A Dynamic Politico-Economic Model of Intergenerational Contracts We are grateful for valuable...

45

A Dynamic Politico-Economic Model of Intergenerational Contracts Francesco Lancia and Alessia Russo 1 March 3 rd , 2014 Abstract This paper proposes a dynamic politico-economic theory of intergenerational government spend- ing. We embed a repeated voting system in an overlapping generations model with human capital accumulation. The aim is to study how democratic institutions settle intergenerational disagree- ment over the allocation of the public budget. We characterize the Markov-perfect equilibrium of the voting game, as well as its welfare properties. We find that (i) the political empowerment of elderly agents acts as a disciplining mechanism for adults, so as to provide durable public invest- ments; (ii) high elderly-targeted transfers do not necessarily dampen public investments; and (iii) a high degree of intergenerational disagreement over the allocation of the public budget leads to high growth. The equilibrium can reproduce some salient features of intergenerational accounting in the U.S. Keywords: Human capital, intergenerational contract, intergenerational disagreement, Markov- perfect equilibrium, repeated voting, social planner. JEL Classification: D72, E62, H23, H30, H53. 1 Francesco Lancia, University of Vienna, Email: [email protected]. Alessia Russo, University of Oslo, Email: [email protected]. We are grateful for valuable comments from Graziella Bertocchi, Marco Bassetto, Roland Ben- abou, Michele Boldrin, Alejandro Cunat, Vincenzo Denicol` o, B˚ ard Harstad, David K. Levine, Anirban Mitra, Nicola Pavoni, Karl Schlag, Paolo Siconolfi, Kjetil Storesletten, and Fabrizio Zilibotti. We also thank the seminar participants at the NBER Summer Institute Meeting in Income Distribution and Macroeconomics, the 2011 SED Annual Meeting in Ghent, the NSF/NBER/CEME Conference in Mathematical Economics and General Equilibrium Theory in New York, the XV Work- shop on Macroeconomic Dynamics in Vigo, the 2 nd Conference on Recent Development in Macroeconomics in Mannheim, and 8 th Workshop on Macroeconomic Theory in Pavia, as well as the seminar participants at the Bank of Italy, ETH in Zurich and the Universities of Bologna, Louvain, Milan, Modena, Napoli, Oslo, and Vienna for useful discussions. All errors are our own.

Transcript of A Dynamic Politico-Economic Model of Intergenerational Contracts We are grateful for valuable...

A Dynamic Politico-Economic Modelof Intergenerational Contracts

Francesco Lancia and Alessia Russo1

March 3rd, 2014

Abstract

This paper proposes a dynamic politico-economic theory of intergenerational government spend-

ing. We embed a repeated voting system in an overlapping generations model with human capital

accumulation. The aim is to study how democratic institutions settle intergenerational disagree-

ment over the allocation of the public budget. We characterize the Markov-perfect equilibrium of

the voting game, as well as its welfare properties. We find that (i) the political empowerment of

elderly agents acts as a disciplining mechanism for adults, so as to provide durable public invest-

ments; (ii) high elderly-targeted transfers do not necessarily dampen public investments; and (iii)

a high degree of intergenerational disagreement over the allocation of the public budget leads to

high growth. The equilibrium can reproduce some salient features of intergenerational accounting

in the U.S.

Keywords: Human capital, intergenerational contract, intergenerational disagreement, Markov-

perfect equilibrium, repeated voting, social planner.

JEL Classification: D72, E62, H23, H30, H53.

1Francesco Lancia, University of Vienna, Email: [email protected]. Alessia Russo, University of Oslo, Email:[email protected]. We are grateful for valuable comments from Graziella Bertocchi, Marco Bassetto, Roland Ben-abou, Michele Boldrin, Alejandro Cunat, Vincenzo Denicolo, Bard Harstad, David K. Levine, Anirban Mitra, Nicola Pavoni,Karl Schlag, Paolo Siconolfi, Kjetil Storesletten, and Fabrizio Zilibotti. We also thank the seminar participants at the NBERSummer Institute Meeting in Income Distribution and Macroeconomics, the 2011 SED Annual Meeting in Ghent, theNSF/NBER/CEME Conference in Mathematical Economics and General Equilibrium Theory in New York, the XV Work-shop on Macroeconomic Dynamics in Vigo, the 2nd Conference on Recent Development in Macroeconomics in Mannheim,and 8th Workshop on Macroeconomic Theory in Pavia, as well as the seminar participants at the Bank of Italy, ETH in Zurichand the Universities of Bologna, Louvain, Milan, Modena, Napoli, Oslo, and Vienna for useful discussions. All errors are ourown.

Why should I care about future generations? What have they done for me?” (Groucho Marx)

1 IntroductionThe challenges involved in sustaining intergenerational welfare programs are prominent in the

current political debate. In modern societies, electoral campaigns often serve as a battleground,

with opposing parties fiercely defending their positions by either promising more generous pub-

lic spending or arguing the financial unsustainability of public programs. Such political disputes pit

young against old and taxpayers against recipients, especially when balanced-budget restrictions ap-

ply. Accordingly, it becomes crucial to explore (i) how democratic institutions settle intergenerational

disagreement over the allocation of public budgets; and (ii) the extent to which the current welfare

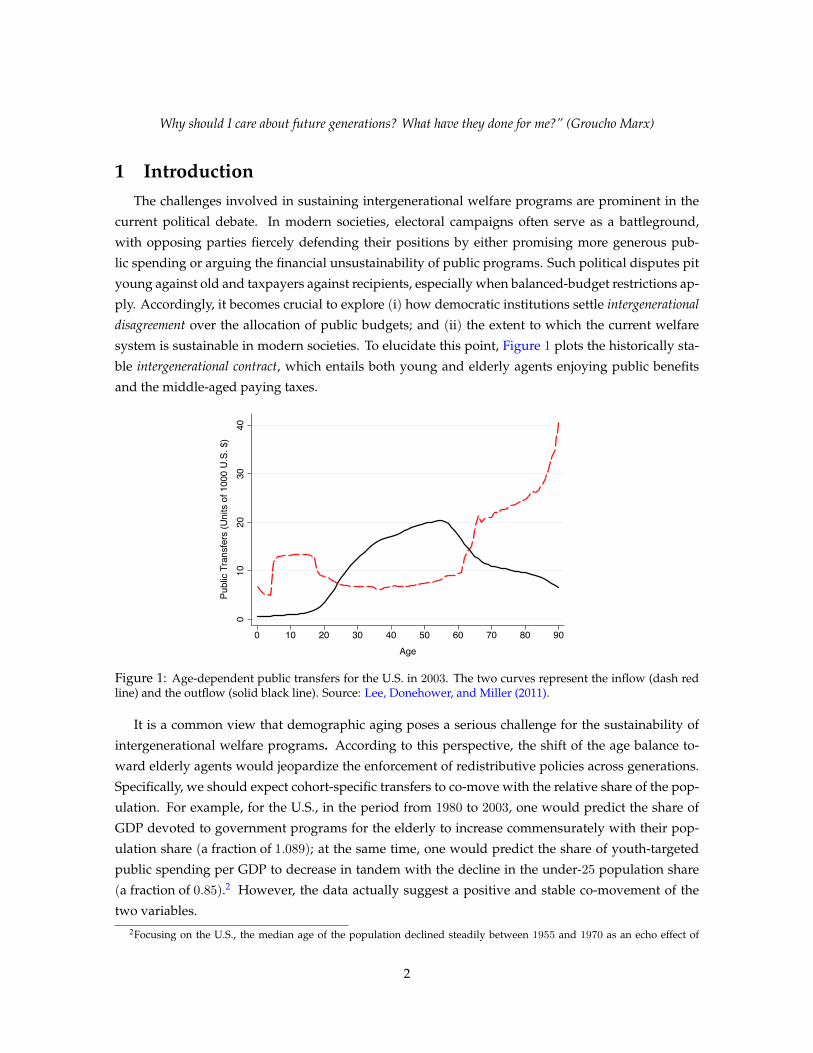

system is sustainable in modern societies. To elucidate this point, Figure 1 plots the historically sta-

ble intergenerational contract, which entails both young and elderly agents enjoying public benefits

and the middle-aged paying taxes.

010

2030

40Pu

blic

Tra

nsfe

rs (U

nits

of 1

000

U.S

. $)

0 10 20 30 40 50 60 70 80 90Age

Figure 1: Age-dependent public transfers for the U.S. in 2003. The two curves represent the inflow (dash redline) and the outflow (solid black line). Source: Lee, Donehower, and Miller (2011).

It is a common view that demographic aging poses a serious challenge for the sustainability of

intergenerational welfare programs. According to this perspective, the shift of the age balance to-

ward elderly agents would jeopardize the enforcement of redistributive policies across generations.

Specifically, we should expect cohort-specific transfers to co-move with the relative share of the pop-

ulation. For example, for the U.S., in the period from 1980 to 2003, one would predict the share of

GDP devoted to government programs for the elderly to increase commensurately with their pop-

ulation share (a fraction of 1.089); at the same time, one would predict the share of youth-targeted

public spending per GDP to decrease in tandem with the decline in the under-25 population share

(a fraction of 0.85).2 However, the data actually suggest a positive and stable co-movement of the

two variables.2Focusing on the U.S., the median age of the population declined steadily between 1955 and 1970 as an echo effect of

2

.05

.055

.06

.065

Shar

e of

GD

P

1980 1984 1988 1992 1996 2000 2004Year

Panel (a)

.041

.042

.043

.044

.045

Shar

e of

GD

P

1980 1984 1988 1992 1996 2000 2004Year

Panel (b)

Figure 2: Cohort-specific public inflow for the U.S. in the period 1980-2003. Panel (a) plots the GDP-ratioof public spending for social security and health case. Panel (b) plots the GDP-ratio of public spending foreducation. Source: Lee, Donehower, and Miller (2011).

As Figure 2 highlights, while public spending on the elderly (including Social Security and health

care) has grown by a factor of 1.196, public spending for the young (including education) has grown

by a factor of 1.06. The scope of this study is to provide a tractable dynamic politico-economic theory

of intergenerational government spending that addresses this seeming puzzle.

Our main idea is driven by the following observation. In a graying society, elderly constituents

show a large propensity to vote and form a single-minded voting block, which makes them an in-

creasingly prized electoral group.3 Insofar as the political imbalance in favor of elderly voters trans-

lates into a large claim over future production, both youth-targeted and elderly-targeted government

spending can be simultaneously implemented as an outcome of the electoral competition. The in-

tuition is the following. Forward-looking voters anticipate that they will peddle their political influence

when they are old and that will be rewarded for the sacrifices they made as adults. Therefore, they provide

youth-targeted public spending, requiring that it be durable and productive. This simple argument can

explain the counter-intuitive simultaneous co-movement of age-targeted public spending and also

the difference from what is expected solely from shifts in the demographic structure. The proposed

mechanism merits two additional qualifications. First, the expected political power assigned to future

elderly constituents also implies a commensurate claim on public spending by current elders, which

may compromise the strategic channel previously highlighted. We show that crowding-out (-in)

effects of elderly-targeted spending on youth-targeted programs ultimately depend on primitives

of the model, such as the intertemporal elasticity of substitution. Second, underlying the mecha-

the baby boom and began to increase in the 1970s. At the same time, the fraction of the elderly – people aged 65+ – inthe population steadily increased, whereas the fraction of youths – people under the age of 25 – in the population steadilydecreased (Source: U.N.). The simultaneous variation in both the median age and the relative cohort size had an impactboth on the financial solvency of the public system – since the share of recipients increased, while the share of contributorsdecreased – and on the outcome of the voting competition – as the population aged, so did the voters.

3As Galasso and Profeta (2004) report, in some countries, the elderly have a higher turnout rate at elections in comparisonto the young and to adults. For example, in the U.S., the turnout rate among those aged 60-69 is twice as high as amongthe young (19-29 years). Furthermore, according to Mulligan and Xala-i-Martin (1996), while young citizens disperse theirpolitical interests among different and often contrasting issues, their older counterparts are likely to target fewer programs,such as Social Security and Medicare, while making their voting decisions.

3

nism is the presumption that credit markets are incomplete because of, for example, the absence of

collateral for the young. These debt constraints inhibit private productive investment and, in turn,

hinder economic growth. Hence, the presence of a political system is justified by the need to restore

such technological possibilities. Interestingly, even with complete markets, private contracts could,

at most, comply with short-term projects, failing to internalize the technological externalities whose

impact outlasts the individual lifespan. Therefore, democratic institutions would also play a crucial

role if markets were complete.

In this paper, we pursue this idea formally by analyzing a dynamic model. Given our focus on

the intergenerational disagreement over public spending, we frame the model as an economy with

overlapping generations comprised of ideologically heterogeneous and selfish agents. Individuals

live for three periods. The young acquire skills and accumulate human capital; adults offer labor

inelastically and partially save their proceeds; and the old retire. From adulthood onwards, agents

exert their voting right. At each time, constituents envision a government of short-lived represen-

tatives in a majoritarian probabilistic voting setting a la Lindbeck and Weibull (1987). The politi-

cians run for office by proposing a fiscal bundle of youth-targeted (forward) and elderly-targeted

(backward) transfers and taxes subject to intra-period balanced budgets.4 Youth-targeted public

spending consists of long-lasting investments, which boost the labor productivity of all future gen-

erations, whereas elderly-targeted transfers serve to subsidize consumption. The aim of political

parties is to win the largest number of votes among the currently living voters, with no concern for

the well-being of unborn generations. To highlight the implications of having politicians with short-

term mandates, we assume that each generation is completely selfish. Furthermore, we abstract

away from commitment technology in the electoral process – that is, no government can bind its suc-

cessors’ policies, regardless of whether or not the successor belongs to the same party. Specifically,

by employing the ”minor causes should have minor effects” principle, we focus on Markov-perfect

equilibria and we characterize the equilibrium politico-economic outcome as the limit of a finite hori-

zon game in which time goes to infinity.5

Our characterization is quite flexible and admits a large class of preferences and technologies.

Despite the model’s simple structure, it generates several interesting results. Moreover, the politico-

economic outcome has the ability to reproduce the salient features of intergenerational accounting in

the U.S., as illustrated in Figure 1 and Figure 2.

To highlight the main findings, let us focus on the basic setup, with human capital as the sole

4We adopt the notion of forward and backward intergenerational transfers as introduced by Rangel (2003). The formerare youth-targeted transfers that generate a cost for the current generation and a benefit for the future one, being crucial forfuture labor productivity. In contrast, the latter are elderly-targeted transfers, generating a cost for the current generationand a benefit for the past one. To single out the impact of political institutions on intergenerational transfers and to highlightthe asynchronous timing of public exchange, we abstract away the provision of public goods – a key element in the politicaleconomy of fiscal policy. See Bassetto (2008) for the role of public good provision in an OLG environment.

5The equilibrium refinement we adopt rules out equilibria in which the current political outcome depends directly on thepast outcome, as in reputation equilibria. This seems appropriate in our setup, where periods are very long (around 30 years)and political competition takes place among different agents at each date. Previous literature has focused on reputationalmechanisms to justify the provision of productive investment. Although trigger strategies may be analytically convenient,they lead to a multiplicity of equilibria. Furthermore, they require coordination among agents and costly enforcement of apunishment technology, which may not work when agents are not patient enough. Finally, they are not robust to refinementsuch as backward induction in a finite horizon economy when time tends to infinity.

4

payoff-relevant state variable. In this stylized economy, the unique source of disagreement among

cohorts lies in the difference in lifespan. Elderly voters aim to maximize the current benefits, whereas

adult constituents also are concerned about next-period wealth. None of them has a personal inter-

est in fostering the stock of human capital in society. Nevertheless, our model predicts that the

existence of a Markov-perfect equilibrium, which attains a growth-enhancing intergenerational contract,

does not require pre-commitment through the establishment of institutions that outlive the current govern-

ment and bind future decision-makers. In a probabilistic voting framework and in the absence of storage

technologies, expected consumption possibilities are related solely to the generations’ prospects for

democratically claiming part of future production via transfers. Accordingly, the empowerment of the

elderly cohort acts as a credible disciplining device for adults to provide public investments. When the relative

political clout of the elderly is large enough, the political outcome entails a self-enforcing intergen-

erational contract with both forward and backward transfers activated in equilibrium. Clearly, the

redistributive scheme works only if the cost of providing forward transfers is at least compensated

by the expected benefit of receiving backward transfers when old. At high values of intertemporal

elasticity of substitution, the model predicts a hump-shaped relationship between the political influ-

ence of elderly voters – and, in turn, the amount of enforced backward transfers – and the provision

of productive transfers – and, in turn, the attained rate of economic growth.

Remarkably, the existence of a growth-enhancing intergenerational contract hinges on the absence

of commitment technology. If the current government invested too little, then the future officeholder

would necessarily punish the generations that were alive under the former government. Indeed,

given the strategic complementarity between human capital and backward transfers, lacking pro-

ductive investments would restrict the public budget possibilities of future constituents. The less the

former government cares for future generations, the harsher the punishment will be. Therefore, it is

the expected punishment that disciplines all governments and discourages them from underinvest-

ment.

When a private storage technology is available, an additional source of intergenerational dis-

agreement arises, which is rooted in the difference in ownership of productive factors, as well as in

the source of income. As a measure of the technological complementarity among assets, the elas-

ticity of factor substitution is also interpreted as a proxy for economic disagreement between workers

and retirees. From this perspective, less complementarity among assets exacerbates the conflict of

interest between different owners of the factors of production. We show that the greater the degree

of economic disagreement over government spending, the lower is the economic growth. Intuitively, when

productive assets are technologically closer complements, the rate of return on physical capital turns

out to be more responsive to a variation of the intergenerational transfers, through a simultaneous

adjustment of both physical and human capital. The increase of the interest rate due to a positive

variation of forward and backward transfers depresses the present value of next-period backward

transfers as internalized by current adults. As a consequence, less economic disagreement implies

a smaller amount of enforced backward transfers and – through their weaker disciplinary valence –

poorer productive investments. Ultimately, this leads to lower economic growth. This effect appears

5

only in overlapping generation economies with long-lasting productive spending – a novelty in the

literature. Furthermore, this finding provides new fundamentals to the theory, which recognizes the

link between the elasticity of substitution in technology and economic growth (Klump and De La

Grandville, 2000).

Finally, we contrast the results with an environment in which intergenerational transfers are del-

egated to a benevolent social planner who attaches independent decaying weights to all future gen-

erations. We emphasize the case of a small open economy in which the electoral competition among

short-term-mandate policy-makers plunges the economy into the efficient allocation. The outcome

hinges on the absence of pecuniary externalities. Indeed, in a closed economy, in which productive

assets are complements, the interdependence of the political wedges via price precludes the possibil-

ity of attaining the efficient allocation via democratic institutions.

Our theoretical mechanism involves two fundamental aspects: (i) the nature of short-term agree-

ments among politicians and current living voters – i.e., the absence of commitment; and (ii) the

prospect of follow-up intergenerational contracts, which serves as a disciplining device to implement

current policies. Clearly, there are many extensions that fit into this setting. Prominent examples of

forward transfers are government decisions on how much to invest in the public infrastructure or

in environmental preservation and R&D. Similar to human capital investments, these programs en-

tail a transfer to future generations that is financed through taxes paid by current generations and

whose benefits are long-lasting. Future compensation through backward transfers can take the form

of pension, health assistance, and, generally, elderly-targeted public good provision.

2 Related LiteratureThis paper augments the literature on dynamic politico-economic models with overlapping gen-

erations that incorporates forward-looking decision makers in a multidimensional policy space (Kru-

sell, Quadrini, and Rıos-Rull, 1997). Previous literature has highlighted altruism (Tabellini, 1991),

public good provision (Bassetto, 2008; Hassler, Storesletten, and Zilibotti, 2007; and Song, Storeslet-

ten, and Zilibotti, 2012), and reputation mechanisms (Bellettini and Berti Ceroni, 1999; and Rangel,

2003) to justify the emergence of an intergenerational contract. While recognizing the theoretical rel-

evance of these channels, we emphasize the role played purely by political institutions and strategic

incentives: The willingness of each adult generation to transfer wealth to the elderly and the young

hinges on its beliefs that the same thing will happen in the subsequent time period via an established

and effective institution, such as democratic voting.

Adopting an approach similar to ours, recent works have developed models of Social Security

in a repeated voting environment. We focus, in particular, on the contributions by Azariadis and

Galasso (2002), Forni (2005), and Gonzalez-Eiras and Niepelt (2008), which are based largely on the

pioneering work of Grossman and Helpman (1998). Unlike in our case, most of their findings exhibit

indeterminacy in equilibrium. Moreover, they have focused only on backward transfers, whereas our

theory recognizes the fundamental link between productive and redistributive public spending as a

social-policy-package deal.

6

Closer in spirit to our work are Gonzalez-Eiras and Niepelt (2012) and Chen and Song (2013). Un-

like in our study, the former analyze a richer demographic environment with elastic labor supply and

endogenous retirement age. Despite this complexity, they find an analytical solution of the Markov-

perfect equilibrium. This comes at the cost of some simplifying assumptions on the parametric form

of preferences and technologies. In the studied case of log-preferences and Cobb-Douglas produc-

tion, strategic effects are mute, and the crowding in of backward transfers on productive investments

is an equilibrium outcome only if the retirement decision is endogenous. As a main departure, we

elucidate contingencies of crowding in and crowding out in the two-sided welfare program for more

flexible preferences and technologies and point out the role of political institutions instead of de-

mographic aging. Chen and Song (2013) develop a dynamic theory of Social Security with sole

private investments in human capital to figure out the puzzling negative correlation between wage

inequality and the size of government. The main prediction is that a larger level of human capital

corresponds to a lower amount of backward transfers. Abstracting from issues of inequality, our

model encompasses the authors’ mechanism as a particular case: With exogenous prices, positive

transfers to the elderly reduce the level of physical capital, which, in turn, increases future payroll

taxes, exactly as human capital does in their framework.

To the best of our knowledge, none of the existing papers have provided an implicit character-

ization of the general-equilibrium politico-economic outcome and posited implications in terms of

welfare analysis, as we do here.6

The remainder of the paper is organized as follows. Section 3 describes the model’s environment.

Section 4 discusses the social planner’s allocation and provides the criterion for the welfare compar-

ison. Section 5 introduces the equilibrium concept. Section 6 presents the main results. Section 7

describes two analytical examples. Section 8 illustrates the quantitative experiments. Finally, Section

9 concludes. All proofs are contained in the Appendix.

3 The ModelConsider an overlapping generation (OLG) economy inhabited by an infinite number of ideolog-

ically heterogeneous agents, living up to three periods: young, adult, and old. i ∈ a, o labels the

adult and elderly cohorts, respectively. Agents of different ages differ in their wealth holdings. Time

is discrete, indexed by t, and runs from zero to infinity. The population grows at a constant rate ν−1;

thus, the mass of the adult generation born at time t− 1 and living at time t is equal to N t−1t = νtN0.

At each time, two short-lived parties, denoted by ιt ∈ Lt,Rt, run for office by proposing a political

platform to maximize the probability of winning the election without commitment to future policies.

6Battaglini and Coate (2007) have explored how pork-barrel spending affects the overall size of government and distortsinvestment in public capital goods. They have focused on the efficiency of the steady-state level of taxation and allocationof the public budget. Unlike us, they have studied an environment in which infinite-living agents make policy decisions bylegislative bargaining.

7

3.1 Households

An agent j born at time t− 1 and living at time t evaluates consumption and ideology according

to the following additive intertemporal (non-altruistic) utility function:

u (cat ) + ςaj,ιt + βEιt[u(cot+1

)+ ςoj,ιt+1

](1)

where β ∈ (0, 1) is the individual discount factor, and Eιt [·] is the expectation operator, which is

conditional on the political platform implemented by the current incumbent party. The random

variable ςij,ιt summarizes the utility derived by agent j belonging to cohort i at time t from political

factors that are orthogonal to consumption (to be discussed later in more detail).

Assumption 1 (Utility) The function u : R+ → R+ is twice continuously differentiable, strictly increasing

and concave, and it satisfies the usual Inada conditions.

cat denotes the consumption at time t when adult, and cot+1 represents the consumption at time

t+ 1 when old. In the first period of life, individuals do not consume. When young, agents spend all

of their time endowment in acquiring skills if productive forward transfers, fιt , are publicly provided,

without having access to private credit markets. In the absence of government intervention, the

debt constraint faced by the young would inhibit human capital formation.7 As adults, individuals

inelastically supply labor and use their income, wtht, taxed at a flat rate, zιt , for consumption and

saving, st. When old, agents retire and consume their total income equal to the sum of savings

capitalized at a gross rate of return Rt+1 and the backward transfers, bιt , that their children pass to

them in the form of a PAYGO system. Thus, the individual budget constraints for the adult and

elderly agents are, respectively, as follows:

cat + st ≤ (1− zιt)wtht (2)

cot+1 ≤ Rt+1st + bιt+1 (3)

At the initial time t = 0, the economy is endowed with an exogenous amount of physical and

human capital, k0, h0. Hence, the budget constraint of the initial adult agent is equal to ca0 =

(1− zι0)w0h0 − s0, whereas the budget constraint of the initial elderly agent is co0 = R0k0 + bι0 .

3.2 Technology

At each time t, the economy produces a single homogeneous private good, Yt ≡ ytN t−1t , combin-

ing aggregate physical capital, Kt ≡ ktN t−1t , which depreciates fully after one period, and aggregate

human capital, Ht ≡ htN t−1t , according to the following technology (expressed in per-capita units):

yt = Θ (kt, ht)

7The debt constraint faced by the young – which is familiar in the literature of self-enforcing contracts – can be motivatedby several factors. For example, Kehoe and Levine (2001) show that debt constraints arise due to the inalienability of cer-tain types of assets, primarily human capital. In this scenario, as in Boldrin and Montes (2005), the presence of a politicalsystem is justified by the need to finance the provision of public spending, which would otherwise preclude the young fromaccumulating human capital.

8

Assumption 2 (Production) The function Θ : R2+ → R+ exhibits a constant return to scale, and it is

strictly monotonic increasing and weakly concave in each of the two inputs with Θ (0, ht), Θ (kt, 0) ≥ 0 and

Θkt,ht , Θht,kt ≥ 0.

By Assumption 2, it follows that yt = htΘ(ktht, 1)≡ htϑ

(kt

)and, in turn, yt = ϑ

(kt

), where

yt and kt refer to the per-efficiency units of the final good and the physical capital, respectively. The

inverse demand functions for factor prices are Θkt = ϑkt and Θht = ϑ(kt

)− ktϑkt . The elasticity

of factor substitution is denoted by ζ. The human capital of an adult born at time t is produced

according to a technology, which combines forward transfers, fιt , and parental human capital, ht, as

complementary factors:

ht+1 = Φ (fιt , ht)

Assumption 3 (Human Capital) The function Φ : R2+ → R+ exhibits a constant return to scale, and it is

strictly monotonic increasing and strictly concave in each of the two inputs with Φ (0, ht), Φ (fιt , 0) ≥ 0 and

Φfιt ,ht , Φht,fιt > 0.

By Assumption 3, a higher level of knowledge attained by one generation reduces the cost of the

next generation to achieve the same level. Furthermore, ht+1 = htΦ(fιtht, 1)≡ htϕ

(fιt

), where fιt

denotes the per-efficiency units of productive transfers. It follows that the growth rate of human

capital is equal to ht+1

ht= ϕ

(fιt

). The marginal impact of forward transfers and parental human

capital on human capital production are Φfιt = ϕfιtand Φht = ϕ

(fιt

)− fιtϕfιt , respectively.8

3.3 Fiscal Constitution

At each date, short-term-mandate governments, democratically elected by their constituents, use

their fiscal authority to transfer income across different age groups. The transfers simultaneously

serve the political scope of the elected representatives and the economic needs of their constituents.

We assume that politicians are prevented from borrowing. Thus, the public balance must hold in

every period, which implies the following:

zιtwthtNt−1t = bιtN

t−2t + fιtN

tt (4)

where the collection zιt , bιt , fιt represents the age-targeted fiscal bundle.9 At each time t, Eq. (4)

reduces the multidimensionality of the political platform to a bi-dimensional plan bιt , fιt, where

the fiscal feasibility conditions require that bιt ∈[0, bt

]and fιt ∈

[0, ft

]with bt ≡ νwtht and ft ≡

8For clarity of exposition, we adopt the following notation. Let xt = x (qt, pt) and pt = p (qt) be functions of the variable

qt. Then, xqt ≡ ∂xt∂qt

and xqt,qt ≡ ∂2xt∂qt∂qt

denote the first and second partial derivative, respectively. Furthermore, dxtdqt

≡∂xt∂qt

+ ∂xt∂pt

∂pt∂qt

represents the total derivative.9In the national accountability of many countries, taxes are transfer-targeted. Social Security contributions cover the bene-

fits of elderly agents, whereas income taxes cover public spending, such as human capital investment. However, in a frame-work with inelastic labor supply and a balanced budget, such an alternative formulation would not compromise the results.

Indeed, Eq. (4) would be equivalent to modeling two separate government budgets, as zbιtwtht =bιtν

and zfιtwtht = νfιt ,where zbιt is the Social Security contribution, and zfιt is the income tax rate.

9

wthtν . The non-negativity constraint for backward transfers can be justified by either the ever-binding

participation constraint of elderly voters or the ability of the older generation to manage an active

lobby group. Suppose that elderly agents were required to pay transfers to future generations. Then,

they would default on their obligations, and the economy would revert to intergenerational autarky.

Definition 1 (Intergenerational Contract) An intergenerational contract is a mutual political agreement

that simultaneously enforces backward and forward transfers.

4 Social Planner AllocationBefore describing the outcome under political competition, we characterize the efficient alloca-

tion implemented by a benevolent social planner who chooses the sequence cat , cot , ft, kt+1, ht+1∞t=0

to maximize the discounted utility of all generations.10 Following Farhi and Werning (2007), the

planner attaches geometrically decaying Pareto weight, δ ∈ (0, 1), to the discounted utility of each

dynasty. Varying δ yields all the allocation possibilities on the Pareto frontier. Given the initial level

of physical and human capital, the sequential formulation of the social planner’s problem is as fol-

lows:

maxcat ,cot+1,ft,ht+1,kt+1∞

t=0

∞∑t=0

δt(u (cat ) + βu

(cot+1

))+β

δu (co0)

subject to the aggregate resource constraint and human capital technology:

cat +cotν

+ νkt+1 + νft −Θ (kt, ht) ≤ 0, ∀t(κtδt

)ht+1 − Φ (ft, ht) ≤ 0, ∀t

(%t+1δ

t+1)

where (κtδt) and(%t+1δ

t+1)

are the associated Lagrangian multipliers. Removing the functional

arguments for expositional clarity, the first-order conditions of the Lagrangian are equal to:

cat : ucat = κt

cot : νβucot = κtδ

ft : νκt = %t+1δΦft

ht+1 : %t+1 = κt+1Θht+1+ %t+2δΦht+1

kt+1 : νκt = κt+1δΘkt+1

together with the transversality conditions – i.e., limt→∞

κtδtkt+1 = 0 and limt→∞

%t+1δt+1ht+1 = 0. Elim-

inating the multipliers from the first-order conditions, the following wedges for the optimal alloca-

tions must be satisfied:

0 = ucat − βΘkt+1ucot+1

(5)

10Gonzalez-Eiras and Niepelt (2008) show that in the absence of binding non-negativity constraints on tax rates, tax distor-tions, and intragenerational inequality, the Ramsey policy with full commitment supports the social planner allocation.

10

Eq. (5) describes the conventional consumption-savings Euler condition and, in turn, the optimal

accumulation of physical capital. The social planner chooses kt+1 to equate the marginal cost in

terms of forgone consumption to the discounted marginal benefits of savings.

0 = νβucot − δucat (6)

The second condition captures the intra-temporal redistribution wedge between the current adult

and elderly cohorts. The social planner is concerned for future generations and does not redistribute

resources from unborn generations to current ones. Thus, the redistributive wedge is entirely de-

termined by the Pareto weight. At each time, the utility of the elderly generation is weighted νβδ ,

reflecting the social planner’s bias toward either adult (δ > νβ) or elderly (δ < νβ) agents. In the

special case with dynastic discounting – that is, if the planner’s weights reflect the discount factor

of the household as well as the cohort size – the optimal policy aims at equalizing the per-capita

consumption of all cohorts in each period.

0 = Φft −Θkt+1

Θht+1

(1− εt+1) (7)

Finally, Eq. (7) describes the productive wedge where εt+1 ≡ νΘkt+1

ΦftΦht+1

Φft+1denotes the intergener-

ational externalities of human capital expressed as a fraction of the cost of investment. Specifically,

it quantifies the impact of productive spending on the utility of adults in terms of current cost and

discounted marginal benefits, through the channels of parental human capital. Despite the infinite

persistence of the productive investment, only the current and subsequent periods matter directly.

Hence, Eq. (7) can be viewed as resulting from a variational (two-period) problem. In other words,

let us think of our variational argument as follows: given the state variables kt, ht and kt+2, ht+2,let us vary kt+1, ht+1 through the controls ft to obtain the highest possible utility.

Definition 2 (Social Planner Allocation) Given the initial conditions k0, h0, the social planner alloca-

tion is defined as a sequencecat , c

ot , ft, kt+1, ht+1

∞t=0

such that for all t ≥ 0, Eqs. (5), (6), and (7), jointly

with the transversality conditions, are satisfied.

5 Politico-Economic EquilibriumWe characterize the politico-economic equilibrium of the economy as a subgame perfect equilib-

rium. Within each time period, the sequence of moves is as follows:

i. A new generation of young people is born.

ii. Before the realization of the ideological shocks among voters, office-seeking candidates demo-

cratically compete by proposing their political platforms.

iii. All uncertainty is realized, and agents vote for their preferred candidates.

iv. The winning candidate implements the proposed political platform.

11

v. Agents save and firms hire workers and rent capital.

vi. The older generation dies; the young and adult generations age and become adult and old, re-

spectively.

Within a given period, the sequential politico-economic game can be viewed as Stackelberg, and

it is solved by backward induction. This procedure entails the standard fixed-point problem, which

nests two interdependent parts. First, given policies, adults determine the individual savings level

and firms produce the homogeneous final good (competitive economic equilibrium). Second, to

maximize the probability of winning the election, short-lived office-seeking politicians promise vot-

ers an age-targeted fiscal bundle (politico-economic equilibrium). We assume that all expectations

about subsequent events are correct and that all promises are honored. The fixed-point problem

requires consistency of the laws of motion for policies that underlie the competitive economic equi-

librium with the political selection.

5.1 Competitive Economic Equilibrium

In a competitive economic equilibrium, each adult individual j chooses her lifetime consumption,

taking factor prices and fiscal policies as given. Maximizing Eq. (1) subject to individual budget

constraints, Eqs. (2) and (3), and the feasibility constraints, cat ≥ 0, cot+1 ≥ 0, and st ≥ 0, yields the

standard Euler condition for savings:

ucat ≥ βEιt[Rt+1ucot+1

](8)

Resulting from Eq. (8), the equilibrium private savings is defined as the functional equation st =

S(Iιt , kt+1, bιt+1

), with Iιt ≡ wtht − νfιt −

bιtν . Hence, conditional on the current and next-period

political platforms, S (·) maps the after-tax earnings for adults and the aggregate savings into the

optimal individual savings. Under full depreciation, the level of saving completely determines the

dynamics of physical capital.

Firms produce in a perfectly competitive environment. They choose the level of inputs to maxi-

mize profits – i.e., maxkt,ht

[Θ (kt, ht) − wtht − Rtkt]. Firms’ optimality and market clearing imply that

factor prices are given by the marginal productivity of each factor:

wt = Θht (9)

Rt = Θkt (10)

Definition 3 (Competitive Economic Equilibrium) Given the initial conditions k0, h0 and the sequence

of policies bιt , fιt∞t=0, a competitive economic equilibrium is defined as a sequence of allocations cat , cot , kt+1, ht+1∞t=0

and factor prices wt, Rt∞t=0 such that for all t ≥ 0:

i. The allocation solves the maximization problem of adults – i.e., Eq. (8) is satisfied;

ii. The factor prices are consistent with the profit maximization of firms – i.e., Eqs. (9) and (10) are satisfied;

12

iii. The market for the private good clears – i.e., cat +cotν + νfιt + νkt+1 = Θ (kt, ht);

iv. The market for physical capital clears – i.e.:

νkt+1 = S(Iιt , kt+1, bιt+1

)(11)

The indirect utility of any individual belonging to the adult and elderly cohorts is, respectively,

equal to:

Waιt≡ u

(Ca(kt, ht, kt+1, bιt , f ιt

))+βEιt

[u(Co(kt+1, ht+1, bιt+1

))](12)

and

Woιt≡ u

(Co(kt, ht, bιt

))(13)

where the individual consumption levels, cat = Ca (kt, ht, kt+1, bιt , fιt) ≡ Iιt − νkt+1 and cot+1 =

Co(kt+1, ht+1, bιt+1

)≡ νRt+1kt+1 + bιt+1

, are obtained by plugging Eqs. (9), (10), and (11) into Eqs.

(2) and (3). When taxation and public spending are precluded, intergenerational autarky yields

Wt ≡ maxstu (cat ) + βu

(cot+1

)| It = wth0.

Definition 4 (Equilibrium Feasible Allocation) Given the initial conditions k0, h0, an equilibrium fea-

sible allocation is a sequence of competitive economic equilibrium allocations cat , cot , kt+1, ht+1∞t=0, factor

prices wt, Rt∞t=0, and policies bιt , fιt∞t=0 that satisfy the balanced budget constraint, Eq. (4), and the

fiscal feasibility conditions at each time t.

5.2 Electoral Competition

In this section, we describe how short-lived office-seeking parties interact in electoral compe-

titions. Public policies are chosen through a repeated voting system according to majority rule.

The young have no political power. The utility derived from political factors, ςij,ιt , embeds two

components: an idiosyncratic ideological bias, σij , and an aggregate ideological bias, η. Formally,

ςij,ιt =(σij + η

)Iιt , where Iιt is an indicator function such that IRt = 1 and ILt = 0. A zero value of

ςij,ιt indicates the neutrality of voters’ ideology, whereas a positive value reveals that an individual

j prefers the candidate belonging to party Rt to the candidate’s opponent. Precisely, the random

variable σij reflects the voters’ opinions about the candidate’s positions (e.g., civil rights, pro-market

rules, religious issues) and personal characteristics (e.g., honesty, leadership, trustworthiness). As

it is drawn from cohort-specific distributions, individuals belonging to the same cohort may vote

differently. The additional random variable η measures the average candidates’ popularity. Thus,

individuals belonging to different cohorts may support the same party. For simplicity, we assume

both shocks to be i.i.d. over time and uniformly distributed with densities σi and η, respectively.

By modeling the political mechanism as a probabilistic voting model a la Lindbeck and Weibull

(1987) – adapted to an OLG environment with intergenerational transfers – at each time t, the parties

propose the same political platform in equilibrium. No candidate is able to change current policies

to obtain a net gain in the number of votes. Hence, they set policies so that the marginal effect on the

13

probability of being (re)elected of the last unit invested is actually zero.11 Using Eqs. (12) and (13),

the equilibrium political platform maximizes a weighted sum of the adult and elderly voters’ utility

as follows:

νWat (kt, ht, kt+1, bt, ft, bt+1) + φWo

t (kt, ht, bt) (14)

The parameter φ ≡ σo

σa ∈ [0,∞) has a structural interpretation: it is a synthetic measure that captures

the political clout – or single-mindedness – of voters belonging to the elderly cohort relative to the

adult cohort. In the limit, when φ approaches infinity, the dictatorship of old agents shapes the insti-

tutional process. The elderly cohort forms a single-minded ideological block, ready to compromise

their partisan loyalties in return for particularistic benefits. When φ = 0, the opposite holds. That

is, the adults hold the only relevant ideological position in the political competition.12 As Eq. (14)

displays, the adoption of a probabilistic voting framework acknowledges not only political factors,

but also demographic characteristics. The pure mass effect is summarized by the relative cohort size,

which weights the indirect utility of each generation.

5.3 Markov-Perfect Equilibrium

We now characterize the subgame perfect equilibrium of the intergenerational voting game. At

each time t, the implementation of a political platform induces dynamic linkages of policies across

periods through the evolution of the asset variables. Fully rational voters internalize such dynamic

effects, which influence their strategic position over time. In principle, the construction of policies

contingent on alternative histories and enforced by reputation mechanisms allows for multiple sub-

game perfect equilibria. We rule out such mechanisms and focus instead on differentiable stationary

Markov policies as equilibrium refinement.13 The payoff-relevant state variables for the political can-

didates are the assets held by the pivotal constituents at each time – i.e., physical and human capital.

In a probabilistic voting environment, when voters condition their strategies on those assets, the

intergenerational contract is enforced and sustained even in a finite-horizon economy. Thus, the

equilibrium characterized here corresponds to the limits of a finite-horizon game. The objects we

are interested in are the intergenerational policy rules and the rules governing the evolution of both

physical and human capital.

Definition 5 (Markov-Perfect Equilibrium) Given the initial conditions k0, h0, a Markov-perfect equi-

librium is an equilibrium feasible allocation such that, for each t ≥ 0, the differentiable policy rules B :

R+ × R+ →[0, bt

]and F : R+ × R+ →

[0, ft

]and the private decision rule K : R+ × R+ → R+ satisfy

the following points:11Probabilistic voting has been extensively studied both theoretically and empirically. Stromberg (2008) adopts this type of

electoral competition to study presidential races in the U.S. and shows the suitability of the model in explaining candidates’behavior. An explicit microfoundation of the probabilistic voting game is provided in the supplementary material in AppendixB.

12An alternative interpretation of φ is in terms of effectiveness of intergenerational political power. On the one hand, itreflects the existence of formal institutions committed to guaranteeing active and passive political participation (i.e., candidacyage, electoral rules, lobby power, voting enfranchisement). On the other hand, it measures how informal institutions alter theage-cohorts’ representativeness (i.e., civil society, clientelism, corruption, social norms, culture).

13Markov perfectness implies that outcomes are history-dependent only on the fundamental state variables. The stationarypart is introduced to focus on equilibrium policy rules that do not depend on calendar time. The differentiable part is aconvenient requirement to avoid the multiplicity of equilibrium outcomes and to give clear positive predictions.

14

i. The policy rules B (kt, ht) and F (kt, ht) are equal to the

arg maxbt,ft

νWat (kt, ht, kt+1, bt, ft, bt+1) + φWo

t (kt, ht, bt)

subject to bt+1 = B (kt+1, ht+1), with kt+1 = K (bt, ft) and ht+1 = Φ (ft, ht);

ii. The private decision rule K (bt, ft) satisfies the functional equation

∆k (bt, ft, kt+1) ≡ νK (bt, ft)− S (It,K (bt, ft) ,B (K (bt, ft) ,Φ (ft, ht))) = 0 (15)

The first equilibrium condition requires the political control variables, bt, ft, to be chosen to

maximize the party’s objective function, constrained to fiscal feasibility requirements, the policy rule

of the next period, the physical capital market clearing condition, and the human capital technol-

ogy. The second condition requires that, if the equilibrium exists, it must satisfy the fixed-point

requirement – i.e., Eq. (15). Upon the existence of a Markov-perfect equilibrium, the partial deriva-

tives of the recursive formulation of the decision rule for private savings – i.e., Kbt ≡ −∆kbt

∆kkt+1

and

Kft ≡ −∆kft

∆kkt+1

– quantify the private sector’s responsiveness to a one-shot deviation of the govern-

ment when voters rationally expect future backward transfers to be set according to B (kt+1, ht+1).

Condition 1 (Uniqueness of Competitive Economic Equilibrium) If ∆k (bt, ft, kt+1) = 0, then ∆kkt+1

>

0.

Condition 1 is necessary and sufficient for a unique intersection point kt+1 solving ∆k (bt, ft, kt+1) =

0. It has a simple interpretation: the elasticity of variation of the interest rate and backward transfers

on the decision to save must be sufficiently large at the solution so that the income effect will not

dominate the substitution effect too much.

Applying Definition 5 yields the following system of first-order conditions with respect to bt, ft:

bt : 0 = φucot − ucat + νβucot+1

(dBt+1

dbt+ νkt+1

dRt+1

dbt

)+ λt (16)

ft : 0 = −νucat + βucot+1

(dBt+1

dft+ νkt+1

dRt+1

dft

)(17)

where λt denotes the multiplier of the non-negativity constraint of bt. Eqs. (16) and (17) depict how

politicians strategically manipulate future policies through their current decisions on the fiscal plat-

form. We disentangle the dynamic effects into two parts. The total derivatives dBt+1

dbt= Bkt+1

Kbt anddBt+1

dft= Bkt+1

Kft+Bht+1Φft capture the strategic effects generated by a variation of the current level of

intergenerational transfers on the next-period amount of backward transfers through the channels of

physical and human capital. The total derivatives dRt+1

dbt= Rkt+1Kbt and dRt+1

dft= Rkt+1Kft+Rht+1Φft

pin down the general-equilibrium effects generated by a variation of the current level of intergenera-

tional transfers on the next-period rate of return on capital.

15

According to Eq. (16), the solution for the backward transfers features three components: (i) the

direct effect on the individual consumption of redistributing resources from tax-payers to tax recip-

ients; (ii) the expected benefits on the consumption of the next-period elderly voters; and (iii) the

tightness of the fiscal constraint relative to the non-negativity of backward transfers. Eq. (17) yields

the trade-off for the current adults between public investments and private savings. On the one

hand, an increase in the total fiscal burden raises the opportunity cost of saving. On the other hand,

the sacrifices suffered by the current taxpayers will be rewarded by higher next-period consumption

through an adjustment of backward transfers and a positive variation in the market interest rate.

6 Intergenerational ContractsIn this section, we characterize the Markov-perfect equilibrium under two headings. To highlight

the main mechanism at work, the first analyzes the basic setup with human capital as the sole payoff-

relevant state variable. The second adds physical capital to the analysis and discusses how elderly

voters’s private wealth alters the politico-economic outcome.

6.1 Human Capital

In this context, we abstract away the general-equilibrium effects via prices, and we isolate the

institutional channel of political competition as the sole determinant of the emergence of a growth-

enhancing intergenerational contract.14 The absence of physical capital destroys the dynamic link-

ages across backward policies. Assuming interior solutions, the redistributive wedge is determined

entirely by the political clout of currently living voters. The equilibrium condition described by Eq.

(16) boils down to the following:

0 = φucot − ucat (18)

Agents’ consumption turns out to be a constant share of the total outcome. The higher the degree

of elderly voters’ relative single-mindedness – i.e., the larger the φ – the lower will be the marginal

rate of intergenerational substitution,ucotucat

, which measures the consumption tightness among agents.

Thus, elderly voters’ bigger relative political clout implies a larger share of public resources devoted to backward

transfers and, in turn, a more unbalanced distribution of consumption in their favor. At the same time, Eq.

(17) collapses to the following:

0 = −νucat + βucot+1Bht+1

Φft (19)

According to Eq. (19), the marginal cost of current taxation borne by adults will be offset by the

marginal benefits of larger next-period consumption. Expected consumption possibilities are related

to the generations’ prospect of democratically claiming part of the future returns of current public

investments via backward transfers.

Proposition 1 (Political Empowerment) An intergenerational contract is enforced if and only if φ > 0,

and it satisfies Bht > 0 and Fht > 0.14The absence of a general-equilibrium effect can be derived as an equilibrium outcome in the context of small open

economies. The link between strategic effects and international capital mobility is further explored in Section 7.1, wherewe provide analytical solutions of the equilibrium policy rules.

16

The proof for the result is the following. In the absence of physical capital, elderly agents have

no private wealth, and bt = 0 whenever φ = 0 for each date t. This implies that Bht+1= 0 and,

by inspecting Eq. (19), there is no productive investment – i.e., ft = 0. In contrast, suppose that

φ > 0 and ft = 0; then, from Eq. (18), bt > 0 for each period t. This cannot be an equilibrium,

as ft = 0 and, in turn, ht+1 = 0 implies bt+1 = 0. The second part of the Proposition hinges on

the forward-looking behavior of constituents and on Assumption 3: accordingly, the sole way to

maximize the voters’ utility entails a positive equilibrium relation between human capital and both

sides of intergenerational transfers. Thus, in equilibrium, backward and forward transfers become

increasing functions of the stock of human capital.

The discontinuity of the mapping F (ht) at φ = 0 highlights the dramatic impact of democratic

institutions in settling intergenerational disagreements and, in turn, enforcing intergenerational con-

tracts. Although our economy encompasses the well-known median voter framework as a degener-

ative case of political competition, Proposition 1 stresses a new neat prediction: when elderly agents

are disempowered – i.e., φ = 0 – voters fail to support productive and durable public spending,

although a growth-enhancing technology is at their disposal. Thus, the economy reverts to inter-

generational autarky. In contrast, if the elderly constituents actively participate in the public debate,

then they will extract a political rent in the form of backward transfers by exerting their electoral in-

fluence. At the same time, adult voters will support productive policies, as they are entitled to grab

a larger share of the next-period production.

In our model, the agents’ concern for future backward transfers is key to enforcing the intergen-

erational contract, given the lack of intergenerational altruism. Therefore, the existence of a Markov-

perfect equilibrium that attains a growth-enhancing intergenerational contract does not require pre-

commitment through the establishment of an institution that outlives the current government and

binds future decision-makers. Rather, the empowerment of the elderly cohort acts as the sole disciplining

mechanism for adults to support public investments.15

6.1.1 Political Power and Growth

In view of Proposition 1, the two redistributive sides of the intergenerational contract are strongly

interrelated. To investigate the nature of such a link, let ρ+ ≡ φBht+1

Bht+1

,φ and ρ− ≡ucot+1

ucot

ddφ

(φucotucot+1

)denote the elasticities of the variation of φ, respectively, on the marginal impact of human capital on

backward transfers and on the marginal rate of substitution between the current and next-period

elderly cohort, weighted by the relative political clout of the elderly voters.

Proposition 2 (Single-Mindedness and Growth) dftdφ≥ (<) 0 if and only if ρ+≥ (<) ρ−.

Proof (See Appendix).15In an OLG economy inhabited by finitely lived players, the assumption of a three-period lifespan might appear unnec-

essarily restrictive. In a more general framework with T periods, the working-age cohorts would support human capitalinvestment to increase their future wealth, just as they were willing to accumulate physical capital in the presence of storagetechnology. These incentives arise irrespective of the implemented voting mechanism that assigns political voice to differentgenerations (see Chen and Song, 2013). Although the extension of the model to a T -period setting would partially under-mine the quantitative impact of the strategic channel, our mechanism remains in place from a qualitative perspective. Indeed,before retiring, the working-aged still have incentives to politically support forward transfers to offspring and increase rentopportunities after retiring.

17

An increase in φ has a two-fold impact on the intergenerational contract. On the one hand, it

alters the distribution of consumption in favor of the current elderly constituents: a higher degree

of elderly voters’ relative single-mindedness positively affects the amount of enforced backward

transfers and, in turn, the consumption level of retirees, measured by ρ−. On the other hand, it

improves the future political ability of current adults to extract an electoral rent – in the form of social

insurance – generated by current public investments, quantified by ρ+. Proposition 2 predicts that

if the latter effect prevails, then the larger φ, the more resources are allocated to growth-enhancing

technology. Therefore, as long as redistribution is crucial to reaching social consensus for growth-oriented

policies, higher redistribution of public resources may enhance growth. From this perspective, our theory

reconciles the existing literature’s contrasting conclusions, which have emphasized a relation of both

strategic complementarity and substitutability between intergenerational welfare programs.16

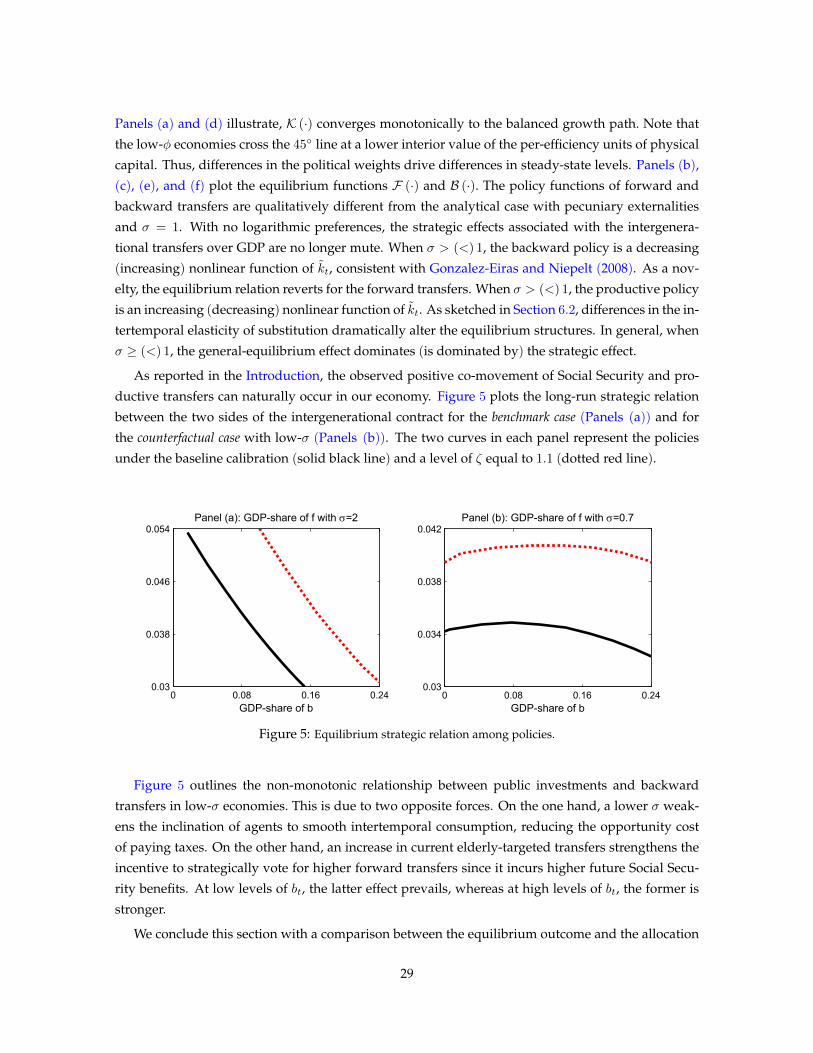

To further qualify the properties of the equilibrium policy rules, Figure 3 graphs forward transfers

against backward transfers, as captured by a variation of φ, for two different levels of intertemporal

elasticity of substitution.17

0 0.2 0.4 0.60.04

0.05

0.06

0.07

0.08Panel (a): GDP-share of f

GDP-share of b0 0.2 0.4 0.6

0.04

0.06

0.08

0.1

0.12Panel (b): GDP-share of f

GDP-share of b

Figure 3: Intergenerational redistribution and economic growth. Panels (a) and (b) plot the equilibrium relationbetween B (ht) and F (ht) in per-efficiency units, when the inverse of the intertemporal elasticity of substitutionacquires the values 0.7 and 2, respectively.

Two observations can be made. First, when agents’ utility is less responsive to changes in con-

sumption, the model predicts a hump-shaped relationship between the provision of backward and

forward transfers and, in turn, the rate of economic growth. Indeed, at low levels of elderly single-

mindedness, an increase in φ induces a variation in ρ+ that offsets the variation in ρ−. The overall

effect reverses at high levels of the relative political clout of elderly constituents (Panel (a)). Second,

16Following the pioneering work of Becker and Murphy (1988), Rangel (2003) emphasizes how voters support publicinvestment because a trigger strategy links investment spending to the future provision of public pensions. Furthermore,Gonzalez-Eiras and Niepelt (2012) have documented the boost of the GDP share of Social Security transfers and public in-vestment as a response to a large increase in the retirement age. In contrast, recent politico-economic models of growth(Alesina and Rodrick, 1994; Persson and Tabellini, 1994; and Azzimonti, 2011) have suggested that political disagreementover the composition of public expenditures leads to extensive redistribution, which depresses growth. As long as partiescompete to retain power via the democratic process, politicians tend to be endogenously short-sighted, and the economyexperiences underinvestment in productive assets.

17Appendix B provides the quantitative framework to replicate Figure 3.

18

the model also predicts that a higher curvature of utility over consumption implies a monotonically

decreasing relation between sustainable public investments and pro-elderly spending (Panel (b)).

6.2 Physical Capital

When a private storage technology is available, the definition of property rights on produc-

tion inputs creates divergent economic interests among cohorts, straining intergenerational coop-

eration. Furthermore, the general-equilibrium effects may add to the analysis and shape the politico-

economic outcome in tandem with the strategic effects. Nevertheless, we show that the core re-

sults of an economy with sole human capital still characterize an environment with savings. As in

Proposition 1, if φ > 0, then an intergenerational contract exists. By contrast, the following remark

acknowledges the case with φ = 0.

Remark 1 (Indeterminacy) When φ = 0, there exists a continuum of undetermined intergenerational con-

tracts.

In the case of adults’ dictatorship, the marginal utility of middle-aged voters is invariant to

changes in the fiscal bundle since agents privately respond through an automatic adjustment of sav-

ings decisions. Therefore, indeterminacy affects the equilibrium outcome. A way to break down

indeterminacy is to introduce some degree of commitment. This is what probabilistic voting does.18

When φ > 0, the political sustainability of the intergenerational contract – either in the presence

or in the absence of general-equilibrium effects – does not rely on self-fulfilling expectations of fu-

ture agreements, but on politico-economic fundamentals that are payoff-relevant state variables for

future constituents. The equilibrium policies directly affect the marginal utility of current elderly

agents and, in turn, the marginal rate of intergenerational substitution. Therefore, the enforced inter-

generational transfers uniquely pin down the consumption level of the old cohort.

Proposition 3 (Necessary Condition) In any intergenerational contract enforced as a Markov-perfect equi-

librium, the dynamic effects of forward transfers are larger than the dynamic effects of backward transfers.

Proof (See Appendix).

Proposition 3 reveals the intertemporal structural relations among policies, which guarantee the

simultaneous enforcement of forward and backward transfers via democratic elections. The sum of

the marginal impacts of public investments on next-period backward benefits and prices is required

to be larger than the sum of the marginal impacts generated by current backward transfers. By con-

trast, if dBt+1

dft+ νkt+1

dRt+1

dftwere smaller or equal to dBt+1

dbt+ νkt+1

dRt+1

dbt, then to maximize the voters’

utility, it would be sufficient to support intergenerational cooperation over backward transfers with-

out investments.18The literature has proposed alternative ways to break down indeterminacy. For example, Azariadis and Galasso (2002)

have established a fiscal constitution, which allows generations to use veto power. However, a general critique asks why asociety that can agree on sophisticated constitutional constraints is not able to agree on the efficient outcome in the first place.Closer to the spirit of this paper are Bassetto (2008) and Gonzalez-Eiras and Niepelt (2008). Whereas the former deals withindeterminacy by assuming that policies are the outcome of a bargaining process, the latter obtains a unique politico-economicequilibrium by modeling political competition with probabilistic voting. We adopt a solution similar to that of Gonzalez-Eirasand Niepelt, and we obtain a unique Markov-perfect equilibrium in a multidimensional state space.

19

To highlight how the dynamic effects influence the enforced intergenerational contract, we rewrite

the political first-order conditions in per-efficiency units by adopting the notation introduced in Sec-

tion 3.2. The state space conveniently reduces to a one-dimensional space, with kt as the state vari-

able. Assuming an interior solution, an envelope argument implies that Eq. (16) now reads as

follows:

0 = φucot −

1− νϕtRt+1

Bkt+1Kbt︸ ︷︷ ︸

Sbt

−

Gbt︷ ︸︸ ︷ν2 kt+1

Rt+1Rkt+1

Kbt

ucat = 0 (20)

where Sbt and Gbt denote, respectively, the strategic and the general-equilibrium effects in per-efficiency

units, generated by bt. Eq. (20) yields the political redistributive wedge, where Υt ≡ 1 − Sbt − Gbtrepresents the endogenous political weight of adult voters as internalized by politicians. A change

in the ratio Υtφ spawns relevant implications in terms of intergenerational inequality. Formally,

higher (lower) endogenous political weight of adult relative to elderly voters corresponds to a higher

(lower) marginal rate of intergenerational substitution and, in turn, to a more skewed distribution of

consumption in favor of the adult (elderly) cohort. Suppose, for example, that Gbt = 0 because of the

negligible impact of assets on prices; then the following Proposition holds.

Proposition 4 (Strategic Substitutability) When the general-equilibrium effects are mute, the Markov-

perfect equilibrium satisfies Bkt+1< 0.

Proof (See Appendix).

When pecuniary externalities are absent, Proposition 4 establishes a decreasing relation between

elderly-targeted transfers and asset variables. Note that, if φ = 0, then Bkt+1= −νR and multi-

ple stationary equilibria – indexed by a free parameter – emerge, consistent with Remark 1. In this

context, the equilibrium policies are obtained as the maximization of adults’ life-cycle utility. The

middle-aged face a trade-off between a more generous next-period Social Security – as measured

by Sbt – and a more effective self-insurance through private savings. In equilibrium, this scheme

prompts a strategic substitutability between public subsidies and private assets. When φ > 0, the

backward policies are set so as to maximize adults’ life-cycle utility in tandem with current elderly

voters’ short-term gains. This additional component weakens the initial trade-off. However, it does

not overturn the substitutability relation between private savings and backward transfers. This out-

come departs from the complementarity result obtained by Grossman and Helpman (1998) for high

levels of elderly political weight, and it hinges on the nonlinearity of voters’ preference.

When the channel of prices is activated, voters also anticipate the general-equilibrium effects

induced by backward policies. By Condition 1, intergenerational transfers have an unambiguous

depressive impact on the accumulation of the asset variable that boosts the rate of return on capital.

Therefore, Gbt is non-negative and partially offsets the strategic benefits via policies. As will be quan-

tified in Section 8 – depending on the intertemporal elasticity of substitution – such a counteracting

force may alter the strategic substitutability relation between private savings and social insurance.

20

We will also document that the magnitude of enforced backward transfers depends negatively on

the degree of complementarity among productive assets.

We conclude this section by taking a closer look at the intergenerational externalities associated

with productive investments. Combining Eqs. (16) and (17) with the equilibrium response of the

saving rate to a variation of current policies – Kbt and Kft – yields the political productive wedge:

0 = ϕft −Rt+1

wt+1(1− εt+1) (21)

where εt+1 ≡ 1 − νϕtwt+1

Rt+1

φucot(It+ϕt

bt+1Rt+1

)ucat−Itφucot

quantifies the human capital externalities in the

politico-economic equilibrium, expressed as a fraction of the cost of investment.19 Eq. (21) illustrates

an interesting property. When εt+1 > 0, office-seeking politicians internalize, at least to some ex-

tent, the inter-temporal externalities generated by current forward transfers. Due to the overlapping

demographic structure and the presence of parental human capital, politicians evaluate the utility

of current living voters, anticipating the expectation of future generations over policies that will be

credibly proposed by future governments. An inspection of Eq. (21) shows that, ceteris paribus,

larger expected backward transfers correspond to greater εt+1 – that is, to a stronger internalization

of the human capital externalities through the channel of rent extraction. It leads to more disci-

plined politicians and to higher economic growth. However, as the amount of enforceable backward

transfers is called into question by technological complementarity, so is its disciplinary impact on

enforceable forward transfers. We return to this point in Section 8.

To sum up: for our theory to apply, the following two fundamental elements of the model must

be identified: (i) the prospect of follow-up intergenerational contracts, which serves as a disciplining device

to implement current policies; and (ii) the nature of short-term agreements among politicians and current

constituents – i.e., the absence of commitment. To clarify the role of commitment, suppose that policy-

makers were able to sign binding long-term agreements with current living voters. Because repre-

sentatives run for office with the aim of being elected following the current political campaign, the

intergenerational contract they may commit to will be, at most, a two-period agreement. In the best

scenario, they will promise current adults that they will fully expropriate the next-period generation

and use the proceeds to subsidize current adults’ consumption when they are old. As a consequence,

the amount of pledgeable income devoted to productive investment would be such that the marginal

rate of transformation equals the opportunity cost of savings, disregarding the effects of externalities

associated with forward transfers. In contrast, in a politico-economic equilibrium without commit-

ment, εt+1 may differ from zero and attain higher economic growth.

19When εt+1 = 0, Eq. (21) is equivalent to the necessary condition of a competitive equilibrium with no credit marketconstraints, where the young can borrow money at the market interest rate.

21

7 Illustrative ExamplesWe now explore the properties of the politico-economic equilibrium under two different economic

environments by providing analytical solutions of the equilibrium policy rules and inspecting their

welfare properties. In the first case, we examine a small open economy. The negligible impact of

domestic capital formation on the world interest rate implies the absence of general-equilibrium ef-

fects. In the second case, we focus on a closed economy. The lack of international capital mobility

gives rise to general-equilibrium effects via prices. We emphasize that democratic institutions en-

force an efficient intergenerational contract when the sole strategic effects influence the economic

system. In both examples, the Markov-perfect equilibrium is obtained as the limit of a finite-horizon

equilibrium whose characteristics do not significantly depend on the time horizon, as long as it is

long enough. We parameterize (i) the preferences over private consumption as the logarithmic type,

u (c) = log (c); and (ii) the human capital and the final good technologies as the Cobb-Douglas form,

ht+1 = Ahθt f1−θt and yt = Bkαt h

1−αt , respectively, with α, θ ∈ (0, 1), and the factor productivity

parameters A, B ≥ 1.

7.1 Small Open Economy

Capital is perfectly mobile. We denote the (exogenous) world interest rate by R and the workers’

per-efficiency wage byw. In a competitive equilibrium, kt =(αBR

) 11−α ht andw = (1− α)B

(αBR

) α1−α .

Hence, the world interest rate uniquely pins down the ratio of the factors of production. According

to Eq. (17), the political productive wedge collapses to dBt+1

dft= νR. Furthermore, from Eq. (16), the

endogenous weight that politicians attach to adults simplifies to Υt+1 = 1 − νRdBt+1

dbt. Proposition 3

predicts that dBt+1

dft> dBt+1

dbt– that is, the strategic effect generated by a variation on current public

investment in the next-period backward benefits is required to be larger than the strategic linkage

between the two successive backward policies.

Lemma 1 (Human Capital Externality) Let m : R+ → R+ be a differentiable single-valued mapping

m(ψ(j)) ≡(AθνR ψ(j) + wA(1−θ)

R

) 1θ

with ψ(1) ≡(wA(1−θ)(φ+αβ(φ+ν))

R(1+αβ)(φ+ν)

) 1θ

as the initial condition. For R >

Aνθ, the first-order nonlinear equation ψ(j+1) = m(ψ(j)) has a unique, locally stable, fixed point equal to ψ.20

Proof (See Appendix).

The fixed point ψ analytically quantifies the human capital externalities as internalized by policy-

makers when proposing their welfare programs. A natural comparative statics is that ψ is decreasing

in the market interest rate. This is intuitive since higher a return of private assets discourages agents

from supporting intergenerational welfare schemes. Furthermore, in the limit, when the share of

parental human capital θ approaches zero, human capital externalities vanish. Let R (φ) ≡ φ+νββ ϕ

denote the implicit net return of Social Security in equilibrium, where ϕ is the economy growth rate.

Using Lemma 1, the following Proposition holds.

20The subscript in the parentheses denotes the number of iterations.

22

Proposition 5 (Equilibrium in a Small Open Economy) WhenR = R (φ), there exists a unique Markov-

perfect equilibrium characterized by the following set of policy functions and laws of motion for the state vari-

ables:

i. bt = B (kt, ht) = − ν2R(1+β)φ+ν(1+β)kt + φν

φ+ν(1+β)

(w + νθ

1−θψ)ht;

ii. ft = F (ht) = ψht;

iii. kt+1 = Rβφ+νβkt +

βR(w−νψ)(φ+ν(1+β))−φ(βR+νAψ1−θ)(w+ θν1−θψ)

νR(1+β)(φ+νβ) ht;

iv. ht+1 = Aψ1−θht.

Proof (See Appendix).

When R = R (φ), agents are indifferent between individual savings and Social Security. The

Markov-perfect equilibrium delivers intergenerational transfers, the strategic effects of which are not

mute. At each time, politicians can influence future policies by varying capital formation through

the current fiscal platform. Consistent with Proposition 4, backward transfers turn out to be a non-

increasing linear function of physical capital and an increasing linear function of human capital. The

equilibrium predictions for forward transfers are easily illustrated. Assumption 3 reveals that the

sole way to maximize the utility of adult constituents requires a positive relation between human

capital and forward transfers. Since the political preferences of the old do not depend on productive

spending, physical capital retained by elderly constituents is not a payoff-relevant state variable for

forward-oriented policies. Moreover, public investments are not influenced by the degree of single-

mindedness among cohorts. This result is an application of Proposition 2 to a small open economy.

Under perfect capital mobility, adults privately respond to a reassessment of relative political clout

by optimally reallocating consumption over time through an automatic adjustment of savings deci-

sions. Inasmuch as the borrowing constraint does not bind, voters always freely allocate their wealth

holdings. Finally, the rate of economic growth amounts to ϕ = Aψ1−θ, and the long-term solution

converges to the balanced growth path in one period.21

Note that there can be no intergenerational contracts with R > R (φ). In this circumstance, voters

would replace social insurance with self-insurance through private saving, accumulating an ever-

increasing stock of physical capital. As elderly agents become richer, they would be required to

use part of their proceeds to subsidize the consumption of future generations, thereby violating the

feasibility constraint of backward transfers. In contrast, it is possible that R < R (φ). In this context,