224078_AR_2016-2017-KALAHANDI.pdf - Directorate of ...

86

AUDIT REPORT 07-02-2017 LOCAL FUND AUDIT, KALAHANDI, ODISHA CATEGORY : Panchayat Samiti,General Audit Report No : 224078/AR/2016-2017-KALAHANDI PARA: 1 TITLE SHEET 1 Name of the Institution : M.Rampur P.S 2 Year of Accounts under Audit : 2015-2016 3 Name of the Local Authority during the year of A/Cs : SRI BASUDEV NAYAK,OAS -I-JB FROM 01-04-15 TO 31-03-16 Name of the Local Authority at the time of Audit : SRI BASUDEV NAYAK,OAS -I-JB 4 Duration of Audit : 29-08-2016 To 04-11-2016 (Mandays Consumed :- 30) 5 Name of the Auditors : JAYA KRISHNA PANDA - Lead Auditor(29-08-2016 to 04-11-2016) SANA KUMAR JANI - Auditor(29-08-2016 to 04-11-2016) 6 Name of the Reviewing Officer : DINABANDHU BEHERA(Audit Superintendent) 7 Date of submission of report by Reviewing officer : 08-12-2016 8 Entry Conference Date : 17-08-2016 9 Exit Conference Date : 25-01-2017 10 Name of the District Audit Officer : BIBHUTI BHUSAN RATH 11 Date of approval of report by District Audit Officer : 07-02-2017 1 / 86

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of 224078_AR_2016-2017-KALAHANDI.pdf - Directorate of ...

AUDIT REPORT 07-02-2017

LOCAL FUND AUDIT, KALAHANDI, ODISHA

CATEGORY : Panchayat Samiti,General Audit Report No : 224078/AR/2016-2017-KALAHANDI

PARA: 1 TITLE SHEET

1 Name of the Institution : M.Rampur P.S

2 Year of Accounts under Audit : 2015-2016

3 Name of the Local Authority during the year of A/Cs : SRI BASUDEV NAYAK,OAS -I-JBFROM 01-04-15 TO 31-03-16

Name of the Local Authority at the time of Audit : SRI BASUDEV NAYAK,OAS -I-JB

4 Duration of Audit : 29-08-2016 To 04-11-2016 (Mandays Consumed :- 30)

5 Name of the Auditors : JAYA KRISHNA PANDA - Lead Auditor(29-08-2016 to 04-11-2016)SANA KUMAR JANI - Auditor(29-08-2016 to 04-11-2016)

6 Name of the Reviewing Officer : DINABANDHU BEHERA(Audit Superintendent)

7 Date of submission of report by Reviewing officer : 08-12-2016

8 Entry Conference Date : 17-08-2016

9 Exit Conference Date : 25-01-2017

10 Name of the District Audit Officer : BIBHUTI BHUSAN RATH

11 Date of approval of report by District Audit Officer : 07-02-2017

1 / 86

AUDIT REPORT 07-02-2017

PARA: 2 PHYSICAL VERIFICATION

Slno Items Date Of Physicalverification Before /After Transaction

Physical Balance Balance As per CashBook / StockRegister

Reference To ThePage No Of CashBook / StockRegister

Discrepancies If Any

1 Measurement Books 29-08-2016 1 1 PAGE 36 Nil

2 Cash in hand 29-08-2016 0.94 0.94 PRIASoft cash book Nil

3 Others

4

5 ServicePostageStamps

29-08-2016 1580 1580 PAGE 43 Nil

6 MiscellaneousReceipt Books

29-08-2016 10 10 PAGE 31 Nil

Comments

POM No.01/ dt.29.08.2016

As per Rule 20 of Orissa Local fund Audit Act the physical verification of Cash in hand, unused MBs, Unused postage stamps, unused Receipt books etc wasconducted before transaction. The physical verification of cash was conducted on the date of commencement of audit i.e. on 29.08.16 as the cash book was madeup to date.

2 / 86

AUDIT REPORT 07-02-2017

PARA: 3 LIST OF VERIFIED RECORDS

A : List Of Verified Records/RegisterSlno List Records/Register Rules Form No1 T.A. Bill for members of the Samiti Rule 88(b) Form No.-XXXIX2 Muster Roll Rule 85(1) Form No.-XXXVII & XXXVIII3 Stock Register of MBs Rule 80(2)4 Measurement Books Rule 80(1) Form No.-XXXIV5 Register of Administrative Approval Rule 76(4) Form No.-XXXIII6 Register of Estimates Rule 76(4) Form No.-XXXII7 Stock Book Rule 71 Form No.-XXV-A8 Log Book Rule 60 Form No.-XXII9 Stationery Account Rule 56 Form No.-XXI10 Stamp Account Rule 56 Form No.-XX11 Cash Book Rule 32 Form No.-X12 Guard file for paid vouchers Rule 2013 Bill Register Rule 18(1) Form No.-V14 Allotment Register Rule 11 Form No.-IV15 Pass Books Rule 716 Misc. Receipts Rule 6(2) Form No.-II17 Grant-in-Aid Register Rule 5(4) Form No.-I18 P.L. Account Rule 5(2)

B : List of Records/Registers not Produced to AuditSlno List Records/Register Rules Form No1 Completion Certificate Rule 80(1) Form No.-XXXV2 Issue of Tender orders Rule 74(3)(d) Form No.-XXIX3 Execution of agreements with the

ContractorsRule 74(3)(d) Form No.-XXX

4 Execution of agreements with theother agencies other thanContractors.

Rule 74(3)(e) Form No.-XXXI

5 Forms to be used by theContractors for submission ofTenders

Rule 74(1) Form No.-XXVI to XVIII

6 Register of lapsed Deposits Rule 64 Form No.-XXIV7 Register of Cheques and Drafts

receivedRule 63 Form No.-XXIII

8 Register of Immovable Properties Rule 49 Form No.-XVIII9 Revenue Register Rule 51 Form No.-XIX10 Loan Register Rule 46 Form No.-XVI11 Appropriation of Loan Register Rule 47(1) Form No.-XVII12 Register of Securities Rule 45(1) Form No.-XV13 Deposit Ledger Rule 44 Form No.-XIII, XIV14 Register of Outstanding Advances Rule 43 Form No.-XII15 Register of Advances Rule 42(1) Form No.-XI16 Indemnity bond executed Rule 31(3) Form No.-IX17 Cheque Books Rule 2218 Permanent Advance Cash Book Rule 21 Form No.-VIII19 Guard file for supply Rule 18(4)20 Order Book Rule 18(3) Form No.-VI or VII

C : List of Records/Registers not MaintainedSlno List Records/Register Rules Form No

D : List of Records/Registers not RequiredSlno List Records/Register Rules Form No1 Receipts for taxes Rule 6(3) Form No.-III

Comments

POM NO.01/29.08.16

Besides those the following records were verified in course of audit.

3 / 86

AUDIT REPORT 07-02-2017

1.PL A/C Cash Book.

2.MISC Cash Book.

3.CC Road Cash Book.

4.BRGF Cash Book.

5.MPLAD Cash Book.

6.MLALAD Cash Book.

7.WODC Cash Book.

8.NREGA Cash Book.

9.RLTAP Cash Book.

10.Hon.Cash Book.

11.SPF,SDP Cash Book.

12IHHL/TSC Cash Book.

13.TFC Cash Book.

14.IAP Cash Book.

15.BKBK Cash Book.

16.NRLM Cash Book.

17.RTI cash book.

18.IAY/MO KUDIA Cash Book.

19.BKSS Cash book.

20.MADA Cash book.

21.PMGSY Cash book.

22.Staff Salary cash book.

23.Teachers salary cash book.

24.OAP.ODP,NOAP CASH BOOK.

25.NFBS CASH BOOK.

26.PMS CASH BOOK.

27.MDM Cash book.

Non Maintenance of accounts and records and register

As per the provision made in Panchayat Samiti Act.1959 and Odisha Panchayat Samiti accounting procedure rules 2002 ,the following records and registerrelating to the year 2015-16 ,was not maintained The local authority was asked the reason for non-maintenance of their prescribed records,to which the localauthority replied that, henceforth the records will be maintained. The details of records not maintained with corresponding Rules and remarks for non-maintain arefurnished below.

Sl.No Name of the accountregister/records

Corresponding Rules Remarks

1 Budget of the Samiti Sec-24(1)(2) pf P.S Act.1959 Non- preparation of annual budget reduced accountabilityand smooth financial control at the level of P.S , Budget, isthe statutory requirement without it the expendituremechanism will fail, and the expenditurebecome un-authorised

2 Security deposit Ledger Rule-44 of PSAP Rules Non-preparation of SD ledger results failure in monitoring ofSD refund and attract the risk of double paymentto executants.

4 / 86

AUDIT REPORT 07-02-2017

3 Property Register Rule-49 Due to non-maintenance of property register. The exactposition of the property of the P.S such as land, ponds,market complex could not be ascertained. In due course therevenue generated from the properties shall be nullified.

4 Asset register Govt. Instruction as per scheme guideline Due to non-maintenance of the asset register the true pictureof the assets created under various schemes could not beensured in the periodical reporting. Thus, no consolidateddatabase on assets created. Could be made possible

5 Bank reconciliation statement G.O NO.5302/PR 23.04.2009, 690/F.dt.21.01.2009,13000/PR dt.25.07.14 , 14261/ PR20.05.2013 Rule-33 of PSAP Rules

Due to non-reconciliation of the difference between closingbalance of all Pass Books and all Cash. Due tonon-reconciliation of the difference between closing balanceof all Pass Books and all Cash Books the possibility offinancial fraud cannot be ruled out. .Further the closingbalance of the cash book will be over stated or under statedresulting incorrect picture of cash management.

6 Outstanding advance ledger Rule-43 Due to non-maintenance of outstanding advance ledger, theP.S authorities could not keep watch over the defaultingadvance holder there by leading to huge accumulation ofoutstanding advance rolling un-adjusted for years together

7 Allotment register of development funds

Rule-11 Due to non-maintenance of allotment register of schemefunds the P.S authorities could not keep watch over the receipt of scheme funds

8 Audit compliance register Due to non-maintenance of audit compliance register, theposition of audit Paras awaiting for settlement could not beascertained the cash book will be over stated or under statedresulting incorrect picture of cash management.

9 Receipt Expenditure statement. Receipt expenditure is a vital part of the account which actsas a mirror of the account in Toto. Non-maintenance of thesame may lead to

10 Grant-in aid register 5(4) As per PSAP rule 2002, Rule 5.4 A register in Form No. 1should be maintained to show the details of grants receivedanddrawn.

5 / 86

AUDIT REPORT 07-02-2017

PARA: 4 FINANCIAL POSITION

M.Rampur P.S - 2015-2016

Slno Name of theCash Book

OB as onDate

OpeningBalance(In Rs:)

Receiptduring theYearunderAudit(InRs:)

Total(InRs:)

Expenditure duringthe YearunderAudit(InRs:)

ClosingBalance asper Audit(DD MM YYYY)

ClosingBalance(In Rs:)(AUDIT)

ClosingBalance asper (DD MM YYYY)Cash Book

ClosingBalance(InRs:)(CASH BOOK)

Difference(In Rs:)

Remarks

1 PS ACCOUNT 01-04-2015 223087693.25

96425342.81

319513036.06

172615343.00

31-03-2016 146897693.06

31-03-2016 144277416.06

2620277.00

2 GOVTACCOUNT

01-04-2015 27888271.03

47045512.00

74933783.03

41757759.00

31-03-2016 33176024.03

31-03-2016 32773010.03

403014.00

GRANDTOTAL

250975964.28

143470854.81

394446819.09

214373102.00

180073717.09

177050426.09

3023291.00

Comments

Details of closing balance furnished below.

1. In Bank:- Rs.176750424.91

2. In Cash . :- Rs. 0.94

3. In P.L.:- Rs. 300000.24

Total:- Rs.177050426.09

HEAD OF ACCOUNT CASH IN HAND BANK ACCOUNT SCHEME

11703064078-State Bank of India 14627389.00BKBK

BKBK Total 0.00 14627389.00

11703064056-State Bank of India 1901376.00BRGF

BRGF Total 0.00 1901376.00

30889662073-State Bank of India 3258974.00CC road

CC road Total 0.00 3258974.00

Cash In Hand 0.11 CRF

11703063993-State Bank of India 1449850.00CRF

32438824311-State Bank of India 136250.00CRF

CRF Total 0.11 1586100.00

11703063993-State Bank of India 1691.00Election

32842815168-State Bank of India 482593.00Election

Election Total 0.00 484284.00

35274661481-State Bank of India 16411805.00GGY

GGY Total 0.00 16411805.00

33173292637-State Bank of India 199726.00HON

HON Total 0.00 199726.00

30889662186-State Bank of India 12643235.00IAP

IAP Total 0.00 12643235.00

6 / 86

AUDIT REPORT 07-02-2017

32438799428-State Bank of India 1351955.00IAY

11703064001-State Bank of India 2250857.00IAY

IAY Total 0.00 3602812.00

84004369218-UTKAL GRAMYA BANK 270848.00IEC

IEC Total 0.00 270848.00

11703063993-State Bank of India 34454.00KL

33173264064-State Bank of India 221568.00KL

KL Total 0.00 256022.00

11703063993-State Bank of India 1138280.00MADA

12174057937-UTKAL GRAMYA BANK 1000000.00MADA

12206010111-UTKAL GRAMYA BANK 1000000.00MADA

32438823260-State Bank of India 1641226.00MADA

11842162236-State Bank of India 154971.00MADA

MADA Total 0.00 4934477.00

Cash In Hand 0.80 MGNREGS

31087730605-State Bank of India 114179.19MGNREGS

MGNREGS Total 0.80 114179.19

31715870870-State Bank of India 6814402.00MLALAD

MLALAD Total 0.00 6814402.00

30809682469-State Bank of India 2792425.00MO KUDIA

MO KUDIA Total 0.00 2792425.00

30889662222-State Bank of India 2373196.00MPLAD

MPLAD Total 0.00 2373196.00

31715869468-State Bank of India 72870.00NRLM

35277326427-State Bank of India 99322.00NRLM

32695659769-State Bank of India 134587.00NRLM

NRLM Total 0.00 306779.00

11703064067-State Bank of India 1819157.00RLTAP

RLTAP Total 0.00 1819157.00

11703068164-State Bank of India 10740.98RTI

RTI Total 0.00 10740.98

33700118901-State Bank of India 90180.00TSC

30889662493-State Bank of India 102729.00TSC

TSC Total 0.00 192909.00

84013698255-UTKAL GRAMYA BANK 229454.00SDP

SDP Total 0.00 229454.00

31715872040-State Bank of India 16453121.00SFC

SFC Total 0.00 16453121.00

33700128374-State Bank of India 1376524.00SPF

SPF Total 0.00 1376524.00

11842162236-State Bank of India 1815827.00MISC

12206010111-UTKAL GRAMYA BANK 2842865.00MISC

32537634485-State Bank of India 13379517.00MISC

7 / 86

AUDIT REPORT 07-02-2017

11703063993-State Bank of India 3872436.20MISC

12174057937-UTKAL GRAMYA BANK 2775232.00MISC

MISC Total 0.00 24685877.20

11703063993-State Bank of India 126686.00PMGAY

PMGAY Total 0.00 126686.00

31715868352-State Bank of India 15275833.00SC/ST Dev

SC/ST Dev Total 0.00 15275833.00

11703068051-State Bank of India 2802678.54THFC

THFC Total 0.00 2802678.54

30546332512-State Bank of India 8426405.00WODC

WODC Total 0.00 8426405.00

TOTAL 0.91 143977414.91

PL account 300000.24

TotAL PS account 0.91 144277415.15

GOVT ACCOUNT

912010005438261-AXIS Bank 1176931.00MDM

30746223889-State Bank of India 6059904.00MDM

MDM Total 0.00 7236835.00

32842812860-State Bank of India 542753.00NFBS

NFBS Total 0.00 542753.00

30746215982-State Bank of India 911622.00NOAP

34778931556-State Bank of India 23332370.00NOAP

NOAP Total 0.00 24243992.00

33173295504-State Bank of India 388064.00PMS

PMS Total 0.00 388064.00

32309533512-State Bank of India 35422.00SSA

SSA Total 0.00 35422.00

11703063993-State Bank of India 12262.00TEACHER SALARY

TEACHER SALARY Total 0.00 12262.00

Cash In Hand 0.03 SSAOC

11703063993-State Bank of India 137582.00SSAOC

11703063256-State Bank of India 176100.00SSAOC

SSAOC Total 0.03 313682.00

TOTAL 0.03 32773010.00

GRANT TOTAL 0.94 177050425.15

GRANT TOTAL 177050426.09

DETAILS OF DISCREPANCY BETWEEN THE CASH BOOK AMOUNT AND THE AUDIT AMOUNT IN RESPECT OF DIFFERENT CASH BOOKS OF P. S ACCOUNT

Name of the grant Discrepancy due to

Grants not taken tocash book

Excess grantsshown in the cash

book

Expenditure notreflected in the cash

book

Total:-

8 / 86

AUDIT REPORT 07-02-2017

IAP 636304 -636304

MPLAD -360000 -360000

BRGF 40991 26227 14764

WODC 19405 200000 -180595

MO KUDIA 105000 360000 -255000

ELECTION -232500 -232500

MISC 3930088 3930088

KL 62173 494990 -432817

Total:- 1847636

Bank int. not taken to cash book 773952 773952

Bank charges not taken to cash book 1311 -1311

C.B of all grants as per Cash Books 144277416.06

Total 4931609.00 -592500.00 1718832.00 146897693.06

DETAILS OF DISCREPANCY BETWEEN THE CASH BOOK AMOUNT AND THE AUDIT AMOUNT IN RESPECT OF DIFFERENT CASH BOOKS OF GOVT. ACCOUNT

Sl.No Description Amount01 Closing Balance as per all Cash Books 32773010.0302 Add difference as per last audit report 14262.0003 Allotment received but not taken to Cash Book 390000.0004 Bank charges deducted but not reflected in Cash Book (-) 1311.00 Total 33176024.03In response to objection memo regarding reconciliation of bank account ) vide POM 06/28.09.16 POM No 10/07.10.16 (relating to previous year discrepancy) localauthority agreed to reconcile the same . But the same was not done till the date of exit conference. Hence the local authority is advised to takes necesary steps forearly settlement

Discrepancy between cash book & pass book (PL ACCOUNT) POM NO11/13.10.16

On scrutiny of the PL account cash book with reference to the treasury pass book, a discrepancy of Rs 62000 was noticed between the Pass Book and the CashBook figures . Necessary steps may be taken to ascertain the head of account & necessary reconciliation may be made in the PL account cash book. During theExit Confeence the BDO assured to work out and settle the difference

PL account as per cash book 300000.24

PL account as per pass book 362000.24

Difference 6200

Persistent irregularities w.r.to financial management in the PS

The following persistent irregularities were noticed during the year under audit.

1. Despite objections raised in the previous Audit Reports and in contravention to provision under Rule-33 of P.S.A.P. Rules-2002, not a single pass book orstatement of bank accounts was compared and verified by the B.D.O. after receipt of the same from the banks with the entries of the cash books to ensurecorrectness of remittances.

2. In violation of Rule-36(1) of the P.S.A.P. Rules-2002, neither the register of receipt and expenditure nor the detailed head wise analysis of the closing balancewas maintained by the local authority on the basis of the supporting records.

3. In contravention of Rule-36(2) of the P.S.A.P. Rules-2002, not a single entry was attested by the B.D.O. in the receipt and expenditure side of the Cash Book afterbeing satisfied about the correctness of the same with reference to the supporting documents and registers.

4. As per Rule-36(2)(e) of the P.S.A.P. Rules-2002, the B.D.O. / A.B.D.O. / Chairman (or who so ever he desires) shall verify the cash balance in the chest with thebalance in the Cash Book at the end of each month and record the same with his signature and date with a certificate. In case of any difference between thephysical balance and the Cash Book balance, the same shall be explained. Such non-conduct of physical verification at the end of the each month violates theabove rule. Further it was stressed upon to maintain annual receipt and expenditure register soon on priority basis.

5. As per rule -3 OGFR all transactions must be brought to account without delay. While working on the financial position the audit observed that the interestsaccrued by different bank accounts are booked as receipt once during the year in consolidated manner. This habit should be changed and regularity should bemaintained. As per rule-9 of OGFR, financial propriety should be maintained while incurring expenditure. But it is not properly adhere to. This habit should beavoided .As per O.M number -2983/PR Dt.22.03.2000 & Vide letter No 13000/25.12.13 of PR Dep't. instruction has been issued to maintain one-savings account forone scheme. In course of audit it was noticed that the same rule has been violated. One-savings account deals with several schemes & vice-versa. Further GO No

9 / 86

AUDIT REPORT 07-02-2017

14261/Dt 20.05.13 it is clearly mentioned that multiple account for one-scheme goes against rule &poses difficulty in reconciliation the BDO shall maintain & operatesavings account for one-scheme. But the same instruction has been violated. Local authority should take suitable steps to follow the Govt. instructions.

Maintenance of Flexi Account in banks w.r.t. Scheme funds (pom no 02/29.08.16 page 3)

These days Banks are offering facilities to better higher returns on Savings account through Flexi Deposits. It helps earn high returns of a fixed deposit on surplusmoney in the Savings Account. The Principal Secretary to Govt., Finance Department in his Letter No.35425(42)/F Dt.12.10.12 instructed on investment of schemefunds in bank account by the implementing agency of centrally sponsored plan schemes above a threshold limit in fixed deposit through flexi account system may beimmediately adopted .By the Flexi accounting system the entire fund besides a nominal amount like Rs1,00,000/- only will be converted to temporary fixed depositswhile balance will lie in savings banks accounts .On requirements the entire amount can be drawn and utilized as good as like a savings bank account , Formaintenance of Flexi account in case of Scheme fund . In response to objection memo local authority replied that no flexi account maintained during 2015-16.However instruction noted for future guidance.

Annual budget (pom no 02/29.08.16)

As per Section-24(1) of the Odisha Panchayat Samiti Act, 1959 Budget shall be sanctioned by the PS and vide section 24(2) the Budget stands valid unlessmodified by the Dist. Collector. But in M.Rampur PS it is observed that no Budget is prepared for the planed expenditure. However for the Non-Planned Expenditurefavoring the head of account salaries is prepared regularly. In absence of the proper Budget Audit is unable to compare the Budgeted receipt and expenditure withthe actual receipt and expenditure. Non-preparation of the Budget makes spending authorities unrestrained & thereby the possibility of financial irregularitiesbecomes more transient & highly affects the maintenance of accounts. Different Schemes launched for public usages by the Higher Administrative PlanningAuthorities are executed aimlessly. Audit suggests Annual Budget be prepared and produced to the audit positively forthwith. In response to objection memo page 2local authorities replied that during 2015-16 no annual budget was prepared. Instruction noted for future guidance.

ABSTRACT OF PS ACCOUNT( DETAIL IN PARA 18.1)

The abstract of receipt expenditure position of PS account of M.Rampur PS with major heads is furnished below.

MAJOR HAEDS OB as 01.04.15 Receipt during theyear 2015-16

Total Expenditure during theyear 2015-16

CB as on 31.03.16

Grants 198141394.09 81400099.81 279541493.90 165119549.00 114421944.90

Other than grants 6399336.58 5867469.00 12266805.58 7137675.00 5129130.58

Own source 948252.59 604590.00 1552842.59 358119 1194723.59

Interest 17598709.99 8553184 26151893.99 26151893.99

Total 223087693.25 96425342.81 319513036.06 172615343.00 146897693.06

Abstract of bank interest

Bank interest credited into the pass book 7779232.00

Bank interest not credited into the pass book 773952.00

Total 8553184.00

ABSTRACT OF GOVT. ACCOUNT( DETAIL IN PARA 18.2)

Govt account

MAJOR HEADS OB AS ON 01.04.15 RECEIPT DURING THEYEAR 2015-16

TOTAL EXPENDITURE DURINGTHE YEAR 2015-16

CB AS ON 31.03.16

GRANTS 0 0

OTHER THAN GRANTS 25124857.03 46543185.00 71668042.03 41757759.00 29910283.03

BANK INT 2763414 502327 3265741 3265741

Total 27888271.03 47045512.00 74933783.03 41757759.00 33176024.03

10 / 86

AUDIT REPORT 07-02-2017

PARA: 5 DETAILS OF CLOSING BALANCE AS PER BANK PASS BOOKS & CASH BOOK BANK BALANCE FIGURE

M.Rampur P.S - 2015-2016

Slno Name of the Bank A/C No. ClosingBalance DateAs on(dd/mm/yyyy)

ClosingBalance in PassBook(In Rs:) (A)

ClosingBalance inBank DateCash Book(dd/mm/yyyy)

ClosingBalance inBank asmentioned inCash Book(InRs:) (B)

Difference(InRs:)(A-B)

Remarks

1 ALL ACCOUNTS 01-04-2015 186731717.46 31-03-2016 176750424.91 9981292.55

GRAND TOTAL 186731717.46 176750424.91 9981292.55

Reconciliation

Slno Name of the Bank A/C No. Closing BalanceDate As on(dd/mm/yyyy

ClosingBalance inPassBook(In Rs:)(A)

Closing Balancein Bank DateCash Book(dd/mm/yyyy)

ClosingBalance inBank asmentioned inCashBook(InRs:) (B)

Difference(InRs:)(A-B)

Remarks

1 SBI 30746215982 31-03-2016 739222.00 31-03-2016 911622.00 -172400.00NOAP

2 SBI 34778931556 31-03-2016 23370752.00 31-03-2016 23332370.00 38382.00NOAP

3 SBI 30889662186 31-03-2016 12662456.00 31-03-2016 12643235.00 19221.00IAP

4 SBI 30889662073 31-03-2016 3662966.00 31-03-2016 3258974.00 403992.00CC ROAD

5 SBI 31715872040 31-03-2016 16731082.00 31-03-2016 16453121.00 277961.00SFC

6 UGB 84013698255 31-03-2016 224500.00 31-03-2016 229454.00 -4954.00SDP

7 SBI 30889662222 31-03-2016 1700383.00 31-03-2016 2373196.00 -672813.00MPLAD

8 SBI 11703064056 31-03-2016 2062422.00 31-03-2016 1901376.00 161046.00BRGF

9 SBI 30546332512 31-03-2016 8224748.00 31-03-2016 8426405.00 -201657.00WODC

10 SBI 11703068051 31-03-2016 2408999.54 31-03-2016 2802678.54 -393679.00THFC

11 SBI 11703064078 31-03-2016 14295484.00 31-03-2016 14627389.00 -331905.00BKBK

12 SBI 31715868352 31-03-2016 15620799.00 31-03-2016 15275833.00 344966.00SC/ST DEV

13 SBI 30809682469 31-03-2016 2742425.00 31-03-2016 2792425.00 -50000.00MO KUDIA

14 SBI 32438824311 31-03-2016 136150.00 31-03-2016 136250.00 -100.00CRF

15 SBI 32842815168 31-03-2016 249853.00 31-03-2016 482593.00 -232740.00ELECTION

16 SBI 11703064001 31-03-2016 2440857.55 31-03-2016 2250857.00 190000.55IAY

17 SBI 33173295504 31-03-2016 407124.00 31-03-2016 388064.00 19060.00PMS

11 / 86

AUDIT REPORT 07-02-2017

18 SBI 31715870870 31-03-2016 6714302.00 31-03-2016 6814402.00 -100100.00MLALAD

19 SBI 11842162236 31-03-2016 3171555.83 31-03-2016 1970798.00 1200757.83MADA

20 SBI 33173264064 31-03-2016 221328.00 31-03-2016 221568.00 -240.00KL

21 SBI 31087730605 31-03-2016 113440.81 31-03-2016 114179.19 -738.38MGNREGS

22 SBI 11703064067 31-03-2016 1819082.00 31-03-2016 1819157.00 -75.00RLTAP

23 SBI 32309533512 31-03-2016 34827.00 31-03-2016 35422.00 -595.00SSA

24 SBI 30746223889 31-03-2016 6038721.00 31-03-2016 6059904.00 -21183.00MDM

25 UGB 12174057937 31-03-2016 6927883.60 31-03-2016 3775232.00 3152651.60Misc

26 SBI 33700118901 31-03-2016 94976.00 31-03-2016 90180.00 4796.00TSC

27 AXIS Bank Bhawnipatna 912010005438261

31-03-2016 981289.04 31-03-2016 1176931.00 -195641.96MDM

28 SBI 32438823260 31-03-2016 1641126.00 31-03-2016 1641226.00 -100.00MADA

29 UGB 12206010111 31-03-2016 4696510.00 31-03-2016 3842865.00 853645.00MADA

30 SBI 32537634485 31-03-2016 17336894.00 31-03-2016 13379517.00 3957377.00MISC

31 SBI 11703063256 31-03-2016 372349.00 31-03-2016 176100.00 196249.00SSAOC

32 SBI 11703063993 31-03-2016 8313350.11 31-03-2016 6773241.20 1540108.91KL

33 SBI 11703068164 31-03-2016 10740.98 31-03-2016 10740.98 0.00RTI

34 UGB 84004369218 31-03-2016 270848.00 31-03-2016 270848.00 0.00IEC

35 SBI 35277326427 31-03-2016 99322.00 31-03-2016 99322.00 0.00NRLM

36 SBI 32438799428 31-03-2016 1351955.00 31-03-2016 1351955.00 0.00IAY

37 SBI 30889662493 31-03-2016 102729.00 31-03-2016 102729.00 0.00TSC

38 SBI 33173292637 31-03-2016 199726.00 31-03-2016 199726.00 0.00HON

39 SBI 33700128374 31-03-2016 1376524.00 31-03-2016 1376524.00 0.00SPF

40 SBI 32695659769 31-03-2016 134587.00 31-03-2016 134587.00 0.00NRLM

41 SBI 32842812860 31-03-2016 542753.00 31-03-2016 542753.00 0.00NFBS

42 SBI 31715869468 31-03-2016 72870.00 31-03-2016 72870.00 0.00NRLM

43 SBI 35274661481 31-03-2016 16411805.00 31-03-2016 16411805.00 0.00GGY

Total 186731717.46 176750424.91 9981292.55

Bank reconciliation

As per G.O. No.690/FIN, Dt.21.01.2009 of Principal Secretary to Govt., Finance Dep't., it has been categorically specified that the Local Authority of the PanchayatSamiti must have to prepare reconciliation statement between Cash Book figure and Pass Book figure at the end of each month. As per GO NO 5352/PR/ 11.02.09BDO should take necessary steps for analysis of cash at his level. Vide letter No 14261/20.05.2014 Para (5) it is clearly mentioned that the DDO concerned shallmake reconciliation of scheme-wise Cash book vis-à-vis scheme-wise bank Pass book & cheque register in the 1st week of every month without fail & a certificate to

12 / 86

AUDIT REPORT 07-02-2017

that effect shall be recorded in the scheme cash book with countersignature of the head of the office (PD DRDA, BDO, DPO, EO etc as cash may be). Similarly, atthe end of the financial year , DDO shall work out & record prominently, at the end of the financial year, DDO shall work out & record prominently, the openingbalance & closing balance of each & individual scheme. The interest accrued in scheme wise bank account should take to concerned scheme cash book. Vide GONO 25357 Dt 11.10.2013 in job chart of accounts officer of Block is communicated. In the job chart of the account officer it is clearly mentioned that he shouldensure certificate by DDO in the 1st week of every month without fail. At the end of the financial year, he shall work out & record prominently, the opening balance &closing balance. But the same procedure has not been adopted in this institution.

The detail of bank reconciliation between bank balance as per cash book and pass book is furnished below:-

1OAP/ODP SBI-30746215982

i. Closing balance as per cash book on dt.31.03.16 911622

ii. Receipt shown in cash book but not deposited in pass book R-39/17.3.16 -172400

Total 739222

iii. Closing balance as per pass book on dt. 31.03.16 739222

2OAP/ODP SBI-34778931556

i. Closing balance as per cash book on dt.31.03.16 23332370

ii. Amount taken less in cash book( cash book R-13/4.8.15 Where,in place ofRs.4109100 taken as Rs.4070100)

39000

Bank charge not reflected on cash book,on dt.12.11.15 -618

Total:- 23370752

Closing balance as per pass book on dt. 31.03.16 23370752

3IAP SBI-30889662186

i. Closing balance as per cash book on dt.31.03.16 12643235

ii. Amount drawn from pass book but not shown in cash book

Lt.No.-2/10.4.15 161630

Lt.No.-24/8.6.15 245415

Lt.No.-59/2.7.15 213606

620651 -620651

iii. Excess payment shown in cash book Where,as per P-42/8.6.15=297818,but drawnfrom pass book Lt.N0.-43/8.6.15=297813

5

iv. Less payment shown in cash book

Where,as per P-117/7.10.15=267022,but drawn from pass bookLt.N0.-120/16.10.15=281218

14196

Where,as per P-89/14.9.15=44676,but drawn from pass bookLt.N0.-92/14.9.15=46138

1462

13 / 86

AUDIT REPORT 07-02-2017

15658 -15658

v. O.B difference 655525

Total:- 12662456

vi. Closing balance as per pass book on dt. 31.03.16 12662456

4C.C ROAD SBI-30889662073

i. closing balance as per cash book on dt.31.03.16 3258974

ii. Amount shown in cash book but not drawn from pass book

p-2/10.04.15 Rs.161630.00 & P.24/08.06.15 Rs.245415.00 407045

p-92/23.02.16 As per Lt.No.90/24.2.16 drawn from pass book Rs.8000 but shown inCash book Rs.5000

-3000

iii. O.B difference -53

Total:- 3662966

iv. Closing balance as per pass book on dt. 31.03.16 3662966

5SFC SBI-31715872040

i. closing balance as per cash book on dt.31.03.16 16453121

ii. Deposited in pass book but not taken in cash book

Interest/25.6.15 251239

iii. Drawn from pass book but not reflected in Cash book

Lt.No.-5/23.3.16 -7000

iv Taken in cash book but not drawn from pass book

Lt.N-5/P-57/23.2.16 2000

v O.B difference 31722

Total:- 16731082

vi. Closing balance as per pass book on dt. 31.03.16 16731082

6SDP SBI-84013698255

i. closing balance as per cash book on dt.31.03.16 229454

ii. Excess receipt taken in Cash book -4924

where same interest taken two times as R-3/31.12.15=Rs.4924 &R-4/31.12.15=Rs.4924

iii. Adjusted from O.B -461995

iv. O.B difference 461965

Total:- 224500

v. Closing balance as per pass book on dt. 31.03.16 224500

7MP.LAD SBI-30889662222

14 / 86

AUDIT REPORT 07-02-2017

i. closing balance as per cash book on dt.31.03.16 2373196

ii. Exces reiceived shown in cash book -360000

Where Rs.1485372 deposited in pass book on dt.31.07.15 but reflected in Cash bookRs.1845372 as R-2 on 31.7.15

iii. Bank charge not reflected in Cash book on dt.28.1.16 -229

iv Lt.No.-5/31.3.16 encashed on dt.4.4.16 35434

v. O.B difference -348018

Total:- 1700383

vi. Closing balance as per pass book on dt. 31.03.16 1700383

8BRGF SBI-11703064056

i. closing balance as per cash book on dt.31.03.16 1901376

ii. Deposited in pass book but not taken in cash book

Cash deposited on dt.20.4.15 40991

iii. O.B difference 12230

iv. Drawn from pass book but not shown in cash book

Lt.No.-55/16.9.15 -24227

Lt.No.-105/26.2.16 -2000

Where as per Adv.No.105/26.2.16 drawn from pass book Rs,3000 but shown in cashbook p-54/26.2.16 Rs.1000

v. Reflected in Cash book but not drawn from pass book

p-43/3.10.15 7500

p52/4.2.16 126552

Total:- 2062422

vi. Closing balance as per pass book on dt. 31.03.16 2062422

9WODC SBI-30546332512

i Closing balance as per cash book on dt.31.03.16 8426405

ii Bank commission not reflected in cash book

30.4.15 -253

1.10.15 -285

16.3.16 -258

16.3.16 -286

iii. Deposited in pass book but not taken in cash book

XFER,DP/25.20.16 19405

iv. Grant/31.3.16 Encashed on dt.4.4.16 -200000

v. O.B difference -19980

Total:- 2802678.54

15 / 86

AUDIT REPORT 07-02-2017

vi. Closing balance as per pass book on dt. 31.03.16 8224748

10THFC SBI-11703068051

i. Closing balance as per cash book on dt.31.03.16 2802678.54

ii. Drawn from pass book but not shown in cash book

Lt.no.-61/16.11.15 -236187

Lt.no.-62/24.11.15 -390057

Lt.No.-63/2.12.15 -23912

iii. Lt.No.-87/31.3.15 encashed on dt.4.4.16 160668

O.B difference 95809

Total:- 2408999.54

iv. Closing balance as per pass book on dt. 31.03.16 2408999.54

11BKBK SBI-11703064078

i. closing balance as per cash book on dt.31.03.16 14627389

ii. Drawn from pass book but not shown in cash book

Lt.No.-43/3.10.15 -7500

Lt.No.-3/4.2.16 -126552

Panchanana Bisoi/19.3.16 -181514

iii. Reflected in Cash book but not drawn from pass book

Lt.No.-55/P-54/16.9.15 drawn from BRGF Cash Book A/c 24277

Lt.No.-137/p-116 encashed on dt.2.4.16 134452

iv. O.B difference -175068

Total:- 14295484

v. Closing balance as per pass book on dt. 31.03.16 14295484

12ST/SC Development SBI-31715868352

i. closing balance as per cash book on dt.31.03.16 15275833

ii. Deposited in pass book but not taken in cash book

Interest on dt.25.12.16 345266

iii. O.B difference -300

Total:- 15620799

iv. Closing balance as per pass book on dt. 31.03.16 15620799

13BPGY SBI-30809682469

i. Closing balance as per cash book on dt.31.03.16 2792425

ii. Drawn from pass book but not shown in cash book

Lt.No.-2367/9.11.15 -125000

Lt.No.-2386/17.11.15 -50000

16 / 86

AUDIT REPORT 07-02-2017

Lt.No.-Pira Majhi/18.11.15 -50000

Lt.No.-2412/20.11.15 drawn on 20.11.15 -125000

Lt.no.-2301/2.11.15 drawn on 02.11.15 -10000

iii. Shown in cash book but not drawn from pass book

P-14/25.5.15(Basanti Rana) P/22.dt.02.06.15 Rs.60000.00, P/23 dt.03.06.15Rs.135000.00

195000

P-95/31.3.16 difference 67863

iv. Shown excess payment in cash book on 31.03.2016 55000

Where two times taken payment as per Lt.No.-1374/18.8.15 on p-94/31.3.16=(-)50000& P-54/18.8.15=(-)50000 Ramesh Majhi/31.3.16 cheque encashed on 4.4.16

50000

vi. Adjusted from O.B(Previous year payment paid during the year 2015-16

J-33475109/4.4.15 450000

J-33475591/4.4.15 825000

vii. O.B difference -1332863

Total:- 2742425

viii. Closing balance as per pass book on dt. 31.03.16 2742425

14CRF SBI-32438824311

i. Closing balance as per cash book on dt.31.03.16 136250

ii. O.B difference -100

Total:- 136150

iii. Closing balance as per pass book on dt. 31.03.16 136150

15ELECTION SBI-32842815168

i. Closing balance as per cash book on dt.31.03.16 482593

ii. Shown in cash book but not deposited in pass book

Same amount taken as receipt two times -232500

ECS-120/26.2.16=232500

& R-6/26.2.16=2325000

iii. O.B difference -240

Total:- 249853

iv. Closing balance as per pass book on dt. 31.03.16 249853

16IAY/FRA SBI-11703064001

i. Closing balance as per cash book on dt.31.03.16 2250857

ii. Cheque issued on 31.3.16 but, encashed during 2016-17 upendra mahanand/2.4.16 10000

Lt.no.-439/2.4.16 180000

17 / 86

AUDIT REPORT 07-02-2017

iii. O.B difference 0.55

Total:- 2440857.55

iv. Closing balance as per pass book on dt. 31.03.16 2440857.55

17PMS SBI-33173295504

Closing balance as per cash book on dt.31.03.16 388064

O.B difference 19060

Total:- 407124

Closing balance as per pass book on dt. 31.03.16 407124

18MLALAD SBI-31715870870

Closing balance as per cash book on dt.31.03.16 6814402

O.B difference (-)100100

Total:- 6714302

Closing balance as per pass book on dt. 31.03.16 6714302

19MADA SBI-11842162236

Closing balance as per cash book on dt.31.03.16 1970798

O.B difference 1355728.83

Drawn from pass books but not reflected in the cash book

Lt No 09/31.12.15 75389

Lt No 11/17.12.15 79582

154971 -154971

Total:- 3171555.83

Closing balance as per pass book on dt. 31.03.16 3171555.83

20KL Grants SBI-33173264064

Closing balance as per cash book on dt.31.03.16 221568

O.B difference -240

Total:- 221328

Closing balance as per pass book on dt. 31.03.16 221328

21MGNREGS SBI-31087730605

Closing balance as per cash book on dt.31.03.16 114179.19

O.B difference -738.38

Total:- 113440.81

Closing balance as per pass book on dt. 31.03.16 113440.81

22RLTAP SBI-11703064067

Closing balance as per cash book on dt.31.03.16 1819157

O.B difference -75

18 / 86

AUDIT REPORT 07-02-2017

Total:- 1819082

Closing balance as per pass book on dt. 31.03.16 1819082

23SSA SBI-32309533512

Closing balance as per cash book on dt.31.03.16 35422

O.B difference -595

Total:- 34827

Closing balance as per pass book on dt. 31.03.16 34827

24MDM SBI-30746223889

Closing balance as per cash book on dt.31.03.16 6059904

O.B difference Cash book 5825413-Pass book 5804230.00 -21183

Total:- 6038721

Closing balance as per pass book on dt. 31.03.16 6038721

25MADA SBI-12174057937

Closing balance as per cash book on dt.31.03.16 3775232

O.B difference Cash book 3506214-Pass book 6658568.60 3152651.6

Total:- 6927883.60

Closing balance as per pass book on dt. 31.03.16 6927883.6

26TSC SBI-33700118901

Closing balance as per cash book on dt.31.03.16 90180

O.B difference Cash book 154145-Pass book 158941.00 4796

Total:- 94976

Closing balance as per pass book on dt. 31.03.16 94976

27MDM Axis bank-912010005438261

Closing balance as per cash book on dt.31.03.16 1176931

O.B difference Cash book 1176931-Pass book 942897.04 -234033.96

bank int not taken to cash book

30.06.15 9403

26.09.15 9184

26.12.15 9589

31.03.16 10216

38392 38392

Total:- 981289.04

Closing balance as per pass book on dt. 31.03.16 981289.04

28MADA SBI-32438823260

Closing balance as per cash book on dt.31.03.16 1641226

19 / 86

AUDIT REPORT 07-02-2017

O.B difference Cash book 1018464-Pass book 707199 -311265

MADA/2015-16/P/2/ 06.04.15 the previous year ob reconciled 311165

Total:- 1641126

Closing balance as per pass book on dt. 31.03.16 1641126

29MADA SBI-12206010111

Closing balance as per cash book on dt.31.03.16 3842865

O.B difference Cash book 3842865-Pass book 4514139 671274

bank int not taken to cash book

03.06.15 89541

31.12.15 92830

182371 182371

Total:- 4696510

Closing balance as per pass book on dt. 31.03.16 4696510

30MADA SBI-32537634485

Closing balance as per cash book on dt.31.03.16 13379517

Grant deposited on 30.03.16 but not reflected in the cash book 3955000

In R-15/30.11.15 the actual deposit in pass book is Rs 18197 but in the cash book asRs 19197

-1000

shown expenditure vide P-108/31.03.16 but not drawn from the pass book till 31.03.16 27289

Recept shown in the cash book vide R-15/30.11.15 -23912

Total:- 17336894

Closing balance as per pass book on dt. 31.03.16 17336894

31Staff salary SBI-11703063256

Closing balance as per cash book on dt.31.03.16 176100

OB difference 196879

Bank charges on 12.03.16 not reflected in the cash book -630

Total:- 372349

Closing balance as per pass book on dt. 31.03.16 372349

32MISC SBI-11703063993

20 / 86

AUDIT REPORT 07-02-2017

Closing balance as per cash book on dt.31.03.16 6773241.2

O.B difference Cash book 21067560.2-Pass book 23016574.11 1949013.91

Deposited in the pass book but not reflected in the cash book

RTGS 31.08.15 43173

DEO,KLD 25.02.16 10000

GPSA PD 16.03.16 9000

62173 62173.00

Shown in the cash book vide P-51/30.11.15 but not drawn from pass book 23912.00

Ch No 876673 drawn on 22.05.15 but not reflected in the cash book -380000.00

Withdrawn from pass book but not reflected in the cash book -114990.00

Total:- 8313350.11

Closing balance as per pass book on dt. 31.03.16 8313350.11

ABSTRCT OF RECONCILIATION

Closing Balance in Bank as mentioned in CashBook

176750424.91

Un reconciled OB 7186002.55

INT NOT TAKEN IN CASH BOOK 812344.00

GRANT /RECEIPT NOT TAKEN IN THE CASHBOOK

3604157.00

BANK CHARGES NOT TAKEN TO CASH BOOK -2559.00

WITHDRAWAL NOT REFLECTED IN THE CASHBOOK

-2848214.00

PAYMENT MADE IN 2015-16 BUT not ENCAHED 31.03.16 386102.00

AMOUNT WRONGLY RAISED IN BANK POSITION IN PROCESS OF RECONCILIATION 843460.00

Closing Balance in Pass Book 186731717.4

Special attention of local authority is drawn on the accounts having negative balance in Pass Book A/c

In course of audit it was noticed that some pass book balances shown in the cash book as on 31.03.16 is are less than the actual amount remain in the pass bookas on 31.03.16. In this case there is apprehension of misappropriation. Local authority is requested to reconcile the following pass book on priority basis as the cashbook balance is more than pass book balance. In failure of which, the matter will be brought to the notice of the higher authorities.

Name of the Bank A/C No. ClosingBalance in

PassBook (In Rs:)

(A)

ClosingBalance in

Bank asmentioned in

CashBook(InRs:) (B)

Difference(In Rs:)(A-B) Remarks

SBI 30746215982 739222.00 911622.00 -172400.00 NOAP

21 / 86

AUDIT REPORT 07-02-2017

UGB 84013698255 224500.00 229454.00 -4954.00 SDP

SBI 30889662222 1700383.00 2373196.00 -672813.00 MPLAD

SBI 30546332512 8224748.00 8426405.00 -201657.00 WODC

SBI 11703068051 2408999.54 2802678.54 -393679.00 THFC

SBI 11703064078 14295484.00 14627389.00 -331905.00 BKBK

SBI 30809682469 2742425.00 2792425.00 -50000.00 MO KUDIA

SBI 32438824311 136150.00 136250.00 -100.00 CRF

SBI 31715870870 6714302.00 6814402.00 -100100.00 MLALAD

SBI 33173264064 221328.00 221568.00 -240.00 KL

SBI 31087730605 113440.81 114179.19 -738.38 MGNREGS

SBI 11703064067 1819082.00 1819157.00 -75.00 RLTAP

SBI 32309533512 34827.00 35422.00 -595.00 SSA

SBI 30746223889 6038721.00 6059904.00 -21183.00 MDM

SBI 32438823260 1641126.00 1641226.00 -100.00 MADA

SBI 1170306325 372349.00 176100.00 -176100.00 SSAOC

AXIS Bank Bhawnipatna 912010005438261

990537.04 1176931.00 -186393.96 MDM

48045275.39 50358308.73 -2313033.34

In response to objection memo no 12/13.10.16 local authority replied that necessary reconciliation will be made & compliance will be produced at the time of exitconference.

in response to objection memo local authority agree to reconcile the same & to produce the compliance at the time of exit conference. But till Exit Conference noreconciliation was made which was brought to the notice of the BDO in course of discussion in the conference . However, BDO assured to take steps after theongoing election process is over. Therefore it is once upon impressed that the reconciliation process be completed within one month and fact reported to audit forbetter appreciation .

Since the local authority has failed to reconcile the negative balance in the Pass Book on priority basis till the end of exit conference the fact was reported toCollector Kalahandi vide this Office Letter No.492/07.02.17 to issue necessary direction to BDO, M.Rampur P.S to reconcile the negative balance on priority basis

22 / 86

AUDIT REPORT 07-02-2017

PARA: 6 STOCK POSITION

M.Rampur P.S - 2015-2016

Slno Material/ Item OpeningBalance

Receipt Issued ClosingBalance As perAudit

As per stockregister

Remarks

Comments

Ref. Memo No.05/27.09.2016 & 09/07.10.16 on idle stock materials

In pursuance to the POM cited above, the local authority directed Asst. Engineer, M.Rampur to conduct physical verification of stock which were remaining in thestock since long in idle condition. . As per direction, the Asst. Engg. had carried out a physical verification on 06.10.16. The result of physical verification isfurnished below.

Slno Material/ Item Closing Balance

As stock register

Actual physicalposition

Difference Rate per unit Total Cost Remarks

1 8MM MS Rod 1.26 0 1.264200 5292 SRP.34

2 MS DOOR 3 3 0.002288 0 SRP 129

3 4X7 DOOR 3 0 3.003172 9516 SRP111

4 3.6X6.6 DOOR 6 6 0.002652 0 SRP104

5 100MM HP 35 11 24.00200 4800 SRP77

6 CHULLAH 252 252 0.00100 0 SRP73

7 ROLLING SHUTTER 2 2 2.005700 11400 SRP15

8 MS WINDOW 4X4 8 8 0.003848 0 SRP124

9 DISPLAY BOARD 35 0 35.00810 28350 SRP117

10 SKY LIGHT 313 192 121.00100 12100 SRP54

11 MS WINDOW 3X4 4 4 0.003016 0 SRP138

12 MSWINDOW 3X4 1 1 0.002912 0 SRP81

Total 71458

As per PSAP rule 65 of PSAP Rules and read with Rule 103 of OGFR , the Block Development Officer and the store-keeper shall be responsible for the custody ofstores and their safety for which necessary arrangement shall be made by the Block Development Officer to keep them in efficient and good condition protectingthem from loss, damage and deterioration.

As per the physical verification, there are two rolling shutters but not in usable condition and 210 nos.of sky lights out of which 18 no are damaged.

Accordingly, as per the aforesaid rules i.e PSAP rule 65 & OGFR rule 103 the persons who have not handed over charges to their successor & subsequently led thestock to deterioration are held responsible for the same.

Necessary steps may be taken to recover the amount from persons responsible as mentioned below

1. Sri Rameswar Majhi, Ex.Head Clerk

2. Sri Dibakar Bag, Sr.Clerk

3.Loknath Das, Ex.Sr.Clerk

Slno Material/ Item Closing Balance Asstock register

Actual physicalposition

Difference Rate per unit Total Cost Person responsible

23 / 86

AUDIT REPORT 07-02-2017

1 8MM MS Rod 1.26 0 1.264200 5292 Rameswar Majhi, EX HC

2 4X7 DOOR 3 0 3.003172 9516 Rameswar Majhi, EX HC

3 DISPLAY BOARD 35 0 35.00810 28350 Rameswar Majhi, EX HC

43158 Rameswar Majhi, EX HCTotal

4 ROLLING SHUTTER 2 2 2.005700 11400 LN Das, EX-Sr. clerk

11400 LN Das, EX-Sr. clerk Total

5 100MM HP 35 11 24.00200 4800 D.Bag, EX-Sr. clerk

6 SKY LIGHT 313 192 121.00100 12100 D.Bag, EX-Sr. clerk

16900 D.Bag, EX-Sr. clerk Total

71458 Grand Total

Further local authority may take suitable steps to utilise the following stocks to avoid further loss.

Slno Material/ Item Closing Balance As stock register Rate per unit Total Cost Remarks

2 MS DOOR 32288 6864 SRP 129

4 3.6X6.6 DOOR 62652 15912 SRP104

6 CHULLAH 252100 25200 SRP73

8 MS WINDOW 4X4 83848 30784 SRP124

11 MS WINDOW 3X4 43016 12064 SRP138

12 MSWINDOW 3X4 12912 2912 SRP81

93736 Total

In response to POM no local authority replied that the defaulter officials will be intimated for recovery & AE has been directed to utilse the stock in good condition indifferent developmental ongoing projects.

Responsible Person for this paragraph

Slno Name Designation Adress Amount(In Rs:)1 RAMESWAR MAJHI, EX

HCEX HEAD-CLERK AT PRESENT

HEAD-CLERK NARLABLOCK DIST KALAHANDI

43158.00

2 Dibakara Bag, Ex-Sr clerk Ex-Sr clerk At present ORS Collectorate Kalahandi

16900.00

3 Lokanath Das, Ex-Sr Clerk Sr clerk At present Sr. Clerk Civilsupply Office, kalahandi

11400.00

24 / 86

AUDIT REPORT 07-02-2017

PARA: 7 INVESTMENT

M.Rampur P.S - 2015-2016 Slno Opening

Balance ofInvestment as on (DD MM YYYY)

OpeningBalance(InRs:)

AmountEncashedduring theYear underAudit(InRs:)

Total(In Rs:) AmountInvested during theYear underAudit(InRs:)

ClosingBalance asper (DD MM YYYY)Audit

ClosingBalanceAudit(InRs:)

ClosingBalance asper (DD MM YYYY)InvestmentLedger

ClosingBalanceInvestmentLedger(InRs:)

Difference(In Rs:)

Remarks

1 01-04-2015 80560.00 0.00 80560.00 0.00 31-03-2016 80560.00 31-03-2016 80560.00 0.00

GRANDTOTAL

80560.00 0.00 80560.00 0.00 80560.00 80560.00 0.00

DETAILS OF CB ON INVESTMENT & Comments :

DETAILS OF CB ON INVESTMENT & COMMENTS:

Details of Investment Position for 2014-15.

1.Panchayat Industry Saw Mill,M.Rampur----50000.00

2.Tribal Dev. Co-operative Society,M.Rampur.---25000.00

3.12 Year N.D.C.-------5560.00

Total---80560.00

No fresh investment was made during the year under audit . It is seen from the last and previous audit report that a sum of Rs80560.00 was invested with the threedifferent organization ,the local authority is requested to make necessary correspondences with the authority where the amount is invested in order to get back theinvested amount along with the amount of dividends accrued there on.

In response to objection memo local authority replied that necessary correspondence has been made with Dist. Co-operative society in this regard vide LetterNo.1653/dated.24.09.16 for necessary action . However, the local authority is advised to peruse and follow till the matter is settled

25 / 86

AUDIT REPORT 07-02-2017

PARA: 8 ADVANCE

M.Rampur P.S - 2015-2016 Slno Advance

Outstandingas on (DD MM YYYY)

CashbookName

AdvanceOutstanding (In Rs:)

AdvancePaid during theYearunderAudit(InRs:)

Total(In Rs:) Advanceadjustedduring theYearunderAudit(InRs:)

AdvanceOutstanding as per(DD MM YYYY)Audit

AdvanceOutstanding Audit(In Rs:)

AdvanceOutstanding as per(DD MM YYYY)CashBook

AdvanceOutstanding CashBook(InRs:)

Difference(In Rs:)

Remarks

1 01-04-2015 govtaccountcash book

20336401.00

31434200.00

51770601.00

4233500.00

31-03-2016

47537101.00

31-03-2016

47537101.00

0.00

2 01-04-2015 PSaccountcash book

3732870.00

104665.00

3837535.00 88665.00 31-03-2016

3748870.00

31-03-2016

3748870.00

0.00

GRAND TOTAL 24069271.00

31538865.00

55608136.00

4322165.00

51285971.00

51285971.00

0.00

Comments :

The cash book wise outstanding advance position furnished below.

Govt account

MDM 5000

NOAP 47270500

STAFF 261601

Total 47537101

PS account

CRF 7918

MGNREGS 36037

TFC 0

NRLM 0

IAY 50000

MISC 3654915

Total 3748870

Grant total 51285971

In last year audit report Rs 30000 outstanding advance not reflected in the outstanding advance position as on 31.03.15. However the same amount has beenadjusted during the year 2015-16.

Year wise break up of outstanding advance

Sl No Year Govt. A/Cs P.S A/Cs Total

1Since inception upto 2010-11 2666013652069.67 3918670.67

22010-11 0 00.00

32011-12 0 00.00

26 / 86

AUDIT REPORT 07-02-2017

42012-13 0 50005000.00

52013-14 659600 0659600.00

62014-15 18392700 3180018424500.00

72015-16 28218200 6000028278200.00

Total 47537101 3748870 51285971

The details of the advance paid during the year 2015-16 & remain unadjusted till 31.03.16 is furnished below.

ADVANCE PAID DURING 2015-16 & REMAIN OUTSTANDING AS ON 31.03.16 (PS Account)

GANESH PRASAD PUHAN

Date Voucher Details Amount

28/12/2015 OWN/2015-16/P/65 ADVANCED TO SRI G.P.PUHAN,CP TOWARDS SHIFTING OF EXISTINGOSWAN ROOM AT DBMFC.Cheque No/DD No.:48 28/12/2015 State Bank of India(11703063993)

10000.00

Total 10000.00

PANCHANAN SUAR

30/11/2015IAY/2015-16/P/140 ADVANCED TO P.SUAR TOWARDS MASON TRAINING. 50000.00

Total 50000.00

Total 60000.00

ADVANCE PAID DURING 2015-16 & REMAIN OUTSTANDING AS ON 31.03.16

BAIBASUTA SAHU

Date Voucher Narration Advance paid

12/06/2015NOAPS/2015-16/P/21 Advance for pension 151300.00

14/08/2015NOAPS/2015-16/P/42 Advance for pension 148800.00

14/09/2015NOAPS/2015-16/P/58 Advance for pension 149700.00

14/10/2015NOAPS/2015-16/P/85 Advance for pension 149700.00

15/01/2016NOAPS/2015-16/P/135 Advance for pension 252200.00

15/03/2016NOAPS/2015-16/P/159 Advance for pension 151800.00

15/07/2015NOAPS/2015-16/P/32 Advance for pension 150900.00

15/11/2015NOAPS/2015-16/P/106 Advance for pension 148500.00

15/12/2015NOAPS/2015-16/P/115 Advance for pension 151800.00

Closing Balance : 1454700.00

BAISAKHU HARIJAN

15/02/2016NOAPS/2015-16/P/146 Advance for pension 151800.00

Closing Balance : 151800.00

BHARATI RANA

12/06/2015NOAPS/2015-16/P/17 Advance for pension 168900.00

14/08/2015NOAPS/2015-16/P/47 Advance for pension 163200.00

14/10/2015NOAPS/2015-16/P/87 Advance for pension 162600.00

15/01/2016NOAPS/2015-16/P/130 Advance for pension 270700.00

27 / 86

AUDIT REPORT 07-02-2017

15/03/2016NOAPS/2015-16/P/170 Advance for pension 162900.00

15/07/2015NOAPS/2015-16/P/28 Advance for pension 162900.00

15/11/2015NOAPS/2015-16/P/97 Advance for pension 161700.00

15/12/2015NOAPS/2015-16/P/109 Advance for pension 162900.00

Closing Balance : 1415800.00

DIBAKARA SAHU

14/10/2015NOAPS/2015-16/P/79 Advance for pension 322000.00

15/01/2016NOAPS/2015-16/P/129 Advance for pension 523000.00

15/03/2016NOAPS/2015-16/P/171 Advance for pension 314200.00

15/11/2015NOAPS/2015-16/P/94 Advance for pension 315400.00

15/12/2015NOAPS/2015-16/P/120 Advance for pension 314200.00

Closing Balance : 1788800.00

FAGUNA GAHIR

14/08/2015 NOAPS/2015-16/P/41 Advance for pension 135700.00

15/02/2016 NOAPS/2015-16/P/150 Advance for pension 185700.00

16/01/2016 NOAPS/2015-16/P/140 PRINTING OF FORMS UNDER OAP. 20000.00

18/03/2016 NOAPS/2015-16/P/174 Advance for pension 36400.00

22/05/2015 NOAPS/2015-16/P/5 DISBURSEMENT OF 1ST PAYMENT. 150600.00

23/11/2015 NOAPS/2015-16/P/107 1ST PAYMENT OF OAP. 118200.00

Closing Balance : 646600.00

GOPAL BIBHAR

15/12/2015 NOAPS/2015-16/P/108Advance for pension 157000.00

Closing Balance : 157000.00

HARISANKAR MISHRA

12/06/2015NOAPS/2015-16/P/13 Advance for pension 145700.00

14/08/2015NOAPS/2015-16/P/50 Advance for pension 144500.00

14/09/2015NOAPS/2015-16/P/67 Advance for pension 144200.00

14/10/2015NOAPS/2015-16/P/81 Advance for pension 144200.00

15/03/2016NOAPS/2015-16/P/163 Advance for pension 142700.00

15/07/2015NOAPS/2015-16/P/37 Advance for pension 146000.00

15/11/2015NOAPS/2015-16/P/99 Advance for pension 142400.00

15/12/2015NOAPS/2015-16/P/116 Advance for pension 142700.00

Closing Balance : 1152400.00

HUTAPATI MAJHI

15/02/2016NOAPS/2015-16/P/151 Advance for pension 259300.00

Closing Balance : 259300.00

JARASANDHA SABAR

12/06/2015NOAPS/2015-16/P/10 Advance for pension 214800.00

14/08/2015NOAPS/2015-16/P/53 Advance for pension 212000.00

15/02/2016NOAPS/2015-16/P/156 Advance for pension 218300.00

15/07/2015NOAPS/2015-16/P/39 Advance for pension 212900.00

28 / 86

AUDIT REPORT 07-02-2017

Closing Balance : 858000.00

JITESH KUMAR TRIPATHY

15/02/2016NOAPS/2015-16/P/145 Advance for pension 162900.00

Closing Balance : 162900.00

KALYAN SAHU

12/06/2015NOAPS/2015-16/P/18 Advance for pension 292200.00

14/08/2015NOAPS/2015-16/P/46 Advance for pension 279600.00

14/09/2015NOAPS/2015-16/P/62 Advance for pension 280500.00

15/02/2016NOAPS/2015-16/P/155 Advance for pension 178300.00

15/07/2015NOAPS/2015-16/P/35 Advance for pension 282300.00

Closing Balance : 1312900.00

KRUSHNA MOHAN DASH

12/06/2015NOAPS/2015-16/P/14 Advance for pension 334000.00

14/08/2015NOAPS/2015-16/P/49 Advance for pension 320500.00

14/09/2015NOAPS/2015-16/P/66 Advance for pension 322000.00

14/10/2015NOAPS/2015-16/P/83 Advance for pension 280500.00

15/01/2016NOAPS/2015-16/P/136 Advance for pension 464800.00

15/02/2016NOAPS/2015-16/P/148 Advance for pension 279600.00

15/03/2016NOAPS/2015-16/P/161 Advance for pension 329600.00

15/07/2015NOAPS/2015-16/P/29 Advance for pension 332500.00

15/11/2015NOAPS/2015-16/P/101 Advance for pension 276900.00

15/12/2015NOAPS/2015-16/P/110 Advance for pension 280500.00

Closing Balance : 3220900.00

LAXMIKANTA MANHIRA

12/06/2015 NOAPS/2015-16/P/23 Advance for pension 191500.00

14/08/2015 NOAPS/2015-16/P/45 Advance for pension 185400.00

14/09/2015 NOAPS/2015-16/P/61 Advance for pension 185700.00

14/10/2015 NOAPS/2015-16/P/76 Advance for pension 185700.00

15/01/2016 NOAPS/2015-16/P/131 Advance for pension 307900.00

15/03/2016 NOAPS/2015-16/P/169 Advance for pension 185700.00

15/07/2015 NOAPS/2015-16/P/27 Advance for pension 186600.00

15/11/2015 NOAPS/2015-16/P/92 Advance for pension 183900.00

15/12/2015 NOAPS/2015-16/P/122 Advance for pension 185700.00

Closing Balance : 1798100.00

MUKESH PUTEL

12/06/2015 NOAPS/2015-16/P/11 Advance for pension 123000.00

14/08/2015 NOAPS/2015-16/P/52 Advance for pension 120600.00

14/09/2015 NOAPS/2015-16/P/69 Advance for pension 119700.00

14/10/2015 NOAPS/2015-16/P/74 Advance for pension 119700.00

15/01/2016 NOAPS/2015-16/P/132 Advance for pension 196300.00

15/02/2016 NOAPS/2015-16/P/152 Advance for pension 118500.00

15/03/2016 NOAPS/2015-16/P/165 Advance for pension 118500.00

15/07/2015 NOAPS/2015-16/P/38 Advance for pension 120900.00

29 / 86

AUDIT REPORT 07-02-2017

15/11/2015 NOAPS/2015-16/P/103 Advance for pension 117900.00

15/12/2015 NOAPS/2015-16/P/111 Advance for pension 118500.00

Closing Balance : 1273600.00

PRAMILA TANDI

14/09/2015NOAPS/2015-16/P/70 Advance for pension 214100.00

14/10/2015NOAPS/2015-16/P/75 Advance for pension 214100.00

15/01/2016NOAPS/2015-16/P/134 Advance for pension 363300.00

15/03/2016NOAPS/2015-16/P/166 Advance for pension 218300.00

15/11/2015NOAPS/2015-16/P/102 Advance for pension 212300.00

15/12/2015NOAPS/2015-16/P/114 Advance for pension 218300.00

Closing Balance : 1440400.00

PARAMESWAR SENAPATI

12/06/2015 NOAPS/2015-16/P/20 Advance for pension 222000.00

15/01/2016 NOAPS/2015-16/P/133 Advance for pension 356700.00

15/02/2016 NOAPS/2015-16/P/153 Advance for pension 214500.00

15/03/2016 NOAPS/2015-16/P/160 Advance for pension 214500.00

15/07/2015 NOAPS/2015-16/P/34 Advance for pension 216900.00

15/12/2015 NOAPS/2015-16/P/112 Advance for pension 214500.00

Closing Balance : 1439100.00

PRASANTA BAGARTY

12/06/2015 NOAPS/2015-16/P/22 Advance for pension 135900.00

14/09/2015 NOAPS/2015-16/P/57 Advance for pension 139000.00

14/10/2015 NOAPS/2015-16/P/88 Advance for pension 139000.00

15/01/2016 NOAPS/2015-16/P/126 Advance for pension 232800.00

15/03/2016 NOAPS/2015-16/P/168 Advance for pension 138400.00

15/07/2015 NOAPS/2015-16/P/25 Advance for pension 140200.00

15/11/2015 NOAPS/2015-16/P/95 Advance for pension 137800.00

15/12/2015 NOAPS/2015-16/P/119 Advance for pension 138400.00

Closing Balance : 1201500.00

RAMKRUSHNA SAHU

12/06/2015NOAPS/2015-16/P/12 Advance for pension 184400.00

14/08/2015NOAPS/2015-16/P/51 Advance for pension 180400.00

14/09/2015NOAPS/2015-16/P/68 Advance for pension 181000.00

14/10/2015NOAPS/2015-16/P/82 Advance for pension 181000.00

15/01/2016NOAPS/2015-16/P/124 Advance for pension 294500.00

15/03/2016NOAPS/2015-16/P/164 Advance for pension 178300.00

15/07/2015NOAPS/2015-16/P/33 Advance for pension 182200.00

15/11/2015NOAPS/2015-16/P/100 Advance for pension 178300.00

15/12/2015NOAPS/2015-16/P/118 Advance for pension 178300.00

Closing Balance : 1738400.00

ROHITA SAHU

12/06/2015 NOAPS/2015-16/P/16 Advance for pension 275900.00

14/08/2015 NOAPS/2015-16/P/48 Advance for pension 260200.00

30 / 86

AUDIT REPORT 07-02-2017

14/09/2015 NOAPS/2015-16/P/64 Advance for pension 261100.00

14/10/2015 NOAPS/2015-16/P/84 Advance for pension 261100.00

15/01/2016 NOAPS/2015-16/P/138 Advance for pension 431100.00

15/03/2016 NOAPS/2015-16/P/162 Advance for pension 259300.00

15/07/2015 NOAPS/2015-16/P/36 Advance for pension 264400.00

15/11/2015 NOAPS/2015-16/P/105 Advance for pension 256600.00

15/12/2015 NOAPS/2015-16/P/113 Advance for pension 259300.00

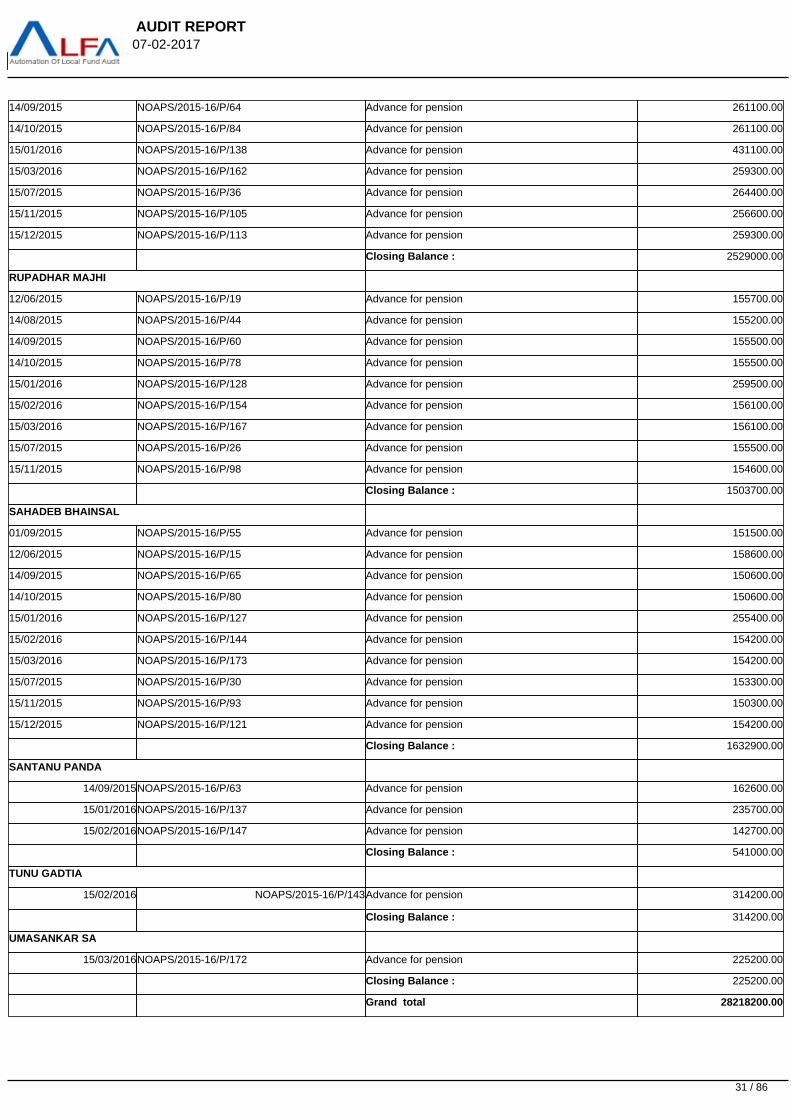

Closing Balance : 2529000.00

RUPADHAR MAJHI

12/06/2015 NOAPS/2015-16/P/19 Advance for pension 155700.00

14/08/2015 NOAPS/2015-16/P/44 Advance for pension 155200.00

14/09/2015 NOAPS/2015-16/P/60 Advance for pension 155500.00

14/10/2015 NOAPS/2015-16/P/78 Advance for pension 155500.00

15/01/2016 NOAPS/2015-16/P/128 Advance for pension 259500.00

15/02/2016 NOAPS/2015-16/P/154 Advance for pension 156100.00

15/03/2016 NOAPS/2015-16/P/167 Advance for pension 156100.00

15/07/2015 NOAPS/2015-16/P/26 Advance for pension 155500.00

15/11/2015 NOAPS/2015-16/P/98 Advance for pension 154600.00

Closing Balance : 1503700.00

SAHADEB BHAINSAL

01/09/2015 NOAPS/2015-16/P/55 Advance for pension 151500.00

12/06/2015 NOAPS/2015-16/P/15 Advance for pension 158600.00

14/09/2015 NOAPS/2015-16/P/65 Advance for pension 150600.00

14/10/2015 NOAPS/2015-16/P/80 Advance for pension 150600.00

15/01/2016 NOAPS/2015-16/P/127 Advance for pension 255400.00

15/02/2016 NOAPS/2015-16/P/144 Advance for pension 154200.00

15/03/2016 NOAPS/2015-16/P/173 Advance for pension 154200.00

15/07/2015 NOAPS/2015-16/P/30 Advance for pension 153300.00

15/11/2015 NOAPS/2015-16/P/93 Advance for pension 150300.00

15/12/2015 NOAPS/2015-16/P/121 Advance for pension 154200.00

Closing Balance : 1632900.00

SANTANU PANDA

14/09/2015NOAPS/2015-16/P/63 Advance for pension 162600.00

15/01/2016NOAPS/2015-16/P/137 Advance for pension 235700.00

15/02/2016NOAPS/2015-16/P/147 Advance for pension 142700.00

Closing Balance : 541000.00

TUNU GADTIA

15/02/2016 NOAPS/2015-16/P/143Advance for pension 314200.00

Closing Balance : 314200.00

UMASANKAR SA

15/03/2016NOAPS/2015-16/P/172 Advance for pension 225200.00

Closing Balance : 225200.00

Grand total 28218200.00

31 / 86

AUDIT REPORT 07-02-2017

As per provision of SR 509 of OTC (volume 1) and Rule 40 & 41 of OPSAP rules 2002 advance to contractors/ executants may be granted as per schemeguidelines and the amount shall be regularly and promptly adjusted within one month. A second advance for any work was also not to be granted unless the firstadvance had been accounted for. Provision under Rule 42 of OPSAP also requires quarterly reviews of the outstanding advances by the DDOs. Rule 14 of OGFRprovides that every officer whose duties to render accounts on returns in respect of public money is responsible for their completeness and strict accuracy. As perthe G.O No. 2221/F dt.7.3.2002 of Govt. in Finance Deptt.Govt. Of Odisha BBSR the advance outstanding for more than one year is treated as a loss to the auditeeinstitution and recoverable. In view of the above facts it is suggested that the above amount is suggested recovery from the advance holder and AdvanceSanctioning Authority on 50:50 basis as per the Letter no-15179/DLFA dt. 28.09.2013 of the Directorate of Local Fund Audit Odisha Bhubaneswar. As on 31.03.16the unadjusted advance out of the advance paid during the year 2014-15 is Rs 18424500 (Govt account 18392700 +PS account 31800). The detail of the same isfurnished below.

Outstanding advance of Govt. A/Cs for the year 2014-15.

Vr. No/Date Name of the Advance Holder Purpose Amount Sanactioning Authority

71/14.8.14 Baibasuta Sahu,GRS OAP/ODP 148200 Khirod Kumar Behera,BDO

93/26.8.14 -do- OAP/ODP 148200 Khirod Kumar Behera,BDO

Total 296400

84/14.8.14 Bharati Rana,GRS OAP/ODP 160500 Khirod Kumar Behera,BDO

98/26.8.14 -do- OAP/ODP 160500 Khirod Kumar Behera,BDO

Total 321000

127/15.11.14 Dinesh Pathak OAP/ODP 258000 Niranjan Nayak,BDO

Total 258000

54/15.7.14 Dusmata Pal OAP/ODP 254500 Khirod Kumar Behera,BDO

70/14.8.14 -do- OAP/ODP 313900 Khirod Kumar Behera,BDO

Total 568400

16/15.4.14 Girish Sabar OAP/ODP 322000 Khirod Kumar Behera,BDO

25/15.5.14 -do- OAP/ODP 313300 Khirod Kumar Behera,BDO

47/13.6.14 -do- OAP/ODP 319600 Khirod Kumar Behera,BDO

67/15.7.14 -do- OAP/ODP 316300 Khirod Kumar Behera,BDO

Total 1271200

34/15.5.14 Gopal Bag OAP/ODP 33000 Khirod Kumar Behera,BDO

46/13.6.14 -do- OAP/ODP 33300 Khirod Kumar Behera,BDO

56/15.7.14 -do- OAP/ODP 151900 Khirod Kumar Behera,BDO

83/14.8.14 -do- OAP/ODP 33300 Khirod Kumar Behera,BDO

101/26.8.14 -do- OAP/ODP 33300 Khirod Kumar Behera,BDO

32 / 86

AUDIT REPORT 07-02-2017

Total 284800

82/14.8.14 Gopal Bibhar OAP/ODP 151300 Khirod Kumar Behera,BDO

88/26.8.14 -do- OAP/ODP 151300 Khirod Kumar Behera,BDO

Total 302600

91/26.8.14 Jarasandha Sabar,PEO OAP/ODP 210300 Khirod Kumar Behera,BDO

121/15.10.14 -do- OAP/ODP 213600 Niranjan Nayak,BDO

136/15.11.14 -do- OAP/ODP 217500 Niranjan Nayak,BDO

142/15.12.14 -do- OAP/ODP 217800 Niranjan Nayak,BDO

Total 859200

105/9.9.14 Jitesh Kumar Tripathy,APO OAP/ODP 114600 Khirod Kumar Behera,BDO

141/15.12.14 -do- OAP/ODP 160800 Niranjan Nayak,BDO

Total 275400

7/15.4.14 Kalyan Sahu OAP/ODP 302800 Khirod Kumar Behera,BDO

27/15.5.14 -do- OAP/ODP 292300 Khirod Kumar Behera,BDO

89/26.8.14 -do- OAP/ODP 313900 Khirod Kumar Behera,BDO

114/15.10.14 -do- OAP/ODP 305200 Niranjan Nayak,BDO

135/15.11.14 -do- OAP/ODP 289300 Niranjan Nayak,BDO

144/15.12.14 -do- OAP/ODP 290800 Niranjan Nayak,BDO

Total 1794300

120/15.10.14 Kanakram Pradhani OAP/ODP 183500 Niranjan Nayak,BDO

134/15.11.14 -do- OAP/ODP 182600 Niranjan Nayak,BDO

151/15.12.14 -do- OAP/ODP 182600 Niranjan Nayak,BDO

Total 548700

80/14.8.14 Krushna Mohan Das,PEO OAP/ODP 347800 Khirod Kumar Behera,BDO

100/26.8.14 -do- OAP/ODP 371500 -do-

119/15.10.14 -do- OAP/ODP 348700 -do-

131/15.11.14 -do- OAP/ODP 326200 Niranjan Nayak,BDO

155/15.12.14 -do- OAP/ODP 337300 Niranjan Nayak,BDO

33 / 86

AUDIT REPORT 07-02-2017

Total 1731500

57/15.7.14 Laxmikanta Manhira OAP/ODP 179700 Khirod Kumar Behera,BDO

72/14.8.14 -do- OAP/ODP 179400 Khirod Kumar Behera,BDO

92/26.8.14 -do- OAP/ODP 179400 Khirod Kumar Behera,BDO

147/15.12.14 -do- OAP/ODP 186900 Niranjan Nayak,BDO

Total 725400

129/15.11.14 Manoj Ku Swain,GPTA OAP/ODP 186900 Niranjan Nayak,BDO

Total 186900

123/15.10.14 Mohan Jani,PEO OAP/ODP 256200 Niranjan Nayak,BDO

132/15.11.14 -do- OAP/ODP 258300 Niranjan Nayak,BDO

153/15.12.14 -do- OAP/ODP 258000 Niranjan Nayak,BDO

Total 772500

73/14.8.14 Mukesh Putel OAP/ODP 116300 Khirod Kumar Behera,BDO

97/26.8.14 -do- OAP/ODP 116300 Khirod Kumar Behera,BDO

112/15.10.14 -do- OAP/ODP 117800 Niranjan Nayak,BDO

137/15.11.14 -do- OAP/ODP 118400 Niranjan Nayak,BDO

152/15.12.14 -do- OAP/ODP 118400 Niranjan Nayak,BDO

Total 587200

143/15.12.14 N.Sahu.BPMO OAP/ODP 149700 Niranjan Nayak,BDO

Total 149700

65/15.7.14 P Senapati OAP/ODP 222000 Khirod Kumar Behera,BDO

85/14.8.14 -do- OAP/ODP 227400 Khirod Kumar Behera,BDO

99/26.8.14 -do- OAP/ODP 227400 Khirod Kumar Behera,BDO

108/15.10.14 -do- OAP/ODP 231300 Niranjan Nayak,BDO

156/15.12.14 -do- OAP/ODP 225600 Niranjan Nayak,BDO

Total 1133700

81/14.8.14 Phaguna Gahir OAP/ODP 210300 Khirod Kumar Behera,BDO

Total 210300

34 / 86

AUDIT REPORT 07-02-2017

76/14.8.14 Prasanta Bagarty,GRS OAP/ODP 143200 Khirod Kumar Behera,BDO

94/26.8.14 -do- OAP/ODP 143200 Khirod Kumar Behera,BDO

145/15.12.14 -do- OAP/ODP 144700 Niranjan Nayak,BDO

Total 431100

125/15.11.14 Rabinarayan Nandi OAP/ODP 150000 Niranjan Nayak,BDO

Total 150000

51/13.6.14 Ramkrushna Sahu OAP/ODP 183500 Khirod Kumar Behera,BDO

62/15.7.14 -do- OAP/ODP 182900 Khirod Kumar Behera,BDO

78/14.8.14 -do- OAP/ODP 181700 Khirod Kumar Behera,BDO

96/26.8.14 -do- OAP/ODP 181700 Khirod Kumar Behera,BDO

Total 729800

42/13.6.14 Rohit Sahu OAP/ODP 254100 Khirod Kumar Behera,BDO

59/15.7.14 -do- OAP/ODP 249000 Khirod Kumar Behera,BDO

74/14.8.14 -do- OAP/ODP 249900 Khirod Kumar Behera,BDO

90/26.8.14 -do- OAP/ODP 249900 Khirod Kumar Behera,BDO

Total 1002900

113/15.10.14 Rupdhar Majhi,PEO OAP/ODP 154300 Niranjan Nayak,BDO

128/15.11.14 -do- OAP/ODP 156100 Niranjan Nayak,BDO

146/15.12.14 -do- OAP/ODP 157300 Niranjan Nayak,BDO

Total 467700

28/15.5.14 Sahadev Bhainsal OAP/ODP 147000 Khirod Kumar Behera,BDO

45/13.6.14 -do- OAP/ODP 152400 Khirod Kumar Behera,BDO

58/15.7.14 -do- OAP/ODP 146400 Khirod Kumar Behera,BDO

75/14.8.14 -do- OAP/ODP 146400 Khirod Kumar Behera,BDO

102/26.8.14 -do- OAP/ODP 146400 Khirod Kumar Behera,BDO

122/15.10.14 -do- OAP/ODP 150900 Niranjan Nayak,BDO

130/15.11.14 -do- OAP/ODP 154200 Niranjan Nayak,BDO

150/15.12.14 -do- OAP/ODP 152700 Niranjan Nayak,BDO

35 / 86

AUDIT REPORT 07-02-2017

Total 1196400

29/15.5.14 Santanu Panda OAP/ODP 134800 Khirod Kumar Behera,BDO

66/15.7.14 -do- OAP/ODP 135100 Khirod Kumar Behera,BDO

77/14.8.14 -do- OAP/ODP 141400 Khirod Kumar Behera,BDO

95/26.8.14 -do- OAP/ODP 141400 Khirod Kumar Behera,BDO

109/15.10.14 -do- OAP/ODP 145600 Niranjan Nayak,BDO

133/15.11.14 -do- OAP/ODP 141700 Niranjan Nayak,BDO

154/15.12.14 -do- OAP/ODP 141700 Niranjan Nayak,BDO

Total 981700

124/15.11.14 Surendra Ku. Parida OAP/ODP 145600 Niranjan Nayak,BDO

Total 145600

37/13.6.14 Thabira Rana OAP/ODP 142900 Khirod Kumar Behera,BDO

Total 142900

40/13.6.14 Tunu Gadtia OAP/ODP 152500 Khirod Kumar Behera,BDO

Total 152500

79/14.8.14 Umasankar Sa OAP/ODP 155900 Khirod Kumar Behera,BDO

103/26.8.14 -do- OAP/ODP 155900 Khirod Kumar Behera,BDO

138/15.11.14 -do- OAP/ODP 164000 Niranjan Nayak,BDO

139/15.11.14 -do- OAP/ODP 38400 Niranjan Nayak,BDO

148/15.12.14 -do- OAP/ODP 162500 Niranjan Nayak,BDO

149/15.12.14 -do- OAP/ODP 38100 Niranjan Nayak,BDO

Total 714800

110/15.10.14 Manoj Ku Swain,GPTA OAP/ODP 100Niranjan Nayak,BDO

Total 100

Grand Total Total 18392700

P.S A/cs outstanding advance for the year 2014-15

Vr. No/date Advance holder PurposeAmount Sanctioning authority

56/29.12.14 Jitendra Kumar Sethy,Driver Fuel 10000Niranjan Nayak,BDO

36 / 86

AUDIT REPORT 07-02-2017

62/24.2.15 Sanjukta Sahu,MI NFSA 21800Niranjan Nayak,BDO

Total 31800

Total 18424500

Ref memo No 02/29.08.16,05/27.09.16

Ref:-POM No 14/14.10.16

In response to POM as mentioned above it was noticed that the undisbursed amount of Rs 758100 was deposited in the bank account during 2016-17 & cashier Srikishor Bishi has received Rs 361200. Local authority may take suitable steps to adjust outstanding advance of Rs 21912600.

VR No. Date Name of the Employee For the period AmountAdvance

AmountDisbursethrough

Acqittance

AmountRefunded

Deposited in bank

Umashankar Sa, PEO 1/2015 194900 180600 14300 on 02.05.16

Umashankar Sa, PEO 2/2015 191600 180600 11000

Umashankar Sa, PEO 3/2015 188600 180600 8000

Umashankar Sa, PEO 4/2015 194900 180600 14300

Umashankar Sa, PEO 5/2015 259200 240800 18400

131/15.01.16 Baibasuta Sahu, GRS 1/2016 252200 234000 18200 on 09.09.16

159/15.03.16 Baibasuta Sahu, GRS 3/2016 151800 141600 10200

71/14.8.14 Baibasuta Sahu, GRS 8/2014 148200 138600 9600on 30.05.16

Hari Shankar Mishra, GRS 6/2015 145700 145500 200 on09.09.16

Hari Shankar Mishra, GRS 7/2015 146000 139100 6900

Hari Shankar Mishra, GRS 8/2015 144500 126700 17800

Hari Shankar Mishra, GRS 9/2015 144200 137500 6700

Hari Shankar Mishra, GRS 10/2015 144200 128300 15900

Hari Shankar Mishra, GRS 11/2015 142400 127400 15000

Hari Shankar Mishra, GRS 12/2015 142700 133600 9100

Hari Shankar Mishra, GRS 3/2016 142700 126900 1580016.09.16

Rohit Kumar Sahu, GRS 1/2016 431100 412500 1860016.09.16

Rohit Kumar Sahu, GRS 3/2016 259300 259200 10016.09.16

Laxmikanta Manhira, GRS 7/2014 179700 168800 10900On 10.08.16

Laxmikanta Manhira, GRS 8/2014 179400 168500 10900On 10.08.16

Laxmikanta Manhira, GRS 6/2015 191500 182100 9400 on 20.08.16

Laxmikanta Manhira, GRS 7/2015 186600 172100 14500

Laxmikanta Manhira, GRS 8/2015 185400 164600 20800

Laxmikanta Manhira, GRS 9/2015 185700 170300 15400

Laxmikanta Manhira, GRS 10/2015 183900 159500 24400

Laxmikanta Manhira, GRS 11/2015 183900 159500 24400

Laxmikanta Manhira, GRS 12/2015 185700 179600 6100

Laxmikanta Manhira, GRS 1/2016 307900 280900 27000

37 / 86

AUDIT REPORT 07-02-2017

Laxmikanta Manhira, GRS 3/2016 185700 165300 20400

Prasanta Ku Bagarty, GRS 7/2015 140200 138500 1700 on 20.08.16

Prasanta Ku Bagarty, GRS 9/2015 139000 137700 1300

Prasanta Ku Bagarty, GRS 10/2015 139000 135000 4000

Prasanta Ku Bagarty, GRS 11/2015 137800 131700 6100

Prasanta Ku Bagarty, GRS 12/2015 138400 138200 200

Prasanta Ku Bagarty, GRS 1/2016 232800 232400 400

Prasanta Ku Bagarty, GRS 3/2016 138400 138300 100

54/15.7.14 Dusmanta Pal, GRS 7/2014 254500 254300 200On 10.08.16

70/14.8.14 Dusmanta Pal, GRS 8/2014 313900 298100 15800On 08.08.16

Sahadev Bhainsal, PEO 1/2015 834300 770400 6390024.06.16

Manoj Ku Swain, GPTA 11/2014 186900 168500 1840028.07.16

Rabinarayan Nandi, JE 11/2014 150000 144300 570028.07.16

Kalyan KU Sahu, PEO 4, 5/2014 595100 545200 49900On 08.08.16

84/14.8.14 Bharati Rana, GRS 8/2014 160500 308700 12300 On 08.08.16

98/26.8.14 Bharati Rana, GRS 9/2014 160500

Bharati Rana, GRS 6,7,8,10,11,12/2015 &1,3/2016

1415800 1326700 89100on 09.09.16

Faguna Gahir, PEO 2/2016 185700 162200 23500on 05.05.16

Baisakhu Harijan, GPTA 2/2016 151800 141000 10800on 09.05.16

Mukesh Putel, PEO 1 to 5/2014 782800 738400 44400on 03.05.16

Mukesh Putel, PEO 1 to 5/2015 612900 596900 16000on 03.05.16

12449900 11691800 758100

received by cashier

Umashankar Sa, PEO 8/2014 155900 151800 4100

Umashankar Sa, PEO 9/2014 155900 144900 11000

Umashankar Sa, PEO 10/2014 193400 191700 1700

Umashankar Sa, PEO 11/2014 202400 183900 18500

Umashankar Sa, PEO 12/2014 200600 180900 19700

Parameswar Senapati, PEO 6/2014 224700 209100 15600

Parameswar Senapati, PEO 7/2014 222000 208900 13100

Parameswar Senapati, PEO 8/2014 227400 219400 8000

Parameswar Senapati, PEO 9/2014 227400 213100 14300

Parameswar Senapati, PEO 12/2014 225600 213900 11700

Parameswar Senapati, PEO 1/2016 356700 344000 12700

Parameswar Senapati, PEO 2/2016 214500 201700 12800

Parameswar Senapati, PEO 3/2016 214500 204900 9600

Parameswar Senapati, PEO 12/2015 214500 207500 7000

Parameswar Senapati, PEO 10/2014 231300 211800 19500

93/26.8.14 Baibasuta Sahu, GRS 9/2014 148200 141000 7200

21/12.06.15 Baibasuta Sahu, GRS 6/2015 151300 150300 1000

32/15.07.15 Baibasuta Sahu, GRS 7/2015 150900 146200 4700

38 / 86

AUDIT REPORT 07-02-2017

42/14.08.15 Baibasuta Sahu, GRS 8/2015 148800 147100 1700

58/14.09.15 Baibasuta Sahu, GRS 9/2015 149700 149200 500

85/14.10.15 Baibasuta Sahu, GRS 10/2015 149700 149400 300

106/15.11.16 Baibasuta Sahu, GRS 11/2015 148500 145500 3000

115/15.12.15 Baibasuta Sahu, GRS 12/2015 151800 143400 8400

Rohit Kumar Sahu, GRS 8/2014 249900 247000 2900

Rohit Kumar Sahu, GRS 9/2014 249900 244900 5000

Rohit Kumar Sahu, GRS 6/2015 275900 274700 1200

Rohit Kumar Sahu, GRS 7/2015 264400 263000 1400