12-2021.pdf - icmai-wirc.in

52

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of 12-2021.pdf - icmai-wirc.in

WIRC BULLETIN – DECEMBER 2021

2

CMA P. Raju Iyer, Vice President ICAI addressing the participants during Discussion Meeting organized by Ahmedabad Chapter on 17th Nov. 2021. Also seen CMA Ashish Bhavsar, RCM-WIRC, CMA Chittaranjan Chattopadhyay, CCM-ICAI and CMA B.B. Goyal-Advisor, ICWAI MARF

CMA Dinesh Kumar Birla, Chairman WIRC delivering his welcome speech at CMA Conclave - Goa 2021.

Western India Regional Council wishes all its Members and Students

Cover Stories • EnvisioningLifeBeyondCOVID-19 CMAN.Rajaraman 6 • ImpactofCOVID19onIndianaswellasGlobalEconomy CMAJayMehta 9 • TradeandTradeFinanceintheCOVID-19crisis CMACS(Dr.)SubirKumarBanerjee 10 • FinancingIndia’sEconomicGrowthPostPandemic CMA(Dr.)S.K.Gupta 13CFO Speakes • CMAs,atHelmasapolicymaker(Ministry-Govt.ofIndia) CMAPawanKumar 15 • CMAs,atHelmasaBusinessEnhancer(PublicSectorUndertaking.... CMAS.M.Choudhury 17 • CMAs,atHelmasaFinanceHead(StateGovt.undertakings) CMASandeepModi 20Articles • WhytheAmericaneconomistscouldnotsuggestaright.... CMADr.GirishJakhotiya 22 • VirtualCFOADomainofCostandManagementAccountant CMADr.AshishThatte 23 • SugarcaneCultivation CMALt.DhananjayKumarVatsyayan 25 • GstImpactonExporters CMAAshokNawal 29 • ForeignInstitutionalInvestments CMAJyotiChaudhary 34 • MISReportsforRawMaterialCostincludingmonitoring,controlling CMARajeshKapadia 39 • HowtofaceanInterview? 42 • What’sNew 43 • StudentsGlossary 48 • Report on CMA Conclave – Goa 2021 49Chapter News 50In

side

the

Bul

leti

n

WIRC BULLETIN – DECEMBER 2021

3

DearProfessionalColleagues,

Namaste !!

“Everybody say mistakes is the First Step of success but the fact is correction of mistake is the First Step of success.”

– A.P.J. Abdul Kalam

ItakethisopportunitytocongratulateCMAShriP.RajuIyeronbeingelectedasPresidentandCMAShriVijenderSharmaasVicePresidentofourInstitute.Weare sure that under their able leadership our Institute will achieve greater heights andsetnewbenchmarksinthedevelopmentofourprofession.

Studentsarehavingexamsfrom8thDecember.WIRChascreatedahelpdeskforthestudentsappearinginDecember2021examsforassistingtheminresolvingproblemsbeingfacedbythem.MyBestwishestothem.

Wearrangedatwodays’seminar“CMAConclave-Goa2021”atGoaon27th&28thNovember2021forthebenefitofMemberswhohadminimuminteractionswiththeirProfessionalpeers,duetoPandemicinducedlockdown.ThemeoftheConclave was “Unconventional Opportunities under IBC, 2016”. Conclave wasinauguratedat theauspicioushandsofShriRiteshKavdia,ExecutiveDirector,InsolvencyandBankruptcyBoardofIndia.CMABiswarupBasu,PresidentofICAIcouldnotmakeittoattendphysicallyintheprogramme.However,headdressedthe participants through online.

Well-knownexpertsthroughout5TechnicalSessionsgaveextensive&exhaustivepresentationwiththeirprofessionaltouch&input.ShriRiteshKavdia,ExecutiveDirector,InsolvencyandBankruptcyBoardofIndiawasthespeakerinthefirsttechnicalsession,onthetopiconQuinquennialofInsolvencyandBankruptcyCode2016.

CMAChitraleeGoswami,ChiefGeneralManager&Head ofFinance,OnshoreEngineeringServices,ONGCandAdvisorFinancetoDirector(Onshore),ONGC,presentedviewsofstakeholderslikehomebuyersthroughtheCasestudies.

Inthe2ndSessiononCrossBorderandGroupInsolvency&Personal&PartnerInsolvencyEnhancingtheTerritoriesSupportservicestoIBCEcosystem,CMAIPDushyantDave,ShriAnilGoel,InsolvencyProfessionalswerethespeakers.

Inthe3rdSessionCMAAshokNawalofferedhisviewsonOpportunitiesforCMAsinprovidingsupportservicestoIP’sandotherstakeholdersinIBC.HeemphasizedthatforprovidingsuchservicesCMAneednotbeIPalways.

4thSessionwason“ForensicAuditof“PUFE”transactionunderIBC2016”.ShriAnilGoel,InsolvencyProfessionalandCMAIPRVHarshadSDeshpande,werethespeakers.ShriAnilGoeladdressedtheregulatoryframework,keyapproachofForensicAuditwithrespecttoPUFEtransactionsinIBCanddiscussedtheredflags,internalcontrolsreview,useofITtools,auditstepsandcheckliststoassistForensic Auditors and RPs.

Fro

m th

e D

esk

oF

Cha

irm

an

3

WIRC BULLETIN – DECEMBER 2021

4

In the 5thSession onRegisteredValuersEcosystemandValuationProfession,CMAR.K.PatelandVr.KedarChikodiwerethespeakers.

CMA RV R.K. Patel presented history of valuation profession, need of unifiedregulatorystructureforvaluationprofession,benefitsofpresentregulatoryregimeundertheRules,practicalaspectspertainingtovaluationsuchasdutiesofvaluer,parameterstojudgequalityofvaluationreport,extentoflimitations,caveatsanddisclaimerstobeusedinvaluationreportandbeneficialpurposeforwhichvaluationreportmaybeused.Vr.KedarChikodiexplainednewregulatoryframeworkundertheRulesandstressedtheneedofrecognizingcontextofvaluation.

ValedictorysessionwaschairedbyCMASunilBagi,GM-Finance,GoaShipyardLtd.GoodnumberofCMAsfromthroughouttheregiontookbenefitoftheConclave.

I would like to update on P.D. activities at WIRC during the month of November:

• Webinar on Business Intelligence and Power BI-Tool of Data Analysis &VisualizationjointlywithPimpri-Chinchwad-AkurdiChapterandKolhapur-SangliChapteron13thNovember2021.Shri.SuryakantMore,Proprietor-SoftMoreEnterprises,Kolhapurwasthespeaker.

• Webinarwasorganizedontheoccasionof InternationalMen’sDayon19thNovember,2021.Mr.NileshZope,RetiredLieutenantCommander–IndianNavywasthespeaker.

• WebinaronUsingthePowerofDataAnalyticsandDashboardforImprovingOrganisation Profitability was organized jointly with Pimpri-Chinchwad-AkurdiChapterandKolhapur-SangliChapteron20thNovember,2021.Dr.B.A.N.Sharma-Founder,CEOofClearMeasurementSolutionsPvt.Limited,wasthespeaker.

• WebinarSeriesonESGwasorganizedon30thNovember2021&1stDecember2021.Mr.SonalVerma,Partner-ESG&GlobalLeader(Markets&Strategy)Dhir&DhirAssociateswasthespeaker.

LookingforwardtoyoursuggestionstoimprovethequalityofservicesofWIRC.

IwishMerryChristmastoalltheMembers,Studentsandtheirfamilies.

TheNewYearstandsbeforeus,likeaChapterinaBook,waitingtobewritten.Wecanwritethatstorybysettinggoals.ByeBye2021andWelcomeNewYear2022.

Stay safe, Stay healthy.

With Best Wishes,

CMA Dinesh Kumar BirlaChairman, ICAI-WIRC

WIRC BULLETIN – DECEMBER 2021

5

MyDearCMAs’

“The highest education is that which does not merely give us information, but makes our life in harmony with all existence”

– Rabindranath Tagore

Ihopeyouarewell,stayingsafeandhealthywithyourlovedones.MysincererequesttoalltokeeputmostprecautionsagainstthenewCOVIDvariant‘Omicron’,makemaskandsanitizer,amustfeatureofyourdailyroutineandlife

ThetitleoftheDecembermonthBulletin-“FinancingtheGrowthofIndianEconomy”.ThisBulletinbecameenrichwiththevaluablecontributionofoureminentresourcepersons.

India’sEconomicadvisorycouncil(EAC)toPrimeMinisterNarendraModiexpectsthecountry’sgrowthtorangebetween7%and7.5%inthenextfiscalyearandthatthenextbudgetshouldhaveaclearroadmapforprivatisingstate-ownedassets.Thegovernmentalso expects the economy to grow 10.5% in the current fiscal year following a recordcontractionof7.3%lastyear

Asexpectedby theEAC, thecontact intensivesectorsaconstructionshouldrecover in2022-23.Oncecapacityutilizationimproves,privateinvestmentsshouldalsorecover

Recent indicatorssuchas taxcollection,exportgrowth, retail salesandpowerdemandpointtowardsabetterthanexpectedrecovery,leadingsomeeconomiststoreviseIndia’sgrowth projection upwards.

TheEACexpected,theUnionBudget2022-23shouldnothaveunrealisticrevenuetargetsandthatitshouldplantospendanyextrarevenuetobuildassets.

Further,theReserveBankofIndia(RBI)hasloweredthegrowthprojectionforthecurrentfinancial year to 9.5 per cent from10.5 per cent estimated earlier,while the IMFhasprojectedagrowthof9.5percentin2021and8.5percentinthenextyear.

TheCMAs’obviouslybeanenergyboosterfortheentrepreneursandindustriestoachievethe target.

IamverymuchthankfultoallourwellwishersincludingTeamWIRCtomakeithappenwithintheduetimeline.Iexpectthesamespirittocontinueinoursuccessiveissues.Withallyoursupportandcooperation,Iamsuretomakethisprojectarousingsuccess.

FromthecurrentmonthwehavestartedInterviewofCMAsholdingHighportfoliosinvariousministries likeExecutiveDirector&CFO etc and alsoCFOs achieved greaterheights and reached a respectable position in public and private sectors.

InadditiontoabovewehavestartedStudentsCornerfromCurrentissueforthebenefitofupcomingCMAs.

OnbehalfofWIRCofICAI,IwishallofyouahappyMerryChristmasandaprosperousNewYearinadvance,praythealmightyforyourgoodhealthandhappiness.

CMA Arindam GoswamiChairman, Editorial BoardFr

om

Des

k o

F C

hie

F eD

itor

WIRC BULLETIN – DECEMBER 2021

6

1. COVID-19isawatershedeventofourera.Ithascausedwidespreaddevastationof lifeand livelihoodandit isstill haunting the global economy in several ways. ThereareveryfewparallelsofashocklikeCOVID-19inhistorywhichleftpolicymakerswithnotemplatetonavigate through the crisis. Both health systems and human endeavor to deal with the crisis were stretched beyond allowable limits.

2. Thepandemichas inducedseveralstructuralchangeswhich have significantly altered the way we work,live, and organize businesses. With greater shift towork from home, technology has gained potential toboost productivity, by saving on travel time, boosting salesononlineplatforms,andacceleratingthepaceofautomation.

3. Global supply chain is undergoing significant shifts;companies and various authorities must be nimble enough to capitalize on these opportunities. Automation androboticswillthreatenlow-skilledworkersandthosein the contact intensive sectors.

4. Atanotherlevel,thepandemichasaffectedthepoorandvulnerable more, especially in emerging and developing economies. Daily wage earners, service and informalsectorworkerswerebadlyhit.Theiremploymentandincome opportunities were curtailed.

5. Technologyadoptionwhichwasearlierlimitedtocoresectors has now permeated to several other areas, viz. education, health, entertainment, retail trade and offices.Thepandemichasalsocauseddisruptionsandinduced reallocation of labor and capital within andacross sectors. The firms which were quick to adopttechnology andwere flexible in working from off-siteare attracting more capital and labor.

The Indian Scenario6. Let us now turn to the Indian scenario. In the post-

pandemicworld,India’sprospectsareunderpinnedbyseveraldynamicsectorswhichbrieflytouchuponsomeofthem.

7. First, information technology (IT) services andinformationtechnology-enabledservices(ITES)backedby entrepreneurial capabilities and innovative solutions have emergedaskey strength of the Indian economyovertheyears.ThereisagrowingleagueofUnicornsinIndiareflectingitspotentialfortechnology-ledgrowth.The countryhasadded severalunicornsover the lastyear to become the third largest start up ecosystem in the world. Underpenetrated Indian markets and

largeITtalentpoolprovideanunprecedentedgrowthopportunity for new age firms. Further, the COVIDpandemic has provided a new impetus to technology-driven companies such as fintech, EdTech andHealthtechwhich are likely to see increased fundingactivity in the coming years.

8. Second, India’s digital momentum is expected tocontinue with a strong demand in areas such as cloud computing, customer troubleshooting, data analytics, workplace transformation, supply chain automation,5G modernization and cyber security capabilities.India has the natural advantage to benefit from theemergingtrendsintheseareas.Thedrivetowardsfullfiberisationoftheeconomymustgohandinhandwiththe establishment of data centers across the nationfor data storage and processing. Ensuring universal,affordable, and fast broadband internet access allthrough the country can play a critical role in advancing productivity and employment opportunities. Various initiatives taken by the government, namely DigitalIndia,make in India,Start-up India,Skill India,andInnovation Fund have created a conducive eco-system forfastergrowthinthedigitalsector.

9. Third, thepandemichasbrought to focuswhat Indiacan achieve inmanufacturing. In the pharmaceuticalsector for the first time in history, vaccines weredeveloped and administered within a year with India remainingaforerunnerandagloballeaderinvaccinemanufacturing.InvestorshaveshownconfidenceintheProductionLinked Incentive (PLI) scheme introducedby the government. Following this initiative, India is now home to almost all the leading global mobile phone manufacturersandduringtherecentperiod,Indiahasturnedfrombeinganimportertoanexporterofmobilephones.Thistrendislikelytospillovertoothersectorsalso. The presence of global players would help inenhancingIndia’sshareinGlobalValueChain(GVC)and building up a resilient supply chain network.Greater GVC participation would also enhance the competitivenessofIndia’s largeandMicro,SmallandMediumEnterprise(MSME)supplierbase.

10. Fourth, the global push towards green technology, though disruptive, can create new opportunities in several sectors. For example, the automobile sectoris moving towards electric vehicles. With greater innovation, electric vehicles are slowly converging to internal combustion engines (ICE) in cost andperformance.ThebiggestElectricVehiclecarmakeris

Envisioning Life Beyond COVID-19

CMA N. Rajaraman

E-mail:[email protected]

WIRC BULLETIN – DECEMBER 2021

7

notfromthetraditionalcarmakercompanies.Similarcreative disruption is also visible in the two-wheelers space. With supportive policies, greener technologies canyieldeconomicandenvironmentalbenefits.

11.Fifth, India’s energy sector is also witnessingsignificantchurningandtechnologicaltransformation.AsIndiagrowsrapidly,itsenergydemandisexpectedtopickupsoon.Currently,a largepartof theenergydemandismetfromfossilfuels,withsignificantimportdependence. India aims to increase the share of non-fossil fuels to 40per cent (450GW) of total electricitygeneration capacity by 2030, as part of the goals setundertheParisagreementwithintheUnitedNationsFrameworkConventiononClimateChange(UNFCCC).With a view to give a boost to the agriculture sector and to reduce environmental pollution, the Government had launchedtheEthanolBlendedPetrol (EBP)Program,whichwouldhelpincleanerairbesidessavingonfuelimports.Thedrivetowardsrenewableenergyisastepintherightdirectionbothforenergysecurityaswellasenvironmentalsustainability,whicharecriticalforourlong-term economic growth.

12.Sixth, in the post-pandemic period, global trade willremain vital for faster recovery. Reflecting congenialpolicy environment and supportive external demand,India’s exports have rebounded, with a broad-baseddouble-digit growth during the first half of 2021-22.India’s exports of agricultural commodities, includingGeographical Indications (GI) certified products tonewerdestinations,offerfavorableprospectsforoverallexport. To strengthen the export potential, there is aneed to enhance the share of high-tech engineeringexports to achieve an ambitious engineering exporttargetofUS$200billionby2030

13.Toachieveourobjectivesinalltheareasoutlinedsofar,weneedabigpushtoinfrastructureparticularlyinareasofhealth,education,lowcarbon,anddigitaleconomyinaddition to transport and communication. In addition, thewarehousing and supply-chain infrastructurewillbe critical to bolster value addition and productivity in the agriculture and horticulture sector. This willcreate employment opportunities in semi-urban and rural areas and promote inclusive growth. Investment in intangible capital such as research and development and skill upgradation of human resource has strongand positive impact on productivity. Some empiricalevidence suggests that the impact of investment inintangible capital on labor productivity is more than investmentintangiblecapital.4

14.Seventh,adynamicandresilientfinancialsystemisattherootofastrongereconomy.India’sfinancialsystemhastransformedrapidlytosupportthegrowingneedsof the economy.While banks have been the primarychannels of credit in the economy aimed at growth,but recent trendssuggest increasingroleofnon-bankfunding channels. Assets of non-banking financialintermediaries like NBFCs and mutual funds havebeengrowing;fundingthroughmarketinstrumentslike

corporatebondshasalsobeenincreasing.Thisisasignofasteadilymaturingfinancialsystem–movingfroma bank-dominated financial system to a hybrid one.Substantialprogresshasbeenmadetofortifyinternaldefensemechanismoffinancialinstitutionstoidentify,measureandmitigaterisks.

Towards a more Inclusive and Sustainable Economy15.History shows that the impact of pandemics, unlike

financial and banking crises, could be a lot moreasymmetric by affecting the vulnerable segmentsmore.TheCOVID-19pandemicisnoexception.Withincountries, contact-intensive service sectors employing large number of informal, low-skilled, and low-wageworkershavebeenhitharder.Inseveralemerginganddeveloping economies, lack of health care access hasdisproportionately affected the family budget of thepoor.Eveneducationwhichwasprovidedonlineduringthepandemicexcludedthelow-incomehouseholdsdueto the lack of requisite skills and resources. Overall,there are evidence across countries that the pandemic may have severely dented inclusivity.

16.The global recovery has also been uneven acrosscountries and sectors. Advanced economies have normalized faster on the back of higher pace ofvaccination and larger policy support. Emerging anddeveloping economies are lagging due to slow access to vaccine and binding constraints on policy support. Multilateralismwilllosecredibilityifitfailstoensureequitableaccesstovaccineacrosscountries.Ifwecansecurethehealthandimmunityofthepoor,wewouldhave made a great leap towards inclusive growth. Globalco-operationremainsvitalforrapidprogressonthisfront.

17. Needless to add that inclusive growth in the post pandemic world will require cooperation and participationofallstakeholders.InIndia,collaborativeeffort of various stakeholders is helping accomplisha seemingly difficult task of accelerating the paceof vaccination. The private sector is developing andmanufacturing the vaccines; the Union Governmentis centrallyprocuringand supplying it; and the stategovernments are delivering and administering it in every nook and corner of the country. India is nowadministeringarecordofaboutonecroredosesofthevaccineeverydayacrossallsegmentsofthepopulation.

18.Amajorchallengetoinclusivenessinthepostpandemicworldwouldcomefromthefilliptoautomationprovidedby the pandemic itself. Greater automation wouldlead to overall productivity gain, but it may also lead toslackinthelabormarket.Suchascenariocallsforsignificant skilling/training of ourworkforce.We alsoneedtoguardagainstanyemergenceof“digitaldivide”asdigitizationgainsspeedafterthepandemic.Further,the need for professional human resources trained inscience, technology, engineering, and mathematics (STEM) is rising briskly. Major technology-based

WIRC BULLETIN – DECEMBER 2021

8

firmshaveexpressedtheirintentiontohiremanynewprofessionalswith skills in these areas. In the short-term,thesupplyofsuchaworkforcecannotbeincreasedby the traditional educational system, and thus there is aneedforcloseinvolvementofcorporatesinthedesignandimplementationofcoursessuitabletothechangingindustrial landscape.

19.Aswe recover,wemust dealwith the legacies of thecrisis and create conditions for strong, inclusive, andsustainable growth. Limiting the damage that thecrisis inflicted was just the first step; our endeavorshould be to ensure durable and sustainable growth in the post-pandemic future. Restoring durability ofprivate consumption, which has remained historically themainstayofaggregatedemand,willbecrucialgoingforward.Moreimportantly,sustainablegrowthshouldentailbuildingonmacrofundamentalsviamediumterminvestments, sound financial systems, and structuralreforms.TheProductionLinkedIncentive(PLI)schemeannouncedbytheGovernmentforcertainsectorsisanimportantinitiativetoboostthemanufacturingsector.It is necessary that the sectors and companies which benefit from this scheme utilize this opportunity tofurther improve their efficiency and competitiveness.

In otherwords, the gains from the scheme should bedurableandnotoneoff.

20.Again, for growth to be sustainable, a transitiontowardsgreener futurewill remain critical.Theneedforcleanandefficientenergysystems,disasterresilientinfrastructure, and environmental sustainabilitycannot be overemphasized. Due consideration should be giventoindividualcountryroadmapskeepinginmindcountry-specificfeaturesandtheirstageofdevelopmentwhile adopting policies towards climate resilience.

Conclusion21. Overall, while the pandemic has created enormous

challenges, it can also act as an inflection point toalterthecourseofdevelopment.Enhancedadoptionoftechnology will give impetus to productivity, growth, and income. Leveraging technology in implementinggovernment schemes, training, and skill developmentprogramfortheunemployed,promotingwomenfriendlyworkatmosphereandsupportingeducationofthepoorandmarginalized sectionswould be areas of focus asweembarkonour journeybeyondCOVID-19. Incomeand job creation with digitalization and innovation can bringaboutanewageofprosperityformanypeople.

WIRC Associate Members – November 2021M.No. NAME CITY

51356 HareshKantilalPrajapati Palanpur

51359 AbaBabanJagadale Satana

51362 VasantDinkarTondwalkar Aurangabad

51366 Keyur Kishorbhai Chhag Ahmedabad

51367 RameshKumarJha Satna

51370 Mohit Chandrabhan Goswami Mumbai

51376 TruptiVishwanathRedkar Mumbai

51378 AkshayDnyandevGhagre Panvel

51387 ShivshankarPanda BadlapurEast

51398 AkankshaRajeshDurve Vadodara

51401 IndraneelVasudeoJadhav Pune

51407 JaydipHarshadraiKikani Ahmedabad

51419 RadheshyamLalitkumarSharma Aurangabad

51421 PratibhaDilipkumarOjha Kalyan

M.No. NAME CITY

51428 RajanPravinkumarRathod Surat

51432 ArwaShabbirKanchwala Mumbai

51436 VinayakBhalchandraPanchal Mumbai

51442 AnandKukreti Surat

51450 RupeshSunilKale Sangli

51456 SavananiSoniShaukinbhai Ahmedabad

51457 HarshHemantRathod Surat

51462 ForamKiritkumarTrivedi Adipur

51470 LiladharShriramDevdhar Dombivili

51471 SachinDeepakRathor Aurangabad

51472 JankiRohitKumarAcharya Ahmedabad

51474 TejasVishwasAsawadekar Pune

51481 SachinNatubhaiWaghela Mumbai

51482 UjjwalSoni Gadarwara

WIRC BULLETIN – DECEMBER 2021

9

Impact of COVID 19 on Indian as well as Global Economy

CMA Jay Mehta

Mob.:8690611515E-mail:[email protected]

NEW DELHI: TheUnion Cabinet onMonday approvedRs. 30,600 crore government guarantee for theNationalAssetReconstructionCompany(NARCL), therebypavingthewayforoperationalisationofbadbank.Theproposalhascomeasawelcomemoveforthebankingsector which has been reeling under the weight of badloans.Oneofthekeyideasbehindformationofbadbanksistode-stressthebalancesheetsofthebanks.Lastmonth,theIndianBankingAssociation(IBA)movedanapplicationtotheReserveBankofIndia (RBI) fora licencetosetupa Rs.6,000-croreNARCL.

• Whatisabadbank A bad bank is a corporate structure that isolates

risky assets held by banks in a separate entity. It isestablishedtobuynon-performingassets(NPAs)frombankatpricethatisdeterminedbythebadbankitself.

In Budget 2021-22, finance minister NirmalaSitharamanhadannouncedsettingupofabadbankaspartofresolutionofbadloansworthaboutRs.2lakhscrore.

As per the announcement made on Thursday, thebadbankorNARCLwillpayupto15percentoftheagreedvalue forthe loans incashandtheremaining85percentwouldbegovernment-guaranteedsecurityreceipts.

Thegovernmentguaranteedwouldbeinvokedifthereis loss against threshold value.

• Howbandbankwillbenefitbusinesses,consumers Ifabankhashighnon-performingassets(NPs),alarge

partofitsprofitswouldbeutilizedtocutlosses.Asaresult, any bankwith highNPAs is likely to becomemore risk averse and would be less willing to lendmoney to borrowers. It would become more difficultfor businesses and consumers to take loans frombank,therebyimpactingtheoverallrobustnessoftheeconomy.

Moreover,inIndia,alargeportionofNPAsiswiththegovernment-owned public sector banks. In the past,thegovernmenthadtoinfusefreshcapitaltoimprovethefinancialhealthofPSBs.Thegovernmentinfusingfreshcapital inPSBs.Thegovernment infusing freshcapitalinPSBsmeanslessmoneyforotherschemes.

• HowmuchNPAsdobankshave AsofMarch2021,thetotalbad loans inthebanking

systemamountedtoRs.8.35lakhcrore.

AccordingtoReserveBank’sfinancialstabilityreport,thegrossnon-performingassets(GNPA)andnetNPA(NNPA)rationsremainedstableduringthesecondhalfof2020-21,amountingto7.5percentand2.4percentrespectively in March 2021.

A stress test conducted by RBI showed that GNPA ratio forscheduledcommercialbanks(SCBs)mayjumpfrom7.48percentinMarch2021to9.8percentbyMarch2022 under severe stressed condition.

• HowmuchbadloansforNARCL? Thevalueofbadloansbeingcarvedoutofbankbooks

fortransfertotheNARCLisaroundRs.2lakhcrore.AboutRs.90000croreinbadloanswillbetransferredinthefirstphase.TheguaranteeofRs.30600crorewillcovertheentirepoolofRs.2lakhcrore.

Thegovernmentguaranteewillbevalidforaperiodoffive years and the condition precedent for invocationof the guaranteewill be resolution or liquidation. Todisincentivizedelayinresolution,NARCLhastopayaguaranteefeewhichincreaseswiththepassageoftime.

• Comparisonwithglobalpeers AsperWorldBankdata,shareofNPAtogrossloans

inIndiaissignificantlyhighercomparedtodevelopedwesterneconomies.Italsoexceedsmostotheremergingeconomies.

• Capitaladequacyratioof16% Further, the capital to risk-weighted assets ratio

(CRAR)ofSCBsincreasedby130bpsfrom14.7percentin March 2020 to per cent in March 2021, with PVBs improvingtheirratiosevenfurther.

CRAR measures a bank’s financial stability bymeasuring its available capital as percentage of itsweightedcreditriskexposure.

AhigherCRARshowsthatthebankisbettercapitalisedto handle NPAs.

Asperthefinancialstabilityreport,underthebaselineand the to stress scenarios, the system level CRAR held upwell,moderatingby30basispointsbetweenMarch2021 and March 2022 under the Vaseline scenario and by 130bps and 256 bps, respectively, under the twostress scenarios.

However, even though the level of CRAR reduces insevere stress condition but remains above the regulatory minimumof9percentasofMarch2022.

WIRC BULLETIN – DECEMBER 2021

10

Trade and Trade Finance in the COVID-19 crisis

CMA (Dr.) Subir Kumar Banerjee

Mob.:9820113419 E-mail:[email protected] No. 3

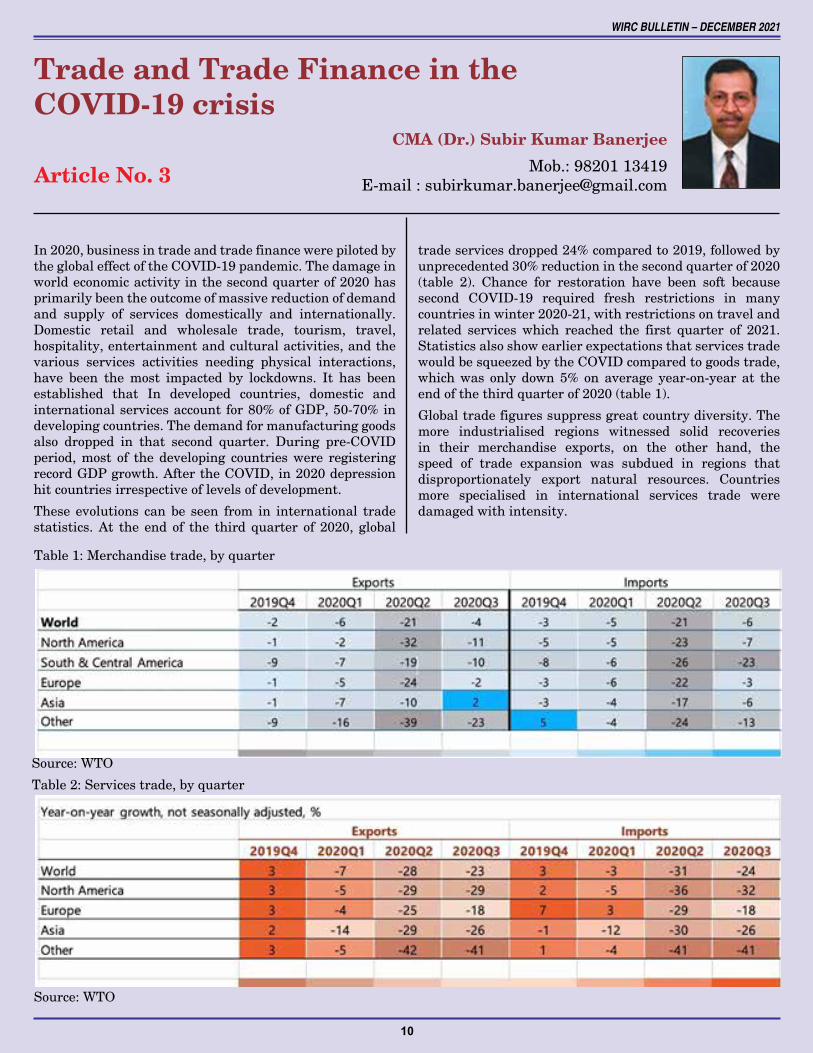

In2020,businessintradeandtradefinancewerepilotedbytheglobaleffectoftheCOVID-19pandemic.Thedamageinworldeconomicactivityinthesecondquarterof2020hasprimarilybeentheoutcomeofmassivereductionofdemandand supply of services domestically and internationally.Domestic retail and wholesale trade, tourism, travel, hospitality, entertainment and cultural activities, and the various services activities needing physical interactions, have been themost impacted by lockdowns. It has beenestablished that In developed countries, domestic and internationalservicesaccountfor80%ofGDP,50-70%indevelopingcountries.Thedemandformanufacturinggoodsalso dropped in that second quarter. During pre-COVIDperiod,most of the developing countrieswere registeringrecordGDPgrowth.AftertheCOVID,in2020depressionhitcountriesirrespectiveoflevelsofdevelopment.

These evolutions canbe seen from in international tradestatistics.At the end of the thirdquarter of 2020, global

tradeservicesdropped24%comparedto2019,followedbyunprecedented30%reductioninthesecondquarterof2020(table 2). Chance for restoration have been soft becausesecond COVID-19 required fresh restrictions in manycountries in winter 2020-21, with restrictions on travel and related serviceswhich reached the first quarter of 2021.StatisticsalsoshowearlierexpectationsthatservicestradewouldbesqueezedbytheCOVIDcomparedtogoodstrade,whichwas only down5%onaverage year-on-year at theendofthethirdquarterof2020(table1).

Globaltradefiguressuppressgreatcountrydiversity.Themore industrialised regions witnessed solid recoveries in their merchandise exports, on the other hand, thespeed of trade expansion was subdued in regions thatdisproportionately export natural resources. Countriesmore specialised in international services trade were damaged with intensity.

Table1:Merchandisetrade,byquarter

Source:WTO

Table2:Servicestrade,byquarter

Source:WTO

WIRC BULLETIN – DECEMBER 2021

11

Internationalorganisations’currentexpectations,includingtheWTO,anoveralldropofworldgoodstradeandservicesofbetween-7%to-10%.Thebaselineoutlookfor2021isoneof relativelymassiverestoration(aroundof6-8%growth)butexpectationwillbemodifiedinthespringtoconsiderofthepaceofvaccinationandofglobaldemand.

Whatishappeninginshort-termtradefinancing?Short-term (ST) trade finance products which providesdeferred payment over a period of less than one year(usually less than 180 days) are the usual form of tradefinance.These loans are at risk during periods ofCOVIDresulting of surge of prices and bring downsupplyavailability (OECD, May 2020[3]). Few information isofficiallypublished forST trade finance.This is because,asmostof these finance issuppliedbytheprivatesectorandcomesinmanyways(intra-firmfinancing, inter-firmfinancing,ormorededicatedtoolssuchaslettersofcredit,advance payment guarantees, performance bonds, andexportcreditinsuranceorguarantees).

Intheperiodduringthe2007-2009slowdown/crisis,ShortTermtradefinancereducedinabigwaybecauseofpressuresonprivateinstitutions’liquidity,thatresultedinincreasedcostsoftradefinance.Ontheotherhand,banks’liquidityhasnoproblemafterappearanceofCOVIDin2020.Because,after crisis of 2007-09, for a decade, all leading financialauthorities of major countries squeezed legislations withhighcapitalbuffersleadingtobankingsystemsaresaferin2020.TheTEDspread(isanacronymformedfromT-BillandED,thetickersymbolfortheEuro-dollarfuturescontract).TEDspreadisthedifferencebetweentheinterestratesoninterbank loansandonshort-termU.S.governmentdebt(“T-bills”) which is usually a broad liquidity indicator ofST trade finance.The TED spread initially boosted up to1.46%(itshighestlevelsincethe2007-2009crisis),andatthebeginningoftheCOVID,itimmediatelyreducedtoitslevelsbeforeCOVIDandcontinuedtolowsincethen.Wecan conclude that opposed to what we saw during the 2007-2009Crisis,thecostofSTtradeliquidityhasnotgoneupandampleliquidityopportunitiesisavailabletoexportersinthebankingsystem.

However, exporters have their challenges in getting STfinancingintheprivatemarket.IntheUnitedStates,theWallStreetJournal(JulieSteinberg,Sep2020[6])revealeda 60% surge in rejected applications for trade creditinsurance.Also, the InternationalChamberofCommerce(ICC)revealedacurtailmentofbanksfromfinancialsectorshas“highrisk”alongwithboostinthecostofSTfinancingfor SMEs (ICC, Nov 2020[7]). Export Credit Agencies(ECAs) are witnessing boost in the demand for their STproducts.Asaresult,43%ofECAshaverevealedgrowthintheirbusiness,mainly inSTproducts.USEximrecorded112% surge in working capital guarantees and a 12%increment inSTexport credit insuranceduring the2020fiscalyear.Simultaneously,GermanECA(EulerHermes)revealedthatithadseenamassiveboostover33%inthenumberofapplicationsforexportcreditguaranteesforthefirsthalfof2020.Theseindicatethateventhoughlendinginstitutions may have ample liquidity to offer funds to

exporters,theirriskassumingmayhavereducedresultingin limited availability of trade finance for exporters anda policy towards governments performing via respectiveECAs.

WhatishappeninginMLTexportfinancing?

Medium-andlong-term(MLT)exportfinancingismainlyutilised for the funding of basic equipment which needbig repayment periods. Most ECAs and multilateralinstitutionsfundtheseprojectsinMLTfinancingcomparedtoSTfinancing.Gradually,privatemarketareencroachingMLTfinancing.However,thereisavailableinformationonexportcreditsbyOECDcountriesinMLTexportfinancing.When observing at this non-comprehensive data, it is felt that the volume of export credits and the number oftransactions have reduced in 2020, with negative (-34%)volume and also (-15%) in number of deals. In the firsthalfof2020,theGermanECAdisclosedareductioninthevolumeofcoverbecauseofthelowernumberofbig-ticketprojects, mainly in the transportation sector in cruise ships, aircraft. The Canadian ECA has witnessed its financingandinvestmentactivityreducedby16%,mainlybecauseofa30%reductioninloanssinceofdiminutionintheoil,gasandminingsectorduringthefirstthreequartersof2020.

Tradefinancedatalacking,butdemandforsupport upHowever, it is difficult tomake comparison of trade andtradefinancedata,becausethereisstillnosoloexhaustivesetof combinedstatistics for trade finance.From2008-9,international agencies like the Berne Union and othershavemadebigeffortstogatherdependableandexhaustiveinformation in their own zones of activities. However,information on bank-intermediated trade finance, likestructured finance (letters of credit and the like) orsupplychain finance,arestill lacking.For2020, it isnotpracticable to predict accurately as to worldly the supply oftradefinancehaddroppedmorethantrade,asaresult,contributingspecificallytothatfallintradeflows.

However,manyprominentfinancialinstitutionswhichareeminentinreducingcross-bordertradefinancerisks, likeECAsandmultilateraldevelopmentbanks,haverevealedasuddenspurtinthedemandfortheirservicesandfacilities,with insomecasesandcountries,backingthesegesturesbeingimportanttomaintainingthechannelsoftradeopenatthetopoftheongoingCOVID.

At the top of theCOVIDposition, during administrationrestrictions, manufactures and traders engaged in worldsupply chains dealt got massive disturbance of supplychannels, operational disruptions of shipping goods, andproblems in channeling trade, customs, ports documents requiredtoprocesstransactionsphysicallyandfinancially.They eventually innovate, evolving creative, for timebeing,andnextbestsolutionstoavoidthesebarriers.Thecircumstancesoftenedabitonthecrucialroutesoftradeinsummer2020,attheexitofthefirstwaveofshutdowns.Simultaneously, it was crystal for numerous economicoperators,which included trade finance institutions, thatthehealthproblemwillremainformoretime.Alsorevealed

WIRC BULLETIN – DECEMBER 2021

12

and that adhoc supplement of the terms of payments bycreditors would be not enough to handle with a more extension time of strain. Bankers and trade financierspredicted payment strain which would reach outside the rangeofthesectorsinitiallyeffectedbytheCOVID(airlines,aeronautics,tourismetc).

Sovereign and corporate risk uptickIn many countries, sovereign risk downgraded withcorporaterisk.Itresultedinadditionalwarningonoverseaslending.Onemustadmitthatthefinancialsectorhasbackedmaincustomersatthetimeofcrisis–theywereinabetterand comfortable position to do so than during the globalfinancialcrisis(GFC).However,indigenously,thedemandforbanks’lendingsurpassedthatitalsodemonstratedthemore unwillingness to engage in overseas trade operations.

Inorder toavoid the ‘scissors’ effect (iswhat takesplacewhenRevenuesandExpensesmoveindifferentordivergingdirections) to boost demand and reluctance of supply offinancerelatedtoincrementalriskaversion,governments,ECAs and international financial institutions massivelyintervened to back private markets. They have suppliedrobustamountsof trade financeguaranteesand liquidityin developing countries. The governments introducedpaymentdeferral schemes, alongwithdictatingdomesticlending support to companies. Big central banks havereleased foreignexchangetoothercentralbanksthroughswap agreements.

WTOincreasesprofileoftradefinancesupportDuringCOVID,theWTOhasincreasedtheprofileoftrade

financeatapolicylevel,asoneofthemanycrucialissuesneedingglobalbackingandmutualunderstanding.OnJuly1, 2020, the then Director General of theWTO releaseda joint statement with six other heads of MultilateralDevelopment Bank (MDB) with assurance of biggercoordinationinbackingtotradefinancemarkets,speciallyto developing countries. Simultaneously, the DirectorGeneral agreed to jointly operate with the private sector (theInternationalChamberofCommerceandtheG20)withtheidenticaltargetofclubbingresourcesandbackingtradefinancemarkets.Thepresenceofpublicsectorinstitutionsinmarketshasbeenveryprominent,anditmakesasteadyeffecttomarkets.

InNovember2020,theWTOagainpinpointedtheproblemsof trade finance in presence of G20 Leaders requestingfor extended boost in support of trade finance into 2021.Therewerebarriers for2021 includenot jointbackingofimports and exports of vaccines against COVID-19. TheG20supremosknewthesechallenges.Themainagendainthissummitwastomaintainandpusheffortssothattherecoveryofglobal trade flowsareexpedited.Thepositivenews is that they are still engaged in this mission.

Reference1. https://www.berneunion.org/Articles/Details/540/

Trade-and-trade-finance-in-the-COVID-19-crisis

2. Trade finance in the COVID era: Current and future challenges (oecd.org)

3. Trade Finance in the COVID era: Current and future challenges (enterprisegreece.gov.gr)

WIRC Help Desk - CMA ExaminationsWIRChasdecidedtocreateaHelpDeskforthestudentswhoareappearingforDecember,2021Examinationsanditwillstartfunctioningwithimmediateeffect.ThefollowingStaffmembersareavailableforattendingtheproblemsfacedbythestudentsregisteredintheWIRCRegion.

Mr. D.G. Vanjari - M: 98921 85588Mrs.RakshaVanjara-M:9372036890Mrs.LataBhagwat- M:9372167164

Incaseyourproblemsarenotattendedsatisfactorilyyouareherebyrequestedtosendamailto [email protected]

StudentsappearingfortheDecember,2021Examinationsareherebyrequestedtomakeuseof the Help Desk created by WIRC of ICAI

With best wishes

CMA Arindam GoswamiChairman,

Students Members Co-ordination Committee

CMA Dinesh Kumar BirlaChairman,

WIRC- ICAI

WIRC BULLETIN – DECEMBER 2021

13

Financing India’s Economic Growth Post Pandemic

CMA (Dr.) S. K. Gupta

Mob.:9810162341 E-mail:[email protected]

The PerspectiveIndia’s economy is struggling to emerge from the shock ofthe pandemic, with the shadow of a possible third wave ofinfections looming large. Besides responding to this threatby stepped-up vaccination efforts, what else should be onpolicymakers’ minds? Perhaps the strategies for prudentfinancial management including identifying sources forgenerating and infusing required funds into the economyoughttobeaprimaryconcernintryingtogetIndiabackontoa rapid growth path. Armed with necessary macro and micro growth drivers, the stage is set for India’s investment cycletokickstartandcatalyzeitsrecoverytowardsbecomingthefastestgrowingeconomyintheworld.

TherearesignsofdeepmalaiseintheIndianeconomy.Growthisslowingsignificantlyandthereiscurrentlylittlefiscalspaceavailable to the government to spend more. Corporate and household debt is rising, and there is deep distress in parts of the financial sector., especially amongst youth, seems tobegrowing,asistheaccompanyingriskofyouthunrest.ButprobablymuchmorewillbeneededtoprovideneededfinancialgreaseforthewheelsoftheIndianeconomy.Aconcertedefforttocreateandexpandnewplatformsforbusinessfinanceoughttobeatoppriorityforpolicymakers.

India’sgrowthwilltakeoffwhenfirmsofallsizescanbetteraccessfinancialresourcesfordailyoperationsandinvestmentsthat will aid their individual growth trajectories. India’sdecade-long credit collapse is a symptom of deep structuralproblemswithitsinstitutionsoffinancialintermediation

Financing India’s Growth RevivalThe pandemic has plunged the Indian economy into acontraction, and government revenues have taken a majorhit.Supporting thecountry’snascenteconomicrecoverywillrequireamassivespendingpackage.Howwillthegovernmentfundthestimulus.Indiahasundertakensignificantstructuralreforms to turn the crisis into an opportunity and emergestronger. Among themost notable reforms, PLI schemes toboost manufacturing, and National Infrastructure Pipelinecomplemented by the National Monetization Pipeline and PM GatiShaktiwouldhelpenhanceIndia’sglobalcompetitivenessandsetastrongfoundationforsustainingIndia’spostCovideconomic growth.

InresponsetotheCOVID-19shock,thegovernmentandtheReserveBankofIndiatookseveralmonetaryandfiscalpolicymeasurestosupportvulnerablefirmsandhouseholds,expandservicedelivery(withincreasedspendingonhealthandsocialprotection)andcushiontheimpactofthecrisisontheeconomy.Thanks inpart to theseproactivemeasures, the economy isexpectedtorebound-withastrongbaseeffectmaterializinginFY22-andgrowthisexpectedtostabilizeataround7percentthereafter.

Re-energizing credit for sustained economic recoveryIndiaisoftendescribedasan‘investment-led’economy.Givenits stage of development, sustained investment is neededfor sustained economic growth. Availability of credit is aprerequisiteforinvestments.Variousmeasuresannouncedbythe governmentand theRBI to dealwith the impact of thepandemic,arenecessaryanduseful.Theywouldhelpbanksremainonanevenkeelastheeconomyrecovers.However,toensuresustainedgrowth,thatis,realGDPofover7%,whichiswidelyacceptedastheaspirationforIndia,thestructuralcollapseofcreditoverthelastdecadewillhavetobeaddressed.

Strengtheningthebankingsystem,whichisstrugglingwithastubborn bad-loan problem, is a crucial ingredient in reviving theeconomy.Buttheformthebankrescueplanwilltakecansignificantly affect its effectiveness. Should there be a bankrecapitalizationplaninthebudget?Orshouldthegovernmentannounceprivatizationofmajorstate-ownedbanks?Comparedto other large economies around the globe, India does not have the credit institutions in place to support the real economy on the scale its growth needs demand. The savings ratio a bigdeterminant of economic activity. Investment depends onsavingrateIfpeoplesavemore,itenablesthebankstolendmoretofirmsforinvestment.WeneedaGrossFixedCapitalFormationof50%ofGDPtogrowat10%pa,but thecreditdelivered to the real economy for this level of investment iszilch:zerofrom2011-12to2019-20.

The government and the Central Bank have undertakenvariousmeasures to protect the banking and finance sectorfrom the adverse impact of the Covid-19 crisis. However,despite historically low interest rates, credit growth has been rather low in recent quarters.

Infrastructure: An enabler of growth Infrastructureisinextricablylinkedtogrowthbyitsinherentability to support livelihoods, drive businesses, generate employment and, in effect, determine the quality of life.Investment in infrastructure ishencepivotal foracceleratedand inclusive socio-economic development of a country.Synergizing MSME-specific infra projects with overallAtmanirbhar Bharat Mission and National InfrastructurePipeline investment (NIP) goals would lead to significantlybetter outcomes.

Investment into creating world-class infrastructure hingeson availability of long-term capital at scale. Financing ofinfrastructureinvestmentsatthescaleenvisagedunderNIPnecessitates a re-imagined approach, and looking beyondthe traditional sources or models of financing. This is whyNIP emphasized on innovative mechanisms–such as asset monetization– for generating additional capital. A sizeable

WIRC BULLETIN – DECEMBER 2021

14

inventory of infrastructureassetshasbeen createdover thepast decade through public investments, which can now be leveragedfortappingprivatesectorinvestmentandefficiencies.TheneedforadoptionofsuchalternativemechanismshasonlybeenfurtherpronouncedinthewakeofCovid-19.

TheIndiancreditdeliverymechanismhaslaggedtheUSandChinaisprovidingcredittotherealeconomy.TheUS,whichhas a very active bond market for corporates, still deliverscredittotherealeconomyinexcessof200%ofGDP.InChina,wheredomesticcredittotherealeconomywas50%ofGDPhasgonetonearly200%GDPpresently.comparedtootherlargeeconomies around the globe, India does not have the credit institutions in place to support the real economy on the scale its growth needs demand over the past decade, investment peaked at 34 percent of GDP in 2011-12 before starting aseculardeclineacross theprivate andpublic sectors to 32.2percentofGDPin2018-19,30percentofGDPin2019-20and28percentofGDPin2020-21withacorrespondingnegativeimpact on growth over the last nine quarters.

Deleveraging the public sectorMore heartening is the government’s recent initiative tomonetize operational assets of the public sector by leasingthem on a long-term basis to private investors. This willsubstitute private for public sector capital and provide anexitoptionforpublicsectorcapital.MisdirectedstimulusthatreliesheavilyonliquidityinfusionwhendemandisdepressedandincentivizingloandefaultsbyroutinelywritingoffNPAsthreaten financial stability and economic recovery. post-Covid-19 there is the possibility of a largermacroeconomic-financial stimulus than India has seen for a long time. Acalibrated stimulus that rises as supply conditions improve, can lead marginal propensities to spend to rise above those to save, and trigger a switch to a higher growth path.

Whatshouldbethefocus?• Investmentisafundamentalvariableamongthesources

ofeconomicgrowth.

• Thesemayincludepeople,knowledgebases,institutionalcapacityortheobviousphysicalcapitalitself.

• The efficiency of the process of savings generation andchannelizing them into productive investment is crucial forsustainedeconomicgrowth.

Whatneedstobedone?• Indianbanksshouldbegivenmore freedomto tapbond

marketsforfundinglonger-termloans.

• Thiswillallowmarketstosendbetterpricesignalsaboutbankportfolios.

• ThereisadireneedforacorporatebondmarketinIndiathatwillallowfirmstoborrowmoredirectlyfromsavers.

• This does not stop at long-term borrowing, but othershort-term borrowing can also benefit from newmarketplatforms.

• India’sfinancialsystemregulatoryarchitecturealsoneedsto be enhanced.

• This involves not just external oversight by financialregulators but also strong corporate governance, with greater disclosure and transparency.

• Auditorsandratingagenciesalsoneedtostepupanddotheir jobs better.

• Thegovernmentcanfacilitatethisbyraisingandenforcingstandardsfortheprivatesectormonitoringinstitutions.

• Thechallengenowismovingbeyondimprovingfiscalpolicyor monetary policy and addressing the political component too.

ConclusionTheCovid-19pandemichasposedimmenseeconomicchallengesandhaselicitedastrongandcomprehensiveresponsefromthegovernment and the RBI. While close attention needs to be giventotherecoveryfromthepandemic,long-termstructuralissues in credit shouldnotbeoverlooked.Theeconomymaybouncebackfromthepandemic,buttheresultinggrowthwillnot be sustained, unless these structural issues are resolved. Financial sector ismeant to sub-serve theneeds of the realeconomy and cannot drive growth by itself. We have seenthepitfallsofthefinancialeconomyracingaheadoftherealeconomyintheformoftheGlobalFinancialCrisis.

TheIndianfinancialsystem,thus,needstolookatnewwaysofdoingbusiness, in termsofknowledge-basedbankingandbetter management of information. It is necessary to tailorthenewinstitutionalfundstolongterminvestments.Besides,the next stage of industrial financing would depend on anaccelerated development of the bondmarket facilitating thesecuritizationofcorporatelending.

Indianeedstolayoutacredibleroadmapandtimeframeoverwhich itwill return to fiscal rectitude.As suggested by theFRBM committee, a commitment to bring public debt down to a target level over themedium term, and the creation ofa watchdog institution like a fiscal council to limit creativeaccounting, will ensure India has some fiscal space to acttoday. Of course, India has consistently postponed fiscalconsolidation when consolidation has required hard choices.

References• Beck,T.,Levine,R.andLoayza,N.(2000).“Financeand

Source of Growth”, Journal of Financial Economics, 58 (1-2): pp. 261- 300.

• Demetriades, P.O and Hussein, K.A. (1996). “DoesFinancial Development Causes Economic Growth? Time Series Evidence from 16 Countries” Journal of Development Economic, 1996, pp. 387-411.

• Dickey,D.A.andFuller,W.A. (1981).“LikelihoodRatioStatistics for Autoregressive Time Series with a Unit Root”, Econometrica, 49, pp. 1057-72.

• Goldsmith,R.(1969).FinancialStructureandDevelopment,1969,NewHaven,CT:YaleUniversityPress.

• Graff,M. (1999). “Financial Development and EconomicGrowth–AnewEmpiricalAnalysis”.Dresdendiscussionpaper series in Economics, 1999.

WIRC BULLETIN – DECEMBER 2021

15

1. What do you feel about your role as CFO of mid-sizecompany?

IamworkingasaJointDirectorinJuniorAdministrativeGrade (JAG) level inGovernmentof India.Presently,being posted in the Department of Pharmaceuticals(DoP),MinistryofChemicals&Fertilizers,holdingthechargeofPricingDivision.TheDivisionlooksafterthePolicyIssuesofthefunctionsofNationalPharmaceuticalPricingAuthority (NPPA),whichisanattachedofficeofDoP.Therefore, it ismoreofadministrativenaturerather than technical one.

Besides that, I am also working as part timeGovt. Nominee Director for some PSUs under theadministrativecontrolof thedepartment.Thoughnotdirectly involved as Financial functionary, as a parttimedirectorofPSUs,Ihavetolookafterthevariousfunctionsofthesecompanies,includingthoseoffinancialone. I am supposed to record my critical observations in the line of Government’s interests and decisions.Clearly, these involve the comments on financialmattersalso,withintheGovernmentframework.

2. WhatinspireyoutopursingCMAqualification? I am a Graduate and Post Graduate in Mathematics

with specialization in Graph Theory and OperationsResearch. Given my special interest in mathematics and influenceofmylatefatherasfinanceofficerinHeavyEngineeringCorporation(HEC),choosingthecourseofCost Accountancy was only natural. It gives me edge inanalysingthefinancialandeconomicaspectsoftheissues coming as such.

3. How the CMA qualification helps you in yourcareerpath?

RightnowasamemberofIndianCostAccountsService,mycareerpathbeginswithCMAitself,thoughduringthe course of the Government Service I may assumeseveral other roles, but seeds are always the same, that is CMA. It gives me distinct identity among the various officersfromotherServicesandaccordinglyputsonustoimpartdistinctiveperformance,parallelyconformingto establish generalistic standards as well.

4. How would you evaluate the role of CMA inmanufacturingindustry?

Manufacturingindustrybroadlyinvolvesstandardisedproduction and job based production. Both of theseprocesses requireactiveanalysisof costand financial

records. During my posting in Audit Commissionerate ofCentralGST, itwas realised that such recordsaremuchinneedtosatisfythequeriesraisedbythegovt.authorities.This is inadditiontotheir inevitableroleforinternalcontrolsaswell.

5. How a CMA can helpful to industry in Cost Control and Cost Saving, especially manufacturing industry?

As I pointed out in previous question, active analysis involves the capturing, recording and compiling the cost dataatlowerlevels.Thereafter,atmiddlelevels,thesedata are analysed at various steps and meaningfulinformationaregeneratedforthepurposeofdecisionsto be made by the Top management. This is quitehelpfulincostcontrolagainsttheprescribedstandards.Similarly, proper recording and analysis helps toidentify wasteful and unnecessary expenditures, onwhichthehighermanagementmaytakedecisions fortheirsavings.Needlesstosaythatforallthisprocesses,CMAsaremostproficientatvariouslevels

6.How aCMA’s role is important formanagementunder COVID situation to improve productive andprofitability?

Continuingwithmypreviousopinion,itmustbekeptinmind that better control and savings automatically lead to improved productivity and profitability. However,this unprecedented pandemic situation has not only posed new challenges in the way of carrying out thevarious activities, but also provided us the opportunity toadoptthenewtoolsandtechniquesforthesame.Asagovernmentofficer,Ihavefoundmyselfquiteeffectivein handling the departmental work, when it is wellknown that DoP had 24X7 role in those challengingdays.ThereisnoreasonthatCMAscan’tdothesamefortheirrespectiveorganisations.

7. What are your views about statutory cost records maintenanceandcostaudit?

PresentsystemisOk

8. Does the Cost Audit create value addition for industry?

Yes, as it gives inner look at the performance of theorganisationagainstvariousparametersofoperations.

9. How the performance appraisal report by cost auditor which is laid down in earlier rules 2011 willbeusefultoindustry?

CMAs at Helm as a policy maker (Ministry - Govt. of India)

CMA Pawan Kumar, ICoAS

JointDirector, DepartmentofPharmaceuticals

WIRC BULLETIN – DECEMBER 2021

16

The performance appraisal report by Cost Auditoris to be submitted to Board / Top Management andis confidential in nature. It contains the informationabout various cost drivers that may have impact on performance,profitabilityandstrategicoutlookof thecompany. Naturally, it gives a good analytical and decisiontoolformanagementofthecompany.Strategicoutlook gives an overall approach to whole of theindustrytoaddressgreyareasoftheirperformanceaspointed out by the Cost Auditors

10. Your message to young CMAs. ThoughbeingCMAisyourcorecompetence,butalways

be ready toaccept the challenges toget intoarenaofnewknowledgeandworkingexperience.

11. What do feel about your role as Head Finance for a Corporate Services of the country’s largest PSU andamultinationalcompany?

AsIamnotincorporatesector,anypracticalexperiencecannot be shared.However, it can be easily assumedthatasaheadofanywingororganization,challengesaremoreofgeneralisticnature,ofcoursethetechnical

competence will always be required. Major challenges are tokeepthefinancedivisioninlinewithorganisationalgoals by application of regular innovative methods,creativities and initiatives and yes, not leaving alone the360degrees’interpersonalrelationships.

12. What inspired you to pursing CMA with other professionalqualification?

Being CMA has an edge in analysis and understandings offinancialresults.Itisbutnaturaltohaveitpursuedwithotherprofessionalqualifications.

13. How the CMA can be helpful in direct taxation to taxpayeraswellasgovernment?

By dint of their knowledge and exposure, a CMA isno less efficient in servicing the taxpayers in directtaxation,whencomparedtotheircounterpartslikeCAsand others. By stressing on ethical practices in this field,usefulcontributiontothegovernmentcanalsobeensured.

Asaprofessionalbody,CMAscanoffertheirvaluablesuggestions to the government.

Membership FeesMembersarerequestedtopaytheirMembershipFees.

UseFollowingmethodswhilemakingtheMembershipFee,online.Pleasenotethatyouhavetoinclude18%GSTwhilemakingthepayment.

1. MakethepaymentdirectlythroughOnlinePaymentthroughInstitutewebsite:-

Link-https://eicmai.in/MMS/PublicPages/UserRegistration/Login-WP.aspx

Incaseofanytroublewhilemakingthepaymentonline,pleasetrytoavoidmakingdoublepayment.

2. You canmake the payment atWIRCbyChequedrawn in favour ofICAI-WIRCfortherequisiteamount.

(ChequedrawninfavourofWIRCofICAIyoucansendbyposttoWIRC)

3. YoucanalsomakethepaymentinthenearestChapter.

WIRC BULLETIN – DECEMBER 2021

17

CMAs at Helm as a Business Enhancer (Public Sector Undertaking - Govt. of India)

CMA S. M. ChoudhuryDirector Finance,

SouthEasternCoalfieldsLtd,Bilaspur

1. Despite the current uncertain situation due to COVID-19, SECL, the largest Coal producing subsidiary of Coal India Limited, has been able to excel in coal production. What are the significant contributions and achievements that deserve mention?

Ans.:DuringunprecedentedCOVID-19pandemicandnecessitating complete lockdown, our coalmines keptrunning and producing coal to meet the energy needs ofthenation.Theuninterruptedenergysupplyplayedakeyrolenotonlysupportedtheburdenedhealthcareinfrastructure and a huge population locked in theirhomes;butalsoplayedavitalroleinfastpacedrevivaloftheeconomythereafter.Energyactsacatalysttoboostindustrial and domestic activities. In India primary energy requirement is largely dependent on thermal power.AllGovtmachineriesatCentreandStatehavetakenvariousmeasuresbyofferingeconomicstimuluspackages,policymeasuresetctorevivetheeconomy.Inourcompanyalso,wehavetakenvariousinitiativessuchasremovaloftriggerlevelrestrictionsincoalsuppliesunder fuel supply agreements, reduction in reserveprices for e-auctionplatforms, offering coal for importsubstitutions at affordable prices, softening financialcoveragesandpaymentmechanismsetc.Suchmeasureshelped our customers in ensuring power generation and sustainable thermal power supply to meet energy demand,apartfromfulfillingthefeedstockdemandinvarious industries.

Despite the unprecedented situations limiting the operations, our company has performed fairlywell inachieving important milestones and holding leadership position as the largest coal producing company in India.

2. Which innovative projects are there in your pipeline for the next 2 to 3 years to promote Coal sector?

Ans.:Inordertoachieve1BillionTonnecoalproductionby Coal India as a whole, our company, the largest coal producing subsidiary of Coal India had beenacknowledging that coal evacuationwouldbeamajorchallengeatvariouscoalfields.Itisafactthatlogisticssupportandconnectivitythroughrail/roadtothemineshadneverbeendevelopedalongthelineofexpansionof

coal mines. Anticipating the upcoming coal evacuation challengesandbulktransportconstraints,ourcompanyhas takenmany steps tohandle voluminousdispatchthroughenvironmentfriendlyin-pitconveyingsystemup to the coal handling plants. Concurrently, steps have also been taken to load coal through RapidLoadingSystems(RLS)intotheSILOsthroughbunkerarrangementsfordispatchingthroughrailnetwork.Inthisdirection,twomajorsubsidiarieshavebeenformedto develop two separate rail corridors through three major coalfields viz., Mand-Raigarh, Korba, Korea-Rewa and to provide rail connectivity to the trunkrail line of Indian Railways. After coal extraction, itis always challenging to move voluminous coal up to thedeliverypointinsidetheminestocontainfugitiveemissions. In this direction, Tenders for all loadingarrangementsandfeeder-linkshavebeeninvitedundertheFirstMileConnectivity(FMC)projects,asenvisagedintherespectiveprojectreportsforthemines.AllsuchoutsourcingworksfortheNine(9)FMCprojectsalongwithraillinkstoloadingpointshavebeenawardedandlikelybecompletedwithinnexttwoyearsatsixmineswithanestimatedinvestmentofabout₹4,000crorestoevacuateadditional60to70milliontonnesofcoaloutofthesemines.

Further,stepshavealsobeentakentostrengthenandwiden 137 km of road in the periphery of theminesapart from the external roads associated with coalevacuation,throughstategovt/districtadministrationon deposit basis.

3. What is the future outlook for the Coal Sector in IndiaforthecomingyearsandSECL’sroleinit?

Ans.: Even though renewables are likely to a takea larger share of the burden of power generation, itis unlikely that wind and solar power will wipe outthe need for fossil fuel-based power generation andtherefore,ThermalPowerwillcontinuetomeetIndia’sbase loadpowerneeds fora foreseeable future.SECLhaving a dominant position in coal production in the countryhasasignificantroletoplayinpowerneedsofthe nation in the coming years.

4. SECL has sanctioned various proposals to helpin the fight against COVID-19 under CSR. What

WIRC BULLETIN – DECEMBER 2021

18

other societal development do SECL is focussing onthesedays?

Ans.: During unprecedented pandemic in the formof Corona Virus, till date SECL has contributedaround Rs. 54 Crores towards providing variousinfrastructure like Ambulances, establishing oxygenplants,temporaryhospitals,providingfoodtomigrantsetc.andstill contributing towards thesame.ApartofCovid-19 related activities, SECL is also taking upvarious societal development activities like providingresidential skill development training to youths inthe operating districts of SECL through CIPET,establishing smart classrooms in the Govt. schools in SECL operating districts, providing tri cycles todifferently abled persons and many other activitiesin the SECL operating districts. The company alsocontributes to societal development in remote mining areas as a whole ecosystem develops around with the functioning of projects. Bedsides, the company alsoprovidesemploymentandotherrehabilitationfacilitiesto Project Affected Families, which in turn ensuressocietal development in the long run.

5. Please share with us the highlights of SECL supporttowardsvariousGovernmentinitiatives?

Ans.: The Govt has introduced several initiativeslike Digital Payments, MSME Policy, GeM (Govt. eMarketPlace)Portal,MakeInIndiapolicy,Vocationaltraining under Apprenticeship Act etc. to promote Digital Payments, support Domestic industries in India and to provide training to unemployed. SECLhas completely stopped business transactions in Cash topromoteDigitalPayments,madeMSMEpolicyandMakeinIndiapolicyascompulsoryinthecontractsandprocurements to promote domestic industries, made it compulsory to purchase the goods/services throughGeM portal andEvery yearwe are engaging varioustradeapprentices for providing Industrial trainingasper Apprentice Act.

6. Give our readers, a sense ofwhat is happeningin the Coal industry since the coronavirus pandemic outbreak. What are the main areas of impact and how the company has responded to thechallenges?

Ans.:TheunforeseencircumstancesduetoCOVID-19outbreak had necessitated social distancing andworking with staggered staff during the lockdownperiods.ThestrictlockdownenforcedtocontainspreadofCOVID-19intheregionalsoledtologisticalissues,shortageofmanpower resulting in failureofawardedcontract at mega mines. Despite all these unprecedented challenges, the company rose to the occasion and addressed the contractual failure in removing OB atmega mines by deploying departmental equipments as an alternative measure to ramp-out coal production. Thenationwide lockdownand thereupon intermittent

regionallockdownacrossthenationledtoslowdownineconomicactivitiesandhence,thedemandofcoalhaddropped sharply and suddenly.

However, we were anticipating the unprecedenteddemand of power coming up in the later months asthe economy picks up pace across the country withfalling active cases of COVID and massive roll-outof vaccination program in India. The company wasprepared with enough coal stock and measures toquicklyrampupproduction.

7. How are you pushing and supplementing the efforts of the Govt. towards ‘Aatma-Nirbhar Bharat’?

Ans.: Indiameetscloseto80percentofitselectricityneeds through coal-fired power plants, which isdependent on imports to meet its needs despite having thefifthlargestrecoverablecoalreservesintheworld.SECLhasplannedfewprojectsunderMineDeveloperandOperator (MDO)modelwhich can reduce importdependency and fulfil Atma-Nirbhar philosophy andconserve precious foreign exchange. MDO, with itstechnicalexpertise,enablesfasteroperationalizationofthecoalblocks.InSECL,threeOpencastprojectsandoneUGProjecthavebeenidentifiedforMDOmodeofoperation.

8. Going forward, how do you envisage the growth ofcoalsectorandSECLby2030?

Ans.: The year 2030, gains significance as India hascommitted at COP21 under Intended NationallyDetermined Contributions (INDCs) inter alia toenhancepowergenerationcapacitybasedonnon-fossilfuelsourcesto40%ofthetotalgenerationmix.Further,under the 19th Electric Power Survey, the electricalenergyrequirementhasbeenprojectedat2400BUandpeakelectricitydemandat340GWin theyear2029-30.Thestudyshowsthattheinstalledcapacityislikelyto be 831GW, inwhich share of coal and lignite willbe 32%of energymix i.e., 267GW,Solar at 300GW(36%) andWind at 140GW (17%).But coalwill stillcontribute50%ofelectricitygenerationin2030andthesamewouldentailfastpacedgrowthinSECLalso.

SECL also taking various diversification initiativeslikeestablishmentofSolarPowerPlants,SurfaceCoalgasificationplantstoextractAmmoniaandMethanol,extracting Sand from Over Burden, and forwardintegration like Establishment of Thermal Powerplants, etc.

9. Being a mining company, how are you addressing the issue related to pollution-control and planning foreco-friendlymining?

Ans.: Environmental management for sustainabledevelopment is the prime concern of SECL and itis achieved by every employee’s contribution andresponsibility towards environmental performance.

WIRC BULLETIN – DECEMBER 2021

19

To achieve this objective, various participativeinitiatives are being practiced and promoted, e.g. Coal is transported by closed conveyors and loaded into railwagonsthroughSILOsatitsmegaminesnamelyGevra,Dipka&KusmundaOCProjects.Thecompanyis also shifting towards new clean coal technologieslike introductionof surfaceminer inOpencastmines,introduction of highwall technology, introduction ofContinuousminerinundergroundmines,Fixedwatersprinklers,mobilewatersprinklershavebeendeployedfordustsuppression,truckmountedlongrangefoggingmachines, Mechanical Road Sweeping machines etc.Further, the company has also installed Continuous Ambient Air QualityMonitoring Systems (CAAQMS)with digital display arrangements for constantmonitoringofambientairquality.

SECL in association with Govt. Forest Department,doing planation activities in our leased land. SECLis also developing various Eco-Parks in ourmines toprotect environment, water conservation. Various scientific studies are continuously being taken up forstudy on assessment on Ecology and Biodiversity atvarious mines.

SECLisgoingtoinstallvariousSolarpowerplantsonnon-residential buildings at various areas and Mounted Grid connected solar plants for supply of power tomines. SECL is going to purchase 25nos of ElectricVehiclesonpilotprojectbasistoreduceCO2emissions.Further, we are also converting all the existing/oldenergy equipment’s with LED fitting with timers formore illumination with less energy usage.

10. Please suggest in what ways Cost & Management Accountants (CMAs) may offer their expertise more effectively to give SECL a competitive edge.

Ans.: We know that Cost Accounting is a process ofcollecting, analyzing, summarizing and evaluating various alternative courses of action, with a goal toadvise management on the most appropriate course of action based on the cost efficiency and capability.CMAs with their expertise provide the detailed costinformationthatmanagementneedstocontrolcurrentoperationsandplanforthefuture.Incoalsector,costanalysis is of utmost importance for newly identifiedcoalblocks,expansionofexistingmines,analysisofloss-makingminesetc.whichrequiresprofessionalexpertiseof Cost & Management Accountants (CMAs). SECL,with itsmajority of financeworkforce being qualifiedCMAs, naturally has a competitive edge with their activeroleincostcontrol,costefficiencyandinformedmanagement decisions for shutdown vs continue,dispatch point finalisation for lowest transportationcost to consumers, etc. CMAs are also a valuable asset tothecompanywiththeirprofessionalexpertise,whenthe company is looking forward to business decisionsof forward integration to thermalpowerprojects, coal

gasification or diversification into new business likesolar power plants, alumina production, OB to sandplants, etc.

11. What are the various ways your organization can integrate with our Institute for the diverse avenuesinprofessionaldevelopmentmatters?

Ans.:Atpresent, ICAI (InstituteofCostAccountantsof India) is offering Industrial Training to studentspursuing CMA. We, as a manufacturing/miningindustry, are providing industrial training to the students while pursuing CMA. As a Director Finance ofthecompany,Ibelieveinthestatement“Knowledgeis power”. At present, the world is growing fasterand rapid changes are taking place in the educationsystemandalsoatprofessionalworkplace.Assuch, Iencourage all the Finance executives of the companytopursuevariousskill enhancementcourses for theirprofessionDevelopmentwhileworkinginthecompany.We also conduct various training sessions at our companytoupdatetheknowledgefortheirprofessionalDevelopment. We also encourage and nominate finance executives to pursue various certificationcourses/seminars conducted by the Institute of CostAccountants of India. Moreover, the company isactively associated with practisingmembers of ICAI,as it regularly seeks them for various consultancyworks, Internal Audits, etc. Therefore, consideringthe symbiotic relationship of mutualism betweenSECLand ICAI,wemay look forward to avenues forcontinued professional development of ICAImembersservinginthecompanyaswellasavailingprofessionalexpertiseandconsultancyofICAImembersinpractiseover diverse areas, enhancing overall efficiency andcapabilityofboththeorganisation.

Dear CMA Colleagues,

WIRCisplanningtosendonlyE-copyoftheWIRCBulletinfromJanuary2022onwards.If any member requires the Hard Copy infuture, please write to WIRC ([email protected]) with Name, Membership Numberand Address to enable us to send the same.

With regards,

CMA Arindam Goswami, Chief Editor - WIRC Bulletin

WIRC BULLETIN – DECEMBER 2021

20

CMAs at Helm- As a strategist (State Govt. undertakings)

CMA Sandeep Modi

ExecutiveDirector(Finance),ChhattisgarhStatePowerHoldingCo.Ltd.

1. Despite the current uncertain situation due to COVID-19, the CSPHCL (erstwhile Chhattisgarh state Electricity Board), the only power utility of Chhattisgarh has been able to excel in enhancing production and sales. What more significant achievementsthatdeservemention?

A.:DuringCOVID-19,thePowerCompaniesofChhattisgarhworked continuously without interruption. ThepersonnelofPowerCompaniesworked likeFront-lineworkersinurbanandruralareas.ThePowerHouseswere running continuously. Despite Pandemic, we were able tomaintain regular supply of power. Moreover,domesticconsumersweregiven50%rebateupto400units which helped them to sustain the income losses inCOVID-19time.Tillnow,aboutRs.2000Crorehavebeenprovidedasrebatetoabout40LakhconsumersoftheState.

2. Which innovative projects are there in your pipeline for the next 2 to 3 years to promote Indianpowersector?

A.:Revampedpowerdistributionsector schemehasbeentaken up to modernize and strengthen the powerinfrastructure. All the consumersexceptagriculturalconsumers, will be connected through smart meters with an estimated cost of Rs. 9600 Crore. This willreducethecommerciallossessituationoftheCompany.Theprojectistargetedtobecompleteintheyear2025.

3. How Artificial Intelligence (AI) can improve resilienceinpowersectorinthepost-Covidera?

Asearliersaid,thesmartmeterswillbeabletoconnect/disconnect the power connection remotely. Meter reading /billgeneration&distributionandprepaidservicescanbetakenuptoimprovethecustomerservices.ArtificialIntelligencecanbetakenupefficientlyinPowerHousesalso.

4. What is the future outlook for the IndianPowerSector for the next couple of years and CSPHCL’srolebehindit?

A.:Future of power sector looks bright as by 2026-27,all India power generation installed capacity, will be nearly 620 GW, 38% of which will be from coal and44%fromrenewableenergy.CSPHCLisanimportantpartner in this journey. The State power generationcapacityisabout3000MW.Thepush-fortechnologicalcompatibility is on transmission and distribution sector innearfuture.

5. CSPHCL contributed Rs 3 cr. to help in the fight against COVID-19, to Chief Minister relief Fund. What other societal development do CSPHCL is focussingonthesedays?

A.: In fact, employees ofPowerCompanieshavedonatedtheir one day salary to fight against COVID-19.The Generation Company has built an environmentexperiment block in which environmental standard,water,air,effluent gases,criticalwastageandsoundmonitoringisbeingdoneatABBThermalPowerPlant,Marwa.

6. Please sharewithus thehighlights ofCSPHCLsupporttowardsGovernmentinitiatives?

A.:Chhattisgarh State Power Companies are supportingvarious Govt. Initiatives in power sector. The Govt.Supportstobelowpovertylineconsumers,agricultureconsumersanddomesticconsumersthrough“HalfBijaliBillYojna”isbeingimplementedbyPowerCompanies.

7. Give our readers, a sense of what is happening in the power industry since the pandemic coronavirus outbreak. What are the main areas ofimpact?

A.:ThepowerindustriesisdealingwithuncertaindemandinPendamic.Thedemandgoesdownduringlockdownperiod, then surges again when restrictions are removed. The power generation and procurement planningbecomedifficult.Thecashflowisalsoeffectedassomerebatesispassedontotheconsumerswithflexibilityin payment terms. During low demand, addressing the fixedcostpaymenttopowerproducers,causesdifficultsituation.

8. How is your esteemed organization responding to these challenges and what are the timelines that they are looking at in terms of the current situation?

A.:The organization is taking the challenges patiently.Thecash flowmis-matchhasbeendealtefficientlysofar.Theprojectscompletionremainsachallengeduetolabourshortagesometimesinlockdownsituationandintervening period.

9. Going forward, how do you envisage the growth ofCSPHCLby2030?

A.:TheChhattisgarhPowerCompaniesenvisagestofullfillthe power demand of the State to maintain “ZERO”

WIRC BULLETIN – DECEMBER 2021

21

power cut status, to be able to provide connection on demandandexpandtotherenewablesourcesofenergyparticularly in solar power.

10. What more eco-friendly and cost-effective measures are you planning to make our Nation proud?

A.:ThepowerplantsoftheStatearetobeequippedwithFGD system to control the environmental pollution. Thepowerprocurementisincreasingcontinuouslyfromrenewablesourcessuchassolar,miniHydelandBio-mass power plants.

11. Please suggest in what ways Cost & Management Accountants (CMAs) may offer their expertise more effectively to give CSPHCL a competitive edge.

A.:The Cost and Management Accountants can maketransparency in the cost of energy production &consumption, losses & conservation potential andenergy related tasks. There services can be useful inclimatechangesprojectsandenergyefficiency.Indiaisone of the largestandmost compact power sector intheworld.However, the sector still faces significantchallenges.The total lossesofPowerDistributionCo.isestimatedtoRs.90000CroreintheFY2020-21.TheroleofStateElectricityRegulatoryCommission,direct

benefit transfer and operational reforms can be dealtwiththehelpofCMAexpertise.

12. What are the various ways your organization can integrate with our Institute for the diverse avenuesinprofessionaldevelopmentmatters?

A.:CSPHCL can take the help of institution(ICMAI) forvarious training programme to Finance Executives,nonFinanceExecutivesandworkingstaff.Specificallydesigned Seminar/Workshop on power sector can beorganizedtoimprovetheskillofthepersonnel.

13. In the Paris Agreement India has committed to an Intended Nationally Determined Contributions target of achieving 40% of its total electricitygeneration from non-fossil fuel sources by 2030. How CSPHCL can help the nation to achieve the target?

A.:TheChhattisgarhPowerCompaniesarecommittedtotarget commitment of Paris Agreement. The presentGenerationcapacityofCGPowerCompanyofnonfossilsourcesisonly5%oftotalinstalledcapacity.ThePowerCompaniesaresettoprocurepowerfromthenonfossilsourcesintheguidanceofSERCandstrivetoachievethe targetofpowerprocurement from non fossil fuelsources

THE INSTITUTE OF COST ACCOUNTANTS OF INDIA(Statutory Body under an Act of Parliament)

WESTERN INDIA REGIONAL COUNCILJointlywith

WESTERN INDIA REGIONAL COUNCILof

THE INSTITUTE OF COMPANY SECRETARIES OF INDIA(Statutory Body under an Act of Parliament)

organizes

Cycle ExpeditionHealth isWealth!Professionals alsohave realized importance of having goodhealth especially duringPandemictime.WIRCofICAIjointlywithWIRCofICSIhasorganizedCycleExpeditionfromPunetoWIRC,Mumbai(distancearound160km)onSaturday,25thDecember2021.

ItWillhave3stages:

1. Pune-Lonavlaaround60km.,MembersfromPuneandPCMCwilljoin/exit, Breakfast

2. LonavlatoVashi-60km.,MembersfromPCMCandNaviMumbaiwilljoin/exit, LunchatNaviMumbai

3. NaviMumbaitoWIRC,Fort-40km.,MembersfromNaviMumbai/Mumbaiwilljoin/exit ClosingCeremony-5.30p.m.

Felicitationofparticipants-Sunday26thDecember2021Forregistration&[email protected]

With regards CMA Dinesh Kumar Birla CMA Harshad Deshpande Chairman,WIRC-ICAI Chairman–PDCommittee,WIRC-ICAI

WIRC BULLETIN – DECEMBER 2021

22

Management WisdomArticle 11: Why the American economists could not suggestarightmedicinefortheirailingeconomy?

CMA (Dr.) Girish JakhotiyaMob.:+919820062116

E-mail:[email protected]