Accounting and power in religious institutions: Verona’s Santa Maria della Scala monastery in the...

32

1 PRE-PRINT – NOT FOR RETAIL DISTRIBUTION Accounting and power in religious institutions: Verona’s Santa Maria della Scala monastery in the Middle Ages Chiara Leardini Gina Rossi All rights reserved. This file is circulated by the authors with the sole purpose of fa- cilitating collaborative peer discussion. For any comments, please write to: [email protected] [email protected] For any other purpose, including quoting, please refer to the published version. Please cite as: Leardini, C. & Rossi, G. (2013), “Accounting and power in religious in- stitutions: Verona’s Santa Maria della Scala monastery in the Middle Ages”, Accounting History, 18(3: 415-427 To link to this article: http://dx.doi.org/10.1177/1032373213487336

Transcript of Accounting and power in religious institutions: Verona’s Santa Maria della Scala monastery in the...

1

PRE-PRINT – NOT FOR RETAIL DISTRIBUTION

Accounting and power in religious institutions: Verona’s

Santa Maria della Scala monastery in the Middle Ages

Chiara Leardini

Gina Rossi

All rights reserved. This file is circulated by the authors with the sole purpose of fa-

cilitating collaborative peer discussion. For any comments, please write to:

For any other purpose, including quoting, please refer to the published version.

Please cite as:

Leardini, C. & Rossi, G. (2013), “Accounting and power in religious in-

stitutions: Verona’s Santa Maria della Scala monastery in the Middle

Ages”, Accounting History, 18(3: 415-427

To link to this article: http://dx.doi.org/10.1177/1032373213487336

2

Accounting and power in religious institutions: Verona’s Santa Maria della Scala monastery in the Middle Ages

Chiara Leardini (corresponding author) University of Verona

Via dell’Artigliere 19, 37100 Verona, Italy

Phone: 0458028222 - Fax: 0458028488

Email: [email protected]

Gina Rossi University of Udine Via Tomadini 30/A, 33100 Udine, Italy

Phone: 0432249349 - Fax: 0432249329

Email: [email protected]

3

Accounting and power in religious institutions: Verona’s Santa Maria della Scala monastery in the Middle Ages

Abstract

The relation between accounting and power in religious institutions has re-

ceived little attention by accounting historians. The present article therefore

studies the case of the Santa Maria della Scala monastery in Verona (Italy) dur-

ing the Middle Ages, to explore whether and how accounting might support the

domination structure and facilitate power relations within the organisation. A

documentary analysis of primary and secondary sources confirms that account-

ing played a key role in reinforcing both hierarchical and horizontal power re-

lation among friars.

Keywords

Accounting practices, power relations, domination structure, religious

institutions, Middle Ages.

Introduction

Historical research on the role of accounting within organisations has focused most-

ly on firms and government organisations, rather than on religious entities (Prieto et

al., 2006). Despite a few country-specific assessments of accounting systems in reli-

gious institutions, Carmona and Ezzamel (2006) highlight that in published interna-

tional literature, research on the relationship between accounting and religion or re-

ligious institutions is in short supply. They also distinguish studies with an historical

versus contemporary focus and recognise that scholars tend to favour research on

contemporary religious institutions.

In another study, which explores accounting and accountability practices in the

Society of Jesus, Quattrone (2004) suggests a different dual categorisation of ac-

counting and religion studies. First, one group of studies focuses on the non-profit

4

status of religious organisations (e.g., Swanson and Gardner, 1988), comparing their

accounting practices with those used by for-profit organisations. These works claim

that even in religious entities, accounting practices play an active role in the man-

agement process by guiding and sustaining the pursuit of the organisation’s goals.

Second, in examining accounting according to the sacred/profane dichotomy, other

authors assign accounting practices to the profane and suggest the need to separate

accounting and administration from religious functions (Booth, 1993; Laughlin,

1988). Yet research consistently confirms accounting’s key role in religious organi-

sations, in that it helps them build an identity and fosters individual spirituality

(Cordery, 2006; Jacobs, 2005; Jacobs and Walker, 2004).

Finally, another recent examination of research into accounting and religion, pub-

lished in Accounting History, identifies two groups of studies (Bisman, 2012). The

slightly larger group looks at Judeo-Christian religions; the smaller one considers

other religions and belief systems.

Even within all these classifications and studies though, a topic that has received

little attention is the relationship between accounting and power in religious institu-

tions. A concern about good bookkeeping often is reflected in the need to manage

power relations, especially within monasteries, where bookkeeping was so prevalent

that it became the subject matter of many important treatises written by friars (Flori,

1636; Pietra, 1586). The monasteries were ‘a place of residence for a community liv-

ing under religious vows’, whose members ‘dedicate their lives to God, and had tak-

en vows of poverty, chastity and obedience’ (Dobie, 2008, p. 142). For these com-

5

munities, bookkeeping played two key roles. First and foremost, it was an instru-

ment for keeping track of events by recording episodes and documenting facts

through financial measurements. Second, within the hierarchical organisation of

monasteries, accounting practices provided support for hierarchical relations (Quat-

trone, 2004).

This article related to historical studies and covers a period that has received rela-

tively little attention in international debates about accounting and religion. Specifi-

cally, it aims to explore whether and how accounting might facilitate power relations

(both hierarchical/vertical and non-hierarchical/horizontal) within monasteries in the

Middle Ages. In particular, this study assumes that accounting played a role in en-

forcing power relations within the organisational structure of monasteries.

To achieve this objective, this article considers the case of S. Maria della Scala

monastery, a religious institution in Verona (Italy). In accepting the recommendation

to transcend ‘the age of modernity’ (Walker, 2005, p. 233), this article adopts the

Middle Ages as the period under consideration. The analysis, conducted with a syn-

chronic approach, is based on examinations of both primary and secondary sources.

The primary sources consist of archival material related to the convent of Santa Ma-

ria della Scala, which survived for the entire period under review. Particularly useful

for the purpose of the research were the Constitutiones preserved in the Archives of

San Marcello in Rome, which describe the prevailing norms that governed the or-

ganisation and revealed the domination structure of the Santa Maria della Scala

monastery. In addition, accounting books from the Middle Ages held at the State

6

Archives of Verona were used to analyse how accounting facilitated the exercise of

power within the monastery. Secondary sources then helped define the theoretical

framework and clarify the relationship between accounting and power.

The remainder of this article is structured as follows: The next section describes

the research framework and discusses the role of accounting in religious institutions,

with a particular focus on accounting and power relations. The subsequent introduc-

tion of the S. Maria della Scala monastery in Verona in the Middle Ages outlines its

historical context, organisational structure and domination structure. Then, with a

focus on the relation between accounting and domination structure, the next section

describes the role that accounting played in power enforcement at S. Maria della

Scala during the Middle Ages. Moving from the theoretical framework and histori-

cal evidence, this article then offers an overview of the key findings and describes

some contributions and further research developments.

The accounting–power paradigm in religious institutions

Over time, accounting history literature has increasingly abandoned traditional

narrative methods and adopted ‘other styles of research informed by critical and so-

ciological theories whereby the political, institutional and social implications of ac-

counting are interpreted, expounded or unmasked’ (Bisman, 2012, p. 8). In particu-

lar, recent studies regard accounting as an instrument of power and domination

(Carnegie and Napier, 1996), capable of contributing to the construction and the

maintenance of an existing social order, as well as to changes in that order within

organisations (Stacchezzini, 2012).

7

This article draws on a sociological perspective (Giddens, 1984) and studies by

Macintosh and Scapens (1990, 1991) to investigate the role of accounting in balanc-

ing power relations within an organisation. This perspective was used for the first

time by Riccaboni et al (2006) to explore the fourteenth-century case of the Opera

Metropolitana di Siena. The present paper draws on their findings to search for and

discuss issues of accounting and power in a religious organisation during the Middle

Ages in a different way compared to contributions drawn on the governmentality

framework (Sargiacomo, 2008; 2009; Lai et al. 2012). The paper adds new insights

to the Riccaboni et al (2006) perspective extending the analysis to non-hierarchical

power relations—that is, power relations among peers.

Giddens’s (1984) structuration theory is based on the idea that social systems are

produced and reproduced across time and space through the actions of human agents

influenced by specific structures, such as codes and rules that shape and bind social

behaviour when agents interact in specific time–space settings. Social actions are in-

fluenced by three intertwined structural dimensions that contribute to maintain the

social order: signification, legitimation and domination. According to Macintosh and

Scapens (1990, p. 462), accounting systems represent modalities of structuration in

each of these three dimensions:

In the signification dimension, management accounting systems are the in-

terpretative schemes which managers use to interpret past results, take ac-

tions, and make plans. In the domination dimension, management account-

ing systems are a facility that management at all levels can use to co-

8

ordinate and control other participants. And in the legitimation dimension,

management accounting systems communicate a set of values and ideals

about what is approved and what is disapproved; justify the rights of some

participants to hold others accountable; and legitimate the use of certain

rewards and sanctions.

For this study, the focus is the domination structure, which involves resources used

to produce power, or as Giddens (1984, p. 257) defines it, ‘the capacity to achieve

outcomes’.

Command over accounting is a resource of power. By making it possible to rec-

ord facts and events through written entries, accounting facilitates the process by

which superiors hold subordinates accountable for their activities. As Carmona et al.

(1997, p. 412) observe, through accounting, ‘modes of surveillance are expanded by

virtue of the ability to convert everything into writing and to exercise judgement

regularly through written reports and directives’. Nevertheless, the notion of a dia-

lectic of control suggests that subordinates are not completely lacking in power

compared with their superiors. In particular, command over accounting grants sub-

ordinates the ability to influence the actions of their superiors, allowing them to

choose what information to communicate and what to hide.

Accounting thus can be interpreted as a power-knowledge element, capable of

underpinning power structures within organisations, supporting relationships of de-

pendence and autonomy and facilitating the exercise of power in social relation-

ships. Furthermore, the exercise of power in a social system specifically identified in

9

a particular time–space relates to the presence of asymmetries in the distribution of

resources. Relevant resources in this respect include allocative resources, which

arise from command over physical goods, possession of skills and knowledge or ac-

cess to information, and authoritative resources, which arise from the ability to ex-

ercise power over people by organising and controlling their activities.

Any analysis of the relationships of dependence between superiors and subordi-

nates, considering the asymmetric distribution of authoritative resources within the

organisation, can consider only some of the power relations established within the

organisation. Therefore, this analysis focuses on the hierarchical relationships be-

tween individuals or groups, based on a definition of power as the ‘ability to get

things done’ (Macintosh and Scapens, 1990, p. 461).

The hierarchical structure typical of monasteries in the Middle Ages suggests the

particular potential interest of verifying the existence of a link between accounting

systems and hierarchical power relations or structures in monastic organisations. But

within the monasteries, power relations are not only hierarchical; they also include

instances of peer power relations (non-hierarchical/horizontal) among friars. Analys-

ing this type of relationship demands a second, different conception of power, as

proposed by Mintzberg (1984). With reference to studies by Kanter (1977) and Rus-

sel (1938), this author defines power as ‘the capacity of individuals or groups to ef-

fect, or affect, organization outcomes’ (Mintzberg, 1984, p. 208).

The peer power relations among friars do not point to a notion of power as the

domination or formal authority of superiors over subordinates, based on the posses-

10

sion of authoritative resources. Instead, they lend themselves to being read as rela-

tions between individuals (or perhaps even between professionals) who carry out

specialised activities with professional autonomy and who, according to their skills

and knowledge, have the ability to influence and affect the results of the organisa-

tion and determine its proper (or mal-) functioning. These peer power relations also

are based on allocative resources, because some members of the organisation have

knowledge, whereas others do not (Bacharach and Lawler, 1980; Mintzberg, 1979).

The S. Maria della Scala monastery in Verona in the Middle Ages: domination

structure

The Middle Ages were a period of socio-economic prosperity for Verona; the

city enjoyed political stability during this time under the domination of the Della

Scala family (Barbieri, 1988; Varanini, 1988). The Santa Maria della Scala monas-

tery, founded by the Servi di Maria Order (hereinafter, the Order), evidently operat-

ed in a context of great favour with the local community and the Della Scala family

(Citeroni, 1998, 2006; Dal Pino, 1972; De Sandre Gasparini, 1988). In 1324,

Cangrande della Scala, Prince of Verona, donated a tract of land in the city centre to

the Servi di Maria friars so that they might build a church, hold religious services,

preach sermons and take care of souls (cura animorum).

All internal relations were regulated by the Regula Sancti Augustini, the Constitu-

tiones Antiquae fratrum servorum sancte Mariae and the Constitutiones Novae, the

main legislative texts of the Servi di Maria Order during the period in question (Dal

Pino, 1965). These primary sources enable the present analysis of the domination

11

structure, by revealing the role of power and the resources allocated to each member

of the monastery, which belonged to the Servi di Maria Order that held its seat in

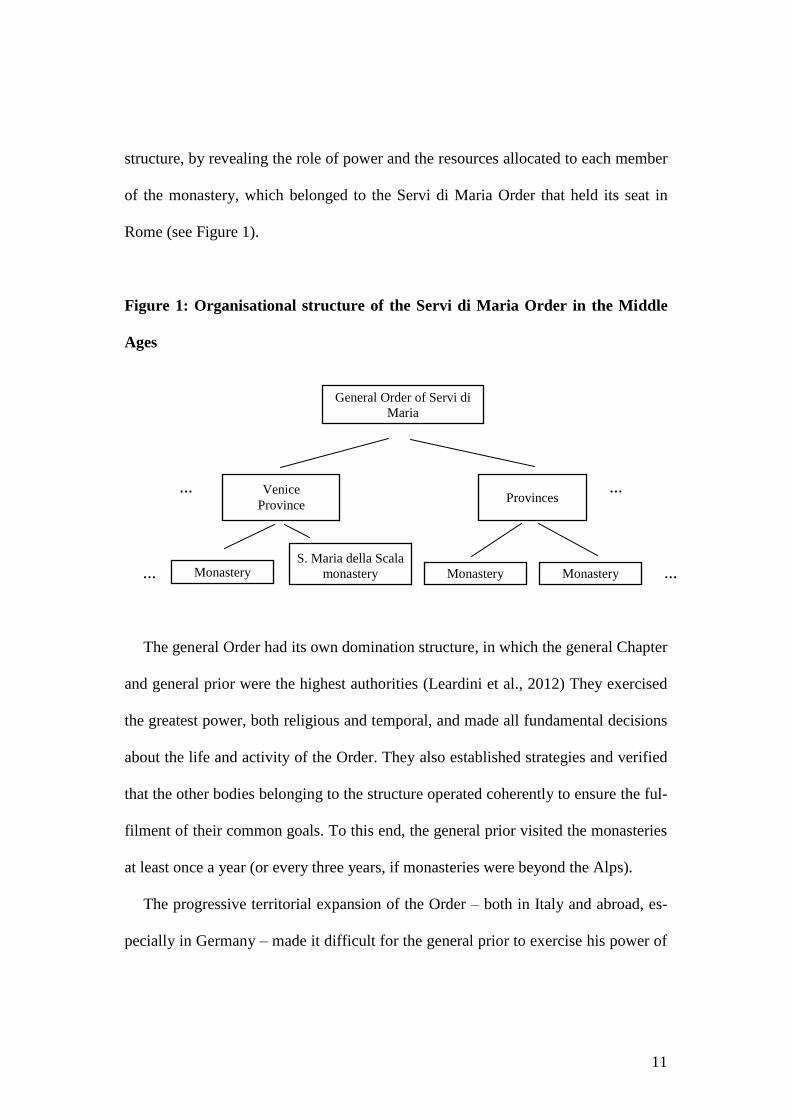

Rome (see Figure 1).

Figure 1: Organisational structure of the Servi di Maria Order in the Middle

Ages

The general Order had its own domination structure, in which the general Chapter

and general prior were the highest authorities (Leardini et al., 2012) They exercised

the greatest power, both religious and temporal, and made all fundamental decisions

about the life and activity of the Order. They also established strategies and verified

that the other bodies belonging to the structure operated coherently to ensure the ful-

filment of their common goals. To this end, the general prior visited the monasteries

at least once a year (or every three years, if monasteries were beyond the Alps).

The progressive territorial expansion of the Order – both in Italy and abroad, es-

pecially in Germany – made it difficult for the general prior to exercise his power of

…

… … Provinces

Monastery Monastery Monastery

General Order of Servi di

Maria

Venice

Province

S. Maria della Scala

monastery …

12

management and control personally and thus increased the need for a closer admin-

istrative supervision. For this reason, the territory in which the Order operated was

subdivided into provinces or local units, which had some level of autonomy. At the

head of each local unit was a provincial prior, elected by the provincial Chapter eve-

ry three years. The general prior gave the provincial prior a mandate to supervise –

in both economic and spiritual terms – the local monasteries. In this sense, the pro-

vincial prior was the vicar in loco of the general prior, vested with spiritual, discipli-

nary and managerial powers. In accordance with the Constitutiones, the provincial

prior visited the monasteries at least three times a year and, on these occasions, as-

sessed the administration of the monasteries. The Santa Maria della Scala monastery

belonged to the province of Venice.

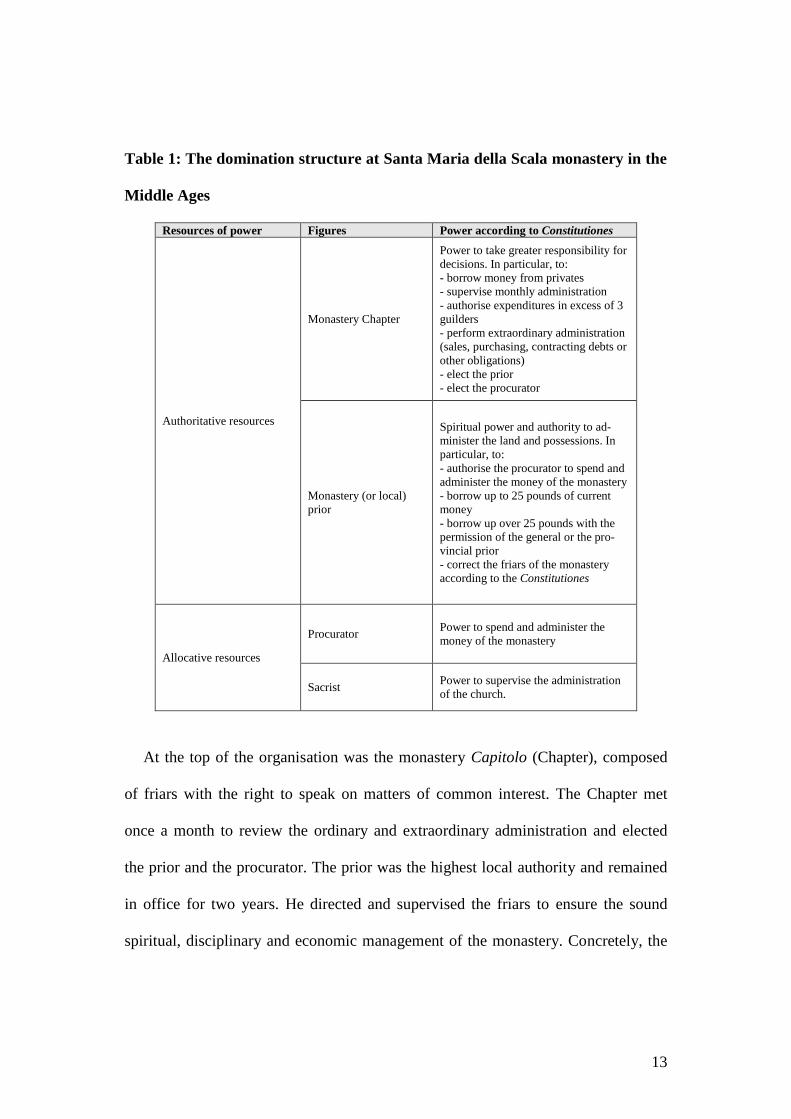

At the local level, each monastery had a well-defined domination structure. Re-

ferring to the distinction between authoritative and allocative resources proposed by

Giddens (1984), the domination structure in the convent of Santa Maria della Scala

in the Middle Ages can be depicted as in Table 1.

13

Table 1: The domination structure at Santa Maria della Scala monastery in the

Middle Ages

Resources of power Figures Power according to Constitutiones

Authoritative resources

Monastery Chapter

Power to take greater responsibility for

decisions. In particular, to:

- borrow money from privates

- supervise monthly administration

- authorise expenditures in excess of 3

guilders

- perform extraordinary administration

(sales, purchasing, contracting debts or

other obligations)

- elect the prior

- elect the procurator

Monastery (or local)

prior

Spiritual power and authority to ad-

minister the land and possessions. In

particular, to:

- authorise the procurator to spend and

administer the money of the monastery

- borrow up to 25 pounds of current

money

- borrow up over 25 pounds with the

permission of the general or the pro-

vincial prior

- correct the friars of the monastery

according to the Constitutiones

Allocative resources

Procurator Power to spend and administer the

money of the monastery

Sacrist Power to supervise the administration

of the church.

At the top of the organisation was the monastery Capitolo (Chapter), composed

of friars with the right to speak on matters of common interest. The Chapter met

once a month to review the ordinary and extraordinary administration and elected

the prior and the procurator. The prior was the highest local authority and remained

in office for two years. He directed and supervised the friars to ensure the sound

spiritual, disciplinary and economic management of the monastery. Concretely, the

14

prior monitored his brothers and directed the religious offices. He had the power to

administer land and property, authorise expenditures of the convent’s money and

borrow money.

All the friars in the monastery were under the direct supervision of the prior. The

hierarchical power exercised by superiors on subordinates was legitimated by a form

of legal authority (Weber, 1978), strengthened within the religious orders by the fri-

ars’ vow of obedience. The friars (as well as the local and provincial priors) subject-

ed themselves to the authority of superiors, as set out in the Constitutiones.

Within the monastery, the exercise of power was related not only to authoritative

resources but also to the possession of allocative resources. With regard to the latter,

it was normal for each friar to carry out a specific assignment, either a repetitive or a

skilled task, according to his capabilities but still under the supervision of the prior.

This task organisation led to specialised knowledge, the possession of which offered

a source of power (Bacharach and Lawler, 1980; Mintzberg, 1979). In this sense,

decision-making power was decentralised and attributed to the friars as ‘experts’ in

certain specific activities (e.g., sale of goods, preaching) that they would carry out in

the interests of the monastery. Rather than power conceived of as the authority to is-

sue commands, this form implies power as an ability to effect organisational out-

comes, in which the technical skills and knowledge of experts dominate. In peer re-

lationships that develop inside the convent, professionalisation thus can be a source

of power (Birkett and Evans, 2005).

15

The Constitutiones highlight these functions. In particular, for the analysis of the

domination structure, the most important figures are the procurator (procurator), and

the sacrista (sacrist). The procurator was elected by a majority of the friars during

the Chapter and remained in office for no more than a biennium. The Constitutiones

recognise that the procurator maintained command over all the money of the monas-

tery, which he could spend with the permission of the prior. Thus the procurator act-

ed as a treasurer and controlled the proceeds and expenses of the monastery. Fur-

thermore, the Constitutiones grant the procurator the power to command information

about the financial situation of the monastery, through the periodic recording of re-

ceipts and payments. To prevent any distortion of this kind of power, the Constitu-

tiones require that the procurator reported on his office every month before the

Chapter. However, less information is available about the figure of sacrist. The Con-

stitutiones attribute to him the power to supervise the church with prudentia et solic-

itudo (prudence and diligence) and specify that he had command over sacred vest-

ments and furnishings.

Accounting and power relations within the monastery.

This section reviews accounting’s role in the enforcement of power relations

during the Middle Ages, with specific reference to the convent of Santa Maria della

Scala. Verifying this predicted role requires further analyses of the primary sources.

However, the only sources that have survived the passage of time and operations to

prune or reorganise the archives are income and expense books (Bandini, 1984).

16

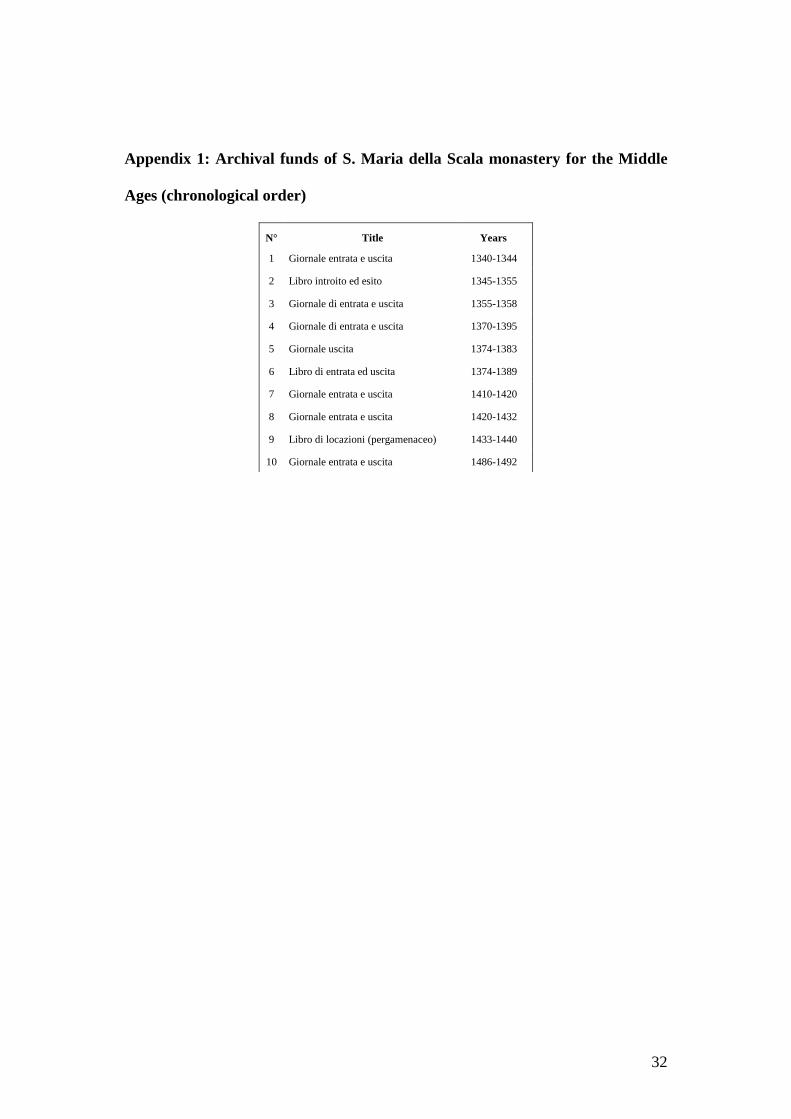

Letters, acts of processes, Libri dei Partiti and similar texts have not survived (see

Appendix 1).

The accounting books contain records of income received and expenses paid by

the monastery’s procurator during 1340–1492, compiled using an upside-down book

method: one part contains records of monthly income, and the other features expend-

itures (Landi, 1996). The most ancient books were compiled in Latin; the more re-

cent texts were vernacular. Each leaf of each book is headed Introitus (income) or

Exitus (expense), with the month and year in Roman numerals; on the left a blank

space is reserved for explanatory notes about certain book-keeping entries (e.g., rent

income, non gabelate income). This study uses these accounting books to under-

stand whether and how accounting functioned as a facility of power, by enforcing an

asymmetrical distribution of authoritative and allocative resources.

Accordingly, this analysis focuses on two relationships, within the domination

structure of the monastery, that were particularly sensitive to the enforcement func-

tion of accounting: between the prior and friars and between the procurator and sac-

rist.

The role of accounting in power relations between the prior and the friars

In the convent of Santa Maria della Scala, accounting was a facility that the pri-

or could use to coordinate and control the subordinates (see Figure 2).

17

Figure 2: Organisational structure of the Santa Maria della Scala Monastery in

the Middle Ages

The prior held control over the administration. To exercise this power easily, he

would need information about the activities performed by each friar, to assess his

individual achievements and responsibilities. The method of accounting increased

the authoritative resources of the prior and strengthened his power by giving him

precise control over the activities performed by each of his subordinates. Specifical-

ly, the precision, diligence and analytical detail recorded about each income and ex-

pense entry enabled the prior to enquire about the origin of incomes and expenses,

and thus the quantum (measure) and the modus (way) in which each friar contribut-

ed to the sound administration of the monastery. Details of income entries allowed

the prior to assess the relationship between factors of production and performance

(e.g., land, goods produced, friars engaged in seeking donations, funds collected by

virtue of their ability). Thus he could coordinate more effectively the activities of his

subordinates, assigning to each of them to their most suited task. For example, dur-

ing their stays at the convent in Verona, friar Martino da Todi served as the sacrist,

Prior

Friars (procurator, sacrist, canaparius, questuant, schoolmaster, kitchener, predicant, other friars)

18

friar Bonaventura was the canaparius, and friar Pietro da Isola della Scala was the

questuante (beggar).

Despite the lack of documentary proofs, the analysis of accounting books re-

vealed that the prior could also conduct more complex evaluations too. For example,

he could calculate the total amount cashed during the questua indumentorum (beg-

ging for clothes) and, at the same time, the total expenses related to purchases of

garments for the friars engaged in that questua. The balance of income and expenses

indicated whether a given activity had ultimately generated income or diverted funds

from other important monastic activities.

A relationship of authoritative power particularly reinforced by accounting was

that between the prior and one of his subordinates, the procurator. The procurator

was authorised by the prior to spend and manage the money of the convent. Evi-

dence of this mandate comes from the accounting entries of income and expenses,

which are preceded by the first singular person verb: recevi (I received) or spesi (I

spent):

Anchora recevi adì XXVI dottobre per fitto duna chasa la quale ci lasciò

maestro Simeone orefice da Santa Maria in Organo e daci di fito la deta

chasa a lanno sol. XVI, den. VIII [The twenty-sixth day of October, I

received a sum deriving from the annual lease of the house donated by

Lord Simeone da Santa Maria in Organo, the goldsmith].

19

Anchora spesi adì XXVIIII di dicenbre in piscio per convento e fo per la

villia di Natale sol. V [The twenty-fourth of December I spent a sum for

fish for the Christmas Eve].

Accounting thus facilitated the power of the prior over the procurator, due to both

the manner in which entries were compiled and the content of the annotations.

The analytical and detailed recognition of income and expenses (instead of totals

only) allowed the prior to check regularly whether the procurator had managed the

money of the convent in a manner consistent with his delegation and authorisation

(Pastore and Garbellotti, 2001). Particularly useful for this purpose were the order in

which accounting books were compiled (incomes separate from expenses), the

chronological succession of records on a monthly basis and the structure of the re-

cording (time–reason–amount).

Another practice involved highlighting, with special annotations (or clauses) on

the board of the page, incomes or expenses with particular importance for manage-

ment purposes, which strengthened the prior’s ability to control the work of the

procurator. For example, the addition of the word ‘nota’ before the record of a pur-

chase of tiles for the restoration of the church’s roof immediately allowed the prior

to verify the extraordinary expenses incurred by the procurator for the convent.

Nota. Item expendi die XVIIII mensis in sex miliaria tegularum pro

ecclesia seliçanda lib. XXII, sol. X [Noteworthy. The twenty-fourth of

the month, I spent a sum for some tiles for the roof of the church].

20

Finally, the frequency of records that show in detail the intended use of the goods

purchased further strengthens the sense that accounting supported the exercise of

power of the prior over the procurator. They show in particular that the prior had the

authority to judge the merits of the expenses made (Benassi et al., 1984):

Item expendi in rapis causa fatiendi composite lib. III, sol. V [I expend-

ed for some turnips in order to prepare a compote].

In primis dedi fratri Bonaventure quos expendit in uno cultello causa in-

cidendi carnes lib. XVI [I gave to friar Bonaventura the money that he

spent for a knife in order to cut the meat].

This analysis of medieval accounting books therefore shows how accounting sup-

ported the knowledge of the prior and reinforced the authoritative power assigned to

him by the domination structure.

The role of accounting in power relations among friars

Accounting also enforced the exercise of power among peers, by strengthening

the allocative resources of some friars. This key role of accounting was particularly

evident in the relation between sacrist and procurator. Both held power based on al-

locative resources: The procurator had command over information related to the

movements of money received and spent by the monastery. The chronological order

and recording of incomes and expenditures in separate pages of accounting books

facilitated this control, because they allowed the procurator to calculate partial cash

balances at any moment. The sacrist, according to Constitutiones, instead held

command over church property. The accounting books of the income and expenses

21

of the sacristy for the Middle Ages, as repeatedly cited in the accounting books kept

by the procurator, did not survive, but their very existence shows that the sacrist had

the power to manage the money received by the church (e.g., donations, sales of

candles). Accounting acted as a facilitator by allowing the sacrist to know exactly

how much money he could manage. The sacrist could decide how much money to

transfer to the convent and how much to keep for the management of the church, on

the basis of accounts that he was holding. Indirect confirmation of this ability came

from the records contained in the accounting books compiled by the procurator:

Item habui de sacristia, scilicet, de lucro candelarum venditis in

ecclesia a XVIII die mensis marcii usque a diem VI mensis madii lib.

VIII, sol. VIII [I had from the sacristy a sum deriving from the candles

sold from the eightenth day of March to the sixth day of May].

The money received in the sacristy was managed directly by the sacrist and

transferred to the procurator, according to the needs of the convent. In particular,

when the incomes were not sufficient to meet additional expenditures during the

month, the procurator could ask for money from the sacrist. This request was noted

by the procurator in the accounting books, under the heading pro expensis faciendis

(expenses to be met).

Item recepi a sacrista die XVIII pro expensis faciendis lib. X [The

eighteenth day of the month, I recived a sum from the sacristy for

expenses to be met].

22

A check of the accounting records confirmed that such withdrawals effectively came

to pass when the expenses had consumed almost entirely the funds available to the

procurator (Alberti et al., 2008).

In conclusion, accounting attributed to the sacrist more power than that provided

by the domination structure outlined by the Constitutiones. Although the Constitu-

tiones already attributed to the procurator command over all the money of the con-

vent, accounting supported a shift of power from the procurator to the sacristan in

terms of control over money received by the church by selling candles or through of-

ferings from the faithful.

Contributions and further developments

This article has sought to contribute to the international debate about accounting and

religion by analysing, from a historical perspective, the relations between accounting

and power in the Santa Maria della Scala monastery in Verona during the Middle

Ages. To this end, primary and secondary sources served to identify the domination

structure that characterised the organisation and to reveal whether and how account-

ing helped reinforce this structure.

The case study confirms the hypothesis that accounting supported, at the local

level (within the monastery), the exercise of power by the Chapter and the prior,

based on authoritative resources (hierarchical power relations). Accounting also fa-

cilitated control over the functioning of the monastery and the activities carried out

by each friar.

23

As an innovative contribution, this study shows that accounting supported peer

power relations among friars who performed specialised tasks. The accounting data

enforced the allocative resources of the procurator and the sacrist, as well as their

ability to effect organisational outcomes.

The validity of the conclusions reached herein for the Middle Ages period also is

reinforced by the finding that accounting continued to support power relations with-

in the monastery, in the same way and for centuries. For example, information con-

tained in a primary, non-accounting source – the Libro dei Partiti (Book of the par-

ties) – which reported on resolutions adopted by the Chapter. The first original that

has survived refers to the period 1684–1727. It describes the definition of the differ-

ent tasks of religious members, the acceptance or rejection of new monks in the

monastery, the punishment of friars who had not maintained appropriate behaviours

and the roles assigned in contractual disputes relating to the purchase, sale and rent

of land. An analysis of this source reveals that accounting continued to play the

same role, as a facility in relations of power, even at the turn of the seventeenth and

eighteenth centuries.

Specifically, with reference to hierarchical power relations, the Libro dei Partiti

confirms that accounting books granted the prior the power to control the work of

the friars. On several occasions, the Libro dei Partiti shows how the prior used the

income and expense book to verify the work performed by each friar and ascertain

responsibility for possible monetary shortages.

24

In reference to peer power relations, the text often reveals how the power of sac-

rists grew stronger through the accounting book of the sacristy. The Libro dei Partiti

shows for example that the sacrist anticipated transferring to the procurator some

money for the monastery’s expenses. He decided what amount to transfer, according

to the availability of money, as evidenced in the register of the sacristy. The same

book was then used to monitor the repayment of the loan.

Considering that the domination structure and characteristics of accounting at the

turn of the seventeenth and eighteenth century were not significantly different from

those in the Middle Ages (Alberti et al., 2010), this ad probandum analysis of the

Libro dei Partiti confirms the findings outlined previously. That is, the case of S.

Maria della Scala, in the Middle Ages and over time, supports the hypothesis that

accounting has been a facility of power for the monastery, in both hierarchical and

horizontal power relations. In addition, it highlights that within the monastery,

though friars officially represented the same level and fell equally under the reli-

gious and administrative authority of the prior, accounting shifted the power among

them, enforcing the position of some friars over others.

Because this study draws its conclusions from an analysis of documents at the lo-

cal level (within the monastery), no conclusions can be drawn regarding the relation

between accounting and power at the provincial or general level of the Order of Ser-

vi di Maria. For this reason, further developments of this work should attempt an

analysis of the role that accounting played in supporting the domination structure of

the Order.

25

Aknowledgements

The Authors are grateful to Professor Alessandro Lai for his suggestions, as well

as to the three anonimous reviewers for the helpful feedback they provided. Sincere

thanks are offered to fra Sergio Pachera and Vinicio Filippi for thei help in

collecting primary and secondary sources. Although this article is the result of a

group effort, Chiara Leardini authored Introduction, The accounting–power

paradigm in religious institutions, The Santa Maria della Scala monastery in Verona

during the Middle Ages: domination structure; Gina Rossi authored Accounting and

power relations within the monastery, Contributions and further developments.

26

References

Alberti GB, Leardini C and Rossi G (2008) L’azienda convento nei registri contabili

di Santa Maria della Scala a Verona. 1345-1355. Padova: Cedam.

Alberti GB, Leardini C and Rossi G (2010) I registri di entrata e uscita del convento

di Santa Maria della Scala a Verona: l’attività di rendicontazione a supporto del

controllo e dell’amministrazione negli enti religiosi. Contabilità e cultura

aziendale X (1): 32–55.

Bacharach SB and Lawler EJ (1980) Power and politics in organizations. San

Francisco: Jossey-Bass.

Bandini G (1984) Archivi e chiesa. Lineamenti di archivistica ecclesiastica e

religiosa. Bologna: Patron.

Barbieri G (1988) Economia, finanza e tenore di vita nella Verona scaligera. In:

Varanini GM (eds., Gli Scaligeri (1277-1387). Verona, pp.329–41.

Benassi V, Dias OJ and Faustini FM (1984) I Servi di Maria. Breve storia

dell’ordine. Roma.

Birkett WP and Evans E (2005) Theorising professionalisation: a model for organis-

ing and understanding histories of the professionalising activities of occupational

associations of accountants. Accounting History 10 (1): 99–127.

Bisman JE (2012) Surveying the landscape: The first 15 years of Accounting Histo-

ry as an international journal. Accounting History 17(1): 5–34.

Booth P (1993) Accounting in Church: A Research Framework in Agenda”.

Accounting, Auditing and Accountability Journal 6(4): 37–67.

27

Carmona S, Ezzamel M and Gutiérrez F (1997) Control and cost accounting

practices in the Spanish Royal Tobacco Factory. Accounting, Organizations and

Society 22(5): 411–46.

Carmona S and Ezzamel M (2006) Accounting and religion: a historical perspective.

Accounting History 11(2): 117–27.

Carnegie GD and Napier CJ (1996) Critical and Interpretative Histories: Insights

into Accounting Present and Future through its Past. Accounting, Auditing and

Accountability Journal 9(3): 7–39.

Citeroni R (1998) L’ordine dei servi di Santa Maria nel Veneto. Tre insediamenti

trecenteschi: Venezia (1316), Verona (1324), Treviso (1346). Roma: Edizioni

Marianum.

Citeroni R (2006) Il convento di Santa Maria della Scala e la società veronese. In:

Sandrini A (eds.) Santa Maria della Scala. La grande “fabbrica” dei Servi di

Maria in Verona, pp.101–122.

Cordery C (2006) Hallowed treasures: sacred, secular and the Wesleyan Methodists

in New Zealand 1819-1840. Accounting History 11(2): 199–220.

Dal Pino AM (1965) Le Constitutiones antiquae fratrum servorum Sanctae Mariae.

Presentazione ed analisi. Roma: Edizioni Marianum.

Dal Pino F (1972) I frati servi di Maria dalle origini all’approvazione (1233 ca. -

1304). I. Storiografia-Fonti-Storia, Louvain, pp.759–1339.

28

De Sandre Gasparini G (1988) Istituzioni ecclesiastiche, religiose e assistenziali

nella Verona scaligera tra potere signorile e società. In: Varanini GM (eds.) Gli

Scaligeri (1277-1387). Verona, pp.393–403.

Dobie A (2008) The Development of Financial Management and Control in

Monastic Houses and Estates in England c. 1200-1540. Accounting, Business &

Financial History 18(2): 141–59.

Flori L (1636) Trattato del modo di tenere il libro doppio domestico con suo

essemplare composto dal P. Lodovico Flori della Compagnia di Gesù per uso

delle case e dei collegi della medesima Compagnia nel Regno di Sicilia. Palermo:

Decio Cirillo.

Giddens A (1984) The Constitution of Society. Cambridge: Polity Press.

Jacobs K and Walker SP (2004) Accounting and Accountability in the Iona

Community. Accounting, Auditing and Accountability Journal 17(3): 361–81.

Jacobs K (2005) The Sacred and the Secular: Examining the Role of Accounting in

the Religious Context. Accounting, Auditing & Accountability Journal 18(2):

189–209.

Kanter RM (1977) Men and women of the corporation. New York: Basic Books.

Lai A, Leoni G and Stacchezzini R (2012), Governmentality rationales and calcula-

tive devices: the rejection of a seventeenth-century territorial barter proposed by

the King of Spain. Accounting History 17(3-4): 369–392.

Landi F (1996) Il paradiso dei monaci. Accumulazione e dissoluzione dei patrimoni

del Clero regolare in età moderna. Roma: La Nuova Italia Scientifica.

29

Laughlin R (1988) Accounting in its Social Context: an Analysis of the Accounting

Systems in the Church of England. Accounting, Auditing and Accountability

Journal l.1(2): 19–42.

Leardini C, Rossi G, Cantele S, Filippi V and Moggi S (2012) Contabilità e Ordine

Generale dei Servi di Maria nel Medioevo. Roma: RIREA Historica.

Macintosh NB and Scapens RW (1990) Structuration Theory in Management

Accounting. Accounting, Organizations and Society 15(5): 455–77.

Macintosh NB and Scapens RW (1991) Management Accounting and Control

Systems: A Structuration Theory Analysis. Journal of Management Accounting

Research 13: 131–58.

Mintzberg H (1979) The structuring of organizations: A synthesis of the research.

Engelwood Cliffs, N.J.: Prentice Hall.

Mintzberg H (1984) Power and Organization Life Cycles. The Academy of

Management Review 9(2): 207–24.

Pastore A and Garbellotti M (2001) L’uso del denaro. Patrimoni e amministrazione

nei luoghi pii e negli enti ecclesiastici in Italia. Bologna: Il Mulino.

Pietra A (1586) Indirizzo degli economi o sia ordinatissima istruttione de

regolamente formare qualunque scrittura in un libro doppio. Aggiuntovi

l’essemplare di un Libro nobile co ‘l suo Giornale ad uso della Congregation

Cassinese dell’Ordine in San Benedetto. Mantova: Francesco Osanna.

30

Prieto B, Matè L and Tua J (2006) The accounting records of the Monastery of Silos

throughout the eighteenth century: the accumulation and management of its

patrimony in the light or its accounting books. Accounting History 11(2): 221–56.

Quattrone P (2004) Accounting for God: accounting and accountability practices in

the Society of Jesus (Italy, XVI-XVII centuries). Accounting, Organizations and

Society 29(7): 327–360.

Riccaboni A, Giovannoni E, Giorgi A and Moscadelli S (2006) Accounting and

Power: Evidence from the Fourteenth Century. Accounting History 11(1): 41–62.

Russel B (1938) Power: A new social analysis. London: George Allen and Unwin.

Sargiacomo M (2008) Accounting and the «art of government»: Margaret of Austria

in Abruzzo (1539-86). European Accounting Review 17(4): 667–695.

Sargiacomo M. (2009) Accounting for the «good administration of justice»: the

Farnese state of Abruzzo in the sixteenth century. Accounting History 14(3): 235–

267.

Stacchezzini R (2012) Accounting e potere. Il contributo interpretativo del

governmentality framework. Milano: Franco Angeli.

Swanson GA and Gardner JC (1988) Not-For-Profit Accounting and Auditing in the

Early Eighteenth Century: Some Archival Evidence. The Accounting Review

LXIII(3): 436–47.

Varanini GM (1988) Gli Scaligeri, il ceto dirigente veronese, l’élite internazionale.

In: Varanini GM (ed.) Gli Scaligeri (1277-1387). Verona, pp.113–24.

31

Walker SP (2005) Accounting in History. Accounting Historians Journal 32(2):

233–259.

Weber M (1978) Economy and Society. Roth G and Wittich C (eds.). Berkeley:

University of California Press.

32

Appendix 1: Archival funds of S. Maria della Scala monastery for the Middle

Ages (chronological order)

N° Title Years

1 Giornale entrata e uscita 1340-1344

2 Libro introito ed esito 1345-1355

3 Giornale di entrata e uscita 1355-1358

4 Giornale di entrata e uscita 1370-1395

5 Giornale uscita 1374-1383

6 Libro di entrata ed uscita 1374-1389

7 Giornale entrata e uscita 1410-1420

8 Giornale entrata e uscita 1420-1432

9 Libro di locazioni (pergamenaceo) 1433-1440

10 Giornale entrata e uscita 1486-1492