在全球价值链 时代 以贸易促发展

312

年世界发展报告 世界银行集团旗舰报告 概述 在全球价值链 时代 以贸易促发展

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of 在全球价值链 时代 以贸易促发展

年世界发展报告

世界银行集团旗舰报告

SKU 33362

概述

在全球价值链

时代

以贸易促发展

年世界发展报告

世界银行旗舰报告

概述

在全球价值链

时代

以贸易促发展

本出版物包含了《2020年世界发展报告:在全球价值链时代以贸易促发展》的内容概述,doi: 10.1596/978=1 =4648-1457-0。完整报告出版后,其 PDF 电子版将在 https://openknowledge.worldbank.org/ 和 http://documents.worldbank.org/提供,纸质报告可通过www.amazon.com订购。引用、复制和改编本报告时请使用报告的最终版本。

© 2020 国际复兴开发银行 / 世界银行

1818 H Street NW, Washington DC 20433电话:202-473-1000; 网址:www.worldbank.org部分版权所有

本报告是世界银行工作人员的成果,其中也包括外部人员的贡献。本著作的发现、阐释和结论未必反映世界银行、

世界银行执行董事会或其所代表的国家的观点。世界银行不保证本报告数据的准确无误。本报告所附地图显示的

疆界、颜色、名称和其他信息并不表示世界银行对任何地区的法律地位的看法,也不意味着对这些疆界的认可或

接受。

此处的任何条款都不构成、也不应被视为世界银行对任何权利或特权的限制或放弃;世界银行明确保留这些

权利和特权。

权利和许可

本著作可以根据知识共享 3.0 政府间组织许可(CC BY 3.0 IGO)授权使用 http://creativecommons.org/

licenses/by/3.0/igo。根据该许可,在下列条件下,使用者可以复制、发行、传播、改编本著作,包括用于商业用途:

标明出处——请按如下方式引用本报告内容:世界银行,2020。《2020 年世界发展报告:在全球价值链时代以

贸易促发展》概述。世界银行,华盛顿。许可:知识共享引用许可协议 CC BY 3.0 IGO。

翻译——若要翻译本著作,请在标明出处的同时加上下列免责声明:本翻译不是世界银行的作品,不应被视为

世界银行的官方译本,世界银行对翻译中的任何内容或错误概不负责。

改编——若要改编本报告,请在标明出处的同时加上下列免责声明:这是对世界银行原著的改编。本改编作品中

的观点和看法完全是改编者的责任,世界银行对改编内容不表示认可。

第三方内容——世界银行未必对本报告所有内容拥有知识产权。因此,世界银行不保证使用本著作中第三方所有

的内容不会侵犯第三方权利,由此引起的赔偿风险由使用者全权承担。如果你想使用著作中的第三方内容,你要

负责确定是否需要获得知识产权所有者的许可。这类内容的例子包括但不限于表格、示图和图片。

所有关于版权和许可的询问,请联系世界银行出版部。地址:World Bank Publications, The World Bank Group,

1818 H Street NW, Washington, DC 20433, USA;电子邮件:[email protected]。

封面图片:封面图片为描绘国际贸易流动的交互式可视化截图,其中每个点代表 10 亿美元的贸易值。该交互式

地图由数据可视化专家Max Galka,通过他的博客 Metrocosm 提供:http://metrocosm.com/map-international-

trade/.Max Galka 许可使用;再次使用需要再次申请许可。

封面设计:Kurt Niedermeier, Niedermeier Design, 西雅图,华盛顿。

内页设计:George Kokkinidis, Design Language, 布鲁克林,纽约与 Kurt Niedermeier, Niedermeier Design, 西雅图,华盛顿。

什么是全球价值链(GVC)?全球价值链是指将生产过程分割并分布在不同国家。企业专注于特定环节,不生产整个产品。

全球价值链如何发挥作用?

企业之间的业务往来通常都建立在持久关系基础之上。

经济基本面驱动国家是否参与全球价值链,而政策对提高参与度、拓宽利益面很重要。

2020年世界发展报告: 在全球价值链时代以贸易促发展

国界

原材料服务生产要素

零部件半成品

产成品

出口 出口 供消费出口

国界

国界

C 67M 0Y 98K 51

C 27M 81Y 8K 30

C 90M 60Y 0K 5

C 48M 40Y 0K 0

C 0M 100Y 65K 4

C 2M 4Y 23K 5

C 0M 30Y 100K 0

C 55M 25Y 0K 0

C 0M 62Y 100K 0

C 74M 0Y 32K 0

C 24M 0Y 98K 8

C 7M 68Y 8K 16

驱动因素 结果

全球

价值链

高度专业化

政策

:社

会与

环境

保护

政

策:

开放

•

互

连互

通

•

合作

企业间关系

地

域

禀

赋

体制

市

场规

模

环

境

削

减贫

困

经济

增长

与就业 不

平等

概述 | 1

概述

全球价值链的兴起推动了 1990 年后国际贸易

快速增长。这一增长促就了前所未有的经济差

距的缩小:穷国经济出现更快速增长,并开始

追赶富国。贫困大幅下降。

这些收益来源于生产过程分散在各国以及企业间联系

的加强。随着企业在任何可能的地方寻求效率,零部件

开始在全球各地穿梭。孟加拉国、中国、越南等参与全球

价值链的国家的生产率和收入都有所提高。而且正是在

这些国家,贫困人口也大幅减少。

但时至今日,不能再想当然地认为贸易仍将是促进繁

荣的力量。自 2008 年全球金融危机以来,贸易增长乏力,

全球价值链扩张放缓。过去十年没有发生像 20 世纪

90 年代那样的变革性事件——中国和东欧融入全球

经济,乌拉圭回合(Uruguay Round)、北美自由贸易

协定(NAFTA)等重大贸易协定达成。

与此同时,劳动密集型、贸易拉动式增长的成功模

式面临两个潜在的严重威胁。首先,自动化和 3D 打印

等节约劳动力的技术的到来可以缩短生产和消费者之间

的距离,减少对国内外劳动力的需求。其次,大国之间

的贸易冲突可能导致全球价值链的收缩或分裂。

对于正在寻求参与全球价值链、获取新技术、并实

现增长的发展中国家来说,这意味着什么?是否仍然可

以通过全球价值链促进发展?这是本报告探讨的中心

问题。本报告研究了全球价值链对经济增长、就业和削

减贫困的贡献程度,以及其对不平等和环境恶化的影响。

本报告阐述了国家政策如何能够重振贸易增长,并确保

全球价值链成为发展的推动力量,而非背离力量。最后,

本报告指出了国际贸易体系中引起国家间分歧的不足

之处,并提供了通过更大规模的国际合作来消除这些分歧

的路线图。

本报告的结论是,只要发展中国家深化改革,工业

国奉行开放、可预测的政策,全球价值链就能继续促进

增长、创造更好的就业岗位和削减贫困。技术变革对贸

易和全球价值链可能是利大于弊。如果所有国家都加强

社会和环境保护,参与全球价值链的收益就可以被广泛

共享、并且得以持续。

只要发展中国家深化改革,工业国奉行开放、可预测的政策,全球价值链就能继续促进增长、创造更好的就业

岗位和削减贫困。

除非恢复政策的可预测性,否则全球价值链

可能停止增长

全球价值链已经存在了几个世纪。但全球价值链在

1990 年到 2007 年期间增长最为迅速,原因是交通、

信息和通信领域技术进步,以及贸易壁垒降低吸引制造

企业将生产流程延伸至国境之外(图 O.1)。全球价值

链的增长主要集中在机械、电子和交通行业,以及在这

些行业拥有专长的地区:东亚、北美和西欧。这些地区

的大多数国家参与复杂的全球价值链,提供先进的产品

和服务,并开展创新活动(地图 O.1)。相比之下,非洲、

拉美和中亚的许多国家仍在生产供其他国家进一步加工

的初级产品。

然而,近年来贸易和全球价值链增长放缓(图 O.1)。

原因之一是经济增长总体放缓,特别是投资方面。另一

个原因是贸易改革步伐放缓,甚至出现倒退。而且,

最具活力的地区和行业的生产分散化已经成熟。中国的

国内生产正在增加。1 蓬勃发展的页岩油行业使美国在

2010 年至 2015 年间的石油进口减少了四分之一,并略

微降低了其将制造业生产外包的动机。2

图 O.1 全球价值链贸易在 20世纪 90年代增速很快,但在 2008年全球金融危机之后出现停滞

资 料 来 源:《2020 年 世 界 发 展 报 告》工 作 组 根 据 Eora26 数 据 库 (https://worldmrio.com/) 和 Johnson 和 Noguera(2017)的数据计算的

结果。

注释:详细内容参见图 1.2。

30

35

40

45

50

55

1970

1975

1980

1985

1990

1995

2000

2005

2010

2015

全球价值链占全球贸易的份额

(%)

资料来源:《2020 年世界发展报告》工作组根据 2015 年全球价值链分类数据计算的结果(参见本报告正文的专栏 1.3)。

注释:一个国家的全球价值链关联类型基于 (1) 该国的全球价值链参与率,(2) 该国贸易所专注的行业,和 (3) 创新措施。详情请参见本报告正文的图 1.6。

地图 O.1 所有国家都参与了全球价值链——参与方式却不尽相同

2 | 2020 年世界发展报告

低参与率

有限初级产品

大量初级产品

初级制造业

先进制造业与服务业

创新活动

无数据

全球价值关联,2015 年

IBRD 44640,2019 年 8 月

概述 | 3

全球价值链促进收入和就业增长,因此参与全球价值

链有助于削减贫困。5 总体来说,贸易主要通过增长来削

减贫困。由于全球价值链带来的经济增长收益往往要大于

最终产品贸易带来的经济增长收益,全球价值链削减贫困

的效果也大于标准贸易。例如,在墨西哥和越南,全球价

值链参与程度越高的地区,其削减贫困的幅度也越大。

全球价值链的收益没有被平等分享,且全球

价值链可能会破坏环境

参与全球价值链的收益并没有在国家之间和国家内部平

均分配。将零部件和任务外包给发展中国家的大型企业

的加价幅度和利润都在上升,意味着参与全球价值链降

低的成本并没有传递给消费者,而且这一比例越来越大。6

与此同时,发展中国家生产商的加价幅度正在下降。

这种对比在如美国和印度的服装公司的加价幅度上

就很明显。在国家内部,与较低收入国家进行贸易和技

术变革促使增加值从劳动力重新分配给资本。劳动力市

近期的保护主义的抬头也对全球价值链的演变产生

了影响。保护主义可能会促使现有的全球价值链回流到

本国或转移到新地点。除非恢复政策的可预测性,否则

全球价值链的扩张可能会停滞不前。当未来的市场准入

具有不确定性时,企业就会有动机推迟投资计划,直到

不确定性消除。

全球价值链可以提高收入,创造更好的就业

岗位和削减贫困

高度专业化可以提升效率,而持久的企业间关系有助于

沿价值链的技术扩散、以及资本和生产要素的获取。例如,

在埃塞俄比亚,参与全球价值链的公司的生产率是参与

标准贸易的相似公司的两倍多。其他发展中国家的企业

也通过参与全球价值链实现了生产率的显著增长。据估

计,全球价值链参与率每增加 1%,人均收入增长将超过

1%,远高于标准贸易带来的 0.2% 收入增长。通常情况下,

当一个国家的出口从初级产品转向用进口的生产要素产

出的基本工业品(例如用进口的纺织品产出的服装)时

(图 O.2),增长幅度最大,孟加拉国、柬埔寨和越南

的情况就是如此。

然而,如果不向逐步复杂的其他参与形式转化,这些

高增长率最终将无法持续。但是,从初级制造业到更先

进的制造业和服务业、并最后迈进到创新活动(本报告

中使用的全球价值链分类将在本报告正文部分的专栏 1.3

中作进一步解释)的过渡对技能、互连互通和监管机构

的要求也越来越高。

全球价值链也提供了更好的工作岗位,但它与就业

的关系更为复杂。全球价值链中的企业往往比其他企业

(尤其是非贸易企业)的生产率和资本密集度更高,

因此其生产流程的劳动密集度较低。然而,生产率的提

高导致企业产出增加,从而增加企业就业。3 其结果是,

全球价值链与发展中国家的结构性转型相关,将劳动力

从生产率较低的活动中解放出来,投入到生产率更高的

制造业和服务业活动之中。全球价值链中的公司不同寻

常的另一面是:在许多国家,它们往往比非全球价值链

公司雇佣更多女性。4 因此,它们对提高女性就业这一更

广泛的发展利益作出了贡献。

图 O.2 当国家参与初级制造业全球价值链时,人均 GDP增长最快

资料来源:《2020 年世界发展报告》工作组根据 Eora (https://worldmrio.com/) 和世界银行的世界发展

指标(WDI)数据库 (https://datacatalog.worldbank.org/dataset/world-development-indicators) 的数据

计算的结果。

注释:本事件研究量化了全球价值链参与从较低阶段转向较高阶段后的 20 年里人均实际 GDP 的累计

变化。关于量化方法,请参见本报告正文中的专栏 3.3。

57

48

32

0

10

20

30

40

50

60

事件年 21 3 4 65 8 97 10 11

事件之后年份

12 13 15 17 1914 16 18 20

人均

GD

P 的累计变化(

%)

初级制造业

先进制造业与服务业

创新活动

4 | 2020 年世界发展报告

风险。但目前的证据表明,这些技术总体而言在促进贸

易和全球价值链增长。

创新催生了全新的贸易商品和服务,进而促进了更

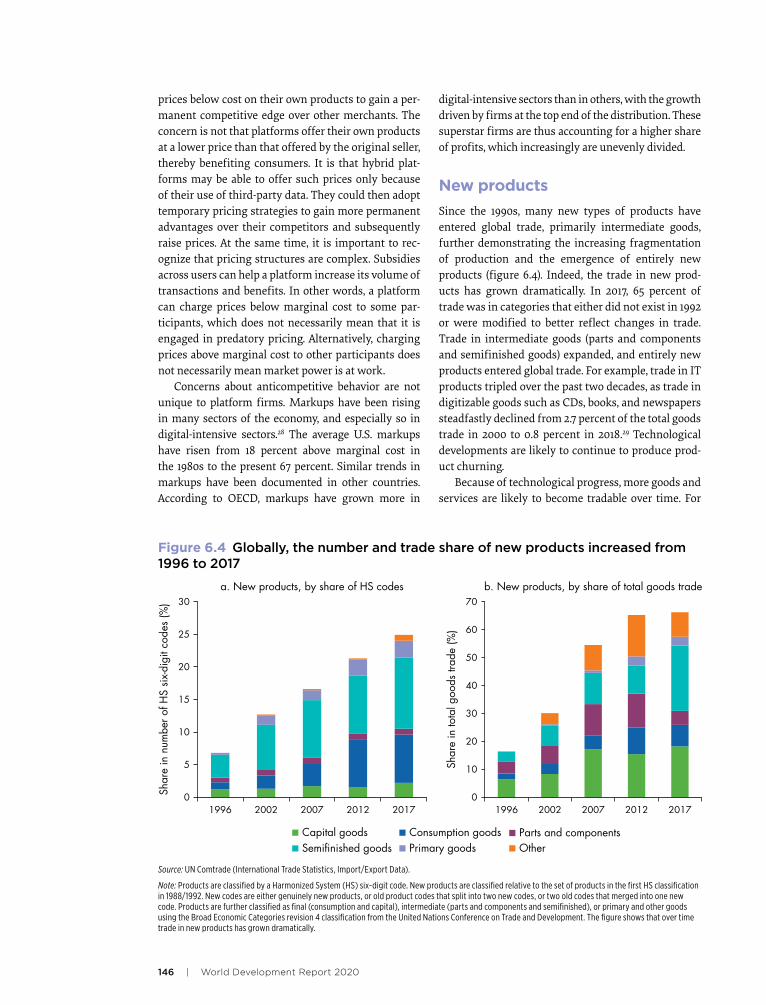

快的贸易增长。2017 年,65% 的贸易属于 1992 年尚不

存在的类别。出人意料的是,新的生产技术也有可能推

动贸易。

自动化确实鼓励各国减少使用劳动密集型的生产

方法,并降低了对发展中国家劳动密集型产品的需求。

然而,将业务回流国内的证据有限,9 而且关于自动化 10

和 3D 打印 11 的证据表明,这些技术有助于提高生产率、

扩大生产规模。因此,它们增加了从发展中国家进口生

产要素的需求(图 O.3)。

同样,数字平台公司正在降低贸易成本,促使小企业

更容易走出本土市场、向全世界销售商品和服务。但有

迹象表明,平台公司日益增强的市场势力正在对贸易收

益的分配产生影响。12

国家政策可以提高全球价值链的参与度

从原则上讲,将汽车、电脑等复杂产品拆分,可以让各

国专注于更简单的零部件和任务,让处于发展初期的国

家更容易参与贸易。但是,并不能就此确保一个国家有

能力参与全球价值链。

全球价值链的参与程度由要素禀赋、地理位置、市场

规模和体制所决定。但单单这些基本面还不足以一锤定

音,政策也发挥重要作用。吸引外国直接投资(FDI)

的政策可以弥补资本、技术和管理技能的不足。13 在国内

实现贸易自由化、并与外国进行贸易自由化谈判可以突

破国内市场规模小的局限,使公司和农场摆脱国内需求

和当地生产要素不足的限制。改善交通和通信基础设施、

并在这些服务中引入竞争可以消除偏远区位的劣势。14

此外,参与深度一体化协议可以促进体制和政策改革,

特别是在技术和财政支持作为补充的情况下。15

基于对参与全球价值链的各种驱动因素的分析,

本报告指出可以推动一个国家融入更先进的全球价值链的

一系列政策(图 O.4)。重要的是,各国的政策可以而且

场上的不平等也可能逐渐加剧,熟练工人的报酬越来越

高,而非熟练工人的工资却停滞不前。7 女性也面临挑战:

全球价值链虽为女性提供更多就业机会,但它们的玻璃

天花板似乎更低。女性一般在低附加值部门任职;女企

业主和女经理难觅踪影。8

全球价值链也可对环境产生有害影响。与标准贸易

相比,全球价值链的主要环境成本与规模不断扩大、

距离越来越远的中间产品贸易相关。这导致运输过程的

二氧化碳排放量更高(相对于标准贸易而言),以及货

物包装产生过量废弃物(尤其是电子产品和塑料行业)。

全球价值链带来的增长也会对自然资源造成压力,特别

是伴随着生产或能源补贴所导致的生产过剩。从更积极

的方面来看,数据并没有证实企业可能选择将污染最严

重的生产环节放在环境规范较为宽松的国家。

新技术总体上对贸易和全球价值链有推动

作用

新产品,自动化、3D 打印等新的生产技术,以及数字

平台等新的分销技术的出现,既创造了机遇,也带来了

图 O.3 自动化增加了工业化国家从发展中国家的进口

资料来源:Artuc, Bastos 和 Rijkers(2018)。

注释:此图反映了 1995 年至 2015 年期间工业化国家各行业从发展中国家物料进口因自动化而引发

的增长。零部件进口的变化以对数点来度量;对数点每增加 0.10 大致相当于进口增加 10%。

0

2

4

6

8

10

行业(按自动化程度自低到高排列)

其他非制造业

从发展中国家零部件进口的变化 %

公用事业建筑农业教育矿业纺织

木材、造纸、印刷

其他制造业食品化工机械电子金属

橡胶与塑料汽车

概述 | 5

进战略,吸引了大型跨国公司对全球价值链的转型性

投资。

过高的汇率和限制性的劳动法规提高了劳动力成本,

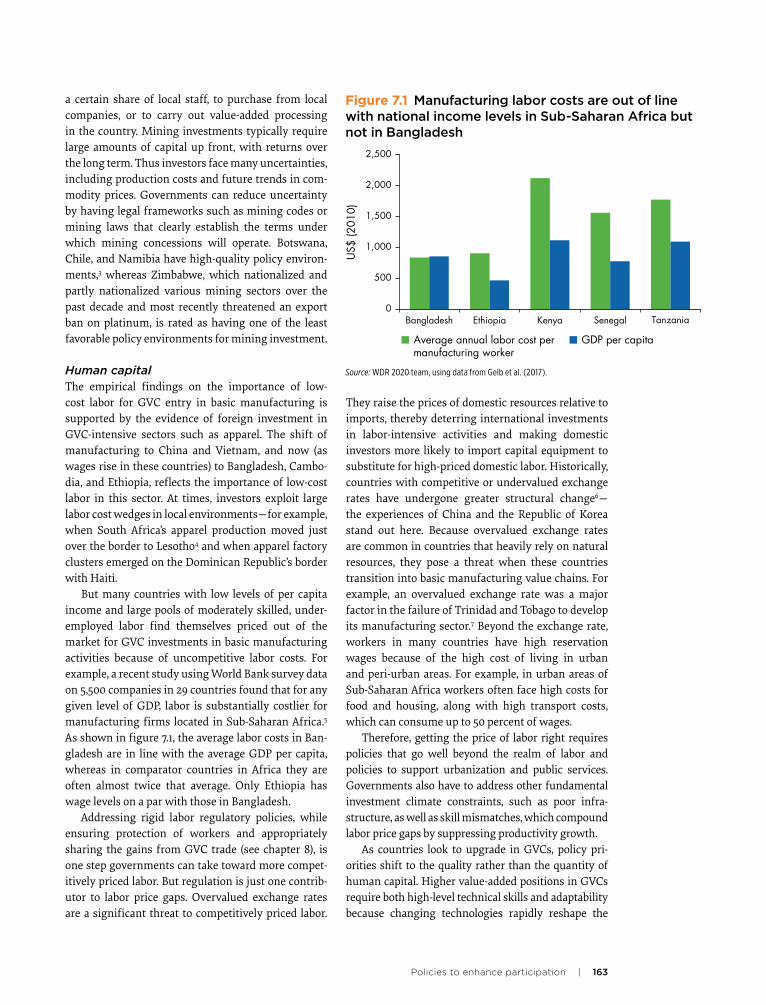

使劳动力充裕的国家无法充分利用其禀赋优势。例如,

孟加拉国制造业劳动力成本与人均收入相当,而非洲许

多国家的劳动力成本是其人均收入的两倍还多。

通过贸易自由化与市场连接有助于各国扩大市场规

模,获得生产所需的生产要素。例如,秘鲁的生产率快

速提升、全球价值链出口的增长和多元化与其在本世纪

头十年单方面大幅削减关税有关。16 贸易协定可以扩大市

应该根据其具体情况和参与全球价值链的具体形式来量身

定制。

在参与全球价值链的所有阶段吸引外国直接投资至

关重要。它需要开放、对投资者的保护、稳定、有利的

商业环境,并在某些情况下要投资促进。一些国家,

如从商品行业的外国投资中受益的东南亚国家,仍然限

制针对服务业的外国投资。另一些国家试图通过免税

和补贴吸引投资,但这些措施可能引起贸易伙伴的不

满,其净收益可能不一定是正值。尽管如此,哥斯达

黎加、马来西亚和摩洛哥等国通过采用成功的投资促

资料来源:《2020 年世界发展报告》工作组。

注释:ICT = 信息与通信技术;NTM = 非关税措施。

图 O.4 向更为复杂的全球价值链参与方式转型:国家政策示例

标准认证:建立合规性评价制度

地理位置

禀赋

基本面

体制

治理:促进政治稳定性 治理:改善政策可预测性,寻求达成深度贸易协议

基本信息与通信技术(ICT)互联互通:ICT 服务自由化,ICT 基础设施投资

贸易基础设施:海关改革,运输服务自由化,

投资建设港口和道路

外国直接投资:采取支持性投资政策,改善营商环境

政策重点

先进 ICT服务:扩大高速宽带覆盖

先进的物流服务:投资建设多式联运基础设施

市场规模

生产要素的获取:减少关税/

非关税措施(NTM),改革服务

市场准入:寻求达成贸易协定

标准化:统一标准或互相接受标准

市场准入:深化贸易协议,将投资和服务纳入其中

知识产权:确保保护到位合同:加强执行力度

融资:拓宽从银行融资的渠道 融资:拓宽股权融资渠道

劳动力成本:避免法规僵化和汇率错配 高级技能:围绕创新的教育,对外国人才开放技术和管理技能:

教育,培训,对外国技能开放

先进制造业和服务业转向创新活动 初级产品转向初级制造业 初级制造业转向先进制造业和服务业

6 | 2020 年世界发展报告

的利益需要额外的支持,例如通过农业推广服务、获得

风险管理工具(例如保险)、以及通过生产者组织协

调来扩大规模。

为了全球价值链在全国范围内改善商业和投资环境

可能费钱耗时,这促使许多国家设立经济特区来打造

“卓越岛”。但到目前为止的成果表明,成功的经济特

区相对较少,而且只有在应对特定的市场和政策失灵时

才取得成功。即便是在一个有限的地理区域,要想所有

条件都得到满足需要精心的规划和实施,以确保所需的

资源——如劳动力、土地、水、电和电信——随时可用,

监管壁垒最小化,并实现无缝的互联互通。少数成功案

例,如中国、巴拿马、阿联酋和当下埃塞俄比亚的经济

特区计划,以及大量未能吸引投资或实现增长的经济

特区案例,为如何利用经济特区促进发展提供了重要的

经验教训。

其他政策有助于确保全球价值链的利益得到

共享和持续

除促进参与全球价值链的政策外,还需要互补性政策来

分享全球价值链的利益并降低成本。这些政策包括帮助

那些可能受到结构性变化伤害的工人的劳动力市场政策;

确保遵守劳动法规的保障机制;以及环保措施。

随着全球价值链的扩张,一些工人将会受益,但一

些地区、行业和岗位的工人可能会遭受损失。调整援助

(adjustment assistance)将帮助工人适应全球价值链

给生产和分销方式带来的变化,它在中高收入国家尤其

重要。调整政策可以包括促进劳动力流动和帮助工人具

备找到新工作的能力。18 由于结构性变化导致的失业往

往具有持续性,工资保险可以让工人从事薪资较低的工

作而不遭受收入损失,从而带来更好的长期结果。例如,

丹麦成功的“灵活保障”(flexicurity)模式给予雇主

几乎不受限制的雇佣和解雇工人的自由,但同时通过慷

慨的失业福利和积极劳动力市场政策为工人提供支持。

劳动法规,如果设计和实施得当,可以帮助确保工

人的安全和健康。私营企业可以做出贡献,尤其是当其

场准入,也对包括孟加拉国、多米尼加共和国、洪都拉斯、

莱索托、马达加斯加和毛里求斯在内的许多国家参与全

球价值链起到了关键的催化作用。由于商品和服务经济

间的联系日益紧密,改革电信、金融、交通和一系列商

业服务领域的服务政策应是促进全球价值链活动战略的

一部分。

对于许多在全球价值链上交易的商品来说,延迟一

天相当于被征收超过 1% 的关税。改善海关和边境手续、

促进运输物流服务竞争、加强港口结构和治理都可以

降低与时间和不确定性相关的贸易成本,缓解地理位置

偏远带来的劣势。

全球价值链的蓬勃发展有赖于企业网络的灵活结构,

因此还应对合同的执行予以关注,以确保网络内的法律

安排的稳定性和可预测性。知识产权保护对更具创新性

和复杂性的价值链尤其重要。加强国家认证和检测能力

来确保符合国际标准也可以促进全球价值链的参与。

在当今的全球价值链背景下,税收激励、补贴和当

地成分要求等传统产业政策可能造成生产模式的扭曲。

采取其他积极政策更有前景,尤其是解决市场失灵问题的

政策:

• 为了加强国内支持价值链升级的能力,各国应对人力

资本进行投资。17 例如马来西亚由行业主导的槟城技能

发展中心。该中心为马来西亚在电子和工程全球价值

链的升级提供了重要支持。

• 有针对性的政策可以有效地解除参与全球价值链贸

易的限制。例如,在孟加拉国,保税仓库的引进和

“背对背”信用证(确保流动资金的获取)被认为是

该国融入服装行业全球价值链的催化剂。

• 各国可通过支持培训和能力建设、向领先企业提供有

关供应机会的信息,帮助国内中小企业与全球价值链

领先企业建立联系。智利和几内亚的矿业、肯尼亚和

莫桑比克的农业、捷克共和国的电子和汽车行业内均

有供应商联系项目的成功案例。

• 对于参与农业价值链的国家来说,支持小农户融入价值

链的政策尤为重要。在非洲,农业提供了 55% 的就业

岗位,也是贫困人口超过 70% 的收入来源。确保小农户

概述 | 7

的影响可能非常巨大——超过 3000 万人可能会被迫陷

入贫困(日收入水平低于 5.50 美元),全球收入的下降

可能高达 1.4 万亿美元。不过,即使保持现状,引发冲

突的贸易做法也可能造成不利影响。

为了保持有益的贸易开放,“两条腿走路”很重要。

第一要务是深化传统贸易合作,消除商品和服务贸易的

剩余壁垒以及补贴、国有企业活动等导致贸易扭曲的措

施。同时,应将合作范围从贸易政策扩大至税收、监管

和基础设施领域。

深化传统合作

展望未来,首要任务应该是深化传统贸易规则和承诺。

迄今为止,国际合作所带来的商品和服务贸易的开放

程度参差不齐。农业和服务业的贸易自由化迟迟未至,

一些工业产品仍然在某些市场受到限制或面临非关税

措施。贸易优惠降低了主要影响最贫穷国家的某些

关税——但并没有降低这些国家征收的进口关税。对发

展中国家的特殊和差别待遇在某些案例中导致这些国家

改革步伐缓慢,最终阻碍其参与全球价值链和融入全球

经济。

此外,世界上一些最大的市场为了保护高附加值产

品而出台的关税升级正在抑制发展中国家的农业和劳动

密集型行业(如服装与皮革)的加工活动。特惠贸易协

定中的限制性原产地规则缩减了采购选择范围。补贴和

国有企业扭曲竞争,且现有规则并不保证竞争中立。

在服务业方面,除了单方面采取的行动外,国际谈判在

实现贸易自由化上几乎没有取得进展。与全球价值链相

关的重要服务,如航空和海运(这些服务最需要协调一

致的自由化)由于既得利益集团的抵抗而被排除在谈判

之外。

如果发展中国家中的主要贸易国以平等伙伴、甚至是

领导者的身份参与谈判,而不是寻求特殊和差别待遇;

如果工业大国继续相信基于规则的谈判,而不是采取单

边保护措施;如果所有国家共同制定一个反映发展和商

业要务的谈判议程,传统贸易谈判就可能会带来更有实

际意义的结果。

扩大税收、竞争和数据流动领域的合作

在如今这个时代,企业在全球运营,生产分散,知识

产权等无形资产增加,对资本征税变得越来越困难。

消费者对公司全球业务的劳动条件敏感时。在建立和

监测适当的劳动标准方面,由国际合作支持的国家政策

也可发挥重要作用。在越南,国际劳工组织和国际金融

公司 (ILO-IFC) 面向企业的“更好的工作”项目(Better

Work Programme),配合政府对未能达到主要劳工标

准的公司的披露,让工人的工作条件得以改善。19

为环境恶化定价可以防止全球价值链加大资源的不

当配置。20 商品价格应同时反映其经济和社会环境成本。

对环境损害适当定价也将鼓励在环境友好型商品和生产

过程方面的创新。减少能源和生产补贴等造成的扭曲、

转向征收碳税将改善资源配置并减少二氧化碳排放。21

此外,环境监管,特别是针对特定行业和污染物的监管,

可以遏制与全球价值链相关的生产和运输造成的损害。

国际合作有助于在参与全球价值链中获益

在全球价值链的世界中,国际贸易体系尤为重要。全球

价值链跨越国界,一个国家的政策行为或不作为可能影

响到其他国家的生产者和消费者。国际合作有助于应对

各国政策的溢出效应,实现更好的发展成果。当商品和

服务数次跨越国界时,贸易保护导致的费用会被放大,

因此协调一致地降低贸易壁垒对全球价值链的好处甚至

比对标准贸易的好处更大。鉴于外国投资与全球价值链

之间有着不可分割的联系,创造一个开放和安全的投资

环境对参与全球价值链至关重要,特别是对资本匮乏的

国家而言。

以规则为基础的贸易体系令发展中国家获益匪浅,

尤其是这一体系中对贸易歧视的抵制、对改革的激励、

全球市场准入以及发生贸易争端时的申诉机制——甚至

是针对贸易大国的申诉。然而,国际贸易体系目前正承

受着巨大的压力。发展中国家 30 年来以贸易为主导的

追赶式增长推动了各国经济实力的变化,加剧了各国内

部的收入不平等。各国经济规模日益对等使其保护水平

的持续不对等性得到明显缓解。与此同时,过去适应过

变化的贸易体系近年来举步维艰,最明显的例子是多哈

谈判的失败。欧盟和北美自由贸易协定等地区性倡议也

受到成员国分歧的影响。

美国和中国之间的贸易冲突正导致保护主义和政策

的不确定性,并开始扰乱全球价值链。如果贸易冲突恶

化,并导致投资者信心下滑,全球经济增长和贫困所受

8 | 2020 年世界发展报告

合作应确保税收收入的公平获得——富国需要依靠税收

帮助失业的产业工人,而穷国需要用税收建设基础设施。

最终,各国联合起来推广基于目的地的征税方式可以

消除企业对利润的转移和国家在税收方面竞争的动机,

但需要考虑到这种做法对小型发展中国家的税收收入的

影响。与此同时,其他防止税基侵蚀和收入转移的措施

可以缓解与国内资源调动相关的挑战。

消费者越来越担心数据流动和数字公司的国际扩张,

二者在全球价值链中都发挥了重要作用。其风险包括基

于数据的服务中的侵犯隐私行为,以及基于平台的服务

中的反竞争行为。各国政府正在制定数据本地化法律以

限制数据的跨境流动,并为国内数据的处理制定严格的

规则。关于竞争的法律仍然明确地聚焦于国内,双边或

地区性贸易协定中的合作也受到了限制。解决方案可能

是一种新型的议价:出口企业做出监管承诺,保护海外

消费者的利益,以换取进口国的市场准入承诺,最近一

些关于数据流动的协议就体现了这种模式。

但发展中国家不应被排除在此类安排之外,因为这

将削弱它们在全球价值链中的参与。国际支持可以帮助

它们在对出口有益的方面(例如基于数据的服务)作出

监管承诺,并在它们开放市场时获得贸易伙伴的承诺

(例如实施竞争政策)。

最后,基础设施投资方面的协作失败会影响到全球

价值链的投资、扩张和升级,尤其是在最贫穷的国家。

从全球范围来看,由于对贸易伙伴的额外利益不加考虑,

很多国家在贸易相关的基础设施方面投资不足。接壤

国家同时采取行动加快贸易速度,收益会更大。例如,

在危地马拉和洪都拉斯加入关税同盟且同意接受同样

的电子文件后,两国边界的延误时间从 10 小时减少到

15 分钟。世界贸易组织的《贸易便利化协定》鼓励各国

在提高贸易便利化方面进行协调,并为低收入国家所需

的投资提供资金援助。类似的方法可能有助于在交通、

能源、通信基础设施等其他投资领域实现协同效应。

注释

1. Constantinescu, Mattoo 和 Ruta(2018)。

2. Constantinescu, Mattoo 和 Ruta (2018)。

3. 在越南,同时从事进口和出口业务的公司雇佣的工人要多

于只出口的公司和不参与贸易的公司,此分析控制了行业

和省份的固定效应、以及国家和外国所有权。在墨西哥,

与买家有关系的公司、以及从事进口和出口公司的提供的

就业岗位也多于只进口或只出口的公司。即使考虑到公司

的所处地区、行业和外国所有权等特征,这一结果仍然成立。

因此,在一国范围内,同时从事进口和出口公司雇佣的工人

数量要高于参与单向贸易的公司或不参与贸易的公司。

4. Rocha 和 Winkler (2019)。

5. 增长的贫困弹性取决于多种因素,包括其发生率(不平等

的变化);土地、财富和收入的初次分配;穷人的受教育

水平;以往其他形式的公共投资;以及包括工会在内的地

方机构(Ferreira, Leite 和 Ravallion(2010);Ravallion

和 Datt(2002))。另请参见 Dollar 和 Kraay(2002)

和 Ferreira 和 Ravallion(2008)。

6. 当市场不是完全竞争时,因为价格更高,或者成本更低,

或者两者兼而有之,加价幅度可能会增加,这意味着公司

可以影响价格。企业加价的影响取决于成本的下降或参与

全球价值链的收益是否通过较低的价格完全传递给消费者。

7. Feenstra 和 Hanson(1996, 1997);Verhoogen(2008)。

8. Rocha 和 Winkler (2019)。

9. Oldenski(2015)提供的证据表明,回流在美国并不普遍。

10. Artuc, Bastos 和 Rijkers(2018)。

11. Freund, Mulabdic 和 Ruta(2018)。

12. 请参见 Chen 和 Wu(2018);Garicano 和 Kaplan(2001);

Höppner 和 Westerhoff(2018)。

13. 外国直接投资与资本、技术和管理技能之间的正相关性仅

由制造行业参与全球价值链所驱动。外国直接投资的流入

与各国农业、初级产品或服务业融入全球价值链之间没有

概述 | 9

关联。这一发现表明,追求效率或寻找市场的外国直接投

资在国际上寻找具有成本竞争力的目的地和潜在出口平台

方面可能发挥更有利的作用。关于双边外国直接投资存量

与双边后向参与全球价值链、以及双边贸易总额正相关的

进一步证据,请参见 Buelens 和 Tirpak(2017)。

14. 亚太经合组织(APEC)和世界银行(World Bank)(2018)。

15. 根据 Johnson 和 Noguera(2017),欧盟和其他特惠贸易

协定,特别是深度贸易协定,在降低双边增加值占出口总

额的比例方面发挥了重要作用,这是全球生产分散化增加

的一个迹象。

16. Pierola, Fernandes 和 Farole(2018)。

17. Eora 数据库(https://worldmrio.com/)的证据显示各国

人均 GDP 与前向全球价值链参与之间呈 U 型关系。

18. Bown 和 Freund(2019)。

19. Hollweg(2019)。

20. Gollier 和 Tirole(2015);Nordhaus(2015)。

21. Cramton等人(2017);Farid等人(2016);Weitzman(2017)。

参考文献

APEC (Asia–Pacific Economic Cooperation) and World Bank. 2018. “Promoting Open and Competitive Markets in Road Freight and Logistics Services: The World Bank Group’s Markets and Competition Policy Assessment Tool Applied in Peru, the Philippines, and Vietnam.” Unpublished report, World Bank, Washington, DC.

Artuc, Erhan, Paulo S. R. Bastos, and Bob Rijkers. 2018. “Robots, Tasks, and Trade.” Policy Research Working Paper 8674, World Bank, Washington, DC.

Bown, Chad P., and Caroline L. Freund. 2019. “Active Labor Market Policies: Lessons from Other Countries for the United States.” PIIE Working Paper 19–2 (January), Peterson Institute for International Economics, Washington, DC.

Buelens, Christian, and Marcel Tirpák. 2017. “Reading the Footprints: How Foreign Investors Shape Countries’ Participation in Global Value Chains.” Comparative Economic Studies 59 (4): 561–84.

Chen, Maggie Xiaoyang, and Min Wu. 2018. “The Value of Reputation in Trade: Evidence from Alibaba.” Paper presented at Workshop on Trade and the Chinese Economy, King Center on Global Development, Stanford University, Stanford, CA, April 12–13.

Constantinescu, Ileana Cristina Neagu, Aaditya Mattoo, and Michele Ruta. 2018. “The Global Trade Slowdown: Cyclical or Structural?” World Bank Economic Review. Published electronically May 23. https://doi.org/10.1093 /wber/lhx027.

Cramton, Peter, David J. MacKay, Axel Ockenfels, and Steven Stoft, eds. 2017. Global Carbon Pricing: The Path to Climate Cooperation. Cambridge, MA: MIT Press.

Dollar, David, and Aart Kraay. 2002. “Growth Is Good for the Poor.” Journal of Economic Growth 7 (3): 195–225.

Farid, Mai, Michael Keen, Michael G. Papaioannou, Ian W. H. Parry, Catherine A. Pattillo, and Anna Ter-Martirosyan. 2016. “After Paris: Fiscal, Macroeconomic, and Financial Implications of Global Climate Change.” IMF Staff Discussion Note 16/01 (January), International Monetary Fund, Washington, DC.

Feenstra, Robert C., and Gordon H. Hanson. 1996. “Foreign Investment, Outsourcing, and Relative Wages.” In The Political Economy of Trade Policy: Papers in Honor of Jagdish Bhagwati, edited by Robert C. Feenstra, Gene M. Grossman, and Douglas A. Irwin, 89–128. Cambridge, MA: MIT Press.

————. 1997. “Foreign Direct Investment and Relative Wages: Evidence from Mexico’s Maquiladoras.” Journal of International Economics 42 (3–4): 371–93.

Ferreira, Francisco H. G., Phillippe George Leite, and Martin Ravallion. 2010. “Poverty Reduction without Economic Growth? Explaining Brazil’s Poverty Dynamics, 1985–

2004.” Journal of Development Economics 93 (1): 20–36. Ferreira, Francisco H. G., and Martin Ravallion. 2008. “Global

Poverty and Inequality: A Review of the Evidence.” Policy Research Working Paper 4623, World Bank, Washington, DC.

Freund, Caroline L., Alen Mulabdic, and Michele Ruta. 2018. “Is 3D Printing a Threat to Global Trade? The Trade Effects You Didn’t Hear About.” Unpublished working paper, World Bank, Washington, DC.

Garicano, Luis, and Steven N. Kaplan. 2001. “The Effects of Business-to-Business E-Commerce on Transaction Costs.” Journal of Industrial Economics 49 (4): 463–85.

Gollier, Christian, and Jean Tirole. 2015. “Negotiating Effective Institutions against Climate Change.” Economics of Energy and Environmental Policy 4 (2): 5–27.

Hollweg, Claire H. 2019. “Firm Compliance and Public Disclosure in Vietnam.” Policy Research Working Paper, World Bank, Washington, DC.

Höppner, Thomas, and Phillipp Westerhoff. 2018. “The EU’s Competition Investigation into Amazon Marketplace.” Kluwer Competition Law Blog, November 30, Wolters Kluwer, Alphen aan den Rijn, The Netherlands. http://competitionlawblog.kluwercompetitionlaw.com/2018/11/30/the-eus-competition-investigation-into-amazon-marketplace/.

ILO (International Labour Organization) and IFC (International Finance Corporation). 2016. “Progress and Potential: How Better Work Is Improving Garment Workers’ Lives and Boosting Factory Competitiveness.” Inter national Labour Office, Geneva. https://betterwork .org/dev/wp-content/uploads/2016/09/BW-Progress-and -Potential_Web-final.pdf.

10 | 2020 年世界发展报告

Johnson, Robert Christopher, and Guillermo Noguera. 2012. “Accounting for Intermediates: Production Sharing and Trade in Value Added.” Journal of International Economics 86 (2): 224–36.

————. 2017. “A Portrait of Trade in Value-Added over Four Decades.” Review of Economics and Statistics 99 (5): 896–911.

Nordhaus, William. 2015. “Climate Clubs: Overcoming Free-Riding in International Climate Policy.” American Economic Review 105 (4): 1339–70.

Oldenski, Lindsay. 2015. “Reshoring by U.S. Firms: What Do the Data Say?” PIIE Policy Brief 15–14 (September), Peterson Institute for International Economics, Washington, DC.

Pierola, Martha Denisse, Ana Margarida Fernandes, and Thomas Farole. 2018. “The Role of Imports for Exporter Performance in Peru.” World Economy 41 (2): 550–72.

Ravallion, Martin, and Guarav Datt. 2002. “Why Has Economic Growth Been More Pro-Poor in Some States of India than Others?” Journal of Development Economics 68 (2): 381–400.

Rocha, Nadia, and Deborah Winkler. 2019. “Trade and Female Labor Participation: Stylized Facts Using a Global Dataset.” Background paper, World Bank-World Trade Organization Trade and Gender Report, World Bank, Washington, DC.

Verhoogen, Eric A. 2008. “Trade, Quality Upgrading, and Wage Inequality in the Mexican Manufacturing Sector.” Quarterly Journal of Economics 123 (2): 489–530.

Weitzman, Martin L. 2017. “How a Minimum Carbon-Price Commitment Might Help to Internalize the Global Warming Externality.” In Global Carbon Pricing: The Path to Climate Collaboration, edited by Peter Cramton, David J. C. MacKay, Axel Ockenfels, and Steven Stoft, 125–48. Cambridge, MA: MIT Press.

生态审计

环境效益声明

世界银行集团致力于减少生态足迹,为此,我们采用电子发行办法和按需打印

技术,后者遍布全球的地区中心。这些综合举措能够降低印量,缩短运输距离,

进而减少纸与化学品消耗、温室气体排放和废弃物的产生。

我们遵循“绿色出版倡议”推荐的用纸标准。世行出版的大部分书籍使用森林

管理委员会(FSC)认证的纸张,基本上所有用纸含有 50-100% 的回收纤维。

图书纸张的回收纤维亦或漂白,亦或使用完全无氯(TCF)、无氯处理(PCF)

或者增强型无元素氯(EECF)工艺漂白。

有 关 世 行 环 境 理 念 的 更 多 信 息, 可 参 见 http://www.worldbank.org/

corporateresponsibility。

SKU 33362

全球价值链推动了 1990年后国际贸易的迅猛增长,

现在几乎占据了全球贸易的半壁江山。这一变化促成

了前所未有的经济差距的缩小:穷国经济快速增长,

并开始赶上富国。

但自 2008年全球金融危机以来,贸易增长乏力,全球

价值链扩张放缓。同时贸易拉动型增长模式正面临严

重威胁。新技术可以缩短生产和消费者之间的距离,

减少对劳动力的需求。大国之间的贸易冲突可能导致

全球价值链走向收缩或分裂。

《2020年全球发展报告:在全球价值链时代以贸易

促发展》探讨了全球价值链和贸易是否仍是促进发展

的途径这一问题。报告的结论是,现阶段的技术变革

利大于弊。只要发展中国家深化改革、促进参与全球

价值链,工业国奉行开放、可预测的政策,所有国家

重振多边合作,全球价值链就能继续促进增长、创造

更好的就业机会和削减贫困。

A World Bank Group Flagship Report

A World Bank Group Flagship Report

© 2020 International Bank for Reconstruction and Development / The World Bank1818 H Street NW, Washington, DC 20433Telephone: 202-473-1000; Internet: www.worldbank.org

Some rights reserved

1 2 3 4 22 21 20 19

This work is a product of the staff of The World Bank with external contributions. The findings, interpretations, and conclusions expressed in this work do not necessarily reflect the views of The World Bank, its Board of Executive Directors, or the governments they represent. The World Bank does not guarantee the accuracy of the data included in this work. The boundaries, colors, denominations, and other information shown on any map in this work do not imply any judgment on the part of The World Bank concerning the legal status of any territory or the endorsement or acceptance of such boundaries.

Nothing herein shall constitute or be considered to be a limitation upon or waiver of the privileges and immunities of The World Bank, all of which are specifically reserved.

Rights and Permissions

This work is available under the Creative Commons Attribution 3.0 IGO license (CC BY 3.0 IGO) http://creativecommons.org/licenses/by/3.0/igo. Under the Creative Commons Attribution license, you are free to copy, distribute, transmit, and adapt this work, including for commercial purposes, under the following conditions:

Attribution—Please cite the work as follows: World Bank. 2020. World Development Report 2020: Trading for Development in the Age of Global Value Chains. Washington, DC: World Bank. doi:10.1596/978-1-4648-1457-0. License: Creative Commons Attribution CC BY 3.0 IGO

Translations—If you create a translation of this work, please add the following disclaimer along with the attribution: This translation was not created by The World Bank and should not be considered an official World Bank translation. The World Bank shall not be liable for any content or error in this translation.

Adaptations—If you create an adaptation of this work, please add the following disclaimer along with the attribution: This is an adaptation of an original work by The World Bank. Views and opinions expressed in the adaptation are the sole responsibility of the author or authors of the adaptation and are not endorsed by the World Bank.

Third-party content—The World Bank does not necessarily own each component of the content contained within the work. The World Bank therefore does not warrant that the use of any third-party-owned individual component or part contained in the work will not infringe on the rights of those third parties. The risk of claims resulting from such infringement rests solely with you. If you wish to re-use a component of the work, it is your responsibility to determine whether permission is needed for that re-use and to obtain permission from the copyright owner. Examples of components can include, but are not limited to, tables, figures, or images.

All queries on rights and licenses should be addressed to World Bank Publications, The World Bank Group, 1818 H Street NW, Washington, DC 20433, USA; e-mail: [email protected].

ISSN, ISBN, e-ISBN, and DOI:

SoftcoverISSN: 0163-5085ISBN: 978-1-4648-1457-0e-ISBN: 978-1-4648-1495-2DOI: 10.1596/978-1-4648-1457-0

HardcoverISSN: 0163-5085ISBN: 978-1-4648-1494-5DOI: 10.1596/978-1-4648-1494-5

Cover image: The cover image is a screen capture of an interactive visualization depicting the flow of international trade, with each dot representing US$1 billion in value. The interactive map was created by data visualization expert Max Galka, from his Metrocosm blog: http://metrocosm.com/map-international-trade/. Used with the permission of Max Galka; further permission required for reuse.

Cover design: Kurt Niedermeier, Niedermeier Design, Seattle, Washington.

Interior design: George Kokkinidis, Design Language, Brooklyn, New York, and Kurt Niedermeier, Niedermeier Design, Seattle, Washington.

Library of Congress Control Number: 2019952802

Contents | iii

xi Foreword

xiii Preface

xv Acknowledgments

xvii Abbreviations

xx Part I: Overview1 Overview2 The expansion of GVCs could stall unless policy predictability is restored3 GVCs boost incomes, create better jobs, and reduce poverty3 The gains from GVCs are not equally shared, and GVCs can hurt the environment4 New technologies on balance promote trade and GVCs4 National policies can boost GVC participation6 Other policies can help ensure GVC benefits are shared and sustainable7 International cooperation supports beneficial GVC participation8 Notes9 References

12 Part II: Global value chains: What are they?14 Chapter 1: The new face of trade16 What is a global value chain?19 The evolution of GVC participation23 How are GVCs distributed across regions?26 Which countries have accounted for most of the GVC expansion?26 How are GVCs distributed across sectors?30 A few large trading firms account for most GVC trade34 Notes34 References

36 Chapter 2: Drivers of participation39 Factor endowments matter46 Market size matters49 Geography matters53 Institutional quality matters54 Transitioning up the GVC typology59 Notes60 References

Contents

iv | Contents

64 Part III: What are the effects of GVCs?66 Chapter 3: Consequences for development68 Economic growth76 Employment80 Poverty and shared prosperity82 Distribution of gains90 The gender gap92 Taxation 93 Notes96 References

102 Chapter 4: Macroeconomic implications103 Synchronizing economic activity105 Propagating shocks106 Synchronizing inflation107 Reducing the effect of devaluations111 Mitigating trade diversion and increasing trade112 The return of protectionism115 Notes115 References

118 Chapter 5: Impact on the environment119 Scale effects of trade and growth124 Changes in the composition of production128 Relational GVCs and production techniques130 Green goods 132 Notes132 References

136 Chapter 6: Technological change137 Declining trade costs146 New products147 Automation anxiety153 Openness and innovation153 Export-led industrialization154 Notes154 References

158 Part IV: What domestic policies facilitate fruitful participation?

160 Chapter 7: Policies to enhance participation162 Facilitating participation175 Policies to enhance benefits186 Policies for upgrading 189 Notes190 References

194 Chapter 8: Policies for inclusion and sustainability195 Sharing the gains202 Managing adjustments 204 Environmental sustainability 209 Notes210 References

Contents | v

214 Part V: How can international cooperation help?216 Chapter 9: Cooperation on trade218 The case for cooperation221 Deepening trade cooperation235 Notes236 References

238 Chapter 10: Cooperation beyond trade239 Taxes242 Regulation246 Competition policy251 Infrastructure 254 Notes255 References

259 Appendix A: Databases used in this Report

265 Appendix B: Glossary

Boxes3.5 79 GVC participation can lead to indirect

welfare improvements for women3.6 82 Does GVC participation lead to

human capital accumulation?3.7 89 Home-based work in GVCs4.1 105 The Japanese earthquake and the

costs of supply chain disruptions4.2 108 Blunting the effects of devaluation on

Turkey’s exports4.3 110 Trade imbalances in using value-

added data5.1 125 The ban on plastics by China

disrupted the waste GVC5.2 127 Virtual water5.3 128 Toward sustainable fashion5.4 130 Demanding environmental standards

in GVC upstream firms6.1 139 Digital innovation and agricultural

trade 6.2 143 GVC linkages and cross-border

connections between people move together

6.3 150 Fully automating the production of hearing aids

6.4 152 Mexico and technological change7.1 164 Determinants of efficiency-seeking

investment7.2 169 Foreign services firms in India’s

manufacturing value chains

1.1 17 Defining global value chains 1.2 17 Measuring global value chains1.3 22 Types of GVC participation1.4 30 A firm-level approach to GVCs2.1 38 Vietnam’s integration in the

electronics GVC 2.2 40 Modeling results on the drivers of

GVC participation2.3 45 Sharing suppliers: How foreign firms

benefit domestic firms2.4 45 How liberalizing trade and FDI

helped China move up in GVCs 2.5 49 Trade preferences as catalytic aid?2.6 55 PTAs and GVCs: The role of rules of

origin 2.7 57 Most important determinants of GVC

participation, by taxonomy group and region

3.1 71 Dynamic estimations of the relationship between GVC participation and per capita income growth

3.2 73 Mining GVCs: New opportunities and old obstacles for local suppliers from developing countries

3.3 75 Assessing outcomes of GVC participation using event studies

3.4 76 Skills and upgrading in Cambodia’s apparel value chain

vi | Contents

7.3 176 Local content requirements are a mismatch in the global auto industry

7.4 178 Supplier development programs help deliver inclusive, sustainable GVCs

7.5 180 Building a workforce with industry-specific skills: Penang Skills Development Centre

7.6 183 Clarifying the terminology: SEZs versus industrial parks

7.7 184 Comparing SEZ experiences: China, India, and Sub-Saharan Africa

7.8 188 Costa Rica moves into the medical devices GVC

8.1 197 Taking advantage of comparative advantage: Agribusiness GVCs deliver more and better jobs in Côte d’Ivoire and Rwanda

8.2 199 A tale of two economic zones: Initiatives to promote women’s employment in garment GVCs in Bangladesh and Jordan

8.3 201 Transparency promotes compliance with labor standards and improves working conditions

8.4 206 Cost-effectiveness and equitability of environmental regulation

8.5 208 Green industrial parks support sustainable production and attract better investors

9.1 218 Special and differential treatment for developing countries

9.2 219 A story of the demise of most-favored-nation status foretold?

9.3 231 The impact of Brexit on GVC trade9.4 234 How the African Continental Free

Trade Area can support integration into GVCs

10.1 252 International cooperation on transport infrastructure

FiguresO.1 2 GVC trade grew rapidly in the 1990s

but stagnated after the 2008 global financial crisis

O.2 3 GDP per capita grows most rapidly when countries break into limited manufacturing GVCs

O.3 4 Automation in industrial countries has boosted imports from developing countries

O.4 5 Transitioning to more sophisticated participation in GVCs: Some examples of national policy

1.1 16 Where do bicycles come from?1.2 19 GVC trade grew rapidly in the 1990s

but stagnated after the 2008 global financial crisis

1.3 20 The ICT revolution spurred the emergence of GVCs

1.4 20 From 1948 to 2016, tariffs dropped thanks to multilateral and regional trade agreements

1.5 21 Country transitions between different types of GVC participation, 1990–2015

1.6 23 Average backward and forward GVC participation across taxonomy groups

1.7 24 GVC activities increased globally and regionally from 1990 to 2015

1.8 25 Global production networks are organized around three main regions, 2018

1.9 26 A handful of countries drove global GVC expansion from 1990 to 2015

1.10 27 GVC participation by sector, 1995 and 2011

1.11 28 A handful of sectors drove global GVC expansion from 1995 to 2011

1.12 29 Services are playing a growing role in GVCs

1.13 29 GVCs expanded in both the agriculture and food industries from 1990 to 2015

1.14 32 Firms that both import and export dominate GVC participation

1.15 33 Foreign direct investment accompanied the fragmentation of production from 1970 to 2018

B2.1.1 38 Vietnam’s backward GVC integration increased from 2000 to 2015 as tariffs declined and foreign direct investment expanded

Contents | vii

B2.2.1 40 What explains backward and forward GVC participation?

B2.2.2 42 What explains a country-sector’s GVC participation levels and gross exports?

2.1 43 Countries specializing in limited manufacturing rely on low labor costs, and countries specializing in commodities derive almost a fifth of GDP from natural resources

2.2 43 Increases in labor costs and capital stock accompany upgrading in GVCs

B2.3.1 45 In Bangladesh, local suppliers grew as FDI grew from 1985 to 2003

B2.4.1 45 Domestic value added in exports from China increased from 2000 to 2007

2.3 46 FDI increases and tariff declines accompany GVC upgrading

2.4 48 Manufacturing tariffs are high and preferential trading partners few in countries connected to commodity GVCs

B2.5.1 50 Four stories of AGOA apparel exports from Africa

2.5 52 Connectivity is associated with specialization in more advanced GVCs

2.6 52 Improving customs and introducing electronic systems are as important as infrastructure for African trade

B2.6.1 56 Mauritius’s exports of apparel to the United States, by origin of fabric, 2001–15

3.1 69 GVC participation is associated with growth in exports and incomes

3.2 69 GVC participation is associated with growth in productivity

3.3 70 Firms that both export and import are more productive

B3.1.1 71 GVC trade is associated with larger per capita income than non-GVC trade

3.4 72 GVC firms with relationships receive more assistance

3.5 74 GDP per capita grows most rapidly when countries break into limited manufacturing GVCs

3.6 77 In Ethiopia, GVC firms are relatively more capital-intensive but their employment is increasing fastest

3.7 78 In Mexico, employment expansion is more strongly linked to GVC expansion than non-GVC trade

3.8 79 Worldwide, GVC firms hire more women than non-GVC firms

3.9 81 The boost to wages is largest in countries after they first enter limited manufacturing GVCs

3.10 81 GVC participation is associated with poverty reduction

3.11 82 In municipalities in Mexico, the expanded presence of GVC firms is more strongly associated with poverty reduction than the presence of firms that export only or import only

3.12 83 In Vietnam, poverty reduction was greater in locations with a higher presence of GVC firms

3.13 84 Rising income inequality is a greater problem for countries breaking into the innovation stages of GVC engagement

3.14 84 A majority worldwide views trade and international business ties positively, but skepticism grew from 2002 to 2014

3.15 85 Increasing GVC participation is associated with rising markups in developed countries but falling markups in developing countries

3.16 85 In Ethiopia, firms entering GVCs experience greater declines in markups, 2000–2014

3.17 86 GVCs have contributed to the declining labor share within countries

3.18 90 Women are more likely to be production workers and less likely to own or manage GVC firms

3.19 91 Gender equality in business regulations ensures that women are more fairly rewarded

3.20 92 Corporate income tax rates have declined by almost 50 percent since 1990

3.21 93 As a share of GDP, non-OECD countries lose the most from profit shifting

4.1 104 In all income groups, countries’ economic activity has become more synchronized since the mid-1990s

4.2 104 Greater synchrony of economic activity is associated with GVCs

4.3 106 The synchrony of inflation increased between 1988 and 2010

viii | Contents

4.4 107 GVCs are associated with greater inflation synchrony in some countries

4.5 107 Trade in intermediate inputs increased the weight of global factors in inflation formation from 1983 to 2006

4.6 108 Export boosts tend to coincide with import boosts—more now than 30 years ago

4.7 109 With GVCs, devaluations can have complex consequences

4.8 109 GVCs dampen the reaction of export volumes to currency movements

B4.3.1 110 Computing bilateral trade balance in gross exports or in value-added exports matters

4.9 114 The multilateral dimension of the U.S.–China trade war

4.10 115 Impact of U.S. tariffs on imports from China

5.1 120 The complexity of producing the Pedego Conveyor electric commuter bike in Vietnam with parts from all over the world

5.2 121 Production-related CO2 emissions drop in countries that recently transitioned into advanced GVCs and innovation hubs

5.3 122 International shipping emissions are increasing

5.4 124 The world produced 50 million metric tons of e-waste in 2018

5.5 126 U.S. output has increasingly shifted away from polluting goods, but imports have done so even faster

B5.3.1 128 Swedish lead firms in apparel and textiles produce a lot of value added with little CO2, and their suppliers produce a lot of CO2 with little value added

6.1 142 Large platform companies are concentrated in North America and Asia

B6.2.1 143 Relationship of exports and GVC participation to online foreign connections

6.2 144 From 2013 to 2015, U.S. exports to Latin America through eBay increased after the introduction of machine translation

6.3 145 Effects of an e-commerce program on the number of buyers and online transactions in Chinese villages

6.4 146 Globally, the number and trade share of new products increased from 1996 to 2017

6.5 147 Robot adoption is greater in high-income countries and in sectors in which tasks are easily automated

6.6 149 Automation in industrial countries has boosted imports from developing countries

6.7 150 Trade in hearing aids increased with the adoption of 3D printing in 2007

6.8 150 Higher robot density is associated with lower shares of income for labor

6.9 151 Change in U.S. employment in robot-intensive industries, by occupation, 1990–2010

B6.4.1 152 Automation reduces the wage employment of high school graduates

7.1 163 Manufacturing labor costs are out of line with national income levels in Sub-Saharan Africa but not in Bangladesh

B7.1.1 165 MNCs involved in efficiency-seeking FDI are more selective

7.2 166 Better-quality investment promotion agencies attract more FDI inflows

7.3 167 Nontariff measure use increases by development status

7.4 171 Shipping delays matter more for products with complex value chains

7.5 171 Customs reform can reduce delay and expand imports: Evidence from Albania

7.6 172 Contract enforcement intensity is higher in services sectors: Evidence from the United States

7.7 173 Share of “other business services” in intermediate inputs is low in poor countries

7.8 174 Certification had long-lasting effects on quality in Mali’s cotton sector

7.9 175 Subsidies account for more than half of distortionary trade policy instruments worldwide

7.10 177 The share of locally supplied inputs in GVCs varies by sector and country

7.11 179 Lack of financing impedes low-income country suppliers the most from entering or moving up in GVCs

7.12 181 Managerial know-how is associated with greater GVC participation in Mexico

Contents | ix

9.6 225 Low-income countries are penalized by tariff escalation both at home and in their destination markets

9.7 226 A majority of PTAs protect investors from discrimination and expropriation

9.8 228 Agricultural producer support converged across some high-income and lower-income countries from 2000 to 2017

9.9 230 Deep trade agreements are associated with GVC integration

B9.3.1 231 Trade impacts of membership in the European Union on the United Kingdom and other EU members

B9.4.1 235 AfCFTA members benefit from reductions in tariffs, nontariff measures, and implementation of the World Trade Organization’s Trade Facilitation Agreement

10.1 243 Regulatory commitments by exporters can be exchanged for import liberalization commitments

10.2 244 Countries’ restrictions on data flows increased from 2006 to 2016

10.3 247 Cartel episodes and significant overcharges have been observed across all regions

10.4 248 The European Commission has imposed large fines on car parts cartels since 2013

B10.1.1 252 Impact of China’s Belt and Road Initiative transport projects with and without input–output linkages

7.13 187 Different policy priorities underpin the transitions between types of GVC participation

B7.8.1 188 Costa Rica’s medical device exports have increased in volume and sophistication since 2000

B8.3.1 201 Working conditions improved in apparel sector firms participating in the ILO-IFC Better Work Vietnam program

8.1 203 Denmark invests more than other OECD countries to support workers

8.2 204 Industrial development was uneven across regions of Mexico during the period of strong international market integration

B8.5.1 208 The number of eco-industrial parks grew rapidly from 1985 to 2015

B9.2.1 219 Shifts in trade shares and changes in policy stances of the United Kingdom and the United States since 1800

9.1 221 Attitudes toward trade differ in the sluggish North and the dynamic South

9.2 221 Corporate tax rates and personal income tax rates for the top 1 percent have fallen, but the rate for the median worker increased in 65 economies between 1980 and 2007

9.3 223 Tariffs have been liberalized across sectors, but pockets of protection remain

9.4 223 There is room for further liberalization9.5 224 Most countries impose higher tariffs

on semifinished and finished goods

MapsO.1 2 All countries participate in GVCs—

but not in the same way1.1 21 All countries participate in GVCs—

but not in the same way2.1 53 Growth in Internet density and

exporter firm density across provinces in China, 1999 and 2007

3.1 78 In Vietnam, employment expansion was linked to GVC firms

3.2 88 In Mexico and Vietnam, GVCs are spatially concentrated

B5.2.1 127 Global water savings associated with international trade in agricultural products, 1996–2005

5.1 131 Supply chain of a solar photovoltaic company

6.1 140 4G network coverage, 20186.2 142 Top e-commerce platforms, by traffic

share, 20196.3 148 A substantial share of exports from

developing countries is in goods that can be produced by robots

7.1 169 Services trade remains restricted in many countries

x | Contents

6.1 141 Ten largest global companies, by market capitalization, 2011, 2015, and 2019

9.1 222 Policy rationale, externalities, and cooperative solutions

B9.3.1 232 Changes in the United Kingdom’s bilateral trade with the European Union under three Brexit scenarios

9.2 233 Existing trade agreements in Africa are relatively shallow

10.1 246 Regulation of international transfers of personal information, by privacy regime

Tables2.1 48 South Asian countries impose higher

barriers to trade on each otherB2.7.1 57 Backward GVC participation and

determinants, by taxonomy groupB2.7.2 58 Backward GVC participation and

determinants, by region and group of countries

3.1 91 Sample of results from case studies on gender in specific GVCs

B5.3.1 129 Total reported savings generated by the Sweden Textile Water Initiative in its five partner countries, 2015–17

5.1 132 Estimation of value added at stages of the supply chain of a solar photovoltaic module

Foreword | xi

Around the world, the process of delivering goods and services to consumers has become spe-cialized to a degree no one could have ever imagined. Businesses focus on what they do best in their home markets and outsource the rest. Samsung makes its mobile phones with parts from 2,500 suppliers across the globe. One country—Vietnam—produces more than a third of those phones, and it has reaped the benefits. The provinces in which the phones are produced, Thai Nguyen and Bac Ninh, have become two of the richest in Vietnam, and poverty there has fallen dramatically as a result.

The face of global trade has been transformed in the three decades since the World Bank’s last major World Development Report on the subject. Until 2008, global value chains (GVCs) expanded rapidly. The expansion was revolutionary for many poorer countries, which boosted growth by joining a GVC, thereby eliminating the need to build whole industries from scratch. The experience of the last three decades has proven that it pays to specialize.

Yet GVCs are at a crossroads. Their growth has leveled off since 2008, when GVCs peaked at 52 percent of global trade. The reasons are complex. Slowing global growth and investment are one factor. And value chains have matured, making further specialization more challeng-ing. Meanwhile, the push toward international trade liberalization has stalled. The growth of automation and other labor-saving technologies such as 3D printing may encourage countries to reduce production abroad. Unless trade liberalization is reinforced, value chains are unlikely to expand.

Under the circumstances, do GVCs still offer developing countries a clear path to progress? That’s the main question explored in the 2020 World Development Report. And the answer is yes: developing countries can achieve better outcomes by pursuing market-oriented reforms spe-cific to their stage of development.

This Report offers a detailed perspective on GVCs. It covers not only the degree to which they contribute to economic growth and poverty reduction, but also the extent to which they lead to inequality and environmental degradation. It discusses how new technologies are reshaping trade, finding that automation will help rather than hurt trade. It also raises concerns about the inadequacies in the global trading system that are fueling disagreements among nations.

In particular, the Report highlights what can be done by countries that have been largely left out of the GVC revolution. Important steps such as speeding up customs procedures and reducing border delays can yield big benefits for countries making the transition from simply exporting commodities to basic manufacturing. Strengthening the rule of law reinforces trade as well. Also helpful are investments that improve connectivity by modernizing communica-tions and roads, railways, and ports. Liberalizing road, sea, and air transport is also important, and it is often less costly.

In the meantime, knowledge and services have become integral to global production, delivering important benefits to developing countries through the supply chain. In Colom-bia, a program led by a multinational firm induced suppliers to upgrade their coffee farms while planting trees and incorporating more efficient and sustainable practices. About 80,000

Foreword

xii | Foreword

farmers and 1,000 villages benefited from the program: the quality of coffee improved, while farmers’ profits increased by 15 percent.

Overall, participation in global value chains can deliver a double dividend. First, firms are more likely to specialize in the tasks in which they are most productive. Second, firms are able to gain from connections with foreign firms, which pass on the best managerial and technolog-ical practices. As a result, countries enjoy faster income growth and falling poverty.

All countries stand to benefit from the increased trade and commerce spurred by the growth of GVCs.

David R. MalpassPresidentThe World Bank Group

Preface | xiii

Preface

The growth of international trade and the expansion of global value chains (GVCs) over the last 30 years have had remarkable effects on development. Incomes have risen, productivity has gone up—particularly in developing countries—and poverty has fallen. The fragmentation of production and knowledge transfer inherent in GVCs are in no small part responsible for these advances. Hyperspecialization by firms at different stages of value chains enhances efficiency and productivity, and durable firm-to-firm relationships foster technology transfer and access to capital and inputs along value chains. GVCs account for around half of world trade today.

At this moment, however, there is reason to worry that this trade-led path to development is under threat. Although trade bounced back after the global financial crisis of 2008, the high growth rates of the 1990s and 2000s have remained elusive. GVC trade—trade in intermediate products—also stalled in 2008, with only modest, intermittent periods of growth since. There are many reasons for this shift, but one is that trade reform has languished and in some cases is even being reversed.

Countries can do much on their own to reinvigorate world trade and GVC expansion. With that in mind, this Report sets out a comprehensive domestic agenda for governments: invest-ments in connectivity, improvements in business climate, and unilateral reductions in trade and investment barriers.

But there is much that countries need to do together to improve the current system. Coor-dinated trade liberalization is overdue in agriculture and services, the rules applied to foreign investment are uneven, and subsidies and state-owned enterprises are distorting competition.

Unfortunately, international cooperation, too, has begun to falter. Many people are disen-chanted with free trade. Some communities have experienced declining wages and unemploy-ment. Businesses are complaining about the limitations of the current multilateral system in dealing with their concerns about lack of access to large markets, the increasing use of “behind-the-border” measures, and “unfair” competition. Governments are inclined to respond by using trade policy as a tool for social protection and to address inadequacies in the current trade rules.

This Report argues that reinvigorating the international trade system will require gov-ernments in certain advanced countries to first look inward to address the discontent and inequality associated with openness. More generally, advanced economies need to rethink the priorities of the welfare state to better help workers adjust to structural change.

Developing countries as well need to expand social assistance and improve compliance with labor regulations in order to extend the jobs and earnings gains from participation in GVCs to more people across society. They also need to take steps to ensure that their domestic firms benefit from knowledge transfer from lead global firms. Finally, all countries need to ensure that the growth associated with trade does not lead to environmental degradation.

Meanwhile, governments need to cooperate with one another beyond the traditional trade issues to ensure that trade and GVCs can deliver for development. Cooperation on corporate taxes will enable governments to better tax capital in a global, digitalized economy, so that they

xiv | Preface

have the resources to finance infrastructure projects and social policies. Improved cooperation on competition issues is needed to ensure that firms enjoy a level playing field globally. And finally, new models of cooperation are needed for data flows to strike a balance between the privacy of citizens and the needs of business and innovators.

The expansion of trade and GVCs is at an inflection point. There is still time to reinvigorate growth, trade, and GVCs. Trade is vital for development, but it needs rules to function smoothly. And those rules require cooperation by governments. This Report offers governments a road map for action.

Pinelopi Koujianou GoldbergChief EconomistThe World Bank Group

Acknowledgments | xv

This year’s World Development Report (WDR) was prepared by a team led by co-directors Caroline Freund and Aaditya Mattoo (World Bank) and Pol Antràs (Harvard University). Daria Taglioni served as task team leader of the project and as a member of the Report’s leadership. Overall guidance was provided by the chief economist of the World Bank, Pinelopi Koujianou Goldberg. The Report is sponsored by the Bank’s Development Economics Vice Presidency.

The core team was composed of Erhan Artuc, Paulo Bastos, Davida Connon, François de Soyres, Thomas Farole, Ana Margarida Fernandes, Michael J. Ferrantino, Bernard Hoekman, Claire H. Hollweg, Melise Jaud, Hiau Looi Kee, Bob Rijkers, and Deborah Winkler.

Members of the extended team—Jessie Coleman, Jan De Loecker, Leonardo Iacovone, Kåre Johard, Madina Kukenova, Michele Mancini, Alen Mulabdic, Nadia Rocha, Michele Ruta, Marijn Verhoeven, Michael D. Wong, and Douglas Zhihua Zeng—provided invaluable contributions to the Report. Sources of additional input were Emma Aisbett, Emmanuelle Auriol, Gaëlle Balineau, Christopher Barrett, Benoit Blarel, Alessandro Borin, Fabrizio Cafaggi, Jieun Choi, Ileana Cristina Constantinescu, Wim Douw, Roberto Echandi, Jakob Engel, Dominik Englert, Marianne Fay, Vivien Foster, Sebastián Franco-Bedoya, Emiko Fukase, Gary Gereffi, Tania Priscilla Begazo Gomez, Stephane Hallegatte, Armando Heilbron, Dirk Heine, Etienne Raffi Kechichian, Jana Krajčovičovà, Peter Kusek, Somik Lall, Arik Levinson, Yan Liu, Rocco Macchiavello, Maryla Maliszewska, Julien Martin, Denis Medvedev, Josepa Miquel-Florensa, Antonio Nucifora, Carlo Pietrobelli, Obert Pimhidzai, Christine Qiang, Tom Reardon, Kirstin Ingrid Roster, Gianluca Santoni, Abhishek Saurav, Kateryna Schroeder, Victor Steenbergen, Michael A. Toman, and Gonzalo Varela.

Research assistance was provided by Vicky Chemutai, Alexandre Gaillard, Chiara Liardi, Julien Maire, Mitali Nikore, Nicolás Gómez Parra, Xiomara Pulido Ramírez, Juan Miguel Jiménez Riveros, Alejandro Forero Rojas, Maria Filipa Seara e Pereira, Guillaume Sublet, Nicolás Santos Villagrán, and the World Bank’s Digital Development program.

The team would like to thank the following colleagues for their guidance during preparation of the Report: Rabah Arezki, Asli Demirgüç-Kunt, Shanta Devarajan, Simeon Djankov, Deon Filmer, Mary Hallward-Driemeier, Daniel Lederman, William Maloney, Martin Rama, Halsey Rogers, Hans Timmer, and Albert Zeufack. The Macroeconomics, Trade, and Investment Global Practice of the Equitable Growth, Finance, and Institutions (EFI) Vice Presidency provided the Report team with support.

The team also benefited at an early stage from consultations on emerging themes with experts from the Bank of Italy, European Commission, French Development Agency, German Agency for International Cooperation (GIZ), German Federal Ministry for Economic Cooper-ation and Development (BMZ), International Trade Centre, Japan International Cooperation Agency, Organisation for Economic Co-operation and Development, Swedish Chamber of Com-merce, Swedish International Development Cooperation Agency, U.K. Department for Inter-national Development, United Nations Industrial Development Organization, U.S. Agency

Acknowledgments

for International Development, and World Trade Organization. An event kindly organized by GIZ and BMZ gave the WDR team a unique opportunity to discuss the Report’s themes with a diverse range of experts from government, civil society, and the private sector.

Bruce Ross-Larson provided developmental guidance in drafting the Report, which was edited by Sabra Ledent and proofread by Gwenda Larsen. Kurt Niedermeier was the prin-cipal graphic designer, with support from Bill Pragluski and Patrick Ibay. Mikael Reventar, Anushka Thewarapperuma, and Roula Yazigi, together with Chisako Fukuda, offered guid-ance, services, and support on communication and dissemination. Special thanks go to Stephen Pazdan, who coordinated and oversaw production of the Report and to the World Bank’s Formal Publishing Program. The team would also like to thank Mary Fisk, who facil-itated translation of the overview; Patricia Katayama, who oversaw the overall publication process; and Deb Barker, who managed the printing and electronic conversions of the book and its overview booklets. The team would also like to thank Marcelo Buitron, Michelle Chester, María del Camino Hurtado, Rashi Jain, Gabriela Calderon Motta, Alejandra Ramon, and Consuelo Jurado Tan for fulfilling their coordinating roles.

Background and related research, along with dissemination, have been generously sup-ported by the KDI School Partnership trust fund, the World Bank’s Knowledge for Change Program (KCP, a multidonor trust fund), Strategic Research Program, Umbrella Facility for Trade, and Multidonor Trust Fund for Trade and Development.

During preparation of the Report, government officials, researchers, and representa-tives of civil society organizations (CSOs) attended consultations in Belgium, Chile, China, France, Germany, India, Poland, Sweden, Turkey, the United Kingdom, and the United States. Participants were drawn from many more countries as well. In addition, a diverse group of CSOs participated in two CSO Forum sessions on this Report held during the 2019 World Bank/International Monetary Fund Spring Meetings and in an e-forum held in March 2019. The team is grateful to these CSOs for their input and to those who took part in these events for their helpful comments and suggestions. Special thanks go to those organizations and individ-uals who provided written comments and engaged directly with the team, including the Con-sumer Unity and Trust Society International, International Trade Union Confederation, ISEAL Alliance, Save the Children, and Women in Informal Employment: Globalizing and Organizing (WIEGO). In addition, the team is grateful for those who submitted comments in response to blogs posted on the topic. Steve Commins provided support during consultations with think tanks and CSOs. Further information on these events is available at http://www.worldbank.org /wdr2020.

The team is grateful as well to the many World Bank colleagues who provided written com-ments during the formal Bank-wide review process. Those comments proved to be invaluable guidance at a crucial stage in the Report’s production.

Team members would also like to thank their families for their support during the prepara-tion of this Report.

Finally, the team apologizes to any individuals or organizations that contributed to this Report but were inadvertently omitted from these acknowledgments.

xvi | Acknowledgments

Abbreviations | xvii

AfCFTA African Continental Free Trade Area AGOA African Growth and Opportunity ActALMP active labor market policyAPEC Asia–Pacific Economic CooperationASCM Agreement on Subsidies and Countervailing MeasuresASEAN Association of Southeast Asian NationsAVE ad valorem equivalentBCRs Binding Corporate RulesBEAT Base Erosion and Anti-abuse TaxBEC Broad Economic CategoriesBEPS base erosion and profit shiftingBIT bilateral investment treatyBPO business processing outsourcingBRI Belt and Road InitiativeCBPRs Cross-Border Privacy RulesCCAC Competition and Consumer Affairs Commission (Guyana)CLOUD Act Clarifying Lawful Overseas Use of Data ActCO2 carbon dioxide COMESA Common Market for Eastern and Southern AfricaCORFO Chilean Innovation AgencyCPEA Cross-border Privacy Enforcement ArrangementCPI consumer price indexCPTPP Comprehensive and Progressive Agreement for Trans-Pacific Partnership CVDs countervailing dutiesDBCFT destination-based cash flow taxDLTs distributed ledger technologies DR–CAFTA Dominican Republic–Central America Free Trade AgreementDST digital services taxDTA domestic tariff areaDTRI Digital Trade Restrictiveness IndexEAC East African CommunityEBA Everything but ArmsECOWAS Economic Community of West African StatesECTEL Eastern Caribbean Telecommunications AuthorityEEA European Economic AreaEEC European Economic CommunityEIP eco-industrial parkEKC environmental Kuznets curveEPZ export processing zoneESG environmental, social, and governance

Abbreviations

xviii | Abbreviations

EU European UnionFAO Food and Agriculture Organization (of the UN)FDI foreign direct investmentfintech financial technologyFTA free trade agreementFVA foreign value addedGATS General Agreement on Trade in ServicesGATT General Agreement on Tariffs and TradeGDP gross domestic productGDPR General Data Protection Regulation GHG greenhouse gasGLoBE global antibase erosionGm3 billion cubic meters GVC global value chainHCI Human Capital IndexHS Harmonized SystemICT information and communication technologyIFC International Finance CorporationILO International Labour OrganizationIMF International Monetary FundIMO International Maritime OrganizationINEGI National Institute of Statistics and Geography (Mexico)IP intellectual propertyIPA investment promotion agencyIPRs intellectual property rightsISCO International Standard Classification of OccupationsISDS investor-state dispute settlementISIC International Standard Industrial ClassificationISO International Organization for StandardizationIT information technologyITC International Trade CentreITKIB Istanbul Textile and Apparel Exporter AssociationsLDCs least developed countriesLPI logistics performance indexm3 cubic metersMENA Middle East and North AfricaMFA Multifibre ArrangementMFN most favored nationMIDP Motor Industry Development ProgrammeMMT million metric tonsMNC multinational corporationMNE multinational enterpriseMOU memorandum of understandingMRIO multiregion input–outputNAFTA North American Free Trade Agreement NEC not elsewhere classifiedNEET not in employment, education, or trainingNOx nitrogen oxidesNTB nontariff barrierNTM nontariff measureOECD Organisation for Economic Co-operation and Development

Abbreviations | xix

PEA Privacy Enforcement AuthorityPHE pollution haven effectPHH pollution haven hypothesisPPP purchasing power parityPSDC Penang Skills Development CentrePTA preferential trade agreementPV photovoltaicPWT Penn World TableQIZ qualified industrial zoneR&D research and developmentRTA regional trade agreementRVC regional value chainSACU Southern African Customs UnionSAR special administrative regionSCC Standard Contractual ClauseSDG Sustainable Development GoalSDT special and differential treatment SEV Samsung Electronics VietnamSEVT Samsung Electronics Vietnam-Thai NguyenSEZ special economic zoneSida Swedish International Development Cooperation AgencySMEs small and medium enterprisesSO2 sulfur dioxideSOE state-owned enterpriseSPS sanitary and phytosanitarySTE state trading enterpriseSTWI Sweden Textile Water InitiativeSystem-GMM System Generalized Method of MomentsTBT technical barrier to tradeTEN-T Trans-European Transport NetworkTFA textile, footwear, and apparel TFA Trade Facilitation AgreementTFP total factor productivityTiVA Trade in Value AddedTRIMs Agreement on Trade-Related Investment MeasuresTRIPS Agreement on Trade-Related Aspects of Intellectual Property RightsUN United NationsUNCTAD United Nations Conference on Trade and DevelopmentUNIDO United Nations Industrial Development OrganizationUSAID U.S. Agency for International DevelopmentUSCBTTA U.S.–Cambodia Bilateral Textile Trade Agreement USMCA United States–Mexico–Canada AgreementVAT value added taxWAEMU West African Economic and Monetary UnionWDI World Development Indicators (database)WEO World Economic Outlook (database)WIOD World Input–Output DatabaseWITS World Integrated Trade Solution (database)WTO World Trade Organization

All dollar amounts are U.S. dollars unless otherwise indicated.

PART I

OverviewPART I

What is a global value chain (GVC)?A global value chain breaks up the production process across countries. Firms specialize in a specific task and do not produce the whole product.

How do GVCs work?Interactions between firms typically involve durable relationships.

Economic fundamentals drive countries’ participation in GVCs. But policies matter—to enhance participation and broaden benefits.

World Development Report 2020: Trading for Development in the Age of

Global Value Chains

Semifinished goods

Bo

rder

Bo

rder

Bo

rderRaw materials

Services inputsParts and components Finished goods

Exports Exports Exports forconsumption

C 67M 0Y 98K 51

C 27M 81Y 8K 30

C 90M 60Y 0K 5

C 48M 40Y 0K 0

C 0M 100Y 65K 4

C 2M 4Y 23K 5

C 0M 30Y 100K 0

C 55M 25Y 0K 0

C 0M 62Y 100K 0

C 74M 0Y 32K 0

C 24M 0Y 98K 8

C 7M 68Y 8K 16

Policies: Social and e

nv

iron

me

nta

l pro

tection

G

eogra

phy Endow

men

ts

Institutions M

arket

size

Gro

wth

and Inequality

En

vironm

ent reductio

n

Pove

rty

Drivers Outcomes

GVC

Hyp

erspecialization

Firm

-to-firm relationsh

ips Polic

ies:

O

pe

nn

ess

•

Co

nnect

ivity

• Cooperation

j

obs

Overview | 1

Overview

International trade expanded rapidly after 1990, powered by the rise of global value chains (GVCs). This expansion enabled an unprecedented con

vergence: poor countries grew faster and began to catch up with richer countries. Poverty fell sharply.

These gains were driven by the fragmentation of production across countries and the growth of connections between firms. Parts and components began crisscrossing the globe as firms looked for efficiencies wherever they could find them. Productivity and incomes rose in countries that became integral to GVCs—Bangladesh, China, and Vietnam, among others. The steepest declines in poverty occurred in precisely those countries.

Today, however, it can no longer be taken for granted that trade will remain a force for prosperity. Since the global financial crisis of 2008, the growth of trade has been sluggish, and the expansion of GVCs has slowed. The last decade has seen nothing like the transformative events of the 1990s—the integration of China and Eastern Europe into the global economy and major trade agreements such as the Uruguay Round and the North American Free Trade Agreement (NAFTA).

At the same time, two potentially serious threats have emerged to the successful model of labor intensive, tradeled growth. First, the arrival of laborsaving technologies such as automation and

3D printing could draw production closer to the consumer and reduce the demand for labor at home and abroad. Second, trade conflict among large coun-tries could lead to a retrenchment or a segmentation of GVCs.

What does all this mean for developing countries seeking to link to GVCs, acquire new technologies, and grow? Is there still a path to development through GVCs? Those are the central questions explored in this Report. It examines the degree to which GVCs have contributed to growth, jobs, and reduced pov-erty—but also to inequality and environmental degra-dation. It spells out how national policies can revive trade growth and ensure that GVCs are a force for development rather than divergence. Finally, it iden-tifies inadequacies in the international trade system that have fomented disagreements among nations and provides a road map to resolving them through greater international cooperation.

This Report concludes that GVCs can continue to boost growth, create better jobs, and reduce poverty, provided that developing countries undertake deeper reforms and industrial countries pursue open, pre-dictable policies. Technological change is likely to be more of a boon than a curse for trade and GVCs. The benefits of GVC participation can be widely shared and sustained if all countries enhance social and environmental protection.

GVCs can continue to boost growth, create better jobs, and reduce poverty—provided that developing countries undertake deeper reforms and industrial countries pursue open, predictable policies.

lower trade barriers induced manufacturers to extend production processes beyond national borders (figure O.1). GVC growth was concentrated in machinery, electronics, and transportation, and in the regions specializing in those sectors: East Asia, North America, and Western Europe. Most countries in these regions participate in complex GVCs, producing advanced manufactures and services, and engage in innovative activities (map O.1). By contrast, many countries in Africa, Latin America, and Central Asia still produce commodities for further processing in other countries.

In recent years, however, trade and GVC growth have slowed (figure O.1). One reason is the decline in overall economic growth, and especially investment. Another reason is the slowing pace and even reversal of trade reforms. Furthermore, the fragmentation of production in the most dynamic regions and sectors has matured. China is producing more at home.1 In the United States, a booming shale sector reduced oil imports by one-fourth between 2010 and 2015 and slightly reduced the incentives to outsource manufac-turing production.2

Recent increases in protection could also affect the evolution of GVCs. Protectionism could induce reshor-ing of existing GVCs or their shifts to new locations. Unless policy predictability is restored, any expansion of GVCs is likely to remain on hold. When future access to markets is uncertain, firms have an incentive to delay investment plans until uncertainty is resolved.

Figure O.1 GVC trade grew rapidly in the 1990s but stagnated after the 2008 global financial crisis

Sources: WDR 2020 team, using data from Eora26 database; Borin and Mancini (2019); and Johnson and Noguera (2017). See appendix A for a description of the databases used in this Report.

Note: See figure 1.2 in chapter 1 for details. Unless otherwise specified, GVC participation measures used in this and subsequent figures throughout the Report follow the methodology from Borin and Mancini (2015, 2019).

30

1970

1975

1980

1985

1990

1995

2000

2005

2010

2015

35

40

45

50

55G

VC s

hare

of g

loba

l tra

de (%

)

2 | World Development Report 2020

Source: WDR 2020 team, based on the GVC taxonomy for 2015 (see box 1.3 in chapter 1).

Note: The type of a country’s GVC linkages is based on (1) the extent of its GVC participation, (2) its sectoral specialization in trade, and (3) its engagement in innovation. Details are provided in figure 1.6 in chapter 1.

Map O.1 All countries participate in GVCs—but not in the same way

Low participation

Limited commodities

High commodities

Limited manufacturing

GVC linkages, 2015

Innovative activities

Data gaps

Advanced manufacturingand services

IBRD 44640 | AUGUST 2019

The expansion of GVCs could stall unless policy predictability is restoredGVCs have existed for centuries. But they grew swiftly from 1990 to 2007 as technological advances—in trans-portation, information, and communications—and

Overview | 3

trade. In Mexico and Vietnam, for example, the regions that saw more intensive GVC participation also saw a greater reduction in poverty.

The gains from GVCs are not equally shared, and GVCs can hurt the environmentThe gains from GVC participation are not distributed equally across and within countries. Large corpora-tions that outsource parts and tasks to developing countries have seen rising markups and profits, sug-gesting that a growing share of cost reductions from GVC participation are not being passed on to consum-ers.6 At the same time, markups for the producers in developing countries are declining. Such a contrast is evident, for example, in the markups of garment firms in the United States and India, respectively.

Within countries, exposure to trade with lower- income countries and technological change contribute to the reallocation of value added from labor to capital. Inequality can also creep upward in the labor market, with a growing premium for skilled work and stag-nant wages for unskilled work.7 Women also face chal-lenges: GVCs may offer more women jobs, but they seem to have even lower glass ceilings. Women are

GVCs boost incomes, create better jobs, and reduce povertyHyperspecialization enhances efficiency, and durable firm-to-firm relationships promote the diffusion of technology and access to capital and inputs along chains. For example, in Ethiopia firms participat-ing in GVCs are more than twice as productive as similar firms that participate in standard trade. Firms in other developing countries also show significant gains in productivity from GVC partici-pation. A 1 percent increase in GVC participation is estimated to boost per capita income by more than 1 percent, or much more than the 0.2 percent income gain from standard trade. The biggest growth spurt typically comes when countries transition out of exporting commodities and into exporting basic manufactured products (for example, garments) using imported inputs (for example, textiles) (figure O.2), as has happened in Bangladesh, Cambodia, and Vietnam.

Eventually, however, these high growth rates can-not be sustained without moving to progressively more sophisticated forms of participation. But the transitions from limited manufacturing to more advanced manufacturing and services, and finally to innovative activities (the GVC taxonomy used in this Report is explained further in box 1.3 in chapter 1), become increasingly more demanding in terms of skills, connectivity, and regulatory institutions.

GVCs also deliver better jobs, but the relationship with employment is complex. Firms in GVCs tend to be more productive and capital-intensive than other (especially nontrading) firms, and so their pro-duction is less job-intensive. However, the enhanced productivity leads to an expansion in firm output and thus to increases in firm employment.3 As a result, GVCs are associated with structural transfor-mation in developing countries, drawing people out of less productive activities and into more produc-tive manufacturing and services activities. Firms in GVCs are unusual in another respect: across a wide range of countries, they tend to employ more women than non-GVC firms.4 They contribute therefore to the broader development benefits of higher female employment.

Because they boost income and employment growth, participation in GVCs is associated with a reduction in poverty.5 Trade in general reduces pov-erty primarily through growth. Because gains in eco-nomic growth from GVCs tend to be larger than from trade in final products, poverty reduction from GVCs also turns out to be greater than that from standard