A n alyst M e e t N o te Hindustan Unilever

10

Analyst Meet Note We attended HUL’s Annual Investor Meet ‘Winning in the new Decade’. The management re-emphasized its five fundamental growth pillars 1) Purposeful Brands 2) Improved Penetration), 3) Impactful innovations, 4) Design for Channel 5) Fuel for growth. HUL’s key focus on people, supply- demand, cost efficiency and technology is expected to accelerate growth and strengthen leadership position in most categories it operates in. We have introduced FY24E EPS at Rs 50.5 – implying 14% CAGR over FY21. We have upward revised our TP to Rs 3,032 (60x FY24E) and upgraded rating to Accumulate. Key highlights are as follows- WiMi- ‘Winning in Many Indias’ strategy classifies the country as 15 consumer clusters for distinctive product development, pricing and marketing. It helps to capture data and understand regional demand of product better and provides insights to develop different SKUs, packs and labels to meet customer need. The company has created 16 Country Category Business Teams (CCBT) which identified focus districts and focus portfolios for driving distribution, increasing penetration. WiMi strategy helped HUL understand demand shifts induced by reverse migration, resurgence of neighbourhood stores over supermarkets and growth of e- commerce during the pandemic. DART View WiMi strategy has remained a key driver in NPD’s and helped HUL gaining more insights about the consumer behaviour. We believe that the strategy would continue to help HUL to analyse pulse of consumer demand and penetrate deep in the domestic market. Structural drivers for domestic FMCG intact- Per capita consumption of FMCG in India is relatively low compared to 10x in Thailand, 6x in Philippines, 3x in China and 2x in Indonesia. Body wash is just 2% penetrated category, hair conditioner ~6%, facewash ~19%, Health food drink (~25%) implying huge headroom for growth. Moreover, while ~61% of the population is in rural, share of rural consumption is low ~31%, implying tremendous scope for penetration. Favourable demographics, higher disposable income, rise in internet users, changing lifestyles will further drive growth. DART View In the long run, we believe that the penetration of niche categories would improve. HUL, being dominant player in the domestic consumer market, is likely to grow faster in low penetrated categories with the help of its vast distribution network. FINANCIALS (Rs Mn) Particulars FY20A FY21A FY22E FY23E FY24E Revenue 387,850 459,960 509,018 556,497 618,323 Growth (%) 1.5 18.6 10.7 9.3 11.1 EBITDA 96,000 113,240 126,513 144,065 164,692 OPM (%) 24.8 24.6 24.9 25.9 26.6 PAT 69,350 81,810 90,064 103,133 118,739 Growth (%) 10.7 18.0 10.1 14.5 15.1 EPS (Rs.) 29.5 34.8 38.3 43.9 50.5 Growth (%) 10.7 18.0 10.1 14.5 15.1 PER (x) 95.2 80.7 73.3 64.0 55.6 ROANW (%) 85.9 28.7 18.8 21.0 23.6 ROACE (%) 93.3 27.1 16.9 19.0 21.3 CMP Rs 2,811 Target / Upside Rs 3,032 / 8% NIFTY 17,378 Scrip Details Equity / FV Rs 2,350mn / Rs 1 Market Cap Rs 6,604bn USD 89.9bn 52-week High/Low Rs 2,825/ 2,000 Avg. Volume (no) 1,437,540 Bloom Code HUVR IN Price Performance 1M 3M 12M Absolute (%) 18 18 32 Rel to NIFTY (%) 11 7 (18) Shareholding Pattern Dec'20 Mar'21 Jun'21 Promoters 61.9 61.9 61.9 MF/Banks/FIs 10.7 10.7 10.7 FIIs 14.9 15.0 15.1 Public / Others 12.5 12.5 12.2 HUL Relative to SENSEX VP - Research: Sachin Bobade Tel: +91 22 40969731 E-mail: [email protected] Associate: Nikhat Koor Tel: +91 22 40969764 E-mail: [email protected] 70 80 90 100 110 120 Sep-20 Oct-20 Nov-20 Dec-20 Jan-21 Feb-21 Mar-21 Apr-21 May-21 Jun-21 Jul-21 Aug-21 Sep-21 HUVR SENSEX Hindustan Unilever Accumulate September 10, 2021

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of A n alyst M e e t N o te Hindustan Unilever

An

aly

st M

ee

t N

ote

We attended HUL’s Annual Investor Meet ‘Winning in the new Decade’. The management re-emphasized its five fundamental growth pillars 1) Purposeful Brands 2) Improved Penetration), 3) Impactful innovations, 4) Design for Channel 5) Fuel for growth. HUL’s key focus on people, supply-demand, cost efficiency and technology is expected to accelerate growth and strengthen leadership position in most categories it operates in. We have introduced FY24E EPS at Rs 50.5 – implying 14% CAGR over FY21. We have upward revised our TP to Rs 3,032 (60x FY24E) and upgraded rating to Accumulate. Key highlights are as follows- WiMi- ‘Winning in Many Indias’ strategy classifies the country as 15 consumer clusters for distinctive product development, pricing and marketing. It helps to capture data and understand regional demand of product better and provides insights to develop different SKUs, packs and labels to meet customer need. The company has created 16 Country Category Business Teams (CCBT) which identified focus districts and focus portfolios for driving distribution, increasing penetration. WiMi strategy helped HUL understand demand shifts induced by reverse migration, resurgence of neighbourhood stores over supermarkets and growth of e-commerce during the pandemic. DART View WiMi strategy has remained a key driver in NPD’s and helped HUL gaining more insights about the consumer behaviour. We believe that the strategy would continue to help HUL to analyse pulse of consumer demand and penetrate deep in the domestic market. Structural drivers for domestic FMCG intact- Per capita consumption of FMCG in India is relatively low compared to 10x in Thailand, 6x in Philippines, 3x in China and 2x in Indonesia. Body wash is just 2% penetrated category, hair conditioner ~6%, facewash ~19%, Health food drink (~25%) implying huge headroom for growth. Moreover, while ~61% of the population is in rural, share of rural consumption is low ~31%, implying tremendous scope for penetration. Favourable demographics, higher disposable income, rise in internet users, changing lifestyles will further drive growth. DART View In the long run, we believe that the penetration of niche categories would improve. HUL, being dominant player in the domestic consumer market, is likely to grow faster in low penetrated categories with the help of its vast distribution network.

FINANCIALS (Rs Mn) Particulars FY20A FY21A FY22E FY23E FY24E

Revenue 387,850 459,960 509,018 556,497 618,323

Growth (%) 1.5 18.6 10.7 9.3 11.1

EBITDA 96,000 113,240 126,513 144,065 164,692

OPM (%) 24.8 24.6 24.9 25.9 26.6

PAT 69,350 81,810 90,064 103,133 118,739

Growth (%) 10.7 18.0 10.1 14.5 15.1

EPS (Rs.) 29.5 34.8 38.3 43.9 50.5

Growth (%) 10.7 18.0 10.1 14.5 15.1

PER (x) 95.2 80.7 73.3 64.0 55.6

ROANW (%) 85.9 28.7 18.8 21.0 23.6

ROACE (%) 93.3 27.1 16.9 19.0 21.3

CMP Rs 2,811

Target / Upside Rs 3,032 / 8%

NIFTY 17,378

Scrip Details

Equity / FV Rs 2,350mn / Rs 1

Market Cap Rs 6,604bn

USD 89.9bn

52-week High/Low Rs 2,825/ 2,000

Avg. Volume (no) 1,437,540

Bloom Code HUVR IN

Price Performance 1M 3M 12M

Absolute (%) 18 18 32

Rel to NIFTY (%) 11 7 (18)

Shareholding Pattern

Dec'20 Mar'21 Jun'21

Promoters 61.9 61.9 61.9

MF/Banks/FIs 10.7 10.7 10.7

FIIs 14.9 15.0 15.1

Public / Others 12.5 12.5 12.2

HUL Relative to SENSEX

VP - Research: Sachin Bobade Tel: +91 22 40969731

E-mail: [email protected]

Associate: Nikhat Koor Tel: +91 22 40969764

E-mail: [email protected]

70

80

90

100

110

120

Se

p-2

0

Oct-

20

Nov-2

0

Dec-2

0

Jan

-21

Fe

b-2

1

Ma

r-21

Ap

r-21

Ma

y-2

1

Jun

-21

Jul-2

1

Au

g-2

1

Se

p-2

1

HUVR SENSEX

Hindustan Unilever

Accumulate

September 10, 2021

September 10, 2021 2 Hindustan Unilever

Beauty & Personal Care segment (BPC) grew 70% during FY11-20. Six major brands (Dove, Lux, Ponds, Glow & Lovely, Clinic Plus+, Lifebuoy) accounted for > Rs 10bn turnover. There is significant headroom for growth in Skin cleansing segment- hand wash penetration stands at ~30%, face wash ~19%, while body wash is ~2%. HUL is driving penetration in rural India with its sachetization strategy, differentiated product mix and locally relevant communication. It is focused on market development and driving premiumization. eg. Launched Dove body wash with moisturizer to upgrade Soap users, addressing hair tangling issue by proposing ‘shampoo+conditioner’. For E-com channel, it has also introduced premium innovative products like Lakme sheet masks, TRESemme hair mask and hair serum. HUL is strengthening Naturals space through Indulekha, Glow& Lovely Ayurvedic cream, Love, Beauty& Planet, Lever Ayush toothpaste, etc. DART View We believe that HUL has higher brand loyalty in this segment compared to peers. The discretionary categories like skincare, deodorants, color cosmetics, which was severely impacted during Covid are likely to post strong growth on favourable base. In the long run, with brand investment and growing penetration, we believe that the BPC segment would grow faster. However, in the near term, the company is likely to witness few hurdles like lower demand from rural areas and increase in saving rate due to fears of third Covid wave. Home care segment- During FY11-20, turnover increased 2.3x. Surf excel and Rin are ranked #1 and #2 respectively in brand equity- fabric solutions, Vim tops in brand equity in Dishwash. HUL is focused on growing its core brands in Home care- Surf turnover is > Rs 50bn while Rin and Vim turnover crossed Rs 10bn. Mass, mid and premium segment contribution of laundry market is 72/14/14% respectively in volume terms. HUL has strong share in premium laundry segment (Surf Excel) 3.0x and mid segment (Rin, Sunlight) share is 1.6x, implying huge scope to drive penetration. HUL will be driving premiumization with detergent liquids and fabric conditioners, through its WiMi strategy. Liquids are under- penetrated category and fetch higher realization. In order to reduce plastic use , HUL has launched ‘Smart Fill’ machine for Surf excel liquid, Comfort and Vim gel. Customers are offered discounts on MRP as an incentive. DART View Innovation has remained a key in laundry for HUL in the past. Its entry in liquid, fabric conditioners and innovations across washing machine suitable products is helping the premium end grow faster compared to overall portfolio. Going ahead, we expect the premium portfolio to continue to register higher growth and enhance margins. Foods & Refreshment- Category penetration of Tomato Ketchup (40%), Coffee (27%), HFD (25%), Soups (7%), Peanut butter (1%) is very low, which offers opportunity for expansion.

Through impactful advertisements, HUL highlights the nutritional benefit of Horlicks and Boost. It has introduced high science based innovations like Horlicks Diabetes Plus and Women’s Plus considering lifestyle diseases in Indians. It aims to increase direct coverage and E-Com contribution 2x by Dec’21 and plans to reach 10x villages in 2021 vs 2019 through Shakti entrepreneurs.

To drive Out of Home consumption impacted by Covid, HUL tied up with Pizza Hut to add Kwality walls ice cream in its menu and partnered with delivery partner Swiggy and E-com channel- Amazon for ice cream sales. Ice cream cabinets are likely to increase 12x from 2015-25 ensuring accelerated availability.

September 10, 2021 3 Hindustan Unilever

HUL aims to drive growth and gain market share in tea through premiumization, expansion to health segments like green tea and upgrading consumers from loose to packaged tea.

Coffee category penetration in North is 17% while it is 87% in South. HUL has launched beaten Bru coffee in the North. It has launched premium filter coffee and Bru Veda in South.

Kissan Ketchup and Jam continue to be the market leader. HUL has introduced Kissan Peanut butter , Knorr Chicken Cubes recently to drive Foods segment.

By providing Unilever Food solutions to chefs in restaurants, HUL plans to tap seasonings/value added sauces (Rs 25bn market).

HUL has partnered with Sahyadri farms for tomato cultivation program which will help to maximize yield, reduce wastage, double farmers’ income by 2023 by crop planning and technological access.

DART View We believe that the Food business would continue to witness double digit growth in the long run driven by – (1) low penetration (2) changing consumer habits (3) favourable demographic mix (4) unorganised to organised shift. HUL being a dominant player in the foods business is likely to gain benefits from increase in demand. We continue to believe that the GSK portfolio has high potential and it would grow faster post normalization of domestic market. Further, GSK Consumer portfolio is margin accretive, we expect improvement in overall margins over the long run.

Strong Brand Portfolio

Source: DART, Company

GT and MT channel: The management indicated that while contribution of General trade is likely to come down going ahead, it will still remain a dominant channel due to familiarity, convenience and credit offered. However, GT needs to adopt technology to thrive. Modern trade which was impacted due to Covid, is likely to bounce back as mobility and vaccination picks up pace. Modern trade is yet to expand in Tier 2/3 towns. As part of its digitization journey, HUL runs the eB2B ordering app Shikhar, which currently has 6 lakh retailers on board and contributes to 10%+ orders. Through partnership with SBI, HUL is also working to provide easy access to affordable credit to small retailers.

September 10, 2021 4 Hindustan Unilever

DART View Going ahead, we believe that E-com and MT would grow faster considering lower penetrations of these channels. However, GT is likely to remain a key channel for the domestic consumer industry and the contribution would not decline significantly. Recent measures like tie up with JioMart are making HUL future ready to increase reach in the areas where it does not have direct connect. Hence, in the long run, HUL is likely to gain maximum benefit of change in channel dynamics. Margins to remain stable: Management alluded that tea prices are not likely to witness further inflation, crude and crude derivatives are stable. The company has taken judicious price increases in Q2FY22 across laundry, tea and skin cleansing portfolio. This, coupled with cost saving, premiumization and nutrition synergies is expected to result in 24-25% EBITDA margins.

DART View Over FY11-21 HUL was able to increase margins from 13.6% to 24.6%. This can be attributed to premiumization, brand strength which helped it to pass on prices, operational efficiencies and cost control measures. Going ahead, we believe that the company can further expand margins with the above measure and addition of high margin portfolios like GSK, Indulekha, etc. We believe that the premiumization and operational efficiencies would continue to remain dominant levers of margin expansion for HUL. Deflation in commodity prices would remain key and can boost margins, exceeding management expectation. Other highlights –

HUL has a wide and resilient portfolio of +50 brands across 15 categories, sold to ~8mn outlets. In the last decade, 16 new brands have been added. The company enjoys category leadership in 80% of the portfolio.

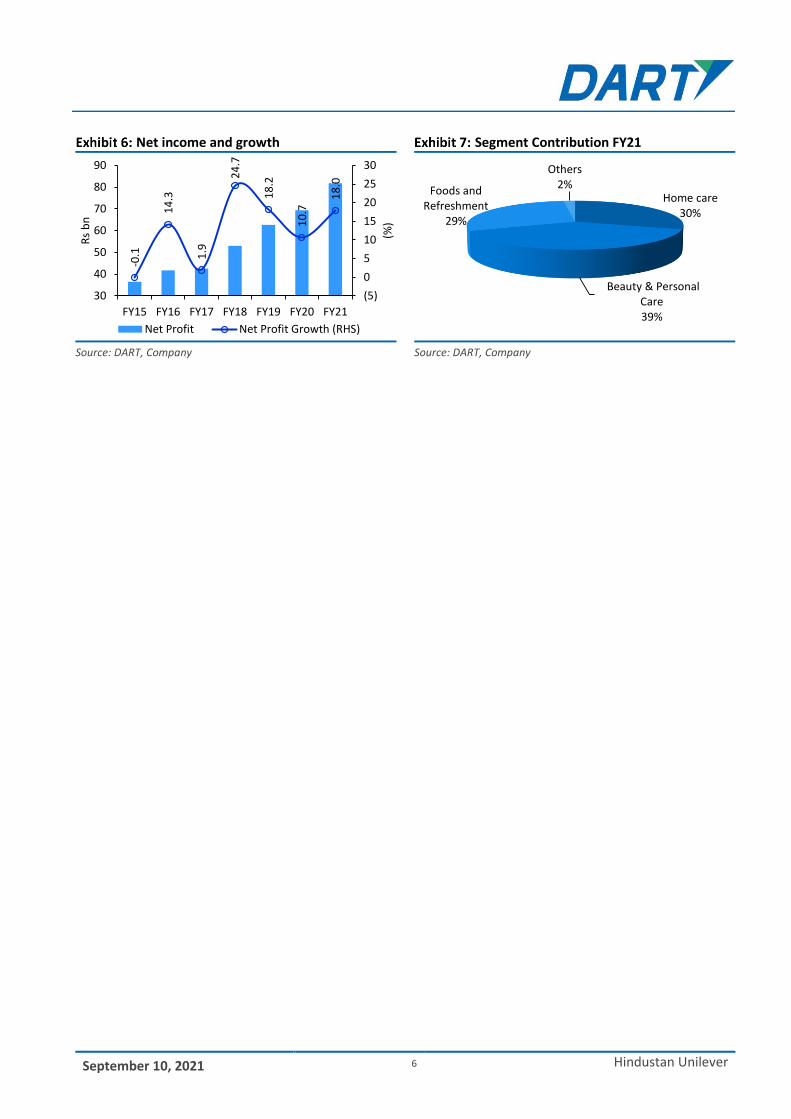

Revenue increased at a CAGR of 9% to Rs 460bn during FY11-21 despite demonetization, GST, rural slowdown and Covid-19. During the last decade, the company acquired Indulekha, Aditya Milk, VWash brand and most significant being Horlicks from GSK-Consumer Healthcare. Consequently, revenue share of F&R division increased from 19% in FY11 to 29% in FY21. Contribution of Beauty and Personal Care segment decreased from 51% to 40%, while that of Home Care segment stood at 31%.

During FY11-21, HUL maintained asset light business model (Capex 2% turnover), improvement in working capital and ROCE (Excl GSK merger) of 93%. It aims to build an intelligent enterprise by leveraging Data, tech & analytics, Leverage R&D expertise for superior products and ensure agility in supply chain for superior execution in market

It expects to deliver competitive growth ahead of peers, modest margin expansion which should aid double digit EPS growth for next decade.

Shakti entrepreneurs totalled 1.36 lakhs in 2020 – 2x from 2016 levels, and covering 18 states.

The management assured that its distributors remain extremely important for the company. It does not intend to rationalize its distributors, tie-up with Jiomart is to enhance direct reach.

September 10, 2021 5 Hindustan Unilever

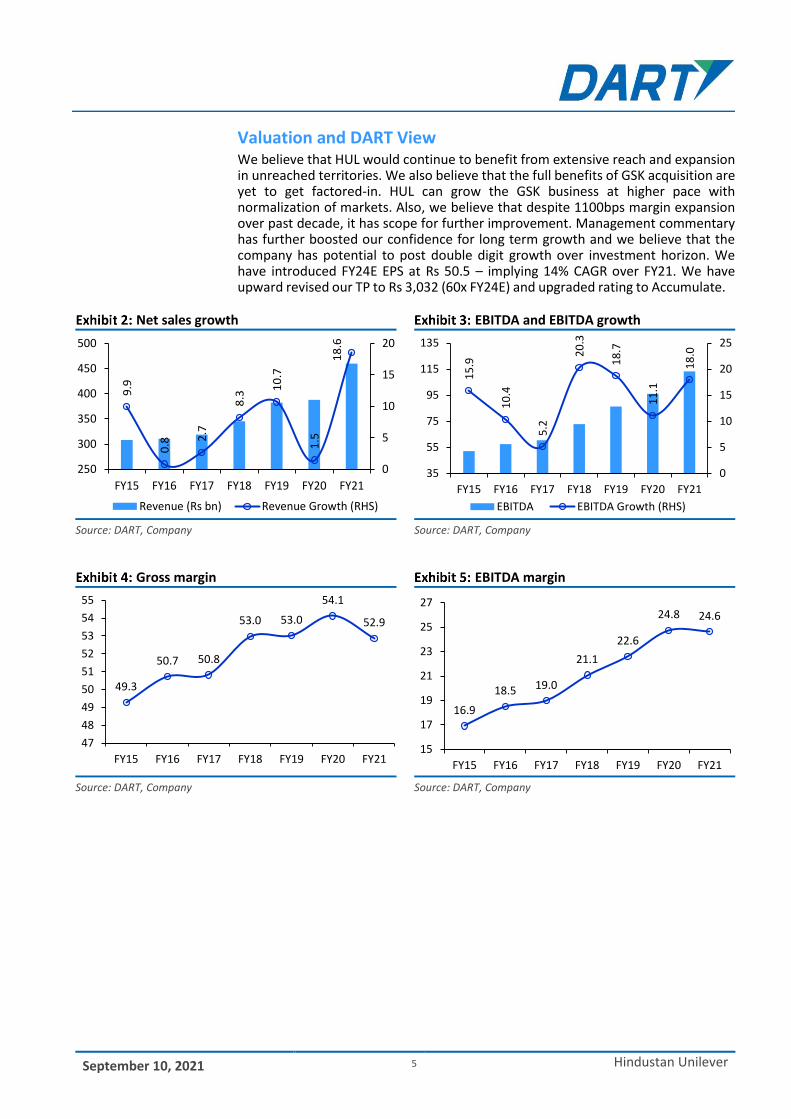

Valuation and DART View We believe that HUL would continue to benefit from extensive reach and expansion in unreached territories. We also believe that the full benefits of GSK acquisition are yet to get factored-in. HUL can grow the GSK business at higher pace with normalization of markets. Also, we believe that despite 1100bps margin expansion over past decade, it has scope for further improvement. Management commentary has further boosted our confidence for long term growth and we believe that the company has potential to post double digit growth over investment horizon. We have introduced FY24E EPS at Rs 50.5 – implying 14% CAGR over FY21. We have upward revised our TP to Rs 3,032 (60x FY24E) and upgraded rating to Accumulate.

Net sales growth EBITDA and EBITDA growth

Source: DART, Company Source: DART, Company

Gross margin EBITDA margin

Source: DART, Company Source: DART, Company

9.9

0.8 2

.7

8.3

10

.7

1.5

18

.6

0

5

10

15

20

250

300

350

400

450

500

FY15 FY16 FY17 FY18 FY19 FY20 FY21

Revenue (Rs bn) Revenue Growth (RHS)

15

.9

10

.4

5.2

20

.3

18

.7

11

.1

18

.0

0

5

10

15

20

25

35

55

75

95

115

135

FY15 FY16 FY17 FY18 FY19 FY20 FY21

EBITDA EBITDA Growth (RHS)

49.3

50.7 50.8

53.0 53.0

54.1

52.9

47

48

49

50

51

52

53

54

55

FY15 FY16 FY17 FY18 FY19 FY20 FY21

16.9

18.5 19.0

21.1

22.6

24.8 24.6

15

17

19

21

23

25

27

FY15 FY16 FY17 FY18 FY19 FY20 FY21

September 10, 2021 6 Hindustan Unilever

Net income and growth Segment Contribution FY21

Source: DART, Company Source: DART, Company

-0.1

14

.3

1.9

24

.7

18

.2

10

.7

18

.0

(5)

0

5

10

15

20

25

30

30

40

50

60

70

80

90

FY15 FY16 FY17 FY18 FY19 FY20 FY21

(%)

Rs

bn

Net Profit Net Profit Growth (RHS)

Home care 30%

Beauty & Personal Care 39%

Foods and Refreshment

29%

Others2%

September 10, 2021 7 Hindustan Unilever

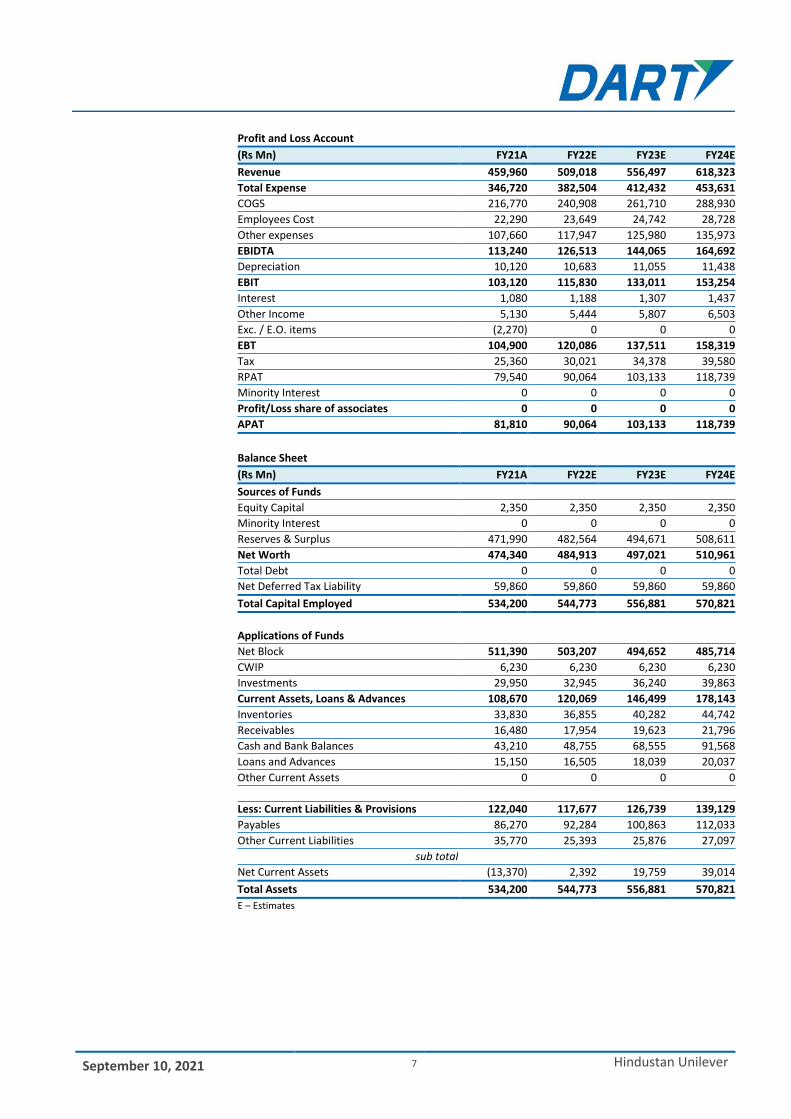

Profit and Loss Account

(Rs Mn) FY21A FY22E FY23E FY24E

Revenue 459,960 509,018 556,497 618,323

Total Expense 346,720 382,504 412,432 453,631

COGS 216,770 240,908 261,710 288,930

Employees Cost 22,290 23,649 24,742 28,728

Other expenses 107,660 117,947 125,980 135,973

EBIDTA 113,240 126,513 144,065 164,692

Depreciation 10,120 10,683 11,055 11,438

EBIT 103,120 115,830 133,011 153,254

Interest 1,080 1,188 1,307 1,437

Other Income 5,130 5,444 5,807 6,503

Exc. / E.O. items (2,270) 0 0 0

EBT 104,900 120,086 137,511 158,319

Tax 25,360 30,021 34,378 39,580

RPAT 79,540 90,064 103,133 118,739

Minority Interest 0 0 0 0

Profit/Loss share of associates 0 0 0 0

APAT 81,810 90,064 103,133 118,739

Balance Sheet

(Rs Mn) FY21A FY22E FY23E FY24E

Sources of Funds

Equity Capital 2,350 2,350 2,350 2,350

Minority Interest 0 0 0 0

Reserves & Surplus 471,990 482,564 494,671 508,611

Net Worth 474,340 484,913 497,021 510,961

Total Debt 0 0 0 0

Net Deferred Tax Liability 59,860 59,860 59,860 59,860

Total Capital Employed 534,200 544,773 556,881 570,821

Applications of Funds

Net Block 511,390 503,207 494,652 485,714

CWIP 6,230 6,230 6,230 6,230

Investments 29,950 32,945 36,240 39,863

Current Assets, Loans & Advances 108,670 120,069 146,499 178,143

Inventories 33,830 36,855 40,282 44,742

Receivables 16,480 17,954 19,623 21,796

Cash and Bank Balances 43,210 48,755 68,555 91,568

Loans and Advances 15,150 16,505 18,039 20,037

Other Current Assets 0 0 0 0

Less: Current Liabilities & Provisions 122,040 117,677 126,739 139,129

Payables 86,270 92,284 100,863 112,033

Other Current Liabilities 35,770 25,393 25,876 27,097

sub total

Net Current Assets (13,370) 2,392 19,759 39,014

Total Assets 534,200 544,773 556,881 570,821

E – Estimates

September 10, 2021 8 Hindustan Unilever

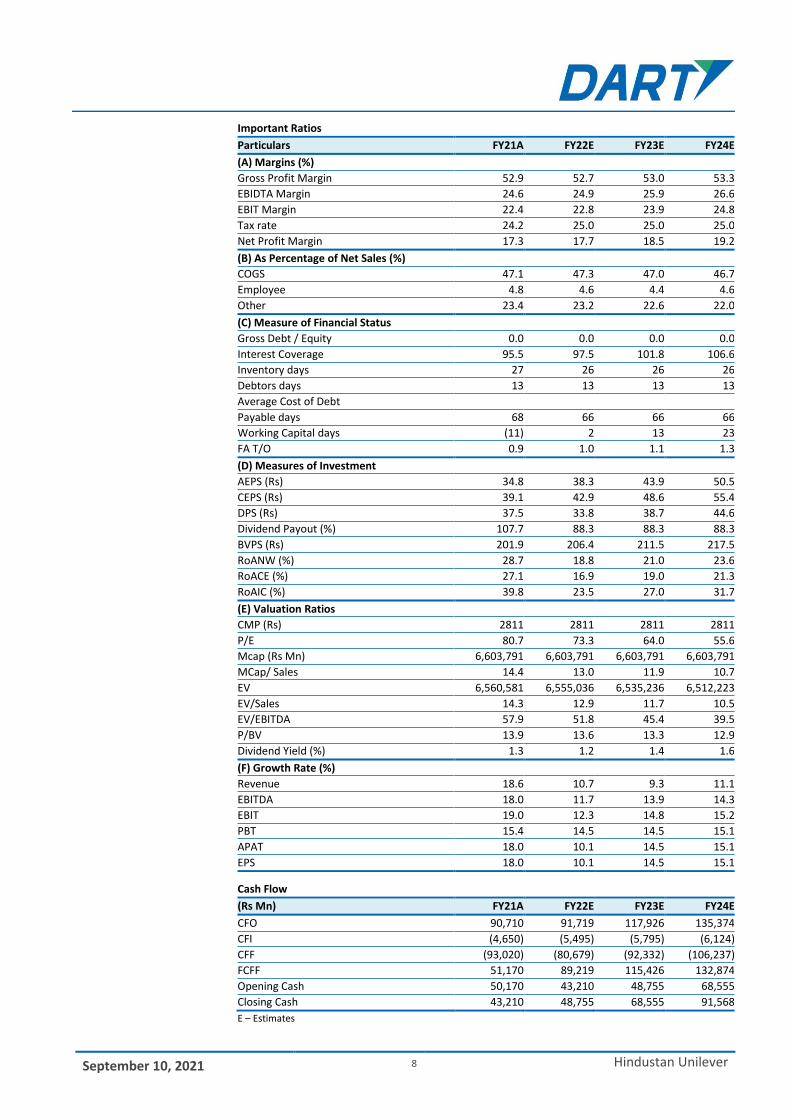

Important Ratios

Particulars FY21A FY22E FY23E FY24E

(A) Margins (%)

Gross Profit Margin 52.9 52.7 53.0 53.3

EBIDTA Margin 24.6 24.9 25.9 26.6

EBIT Margin 22.4 22.8 23.9 24.8

Tax rate 24.2 25.0 25.0 25.0

Net Profit Margin 17.3 17.7 18.5 19.2

(B) As Percentage of Net Sales (%)

COGS 47.1 47.3 47.0 46.7

Employee 4.8 4.6 4.4 4.6

Other 23.4 23.2 22.6 22.0

(C) Measure of Financial Status

Gross Debt / Equity 0.0 0.0 0.0 0.0

Interest Coverage 95.5 97.5 101.8 106.6

Inventory days 27 26 26 26

Debtors days 13 13 13 13

Average Cost of Debt

Payable days 68 66 66 66

Working Capital days (11) 2 13 23

FA T/O 0.9 1.0 1.1 1.3

(D) Measures of Investment

AEPS (Rs) 34.8 38.3 43.9 50.5

CEPS (Rs) 39.1 42.9 48.6 55.4

DPS (Rs) 37.5 33.8 38.7 44.6

Dividend Payout (%) 107.7 88.3 88.3 88.3

BVPS (Rs) 201.9 206.4 211.5 217.5

RoANW (%) 28.7 18.8 21.0 23.6

RoACE (%) 27.1 16.9 19.0 21.3

RoAIC (%) 39.8 23.5 27.0 31.7

(E) Valuation Ratios

CMP (Rs) 2811 2811 2811 2811

P/E 80.7 73.3 64.0 55.6

Mcap (Rs Mn) 6,603,791 6,603,791 6,603,791 6,603,791

MCap/ Sales 14.4 13.0 11.9 10.7

EV 6,560,581 6,555,036 6,535,236 6,512,223

EV/Sales 14.3 12.9 11.7 10.5

EV/EBITDA 57.9 51.8 45.4 39.5

P/BV 13.9 13.6 13.3 12.9

Dividend Yield (%) 1.3 1.2 1.4 1.6

(F) Growth Rate (%)

Revenue 18.6 10.7 9.3 11.1

EBITDA 18.0 11.7 13.9 14.3

EBIT 19.0 12.3 14.8 15.2

PBT 15.4 14.5 14.5 15.1

APAT 18.0 10.1 14.5 15.1

EPS 18.0 10.1 14.5 15.1

Cash Flow

(Rs Mn) FY21A FY22E FY23E FY24E

CFO 90,710 91,719 117,926 135,374

CFI (4,650) (5,495) (5,795) (6,124)

CFF (93,020) (80,679) (92,332) (106,237)

FCFF 51,170 89,219 115,426 132,874

Opening Cash 50,170 43,210 48,755 68,555

Closing Cash 43,210 48,755 68,555 91,568

E – Estimates

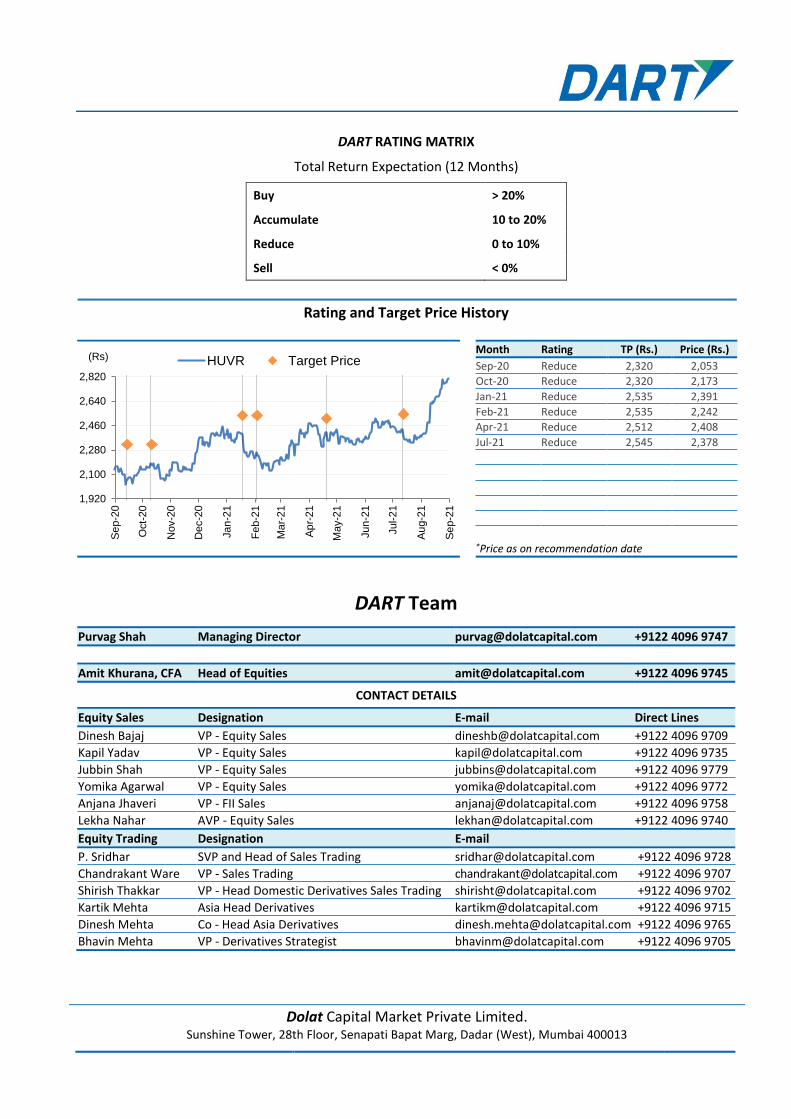

DART RATING MATRIX

Total Return Expectation (12 Months)

Buy > 20%

Accumulate 10 to 20%

Reduce 0 to 10%

Sell < 0%

Rating and Target Price History

Month Rating TP (Rs.) Price (Rs.)

Sep-20 Reduce 2,320 2,053

Oct-20 Reduce 2,320 2,173

Jan-21 Reduce 2,535 2,391

Feb-21 Reduce 2,535 2,242

Apr-21 Reduce 2,512 2,408

Jul-21 Reduce 2,545 2,378

*Price as on recommendation date

DART Team

Purvag Shah Managing Director [email protected] +9122 4096 9747

Amit Khurana, CFA Head of Equities [email protected] +9122 4096 9745

CONTACT DETAILS

Equity Sales Designation E-mail Direct Lines

Dinesh Bajaj VP - Equity Sales [email protected] +9122 4096 9709

Kapil Yadav VP - Equity Sales [email protected] +9122 4096 9735

Jubbin Shah VP - Equity Sales [email protected] +9122 4096 9779

Yomika Agarwal VP - Equity Sales [email protected] +9122 4096 9772

Anjana Jhaveri VP - FII Sales [email protected] +9122 4096 9758

Lekha Nahar AVP - Equity Sales [email protected] +9122 4096 9740

Equity Trading Designation E-mail

P. Sridhar SVP and Head of Sales Trading [email protected] +9122 4096 9728

Chandrakant Ware VP - Sales Trading [email protected] +9122 4096 9707

Shirish Thakkar VP - Head Domestic Derivatives Sales Trading [email protected] +9122 4096 9702

Kartik Mehta Asia Head Derivatives [email protected] +9122 4096 9715

Dinesh Mehta Co - Head Asia Derivatives [email protected] +9122 4096 9765

Bhavin Mehta VP - Derivatives Strategist [email protected] +9122 4096 9705

1,920

2,100

2,280

2,460

2,640

2,820

Se

p-2

0

Oct-

20

Nov-2

0

Dec-2

0

Jan

-21

Fe

b-2

1

Ma

r-21

Ap

r-21

Ma

y-2

1

Jun

-21

Jul-2

1

Au

g-2

1

Se

p-2

1

(Rs) HUVR Target Price

Dolat Capital Market Private Limited. Sunshine Tower, 28th Floor, Senapati Bapat Marg, Dadar (West), Mumbai 400013

Our Research reports are also available on Reuters, Thomson Publishers, DowJones and Bloomberg (DCML <GO>)

Analyst(s) Certification The research analyst(s), with respect to each issuer and its securities covered by them in this research report, certify that: All of the views expressed in this research report accurately reflect his or her or their personal views about all of the issuers and their securities; and No part of his or her or their compensation was, is, or will be directly or indirectly related to the specific recommendations or views expressed in this research report.

I. Analyst(s) and Associate (S) holding in the Stock(s): (Nil)

II. Disclaimer: This research report has been prepared by Dolat Capital Market Private Limited. to provide information about the company(ies) and sector(s), if any, covered in the report and may be distributed by it and/or its affiliated company(ies) solely for the purpose of information of the select recipient of this report. This report and/or any part thereof, may not be duplicated in any form and/or reproduced or redistributed without the prior written consent of Dolat Capital Market Private Limited. This report has been prepared independent of the companies covered herein. Dolat Capital Market Private Limited. and its affiliated companies are part of a multi-service, integrated investment banking, brokerage and financing group. Dolat Capital Market Private Limited. and/or its affiliated company(ies) might have provided or may provide services in respect of managing offerings of securities, corporate finance, investment banking, mergers & acquisitions, financing or any other advisory services to the company(ies) covered herein. Dolat Capital Market Private Limited. and/or its affiliated company(ies) might have received or may receive compensation from the company(ies) mentioned in this report for rendering any of the above services. Research analysts and sales persons of Dolat Capital Market Private Limited. may provide important inputs to its affiliated company(ies) associated with it. While reasonable care has been taken in the preparation of this report, it does not purport to be a complete description of the securities, markets or developments referred to herein, and Dolat Capital Market Private Limited. does not warrant its accuracy or completeness. Dolat Capital Market Private Limited. may not be in any way responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report. This report is provided for information only and is not an investment advice and must not alone be taken as the basis for an investment decision. The investment discussed or views expressed herein may not be suitable for all investors. The user assumes the entire risk of any use made of this information. The information contained herein may be changed without notice and Dolat Capital Market Private Limited. reserves the right to make modifications and alterations to this statement as they may deem fit from time to time. Dolat Capital Market Private Limited. and its affiliated company(ies), their directors and employees may; (a) from time to time, have a long or short position in, and buy or sell the securities of the company(ies) mentioned herein or (b) be engaged in any other transaction involving such securities and earn brokerage or other compensation or act as a market maker in the financial instruments of the company(ies) discussed herein or act as an advisor or lender/borrower to such company(ies) or may have any other potential conflict of interests with respect to any recommendation and other related information and opinions. This report is neither an offer nor solicitation of an offer to buy and/or sell any securities mentioned herein and/or not an official confirmation of any transaction. This report is not directed or intended for distribution to, or use by any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution, publication, availability or use would be contrary to law, regulation or which would subject Dolat Capital Market Private Limited. and/or its affiliated company(ies) to any registration or licensing requirement within such jurisdiction. The securities described herein may or may not be eligible for sale in all jurisdictions or to a certain category of investors. Persons in whose possession this report may come, are required to inform themselves of and to observe such restrictions.

For U.S. Entity/ persons only: “This Report is considered independent third-party research and was prepared by Dolat Capital Market Private Limited, with headquarters in India. The distribution of this Research is provided pursuant to the exemption under Rule 15a-6(a) (2) and is only intended for an audience of Major U.S. Institutional Investors (MUSIIs) as defined by Rule 15a-6(b)(4). This research is not a product of StoneX Financial Inc. Dolat Capital Market Private Limited has sole control over the contents of this research report. StoneX Financial Inc. does not exercise any control over the contents of, or the views expressed in, any research reports prepared by Dolat Capital Market Private Limited and under Rule 15a-6(a) (3), any U.S. recipient of this research report wishing to affect any transaction to buy or sell securities or related financial instruments based on the information provided in this research report should do so only through StoneX Financial Inc. Please contact Paul Karrlsson-Willis at +1 (407) 741-5310 or email [email protected] and/or Igor Chernomorskiy at +1 (212)379-5463 or email [email protected]. Under no circumstances should any U.S. recipient of this research report effect any transaction to buy or sell securities or related financial instruments through the Dolat Capital Market Private Limited.”

Dolat Capital Market Private Limited.

Corporate Identity Number: U65990DD1993PTC009797 Member: BSE Limited and National Stock Exchange of India Limited.

SEBI Registration No: BSE - INZ000274132, NSE - INZ000274132, Research: INH000000685 Registered office: Unit no PO6-02A - PO6-02D, Tower A, WTC, Block 51, Zone-5, Road 5E, Gift City, Gandhinagar, Gujarat – 382355

Board: +9122 40969700 | Fax: +9122 22651278 | Email: [email protected] | www.dolatresearch.com