that more publications on newly

introduced Islamic banking system should be made publicly available.

An Empirical Survey of Potential Customers’ Perception

towards Islamic Bank

Page 36 of 37

REFERENCES

Ahmed, A.; Rehman, K.; Saif, M. I. (2010). Islamic Banking Experience of Pakistan: Comaprison

between Islamic and Conventional Banks. 2.

Ashraf, M. (2013). Development and Growth of Islamic Banking in Pakistan , 3145.

Awan, H. M., Bukhari, K. S., & Iqbal, A. (2011). Service Quality and Customer Satisfaction in the

Banking Sector. A Comparitive Study of Conventional and Islamic Banks in Pakistan. Journal of

Islamic Marketing , 12-20.

Bashir, M. S. (2013). Analysis of Customer Satisfaction with the Islamic Banking Sector: Case of

Brunei Darussalam. Asian Journal of Business and Management Sciences , 38-50.

Butt, I., Saleem, N., Ahmed, H., Altaf, M., Jaffer, K., & Mahmood, J. (2011). Barriers to adoption of

Islamic Banking in Pakistan. Journal of Islamic Marketing , 259-273.

Gait, A.H; Worthington A.C. (2007). A Primer on Islamic Finance: Definitions, Sources, Principles

and Methods. School of Accounting and Finance Working Paper Series , 05-07.

Imran, M., Samad, S. A., & Masood, R. (2010). Awareness Level of Islamic Banking in Pakistan's

Two Largest Cities. Journal of Managerial Sciences , 1-20.

Kadubo, A. (2010). Factors Influencing Development of Islamaic Banking in Kenya , 14.

Khan, H. N., & Asghar, N. (2012). Customer Awareness and Adoption of Islamic Banking in

Pakistan. 360.

Khan, N. & Ahmed, Z. (2014). Perception of potential customers about islamic banking. Banking

Journal , 18-20.

Khattak, N., & Rehman, K. (2010). Customer Satisfaction and Awareness of Islamic banking .

African Journal of Business Management Vol. 4(5) , 662-671.

Kishada, Z. M., & Wahab, N. A. (2013). Factors Affecting Customers' Loyalty in Islamic Banking:

Evidence from Malaysian Banks. , 1.

Kishada, Z., & Wahab, N. (2013). Factors Affecting Customers' Loyalty in Islamic Banking:

Evidence from Malaysian Banks. 265.

Zainol, Z., & Shaari, R. (2008). A Comparative Analysis of Bankers' Perceptions on Islamic

Banking. International Journal of Business and Management , 157-1