Bahasa

Halaman

Hukum

CSR, Sustainability, Ethics & GovernanceSeries Editors: Samuel O. Idowu · René Schmidpeter

Nicholas CapaldiSamuel O. IdowuRené Schmidpeter Editors

Dimensional Corporate GovernanceAn Inclusive Approach

26/10/2020 Dimensional Corporate Governance | SpringerLink

https://link.springer.com/book/10.1007%2F978-3-319-56182-0 1/4

Dimensional Corporate Governance

An Inclusive Approach

Editors(view affiliations)

Nicholas CapaldiSamuel O. IdowuRené Schmidpeter

Book

11 Citations10k Downloads

Part of the CSR, Sustainability, Ethics & Governance book series (CSEG)

ChaptersAbout

Table of contents

1. Front MatterPages i-xxxviiPDF

2. Business and Society

1. Front MatterPages 1-1PDF

2. Global Institution of Business? Comparing Role-of-Business Expectations in USA,South Korea, Hong Kong and SingaporeRandal S. Franz, Donghun “Don” LeePages 3-20

3. Justifying CEO Pay Ratios: Analysing Corporate Responses to Bloomberg’s Listing ofStandard & Poor’s 500 Pay RatiosManuel Castelo Branco, Catarina Delgado

26/10/2020 Dimensional Corporate Governance | SpringerLink

https://link.springer.com/book/10.1007%2F978-3-319-56182-0 2/4

Pages 21-364. The Banality of Good and Evil: Ethics Courses in Business Management Education

Mary GodwynPages 37-48

5. Ethics, Values and Corporate Cultures: A Wittgensteinian Approach in UnderstandingCorporate ActionFriedrich GlaunerPages 49-59

3. Corporate Governance

1. Front MatterPages 61-61PDF

2. Corporate Governance Regulatory Framework in Nigeria: The Offerings and ChallengesBenjamin J. InyangPages 63-78

3. Board Composition and Corporate Governance Mechanisms in the Nigerian BankingSectorAdebimpe Lincoln, Oluwatofunmi Adedoyin, Janet LaugharnePages 79-102

4. Corporate Social Responsibility, Shared Territorial Governance and Social Innovation:Some Exemplary Italian PathsMara Del BaldoPages 103-120

5. Corporate Governance in Brazilian Companies: The Influence of the Founder in theFinancial DecisionsLiliane Segura, Henrique Formigoni, Rute Abreu, Fátima DavidPages 121-137

4. Corporate Social Responsibility and Reporting Corporate SocialResponsibility

1. Front MatterPages 139-139PDF

2. The Concept of Value Beyond Economics: Social and Philosophical Roots for CorporateSocial ResponsibilityMassimo Costa, Patrizia TorrecchiaPages 141-149

3. Corporate Social Responsibility Management System: A Beverage Industry Case StudyRita Almeida, Fátima David, Rute AbreuPages 151-173

4. Choice, Freedom and Responsibility in Public Administration: The Need for CSRReporting of Core ActivitiesPaolo D’Anselmi, Athanasios Chymis, Massimiliano Di BitettoPages 175-187

5. Development of an Indicator of Economic, Environmental and Societal Development(IDEES) Concept for SMEs: A Case Study in the Hotel and Restaurant Business SectorPhilippe Callot

26/10/2020 Dimensional Corporate Governance | SpringerLink

https://link.springer.com/book/10.1007%2F978-3-319-56182-0 3/4

Pages 189-2046. Corporate Social Responsibility in Indian Apparel Industry

Archana GandhiPages 205-212

5. Sustainability and Financial Performance

1. Front MatterPages 213-213PDF

2. The Impact of Sustainability Practices on the Financial Performance: Evidence fromListed Oil and Gas Companies in NigeriaAbubakar M. DemboPages 215-233

3. Design and Development of Ergonomic Workstation for Pregnant Workers inReadymade Garment IndustryNoopur Anand, Archana Gandhi, Vipul Verma, Sarablin KaurPages 235-250

4. Proposed Integrated Measurement Standard to Measure Sustainability Performance:Evidence From IndonesiaKurnia Perdana, Juniati GunawanPages 251-267

6. Summary

1. Front MatterPages 269-269PDF

2. Dimensional Corporate Governance: An Inclusive Approach in SummarySamuel O. Idowu, Nicholas Capaldi, René SchmidpeterPages 271-274

7. Back MatterPages 275-281PDF

About this book

Introduction

This book explores different dimensions of the field of corporate governance and socialresponsibility. It discusses how business and society perceive and relate to CSR; how the field hascontinued to reshape modern corporate boardrooms in both the advanced and emergingeconomies; how CSR has transformed the manner in which modern corporate entities disclose thenon-financial information aspect of their operations to the world at large; and the way in whichsustainable development has continued to contribute to improving the quintuple bottom line -people, planet, prosperity, partnership and peace - of 21st century corporate entities. Further, thebook also provides evidence of how these aspects of corporate social responsibility are depicted indifferent forms in eleven nations around the globe.

26/10/2020 Dimensional Corporate Governance | SpringerLink

https://link.springer.com/book/10.1007%2F978-3-319-56182-0 4/4

© 2020 Springer Nature Switzerland AG. Part of Springer Nature.

Not logged in Not affiliated 139.0.252.23

Keywords

CSR responsible management sustainable business models greenwashing fraudethical values and profit stakeholder interest

Editors and affiliations

Nicholas Capaldi (1) Samuel O. Idowu (2) René Schmidpeter (3)

1. College of Business, Loyola University New Orleans, , New Orleans, USA2. Guildhall Faculty of Business and Law, London Metropolitan University, , London, UnitedKingdom3. Cologne Business School, , Cologne, Germany

Bibliographic information

DOI https://doi.org/10.1007/978-3-319-56182-0Copyright Information Springer International Publishing AG 2017Publisher Name Springer, ChameBook Packages Business and Management Business and Management (R0)Print ISBN 978-3-319-56181-3Online ISBN 978-3-319-56182-0Series Print ISSN 2196-7075Series Online ISSN 2196-7083Buy this book on publisher's site

��������� ������ �������� ������ �������������

���������������������������������� !�"# �$%$%�#$�&���$�'(����� ( ))��� ���� *�&

+,-./0123415106,7893:1;<=03>?3@6/A<7B93C=DE3:-.;,65=F=G7H93

8?34/00=I=3/J3K<2,D=22L3M/N/013OD,P=G2,FN3+=A3>G0=1D2L3L3+=A3>G0=1D2L3O:QB?3R<,06.1003S1-<0FN3/J3K<2,D=2231D63M1AL3M/D6/D3T=FG/5/0,F1D3OD,P=G2,FNL3L3M/D6/DL3OD,F=6U,DI6/;H?34/0/ID=3K<2,D=223:-.//0L3L34/0/ID=L3R=G;1DN

VWXYZ[Z\][]_ZXa

+,-./0123415106,3,23M=I=D6G=b:/<0E3c,2F,DI<,2.=634.1,G3,D3K<2,D=223dF.,-231F3M/N/013OD,P=G2,FNL+=A3>G0=1D2?3e=3102/32=GP=23123c,G=-F/G3/J3F.=3+1F,/D1034=DF=G3J/G3K<2,D=223dF.,-2?3e=3F1<I.F5G=P,/<20N31Ff3F.=3OD,P=G2,FN3/J3g<0213A.=G=3.=3A123T-S1G0,D3C=2=1G-.3hG/J=22/G3/J3M1Ai34/0<;j,1OD,P=G2,FNi3k<==D234/00=I=L34,FN3OD,P=G2,FN3/J3+=A3l/Gmi3g.=3OD,F=63:F1F=23T,0,F1GN3Q-16=;N31Fn=2F3h/,DFL31D63F.=3+1F,/D103OD,P=G2,FN3/J3:,DI15/G=?[hG/J=22/G3415106,3G=-=,P=63.,23K?Q?3JG/;3F.=OD,P=G2,FN3/J3h=DD2N0P1D,131D63.,23h.?c?3JG/;34/0<;j,13OD,P=G2,FN?3e,235G,D-,5103G=2=1G-.31D6F=1-.,DI3,DF=G=2F3,23,D35<j0,-35/0,-N31D63,F23,DF=G2=-F,/D3A,F.35/0,F,-1032-,=D-=L35.,0/2/5.NL301ALG=0,I,/DL31D63=-/D/;,-2?3e=3,23F.=31<F./G3/J3o3j//m2L3/P=G3pq31GF,-0=2L31D63=6,F/G3/J32,r31DF./0/I,=2?e=3,2313;=;j=G3/J3F.=3=6,F/G,103j/1G63/J32,r3s/<GD10231D63.1232=GP=63;/2F3G=-=DF0N3123=6,F/G/J3tuvwxyz{||}x~�z�u}~��~w�?[hG/J=22/G3415106,3,23F.=3G=-,5,=DF3/J3IG1DF23JG/;3F.=3+1F,/D10dD6/A;=DF3J/G3F.=3e<;1D,F,=2L3g.=3T=00/D3S/<D61F,/DL3g.=3O?:?3c=51GF;=DF3/J3d6<-1F,/DL3g.=K/1G63/J3C=I=DF23/J3M/<,2,1D1L31D63F.=3�/.D3g=;50=F/D3S/<D61F,/D31;/DI3/F.=G2?3e=3,231D,DF=GD1F,/D100N3G=-/ID,�=632-./01G31D63136/;=2F,-35<j0,-35/0,-N325=-,10,2F3/D32<-.3,22<=23123.,I.=G=6<-1F,/DL3j,/b=F.,-2L3j<2,D=223=F.,-2L31JJ,G;1F,P=31-F,/DL31D63,;;,IG1F,/D?[hG/J=22/G3415106,�2G=-=DF35<j0,-1F,/D23,D-0<6=31GF,-0=23/D3-/G5/G1F=32/-,103G=25/D2,j,0,FNL3F.=3=F.,-23/J3JG==3;1Gm=F2/-,=F,=2L31D631D3,DF=00=-F<103j,/IG15.N3/J3�/.D3:F<1GF3T,003,D3-/DD=-F,/D3A,F.3A.,-.3.=3A12G=-=DF0N3,DF=GP,=A=63/D34b:hQ+�23K//mD/F=2?

:1;<=03>3@6/A<3,2313:=D,/G3M=-F<G=G3,D3Q--/<DF,DI31D634/G5/G1F=3:/-,103C=25/D2,j,0,FN31F3M/D6/DR<,06.1003:-.//03/J3K<2,D=223�3M1AL3M/D6/D3T=FG/5/0,F1D3OD,P=G2,FNL3OU?3e=3G=2=1G-.=23,D3F.=J,=0623/J34/G5/G1F=3:/-,103C=25/D2,j,0,FN374:C9L34/G5/G1F=3R/P=GD1D-=L3K<2,D=223dF.,-231D6Q--/<DF,DI31D63.1235<j0,2.=63,D3j/F.35G/J=22,/D1031D631-16=;,-3s/<GD10232,D-=38�p�?3e=3,231JG==;1D3/J3F.=34,FN3/J3M/D6/D31D6313M,P=GN;1D3/J3F.=3n/G2.,5J<034/;51DN3/J34.1GF=G=6:=-G=F1G,=231D63Q6;,D,2FG1F/G2?3:1;<=03,23F.=3c=5<FN34d>31D63S,G2F3�,-=3hG=2,6=DF3/J3F.=3R0/j104/G5/G1F=3R/P=GD1D-=3@D2F,F<F=?3e=3.1230=632=P=G103=6,F=63j//m23,D34:CL3,23F.=3d6,F/Gb,Db4.,=J3/JFA/3:5G,DI=G�23G=J=G=D-=3j//m23�3F.=3dD-N-0/5=6,13/J34/G5/G1F=3:/-,103C=25/D2,j,0,FN31D63F.=c,-F,/D1GN3/J34/G5/G1F=3:/-,103C=25/D2,j,0,FN31D631D3d6,F/Gb,Db4.,=J3/J3F.=3@DF=GD1F,/D103�/<GD10/J34/G5/G1F=3:/-,103C=25/D2,j,0,FN?3e=3,23102/313:=G,=23d6,F/G3J/G3:5G,DI=G�23j//m23/D34:CL:<2F1,D1j,0,FNL3dF.,-231D63R/P=GD1D-=?3>D=3/J3.,23=6,F=63j//m23A/D3F.=3;/2F3><F2F1D6,DI3K<2,D=22C=J=G=D-=3j//m3QA1G63/J3F.=3Q;=G,-1D3M,jG1GN3Q22/-,1F,/D37QMQ93,D3Bq8�31D631D/F.=G3A123G1Dm=68pF.3,D3F.=3Bq8q3g/53�q3:<2F1,D1j,0,FN3K//m23jNL3�}�v~x���z��x��~�x���z�u��}x�}vxwx��z��}��~��x�t~��~}����3:1;<=03,2313;=;j=G3/J3F.=34/;;,FF==3/J3F.=34/G5/G1F=3R/P=GD1D-=3:5=-,103@DF=G=2FRG/<53/J3F.=3KG,F,2.3Q-16=;N3/J3T1D1I=;=DF37KQT9?3e=3,23/D3F.=3d6,F/G,103K/1G623/J3F.=@DF=GD1F,/D103�/<GD103/J3K<2,D=223Q6;,D,2FG1F,/DL341D16131D63Q;J,F=1FG<3d-/D/;,-3�/<GD10LC/;1D,1?3:1;<=03.1236=0,P=G=6313D<;j=G3/J3U=ND/F=3:5==-.=231F3D1F,/D1031D63,DF=GD1F,/D10-/DJ=G=D-=231D63A/Gm2./523/D34:C31D63.123/D3FA/3/--12,/D23Bqqp31D63Bq8�3A/D3d;=G106�2e,I.0N34/;;=D6=63M,F=G1F,3+=FA/Gm3QA1G623J/G3dr-=00=D-=?3g/361F=L3:1;<=03.123=6,F=632=P=G10j//m23,D3F.=3J,=063/J34:CL3:<2F1,D1j,0,FN31D63R/P=GD1D-=31D63.123AG,FF=D3J/<G3J/G=A/G623F/3j//m2?

��������� ������ �������� ������ �������������

���������������������������������� !�"# �$%$%�#$�&���$�'(����� ( ))��� ���� ��&

*+,-,-+./012340+567804+.917:40;62<+=>?+@607+AB+./012340+567804?

5A7+;A334<+12+5A7+6BB1;1674<+CD,?E-?CFG?CE-

.6H84;+I6J+J40K4<+6J+62+4L74026;+4L6H1240+7A+7I4+BA;;A9123+MN+M21K40J1714J+O+.82<40;62<P+M;J740P=23;16+Q8JR12+62<+@;SHA87I?+T4+1J+U800427;S+62+4L74026;+4L6H1240+67+QAV407+>A0<A2+M21K40J17SP=V40<442P+W44JJ1<4+M21K40J17SP+X1<<;4JV0A83I+62<+.I4BB14;<+T6;;6H+M21K40J17SP+MN?

Q42Y+.UIH1</4740+IA;<J+7I4+Z0?+[840342+X4S40+\2<A94<+]I610+AB+27402671A26;+_8J124JJ+\7I1UJ62<+]A0/A0674+.AU16;+Q4J/A2J1V1;17S+67+]A;A324+_8J124JJ+.UIAA;+]_.a?+T4+1J+6;JA+6+/0AB4JJA0+67+7I4562b123+M21K40J17S+AB+c1262U4+62<+\UA2AH1UJ+6J+94;;+6J+7I4+<104U7A0+AB+7I4+]42740+BA0+=<K62U4<.8J76126V;4+X62634H427+]=.Xa+67+]_.?+T4+1J+6+J4014J+4<17A0+BA0+./012340dJ+].QP+.8J76126V1;17SP\7I1UJ+62<+>AK40262U4+VAARJP+6+J4U71A2+4<17A0+AB+7I4+\2USU;A/4<16+AB+]A0/A0674+.AU16;Q4J/A2J1V1;17S+\].Qa+62<+62+4<17A0+AB+7I4+Z1U71A260S+AB+]A0/A0674+.AU16;+Q4J/A2J1V1;17S+Z].Qa?T1J+04J460UI+62<+746UI123+6U71K1714J+BAU8J+A2+7I4+H62634H427+AB+]A0/A0674+.AU16;+Q4J/A2J1V1;17SP127402671A26;+/40J/4U71K4J+A2+].QP+.AU16;+22AK671A2+62<+.8J76126V;4+\2704/042480JI1/+6J+94;;+6J7I4+04;671A2JI1/+V479442+V8J124JJ+62<+JAU147S?+T4+I6J+/8V;1JI4<+91<4;S+62<+1J+7I4+4<17A0+AB+7I4>40H62+H62634H427+J4014J+A2+]A0/A0674+.AU16;+Q4J/A2J1V1;17S+67+./012340+>6V;40?+

efghfijklmnfopfqriksltfiq

_AAR+W17;4+Z1H42J1A26;+]A0/A0674+>AK40262U4

_AAR+.8V717;4+=2+2U;8J1K4+=//0A6UI

\<17A0J+51UIA;6J+]6/6;<1+

.6H84;+u?+<A98+

Q42Y+.UIH1</4740+

.4014J+W17;4+].QP+.8J76126V1;17SP+\7I1UJ+v+>AK40262U4

.4014J+=VV04K1674<+W17;4+].QP+.8J76126V1;17SP+\7I1UJ+v+>AK40262U4

Zu+I77/Jwxx<A1?A03xC-?C--yxGyDzEzECGzF{CD,z-

]A/S013I7+2BA0H671A2+./012340+27402671A26;+@8V;1JI123+=>+,-Cy

@8V;1JI40+56H4+./012340P+]I6H

4_AAR+@6UR634J+_8J124JJ+62<+X62634H427+_8J124JJ+62<+X62634H427+Q-a

T60<UAK40+._5+GyDzEzECGzF{CDCzE

.AB7UAK40+._5+GyDzEzECGzDFD|{zE

4_AAR+._5+GyDzEzECGzF{CD,z-

.4014J+..5+,CG{zy-yF

.4014J+\z..5+,CG{zy-DE

\<171A2+58HV40+C

58HV40+AB+@634J+}}}~ P+,DC

58HV40+AB+;;8J70671A2J+CD+Vx9+1;;8J70671A2JP+-+1;;8J70671A2J+12+UA;A80

WA/1UJ+]A0/A0674+>AK40262U4+

_8J124JJ+\7I1UJ+

]A0/A0674+.AU16;+Q4J/A2J1V1;17S+

]A0/A0674+\2K10A2H4276;+X62634H427+

.8J76126V;4+Z4K4;A/H427+

_8S+7I1J+VAAR+A2+/8V;1JI40�J+J174

1

PROPOSED INTEGRATED MEASUREMENT STANDARD TO MEASURE SUSTAINABILITY PERFORMANCE: EVIDENCE FROM INDONESIA

Abstract This study introduces a new integrated measurement standard to comprehensively measure sustainability performance., It which is comprised comprises of a balanced scorecard and three internationally leading sustainability standards: Global Reporting Initiatives (GRI), ISO 26000 and United Nation Global Compact (UNGC). to comprehensively measure sustainability performance. These integrated guidelines cover four aspects, namely economical, social, environmental, and the well-being. Samples were taken from Indonesian companies which that had participated in the Indonesia Sustainability Reporting Awards (ISRA). The 2010 and 2011 sustainability reports are were examined using these integrated measurement standards (IMS). The results of a content analysis showed that the trend of disclosing sustainability had tended to increase over the past two years. The disclosure scores are were considered medium to high profile, with the indication that the sustainability performance of state-owned companies is was higher than that of private companies; publicly-listed companies obtained higher scores of disclosures than did non-listed companies; and manufacturing industries received the highest scores followed by service and energy industries respectively.

Keywords: integrated measurement standard, sustainability disclosure, content analysis.

INTRODUCTION

The main purpose of business is profit. The word profit not only refers to short-term and temporary profit, but also long-term profit with its impact on the increasing the value of a company. Once these aims are reached, the company will be sustainable. On the other hand, there is a changing paradigm that states that long-term profit is not only about the amount of profit, but also about non-monetary factors. Companies that integrate sustainability into their strategies can achieve higher non-financial profits. Those profits may serve as a good corporate image for all stakeholders, influence the customers’ perceptions, maintain the customers’ loyalty and attract new customers, attract the best candidates for vacant staff positions, and increase the motivation and commitment of the employees (Maignan et al, 1999; Sharma et al, 2009). Sustainability can also leverage social legitimacy and environmental endorsement in comprehensive ways, decrease the cost of production, and ultimately increase the competitive advantage of the corporation (Branco and Rodrigues, 2007; Garriga and Mele, 2004; Porter and Kramer, 2006; Meehan et al, 2006).

Stakeholder theory states that sustainability performance will be affected by social legitimacy, in which one of the strategic decisions taken into consideration is the increasing stakeholder’s demands (Garriga and Mele, 2004; Hanke and Stark, 2009; Latteman et al, 2009). NGOs and society are legitimate elements which can interrupt or interfere with business operations, so their existence should not be ignored. Governments can also interrupt or interfere with business operations through regulations, and if companies do not accommodate their stakeholders’ demands, financial institutions will be affected in their financial performance

��������� ������ �������� ������ �������������

���������������������������������� !�"# �$%$%�#$�&���$�'(����� ( ))��� ���� ��&

*+,-./

012345164789:6;<6;7=39>6?3;474@3

A49B4@8C51?39A<<;67@D

EFGHIJKLMGNO+PQQGRGPHGISKT

UGVWIRPK+XPYPRFGZP[\NR+]+_FIO\NSa+ZVW[GFYNHNJ

bIIc

.,+XGHPHGISK

..c+dIOSRIPFK

ePJH+IQ+HWN+XZf+Z\KHPGSPgGRGHhf+EHWGVK+i+jIMNJSPSVN+gIIc+KNJGNK+LXZEjT

XWPYHNJKkgI\H

l7m8396n9@64=34=5

ePoN+++++IQ+++,UNpH

.+qJISH+rPHHNJePoNK+GspppMGGedq

,+tC514355974u9v6@13=w

.+qJISH+rPHHNJePoNK+.s.edq

,+jRIgPR+_SKHGH\HGIS+IQ+b\KGSNKKx+XI[YPJGSo+IRNsIQsb\KGSNKK+EpYNVHPHGISK+GS+yZkfZI\HW+zIJNPf+{ISo+zISo+PSF+ZGSoPYIJN

��������� ������ �������� ������ �������������

���������������������������������� !�"# �$%$%�#$�&���$�'(����� ( ))��� ���� ��&

*+,-+./01/23+,45/67,89:,/;67,</=>>?+8>@/ABCD

A1/E:@FGHIG,8/JKL/?+I/*+FG7@M/N,+.I@G,8/J73O73+F>/*>@O7,@>@/F7/P.77QR>38S@/=G@FG,8/7H0F+,-+3-/T/?773S@/UDD/?+I/*+FG7@V+,:>./J+@F>.7/P3+,W75/J+F+3G,+/6>.8+-7?+8>@/CXBAY

Z1/[9>/P+,+.GFI/7H/\77-/+,-/K]G.M/KF9GW@/J7:3@>@/G,/P:@G,>@@/V+,+8>Q>,F/K-:W+FG7,V+3I/\7- I,?+8>@/A_BZ

U1/KF9GW@5/a+.:>@/+,-/J73O73+F>/J:.F:3>@M/N/bGFF8>,@F>G,G+,/NOO37+W9/G,/c,->3@F+,-G,8J73O73+F>/NWFG7,23G>-3GW9/\.+:,>3?+8>@/ZdBUd

A1/efghfgijklmfnkgoiopk

X1/237,F/V+FF>3?+8>@/YXBYX?62

C1/J73O73+F>/\7]>3,+,W>/*>8:.+F73I/23+Q>73q/G,/rG8>3G+M/[9>/LHH>3G,8@/+,-/J9+..>,8>@P>,s+QG,/E1/t,I+,8?+8>@/YAB_

A1/P7+3-/J7QO7@GFG7,/+,-/J73O73+F>/\7]>3,+,W>/V>W9+,G@Q@/G,/F9>/rG8>3G+,/P+,qG,80>WF73N->RGQO>/=G,W7.,5/L.: +F7H:,QG/N->-7IG,5/E+,>F/=+:89+3,>?+8>@/_dBXDC

Z1/J73O73+F>/07WG+./*>@O7,@GRG.GFI5/09+3>-/[>33GF73G+./\7]>3,+,W>/+,-/07WG+./t,,7]+FG7,M07Q>/Ku>QO.+3I/tF+.G+,/?+F9@V+3+/6>./P+.-7?+8>@/XDABXCD

U1/J73O73+F>/\7]>3,+,W>/G,/P3+4G.G+,/J7QO+,G>@M/[9>/t,H.:>,W>/7H/F9>/27:,->3/G,/F9>2G,+,WG+./6>WG@G7,@=G.G+,>/0>8:3+5/v>,3Gw:>/273QG87,G5/*:F>/NR3>:5/2xFGQ+/6+]G-?+8>@/XCXBXA_

Z1/efghfgijklyfpzi{l|k}hfo}z~z{zj�lio�l|khfgjzo�lefghfgijklyfpzi{|k}hfo}z~z{zj�

X1/237,F/V+FF>3?+8>@/XAdBXAd?62

C1/[9>/J7,W>OF/7H/a+.:>/P>I7,-/KW7,7QGW@M/07WG+./+,-/?9G.7@7O9GW+./*77F@/H73/J73O73+F>07WG+./*>@O7,@GRG.GFIV+@@GQ7/J7@F+5/?+F3G4G+/[733>WW9G+?+8>@/XZXBXZd

A1/J73O73+F>/07WG+./*>@O7,@GRG.GFI/V+,+8>Q>,F/0I@F>QM/N/P>]>3+8>/t,-:@F3I/J+@>/0F:-I*GF+/N.Q>G-+5/2xFGQ+/6+]G-5/*:F>/NR3>:?+8>@/XUXBX_A

Z1/J97GW>5/23>>-7Q/+,-/*>@O7,@GRG.GFI/G,/?:R.GW/N-QG,G@F3+FG7,M/[9>/r>>-/H73/J0**>O73FG,8/7H/J73>/NWFG]GFG>@

��������� ������ �������� ������ �������������

���������������������������������� !�"# �$%$%�#$�&���$�'(����� ( ))��� ���� %�&

*+,-,./01234-567.189+2+36,3.:9;5637.<+33656-6+2,./6.=68488,*+>43.?@AB?C@

AD./4E4-,F5428.,G.+2.H2I6J+8,K.,G.LJ,2,56J7.L2E6K,25428+-.+2I.M,J648+-./4E4-,F5428NH/LLMO.:,2J4F8.G,K.M<L3P.1.:+34.M8QI;.62.894.R,84-.+2I.S438+QK+28.=Q362433.M4J8,K*96-6FF4.:+--,8*+>43.?CTBUVW

XD.:,KF,K+84.M,J6+-.S43F,236Y6-68;.62.H2I6+2.1FF+K4-.H2IQ38K;1KJ9+2+.Z+2I96*+>43.UVABU?U

AD.[\]_a_bcde_afega_ah_ceijklmkn_ahj

?D.oK,28.<+884K*+>43.U?pBU?p*/o

UD.q94.H5F+J8.,G.MQ38+62+Y6-68;.*K+J86J43.,2.894.o62+2J6+-.*4KG,K5+2J4P.LE6I42J4.GK,5r6384I.s6-.+2I.Z+3.:,5F+2643.62.t6>4K6+1YQY+u+K.<D./45Y,*+>43.U?ABUpp

pD./436>2.+2I./4E4-,F5428.,G.LK>,2,56J.v,Ku38+86,2.G,K.*K4>2+28.v,Ku4K3.62S4+I;5+I4.Z+K5428.H2IQ38K;t,,FQK.12+2I7.1KJ9+2+.Z+2I967.w6FQ-.w4K5+7.M+K+Y-62.x+QK*+>43.UpABUAV

*+>4.....,G...Ut4y8

zbm\e{]ebmm|

}akmf\h ma

q963.Y,,u.4yF-,K43.I6GG4K428.I654236,23.,G.894.G64-I.,G.J,KF,K+84.>,E4K2+2J4.+2I.3,J6+-K43F,236Y6-68;D.H8.I63JQ3343.9,~.YQ362433.+2I.3,J648;.F4KJ46E4.+2I.K4-+84.8,.:MS�.9,~.894.G64-I.9+3J,2862Q4I.8,.K439+F4.5,I4K2.J,KF,K+84.Y,+KIK,,53.62.Y,89.894.+IE+2J4I.+2I.454K>62>4J,2,5643�.9,~.:MS.9+3.8K+23G,K54I.894.5+224K.62.~96J9.5,I4K2.J,KF,K+84.42868643.I63J-,34.8942,2BG62+2J6+-.62G,K5+86,2.+3F4J8.,G.8946K.,F4K+86,23.8,.894.~,K-I.+8.-+K>4�.+2I.894.~+;.62.~96J93Q38+62+Y-4.I4E4-,F5428.9+3.J,2862Q4I.8,.J,28K6YQ84.8,.65FK,E62>.894.�Q628QF-4.Y,88,5.-624.BF4,F-47.F-+2487.FK,3F4K68;7.F+K824K396F.+2I.F4+J4.B.,G.U?38.J428QK;.J,KF,K+84.42868643D.oQK894K7.894Y,,u.+-3,.FK,E6I43.4E6I42J4.,G.9,~.89434.+3F4J83.,G.J,KF,K+84.3,J6+-.K43F,236Y6-68;.+K4.I4F6J84I.62I6GG4K428.G,K53.62.4-4E42.2+86,23.+K,Q2I.894.>-,Y4D

�jd�mkf]

:MS K43F,236Y-4.5+2+>454283Q38+62+Y-4.YQ362433.5,I4-3>K442~+3962>GK+QI

4896J+-.E+-Q43.+2I.FK,G6838+u49,-I4K.6284K438

�f mk]e_afe_llc_ ma]

��������� ������ �������� ������ �������������

���������������������������������� !�"# �$%$%�#$�&���$�'(����� ( ))��� ���� *�&

+,-./0123415106,7893:1;<=03>?3@6/A<7B93C=DE3:-.;,65=F=G7H93

8?34/00=I=3/J3K<2,D=22L3M/N/013OD,P=G2,FN3+=A3>G0=1D2L3L3+=A3>G0=1D2L3O:QB?3R<,06.1003S1-<0FN3/J3K<2,D=2231D63M1AL3M/D6/D3T=FG/5/0,F1D3OD,P=G2,FNL3L3M/D6/DL3OD,F=6U,DI6/;H?34/0/ID=3K<2,D=223:-.//0L3L34/0/ID=L3R=G;1DN

VWXYZ[Z\][]_ZXa

+,-./0123415106,3,23M=I=D6G=b:/<0E3c,2F,DI<,2.=634.1,G3,D3K<2,D=223dF.,-231F3M/N/013OD,P=G2,FNL+=A3>G0=1D2?3e=3102/32=GP=23123c,G=-F/G3/J3F.=3+1F,/D1034=DF=G3J/G3K<2,D=223dF.,-2?3e=3F1<I.F5G=P,/<20N31Ff3F.=3OD,P=G2,FN3/J3g<0213A.=G=3.=3A123T-S1G0,D3C=2=1G-.3hG/J=22/G3/J3M1Ai34/0<;j,1OD,P=G2,FNi3k<==D234/00=I=L34,FN3OD,P=G2,FN3/J3+=A3l/Gmi3g.=3OD,F=63:F1F=23T,0,F1GN3Q-16=;N31Fn=2F3h/,DFL31D63F.=3+1F,/D103OD,P=G2,FN3/J3:,DI15/G=?[hG/J=22/G3415106,3G=-=,P=63.,23K?Q?3JG/;3F.=OD,P=G2,FN3/J3h=DD2N0P1D,131D63.,23h.?c?3JG/;34/0<;j,13OD,P=G2,FN?3e,235G,D-,5103G=2=1G-.31D6F=1-.,DI3,DF=G=2F3,23,D35<j0,-35/0,-N31D63,F23,DF=G2=-F,/D3A,F.35/0,F,-1032-,=D-=L35.,0/2/5.NL301ALG=0,I,/DL31D63=-/D/;,-2?3e=3,23F.=31<F./G3/J3o3j//m2L3/P=G3pq31GF,-0=2L31D63=6,F/G3/J32,r31DF./0/I,=2?e=3,2313;=;j=G3/J3F.=3=6,F/G,103j/1G63/J32,r3s/<GD10231D63.1232=GP=63;/2F3G=-=DF0N3123=6,F/G/J3tuvwxyz{||}x~�z�u}~��~w�?[hG/J=22/G3415106,3,23F.=3G=-,5,=DF3/J3IG1DF23JG/;3F.=3+1F,/D10dD6/A;=DF3J/G3F.=3e<;1D,F,=2L3g.=3T=00/D3S/<D61F,/DL3g.=3O?:?3c=51GF;=DF3/J3d6<-1F,/DL3g.=K/1G63/J3C=I=DF23/J3M/<,2,1D1L31D63F.=3�/.D3g=;50=F/D3S/<D61F,/D31;/DI3/F.=G2?3e=3,231D,DF=GD1F,/D100N3G=-/ID,�=632-./01G31D63136/;=2F,-35<j0,-35/0,-N325=-,10,2F3/D32<-.3,22<=23123.,I.=G=6<-1F,/DL3j,/b=F.,-2L3j<2,D=223=F.,-2L31JJ,G;1F,P=31-F,/DL31D63,;;,IG1F,/D?[hG/J=22/G3415106,�2G=-=DF35<j0,-1F,/D23,D-0<6=31GF,-0=23/D3-/G5/G1F=32/-,103G=25/D2,j,0,FNL3F.=3=F.,-23/J3JG==3;1Gm=F2/-,=F,=2L31D631D3,DF=00=-F<103j,/IG15.N3/J3�/.D3:F<1GF3T,003,D3-/DD=-F,/D3A,F.3A.,-.3.=3A12G=-=DF0N3,DF=GP,=A=63/D34b:hQ+�23K//mD/F=2?

:1;<=03>3@6/A<3,2313:=D,/G3M=-F<G=G3,D3Q--/<DF,DI31D634/G5/G1F=3:/-,103C=25/D2,j,0,FN31F3M/D6/DR<,06.1003:-.//03/J3K<2,D=223�3M1AL3M/D6/D3T=FG/5/0,F1D3OD,P=G2,FNL3OU?3e=3G=2=1G-.=23,D3F.=J,=0623/J34/G5/G1F=3:/-,103C=25/D2,j,0,FN374:C9L34/G5/G1F=3R/P=GD1D-=L3K<2,D=223dF.,-231D6Q--/<DF,DI31D63.1235<j0,2.=63,D3j/F.35G/J=22,/D1031D631-16=;,-3s/<GD10232,D-=38�p�?3e=3,231JG==;1D3/J3F.=34,FN3/J3M/D6/D31D6313M,P=GN;1D3/J3F.=3n/G2.,5J<034/;51DN3/J34.1GF=G=6:=-G=F1G,=231D63Q6;,D,2FG1F/G2?3:1;<=03,23F.=3c=5<FN34d>31D63S,G2F3�,-=3hG=2,6=DF3/J3F.=3R0/j104/G5/G1F=3R/P=GD1D-=3@D2F,F<F=?3e=3.1230=632=P=G103=6,F=63j//m23,D34:CL3,23F.=3d6,F/Gb,Db4.,=J3/JFA/3:5G,DI=G�23G=J=G=D-=3j//m23�3F.=3dD-N-0/5=6,13/J34/G5/G1F=3:/-,103C=25/D2,j,0,FN31D63F.=c,-F,/D1GN3/J34/G5/G1F=3:/-,103C=25/D2,j,0,FN31D631D3d6,F/Gb,Db4.,=J3/J3F.=3@DF=GD1F,/D103�/<GD10/J34/G5/G1F=3:/-,103C=25/D2,j,0,FN?3e=3,23102/313:=G,=23d6,F/G3J/G3:5G,DI=G�23j//m23/D34:CL:<2F1,D1j,0,FNL3dF.,-231D63R/P=GD1D-=?3>D=3/J3.,23=6,F=63j//m23A/D3F.=3;/2F3><F2F1D6,DI3K<2,D=22C=J=G=D-=3j//m3QA1G63/J3F.=3Q;=G,-1D3M,jG1GN3Q22/-,1F,/D37QMQ93,D3Bq8�31D631D/F.=G3A123G1Dm=68pF.3,D3F.=3Bq8q3g/53�q3:<2F1,D1j,0,FN3K//m23jNL3�}�v~x���z��x��~�x���z�u��}x�}vxwx��z��}��~��x�t~��~}����3:1;<=03,2313;=;j=G3/J3F.=34/;;,FF==3/J3F.=34/G5/G1F=3R/P=GD1D-=3:5=-,103@DF=G=2FRG/<53/J3F.=3KG,F,2.3Q-16=;N3/J3T1D1I=;=DF37KQT9?3e=3,23/D3F.=3d6,F/G,103K/1G623/J3F.=@DF=GD1F,/D103�/<GD103/J3K<2,D=223Q6;,D,2FG1F,/DL341D16131D63Q;J,F=1FG<3d-/D/;,-3�/<GD10LC/;1D,1?3:1;<=03.1236=0,P=G=6313D<;j=G3/J3U=ND/F=3:5==-.=231F3D1F,/D1031D63,DF=GD1F,/D10-/DJ=G=D-=231D63A/Gm2./523/D34:C31D63.123/D3FA/3/--12,/D23Bqqp31D63Bq8�3A/D3d;=G106�2e,I.0N34/;;=D6=63M,F=G1F,3+=FA/Gm3QA1G623J/G3dr-=00=D-=?3g/361F=L3:1;<=03.123=6,F=632=P=G10j//m23,D3F.=3J,=063/J34:CL3:<2F1,D1j,0,FN31D63R/P=GD1D-=31D63.123AG,FF=D3J/<G3J/G=A/G623F/3j//m2?

��������� ������ �������� ������ �������������

���������������������������������� !�"# �$%$%�#$�&���$�'(����� ( ))��� ���� ��&

*+,-,-+./012340+567804+.917:40;62<+=>?+@607+AB+./012340+567804?

5A7+;A334<+12+5A7+6BB1;1674<+CD,?E-?CFG?CE-

.6H84;+I6J+J40K4<+6J+62+4L74026;+4L6H1240+7A+7I4+BA;;A9123+MN+M21K40J1714J+O+.82<40;62<P+M;J740P=23;16+Q8JR12+62<+@;SHA87I?+T4+1J+U800427;S+62+4L74026;+4L6H1240+67+QAV407+>A0<A2+M21K40J17SP=V40<442P+W44JJ1<4+M21K40J17SP+X1<<;4JV0A83I+62<+.I4BB14;<+T6;;6H+M21K40J17SP+MN?

Q42Y+.UIH1</4740+IA;<J+7I4+Z0?+[840342+X4S40+\2<A94<+]I610+AB+27402671A26;+_8J124JJ+\7I1UJ62<+]A0/A0674+.AU16;+Q4J/A2J1V1;17S+67+]A;A324+_8J124JJ+.UIAA;+]_.a?+T4+1J+6;JA+6+/0AB4JJA0+67+7I4562b123+M21K40J17S+AB+c1262U4+62<+\UA2AH1UJ+6J+94;;+6J+7I4+<104U7A0+AB+7I4+]42740+BA0+=<K62U4<.8J76126V;4+X62634H427+]=.Xa+67+]_.?+T4+1J+6+J4014J+4<17A0+BA0+./012340dJ+].QP+.8J76126V1;17SP\7I1UJ+62<+>AK40262U4+VAARJP+6+J4U71A2+4<17A0+AB+7I4+\2USU;A/4<16+AB+]A0/A0674+.AU16;Q4J/A2J1V1;17S+\].Qa+62<+62+4<17A0+AB+7I4+Z1U71A260S+AB+]A0/A0674+.AU16;+Q4J/A2J1V1;17S+Z].Qa?T1J+04J460UI+62<+746UI123+6U71K1714J+BAU8J+A2+7I4+H62634H427+AB+]A0/A0674+.AU16;+Q4J/A2J1V1;17SP127402671A26;+/40J/4U71K4J+A2+].QP+.AU16;+22AK671A2+62<+.8J76126V;4+\2704/042480JI1/+6J+94;;+6J7I4+04;671A2JI1/+V479442+V8J124JJ+62<+JAU147S?+T4+I6J+/8V;1JI4<+91<4;S+62<+1J+7I4+4<17A0+AB+7I4>40H62+H62634H427+J4014J+A2+]A0/A0674+.AU16;+Q4J/A2J1V1;17S+67+./012340+>6V;40?+

efghfijklmnfopfqriksltfiq

_AAR+W17;4+Z1H42J1A26;+]A0/A0674+>AK40262U4

_AAR+.8V717;4+=2+2U;8J1K4+=//0A6UI

\<17A0J+51UIA;6J+]6/6;<1+

.6H84;+u?+<A98+

Q42Y+.UIH1</4740+

.4014J+W17;4+].QP+.8J76126V1;17SP+\7I1UJ+v+>AK40262U4

.4014J+=VV04K1674<+W17;4+].QP+.8J76126V1;17SP+\7I1UJ+v+>AK40262U4

Zu+I77/Jwxx<A1?A03xC-?C--yxGyDzEzECGzF{CD,z-

]A/S013I7+2BA0H671A2+./012340+27402671A26;+@8V;1JI123+=>+,-Cy

@8V;1JI40+56H4+./012340P+]I6H

4_AAR+@6UR634J+_8J124JJ+62<+X62634H427+_8J124JJ+62<+X62634H427+Q-a

T60<UAK40+._5+GyDzEzECGzF{CDCzE

.AB7UAK40+._5+GyDzEzECGzDFD|{zE

4_AAR+._5+GyDzEzECGzF{CD,z-

.4014J+..5+,CG{zy-yF

.4014J+\z..5+,CG{zy-DE

\<171A2+58HV40+C

58HV40+AB+@634J+}}}~ P+,DC

58HV40+AB+;;8J70671A2J+CD+Vx9+1;;8J70671A2JP+-+1;;8J70671A2J+12+UA;A80

WA/1UJ+]A0/A0674+>AK40262U4+

_8J124JJ+\7I1UJ+

]A0/A0674+.AU16;+Q4J/A2J1V1;17S+

]A0/A0674+\2K10A2H4276;+X62634H427+

.8J76126V;4+Z4K4;A/H427+

_8S+7I1J+VAAR+A2+/8V;1JI40�J+J174

��������� ������ �������� ������ �������������

���������������������������������� !�"# �$%$%�#$�&���$�'(����� ( ))��� ���� &�&

2

It is important for a company to disclose its entire sustainability performance to its stakeholders and the most effective communication instrument for this is an annual report or a sustainability report (Branco and Rodriguez, 2007; Dhaliwal et al, 2011). A Sustainability report is also a strategy for a company to disclose its sustainability performance to its stakeholders (Golob and Barlet, 2007; Dhaliwal et al, 2011). Previous research states that the publishing of the social performance was advantageous for both the company and its stakeholders.

The evaluation of strategy, process and policy are is important to ensure the quality and quantity of the program. Hence, several stages of performance measurements are needed to evaluate a company’s CSR performance. This The performance measurement is a process of recording and evaluating of application accomplishments gaining the mission accomplishment through the results of a process. (Wood, 2010; Panayiotou, 2009).

The performance measurement of a company is a system that aims to help it accomplish its strategy by using financial and nonfinancial measurements. Performance measurement can be undertaken through a number of approaches and knowledge. Generally, the performance measurement has the following purposes:

1. To communicate the company’s strategy. 2. To measure both financial and non-financial performances, so that strategic accomplishment

can be achieved. 3. To accommodate better understanding between middle and low level management and also

to motivate the congruence of personal goals. 4. As an instrument to reach satisfaction based on individual approach and rational collective

ability. (McLoughin et al, 2009).

It is important for the company to acknowledge the quality of sustainability performance, . the The feedback and suggestions can become input for the improvement of strategic decisions, processes and sustainability policy policies in a the company. Thus, this study proposes a new integrated measurement standard (IMS) (Perdana and Gunawan, 2014) to comprehensively measure sustainability performances, covering four aspects of economical, social, environmental and the well--being.

Literature Review

Sustainability should be based on the whole of the company value chain. Each activity should provide some sustainable impact on the company; from planning, determination of strategies, formulation of programmes, systems and policies, processes and execution (Panayiotou et al, 2009; Butler et al, 2011; Gates and Germain, 2011). Furthermore, the measurement of sustainability performance is considered a significant constraintconstraint, as there is no decision yet as to which instrument is best to measure sustainability.

Previous research considered the integration of sustainability with corporate strategy in order to identify the stimulation of the social and environmental performance and also manage the positive and negative effects of the performance. Corporations wish to gain significant contributions for the society. A Sstrategic business units were dividedintegrated integrated into eight sustainable performance measurements, which are were measured by through

3

stakeholders’ responds responses, and the it shall results showed an the impact on a the long-term financial performance of the company.

Another prior study examined the integration of a balanced scorecard with GRI by using CSR performance disclosures in the annual report. The findings in this study are were more detailed on aspects of the integration of economic, environmental, social and governance reporting organizations and companies to evaluate the performance of the company. Some instruments such as GRI, UNGC, ISO 26000, UNEP-FI and OECD are integrated in this study. Integrated instruments are used simply because all aspects can be integrated into the sustainability perspective (Panayiotou et al, 2009; Hrebicek et al, 2011).

Prior studies attempted to develop reference models for measuring corporate sustainability performance by complementarity, shortcomings and strengths of eight well- known sustainability measurement initiatives alongside an extant corporate sustainability literature review (Delai and Takahashi, 2011).

Methodology

Forty six companies which that had published sustainability reports that were published in Indonesia, and which had participated in the Indonesian Sustainability Reporting Award (ISRA) in 2010 and 2011 have beenwere selected as the unit analysis of this study.

The measuring process of the sustainability performance used integrated measurement standardd by examining the sustainability disclosures quantity based on each indicator that are listed in the guidelines. Finally the scoring system is was taken from the previously established scoring guidelines and criteria.

Scoring Process

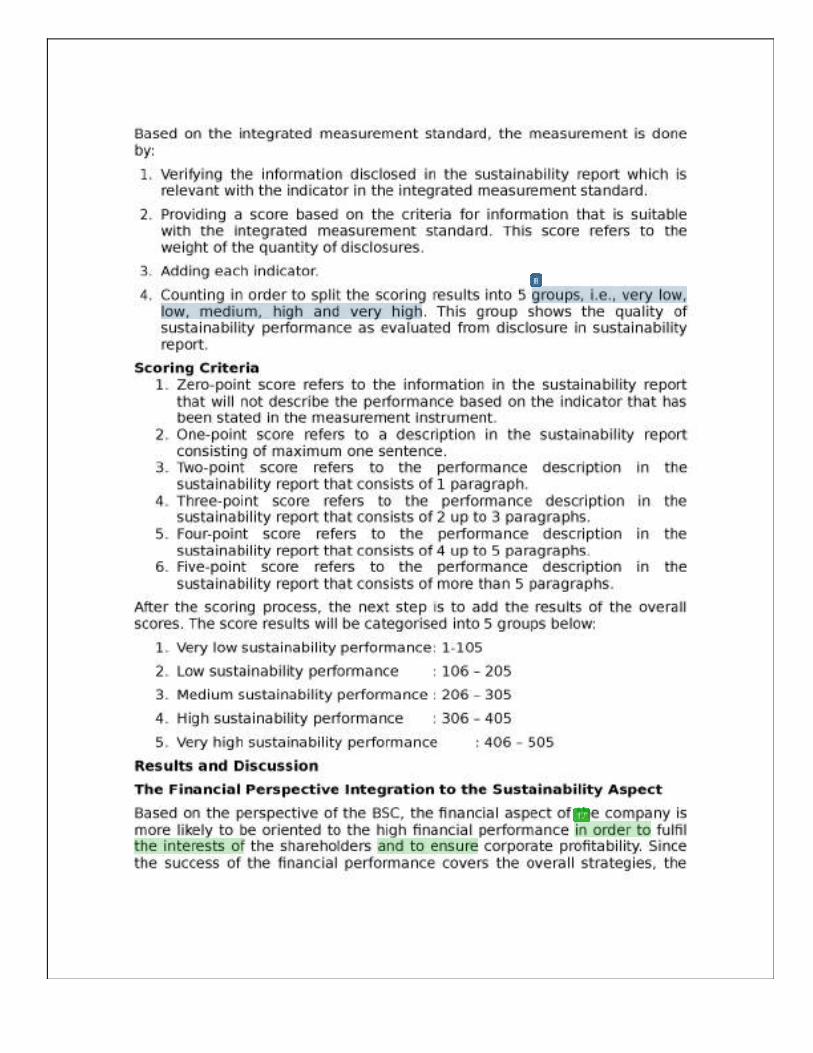

Based on the integrated measurement standard, the measurement is was done by:

1. Verifying the information disclosed in the sustainability report which is relevant with the indicator in the integrated measurement standard.

2. Providing a score based on the criteria for information that is suitable with the integrated measurement standard. This score refers to the weight of the quantity of disclosures.

3. Adding each indicator. 4. Counting in order to split the scoring results into 5 groups, i.e., very low, low, medium, high

and very high. This group shows the quality of sustainability performance as evaluated from disclosure in sustainability report.

Scoring Criteria 1. Zero-point score refers to the information in the sustainability report that will does not

describe the performance based on the indicator that has been stated in the measurement instrument.

2. One-point score refers to a description in the sustainability report consisting of a maximum one sentence.

3. Two-point score refers to the performance description in the sustainability report that consists of 1 paragraph.

4

4. Three-point score refers to the performance description in the sustainability report that consists of 2 up to 3 paragraphs.

5. Four-point score refers to the performance description in the sustainability report that consists of 4 up to 5 paragraphs.

6. Five-point score refers to the performance description in the sustainability report that consists of more than 5 paragraphs.

After the scoring process, the next step is to add the results of the overall scores. The score results will be categorisedcategorized into 5 groups below:

1. Very low sustainability performance : 1-105 2. Low sustainability performance : 106 – 205 3. Medium sustainability performance : 206 – 305 4. High sustainability performance : 306 – 405 5. Very high sustainability performance : 406 – 505

Results and Discussion

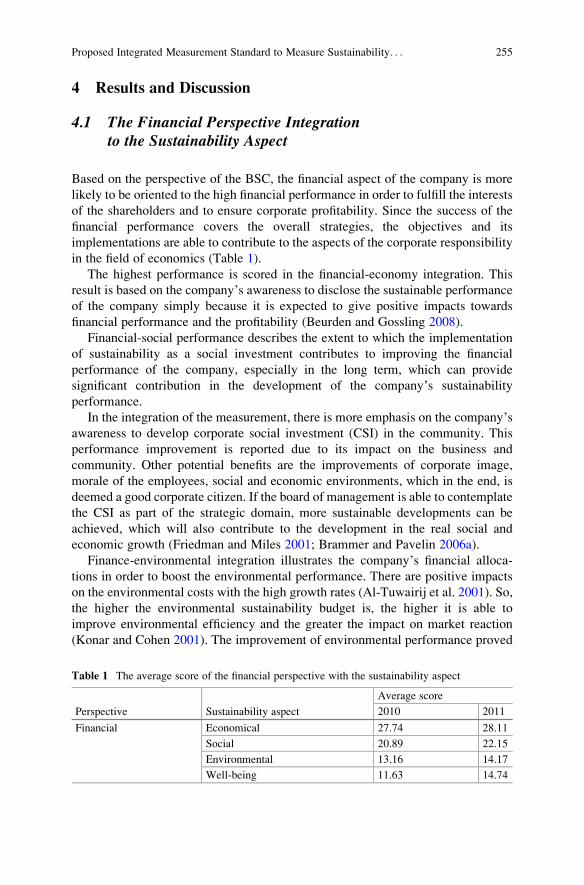

The Financial Perspective Integration to the Sustainability Aspect

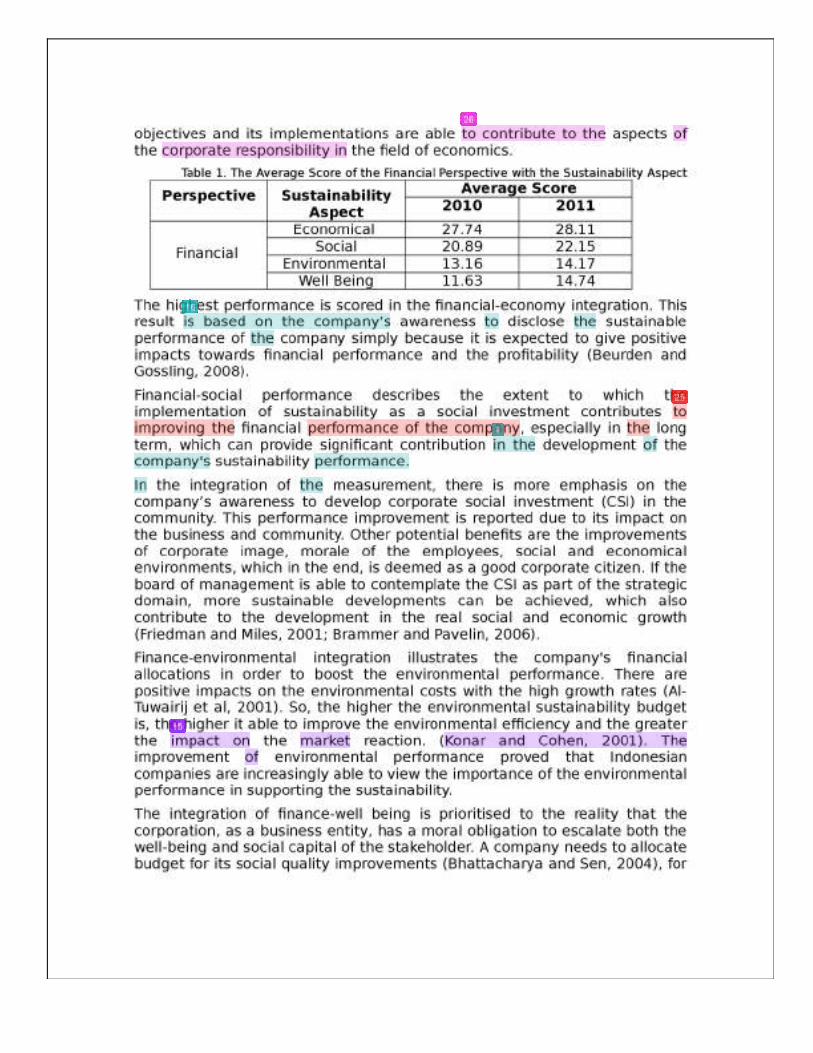

Based on the perspective of the BSC, the financial aspect of the company is more likely to be oriented to the high financial performance in order to fulfilfulfill the interests of the shareholders and to ensure corporate profitability. Since the success of the financial performance covers the overall strategies, the objectives and its implementations are able to contribute to the aspects of the corporate responsibility in the field of economics.

Table 1. The Average Score of the Financial Perspective with the Sustainability Aspect

Perspective Sustainability Aspect Average Score

2010 2011

Financial

Economical 27.74 28.11

Social 20.89 22.15

Environmental 13.16 14.17

Well Well-Being 11.63 14.74

The highest performance is scored in the financial-economy integration. This result is based on the company’s awareness to disclose the sustainable performance of the company simply because it is expected to give positive impacts towards financial performance and the profitability (Beurden and Gossling, 2008).

Financial-social performance describes the extent to which the implementation of sustainability as a social investment contributes to improving the financial performance of the company, especially in the long term, which can provide significant contribution in the development of the company's sustainability performance.

In the integration of the measurement, there is more emphasis on the company’s awareness to develop corporate social investment (CSI) in the community. This performance improvement is reported due to its impact on the business and community. Other potential benefits are the improvements of corporate image, morale of the employees, social and economical environments, which in the end, is deemed as a good corporate citizen. If the board of

5

management is able to contemplate the CSI as part of the strategic domain, more sustainable developments can be achieved, which will also contribute to the development in the real social and economic growth (Friedman and Miles, 2001; Brammer and Pavelin, 2006).

Finance-environmental integration illustrates the company's financial allocations in order to boost the environmental performance. There are positive impacts on the environmental costs with the high growth rates (Al-Tuwairij et al, 2001). So, the higher the environmental sustainability budget is, the higher it is able to improve the environmental efficiency and the greater the impact on the market reaction. (Konar and Cohen, 2001). The improvement of environmental performance proved that Indonesian companies are increasingly able to view the importance of the environmental performance in supporting the sustainability.

The integration of financefinancial -well beingwell-being is prioritisedprioritized to the realityso that the corporation, as a business entity, has a moral obligation to escalate both the well-being and social capital of the stakeholder. A company needs to allocate budget for its social quality improvements (Bhattacharya and Sen, 2004), for example to provide worship and sports facilities, a safe working environment and to promote the quality within the community.

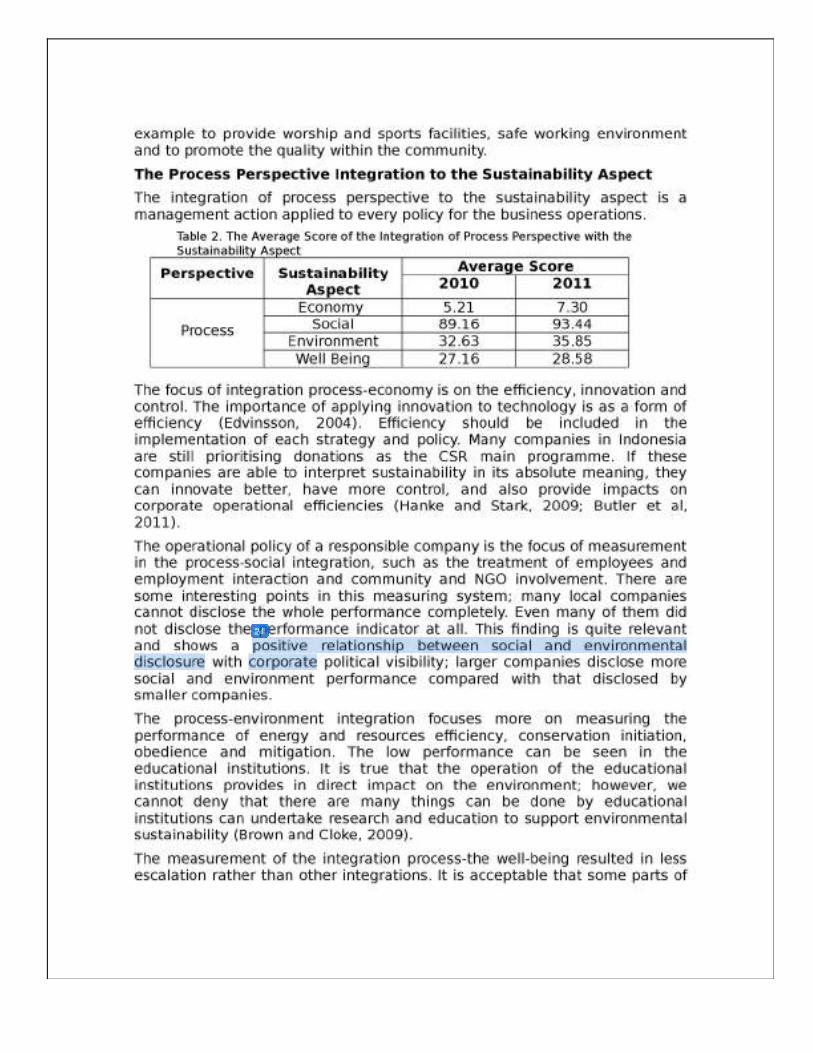

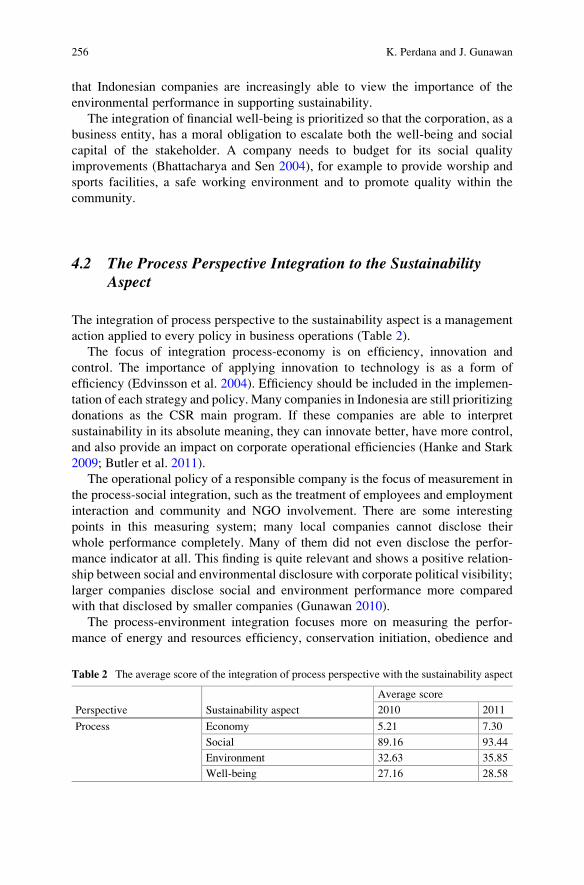

The Process Perspective Integration to the Sustainability Aspect

The integration of process perspective to the sustainability aspect is a management action applied to every policy for in the business operations.

Table 2. The Average Score of the Integration of Process Perspective with the Sustainability Aspect

Perspective Sustainability Aspect Average Score

2010 2011

Process

Economy 5.21 7.30

Social 89.16 93.44

Environment 32.63 35.85

Well Well-Being 27.16 28.58

The focus of integration process-economy is on the efficiency, innovation and control. The importance of applying innovation to technology is as a form of efficiency (Edvinsson, 2004). Efficiency should be included in the implementation of each strategy and policy. Many companies in Indonesia are still prioritisingprioritizing donations as the CSR main programme. If these companies are able to interpret sustainability in its absolute meaning, they can innovate better, have more control, and also provide an impacts on corporate operational efficiencies (Hanke and Stark, 2009; Butler et al, 2011).

The operational policy of a responsible company is the focus of measurement in the process-social integration, such as the treatment of employees and employment interaction and community and NGO involvement. There are some interesting points in this measuring system; many local companies cannot disclose their whole performance completely. Even manyMany of them did not even disclose the performance indicator at all. This finding is quite relevant and shows a positive relationship between social and environmental disclosure with corporate political visibility; larger companies disclose more social and environment performance more compared with that disclosed by smaller companies.

6

The process-environment integration focuses more on measuring the performance of energy and resources efficiency, conservation initiation, obedience and mitigation. The lLow performance can be seen in the educational institutions. It is true that the operation of the educational institutions provides in a direct impact on the environment; however, we cannot deny that there are many things that can be done by educational institutions that can undertakethrough research and education to support environmental sustainability (Brown and Cloke, 2009).

The measurement of the integration process, -the well-being often resulted in less escalation, therefore, rather than other integrations. It is acceptable that some parts of the indicators are incidental and long-term facilities provision. So, the increasing frequency for each inficator is needed here. Frequency improvement will increase the corporate advantages and also the quality value of the stakeholders (Bremmer and Pavelin, 2006).

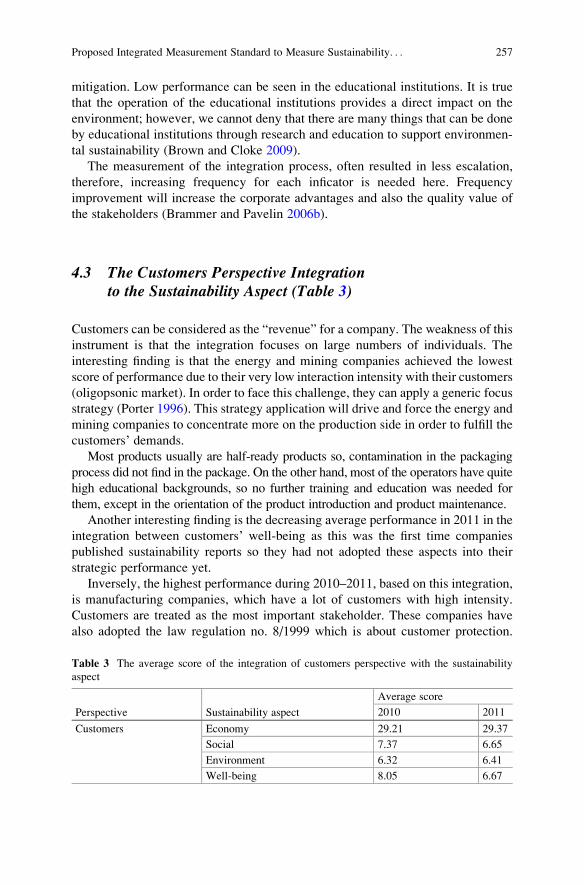

The Customers Perspective Integration to the Sustainability Aspect

Table 3. The Average Score of the Integration of Customers Perspective with the Sustainability Aspect

Perspective Sustainability Aspect Average Score

2010 2011

CUSTOMERS

Economy 29.21 29.37

Social 7.37 6.65

Environment 6.32 6.41

Well-being 8.05 6.67

Customers can be considered as the “revenue” for a company. The weakness of this instrument is that the integration focuses on large numbers of individuals. The interesting finding is that the energy and mining companies achieved the lowest score of performance due to their very low interaction intensity with their customers (oligopsonic market). In order to face this challenge, they can apply a generic focus strategy (Porter, 1996). This strategy application will drive and force the energy and mining companies to concentrate more on the production side in order to fulfilfulfill the customers’ demands.

Most products usually are half-ready products or intangible products, so, no contamination in the packaging process did not find in the was founding the package. Other On the other hand, most of the operators have quite high educational backgrounds, so no further training and educations are was needed for them, except in the orientation of the product introduction and product maintenance.

Another interesting finding is the decreasing average performance in 2011 in the integration between customers’- well well-being as this was the first time for companyies to published sustainability reports so they have had not adopted those these aspects into their strategic performance yet.

Inversely, the highest performance during 2010-2011, based on this integration, is manufacturing companies, which have a lot of customers with high intensity. Customers are treated as the most important stakeholder. These companies have also adopted the law regulation no. 8/1999 regarding customer protection. Therefore the company’s strategic interaction focus is customer satisfaction. Many efforts have been done undertaken to maintain

7

this, such as by conducting an education about the function of the products so that customers will obtain the product value optimally.

The Perspective Integration of Growth and Learning to the Sustainability Aspect

Table 4. The Average Score of the Integration of Process Perspective with the Sustainability Aspect

Perspective Sustainability Aspect Average Score

2010 2011

Growth and

Learning

Economy 8.80 8.19

Social 13.15 14.93

Environment 12.00 12.11

Well Well-Being 16.75 17.07

The increasing average performance in the integration showed that these companies are trying to increase the capacity and ability of the employees’ performance in every side toward sustainability. Performance will generally increase mostly because:

1. The increasing awareness and knowledge about the concept and philosophy of sustainability and the governance coming from the Boards of Directors and Commissioners;

2. The awareness and knowledge as the fundamental programme which needs to be applied and avowed as the company’s performance;

3. The new initiatives that are suitable for the company’s culture so that they can be applied properly and become the company’s characteristic;

4. Technology is used by the employees. An efficient company will certainly require its employees to be highly competent. It needs a network of information and modern technology.

Overall, the lowest performance is shown by educational institutions and transportation companies due to the fact that they use fewer vehicles with unleaded fuel, do not use 3Rs materials and undertake fewer actions in preventing pollution and the waste. They do not provide much of a contribution for the ecosystem recovery as well. Only educational institutions do focus on the main activity: learning and researching.

On other hand, the important fact in this integration is the initiation from the top management of the telecommunication company to determine regulation for protecting the environment by preventing the ecosystem, such as green ecosystem. This strategy can be applied in every branch office and some strategic locations in the town centrecenter. Another way is by and also using unleaded fuel for each company’s vehicle even though the company’s operation has indirectly affected the environment with its pollution.

Overall Sustainability Performance Analysis

Table 5. Sustainability Performance of ISRA Participant in 2010 and 2011

No SUSTAINABILITY PERFORMANCE

Participants in 2010 Participants in 2011

% %

1 Very high 1 5.26 1 3.70

2 High 11 57.89 16 59.26

3 Medium high 7 36.84 10 37.04

8

4 Low 0 0 0 0

5 Very low 0 0 0 0

Based on the measurement of all companies that participated in the ISRA in 2010 and 2011, most of them resulted in the a medium high performance. This fact shows us that sustainability has been integrated within the company’s strategy (Butler et al, 2011; Delai and Takahashi, 2011). The development of the sustainable performance shows there are six companies that have successfully received the medium high predicate in 2010 and continued to become the high predicate in 2011. In the meanwhile, the other 12 companies have successfully developed their sustainable performance values.

The ten new ISRA participants in 2011 can be divided into two groups, four companies with high performance, and six companies with medium performance. Based on the results of the performance measurement, it has fulfilled three criteria of the sustainable report required by GRI which can be described as:

1. A benchmarking and sustainable performance measurement which complies with the law, norms, codes, performance standard and voluntary initiatives;

2. A demonstration of the involvement of the organisationorganization to sustainable development

3. A comparison between the performance in one organisationorganization and another organisationorganization during a specific time (GRI, 2006)

A Company’s Sustainable Performance Comparison based on Ownership

This analyzes eight state-owned and nine private companies and the sustainability performance of these companies in 2010 and 2011.

Table 6. The Average Score of Corporate Sustainability Performance Based on Ownership

Ownership Average Score in 2010 Average Score in 2011

State-Owned 336.62 368.75

Private 301.00 324.22

The sustainability performance of the state-owned companies was higher than the private companies. The average performance of the state-owned companies in 2010 and 2011 show a high performance. The private companies had the a medium predicate in 2010, but their performance increase resulted in a high sustainability performance in 2011.

This situation occurred since those state-owned companies are obliged to implement the mandatory of social responsibility based on the regulation No. 40/2007 Chapter 74 paragraph 1-4, No.25/2007 Chapter 15b and the government rules No.47/2012 about corporate social responsibility. In order to meet those requirements, they need to implement the CSR towards through integrated sustainability in the management strategy in order to pursue the sustainability and performance, which will be reported in a form of sustainability report.

A sSustainability report is also required by BAPEPAM LK based on the regulation No. X.K.6 about Bapepam Policy and LK number: Kep-431/BL/2012 about Issuer Annual Report for listed companies. Throughout sState-owned company companies, which joins joined the ISRA in 2010 and 2011, are also as listed companycompanies. The Bapepam policy regulatepolicy regulates

9

that the CSR performance be disclosed in the annual report and shall be reported to the Bapepam in a separated chapter or published independently as a sustainability Reportreport. It can be concluded that state-owned companies have higher performance than private-owned companies due to their purpose need to comply the government’s rules, where on the other hand the government actually is the main shareholder.

Based on the agency theory, a company will be supported to run upon thebased on stakeholder expectation and managers should will be motivated to improve the performance and, as the a result, in the end, it will increase the value of the company. Then, the larger companies, with higher institutional ownershipownership, will indicate their ability desire to monitor the management. A big amount oflarge share ownerships has a vital meaning in when monitoring the performance of managers. By applying the ownership consent, big stakeholders will be able to effectively monitor the team and later, it will increase the company’s performance (Palazzo and Scherer, 2006; Navisi and Naiker, 2006)

Comparison of Sustainability Performances based on Business Types

This part will describe the comparison of sustainable performances based on the types of business in 2010 and 2011. ISRA participants can be grouped based on their type of business into five: seven mining companies, two plantation companies, four service companies, two manufacturing companies and two energy companies.

In the Table 7, there are some groups that have increased their sustainability performance, and the highest value in 2010 and 2011 is was achieved by manufacture manufacturing companies. On the other hand, the lowest performance achieved during two years is was achieved by energy companies. The detail is described below:

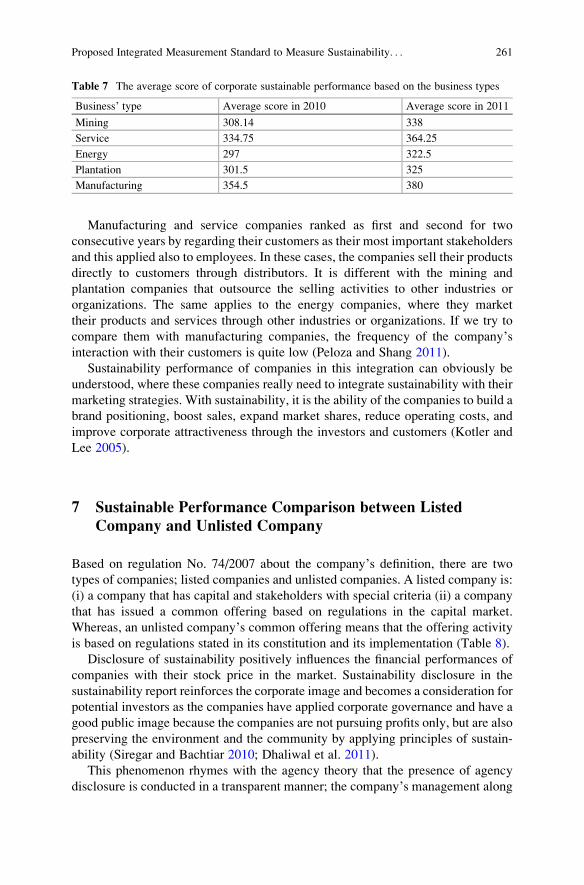

Table 7. The Average Score of Corporate Sustainable Performance based on the Business Types

Business’ Type Average Score in 2010 Average Score in 2011

Mining 308.14 338

Service 334.75 364.25

Energy 297 322.5

Plantation 301.5 325

ManufactureManufacturing 354.5 380

Manufacture Manufacturing and service companies ranked as the first and second ranks for the consecutive two consecutive years have by regarded regarding their customers as their most important stakeholders and this applies applied also to employees as well. In this these cases, those companies sell their products directly to the customers through distributors. It is different with the mining and plantation companies that manage outsource the selling activities to other industries or organisationsorganizations only. The same applies to the energy companies, where they market their products and services to through other industries or organisationsorganizations. If we try to compare them with manufacture manufacturing companies, the frequency of the company’s interaction with their customers is quite low (Peloza and Shang, 2011).

10

Sustainability performance of companies in this integration can obviously be understood, that where those these companies really need to integrate sustainability with their marketing strategies. With sustainability, it is the able ability for of the companies to build a brand positioning, boost sales, expand market shares, reduce operating costs, and improve corporate attractiveness through the investors and customers (Kotler and Lee, 2005).

Sustainable Performance Comparison between Listed Company and Unlisted Company

Based on the regulation No.74/2007 about the company’s definition, there are two types of companies; listed company companies and unlisted companycompanies. Listed A listed company is: (i) a company that has a capital and stakeholders with special criteria (ii) a company that has applies issued a common offering (issue) based on regulations in the capital market. Vice versaWhereas, an unlisted company’s has the different definition. A common offering means that the offering activity is based on the regulations stated in the its constitution and its implementation.

Table 8. The Average Score of the Corporate Sustainable Performance Based On Status

Status Average Score in 2010 Average Score in 2011

Listed 287.80 318.00

Unlisted 330.25 357.33

Disclosure of sustainability positively influences the relationship between financial performances of companies with their stock price in the market. Sustainability disclosure in the sustainability report reinforces the corporate image and becomes a consideration for potential investors as the companies have applied corporate governance and have a good public appearance image because the companies do are not pursue pursuing profits only, but are merely also preserve preserving the environment and the community by applying principles of sustainability (Siregar and Bachtiar, 2010; Dhaliwal et al, 2011).

This phenomenon rhymes with the agency theory that the presence of agency disclosure is conducted in a transparent manner; the company’s management along with its sustainability disclosure give the impression to its shareholders that the company continues to grow sustainably. Therefore, it can be concluded that sustainability has a positive impact on the stock price and the disclosure of the sustainability provides a positive influence on the relationship between financial performance and stock price in the market. This positive effect is not obtained by private companies. (Siregar and Bachtiar, 2010)

Conclusion Many companies in Indonesia only understand sustainability in the applianceits impact on the of triple bottom line. This generates a lack of understanding, that the well-beingwell-being is an integral part of corporate sustainability, which results in it receiving a less serious attention. It can be recognised seen throughfrom the low performance of the the well-beingwell-being.

Based on the analysis and discussion, it can be concluded that no sample was awarded low or very low sustainability performance. The majority of companies already have medium and high score for sustainability performance and one company achieved a very high performance. The sustainability performance of all companies in 2010, increased to by an average of 11.6 points the following year.

11

The average value of the sustainable performance in companies, especially showed that manufacturing companies has had the highest ranking, with the performance of service companies ranked second, followed by those of mining companies, plantation companies and energy companies. This The factor that contributes contributed a huge influence to was the perspective of the customers-sustainability. The more interaction companies have with their customers, the higher the company’s performance.

The average value in the sustainability performance of listed companies is was higher than that of unlisted companies. There is was a positive relationship between the disclosures of the corporate social performance and the corporate visibility. These companies disclosed more information about their sustainability activities than smaller companies. The government requires listed companies to report their sustainability activities in a dedicated chapter in their annual report or in a separate sustainability report. The result is that larger companies, through disclosures of sustainability performance, are, more disclosures of sustainability performance will likely to be revealedseen.

Limitation The limitation of this study is dependency dependent of upon the performance assessment to and the quality of the report disclosure. So, if a company cannot improve the quality of the its reporting quality, the performance cannot be measured properly.

References

Al-Tuwairij, SA, Christensen, TE, and Hughes II, K.E. (2001) ’The Relations Among Environmental Disclosure, Environmental Performance adn Economic Performance: A Simultanious Equation Approach’, Accounting, Organizations and Society, Vol. 29, Iss. 5-6, pp 447-471

Bhattacharya, CB, and Sen, S. (2004) ‘Doing Better at Doing Good: When, Why and How Consumers Respond to Corporate Social Initiatives’,California Management Review Vol. 47, No 1, pp 9-24.

Beurden, PV, and Gossling, T. (2008) ‘The Worth of Value-A Literature Review on the Relation Between Corporate Social and Financial Performance’, Journal of Business Ethics Vol 82 pp 407-424.

Brammer, SJ, and Pavelin, S. (2006) ‘Corporate Reputation and Social Performance: the Importance of Fit’, Journal of Management Studies. Vol 43:3, pp 435-455.

Branco, M C, and Rodrigues, LL. (2007) ‘Positioning Stakeholder Theory Within The Debate on Corporate Social Responsibility’, Journal of Business Ethics and Organization Studies, Vol. 12, No. 1, pp. 5-15.

Branco, M C, and Rodrigues, LL. (2008) ‘Social Responsibility Disclosure: A Study of Proxies For Public Company Visibility of Portugese Banks’, The British Accounting Review. Vol. 40, Iss. 2. Pp 161-181.

Brown, E, and Cloke, J. (2009) ‘Corporate Social Responsibility in Higher Education’, An International Journal for Critical Geographies. Vol 8(3). Pp 474-483.

12

Butler, JB, Henderson, SC, and Raiborn, C. (2011) ‘Sustainability and Balanced Scorecard; Integrating Green Measures into Business Reporting’, Management Accounting Quarterly Vol. 12, No. 2, pp 1-10

Delai, I, and Takahashi, S. (2011) ‘Sustainability Measurement System: A Reference Model Proposal’, Social Responsibility Journal, Vol. 7 No. 3 2011, pp. 438-471.

Dhaliwal, DS, Li, OZ, Tsang, A, and Yang, YG. (2011) ‘Voluntary Nonfinancial Disclosure and the Cost of Equity Capital: The Initiation of Corporate Social Responsibility’, The Accounting Review Vol. 86, No 1, pp. 59-100.

Ebben, J J,and Johnson, A C. (2005), ‘Efficiency, Flexibility, or Both? Evidence Linking Strategy to Performance in Small Firms’, Strategic Management Journal.,Vol. 26, Iss. 13, pp. 1249–1259.

Edvinsson, L, Dvir, R, Roth, N, and Pasher, E. (2004) ‘Innovations: The New Unit of Analysis in the Knowledge Era: The Quest and Context for Innovation Efficiency and Management of IC’, Journal of Intellectual Capital, Vol. 5 Iss: 1, pp.40 – 58

Friedman, AL, and Miles, S. (2001) ‘Socially Responsible Investment and Corporate Social and Environmental Reporting in the UK: An Exploratoey Study’, The British Accounting Review Vol 33, Iss. 4, pp 523-548.

Gates, S, and Germain, C. (2010) ‘Integrating Sustainability Measure into Strategic Performance Measurement System: An Empirical Study’, Management Accounting Quarterly Vol 11 No 3 pp. 1-10.

Garriga, E, and Mele, D. (2004). ‘Corporate Social Responsibility Theory; Mapping the Territory’, Journal of Business Ethic Vol 53 pp 51-71

Golob, U, and Barlett JL. (2007) ‘Comunicating About Corporate Social Responsibility: A Comparative Study of CSR Reporting in Australia and Slovenia’, Public Relation Review, Vol 33.

Global Reporting Initiatives (2010). ‘GRI and ISO 26000: How To Use the GRI Guidelines in Conjunction with ISO 26000’, Global Reporting Initiatives.

Global Reporting Initiatives (2011) ‘Sustainability Reporting Guidelines ver 3.1’,Global Reporting Initiatives.

Gunawan, J. (2007) ‘Corporate Social Disclosures by Indonesian Listed Companies: A Pilot Study’, Social Responsibility Journal, Vol. 3 Iss: 3, pp.26 - 34

Gunawan, J. (2010). ‘Perception of Important Information in Corporate Social Disclosures: Evidence from Indonesia’, Social Responsibility Journal Vol. 6 Iss. 1, pp. 62-71,

Hanke, T, and Stark, W, (2009) ‘Strategy Development: Conceptual Framework on Corporate Social Responsibility’, Journal Of Business Ethics.Vol 3 No 5 pp. 21-40.

Hrebicek, J., Soukopva, J., Stencl, M., Trenz, O., (2011).”Integration of Economic, Environmental,

Social and Corporate Governance Performance and Reporting In Enterprises”. Acta

Universitatis Agriculturae Et Silviculturae Mendelianae Brunensis Vol LIX, No 7, 2011.

13

Idowu, SO, and Towler, BA. (2004) ‘A Comparative Study of the Contents of Corporate Social Responsibility Reports of UK Companies’, Management of Environmental Quality: An International Journal, Vol. 15, pp.420 - 437

ISO 26000 (2010)‘International Standard, Guidance on Social Responsibility’

Jamali, D, Safieddine, AM, and Rabbath, M. (2008) ‘Corporate Governance And Corporate Social Responsibility Synergies And Interrelationships’, Corporate Governance-An International Review, vol. 16, no. 5.

Kaplan, RS. (2010) ‘Conceptual Foundations of the Balanced Scorecard’,Working paper. Harvard Business School.

Kaplan, RS, and Norton,DP. (1996) ‘Using the Balanced Scorecard as a Strategic Management System’, Harvard Business Review (January-February)

Kaplan, RS, and Norton,DP. (1993) ‘Putting the Balanced Scorecard to Work’, Harvard Business Review (September-October)

Kaplan, RS, and Norton,DP. (1992) ‘The Balanced Scorecard; Measure that Drive Performance’, Harvard Business Review (January-February)

Konar, S, and Cohen, MA. (2001) ‘Does The Market Value Environmental Performance?’, The Review of Economics and Statistics. Vol. 83(2), pp 281-289.

Kotler, P, and Lee, N. (2005) ‘Corporate Social Responsibility: Doing the Most Good for Your Company and Your Cause’, John Wiley and Son.

Krippendorff, K. (2004). ‘Content Analysis; An Introduction to Its Methodology’. Sage Publication Inc.

Maignan, I, Ferrell, OC, and Hult, GTM.(1999) ‘Corporate Citizenship: Cultural Antecedents and Business Benefits’, Journal Acad Mark Sci, 26 (4), 455-469.

McLoughin, J, Kaminski, J, and Sodagar, B. (2009) ‘A Strategic Approach To Social Impact Measurement of Social Enterprises The SIMPLE Metodology’, Social Enterprise Journal Vol 5, Iss. 2, pp 154-178.

Meehan, J, Meehan, K, and Richards, A. (2006) ‘Corporate Social Responsibility: The 3C-SR Model’, International Journal of Social Economics. Vol 33, No. 5/6 pp 386-398.

Navissi, F, and Naiker, V. (2006)‘ Institutional Ownership and Corporate Value’, Journal of Managerial Finance, Vol. 32, No.1, pp.247-256.

Orlitzki, M, Schmidt, FL, Rynes, SL. (2005) ‘Corporate Social and Financial Performance: A Meta Analysis’, Organization Studies. Vol 24(3), pp 403-441.

Panayiotou, NA, Aravossis, K, and Moschou, P. (2009) ‘A New Methodology Approach for Measuring Corporate Social Responsibility Performance’, Water Air Soil Pollut: Focus 9:129-139.

Palazzo, G, and Scherer, AG. (2006) ‘Corporate Legitimacy as Deliberation: A Communicative Framework’, Journal of Business Ethics 66: Iss. 3, pp.71-88

14

Peloza, J, and Shang, J. (2011) ‘Investing in CSR to Enhance Customer Value’, The Harvard Law School Forum, Corporate Governance and Financial Regulation.

Perdana, K, and Gunawan, J. (2014) ‘Integration of Balanced Scorecard, ISO 26000, United Nation Global Compact and Global Reporting Initiatives: Building an Integrated Measurement Standard for Measuring Sustainability Performance’, Proceeding International Conference on Governance, Fakultas Ekonomi Universitas Trisakti, Jakarta

ISBN 978-979-3634-24-1.

Porter, ME. (1996). ‘What is Strategy?’, Harvard Business Review 96(6)61-78

Raar, J. (2002) ‘Environmental Initiatives: Towards Triple-Bottom Line Reporting. Corporate Communications’, An International Journal, vol. 7, no. 3, pp. 169-183.

Siregar, SV, and Bachtiar, Y (2010) ‘Corporate Social Reporting: Empirical Evidence From Indonesia Stock Exchange’, International Journal of Islamic and Middle Eastern Finance and Management, Vol. 3 Iss: 3, pp.241 – 252

Undang-Undang Nomor 40 (2007) Tentang Perseroan Terbatas.

Undang-Undang Nomor 25 (2007) Tentang Penanaman Modal.

Undang-Undang Nomor 8 tahun (1999) Tentang Perlindungan Konsumen

Wood, DJ. (2010) ‘Measuring Corporate Social Performance: A Review’, International Journal of Management Reviews. Vol 12 Iss. 1 pp. 50-84

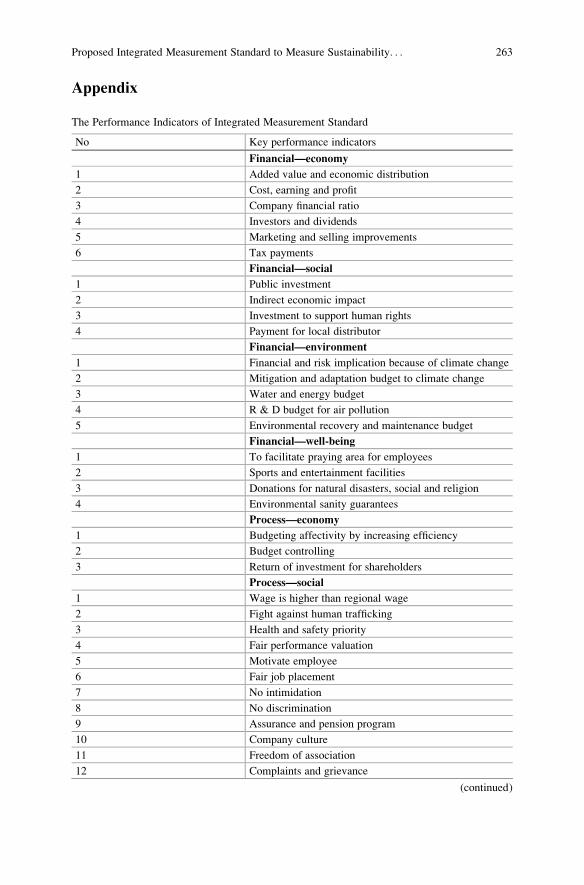

Appendix

The Performance Indicators of Integrated Measurement Standard No Key Performance Indicators

Financial – economy

1 Added value and economic distribution

2 Cost, earning and profit

3 Company financial ratio

4 Investors and dividends

5 Marketing and selling improvements

6 Tax payments

Financial – social

1 Public investment

2 Indirect economic impact

3 Investment to support human rights

4 Payment for local distributor

Financial – environment

1 Financial and risk implication because of climate changingchange

15

2 Mitigation and adaptation budget to the climate changingchange

3 Water and energy budget

4 R & D budget for the air pollution

5 Environmental recovery and maintenance budget

Financial – well well-being

1 To facilitate praying area for the employees

2 Sports and entertainment facilitation facilities

3 Donations for natural disasters, social and religion

4 Environmental sanity guarantees

Process – economy

1 Budgeting affectivity by increasing efficiency

2 Budget controlling

3 Return of investment for shareholders

Process – social

1 Wage is higher than regional wage

2 Fight against human trafficking

3 Health and safety priority

4 Fair performance valuation

5 Motivate employee

6 Fair job placement

7 No intimidation

8 No discrimination

9 Assurance and pension program

10 Company culture

11 Freedom of association

12 Complaints and grievance

13 Security assistance

14 Against child labor

15 Liberation of sliveryslavery

16 Discipline and preventive disobedience

17 Anti-corruption, bribery and collusion

18 Fair competition and anti-monopoly

19 Community involvement

20 Obedience to government’s rules

21 The decrease of fine/punishment

22 Effort of decreasing the negative effects in society

23 Woman empowerment

24 Supporting the society’s organization

25 Local worker acceptance

26 Carrier development

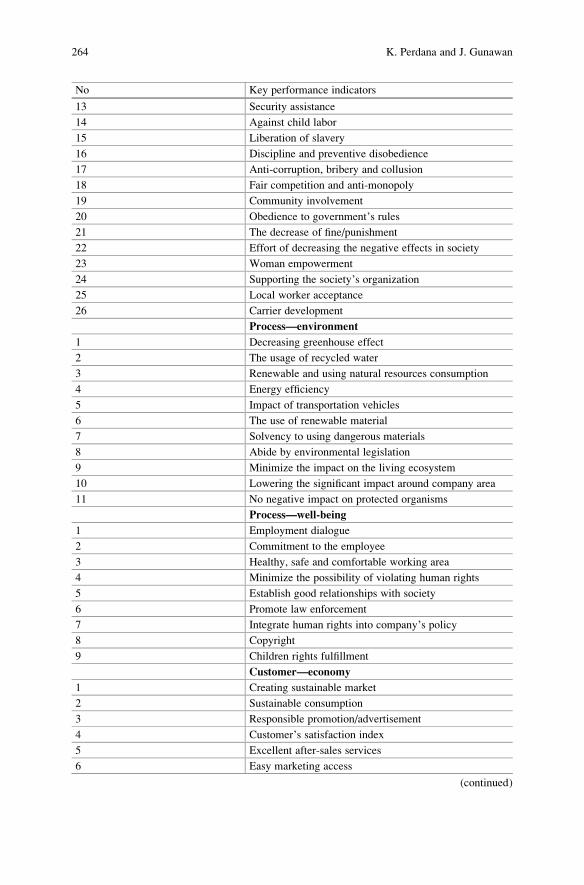

Process – environment

1 Decreasing greenhouse effect

16

2 The using usage of recycled water

3 Renewable and using natural resources consumption

4 Energy efficiency

5 Impact of transportation vehicles

6 The using use of renewable material

7 Solvency to using dangerous materials

8 Abide by environmental legislation

9 Minimize the impact to on the living ecosystem

10 Lowering the significant impact aroundimpact around company area

11 No negative impact to theon protected organisms

Process – well well-being

1 Employment dialogue

2 Commitment to the employee

3 Healthy, safe and comfortable working area

4 Minimize the possibility of violating the human rights

5 Establish good relationships with society

6 Promote law enforcement

7 Integrate human rights into company’s policy

8 Copyright

9 Children rights fulfillment

Customer - economy

1 Creating sustainable market

2 Sustainable consumption

3 Responsible promotion/advertisement

4 Customer’s satisfaction index

5 Excellent afterExcellent after-sales services

6 Easy marketing access

7 Product quality

8 Continuous improvement

9 Product reliabilityProduct reliability

Customer – social

1 Brand or product labeling product

2 Education and awareness

3 Response to customer’s complaints

Customer – environment

1 Involving customers to in maintaining the environment

2 Re-withdrawal packaging

3 Innovation of green products

Customer – well well-being

1 Customer’s protection and privacy

2 Customer’s health and safety

17

Learning &development - economy

1 Good governance

2 Employee’s technology access

3 AcknoledgeAcknowledge to the rights of the community.

Learning and development - social

1 Training and research for human rights

2 Employee’s training and education

3 Corporation agreement with employees

4 Training and education of on anti-corruption

Learning and development - environment

1 Initiative in using the renewable energy

2 Initiative in using the renewable materials

3 Initiative in preventing pollution/waste

4 Initiative in ecosystem recovery

Learning and development - well well-being

1 Obedience to society’s norm

2 Comprehensive research about the stakeholder

3 Anticipate working accidents

4 Commitment to public

5 Carrier development

PROPOSED INTEGRATEDMEASUREMENT STANDARD

TO MEASURESUSTAINABILITY

PERFORMANCE: EVIDENCEFROM INDONESIA

by Juniati Gunawan

Submission date: 19-Dec-2018 03:38PM (UTC+0700)Submission ID: 1059145329File name: nsional_Corporate_Governance_Full_Paper_book_chapter_JG___KP.pdf (170.95K)Word count: 6096Character count: 35621

6%SIMILARITY INDEX

4%INTERNET SOURCES

4%PUBLICATIONS

1%STUDENT PAPERS

1 <1%

2 <1%

3 <1%

4 <1%

5

PROPOSED INTEGRATED MEASUREMENT STANDARD TOMEASURE SUSTAINABILITY PERFORMANCE: EVIDENCEFROM INDONESIAORIGINALITY REPORT

PRIMARY SOURCES

Ivete Delai, Sérgio Takahashi. "Sustainabilitymeasurement system: a reference modelproposal", Social Responsibility Journal, 2011Publicat ion

Submitted to Hofstra UniversityStudent Paper

Joseph, Corina, Juniati Gunawan, YussriSawani, Mariam Rahmat, Josephine AvelindNoyem, and Faizah Darus. "A comparativestudy of anti-corruption practice disclosureamong Malaysian and Indonesian CorporateSocial Responsibility (CSR) best practicecompanies", Journal of Cleaner Production,2016.Publicat ion

link.springer.comInternet Source

redete.org

<1%

6 <1%

7 <1%

8 <1%

9 <1%

10 <1%

11 <1%

12 <1%

13 <1%

14 <1%

15 <1%

Internet Source

"Corporate Social Responsibility andGovernance", Springer Nature America, Inc,2015Publicat ion

eprints.hud.ac.ukInternet Source

parlinfo.aph.gov.auInternet Source

eprints.nottingham.ac.ukInternet Source

www.ioe-emp.orgInternet Source

ml.scribd.comInternet Source

www.theibfr.comInternet Source

www.publishing.globalcsrc.orgInternet Source

www.coursehero.comInternet Source

www.ndirseo.comInternet Source

16 <1%

17 <1%

18 <1%

19 <1%

20 <1%

21 <1%

22 <1%

23 <1%

24

ivythesis.typepad.comInternet Source

etheses.dur.ac.ukInternet Source

Janine Hogan, Sumit Lodhia. "Sustainabilityreporting and reputation risk management: anAustralian case study", International Journal ofAccounting & Information Management, 2011Publicat ion

www.wseas.usInternet Source

www.crrconference.orgInternet Source

eprints.usq.edu.auInternet Source

Merve Kiliç, Cemil Kuzey, Ali Uyar. "The impactof ownership and board structure on CorporateSocial Responsibility (CSR) reporting in theTurkish banking industry", CorporateGovernance: The international journal ofbusiness in society, 2015Publicat ion

www.emrbi.orgInternet Source

Hichem Khlif, Achraf Guidara, Mohsen Souissi.

<1%

25 <1%

26 <1%

27 <1%

28 <1%

29 <1%

30 <1%

"Corporate social and environmental disclosureand corporate performance", Journal ofAccounting in Emerging Economies, 2015Publicat ion

docslide.usInternet Source

Mia Mahmudur Rahim. "Legal Regulation ofCorporate Social Responsibility", SpringerNature America, Inc, 2013Publicat ion

collections.plymouth.ac.ukInternet Source

www.researchgate.netInternet Source

Ana Patrícia Duarte, Carla Mouro, JoséGonçalves das Neves. "Corporate socialresponsibility: mapping its social meaning",Management Research: Journal of theIberoamerican Academy of Management, 2010Publicat ion

International Journal of Bank Marketing,Volume 34, Issue 4 (2016)Publicat ion

CSR, Sustainability, Ethics & GovernanceSeries Editors: Samuel O. Idowu · René Schmidpeter

Nicholas CapaldiSamuel O. IdowuRené Schmidpeter Editors

Dimensional Corporate GovernanceAn Inclusive Approach

CSR, Sustainability, Ethics & Governance

Series editors

Samuel O. Idowu, London Metropolitan University, London, United Kingdom

Rene Schmidpeter, Cologne Business School, Germany

More information about this series at http://www.springer.com/series/11565

Nicholas Capaldi • Samuel O. Idowu •Rene Schmidpeter

Editors

Dimensional CorporateGovernance

An Inclusive Approach

EditorsNicholas CapaldiCollege of BusinessLoyola University New OrleansNew Orleans, LA, USA

Samuel O. IdowuGuildhall Faculty of Business and LawLondon Metropolitan UniversityLondon, United Kingdom

Rene SchmidpeterCologne Business SchoolCologne, Germany

ISSN 2196-7075 ISSN 2196-7083 (electronic)CSR, Sustainability, Ethics & GovernanceISBN 978-3-319-56181-3 ISBN 978-3-319-56182-0 (eBook)DOI 10.1007/978-3-319-56182-0

Library of Congress Control Number: 2017942956

This book was advertised with a copyright holder in the name of the author(s) in error, whereas thepublisher holds the copyright.

© Springer International Publishing AG 2017This work is subject to copyright. All rights are reserved by the Publisher, whether the whole or part ofthe material is concerned, specifically the rights of translation, reprinting, reuse of illustrations,recitation, broadcasting, reproduction on microfilms or in any other physical way, and transmissionor information storage and retrieval, electronic adaptation, computer software, or by similar ordissimilar methodology now known or hereafter developed.The use of general descriptive names, registered names, trademarks, service marks, etc. in thispublication does not imply, even in the absence of a specific statement, that such names are exemptfrom the relevant protective laws and regulations and therefore free for general use.The publisher, the authors and the editors are safe to assume that the advice and information in thisbook are believed to be true and accurate at the date of publication. Neither the publisher nor theauthors or the editors give a warranty, express or implied, with respect to the material containedherein or for any errors or omissions that may have been made. The publisher remains neutral withregard to jurisdictional claims in published maps and institutional affiliations.

Cover illustration: eStudio Calamar, Berlin/Figueres

Printed on acid-free paper

This Springer imprint is published by Springer NatureThe registered company is Springer International Publishing AGThe registered company address is: Gewerbestrasse 11, 6330 Cham, Switzerland

Dedicated to All Members of the GlobalCorporate Governance Institute Worldwide

Foreword

The Global Corporate Governance Institute came into existence as the confluence

of two streams of research: Corporate Governance and Corporate Social Respon-

sibility. The former field has existed for over a century in Anglo-American Law,

and the latter field came into prominence in the 1980s. Events since 1989 have

made this confluence necessary. There are since the 1989 fall of the Berlin Wall

very few places in the world where centrally planned economies are advocated.

Almost everywhere there is the recognition of the importance of the promise of

economic growth and development as the product of a market economy. At the

same time, globalisation, the recognition of an inescapable global marketplace,

became part of the public consciousness. But globalisation brings contagion—both

its promise and its problems cannot be contained. It is no longer possible to be

provincial.

Nor is it possible to understand these issues through the lens of one discipline. It

is no longer possible to engage in the evolution of legal thought in abstraction from

competing and sometimes conflicting legal traditions. The social sciences such as

economics and traditional business school disciplines such as finance, management

and marketing are forced to confront normative issues for which they are

ill-equipped intellectually.

How are we to understand ‘social’ institutions? In what sense is a corporation

(or firm) a ‘social’ entity, specifically as opposed to a ‘commercial’ entity? How do

corporations relate to other social institutions (including political and legal ones)?

What does it mean to evaluate the performance of social institutions in general and

commercial ones in particular? How are we thereby to make sense of the notion of

‘improving’ performance? Advocacy of what future practice should be in evolving

and novel contexts is not a form of research (i.e. not descriptive) but a normative

activity. There is nothing inherently illegitimate about advocacy or normative

activity. But it is intellectually dishonest to present this as ‘research’. To what

extent do activist organisations misrepresent the facts and to what extent is advo-

cacy a mask for a private political agenda?

Scholars view CSR as a form of value creation (sustainable business model), risk

management or philanthropy. While all of these perspectives are useful, these

vii

perspectives merely focus on the fact that corporations impact other social institu-

tions. Might corporations have a positive obligation to transform other social

institutions? Are corporations constrained to prioritise the production of profitable

products or services?

As Schumpeter pointed out long ago, markets reflect a process of creative

destruction. In the light of what Schumpeter had to say, we need to ask if we are

researching the right questions. To what extent is our thinking constrained by

inherited philosophical prejudice? Could this be by inherited cultural or geograph-

ical or historical bias? What institutions or institutional structures can be exported?

Are we seeking a universal model or might we welcome a continuum of

approaches?

We seek to turn the page and engage scholars from every discipline and every

perspective to come together to grapple with what may be the epicentre of the major

commercial, political and social issues of our time.

Global Corporate Governance Institute

New Orleans, USA

Nicholas Capaldi

viii Foreword

Foreword: Global Corporate Governance:

Global Cosmetics?

For CSR, the efforts of Samuel O. Idowu and colleagues have put in place a

formidable background literature for CSR, including the Encyclopaedia of CSRand the Dictionary of CSR (Idowu et al. 2009, 2011, 2013, 2014). This has provided

a well-documented vocabulary. The diversity of CSR is such that the same words

are used with different meanings and contexts. CSR tends to be defined in terms of

companies going beyond legal minimum requirements, and as such legal require-

ments vary around the world, we encounter varied cases. We need to explore central

concepts around Responsibility, recognising that theory and practice can be very

different. We must walk the talk, avoiding claims of academic detachment. We

share an understanding of individual responsibility for our actions. Social respon-

sibility, taking responsibility for the needs of others, may be less clear.

Management tends to be anything but Responsible. The culture is based on

Irresponsibility, starting with protection of Limited Liability. We see an increased

tendency to outsource responsibility. Profitability is maximised while commitments

are restricted. This has accelerated with privatisation.