&29,' - ICMAB

75

The Institute of Cost and Management Accountants of Bangladesh (A statutory body under the Ministry of Commerce, GoB) ISSN 1817-5090 92/80( ;/9,,, 180%(5 0$5&+$35,/ 67$< +20( ,-2 , &29,'

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of &29,' - ICMAB

The Institute of Cost and Management Accountants of Bangladesh(A statutory body under the Ministry of Commerce, GoB)

ISSN

181

7-50

90

Bi-monthly Journal of the ICMABISSN 1817-5090NUMBER-02, MARCH-APRIL 2020

VOLUME XLVIII

Mr. Ruhul Ameen FCMA

w Mr. G M Omar Faruque Chowdhury FCMA

w Dr. Md. Saiful Alam FCMA

Mr. Md. Mahbub-Ul-AlamExecutive Director, ICMAB

Mr. Md. Abdul Maleque

Mr. Sami Al Mehedi

Md. Amirul Islam

Modina Printers & Publishers278/3, Elephant Road, Katabon, Dhaka-1205.

Ph.: +88 02 9635081, Email: [email protected]

The Institute of Cost and Management Accountants of Bangladesh

ICMA Bhaban, Nilkhet, Dhaka-1205, GPO Box No. 2629Tel.: 9615460 & 9611799E-mail: [email protected], [email protected]

Editor

Associate Editors

Publisher

All supervision

Photography

Design & Graphics

Editorial Office

Contents

01Editorial

02From the President’s Desk

04Corporate Governance and its Implications for the Banking Sector of Bangladesh

10Income Tax Disputes Resolution through ADR: Bangladesh Perspective

18Stakeholders’ Perceptions towards Sustainability Reporting Practices of Listed Manufacturing Companies: Evidence from Bangladesh

30The Effect of Marketing Mix (7Ps’) on Tourists’ Satisfaction: A Study on Cumilla

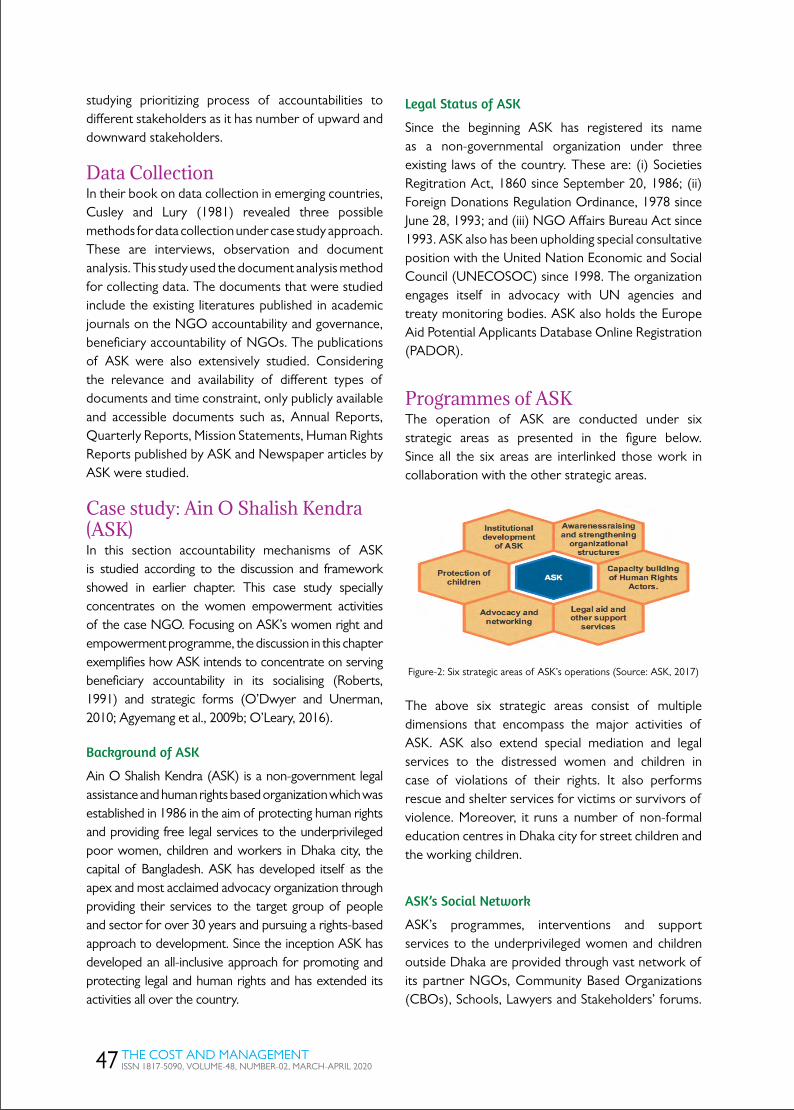

41Beneficiary Accountability of NGOs: A Case Study on a Women EmpowermentBased Advocacy NGO

54Alternative Investments

55IFRS Update

57Update on Dhaka Stock Market

59CMA Students’ World

61ICMAB News

69Introducing The New Editorial Board

All rights reserved. No part of this publication may be reproduced, duplicated or copied by any means without the prior consent of the holder of the copyright, requests for which should be addressed to the publisher.

EDITORIAL

We are passing the March-April issue of the Cost and Management Accountants at such a time when the

entire world is struggling to prevent the transmission of novel corona viral disease (COVID-19). Like any other virus it cannot be fully eradicated but it can be controlled through developing higher immune power in our body. We cannot sanitize the whole world but we can sanitize our hands, feet, body and things around us by proper cleaning. We also can develop higher immunity through meditation and prayer, proper exercise and healthy food and a stress free life. Instead of these we are spreading panic and approaching a wrong way. This reminds me of the story of shoe discovery which cover our feet instead of covering the whole earth to protect us from dust.

The American Center for Disease Control and Prevention (CDC) stated that the genetic structure of the new virus has been changing rapidly. So, the world will have to wait one or more years for the vaccine of COVID-19. Hence, the World Health Organization (WHO) declared that the best way to prevent the spread of COVID-19 is to maintain ‘social distance’. Therefore, various countries already have adopted rigorous programs like lockdowns or shutdowns. Consequently, economic activity is gradually deteriorating around the world. Every day large number of people are joining to the procession of unemployment. The resultant situation is already creating multidimensional humanitarian crisis.

WHO appealed to the global leaders for reconsidering the way of our lifestyle and business approach. So as to adopt with the changing situation, we can move towards the virtual solutions like e-commerce, e-learning and telemedicine. Because, human civilization has already reached the entrance of the Fourth Industrial Revolution through the uses of Artificial Intelligence (AI), Internet of Things (IoT), Robotics and Computer Clouding. China has set a remarkable achievement in the field of digital economy. At the conference of the Association for the Advancement of Artificial Intelligence in New York in early February, Chinese researchers announced that consumer behavior in China has already been altered and may not revert. Alibaba’s CEO Yong Zhang noted: “We are confident in the ongoing digitalization of China’s economy”. Incidentally, the state of e-commerce in Bangladesh is encouraging. The world's largest e-commerce company- Alibaba, already entered our market with the acquisition of Daraj. According to media

reports, the Gross Merchandising Value (GMV) has increased several times in Bangladesh within last few months.

Besides, the COVID-19 infection is forcing us to think about our office management system. Because, the US CDC opined that the persons with symptoms of COVID-19 should stay at home. In this regard, “Remote Work” can be considered essentially relevant for today’s economy. A remote worker is someone who works at home instead of a traditional office. The World Economic forum referred to ‘remote work’ as “one of the biggest drivers of transformation of business. Various studies reveal that remote workers are considerably more productive than traditional office employees. As well, hiring remote workers can result in huge business savings by reducing in real estate costs together with office management costs, transportation cost and other relevant costs for employees. Moreover “Remote Work” is also a greener approach, because it could decrease huge volume of oil and gas burning. Thus, remote work can control tons of greenhouse gas emissions.

For ensuring e-commerce and Remote Work services, it is necessary to confirm sound internet facilities. In this regard, the preparation of Bangladesh is promising. Bangladesh already connected with two submarine cables and waiting for joining with the third submarine cable. Moreover, Bangladesh launched its first commercial satellite named Bangabandhu Satellite-1 into the space. Besides, with the aim of expand IT-based business and employment opportunities, the establishment of 100 economic zones along with the creation of sufficient number of high-tech parks are in progress. If we can be able to adopt such suitable virtual techniques in our economy, coronavirus may lead to more efficient opportunities and perhaps make possible better work practices and profits.

This journal has been striving for creating a platform of exploring the scholarly thoughts and insight of honorable members, Accounting scholars and other prospective academics and relevant researchers with the purpose of improving the national economy as well as our professional skill. We intensely believe that our esteemed members, academics and relevant researchers will come forward with pragmatic economic and social research articles. Which can be supportive for our state and corporate policy makers to get realistic direction for adopting with the current situation, as well take our journal to a new height.

Ruhul Ameen FCMA

Bi-monthly Journal of the ICMABISSN 1817-5090NUMBER-02, March-April 2020

VOLUME XLVIII

1 THE COST AND MANAGEMENTISSN 1817-5090, VOLUME-48, NUMBER-02, MARCH-APRIL 2020

2 THE COST AND MANAGEMENTISSN 1817-5090, VOLUME-48, NUMBER-02, MARCH-APRIL 2020

I would like to remember with deep respect our Father of the Bengali Nation

Bangabandhu Sheikh Mujibur Rahman, the vivacious leader, the architect of independent Bangladesh and the greatest Bengali of all times, at his 100th birth anniversary. We should work all together to materialize his dream for building the country as “Sonar Bangla”.

I would like to remember with deep respect the ‘The Historic 7th March Speech’ by the Father of the Nation Bangabandhu Sheikh Mujibur Rahman on 7th March, 1971. His historic speech is often considered as one of the most influential speeches over the world as part of the world’s documentary heritage in 2017. The speech of Bangabandhu paved the way for independent Bangladesh in 1971.

In the meantime, we know that COVID-19 is touching every corner of our lives

From thePresident’s Desk

throughout the world. It is continuing to cause unprecedented challenges to our humanity, in terms of the public healthcare and economic stability. All companies are now facing unexpected and extreme challenges during this pandemic. It also now causes critical challenges to our accounting profession.

The business environment is being extremely affected due to reducing the volume of transactions, liquidity shortage, inefficiency in cash management and histrionic decrease of profits. Companies are under extreme pressure to meet company’s goals, objectives and expected returns. Layoffs and downsizing are driving employees under financial pressures as the business environment and market condition are changing rapidly due to COVID 19.

We should not assume to solve all of our difficulties today and we have to live with

3 THE COST AND MANAGEMENTISSN 1817-5090, VOLUME-48, NUMBER-02, MARCH-APRIL 2020

uncertainty against the corona virus may be for indefinite period of time. But as a profession, we are providing the essential services to the global economy and society to restore the economy back to normal. I express my heartfelt thanks to Government for providing enormous stimulus packages in different sectors of Bangladesh to make the economic and financial condition stable. Professional accountants can also play a big role with the government's efforts to tackle the damages done by the coronavirus outbreak in Bangladesh. Our profession, with the global leaders and other professional bodies of accountants, is trying to join the efforts in restoring the economy. Moreover, we should develop a widely agreed upon conceptual framework (focusing the problems, challenges, reporting and other materials issues during the pandemic) considering the demand of various stakeholders. I am also expecting that the professionals will exercise the ethical practices with integrity and refrain from financial engineering.

The coronavirus might be an opportunity for the accounting, auditing and consulting regime to further grow under digital platforms and you will be happy to know that ICMAB is now offering online education, training and CPDs in a limited scale. In the meantime, we have successfully organized pre-budget discussion on national budget 2020-21 and international webinar on the theme “The challenges and Role of Professional Accountants amid and post COVID-19 era” using the digital platforms and provide the online CPD opportunities to enhance the knowledge of members. We are also trying to stand with our beloved members and students by giving financial assistance and engaging doctor’s service when necessary.

It is very unfortunate that the cost audit in all public limited companies has not yet been

ensured although notice was issued in this regard in 2001 under an act of Parliament . But, we are trying to pursue our Government to take necessary steps to implement cost audit in all public limited companies.

We are also planning to make a strategic plan 2020 to develop our institute in a new height and we have the plan to reform the existing education and examination systems, developing the course curriculum considering market demand, introducing the timely soft skill development programs, developing the qualified CMAs having technical and soft skills, creating the job opportunities for CMAs through meeting with employers, policy makers, business leaders, media and other segments, organizing more international conferences and seminars, and CPDs with joint collaboration using online platforms, provide training facilities on timely demanding issues, extending the scope of professional services for the members, implementation of cost audit in all sectors of the country and maintain liaison with the government officials for the development of the institute.

I am expecting that the world as well as Bangladesh would overcome the pandemic very soon and will restart a fresh journey of growth again with you all. I am seeking your full hearted support, cooperation, guidance and blessing to face the challenges due to COVID 19 and I firmly believe that with your continued support and blessing we will implement our strategic plan and uphold the image of the CMA profession in a new height.

“Keep our distance, wash our hands, think of others and play our part. All together.”

Md. Jasim Uddin Akond FCMA

AbstractCorporate governance plays an important role in economic growth and development. The governance of banks is of particular importance given their critical role in the financial system. Bank management has the responsibility to safeguard depositors’ money as well as to maximize shareholders interest. A sound banking system requires more prudential regulation and competitive banking environment. To be competitive banks must ensure corporate governance. In this context, the major objective of the study are to identify the critical factors responsible for governance in Bangladesh banking sector. Accordingly the study finds out nine critical factors contributing to the governance in Bangladesh banking sector and highlights on some issues on the governance practices in banks.

Key words: Corporate Governance, Banking Sector, Accountability, Transparency, Ethics.

Introduction and backgroundThere is no doubt that corporate governance plays an important role in economic growth and development. The governance of banks is of particular importance given their critical role in the financial system, channeling the public’s savings and providing the main source of funding for business. The impact of failure in banking can have immense costs. The growing importance of international standards and codes, such as the OECD Principles of Corporate Governance, Basel guidelines, have given both developed and developing countries an opportunity

Corporate Governance and its Implications for the Banking Sector of Bangladesh

Ashraf Al MamunAssociate Professor

Bangladesh Institute of Bank ManagementMirpur-2, Dhaka – 1216.

E-mail: [email protected]

GOVERNANCECORPORATE

4 THE COST AND MANAGEMENTISSN 1817-5090, VOLUME-48, NUMBER-02, MARCH-APRIL 2020

to benchmark their progress towards strengthening their financial systems by improving governance. As banks are the main provider of finance to enterprises, their failure in that role can have a devastating effect upon growth, and ultimately thereby upon the need to tackle poverty (The World Bank, 2004).

Banks in any country are considered as the lifeline of the economy. Lack of corporate governance may pose serious threat to the economy as well as sustainability of banks. “Banks are institutions where people, rich and poor keep their money for safe custody as well as for getting benefits in the form of profit or interest (Ahmed 1998)”. Banks are the trustees of the depositors and depositors’ money are invested to generate profit which may ensure shareholders’ expectation. In doing so all the banks should run their businesses in a transparent and accountable way, which establishes good corporate governance. In this context, the role of corporate governance in the banking sector is considered critical to the sustainable growth in the banking sector.

Improving transparency, better disclosure of financial information, enhanced regulatory oversight and stronger corporate governance, including measures to improve accountability and better align shareholder and manager interests are necessary for better functioning of banks. Moreover, their impact has been reinforced by growing shareholder awareness of the importance of good governance and their increasing willingness to take action to hold managers accountable for their stewardship. These are all positive signs. However, this is a huge and complex task with many different facets. Looking forward, two areas need greater attention are, firstly, the corporate governance of banks- and, secondly, the need to promote the reform agenda at the international level and, in particular, within the developing world.

The need to regulate banking transactions is not new. Indeed, it exists in one of the earliest codes of law. But, in today’s modern world, the importance of banks has grown enormously: indeed, the special nature of modern banking institutions makes it not just desirable, but necessary, to take a broad view of corporate governance – one that promotes transparency and accountability as an integral part of sound financial regulation. In the broad sense of the term, corporate governance deals with all of the factors and forces,

both internal and external to the organization, that work to harmonize the interests of managers and shareholders (Baysinger and Hoskisson 1990). Corporate governance seeks to the harmonization of interests of managers and shareholders. The separation of ownership from control in modern corporations has led to some interesting questions and much debate among researchers and practicing managers (Baysinger and Hoskisson 1990; Berle and Means 1932; Johnson, Daily, and Ellstrand 1996; Zahra and Perace 1989).

As the banking sector has diversified into new products and services, and as it has grown in overseas representation and in the nature and scope of the risk it manages, so there is an even greater need for a sound framework of regulation and governance – one that balances protection for consumers and the wider economy with adequate incentives for taking on appropriate levels of risk. In fact, while bank governance has arguably had a lower profile than corporate governance, it raises all the usual ‘good governance’ questions. Moreover, there are some specific characteristics of banks that make good governance especially important:

n By their nature, banks manage liquidity and risk on highly leveraged balance sheets, and instability in banks can have a serious systemic impact

n Instability in the financial sector can, in turn, have a significant impact on the rest of the economy

n In addition, the complexity of many bank transactions means that good quality accounts and financial reporting are vital to ensure appropriate levels of transparency

n And, finally, there is also a particular risk of moral hazard in the operation of banks – particularly in being considered “too big to fail”.

Banking sector in Bangladesh is at present going through a transition. To catch-up with the tide banks must operate in a way so that it can maximize its earnings and take care of the different stakeholders properly. To ensure that the banking is moving on a right track, proper compliance of the existing regulatory and other national and international guidelines should be practiced.

The banking sector in Bangladesh comprises of four types of scheduled banks, namely, state-owned

5 THE COST AND MANAGEMENTISSN 1817-5090, VOLUME-48, NUMBER-02, MARCH-APRIL 2020

commercial banks (SCBs), state-owned development financial institutions (DFIs), private commercial banks (PCBs) and foreign commercial banks (FCBs). According to Bangladesh Bank annual report 2017-2018 (as on 30 June 2018) there are 57 banks with 9654 branches in operation in the banking sector of Bangladesh. Moreover, few banks are in the process of obtaining license from the Bangladesh Bank, the central bank. The structure of Bangladesh banking is in the process of change i.e. more and more private commercial banks are entering into the market while SCBs are also in the process of either corporatization or complete privatization. Hence, the SCBs and PCBs in Bangladesh are introducing new banking products and services to be competitive in the market. For the SCBs, the overall performance is not satisfactory due to the fact that they had to comply with different government guidelines, political considerations etc. ignoring the fact that they must do their business in accountable and transparent way as the stakeholders of these banks are the people of Bangladesh. Again the PCBs are doing business sometimes by sacrificing the accountability and transparency. In recent past Bangladesh banking experienced some scams (Hallmark, Bismillah group, malpractices with bank funds etc.) which indicates lack of governance in their banking operations. Several measures have been taken by the Bangladesh Bank to put in place good corporate governance in the banks. These include regulation limiting the tenure of Board of Directors; appointment of independent directors in the boards of the banks by the Bangladesh Bank; limiting the number of Directors; fit and proper test for appointment of Board Members and Chief Executive Officer of the PCBs; constitution of audit committee of the Board and disclosure requirements. The role and functions of the Board of Directors and the Management of the banks have been redefined specifying the powers of the Management and the Board.

As the banking sector is being diversified into new products and services, so there is an even greater need for a sound framework of regulation and governance – one that balances protection for consumers and the wider economy with adequate incentives for taking on appropriate levels of risk. In fact, while bank governance has arguably had a lower profile than corporate governance, it raises all the usual ‘good governance’ questions. Therefore, it is relevant to focus on the factors responsible for ‘good governance’

i.e. transparency, disclosure, accountability, and ethics in banking.

A number of laws and regulations are in existence to regulate the banking sector of Bangladesh for ensuring corporate governance, such as, Bangladesh Bank Order, 1972 (P.O.No.127 of 1972); Bangladesh Bank (Nationalization) Order 1972 (P.O. No. 26 of 1972) as amended by Bangladesh Banks (Nationalization) (Amendment) Ordinance, 1977 (Ordinance No. 28 of 1977); Bank Company Act, 1991 (Act No.XIV of 1991), amended up to 2013; Financial Institutions Act, 1993 (Act No.XXVII of 1993); Financial Institutions Regulations Rules 1994; Foreign Exchange Regulation Act, 1947 (Act No.VIII of 1947); Money Laundering Prevention Act 2002 (Act No.VII of 2002); Negotiable Instruments Act, 1881 (Act No.XXVI of 1881); Negotiable Instruments (Amendment) Act, 1994 (Act No.XIX of 1994); Bankruptcy Act, 1997 (Act No.X of 1997); Bankruptcy Rules, 1997; Artha Rin Adalat Ain [Money Loan Court Act], 1990 (Act No.IV of 1990); Artha Rin Adalat Bidhan [Money Loan Court Rules], 1990; and Companies Act, 1994 (Act No.XVIII of 1994).

Objectives of the studyBased on the above discussions this study has the following objectives, the major objective of this study is to identify the critical factors responsible for governance in Bangladesh banks.

Methodologies and scope of the studyThe study is limited only to perception of the bankers for ensuring good governance in overall banking operation in Bangladesh. An opinion survey was conducted from the participants of the training course of the Bangladesh Institute of Bank Management (BIBM) regarding the factors responsible for ensuring good governance in banking sector of Bangladesh. To make the sample representative, the questionnaire (Annex) has been distributed among 250 officials of different commercial banks (SCBs, DFIs, PCBs, and FCBs) operating in Bangladesh in the rank starting from Senior Officer to Deputy General Manager or equivalent positions. Of them 211 bank officials responded (response rate 84%). The responses are processed using Factor Analysis (Principal Component Analysis) technique in the SPSS. The study was

6 THE COST AND MANAGEMENTISSN 1817-5090, VOLUME-48, NUMBER-02, MARCH-APRIL 2020

conducted during 2019. As this study uses questionnaire survey, hence the principal source of data is primary. Secondary data is collected from different sources such as literatures, articles, publications, annual reports, Bangladesh Bank Circulars, and web sites.

The questionnaire comprises 9 factors identified by the researcher to measure the banker’s opinion on the governance in banks. The respondents are then requested to rank the 9 factors in order of their significance. For measuring the answer, a five-point Likert scale as mentioned below is used:

Strongly agree – 5; Agree – 4; Uncertain – 3; Disagree – 2; and Strongly disagree -1

The Likert scale is a convenient measurement to quantify the qualitative judgment such as opinion, perception, attitude of the respondents and it was also used in different studies e.g. (Beattie et al., 1999) and (Hussey and Lan, 2001).

Analysis and FindingsA well governed banking sector requires a legal, ethical and rational system of activities. To cope pace with the increased competition every commercial organization requires accountable and transparent system. Banks make business of trust and to do that they need to be accountable and transparent in their operation as well as reporting. To make the banks accountable and transparent, the central bank is strengthening its supervision and monitoring on a continuous basis. Not only the central bank has the responsibility to ensure good governance in the banking system but also all concerned should perform their duties in a legal and ethical manner.

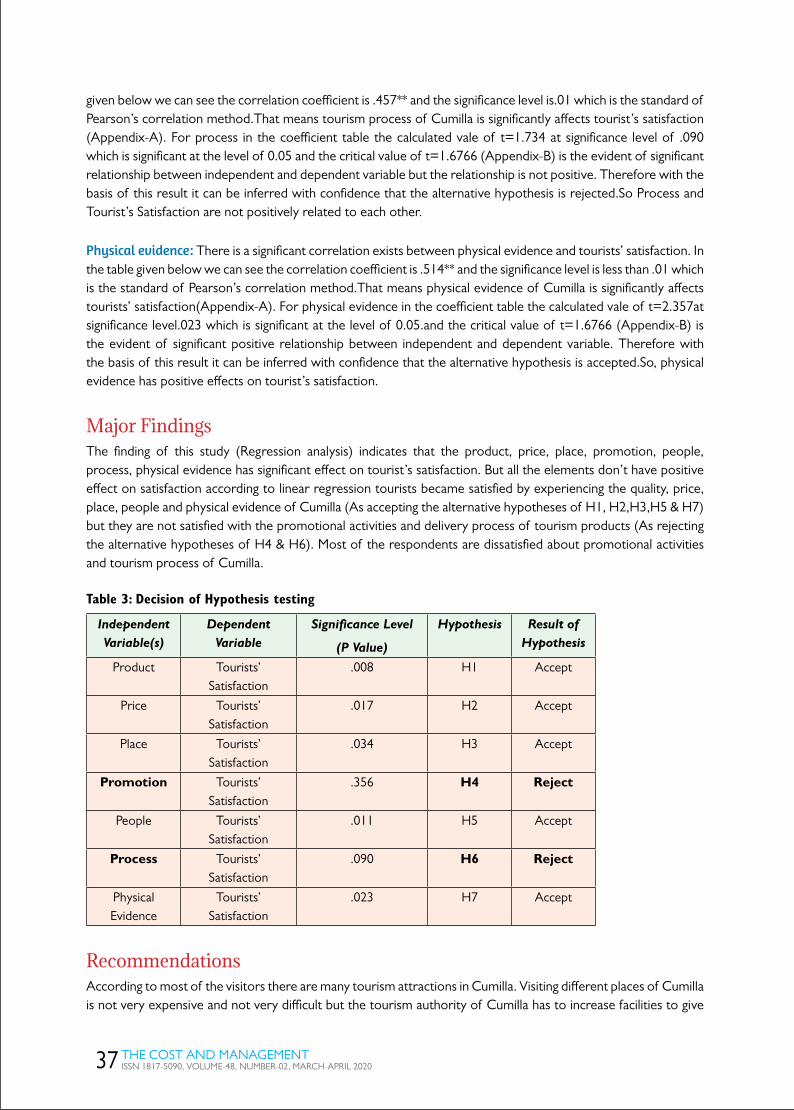

By applying the technique of factor analysis (principal component analysis) the study have identified nine major contributing factors for ensuring better governance in the banking sector of Bangladesh. Based on the factor-wise average scores, ranks were obtained for nine factors as shown in the following table:

Table: Ranking of the Factors Contributing to Corporate Governance in Bangladesh Banking Sector

Name of the Factors Average Score Rank

Transparent Relationship Between Banks And Their Clients 2.958 1

Credit Administration, Monitoring And Recovery 2.860 2

Clearly Defined Management Structure And Policy 2.638 3

Exposure Concentration And Bias-Less Judgment 2.464 4

Independence And Competence In Risk Analysis 2.446 5

Mechanism Of Minimizing Conflict Among Stakeholders 2.359 6

Information Disclosure To Clients And Information On Market Risk 2.255 7

Obligation To Offer Higher Standard Service And Harmony Among Stakeholders 2.062 8

Credit Assessment And Board’s Role 1.858 9

Source: Result of the opinion survey.

The ranking of the factors reveals that “Transparent Relationship Between Banks and Their Clients” (score 2.958, rank 1) considered most important in case of governance in Bangladesh banking sector. It signifies that depositors, customers, and the public are adequately informed about the strength(s) and weakness(es) of bank and full disclosure is made to depositors, customers, and the public that bank’s directors and managers are adequately safeguarding depositors’ fund.

“Credit Administration, Monitoring And Recovery” (score 2.860, rank 2) reflects that the methods of loan authorization and lending limits are clearly spelled out, personnel assigned to credit risk management functions have relevant training, there is a separate section to follow up and monitor loans and there is a separate unit in bank to recover debt.

“Clearly Defined Management Structure And Policy” (score 2.638, rank 3) shows that management structure

7 THE COST AND MANAGEMENTISSN 1817-5090, VOLUME-48, NUMBER-02, MARCH-APRIL 2020

i.e. responsibilities, reporting lines, qualifications, experiences etc. is clearly defined, appointment, posting, transfer and promotion of the employees are very much transparent, and remuneration policies, executive compensation, bonuses, are fairly transparent.

“Exposure Concentration And Bias-Less Judgment” (score 2.464, rank 4) shows that exposure concentration (lending and deposit) is disclosed and credit approval is largely based on quantitative or objective judgment and personal biasness does not happen. “Independence And Competence In Risk Analysis” (score 2.446, rank 5) signifying that there are some provision to train the directors and senior management of bank to understand and manage risks and there is an officer(s) assigned to monitor and report on corporate governance compliance and that they can act independently.

The remaining four factors i.e. “Mechanism of Minimizing Conflict Among Stakeholders” score 2.359, rank 6), “Information Disclosure To Clients And Information On Market Risk” (score 2.255, rank 7), “Obligation To Offer Higher Standard Service And Harmony Among Stakeholders” (score 2.062, rank 8) and “Credit Assessment And Board’s Role” (score 1.858, rank 9) also has significant influence on the overall accountability and transparency in Bangladesh banking sector.

Most of the factors that are required to ensure accountability and transparency in banking sector are at this moment present in the banking system. Even after that, it is generally spoken that in Bangladesh, banking environment is not sound. Several measures have been taken by the Bangladesh Bank to put in place good corporate governance in the banks. These include regulation limiting the tenure of Board of Directors; appointment of independent directors in the boards of the banks by the Bangladesh Bank; limiting the number of Directors in the boards; fit and proper test for appointment of Board Members and Chief Executive Officer of the PCBs; constitution of audit committee of the Board and disclosure requirements. The role and functions of the Board of Directors and the Management of the banks have been redefined specifying the powers of the Management and the Board. Also the Bangladesh Bank issued different manuals for management of the

six core risks (asset-liability risk, credit risk, money laundering risk, internal control and compliance risk, foreign exchange risk, and IT risk) to properly guide the banking sector.

Issues related to the governance practices in banks in BangladeshNot always, the profitability and assets quality figures only matter for a bank but also the management’s attitude, ethics and concern for the society matters. Most private banks’ lending is concentrated in the urban areas. How can the banking sector trade off the following two conflicting situations:

v A more privatized banking sectorv Extending banking services in the rural areas

Private banks should extend their services to the rural areas to be accountable because their deposits are not coming only from urban areas. Here remains the question of economic operation. They should also find test of economic operation and the answer because not all their activities are economically viable. Controlling operating costs is a major focus for all the commercial banks. For the SCBs inefficiency expense is a threat. On the other hand, for PCBs over spending to increase efficiency also must be taken into consideration because it creates social imbalance and as such it may not be transparent. Banking sector requires efficiency but becoming too aggressive, dynamic and efficient CEOs might sometimes create destruction for the overall banking sector. Payment must be related to performance. CEOs must earn their remuneration. The operation of the FCBs is limited to a few people and they are not extending their operation to agricultural sector and not even they have any rural operation. Foreign banks do not have shareholders in Bangladesh. They are in the same tax bracket but with operation in more profitable areas. Also, depositors having a smaller amount do not get any interest and moreover small depositors are charged with bank charges, so their degree of operational accountability and transparency begs a question.

ConclusionThis study is only an indicative study of corporate Bangladesh banking sector. There is scope for further study in the area of ensuring corporate governance in this sector. The study reflects the bankers’

8 THE COST AND MANAGEMENTISSN 1817-5090, VOLUME-48, NUMBER-02, MARCH-APRIL 2020

opinion and perception about the factors critical for good governance in Bangladesh banking sector. A separate study considering the external perception (shareholders’ view) regarding accountability and transparency would certainly provide a complete picture. The adoption and implementation of the Code of Corporate Governance by the banking sector can enhance the degree of accountability and transparency in this sector.

Bangladesh banking sector is now facing strong demands for improvement in the following four aspects: (i) Transparency, (ii) Accountability, (iii) Information Disclosure, and (iv) Ethics. There can be no doubt that, in the future, a great competitive gap will open up between those banking companies that actively undertake reform of their governance and those that neglect to do so.

References

Ahmed, S. (1998). “First Nurul Matin Memorial Lecture on Ethics in

Banking”, Bank Parikrama, Vol. XXIII, March & June.

Bangladesh Bank, Annual Report (2017-2018), “Department of Public

Relations and Publications”, Bangladesh Bank, Dhaka.

Baysinger, B.D., and Hoskisson, R.E, (1990), “The Composition of

boards of directors and strategic control: Effects on corporate

strategy”, Academy of Management Review, 15: 72-87.

Beattie, V., Brandt, R and Fearnley, S., 1999), “Perceptions of Auditor

Independence: UK Evidence”, Journal of International Accounting,

Auditing and Taxation 8(1). 67-107.

Berle, A.A., and Means, G. C., (1932), The Modern Corporation and

Private Property. New York: Macmillan

Hussey, R. and Lan, G., (2001), “An Examination of Auditor

Independence Issues from the Perspective of UK Finance

Directors”, Journal of Business Ethics 32. 169-178.

Johnson, J. L., Daily, C. M., and Ellstrand, A.E., (1996), “Boards of

directors: A review and research agenda”, Journal of Management,

22: 409-38

The World Bank, 2004. Found in www.gcgf.org

Zahra, S.A., and Pearce, J.A., II, (1989), “Boards of directors and

corporate financial performance: A review and integrative model”,

Journal of Management, 15: 291-334.

Annexure

Questionnaire for Opinion Survey of Bankerson “Factors influencing corporate governance in

banks”

Name (Optional):

Designation:

Bank:

Please indicate by tick mark (√) the extent to which you support the statement in the following scale that best reflect your perception and judgment. (All the information will be used for research purpose only).

Strongly agree 5

Agree 4

Uncertain 3

Disagree 2

Strongly disagree 1

SL. Particulars Response

1 2 3 4 5

1 Factor 1: Information Disclosure To Clients And Information On Market Risk

2 Factor 2: Credit Assessment And Board’s Role

3 Factor 3: Credit Administration, Monitoring And Recovery

4 Factor 4: Independence And Competence In Risk Analysis

5 Factor 5: Transparent Relationship Between Banks And Their Clients

6 Factor 6: Clearly Defined Management Structure And Policy

7 Factor 7: Exposure Concentration And Bias-Less Judgment

8 Factor 8: Obligation To Offer Higher Standard Service And Harmony Among Stakeholders

9 Factor 9: Mechanism Of Minimizing Conflict Among Stakeholders

9 THE COST AND MANAGEMENTISSN 1817-5090, VOLUME-48, NUMBER-02, MARCH-APRIL 2020

AbstractAlternative Dispute Resolution (ADR) system is common place in settling revenue disputes in the tax administrations around the world. Bangladesh joined the club in 2011. Unlike the conventional dispute resolution mechanism, ADR facilitates settlement of disputes in a quick and cost effective manner. The system seems to be working efficiently in countries like the UK, Australia and other countries. In Bangladesh it is observed that though ADR system is in operation and gradually gaining ground the success of ADR as a tax dispute settlement forum seems to be a bit slow. The present article discusses the background of the introduction of the ADR system and the success of the same so far.

Key words: Income tax, Dispute settlement, Alternative dispute resolution, Bangladesh income tax department.

Tax is at the heart of our societies. A well-functioning tax system is the foundation stone of the citizen-state relationship, establishing powerful links based on accountability and responsibility. It is also critical for inclusive growth and for sustainable development, providing governments with the resources to invest in infrastructure, education, health, and social protection systems.

------Angel Gurria, Secretary General, OECD

Income Tax Disputes Resolution through ADR: Bangladesh Perspective

Dr. Sams Uddin AhmedCommissioner of Taxes

10 THE COST AND MANAGEMENTISSN 1817-5090, VOLUME-48, NUMBER-02, MARCH-APRIL 2020

Part I: IntroductionThe traditional dispute resolution system in Bangladesh

is the adversarial system as developed in England by

Common Law. Taxation litigation is not an exception.

But the adversarial system is time consuming, full of

procedural complexities and expensive (Caenegem,

1999). This negative feature of the dispute resolution

system provides a perception among the taxpayers

that the income tax department is not taxpayer

friendly and consequently mars the investment climate

discouraging the FDIs and even local entrepreneurs.

Besides, a large amount of tax revenue cannot be

collected because of the pendency of the tax disputes

in the higher dispute resolution forum (Bangladesh

Protidin, 2020).These cases could have been settled

easily and speedily if there would be any dispute

settling forum that facilitates quick disposal of tax

litigations. Against this backdrop there is no gainsay

that alternative dispute resolution system is by far the

best system to resolve revenue cases in an accelerated

manner without wasting time and resources. Realizing

the truth the NBR introduced the ADR system in

2011.

After its introduction the ADR system faces challenge

since the number of cases resolved through ADR

is not very enterprising. Since the introduction of

the ADR system in the income tax department of

Bangladesh, the system does not seem to be a success

in terms of dispute settlements and the collection of

revenue as well. The purpose of the present article is

to delve into the matter why ADR is not experiencing

expected success in settling income tax disputes in

Bangladesh. The article is arranged as follows: Part I

gives an introduction. Part II narrates the tax dispute

resolution process in Bangladesh. Part III discusses the

introduction of ADR in the NBR. Part IV examines

the issue of success and failure of ADR in Bangladesh.

Finally part V gives a conclusion.

Part II: Tax Dispute Settlement Process in Bangladesh: The Protraction ContinuesThe legal system of Bangladesh is adversarial system

based on the Common Law of England. In this system

the judge plays the role of an umpire and passes

judgment in favor of the party who plays well i.e.,

the party who can defend her case well by producing

enough evidences and arguments. The present legal

frameworks and the bulk of statutes were crafted

by the English jurists and parliamentarians during

the British rule in the then Indo-Pak subcontinent.

Likewise in 1922 Income Tax Act was made by the

British people to impose and collect tax in the country.

That law continued until 1984 when the new Income

Tax Ordinance was adopted.

Income Tax Ordinance (ITO) 1984 prescribes the

legal provisions how to settle income tax disputes

between the assesse and the income tax department.

The process starts from the submission of income

tax returns. Under the ITO, there are two systems of

submission of return. One is under the universal self-

assessment system and the other is under the normal

system. When the assesse submits returns under

the normal system the DCT goes for administrative

assessment.

He issues notice to the assesse, takes hearing of

the assesse and finalizes the assessment. Under the

universal self-assessment system a few number of

returns are selected for audit with the prior approval

of the NBR and the DCT goes for making normal

assessment issuing notice of hearing to the assesse.

In both the cases, if the assesse is not happy with the

assessment order of the DCT she can prefer appeal

to the first appellate authority as per legal provisions.

This is called the first appeal. If the assesse is not happy

with the order of the first appellate authority then she

can file second appeal to the Taxes Appellate Tribunal.

The order of the Tribunal is final if the order relates

to the question of fact. If there is any question of law

then the assesse can prefer appeal to the High Court

Division (HCD) of the Supreme Court of Bangladesh.

If there is any law point and the department is

aggrieved, it can prefer reference application to the

HCD. The assesse can file writ petition with the HCD

in appropriate cases. In some cases a dispute can go

to the Appellate Division of the Supreme Court of

Bangladesh for decision.

11 THE COST AND MANAGEMENTISSN 1817-5090, VOLUME-48, NUMBER-02, MARCH-APRIL 2020

So it is evident that for a tax dispute to be settled in the traditional dispute resolution forum takes necessitates several steps that takes long time, human hour and also cost. The following chart shows the time necessary for disposing of income tax disputes in different forums.

Besides, often huge amount of revenue remains uncollected due to pendency of cases in the higher dispute resolution forums. In a report published in the daily Bengali vernacular Bangladesh Protidin on March 2, 2020 it

Income Tax Dispute Resolution System in Bangladesh

Appellate Division of the Supreme Courte of Bangladesh

Question of Law

High Court Division of the Supreme Courte of Bangladesh

Question of Law

Taxes Appellate Tribunal

Assessee

Assesse files appeal against the order of the DCT

Deputy Commissioner of Taxes

Commissioner of Taxes(Appeals)

Files Return

Supreme Court of Bangladesh

No statutory time limit. But generally 2-3 years.

Average 10 months

Average 9 months

Average one yearDeputy Commissioner of Taxes

Commissioner of Taxes (Appeals)

Taxes Appellate Tribunal

High Court Division

Time Involved in Settling Tax Dispute through Tradition Forums

Appellate Division

12 THE COST AND MANAGEMENTISSN 1817-5090, VOLUME-48, NUMBER-02, MARCH-APRIL 2020

is revealed that as of 2019 -2020 fiscal year revenue cases involving both direct and indirect cases stood at a number of twenty seven thousands seven twenty five hundred and the amount of revenue involved is forty one thousands crores taka. Among these cases the amount of income tax involved stands to the tune of taka twelve thousands nine hundred seventeen crores. These cases are pending before the HCD, Appellate Division of the Supreme Court of Bangladesh and in the respective taxes Appellate Tribunals. It has been reported that a section of dishonest business people take the cases to the higher forum to prolong tax collection and in some cases not to pay their fair amount of taxes. As a result it is creating pressure on the treasury of the government (Munna, 2010). The law officer of the NBR informed that if the cases were disposed of in a timely manner then the government could have collected huge amount of revenue. The statistics furnished presents the dismal picture of prolongation of revenue cases increasing time and costs for the taxpayers and the government simultaneously. Against this backdrop, it is worthwhile to look for alternative dispute resolution mechanism which is known as ADR.

Part III: ADR in the Income Tax Department of BangladeshSettling disputes through ADR is as old as the history of litigations and conflicts in the society. The ADR system can be traced back to 450 BC when the Roman Twelve Tables prescribed ADR to settle dispute (Gulfam, 2014). The traditional dispute resolution mechanisms do have their limitations in terms of time and cost involved in settling the disputes. ADR is common in the family matters and in large commercial disputes. The limitations of the traditional court system helped in the development of the ADR system. As the Irish Law Commission Report (2010) states, “It is clear that, from one perspective, the word—alternative refers to looking outside the courtroom setting to resolve some disputes. In this respect, the Commission fully supports the long-standing approach of the legal profession and of the courts that, where it is appropriate, parties involved in civil disputes should be encouraged to explore whether their dispute can be resolved by agreement, whether directly or with the help of a third party mediator or conciliator, rather than by proceeding to a formal—winner v loser‖ decision by a court. This

happens every day in the courts, in family litigation, in large and small commercial claims and in boundary and other property disputes between neighbours.”A democratic society must ensure access to justice for its citizens. The constitution of the people’s republic of Bangladesh like all other democratic countries, ensures the provision of access to justice to realize the fundamental right of the people of Bangladesh. Access to justice can be ensured through wider choice of avenues of dispute settlement mechanisms. In this respect the Irish Law Commission in its Consultation Paper noted, —In promoting access to justice, a modern civil justice system should offer a variety of approaches and options to dispute resolution. Citizens should be empowered to find a satisfactory solution to their problem which includes the option of a court-based litigation but as part of a wider ’menu of choices‘.

ADR is the part of the formal legal system of Bangladesh. Sajal (2015) notes, “ADR system has been introduced within the formal justice system to minimize inordinate delays and to reduce undue litigation costs.” Presently, in the civil matters, ADR is found in the Civil Procedure Code, Artha Rin Adalat Ain, 2003, The Family Courts Ordinance, 1985, Village Court Act, 2006, Code of Criminal Procedure, 1898 and Arbitration Act, 2001, The Value Added Tax Act, 1991, The Legal Aid Rules, 2015,The Conciliation of Disputes (Municipal Areas) BoardAct, 2004.The Labor Act, 2006,The EPZ Trade Union and Industrial Relation Act, 2004. From the very inception of the pilot project of ADR in the Family Court the ADR system witnessed success to a considerable extent (Gulfam, 2014). Though not an alternative for a formal judicial system, ADR program is commonly used by most of the tax administrations in the world to settle tax disputes. For example in the UK ADR system was introduced as a pilot project in 2011. Since its introduction the ADR system is considered to be a huge success both by the department and the taxpayers as well (EY, 2014).The UK tax administration is now seriously thinking to extend the use the ADR to resolve tax dispute involving factual rather than technical issues, the litigation that involves cost in regular forum, cases involving uncertainties of facts, cases involving lack of clarity and understanding regarding the parties’ respective technical position. In Australia the ADR in settling tax disputes is very effective (Sourdin, 2015). According to Australian

13 THE COST AND MANAGEMENTISSN 1817-5090, VOLUME-48, NUMBER-02, MARCH-APRIL 2020

Taxation Office (2017) ADR is cost-effective, informal, consensual and speedy way to resolve disputes. The ATO uses three types of ADR namely in-house facilitation is the ATO’s version of mediation, and is a free service where a trained independent ATO facilitator assists participants to negotiate their dispute in large, complex disputes the ATO may consider engaging an external practitioner to conduct ADR can also be initiated by the courts or tribunals in litigation cases. Mediation, conciliation and early neutral evaluation are the most commonly used in tax and superannuation disputes.

However, in line with the successful introduction of ADR system in the formal legal system of Bangladesh, the National Board of Revenue (NBR) introduced ADR system in the income tax department through Finance Act 2011 to settle income tax disputes. New chapter XVIIIB that contains sections 52F to 52S and the newly added sections deal with the detailed provisions of dispute settlement through ADR. Regarding the ADR, the NBR states, “Alternative Dispute Resolution (ADR) is a process of resolving disputes within shortest possible time beyond the regular course of business followed by Appeal/Tribunal/Court. This is a platform for holistic and multilateral discussion with the third party in resolving disputes. This benefits both the taxpayers and the government. It reduces the cost of trial as well as facilitating the government in collecting revenue within shortest possible time. This is a speedy way of resolving disputes. Following a global trend of success of ADR in tax administration Bangladesh has introduced this method in 2011-2012 financial year.” ADR was introduced for resolving disputes involving both direct and indirect taxes in Bangladesh. According to section 152F any dispute of an assessee lying with any income tax authority, Taxes Appellate Tribunal or Court may be resolved through ADR. It means that cases pending at the High Court Division or Appellate Division of Supreme Court are also qualified to apply at ADR. The aggrieved assessee may apply at ADR obtaining permission from the concerned Court. The proceeding of such appeal or reference shall remain stayed till the disposal of the application for ADR. According to section 152II where an assessee has filed an application for ADR for any income year and for the same income year, the Deputy Commissioner of Taxes has filed an appeal before the Appellate Tribunal or the Commissioner has made a reference before the High Court Division and no decision has been made in that respect by the Appellate Tribunal or High Court Division as the case may be, the proceeding of such appeal or reference shall remain stayed till disposal of the application for ADR. It follows that the assesse has been given a wide range of privilege in resorting to ADR before the same is resolved by the traditional dispute resolution forums. Before filing ADR application the assessee must pay the tax as per the income tax return under the provision of section 74 of the Income Tax Ordinance 1984. In the ADR system a facilitator is nominated by the NBR who sits with the taxpayer and the representative of the income tax commissioner to settle the agitated issues. If agreement is reached the facilitator passes an order and the order is binding on the parties. The taxpayer has to pay the tax within the stipulated time failing which the order stands null and void. If there is no agreement the assesse can go for traditional dispute resolution as per the provision of law. Following chart delineates the statistics of the cases brought to ADR and disposed of by the same since the inception of the ADR system in Bangladesh.

Source: National Board of Revenue

14 THE COST AND MANAGEMENTISSN 1817-5090, VOLUME-48, NUMBER-02, MARCH-APRIL 2020

The ADR system in Bangladesh appears to be very brief compared to the traditional dispute settlement system. The following diagram shows the ADR process of disposal.

Source: National Board of Revenue

Part IV: Is ADR a Success in Bangladesh?It is observed that in recent years ADR in tax matter is becoming popular around the world. Countries like India, Australia, and the UK all are gradually promoting ADR in tax disputes to reduce the time and financial cost of both the taxpayers and the governments. From the statistics furnished in the previous section it is observed that during six years of its operation only 998 cases were brought before the ADR forum for settlement. Among

15 THE COST AND MANAGEMENTISSN 1817-5090, VOLUME-48, NUMBER-02, MARCH-APRIL 2020

the cases 597 cases were fully agreed on by both the

parties. Most of the cases were individual income tax

cases. The NBR is working hard to make the ADR

system popular among the taxpayers. Anecdotal

evidence shows that taxpayers, particularly the

income tax practitioners do not feel interested to go

to ADR forum and even if they go and agree with the

ADR decisions they do not abide by the order of the

ADR facilitator. Under the circumstances ADR can be

seen as another forum to protract the litigations. For

as mentioned earlier the other options of taking the

litigation to the traditional forums are not closed. So

if a taxpayer feels that the ADR order might not be in

her favor, she opts out of the ADR. One important

issue is the neutrality of the facilitator of the ADR

proceeding. So far there is no complain regarding

the neutrality of the facilitators. But there should be

a system of monitoring in this respect. Among the

weaknesses of the ADR system some important issues

have been identified by the researchers. For example,

Islam (2019) identities inter alia absence of proper

institutional tricks, lack of appropriate training of the

lawyers and judges, lack of proper education of the

people, negative attitude of the lawyers towards ADR

system, lack of awareness among the stakeholders

and to some extent corruption in the mechanism.

For income tax department it might seem early to

make any hasty comments regarding the success

and failure of the ADR system. But the NBR should

move more quickly to address the issues mentioned

in this article to make the ADR system a successful

one. It is to be mentioned that the tax lawyers of

Bangladesh expressed their opinion regarding the

institutional structure of the ADR system when on

the eve of its launcing.The lawyers were not against

the ADR system. But the demanded that the system

should be introduced in separate institutional frame

work (The Daily Star, 2011). It seems that they like

separate institutional framework like the Taxes

Appellate Tribunal, independent of the NBR. In fact

it is a question of tax dispute system design. It can be

argued that this is not important whether the ADR is

separate or not. What is important was the vision of

the NBR that it took the timely step to go for ADR.

The current system can be reviewed by a committee

of expert regarding its institutional perspective.

Currently, the ADR system lacks adequate manpower

and logistic supports. Anecdotal evidence supports

this statement. Besides the NBR should make

necessary arrangement to impart adequate training

to the officers and the lawyers regarding the effective

method of conducting ADR proceeding. The

facilitators should have the same opportunity and

bent for training to gain enough skill to facilitate ADR

cases.

Part V: ConclusionADR in Bangladesh has now gained ground because of its certainty, efficiency, timeliness and cost effectiveness. Islam (2019) states, “The ADR mechanism is very remarkable and successful development in Bangladesh to resolve the disputes inalternative way. When a dispute is solved amicably with thesaving of time and cost of the litigants then it ensures theimpartiality, integrity and authenticity of the ADRmechanisms.” Gearing the earlier resolution of income tax disputes is an important mission of the NBR. Settling disputes earlier saves time and money for taxpayers and the income tax department. ADR also provides certainty for assessees. It will facilitate the NBR’s capacity to contribute to the economic and social wellbeing of Bangladesh by encouraging willing participation in our income tax system. For the success of the ADR system it is necessary that the department be more responsive to the taxpayers, their advisors, the legal profession and other stakeholders in the income tax system. The taxpayers should also be aware of the benefit of the ADR system and also the tax advisers should come forward by making the taxpayers aware of the benefit of the system. By referring to a research on ADR in Australia Sourdin (2015) states, “The research… showed that there was a perception among some survey respondents that, in order for an ADR process to be beneficial, everyone has to ‘come to the table with an open mind’. It was suggested that in some circumstances participants had not engaged in good faith or appropriately. It was also noted that there should be clear guidelines as to when ADR is appropriate, as it may not be appropriate for all cases.” It is expected that the ADR in the income tax department of Bangladesh will be more prominent and much liked forum for early resolution of income tax disputes in coming days.

16 THE COST AND MANAGEMENTISSN 1817-5090, VOLUME-48, NUMBER-02, MARCH-APRIL 2020

References

Bento, Barbara and Taylor, Mark. How alternative dispute resolution

is used to settle cases, Taxation (26 November 2019). https://

www.taxation.co.uk/articles/taylor-digital

Gulfam, Mahua.Introducing Alternative Dispute Resolution (ADR)

in Criminal Justice System: Bangladesh Perspective, (2014),

Banglavision, 13(1), 205-2016. http://bv-f.org/17.%20BV%20

Final.-13.pdf

Govind, Sriram and Samira Varanasi. 2013. ‘Dispute Resolution in Tax

Matters: An India-UK Comparative Perspective’, 9 International

Taxation, 9,313-324.

Hidaya, Khoirul. Indonesian Tax Dispute Resolution in Cooperative

Paradigm Compared to United Kingdom and Australia, 2018 IOP

Conf. Ser.: Earth Environ. Sci. 175 012203. https://iopscience.iop.

org/article/10.1088/1755-1315/175/1/012203/pdf

Income Tax Ordinance 1984.

Islam, Sanjida and Sultana, Rajia.2019.The effectiveness of alternative

dispute resolution in Bangladesh: A critical analysis, International

Journal of Multidisciplinary Research and Development, 6(3), 108-

109.

Law Reform Commission, Alternative Dispute Resolution: Mediation

and Conciliation (Report, LRC 98-2010). https://www.lawreform.

ie/_fileupload/Reports/r98ADR.pdf

Mc Donough, Kirsten J. 1993.Resolving Federal Tax Disputes through

ADR, Dispute Resolution Journal, 48(2).

Munna, Arafat, 41000crores Taka in the Case Net (Bangladesh Protidin,

March 2, 2010). https://www.bd-pratidin.com/

Palin, Adam, Keeping Dispute out of the Courtroom, Financial Times,

April 24, 2015<https://www.ft.com/content/a0b3d276-e807-

11e4-9960-00144feab7de>.

Pandey, Pranab Kumar and Mollah, Md, Awal Hossain. 2011. The judicial

System of Bangladesh: an Overview from Historical Viewpoint,

International Journal of Law and Management 53(1):6-31. https://

www.researchgate.net/publication/235250895_The_judicial_

system_of_Bangladesh_An_overview_from_historical_viewpoint

Sajal, Imtiaz Ahmed, ‘ADR Mechanism in Ordinary Civil Courts of

Bangladesh’ (Bangladesh Law Digest, October 7, 2015) <http://

bdlawdigest.org/adr-in-civil-justice-system-in-bangladesh.html>

Star Business Report. Tax lawyers for keeping ADR outside NBR, The

Daily Star (27 June 2011). https://www.thedailystar.net/news-

detail-191788

Sourdin, Tania, Evaluating Alternative Dispute Resolution (ADR)

in Disputes About Taxation (December 1, 2015). 34(1) The

Arbitrator & Mediator 19-31. Available at SSRN: https://ssrn.

com/abstract=2756313

Van Caenegem, William, “Advantages and disadvantages of the

adversarial system in criminal proceedings” (1999). Law Faculty

Publications. Paper 224 <http://epublications.bond.edu.au/

law_pubs/224>.

17 THE COST AND MANAGEMENTISSN 1817-5090, VOLUME-48, NUMBER-02, MARCH-APRIL 2020

Stakeholders’ Perceptions towards Sustainability Reporting Practices of Listed Manufacturing

Companies: Evidence from Bangladesh

Dr. Mohammed Fazlur Rahman Khan(Member of 24th BCS General Education Cadre)

Assistant Professor (Accounting)

Mymensingh Govt. College

Mymensingh, Bangladesh.

e-mail: [email protected]

Abstract

Sustainability Reporting has become increasingly relevant to the enterprise in ensuring environmental protection. Accordingly, target 12.6 of the SDG12 specifically advises to integrate sustainability information into the reporting cycle of companies. But, disclosure of sustainability information is largely depending on the expectations of stakeholders, because Sustainability Reporting is still unregulated in developing economies like Bangladesh. Therefore, recent Sustainability Reporting literature emphasizes the importance of exploring the perceptions of both managerial and non-managerial stakeholder groups regarding Sustainability disclosures. But, very few studies have been carried out that examined both managerial and non-managerial stakeholders’ views towards Sustainability Reporting practices in the context of developing countries. And so, the study aimed at exploring the perceptions of five selected managerial and non-managerial stakeholder groups regarding the various aspects of the reporting practices of the listed manufacturing companies in Bangladesh, by arranging a series of interviews with the help of a structured questionnaire. The study revealed that most of the selected stakeholders considered Sustainability Reporting as a significant tool for reducing environmentally hazardous activities of the companies. But stakeholder believed that external audit is essentially necessary for ensuring credibility of sustainability disclosures. Besides, maximum survey participants opined that Sustainability Reporting should be a mandatory task for the listed manufacturing companies in Bangladesh. The study included only 85 respondents from five stakeholder groups that were slightly different in sample sizes.

Keywords: Sustainability Reporting, Stakeholder, Stakeholders’ perceptions.

18 THE COST AND MANAGEMENTISSN 1817-5090, VOLUME-48, NUMBER-02, MARCH-APRIL 2020

1.Background of the Study On 1st January 2016 the world takeoff for an exclusive journey of universal development in the name of the Sustainable Development Goals (SDGs). The SDGs incorporated 17 Goals with 169 associated Targets that can be utilized to frame the national and international agenda to end poverty and tackle climate change by 2030 (Khan, 2016). According to the UN Conference on Trade and Development (UNCTAD), at the beginning stage of investment in SDG-relevant sectors, developing countries alone face an annual gap of $2.5 trillion. So it is clear that the SDGs will not be achieved without engaging businesses. Because, as a key stakeholder, business organizations have a vital role in the sustainable development process either negative or positive. Consequently, the SDGs clearly call on all businesses to measure and report their impacts on sustainable development (DSE, 2019). Sustainability reporting is an emerging significant tool in introducing social and environmental cost and other relevant Sustainability information of the organizations to their stakeholders which is necessary to identify the ways of reducing or avoiding such cost and hazards for achieving sustainable development (Gray et al., 1995). Accordingly, SR is specified in target 12.6 of the SDG 12 (Responsible consumption and production) which exactly advises to encourage companies, to integrate sustainability information into their reporting cycle in order to apply their creativity that improve business approach as well reducing their footprint and minimizing overall impacts. It can provide a broader view of a company’s performance than financial disclosure alone (DSE, 2019).

On the other hand, The Labor Force Survey 2018 revealed that only about 13% people of the Bangladeshi labor market are engaged in institutional work. And about 4.2% of the total workforce is unemployed. (BBS, 2018). Therefore, Bangladesh has been striving for employment-intensive industrialization since its independence. Consequently, with a view to accelerating the pace of industrialization in the country, the ‘Outline Perspective Plan of Bangladesh (2010-2021): Making Vision 2021 A Reality’ have also recognized the importance of manufacturing as vehicle of reducing unemployment. Hence, the growth in manufacturing sector stood at about 9 percent in FY 2016-2017 (GoB, 2018). But, Bangladesh has not been achieved sufficient structural industrial transformation,

and insufficient consideration has been given to the sustainable consumption and production (Nath, 2012). The consequence of largely unregulated industrial development has caused in many adverse sustainability effects in Bangladesh (Alam, 2009). The toxic discharges from manufacturing industries pollute both surface and ground water sources. Thus industrial development of Bangladesh is taking high toll on its natural resources (Ahmad, 2012). But it is not expected to have more corporate profit at the cost of sustainability. (Enahoro, 2009).

Since SR has the potentiality to enhance accountability of the corporate organizations regarding sustainable development, it is essential to realize the reasons of SR is, or is not evolving in developing countries like Bangladesh (Belal & Cooper, 2011). Therefore, within the last few decades SR has become a popular field of research around the world (Yaftian, 2011). But, most of the previous studies of SR were focused on developed countries and very few studies have been carried out in the context of developing countries like Bangladesh (Belal & Owen, 2007). However, SR studies in Bangladesh are mainly determined by the volume of disclosure that using secondary data (Imam, 2000). Moreover, disclosure of sustainability information in Bangladesh is still voluntary in nature. As a result, several scholars (Islam & Deegan, 2008) have called for more direct engagement-based studies in developing countries like Bangladesh by using primary data. Besides, latest literature emphasizes the importance of exploring the perceptions of both managerial and non-managerial stakeholder groups regarding SR. Some very recent studies concentrate on the perceptions of multiple stakeholder groups (Belal & Cooper, 2011).

But, so far researcher’s knowledge goes, there is little evidence of comprehensive recent study that examined the perceptions of both managerial and non-managerial stakeholders’ views regarding the significance of SR and credibility as well adequacy or inadequacy of existing regulatory frameworks of SR of the listed manufacturing companies in Bangladesh context. So, there is ample opportunity to carry out an inclusive research in this field. In addressing the gap in the existing literature, present study aimed at exploring the perceptions of 85 managerial and non-managerial stakeholders regarding various aspects of

19 THE COST AND MANAGEMENTISSN 1817-5090, VOLUME-48, NUMBER-02, MARCH-APRIL 2020

SR practices of the listed manufacturing companies in Bangladesh.

2. Objectives of the StudyThe objective of the study is to explore the perceptions of the multiple stakeholder groups regarding the significance, credibility and regulatory frameworks of Sustainability Reporting practices of listed companies in Bangladesh context.

3. Literature Review Rudyanto and Siregar (2018) conducted a study on “The effect of stakeholder pressure and corporate governance on the sustainability report quality” in Indonesia by using multiple regression method. The study revealed that pressure from consumers and employee positively affects the quality of sustainability reports of the companies. But pressure from shareholders has no effect on the quality of sustainability report. Zhao (2011) conducted a study on environmental reporting practices in a Chinese context. The researcher used content analysis, questionnaire survey and in-depth interview methods for conducting the study. The study reveals that the regulatory requirements and other national and international corporate issues influence the SEAR practice in China. Haque (2011) conducted a comprehensive study on ‘Climate change related corporate governance disclosure practices in Australia’. Attempt has been made to evaluate the nature of the climate change related corporate governance disclosure practices of the companies and to know the perception of the stakeholders regarding the reporting and to investigate the reasons for the practices. In this study the researcher used content analysis method, in-depth interview and survey methods. The study identified some reasons for the low level of climate change related corporate disclosures practices of the Australian companies. Belal and Robrets (2010) conducted a study with the aim of exploring the perceptions of non-managerial stakeholders regarding corporate social reporting in the context of a developing country, Bangladesh. By the help of a series of semi-structured interviews the study reveals that CSR is evolving in Bangladesh as a response of pressures from international markets and

is producing largely cosmetic responses. Clarkson et al. (2008) had a study on Revisiting the relation between environmental performance and environmental disclosure: an empirical analysis and revealed that sustainability report is made to assist decision makers and stakeholders by translating ecological, economic and social data. However, decision makers and stakeholders have to make sure that the sustainability report made by corporation is transparent Diouf and Boiral (2017) conducted a study on ‘The quality of sustainability reports and impression management: A stakeholder perspective’ with the purpose of analyzing the perceptions of the quality of GRI reports held by stakeholders involved in the field of socially responsible investment (SRI)’. The study revealed that the perceptions of SRI practitioners shed more light on the elastic and uncertain application of the GRI principles in determining the quality of sustainability reports. Belal and Owen (2007) carried out a study in order to determine the views of Bangladeshi managers on the current state of, and future prospects for, social reporting in the country. This study utilizes a primary research method such as interviews to investigate disclosure practices within the context of a developing country like Bangladesh. The results of their study revealed that managers’ major motivation for social reporting practices lies in a desire on the part of corporate management to manage powerful stakeholder groups such as multinational companies. Islam (2009) conducted a broad based study on by using in-depth interview, Annual Report Content Analysis and survey methods. The study also uses the legitimacy theory, stakeholder theory and institutional theory. The study reveals that social responsibility initiative of BGMEA respond directly to the concerns of multinational buying companies and media have influence upon corporate social and environmental disclosure practices. The study also reveals that Global and local NGOs can positively use the media to effect change in the disclosure practices of the organizations. Yaftian (2011) examined CSR practices in corporate annual reports and needs of Iranian stakeholders regarding CSR information. The study used content analysis method. Questionnaires survey method was also used to investigate the CSR information needs of stakeholders. The study revealed that annual reports were perceived as the main source of CSR information, and stakeholders

20 THE COST AND MANAGEMENTISSN 1817-5090, VOLUME-48, NUMBER-02, MARCH-APRIL 2020

believed that CSR disclosures were sufficient among the sample companies. Hossain et al. (2006) revealed that a very few companies in Bangladesh are making efforts to provide Sustainability information on a voluntary basis by using questionnaire survey and content analysis method. Teoh and Thong (1984) conducted a study based on interview questionnaire survey. The study reveals that social reporting lags behind corporate social involvement Assaduzzaman et al. (2014) conducted a study on “Corporate Environmental Reporting (CER) Practices: Empirical Evidence from Selected Non-financial Companies in Bangladesh”. The study investigated the perceptions of 40 senior accounts executives of sample companies regarding the environmental reporting practices of the listed companies in Bangladesh by using a structured questionnaire. Besides, the study used a convenience sampling process to collect primary data. The study showed that survey respondents felt strong need for environmental disclosure in the corporate annual reports.

The review of relevant literature revealed that over the past few decades a number of studies have been conducted on SR practices of the corporate organizations, majority of which have been done in the context of developed countries. But a small number of studies conducted in Bangladesh context. it is also revealed that recent SR literature emphasizes the importance of exploring the perceptions of both managerial and non-managerial stakeholder groups regarding SR. However, some studies concentrate on the perceptions of multiple stakeholder groups in this country, but there are few studies that examined non-managerial stakeholders’ perceptions of SR in Bangladesh context. As per author’s knowledge goes there is a handful studies that exploring the perceptions of multiple stakeholder groups regarding various aspects of SR of the listed manufacturing companies in Bangladesh context.

4.Research Methods4.1 Overview

The study approach is descriptive in nature, and primary data has been used in this study. The study employed questionnaire survey method in investigating the manifold perceptions of multiple stakeholder

groups regarding various aspects of SR practices of the listed manufacturing companies in Bangladesh.

4.2 Study Population

The population of this study comprises all the manufacturing companies of Cement, Tannery, Textiles and Pharmaceuticals industries which are listed on the Dhaka Stock Exchange (DSE). In addition, survey population of this research includes all the members of the key stakeholder groups of the listed manufacturing companies like Accounts Executives and Internal Auditors of sample companies, Because, their activities are closely related in preparing the financial reports of the companies. Besides, Professional Accountants (ACA/FCA) play an significant role in the verification of disclosures of listed companies, and Environmental Activists have an important role in improving the corporate environmental conditions, as well, Member of the Regulatory Bodies [top or mid-level officials of the Bangladesh Securities and Exchange Commission (BSEC), Ministry of Environment, Forest and Climate Change, the Bangladesh Bank (BB) and the National Board of Revenue (NBR)] have the influence in framing the disclosure rules in Bangladesh with which companies bound to comply. Consequently, these groups are also included in this study.

4.3 Sample Size and Sampling Techniques

Based on the purposive sampling method, five companies from each of the four selected industrial sectors (Cement, Tannery, Textiles and Pharmaceuticals) were included in this study. To achieve the advantage of an in-depth research, a total number of 85 respondents were taken from five selected stakeholder groups. Chief Financial Officer (CFO) or one Senior Accounts Executive and Head of Internal Audit or one Senior Executive (internal audit) from each of the sample companies, 20 professional accountants (ACA/FCA), 15 officials from different regulatory bodies including 2 Deputy Directors of the Directorate of Environment, 2 Deputy Secretary and one Joint Secretary of the Ministry of Environment, Forest and Climate Change, 3 Directors of the BSEC, 2 Joint Directors of Bangladesh Bank, 3 Deputy Commissioner of Taxes, one joint Commissioner of Taxes and one Additional Commissioner of Taxes of the NBR, and 10 Environmental Activists were taken into consideration. Respondents were selected on the basis of convenience of data collection.

21 THE COST AND MANAGEMENTISSN 1817-5090, VOLUME-48, NUMBER-02, MARCH-APRIL 2020

Table: 4.1 Details of selected respondents

Strata

No.Category of Respondents

Company wise

respondents

Sample

respondents

1 Chief financial Officer (CFO)/ Senior Accounts Executive 1 20

2 Head of Internal Audit / Senior Executive (internal audit) 1 20

3

Member of the Regulatory Bodies

–15

Officials of Ministry of Environment Forest and Climate

Change (#)

Directorate of Environment (2)

BSEC (3)

Bangladesh Bank (2)

NBR (5)

4 External Auditors (ACA/FCA) - 20

5 Environmental Activists - 10

Total respondents 85

4.4 Primary Data Sources

4.4.1 Questionnaire

The present study used a structured questionnaire in exploring the perceptions of stakeholders regarding SR. The questionnaire was divided into two parts. The first part of the questionnaire contained eight demographic questions. The second part of the questionnaire proceeds with the questions on the Significance of SR practices in improving the sustainability performance of the companies. The questionnaire also included questions on the Credibility issue, needs of external audit of sustainability disclosures and sufficiency of existing Regulatory Frameworks for SR practices in Bangladesh. Most of the questions of the questionnaire were designed by using a five-point Likert Scale. and were close-ended.

4.4.2 Actual field Work and Administration of Survey Instruments

4.4.2.1 Interview Procedures

The primary data were collected through e-mail survey with a structured questionnaire. The interviews took place between mid-September, 2019 and mid-December, 2019.

4.4.3 Statistical Techniques of Analysis

Quantitative data were analyzed by using appropriate statistical techniques such as frequency, mean, standard deviation, percentage etc. through SPSS program (Version-15).

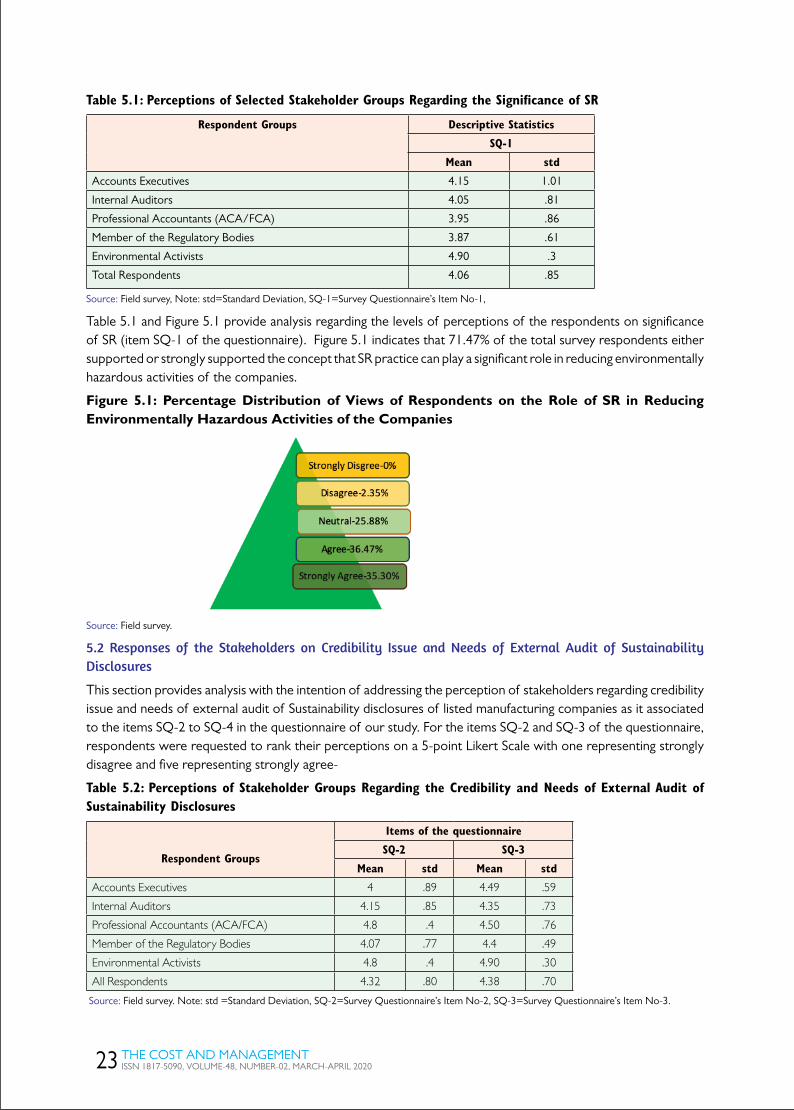

5. Data Analysis and Presentation The aim of this segment is to provide analysis on manifold perception of the survey respondents regarding SR practices of the listed manufacturing companies in Bangladesh.