Bahasa

Halaman

Hukum

L 336/16 I EN Official Journal of the European Communities 8 . 12 . 97

COMMISSION DECISION

of 30 July 1997

declaring a concentration compatible with the common market and the functioning of the EEAAgreement

(Case No IV/M.877 — Boeing/McDonnell Douglas )

(Only the English text is authentic )

(Text with EEA relevance )

( 97/816/EC )

Company (Boeing ) would acquire control withinthe meaning of Article 3 ( 1 ) ( b ) of the MergerRegulation of the whole of McDonnell DouglasCorporation (MDC).

(2 ) After examination of the notification, theCommission decided on 7 March 1997 to continuethe suspension of the concentration until a finaldecision was reached . The Commissionsubsequently concluded that the proposedconcentration falls within the scope of the MergerRegulation and raised serious doubts as to itscompatibility with the common market, and bydecision of 19 March 1997 it accordingly initiatedproceedings pursuant to Article 6 ( 1 ) ( c ) of theMerger Regulation .

THE COMMISSION OF THE EUROPEAN COMMUNITIES,

Having regard to the Treaty establishing the EuropeanCommunity,

Having regard to the European Economic Area (EEA)Agreement, and in particular Article 57 ( 1 ) thereof,

Having regard to Council Regulation (EEC ) No 4064/89of 21 December 1989 on the control of concentrationsbetween undertakings ( ! ), as amended by the Act ofAccession of Austria , Finland and Sweden, and inparticular Article 8 (2 ) thereof,

Having regard to the Agreement between the EuropeanCommunities and the Government of the United States ofAmerica regarding the application of their competitionlaw ( 2 ), and in particular Articles II and VI thereof, I. THE PARTIES

Having regard to the Commission decision of 19 March1997 to initiate proceedings in this case,

Having given the undertakings concerned the opportunityto make known their views on the objections raised bythe Commission,

Having regard to the opinion of the Advisory Committeeon Concentrations ( 3 ),

Whereas :

( 1 ) On 18 February 1997, the Commission receivednotification of a proposed concentration pursuantto Article 4 of Regulation (EEC ) No 4064/89(Merger Regulation ) by which the Boeing

( 3 ) Boeing is a United States corporation whose sharesare publicly traded . Boeing operates in twoprincipal areas : commercial aircraft, and defenceand space . Commercial aircraft operations involvedevelopment, production and marketing ofcommercial jet aircraft and providing relatedsupport services to the commercial airline industryworldwide . Defence and space operations involveresearch, development, production, modificationand support of military aircraft and helicopters andrelated systems, space systems and missile systems,rocket engines, and information services .

( 4 ) MDC is a US corporation whose shares arepublicly traded . MDC operates in four principalareas : military aircraft; missiles, space andelectronic systems; commercial aircraft; andfinancial services . Operations in the first twoindustry areas involve the design, development,production and support of the following majorproducts : military transport aircraft; combataircraft and training systems; commercial andmilitary helicopters and ordnance; missiles;

(') OJ L 395 , 30 . 12 . 1989, p. 1 ; corrected version OJ L 257,21 . 9 . 1990, p. 13 .

( 2 ) OJ L 95 , 27. 4 . 1995 , p . 47.( 3 ) OJ C 372 , 9 . 12 . 1997.

Official Journal of the European Communities L 336/178 . 12 . 97 1 EN |

satellites ; launching vehicles and space stationcomponents and systems; lasers, sensors ; andcommand, control, communications, andintelligence systems . In the commercial aircraft areaMDC designs, develops, produces, modifies andsells commercial jet aircraft and related spare parts .MDC is also engaged in aircraft financing andcommercial equipment leasing and in thecommercial real estate market, for itself and forcommercial customers .

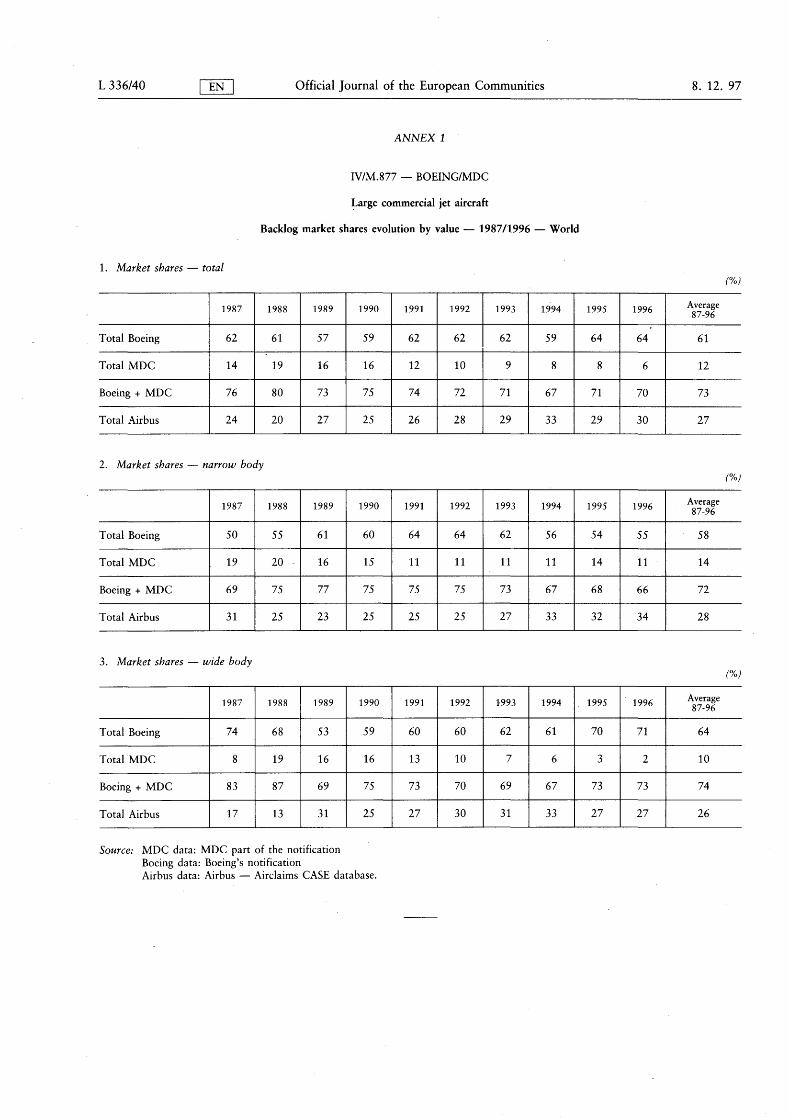

competitive structure is very similar . According toBoeing's 1997 Current Market Outlook, Europeanairlines will account for about 30 % of cumulatedforecast world demand over the next ten years .The average market shares of Boeing and MDC inthe EEA over the last 10 years have been 54% and12% respectively ( in the world 61% and 12%respectively). As far as the existing fleet in servicein the EEA is concerned, Boeing has a share ofabout 58% , MDC about 20%, and Airbus about21 % ( 5 ) (corresponding world figures are 60% ,24%, and 14% ).

II . THE OPERATION

( 5 ) On 14 December 1996, Boeing and MDC enteredinto an agreement by which MDC would become awholly owned subsidiary of Boeing .

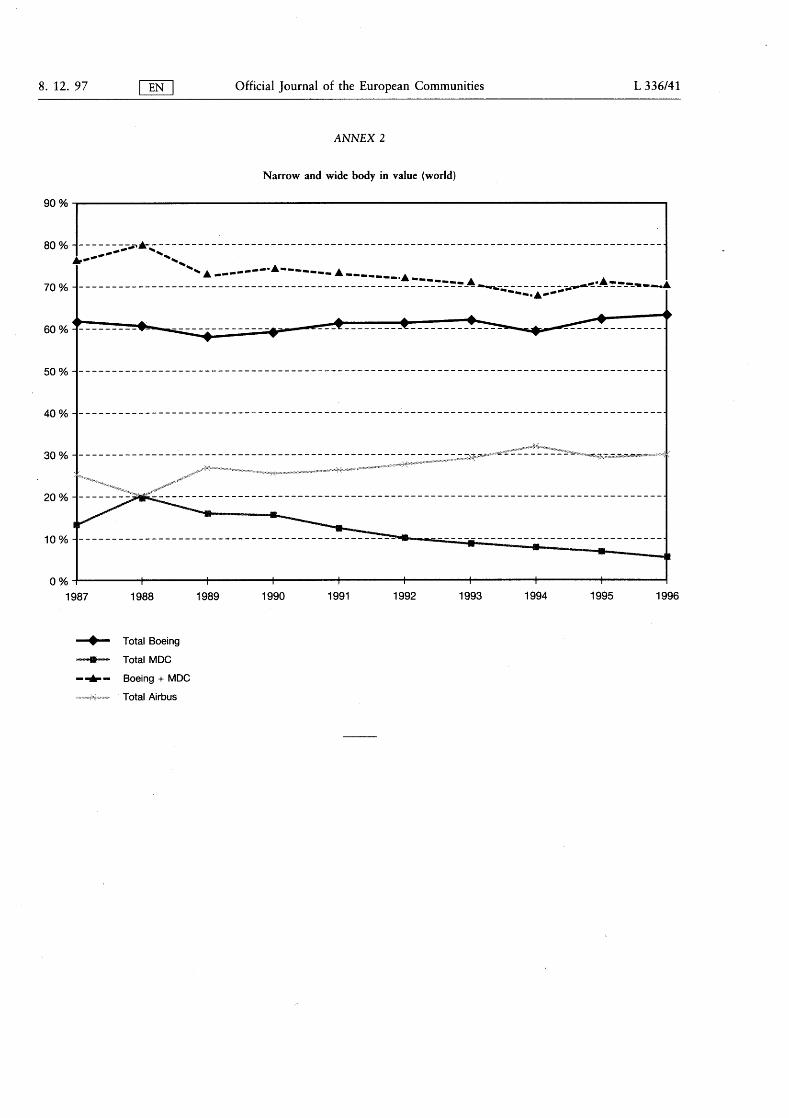

( 10 ) It is therefore evident that the operation is of greatsignificance in the EEA as it is in the world marketof which the EEA is an important part.

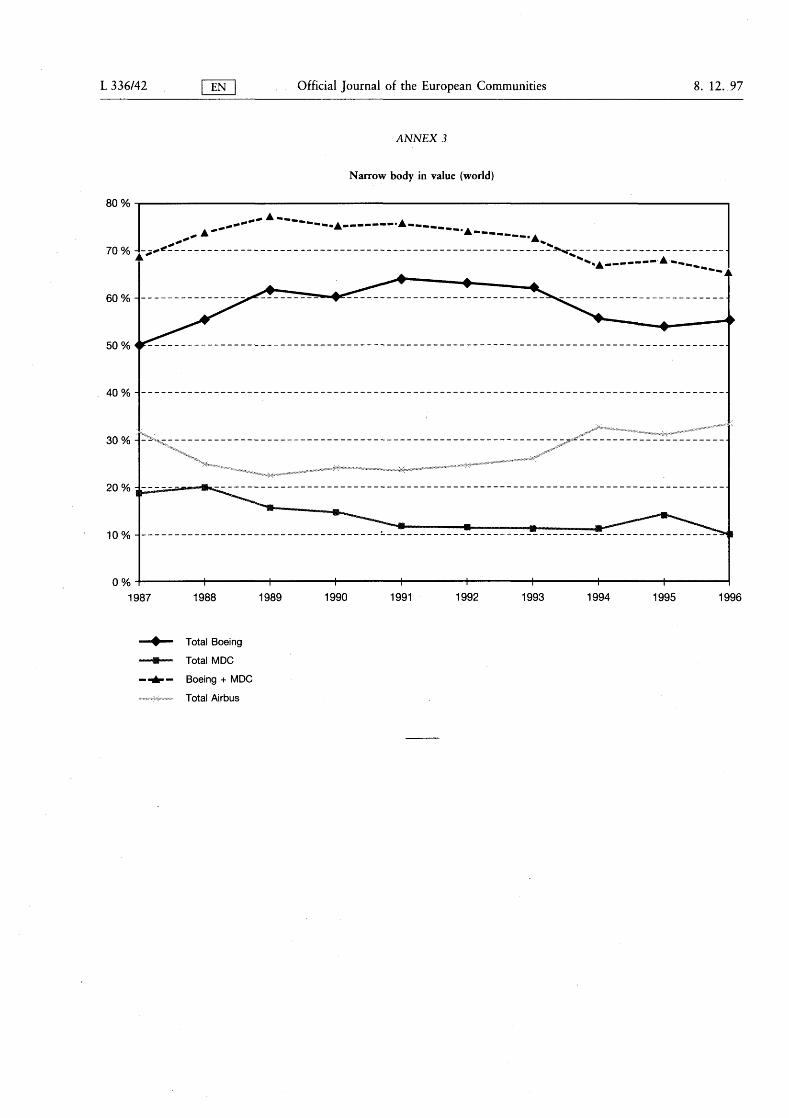

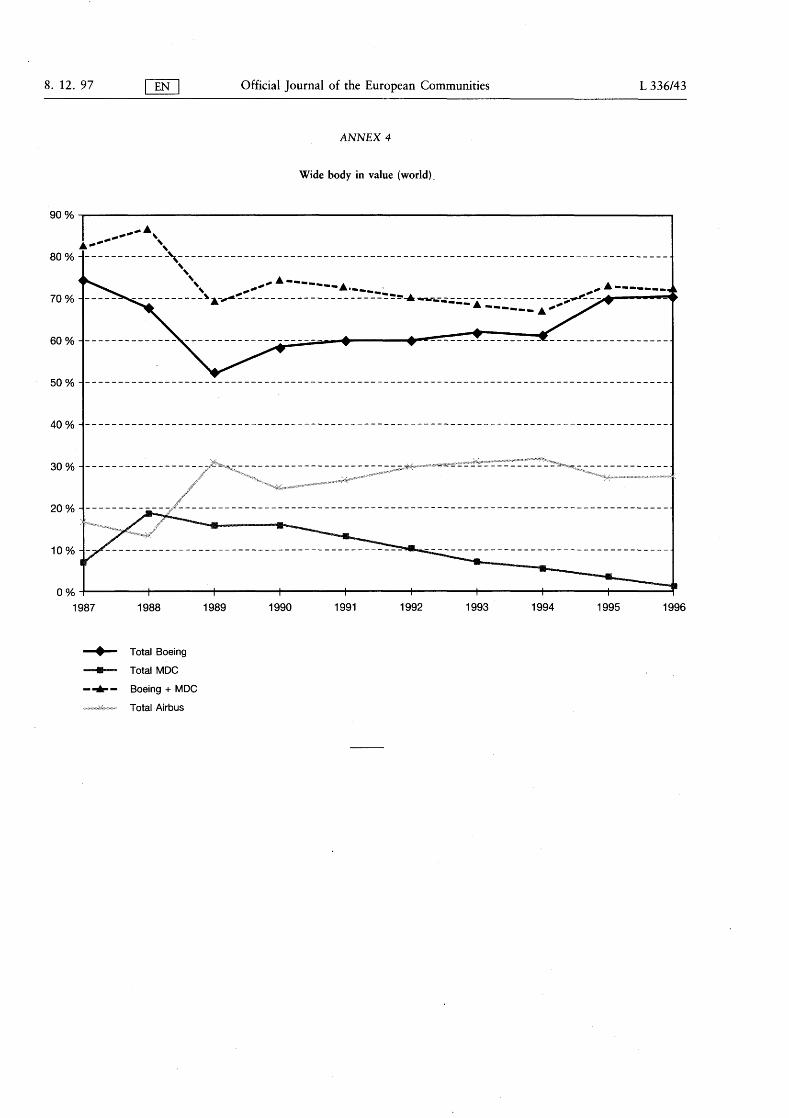

VI . COOPERATION WITH THE US AUTHORITIES

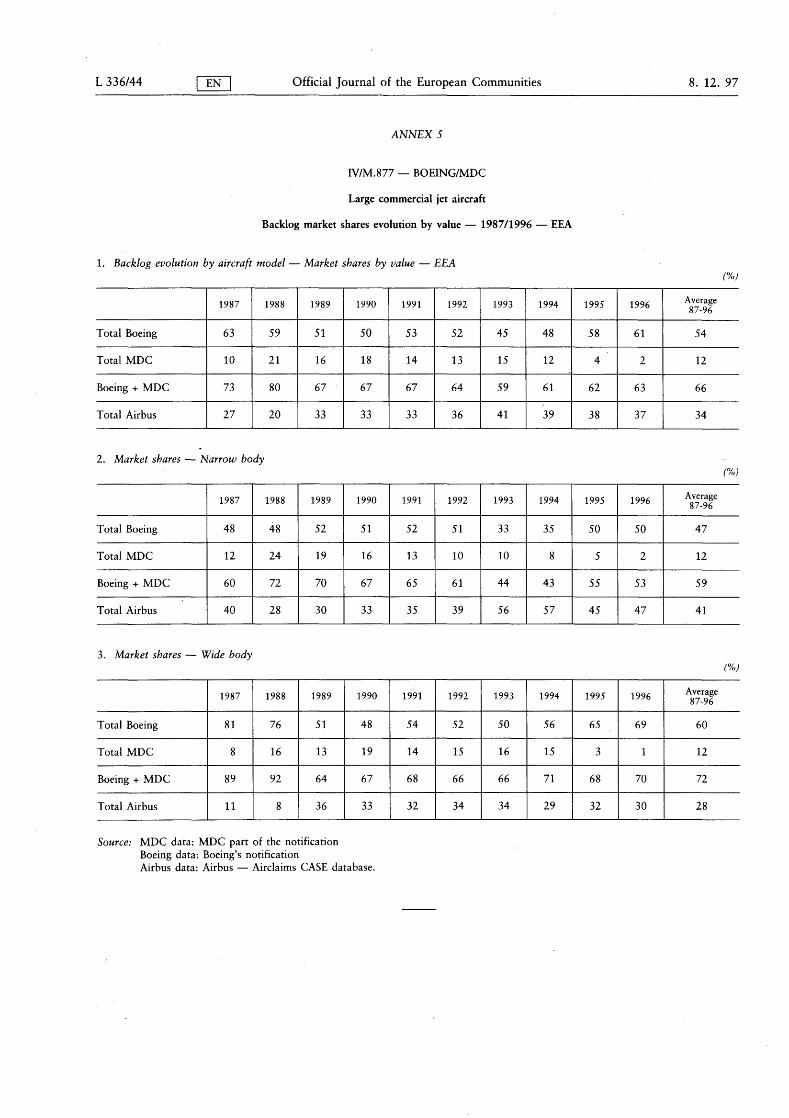

III . THE CONCENTRATION

( 6 ) The operation constitutes a concentration withinthe meaning of Article 3 of the Merger Regulationsince Boeing acquires within the meaning ofArticle 3 ( 1 ) ( b ) of the Regulation control of thewhole of MDC.

IV. THE COMMUNITY DIMENSION

( 7 ) Boeing and MDC have a combined aggregateworldwide turnover in excess of ECU 5 billion(Boeing ECU 17 billion, MDC ECU 11 billion ).Each of them has a Community-wide turnover inexcess of ECU 250 million (Boeing [. . .] ( 4 ), MDC[. . .]), but they do not both achieve more than twothirds of their aggregate Community-wide turnoverwithin one and the same Member State . Thenotified operation therefore has a Communitydimension .

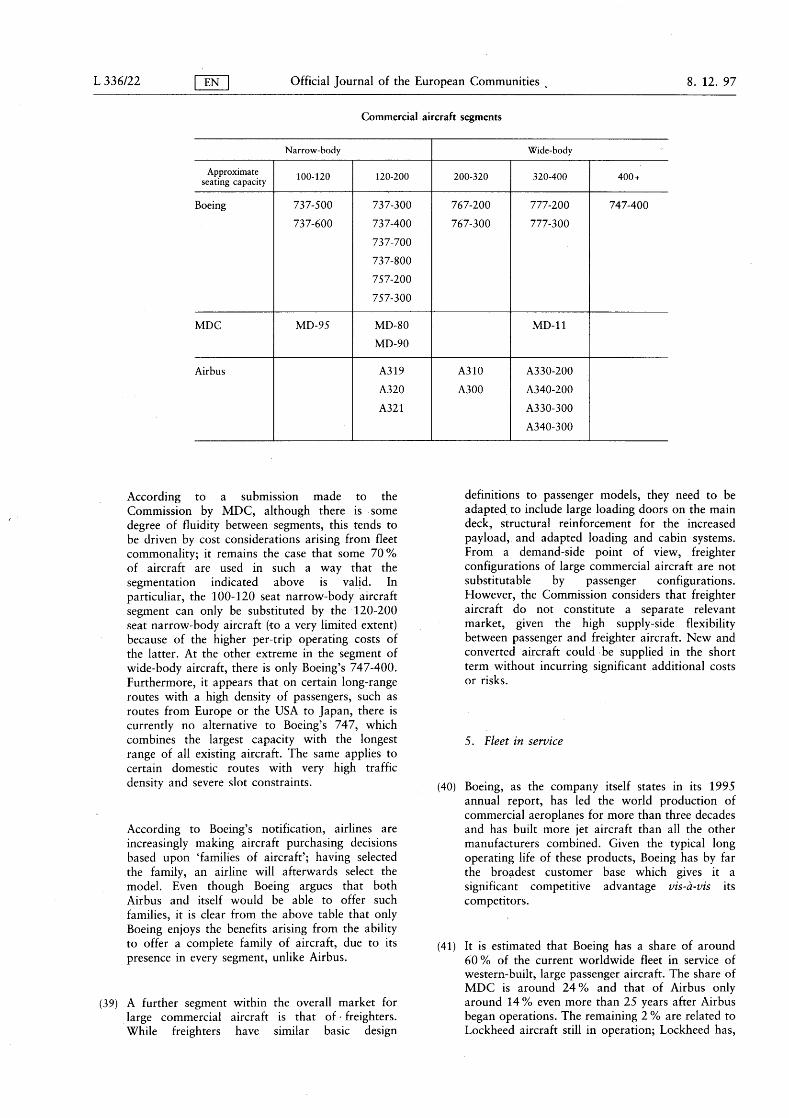

( 11 ) In compliance with the Agreement between theEuropean Communities and the Government of theUnited States of America regarding the applicationof their competition laws ('the Agreement'), theEuropean Commission and the Federal TradeCommission have carried out all necessarynotifications . Pursuant to Article VI of theAgreement, the European Commission has soughtan appropriate way to take account of importantnational interests of the United States, particularlythose stemming from the consolidation of the USdefence industry. Furthermore , pursuant toArticle VI of the Agreement, the EuropeanCommission notified to the US authorities on26 June 1997 its preliminary conclusions andconcerns and asked the Federal Trade Commissionto take account of the European Union's importantinterests in safeguarding competition in the marketfor large civil aircraft . Chairman Pitofsky of theFederal Trade Commission responded with a letterthe same day indicating that the Federal TradeCommission would take into account the expressedinterests of the European Communities whenreaching its decision . On 1 July 1997, the FederalTrade Commission reached a majority decision notto opposte the merger .

V. THE IMPACT OF THE OPERATION WITHINTHE EUROPEAN ECONOMIC AREA

( 8 ) Not only does the operation have a Communitydimension within the legal sense of the MergerRegulation (Section IV above ), it also has animportant economic impact on the largecommercial jet aircraft market within the EEA, aswill be shown below in Section VII 'Competitiveassessment '.

( 9 ) The relevant market for the purposes of assessingthe operation is the world market for largecommercial jet aircraft . The EEA is an integral andimportant part of this world market, and its

( 12 ) On 13 July 1997, pursuant to Articles VI and VIIof the Agreement, the US Department of Defenceand Department of Justice, on behalf of the USGovernment, informed the European Commissionof concerns that : ( i ) a decision prohibiting theproposed merger could harm important US defenceinterests; ( ii ) despite any measures the Commissioncould impose on a third party purchaser, adivestiture of Douglas Aircraft Company (DAC )( 4 ) In the published version of the Decision, some information

has hereinafter been omitted, pursuant to the provisions ofArticle 17 (2 ) of Regulation (EEC) No 4064/89 concerningnon-disclosure of business secrets . ( 5 ) Source: UK Department of Trade and Industry.

Official Journal of the European Communities 8 . 12 . 97L 336/18 1 EN

( trade-offs between fewer flights with largeraircraft, and the converse ), and the availability ofairport slots . Technical characteristics will includerange, capacity, performance and reliability, fleetcommonality ( that is , the degree of facility withwhich new aircraft can be integrated into existingfleets ), and maintenance and service networks .Finally, alternative aircraft will be evaluated on thebasis of net present value according to purchaseprice, forecast operating revenues and costs, andresidual value .

would be likely to be unsuccessful in preservingDAC as a stand-alone manufacturer of newaircraft, resulting in an inefficient disposition ofwhatever of DAC's new aircraft manufacturingoperations that potentially could be salvaged byBoeing, and in the loss of employment in theUnited States ; and ( iii ) any divestiture of DAC to athird party that would not operate DAC as amanufacturer of new aircraft would beanti-competitive in that it would create a firm withthe incentive and means to raise price and diminishservice in respect of the provision of spare partsand service to DAC's fleet-in-service , a largeportion of which is owned by US airlines . TheCommission took the above concerns intoconsideration to the extent consistent withCommunity law. In particular, as far as US defenceinterests are concerned, the Commission has in anyevent limited the scope of its action to the civil sideof the operation since it has not established that adominant position has been strenghtened orcreated in the defence sector as a result of theproposed concentraion . The Commission has notpursued further the concerns it expressed in its'Statement of objections' concerning the effect ofthe concentration on the international market forfighter aircraft . As far as DAC is concerned, theCommission, for reasons outlined below, has notconsidered a divestiture as a remedy to resolve thecompetition problems created by theconcentration .

( 15 ) It is widely accepted that the regional jet market( including, for example, Fokker, Bombardier andBritish Aerospace models ) is distinct from the largecommercial jet aircraft market on which Boeing,MDC and Airbus are active . None of the latterthree manufacturers have products below the 100seat/1 700 nautical mile maximum-rangethresholds, which are considered to be theapproximate combined upper limits for the specificrequirements of regional carriers . For the mostpart, regional jets are incompatible with families oflarge jets in terms of range, operatingcharacteristics, cargo carrying, and so on . Majorairlines acquiring regional jets use them in specificregional applications or subsidiaries (examplesbeing British Airways and Swissair/Crossair ).

( 16 ) It is also widely accepted that the only aircraftconcerned are Western-built jets, sincenon-Western aircraft ( such as the Russian Ilyushin )

VII . COMPETITIVE ASSESSMENT cannot compete on technical grounds in theircurrent versions, for reasons of reliability,after-sales service and public image .

A. RELEVANT PRODUCT MARKETS

( 13 ) The concentration affects the market for largecommercial jet aircraft .

1 . New large commercial aircraft

The notifying party identified the relevant productmarkets as 'narrow-body and wide-bodycommercial jet aircraft '. The Commission'sinvestigation has revealed that varying opinionsexist on the part of manufacturers and customersas to the appropriate segmentation of the overallmarket . Segmentation of the large commercial jetaircraft market cannot be definitive , in view of thecomplexity of the demand-side purchasing criteriaalready enumerated . However, the narrow-body(or single-aisle ) and wide-body (or twin-aisle )distinction proposed by the notifying party seemsto be generally accepted as a valid segmentation .Narrow-body aircraft have as operatingcharacteristics a range of approximately 2 000 to4 000 nautical miles and seating capacity for about100 to 200 passengers , whilst for wide-bodyaircraft the corresponding parameters are 4 000 to8 000 + nautical miles and 200 to 400 + passengers .A further segmentation of the narrow-body andwide-body markets is given below (paragraph 38 ).

( 14 ) From the demand side , a customer will generallyapproach a purchasing decision in several stages,considering firstly operating requirements, thentechnical requirements, and finally economic andfinancial aspects . Operating criteria will includeroutes to be flown ( traffic density and distance ),optimal seating or loading and flight frequency

8 . 12 . 97 PEN Official Journal of the European Communities L 336/19

and separate from the market for new aircraft onwhich Boeing and MDC are active. The market forsecond-hand aircraft will not, therefore, be takeninto account in what follows .

It is therefore concluded that there are twoseparate relevant markets within the overall marketfor large commercial jet aircraft, the market fornarrow-body aircraft and the market forwide-body aircraft . Since the structure of thenarrow-body and the wide-body markets is similarand the competition problems resulting from theproposed merger are the same for both markets,the Commission will assess below the effects of themerger on both markets together.

B. RELEVANT GEOGRAPHIC MARKET

( 20 ) Large commercial jet aircraft are sold and operatedthroughout the world under similar conditions ofcompetition . Relative transportation costs ofdelivery are negligible . Therefore, the Commissionconsiders that the geographic market for largecommercial jet aircraft to be taken into account isa world market.

C. EFFECTS OF THE CONCENTRATION ON THEMARKET FOR LARGE COMMERCIAL JETAIRCRAFT

2 . Second-hand aircraft

( 17) As already stated, the overall product marketconsists of large commercial jet aircraft . Thereexist significant sales of these aircraft on asecond-hand basis . It is estimated that about 30%of passenger aircraft delivered change airlineswhilst remaining in passenger use; over two thirdsof total demand for freighters is met by theconversion of used passenger aircraft . However, inline with previous practice of the Commission(Commission Decision 91/619/EEC of 2 October1991 in Case IV/M.053 — Aerospatiale-Alenia/deHavilland ) ( 6 ), it is appropriate to consider thesecond-hand aircraft market as separate from thenew aircraft market.

( 18 ) Firstly, it must be noted that in any eventconstraints due to the inherent longevity of thegoods in question should be distinguished fromconstraints arising from competitive pressures dueto the availability of goods from alternativesuppliers . In the large commercial jet aircraftsector, where the life-span of the products can beover 20 years, the existence of a large fleet inservice will per se impose (probably cyclical )constraints on the opportunities for manufacturersto sell new aircraft .

( 19 ) As far as the actual market for second-hand, largecommercial jet aircraft is concerned, itscharacteristics indicate that it is separate from thatfor new aircraft . The capital prices of second-handaircraft are lower, whereas the running costs tendto be higher, and such aircraft clearly have ashorter life . The Commission's investigation hasrevealed that used aircraft may be a feasiblealternative for smaller airlines where limitedfinancial resources constrain them to buy otherequipment . For large airlines, used aircraft typicallycannot be acquired in sufficient numbers orconfiguration commonality to meet longer-termrequirements; whilst used aircraft can sometimesmeet specific short-term needs , they tend to becomplements to, rather than substitutes for, newaircraft . Therefore , sales of second-hand aircraftmust be considered to constitute a market distinct

I. Current structure of the market for largecommercial jet aircraft

1 . The competitors

(21 ) There are currently three competitors on theworldwide market for large commercial jet aircraft :Boeing, Airbus and MDC.

(22 ) Boeing is a fully integrated aerospace company,active in all aerospace sectors : commercial, defenceand space ( see above ). Boeing is the world'sleading company in large commercial jet aircraft,sales of which represent about 70% of itsrevenues .

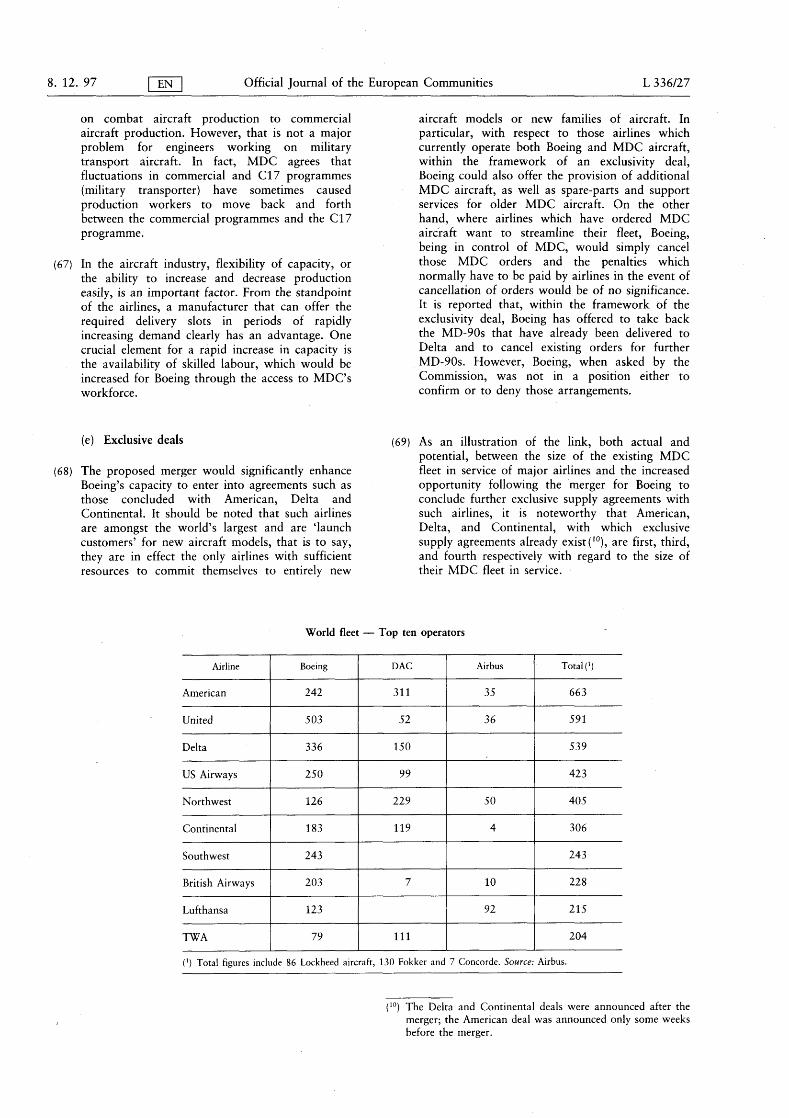

(23 ) MDC is another fully integrated aerospacecompany, also active in all sectors of aerospace ( seeabove ). MDC is the world 's third largestmanufacturer of large commercial jet aircraft, aswell as the world's leading producer of militaryaircraft and the second leading defence firm in theworld . Of its 1996 turnover, around 70% camefrom military and space businesses and the restwas related to large commercial jet aircraft .

(24 ) Airbus Industrie is the world's second largestproducer of large commercial jet aircraft . Airbuswas established in December 1971 as agroupement d'interet economique (GIE), or aconsortium of economic interests . The members ofthe Airbus consortium include privately ownedDaimler-Benz Aerospace Airbus of Germany(DASA) ( 37,9% ) and British Aerospace (20% ),respectively, and government-owned Aerospatialeof France ( 37,9% ) and CASA of Spain (4,2% ).The partnership is unique in that each memberoperates under the laws of the country in which it( 6 ) OJ L 334 , 5 . 12 . 1991 , p . 42 .

L 336/20 1 EN Official Journal of the European Communities 8 . 12 . 97

purchases would amount to US $ 307,5 billion, ofa total market potential that would reach US $1 100 billion.

is incorporated . Partners finance their ownresearch, development and production of aircraft,while Airbus Industrie oversees the marketing andservicing of aircraft . Fully equipped sections ofAirbus aircraft are manufactured at separatelocations throughout Europe, then transported toFrance or Germany for final assembly . Forexample, Aerospatiale manufactures the cockpit,DASA produces fuselage sections and aircraftwings are manufactured by British Aerospace .Work is distributed according to the corecompetences of each partner .

3 . Market shares

(28 ) With respect to the calculation of market shares ,the notification does not propose one specificmethod of calculation but provides figures for eachof the last 10 years on backlog, new firm ordersand net orders both in terms of value and units ofaircraft . Backlog data is widely seen as the bestindicator of market position in this industry; tohave a complete picture of the market, thedevelopment of this indicator over the last 10 yearsneeds to be evaluated . The yearly backlog reflectsthe development of net orders (number of newfirm orders minus number of cancelled orders )over a certain period . It is also appropriate to basethe analysis on the backlog in terms of value andnot in terms of units in order to take into accountthe different prices and sizes of the various types ofaircraft . This is necessary since, for the purpose ofcalculation of market shares the same weightcannot be given to, for example, a Boeing 737-300with a price range of US $ 38 to 44 million as to aBoing 747-400 with a price range of US $ 156 to182 million . Value shares are calculated in USdollars, since this is the currency in which pricesare expressed in this market .

(29 ) According to the figures provided in thenotification and by Airbus, the worldwide marketshares in the overall market for large commercialjet aircraft in terms of backlog value as of31 December 1996 are the following (seeAnnex 1 ):

2 . The customers

(25 ) Customers of large commercial jet aircraft areairlines ( including scheduled and non-scheduledoperators ) and leasing companies . 561 airlinesoperating western aircraft from manufacturerswhich are still on the market have been identified,of which 246 airlines operate more than fiveaircraft . However, relatively few of these purchaseaircraft in a given year . Even over a longer period,demand tends to remain concentrated among a fewvery large companies ; for example, during theperiod 1992 through 1996, Boeing's five largestcustomers accounted for more than [. . .] of itssales for each year. Furthermore , it is estimatedthat half the world jetliner fleet is operated by the12 largest airlines . Leasing companies account foran estimated 20 % of demand .

(26 ) The demand for large civil jet aircraft is driven bythe demand for air transportation, which has beengrowing in a cyclical but steady manner since itsbeginnings in the late 1950s . Among the latestmain factors that have contributed to the industrygrowth, developments such as the air transportliberalization process within the Community andthe additional demand from China and the formereastern block are to be emphasized .

(27) The market is in a process of expansion and stronggrowth in demand is predicted, althoughconditioned by the cyclical nature of the industry .In its 1997 Current Market Outlook, Boeingforecasts that over the next 10 years the totalmarket potential is 7 330 aircraft or the equivalentof US $ 490 billion ( in 1996 US dollar terms ).Most of this demand will correspond to three mainregional areas : Asia-Pacific (1 750 aircraft), NorthAmerica (2 460 aircraft ) and Europe ( 7 ); customersfrom the latter are expected to purchase 2 070aircraft or an equivalent US $ 137 billion . In otherwords , European customers will account for morethan 28 % of the cumulated demand. If thispercentage remained stable, in 20 years ( 18according to MDC), the value of European

(%)

Boeing 64

Airbus 30

MDC 6

Total 100

( 30 ) Although the notification includes the BritishAerospace RJ products line and the Fokker 70/100in the segment for narrow-body aircraft, it is theview of the Commission that these types of aircraftare in a different market (see above ). In any event,it makes no significant difference whether or notthe British Aerospace and the Fokker aircraft areto be included in the market for large commercialaircraft, given their marginal position . Similarly,existing Russian aircraft ( such as the Ilyushin ) arenot to be included either, since , although they havereached a certain stage of technical development, itappears that they do not yet constitute a realalternative , for reasons of reliability, after-salesservice and public image .

( 7 ) In Boeing's report this term refers to continental Europe,excluding former Soviet Union States and including Turkey.

8 . 12 . 97 EN Official Journal of the European Communities L 336/21

( 31 ) For the period 1987 to 1996 , the average shares ofthe backlog were the following:

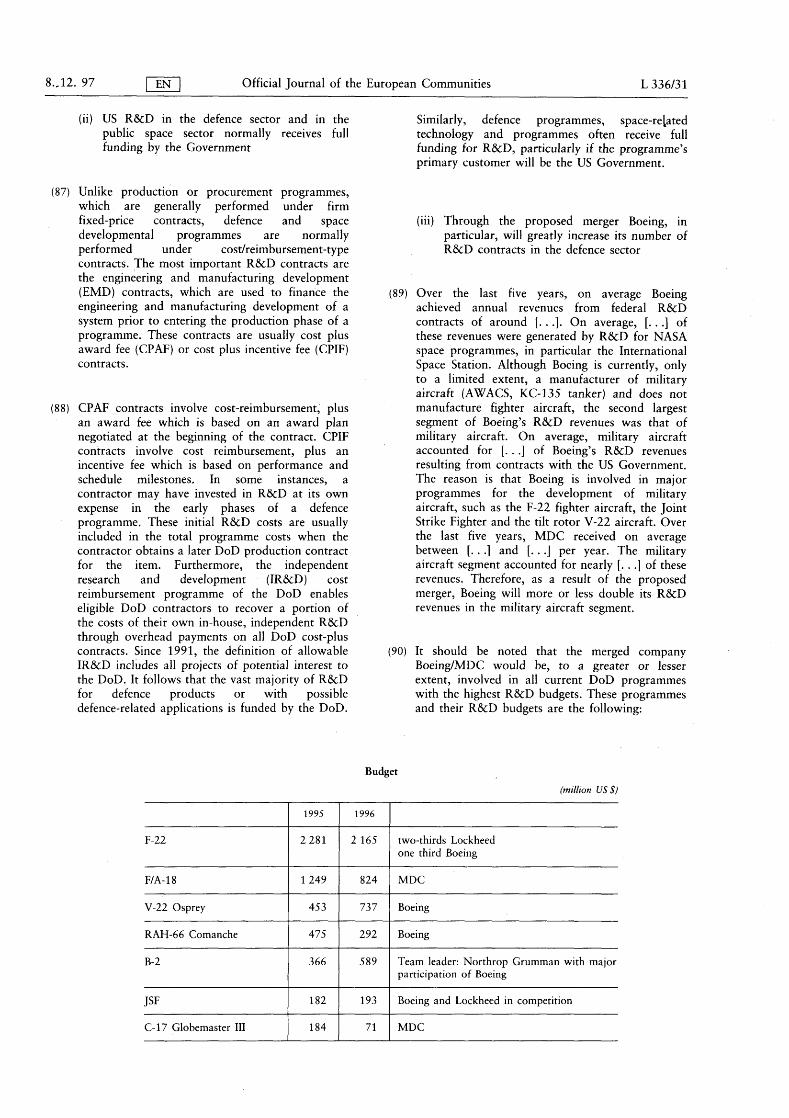

(%)

Boeing 61

Airbus 27

MDC 12

Total 100

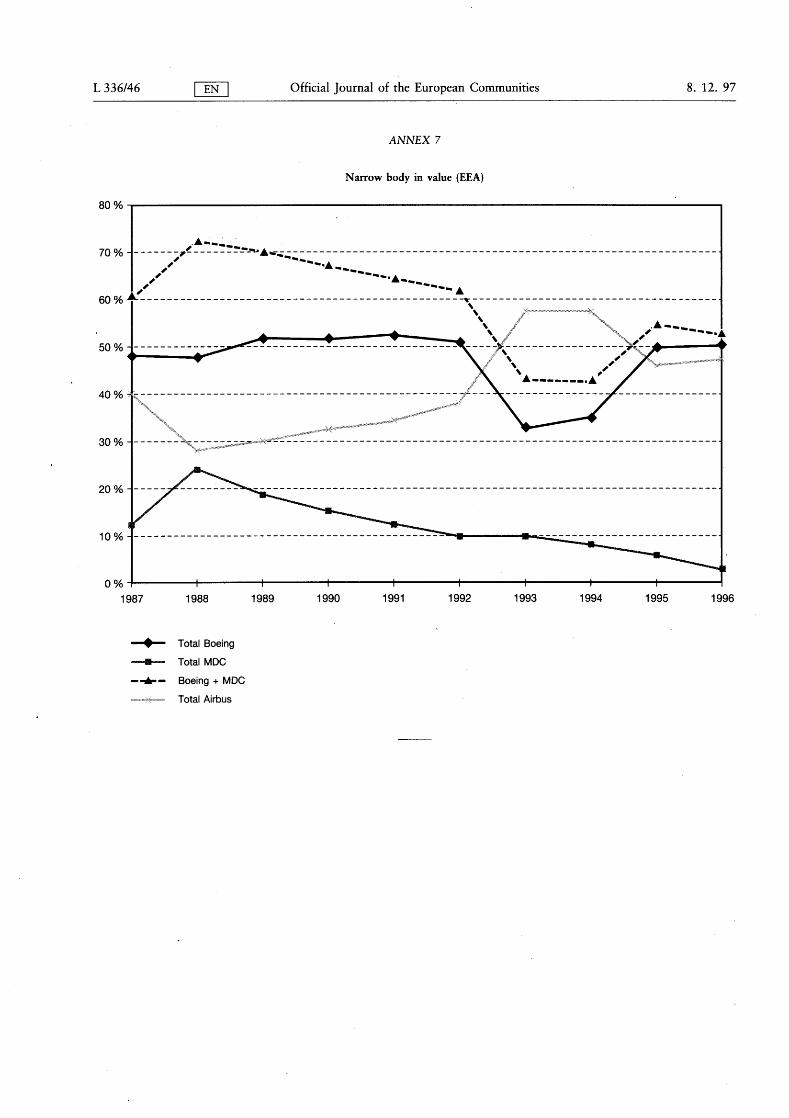

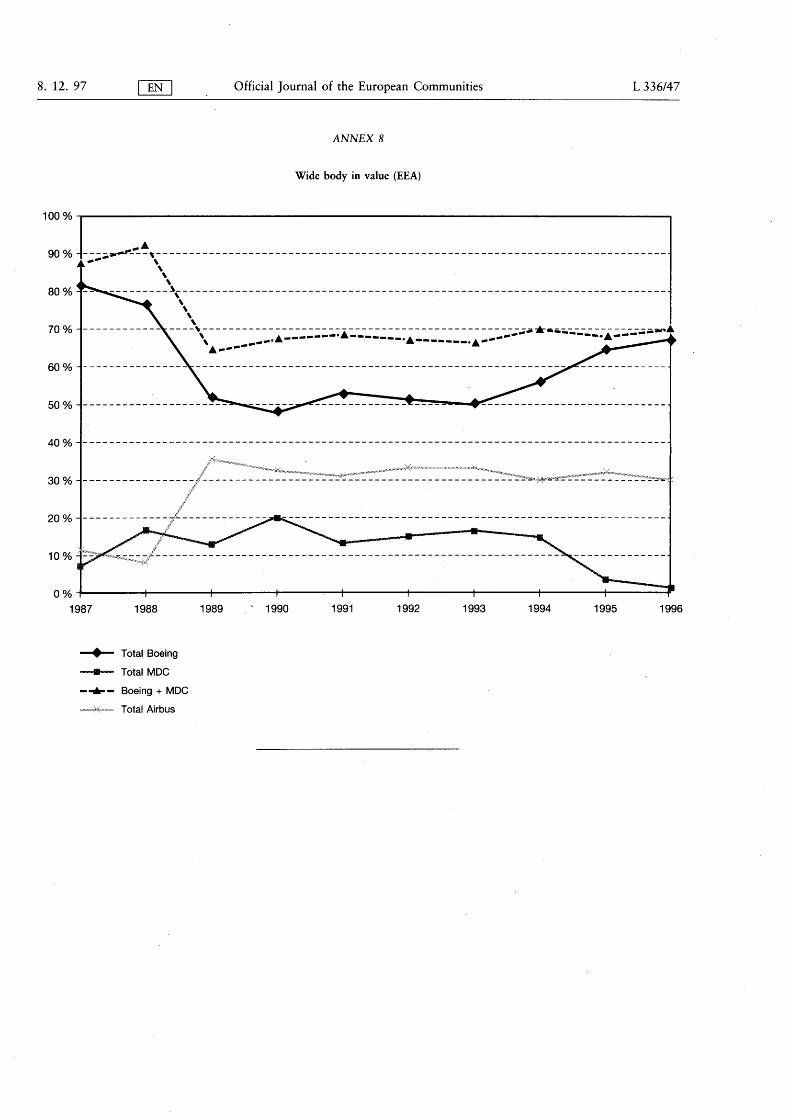

1989, the market share of Airbus showed a slightincrease whilst MDC's market share decreasedcontinuously from 1988 from around 20% to 2% .In the wide-body market between 1987 and 1989there was a significant increase in the share ofAirbus from around 11% to around 36%,followed by a more or less stable share of theorder of 30% . For Boeing in 1989 there was asignificant decrease to around 51%, followed by acontinuous increase to about 69% . For MDCthere was a continuous decrease from around 19%in 1990 to around 1% in 1996 . In thenarrow-body market, from 1989 Airbus increasedits market share to around 47% , Boeing's sharewas more or less stable at around 50% andMDC's share decreased from around 19% to2% .

( 36 ) The overall world-wide assessment leads to theconclusion that, after a significant improvement inthe late 1980s and early 1990s, Airbus maintainedits position in large commercial aircraft on thesame level . Boeing increased its market shareduring the 1990s to more than 60% whilst therewas a continuous decrease in the market share ofMDC, in particular in the wide-body market . Thecombined market share of Boeing and MDC from1989 was more or less stable at around 70% .

( 37 ) The very high market shares of Boeing alreadyindicate a strong position in the overall market forlarge commercial aircraft as well as in the twomarkets proposed in the notification . Furthermore,after making an inroad into Boeing's position inthe 1980s , Airbus was not able significantly toimprove its position during the 1990s whilstBoeing, already starting from a high level , was ableto increase its market share more or lesscontinuously during this period . This indicates thatit was difficult for Airbus to attack Boeing'sposition in the market even after having gained amarket share of nearly 30% in the 1980s . This isalso reflected by the fact that Airbus has notsucceeded in making a significant inroad in most ofthe top 10 operators' fleets ( see table inparagraph 69 ). The market power of Boeing,allowing it to behave to an appreciable extentindependently of its competitors , is an illustrationof dominance, as defined by the Court of Justice ofthe European Communities in its judgment in Case322/81 Michelin v. Commission ( 8 ).

( 32 ) As can be seen from the table in Annex 1 and thegraph in Annex 2, there was an increase in theshare of Airbus from around 24% in 1987 toaround 27% in 1989 . Since 1989, the share ofAirbus has remained more or less stable . There wasa decrease of Boeing's share in 1989, followed byan increase over the years until 1996 ( from 57%to 64% ). In contrast, there was a continuousdecrease in MDC's share from around 19% in1988 to around 6% in 1996 .

( 33 ) The development in both the wide-body andnarrow-body markets was similar to that in theoverall market ( see Annex 1 and the graphs inAnnexes 3 and 4 ). In the wide-body market, in1989, there was a significant increase in the shareof Airbus from 13 % to 31 %, largely due to ordersfor the new A 330 and A 340 models ; this wasfollowed by a more or less stable share of theorder of 30% . For Boeing in 1989 there was asignificant decrease to around 50 % , followed by acontinuous increase to more than 70% . For MDCthere was a continuous decrease from around 20 %to around 2% . In the narrow-body market, from1989 Airbus increased its market share to over30% . Boeing's share was more or less stable ataround 55 % and MDC's share decreased from19% to 11% .

( 34 ) The market structure within the EEA shows moreor less the same pattern as the world market ( seeAnnex 5 ) as the following table illustrates :

(%)

Backlog 31 . 12 . 1996 Average 1987/1996

Boeing 61 54

Airbus 37 34

MDC 2 12

Total 100 100 4 . Market segments

( 38 ) Within the overall large commercial jet aircraftmarket, a number of segments can be identified.The following table illustrates what amounts to anapproximate consensus within the industry ( 9 ) onthis segmentation .

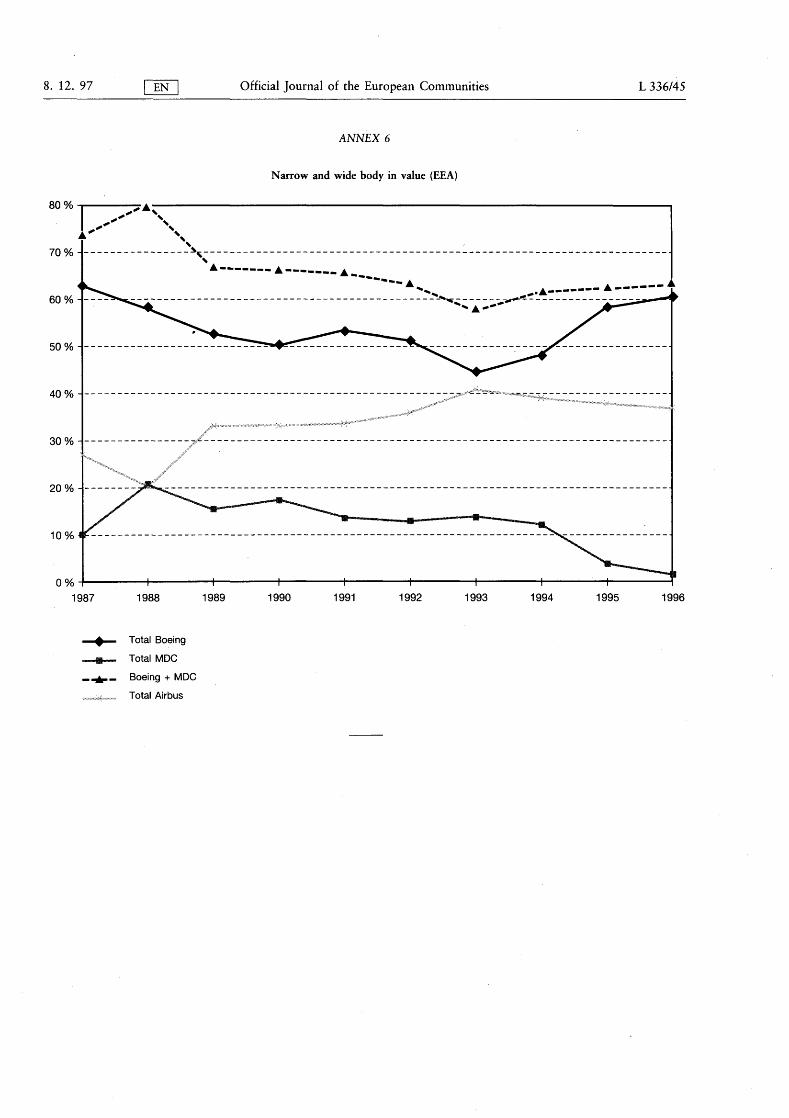

( 35 ) As evidenced in the tables in Annex 5 and thegraphs in Annexes 6 , 7 and 8 , in the EEA thedevelopment in the overall market and in both thewide-body and narrow-body markets was similarto that in the world market. In the overall market,from 1989 Boeing increased its market sharecontinuously from around 50% to over 60% .After a significant increase from 20 % to 33 % in

( 8 ) [ 19831 ECR 3461 .( 9 ) Including Boeing itself ( 1997 Current Market Outlook).

L 336/22 | EN Official Journal of the European Communities 8 . 12 . 97

Commercial aircraft segments

Narrow-body Wide-body

Approximateseating capacity

100-120 120-200 200-320 320-400 400 +

Boeing 737-500 737-300 767-200 777-200 747-400

737-600 737-400

737-700

737-800

757-200

757-300

767-300 777-300

MDG MD-95 MD-80

MD-90

MD-11

Airbus A319

A320

A321

A310

A300

A330-200

A340-200

A330-300

A340-300

definitions to passenger models, they need to beadapted to include large loading doors on the maindeck, structural reinforcement for the increasedpayload, and adapted loading and cabin systems .From a demand-side point of view, freighterconfigurations of large commercial aircraft are notsubstitutable by passenger configurations .However, the Commission considers that freighteraircraft do not constitute a separate relevantmarket, given the high supply-side flexibilitybetween passenger and freighter aircraft . New andconverted aircraft could be supplied in the shortterm without incurring significant additional costsor risks .

According to a submission made to theCommission by MDC, although there is somedegree of fluidity between segments, this tends tobe driven by cost considerations arising from fleetcommonality; it remains the case that some 70%of aircraft are used in such a way that thesegmentation indicated above is valid . Inparticuliar, the 100-120 seat narrow-body aircraftsegment can only be substituted by the 120-200seat narrow-body aircraft (to a very limited extent )because of the higher per-trip operating costs ofthe latter . At the other extreme in the segment ofwide-body aircraft, there is only Boeing's 747-400 .Furthermore , it appears that on certain long-rangeroutes with a high density of passengers, such asroutes from Europe or the USA to Japan, there iscurrently no alternative to Boeing's 747, whichcombines the largest capacity with the longestrange of all existing aircraft . The same applies tocertain domestic routes with very high trafficdensity and severe slot constraints .

5 . Fleet in service

(40 ) Boeing, as the company itself states in its 1995annual report, has led the world production ofcommercial aeroplanes for more than three decadesand has built more jet aircraft than all the othermanufacturers combined . Given the typical longoperating life of these products, Boeing has by farthe broadest customer base which gives it asignificant competitive advantage vis-a-vis itscompetitors .

According to Boeing's notification, airlines areincreasingly making aircraft purchasing decisionsbased upon 'families of aircraft '; having selectedthe family, an airline will afterwards select themodel . Even though Boeing argues that bothAirbus and itself would be able to offer suchfamilies, it is clear from the above table that onlyBoeing enjoys the benefits arising from the abilityto offer a complete family of aircraft, due to itspresence in every segment, unlike Airbus .

(41 ) It is estimated that Boeing has a share of around60 % of the current worldwide fleet in service ofwestern-built , large passenger aircraft . The share ofMDC is around 24% and that of Airbus onlyaround 14% even more than 25 years after Airbusbegan operations . The remaining 2 % are related toLockheed aircraft still in operation; Lockheed has,

( 39 ) A further segment within the overall market forlarge commercial aircraft is that of • freighters .While freighters have similar basic design

8 . 12 . 97 I EN Official Journal of the European Communities L 336/23

however, no longer been active in the productionof commercial aircraft since 1984 . It is true thatthe existence of a large fleet in service is not aguarantee of the success of a supplier ofcommercial aircraft , particularly when a supplieroffers only a limited range of aircraft types .However, where a large fleet in service is combinedwith a broad product range , the existing fleet inservice can be a key factor which may oftendetermine decisions of airlines on fleet planning oracquisitions . Cost savings arising fromcommonality benefits , such as engineering sparesinventory and flight crew qualifications, are veryinfluential in an airline's decision-making processfor aircraft type selections and may frequently leadto the acquisition of a certain type of aircraft evenif the price of competing products is lower . Theimportance of the existing fleet in service for thechoice of new aircraft has been underlined by allairlines which replied to the Commission'squestions on this point .

(42 ) In this context, it should be noted that Boeing hasnot only by far the largest fleet in service , but alsoby far the broadest product range and it offers afamily of aircraft which covers all conceivablesegments of large commercial aircraft .

airline when Delta agreed to purchase exclusivelyBoeing aircraft for the next 20 years . Delta placed106 firm aircraft orders until the year 2006,including ten 767-300ERs, five 757/200 twin jets,seventy next-generation 737s and twenty-one767-400ERXs. The total order is valued at US $6,7 billion . The plan also includes 124 optionswith an estimated value of US $ 8,3 billion, as wellas 414 rolling options for aircraft until 2018 .Finally, on 10 June 1997, Continental agreed inprinciple on 35 firm orders and further purchaseoptions from Boeing, with a condition thatContinental will meet all its large aircraft supplyrequirements exclusively from Boeing for the next20 years .

(45 ) The fact that three of the biggest airlines in theworld have locked themselves into a 20-yearsupply agreement with a single supplier is alreadyan indication that Boeing enjoys a dominantposition in the large commercial aircraft market.Furthermore it is likely that those three deals werefacilitated by the proposed merger ( as explainedbelow). Although, as indicated, the customers areto receive economic benefits from the deals , theseare likely to be more than offset by the rigidityincurred by being locked into a single supplier forso long a period, during which it might prove to bethe case that competitors ' prices become lower,their technology and related services superior.

(46 ) The existing exclusive deals between Boeing andthe three airlines in question will have importantforeclosure effects on the worldwide market forlarge commercial jet aircraft over the next 20years . It is estimated that 14 400 new aircraft willbe delivered worldwide between 1997 and 2016,of which about 2 400 are on firm order withBoeing, MDC or Airbus . There thus remains anopen market for about 12 000 aircraft . However,Boeing's exclusive deals including options andpurchase rights , account for an estimated 13% ofthis open market (or over 30 % of the USmarket ).

6 . Exclusive deals

( 43 ) Boeing has recently entered into exclusivearrangements for the supply of large commercialjet aircraft to American Airlines (American ), DeltaAirlines (Delta ), and Continental Airlines(Continental ). In November 1996 , American andBoeing agreed on a long-term partnership that willmake Boeing the exclusive supplier of jet aircraft toAmerican until the year 2018 . American placedfirm orders for 103 aircraft, including 75 ordersfor the next generation 737 family of jetliners,twelve orders for the 777-200, twelve 757s andfour 767-300ERs. Based on Boeing's list prices, theorder is valued at about US $ 6,6 billion . Americanalso obtained price-protect 'purchase rights ' for527 additional jets during the more than 20-yearexclusivity period . These purchase rights enableAmerican to determine when it wants to exerciseits options to buy aircraft, with as little as 15months advance notice before delivery fornarrow-body aircraft and 18 months beforedelivery for wide-body aircraft , compared to thetraditional 18 to 36 month delivery period . It hasbeen reported that American did not have to payfor these purchase rights but received them inexchange for the commitment to buy only Boeingjets . At the same time, it appears that Boeingoffered retroactive price reductions on aircraftpurchased by American in previous campaigns .

(44 ) On 20 March 1997, Boeing concluded a secondlong-term exclusive arrangement with a major

7. Future market growth

( 47 ) The parties have argued that the supply ofsecond-hand aircraft and the purchasing power ofairlines already constrain Boeing's market power,and will continue to do so .

The Commission's view that second-hand aircraftare not in general effective substitutes for newaircraft has already been explained ( see above ).This is particularly likely to hold true over the next20 years, when demand for aircraft is expected togrow by more than 80% . Second-hand aircraftcould not possibly meet more than a fraction of

L 336/24 | EN Official Journal of the European Communities 8 . 12 . 97

this growing demand, particularly given that a highproportion (more than 80% ) of the existing worldfleet in service will need to be retired and replacedduring this same period .

aircraft, as described above, in particular theexisting market shares of Boeing, the size of itsfleet in service, the recent conclusion of long-termexclusive supply deals with major customers, andthe lack of potential new entrants, the Commissionhas reached the conclusion that Boeing alreadyenjoys a dominant position on the overall marketfor large commercial aircraft as well as on themarkets for narrow-body and wide-body aircraft .

The anticipated market growth will also lessenwhatever buying power airlines are able toexercise . During a period when demand for airtransport is forecast to increase very significantly (a5 % annual rate is foreseen ), airlines in trying tomeet this demand will to an extent find themselvesvying with each other to obtain new aircraft,which will put them in a less favourablenegotiating position vis-a-vis suppliers .Furthermore, the buying power of airlines vis-a-visBoeing is, in any event, limited given Boeing'smonopoly in the largest wide-body segment and, atleast after the proposed concentration, in thesmallest narrow-body segment .

II . Strengthening of Boeing's dominant position

( 53 ) The proposed concentration would lead to astrengthening of Boeing's dominant position inlarge commercial aircraft through:

— the addition of MDC's competitive potential inlarge commercial aircraft to Boeing's existingposition in this market,

— the large increase in Boeing's overall resourcesand in Boeing's defence and space businesswhich has a significant spill-over effect onBoeing's position in large commercial aircraftand makes this position even less assailable .

8 . Potential competition

(48 ) In its notification Boeing states that there arepotential new entrants to the large commercial jetaircraft market, particularly companies situated inRussia , India and the Far East (China , Japan,South Korea and Indonesia ).

(49 ) However, Boeing itself effectively admits that thereare massive barriers to entry to this market. Initialdevelopment and investment costs are huge (overUS $ 10 billion to develop a new wide-body jet,according to Boeing). The production process itselfis characterized by very significant learning curveeffects and economies of scale and scope , whichmust be attained if a new entrant is to competeeffectively over time . Very strict safety regulationsneed to be complied with at US, European andother national levels .

( 50 ) Again, in Boeing's notification potential entrantswhich are identified are likely to be active mainlyin the regional jet market, and as such will notcompete on the large commercial jet market ( seeabove under market definition ). This is confirmedby replies from ( for example ) Far Easterncompanies supplied to the Commission ; suchcompanies are involved either in the regional jetmarket, or are subcontractors to Boeing for largejet aircraft programmes .

( 51 ) It can therefore be excluded that potentialcompetition will have any significant impact on thepresent competitive situation over the foreseeablefuture .

1 . Impact of MDC's commercial aircraft business

( 54 ) The immediate effect of the proposedconcentration would be that :

( a ) Boeing would increase its market share in theoverall market for large commercial aircraftfrom 64% to 70% ;

( b ) by taking over the activities of MDC, Boeingwould , in future , be faced with only onecompetitor in this market;

( c ) Boeing would increase its customer base from60% to 84% of the current fleet in service;

( d ) Boeing would increase its capactiy incommercial aircraft, particularly in terms ofskilled work force;

( e ) Boeing would increase its ability to induceairlines to enter into exclusivity deals, therebyfurther foreclosing the market .

( a ) Increase in market share

( 55 ) In the overall market for large commercial aircraft,Boeing would increase its market share in terms ofcurrent backlog from 64% to 70% . In thewide-body market, there would be an increasefrom 71% to 73% . In the narrow-body market,Boeing's market share would increase from 55 %to 66% .

9 . Conclusion

( 52 ) In view of the various characteristics of the currentstructure of the markets for large commercial jet

8 . 12 . 97 , 1 EN | Official Journal of the European Communities L 336/25

Airbus, MDC had been in competition for all or apart of the orders . Out of the 20 airlines, 13 statedthat competition from MDC had an influence onthe outcome of their negotiations with the winnerof the bid in terms of a better price or betterpurchasing conditions . Two airlines stated that thisinfluence was of major importance and three statedthat this influence was of minor importance . Sevenairlines stated that the influence of MDC'scompetition was of significant importance .

This is confirmed by a study conducted by LexeconLtd . on behalf of Airbus and presented at theHearing, in which 52 aircraft-supply competitionsbetween 1994 and 1996 were analysed, comparingthose in which MDC participated with those inwhich it did not participate . In this study, it wasfound that the MDC presence led to a reduction ofover 7 % in the realized price as compared with thelist price as far as orders placed with Airbus wereconcerned .

(56 ) Furthermore, Boeing would add to itsalready-existing monopoly in the largest wide-bodysegment a further monopoly in the smallestnarrow-body segment of aircraft with 100 to 120seats . This segment is particularly important sinceit is , to a great extent, used by large airlines to feedtheir hubs and to achieve profitable operations onlow-traffic routes . On these routes, it is difficult tosubstitute aircraft of 100 to 120 seats by largernarrow-body aircraft such as the Airbus 319, dueto the higher per-trip operating costs of the latter .For the time being, the only competing aircraft inthe smallest narrow-body segment are the Boeing737-500 and 737-600 and the MD-95 . It has to benoted that, even if Airbus has undertaken somediscussions with China and other Asiamanufacturers about the development of a100-seater, these negotiations are still at an earlystage and the investment decision will depend onmarket and development scenarios; consequently,this project is not likely to have any influence inthe market in the foreseeable future . Boeing wouldalso achieve a near monopoly in the freightersegment. For deliveries of new freighters in theperiod 1990-96, the average annual world-widemarket shares of Boeing and MDC were 67 % and23 % respectively, that is 90 % combined .

( ii ) However, today MDC is no longer a real forcein the market for the sale of new aircraft on astand-alone basis

( 57 ) However, since, as outlined below, MDC is nolonger a real force in the market for commercialaircraft , and in the absence of another potentialbuyer of its commercial aircraft business , it is likelythat Boeing would have obtained, over time, amonopoly in the 100 to 120 seats segment and anear monopoly in the freighter segment evenwithout the present concentration .

( b ) Competitive potential of MDC

( i ) The competitive influence of MDC was in thepast greater than reflected by its marketshare

( 59 ) The Douglas Aircraft Company (DAC), whichoperates the commercial aircraft business of MDC,generated in 1996 operating earnings of US $ 100million as compared with US $ 39 million andUS $ 47 million in 1995 and 1994 respectively .Furthermore, DAC has still a firm backlog of US $7 billion . However, it appears that the operatingearnings of DAC were essentially related to DAC'sspare parts and product support business ratherthan to the sale of new aircraft . In contrast to thebroader and more modern families of aircraftoffered by Boeing and Airbus, DAC currentlyoffers only three types of narrow-body and onetype of wide-body aircraft which do not provide ,according to Boeing, significant commonalitybenefits and are all themselves derivatives of earlierDouglas models, rather than entirely new designs .It appears that these are the main reasons for thecontinuous decline of DAC's market shares .Furthermore , the current backlog covers only alimited period of future production . Since thecancellation of the MDXX program in October1996, DAC has virtually received no new firmorders . This reflects the perception of airlines thatMDC is no longer committed to the commercialaircraft business and may leave the market overtime . In this context, it is also important that DAClost over the last nine months its core customersAmerican, Northwest Airlines , Delta andContinental, the four largest operators of DACaircraft . The loss of these 'mainstream' airlinecustomers, which are points of reference for othersand one of which, Delta , was even the launchcustomer for the MD90, gave a further signal tothe market that DAC would have no prospects in

( 58 ) Although, as outlined above, the market share ofMDC has been continuously declining, it appearsthat the impact of MDC on the conditions ofcompetition in the market for large commercialaircraft was higher than reflected by its marketshare in 1996 .

The Commission has received replies from 31airlines which have all purchased new largecommercial aircraft over the last five years . Two ofthem purchased only MDC aircraft . Out of theremaining 29 airlines, 20 stated that in those caseswhere they had placed orders with Boeing or

L 336/26 EN Official Journal of the European Communities 8 . 12 . 97

the market for large commercial aircraft . In thesecircumstances, it has to be concluded that DAC istoday no longer a real force in the market on astand-alone basis .

Through Boeing's preferential access to the largeexisting customer base of DAC, as outlined below,Boeing would be in an advantageous position toreplace, over time, DAC aircraft which are inservice today .

( iii ) It is unlikely that a third party would acquireMDC's commercial aircraft business

( 60 ) In theory, without the merger DAC could havebeen a candidate for a take-over by otheraerospace companies . [...]. However, DAC'sposition on the market deteriorated dramatically in1997. Extensive market enquiries carried out bythe Commission made it clear that it is in practicehighly unlikely that a third party would acquireDAC. It appears that this is inter alia due to thedeterioration of the situation of DAC. NeitherAirbus , the only competitor left in the market forlarge commercial aircraft , nor one of its parentcompanies showed an interest in the acquisition ofDAC. Furthermore, no other potential buyers wereinterested in entering the market for largecommercial aircraft through the acquisition ofDAC. It appears , therefore, that, given the currentcompetitive situation of DAC, only Boeing isprepared to take over MDC's commercial aircraftbusiness .

( c ) Fleet in service

( 62 ) Boeing would increase its share in the existing fleetin service from 60% to 84% (as opposed to only14 % for Airbus ) and would, therefore, increase itslong-term relationships with customers and itsposition in customer support . It would alsosignificantly broaden its customer base . It appearsthat out of the 561 airlines operating Boeing,MDC and Airbus aircraft at the end of 1996, 75operators use only MDC aircraft and 10 operatorsuse only MDC and Airbus aircraft . In addition tothe 316 airlines operating only Boeing aircraft, the50 airlines operating Boeing and MDC, the 62airlines operating Boeing and Airbus and the 26airlines operating Boeing, MDC and Airbus (only22 airlines operate exclusively Airbus ), Boeingwould also get access to a further 85 airlines whichdo not as yet operate Boeing aircraft .

( 63 ) The opportunity for closer contacts with thoseairlines resulting from ongoing support activitiescould provide opportunities for future sales byallowing Boeing to influence customer needs .However, it has to be recognized that Boeingalready has close contacts with a large number ofairlines through its own product supportactivities .

( 64 ) In general, the acquisition of MDC's spare-partsand maintenance business may confer on Boeingsignificant additional leverage over existing MDCaircraft users, whose combined MDC fleetsconstitute , as already stated, 24% of the totalaircraft fleet worldwide .

( iv ) The competitive potential of MDC'scommercial aircraft business can, however, bea significant factor in the market when it isintegrated into the Boeing group

( 61 ) Boeing has stated that it could decide on thecontinuation or discontinuation of DAC's productlines only once it has had access to DAC's internaldata . According to Boeing such a decision would,furthermore, depend on a number of differentfactors including social and politicalconsiderations . There are, however, indicationsthat Boeing could, despite the current difficultsituation of DAC, decide to continue all or some ofDAC's product lines, at least for a certain time . Inthe event that Boeing continues production ofDAC aircraft , the existing negative perception ofMDC's prospects could be removed . That couldequally remove the reluctance, to a certain extent,on the part of airlines to buy DAC aircraftstemming from uncertainty about the future of itscommercial aircraft business . As a part of theBoeing Group, DAC aircraft could be marketedtogether with Boeing aircraft and Boeing would beable to decide when to put DAC aircraft into acompetition and when not.

If, by contrast, Boeing were to decide to phase outproduction of all or some DAC aircraft over time,Boeing would be better placed than Airbus to gainthe market shares freed by such a decision .

( d ) Use of MDC's capacity

( 65 ) According to Boeing only [. . .] of its productioncapacity is in use, which leaves spare capacity of[...]. However, it appears that these figures areonly related to tooling capacity and not existingworkforce . There are indications that Boeing seeksin particular access to MDC's engineers for its owncommercial aircraft development and production .In MDC's 1996 annual report, it is reported inrelation to a plan for a future commercial jetliner,that several hundred engineers of MDC beganwork for Boeing on this project in December1996 .

( 66 ) The Commission accepts that it is relativelydifficult to transfer engineering personnel working

8 . 12 . 97 1 EN Official Journal of the European Communities L 336/27

on combat aircraft production to commercialaircraft production . However, that is not a majorproblem for engineers working on militarytransport aircraft . In fact, MDC agrees thatfluctuations in commercial and CI 7 programmes(military transporter ) have sometimes causedproduction workers to move back and forthbetween the commercial programmes and the CI 7programme.

( 67 ) In the aircraft industry, flexibility of capacity, orthe ability to increase and decrease productioneasily, is an important factor. From the standpointof the airlines, a manufacturer that can offer therequired delivery slots in periods of rapidlyincreasing demand clearly has an advantage . Onecrucial element for a rapid increase in capacity isthe availability of skilled labour, which would beincreased for Boeing through the access to MDC'sworkforce .

aircraft models or new families of aircraft . Inparticular, with respect to those airlines whichcurrently operate both Boeing and MDC aircraft,within the framework of an exclusivity deal ,Boeing could also offer the provision of additionalMDC aircraft , as well as spare-parts and supportservices for older MDC aircraft . On the otherhand, where airlines which have ordered MDCaircraft want to streamline their fleet, Boeing,being in control of MDC, would simply cancelthose MDC orders and the penalties whichnormally have to be paid by airlines in the event ofcancellation of orders would be of no significance .It is reported that, within the framework of theexclusivity deal , Boeing has offered to take backthe MD-90s that have already been delivered toDelta and to cancel existing orders for furtherMD-90s . However, Boeing, when asked by theCommission, was not in a position either toconfirm or to deny those arrangements .

( e ) Exclusive deals

( 68 ) The proposed merger would significantly enhanceBoeing's capacity to enter into agreements such asthose concluded with American, Delta andContinental . It should be noted that such airlinesare amongst the world's largest and are ' launchcustomers ' for new aircraft models, that is to say,they are in effect the only airlines with sufficientresources to commit themselves to entirely new

(69 ) As an illustration of the link, both actual andpotential, between the size of the existing MDCfleet in service of major airlines and the increasedopportunity following the merger for Boeing toconclude further exclusive supply agreements withsuch airlines , it is noteworthy that American,Delta , and Continental , with which exclusivesupply agreements already exist ( I0 ), are first, third,and fourth respectively with regard to the size oftheir MDC fleet in service .

World fleet — Top ten operators

Airline Boeing DAC Airbus Total 0 )

American 242 311 35 663

United 503 52 36 591

Delta 336 150 539

US Airways 250 99 423

Northwest 126 229 50 405

Continental 183 119 4 306

Southwest 243 243

British Airways 203 7 10 228

Lufthansa 123 92 215

TWA 79 111 204

(') Total figures include 86 Lockheed aircraft, 130 Fokker and 7 Concorde . Source: Airbus .

( 10 ) The Delta and Continental deals were announced after themerger ; the American deal was announced only some weeksbefore the merger .

L 336/28 | EN Official Journal of the European Communities 8 . 12 . 97

( b ) an increase in Boeing's access to publiclyfunded R&D and intellectual propertyportfolio;

( c ) an increase in Boeing's bargaining powervis-a-vis suppliers;

( d ) opportunities for offset and 'bundling deals '.

It is also noteworthy that prior to thoseagreements, exclusivity deals had never before beenentered into in the large commercial aircraft sectorand that their duration itself is unprecedented .

( 70 ) More generally, Boeing's broader product rangeafter the merger, its financial resources and itshigher capacity which enables it to respond toairlines ' needs for deliveries on a short lead timewould, in combination, significantly increaseBoeing's ability to induce airlines to enter intoexclusive deals . It should be noted that it would beimpossible for Airbus to offer exclusive dealsbecause Airbus is unable to offer a full ' family' ofaircraft .

( a ) Financial resources

( 73 ) Following the concentration, Boeing will becomethe largest integrated aerospace company in theworld with estimated 1997 revenues in excess ofUS $ 48 billion . Based on the figures for 1995 ,Boeing's commercial aircraft operations accountedfor around 70% of its total business . For MDCthe ratio is just the opposite; around 70% of itstotal business was related to defence and spaceoperations . Without taking into account therecently completed acquisition of RockwellDefence and Aerospace, Boeing will approximatelytriple its defence and space activities through theproposed take-over of MDC. This will significantlyincrease Boeing's ability to cope with the economiccycles in commercial aircraft given that, despitebudget constraints in recent years, revenuesachieved in the defence and space sector appear tobe much more stable than those generated in thecommercial sector.

( 74 ) Since Airbus is a groupement d'interet economique( GIE) and as such does not publish its ownfinancial accounts , a detailed financial comparisonbetween Airbus and Boeing or MDC is notpossible . However, the relative magnitude of thethree organizations is indicated by their respectivetotal turnover figures for 1996 .

( 71 ) The potential effect of exclusive deals with theworld 's top ten airlines would be to block over40 % of the worldwide market (based on thoseairlines' existing fleet in service as a proportion ofthe worldwide fleet ). Such a scenario is quitefeasible, since there could be a knock-on effectwereby further large airlines would not want tomiss out on the apparent advantages accruing totheir competitors who have already entered intoexclusive deals . The result could be a splitworldwide market, with the biggest airlines withthe largest fleets exclusively controlled by Boeingfollowing the merger, leaving competition possibleonly for the supply of the aircraft requirements ofsmaller airlines .

(billion US $)

Furthermore, those deals are likely to have anextended effect beyond their already verylong-frame, given the very long operating lifetypical of the industry's products . Thus, Boeingestimates that aircraft designed after 1980 mayhave an operating life of between 28 and 31 years .This implies in fact that aircraft bought in the lastyears of the deal , even if it is not renewed, couldcover the airlines ' needs up to the years 2045 to2047. Moreover, it is also reasonable to considerthat after such an extremely long period ofpurchasing exclusively from Boeing, airlines wouldprobably not be inclined to face the costs ofswitching to a different family of aircraft .

Airbus 8,9

Boeing 22,7MDC 13,8

The aerospace turnover of each of the four Airbuspartners in 1996 was as follows :

(billion US $)

Aerospatiale 10,1BAC 11,6

DASA 8,8CASA 0,9

2 . Overall effects resulting from the defence andspace business of MDC

( 72 ) The overall effects resulting from the take-over ofMDC's defence and space business would lead to astrengthening of Boeing's dominant positionthrough :

(a ) an increase in Boeing's overall financialresources;

However, despite arguments to the contrary madeby Boeing, it is not appropriate to include theturnover of the four Airbus partners in that ofAirbus . As far as turnover from military aerospaceactivities is concerned, it is important to note that

8 . 12 . 97 | EN Official Journal of the European Communities L 336/29

( 75 ) The soundness of the financial structures of bothBoeing and MDC are indicated by their ratios ofdebt to equity (US $ 4,1:10,5 billion and US $3,4:3,0 billion respectively ) ( 11 ).

( 76 ) The following 1996 operating results indicate theindividual and combined strength of Boeing andMDC ( 12 ):

the four Airbus partners do not together constitutean integrated business entity, as do both Boeingand MDC, which are individual stand-alonecompanies . Moreover, the only Airbus partnerwith significant non-aerospace connected activitiesis DASA, which is part of the Daimler-Benz group .It is clear that Daimler-Benz would not find iteconomically rational to use its other activities(mainly motor vehicle manufacture ) to subsidizeAirbus to any significant extent, particularly sinceits shareholding is only about 37% ( see above ).

( n ) Source: Boeing and MDC Annual Reports 1996 .( 12 ) Source: Boeing and MDC Annual Reports 1996 .

Boeing MDC Combined

Profits 1,4 0,79 2,19

Cash flow \( beginning of year pluschanges = year-endbalance ) 3,73 + 0,64 = 4,37 0,8 + 0,3 = 1,1 4,53 + 0,94 = 5,47

( 77) Including MDC, Boeing's pre-tax profits have beenforecast by Lehman Brothers to climb from US $4,4 billion in 1997 to US $ 7,3 billion in 2000, onsales of US $ 54,8 billion in that year . With respectto cash, Lehman Brothers state that 'Boeing couldhave US $ 15 billion in cash on the balance sheetby the end of the decade, and early in the nextcentury they could have in the mid US $ 20 billionrange' ( 13 ).

zero-profit or below-cost levels within the mid-sizesegment, financed by the higher margins achievedin the smallest and largest segments . Besides suchturnover, cash and profits combination, thedoubling of governmental-funded military R&Dand the tripling of Boeing's general revenuesgenerated in the defence and space sector willincrease the scope of cross-subsidization ofBoeing's sales in commercial aircraft in cases whereBoeing wants to meet specific competition ( such asin the mid-size segment of the wide-body market ).

( 79 ) A possible example of such pricing tactics alreadyemployed by Boeing in fact involved the 737 modelitself. Concerning an order for new commercial jetaircraft placed by Scandinavian Airline Systems( SAS ) in March 1995 , the newspaper TheWashington Post has reported ( 15 ):

( 78 ) The accounts of Boeing and MDC are nottransparent with regard to the profit marginsachieved on their various individual models .Financial analysts calculate that significantdifferences exist between the profit margins madeby Boeing on its various models . In particular, it isestimated that margins are significantly higher( around 30% ) on the 737 and 747 models ( thesmallest and largest respectively ) than on the 757and 767 models ( the mid-size aircraft ); wheremargins are estimated at around 18 % ( 14 ). Thisprobably reflects the near-monopoly position ofBoeing in the smallest and largest segments ( seeabove, under passenger aircraft market definition ).Boeing is therefore probably able to cross-subsidizesales of mid-sized aircraft , where competition isstronger, because of the higher margins it achieveson the smallest and largest aircraft where there arefewer or no competing aircraft . It can therefore beanticipated that, with the addition of productsfrom MDC, Boeing would have opportunities,where it thought appropriate , to set prices at

'SAS's internal evaluating committee hadrecommended the purchase of 50 of Douglas'proposed new 100-seat MD-95 jetliners forUS $ 20 million each . Instead , [SAS Chairman]said that SAS would order 35 of a new versionof Boeing's venerable 737 at about US $ 19million per plane, a steep discount fromBoeing's list price . " It was clear that Boeing'sstrategy was to prevent Douglas from everlaunching the MD-95 ", recalled one salesmaninvolved in the competition .'

( 13 ) Source : Lehman Brothers, 22 April 1996 .( H ) Source : Lehman Brothers , 22 April 1996 . ( 15 ) Source : The Washington Post, 5 April 1997.

L 336/30 [ EN Official Journal of the European Communities 8 . 12 . 97

This is the case, in particular, with respect to R&Dfor military aircraft .

( 80 ) According to data supplied by Boeing, the lowestpublished 1996 price for a 100-seater 737 aircraftwould be US $ 32 million . On the assumption thatfinancial analysts' calculations of a profit marginof about 30% on a Boeing 737 aircraft areapproximately correct ( 16 ), an actual sales price toSAS of US $ 19 million per aircraft would implythat no profit whatsoever accrued to Boeing onthis particular transaction (US $ 32 million less30% = approximately US $ 22 million).

( 81 ) It is clear that, as already stated, the addition ofproducts from MDC (in particular thesmall-segment MD-95 ) and the large increase in itsoverall resources would enhance Boeing'sopportunities to engage in such pricing practices,especially in view of its strong, and increasinglystrengthening, cash-flow position as outlinedabove .

( i ) R&D in the US aerospace industry is, to alarge extent, funded by the Government

( 84 ) According to figures compiled by the AerospaceIndustries Association of America, in the UnitedStates total R&D (federal and company funding)which is performed by industry amounts onaverage to 3 to 4% of net sales of manufacturingcompanies . By contrast, in the aerospace sector,total US industrial R&D amounts to 12 to 14% ofnet sales . Across industry as a whole, companiesfund around 80 % of total industrial R&D, whilstfederal funding represents around 20% . In theaerospace industry, the ratio is again completelydifferent : around 60% of total industrial R&D isfunded by the US Government and only 40% bycompanies themselves .

( 85 ) In 1994, the federal funds for industrial R&D inthe overall aerospace sector amounted to US $ 8,8billion . Out of this amount, around US $ 8 billionwas spent on development, the remainder beingattributed to basic and applied research. The mainsources for funding industrial R&D were the DoDand NASA. DoD's total budget for aeronauticsR&D (for aircraft and related equipment )amounted to US $ 6,8 billion and NASA's budgetfor aeronautics R&D amounted to US $ 1,5billion . The figures for 1995 were US $ 7,1 billionand US $ 1,3 billion respectively . DoD's primecontract awards for research, development, testand evaluation (RDT&E) related to aircraftamounted to US $ 5,8 billion in 1994 and tonearly the same amount in 1995 .

( 82 ) A past example of Boeing's preparedness to use itsoverall strength in resources to pressurize not justcompetitors but also customers can be found in aletter addressed to a Japanese aircraft leasingcompany on signing an order for Airbus aircraft,as reported at the Hearing :

'I want you to know that the Boeing Companytakes such a decision . . . extremely seriously.This not only comes as a shock to me and mycolleagues here, but will surely have a negativeimpact on the future of the long-termrelationship our two companies have enjoyedover the many years '.

'. . . More significantly, it could haveundesirable implications for the Japan Americaaerospace industry cooperation'.

( signed Mr Ronald Woodard, BoeingCommercial Airplane, Group President,17 December 1996 ).

( b ) Access to publicly-funded R&D

( 86 ) In general, DoD's expenditure for R&D is muchlarger than those of the European Ministries ofDefence (MoDs). In 1996 , the total DoDappropriation for R&D was US $ 34,8 billion . Bycontrast, the total combined R&D budget for theMoDs in the Community (excluding Austria ,Sweden and Finland ) amounted to US $ 11,7billion . Out of this amount, US $ 10,6 billion wasaccounted for by the MoDs of France, Germanyand the United Kingdom, the countries of the mainAirbus partners . With respect to space activities,the relationship is similar . In 1996, the totalbudget of NASA was US $ 13,8 billion . Bycontrast, the contribution of the Member States tothe budget of the European Space Agency (ESA),which represents by far the largest part of thespace budget within the Community, was US $ 3,1billion . Furthermore these figures , which are clearlydisproportionate, are not even strictly comparablesince the MoDs in the Community do notnecessarily coordinate their behaviour as a matterof course .

( 83 ) The large increase in its defence and space activitieswill give Boeing a much greater access to R&Dwhich is funded by the US Department of Defence(DoD ), the National Aeronautics and SpaceAdministration (NASA) or other public bodies .

( 16 ) Source : Lehman Brothers , 22 April 1996 .

8..12 . 97 1 EN Official Journal of the European Communities L 336/31

Similarly, defence programmes, space-relatedtechnology and programmes often receive fullfunding for R&D, particularly if the programme'sprimary customer will be the US Government .

( ii ) US R&D in the defence sector and in thepublic space sector normally receives fullfunding by the Government

( 87) Unlike production or procurement programmes,which are generally performed under firmfixed-price contracts, defence and spacedevelopmental programmes are normallyperformed under cost/reimbursement-typecontracts . The most important R&D contracts arethe engineering and manufacturing development(EMD) contracts, which are used to finance theengineering and manufacturing development of asystem prior to entering the production phase of aprogramme . These contracts are usually cost plusaward fee (CPAF ) or cost plus incentive fee (CPIF )contracts .

( iii ) Through the proposed merger Boeing, inparticular, will greatly increase its number ofR&D contracts in the defence sector

( 89 ) Over the last five years, on average Boeingachieved annual revenues from federal R&Dcontracts of around [...]. On average, [. . .] ofthese revenues were generated by R&D for NASAspace programmes, in particular the InternationalSpace Station . Although Boeing is currently, onlyto a limited extent, a manufacturer of militaryaircraft (AWACS, KC-135 tanker) and does notmanufacture fighter aircraft , the second largestsegment of Boeing's R&D revenues was that ofmilitary aircraft . On average , military aircraftaccounted for [. . .] of Boeing's R&D revenuesresulting from contracts with the US Government .The reason is that Boeing is involved in majorprogrammes for the development of militaryaircraft , such as the F-22 fighter aircraft, the JointStrike Fighter and the tilt rotor V-22 aircraft . Overthe last five years , MDC received on averagebetween [. . .] and [. . .] per year. The militaryaircraft segment accounted for nearly [. . .] of theserevenues . Therefore, as a result of the proposedmerger, Boeing will more or less double its R&Drevenues in the military aircraft segment .

( 90 ) It should be noted that the merged companyBoeing/MDC would be, to a greater or lesserextent, involved in all current DoD programmeswith the highest R&D budgets . These programmesand their R&D budgets are the following:

( 88 ) CPAF contracts involve cost-reimbursement, plusan award fee which is based on an award plannegotiated at the beginning of the contract . CPIFcontracts involve cost reimbursement, plus anincentive fee which is based on performance andschedule milestones . In some instances, acontractor may have invested in R&D at its ownexpense in the early phases of a defenceprogramme . These initial R&D costs are usuallyincluded in the total programme costs when thecontractor obtains a later DoD production contractfor the item. Furthermore , the independentresearch and development (IR&D ) costreimbursement programme of the DoD enableseligible DoD contractors to recover a portion ofthe costs of their own in-house , independent R&Dthrough overhead payments on all DoD cost-pluscontracts . Since 1991 , the definition of allowableIR&D includes all projects of potential interest tothe DoD . It follows that the vast majority of R&Dfor defence products or with possibledefence-related applications is funded by the DoD.

Budget(million US $)

1995 1996

F-22 2 281 2 165 two-thirds Lockheedone third Boeing

F/A-18 1 249 824 MDC

V-22 Osprey 453 737 Boeing

RAH-66 Comanche 475 292 Boeing

B-2 366 589 Team leader : Northrop Grumman with majorparticipation of Boeing

JSF 182 193 Boeing and Lockheed in competition

C- 1 7 Globemaster III 184 71 MDC

L 336/32 | EN Official Journal of the European Communities 8 . 12 . 97

applications, advanced tooling, manufacturing andautomation in the manufacture of electronicproducts resulting from its commercialprogrammes on military programmes such as theF-22, V-22 and RAH-66 . Although Boeing assertsthat there are no significant benefits for thecommercial sector resulting from know-how gainedin military programmes, these examples prove,however, a cross fertilization of know-howbetween the commercial and military sectors .

( 91 ) It appears that the most important aircraftprogrammes in the foreseeable future will be theJoint Strike Fighter (JSF), the F-22 and the F/A-18 .System leader for the F-18 is MDC and the F-22 isdeveloped by Lockheed and Boeing together. Thefinal contract for the JSF is currently incompetition between Boeing and Lockheed . TheCommission considers that the merged company,Boeing/MDC, would have, after the merger, abetter chance of becoming the final primecontractor for the development of the JSF, giventhe combination of their technological resources ,

(v ) Through the proposed merger Boeing willgreatly increase the benefits obtained from thetransfer of military technology to commercialaircraft

( 94 ) Much technology developed in the defence sectorcan be applied to commercial aircraft uses . Themain increase in Boeing's military R&D will berelated to military aircraft and, in particular, tofighter aircraft . Although fighter aircrafttechnology is not wholly transferable because ofthe more compact packaging of systems, thattechnology can, however, be transferred to a largeextent. The following list provides an estimate byLockheed Martin of the percentages of a numberof fighter aircraft systems or types of technologythat are transferable to commercial applications :

( iv ) The large increase in Boeing's defence R&Dwill confer a number of general competitiveadvantages on the company

(92 ) As discussed below, an obvious advantage resultingfrom defence R&D for a manufacturer ofcommercial aircraft is the- possible transfer oftechnology, developed under public funding to thecommercial sector . However, technology transfersare not the only means by which manufacturers ofcommercial aircraft benefit from military R&D.The extensive participation of private companies inhighly sophisticated military R&D projects helpstrain technical personnel in those companies andtherefore increases general know-how. MilitaryR&D also pays for basic equipment, such as highlyspecialized tools, that may later be used forcommercial aeronautics work . And even if amilitary R&D project does not lead to a specifictechnological advance (' failed programmes'), it mayhave commercial utility to the company thatcarried it out by informing the company ofresearch 'dead-ends' that should be avoided .

— navigational aids ( 100% )

— general avionics ( 30% )

— cockpit displays ( 100% )

— avionic software processes ( 80% )

— sub-systems technology ( 90% )

— sub-systems hardware ( 10% )

— flight control techniques ( 60% )

— composite materials ( 60 to 100% )

— advanced structural metallics ( 100% ).

( 93 ) Such increases in general know-how will , inparticular, arise in the areas of design andmanufacturing processes . For example , the USDoD is supporting a major programme on the useof synthetic environments design technology whichlinks advanced CAD/CAM systems with productmodelling and simulation and which willsignificantly reduce the time and risk involved inputting new aircraft into production . Thesetechniques are equally applicable to civilprogrammes . Other examples are the know-howfor applying new composites technology onmilitary programmes such as the V-22 , F-22 andthe B-2 , which provided the knowledge required todesign and manufacture composites structures nowused for the B-777, or the design manufacturingand producibility simulation, an engineering systemdeveloped by MDC over the course of its militaryprogrammes which leads to a significant reductionin the timing of the overall design cycle and was amodel for the development of the MD-XX. In thiscontext, it should be noted that Boeing, in its replyto the Statement pursuant to Article 18 , stated thatit used know-how in computing and software

( 95 ) It is true, as stated by Boeing and MDC, that arecipient of public funding for military R&D mayoften subcontract a significant amount of the workinvolved . However, this does not reduce theopportunity for a prime contractor, such as Boeingor MDC, to gain full advantage of the know-howand technological expertise generated by suchprogrammes, since the prime contractor willalways have access to full details of the R&D workcarried out. It is in any event questionable to whatextent and with what frequency publicly fundedR&D work is put out to subcontractors . Forexample , MDC stated that composites are usually

Official Journal of the European Communities L 336/338 . 12 . 97 1 EN

above, would over time confer on it a significantcompetitive advantage vis-a-vis its only remainingcompetitor in large commercial aircraft .

developed by material suppliers and not byBoeing or MDC. However, in the frameworkof the DoD-funded manufacturing technologyprogramme, the development of low-costcomposites was contracted to Boeing for fuselageapplications and to MDC for wing applications .That manufacturing technology programme wasthe most important part of the DoD's 1996 budgetfor technology transfer initiatives for which a totalof US $ 1 768 million was requested .

( 99 ) The Commission considers that to be especiallytrue since in the United States the line between thedefence and civil aircraft programmes is much lessclear than in the European Union, because of theUS policy that defence , space and commercialtechnology are highly linked . For instance, inAugust 1995 , the National Space and TechnologyCouncil stated :( 96 ) Besides its leading position in fighter aircraft,

MDC is also one of the leading manufacturers ofmilitary transport aircraft . It appears thattechnology developed in the military transportsector can be fully used for commercialapplications . MDC recently announced that it hasdecided to produce a commercial version of itsC-17 military transport aircraft . In this context, ahistoric example is the Boeing 747 which wasdeveloped at its initial stage for a militarytransport competition .

' the significant basic technological commonalitybetween military and civil aviation productsand services must be exploited to increase theproductivity and efficiency of our R&Ddevelopment activities . This requiresgovernment and industry, working together, toactively seek technological goals that arecommon to both civil and militaryapplications . . . DoD, the Federal AviationAdministration (FAA) and NASA must expandtheir focus on encouraging this earlyconsideration of dual-use applications intechnology development programmes .'

Again in a December 1995 Congressional ResearchService Report it was stated:

'In DoD, dual-use technology development wasemphasized, both to expand the commercialmanufacturing base for producing militaryproducts and to help exploit militarytechnology for civilian purposes '.

( 97 ) With respect to commercial applications of militarytechnology, Boeing has stated that, in terms of the1992 Bilateral Agreement on Large Civil Aircraftbetween the Community and the US, it has derivedno identifiable benefits to commercial programmesfrom its defence and other US Governmentprogrammes during the period since 1993 .However, Boeing in a statement during the oralhearing on 13 June 1997 admitted that there existsat least a broad commonality between military andcommercial research applications . Boeing hasclaimed that such commonality benefits the wholeindustry rather than individual companies such asitself. However, this seems highly unlikely, giventhat military research contracts are subject tosecurity and confidentiality rules . In particular,NASA has made use of ' limited exclusive rightsprovisions ' which provide for protection ofinformation from non-government partiesparticipating in agreements with NASA. Forexample , many programmes concerning the highspeed civil transport (HSCT), the proposedsuccessor to Concorde, are protected from publicdisclosure for at least five years .

Many such examples could be provided of the USAdministration 's emphasis on dual-use technology;if there were no transfer between military and civilapplications in the aerospace sector, such adual-use policy would make no sense .