Bahasa

Halaman

Hukum

RDI/EDEXCEL

BTEC Higher Nationals

Programme: Business Management

Module 2: Managing Financial Resources

& Decisions _( Level 4)

Assignment

Date for Submission: 18th February 2013

The submission portal will close at 23.59 (GMT) on 18th February 2013

Tutor: Michael Lloyd- William

You are the finance director of Ambalata public limited company a (fictional) company,

manufacturing street cleaning equipment.

You have been given responsibility for making decisions about the financing and viability of a new

line of low emission street cleaning vehicles. Initial estimates by the company’s market research

department suggest that there is likely to be significant demand for such vehicles from local

authorities both in the UK and abroad. In order to assist you in making relevant decisions you have

assembled a range of documents. These are included as appendices to this assignment and you

should refer to these appendices as you seek to answer the assignment questions below. The

documents are as follows.

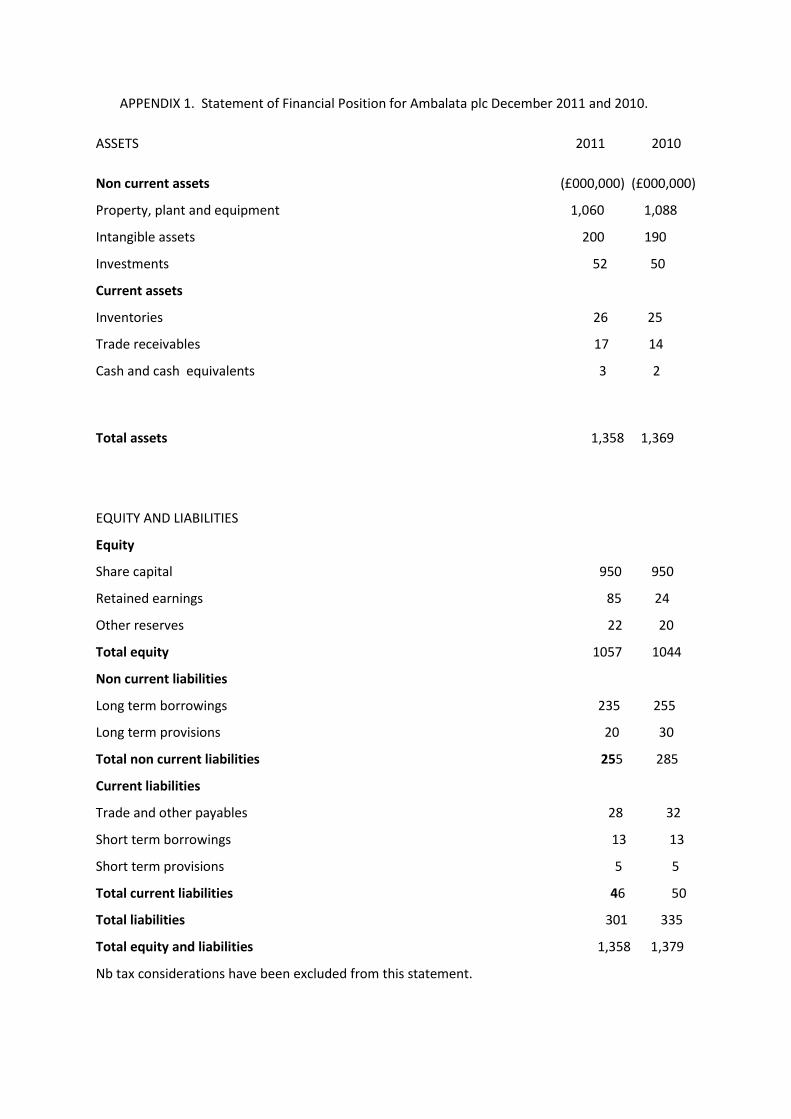

APPENDIX 1. Statement of Financial Position for Ambalata plc at 31st December 2011 (Figures for

December 2010 also given for comparison).

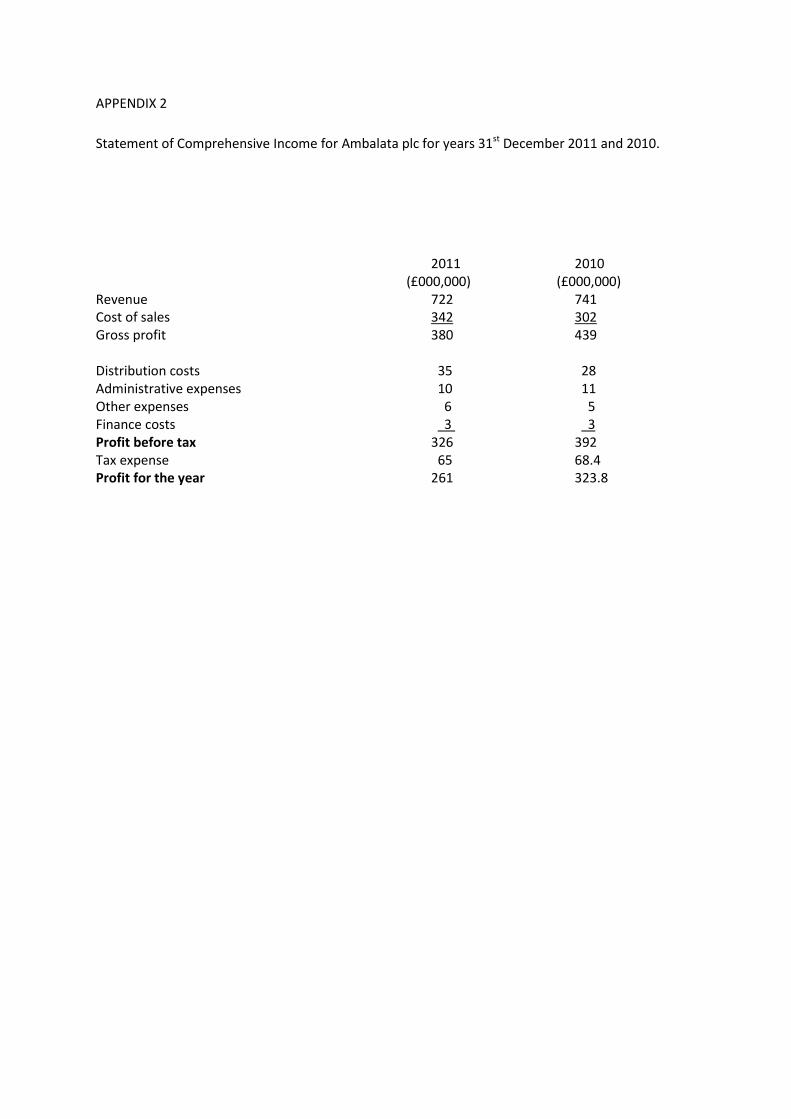

APPENDIX 2. Statement of Comprehensive Income for Ambalata plc for year to 31st December 2011

{with 2010 figures for comparison).

APPENDIX 3. Cash flow forecast for an existing Ambalata factory for the next six months.

APPENDIX 4. Cash flows projected for the proposed investment in the new line of vehicles over the

next five years.

ASSIGNMENT REQUIREMENT

Task 1

You should draft a paper setting out sources of finance that are potentially available for Ambalata

to finance their possible investment in new vehicles South America.

This paper should include

i) A table setting out the main features of two long term and two short term sources of

finance, including the main advantages and disadvantages of each of the sources .

( LO 1.1 ,1.2,2.1)

ii) A recommendation concerning which source(s) you would propose using to finance the

proposed investment, were it to go ahead, along with brief reasons for your

recommendation. ( LO 1.3)

Task 2

i) If you decided to raise the £100 million capital required cost for the proposed investment

with half being equity and half debt explain briefly what impact your decision would

have upon the financial statements contained in Appendices 1 and 2. ( LO 2.4,4.1)

ii) Using an appropriate formula, explain what is meant by the concept of the weighted average

cost of capital (WACC). Assuming the above split of equity and debt calculate the

weighted cost of new capital to be raised by Ambalata if the rate of interest on the debt

is expected to be 5% and the cost of equity 8%. ( LO 2.1)

Task 3.

i) Using the figures provided in Appendix 4 calculate both the payback and net present value

of the proposed investment. ( LO 3.3)

ii) Based upon your calculations in (i) above, state what recommendation you would make

about the investment and why? What reservations might you have about how reliable

your recommendation is likely to be? ( LO 3.3)

iii) The figures in Appendix 3 have had to be produced making a number of assumptions about

cost faced by Ambalata and prices that they might charge

a) Define the concept of unit cost and explain briefly how they can be calculated.(LO

3.2)

b) Discuss what factors should be taken into account by an organisation such as

Ambalata when setting prices for their output.( LO 3.2)

Task 4

One of your roles as finance director is to be ultimately responsible for both the profitability and

liquidity of all of Ambalata ‘s operations. Appendix 3 provides a 6 month cash flow forecast for one

of Ambalata ’s existing factories.

i) Comment on the main trends and messages contained within the cash flow forecast.

(LO 2.2,3.1)

ii) Identify different groups who may have an interest in the factory’s cash flow statement and

discuss the different interests that these different groups may have.(LO 2.3)

iii) Explain why a company may be profitable but run into problems with its liquidity.(LO 2.2)

Task 5

i) Using a maximum of four financial ratios analyse Ambalata ’s profitability and liquidity

performance 2010 /11 based upon the financial statements given in Appendices 1 and 2.

(LO 4.1, 4.3)

ii) Ambalata is a public limited company. What are the main differences in the financial

statements of sole traders, partnerships and limited companies? (LO 4.2)

Word limit; 3,500 words, excluding tables, references, footnotes etc

APPENDIX 1. Statement of Financial Position for Ambalata plc December 2011 and 2010.

ASSETS 2011 2010

Non current assets (£000,000) (£000,000)

Property, plant and equipment 1,060 1,088

Intangible assets 200 190

Investments 52 50

Current assets

Inventories 26 25

Trade receivables 17 14

Cash and cash equivalents 3 2

Total assets 1,358 1,369

EQUITY AND LIABILITIES

Equity

Share capital 950 950

Retained earnings 85 24

Other reserves 22 20

Total equity 1057 1044

Non current liabilities

Long term borrowings 235 255

Long term provisions 20 30

Total non current liabilities 255 285

Current liabilities

Trade and other payables 28 32

Short term borrowings 13 13

Short term provisions 5 5

Total current liabilities 46 50

Total liabilities 301 335

Total equity and liabilities 1,358 1,379

Nb tax considerations have been excluded from this statement.

APPENDIX 2

Statement of Comprehensive Income for Ambalata plc for years 31st December 2011 and 2010.

2011 2010 (£000,000) (£000,000) Revenue 722 741 Cost of sales 342 302 Gross profit 380 439 Distribution costs 35 28 Administrative expenses 10 11 Other expenses 6 5 Finance costs 3 3 Profit before tax 326 392 Tax expense 65 68.4 Profit for the year 261 323.8

APPENDIX 3

Month 1 (£,000)

Month 2 (£,000)

Month 3 (£,000)

Month 4 (£,000)

Month 5 (£,000)

Month 6 (£,000)

Sales 1,350 1,750 1,960 3,080 3,350 2,050

PAYMENTS

Wages and salaries 850 850 850 1,460 1,460 1,460

Supplies 450 750 970 1,070 1,240 1,890

Rent and rates 80 80 80 80 80 80

Advertising 50 50 50 50 50 50

Miscellaneous 10 10 10 15 15 15

TOTAL 1,440 1,740 1,960 2,675 2,845 3,495

Receipts minus payments

(90) 10 0 405 505 (1,445)

Balance brought forward

750 660 670 670 1075 1580

Balance carried forward

660 670 670 1075 1580 135

APPENDIX 4

nb Ambalata uses a discount rate of 6% when appraising projects using discounted cash flow analysis

Anticipated capital cost (in year zero) £100,000,000

Year Cash Inflow

(£000) Cash Outflow

(£000)

1 81,500 47,000

2 133,100 58,100

3 159,800 62,900

4 165,900 68,900

5 198,500 92,300

Assessment Criteria for Pass

To achieve a pass you must meet all of the assessment criteria as stated

below. Failure to cover all of the assessment criteria will result in a referral

grade and you be required to re-submit your assignment.

Further guidance on completion of your assignment can be found in the

guidance notes which are posted on the group learning space by your

module tutor. For additional support please post questions onto the group

learning space, or email your module tutor

Learning

Outcomes/

Assessment

Criteria

Criteria Met

For tutor

use

(you may

wish to use

this in your

preparation

for your

assignment

submission)

LO 1 Understand the sources of finance available to a business

1.1 identify the sources of finance available to a business Task 1 i

1.2 assess the implications of the different sources Task 1 i

1.3 evaluate appropriate sources of finance for a business project Task 1 ii

LO2 Understand the implications of finance as a resource within a business

2.1 Analyse the costs of different sources of finance Task 1 I; task

2 ii

2.2 explain the importance of financial planning Task 4 I, task

4.iii

2.3 assess the information needs of different decision makers Task 4 ii

2.4 explain the impact of finance on financial statements Task 2 i

LO3 Be able to make financial decisions based on financial information

3.1 analyse budgets and make appropriate decisions Task 4 i

3.2 explain the calculation of unit costs and make pricing decisions using relevant information

Task 3 iii

3.3 assess the viability of a project using investment and appraisal techniques

Task 3 i and

ii

Be able to evaluate the financial performance of a business

4.1 discuss the main financial statements Task 2 i;

Task 5

4.2 compare appropriate formats of financial statements for different types of business

Task 5 ii

4.3 interpret financial statements using appropriate ratios and comparisons, both internal and external

Task 5 i

Assessment Criteria for Merit

To achieve a Merit all of the Pass criteria need to be met, then the tutor

will assess whether you have met the Merit Criteria. Each of the Merit

criteria must have been met at least once within the assignment.

The following statements are examples of how a merit may be achieved,

if you do meet the Merit Criteria by showing you have reached this level in

other ways then credit will be awarded for this. You will need to meet M1,

M2, M3 at least once.

Effective judgments have been made on the basis of accurate

cash flow forecasting

Good knowledge of working capital/liquidity management has

been displayed

Good knowledge of appropriate sources of long term finance are

displayed

M1

Effective use has been made of appropriate investment appraisal techniques and other calculations eg WACC

M2

A clear, concise and logical flow has been achieved

Use of Harvard referencing throughout

Relatively few omissions and confusions exist

M3

Assessment Criteria for Distinction

To achieve a Distinction you have met all of the Pass and the Merit

criteria. Each of the Distinction criteria must be met at least once within

the assignment.

The following statements are examples of how a Distinction may be

achieved, if you do meet the Distinction Criteria by showing you have

reached this level in other ways then credit will be awarded for this. You

will need to meet D1,D2,D3 at least once.

A reflective approach will be evident throughout and in particular in areas like evaluation of sources of business finance and uses /limitations of investment appraisal techniques

D1

Independent research, outside of what has been provided in

class, has been utilised to prepare a thorough set of answers

D2

Ideas are evaluated for their validity & realism in the context of

the answers

An attempt is made at an evaluation of optimal approaches to

financial management conclusions

D3

Top Related

Copyright © 2022 FDOKUMEN