Introduction of HIGEN \(English_131001_Rev2\).ppt [\310\243 ...

Upload

khangminh22Category

view

5download

0

.I

I

I

. .

.-

I11III

..

m

m

KPP~DKomIt. Pemantauan Pelaksanaan Otonoml D..rahReg/ollal Autonomy Watch

.The Asia Foundation

Supported by:

AustralianAlD~

This 2011 report on Local Economic Governance (LEG) is the fruit of a cooperation effort between KPPOD (Komite Pemantauan Pelaksanaan Otonomi Daerah, or Regional Autonomy Watch) and The Asia Foundation. The members of the KPPOD team were Sigit Murwito, Riyanto, Firman Bakrie, Robert Endi Jaweng and Boedhi Reza, with P. Agung Pambudhi acting as coordinator, while the Asia Foundation team consisted of Mochamad Mustafa, Romawati Sinaga and Ronaldo Oktaviano, coordinated by Erman A. Rahman and supported by Frida Rustiani, Hari Kusdaryanto, R. Alam Surya Putra, Aryasatyani Sintadewi and Hesti Wulandari.

This report is based on the results of a survey of business operators carried out by Nielsen Indonesia. In addition, the Jawa Pos Institute of Pro-Otonomi (JPIP) performed a qualitative study to complement the quantitative survey. The analysis and writing of the report was done jointly by KPPOD and The Asia Foundation. Valuable input and suggestions from Prof. Dr. Suahasil Nazara and Prof. Dr. Robert Simanjuntak, both of the University of Indonesia, Faculty of Economics, have been taken into consideration in the writing of the report.

Funding for this undertaking has been provided by the Australian Agency for International Development (AusAID). However, AusAID is exempted from responsibility for the material contained in this report.

iiiKPP D

Decentralization has been underway in Indonesia for more than ten years, but recently many have challenged the how effectively decentralization – and even democratization – is being implemented. Deterioration in the quality of public services, the many corruption cases involving local governments, and low economic growth rates in some regions have prompted discourse about whether the country is making a reversal away from decentralization and democratization.

We recognize that the move toward regional autonomy has not been without its faults. Nevertheless, a choice was made to strengthen democracy and move towards local autonomy based on the problems created by the centralistic, authoritarian system of the previous regime. Yet it is unfair to judge regional autonomy a failure after it has been implemented for such a short time, and under a somewhat inconsistent policy framework.

Since 2001, the Regional Autonomy Watch (KPPOD) and The Asia Foundation have aimed to present a clear picture of the quality of regional economic governance from the perspective of business owners. Our studies provide input to government at the central, provincial and regional/municipal levels, as well as information to other stakeholders regarding efforts that can be undertaken to promote improve economic growth under regional autonomy.

This year’s study finds significant variation among regions in the quality of economic governance. This indicates that despite many limitations, some regions have used the opportunities provided by autonomy to foster good governance while others have not. It is hoped that this present study, and the awards presented to regencies and municipalities with the best performance, will promote a healthy competition among regional leaders. It is also envisioned that local governments whose performance is still low can learn from their neighbors who are doing better, and be inspired to improve.

We recognize that improving economic governance requires a strong commitment and hard work, not only from the heads of regions but from all ranks of government officials, politicians, business owners and other stakeholders. This study can help set priorities for reform of local economic governance, identifying areas for immediate improvement that are relatively easy to achieve but have the potential of significant impact. Other aspects may need more time for improvement.

Preface

iv

KPPOD and The Asia Foundation would like to thank all parties who supported this study being conducted, and particularly the Government of Australia (AusAID) for its funding support. We hope that this small contribution will encourage improvements in decentralized governance in Indonesia.

Jakarta, June 2011

P. Agung Pambudhi Robin BushExecutive Director Country RepresentativeRegional Autonomy Watch/KPPOD The Asia Foundation

vKPP D

Preface iiiTable of Contents ................................................................................................................................................ vList of Tables .................................................................................................................................................... viiiList of Graphs ..................................................................................................................................................... ixList of Boxes .......................................................................................................................................................xiiList of Terms and Abbreviations ..................................................................................................................xiiiExecutive Summary .......................................................................................................................................... xv

1. INTRODUCTION .........................................................................................................................................1 1.1 Background .............................................................................................................................................1 1.2 Research Objectives ................................................................................................................................2 1.3 Results of the Study ...............................................................................................................................2

2. METHODOLOGY.........................................................................................................................................3 2.1 Conceptual Framework .........................................................................................................................3 2.2 Indicators of Local Economic Governance .........................................................................................4 2.3 Research Locations .................................................................................................................................4 2.4 Research Instruments ............................................................................................................................5 2.5 Weighting of Indicators Forming the Local Economic Governance Index ....................................6 2.6 Sampling ..................................................................................................................................................7 2.7 Construction of LEG Index ...................................................................................................................7

3. CHARACTERISTICS OF RESPONDENTS AND FIRMS ...................................................................9 3.1 Characteristics of Respondents ............................................................................................................9 3.2 Characteristics of Firms .........................................................................................................................9 3.3 Firms' Performance and Plans ............................................................................................................11

4. LAND ACCESS ...........................................................................................................................................13 4.1 Background ...........................................................................................................................................13 4.2 Land ownership ....................................................................................................................................14 4.3 Time Needed to Process Land Certificates .......................................................................................14 4.4 Perceived Ease of Obtaining Land ....................................................................................................15 4.5 Land Eviction Cases .............................................................................................................................16 4.6 Land Conflict Cases .............................................................................................................................17 4.7 Significance of Land Problems on Business .....................................................................................17 4.8 Land Access Sub-Index .......................................................................................................................18

Table of Contents

vi

5. LOCAL INFRASTRUCTURE ...................................................................................................................21 5.1 Background ...........................................................................................................................................21 5.2 Quality of Local Infrastructure ...........................................................................................................21 5.3 Time Needed to Repair Damaged Infrastructure ............................................................................23 5.4 Frequency of Blackouts and Level of Generator Ownership .........................................................25 5.5 Obstruction Level of Infrastructure for Firm Performance ............................................................26 5.6 Local Infrastructure Sub-Index...........................................................................................................26

6. BUSINESS LICENSING ............................................................................................................................31 6.1 Background ...........................................................................................................................................31 6.2 Level of Permit Ownership .................................................................................................................31 6.3 Time Needed to Obtain TDP ..............................................................................................................32 6.4 Perceived Level of Difficulty of Obtaining TDP ..............................................................................33 6.5 Cost of TDP and Firms’ Perceptions of Cost as an Obstacle to Business ....................................33 6.6 Licensing Services Free from Collusion, Efficient and Free from Illegal Changes .....................34 6.7 Availability of Complaint Mechanisms ............................................................................................35 6.8 Obstruction Level of Business Licensing for Business Performance ............................................36 6.9 Business Licensing Sub-Index ............................................................................................................36

7. LOCAL-LEVEL REGULATIONS .............................................................................................................39 7.1 Background ...........................................................................................................................................39 7.2 Methodology and Variables Forming the Local-Level Regulations Sub-Index ..........................39 7.3 Characteristics of the Local-Level Regulations Studied .................................................................40 7.4 Juridical Problems ................................................................................................................................41 7.5 Substance Problems .............................................................................................................................42 7.6 Principle Problems ...............................................................................................................................43 7.7 Local-Level Regulations Sub-Index ...................................................................................................44

8. TRANSACTION COSTS ...........................................................................................................................49 8.1 Background ...........................................................................................................................................49 8.2 Obstruction Level of Local Taxes and Local User Charges on Firm Performance .....................49 8.3 Official Costs for Inter-regional Commodity Distribution Activities ...........................................51 8.4 Level of Payment of Donations to Local Governments ..................................................................52 8.5 Security Costs ........................................................................................................................................53 8.6 Impact of Transaction Costs on Business Activities ........................................................................54 8.7 Transaction Costs Sub-Index ..............................................................................................................54

9. CAPACITY AND INTEGRITY OF REGENTS/MAYORS ..................................................................59 9.1 Background ...........................................................................................................................................59 9.2 Understanding by Regents/Mayors of Business Problems and Professionalism of Local Government Officials ................................................................................................................59 9.3 Attitude and Character of Regents/Mayors toward Corruption .................................................61 9.4 Leadership Character of Regents/Mayors .......................................................................................62 9.5 Capacity and Integrity of Regents/Mayors as Obstacles to Business Performance ..................62 9.6 Sources of Information regarding Behavior of Regents/Mayors ..................................................63 9.7 Capacity and Integrity of Regents/Mayors Sub-Index ..................................................................63

viiKPP D

10. LOCAL GOVERNMENT AND BUSINESS INTERACTION ............................................................67 10.1 Background ...........................................................................................................................................67 10.2 Awareness of Communication Forums ............................................................................................67 10.3 Level of Business Problem Solving by Local Governments ...........................................................68 10.4 Level of Local Government Support for Business ...........................................................................69 10.5 Level of Non-Discriminatory Local Government Policies .............................................................71 10.6 Level of Local Government Policies’ Influence on Business Expenditures and Level of Uncertainty for the Business Community ........................................................................................71 10.7 Obstruction Level of Interaction between Local Governments and Businesses ........................72 10.8 Local Government and Business Interaction Sub-Index ................................................................72

11. BUSINESS DEVELOPMENT PROGRAMS (BDP) ..............................................................................77 11.1 Background ...........................................................................................................................................77 11.2 Level of Awareness of Existence of BDP ..........................................................................................77 11.3 BDP Participation Level ......................................................................................................................79 11.4 Level of Benefits of BDP ......................................................................................................................80 11.5 Impact of BDP on Firm Performance ................................................................................................81 11.6 Role of Local Governments in Addressing Problems of Raw Material Supply and Distribution of Products ......................................................................................................................81 11.7 Business Development Programs Sub-Index ...................................................................................83

12. SECURITY AND CONFLICT RESOLUTION ......................................................................................87 12.1 Background ..........................................................................................................................................87 12.2 Level of Theft Incidents at Business Sites .........................................................................................87 12.3 Quality of Police Handling of Crimes ...............................................................................................88 12.4 Quality of Police Handling of Labor Demonstrations ...................................................................88 12.5 Obstruction Level of Security for Business Performance ...............................................................89 12.6 Security and Conflict Resolution Sub-Index ....................................................................................89

13. LOCAL ECONOMIC GOVERNANCE INDEX ....................................................................................93 13.1 Weights of Indicators Forming the Local Economic Governance Index ......................................93 13.2 Local Economic Governance Index ...................................................................................................93

14. CONCLUDING REMARKS AND RECOMMENDATIONS ............................................................99

APPENDIX ........................................................................................................................................................101

viii

Table 5.1 Quality of Local Infrastructure, by Province (Percentages Stating “Poor” and “Very Poor”) ..............................................................................................................................................22

Table 5.2 Time Needed to Repair Damaged Infrastructure, by Province (in Days) .............................24Table 7.1 14 Assessment Criteria for Local-Level Regulations with Assigned Weight ..........................40Table 7.2 Types and Composition of Local-Level Regulations Examined ............................................41Table 7.3 Substance Problems in Regulations on Basic Business Permits (in Percentages) ................43Table 8.1 Levels of Payment of Local Taxes and User Charges, by Scale and Sector of Business (in Rp/Worker/Year) ...................................................................................................................50Table 8.2 Level of Objections to Local User Charges and Local Taxes, for East Java, NTB and NTT, 2007 and 2011 (in Percentages) ..........................................................................................51Table 8.3 Official and Unofficial Commodity Distribution Costs, by Regional Characteristics and Locations (in Rupiah) ............................................................................................................52Table 9.1 Comparison of Business Operators’ Perception of the Leadership and Integrity of

Regents/Mayors, for East Java, NTB and NTT, 2007 and 2011 (in Percentages) .................60Table 10.1 Level of Trust in Local Government Support to Business Operators, by Province (in Percentages) ..............................................................................................................................69Table 10.2 Assessment of Local Governments Support for the Business Community, by Scale of Business (in Percentages) .............................................................................................................70Table 10.3 Positive Impact of Local Government Policies and Interaction Between Local

Governments and Business Operators for Firm Performance, by Scale of Business (in Percentages) ..............................................................................................................................72Table 11.1 Level of Awareness on Existence of BDPs, by Scale of Business (in Percentages) ..............78Table 11.2 Level of Awareness on Existence of BDPs, by Region Characteristics (in Percentages) .....79Table 11.3 Participation Level of BDPs, by Scale of Business (Proportions on BDP Programs’

Awareness, in Percentages)..........................................................................................................80Table 11.4 Level of Benefit of BDPs, by Scale of Business (Proportions on BDP Programs’

Participation, in Percentages) ......................................................................................................80Table 12.1 Quality of Police in Handling Worker Demonstrations, by Scale of Business (in Percentages) ..............................................................................................................................89Table 13.1 Weights of Local Economic Governance Sub-Indices/Dimensions ......................................93

List of Tables

ixKPP D

Graph 2.1 Coverage of LEG Studies: 2007-2011 ............................................................................................5Graph 2.2 Stages in Calculation of Final Index .............................................................................................7Graph 3.1 Level of Education of Respondents (in Percentages) .................................................................9Graph 3.2 Scale of Business, 2007 and 2011 (in Percentages) ....................................................................10Graph 3.3 Sector of Business, 2007 and 2011 (in Percentages) ..................................................................10Graph 3.4 Firms Received Loan from Banks (in Percentages) ..................................................................11Graph 3.5 Firms’ Financial Condition (in Percentages) .............................................................................11Graph 3.6 Firms’ Performance in The Last Three Years (in Percentages) ...............................................12Graph 4.1 Business Premises’ Status (in Percentages) ................................................................................14Graph 4.2 Business Premises’ Ownership (in Percentages) ......................................................................14Graph 4.3 Time Needed to Obtain Land Certificates, by Province (in Weeks) ......................................15Graph 4.4 Level of Difficulty in Arranging Land Use Permits and Level of Difficulty in Obtaining Business Land, by Province (in Percentages) .........................................................15Graph 4.5 Level of Difficulty in Arranging Land Use Permits and Level of Difficulty in Obtaining Business Land, by Region Characteristics (in Percentage) ...................................16Graph 4.6 Levels of Perceived Likelihood of Eviction and Frequency of Occurrence of Eviction, by Province (in Percentages) ........................................................................................................17Graph 4.7 Level of Obstruction of Business Performance Due to Land Access Problems and to Legal Certainty of Land Ownership, by Province (in Percentages) ..................................17Graph 4.8 Land Access Sub-Index .................................................................................................................19Graph 5.1 Quality of Local Infrastructure, by Region Characteristics (Percentages Stating “Good” and “Very Good”) ...........................................................................................................23Graph 5.2 Time Needed to Repair Damaged Infrastructure, by Region Characteristics (in Days) .....25Graph 5.3 Frequency of Water Supply Not Running per Week, by Province ........................................26Graph 5.4 Frequency of Blackouts and Level of Generator Ownership, by Province ...........................26Graph 5.5 Local Infrastructure Sub-Index and Population Density .........................................................27Graph 5.6 Local Infrastructure Sub-Index ....................................................................................................28Graph 6.1 Level of Ownership of Basic Business Permits, by Scale of Business (in Percentages) .......32Graph 6.2 Time Needed to Obtain TDP, by Province (in Days) ...............................................................32Graph 6.3 Perceived Level of Difficulty of Obtaining TDP, by Scale of Business (in Percentages) .....33Graph 6.4 Cost to Arrange TDP and TDP Cost Perceived as Obstacle, by Province (in Thousand Rp and Percentages) ......................................................................................................................34Graph 6.5 Perceived Quality of Licensing Services (in Percentages) .......................................................35Graph 6.6 Knowledge about Complaint Handling Mechanisms, by Province (in Percentages) .........35Graph 6.7 Business Licensing Sub-Index .....................................................................................................37Graph 7.1 Categorization of Local-Level Regulations Studied (in Percentages) ....................................41Graph 7.2 Juridical Problems on Local-Level Regulations Studied (in Percentages) ............................41

List of Graphs

x

Graph 7.3 Juridical Problems on Local-Level Regulations Studied Concerning Basic Business Permits (in Percentages) ...............................................................................................................42

Graph 7.4 Substance Problems on Local-Level Regulations Studied (in Percentages) .........................43Graph 7.5 Principle Problems on Local-Level Regulations Studied (in Percentages) ...........................44Graph 7.6 Local-Level Regulations Sub-Index ............................................................................................46Graph 8.1 Level of Objection to Local Taxes and User Charges, by Province (in Percentages) ...........50Graph 8.2 Payments and Objecting to Payments of Donations to Local Governments, by Province (in Percentages) ........................................................................................................53Graph 8.3 Paying and Objecting to Additional Security Costs (in Percentages) ....................................53Graph 8.4 Obstruction Level of Transaction Costs, by Province (in Percentages) ....................................54Graph 8.5 Transaction Costs Sub-Index .......................................................................................................56Graph 9.1 Understanding by Regents/Mayors of Business Problems and Regent/Mayors Selected Local Government Officials Professionally, by Province (in Percentages) ...........60Graph 9.2 Regents/Mayors do NOT Engage in Activities for Personal Gain and Regents/Mayors

Act Firmly Against Corruption by Staffs, by province (in Percentages) ...............................61Graph 9.3 Leadership Character of Regents/Mayors, by Province (in Percentages) ............................62Graph 9.4 Sources of Information In Regards to Behavior of Regents/Mayors (in Percentages) .......63Graph 9.5 Capacity and Integrity of Regents/Mayors Sub-Index............................................................64Graph 10.1 Level of Awareness of Communication Forum, by Province (in Percentages) ....................68Graph 10.2 Level of Awareness of Communication Forum, by Scale of Business and Region

Characteristics (in Percentages) ...................................................................................................68Graph 10.3 Assessment of Local Government Commitment to Promoting Investment, by Province (in Percentages) ........................................................................................................70Graph 10.4 Assessment of Non-Discriminatory Local Government Policies, by Province (in Percentages) ..............................................................................................................................71Graph 10.5 Local Government and Business Interaction Sub-Index..........................................................74Graph 11.1 Level of Awareness on Management and Manpower Training Programs, by Province (in Percentages) ........................................................................................................78Graph 11.2 Main Obstacle in Obtaining Raw Materials (in Percentages) .................................................81Graph 11.3 Local Governments’ Actions to Overcome The Constraints of Raw Materials’ Access (in Percentages) .................................................................................................................82Graph 11.4 Constraint in Distribution/Marketing of Products (in Percentages) .....................................82

xiKPP D

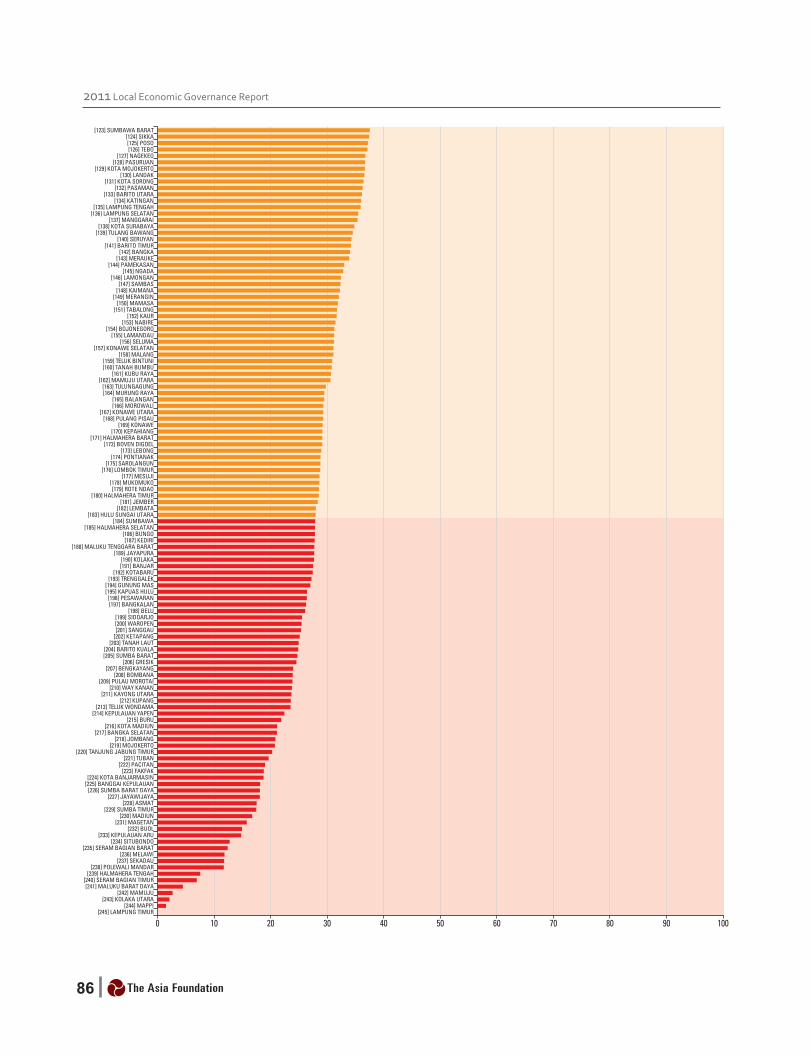

Graph 11.5 Local Governments Actions to Overcome Impediments to The Distribution of Products (in Percentages) .............................................................................................................83Graph 11.6 Business Development Programs Sub-Index ............................................................................85Graph 12.1 Level of Theft Incidents at Business Sites (in Percentages) .....................................................88Graph 12.2 Quality of Police in Crimes Handling, by Scale of Business (in Percentages) ......................88Graph 12.3 Obstruction Level of Security and Conflict Resolution for Business Performance (in Percentages) ..............................................................................................................................89Graph 12.4 Security and Conflict Resolution Sub-Index ..............................................................................91Graph 13.1 Kota Blitar’s Spider Diagram .......................................................................................................94Graph 13.2 LEG Index and Regional Characteristics ...................................................................................94Graph 13.3 LEG Index and Population Density ............................................................................................94Graph 13.4 LEG Index and GRDP Per Capita ...............................................................................................95Graph 13.5 LEG Index and Proliferation of Regions ....................................................................................95Graph 13.6 Local Economic Governance Index .............................................................................................96

xii

Box 4.1 Variables Forming the Land Access Sub-Index .............................................................................18Box 5.1 Variables Forming the Local Infrastructure Sub-Index ................................................................27Box 6.1 Variables Forming Business Licensing Sub-Index ........................................................................36Box 8.1 Variables Forming Transaction Costs Sub-Index ..........................................................................54Box 9.1 Variables Forming Capacity and Integrity of Regents/Mayors Sub-Index ..............................63Box 10.1 Variables Forming Local Government and Business Interaction Sub-Index ............................72Box 11.1 Variables Forming the Business Development Programs (BDP) Sub-Index .............................83Box 12.1 Variables Forming Security and Conflict Resolution Sub-Index ................................................89

List of Boxes

xiiiKPP D

APBD : Anggaran Pendapatan dan Belanja Daerah (Local Government Budget)APBN : Anggaran Pendapatan dan Belanja Negara (National Budget) Babel : Bangka BelitungBDP : Business Development ProgramsBPD : Badan Pertanahan Daerah (Regional Land Agency) BPN : Badan Pertanahan Nasional (National Land Agency)BPS : Badan Pusat Statistik (Central Bureau of Statistics)BUMD : Badan Usaha Milik Daerah (Local Government-Owned Enterprise Corporation)BUMN : Badan Usaha Milik Negara (State-Owned Enterprise, SOE)CU : Credit UnionCSR : Corporate Social ResponsibillityFGD : Focus Group DiscussionGDP : Gross Domestic ProductGRDP : Gross Regional Domestic ProductHGB : Hak Guna-Bangunan (Leasehold rights)HGU : Hak Guna-Usaha (Leasehold land right for business)HM : Hak Milik (Proprietary rights)HO : Hinder Ordonantie (Nuisance Permit)IMB : Izin Mendirikan Bangunan (Building Permit)IPM : Indeks Pembangunan Manusia (Human Development Index, HDI)JPIP : Jawa Pos Institute of Pro-OtonomiKabupaten : Regency KKN : Korupsi, Kolusi dan Nepotisme (Corruption, Collusion and Nepotism)Kota : MunicipalityKPK : Komisi Pemberantasan Korupsi (Corruption Eradication Commission)KPPOD : Komite Pemantauan Pelaksanaan Otonomi Daerah (Regional Autonomy Watch)LEG : Local Economic GovernanceLPEM-FEUI : Lembaga Penyelidikan Ekonomi dan Masyarakat - Fakultas Ekonomi Universitas

Indonesia (Institute for Economics and Social Research-Faculty of Economics University of Indonesia)

MOF : Ministry of FinanceMOHA : Ministry of Home AffairsNTB : Nusa Tenggara Barat (West Nusa Tenggara) NTT : Nusa Tenggara Timur (East Nusa Tenggara)Ormas : Organisasi Masyarakat (Mass organization)OSS : One Stop Shop for Business LicensingPAD : Pendapatan Asli Daerah (Locally-Generated Revenue)

List of Terms and Abbreviations

xiv

PDAM : Perusahaan Daerah Air Minum (Municipal Waterworks)Pemda : Pemerintah Daerah (Local Government)Perbup : Peraturan Bupati (Regent Regulation)Perda : Peraturan Daerah (Local Regulation) Permendag : Peraturan Menteri Perdagangan (Minister of Trade Regulation)Permendagri : Peraturan Menteri Dalam Negeri (Minister of Home Affairs Regulation)Permenpan : Peraturan Menteri Negara Pendayagunaan Aparatur Negara (Regulation from Minister

for Supervision of the State Apparatus)Perwali : Peraturan Walikota (Mayoral Regulation)PJ-PPUS : Penyedia Jasa Program Pengembangan Usaha Swasta (Private Business Development

Program Service Provider) PLN : Perusahaan Listrik Negara (State Power Company)PO : Perusahaan Perorangan (Sole Proprietorship)PP : Peraturan Pemerintah (Government Regulation) PT : Perusahaan Terbatas (Limited Liability Company)PT Tbk : Perusahaan Terbuka (Publicly Listed Corporation)PTSA : Pelayanan Terpadu Satu Atap (“One Roof” One Stop Shop for business licensing)PTSP : Pelayanan Terpadu Satu Pintu (“One Door” One Stop Shop for business licensing)SD : Sekolah Dasar (Elementary School)Seknas FITRA : Sekretariat Nasional Forum Indonesia untuk Transparansi Anggaran (National

Secretariat-Indonesian Forum for Budget Transparency)SITU Surat Izin Tempat Usaha (Business Location Permit)SIUP : Surat Izin Usaha Perdagangan (Trading Business License)SLTP : Sekolah Lanjutan Tingkat Pertama (Junior High School)SP3 : Sumbangan Pihak Ketiga (Third-Party Contribution)Sumbar : Sumatera Barat (West Sumatera)TDI : Tanda Daftar Industri (Certificate of Industrial Registration)TDP : Tanda Daftar Perusahaan (Certificate of Company Registration) THR : Tunjangan Hari Raya (Religious Holiday Allowance)Tramtib : Ketentraman dan Ketertiban Masyarakat (Public Order and Tranquility) UD : Usaha Dagang (Trading Business)SME : Usaha Kecil dan Menengah (Small and Medium-Scale Businesses)UMK : Usaha Mikro dan Kecil (Micro and Small-Scale Businesses)UU : Undang-undang (Law, Act)

xvKPP D

This 2011 study of Local Economic Governance (LEG) is aimed at giving a portrayal of the quality of local economic governance in 245 regencies/municipalities in 19 provinces in Indonesia.1 It is hoped that this study will serve as a basis for local governments at the local level to prioritize reforms and improvements in their performance in various aspects of local economic governance. It is also expected that this study will create an atmosphere of healthy competition among regencies/municipalities. For the provincial governments, the results of this study can be used as an instrument to monitor the performance of local governments and to set priorities – in terms of aspects of LEG and of location – in facilitation and support for regencies/municipalities in improving their performance. For business operators, the results of the LEG study are expected to provide information on the quality of economic governance in the respective regencies/municipalities that will help them make decisions on investment and business development.

This study uses the same methodology as the 2007 LEG study of 15 provinces and the 2008 and 2010 study in Aceh. In the period 2001-2005, Komite Pemantauan Pelaksanaan Otonomi Daerah (KPPOD or Regional Autonomy Watch) and The Asia Foundation conducted annual studies on “Local Investment Attractiveness”, with the number of regencies/municipalities examined rising steadily from 90 regions (2001) to 228 (2005). The study methodology then underwent significant changes; the indicators used focused on various aspects of local economic governance, rather than on investment attractiveness. As it uses the same methodology, design and survey instruments as the three previous studies, the results of this 2011 LEG study can be compared with those of the 2007 LEG study and the 2008 and 2010 Aceh LEG studies. Thus, with the completion of this 2011 LEG study, the views of business operators in nearly all regencies/municipalities in Indonesia are now available,2 though in different time frames. Furthermore, changes in the perceptions of business operators in regencies/municipalities in four provinces – Aceh, East Java, West Nusa Tenggara and East Nusa Tenggara – can be measured, because these regions have had two LEG studies in two different years.

The criteria used in the 2011 LEG study included nine indicators, most of which are within the authority of the regency/municipality governments. The variables used are grouped into the following nine aspects: (i) Land access; (ii) Local infrastructure; (iii) Business licensing; (iv) Local-

1 The nineteen provinces included in this 2011 LEG study are Papua, West Papua, Maluku, North Maluku, Southeast Sulawesi, Central Sulawesi, West Sulawesi, South Kalimantan, Central Kalimantan, West Kalimantan, East Nusa Tenggara (NTT), West Nusa Tenggara (NTB), East Java, Banten, Lampung, Bengkulu, Bangka Belitung, Jambi, and West Sumatera.

2 According to data from the Ministry of Home Affairs (May 2010), there are 267 regencies/municipalities in the 19 provinces targeted in this 2011 LEG study. However, 22 regencies/municipalities in West Sumatera, East Nusa Tenggara, West Papua and Papua were not surveyed or analyzed because they had recently experienced natural disasters, were deemed unsafe, or had a low response rate.

Executive Summary

xvi

level regulations; (v) Transaction costs; (vi) Capacity and integrity of regents/mayors; (vii) Local government and business interaction; (viii) Business development programs (BDPs); and (ix) Security and conflict resolution. These nine aspects are chosen because they accurately reflect LEG, are not endowment factors, and, insofar as possible, are within the authority of the regency/municipality governments. Furthermore, the indicators that are measured are operational and practical, rather than indicators of outcomes or impacts, and therefore can be addressed in a relatively short time.

Data gathered through direct interviews and analyses of local level regulations were then used to calculate the sub-indices for each aspect of LEG, and then the final index. Apart from the aspect of quality of local-level regulations, which was examined through analysis of secondary data, a firm survey (direct interviews with 40 to 50 business operators in each regency/municipality) was performed to obtain data on the other eight aspects. The sub-index indicating the performance of one regency/municipality in one aspect of LEG is compared with the other localities by calculating the average of the variables included in one sub-index after normalization. The final index was calculated using weighting to reflect the importance of one sub-index compared to the others based on firms’ perceptions. To complement the survey results, qualitative studies were conducted by the Jawa Pos Institute of Pro-Otonomi (JPIP), as well as focus group discussions (FGDs) by KPPOD in a number of regions.

Based on business operators’ perceptions, infrastructure is the most important aspect of LEG, so it has been given the greatest weight in calculating the final LEG index. The weights for the respective sub-indices are based on the percentages of perceptions of business operators who feel that the particular sub-index (dimension or aspect of LEG) is a major constraint for business activities. Infrastructure received the greatest weight, 38%, followed by business development programs (BDPs) with a weight of 14%, local government and business interaction (13%), land access (9%), business licensing (8%), and transaction costs (7%). In contrast, capacity and integrity of regents/mayors, local level regulations and security and resolution of business conflicts each received weights of less than 5%.

The survey was conducted in August 2010 to January 2011 with respondents from 12,391 firms. The 2006 Economic Survey (Central Bureau of Statistics, BPS) was used as a sampling frame to select the respondents. Most of the respondents are the owners of their businesses (68%), manager-level employees (25%) and directors (8%). In terms of scale of business of the companies surveyed, small businesses (with 5 to 19 workers) dominated, at 58%, followed by 36% medium-sized businesses, 4% large companies and 2% micro scale enterprises (with fewer than five workers).

Land access – a basic prerequisite for doing business – is still seen as a major problem, especially in urban areas. Most firms own the land on which they do business. Nevertheless, on average one out of three business operators expressed difficulties in accessing land, and roughly one out of four had difficulties in arranging land use permits. Business operators in municipality areas found it relatively more difficult to obtain business land than those in regencies. In terms of the length of time needed to arrange a land certificate, there were significant differences between regions. More time was needed in Western Indonesia (Java and Sumatera, with the highest provincial average of 16 weeks in Bangka-Belitung) than in Eastern Indonesia (Kalimantan, Sulawesi, Nusa Tenggara, Maluku and Papua), with the shortest times, only four weeks, in Central Sulawesi and South Kalimantan. Most business operators considered the risks of eviction and conflict of land to be low. For the land access sub-index, Kolaka Utara in North Sulawesi was the best, while Tebo in Jambi had the lowest performance. Five of the eight regencies/municipalities in the province of Banten were among the 20 regions ranked lowest for this sub-index.

xviiKPP D

Infrastructure, deemed to be the main constraint to business performance, is still considered poor by a lot of business operators. Of the five types of infrastructure examined, telephone and electricity – neither of which is under the authority of the local governments – were considered relatively good by business operators, with 22% and 34% of respectively regarding these as poor. On the contrary, quality of roads, water supply and streetlights are considered in bad quality by over 40% business operators. Business operators in Jambi, West Kalimantan, Central Kalimantan and Papua have to wait 100 days or even longer for damaged roads to be repaired, while in West Sumatera such repairs take less than 20 days. On average, blackouts occur around three times per week, and in Maluku, NTB, West Kalimantan and West Sulawesi they range between five and seven times per week. Regencies/municipalities in East Java dominate the 20 highest ranked regions for the local infrastructure sub-index, with Kota Blitar in first place. In contrast, all of the 20 lowest ranked localities for this sub-index are regencies (no municipality) in Eastern Indonesia, with Waropen (Papua) in last place.

Many business operators still do not have licenses, though most business operators feel that business licensing services are good. Overall, more than 70% of firm feel that business licensing services in their areas are free from collusion, free from illegal levies, and efficient. However, this positive perception of these services is not reflected in the level of permit ownership. Certificates of Company Registration (Tanda Daftar Perusahaan, TDP) – which are mandatory for all business – are held by only around half of the business operators who were interviewed. Similarly, Trading Business Licenses (Surat Izin Usaha Perdagangan, SIUP) – required by most banks to arrange loans – are held by only 58% of business operators. The average time required to arrange a TDP is 11 days, whereas the standard set by the Ministry of Trade is only three days. The costs borne by business operators to obtain TDP are also relatively high, at nearly Rp 500 thousand. Yet the fee set by the central government is only Rp 100 thousand for a sole proprietorship (PO) – the category of most respondents in this study. Lampung Utara (Lampung) is ranked the highest for this sub-index, while Gunung Mas (Central Kalimantan) is the lowest. Among the “top 20” in the business licensing sub-index are nine regencies/municipalities located in East Java and four in South Kalimantan. On the other hand, the “bottom 20” for this sub-index are dominated by regencies (with not one municipality) outside Java (only one regency in East Java).

There are still many problematic local-level regulations. A study was conducted of 1,480 local-level regulations – including local regulation (perda) and regent/mayor regulations/decrees – that affect the business community, examining three aspects: juridical, substance and principle. Juridical problems were considered the worst. No fewer than 1,192 regulations (81%) were identified as having at least one problem from the juridical perspective. Around 72% of all the regulations examined have outdated juridical references; the local-level regulations failed to refer to the most recent versions of the higher-level regulations. Moreover, 35% of all regulations examined were also legally incomplete. In terms of substance, 21% of regulations were found to lack clarity on time, cost and procedural standards (or fee structure and standards). Many regulations relating to business licensing have problems in these aspects. With regard to principles, 17% of regulations were identified as creating negative economic impacts. Most of the problematic regulations are ones that regulate commodity trading. Kubu Raya (West Kalimantan) was the best regency for the local-level regulations sub-index, while Kotabaru (South Kalimantan) had the lowest score.

One impact of these problematic regulations is transaction costs, which increase the costs borne by companies and thus reduce their competitiveness. Official transaction costs (those based on local-level regulations) include taxes, user charges and donations (third-party contributions or SP3). Due to the economies of scale the amounts of taxes and user charges per worker paid by business operators are inversely correlated with the scale of business. Micro-scale businesses pay user charges of around

xviii

Rp 48 thousand/worker and taxes of Rp 65 thousand/worker, while large businesses pay only Rp 14 thousand and Rp 26 thousand per worker for user charges and taxes, respectively. Even so, fewer than 10% of business operators felt these local taxes and user charges were burdensome. Meanwhile, for inter-region movement of goods, roughly one out of two business operators pay official levies, and around one out of four pay unofficial levies. Two newly established regencies, Kolaka Utara (Southeast Sulawesi) and Sumba Barat Daya (NTT), share the highest ranking for the transaction costs sub-index. At the other end of the scale, six of the eight regencies/municipalities in the province of Banten are among the 20 ranked lowest, with Serang in last place.

Generally, business operators’ level of trust in the capacity and integrity of their regents/mayors is fairly high. Around two out of three firms feel that their regents/mayors have a good understanding of the problems of the business community and that the regents/mayors appoint staff with appropriate expertise. A similar proportion was found for business operators’ perceptions that their regents/mayors have strong integrity and take firm action against their staff who engages in corruption. However, this resolute action against staffs does not correlate with the perceived integrity of the regents/mayors themselves. Overall, around three out of four business operators felt that their regents/mayors were strong, respected figures and good role models. Three regencies in Southeast Sulawesi – Buton, Buton Utara and Wakatobi – were in the highest ranking for this sub-index. In contrast, four regencies each in Papua and NTT were among the 20 regions ranked lowest, with Merangin (Jambi) receiving the lowest sub-index score.

Firms’ perception of interaction between local governments and the business community is not too bad. Although only around one out of four business operators are aware of the existence of a communication forum, which is a vehicle for local governments to discuss and seek solutions for the problems of the business community, generally a majority of business operators have positive views of their local governments’ support for the private sector. However, the trust level tends to be lower for smaller-scale businesses. Around 59% of large business operators stated that their local governments provide facilities to support business development, while only around 47% of micro business operators made this statement. With regard to investment promotion, more than half of business operators feel that their local governments have promoted investment and created equal opportunities (non-discriminatory). Kota Probolinggo (East Java) was the best for this sub-index, while Seram Bagian Barat (Maluku) received the lowest score.

Business Development Programs (BDPs) remain relatively unknown, though business operators feel they significantly influence firm performance. Business operators’ level of knowledge of the various BDP activities – business management training, manpower training, promotion of local products, connecting small, medium and large businesses, training in applying for loans and matchmaking of business partners – remains very low. The BDP activity best known by business operators is manpower training, though only 24% of firms are aware of it, and this activity is more familiar to large businesses than to micro and small business operators, who are actually the main target of this program. It is interesting to examine further the efforts made by the regency/municipality governments in West Sumatera, six of which are among the 20 regions ranked highest for this sub-index. According to the results of the FGD held there, most of these local governments facilitate the corporate social responsibility (CSR) activities of private companies to help business operators, rather than financing BDP activities from their own budgets. Lumajang (East Java) has the highest score for the BDP sub-index, while Lampung Timur (Lampung) has the lowest.

xixKPP D

Although the incidence of thefts in business sites are relatively high, firms’ perceptions on the police performance in dealing with crime rases and demonstrations are quite positive. Only 3% of business operators stated that these aspects create problems. However, one out of five business operators were aware of thefts affecting businesses. Regarding the quality of police handling of crimes, around three out of four business operators felt that the police act promptly and minimize losses to companies. Kolaka Utara (Southeast Sulawesi) is the regency with the highest score for this sub-index, while Lampung Timur (Lampung) received the lowest.

Kota Blitar received the highest ranking for the overall Local Economic Governance Index, with ten other regencies/municipalities in East Java among the “top 20”. Kota Blitar also received the highest score in the 2007 LEG study. Of the nine aspects forming the final LEG Index, Kota Blitar was considered particularly good in the sub-indices of infrastructure (ranked first), local government and business interaction (sixth), capacity and integrity of regents/mayors (12th), and business licensing (14th). Furthermore, ten other regions in the province of East Java were among the top 20 in the overall LEG index: Kota Probolinggo, Kota Batu, Magetan, Probolinggo, Lamongan, Tulungagung, Blitar, Kota Kediri, Ngawi and Nganjuk.

In contrast, the 20 regions with the lowest overall LEG indices were regencies (no municipality) outside Java, mainly in Eastern Indonesia. Kabupaten Waropen was judged by its business operators as having the lowest quality of LEG among the 245 regencies/municipalities studied. Further, four other regencies in Papua – Mappi, Sarmi, Asmat and Keerom – were also among the 20 lowest-ranked regions. Apart from the province of Papua, Maluku also had quite a few regencies in this list. Two adjoining regencies, Seram Bagian Barat and Seram Bagian Timur, were ranked second and third from the bottom. Maluku Barat Daya and Maluku Tenggara Barat were also among the bottom ten.

The imbalance in LEG between relatively developed regions and disadvantaged regions requires special attention. Overall, the LEG indices are relatively higher in Western Indonesia (except Banten and Jambi) than in Eastern Indonesia (except Central Sulawesi and South Kalimantan); higher in municipalities than in regencies; and higher in regions with high gross regional domestic product (GRDP) per capita than in those with low GRDP. This situation is clearly cause for concern; we hope that the quality of governance in relatively disadvantaged regions can improve, so as to create opportunities to increase private investment, which will in turn stimulate local economic development and thereby reduce poverty. What we see, however, is the opposite: governance in disadvantaged regions is poorer, so it is likely that the disparity between developed and disadvantaged regions will in fact increase.

LEG in newly created autonomous regions also tends to be fairly low; as well as the gap between “rich” and “poor” regions, “older” regions tend to have slightly higher LEG indices when being compared to “younger” regions. The average LEG index of the 98 regions that experienced no administrative partitioning at all was 65.9 – slightly higher than the average of 63.3 for the 56 parent regions from which new regions had been created. Furthermore, the average LEG index for autonomous regions newly created after decentralization was only 59.5. This indicates that the creation of new administrative regions has not yet contributed to improving the quality of local economic governance.

xx

1KPP D

1.1 Background

The decentralization process is occurring in a time of increasingly tight global competition. Private investment is a critical driver of the economy. Steadily increasing private investment is essential for job creation and sustainable reduction of poverty. A conducive business climate is a crucial prerequisite for attracting and maintaining investment in a given region.

The Indonesian investment climate has shown improvement, though further improvement is needed. According to Doing Business 2011 (World Bank, 2010), among the 183 countries surveyed, Indonesia was ranked number 121, down from 115 the previous year. In the Global Competitiveness Report 2010-2011 (World Economic Forum, 2010), Indonesia is ranked number 44 (of 139 countries), up from number 54 the year before. However, compared with other countries in Southeast Asia, Indonesia is still far behind Thailand and Malaysia, and roughly on a par with Vietnam (which has a higher score in Doing Business but lower in the Global Competitiveness Report).

The decentralization process that has taken place in the past ten years creates new challenges for Indonesia. Decentralization provides wide-ranging authority to sub-national governments, especially regencies/municipalities, including with respect to the investment climate. This authority can be used to simplify licensing procedures, revoke regulations and levies that burden or disrupt the business community, encourage small business development and provide adequate infrastructure. These aspects

1. Introduction

of economic governance need to be continually upgraded to improve Indonesia’s investment climate.

KPPOD, together with The Asia Foundation, is working continuously to promote improved local economic governance in order to improve the investment climate in Indonesia. One part of this effort is a series of studies relating to the investment climate of regions in Indonesia. This was first done in 2001 with annual studies on Investment conpetitiveness of Regions, which were refined starting in 2007 as studies of Local Economic Governance (LEG). In 2007, the LEG study was conducted in 243 regencies/municipalities in Indonesia. The same methodology was also used for LEG studies of 23 regencies/municipalities in Aceh in 2008 and 2010 (also including two regencies in the island of Nias, North Sumatra).

This 2011 LEG study uses the same methodology that was employed in 2007 to 2010 and was conducted in 245 regencies/municipalities in 19 provinces of Indonesia. This study, conducted in 2010-2011, included 16 provinces that were not covered in the previous studies, as well as three provinces that were covered in the 2007 LEG study: East Java, West Nusa Tenggara (NTB) and East Nusa Tenggara (NTT). With the completion of this study, nearly all regencies/municipalities in 32 provinces in Indonesia (all provinces except Jakarta, which is administratively at province level) have been covered, and a complete picture of local economic governance conditions in Indonesia has been obtained.

2011 Local Economic Governance Report

2

1.2 Research Objectives

This study of local economic governance (LEG) is aimed at providing a portrayal of the quality of local governance, which strongly affects the business climate in regencies/municipalities. This portrayal of LEG in the respective regencies/municipalities is based on nine sub-indices (groups of indicators) that are believed to be under the direct control of the regency/municipality governments and not based on endowment factors, which can be improved and generate quick observable results.

We hope that local governments will use this LEG study as a basis for implementing governance reform. Based on this study, local governments can identify and prioritize factors considered important by business operators and formulate policies and reform efforts for business climate improvement in their respective districts. These efforts toward improvement should be undertaken jointly with other stakeholders in the regions through constructive dialogue between business operators and governments to overcome the obstacles to doing business in the regions.

It is hoped that governments at all levels will facilitate a cross learning process, based on good practices already implemented throughout Indonesia. The results of this study should also promote healthy competition among regions in creating a conducive business climate, which will, in turn, ultimately enhance national economic competitiveness. It is hoped that provincial governments and the central government will facilitate joint learning processes so that each

regency/municipality can learn from others that are more advanced. Both the central and the provincial governments can use the results of this study as part of their monitoring and evaluation of the performance of local governments. Furthermore, the study results can also be used to provide incentives and disincentives – both fiscal and non-fiscal – to local governments. Priorities in facilitation and support for regency/municipality governments in improving their performance – in terms of aspects of LEG and of location – can also be planned based on the results of this study.

This study will also be useful for business operators. The results of this LEG study are expected to provide information on the quality of economic governance in the respective regencies/municipalities that will help business operators make decisions on investment and business development.

1.3 Results of the Study

There are three major results of this study. It is expected that these three study results will be useful to all parties concerned in the efforts to create a conducive investment climate in the regions:(1) A ranking of the regencies/municipalities

surveyed based on local economic governance to support a positive business climate.

(2) An overview of the problems faced by the business community in conducting their business activities in the regions, as related to local government policies.

(3) Policy recommendations for improvement of the business climate in the regions.

3KPP D

2.1 Conceptual Framework

The methodology used in this study is the same as that used in the 2007 study of local economic governance (LEG) in 15 provinces and the 2008 Aceh LEG study and the 2010 Aceh-Nias LEG study. The indicators that are used focus on various aspects of local economic governance, rather than on investment attractiveness. Since they all use the same methodology, the results of this 2011 LEG study can be compared with those of both the 2007 LEG study and the 2008 and 2010 Aceh LEG studies.

The LEG study focuses on the perspectives of the business community regarding various aspects of policies, institutions and services at the regency/municipality level. “Local economic governance” refers to the policies of local governments that regulate the activities of the business community in the regions in accordance with their authority. This study examines the policies, institutions and services of local governments in line with the needs of the business community as positive conditions for creation of a healthy business climate in their regions.

The LEG study is not focused on outcomes indicators. This survey is aimed at identifying how the local governments provide services for business activity. This study is therefore different from other surveys that focus mainly on outcomes not under the direct control of local governments, such as employment rate, Human Development Index, and economic growth rate.

2. Methodology

The indicators selected are, insofar as possible, ones that are under local government control, rather than endowment factors. Endowment factors, do certainly affect the investment climate, but they cannot be changed by local governments, or at least take a very long time to change. Therefore, such factors are not selected as indicators in this study.

However, several very important indicators under central government control are still used in this study because they strongly influence the business climate. For instance, several business security indicators remain under control of the police, as a central government agency in the districts. The same applies for land access indicators, which remain under National Land Agency (BPN) authority and are not decentralized; this includes forest and mining concessions. Nevertheless, local governments can, to some extent, influence their performance through more intensive coordination with these central government agencies.

It is hoped that the indicators selected can be immediately adopted, improved and produce tangible results. This LEG study was undertaken to provide information for local governments to prioritize reform of economic governance in their districts. Thus, one of the criteria used in selecting the indicators is that reform ought to be mostly of an operational nature and generate noticeable results in a relatively short time. Besides making it easier for local governments to carry out the required improvements, this should also facilitate non-government stakeholders, such as the business community and civil society, in advocating for policies.

2011 Local Economic Governance Report

4

2.2 Indicators of Local Economic Governance

Based on the various considerations outlined above and on theories of how local economic governance influences economic performance, particularly for private businesses, nine indicators have been selected for measuring LEG, as follows:

1) Land Access strongly affects businesses, as companies will not make new investments if they do not have access to land. At the same time, existing business activities are affected if there is no certainty about the status of their land.

2) Local Infrastructure – good quality district roads, power supply, street lighting, water supply and telecommunication – is a prerequisite for business activities to operate effectively and efficiently. Conversely, poor infrastructure quality increases the cost for businesses to invest and develop.

3) Simple and inexpensive Business Licensing will encourage development of new businesses. In contrast, a difficult, long and expensive business licensing procedure discourages businesspersons from arranging licenses and impedes the growth of new business activities.

(4) Quality of Local-Level Regulations is an indicator of local governments’ policy framework for developing the economy of their districts. Complicated and confusing local level regulations are an obstacle to business in districts, as they lead to uncertainties and restrict trade and market access.

(5) High Transaction Costs in the form of taxes, user charges and other transaction costs, both legal and illegal, may become obstacles to business in districts if they are imposed solely to increase local revenue without taking into

account their impact on business development. On the other hand, transaction costs will not become obstacles when they are enforced based on explicit reasons, properly implemented, and the proceeds are directed toward improving public services.

(6) Capacity and Integrity of Regents/Mayors is critical to guarantee effective implementation of government policies. Trusted and capable regional heads enhance investor confidence and will probably implement investment-friendly policies.

(7) Local Government and Business Interaction is extremely important for guaranteeing that policies and public investments undertaken by local governments are in line with the needs of business operators. In contrast, ineffective interaction between local governments and businesses may lead to policy implementation that impedes business growth.

(8) Business Development Programs (BDPs) carried out by local governments can be an effective method to enhance management capacity and skill of workers, and to connect business operators with markets outside their districts.

(9) Security and Conflict Resolution are critical aspects in the investment climate. It is difficult for business operators to stay in business if they often face security disturbances. Likewise, a good mechanism for resolution of conflicts or business disputes enhances investors’ confidence in starting and doing business.

2.3 Research Locations

The study was conducted in 260 regencies/municipalities located in 19 provinces. Three of the 19 provinces were also surveyed in LEG 2007,3 i.e. East Java, West Nusa Tenggara (NTB) and East

_______________________________________________________________3 The LEG study covered all 243 regencies/municipalities in 15 provinces of Indonesia: North Sumatra, Riau, Riau Islands, South

Sumatra, West Java, Central Java, Yogyakarta, East Java, Bali, NTB, NTT, East Kalimantan, South Sulawesi, North Sulawesi, and Gorontalo. The 2008 Aceh LEG study covered all 23 regencies/municipalities in Aceh. The 2010 Aceh-Nias LEG study covered all 23 regencies/municipalities in Aceh and two regencies on the island of Nias.

Survey of Businesses in 245 Regencies/Municipalities in Indonesia

5KPP D

Nusa Tenggara (NTT), while the other 16 had not previously been surveyed. Based on data from the Directorate General of Public Administration in the Ministry of Home Affairs (May 2010), there are 267 regencies/municipalities in these 19 provinces. However, the survey was not carried out in seven regencies in West Sumatra (Sumbar) and Papua,4 so only 260 regencies/municipalities were covered.

Analysis was performed for 245 regencies/municipalities. Of the 260 regions surveyed, 155

could not be analyzed for various reasons. In several regencies, the response rates for certain variables were very low, making it impossible to compare them equivalently with other regions. Further, in certain regencies over 80% of the firms who were interviewed were micro business operators with fewer than four workers, who were considered to have very little interaction with their local governments and to lack adequate understanding about local economic governance. For these two reasons, 15 regencies were excluded from the analysis in this study.

Various regional characteristics are represented by the 245 localities analyzed. Of the 245 regions analyzed, 202 (82%) are regencies and 43 (18%) are municipalities. Overall, 106 of these regions (43%) are located in Western Indonesia (Java and Sumatra) and 139 (57%) in Eastern Indonesia (Kalimantan, Sulawesi, Nusa Tenggara, Maluku and Papua). In terms of regional typology, they are divided into 190 mainland regions (78%) and 55 (22%) with island characteristics. Among the regions analyzed are 98 newly-created

administrative districts (40%), 56 (23%) that were the parent districts of newly-established districts, and 91 (37%) that have not undergone such partitioning. This variety allows an analysis of the impact of these of characteristics on local economic governance, and also of the correlation between economic indicators and population.

2.4 Research Instruments

This 2011 LEG Study uses two data sources: a firm survey and secondary data. The firm survey of selected businesspersons in each regency/

W Sumatra

Banten

Jambi Babel

Lampung

E Java NTB

NTT

Bengkulu

W Kalimantan

C KalimantanW Sulawesi

S Kalimantan

SE Sulawesi

C Sulawesi

N Maluku

Maluku

W Papua

Papua

Graph 2.1 Coverage of LEG Studies: 2007-2011

_______________________________________________________________4 The Mentawai Islands (West Sumatra) were not surveyed due to a recent natural disaster, while Puncak Jaya, Tolikara, Mamberamo

Raya, Yalimo, Nduga, and Puncak (all in Papua) were excluded from the survey for security reasons.5 The regencies that could not be analyzed were Sabu Raijua and Sumba Tengah (NTT), Buru Selatan (Maluku), Raja Ampat,

Tambrauw, and Maybrat (West Papua), and Paniai, Yahukimo, Pengunungan Bintang, Supiori, Mamberamo Tengah, Lanny Jaya, Dogiyai, Deiyai and Intan Jaya (Papua).

2011 Local Economic Governance Report

6

municipality was carried out through direct interviews (face-to-face) over the period of September 2010-January 2011 to obtain data – perception and quantitative – to measure performance in eight LEG indicators. To measure the indicators for the local-level regulations sub-index, local-level regulations affecting business in each regency/municipality were analyzed. Secondary socio-economic data were collected to complement the firm survey results and local-level regulation assessments.

A questionnaire was used for the firm survey. The questionnaire used in the 2011 LEG study was the same one used in the 2007 LEG study and the 2008 and 2010 Aceh LEG studies, with some minor modifications and simplifications to make things easier for interviewers and respondents. The questionnaire includes questions to obtain both data on businesspersons’ perceptions and quantitative (numerical) data on eight LEG indicators. For instance, respondents were asked about how often they experience blackouts while at work and whether they have generator sets; also asked was their perception about the quality of existing electricity supply.

To complement the firm survey and the analysis of local-level regulations, qualitative studies and focus group discussions (FGD) were conducted in several regions. The qualitative studies were conducted by the Jawa Pos Institute of Pro-Otonomi (JPIP) in February-April 2011 in 15 regencies/municipalities in the provinces of East Java, NTB and NTT.6 These qualitative studies were conducted by interviewing key informants from local governments, business associations and business operators. In addition, secondary data, such as local legal products and programs conducted in the regions, were collected and analyzed. As well as the qualitative studies conducted by JPIP, KPPOD also held FGDs with relevant stakeholders in March 2011 in East Java,

West Kalimantan, West Papua, NTT and West Sumatra to discuss the preliminary findings of the firm surveys.

Qualitative analysis scorecards were used to assess local-level regulations. Various regulations issued by local governments – including Local Regulations (perda),7 Regulations and Decrees of Regents/Mayors and Circular Letters from Regents/Mayors – relating to the business community were collected and assessed. Scorecards based on the indicators and variables were used to evaluate problems with each policy. An assessment weighting is provided on each aspect of each regulation, based on possible impact on economic activities. A more detailed explanation on this is included in the discussion on the Local-Level Regulations sub-index (Chapter 7).

2.5 Weighting of Indicators Forming the Local Economic Governance Index

The weights for each sub-index are based on percentages of business operators’ perceptions of the extent to which a given sub-index (LEG dimension) is a major obstacle to doing business. Although all nine sub-indices and their supporting variables are important aspects of local economic governance, business operators felt that certain sub-indices were more important than others. Based on these weights and priorities, it is hoped that governments can have a more accurate reference for determining the priorities of policies to be undertaken in improving the performance of economic governance in their regions. The weights for each sub-index are explained in Chapter 13 (Local Economic Governance Index).

The calculation of the overall 2011 LEG index uses different weights from those in the 2007 LEG study. The main reason for using different weights from those in the previous studies was to observe the changes in the issues faced by the business

_______________________________________________________________6 Qualitative studies were undertaken in Tuban, Jombang, Lumajang, Sampang, Kota Blitar, and Kota Surabaya (East Java); Bima,

Sumbawa Barat, Lombok Barat and Kota Mataram (NTB); and Timor Tengah Utara, Manggarai, Belu, Kota Kupang and Sumba Barat (NTT).

7 Local regulation (peraturan daerah or perda) is the highest level of legal document. It must be discussed and passed by the legistative council (DPRD) and signed into law by the executive.

Survey of Businesses in 245 Regencies/Municipalities in Indonesia

7KPP D

community over the course of four years. Also, most of the regions surveyed were different regions from before, so the problems faced by the business community were different as well.

2.6 Sampling

The respondents targeted in this survey represent businesspersons from all non-primary business sectors: services, production and trading. Services, production and trading are the key economic sectors that most often come into contact with the government. Businesspersons engaged in agriculture, forestry and fishery were not selected as respondents for this survey. The reason for not including these primary business sectors is that the handling of those sectors by government is very different. However, business activities for processing agricultural, forest and fishery products are included in this survey, while government-owned enterprises (BUMN/BUMD), government agencies engaged in education and health care services and other public services are excluded from the survey.

In terms of business scale, this survey originally focused only on business of small, medium and large scale, but eventually also included micro-scale enterprises. This was because some districts did not have sufficient numbers of small (5-19 workers), medium-scale (20-99 workers) and large (more than 99 workers) businesses to serve as a sample. So that each district would be adequately represented, micro-scale businesses (less than 5 workers) were also interviewed, though businesses with only one worker were excluded from the analysis.8

The 2011 LEG study used the 2006 Economic Survey9 as its sample frame. The 2006 Economic Survey was also used as the sampling frame for the three previous LEG studies. Proportional random sampling was used to obtain samples representing

the sectors and scales of business10 that are the focus of the survey.