A Report On Internship at Global IME Bank Limited (Gyaneshwor Branch

42

A Report On Internship at Global IME Bank Limited (Gyaneshwor Branch) Submitted to Pitamber Lamichhane Faculty of Management Pokhara University Submitted by Sumit Kumar Shah 1

Transcript of A Report On Internship at Global IME Bank Limited (Gyaneshwor Branch

A Report

On

Internship at Global IME Bank Limited(Gyaneshwor Branch)

Submitted to

Pitamber Lamichhane

Faculty of Management

Pokhara University

Submitted by

Sumit Kumar Shah

1

December, 2013

ACKNOWLEDGEMENT

This report has been prepared to fulfill the partial

requirement for the degree, Bachelors of Business

Administration in Banking and Insurance (BBA-BI) 6th

semester of Pokhara University. For this, I would like to

acknowledge the effort of Apex College for offering such a

great program to enhance the research skill and quality of

management education.

Working with this report has been very interesting. I am

forever indebted to all those who gave me valuable

suggestions, stimulating ideas, constructive comments and

encouragements throughout this report writing. First of all,

I am deeply indebted to my supervisor Mrs. Manisha Shah and

Mrs. Rebha K.C for their time and effort in my internship

period at Global IME Bank, Gyaneshwor, and for their

invaluable advice and consultations, during the analysis and

overall processes of writing this report. Their constructive

comments and assistance was vital to how this report looks

today.

2

Special thanks and appreciation goes to my respected sir Mr.

Prabhakar Pokharel, from Customer Service Department.

Without his encouragement and advices, I could not have

performed well at the branch and so does with the report

writing.

Sincere thanks to all staffs and employees of Global IME

Bank, Gyaneshwor branch. Without their coordination, this

report would not have been complete.

Thank you very much to all of you for your kind cooperation,

inspiration and for providing information.

EXECUTIVE SUMMARY

This research study is done with the main purpose of

analyzing closely the first hand experience of my internship

and to forward the gained experience towards the person

eager to know about the internship program as well as its

idea. This report tries to explore the every single aspect

3

of an internship and about the intern. This report will also

give light to the performance of the selected commercial

banks in regards to the selected internship destination.

The report is organized in four parts/chapters, where each

chapter deals with distinct subject matter under one

purpose. The first chapter is about the internship program,

objective of doing the internship as well as the limitations

faced at the place. The chapter two is all about the bank

(Global IME Bank Ltd.) its values, missions along with its

products and services available in the market. After

following chapter two, chapter three deals with the major

internship experience, SWOT analysis of the bank followed by

the branch/department analysis (Gyaneshwor Branch). The

report will end up by a brief summary of the overall report

along with conclusion and some recommended suggestions as a

part of the internship evaluation of the branch.

4

ABBRIVIATIONS

ATM : Automated Teller Machine

BBA-BI : Bachelor in Business Administration for Banking and Insurance

BOD : Board of Directors

CBS : Core Banking Solution

CSD : Customer Services Department

ECC : Electronic Check Clearing

FAU : Financial Advisory Unit

FD : Fixed Deposit

FTR : Financial Transaction Report

GBL : Global Bank Limited

GIBL : Global IME Bank Limited

HRM : Human Resource Management

IME : International Money Exchange

LC : Letter of Credit

MF : Mutual Fund & Micro Finance

NPN : National Payment Network

NRB : Nepal Rastra Bank

OD : Over Draft

PG : Personal Guarantee

5

PL : Personal Loan

POS : Point of Sale

SWIFT : Society for Worldwide Interbank Financial Telecommunication

SME : Small Medium Enterprises

TABLE OF CONTENTS

ABBRIVIATIONS

ACKNOWLEDGEMENT

EXECUTIVE SUMMARY

Contents

Page no.

Chapter 1Introduction to Internship

7-10

1.1 About Internship 7

1.2 Organization Selection

8

1.3 Objectives of Internship

8

1.4 Limitations of Internship 9

6

1.5 Placement and Duration

9

Chapter 2Global IME Bank Limited

11-19

2.1 Bank Overview 11

2.2 Promoters and Shareholders Structure

12

2.3 Vision, Mission, and Values13

2.3.1 Vision 132.3.2 Mission 132.3.3 Core Values 13

2.4 Board of Directors BOD 13

2.5 Financial Highlights `

14

2.6 Branch Workforce and Services Offered

142.6.1 Branch Workforce (Gyaneshwor)142.6.2 Products and Services Offered15

2.7 Current and Future Planning17

Chapter 37

Internship Experience 19-24

3.1 Overview 19

3.2 SWOT Analysis 20

3.2.1 Strength 213.2.2 Weakness 223.2.3 Opportunities 223.2.4 Threats 23

3.3 Departmental/Branch Analysis 24

Chapter 4Summary, Conclusion and Recommendations

25-27

4.1 Summary 25

4.2 Conclusion 26

4.3 Recommendations 27

References

8

CHAPTER ONEINTRODUCTION TO INTERNSHIP

1.1 About Internship

Bachelor in Business Administration for Banking and Insurance

(BBA-BI) is a specialized stream offered by Pokhara

University and its major emphasis of its subject matter is

hence given towards the study of the fundamentals of these

two industries i.e. Banking and Insurance. The course BBA-BI,

within its predefined period has number of theoretical

subject matters along with a practical learning aspect called

Internship compulsory to be completed for the achievement of

the degree in BBA-BI. It has provided a practical platform

for developing creative side of students in the specialized

field of banking as well as in insurance.

During the program, students are required to prepare a report

in every semester, which in turn has helped the students to

develop their analytical skills through practical basis. The

internship provides the students a chance to work in the

reputed organizations, where the students can implement their

theoretical knowledge in the real situation. This has helped

9

the students to experience the actual job situation and is

also a type of the job training.

Internship is the short period activity performed by the

candidates from various educational backgrounds to work and

to learn at the same time while they are provided eligibility

by the concerned officials or authority. In my case, my

college, Apex College, has issued a kind of letter stating

the nature of internship on my behalf so that I can be

eligible.

Practical based knowledge is very necessary to cope up with

the external environment. In other words, internship has been

a window to the outer world. And that is why internship has

been a wonderful experience for me. It is the medium through

which I get the chance to apply my theoretical knowledge into

the realistic field. It is obvious that only the theoretical

knowledge is not sufficient to tackle with real time

problems. So to update with knowledge, practical knowledge is

very necessary.

In my internship period, I have utilized all my efforts in

creating an excellent impression towards my mentors and my

supervisor along with collecting as much information and

ideas as I could from the first hand experience. It was a

wonderful opportunity indeed to do field work and learn from

it which has a great deal in my career life.

10

1.2 Organizational Selection

The maximum focus of the program BBA-BI is on the banking and

financial institution analysis. Since it is the centre point

of my study background, I have decided to carry my internship

at a reputed financial institution from the Kathmandu

locality. From amongst different banks and other financial

institution, I favourite Global IME Bank Limited in this

regard. It is so because, the bank has recently merged with

two other financial institutions as well as it is one of the

oldest and strongest banks in Nepal.

After deciding the bank to do my internship, I have complied

with all other essential procedures along with the documents

required to drop a request letter at the corporate office of

the bank. The Human Resource Manager (HRM) has then referred

me to Gyaneshwor branch. I have started to work at the given

branch the day after tomorrow I got the permission letter

from the HR Manager of GIBL, Mrs Anamika Singh, from the date

29th July, 2013.

1.3 Objectives of Internship

The foremost important objective of internship is to apply

the theoretical education into practical field to bridge the

gap of understanding about the subject matter. On the other

hand, followings are the cited objectives of my internship;

11

Get the attention from the supervisor and other officials

by complying with the stated rules, regulations of the

institution and outperforming the expectation of them.

To be familiar with the real work environment of banking

sector.

To recognize the whole operational mechanism of the

banking industry.

Considerate the customers desires as a service seekers

and the methods to fulfil such urges.

To analyse the core strength as well as weakness of

Global IME Bank and at the same time opportunity and

threats prevailing in the banking sector.

The application of theoretical knowledge into practical

implication and gain experiences.

1.4 Limitations

This report was being prepared while my internship was in

effect. Thus, any kind of limitations are the direct result

of the limitations form my on going internship program. Some

of the limitations are presented here;

Detailed analysis of the operations of the bank was not

available due to the restrictive bank policies for the

interns.

Although most of the operational areas of the branch are

covered, still some central banking procedures are not

12

fully participated and practiced due to the internship

time constraint.

Some data such as branch operating costs, rental expenses

etc. could not be reached due to the policies of the

bank.

As far as possible, the report will provide with enough

materials to understand about the bank and its operations

and will explore about my internship experience.

1.5 Placement and Duration

My internship period was of eight weeks (29th July – 29

September). Within this time frame, I was placed at

different departments of the branch. Since my study

background is quit similar with my internship destination,

it gave me the major advantage to learn and adapt with the

banking culture and to act like one of their own.

Eight weeks are not sufficient enough to understand the

whole operating mechanism of the bank, though I have managed

to integrate with the various placements within the limited

time. These eight weeks of internship had really been

noticeably knowledgeable and fruitful for me to gain at

least brief understanding of the modern banking business.

Followings are the departments where I have worked and

explored about:

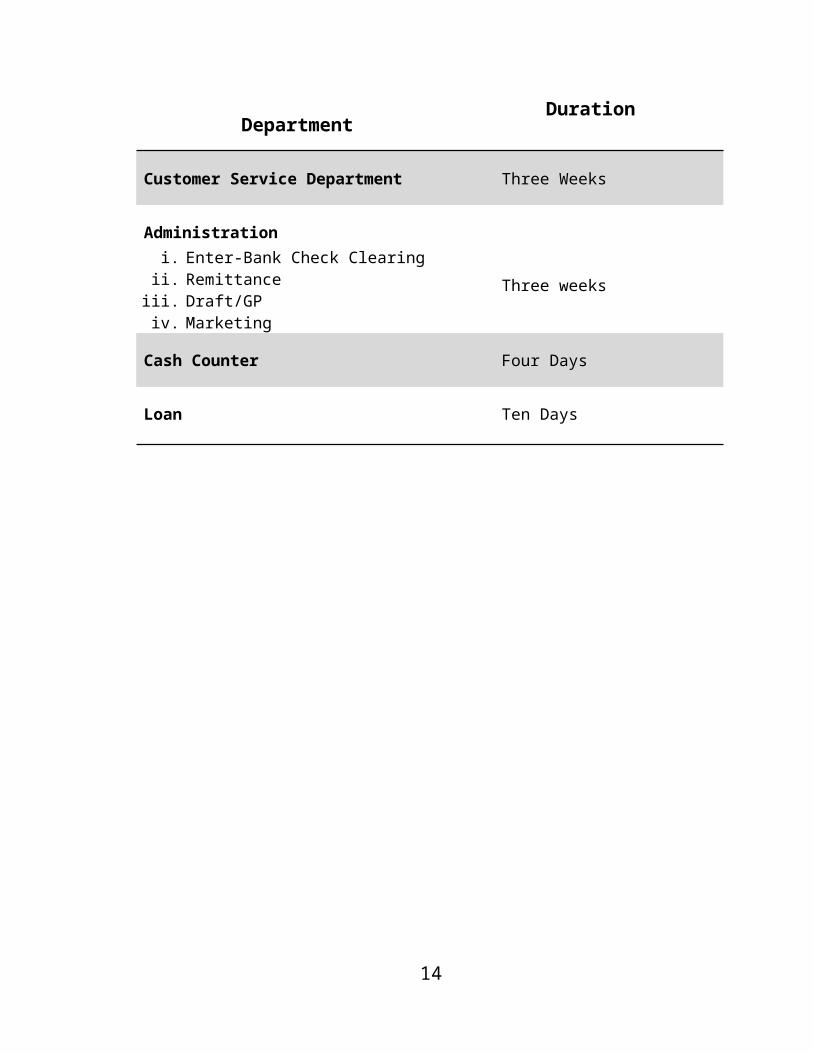

13

DepartmentDuration

Customer Service Department Three Weeks

Administrationi. Enter-Bank Check Clearingii. Remittanceiii. Draft/GPiv. Marketing

Three weeks

Cash Counter Four Days

Loan Ten Days

14

CHAPTER TWOGLOBAL IME BANK LIMITED

2.1 Bank Overview

Global Bank Limited (GBL) was established in 2007 as an ‘A’

class commercial bank in Nepal which provides entire

commercial banking services. The bank was established with

the largest capital base at the time with a paid up capital

of NPR 1.0 billion. The paid up capital of the bank has

since been increased to NPR 2.25 billion. The bank’s shares

are publicly traded as an ‘A’ category company in the Nepal

Stock Exchange.

The current name of the Bank, Global IME Bank Ltd., is

emerged after successful merger of Global Bank Ltd (an “A”

class commercial bank), IME Financial Institution (a “C”

class finance company) and Lord Buddha Finance Ltd. (a “C”

class finance company).

Pursuant to the liberalized economic policy of the

government, majority of the commercial banks have

established their head office in the Kathmandu valley.

Witnessing the incredible potential the country offers

outside the capital, the promoters have established the bank

in Birgunj, the commercial hub of the nation. It is in line

15

with the aim of the bank to be “The Bank for All” by giving

necessary impetus to the economy through world class banking

service.

For the day to day operations, the bank has been using the

world renowned FINACLE software that provides real time

access to customer database across all branches and

corporate locations of the bank. This state of the art

customer database has also been linked to a Management

Information System that provides easy reach to all possible

database information for balanced and informed decision

making. A disaster recovery system (DRS) of the Bank has

also been established in the Western Region of Nepal (200

KMS west of Kathmandu).

The bank has been able to achieve excellent diversification

of its assets. A well balanced distribution of exposure in

areas of national interest has been possible through long

term forecasting and timely strategic planning. The bank has

diversified interests in hydro power, manufacturing,

textiles, services industry, aviation, exports, trading and

microfinance projects, just to mention a few.

The exemplary performance of the bank in these last five

years has elevated it to a premier status in the industry.

The bank has been handling government transactions and is

officially among the only 5 banks in Nepal to do so. The

bank has been able to earn the trust and confidence of the

16

public, which is reflected in the large and ever expanding

customer base of the bank. Through all this the bank has

been able to truly achieve its vision of being “The Bank for

All”. Even with all this success, the bank remains

internally focused towards manpower development, product

innovation and process innovation etc. to have a strong and

solid foundation, which are ongoing and continuous

improvement initiatives undertaken by the management and

staff alike.

2.2 Promoters and Shareholders Structure

GBL has been promoted by a group of prominent indigenous

entrepreneurs who have written a history of success in their

field of ever growing business. The promoters of the bank

include renowned, well established and respected

businessmen/industrialists in Nepal from a variety of

different sectors that include finance, remittance, trading,

export, automotive services, manufacturing, media services

and hydropower to name a few. The collective experience of

the promoters have been realized to customize the bank’s

offerings and services to compete with best in the banking

industry and instill a culture based on our core values of

integrity, business ethics, teamwork, respect, humility,

professionalism, loyalty and good governance.

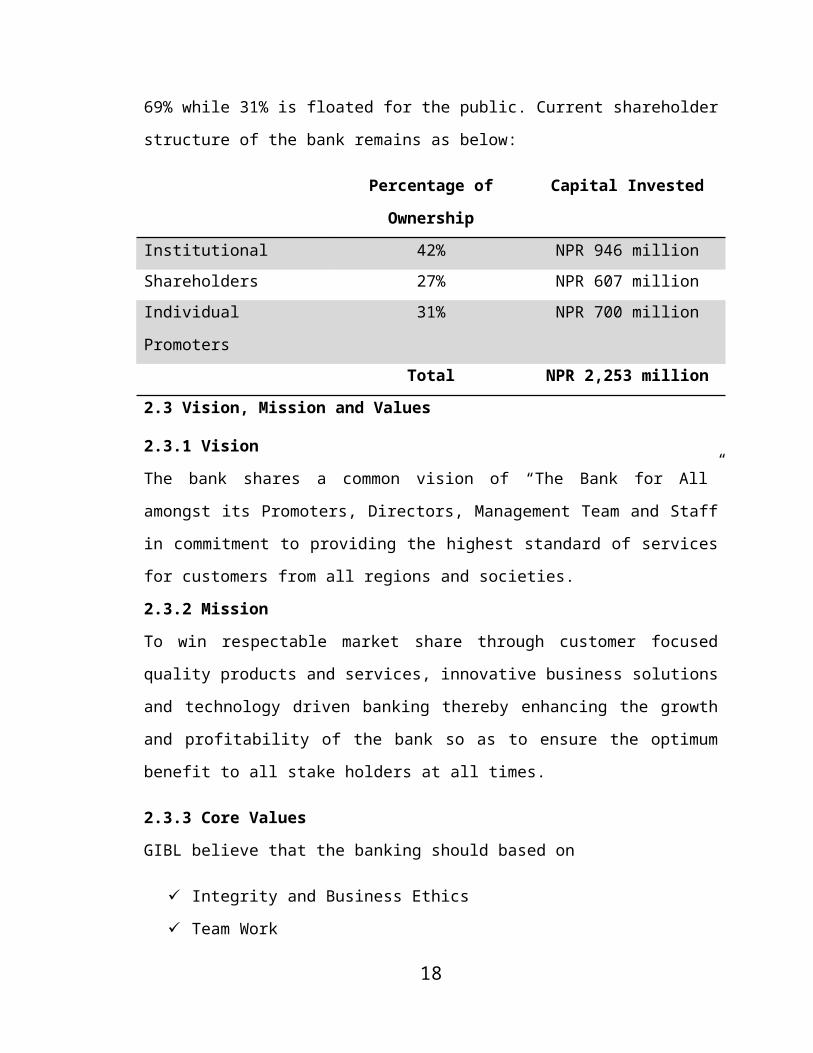

Authorized Capital of Global IME Bank is NPR 3,000 million

and Paid up Capital is NPR 2,253 million. The promoters hold

17

69% while 31% is floated for the public. Current shareholder

structure of the bank remains as below:

Percentage of

Ownership

Capital Invested

Institutional 42% NPR 946 millionShareholders 27% NPR 607 millionIndividual

Promoters

31% NPR 700 million

Total NPR 2,253 million

2.3 Vision, Mission and Values

2.3.1 Vision

The bank shares a common vision of “The Bank for All”

amongst its Promoters, Directors, Management Team and Staff

in commitment to providing the highest standard of services

for customers from all regions and societies.

2.3.2 Mission

To win respectable market share through customer focused

quality products and services, innovative business solutions

and technology driven banking thereby enhancing the growth

and profitability of the bank so as to ensure the optimum

benefit to all stake holders at all times.

2.3.3 Core Values

GIBL believe that the banking should based on

Integrity and Business Ethics

Team Work

18

Respect and Humility

Professionalism

Good Governance

Loyalty

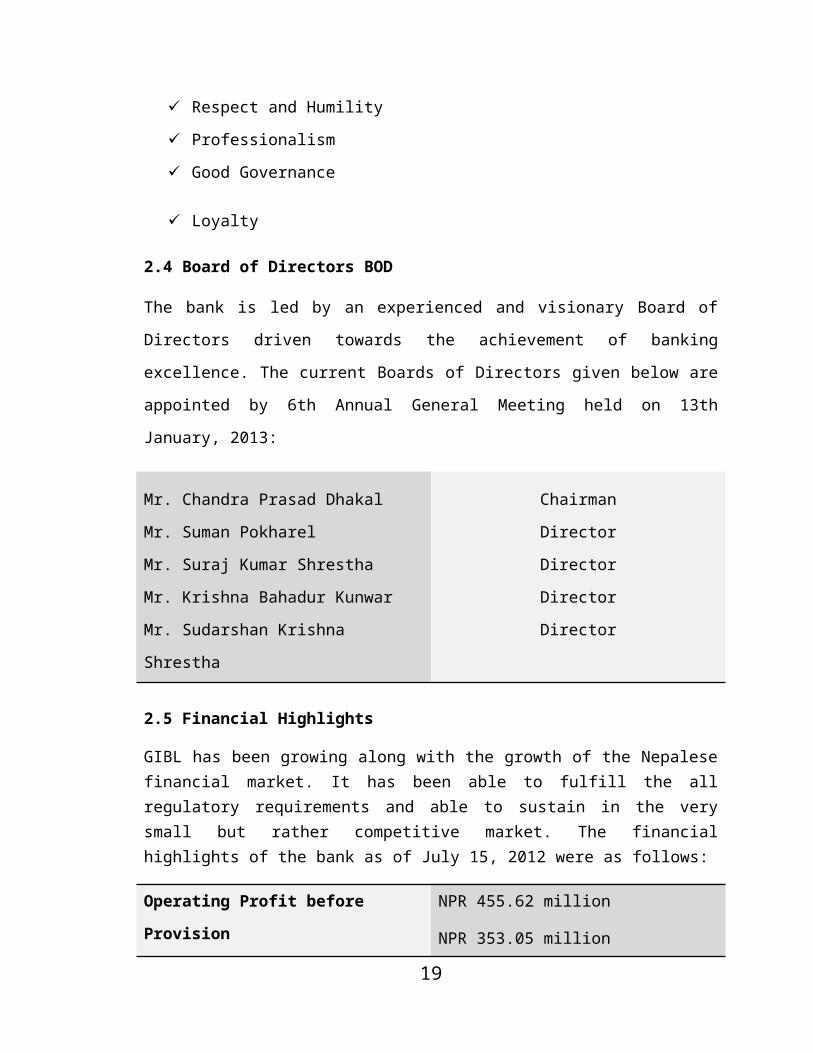

2.4 Board of Directors BOD

The bank is led by an experienced and visionary Board of

Directors driven towards the achievement of banking

excellence. The current Boards of Directors given below are

appointed by 6th Annual General Meeting held on 13th

January, 2013:

Mr. Chandra Prasad Dhakal

Mr. Suman Pokharel

Mr. Suraj Kumar Shrestha

Mr. Krishna Bahadur Kunwar

Mr. Sudarshan Krishna

Shrestha

Chairman

Director

Director

Director

Director

2.5 Financial Highlights

GIBL has been growing along with the growth of the Nepalesefinancial market. It has been able to fulfill the allregulatory requirements and able to sustain in the verysmall but rather competitive market. The financialhighlights of the bank as of July 15, 2012 were as follows:

Operating Profit before

Provision

NPR 455.62 million

NPR 353.05 million

19

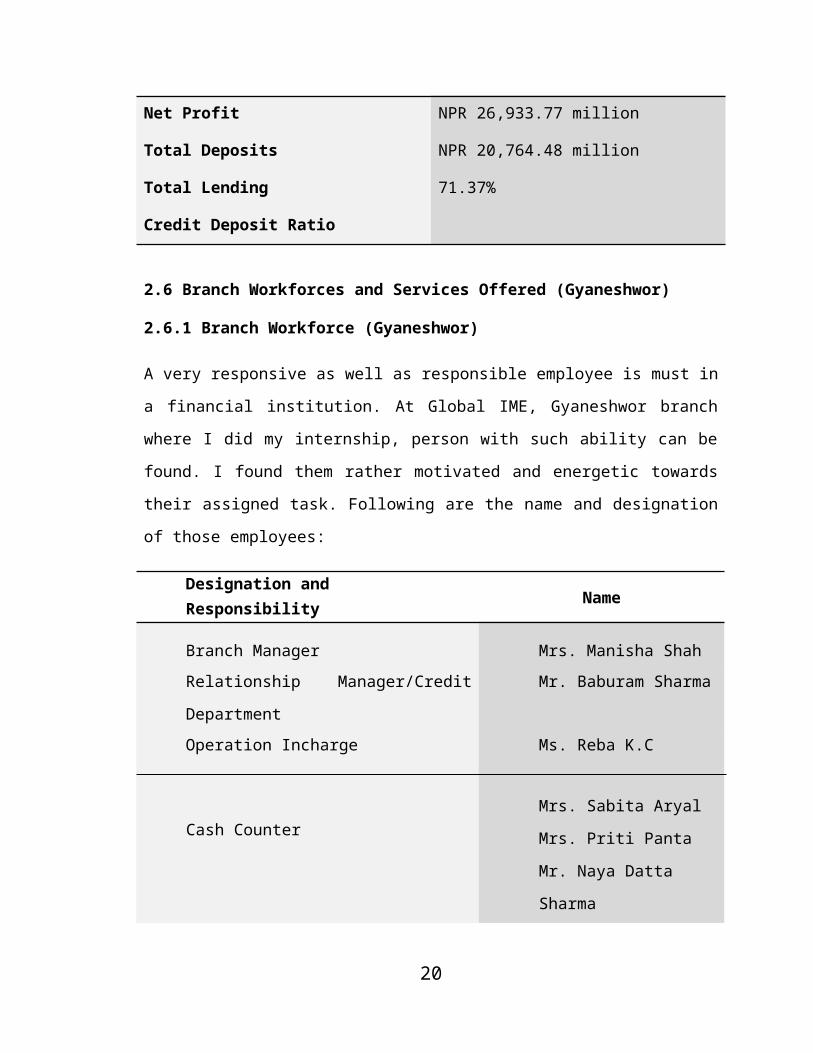

Net Profit

Total Deposits

Total Lending

Credit Deposit Ratio

NPR 26,933.77 million

NPR 20,764.48 million

71.37%

2.6 Branch Workforces and Services Offered (Gyaneshwor)

2.6.1 Branch Workforce (Gyaneshwor)

A very responsive as well as responsible employee is must in

a financial institution. At Global IME, Gyaneshwor branch

where I did my internship, person with such ability can be

found. I found them rather motivated and energetic towards

their assigned task. Following are the name and designation

of those employees:

Designation and Responsibility Name

Branch Manager Mrs. Manisha ShahRelationship Manager/Credit

Department

Mr. Baburam Sharma

Operation Incharge Ms. Reba K.C

Cash CounterMrs. Sabita Aryal

Mrs. Priti Panta

Mr. Naya Datta

Sharma

20

Customer Service Department Mr. Prabhakar

Pokharel

Inventory Department Mr. Bikash

Shrestha2.6.2 Product and Services Offered

The bank offers a complete range of banking products in

deposits, lending, trade finance and remittances. The bank’s

deposit product portfolio encompasses customer tailored

saving deposits, fixed deposits, call and current deposits.

The lending product portfolio includes commercial loan

products such as demand loans, cash credits, overdrafts,

trust receipts and term loans, whereas a complete portfolio

of personal and retail credit products are also provided by

the bank. Non-fund based products such as bank guarantees

and letters of credit are also available to the bank’s

customers.

2.6.2.1 Deposit Products

Saving Deposit Products ofGIBL are given below:

Global Super Savings Global Savings Plus Global Subhlabh Bachat Global Nari Bachat Global Students Saving

Account

Global Future Star Deposit

Global Senior Citizen Account

Global karmachari Bachat Global Janmabhumi Bachat Global Remittance Deposit

Khata Global Normal Savings Foreign Currency Savings

Deposit Account

21

Fixed Deposit Products ofGIBL are as follows:

Global Karmachari Awakas Muddhati Khata

Global General Fixed Deposit

Current Deposit Accounts ofGIBL are cited below:

Global Current Deposit Global Convertible

Foreign Currency Current Deposit Scheme

2.6.2.2 Loans and Advances

GIBL offers the following types of Consumer/Personal Loans: Global Home Loan Global Auto Loan Global Hire Purchase Loan Global Education Loan Global Mortgage Loan

(Personal) Loan Against Fixed

Deposit (FD)

Global IME Bank has a special loan product under small business:

SME Loan

GIBL has the following types of Corporate Loans:

Followings are the funded facilities offered by GIBL; Fixed Term Loan Working Capital Loan Overdraft

Import Credit Export Credit

Demand Loan Cash Credit

Revolving Non-Revolving

Pledge LoanGIBL provides following

types of Non Funded

Loan/Trade Services:

Letter of Credits (LC)

Import LC Export LC

Guarantees

Bid Bond Guarantees Performance Bond

Guarantees Advance Payment

Guarantees

Documentary Collection

2.6.2.3 Remittance

Global IME Bank is

providing fastest, most

reliable and most secured

22

remittance facilities of

domestic remittance through

its wide network of more

than 200 locations.

Domestic Remittance

Global Remit IME Remit

Outward Remittances

Swift Bank Draft

Indian Rupee Draft Arrangement

FCY Draft Arrangement

Managers Cheques Anywhere Branch BankingServices

23

2.6.2.4 Other Services

Along with the above products and services, GIBL has been

able to deliver the followings:

Mobile Banking

E-Banking

ATM VISA Cards

Online Payment System

Branchless Banking

SMS Banking

Apart from this, the bank has more than 32 National Payment

Networks (NPN) and 7 member banks throughout the country

along with more than 35 ATM locations inside the Kathmandu

valley and more than 40 ATM locations outside the Kathmandu

valley.

24

2.6.2.5 Outward Clearing Transaction Maintenance

The clearing of checks drawn by the customers first go

through the Electronic Check Clearance (ECC) device. The

image captured by the device shows the actual and exact

physical presence. Each check clearance cost rupees 2 to

rupees 5 to the bank and takes about a day or two for fund

transfer to payees account. The check is transfer to more

than one party, they are i) bank upon who the check is

presented, ii) clearing house of Nepal Rastra Bank, and iii)

the bank of whose check is presented.

2.7 Current and Future Planning

Increasing lending to the small businesses segment and to

agriculture sector has remained the prime target of Global

IME Bank. Separate products aiming these segments to lend

from Rs. 50 thousand to Rs. 500 thousand has already been

implemented by the bank. Customers are attracted to these

schemes as is anticipated. It believes in giving the best

contribution for the development of agriculture sector as

well through this product. In both of these products,

insurance coverage is correspondingly provided against

accidental death as well as incapacitation due to terminal

dieses. This has remained a big attraction.

Going forward, in line with the vision of the bank ‘The Bank

for All’, the following areas are on the priority for

execution /continuation in the following year.

25

To continue with expansion of small business loan and

agricultural loan. A new Branch in Nepalgunj Pushpalal

Chowk is recently opened with the objective to provide

special attention on agricultural loan.

To improve on the accretion of savings deposit portion in

deposit mix. The change in the deposit mix has been very

much instrumental in better management of banks’

resources. Efforts are underway to improve proportion of

the current and savings deposits, for which emphasis is

being provided with due planning in handling remittance

and other major sources of saving deposits.

To continue effort is also being provided to improve the

quality of consumer and business loan. Increasing focus

is also provided in acquiring due market share in export

business. Global has become the first bank to have

initiated providing export financing against refinance

facility received from Nepal Rastra Bank.

To continue mobile banking, internet banking and card

related services with enhanced technological facilities.

Customers using out mobile banking services have crossed

50 thousand and is increasing.

To extend branchless banking facility in rural areas

where banking service is not yet available. The bank has

already started Branchless Banking services from

26

Mainapokhara of Bardia District. This program is targeted

to expand to other places throughout the country.

To continue participation in micro finance (deprived

sector) activities. In partnership with 9 other financial

institutions, altogether, they are preparing to set up a

separate micro-finance institution. Preliminary approval

has been received from Nepal Rastra Bank to establish the

same in Nuwakot.

Study is being made to establish a separate Financial

Advisory Unit under the Credit Department to provide

financial advisory services as well as technical advices

to small and medium enterprises/projects.

Mutual Funds project shall be initiated as is mandated by

the last annual general meeting amending the object

clause. Application requesting for approval has already

been submitted to the regulatory authority. Since this

would also require assistance of merchant banking

activities, probable investment in a feasible entity has

been thought of.

27

CHAPTER THREEINTERNSHIP EXPERIENCES

3.1 Overview

It is very essential to select the good organization for

internship. When my internship period was near I was in

confusion where to apply, how to apply, whether I will get

opportunity or not and many other questions were arising

inside my head. Instead of these obstacles, I knew what

field is most appropriate for my background of study. And

then I made up my choice of doing the internship at Global

IME Bank near my location.

I got the approval from the bank to become the intern. I was

placed in Gyaneshwor branch. During the 2 months internship

period, I have gone through every single department along

with its activities in-depth.

It was Customer Service Department from where I have

commenced my first day of internship. Here, I learned

following tasks:

Balance Inquiry

Statement Request

All sorts of filings

Cheque book issuance and compiling

28

Register Maintenance

Document scanning and emailing

Application and letter writing for inside and outside

purpose

Filling forms and studying the forms and application

Customer requests and inquiries handlings etc.

While I shifted to the loan administration department, I

didn’t leave the rest of my day sitting at the desk. Loan

department, from my perspective, is the much complex place

of any bank. Here, I took my time by understanding the

almost every general procedure of loan administration

procedure. I came to apply my theoretical knowledge with

empirical practice. I learned loan documentation, loan

review, loan enquiry, loan guidelines reviews and many

others. I also studied some of the files of home loan,

vehicle loan, overdraft, letter of credit and bank guarantee

in the credit department. I also helped to make the

documents required for the loan departments, typing some

documents as requested by the branch officials.

With the reasonable guidance of the bank officials and my

supervisor, I have achieved my each single objectives as

well as motives I have expected from my internship program

at the Global IME Bank. This two month internship really

helped me to develop managerial and interpersonal skills of

29

my own. I was able to learn the bank culture, work

environment and working procedure of Global IME Bank.

I have also realized that two months is not good enough to

meet overall knowledge of banking business, but these two

months of internship had really transformed me and my

thinking capacity along with this it was very knowledgeable

and energizing for me to get the chance to do my internship

at Global IME Bank.

I am also happy with performance at the bank in this due

time period. I am glad knowing that every single bank

officials have appreciated my way of doing the tasks as well

as supported me and encouraged me for what I was doing. It

was really great deal for me to engage with banking

activities with the qualified and interesting members of the

Global IME Bank.

3.2 SWOT Analysis

SWOT is an acronym used to describe the particular strength,

weakness, opportunity and threats and is strategic factors

for a specific company. SWOT analysis should not only result

in the identification of corporation ‘s distinctive

competency-the particular capabilities and resources that

firm posses and the superior way in which that are used but

also in the identification of opportunities that the firm is

not currently able to take advantage of due to lack of

appropriate resources.30

Strength and weakness are related to the internal

environment of the organization while threat and

opportunities are related to the external environment. The

components of internal environment viz. organizational

strategy, culture, structure, labor unions, organizational

activities shows the strength and weakness of that

organization and these components are in hand of

organization’s control to some extent. Similarly, the

components of external environment that affects the

organization are physical environment, economic environment,

political/legal environment, technological environment,

global business environment, trade union environment etc.

(somewhat referred as PEST). The factors are not in the hand

of organization’s control and there is no way to change the

organization as per external environment to huge extent.

With the SWOT analysis it becomes easy for management to

know if a particular activity is cost effective in

comparison with competitors or competitive to its rivals in

terms of product differentiation. Thus, managers use

information derived from SWOT analysis to develop specific

and effective strategies. Effective strategies are ones that

exploit external opportunities and organization strengths

neutralize environment threats and protect or overcome

organizational weakness.

3.2.1 Strength

31

The services like e-banking, e-services, mobile recharge,

reliable services, diversified branches, services in the

rural areas are the major strength in the competitive

scenario. Similarly, highly dignified members in the BOD and

public trust towards bank are also the strength to the bank.

Some other strength aspects of the bank are:

A strong customer base, which includes depositors and big

institutional clients.

Experienced, trained and highly motivated staffs

Being the ‘A’ class financial institution and government

owned bank, customer feel secure with the bank.

Infrastructural and technological advancement as per the

need and demand of the global banking industry.

Along with the lower interest rate in the deposit as

compared to other institution, it has attracted the

customers.

In course of lending, GIBL provides the loan to the

customers with low service charge and interest rate as

compared to other institution.

3.2.2 Weakness

In the course of operation, each and every organization has

some weakness. The major indicator to measure the weakness

of any organization is the level of customer satisfaction

and dissatisfaction. The major weakness of GIBL is the

32

proper maintenance of CSD (help desk) and major complains

are linked with the CSD. As there is the proverb that:

“First impression is the last impression” but GIBL is unable

to maintain that. The structure as well as the furniture is

too traditional. But the bank is in continuous improvement.

Some other weaknesses are pointed as below:

Slow processing of documents due to which sometimes

customers are disappointed.

The bank has less numbers of ATM booths as compared to

the other financial institutions

The bank has less number of cash counters

It takes long time to provide the ATM to their customers

similarly the technical failure of the ATM system is

another heating problem

Bank (specifically the Gyaneshwor Branch) is not showing

keen interest for marketing strategies to foster their

products

3.2.3 Opportunities

Our country Nepal is a developing country and is in the pace

of developing. About only 25-30% people are touched with

banking activities. Rest 70% people are the source of

opportunities to the banks to bring them in touch. GIBL only

covers less than 40 districts of our country. So the

opportunities for this bank are unlimited but it just relies

33

on how to manage and diversify that opportunity. Higher

public trust towards bank acts as the precious stone for the

progress of the bank. Other opportunities of the bank are as

follows:

Capturing the market by taking advantage of weak

competition

Increasing demand of consumer loan

Service provided through the Branchless Banking System

where the bank has not been reached. This unique feature

has attracted the customers too

Innovation and technological advancement in today’s

scenario is another lucrative opportunity

Unity among the employee is the good sign of organization

as in the modern environment HR are taken as the sharp

weapon for competitive advantages

Retaining customers and providing quality assurance

3.2.4 Threats

Regular updating and ever changing technology come up with

threat. Likewise, lack of investment opportunities, unstable

political situation, decreasing flow of remittance because

of hundis are other threats for bank. However, the current

liquidity crisis, rising in value of dollars, illegal

34

markets are also acting as major threats. Similarly,

cooperatives etc. has been challenges for the banks because

they provides the loan with weak collateral and low interest

and take deposits providing high interest. Below points

oversees more about threats:

Entrance of international banks

Unstable socio-economic and political conditions of the

country, decreasing attractiveness of new investment

There is rise in number of financial institutions leading

to cut-throat competition in the domestic banking sector

Many local competitors

3.3 Department Analysis

Though the bank is trying to change as per the demand of

time and customer’s need, but the pace of development and

changing the structure and layout is too slow. Bank is

responding to the need of customers to some extend but

response rate is still slow. If it is to be continuing then

it may lead to the downgrading of that bank because the

competition is high in too small area. Thus, quick respond

towards the customer is more prominent.

35

In the course of my experience in the internship, I found

the staffs in the bank very much energetic and complying to

their responsibility the best possible way they could. Also

the CSD is the most tactical and humanistic place to work

provided the person I was with while at the CSD desk. Mr.

Prabhakar Pokharel, CSD department, has the all abilities

and skills to deal with all sorts of customers along with

assisting the other officials from the branch. He has been

able to deliver his instant service in any scenario and

cases it may or may not arise. The devotion of employees

towards their work, loyalty, co-working habit, friendly

behavior, less absenteeism has been the good aspects of all

I can expect.

Some due diligence is required at the operational level of

Gyaneshwor branch. In my course of internship, I have found

two huge mistakes and carelessness by the operation

department in check processing and FTR safe keeping.

Altogether, I found the branch and its every officials, a

very busy place and hardworking. They really are committed

towards the prosperity of the bank and growth of the banking

services as a whole.

36

CHAPTER FOURSUMMARY, CONCLUSION AND RECOMMENDATION

4.1 Summary

Global IME Bank- The Bank for All, has more than 63 years of

experience. With the noble guidance of board of directors

and combined efforts of the management and employees, the

bank has witnessed turnaround in different parameters i.e.

profitability, loan recovery, service quality including

system reform and modernization of the bank.

GIBL is committed towards the satisfaction of its customers

by providing modern banking facilities. At the same time,

the bank is equally committed to the economic growth and

development of the country. The bank aims to reach every

rural and urban corner of Nepal to accommodate the

requirement of people. The bank’s extensive branch network

and international connections are designed to transact

banking activity between any part of the country and any

part of the world. The bank has earned a glory of making

available the services to almost all the top business houses

of the country and it occupies one of the leading positions

37

among banks in Nepal. The bank is still pursuing to

accommodate as many clients as far as possible. It is always

committed to offer quality products and services to its

customers. All customers are treated with utmost courtesy as

valued clients. Besides, the bank is trying to establish the

lifelong relationship with the clients.

It was a nice experience of learning in such a short period

of time at GIBL, the chance to explore the real world

situation of the banking industry. I got the opportunity to

develop managerial and analytical skills. The experience is

really fruitful and it helps me to increase my horizon of

skills and knowledge and to build my confidence at work.

4.2 Conclusion

The internship of two months has provides with an immense

opportunities to explore the practical knowledge that was

confined with the bookish and theoretical knowledge. Some

conclusion driven from the internship experiences are listed

below in the following points:

38

This bank provides effective service to customer by using

all the modern technology like ATMs, SWIFT technology,

SMS banking etc.

Proper management of HR with variety of facility

available to personnel working in the organization.

Able to create strong impact upon customer by opening

more branches as well as branchless banking system.

Bank is maintaining good financial position although

providing lot of credit facility to customers to fulfil

their dreams.

Facilitating the rural areas of Nepal.

Providing and introducing new service and facility by

understanding the customer needs and wants.

4.3 Recommendation

39

It has been a great experience working at Global IME Bank at

Gyaneshwor branch, where I gained a lot practical knowledge

about banking activities and procedure that will help me in

near future. The whole activities of GIBL are appreciable

one but nevertheless I come up some glitches and the

personal recommendations for such glitches are provided

below:

Thus looking at the flow of customers, there should be

more cash payment counters. It is found that the

customers need to wait a long sometime for deposit and

withdrawals of cash.

The services and product of the bank are as per the

demand of customers. But lacking is that they should be

provided as quick as possible i.e. response rate should

be high

Although bank has stored all the documents and records

needed in the future for them but it need to be managed

properly

Provision for trainings are also recommended so as to

cope up with new sorts of difficulties found at the upper

level of the bank

Human Resource supervision as well as apprise process of

GIBL is rather unhealthy from the employee point of view.

The appraisal report should be prepared by the branch

40

manager of supervisor at high level authority rather than

from the head office by the person who does not even

visit the branch once in a month.

Above are some of my recommendations and suggestions for the

branch and the person who are responsible for managing the

concerned branch. Not to mention that, GIBL is the bank that

every one can count on for their financial security. As well

as, the bank has done major achievement in the due course to

advance its reach to the general public. I would like to

place my best of wishes for the success and prosperity of

Global IME Bank Limited.

REFERENCE

Web Sites

www.globalimebank.com

Books and Reports

Annual Report of Global IME Bank Ltd. 2012

41

42