PAM PT.KAI(1)

38

EVALUASI SISTEM INFORMASI PEMBAYARAN REKENING AIR PADA PDAM DKI JAKARTA Kevin Baihaqi Putra Manoto Binus University, Jakarta, Indonesia, 11480 Dwi Prawira Herlambang Binus University, Jakarta, Indonesia, 11480 Dan Rizki Yut Bagus Koesdinar Binus University, Jakarta, DKI Jakarta, 11480, Indonesia

-

Upload

ali-saiful -

Category

Documents

-

view

108 -

download

6

description

pengukuran, kapabilitas, assessment, untuk kamu, yang sedang, bingung ngerjain tesis atau skripsi

Transcript of PAM PT.KAI(1)

EVALUASI SISTEM INFORMASI

PEMBAYARAN REKENING AIR PADA

PDAM DKI JAKARTA

Kevin Baihaqi Putra Manoto

Binus University, Jakarta, Indonesia, 11480

Dwi Prawira Herlambang Binus University, Jakarta, Indonesia, 11480

Dan

Rizki Yut Bagus Koesdinar

Binus University, Jakarta, DKI Jakarta, 11480, Indonesia

Abstrak

Tujuan Penelitian, ialah untuk menganalisis sistem informasi pembayaran rekening air yang sedang berjalan pada PDAM DKI Jakarta dan mengidentifikasi kelemahan dari sistem informasi pembayaran rekening air. Metodologi Penelitian yang digunakan adalah penelitian kepustakaan dan penelitian lapangan seperti wawancara, observasi, checklist, studi dokumentasi. Hasil yang dicapai dari evaluasi sistem informasi pembayaran rekening air berupa hasil analisa data yang disajikan dalam bentuk temuan masalah, potensi resiko, dan rekomendasi sebagai tindakan perbaikan. Simpulan dari hasil evaluasi sistem informasi pembayaran rekening air sudah berjalan dengan baik namun masih terdapat beberapa kekurangan dalam manajemen IT yang harus diperbaiki agar proses pembayaran rekening air yang berjalan dalam perusahaan dapat lebih maksimal. Kata kunci : evaluasi, sistem informasi, pembayaran rekening air

1. Pendahuluan

Perkembangan Teknologi Informasi (TI) ditandai dengan berkembangnya

pemanfaatan teknologi informasi. Kini, teknologi informasi tidak hanya digunakan

untuk proses operasional sehari-hari, tetapi juga dapat memberikan keuntungan yang

kompetitif bagi organisasi dan informasi. Dukungan teknologi informasi dalam

perusahaan juga dapat menciptakan keunggulan bersaing.

Bumi dikenal sebagai “Planet Air” lantaran 70% permukaan bumi tertutup air, air

memiliki manfaat yang sangat besar bagi manusia. Manfaat sangat nyata dapat kita

lihat dari segi kesehatan. Oleh sebab itu banyak orang mengeksploitasi air secara

berlebihan untuk memenuhi kebutuhan sehari-hari.

Salah satu teknologi informasi yang dibutuhkan oleh perusahaan air adalah teknologi

yang berhubungan pada sistem pembayaran rekening air. Sistem pembayaran ialah

seperangkat komponen yang secara bersama-sama membentuk satu kesatuan yang

diperlukan dalam perpindahan nilai uang dari satu pihak ke pihak lain. Seperti halnya

penerapan teknologi pada bidang rekonsiliasi pembayaran, dimana sistem ini

digunakan untuk mencocokkan data-data yang terkait dengan kebutuhan perusahaan.

Karena ada kemungkinan perbedaan data antara satu dengan yang lain, duplikasi data,

dan data yang hilang, sehingga dapat menimbulkan resiko berupa kerugian

perusahaan, menyebabkan proses bisnis yang tidak optimal, kerugian financial dan

penurunan reputasi perusahaan.

Perusahaan Daerah Air Minum (PDAM) merupakan badan usaha milik

negara atau daerah yang memberikan jasa pelayanan dan menyelenggarakan

kemanfaatan di bidang air minum. Pada tahun 1997, pemerintah memutuskan untuk

bekerja sama dengan dua mitra operator swasta asing untuk mengelola dan

menyediakan air bersih untuk warga DKI Jakarta. Kedua pihak tersebut adalah

Thames Overseas Ltd (PT.Thames PAM Jaya/PT.TPJ) berasal dari Inggris yang

kemudian pada tahun 2008 terjadi penjualan salah satu saham di dalam PT Thames

Jaya kepada perusahaan asal Singapura., PT Acuatico Ltd dan pihak lainnya adalah

Ordeo Suez Lyonnaise de enax (PT. Palyja) yang berasal dari Perancis. Perjanjian

kerja sama ini mengikat kedua belah pihak selama 25 tahun dengan bentuk konsesi

modifikasi. Hal ini berarti mitra swasta akan diberikan hak pengelolahan penuh untuk

seluruh sistem pelayanan PAM Jaya, baik yang sudah mempunyai jaringan perpipaan

maupun daerah yang baru sama sekali.

Di dalam perjanjian kerjasama yang berbentuk konsesi, operator swasta yang

mendapatkan hak penuh pengelolahan, akan memberikan kompensasi biaya kepada

pihak pemerintah, antara lain bentuk : i) deviden apabila ada saham pemerintah dalam

pembiayaan investasi, ii) usage fee untuk biaya penyewaan aset yang diserahkan, iii)

untuk pembayaran hak pengelolahan sistem. Klausul-klausul didalam kontrak

perjanjian secara lengkap mencantumkan : i) target teknis yang hendak dicapai, ii)

hak dan kewajiban pihak yang berjanji, iii) bench mark pelayanan yang harus

dipenuhi dan sanksi yang berlaku, iv) alokasi resiko, v) penyelesaian perselisihan dan

yang paling penting adalah ,vi) formulasi tarif yang harus disepakati. Oleh karena itu,

pembahasan analisis ini berkaitan dengan judul “EVALUASI SISTEM INFORMASI

PEMBAYARAN REKENING AIR PADA PDAM DKI JAKARTA”.

2. Metodologi

Metode penelitian yang digunakan dalam penulisan skripsi ini antara lain:

1. Studi Kepustakaan (Library Research)

Penelitian kepustakaan dilakukan dengan mencari dan mengumpulkan data

dan informasi dari berbagai media seperti media cetak dan media elektronik

seperti internet.

2. Metode penelitian lapangan

Metode penelitian lapangan merupakan metode yang dilakukan peneliti

dengan cara meneliti langsung di perusahaan untuk mendapatkan data yang

diperlukan dengan cara:

a. Wawancara (interview)

Wawancara merupakan kegiatan pengumpulan data dengan cara tanya

jawab secara langsung dengan pihak – pihak yang bersangkutan dalam

perusahaan untuk mendapatkan informasi yang diperlukan.

b. Pengamatan (observation)

Observasi merupakan kegiatan pengumpulan data dengan cara melakukan

pengamatan dan peninjauan secara langsung terhadap obyek yang diteliti

dari perusahaan tersebut.

c. Checklist

Merupakan teknik pengumpulan data yang dilakukan dengan cara memberi

seperangkat pertanyaan atau pernyataan tertulis kepada responden untuk

dijawab.

d. Studi dokumentasi (Review Documentation)

Merupakan proses penelusuran terhadap dokumen – dokumen yang

dijadikan sebagai temuan – temuan atau bukti – bukti audit.

2.1 Ruang Lingkup

Dalam pembuatan skripsi ini berdasarkan latar belakang yang sudah

dijelaskan di atas, maka diperlukan pembatasan ruang lingkup penelitian,

diantaranya :

1. Evaluasi terhadap sistem informasi rekonsiliasi pembayaran rekening.

2. Penelitian ini dilakukan dengan menggunakan standar COBIT versi 4.1

untuk mengukur proses sistem informasi rekonsiliasi pembayaran

rekening.

2.2 Profil Perusahaan

Untuk memenuhi kebutuhan air kota Jakarta (Batavia) pada tahun 1843

oleh Pemerintah Hindia Belanda pengadaan air bersih berasal dari sumur

bor atau artesis. Hingga pada tahun 1928 – 1920, telah ditemukan sumber

mata air Ciburial di daerah Ciomas Bogor oleh Pemerintah Hindia Belanda

dengan kapasitas 484 l/dt, bersamaan dengan berdirinya Gementeestaat-

waterleidengen van Batavia, kantor pemerintah yang menangani

penyediaan air bersih di Jakarta). Pada tanggal 23 Desember 1922, untuk

pertama kalinya air yang berasal dari Ciburial Bogor dialirkan ke kota

Batavia (Jakarta), dan pada tanggal tersebut dijadikan sebagai hari PAM

JAYA. Pada tahun 1945 – 1963 pelayanan air minum dilaksanakan oleh

Dinas Saluran Air Minum Kota Praja dibawah Kesatuan Pekerjaan Umum

Kota Praja. Pada tanggal 30 April 1977, PAM JAYA disyahkan

berdasarkan PERDA DKI Jakarta No. 3/1977. Dan pada tanggal 2

Nopember 1977, PAM JAYA dikukuhkan oleh SK Mendagri No.

PEM/10/53/13350 diundangkan dalam Lembaran DKI Jakarta No. 74 tahun

1977.

PAM JAYA memiliki Nomor Pokok Wajib Pajak (NPWP)

01.000.516.3.073.000. Di Tahun 1997, tepatnya tanggal 6 Juni,

Penandatanganan Perjanjian Kerjasama PAM JAYA dengan 2 Mitra Swasta

selama 25 tahun yaitu PT. Garuda Dipta Semesta yang saat ini menjadi PT.

PAM LYONNAISE JAYA (PT. PALYJA) dan PT. Kekar Pola Airindo

yang saat ini menjadi PT. THAMES PAM JAYA (PT.TPJ). Pada 1 Februari

1998, Operasional secara penuh pelayanan air minum pada wilayah usaha

dilaksanakan oleh 2 Mitra Swasta. Setelah melalui negosiasi Perjanjian

Kerjasama direvisi dinyatakan kembali (Amended & Restated) dengan

Perjanjian Kerjasama 22 Oktober 2001. Penandatanganan kesepakatan

Addendum Perjanjian Kerjasama 2001 untuk Wilayah Barat (PT. PALYJA)

pada tanggal 24 Desember 2004. Dan Penandatanganan kesepakatan

Addendum Perjanjian Kerjasama 2001 untuk Wilayah Timur pada tanggal 7

Oktober 2005.

Kerjasama dengan swasta sebagai upaya meningkatkan kinerja PAM JAYA

dimana dalam era globalisasi diperlukan keikutsertaan swasta, adapun

peningkatan kinerja yang diharapkan dari kerjasama ini :

a. Private sector membawa dana segar untuk mengelola secara efisien

dan mempercepat pembangunan.

b. PAM JAYA dapat meningkatkan kinerja dengan pelayanan yang lebih

baik serta tarif air minum yang masih terjangkau oleh masyarakat kota

Jakarta.

Sungai Ciliwung sebagai batas wilayah pelayanan, wilayah timur

sungai Ciliwung oleh PT. Thames PAM JAYA (Thames Water Overseas

Ltd., Inggris) dan sebelah barat sungai Ciliwung oleh PT. PAM Lyonnaise

Jaya (Lyonnaise des Eaux Perancis). Efektif kerjasama dilaksanakan sejak

tanggal 1 Februari 1998 periode kerjasama selama 25 tahun dan PAM

JAYA secara ekslusif menunjuk kepada kedua mitra swasta untuk

mengoperasikan, memelihara dan mengembangkan sistem penyediaan air

bersih kota DKI Jakarta. Dan pada akhir kerjasama seluruh sistem dan aset

akan dikembalikan kepada PAM JAYA. Sistem Rekonsiliasi Rekening Air

Minum ini diterapkan untuk melayani kebutuhan pengolahan rekonsiliasi.

Dirancang dengan menggunakan konsep berbasis thin client dengan

database Informix Dynamic Service 9.40 untuk pelayanan data yang

terintegrasi dengan sebuah server. Program dibuat dengan bahasa

pemograman Informix 4GL (Four Generation Language), pemilihan

database Informix dilatar belakangi kecepatan dan kemampuan Informix

database dalam paralel prosessing yang dapat meningkatkan kecepatan

proses tergantung dari resource hardware yang tersedia

2.3 Evaluasi

Proses evaluasi di lakukan pada sistem rekonsiliasi yang di miliki oleh

PDAM. Evaluasi di lakukan dengan membuat framework perencanaan apa

saja yang di lakukan untuk memperoleh data-data yang dibutuhkan.

Tujuan dari Evaluasi Sistem Informasi Rekonsiliasi pada PDAM DKI

Jakarta adalah sebagai berikut :

1) Melakukan evaluasi terhadap prosedur sistem informasi rekonsiliasi

pembayaran rekening pada Perusahaan Daerah Air Minum (PDAM) DKI

Jakarta.

2) Mengetahui apakah sistem informasi rekonsiliasi pembayaran yang

sedang berjalan telah terintegrasi dengan baik.

3) Memberikan rekomendasi dan saran yang dapat digunakan untuk

memperbaiki kelemahan – kelemahan yang ada pada sistem agar aset

dalam perusahaan dapat terlindungi dengan baik.

Berikut ini adalah hasil evaluasi dari Sistem Informasi Rekonsiliasi

pada PDAM DKI JAKARTA yang dilakukan dengan menggunakan kerangka

kerja COBIT 4.1 dengan menyertakan Audit Checklist dan pengukuran

Maturity Level sehingga menimbulkan beberapa temuan, yaitu:

1. Pengukuran Maturity Level

a. Hasil Pengukuran Maturity Level pada domain Planning and

Organization (PO)

No. Type Perhitungan Hasil

1. PO1 3 + 3 + 3 + 3 + 3 + 2

∑ Pertanyaan = 6

2,83

2. PO2 3 + 2 + 2 + 2

∑ Pertanyaan = 4

2,25

3. PO3 2 + 1 + 4 + 4 + 4 3

∑ Pertanyaan = 5

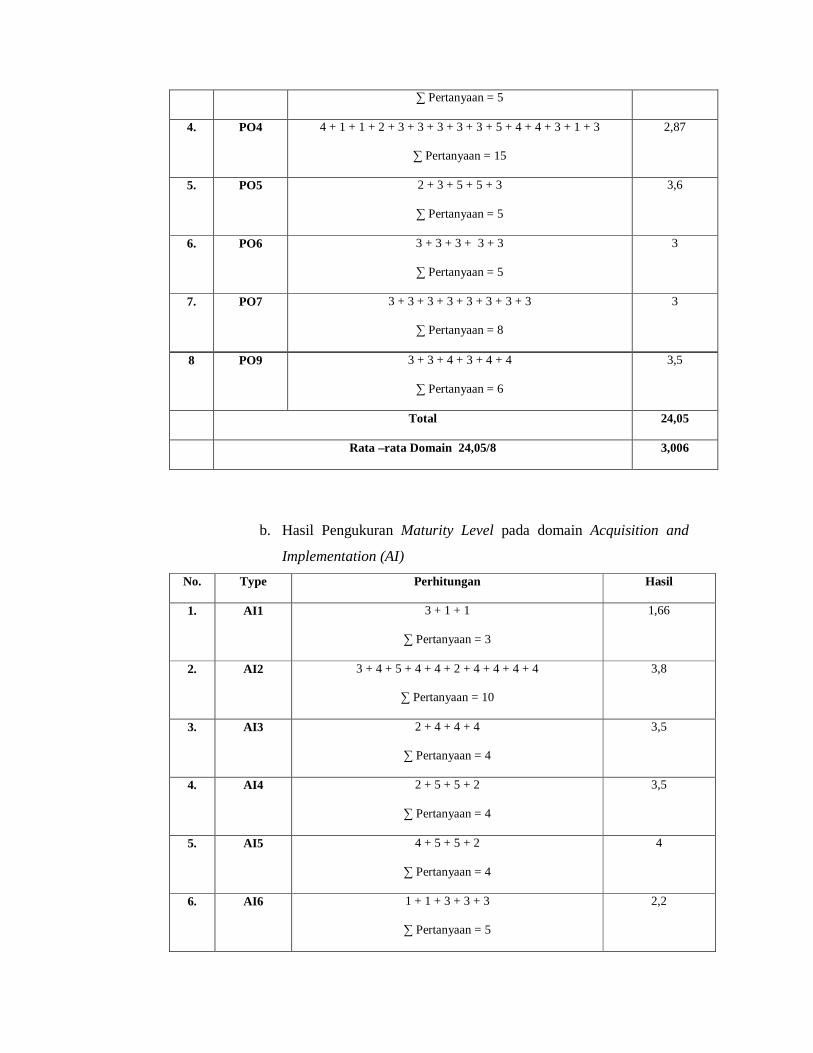

4. PO4 4 + 1 + 1 + 2 + 3 + 3 + 3 + 3 + 3 + 5 + 4 + 4 + 3 + 1 + 3

∑ Pertanyaan = 15

2,87

5. PO5 2 + 3 + 5 + 5 + 3

∑ Pertanyaan = 5

3,6

6. PO6 3 + 3 + 3 + 3 + 3

∑ Pertanyaan = 5

3

7. PO7 3 + 3 + 3 + 3 + 3 + 3 + 3 + 3

∑ Pertanyaan = 8

3

8 PO9 3 + 3 + 4 + 3 + 4 + 4

∑ Pertanyaan = 6

3,5

Total 24,05

Rata –rata Domain 24,05/8 3,006

b. Hasil Pengukuran Maturity Level pada domain Acquisition and

Implementation (AI)

No. Type Perhitungan Hasil

1. AI1 3 + 1 + 1

∑ Pertanyaan = 3

1,66

2. AI2 3 + 4 + 5 + 4 + 4 + 2 + 4 + 4 + 4 + 4

∑ Pertanyaan = 10

3,8

3. AI3 2 + 4 + 4 + 4

∑ Pertanyaan = 4

3,5

4. AI4 2 + 5 + 5 + 2

∑ Pertanyaan = 4

3,5

5. AI5 4 + 5 + 5 + 2

∑ Pertanyaan = 4

4

6. AI6 1 + 1 + 3 + 3 + 3

∑ Pertanyaan = 5

2,2

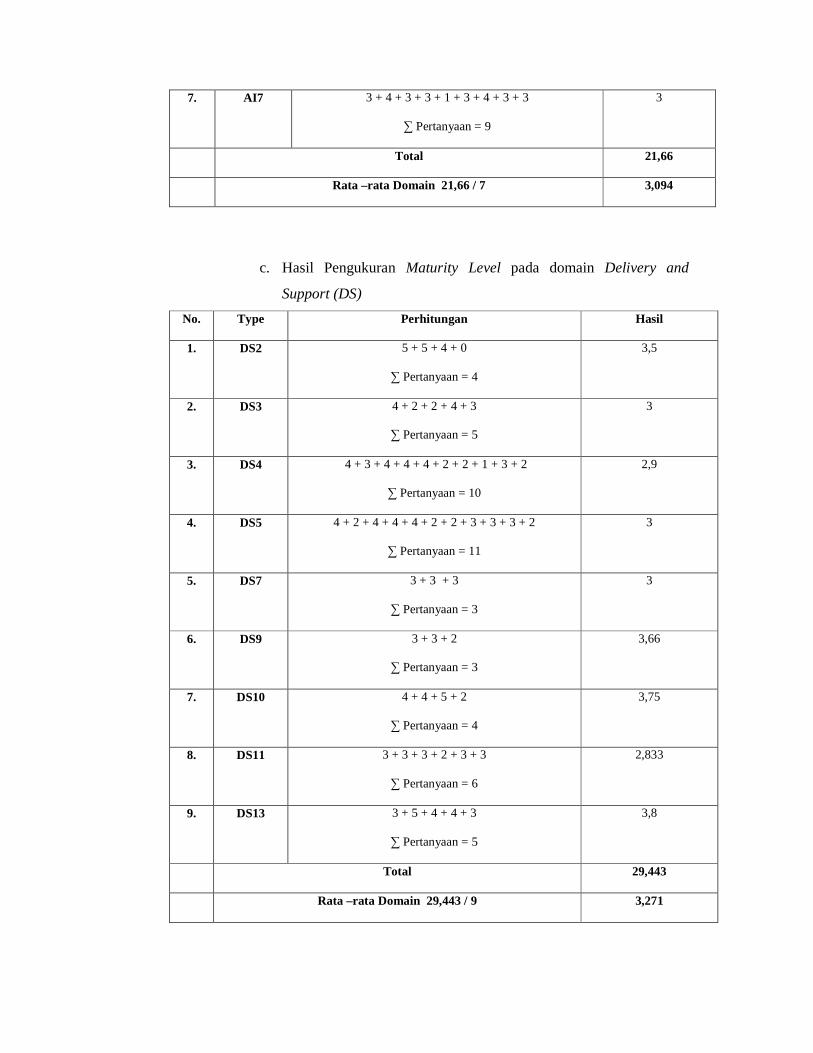

7. AI7 3 + 4 + 3 + 3 + 1 + 3 + 4 + 3 + 3

∑ Pertanyaan = 9

3

Total 21,66

Rata –rata Domain 21,66 / 7 3,094

c. Hasil Pengukuran Maturity Level pada domain Delivery and

Support (DS)

No. Type Perhitungan Hasil

1. DS2 5 + 5 + 4 + 0

∑ Pertanyaan = 4

3,5

2. DS3 4 + 2 + 2 + 4 + 3

∑ Pertanyaan = 5

3

3. DS4 4 + 3 + 4 + 4 + 4 + 2 + 2 + 1 + 3 + 2

∑ Pertanyaan = 10

2,9

4. DS5 4 + 2 + 4 + 4 + 4 + 2 + 2 + 3 + 3 + 3 + 2

∑ Pertanyaan = 11

3

5. DS7 3 + 3 + 3

∑ Pertanyaan = 3

3

6. DS9 3 + 3 + 2

∑ Pertanyaan = 3

3,66

7. DS10 4 + 4 + 5 + 2

∑ Pertanyaan = 4

3,75

8. DS11 3 + 3 + 3 + 2 + 3 + 3

∑ Pertanyaan = 6

2,833

9. DS13 3 + 5 + 4 + 4 + 3

∑ Pertanyaan = 5

3,8

Total 29,443

Rata –rata Domain 29,443 / 9 3,271

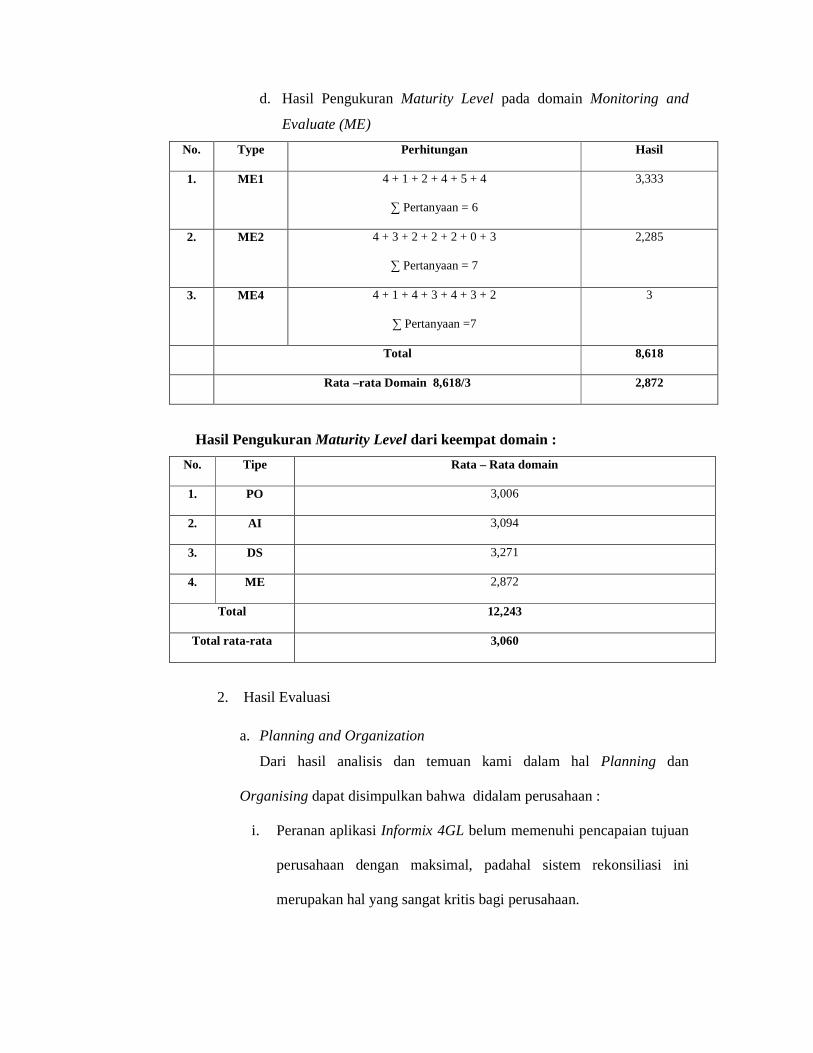

d. Hasil Pengukuran Maturity Level pada domain Monitoring and

Evaluate (ME)

No. Type Perhitungan Hasil

1. ME1 4 + 1 + 2 + 4 + 5 + 4

∑ Pertanyaan = 6

3,333

2. ME2 4 + 3 + 2 + 2 + 2 + 0 + 3

∑ Pertanyaan = 7

2,285

3. ME4 4 + 1 + 4 + 3 + 4 + 3 + 2

∑ Pertanyaan =7

3

Total 8,618

Rata –rata Domain 8,618/3 2,872

Hasil Pengukuran Maturity Level dari keempat domain :

No. Tipe Rata – Rata domain

1. PO 3,006

2. AI 3,094

3. DS 3,271

4. ME 2,872

Total 12,243

Total rata-rata 3,060

2. Hasil Evaluasi

a. Planning and Organization

Dari hasil analisis dan temuan kami dalam hal Planning dan

Organising dapat disimpulkan bahwa didalam perusahaan :

i. Peranan aplikasi Informix 4GL belum memenuhi pencapaian tujuan

perusahaan dengan maksimal, padahal sistem rekonsiliasi ini

merupakan hal yang sangat kritis bagi perusahaan.

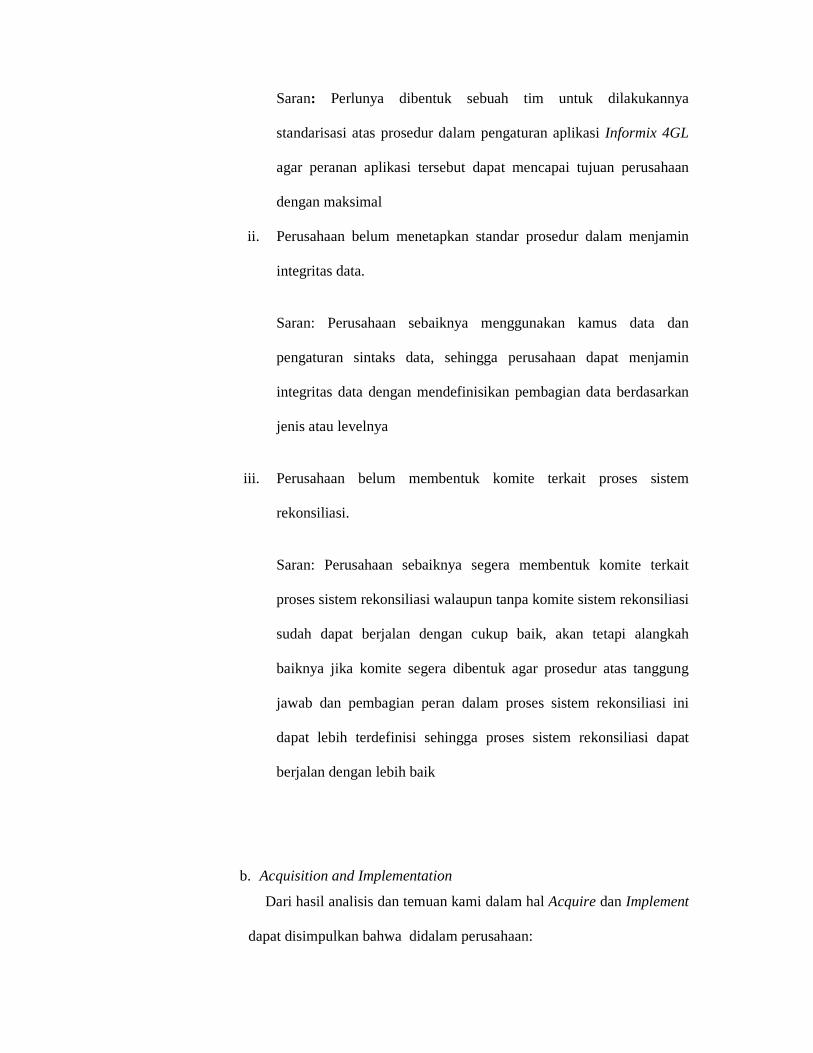

Saran: Perlunya dibentuk sebuah tim untuk dilakukannya

standarisasi atas prosedur dalam pengaturan aplikasi Informix 4GL

agar peranan aplikasi tersebut dapat mencapai tujuan perusahaan

dengan maksimal

ii. Perusahaan belum menetapkan standar prosedur dalam menjamin

integritas data.

Saran: Perusahaan sebaiknya menggunakan kamus data dan

pengaturan sintaks data, sehingga perusahaan dapat menjamin

integritas data dengan mendefinisikan pembagian data berdasarkan

jenis atau levelnya

iii. Perusahaan belum membentuk komite terkait proses sistem

rekonsiliasi.

Saran: Perusahaan sebaiknya segera membentuk komite terkait

proses sistem rekonsiliasi walaupun tanpa komite sistem rekonsiliasi

sudah dapat berjalan dengan cukup baik, akan tetapi alangkah

baiknya jika komite segera dibentuk agar prosedur atas tanggung

jawab dan pembagian peran dalam proses sistem rekonsiliasi ini

dapat lebih terdefinisi sehingga proses sistem rekonsiliasi dapat

berjalan dengan lebih baik

b. Acquisition and Implementation

Dari hasil analisis dan temuan kami dalam hal Acquire dan Implement

dapat disimpulkan bahwa didalam perusahaan:

i. Perusahaan belum memiliki laporan analisi resiko yang berkaitan

dengan proses rekonsiliasi.

Saran: Perusahaan harus segera membuat laporan analisis resiko

yang berkaitan dengan proses rekonsiliasi agar perusahaan memiliki

persiapan dalam menghadapi resiko-resiko yang akan dihadapi

ii. Dalam waktu dekat perusahaan belum memiliki rencana yang

matang dalam proses perubahan. Perubahan atas suatu proses sangat

diperlukan terutama pada jaman yang sudah sangat maju ini agar

perusahaan tetap dapat menjalankan proses bisnisnya dengan baik.

Saran: Perusahaan perlu membuat rencana yang matang untuk

perubahan-perubahan terkait proses rekonsiliasi yang akan datang.

Dan juga perlunya penilaian atas dampak-dampak jika perubahan

dilakukan agar perusahaan dapat memahami perubahan tersebut

c. Delivery and support

Dari hasil analisis dan temuan kami dalam hal Deliver dan Support

dapat disimpulkan bahwa didalam perusahaan:

i. Perusahaan sama sekali tidak memiliki wewenang untuk mengawasi

performa dari rekanan perusahaan (Mitra) terkait proses rekonsiliasi

Saran : Perusahaan perlu membuat perubahan terhadap perjanjian

kerja sama dengan rekanan (Mitra) agar perusahaan memiliki

wewenang dalam melakukan pengawasan terhadap performa rekanan

(Mitra) terkait proses rekonsiliasi

ii. Perusahaan masih belum memiliki kepastian akan standard dari kinerja

perusahaan, sehingga pada masa mendatang perusahaan belum

memiliki antisipasi untuk men-support kinerjanya terkait proses

rekonsiliasi

Saran : Perusahaan harus melakukan pengukuran dan pelaporan

terhadap hasil dari kinerja yang sudah dicapai oleh perusahaan, dari

hasil tersebut perusahaan dapat melakukan evaluasi dan menentukan

standard yang ingin dicapai perusahaan serta memiliki antisipasi

untuk men-support kinerja dan kapasitas pada masa mendatang

iii. Perusahaan masih belum memaksimalkan pengelolaan data mengenai

penyimpanan, back up data , pertukaran data yang sensitive dan

restorasi terhadap data perusahaan yang ada.

Saran: Perusahaan harus memiliki media untuk penyimpanan data

seperti flashdisk atau harddisk external yang nantinya tanggung

jawab penyimpanannya diberikan kepada pihak yang dapat

dipercayai dan back up data secara berkala guna untuk pemulihan

data jika sewaktu-waktu terjadi ancaman yang tidak terduga. Perlu

juga dilakukannya pengawasan terhadap pertukaran data yang

sensitif terutama dari segi keamanannya terhadap pihak yang tidak

bertanggung jawab maupun ancaman-ancaman dari segi teknis

(seperti virus, Trojan, worm, dsb)

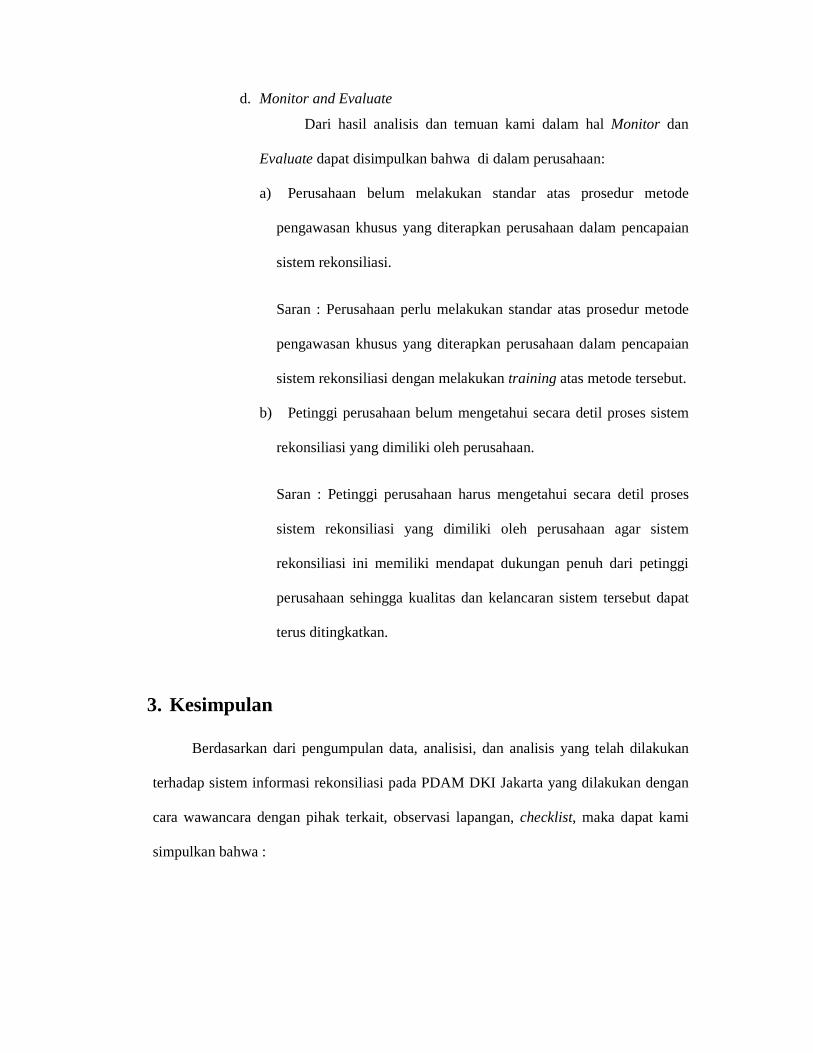

d. Monitor and Evaluate

Dari hasil analisis dan temuan kami dalam hal Monitor dan

Evaluate dapat disimpulkan bahwa di dalam perusahaan:

a) Perusahaan belum melakukan standar atas prosedur metode

pengawasan khusus yang diterapkan perusahaan dalam pencapaian

sistem rekonsiliasi.

Saran : Perusahaan perlu melakukan standar atas prosedur metode

pengawasan khusus yang diterapkan perusahaan dalam pencapaian

sistem rekonsiliasi dengan melakukan training atas metode tersebut.

b) Petinggi perusahaan belum mengetahui secara detil proses sistem

rekonsiliasi yang dimiliki oleh perusahaan.

Saran : Petinggi perusahaan harus mengetahui secara detil proses

sistem rekonsiliasi yang dimiliki oleh perusahaan agar sistem

rekonsiliasi ini memiliki mendapat dukungan penuh dari petinggi

perusahaan sehingga kualitas dan kelancaran sistem tersebut dapat

terus ditingkatkan.

3. Kesimpulan

Berdasarkan dari pengumpulan data, analisisi, dan analisis yang telah dilakukan

terhadap sistem informasi rekonsiliasi pada PDAM DKI Jakarta yang dilakukan dengan

cara wawancara dengan pihak terkait, observasi lapangan, checklist, maka dapat kami

simpulkan bahwa :

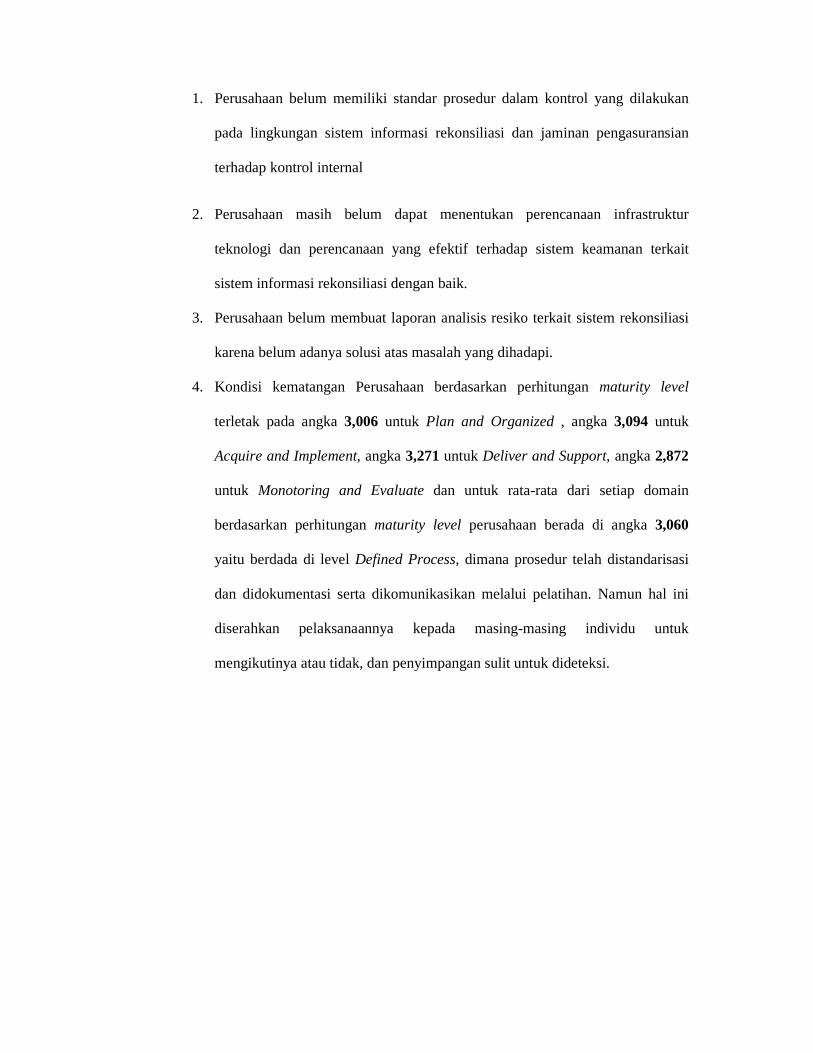

1. Perusahaan belum memiliki standar prosedur dalam kontrol yang dilakukan

pada lingkungan sistem informasi rekonsiliasi dan jaminan pengasuransian

terhadap kontrol internal

2. Perusahaan masih belum dapat menentukan perencanaan infrastruktur

teknologi dan perencanaan yang efektif terhadap sistem keamanan terkait

sistem informasi rekonsiliasi dengan baik.

3. Perusahaan belum membuat laporan analisis resiko terkait sistem rekonsiliasi

karena belum adanya solusi atas masalah yang dihadapi.

4. Kondisi kematangan Perusahaan berdasarkan perhitungan maturity level

terletak pada angka 3,006 untuk Plan and Organized , angka 3,094 untuk

Acquire and Implement, angka 3,271 untuk Deliver and Support, angka 2,872

untuk Monotoring and Evaluate dan untuk rata-rata dari setiap domain

berdasarkan perhitungan maturity level perusahaan berada di angka 3,060

yaitu berdada di level Defined Process, dimana prosedur telah distandarisasi

dan didokumentasi serta dikomunikasikan melalui pelatihan. Namun hal ini

diserahkan pelaksanaannya kepada masing-masing individu untuk

mengikutinya atau tidak, dan penyimpangan sulit untuk dideteksi.

Daftar Pustaka

[1] Arikunto, Suharsimi dan Jabar, Safruddin Abdul. (2010). Evaluasi Program

Pendidikan Pedoman Praktis Bagi Mahasiswa dan Praktisi pendidikan. Jakarta :

Bumi Aksara.

[2] Arifin, Zainal, (2010). Evaluasi Pembelajaran Prinsip, Teknik, Prosedur. Bandung :

Remaja Rosdakarya.

[3] Bachrudin, Sahrir. (2008).” Implementasi SAI Kanwil Depag Sulut”. Retrieved (04-

20-2008) from http://opini-manadopost.blogspot.com/2008/04/implementasi-sai-

kanwil-depag-sulut.html.

[4] Bin Ladjamudin, Al bahra. (2005). Konsep Sistem Basis Data dan Implementasinya.

Yogyakarta: Graha Ilmu.

[5] Edelhauser, Eduard. (2011). IT&C Impact on the Romanian Business and

Organizations. Informatica Economica, Volume 15 (2). Retrieved (09-20-2011) from

http://media.proquest.com

[6] Gelinas,Jr., Ulric J., Dull, Richard B. (2010). Accounting Information Systems. (8th

edition). South Western : Cengage Learning.

[7] Gondodiyoto, Sanyoto. (2007). Audit Sistem Informasi & Pendekatan Cobit. Jakarta :

Mitra Wacana Media.

[8] Gondodiyoto, Sanyoto. (2007). Audit Sistem Informasi: Pendekatan Cobit, Edisi

Revisi. Jakarta : Mitra Wacana Media.

[9] Herawati, Evy. (2009). Audit Sistem Informasi Aplikasi Penjualan Tunai Pada PT.

AJ. CommIT Journal, 3(2), 86.

[10] Husni, Hari Setiabudi. (2010). Evaluasi Pengendalian Sistem Informasi Penjualan

pada PT. XYZ. ComTech, 1(2), 971.

[11] Indrajit, R. E. (2004). Kajian Strategis Cost Benefit Teknologi Informasi. Yogyakarta

: Penerbit Andi.

[12] Jogiyanto H. M. (2009). Sistem Teknolgi Informasi, Edisi Ketiga. Yogyakarta : Andi.

[13] Jones, Frederick L, dan Rama, Dasaratha V. (2006). Accounting Information

Systems. Canada : South-Western College Publishing.

[14] Henny Hendarti. (2008). Korelasi Antara Efektifitas Sistem Informasi KRS Online

dengan Kepuasan Mahasiswa Universitas Bina Nusantara. Jurnal Piranti Warta,

11(2), 161 – 179.

[15] Prasojo, M. (2005). Audit Sistem Informasi untuk Menciptakan Good Corporate

Governance Ditinjau dari Profesi External Auditor, Seminar Nasional Mahasiswa

Jurusan Akuntansi. Retrieved (05-12-2005) from Universitas Katholik Widya

Mandala, Surabaya.

[16] Putra, I N. B. (2009). Audit Sistem Informasi Perpustakaan Menggunakan Standar

COBIT 4.1 Domain Acquire and Implement (Studi Kasus: STIKOM Surabaya), Tugas

Akhir, Program Sarjana, Program Studi Sistem Informasi. Retrieved (07-24-2009)

from Sekolah Tinggi Manajemen Informatika & Teknik Komputer Surabaya,

Surabaya

[17] Romney, Marshall P. Paul John Steinbart. (2008). Accounting Information Systems

(10th edition). USA : Prentice Hall.

[18] Sarosa, S. (2009). Sistem Informasi Akuntansi. Jakarta: Gramedia Widiasarana

Indonesia.

[19] Santo F.Wijaya, Hendra Alianto. (2012). Esensi Dan Penerapam Erp Dalam Bisnis.

Yogyakarta : Graha Ilmu.

[20] Sarno, R. (2009). Audit Sistem & Teknologi Informasi, Surabaya : ITS Press.

[21] Sarno, R. (2009). Strategi Sukses Bisnis dengan Teknologi Informasi Berbasis

Balanced Scorecard & COBIT. Surabaya : ITS Press.

[22] Sarwoto. (2008). Dasar-dasar Organisasi dan Manajemen. Jakarta : PT. Ghalia

Indonesia.

[23] Sawka, Michael N. (2005). p.10 “Healthy humans regulate daily water balance

remarkably well across their lifespan despite changes in biological development and

exposure to stressors on hydration status.” Retrieved (02-19-2005) from

http://search.proquest.com/docview/212334059/fulltextwithgraphics/136F6F69B9C5

A333E5F/1?accountid=31532.

[24] Surendro, K. (2004). Audit Sistem Informasi Rumah Sakit dengan Menggunakan

Acuan COBIT. Gematika Jurnal Manajemen Informatika, 6(1), 1-9.

[25] Wibisono, Dermawan. (2006). Riset Bisnis, Panduan bagi Praktisi dan Akademisi.

Jakarta : Gramedia Puskata Utama.

[26] ”Konsep Dasar Sistem Informasi”, http://blackice89.blogspot.com/2007/12/konsep-

dasar-sistem-informasi.html

[27] “E- commerce”. Encarta. http://microsoft.encarta.com.

[28]”Chapter 1- Sistem Informasi : Konsep dan Management”,

http://ridobelajar.files.wordpress.com/2007/10/ch01revisi.ppt

http://opini-manadopost.blogspot.com/2008/04/implementasi-sai-kanwil-depag-sulut.html

Evaluation Information System of Water

Account Payment in

PDAM DKI JAKARTA

Kevin Baihaqi Putra Manoto

Binus University, Jakarta, Indonesia, 11480

Dwi Prawira Herlambang Binus University, Jakarta, Indonesia, 11480

And

Rizki Yut Bagus Koesdinar

Binus University, Jakarta, DKI Jakarta, 11480, Indonesia

Abstract Research purposes, is to analyze the water bill payment information system that is running on PDAM Jakarta and identify weaknesses of the system water bill payment information. The research methodology used was literature research and field research such as interviews, observations, checklists, study documentation. The results obtained from the evaluation of information systems in the form of water bill payment data analysis presented in the form of finding the problem, potential risks, and recommendations for corrective action. The conclusions of the evaluation system of water bill payment information has been running well but there are still some deficiencies in IT management which must be corrected for water bill payment process that runs in a company can get more leverage. Key words: evaluation, information systems, payment of water bill

1. Introduction

Development of Information Technology (IT) is characterized by the development of

information technology utilization. Today, information technology is not only used to process

daily operations, but also can provide a competitive advantage for the organization and

information. Information technology support within the company can also create competitive

advantage.

Earth is known as the "Water Planet" because 70% of the earth's surface covered in water,

water has enormous benefits for humans. Very real benefits can be seen in terms of health.

Therefore many people exploit the extra water to meet daily needs.

One of the technologies of information needed by water companies are technology related to

the water bill payment system. Payment system is a set of components that together form a

unity that is required in the transfer of value for money from one party to another party. As

with any technology implementation in the field of reconciliation of payments, where the

system is used to match the data related to the needs of the company. Because there is the

possibility of differences in data between one another, duplication of data, and missing data,

so that may pose risks of the company's losses, which do not lead to optimal business

processes, financial losses and a decrease in the company's reputation.

Perusahaan Daerah Air Minum (PDAM) is a state-owned enterprises or areas that

provide services and held a benefit in the field of drinking water. In 1997, the government

decided to cooperate with the two partners of foreign private operators to manage and provide

clean water to residents of Jakarta. Both parties are Thames Overseas Ltd (PT.Thames PAM

Jaya / PT.TPJ) came from England and then in 2008 the sale of a stake in PT Thames Jaya to

Singapore-based companies., PT Acuatico Ltd and others are Ordeo Suez Lyonnaise de enax

(PT Palyja) derived from the French. Cooperation agreement is binding on both parties for 25

years with a modified form of concession. This means that the private partner will be given

full rights to the entire system pengelolahan service PAM Jaya, both of which already has a

network of piping and a new area altogether.

In the cooperation agreement in the form of concessions, the private operators who have full

rights pengelolahan, will compensate the cost to the government, among other forms of: i)

any stock dividend when the government in financing the investment, ii) usage fee for the

rental cost of the asset transferred, iii) pengelolahan right to payment systems. Clauses in the

contract in full agreement include: i) technical targets to be achieved, ii) the rights and

obligations of the parties that promise, iii) the service bench mark to be met and the

applicable sanctions, iv) the allocation of risk, v) settlement of disputes and the most

important thing is, vi) formulation of tariff to be agreed. Therefore, the discussion of this

analysis deals with the title "EVALUATION INFORMATION SYSTEM OF WATER

ACCOUNT PAYMENT IN PDAM DKI JAKARTA”

2. Methodology

The research method used in the writing of this thesis are:

1. Library Studies (Library Research)

Library research done by finding and collecting data and information from

various media such as print and electronic media like the Internet.

2. Field research methods

Method is a method of field research conducted by researchers examined

directly in the company to obtain the data needed by:

a. Interview (interview)

The interview is a data collection activities by direct questioning by the

parties - the parties concerned in the company to obtain necessary

information.

b. Observations (observation)

Observation is an activity by means of data collection and review of direct

observation of the object under study from the company.

c. Checklist

A data collection technique that is done by giving a set of questions or a

written statement to the respondent to answer.

d. Study documentation (Documentation Review)

Is the process of searching for documents - documents that serve as the

findings - findings or evidence - audit evidence.

2.1 Scope

In the making of this thesis is based on the background described

above, the necessary restrictions on the scope of research, including:

1. Evaluation of information systems reconciliation bill payment.

2. The research was carried out using standard COBIT version 4.1 to

measure the process of reconciliation payment account information

system.

2.2 Company Profiles

To meet the water needs of Jakarta (Batavia) in 1843 by the Dutch East

Indies government supply of water comes from wells drilled or artesian.

Until the year 1928 - 1920, has found the fountain Ciburial Ciomas Bogor

area by the Government of the Netherlands East Indies with a capacity of

484 l / dt, together with the establishment Gementeestaat-waterleidengen

van Batavia, government offices that deal with water supply in Jakarta).

On December 23, 1922, for the first time water from Bogor Ciburial

flowed into the city of Batavia (Jakarta), and by that date used as PAM

JAYA day. In the year 1945 - 1963 water supply services carried out by

the Office of Drinking Water Channels under the Unity Township

Municipal Public Works. On 30 April 1977, PAM JAYA approved by

Regional Regulation No. DKI Jakarta. 3/1977. And on November 2,

1977, PAM JAYA inaugurated by Minister of Home Affairs No. SK.

PEM/10/53/13350 promulgated in the Gazette No. DKI Jakarta. 74 in

1977.

PAM JAYA have a Taxpayer Identification Number (TIN)

01.000.516.3.073.000. In 1997, the exact date is June 6, PAM JAYA

Signing of Cooperation Agreement with two private partners for 25 years,

PT. Garuda Dipta Universe which is currently a PT. PAM Lyonnaise Jaya

(PT PALYJA) and PT. Stump Airindo pattern that is currently the PT.

THAMES PAM JAYA (PT.TPJ). On February 1, 1998, fully operational

water supply in the area of business carried out by two private partners.

After negotiations revised Restated Cooperation Agreement (Amended

and Restated) by October 22, 2001 Cooperation Agreement. Signing of

Cooperation Agreement Addendum agreement in 2001 for Western

Region (PT PALYJA) on December 24, 2004. The signing of the

agreement and Addendum to the Cooperation Agreement in 2001 Eastern

Conference on October 7, 2005.

Cooperation with the private sector as an effort to improve the

performance of PAM JAYA where necessary in the era of globalization

of private participation, while the increase in the expected performance of

this agreement:

a. Private sector brings fresh funds to efficiently manage and accelerate

development.

b. PAM JAYA can improve performance with better service and water

rates are still affordable by the people of Jakarta.

Ciliwung River as its service area boundary, the eastern river Ciliwung by

PT. Thames PAM JAYA (Thames Water Overseas Ltd., UK) and west of

the river Ciliwung by PT. PAM Lyonnaise Jaya (Lyonnaise des Eaux

France). Implemented effective cooperation from the date of February 1,

1998 for 25-year period of cooperation and PAM JAYA refer exclusively

to the private partner to operate, maintain and develop water supply

systems of Jakarta city. And at the end of the cooperation of all the

systems and assets would be returned to the PAM JAYA. Drinking Water

Account Reconciliation System was implemented to serve the needs of

the reconciliation process. Designed using the concept of database-based

thin client with Informix Dynamic Service 9:40 for the data service that is

integrated with a server. Programs created with Informix 4GL

programming language (Four Generation Language), the selection of

background Informix database speed and ability to Informix databases in

parallel processing which can improve the speed of the process depends

on the available hardware resources.

2.3 Evaluation

The evaluation process is done on a system of reconciliation

which is owned by the taps. Evaluation is done by creating a

framework in planning what to do to obtain the required data.

The purpose of the Evaluation Information System Reconciliation on

PDAM Jakarta are as follows:

1) Conduct an evaluation of information systems procedures

reconciliation payment on account of Regional Water

Company (PDAM) DKI Jakarta.

2) Determine if the reconciliation payment information system

that is running well integrated.

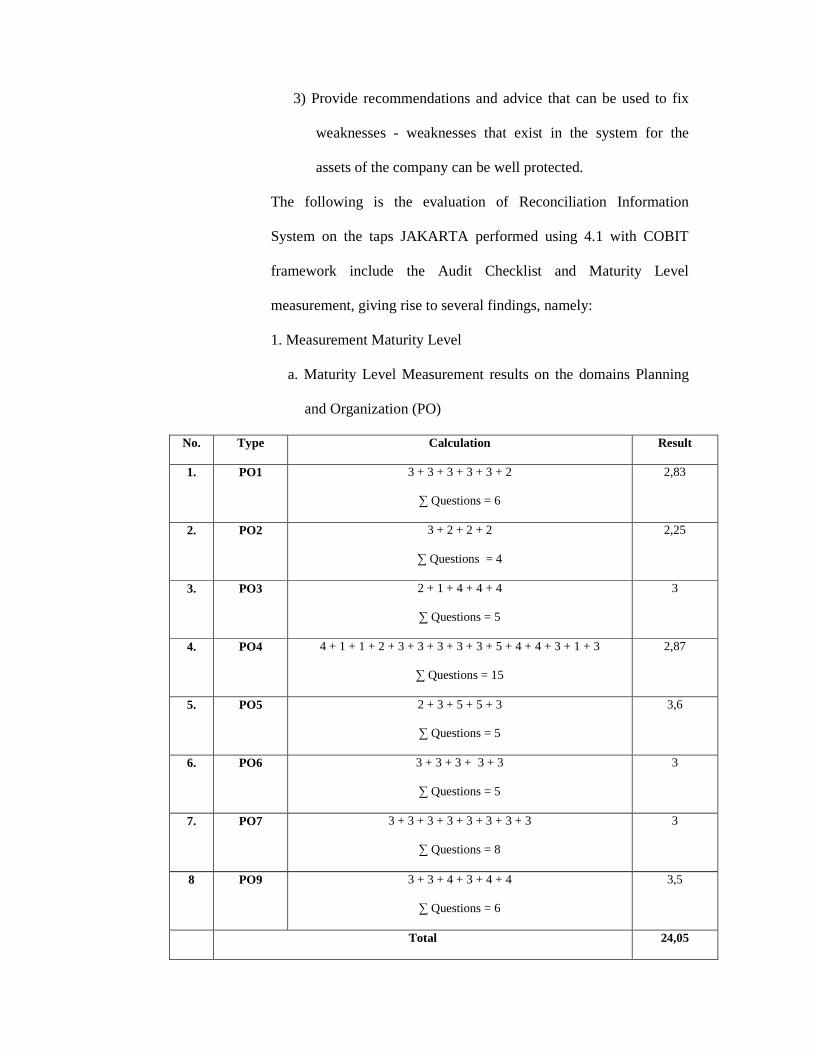

3) Provide recommendations and advice that can be used to fix

weaknesses - weaknesses that exist in the system for the

assets of the company can be well protected.

The following is the evaluation of Reconciliation Information

System on the taps JAKARTA performed using 4.1 with COBIT

framework include the Audit Checklist and Maturity Level

measurement, giving rise to several findings, namely:

1. Measurement Maturity Level

a. Maturity Level Measurement results on the domains Planning

and Organization (PO)

No. Type Calculation Result

1. PO1 3 + 3 + 3 + 3 + 3 + 2

∑ Questions = 6

2,83

2. PO2 3 + 2 + 2 + 2

∑ Questions = 4

2,25

3. PO3 2 + 1 + 4 + 4 + 4

∑ Questions = 5

3

4. PO4 4 + 1 + 1 + 2 + 3 + 3 + 3 + 3 + 3 + 5 + 4 + 4 + 3 + 1 + 3

∑ Questions = 15

2,87

5. PO5 2 + 3 + 5 + 5 + 3

∑ Questions = 5

3,6

6. PO6 3 + 3 + 3 + 3 + 3

∑ Questions = 5

3

7. PO7 3 + 3 + 3 + 3 + 3 + 3 + 3 + 3

∑ Questions = 8

3

8 PO9 3 + 3 + 4 + 3 + 4 + 4

∑ Questions = 6

3,5

Total 24,05

Domain Average 24,05/8 3,006

b. Maturity Level Measurement results on the domain Acquisition

and Implementation (AI)

No. Type Calculation Result

1. AI1 3 + 1 + 1

∑ Questions = 3

1,66

2. AI2 3 + 4 + 5 + 4 + 4 + 2 + 4 + 4 + 4 + 4

∑ Questions = 10

3,8

3. AI3 2 + 4 + 4 + 4

∑ Questions = 4

3,5

4. AI4 2 + 5 + 5 + 2

∑ Questions = 4

3,5

5. AI5 4 + 5 + 5 + 2

∑ Questions = 4

4

6. AI6 1 + 1 + 3 + 3 + 3

∑ Questions = 5

2,2

7. AI7 3 + 4 + 3 + 3 + 1 + 3 + 4 + 3 + 3

∑ Questions = 9

3

Total 21,66

Domain Average 21,66 / 7 3,094

c. Measurement results on the domain Maturity Level Delivery

and Support (DS)

No. Type Calculation Result

1. DS2 5 + 5 + 4 + 0

∑ Questions = 4

3,5

2. DS3 4 + 2 + 2 + 4 + 3 3

∑ Questions = 5

3. DS4 4 + 3 + 4 + 4 + 4 + 2 + 2 + 1 + 3 + 2

∑ Questions = 10

2,9

4. DS5 4 + 2 + 4 + 4 + 4 + 2 + 2 + 3 + 3 + 3 + 2

∑ Questions = 11

3

5. DS7 3 + 3 + 3

∑ Questions = 3

3

6. DS9 3 + 3 + 2

∑ Questions = 3

3,66

7. DS10 4 + 4 + 5 + 2

∑ Questions = 4

3,75

8. DS11 3 + 3 + 3 + 2 + 3 + 3

∑ Questions = 6

2,833

9. DS13 3 + 5 + 4 + 4 + 3

∑ Questions = 5

3,8

Total 29,443

Domain Average 29,443 / 9 3,271

d. Measurement results on the domain Maturity Level Monitoring

and Evaluate (ME)

No. Type Calculation Result

1. ME1 4 + 1 + 2 + 4 + 5 + 4

∑ Questions = 6

3,333

2. ME2 4 + 3 + 2 + 2 + 2 + 0 + 3

∑ Questions = 7

2,285

3. ME4 4 + 1 + 4 + 3 + 4 + 3 + 2

∑ Questions =7

3

Total 8,618

Domain Average 8,618/3 2,872

Maturity Level Measurement results of the four domains:

No. Type Domain Average

1. PO 3,006

2. AI 3,094

3. DS 3,271

4. ME 2,872

Total 12,243

Total Average 3,060

2. Evaluation results

a. Planning and Organization

From the analysis and our findings in terms of Planning and

Organising can be concluded that within the company:

i. Informix 4GL application role has not met the achievement

of corporate objectives to the maximum, but this

reconciliation system is very critical for the company.

Recommendation: Need set up a team to undertake the

standardization of the procedures in Informix 4GL

application settings so that the role of such applications can

achieve corporate goals with maximum

ii. The Company has not set the standard procedure to

guarantee data integrity.

Recommendation: Companies should use the data dictionary

and syntax arrangement of data, so the company can ensure

the integrity of the data by defining the distribution of the

data by type or level

iii . The Company has not formed a committee related to the

process of reconciliation system.

Recommendation: The company should immediately form a

committee related to the process of reconciliation systems

even without the committee was able to reconcile the system

works quite well, but it would be nice if the committee was

immediately formed that the procedure for the division of

roles and responsibilities in the process of reconciliation

systems can be better defined so that the system

reconciliation can work better

b. Acquisition and Implementation

From the analysis and our findings in terms Acquire and

Implement it can be concluded that within the company:

i. The Company does not have the report analyzes the risks

associated with the reconciliation process.

Recommendation: The Company shall promptly make a report

analyzes the risks associated with the reconciliation process

that the company has a preparation to face the risks to be

faced

ii. In the near future the company has no plans to mature in the

process of change. An amendment to a process is needed,

especially in the era of highly developed is that companies

can still run the business properly.

Recommendation: Companies need to create a plan that is ripe

for changes related to the reconciliation process to come.

And also the need for an assessment of the impacts if

changes are made so the company can understand the

changes

c. Delivery and support

From the analysis and our findings in terms Deliver and

Support can be concluded that within the company:

i. The Company did not have the authority to supervise the

performance of the company partners (Partners) related to

the process of reconciliation

Recommendation: Companies need to make changes to the

agreement of cooperation with partners (Partners) that the

company has the authority to supervise the performance of

partners (Partners) relating to the reconciliation process

ii. Companies still do not have the assurance of standards of

performance of the company, so that in future the company

does not have the anticipation for the performance-related

support to the reconciliation process

Recommendation: Companies should make the measurement

and reporting of the results of performance already achieved

by the company, the results of the company can evaluate and

determine the standards to be achieved and have the

anticipation for the company to support the performance and

capacity in the future

iii. Companies are still not maximizing the storage of data

management, data backup, data exchange and restoration of

sensitive corporate data available.

Recommendation: Companies should have a medium for data

storage such as flash or external hard drive storage that will

be the responsibility given to those which can be trusted and

back up data regularly in order to restore the data if at any

time of the threat of the unexpected. There should also do

surveillance of the exchange of sensitive data, especially in

terms of security against casual and irresponsible threats of

technical terms (such as viruses, Trojans, worms, etc.)

d. Monitor and Evaluate

From the analysis and our findings in terms of Monitor and

Evaluate can be concluded that in the company:

i. The Company has not made the standard procedures applied

to specific methods of monitoring the company in achieving

reconciliation system.

Recommendation: Companies need to perform the standard

procedures applied to specific methods of monitoring the

company in achieving reconciliation system by conducting

training on the method.

ii. the company officials are not yet know in detail the process

of reconciliation of systems owned by the company.

Recommendation: the officer must know in detail the

company's systems process of reconciliation which is owned

by the company in order to reconcile the system has received

full support from company officials that the quality and

continuity of the system can be improved.

3. Conclusion

Based on the data collection, analisisi, and analysis has been conducted on

information systems at PDAM Jakarta reconciliation by way of interviews with

relevant parties, field observations, checklists, then we can conclude that:

1. Companies do not have a standard procedure performed in the environmental

control system and security information pengasuransian reconciliation of

internal controls

2. Companies are still not able to determine the technological infrastructure

planning and effective planning for information systems security system

associated with a good reconciliation.

3. The Company has not made a report related to risk analysis of reconciliation

systems because there is no solution to the problem at hand.

4. The company is based on the calculation of the condition of maturity is the

maturity level figures for the Plan and Organized 3.006, 3.094 rate for Acquire

and Implement, the number 3.271 to Deliver and Support, the rate of 2.872 to

Monotoring and Evaluate and for the average of each maturity level domain

based on the calculation of the company is 3.060 in the barrel-chested figure in

Process Defined level, where the procedure has been standardized and

documented and communicated through training. However this implementation

is left to each individual to follow it or not, and the deviation is difficult to

detect.

References

[1] Arikunto, Suharsimi dan Jabar, Safruddin Abdul. (2010). Evaluasi Program

Pendidikan Pedoman Praktis Bagi Mahasiswa dan Praktisi pendidikan. Jakarta :

Bumi Aksara.

[2] Arifin, Zainal, (2010). Evaluasi Pembelajaran Prinsip, Teknik, Prosedur.

Bandung : Remaja Rosdakarya.

[3] Bachrudin, Sahrir. (2008).” Implementasi SAI Kanwil Depag Sulut”. Retrieved

(04-20-2008) from http://opini-

manadopost.blogspot.com/2008/04/implementasi-sai-kanwil-depag-sulut.html.

[4] Bin Ladjamudin, Al bahra. (2005). Konsep Sistem Basis Data dan

Implementasinya. Yogyakarta: Graha Ilmu.

[5] Edelhauser, Eduard. (2011). IT&C Impact on the Romanian Business and

Organizations. Informatica Economica, Volume 15 (2). Retrieved (09-20-2011)

from http://media.proquest.com

[6] Gelinas,Jr., Ulric J., Dull, Richard B. (2010). Accounting Information Systems.

(8th edition). South Western : Cengage Learning.

[7] Gondodiyoto, Sanyoto. (2007). Audit Sistem Informasi & Pendekatan Cobit.

Jakarta : Mitra Wacana Media.

[8] Gondodiyoto, Sanyoto. (2007). Audit Sistem Informasi: Pendekatan Cobit,

Edisi Revisi. Jakarta : Mitra Wacana Media.

[9] Herawati, Evy. (2009). Audit Sistem Informasi Aplikasi Penjualan Tunai Pada

PT. AJ. CommIT Journal, 3(2), 86.

[10] Husni, Hari Setiabudi. (2010). Evaluasi Pengendalian Sistem Informasi

Penjualan pada PT. XYZ. ComTech, 1(2), 971.

[11] Indrajit, R. E. (2004). Kajian Strategis Cost Benefit Teknologi Informasi.

Yogyakarta : Penerbit Andi.

[12] Jogiyanto H. M. (2009). Sistem Teknolgi Informasi, Edisi Ketiga. Yogyakarta

: Andi.

[13] Jones, Frederick L, dan Rama, Dasaratha V. (2006). Accounting Information

Systems. Canada : South-Western College Publishing.

[14] Henny Hendarti. (2008). Korelasi Antara Efektifitas Sistem Informasi KRS

Online dengan Kepuasan Mahasiswa Universitas Bina Nusantara. Jurnal Piranti

Warta, 11(2), 161 – 179.

[15] Prasojo, M. (2005). Audit Sistem Informasi untuk Menciptakan Good

Corporate Governance Ditinjau dari Profesi External Auditor, Seminar

Nasional Mahasiswa Jurusan Akuntansi. Retrieved (05-12-2005) from

Universitas Katholik Widya Mandala, Surabaya.

[16] Putra, I N. B. (2009). Audit Sistem Informasi Perpustakaan Menggunakan

Standar COBIT 4.1 Domain Acquire and Implement (Studi Kasus: STIKOM

Surabaya), Tugas Akhir, Program Sarjana, Program Studi Sistem Informasi.

Retrieved (07-24-2009) from Sekolah Tinggi Manajemen Informatika &

Teknik Komputer Surabaya, Surabaya

[17] Romney, Marshall P. Paul John Steinbart. (2008). Accounting Information

Systems (10th edition). USA : Prentice Hall.

[18] Sarosa, S. (2009). Sistem Informasi Akuntansi. Jakarta: Gramedia

Widiasarana

Indonesia.

[19] Santo F.Wijaya, Hendra Alianto. (2012). Esensi Dan Penerapam Erp Dalam

Bisnis. Yogyakarta : Graha Ilmu.

[20] Sarno, R. (2009). Audit Sistem & Teknologi Informasi, Surabaya : ITS Press.

[21] Sarno, R. (2009). Strategi Sukses Bisnis dengan Teknologi Informasi Berbasis

Balanced Scorecard & COBIT. Surabaya : ITS Press.

[22] Sarwoto. (2008). Dasar-dasar Organisasi dan Manajemen. Jakarta : PT. Ghalia

Indonesia.

[23] Sawka, Michael N. (2005). p.10 “Healthy humans regulate daily water balance

remarkably well across their lifespan despite changes in biological

development and exposure to stressors on hydration status.” Retrieved (02-19-

2005) from

http://search.proquest.com/docview/212334059/fulltextwithgraphics/136F6F69

B9C5A333E5F/1?accountid=31532.

[24] Surendro, K. (2004). Audit Sistem Informasi Rumah Sakit dengan

Menggunakan Acuan COBIT. Gematika Jurnal Manajemen Informatika, 6(1),

1-9.

[25] Wibisono, Dermawan. (2006). Riset Bisnis, Panduan bagi Praktisi dan

Akademisi. Jakarta : Gramedia Puskata Utama.

[26]”Konsep Dasar Sistem Informasi”,

http://blackice89.blogspot.com/2007/12/konsep-dasar-sistem-informasi.html

[27] “E- commerce”. Encarta. http://microsoft.encarta.com.

[28]”Chapter 1- Sistem Informasi : Konsep dan Management”,

http://ridobelajar.files.wordpress.com/2007/10/ch01revisi.ppt

http://opini-manadopost.blogspot.com/2008/04/implementasi-sai-kanwil-depag-

sulut.html