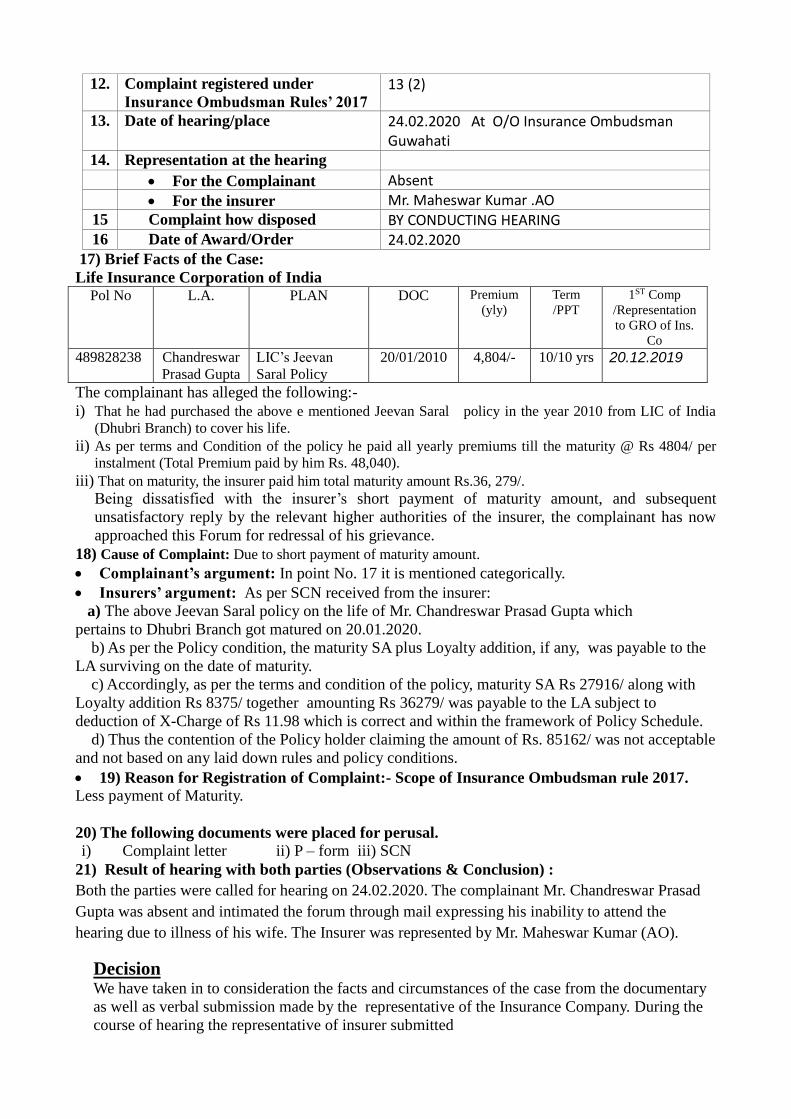

16(1)/17 OF THE INSURANCE OMBUDSMAN RULE 2017) Mr ...

128

Page1 PROCEEDINGS BEFORE - THE INSURANCE OMBUDSMAN, STATE OF UP (UNDER RULE NO: 16(1)/17 OF THE INSURANCE OMBUDSMAN RULE 2017) Mr. Gopal Chandra Sharma……. ………………..……....………………. Complainant V/S Bajaj Allianz Life Insurance Co Ltd..…..…....……………………………Respondent COMPLAINT NO: LCK-L-006-1920-0176 Order No. IO/LCK/A/LI/0431/2019-20 1. Name & Address of the Complainant Mr. Gopal Chandra Sharma Gomti Nagar Lucknow 2. Policy No: Type of Policy Duration of policy/DOC 0027574660, 0034549794 New Unit Gain EasyPension Plus,Capital Unit Gain 28.09.2006, 28.12.2006 3. Name of the insured Name of the policyholder Mr. Gopal Chandra Sharma Mrs. Asha Sharma 4. Name of the insurer Bajaj Allianz Life Insurance Co. Ltd. 5. Date of Repudiation/Rejection - 6. Reason for repudiation/Rejection - 7. Date of receipt of the Complaint - 8. Nature of complaint Payment of Mty and interest thereon 9. Amount of Claim 10. Date of Partial Settlement 11. Amount of relief sought 12. Complaint registered under Rule Rule No. 13(1)(b) of Ins. Ombudsman Rule 2017 13. Date of hearing/place On 28.02.2020 , 10.30 am at Lucknow 14. Representation at the hearing a) For the Complainant Mr. Gopal Chandra Sharma b) For the insurer Mr. Amit Khanna 15. Complaint how disposed Dismissed 16. Date of Award/Order 28.02.2020 17. Mr. Gopal Chandra Sharma (Complainant) has filed a complaint against Bajaj Allianz Life Insurance Co. Ltd. (Respondent) alleging maturity payment not paid and interest on it.

-

Upload

khangminh22 -

Category

Documents

-

view

3 -

download

0

Transcript of 16(1)/17 OF THE INSURANCE OMBUDSMAN RULE 2017) Mr ...

Pag

e1

PROCEEDINGS BEFORE - THE INSURANCE OMBUDSMAN, STATE OF UP

(UNDER RULE NO: 16(1)/17 OF THE INSURANCE OMBUDSMAN RULE 2017)

Mr. Gopal Chandra Sharma……. ………………..……....………………. Complainant

V/S

Bajaj Allianz Life Insurance Co Ltd..…..…....……………………………Respondent

COMPLAINT NO: LCK-L-006-1920-0176 Order No. IO/LCK/A/LI/0431/2019-20

1. Name & Address of the Complainant Mr. Gopal Chandra Sharma

Gomti Nagar

Lucknow

2. Policy No:

Type of Policy

Duration of policy/DOC

0027574660, 0034549794

New Unit Gain EasyPension Plus,Capital

Unit Gain

28.09.2006, 28.12.2006

3. Name of the insured

Name of the policyholder

Mr. Gopal Chandra Sharma

Mrs. Asha Sharma

4. Name of the insurer Bajaj Allianz Life Insurance Co. Ltd.

5. Date of Repudiation/Rejection -

6. Reason for repudiation/Rejection -

7. Date of receipt of the Complaint -

8. Nature of complaint Payment of Mty and interest thereon

9. Amount of Claim

10. Date of Partial Settlement

11. Amount of relief sought

12. Complaint registered under Rule Rule No. 13(1)(b) of Ins. Ombudsman Rule

2017

13. Date of hearing/place On 28.02.2020 , 10.30 am at Lucknow

14. Representation at the hearing

a) For the Complainant Mr. Gopal Chandra Sharma

b) For the insurer Mr. Amit Khanna

15. Complaint how disposed Dismissed

16. Date of Award/Order 28.02.2020

17. Mr. Gopal Chandra Sharma (Complainant) has filed a complaint against Bajaj Allianz Life

Insurance Co. Ltd. (Respondent) alleging maturity payment not paid and interest on it.

Pag

e2

MS

COMPLAINT NO: LCK-L-006-1920-0176 Order No. IO/LCK/A/LI/ 0431/2019-20

Brief Facts of the Case:-

18. Mr. Gopal Chandra Sharma has lodged his complaint stating that he had two policies with

Bajaj Alianz Life Insurance Co. Ltd. He has deposited total one premium only under the policies.

He visited RIC`s office to know about his policies. They gave him account statement and

assured him more benefits even if he did not deposit premiums. As he was not in a position to

deposit renewal premiums, he waited till maturity. On maturity, company has not replied his

letters. Nothing was heard from them. The complainant initially lodged his complaint for

maturity payment but when amount was received by him, he claimed for interest of his deposit

money under the policies. Being aggrieved, the complainant approached this forum for the

redressal of his grievance.

Written reply/SCN:-

19. In their SCN/reply , the RIC has stated in their mail to the complainant with c.c. to us that

they have cancelled the policies since inception and amount was paid to the complainant

through cheque on 06.08.2010 for Rs. 10667/= and rest amount through NEFT on 22.01.2019

and 28.01.2019. Detailed SCN was not received.

20. The complainant has filed a complaint letter, annexure VI A, correspondence with respondent

while respondent has not filed SCN with enclosures.

21. I have heard the complainant as well as respondent representative and perused the record.

Findings:-

22. Admittedly the complainant had taken 2 policies with an annual premium of Rs. 30,000/- and

Rs. 51,000 with commencement date 28.09.2016 respectively. One premium was paid thereafter

due to personal reasons complainant did not continue with the policy. He approached the

respondent and other officers in the government of India. Complainant received the refund of his

Pag

e3

amount in the month of January, 2019 but without any interest. Accordingly he has prayed for

interest on the deposited amount.

COMPLAINT NO: LCK-L-006-1920-0176 Order No. IO/LCK/A/LI/ 0431/2019-20

23. As per the respondent following were made:-

Policy No.

Voucher No. Bank Name

Payment

Mode

Cheque

No.

Amount

Cheque

Date

Payment

Date

0027574660 1260123 UTI Bank Ltd Cheque 233365 10667 6/8/2010 6/8/2010

Policy No.

Payment Type Bank Name

Account No.

UTR Amoun

t

Payment

Date

Payment

Mode

0027574660 CI UCO Bank 16540100002846 SIN00101Q4949371 19333 22/01/2019 NEFT

Policy No.

Payment Type Bank Name

Account No.

UTR Amount

Payment

Date

Payment

Mode

0034549794 CI UCO Bank 16540100002846 SIN00101Q4967948 51000 28/01/2019 NEFT

24. Now it is to be looked into as to whether the complainant entitled for any interest on the

amount refunded by the respondent.

25. Admittedly only one premium was paid by the complainant thereafter he discontinued the

policy. The payment was made treating the policies cancelled since inception. Policies were not

revivable. In such circumstances since policies itself got cancelled since inception although

amount remained with the respondent but the complainant cannot claim any interest on the

premium amount. Refund of premium amount itself is a good gesture from the respondent. In

such circumstances complaint is liable to be dismissed.

Order:-

26. Complaint is dismissed.

Pag

e4

COMPLAINT NO: LCK-L-006-1920-0176 Order No. IO/LCK/A/LI/ 0431 /2019-20

27. Let the copy of award be given to both the parties.

Date: 28.02.2020 Justice Anil Kumar Srivastava

Place: Lucknow (Insurance Ombudsman)

PROCEEDINGS BEFORE - THE INSURANCE OMBUDSMAN, LUCKNOW

(UNDER RULE NO: 16(1)/17 OF THE INSURANCE OMBUDSMAN RULE 2017)

Mr. Chandra Datta..……....………………………………………………………. Complainant

V/S

L.I.C. of India……..…...……………..……………………..………..…..………...Respondent

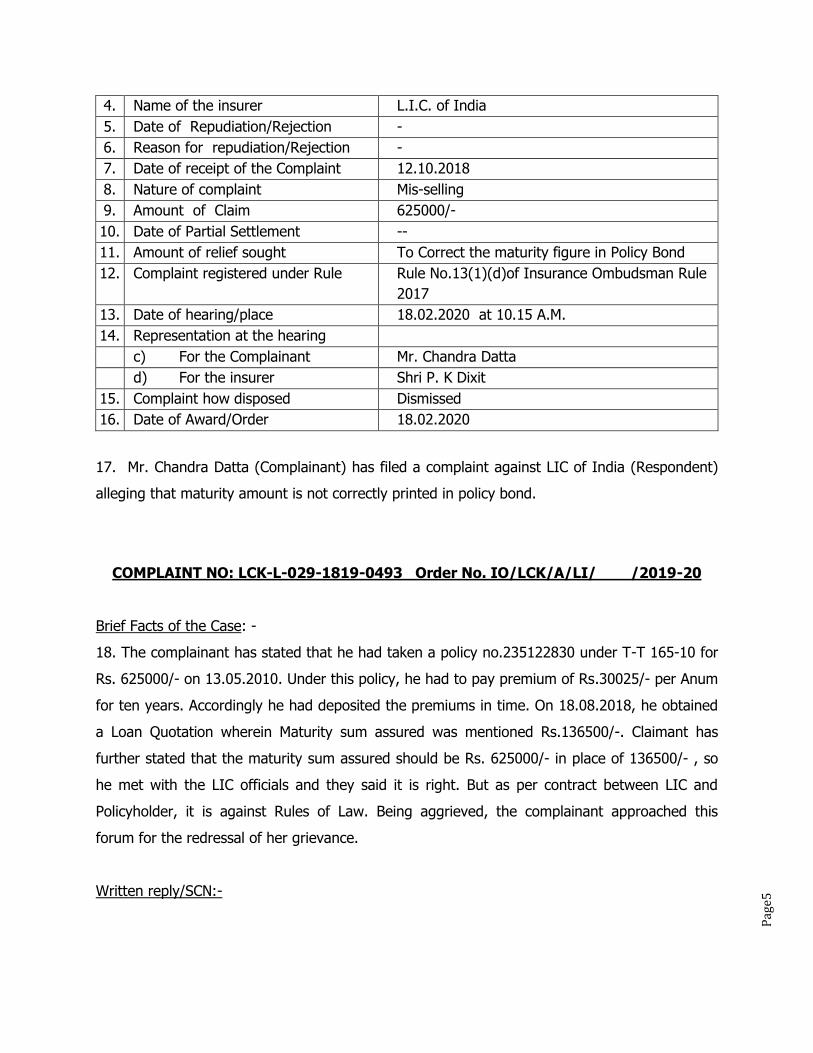

COMPLAINT NO: LCK-L-029-1819-0493 Order No. IO/LCK/A/LI/0377/2019-20

1. Name & Address of the Complainant Mr. Chandra Datta

M-22 , Indra Nagar

Kanpur -208026

2. Policy No:

Type of Policy

DOC /DOR

DOD

Duration of policy

235122830

Jeevan Saral

26.04.2010

--

10 years

3. Name of the insured

Name of the policyholder

Mr. Chandra Datta

Mr. Chandra Datta

Pag

e5

4. Name of the insurer L.I.C. of India

5. Date of Repudiation/Rejection -

6. Reason for repudiation/Rejection -

7. Date of receipt of the Complaint 12.10.2018

8. Nature of complaint Mis-selling

9. Amount of Claim 625000/-

10. Date of Partial Settlement --

11. Amount of relief sought To Correct the maturity figure in Policy Bond

12. Complaint registered under Rule Rule No.13(1)(d)of Insurance Ombudsman Rule

2017

13. Date of hearing/place 18.02.2020 at 10.15 A.M.

14. Representation at the hearing

c) For the Complainant Mr. Chandra Datta

d) For the insurer Shri P. K Dixit

15. Complaint how disposed Dismissed

16. Date of Award/Order 18.02.2020

17. Mr. Chandra Datta (Complainant) has filed a complaint against LIC of India (Respondent)

alleging that maturity amount is not correctly printed in policy bond.

COMPLAINT NO: LCK-L-029-1819-0493 Order No. IO/LCK/A/LI/ /2019-20

Brief Facts of the Case: -

18. The complainant has stated that he had taken a policy no.235122830 under T-T 165-10 for

Rs. 625000/- on 13.05.2010. Under this policy, he had to pay premium of Rs.30025/- per Anum

for ten years. Accordingly he had deposited the premiums in time. On 18.08.2018, he obtained

a Loan Quotation wherein Maturity sum assured was mentioned Rs.136500/-. Claimant has

further stated that the maturity sum assured should be Rs. 625000/- in place of 136500/- , so

he met with the LIC officials and they said it is right. But as per contract between LIC and

Policyholder, it is against Rules of Law. Being aggrieved, the complainant approached this

forum for the redressal of her grievance.

Written reply/SCN:-

Pag

e6

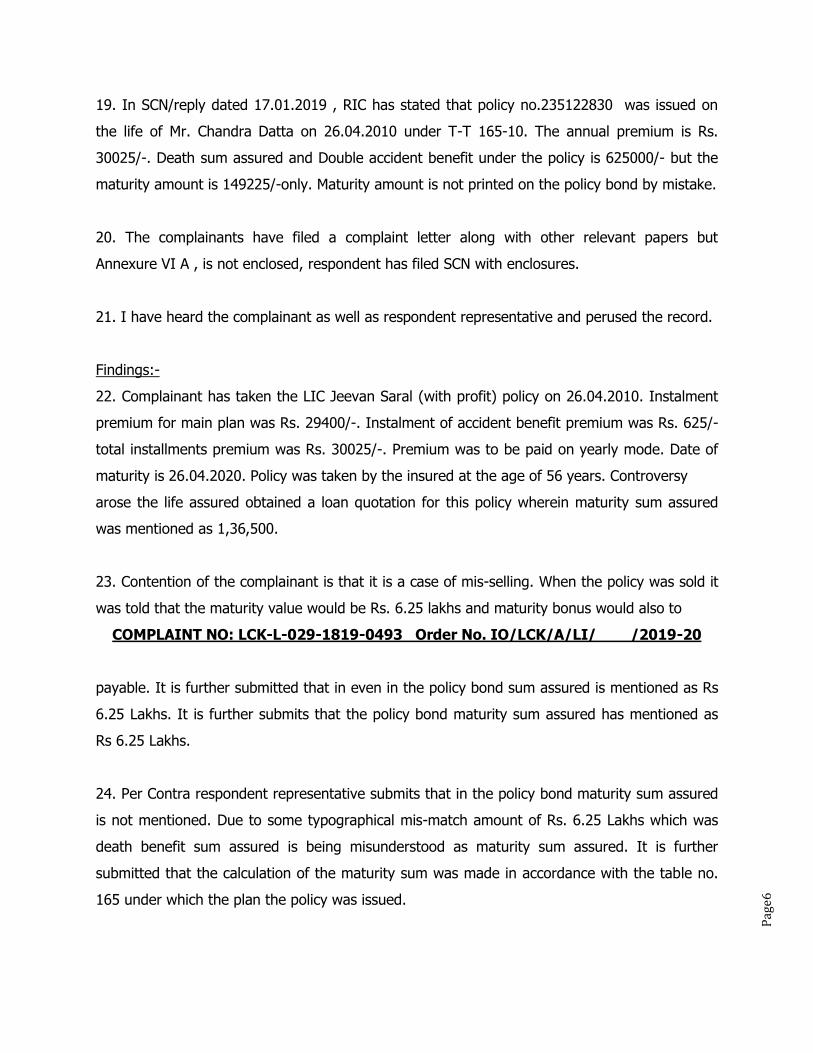

19. In SCN/reply dated 17.01.2019 , RIC has stated that policy no.235122830 was issued on

the life of Mr. Chandra Datta on 26.04.2010 under T-T 165-10. The annual premium is Rs.

30025/-. Death sum assured and Double accident benefit under the policy is 625000/- but the

maturity amount is 149225/-only. Maturity amount is not printed on the policy bond by mistake.

20. The complainants have filed a complaint letter along with other relevant papers but

Annexure VI A , is not enclosed, respondent has filed SCN with enclosures.

21. I have heard the complainant as well as respondent representative and perused the record.

Findings:-

22. Complainant has taken the LIC Jeevan Saral (with profit) policy on 26.04.2010. Instalment

premium for main plan was Rs. 29400/-. Instalment of accident benefit premium was Rs. 625/-

total installments premium was Rs. 30025/-. Premium was to be paid on yearly mode. Date of

maturity is 26.04.2020. Policy was taken by the insured at the age of 56 years. Controversy

arose the life assured obtained a loan quotation for this policy wherein maturity sum assured

was mentioned as 1,36,500.

23. Contention of the complainant is that it is a case of mis-selling. When the policy was sold it

was told that the maturity value would be Rs. 6.25 lakhs and maturity bonus would also to

COMPLAINT NO: LCK-L-029-1819-0493 Order No. IO/LCK/A/LI/ /2019-20

payable. It is further submitted that in even in the policy bond sum assured is mentioned as Rs

6.25 Lakhs. It is further submits that the policy bond maturity sum assured has mentioned as

Rs 6.25 Lakhs.

24. Per Contra respondent representative submits that in the policy bond maturity sum assured

is not mentioned. Due to some typographical mis-match amount of Rs. 6.25 Lakhs which was

death benefit sum assured is being misunderstood as maturity sum assured. It is further

submitted that the calculation of the maturity sum was made in accordance with the table no.

165 under which the plan the policy was issued.

Pag

e7

25. No doubt policy was issued under the approval of IRDA. As per the circular no.

ACTL/1934/4 of the LIC the plan in question was issued under the table no. 165 wherein the

basic core factor is that it provides to the policy holder high risk covered with a smooth return,

Liquidity and lots of flexibility. It is also provided in the plan in conventional products premium

rates are given per 1000/- sum assured for different entry ages and terms. Under this product

death cover will be same irrespective of at entry and term but the sum payable at maturity will

differ for different entry ages and terms. This policy also provides for loyalty additions. Loyalty

additions will be declared after the policy has been in full form for at least 10 years. On Maturity

the life insured will get the maturity sum assured plus loyalty addition if any.

26. The only point to be looked into is as to whether the complainant take an advantage of

non- mentioning of maturity sum assured in the policy bond. We can read the bond and find

that 2 sums are mentioned in the policy bond which is Rs 6.25 Lakhs each. They are meant for

death benefit sum assured under main plan and accident benefit sum assured. Column relating

to maturity sum assured is lying vacant. When nothing is printed in this column how it would be

presumed that it was Rs 6.25 Lakhs? Policy bond was generated through computer and the

entries are made on a printed form. Little mis-match that is printing of an amount of Rs 6.25

Lakhs on a higher side with a few millimeters difference cannot extend a benefit or right to the

complainant. It is settled legal position that a party cannot take the advantage of a printing or

typographical error in the agreement. A presumption cannot be raised in favor of the

COMPLAINT NO: LCK-L-029-1819-0493 Order No. IO/LCK/A/LI/0377/2019-20

complainant. It is more important that the basic features of table no. 165 are in public domain.

In that situation it cannot be accepted that any mis-selling was done with the complainant who

himself is a retired employee.

27. Accordingly I am of the view that the payment of Rs. 149225/- was offered by the

respondent LIC to the complainant in accordance with the terms and conditions of the policy

bond which is justifiable. It doesn‟t require any interference. Accordingly complaint is liable to

be dismissed.

Pag

e8

Order:-

28. Complaint is dismissed.

29. Let the copy of award be given to both the parties.

Date: 18.02.2020 (Justice Anil Kumar Srivastava)

Place: Lucknow Insurance Ombudsman

PROCEEDINGS BEFORE - THE INSURANCE OMBUDSMAN, STATE OF UP

(UNDER RULE NO: 16(1)/17 OF THE INSURANCE OMBUDSMAN RULE 2017)

Mr. Lal Sahab Yadav………………..……....………………………….………. Complainant

V/S

Bajaj Alianz Life Insurance Co. Ltd……....................…………………………Respondent

COMPLAINT NO: LCK-L-006-1819-0001 Order No. IO/LCK/A/LI/ 0387/2019-20

1. Name & Address of the Complainant Mr. Lal Sahab Yadav,

Chota Baghara,

Allahabad

2. Policy No:

Type of Policy

Duration of policy/DOC

0078806501

-

Matured

3. Name of the insured

Name of the policyholder

Mr.Lal Sahab Yadav

Mr. Lal Sahab Yadav

Pag

e9

4. Name of the insurer Bajaj Alianz Life Insurance Co. Ltd.

5. Date of Repudiation/Rejection -

6. Reason for repudiation/Rejection -

7. Date of receipt of the Complaint 03.04.2018

8. Nature of complaint Maturity amount less paid

9. Amount of Claim Rs.25,000/=

10. Date of Partial Settlement Rs.16915/=

11. Amount of relief sought Balance amount with interest

12. Complaint registered under Rule Rule No. 13(1)(b) of Ins. Ombudsman

Rule 2017

13. Date of hearing/place On 20.02.2020 at 10.30 am at

Lucknow

14. Representation at the hearing

a) For the Complainant Absent

b) For the insurer Mr. Amit Khanna

15. Complaint how disposed Dismissed

16. Date of Award/Order 20.02.2020

17. Mr. Lal Sahab Yadav (Complainant) has filed a complaint against Bajaj Alianz Life

Insurance Co. Ltd. (Respondent) alleging that less maturity amount was paid to him.

YKS

COMPLAINT NO: LCK-L-006-1819-0001 Order No. IO/LCK/A/LI/ /2019-20

Brief Facts of the Case:-

18. Mr. Lal Sahab Yadav has lodged his complaint on 03.04.2018 stating that he has

received less amount of maturity. The complainant has stated that he had deposited

Rs.25000/= as single premium for 10 years as per terms of policy but on maturity he

received less amount. He has received only Rs.16915/= against Rs. 25,000/=

deposited by him for 10 years. He approached RIC but was not satisfied. Being

aggrieved he has approached this forum for the redressal of his grievance.

Pag

e10

Written reply/SCN:-

19. In their SCN/reply the RIC has stated that total amount payable under the policy

has been paid to the complainant and no amounts are due or payable in any manner.

It is submitted that being an advocate himself, the complainant was able to assess the

terms and conditions of the said policy, which was unit linked, the details of charges in

respect of the said policy have been clearly provided therein. Single premium amount

was fully invested in the Equity Index Fund II as per the proposal form, the same was

allocated accordingly and on maturity the fund value, as on the date of maturity, was

paid to the complainant.

20. The complainant has filed a complaint letter, annexure VI A, correspondence with

respondent while respondent has filed SCN with enclosures.

21. Despite notice complainant is not present. I have heard the respondent

representative and perused the record.

Findings:-

22. Complainant has taken a policy “Bajaj Alliance New Unit Gain Plus-SP” dated

18.12.2007 where in one single premium of Rs. 25,000/- was paid. Sum Assured was

Rs. 1,25,000/-. On maturity complainant received only Rs. 16915/- on 05.01.2018.

23. Respondent submits that it was a „Unit Link Policy‟ wherein the maturity value was

to be calculated in accordance with the NAV. The fund value was paid as was existing

on the date of maturity. The single premium amount was equity index fund-II.

Payment was made in

COMPLAINT NO: LCK-L-006-1819-0001 Order No. IO/LCK/A/LI/ 0387/2019-20

accordance with the terms and conditions of the policy bond. I do not find any merit in

the complaint which is liable to be dismissed.

Pag

e11

Order:-

24. Complaint is dismissed.

25. Let the copy of award be given to both the parties.

Date: 20.02.2020 (Justice Anil Kumar Srivastava)

Place: Lucknow Insurance Ombudsman

PROCEEDINGS BEFORE - THE INSURANCE OMBUDSMAN, STATE OF UP

(UNDER RULE NO: 16(1)/17 OF THE INSURANCE OMBUDSMAN RULE 2017)

Dr. Dingur Mal Mishra…………. ………………..……....………………. Complainant

V/S

Life Insurance Corp. of India…………………....…....…………………………Respondent

COMPLAINT NO: LCK-L-029-1819-0457 Order No. IO/LCK/A/LI/ 0354/2019-20

1. Name & Address of the Complainant Dr. Dingur Mal Mishra

Civil Lines

Sultanpur

2. Policy No:

Type of Policy

Duration of policy/DOC

236794052

Wealth Plus

08.05.2010

3. Name of the insured

Name of the policyholder

Dr. Dingur Mal Mishra

Dr. Dingur Mal Mishra

4. Name of the insurer Life Insurance Corp. of India

5. Date of Repudiation/Rejection -

6. Reason for repudiation/Rejection -

7. Date of receipt of the Complaint 06.11.2018

8. Nature of complaint Maturity Amount less paid

Pag

e12

9. Amount of Claim

10. Date of Partial Settlement

11. Amount of relief sought

12. Complaint registered under Rule Rule No. 13(1)(b) of Ins. Ombudsman Rule

2017

13. Date of hearing/place On 14.02.2020 , 10.30 am at Lucknow

14. Representation at the hearing

a) For the Complainant Absent

b) For the insurer Mr. Heera Singh

15. Complaint how disposed Dismissed

16. Date of Award/Order 14.02.2020

17. Dr. Dingur Mal Mishra (Complainant) has filed a complaint against Life Insurance Corp. of

India (Respondent) alleging that less amount was paid on maturity.

MS

COMPLAINT NO: LCK-L-029-1819-0457 Order No. IO/LCK/A/LI/ /2019-20

Brief Facts of the Case:-

18. Dr. Dingur Mal Mishra has lodged his complaint on 06.11.2018 stating that less amount was

paid by the Life Ins. Corp. of India on maturity of his policy. The complainant has stated that he

deposited Rs.75000/= as single premium for 8 years but on maturity of the said policy he

received only Rs.75969 /= as maturity amount of the policy. He further stated that at proposal

stage agent assured him to get highest NAV for policy period. The complainant has written

many letters for receiving less payment but he received no response from RIC. The complainant

was not satisfied. Being aggrieved he has approached this forum for the redressal of his

grievance.

Written reply/SCN:-

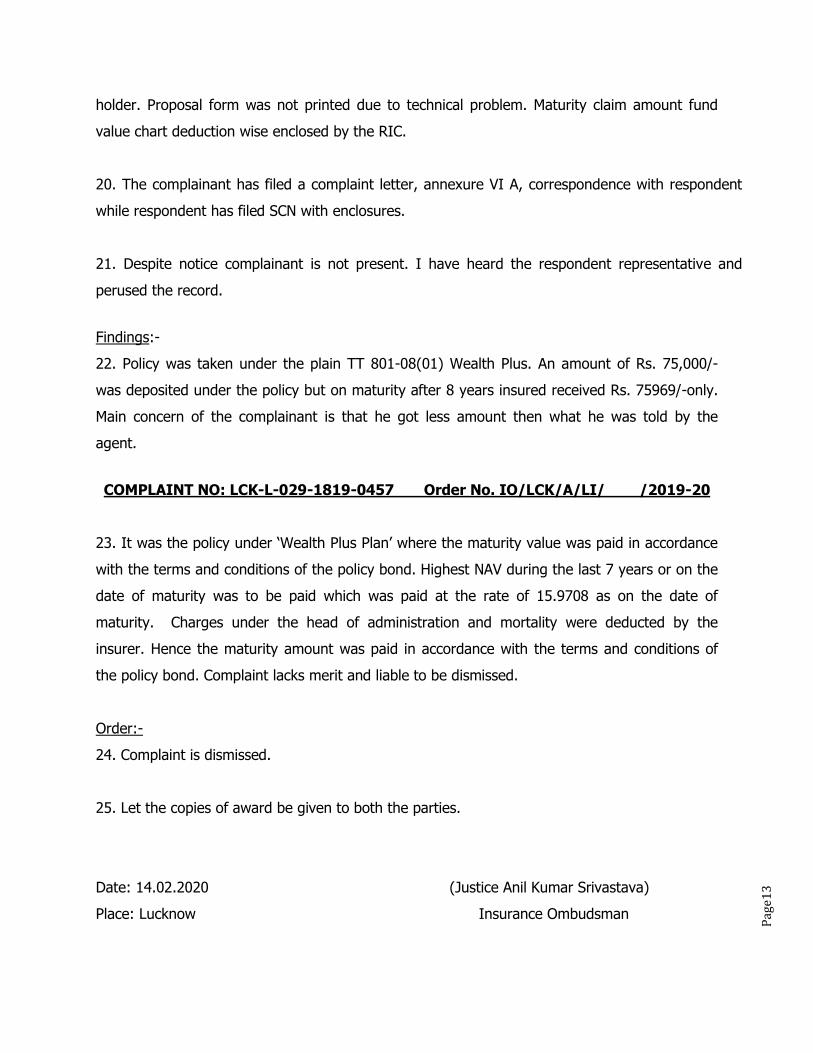

19. In their SCN/reply, the RIC has stated that the company has received complaint on

06.12.2018 regarding maturity payment of „wealth Plus policy‟. AS per terms and conditions of

the policy, risk premium was chargeable every month, and at the time of proposal the age of

the complainant was 60 years. There is two years extended life cover under this policy after

completion of policy term. After deduction as per rules maturity amount was paid to the policy

Pag

e13

holder. Proposal form was not printed due to technical problem. Maturity claim amount fund

value chart deduction wise enclosed by the RIC.

20. The complainant has filed a complaint letter, annexure VI A, correspondence with respondent

while respondent has filed SCN with enclosures.

21. Despite notice complainant is not present. I have heard the respondent representative and

perused the record.

Findings:-

22. Policy was taken under the plain TT 801-08(01) Wealth Plus. An amount of Rs. 75,000/-

was deposited under the policy but on maturity after 8 years insured received Rs. 75969/-only.

Main concern of the complainant is that he got less amount then what he was told by the

agent.

COMPLAINT NO: LCK-L-029-1819-0457 Order No. IO/LCK/A/LI/ /2019-20

23. It was the policy under „Wealth Plus Plan‟ where the maturity value was paid in accordance

with the terms and conditions of the policy bond. Highest NAV during the last 7 years or on the

date of maturity was to be paid which was paid at the rate of 15.9708 as on the date of

maturity. Charges under the head of administration and mortality were deducted by the

insurer. Hence the maturity amount was paid in accordance with the terms and conditions of

the policy bond. Complaint lacks merit and liable to be dismissed.

Order:-

24. Complaint is dismissed.

25. Let the copies of award be given to both the parties.

Date: 14.02.2020 (Justice Anil Kumar Srivastava)

Place: Lucknow Insurance Ombudsman

Pag

e14

PROCEEDINGS BEFORE - THE INSURANCE OMBUDSMAN, LUCKNOW

(UNDER RULE NO: 16(1)/17 OF THE INSURANCE OMBUDSMAN RULE 2017)

Mrs. Urmila Tripathi..……...............................................………………. Complainant

V/S

L.I.C. of India……..…...……………..………………….…..………..…..………...Respondent

COMPLAINT NO: LCK-L-029-1819-0494 Order No. IO/LCK/A/LI/ 0384/2019-20

1. Name & Address of the Complainant Mrs. Urmila Tripathi

M-22 , Indra Nagar

Kanpur -208026

2. Policy No:

Type of Policy

DOC /DOR

DOD

Duration of policy

235123064

Jeevan Saral

27.04.2010

--

10 years

3. Name of the insured

Name of the policyholder

Mrs. Urmila Tripathi

Mrs. Urmila Tripathi

4. Name of the insurer L.I.C. of India

5. Date of Repudiation/Rejection -

6. Reason for repudiation/Rejection -

7. Date of receipt of the Complaint 03.12.2018

8. Nature of complaint Mis-selling

9. Amount of Claim 625000/-

10. Date of Partial Settlement --

11. Amount of relief sought To Correct the maturity figure in Policy Bond

12. Complaint registered under Rule Rule No.13(1)(d)of Insurance Ombudsman Rule

2017

13. Date of hearing/place 18.02.2020 at 10.15 A.M.

14. Representation at the hearing

e) For the Complainant Shri Chandra Datta

f) For the insurer Shri P K Dixit

Pag

e15

15. Complaint how disposed Dismissed

16. Date of Award/Order 18.02.2020

17. Mrs. Urmila Tripathi Complainant) has filed a complaint against LIC of India (Respondent)

alleging that maturity amount is not correctly printed in policy bond.

COMPLAINT NO: LCK-L-029-1819-0494 Order No. IO/LCK/A/LI/ /2019-20

Brief Facts of the Case: -

18. The complainant has stated that she had taken a policy no.235123064 under T-T 165-10 for

Rs. 625000/- on 13.05.2010. Under this policy, she had to pay premium of Rs.30025/- per

annum for ten years. Accordingly she had deposited the premiums in time. On 18.08.2018, she

obtained a Loan Quotation wherein Maturity sum assured was mentioned as Rs.1,65,650/-.

The complainant has further stated that the maturity sum assured should be Rs. 6,25,000/- in

place of 1,65,650/-, so she met with the LIC officials and they said it is right. But as per

contract between LIC and Policyholder, it is against Rules of Law. Being aggrieved, the

complainant approached this forum for the redressal of her grievance.

Written reply/SCN:-

19. In SCN/reply dated 17.01.2019 , RIC has stated that policy no.235123064 was issued on

the life of Mrs. Urmila Tripathi on 27.04.2010 under T-T 165-10. The annual premium is Rs.

30025/-. Death sum assured and Double accident benefit under the policy is 625000/- but the

maturity amount is 1,85,200/-only. Maturity amount is not printed on the policy bond by

mistake.

20. The complainants have filed a complaint letter along with other relevant papers but

Annexure VI A, is not enclosed, respondent has filed SCN with enclosures.

21. I have heard the complainant as well as respondent representative and perused the record.

Pag

e16

Findings:-

22. Complainant has taken the LIC Jeevan Saral (with profit) policy on 27.04.2010. Installments

premium for main plan was Rs. 29,400/- while instalments accident benefit premium was Rs.

625/- total installments premium was Rs. 30025/-. Premium was to be paid on yearly mode.

Date of maturity was 27.04.2020. Policy was taken by the insured at the age of 53 years.

23. Controversy arose when the life assured obtained a loan quotation from LIC Branch wherein

Maturity Sum Assured was mentioned as 1,65,650/-. Contention of the complainant is that it is

COMPLAINT NO: LCK-L-029-1819-0494 Order No. IO/LCK/A/LI/ /2019-20

a case of mis-selling. When the policy was sold it was told with the sum assured and the

maturity value would be Rs. 6.25 lakhs and maturity bonus would also to be payable. It is

further submitted that even in the policy bond sum assured is mentioned as Rs 6.25 Lakhs. It is

further submitted that the policy bond maturity sum assured has mentioned as Rs 6.25 Lakhs.

24. Per Contra respondent representative submitted that in the policy bond maturity sum

assured is not mentioned. Due to some typographical mis-match amount of Rs. 6.25 Lakhs

which was death benefit sum assured is being misunderstood as maturity sum assured. It is

further submitted that the calculation of the maturity sum was made in accordance with the

table no. 165 under which the plan the policy was issued.

25. No doubt policy was issued under the approval of IRDA. As per the circular no.

ACTL/1934/4 of the LIC the plan in question was issued under the table no. 165 wherein the

basic core factor is that it provides to the policy holder highly covered with a smooth return,

Liquidity and lots of flexibility. It is also provided in the plan in conventional products premium

rates are given per 1000/- sum assured for different entry ages and terms. Under this product

death cover will be same irrespective of at entry and term but the sum payable at maturity will

differ for different entry ages and terms. This policy also provides for loyalty additions. Loyalty

additions will be declared after the policy has been in full form for at least 10 years. On Maturity

the life insured will get the maturity sum assured plus loyalty addition if any. The only point to

be looked into as to whether the complainant takes advantage of non- mentioning of maturity

Pag

e17

sum assured in the policy bond. We can read the bond and find that 2 sums are mentioned in

the policy bond which is Rs 6.25 Lakhs each meant for death benefit sum assured under main

plan and accident benefit sum assured. Column redressing to maturity sum assured is lying

vacant. When nothing is printed in this column how it can would be presumed that it was Rs

6.25 Lakhs. The policy bond was generated through computer and the entries are made on a

printed form. Little mis-match that is printing of an amount of Rs 6.25 Lakhs on a higher side

with a few millimeters difference cannot extend a benefit or right to the complainant. It is

settled legal position that a party cannot take the advantage of a printing or typographical error

in the agreement. A presumption cannot be raised in favor of the complainant. It is more

COMPLAINT NO: LCK-L-029-1819-0494 Order No. IO/LCK/A/LI/0384/2019-20

important that the basic features of table no. 165 are in public domain. In that situation it

cannot be accepted that any mis-selling was done with the complainant who himself is a retired

employee.

26. Accordingly I am of the view that the payment of Rs. 185200/- was offered by the

respondent LIC to the complainant in accordance with the terms and conditions of the policy

bond which is justifiable. It doesn‟t require any interference. Accordingly complaint is liable to

be dismissed.

Order:-

27. Complaint is dismissed.

28. Let the copy of award be given to both the parties.

Date: 18.02.2020 (Justice Anil Kumar Srivastava)

Place: Lucknow Insurance Ombudsman

Pag

e18

PROCEEDINGS BEFORE - THE INSURANCE OMBUDSMAN, STATE OF UP

(UNDER RULE NO: 16(1)/17 OF THE INSURANCE OMBUDSMAN RULE 2017)

Mr. Anoop Kumar Sinha…………. ………………..……....………………. Complainant

V/S

Life Insurance Corp. of India…………………....…....…………………………Respondent

COMPLAINT NO:LCK-L-029-1819-0528 Order No. IO/LCK/A/LI/0362/2019-20

1. Name & Address of the Complainant Mr. Anoop Kumar Sinha

Faizabad Road

Lucknow

2. Policy No:

Type of Policy

Duration of policy/DOC

214735077

Jeevan Nidhi

11.12.2004

3. Name of the insured

Name of the policyholder

Mr. Anoop Kumar Sinha

Mr. Anoop Kumar Sinha

4. Name of the insurer Life Insurance Corp. of India

5. Date of Repudiation/Rejection -

6. Reason for repudiation/Rejection -

7. Date of receipt of the Complaint 01.01.2019

8. Nature of complaint Maturity not settled

9. Amount of Claim Pension Plan

10. Date of Partial Settlement

11. Amount of relief sought

12. Complaint registered under Rule Rule No. 13(1)(b) of Ins. Ombudsman Rule

2017

13. Date of hearing/place On 14.02.2020 , 10.30 am at Lucknow

14. Representation at the hearing

a) For the Complainant Mr. Anoop Kumar Sinha

Pag

e19

b) For the insurer Mr. Rishi Mishra

15. Complaint how disposed Dismissed as settle

16. Date of Award/Order 14.02.2020

17. Mr. Anoop Kumar Sinha (Complainant) has filed a complaint against Life Insurance Corp. of

India (Respondent) alleging that maturity claim of the policy was not settled by the LIC.

COMPLAINT NO: LCK-L-029-1819-0528 Order No. IO/LCK/A/LI/ /2019-20

Brief Facts of the Case:-

18. Mr. Anoop Kumar Sinha has lodged his complaint on 01.01.2019 stating that maturity claim

of his policy was not settled by the Corporation. The complainant has stated that on maturity

of the policy he has submitted all requirement as consent letter for pension and for payment of

1/3rd commutation amount but the claim was not settled. The complainant visited branch office

where it was confirmed by concerned officer that there was some mismatch in policy master

but no written response was received from RIC. The complainant was not satisfied. Being

aggrieved he has approached this forum for the redressal of his grievance.

Written reply/SCN:-

19. In their SCN/reply, the respondent has stated that due to technical mistake of policy master

commutation amount and annuity was not paid but now commutation value with penal interest

has been paid to the complainant and Zonal Office has started to make annuity payment as per

option requested by the annuitant.

20. The complainant has filed a complaint letter, annexure VI A, correspondence with

respondent while respondent has filed SCN with enclosures.

21. I have heard the complainant as well as respondent representative and perused the record.

Pag

e20

Findings:-

22. Undisputedly the insured had taken „LIC Jeevan Nidhi Plan‟ which got matured on

11.12.2017 but neither the pension nor commutation amount was paid to the insured. It is

admitted by the LIC that due to incorrect policy master payment could not be made. Payment

of Rs. 59991/- has been made on 18.09.2019 which includes penal interest at the rate of 8.25

percent amounting to Rs. 4759/-. Now pension is regularly being paid. Complainant submits

that he wants that the amount be paid to him one time in lump sum. It is submitted by the

respondent representative that onetime payment cannot made after maturity except on medical

grounds.

COMPLAINT NO: LCK-L-029-1819-0528 Order No. IO/LCK/A/LI/0362 /2019-20

23. Having considered the submission I am of the view that the LIC had already made the

payment of commutation value along with penal interest. Now the pension is being paid

regularly. As per terms and conditions of policy bond, policy cannot be surrendered after

maturity except on exceptional grounds of illness. No such ground is taken by the complainant.

Hence, now policy cannot be surrendered. Complaint is to be disposed off accordingly.

Order:-

24. Complaint is disposed off.

25. Let the copy of award be given to both the parties.

Date: 14.02.2020 (Justice Anil Kumar Srivastava)

Place: Lucknow Insurance Ombudsman

Pag

e21

PROCEEDINGS BEFORE - THE INSURANCE OMBUDSMAN, STATE OF UP

(UNDER RULE NO: 16(1)/17 OF THE INSURANCE OMBUDSMAN RULE 2017)

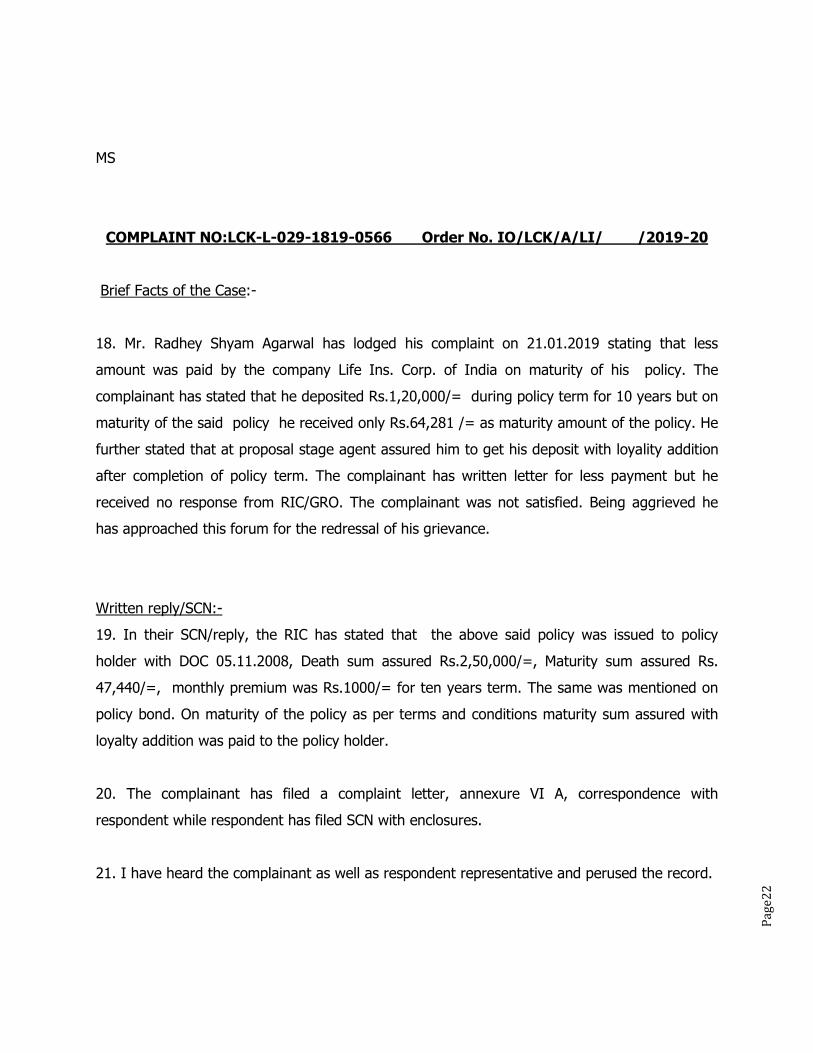

Mr. Radhey Shyam Agarwal…… ………………..……....………………. Complainant

V/S

Life Insurance Corp. of India…………………....…....…………………………Respondent

COMPLAINT NO:LCK-L-029-1819-0566 Order No. IO/LCK/A/LI/0364 /2019-20

1. Name & Address of the Complainant Mr. Radhey Shyam Agarwal

Rajajipuram

Lucknow

2. Policy No:

Type of Policy

Duration of policy/DOC

216844235

Jeevan Saral

05.11.2008

3. Name of the insured

Name of the policyholder

Mr. Radhey Shyam Agarwal

Mr. Radhey Shyam Agarwal

4. Name of the insurer Life Insurance Corp. of India

5. Date of Repudiation/Rejection -

6. Reason for repudiation/Rejection -

7. Date of receipt of the Complaint 21.01.2019

8. Nature of complaint Maturity Amount less paid

9. Amount of Claim

10. Date of Partial Settlement

11. Amount of relief sought

12. Complaint registered under Rule Rule No. 13(1)(b) of Ins. Ombudsman Rule

2017

13. Date of hearing/place On 14.02.2020 , 10.30 am at Lucknow

14. Representation at the hearing

a) For the Complainant Mr. Radhey Shyam Agarwal

b) For the insurer Mr. Rishi Mishra

15. Complaint how disposed Dismissed

16. Date of Award/Order 14.02.2020

17. Mr. Radhey Shyam Agarwal (Complainant) has filed a complaint against Life Insurance

Corp. of India (Respondent) alleging less amount paid on maturity.

Pag

e22

MS

COMPLAINT NO:LCK-L-029-1819-0566 Order No. IO/LCK/A/LI/ /2019-20

Brief Facts of the Case:-

18. Mr. Radhey Shyam Agarwal has lodged his complaint on 21.01.2019 stating that less

amount was paid by the company Life Ins. Corp. of India on maturity of his policy. The

complainant has stated that he deposited Rs.1,20,000/= during policy term for 10 years but on

maturity of the said policy he received only Rs.64,281 /= as maturity amount of the policy. He

further stated that at proposal stage agent assured him to get his deposit with loyality addition

after completion of policy term. The complainant has written letter for less payment but he

received no response from RIC/GRO. The complainant was not satisfied. Being aggrieved he

has approached this forum for the redressal of his grievance.

Written reply/SCN:-

19. In their SCN/reply, the RIC has stated that the above said policy was issued to policy

holder with DOC 05.11.2008, Death sum assured Rs.2,50,000/=, Maturity sum assured Rs.

47,440/=, monthly premium was Rs.1000/= for ten years term. The same was mentioned on

policy bond. On maturity of the policy as per terms and conditions maturity sum assured with

loyalty addition was paid to the policy holder.

20. The complainant has filed a complaint letter, annexure VI A, correspondence with

respondent while respondent has filed SCN with enclosures.

21. I have heard the complainant as well as respondent representative and perused the record.

Pag

e23

Findings:-

22. Undisputedly the insured has taken the plan „Jeevan Saral (with profits) wherein he

deposited an amount of Rs. 1000/- per month for 10 years but on maturity he got Rs. 64281/-

only. Main grievance of the complainant is that he had received the amount which is less than

the amount deposited by him.

COMPLAINT NO:LCK-L-029-1819-0566 Order No. IO/LCK/A/LI/0364 /2019-20

23. Policy in question was a term policy wherein the policy bond itself maturity sum assured as

mentioned as Rs. 47440/- only. On the basis of the terms and conditions of the policy bond

calculation was made wherein loyalty bonus of Rs. 16841/- was paid. Accordingly the payment

was made in according to the terms and conditions of the policy bond. Complaint is devoid of

any merit and is liable to be dismissed.

Order:-

24. Complaint is dismissed.

25. Let the copy of award be given to both the parties.

Date: 14.02.2020 (Justice Anil Kumar Srivastava)

Place: Lucknow Insurance Ombudsman

Pag

e24

PROCEEDINGS BEFORE - THE INSURANCE OMBUDSMAN, STATE OF UP

(UNDER RULE NO: 16(1)/17 OF THE INSURANCE OMBUDSMAN RULE 2017)

Mr. Om Prakash Kapoor…… ………………..……...........………………. Complainant

V/S

Life Insurance Corp. of India…………………....…....…………………………Respondent

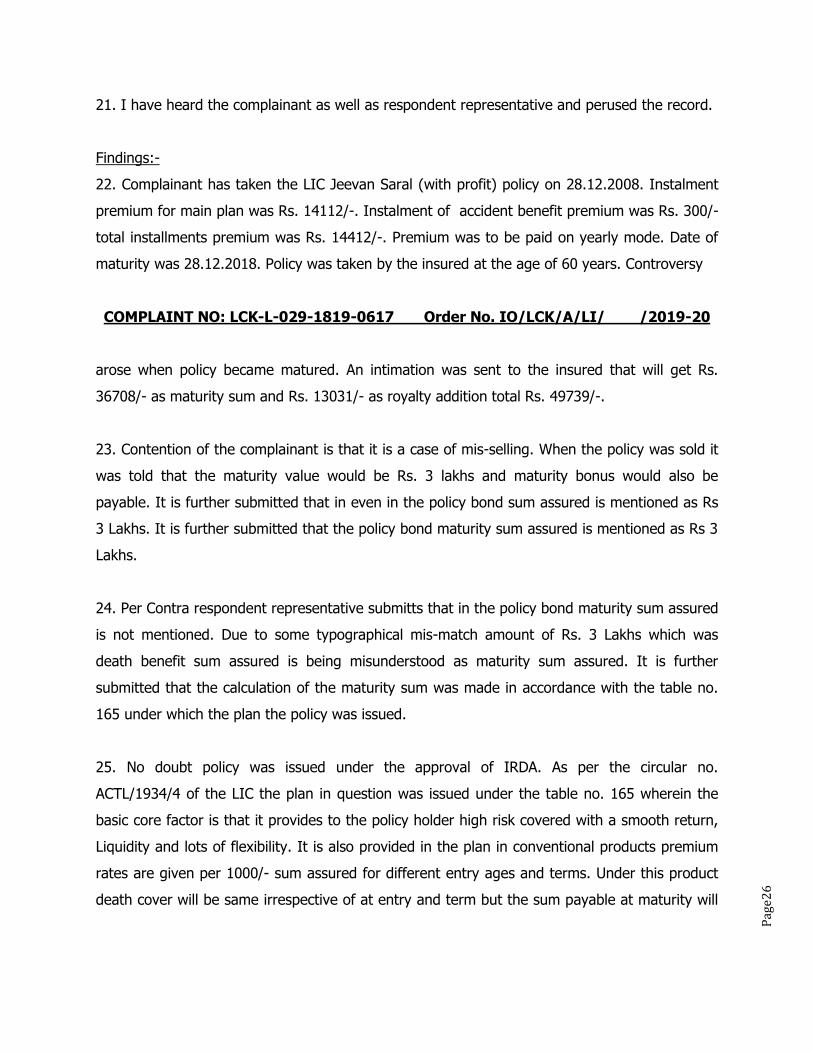

COMPLAINT NO: LCK-L-029-1819-0617 Order No. IO/LCK/A/LI/ 0383/2019-20

1. Name & Address of the Complainant Mr. Om Prakash Kapoor

Pheel Khana

Kanpur

2. Policy No:

Type of Policy

Duration of policy/DOC

234713489

Jeevan Saral

28.12.2008

3. Name of the insured

Name of the policyholder

Mr. Om Prakash Kapoor

Mr. Om Prakash Kapoor

4. Name of the insurer Life Insurance Corp. of India

5. Date of Repudiation/Rejection -

6. Reason for repudiation/Rejection -

7. Date of receipt of the Complaint 22.02.2019

8. Nature of complaint Maturity Amount less paid

9. Amount of Claim

10. Date of Partial Settlement

11. Amount of relief sought

12. Complaint registered under Rule Rule No. 13(1)(b) of Ins. Ombudsman Rule

2017

13. Date of hearing/place On 18.02.2020 , 10.30 am at Lucknow

14. Representation at the hearing

a) For the Complainant Mr Vikas Kapoor

b) For the insurer Sri Pramod Kumar Dixit

Pag

e25

15. Complaint how disposed Dismissed

16. Date of Award/Order 18.02.2020

17. Mr. Om Prakash Kapoor (Complainant) has filed a complaint against Life Insurance Corp. of

India (Respondent) alleging that less amount was paid on maturity.

COMPLAINT NO: LCK-L-029-1819-0617 Order No. IO/LCK/A/LI/ /2019-20

Brief Facts of the Case:-

18. Mr. Om Prakash Kapoor has lodged his complaint on 22.02.2019 stating that less amount

was paid by the Life Ins. Corp. of India on maturity of his policy. The complainant has stated

that when he purchased the said policy it was mentioned in policy documents and also as

explained by his advisor, the policy term was 10 years, sum assured at maturity 3 lakhs, and

loyalty bonus was Rs.50 per thousand but he got only Rs.36,708/= at maturity . At the time of

purchasing this policy, if maturity amount would have been mentioned on policy bond, the

complainant would have never bought this policy or he would have opted for cooling off

cancellation. The complainant has approached RIC through e-mail but no response was

received from them. Being aggrieved he has approached this forum for the redressal of his

grievance.

Written reply/SCN:-

19. In their SCN/reply, the RIC has stated that the policy no.234713489 was issued with doc

28.12.2008, death sum assured Rs.3,00,000/=, Yearly premium Rs.14,412/, Plan term 165-10.

Under the policy maturity sum assured was Rs.36708/= but on bond death sum assured and

double accidental benefit was mentioned. Maturity sum assured was not mentioned on the

policy bond due to mistake.

20. The complainant has filed a complaint letter, annexure VI A, correspondence with

respondent while respondent has filed SCN with enclosures.

Pag

e26

21. I have heard the complainant as well as respondent representative and perused the record.

Findings:-

22. Complainant has taken the LIC Jeevan Saral (with profit) policy on 28.12.2008. Instalment

premium for main plan was Rs. 14112/-. Instalment of accident benefit premium was Rs. 300/-

total installments premium was Rs. 14412/-. Premium was to be paid on yearly mode. Date of

maturity was 28.12.2018. Policy was taken by the insured at the age of 60 years. Controversy

COMPLAINT NO: LCK-L-029-1819-0617 Order No. IO/LCK/A/LI/ /2019-20

arose when policy became matured. An intimation was sent to the insured that will get Rs.

36708/- as maturity sum and Rs. 13031/- as royalty addition total Rs. 49739/-.

23. Contention of the complainant is that it is a case of mis-selling. When the policy was sold it

was told that the maturity value would be Rs. 3 lakhs and maturity bonus would also be

payable. It is further submitted that in even in the policy bond sum assured is mentioned as Rs

3 Lakhs. It is further submitted that the policy bond maturity sum assured is mentioned as Rs 3

Lakhs.

24. Per Contra respondent representative submitts that in the policy bond maturity sum assured

is not mentioned. Due to some typographical mis-match amount of Rs. 3 Lakhs which was

death benefit sum assured is being misunderstood as maturity sum assured. It is further

submitted that the calculation of the maturity sum was made in accordance with the table no.

165 under which the plan the policy was issued.

25. No doubt policy was issued under the approval of IRDA. As per the circular no.

ACTL/1934/4 of the LIC the plan in question was issued under the table no. 165 wherein the

basic core factor is that it provides to the policy holder high risk covered with a smooth return,

Liquidity and lots of flexibility. It is also provided in the plan in conventional products premium

rates are given per 1000/- sum assured for different entry ages and terms. Under this product

death cover will be same irrespective of at entry and term but the sum payable at maturity will

Pag

e27

differ for different entry ages and terms. This policy also provides for loyalty additions. Loyalty

additions will be declared after the policy has been in full form for at least 10 years. On Maturity

the life insured will get the maturity sum assured plus loyalty addition if any.

26. The only point to be looked into is as to whether the complainant takes an advantage of

non- mentioning of maturity sum assured in the policy bond. We can read the bond and find

that 2 sums are mentioned in the policy bond which is Rs 3 Lakhs each. They are meant for

death benefit sum assured under main plan and accident benefit sum assured. Column relating

to maturity sum assured is lying vacant. When nothing is printed in this column how it would be

COMPLAINT NO: LCK-L-029-1819-0617 Order No. IO/LCK/A/LI/0383 /2019-20

presumed that it was Rs 3 Lakhs? Policy bond was generated through computer and the entries

are made on a printed form. Little mis-match that is printing of an amount of Rs 3 Lakhs on a

higher side with a few millimeters difference cannot extend a benefit or right to the

complainant. It is settled legal position that a party cannot take the advantage of a printing or

typographical error in the agreement. A presumption cannot be raised in favor of the

complainant. It is more important that the basic features of table no. 165 are in public domain.

In that situation it cannot be accepted that any mis-selling was done with the complainant who

himself is a retired employee.

27. Accordingly I am of the view that the payment of Rs. 49739/- was offered by the

respondent LIC to the complainant in accordance with the terms and conditions of the policy

bond which is justifiable. It doesn‟t require any interference. Accordingly complaint is liable to

be dismissed.

Order:-

28. Complaint is dismissed.

29. Let the copy of award be given to both the parties.

Date: 18.02.2020 (Justice Anil Kumar Srivastava)

Place: Lucknow Insurance Ombudsman

Pag

e28

PROCEEDINGS BEFORE - THE INSURANCE OMBUDSMAN, STATE OF UP

(UNDER RULE NO: 16(1)/17 OF THE INSURANCE OMBUDSMAN RULE 2017)

Mr. Sunder Lal…………. ………………..……………….…....………………. Complainant

V/S

Life Insurance Corp. of India …….…..…....……………………………..…………Respondent

COMPLAINT NO: LCK-L-029-1819-0618 Order No. IO/LCK/A/LI/ 0378/2019-20

1. Name & Address of the Complainant Mr. Sunder Lal

Rawatpur

Kanpur

2. Policy No:

Type of Policy

Duration of policy/DOC

234258911

Jeevan Saral

26.12.2008

3. Name of the insured

Name of the policyholder

Mr. Sunder Lal

Mr. Sunder Lal

4. Name of the insurer Life Insurance Corp. of India

5. Date of Repudiation/Rejection -

6. Reason for repudiation/Rejection -

7. Date of receipt of the Complaint 20.02.2019

8. Nature of complaint Amount less paid on maturity

9. Amount of Claim

10. Date of Partial Settlement

11. Amount of relief sought

12. Complaint registered under Rule Rule No. 13(1)(b) of Ins. Ombudsman Rule

2017

13. Date of hearing/place On 18.02.2020 , 10.30 am at Lucknow

14. Representation at the hearing

a) For the Complainant Mr. Sunder Lal

b) For the insurer Shri P.K Dixit

Pag

e29

15. Complaint how disposed Dismissed

16. Date of Award/Order 18.02.2020

17. Mr. Sunder Lal (Complainant) has filed a complaint against Life Insurance Corp. of India

(Respondent) alleging that less amount was paid on maturity.

MS

COMPLAINT NO: LCK-L-029-1819-0618 Order No. IO/LCK/A/LI/ /2019-20

Brief Facts of the Case:-

18. Mr. Sunder Lal has lodged his complaint on 20.02.2019 stating that less amount was paid

by the Life Ins. Corp. of India on maturity of his policy. The complainant has stated that he

deposited Rs.1,83,720/= as Rs. 1531/= per month (ecs mode) premiums for 10 years but on

maturity of the said policy he received only Rs.1,21,320 /= against his initial amount deposited

by him. He further stated that he was expecting to get his money with reasonable interest in

ten years long time but he got lesser amount. He approached RIC/GRO but was not satisfied.

Being aggrieved he has approached this forum for the redressal of his grievance.

Written reply/SCN:-

19. In their SCN/reply , the RIC has stated that under the said policy death sum assured is

Rs.3,75,000/= and maturity sum assured Rs. 89,535/= but due to printing mistake maturity

sum assured was not mentioned on policy bond.

20. The complainant has filed a complaint letter, annexure VI A, correspondence with respondent

while respondent has filed SCN with enclosures.

21. I have heard the complainant as well as respondent representative and perused the record.

Findings:-

Pag

e30

22. Complainant has taken the LIC Jeevan Saral (with profit) policy on 26.12.2008. Instalment

premium for main plan was Rs. 1499.75/-. Instalment accident benefit premium was Rs.

31.25/- total installments premium was Rs. 1531/-. Premium was to be paid on monthly mode.

Date of maturity was 26.12.2018. Policy was taken by the insured at the age of 56 years.

Controversy arose when policy became matured and an amount of Rs. 121320/- was sent to his

bank account as maturity amount.

23. Contention of the complainant is that it is a case of mis-selling. When the policy was sold it

was told that the maturity value would be Rs. 3.75 lakhs and maturity bonus would also to be

payable. It is further submitted that even in the policy bond sum assured is mentioned as Rs

COMPLAINT NO: LCK-L-029-1819-0618 Order No. IO/LCK/A/LI/ 0378/2019-20

3.75 Lakhs. It is further submitted that in the policy bond maturity sum assured is mentioned as

Rs 3.75 Lakhs.

24. Per Contra respondent representative submits that in the policy bond maturity sum assured

is not mentioned. Due to some typographical mis-match amount of Rs. 3.75 Lakhs which was

death benefit sum assured is being misunderstood as maturity sum assured. It is further

submitted that the calculation of the maturity sum was made in accordance with the table no.

165 under which the plan the policy was issued.

25. No doubt policy was issued under the approval of IRDA. As per the circular no.

ACTL/1934/4 of the LIC the plan in question was issued under the table no. 165 wherein the

basic core factor is that it provides to the policy holder high risk covered with a smooth return,

Liquidity and lots of flexibility. It is also provided in the plan in conventional products premium

rates are given per 1000/- sum assured for different entry ages and terms. Under this product

death cover will be same irrespective of at entry and term but the sum payable at maturity will

differ for different entry ages and terms. This policy also provides for loyalty additions. Loyalty

additions will be declared after the policy has been in full form for at least 10 years. On Maturity

the life insured will get the maturity sum assured plus loyalty addition if any.

Pag

e31

26. The only point to be looked into is as to whether the complainant takes an advantage of

non- mentioning of maturity sum assured in the policy bond. We can read the bond and find

that 2 sums are mentioned in the policy bond which is Rs 3.75 Lakhs each. They are meant for

death benefit sum assured under main plan and accident benefit sum assured. Column relating

to maturity sum assured is lying vacant. When nothing is printed in this column how it would be

presumed that it was Rs 3.75 Lakhs? Policy bond was generated through computer and the

entries are made on a printed form. Little mis-match that is printing of an amount of Rs 3.75

Lakhs on a higher side with a few millimeters difference cannot extend a benefit or right to the

complainant. It is settled legal position that a party cannot take the advantage of a printing or

typographical error in the agreement. A presumption cannot be raised in favor of the

COMPLAINT NO: LCK-L-029-1819-0618 Order No. IO/LCK/A/LI/ 0378 /2019-20

complainant. It is more important that the basic features of table no. 165 are in public domain.

In that situation it cannot be accepted that any mis-selling was done with the complainant who

himself is a retired employee.

27. Accordingly I am of the view that the payment of Rs. 121320/- was offered by the

respondent LIC to the complainant in accordance with the terms and conditions of the policy

bond which is justifiable. It doesn‟t require any interference. Accordingly complaint is liable to

be dismissed.

Order:-

28. Complaint is dismissed.

29. Let the copy of award be given to both the parties.

Date: 18.02.2020 (Justice Anil Kumar Srivastava)

Place: Lucknow Insurance Ombudsman

Pag

e32

PROCEEDINGS BEFORE - THE INSURANCE OMBUDSMAN, STATE OF UP

(UNDER RULE NO: 16(1)/17 OF THE INSURANCE OMBUDSMAN RULE 2017)

Mr. Anil Kapur…………. ……………………………..…..……....………………. Complainant

V/S

Star Union Dai-ichi- Life Insurance Co. Ltd…..…....…………………………Respondent

COMPLAINT NO: LCK-L-045-1819-0260 Order No. IO/LCK/A/LI/0344/2019-20

1. Name & Address of the Complainant Mr. Anil Kapur

Hazratganj

Lucknow

2. Policy No:

Type of Policy

Duration of policy/DOC

00645131

Dhan Suraksha (Unit Linked)

24.05.2013

3. Name of the insured

Name of the policyholder

Mr. Anil Kapur

Mr. Anil Kapur

4. Name of the insurer Star Union Dai-ichi- Life Insurance Co. Ltd.

5. Date of Repudiation/Rejection -

6. Reason for repudiation/Rejection -

7. Date of receipt of the Complaint 31.07.2018

8. Nature of complaint Amount less paid

9. Amount of Claim -

10. Date of Partial Settlement -

11. Amount of relief sought -

12. Complaint registered under Rule Rule No. 13(1)(b) of Ins. Ombudsman Rule

2017

13. Date of hearing/place On 11.02.2020 , 10.30 am at Lucknow

14. Representation at the hearing

a) For the Complainant Mr. Anil Kapur

b) For the insurer Anis Aslam Kazi

Pag

e33

15. Complaint how disposed Dismissed

16. Date of Award/Order 11.02.2020

17. Mr. Anil Kapur (Complainant) has filed a complaint against SBI Life Insurance Co. Ltd.

(Respondent) alleging less amount paid on maturity.

MS

COMPLAINT NO: LCK-L-045-1819-0260 Order No. IO/LCK/A/LI/ 0344/2019-20

Brief Facts of the Case:-

18. Mr. Anil Kapur has lodged his complaint on 31.07.2018 stating that less amount was paid by

the company Star Union Dai-ichi- Life Ins. Co. Ltd. on maturity of his policy. The complainant

has stated that he deposited Rs.25000/= as annual premium for 5 years but on maturity of the

said policy he received only Rs.1,16,805.25 /= against Rs. 125000/= deposited by him. He

further stated that at proposal stage agent assured him to get at least double of his deposit.

The complainant has made many efforts to get his maturity and when he received his maturity

amount he was surprised and he approached RIC but was not satisfied. Being aggrieved he has

approached this forum for the redressal of his grievance.

Written reply/SCN:-

19. In their SCN/reply, the RIC has stated that the complainant had submitted the proposal

form for purchasing SUD Life Dhan Suraksha Premium 3 with the company and policy was

issued. The complainant is very well educated to understand the policy documents which

contain various details. The complainant has duly paid all the premiums and now making false

allegations after completion of the policy term. The said plan is unit linked insurance plan

wherein the risk in investment portfolio is borne by policy holder. Investment in the unit is

subject to market and others risks and maturity benefits are equivalent to the fund value as on

the date of maturity. The company hereby submits that upon payment of the maturity benefits

on 29.05.2018 the company has duly discharged its liability under the policy.

Pag

e34

20. The complainant has filed a complaint letter, annexure VI A, correspondence with

respondent while respondent has filed SCN with enclosures.

21. I have heard the complainant as well as respondent representative and perused the record.

Findings:-

22. The insurance cover of the complainant is connected with the loan taken by him from Bank

of India. There is no dispute that the policy was taken by the insured and policy bond was sent

COMPLAINT NO: LCK-L-045-1819-0260 Order No. IO/LCK/A/LI/ 0344/2019-20

to him. Total premium paid in 5 years was 1.25 lakhs while the payment of Rs. 116805.25 was

made on maturity. It was a Unit Linked Policy wherein the value was assessed on the basis of

units. Complainant main concern is about the harassment made by the bank as well as

insurance company. It is admitted that the payment was made in the insured account on

31.05.2018. So far as harassment by bank is concerned, insured would be at liberty to

approach the proper forum. Payment is made in accordance with the terms and conditions with

the policy bond. Deductions were made under different heads of charges as per the terms and

conditions of the policy bond. Accordingly I do not find any merit in the complaint which is

liable to be dismissed.

Order:-

23. Complaint is dismissed.

24. Let copy of award be given to both the parties.

Date: 11.02.2020 (Justice Anil Kumar Srivastava)

Place: Lucknow Insurance Ombudsman

Pag

e35

PROCEEDINGS BEFORE - THE INSURANCE OMBUDSMAN, LUCKNOW

(UNDER RULE NO: 16(1)/17 OF THE INSURANCE OMBUDSMAN RULE 2017)

Mr. Ram Prakash ………………………………....……....………………. Complainant

VS

Life Insurance Corporation of India…………………………………………...Respondent

COMPLAINT NO: LCK-L-029-1819-0341 Order No. IO/LCK/A/LI/0317/2019-20

1. Name & Address of the Complainant Mr. Ram Prakash

538K / 1557 ,

Triveni Nagar- II,

Sitapur Road

Lucknow- 226020 (U.P.)

2. Policy No:

Type of Policy

DOC /DOR

DOD

Duration of policy

219125727

Wealth Plus Plan

31.03.2010

N/A

08 years

3. Name of the insured /

Name of the policyholder

Mr. Ram Prakash

Mr. Ram Prakash

4. Name of the insurer Life Insurance Corporation of India

5. Date of Repudiation/Rejection N/A

6. Reason for repudiation/Rejection N/A

7. Date of receipt of the Complaint 03.10.2018

8. Nature of complaint Maturity not received

9. Amount of Claim Maturity Value 65000/-

10. Date of Partial Settlement -

11. Amount of relief sought Maturity Value

12. Complaint registered under Rule Rule No.13(1)(f)of Insurance Ombudsman

Rule 2017

13. Date of hearing/place 04.02.2020 at 10.15 A.M.

Pag

e36

14. Representation at the hearing

a) For the Complainant Mr. Ram Prakash

b) For the insurer Mr. Rishi Misra

15. Complaint how disposed Closed

16. Date of Award/Order 04.02.2020

17. Mr. Ram Prakash (Complainant) has filed a complaint against Life Insurance Corporation of

India. (Respondent) alleging that Maturity value of his policy is not being made.

YKS

COMPLAINT NO: LCK-L-029-1819-0341 Order No. IO/LCK/A/LI/ 0317 /2019-20

Brief Facts of the Case:-

18. As per the complaint, complainant had taken one policy no. 219125727 under „Wealth Plus

Plan‟ for Rs. 65000/- with single premium of Rs.50000/- for 08 years term on 31.03.2010 from

LIC of India. Policy matured on 31.03.2018, hence he has deposited Original Policy bond with

other relevant papers with LIC on 12.03.2018 at Trans Gomti Branch Lucknow. After vigorous

follow-up, complainant came to know that the aforesaid policy has already been surrendered by

the employees of LIC at his own in 2014 without original policy bond and consent letter of the

policy holder and part amount was used for new business from the proceeds. Being aggrieved,

the complainant approached this forum for the redressal of his grievance.

Written reply/SCN:-

19. In SCN/reply dated 03.02.2020, RIC has informed that grievance has been resolved and

Branch has paid following amount to policy holder through NEFT on 01.02.2020.

Maturity claim amount as on 31.03.2018 Rs. 65050/-

(Considering Units 4207.102, NAV Rs. 15.4619)

Interest Thereon Rs. 7058/-

TOTAL Rs. 72108/-

They further informed that the delay has occurred due to Technical reason.

Pag

e37

20. The complainants have filed a complaint letter, Annexure VI A along with other relevant

papers while respondent has filed SCN with enclosures.

21. I have heard the complainant as well as respondent representative and perused the record.

Findings:-

22. Undisputedly complainant had taken the policy under „Wealth Plus Plan‟ on 31.03.2010.

Duration was 8 years. It is alleged that the policy was surrendered in 2014 due to the fault of

the respondent. However respondent has paid an amount of Rs.72108/- to the complainant on

01.02.2020. It includes interest amount of Rs. 7058/-. Since payment has already been made

complaint become infructuous and is liable to be closed.

COMPLAINT NO: LCK-L-029-1819-0341 Order No. IO/LCK/A/LI/ 0317/2019-20

Order:-

23. Complaint is closed.

24. Let copy of award be given to both the parties.

Date: 04.02.2020 (Justice Anil Kumar Srivastava)

Place: Lucknow Insurance Ombudsman

Pag

e38

PROCEEDINGS BEFORE - THE INSURANCE OMBUDSMAN, LUCKNOW

(UNDER RULE NO: 16(1)/17 OF THE INSURANCE OMBUDSMAN RULE 2017)

Mr. Shiv Singh ………………………………....……....………………………. Complainant

VS

Life Insurance Corporation of India…………………………………………...Respondent

COMPLAINT NO: LCK-L-029-1920-0181 Order No. IO/LCK/A/LI/ 0422/2019-20

1. Name & Address of the Complainant Mr. Shiv Singh

S/O Sri Duniya Singh

69; Gayatri Nagar

Sanigavon Road

Kanpur- 208021 (U.P.)

2. Policy No:

Type of Policy

DOC

DOD

Duration of policy

234613739;234613773;234613741;

235268853;234613738;235268855

235268851;234613740 & 234613787

Wealth Plus Plan & Last one Jeevan Saral

29.09.2008;30.09.2008;29.09.2008

27.08.2010;29.09.2008;27.08.2010

27.08.2010;29.09.2008 & 29.09.2008

N/A

10-20 years & last one 16 years

3. Name of the insured /

Name of the policyholder

Mr. Shiv Singh

Mr. Shiv Singh

4. Name of the insurer Life Insurance Corporation of India

5. Date of Repudiation/Rejection N/A

6. Reason for repudiation/Rejection N/A

7. Date of receipt of the Complaint 03.07.2018

8. Nature of complaint Maturity not received

9. Amount of Claim Maturity Value 410208/-with interest

10. Date of Partial Settlement -

Pag

e39

11. Amount of relief sought Maturity Value

12. Complaint registered under Rule Rule No.13(1)(f)of Insurance Ombudsman

Rule 2017

13. Date of hearing/place 27.02.2020 at 10.15 A.M.

14. Representation at the hearing

a) For the Complainant Mr. Shiv Singh

b) For the insurer Ramakanti

15. Complaint how disposed Allowed

16. Date of Award/Order 27.02.2020

YKS

COMPLAINT NO: LCK-L-029-1920-0181 Order No. IO/LCK/A/LI/ /2019-20

17. Mr. Shiv Singh (Complainant) has filed a complaint against Life Insurance Corporation of

India. (Respondent) alleging that his policies were surrendered and amount adjusted in some

other policies.

Brief Facts of the Case:-

18. As per the complaint, complainant had taken aforesaid nine policies (Except Last One)

under ULIP plan with single premium of Rs.50000/- each for 10 & 20 years term on aforesaid

dates from LIC of India. Last policy no.234613787 was issued under Jeevan Saral for 16 years

on 29.09.2008. Claimant has got all policies bonds and is in his possession. Further claimant has

come to know from Local Newspapers that LIC has cheated to several LIC customers of that

particular branch no. CBO-8by transferring the customer‟s premium money into their personal

account instead of LIC account. Claimant has lodged written complaint against LIC Agent Mr.

Gajendra Singh. After vigorous follow-up, complainant came to know that the aforesaid policy

has already been surrendered by the employees/agent of LIC at his own without original policy

bond and consent letter of the policy holder and amount was used for new business from the

proceeds. Being aggrieved, the complainant approached this forum for the redressal of his

grievance.

Pag

e40

Written reply/SCN:-

19. In SCN/reply dated 25.02.2020, RIC has stated that aforesaid policies were issued on the

life of Mr. Shiv Singh. Departmental enquiry is being conducted against Agent and reply of Legal

Notice has already been given through our panel Advocate Sri Rajesh Pandey. Respondent has

further stated that since Complainant has not given NEFT and other details, hence payment

could not be made.

20. The complainants have filed a complaint letter along with other relevant papers while

respondent has filed SCN with enclosures. Annexure VI A not enclosed.

21. I have heard the complainant as well as respondent representative and perused the record.

COMPLAINT NO: LCK-L-029-1920-0181 Order No. IO/LCK/A/LI/ 0422/2019-20

Findings:-

22. It is a case which relates to the fraud, having been played by one Mr. Gajendra Singh,

agent of the respondent LIC.

23. The following chart is submitted by the respondent LIC:-

S No Policy No. Status T-T No. of

units

DOC Mty Date Fund

Type

SA/Inst Prem

1

234613739 Surrendered on 28.12.2011 for Rs

57358/-

191-20-

01

4755.095

29.09.2008

29.09.2028

Growth

0/50000

Single Prem.

2 234613773 Surrendered on 01.02.2012 for Rs

62586/-

191-10-

01

4752.124

30.09.2008

30.09.2018

Growth

0/50000

Single Prem.

3

234613741 Surrendered on 02.01.2012 for Rs

56825/-

191-20-01 4755.095 29.09.2008 29.09.2028 Growth

0/50000

Single Prem.

4 235268853 Surrendered on 07.11.2013 for Rs

48166/- Lying in stale

191-20-01 3354.871 27.08.2010 27.08.2020 Growth

0/50000

Single Prem.

5 234613738 Surrendered on 13.07.2012 for Rs

64182/-

191-20-01 4744.392 29.09.2008 29.09.2028 Growth

0/50000

Single Prem.

Pag

e41

6 235268855 Surrendered on 26.10.2013 for Rs

48195/- Lying in Stale as per Branch

Record

191-10-01 3354.871 27.08.2010 27.08.2020 Growth

0/50000

Single Prem.

7 235268851 FP Cheque Dishonored 191-10-01 0 27.08.2010 27.08.2020 Growth

0/50000

Single Prem.

8 234613740 Surrendered on 18.01.2012 For Rs

59571/-

191-20-01 4753.432 29.09.2008 29.09.2028 Growth

0/50000

Single Prem.

9 234613789 Policy is issued in the name of Madhu

Lata nominee is Shiv Singh Husband,

This is in Lapsed Condition Premium is

unpaid since 09/2009 cannot be revived

165-16-16 28.09.2008 28.09.2024 212500 Death

SA/10208 Yly

24. It is clear from the chart in the SCN that the complainant insured had taken policies from

serial 1 to 9 to the respondent LIC. We can classify the policies in the following manner. Policy

mentioned at serial no. 1 to 6 and 8 were undisputedly taken by the insured. These policies

were under” wealth Plus Plan.” The policies had never been surrendered by the complainant.

Letter dated 09.01.2019 written by the insurance company to the insured reads as under:-

COMPLAINT NO: LCK-L-029-1920-0181 Order No. IO/LCK/A/LI/ 0422/2019-20

सेवा मे:-

श्री शिव शस िंह

69 गयात्री नगर सननगावओिं रोड, कानऩरु- 208021

महोदय

ववषय:- आऩकी ऩॉशऱसीस के भगूतान के सिंदभभ मे

सऺम अधधकारी से स्वीकृती शमऱने के ऩियत आऩको सधूित ककया जाता है कक आऩकी ननम्नशऱखित ऩॉशऱसीस

के अिंतगभत आऩकी शिकायत के सिंदभभ मे आऩको भगुतान ककया जाना है

क्र स० ऩाशऱसी स० राशि

1 234613738 64182.00

2 234613739 57358.00

3 234661374 59571.00

Pag

e42

4 234613741 55000+1825(stale)

=56825.00

5 234613773 53206.00

6 235268853 48166.00 (stale)

7 235268855 48195.00 (stale)

8 235268851 िेक अनाद्रथ

( अत: देय नहीिं है)

आऩ से अनरुोध है की NEFT द्वारा भगूतान प्राप्त करने हेत ुआऩ ननम्नशऱखित आवश्यकता प्रऩत्र ऩरू्भ कर

िािा मे प्रश्ततु करे जजसस ेकी भगुतान की प्रकक्रया की जा सके

25. It is admitted by the insurance company that a vigilance enquiry is pending against the

agent regarding fraud having been committed by him. Surrender amount of the policies was not

paid to the complainant rather was transferred to the account of some other person. It is also

admitted in the letter dated 09.01.2019 and SCN that the surrender value as on the date of the

alleged surrender is to be paid by the insurance company. At this stage it would be relevant to

mention that the complainant insured had never applied for surrender in 2012 rather it was a

matter of enquiry as to who had applied for surrender and in whose account was paid if the

COMPLAINT NO: LCK-L-029-1920-0181 Order No. IO/LCK/A/LI/0422/2019-20

payment was made by the LIC but the record shows that the complainant applied for the

surrender of policies on 15.06.2017. Hence, complainant would be entitled for the surrender

value as on 15.06.2017.

26. It is further relevant that one policy no. 235268851 is not in existence as the cheque of

premium got dishonored. Complainant submits that he had paid the amount in cash to his

agent name Gajendra Singh but he received the receipt from LIC wherein it is mentioned that

payment was made through cheque which got dishonored. It is a matter of enquiry as to who

had issued the cheque which was dishonored and if it is established that complainant had made

the payment in cash and someone else had issued cheque in that case complainant would be

entitled for the surrender value as prevalent on 15.06.2017 alongwith penal interest @ 8.25

percent per annum.

Pag

e43

27. Another policy was 234613789 is “Jeevan Saral” in the name of complainant‟s wife Madhu

Lata. It is submitted that complainant had paid all the premium to the agent but only first

receipt and receipt of premium dated 28.09.2016 are on record. This receipt is also not issued

by the LIC. It is also on matter of enquiry. Result of enquiry would decide the fate of this policy.

28. Having considered the submission and discussion made above I am of the view that

complaint is liable to be partially allowed.

Order:-

29. Complaint is partially allowed. Respondents are directed to make the payment of policy no.

1 to 6 and 8 as surrender value as on 15.06.2017 with penal interest @ 8.25 percent per

annum w.e.f 15.06.2017 till the date of actual payment.

30. Fate of policy no 235268851 and 234613789 shall be subject to decision of vigilance enquiry

as observed in the body of order.

31. This order shall not affect the vigilance enquiry. LIC would be at liberty to get the legal

formalities completed from the complainant.

COMPLAINT NO: LCK-L-029-1920-0181 Order No. IO/LCK/A/LI/ 0422/2019-20

32. Let the copy of award be given to both the parties.

Date: 27.02.2020 Justice Anil Kumar Srivastava

Place: Lucknow (Insurance Ombudsman)

Pag

e44

PROCEEDINGS BEFORE - THE INSURANCE OMBUDSMAN, LUCKNOW

(UNDER RULE NO: 16(1)/17 OF THE INSURANCE OMBUDSMAN RULE 2017)

Mr. Suresh Kumar Gupta………………....…….....................………………. Complainant

VS

Life Insurance Corporation of India…………………………..…………………...Respondent

COMPLAINT NO: LCK-L-029-1819-0591 Order No. IO/LCK/A/LI/ 0386/2019-20

1. Name & Address of the Complainant Mr. Suresh Kumar Gupta

715 , Azad Mohal

Sadar Bazar

Lucknow -226002 (U.P.)

2. Policy No:

Type of Policy

DOC /DOR

DOD

Duration of policy

212121310

Jeevan Sanchay Plan

………….

N/A

20years

3. Name of the insured /

Name of the policyholder

Mr. Suresh Kumar Gupta

Mr. Suresh Kumar Gupta

4. Name of the insurer Life Insurance Corporation of India

5. Date of Repudiation/Rejection N/A

6. Reason for repudiation/Rejection N/A

7. Date of receipt of the Complaint 04.02.2019

8. Nature of complaint Less Maturity payment

9. Amount of Claim 55000/-

10. Date of Partial Settlement 93000/-

11. Amount of relief sought S.B. payment Rs 20000/-+ Loyalty Addition

35000/- (TOTAL 55000/-)

12. Complaint registered under Rule Rule No.13(1)(a)of Insurance Ombudsman

Rule 2017

13. Date of hearing/place 20.02.2020 at 10.15 A.M.

Pag

e45

14. Representation at the hearing

a) For the Complainant Mr. Suresh Kumar Gupta

b) For the insurer Mr. Rishi Misra

15. Complaint how disposed Dismissed

16. Date of Award/Order 20.02.2020

17. Mr. Suresh Kumar Gupta (Complainant) has filed a complaint against Life Insurance

Corporation of India. (Respondent) alleging that he has received less maturity amount of his

policy.

COMPLAINT NO: LCK-L-029-1819-0591 Order No. IO/LCK/A/LI/ 0386/2019-20

Brief Facts of the Case:-

18. As per the complaint, complainant had taken one policy no. 212121310 for Rs. 50000/-

under “Jeevan Sanchay Plan” from LIC of India for 20 years. As per policy condition, he had to

get 20% survival benefit payment after 05, 10 and 15 years and balance 40% on maturity.

Complainant had received three survival benefit of 10000/- each. Thereafter on maturity he

received a mail from LIC intimating that a Bonus of Rs. 70000/- is due for payment. Hence he

had submitted all claim papers with LIC. Claimant has received Rs 93000/- only (70000/-

against Bonus and Rs. 23000/-against balance maturity amount) through NEFT. Hence he has

received less maturity amount of Rs 53000/-. Being aggrieved, the complainant approached this

forum for the redressal of his grievance.

Written reply/SCN:-

19. In SCN/reply dated 17.02.2020, RIC has stated that claimant has taken a policy under

Jeevan Sanchay Plan for 20 years. Survival benefit were payable at the interval of every five

years(i.e 5 years, 10 years and 15 years from DOC )as 20% of sum assured .On life assured

surviving at the date of maturity 40%of the sum assured along with accrued Guaranteed

Additions and Loyalty Addition would be payable. Under this plan guaranteed addition was

Pag

e46

Rs.70 per thousand at the end of each policy anniversary. Hence fallowing payments have been

made-

S.B due after 05 years Rs. 10000/-

S.B due after 10 years Rs. 10000/-

S.B. due after 15 years Rs. 10000/-

Maturity claim paid 20000/- (40% of S.A.)

70000/- (Guaranteed addition @70/- per thousand)

3000/- (Loyalty addition)

-------------------

93000/-

------------------------

Hence correct amount has been paid to claimant.

COMPLAINT NO: LCK-L-029-1819-0591 Order No. IO/LCK/A/LI/ 0386/2019-20

20. The complainant has filed a complaint letter along with other relevant papers. But

respondent has not filed SCN with enclosures.

21. I have heard the complainant as well as respondent representative and perused the record.

Findings:-

22. Admittedly complainant had a policy under 125(Jeevan Sanchay) with term of 20 years and a

sum assured Rs. 50,000/-. He received 3 instalments of survival benefit Rs. 10,000/- each. On

maturity he got the balance sum assured i.e. Rs. 20,000/-, Rs. 70,000/- as bonus, Rs. 3000/- as

loyalty addition. It appears that due to some mis-conception complainant is claiming Rs. 35,000/-

as loyalty addition. Payment has been made in accordance with the terms and conditions of the

policy bond. Accordingly complaint lacks merit and is liable to be dismissed.

Order:-

23. Complaint is dismissed.

24. Let the copy of award be given to both the parties.

Date: 20.02.2020 (Justice Anil Kumar Srivastava)

Place: Lucknow Insurance Ombudsman

Pag

e47

PROCEEDINGS BEFORE - THE INSURANCE OMBUDSMAN, LUCKNOW

(UNDER RULE NO: 16(1)/17 OF THE INSURANCE OMBUDSMAN RULE 2017)

Mr. Suresh Kumar Gupta………………....…….....................………………. Complainant

VS

Life Insurance Corporation of India…………………………..…………………...Respondent

COMPLAINT NO: LCK-L-029-1819-0591 Order No. IO/LCK/A/LI/ 0386/2019-20