Advanced Auditing and Professional Ethics - Srinivasa Academy

409

Final Course (Revised Scheme of Education and Training) Study Material (Modules 1 to 3) PAPER 3 Advanced Auditing and Professional Ethics MODULE – 1 BOARD OF STUDIES THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA © The Institute of Chartered Accountants of India

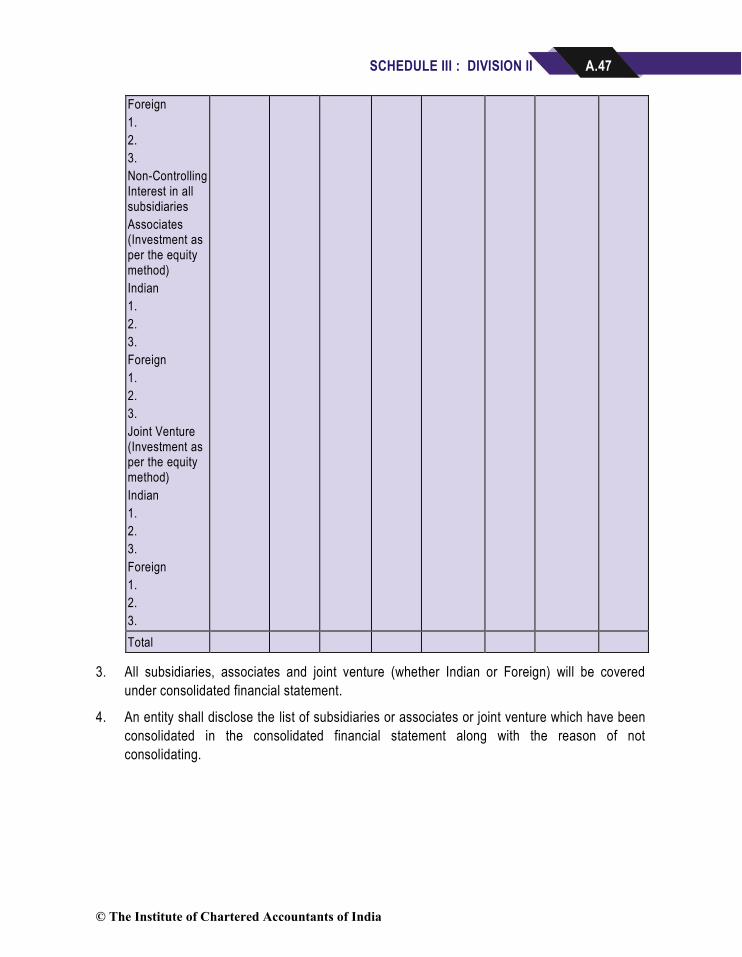

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of Advanced Auditing and Professional Ethics - Srinivasa Academy

Final Course (Revised Scheme of Education and Training)

Study Material (Modules 1 to 3)

PAPER 3

Advanced Auditing and Professional Ethics

MODULE – 1

BOARD OF STUDIES THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA

© The Institute of Chartered Accountants of India

ii This study material has been prepared by the faculty of the Board of Studies. The objective of the study material is to provide teaching material to the students to enable them to obtain knowledge in the subject. In case students need any clarifications or have any suggestions for further improvement of the material contained herein, they may write to the Director of Studies. All care has been taken to provide interpretations and discussions in a manner useful for the students. However, the study material has not been specifically discussed by the Council of the Institute or any of its Committees and the views expressed herein may not be taken to necessarily represent the views of the Council or any of its Committees. Permission of the Institute is essential for reproduction of any portion of this material.

© The Institute of Chartered Accountants of India

All rights reserved. No part of this book may be reproduced, stored in a retrieval system, or transmitted, in any form, or by any means, electronic, mechanical, photocopying, recording, or otherwise, without prior permission, in writing, from the publisher. Edition : August, 2019

Website : www.icai.org

E-mail : [email protected]

Committee/ : Board of Studies

Department

ISBN No. :

Price (All Modules) : `

Published by : The Publication Department on behalf of The Institute of Chartered Accountants of India, ICAI Bhawan, Post Box No. 7100, Indraprastha Marg, New Delhi 110 002, India.

Printed by :

© The Institute of Chartered Accountants of India

iii

BEFORE WE BEGIN …

Evolving Role of a CA. - Shift Towards Strategic Decision Making

The traditional role of a chartered accountant restricted to accounting and auditing, has now changed substantially and there has been a marked shift towards strategic decision making and entrepreneurial roles that add value beyond traditional financial reporting. The primary factors responsible for the change are the increasing business complexities on account of plethora of laws, borderless economies consequent to giant leap in e-commerce, emergence of new financial instruments, emphasis on corporate social responsibility, significant developments in information technology, to name a few. These factors necessitate an increase in the competence of chartered accountants to take up the role of not merely an accountant or auditor, but a global solution provider. Towards this end, the scheme of education and training is being continuously reviewed so that it is in sync with the requisites of the dynamic global business environment; the competence requirements are being continuously reviewed to enable aspiring chartered accountants to acquire the requisite professional competence to take on new roles.

Skill Requirements at Final Level

Under the Revised Scheme of Education and Training, at the Final Level, you are expected to not only acquire professional knowledge but also the ability to apply such knowledge in problem solving. The process of learning should also help you inculcate the requisite professional skills, i.e., the intellectual skills and communication skills, necessary for achieving the desired professional competence.

Auditing – Core and Practical Subject

Auditing has been conceived of to provide a highly useful technical service to the economy to know performances in financial and other appropriate terms in a reliable manner. It is needless to say that multitudes of significant decisions in the economic society are taken based on the financial information and, therefore, ensuring reliability of such information is an imperative necessity. Audit is a subject that requires a lot of quick and logical application of mind to answer practical problems. It is one of the most practical-oriented subjects in the C.A. curriculum. This paper aims to provide knowledge of generally accepted auditing procedures and of techniques and skills needed to apply them in audit engagements. A good knowledge of the subject would provide a strong foundation to students while pursuing the Chartered Accountancy course. A good understanding of the theoretical concepts, particularly, in the context of auditing standards would make practical training an enriching and enjoying experience. While studying this paper, students are advised to integrate the knowledge acquired in other subjects in a meaningful manner along with practical training. Such learning would only help a student to become a better professional.

© The Institute of Chartered Accountants of India

iv

Know your syllabus and Study Material

The Study Material of Advanced Auditing and Professional Ethics subject has been designed having regard to the needs of home study and distance learning students. The study material deals with the conceptual theoretical framework in detail. In each chapter, the topic has been covered in a step by step approach. The text has been explained, where appropriate, through illustrations, diagrams, tables, flowcharts, screenshots etc. You should go through the chapter carefully ensuring that you understand the topic and then test your knowledge by attempting question.

The Study Material has been divided into eighteen chapters in line with the syllabus and further bifurcated into three modules for the easy handling and convenience of students. For bare text of Guidance Notes and Auditing Standards, the students are advised to refer the “Auditing Pronouncements” which has been separately published by the Board of Studies. For understanding the coverage of the syllabus, it is important to read the study material along with the Study Guidelines.

Framework of Chapters – Uniform Structure Comprising of Specific Components

Efforts have been made to present each topic of the syllabus in a lucid manner. Care has been taken to present the chapters in a logical sequence to facilitate easy understanding by the students.

Structure of the Study Material

The content for each chapter/unit at the Final level has been structured in the following manner –

S. No.

Components of Each Chapter

About the Component

1. Learning Outcomes Learning outcomes which you need to demonstrate after learning each topic have been detailed in the first page of each chapter/unit. Demonstration of these learning outcomes would help you to achieve the desired level of technical competence.

2. Chapter Overview As the name suggests, this chart/table would give a broad outline of the contents covered in the chapter.

3. Introduction A brief introduction is given at the beginning of each chapter/unit which would help you get a feel of the topic.

4. Content The concepts and provisions of law/standard are explained in student-friendly manner with the aid of Examples/illustrations/diagrams/flow charts. These value additions would help you develop conceptual clarity and get a

© The Institute of Chartered Accountants of India

v

good grasp of the topic. Diagrams and Flow charts would help you understand the concept/provision in a better manner. Illustrations would help you understand the application of concepts/provisions.

5. Exercise Questions with Answers and MCQs / Test Your Knowledge

Exercising questions and answers alongwith MCQs would help you to apply what you have learnt in problem solving. In effect, it would sharpen your application skills and test your understanding as well as your application of concepts/provisions.

Attention is invited to the Significant Additions/Modifications made in this edition of the Study Material which are given on the next page.

We hope that these student-friendly features in the Study Material makes your learning process more enjoyable, enriches your knowledge and sharpens your application skills.

Happy Reading and Best Wishes!

© The Institute of Chartered Accountants of India

vi

SIGNIFICANT ADDITIONS/ MODIFICATIONSIN THE REVISED EDITION

Students are advised to refer Multiple Choice Questions (MCQs) inserted at the end of each of the Chapters after Theoretical Questions under heading Test Your Knowledge.

Chapter No.

Chapter Name Section / Sub-Section wherein Additions / Modifications have been done

Page Number

5 Company Audit

Insertion of Example on Section 139(2) Rotation of Auditors

5.15

Insertion of Tabular Presentation explaining Manner and Procedure of Selection and Appointment of Auditors 5.20, 5.21

12 Cost Audit 5.42

14.1 Financial Statements 5.44

14.4 Constitution of National Financial Reporting Authority

5.47

© The Institute of Chartered Accountants of India

vii

SYLLABUS

PAPER – 3 : ADVANCED AUDITING AND PROFESSIONAL ETHICS

(One paper – Three hours – 100 marks)

Objective:

(a) To acquire the ability to analyse current auditing practices and procedures and apply themin auditing engagements;

(b) To acquire the ability to solve cases relating to audit engagements.

Contents:

1. Auditing Standards, Statements and Guidance Notes: Engagement & Quality ControlStandards, Statements and Guidance Notes on Auditing issued by the ICAI; Elements of System ofQuality Control, Leadership Responsibilities for Quality within the Firm, Acceptance andContinuance of Clients Relationships and Specific Engagements, Engagement Performances, etc.(SQC 1 Quality Control for Firms that Perform Audits and Reviews of Historical FinancialInformation and Other Assurance and Related Services Engagements).

2. Audit Planning, Strategy and Execution: Planning the Flow of Audit Work; Audit Strategy,Audit Plan, Audit Programme and Importance of Supervision; Principal’s Ultimate Responsibility;Extent of Delegation; Control over Quality of Audit Work; Analytical Procedures Prior to Audit aswell as towards finalization; Concept of Principal Auditor and Other Auditor, Acceptance asPrincipal Auditor, Procedures to be Performed by Principal Auditor, Co-ordination between thePrincipal Auditor and Other Auditor (SA 600 Using the Work of Another Auditor); Concept ofInternal Audit Functions and its evaluation, Using the work of the internal audit function, UsingInternal Auditors to Provide Direct Assistance (SA 610 Using the Work of Internal Auditors);Auditor's Expert – Meaning, Need for an Auditor’s Expert, Understanding the Auditor’s Expert,Agreement with the Auditor’s Expert, Adequacy of the Auditor’s Expert’s Work (SA 620 Using theWork of an Auditor’s Expert).

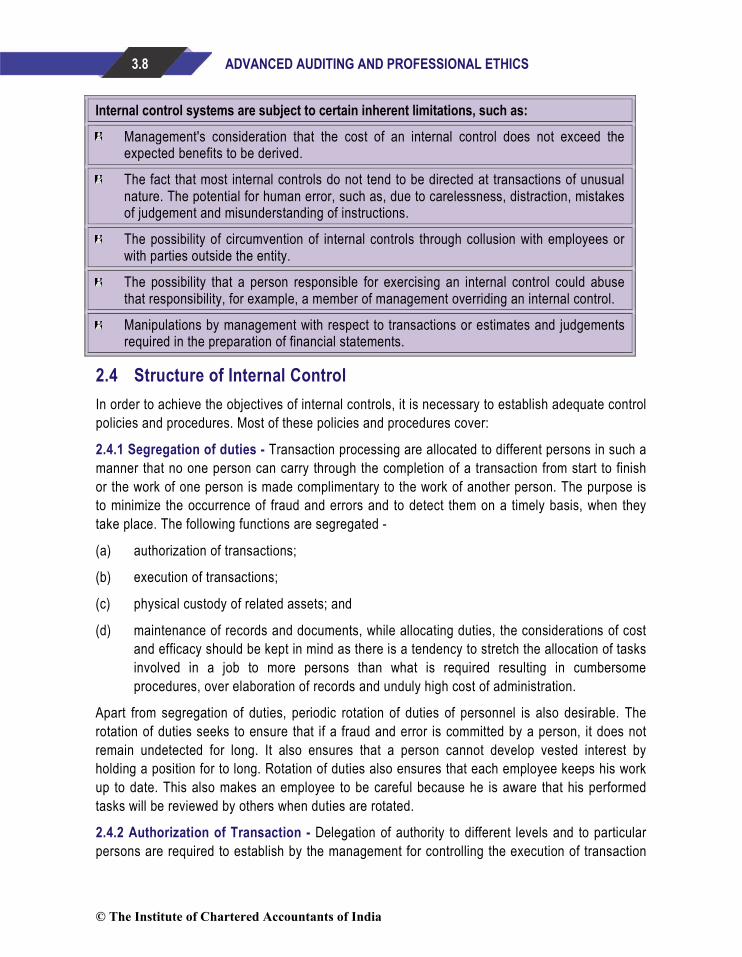

3. Risk Assessment and Internal Control: Evaluation of Internal Control Procedures;Components of Internal Controls; Internal Control and Risk Assessment; Risk-Based Audit- AuditRisk Analysis, General Steps; Internal Audit; Reporting on Internal Control Weaknesses (SA 265Communicating Deficiencies in Internal Control to Those Charged With Governance andManagement); Framework on Reporting of Internal Controls.

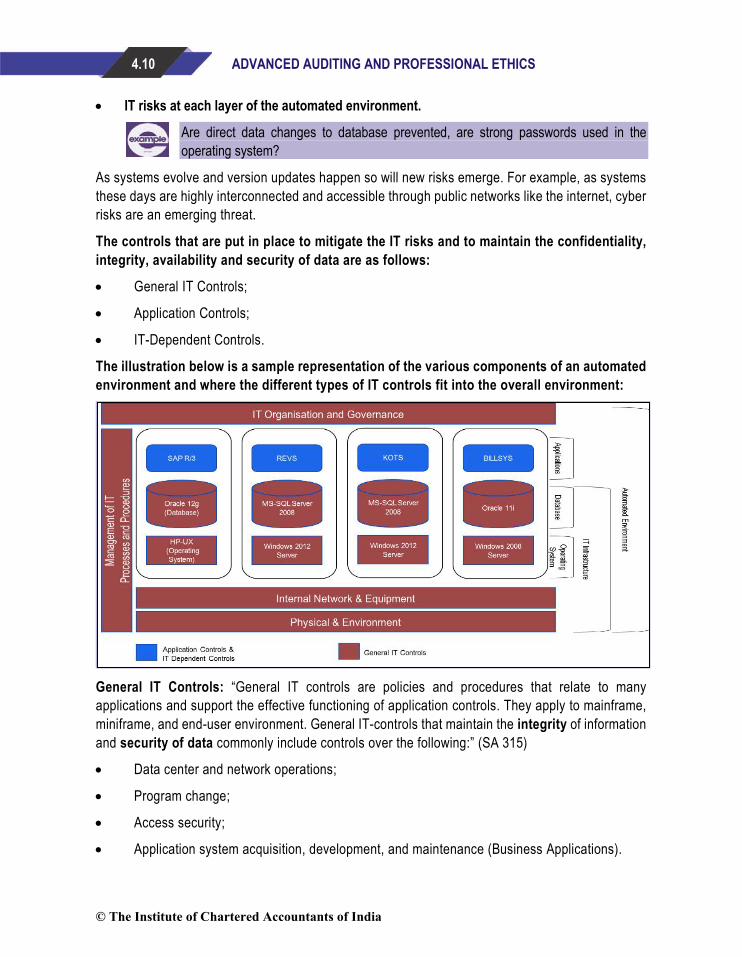

4. Special aspects of Auditing in an Automated Environment: Key Features of AutomatedEnvironment, Related Risks and Controls, Standards, Guidelines and Procedures, Using RelevantFrameworks and Best Practices, Understanding and Documenting Automated Environment,

© The Institute of Chartered Accountants of India

viii Enterprise Risk Management Overview, Assessing IT-Related Risks and Controls, Evaluating Risks and Controls at Entity Level and Process Level, Considerations of Automated Environment at each Phase of Audit Cycle, Using Relevant Analytical Procedures and Tests Using Data Analytics, Key Concepts of Auditing in Real-Time Automated Environments such as E-Commerce, ERP, Core Banking, etc..

5. Audit of Limited Companies: Application of Relevant Provisions under the Companies Act, 2013 relating to Audit and Auditors and Rules made thereunder; Powers/rights, Duties of Auditors; Branch Audit; Significance of True and Fair View; Dividends and Divisible Profits- Financial, Legal, and Policy Considerations; Depreciation; Special Features of Audit of Limited Liability Partnerships (LLPs)- Eligibility for Audit, Appointment of Auditor, Remuneration, etc. Audit Report under the Companies Act, 2013; Reporting under CARO.

6. Audit Reports: Basic Elements of Auditor’s Report; Types of Opinion; Notes on Accounts; Distinction between Notes and Qualifications; Distinction between Audit Reports and Certificates; Communication to Management and those Charged with Governance; Self Review Threats; Drafting of Different Types of Audit Reports.

7. Audit Committee and Corporate Governance: Audit committee; Role of Auditor in Audit Committee and Certification of Compliance of Corporate Governance; Compliances with Laws and Regulations (SA 250 Consideration of Laws and Regulations in an Audit of Financial Statements); Disclosure requirements including those of SEBI; Regulatory requirements of Corporate Governance, Report on Corporate Governance.

8. Audit of Consolidated Financial Statements: Provisions under the Companies Act, 2013 in respect of Accounts of Companies and Rules made thereunder; Audit of Consolidated Financial Statements - Responsibility of Parent Company, Auditor of the Consolidated Financial Statements; Audit Considerations - Permanent Consolidation, Current Period Consolidation; Reporting.

9. Special Features of Audit of Banks, Insurance & Non Banking Financial Companies

10. Audit under Fiscal Laws: Audit under Fiscal Laws, viz, Direct and Indirect Tax Laws including Documentation for Form 3CD etc.

11. Audit of Public Sector Undertakings: Special features, Directions of Comptroller and Auditor General of India; Concept of Propriety Audit; Performance Audit; Comprehensive Audit.

12. Liabilities of Auditors: Professional Negligence; Civil Liabilities; Criminal Liabilities; Liabilities under Different Statutes - for example Income Tax Act, Companies Act.

13. Internal Audit, Management and Operational Audit: Provisions of Internal Audit as per Companies Act, 2013; Scope of Internal Auditing; Relationship between Internal and External Auditor; Basics of Internal Audit Standards issued by the ICAI; Drafting of Internal Audit Report; Management Audit and Operational Audit.

© The Institute of Chartered Accountants of India

ix 14. Due Diligence, Investigation and Forensic Audit: Due Diligence Review; Audit versus Investigation; Steps for Investigation; Types of Investigation; Procedure, Powers, etc. of Investigator; Types of Fraud, Indicators of Fraud, Follow-up thereof; Forensic Audit- meaning, difference between Statutory Audit and Forensic Audit, Forensic Audit Techniques, Forensic Audit Report etc.

15. Peer Review and Quality Review

16. Professional Ethics: Code of Ethics with special reference to the relevant provisions of the Chartered Accountants Act, 1949 and the Regulations thereunder.

Note:

(i) The specific inclusions/exclusions, in any topic covered in the syllabus, will be effected every year by way of Study Guidelines.

(ii) The provisions of the Companies Act, 1956 which are still in force would form part of the syllabus till the time their corresponding or new provisions of the Companies Act, 2013 are enforced.

(iii) If new legislations/ Engagement and Quality Control Standards /Guidance Notes/Statements are enacted in place of the existing legislations, the syllabus would include the corresponding provisions of such new legislations with effect from a date notified by the Institute. The changes in this regard would also form part of Study Guidelines.

© The Institute of Chartered Accountants of India

x

CONTENTS

MODULE – 1

Chapter 1: Auditing Standards, Statements and Guidance Notes – An Overview

Chapter 2: Audit Planning, Strategy and Execution

Chapter 3: Risk Assessment and Internal Control

Chapter 4: Special Aspects of Auditing in an Automated Environment

Chapter 5: Audit of Limited Companies

Chapter 6: Audit Reports

MODULE – 2

Chapter 7: Audit Committee and Corporate Governance

Chapter 8: Audit of Consolidated Financial Statements

Chapter 9: Audit of Banks

Chapter 10: Audit of Insurance Companies

Chapter 11: Audit of Non Banking Financial Companies

Chapter 12: Audit under Fiscal Laws

MODULE – 3

Chapter 13: Audit of Public Sector Undertakings

Chapter 14: Liabilities of Auditors

Chapter 15: Internal Audit, Management and Operational Audit

Chapter 16: Due Diligence, Investigation and Forensic Audit

Chapter 17: Peer Review and Quality Review

Chapter 18: Professional Ethics

© The Institute of Chartered Accountants of India

xi

DETAILED CONTENTS MODULE – 1

CHAPTER-1: AUDITING STANDARDS, STATEMENTS & GUIDANCE NOTES-AN OVERIVEW

LEARNING OUTCOMES ........................................................................................................... 1.1

CHAPTER OVERVIEW ............................................................................................................. 1.1

Contents:

1. Introduction ................................................................................................................. 1.2

2. Historical Retrospect .................................................................................................... 1.2

3. Auditing and Assurance Standards Board-Scope and Functions ................................... 1.3

3.1 Setting up of AASB ......................................................................................... 1.3

3.2 Scope and Functions of AASB ........................................................................ 1.4

3.3 Scope of SAs .................................................................................................. 1.4

3.4 Procedure for Issuing SAs ............................................................................... 1.5

3.5 Compliance with the SAs ................................................................................ 1.5

3.6 Linkage between SAs and Disciplinary Proceedings ........................................ 1.5

4. Framework of Standards and Guidance Notes on Related Services .............................. 1.6

5. Quality Control and Engagement Standards ................................................................. 1.8

5.1 Structure of SAs ........................................................................................... 1.11

6. Guidance Notes ......................................................................................................... 1.11

6.1 Guidance Note on Tax Audit under Section 44AB of the Income-Tax Act ........ 1.11

6.2 Guidance Note on Audit of Internal Financial Controls over

Financial Reporting ....................................................................................... 1.12

7. Guidance Note(s) on Related Services ....................................................................... 1.12

8. Authority Attached to the Documents issued by the Institute/MCA ............................... 1.12

8.1 Statements ................................................................................................... 1.13

8.2 Guidance Notes ............................................................................................ 1.13

© The Institute of Chartered Accountants of India

xii 8.3 Accounting Standards and Standards on Auditing .......................................... 1.13

8.4 Accounting Standards ................................................................................... 1.14

8.5 Ind AS .......................................................................................................... 1.16

9. SQC 1- Quality Control for Firms that Perform Audits and Reviews of Financial Statement and Other Assurance and Related Services Engagements ......................... 1.19

10. SAs -Brief Overview ................................................................................................... 1.24

10.1 SA 200: Overall Objectives of the Independent Auditor and the Conduct of an Audit in accordance with Standards on Auditing ..................... 1.24

10.2 SA 210: Agreeing the Terms of Audit Engagements ....................................... 1.24

10.3 SA 220: Quality Control for an Audit of Financial Statements ......................... 1.25

10.4 SA 230: Audit Documentation........................................................................ 1.25

10.5 SA 240: The Auditor’s Responsibility Relating to Fraud in an Audit of Financial Statements ........................................................................ 1.25

10.6 SA 250: Consideration of Laws and Regulations in an Audit of Financial Statements .................................................................................... 1.26

10.7 SA 260: Communication with Those Charged with Governance ..................... 1.26

10.8 SA 265: Communicating Deficiencies in Internal Control to Those Charged with Governance and Management ....................................... 1.26

10.9 SA 299: Responsibility of Joint Auditors ........................................................ 1.27

10.10 SA 300: Planning an Audit of Financial Statements ........................................ 1.27

10.11 SA 315: Identifying and Assessing the Risks of Material Misstatement Through Understanding the Entity and Its Environment .................................. 1.27

10.12 SA 320: Materiality in Planning and Performing an Audit ............................... 1.27

10.13 SA 330: The Auditor’s Responses to Assessed Risks ................................... 1.28

10.14 SA 402: Audit Considerations Relating to an Entity Using a Service Organisation ..................................................................................... 1.28

10.15 SA 450: Evaluation of Misstatements Identified During the Audit .................... 1.28

10.16 SA 500: Audit Evidence ................................................................................ 1.28

10.17 SA 501: Audit Evidence—Specific Considerations for Selected Items ............. 1.29

10.18 SA 505: External Confirmations ..................................................................... 1.29

© The Institute of Chartered Accountants of India

xiii 10.19 SA 510: Initial Audit Engagements- Opening Balances ................................. 1.29

10.20 SA 520: Analytical Procedures ...................................................................... 1.30

10.21 SA 530: Audit Sampling ................................................................................ 1.30

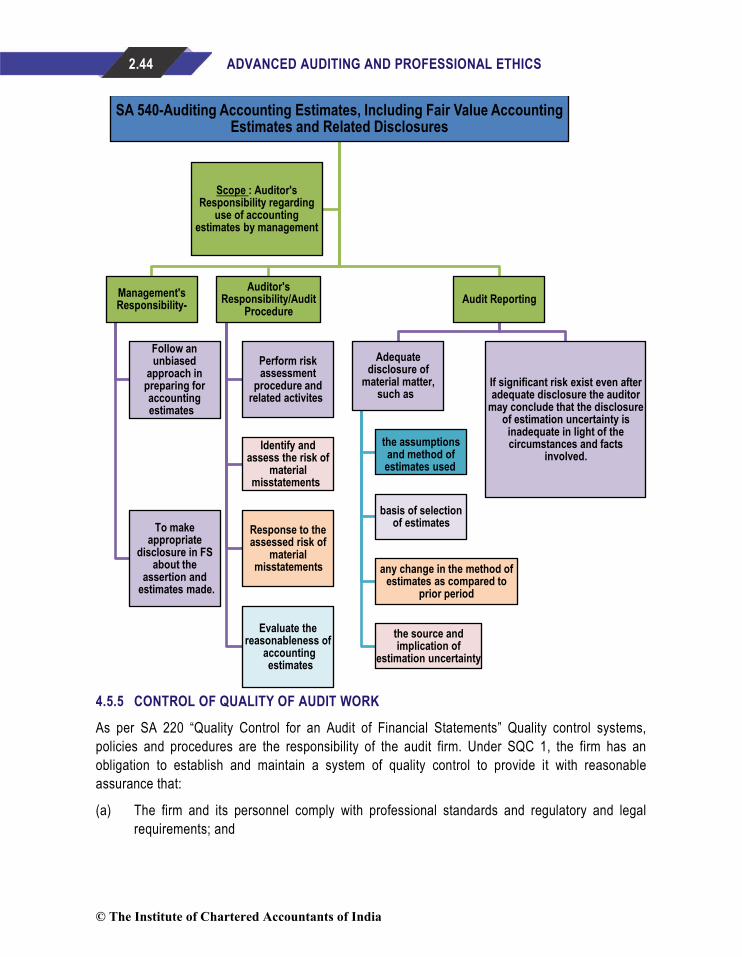

10.22 SA 540: Auditing Accounting Estimates, Including Fair Value Accounting Estimates, and Related Disclosures ............................................ 1.30

10.23 SA 550: Related Parties ................................................................................ 1.31

10.24 SA 560: Subsequent Events .......................................................................... 1.31

10.25 SA 570 Going Concern ................................................................................. 1.31

10.26 SA 580: Written Representations................................................................... 1.31

10.27 SA 600: Using the Work of Another Auditor ................................................... 1.32

10.28 SA 610: Using the work of Internal Auditors ................................................... 1.33

10.29 SA 620: Using the Work of an Auditor’s Expert .............................................. 1.33

10.30 SA 700: Forming an Opinion and Reporting on Financial Statements ............. 1.33

10.31 SA 701: Communicating Key Audit Matters in the Independent Auditor’s Report ........................................................................ 1.34

10.32 SA 705: Modifications to the Opinion in the Independent Auditor’s Report ...... 1.34

10.33 SA 706: Emphasis of Matter Paragraphs and Other Matter Paragraphs in the Independent Auditor’s Report ............................................ 1.34

10.34 SA 710: Comparative Information—Corresponding Figures and Comparative Financial Statements ......................................................... 1.35

10.35 SA 720: The Auditor’s Responsibility Relating to Other Information ................ 1.35

TEST YOUR KNOWLEDGE .................................................................................................... 1.36

CHAPTER-2: AUDIT PLANNING, STRAEGY & EXECUTION

LEARNING OUTCOMES ........................................................................................................... 2.1

CHAPTER OVERVIEW ............................................................................................................. 2.1

Contents:

1. Commencing an Audit .................................................................................................. 2.2

1.1 Benefits/Advantages of Planning in an Audit of Financial Statements ............... 2.2

© The Institute of Chartered Accountants of India

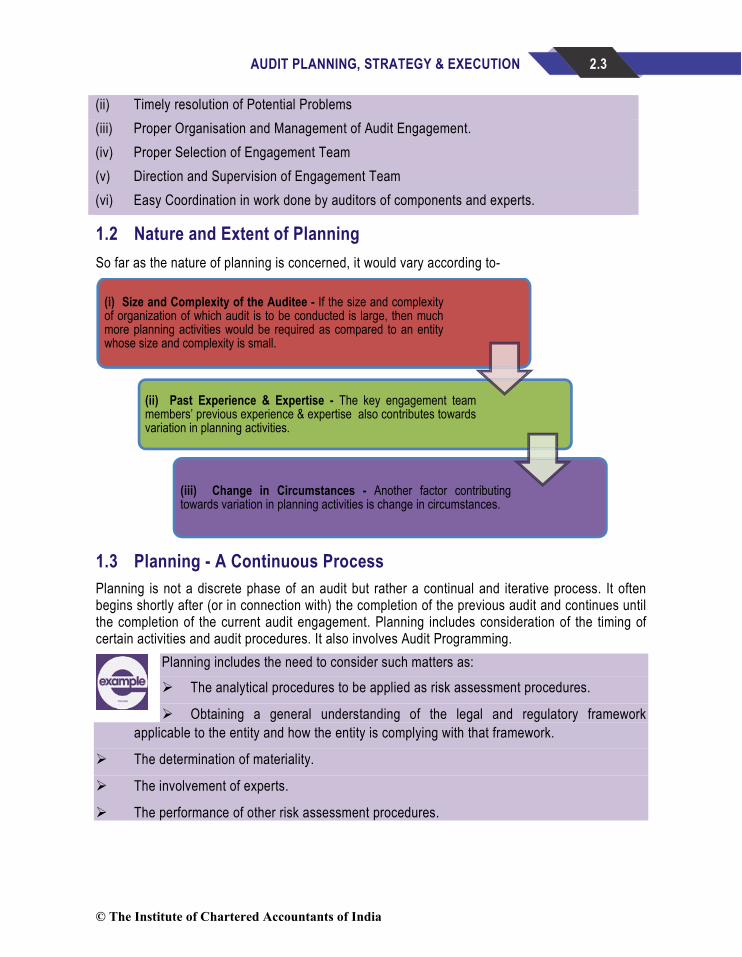

xiv 1.2 Nature and Extent of Planning ......................................................................... 2.3

1.3 Planning - A Continuous Process .................................................................... 2.3

1.4 Overall Audit Strategy and Audit Plan - Responsibility of the Auditor ................ 2.4

1.5 Acceptance and Continuance of Client Relationships and Audit engagements .. 2.4

1.6 Contents of an Audit Plan ............................................................................... 2.5

1.7 Changes to Planning Decisions ....................................................................... 2.5

2. Overall Audit Strategy .................................................................................................. 2.6

2.1 Factors while establishing Overall Audit Strategy ............................................. 2.6

2.2 Benefits of Overall Audit Strategy .................................................................... 2.6

2.3 Considerations in Establishing the Overall Audit Strategy ................................ 2.7

2.4 Documenting the Audit Plan ........................................................................... 2.9

2.5 Relationship between the Overall Audit Strategy and the Audit Plan ................. 2.9

3. Audit Programme ....................................................................................................... 2.10

3.1 Formulating an Audit Programme .................................................................. 2.10

3.2 Drawing up the Audit Programme .................................................................. 2.12

4. Audit Execution .......................................................................................................... 2.13

4.1 Execution Planning ....................................................................................... 2.13

4.2 Risk and Control Evaluation .......................................................................... 2.13

4.3 Testing ........................................................................................................ 2.14

4.4 Reporting...................................................................................................... 2.14

4.5 Other Important Considerations ..................................................................... 2.14

TEST YOUR KNOWLEDGE .................................................................................................... 2.47

CHAPTER-3: RISK ASSESSMENT AND INTERNAL CONTROL

LEARNING OUTCOMES ........................................................................................................... 3.1

CHAPTER OVERVIEW ............................................................................................................. 3.2

Contents:

1. Introduction ................................................................................................................. 3.2

© The Institute of Chartered Accountants of India

xv 2. Internal Control System - Nature, Scope, Objectives and Structure ............................... 3.5

2.1 Nature of Internal Control ................................................................................ 3.5

2.2 Scope of Internal Controls ............................................................................... 3.6

2.3 Objectives of Internal Control System .............................................................. 3.6

2.4 Structure of Internal Control ............................................................................ 3.8

3. Components of Internal Controls ................................................................................ 3.10

3.1 Control Environment ..................................................................................... 3.10

3.2 Entity’s Risk Assessment Process ................................................................. 3.11

3.3 Control Activities ........................................................................................... 3.13

3.4 Information System, including the Related Business Processes, Relevant to Financial Reporting, and Communication ................................... 3.14

3.5 Monitoring of Controls ................................................................................... 3.14

4. Review of the system of Internal Controls ................................................................... 3.17

5. Methods of Recording ................................................................................................ 3.19

5.1 Questionnaire ............................................................................................... 3.19

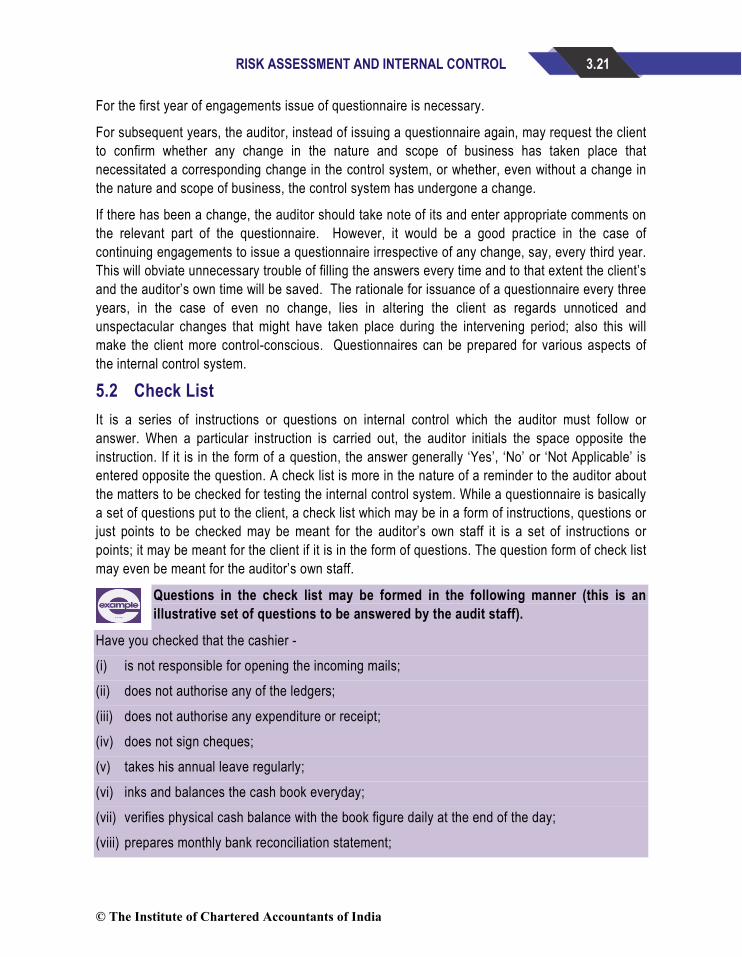

5.2 Check List .................................................................................................... 3.21

5.3 Flow Chart .................................................................................................... 3.22

6. Internal Control and Risk Assessment ........................................................................ 3.29

6.1 Preliminary Assessment of Control Risk ........................................................ 3.31

6.2 Relationship between the Assessments of Inherent and Control Risk: ............ 3.35

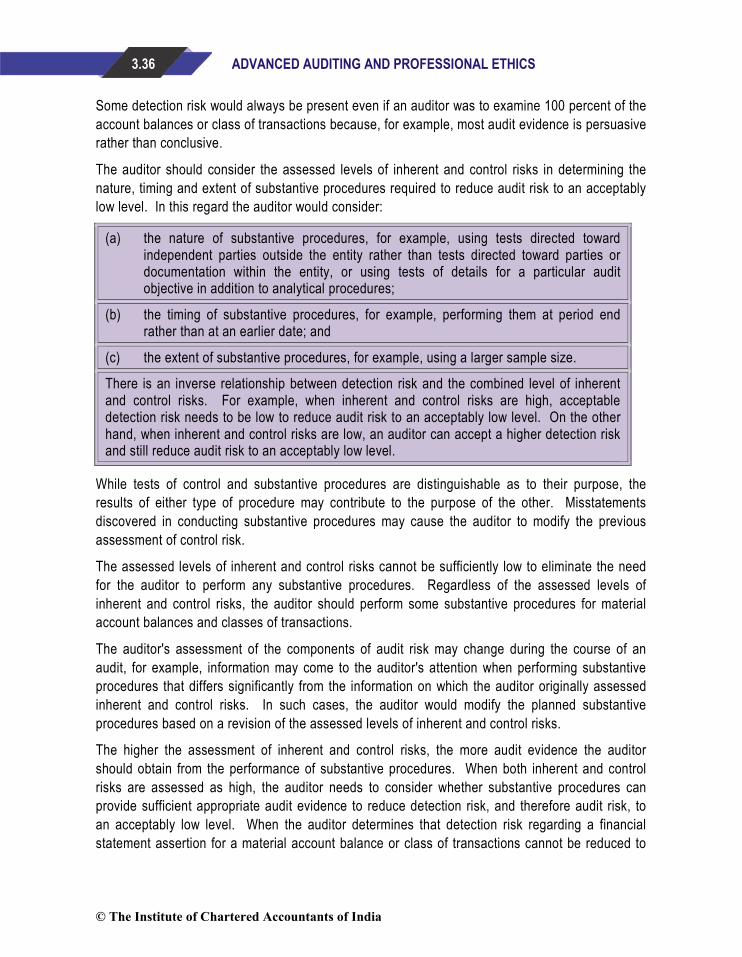

6.3 Detection Risk .............................................................................................. 3.35

7. Internal Control Assessment & Evaluation .................................................................. 3.38

8. Reporting to clients on Internal Control Weaknesses .................................................. 3.39

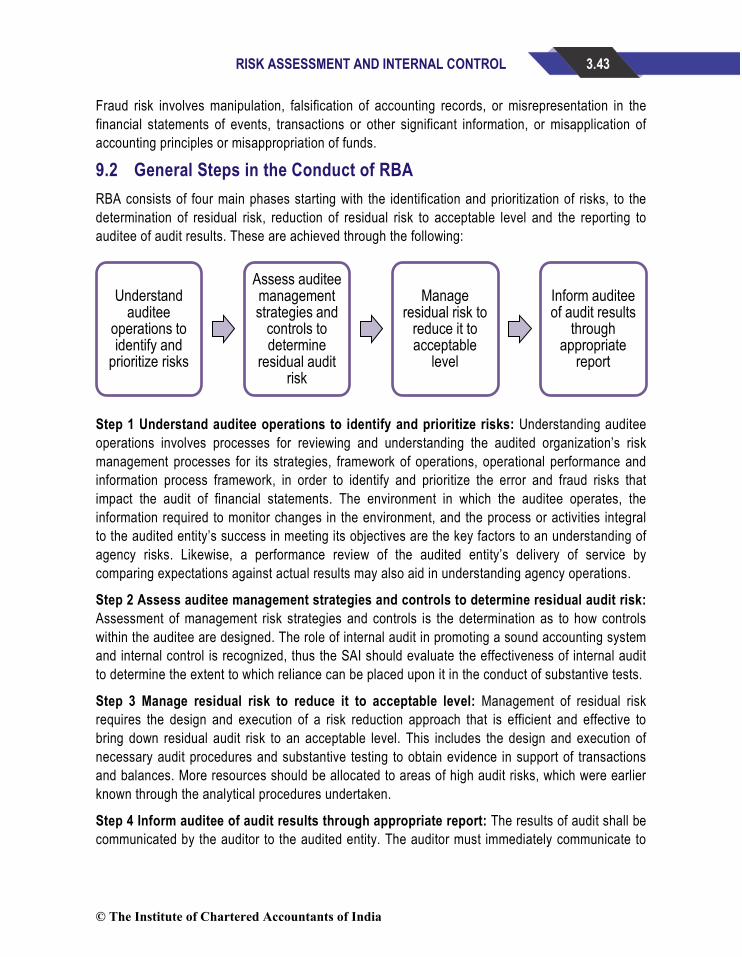

9. Risk Based Audit ....................................................................................................... 3.41

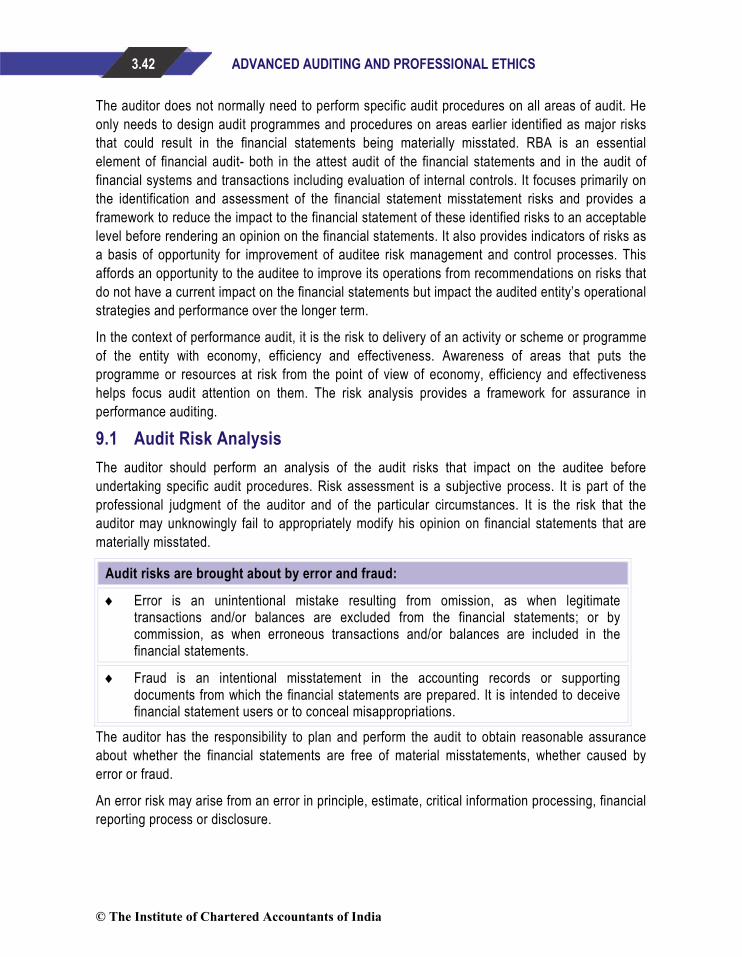

9.1 Audit Risk Analysis ....................................................................................... 3.42

9.2 General Steps in the Conduct of RBA ............................................................ 3.43

10. Frameworks of Internal Control .................................................................................. 3.44

10.1 International Internal Control Frameworks: .................................................... 3.45

TEST YOUR KNOWLEDGE .................................................................................................... 3.49

© The Institute of Chartered Accountants of India

xvi CHAPTER 4: SPECIAL ASPECTS OF AUDITING IN AN AUTOMATED ENVIRONMENT

LEARNING OUTCOMES ........................................................................................................... 4.1

CHAPTER OVERVIEW ............................................................................................................. 4.2

Contents:

1. Key Features of an Automated Environment ................................................................ 4.2

2. Key concepts of Auditing in Real-Time Environment such as E-Commerce, ERP, Core Banking, etc. ............................................................ 4.4

3. Understanding and Documenting Automated Environment ........................................... 4.5

4. Consideration of Automated Environment at each phase of Audit Cycle ........................ 4.6

5. Enterprise Risk Management Overview ........................................................................ 4.7

6. Assessing IT-related Risks and Controls ..................................................................... 4.9

7. Evaluating Risks and Controls at Entity Level and Process Level ................................ 4.12

8. Using relevant Analytical Procedures and Tests using Data Analytics ......................... 4.16

9. Standards, Guidelines and Procedures-using Relevant Frameworks and Best Practices ................................................................................. 4.17

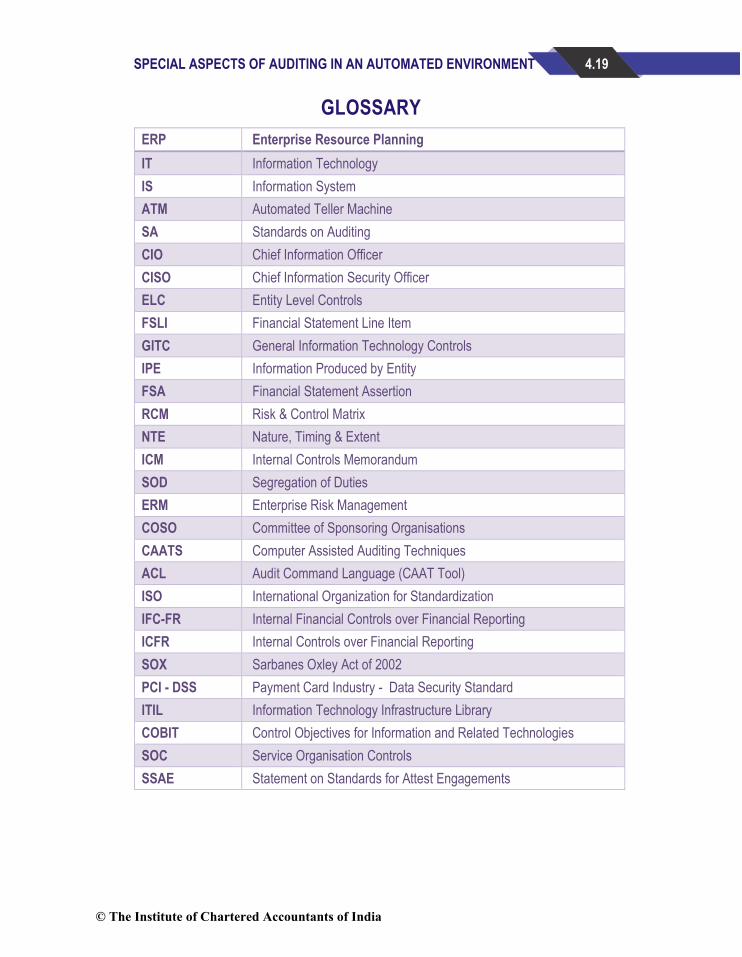

GLOSSARY ............................................................................................................................ 4.19

TEST YOUR KNOWLEDGE .................................................................................................... 4.20

CHAPTER-5: COMPANY AUDIT

LEARNING OUTCOMES ........................................................................................................... 5.1

CHAPTER OVERVIEW ............................................................................................................. 5.2

Contents:

1. Appointment of Auditors ............................................................................................... 5.2

1.1 Appointment of First Auditors ......................................................................... 5.3

1.2 Appointment of Subsequent Auditors/Re-appointment of Auditors .................. 5.5

1.3 Filling of a Casual Vacancy ............................................................................ 5.6

2. Eligibility, Qualifications and Disqualifications of an Auditor ......................................... 5.7

3 Rotation of Auditors .................................................................................................. 5.14

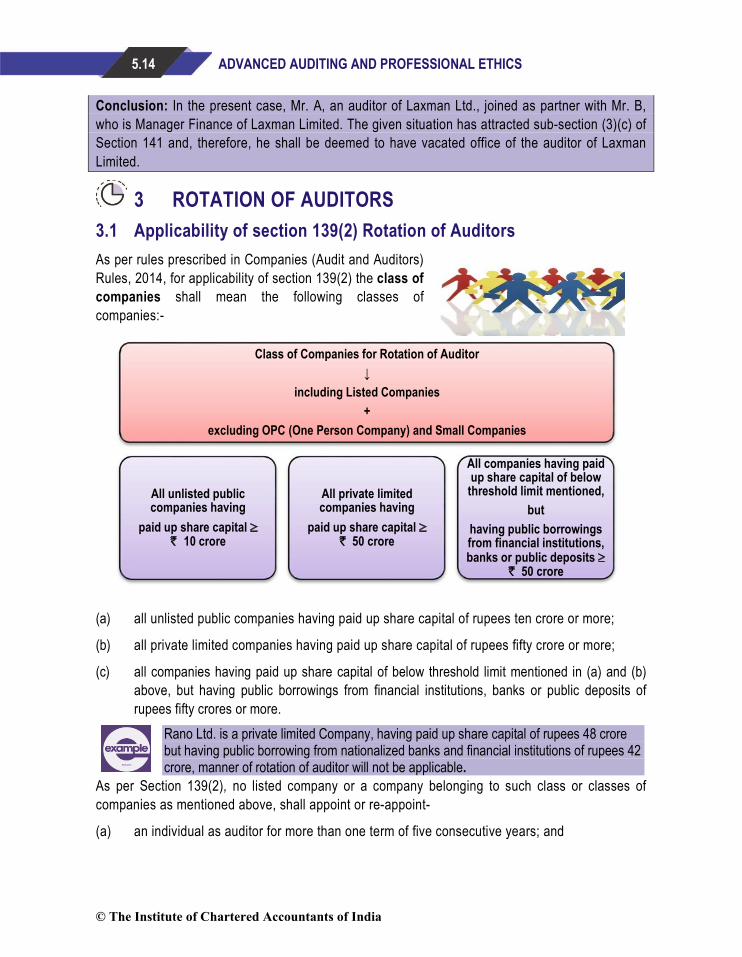

3.1 Applicability of section 139(2) Rotation of Auditors ....................................... 5.14

© The Institute of Chartered Accountants of India

xvii 3.2 Manner of Rotation of Auditors by the

Companies on Expiry of their Term .............................................................. 5.17

4. Provisions relating to Audit Committee ...................................................................... 5.19

4.1 Applicability of section 177 i.e. Constitution of Audit Committee .................... 5.19

4.2 Manner and procedure of selection and appointment of auditors ................... 5.20

5. Auditor’s Remuneration ............................................................................................. 5.21

6. Removal of Auditors .................................................................................................. 5.22

6.1 Removal of Auditor before Expiry of Term .................................................... 5.22

6.2 Appointment of Auditor other than retiring Auditor: ........................................ 5.22

7. Ceiling on Number of Audits ...................................................................................... 5.23

8. Powers/Rights of Auditors ......................................................................................... 5.26

8.1 Powers / Rights of Comptroller and Auditor-General of India ......................... 5.30

9. Duties of Auditors ..................................................................................................... 5.31

10. Joint Audit ................................................................................................................ 5.37

11. Audit of Branch Office Accounts ................................................................................. 5.38

12. Cost Audit ................................................................................................................. 5.39

13. Punishment for non-compliance ............................................................................... 5.42

14. Final Accounts Preparation and Presentation ............................................................ 5.43

14.1 Financial Statements ................................................................................... 5.43

14.2 Consolidated Financial Statement ................................................................ 5.45

14.3 Penalty for contravention ............................................................................. 5.46

14.4 Constitution of National Financial Reporting Authority ................................... 5.47

14.5 Form of the Balance Sheet ............................................................................ 5.50

15. Significance of True and Fair ..................................................................................... 5.52

16. Divisible Profits, Dividends and Reserves .................................................................. 5.54

16.1 Depreciation under Section 123 of the Companies Act, 2013 read with Schedule II to the Companies Act, 2013 ........................................ 5.54

16.2 Law relating to dividends .............................................................................. 5.55

© The Institute of Chartered Accountants of India

xviii 16.3 Right to dividend, rights shares and bonus shares to be held in

abeyance pending registration of transfer of shares ...................................... 5.61

16.4 Power to close register of members or debenture-holders or other security holders .............................................................................. 5.61

16.5 Interim Dividend ........................................................................................... 5.62

16.6 Payment of dividend and the Income tax Act ................................................ 5.62

16.7 Audit procedure for “Payment of Dividend”: .................................................. 5.63

16.8 Reserves ..................................................................................................... 5.64

16.9 Deferred Taxation ........................................................................................ 5.65

16.10 Non-provision of Tax in the Accounts ........................................................... 5.65

17. Depreciation ............................................................................................................. 5.69

18. Salient features of Limited Liability Partnerships (LLP) Audit ....................................... 5.70

19. Audit Report ............................................................................................................. 5.73

19.1 Reporting Under CARO, 2016 ...................................................................... 5.73

Appendix 1: Comprehensive Case Studies on CARO 2016 .............................................. 5.79

Appendix-2: Key Aspects discussed in Guidance Note on Internal Financial Control over Financial Reporting .............................................................................. 5.88

TEST YOUR KNOWLEDGE ............................................................................................................... 5.91

Schedule III ................................................................................................................................... A1-A47

CHAPTER-6: AUDIT REPORTS

LEARNING OUTCOMES ........................................................................................................... 6.1

CHAPTER OVERVIEW ............................................................................................................. 6.1

Contents:

1. Introduction ................................................................................................................. 6.2

2. The Auditor’s Report on Financial Statements .............................................................. 6.2

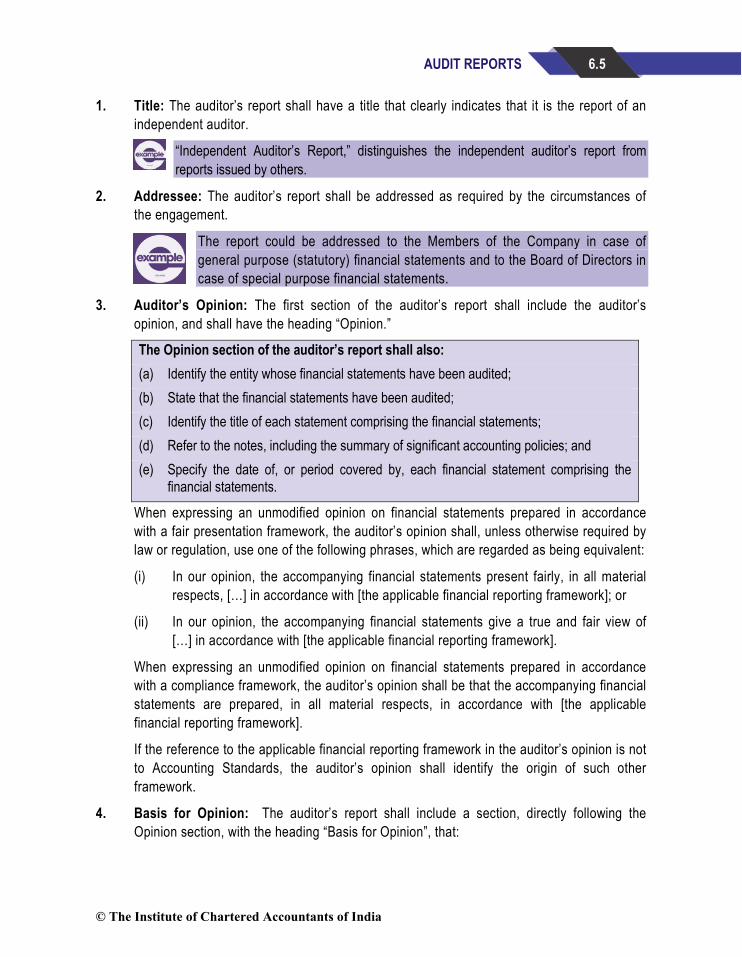

3. SA-700, “Forming an Opinion and Reporting on the Financial Statements” .................... 6.3

3.1 Purpose .......................................................................................................... 6.4

3.2 Basic Elements of the Auditor’s Report ............................................................ 6.4

© The Institute of Chartered Accountants of India

xix 3.3 Auditor’s Report Prescribed by Law or Regulation ........................................ .6.12

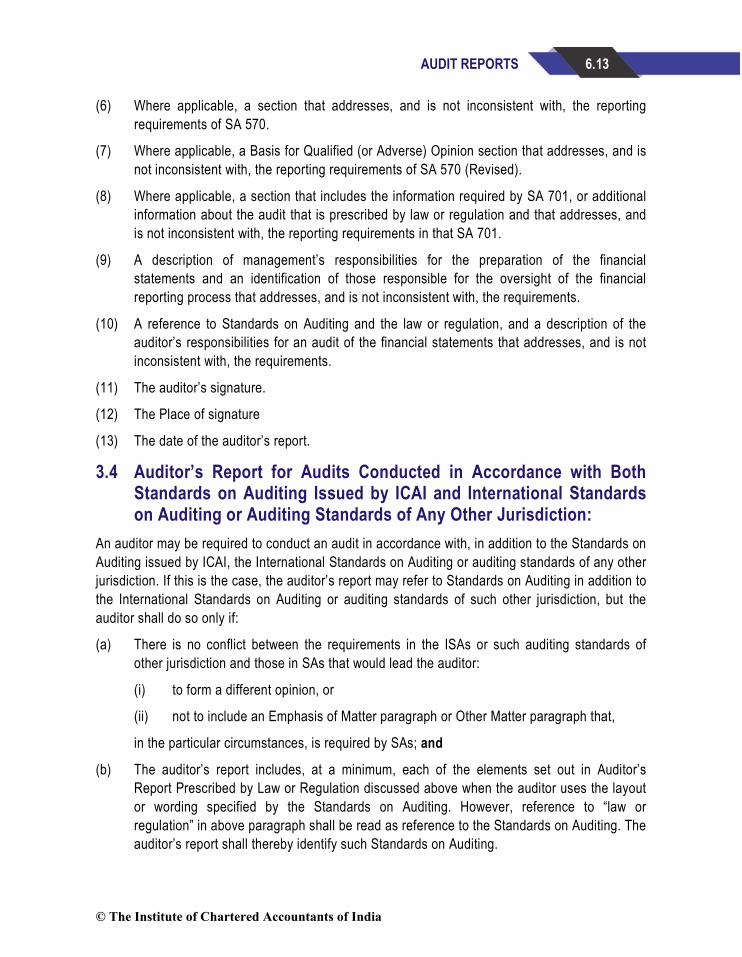

3.4 Auditor’s Report for Audits Conducted in accordance with both Standards on Auditing issued by ICAI and International Standards on Auditing or Auditing Standards of any other jurisdiction .................................. 6.13

4. SA 701, “Communicating Key Audit Matters in the Independent Auditor’s Report” ....... 6.14

4.1 Purpose ........................................................................................................ 6.14

4.2 Scope ........................................................................................................... 6.14

4.3 Determining Key Audit matters ...................................................................... 6.15

4.4 Communicating Key Audit matters: ................................................................ 6.15

5. SA 705, “Modifications to the opinion in the Independent Auditor’s Report” ................. 6.16

5.1 Types of modified opinions ............................................................................ 6.16

5.2 Objective ...................................................................................................... 6.16

5.3 Circumstances when a Modification to the Auditor’s Opinion is required ........ 6.17

5.4 Determining the type of Modification to the Auditor’s Opinion ......................... 6.17

5.5 Consequence of an inability to obtain Sufficient Appropriate Audit Evidence due to a Management-Imposed Limitation after the Auditor has accepted the Engagement ........................................................................................... 6.19

5.6 If the Auditor Decides to Withdraw ................................................................ 6.20

5.7 Other Considerations Relating to an adverse opinion or Disclaimer of opinion 6.20

5.8 Form and Content of the Auditor’s Report when the opinion is modified ......... 6.20

5.9 Communication with those charged with Governance .................................... 6.23

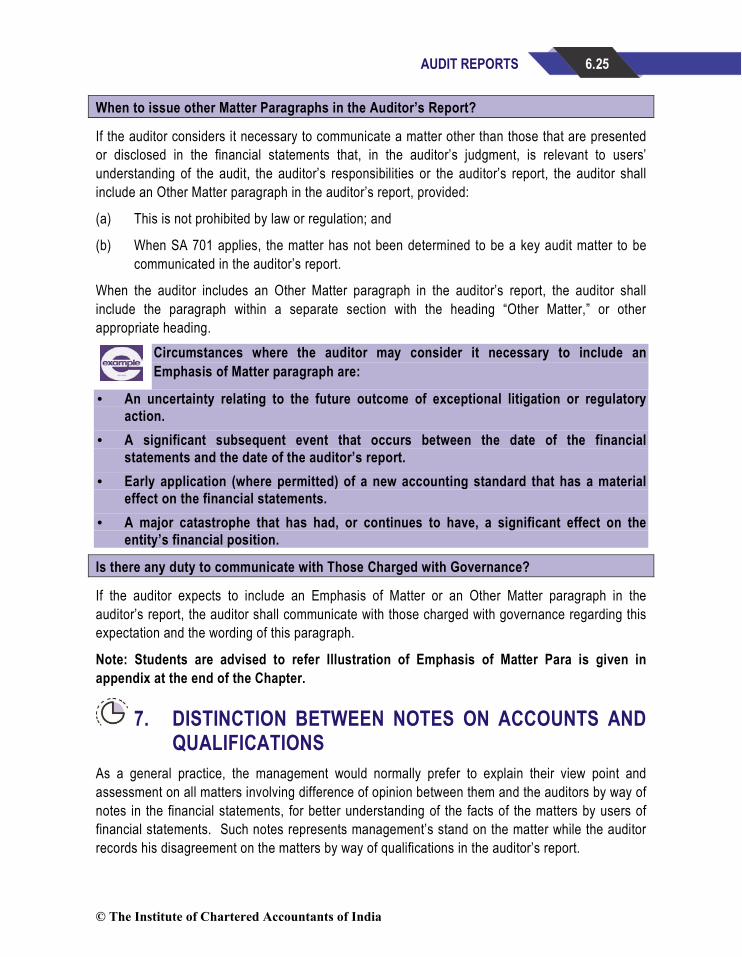

6. SA 706, “Emphasis of Matter Paragraphs and Other Matter Paragraphs in the Independent Auditor’s Report” ........................................................ 6.23

6.1 Objective ...................................................................................................... 6.23

6.2 When to give Emphasis of Matter Paragraphs in the Auditor’s Report?........... 6.24

6.3 When the auditor includes an Emphasis of Matter Paragraph in the Auditor’s Report .................................................................................. 6.24

7. Distinction between Notes on Accounts and Qualifications .......................................... 6.25

8. Distinction between Audit Report and Certificate ........................................................ 6.26

9. Communication to Management and those charged with Governance ......................... 6.27

© The Institute of Chartered Accountants of India

xx 9.1 When all of those charged with Governance are involved

in managing the entity ................................................................................... 6.28

9.2 Matters to be communicated ......................................................................... 6.28

9.3 Planned Scope and Timing of the Audit ......................................................... 6.28

9.4 Significant findings from the Audit ................................................................. 6.29

10. Self Review Threats ................................................................................................... 6.29

10.1 Meaning- Self Review Threats ....................................................................... 6.30

10.2 Safeguards that may eliminate or reduce such threats to an acceptable level fall into two board categories ................................................................ 6.30

11. Reporting Requirements in case of Comparative Information ...................................... 6.30

11.1 Audit Procedures for Comparative Information ............................................... 6.31

11.2 Audit Reporting ............................................................................................. 6.31

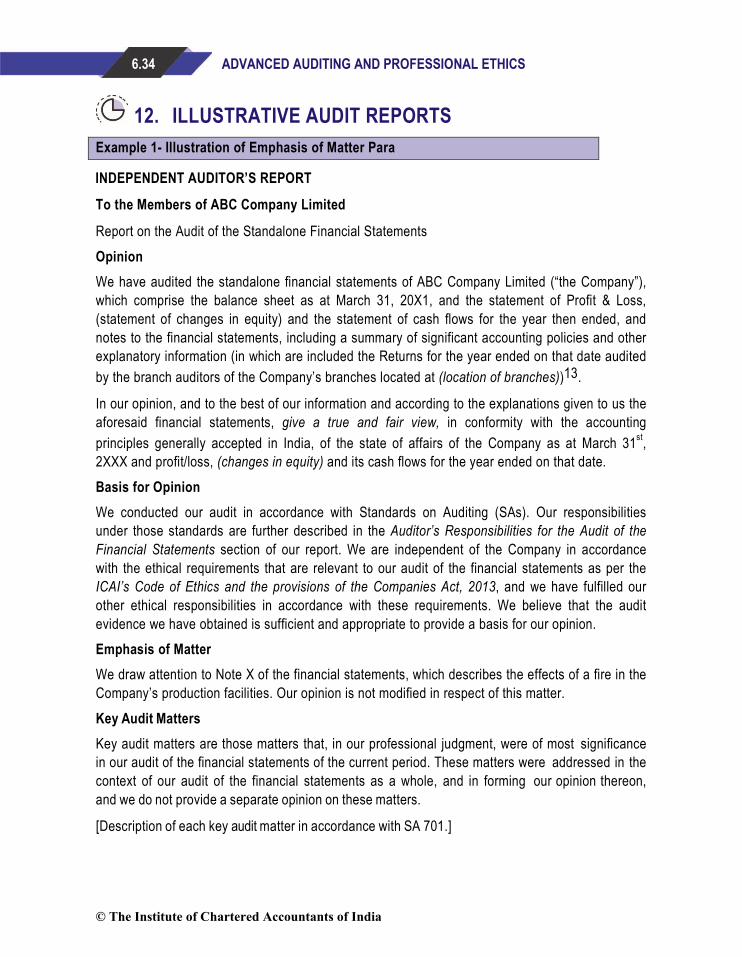

12. Illustrative Audit Reports ............................................................................................ 6.34

TEST YOUR KNOWLEDGE ............................................................................................ 6.49

© The Institute of Chartered Accountants of India

1 AUDITING STANDARDS, STATEMENTS AND GUIDANCE NOTES - AN OVERVIEW

LEARNING OUTCOMES

After studying this chapter, you will be able to: Apply logical, critical and creative thinking to analyse, synthesise and

apply theoretical knowledge, and technical skills to conduct Audit & Assurance as per Engagement and Quality Control Standards.

Determine and apply knowledge of Auditing Standards to your professional practice and/or further study.

Understand the requirements of each Standard to conduct Audit in Accordance with Standards.

Auditing Standards, Statements & Guidance Notes

IFAC - IAASB ICAI - AASB

Engagement and Quality Control

StandardsGuidance Notes Statements

CHAPTER OVERVIEW

© The Institute of Chartered Accountants of India

1.2 ADVANCED AUDITING AND PROFESSIONAL ETHICS

1. INTRODUCTION The past decade has been one of unprecedented change in the global economy and capital markets. Key aspects of the current business environment include a globalized, highly competitive, expanding economy; explosive growth in the development and use of technology; dramatic increases in new economy service- and technology-based businesses with predominantly intangible assets; unparalleled expansion in the number of public entities; large increases in the number of individuals who directly or indirectly own equity securities; and unprecedented growth in the market value of those securities.

The expanded use of technology in both the operating and financial systems of companies also has significantly affected the audit environment, forcing audit firms to recruit, train and deploy a large number of information technology specialists to support their audit efforts. It also has caused firms to reconsider their audit methods and techniques in an effort to harness technology to improve audit efficiency and effectiveness. In the changing environment, it is obvious that a professional accountant should to adhere to standards and procedures laid down by the professional accountancy bodies of which he is a member while discharging his duties in a responsible manner. In this direction, the role of a professional accounting body is to lay down such standards and procedures with the aim of providing guidance to members. The Institute of Chartered Accountants of India (ICAI) has been formulating auditing and accounting standards for the guidance of its members on its own volition in the larger interests of the society. In this chapter, we provide an overview of auditing standards and guidance notes issued by the Institute from time to time. Though these standards and guidance notes have been dealt at appropriate places, the main purpose is to acquaint and inculcate appreciation on the part of students in a focused manner as to significance of the standards in their day to day auditing activities. Towards the end of the Chapter, the clarification issued by the Council of the Institute is also included, which would go a long way in understanding as well as significance to the mandatory status of “Statements” and “Standards”.

2. HISTORICAL RETROSPECT The Institute, since its inception, has been committed to research in the field of accountancy. As early as in 1955, the Council set up the Research Committee. The Council at that point of time felt the necessity to establish such a Committee to deal with the growing complexities of the problems faced by membership at large and with a view to ensuring the highest of traditions and technical competence in the discharge of the duties by chartered accountants.

© The Institute of Chartered Accountants of India

1.3 AUDITING STANDARDS, STATEMENTS AND GUIDANCE NOTES - AN OVERVIEW

As back as in 1964, the Council published the “Statement on Auditing Practices” as prepared by the Research Committee not only for the benefit of its members but also for others outside the profession, who might be interested in this subject. It was hoped that this Statement would provide valuable guidance in the performance of audits, particularly of companies. The Council of the Institute fully realised that techniques of accounting and auditing had undergone and were undergoing important changes. Since the members were expected to keep pace with recent developments, this Statement attempted to set out practices which were generally accepted in other countries and which the Council considered desirable in the light of prevailing circumstances in India. The issuance of the Statement on Auditing Practices might be considered as a path break as far as establishing sound auditing practices is concerned.

3. AUDITING AND ASSURANCE STANDARDS BOARD – SCOPE AND FUNCTIONS

The Following are the important points as regards scope and functions of Auditing and Assurance Standards Board –

3.1 Setting up of AASB The International Federation of Accountants (IFAC) came into existence in 1977 and constituted International Auditing Practices Committee (IAPC) to formulate International Auditing Guidelines. These guidelines were later on converted into International Standards on Auditing (ISA). Considering the developments in the field of auditing at international level, the need for issuing Standards and Guidance Notes in tandem with international standards but conforming to national laws, customs, usages and business environments was felt. With this objective, our Institute constituted the Auditing Practices Committee (APC) on September 17, 1982, to spearhead the new framework of Statements on Standard Auditing Practices (SAPs) and Guidance Notes (GNs) inter alia to replace various chapters of the old omnibus Statement on Auditing Practices issued in 1964.

International Auditing and Assurance Standards Board (IAASB): The IFAC Board has established the IAASB to develop and issue, in the public interest and under its own authority, high quality auditing standards for use around the world. The IAASB functions as an independent standard-setting body under the auspices of IFAC.

Auditing and Assurance Standards Board: ICAI is a member of the IFAC and is committed to work towards the implementation of the guidelines issued by the IFAC. ICAI constituted the AASB (erstwhile Auditing Practices Committee) to review the existing auditing practices in India and to develop Engagement and Quality Control Standards (erstwhile Statements on Standard Auditing Practices) so that these may be issued by the Council of the Institute.

© The Institute of Chartered Accountants of India

1.4 ADVANCED AUDITING AND PROFESSIONAL ETHICS

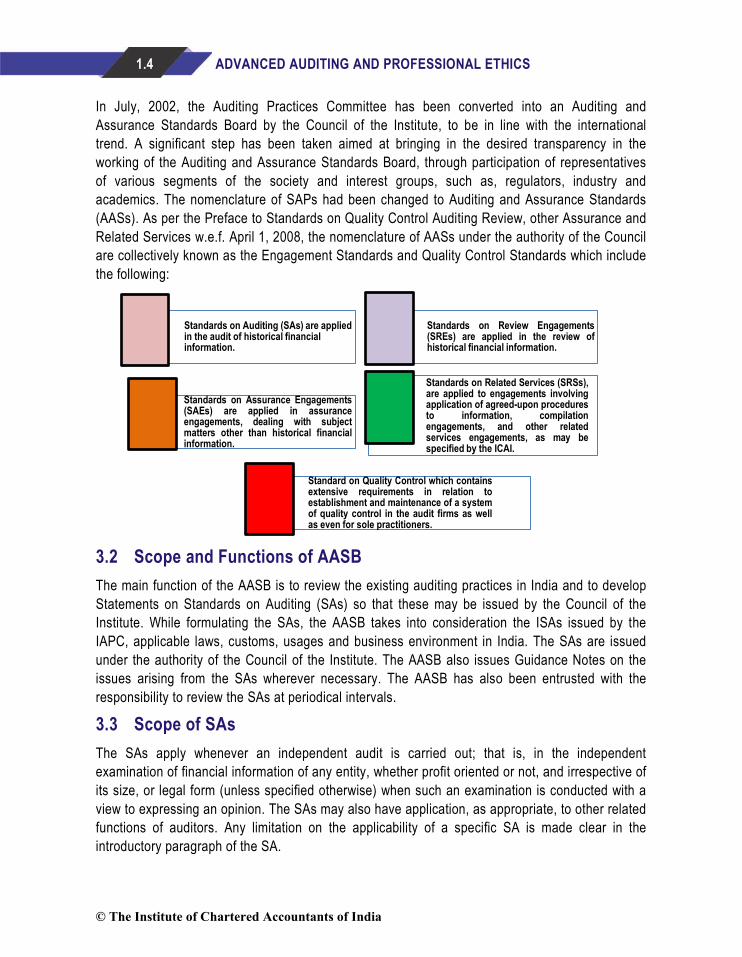

In July, 2002, the Auditing Practices Committee has been converted into an Auditing and Assurance Standards Board by the Council of the Institute, to be in line with the international trend. A significant step has been taken aimed at bringing in the desired transparency in the working of the Auditing and Assurance Standards Board, through participation of representatives of various segments of the society and interest groups, such as, regulators, industry and academics. The nomenclature of SAPs had been changed to Auditing and Assurance Standards (AASs). As per the Preface to Standards on Quality Control Auditing Review, other Assurance and Related Services w.e.f. April 1, 2008, the nomenclature of AASs under the authority of the Council are collectively known as the Engagement Standards and Quality Control Standards which include the following:

3.2 Scope and Functions of AASB The main function of the AASB is to review the existing auditing practices in India and to develop Statements on Standards on Auditing (SAs) so that these may be issued by the Council of the Institute. While formulating the SAs, the AASB takes into consideration the ISAs issued by the IAPC, applicable laws, customs, usages and business environment in India. The SAs are issued under the authority of the Council of the Institute. The AASB also issues Guidance Notes on the issues arising from the SAs wherever necessary. The AASB has also been entrusted with the responsibility to review the SAs at periodical intervals.

3.3 Scope of SAs The SAs apply whenever an independent audit is carried out; that is, in the independent examination of financial information of any entity, whether profit oriented or not, and irrespective of its size, or legal form (unless specified otherwise) when such an examination is conducted with a view to expressing an opinion. The SAs may also have application, as appropriate, to other related functions of auditors. Any limitation on the applicability of a specific SA is made clear in the introductory paragraph of the SA.

Standards on Auditing (SAs) are applied in the audit of historical financial information.

Standards on Review Engagements(SREs) are applied in the review ofhistorical financial information.

Standards on Assurance Engagements(SAEs) are applied in assuranceengagements, dealing with subjectmatters other than historical financialinformation.

Standards on Related Services (SRSs),are applied to engagements involvingapplication of agreed-upon proceduresto information, compilationengagements, and other relatedservices engagements, as may bespecified by the ICAI.

Standard on Quality Control which containsextensive requirements in relation toestablishment and maintenance of a systemof quality control in the audit firms as wellas even for sole practitioners.

© The Institute of Chartered Accountants of India

1.5 AUDITING STANDARDS, STATEMENTS AND GUIDANCE NOTES - AN OVERVIEW

3.4 Procedure for issuing SAs Broadly, the following procedure is adopted for the formulation of SAs:

3.5 Compliance with the SAs While discharging their attest function, it is the duty of the members of the Institute to ensure that the SAs are followed in the audit of financial information covered by their audit reports. If for any reason a member has not been able to perform an audit in accordance with the SAs, his report should draw attention to the material departures therefrom. Auditors are expected to follow SAs in the audits commencing on or after the date specified in the Standard. Further, compliance of SAs are mandatory requirement as per the Companies Act, 2013.

3.6 Linkage between SAs and Disciplinary Proceedings The SAs (as well as other statements on auditing) represent the generally accepted procedure(s) of audit. As such, a member who does not perform his audit in accordance with these statements and fails to disclose the material departures there from, becomes liable to the disciplinary proceedings of the Institute under Clause (9) of Part I of the Second Schedule to the Chartered Accountants Act, 1949 (as amended by the Chartered Accountants (Amendment) Act, 2006), which specifies that a member of the Institute engaged into practice shall be guilty of professional misconduct if he “fails to invite attention to any material departure from the generally accepted procedure of audit applicable to the circumstances”.

1. The AASB determines the broadareas in which the SAs need to beformulated and the priority in regard tothe selection thereof.

2. In the preparation of SAs, the AASB is assisted byStudy Groups constituted to consider specificsubjects. In the formation of Study Groups, provisionis made for participation of a cross-section ofmembers of the Institute.

3. On the basis of the work of the StudyGroups, an exposure draft of the proposedSA is prepared by the Committee andissued for comments by members of theInstitute.

4. After taking into consideration thecomments received, the draft of theproposed SA is finalised by theAASB and submitted to the Councilof the Institute.

5. The Council of the Institute considers the final draft of the proposedSA, and, if necessary, modifies the same in consultation with the AASB.The SA is then issued under the authority of the Council.

© The Institute of Chartered Accountants of India

1.6 ADVANCED AUDITING AND PROFESSIONAL ETHICS

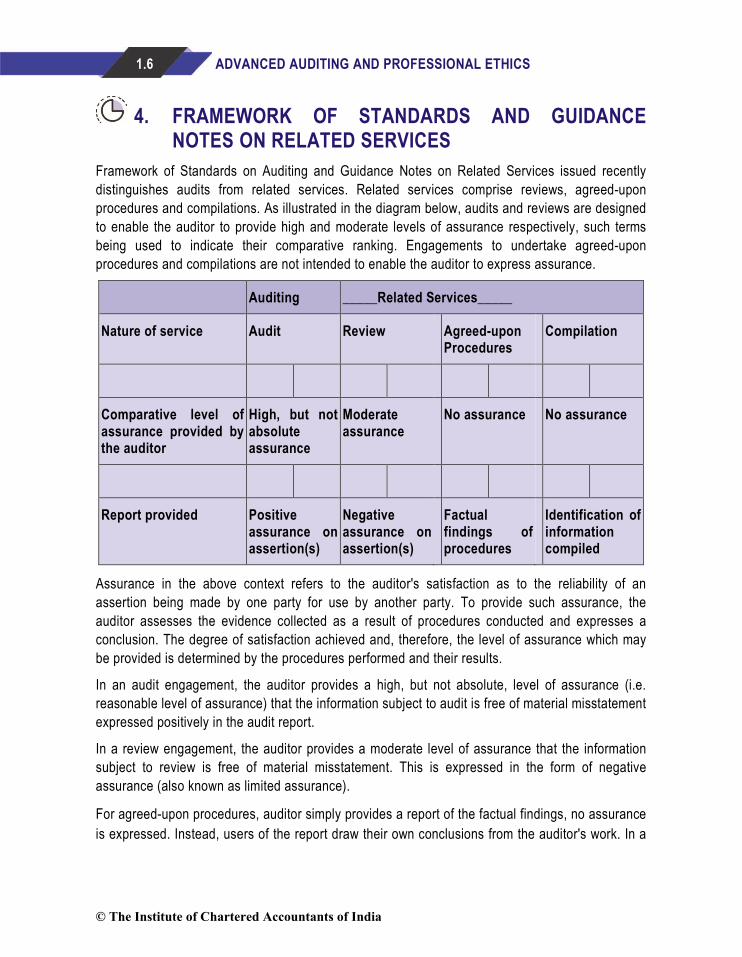

4. FRAMEWORK OF STANDARDS AND GUIDANCE NOTES ON RELATED SERVICES

Framework of Standards on Auditing and Guidance Notes on Related Services issued recently distinguishes audits from related services. Related services comprise reviews, agreed-upon procedures and compilations. As illustrated in the diagram below, audits and reviews are designed to enable the auditor to provide high and moderate levels of assurance respectively, such terms being used to indicate their comparative ranking. Engagements to undertake agreed-upon procedures and compilations are not intended to enable the auditor to express assurance.

Auditing _____Related Services_____

Nature of service Audit Review Agreed-upon Procedures

Compilation

Comparative level of assurance provided by the auditor

High, but not absolute assurance

Moderate assurance

No assurance No assurance

Report provided Positive assurance on assertion(s)

Negative assurance on assertion(s)

Factual findings of procedures

Identification of information compiled

Assurance in the above context refers to the auditor's satisfaction as to the reliability of an assertion being made by one party for use by another party. To provide such assurance, the auditor assesses the evidence collected as a result of procedures conducted and expresses a conclusion. The degree of satisfaction achieved and, therefore, the level of assurance which may be provided is determined by the procedures performed and their results.

In an audit engagement, the auditor provides a high, but not absolute, level of assurance (i.e. reasonable level of assurance) that the information subject to audit is free of material misstatement expressed positively in the audit report.

In a review engagement, the auditor provides a moderate level of assurance that the information subject to review is free of material misstatement. This is expressed in the form of negative assurance (also known as limited assurance).

For agreed-upon procedures, auditor simply provides a report of the factual findings, no assurance is expressed. Instead, users of the report draw their own conclusions from the auditor's work. In a

© The Institute of Chartered Accountants of India

1.7 AUDITING STANDARDS, STATEMENTS AND GUIDANCE NOTES - AN OVERVIEW

compilation engagement, although the users of the compiled information derive some benefit from the involvement of a member of the Institute, no assurance is expressed in the report. Objective of an audit is to enable the auditor to express an opinion whether the financial statements are prepared, in all material respects, in accordance with an identified financial reporting framework "give a true and fair view". Absolute assurance in auditing is not attainable as a result of such factors as the need for judgement, the use of test checks, the inherent limitations of any accounting and internal control systems and the fact that most of the evidence available to the auditor is persuasive, rather than conclusive, in nature.

The objective of a review of financial statements is to enable an auditor to state whether, on the basis of procedures which do not provide all the evidence that would be required in an audit, anything has come to the auditor's attention that causes the auditor to believe that the financial statements are not prepared, in all material respects, in accordance with an identified financial reporting framework. While a review involves the application of audit skills and techniques and the gathering of evidence, it does not ordinarily involve on assessment of accounting and internal control systems, tests of records and of responses to inquiries by obtaining corroborating evidence through inspection, observation, confirmation and computation, the auditor attempts to become aware of all significant matters, the procedures of a review make the achievement less likely than in an audit engagement, thus the level of assurance provided in a review report is correspondingly less than that given in an audit report.

In an engagement to perform agreed-upon procedures and auditor is engaged to carry out those procedures of an audit nature to which the auditor and the entity and any appropriate third parties have agreed and to report on factual findings.

The report is restricted to those parties that have agreed to the procedures to be performed since others, unaware of the reasons for the procedures, may misinterpret the results. In a compilation engagement, a member of the Institute is engaged to use accounting expertise as opposed to auditing expertise to collect, classify, and summaries financial information.

The procedures employed are not designed and do not enable the member to express any assurance on the financial information. However, users derive some benefit as a result of the member's involvement because the service has been performed with due professional skill and care. An auditor is associated with financial information when the auditor attaches a report to that information or consents to the use of the auditor's name in a professional connection. If the auditor is not associated in this manner, third parties can assume no responsibility of the auditor.

© The Institute of Chartered Accountants of India

1.8 ADVANCED AUDITING AND PROFESSIONAL ETHICS

5. QUALITY CONTROL AND ENGAGEMENT STANDARDSDiagrammatic Representation of the Structure of Standards Under the New Preface

AUDITING STANDARDS - AN OVERVIEW

Auditing and Assurance Standard Board - (AASB)- Scope / Objective STRUCTURE OF

PRONOUNCEMENTS ISSUED BY AASB

FRAMEWORK FOR AUDIT & ASSURANCE & OTHER SERVICES ENGAGEMENTS –

Scope/ Objective/ Definitions/ Requirements

Standard for Quality Control

(SQC 01 - 99)

Standards on Auditing (SA 100-999) - aspects covered in series: Introductory Matters SA100 - 199

General Principles and Responsibilities SA200 - 299 Risk Assessment and Response to Assessed Risk SA300 - 499

Audit Evidence SA500 - 599 Using Work of Others SA600 - 699

Audit Conclusions and Reporting SA700 – 799 Specialised Areas SA800 - 899

Standard on Assurance Engagements

SAE (3000-3699)

Standards on Related Services

SRS- 4000 & 4699

Standards on Review Engagements (SRE 2000 -2699)

© The Institute of Chartered Accountants of India

1.9 AUDITING STANDARDS, STATEMENTS AND GUIDANCE NOTES - AN OVERVIEW

The Council of the ICAI has issued following Quality Control and Engagement Standards:

S. No. No. of Standard Title of the Standard 1 SQC 1 Quality Control for Firms that Perform Audits and Reviews of

Historical Financial Information, and Other Assurance and Related Services Engagements

2 SA 200 Overall Objectives of the Independent Auditor and the Conduct of an Audit in Accordance with Standards on Auditing

3 SA 210 Agreeing the Terms of Audit Engagements 4 SA 220 Quality Control for an Audit of Financial Statements 5 SA 230 Audit Documentation 6 SA 240 The Auditor’s responsibilities Relating to Fraud in an Audit of

Financial Statements 7 SA 250 Consideration of Laws and Regulations in an Audit of Financial

Statements 8 SA 260 Communication with Those Charged with Governance 9 SA 265 Communicating Deficiencies in Internal Control to Those Charged

with Governance and Management 10 SA 299 Joint Audit of Financial Statements 11 SA 300 Planning an Audit of Financial Statements 12 SA 315 Identifying and Assessing the Risks of Material Misstatement

through Understanding the Entity and its Environment 13 SA 320 Materiality in Planning and Performing an Audit 14 SA 330 The Auditor’s Responses to Assessed Risks 15 SA 402 Audit Considerations Relating to an Entity Using a Service

Organization 16 SA 450 Evaluation of Misstatements Identified during the Audits 17 SA 500 Audit Evidence 18 SA 501 Audit Evidence - Specific Considerations for Selected Items 19 SA 505 External Confirmations 20 SA 510 Initial Audit Engagements-Opening Balances 21 SA 520 Analytical Procedures 22 SA 530 Audit Sampling 23 SA 540 Auditing Accounting Estimates, Including Fair Value Accounting

© The Institute of Chartered Accountants of India

1.10 ADVANCED AUDITING AND PROFESSIONAL ETHICS

Estimates, and Related Disclosures 24 SA 550 Related Parties 25 SA 560 Subsequent Events 26 SA 570 Going Concern 27 SA 580 Written Representations 28 SA 600 Using the Work of Another Auditor 29 SA 610 Using the Work of Internal Auditors 30 SA 620 Using the Work of an Auditor’s Expert 31 SA 700 Forming an Opinion and Reporting on Financial Statements 32 SA 701 Communicating Key Audit Matters in the Independent Auditor’s

Report 33 SA 705 Modifications to the Opinion in the Independent Auditor’s Report 34 SA 706 Emphasis of Matter Paragraphs and Other Matter Paragraphs in

the Independent Auditor’s Report 35 SA 710 Comparative Information – Corresponding Figures and

Comparative Financial Statements 36 SA 720 The Auditor’s Responsibility in Relation to Other Information 37 SA 800 Special Considerations-Audits of Financial Statements Prepared

in Accordance with Special Purpose Framework 38 SA 805 Special Considerations-Audits of Single Purpose Financial

Statements and Specific Elements, Accounts or Items of a Financial Statement

39 SA 810 Engagements to Report on Summary Financial Statements 40 SRE 2400 Engagements to Review Historical Financial Statements 41 SRE 2410 Review of Interim Financial Information Performed by the

Independent Auditor of the Entity 42 SAE 3400 The Examination of Prospective Financial Information 43 SAE 3402 Assurance Reports on Controls At a Service Organisation 44 SAE 3420 Assurance Engagements to Report on the Compilation of Pro

Forma Financial Information Included in a Prospectus 45 SRS 4400 Engagements to Perform Agreed Upon Procedures Regarding

Financial Information 46 SRS 4410 Compilations Engagements

© The Institute of Chartered Accountants of India

1.11 AUDITING STANDARDS, STATEMENTS AND GUIDANCE NOTES - AN OVERVIEW

5.1 Structure of SAs SAs are structured in the particular manner:

• Introduction: It includes the purpose, scope, and subject matter as well as the responsibilities of the auditor and others in that context.

• Objective: It includes the objective of the auditor in the audit area addressed by that particular SA.

• Definitions: For higher understanding of the SAs, pertinent terms are delineated in each SA.

• Requirements: Every objective is shored up by clearly stated requirements. Requirements are always expressed by the phrase “the auditor shall.”

• Application and Other Explanatory Material: The application and other explanatory material explains more exactly what is meant by a requirement or is intended to cover, or includes examples of procedures that can be appropriate under certain circumstances.

(Students may note that the above mentioned Quality Control and Engagement Standards are reproduced in Auditing Pronouncements)

6. GUIDANCE NOTES Various technical committees of the Institute are involved in the task of issuing guidance notes on topics relating to accounting and auditing for guidance of the members. Some of the important topics in auditing on which guidance notes have been issued are discussed below:

6.1 Guidance Note on Tax Audit under Section 44AB of the Income-Tax Act This Guidance Note was first issued by the Taxation Committee in 1985 and was revised from time to time by the Direct Taxes Committee. Refer to Chapter 12 for a detailed discussion.

The clarifications and explanations contained in this Guidance Note are not intended to be exhaustive and the auditors should exercise their professional judgment and experience on various matters on which they are

© The Institute of Chartered Accountants of India

1.12 ADVANCED AUDITING AND PROFESSIONAL ETHICS required to report under the Order. Further, the Order is also not intended to limit the duties and responsibilities of auditors but only requires a statement to be included in the audit report in respect of the matters specified therein.

Students are advised to refer Chapter 6 Audit Reports and Auditing Pronouncements for details.

6.2 Guidance Note on Audit of Internal Financial Controls over Financial Reporting

To help the members properly understand and perform the various aspects of reporting responsibility related to audits of internal financial controls over financial reporting, the Auditing and Assurance Standards Board of the Institute of Chartered Accountants of India has brought out this Guidance Note on Audit of Internal Financial Controls Over Financial Reporting. The Guidance Note covers aspects such as Scope of reporting on internal financial controls under Companies Act 2013, essential components of internal financial controls, Technical guidance on audit of internal financial controls, Implementation guidance on audit of internal financial controls.

The Companies Act, 2013 has introduced some new requirements relating to audits and reporting by the statutory auditors of companies. One of these requirements is given under Section 143(3)(i) of the Act which requires the statutory auditor to state in his audit report whether the company has adequate internal financial controls system in place and the operating effectiveness of such controls. The section has cast onerous responsibilities on the statutory auditors because reporting on internal financial controls is not covered under the Standards on Auditing issued by the ICAI.

7. GUIDANCE NOTE(S) ON RELATED SERVICES The framework for auditing and related services makes it clear that there can be different layers of assurance depending upon the nature of services being performed by the chartered accountant. Related Services comprise of Review engagements, Agreed upon Procedures and Compilation Engagement. Reviews engagements involve providing moderate assurance (or negative assurance) but other two services, viz., and compilation and agreed upon procedures provide no assurance at all. The Institute has issued guidance notes covering these aspects of related services in a comprehensive manner.

8. AUTHORITY ATTACHED TO THE DOCUMENTS ISSUED BY THE INSTITUTE/MCA

The Institute has, from time to time, issued ‘Statements’ and ‘Guidance Notes’ on a number of matters. With the formation of the Accounting Standards Board and the Auditing and Assurance Standards Board, Accounting Standards and Standards on Auditing have also been issued. The level of authority attached to these documents and the degree of compliance required in respect thereof has been explained by the Institute through its various announcements issued from time to time.

© The Institute of Chartered Accountants of India

1.13 AUDITING STANDARDS, STATEMENTS AND GUIDANCE NOTES - AN OVERVIEW

8.1 Statements The ‘statements’ have been issued with a view to securing compliance by members on matters which in the opinion of the council of the institute are critical for the proper discharge of their functions. ‘statements’ therefore are mandatory. Accordingly, while discharging their attest function, it is the duty of the members of the institute-

(a) to examine whether ‘Statements’ relating to accounting matters are complied with in the presentation of financial statements covered by their audit. In the event of any deviation from such ‘Statements’, it is their duty to make adequate disclosures in their audit reports so that the users of financial statements may be aware of such deviations; and

(b) to ensure that the ‘Statements’ relating to auditing matters, are followed in the audit of financial information covered by their audit reports. If, for any reason, a member, has not been able to perform an audit in accordance with such ‘Statements his report should draw attention to the material departures there from.

8.2 Guidance Notes ‘Guidance Notes’ are primarily designed to provide guidance to members on matters which may arise in the course of their professional work and on which they may desire assistance in resolving issues which may pose difficulty. Guidance notes are recommendatory in nature. A member should ordinarily follow recommendations in a guidance note relating to an auditing matter except where he is satisfied that in the circumstances of the case, it may not be necessary to do so. Similarly, while discharging his attest function, a member should examine whether the recommendations in a guidance note relating to an accounting matter have been followed or not. If the same have not been followed, the member should consider whether keeping in view the circumstances of the case, a disclosure in his report is necessary. There are, however a few guidance notes in case of which the Council has specifically stated that they should be considered as mandatory on members while discharging their attest function.

8.3 Accounting Standards and Standards on Auditing The ‘accounting standards’ and ‘Standards on Auditing’ establish standards which have to be complied with to ensure that financial statements are prepared in accordance with generally accepted accounting standards and that auditors carry out their audit in accordance with the generally accepted auditing practices. They become mandatory on the dates specified in the respective document or notified by the council.

There can be situations in which certain matters are covered both by a ‘Statement’ and by an ‘Accounting Standard’/ ‘Standards on Auditing. In such a situation, the ‘Statement’ prevails till the time the relevant ‘Accounting Standard’/ Standards on Auditing becomes mandatory. Once an ‘Accounting Standard’/ ‘Standards on Auditing’ becomes mandatory, the concerned ‘Statement’ or the relevant part thereof automatically stands withdrawn.

© The Institute of Chartered Accountants of India

1.14 ADVANCED AUDITING AND PROFESSIONAL ETHICS Standards on Auditing (SAs) establish standards, which have to be complied with to ensure that auditors carry out their duties in accordance with the generally accepted auditing practices. They become operative (i.e., mandatory) in respect of audit of all enterprises on the dates specified in the respective SAs or notified by the Council. The duties of the members of the Institute in relation to operative SAs are similar to those in respect of ‘Statements’ relating to auditing matters.

8.4 Accounting Standards Accounting Standards are formulated by the Accounting Standards Board and issued by the Council of the Institute. The Accounting Standards are issued for use in the presentation of ‘general purpose financial statements’ which are issued to the public by such ‘commercial, industrial or business enterprises’ as may be specified by the Institute from time to time and subject to the attest function of its members. They become mandatory on the dates specified in the respective Accounting Standards or notified by the Council in this behalf.

(a) The term ‘General Purpose Financial Statements’ includes balance sheet, statement of profit and loss and other statements and explanatory notes which form part thereof, issued for the use of shareholders/members, creditors, employees and public at large.