A Review of the Corporate Insolvency Framework - GOV.UK

663

Summary of Responses: A Review of the Corporate Insolvency Framework September 2016

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of A Review of the Corporate Insolvency Framework - GOV.UK

Summary of Responses:

A Review of the Corporate Insolvency Framework September 2016

2

1. Executive summary Introduction 1.1. In May 2016 the Government published a consultation seeking views on measures to

update the UK’s corporate insolvency regime. The proposed changes should facilitate the rescue of a greater number of viable, financially distressed companies.1 The UK’s corporate insolvency regime is highly regarded internationally (ranked as one of the top 15 in the world by the World Bank), but Government wants to ensure it continues to deliver the best possible outcomes for business.2

1.2. The consultation ran from May to July 2016. During the consultation period officials met with a wide range of stakeholders, including at two roundtable events held in June 2016 at which representatives from law firms, trade bodies, creditor organisations, banks, regulators, academia and industry were present.

1.3. 71 written responses were received from a range of interested organisations and individuals. These responses will help shape the Government’s policy to enable the rescue of viable distressed businesses, and we are very grateful for the time respondents took to provide constructive feedback on the proposals. Government looks forward to maintaining this dialogue with stakeholders over the coming months, and is continuing to consider the proposals in the light of the responses received.

1.4. This paper provides a summary of respondents’ views. The full responses can be found at Annex 2. Some respondents asked that their responses be kept confidential or provided responses that could not be published (e.g. for copyright reasons). They have not been listed in Annex 1 and their responses have not been published in Annex 2, but they have been included in the analysis below.

Background

1.5. The consultation sought views on four proposed areas for reform of the UK’s corporate

insolvency framework:

• Creation of a new moratorium period for financially distressed (but ultimately viable) companies. Creditors would not be able to take action against the company in this

1 A Review of the Corporate Insolvency Framework: https://www.gov.uk/government/uploads/system/uploads/attachment_data/file/525523/A_Review_of_the_Corporate_Insolvency_Framework.pdf 2 Doing Business - Economy Rankings: http://www.doingbusiness.org/rankings Full report available at: http://www.doingbusiness.org/~/media/GIAWB/Doing%20Business/Documents/Annual-Reports/English/DB16-Full-Report.pdf

A Review of the Corporate Insolvency Framework: summary of responses

3

period, during which it would be making preparations to restructure;

• Provision to require essential suppliers to continue to supply to a financially distressed company on existing terms and not use termination clauses or demand ‘ransom’ payments;

• Creation of a ‘new restructuring plan’ – a company rescue vehicle that would enable (for the first time in the UK) a ‘cram down’ of classes of dissenting creditors;

• Measures to encourage ‘rescue finance’ (money lent to a company in an insolvency procedure to assist in its survival).

An overview of responses

1.6. Stakeholders welcomed Government’s exploration of reforms that could improve the

restructuring tools available to companies. While there was broad support for the principles behind the proposals, a range of views were expressed on the technical detail. Government will continue to liaise with stakeholders while establishing this detail, considering policy options further and refining the proposals in light of responses received to this consultation.

A new moratorium period: Two thirds of respondents who commented on this proposal agreed in principle that the introduction of a pre-insolvency temporary moratorium would facilitate business rescue. Stakeholders provided helpful feedback on the proposed length of the moratorium period, its supervision, and on suggested safeguards. Essential supplies: There was support for the broad objective of helping businesses to continue trading through the restructuring process. Over half of the 24 respondents who commented on whether the proposal would bring about more business rescues thought that it would do so. Respondents provided constructive comments on how the proposal might operate in practice, and on how the associated safeguards for suppliers might be strengthened. A new restructuring plan: There was support for the principle of the proposal, and agreement that a restructuring plan which could be made binding in the face of opposition by a minority of creditors would be a valuable addition to the insolvency framework. Stakeholders provided a range of valuable perspectives on how the new plan might operate in practice.

A Review of the Corporate Insolvency Framework: summary of responses

4

Rescue finance : In 2009, the Government published a consultation which included proposals relating to super-priority for rescue funding in administrations and CVAs.3 As a result of responses received to that consultation, the proposals were not taken forward at that time. Given changes in market conditions, the Government believed that it was appropriate to seek views again from interested parties. Responses to this consultation indicated that a lack of finance rarely prevents the rescue of viable businesses; the existing framework does permit rescue financing, and there is currently a market for rescue finance.

2. Summary of responses: moratorium General views on the proposal

2.1 The majority (67%) of respondents who commented on this proposal expressed their

support for the introduction of a preliminary moratorium during which viable distressed businesses could consider their options for rescue. Of those who supported the proposal, 37% (16 respondents) agreed with the proposal as outlined in the consultation document. 63% (27 respondents) agreed in principle that a moratorium would promote business rescue, but felt that the detail of the proposal needed refining.

2.2 Those who supported the proposal felt that a new moratorium, upstream of formal insolvency, could encourage directors to act earlier to tackle financial difficulties. A turnaround professional commented that: ‘the very existence of a moratorium may encourage earlier intervention and consensual commercially negotiated solutions without even having to resort to a formal moratorium’.

2.3 A common view – both among those who supported the moratorium and those who opposed it – was that safeguards for creditors needed to be strengthened.

Obtaining and dissolving the moratorium

2.4 29 of the 44 respondents (66%) who commented on the process of filing to court to

obtain a moratorium agreed that this was the most efficient way in which a business could gain relief from creditor action. There was widespread concern that a full court hearing could involve costs and delay, at a time in a company’s life cycle when speed is crucial.

2.5 20 of the 35 respondents (57%) who expressed a view on how creditors could best seek

to dissolve the moratorium if their interests were not protected agreed that doing so in

3 Encouraging Company Rescue - a consultation: http://webarchive.nationalarchives.gov.uk/20140311023846/http://www.insolvencydirect.bis.gov.uk/insolvencyprofessionandlegislation/con_doc_register/compresc/compresc09.pdf

A Review of the Corporate Insolvency Framework: summary of responses

5

court was the most appropriate option. Those who disagreed highlighted that access to court and the costs of mounting a challenge could be problematic.

Eligibility tests and qualifying criteria

2.6 24 of the 63 respondents (38%) who expressed a view in relation to this question agreed that the proposed eligibility tests and qualifying criteria provided the right level of protection for suppliers and creditors. 13 respondents (21%) felt that there was insufficient detail in the consultation document. 25 respondents (41%) felt that the proposed tests and criteria did not provide sufficient protection to those dealing with the company.

2.7 Several respondents noted that the test proposed in the consultation document (i.e. that a company must demonstrate ‘that it is already or imminently will be in financial difficulty, or is insolvent’) could be more clearly defined.

Rights and responsibilities of creditors and direct ors

2.8 20 of the 58 respondents (34%) who commented on the proposed rights and

responsibilities for creditors and directors agreed that they strike the right balance between safeguarding creditors and increasing the chance of business rescue. 32 respondents (55%) did not think that the safeguards were sufficient as drafted, and 6 respondents (10%) thought that insufficient detail was provided in the consultation document to make a judgement.

2.9 Respondents had mixed views on the proposal to suspend director liability. One respondent noted that: ‘it would be anomalous if directors operated under one regime in an informal moratorium and under a different regime in a statutory moratorium’. Government is further considering the costs and benefits of suspending liability for wrongful trading during the moratorium period.

2.10 Several respondents commented that creditors should have the right to challenge the moratorium in court. Government has noted stakeholder concerns, and is considering whether creditors should have a general right to apply to court during the moratorium if they think that their interests have been unfairly harmed.

2.11 Discussion also focused on the issue of whether a moratorium supervisor should be eligible to be an office-holder for the company during any insolvency or restructuring proceedings that may immediately follow on from the moratorium. Views were mixed, and some respondents noted that the requirement for a new office-holder would lead to delay and increased costs. Others felt that the requirement for a new office-holder was an important safeguard, and that it would help to ensure that the supervisor acted independently during the moratorium.

A Review of the Corporate Insolvency Framework: summary of responses

6

Duration, extension and cessation of the moratorium

2.12 The majority of respondents (76%) who commented on this issue disagreed with the

proposals for the length, extension and cessation of the moratorium as outlined in the consultation document.

2.13 Several alternatives were proposed by the 41 respondents who disagreed with the proposed length. Most thought that it should be shorter than three months, citing difficulties with funding a lengthy moratorium period, and suggesting that a shorter period would reduce the risk of abuse.

2.14 The most common length suggested was 21 days (proposed by seven respondents), then ‘variable depending on size of company’ (five respondents). Others fell somewhere in the middle, maintaining that 21 days was too short, but that three months was too long. Three respondents thought that the moratorium should be longer than three months, commenting that, for example, it would not be possible to negotiate and sanction a scheme of arrangement within that window.

2.15 Respondents commented on the suggested process for extending the moratorium. Of the 36 who expressed an opinion, 21 (58%) were of the view that the agreement of all secured creditors should not be a requirement. Alternatives proposed were the same majority as required for the new restructuring plan, or that an extension could be approved by court if secured creditor agreement could not be obtained.

2.16 There were a number of comments on the proposal to subtract the length of the moratorium from the 12-month period permitted for a subsequent administration. 16 of the 19 respondents who raised this issue said that a subsequent administration should not be shortened. They noted that this could cause practical administrative difficulties, might act as a disincentive for those considering a moratorium, and suggested that insolvency practitioners would be less likely to take on post-moratorium administrations if they knew that they would have less time to conduct them than if there had not been a moratorium.

The supervisor

2.17 Of the 52 respondents who expressed an opinion on the qualification requirements for a

supervisor, 31 (60%) were of the view that appropriate supervision of the moratorium period could only be provided by a licensed insolvency practitioner. These respondents felt that insolvency practitioner supervision would constitute an important safeguard, and suggested that it would be crucial for obtaining and maintaining creditor confidence in the moratorium procedure.

A Review of the Corporate Insolvency Framework: summary of responses

7

Dealing with the costs of the moratorium

2.18 39 of the 53 respondents (74%) who commented on how the costs of the moratorium

should be dealt with agreed with the proposals outlined in the consultation document. Eight respondents (15%) disagreed, and six respondents (12%) felt that there was insufficient detail in the consultation document. Government is continuing to consider this matter.

Allowing creditors to request information 2.19 Of the 59 respondents who commented on this proposal, 44 (75%) agreed that there

was benefit in allowing creditors to request information.

2.20 34 of the 35 respondents who commented explicitly on the need for safeguards and exemptions agreed that these would be necessary. Respondents agreed that the time and cost burden of dealing with unreasonable requests should be minimised, and that exemptions would be needed for dealing with commercially sensitive information.

2.21 21 respondents suggested that regular updates should be given, either by the supervisor or via a creditor portal, rather than creditors having a freestanding ability to request information. It was felt that this would guard against the risk of demands for information proving a distraction and hindering progress during the moratorium period. Others suggested that the supervisor should act as arbiter of what does or does not constitute a reasonable request.

A Review of the Corporate Insolvency Framework: summary of responses

8

3. Summary of responses: essential supplies Definition of essential contracts

3.1 47% of the 59 respondents who answered this question agreed with the criteria under

consideration for an essential contract.

3.2 41% of respondents disagreed with the proposed criteria under consideration for an essential contract as drafted. Several respondents suggested that a ‘one size fits all’ approach would not work. Some respondents also commented that the criteria as drafted were too debtor-friendly.

3.3 A number of respondents stipulated that some suppliers should be carved out. In particular, some respondents stated that the provision of finance and of financial services should be excluded from the proposals. It was also suggested that suppliers should be able to request a personal guarantee from the company’s directors.

3.4 12% of respondents felt that there was insufficient detail in the consultation document to make a judgement on the criteria for an essential contract. Some questioned how the proposals would be enforceable in relation to international suppliers and what would happen if a supplier suffered production difficulties.

3.5 24 respondents answered separately on whether the proposal would bring about more business rescues. 13 respondents thought that it would increase the number of successful rescues, whereas 11 respondents thought that it would not.

Court’s role and safeguards for suppliers 3.6 Of all respondents, 31% felt that the court’s role in the process and a supplier’s ability to

challenge their designation as ‘essential’ were sufficient safeguards to ensure that a supplier would be paid when required to continue supplying.

3.7 69% of respondents did not agree that the proposals as drafted offered sufficient safeguards for suppliers. A number of respondents commented on the additional burden that the proposals may place on the courts, and questioned whether the courts would have the requisite resources to deal with the potential increased workload. Government notes stakeholder concerns, and is continuing to consider the matter.

A Review of the Corporate Insolvency Framework: summary of responses

9

4. Summary of responses: a new restructuring plan Standalone procedure vs. extension of an existing p rocedure 4.1. 41% of the 68 respondents who commented on this issue were in support of a new

restructuring plan operating as a standalone procedure, rather than as an extension of an existing procedure (e.g. a CVA). They suggested that this would promote flexibility and allow a wider range of companies to benefit from the plan. Several respondents who supported a standalone process suggested that it would be more effective if it was viewed as a ‘restructuring’ process rather than as an ‘insolvency’ procedure.

4.2. The respondents who disagreed and felt that the restructuring plan should operate within the existing CVA framework made up 22% of the replies (15 responses).

4.3. A number of respondents commented that the procedure should not be time-limited to 12 months, and that it should instead be flexible in length.

4.4. Seven of the 68 respondents who answered this question queried the need to introduce a further procedure (whether standalone or as an extension to an existing process), as they felt that existing provisions were sufficient.

Views on cram down 4.5. 42 of the 69 respondents (61%) who answered this question agreed with the principle that

a court-approved ‘cram down’ should be possible in some circumstances. Many respondents agreed with the suggestion that creditors should be grouped in court-approved classes. The proposed voting requirements (at least 75% of creditors by value and more than 50% of each remaining class by number) were generally felt to be suitable. A number of respondents envisaged that this option would be used mainly by large companies because of costs. Others commented that protections would be needed to ensure that junior creditors’ rights were not unfairly expropriated.

4.6. A number of respondents who supported the proposals suggested that shareholders should be included in the ‘cram down’. It was also suggested that it could be more cost effective to go straight to the courts without junior creditors voting.

4.7. Some respondents opposed the idea that a restructuring plan should be universally binding on the grounds that existing creditors’ rights should be recognised and the existing priority of claims should be respected.

Safeguards for creditors, including the role of the court 4.8. Over half of the 68 respondents who answered this question felt that the proposed

safeguards offered sufficient protection for creditors. Many felt that court involvement was

A Review of the Corporate Insolvency Framework: summary of responses

10

fair and offered sufficient protection.

4.9. However 15% of respondents (10 responses) felt that the proposals as drafted would not provide sufficient protection for creditors. They expressed their concern that the courts may not be resourced to deal with the likely increase in applications and the costs associated with the new process. A further concern expressed was that the safeguards as drafted provided sufficient protection for larger creditors but were not sufficient for smaller creditors.

Valuation

4.10. 40% of the 69 respondents who answered this question agreed with the proposal that there should be a minimum liquidation value test for determining the fairness of a plan which is being crammed down onto dissenting classes. There was widespread recognition from all respondents that valuation is a contentious topic. Over a quarter of respondents argued that liquidation is not the right comparator, and that a ‘next best alternative’ value should be used instead. Government is continuing to consider the issue.

A Review of the Corporate Insolvency Framework: summary of responses

11

5. Summary of responses: rescue finance Background

5.1. In 2009, the then Government published a consultation which included proposals relating

to super-priority for rescue funding in administrations and CVAs.4 As a result of responses received, these proposals were not taken forward. Given changes in market conditions, Government believed that it was appropriate to seek views again from interested parties in this consultation.

5.2. Of the 52 respondents who commented on rescue finance, 38 (73%) disagreed with the proposals. Several respondents commented to the effect that a lack of rescue finance rarely prevents business rescue, and that as long as a business is truly viable, there is no shortage of funding available. The existing framework does permit rescue finance, and there is currently a market for rescue financing. 23 respondents were concerned that any changes made to the order of priority would have a negative impact on the lending environment by increasing the cost of borrowing.

4 Encouraging Company Rescue - a consultation: http://webarchive.nationalarchives.gov.uk/20140311023846/http://www.insolvencydirect.bis.gov.uk/insolvencyprofessionandlegislation/con_doc_register/compresc/compresc09.pdf

A Review of the Corporate Insolvency Framework: summary of responses

12

6. Annex A: list of respondents

Organisation Category

Akin Gump Stauss Hauer & Feld LLP

Legal representative

AlixPartners Large business

Allen & Overy LLP Large business

APPG on Fair Business Banking Other

BBA Business representative organisation/trade body

Be Rescued (Business) Consultants Ltd

Micro business

Dr Bolanle Adebola Individual

Bristol Wessex Billing Services Ltd Large business

British Property Federation Business representative organisation/trade body

Bryan, Mansell & Tilly LLP Small business

Chartered Institute of Credit Management (CICM)

Charity or social enterprise

Clarke Bell Ltd Small business

Clifford Chance LLP Large business/legal representative

CMS Cameron McKenna LLP Legal representative

Co-Operatives UK Business representative organisation/trade body

Deloitte LLP Large business

Ernst & Young LLP Large business

European Association of Certified Turnaround Professionals

Business representative organisation/trade body

A Review of the Corporate Insolvency Framework: summary of responses

13

Faculty of Advocates Legal representative

Federation of Small Businesses Business representative organisation/trade body

Finance & Leasing Association (FLA)

Business representative organisation/trade body

Grant Thornton Large business

ICAEW Other - licensing and regulatory body

ICAS Other - a regulator of insolvency practitioners

Insolvency Lawyers’ Association Legal representative

Insolvency Practitioners Association Other - Recognised Professional Body for the authorisation and regulation of Insolvency Practitioners

Professor Jennifer Payne, University of Oxford

Individual

K2 Business Partners Ltd Micro business - specialising exclusively in turnaround

KPMG Large business

Lancaster University University faculty

Land Registry Central Government

Loan Market Association Business representative organisation/trade body

Mark Homan Individual

Mazars LLP Large business

Menzies Other - accountancy firm

Michael Pangley Individual

Mira Makar member SME Alliance Ltd

Moore Stephens Large business

A Review of the Corporate Insolvency Framework: summary of responses

14

Nottingham Trent University Other - academic institution

Pension Protection Fund Other - a statutory corporation established under the provisions of the Pensions Act 2004

Peter Bloxham Individual

Pinsent Masons LLP Legal representative

PwC Large business

R3 Business representative organisation/trade body

Rachel Lai and John Cullen Individuals

ReSolve Partners Limited Small business

RWE npower Large business

Sarah Paterson Individual

Secured Transactions Law Reform Project (STLRP)

Other

Squire Patton Boggs LLP Legal representative

Stephens Scown LLP Legal representative

The Asset Based Finance Association (ABFA)

Business representative organisation/trade body

The Bar Council Legal representative

The Chancery Judges Other - judicial

The City of London Law Society Business representative organisation/trade body

The Law Society Professional body

Tokio Marine Credit Division Other - credit insurer

Turnaround Management Association (TMA)

Business representative organisation/trade body

A Review of the Corporate Insolvency Framework: summary of responses

15

7. Annex B: responses to the Government’s Review of the Corporate Insolvency Framework (May-July 2016)

A Review of the Corporate Insolvency Framework: a consultation on options for reform

A Review of the Corporate Insolvency Framework response form

The consultation response form is available electronically on the consultation page: https://www.gov.uk/government/consultations/a-review-of-the-corporate-insolvency-framework (until the consultation closes).

The closing date for this consultation is 06/07/2016.

The form can be submitted online/by email or by letter to:

Policy Unit The Insolvency Service 4 Abbey Orchard Street London SW1P 2HT Tel: 0207 291 6879 Email: [email protected]

The Department may, in accordance with the Code of Practice on Access to Government Information, make available, on public request, individual responses.

Information provided in response to this consultation, including personal information, may be subject to publication or release to other parties or to disclosure in accordance with the access to information regimes. Please see page 9 for further information. If you want information, including personal data, that you provide to be treated in confidence, please explain to us what information you would like to be treated as confidential and why you regard the information as confidential. If we receive a request for disclosure of the information we will take full account of your explanation, but we cannot give an assurance that confidentiality can be maintained in all circumstances. An automatic confidentiality disclaimer generated by your IT system will not, of itself, be regarded as binding on the department.

I want my response to be treated as confidential ☐

Comments:

A Review of the Corporate Insolvency Framework: a consultation on options for reform

Questions Name: Jeff Naylor

Organisation (if applicable): AlixPartners

Address: The Zenith Building, 26 Spring Gardens, Manchester, M2 1AB

Respondent type

Business representative organisation/trade body

Central Government

Charity or social enterprise

Individual

X Large business (over 250 staff)

Legal representative

Local Government

Medium business (50 to 250 staff)

Micro business (up to 9 staff)

Small business (10 to 49 staff)

Trade union or staff association

Other (please describe)

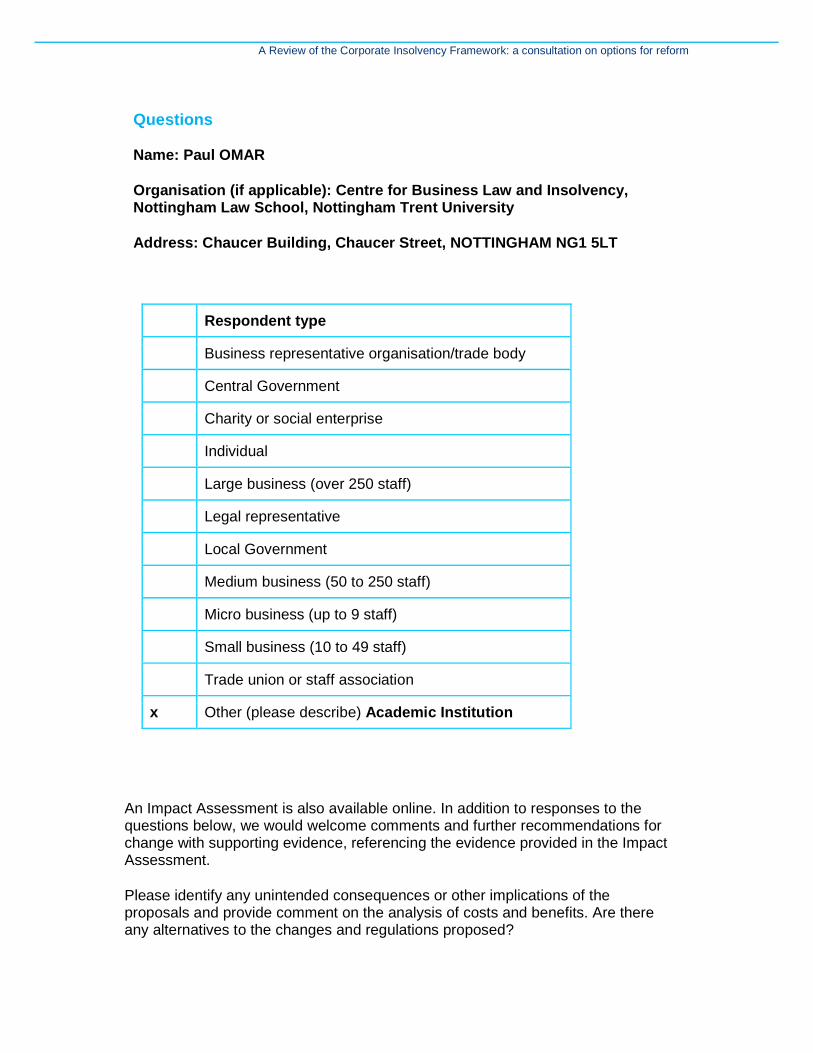

An Impact Assessment is also available online. In addition to responses to the questions below, we would welcome comments and further recommendations for change with supporting evidence, referencing the evidence provided in the Impact Assessment.

Please identify any unintended consequences or other implications of the proposals and provide comment on the analysis of costs and benefits. Are there any alternatives to the changes and regulations proposed?

A Review of the Corporate Insolvency Framework: a consultation on options for reform

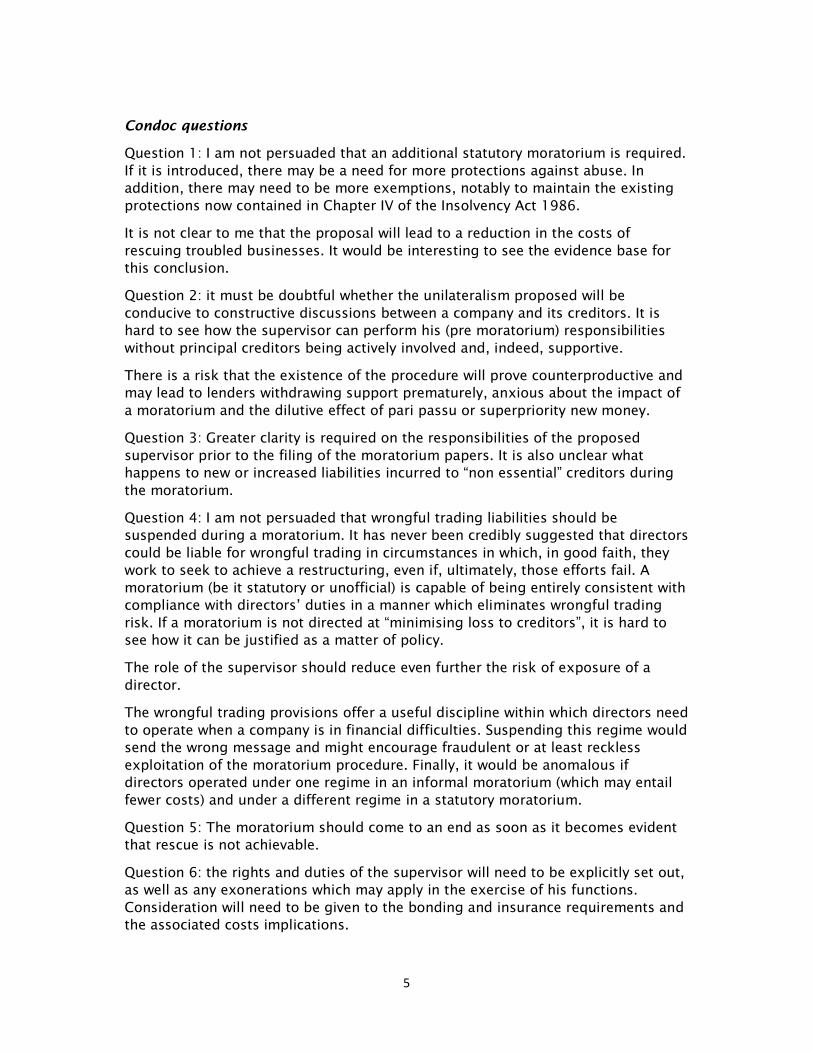

The Introduction of a Moratorium

1) Do you agree with the proposal to introduce a preliminary moratorium as a

standalone gateway for all businesses?

Although a moratorium would provide valuable time for troubled companies to

formulate a restructuring plan, there are potentially significant problems that such

moratoriums may create that will require safeguards to be put in place before such

moratoriums are made available.

In particular, the protection of creditors is crucial as their position may be

significantly worsened during the lifetime of the moratorium and few safeguards

have been advanced against this in the proposals. The circumstances envisaged by

the proposals for businesses that would require such a moratorium, actual or

anticipated “imminent financial difficulty or insolvency” implies that the business

must have made losses or experienced some cash-flow crisis. Unless this crisis was

very transitory in nature, then losses or cash outflows will continue during the

moratorium.

Unless rescue finance has been obtained, or working capital introduced by the

directors or shareholders for the moratorium period, then losses incurred in trading

during a moratorium would be borne by the secured floating charge holder, or by

the unsecured creditors. If a restructuring cannot be successfully implemented,

then those creditors may seek to hold the directors or Supervisor responsible for

the deterioration in their position. It is proposed that the directors are to be

exempt from wrongful trading consequences during a moratorium. In such

circumstances, the Supervisor will need to be satisfied that the legislation protects

him from liability for losses caused to creditors. Alternatively, is it envisaged that

the Supervisor (or Directors) will need to take out insurance to cover such losses?

The proposals are also silent on the issue of unsecured trade creditors who have

supplied goods which are subject to reservation of title clauses, and whether such

clauses would be enforceable following a company entering a moratorium. In an

insolvency scenario, such suppliers would be entitled (should their claims be valid)

to receive either their goods back or the invoice value of those goods. If no

provisions are put in place to protect such suppliers, then they will be forced to

stand by whilst the goods are used to fund the working capital requirements of the

business during the moratorium. Such an inconsistency would be resented by

creditors, and may lead companies to seek a moratorium where not appropriate,

for the advantages this would bring.

A Review of the Corporate Insolvency Framework: a consultation on options for reform

Whilst it is noted that the intention of a moratorium provision is to encourage

directors to address the company’s problems at an earlier stage, rather than when

the value of its business has been damaged and its financial position has

deteriorated, it is a concern that directors may seek to use the moratorium in

circumstances where it is not warranted. It is vital that creditors are given

confidence that the professional advisers to the business are regulated and

appropriately qualified whose role is to protect their interests. For this reason, we

believe that qualified and licensed insolvency practitioners would be the

appropriate individuals to perform this function.

There is also a concern that where a moratorium is made available to all

businesses, then access to that moratorium will become a default course of action

followed by businesses even where not appropriate. Empirical research in the

United States (The Success of Chapter 11: A Challenge to the Critics by Elizabeth

Warren and Jay Lawrence) shows that size is the true defining factor that

determines whether US companies use Chapter 11 or Chapter 7 (liquidation

proceedings). Among companies filing for bankruptcy with $1 million or more of

debt, 95% begin in Chapter 11.

That same research shows that small businesses are unable to afford the cost of

Chapter 11 proceedings and therefore elect to liquidate the business and not seek a

restructure or rescue; 97% of companies sampled by Warren & Lawrence entering

Chapter 7 (i.e. liquidation) had less than $500,000 of assets. One of the strengths of

the current UK insolvency regime is the ability for SMEs to have affordable access to

rescue procedures. The proposed changes to the UK insolvency framework will

increase the level of court involvement, which implies a greater level of cost. The

low take up of the existing CVA moratorium suggests that SMEs are less likely to

derive benefit from the moratorium even if access to it is broadened to all

insolvency procedures.

2) Does the process of filing to court represent the most efficient means for

gaining relief for a business and for creditors to seek to dissolve the

moratorium if their interests aren’t protected?

There is no doubt that the court could provide an appropriate facility for both the application for and recording of a moratorium, and for any appeal by creditors or the parties against the moratorium. However, given the current shortage of available Court time in the UK, any such proposals would have to be accompanied by a significant investment in the expansion of court resource.

A Review of the Corporate Insolvency Framework: a consultation on options for reform

In the US, where Chapter 11 applications which are the most analogous to the proposals are used, there are specialist bankruptcy courts. To implement a moratorium system which is intended to facilitate the swift production of restructuring plans at an early stage of a company’s financial difficulties, any challenges to the moratorium or actions taken by the company or Supervisor must be dealt with expeditiously. This will require significant investment in court resources should the proposals be implemented. In addition, as mentioned above, empirical research in the US shows that one of the factors that discourages businesses from seeking the protection of a moratorium from their creditors is cost. If the costs of seeking to obtain a moratorium and defending it against the challenges of creditors are to be made through the court, there is a real risk that access to restructuring tools will be restricted to larger businesses. A corresponding concern is that the ability to challenge inappropriate moratorium applications or conduct of the company will likewise be restricted to creditors above a certain size, because of the cost of access.

An additional concern raised by the consultation proposals is that the process of directors selecting a supervisor and seeking for them to obtain protection of a moratorium from creditors is to be done with minimal contact with creditors, other than major secured creditors. The reason for not consulting creditors ahead of a moratorium is clear; to prevent them taking unilateral action that might harm the value of the business. And yet the necessary secrecy in the period leading up to a pre-packaged administration sale is one of the factors that creditors are most unhappy about, leading to criticism that creditors’ rights are being abused. Again, this means that the Supervisor must be able to have the confidence of creditors.

3) Do the proposed eligibility tests and qualifying criteria provide the right level

of protection for suppliers and creditors?

Although the proposals state that the moratorium is not intended to allow failing businesses to merely buy time with creditors where there is no realistic prospect of a rescue or compromise being reached; in reality at the point at which a moratorium is applied for, the deliverability of a rescue or restructuring of the company will very likely be uncertain, as little contact will have been made with creditors. The presence of key drivers of a successful restructuring; creditor willingness to forgive debt, a viable business, and availability of working capital finance, will in many cases only be made clear after the moratorium has been applied for and put in place.

Eligibility test The requirement that the business must be already or imminently be in financial difficulty or insolvent may lead to businesses delaying seeking a moratorium until

A Review of the Corporate Insolvency Framework: a consultation on options for reform

they are already in significant difficulty. It is difficult to reconcile this requirement with the aim of promoting the early address by directors of corporate distress. The exclusion of banks and insurance companies appears sensible. The availability of working capital and funding to enable the trading on during a moratorium is a concern that will have to be addressed by the government as part of these proposals. Without available specialist rescue finance, it is likely that the bulk of cases where a moratorium might be of use will be prevented from achieving this due to the lack of such funding. In addition at the outset of the moratorium it will be very difficult to show there is a reasonable prospect that a compromise or arrangement can be agreed with its creditors, without being aware of the views of those creditors. Conversely, the requirement to consult with senior secured lenders before seeking the protection of a moratorium presents an obvious challenge to legislators; what prevents the secured lender from taking enforcement action to protect their interests, particularly if they believe their position may be undermined by the potential costs of the procedure taking priority over their repayment?

4) Do you consider the proposed rights and responsibilities for creditors and

directors to strike the right balance between safeguarding creditors and

deterring abuse while increasing the chance of business rescue?

We have concerns that in practice the timescale may act against the protection of creditors’ rights. There is no statement in the proposals as to the date by which the business seeking a moratorium will have to notify its creditors that a moratorium is in place. Assuming that the current notification standard of five business days is applied, it may be more than a week after the moratorium has commenced that a creditor finds out that it is in place. This would then give them less than 21 days to make an application to court to contest it. As noted above our concern regarding court resource is that such applications should be heard within a reasonable period of time, particularly if the supplier has been deemed an essential supplier. Without prompt access to court, there is a risk that creditor rights may not be adequately protected or could even be eroded.

Also as previously noted, it is not clear what protection is to be given to suppliers who have provided goods subject to reservation of title clauses or who hold liens. If they have no protection, then they would be forced to watch their stock being used by the company in the moratorium. However, if their rights are enforceable, this would increase the working capital requirement that the business would need to fund its trading during the moratorium period, as such stock would then have to be paid for. Clarity on the approach to such matters in a moratorium will be essential before any legislation is enacted.

A Review of the Corporate Insolvency Framework: a consultation on options for reform

We agree that the company should as a matter of course consult with its largest secured creditors before making application for a moratorium. Particularly where those secured creditors are also the only practical source of funding for the moratorium period, this will be an imperative. However, as noted above, what prevents a notified secured lender from then taking enforcement action to protect their interests, particularly if they believe their position may be undermined by the potential costs of the procedure taking priority over their repayment?

The exception from claims for wrongful trading under section 214 of the Insolvency Act 1986 during a moratorium will need careful construction. It is unlikely that a business seeking protection from a moratorium will be profitable or cash generative during the moratorium period, and therefore its net liabilities to creditors will be increasing. Unless such increases in liability are covered by rescue finance, then should a restructuring plan not be accepted by creditors, those creditors whose interests have been prejudiced during the moratorium will wish to know who will recompense them for their losses. This makes the requirement for an appropriately qualified and licensed insolvency professional to act as Supervisor all the more critical, and highlights the need for them to be adequately protected to enable them to accept appointment.

The protection of creditor interests during the moratorium is a real concern, particularly where creditors are forced to continue trading with the company as an essential supplier, in circumstances where they would might prefer to seek a more profitable or long term business relationship elsewhere, but are prevented from doing so by their designation. Their ability to challenge the decision of the court will be unhelpful if they are not able to do so within reasonable timescales, or at reasonable cost. Pensions Often one of the largest unsecured creditors of the company may arise in cases where the company had a defined benefit pension scheme. Pension schemes, and treatment of the debts owed to them have been very high profile of late, due to cases such as BHS, Lehman and Nortel. However, there is no mention of pension schemes in either the consultation document or the impact assessment that accompanies it. It is unclear whether obtaining a moratorium would become an insolvency event for Pension Protection Fund purposes. If so, the PPF would in most such cases be the largest creditor, whose size of vote would determine whether any restructuring plan would be approved. However, it is also unclear whether or not in such circumstances their rights could be crammed down. Nor is it clear whether or not the moratorium would prevent the Pension Regulator (tPR) from using its moral hazard powers. It is crucial that the treatment of a defined benefit pension scheme under a moratorium is clarified as part of any legislation to bring these proposals into effect. It would seem logical to make the position of a pension scheme

A Review of the Corporate Insolvency Framework: a consultation on options for reform

consistent with that under a formal insolvency process, to be sure that abuse of the pension scheme does not occur.

5) Do you agree with the proposals regarding the duration, extension and

cessation of the moratorium?

The duration of the moratorium of three months does not appear an adequate amount of time to formulate detailed plans to put in front of creditors for a business of any size. Empirical research in the United States (The Success of Chapter 11: A Challenge to the Critics by Elizabeth Warren and Jay Lawrence) stated that 82% of successful small business restructurings under Chapter 11 took longer than 6 months to complete. Firstly, the period of three months will in practice be a shorter time, as the necessary notification period to creditors to enable them to vote on the proposals, or on any extension to the moratorium will have to take place in the three month period. There is a real risk that major creditors may use their voting power to block the extension of the moratorium, particularly secured creditors who are not fully secured, or who believe any extension of the moratorium will further diminish their position. It may be prudent to include an option to seek the permission of the court to extend the moratorium. Conversely, in addition to the proposals for extension moratoriums, we propose that in accordance with the current CVA procedure, the Supervisor of a moratorium should have a duty to apply to court to seek the end of the moratorium, should they believe that the reasons for the moratorium’s commencement are no longer valid.

6) Do you agree with the proposals for the powers of and qualification

requirements for a supervisor?

It is vital that the supervisor commands the confidence of the creditors and company in balancing the rights and responsibilities of each. The proposal that a Supervisor may be someone other than a licensed insolvency practitioner or equivalent is a concern, for the reasons detailed in our answers to previous questions. Although the restriction of the Supervisor from taking a subsequent role in a formal insolvency process would prevent a potential conflict of interest for the Supervisor, it would create an additional conflict of interest, insofar that the Supervisor may have an interest in retaining or extending the moratorium where there is no real prospect of a successful outcome, and not be objective in making such a decision.

A Review of the Corporate Insolvency Framework: a consultation on options for reform

It is unclear from the proposals whether the current rule that “an insolvency practitioner who previously acted as supervisor would be prevented from taking an appointment” would apply to another IP from the same firm. However, should it be felt that there should be no connection between the Supervisor and a subsequently appointed insolvency practitioner, this would cause increased costs due to the time required for the staff involved to become familiar with the company, and passing on all the relevant knowledge. Further detail is required when formulating the requirements for the supervisor and we believe that he should be qualified, licensed and have a bond and also that matters regarding his selection and any veto by creditors are covered to ensure that he is able to have the confidence of creditors

7) Do you agree with the proposals for how to treat the costs of the

moratorium?

It is correct to seek to ensure that those who trade with the business during the moratorium are adequately protected. However provision of such protection may be at the expense of other creditors, particularly secured creditors who hold a floating charge. As previously noted there is a risk that losses incurred during the moratorium period may lead to an impairment of the creditors’ positions. Given that one of the conditions to enable an application for a moratorium is the availability of funding for that period, the potential for unpaid costs to exist at the end of the moratorium suggests that this condition has not been met. It must be considered whether in such circumstances it is correct that secured or other creditors should meet those costs, or whether they should be met from those responsible for the trading, via insurance or a bond.

8) Is there a benefit in allowing creditors to request information and should the

provision of that information be subject to any exemptions?

The provision of information to creditors is important to give creditors an overview of the procedure and help them gain confidence in the process. However the provision of such information must be balanced against the cost of its provision and to ensure that what is provided is of genuine value to creditors. We propose that in the moratorium creditors are provided with information, but that it should be prescribed in both its contents and frequency to prevent creditors from adding additional cost to the process without generating additional value from the information that is provided. There is a real danger that the provision of information may become a distraction from the primary focus in the moratorium period.

A Review of the Corporate Insolvency Framework: a consultation on options for reform

Any intention to extend this proposed provision to current insolvency procedures should be balanced against the additional costs that may be added to those procedures, particularly where information may be requested by creditors who may not be the stakeholders who are bearing such costs. There should be safeguards put in place to prevent creditors who have no stake in the process from requesting information to frustrate the process or (for example from competitors) to serve their own agendas. This may have a detrimental effect where there is a sale of the business being attempted in an insolvency process.

Helping Businesses Keep Trading through the Restructuring Process

9) Do you agree with the criteria under consideration for an essential contract,

or is there a better way to define essential contracts? Would the continuation

of essential supplies result in a higher number of business rescues?

The protection of businesses by enabling them to compel critical suppliers to

provide goods or services required for the continuation of trade will be of benefit to

many businesses seeking to restructure. We believe that providing an open

definition of what constitutes an essential supply will both enable the court to

determine this on the basis of the circumstances of the case in case of challenge,

and future proof legislation against changes brought by technology or other market

forces which may create new essential utilities.

10) Do you consider that the Court’s role in the process and a supplier’s ability to

challenge the decision, provide suppliers with sufficient safeguards to ensure

that they are paid when they are required to continue essential supplies?

It is possible that the designation of a supplier as essential may prove onerous to

them, should they wish to reassign their resources to more profitable or potentially

longer term trading partners, and that the cost of challenging the matter in court

restricts their rights.

It is not confirmed in the proposal is whether or not the continued supply will be on

the same terms as was made prior to the moratoriums or whether the supply will be

able to change those terms.

As previously noted the operation of this proposal will be dependent on access to

the court at reasonable cost, and within acceptable timeframes, which requires

additional sufficient court resources to facilitate this. It is not made clear what

would happen if the supplier refused to provide goods or services, notwithstanding

A Review of the Corporate Insolvency Framework: a consultation on options for reform

their designation as essential. It would not take very long before such non supply

would cripple a trading business, so court intervention would have to be almost

immediate, if it was to be of help.

Also, contemporary supply chains often cross borders, and involve companies from

other jurisdictions. Is it envisaged that such suppliers could be compelled to

continue to provide goods or services?

Developing a Flexible Restructuring Plan

11) Would a restructuring plan including these provisions work better as a standalone procedure or as an extension of an existing procedure, such as a CVA?

The CVA procedure was first brought in as part of the 1986 Act, and its practices have been established and confirmed over time by case law. It is a mature procedure which is well understood by creditors and companies, and therefore the addition of a change to enable the binding of all creditors to a restriction plan, and to enforce the will of the majority against a minority of dissenting creditors would be sensible to operate as an extension of a CVA. In addition, the availability of a moratorium prior to a CVA would give the time and capacity to formulate a plan that would be acceptable to all creditors and we believe would lead to greater use of the CVA procedure.

12) Do you agree with the proposed requirements for making a restructuring

plan universally binding in the face of dissention from some creditors?

If dissenting creditors would not be worse off under the restructuring than they would have been in a liquidation, then making a restructuring plan binding would make little difference to them. The issue which will be most difficult, and which will need to be carefully implemented, will be determining which creditors can be deemed to have an economic stake and which do not.

13) Do you consider the proposed safeguards, including the role of the court, to

be sufficient protection for creditors?

As stated above we believe that the proposed safeguards including the role of the court will provide sufficient creditors protection against the cram-down of their rights. In addition, we believe that secured creditors whose security has no value given the existence of more senior secured creditors should be prevented from blocking a restructuring plan, and should be treated in a similar way to unsecured creditors.

A Review of the Corporate Insolvency Framework: a consultation on options for reform

14) Do you agree that there should be a minimum liquidation valuation basis

included in the test for determining the fairness of a plan which is being crammed down onto dissenting classes?

The valuations which are used by the court to ensure the creditors are not prejudiced by the use of a cram-down procedure will be of great importance, and we support the development of a set of consistent bases of valuations which can be used not only in these circumstances, but across a wider range of insolvency processes, in order that creditors can obtain greater information from, and confidence in such valuations. Valuations are however subjective and theoretical exercises and do not always result the forecast outcome so some caution is required here.

Rescue Finance

15) Do you think in principle that rescue finance providers should, in certain circumstances, be granted security in priority to existing charge holders, including those with the benefit of negative pledge clauses? Would this encourage business rescue?

As is noted in chapter 10 of the proposals on rescue finance, the structure of UK

borrowing is different to many other countries who have more widespread

availability of rescue finance. In particular, the customary UK use of floating charges

which cover all or significantly all of the assets of the company inhibit the seeking

of rescue finance for a troubled business. In practice, companies who are in a

position to require a moratorium have few if any unpledged assets, and the value

of the pledged security is frequently approached or even exceeded by borrowings

against those assets.

Although a negative pledge clause may inhibit further lending in some cases, in

practice most lenders who hold a floating charge lend to a greater degree than

would otherwise be the case. There is a real risk that should lenders believe that

the assets backing their lending may be primed by rescue finance providers, they

may factor this into their calculations when making finance available to companies.

Consequently there may be a knock on reduction in lending facilities, which may do

more harm to troubled businesses.

16) How should charged property be valued to ensure protection for existing

charge holders?

A Review of the Corporate Insolvency Framework: a consultation on options for reform

If super priority is to be given to providers of rescue finance, then existing security holders must be protected via a prudent valuation of the assets which the existing lender has a charge over, in determining whether there is equity. We suggest that the liquidation valuation basis which is been suggested for creditors in a cram-down could be utilised to provide a prudent basis in determining whether or not there is equity available for rescue finance to be pledged against.

17) Which categories of payments should qualify for super-priority as ‘rescue

finance’?

By providing for the costs of the moratorium (including trading costs) to be met as an expense, those costs are already being given super-priority. The Government should exercise caution before permitting priority over existing lending, due to the possibility that such lenders may seek to reduce perceived exposure to any payments that may end up being given priority over the repayment of their debt.

Impact on SMEs

18) Are there any other specific measures for promoting SME recovery that

should be considered?

The SME community are an integral part of the UK economy, and of great importance to it. Due to the interdependence of the business and its owners, in many cases help is only sought at a later stage, after a restructure outside insolvency becomes impossible. In part this is also due to cost, in our opinion the existing small company moratorium available prior to a CVA is underutilised not only because of the inability to bind secured creditors, but also because of the cost of procedure relative to the size of the firm. This adverse factor will be shared by any moratorium process. In addition, we do not consider that the widening of the pool of expertise to SMEs will necessarily be helpful, as the specialist knowledge and advice provided by insolvency practitioners, and the licensed and regulated nature of their profession provides additional safeguards over those offered by accountants or solicitors who have not obtained additional qualification as an insolvency practitioner. The general lack of SME director expertise in restructuring means they are in particular need of proper advice on all options.

A Review of the Corporate Insolvency Framework: a consultation on options for reform

Do you have any other comments that might aid the consultation process as a whole? Comments on the layout of this consultation would also be welcomed.

In seeking to enable rescue finance, one source of funding that does not appear to have been considered is the equity of the company. By allowing creditors to take an equity stake in the company in recompense for providing finance to the company, or for accepting a write down of their debt, this may assist in finding a restructuring solution.

Thank you for taking the time to let us have your views. We do not intend to acknowledge receipt of individual responses unless you tick the box below.

Please acknowledge this reply

At BIS we carry out our research on many different topics and consultations. As your views are valuable to us, would it be okay if we were to contact you again from time to time either for research or to send through consultation documents?

X Yes No

0010023-0016973 BK:36524673.2 1

1. Introduction

(a) Allen & Overy LLP is a global law firm headquartered in London with operations across Europe, the

U.S, Asia, Africa and Australasia. Our restructuring practice is a global practice acting on a wide

range of domestic and international restructuring and insolvency transactions for debtors, creditors,

sponsors, insolvency practitioners and other stakeholders. Our market tends to be large and complex

cross-border transactions and we are rarely involved in situations involving small and medium sized

enterprises.

(b) We set out below a summary of our comments followed by more detailed responses to the specific

questions set in the consultation.

2. Summary comments

(a) We welcome the opportunity to consider the current UK insolvency regime framework, in particular

in relation to companies on the verge of financial difficulty. Although the business rescue culture is

a well-established part of UK insolvency and restructuring practice and there are some very useful

statutory tools available to UK and foreign companies that can fall within the UK’s broad

jurisdiction, other jurisdictions, particularly in Europe, are busy updating their restructuring regimes

(often mirroring certain elements of the UK regime) and it is clearly important that the UK

continually considers how its own regime can be further improved. The existing UK corporate

insolvency regime is flexible, effective and internationally well-regarded. We also note that the

variety of formal and informal insolvency process in the UK, including contractual/consensual

workouts, CVAs, schemes of arrangement and administrations preserve the necessary flexibility for

a distressed company to negotiate and implement bespoke arrangements in order to best preserve

value for all of its stakeholders. We consider therefore that a strong case needs to be made for any

legislative change particularly those of the magnitude set out in the consultation.

(b) The four proposals in the consultation are high level and would represent a material change to the

UK restructuring and insolvency regime. The detail of formal legislative proposals will need careful

consideration before they can proceed to implementation. The proposals address a range of issues

that may arise for companies in financial difficulty, but will not necessarily be relevant in each

situation. The problems faced by small and medium sized enterprises in financial difficulty are

different from those faced by large businesses and some proposals will be more relevant for one or

the other.

(c) For large corporate restructurings we consider that the ability to effect “cross-class” cram-down of

out of the money creditors could improve the current regime. However, we don't consider the need

for and benefit of the other proposals to be as clear in large corporate restructurings.

(d) The moratorium, supply of essential services and the rescue financing proposals are, to some extent,

inter-dependent. The moratorium arguably necessitates the proposals in respect of the supply of

essential services and rescue financings. The moratorium proposal should also be considered in the

wider context of how finance is provided to companies and how different stakeholders would react

to the introduction of a moratorium. In the context of large corporate restructurings we do not

consider this proposal to be necessary and, if implemented, would represent a very debtor friendly

shift in the legal framework with insufficient protections for creditors.

(e) The proposals regarding the supply of essential services are, in the context of large corporate

restructurings, not necessary and, in our view, the existing framework for the supply of essential

services (which has only been extended relatively recently) is sufficient. Applying the regime to a

0010023-0016973 BK:36524673.2 2

potentially very broad range of suppliers, however big or small, could have a disproportionate effect

and very robust protections would be required in order to render the proposal balanced as between

the interests of the debtor and its suppliers. In particular, trade suppliers (who are often small and

medium sized enterprises not well placed to absorb losses and increased risk) should not be forced to

incur further credit risk on a financially distressed company. To the extent this is to be introduced

certain contracts will also need to be excluded particularly those contracts relating to the provision of

funding or hedging transactions.

(f) The UK has, to some extent, lead the way in promoting a rescue culture for companies in or

approaching financial distress. CVAs, schemes of arrangement and administrations all offer

companies with a large degree of flexibility to rescue their businesses either pre-insolvency or

quickly through an insolvency process.

(g) Schemes of arrangement have developed naturally over time – their use now is far more prevalent

and covers far more situations than it would have done even 5 years ago, for example. There is a

clear gap in the scheme legislation, however – cross-class cram-down is not possible even for out of

the money stakeholders. We therefore consider a new procedure similar to a scheme but with such a

mechanism permitted would provide a useful restructuring tool.

(h) The rescue finance proposal raises a number of issues that would need to be worked through before a

proposal could be fully considered and we have concerns that adding such a regime to the existing

statutory framework could have unintended consequences. In addition, the need for such rescue

financing arrangements in the context of large corporate restructurings has not, in our view, been

demonstrated so as to justify the potential interference with the rights of secured creditors.

(i) We do have additional concerns that the complexity of the four proposals will not address the

problems with the current statutory regime for small and medium sized enterprises in financial

difficulty.

(j) Finally, we note that the consultation was issued prior to the outcome in the European Referendum

and the UK’s decision to leave the EU. It is too early to tell yet what impact this will have on

European legislation such as the European Regulation on Insolvency Proceedings. Until it is known

what “exit model” the UK will be pursuing, it would seem premature to adopt a new business rescue

tool that is intended to have the benefit of EU recognition.

3. The introduction of a new moratorium to help business rescue

(a) Do you agree with the proposal to introduce a preliminary moratorium as a standalone

gateway for all businesses?

General observations

As discussed above, our experience of the UK corporate insolvency regime centres around larger

businesses with complex financing arrangements and multiple stakeholders. We question whether

the proposed moratorium would benefit such businesses, given the current framework and in

particular the rights of lenders to take enforcement action and the risks to lenders that taking

enforcement action could result in significant losses for all stakeholders. Security enforcement

generally requires an instruction from a significant majority of creditors (typically 66.6% in a bank

syndicate and 25% in a bond issue). The broad support required for such enforcement action against

large companies often necessitates early dialogue between groups of creditors and a financially

distressed company but also reduces the likelihood of action by small groups of hostile creditors.

Infringing the rights of secured creditors, particularly in circumstances where management may no

longer be trusted to run the business prudently, must be considered very carefully. One potential

option would be for secured creditor consent to be obtained before a moratorium could be sought.

0010023-0016973 BK:36524673.2 3

Moreover, trade creditors often base their lending decisions on different criteria to high yield bond

lenders or syndicated bank lenders and generally lend on shorter contractual terms with greater

flexibility to reduce or pull credit lines. Again, the flexibility of trade creditors to pull their credit

lines incentivises a financially distressed company to enter into early negotiations with such creditors

or to demonstrate that negotiations with its other long-term creditors are progressing. The proposed

statutory moratorium risks unintentionally minimising the importance of such early negotiations as

the directors and the company have a statutory ‘fallback’ procedure to rely on in the face of

threatened creditor action. This position has the potential to incentivise lenders, and in particular

trade finance suppliers, to pull lines earlier and more aggressively at the first signs of financial

distress in an effort to avoid being ‘caught’ by a potentially lengthy moratorium. This could

incentivise a ‘rush to the exit’ on the part of trade creditors in particular and the opportunities for the

company to engage in consensual negotiations with creditors (which are often necessarily complex

and lengthy) could be greatly reduced. In our experience, in larger business restructurings, the focus

is on the capital structure and often trade creditor arrangements are left unaffected.

It is our experience that the process of agreeing contractual standstill arrangements between a

company and (certain) of its creditors is in itself proof of positive action being taken by a company

in financial distress. Even if a contractual standstill is not signed, de facto standstill arrangements are

not unusual in the market and often provide a stable platform from which to negotiate a wider

restructuring of the company’s financial indebtedness. A statutory moratorium process would almost

certainly involve some degree of ‘stigma’ for the company which would in itself reduce the

likelihood of existing financing arrangements continuing following the moratorium period. Along

with the risks of a ‘rush to the exit’ outlined above, this would incentivise a company to enter into a

moratorium before discussions with (certain) creditors began. This would reduce trust between

stakeholders, effectively mandating an exit from the moratorium by way of a more formal process,

such as a CVA, scheme of arrangement or administration. Trust with creditors would be further

reduced given that a moratorium of this nature inherently prefers shareholders over creditors as the

rights of creditors are compromised for a potentially long period while a financially distressed

company is enabled to continue trading where it otherwise may not have been able to do so. On these

grounds and given the increasing complexity of financing structures, a statutory moratorium

mechanism seems to us to be a blunter and more aggressive tool than the existing option to negotiate

a contractually-based standstill between (certain) creditors.

Specific considerations

The proposed moratorium needs further detail in relation to the following areas, which will raise

difficulties in the context of a large financial restructuring:

1. Protections for set-off, netting and financial collateral will be required in relation to the proposed

moratorium.

2. The treatment of creditors with rolling debts (such as those lenders under RCF/working capital

facilities) will need to be clarified. Would a rolling debt automatically expire (or be rolled) during

the moratorium period? In either situation, the liquidity position of the company could be affected

during the moratorium, which in itself would impact the proposed criteria for continuing the

moratorium.

3. The new concepts of directors’ liability need to be considered in detail. As discussed below, the

current moratorium proposals to reduce potential directors’ liability should be reviewed extremely

carefully to avoid potential unintended consequences.

4. As discussed below, the role of the supervisor should be defined carefully and striking the correct

balance between the company and creditors will be crucial to the success of the proposed

moratorium.

0010023-0016973 BK:36524673.2 4

5. The role of the court in the proposed moratorium should be clearly defined, particularly in relation to

any tests that must be applied by the court to enter/exit/continue the moratorium. The proposal seeks

to balance enough court involvement to police the process adequately and engender confidence

among all stakeholders, but while limiting court involvement so as not to make the procedure

prohibitively cumbersome and expensive, waste precious costs and stakeholder time. The detail of

what the court is bound to consider in relation to the moratorium procedure will affect how well this

balance is struck.

6. The eligibility requirements that engage the proposed moratorium should not be unnecessarily

restrictive. In particular we suggest the availability of a moratorium should not be limited to UK

incorporated companies or EEA incorporated companies with their centre of main interests in an

EEA state (assuming of course that these concepts remain relevant following the outcome of the

European referendum). We would suggest instead that further consideration is given to the eligibility

criteria of the moratorium, perhaps giving the English Court jurisdiction to grant a moratorium based

on the ‘sufficient connection test’ which is currently used when approaching schemes of

arrangement.

7. There is a separate issue regarding the recognition of the proposed moratorium outside of the UK. In

restructurings of the size and complexity envisaged by the proposals there is likely to be some cross

border aspect to the business being restructured.

(b) Does the process of filing to court represent the most efficient means for gaining relief for a

business and for creditors to seek to dissolve the moratorium if their interests aren’t

protected?

The process of filing to court is an efficient means for a company to obtain such wide-ranging relief

against its creditors. However, preparing the documentation required for such an application is likely

to be an intensive and time consuming process. In practice, we suggest that a company is likely to

have consulted at least a subsection of its creditors before applying to court and that this will add to

the cost and time required to initiate a moratorium. For larger businesses, we would expect some

degree of stakeholders being made aware of a pending application. The option for creditors to

challenge the moratorium in a court hearing provides a robust mechanism for challenge but is

weighted in favour of the debtor. Creditors would need to expend time and resources challenging

any moratorium. For example, a company will need to plan for any potential creditor challenge that

may be made in court during the moratorium period. Because the proposed moratorium is so wide-

ranging, this will mean that a company is forced to plan a response to all of its creditors. This has the

potential to make the preparation for a moratorium application more onerous than a contractual

arrangement that targets certain creditors only.

The current proposal allows a company to apply for the relief of a moratorium without giving prior

notice to any creditor and does not allow for creditors to challenge the moratorium before it becomes

effective and the challenge period is limited to the first 28 days of the moratorium period. For

creditors with short-dated instruments or with imminent maturity dates and for those creditors who

provide ‘essential supplies’, this proposal drastically reduces certainty of rights in relation to any

company in financial or possible financial distress. We see this as potentially problematic,

particularly for companies whose financial condition is tied to volatile or cyclical markets, such as

commodities.

The proposal as drafted is very debtor friendly.

(c) Do the proposed eligibility tests and qualifying criteria provide the right level of protection for

suppliers and creditors?

0010023-0016973 BK:36524673.2 5

The proposal states that the company must demonstrate that it ‘is already or imminently will be in

financial difficulty, or is insolvent’. While this seems a sensible test for a moratorium, providing a

definition in statute for this eligibility will prove extremely difficult. Any attempt to impose a

statutory requirement for a valuation, for example, will reduce the speed and efficacy of the

moratorium relief and will impose greater costs on companies. Additionally, it will be difficult for a

company to prove that it has ‘sufficient funds to carry on its business during the moratorium,

meeting current obligations as and when they fall due as well as any new obligations that are

incurred.’ If this test remains as drafted then it is likely that companies in the most severe need of the

benefit of a moratorium are likely to be unable to satisfy the test because they may have payment

defaults outstanding or expect potential payment defaults during the moratorium period. Similarly,

while the ‘no creditor worse off’ test is a test seen in other jurisdictions, we query how will the test

be framed and at what times and against what comparator are creditors’ rights compared.

The final qualifying condition for the moratorium, that ‘at the outset there is a reasonable prospect

that a compromise or arrangement can be agreed with its creditors’ seems to reduce the potential

benefits of the moratorium. For directors to reach such a conclusion for large businesses with

complex capital structures, some degree of consultation would almost certainly had to have occurred.

In such circumstances, those creditors are unlikely to wish to give up rights without having

negotiated some form of agreement, much as is the case under the current system. However, because

of the ‘no creditor worse off’ and ‘sufficient funds tests’ and because of the wide ranging nature of

the moratorium, almost all, if not all, creditors will need to be consulted prior to the moratorium

application. This will mean that the negotiation for a moratorium may in fact be more onerous than

for a contractual standstill and involve a number of inter-creditor negotiations which would be

unnecessary for a contractual standstill.

Finally, the process for the supervisor to monitor the qualifying conditions during the moratorium is

likely to be costly and time consuming, particularly in circumstances where a company is in

financial distress.

(d) Do you consider the proposed rights and responsibilities for creditors and directors to strike

the right balance between safeguarding creditors and deterring abuse while increasing the

chance of business rescue?