Bahasa

Halaman

Hukum

University of WollongongResearch Online

University of Wollongong Thesis Collection University of Wollongong Thesis Collections

2002

The moral reasoning of public accountants in thedevelopment of a code of ethics: the case ofIndonesiaLindawatiUniversity of Wollongong

Research Online is the open access institutional repository for theUniversity of Wollongong. For further information contact the UOWLibrary: [email protected]

Recommended CitationLindawati, The moral reasoning of public accountants in the development of a code of ethics: the case of Indonesia, Master ofCommerce (Hons.) thesis, School of Accounting and Finance, University of Wollongong, 2002. http://ro.uow.edu.au/theses/2305

The Moral Reasoning of Public Accountants in the Development of a Code of Ethics: the Case of Indonesia

A thesis submitted in partial fulfilment of the requirements for the · award of the degree

HONOURS MASTER OF COMMERCE

From

UNIVERSITY OF WOLLONGONG

By

LINDAWATI, M COM (Ace)

DEPARTMENT OF ACCOUNTANCY 2002

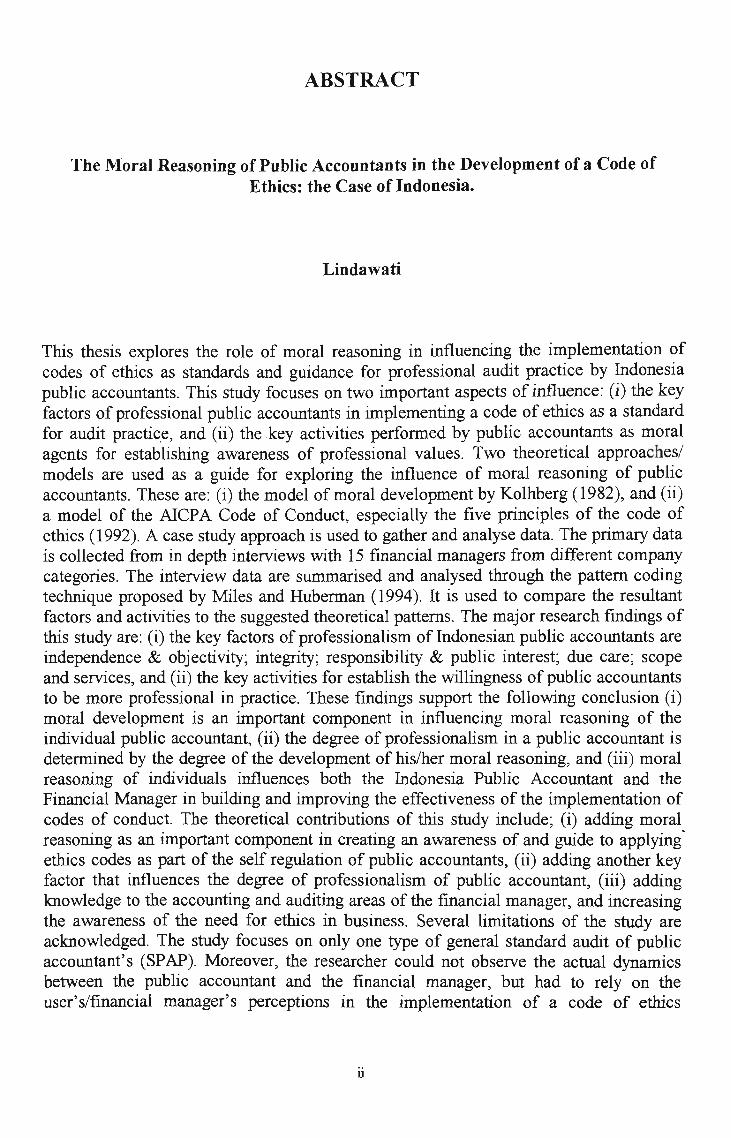

ABSTRACT

The Moral Reasoning of Public Accountants in the Development of a Code of Ethics: the Case of Indonesia.

Lindawati

This thesis explores the role of moral reasoning in influencing the implementation of codes of ethics as standards and guidance for professional audit practice by Indonesia public accountants. This study focuses on two important aspects of influence: (i) the key factors of professional public accountants in implementing a code of ethics as a standard for audit practic.e, and (ii) the key activities performed by public accountants as moral agents for establishing awareness of professional values. Two theoretical approaches/ models are used as a guide for exploring the influence of moral reasoning of public accountants. These are: (i) the model of moral development by Kolhberg (1982), and (ii) a model of the AICP A Code of Conduct, especially the five principles of the code of ethics (1992). A case study approach is used to gather and analyse data. The primary data is collected from in depth interviews with 15 financial managers from different company categories. The interview data are summarised and analysed through the pattern coding technique proposed by Miles and Huberman ( 1994 ). It is used to compare the resultant factors and activities to the suggested theoretical patterns. The major research findings of this study are: (i) the key factors of professionalism of Indonesian public accountants are independence & objectivity; integrity; responsibility & public interest; due care; scope and services, and (ii) the key activities for establish the willingness of public accountants to be more professional in practice. These findings support the following conclusion (i) moral development is an important component in influencing moral reasoning of the individual public accountant, (ii) the degree of professionalism in a public accountant is determined by the degree of the development of his/her moral reasoning, and (iii) moral reasoning of individuals influences both the Indonesia Public Accountant and the Financial Manager in building and improving the effectiveness of the implementation of codes of conduct. The theoretical contributions of this study include; (i) adding moral reasoning as an important component in creating an awareness of and guide to applying· ethics codes as part of the self regulation of public accountants, (ii) adding another key factor that influences the degree of professionalism of public accountant, (iii) adding knowledge to the accounting and auditing areas of the financial manager, and increasing the awareness of the need for ethics in business. Several limitations of the study are acknowledged. The study focuses on only one type of general standard audit of public accountant's (SPAP). Moreover, the researcher could not observe the actual dynamics between the public accountant and the financial manager, but had to rely on the user's/financial manager's perceptions in the implementation of a code of ethics

11

expressed in the interview data and through supporting evidence. The study also suggests some fruitful areas for further investigation into other aspects of the role of moral reasoning in this important influence on achieving awareness between public accountant and financial managers within the implementation of ethics codes as standard professional practice in general, and on Indonesia's public accountant in particular.

CERTIFICATE

I, Lindawati, hereby certify that this work is my own and has not been submitted for a degree to any other university or institution.

lll

ACKNOWLEDGMENTS

This study would never finish without assistance of many people. First and foremost, I

am very grateful to my supervisor Professor Michael Gaffikin for his guidance, help and

encouragement during the entire period of this research. He worked feverishly to invent a

new language to critique my meagre linguistic efforts. My thanks also go to the staff of

Department of Accountancy at Wollongong University for their support.

I am thankful to the companies in Indonesia and individuals who participated in the

study. Without their co-operation this study would not have been possible.

I thank Kim Darisma for her constructive comments and suggestions regarding to

revisions of structure and grammar of my English languages. I am also thankful to

Robbyn Ngui, as International Student Adviser Student Services University of

Wollongong for her support and guidance in solving the problems of my life during my

study at University of Wollongong.

I am most thankful for the continuous support provided by my husband, Budiyono and

my mother, Mrs Nursiah, for her patience and help in taking care of my daughter,

Adinda, my son, Aldi and my little daughter, Aulia during the day, while I studied in

Australia. Finally, my deepest appreciation goes to Djoko Wintoro for his guidance and

reviewing the findings; his enthusiasm and support motivated me to complete this task.

lV

Last, but not least, I am very grateful to ALLAH Most Gracious, Most Merciful.

Alhamdullilah ya Robbal Alamin; praise be to God, the Cherisher and Sustainer of the

world.

v

Table of Contents

Chapter 1 Introduction

Background ........ ........ ...... ...... ......... ......... .. ....... ..... .... .. ........... .. ... .. .... ...... .. · .... · · · · · · · · · · · · · · · 1 Theoretical Development ............ ........... . _. .. .. .......... ... .. ..... ... ..... .. .... ... .. ... .... ...... ..... ... .... .. 2 Statement of the Problem .... ... .... ...... ... .......... ... .... ... ... .... ..... .. ..... .. .... ........ .... .... · · · · · · · · · · · · · · 6 The Purpose of the Study .... ..... ...... .. ..... ..... .. ... .. ....... ... ... ... ... .. ... .... ........ ... ... .... ...... · · · · · · · · · 8 Study Approach ... .. ...... .... .......... ..... .... .. .... .... .... ..... ... ....... ..... .... .. .. .. ... .. ..... .. .... ..... .. ... .... . 9 Contribution of this Study . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10 Limitation of this Case Study ............ ..... .... ... .. .... ..... ..... ... ......... .......... ..... ..... ...... ... .... ... 11 The Structure of this Thesis . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

Chapter 2 Literature Review

Introduction . . . . . . . . .. . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14 Moral & Morality . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15 Definition and Characteristics . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15 The Categories of Moral Perspectives . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22 The General Role of Morals . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27 Moral Judgment (Bad and Good Morals) ........ ..... .. .... .. ...... ...... ..... ..... ..... .... ........ .. 29 Summary .... ... ........ .. ....... .. .... ... .. .. .. ..... ........ ... .. .... .. .. .... .. ...... ... ..... .. ... .... ....... .. ... ... ... 33

The Role of Moral Reasoning . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 34 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 34 Definition and Characteristics ........ .. ........ ..... ..... ........ ....... ..... ..... ............... ........... 35 Theoretical Approach of Moral Reasoning . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36 Process ofMoral Reasoning (Individual Moral Development) .. ... .. .. ...... ........ .... .. 39 Summary ... ... ...... .... ...... ... ..... ...... ... ..... ...... ..... ..... .... ... .. ........ .... ..... .... ........ ... .... ... ... . 46

Ethics in Accounting (Theoretical Perspectives) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4 7 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . .. . . .. . .. . . . . . . . . . . 4 7 The Definition and Characteristics of Ethics ..... ..... .... .... ..... ......... ..... .... .............. .. 48 The Process of Ethics in Accounting ... .... ................... ....... ..... ................ ... ....... .. .. . 52 The Categories of Ethics in Accounting (Philosophical Foundation) .. ........ ... ...... 55 Implementation of Ethics in Accounting . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 61 Contribution ofEthics to Accounting. ........ .... .... .... .... .. ...... ..... ..... ..... .... .. .. .. .... ..... . 65 Summary .... .... ..... .. ... ... ....... ... .. ... ... ..... .... ..... .. ..... .. .. ........ ... ... ... ... .. ..... .. .... ....... ... .... . 67

Ethics in Public Accounting Practice (Applied Ethics) ... ....... ...... ... .. ... ....... .. ...... ... ..... .. 68 Introduction .... .... ....... ... ...... .. ....... ... ... ...... .... ... ......... .. ......... .... .... ... ..... .... .... ....... .... 68 The Importance of Ethics in the Public Accounting Profession... ..... .... ..... .... ....... 70 The Development of Professional Ethics of Public Accountants. .... ... .. .. ... .. ... .. .... . 73

V1

The United States Code of Professional Conduct . . . . . . . . . . .. . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 77 Principles of Professional Conduct. .... ............ ........... .... ...... .. .... .......... .... .. 78 Rules of Professional Conduct . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 80

Summary... ..... .. .. ..... ... ...... ..... ........ ... ........ .. .. ....... ..... .... ... .... ... ................... .. ....... ... . 83 Conclusion . . . . . .. . . . . . .. . . .. . . . . . . . . . . . . . . . . . . . . .. . . . . . . . .. . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 84

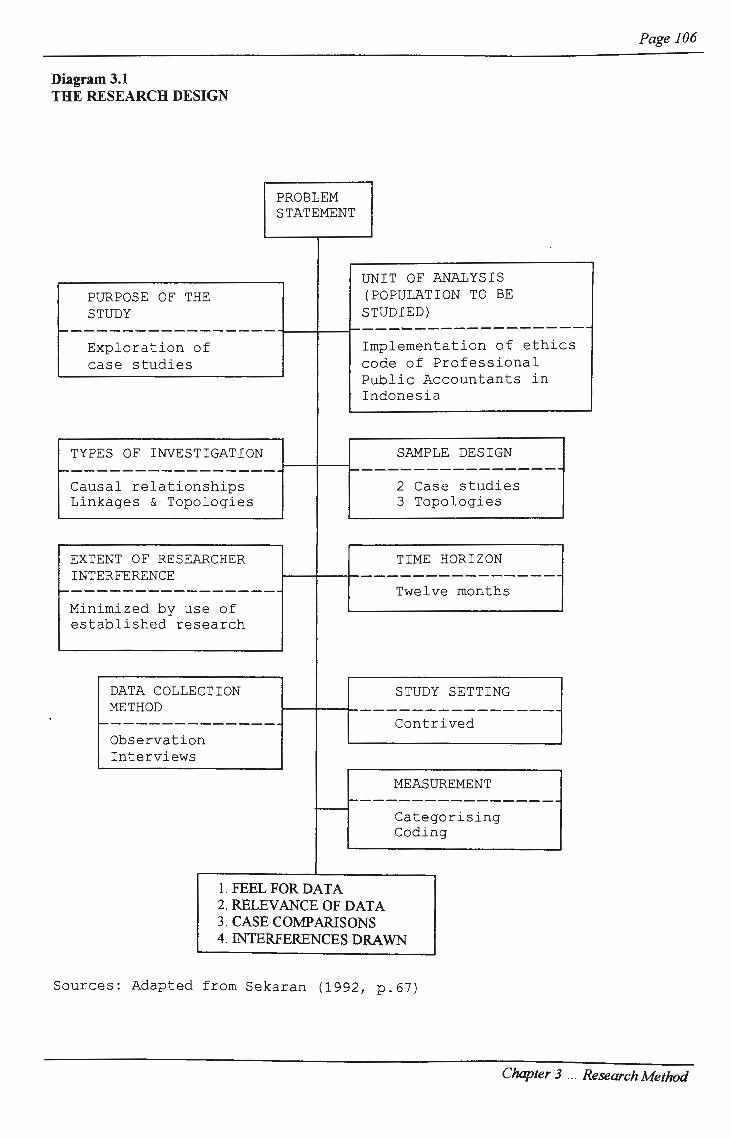

Chapter 3 Research Method

Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 87 Research Method Employed . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 88

Sample ... .............. ...... ....... .... .... ... .... ... .. ......... ......... .... ......... .. ... .. ............. ... ..... ... ... 88 Case Study . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . 90

Case Study Design ... ..... . :. .. .. .... .... ...... ......... .. ... ........ ..... ......................... .. .... .... .. ............ 91 Validity of Case Study Research . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 93

Issues of Case Study . ... . .. . . ... .. . . . . . . . . . . . .. .. . . . .. ... . .. . . .. . . . . . . . . .. . . .. .. . . .. . .. ... .. .. . . .. . . . .. . . . . . . . .. .. 95 Summary ........ ..... .. ....... .. ...... .. ... ............ ...... ....... ... ... .. ... ... ..... ... ... .. .... .... ...... ...... .. ... 95

Data Collection . . . . .. .. . .. . . . .. .. .. . . . .. . . . . . .. . .. . . . . . . . . . .. . .. . . .. . .. . . .. . . . . . . . .. . . . . .. . . . .. . .. .. . .. .. . . . .. . . . . .. . .. . . . . . . 95 Sources and Technique of Data Collection .... .. ... .. .. ...... ............................... ...... ... 96

Interviewing . . .. . . .. . . . .. .. .. .. . . . .. .. . . . .. . . .. . .. . . . .. . . . .. . . . . .. . .. . .. . . .. . . . . .. . .. . .. . .. . . . . .. . . . . . .. . .. 97 Interview Techniques .............. ........... .... ................ ...... ... ........ .. ... .... .... .... . 97 Interview Structures .. ... ... ............ ... .......... ....... ........ ....... ...................... .. .. .. 100

Summary ....................................................................................... ......................... 102 Research Design .. .. . . .. . .. . . .. .. . . . . . . . . .. .. .. .. . . .. . .. .. . . . . . . . .. .. . . . . . . . . . . .. . . .. . . . . .. .. .. .. . .. .. . .. . . . .. . . .. . .. .. . .. .. . 103 Data Analysis ........................................................................................ ..... ... ............ ... .. 107

Techniques of Analysis .. ... .. .. .... .... ...... .............................................. ..... .. ..... ... .. ... 108 Conclusion . . . . .. . . . .. . . . . . . . . .. . .. . . . . . . . . . .. . . .. . .. . . . .. . .. . .. . .. . .. . . . . . . .. .. . . . . .. .. . . . . . . .. .. . . . .. . .. .. . . . . .. . .. .. . . . . .. .. . 109

Chapter 4 The IAI and the Development of Public Accounting in Indonesia

Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 110 History and Development of the IAI . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 111

A Brief History of the IAI ... ........ ... .......... .............. .. ....... ............ .......... .... ......... ... 114 Membership ofIAI ... ...... ... ...... ... .... ............ ....... ..... ... .. .... .... .................... ...... .... .. .. 116 Scope and Nature of the Public Accountant's Work .. .... .......... ...... ..... .. ...... ..... .. ... 117

The Role and Responsibility of Public Accounting ....................................................... 122 The Development of the Ethics Code in Indonesia .... ... ........... .. .... .... ... .. ... .. ... .. .. ...... .... 124

Assertion of Ethics Profession .. ... ..... ...... .. ....... .. .... ... .. ... .. ... .. .. .... .. ......... ...... ....... .. . 125 The Principle of Ethics ........ .. .... .... .. ... .. ... .. ..... ....... ..... .... ..... .... ......... ... ....... ... ....... . 129 The Rules of Ethics ..... ...... .. ......... ...... .... ........... ..... ... ... ... ... .... ...... ........ ....... .. ......... 131

Conclusion ... .... ...... ....... .. .... ... ... ......... ... .... ..... .. .... .. ..... ...... .......... ..... ... .... ...... .... .. .. .... ..... 135

Vll

Chapter 5 Analysis

Introduction ....... ....... ... .. ... .. .. ... ........... .... ... ... ...... .. ...... ......... ... ... ...... ..... ... ... ... .. .. ..... .... .... 137 Data Descriptions .. ... .. ............. ............ ... ...... .. .... .... .. .... ....... .. .. ....... ... ....... ..... ............. .... 138

The criteria of interviewees respondent ........ ...... .... ... ..... .. .... ...... ..... .............. .... ... . 139 Ethics Codes for Accountants in Indonesia .. ..... ... .... ...... .. ..... .. .... ... ..... .... ... ... ........ 140 Implementation and Interview Results .. .... ... ..... .... ....... ......... .. ..... .. ..... ..... .. ... .... .... 142

Meas~~:i~:(. ::: : :: :: ::::::::::: : :::::::::::: : :::::::::::::: :: : :: : : :::::::::::: : : ::::: :: ::: ::::::: : :: : : : ::::: : : : ::: : :: : : : :: : : i ~~ The Utilities of Measurement ............... .. ... .. .... ........ ..... ........ ... ... .. .... ... ... ............ ... 159 Types of Standard Measurement ... ..... .... ... ... ...... .. .... .. ... ..... .. ... .... ..... .. ..... .. ... ... ... .. . 159

The Principles of the Ethics Code Model as Standard Measurement ... ... ..... 160 The Individual Moral Development Model as Standard Measurement ... ..... 164

The Results of Measurement . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16 7 The Result of Measurement in Family-Owned, State-Owned, and Foreign-Owned Companies ....... .... ... ... ......... .... ........ .. ..... ..... .... .. ... .. ....... .... ..... ..... .. 168 General Result of Measurement in Indonesia .... ... .. ... .......... ..... .. .. ........ .. ... ... .. ..... .. 178 Implementation and Obstruction of the Code of Ethics .. .... ......... ...... ... ... ... .. ... .... . 179 Obedience of the Code of Ethics . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 181

Summary .. .... ....... ... ........ .. .. .... ..... .... .... ....... ............ ......... ............ ...... .... ... ... ......... .... .. .... 183 Analysis .... .. .. .... ... ....... ..... ..... .... .. .... ..... .... ..... ..... .... ..... ... ... ............. ... ........... .... ... ... .... .... . 185

Professional Approach . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 186 Individual Approach .... .... .. ... ........ ........ ... ........ ...... ......... .. ... ........ .. .... .... .... ..... ....... 197 Summary .. .............. ... .. .... .... ... .. ... ...... .. .... ... ..... ..... .. .. ... ... .... .... ... .. ....... ... .. ...... ...... ... 206

Chapter 6 Research Findings and Conclusion

Introduction .. ........ ... .. ... ..... .......... .... .. ... ........ .... .. .. .. .... ... ... ..... ........... .. ...... ..... .... .. ..... ...... 214 Research Finding ....... .. ... ..... ...... .. ...... ...... .... .. .............. .... ... ... .. ..... ... ..... ... .............. .... .. .. 216

The influence of moral development on the moral reasoning process of the public accountant in implementing the principles of the code of conduct . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . .. .. .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 217 The level of the public accountant' s moral reasoning as a moral agent ... ........ ..... 220 The key activities performed by both the Indonesia Public Accountant and the Financial Manager to build and improve the effectiveness in the implementation of the principles of the code of conduct in developing and achieving professional practices ........ ....... ....... .. ... ... ... 221

Establishing a conducive cultural condition ... ... ....... ... .. ..... ..... .. ...... ....... .. ..... 222 The existence of control from a professional body (IAI), government, and the public .. ... ... ... .. .... ....... ............. .. .. ... ...... .. ...... .... .. ..... .... ... 223

V11l

Importance of this research ...... .. ... .... ....... .... .. .......... ..... .. .... ................. ..... .... .. ........ ....... 224 Theoretical Contributions ...... .............. ... ..... ........ ... .. ..... ... .... ... ....... .... .. .... ... .. .. .. .... 225

Contribution Theory for the Ethics Codes ........ ....... ..... ... ....... ... ............... ..... 225 Contribution for Moral Development Theory ........ .. .. ... .. .... .. ...... ............ ... ... . 227 Contribution Towards Audit Practice in Indonesia's Companies ...... .. .... ... ... 228

General Contribution Towards Audit Practice in Indonesia ................. 228 C .b . .!:'. F. . 1 ontn ut10n 1or mancia Managers ...... ..... ... .... .... .. ... ...... ... ... .. ....... .... 231

Methodological Consideration .... ......... .. ......... ......... ...... .. ... ...... ....... ......... ... ... ...... 231 The Limitations of the Research .. .. ................. ............ .... .. ... .... ................. ... .. ....... ..... ... . 232 Future Research .. .... ..... ... ..... ....... ..... ......... ..... .......... .... ......... ........... ... .. ... ...... .... .... .... .... 233 Conclusion .. .. ................ ... .. ... ...... ... ....................... ... .. .. .... ....... ..... .. ... .. .......... ..... .. ..... ... .. 234

Bibliography .. .. .... .. .. .... .... ... .... ................... .... ... ... .... .. ............. ... .... ......... .. ... ... ... ... ... . 237

Appendices

Appendix 5 .1 Appendix 5.2

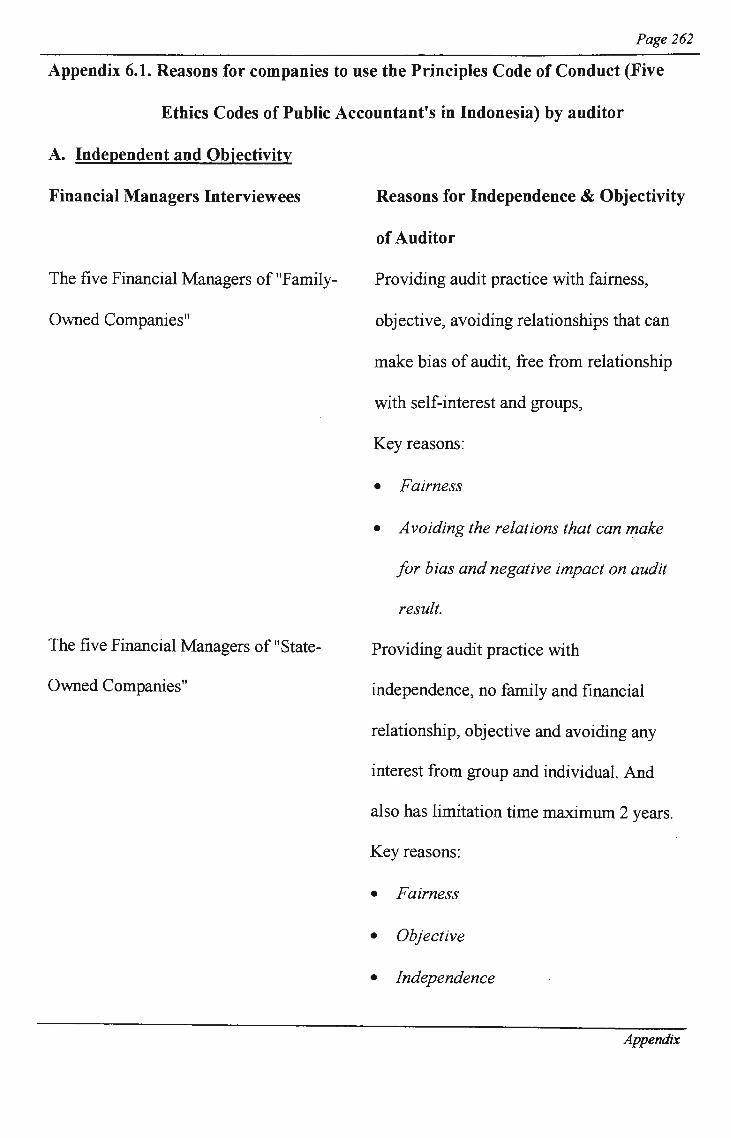

Appendix 5.2.1 : Appendix 6 .1

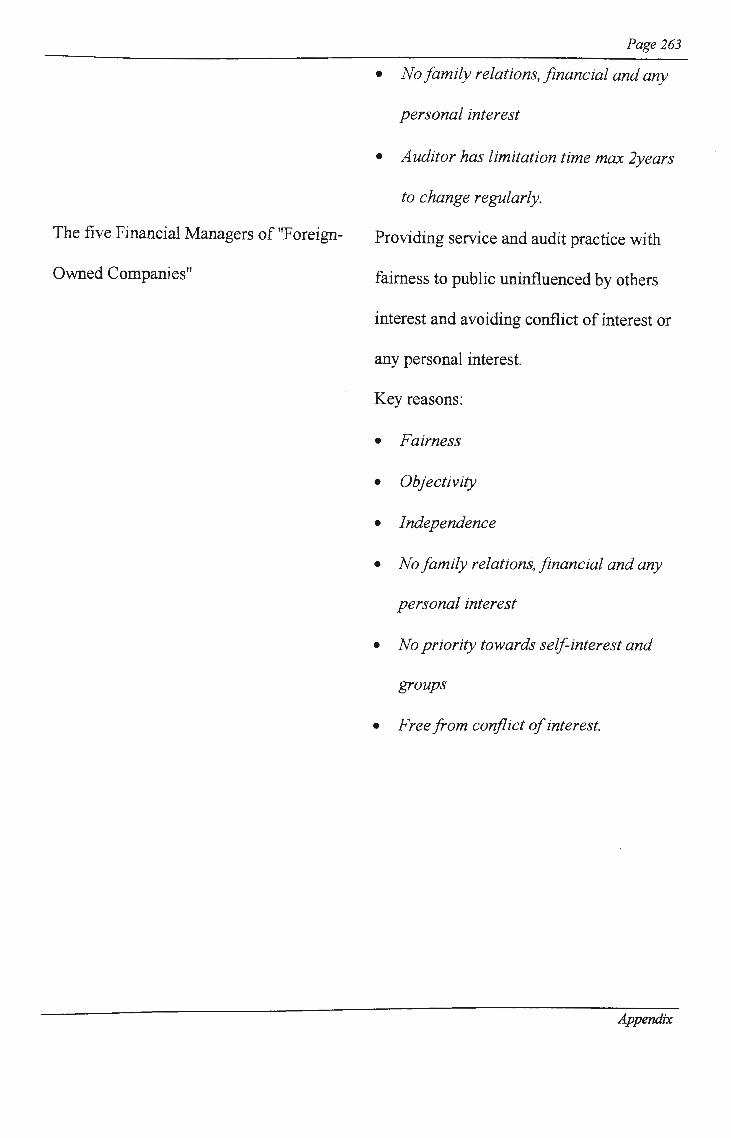

Appendix 6 .1.1 :

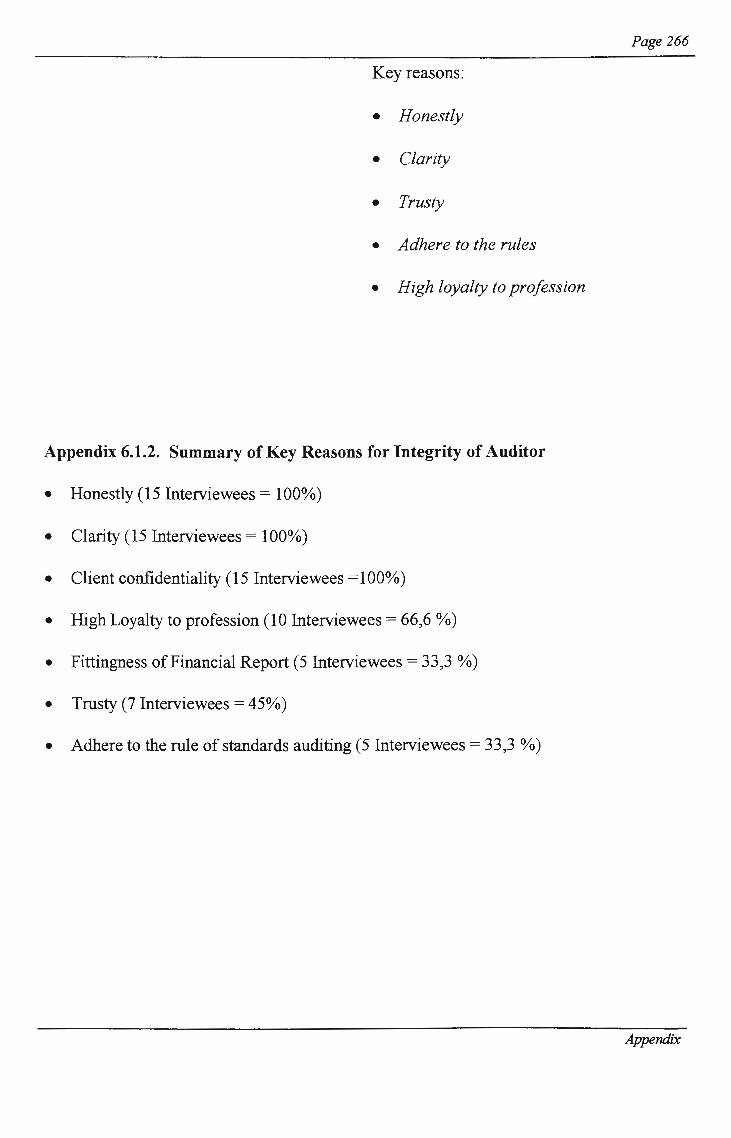

Appendix 6.1.2 : Appendix 6 .1. 3 :

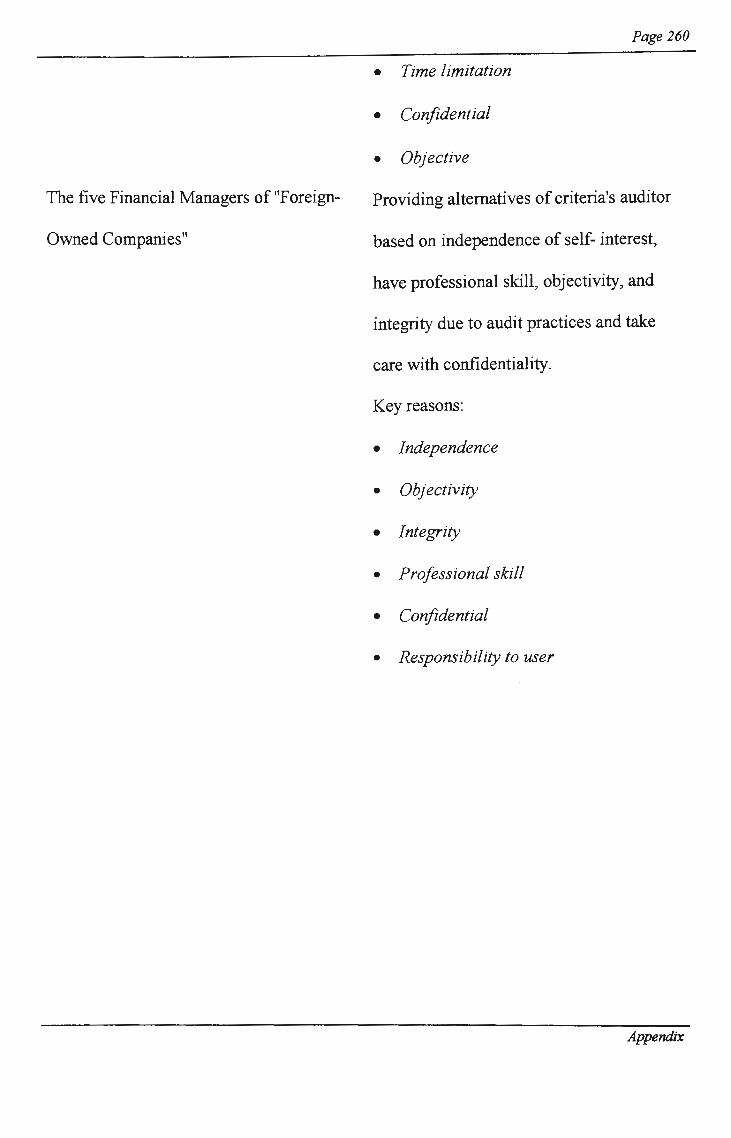

List of Interview Questions ........... ... ... ........... .. .......... .. .... ..... .... .... ... 257 Reasons Companies within determines auditor's criteria to perform audit practices ...... ........ .. ... ..... ..... .. ....... .... .... .................. 259 Summary of Key Reasons for issuing auditor's criteria .... ... .. .... .... 261 Reasons for companies to use the Principles Code of Conduct (Five Ethics Codes of Public Accountant's in Indonesia) by auditor ............. ......... .. .. .. .. .............. ....... .... .... .. ... ....... 262 Summary of Key Reasons for Independence & Objectivity of Auditor .. ......... .... .. ... .. .. .. .. .. .... .......... ..... ...... ..... .... ... ... 264 Summary of Key Reasons for Integrity of Auditor ... .. ... ... ...... .. ...... 266 Summary of Key Reasons for Responsibility of Auditor

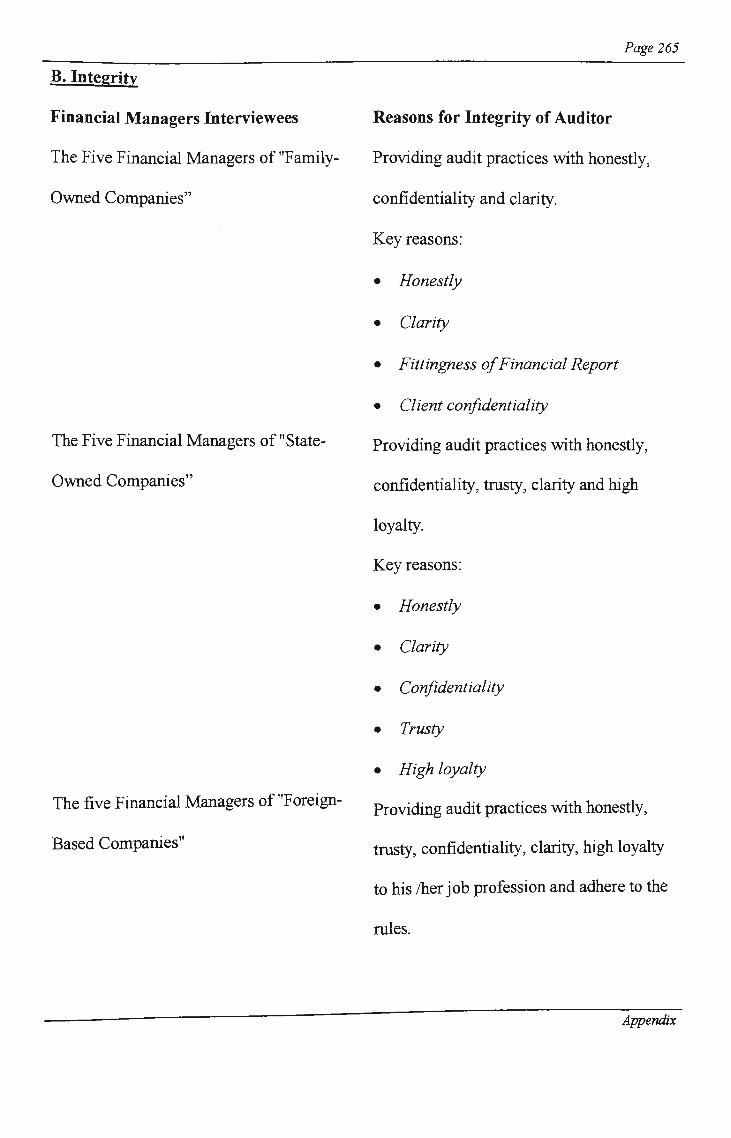

··· ···· ··· ·· ··········· ·············· ···· ········ ······ ··· ···· ··· ······ ····· ······· ······ ·· ··· ·· ···· ··· ··· · 269 Appendix 6.1.4 : Summary of Key Reasons for Due Care of Auditor .. ............ ...... .. .. 271 Appendix 6.1.5.: Summary of Key Reasons for Scope and Services of

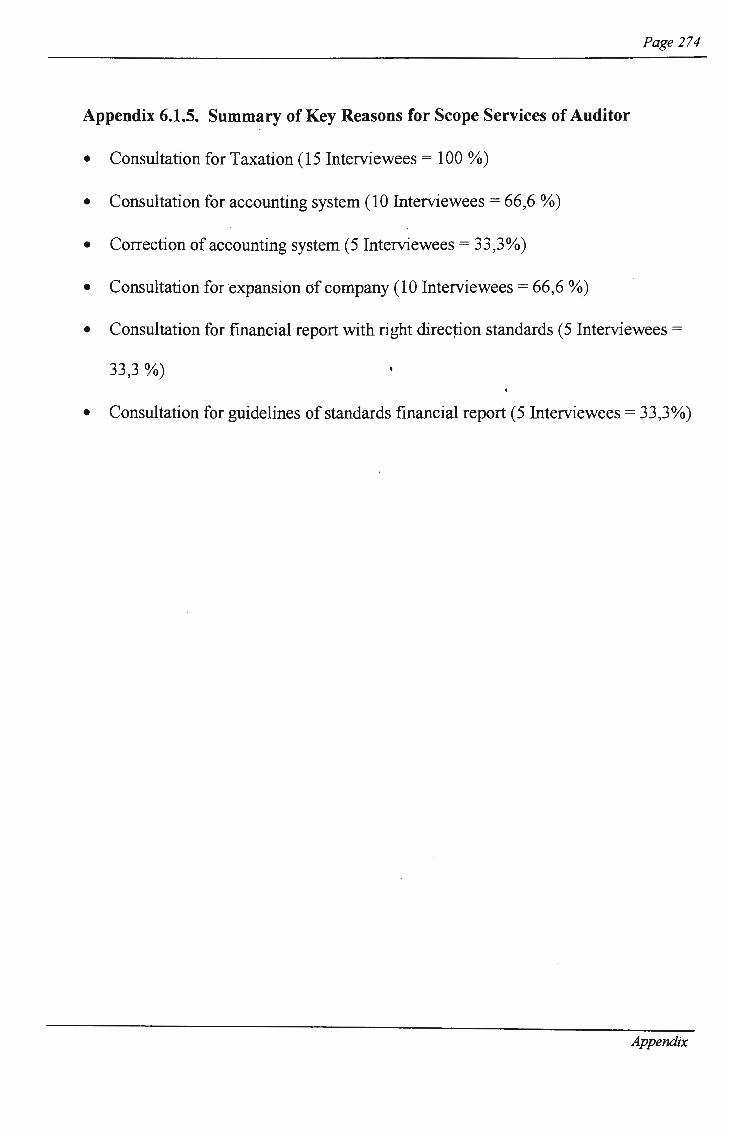

Auditor ................. ... ... ...... .... ... .... .... .. .................... ... .... .... ............. ... 274

List of Tables

Table 3.1 Table 3.2 Table 3.3 Table 3.4 Table 4.1

Tactics For Case Studies ........ ... .... .. ... ........... .... ..... .... ....... .. .. ..... ..... .. .. ..... 92 Interview Question Design . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 99 Summary of Variables ............. .. ... ... ... ........ ..... ....... ..... ..... ... ......... ........ ... 105 Overview of Dependent Variables .. ........ ....... .. ....... .... .. ..... .... .. ... .. ........... 105 The Six Assertions of Professional Ethics .... .. .... ... ... .... ... .. ... ......... .... .... .. 126

lX

Table 5.1

Table 5.2

Table 5.3

Table 5.4 Table 5.5

Table 5.6 Table 5.7

Table 5.8 Table 5.9

Table 5.10: Table5.11:

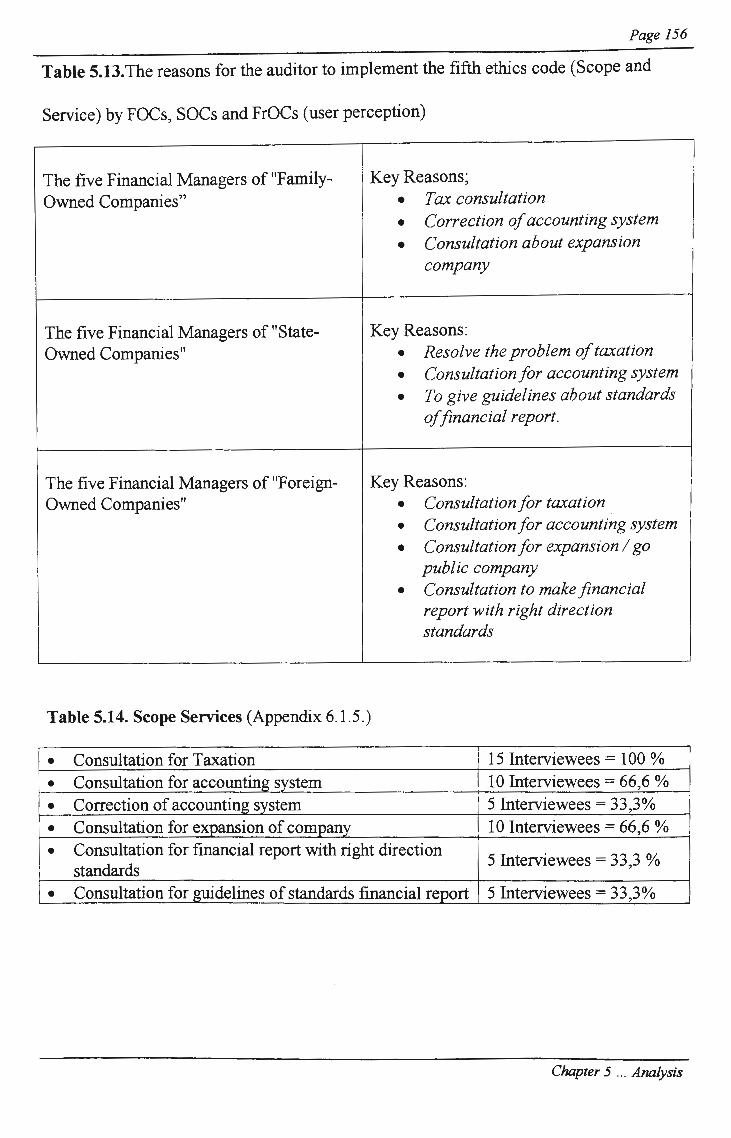

Table 5.12: Table 5.13 :

Table 5.14 :

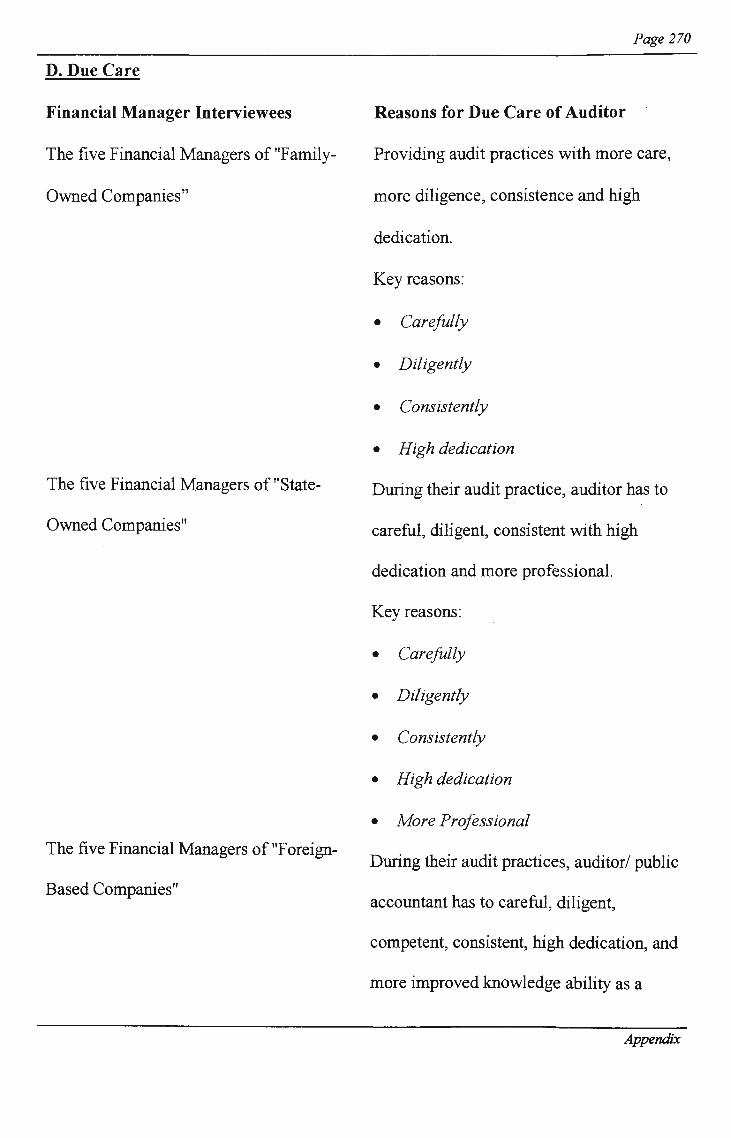

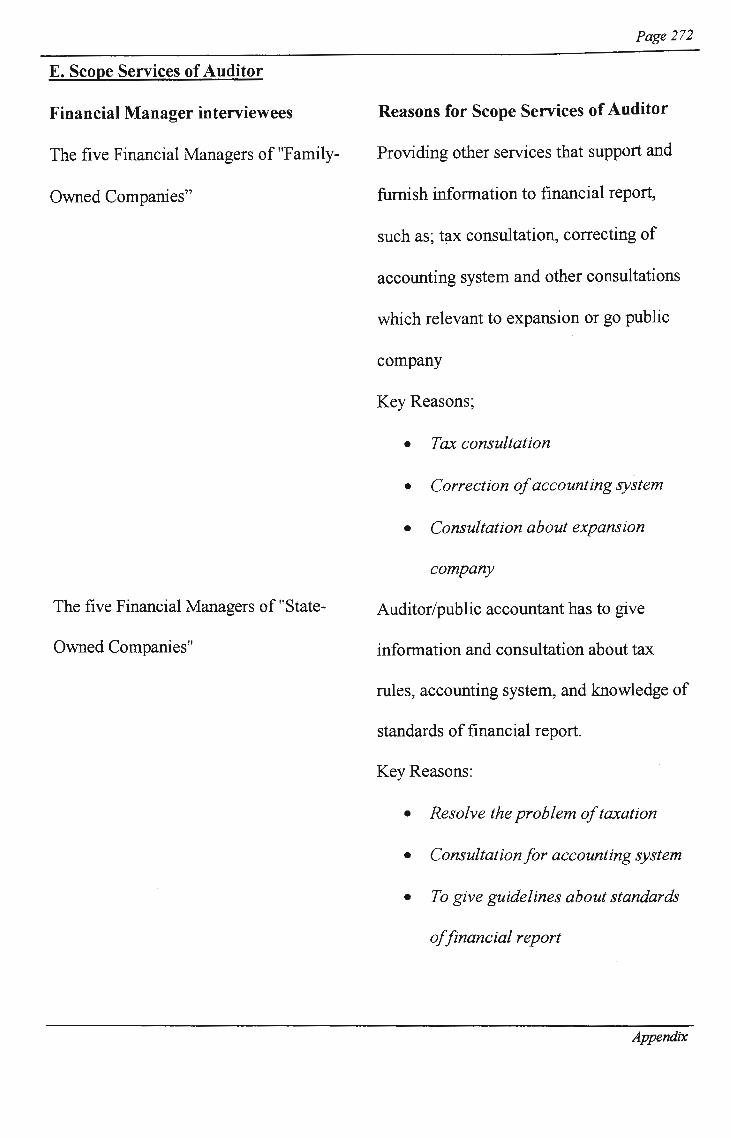

The Reasons for selection criteria of auditors by interviewees from FOCs ........ .... ................ ............. .... .... .. ..... .. .... .. .... ...... 150 The Reasons for selection criteria of auditors by interviewees from SOCs ..... ......... ..... ..... ......... .... .. .... ................. .............. 150 The Reasons for selection criteria of auditors by interviewees from FrOCs ..... .. .... .. ... .. ... ......... ... .... ..... ..... ... ....... ..... ........... 150 Summary of Key Reasons for Issuing Auditor's Criteria ........... ....... .. .... 151 The reasons for auditors to implement the first ethics code (Independence and Objectivity) by FOCs, SOCs, and FrOCs ................. 152 Independence and Objectivity ....... .. .... .. .... .. ... .. ... ......... ... ..... ..... .... ........ .. . 152 The Reasons for auditors to implement the second ethics code (Integrity) by FOCs, SOCs and FrOCs ..... .. .... .. ........ ..... .. ............... 153 Integrity ... ................. .... ... ...... ......... ...... ........ ...... ...... .... .. ... ... .... ... ..... ..... ... 153 The Reasons for auditors to implement the third ethics code (Responsibility) by FOCs, SOCs and FrOCs ........................................... 154 Responsibility . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 154 The Reasons for auditors to implement the fourth ethics code (Due Care) by FOCs, SOCs and FrOCs ................................................... 155 Due Care .. ... ......... ... ... .... ........... .. ....... .... .. ...... ...... ..... ....... ........................ 155 The Reasons auditors to implement the fifth ethics code (Scope and Services) by FOCs, SOCs and FrOCs .. ...... .. .. ......... ............ .. 156 Scope and Services ..... ..... ... ..... .. .... .... ........ ......... ....... ............. ... ..... ...... .. . 156

List of Diagrams

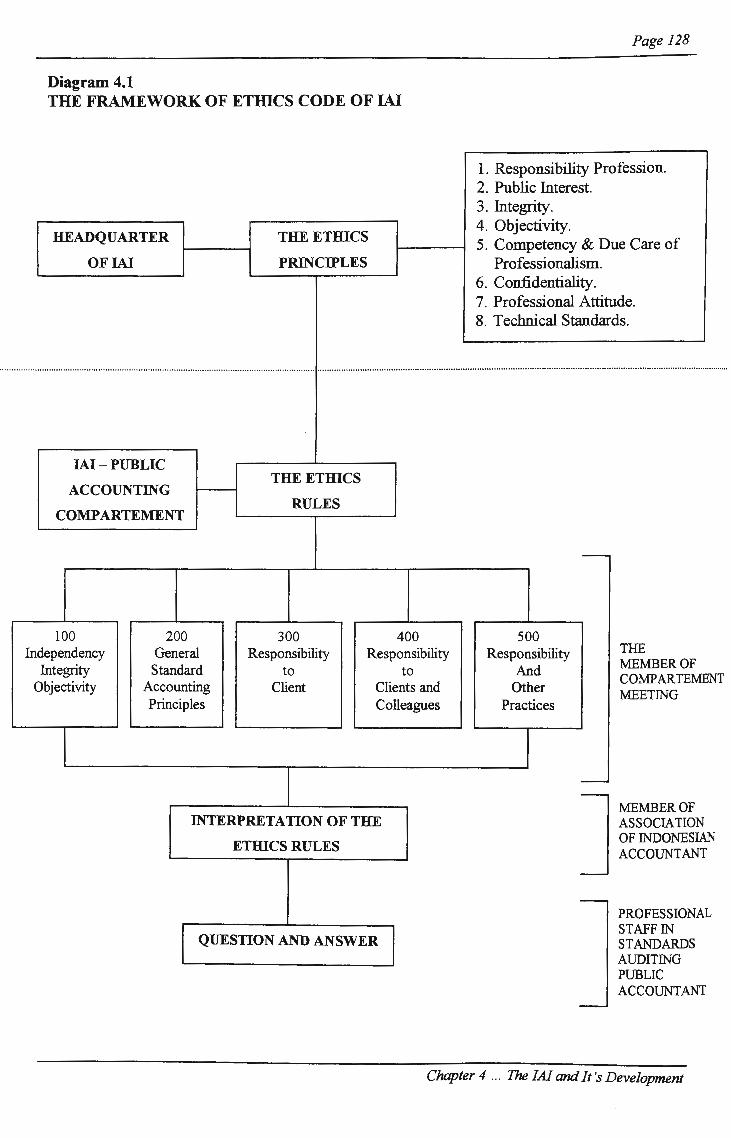

Diagram 3 .1: The Research Design . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 106 Diagram 4.1: The Framework of Ethics Code ofW ...... .... ... .. ....... .... .............. .... ...... 128 Diagram 5 .1: Flowchart of The Relationship between Professional

Approach and Individual Approach .......... ............... .... .. .... .. .................. 213

x

Background

CHAPTER I

INTRODUCTION

Page 1

An auditor is an accounting professional, who supposedly performs his/her duties in a

professional manner. This can be achieved by applying standards or principles of

accounting and auditing correctly, and abiding by the ethical codes. These regulations

and guidelines have been specifically prepared and enforced by professional bodies

on their members. They are intended to avoid any fraudulent conduct and improve

professional quality as well as a commitment to solving problems. For example, the

ability to cope with difficult situations in a manner beneficial to clients is a reflection

of professionalism (Nixon, 1994, p.2).

Currently, there are many debatable issues related to the extent that public

accountants have rendered their services -- such as providing information in the form

of financial reports to the users. In fact, as one of economic agents, public

accountants so . frequently face complicated situations that they are tempted to choose

their self-interest (for the client's benefit) rather than the public interest (observing

rules of conduct). This is a moral dilemma that often poses great difficulties for

accounting professionals. For this reason, in order to cope with this dilemma,

regulations, standards, principles and ethical codes, devised by professional bodies

Chapter 1 .. . Introduction

Page2

are needed by all public accounting practitioners as guidelines for serving society

(users).

In principle, professional accounting body ethical codes have seven aspects, which

need to be considered. In the USA, the AICPA have listed these as independence,

objectivity and integrity, public interest, responsibility, due care and scope and nature

of services (AICPA, 1992). Therefore, professional ethics are more than just

instrumental to the maintenance of a moral, ethical and honest image among the

public: professional bodies need to ensure that the trust of society is upheld. The

maintenance of high professional ethical standards relies on an understanding of the

moral reasoning process. This moral reasoning process forms part of the entire moral

consciousness of an individual's belief system and from which a decision is made

when an individual is facing difficult dilemmas (Au and Wong, 2000). Hence, in this

thesis, the moral reasoning process of professional accountants is investigated by

utilising the theory of ethical development.

Theoretical Development

Most public accountants would think it ridiculous to expect their actions to damage a

client. However, it is possible that as a result of strictly following the professional

Code of Conduct a public accountant could allow clients to be defrauded . . Hence,

most public accountants who desire to protect a client from harm may find that

following the Code would lead to a moral conflict.

Chapter 1 ... Introduction

Page 3

On one hand, taking care of client interests disregarding existing ethical rules or

values ethics can be considered as prioritising self-interest. The practice can be

related to improving financial benefit of public accountants. On the other hand

placing a higher priority on public interest (users) by upholding the ethical rules and

values might cause harm to clients, which could even encourage them to get involved

in more fraudulent conduct. Consequently, these different conditions will create a

moral confli.ct for public accountants. Therefore, the quality of actions chosen by

professional accountants is determined· by how far they understand the meaning of

and utilise codes of conduct and the principles underlying them. Moral reasoning as, a

development process of moral levels of public accountants (from cognition-judgment

to moral action) will influence decision making of public accountants in action.

Moral reasoning can be defined as the arguments about how people should act or give

reasons to justify or criticize behaviour. The reason is offered to show why that kind

of action is believed to be wrong or why that judgment is thought to be correct. Thus,

moral reasoning involves offering reasons for or against moral beliefs in an attempt to

show that those beliefs are either correct or mistaken. (Fox and DeMarco, 1990, p.4).

Furthermore, the definition of moral reasoning is an argument that means a reason or

a series of reasons that aims to support a particular claim, which is called the

conclusion. Hence, these arguments consist of reason and conclusion (Thompson,

1998, p.5). For example, in particular ethical issues, moral reasoning arises from

demonstrating an action or behaviour which is led by thought that stimulates a

question "What ought I to do", not "What shall I do", and several issues such as,

Chapter 1 .. . Introduction

Page 4

considering the consequences of various courses of action, or some weighing of the

conflicting responsibilities, and attempting to come to a conclusion on the issues

(Thompson, 1998, p.6). From the definition above, it can be concluded that reasoning

consists of three points of view, such as; (a). Thinking about what peoples should do

and why peoples should do it; (b ). Forming ideas to describe and evaluate actions,

and ( c ). Judging a particular action by means of a general rule.

Additionally, moral reasoning is an argument of an individual that has the objectives

of explaining the process by which ethical decision making of that individual is made,

or describing a process of establishing behaviour or action based on individual moral

judgment (cognition-judgement-action process). Thus, the moral reasoning process

of an individual can also be understood by examining how individuals internalize

moral standards (Adams, Malone, James, 1995, p.3).

In principle, theoretical development of moral reasomng can be explored by

describing a model individual's moral development from some scholars. According to

Kohlberg ( 1976), moral development occurs at three levels with each level having

two distinct stages. These stages determine the level of moral reasoning used by

individuals in distinguishing right actions from wrong actions. Level 1: Pre

conventional contains Stage 1 - Physical consequence of actions, avoidance of

punishment; and Stage 2 - Satisfaction of one's own needs. Level 2: Conventional

involves Stage 3 - Desire to please others and Stage 4 - Respecting authority and

preserving the rules of society. Level 3: Post-conventional embraces Stage 5 -

Chapter I ... Introduction

Page 5

Morality of contracts, individual rights and democratically accepted law and Stage 6

- Universal moral and ethical principles (Kohlberg, 1976). Furthermore, Kohlberg

maintains that these stages are sequential such that a person does not enter into a later

stage until the person has passed through each of the previous stages.

However, Gilligan criticized Kohlberg for his focus only on justice and argues,

instead, there is also ethics of care, which may be the framework that females are

more likely to work from. Moreover, Johnson' s Moral Imagination Model argued

that action is the reflection of a conscious form of character and motivations.

According to Johnson (1993) the moral imagination model proposes ways that ethics

education can lead to appropriate moral action through strengthening character and

self awareness, developing ethics sensibility, cultivating ethical reasoning and critical

thinking skills, engendering qualities of emotional empathy, and understanding the

effects of organizational policies and economic incentives on ethical behaviour. In

addition, other scholars such as Sweeney (1995) argued that moral development

theory attempts to explain the cognitive framework underlying individual decision

making in the context of an ethical dilemma.

Based on statements of objectivity of moral reasoning it can be underlined that moral

reasoning is influenced by levels of an individual ' s moral development. Thus, the

higher the individual moral development, the higher her level of moral reasoning.

Consequently, the higher level of moral reasoning will influence an individual ' s

ethical decision making on behaviour or action and hence supports an individual's

Chapter 1 .. . Introduction

Page6

choice to apply rules of code of conduct with full awareness. Obviously, the

implementation of a mle or ethics codes is similar to establishing performance of

individual ethical decision-making.

Thus, the process of moral reasonmg is precisely a process of individual moral

reasoning toward a consciousness of ethical decision making to be made to create

actions or behaviour in society. Moreover, ethical decision-making has been

influenced by personal variables (gender, age, socio politic, socio economic and

ethics education), and professional variables (firm size, culture, and job satisfaction).

Therefore, a decision of ethics (judgment good or bad and wrong or mistake) should

need the highest moral level that can be achieved with individual moral development

and some variables involved.

Statement of the Problem

Not much is known about an auditor' s need of moral reasoning as a basis for moral

argument to achieve the process of ethical decision making in performing an audit of

financial reports or providing other services to users. Therefore, this study is

essentially exploratory. In this thesis, moral reasoning in the context of moral

argument is defined as the arguments of people about how people should act or give a

reason to justify or criticise a behaviour. Suggestions are made to show why one kind

of action is believed to be wrong or why a judgment is thought to be correct. (Fox and

DeMarco, 1990) Moreover, another definition of moral reasoning is a process of

deciding whether an action, or decision is right or wrong (Thomspon, 1998). As a

Chapter 1 ... Introduction

Page 7

result, this definition of moral reasoning implies that there are three points of view

such as, thinking about what people should do and why people should do it; forming

ideas to describe and evaluate actions; and judging a particular action by means of a

general mle. Thus, this thesis focuses on two important aspects: (i) an investigation of

the extent that the moral reasoning of public accountants influences the

implementation of ethical codes, especially a Code of Conduct, that consists of

responsibility; independence and objectivity; integrity; public interest; due care; and

scope and nature of services (AICP A, 1992), and (ii) an analysis of the problem

solving to improve the effectiveness of the implementation of ethical codes (Code of

Conduct). This leads to major research questions:

1. To what extent public accountants' consciousness determined an appropriate code

of conduct in Indonesia?

2. What actions will improve the effectiveness of the implementation of principles

of a code of conduct in providing audit services and other services to users?

The propositions of this study are expressed in the following terms:

1. Consciousness of public accountants is defined as the extent to which moral

reasoning of public accountants influences ethical decision~making Gudgements

of good or bad and of right or wrong behaviour) towards the upholding of a

principle codes of conduct.

2. The principles of a code of conduct that contain seven ethical codes of

professional accountants that address moral and ethical behaviour regarding

activities, attitudes, and procedures involved in most aspects of professional

conduct.·

Chapter I ... Introduction

Page 8

3. The attributes of codes of conduct by which the major duties of accountants will

be designed to monitor and measure performance of public accountants.

4. The key factors of the level of moral reasoning of professional public accountants

are defined in respect of the increase of the level of individual moral development

of public accountants.

5. Key effectiveness is defined as the adherence of public accountants to appropriate

codes of conduct, and consequently, the improvement of implementations of

codes of conduct is achieved.

The Purpose of the Study

The purpose of this study is to investigate the role played by moral reasoning in

influencing the ethical decision-making process of public accountants in

implementing codes of conduct (ethics codes). In other words, it investigates the

relationship between moral development and ethical decision making in the context

of a public accountant's ethical code in developing countries where social, political

and economic environments are influenced by a high level of corrupt, collusive and

nepotistic culture. The investigation focuses on two critical aspects: the development

of moral reasoning of public accountants as moral agents, and the key activities they

perform to improve the implementation of a code of conduct.

Kohlberg' s individual moral development model (1982) is used to identify and

investigate the influence of moral reasoning by public accountants in relation to the

development of professional ethical codes of practice. The stages of the principle

Chapter 1 .. . Introduction

Page 9

code of conduct development proposed by the AICPA (1992) are used to identify the

improvement of effectiveness of implementation of the principle code of conduct by

public accountants in developing and achieving professional practices.

Study Approach

Ethics have recently become an interesting topic in accounting (Francis, 1990; Alam,

1991; Gambling and Karim, 1991; Chua and Degeling, 1993 ). Various researchers, in

essence argue that ethics should be cohesively implanted in accounting practices,

particularly in auditing practices, because ethics clearly signals and distinguishes

right from wrong, good from bad, and justice from injustice. Thus, the importance of

its presence in accmmting lies primarily in its real effects on an individual society.

Further, many researchers who study ethics in an accounting and auditing context use

empirical research or quantitative method to describe the behaviour of accountants in

public accounting (Ponemon and Gabhart, 1993; Bernardi, 1994 who tested

accountants reactions to specific auditing problems), as well as in industry

(Etherington and Schulting, 1995, who were interested in assessing the moral

development of CMAs and comparing the moral development of male and female

CMAs ). However, quantitative approaches have tended to neglect qualitative factors

in the implementation of ethics in accoimting. This is a major issue, which this thesis

will investigate by conducting qualitative research, in the form of a case study.

In this thesis, the discussion regarding implementation of ethics in accounting

practices focuses more on the specific scope of ethics in ethical codes or principles of

Chapter I .. . Introduction

Page 10

conduct for professional public accountants (AlCPA, 1992), and utilises qualitative

method to resolve the ethical codes problem. According to Lemon ( 1996), qualitative

research is several lines of empirical research that enable researchers to examine the

behaviour of professional public accountants in relation to culture, social issues,

gender issues, environmental issues, employment issues such as downsizing, codes of

conduct and corporate morality.

In this thesis, a qualitative approach is used to explore the existence of problems. A

case study is used to explore the factors that influence the consciousness of

professional public accountants in performing with principle codes of conduct, and

how professional public accountants improve effectiveness in the implementation of

suitable principles codes of conduct. According to Wintoro (2000, p.18) there are 3

basic reasons for this. First, the case study is a rigorous research method for exploring

individual behaviour, especially the relationship between individuals (Orum, Feagin

and Sjoberg, 1991; Hamel, 1992); and uses primary and secondary data in answering

the research questions (Yin, 1994 ). Secondly, the case study is a relevant research

method to use in the early stage of research on particular topics (Hill, 1993). Thirdly,

the relationship between the public accountant and client can be considered as a

business relationship (Kozak and Cohen, 1977; Lewin and Johnston, 1997).

Contribution of this Study

As a result, this study contributes, at least, three things. First, it helps develop the

knowledge through the introduction of new variable, namely, the level of

Chapter I ... Introduction

Page 11

consciousness of moral reasoning through an individual moral development model,

and of the key effectiveness in improving the implementation of codes of conduct.

Second, at the practical level, this study is expected to provide a confirmation of the

high level of awareness of public acco1mtants to perform consistently with ethical

codes. Empirical evidence is provided of the factors of the level of awareness of

public accountants as proposed by Kohlberg (1982) in their individual moral

development and empirical evidence is provided supporting an improvement in the

implementation of codes of conduct.

Third, it contributes to regulation or justice/law by providing useful information for

the regulators of public accountants in Indonesia that issue regulations or rules to

increase the implementation of codes of conduct in practice; increase the rules and

penalties of accounting bodies and government on public accountants that have

behaved fraudulently; and for public accountants who will demonstrate their

awareness of the need to improve and establish appropriate codes of conduct.

Limitation of this Case Study

The limitation of this research is related to the Indonesian case study and the data

collection methods. First, in a case study, the implementation of principles of codes of

conduct by public accountant is very specific. This is because Indonesian society is

strongly influenced by social, political, cultural and economic conditions that

characterise nearly all developing countries, in particular the culture of collusion,

Chapter 1 ... Introduction

Page 12

nepotism and corruption that strongly influences almost all business activities.

Moreover, Indonesian society is one of the Asian countries so influenced by Eastern

culture that it is quite difficult to become an open-minded society, and hence is not

open to all business activities. Therefore, the findings of this research are too limited

to be generalised. Secondly, the primary data are only gathered through the

conducting of semi-structured interviews with clients (users). The researcher

obviously could not observe at first hand, the actual implementation of principles of

codes of conduct by public accountants, because the information discussed between

clients and public accountants is confidential and unavailable to outside persons.

Hence, the information merely reports regarding their auditing practices. Therefore,

the researcher must accept the statements they make and the data analysis must be

limited to the interview results.

The Structure of this Thesis

This thesis is presented in six chapters. Chapter 2 develops the establishment of the

underlying theories of morals and morality, especially moral reasoning, the

development of ethics in accounting (professional ethics), and how ethics contributes

to the professional accountant (CPA). Studies related to each variable are reviewed

and characteristics are identified for use in the study.

Chapter 3 is a discussion of the research method employed. The validity and

applicability of the case study approach including the interview and questionnaire

design as well as the interpretation process are discussed. Then, chapter 4 is an

Chapter 1 ... Introduction

Page 13

overview of the historical development of public accountants in Indonesia and

includes the process of the development and improvement of standards, principles

and regulation of the accounting profession, particularly ethical codes (principles

codes of conduct). The analysis, interpretation and discussions of each individual case

study of the implementation of principles code of conduct by public accountants in

Indonesia is presented in chapter 5. Finally, chapter 6 is a summary of the findings

and a discussion of recommendation and conclusions based upon the findings.

Chapter 1 ... Introduction

Introduction

CHAPTER2

LITERATURE REVIEW

Page 14

This chapter provides a literature review of the role of "morals", especially moral

reasoning by individuals in making ethical decision in action. Therefore, this chapter

is divided into 5 sections. The first section contains a literature review that discusses

morals and morality in general. The second section follows the development of

research on the role of mora~ reasoning in implementing judgments (ethical decision

making). This section reviews research relating to identifying theoretical approaches,

ethical decision-making and implementation, and also focuses on the process of moral

reasoning of individuals that can be explored through understanding of the

individual 's moral development model. The third section discusses research

associated with the development of ethics in accounting practices. And the fourth

section summarizes studies relating to applied ethics in public accounting. This

section addresses several issues related to ethical codes as fundamental for the

practice of professionals. The case of the development of a professional code of ethics

in the United States of America is used to illustrate some of the problems encountered

in developing a code and how these problems can be resolved. Finally, the last section

addresses the relationship between moral reasoning and ethical decision making in

the implementation of ethical codes by professional accountants.

Chapter 2 .. . Literature Review

Moral & Morality

Introduction

Page 15

Many recent philosophical papers have concentrated on the discussion about the

establishment of morals and morality. This discussion has been based on identifying

several aspects, such as attitudes, problems and principles, which determine the

concept of morals and morality. However, there has been no consistency in the use of

the words "moral" and "morality" in many disciplines. In fact, the words 'morals' and

'morality' have different meanings. According to Whiteley (1970, p.21) any

acceptable way of defining morals and morality must isolate something, which plays

a distinctive part in human life, and must enable us to distinguish matters of morality

(right and wrong) from matters of taste or preference and matters of convenience or

expediency. The difference between morals and morality is important to comprehend.

Therefore, this section provides a definition of morals and morality as well as a

discussion of the role, and the judgment of morals, in general.

Definition and Characteristics

What is Moral?

A definition of morals depends on the purpose the definition is intended to serve, and

in what contexts it is to be used. Furthermore, a definition of moral should not be

judged as correct or incorrect, but should be judged as suitable or unsuitable (Baier,

1958, p.12)

Chapter 2 ... Literature Review

Page 16

Moral is defined as

The way in which in one combination it contrasts with one set of epithets, whereas in another combination it contrasts with a different set: a moral duty can be contrasted with a legal duty; on the other hand, moral considerations may be opposed to legal, prudential or aesthetic consideration (Wallace & Walker, 1970, p.14)

For Whiteley (1970), there are two possible ways to define 'moral ' . The first possible

way is that suggested by the etymology of moral, ethical and similar words. As an

example, the morality of a community consists of those ways of behaviour, which

each member of the community is taught, bidden and encouraged to adopt by the

other members. The second possible way of defining 'moral ' is based on an

individual (agent) viewpoint that means content of conscience. In other words,

morality is not only concerned with what people insist that I should do, but also

concerns what I insist that I should do.

Moreover, the definition of moral from a linguistics perspective has several meaning

aspects, such as

Of or concerned with the judgment or instruction of goodness or badness of character and behavior; Conforming to established standards of good behavior; A rising from conscience; Having psychological rather than tangible effect; Based on likelihood rather than evidence; The principle taught by a story or event and Rules or habits of conduct, especially of sexual conduct (Encarta Encyclopedia. CD-ROM, Encarta Encyclopedia, January 1998).

Furthermore, Webster' s Dictionary (1992) defines moral as a concept dealing with or

capacity to make the distinction between right and wrong in conduct. In other words,

Chapter 2 ... Literature Review

Page 17

moral implies conformity with the generally accepted standards of goodness or

rightness in conduct or character. Donagan argued that,

Moral has known as intuitionism and 'has been widely advanced as connecting the conception of morality as a system of specific precepts binding upon rational creatures as such with the conception of it as an unselfconscious disposition of affection and conduct ( 1977, p.17)

It is clear that several interpretations of the definition of moral can be drawn together

into one important conclusion that moral involves a judgment of goodness or badness,

and rightful or wrongful behaviour. This judgment should exist within every

individual as a rational creature who possesses a conscience. And also, moral includes

the involvement of social constraints, which would encourage people to decide on

their judgment, thus the expected condition of their society would be established.

Several reviews of various definitions given above might provide an adequate

account of 'moral' as a term of approval, but provide a quite inadequate account of

'moral' as a classificatory term.

What is Morality?

Morality is "a guide to conduct acceptable to all rational people that means a code of

conduct that all rational men would accept" (Gert, 1973). Moreover, Baier (1958)

argued that moral quality or character, is the rightness or wrongness of an action and

also the character of being in accordance with the principles or standards of right

conduct. Additionally, Robber's argument (cf Baier, 195 8, p.314) about morality is

Chapter 2 ... Literature Review

Page 18

that it is a system of principles whose acceptance by everyone as overruling the

dictates of self-interest and is in the interest of everyone alike. Following the rules of

morality, however, is not, of course, identical with following self-interest. If it were,

there could be no conflict between morality and self-interest and there would be no

point in having moral rules overriding self-interest. In spite of this, it is also right in

saying that the application of this system of rules is in accordance with the reason

only in social conditions that is when there are well-established ways of behaviour.

Furthermore, morality has other definitions, namely: the quality of being moral; a

system of ideas of right and Wrong conduct and also Virtuous conduct (Encarta

Encyclopedia. CD-ROM, Encarta Encyclopedia, January 1998). Moreover, The

Webster Dictionary defines morality as the character of being in accordance with the

principles or standards of right conduct. MacDonald (1995) defines morality as a

system of rules that modifies our behaviour in social situations. It is about the doing

of good instead of harm, and it sets some standard of virtuous conduct.

In spite of the definitions of morality mentioned above, morality also can be defined

in accordance with several reasonable conceptions that will be used as a base of

thought and understanding. Morality is innate and underpins the development of some

concepts. According to Whiteley (1970, p.23) the concept of morality is a

sociological or political concept that defines rules in the life of societies. Therefore,

morality can be explored based on its function, its relationship with religion,

economics and government. Durkheim (cf Etzioni, A, 1988, p. 8) argued that,

Chapter 2 .. . Literature Review

Page 19

"morality is a system of rules and values provided by society, imbedded in its culture

and that individual acquires these as part of the general transmission of culture".

Morality based on the psychological point of view is

A certain factor in the consciousness and conduct of individuals. It is a suitable concept for those who are concerned with, moral endeavor, aspiration and struggle with the nature, development and influence of the conscience. (Solomon, 1984, p.28)

Moreover, from the religious point of view as explained in the Western intellectual

tradition, the first reasonably clear conception of morality is as a standard for judging

systems of mores, or in other words, the concept of morality is based on common law

that applies to every rational and knowledgeable individual. This view seems to have

been formed by some philosophers, namely the Stoics, Cicero, Aristotle, and through

religious tradition (Donagan, 1977). At the beginning, the Stoics and Cicero

explained that before there was a written law that must be applied, naturally and

universally, there was established a highest law and truth that originated from the

highest substance or thing (a God) commonly called Zeus and Jupiter. They believed

that, every rational individual whom obviously possesses a divine mind would

automatically construct a divine law to be applied on their life regulation.

The Stoic ideal as described by Diogenes Laetius was,

To be in accordance with Nature, that is in accordance with the nature of man and that of the universe, doing nothing which the universal law is wont to forbid, that is, the right reason which pervades all things and is coextensive with Zeus (1998, p.2)

Chapter 2 ... Literature Review

Page 20

There is another similar argument mentioned by the scholar, Cicero (Cicereo, de

Legibus, II, 4, 10) argued that

Before there was a written law reason existed, having sprung from the nature of things, impelling (men) to right action, and summoning (them) from wrongdoing. This reason began to be law, not when it was written down, but it originated; and it originated simultaneously with the divine mind. Hence the true and supreme law having to do with commanding and forbidding is the right reason of Jupiter and highest. (cf Donagan, 1977, p.3)

The true and supreme law was held to be both willed by the highest of the gods and

enjoined by reason. These two characteristics are inseparable, because the divine law

expresses the divine mind, which is necessarily rational. Hence, t.he point of view of

moral philosophy, the one that is fundamental, is rationality (Etzioni, 1988, p.10).

However, since the birth and development of western religion, those descriptions of

law by the Stoics and Cicero mentioned above have been criticized by several groups,

especially the Christian and Jews. They place more emphasis on existing law and also

truth as originating from the divine commands that in the end actually originated from

the highest substance, that is God, as an expression of divine law. A divine command

expresses divine law if and only if it expresses divine reason. And if it can be

assumed, as it was by the Stoics, that human reason is in principle adequate for the

direction of human life, it follows that so far as it has to do with the regulation of

human life, the context of the divine law can be ascertained by natural human reason,

and its force appreciated, without any direct reference to the gods at all. By contrast,

divine commands that do not express divine law can only be known by revelation,

whether from the mouth of the god himself, or through intermediaries (Donagan,

Chapter 2 ... Literature Review

Page 21

1977, p.5). Thus, this universal or common code is what Jews and Christians came to

refer to as morality or the moral law and which also became known as the law of

nature and natural law. This is because they believed that the moral law applies to

people by virtue of his/her nature as a rational being, and is known to them primarily

by the exercise of natural human reason. The philosopher, Aristotle, also supported

those matters mentioned above The Aristotelian way believed that the conception of

morality as virtue is not an alternative to a conception of it as law. The conception of

morality as virtue presupposes that, in situations calling for moral choice, practical

wisdom can determine whether or not a given choice accords with a rationally

determined mean (cf Donagan, 1977, p. 7)

Even though, endorsed by the Stoics, and Jewish and Christian religious traditions,

the conception of morality as a common law to all rational creatures by virtue of their

rationality, is not religious-itself. Ultimately, morality is a system of laws or percepts,

binding upon rational creatures as such, the content of which is ascertainable by

human reason (Donagan, 1977). Basically, it can be concluded that the definition of

morality is a rule or as a system or laws which governs each individual on how to

morally behave, or rules or norms that are applied within society, that must be obeyed

by every rational individual consciously. From the discussion above, it can be seen

that moral and morality are different. Moral relates to conscience, character and

conduct of life, whilst morality relates to rules, law or systems that are commonly

applied within society to establish expected conditions.

Chapter 2 ... Literature Review

Page 22

However, further discussion in this study concentrates on the scope of morals,

because moral issues have the aim of exploring individuals as rational creatures, who

must be able to judge which is good or bad, and which is right or wrong for all their

desire and intention in their behaviour. In other words, individuals with morals should

be able to obey the applied rule or system consciously. Based on this line of

reasoning, comprehension of moral issues will be important.

The Categories of Moral Perspectives

Before further discussion in relation to the scope of morals, this chapter provides a

wider understanding of the difference of moral definitions when viewed from several

different perspectives or points of view. Preceding scholars have classified the

meaning of moral from several different perspectives of knowledge; philosophical,

psychological, social and economic perspectives.

First, the Philosophical perspective provides a consideration of the various kinds of

questions that arise in thinking about how one ought to live one's life, especially

finding out how to justify what is right, good, worthwhile, or just, and precisely what

such judgments means (Glickman, 1976, p.4). Philosophical perspectives argue that

because morality involves deliberation due to possible courses of action, a vast range

of empirical knowledge about action, desire, and reasoning is centrally relevant to

moral philosophy (Johnson, 1996).

Chapter 2 ... Literature Review

Page 23

Secondly, the Psychological perspective alleges to be a merely empirical discipline

describing contingent facts about how people actually are motivated, how they

understand things, and the factors that affect their moral reasoning (Johnson, 1996,

p.46). In other words, a psychological perspective means the psychology of human

moral understanding, which includes empirical inquiry into the conceptual system

that underlies moral reasoning. Moreover, the psychology of moral understanding can

give profound insights into the origin, nature, and structure of basic moral concepts

and into the ways to reason with those concepts. Thus, Johnson (1996, p.50) says that

a comprehensive moral psychology perspective includes at least the following types

of inquiry; personal identity; human behaviour and motivation; moral development;

conceptualization; reasoning; and affection. Moreover, moral psychology explores

what is involved in making moral judgments, and it will thereby cultivate in a certain

wisdom that comes from knowing about the nature and limits of human

understanding, a wisdom that will help us live morally insightful and sensitive lives.

Thirdly, another perspectives are the Social perspective. This explores morals as

human nature wherein individuals are assumed to be born with an unsavory

predisposition and not at all inclined to live harmoniously with one another. They

must be inoculated with values to develop their moral character, and authority is

needed to keep the lid on social order (Etzioni, 1988, p.8). This is similar to Parson's

description (cf Etzioni, 1988, p.8) that the core concept is functionalism. This means

that the acts of individuals are affected and evaluated in terms of their contribution to

the social order, which in tum is introduced into the individuals via socialization and

Chapter 2 ... Literature Review

Page 24

reinforced by social control. Social scientists (cf. Etzioni, A, 1988, p.9) have a simple

answer: that those who violate the values are either re-educated to embrace it, or

punished until they abide by it, and others are deterred from transgressing. Morality

motivates people to worry about public goods, to forgo free rides. It is clearly an

important way to shore up the commons and one that keeps the need for government

intervention low, including the need to generated inducements.

Fourthly, based on the Economic perspective that which is moral will be explored

with two paradigms, namely the neoclassical paradigm and the deontological

paradigm.

The neoclassical paradigm is a utilitarian, rationalist and individualist paradigm. It

sees individuals as seeking to maximize their utility and rationally, choosing the best

means to serve goals (Etzioni, 1988, p.2). The neoclassical paradigm is that people

seek to maximize one utility whether it is pleasure, happiness, consumption or merely

a formal notion of a unitary goal. These assume that people pursue at least two

irreducible "utilities" and have two sources of valuation; pleasure and morality

(Etzioni, 1988, p.3). Moreover, the model of the neoclassicists is self-oriented,

rational behaviour that is assumed to occur within the context of personality structure

and society. Additionally, other neoclassicists argued that moral commitments deeply

affects all behaviour, economic included (Wimich, 1984, p.994). The neoclassical

paradigm does not merely ignore the moral dimension but actively opposes its

Chapter 2 .. . Literature Review

Page 25

inclusion. Thus, it is stressed that various individuals may have different rankings of

preference over a field of choice, but none can be deemed to be better (Etzioni, 1988).

Finally, the deontological paradigm emerged as a suggested paradigm that begins

with the multiple self as a primary concept, but went on to seek specific theorems

about the social and intrapsychic conditions under which one part of the self is more

powerful than the other. Moreover, the essence of the deontological position is the

notion that actions are morally right when they conform to a relevant principle or duty

(Etzioni, 1988, p.13). The deontological paradigm assumes that people have at least

some significant involvement in the community (neoclassical paradigm would say

"surrender of sovereignty"), a sense of shared identity and commitment to values; a

sense that "We are members of one another" (Etzioni, 1988, p.7). The deontological

paradigm assumes that individuals experience perpetual inner tension generated by

conflict among their various basic urges (or desires), among their various moral

commitments and between their urges and their moral commitments (Etzioni, 1988,

p.11). Deontology stresses that the moral status of an act should not be judged by its

consequences, the way utilitarian do, but by the intention. For example, a person who

sets out to defame another is acting immorally, whether or not the person succeeds in

actually damaging the one he or she seeks to defame. The deontology paradigm is

used as the criterion for judging the morality of an act, not the ends it aspires to

achieve, nor the consequences, but the moral duty it discharges or disregards (Guy,

1990; Etzioni, 1988)

Chapter 2 ... Literature Review

Page 26

Finally, the importance of the deontology paradigm is that a major source of the

conflict is in the self as commitment to discharge one' s duties and more generally to

act morally. There is more to life than a quest to maximize one's satisfaction.

From the several perspectives explained above, it could be concluded that human

beings can be moral creatures because there are several concepts underlying their

behaviour, or there are several issues involved. From the psychology perspective,

moral is a form of system that gives an argument as to how people actually think and

behave morally. As a result, this concept will produce reasoning for individuals

within every activity; so people can live more morally, rightful and sensitive lives.

Moreover, a philosophical approach explores how to create harmonious lives in

societies, with focus on how people ought to think and behave morally.

Consequently, moral behaviour can be achieved through the development of moral

character, and through the existences of rules or regulation, subsequently;

expectations of societies can be realized. Moreover, the economic perspectives

describes moral with two concepts. Similar to the definition of economic behaviour

the concept is maximalisations of utility with minimise of sacrifice; then moral can be

influenced by economic behaviour (self oriented). Hence, this matter sometimes is

biased to a few situations because moral only focused to satisfy self -interest.

Consequently, to balance this concept is the deontological concept, which is focused

on obligation or duty, oriented to attain harmonization of lives.

Chapter 2 .. . Literature Review

Page 27

Therefore, morals could be described as the way of life of human beings whose lives

have been greatly influenced by their perspective, such as their understanding of

education and knowledge, which then evolves from the development of their moral

psychology, and their social economic condition which then evolves into the

development of their social morals. From the argument above it can be seen that the

role of morals is very significant and essential, particularly as guidance and

motivation for human beings to come to good and proper decisions in all their

conscious behaviour.

The General Role of Morals

As discussed before, the role of morals 1s very important for every individual

because, fundamentally, human beings always are in search of objectives and

satisfaction and fulfillment as individuals or as social creatures. Therefore, it can be

argued that there exists an approach or means that behaves as controller or balancer of

it all, which is described as morals. Then, naturally the role of morals is essential in

forming an expected condition in people lives by making good and proper decisions

and having good behaviour, according to the culture. As Buttler and Hume observed

(cf. Nielsen, 1974, p.191) the human being is a part of human society and people

normally tend to consider the welfare to others as well as their own welfare. Thus,

people are moral primarily because they have been conditioned to be moral.

In fact, many people often do what is right and what is wrong. It has been shown that

nature cannot be responsible for this fact, for human morality cannot consist in simply

Chapter 2 .. . Literature Review

Page 28

following nature ' s prompting or inclinations. The cause of human beings' morals is

their moral reasoning. According to Baier (1958, p.258), there are within people two

forces, reason and desire, capable of pushing people in opposite directions, and

reason is always on the side of morality. Reason inclines us toward satisfying the

demands of morality; desire inclines us the other way. In other words, if reason is

stronger, people are moral; if desire is stronger, people are immoral.

Moreover, based on human psychology, human nature certainly means that people

have a conscience and this conscience not only causes people to act in certain ways,

but also is in fact a norm of action. Nielsen (1974, p.192) argued that conscience

guides as well as goads, the deliverances of conscience are both actions - evoking

and a source of moral knowledge. Also, conscience tells the moral agent what to do

even in specific situations. According to Baier (1958, p.260) people should be moral

because they will not be happy if they do not behave morally. Being moral is at least

a necessary condition for being happy. If people ignore the dictates of their

conscience, then they will not be happy. Therefore, morals that emerge by any reason

will have important roles in regulating or inventing balance, creating joyful and

peaceful relationships within the society.

Consequently, if everyone acts morally, or generally act morally, people will able to

attain more of what they want That means in a moral community more good will be

realized than in a non-moral collection of people. Hence, in the interest of realizing a

commodious life for all, voluntary self-sacrifice is sometimes necessary, but the best

Chapter 2 ... Literature Review

Page 29

possible life for everyone is attainable only if people act morally. Additionally, the

greatest possible good is realized only when everyone puts aside their own self

interest when it conflicts with the common good (Nielsen, 1974, p.200).

Finally, moral roles are required within the living of society, in order to regulate that

culture and way of life. But in some particular cases, especially when morals conflict

with a human' s personal interest, then sometimes morals is set aside and the role of

morals become unclear. Conversely, individual awareness is important, especially

when deciding moral judgments, in order for morals to have their role.

Moral Judgment (Bad and Good Morals)

It is clearly understood that morals have an important role to manage or maintain the

equilibrium between human being as social creatures and an individual that has

personal concerns. For that reason, in the determination of a moral decision it is

significant to determine whether it is a good or poor decision. Hence the undertaken

decision will result in a suitable behaviour that is conformable with a way of life.

According to some philosophers' perceptions, there are several different angles

regarding conceptualizing and comprehending moral judgment. One classification

claims a moral decision as a result of the existence of a pure reason from each

individual. That claim refers to the good reason that is decided by each individual in

his/her action and behaviour. As has been explained by Toulmin (1950) a moral

judgment asserts the existence or non-existence of good reason. The term 'good

reason' that is being used here is a reason for doing the action. Good reason means

Chapter 2 ... Literature Review

Page 30

unequivocally good reason for doing the action, and also it must refer to morally good

reason. Some scholars argue that moral decisions are established from the foundation

of the logical process of human beings ' ideas. Further, human beings have always

been challenged with sets of decisions that must be chosen, before something is done.

As has been explained by Baier (1958, p.265) moral judgments are practical

judgments which have four main logical features such as, (a) they can be mutually

contradictory; (b) they are capable of guiding a moral agent in the search of the