5:30 pm 1. Audit Serv - Chapel Hill-Carrboro City Schools

195

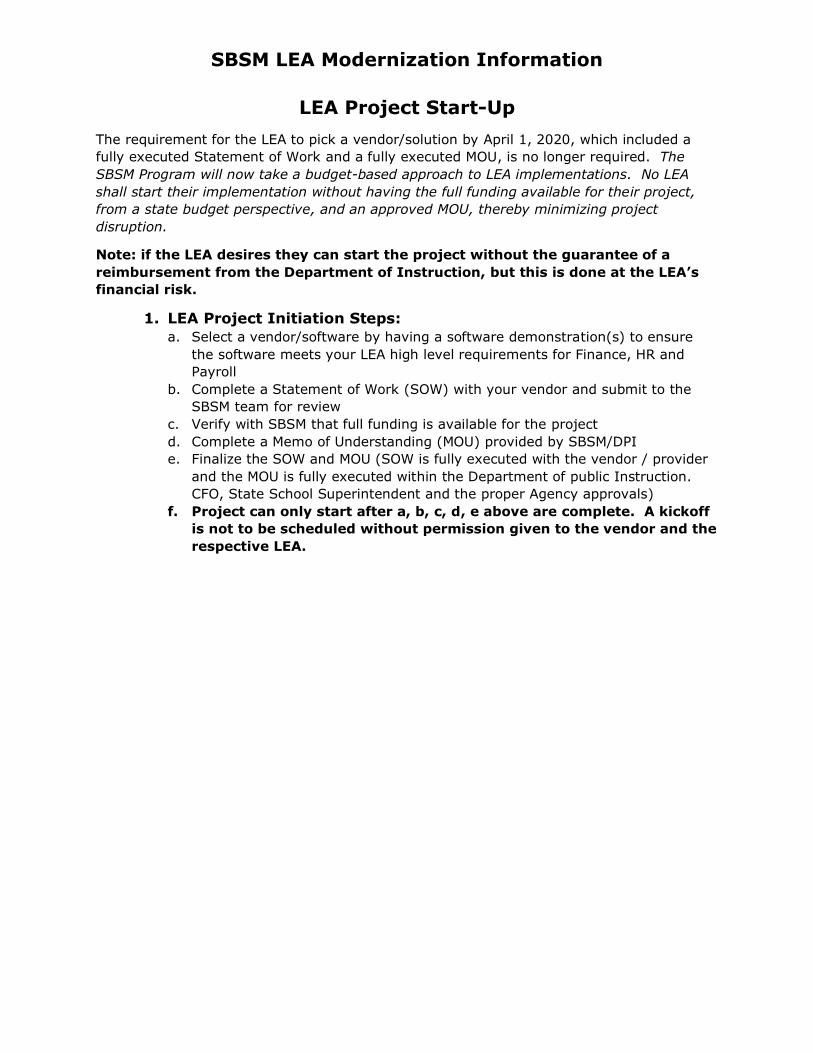

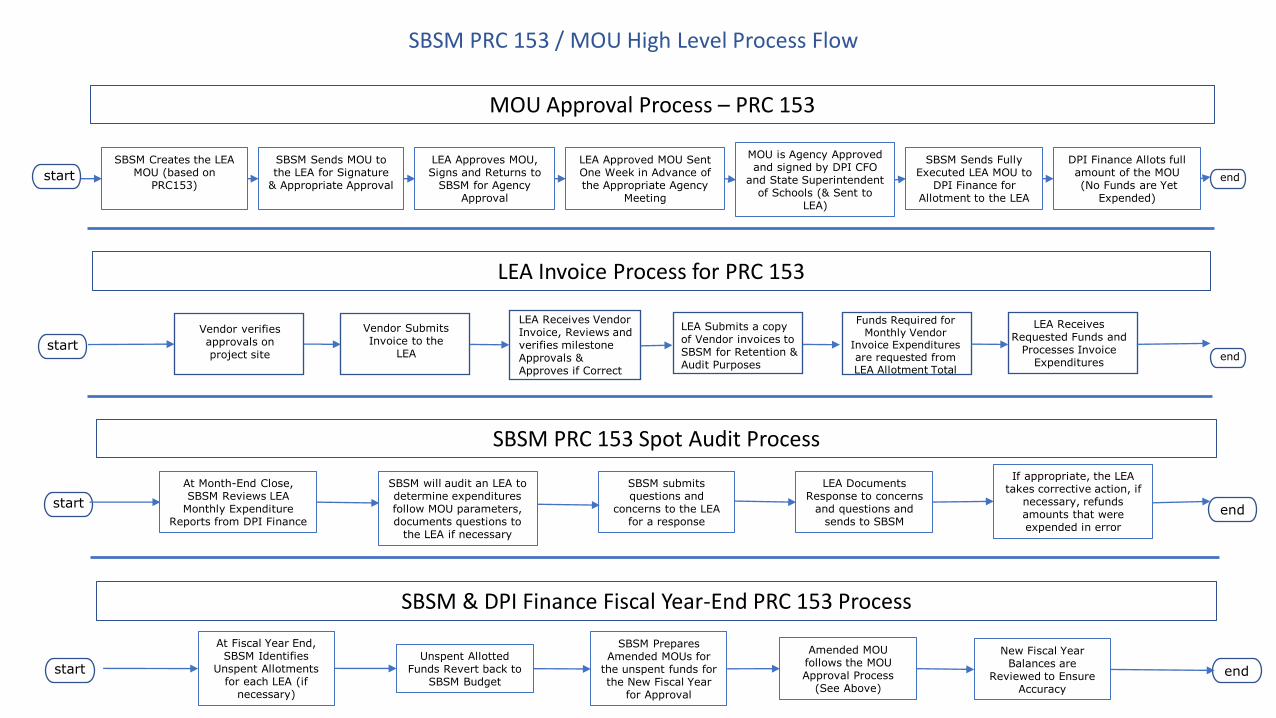

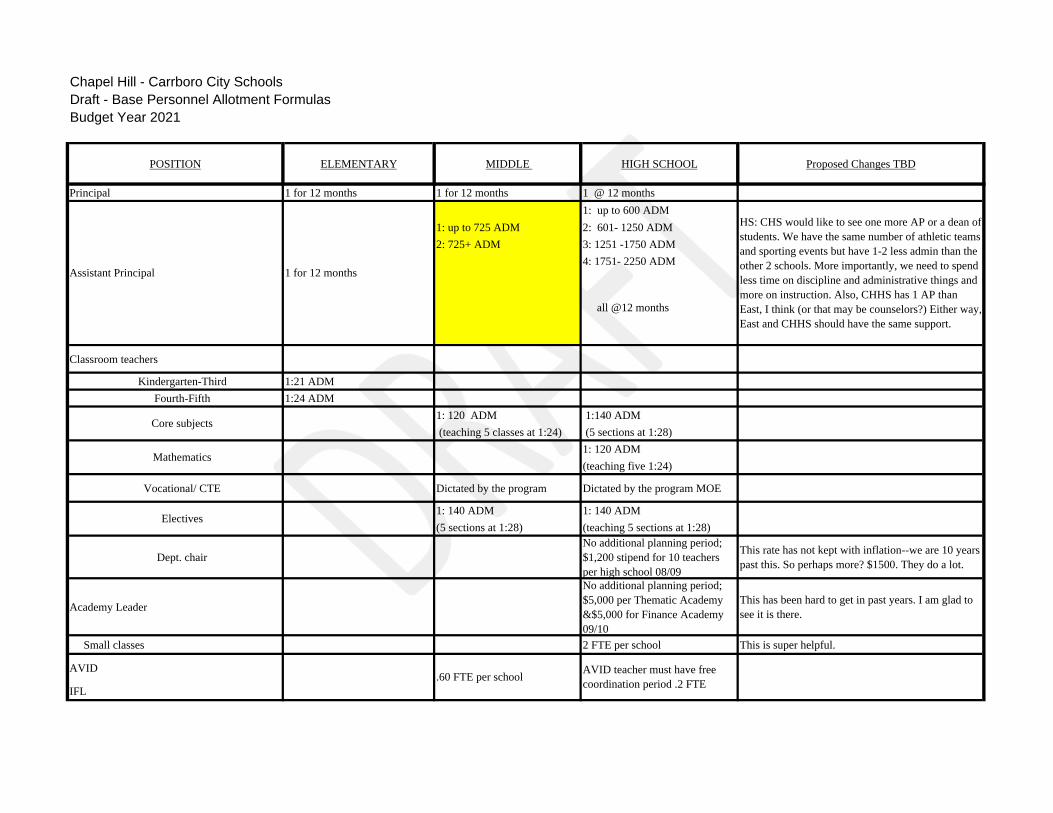

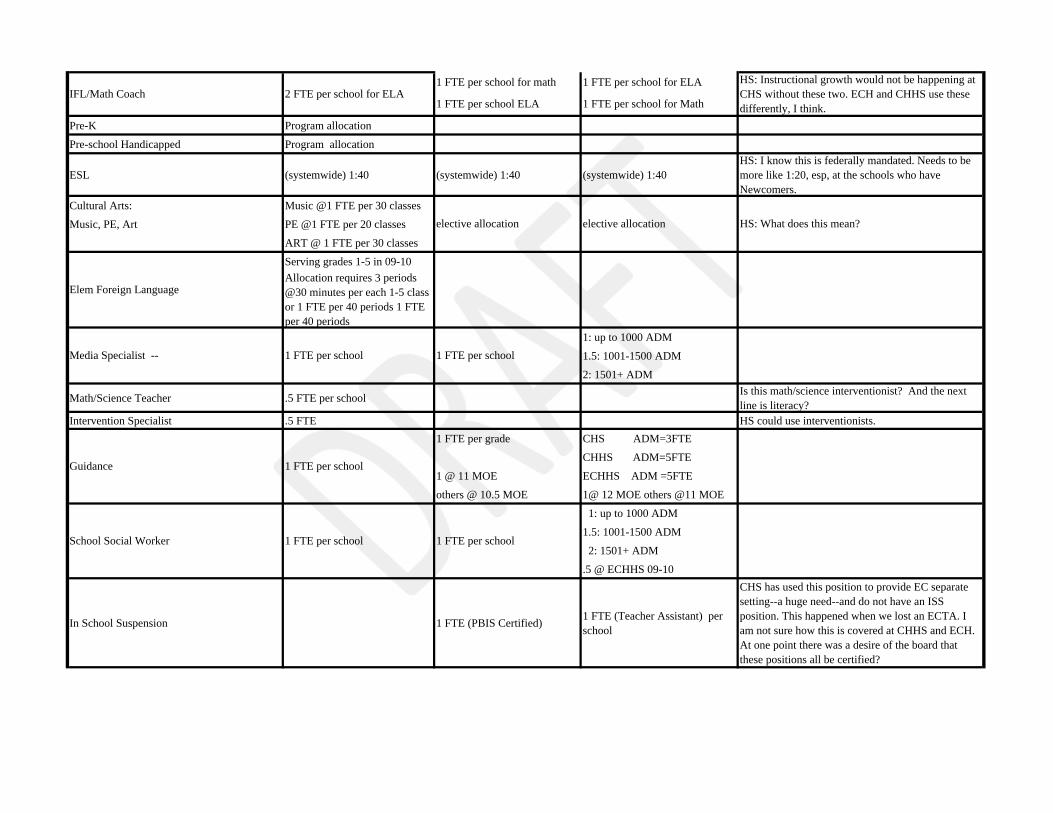

Chapel Hill-Carrboro City Schools Finance Committee Meeting Date: May 11, 2020 Place: Virtual Time: 5:30 p.m. 1. Audit Services RFP Committee Report Report on the findings of the Audit RFP review committee and discuss best option(s) to bring forward to the BOE as a recommendation for external audit services for the fiscal year ended 6/30/20. A one page summary of the committee’s review and each firm’s proposal is attached. 2. Review of the NC School Business Systems Modernization Office’s MOU Discussion surrounding the requirement for CHCCS to update the Memorandum of Understanding with NCDPI relating to participation in the State-wide ERP pilot program. In order to receive continued State funding next year to continue our modernization work, NCDPI requires an updated MOU to be executed and brought before the NC State Board of Education in June. A summary of the requirements, flowchart, and MOU is attached. 3. Update on the continued work on Base Personnel Allotment Formulas Continued discussion surrounding the adoption of Base Allotment Formulas to be included in the BOE’s final approved 2020-2021 Budget. Work is continuing, a copy of the most recent draft is attached.

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of 5:30 pm 1. Audit Serv - Chapel Hill-Carrboro City Schools

Chapel Hill-Carrboro City Schools Finance Committee Meeting

Date: May 11, 2020 Place: Virtual Time: 5:30 p.m.

1. Audit Services RFP Committee Report

Report on the findings of the Audit RFP review committee and discuss best option(s) to bring forward to the BOE as a recommendation for external audit services for the fiscal year ended 6/30/20. A one page summary of the committee’s review and each firm’s proposal is attached.

2. Review of the NC School Business Systems Modernization Office’s MOU

Discussion surrounding the requirement for CHCCS to update the Memorandum of Understanding with NCDPI relating to participation in the State-wide ERP pilot program. In order to receive continued State funding next year to continue our modernization work, NCDPI requires an updated MOU to be executed and brought before the NC State Board ofEducation in June. A summary of the requirements, flowchart, and MOU is attached.

3. Update on the continued work on Base Personnel Allotment Formulas Continued discussion surrounding the adoption of Base Allotment Formulas to be includedin the BOE’s final approved 2020-2021 Budget. Work is continuing, a copy of the most recent draft is attached.

AS&W TPS&A M&J S&P

Audit Year 6/30/2020 47,500$ 49,500$ 39,000$ 50,398$

Audit Year 6/30/2021 48,500 49,500 40,000 51,910

Audit Year 6/30/2022 49,500 49,500 41,000 53,467

3 Year Totals 145,500$ 148,500$ 120,000$ 155,775$

Audit Year 6/30/2020 Cost Ranking 2 3 1 4

3 Year Cummulative Cost Ranking 2 3 1 4

Audit Approach 8.9 8.3 8.9 5.5

Governmental Audit Experience 9.4 8.7 6.7 7.4

Specialized Skills ‐ NC LEA Specific 9.5 8.8 7.6 5.9

Availability During the Year for Consultation 9.1 7.7 2.5 6.0

Ability to Perform Additional Work 9.1 8.1 6.2 5.6

Average Score 9.2 8.3 6.4 6.1

Ranking 1 2 3 4

Jonathan Scott ‐Finance Ellen Hines ‐ Finance

Kelly Glosson ‐ Instructional Services Justin Kiser ‐ Finance/EC

Denise Buckley ‐ Finance Amy Langenderfer ‐ Community Schools

Amanda Bales ‐ Finance Tami Zubler ‐ Pre K/ Headstart

Laverne Riggsbee ‐ East Chapel Hill High School Linda Fyle ‐ Scroggs Elementary School

Julie Walker ‐ McDougle Middle School Marie Williams‐Skinner ‐ Human Resources

Rochell Selvey ‐ Finance

Committee Members:

Bid Tabulation/Comparison for Audit RFP for 6/30/20

May 6, 2020

Base Audit Fees (Including Financial Statements):

Other Decision Factors:

CHAPEL HILL-CARRBORO

CITY SCHOOLS

Proposal for Audit Services

First Section

June 30, 2020, 2021 and 2022

Table of contents

Introduction ............................................................................................................................. 1

Firm Background ..................................................................................................................... 2

Services Requested ................................................................................................................... 3

Audit Approach ........................................................................................................................ 3

Requested Information ............................................................................................................. 4

Most Recent Peer Review Letter .............................................................................................. 13

Independence Policy ................................................................................................................. 14

1 | P a g e

Certified Public Accountants

ANDERSON SMITH & WIKE PLLCA S W

Dear Mr. Scott,

Thank you for giving Anderson Smith & Wike PLLC the opportunity to bid on the audit services

for Chapel Hill-Carrboro City Schools. We are a service-oriented accounting firm and our largest

practice area is in providing audit services to school districts. In fact, we audit more school

districts in North Carolina than any other firm. Since we serve so many school districts

throughout the state we are able to ensure that our clients are well-informed relating to any

pending or actual changes in the industry. We truly feel that we are a valuable resource for our

clients.

On behalf of Anderson Smith & Wike PLLC, we are all very pleased to be able to provide you

with this proposal for the audit of the basic financial statements of Chapel Hill-Carrboro City

Schools for the years ending June 30, 2020, 2021 and 2022.

If you have any questions, or would like to discuss the proposal in more detail, do not hesitate to

call. I can be reached at (910) 997-1418.

Sincerely,

Dale Smith, CPA

Anderson Smith & Wike PLLC

2 | P a g e

Firm Background

Anderson Smith & Wike PLLC is a full-service accounting firm serving clients throughout North

Carolina. With offices in Gastonia, Statesville, Rockingham and West End, we are dedicated to

providing our clients with professional, personalized services and guidance in a wide range of

financial and business needs.

Our firm’s five partners (Ken Anderson, Dale Smith, Michael Wike, Adam Scepurek and Vince

Quinn) have an average of over 20 years of public accounting experience, with the majority of

those years spent focusing on providing services to governmental entities. Our current practice,

as you will see in our proposal, includes a strong concentration in audit services provided to

governmental entities, particularly school districts. Unlike most firms, governmental audits and

related services are the key practice area in our firm and is where we focus the majority of our

efforts and training. In addition, Anderson Smith and Wike PLLC is a strong supporter of

NCASBO having presented classes at each of the last seven winter conferences held in

Greensboro.

Anderson Smith and Wike PLLC prides itself in customer service. We are able to combine

extensive experience and industry specific knowledge with hands-on service to provide a

superior level of customer service. At Anderson Smith and Wike PLLC our clients never feel as

if they are simply a number, as we value each and every client – no matter how large or how

small.

The firm is a member of the North Carolina Association of Certified Public Accountants

(NCACPA) and the American Institute of Certified Public Accountants (AICPA). As such, we

comply with all peer review requirements of the AICPA.

3 | P a g e

Services Requested

Anderson Smith & Wike PLLC will provide the following services for Chapel Hill-Carrboro

City Schools:

• Audit of the basic financial statements of Chapel Hill-Carrboro City Schools for the years

ending June 30, 2020, 2021 and 2022 in accordance with auditing standards generally

accepted in the United States of America and the standards applicable to financial audits

contained in Government Auditing Standards, issued by the Comptroller General of the

United States.

• In conjunction with the audit of the basic financial statements, we will consider Chapel

Hill-Carrboro City Schools’ internal control over financial reporting and test its

compliance with certain provisions of laws, regulations, contracts, and grants as required

by the U.S. Office of Management and Budget (OMB) Uniform Guidance and the State

Single Audit Implementation Act.

• Preparation of the audited basic financial statements for Chapel Hill-Carrboro City

Schools for the years ending June 30, 2020, 2021 and 2022.

• Preparation of the Federal Data Collection Form.

• Issuance of a management letter detailing internal control deficiencies, if any, that are

noted during the course of the audit of the basic financial statements.

• Preparation of an Auditor Communications Letter.

Audit Approach

Our audit approach is designed to make the audit as efficient and effective as possible. We strive

to coordinate and schedule the audit such that the day-to-day work flow of the school board

employees is disrupted as little as possible. In addition, our planning and scheduling efforts

enable us to complete the audit fieldwork efficiently without needing multiple “return visits” to

gather additional information. We feel our extensive school board audit experience coupled with

on-site, partner service is what enables Anderson Smith & Wike PLLC to achieve these

efficiencies.

We will utilize standardized Governmental Audit Programs as well as Federal and State

Compliance Supplements as published by the applicable Federal grantor agency or North

Carolina’s Local Government Commission. Our tests will be performed utilizing various

sampling techniques as deemed appropriate for the specific objective of the test being performed.

4 | P a g e

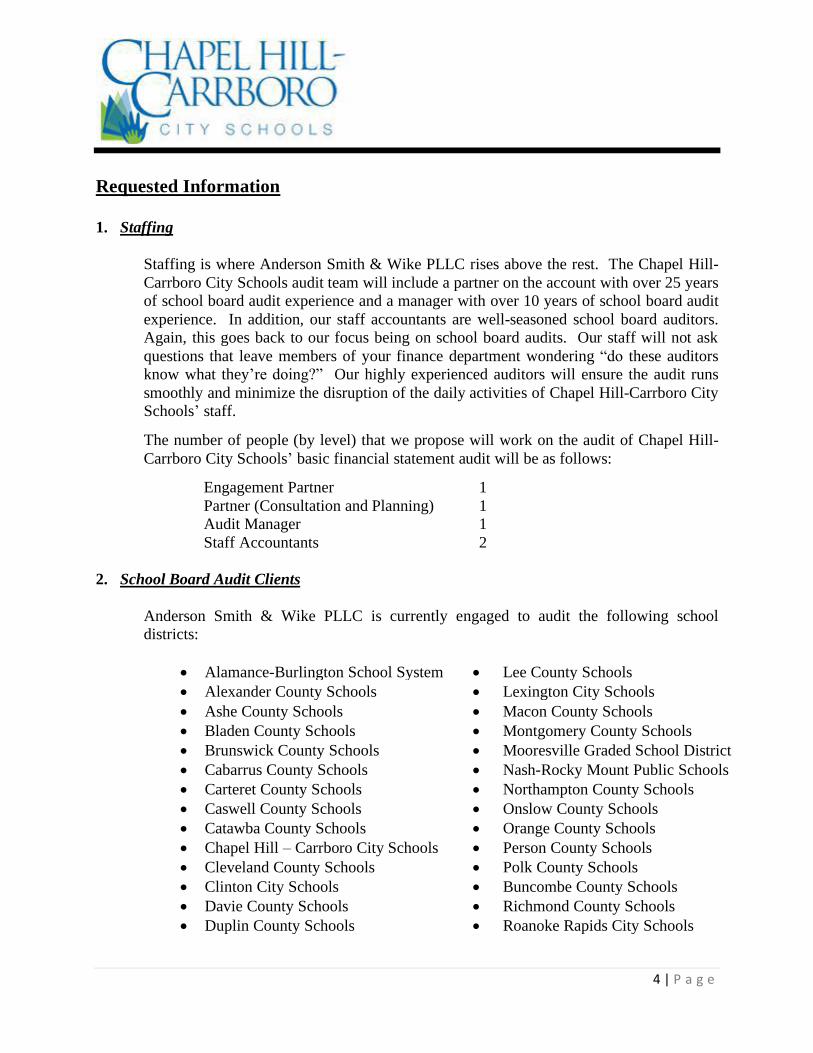

Requested Information

1. Staffing

Staffing is where Anderson Smith & Wike PLLC rises above the rest. The Chapel Hill-

Carrboro City Schools audit team will include a partner on the account with over 25 years

of school board audit experience and a manager with over 10 years of school board audit

experience. In addition, our staff accountants are well-seasoned school board auditors.

Again, this goes back to our focus being on school board audits. Our staff will not ask

questions that leave members of your finance department wondering “do these auditors

know what they’re doing?” Our highly experienced auditors will ensure the audit runs

smoothly and minimize the disruption of the daily activities of Chapel Hill-Carrboro City

Schools’ staff. The number of people (by level) that we propose will work on the audit of Chapel Hill-

Carrboro City Schools’ basic financial statement audit will be as follows:

Engagement Partner 1

Partner (Consultation and Planning) 1

Audit Manager 1

Staff Accountants 2

2. School Board Audit Clients

Anderson Smith & Wike PLLC is currently engaged to audit the following school

districts:

• Alamance-Burlington School System • Lee County Schools

• Alexander County Schools • Lexington City Schools

• Ashe County Schools

• Bladen County Schools

• Brunswick County Schools

• Cabarrus County Schools

• Carteret County Schools

• Caswell County Schools

• Catawba County Schools

• Chapel Hill – Carrboro City Schools

• Cleveland County Schools

• Clinton City Schools

• Macon County Schools

• Montgomery County Schools

• Mooresville Graded School District

• Nash-Rocky Mount Public Schools

• Northampton County Schools

• Onslow County Schools

• Orange County Schools

• Person County Schools

• Polk County Schools

• Buncombe County Schools

• Davie County Schools

• Duplin County Schools

• Richmond County Schools

• Roanoke Rapids City Schools

5 | P a g e

2. School Board Audit Clients (continued)

• Gaston County Schools

• Halifax County Schools

• Haywood County Schools

• Hickory City Schools

• Hoke County Schools

• Kannapolis City Schools

• Johnston County Schools

• Bertie County Schools

• Granville County Schools

• Rockingham County Schools

• Rutherford County Schools

• Scotland County Schools

• Union County Public Schools

• Weldon City Schools

• Chatham County Schools

• Surry County Schools

• Davidson County Schools

• Jackson County Schools

• Yancey County Schools

• Stanly County Schools

• Wilson County Schools

• Madison County Schools

• Graham County Schools

• Arapahoe Charter School

• Currituck County Schools

• Avery County Schools

3. Additional Professional Services

Our auditors have provided additional professional services to numerous school boards

throughout their careers. A brief listing of these past engagements follows. Please

contact Dale Smith if additional information is needed relating to any of these

engagements.

• Analysis of ABC Transfers – waivers

• Agreed-Upon Procedures Engagements

• Assistance with GASB 34/68/75 Implementation

• Assistance with ASBO and GFOA Submissions

• Bank Reconciliations

• Bookkeeping Services

• Budget Consultation and Assistance

• Capital Asset Reconciliation

• Capital Asset Software Consulting

• Fraud Investigations

• Internal Control Assessments

• Modification to Accounting Policies and Procedures Manual

• Meeting with County Commissioners

• Assistance with Sales Tax Refund Claims

• School Bookkeeper and Principal Training

• Set up of Fund 8 – Other Special Revenue Fund

• Training for Board of Education members

6 | P a g e

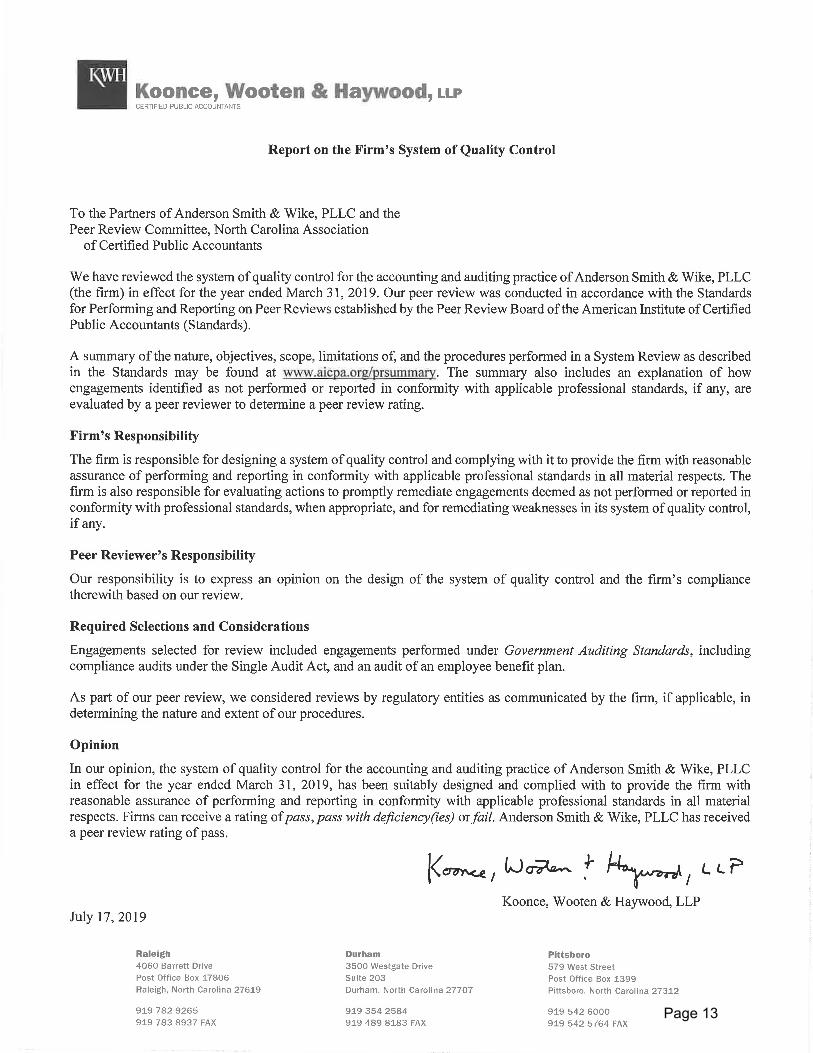

4. Peer Review

Anderson Smith & Wike PLLC is a member of the North Carolina Association of

Certified Public Accountants (NCACPA) and the American Institute of Certified Public

Accountants (AICPA). As such, we comply with all peer review requirements of the

AICPA and have included a copy of our most recent peer review letter. A copy of our

most recent peer review letter can be found on page 13.

5. Key Audit Team Members

Dale Smith, CPA – Partner Dale began his career with Dixon Hughes PLLC in 1994 and immediately focused on

audits of school boards. Throughout his career he has worked on school board audits of

all sizes and all levels of complexity. Based on his past experience, Dale has the

technical expertise required to audit a school board such as Chapel Hill-Carrboro City

Schools. Equally important as the technical abilities, Dale understands the demands and

pressures the staff of Chapel Hill-Carrboro City Schools encounter on a daily basis. He

will work with your staff to ensure that the audit progresses smoothly. Dale has experience on the audits of the following boards of education (please note that

dates may not be exact):

Scotland County Schools (1995-2007, 2010-2019)

Moore County Schools (1995-2007)

Bladen County Schools (1996-2007, 2011-2015)

Montgomery County Schools (1997-2007, 2010-2019)

Richmond County Schools (1994-2007, 2012-2019)

Harnett County Schools (1998-2007)

Northampton County Schools (1999-2007, 2010-2019)

Onslow County Schools (2004-2007, 2014-2019)

Brunswick County Schools (2007, 2012-2013)

Chatham County Schools (2007, 2015-2019)

Iredell-Statesville Schools (2008)

Alamance-Burlington School System (2008-2013, 2019)

Hoke County Schools (2008-2019)

Orange County Schools (2008-2019)

Roanoke Rapids Graded School District (2008-2015)

Weldon City Schools (2008-2019)

Union County Public Schools (2008-2013)

Polk County Schools (2009)

Chapel Hill-Carrboro City Schools (2009-2019)

7 | P a g e

5. Key Audit Team Members (continued)

Bertie County Schools (2009-2010, 2016-2019)

Ashe County Schools (2010)

Duplin County Schools (2011-2012)

Granville County Schools (2014, 2016-2019)

Nash-Rocky Mount Public Schools (2012-2019)

Lee County Schools (2012-2019)

Rockingham County Schools (2013-2019)

Arapahoe Charter School (2017-2019)

Adam Scepurek, CPA – Partner Adam began his career with Dixon Hughes PLLC in 2000 and joined Anderson Smith &

Wike PLLC in 2012. He has focused on audits of school boards for the past 18 years. He

has concentrated primarily in the area of auditing and has developed a strong proficiency

in financial reporting and auditing standards along with an extensive grasp of

governmental accounting, state and federal compliance requirements and business

management. Adam has been involved in the audits of numerous Boards of Education of

various sizes ranging from districts with fewer than 5 schools all the way up to 50+

schools. Adam has broad experience with single audits, special grants, school food

service operations, creation of Fund 8 – Other Special Revenue Fund, fixed asset issues,

and other areas as they pertain to boards of education and individual schools. Adam has experience on the audits of the following boards of education (please note that

the dates may not be exact):

Moore County Schools (2001-2011)

Richmond County Schools (2001-2011)

Montgomery County Schools (2001-2009, 2012-2013)

Harnett County Schools (2003-2011)

Brunswick County Schools (2007-2019)

Beaufort County Schools (2007-2011)

Carteret County Schools (2007-2008, 2012-2019)

Northampton County Schools (2003-2008, 2012-2013)

Scotland County Schools (2004-2008, 2012-2013)

Onslow County Schools (2007-2008, 2012)

Lee County Schools (2001-2011)

Bladen County Schools (2005-2019)

Chatham County Schools (2007-2011)

Cabarrus County Schools (2012-2019)

Halifax County Schools (2011-2013)

8 | P a g e

5. Key Audit Team Members (continued)

Roanoke Rapids Graded Schools (2012-2019)

Orange County Schools (2012-2013)

Union County Schools (2012-2019)

Duplin County Schools (2012-2019)

Clinton City Schools (2014-2019)

Johnston County Schools (2015-2019)

Graham County Schools (2016-2019)

Caswell County Schools (2016-2019)

Sampson County Schools (2017-2019)

Yancey County Schools (2017-2019)

Currituck County Schools (2019) Wilson County Schools (2019)

Paul Carson, CPA – Audit Manager Paul began his career with Norris, Stewart & Ralston, P.A .in 2008 and joined Anderson

Smith & Wike PLLC in 2010. He has focused on school board audits for the past 10

years and has developed a strong proficiency in financial reporting, auditing standards,

and accounting principles significant to school districts. Paul has extensive experience

with single audits, special grants, school food service operations, individual school

controls and procedures, fixed asset issues, school district fraud investigations and other

areas as they pertain to school districts. Paul has experience on the audits of the following boards of education (please note that

the dates may not be exact):

Hoke County Schools (2008-2019)

Orange County Schools (2008-2019)

Weldon City Schools (2008-2019)

Alamance-Burlington School System (2008-2013, 2019)

Roanoke Rapids Graded School District (2008, 2010-2013)

Scotland County Schools (2009-2019)

Chapel Hill-Carrboro City Schools (2009-2019)

Onslow County Schools (2009-2010, 2014-2019)

Northampton County Schools (2009-2019)

Mooresville Graded School District (2009-2010, 2016)

Bertie County Schools (2009-2010, 2016-2019)

Halifax County Schools (2010-2017)

Montgomery County Schools (2010-2019)

Union County Public Schools (2010)

Macon County Schools (2010)

9 | P a g e

5. Key Audit Team Members (continued)

Bladen County Schools (2011-2013)

Hickory City Public Schools (2011)

Polk County Schools (2011-2012)

Ashe County Schools (2011-2012)

Duplin County Schools (2011)

Richmond County Schools (2012-2019)

Nash-Rocky Mount Public Schools (2012-2019)

Lee County Schools (2012-2019)

Brunswick County Schools (2012-2013)

Carteret County Schools (2012)

Rockingham County Schools (2013-2019)

Granville County Schools (2014, 2016-2019)

Chatham County Schools (2015-2019)

Arapahoe Charter School (2017-2019)

6. Educational Background and Professional Memberships of Audit Team

Dale Smith, CPA

Education

UNCC, Bachelor of Science in Accountancy, 1993

Memberships

Member of the AICPA

Member of the NCACPA

Recent Continuing Education Relevant to School Board Audits

Governmental Accounting and Reporting (2016, 2017, 2019)

Auditing Developments (2019)

The Detection and Prevention of Fraud in Financial Statements (2019)

Accounting Fraud – Recent Cases (2019)

Internal Control and Fraud Detection: A Practical Guide (2019)

Accounting for Pensions and Postretirement Benefits (2017)

Government Auditing (2014, 2016, 2017, 2019)

NCASBO Instructor – Internal Audit Function (2014, 2015)

NCASBO Instructor – PTO’s, PTA’s, Booster Clubs & Advertising (2013)

NCASBO Instructor – Fraud and Segregation of Duties (2013, 2015)

NCASBO Instructor – Preparing for an Audit (2015, 2019)

NCASBO Instructor – Central Office & Individual Schools Controls (2011, 2012)

NCASBO Instructor – Individual Schools and PTO Internal Controls (2017)

NCASBO Instructor – Crowdfunding, PTO’s, PTA’s, Booster Clubs (2018)

10 | P a g e

6. Educational Background and Professional Memberships of Audit Team (continued)

Adam Scepurek, CPA

Education

UNCW, Bachelor of Science in Accountancy, 1999

UNCW, Masters of Science in Accountancy, 2000

Memberships

Member of the AICPA

Member of the NCACPA

Recent Continuing Education Relevant to School Board Audits

Local Government Auditing, Reporting & Review (2019)

Government Auditing (2017 & 2018)

Auditing Developments (2018)

Full Disclosure in Financial Reporting (2018)

Detection and Prevention of Fraud in Financial Statements (2018)

Government Auditing – Green Book – Information and Monitoring (2018)

Ethics for NC CPA’s (2017 & 2018)

Governmental GAAP – Fund Accounting (2017)

Introduction to Governmental GAAP (2017)

Governmental Accounting and Reporting (2016)

Accounting for Pension and Post-Retirement Benefits (2016)

Paul Carson, CPA

Education

Appalachian State University, Bachelor of Science in Business Administration in

Accounting, 2007

Memberships

Member of the AICPA

Recent Continuing Education Relevant to School Board Audits

Government Accounting: Principles and Financial Reporting (2019)

Auditing Developments (2017, 2019)

Major Changes to Auditing Standards (2019)

The Detection and Prevention of Fraud in Financial Statements (2019)

Government Auditing (2018)

Internal Control and Fraud Detection (2018)

Assessing the Reliability of Computer-Processed Data (2017)

11 | P a g e

7. Professional Experience of Assigned Personnel

Our auditors have experience in auditing the following governmental funds, federal

programs, and state programs:

• Funds

▪ State Public School Fund

▪ Federal Grants Fund

▪ Current Expense Fund

▪ Capital Outlay Fund

▪ School Food Service Fund

▪ Child Care Fund

▪ Other Special Revenue Fund

▪ Individual Schools Fund

▪ Scholarship and Agency Funds

• Federal Programs

▪ Child Nutrition Cluster

▪ Food Distribution - Commodities

▪ Title I Cluster

▪ Special Education Cluster

▪ Supporting Effective Instruction (Improving Teacher Quality)

▪ Head Start

▪ 21st Century

▪ Reading First

▪ Workforce Investment Act

▪ Magnet Schools

▪ Upward Bound

▪ Migrant Education

▪ Title II, Math and Science Partnership

▪ Impact Aid

▪ Various ARRA Grants

• State Programs

▪ State Public School Fund

▪ School Technology

▪ Driver Training

▪ Career and Technical Education

▪ Textbooks

▪ North Carolina Pre-K Program

▪ Smart Start

▪ Public School Building Capital Fund

▪ Public School Capital Fund - Lottery

12 | P a g e

8. Specialized Skills, Training and Background

Please refer to items 5, 6, and 7.

9. References

We encourage you to contact the Finance Officer at any of the school districts listed

in item #2 above as we are confident that all of the districts we audit are satisfied

with our services. However, we’ve included four finance officers along with their

contact information for your convenience.

• Tina Edmonds, Finance Officer

Richmond County Schools 910-582-5860

• Beth Day, Chief Financial Officer

Granville County Schools

919-693-4613

• Jeff Hollamon, Chief Financial Officer

Onslow County Schools

910-455-2211

• Freyja Cahill, Chief Financial Officer

Brunswick County Schools

910-253-2900

10. Independence Policy

Anderson Smith & Wike PLLC has implemented an independence policy in accordance

with AICPA and Government Auditing Standards requirements. Our Independence,

Integrity and Objectivity policy can be found starting on page 14.

11. Liability Insurance Coverage

Anderson Smith & Wike PLLC has a standard professional liability insurance policy.

Based on discussions with our professional liability insurance provider and legal counsel,

we feel our liability insurance coverage is sufficient.

12. Regulatory Actions

See item 4 for discussion regarding our participation in AICPA peer review program and

see page 13 for our most recent peer review report. There have been no other reviews

during this period.

Page 13

14 | P a g e

ANDERSON SMITH & WIKE PLLC

I. INDEPENDENCE, INTEGRITY AND OBJECTIVITY

It is the policy of our firm that all professional personnel be familiar with and adhere to the

independence, integrity and objectivity rules, regulations, interpretations, and rulings of the

AICPA, the North Carolina State Board of Accountancy, the North Carolina Association of

Certified Public Accountants and state statutes. Furthermore, it is the policy of our firm that, for

engagements that are subject to Government Auditing Standards and other regulatory agencies,

all professional personnel be familiar with and adhere to the independence rules included in

those standards and that personnel will always act in the public interest. In this regard, any

transaction, event, circumstance, or action that would impair the firm’s independence or violates

its integrity and objectivity policy, on a compilation, review, audit, or attestation (including

forecast and projection) engagement is prohibited. Additionally, when the firm and its

professional personnel encounter situations that raise independence concerns, but such situations

are not specifically addressed by independence, integrity, and objectivity rules, the firm will

evaluate the situation by referring to the Conceptual Framework for AICPA Independence

Standards and applying professional judgment to determine whether independence, in fact or

appearance, is affected.

Although not necessarily all-inclusive, the following are considered to be prohibited transactions

and relationships:

1. Investments by any owner or professional employee in a client’s business during the period

of a professional engagement, including a commitment to acquire any direct or material

indirect financial interest in a client.

2. An investment in an entity or property by any of the following individuals and the client (or

the client’s officers or directors, or any owner who has the ability to exercise significant

influence over the client) that enables them to control (as defined by GAAP for consolidation

purposes) the entity or property:

a. An individual on an attest engagement team.

b. An individual in a position to influence the attest engagement by doing any of the

following:

i. evaluating the performance or recommending the compensation of the attest

engagement member,

ii. directly supervising or managing the attest engagement member and all of that

member’s superiors,

iii. consulting with the attest engagement team about technical or industry-related issues

specific to the engagement, or

15 | P a g e

iv. participating in or overseeing quality control activities, including internal monitoring,

with respect to the attest engagement.

c. A member or manager who provides nonattest services to the attest client beginning once

he or she provides ten or more hours of nonattest services to the client within any fiscal

year and ending on the later of the date:

i. the firm signs the report on the financial statements for the fiscal year during

which those services were provided , or

ii. he or she no longer expects to provide ten or more hours of nonattest services to

the attest client on a recurring basis.

d. A member in the office in which the lead attest engagement partner primarily practices

with respect to the attest engagement.

3. Borrowing from or loans to a client, or client’s personnel, during the period of a professional

engagement by any of the individuals listed in items 2.a.-d.

4. Accepting or offering gifts or entertainment from or to a client unless reasonable in the

circumstances and approved by the managing member.

5. Certain family relationships between professional personnel and client personnel. (Consult

the managing member for a ruling on these.)

Notwithstanding the preceding policy and list of prohibited transactions and relationships, at the

managing member’s discretion, certain prohibitions can be waived if it is deemed to be in the

best interest of the firm. However, in so doing, the engagement service performed for the client

must be limited to that allowed by AICPA professional literature.

The procedures listed below are followed to ensure compliance with this policy:

1. All professional personnel are required to sign a representation letter when hired (and

annually thereafter) that acknowledges their familiarity with the firm’s independence,

integrity, and objectivity policy and procedures. Independence and ethics training is provided

for all personnel at least every three years. Such training covers the firm’s independence and

ethics policies and procedures and the independence and ethical requirements of all

applicable regulators.

2. All professional personnel are required to notify the managing member of any potential

prohibited transaction or violation of an independence, integrity or objectivity rule as soon as

they become aware of such a situation. To acknowledge that responsibility, all professional

personnel are required when hired (and annually thereafter) to sign a representation letter and

to list known situations that could impair independence or that violate the firm’s integrity and

objectivity policy. (The firm library contains the authoritative rules on independence,

integrity and objectivity that govern our firm. That literature and the advice of the managing

16 | P a g e

member should be consulted when an employee is not sure if a transaction, event,

circumstance, or action should be reported.)

3. All professional personnel are required to review the firm’s client list annually for possible

violations. The list of clients is maintained by the managing member and additions to the list

are entered as soon as new clients are accepted. When hired (and annually thereafter), all

professional personnel are required to sign a representation that confirms this responsibility.

4. If our firm is engaged as principal auditor and another firm is engaged to audit a subsidiary,

branch, division, governmental component unit, or to perform procedures on an element or

account grouping within a client’s financial statement, the engagement team is required to

obtain a written representation regarding the other firm’s independence with respect to our

client. The auditing manuals used by the firm contain examples of representation letters to

use in such situations. Furthermore, in a review or attestation engagement, if another firm

performs work on a segment of the engagement, a representation (either written or oral)

regarding the other firm’s independence is required. The engagement programs in the

accounting and auditing manuals used by our firm contain steps to ensure compliance with

this procedure.

5. The engagement member (or the in-charge accountant) has the primary responsibility for

determining if there are unpaid fees on any of his clients that would impair the firm’s

independence. The engagement work programs and standard forms used by the firm contain

steps to ensure compliance with this procedure. The firm’s client accounts receivable listing

and the engagement member’s knowledge of unbilled fees should be considered in making

this determination. In addition, the managing member has secondary responsibility to review

the firm’s accounts receivable listing on a periodic basis to identify potential independence

problems.

6. The engagement member has the primary responsibility to identify all nonattest services

performed for an attest service client [including services performed by entities closely

aligned through common employment] and for determining if such nonattest services impair

independence with respect to that client. Reviewing nonattest services performed for attest

clients includes obtaining and documenting an understanding with the client regarding the

client’s responsibilities for the nonattest services performed by the firm. Where applicable,

this includes determining whether such nonattest (nonaudit) services impair independence

under the independence rules in Government Auditing Standards for ongoing, planned, and

future audits. Firm engagement work programs for all attest, as well as compilation

engagements, include steps to ensure compliance with this procedure.

7. The engagement member has the primary responsibility for determining whether actual or

threatened litigation has an effect on the firm’s independence with respect to the client. The

firm’s independence could be impaired by litigation (a) between the client and the firm, (b)

with the client company’s securities holders, and (c) from other third parties.

8. If our firm is engaged as principal auditor to report on the basic financial statements of a

financial reporting entity, all professional personnel must be independent of the financial

reporting entity. If our firm is engaged as principal auditor to report on a major fund,

17 | P a g e

nonmajor fund, internal service fund, fiduciary fund, or component unit of the financial

reporting entity, all professional personnel must be independent of the fund or entity the firm

reports on. The engagement member has the primary responsibility for determining whether

the firm’s relationship with entities in the governmental financial statements has an effect on

independence.

9. The managing member has the primary responsibility for determining whether the firm was a

party to a cooperative arrangement with a client that was material to the firm or the client.

10. The managing member is responsible for obtaining the representation letters, reviewing for

completeness, and for resolving questions relating to independence, integrity, and objectivity

matters (including questions from the representation letters and those from other sources) and

is available to provide guidance. In so doing, the managing member should, when necessary,

consult the AICPA or the North Carolina Association of Certified Public Accountants for

assistance in interpreting independence, integrity and objectivity rules. Documentation of the

resolution of an independence, integrity and objectivity matter should be filed in the client’s

permanent workpaper files. The managing member is also responsible for determining

actions to be taken when professional personnel violate firm independence policies and

procedures. The action for each incident is determined based on its unique circumstances and

may include eliminating a personal impairment, additional training, reprimand letter, or

termination.

11. The managing member is also responsible for monitoring the firm’s independence of attest

clients at which owners or other senior personnel have been offered management positions or

have accepted offers of employment. The independence, integrity, and objectivity

questionnaire used by the firm and the client acceptance checklists used by the firm in attest

engagements include questions to help ensure compliance with this requirement.

12. To ensure that independence is properly considered at the engagement level, the work

programs and standard forms in the accounting and auditing manuals used by the firm

contain steps that require a determination of independence on each new and recurring client.

Furthermore, these manuals contain reporting guidance for those types of engagements where

a lack of independence is allowed.

13. At least annually, the managing member reviews our independence, integrity, and objectivity

policy and procedures to determine if they are appropriate and operating effectively. This

review is performed and documented by reviewing the applicable section of the “Monitoring

Questionnaire” in Chapter 12 of PPC’s Guide to Quality Control. Changes, if necessary, to

the system are made based on the results of the review.

CHAPEL HILL-CARRBORO

CITY SCHOOLS

Proposal for Audit Services

Second Section

June 30, 2020, 2021 and 2022

Table of Contents

Type of Audit Programs ........................................................................................................... 1

Audit Sampling ........................................................................................................................ 1

Use of Computer Specialist ...................................................................................................... 1

Organization of the Audit Team ............................................................................................... 1

Information to be Included in the Management Letter .............................................................. 1

Assistance from Chapel Hill-Carrboro City Schools ................................................................. 2

Tentative Schedule ................................................................................................................... 2

Use of Internal Audit Staff ....................................................................................................... 2

Fee Quote ................................................................................................................................. 3

Other Information .................................................................................................................... 4

Summary of Audit Costs .......................................................................................................... 4

1 | P a g e

1. Type of Audit Programs

We will utilize standardized Governmental Audit Programs as well as Federal and State

Compliance Programs as published by the applicable Federal grantor agency or North

Carolina’s Local Government Commission.

2. Audit Sampling

Our tests will be performed utilizing various sampling techniques as deemed appropriate

for the specific objective of the test being performed. We will use audit sampling for

compliance and cash disbursement testing.

3. Use of Computer Specialist

Our engagement team will evaluate Chapel Hill-Carrboro City Schools’ information

technology system as required by our professional standards.

4. Organization of the Audit Team

Please see the First Section of the Proposal for Audit Services for detailed information

regarding the audit team. The following schedule details the approximate percentage of

time to be spent on the audit by each member of the audit team.

Partner 25 - 30%

Manager / Staff Accountants 70 - 75%

Clerical 3 – 5%

5. Information to be Included in the Management Letter

Certain items are required by our professional standards, the State Single Audit

Implementation Act, and OMB Uniform Guidance to be reported to management. We

will conform with these requirements. Any items noted during the audit for potential

inclusion in the management letter will be discussed in detail with the Finance Officer

prior to issuance.

2 | P a g e

6. Assistance from Chapel Hill-Carrboro City Schools

We will prepare a comprehensive listing of requested client prepared items prior to

commencement of interim fieldwork and again prior to commencement of final

fieldwork. In addition to the items detailed in the RFP, we expect the accounting staff to

provide various other items, such as:

• Monthly retirement reports and various other payroll-related reports

• Inventory and capital asset listings

• Various employee payroll information as part of our compliance audit

• Assistance pulling vendor invoices and related documentation

7. Tentative Schedule

We will coordinate the exact scheduling of fieldwork with the Finance Officer.

However, the following schedule is anticipated:

Audit Planning / Compliance / Internal Control Testing Procedures ...... May and June

Year End Audit Fieldwork ...................................................... September and October

Draft of Financial Statements Available ................................ …………………October

Issuance of Audit Report…… .................................................... October or November

8. Use of Internal Audit Specialists

We will evaluate the work of any internal audit staff employed by the Board as part of

our audit planning process.

3 | P a g e

9. Fee Quote

We commit to the following fee schedule for the audit of the basic financial statements

of Chapel Hill-Carrboro City Schools. In addition to the amount below, we will bill for

travel, postage and other reasonable out-of-pocket costs. We understand that the first

year is binding while the other years are estimated “not to exceed” amounts.

Year Ending June 30, Audit Fee

2020 47,500$

2021 48,500

2022 49,500

Although not requested, we would also perform the June 30, 2023 and 2024 audits at the

same price as the June, 30 2022 audit if the district wished to continue the relationship

with us. As part of our audit we prepare a budget of anticipated time to be spent on each

individual part of the audit. We utilized our past experience with the district to prepare

our budget for the audit of the basic financial statements of Chapel Hill-Carrboro City

Schools. Accordingly, our proposed audit fee is based on our budget. Listed below is a summary of our hourly budget by audit area.

Partner Manager Staff Total

Audit planning 8 12 5 25

Compliance 20 35 35 90

Risk assessment 3 6 3 12

Year-end Fieldwork 35 85 95 215

Report preparation 30 15 5 50

Review and finalization 10 8 5 23

106 161 148 415

Hourly Rate 175$ 125$ 100$

Budgeted cost 18,550$ 20,125$ 14,800$ 53,475$

Discount offered to the district (5,975)

Fee quote 47,500$

4 | P a g e

10. Other Information

We greatly value our relationship with the school system and sincerely desire to continue

as the district’s external auditors. We have always made Chapel Hill-Carrboro City

Schools a top priority each year when preparing our schedule and feel that we have

provided excellent service to the district. In a good-faith effort to show our desire to

continue this relationship, we have reduced our fee in this proposal by approximately

10% from last year’s audit fee.

While considering these audit proposals, a few other things to keep in mind that we feel

significantly distinguish Anderson Smith & Wike PLLC from other audit firms are:

a. Experience matters, and the partner in charge of the engagement will be on site for

the majority of your audit fieldwork. With most firms, the partner typically spends

very little time on site while the audit work is being completed, primarily due to

budgeting constraints. This results in most firms sending their less-experienced,

lower-rate staff members to do as much of the work as possible.

b. School board auditing is by far our firm’s primary practice area. At most firms,

governmental auditing, including school boards, is not a major focus.

c. As part of the audit each year, we try to incorporate an element of “unpredictability”.

This includes looking at new areas within the district for compliance with local, State

or federal guidelines, and looking deeper at areas for which issues may have been

noted at one of our other school board audit clients. We also encourage suggestions

from administration and Board members for specific areas that they would like us to

address.

d. The partner in charge and manager will both be available throughout the year for

routine consultations and to offer assistance with any accounting and auditing issues

that may arise. We do not believe in “nickel and diming” the district for these routine

consultations and do not charge extra for providing this service unless a significant

time commitment becomes necessary, at which time we would consult with

management before beginning such work.

11. Summary of Audit Costs

For the year ending June 30, 2020, we estimate the base audit fee to comprise $43,000 of

the total fee while financial statement preparation will comprise $4,500 of the fee. In

addition to the amount below, we will bill for travel, postage and other reasonable out-of-

pocket costs. Any extra audit or nonattest services that we may be requested to provide

would be billed at the rates shown in the fee quote in item 9. If we encounter any

unexpected circumstances outside the normal scope of the audit or if the scope of the

audit is modified, we will consult with the management of Chapel Hill-Carrboro City

Schools prior to performing any procedures that would require additional billings.

Chapel Hill-Carrboro

City Schools

Proposal to Provide Auditing Services

Fiscal Years Ended June 30, 2020 through 2022 May 6, 2020

Mauldin & Jenkins, LLC

James W. Bence, CPA, Partner Timothy M. Lyons, CPA, Partner 200 Galleria Parkway, Suite 1700 508 Hampton Street, Suite 100 Atlanta, Georgia 30339 Columbia, SC 29201 Office: (770) 955‐8600 Office: (803) 799‐5810 Email: [email protected] [email protected]

Toll Free Phone No: (800) 277‐0080

Web: www.mjcpa.com

Baker County

Schools

Bartow County Schools

Troup County Schools

City Schools of Decatur

Hamilton County

Department of Ed.

Thomas County Schools Clayton County

Schools

Emanuel County Schools

Savannah Chatham County

Public School System

Dodge County Schools

Paulding County

Schools

Butts County Schools

Marlboro County School District

Hancock County Schools

Bristol City Schools

Buford City Schools

Highland County

Schools

Harris County Schools

Putnam County Schools

Lexington School

District 4

Carroll County Schools

Sumter County

Schools

Atlanta Public Schools

Glynn County

Schools

Forsyth County Schools

Rome City Schools

Douglas County Schools

Cobb County Schools

Polk County

Schools

Peach County Schools

Cherokee County Schools Manatee County

Schools

Twiggs County Schools

Henry County

Schools

DeKalb County Schools

Lee County Schools

Walton County

Schools

Ware County Schools

Marietta City

Schools

Carrollton City Schools

Rockdale County Schools

Camden County

Schools

Gainesville

City Schools

Cartersville City Schools

Jefferson City Schools

Marion County Schools

Clay County Schools

Bleckley County

Schools

Richland County

School District 1

Fayette County Schools

Oconee County Schools

Murray County Schools

Fannin County Schools

Over 500 Governmental Units Served

We Do Things Right & We Do the Right Things

Chapel Hill‐Carrboro City Schools Proposal to Serve

Table of Contents Transmittal Letter ................................................................................................................................ 1

1 Atlanta & Columbia Offices at a Glance ...................................................................................... 3 Serving Governments for A Century Leaders in the Governmental Industry

2 Current and Prior Governmental Audit Clients ............................................................................ 6 What makes us stand apart Experience with Local Governments Comprehensive Annual Financial Report (CAFR) Experience

3 Additional Services Provided ..................................................................................................... 14 Audits of Federally Funded Programs (Single Audits) Governmental Attestation Services Governmental IT Solutions Governmental Advisory Services

4 Mauldin & Jenkins’ Quality Control Program ............................................................................ 18 5 Proposed Engagement Team’s Professional Experience ............................................................ 21

Turnover and Audit Continuity The Mauldin & Jenkins Difference – Depth of Resources Other Staff Resources Other Staff Auditors & Accountants

6 Education and Training of Engagement Team ........................................................................... 32 7 Experience of Engagement Team .............................................................................................. 34 8 Specialized Skills of Engagement Team ..................................................................................... 35 9 Client References ...................................................................................................................... 36 10 Mauldin & Jenkins’ Independence Policies ................................................................................ 38 11 Mauldin & Jenkins’ Insurance Policies ....................................................................................... 38 12 Regulatory Actions ................................................................................................................... 38

Other Information .............................................................................................................................. 39 Free Continuing Education Governmental Newsletters High Percentage of Partner & Manager Involvement Workflow Program – Suralink Remote Audits

Closing ............................................................................................................................................... 43

Appendix A – Copy of Mauldin & Jenkins’ Policy and Procedures Regarding Independence

Chapel Hill‐Carrboro City Schools Proposal to Serve

INDUSTRY EXPERTISE / PROACTIVE SERVICE / PROVEN RESULTS

1

Transmittal Letter May 6, 2020

Chapel Hill‐Carrboro City Schools Attn: Jonathan Scott, Finance Officer 750 S. Merritt Mill Road Chapel Hill, North Carolina 27516 Ladies and Gentlemen: We are pleased to submit a proposal, to provide annual financial and compliance auditing services for Chapel Hill‐Carrboro City Schools (the “School District” or “CHCCS”). It is our understanding that the School District is requesting proposals from qualified firms of certified public accountants to establish a contract for the audit of the School District’s financial statements. The contract for such audit services will be for three consecutive years beginning with the fiscal year ended June 30, 2020 and ending with the fiscal year ended June 30, 2022. We have read the Request for Proposals (RFP) and fully understand its intent and contents. We understand the time frame for performance of the annual financial audits as stipulated by the School District, and fully intend and expect to satisfy all objectives. As professionals serving the public sector, Mauldin & Jenkins is qualified to serve CHCCS. We believe that Mauldin & Jenkins is the leader in auditing state and local governments in the southeast. This leadership was achieved by recognizing that we are an important part of our client's success, with our objective being to ensure that accurate information is reported to the Board, management, and its citizens. Given the complexities of the School District’s financial operations and the ongoing significant changes in accounting standards, we feel that it is extremely important that you select an accounting firm that is focused and extremely experienced in the governmental industry. We differentiate ourselves from our peers in the following ways:

Experience with Governments. As auditors for more governments in the Southeast than most other firms, our professionals are thoroughly versed in the complex governmental arena, and have consistently provided the highest quality of service to our government clients. We serve approximately:

500 state and local governments across the Southeast.

62 school districts and 40 charter schools.

126 cities and 57 counties.

48 state agencies, authorities, commissions, colleges, and departments.

131 governments currently awarded Certificates of Achievement for Excellence in Financial Reporting by GFOA and/or ASBO.

Mauldin & Jenkins provides over 100,000 hours of service to approximately 500 governmental units in the Southeast on an annual basis, utilizing over 100 professionals.

Chapel Hill‐Carrboro City Schools Proposal to Serve

INDUSTRY EXPERTISE / PROACTIVE SERVICE / PROVEN RESULTS

2

Nationally Recognized. While the focus of our governmental practice remains on each of our state and local clients, we are proud of our national recognition and track record of significant contributions to the governmental industry. Our national service includes the Government Audit Quality Center with the AICPA, an appointment to the Governmental Accounting Standards Advisory Council (GASAC) and, in January 2020, our own Joel Black accepted the nomination to become the next Chairman of the Governmental Accounting Standards Board.

Service to North Carolina Governments. We continue to grow our governmental practice in North Carolina, serving the state with teams from our Atlanta and Columbia offices. We recognize the concerns the School District may have in selecting a Firm that does not have a physical location in the State. However, we will strive to allay those concerns in our proposal. Furthermore, we believe that in the current environment and given all of the uncertainty and complexity brought about by the COVID‐19 pandemic, it is far more important for you to select a Firm with governmental expertise that can be combined with technology resources to conduct audits in any environment. We have a team dedicated to serving North Carolina and the School District will be served just as well as if we had an office within a few miles.

Staffing. Our staff retention rates are considered to be among the best in the profession (and much

better than national and other regional firms). This fact, coupled with our vast array of government clients, results in a staff pool highly experienced with governmental entities with the definite capacity to serve CHCCS. We are able to not only provide consistency with the partner and manager on our engagement teams, but seniors as well.

Education. Mauldin & Jenkins’ clients have the opportunity to register and receive approximately

thirty (30) hours of continuing education on an annual basis, free of charge. We take our experience in serving governments, and choose timely and relevant topics to provide ongoing education to our clients. Sessions are limited to clients only.

Chapel Hill‐Carrboro City Schools would be a very important client to Mauldin & Jenkins and one that we would be proud to serve. Again, on behalf of Mauldin & Jenkins, we are excited about this opportunity to work with the School District in order to help meet the continuing challenges you face. Thank you very much for allowing us to present our proposal. This proposal represents a firm offer for 90 days from the date of the proposal. As a partner with Mauldin & Jenkins, Tim Lyons is authorized to bind, and make representations for the Firm. Tim will be the ultimate party responsible for the quality of the report and working papers. Please contact us at (803) 799‐5810, 508 Hampton Street, 1st Floor, Columbia, South Carolina, 29201 if you have any questions about this proposal or any related matters.

Sincerely, MAULDIN & JENKINS, LLC Timothy M. Lyons, CPA, CGMA Partner

Chapel Hill‐Carrboro City Schools Proposal to Serve

INDUSTRY EXPERTISE / PROACTIVE SERVICE / PROVEN RESULTS

3

1. Atlanta & Columbia Offices at a Glance Mauldin & Jenkins was formed in Albany, Georgia in 1918 and has been actively engaged in governmental auditing for over a century. Mauldin & Jenkins is considered to be one of the largest locally owned provider of audit and accounting services in the Southeast, and one of the largest certified public accounting firms in the country. Mauldin & Jenkins services clients throughout the Southeastern United States. Mauldin & Jenkins serves clients whose operations span the entire U.S.A. Mauldin & Jenkins is considered to be a large regional firm with offices in the following eight communities:

Atlanta

Macon

Albany

Savannah

Chattanooga

Columbia

Bradenton

Birmingham

Our current footprint of governmental clients extends as far northeast as Gates County in North Carolina (on the Virginia line) to Gulfport, Mississippi to Islamorada, Florida in the Florida Keys. Other key information relative to the size and experience of Mauldin & Jenkins is as follows:

90 – total number of water and sewer systems being served by the Firm across the southeast

300,000 ‐ approx. total hours of service provided annually to clients of the Firm

85,000 ‐ approx. total hours of service provided annually to governmental clients of the Firm

40% ‐ percentage of governmental practice as compared to Firm’s attestation practice

25% ‐ percentage of governmental practice as compared to Firm’s overall practice

400 ‐ approx. total governmental entities served in past three (3) years

280 ‐ total number of Firm personnel

115 ‐ total clients served who obtain the GFOA / ASBO Certificates

44 ‐ total clients with publicly issued debts in excess of $50 million

52 ‐ total number of Firm partners

11 ‐ total number of governmental partners & directors

11 ‐ total number of governmental managers

90 ‐ total number of professionals with current governmental experience The goal of our government practice is to help governments improve their financial processes and strategies so that they can in turn achieve their goal of improving the lives of their citizens. This shared

Chapel Hill‐Carrboro City Schools Proposal to Serve

INDUSTRY EXPERTISE / PROACTIVE SERVICE / PROVEN RESULTS

4

commitment to the goals of our clients has resulted in a significant government clientele. As noted in our transmittal letter, we currently serve approximately 400 governments in the Southeast.

Serving Governments For A Century Mauldin & Jenkins’ commitment to government began when our firm was established in 1918. Since then, we have viewed service to governments as significant to the overall success of the firm. Today, the governmental sector is an industry that has been specifically identified for our continued growth in professional services. Accordingly, all professionals, from entry‐level accountants to partners (who select the governmental practice spend 100% of their time in this area.

As noted previously, Mauldin & Jenkins employs 22 partners, directors and managers who dedicate 100% of their time serving government clients. We also have numerous additional professionals with current experience in providing services to governmental entities – many of whom spend their time exclusively on government clients. Mauldin & Jenkins’ dedicated professionals can bring a comprehensive understanding of the issues that face government entities as well as “bench strength” at all levels, allowing us to respond swiftly and effectively to your evolving needs.

The goal of our government practice is to help governments improve their financial processes and strategies so that they can in turn achieve their goal of improving the lives of their citizens. This shared commitment to the goals of our clients has resulted in a significant government clientele. As noted in our transmittal letter, we currently serve approximately 500 governments in the Southeast. We know of no other firm that can match our experience. The Columbia Office will act as the lead in providing services to CHCCS, with additional resources coming from Atlanta Office. As we noted in the transmittal letter, we recognize the concern the School District may have in utilizing the services of a certified public accounting firm whose office may be further away from the School District; however, we believe by using the individuals mentioned in this proposal that this problem is 100% mitigated. These individuals, Mr. Tim Lyons, Mr. James Bence, Mr. Adam Fraley, and Mr. Will Derzis, are known for their involvement with governmental units and have significant experience providing services to governments in North Carolina. Furthermore, as the situation continues to evolve regarding the COVID‐19 pandemic and the spread of the novel coronavirus, we are deploying more and more resources into the remote audit environment and the feedback from our clients has been incredibly positive. We have the expertise and experience to conduct the School District’s audit from anywhere – onsite in Chapel Hill, North Carolina or 100% remotely. And, the combination of our expertise with the technological tools in which we have invested, results in significant savings to our governmental clients which is exactly what is needed during times of budgetary uncertainty.

Chapel Hill‐Carrboro City Schools Proposal to Serve

INDUSTRY EXPERTISE / PROACTIVE SERVICE / PROVEN RESULTS

5

Regardless of the location, if requested by the School District, we will be on‐site for the interim procedures, final fieldwork, wrap up meetings with management, and for presentation of the audit to the Board. We are always available to all of our clients through phone calls throughout the year. As our proposed engagement team spends 100% of their year serving governmental clients, you will never have to compete with tax season or other industry seasons for guidance, clarification, or assistance from your proposed team! We find that our local clients do not visit the auditor’s office and having a firm willing to come to you is more valuable than a local office. The Atlanta and Columbia office employs 61 professionals with current experience in providing services to governmental entities and who will meet the continuing professional education requirements set forth in the U.S. General Accounting Office Government Auditing Standards. A further profile of the two offices and the firm’s professional staff as a whole is as found in the table on the following page.

Professional Staff by Level Atlanta Columbia Firm‐Wide

Partners 16 7 46

Managers 22 3 40

Supervisors / Senior 16 2 75

Other Staff & Consultants 56 14 122

Total 110 26 283

Mauldin & Jenkins is a Leader in the Industry

We routinely reinvest in the government industry. Nationally, we are members of the AICPA’s Government Audit Quality Center and we have partners who participated in national task forces for that Center and Joel Black recently appointed the Chair of Governmental Accounting Standards Board. He was recently appointed to the AICPA’s State and Local Government Expert Panel. We have also instructed at several national AICPA government and not‐for‐profits conferences, and Joel is on the AICPA committee for the annual Government and Not for Profit Training Program. This has led to Mauldin & Jenkins being recognized both within the State of Georgia and nationally as leaders in serving government clients.

Chapel Hill‐Carrboro City Schools Proposal to Serve

INDUSTRY EXPERTISE / PROACTIVE SERVICE / PROVEN RESULTS

6

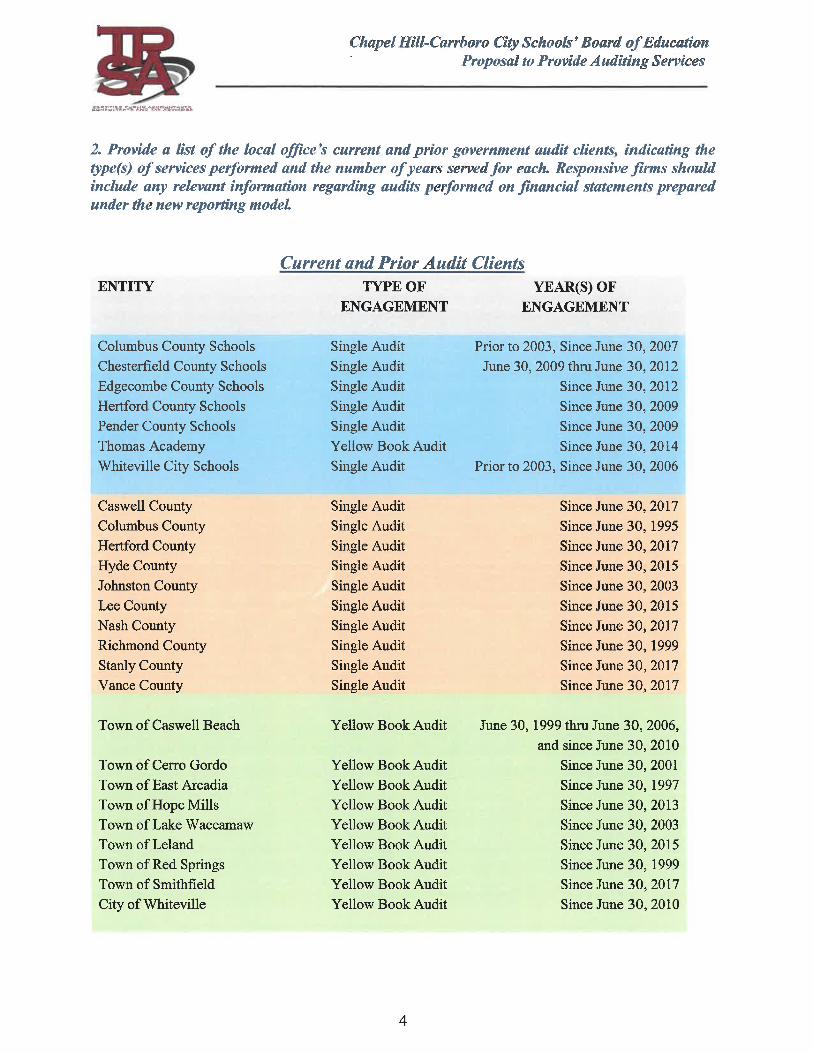

2. Current and Prior Governmental Audit Clients

Mauldin & Jenkins has experienced nearly 500 governmental client transitions in the past seventeen (17) years.

We recognize changing audit organizations creates an opportunity as well as a challenge to governmental units. Fundamental principles and goals of all M&J audits:

Experience. Our experience enables us to focus on the areas of your organization that possess the greatest risk. Each and every person assigned to the engagement will bring extensive governmental experience relative to their time with the firm. Essentially, our youngest staff persons oftentimes have more current governmental experience than higher level people in other firms.

Communication. Our emphasis on planning and communication allows for an efficient and effective audit process in which everyone involved knows their roles and expectations. Further, we like to communicate with our clients, and want to hear their concerns, questions and thoughts as they develop, and address such matters at that time. This helps avoid surprises to all respective parties.

Year‐long Support. We encourage your staff to take advantage of our accessible staff throughout the year for questions that may arise. Our people, working with you and your staff, can provide proactive advice on new accounting or GAAP pronouncements and their potential impact; help with immediate problems including answers to questions; and share insights and best practices to assist you in planning for your future success.

Learning Before Testing. We do not take a cookie‐cutter approach to our audits. Initially, we spend time visiting, inquiring, listening and learning before we ever begin the first audit tests.

Tailoring Our Approach. Once we obtain an understanding of the intricacies of a client’s operations, we tailor our audit approach to minimize unnecessary time and effort in the audit process, and avoid disruptions to client personnel.

Decisions Made in the Field. Issues, as they arise, are dealt with immediately and not accumulated until the end of the audit. This is accomplished by having seasoned governmental partners and managers in the field during the course of the engagement.

Flexible. We understand the demands client personnel have on a daily basis. We have the resources available to accommodate any special requests or timing relative to the conduct of the annual audit, and still meet required specified deadlines. We understand plans can change, and we are open to making any change in scheduling requested by our clients.

Reviews in the Field. Our goal is to conduct and review audits in the field. We find that to be

the most effective and efficient approach to client service. Because our partners and managers

are directly involved in the engagement during fieldwork, we can proactively identify significant issues immediately and resolve them with management so the engagement is essentially complete when fieldwork ends.

Working Toward a Common Goal. Considering all of the above thoughts, our ultimate goal and objective is to provide excellent client service with the least amount of disruption to our clients. We tailor our approach to provide for everyone to work smarter so our clients do not have to work harder.

Chapel Hill‐Carrboro City Schools Proposal to Serve

INDUSTRY EXPERTISE / PROACTIVE SERVICE / PROVEN RESULTS

7

Experience with Local Governments As noted before, the Columbia and Atlanta Offices will be providing the engagement team to serve the School District. Below is a list of the current governmental clients served by these offices. It should be noted that all of our governmental clients report under the most recent and applicable governmental accounting standards as issued by Governmental Accounting Standards Board (GASB).

No. Entity Years Served No. Entity Years Served

1) Aiken, South Carolina 2015 ‐ current 27) Hollywood, South Carolina 2018 ‐ current

2) Alpharetta 2005 ‐ current 28) Jefferson 2010 ‐ current

3) Asheville, North Carolina 2019‐current 29) Johns Creek 2008 ‐ current

4) Austell 2008 ‐ current 30) Kennesaw 2008 ‐ current

5) Baldwin 2015 ‐ current 31) Lawrencevil le 2013 ‐ current

6) Ball Ground 2006 ‐ current 32) Lilburn 2005 ‐ current

7) Beaufort, South Carolina 2012 ‐ current 33) Loris, South Carolina 2016 ‐ current

8) Black Mountain, North Carolina 2019‐current 34) Milton 2007 ‐ current

9) Braselton 2015 ‐ current 35) Monroe 2006 ‐ current

10) Brookhaven 2013 ‐ current 36) New Bern, North Carolina 2016 ‐ current

11) Cedartown 2015 ‐ current 37) Orangeburg, South Carolina 2017 ‐ current

12) Chamblee 2010 ‐ current 38) Peachtree Corners 2013 ‐ current

13) Chapin, South Carolina 2017 ‐ current 39) Powder Springs 2009 ‐ current

14) Charleston, South Carolina 2016 ‐ current 40) Riverdale 2011 ‐ current

15) Chattahoochee Hil ls 2008 ‐ current 41) Rockmart 2012 ‐ current

16) Clarkston 2005 ‐ current 42) Rome 2005 ‐ current

17) Clover, South Carolina 2017 ‐ current 43) Roswell 2004 ‐ current

18) College Park 2008 ‐ current 44) Sandy Springs 2006 ‐ current

19) Decatur 2002 ‐ current 45) Selma, North Carolina 2015 ‐ current

20) Doravil le 2011 ‐ current 46) Social Circle 2008 ‐ current

21) Duluth 2007 ‐ current 47) South Fulton 2017 ‐ current

22) Fairburn 2010 ‐ current 48) Stonecrest 2017 ‐ current

23) Forest Park 2008 ‐ current 49) Summervil le, South Carolina 2015 ‐ current

24) Garner, North Carolina 2018 ‐ current 50) Suwanee 2010 ‐ current

25) Goose Creek, South Carolina 2017 ‐ current 51) Toccoa 2010 ‐ current

26) Hardeeville, South Carolina 2018 ‐ current 52) Vil la Rica 2015 ‐ current

Municipalities

No. Entity Years Served No. Entity Years Served

1) Athens‐Clarke County 2005 ‐ current 14) Greenville County, South Carolina 2019 ‐ current

2) Barrow County 2011 ‐ current 15) Gwinnett County 2004 ‐ current

3) Beaufort County, South Carolina 2016 ‐ current 16) Halifax County, North Carolina 2018 ‐ current

4) Calhoun County, South Carolina 2019‐current 17) Jackson County 2017 ‐ current

5) Cherokee County 2006 ‐ 2015 18) Lancaster County, South Carolina 2014 ‐ current

6) Colleton County, Sourth Carolina 2014 ‐ current 19) Laurens County, South Carolina 2014 ‐ current

7) Darlington County, South Carolina 2016 ‐ current 20) Lumpkin County 2007 ‐ current

8) DeKalb County 2012 ‐ current 21) Madison County, North Carolina 2018 ‐ current

9) Douglas County 2017 ‐ current 22) Oconee County, South Carolina 2013 ‐ current

10) Edgefield County, South Carolina 2014 ‐ current 23) Orange County, North Carolina 2016 ‐ current

11) Floyd County 2006 ‐ current 24) Paulding County 2010 ‐ current

12) Forsyth County 2009 ‐ current 25) Walton County 2008 ‐ current

13) Gates County, North Carolina 2018 ‐ current 26) Washington County, North Carolina 2018

Counties:

Chapel Hill‐Carrboro City Schools Proposal to Serve

INDUSTRY EXPERTISE / PROACTIVE SERVICE / PROVEN RESULTS

8

No. Entity Years Served No. Entity Years Served

1) Atlanta Independent School System 2009 ‐ current 17) Florence 1 School District 2019 ‐ current

2) Atlanta Heights Charter Academy 2015 ‐ current 18) Fulton County Board of Education 2006 ‐ current

3) Bartow County Board of Education 2010 ‐ current 19) Georgia Online Academy 2012 ‐ current

4) Brighten Academy 2008 ‐ current 20) Gwinnett County Board of Education 2007 ‐ current

5) Cherokee Charter Academy 2015 ‐ current 21) International Charter School of Georgia 2019 ‐ current

6) City of Buford Board of Education 2013 ‐ current 22) Jefferson County Schools 2015 ‐ current

7) City of Carrollton Board of Education 2010 ‐ current 23) Lexington School District Four 2019

8) City of Cartersvil le Board of Education 2009 ‐ current 24) Marlboro County School District 1996 ‐ current

9) City of Decatur Board of Education 2004 ‐ current 25) Pataula Charter Academy 2015 ‐ current

10) City of Gainesvil le Board of Education 2015 ‐ current 26) Paulding County Board of Education 2012 ‐ current

11) City of Marietta Board of Education 2009 ‐ current 27) Richland County School District One 1996 ‐ current

12) City of Rome Board of Education 2006 ‐ current 28) Scinti l la Charter Academy 2016 ‐ current

13) Cobb County School District 2010 ‐ current 29) Sumter County School District 2018 ‐ current

14) Coweta Charter Academy 2015 ‐ current 30) Troup County Board of Education 2008 ‐ current

15) Douglas County Board of Education 2008 ‐ current 31) Troup County Col lege & Career Academy 2015 ‐ current

16) Forsyth County Schools 2005 ‐ current 32) Walton County Board of Education 2008 ‐ current

School Districts:

No. Entity Years Served No. Entity Years Served

1) Atlanta Development Auth. 2005 ‐ current 23) Gwinnett Convention and Visitors Bureau 2004 ‐ current

2) Austell Natural Gas System 2008 ‐ current 24) Gwinnett County Airport Auth. 2004 ‐ current

3) Barrow County Water & Sewer Authority 2001 ‐ current 25) Gwinnett County BOE Charter Schools 2005 ‐ current

4) Chatsworth Water Works Commission 2007 ‐ current 26) Gwinnett County Development Auth. 2005 ‐ current

5) Chattahoochee River 911 Auth. 2008 ‐ current 27) Gwinnett County Public Facil ities Auth. 2004 ‐ current

6) Cherokee County Airport Auth. 2008 ‐ current 28) Gwinnett County Public Library 2004 ‐ current

7) City of East Point Retirement Plan 2006 ‐ current 29) Gwinnett County Recreation Auth. 2004 ‐ current

8) City of Sandy Springs Development Auth. 2008 ‐ current 30) Gwinnett County Water and Sewerage Auth. 2004 ‐ current

9) Classic Center Auth. of Clarke County 2004 ‐ current 31) Gwinnett Online Campus 2006 ‐ current

10) Cobb County ‐ Marietta Water Authority 2008 ‐ current 32) Halifax Tourism Development Autority 2018 ‐ current

11) Cobb County‐Marietta Water Auth. Pension 2013 ‐ current 33) Halifax‐Northampton Regional Airport Auth. 2018 ‐ current

12) DeKalb County Public Library 2010 ‐ current 34) Heart of Georgia Altamaha Regional Commission 2008 ‐ current

13) Development Auth. of Cherokee County 2004 ‐ current 35) Historic Roswell Convention & Visitors Bureau 2006 ‐ current

14) Development Auth. of City of Roswell,GA 2006 ‐ current 36) Lumpkin County Hospital Auth. 2007 ‐ current

15) Development Auth. of Lumpkin County 2007 ‐ current 37) Lumpkin County Water & Sewerage Auth. 2007 ‐ current

16) Downtown Atlanta Revital ization 2009 ‐ current 38) Madison Tourism Development Authority 2018 ‐ current

17) Evermore Community Improvement District 2015 ‐ current 39) MARTA/ATU Local 732 Employees Retirement 2008 ‐ current

18) Forsyth County Public Library 2009 ‐ current 40) Northeast Georgia Regional Commission 2012 ‐ current

19) Friends of Bulloch 2006 ‐ current 41) Riverdale Downtown Development Auth. 2011 ‐ current

20) Georgia Charter Educational Foundation 2015 ‐ current 42) Sandy Springs Hospital ity Board 2006 ‐ current

21) Georgia Superior Court Clerk's Coop. Auth. 1995 ‐ current 43) Toccoa‐Stephens County Public Library 2006 ‐ current

22) Gwinnett Civic/Cultural Center Operations 2004 ‐ current 44) Town Center Area Community Imp. District 2012 ‐ current

45) Walton County Water & Sewerage Auth. 2008 ‐ current

Other Governmental Entities