Bahasa

Halaman

Hukum

THE RELATIVE USE OF FORMAL AND INFORMAL INFORMATION IN THE

EVALUATION OF INDIVIDUAL PERFORMANCE

by

GENE H. JOHNSON, B.B.A., M.S. in Acct.

A DISSERTATION

IN

BUSINESS ADMINISTRATION

Submitted to the Graduate Faculty of Texas Tech University in Partial Fulfillment of the Requirements for

the Degree of

DOCTOR OF PHILOSOPHY

December, 1986

•

//^,;¥

(c) 1986 Gene H. Johnson

ACKNOWLEDGMENTS

Funding for this research project was provided by the

National Association of Accountants, and was especially

beneficial in that it allowed the author to complete the

project in a timely manner. Subjects for the project were

provided by the research entity which must, for the sake of

anonymity, remain unnamed. Nonetheless, their partici

pation is greatly appreciated.

Early conceptual development of the project was

facilitated by a number of individuals, including the

doctoral students and Professors Don Clancy and Frank

Collins of Texas Tech University. Also helpful were the

experiences of Louis Johnson, John Johnson, Sam Nichols,

Darrell Adams, and Del Shumate. The members of the

committee provided valuable guidance and support throughout

the project; and although not a member of the committee.

Professor Roy Howell provided valuable assistance with data

analysis. Finally, Professor Donald K. Clancy served not

only as committee chairman but also as a role model/mentor

for the author. His participation made the project

interesting, educational, and enjoyable.

11

CONTENTS

ACKNOWLEDGMENTS ii

ABSTRACT vi

LIST OF TABLES viii

LIST OF FIGURES ix

I. INTRODUCTION AND BACKGROUND 1

Formal and Informal Information 2

Performance Evaluation 4

Purpose, Objectives, and Significance . . 6

Organization 7

II. PREVIOUS STUDIES OF INFORMATION

FOR PERFORMANCE EVALUATION 8

Goals and Goal-Directed Behavior 9

Early Studies on Performance Measures . . 11

Budget-Based Studies 17

Contingency Theory 19

Agency Theory 21

Markets and Hierarchies 22

Managerial Performance Appraisal 25

Informal Information 30

Summary 3 3

111

III. DISCUSSION OF VARIABLES AND RELATIONSHIPS:

MODEL DEVELOPMENT 36

Theoretical Perspective 36

Potential Explanatory Variables 41

Research Perspective 42

The Relative Use of Formal and

Informal Information 44

Attitudes Toward Formal and

Informal Information 45

Locus of Control 49

Role Stress 51

Leadership Style 54

Other Relationships Among

Explanatory Variables 57

Variables of Interest: Summary 58

Hypotheses 59

The Research Model 61

IV. RESEARCH METHODOLOGY 64

A Two-Phase Field Study 64

Phase One: Development of the Instrument . 66

Phase Two: A Single-Entity Sample . . . . 73

Statistical Analysis - LISREL 78

V. EMPIRICAL RESULTS 86

Verification of the Research Constructs . 86

Demographics and Other Potential

Explanatory Variables 100

iv

Testing Hypotheses with LISREL 103

Tests of Hypotheses 105

Stress as an Endogenous Variable:

A Fitted Model 109

VI. SUMMARY AND CONCLUSIONS 114

Summary of Findings 114

Implications of the Use of

Informal Information 119

Implications of the Relationships

Among the Variables 120

Policy Implications 121

Limitations of the Study 123

Suggestions for Future Research 124

REFERENCES 127

APPENDICES

A. INTERVIEW SCHEDULE 138

B. QUESTIONNAIRE 140

C. ANALYSIS OF DEMOGRAPHIC VARIABLES 147

D. THE NULL MODEL 150

E. THE ATTITUDES MODEL 153

F. THE FITTED MODEL 156

V

ABSTRACT

Individual performance evaluation is a critical

managerial function. Judgments of individual performance

are evident in certain managerial decisions, such as those

regarding the pay, promotion, and termination of

subordinates. While much has been written about the

measurement of performance and about performance-appraisal

techniques, little is known about the information managers

use in evaluating individual performance. Accordingly,

this study was conducted for two reasons: 1) to study the

extent to which informal information (unofficial, or

"non-sanctioned") is used in individual performance

evaluation, and 2) to examine the relationships among a

number of explanatory variables and the relative use of

formal and informal information. '

A questionnaire was used to measure the relative use

of formal and informal information in performance-related

decision making (the dependent variable), attitudes toward

the information used (ATTITUDES), role stress, two

dimensions of superior's leadership style (structure and

consideration), and one personality variable (locus of

control). The responses indicate that informal information \

vi

is used relatively more than formal information in the |

evaluation of individual performance. Further, the

managers perceived the informal information easier to use

and understand, more qualitative, and more confidential

than the formal information.

Covariance structural equations modeling (LISREL) was

used to study the relationships among the research

variables. As hypothesized, attitudes toward the

information are strongly related to the relative use of

formal and informal information. The hypothesized

relationship between the research variable ATTITUDES and

role stress, and the influences of leadership style and

locus of control on stress are also supported. Not

supported by the data, however, are the hypothesized

relationships among the relative use of formal and informal

information and role stress, leadership style, and locus of

control, and the hypothesized relationships among

ATTITUDES, leadership style, and locus of control.

The findings suggest a discrepancy between the

formally agreed upon rules of governance in organizations

and the true system of rewards. Contractual disputes and

other dysfunctional consequences are implied. However,

another plausible explanation is that the informal

information is necessary in order to compensate for the

inadequacies of the formal information. Thus, the formal

and informal information may be complementary.

vii

LIST OF TABLES

4.1: Non-Response Bias Test Results 77

5.1: Responses to RUFI Items 87

5.2: Tests For Differences in RUFI Responses . . . . 89

5.3: Correlations Among RUFI Responses 90

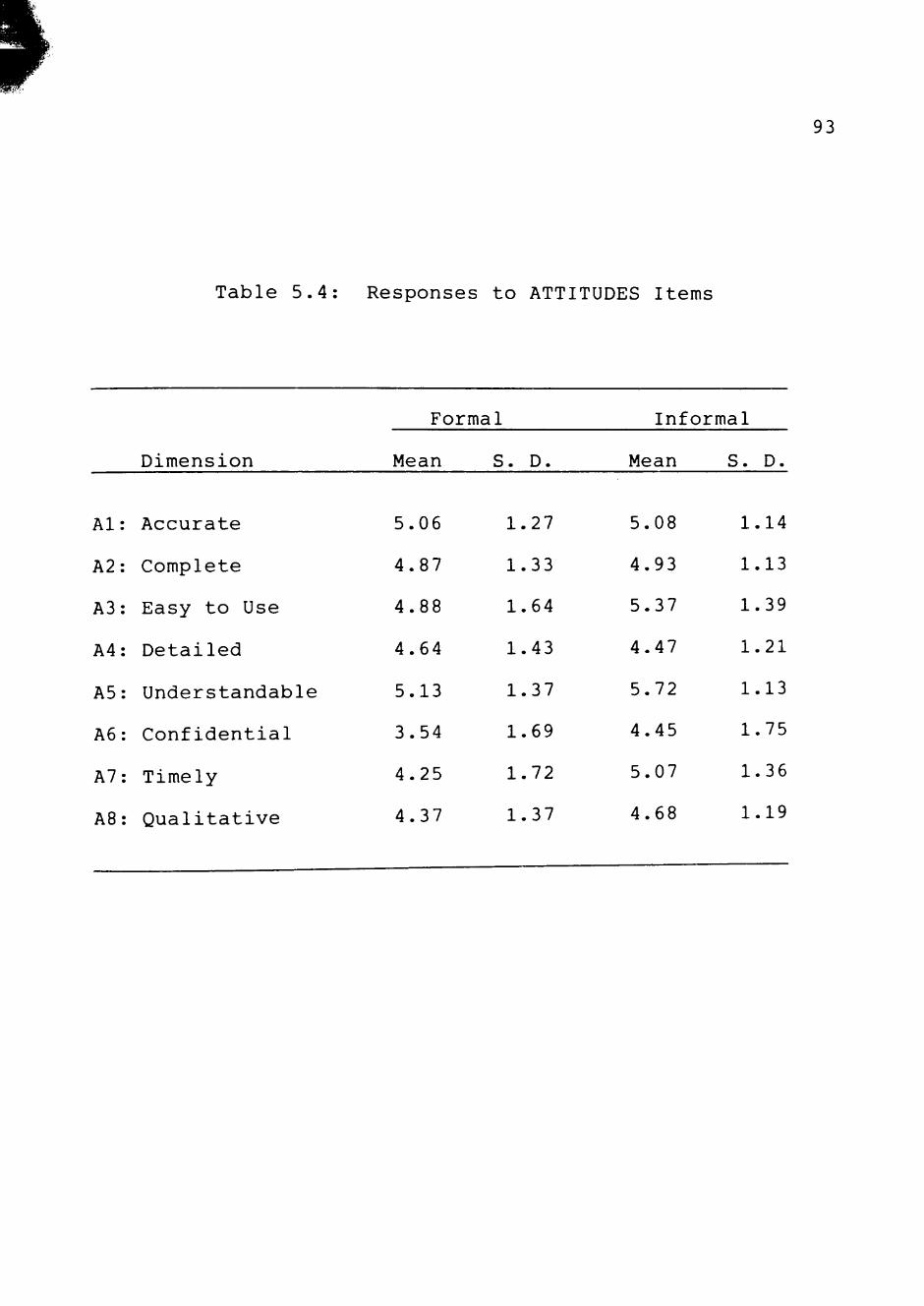

5.4: Responses to ATTITUDES items 93

5.5: Tests for Differences in ATTITUDES Responses . 95

5.6: Initial Factor Loadings: ATTITUDES 97

5.7: Promax Rotated Factor Loadings: ATTITUDES . . . 98

5.8: Tests for Differences by Department 101

5.9: Tests for Differences by Faction 102

5.10: Tests of Direct Hypotheses 106

5.11: Preliminary Tests of Indirect Hypotheses . . . 108

5.12: Sequential Tests of Indirect Hypotheses . . . . 110

5.13: Total Effects: The Fitted Model 112

Vlll

LIST OF FIGURES

3.1: Preliminary Theoretical Model 37

3.2: Theoretical Model 39

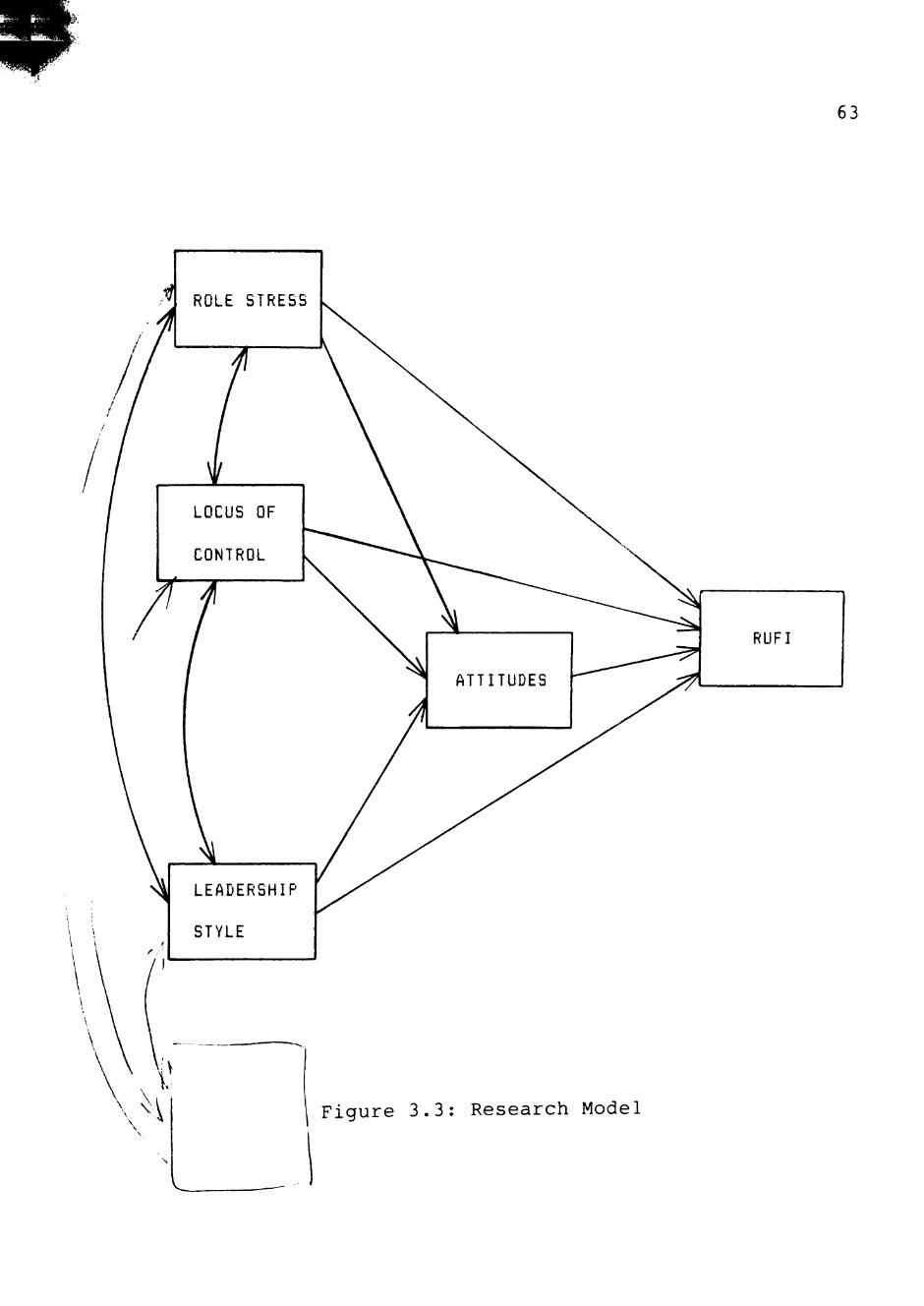

3.3: Research Model 63

4.1: The LISREL Model 81

4.2: LISREL Notation 83

4.3: LISREL Equations 85

5.1: The Fitted Model 113

6.1: The Research Model in Context 117

IX

CHAPTER I

INTRODUCTION AND BACKGROUND

Individual performance evaluation is a critical

managerial function. Many business decisions are

influenced by evaluations of individuals' past performance

and expectations of individuals' future performance.

Generally, the accounting role in the performance

evaluation process is through the use of accounting reports

as measures of performance. However, the task of

performance measurement is situational and decisions are

made by individuals. Accordingly, the type of information

obtained by an evaluator, and the extent to which each type

of information is used in arriving at a decision vary from

situation to situation and from individual to individual.

Many organizations have attempted to structure the

performance evaluation process (or related decisions such

as pay, promotion, termination, etc.) by adopting policies,

procedures, guidelines, and standards. These "formal"

systems are designed to produce a performance report and

are intended to support personnel decisions. However, the

individuals who make the decisions are subject to a variety

of influences such as additional information and the

opinions of others. It is naive to assume that individuals

rely strictly on the output of formal information systems

when making performance related judgments and decisions.

This study addresses the relative use of formal and

informal (other) information in the evaluation of

individual performance and the relationships among relative

reliance on informal information and a number of potential

explanatory variables.

Formal and Informal Information

Information can be classified in a variety of ways.

In studying organizations it may be useful to classify

information according to function (operations support,

external reporting, decision support, etc.). It may also

be useful to classify information as either formal or

informal [Banbury and Nahapiet, 1979; Clancy and Collins,

1979; Dirsmith and Covaleski, 1985; Jiambalvo, Watson, and

Baumler, 1983]. Formal information systems can be thought

of as those "sanctioned" by senior management, the output

of which becomes a part of "organizational awareness"

[Clancy and Collins, 1979]. Formal systems are

characterized by policies, procedures, and other

documentation. A formal performance evaluation information

system would frequently involve accounting and/or personnel

department participation with performance represented

numerically. Suggestions or guidelines as to the factors

to be considered and the "weight" to be assigned to each

factor when making performance judgments would often be

included.

The output of formal systems can be referred to as

formal information. Accordingly, any other data relevant

to a decision is informal information. Informal

information systems need not be documented, sanctioned, or

otherwise "official" in order to be relied upon. Unlike

formal systems, informal information systems are difficult i

to characterize. Such systems range from detailed records

maintained methodically, to hearsay, rumor, and memory.

Informal systems may even be computerized. Informal

information may be indirectly incorporated into an

"official" system, reflected primarily as adjustments or

modifications to formal information, or overtly relied upon

and incorporated into the formal system. Informal

information may affect decisions but otherwise never be

documented or made known to others. Also, informal

information may be in non-numeric form, and in fact, may be

perceived by some managers as the antithesis to formally

measured performance. The only distinguishing factor is

that informal information is not produced or required by

the formal system.

It is likely that the accounting function in an

organization is a part of the formal information system,

although accountants' participation in an informal system

is not precluded. It is also likely that performance

related decisions are based on both formal and informal

information.

Performance Evaluation

Performance evaluation is a process that serves

judgmental purposes (retention, promotion, and reward) and

developmental purposes (planning, training and development,

and superior/subordinate communications) [Jiambalvo et al.,

1983] . The part of the evaluation process involving

accounting is the measurement process, which results in

numerical representations of events and transactions

[Flamholtz, 1980]. Performance measurement involves the

application of both procedural rules and instruments to

observable characteristics of performance. The performance

measurement process may be formal or informal just as other

aspects of the evaluation process may be formal or

informal. In formal performance measurement the rules and

instruments have been established and sanctioned by senior

management. With informal performance measurement either

the instrument or the procedural rules of application, or

both, will not be sanctioned. Judgment may or may not be

involved in application of the instruments and rules.

Performance evaluation is intertwined with other

business activities. Company commitments are based upon

assumptions of individuals' future performance. Production

scheduling and other resource allocation decisions are

affected by perceptions of the performance of the

individuals involved. Virtually any business-related

decision is in some way affected by the decision maker's

judgments and expectations about individuals' performance.

Accordingly, performance evaluation is likely to be a

continual process rather than a periodic exercise.

However, the evaluation of performance assumes a periodic

nature because the intensity of the process is much greater

at some times than others. There are specific periodic

decisions made by managers in which performance judgments

are manifest, such as pay, promotion, and termination

decisions. Also, many businesses require managers to

document evaluations of subordinates' performance at

regular intervals or specified times regardless of the need

for pay increase, promotion, or termination.

Performance evaluation is by necessity a judgmental

process. The evaluator will consider the pattern of

performance measures and must make a judgment regarding the

quality of the overall performance: poor, adequate, good,

or outstanding. When the evaluator is the superior to the

person evaluated, the judgments made will influence

decisions on retention, salary, promotion, and assignment.

Jiambalvo et al. [1983] classified performance

evaluation processes as formative ("coaching" purposes) and

summative (a necessary precedent to pay and promotion

decisions). The concept of "summative evaluation"

[Jiambalvo et al., 1983; Zedeck and Kafry, 1977] is

particularly useful in the following discussions.

Purpose, Objectives, and Significance

The purpose of this study was to improve our

understanding of the sources of information relied upon by

individuals in making performance related decisions in

organizations. It was intended to gather and interpret

evidence regarding the relative use of formal and informal

information. More specifically, there were two research

objectives:

1. To examine the extent to which informal

information is relied upon relative to formal

information (RUFI) in performance-related

decision making, and

2. To study the relationships among a number of

a priori explanatory variables and RUFI.

The results contribute to the small body of informal

information systems literature, and may stimulate

additional research efforts and contribute toward

improvement in both systems design and performance

measurement. Empirical evidence of the relative importance

of informal information systems in the accounting

literature is scarce—few published works have been

located.

7

Organization

In the following chapter, selected relevant works are

reviewed and discussed. Chapters III and IV provide

discussions of the relationships among the variables of

interest and the research methodology applied. The

empirical results are presented in Chapter V, and the

conclusions and implications are discussed in Chapter VI.

CHAPTER II

PREVIOUS STUDIES OF INFORMATION

FOR PERFORMANCE EVALUATION

Performance evaluation and performance information

utilization research has generated a substantial

literature. Selected representative works on goals and

goal-directed behavior demonstrate individuals' needs for

performance related information. Early studies on

organizational performance measures and budget-based

studies illustrate the importance of performance-related

information and suggest a need for informal information.

When applied to information systems in organizations,

contingency theory provides a framework for discussing a

number of factors with the potential to influence the

systems' effectiveness. From a total labor force

perspective, both agency theory and the markets and

hierarchies paradigm are consistent with informal

information usage. Finally, research addressing managerial

performance measurement and appraisal, and studies of

informal information in organizations are particularly

relevant.

8

Goals and Goal-Directed Behavior

One way in which individual performance evaluation

influences the attitudes and actions of individuals is

through communication of the results. The information

exchanged facilitates individuals' goal setting processes

and constitutes feedback (knowledge of the results of

goal-directed behavior).

Goals and goal-directed behavior were discussed by

Lewin, Dembo, Festinger, and Sears [1944] in relation to

their concept of "level of aspiration," and their

associated "resultant valence theory." Lewin et al.,

hypothesized that the choice of level of aspiration is the

result of three factors: the seeking of success, the

avoiding of failure, and a probability of success judgment.

The strength of each of these three factors is dependent

upon situational influence and individual characteristics.

Thus, levels of aspiration (goals) are a function of an

individual's perceptions and attitudes regarding the

desirability and likelihood (valences) of success vs.

failure in goal attainment. Further, levels of aspiration

are altered as information and experience influence

perceptions and attitudes.

In addition to facilitating goal setting, the revealed

output of both performance measurement and evaluation

provides the subordinate with knowledge of the results of

goal-directed behavior (feedback), which is related

10

strongly to performance [Becker, 1978; Locke, 1968; Erez,

1911J Locke, Shaw, Saari, and Latham, 1981; Cook, 1967;

Pavett, 1983; Ilgen, Fisher, and Taylor, 1979]. Based on a

comprehensive review of goal setting and task performance

in laboratory and field studies, Locke, Shaw, Sari, and

Latham [1981] noted that performance is effected (improved)

only when goals are set and feedback is provided:

Goal setting is most likely to improve task performance when the goals are specific and sufficiently challenging, the subjects have sufficient ability (and ability differences are controlled), feedback is provided to show progress in relation to the goal, rewards such as money are given for goal attainment, the experimenter or manager is supportive, and assigned goals are accepted by the individual [p. 125; emphasis added].

Since goals are determined by individuals' perceptions

and attitudes regarding future outcomes and likelihoods

[Lewin et al., 1944], goals must be expected to change over

time as information and experience influence perceptions

and attitudes. Although not explicitly recognizing the

influence of information on performance through goal

setting. Cook [1967] studied the effects of frequency of

feedback on attitudes and performance. In a simulated

business setting, student subjects receiving performance

reports more frequently were more successful and had more

positive attitudes than other student subject participants.

In spite of methodological weaknesses in Cook's study as

discussed by Becker [1967] and Jensen [1967], the study

11

provides empirical evidence of the need for, and importance

of, timely feedback regarding performance.

Relevance to the current study

Performance-related information has been found to be

important in improving performance through its influence on

goal setting and on goal-directed behavior. A number of

characteristics of the information, such as timeliness, are

also important. Information, formal or informal, should be

frequent, specific, involve the job challenges, and concern

subordinates' abilities and the use thereof. The

information should relate to agreed upon goals and evidence

the performance-reward relationship. Of particular

relevance to this study is the implication that perceptions

regarding certain characteristics, or attributes of the

information are indicative of the information's usefulness.

Accordingly, the relative use of formal and informal

information is likely to be influenced by perceptions

regarding certain attributes of both the formal and

informal information.

Early Studies on Performance Measures

Some work has focused on the measurement and control

of various parts of an organization (segments, divisions,

profit centers, investment centers) rather than on

individuals. The performance of certain organizational

12

components is often a primary determinant of, or surrogate

for, the individual performance of segment management.

However, the influence of organizational performance

measures may be widespread. Hopwood [1972, 1974]

identified a "contagion" effect in the use of accounting

information. The suggested result is a "trickle-down" of

the influence of measured organizational performance.

Ridgway [1956] and Tiessen and Waterhouse [1983] suggest

that organizational performance measures influence

behaviors and attitudes even when the information is not

intended to be used as a measure of individual performance.

The following discussion indicates how early behavioral

researchers questioned the practice of performance

measurement and noted dysfunctional behavior associated

with single numeric representations of performance.

Single Performance Measures

Argyris [1952] reported a tendency of workers to

manipulate production scheduling in order to obtain the

desired effect on measured performance in spite of the

potentially negative economic consequences to the firm.

Blau [1955] observed similar behavior in a service oriented

organization. Simon, Guetzkow, Kozmetsky, and Tyndall

[1954] noticed that the use of standard cost as a single

performance criterion often led to considerable

inefficiencies. Employees spent time and effort on the

13

nonproductive practice of arguing the accuracy and

appropriateness of the numbers. Apparently, a general lack

of trust had resulted from a history of errors and problems

related to the allocation of uncontrollable, or indirect

costs. Studies in the Soviet Union [Granick, 1954;

Berlinger, 1956; Horwitz, 1970] support the basic

conclusion that single measures of performance are often

accompanied by dysfunctional behavioral consequences.

Relevance to the current study. When formal systems

have single performance measures, managers will need to

supplement the formal system with additional criteria in

evaluating their subordinates in order to counteract the

negative effects of the single measure.

Multiple and Composite Measures

The use of multiple measures of performance (a number

of single measures of different aspects of performance) is

currently espoused in the normative literature [Horngren,

1982]. Closely related to the multiple measures approach

is the use of a composite measure of performance, which is

the result of mathematically combining a number of

performance measures into a single score. A composite

measure is a known function of multiple measures. Using

either multiple measures or composite scores, it is argued

in the normative literature that the dysfunctional

consequences of single measures can be avoided [Horngren,

14

1982]. However, the added complexity may be accompanied by

a different set of behavioral concerns.

Ridgway [1956] hypothesized that when faced with

multiple performance criteria (multiple measures), an

individual may experience ambiguity. If a particular

action has equally desirable results on all criteria, there

is no ambiguity. Typically, however, there are conflicts,

tradeoffs, and compromises. If the individual knows how

the multiple measures will be reflected in some overall

(composite) measure of performance, again there is no

ambiguity. But, if the individual is unaware of how the

multiple measures are to be combined, the employee will be

forced to use judgment in deciding where to expend

resources. Based on his review of the literature, Ridgway

concluded:

Quantitative performance measurements—whether single, multiple, or composite--are seen to have undesirable consequences for over-all organizational performance [p. 247].

Perhaps more importantly, Ridgway continues to note another

very important behavioral concern:

Even where performance measures are instituted purely for purposes of information, they are probably interpreted as definitions of the important aspects of that job or activity and hence have important implications for the motivation of behavior [p. 247].

Rosen and Schneck [1967] referred to Ridgway's

summarization of the behavioral problem(s) associated with

multiple measures of performance. They were unable to add

15

any additional sources of information pertinent to the use

of either multiple or composite performance, but again

concluded:

Dysfunctions to the organization result from the use of single, multiple, and composite measures of performance. Single measures may not be properly selected or broad enough to coincide with the organization's goals. To be effective, multiple measures must be arranged in their degree of importance. Otherwise, in situations of ambiguity, employees may not focus on the one measure that gives the most desirable results for the organization. Composite measures also have potentially unfavorable effects, depending upon how management uses them [p. 14] .

Relevance to the current study. Even multi

dimensional measurements are inadequate representations of

performance when the behavioral consequences are

considered. The measurements can produce ambiguity and/or

result in dysfunctional consequences to the organization

whether or not they are presented as indicators of

performance. Again, the implication is that informal

information is needed to supplement the formal information.

Return on Investment (ROI)

Primarily because of a widespread move toward

organizational decentralization that began in the 1950s, a

particular composite performance measure relating income to

investment, return on investment (ROI), became popular with

companies in the 1960s [Mauriel and Anthony, 1966]. A

broad-based survey of United States businesses provided

16

Mauriel and Anthony the information necessary to reach

their most significant complaint about practice:

. . . that generally accepted accounting principles, including any internal company rules and procedures intended to govern the reporting to outsiders of financial data on the firm as a whole, tend to influence very strongly the methods used in calculating an investment center's profit and investment base [p. 99].

They continue to explain how the accounting distortions are

likely to produce incentives to favor the short-run

operations over the long-run growth of the organization.

The authors also consider the problems associated with the

use of ROI in determining executive compensation.

Mauriel and Anthony call for internal accounting

procedures based on the internal needs of the organization.

Similarly, Rappaport [1978] argues for the design of

incentive systems in such a manner as to avoid the

short-term emphasis of the "simplistic rhetoric of

accounting numbers" (ROI, earnings per share, or some other

measure of profit).

Reece and Cool [1978] replicated the Mauriel and

Anthony study and found that the use of GAAP-based ROI had

increased in use over a decade. In spite of a number of

critical flaws, ROI had become deeply ingrained in the

divisional performance evaluation process (only 3% of the

companies with investment centers reported no influence of

ROI on performance, and 74% of the companies surveyed

reported having investment centers). Also, GAAP-based

17

reports were deeply ingrained as performance measures (40%

of the companies reported no differences and/or

adjustments).

Relevance to the current study. Although widely

criticized in the literature, ROI and GAAP-based reports

strongly influence performance measurement and evaluation

practices in organizations. The inadequacies of numeric

representations of performance and the measurement error

attributable to the influence of GAAP are reflected in ROI.

Informal information is necessary to adjust for both.

Budget-Based Studies

Budgeting activities are pervasive in business just as

budget-based studies are abundant in the literature. Four

of these, regarding individual performance evaluation and

budgets, are particularly relevant to this study.

Argyris [1953] recognized the control function of

budgets, the pervasive influence of budgets in

organizational decision making, and the use of budgets in

individual performance evaluation:

Budgets are accounting techniques designed to control costs through people. As such their impact is felt by everyone in the organization. They are continuously being brought into the picture when anyone is trying to determine, plan, and implement an organizational policy or practice. Moreover, budgets frequently serve as a basis for rewarding and penalizing those in the organization [p. 97; emphasis on original].

18

Hopwood [1972, 1974] gathered empirical evidence

regarding the use of accounting information in performance

evaluation. He hypothesized that there were three distinct

styles of using budgeted and actual cost information:

budget constrained, profit conscious, and nonaccounting.

The Ohio State University leadership behavior descriptive

questionnaire (LBDQ) was used to measure various dimensions

of managerial style. Hopwood concluded that a manager is

more likely to be seen as using a budget constrained style

of evaluation if that manager has a leadership style low in

consideration and high in initiation of structure,

particularly if a budget constrained style is used by the

manager's superior (the contagion effect).

Otley [1978] replicated and extended Hopwood's earlier

study. Otley was particularly interested in the effects of

such intervening variables as the interactions among style

of budget use, budget accuracy, and profitability. He

concluded that it is inappropriate to use differences in

budget style to explain differences in performance because

both depend upon the state of the economic environment, and

pointed toward the need for:

. . . a more contingent theory of budgetary control based on differences in organizational types, the environmental circumstances in which they operate, and the norms and values current both within the organization itself and within the society in which it is set [p. 146].

19

Relevance to the current study

In spite of potential dysfunctional consequences,

budgets often constitute a large part of the formal

performance evaluation support system. Individual

variation in the use of budgetary information implies

individual variation in the use of other information as

well. If there are no other formal sources of performance

related information, informal information will be sought to

compensate for any perceived information inadequacies. In

explaining individual variation in the use of accounting

information, perceptions regarding the individual's

superior are particularly important (the contagion effect),

but there are a number of other potential influences.

Accordingly, the relative use of formal and informal

information in individual performance evaluation is

contingent upon such factors as superior's leadership

style, organizational type, environmental circumstance, and

norms and values.

Contingency Theory

Contingency theory has been applied to the study of a

variety of organizational phenomena. Hunt [1984] discusses

the contingency theory of organizational leadership, noting

its dominance as a research paradigm since the late 1960s.

Waterhouse and Tiessen [1978] suggest a contingency

framework for research in management accounting systems.

20

Relevant to this study is the research concerning

organizational structural contingencies.

Ford and Slocum [1977] summarize the literature

pertaining to the influence of size, technology, and

environment on the structure of organizations. The authors

measured four dimensions of organizational structure:

complexity, centralization, administrative intensity, and

formalization. Formalization was defined as:

. . . the degree to which rules and procedures within a system are specified and/or adhered to. As a strategy of control, it emcompasses both the existence of rules or procedures, whether or not they are codified, and the degree of variation allowed therein [p. 562].

Formalization was found to be positively related to both

technology (task routineness) and size (number of members),

and negatively related to environment (perceived

uncertainty).

Relevance to the current study

Contingency theory suggests that organizational

structures are dependent upon certain organizational and

environmental variables. Information systems are

organizational structures. Thus, formal and informal

systems of performance related information may be

contingent upon organizational and environmental variables.

Also, performance evaluation is based on information from a

variety of sources, formal and informal. Since

21

characteristics of both the formal and informal information

systems are contingent upon organizational and

environmental variables, the relative use of formal and

informal information is likely to vary due to

organizational and environmental variables.

Agency Theory

Agency theorists such as Arrow [1963; 1964; 1974],

Jensen and Meckling [1976] , and Demski and Feltham [1978]

view organizations:

. . . simply as a focus for a complex process in which the conflicting objectives of individuals are brought into equilibrium within the framework of contracts. In this sense, the behavior of an organization is like the behavior of a market in that it is the outcome of a complex equilibrium seeking process [Tiessen and Waterhouse, 1983; p. 254].

The fundamental principal/agent relationships are based on

contractual specifications of pay-off and risk sharing, and

the monitoring of behaviors is recognized to be imperfect

and costly. Pay-off is determined in accordance with

completely specified, contractual procedures for

performance measurement. Alterations in the

principal/agent relationship constitute renegotiation of

the employment contract.

22

Relevance to the current study

Agency theory does not preclude individual performance

evaluation nor the influence of informal information.

Performance measurement and pay-off are contractually

determined but the renegotiation process is not. The

result of individual performance evaluation is manifest in

the contract renegotiation process. Since renegotiation is

not contractually specified, performance evaluation

processes are by definition informal (non-contractual).

While agency theory is not inconsistent with the study

of information for performance evaluation, much of the

relationship between formal and informal information goes

beyond the hypothesized contractual relationships.

Markets and Hierarchies

The markets and hierarchies paradigm "is a positive

theory which seeks to explain the structure of markets and

hierarchies, and the division of activity between markets

and hierarchies" [Tiessen and Waterhouse, 1983; p. 258].

Based largely on the works of Williamson [1964, 1971, 1973,

1975], the markets and hierarchies paradigm emphasizes

information, structure, and control. Generally, the theory

suggests that hierarchies supplant markets when the market

transaction and contract enforcement costs become too

great. Regarding labor in organizations, hierarchies are

an alternative to a set of separate and individual

23

contracts. The hierarchical form of organization includes

an "internal labor market," membership in which

(employment) constitutes acceptance of an incomplete social

contract with the organization.

Subordinate managers have local information not

available to senior managers because they are closer to the

operations of their subdivisions. This information about

conditions and opportunities will be withheld (called

"information impactedness") unless senior managers offer

sufficient rewards in the form of opportunities and

security. Further, subordinates must learn specialized

skills, procedures, and language that have little value

outside the specific organization. In order to induce the

specialized learning, senior management must offer rewards

and continuity. The communication of local information and

the specialized learning become part of the performance

history of the subordinate.

The primary purposes for ex post accounting measures

in internal labor markets are "to assist in constructing

performance histories and in settling disputes" [Tiessen

and Waterhouse, 1983; p. 265]. While accounting numbers

may be arbitrary and unfair:

Other internal labor market customs and rules will simply adjust to compensate for the possibly undesirable direct effects of the accounting measures [Tiessen and Waterhouse, 1983, p. 265].

24

Relevance to the current study

Performance histories are not limited to a series of

accounting measurements, and "internal labor market customs

and rules" will require the consideration of informal

information in performance related decisions. Formal

performance information is included in the concept of

sanctioned performance history hypothesized in the

hierarchies and markets literature. While the terminology

differs, the substance and intent are similar. The

proportion of formal performance systems that are concerned

with long-run performance instead of short-term performance

measures is an empirical question already researched.

Reece and Cool [1978] and other findings indicate that the

majority of performance measures (circa 1978) are short-run

in nature. Thus, the markets and hierarchies paradigm does

provide a theory for why informal information is necessary

in the performance evaluation process. Since performance

measures are short-run in practice, informal information on

long-run performance and local information sharing is

necessary for performance evaluation. Further, since the

observed performance measures are GAAP-based, they must be

informally adjusted to make an equitable judgment on

performance.

25

Managerial Performance Appraisal

Performance appraisal, "which consists of the

observation and evaluation of an employee's work behavior

or the results of that behavior by someone," is the most

frequently used method of measuring employee performance

[Heneman, Schwab, Fossum, and Dyer, 1980; p. 116].

Periodic, all-purpose performance appraisal is a primary

subject in both descriptive and normative managerial

literature.

The normative literature addresses individual

performance in organizations from two approaches. First,

writers such as Landy and Farr [1983] and Heneman, Schwab,

Fossum, and Dyer [1980], emphasize measurement. Others,

typified by Lawler [1981] and Kane and Lawler [1979],

emphasize the subjective nature of the process. To the

former, periodic performance appraisal is the most common

method of performance measurement. To the later, periodic

performance appraisal serves a variety of purposes,

primarily developmental and reward allocation. Some

writers suggest that development and reward allocation are

incompatible functions [Kane and Lawler, 1979], while

others suggest that the tv;o functions may be inseparable

[Marshall, 1978].

Of particular relevance to this study are two surveys

of managerial performance appraisal practices and

techniques. A 1977 report by The Conference Board [Lazer

26

and Wikstrom, 1977] addressed current managerial

performance appraisal practices and existing performance

appraisal information systems. The study indicated that

managers were appraised annually (90%) and appraised by

their immediate superior (95%). A variety of techniques

was used to evaluate performance, the most common being

objective setting or MBO (management by objectives),

ratings, critical incident, checklists, and rankings or

comparisons. Further, 71% of the companies were found to

have formal appraisal systems for mid-to-low-level

management. Eight general categories of stated objectives

characterized the formal systems (presented in decreasing

frequency of occurrence):

Management development Performance measurement Performance improvement Compensation administration Identifying potential Feedback Manpower planning Communications [p. 11]

However, the actual uses of the performance appraisal

information were found to be quite different. The

responses were summarized into six groups (decreasing

frequency):

Performance feedback Compensation administration Promotion decisions Identifying management manpower needs Manpower planning Validation of selection procedures [p. 11]

27

A third ordering was suggested by a follow-up study of the

priorities associated with each of the six groups of uses

of performance appraisal (decreasing priority):

Compensation administration Performance feedback Identifying management development needs Promotion decisions Manpower planning Validation of selection procedures [p. 11]

The discrepancy between the stated objectives and the

actual use of the formal performance appraisal information

was attributed to dissatisfaction with the formal system.

A number of problems with the formal system was suggested,

with "conflicting multiple uses" being the most prevalent.

Even though the subjects seemed to perceive performance

appraisal for compensation adjustment purposes to differ

from performance appraisal for developmental purposes, the

data indicate that more than three-fourths of the companies

used the same appraisals for both.

Finally, the study found that "the performance of

managers not currently covered by a formal performance

appraisal system is still evaluated," citing a number of

subjects' descriptions of alternative (informal) appraisal

techniques:

Personal observation by the department head -nothing in writing

Our appraisal of managers consists of periodic visits with the supervisor, generally at salary evaluation time . . .

Seat of the pants

28

Since our management group is fairly small, we still enjoy an intimate set of supervisor-subordinate relations.

Performance evaluation, therefore, is an ongoing continuous activity rather than a fixed event occurring once a year

By their immediate supervisors, in whatever way the supervisor considers appropriate

Unwritten, mental appraisal

Observation by immediate supervisor, and confirmed by next highest supervisor. This is not usually written or even communicated . . . the "no news is good news" syndrome

Function of individual's manager's philosophy and techniques

What the boss's "tummy" tells him [Lazer and Wikstrom, 1977; page 23; subjects' descriptions deleted]

The findings reported by The Conference Board were

largely supported by a more recent report of the American

Management Associations (AMA) [Eichel and Bender, 1984].

Annual evaluations remained prevalent, particularly when

related to compensation adjustment. Goal setting, essays,

and critical incidents, respectively, continued to be the

three most commonly used techniques of performance

appraisal, but two new techniques, graphic ratings and BARS

(behaviorally anchored rating scales) were evident in

practice. Seven primary uses for performance evaluation

were identified (decreasing frequencies):

Compensation Counselling Training & development Promotion

29

Manpower planning Retention/discharge

Validation of selection technique [p. 12]

Again, the authors suggest that performance evaluation for

salary administration purposes differs from performance

evaluation for improvement and developmental purposes.

The AMA study did not specifically address sources of

information used in performance evaluation but did note

that the current legal environment required the use of a

formal, documented performance appraisal system emphasizing

quantification, replication, and standardization.

Relevance to the current study

Normative literature regarding performance

measurement, evaluation, and appraisal is abundant and

diverse. Both of the descriptive studies, however, suggest

that performance evaluation (appraisal) for compensation

related purposes is not the same as performance evaluation

for training and developmental purposes. Also, Lazer and

Wikstrom noticed a discrepancy between the formally stated

objectives of performance appraisal system and the actual

use of the information. Inadequacies of the formal

information are the identified causes of the discrepancy;

use of informal information to compensate for the

inadequacies is a likely result.

30

Informal Information

Four studies directly addressing informal information

in organizations have been identified. Clancy and Collins

[1977, 1979] report the results of a two-stage study (case

and questionnaire) of informal accounting information

systems. They defined a formal accounting information

system as:

. . . that which collects, stores, analyzes and reports events, typically of an economic and quantitative nature . . . (and) normally legitimized by top management [Clancy and Collins, 1979, pp. 21-22].

Informal accounting information systems were

"non-legitimized" or personally maintained. They found

that about 85% of the sampled managers kept an informal

system of records and, while the informal records were

important in control and evaluation, the records were

considered less important than the formal reports. The

questionnaire used by Clancy and Collins solicited

subjects' perceptions about a number of characteristics of

both the formal and informal information systems, such as

accuracy, understanding, importance, and level of detail.

Using the questionnaire data, Clancy and Collins determined

that the subjects perceived formal and informal information

systems as distinct and separate, and identified a number

of relevant characteristics. However, they were not able

to support their a priori expectations that the existence

of informal information systems would be correlated with

31

certain formal system characteristics. Generally, Clancy

and Collins conclude that informal a ccounting systems are

"a useful_and necessary adjunct to formal_systems rather

than an unnecessary dissipation of resources." Even though

the informal records were less important, both systems were

perceived to be useful and desirable by the subjects.

Collins and Johnson [1986] report the results of an

exploratory case study of organizational communication,

noting the importance of general, informal communication

activity. They suggest that general, informal

communications provide a "linking" function between j

organizational problems and solutions.

Based on series of interviews with individuals in

public accounting firms, Dirsmith and Covaleski [1985]

observed that "[all] individuals concurred that informal

communication networks were much in evidence" [p. 154;

emphasis on original], and that "[the] most mentioned theme

of informal communications was compensation" [p. 155] .

However, they disagreed with the conclusions of Clancy and

Collins [1979] regarding the complementarity of formal and

informal information systems. Instead they attribute

aberrant behavior to inaccuracies with, and perceptions

about, the informal information. However, the disagreement

may be one of semantics. Dirsmith and Covaleski suggest a

third "category" of information--nonformal. Nonformal

communications are seen to be distinct in that they are

32

associated with the formally recognized, "sanctioned"

practice of mentoring. What may have been "nonformal" to

Dirsmith and Covaleski may well have been "informal" to

Clancy and Collins.

Dirsmith and Covaleski's conclusions are also

inconsistent with the more recent findings of Collins and

Johnson [1986] regarding the importance of informal

communication activity. But again, the apparent

discrepancy is explainable. Collins and Johnson studied a

significantly less mature, formalized entity than the CPA

firms studied by Dirsmith and Covaleski. Accordingly, the

extent to which the formal performance evaluation support

system had been developed differed greatly.

Relevance to the current study

Researchers agree as to the pervasiveness of informal

information in organizations but disagree about its

effects. Informal information systems have been inferred

to complement formal information systems, and informal

communication activity has been demonstrated to be

beneficial to organizations. However, informal i

communications have also been shown to be dysfunctional.

While none of the studies of informal information activity

directly address performance evaluation, their inconsistent

conclusions suggest situational variability and semantic

difficulty in the study of informal information.

33

Summary

The evaluation of individual performance plays an

important role in organizations. Performance evaluation

influences goal setting and provides feedback regarding

goal-directed behavior. However, the relationships among

goals, performance, and feedback are situational.

Early studies on performance measures (single,

multiple, and composite) conclude that measures of various

aspects of organizational activity influence the behavior

of individuals even in cases in which the measures are not

intended to do so. Further, early budget studies indicate

the importance of budgets to individuals in organizations,

particularly because of their frequent use in pay and

promotion decision making. Also suggested is that some

effects "filter down" the organization thereby influencing

the behaviors of lower management. Potentially, the

dysfunctional consequences of organizational performance

measurement and the influences of budgeting will be evident

throughout the organization.

Periodic performance appraisals are pervasive.

Performance appraisals are used for a variety of purposes,

but the two most important and most frequent uses of

appraisals are compensation administration and feedback

(including counseling and development). In most formal

systems, and according to a great deal of the normative

literature, a single appraisal is intended to serve many

34

purposes. However, research has suggested that performance

appraisal for the purpose of compensation adjustment should

not be the same thing as performance appraisal for training

and developmental purposes. Since periodic performance

appraisals are incapable of supporting both salary

administration and training and development, superiors must

use additional information in at least one of the

processes.

From a total labor force perspective, the markets and

hierarchies literature recognizes the potential for

dysfunctional behavioral consequences of the use of

accounting measures alone because they are short-run in

nature, and suggests the role of informal information in

compensating for formal system inadequacies. This

complementary relationship between formal and informal

information is supported by Clancy and Collins [1979] and

Collins and Johnson [1986] , but disputed in Dirsmith and

Covaleski [1985].

Individual performance evaluation is influenced by a

number of situational and individual factors. Accordingly,

the relative use of formal and informal information in

performance evaluation is likely to be related to, or

contingent upon, a number of situational and individual

factors, or explanatory variables of interest. In the

following chapter, the dependent variable (relative use of

formal and informal information in individual performance

35

evaluation) and the explanatory variables of interest are

discussed, and illustrations of the expected relationships

among the variables are provided.

CHAPTER III

DISCUSSION OF VARIABLES AND RELATIONSHIPS

MODEL DEVELOPMENT

In this chapter, the research perspective is explained

and the variables of interest are discussed. Then,

hypotheses are stated in order to specify the a. priori

relationships among the variables, and a research model is

provided to illustrate the hypothesized relationships. In

the following chapter, the research methodology is

explained, and data gathering and analysis are discussed.

Theoretical Perspective

Performance information is relied upon in making

judgments about an individual's performance, and

performance judgments as a summative evaluation are a

primary determinant of performance related decisions

[Jiambalvo, Watson, and Baumler, 1983; Howell, 1976; Zedeck

and Kafry, 1977]. Therefore, performance evaluation is an

intervening variable between the relevant information and

performance-related decisions, such as pay, promotion, and

termination. Figure 3.1 (following page) illustrates these

basic relationships.

36

37

Performance

I n f o r m a t i on

Pe r fo rmance

E v a l u a t i on

Pay, P r o m o t i o n , or

T e r m i n a t i o n D e c i s i o n

Figure 3 . 1 : Preliminary Theoret ical Model

38

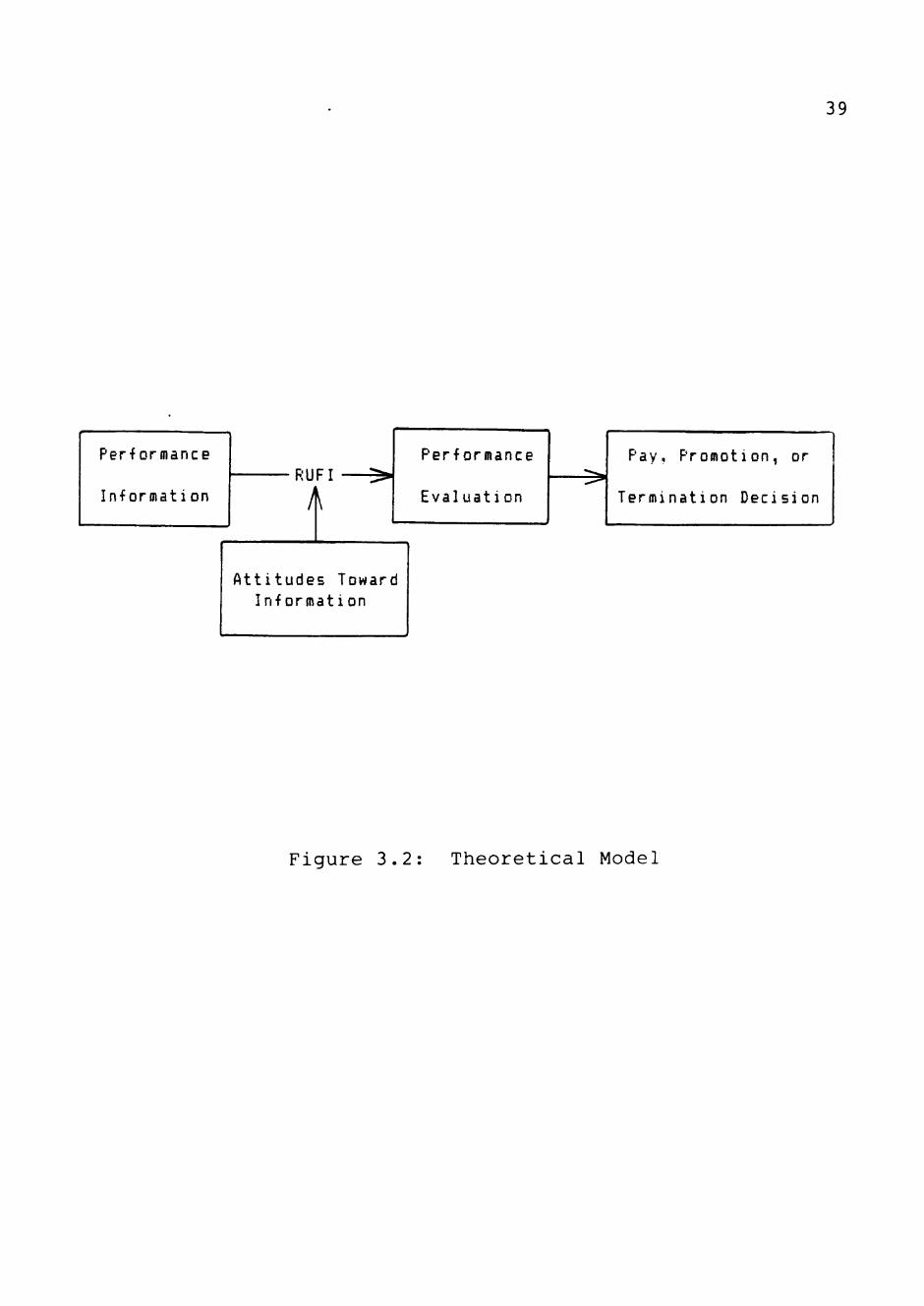

One characteristic of the relationship between

performance information and performance evaluation is the

relative use of formal and informal information (RUFI).

Variation in RUFI may evidence moderating effects of a

number of factors on the relationship betv/een information

and evaluation. From an individual decision-maker's

perspective, RUFI may be partially determined by that

individual's attitudes toward the information. Variance in

RUFI may be partially attributable to variation in

individuals' attitudes toward the information (ATTITUDES).

With the addition of the moderating variable (ATTITUDES)

and in illustration of the variable of interest (RUFI),

Figure 3.2 (following page) depicts the theoretical model.

Since the design of jobs influences the approach and

content of performance evaluation, variation in RUFI may

also be attributable to variation in the nature and content

of the individuals' organizational function. The nature

and content of jobs vary both within and among

organizations. Organizational size, technology, and

environment are likely to influence the design of jobs from

organization to organization. Delineation of

responsibilities within organizations (sales, production,

support, etc.) is likely to influence the design of jobs

within organizations. Of primary concern in this study,

however, are the individually-oriented factors that

influence RUFI. Thus, the models presented in this chapter

39

Per formance

I n f o r m a t i on RUFI

A

Per fo rmance

E v a l u a t i on • ^

Pay, P r o m o t i o n , or

T e r m i n a t i o n D e c i s i o n

A t t i t u d e s Toward I n f o r m a t i o n

Figure 3 . 2 : T h e o r e t i c a l Model

40

do not depict the influence of variation in job design on

RUFI, and the sampling procedures discussed in the

following chapter were designed to control for both

interorganizational and intraorganizational variation in

the nature of the individuals' jobs.

In this study, attitudes toward the information (and

other individually-oriented factors) are expected to

moderate the relationship between information and

evaluation. The relative use of formal and informal

information (RUFI) is descriptive of the relationship

between information and evaluation, and variation in RUFI

indicative of moderating effects on that relationship.

Finally, the results of performance evaluation are presumed

to be manifest in pay, promotion, and termination

decisions.

Under the hierarchies and markets theory [Tiessen and

Waterhouse, 1983] , a performance history is a necessary

part of an "internal labor market" that encourages

subordinates to reveal private information. In a dynamic

setting, the results of performance decisions become part

of the performance history of the employee. Thus, the

relationships illustrated in the theoretical models may not

be unidirectional as indicated. The static, unidirectional

models are presented in order to emphasize the primary

41

theoretical relationships. Of primary concern in this

study is the formal/informal classification, regardless of

the current/historical nature of the information.

Potential Explanatory Variables

In addition to ATTITUDES, there are a number of

measurable personality traits and other individually-

oriented variables with the potential of explaining

variation in RUFI. Possibilities include perceived role

stress; leadership style; the "needs" variables of power,

achievement, and affiliation; Jungian type;

Machiavellianism; authoritarianism; and demographic

variables such as age, tenure, and sex. Included in this

study, however, are only those variables for which an

a priori statement of casual relationship with RUFI could

be provided. Previous discussions justified the inclusion

of ATTITUDES as an explanatory variable. The following

discussion of the research perspective adopted explains why

role stress and superiors' leadership style are included.

One additional variable, locus of control, is included

since an extensive theoretical articulation and a pervasive

empirical base support a priori specification of the

relationships among locus of control and the other research

constructs of interest.

42

Research Perspective

Some researchers (see Collins and Clancy [1980]; *

Collins [1982]; Collins, Seller, and Clancy [1984]; Collins

and Johnson [1986]; Collins, Munter, and Finn [1983]) have

adopted the role perspective suggested by Katz and Kahn

[1967], viewing organizations as dynamic, interactive

systems capable of being described in terms of roles and

norms. Roles and norms are closely related concepts; the

former referring to a sets of behaviors and the latter

representing limitations, or expectations about the former.

Collins and Clancy [1980] note that "roles exist in

relationship to other roles," [p. 1] and recognize the

particular importance of the role-related expectations of

"salient" others [p. 2]. In a business setting, an

individual's superior is likely to be a particularly

salient other. Thus, both perceived role stress and

perceived leadership style (superiors') are likely to be

useful explainers of attitudes and behaviors of individuals

in organizations.

The influence of extraorganizational factors on

individual behavior (the external environment) is not

inconsistent with the research perspective. Norms and

roles are the result of both internal and external

influences. External influence is evident in the

subsystems within an organization [Katz and Kahn, 1967;

Collins and Clancy, 1980], and therefore is reflected in

43

individuals' attitudes toward those systems. Collins

[1982, p. 1] suggests that certain information-providing

subsystems "are useful in communicating role expectations."

Thus, additional external influence is evident in

individuals' role-related perceptions. Finally,

organizational attributes such as size, structure, and

technology also evidence external influence. To the extent

that individuals' perceptions and attitudes vary among

organizations, organizational variables such as size,

structure, and technology, are potentially useful

explanatory variables. Organizational variables are not

useful, however, in explaining variation within

organizations.

This study focuses on RUFI and on individually-

oriented factors that influence RUFI. Subjects' attitudes

and perceptions constitute the primary empirical evidence.

Also, a role perspective is adopted both in discussing

information systems in organizations and in studying the

attitudes of individuals. Thus, the role related variables

of role stress and perceived superiors' leadership style

are included as explanatory variables. Finally, a

personality variable, locus of control is of interest

largely because of the vast empirical history of the

construct and the intuitive appeal of locus of control as

an explanatory variable. Beginning with the dependent

44

variable, RUFI, discussions of each of the research

variables of interest follow.

The Relative Use of Formal and Informal Information

As previously stated, there are two primary research

objectives:

1. To examine the extent to which informal

information is relied upon relative to formal

information (RUFI) in performance-related

decision making, and

2. To study the relationships among a number of

a. priori explanatory variables and RUFI.

The dependent variable of interest, THE RELATIVE USE OF

FORMAL AND INFORMAL INFORMATION (RUFI), is operationally

defined as the extent to which formal information is

perceived to be relied upon relative to informal

information in performance-related decision-making in

organizations. This variable directly addresses the first

research objective; explained variation in RUFI addresses

the second.

RUFI is of particular relevance to anformation systems

analysis and design. In fact, RUFI might be considered as

a measure of the influence of the formal, or official,

system of performance information. Heavy reliance on

formal information (relative to informal) suggests that an

45

organization's formal system influences managers' judgments

greatly. Conversely, relatively heavy reliance on informal

information suggests that the formal system has less

influence. Positive and normative issues arise: To what

extent i_s the formal information relied upon (relative

to informal) and what factors explain the variation in use;

and to what extent should the formal information be

relied upon (relative to informal) and how can the reliance

be influenced? This study addresses the subject from a

positive research perspective.

In order to provide comparability, a definition of the

term "informal" similar to that applied by Clancy and

Collins [1979] is used in this study. Accordingly,

informal information is defined by default, as that which

is not formal. Formal information is that information

produced or required by official, "sanctioned" information

systems. All other information is informal. A large part

of the variation in RUFI is expected to be attributable to

attitudes toward both the formal (official) information and

the informal (other) information relied upon.

Attitudes Toward Formal and Informal Information

Perhaps most relevant to the designers of information

systems are the relationships among attitudes toward formal

and informal information and RUFI. Descriptive conclusions

46

and normative suggestions are likely to concern certain

attributes of the information, such as timeliness,

completeness, accuracy or confidentiality. Clancy and

Collins [1979] suggest several reasons for the informal

collection of accounting information, many of which refer

to formal system inadequacies:

1. Limitations of the formal information system. a. Reports not tailored to individual user

needs b. Untimely (tardy) reporting c. Lack of data reliability d. Inappropriate level of data aggregation

or grouping regarding individual user needs

2. Limitations of the organizational environment. a. Lack of trust between report users and

preparers b. The need for a defense mechanism in

their performance evaluation involving formal system data ("covering tracks")

c. A perceived need on the part of managers for information confidentiality

d. Failure of formal system to measure personalized manager goals

e. Informal accounting records may be helpful in learning (memorizing) currently important operational information [pp. 23-24].

While certain characteristics or attributes may be

more important than others, individuals are likely to have

a general attitude toward formal and informal information.

Perceptions regarding certain characteristics of the

information are indicative of such a general attitude. As

indicated in the following descriptive categories, there

may be a wide range of general attitudes toward informal

performance information:

iX

v

47

1. Highly negative: Informal information used in

performance evaluation is inherently bad.

If the information was any good, it could

easily be included in the formal system.

2. Mildly negative: Informal information is a

necessary evil. Even the most detailed,

bureaucratic formal system will not be able

to measure all the significant aspects of a

manager's performance.

3. Mildly positive: Informal information in

performance evaluation is necessary for the

exercise of good management. Good and poor

performance can be hidden in the details of

formal systems because the formal system cannot

consider all significant aspects of performance

and the unique facts and circumstances of each

manager.

4. Highly positive: Informal information is

most often an accurate indicator of performance.

Informal information is critical for the exercise

of good supervision of employees. Without

informal information, a manager is blinded by the

formal reports.

48

Attitudes toward the formal system may vary as well:

1- Highly negative: Formal performance measurement

systems are highly bureaucratic, satisficing

procedures with dysfunctional consequences.

2. Mildly negative: Formal performance measurement

systems do tell us something about performance,

but are far from complete.

3- Mildly positive: Formal systems are necessary

for adequate control, but some supplementary

information is needed.

4. Highly positive: Formal performance measurement

is a useful exercise in good management, and need

not be supplemented with additional information.

Perceptions regarding such attributes as completeness,

accuracy, usefulness, understandability, and

confidentiality of both formal and informal information

reflect individuals' general attitudes toward each. Thus,

the research construct, ATTITUDES, consists of two

dimensions—attitudes toward formal information and

attitudes toward informal information. Variation in

ATTITUDES is expected to explain a significant part of the

variation in RUFI. Generally, relatively positive

attitudes toward formal (informal) information is expected

to result in relatively greater reliance on formal

(informal) information.

49

Locus of Control

The concept of locus of control refers to individuals'

attributions regarding the control over events. Internals

attribute control to themselves, whereas externals

attribute control to outside forces. Spector [1982]

summarized the empirical research as follows:

. . . locus of control is related to motivation, effort, performance, satisfaction, perception of the job, compliance with authority, and supervisory style [p. 482].

Brownell [1979; 1981; 1982b] studied locus of control

as a moderator of the relationship between participation in

budgeting and organizational effectiveness (performance).

Brownell justified the treatment of locus of control as a

personality variable "simply as a function of the sheer

weight of evidence concerning the wide variety of

situations across which predictions regarding locus of

control have been confirmed" [1979; p. 41]. In general,

budgetary participation was found to have a positive effect

on the performance of internals and a negative effect on

the performance of externals [1981]. Since the budget is

often an important component related to performance

evaluation, the findings of Brownell suggest that locus of

control is relevant to this study as well.

Licata, Strawser, and Welker [1986] report the results

of an experiment that supports their hypothesis that

internal managers allow subordinates greater participation

50

in budgeting than do external managers. In another

experiment, Goodstadt and Hjelle [1973] found internals

exhibiting a personal, persuasive style of supervision and

externals exhibiting a coercive style. Both experiments

suggest that internals use a more flexible, subordinate

oriented managerial style. Implied is the use of a wider

range of information in performance related decision making

by internals than by externals.

Licata et al. suggest that:

It is conceivable that a supervisor involved in budget preparation may have a choice as to the amount of influence he will allow the subordinate to have on his determination of the budget and, further, that locus of control may affect the superior's behavior . . . biasing either toward or away from the subordinate's performance expectations [pg. 113].

The logical extension is that locus of control may affect

the superior's behavior regarding the evaluation of the

subordinate's performance as well.

In explaining the relative use of formal and informal

information systems, LOCUS OF CONTROL may be significant

not just because of relationships with other performance

related variables. In a laboratory experiment, Harvey,

Barnes, Sperry, and Harris [1974] found that internals

perceive more alternatives in a choice situation than do

externals. Accordingly, informal information systems are

more likely to be considered viable alternatives, or

supplements to the formal system by internals than by

51

externals. Conversely, externals may rely more on formal

systems than do internals because they are relatively less

able to perceive alternatives and are more likely to accept

what information is placed before them by the formal

system. Also, internals have been shown to exhibit less

conformity than externals [Crowne and Liverant, 1963].

Again, internals would be expected to rely relatively less

on formal information than do externals, particularly if

the individuals perceive pressure to conform to the formal

system.

Generally, externals are expected to have more

favorable attitudes toward, and rely relatively more on

formal information, whereas internals are expected to have

more favorable attitudes toward, and rely relatively more

on informal information systems.

Role Stress

Role stress is best defined as the strain that results

from one or both of two situations: role conflict and role

ambiguity [Kahn, Wolfe, Quinn, Snoek, and Rosenthal, 1964].

Based on their review of the literature. Van Sell, Brief,

and Schuler [1981] defined role conflict as "incongruity of

expectations associated with a role" [p. 44], but were

unable to provide a specific definition for role ambiguity,

noting the lack of an elaborate conceptualization in the

literature (see also McGrath [1976] and Sarbin and Allen

52

[1968]). The following forms of role ambiguity are

suggested by Van Sell et al:

(a) information is unclear regarding which potential role expectation—A, B, or C—should be performed;

(b) it is understood that expectation A should be met, but information is unclear regarding what behavior will in fact yield A;

(c) the consequences of behavior A are unclear [p. 44] .

Rizzo, House, and Lirtzman [1970] developed a

frequently used role stress measurement instrument and

provided the initial support for interpretation of the

scale's results along the two dimensions of conflict and

ambiguity. High construct validity and continued use of

the scale are supported by a psychometric evaluation

reported by Schuler, Aldag, and Brief [1977] and in the

review and discussion of Van Sell, Brief, and Schuler

[1981]. However, the later are careful to note high

correlation between the two constructs and to suggest

bi-directional causation. More recently, Howell and Wilcox

[1986], caution against separate interpretation of the two

dimensions of the scale on the basis of another

psychometric analysis. In this study, role stress is of

concern as an explanatory variable. Thus, the composition

of stress by dimension is secondary since the type, or

cause, of stress is not of primary concern.

53

Role stress has been studied in relation to a variety

of other research constructs. It has been hypothesized to

be related to budgetary attitudes [Collins, 1978; Collins

and Seller, 1981; Collins, Seller, and Clancy, 1984],

satisfaction [Sapp and Seller, 1980], leadership style

[Rizzo, House, and Lirtzman, 1970; Collins, Anderson, and

White; 1984], employee turnover [Ivancevich and Donnelly,

1975; Sorensen and Sorensen, 1974; Lyons, 1976],

performance [Greene, 1972; Brief and Aldag, 1976; Haas,

1964] , and perhaps most significantly to job satisfaction

(see Van Sell, Brief, and Schuler, [1981] for a review).

The hypothesized psychological and physiological

effects of stress on individuals are diverse. From a